BBK34133 Investment Analysis Prepared by Dr Khairul Anuar. L6 Dividend and Dividend Policy

|

|

|

- Paula West

- 6 years ago

- Views:

Transcription

1 BBK34133 Investment Analysis Prepared by Dr Khairul Anuar L6 Dividend and Dividend Policy

2 What is Dividend Policy Dividend Policy refers to the explicit or implicit decision of the Board of Directors regarding the amount of residual earnings (past or present) that should be distributed to the shareholders of the corporation. This decision is considered a financing decision because the profits of the corporation are an important source of financing available to the firm

3 Types of Dividends Dividends are a permanent distribution of residual earnings of the corporation to its owners. Dividends can be in the form of: Cash Additional Shares of Stock (stock dividend) If a firm is dissolved, at the end of the process, a final dividend of any residual amount is made to the shareholders this is known as a liquidating dividend

4 Distributions to Shareholders 4

5 The clientele effect Different groups of investors, or clienteles, prefer different dividend policies. Firm s past dividend policy determines its current clientele of investors. Clientele effects impede changing dividend policy. Taxes & brokerage costs hurt investors who have to switch companies due to a change in payout policy. 5

6 The information content, or signaling, hypothesis Investors view dividend changes as signals of management s view of the future. Managers hate to cut dividends, so won t raise dividends unless they think raise is sustainable. Therefore, a stock price increase at time of a dividend increase could reflect higher expectations for future EPS, not a desire for dividends. 6

7 Dividends a Financing Decision In the absence of dividends, corporate earnings accrue to the benefit of shareholders as retained earnings and are automatically reinvested in the firm. When a cash dividend is declared, those funds leave the firm permanently and irreversibly. Distribution of earnings as dividends may starve the company of funds required for growth and expansion, and this may cause the firm to seek additional external capital

8 Dividends characteristics A dividend is a discretionary payment made to shareholders The decision to distribute dividends is solely the responsibility of the board of directors Shareholders are residual claimants of the firm (they have the last, and residual claim on assets on dissolution and on profits after all other claims have been fully satisfied)

9 Distributions to Shareholders The company s board of directors declares the dividend that will be paid and decides when the payment will occur: Ex-dividend date Record date Payment date Some companies pay dividends once year while others pay dividends twice a year usually as an interim and a final dividend. Occasionally, a firm may pay a one-time, special dividend that is usually much larger than a regular dividend. 9

10 Mechanics of Cash Dividend Pay Declaration Date this is the date on which the Board of Directors meet and declare the dividend. In their resolution the Board will set the date of record, the date of payment and the amount of the dividend for each share class. when CARRIED, this resolution makes the dividend a current liability for the firm. Date of Record is the date on which the shareholders register is closed after the trading day and all those who are listed will receive the dividend

11 Mechanics of Cash Dividend Pay Ex dividend Date is the date that the value of the firm s common shares will reflect the dividend payment (ie. fall in value) ex means without. At the start of trading on the ex-dividend date, the share price will normally open for trading at the previous days close, less the value of the dividend per share. This reflects the fact that purchasers of the stock on the ex-dividend date and beyond WILL NOT receive the declared dividend. Date of Payment is the date the cheques for the dividend are mailed out to the shareholders

12 Dividend Declaration Time Line x business days prior to the Date of Record Declaration Date Date of Record Date of Payment The Board Meets and passes the motion to create the dividend Ex Dividend Date is determined by the Date of Record. The market value of the shares drops by the value of the dividend per share on market opening compared to the previous day s close

13 Dividend Policy There is no legal obligation for firms to pay dividends to common shareholders Shareholders cannot force a Board of Directors to declare a dividend, and courts will not interfere with the BOD s right to make the dividend decision because: Board members are jointly and severally liable for any damages they may cause Board members are constrained by legal rules affecting dividends including: Not paying dividends out of capital Not paying dividends when that decision could cause the firm to become insolvent Not paying dividends in contravention of contractual commitments (such as debt covenant agreements)

14 Dividend Reinvestment Plans (DRIPs) Also referred to as stock dividends Involve shareholders deciding to use the cash dividend proceeds to buy more shares of the firm DRIPs will buy as many shares as the cash dividend allows with the residual deposited as cash Shareholders can automatically reinvest their dividends in shares of the company s common stock. Firms are able to raise additional common stock capital continuously at no cost and fosters an on-going relationship with shareholders

