Money, Banking, and the Financial System CHAPTER

|

|

|

- Stuart Freeman

- 6 years ago

- Views:

Transcription

1 Money, Banking, and the Financial System 12 CHAPTER

2 Money: What Is It and How Did It Come to Be? Money: A Definition To the layperson, the words income, credit, and wealth are synonyms for money. In each of the next three sentences, the word money is used incorrectly; the word in parentheses is the word an economist would use. 1. How much money (income) did you earn last year? 2. Most of her money (wealth) is tied up in real estate. 3. It sure is difficult to get money (credit) in today s tight mortgage market. In economics, the words money, income, credit, and wealth are not synonyms. The most general definition of money is any good that is widely accepted for purposes of exchange (payment for goods and services) and the repayment of debt.

3 Money: What Is It and How Did It Come to Be? Three Functions of Money Money has three major functions; it is a: Medium of exchange Unit of account Store of value

4 Money: What Is It and How Did It Come to Be? Medium of Exchange A medium of exchange is an object that is generally accepted in exchange for goods and services. In the absence of money, people would need to exchange goods and services directly, which is called barter. Barter requires a double coincidence of wants, which is rare, so barter is costly it requires either much search, or lots of specialized middle-men.

5 Money: What Is It and How Did It Come to Be? Unit of Account In a money economy, a person doesn t have to know the price of an apple in terms of oranges, pizzas, chickens, or potato chips, as in a barter economy. A person needs only to know the price in terms of money. A unit of account is an agreed measure for stating the prices of goods and services. This Table illustrates how money simplifies comparisons. Because all goods are denominated in money, determining relative prices is easy and quick.

6 Money: What Is It and How Did It Come to Be? Store of Value The store of value function is related to a good s ability to maintain its value over time. This is the least exclusive function of money because other goods for example, paintings, houses, and stamps can store value too. At times, money has not maintained its value well, such as during high-inflationary periods. For the most part, though, money has served as a satisfactory store of value. This function allows us to accept payment in money for our productive efforts and to keep that money until we decide how we want to spend it.

7 Money: What Is It and How Did It Come to Be? From a Barter to a Money Economy: The Origins of Money How did we move from a barter to a money economy? Did a king or queen issue an edict: Let there be money? Actually, money evolved in a much more natural, market-oriented manner. Making exchanges takes longer (on average) in a barter economy than in a money economy because the transaction costs are higher in a barter economy since it requires double coincidence of wants. In a barter economy, some goods are more readily accepted than others in exchange.

8 Money: What Is It and How Did It Come to Be? From a Barter to a Money Economy: The Origins of Money Suppose that, of 10 goods A J, good G is the most marketable (the most acceptable) of the 10. On average, good G is accepted 5 of every 10 times it is offered in an exchange, whereas the remaining goods are accepted, on average, only 2 of every 10 times. Given this difference, some individuals accept good G simply because of its relatively greater acceptability, even though they have no plans to consume it. The more people accept good G for its relatively greater acceptability, the greater its relative acceptability becomes, in turn causing more people to accept it.

9 Money: What Is It and How Did It Come to Be? From a Barter to a Money Economy: The Origins of Money This is how money evolved. When good G s acceptance evolves to the point that it is widely accepted for purposes of exchange, good G is money. Historically, goods that have evolved into money include gold, silver, copper, cattle, salt, cocoa beans, and shells. In many of the World War 2 prisoner of war (POW) camps, the cigarette was being used as money among the prisoners.

10 Money: What Is It and How Did It Come to Be? Money, Leisure, and Output Exchanges take less time in a money economy than in a barter economy because a double coincidence of wants is unnecessary: Everyone is willing to trade for money. The movement from a barter to a money economy therefore frees up some of the transaction time, which people can use in other ways. Some will use them to work, others will use them for leisure, and still others will divide the available time between work and leisure.

11 Money: What Is It and How Did It Come to Be? Money, Leisure, and Output Thus, a money economy is likely to have both more output (because of the increased production) and more leisure time than a barter economy. In other words, a money economy is likely to be richer in both goods and leisure than a barter economy. A person s standard of living depends, to a degree, on the number and quality of goods consumed and on the amount of leisure consumed. We would expect the average person s standard of living to be higher in a money economy than in a barter economy.

12 Money: What Is It and How Did It Come to Be? Finding Economics with William Shakespeare in London (1595) It is 1595, and William Shakespeare is sitting at a desk writing the Prologue to Romeo and Juliet. Where is the economics? More specifically, what is the connection between Shakespeare s writing a play and the emergence of money out of a barter economy? For Shakespeare, living in a barter economy would mean writing plays all day and then going out and trying to trade what he had written that day for apples, oranges, chickens, and bread. Would the baker trade two loaves of bread for two pages of Romeo and Juliet?

13 Money: What Is It and How Did It Come to Be? Finding Economics with William Shakespeare in London (1595) Had Shakespeare lived in a barter economy, he would have soon learned that he did not have a double coincidence of wants with many people and that if he were going to eat and be housed, he would need to spend time baking bread, raising chickens, and building a shelter instead of thinking about Romeo and Juliet. In a barter economy, trade is difficult; so people produce for themselves. In a money economy, trade is easy, and so individuals produce one thing, sell it for money, and then buy what they want with the money. A William Shakespeare who lived in a barter economy no doubt spent his days very differently from the William Shakespeare who lived in England in the sixteenth century. Put bluntly: Without money, the world might never have enjoyed Romeo and Juliet.

14 Money: What Is It and How Did It Come to Be? Components of Money Money consists of Currency Deposits at banks and other depository institutions Currency is the notes and coins held by households and firms.

15 Money: What Is It and How Did It Come to Be? Official Measures of Money The two main official measures of money are M1 and M2. M1 consists of currency and traveler s checks and checking deposits owned by individuals and businesses. M2 consists of M1 plus time, saving deposits, money market mutual funds, and other deposits.

16 Money: What Is It and How Did It Come to Be? The figure illustrates the composition of M1 and M2. It also shows the relative magnitudes of the components.

17 Money: What Is It and How Did It Come to Be? Are M1 and M2 Really Money? All the items in M1 are means of payment. They are money. Some saving deposits in M2 are not means of payments they are called liquid assets. Liquidity of an asset measures how quickly the asset can be converted into cash (a means of payment) with little/no loss of value.

18 Money: What Is It and How Did It Come to Be? Deposits are Money but Checks Are Not In defining money, we include, along with currency, deposits at banks and other depository institutions. But we do not count the checks that people write as money. A check is an instruction to a bank to transfer money. Credit Cards Are Not Money Credit cards are not money. A credit card enables the holder to obtain a loan, but it must be repaid with money.

19 Money: What Is It and How Did It Come to Be? Always be prudent when using credit cards.

20 How Banking Developed Just as money evolved, so did banking. The Early Bankers Our money today is easy to carry and transport, but it was not always so portable. For example, when money consisted principally of gold coins, carrying it about was neither easy nor safe. Gold was not only inconvenient for customers to carry, but it was also inconvenient for merchants to accept - gold is heavy. Gold is unsafe to carry around - can easily draw the attention of thieves. Storing gold at home can also be risky.

21 How Banking Developed The Early Bankers Most individuals therefore turned to their local goldsmiths for help because they had safe storage facilities. Goldsmiths were thus the first bankers. They took in other people s gold and stored it for them. To acknowledge that they held deposited gold, goldsmiths issued receipts, called warehouse receipts, to their customers. Once people s confidence in the receipts was established, they used the receipts to make payments instead of using the gold itself. In time, the paper warehouse receipts circulated as money.

22 How Banking Developed The Early Bankers At this stage of banking, warehouse receipts were fully backed by gold; they simply represented gold in storage. Goldsmiths later began to recognize that, on an average day, few people redeemed their receipts for gold. Many individuals traded the receipts for goods and seldom requested the gold itself. In short, the receipts had become money, widely accepted for purposes of exchange. Sensing opportunity, goldsmiths began to lend some of the stored gold, realizing that they could earn interest on the loans without defaulting on their pledge to redeem the warehouse receipts when presented.

23 How Banking Developed The Early Bankers In most cases, however, the gold borrowers also preferred warehouse receipts to the actual gold. Thus the warehouse receipts came to represent a greater amount of gold than was actually on deposit. Consequently, the money supply increased, now measured in terms of gold and the paper warehouse receipts issued by the Goldsmith/bankers. Thus fractional reserve banking had begun. In a fractional reserve system, banks create money by holding on reserve only a fraction of the money deposited with them and lending the remainder. Our modern-day banking operates within such a system.

24 Direct and Indirect Finance Lenders can get together with borrowers directly or indirectly; that is, there are two types of finance: direct and indirect. Direct finance In direct finance, the lenders and borrowers come together in a market setting, such as the bond market. In the bond market, people who want to borrow funds issue bonds. For example, company A might issue a bond that promises to pay an interest rate of 10 percent annually for the next 10 years. A person with funds to lend might then buy that bond for a particular price. The buying and selling in a bond market are simply lending and borrowing. The buyer of the bond is the lender, and the seller of the bond is the borrower.

25 Direct and Indirect Finance Indirect finance In indirect finance, lenders and borrowers go through a financial intermediary, which takes in funds from people who want to save and then lends the funds to people who want to borrow. For example, a commercial bank is a financial intermediary, doing business with both savers and borrowers. Through one door the savers come in, looking for a place to deposit their funds and earn regular interest payments. Through another door come the borrowers, seeking loans on which they will pay interest. The bank, or the financial intermediary, ends up channeling the saved funds to borrowers.

