Mobilising collateral the growing need for counterparty diversification

|

|

|

- Lesley Davidson

- 6 years ago

- Views:

Transcription

1 Mobilising collateral the growing need for counterparty diversification Greater diversification of counterparties in the repo market can halt the decline in liquidity, says Roberto Verrillo at Elixium. Regulatory changes aimed squarely at improving the resilience of financial markets and their participants have had, as an unintended consequence, a direct impact on the pricing and liquidity provided by traditional intermediaries (banks). Balance sheet costs have risen substantially as significantly more capital is now required to support outstanding transactions. These changes have had a disproportionate effect on low margin, high volume businesses, such as repo, which are balance sheet intensive. As a result, balance sheets have been scaled back dramatically and consequently banks have reduced their trading operations and risk appetite. A clear consequence of the reduction and pricing of balance sheets has been a pronounced pass-through of this additional cost from banks to their customers, and a knock on effect on the pricing and liquidity of the underlying assets. More specifically, spreads offered to clients for balance sheet intensive repo transactions have increased to reflect the additional costs incurred by banks by virtue of regulation increasing the overall cost of trading. This has also affected dealers ability to market make because the cost of holding and funding inventory has risen. The demand for initial and variation margin cash and collateral provision/transformation is set to increase dramatically with the adoption of new rules surrounding mandatory margining of uncleared OTC derivatives. Consequently, this has led to question marks around the markets current capacity to satisfy the demand for high quality liquid assets (HQLA) and cash during exceptional market conditions.

2 Looking at this issue in its entirety we can ascertain quite clearly that: Illiquidity in secured and unsecured markets is reported across the spectrum, be it buy-side, sell-side or brokers Current intermediated capacity is stretched and is causing fragmented pricing Intermediated capacity is only likely to deteriorate further There is more than ample liquidity in the form of cash as a result of global quantitative easing (QE) Collateral providers have significant reserves of previously un-lent and unencumbered inventory There is an increasing need for capacity on the back of new margining rules for OTC products The transmission mechanism for collateral transformation to be executed is severely impaired. The potential for more serious market dislocations where collateral provision/transformation can be severely affected in stressed environments is set out more comprehensively in a Bank of England staff working paper (No.609): Here are some selected excerpts:

3 Summary: the risk of demand exceeding supply (Risk 1) Chart 1: Modelled collateral supply/demand for different levels of market stress Based on a series of empirical historical relationships, the green line in Chart 1 shows the made available supply of collateral as a decreasing function of market stress (which we proxy with the quarterly average of the level of the VIX index of equity volatility). Combining the profiles for collateral demand and supply brings us to Risk 1: that is, the possibility that as market stress intensifies, total demand for high-quality collateral eventually exceeds its made available supply. As market stress intensifies, the ability and willingness of these institutions to obtain the leverage necessary to perform this intermediation tends to decrease. This leads to the risk that in future periods of stress although the demand for collateral might not exceed unleveraged end investors ability to supply it collateral may become blocked ; that is, unable to reach those that wish to use it, due to a shortage of intermediation capacity.

4 Risk 2: Can collateral get to where it is most needed? Chart 2 Estimated required intermediation capacity necessary to meet demand for collateral (RIC) versus the maximum intermediation capacity of dealers for different levels of financial stress Sources: Bloomberg, BIS, Dealogic, Data Explorers, ECB, FSB, ICMA, ISLA, SIFMA, SNL and Bank calculations.

5 Although Risk 2 is slightly less likely to crystallise than Risk 1, it is likely to persist (as it can take a long time for new intermediation capacity to come to the market) and thus, could have a significant negative impact on financial stability. In particular, if triggered, Risk 2 will likely prevent collateral from performing its role of supporting market functioning. The consequences of this might include a sudden inability of market participants to obtain collateral to post initial margin on their derivative portfolios, leading to a potentially disorderly unwind of positions and/or inability of leveraged investors (e.g. hedge funds) to fund their positions and continue supporting market liquidity. If Risk 2 crystallised, banks could also experience significant difficulty monetising their liquid asset buffers via repo markets. By facilitating the flow of cash to collateral, and vice-versa, Elixium seeks to release liquidity from counterparties who previously may not have been engaged in secured financing activity. At the recent (08/16) economic policy symposium at Jackson Hole, Minouche Shafik, Deputy Governor, Markets & Banking, Bank of England, and a member of the Monetary Policy Committee (MPC), referenced data below when commenting on monetary policy and its transmission mechanism: It is clear that repo activity has diminished as balance sheet has been constrained while bid/offer spreads have widened to reflect the additional cost. Liquidity in anything other than short dated, balance sheet neutral trades has dried up substantially, with brokers and market professionals all reporting a lack of activity and interest in price making across the interdealer community. The more balance sheet intensive a particular business area is, the higher the hurdle rate for returns should be. In this regard market making (via capital costs for holding positions) and repo stand out. We believe that as this process of re-pricing and charging business areas for the regulatory cost of partaking in certain businesses (and transactions) progresses, the market will find many more institutions cutting back and re-structuring their current business models, or simply pulling out of certain markets or product lines altogether. Clearly, this will exacerbate the problem.

6 Chart 3 Change in Repo market activity since 2013

7 Chart 4 Spread between Repo rates and swap rates The cost of transacting repo has risen and will continue to rise as regulation is implemented.

8 Chart 5 Survey respondent s views of sterling money market functioning The net balance of survey respondents who think secured markets are functioning well has declined in recent years. CSA re-negotiation and Variation Margin (VM) rules the impact on OTC products and collateral markets Buy-side firms will need to be able to source cash collateral for variation margin (VM) on OTC derivatives going forward. Regulation targeting initial margin (IM) and VM for OTC products will come into effect during the first half of Dealers are busy trying to comply with bi-lateral margin rules set out by BCBS/IOSCO that could entail having to amend up to 200,000 CSAs. Each individual CSA may require re-negotiation and could trigger payments based on these amendments, which revolve around dealers wanting to receive cash only as VM. Previously, many of these CSAs were margined using collateral, but as dealers will only get capital relief from daily-exchanged, cash margined VM,

