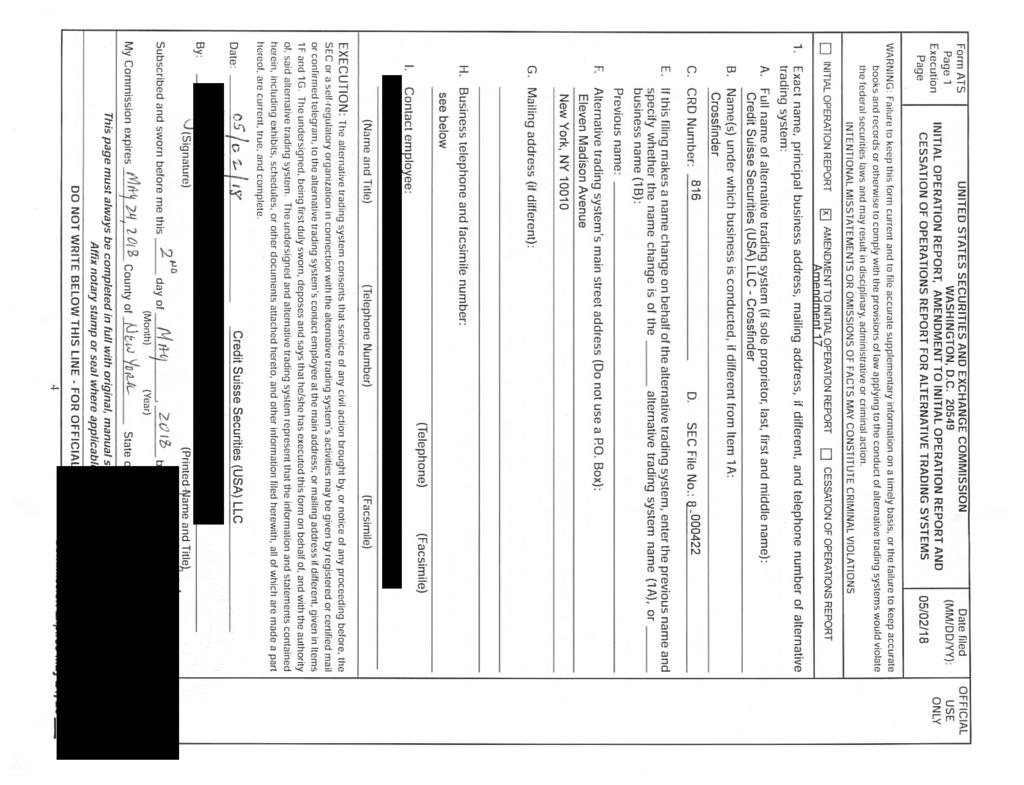

Credit Suisse Securities (USA) LLC CRD No. 816 Form ATS Amendment 17 SEC File No /02/18

|

|

|

- Olivia Clark

- 5 years ago

- Views:

Transcription

1

2

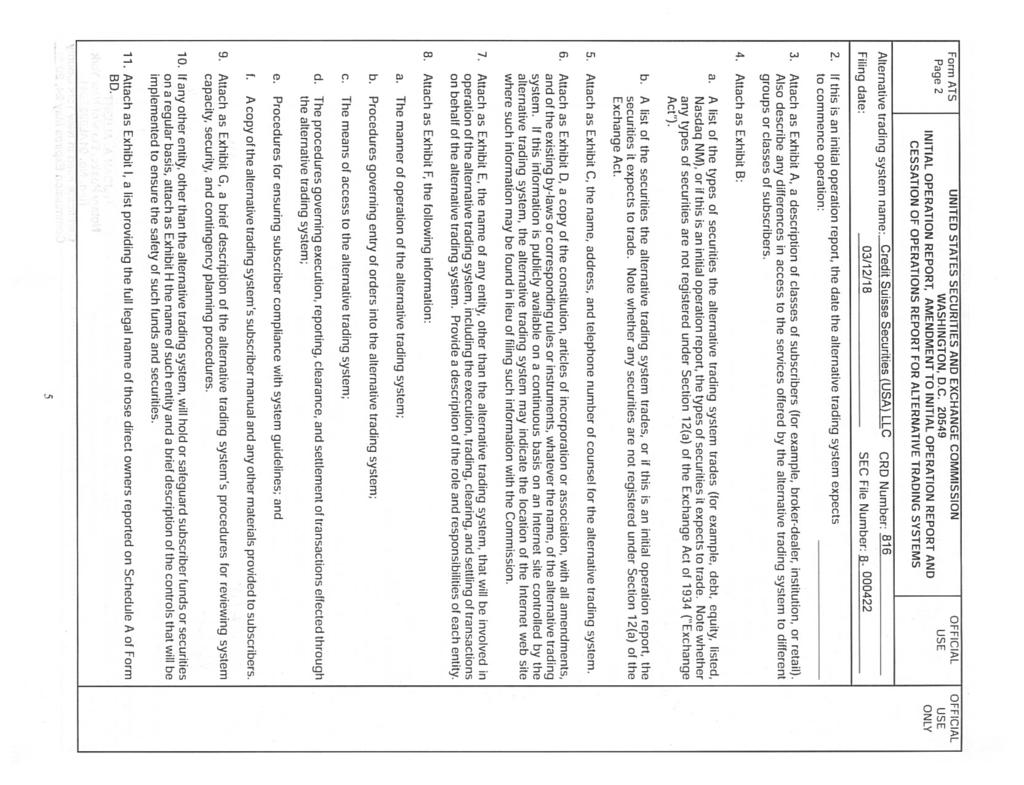

3 Crossfinder Form ATS Table of Contents Exhibit A (Item 3)... 3 Exhibit B (Item 4)... 4 Exhibit C (Item 5)... 5 Exhibit D (Item 6)... 6 Exhibit E (Item 7)... 7 Exhibit F (Item 8) a. The manner of operation of the alternative trading system Introduction... 8 Matching Priority... 8 Order Types and Parameters... 8 Optional Participant Configurations... 9 Minimum Execution Quantity... 9 Locked and Crossed Markets... 9 Order Book Transparency... 9 Outbound Routing... 9 NBBO Price Calculations (Market Data Sources)... 9 Closing Auction Minimum Price Increment / Reg. NMS Rule Crossing Scenario Examples Classification of Crossfinder Participants Scoring Methodology Examples of Crossfinder Classifications (for illustrative purposes only) Order Interaction Rules Conditional Process Terminology in the Conditional Process Conditional Matching Process Conditional Interactions Conditional Matching Priority Conditional Price Overlap Tick Size Pilot Securities Crossing Scenario Examples For Pilot Securities in Test Group Two

4 Communication with Participants Anti-Gaming Trade Reporting Confidentiality Rates b. Procedures governing entry of orders into the alternative trading system c. The means of access to the alternative trading system Fair Access System Problems d. The procedures governing execution, reporting, clearance, and settlement of transactions effected through the alternative trading system e. Procedures for ensuring subscriber compliance with system guidelines f. A copy of the alternative trading system s subscriber manual and any other materials provided to subscribers Exhibit G (Item 9) Capacity Security Contingency Planning Procedures Disaster Recovery Exhibit H (Item 10) Exhibit I (Item 11)

5 Exhibit A (Item 3) A description of classes of subscribers (for example, broker-dealer, institution, or retail). Also describe any differences in access to the services offered by the alternative trading system to different groups or classes of subscribers. Crossfinder is a non-displayed alternative trading system available to Credit Suisse Securities (USA) LLC ( Credit Suisse ) clients and internal trading desks. Clients include buy-side firms (mutual funds, institutional asset managers, hedge funds, etc.) and sell-side firms (broker-dealers who focus on institutional trading, Retail 1, market-making, etc.). Please see Exhibit F on Classification of Crossfinder Participants and Order Interaction Rules for more information on subscribers. 1 See Retail definition in Footnote 2 in Exhibit F. 3

6 Exhibit B (Item 4) a. A list of the types of securities the alternative trading system trades (for example, debt, equity, listed, Nasdaq NM), or if this is an initial operation report, the types of securities it expects to trade. Note whether any types of securities are not registered under Section 12(a) of the Exchange Act of 1934 ( Exchange Act ). Crossfinder accepts orders in National Market System ( NMS ) stocks as defined in Regulation NMS. b. A list of the securities the alternative trading system trades, or if this is an initial operation report, the securities it expects to trade. Note whether any securities are not registered under Section 12(a) of the Exchange Act. A list of NMS stocks can be found on the following websites: Please note that from time-to-time and for various reasons, Crossfinder may disable trading in a given security. 4

7 Exhibit C (Item 5) The name, address, and telephone number of counsel for the alternative trading system. 5

8 Exhibit D (Item 6) A copy of the constitution, articles of incorporation or association, with all amendments, and of the existing by-laws or corresponding rules or instruments, whatever the name, of the alternative trading system. If this information is publicly available on a continuous basis on an Internet site controlled by the alternative trading system, the alternative trading system may indicate the location of the Internet web site where such information may be found in lieu of filing such information with the Commission. The Certificate of Formation and Operating Agreement for were submitted as part of the October 20, 2005 Initial Filing. 6

9 Exhibit E (Item 7) The name of any entity, other than the alternative trading system, that will be involved in operation of the alternative trading system, including the execution, trading, clearing, and settling of transactions on behalf of the alternative trading system. Provide a description of the role and responsibilities of each entity. N/A, Credit Suisse is solely responsible for the operation of Crossfinder. 7

