Financial law reform: purpose and key questions

|

|

|

- Wesley Stafford

- 6 years ago

- Views:

Transcription

1 Conference on Cross-Jurisdictional Netting and Global Solutions Update on Netting in Asia May 12, 2011 London School of Economics and Political Science Peter M Werner Senior Director ISDA pwerner@isda.org 2011 International Swaps and Derivatives Association, Inc. ISDA is a registered trademark of the International Swaps and Derivatives Association, Inc. Financial law reform: purpose and key questions Creating a more stable and predictable legal environment for derivatives trading, close-out netting and related financial collateral arrangements Knowing where you stand : the practical value of increasing legal certainty An abstract goal, but with concrete results: increased market confidence, more liquidity, greater financial stability Key questions: Will my agreement be respected and enforced by a court or arbitration tribunal? Will foreign law governed contracts and foreign based counterparties be treated equally? Will it be enforced as written, both before and after my counterparty s insolvency? How can I protect against the risk of my counterparty s insolvency? Early termination and close-out netting under a master agreement Set-off rights Financial collateral arrangements and other forms of security Guarantees, letters of credit, insurance, credit derivatives 2 1

2 Selected int l legal instruments UNCITRAL Legislative Guide on Secured Transactions UNCITRAL Legislative Guide on Insolvency UN Convention on the Assignment of Receivables in International Trade UN Convention on Contracts for the International Sale of Goods Geneva Securities Convention Hague Securities Convention Hague Choice of Court Convention EU Directive on Financial Collateral Arrangements plus Amending Directive EU Directives on Winding-up of Banks and Insurance Undertakings EU Insolvency Regulation EU Regulation (Rome I) on the Law Applicable to Contractual Obligations EU Regulation (Brussels I) on the Recognition and Enforcement of Judgments in Civil and Commercial Matters Other law reform initiatives affecting international finance (e.g. proposals for EU and UNIDROIT instruments on netting) New York Convention (arbitration in derivatives disputes) 3 Importance and nature of close-out netting The single most important credit risk mitigation technique in the derivatives market Collateral is enforced against net balance and is calculated and taken on assumption netting works A three step process (requires a master agreement): 1. early termination 2. valuation of positions 3. determination of net balance Third step may be effected by contractual set-off, but not necessarily In other words, netting and set-off are related but distinct concepts Close-out netting under ISDA Master Agreement works on basis of conditionality, not set-off Other forms of netting: payment netting and netting by novation 4 2

After applying close-out netting, total credit exposure was $3.6 trillion (0.")

3 Risk reduction through close-out netting Bank for International Settlements, November 2010 As of June 30, 2010, total notional amount of all outstanding OTC derivatives was $582.7 trillion Total gross market value of outstanding OTC derivatives was $24.7 trillion (4.2% of notional amount) After applying close-out netting, total credit exposure was $3.6 trillion (0.6% of notional amount), a reduction of 85.5% from gross market value All banks, Reduction of mark-to-market exposure Jun-98 Jun-99 Jun-00 Jun-01 Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Jun-09 US banks, U.S. Office of the Comptroller of the Currency, 3 rd Quarter 2010 As of September 30, 2010, close-out netting reduced counterparty credit exposure at U.S. banks by 92.1% 69% of the netted credit exposure was covered by collateral Reduction of mark-to-market exposure Mar-96 Mar-98 Mar-00 Mar-02 Mar-04 Mar-06 Mar-08 Mar

4 7 8 4

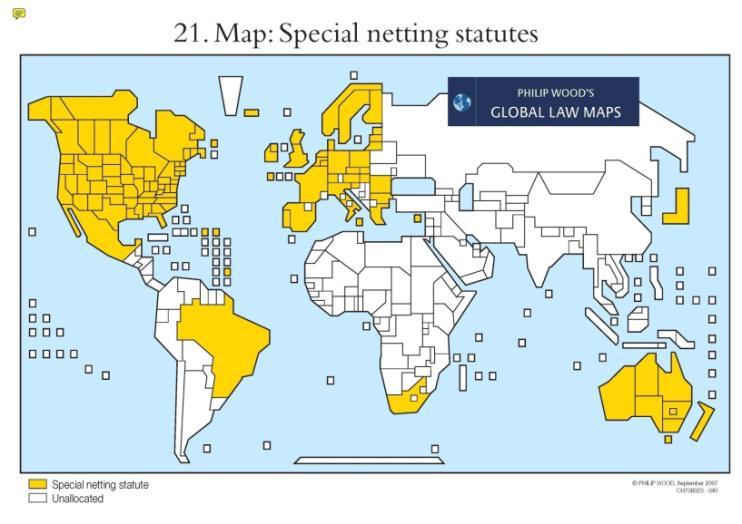

5 Netting legislation - status Country Netting Legislation Lithuania Under Consideration Andorra Adopted Luxembourg Adopted Anguilla Adopted Malta Adopted Argentina Under Consideration Adopted Mauritius Australia Adopted Mexico Adopted Austria Adopted Adopted New Zealand Belgium Adopted Norway Adopted Brazil Adopted Pakistan Under Consideration British Virgin Islands Adopted Peru Adopted Canada Adopted Poland Adopted Chile Under Consideration Portugal Adopted Colombia Adopted Romania Adopted Czech Republic Adopted Russia Adopted Denmark Adopted Seychelles Under Consideration Finland Adopted Slovakia Adopted France Adopted Slovenia Adopted Germany Adopted South Africa Adopted Greece Adopted South Korea Adopted Hungary Adopted Spain Adopted Ireland Adopted Sweden Adopted Israel Adopted Switzerland Adopted *United Kingdom: ISDA provides legal opinions for the laws of England & Wales as well as Scotland. As of February 21, 2009, the UK Banking Act introduced a new insolvency law for all UK jurisdictions providing for a special resolution regime for banks and building societies. This includes specific netting legislation for transactions with such counterparties. With regard to most other counterparties the previous regime remains in place. In England, the enforceability of netting is widely accepted without the need for specific statutory recognition. Please refer to the ISDA netting opinions on English and Scots law respectively. For other jurisdictions without specific netting statutes, eg, Turkey, Netherlands, Hong Kong, please refer to the relevant ISDA netting opinions. Italy Adopted United Kingdom * Adopted (see note) Japan Adopted United States Adopted 9 ISDA netting legislation initiatives Across jurisdictions globally the scope and contents of netting legislation vary significantly, especially regarding: Scope of counterparties eligible Scope of transactions covered Hence current and recent initiatives in: Russia, Kazakhstan, Ukraine, Poland, Czech Republic, Slovakia, Slovenia, Hungary, Lithuania, Bulgaria, Romania, Croatia, Serbia, UK, Pakistan, UAE, Bahrain, Qatar, Colombia, Peru, Mauritius, Nigeria, South Africa, Seychelles, South Korea, China, India, Indonesia, Malaysia, USA, Canada, Australia, New Zealand Relation between collateral transactions and netting legislation 10 5