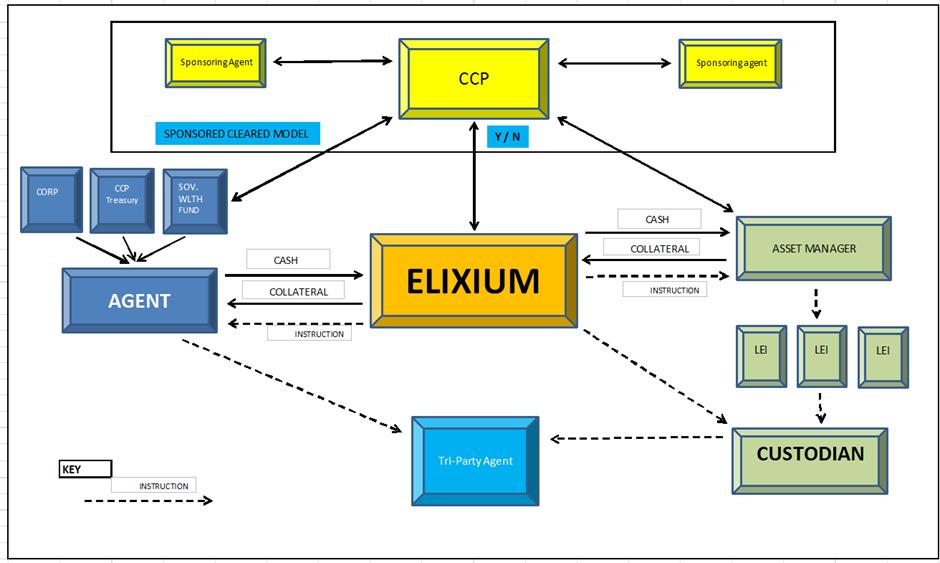

9 the cost to them of receiving collateral becomes prohibitive. Consequently, sell side firms will factor in charges (via wider bid/offer spreads) to reflect their increased cost base. The requirements for all entities that are viewed as systematically important to exchange IM and VM against their OTC portfolios are mandatory. It is estimated that the size of the uncleared market in OTC products to be in the region of USD127 trillion (ISDA). 1 Buy-side firms will need to decide on how they view the implications of having to produce cash/collateral IM/VM vs their OTC portfolios, particularly in times of market stress. The ability to convert collateral to cash, and the markets capacity to enable that process, needs to be considered in light of these imminent regulatory changes. According to a recent Risk magazine article, margin requirements spiked following the Brexit vote: Estimates of the combined (VM) margin call issues by derivatives central counterparties (CCP s) on the day range from $25 billion to $40 billion or more. 2 Elixium liberating capacity Elixium is a global all-to-all electronic marketplace, designed to provide a transparent and unbiased venue for trading collateral and seeking to address the growing issues around liquidity that have been affected by on-going market evolution. Elixium is a regulated marketplace (a Multilateral Trading Facility, or MTF) for collateral and secured deposits, targeted at firms of various size and constituencies, including corporate treasurers, CCPs, asset managers, hedge funds, banks, government issuers, central banks, insurers and agencies. As an MTF, Elixium is characterised by the non-discretionary execution of transactions and is therefore subject to pre-determined rules. 1 1 Initial Margin for Non-Centrally Cleared Swaps: Understanding the Systemic Implications, ISDA November Huge Brexit margin calls stoke intra-day funding fears 31 October 2016

10 Elixium has been designed to address the impact of regulation, balance sheet pressures and deteriorating levels of liquidity in the repo market by providing participants with collateralised liquidity on a fair, transparent, inexpensive and equitable basis. Costs of some investment strategies (such as LDI which is sensitive to the provision and pricing/tenor of finance) have been driven sharply higher by this balance sheet deficiency and intermediary capacity. Elixium has plans to introduce specific solutions in order to increase liquidity for these strategies going forward. Whilst the demand and client benefits are clear, many new counterparties are continuing to face high barriers to entry when seeking to access collateralised liquidity. Elixium has addressed this by adopting a user-friendly modular approach to documentation with the option of either subscribing to Elixium s standard GMRA (with bespoke annexes and rapid All-to-All capability) or utilising existing GMRA documentation between counterparties. Elixium provides a full credit limit framework where the participant retains full control over the credit line, products and firms with whom they are willing to trade. Via intelligent trading tools and analytics, Elixium enables institutions to qualify for credit slippage, view depth and liquidity across tenors and collateral baskets, and offer varied execution functionality. Elixium uses standardised products and processes. Firms will have access to a range of maturities, currencies and collateral baskets and will be able to facilitate collateral upgrades and new trading strategies via cleared, tri-party and domestic settlement. Following mandatory margining of un-cleared OTC products (EMIR), demand for efficient initial and variation margin collateral transformation, is set to increase dramatically. Elixium facilitates this process and will provide a marketplace through which cash or collateral can be sourced from a much more diverse counterparty base than is currently the norm. Over the coming months, Elixium will expand its initial offering to more than 40 collateral baskets covering fixed income and equities in GBP EUR USD CAD JPY and EMs.

11 The system will be launched in various stages: Auction, using standard collateral baskets and a fixed rate. CLOB (central limit order book) where we will endeavor to standardise maturity dates where possible in order to concentrate liquidity away from balance sheet sensitive dates, weekends, bank holidays etc. IOI (Indication of Interest) where a participant can express a bid/offer in a particular date run to suit his cash flow needs. Collateral Transformation, which will enable participants to swap collateral credit in exchange for a fee. In summary, Elixium has been designed to provide: A transparent, unbiased, regulated, all-to-all marketplace. A reduction in counterparty credit risk through collateralisation. Rapid growth and diversity of counterparty base and access to new supplies of cash and collateral. Specific trading solutions to facilitate implementation of certain strategies. An efficient conduit to raise/invest cash/collateral on a secured basis to manage margin and cashflow and to demonstrate best price execution. Accelerated counterparty on-boarding. Tri-party, cleared and domestic settlement methodology. Pre-trade anonymity in a MTF with a robust credit framework. Collateral transformation functionality for HQLA with NSFR (Net Stable Funding Ratio) and LCR (Liquidity Coverage Ratio) benefits. Roberto Verrillo Head of Strategy and Markets, Elixium Sales: +44 (0) / 1585

12

LGIM DAT consultation response

LGIM DAT consultation response Name: Robert Pace Job title: Senior Solutions Strategy Manager Email: robert.pace@lgim.com Tel: +44 (0)20 3124 3568 Contents Incentives... 3 Markets... 4 Reforms... 4 Access...

LGIM DAT consultation response Name: Robert Pace Job title: Senior Solutions Strategy Manager Email: robert.pace@lgim.com Tel: +44 (0)20 3124 3568 Contents Incentives... 3 Markets... 4 Reforms... 4 Access...

Collateral Management

Collateral Management MANAGE AND UNDERSTAND COLLATERAL MANAGEMENT ISSUES TO ANTICIPATE BUSINESS AND REGULATORY EVOLUTIONS STRATEGY & MANAGEMENT CONSULTING PARIS LONDON LUXEMBOURG ASIA 22 novembre 2016

Collateral Management MANAGE AND UNDERSTAND COLLATERAL MANAGEMENT ISSUES TO ANTICIPATE BUSINESS AND REGULATORY EVOLUTIONS STRATEGY & MANAGEMENT CONSULTING PARIS LONDON LUXEMBOURG ASIA 22 novembre 2016

The BBA is pleased to respond to this consultation on the net stable funding ratio. Please find below are comments on the key issues in the paper.

BBA response to BCBS 271: Basel III: The Net Stable Funding Ratio Introduction The British Bankers Association ( BBA ) is the leading association for UK banking and financial services for the UK banking

BBA response to BCBS 271: Basel III: The Net Stable Funding Ratio Introduction The British Bankers Association ( BBA ) is the leading association for UK banking and financial services for the UK banking

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD)

") Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) As a follow-up to the recommendation in the Committee on the Global Financial System

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) As a follow-up to the recommendation in the Committee on the Global Financial System

Appendix B: HQLA Guide Consultation Paper No Basel III: Liquidity Management

Appendix B: HQLA Guide Consultation Paper No.3 2017 Basel III: Liquidity Management [Draft] Guide on the calculation and reporting of HQLA Issued: 26 April 2017 Contents Contents Overview... 3 Consultation...

Appendix B: HQLA Guide Consultation Paper No.3 2017 Basel III: Liquidity Management [Draft] Guide on the calculation and reporting of HQLA Issued: 26 April 2017 Contents Contents Overview... 3 Consultation...

