THE IMPACT OF DERIVATIVE COLLATERAL POLICIES OF EUROPEAN SOVEREIGNS AND RESULTING BASEL III CAPITAL ISSUES

|

|

|

- Cuthbert Norris

- 5 years ago

- Views:

Transcription

1 THE IMPACT OF DERIVATIVE COLLATERAL POLICIES OF EUROPEAN SOVEREIGNS AND RESULTING BASEL III CAPITAL ISSUES Summary The majority of sovereigns do not post collateral to support their use of over-the-counter ( OTC ) derivatives 1. As a result, dealers regularly have credit exposure arising out of these contracts which is often hedged with the sovereign Credit Default Swaps ( CDS ), and interest rate and foreign exchange swaps and options. This process has been of particular concern in Europe because of the possible ban on the use of sovereign CDS. To assist in highlighting this and other concerns arising out of the practice not to collateralize OTC derivatives, two associations 2 ( the Surveying Associations or SAs ) conducted a survey of dealers earlier this year, regarding their OTC derivatives exposure to European Sovereigns ( ES ). The survey and our analysis reveal the following: Derivatives exposure of dealers to ES may total as much as $70 billion; If dealers were to hedge their ES derivative exposure through single-name ES CDS, it could require as much as 50% of the entire ES open interest; One-way collateral relating to ES derivatives may drain as much as $70 billion from the financial system; The EU s new Short Selling Regulation provides a good basis for the use of ES CDS for hedging the counterparty exposure arising from derivative contracts; and Proposed Basel III rules do not recognize interest rate or foreign exchange products as hedges of ES derivatives exposure for capital charges. The paper will be organized as follows: Current Collateral Practices Current Exposure Management Practices Liquidity Effects of One-Way Credit Support Annex ( CSA ) Dealer Survey European Sovereign CDS Market Size EU Short Selling Regulation Basel Capital Requirements Conclusion 1 In Europe the exceptions are Portugal and the Republic of Ireland 2 The Association of Financial Markets in Europe ( AFME ) and The International Swaps and Derivatives Association ( ISDA ) are the SAs and the SAs along with the International Capital Markets Association ( ICMA ) are referred to as the Associations in this paper.

2 2 Current Collateral Practices Collateral arrangements between participants in the OTC derivatives market are generally governed by the CSA to ISDA s Master Agreement. Typically, each CSA is negotiated separately between dealer and client. For a large majority of frequent users, the CSAs are two-way, ie each entity is required to post collateral to the other to match the net exposure the other entity has to it through the mutual portfolio of OTC derivatives. In one-way CSAs, only one party to the contracts is required to post collateral to the other as exposures arise. The other party, however, has no obligation to post collateral if its positions have a net negative value. A majority of ES have one-way CSAs in place. They have historically used their superior credit and bargaining power to obtain these favorable contracts from dealers. As a result, any exposures that ES might have to dealers are always collateralized. Exposures the dealers have to ES, however, are unsecured. Current Exposure Management Practices Most dealers actively hedge uncollateralized OTC derivatives exposure through the CDS, interest rate swaps and foreign exchange markets. Typically, dealers focus on Expected Potential Exposure ( EPE ) to manage risk. For a single interest rate swap, EPE is a series of calculations along a forward yield curve valuing the remaining tenor of the swap. If a calculation produces a positive result, that amount is multiplied by the probability of default of the counterparty and discounted back to the present. If the result is negative, the amount is set at zero as one cannot benefit from a default of a counterparty. The sum of the positive discounted amounts is EPE. The EPE on a single swap is equivalent to the cost of buying swaptions that would replace the swap upon default at any point along the yield curve. So, at the onset, the size of the EPE needs to be hedged by the use of interest rate products, and the probability of default needs to be hedged by the use of CDS. As exposures increase, CDS become a very valuable tool for hedging risk. For example, in its 2010 annual report, a major international bank revealed it had purchased nearly $7 billion of sovereign CDS to offset its credit exposures to sovereigns around the world. Dealers generally assign the EPE hedging task to their CVA desks where CVA stands for Credit Valuation Adjustment. CVAs adjust mark to market derivatives receivables on dealers balance sheets to reflect the credit strength of each counterparty. An OTC derivatives contract creates a receivable on the books of a dealer when the payments to be made by a counterparty under the contract are above market. These above market cashflows are discounted at rates equal to the sum of the London Interbank Offered Rates ( LIBOR ) and the credit spreads associated with each counterparty for each point in time. The credit spread can be derived from the CDS credit curve for each counterparty. If an OTC derivative receivable grows in value, the growth in value will be booked as trading income. The growth in value, however, increases the credit exposure and EPE to the counterparty. If the credit spreads for the counterparty remain constant, the increase in value of the receivable will be accompanied by an increase in CVA. CVAs are booked as contra assets and increases in CVAs are run through the income statement as expenses or negative trading income.

3 3 As noted above, EPE is hedged through interest rate, foreign exchange and CDS products. In markets where the probabilities of default are rapidly rising, very large interest rate and foreign exchange rate positions can be created very quickly. Desks regularly assess which of the interest rate, foreign exchange or CDS markets is the most efficient and liquid. If a CVA desk were to buy CDS in amounts equal to EPE to the counterparty, it would consider itself hedged. It is interesting to note that a deterioration of a counterparty s credit will have no income statement effect if EPE is hedged but interest rate or foreign exchange movements will change the size of the derivative receivable and thereby have an impact on CVA. Liquidity Effects of One-Way CSA Sovereign entities have been participants in the OTC derivatives markets for decades. When ES first developed trading relationships, much of their derivative activity was tied to capital market business which was prestigious, profitable and consistent with dealers aspirations in the bond market. ES were also premier counterparties. At first, before collateral was a normal provision in the market place, ES accepted only the best credits as counterparties. As more and more OTC derivatives business became subject to collateralization, ES decided they needed collateral protection as well. Most, however, have not been willing to post collateral. In addition to creating credit exposure, the use of one-way CSAs has also created significant liquidity issues for the dealer community. This arises because dealer hedges of OTC derivatives with ES are themselves routinely subject to collateral arrangements. For example, suppose a dealer executes a cross-currency swap with a ES without an initial exchange of principal. The dealer needs to put in place both an FX hedge as well as an interest rate hedge. The FX hedge is transacted in the interbank market through a short-date forward contract. This exposure is subject to collateral. The interest rate hedge is executed through futures or government bonds. Either such hedge requires collateral. These temporary hedges are eventually offset through other OTC contracts, which will also require collateral. If the dealer has exposure to ES, its hedges will create opposite exposure and will need to be collateralized by the dealer. A reasonably good proxy for the amount of collateral that the dealer has to post is the amount of exposure EPE - it has to its ES counterparties. If no collateral relationships existed between dealers and ESs, dealers would receive a liquidity benefit to the extent the ESs have credit exposure to the dealers. The one-way CSA eliminates the possibility of this benefit for the dealers.