26 Depository Institutions A depository institution is a firm that accepts deposits from households and firms and uses the deposits to make loans to other households and firms. The deposits of three types of depository institution are part of the nation s money: Commercial banks Thrift institutions Money market mutual funds

27 Depository Institutions Commercial Banks A commercial bank is a private firm that is licensed to receive deposits and make loans. A commercial bank s balance sheet summarizes its business and lists the bank s assets, liabilities, and net worth. The objective of a commercial bank is to maximize the net worth of its stockholders, by making profits.

28 Adverse Selection and Moral Hazard Problems When it comes to lending and borrowing, both adverse selection and moral hazards can arise. Both are the result of asymmetric information. Asymmetric information relates to one side of a transaction having information that the other side does not have. Suppose Rahima is going to sell her house. As the seller of the house, she has more information about the house than potential buyers. Rahima knows whether the house has plumbing problems, cracks in the foundation, and so on. Potential buyers do not.

29 Adverse Selection and Moral Hazard Problems The effect of asymmetric information can be either an adverse selection problem or a moral hazard problem. The adverse selection problem (hidden type) occurs before the loan is made, and the moral hazard problem (hidden action) occurs afterward. Before the loan is made An adverse selection problem occurs when the parties on one side of the market, having information not known to others, self-select in a way that adversely affects the parties on the other side of the market. Think of it this way: Two people want a loan. One person is a good credit risk, and the other is a bad credit risk. The person who is the bad credit risk is the person more likely to ask for the loan.

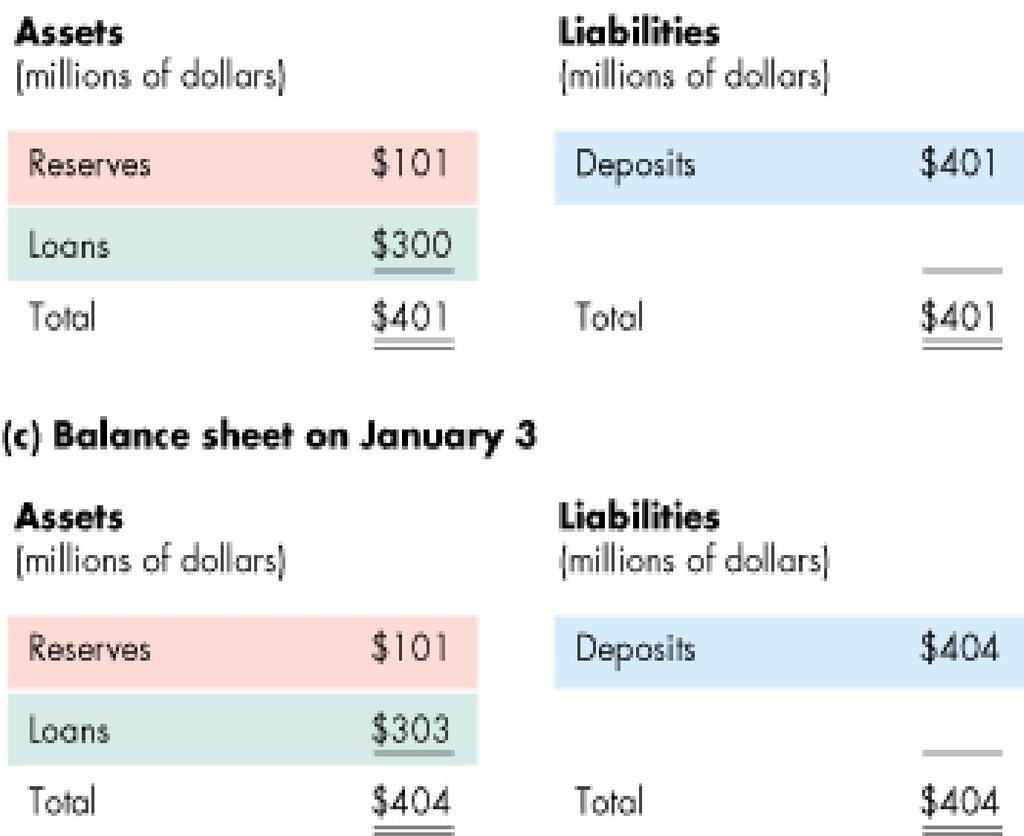

30 Adverse Selection and Moral Hazard Problems Before the loan is made Suppose two people, Selim and Salina, want to borrow Tk. 100,000, and Malek has Tk. 100,000 to lend. Salina wants to borrow the Tk. 100,000 to buy a piece of equipment for her small business. She plans to pay back the loan, and she takes her loan commitments very seriously. She is the Good type. Selim wants to borrow the Tk. 100,000 so that he can gamble. He will pay back the loan only if he wins big gambling. He is not the type of person who takes his loan commitments seriously. He is the Bad type. Who is more likely to ask Malek for the loan, Selim or Salina? Selim is because he knows that he will pay back the loan only if he wins big in gambling; he sees a loan as essentially free money. Heads, Selim wins; tails, Malek loses!

31 Adverse Selection and Moral Hazard Problems Before the loan is made If Malek can t separate the good types from the bad types, what can he do? He might just decide not to give a loan to anyone. In other words, his inability to solve the adverse selection problem may be enough for him to decide not to lend to anyone. At this point, a financial intermediary can help. A bank does not require Malek to worry about who will and who will not pay back a loan. Malek needs simply to turn over his saved funds to the bank, in return for the bank s promise to pay him say a 5 percent interest rate per year. Then, the bank takes on the responsibility of trying to separate the good types from the bad ones. The bank will run a credit check on everyone; the bank will collect information on who has a job and who doesn t; the bank will ask the borrower to put up some collateral on the loan; and so on. In other words, the bank s job is to solve the adverse selection problem.

32 Adverse Selection and Moral Hazard Problems After the loan is made The moral hazard problem exists when one party to a transaction changes his or her behavior in a way that is hidden from and costly to the other party. Suppose you want to lend some saved funds. You give Selim a Tk. 100,000 loan because he promised you that he was going to use the funds to help him get through university. Instead, once Selim receives the money, he decides to use the funds to buy some clothes and take a vacation to Thailand. Because of such potential moral hazard problems, you might decide to cut back on granting loans. You want to protect yourself from borrowers who do things that are costly to you.

33 Adverse Selection and Moral Hazard Problems After the loan is made Again, a financial intermediary has a role to play. A financial intermediary, such as a bank, might try to solve the moral hazard problem by specifying that a loan can only be used for a particular purpose (e.g., paying for university). It might require the borrower to provide regular information on and evidence of how the borrowed funds are being used, giving out the loan in installments (Tk. 10,000 this month, Tk. 10,000 next month), and so on.

34 Financial Regulation There are four main balance sheet rules: Capital requirements Reserve requirements Deposit rules Lending rules