E.ON General Statement to Margin requirements for non-centrally-cleared derivatives

E.ON AG Avenue de Cortenbergh, 60 B-1000 Bruxelles www.eon.com Contact: Political Affairs and Corporate Communications E.ON General Statement to Margin requirements for non-centrally-cleared derivatives

E.ON AG Avenue de Cortenbergh, 60 B-1000 Bruxelles www.eon.com Contact: Political Affairs and Corporate Communications E.ON General Statement to Margin requirements for non-centrally-cleared derivatives

Baseline report on solutions for the posting of non-cash collateral to central counterparties by pension scheme arrangements

Baseline report on solutions for the posting of non-cash collateral to central counterparties by pension scheme arrangements A report for the European Commission prepared by Europe Economics and Bourse

Baseline report on solutions for the posting of non-cash collateral to central counterparties by pension scheme arrangements A report for the European Commission prepared by Europe Economics and Bourse

EPTF. Godfried De Vidts Chairman, ICMA European Repo & Collateral Council Brussels, 19 May 2016

EPTF Godfried De Vidts Chairman, ICMA European Repo & Collateral Council Brussels, 19 May 2016 International Capital Market Association (ICMA) Introduction to ICMA» ICMA s mission is to promote resilient

EPTF Godfried De Vidts Chairman, ICMA European Repo & Collateral Council Brussels, 19 May 2016 International Capital Market Association (ICMA) Introduction to ICMA» ICMA s mission is to promote resilient

IMPACT OF RECENT REGULATION ON REPO MARKET ACTIVITY FROM THE PERSPECTIVE OF A NON BANK PARTICIPANT

IMPACT OF RECENT REGULATION ON REPO MARKET ACTIVITY FROM THE PERSPECTIVE OF A NON BANK PARTICIPANT Key Takeaways Repo is a key tool for Insurance Companies to manage duration & liquidity risks The Repo

IMPACT OF RECENT REGULATION ON REPO MARKET ACTIVITY FROM THE PERSPECTIVE OF A NON BANK PARTICIPANT Key Takeaways Repo is a key tool for Insurance Companies to manage duration & liquidity risks The Repo

Collateralized Banking

Collateralized Banking A Post-Crisis Reality Dr. Matthias Degen Senior Manager, KPMG AG ETH Risk Day 2014 Zurich, 12 September 2014 Definition Collateralized Banking Totality of aspects and processes relating

Collateralized Banking A Post-Crisis Reality Dr. Matthias Degen Senior Manager, KPMG AG ETH Risk Day 2014 Zurich, 12 September 2014 Definition Collateralized Banking Totality of aspects and processes relating

29 January Dear Commissioner, Re: Call for evidence on EU regulatory framework for financial services

29 January 2016 Jonathan Hill, Lord Hill of Oareford Commissioner Financial Stability, Financial Services and Capital Markets Union European Commission Rue de la Loi / Wetstraat 200 1049 Brussels Belgium

29 January 2016 Jonathan Hill, Lord Hill of Oareford Commissioner Financial Stability, Financial Services and Capital Markets Union European Commission Rue de la Loi / Wetstraat 200 1049 Brussels Belgium

Liquidity in the bond & credit markets

Liquidity in the bond & credit markets Franck Motte Global Head of Euro Rates, HSBC Liquidity in the bond & credit markets Certain / existing/ / agreed Recent trends in market liquidity : converging views

Liquidity in the bond & credit markets Franck Motte Global Head of Euro Rates, HSBC Liquidity in the bond & credit markets Certain / existing/ / agreed Recent trends in market liquidity : converging views

Guidance to completing the LCR module of Form LCR

Guidance to completing the LCR module of Form LCR LIQUIDITY COVERAGE RATIO GUIDANCE Introduction The Liquidity Coverage Ratio ( LCR ) promotes the short-term resilience of the liquidity risk profile of

Guidance to completing the LCR module of Form LCR LIQUIDITY COVERAGE RATIO GUIDANCE Introduction The Liquidity Coverage Ratio ( LCR ) promotes the short-term resilience of the liquidity risk profile of

REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL

EUROPEAN COMMISSION Brussels, 19.10.2017 COM(2017) 604 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL under Article 29(3) of Regulation (EU) 2015/2365 of 25 November 2015 on

EUROPEAN COMMISSION Brussels, 19.10.2017 COM(2017) 604 final REPORT FROM THE COMMISSION TO THE EUROPEAN PARLIAMENT AND THE COUNCIL under Article 29(3) of Regulation (EU) 2015/2365 of 25 November 2015 on

Incentage Customer Event Zurich

www.strate.co.za Strate Collateral Management Services Incentage Customer Event Zurich Presented by : Ant van Eden (Strategic Projects Director) Date: 6 November 2104 Key Drivers Requiring Greater Collateralisation

www.strate.co.za Strate Collateral Management Services Incentage Customer Event Zurich Presented by : Ant van Eden (Strategic Projects Director) Date: 6 November 2104 Key Drivers Requiring Greater Collateralisation

Managing capital and liquidity impacts on collateral management

Managing capital and liquidity impacts on collateral management Ben Watson ben.watson@maroonanalytics.com www.maroonanalytics.com About your presenter Ben Watson has worked for more than 20 years as a

Managing capital and liquidity impacts on collateral management Ben Watson ben.watson@maroonanalytics.com www.maroonanalytics.com About your presenter Ben Watson has worked for more than 20 years as a

THE IMPACT OF DERIVATIVE COLLATERAL POLICIES OF EUROPEAN SOVEREIGNS AND RESULTING BASEL III CAPITAL ISSUES

THE IMPACT OF DERIVATIVE COLLATERAL POLICIES OF EUROPEAN SOVEREIGNS AND RESULTING BASEL III CAPITAL ISSUES Summary The majority of sovereigns do not post collateral to support their use of over-the-counter

THE IMPACT OF DERIVATIVE COLLATERAL POLICIES OF EUROPEAN SOVEREIGNS AND RESULTING BASEL III CAPITAL ISSUES Summary The majority of sovereigns do not post collateral to support their use of over-the-counter

Navigating the Future Collateral Roadmap By Mark Jennis

Navigating the Future Collateral Roadmap By Mark Jennis Policymakers around the world have enacted new rules and legislation, such as the Dodd-Frank Act (DFA) in the United States, European Market Infrastructure

Navigating the Future Collateral Roadmap By Mark Jennis Policymakers around the world have enacted new rules and legislation, such as the Dodd-Frank Act (DFA) in the United States, European Market Infrastructure

Reality Shares DIVS ETF DIVY (NYSE Arca, Inc.)

") Reality Shares DIVS ETF DIVY (NYSE Arca, Inc.) SUMMARY PROSPECTUS February 28, 2018 Before you invest in the Fund, as defined below, you may want to review the Fund s prospectus and statement of additional

Reality Shares DIVS ETF DIVY (NYSE Arca, Inc.) SUMMARY PROSPECTUS February 28, 2018 Before you invest in the Fund, as defined below, you may want to review the Fund s prospectus and statement of additional

Consultation paper on further considerations for the implementation of the NSFR in the EU

8 July 2016 European Commission Directorate General for Financial Stability, Financial Services, and Capital Markets Union (DG FISMA) Rue de Spa 2 1000 Brussels Belgium Submitted by e-mail RE: Consultation

8 July 2016 European Commission Directorate General for Financial Stability, Financial Services, and Capital Markets Union (DG FISMA) Rue de Spa 2 1000 Brussels Belgium Submitted by e-mail RE: Consultation

Regulatory Landscape and Challenges

TITLE: Regulatory Landscape and Challenges AUTHOR: Adrian Orr Chief Executive EVENT PRESENTATION: September 2012 PG 2 Overview Significant regulatory and legislative reform globally: banking, insurance,

