CODA BLOCK EXECUTION QUALITY REPORT EXECUTIVE SUMMARY. Contents

|

|

|

- Blake Simpson

- 5 years ago

- Views:

Transcription

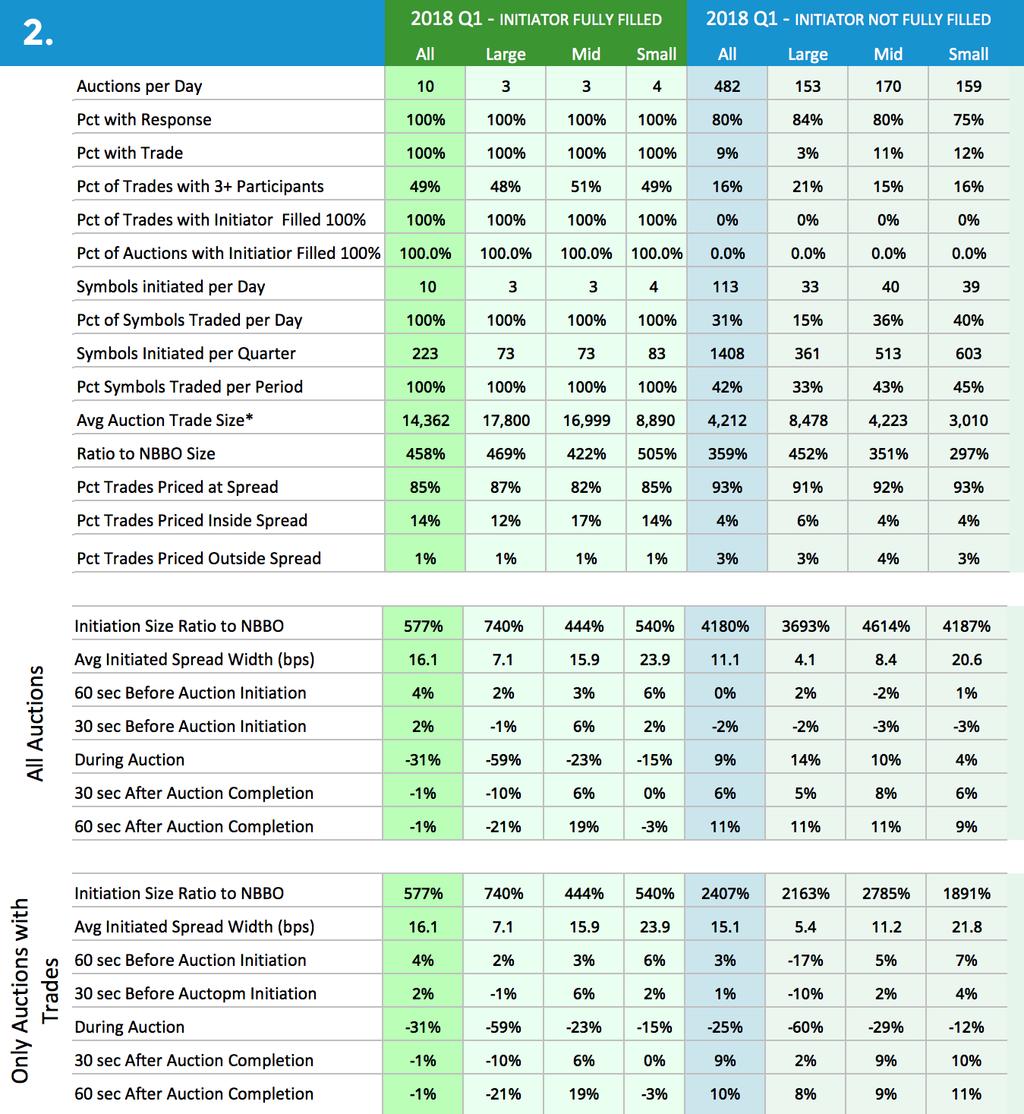

1 CODA BLOCK EXECUTION QUALITY REPORT Contents Executive Summary Metric Definitions Methodology Results and Conclusions Appendix - Comprehensive Data Tables EXECUTIVE SUMMARY This is the first quarterly report by ViableMkts of execution quality for CODA Block auctions. CODA Block is a US equity ATS which operates an on-demand, institutional auction trading facility. In this report, the metrics for both market impact and information leakage can be judged benign, showing that initiating auctions on the CODA Block platform could be a valuable tool for trading institutional size with little or no downside and potentially large benefits. This report was constructed by analyzing 9 months of CODA Block auction initiations, orders and trades - a period which included over 96,000 auctions initiated in over 2,000 symbols, and over 53,000,000 shares traded in nearly 1,000 symbols. The analysis separates out auctions that were initiated with and without resulting trades, and measures both the execution quality of trades as well as the movement of the National Best Bid and Offer (NBBO) before, during and after the auction.

2 ViableMkts: CODA Block Auction Analysis This analysis report was prepared by ViableMkts based on data provided by CODA Markets, Inc. Based upon the analysis of statistically significant data, ViableMkts has concluded that initiating auctions does not create significant information leakage and, furthermore, that auctions which result in trades are beneficial to the initiator, particularly when attempting to trade substantial quantities relative to the displayed market. This is based on the following highlights of the findings. Auction Initiation At all three market capitalization groups, we find evidence that initiating an auction on CODA Block results in minimal information leakage. Despite an average order size roughly 4,115% of the displayed size at the NBBO for the last quarter (with CODA Block ticker-only alerts sent to qualified subscribers), the move in the midpoint of the NBBO for all initiated auctions was only 6% of the bid-offer spread at 30 seconds later and 1 60 seconds later. Considering that these small movements take place despite the likelihood of some clients trading outside of CODA Block, particularly when they are not completely filled, it is reasonable to conclude that initiating an auction does not leak the direction and size of the order to the market. It is particularly compelling that the market moved only 11% of the spread after 60 seconds, on average, for auctions where the initiator was not completely filled. This was despite the initiator attempting to trade 4,18 of the displayed liquidity. This confirms the hypothesis that those responding to the auction are unable to discern that a larger order lurked behind. The implication is that traders trying to fill large-sized orders should strongly consider using CODA Block as a tool for finding latent liquidity. 2

3 ViableMkts: CODA Block Auction Analysis Auction Trades At all three market capitalization groups, we find evidence that auctions which result in trades on CODA Block provide valuable liquidity at a reasonable price. Despite an average fill quantity in the first quarter of 403% of the NBBO order size, 97% of all executions took place at or better than the NBBO. In addition, despite the fact that, on average, auctions were filled when the price of the stock moved towards the auction initiator by 26% of the spread during the auction (lower if the initiator was buying and higher if selling), after the auction the stocks moved in favor of the trade slightly (7% of the spread at 30 seconds and 8% at 60 seconds). Were there to be a move against the initiator after purchasing or selling, that would have been indicative of adverse selection, but that was not the case. It is also worth noting that the data for small cap stocks was even more compelling. Trades occurred despite only a 12% of the spread move towards the initiator during the auction, and the post-auction move was slightly more positive. In addition, small cap stock auctions resulted in trades 14% of the time, which was a higher success rate than for larger cap stocks. Conclusion The data shows that using CODA Block generally did not create adverse market moves when initiating an auction and, when successful, the liquidity found by the process was incrementally valuable and did not suffer post-trade adverse selection on average. The statistics analyzed have been quite consistent across market capitalization groups for each of the past 3 quarters of data. 3