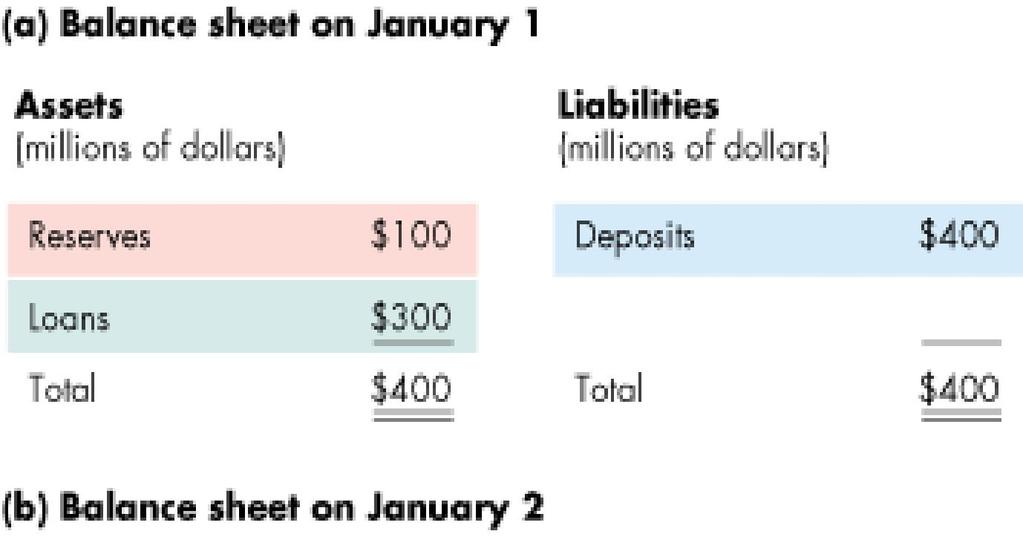

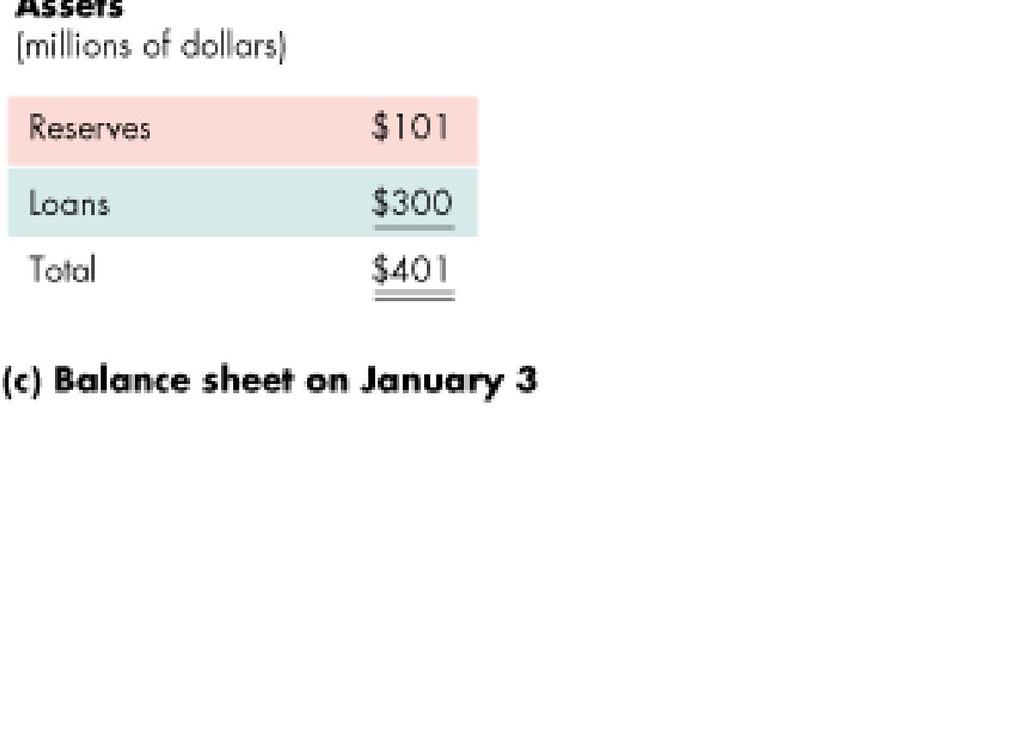

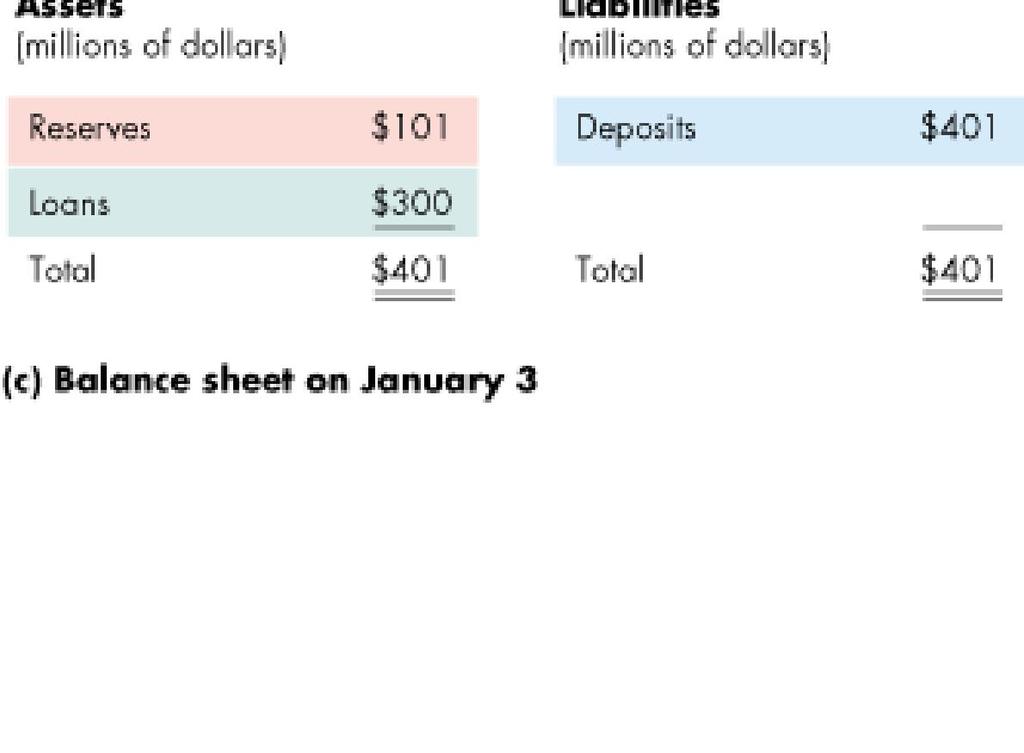

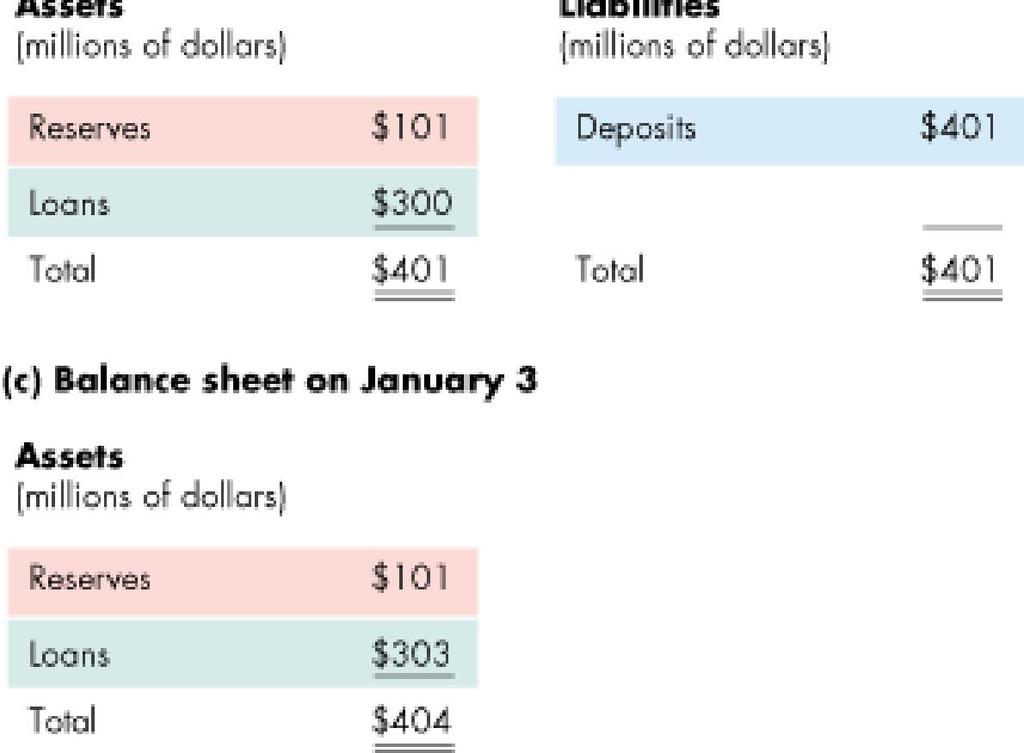

35 How Banks Create Money To achieve its objective, a bank makes (risky) loans at an interest rate higher than that paid on deposits. But the banks must balance profit and prudence; loans generate profit, but depositors must be able to obtain their funds when they want them. Banks funds come from their assets, which we divide into two important parts: reserves and loans. Reserves are the cash in a bank s vault and the bank s deposits at Federal Reserve Banks. Bank assets also include buildings and equipment, liquid assets, investment securities, and loans.

36 How Banks Create Money Reserves: Actual and Required The fraction of a bank s total deposits held as reserves is the reserve ratio. The required reserve ratio is the fraction that banks are required, by regulation, to keep as reserves. Required reserves are the total amount of reserves that banks are required to keep. Excess reserves equal total reserves minus required reserves.

37 How Banks Create Money Creating Deposits by Making Loans in a One-Bank Economy When a bank receives a deposit of currency, its reserves increase by the amount deposited, but its required reserves increase by only a fraction (determined by the required reserve ratio) of the amount deposited. The bank has excess reserves, which it loans. These loans can only end up as deposits in our one and only bank, where they boost deposits without changing total reserves, which creates money.

38 How Banks Create Money This Figure illustrates how one bank create money by making loans.

39 How Banks Create Money The Deposit Multiplier The deposit multiplier is the amount by which an increase in bank reserves is multiplied to calculate the increase in bank deposits. The deposit multiplier = 1/Required reserve ratio.