15 Stock Dividends Stock dividends simply amount to distribution of additional shares to existing shareholders They represent nothing more than recapitalization of earnings of the company. (that is, the amount of the stock dividend is transferred from the R/E account to the common share account. Because of the capital impairment rule stock dividends reduce the firm s ability to pay dividends in the future

16 Stock Dividends Implications reduction in the Retained earnings account reduced capacity to pay future dividends proportionate share ownership remains unchanged shareholder s wealth (theoretically) is unaffected Effect on the Company conserves cash serves to lower the market value of firm s stock modestly promotes wider distribution of shares to the extent that current owners divest themselves of shares...because they have more adjusts the capital accounts dilutes EPS Effect on Shareholders proportion of ownership remains unchanged total value of holdings remains unchanged if former DPS is maintained, this really represents an increased dividend payout 16

17 Stock Dividends Example ABC Company Equity Accounts as at February xx, 20x9 Common stock (21,500) $5,000,000 Retained earnings 20,000,000 Net Worth $25,000,000 The company, on March 1, 20x9 declares a 10 percent stock dividend when the current market price for the stock is $40.00 per share. This stock dividend will increase the number of shares outstanding by 10 percent. This will mean issuing 21,500 shares. The value of the shares is: $40.00 (21,500) = $860,000 This stock dividend will result in $860,000 being transferred from the retained earnings account to the common stock account: 17

18 Share Repurchases Repurchases: Buying own stock back from stockholders. Simply another form of payout policy. An alternative to cash dividend where the objective is to increase the price per share rather than paying a dividend. Since there are rules against improper accumulation of funds, firms adopt a policy of large infrequent share repurchase programs. 18

19 Stock Repurchases Reasons for repurchases: As an alternative to distributing cash as dividends. To dispose of one-time cash from an asset sale. To make a large capital structure change. To use when employees exercise stock options. 19

20 Repurchased Shares called treasury stock non-voting may not receive dividends if not retired, can be resold unlike the U.S., (in some countries shares repurchased are cancelled eg. Canada)

21 Repurchase Example Scenario: Company A: Current earnings=$4.4m, Current no of shares=1.1 m shares Current share price = $20 Repurchase = 100,000 shares (0.1 m shares) Current EPS = [total earnings] / [# of shares] = $4.4 m / 1.1 m = $4.00 Current P/E ratio = $20 / $4 = 5X EPS after repurchase of 100,000 shares = $4.4 m / 1.0 = $4.40 Expected market price after repurchase: = [p/e] x [EPSnew] = [5] x [$4.40] = $22.00 per share

22 Effects of A Share Repurchase EPS should increase following the repurchase if earnings after-tax remains the same should result with a higher market price per outstanding share shareholders not selling their shares back to the firm will enjoy a capital gain if the repurchase increases the share price

23 Share repurchase as a signal The announcement of an intended repurchase might send a signal that affects stock price, and the previous events that led to cash available for a distribution affect stock price 23

24 Summary of Dividends vs. Repurchases 24

25 Dividend Versus Retention of Cash Agency costs of retaining cash There is no benefit to shareholders when a firm holds cash above and beyond its future investment or liquidity needs. Managers may use this cash inefficiently by continuing money-losing pet projects, paying excessive executive perks or overpaying for acquisitions. Leverage is one way to reduce a firm s access cash. Paying out cash can boost the share price by reducing managers ability and temptation to waste resources. 25

26 Advice for the Financial Manager Overall, as a financial manager, you should consider the following when making payout policy decisions: For a given payout amount, try to maximise the after-tax payout to the shareholders. Repurchases and dividends are often taxed differently and one can have an advantage over the other. Repurchases and special dividends are useful for making large, infrequent distributions to shareholders - neither implies any expectation of repeated payouts. Starting and increasing a regular dividend is seen by shareholders as an implicit commitment to maintain this level of regular payout indefinitely. 26

27 Advice for the Financial Manager Because regular dividends are seen as an implicit commitment, they send a stronger signal of financial strength to shareholders - However, this signal comes with a cost because regular payouts reduce a firm s financial flexibility. Be mindful of future investment plans - There are transaction costs associated with both distributions and raising new capital, so it is expensive to make a large distribution and then raise capital to fund a project. 27