4 ViableMkts: CODA Block Auction Analysis METRIC DEFINITIONS Market Move Market move, for the context of this report, is the movement of the midpoint of the NBBO from immediately before the time period specified. For the report, the following Mid Moves were measured: Pre-Auction (both 60 seconds and 30 seconds before the auction was initiated to the initiation time) During Auction (for the entire duration of the auction from initiation until either trade or cancel messages sent out) Post-Auction (both 60 seconds and 30 seconds after the time the auction concluded) Spread Metrics The Bid-Offer Spread, for the purpose of this paper, is represented by the NBBO as reported by the SIP, which aggregates the top-of-book from all registered securities exchanges. The metrics calculated include: Average spread of all initiated auctions Average spread of all auctions that resulted in trades Ratio of the order size to the size at the NBBO aggregated across exchanges Execution price relative to the spread at the far side (the offer for buy orders and bid for sell orders). Other Descriptive Metrics In addition to the foregoing, the following additional descriptive metrics were calculated to provide context for the analysis: Auctions per day % of auctions with responses % of auctions with a trade % of trades/auctions where initiator was filled 10 Symbols with auctions per day Average trade size 4

5 ViableMkts: CODA Block Auction Analysis METHODOLOGY ViableMkts analyzed anonymized auction data, namely initiating orders, responding orders, and resulting auction execution or non-execution data on the CODA Block platform based on all the metrics defined above. For each quarter, auctions were analyzed in total and within market capitalization groups of Large (>$10 bln+), Mid ($2 bln-$10 bln) and Small (< $2 bln). Auctions were categorized as all auctions and auctions with trades. Within the auctions with trades, in the last quarter, ViableMkts analyzed auctions where the initiator was completely filled vs those with partial fills. ViableMkts looked at the market moves in each of the time periods and stock categories for patterns that would indicate adverse selection or information leakage. Adverse Selection For the purpose of this report, we defined adverse selection as situations where the market moved against orders which resulted in executions, from the perspective of the auction initiator. Information Leakage For the purpose of this report, we defined information leakage as the tendency of the market to move in the direction that the auction initiator was attempting to trade either during or after the auction. This metric needs to be analyzed, however, in the context that the auction initiator could (and often does) trade on multiple venues after the auction, particularly if it fails to execute their orders. RESULTS & CONCLUSIONS Adverse Selection Analysis In all three quarters analyzed - and across large, mid and small cap stocks - the data shows little to no adverse selection for trades from initiated auctions. Overall and in most cases, the data shows that the market moved positively when fills were received by CODA Block initiators, and the adverse moves that occurred were small. 5

6 ViableMkts: CODA Block Auction Analysis 12% 1 8% 6% 4% 2% -2% 2018 Q1 % OF SPREAD MOVEMENT 2018 Q1 Adverse Selection -4% All Large Mid Small 30 Seconds 60 Seconds 2017 Q % OF Q4 Adverse SPREAD Selection MOVEMENT 25% 2 15% 1 5% All Large Mid Small Small 2017 Q4 Series1 Series2 6

7 ViableMkts: CODA Block Auction Analysis 12% 1 8% 6% 4% 2% -2% -4% 2017 Q % OF Q3 Adverse SPREAD Selection MOVEMENT -6% All Large Mid Small 30 Seconds 60 seconds In addition, in the first quarter of 2018, we also analyzed adverse selection for trades where the auction initiator was completely filled. This was added to ensure that cases where the order was completely filled were due to finding latent liquidity, rather than due to adverse selection. (Which would be described as buying in a falling market or selling in a rising one.) The data, however, does not show significant adverse selection in this case, showing only 1% overall and only showing any material adverse move in large cap stocks. (Although, at 21% of spread, an adverse move is not very material) Q1 Q1 % Auction OF SPREAD Initiator MOVEMENT Fully Filled 25% 2 15% 1 5% -5% -1-15% -2-25% All Large Mid Small 30 Seconds 60 Seconds 7

8 ViableMkts: CODA Block Auction Analysis Trade Quality Analysis In all three quarters analyzed, the trades executed, despite being for much larger than the quantity displayed at the NBBO, were done at or better than the NBBO 97% of the time or greater. Most trades were executed at the spread, but there were some trades inside the spread with a very small amount outside of the spread, as depicted below. 12 TRADE QUALITY ANALYSIS 2017 Q Q1 Trade Quality Analysis 2017 Q Q All Large Mid Small All Large Mid Small All Large Mid Small 2017 Q Q Q1 % Trades at Spread % Trades Inside Spread % Trades Outside Spread Information Leakage Analysis In all three quarters analyzed, we see no evidence of significant information leakage from initiated auctions. While 8 of the auctions did attract responses in the latest quarter, the movement after the auction, when auction initiators were not fully filled, was only 9% of the spread during the auction, 6% of the spread at 30 seconds after the auction, and 11% of the spread at 60 seconds after the auction. 8

9 ViableMkts: CODA Block Auction Analysis 2018 Q1 INFO LEAKAGE (INITIATOR NOT FULLY FILLED) 2018 Q1 Auction Initiator Not Fully Filled 14% 12% 1 8% 6% 4% 2% All Large Mid Small 2018 Q1 - Initiator Not Fully Filled 30 Seconds 60 Seconds During the auction period. For all auctions, the movement from the time that an auction was initiated to when the auction ended was 8% of the spread, with an additional 6% of the spread after 30 seconds and 1 of the spread after 60 seconds. Thus, despite the average auction initiator in the past quarter seeking to trade 4, 115% of the displayed size available at the NBBO (with CODA Block s ticker-only alert sent to qualified subscribers), the average move from auction initiation to 90 seconds later was only 18% of the spread. Considering that it is highly likely that the auction initiator, who is trying to trade over 40 times the available displayed liquidity, would trade within the 60 seconds after the auction, this shows that the auction itself does not materially leak information. Had, on the other hand, the responders to the auction been aware of such a large order, we would expect to see much more movement. 14% 12% 1 8% 6% 4% 2% 2018 Q1 ALL AUCTIONS POST AUCTION MOVE 2018 Q1 All Auctions Post Auction Move All Large Mid Small 2018 Q1 30 Seconds 60 Seconds 9

3.")

10 ViableMkts: CODA Block Auction Analysis APPENDIX 1. CODA Block Auction Quarterly Data Table (Q Q3 2017) 2. CODA Block Auction Fully Filled & Non-Fully Filled Initiator Data Table (Q1 2018) 3. CODA Block Auction Order & Trade Size Requirements 10

11 ViableMkts: CODA Block Auction Analysis 11

12 ViableMkts: CODA Block Auction Analysis 3. CODA Block Auction Order & Trade Size Requirements Appendix supplied by CODA Markets David Weisberger Head of Equities ViableMkts ABOUT ViableMkts ViableMkts is a strategic advisory firm that provides business analysis, research and guidance to institutions who are focused on successfully adapting to the ever-changing market environment. The firm specializes in financial technology and is comprised of an unparalleled team of proven innovators with an extensive track record of building and delivering financial market solutions. The Principals are former leaders at investment banks, trading platforms, exchanges and technology vendors that cover the gamut of equities, credit, rates, swaps, FX and crypto assets. ViableMkts helps: Sell-side dealers leverage technology to increase inventory velocity, improve sales performance, reduce development time and improve delivery. Buy-side asset managers improve access to liquidity, enhance ability to make and distribute prices and maintain trading compliance while reducing transaction costs. Platforms accelerate validated learning through vetting product concepts, enhancing product design and refining strategy to improve execution. viablemkts.com 12

CODA BLOCK EXECUTION QUALITY REPORT

CODA BLOCK EXECUTION QUALITY REPORT Contents Overview Executive Summary Metric Definitions Methodology Results and Conclusions Appendix Comprehensive Data Tables OVERVIEW Initiating auctions on CODA Block

CODA BLOCK EXECUTION QUALITY REPORT Contents Overview Executive Summary Metric Definitions Methodology Results and Conclusions Appendix Comprehensive Data Tables OVERVIEW Initiating auctions on CODA Block

CODA Markets, INC. CRD# SEC#

Exhibit A A description of classes of subscribers (for example, broker-dealer, institution, or retail). Also describe any differences in access to the services offered by the alternative trading system

Exhibit A A description of classes of subscribers (for example, broker-dealer, institution, or retail). Also describe any differences in access to the services offered by the alternative trading system

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2016

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2016 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2016 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending March 30, 2016

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending March 30, 2016 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending March 30, 2016 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2015

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2015 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2015 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2017

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2017 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2017 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending June 30, 2014