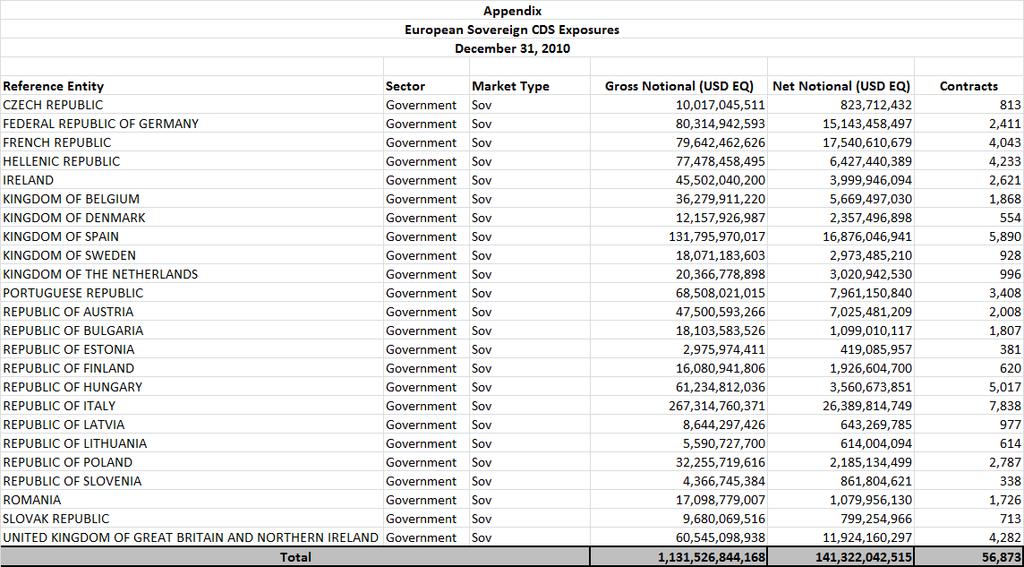

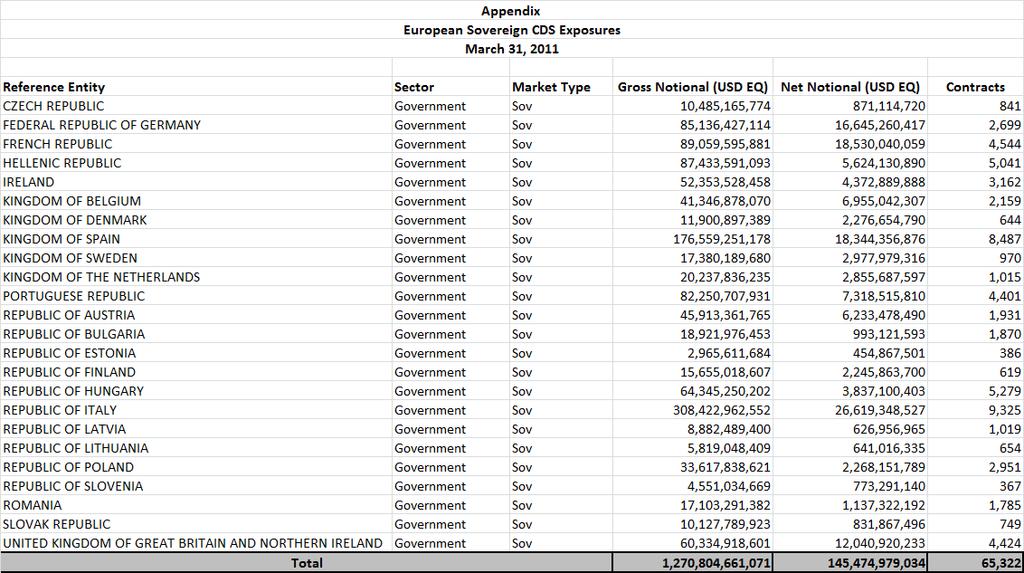

4 4 Dealer Survey This past spring, the SAs worked with the so-called G-14 (14 of the largest derivatives dealers in the world) to make an estimate of CDS hedging needs and losses of liquidity. Ideally, dealers would have provided the amount of CDS required to hedge CVA risk as well as the mark to market exposure for each ES. The mark to market would be a more precise estimate of the liquidity drain caused by each ES. Not surprisingly, despite assurances of anonymity, dealers were only willing to provide the amount of CDS they would have to purchase to hedge their CVA risk to the group of ES as a whole. This information was collected for the three quarters ended, September 2010, December 2010 and March The SAs did not get 100% participation but received responses from 12 firms for March 2011 and from 10 or 11 for the other two dates. To complete the analysis, it was assumed the missing dealers had EPE equal to the average of those that responded. This created the following EPE for the G-14: G-14 EPE to ES September 30, 2010 December 31, 2010 March 31, 2011 $61.4 billion $55.6 billion $56.4 billion These figures are by no means complete. There are, after all, 37 dealer members of LCH, each of which has $1 trillion or more of notional amounts of interest rate contracts outstanding. Presumably, many of these dealers have significant exposure to ES. The SAs used a simple shortcut to make an estimate of this additional exposure. TriOptima, which runs the interest rate derivatives trade repository, estimates that the G-14 represent about 80% of the market for interest rate swaps. Using this simple 80/20 rule to gross up the exposures of the G-14 presented above, one arrives at the following: Estimated Global Dealer EPE to ES September 30, 2010 December 31, 2010 March 31, 2011 $76.8 billion $69.5 billion $70.5 billion European Sovereign CDS Market Size With the help of DTCC, the SAs were able to determine the net notional exposures in the ES CDS marketplace for each quarter end. This is presented in the Appendix for each of the names covered in the survey. The totals are summarized below along with the exposures of the global dealers.

5 5 ES CDS Global Dealer as a % of ES Market EPE to ES CDS Market September 30, 2010 $137.8 Bn $76.8 Bn 55.7% December 31, 2010 $141.3 Bn $69.5 Bn 49.2% March 31, 2011 $145.5 Bn $70.5 Bn 48.5% As can be seen, the estimated exposures of dealers to sovereigns through OTC derivatives are quite significant relative to the size of the CDS market for the names involved. The figures also show that the estimated exposures and the open positions in the CDS market are reasonably constant close to $70 billion and $140 billion, respectively. What is not known is how much of the exposure is actually hedged. It is, however, reasonable to assume that, during this period, the amount of hedging has increased due to turmoil in the market for sovereign risk and the impact of CVA on dealers income statements. EU Short Selling Regulation Policymakers in Europe considered for some time the outright banning of naked CDS in ES reference entities. Partly as a result of industry action, the actual Short Selling Regulation permits the use of ES CDS as a hedge of the counterparty exposure from financial contracts. The regulation will be converted into technical standards by the European Securities Markets Authority ( ESMA ) and the Associations, respectfully, strongly recommend the ESMA respect the clear intent of the Regulation, particularly as regards its identification of financial contracts as exposures that firms might legitimately hedge through CDS. As can be seen, the need for ES CDS for hedging purposes is large and the inability of dealer firms to use ES CDS in this context might create unhealthy concentrations of credit risk and reduce ES access to the OTC derivatives marketplace. Basel Capital Requirements Under Basel II, exposure to sovereign risk was handled under one of two approaches. Under the standardized approach, exposures were given zero risk weighting provided the sovereign was rated AA or above. Under the Internal Model Method ( IMM ), firms were able to develop capital charges using models approved by regulators. As a result, it is believed the exposures mentioned above carried little capital charge until certain ES were downgraded in the past year. Basel III retains the capital charge methodology with respect to sovereign exposure but adds a new capital charge linked to CVA. This capital charge may be computed in one of two ways. First, using a standard approach, a probability of default derived from a counterparty s rating is calculated for annual calendar points and a loss given default assumed. The resulting small percentage is then applied to expected exposure and discounted to the present. The sum of these amounts is then a form of expected losses and is the CVA risk weighted asset amount. Under a modeling approach, dealer firms use credit

6 6 default spreads to calculate probabilities of default. Given the current environment, this approach produces much larger capital charges. Basel III does provide capital relief if positions are hedged with single name CDS. This can only provide even more incentive for dealers to hedge their exposure to sovereigns with CDS. However, there is a very serious shortfall in the Basel III rules regarding CVA hedging. As we have seen, interest rate and foreign exchange products are important means of managing CVA risk. However, they are not considered hedges of CVA risk, and, hence, do not lead to reduced capital charges. To the contrary, they are considered proprietary positions and themselves attract further capital charges. This creates unsatisfactory unintended consequences as it discourages hedging. The industry will continue to promote the correction of this which it views to be a serious error. While ES did not create this rule, the application of the rule would have much less effect if ES posted collateral. Conclusion The Associations believe the use of one- way CSAs by ES has created meaningful credit risks in the financial system and has also drained liquidity from the banking system. The CDS market for ES reference entities is an important hedging tool and it is very important that its use for hedging remains permissible under recent EU legislation. Dealers also hedge EPE risk with interest rate and FX products. Unfortunately use of these products will attract significant capital charges under proposed Basel III rules. Adoption of two-way CSAs by ES would ameliorate all of the issues discussed in this paper and the Associations accordingly recommend that such a change be given careful consideration. An additional benefit we have not discussed is the increased transparency this product would bring to the level of ES indebtedness which is surely not a bad side effect.