6 Certain issues (1) South Korea: Netting legislation in place ( 2005 Debtor Rehabilitation and Bankruptcy Law ), but inconsistencies remain (e.g. re. any type of physical or financial commodity transaction plus corporates, central bank, public law entity, pension funds). India: No netting legislation, but gradual liberalisation via RBI circulars, policy statements etc. Certain products not allowed (e.g., equity, credit). Transactions limited to hedging. Additional problems remain due to inconsistencies with existing primary legislation, esp. re. legislation beyond the remit of RBI, e.g. central bank, certain state and nationalised banks, other government companies and insurance companies. 11 Certain issues (2) China: Close-out netting is not recognised under Chinese law. The 2006 Enterprise Bankruptcy Act recognises insolvency set-off, but subject to several major restrictions. Also, cherrypicking still possible. This far, no further clarifications made by legislator, financial regulators or Supreme Court (e.g. by way of special opinion on interpretation of the 2006 act). Hong Kong: No netting legislation, but netting is recognised under general principles of law. Netting analysis generally regarded positive with regard to financial and corporate counterparties. Problems remain re. insurance companies, funds, central bank, public law entities. Taiwan: No specific legislation. Netting enforceable under general principles of law. Wide scope of transactions and counterparties covered. 12 6

7 Certain issues (3) Malaysia: No netting legislation. Mandatory set-off on insolvency. However, in certain circumstances close-out netting may not be enforceable, esp. during moratoria pursuant to 1998 Danaharta Act and 2005 Deposit Insurance Corporation Act. Otherwise, scope of counterparties (excl. insurance companies) and transactions fairly wide. Indonesia: No netting legislation. Enforceability based on general principles of law, but relatively large degree of uncertainty regarding the material content of legal rules. Otherwise, scope of counterparties and transactions fairly wide. Philippines: No netting legislation. General principles of law apply. However, application of general insolvency law rules is limited to certain counterparties only. 13 Certain issues (4) Japan: Enforceability based on both legislation and general principles. Problems remain re. some types of corporations, funds, public law entities as well as all types of commodity transactions and new products. Australia: Both legislation and general (1998 Payment Systems and Netting Act) principles. Fairly wide scope of counterparties and transactions covered, but proposals for moratorium pending. Middle East:..nothing (almost). Some rudimentary provisions here and there in Bahrain, UAE, Qatar, but not sufficient by any measure. Very good draft bill pending in Pakistan (on netting and collateral). Central Asia:.not much better (esp. Kazakhstan). 14 7

8 Conclusion: We need a global instrument on close-out netting now! 15 Conference on Cross-Jurisdictional Netting and Global Solutions Update on Netting in Asia May 12, 2011 London School of Economics and Political Science Dr Peter M Werner Senior Director ISDA pwerner@isda.org 2011 International Swaps and Derivatives Association, Inc. ISDA is a registered trademark of the International Swaps and Derivatives Association, Inc. 8

Guide to Treatment of Withholding Tax Rates. January 2018

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Guide to Treatment of Withholding Tax Rates Contents 1. Introduction 1 1.1. Aims of the Guide 1 1.2. Withholding Tax Definition 1 1.3. Double Taxation Treaties 1 1.4. Information Sources 1 1.5. Guide Upkeep

Financial wealth of private households worldwide

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

Economic Research Financial wealth of private households worldwide Munich, October 217 Recovery in turbulent times Assets and liabilities of private households worldwide in EUR trillion and annualrate

STOXX EMERGING MARKETS INDICES. UNDERSTANDA RULES-BA EMERGING MARK TRANSPARENT SIMPLE

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

STOXX Limited STOXX EMERGING MARKETS INDICES. EMERGING MARK RULES-BA TRANSPARENT UNDERSTANDA SIMPLE MARKET CLASSIF INTRODUCTION. Many investors are seeking to embrace emerging market investments, because

Reporting practices for domestic and total debt securities

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Last updated: 27 November 2017 Reporting practices for domestic and total debt securities While the BIS debt securities statistics are in principle harmonised with the recommendations in the Handbook on

Summary 715 SUMMARY. Minimum Legal Fee Schedule. Loser Pays Statute. Prohibition Against Legal Advertising / Soliciting of Pro bono

Summary Country Fee Aid Angola No No No Argentina No, with No No No Armenia, with No No No No, however the foreign Attorneys need to be registered at the Chamber of Advocates to be able to practice attorney

Summary Country Fee Aid Angola No No No Argentina No, with No No No Armenia, with No No No No, however the foreign Attorneys need to be registered at the Chamber of Advocates to be able to practice attorney

EQUITY REPORTING & WITHHOLDING. Updated May 2016

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

EQUITY REPORTING & WITHHOLDING Updated May 2016 When you exercise stock options or have RSUs lapse, there may be tax implications in any country in which you worked for P&G during the period from the

FOREIGN ACTIVITY REPORT

FOREIGN ACTIVITY REPORT SECOND QUARTER 2012 TABLE OF CONTENTS Table of Contents... i All Securities Transactions... 2 Highlights... 2 U.S. Transactions in Foreign Securities... 2 Foreign Transactions in

FOREIGN ACTIVITY REPORT SECOND QUARTER 2012 TABLE OF CONTENTS Table of Contents... i All Securities Transactions... 2 Highlights... 2 U.S. Transactions in Foreign Securities... 2 Foreign Transactions in

TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF REGULATIONS No. 3) (JERSEY) ORDER 2017

(CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF REGULATIONS No. 3) (JERSEY) ORDER 2017") Taxation (Implementation) (Convention on Mutual Regulations No. 3) (Jersey) Order 2017 Article 1 TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF

Taxation (Implementation) (Convention on Mutual Regulations No. 3) (Jersey) Order 2017 Article 1 TAXATION (IMPLEMENTATION) (CONVENTION ON MUTUAL ADMINISTRATIVE ASSISTANCE IN TAX MATTERS) (AMENDMENT OF

Quarterly Investment Update First Quarter 2018

Quarterly Investment Update First Quarter 2018 Dimensional Fund Advisors Canada ULC ( DFA Canada ) is not affiliated with [insert name of Advisor]. DFA Canada is a separate and distinct company. Market

Quarterly Investment Update First Quarter 2018 Dimensional Fund Advisors Canada ULC ( DFA Canada ) is not affiliated with [insert name of Advisor]. DFA Canada is a separate and distinct company. Market

APA & MAP COUNTRY GUIDE 2017 DENMARK

APA & MAP COUNTRY GUIDE 2017 DENMARK Managing uncertainty in the new tax environment DENMARK KEY FEATURES Competent authority Danish Tax Office ( SKAT ) APA provisions/ guidance Types of APAs available