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending June 30, 2014 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending June 30, 2014 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

BROKERS: YOU BETTER WATCH OUT, YOU BETTER NOT CRY, FINRA IS COMING TO

November 2017 BROKERS: YOU BETTER WATCH OUT, YOU BETTER NOT CRY, FINRA IS COMING TO TOWN Why FINRA s Order Routing Review Could Be a Turning Point for Best Execution FINRA recently informed its member

November 2017 BROKERS: YOU BETTER WATCH OUT, YOU BETTER NOT CRY, FINRA IS COMING TO TOWN Why FINRA s Order Routing Review Could Be a Turning Point for Best Execution FINRA recently informed its member

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2018

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2018 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2018 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2017

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2017 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2017 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Chapter 8: Transaction costs

Securities Trading: Principles and Procedures Chapter 8: Transaction costs What does it cost to trade? The long-term investor vs. the short-term trader We often differentiate investment and trading activities

Securities Trading: Principles and Procedures Chapter 8: Transaction costs What does it cost to trade? The long-term investor vs. the short-term trader We often differentiate investment and trading activities

SIFMA Board Committee on Equity Market Structure. Recommendations as of July 10, 2014

SIFMA Board Committee on Equity Market Structure Recommendations as of July 10, 2014 Table of Contents Market Complexity... 1 Access Fees... 1 Number of Trading Venues... 1 Order Types... 1 Message Traffic...

SIFMA Board Committee on Equity Market Structure Recommendations as of July 10, 2014 Table of Contents Market Complexity... 1 Access Fees... 1 Number of Trading Venues... 1 Order Types... 1 Message Traffic...

SEC Rule 606 Report Interactive Brokers 3 rd Quarter 2017 Scottrade Inc. posts separate and distinct SEC Rule 606 reports that stem from orders entered on two separate platforms. This report is for Scottrade,

SEC Rule 606 Report Interactive Brokers 3 rd Quarter 2017 Scottrade Inc. posts separate and distinct SEC Rule 606 reports that stem from orders entered on two separate platforms. This report is for Scottrade,

PDQ ATS, INC. CRD# SEC#

Exhibit A A description of classes of subscribers (for example, broker-dealer, institution, or retail). Also describe any differences in access to the services offered by the alternative trading system

Exhibit A A description of classes of subscribers (for example, broker-dealer, institution, or retail). Also describe any differences in access to the services offered by the alternative trading system

NASDAQ ACCESS FEE EXPERIMENT

Report II / May 2015 NASDAQ ACCESS FEE EXPERIMENT FRANK HATHEWAY Nasdaq Chief Economist INTRODUCTION This is the second of three reports on Nasdaq s access fee experiment that began on February 2, 2015.

Report II / May 2015 NASDAQ ACCESS FEE EXPERIMENT FRANK HATHEWAY Nasdaq Chief Economist INTRODUCTION This is the second of three reports on Nasdaq s access fee experiment that began on February 2, 2015.

SEC Rule 606 Report Interactive Brokers 1st Quarter 2018

SEC Rule 606 Report Interactive Brokers 1st Quarter 2018 Scottrade Inc. posts separate and distinct SEC Rule 606 reports that stem from orders entered on two separate platforms. This report is for Scottrade,

SEC Rule 606 Report Interactive Brokers 1st Quarter 2018 Scottrade Inc. posts separate and distinct SEC Rule 606 reports that stem from orders entered on two separate platforms. This report is for Scottrade,

Dark Liquidity Guide. Toronto Stock Exchange TSX Venture Exchange. Document Version: 1.6 Date of Issue: September 1, 2017

Dark Liquidity Guide Toronto Stock Exchange TSX Venture Exchange Document Version: 1.6 Date of Issue: September 1, 2017 Table of Contents 1. Introduction... 4 1.1 Overview... 4 1.2 Purpose... 4 1.3 Glossary...

Dark Liquidity Guide Toronto Stock Exchange TSX Venture Exchange Document Version: 1.6 Date of Issue: September 1, 2017 Table of Contents 1. Introduction... 4 1.1 Overview... 4 1.2 Purpose... 4 1.3 Glossary...

CRYPTO CONFUSION, WALL STREET DELUSION

April 2018 CRYPTO CONFUSION, WALL STREET DELUSION After 30+ years of Wall St experience, I took the plunge into crypto last year to start CoinRoutes with my son (his idea & code) to automate crypto trading

April 2018 CRYPTO CONFUSION, WALL STREET DELUSION After 30+ years of Wall St experience, I took the plunge into crypto last year to start CoinRoutes with my son (his idea & code) to automate crypto trading

Credit Suisse Securities (USA) LLC CRD No. 816 Form ATS Amendment 17 SEC File No /02/18

LLC CRD No. 816 Form ATS Amendment 17 SEC File No /02/18") Crossfinder Form ATS Table of Contents Exhibit A (Item 3)... 3 Exhibit B (Item 4)... 4 Exhibit C (Item 5)... 5 Exhibit D (Item 6)... 6 Exhibit E (Item 7)... 7 Exhibit F (Item 8)... 8 8a. The manner of

Crossfinder Form ATS Table of Contents Exhibit A (Item 3)... 3 Exhibit B (Item 4)... 4 Exhibit C (Item 5)... 5 Exhibit D (Item 6)... 6 Exhibit E (Item 7)... 7 Exhibit F (Item 8)... 8 8a. The manner of

Dark Liquidity Guide Toronto Stock Exchange TSX Venture Exchange

Dark Liquidity Guide Toronto Stock Exchange TSX Venture Exchange Document Version: 1.3 Date of Issue: 2012/09/28 Table of Contents 1.1 Overview... 3 1.2 Purpose... 3 1.3 Glossary... 3 1.4 Dark order types

Dark Liquidity Guide Toronto Stock Exchange TSX Venture Exchange Document Version: 1.3 Date of Issue: 2012/09/28 Table of Contents 1.1 Overview... 3 1.2 Purpose... 3 1.3 Glossary... 3 1.4 Dark order types

Exhibit A to Form ATS Classes of Subscribers

Exhibit A to Form ATS Classes of Subscribers Alternative trading system name: Liquidnet H2O ATS CRD No.: 103987 Filing date: March 4, 2016 SEC File No.: 8-52461 Classes of subscribers; any differences

Exhibit A to Form ATS Classes of Subscribers Alternative trading system name: Liquidnet H2O ATS CRD No.: 103987 Filing date: March 4, 2016 SEC File No.: 8-52461 Classes of subscribers; any differences

Fragmentation in Financial Markets: The Rise of Dark Liquidity

Fragmentation in Financial Markets: The Rise of Dark Liquidity Sabrina Buti Global Risk Institute April 7 th 2016 Where do U.S. stocks trade? Market shares in Nasdaq-listed securities Market shares in

Fragmentation in Financial Markets: The Rise of Dark Liquidity Sabrina Buti Global Risk Institute April 7 th 2016 Where do U.S. stocks trade? Market shares in Nasdaq-listed securities Market shares in

September 18, The UBS ATS has the following classes of participants:

EXHIBIT A Description of classes of subscribers and any differences in access to the services offered by UBS ATS to different groups or classes of subscribers. The UBS ATS has the following classes of

EXHIBIT A Description of classes of subscribers and any differences in access to the services offered by UBS ATS to different groups or classes of subscribers. The UBS ATS has the following classes of

TCA metric #4. TCA and fair execution. The metrics that the FX industry must use.

LMAX Exchange: TCA white paper V1.0 - May 2017 TCA metric #4 TCA and fair execution. The metrics that the FX industry must use. An analysis and comparison of common FX execution quality metrics between

LMAX Exchange: TCA white paper V1.0 - May 2017 TCA metric #4 TCA and fair execution. The metrics that the FX industry must use. An analysis and comparison of common FX execution quality metrics between

Report on the Thematic Review of Alternative Liquidity Pools in Hong Kong. 9 April 2018

Report on the Thematic Review of Alternative Liquidity Pools in Hong Kong 9 April 2018 Table of contents A. Introduction 1 B. ALP industry landscape in Hong Kong 3 1. Overview of ALPs in Hong Kong 3 2.