7

8

9

The Changing Landscape for Derivatives. John Hull Joseph L. Rotman School of Management University of Toronto.

The Changing Landscape for Derivatives John Hull Joseph L. Rotman School of Management University of Toronto hull@rotman.utoronto.ca April 2014 ABSTRACT This paper describes the changes taking place in

The Changing Landscape for Derivatives John Hull Joseph L. Rotman School of Management University of Toronto hull@rotman.utoronto.ca April 2014 ABSTRACT This paper describes the changes taking place in

XVA S, CSA S & OTC CLEARING

XVA S, CSA S & OTC CLEARING Plus the impact of regulation on OTC Derivatives Date November 2016 Author Darren Hooton, Business and Corporate Sales - FICC DEMYSTIFYING SOME OF THE DERIVATIVE MARKET TLA

XVA S, CSA S & OTC CLEARING Plus the impact of regulation on OTC Derivatives Date November 2016 Author Darren Hooton, Business and Corporate Sales - FICC DEMYSTIFYING SOME OF THE DERIVATIVE MARKET TLA

Discounting. Jeroen Kerkhof. 22 September c Copyright VAR Strategies BVBA 1 / 53

Discounting Jeroen Kerkhof 22 September 2010 c Copyright VAR Strategies BVBA 1 / 53 Overview c Copyright VAR Strategies BVBA 2 / 53 Time Value of Money c Copyright VAR Strategies BVBA 3 / 53 Time Value

Discounting Jeroen Kerkhof 22 September 2010 c Copyright VAR Strategies BVBA 1 / 53 Overview c Copyright VAR Strategies BVBA 2 / 53 Time Value of Money c Copyright VAR Strategies BVBA 3 / 53 Time Value

ANALYZING INTEREST RATE EXPOSURE

ANALYZING INTEREST RATE EXPOSURE STEFFAN TSILIMOS INTEREST RATE DERIVATIVES SPECIALIST STSILIMOS1@BLOOMBERG.NET PH: 212-617-8211 2 ARKET ONDITIONS Market Conditions While the market is stabilizing from

ANALYZING INTEREST RATE EXPOSURE STEFFAN TSILIMOS INTEREST RATE DERIVATIVES SPECIALIST STSILIMOS1@BLOOMBERG.NET PH: 212-617-8211 2 ARKET ONDITIONS Market Conditions While the market is stabilizing from

CVA. What Does it Achieve?

CVA What Does it Achieve? Jon Gregory (jon@oftraining.com) page 1 Motivation for using CVA The uncertainty of CVA Credit curve mapping Challenging in hedging CVA The impact of Basel III rules page 2 Motivation

CVA What Does it Achieve? Jon Gregory (jon@oftraining.com) page 1 Motivation for using CVA The uncertainty of CVA Credit curve mapping Challenging in hedging CVA The impact of Basel III rules page 2 Motivation

Hedging CVA. Jon Gregory ICBI Global Derivatives. Paris. 12 th April 2011

Hedging CVA Jon Gregory (jon@solum-financial.com) ICBI Global Derivatives Paris 12 th April 2011 CVA is very complex CVA is very hard to calculate (even for vanilla OTC derivatives) Exposure at default

Hedging CVA Jon Gregory (jon@solum-financial.com) ICBI Global Derivatives Paris 12 th April 2011 CVA is very complex CVA is very hard to calculate (even for vanilla OTC derivatives) Exposure at default

MiFID II: Information on Financial instruments

MiFID II: Information on Financial instruments A. Introduction This information is provided to you being categorized as a Professional client to inform you on financial instruments offered by Rabobank

MiFID II: Information on Financial instruments A. Introduction This information is provided to you being categorized as a Professional client to inform you on financial instruments offered by Rabobank

CVA in Energy Trading

CVA in Energy Trading Arthur Rabatin Credit Risk in Energy Trading London, November 2016 Disclaimer The document author is Arthur Rabatin and all views expressed in this document are his own. All errors

CVA in Energy Trading Arthur Rabatin Credit Risk in Energy Trading London, November 2016 Disclaimer The document author is Arthur Rabatin and all views expressed in this document are his own. All errors

Using Eris Swap Futures to Hedge Mortgage Servicing Rights

Using Eris Swap Futures to Hedge Mortgage Servicing Rights Introduction Michael Riley, Jeff Bauman and Rob Powell March 24, 2017 Interest rate swaps are widely used by market participants to hedge mortgage

Using Eris Swap Futures to Hedge Mortgage Servicing Rights Introduction Michael Riley, Jeff Bauman and Rob Powell March 24, 2017 Interest rate swaps are widely used by market participants to hedge mortgage

Counterparty Credit Risk Management in the US Over-the-Counter (OTC) Derivatives Markets, Part II

Derivatives Markets, Part II") November 2011 Counterparty Credit Risk Management in the US Over-the-Counter (OTC) Derivatives Markets, Part II A Review of Monoline Exposures Introduction This past August, ISDA published a short paper

November 2011 Counterparty Credit Risk Management in the US Over-the-Counter (OTC) Derivatives Markets, Part II A Review of Monoline Exposures Introduction This past August, ISDA published a short paper

ING response to the draft Technical Standards for the Regulation on OTC Derivatives, CCPs and Trade Repositories

ING response to the draft Technical Standards for the Regulation on OTC Derivatives, CCPs and Trade Repositories 3 August 2012 About ING Contact: Jeroen Groothuis Group Public & Government Affairs T +31

ING response to the draft Technical Standards for the Regulation on OTC Derivatives, CCPs and Trade Repositories 3 August 2012 About ING Contact: Jeroen Groothuis Group Public & Government Affairs T +31

COPYRIGHTED MATERIAL. 1 The Credit Derivatives Market 1.1 INTRODUCTION

1 The Credit Derivatives Market 1.1 INTRODUCTION Without a doubt, credit derivatives have revolutionised the trading and management of credit risk. They have made it easier for banks, who have historically

1 The Credit Derivatives Market 1.1 INTRODUCTION Without a doubt, credit derivatives have revolutionised the trading and management of credit risk. They have made it easier for banks, who have historically

PENNSYLVANIA TURNPIKE COMMISSION POLICY AND PROCEDURE

PTC 502005539 (12/05) Policy Subject: 7.7 - Interest Rate Swap Management Policy PENNSYLVANIA TURNPIKE COMMISSION POLICY AND PROCEDURE This is a statement of official Pennsylvania Turnpike Commission Policy

PTC 502005539 (12/05) Policy Subject: 7.7 - Interest Rate Swap Management Policy PENNSYLVANIA TURNPIKE COMMISSION POLICY AND PROCEDURE This is a statement of official Pennsylvania Turnpike Commission Policy

Introduction to Derivative Instruments Part 2

Link n Learn Introduction to Derivative Instruments Part 2 Leading Business Advisors Contacts Elaine Canty - Manager Financial Advisory Ireland Email: ecanty@deloitte.ie Tel: 00 353 417 2991 Fabian De

Link n Learn Introduction to Derivative Instruments Part 2 Leading Business Advisors Contacts Elaine Canty - Manager Financial Advisory Ireland Email: ecanty@deloitte.ie Tel: 00 353 417 2991 Fabian De

Funding Value Adjustments and Discount Rates in the Valuation of Derivatives

Funding Value Adjustments and Discount Rates in the Valuation of Derivatives John Hull Marie Curie Conference, Konstanz April 11, 2013 1 Question to be Considered Should funding costs be taken into account

Funding Value Adjustments and Discount Rates in the Valuation of Derivatives John Hull Marie Curie Conference, Konstanz April 11, 2013 1 Question to be Considered Should funding costs be taken into account

September 28, Japanese Bankers Association

September 28, 2012 Comments on the Consultative Document from Basel Committee on Banking Supervision and the International Organization of Securities Commissions : Margin requirements for non-centrally-cleared

September 28, 2012 Comments on the Consultative Document from Basel Committee on Banking Supervision and the International Organization of Securities Commissions : Margin requirements for non-centrally-cleared

Basel Committee on Banking Supervision. Basel III counterparty credit risk - Frequently asked questions

Basel Committee on Banking Supervision Basel III counterparty credit risk - Frequently asked questions November 2011 Copies of publications are available from: Bank for International Settlements Communications

Basel Committee on Banking Supervision Basel III counterparty credit risk - Frequently asked questions November 2011 Copies of publications are available from: Bank for International Settlements Communications

Derivatives Use Policy. Updated and Approved by the Board of Trustees November 13, 2014

Derivatives Use Policy Updated and Approved by the Board of Trustees November 13, 2014 Originated July 22, 2010 Table of Contents 1. STATEMENT OF PURPOSE... 1 2. SUBORDINATE POLICIES... 1 3. AUTHORIZATIONS...