APA & MAP COUNTRY GUIDE 2017 DENMARK Managing uncertainty in the new tax environment DENMARK KEY FEATURES Competent authority Danish Tax Office ( SKAT ) APA provisions/ guidance Types of APAs available

Summary of key findings

1 VAT/GST treatment of cross-border services: 2017 survey Supplies of e-services to consumers (B2C) (see footnote 1) Supplies of e-services to businesses (B2B) 1(a). Is a non-resident 1(b). If there is

1 VAT/GST treatment of cross-border services: 2017 survey Supplies of e-services to consumers (B2C) (see footnote 1) Supplies of e-services to businesses (B2B) 1(a). Is a non-resident 1(b). If there is

Corrigendum. OECD Pensions Outlook 2012 DOI: ISBN (print) ISBN (PDF) OECD 2012

ISBN (PDF) OECD 2012") OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

OECD Pensions Outlook 2012 DOI: http://dx.doi.org/9789264169401-en ISBN 978-92-64-16939-5 (print) ISBN 978-92-64-16940-1 (PDF) OECD 2012 Corrigendum Page 21: Figure 1.1. Average annual real net investment

Total Imports by Volume (Gallons per Country)

") 10/5/2017 Imports by Volume (Gallons per Country) YTD YTD Country 08/2016 08/2017 % Change 2016 2017 % Change MEXICO 51,349,849 67,180,788 30.8 % 475,806,632 503,129,061 5.7 % NETHERLANDS 12,756,776 12,954,789

10/5/2017 Imports by Volume (Gallons per Country) YTD YTD Country 08/2016 08/2017 % Change 2016 2017 % Change MEXICO 51,349,849 67,180,788 30.8 % 475,806,632 503,129,061 5.7 % NETHERLANDS 12,756,776 12,954,789

Total Imports by Volume (Gallons per Country)

") 1/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 11/2016 11/2017 % Change 2016 2017 % Change MEXICO 50,994,409 48,959,909 (4.0)% 631,442,105 657,851,150 4.2 % NETHERLANDS 9,378,351 11,903,919

1/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 11/2016 11/2017 % Change 2016 2017 % Change MEXICO 50,994,409 48,959,909 (4.0)% 631,442,105 657,851,150 4.2 % NETHERLANDS 9,378,351 11,903,919

Total Imports by Volume (Gallons per Country)

") 7/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 05/2017 05/2018 % Change 2017 2018 % Change MEXICO 71,166,360 74,896,922 5.2 % 302,626,505 328,397,135 8.5 % NETHERLANDS 12,039,171 13,341,929

7/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 05/2017 05/2018 % Change 2017 2018 % Change MEXICO 71,166,360 74,896,922 5.2 % 302,626,505 328,397,135 8.5 % NETHERLANDS 12,039,171 13,341,929

a closer look GLOBAL TAX WEEKLY ISSUE 249 AUGUST 17, 2017

GLOBAL TAX WEEKLY a closer look ISSUE 249 AUGUST 17, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

GLOBAL TAX WEEKLY a closer look ISSUE 249 AUGUST 17, 2017 SUBJECTS TRANSFER PRICING INTELLECTUAL PROPERTY VAT, GST AND SALES TAX CORPORATE TAXATION INDIVIDUAL TAXATION REAL ESTATE AND PROPERTY TAXES INTERNATIONAL

Total Imports by Volume (Gallons per Country)

") 10/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 08/2017 08/2018 % Change 2017 2018 % Change MEXICO 67,180,788 71,483,563 6.4 % 503,129,061 544,043,847 8.1 % NETHERLANDS 12,954,789 12,582,508

10/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 08/2017 08/2018 % Change 2017 2018 % Change MEXICO 67,180,788 71,483,563 6.4 % 503,129,061 544,043,847 8.1 % NETHERLANDS 12,954,789 12,582,508

Total Imports by Volume (Gallons per Country)

") 11/2/2018 Imports by Volume (Gallons per Country) YTD YTD Country 09/2017 09/2018 % Change 2017 2018 % Change MEXICO 49,299,573 57,635,840 16.9 % 552,428,635 601,679,687 8.9 % NETHERLANDS 11,656,759 13,024,144

11/2/2018 Imports by Volume (Gallons per Country) YTD YTD Country 09/2017 09/2018 % Change 2017 2018 % Change MEXICO 49,299,573 57,635,840 16.9 % 552,428,635 601,679,687 8.9 % NETHERLANDS 11,656,759 13,024,144

Total Imports by Volume (Gallons per Country)

") 2/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 11/2017 11/2018 % Change 2017 2018 % Change MEXICO 48,959,909 54,285,392 10.9 % 657,851,150 716,916,480 9.0 % NETHERLANDS 11,903,919 10,024,814

2/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 11/2017 11/2018 % Change 2017 2018 % Change MEXICO 48,959,909 54,285,392 10.9 % 657,851,150 716,916,480 9.0 % NETHERLANDS 11,903,919 10,024,814

Total Imports by Volume (Gallons per Country)

") 12/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 10/2017 10/2018 % Change 2017 2018 % Change MEXICO 56,462,606 60,951,402 8.0 % 608,891,240 662,631,088 8.8 % NETHERLANDS 11,381,432 10,220,226

12/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 10/2017 10/2018 % Change 2017 2018 % Change MEXICO 56,462,606 60,951,402 8.0 % 608,891,240 662,631,088 8.8 % NETHERLANDS 11,381,432 10,220,226

Total Imports by Volume (Gallons per Country)

") 3/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 12/2017 12/2018 % Change 2017 2018 % Change MEXICO 54,169,734 56,505,154 4.3 % 712,020,884 773,421,634 8.6 % NETHERLANDS 11,037,475 8,403,018

3/6/2019 Imports by Volume (Gallons per Country) YTD YTD Country 12/2017 12/2018 % Change 2017 2018 % Change MEXICO 54,169,734 56,505,154 4.3 % 712,020,884 773,421,634 8.6 % NETHERLANDS 11,037,475 8,403,018

Total Imports by Volume (Gallons per Country)

") 3/7/2018 Imports by Volume (Gallons per Country) YTD YTD Country 01/2017 01/2018 % Change 2017 2018 % Change MEXICO 54,235,419 58,937,856 8.7 % 54,235,419 58,937,856 8.7 % NETHERLANDS 12,265,935 10,356,183

3/7/2018 Imports by Volume (Gallons per Country) YTD YTD Country 01/2017 01/2018 % Change 2017 2018 % Change MEXICO 54,235,419 58,937,856 8.7 % 54,235,419 58,937,856 8.7 % NETHERLANDS 12,265,935 10,356,183

Approach to Employment Injury (EI) compensation benefits in the EU and OECD

compensation benefits in the EU and OECD") Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

Approach to (EI) compensation benefits in the EU and OECD The benefits of protection can be divided in three main groups. The cash benefits include disability pensions, survivor's pensions and other short-