Report on the Thematic Review of Alternative Liquidity Pools in Hong Kong 9 April 2018 Table of contents A. Introduction 1 B. ALP industry landscape in Hong Kong 3 1. Overview of ALPs in Hong Kong 3 2.

DALTON STRATEGIC PARTNERSHIP LLP ORDER EXECUTION POLICY DECEMBER 2017

DALTON STRATEGIC PARTNERSHIP LLP ORDER EXECUTION POLICY DECEMBER 2017 General Policy Information Dalton Strategic Partnership (DSP) invests in various asset classes as part of the investment management

DALTON STRATEGIC PARTNERSHIP LLP ORDER EXECUTION POLICY DECEMBER 2017 General Policy Information Dalton Strategic Partnership (DSP) invests in various asset classes as part of the investment management

SEC TICK SIZE PILOT MEASURING THE IMPACT OF CHANGING THE TICK SIZE ON THE LIQUIDITY AND TRADING OF SMALLER PUBLIC COMPANIES

SEC TICK SIZE PILOT MEASURING THE IMPACT OF CHANGING THE TICK SIZE ON THE LIQUIDITY AND TRADING OF SMALLER PUBLIC COMPANIES APRIL 7, 2017 On May 6, 2015, the Securities & Exchange Commission (SEC) issued

SEC TICK SIZE PILOT MEASURING THE IMPACT OF CHANGING THE TICK SIZE ON THE LIQUIDITY AND TRADING OF SMALLER PUBLIC COMPANIES APRIL 7, 2017 On May 6, 2015, the Securities & Exchange Commission (SEC) issued

NYSE American Options Customer Best Execution ( CUBE ) Mechanism Frequently Asked Questions

Mechanism Frequently Asked Questions") NYSE American Options Customer Best Execution ( CUBE ) Mechanism Frequently Asked Questions GENERAL INFORMATION 1. What is CUBE? CUBE is NYSE American Options (the Exchange ) electronic crossing price

NYSE American Options Customer Best Execution ( CUBE ) Mechanism Frequently Asked Questions GENERAL INFORMATION 1. What is CUBE? CUBE is NYSE American Options (the Exchange ) electronic crossing price

Quarterly Scorecard 2nd Quarter 2016 what s INSIDE

ETF Stats Ticker: NAV Symbol: Intraday Symbol: Listing Exchange:.NV.IV NYSE Arca CUSIP: 00162Q 205 Fund Inception: 7/6/2009 Dividends Paid: Quarterly Most Recent Dividend:* $0.289879 Management Fee: 0.37%

ETF Stats Ticker: NAV Symbol: Intraday Symbol: Listing Exchange:.NV.IV NYSE Arca CUSIP: 00162Q 205 Fund Inception: 7/6/2009 Dividends Paid: Quarterly Most Recent Dividend:* $0.289879 Management Fee: 0.37%

Goldman Sachs Presentation to Bernstein Strategic Decisions Conference

Goldman Sachs Presentation to Bernstein Strategic Decisions Conference Comments by Gary Cohn, President and Chief Operating Officer May 31, 2012 Slide 2 Thanks Brad, good morning to everyone. Slide 3 In

Goldman Sachs Presentation to Bernstein Strategic Decisions Conference Comments by Gary Cohn, President and Chief Operating Officer May 31, 2012 Slide 2 Thanks Brad, good morning to everyone. Slide 3 In

Omega/Lynx ATS Subscriber Manual v. 1.6 Effective Date: June 10, 2013

Omega/Lynx ATS Subscriber Manual v. 1.6 Effective Date: June 10, 2013 Revision History Date Description Author August 21, 2008 Standard boardlots (page 4) to change from 100 shares across all traded securities

Omega/Lynx ATS Subscriber Manual v. 1.6 Effective Date: June 10, 2013 Revision History Date Description Author August 21, 2008 Standard boardlots (page 4) to change from 100 shares across all traded securities

TICK SIZE PILOT INSIGHTS

Clearpool Review TICK SIZE PILOT INSIGHTS May 2017 The Securities Exchange Commission (SEC) approved the implementation of the Tick Size Pilot (TSP) to evaluate whether or not widening the tick size for

Clearpool Review TICK SIZE PILOT INSIGHTS May 2017 The Securities Exchange Commission (SEC) approved the implementation of the Tick Size Pilot (TSP) to evaluate whether or not widening the tick size for

POSIT Frequently Asked Questions

POSIT Frequently Asked Questions This document addresses some frequently asked questions about POSIT. POSIT is a registered Alternative Trading System ( ATS ) operated by ITG Inc. ( ITG or the firm ),

POSIT Frequently Asked Questions This document addresses some frequently asked questions about POSIT. POSIT is a registered Alternative Trading System ( ATS ) operated by ITG Inc. ( ITG or the firm ),

Options on CBOT Fed Funds Futures Reference Guide

Options on CBOT Fed Funds Futures Reference Guide Contents Introduction.................................................................... 3 Potential Users of Options on CBOT Fed Funds Futures...............................

Options on CBOT Fed Funds Futures Reference Guide Contents Introduction.................................................................... 3 Potential Users of Options on CBOT Fed Funds Futures...............................

Competing Business Models

Competing Business Models Liquidity Providers (Capital Commitment) None One Many Attain Archipelago B-Trade Brut Instinet Island MarketXT NexTrade REDIBook NYSE Amex Nasdaq Data as of January 2002. Liquidity

Competing Business Models Liquidity Providers (Capital Commitment) None One Many Attain Archipelago B-Trade Brut Instinet Island MarketXT NexTrade REDIBook NYSE Amex Nasdaq Data as of January 2002. Liquidity

IEX FIX Certification Notes for Product Managers

IEX FIX Certification Notes for Product Managers Version: 1.01 Updated: October 3, 01 IEX Group, Inc. 7 World Trade Center 30th Floor New York, NY 10007 Copyright 01 IEX Group, Inc. All rights reserved.

IEX FIX Certification Notes for Product Managers Version: 1.01 Updated: October 3, 01 IEX Group, Inc. 7 World Trade Center 30th Floor New York, NY 10007 Copyright 01 IEX Group, Inc. All rights reserved.

In Detail What is MATCHNow?... 3

May 2017 In Detail What is MATCHNow?... 3 Improve Your Trading... 4 Access Advantages... 4 Cost Advantages... 4 Tactical Advantages... 4 Access to MATCHNow... 5 Order Attributes... 6 Parameters for Liquidity

May 2017 In Detail What is MATCHNow?... 3 Improve Your Trading... 4 Access Advantages... 4 Cost Advantages... 4 Tactical Advantages... 4 Access to MATCHNow... 5 Order Attributes... 6 Parameters for Liquidity

TABLE OF CONTENTS 1. INTRODUCTION Institutional composition of the market 4 2. PRODUCTS General product description 4

JANUARY 2019 TABLE OF CONTENTS 1. INTRODUCTION 4 1.1. Institutional composition of the market 4 2. PRODUCTS 4 2.1. General product description 4 3. MARKET PHASES AND SCHEDULES 5 3.1 Opening auction 5 3.2

JANUARY 2019 TABLE OF CONTENTS 1. INTRODUCTION 4 1.1. Institutional composition of the market 4 2. PRODUCTS 4 2.1. General product description 4 3. MARKET PHASES AND SCHEDULES 5 3.1 Opening auction 5 3.2

Autobahn Equity Americas

http://autobahn.db.com Autobahn Equity Americas US Routing Logic Smarter Liquidity Innovation with Integrity September 2016 This document describes the routing logic used for orders sent to the Autobahn

http://autobahn.db.com Autobahn Equity Americas US Routing Logic Smarter Liquidity Innovation with Integrity September 2016 This document describes the routing logic used for orders sent to the Autobahn

SUMMARY COMPARISON OF CURRENT EQUITY MARKETPLACES

SUMMARY COMPARISON OF CURRENT EQUITY MARKETPLACES The following tables contain summary information on each of the marketplaces that have retained RS to act as a regulation services provider. The information