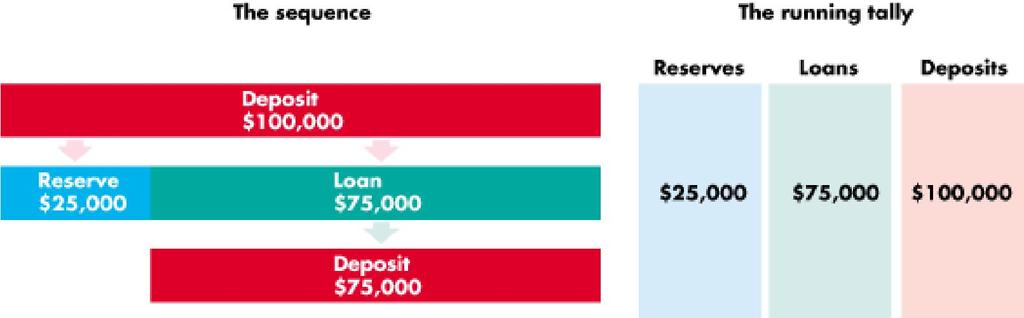

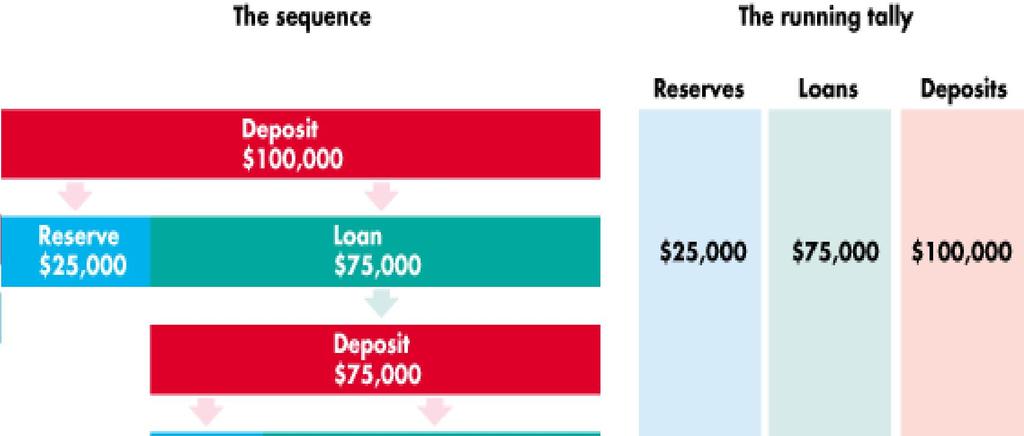

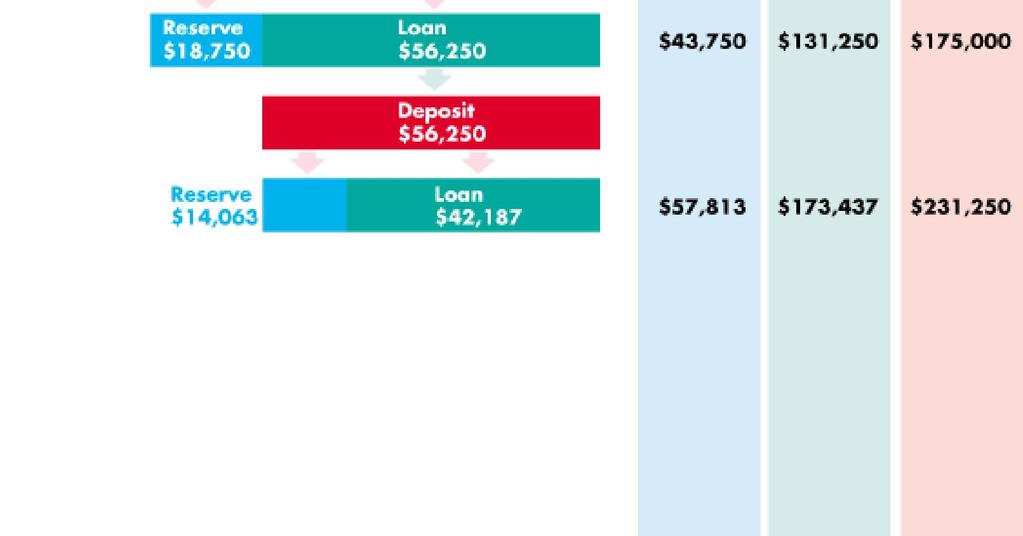

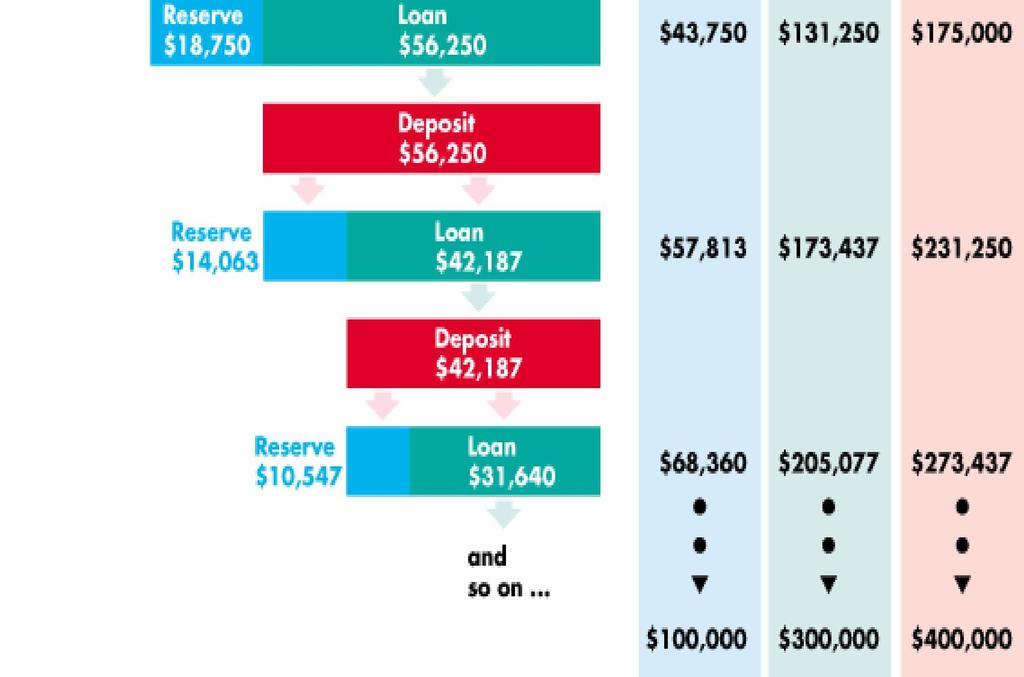

40 How Banks Create Money Creating Deposits by Making Loans with Many Banks With many banks, one bank lending out its excess reserves cannot expect its deposits to increase by the full amount loaned; some of the loaned reserves end up in other banks. But then the other banks have excess reserves, which they loan. Ultimately, the effect in the banking system is the same as if there was only one bank, so long as all loans are deposited in banks.

41 How Banks Create Money This Figure illustrates money creation with many banks.

MONEY, THE PRICE LEVEL, AND INFLATION

25 MONEY, THE PRICE LEVEL, AND INFLATION What is Money? Money is any commodity or token that is generally acceptable as a means of payment. A means of payment is a method of settling a debt. Money has

25 MONEY, THE PRICE LEVEL, AND INFLATION What is Money? Money is any commodity or token that is generally acceptable as a means of payment. A means of payment is a method of settling a debt. Money has

Money, Banking and the Federal Reserve System. Chapter 10

Money, Banking and the Federal Reserve System Chapter 10 Changes for the last few weeks For the next two weeks we will be doing about a chapter a day so we need to pick up the pace a little bit. You will

Money, Banking and the Federal Reserve System Chapter 10 Changes for the last few weeks For the next two weeks we will be doing about a chapter a day so we need to pick up the pace a little bit. You will

Chapter8 3/5/2018. MONEY, THE PRICE LEVEL, AND INFLATION Part 1. In this chapter: Define money and its functions

Chapter8 MONEY, THE PRICE LEVEL, AND INFLATION Part 1 https://www.yahoo.com/finance/news/feds-williams- youre-living-in-an-almost-goldilocks-economy- 191512496.html In this chapter: Define money and its

Chapter8 MONEY, THE PRICE LEVEL, AND INFLATION Part 1 https://www.yahoo.com/finance/news/feds-williams- youre-living-in-an-almost-goldilocks-economy- 191512496.html In this chapter: Define money and its

29 THE MONETARY SYSTEM

29 THE MONETARY SYSTEM WHAT S NEW IN THE FOURTH EDITION: There is a new FYI box on The Federal Funds Rate. There is also a new In the News box on The History of Money. LEARNING OBJECTIVES: By the end of

29 THE MONETARY SYSTEM WHAT S NEW IN THE FOURTH EDITION: There is a new FYI box on The Federal Funds Rate. There is also a new In the News box on The History of Money. LEARNING OBJECTIVES: By the end of

2010 Pearson Addison Wesley CHAPTER 1

CHAPTER 1 Money has taken many forms. What is money today? What happens when the bank lends the money we re deposited to someone else? How does the Fed influence the quantity of money? What happens when

CHAPTER 1 Money has taken many forms. What is money today? What happens when the bank lends the money we re deposited to someone else? How does the Fed influence the quantity of money? What happens when

Macroeconomics CHAPTER 13. Money, Banking, and the Federal Reserve System

Macroeconomics CHAPTER 13 Money, Banking, and the Federal Reserve System What you will learn in this chapter: The various roles money plays and the many forms it takes in the economy. How the actions of

Macroeconomics CHAPTER 13 Money, Banking, and the Federal Reserve System What you will learn in this chapter: The various roles money plays and the many forms it takes in the economy. How the actions of

12/03/2012. What is Money?

Money has taken many forms. What is money today? What happens when the bank lends the money we re deposited to someone else? How does the Bank of Canada influence the quantity of money? What happens when

Money has taken many forms. What is money today? What happens when the bank lends the money we re deposited to someone else? How does the Bank of Canada influence the quantity of money? What happens when

Goals understand what money is understand money creation and the multiple expansion process

375 Chapter 26 MONEY Key Topics what is money fractional reserves the creation of money the money multiplier Goals understand what money is understand money creation and the multiple expansion process

375 Chapter 26 MONEY Key Topics what is money fractional reserves the creation of money the money multiplier Goals understand what money is understand money creation and the multiple expansion process

MONEY, THE PRICE LEVEL, AND INFLATION

24 MONEY, THE PRICE LEVEL, AND INFLATION After studying this chapter, you will be able to: Define money and describe its functions Explain the economic functions of banks Describe the structure and functions

24 MONEY, THE PRICE LEVEL, AND INFLATION After studying this chapter, you will be able to: Define money and describe its functions Explain the economic functions of banks Describe the structure and functions

the Federal Reserve System

CHAPTER 13 Money, Banks, and the Federal Reserve System Chapter Summary and Learning Objectives 13.1 What Is Money, and Why Do We Need It? (pages 422 425) Define money and discuss its four functions. A

CHAPTER 13 Money, Banks, and the Federal Reserve System Chapter Summary and Learning Objectives 13.1 What Is Money, and Why Do We Need It? (pages 422 425) Define money and discuss its four functions. A

MONEY. Economics Unit 4 Macroeconomics Just the Facts Handout

MONEY Economics Unit 4 Macroeconomics Just the Facts Handout Barter Economy A barter economy is an economy with no money. The only way you can get what you want in a barter economy is to trade something

MONEY Economics Unit 4 Macroeconomics Just the Facts Handout Barter Economy A barter economy is an economy with no money. The only way you can get what you want in a barter economy is to trade something

the Federal Reserve System

CHAPTER 14 Money, Banks, and the Federal Reserve System Chapter Summary and Learning Objectives 14.1 What Is Money, and Why Do We Need It? (pages 456 459) Define money and discuss the four functions of