Derivatives Use Policy Updated and Approved by the Board of Trustees November 13, 2014 Originated July 22, 2010 Table of Contents 1. STATEMENT OF PURPOSE... 1 2. SUBORDINATE POLICIES... 1 3. AUTHORIZATIONS...

INTEREST RATE SWAP POLICY

INTEREST RATE SWAP POLICY August 2007 Table of Contents I. Introduction... 1 II. Scope and Authority... 1 III. Conditions for the Use of Interest Rate Swaps... 1 A. General Usage... 1 B. Maximum Notional

INTEREST RATE SWAP POLICY August 2007 Table of Contents I. Introduction... 1 II. Scope and Authority... 1 III. Conditions for the Use of Interest Rate Swaps... 1 A. General Usage... 1 B. Maximum Notional

PA TURNPIKE COMMISSION POLICY

POLICY SUBJECT: PA TURNPIKE COMMISSION POLICY This is a statement of official Pennsylvania Turnpike Policy RESPONSIBLE DEPARTMENT: NUMBER: 7.07 APPROVAL DATE: 05-07-2013 EFFECTIVE DATE: 05-07-2013 7.07

POLICY SUBJECT: PA TURNPIKE COMMISSION POLICY This is a statement of official Pennsylvania Turnpike Policy RESPONSIBLE DEPARTMENT: NUMBER: 7.07 APPROVAL DATE: 05-07-2013 EFFECTIVE DATE: 05-07-2013 7.07

EMIR FAQ 1. WHAT IS EMIR?

EMIR FAQ The following information has been compiled for the purposes of providing an overview of EMIR and is not legal advice. The information is only accurate at date of publication and is subject to

EMIR FAQ The following information has been compiled for the purposes of providing an overview of EMIR and is not legal advice. The information is only accurate at date of publication and is subject to

Case 11-2(a) Instrument 1 Collateralized Debt Obligation

Instrument 1 Collateralized Debt Obligation") Case 11-2(a) Fair Value Hierarchy Family Finance Co. (FFC), a publicly traded commercial bank located in South Carolina, has a December 31 year-end. FFC invests in a variety of securities to enhance returns,

Case 11-2(a) Fair Value Hierarchy Family Finance Co. (FFC), a publicly traded commercial bank located in South Carolina, has a December 31 year-end. FFC invests in a variety of securities to enhance returns,

Counterparty Credit Risk and CVA

Jon Gregory Solum Financial jon@solum-financial.com 10 th April, SIAG Consulting, Madrid page 1 History The Complexity of CVA Impact of Regulation Where Will This Lead Us? 10 th April, SIAG Consulting,

Jon Gregory Solum Financial jon@solum-financial.com 10 th April, SIAG Consulting, Madrid page 1 History The Complexity of CVA Impact of Regulation Where Will This Lead Us? 10 th April, SIAG Consulting,

RBS Collective Investment Funds Ltd Derivatives Risk Management Policy. Part 1: Authorised Corporate Director ( ACD ) Overarching Arrangements

Overarching Arrangements") RBS Collective Investment Funds Ltd Derivatives Risk Management Policy Part 1: Authorised Corporate Director ( ACD ) Overarching Arrangements 1 Contents Policy Statement 3 Derivatives Defined 3 Credit

RBS Collective Investment Funds Ltd Derivatives Risk Management Policy Part 1: Authorised Corporate Director ( ACD ) Overarching Arrangements 1 Contents Policy Statement 3 Derivatives Defined 3 Credit

INTEREST RATE & FINANCIAL RISK MANAGEMENT POLICY Adopted February 18, 2009

WESTERN MUNICIPAL WATER DISTRICT INTEREST RATE & FINANCIAL RISK MANAGEMENT POLICY Adopted February 18, 2009 I. INTRODUCTION The purpose of this Interest Rate Swap and Hedge Agreement Policy ( Policy )

WESTERN MUNICIPAL WATER DISTRICT INTEREST RATE & FINANCIAL RISK MANAGEMENT POLICY Adopted February 18, 2009 I. INTRODUCTION The purpose of this Interest Rate Swap and Hedge Agreement Policy ( Policy )

New challenges in interest rate derivatives valuation Simple is not just simple anymore. Guillaume Ledure Manager Advisory & Consulting Deloitte

New challenges in interest rate derivatives valuation Simple is not just simple anymore Guillaume Ledure Manager Advisory & Consulting Deloitte In the past, the valuation of plain vanilla swaps has been

New challenges in interest rate derivatives valuation Simple is not just simple anymore Guillaume Ledure Manager Advisory & Consulting Deloitte In the past, the valuation of plain vanilla swaps has been

Counterparty Credit Risk under Basel III

Counterparty Credit Risk under Basel III Application on simple portfolios Mabelle SAYAH European Actuarial Journal Conference September 8 th, 2016 Recent crisis and Basel III After recent crisis, and the

Counterparty Credit Risk under Basel III Application on simple portfolios Mabelle SAYAH European Actuarial Journal Conference September 8 th, 2016 Recent crisis and Basel III After recent crisis, and the

Heir to LIBOR. The Background Why? November 2017

November 2017 Heir to LIBOR For many of us in the U.S., the UK Financial Conduct Authority s (FCA) decision to abolish LIBOR by the end of 2021 is a non-event, not to mention it is still four years away

November 2017 Heir to LIBOR For many of us in the U.S., the UK Financial Conduct Authority s (FCA) decision to abolish LIBOR by the end of 2021 is a non-event, not to mention it is still four years away

12th February, The European Banking Authority One Canada Square (Floor 46), Canary Wharf London E14 5AA - United Kingdom

, Canary Wharf London E14 5AA - United Kingdom") 12th February, 2016 The European Banking Authority One Canada Square (Floor 46), Canary Wharf London E14 5AA - United Kingdom Re: Industry Response to the EBA Consultative Paper on the Guidelines on the

12th February, 2016 The European Banking Authority One Canada Square (Floor 46), Canary Wharf London E14 5AA - United Kingdom Re: Industry Response to the EBA Consultative Paper on the Guidelines on the

Research Note. Derivatives Market Analysis: Interest Rate Derivatives

July 2016 Research Note Derivatives Market Analysis: Interest Rate Derivatives Twice a year, the International Swaps and Derivatives Association (ISDA) analyzes interest rate derivatives notional outstanding

July 2016 Research Note Derivatives Market Analysis: Interest Rate Derivatives Twice a year, the International Swaps and Derivatives Association (ISDA) analyzes interest rate derivatives notional outstanding

REAL ESTATE DERIVATIVES: DRIVE TO DERIVE. September 2005

: DRIVE TO DERIVE September 2005 The Townsend Group Institutional Real Estate Consultants Cleveland, OH Denver, CO San Francisco, CA NEW PRODUCTS COULD BE BENEFICIAL TO INVESTORS The $151 trillion global

: DRIVE TO DERIVE September 2005 The Townsend Group Institutional Real Estate Consultants Cleveland, OH Denver, CO San Francisco, CA NEW PRODUCTS COULD BE BENEFICIAL TO INVESTORS The $151 trillion global