TITLE: Regulatory Landscape and Challenges AUTHOR: Adrian Orr Chief Executive EVENT PRESENTATION: September 2012 PG 2 Overview Significant regulatory and legislative reform globally: banking, insurance,

Response of the AFTI. Association Française. des Professionnels des Titres. On European Commission consultation

Paris, 9 September 2009 Response of the AFTI Association Française des Professionnels des Titres On European Commission consultation Possible initiatives to enhance the resilience of OTC Derivatives Markets

Paris, 9 September 2009 Response of the AFTI Association Française des Professionnels des Titres On European Commission consultation Possible initiatives to enhance the resilience of OTC Derivatives Markets

Assessing Capital Markets Union

6 Assessing Capital Markets Union Quarterly Assessment by Paul Richards Summary It is too early to make an assessment of Capital Markets Union, but not too early to give a market view of the tests by which

6 Assessing Capital Markets Union Quarterly Assessment by Paul Richards Summary It is too early to make an assessment of Capital Markets Union, but not too early to give a market view of the tests by which

14 January Secretariat of the Financial Stability Board c/o Bank for International Settlements CH-4002 Basel Switzerland

14 January 2013 Secretariat of the Financial Stability Board c/o Bank for International Settlements CH-4002 Basel Switzerland Submitted to fsb@bis.org Re: Strengthening Oversight and Regulation of Shadow

14 January 2013 Secretariat of the Financial Stability Board c/o Bank for International Settlements CH-4002 Basel Switzerland Submitted to fsb@bis.org Re: Strengthening Oversight and Regulation of Shadow

EFAMA response to the ESMA consultation paper on the clearing obligation for financial counterparties with a limited volume of activity

EFAMA response to the ESMA consultation paper on the clearing obligation for financial counterparties with a limited volume of activity The European Fund and Asset Management Association 1, EFAMA, welcomes

EFAMA response to the ESMA consultation paper on the clearing obligation for financial counterparties with a limited volume of activity The European Fund and Asset Management Association 1, EFAMA, welcomes

Liquidity risk Definition

susceptible to being cleared through a CCP are being cleared in this way. At the same time, the Group has worked to standardise OTC derivatives with a view to increasing the use of CCPs. The exposure to

susceptible to being cleared through a CCP are being cleared in this way. At the same time, the Group has worked to standardise OTC derivatives with a view to increasing the use of CCPs. The exposure to

Senior Credit Officer Opinion Survey on Dealer Financing Terms

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM DIVISION OF MONETARY AFFAIRS DIVISION OF RESEARCH AND STATISTICS For release at 2:00 p.m. EDT March 29, 2012 Senior Credit Officer Opinion Survey on Dealer

BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM DIVISION OF MONETARY AFFAIRS DIVISION OF RESEARCH AND STATISTICS For release at 2:00 p.m. EDT March 29, 2012 Senior Credit Officer Opinion Survey on Dealer

Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016

Page 1 of 93 Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016 Print Summary Results of the September 2016 Survey Summary The September 2016 Senior Credit Officer Opinion Survey

Page 1 of 93 Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016 Print Summary Results of the September 2016 Survey Summary The September 2016 Senior Credit Officer Opinion Survey

SWFs & Securities Lending Podcast January 2017

Hello and welcome to a DerivSource podcast. I m Julia Schieffer, the founder and editor of DerivSource.com. A recently published paper OTC Derivatives Reform: Putting Asset Owners and Sovereign Wealth

Hello and welcome to a DerivSource podcast. I m Julia Schieffer, the founder and editor of DerivSource.com. A recently published paper OTC Derivatives Reform: Putting Asset Owners and Sovereign Wealth

Financial Conduct Authority

Financial Conduct Authority Research Note August 2018 EMIR data and derivatives market policies How EMIR data help regulators better understand the impact of policies Anne-Laure Condat, Alessandro Puce

Financial Conduct Authority Research Note August 2018 EMIR data and derivatives market policies How EMIR data help regulators better understand the impact of policies Anne-Laure Condat, Alessandro Puce

Guideline. Liquidity Adequacy Requirements (LAR) Chapter 2 Liquidity Coverage Ratio Date: June 2017

Chapter 2 Liquidity Coverage Ratio Date: June 2017") Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 2 Date: June 2017 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies Act (TLCA) and subsection

Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 2 Date: June 2017 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies Act (TLCA) and subsection

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD)

") Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) December 2016 As a follow-up to the recommendation in the Committee on the Global Financial

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) December 2016 As a follow-up to the recommendation in the Committee on the Global Financial

Draft Guideline. Liquidity Adequacy Requirements (LAR) Chapter 2 Liquidity Coverage Ratio Date: June 2017February 2019

Chapter 2 Liquidity Coverage Ratio Date: June 2017February 2019") Draft Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 2 Date: June 2017February 2019 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies

Draft Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 2 Date: June 2017February 2019 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at June 30, 2016

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at June 30, 2016 Table of Contents Capital Structure Statement of Financial Position - Step 1 ( Table

Information on Capital Structure, Liquidity Coverage and Leverage Ratios as per Basel-III Framework as at June 30, 2016 Table of Contents Capital Structure Statement of Financial Position - Step 1 ( Table

London, August 16 th, 2010

CESR The Committee of European Securities Regulators Submitted via www.cesr.eu Standardisation and exchange trading of OTC derivatives London, August 16 th, 2010 Dear Sirs, MarkitSERV welcomes the publication

CESR The Committee of European Securities Regulators Submitted via www.cesr.eu Standardisation and exchange trading of OTC derivatives London, August 16 th, 2010 Dear Sirs, MarkitSERV welcomes the publication

MBF1243 Derivatives Prepared by Dr Khairul Anuar. Lecture 2 Mechanics of Futures Markets

MBF1243 Derivatives Prepared by Dr Khairul Anuar Lecture 2 Mechanics of Futures Markets Specification of Futures Contracts Available on a wide range of assets Exchange traded Specifications need to be

MBF1243 Derivatives Prepared by Dr Khairul Anuar Lecture 2 Mechanics of Futures Markets Specification of Futures Contracts Available on a wide range of assets Exchange traded Specifications need to be

STANDARD CHARTERED BANK (HONG KONG) LIMITED. Liquidity Coverage Ratio Current Period. Table 1: Average LCR for the quarter ended 31 st December 2015

LIMITED. Liquidity Coverage Ratio Current Period. Table 1: Average LCR for the quarter ended 31 st December 2015") Liquidity Coverage Ratio Current Period Table 1: Average LCR for the quarter ended 31 st December 2015 Table 2: Average LCR for the quarter ended 30 th September 2015 Table 3: Average LCR for the quarter

Liquidity Coverage Ratio Current Period Table 1: Average LCR for the quarter ended 31 st December 2015 Table 2: Average LCR for the quarter ended 30 th September 2015 Table 3: Average LCR for the quarter

ISDA also advocates for making uncleared margin requirements more risk appropriate. These proposals will be the subject of a separate paper.