SUMMARY COMPARISON OF CURRENT EQUITY MARKETPLACES The following tables contain summary information on each of the marketplaces that have retained RS to act as a regulation services provider. The information

Order Types and Functionality

Date of Issue: May 12, 2017 Contents 1. INTRODUCTION... 3 2. CONTACT... 3 3. TRADING SESSIONS... 3 3.1 Hours of Operation... 3 3.2 Pre-Open and Post-Open Priority and Allocation... 3 3.3 Opening... 3 3.4

Date of Issue: May 12, 2017 Contents 1. INTRODUCTION... 3 2. CONTACT... 3 3. TRADING SESSIONS... 3 3.1 Hours of Operation... 3 3.2 Pre-Open and Post-Open Priority and Allocation... 3 3.3 Opening... 3 3.4

MARKET REGULATION ADVISORY NOTICE

MARKET REGULATION ADVISORY NOTICE Exchange Subject Rule References Rule 539 CME, CBOT, NYMEX & COMEX Pre-Execution Communications Advisory Date Advisory Number CME Group RA1611-5R Effective Dates September

MARKET REGULATION ADVISORY NOTICE Exchange Subject Rule References Rule 539 CME, CBOT, NYMEX & COMEX Pre-Execution Communications Advisory Date Advisory Number CME Group RA1611-5R Effective Dates September

Cboe Europe Ltd. Large in Scale Service (LIS) Service Description. Version 1.2. October Cboe Europe Limited

Service Description. Version 1.2. October Cboe Europe Limited") Cboe Europe Ltd Large in Scale Service (LIS) Service Description Version 1.2 October 2017 1 Contents Introduction... 4 1. Regulation... 4 2. Definitions... 4 3. Workflow... 6 4. Market Model... 7 4.1.

Cboe Europe Ltd Large in Scale Service (LIS) Service Description Version 1.2 October 2017 1 Contents Introduction... 4 1. Regulation... 4 2. Definitions... 4 3. Workflow... 6 4. Market Model... 7 4.1.

US Options Complex Book Process. Version 1.1.1

Complex Book Process Version 1.1.1 October 17, 2017 Contents 1 Overview... 4 2 Complex Order Basics... 5 2.1 Ratios... 5 2.2 Net Price... 5 2.3 Availability of Complex Order Functionality... 5 2.3.1 Eligible

Complex Book Process Version 1.1.1 October 17, 2017 Contents 1 Overview... 4 2 Complex Order Basics... 5 2.1 Ratios... 5 2.2 Net Price... 5 2.3 Availability of Complex Order Functionality... 5 2.3.1 Eligible

MARKET REGULATION ADVISORY NOTICE

MARKET REGULATION ADVISORY NOTICE Exchange Subject Rule References Rule 539 CME, CBOT, NYMEX & COMEX Pre-Execution Communications Advisory Date Advisory Number CME Group RA1718-5 Effective Dates January

MARKET REGULATION ADVISORY NOTICE Exchange Subject Rule References Rule 539 CME, CBOT, NYMEX & COMEX Pre-Execution Communications Advisory Date Advisory Number CME Group RA1718-5 Effective Dates January

Re: Release No , File No. S , Regulation of Non-Public Trading Interest

Goldman, Sachs & Co. lone New York Plaza I New York, New York 10004 Goldman Sachs February 17, 2010 Ms. Elizabeth M. Murphy Secretary Securities and Exchange Commission 100 F Street, N.E. Washington, D.C.

Goldman, Sachs & Co. lone New York Plaza I New York, New York 10004 Goldman Sachs February 17, 2010 Ms. Elizabeth M. Murphy Secretary Securities and Exchange Commission 100 F Street, N.E. Washington, D.C.

Order Handling and Execution Policy Asset Class Specific Appendices Listed Derivatives Agency Execution Appendix

BNP London, Paribas June 2017 CIB Order Handling and Execution Policy Asset Class Specific Appendices Listed Derivatives Agency Execution Appendix BNP PARIBAS CIB GLOBAL MARKETS London, December 2017 Table

BNP London, Paribas June 2017 CIB Order Handling and Execution Policy Asset Class Specific Appendices Listed Derivatives Agency Execution Appendix BNP PARIBAS CIB GLOBAL MARKETS London, December 2017 Table

Fidelity Active Trader Pro Directed Trading User Agreement

Fidelity Active Trader Pro Directed Trading User Agreement Important: Using Fidelity's directed trading functionality is subject to the Fidelity Active Trader Pro Directed Trading User Agreement (the 'Directed

Fidelity Active Trader Pro Directed Trading User Agreement Important: Using Fidelity's directed trading functionality is subject to the Fidelity Active Trader Pro Directed Trading User Agreement (the 'Directed

NATIONAL BANK FINANCIAL INC. BEST EXECUTION PUBLIC DISLOSURE STATEMENT January NBF Best Execution Public Disclosure Statement January

NATIONAL BANK FINANCIAL INC BEST EXECUTION PUBLIC DISLOSURE STATEMENT January 2018 NBF Best Execution Public Disclosure Statement January 2018 1 8 Best Execution Disclosure Changes The following are recent

NATIONAL BANK FINANCIAL INC BEST EXECUTION PUBLIC DISLOSURE STATEMENT January 2018 NBF Best Execution Public Disclosure Statement January 2018 1 8 Best Execution Disclosure Changes The following are recent

An Overview COPYRIGHTED MATERIAL CHAPTER 1

CHAPTER 1 An Overview The Stock Markets The Exchange System NYSE Time Line Listed Stocks The Specialist System Who s Who on the Exchange Floor The SuperDOT System COPYRIGHTED MATERIAL 6 SAMMY CHUA S DAY

CHAPTER 1 An Overview The Stock Markets The Exchange System NYSE Time Line Listed Stocks The Specialist System Who s Who on the Exchange Floor The SuperDOT System COPYRIGHTED MATERIAL 6 SAMMY CHUA S DAY

Deutsche Bank. I. Trading Considerations. Dear Valued Client,

Deutsche Bank Dear Valued Client, Consistent with our best practices, and in connection with various rules and regulations applicable to Deutsche Bank Securities Inc. ( DBSI and, together with its affiliates,

Deutsche Bank Dear Valued Client, Consistent with our best practices, and in connection with various rules and regulations applicable to Deutsche Bank Securities Inc. ( DBSI and, together with its affiliates,

MARKET REGULATION ADVISORY NOTICE

MARKET REGULATION ADVISORY NOTICE Exchange Subject Rule References Rule 539 CME, CBOT, NYMEX & COMEX Pre-Execution Communications Advisory Date Advisory Number CME Group RA1602-5 Effective Dates April

MARKET REGULATION ADVISORY NOTICE Exchange Subject Rule References Rule 539 CME, CBOT, NYMEX & COMEX Pre-Execution Communications Advisory Date Advisory Number CME Group RA1602-5 Effective Dates April

Crypto-Asset Market Structure

Crypto-Asset Market Structure Presentation to UC Berkeley Chapter of Alpha Kappa Psi March 21, 2018 Ian Weisberger, Co-Founder CoinRoutes Outline I. II. Market Structure Overview A. 4 Types Of Markets

Crypto-Asset Market Structure Presentation to UC Berkeley Chapter of Alpha Kappa Psi March 21, 2018 Ian Weisberger, Co-Founder CoinRoutes Outline I. II. Market Structure Overview A. 4 Types Of Markets

Composite+ ALGORITHMIC PRICING IN THE CORPORATE BOND MARKET MARKETAXESS RESEARCH

Composite+ ALGORITHMIC PRICING IN THE CORPORATE BOND MARKET MARKETAXESS RESEARCH David Krein Global Head of Research Julien Alexandre Senior Research Analyst Introduction Composite+ (CP+) is MarketAxess

Composite+ ALGORITHMIC PRICING IN THE CORPORATE BOND MARKET MARKETAXESS RESEARCH David Krein Global Head of Research Julien Alexandre Senior Research Analyst Introduction Composite+ (CP+) is MarketAxess

Trading Tops and Bottom s

Trading Tops and Bottom s How To Trade Like A Professional Series II, Buying Debit Spreads Why Do We Want To Trade Like a Professional? Leverage small sums of money can with potential to turn into large

Trading Tops and Bottom s How To Trade Like A Professional Series II, Buying Debit Spreads Why Do We Want To Trade Like a Professional? Leverage small sums of money can with potential to turn into large

ANNEX. to the. COMMISSION DELEGATED REGULATION (EU) No.../...