MORGAN STANLEY SMITH BARNEY LLC CONSOLIDATED STATEMENT OF FINANCIAL CONDITION AS OF JUNE 30, 2017 (UNAUDITED)

") MORGAN STANLEY SMITH BARNEY LLC CONSOLIDATED STATEMENT OF FINANCIAL CONDITION AS OF JUNE 30, 2017 (UNAUDITED) ******** MORGAN STANLEY SMITH BARNEY LLC CONSOLIDATED STATEMENT OF FINANCIAL CONDITION June

MORGAN STANLEY SMITH BARNEY LLC CONSOLIDATED STATEMENT OF FINANCIAL CONDITION AS OF JUNE 30, 2017 (UNAUDITED) ******** MORGAN STANLEY SMITH BARNEY LLC CONSOLIDATED STATEMENT OF FINANCIAL CONDITION June

Saudi Banks Comments on Margin Requirements for Non-Centrally Cleared Derivatives

Annex Saudi Banks Comments on Margin Requirements for Non-Centrally Cleared Derivatives Bank # 1: The background to the consultative paper is clear, as the policy proposals in the paper seek to ensure

Annex Saudi Banks Comments on Margin Requirements for Non-Centrally Cleared Derivatives Bank # 1: The background to the consultative paper is clear, as the policy proposals in the paper seek to ensure

CHINA CONSTRUCTION BANK (ASIA) CORPORATION LIMITED. Regulatory Disclosures For the year ended 31 December 2017 (Unaudited)

CORPORATION LIMITED. Regulatory Disclosures For the year ended 31 December 2017 (Unaudited)") CHINA CONSTRUCTION BANK (ASIA) CORPORATION LIMITED For the year ended 31 December 2017 (Unaudited) Table of contents Page Key capital ratios 1 Template OVA: Overview of Risk Management 2 Template OV1:

CHINA CONSTRUCTION BANK (ASIA) CORPORATION LIMITED For the year ended 31 December 2017 (Unaudited) Table of contents Page Key capital ratios 1 Template OVA: Overview of Risk Management 2 Template OV1:

Discussion of Replumbing Our Financial System: Uneven Progress

Discussion of Replumbing Our Financial System: Uneven Progress Stephen G. Cecchetti Bank for International Settlements 1. Introduction Professor Duffie has written a wide-ranging and thoughtful paper on

Discussion of Replumbing Our Financial System: Uneven Progress Stephen G. Cecchetti Bank for International Settlements 1. Introduction Professor Duffie has written a wide-ranging and thoughtful paper on

Danish Ship Finance Risk Report 2017

Danish Ship Finance Risk Report 2017 CVR NO. 27 49 26 49 Introduction The objective of the Risk Report is to inform shareholders and other stakeholders of the Group s risk management, including policies,

Danish Ship Finance Risk Report 2017 CVR NO. 27 49 26 49 Introduction The objective of the Risk Report is to inform shareholders and other stakeholders of the Group s risk management, including policies,

Developments in Processing Over-the-Counter Derivatives

Developments in Processing Over-the-Counter Derivatives Natasha Khan* T his article discusses the main findings of the report New Developments in Clearing and Settlement Arrangements for OTC Derivatives

Developments in Processing Over-the-Counter Derivatives Natasha Khan* T his article discusses the main findings of the report New Developments in Clearing and Settlement Arrangements for OTC Derivatives

Adverse Liquidity Effects of the EU Uncovered Sovereign CDS Ban

Research Note Adverse Liquidity Effects of the EU Uncovered Sovereign CDS Ban January 2014 Summary On November 1, 2012, the provisions of Regulation (EU) No 236/2012 of the European Parliament and the

Research Note Adverse Liquidity Effects of the EU Uncovered Sovereign CDS Ban January 2014 Summary On November 1, 2012, the provisions of Regulation (EU) No 236/2012 of the European Parliament and the

Derivative Contracts and Counterparty Risk

Lecture 13 Derivative Contracts and Counterparty Risk Giampaolo Gabbi Financial Investments and Risk Management MSc in Finance 2016-2017 Agenda The counterparty risk Risk Measurement, Management and Reporting

Lecture 13 Derivative Contracts and Counterparty Risk Giampaolo Gabbi Financial Investments and Risk Management MSc in Finance 2016-2017 Agenda The counterparty risk Risk Measurement, Management and Reporting

INTEREST RATE SWAP POLICY

INTEREST RATE SWAP POLICY I. INTRODUCTION The purpose of this Interest Rate Swap Policy (Policy) of the Riverside County Transportation Commission (RCTC) is to establish guidelines for the use and management

INTEREST RATE SWAP POLICY I. INTRODUCTION The purpose of this Interest Rate Swap Policy (Policy) of the Riverside County Transportation Commission (RCTC) is to establish guidelines for the use and management

European Commission Public Consultation on Short Selling

July 2010 European Commission Public Consultation on Short Selling Reply from NASDAQ OMX The NASDAQ OMX Group, Inc. delivers trading, exchange technology, listings and other public company services and

July 2010 European Commission Public Consultation on Short Selling Reply from NASDAQ OMX The NASDAQ OMX Group, Inc. delivers trading, exchange technology, listings and other public company services and

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended December 31, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended December 31, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

Canada Credit Rating Action Plan

January 27, 2014 Canada Credit Rating Action Plan I: Banks Milestones and Action to be taken changes in standards) 1. Reducing reliance on CRA ratings in laws and regulations (Principle I) Based on the

January 27, 2014 Canada Credit Rating Action Plan I: Banks Milestones and Action to be taken changes in standards) 1. Reducing reliance on CRA ratings in laws and regulations (Principle I) Based on the

Solvency Assessment and Management: Pillar 1 - Sub Committee Technical Provisions Task Group Discussion Document 40 (v 3) Risk-free Rate: Dashboard

Risk-free Rate: Dashboard") Solvency Assessment and Management: Pillar 1 - Sub Committee Technical Provisions Task Group Discussion Document 40 (v 3) Risk-free Rate: Dashboard EXECUTIVE SUMMARY 1. INTRODUCTION AND PURPOSE The purpose

Solvency Assessment and Management: Pillar 1 - Sub Committee Technical Provisions Task Group Discussion Document 40 (v 3) Risk-free Rate: Dashboard EXECUTIVE SUMMARY 1. INTRODUCTION AND PURPOSE The purpose

IFRS 13 - CVA, DVA AND THE IMPLICATIONS FOR HEDGE ACCOUNTING

WHITEPAPER IFRS 13 - CVA, DVA AND THE IMPLICATIONS FOR HEDGE ACCOUNTING By Dmitry Pugachevsky, Rohan Douglas (Quantifi) Searle Silverman, Philip Van den Berg (Deloitte) IFRS 13 ACCOUNTING FOR CVA & DVA

WHITEPAPER IFRS 13 - CVA, DVA AND THE IMPLICATIONS FOR HEDGE ACCOUNTING By Dmitry Pugachevsky, Rohan Douglas (Quantifi) Searle Silverman, Philip Van den Berg (Deloitte) IFRS 13 ACCOUNTING FOR CVA & DVA

Managing capital and liquidity impacts on collateral management

Managing capital and liquidity impacts on collateral management Ben Watson ben.watson@maroonanalytics.com www.maroonanalytics.com About your presenter Ben Watson has worked for more than 20 years as a

Managing capital and liquidity impacts on collateral management Ben Watson ben.watson@maroonanalytics.com www.maroonanalytics.com About your presenter Ben Watson has worked for more than 20 years as a

Thoughts on determining central clearing eligibility of OTC derivatives

Financial Stability Paper No. 14 March 2012 Thoughts on determining central clearing eligibility of OTC derivatives Che Sidanius and Anne Wetherilt Financial Stability Paper No. 14 March 2012 Thoughts