10 Exhibit F (Item 8) 8a. The manner of operation of the alternative trading system. Introduction Crossfinder is a non-displayed alternative trading system available to Credit Suisse clients and internal trading desks. Clients include buy-side firms (mutual funds, institutional asset managers, hedge funds, etc.) and sell-side firms (broker-dealers who focus on institutional trading, Retail 2, market-making, etc.). Those clients and internal trading desks are assigned one or more unique system IDs for their order flow(s). Crossfinder treats each system ID as a Participant. Matching Priority Crossfinder s matching engine operates on a price/time priority basis. All executions occur at or within the National Best Bid or Offer ( NBBO ). Priority is subject to the Order Interaction Rules and Optional Participant Configurations below. Conditional Orders and MOCX orders have different matching priority rules, as described in the Conditional Matching Priority and Closing Auction sections below. Order Types and Parameters Crossfinder accepts orders with the following parameters only: Price Instructions: o Market o Limit Time-In-Force: o Immediate-or-Cancel ( IOC ) o Day (Resident) Peg Instructions: o Midpoint Peg o Market Peg (pegged to the Far Touch) o Primary Peg (pegged to the Near Touch) o MOCX (official exchange closing cross price) o No Peg Minimum Quantity: Permitted Round Lot Trading: Permitted Conditional Order Interaction: Permitted 2 For purposes of this document, Retail means retail-originated orders that are sent to Credit Suisse via other brokerdealers. Not all Retail orders will qualify as Retail Investor Orders as defined in the Tick Size Pilot Program. Please see the Tick Pilot Securities section, below. 8

11 Optional Participant Configurations A Participant has the option to request the following configurations for its order flow generally (rather than on an order-by-order basis): Opt-out of interacting with Credit Suisse principal orders Opt-in to Volatility Spread Protection (See Anti-Gaming ) Opt-in to round lot only trading (may also be configured on an order-by-order basis) Opt-out of self-trade prevention Opt-in to Maximum Liquidity IOC 3 Opt-in to interacting with conditional orders (may also be configured on an order-by-order basis) Certain order interaction preferences (See Order Interaction Rules ) Minimum Execution Quantity When an order includes a minimum execution quantity instruction, Crossfinder does not aggregate contra interest to satisfy the minimum quantity. Locked and Crossed Markets Crossfinder does not execute in locked or crossed markets. Order Book Transparency Crossfinder does not send out indications of interest ( IOIs ). Crossfinder does not send out bids or offers, including to the AES smart order router. Crossfinder does accept Conditional Orders and may send an invitation to firm-up in response to a Conditional Order (See Conditional Process ). Outbound Routing Crossfinder does not route orders to other destinations. NBBO Price Calculations (Market Data Sources) Crossfinder generally determines the NBBO using a Credit Suisse system that combines direct market data feeds from market centers. As of the date of this Form ATS filing, Crossfinder receives direct market data feeds from: Nasdaq: Nasdaq, Nasdaq BX, Nasdaq PSX NYSE: NYSE, NYSE Arca, NYSE American, NYSE National CBOE: BZX, BYX, EDGA, EDGX CHX IEX (planned launch May 21, 2018) 3 This configuration allows a Participant to opt-in its IOCs to trade with the entire pool, subject to the Interaction Preferences of the potential counterparty. (See Order Interaction Rules ). This is not applicable to the Conditional Order Process. 9

12 In the event that there is a problem with one or more of the direct market data feeds, the internal system may switch temporarily to the SIP market data feed for the affected market center(s), while continuing to determine the NBBO using the direct market data feeds for all other exchanges. As set forth in Exhibit G, in the event that Crossfinder operates out of its secondary, disaster recovery site, Crossfinder will use the NBBO as published by the SIP for all market centers. Closing Auction Crossfinder accepts orders where the execution for each security will occur at a single point-intime at that security s official closing price on its primary listing exchange ( MOCX orders). Credit Suisse will accept MOCX orders in securities it deems eligible. Matching priority for MOCX orders is based on size/time. Crossfinder will accept MOCX orders for eligible securities up until a pre-determined time prior to the official market-on-close cutoff time of the security s primary listing exchange and will notify Participants of any unmatched interest. Crossfinder will send fill messages once the official closing price is known for an eligible security. In the event of a technical problem on a security s primary listing exchange, Crossfinder will follow that exchange s procedures/instructions for determining the official closing price. The following order attributes govern: MOCX orders must be Resident Orders. MOCX orders must be Market orders. Orders with a Limit Price will be rejected. MOCX orders must be greater than or equal to one round lot in a particular security. MOCX orders with the following parameters will be rejected: Minimum Quantity, Round Lot, and Conditional Order. MOCX orders marked as short sale orders will be rejected. Only the following Participant Configurations will be honored on MOCX orders: o Opt-out of interacting with Credit Suisse principal orders o Opt-out of self-trade prevention MOCX orders and executions will be excluded from the Crossfinder monthly scoring process as described below in Scoring Methodology. Crossfinder Order Interaction Rules as described below will not apply to MOCX orders. Minimum Price Increment / Reg. NMS Rule Crossfinder accepts: Market orders; Limit orders; o Limit orders priced at $1.00 or higher must be expressed in whole pennies; o Limit orders priced at less than $1.00 may be expressed in up to four (4) decimals (e.g., Limit: $0.9876); and 4 Please see the Tick Size Pilot Securities section for information about minimum price increments and crossing logic for securities that are part of the Tick Size Pilot Program ( Pilot Securities ). More information about the Tick Size Pilot Program is available at and 10

13 Market and Limit orders pegged to the National Best Bid or Offer; o Midpoint Peg; o Market Peg (pegged to the Far Touch); and o Primary Peg (pegged to the Near Touch). Orders priced in any manner other than as set forth above will not be accepted. The minimum price increments described above are in compliance with Rule 612 of Regulation NMS. 5 Crossing Scenario Examples The following examples illustrate Crossfinder s order crossing process and apply to both pegged and non-pegged orders. The following examples assume that the interaction settings and order instructions for the buyer and seller would permit a trade to occur, and that the Resting Buy Order and Incoming Sell Order have priority. All executions are bound by the NBBO. Crossfinder provides 100% of price overlap on the execution to the resting orders, unless one of the orders is Retail, then 80% of the overlap goes to the non-retail order and 20% goes to the Retail order. These examples are stand alone and assume no other orders are present. 5 In compliance with Rule 612 of Regulation NMS, Crossfinder will not display, rank, or accept quotations, orders, or indications of interest in any NMS stock priced in an increment smaller than $0.01 if the quotation, order, or indication of interest is priced equal to or greater than $1.00 per share; provided, however, that if the quotation, order, or indication of interest is priced less than $1.00 per share, then the minimum pricing increment is $

14 Assume the NBBO is x Midpoint = Resting Buy Order: Near Touch = Far Touch = Incoming Sell Order: Near Touch = Far Touch = Resting Buy Order* Incoming Sell Order* Execution Price (non-retail) 1. Midpoint Midpoint Midpoint Far Touch (non-retail) Far Touch (Retail) + 3. Far Touch Midpoint (non-retail) Midpoint (Retail) + 4. Far Touch Far Touch (non-retail) Far Touch (Retail) (80% split of x ) (80% split of x 10.10) (80% split of x 10.10) 5. Far Touch Near Touch Near Touch Far Touch * These examples illustrate resting buy orders versus all incoming sell orders. Reverse logic applies to resting sell orders versus all incoming buy orders. + Only Participants in the Retail Client Type that are categorized as Natural will be eligible to receive the price overlap described in this example. Please refer to the Classification of Crossfinder Participants section below for more information. Classification of Crossfinder Participants All Participants accessing Crossfinder are classified into the following categories (each a Category ): Natural ; Plus ; Max ; or Opportunistic Participants are classified separately for liquid and illiquid securities. 6 The Category is used to determine the eligibility of a Participant s orders to interact with orders of other Participants. This classification process seeks to evaluate the quality of the Participant s order flow. Below is a description of the classification process. First, each Participant is assigned a type ( Client Type ) in Crossfinder (See Table below). The Client Type is determined by AES personnel based on information provided about the Participant and/or its order flow characteristics. The Client Type determines the metrics that are applied in 6 This process may result in a Participant being classified in two identical or two different Categories. 12

15 the scoring methodology. The resulting score from the metrics relevant for each Client Type is used to classify the Participant into Natural, Plus, Max, and/or Opportunistic Categories. Client Type Default Category Post-Scoring Category AES Routed Flow Natural Natural, Plus, or Max Retail 7 Natural Natural, Plus, or Max BuySide Routed Flow Natural Natural, Plus, or Max BD Client Routed Flow Plus Plus, Max, or Opportunistic BD Systematic Adder + Max Plus, Max, or Opportunistic BD Systematic Remover + Max Plus, Max, or Opportunistic BD Systematic Mixed + Max Plus, Max, or Opportunistic BD Non-Systematic Max Plus, Max, or Opportunistic BD Exchange Max Plus, Max, or Opportunistic + Direct order flow from Credit Suisse principal trading desks is assigned to one of the three BD (broker dealer) Systematic Client Types. Scoring Methodology A client may have more than one Crossfinder Participant. Each Participant is evaluated individually. The flow from each Participant is evaluated separately for liquid and illiquid securities. The resulting scores may be used to establish the respective liquid and illiquid Categories to which the Participant is assigned. A Participant may be classified into two identical or two different Categories. Scoring is performed monthly and is evaluated against the default Category for a Participant s assigned Client Type. Based on the results, a Participant may (or may not) change Categories for liquid securities, illiquid securities, or both. 8 To be scored, a Participant must execute a pre-determined minimum number of trades (excluding Conditional and MOCX orders and fills) in Crossfinder during the measurement period. Participants who do not execute the minimum number of trades during the measurement period will remain in the Category from the previous month. 7 See Footnote 2. 8 If order flow from a Participant has been categorized as Opportunistic more than once, it will remain in the Opportunistic category for at least three months (the Penalty Box ). At the end of those three months, the Participant s flow will be re-evaluated and categorized in the same manner as other scored Participants. 13