Total Imports by Volume (Gallons per Country)

") 2/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 12/2016 12/2017 % Change 2016 2017 % Change MEXICO 50,839,282 54,169,734 6.6 % 682,281,387 712,020,884 4.4 % NETHERLANDS 10,630,799 11,037,475

2/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 12/2016 12/2017 % Change 2016 2017 % Change MEXICO 50,839,282 54,169,734 6.6 % 682,281,387 712,020,884 4.4 % NETHERLANDS 10,630,799 11,037,475

International Statistical Release

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Regulated Open-ended Fund Assets and Flows Trends

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Regulated Open-ended Fund Assets and Flows Trends

Argentina Bahamas Barbados Bermuda Bolivia Brazil British Virgin Islands Canada Cayman Islands Chile

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

Americas Argentina (Banking and finance; Capital markets: Debt; Capital markets: Equity; M&A; Project Bahamas (Financial and corporate) Barbados (Financial and corporate) Bermuda (Financial and corporate)

International Statistical Release

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Investment Fund Assets and Flows Trends in the

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Investment Fund Assets and Flows Trends in the

Double Tax Treaties. Necessity of Declaration on Tax Beneficial Ownership In case of capital gains tax. DTA Country Withholding Tax Rates (%)

") Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Double Tax Treaties DTA Country Withholding Tax Rates (%) Albania 0 0 5/10 1 No No No Armenia 5/10 9 0 5/10 1 Yes 2 No Yes Australia 10 0 15 No No No Austria 0 0 10 No No No Azerbaijan 8 0 8 Yes No Yes

Total Imports by Volume (Gallons per Country)

") 5/4/2016 Imports by Volume (Gallons per Country) YTD YTD Country 03/2015 03/2016 % Change 2015 2016 % Change MEXICO 53,821,885 60,813,992 13.0 % 143,313,133 167,568,280 16.9 % NETHERLANDS 11,031,990 12,362,256

5/4/2016 Imports by Volume (Gallons per Country) YTD YTD Country 03/2015 03/2016 % Change 2015 2016 % Change MEXICO 53,821,885 60,813,992 13.0 % 143,313,133 167,568,280 16.9 % NETHERLANDS 11,031,990 12,362,256

International Statistical Release

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org) Worldwide Investment Fund Assets and Flows Trends in the

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org) Worldwide Investment Fund Assets and Flows Trends in the

Global Business Barometer April 2008

Global Business Barometer April 2008 The Global Business Barometer is a quarterly business-confidence index, conducted for The Economist by the Economist Intelligence Unit What are your expectations of

Global Business Barometer April 2008 The Global Business Barometer is a quarterly business-confidence index, conducted for The Economist by the Economist Intelligence Unit What are your expectations of

Total Imports by Volume (Gallons per Country)

") 4/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 02/2017 02/2018 % Change 2017 2018 % Change MEXICO 53,961,589 55,268,981 2.4 % 108,197,008 114,206,836 5.6 % NETHERLANDS 12,804,152 11,235,029

4/5/2018 Imports by Volume (Gallons per Country) YTD YTD Country 02/2017 02/2018 % Change 2017 2018 % Change MEXICO 53,961,589 55,268,981 2.4 % 108,197,008 114,206,836 5.6 % NETHERLANDS 12,804,152 11,235,029

PENTA CLO 2 B.V. (the "Issuer")

") THIS NOTICE CONTAINS IMPORTANT INFORMATION OF INTEREST TO THE REGISTERED AND BENEFICIAL OWNERS OF THE NOTES (AS DEFINED BELOW). IF APPLICABLE, ALL DEPOSITARIES, CUSTODIANS AND OTHER INTERMEDIARIES RECEIVING

THIS NOTICE CONTAINS IMPORTANT INFORMATION OF INTEREST TO THE REGISTERED AND BENEFICIAL OWNERS OF THE NOTES (AS DEFINED BELOW). IF APPLICABLE, ALL DEPOSITARIES, CUSTODIANS AND OTHER INTERMEDIARIES RECEIVING

Spain France. England Netherlands. Wales Ukraine. Republic of Ireland Czech Republic. Romania Albania. Serbia Israel. FYR Macedonia Latvia

Germany Belgium Portugal Spain France Switzerland Italy England Netherlands Iceland Poland Croatia Slovakia Russia Austria Wales Ukraine Sweden Bosnia-Herzegovina Republic of Ireland Czech Republic Turkey

Germany Belgium Portugal Spain France Switzerland Italy England Netherlands Iceland Poland Croatia Slovakia Russia Austria Wales Ukraine Sweden Bosnia-Herzegovina Republic of Ireland Czech Republic Turkey

Total Imports by Volume (Gallons per Country)

") 6/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 04/2017 04/2018 % Change 2017 2018 % Change MEXICO 60,968,190 71,994,646 18.1 % 231,460,145 253,500,213 9.5 % NETHERLANDS 13,307,731 10,001,693

6/6/2018 Imports by Volume (Gallons per Country) YTD YTD Country 04/2017 04/2018 % Change 2017 2018 % Change MEXICO 60,968,190 71,994,646 18.1 % 231,460,145 253,500,213 9.5 % NETHERLANDS 13,307,731 10,001,693

DOMESTIC CUSTODY & TRADING SERVICES

Pricing Structure DOMESTIC CUSTODY & TRADING SERVICES A flat custody fee of 20bps per account type per year is applicable to all holdings and cash, the custody fee is collected each month but will be capped

Pricing Structure DOMESTIC CUSTODY & TRADING SERVICES A flat custody fee of 20bps per account type per year is applicable to all holdings and cash, the custody fee is collected each month but will be capped

TAXATION OF TRUSTS IN ISRAEL. An Opportunity For Foreign Residents. Dr. Avi Nov

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

TAXATION OF TRUSTS IN ISRAEL An Opportunity For Foreign Residents Dr. Avi Nov Short Bio Dr. Avi Nov is an Israeli lawyer who represents taxpayers, individuals and entities. Areas of Practice: Tax Law,

Quarterly Investment Update First Quarter 2017

Quarterly Investment Update First Quarter 2017 Market Update: A Quarter in Review March 31, 2017 CANADIAN STOCKS INTERNATIONAL STOCKS Large Cap Small Cap Growth Value Large Cap Small Cap Growth Value Emerging

Quarterly Investment Update First Quarter 2017 Market Update: A Quarter in Review March 31, 2017 CANADIAN STOCKS INTERNATIONAL STOCKS Large Cap Small Cap Growth Value Large Cap Small Cap Growth Value Emerging

International Statistical Release

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). wide Regulated Open-ended Fund Assets and Flows Trends

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). wide Regulated Open-ended Fund Assets and Flows Trends