CHAPTER 14 Money, Banks, and the Federal Reserve System Chapter Summary and Learning Objectives 14.1 What Is Money, and Why Do We Need It? (pages 456 459) Define money and discuss the four functions of

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 3 What Is Money? 3.1 Meaning of Money

Chapter 3 What Is Money? 3.1 Meaning of Money") Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 3 What Is Money? 3.1 Meaning of Money 1) To an economist, is anything that is generally accepted in payment for goods and services or

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 3 What Is Money? 3.1 Meaning of Money 1) To an economist, is anything that is generally accepted in payment for goods and services or

What is Money? Gregory La Blanc

What is Money? Gregory La Blanc Commercial Bank Balance Sheet Loans Deposits Commercial Bank Balance Sheet Cash Deposits Loans Equity Origins of Banking Before banking there was money. What is money? Medium

What is Money? Gregory La Blanc Commercial Bank Balance Sheet Loans Deposits Commercial Bank Balance Sheet Cash Deposits Loans Equity Origins of Banking Before banking there was money. What is money? Medium

The Monetary System CHAPTER. Goals. Outcomes

CHAPTER 29 The Monetary System Goals in this chapter you will Consider what money is and what functions money has in the economy Learn what the Federal Reserve System is Examine how the banking system

CHAPTER 29 The Monetary System Goals in this chapter you will Consider what money is and what functions money has in the economy Learn what the Federal Reserve System is Examine how the banking system

Money and banking (First part) Macroeconomics Money and banking Money and its functions Different money types Modern banking Money creation

Macroeconomics Money and banking Money and its functions Different money types Modern banking Money creation") Money and banking (First part) Macroeconomics Money and banking Money and its functions Different money types Modern banking Money creation 1 What is money? It is a symbol of success, a source of crime,

Money and banking (First part) Macroeconomics Money and banking Money and its functions Different money types Modern banking Money creation 1 What is money? It is a symbol of success, a source of crime,

CHAPTER 10: MONEY, BANKS AND THE FEDERAL RESERVE

CHAPTER 10: MONEY, BANKS AND THE FEDERAL RESERVE Learning Goals To know what is money To know how banks create money To know the structure of the Federal Reserve System To know how the Fed controls the

CHAPTER 10: MONEY, BANKS AND THE FEDERAL RESERVE Learning Goals To know what is money To know how banks create money To know the structure of the Federal Reserve System To know how the Fed controls the

Chapter 1 Why Study Money, Banking, and Financial Markets?

Chapter 1 Why Study Money, Banking, and Financial Markets? MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Markets in which funds are transferred

Chapter 1 Why Study Money, Banking, and Financial Markets? MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Markets in which funds are transferred

ECO 100Y INTRODUCTION TO ECONOMICS

Prof. Gustavo Indart Department of Economics University of Toronto ECO 100Y INTRODUCTION TO ECONOMICS Lecture 15. MONEY, BANKING, AND PRICES 15.1 WHAT IS MONEY? 15.1.1 Classical and Modern Views For the

Prof. Gustavo Indart Department of Economics University of Toronto ECO 100Y INTRODUCTION TO ECONOMICS Lecture 15. MONEY, BANKING, AND PRICES 15.1 WHAT IS MONEY? 15.1.1 Classical and Modern Views For the

Chapter 10: Money and Banking Section 1

Chapter 10: Money and Banking Section 1 Key Terms money: anything that serves as a medium of exchange, a unit of account, and a store of value medium of exchange: anything that is used to determine value

Chapter 10: Money and Banking Section 1 Key Terms money: anything that serves as a medium of exchange, a unit of account, and a store of value medium of exchange: anything that is used to determine value

For instance, some societies used cows as money 1 cow = 2 goats 1 cow = 5 blankets 1 cow = 3 chairs 1 cow = 50 loafs of bread

Money History of Money Barter economy: Goods were exchanged directly for other goods, so there was no money in the economy. It was very difficult to have a lot of exchange going on because of the requirement

Money History of Money Barter economy: Goods were exchanged directly for other goods, so there was no money in the economy. It was very difficult to have a lot of exchange going on because of the requirement

Banking, Liquidity Transformation, and Bank Runs

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

Banking, Liquidity Transformation, and Bank Runs ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 30 Readings GLS Ch. 28 GLS Ch. 30 (don t worry about model

CHAPTER 32 Money Creation

CHAPTER 32 Money Creation A. Short-Answer, Essays, and Problems 1. What is the history behind the idea of a fractional reserve banking system? Early traders used gold in making transactions. They realized

CHAPTER 32 Money Creation A. Short-Answer, Essays, and Problems 1. What is the history behind the idea of a fractional reserve banking system? Early traders used gold in making transactions. They realized

The Monetary System P R I N C I P L E S O F. N. Gregory Mankiw. What Money Is and Why It s Important

C H A P T E R 29 The Monetary System P R I N C I P L E S O F Economics N. Gregory Mankiw What Money Is and Why It s Important Without money, trade would require barter, the exchange of one good or service

C H A P T E R 29 The Monetary System P R I N C I P L E S O F Economics N. Gregory Mankiw What Money Is and Why It s Important Without money, trade would require barter, the exchange of one good or service

Financial Markets and Institutions, 9e (Mishkin) Chapter 2 Overview of the Financial System. 2.1 Multiple Choice

Chapter 2 Overview of the Financial System. 2.1 Multiple Choice") Financial Markets and Institutions, 9e (Mishkin) Chapter 2 Overview of the Financial System 2.1 Multiple Choice 1) Every financial market performs the following function: A) It determines the level of

Financial Markets and Institutions, 9e (Mishkin) Chapter 2 Overview of the Financial System 2.1 Multiple Choice 1) Every financial market performs the following function: A) It determines the level of

ECON 141: Macroeconomics Ch 5: Money and Banking Mohammed Alwosabi

Chapter 5 MONEY, BANKING, AND MONETARY POLICY 1 WHAT IS MONEY Money is anything that is generally accepted as a measure of payment and settling of debt. Money is a stock concept. It is a certain amount

Chapter 5 MONEY, BANKING, AND MONETARY POLICY 1 WHAT IS MONEY Money is anything that is generally accepted as a measure of payment and settling of debt. Money is a stock concept. It is a certain amount

FINANCIAL MARKETS FINANCIAL INSTRUMENTS FINANCIAL INSTITUTIONS. Lecture 2 Monetary policy FINANCIAL MARKETS

FINANCIAL MARKETS FINANCIAL INSTRUMENTS FINANCIAL INSTITUTIONS Lecture 2 Monetary policy FINANCIAL MARKETS markets in which funds are transferred from people who have an excess of available funds to people

FINANCIAL MARKETS FINANCIAL INSTRUMENTS FINANCIAL INSTITUTIONS Lecture 2 Monetary policy FINANCIAL MARKETS markets in which funds are transferred from people who have an excess of available funds to people

Introduction. Learning Objectives. Learning Objectives. Chapter 15. Money, Banking, and Central Banking. Define the fundamental functions of money

Chapter 15 Money, Banking, and Central Banking Introduction About 20 billion new U.S. coins will be put into circulation this year, and new paper currency will be printed as well. These new coins and currency

Chapter 15 Money, Banking, and Central Banking Introduction About 20 billion new U.S. coins will be put into circulation this year, and new paper currency will be printed as well. These new coins and currency

Financial Markets and Institutions, 8e (Mishkin) Chapter 2 Overview of the Financial System. 2.1 Multiple Choice

Chapter 2 Overview of the Financial System. 2.1 Multiple Choice") Financial Markets and Institutions, 8e (Mishkin) Chapter 2 Overview of the Financial System 2.1 Multiple Choice 1) Every financial market performs the following function: A) It determines the level of

Financial Markets and Institutions, 8e (Mishkin) Chapter 2 Overview of the Financial System 2.1 Multiple Choice 1) Every financial market performs the following function: A) It determines the level of

WHAT IS MONEY? Chapter 3. ECON248: Money and Banking Ch.3: What is Money? Dr. Mohammed Alwosabi

Chapter 3 WHAT IS MONEY? MEANING OF MONEY In ordinary conversation, we commonly use the word money to mean income ("he makes a lot of money") or wealth ("she has a lot of money"). Money ( or money supply)

Chapter 3 WHAT IS MONEY? MEANING OF MONEY In ordinary conversation, we commonly use the word money to mean income ("he makes a lot of money") or wealth ("she has a lot of money"). Money ( or money supply)

Macro Money and Banking Essentials WCC

Macro Money and Banking Essentials WCC Barter - a system of exchange in which people directly exchange one good for another without any intermediate step Barter relies on the double coincidence of wants

Macro Money and Banking Essentials WCC Barter - a system of exchange in which people directly exchange one good for another without any intermediate step Barter relies on the double coincidence of wants

Chapter 14: Money, Banks, and the Federal Reserve System

Chapter 14: Money, Banks, and the Federal Reserve System Yulei Luo SEF of HKU March 28, 2016 Learning Objectives 1. De ne money and discuss its four functions. 2. Discuss the de nitions of the money supply.

Chapter 14: Money, Banks, and the Federal Reserve System Yulei Luo SEF of HKU March 28, 2016 Learning Objectives 1. De ne money and discuss its four functions. 2. Discuss the de nitions of the money supply.