ISDA Response to the FSB DAT report Incentives to centrally clear over the counter (OTC) derivatives A post implementation evaluation of the effects of the G20 financial regulatory reforms (the DAT Report)

ISDA Response to the FSB DAT report Incentives to centrally clear over the counter (OTC) derivatives A post implementation evaluation of the effects of the G20 financial regulatory reforms (the DAT Report)

Samba Financial Group Basel III - Pillar 3 Disclosure Report. September 2017 PUBLIC

Basel III - Pillar 3 Disclosure Report September 2017 Basel III - Pillar 3 Disclosure Report as at September 30, 2017 Page 1 of 12 Table of contents Capital Structure Page Statement of financial position

Basel III - Pillar 3 Disclosure Report September 2017 Basel III - Pillar 3 Disclosure Report as at September 30, 2017 Page 1 of 12 Table of contents Capital Structure Page Statement of financial position

TABLE 2: CAPITAL STRUCTURE - December 31, 2015

Frequency : Quarterly Location : Quarterly Financial Statement TABLE 2: CAPITAL STRUCTURE - December 31, 2015 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published

Frequency : Quarterly Location : Quarterly Financial Statement TABLE 2: CAPITAL STRUCTURE - December 31, 2015 Balance sheet - Step 1 (Table 2(b)) All figures are in SAR '000 Assets Balance sheet in Published

IIAC Market Insights Canadian ETF Dynamics, Risks and Outlook

IIAC Market Insights Canadian ETF Dynamics, Risks and Outlook JANUARY 2019 INTRODUCTION Growth of exchange traded funds (ETFs) has accelerated in recent years while ETF industry product offerings have

IIAC Market Insights Canadian ETF Dynamics, Risks and Outlook JANUARY 2019 INTRODUCTION Growth of exchange traded funds (ETFs) has accelerated in recent years while ETF industry product offerings have

Centrally Cleared CFDs: The Buy-Side Perspective

Centrally Cleared CFDs: The Buy-Side Perspective Will Rhode Analyst V08:026 September 2010 www.tabbgroup.com TABB Group Credit Default Swaps: Industry Projections March 2009 1 LCH.Clearnet and Chi-X Europe

Centrally Cleared CFDs: The Buy-Side Perspective Will Rhode Analyst V08:026 September 2010 www.tabbgroup.com TABB Group Credit Default Swaps: Industry Projections March 2009 1 LCH.Clearnet and Chi-X Europe

Loco London precious metals

Loco London precious metals Guide to regulatory and capital considerations for exchange trading and clearing of loco London precious metals SETTING THE GLOBAL STANDARD Introduction This paper has been

Loco London precious metals Guide to regulatory and capital considerations for exchange trading and clearing of loco London precious metals SETTING THE GLOBAL STANDARD Introduction This paper has been

SUMMARY PROSPECTUS SIMT Dynamic Asset Allocation Fund (SDYYX) Class Y

Class Y") January 31, 2018 SUMMARY PROSPECTUS SIMT Dynamic Asset Allocation Fund (SDYYX) Class Y Before you invest, you may want to review the Fund s prospectus, which contains information about the Fund and its

January 31, 2018 SUMMARY PROSPECTUS SIMT Dynamic Asset Allocation Fund (SDYYX) Class Y Before you invest, you may want to review the Fund s prospectus, which contains information about the Fund and its

Systemic Risks in Repo Markets

Systemic Risks in Repo Markets Somnath Chatterjee CCBS, Bank of England 8, November 2013 Outline Repo markets introduction Pro-cyclicality Role of Collateral UK banks aggregate repo activity Margin flows

Systemic Risks in Repo Markets Somnath Chatterjee CCBS, Bank of England 8, November 2013 Outline Repo markets introduction Pro-cyclicality Role of Collateral UK banks aggregate repo activity Margin flows

This was the reason for the introduction of an exemption for pension provision and retirement products in the framework Regulation.

ABI response to the joint Discussion Paper on Draft Technical Standards on risk mitigation techniques for OTC derivatives not cleared by a CCP under the Regulation on OTC Derivatives, CCPs and Trade Repositories

ABI response to the joint Discussion Paper on Draft Technical Standards on risk mitigation techniques for OTC derivatives not cleared by a CCP under the Regulation on OTC Derivatives, CCPs and Trade Repositories

Operational and Computational Challenges in Counterparty Credit Risk

Operational and Computational Challenges in Counterparty Credit Risk Head of CB&S Counterparty and Funding Risk Technology, AG 8 th Annual Banking Credit Risk Management Summit, Feb 3 rd - 5 th 2015 Vienna,

Operational and Computational Challenges in Counterparty Credit Risk Head of CB&S Counterparty and Funding Risk Technology, AG 8 th Annual Banking Credit Risk Management Summit, Feb 3 rd - 5 th 2015 Vienna,

Guideline. Liquidity Adequacy Requirements (LAR) Chapter 5 Liquidity Monitoring Tools Date: May 2014

Chapter 5 Liquidity Monitoring Tools Date: May 2014") Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 5 Date: May 2014 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies Act (TLCA) and subsection

Guideline Subject: Liquidity Adequacy Requirements (LAR) Chapter 5 Date: May 2014 Subsection 485(1) and 949(1) of the Bank Act (BA), subsection 473(1) of the Trust and Loan Companies Act (TLCA) and subsection

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD)

") Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) As a follow-up to the recommendation in the Committee on the Global Financial System

Survey on credit terms and conditions in euro-denominated securities financing and OTC derivatives markets (SESFOD) As a follow-up to the recommendation in the Committee on the Global Financial System

The Association of Corporate Treasurers Interest Representative Register ID:

The Association of Corporate Treasurers Interest Representative Register ID: 64617562334-37 Comments in response to Joint ESMA/EBA/EIOPA Discussion Paper On Draft Regulatory Technical Standards on risk

The Association of Corporate Treasurers Interest Representative Register ID: 64617562334-37 Comments in response to Joint ESMA/EBA/EIOPA Discussion Paper On Draft Regulatory Technical Standards on risk

Basel Committee on Banking Supervision. Liquidity coverage ratio disclosure standards

Basel Committee on Banking Supervision Liquidity coverage ratio disclosure standards January 2014 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2014.

Basel Committee on Banking Supervision Liquidity coverage ratio disclosure standards January 2014 This publication is available on the BIS website (www.bis.org). Bank for International Settlements 2014.

EBA recommendations on the Call for Advice on European Secured Notes. 26 June 2018

EBA recommendations on the Call for Advice on European Secured Notes 26 June 2018 Content 1.Mandate 2.Business case 3.Impact on asset encumbrance 4.SME ESNs 5.Infrastructure ESNs EBA recommendations on

EBA recommendations on the Call for Advice on European Secured Notes 26 June 2018 Content 1.Mandate 2.Business case 3.Impact on asset encumbrance 4.SME ESNs 5.Infrastructure ESNs EBA recommendations on

Collateral upgrade transactions and asset encumbrance: expectations in relation to firms risk management practices

Supervisory Statement LSS2/13 Collateral upgrade transactions and asset encumbrance: expectations in relation to firms risk management practices April 2013 Supervisory Statement LSS2/13 Collateral upgrade

Supervisory Statement LSS2/13 Collateral upgrade transactions and asset encumbrance: expectations in relation to firms risk management practices April 2013 Supervisory Statement LSS2/13 Collateral upgrade

Re: Consultative document: Margin requirements for non-centrally cleared derivatives

Mr David Wright International Organisation of Securities Commissions C/Oquendo 12 28006 Madrid Spain cc: Basel Committee on Banking Supervision 15 March 2013 Dear David, Re: Consultative document: Margin

Mr David Wright International Organisation of Securities Commissions C/Oquendo 12 28006 Madrid Spain cc: Basel Committee on Banking Supervision 15 March 2013 Dear David, Re: Consultative document: Margin

Guideline on Liquidity Risk Management

BOM/BSD 4/January 2000 BANK OF MAURITIUS Guideline on Liquidity Risk Management January 2000 Revised October 2009 Revised August 2010 Revised October 2017 Table of Contents INTRODUCTION... 1 Authority...