COUNTRY COST INDEX JUNE 2013

COUNTRY COST INDEX JUNE 2013 June 2013 Kissell Research Group, LLC 1010 Northern Blvd., Suite 208 Great Neck, NY 11021 www.kissellresearch.com Kissell Research Group Country Cost Index - June 2013 2 Executive

COUNTRY COST INDEX JUNE 2013 June 2013 Kissell Research Group, LLC 1010 Northern Blvd., Suite 208 Great Neck, NY 11021 www.kissellresearch.com Kissell Research Group Country Cost Index - June 2013 2 Executive

Open Day 2017 Clearstream execution-to-custody integration Valentin Nehls / Jan Willems. 5 October 2017

Open Day 2017 Clearstream execution-to-custody integration Valentin Nehls / Jan Willems 5 October 2017 Deutsche Börse Group 1 Settlement services: single point of access to cost-effective, low risk and

Open Day 2017 Clearstream execution-to-custody integration Valentin Nehls / Jan Willems 5 October 2017 Deutsche Börse Group 1 Settlement services: single point of access to cost-effective, low risk and

FTSE Global Equity Index Series

Methodology overview FTSE Global Equity Index Series Built for the demands of global investors Indexes for a global market The FTSE Global Equity Index Series (FTSE GEIS) includes objective, rules-based

Methodology overview FTSE Global Equity Index Series Built for the demands of global investors Indexes for a global market The FTSE Global Equity Index Series (FTSE GEIS) includes objective, rules-based

Real Estate & Private Equity workshop

Real Estate & Private Equity workshop Moderator: Panelists: Joseph Hendry, Managing Director, Brown Brothers Harriman Gautier Despret, Senior Manager, Ernst & Young Patrick Goebel, Counsel, Allen & Overy

Real Estate & Private Equity workshop Moderator: Panelists: Joseph Hendry, Managing Director, Brown Brothers Harriman Gautier Despret, Senior Manager, Ernst & Young Patrick Goebel, Counsel, Allen & Overy

The Global Tax Reset 2017 Audit Committee Symposium

The Global Tax Reset Copyright 2017 Deloitte Development LLC. All rights reserved. 2017 Audit Committee Symposium Anticipate. Navigate. Focus. 1 The Global Tax Reset General context Multinational companies

The Global Tax Reset Copyright 2017 Deloitte Development LLC. All rights reserved. 2017 Audit Committee Symposium Anticipate. Navigate. Focus. 1 The Global Tax Reset General context Multinational companies

Actuarial Supply & Demand. By i.e. muhanna. i.e. muhanna Page 1 of

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

By i.e. muhanna i.e. muhanna Page 1 of 8 040506 Additional Perspectives Measuring actuarial supply and demand in terms of GDP is indeed a valid basis for setting the actuarial density of a country and

Focus on Barrier 16 : Netting Edward Murray, Partner, Allen & Overy LLP

5th Meeting of the CESAME2 Group European Commission, DG Internal Market and Services Tuesday, 2 March 2010, Centre Borschette, Brussels Focus on Barrier 16 : Netting Edward Murray, Partner, Allen & Overy

5th Meeting of the CESAME2 Group European Commission, DG Internal Market and Services Tuesday, 2 March 2010, Centre Borschette, Brussels Focus on Barrier 16 : Netting Edward Murray, Partner, Allen & Overy

When will CbC reports need to be filled?

Who will be subject to CbCR? Country by Country Reporting (CbCR) applies to multinational companies (MNCs) with a combined revenue of euros 750 million or more When will CbC reports need to be filled?

Who will be subject to CbCR? Country by Country Reporting (CbCR) applies to multinational companies (MNCs) with a combined revenue of euros 750 million or more When will CbC reports need to be filled?

Public Pension Spending Trends and Outlook in Emerging Europe. Benedict Clements Fiscal Affairs Department International Monetary Fund March 2013

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

Public Pension Spending Trends and Outlook in Emerging Europe Benedict Clements Fiscal Affairs Department International Monetary Fund March 13 Plan of Presentation I. Trends and drivers of public pension

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA)

") BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA) In the period January - April 2017 Bulgarian exports to the EU increased by 8.6% 2016 and amounted to 10 418.6 Million BGN

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - APRIL 2017 (PRELIMINARY DATA) In the period January - April 2017 Bulgarian exports to the EU increased by 8.6% 2016 and amounted to 10 418.6 Million BGN

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA)

") BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA) In the period January - May 2017 Bulgarian exports to the EU increased by 10.8% 2016 and added up to 13 283.0 Million BGN (Annex,

BULGARIAN TRADE WITH EU IN THE PERIOD JANUARY - MAY 2017 (PRELIMINARY DATA) In the period January - May 2017 Bulgarian exports to the EU increased by 10.8% 2016 and added up to 13 283.0 Million BGN (Annex,

San Francisco Retiree Health Care Trust Fund Education Materials on Public Equity

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

M E K E T A I N V E S T M E N T G R O U P 5796 ARMADA DRIVE SUITE 110 CARLSBAD CA 92008 760 795 3450 fax 760 795 3445 www.meketagroup.com The Global Equity Opportunity Set MSCI All Country World 1 Index

Global Tax Reset Transfer Pricing Documentation Summary. February 2018

Global Tax Reset Transfer Pricing Summary February 2018 Global Tax Reset Transfer Pricing Summary Overview The Global Tax Reset Transfer Pricing Summary ( Guide ) compiles essential country-by-country

Global Tax Reset Transfer Pricing Summary February 2018 Global Tax Reset Transfer Pricing Summary Overview The Global Tax Reset Transfer Pricing Summary ( Guide ) compiles essential country-by-country

APA & MAP COUNTRY GUIDE 2017 CANADA

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

APA & MAP COUNTRY GUIDE 2017 CANADA Managing uncertainty in the new tax environment CANADA KEY FEATURES Competent authority APA provisions/ guidance Types of APAs available APA acceptance criteria Key

ISSUE OF ENDORSEMENTS ATTESTING TO THE RECOGNITION OF A CERTIFICATE OF COMPETENCY

SHIPPING NOTICE 05/2011 (Rev 7) ISSUE OF ENDORSEMENTS ATTESTING TO THE RECOGNITION OF A CERTIFICATE OF COMPETENCY To: OWNERS, MANAGERS, CHARTERERS, CREWING AGENCIES AND MASTERS OF CAYMAN ISLANDS SHIPS

SHIPPING NOTICE 05/2011 (Rev 7) ISSUE OF ENDORSEMENTS ATTESTING TO THE RECOGNITION OF A CERTIFICATE OF COMPETENCY To: OWNERS, MANAGERS, CHARTERERS, CREWING AGENCIES AND MASTERS OF CAYMAN ISLANDS SHIPS

Withholding Tax Handbook BELGIUM. Version 1.2 Last Updated: June 20, New York Hong Kong London Madrid Milan Sydney