16 The Scoring Methodology for each Client Type uses an established combination of: o Alpha Scoring Metrics (at least one of these two metrics is always applied) 1. Short Term Negative Selection 2. Volatility Normalized Alpha AND o Additional Metrics (the metrics deemed to be relevant for a particular Client Type are applied). Depending upon the Client Type, the relevant metrics include three (3) or four (4) of the following: 1. Average Execution Size 2. Average Order Size 3. Average Duration 4. Fill Rate 5. Percentage of Executions with Price Improvement 6. Percentage of Orders Sent at Midpoint 7. Percentage of Aggregate Demi-Blocks 8. Percentage of Too Late To Cancel 9. Percentage of Adding 10. Number of Symbols traded Examples of Crossfinder Classifications (for illustrative purposes only) Participant (system ID) Default Category Liquid / Illiquid Client Description Client Type ABC Teachers Retirement Long Only ABC AES Routed Flow Natural Liquid NATURAL ABC Teachers Retirement Long Only ABC AES Routed Flow Natural Illiquid NATURAL Classification XYZ Management Company Short Term Quant Fund XYZ1 BuySide Routed Flow Plus Liquid PLUS XYZ Management Company Short Term Quant Fund XYZ1 BuySide Routed Flow Plus Illiquid MAX XYZ Management Company Macro Fund XYZ2 AES Routed Flow Natural Liquid NATURAL XYZ Management Company Macro Fund XYZ2 AES Routed Flow Natural Illiquid PLUS 123 Brokerage B/D Systematic Market Making 123MM BD Systematic Adder* Max Liquid MAX 123 Brokerage B/D Systematic Market Making 123MM BD Systematic Adder* Max Illiquid OPP 123 Brokerage B/D Systematic Hedging 123HED BD Systematic Mixed* Max Liquid PLUS 123 Brokerage B/D Systematic Hedging 123HED BD Systematic Remover* Max Illiquid MAX * These Participants Add/Take ratio during the relevant measurement period determines whether they are a BD Systematic Adder, BD Systematic Remover, or BD Systematic Mixed. 14

17 Order Interaction Rules 9 The Participant s Category ( Natural, Plus, Max, Opportunistic ) determines its default interaction eligibility with other Participants. This default interaction eligibility applies unless the client requests that Credit Suisse customize the Participant s configuration. Default System Settings: o AES Routed Flow and BD Client Routed Flow Client Types do not interact with Opportunistic. o All other Client Types are eligible to interact with Natural, Plus, Max, and Opportunistic. Customizable Interaction Preferences and Rules: o All Client Types may request that Credit Suisse configure the Participant s interactions to be eligible or ineligible for any combination of these Categories: Natural, Plus, Max, and Opportunistic. However, a Natural- Only configuration (i.e., the Participant s flow is eligible to interact with Natural flow only) is available only to those Participants whose default Category is Natural. o All Client Types may request a Retail-Only configuration, under which the Participant s flow is eligible to interact only with Retail Client Types that are in the Natural Category. Order flow from two Participants will not trade with each other unless the Interaction Preferences for both Participants overlap. For example, an AES Routed Flow Participant whose interaction preference restricts Opportunistic would not execute against a Participant that is currently classified as Opportunistic, regardless of the Opportunistic Participant s Interaction Preferences. Conditional Process Crossfinder provides a means for finding liquidity through a conditional process. Terminology in the Conditional Process Eligible Firm Order: A Resident order in Crossfinder that is eligible to participate in the conditional process because the order has been opted-in to interacting with Conditional Orders. Conditional Order: A non-executable interest. Participants must set a minimum quantity and Midpoint Peg instructions. IOCs will not be accepted. Participants that enter Conditional Orders may be invited to send Firm-Up Orders (defined below). 9 The Order Interaction Rules do not apply to Conditional or MOCX orders. 15

18 Invitation: A request sent to a Participant, inviting the Participant to send a Firm-up Order in response to the Participant s Conditional Order, if there is a potential match. Firm-Up Order: A firm order sent by a Participant in response to an Invitation. Participants must set a minimum quantity and Midpoint Peg instructions. Day orders will not be accepted. Conditional Matching Process Eligible Firm Order versus Conditional Order: When an Eligible Firm Order is a potential match with a Conditional Order, an Invitation will be sent to the Participant that sent the Conditional Order. The associated Conditional Order will be cancelled. During this firmup period, 10 the portion of the shares of the Eligible Firm Order equal to the Minimum Quantity on the Conditional Order will be locked-up and ineligible to trade with other Crossfinder liquidity. 11 If the recipient of the invitation sends a Firm-Up Order within the firm-up period and the order attributes still overlap, the Firm-Up order will be executed against the Eligible Firm Order. A Firm-Up Order received after the firm-up period expires will be rejected. Any locked-up shares on an Eligible Firm Order that are not executed will be released to the Crossfinder order book. Conditional Order versus Conditional Order: When a Conditional Order is a potential match with another Conditional Order, both Participants will receive an Invitation. The associated Conditional Orders will be cancelled. During this firm-up period, if both Participants respond with a Firm-Up Order and the order attributes still overlap, the orders will be executed. Any Firm-Up Order received after the firm-up period expires will be rejected. Any unexecuted portion of a Firm-Up Order (received within the firm-up period) will be treated as an IOC order in the Crossfinder order book. This may result in multiple fills. Conditional Interactions A two-step process is applied to determine which Conditional Order will receive an Invitation in response to an Eligible Firm Order or a Conditional Order based on Participant Eligibility and Participant Priority. 1. Participant Eligibility The process for identifying when a Participant s Conditional Order is eligible to receive an Invitation is based on the Participant s Crossfinder Category for liquid and illiquid securities ( See Scoring Methodology ) and order interaction eligibility ( See Order Interaction Rules ) in 10 The firm-up period will be identical for all Participants and initially will be less than 2 seconds. 11 Any portion of the Eligible Firm Order that is not locked-up remains eligible to interact with the Crossfinder order book. 16

19 Crossfinder. Only those Participants that are otherwise eligible to interact with each other in Crossfinder may be invited to participate in a potential Conditional Order match. In addition, Participants will be assigned to one of two default conditional categories: Category 1 or Category 2. This is done separately for liquid and illiquid securities (i.e., each Participant will have a default conditional category for liquid securities and a default conditional category for illiquid securities). The default conditional categories and corresponding interactions are described below. Scored Crossfinder Category 12 Default Conditional Category Natural / Plus / Max 1 Opportunistic 2 Resident Order Interactions Default Setting: Resident orders in Crossfinder will not interact with Conditional Orders. Opt-in: Resident orders that have opted-in to interacting with Conditional Orders (i.e., Eligible Firm Orders) may interact with: (i) Conditional Orders in Category 1 only, or (ii) All Conditionals Orders (Categories 1 and 2) Conditional Order Interactions Default Settings: o Conditional Orders in Category 1 will interact with all Eligible Firm Orders and other Conditional Orders in Category 1. o Conditional Orders in Category 2 will only interact with those Eligible Firm Orders described in (ii) above, and those Conditional Orders described in (iv) below. Opt-in: Conditional Orders in Categories 1 and 2 may opt-in to interact with: (iii) Eligible Firm Orders only, or (iv) All Conditional Orders (Categories 1 and 2) and Eligible Firm Orders 2. Participant Priority For every security in which a Participant sends a Conditional Order, the Participant accumulates a real-time daily score based on its firm-up rate ( Symbol Score ). If a Category 1 Participant s Symbol Score falls below a pre-set daily threshold for the corresponding security, the Participant will be moved to Category 2 in that security for the remainder of the day. In addition to the Symbol Score, each Participant also will accrue a real-time, daily cumulative score ( Cumulative Score ) for liquid and illiquid securities, separately, based on its firm-up rate. 12 As described in Classification of Crossfinder Participants and Scoring Methodology, if a Participant has not executed a minimum number of trades to be scored, it will be assigned to the Default Crossfinder Category for its Client Type. 17

20 If a Category 1 Participant s Cumulative Score falls below a pre-set daily threshold for liquid and/or illiquid securities, the Participant will immediately be moved to Category 2 for the respective securities and will remain in Category 2 for a pre-defined penalty period. The daily threshold and penalty period may vary based on the Participant s Crossfinder Category for liquid and illiquid securities. Regardless of a Category 1 Participant s Symbol Score, if its Cumulative Score falls below the daily threshold, the Participant will be moved to Category 2 as described above. Conditional Matching Priority Eligible Firm Orders have priority over Conditional Orders at the same price level. Priority for Conditional Orders is based on price/symbol Score/size/time. Conditional Price Overlap Any Crossfinder match that involves a Firm-Up Order will be priced in a manner consistent with existing Crossfinder logic with respect to price overlap, as described in the Crossing Scenario Examples. An Eligible Firm Order will be treated as a Resting Order when determining whether a Firm Up Order or an Eligible Firm Order receives the benefit of price overlap. Tick Size Pilot Securities Under the U.S. Securities and Exchange Commission s Tick Size Pilot Program 13, Crossfinder will have certain pricing and execution obligations related to orders for securities subject to the Tick Size Pilot Program ( Pilot Securities ). In compliance with the Tick Size Pilot Program, the following additional conditions will apply: Crossfinder will reject orders with limit prices in increments other than $0.05 for Pilot Securities that are part of Test Group One, Test Group Two, or Test Group Three. For orders for Pilot Securities in Test Group One, Crossfinder provides 100% of the price overlap on the execution to the resting order, unless the incoming order is from a Retail Participant that is categorized as Natural, then 80% of the overlap goes to the non-retail order and 20% goes to the Retail order. This pricing logic is consistent with the pricing logic that Crossfinder applies to non-pilot Securities. Price improvement on orders for Pilot Securities in Test Group Two will be available only for orders from those Participants who have attested that the order is a Retail Investor Order (as defined in the Tick Size Pilot Program). See Crossing Scenario Examples for Pilot Securities in Test Group Two, below. Crossfinder will accept only orders designated as Midpoint Peg for Pilot Securities in Test Group Three. Crossfinder will reject all other orders for Pilot Securities in Test Group Three Implementation date was October 3, Price improvement will not be available to orders for Test Group Three securities, which will execute in Crossfinder at midpoint. 18