BOM/BSD 4/January 2000 BANK OF MAURITIUS Guideline on Liquidity Risk Management January 2000 Revised October 2009 Revised August 2010 Revised October 2017 Table of Contents INTRODUCTION... 1 Authority...

Habib Bank AG Zurich. Annual disclosures according to Basel III (Year 2015)

") Annual disclosures according to Basel III (Year 2015) 1 Annual disclosures according to Basel III (Year 2015) 1. Scope of consolidation Scope of consolidation for capital adequacy purposes The scope of

Annual disclosures according to Basel III (Year 2015) 1 Annual disclosures according to Basel III (Year 2015) 1. Scope of consolidation Scope of consolidation for capital adequacy purposes The scope of

EFAMA reply to the EU Commission's consultation on EMIR REFIT

EFAMA reply to the EU Commission's consultation on EMIR REFIT EFAMA 1 welcomes the opportunity to comment on the EU Commission's proposed EMIR refit. We want to congratulate the EU Commission for the excellent

EFAMA reply to the EU Commission's consultation on EMIR REFIT EFAMA 1 welcomes the opportunity to comment on the EU Commission's proposed EMIR refit. We want to congratulate the EU Commission for the excellent

Introduction. Interim Report and Consultation The Alternative Reference Rates Committee

Introduction Interim Report and Consultation The Alternative Reference Rates Committee 1 Alternative Rates Interim Report and Consultation The Alternative Reference Rates Committee 2 Alternative Rates

Introduction Interim Report and Consultation The Alternative Reference Rates Committee 1 Alternative Rates Interim Report and Consultation The Alternative Reference Rates Committee 2 Alternative Rates

Annual Report December 31, 2016

Annual Report December 31, 2016 Goldman Sachs International (unlimited company) Company Number: 02263951 ANNUAL REPORT FOR THE FINANCIAL YEAR ENDED DECEMBER 31, 2016 INDEX Page No. Part I 2 Introduction

Annual Report December 31, 2016 Goldman Sachs International (unlimited company) Company Number: 02263951 ANNUAL REPORT FOR THE FINANCIAL YEAR ENDED DECEMBER 31, 2016 INDEX Page No. Part I 2 Introduction

Point De Vue: Operational challenges faced by asset managers to price OTC derivatives Laurent Thuilier, SGSS. Avec le soutien de

Point De Vue: Operational challenges faced by asset managers to price OTC derivatives 2012 01 Laurent Thuilier, SGSS Avec le soutien de JJ Mois Année Operational challenges faced by asset managers to price

Point De Vue: Operational challenges faced by asset managers to price OTC derivatives 2012 01 Laurent Thuilier, SGSS Avec le soutien de JJ Mois Année Operational challenges faced by asset managers to price

INFORMATION ON THE ORDER EXECUTION POLICY OF PATRIA FINANCE FOR PROFESSIONAL CLIENTS

INFORMATION ON THE ORDER EXECUTION POLICY OF PATRIA FINANCE FOR PROFESSIONAL CLIENTS 1. SCOPE OF BEST EXECUTIONS In accordance with the Markets in Financial Instruments Directive 2014/65/EU ( MiFID II

INFORMATION ON THE ORDER EXECUTION POLICY OF PATRIA FINANCE FOR PROFESSIONAL CLIENTS 1. SCOPE OF BEST EXECUTIONS In accordance with the Markets in Financial Instruments Directive 2014/65/EU ( MiFID II

Securities Lending An Overview. An NSE Presentation By Segun Sanni Head, Client Services Stanbic IBTC

Securities Lending An Overview An NSE Presentation By Segun Sanni Head, Client Services Stanbic IBTC September 2012 Outline 1 2 3 4 Introduction Key Players Benefits of Securities Lending Types of Loans

Securities Lending An Overview An NSE Presentation By Segun Sanni Head, Client Services Stanbic IBTC September 2012 Outline 1 2 3 4 Introduction Key Players Benefits of Securities Lending Types of Loans

LIQUIDITY RISK. 1. Form BA Liquidity risk

473 LIQUIDITY RISK Page no. 1. Form BA 300 - Liquidity risk... 474 2. Regulation 26 - Directives, definitions and interpretations for completion of monthly return concerning liquidity risk (Form BA 300)...

473 LIQUIDITY RISK Page no. 1. Form BA 300 - Liquidity risk... 474 2. Regulation 26 - Directives, definitions and interpretations for completion of monthly return concerning liquidity risk (Form BA 300)...

Opinion of the EBA on Good Practices for ETF Risk Management

EBA-Op-2013-01 7 March 2013 Opinion of the EBA on Good Practices for ETF Risk Management Table of contents Table of contents 2 Introduction 4 I. Good Practices for ETF business 6 II. Considerations for

EBA-Op-2013-01 7 March 2013 Opinion of the EBA on Good Practices for ETF Risk Management Table of contents Table of contents 2 Introduction 4 I. Good Practices for ETF business 6 II. Considerations for

Standard Bank submission on BCBS and IOSCO Consultative Document: Margin requirements for non-centrally-cleared derivatives

Basel Committee on Banking Supervision Bank for International Settlements Basel Switzerland By email: baselcommittee@bis.org Group Governance and Assurance Regulatory Advocacy Standard Bank submission

Basel Committee on Banking Supervision Bank for International Settlements Basel Switzerland By email: baselcommittee@bis.org Group Governance and Assurance Regulatory Advocacy Standard Bank submission

SUMMARY PROSPECTUS Impact Shares NAACP Minority Empowerment ETF Ticker: NACP NYSE ARCA July 17, 2018

SUMMARY PROSPECTUS Impact Shares NAACP Minority Empowerment ETF Ticker: NACP NYSE ARCA July 17, 2018 Before you invest, you may want to review the Fund s Prospectus and Statement of Additional Information,

SUMMARY PROSPECTUS Impact Shares NAACP Minority Empowerment ETF Ticker: NACP NYSE ARCA July 17, 2018 Before you invest, you may want to review the Fund s Prospectus and Statement of Additional Information,

Response to the Joint Discussion Paper on Draft Regulatory Technical Standards

European Securities and Markets Authority www.esma.europa.eu April 2, 2012 Beurs World Trade Center, 20 th floor Beursplein 37, P.O. Box 30173 3001 DD Rotterdam The Netherlands T. +31 (0)10 243 47 47 F.

European Securities and Markets Authority www.esma.europa.eu April 2, 2012 Beurs World Trade Center, 20 th floor Beursplein 37, P.O. Box 30173 3001 DD Rotterdam The Netherlands T. +31 (0)10 243 47 47 F.

Exchange Traded Funds (ETFs)

") Exchange Traded Funds (ETFs) Advisers guide to ETFs and their potential role in client portfolios This document is directed at professional investors and should not be distributed to, or relied upon by

Exchange Traded Funds (ETFs) Advisers guide to ETFs and their potential role in client portfolios This document is directed at professional investors and should not be distributed to, or relied upon by

BVI 1 welcomes the opportunity to present its views on BCBS/IOSCOs consultation on margin requirements for non-centrally-clearfed derivatives.

BVI Bockenheimer Anlage 15 D-60322 Frankfurt am Main Basel Committee on Banking Supervision Bank for International Settlements CH-4002 Basel Switzerland Bundesverband Investment und Asset Management e.v.

BVI Bockenheimer Anlage 15 D-60322 Frankfurt am Main Basel Committee on Banking Supervision Bank for International Settlements CH-4002 Basel Switzerland Bundesverband Investment und Asset Management e.v.