Withholding Tax Handbook BELGIUM Version 1.2 Last Updated: June 20, 2014 Globe Tax Services Incorporated 90 Broad Street, New York, NY, USA 10004 Tel +1 212 747 9100 Fax +1 212 747 0029 Info@GlobeTax.com

Withholding Tax Handbook BELGIUM Version 1.2 Last Updated: June 20, 2014 Globe Tax Services Incorporated 90 Broad Street, New York, NY, USA 10004 Tel +1 212 747 9100 Fax +1 212 747 0029 Info@GlobeTax.com

KPMG s Individual Income Tax and Social Security Rate Survey 2009 TAX

KPMG s Individual Income Tax and Social Security Rate Survey 2009 TAX B KPMG s Individual Income Tax and Social Security Rate Survey 2009 KPMG s Individual Income Tax and Social Security Rate Survey 2009

KPMG s Individual Income Tax and Social Security Rate Survey 2009 TAX B KPMG s Individual Income Tax and Social Security Rate Survey 2009 KPMG s Individual Income Tax and Social Security Rate Survey 2009

World Consumer Income and Expenditure Patterns

World Consumer Income and Expenditure Patterns 2011 www.euromonitor.com iii Summary of Contents Contents Summary of Contents Section 1 Introduction 1 Section 2 Socio-economic parameters 21 Section 3 Annual

World Consumer Income and Expenditure Patterns 2011 www.euromonitor.com iii Summary of Contents Contents Summary of Contents Section 1 Introduction 1 Section 2 Socio-economic parameters 21 Section 3 Annual

n O v e m b e R Securities Industry And Financial Markets Global Addendum 2007 Volume I I No. New York n Washington n London n Hong Kong

ReseaRch RePORT n O v e m b e R 2 7 Securities Industry And Financial Markets Global Addendum 27 Volume I I No. 1 New York n Washington n London n Hong Kong SIFMA RESEARCH AND POLICY DEPARTMENT Michael

ReseaRch RePORT n O v e m b e R 2 7 Securities Industry And Financial Markets Global Addendum 27 Volume I I No. 1 New York n Washington n London n Hong Kong SIFMA RESEARCH AND POLICY DEPARTMENT Michael

CNH and China QFII market: Opportunities and Challenges A Fund Custodian and Administrator's Perspective"

CNH and China QFII market: Opportunities and Challenges A Fund Custodian and Administrator's Perspective" Eric Chow HSBC Securities Services June 2011 2 Agenda About HSBC Securities Services (HSS) Introducing

CNH and China QFII market: Opportunities and Challenges A Fund Custodian and Administrator's Perspective" Eric Chow HSBC Securities Services June 2011 2 Agenda About HSBC Securities Services (HSS) Introducing

Rev. Proc Implementation of Nonresident Alien Deposit Interest Regulations

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

Rev. Proc. 2012-24 Implementation of Nonresident Alien Deposit Interest Regulations SECTION 1. PURPOSE Sections 1.6049-4(b)(5) and 1.6049-8 of the Income Tax Regulations, as revised by TD 9584, require

% 38, % 40, % 2,611 2,

3 DECEMBER 6 OPEN ENDED Number of Net Value of Number of Total Value Total Value Net New Date Authorised/Registered Schemes Registered of Sales of Repurchases Investment Schemes ( mn) Holders ( mn) ( mn)

3 DECEMBER 6 OPEN ENDED Number of Net Value of Number of Total Value Total Value Net New Date Authorised/Registered Schemes Registered of Sales of Repurchases Investment Schemes ( mn) Holders ( mn) ( mn)

Information Leaflet No. 5

Information Leaflet No. 5 REGISTRATION OF EXTERNAL COMPANIES INFORMATION LEAFLET NO. 5 / May 2017 1. INTRODUCTION An external (foreign) limited company registered abroad may establish a branch in the State.

Information Leaflet No. 5 REGISTRATION OF EXTERNAL COMPANIES INFORMATION LEAFLET NO. 5 / May 2017 1. INTRODUCTION An external (foreign) limited company registered abroad may establish a branch in the State.

Frontier Markets and a teaser of what is to come. Peter Elam Håkansson, Chairman and Partner

Frontier Markets and a teaser of what is to come Peter Elam Håkansson, Chairman and Partner The Frontier Markets Have the good old Emerging Markets lost their appeal? We remain convinced that Emerging

Frontier Markets and a teaser of what is to come Peter Elam Håkansson, Chairman and Partner The Frontier Markets Have the good old Emerging Markets lost their appeal? We remain convinced that Emerging

WHY UHY? The network for doing business

The network for doing business the network for doing business UHY has over 6,800 professionals to choose from trusted advisors and consultants operating in more than 250 business centres, based in 81 countries

The network for doing business the network for doing business UHY has over 6,800 professionals to choose from trusted advisors and consultants operating in more than 250 business centres, based in 81 countries

The current state of ICOs

The current state of ICOs A concise overview of ICO overall developments, regions, raised capital and the biggest projects Contents Preface... 2 1. Current ICO developments in Q1 2018... 3 1.1 Raised ICO

The current state of ICOs A concise overview of ICO overall developments, regions, raised capital and the biggest projects Contents Preface... 2 1. Current ICO developments in Q1 2018... 3 1.1 Raised ICO

2009 Half Year Results. August 25, 2009

1 2009 Half Year Results August 25, 2009 2 Caution statement This presentation may contain forward looking statements, which are subject to risk and uncertainty. A variety of factors could cause our actual

1 2009 Half Year Results August 25, 2009 2 Caution statement This presentation may contain forward looking statements, which are subject to risk and uncertainty. A variety of factors could cause our actual

Instruction Deadline. *Settlement Cycle

Argentina Equity & Fixed Income T+0-T+2 SD+1 2:30 SD+1 2:30 Fixed Income (MAECLEAR) T+0-T+2 SD 23:00 SD 23:00 Physical T+0-T+2 SD 23:00 SD 23:00 Australia Equity T+2 SD 5:30 SD 10:30 Fixed Income T+2 SD

Argentina Equity & Fixed Income T+0-T+2 SD+1 2:30 SD+1 2:30 Fixed Income (MAECLEAR) T+0-T+2 SD 23:00 SD 23:00 Physical T+0-T+2 SD 23:00 SD 23:00 Australia Equity T+2 SD 5:30 SD 10:30 Fixed Income T+2 SD

Madeira: Global Solutions for Wise Investments

Madeira: Global Solutions for Wise Investments Double Taxation Treaties Document downloaded from www.ibc-madeira.com DOUBLE TAXATION TREATIES RATIFIED BY PORTUGAL Europe RATIFICATION/ENTRY INTO FORCE AUSTRIA

Madeira: Global Solutions for Wise Investments Double Taxation Treaties Document downloaded from www.ibc-madeira.com DOUBLE TAXATION TREATIES RATIFIED BY PORTUGAL Europe RATIFICATION/ENTRY INTO FORCE AUSTRIA