21 Crossing Scenario Examples For Pilot Securities in Test Group Two The following examples illustrate Crossfinder s order crossing process and apply to both pegged and non-pegged orders for Pilot Securities in Test Group Two. The following examples assume that the interaction settings and order instructions for the buyer and seller would permit a trade to occur, and that the Resting Buy Order and Incoming Sell Order have priority. All executions are bound by the NBBO. Crossfinder provides 100% of price overlap on the execution to the resting order for a Test Group Two security, unless one of the orders is a Retail Investor Order, then 80% of the overlap goes to the non-retail Investor Order and 20% goes to the Retail Investor Order. These examples are stand alone and assume no other orders are present. Test Group Two Securities Assume the NBBO is x Midpoint = Resting Buy Order: Near Touch = Far Touch = Incoming Sell Order: Near Touch = Far Touch = Resting Buy Order* Incoming Sell Order* Execution Price (non-retail) 1 Midpoint Midpoint Midpoint Far Touch (non-retail Investor Order) Far Touch (Retail Investor Order) (80% split of x ) 3 Far Touch Midpoint (non-retail Investor Order) Midpoint (Retail Investor Order) (80% split of x 12.10) 4 Far Touch Far Touch (non-retail Investor Order) Far Touch (Retail Investor Order) (80% split of x 12.10) 5 Far Touch Near Touch Near Touch Far Touch * These examples illustrate resting buy orders versus all incoming sell orders. Reverse logic applies to resting sell orders versus all incoming buy orders. + Only Retail Investor Orders from Participants in the Retail Client Type that are categorized as Natural will be eligible to receive the price overlap described in this example. Communication with Participants During a scoring month, AES personnel may monitor activity in Crossfinder. To the extent that AES personnel notice that a Participant s flow mid-month is trending towards a particular Category, that information may be shared with the Participant, which gives the Participant an opportunity to improve the quality of its order flow. Anti-Gaming Crossfinder employs various anti-gaming measures, for example: 19

22 To reduce the potential for latency arbitrage, Crossfinder generally determines the NBBO through market data sourced directly from most exchanges, as described above, instead of the SIP. Crossfinder s matching engine has a built-in, real-time mechanism designed to prevent order matching if the bid/ask spread of a security significantly differs from its historical norm. Volatility Spread Protection : During periods when market volatility is high, pricing discrepancies may increase between direct data feeds and the SIP. Crossfinder allows Participants to elect to prevent executions when such pricing discrepancies exist. Trade Reporting All Crossfinder trades are reported in real-time to one of the Trade Reporting Facilities ( TRF ), currently the NASDAQ TRF, as Over-the-Counter ( OTC ) transactions. Confidentiality The Crossfinder order book is dark meaning there is no pre-trade transparency to Participants. Credit Suisse has established information security policies and procedures and has implemented internal controls designed to ensure that no employee is permitted to view the live Crossfinder order book. AES product support personnel and technology support personnel have access to Crossfinder s system components, databases, and physical hardware. Like other order data within CSSU, Crossfinder order data is available to certain CSSU risk management, supervisory, and compliance systems. Information in Crossfinder databases may be made available to Compliance and Legal personnel. Credit Suisse may also disclose information in Crossfinder s databases to third parties in certain circumstances, including in response to a regulatory request or a subpoena. Rates AES charges commissions for executions in Crossfinder, except Retail orders which generally may qualify for a rebate or zero cost. Commission rates are negotiated. 8b. Procedures governing entry of orders into the alternative trading system AND 8c. The means of access to the alternative trading system. Matching occurs in Crossfinder during normal market hours 9:30 a.m. to 4:00 p.m. ET. Participants may access Crossfinder through: The AES algorithmic product suite which routes orders via the AES smart order router to a number of venues, including Crossfinder Credit Suisse s market access gateway ( MAGic ) Direct Crossfinder FIX protocol Direct Crossfinder binary protocol 20

23 Fair Access Credit Suisse monitors Crossfinder volume thresholds monthly in compliance with the fair access requirements set forth in Rule 301(b)(5) of Regulation ATS. If Credit Suisse determines that trading in Crossfinder is approaching such volume threshold in a security or securities, Credit Suisse will disable trading in such security(ies). In those circumstances Credit Suisse will provide clients with notice of any securities which may be temporarily disabled for trading. System Problems In the event that Crossfinder experiences systems problems, it may temporarily reject incoming order flow. 8d. The procedures governing execution, reporting, clearance, and settlement of transactions effected through the alternative trading system. When orders are matched, the execution is reported to an exchange TRF as an OTC transaction pursuant to the rules of the TRF to which it is reported. Once reported to a TRF, all executions facilitated through Crossfinder are cleared and settled in the same manner as other Credit Suisse client equity transactions. 8e. Procedures for ensuring subscriber compliance with system guidelines. Participant compliance is enforced in real-time by Credit Suisse systems, which reject ineligible orders (e.g., incorrect symbol; size or notional value exceeding pre-set parameters). 8f. A copy of the alternative trading system s subscriber manual and any other materials provided to subscribers. Crossfinder is a component of Credit Suisse s order routing system and market access system. Participants are not provided with any separate manuals. From time to time, Credit Suisse may send notices to clients about technical updates. Please see attachment Exhibit F-1 in our August 2015 submission for a copy of the current standard form of Credit Suisse Securities (USA) LLC s Electronic Trading Agreement. 21

24 Exhibit G (Item 9) A brief description of the alternative trading system's procedures for reviewing capacity, security, and contingency planning procedures. Capacity Credit Suisse monitors Crossfinder systems on an intra-day basis, including system level resources, database resources, internal application capacity, and network and communications infrastructure capacity, against pre-established thresholds. Under certain circumstances, Credit Suisse may expand system capacity when utilization exceeds capacity requirements or performance related issues exist. Credit Suisse also performs periodic stress testing on the Crossfinder systems. Security Access security controls for Crossfinder must meet the requirements of the standard attached in Appendix 2. Access security for Crossfinder is handled using Credit Suisse-mandated multilayered access control mechanisms that Credit Suisse employs for components of its order management system. Specific controls include physical security, operating system level user authentication and authorization, and Crossfinder specific application level access controls. Crossfinder also follows a set of procedural controls for new account creation and deletion, granting and revoking specific privileges for user accounts, and password aging. See Appendix 1 and 2 for specific details on the aforementioned procedures and controls. As discussed in Exhibit F, the Crossfinder order book is dark meaning there is no pre-trade transparency to Participants. Credit Suisse has established information security policies and procedures and has implemented internal controls designed to ensure that no employee is permitted to view the live Crossfinder order book. AES product support personnel and technology support personnel have access to Crossfinder s system components, databases, and physical hardware. Like other order data within CSSU, Crossfinder order data is available to certain CSSU risk management, supervisory, and compliance systems. Information in Crossfinder databases may be made available to Compliance and Legal personnel. Credit Suisse may also disclose information in Crossfinder s databases to third parties in certain circumstances, including in response to a regulatory request or a subpoena. In addition to electronic security measures, Credit Suisse has written policies governing employee use of confidential information. All employees are required to acknowledge that they have read, understand and agree to adhere to these policies and other relevant employment-related rules and policies. See Appendix 3 for Credit Suisse s policies on employee handling of confidential information. In accordance with Credit Suisse s overall security policy, Crossfinder undergoes a periodic security review to ensure that only authorized personnel have access to the system (including applications, databases, hardware, operating system and network). 22

25 Contingency Planning Procedures In the event of transient conditions which impact normal trading activities (such as temporary power failure or natural disasters) Crossfinder complies with Credit Suisse s business continuity management (BCM) policies and procedures to continue its operations. Credit Suisse performs contingency planning testing annually. See Appendix 4 for more detail on contingency procedures. Disaster Recovery Disaster recovery for Crossfinder is managed as part of Credit Suisse s overall disaster recovery program which includes provisions for secondary site operation. In the event of a major disaster where Credit Suisse s operations are impacted substantially at the primary site and are relocated to a designated secondary, disaster recovery site, Credit Suisse will simplify operations as practicable and minimize a number of components participating in handling of order flow. In accordance with Regulation SCI, Credit Suisse will provide access to this secondary site through the smart order router. As discussed in Section 8a of Exhibit F, Crossfinder determines the NBBO using a Credit Suisse system that combines direct market data feeds from most market centers and the SIP for the other market centers. The connectivity for these direct market data feeds is centralized in the Crossfinder primary data center. In the event Crossfinder operates out of the secondary site, Crossfinder will use the NBBO as published by the SIP. See Appendix 4 for more detail on contingency procedures. Attachments Appendix 1: Appendix 2: Appendix 3: Appendix 4: P Information Security Management for IT (see May 2017 submission) S Access Control and System Security Standard (see May 2017 submission) Credit Suisse Annual Certification & Excerpts from Relevant Manuals (see August 2015 submission) GP Business Continuity Management (BCM) Policy (see May 2017 submission) 23

26 Exhibit H (Item 10) If any other entity, other than the alternative trading system, will hold or safeguard subscriber funds or securities on a regular basis, attach as Exhibit H the name of such entity and a brief description of the controls that will be implemented to ensure the safety of such funds and securities. N/A, Credit Suisse is solely responsible for safeguarding subscriber funds and securities. 24

27 Exhibit I (Item 11) A list providing the full legal name of those direct owners reported on Schedule A of Form BD. As reported on Schedule A of Form BD, the sole member of is Credit Suisse (USA), Inc. 25

September 18, The UBS ATS has the following classes of participants:

EXHIBIT A Description of classes of subscribers and any differences in access to the services offered by UBS ATS to different groups or classes of subscribers. The UBS ATS has the following classes of

EXHIBIT A Description of classes of subscribers and any differences in access to the services offered by UBS ATS to different groups or classes of subscribers. The UBS ATS has the following classes of

CODA Markets, INC. CRD# SEC#

Exhibit A A description of classes of subscribers (for example, broker-dealer, institution, or retail). Also describe any differences in access to the services offered by the alternative trading system

Exhibit A A description of classes of subscribers (for example, broker-dealer, institution, or retail). Also describe any differences in access to the services offered by the alternative trading system

Exhibit A. Institutions and broker-dealers that are clients of ITG Inc. ( ITG ) are eligible to execute in POSIT, including affiliates of ITG.

are eligible to execute in POSIT, including affiliates of ITG.") Exhibit A A description of classes of Subscribers (for example, broker-dealer, institution, or retail). Also describe any differences in access to the services offered by the alternative trading system

Exhibit A A description of classes of Subscribers (for example, broker-dealer, institution, or retail). Also describe any differences in access to the services offered by the alternative trading system

Citi Cross is owned and operated by Citigroup Global Markets Inc. (CGMI)

") Form ATS Page 1 Execution Page UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 INITIAL OPERATION REPORT, AMENDMENT TO INITIAL OPERATION REPORT AND CESSATION OF OPERATIONS REPORT

Form ATS Page 1 Execution Page UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 INITIAL OPERATION REPORT, AMENDMENT TO INITIAL OPERATION REPORT AND CESSATION OF OPERATIONS REPORT

PDQ ATS, INC. CRD# SEC#

Exhibit A A description of classes of subscribers (for example, broker-dealer, institution, or retail). Also describe any differences in access to the services offered by the alternative trading system

Exhibit A A description of classes of subscribers (for example, broker-dealer, institution, or retail). Also describe any differences in access to the services offered by the alternative trading system

Exhibit A to Form ATS Classes of Subscribers

Exhibit A to Form ATS Classes of Subscribers Alternative trading system name: Liquidnet H2O ATS CRD No.: 103987 Filing date: March 4, 2016 SEC File No.: 8-52461 Classes of subscribers; any differences

Exhibit A to Form ATS Classes of Subscribers Alternative trading system name: Liquidnet H2O ATS CRD No.: 103987 Filing date: March 4, 2016 SEC File No.: 8-52461 Classes of subscribers; any differences

Credit Suisse Asia Pacific Crossfinder User Guidelines 2017

Credit Suisse Asia Pacific Crossfinder User Guidelines 2017 July 2017 2 Credit Suisse Crossfinder User Guidelines Asia Pacific Important Matters Relating to Orders Routed to Crossfinder Credit Suisse s

Credit Suisse Asia Pacific Crossfinder User Guidelines 2017 July 2017 2 Credit Suisse Crossfinder User Guidelines Asia Pacific Important Matters Relating to Orders Routed to Crossfinder Credit Suisse s

Autobahn Equity Americas

http://autobahn.db.com Autobahn Equity Americas US Routing Logic Smarter Liquidity Innovation with Integrity September 2016 This document describes the routing logic used for orders sent to the Autobahn

http://autobahn.db.com Autobahn Equity Americas US Routing Logic Smarter Liquidity Innovation with Integrity September 2016 This document describes the routing logic used for orders sent to the Autobahn

POSIT Frequently Asked Questions

POSIT Frequently Asked Questions This document addresses some frequently asked questions about POSIT. POSIT is a registered Alternative Trading System ( ATS ) operated by ITG Inc. ( ITG or the firm ),

POSIT Frequently Asked Questions This document addresses some frequently asked questions about POSIT. POSIT is a registered Alternative Trading System ( ATS ) operated by ITG Inc. ( ITG or the firm ),

SEC Rule 606 Report Interactive Brokers 3 rd Quarter 2017 Scottrade Inc. posts separate and distinct SEC Rule 606 reports that stem from orders entered on two separate platforms. This report is for Scottrade,

SEC Rule 606 Report Interactive Brokers 3 rd Quarter 2017 Scottrade Inc. posts separate and distinct SEC Rule 606 reports that stem from orders entered on two separate platforms. This report is for Scottrade,

Cboe Tick Size Pilot Program FAQ

Cboe Tick Size Pilot Program FAQ Last Updated October 17, 2017 What is the Tick Pilot? On May 6, 2015 the Securities and Exchange Commission ( SEC ) approved, on a pilot basis, a two-year program that

Cboe Tick Size Pilot Program FAQ Last Updated October 17, 2017 What is the Tick Pilot? On May 6, 2015 the Securities and Exchange Commission ( SEC ) approved, on a pilot basis, a two-year program that

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending June 30, 2014

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending June 30, 2014 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending June 30, 2014 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

US Options Complex Book Process. Version 1.1.1

Complex Book Process Version 1.1.1 October 17, 2017 Contents 1 Overview... 4 2 Complex Order Basics... 5 2.1 Ratios... 5 2.2 Net Price... 5 2.3 Availability of Complex Order Functionality... 5 2.3.1 Eligible

Complex Book Process Version 1.1.1 October 17, 2017 Contents 1 Overview... 4 2 Complex Order Basics... 5 2.1 Ratios... 5 2.2 Net Price... 5 2.3 Availability of Complex Order Functionality... 5 2.3.1 Eligible

Morgan Stanley s EMEA Equity Order Handling & Routing. Frequently Asked Questions. (Last Updated: February, 2017)

") Morgan Stanley s EMEA Equity Order Handling & Routing Frequently Asked Questions (Last Updated: February, 2017) This document is part of Morgan Stanley International plc s ( Morgan Stanley ) ongoing efforts

Morgan Stanley s EMEA Equity Order Handling & Routing Frequently Asked Questions (Last Updated: February, 2017) This document is part of Morgan Stanley International plc s ( Morgan Stanley ) ongoing efforts

Morgan Stanley s EMEA Equity Order Handling & Routing. Frequently Asked Questions. (Last Updated: March, 2018)

") Morgan Stanley s EMEA Equity Order Handling & Routing Frequently Asked Questions (Last Updated: March, 2018) This document is part of Morgan Stanley International plc s ( Morgan Stanley ) ongoing efforts

Morgan Stanley s EMEA Equity Order Handling & Routing Frequently Asked Questions (Last Updated: March, 2018) This document is part of Morgan Stanley International plc s ( Morgan Stanley ) ongoing efforts

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2015

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2015 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2015 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2016

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2016 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2016 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending March 30, 2016

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending March 30, 2016 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending March 30, 2016 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

SEC Rule 606 Report Interactive Brokers 1st Quarter 2018

SEC Rule 606 Report Interactive Brokers 1st Quarter 2018 Scottrade Inc. posts separate and distinct SEC Rule 606 reports that stem from orders entered on two separate platforms. This report is for Scottrade,

SEC Rule 606 Report Interactive Brokers 1st Quarter 2018 Scottrade Inc. posts separate and distinct SEC Rule 606 reports that stem from orders entered on two separate platforms. This report is for Scottrade,

NASDAQ CXC Limited. Trading Functionality Guide

NASDAQ CXC Limited Trading Functionality Guide CONTENTS 1 PURPOSE... 1 2 OVERVIEW... 2 3 TRADING OPERATIONS... 3 3.1 TRADING SESSIONS... 3 3.1.1 Time... 3 3.1.2 Opening... 3 3.1.3 Close... 3 3.2 ELIGIBLE

NASDAQ CXC Limited Trading Functionality Guide CONTENTS 1 PURPOSE... 1 2 OVERVIEW... 2 3 TRADING OPERATIONS... 3 3.1 TRADING SESSIONS... 3 3.1.1 Time... 3 3.1.2 Opening... 3 3.1.3 Close... 3 3.2 ELIGIBLE

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2017

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2017 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending September 30, 2017 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

NASDAQ CXC Limited. Trading Functionality Guide

NASDAQ CXC Limited Trading Functionality Guide CONTENTS 1 PURPOSE... 1 2 OVERVIEW... 2 3 TRADING OPERATIONS... 3 3.1 TRADING SESSIONS... 3 3.1.1 Time... 3 3.1.2 Opening... 3 3.1.3 Close... 3 3.2 ELIGIBLE

NASDAQ CXC Limited Trading Functionality Guide CONTENTS 1 PURPOSE... 1 2 OVERVIEW... 2 3 TRADING OPERATIONS... 3 3.1 TRADING SESSIONS... 3 3.1.1 Time... 3 3.1.2 Opening... 3 3.1.3 Close... 3 3.2 ELIGIBLE

Cboe Europe Ltd. Large in Scale Service (LIS) Service Description. Version 1.2. October Cboe Europe Limited

Service Description. Version 1.2. October Cboe Europe Limited") Cboe Europe Ltd Large in Scale Service (LIS) Service Description Version 1.2 October 2017 1 Contents Introduction... 4 1. Regulation... 4 2. Definitions... 4 3. Workflow... 6 4. Market Model... 7 4.1.

Cboe Europe Ltd Large in Scale Service (LIS) Service Description Version 1.2 October 2017 1 Contents Introduction... 4 1. Regulation... 4 2. Definitions... 4 3. Workflow... 6 4. Market Model... 7 4.1.