Chapter 2 Money and the Monetary System

Chapter 2 Money and the Monetary System Chapter Two: Money and the Monetary System CHAPTER PREVIEW The monetary system plays an important role in the operation and development of the financial and economic

Chapter 2 Money and the Monetary System Chapter Two: Money and the Monetary System CHAPTER PREVIEW The monetary system plays an important role in the operation and development of the financial and economic

ECON 3303 Money and Banking Final Exam. MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 3303 Money and Banking Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If Treasury deposits at the Fed are predicted to fall,

ECON 3303 Money and Banking Final Exam Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If Treasury deposits at the Fed are predicted to fall,

The Monetary System: What It Is and How It Works

4 The Monetary System: What It Is and How It Works CHAPTER 5 Inflation Modified by Ming Yi 2016 Worth Publishers, all rights reserved 3 IN THIS CHAPTER, YOU WILL LEARN: The definition, functions, and types

4 The Monetary System: What It Is and How It Works CHAPTER 5 Inflation Modified by Ming Yi 2016 Worth Publishers, all rights reserved 3 IN THIS CHAPTER, YOU WILL LEARN: The definition, functions, and types

Introduction. Learning Objectives. Chapter 15. Money, Banking, and Central Banking

Chapter 15 Money, Banking, and Central Banking Introduction Bear Stearns, Goldman Sachs, Lehman Brothers, Merrill Lynch, and Morgan Stanley have been big names on Wall Street for years. Known as investment

Chapter 15 Money, Banking, and Central Banking Introduction Bear Stearns, Goldman Sachs, Lehman Brothers, Merrill Lynch, and Morgan Stanley have been big names on Wall Street for years. Known as investment

Introduction. Learning Objectives. Learning Objectives. Economics Today Twelfth Edition. Chapter 15 Money Creation and Deposit Insurance

Roger LeRoy Miller Economics Today Twelfth Edition Chapter 15 Money Creation and Deposit Insurance Introduction A quick response by the Federal Reserve to the September 11, 2001 terrorist attacks stabilized

Roger LeRoy Miller Economics Today Twelfth Edition Chapter 15 Money Creation and Deposit Insurance Introduction A quick response by the Federal Reserve to the September 11, 2001 terrorist attacks stabilized

WHAT IS BANK CREDIT? FRACTIONAL BANKING

The Story of Money: Reflect with me for a moment upon the nature of money, wealth and prosperity. And the more time you take reflecting upon it, the more varied and abstract your thoughts concerning money,

The Story of Money: Reflect with me for a moment upon the nature of money, wealth and prosperity. And the more time you take reflecting upon it, the more varied and abstract your thoughts concerning money,

Value of goods and services are measured in terms of the units of money

Chapter 3: Money What is money? Not currency Not income Not wealth Money is anything that is generally accepted in payment for goods & services, or repayment of a debt Functions performed by money: Medium

Chapter 3: Money What is money? Not currency Not income Not wealth Money is anything that is generally accepted in payment for goods & services, or repayment of a debt Functions performed by money: Medium

The Financial Sector Functions of money Medium of exchange Measure of value Store of value Method of deferred payment

The Financial Sector Functions of money Medium of exchange - avoids the double coincidence of wants Measure of value - measures the relative values of different goods and services Store of value - kept

The Financial Sector Functions of money Medium of exchange - avoids the double coincidence of wants Measure of value - measures the relative values of different goods and services Store of value - kept

The Monetary System. Economics CHAPTER. N. Gregory Mankiw. Principles of. Seventh Edition. Wojciech Gerson ( )

") Wojciech Gerson (1831-1901) Seventh Edition Principles of Economics N. Gregory Mankiw CHAPTER 29 The Monetary System In this chapter, look for the answers to these questions What assets are considered

Wojciech Gerson (1831-1901) Seventh Edition Principles of Economics N. Gregory Mankiw CHAPTER 29 The Monetary System In this chapter, look for the answers to these questions What assets are considered

Lecture 6. The Monetary System Prof. Samuel Moon Jung 1

Lecture 6. The Monetary System Prof. Samuel Moon Jung 1 Main concepts: The meaning of money, the Federal Reserve System, banks and money supply, the Fed s tools of monetary control Introduction In the

Lecture 6. The Monetary System Prof. Samuel Moon Jung 1 Main concepts: The meaning of money, the Federal Reserve System, banks and money supply, the Fed s tools of monetary control Introduction In the

International Money and Banking: 2. Banks and Financial Intermediation

International Money and Banking: 2. Banks and Financial Intermediation Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Banks and Financial Intermediation Spring 2018 1 / 15 Banks While

International Money and Banking: 2. Banks and Financial Intermediation Karl Whelan School of Economics, UCD Spring 2018 Karl Whelan (UCD) Banks and Financial Intermediation Spring 2018 1 / 15 Banks While

Banking Basics Table of contents Introduction 4 What is a bank? 6 How do people start banks? 7 How did banking begin? 8 Why are there so many different types of banks? 11 How do I choose a bank? 13 What

Banking Basics Table of contents Introduction 4 What is a bank? 6 How do people start banks? 7 How did banking begin? 8 Why are there so many different types of banks? 11 How do I choose a bank? 13 What

What Makes Money..Money? (HA)

") What Makes Money..Money? (HA) Kyle MacDonald managed to get the house he wanted using barter. To do this, he relied on a coincidence of wants. People wanted what he had, and he wanted what they had. MacDonald

What Makes Money..Money? (HA) Kyle MacDonald managed to get the house he wanted using barter. To do this, he relied on a coincidence of wants. People wanted what he had, and he wanted what they had. MacDonald

Money and the Monetary System

Money and the Monetary System WHAT IS MONEY? Definition of Money Money Any commodity or token that is generally accepted as a means of payment. Any Commodity or Token Something that can be recognized Divided

Money and the Monetary System WHAT IS MONEY? Definition of Money Money Any commodity or token that is generally accepted as a means of payment. Any Commodity or Token Something that can be recognized Divided

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 55

The Financial System 1 / 55") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 55 The financial system consists of those institutions in the economy that matches saving with investment. The financial system

MGT411 Money & Banking Latest Solved Quizzes By

MGT411 Money & Banking Latest Solved Quizzes By http://vustudents.ning.com Which of the following is true of a nation's central bank? It makes important decisions about the nation's tax and public spending

MGT411 Money & Banking Latest Solved Quizzes By http://vustudents.ning.com Which of the following is true of a nation's central bank? It makes important decisions about the nation's tax and public spending

ECON30150 (International Money and Banking) MIDTERM EXAM. March 6, 2017

MIDTERM EXAM. March 6, 2017") ECON30150 (International Money and Banking) MIDTERM EXAM March 6, 2017 There are 50 questions in this exam. You have one hour to complete it. All questions have only one correct answer. There is no negative

ECON30150 (International Money and Banking) MIDTERM EXAM March 6, 2017 There are 50 questions in this exam. You have one hour to complete it. All questions have only one correct answer. There is no negative

General Study Questions re Money and Banking

General Study Questions re Money and Banking 1. Which of the following best describes a clearing house? 2. Which of the following best describes how a clearing house can result in a more stable and uniform

General Study Questions re Money and Banking 1. Which of the following best describes a clearing house? 2. Which of the following best describes how a clearing house can result in a more stable and uniform

CHAPTER 10 Money, Banking, and the Federal Reserve System. CHAPTER 11 Measuring Economic Performance. CHAPTER 12 Economic Changes and Cycles

CHAPTER 10 Money, Banking, and the Federal Reserve System CHAPTER 11 Measuring Economic Performance CHAPTER 12 Economic Changes and Cycles CHAPTER 13 Fiscal and Monetary Policy CHAPTER 14 Taxing and Spending

CHAPTER 10 Money, Banking, and the Federal Reserve System CHAPTER 11 Measuring Economic Performance CHAPTER 12 Economic Changes and Cycles CHAPTER 13 Fiscal and Monetary Policy CHAPTER 14 Taxing and Spending

Reading Essentials and Study Guide

Lesson 2 Monetary Policy ESSENTIAL QUESTION How does the government promote the economic goals of price stability, full employment, and economic growth? Reading HELPDESK Academic Vocabulary explicit openly

Lesson 2 Monetary Policy ESSENTIAL QUESTION How does the government promote the economic goals of price stability, full employment, and economic growth? Reading HELPDESK Academic Vocabulary explicit openly

Chapter 03 Financial Instruments, Financial Markets, and Financial Institutions

Chapter 03 Financial Instruments, Financial Markets, and Financial Institutions Multiple Choice Questions 1. (p. 56) A financial intermediary: a. Is an agency that guarantees a loan? B. Is involved in

Chapter 03 Financial Instruments, Financial Markets, and Financial Institutions Multiple Choice Questions 1. (p. 56) A financial intermediary: a. Is an agency that guarantees a loan? B. Is involved in

Being an economist and the economics of money Not as boring at it sounds. Tony Yates, aged 49 and ¾ [=Jonas Dad]

![Being an economist and the economics of money Not as boring at it sounds. Tony Yates, aged 49 and ¾ [=Jonas Dad]](/thumbs/79/80190727.jpg "Being an economist and the economics of money Not as boring at it sounds. Tony Yates, aged 49 and ¾ [=Jonas Dad]") Being an economist and the economics of money Not as boring at it sounds Tony Yates, aged 49 and ¾ [=Jonas Dad] BEING AN ECONOMIST This is a photo of a robot. People often think of economists as a bit

Being an economist and the economics of money Not as boring at it sounds Tony Yates, aged 49 and ¾ [=Jonas Dad] BEING AN ECONOMIST This is a photo of a robot. People often think of economists as a bit

Function of Financial Markets

Chapter 2 An Overview of the Financial System Function of Financial Markets Perform the essential function of channeling funds from economic players (households, firms and govt.) that have saved surplus

Chapter 2 An Overview of the Financial System Function of Financial Markets Perform the essential function of channeling funds from economic players (households, firms and govt.) that have saved surplus

ECONOMICS. Part V: Money Monetary Equation of Exhange Creation of banking. What does it mean to me? READ Mankiw, Chapter 29, 30, Morton Unit 4

ECONOMICS What does it mean to me? Part V: Money Monetary Equation of Exhange Creation of banking READ Mankiw, Chapter 29, 30, Morton Unit 4 In any society, money is the asset, commodity or token, that

ECONOMICS What does it mean to me? Part V: Money Monetary Equation of Exhange Creation of banking READ Mankiw, Chapter 29, 30, Morton Unit 4 In any society, money is the asset, commodity or token, that

1. Which of the following would not be considered a characteristic of money? D. would be more efficient since people would be more self-sufficient.