Enterprise Europe Network SME growth outlook

Enterprise Europe Network SME growth outlook 2018-19 een.ec.europa.eu 2 Enterprise Europe Network SME growth outlook 2018-19 Foreword The European Commission wants to ensure that small and medium-sized

Enterprise Europe Network SME growth outlook 2018-19 een.ec.europa.eu 2 Enterprise Europe Network SME growth outlook 2018-19 Foreword The European Commission wants to ensure that small and medium-sized

Switzerland Country Profile

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Switzerland Country Profile EU Tax Centre June 2018 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

FTSE Annual Country Classification Review Published: 26 September 2018

FTSE Classification of Markets FTSE Annual Country Classification Review Published: 26 September 2018 Headlines China A to be assigned Secondary Emerging market status commencing June 2019 Iceland to be

FTSE Classification of Markets FTSE Annual Country Classification Review Published: 26 September 2018 Headlines China A to be assigned Secondary Emerging market status commencing June 2019 Iceland to be

Tax Newsflash January 31, 2014

Tax Newsflash January 31, 2014 Luxembourg s New Double Tax Treaties As of 1 January 2014, Luxembourg further enlarged its double tax treaty network with the entry into force of the new double tax treaties

Tax Newsflash January 31, 2014 Luxembourg s New Double Tax Treaties As of 1 January 2014, Luxembourg further enlarged its double tax treaty network with the entry into force of the new double tax treaties

DIVERSIFICATION. Diversification

Diversification Helps you capture what global markets offer Reduces risks that have no expected return May prevent you from missing opportunity Smooths out some of the bumps Helps take the guesswork out

Diversification Helps you capture what global markets offer Reduces risks that have no expected return May prevent you from missing opportunity Smooths out some of the bumps Helps take the guesswork out

Convention on Mutual Administrative Assistance in Tax Matters as amended by the 2010 Protocol

European Treaty Series - No. 127 Convention on Mutual Administrative Assistance in Tax Matters as amended by the 2010 Protocol Strasbourg, 1.VI.2011 Annex B Competent authorities (*) States From A to F

European Treaty Series - No. 127 Convention on Mutual Administrative Assistance in Tax Matters as amended by the 2010 Protocol Strasbourg, 1.VI.2011 Annex B Competent authorities (*) States From A to F

IMPORTANT TAX INFORMATION

00126803 IMPORTANT TAX INFORMATION Dear Hartford Funds Shareholder: The following information about your enclosed 1099-DIV from Hartford Funds should be used when preparing your 2014 tax return. The information

00126803 IMPORTANT TAX INFORMATION Dear Hartford Funds Shareholder: The following information about your enclosed 1099-DIV from Hartford Funds should be used when preparing your 2014 tax return. The information

Information Leaflet No. 5

Information Leaflet No. 5 REGISTRATION OF EXTERNAL COMPANIES INFORMATION LEAFLET NO. 5 / FEBRUARY 2018 ii 1. INTRODUCTION An external (foreign) limited company registered abroad may establish a branch

Information Leaflet No. 5 REGISTRATION OF EXTERNAL COMPANIES INFORMATION LEAFLET NO. 5 / FEBRUARY 2018 ii 1. INTRODUCTION An external (foreign) limited company registered abroad may establish a branch

Global Consumer Confidence

Global Consumer Confidence The Conference Board Global Consumer Confidence Survey is conducted in collaboration with Nielsen 4TH QUARTER 2017 RESULTS CONTENTS Global Highlights Asia-Pacific Africa and

Global Consumer Confidence The Conference Board Global Consumer Confidence Survey is conducted in collaboration with Nielsen 4TH QUARTER 2017 RESULTS CONTENTS Global Highlights Asia-Pacific Africa and

Government of Bermuda Bermuda Shipping and Maritime Authority BERMUDA SHIPPING NOTICE

Government of Bermuda Bermuda Shipping and Maritime Authority 2016-015 BERMUDA SHIPPING NOTICE OFFICER CERTIFICATION AND ISSUE OF ENDORSEMENTS. Summary This notice sets out the general requirements for

Government of Bermuda Bermuda Shipping and Maritime Authority 2016-015 BERMUDA SHIPPING NOTICE OFFICER CERTIFICATION AND ISSUE OF ENDORSEMENTS. Summary This notice sets out the general requirements for

Switzerland Country Profile

Switzerland Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

Switzerland Country Profile EU Tax Centre July 2015 Key tax factors for efficient cross-border business and investment involving Switzerland EU Member State No. Please note that, in addition to Switzerland

15 Popular Q&A regarding Transfer Pricing Documentation (TPD) In brief. WTS strong presence in about 100 countries

In brief. WTS strong presence in about 100 countries") 15 Popular Q&A regarding Transfer Pricing Documentation (TPD) Contacts China Martin Ng Managing Partner Martin.ng@worldtaxservice.cn + 86 21 5047 8665 ext.202 Xiaojie Tang Manager Xiaojie.tang@worldtaxservice.cn

15 Popular Q&A regarding Transfer Pricing Documentation (TPD) Contacts China Martin Ng Managing Partner Martin.ng@worldtaxservice.cn + 86 21 5047 8665 ext.202 Xiaojie Tang Manager Xiaojie.tang@worldtaxservice.cn

CB CROSS BORDER YOUR GOAL. OUR MISSION.

CB CROSS BORDER YOUR GOAL. OUR MISSION. Your Chosen Counsel Because We care We are an international private wealth advisory We specialize in providing offshore solutions crossborderworldwide.com What we

CB CROSS BORDER YOUR GOAL. OUR MISSION. Your Chosen Counsel Because We care We are an international private wealth advisory We specialize in providing offshore solutions crossborderworldwide.com What we

Double tax considerations on certain personal retirement scheme benefits

www.pwc.com/mt The elimination of double taxation on benefits paid out of certain Maltese personal retirement schemes February 2016 Double tax considerations on certain personal retirement scheme benefits

www.pwc.com/mt The elimination of double taxation on benefits paid out of certain Maltese personal retirement schemes February 2016 Double tax considerations on certain personal retirement scheme benefits

Global Forum on Transparency and Exchange of Information for Tax Purposes. Statement of Outcomes

Global Forum on Transparency and Exchange of Information for Tax Purposes Statement of Outcomes 1. On 25-26 October 2011, over 250 delegates from 84 jurisdictions and 9 international organisations and

Global Forum on Transparency and Exchange of Information for Tax Purposes Statement of Outcomes 1. On 25-26 October 2011, over 250 delegates from 84 jurisdictions and 9 international organisations and

Islamic Finance News Forum London, October 17 th, Christine Chardonnens MSCI Barra