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2018

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2018 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2018 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2017

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2017 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Interactive Brokers Rule 606 Quarterly Order Routing Report Quarter Ending December 31, 2017 I. Introduction Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange

Cboe Limit Up/Limit Down FAQ

Cboe Limit Up/Limit Down FAQ Last Updated October 17, 2017 What is Limit Up/Limit Down? On May 31, 2012 the Securities and Exchange Commission (SEC) approved, on a pilot basis, a National Market System

Cboe Limit Up/Limit Down FAQ Last Updated October 17, 2017 What is Limit Up/Limit Down? On May 31, 2012 the Securities and Exchange Commission (SEC) approved, on a pilot basis, a National Market System

Interactive Brokers Quarterly Order Routing Report Quarter Ending June 30, 2007

I. Introduction Interactive Brokers Quarterly Order Routing Report Quarter Ending June 30, 2007 Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

I. Introduction Interactive Brokers Quarterly Order Routing Report Quarter Ending June 30, 2007 Interactive Brokers ( IB ) has prepared this report pursuant to a U.S. Securities and Exchange Commission

Description. Contact Information. Signature. SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C Form 19b-4. Page 1 of * 34

OMB APPROVAL Required fields are shown with yellow backgrounds and asterisks. OMB Number: 3235-0045 Estimated average burden hours per response...38 Page 1 of * 34 SECURITIES AND EXCHANGE COMMISSION WASHINGTON,

OMB APPROVAL Required fields are shown with yellow backgrounds and asterisks. OMB Number: 3235-0045 Estimated average burden hours per response...38 Page 1 of * 34 SECURITIES AND EXCHANGE COMMISSION WASHINGTON,

Information regarding where your orders have been routed for execution is available by contacting your sales representative.

REGULATORY DISCLOSURE STATEMENT The U.S. Securities and Exchange Commission ( SEC ), the Financial Industry Regulatory Authority, Inc. ( FINRA ), and other regulators have various rules and regulations

REGULATORY DISCLOSURE STATEMENT The U.S. Securities and Exchange Commission ( SEC ), the Financial Industry Regulatory Authority, Inc. ( FINRA ), and other regulators have various rules and regulations

Citi Equities Electronic Markets

Citi Match Reference Guide Asia Pacific Citi Match is Citi s crossing / dark pool service for Hong Kong, Japan and Australia. It provides anonymous crossing of buy and sell orders supporting a number of

Citi Match Reference Guide Asia Pacific Citi Match is Citi s crossing / dark pool service for Hong Kong, Japan and Australia. It provides anonymous crossing of buy and sell orders supporting a number of

Virtu Americas LLC Rule 606 Disclosure: Q1 2018

Virtu Americas LLC Rule 606 Disclosure: Q1 2018 Virtu Americas LLC ( VAL or the Firm ) has prepared this report for itself pursuant to a U.S. Securities and Exchange Commission rule requiring all brokerage

Virtu Americas LLC Rule 606 Disclosure: Q1 2018 Virtu Americas LLC ( VAL or the Firm ) has prepared this report for itself pursuant to a U.S. Securities and Exchange Commission rule requiring all brokerage

The Proven Retail Exchange Operator. Bill Cody Director, US Equity Sales Bats Global Markets

The Proven Retail Exchange Operator Bill Cody Director, US Equity Sales Bats Global Markets November 16, 2017 Global Exchange Operator Options #1 U.S. options market Trading home to SPX and VIX options

The Proven Retail Exchange Operator Bill Cody Director, US Equity Sales Bats Global Markets November 16, 2017 Global Exchange Operator Options #1 U.S. options market Trading home to SPX and VIX options

IEX FIX Certification Notes for Product Managers

IEX FIX Certification Notes for Product Managers Version: 1.01 Updated: October 3, 01 IEX Group, Inc. 7 World Trade Center 30th Floor New York, NY 10007 Copyright 01 IEX Group, Inc. All rights reserved.

IEX FIX Certification Notes for Product Managers Version: 1.01 Updated: October 3, 01 IEX Group, Inc. 7 World Trade Center 30th Floor New York, NY 10007 Copyright 01 IEX Group, Inc. All rights reserved.

NASDAQ CXC Limited. Trading Functionality Guide

NASDAQ CXC Limited Trading Functionality Guide CONTENTS 1 PURPOSE... 1 2 OVERVIEW... 2 3 TRADING OPERATIONS... 3 3.1 TRADING SESSIONS...3 3.1.1 Time...3 3.1.2 Opening...3 3.1.3 Close...3 3.2 ELIGIBLE SECURITIES...3

NASDAQ CXC Limited Trading Functionality Guide CONTENTS 1 PURPOSE... 1 2 OVERVIEW... 2 3 TRADING OPERATIONS... 3 3.1 TRADING SESSIONS...3 3.1.1 Time...3 3.1.2 Opening...3 3.1.3 Close...3 3.2 ELIGIBLE SECURITIES...3

Dark Liquidity Guide Toronto Stock Exchange TSX Venture Exchange

Dark Liquidity Guide Toronto Stock Exchange TSX Venture Exchange Document Version: 1.3 Date of Issue: 2012/09/28 Table of Contents 1.1 Overview... 3 1.2 Purpose... 3 1.3 Glossary... 3 1.4 Dark order types

Dark Liquidity Guide Toronto Stock Exchange TSX Venture Exchange Document Version: 1.3 Date of Issue: 2012/09/28 Table of Contents 1.1 Overview... 3 1.2 Purpose... 3 1.3 Glossary... 3 1.4 Dark order types

Dark Liquidity Guide. Toronto Stock Exchange TSX Venture Exchange. Document Version: 1.6 Date of Issue: September 1, 2017

Dark Liquidity Guide Toronto Stock Exchange TSX Venture Exchange Document Version: 1.6 Date of Issue: September 1, 2017 Table of Contents 1. Introduction... 4 1.1 Overview... 4 1.2 Purpose... 4 1.3 Glossary...

Dark Liquidity Guide Toronto Stock Exchange TSX Venture Exchange Document Version: 1.6 Date of Issue: September 1, 2017 Table of Contents 1. Introduction... 4 1.1 Overview... 4 1.2 Purpose... 4 1.3 Glossary...

IEX ATS Subscriber Manual

IEX ATS Subscriber Manual Version: 2.5 Updated: July 13, 2015 Note: IEX plans to begin offering trading and routing during the Pre-Market and Post-Market Sessions in August. Trading and routing during

IEX ATS Subscriber Manual Version: 2.5 Updated: July 13, 2015 Note: IEX plans to begin offering trading and routing during the Pre-Market and Post-Market Sessions in August. Trading and routing during

Virtu Americas LLC Rule 606 Disclosure: Q4 2017

Virtu Americas LLC Rule 606 Disclosure: Q4 2017 Virtu Americas LLC ( VAL or the Firm ) has prepared this report for itself pursuant to a U.S. Securities and Exchange Commission rule requiring all brokerage

Virtu Americas LLC Rule 606 Disclosure: Q4 2017 Virtu Americas LLC ( VAL or the Firm ) has prepared this report for itself pursuant to a U.S. Securities and Exchange Commission rule requiring all brokerage

DRECT Market Guide Version 7.0

DRECT Market Guide Version 7.0 october 2012 DRECT マーケット ガイド 2 CONTENTS 1. Introduction... 3 2. Features... 4 Crossing Engine... 4 Universe Hours Currencies Internal Market Structure and Matching Rules

DRECT Market Guide Version 7.0 october 2012 DRECT マーケット ガイド 2 CONTENTS 1. Introduction... 3 2. Features... 4 Crossing Engine... 4 Universe Hours Currencies Internal Market Structure and Matching Rules

US Options Auction Process. Version 1.0.5

US Options Auction Process Version 1.0.5 October 17, 2017 Contents 1 Introduction... 4 1.1 Overview... 4 2 Cboe Options Auction Information... 4 3 Messaging... 4 3.1 Auction Notification Messages... 4

US Options Auction Process Version 1.0.5 October 17, 2017 Contents 1 Introduction... 4 1.1 Overview... 4 2 Cboe Options Auction Information... 4 3 Messaging... 4 3.1 Auction Notification Messages... 4

Virtu Americas LLC Rule 606 Disclosure: Q3 2017

Virtu Americas LLC Rule 606 Disclosure: Q3 2017 Virtu Americas LLC ( VAL or the Firm ) has prepared this report for itself pursuant to a U.S. Securities and Exchange Commission rule requiring all brokerage

Virtu Americas LLC Rule 606 Disclosure: Q3 2017 Virtu Americas LLC ( VAL or the Firm ) has prepared this report for itself pursuant to a U.S. Securities and Exchange Commission rule requiring all brokerage

In Detail What is MATCHNow?... 3

May 2017 In Detail What is MATCHNow?... 3 Improve Your Trading... 4 Access Advantages... 4 Cost Advantages... 4 Tactical Advantages... 4 Access to MATCHNow... 5 Order Attributes... 6 Parameters for Liquidity

May 2017 In Detail What is MATCHNow?... 3 Improve Your Trading... 4 Access Advantages... 4 Cost Advantages... 4 Tactical Advantages... 4 Access to MATCHNow... 5 Order Attributes... 6 Parameters for Liquidity

Pursuant to Section 19(b)(1) of the Securities Exchange Act of 1934 ( Act ), 1 and Rule

(1) of the Securities Exchange Act of 1934 ( Act ), 1 and Rule") This document is scheduled to be published in the Federal Register on 11/19/2013 and available online at http://federalregister.gov/a/2013-27626, and on FDsys.gov 8011-01p SECURITIES AND EXCHANGE COMMISSION

This document is scheduled to be published in the Federal Register on 11/19/2013 and available online at http://federalregister.gov/a/2013-27626, and on FDsys.gov 8011-01p SECURITIES AND EXCHANGE COMMISSION

* * * * * (b) Except where stated otherwise, the following Order Types are available to all Participants:

Except where stated otherwise, the following Order Types are available to all Participants:") Deleted text is [bracketed]. New text is underlined. The Nasdaq Stock Market Rules 4702. Order Types (a) No change. * * * * * (b) Except where stated otherwise, the following Order Types are available

Deleted text is [bracketed]. New text is underlined. The Nasdaq Stock Market Rules 4702. Order Types (a) No change. * * * * * (b) Except where stated otherwise, the following Order Types are available