Financial Stability Paper No. 14 March 2012 Thoughts on determining central clearing eligibility of OTC derivatives Che Sidanius and Anne Wetherilt Financial Stability Paper No. 14 March 2012 Thoughts

1.2 Product nature of credit derivatives

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

1.2 Product nature of credit derivatives Payoff depends on the occurrence of a credit event: default: any non-compliance with the exact specification of a contract price or yield change of a bond credit

Swap hedging of foreign exchange and interest rate risk

Lecture notes on risk management, public policy, and the financial system of foreign exchange and interest rate risk Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: March 18, 2018 2

Lecture notes on risk management, public policy, and the financial system of foreign exchange and interest rate risk Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: March 18, 2018 2

Basel III - Implementation issues facing the Industry. Patricia Jackson Head of Financial Regulation Advisory EMEIA

Basel III - Implementation issues facing the Industry Patricia Jackson Systemically Important Banks FSB paper on intensive supervision Other elements are under discussion Contains a number of components:

Basel III - Implementation issues facing the Industry Patricia Jackson Systemically Important Banks FSB paper on intensive supervision Other elements are under discussion Contains a number of components:

Practical guidance at Lexis Practice Advisor

Lexis Practice Advisor offers beginning-to-end practical guidance to support attorneys work in specific transactional practice areas. Grounded in the real-world experience of expert practitioner-authors,

Lexis Practice Advisor offers beginning-to-end practical guidance to support attorneys work in specific transactional practice areas. Grounded in the real-world experience of expert practitioner-authors,

Mobilising collateral the growing need for counterparty diversification

Mobilising collateral the growing need for counterparty diversification Greater diversification of counterparties in the repo market can halt the decline in liquidity, says Roberto Verrillo at Elixium.

Mobilising collateral the growing need for counterparty diversification Greater diversification of counterparties in the repo market can halt the decline in liquidity, says Roberto Verrillo at Elixium.

Challenges in Managing Counterparty Credit Risk

Challenges in Managing Counterparty Credit Risk Jon Gregory www.oftraining.com Jon Gregory (jon@oftraining.com), Credit Risk Summit, London, 14 th October 2010 page 1 Jon Gregory (jon@oftraining.com),

Challenges in Managing Counterparty Credit Risk Jon Gregory www.oftraining.com Jon Gregory (jon@oftraining.com), Credit Risk Summit, London, 14 th October 2010 page 1 Jon Gregory (jon@oftraining.com),

City of Portland Interest Rate Exchange Agreement Policy

City of Portland Interest Rate Exchange Agreement Policy City of Portland Philosophy Regarding Use of Interest Rate Exchange Agreements Introduction Interest rate exchange agreements ( Swaps ) and related

City of Portland Interest Rate Exchange Agreement Policy City of Portland Philosophy Regarding Use of Interest Rate Exchange Agreements Introduction Interest rate exchange agreements ( Swaps ) and related

1.0 Purpose. Financial Services Commission of Ontario Commission des services financiers de l Ontario. Investment Guidance Notes

Financial Services Commission of Ontario Commission des services financiers de l Ontario SECTION: INDEX NO.: TITLE: APPROVED BY: Investment Guidance Notes IGN-002 Prudent Investment Practices for Derivatives

Financial Services Commission of Ontario Commission des services financiers de l Ontario SECTION: INDEX NO.: TITLE: APPROVED BY: Investment Guidance Notes IGN-002 Prudent Investment Practices for Derivatives

Best Execution Policy

SUBJECT: BEST EXECUTION OVERVIEW: This policy sets out the rules and responsibilities for the best execution of orders on behalf of clients whom we have classified as professional clients of. TABLE OF

SUBJECT: BEST EXECUTION OVERVIEW: This policy sets out the rules and responsibilities for the best execution of orders on behalf of clients whom we have classified as professional clients of. TABLE OF

PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. December 2012 PILLAR 3 DISCLOSURES For the period ended June 30, 2014 TABLE OF CONTENTS Page No. Index of Tables 2 Introduction 3 Regulatory Capital 7 Capital Structure 8

The Goldman Sachs Group, Inc. December 2012 PILLAR 3 DISCLOSURES For the period ended June 30, 2014 TABLE OF CONTENTS Page No. Index of Tables 2 Introduction 3 Regulatory Capital 7 Capital Structure 8

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended September 30, 2016 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended September 30, 2016 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

CDS on Bclear. Liffe CDS. ECB, Frankfurt. 24 February NYSE Euronext All Rights Reserved

CDS on Bclear Liffe CDS ECB, Frankfurt 24 February 2009 Ade Cordell Chris Jones Director, OTC Services Director, Head of Risk Management NYSE Euronext LCH.Clearnet ACordell@nyx.com Chris.Jones@lchclearnet.com

CDS on Bclear Liffe CDS ECB, Frankfurt 24 February 2009 Ade Cordell Chris Jones Director, OTC Services Director, Head of Risk Management NYSE Euronext LCH.Clearnet ACordell@nyx.com Chris.Jones@lchclearnet.com

Feedback Statement Consultation on the Clearing Obligation for Non-Deliverable Forwards

Feedback Statement Consultation on the Clearing Obligation for Non-Deliverable Forwards 4 February 2015 2015/ESMA/234 Table of Contents 1 Executive Summary... 2 2 Background... 3 3 Results of the consultation...

Feedback Statement Consultation on the Clearing Obligation for Non-Deliverable Forwards 4 February 2015 2015/ESMA/234 Table of Contents 1 Executive Summary... 2 2 Background... 3 3 Results of the consultation...

Credit Risk in Derivatives Products

Credit Risk in Derivatives Products Understand how derivatives work, how they are used and the inherent credit risk experienced by both banks and their customers This in-house course can be presented in-house

Credit Risk in Derivatives Products Understand how derivatives work, how they are used and the inherent credit risk experienced by both banks and their customers This in-house course can be presented in-house

UNDERSTANDING AND MANAGING OPTION RISK

UNDERSTANDING AND MANAGING OPTION RISK Daniel J. Dwyer Managing Principal Dwyer Capital Strategies L.L.C. Bloomington, MN dan@dwyercap.com 952-681-7920 August 9 & 10, 2018 Dwyer Capital Strategies L.L.C.

UNDERSTANDING AND MANAGING OPTION RISK Daniel J. Dwyer Managing Principal Dwyer Capital Strategies L.L.C. Bloomington, MN dan@dwyercap.com 952-681-7920 August 9 & 10, 2018 Dwyer Capital Strategies L.L.C.

PILLAR 3 DISCLOSURES

. The Goldman Sachs Group, Inc. December 2012 PILLAR 3 DISCLOSURES For the period ended December 31, 2014 TABLE OF CONTENTS Page No. Index of Tables 2 Introduction 3 Regulatory Capital 7 Capital Structure

. The Goldman Sachs Group, Inc. December 2012 PILLAR 3 DISCLOSURES For the period ended December 31, 2014 TABLE OF CONTENTS Page No. Index of Tables 2 Introduction 3 Regulatory Capital 7 Capital Structure

Comments on the Basel Committee on Banking Supervision s Consultative Document Fundamental review of the trading book: outstanding issues

February 20, 2015 Comments on the Basel Committee on Banking Supervision s Consultative Document Fundamental review of the trading book: outstanding issues Japanese Bankers Association We, the Japanese

February 20, 2015 Comments on the Basel Committee on Banking Supervision s Consultative Document Fundamental review of the trading book: outstanding issues Japanese Bankers Association We, the Japanese

Credit Valuation Adjustment

Credit Valuation Adjustment Implementation of CVA PRMIA Credit Valuation Adjustment (CVA) CONGRESS IMPLEMENTATION UND PRAXIS Wolfgang Putschögl Köln, 20 th July 2011 CVA in a nutshell Usually pricing of

Credit Valuation Adjustment Implementation of CVA PRMIA Credit Valuation Adjustment (CVA) CONGRESS IMPLEMENTATION UND PRAXIS Wolfgang Putschögl Köln, 20 th July 2011 CVA in a nutshell Usually pricing of

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD)

") Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) December 2016 As a follow-up to the recommendation in the Committee on the Global Financial

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) December 2016 As a follow-up to the recommendation in the Committee on the Global Financial

Bond Basics January 2008

Bond Basics: What Are Interest Rate Swaps and How Do They Work? Interest-rate swaps have become an integral part of the fixed-income market. These derivative contracts, which typically exchange or swap

Bond Basics: What Are Interest Rate Swaps and How Do They Work? Interest-rate swaps have become an integral part of the fixed-income market. These derivative contracts, which typically exchange or swap

The OTC Derivatives Reform: Central Clearing And Implications On Banks' Hedging Policies

The OTC Derivatives Reform: Central Clearing And Implications On Banks' Hedging Policies Cristiano Zazzara, Ph.D. Head of EMEA Application Specialists & Global Risk Solutions Monday, June 16 th, 2014 Permission

The OTC Derivatives Reform: Central Clearing And Implications On Banks' Hedging Policies Cristiano Zazzara, Ph.D. Head of EMEA Application Specialists & Global Risk Solutions Monday, June 16 th, 2014 Permission

Regulatory Landscape and Challenges

TITLE: Regulatory Landscape and Challenges AUTHOR: Adrian Orr Chief Executive EVENT PRESENTATION: September 2012 PG 2 Overview Significant regulatory and legislative reform globally: banking, insurance,

TITLE: Regulatory Landscape and Challenges AUTHOR: Adrian Orr Chief Executive EVENT PRESENTATION: September 2012 PG 2 Overview Significant regulatory and legislative reform globally: banking, insurance,

Derivatives Consulting

Derivatives Consulting Group Part of The DCG quick reference guide to credit event terminology DCG Subject Matter experts Boston Ed Dragon edragon@sapient.com +1.617.963.1576 India Prakash Kini pkini@sapient.com

Derivatives Consulting Group Part of The DCG quick reference guide to credit event terminology DCG Subject Matter experts Boston Ed Dragon edragon@sapient.com +1.617.963.1576 India Prakash Kini pkini@sapient.com

Basel III Pillar 3 Disclosures Report. For the Quarterly Period Ended December 31, 2015

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended December 31, 2015 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy...

BASEL III PILLAR 3 DISCLOSURES REPORT For the quarterly period ended December 31, 2015 Table of Contents Page 1 Morgan Stanley... 1 2 Capital Framework... 1 3 Capital Structure... 2 4 Capital Adequacy...

County Of Sacramento Master Swap Policy

County Of Sacramento Master Swap Policy Approved by the Sacramento County Board of Supervisors December 7, 2004 Resolution No. 2004-1518 County of Sacramento Table of Contents Page Number SECTION 1. Introduction...

County Of Sacramento Master Swap Policy Approved by the Sacramento County Board of Supervisors December 7, 2004 Resolution No. 2004-1518 County of Sacramento Table of Contents Page Number SECTION 1. Introduction...

NEW JERSEY EDUCATIONAL FACILITIES AUTHORITY SWAP AND DERIVATIVE POLICY. Adopted: October 26, 2005

NEW JERSEY EDUCATIONAL FACILITIES AUTHORITY SWAP AND DERIVATIVE POLICY Adopted: October 26, 2005 A. GENERAL NEW JERSEY EDUCATIONAL FACILITIES AUTHORITY SWAP AND DERIVATIVE POLICY 1) Scope and Purpose 2)

NEW JERSEY EDUCATIONAL FACILITIES AUTHORITY SWAP AND DERIVATIVE POLICY Adopted: October 26, 2005 A. GENERAL NEW JERSEY EDUCATIONAL FACILITIES AUTHORITY SWAP AND DERIVATIVE POLICY 1) Scope and Purpose 2)

Comments on the Fair and Effective Markets Review. Remarks by. Jerome H. Powell. Member. Board of Governors of the Federal Reserve System

For release on delivery 10:00 a.m. EST January 20, 2015 Comments on the Fair and Effective Markets Review Remarks by Jerome H. Powell Member Board of Governors of the Federal Reserve System at Making Markets

For release on delivery 10:00 a.m. EST January 20, 2015 Comments on the Fair and Effective Markets Review Remarks by Jerome H. Powell Member Board of Governors of the Federal Reserve System at Making Markets

Arbitrage Activities between Offshore and Domestic Yen Money Markets since the End of the Quantitative Easing Policy

Bank of Japan Review 27-E-2 Arbitrage Activities between Offshore and Domestic Yen Money Markets since the End of the Quantitative Easing Policy Teppei Nagano, Eiko Ooka, and Naohiko Baba Money Markets

Bank of Japan Review 27-E-2 Arbitrage Activities between Offshore and Domestic Yen Money Markets since the End of the Quantitative Easing Policy Teppei Nagano, Eiko Ooka, and Naohiko Baba Money Markets

Evaluating the Use of Interest Rate Swaps by U.S. Public Finance Issuers 1 11

Rating Methodology October 2007 Contact Phone New York Bill Fitzpatrick 1.212.553.4104 Naomi Richman 1.212.553.0014 Gail Sussman 1.212.553.0819 Robert Kurtter 1.212.553.4453 John Nelson 1.212.553.4096

Rating Methodology October 2007 Contact Phone New York Bill Fitzpatrick 1.212.553.4104 Naomi Richman 1.212.553.0014 Gail Sussman 1.212.553.0819 Robert Kurtter 1.212.553.4453 John Nelson 1.212.553.4096

Understanding Bank Returns on Derivative Transactions with Corporate Counterparties. July 10, 2014

Understanding Bank Returns on Derivative Transactions with Corporate Counterparties July 10, 2014 Overview Recent regulatory changes, including Basel III, are have far reaching implications for banks pricing

Understanding Bank Returns on Derivative Transactions with Corporate Counterparties July 10, 2014 Overview Recent regulatory changes, including Basel III, are have far reaching implications for banks pricing

Foreign Exchange, Money Markets and Derivatives

Foreign Exchange, Money Markets and Derivatives Page 1 of 13 Why Attend The global foreign exchange (FX) and money markets are the world s largest markets and pivotal parts of the financial system. In

Foreign Exchange, Money Markets and Derivatives Page 1 of 13 Why Attend The global foreign exchange (FX) and money markets are the world s largest markets and pivotal parts of the financial system. In

Harmonisation of critical OTC derivatives data elements (other than UTI and UPI) second batch consultative report

second batch consultative report") Harmonisation of critical OTC derivatives data elements (other than UTI and UPI) second batch consultative report Respondent name: Contact person: HSBC Bank plc Contact details: Please flag if you do not

Harmonisation of critical OTC derivatives data elements (other than UTI and UPI) second batch consultative report Respondent name: Contact person: HSBC Bank plc Contact details: Please flag if you do not

Response of the AFTI. Association Française. des Professionnels des Titres. On European Commission consultation

Paris, 9 September 2009 Response of the AFTI Association Française des Professionnels des Titres On European Commission consultation Possible initiatives to enhance the resilience of OTC Derivatives Markets

Paris, 9 September 2009 Response of the AFTI Association Française des Professionnels des Titres On European Commission consultation Possible initiatives to enhance the resilience of OTC Derivatives Markets

Deriv/SERV Trade Repository Update DTCC

Deriv/SERV Trade Repository Update Deriv/SERV: Early History Deriv/SERV, a subsidiary of DTCC established in 2003, operates as an at-cost, industry owned, utility provider. Focus on Post-Trade Processing

Deriv/SERV Trade Repository Update Deriv/SERV: Early History Deriv/SERV, a subsidiary of DTCC established in 2003, operates as an at-cost, industry owned, utility provider. Focus on Post-Trade Processing

Swap Markets CHAPTER OBJECTIVES. The specific objectives of this chapter are to: describe the types of interest rate swaps that are available,

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

Research Note. Asia-Pacific Derivatives Survey. April 2019

April 19 Research Note In anticipation of ISDA s 34th Annual General Meeting in Hong Kong, ISDA conducted a survey of derivatives markets in the Asia-Pacific region. The survey reveals that market participants