Counterparty Credit Risk and CVA

Jon Gregory Solum Financial jon@solum-financial.com 10 th April, SIAG Consulting, Madrid page 1 History The Complexity of CVA Impact of Regulation Where Will This Lead Us? 10 th April, SIAG Consulting,

Jon Gregory Solum Financial jon@solum-financial.com 10 th April, SIAG Consulting, Madrid page 1 History The Complexity of CVA Impact of Regulation Where Will This Lead Us? 10 th April, SIAG Consulting,

Description of financial instruments nature and risks

Description of financial instruments nature and risks (i) General Risks This document sets out a non-exhaustive list of risks which may be associated with particular kinds of Investments. This document

Description of financial instruments nature and risks (i) General Risks This document sets out a non-exhaustive list of risks which may be associated with particular kinds of Investments. This document

RISK REPORT 2015 CVR NO

RISK REPORT 2015 CVR NO. 27 49 26 49 INTRODUCTION The purpose of this risk report is to provide a description of 1) risk and capital management and 2) the composition of the total capital and risks in

RISK REPORT 2015 CVR NO. 27 49 26 49 INTRODUCTION The purpose of this risk report is to provide a description of 1) risk and capital management and 2) the composition of the total capital and risks in

Proposed regulatory framework for haircuts on securities financing transactions

Proposed regulatory framework for haircuts on securities financing transactions Instructions for the Quantitative Impact Study (QIS2) for Agent Securities Lenders 5 November 2013 Table of Contents Page

Proposed regulatory framework for haircuts on securities financing transactions Instructions for the Quantitative Impact Study (QIS2) for Agent Securities Lenders 5 November 2013 Table of Contents Page

Basel III: The Liquidity Coverage Ratio and Liquidity Risk Monitoring Tools

P2.T7. Operational & Integrated Risk Management Basel III: The Liquidity Coverage Ratio and Liquidity Risk Monitoring Tools Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com

P2.T7. Operational & Integrated Risk Management Basel III: The Liquidity Coverage Ratio and Liquidity Risk Monitoring Tools Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM www.bionicturtle.com

London Stock Exchange Group response to the CPMI-IOSCO, FSB and BCBS consultation on incentives

London Stock Exchange Group response to the CPMI-IOSCO, FSB and BCBS consultation on incentives to centrally clear OTC Derivatives Introduction The London Stock Exchange Group (LSEG or the Group) is a

London Stock Exchange Group response to the CPMI-IOSCO, FSB and BCBS consultation on incentives to centrally clear OTC Derivatives Introduction The London Stock Exchange Group (LSEG or the Group) is a

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT. Global Debt Issuance Facility. No. 4596

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT Global Debt Issuance Facility No. 4596 USD 12,000,000 Notes linked to UYU/USD FX and the Republica AFAP Dynamic Index (Third Series) due 2026 JPMorgan

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT Global Debt Issuance Facility No. 4596 USD 12,000,000 Notes linked to UYU/USD FX and the Republica AFAP Dynamic Index (Third Series) due 2026 JPMorgan

Principal Listing Exchange for each Fund: Cboe BZX Exchange, Inc.

EXCHANGE TRADED CONCEPTS TRUST Prospectus March 30, 2018 REX VolMAXX TM LONG VIX WEEKLY FUTURES STRATEGY ETF (VMAX) REX VolMAXX TM SHORT VIX WEEKLY FUTURES STRATEGY ETF (VMIN) Principal Listing Exchange

EXCHANGE TRADED CONCEPTS TRUST Prospectus March 30, 2018 REX VolMAXX TM LONG VIX WEEKLY FUTURES STRATEGY ETF (VMAX) REX VolMAXX TM SHORT VIX WEEKLY FUTURES STRATEGY ETF (VMIN) Principal Listing Exchange

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure. For the quarterly period ended June 30, 2018

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended June 30, 2018 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. Main Drivers

Consolidated Citigroup U.S. Liquidity Coverage Ratio Disclosure For the quarterly period ended June 30, 2018 Table of Contents 1. Overview..... 2 2. Liquidity Coverage Ratio Template... 3 3. Main Drivers

INTRODUCTION. London Stock Exchange Group plc Registered in England & Wales No Registered office 10 Paternoster Square, London EC4M 7LS

MIFID REVIEW LSEG Response to CESR MiFID Consultation Paper 10-510 NON-EQUITY MARKETS TRANSPARENCY Kathleen Traynor Head of Regulatory Strategy London Stock Exchange Group 0044 (0) 20 7797 3222 ktraynor@londonstockexchange.com

MIFID REVIEW LSEG Response to CESR MiFID Consultation Paper 10-510 NON-EQUITY MARKETS TRANSPARENCY Kathleen Traynor Head of Regulatory Strategy London Stock Exchange Group 0044 (0) 20 7797 3222 ktraynor@londonstockexchange.com

CDS on Bclear. Liffe CDS. ECB, Frankfurt. 24 February NYSE Euronext All Rights Reserved

CDS on Bclear Liffe CDS ECB, Frankfurt 24 February 2009 Ade Cordell Chris Jones Director, OTC Services Director, Head of Risk Management NYSE Euronext LCH.Clearnet ACordell@nyx.com Chris.Jones@lchclearnet.com

CDS on Bclear Liffe CDS ECB, Frankfurt 24 February 2009 Ade Cordell Chris Jones Director, OTC Services Director, Head of Risk Management NYSE Euronext LCH.Clearnet ACordell@nyx.com Chris.Jones@lchclearnet.com

The Changing Landscape for Derivatives. John Hull Joseph L. Rotman School of Management University of Toronto.

The Changing Landscape for Derivatives John Hull Joseph L. Rotman School of Management University of Toronto hull@rotman.utoronto.ca April 2014 ABSTRACT This paper describes the changes taking place in

The Changing Landscape for Derivatives John Hull Joseph L. Rotman School of Management University of Toronto hull@rotman.utoronto.ca April 2014 ABSTRACT This paper describes the changes taking place in

Overview of Goldman Sachs. February 2019

Overview of Goldman Sachs February 209 Cautionary Note on Forward-Looking Statements This presentation includes forward-looking statements. These statements are not historical facts, but instead represent

Overview of Goldman Sachs February 209 Cautionary Note on Forward-Looking Statements This presentation includes forward-looking statements. These statements are not historical facts, but instead represent

The jurisdiction of this policy is extended to Tokyo Marine Rogge Asset Management Limited.