BX Options Depth of Market

Market Data Feed Version 1.3 BX Options Depth of Market 1. Overview Nasdaq BX Options Depth of Market (BX Depth) is a direct data feed product offered by The Nasdaq BX Options Market, which features the

Market Data Feed Version 1.3 BX Options Depth of Market 1. Overview Nasdaq BX Options Depth of Market (BX Depth) is a direct data feed product offered by The Nasdaq BX Options Market, which features the

ALP Guidelines for MS POOL for the Hong Kong Market

ALP Guidelines for MS POOL for the Hong Kong Market Morgan Stanley Hong Kong Securities Limited ( MSHK ) is licensed by the Securities and Futures Commission ( SFC ), to conduct, inter alia, the regulated

ALP Guidelines for MS POOL for the Hong Kong Market Morgan Stanley Hong Kong Securities Limited ( MSHK ) is licensed by the Securities and Futures Commission ( SFC ), to conduct, inter alia, the regulated

NLS Plus. Version 2.1

NLS Plus Version 2.1 A trade-by-trade data feed with Nasdaq, Nasdaq BX and Nasdaq PSX transactions and consolidated volume information for U.S. exchange-listed equities Page 1 Table of Contents 1 Product

NLS Plus Version 2.1 A trade-by-trade data feed with Nasdaq, Nasdaq BX and Nasdaq PSX transactions and consolidated volume information for U.S. exchange-listed equities Page 1 Table of Contents 1 Product

Pursuant to Section 19(b)(1) of the Securities Exchange Act of 1934 (the Act ), 1 and

(1) of the Securities Exchange Act of 1934 (the Act ), 1 and") SECURITIES AND EXCHANGE COMMISSION (Release No. 34-80683; File No. SR-BatsBZX-2017-34) May 16, 2017 Self-Regulatory Organizations; Bats BZX Exchange, Inc.; Notice of Filing of a Proposed Rule Change to

SECURITIES AND EXCHANGE COMMISSION (Release No. 34-80683; File No. SR-BatsBZX-2017-34) May 16, 2017 Self-Regulatory Organizations; Bats BZX Exchange, Inc.; Notice of Filing of a Proposed Rule Change to

Report on the Thematic Review of Alternative Liquidity Pools in Hong Kong. 9 April 2018

Report on the Thematic Review of Alternative Liquidity Pools in Hong Kong 9 April 2018 Table of contents A. Introduction 1 B. ALP industry landscape in Hong Kong 3 1. Overview of ALPs in Hong Kong 3 2.

Report on the Thematic Review of Alternative Liquidity Pools in Hong Kong 9 April 2018 Table of contents A. Introduction 1 B. ALP industry landscape in Hong Kong 3 1. Overview of ALPs in Hong Kong 3 2.

TMX SELECT INC. NOTICE OF INITIAL OPERATIONS REPORT AND REQUEST FOR FEEDBACK

13.2 Marketplaces 13.2.1 TMX Select Inc. Notice of Initial Operations Report and Request for Feedback TMX SELECT INC. NOTICE OF INITIAL OPERATIONS REPORT AND REQUEST FOR FEEDBACK TMX Select has announced

13.2 Marketplaces 13.2.1 TMX Select Inc. Notice of Initial Operations Report and Request for Feedback TMX SELECT INC. NOTICE OF INITIAL OPERATIONS REPORT AND REQUEST FOR FEEDBACK TMX Select has announced

Section 19(b)(3)(A) * Section 19(b)(3)(B) * Section 19(b)(2) * Rule. 19b-4(f)(1) 19b-4(f)(2) (Title *) Executive Vice President and General Counsel

(3)(A) * Section 19(b)(3)(B) * Section 19(b)(2) * Rule. 19b-4(f)(1) 19b-4(f)(2) (Title *) Executive Vice President and General Counsel") OMB APPROVAL Required fields are shown with yellow backgrounds and asterisks. OMB Number: 3235-0045 Estimated average burden hours per response...38 Page 1 of * 19 SECURITIES AND EXCHANGE COMMISSION WASHINGTON,

OMB APPROVAL Required fields are shown with yellow backgrounds and asterisks. OMB Number: 3235-0045 Estimated average burden hours per response...38 Page 1 of * 19 SECURITIES AND EXCHANGE COMMISSION WASHINGTON,

Self-Regulatory Organizations; The NASDAQ Stock Market LLC; Notice of Filing and Immediate Effectiveness of Proposed Rule Change to Amend Rule 7022(d)

") This document is scheduled to be published in the Federal Register on 01/05/2017 and available online at https://federalregister.gov/d/2016-31936, and on FDsys.gov 8011-01 SECURITIES AND EXCHANGE COMMISSION

This document is scheduled to be published in the Federal Register on 01/05/2017 and available online at https://federalregister.gov/d/2016-31936, and on FDsys.gov 8011-01 SECURITIES AND EXCHANGE COMMISSION

Self-Regulatory Organizations; Cboe BZX Exchange, Inc.; Notice of Filing and Immediate

This document is scheduled to be published in the Federal Register on 01/11/2018 and available online at https://federalregister.gov/d/2018-00309, and on FDsys.gov 8011-01p SECURITIES AND EXCHANGE COMMISSION

This document is scheduled to be published in the Federal Register on 01/11/2018 and available online at https://federalregister.gov/d/2018-00309, and on FDsys.gov 8011-01p SECURITIES AND EXCHANGE COMMISSION

UNITED STATES OF AMERICA Before the SECURITIES AND EXCHANGE COMMISSION

SECURITIES ACT OF 1933 Release No. 10565 / September 28, 2018 UNITED STATES OF AMERICA Before the SECURITIES AND EXCHANGE COMMISSION SECURITIES EXCHANGE ACT OF 1934 Release No. 84314 / September 28, 2018

SECURITIES ACT OF 1933 Release No. 10565 / September 28, 2018 UNITED STATES OF AMERICA Before the SECURITIES AND EXCHANGE COMMISSION SECURITIES EXCHANGE ACT OF 1934 Release No. 84314 / September 28, 2018

NYSE ARCA, INC. Appearances

NYSE ARCA, INC. NYSE REGULATION, v. MORGAN STANLEY & CO. LLC, Complainant, Proceeding No. 20120346239-01 1 August 23, 2018 Respondent. Morgan Stanley & Co. LLC violated: (i) SEA Rules 15c3-5(b) and (c)(1)(ii),

NYSE ARCA, INC. NYSE REGULATION, v. MORGAN STANLEY & CO. LLC, Complainant, Proceeding No. 20120346239-01 1 August 23, 2018 Respondent. Morgan Stanley & Co. LLC violated: (i) SEA Rules 15c3-5(b) and (c)(1)(ii),

Nasdaq BX Options PRISM

Nasdaq BX Options PRISM Frequently Asked Questions Overview Q: What is PRISM? PRISM is the BX Options electronic price improvement mechanism whereby an initiating member submits a two-sided (buy and sell)

Nasdaq BX Options PRISM Frequently Asked Questions Overview Q: What is PRISM? PRISM is the BX Options electronic price improvement mechanism whereby an initiating member submits a two-sided (buy and sell)

Reg NMS. Outline. Securities Trading: Principles and Procedures Chapter 18

Reg NMS Securities Trading: Principles and Procedures Chapter 18 Copyright 2015, Joel Hasbrouck, All rights reserved 1 Outline SEC Regulation NMS ( Reg NMS ) was adopted in 2005. It provides the defining

Reg NMS Securities Trading: Principles and Procedures Chapter 18 Copyright 2015, Joel Hasbrouck, All rights reserved 1 Outline SEC Regulation NMS ( Reg NMS ) was adopted in 2005. It provides the defining

The Cost Of Exchange Services

January 2019 The Cost Of Exchange Services Disclosing the Cost of Offering Market Data and Connectivity as a National Securities Exchange Adrian Facini - Head of Product John Ramsay - Chief Market Policy

January 2019 The Cost Of Exchange Services Disclosing the Cost of Offering Market Data and Connectivity as a National Securities Exchange Adrian Facini - Head of Product John Ramsay - Chief Market Policy

Self-Regulatory Organizations; NASDAQ OMX BX Inc.; Notice of Proposed Rule Change

This document is scheduled to be published in the Federal Register on 04/06/2015 and available online at http://federalregister.gov/a/2015-07750, and on FDsys.gov SECURITIES AND EXCHANGE COMMISSION [Release

This document is scheduled to be published in the Federal Register on 04/06/2015 and available online at http://federalregister.gov/a/2015-07750, and on FDsys.gov SECURITIES AND EXCHANGE COMMISSION [Release

File No. S : Disclosure of Order Handling Information

Via Electronic Mail (rule-comments@sec.gov) Mr. Brent J. Fields Secretary U.S. Securities & Exchange Commission 100 F Street, N.E. Washington, D.C. 20549-1090 Re: File No. S7 14 16: Disclosure of Order

Via Electronic Mail (rule-comments@sec.gov) Mr. Brent J. Fields Secretary U.S. Securities & Exchange Commission 100 F Street, N.E. Washington, D.C. 20549-1090 Re: File No. S7 14 16: Disclosure of Order

Regulatory Notice 10-42

Regulatory Notice 10-42 REG NMS-Principled Rules SEC Approves Amendments to Establish Regulation NMS-Principled Rules in Market for OTC Equity Securities Effective Dates: FINRA Rules 6434, 6437 and 6450:

Regulatory Notice 10-42 REG NMS-Principled Rules SEC Approves Amendments to Establish Regulation NMS-Principled Rules in Market for OTC Equity Securities Effective Dates: FINRA Rules 6434, 6437 and 6450:

Fidelity Active Trader Pro Directed Trading User Agreement

Fidelity Active Trader Pro Directed Trading User Agreement Important: Using Fidelity's directed trading functionality is subject to the Fidelity Active Trader Pro Directed Trading User Agreement (the 'Directed