Money Banking and Financial Markets 4th Edition Cecchetti Test Bank Full Download: http://testbanklive.com/download/money-banking-and-financial-markets-4th-edition-cecchetti-test-bank/ Chapter 02 Money

Money Banking and Financial Markets 4th Edition Cecchetti Test Bank Full Download: http://testbanklive.com/download/money-banking-and-financial-markets-4th-edition-cecchetti-test-bank/ Chapter 02 Money

BOGAZICI UNIVERSITY - DEPARTMENT OF ECONOMICS FALL 2016 EC 344: MONEY, BANKING AND FINANCIAL INSTITUTIONS - PROBLEM SET 2 -

BOGAZICI UNIVERSITY - DEPARTMENT OF ECONOMICS FALL 2016 EC 344: MONEY, BANKING AND FINANCIAL INSTITUTIONS - PROBLEM SET 2 - DUE BY OCTOBER 10, 2016, 5 PM 1) Every financial market has the following characteristic.

BOGAZICI UNIVERSITY - DEPARTMENT OF ECONOMICS FALL 2016 EC 344: MONEY, BANKING AND FINANCIAL INSTITUTIONS - PROBLEM SET 2 - DUE BY OCTOBER 10, 2016, 5 PM 1) Every financial market has the following characteristic.

International Finance

International Finance FINA 5331 Lecture 2: U.S. Financial System William J. Crowder Ph.D. Financial Markets Financial markets are markets in which funds are transferred from people and Firms who have an

International Finance FINA 5331 Lecture 2: U.S. Financial System William J. Crowder Ph.D. Financial Markets Financial markets are markets in which funds are transferred from people and Firms who have an

Economics of Money, Banking, and Financial Markets, 11e (Mishkin) Chapter 2 An Overview of the Financial System. 2.1 Function of Financial Markets

Chapter 2 An Overview of the Financial System. 2.1 Function of Financial Markets") Economics of Money, Banking, and Financial Markets, 11e (Mishkin) Chapter 2 An Overview of the Financial System 2.1 Function of Financial Markets 1) Every financial market has the following characteristic.

Economics of Money, Banking, and Financial Markets, 11e (Mishkin) Chapter 2 An Overview of the Financial System 2.1 Function of Financial Markets 1) Every financial market has the following characteristic.

Chapter 8 An Economic Analysis of Financial Structure

Chapter 8 An Economic Analysis of Financial Structure Multiple Choice 1) American businesses get their external funds primarily from (a) bank loans. (b) bonds and commercial paper issues. (c) stock issues.

Chapter 8 An Economic Analysis of Financial Structure Multiple Choice 1) American businesses get their external funds primarily from (a) bank loans. (b) bonds and commercial paper issues. (c) stock issues.

Stocks and corporate bonds not the most important sources of funds for business

Stocks and corporate bonds not the most important sources of funds for business Stocks and corporate bonds not the most important sources of funds for business Indirect finance through financial intermediaries

Stocks and corporate bonds not the most important sources of funds for business Stocks and corporate bonds not the most important sources of funds for business Indirect finance through financial intermediaries

Chapter Eleven. Chapter 11 The Economics of Financial Intermediation Why do Financial Intermediaries Exist

Chapter Eleven Chapter 11 The Economics of Financial Intermediation Why do Financial Intermediaries Exist Countries With Developed Financial Systems Prosper Basic Facts of Financial Structure 1. Direct

Chapter Eleven Chapter 11 The Economics of Financial Intermediation Why do Financial Intermediaries Exist Countries With Developed Financial Systems Prosper Basic Facts of Financial Structure 1. Direct

The Financial System. Sherif Khalifa. Sherif Khalifa () The Financial System 1 / 52

The Financial System 1 / 52") The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

The Financial System Sherif Khalifa Sherif Khalifa () The Financial System 1 / 52 Financial System Definition The financial system consists of those institutions in the economy that matches saving with

ECOS2004 MONEY AND BANKING LECTURE SUMMARIES

ECOS2004 MONEY AND BANKING LECTURE SUMMARIES TABLE OF CONTENTS WEEK TOPICS 1 Chapter 1: Why Study Money, Banking, and Financial Markets? Chapter 2: An Overview of the Financial System 2 Chapter 3: What

ECOS2004 MONEY AND BANKING LECTURE SUMMARIES TABLE OF CONTENTS WEEK TOPICS 1 Chapter 1: Why Study Money, Banking, and Financial Markets? Chapter 2: An Overview of the Financial System 2 Chapter 3: What

Unit 9: Money and Banking

Unit 9: Money and Banking Name: Date: / / Functions of Money The first and foremost role of money is that it acts as a medium of exchange. Barter exchanges become extremely difficult in a large economy

Unit 9: Money and Banking Name: Date: / / Functions of Money The first and foremost role of money is that it acts as a medium of exchange. Barter exchanges become extremely difficult in a large economy

Trefzger, FIL 240 & FIL 404 Assignment: Debt and Equity Financing and Form of Business Organization

Trefzger, FIL 240 & FIL 404 Assignment: Debt and Equity Financing and Form of Business Organization Please read the following story that provides insights into debt (lenders) and equity (owners) financing.

Trefzger, FIL 240 & FIL 404 Assignment: Debt and Equity Financing and Form of Business Organization Please read the following story that provides insights into debt (lenders) and equity (owners) financing.

Review Material for Exam I

Class Materials from January-March 2014 Review Material for Exam I Econ 331 Spring 2014 Bernardo Topics Included in Exam I Money and the Financial System Money Supply and Monetary Policy Credit Market

Class Materials from January-March 2014 Review Material for Exam I Econ 331 Spring 2014 Bernardo Topics Included in Exam I Money and the Financial System Money Supply and Monetary Policy Credit Market

CHAPTER 31 Money, Banking, and Financial Institutions

CHAPTER 31 Money, Banking, and Financial Institutions Answers to Short-Answer, Essays, and Problems 1. What is money? Explain in terms of the functions of money. Money is whatever performs the three basic

CHAPTER 31 Money, Banking, and Financial Institutions Answers to Short-Answer, Essays, and Problems 1. What is money? Explain in terms of the functions of money. Money is whatever performs the three basic

3. What is Money? Copyright 2007 Pearson Addison-Wesley. All rights reserved. 3-1

3. What is Money? Copyright 2007 Pearson Addison-Wesley. All rights reserved. 3-1 Meaning of Money Money (money supply) anything that is generally accepted in payment for goods or services or in the repayment

3. What is Money? Copyright 2007 Pearson Addison-Wesley. All rights reserved. 3-1 Meaning of Money Money (money supply) anything that is generally accepted in payment for goods or services or in the repayment

Money is anything that is generally accepted as a means of payment. Money eliminates the need for a double coincidence of wants.

EC 201 Lecture Notes 6 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 6 Metropolitan State University Allen Bellas BB Chapter 11 Money and Banking Money is a tremendously important invention for the

EC 201 Lecture Notes 6 Page 1 of 1 ECON 201 - Macroeconomics Lecture Notes 6 Metropolitan State University Allen Bellas BB Chapter 11 Money and Banking Money is a tremendously important invention for the

Savings and Investment

Lecture Notes for Chapter 3 of MACROECONOMICS: An Introduction Savings and Investment Copyright 2000-2009 by Charles R. Nelson 1/8/09 In this chapter we will discuss- How savings becomes investment. Banks

Lecture Notes for Chapter 3 of MACROECONOMICS: An Introduction Savings and Investment Copyright 2000-2009 by Charles R. Nelson 1/8/09 In this chapter we will discuss- How savings becomes investment. Banks

Money and the Banking System

12 Money and the Banking System [Money] is a machine for doing quickly and commodiously what would be done, though less quickly and commodiously, without it. JOHN STUART MILL Contents The Nature of Money

12 Money and the Banking System [Money] is a machine for doing quickly and commodiously what would be done, though less quickly and commodiously, without it. JOHN STUART MILL Contents The Nature of Money

Multiple Choice Identify the letter of the choice that best completes the statement or answers the question.

Chapter 14 - Section I 1. Money functions as all of the following EXCEPT a. a store of value. c. a medium of exchange. b. a monetary standard. d. a measure of value. 2. A mutual coincidence of wants is

Chapter 14 - Section I 1. Money functions as all of the following EXCEPT a. a store of value. c. a medium of exchange. b. a monetary standard. d. a measure of value. 2. A mutual coincidence of wants is

Chapter 1-3. Topics in Financial Decisions. Financial System and the Economy. Financial system affects the economic performance It consists of

Chapter 1-3 Topics in Financial Decisions Financial system affects the economic performance It consists of Financial markets Financial institutions Money How does each of the above affect the economy?

Chapter 1-3 Topics in Financial Decisions Financial system affects the economic performance It consists of Financial markets Financial institutions Money How does each of the above affect the economy?