April 19 Research Note In anticipation of ISDA s 34th Annual General Meeting in Hong Kong, ISDA conducted a survey of derivatives markets in the Asia-Pacific region. The survey reveals that market participants

Pillar 3 and regulatory disclosures Credit Suisse Group AG 2Q17

Pillar 3 and regulatory disclosures Credit Suisse Group AG 2Q17 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse

Pillar 3 and regulatory disclosures Credit Suisse Group AG 2Q17 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse

Course Materials UNDERSTANDING AND MANAGING OPTION RISK

Course Materials UNDERSTANDING AND MANAGING OPTION RISK Dan Dwyer Managing Director Bloomington, Minnesota danieldwyer@firstintegritycapital.com 952-681-7920 August 10 & 11, 2017 Understanding and Managing

Course Materials UNDERSTANDING AND MANAGING OPTION RISK Dan Dwyer Managing Director Bloomington, Minnesota danieldwyer@firstintegritycapital.com 952-681-7920 August 10 & 11, 2017 Understanding and Managing

Glossary of Swap Terminology

Glossary of Swap Terminology Arbitrage: The opportunity to exploit price differentials on tv~otherwise identical sets of cash flows. In arbitrage-free financial markets, any two transactions with the same

Glossary of Swap Terminology Arbitrage: The opportunity to exploit price differentials on tv~otherwise identical sets of cash flows. In arbitrage-free financial markets, any two transactions with the same

December 31, Dear Mr. Stawick:

December 31, 2010 David A. Stawick Secretary of the Commission Commodity Futures Trading Commission Three Lafayette Centre 1155 21st Street, N.W. Washington, DC 20581 Re: Release No. 34-63423, File No.

December 31, 2010 David A. Stawick Secretary of the Commission Commodity Futures Trading Commission Three Lafayette Centre 1155 21st Street, N.W. Washington, DC 20581 Re: Release No. 34-63423, File No.

GUIDANCE FOR CALCULATION OF LOSSES DUE TO APPLICATION OF MARKET RISK PARAMETERS AND SOVEREIGN HAIRCUTS

Annex 4 18 March 2011 GUIDANCE FOR CALCULATION OF LOSSES DUE TO APPLICATION OF MARKET RISK PARAMETERS AND SOVEREIGN HAIRCUTS This annex introduces the reference risk parameters for the market risk component

Annex 4 18 March 2011 GUIDANCE FOR CALCULATION OF LOSSES DUE TO APPLICATION OF MARKET RISK PARAMETERS AND SOVEREIGN HAIRCUTS This annex introduces the reference risk parameters for the market risk component

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended June 30, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

The Goldman Sachs Group, Inc. PILLAR 3 DISCLOSURES For the period ended June 30, 2015 TABLE OF CONTENTS Page No. Index of Tables 1 Introduction 2 Regulatory Capital 5 Capital Structure 6 Risk-Weighted

FINCAD s Flexible Valuation Adjustment Solution

FINCAD s Flexible Valuation Adjustment Solution Counterparty credit risk measurement and valuation adjustment (CVA, DVA, FVA) computation are business-critical issues for a wide number of financial institutions.

FINCAD s Flexible Valuation Adjustment Solution Counterparty credit risk measurement and valuation adjustment (CVA, DVA, FVA) computation are business-critical issues for a wide number of financial institutions.

Compressing over-the-counter markets

Compressing over-the-counter markets Marco D Errico 1 Tarik Roukny 2 1 University of Zurich marco.derrico @ uzh.ch 2 Massachusetts Institute of Technology roukny @ mit.edu Second ESRB Annual Conference

Compressing over-the-counter markets Marco D Errico 1 Tarik Roukny 2 1 University of Zurich marco.derrico @ uzh.ch 2 Massachusetts Institute of Technology roukny @ mit.edu Second ESRB Annual Conference

Break clauses and Derivatives Valuation

Break clauses and Derivatives Valuation Mizuho International Plc 23 rd - 25 th September 2013 Disclaimer This publication has been prepared by Gaël Robert of Mizuho International solely for the purpose

Break clauses and Derivatives Valuation Mizuho International Plc 23 rd - 25 th September 2013 Disclaimer This publication has been prepared by Gaël Robert of Mizuho International solely for the purpose

Consultation response from

CESR Consultation Paper on: Transaction Reporting on OTC Derivatives and Extension of the Scope of Transaction Reporting Obligations Consultation response from The Depository Trust & Clearing Corporation

CESR Consultation Paper on: Transaction Reporting on OTC Derivatives and Extension of the Scope of Transaction Reporting Obligations Consultation response from The Depository Trust & Clearing Corporation

The University of Texas/Texas A&M Investment Management Company Derivative Investment Policy

Effective Date of Policy: August 25, 2016 Date Approved by U. T. System Board of Regents: August 25, 2016 Date Approved by UTIMCO Board: July 21, 2016 Supersedes: approved November 5, 2015 Purpose: The

Effective Date of Policy: August 25, 2016 Date Approved by U. T. System Board of Regents: August 25, 2016 Date Approved by UTIMCO Board: July 21, 2016 Supersedes: approved November 5, 2015 Purpose: The

Link n Learn. EMIR SFT Regulations. Leading Business Advisors

Link n Learn EMIR SFT Regulations Leading Business Advisors Contacts Niamh Geraghty Partner Financial Services Deloitte Ireland E: ngeraghty@deloitte.ie T: +353 417 2649 Natalie Berkecz Senior Manager

Link n Learn EMIR SFT Regulations Leading Business Advisors Contacts Niamh Geraghty Partner Financial Services Deloitte Ireland E: ngeraghty@deloitte.ie T: +353 417 2649 Natalie Berkecz Senior Manager

Aviva Investors response to CESR s Technical Advice to the European Commission in the context of the MiFID Review: Non-equity markets transparency

Aviva Investors response to CESR s Technical Advice to the European Commission in the context of the MiFID Review: Non-equity markets transparency Aviva plc is the world s fifth-largest 1 insurance group,

Aviva Investors response to CESR s Technical Advice to the European Commission in the context of the MiFID Review: Non-equity markets transparency Aviva plc is the world s fifth-largest 1 insurance group,

Monetary and Economic Department OTC derivatives market activity in the first half of 2006

Monetary and Economic Department OTC derivatives market activity in the first half of 2006 November 2006 Queries concerning this release should be addressed to the authors listed below: Section I: Christian

Monetary and Economic Department OTC derivatives market activity in the first half of 2006 November 2006 Queries concerning this release should be addressed to the authors listed below: Section I: Christian

CVA Risk Management Working Group Report -Towards the Introduction of Market-based CVA-

CVA Risk Management Working Group Report -Towards the Introduction of Market-based CVA- June 2017 Japanese Bankers Association Table of contents I. Executive Summary... 1 II. Background and issues... 1

CVA Risk Management Working Group Report -Towards the Introduction of Market-based CVA- June 2017 Japanese Bankers Association Table of contents I. Executive Summary... 1 II. Background and issues... 1

Keynes Animal Spirits in the financial markets

riskupdate GLOBAL The quarterly independent risk review for banks and financial institutions worldwide nov / dec 2012 Keynes Animal Spirits in the financial markets Also in this issue n Black Swans Mean

riskupdate GLOBAL The quarterly independent risk review for banks and financial institutions worldwide nov / dec 2012 Keynes Animal Spirits in the financial markets Also in this issue n Black Swans Mean

SUMMARY PROSPECTUS SIMT Dynamic Asset Allocation Fund (SDYYX) Class Y

Class Y") January 31, 2018 SUMMARY PROSPECTUS SIMT Dynamic Asset Allocation Fund (SDYYX) Class Y Before you invest, you may want to review the Fund s prospectus, which contains information about the Fund and its

January 31, 2018 SUMMARY PROSPECTUS SIMT Dynamic Asset Allocation Fund (SDYYX) Class Y Before you invest, you may want to review the Fund s prospectus, which contains information about the Fund and its