Islamic Finance News Forum London, October 17 th, 2008 Christine Chardonnens MSCI Barra Islamic Indices 1. Construction and methodology highlights, including dividend purification 2. Performance and risk

Islamic Finance News Forum London, October 17 th, 2008 Christine Chardonnens MSCI Barra Islamic Indices 1. Construction and methodology highlights, including dividend purification 2. Performance and risk

Belgium Country Profile

Belgium Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Belgium EU Member State Double Tax Treaties Yes With: Albania Algeria Argentina

Belgium Country Profile EU Tax Centre July 2016 Key tax factors for efficient cross-border business and investment involving Belgium EU Member State Double Tax Treaties Yes With: Albania Algeria Argentina

Austria Country Profile

Austria Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Austria EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

Austria Country Profile EU Tax Centre March 2014 Key tax factors for efficient cross-border business and investment involving Austria EU Member State Yes Double Tax Treaties With: Albania Algeria Armenia

INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING FOR SEAFARERS (STCW), 1978, AS AMENDED

, 1978, AS AMENDED") E 4 ALBERT EMBANKMENT LONDON SE 7SR Telephone: +44 (0)20 7735 76 Fax: +44 (0)20 7587 320 MSC./Circ.64/Rev.5 7 June 205 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING

E 4 ALBERT EMBANKMENT LONDON SE 7SR Telephone: +44 (0)20 7735 76 Fax: +44 (0)20 7587 320 MSC./Circ.64/Rev.5 7 June 205 INTERNATIONAL CONVENTION ON STANDARDS OF TRAINING, CERTIFICATION AND WATCHKEEPING

IRS Reporting Rules. Reference Guide. serving the people who serve the world

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

IRS Reporting Rules Reference Guide serving the people who serve the world The United States has and continues to maintain a policy of not taxing the deposit interest earned by United States (US) nonresidents

Clinical Trials Insurance

Allianz Global Corporate & Specialty Clinical Trials Insurance Global solutions for clinical trials liability Specialist cover for clinical research The challenges of international clinical research are

Allianz Global Corporate & Specialty Clinical Trials Insurance Global solutions for clinical trials liability Specialist cover for clinical research The challenges of international clinical research are

1.1. STOXX TOTAL MARKET INDICES

STOXX INDEX LIST A-Z 1. TOTAL MARKET INDICES 1/14 1.1. STOXX TOTAL MARKET INDICES Regional indices STOXX BRIC TMI STOXX Developed and Emerging Markets TMI STOXX Developed Markets TMI STOXX Emerging Markets

STOXX INDEX LIST A-Z 1. TOTAL MARKET INDICES 1/14 1.1. STOXX TOTAL MARKET INDICES Regional indices STOXX BRIC TMI STOXX Developed and Emerging Markets TMI STOXX Developed Markets TMI STOXX Emerging Markets

International Statistical Release

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Investment Fund Assets and Flows Trends in the

International Statistical Release This release and additional tables of international statistics are available on efama s website (www.efama.org). Worldwide Investment Fund Assets and Flows Trends in the

FY2016 RESULTS. 1 February 2016 to 31 January Inditex continues to roll out its global, fully integrated store and online model.

FY2016 RESULTS 1 February 2016 to 31 January 2017 Inditex continues to roll out its global, fully integrated store and online model. Strong operating performance: Net sales for FY2016 reached 23.3 billion,

FY2016 RESULTS 1 February 2016 to 31 January 2017 Inditex continues to roll out its global, fully integrated store and online model. Strong operating performance: Net sales for FY2016 reached 23.3 billion,

(of 19 March 2013) Valid from 1 January A. Taxpayers

Valid from 1 January A. Taxpayers") Leaflet. 29/460 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under private law for persons without domicile or residence in Switzerland (of 19 March 2013) Valid from 1

Leaflet. 29/460 of the Cantonal Tax Office on withholding taxes applicable to pension benefits under private law for persons without domicile or residence in Switzerland (of 19 March 2013) Valid from 1

Setting up in Denmark

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

Setting up in Denmark 6. Taxation The Danish tax system for individuals rests on the global taxation principle. The principle holds that the income of individuals and companies with full tax liability

AUTOMATIC EXCHANGE OF INFORMATION (AEOI)

") AUTOMATIC EXCHANGE OF INFORMATION (AEOI) As the world becomes increasingly globalised, money can be transferred from one jurisdiction to another with ease. While this may help to facilitate trade and boost

AUTOMATIC EXCHANGE OF INFORMATION (AEOI) As the world becomes increasingly globalised, money can be transferred from one jurisdiction to another with ease. While this may help to facilitate trade and boost

Does One Law Fit All? Cross-Country Evidence on Okun s Law

Does One Law Fit All? Cross-Country Evidence on Okun s Law Laurence Ball Johns Hopkins University Global Labor Markets Workshop Paris, September 1-2, 2016 1 What the paper does and why Provides estimates

Does One Law Fit All? Cross-Country Evidence on Okun s Law Laurence Ball Johns Hopkins University Global Labor Markets Workshop Paris, September 1-2, 2016 1 What the paper does and why Provides estimates

Developing Housing Finance Systems

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

Developing Housing Finance Systems Veronica Cacdac Warnock IIMB-IMF Conference on Housing Markets, Financial Stability and Growth December 11, 2014 Based on Warnock V and Warnock F (2012). Developing Housing

Sweden Country Profile

Sweden Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Sweden EU Member State Double Tax Treaties With: Albania Armenia Argentina Azerbaijan

Sweden Country Profile EU Tax Centre June 2017 Key tax factors for efficient cross-border business and investment involving Sweden EU Member State Double Tax Treaties With: Albania Armenia Argentina Azerbaijan

PREDICTING VEHICLE SALES FROM GDP

UMTRI--6 FEBRUARY PREDICTING VEHICLE SALES FROM GDP IN 8 COUNTRIES: - MICHAEL SIVAK PREDICTING VEHICLE SALES FROM GDP IN 8 COUNTRIES: - Michael Sivak The University of Michigan Transportation Research

UMTRI--6 FEBRUARY PREDICTING VEHICLE SALES FROM GDP IN 8 COUNTRIES: - MICHAEL SIVAK PREDICTING VEHICLE SALES FROM GDP IN 8 COUNTRIES: - Michael Sivak The University of Michigan Transportation Research

MEXICO - INTERNATIONAL TAX UPDATE -

TTN Conference May 2017 MEXICO - INTERNATIONAL TAX UPDATE - Arturo G. Brook Main Taxes Income Tax Value Added Tax Others Agenda DTTs and TIEAs FATCA (IGA) and CRS Choice of Vehicles Income Tax - General

TTN Conference May 2017 MEXICO - INTERNATIONAL TAX UPDATE - Arturo G. Brook Main Taxes Income Tax Value Added Tax Others Agenda DTTs and TIEAs FATCA (IGA) and CRS Choice of Vehicles Income Tax - General