MONEY, BANKS, AND THE FEDERAL RESERVE*

Chapter 10 MONEY, BANKS, AND THE FEDERAL RESERVE* What Is Money? Topic: What Is Money? * 1) The functions of money are A) medium of exchange and the ability to buy goods and services. B) medium of exchange,

Chapter 10 MONEY, BANKS, AND THE FEDERAL RESERVE* What Is Money? Topic: What Is Money? * 1) The functions of money are A) medium of exchange and the ability to buy goods and services. B) medium of exchange,

1. Allocates scarce capital among competing uses 2. Spreads/shares risk 3. Facilitates inter-temporal trade

Chapter 2: The Financial System What it is: What it does: A network of financial intermediaries (banks, S&Ls, credit unions, etc.), facilitators (credit rating agencies, appraisers, etc.), and markets

Chapter 2: The Financial System What it is: What it does: A network of financial intermediaries (banks, S&Ls, credit unions, etc.), facilitators (credit rating agencies, appraisers, etc.), and markets

8.1 Basic Facts About Financial Structure Throughout the World

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 8 An Economic Analysis of Financial Structure 8.1 Basic Facts About Financial Structure Throughout the World 1) American businesses

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 8 An Economic Analysis of Financial Structure 8.1 Basic Facts About Financial Structure Throughout the World 1) American businesses

Chapter 21: Study Questions Key, Version A

Chapter 21: Study Questions Key, Version A Name: Class (day & time): Discussing the concepts and working examples with others is allowable. However, receiving answers from someone else, and turning these

Chapter 21: Study Questions Key, Version A Name: Class (day & time): Discussing the concepts and working examples with others is allowable. However, receiving answers from someone else, and turning these

I. Learning Objectives II. The Functions of Money III. The Components of the Money Supply

I. Learning Objectives In this chapter students will learn: A. The functions of money and the components of the U.S. money supply. B. What backs the money supply, making us willing to accept it as payment.

I. Learning Objectives In this chapter students will learn: A. The functions of money and the components of the U.S. money supply. B. What backs the money supply, making us willing to accept it as payment.

The Federal Reserve System and Open Market Operations

Chapter 15 MODERN PRINCIPLES OF ECONOMICS Third Edition The Federal Reserve System and Open Market Operations Outline What Is the Federal Reserve System? The U.S. Money Supplies Fractional Reserve Banking,

Chapter 15 MODERN PRINCIPLES OF ECONOMICS Third Edition The Federal Reserve System and Open Market Operations Outline What Is the Federal Reserve System? The U.S. Money Supplies Fractional Reserve Banking,

1-1. Chapter 1: Basic Concepts

TEST BANK 1-1 Chapter 1: Basic Concepts 1. Which of the following statements is (are) true? a. A risk-preferring individual always prefers the riskier of two gambles that involve different expected value.

TEST BANK 1-1 Chapter 1: Basic Concepts 1. Which of the following statements is (are) true? a. A risk-preferring individual always prefers the riskier of two gambles that involve different expected value.

Objectives: We will examine the three uses of money. We will study the six characteristics of money. We will analyze the sources of moneys value.

Chapter 10:1 Money Objectives: We will examine the three uses of money. We will study the six characteristics of money. We will analyze the sources of moneys value. Verse of the Day: Act_8:20 But Peter

Chapter 10:1 Money Objectives: We will examine the three uses of money. We will study the six characteristics of money. We will analyze the sources of moneys value. Verse of the Day: Act_8:20 But Peter

Chapter 2. Overview of the Financial System. Chapter Preview

Chapter 2 Overview of the Financial System Chapter Preview Suppose you want to start a business manufacturing a household cleaning robot, but you have no funds. At the same time, Walter has money he wishes

Chapter 2 Overview of the Financial System Chapter Preview Suppose you want to start a business manufacturing a household cleaning robot, but you have no funds. At the same time, Walter has money he wishes

ECON 3303 Exam 4 Summer MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 3303 Exam 4 Summer 2017 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following would not be a way to increase the return

ECON 3303 Exam 4 Summer 2017 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Which of the following would not be a way to increase the return

THE MEANING OF MONEY. Chapter 29. The Monetary System

Chapter 29. The Monetary System THE MEANING OF MONEY Money is the set of assets in an economy that people regularly use to buy goods and services from other people. slide 0 slide 1 The Functions of Money

Chapter 29. The Monetary System THE MEANING OF MONEY Money is the set of assets in an economy that people regularly use to buy goods and services from other people. slide 0 slide 1 The Functions of Money

Chapter 7 The Asset Market, Money, and Prices

1 Chapter 7 The Asset Market, Money, and Prices Learning Objectives A. Define money, discuss its functions, and describe how it is measured in the United States (Sec. 7.1) B. Discuss the factors that affect

1 Chapter 7 The Asset Market, Money, and Prices Learning Objectives A. Define money, discuss its functions, and describe how it is measured in the United States (Sec. 7.1) B. Discuss the factors that affect

How Does the Banking System Work? (EA)

") How Does the Banking System Work? (EA) What do you notice when you enter a bank? Perhaps you pass an automated teller machine in the lobby. ATMs can dispense cash, accept deposits, and make transfers from

How Does the Banking System Work? (EA) What do you notice when you enter a bank? Perhaps you pass an automated teller machine in the lobby. ATMs can dispense cash, accept deposits, and make transfers from

Asymmetric Information and the Role of Financial intermediaries

Asymmetric Information and the Role of Financial intermediaries 1 Observations 1. Issuing debt and equity securities (direct finance) is not the primary source for external financing for businesses. 2.

Asymmetric Information and the Role of Financial intermediaries 1 Observations 1. Issuing debt and equity securities (direct finance) is not the primary source for external financing for businesses. 2.

1. Primary markets are markets in which users of funds raise cash by selling securities to funds' suppliers.

Test Bank Financial Markets and Institutions 6th Edition Saunders Complete download Financial Markets and Institutions 6th Edition TEST BANK by Saunders, Cornett: https://testbankarea.com/download/financial-markets-institutions-6th-editiontest-bank-saunders-cornett/

Test Bank Financial Markets and Institutions 6th Edition Saunders Complete download Financial Markets and Institutions 6th Edition TEST BANK by Saunders, Cornett: https://testbankarea.com/download/financial-markets-institutions-6th-editiontest-bank-saunders-cornett/

Money. What is Money? 3 Uses of Money #1 Medium of Exchange #2 Unit of Account. #3 Store of Value. 6 Characteristics of. Money.

What is Money? Suppose a generous relative gave you a gift of $1000 for your high school graduation. In a short paragraph outline what you would do with the money and the reason behind your decision. Can

What is Money? Suppose a generous relative gave you a gift of $1000 for your high school graduation. In a short paragraph outline what you would do with the money and the reason behind your decision. Can

Money. What is money? What are the three uses of money? What are the six characteristics of money? What are the sources of money s value?

Money What is money? What are the three uses of money? What are the six characteristics of money? What are the sources of money s value? What Is Money? Money is anything that serves as a medium of exchange,

Money What is money? What are the three uses of money? What are the six characteristics of money? What are the sources of money s value? What Is Money? Money is anything that serves as a medium of exchange,

Money. Monetary Economics. Mark Huggett 1. 1 Georgetown. April 17, 2018

Monetary Economics Mark Huggett 1 1 Georgetown April 17, 2018 A longstanding problem is to formally incorporate money into an economic model framework. This is not so easily done because modern currencies

Monetary Economics Mark Huggett 1 1 Georgetown April 17, 2018 A longstanding problem is to formally incorporate money into an economic model framework. This is not so easily done because modern currencies

Economics 311: Money and Banking Midterm #2

Student ID #: Economics 311: Money and Banking Midterm #2 Please answer the following questions to the best of your ability. Remember, this exam is intended to be closed books, notes, and neighbors. No

Student ID #: Economics 311: Money and Banking Midterm #2 Please answer the following questions to the best of your ability. Remember, this exam is intended to be closed books, notes, and neighbors. No

Pindyck and Rubinfeld, Chapter 17 Sections 17.1 and 17.2 Asymmetric information can cause a competitive equilibrium allocation to be inefficient.

Pindyck and Rubinfeld, Chapter 17 Sections 17.1 and 17.2 Asymmetric information can cause a competitive equilibrium allocation to be inefficient. A market has asymmetric information when some agents know

Pindyck and Rubinfeld, Chapter 17 Sections 17.1 and 17.2 Asymmetric information can cause a competitive equilibrium allocation to be inefficient. A market has asymmetric information when some agents know

Money and the. Financial System 14

Money and the Financial System 14 1 The Evolution of Money No exchange, self-sufficient families No money Specialization Exchange: Barter Barter Discover a double coincidence of wants Two traders are willing

Money and the Financial System 14 1 The Evolution of Money No exchange, self-sufficient families No money Specialization Exchange: Barter Barter Discover a double coincidence of wants Two traders are willing

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM To "finance" something means to pay for it. Since money (or credit) is the means of payment, "financial" basically means "pertaining to money or credit." Financial

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM To "finance" something means to pay for it. Since money (or credit) is the means of payment, "financial" basically means "pertaining to money or credit." Financial

Unit 4: Money and Monetary Policy

Unit 4: Money and Monetary Policy 1 Types of PERSONAL Investments Assets- Anything of monetary value owned by a person or business. 2 Bonds vs. Stocks Pretend you are going to start a lemonade stand. You

Unit 4: Money and Monetary Policy 1 Types of PERSONAL Investments Assets- Anything of monetary value owned by a person or business. 2 Bonds vs. Stocks Pretend you are going to start a lemonade stand. You

Money. What is Money? 3 Uses of Money #1 Medium of Exchange #2 Unit of Account. #3 Store of Value. 6 Characteristics of. Money.

What is Money? Suppose a generous relative gave you a gift of $1000 for your high school graduation. In a short paragraph outline what you would do with the money and the reason behind your decision. Can

What is Money? Suppose a generous relative gave you a gift of $1000 for your high school graduation. In a short paragraph outline what you would do with the money and the reason behind your decision. Can

Development Economics 855 Lecture Notes 7

Development Economics 855 Lecture Notes 7 Financial Markets in Developing Countries Introduction ------------------ financial (credit) markets important to be able to save and borrow: o many economic activities

Development Economics 855 Lecture Notes 7 Financial Markets in Developing Countries Introduction ------------------ financial (credit) markets important to be able to save and borrow: o many economic activities