ORDER EXECUTION POLICY (PUBLIC) As of 19 March 2018 1. Policy Statement This document shall outline the principles that apply to the execution of orders in financial instruments on behalf of the funds

ORDER EXECUTION POLICY (PUBLIC) As of 19 March 2018 1. Policy Statement This document shall outline the principles that apply to the execution of orders in financial instruments on behalf of the funds

Pillar 3 Disclosure (UK)

") MORGAN STANLEY INTERNATIONAL LIMITED Pillar 3 Disclosure (UK) As at 31 December 2009 1. Basel II accord 2 2. Background to PIllar 3 disclosures 2 3. application of the PIllar 3 framework 2 4. morgan stanley

MORGAN STANLEY INTERNATIONAL LIMITED Pillar 3 Disclosure (UK) As at 31 December 2009 1. Basel II accord 2 2. Background to PIllar 3 disclosures 2 3. application of the PIllar 3 framework 2 4. morgan stanley

Tax Issues Faced by Financial Institutions

International Fiscal Association USA Branch Young IFA Network Summer Seminar Wednesday, August 2, 2017 Tax Issues Faced by Financial Institutions Emily Fett Senior Manager EY, LLP Jonas Robison Managing

International Fiscal Association USA Branch Young IFA Network Summer Seminar Wednesday, August 2, 2017 Tax Issues Faced by Financial Institutions Emily Fett Senior Manager EY, LLP Jonas Robison Managing

March 15, Japanese Bankers Association

March 15, 2013 Comments on the Second Consultative Document Margin requirements for non-centrally cleared derivatives by the Basel Committee on Banking Supervision and the International Organization of

March 15, 2013 Comments on the Second Consultative Document Margin requirements for non-centrally cleared derivatives by the Basel Committee on Banking Supervision and the International Organization of

CGFS Papers. Committee on the Global Financial System. Repo market functioning. No 59. Report prepared by a Study Group established by the

Committee on the Global Financial System CGFS Papers No 59 Repo market functioning Report prepared by a Study Group established by the Committee on the Global Financial System The Group was chaired by

Committee on the Global Financial System CGFS Papers No 59 Repo market functioning Report prepared by a Study Group established by the Committee on the Global Financial System The Group was chaired by

Brexit CCP Location and Legal Uncertainty

August 2017 Brexit CCP Location and Legal Uncertainty The UK s withdrawal from the European Union (EU), set for March 2019, is now little more than 18 months away. Negotiations between the UK government

August 2017 Brexit CCP Location and Legal Uncertainty The UK s withdrawal from the European Union (EU), set for March 2019, is now little more than 18 months away. Negotiations between the UK government

EXCHANGE TRADED CONCEPTS TRUST. REX VolMAXX TM Long VIX Futures Strategy ETF. Summary Prospectus March 30, 2018, as revised April 25, 2018

EXCHANGE TRADED CONCEPTS TRUST REX VolMAXX TM Long VIX Futures Strategy ETF Summary Prospectus March 30, 2018, as revised April 25, 2018 Principal Listing Exchange for the Fund: Cboe BZX Exchange, Inc.

EXCHANGE TRADED CONCEPTS TRUST REX VolMAXX TM Long VIX Futures Strategy ETF Summary Prospectus March 30, 2018, as revised April 25, 2018 Principal Listing Exchange for the Fund: Cboe BZX Exchange, Inc.

1.0 Purpose. Financial Services Commission of Ontario Commission des services financiers de l Ontario. Investment Guidance Notes

Financial Services Commission of Ontario Commission des services financiers de l Ontario SECTION: INDEX NO.: TITLE: APPROVED BY: Investment Guidance Notes IGN-002 Prudent Investment Practices for Derivatives

Financial Services Commission of Ontario Commission des services financiers de l Ontario SECTION: INDEX NO.: TITLE: APPROVED BY: Investment Guidance Notes IGN-002 Prudent Investment Practices for Derivatives

Deutsche Bank welcomes the opportunity to provide comments on the above consultation.

Secretariat of the Financial Stability Board, c/o Bank for International Settlements CH-4002, Basel, Switzerland 28 November 2013 Deutsche Bank AG Winchester House 1 Great Winchester Street London EC2N

Secretariat of the Financial Stability Board, c/o Bank for International Settlements CH-4002, Basel, Switzerland 28 November 2013 Deutsche Bank AG Winchester House 1 Great Winchester Street London EC2N

Financial Policy Summary and Record of the Financial Policy Committee Meeting on 26 February 2019

Financial Policy Summary and Record of the Financial Policy Committee Meeting on 26 February 2019 Publication date: 5 March 2019 This is the record of the Financial Policy Committee meeting held on 26

Financial Policy Summary and Record of the Financial Policy Committee Meeting on 26 February 2019 Publication date: 5 March 2019 This is the record of the Financial Policy Committee meeting held on 26

Regulatory Impacts on the Nordic Secondary Bonds and Derivatives Market

Regulatory Impacts on the Nordic Secondary Bonds and Derivatives Market ICMA Copenhagen, 27 October 2015 Fredrik Jenestrand, Head of Regulatory Strategy and Implementation, Markets FICC EU s regulatory

Regulatory Impacts on the Nordic Secondary Bonds and Derivatives Market ICMA Copenhagen, 27 October 2015 Fredrik Jenestrand, Head of Regulatory Strategy and Implementation, Markets FICC EU s regulatory

Order Execution Policy Macquarie Investment Management EMEA

Macquarie Investment Management EMEA Version: 2.0 Last approved: December 2017 Last updated: December 2017 Policy owner: Compliance 1. Policy Statement In accordance with regulatory obligations in the

Macquarie Investment Management EMEA Version: 2.0 Last approved: December 2017 Last updated: December 2017 Policy owner: Compliance 1. Policy Statement In accordance with regulatory obligations in the

Thomson Reuters response to CESR consultation Transparency of corporate bond, structure finance product and credit derivatives markets (CESR/O8-1014)

") February 2009 Thomson Reuters response to CESR consultation Transparency of corporate bond, structure finance product and credit derivatives markets (CESR/O8-1014) Thomson Reuters is the world s leading

February 2009 Thomson Reuters response to CESR consultation Transparency of corporate bond, structure finance product and credit derivatives markets (CESR/O8-1014) Thomson Reuters is the world s leading

Consultation on Term SONIA Reference Rates Summary of Responses. The Working Group on Sterling Risk-Free Reference Rates

Consultation on Term SONIA Reference Rates Summary of Responses The Working Group on Sterling Risk-Free Reference Rates November 2018 Term Sonia Reference Rates Consultation - Summary of Responses 1 The

Consultation on Term SONIA Reference Rates Summary of Responses The Working Group on Sterling Risk-Free Reference Rates November 2018 Term Sonia Reference Rates Consultation - Summary of Responses 1 The

Basel Committee on Banking Supervision. Basel III counterparty credit risk - Frequently asked questions

Basel Committee on Banking Supervision Basel III counterparty credit risk - Frequently asked questions November 2011 Copies of publications are available from: Bank for International Settlements Communications

Basel Committee on Banking Supervision Basel III counterparty credit risk - Frequently asked questions November 2011 Copies of publications are available from: Bank for International Settlements Communications

EMIR FAQ 1. WHAT IS EMIR?

EMIR FAQ The following information has been compiled for the purposes of providing an overview of EMIR and is not legal advice. The information is only accurate at date of publication and is subject to

EMIR FAQ The following information has been compiled for the purposes of providing an overview of EMIR and is not legal advice. The information is only accurate at date of publication and is subject to

Response to Consultative DAT Report on Incentives to Centrally Clear OTC Derivatives

Financial Stability Board Bank for International Settlements Centralbahnplatz 2 CH-4002 Basel Switzerland Basel Committee on Banking Supervision Bank for International Settlements Centralbahnplatz 2 CH-4002

Financial Stability Board Bank for International Settlements Centralbahnplatz 2 CH-4002 Basel Switzerland Basel Committee on Banking Supervision Bank for International Settlements Centralbahnplatz 2 CH-4002

Glitnir banki hf. Statement of Assets and Liabilities. 6 February 2009

Glitnir banki hf Statement of Assets and Liabilities Incorporating an estimate of the value of assets and a computation of liabilities 6 February 2009 Disclaimer This document includes a Statement of Assets

Glitnir banki hf Statement of Assets and Liabilities Incorporating an estimate of the value of assets and a computation of liabilities 6 February 2009 Disclaimer This document includes a Statement of Assets