No.../...") EUROPEAN COMMISSION Brussels, 8.5.26 C(26) 2775 final ANNEX ANNEX to the COMMISSION DELEGATED REGULATION (EU) No.../... supplementing Directive 24/65/EU of the European Parliament and of the Council on

EUROPEAN COMMISSION Brussels, 8.5.26 C(26) 2775 final ANNEX ANNEX to the COMMISSION DELEGATED REGULATION (EU) No.../... supplementing Directive 24/65/EU of the European Parliament and of the Council on

MARKET REGULATION ADVISORY NOTICE

MARKET REGULATION ADVISORY NOTICE Exchange CME, CBOT, NYMEX, COMEX & KCBT Subject Pre-Execution Communications Rule References Rule 539 Advisory Date Advisory Number CME Group RA1312-5 Updated Effective

MARKET REGULATION ADVISORY NOTICE Exchange CME, CBOT, NYMEX, COMEX & KCBT Subject Pre-Execution Communications Rule References Rule 539 Advisory Date Advisory Number CME Group RA1312-5 Updated Effective

FX Analytics. An Overview

FX Analytics An Overview FX Market Data Challenges The challenges of data capture and analysis in the FX Market are widely appreciated: no central store of quote, order and trade data a decentralized market

FX Analytics An Overview FX Market Data Challenges The challenges of data capture and analysis in the FX Market are widely appreciated: no central store of quote, order and trade data a decentralized market

ARGENTINA Sovereign & Provincial Bonds technical levels

Monday, August 25, 2014 ARGENTINA Sovereign & Provincial Bonds technical levels Are there opportunities in Argentina s sovereign and provincials? In both sovereign and provincial bonds, we find that the

Monday, August 25, 2014 ARGENTINA Sovereign & Provincial Bonds technical levels Are there opportunities in Argentina s sovereign and provincials? In both sovereign and provincial bonds, we find that the

Interactive Brokers Quarterly Order Routing Report Quarter Ending June 30, 2007

I. Introduction Interactive Brokers Quarterly Order Routing Report Quarter Ending June 30, 2007 Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

I. Introduction Interactive Brokers Quarterly Order Routing Report Quarter Ending June 30, 2007 Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

Research Library. Treasury-Federal Reserve Study of the U. S. Government Securities Market

Treasury-Federal Reserve Study of the U. S. Government Securities Market INSTITUTIONAL INVESTORS AND THE U. S. GOVERNMENT SECURITIES MARKET THE FEDERAL RESERVE RANK of SE LOUIS Research Library Staff study

Treasury-Federal Reserve Study of the U. S. Government Securities Market INSTITUTIONAL INVESTORS AND THE U. S. GOVERNMENT SECURITIES MARKET THE FEDERAL RESERVE RANK of SE LOUIS Research Library Staff study

Best Execution Policy

Best Execution Policy Stephen Avenue Securities Inc. ( SAS ) is committed to using all reasonable efforts to ensure that clients achieve best execution of their orders in respect to all securities, including

Best Execution Policy Stephen Avenue Securities Inc. ( SAS ) is committed to using all reasonable efforts to ensure that clients achieve best execution of their orders in respect to all securities, including

Means the Securities and Exchange Commission (SEC) Means the Nigerian Stock Exchange (NSE)

Means the Nigerian Stock Exchange (NSE)") PROPOSAL FOR MARKET MAKING ON THE NIGERIAN STOCK EXCHANGE DEFINITION The Commission The Exchange Dealing Member Instruments Market Maker Market Making National Best Bid (NBB) National Best Offer (NBO)

PROPOSAL FOR MARKET MAKING ON THE NIGERIAN STOCK EXCHANGE DEFINITION The Commission The Exchange Dealing Member Instruments Market Maker Market Making National Best Bid (NBB) National Best Offer (NBO)

Amendments Respecting Designations and Identifiers

Rules Notice Notice of Approval/Implementation UMIR Please distribute internally to: Institutional Legal and Compliance Senior Management Trading Desk Retail Contact: Theodora Lam Policy Counsel, Market

Rules Notice Notice of Approval/Implementation UMIR Please distribute internally to: Institutional Legal and Compliance Senior Management Trading Desk Retail Contact: Theodora Lam Policy Counsel, Market

Citi Order Routing and Execution, LLC ( CORE ) Order Handling Document

Order Handling Document") Citi Order Routing and Execution, LLC ( CORE ) Order Handling Document CORE s automated systems have been designed and are routinely enhanced to automatically provide the highest level of regulatory compliance

Citi Order Routing and Execution, LLC ( CORE ) Order Handling Document CORE s automated systems have been designed and are routinely enhanced to automatically provide the highest level of regulatory compliance

I. INTRODUCTION BACKGROUND

JOINT CANADIAN SECURITIES ADMINISTRATORS/INVESTMENT INDUSTRY REGULATORY ORGANIZATION OF CANADA STAFF NOTICE 23-311 REGULATORY APPROACH TO DARK LIQUIDITY IN THE CANADIAN MARKET I. INTRODUCTION The publication

JOINT CANADIAN SECURITIES ADMINISTRATORS/INVESTMENT INDUSTRY REGULATORY ORGANIZATION OF CANADA STAFF NOTICE 23-311 REGULATORY APPROACH TO DARK LIQUIDITY IN THE CANADIAN MARKET I. INTRODUCTION The publication

/27/2017 RISK DISCLOSURE STATEMENT FOR FOREX TRADING AND IB MULTI-CURRENCY ACCOUNTS

3024 07/27/2017 RISK DISCLOSURE STATEMENT FOR FOREX TRADING AND IB MULTI-CURRENCY ACCOUNTS Rules of the U.S. National Futures Association ("NFA") require Interactive Brokers ("IB") to provide you with

3024 07/27/2017 RISK DISCLOSURE STATEMENT FOR FOREX TRADING AND IB MULTI-CURRENCY ACCOUNTS Rules of the U.S. National Futures Association ("NFA") require Interactive Brokers ("IB") to provide you with

NASDAQ CXC Limited. Trading Functionality Guide

NASDAQ CXC Limited Trading Functionality Guide CONTENTS 1 PURPOSE... 1 2 OVERVIEW... 2 3 TRADING OPERATIONS... 3 3.1 TRADING SESSIONS... 3 3.1.1 Time... 3 3.1.2 Opening... 3 3.1.3 Close... 3 3.2 ELIGIBLE

NASDAQ CXC Limited Trading Functionality Guide CONTENTS 1 PURPOSE... 1 2 OVERVIEW... 2 3 TRADING OPERATIONS... 3 3.1 TRADING SESSIONS... 3 3.1.1 Time... 3 3.1.2 Opening... 3 3.1.3 Close... 3 3.2 ELIGIBLE

Quarterly Scorecard 1st Quarter 2016 what s INSIDE

ETF Stats Ticker: NAV Symbol:.NV Intraday Symbol:.IV Listing Exchange: NYSE Arca CUSIP: 00162Q 205 Fund Inception: 7/6/2009 Dividends Paid: Quarterly Most Recent Dividend:* $0.2658 Management Fee: 0.37%

ETF Stats Ticker: NAV Symbol:.NV Intraday Symbol:.IV Listing Exchange: NYSE Arca CUSIP: 00162Q 205 Fund Inception: 7/6/2009 Dividends Paid: Quarterly Most Recent Dividend:* $0.2658 Management Fee: 0.37%