Fidelity Active Trader Pro Directed Trading User Agreement Important: Using Fidelity's directed trading functionality is subject to the Fidelity Active Trader Pro Directed Trading User Agreement (the 'Directed

Citi Order Routing and Execution, LLC ( CORE ) Order Handling Document

Order Handling Document") Citi Order Routing and Execution, LLC ( CORE ) Order Handling Document CORE s automated systems have been designed and are routinely enhanced to automatically provide the highest level of regulatory compliance

Citi Order Routing and Execution, LLC ( CORE ) Order Handling Document CORE s automated systems have been designed and are routinely enhanced to automatically provide the highest level of regulatory compliance

CHX ORDER TYPES PRIMER

CHX ORDER TYPES PRIMER The CHX Order Types Primer is informational and summarizes the order types and modifiers offered by the Exchange and the general operation of the Exchange s automated trading facility,

CHX ORDER TYPES PRIMER The CHX Order Types Primer is informational and summarizes the order types and modifiers offered by the Exchange and the general operation of the Exchange s automated trading facility,

Periodic Auctions Book FAQ

Page 1 General What is the Cboe Periodic Auctions book? The Cboe Europe ( Cboe ) Periodic Auctions book is: > A lit order book that independently operates frequent randomised intra-day auctions throughout

Page 1 General What is the Cboe Periodic Auctions book? The Cboe Europe ( Cboe ) Periodic Auctions book is: > A lit order book that independently operates frequent randomised intra-day auctions throughout

Order Types and Functionality

Date of Issue: May 12, 2017 Contents 1. INTRODUCTION... 3 2. CONTACT... 3 3. TRADING SESSIONS... 3 3.1 Hours of Operation... 3 3.2 Pre-Open and Post-Open Priority and Allocation... 3 3.3 Opening... 3 3.4

Date of Issue: May 12, 2017 Contents 1. INTRODUCTION... 3 2. CONTACT... 3 3. TRADING SESSIONS... 3 3.1 Hours of Operation... 3 3.2 Pre-Open and Post-Open Priority and Allocation... 3 3.3 Opening... 3 3.4

BSE Trading Rules July 2012 TRADING RULES FOR EQUITY SECURITIES JULY 2012

TRADING RULES FOR EQUITY SECURITIES JULY 2012 i TABLE OF CONTENTS Page No: CHAPTER 1... 1 INTRODUCTION... 1 1.1 TRADING BOARDS... 1 1.2 TRADING AND SYSTEM OPERATION SESSIONS... 2 1.2.1 Pre-trading Session...

TRADING RULES FOR EQUITY SECURITIES JULY 2012 i TABLE OF CONTENTS Page No: CHAPTER 1... 1 INTRODUCTION... 1 1.1 TRADING BOARDS... 1 1.2 TRADING AND SYSTEM OPERATION SESSIONS... 2 1.2.1 Pre-trading Session...

Nasdaq CXC Subscriber Manual

Nasdaq CXC Limited Nasdaq CXC Subscriber Manual Nasdaq CXC Limited (NCXL) is an alternative trading system (ATS) that operates three trading books; Nasdaq CXC, Nasdaq CX2 (CX2) and Nasdaq CXD (CXD). This

Nasdaq CXC Limited Nasdaq CXC Subscriber Manual Nasdaq CXC Limited (NCXL) is an alternative trading system (ATS) that operates three trading books; Nasdaq CXC, Nasdaq CX2 (CX2) and Nasdaq CXD (CXD). This

AUTOMATED TRADING RULES

AUTOMATED TRADING RULES FEBRUARY 2018 CONTENTS INTRODUCTION 3 ENTERING ORDERS 3 DIVISION OF MARKET 4 TRADING SESSIONS 4 1. TYPES OF TRANSACTIONS 5 1.1 Limit Orders 1.2 Market Orders 1.2.1 Touchline 1.2.2

AUTOMATED TRADING RULES FEBRUARY 2018 CONTENTS INTRODUCTION 3 ENTERING ORDERS 3 DIVISION OF MARKET 4 TRADING SESSIONS 4 1. TYPES OF TRANSACTIONS 5 1.1 Limit Orders 1.2 Market Orders 1.2.1 Touchline 1.2.2

SEC TICK SIZE PILOT MEASURING THE IMPACT OF CHANGING THE TICK SIZE ON THE LIQUIDITY AND TRADING OF SMALLER PUBLIC COMPANIES

SEC TICK SIZE PILOT MEASURING THE IMPACT OF CHANGING THE TICK SIZE ON THE LIQUIDITY AND TRADING OF SMALLER PUBLIC COMPANIES APRIL 7, 2017 On May 6, 2015, the Securities & Exchange Commission (SEC) issued

SEC TICK SIZE PILOT MEASURING THE IMPACT OF CHANGING THE TICK SIZE ON THE LIQUIDITY AND TRADING OF SMALLER PUBLIC COMPANIES APRIL 7, 2017 On May 6, 2015, the Securities & Exchange Commission (SEC) issued

How orders are routed when sent to Autobahn s algorithmic strategies

Autobahn Equity EMEA Routing Logic February 2016 page 1/5 How orders are routed when sent to Autobahn s algorithmic strategies Deutsche Bank s algorithms utilise its Smart Order Router (SOR) and SuperX+

Autobahn Equity EMEA Routing Logic February 2016 page 1/5 How orders are routed when sent to Autobahn s algorithmic strategies Deutsche Bank s algorithms utilise its Smart Order Router (SOR) and SuperX+

NASDAQ ITCH to Trade Options

Market Data Feed Version 4.0 NASDAQ ITCH to Trade Options 1. Overview NASDAQ ITCH to Trade Options (ITTO) is a direct data feed product in NOM2 system offered by The NASDAQ Option Market, which features

Market Data Feed Version 4.0 NASDAQ ITCH to Trade Options 1. Overview NASDAQ ITCH to Trade Options (ITTO) is a direct data feed product in NOM2 system offered by The NASDAQ Option Market, which features

Appendix n: Manual Trades

Early draft proposal for INET Nordic Market Model version effective as of January 3, 2017 Appendix n: Manual Trades For trading on-exchange, the Member can either make Trades in the Order Book or outside

Early draft proposal for INET Nordic Market Model version effective as of January 3, 2017 Appendix n: Manual Trades For trading on-exchange, the Member can either make Trades in the Order Book or outside

Pursuant to Section 11A of the Securities Exchange Act of 1934 ( Act ) 1 and Rule 608

1 and Rule 608") This document is scheduled to be published in the Federal Register on 04/18/2016 and available online at http://federalregister.gov/a/2016-08815, and on FDsys.gov 8011-01p SECURITIES AND EXCHANGE COMMISSION

This document is scheduled to be published in the Federal Register on 04/18/2016 and available online at http://federalregister.gov/a/2016-08815, and on FDsys.gov 8011-01p SECURITIES AND EXCHANGE COMMISSION

NATIONAL BANK FINANCIAL INC. BEST EXECUTION POLICY January NBF Best Execution Policy January

NATIONAL BANK FINANCIAL INC. BEST EXECUTION POLICY January 2018 NBF Best Execution Policy January 2018 1 8 Contents CONTENTS... 2 DEFINITIONS... 3 BEST EXECUTION OVERVIEW... 3 HOURS OF OPERATION FOR TRADING

NATIONAL BANK FINANCIAL INC. BEST EXECUTION POLICY January 2018 NBF Best Execution Policy January 2018 1 8 Contents CONTENTS... 2 DEFINITIONS... 3 BEST EXECUTION OVERVIEW... 3 HOURS OF OPERATION FOR TRADING

NYSE ARCA, INC. June 9, 2017

NYSE ARCA, INC. NYSE REGULATION, Complainant, FINRA Proceeding No. 20130354629-01 1 v. June 9, 2017 CITIGROUP GLOBAL MARKETS INC., Respondent. Respondent violated: (1) Exchange Act Rules 15c3-5(b) and

NYSE ARCA, INC. NYSE REGULATION, Complainant, FINRA Proceeding No. 20130354629-01 1 v. June 9, 2017 CITIGROUP GLOBAL MARKETS INC., Respondent. Respondent violated: (1) Exchange Act Rules 15c3-5(b) and

State Street Global Markets Canada Inc. ( SSGMC ) - Best Execution of Client Orders Disclosure

- Best Execution of Client Orders Disclosure") Global Markets State Street Global Markets Canada Inc. ( SSGMC ) - Best Execution of Client Orders Disclosure Effective Date: January 2, 2018 Last Change Date: January 2, 2018 1 State Street Global Markets

Global Markets State Street Global Markets Canada Inc. ( SSGMC ) - Best Execution of Client Orders Disclosure Effective Date: January 2, 2018 Last Change Date: January 2, 2018 1 State Street Global Markets

Dark markets. Darkness. Securities Trading: Principles and Procedures, Chapter 8

Securities Trading: Principles and Procedures, Chapter 8 Dark markets Copyright 2017, Joel Hasbrouck, All rights reserved 1 Darkness A dark market does not display bids and asks. Bids and asks may exist,

Securities Trading: Principles and Procedures, Chapter 8 Dark markets Copyright 2017, Joel Hasbrouck, All rights reserved 1 Darkness A dark market does not display bids and asks. Bids and asks may exist,

Omega/Lynx ATS Subscriber Manual v. 1.6 Effective Date: June 10, 2013

Omega/Lynx ATS Subscriber Manual v. 1.6 Effective Date: June 10, 2013 Revision History Date Description Author August 21, 2008 Standard boardlots (page 4) to change from 100 shares across all traded securities

Omega/Lynx ATS Subscriber Manual v. 1.6 Effective Date: June 10, 2013 Revision History Date Description Author August 21, 2008 Standard boardlots (page 4) to change from 100 shares across all traded securities

Version Overview