CANADIAN SECURITY TRADERS ASSOCIATION, INC. P.O. Box 3, 31 Adelaide Street East, Toronto, Ontario M5C 2H8

CANADIAN SECURITY TRADERS ASSOCIATION, INC. P.O. Box 3, 31 Adelaide Street East, Toronto, Ontario M5C 2H8 August 25, 2010 Ms. Tracey Stern, Assistant Manager, Market Regulation Ontario Securities Commission

CANADIAN SECURITY TRADERS ASSOCIATION, INC. P.O. Box 3, 31 Adelaide Street East, Toronto, Ontario M5C 2H8 August 25, 2010 Ms. Tracey Stern, Assistant Manager, Market Regulation Ontario Securities Commission

SIX Swiss Exchange Ltd. Directive 3: Trading. of 30/06/2016 Effective from: 17/10/2016

SIX Swiss Exchange Ltd Directive 3: Trading of 30/06/06 Effective from: 7/0/06 Content. Purpose and principle... I General.... Trading day and trading period... 3. Clearing day... 4. Trading hours... II

SIX Swiss Exchange Ltd Directive 3: Trading of 30/06/06 Effective from: 7/0/06 Content. Purpose and principle... I General.... Trading day and trading period... 3. Clearing day... 4. Trading hours... II

AEQUITAS NEO EXCHANGE TRADING POLICIES AMENDMENTS

2017 002 Trading Notice Amendments to Trading Policies Approved AEQUITAS NEO EXCHANGE TRADING POLICIES AMENDMENTS January 26, 2017 In accordance with Schedule 5 of its recognition order dated November

2017 002 Trading Notice Amendments to Trading Policies Approved AEQUITAS NEO EXCHANGE TRADING POLICIES AMENDMENTS January 26, 2017 In accordance with Schedule 5 of its recognition order dated November

Aliceblue Mobile App. User Manual

Aliceblue Mobile App User Manual Introduction Aliceblue Mobile Application gives the Investor Clients of the Brokerage House the convenience of secure and real time access to quotes and trading. The services

Aliceblue Mobile App User Manual Introduction Aliceblue Mobile Application gives the Investor Clients of the Brokerage House the convenience of secure and real time access to quotes and trading. The services

Exhibit A. Institutions and broker-dealers that are clients of ITG Inc. ( ITG ) are eligible to execute in POSIT, including affiliates of ITG.

are eligible to execute in POSIT, including affiliates of ITG.") Exhibit A A description of classes of Subscribers (for example, broker-dealer, institution, or retail). Also describe any differences in access to the services offered by the alternative trading system

Exhibit A A description of classes of Subscribers (for example, broker-dealer, institution, or retail). Also describe any differences in access to the services offered by the alternative trading system

Case: 1:15-cv Document #: 1 Filed: 03/10/15 Page 1 of 20 PageID #:1

Case: 1:15-cv-02129 Document #: 1 Filed: 03/10/15 Page 1 of 20 PageID #:1 IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF ILLINOIS EASTERN DIVISION HTG CAPITAL PARTNERS, LLC, Plaintiff,

Case: 1:15-cv-02129 Document #: 1 Filed: 03/10/15 Page 1 of 20 PageID #:1 IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF ILLINOIS EASTERN DIVISION HTG CAPITAL PARTNERS, LLC, Plaintiff,

Throughout this report reference will be made to different time periods defined as follows:

NYSE Alternext US LLC 86 Trinity Place New York, New York 0006 November, 008 Executive Summary As part of our participation in the Penny Pilot Program ( Pilot ), NYSE Alternext US, LLC, ( NYSE Alternext

NYSE Alternext US LLC 86 Trinity Place New York, New York 0006 November, 008 Executive Summary As part of our participation in the Penny Pilot Program ( Pilot ), NYSE Alternext US, LLC, ( NYSE Alternext

Interactive Brokers Order Routing and Payment for Order Flow Disclosure

Interactive Brokers Order Routing and Payment for Order Flow Disclosure 1. IB S ORDER ROUTING SYSTEM IB does not sell its order flow to another broker to handle and route. Instead, IB has built a real-time,

Interactive Brokers Order Routing and Payment for Order Flow Disclosure 1. IB S ORDER ROUTING SYSTEM IB does not sell its order flow to another broker to handle and route. Instead, IB has built a real-time,

Merrill Edge MarketPro Orders

Merrill Edge MarketPro Orders Use the Order Status window to display order information for an account or group of accounts. TOOLBAR GUIDE 1 2 4 3 5 1 Account selection allows selection of an account or

Merrill Edge MarketPro Orders Use the Order Status window to display order information for an account or group of accounts. TOOLBAR GUIDE 1 2 4 3 5 1 Account selection allows selection of an account or

Penny Quoting Pilot Program Report

Penny Quoting Pilot Program Report Executive Summary The Options Penny Quoting Pilot Program ( Pilot ) has clearly resulted in the reduction of quoted spread width (NBBO) with the majority of the benefit

Penny Quoting Pilot Program Report Executive Summary The Options Penny Quoting Pilot Program ( Pilot ) has clearly resulted in the reduction of quoted spread width (NBBO) with the majority of the benefit

NASDAQ CXC Limited. Trading Functionality Guide

NASDAQ CXC Limited Trading Functionality Guide CONTENTS 1 PURPOSE... 1 2 OVERVIEW... 2 3 TRADING OPERATIONS... 3 3.1 TRADING SESSIONS... 3 3.1.1 Time... 3 3.1.2 Opening... 3 3.1.3 Close... 3 3.2 ELIGIBLE

NASDAQ CXC Limited Trading Functionality Guide CONTENTS 1 PURPOSE... 1 2 OVERVIEW... 2 3 TRADING OPERATIONS... 3 3.1 TRADING SESSIONS... 3 3.1.1 Time... 3 3.1.2 Opening... 3 3.1.3 Close... 3 3.2 ELIGIBLE

PROCEDURES FOR HANDLING CERTAIN DESIGNATED TRADES AS PRINCIPAL

Rules Notice Guidance Note - UMIR Please distribute internally to: Legal and Compliance Trading Contact: Felix Mazer Policy Counsel Telephone: 416.646.7280 Fax: 416.646.7265 e-mail: fmazer@iiroc.ca 09-0224

Rules Notice Guidance Note - UMIR Please distribute internally to: Legal and Compliance Trading Contact: Felix Mazer Policy Counsel Telephone: 416.646.7280 Fax: 416.646.7265 e-mail: fmazer@iiroc.ca 09-0224

Credit Suisse Asia Pacific Crossfinder User Guidelines 2017

Credit Suisse Asia Pacific Crossfinder User Guidelines 2017 July 2017 2 Credit Suisse Crossfinder User Guidelines Asia Pacific Important Matters Relating to Orders Routed to Crossfinder Credit Suisse s

Credit Suisse Asia Pacific Crossfinder User Guidelines 2017 July 2017 2 Credit Suisse Crossfinder User Guidelines Asia Pacific Important Matters Relating to Orders Routed to Crossfinder Credit Suisse s

Cboe Tick Size Pilot Program FAQ

Cboe Tick Size Pilot Program FAQ Last Updated October 17, 2017 What is the Tick Pilot? On May 6, 2015 the Securities and Exchange Commission ( SEC ) approved, on a pilot basis, a two-year program that

Cboe Tick Size Pilot Program FAQ Last Updated October 17, 2017 What is the Tick Pilot? On May 6, 2015 the Securities and Exchange Commission ( SEC ) approved, on a pilot basis, a two-year program that

Version 3.1 Contents

O*U*C*H Version 3.1 Updated April 23, 2018 Contents 2 1 Overview... 2 1.1 Architecture... 2 1.2 Data Types... 2 1.3 Fault Redundancy... 3 1.4 Service Bureau Configuration... 3 2 Inbound Messages... 3 2.1

O*U*C*H Version 3.1 Updated April 23, 2018 Contents 2 1 Overview... 2 1.1 Architecture... 2 1.2 Data Types... 2 1.3 Fault Redundancy... 3 1.4 Service Bureau Configuration... 3 2 Inbound Messages... 3 2.1

TMX SELECT INC. NOTICE OF INITIAL OPERATIONS REPORT AND REQUEST FOR FEEDBACK

13.2 Marketplaces 13.2.1 TMX Select Inc. Notice of Initial Operations Report and Request for Feedback TMX SELECT INC. NOTICE OF INITIAL OPERATIONS REPORT AND REQUEST FOR FEEDBACK TMX Select has announced

13.2 Marketplaces 13.2.1 TMX Select Inc. Notice of Initial Operations Report and Request for Feedback TMX SELECT INC. NOTICE OF INITIAL OPERATIONS REPORT AND REQUEST FOR FEEDBACK TMX Select has announced

Lightspeed Gateway::Books

Lightspeed Gateway::Books Note: Messages on test servers may not reflect this specification. Production messages will be adapted to follow this specification. ECN's all use the same message formats, with

Lightspeed Gateway::Books Note: Messages on test servers may not reflect this specification. Production messages will be adapted to follow this specification. ECN's all use the same message formats, with

MyE214: Global Securities Markets Dr. Sunil Parameswaran January Target Audience: Objectives:

MyE214: Global Securities Markets Dr. Sunil Parameswaran January 4-15-2016 Target Audience: This course is focused at those who are seeking to acquire an overview of Finance, and more specifically a foundation

MyE214: Global Securities Markets Dr. Sunil Parameswaran January 4-15-2016 Target Audience: This course is focused at those who are seeking to acquire an overview of Finance, and more specifically a foundation

CBOT HOLDINGS INC. FORM 425 (Filing of certain prospectuses and communications in connection with business combination transactions) Filed 4/5/2007

Filed 4/5/2007") CBOT HOLDINGS INC FORM 425 (Filing of certain prospectuses and communications in connection with business combination transactions) Filed 4/5/2007 Address 141 WEST JACKSON BLVD CHICAGO, Illinois 60604

CBOT HOLDINGS INC FORM 425 (Filing of certain prospectuses and communications in connection with business combination transactions) Filed 4/5/2007 Address 141 WEST JACKSON BLVD CHICAGO, Illinois 60604

Product Disclosure Statement (Sartorius Capital)

") ADMIRAL MARKETS PTY LTD (Sartorius Capital) Issued by: Admiral Markets Pty Ltd ABN 63 151 613 839 AFSL 410681 Level 10, 17 Castlereagh Street Sydney NSW 2000 Phone number 1300 88 98 66 1 Table of Contents

ADMIRAL MARKETS PTY LTD (Sartorius Capital) Issued by: Admiral Markets Pty Ltd ABN 63 151 613 839 AFSL 410681 Level 10, 17 Castlereagh Street Sydney NSW 2000 Phone number 1300 88 98 66 1 Table of Contents

Producing RTS 27 & 28 Reports

#FIXEMEA2018 Producing RTS 27 & 28 Reports Alex Wolcough Director, Appsbroker Hanno Klein Co-Chair Global Technical Committee and Co-Chair High Performance Working Group, FIX Trading Community, Senior

#FIXEMEA2018 Producing RTS 27 & 28 Reports Alex Wolcough Director, Appsbroker Hanno Klein Co-Chair Global Technical Committee and Co-Chair High Performance Working Group, FIX Trading Community, Senior

PERFORMANCE STUDY 2013

US EQUITY FUNDS PERFORMANCE STUDY 2013 US EQUITY FUNDS PERFORMANCE STUDY 2013 Introduction This article examines the performance characteristics of over 600 US equity funds during 2013. It is based on

US EQUITY FUNDS PERFORMANCE STUDY 2013 US EQUITY FUNDS PERFORMANCE STUDY 2013 Introduction This article examines the performance characteristics of over 600 US equity funds during 2013. It is based on

Dark markets. Darkness. Securities Trading: Principles and Procedures, Chapter 8

Securities Trading: Principles and Procedures, Chapter 8 Dark markets Copyright 2017, Joel Hasbrouck, All rights reserved 1 Darkness A dark market does not display bids and asks. Bids and asks may exist,

Securities Trading: Principles and Procedures, Chapter 8 Dark markets Copyright 2017, Joel Hasbrouck, All rights reserved 1 Darkness A dark market does not display bids and asks. Bids and asks may exist,

Nasdaq Dubai Trading Manual Equities

Nasdaq Dubai Trading Manual Equities Version 3.9 For more information Nasdaq Dubai Ltd Level 7 The Exchange Building No 5 DIFC PO Box 53536 Dubai UAE +971 4 305 5454 Concerned department: Market Operations

Nasdaq Dubai Trading Manual Equities Version 3.9 For more information Nasdaq Dubai Ltd Level 7 The Exchange Building No 5 DIFC PO Box 53536 Dubai UAE +971 4 305 5454 Concerned department: Market Operations

Annual Australian Cash Equity Market

Annual Australian Cash Equity Market ASX Equity Market Turnover Average Total Market Capitalisation and Liquidity (1987 to 212) A$B 1,8 1,6 1,4 1,2 1, 8 6 4 2 11 1 9 8 7 6 5 4 3 2 1 Percentage (%) 1987

Annual Australian Cash Equity Market ASX Equity Market Turnover Average Total Market Capitalisation and Liquidity (1987 to 212) A$B 1,8 1,6 1,4 1,2 1, 8 6 4 2 11 1 9 8 7 6 5 4 3 2 1 Percentage (%) 1987

AMENDMENTS NATIONAL INSTRUMENT MARKETPLACE OPERATION

AMENDMENTS TO NATIONAL INSTRUMENT 21-101 MARKETPLACE OPERATION PART 1 AMENDMENTS 1.1 Amendments (1) This Instrument amends National Instrument 21-101 Marketplace Operation. (2) The definitions in section

AMENDMENTS TO NATIONAL INSTRUMENT 21-101 MARKETPLACE OPERATION PART 1 AMENDMENTS 1.1 Amendments (1) This Instrument amends National Instrument 21-101 Marketplace Operation. (2) The definitions in section

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 3 Repo Market and Securities Lending

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 3 Repo Market and Securities Lending Today: I. What s a Repo? II. Financing with Repos III. Shorting with Repos IV. Specialness and Supply

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 3 Repo Market and Securities Lending Today: I. What s a Repo? II. Financing with Repos III. Shorting with Repos IV. Specialness and Supply

Best Execution and Order Handling Policy

Best Execution and Order Handling Policy OR Taxonomy: Client-related Business Conduct Owner/Issuer: Head Global Trading and Order Generation Why do we have this policy? This policy will set a standard

Best Execution and Order Handling Policy OR Taxonomy: Client-related Business Conduct Owner/Issuer: Head Global Trading and Order Generation Why do we have this policy? This policy will set a standard

FX PRODUCTS. Making a world of forex opportunities accessible to you.

FX PRODUCTS Making a world of forex opportunities accessible to you. In a world of increasing volatility, customers around the globe rely on CME Group as their premier source for managing risk. Formed

FX PRODUCTS Making a world of forex opportunities accessible to you. In a world of increasing volatility, customers around the globe rely on CME Group as their premier source for managing risk. Formed

Order Execution Policy Macquarie Investment Management EMEA

Macquarie Investment Management EMEA Version: 2.0 Last approved: December 2017 Last updated: December 2017 Policy owner: Compliance 1. Policy Statement In accordance with regulatory obligations in the

Macquarie Investment Management EMEA Version: 2.0 Last approved: December 2017 Last updated: December 2017 Policy owner: Compliance 1. Policy Statement In accordance with regulatory obligations in the

NYSEnet. A Strategic Resource for Market Intelligence

NYSEnet A Strategic Resource for Market Intelligence Proprietary Trading Information By using NYSEnet s unique capabilities, you can analyze your company s trading characteristics and evaluate market quality

NYSEnet A Strategic Resource for Market Intelligence Proprietary Trading Information By using NYSEnet s unique capabilities, you can analyze your company s trading characteristics and evaluate market quality