28 Dividend Policy Our Company intends to distribute yearly dividends of RM700 million or up to 90% of our normalized PATAMI, whichever is higher. Dividends will be paid only if approved by our Board out of funds available for such distribution. The actual amount and timing of dividend payments will depend upon our level of cash and retained earnings, results of operations, business prospects, monetization of non-core assets, projected levels of capital expenditure and other investment plans, current and expected obligations and such other matters as our Board may deem relevant. 28

29 Westport dangles 75% dividend carrot September 20, 2013 PETALING JAYA: Westport Holdings Bhd is dangling a 75% dividend payout policy to woo investors to its initial public offering (IPO) of million shares of 10 sen par value. The 75% dividend payout policy is a target we hope to achieve every year, said chief executive officer at the company s prospectus launch in Kuala Lumpur yesterday Divided per share (sen) Dividend payout ratio 70.2% 63.1% 75.0% 75.0% 29

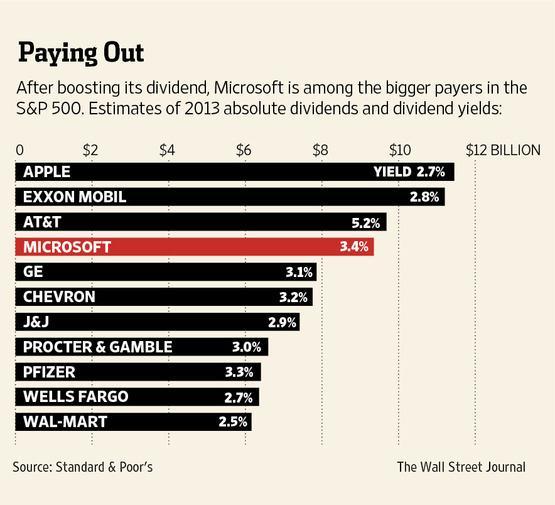

30 Microsoft Boosts Dividend by 22%, Sets $40 Billion Buyback Wall Street Journal, Updated Sept. 17, 2013 Microsoft Corp moved to share more of its cash hoard with shareholders, boosting its quarterly dividend by 22% and renewing a $40 billion authorization to buy back its shares. Microsoft unveiled a $40 billion share buyback plan and boosted its quarterly dividend by 22%, continuing the shareholder-friendly moves it has pushed in recent years. The announcement Tuesday comes two days before a highly anticipated meeting with financial analysts and follow a series of surprise changes at the software giant, including a plan to seek a successor to Chief Executive Steve Ballmer and a $7 billion deal to buy Nokia Corp.'s 2.19% smartphone business. Microsoft has raised its dividend eight times since 2004, in announcements that typically come in September. But the latest increase was greater than predicted by some analysts, who see Microsoft's moves to return cash to shareholders as a way to defuse dissatisfaction with the company's share price. 30

31 31

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L6 - Dividends and Dividend Policy www.mba638.wordpress.com Uses of Free Cash Flow: Distributions to Shareholders 22-2 2 What is Dividend Policy

MBF1223 Financial Management Prepared by Dr Khairul Anuar L6 - Dividends and Dividend Policy www.mba638.wordpress.com Uses of Free Cash Flow: Distributions to Shareholders 22-2 2 What is Dividend Policy

CHAPTER 14 Distributions to shareholders: Dividends and share repurchases. What is dividend policy?

CHAPTER 14 Distributions to shareholders: Dividends and share repurchases Theories of investor preferences Signaling effects Residual model Dividend reinvestment plans Stock dividends and stock splits

CHAPTER 14 Distributions to shareholders: Dividends and share repurchases Theories of investor preferences Signaling effects Residual model Dividend reinvestment plans Stock dividends and stock splits

Distributions to Shareholders

Chapter 14 Distributions to Shareholders Investor Preferences on Dividends Signaling Effects Residual Dividend Model Dividend Reinvestment Plans Stock Repurchases Stock Dividends and Stock Splits 14 1

Chapter 14 Distributions to Shareholders Investor Preferences on Dividends Signaling Effects Residual Dividend Model Dividend Reinvestment Plans Stock Repurchases Stock Dividends and Stock Splits 14 1

Chapter 17 Payout Policy

Chapter 17 Payout Policy Chapter Outline 17.1 Distributions to Shareholders 17.2 Comparison of Dividends and Share Repurchases 17.3 The Tax Disadvantage of Dividends 17.4 Dividend Capture and Tax Clienteles

Chapter 17 Payout Policy Chapter Outline 17.1 Distributions to Shareholders 17.2 Comparison of Dividends and Share Repurchases 17.3 The Tax Disadvantage of Dividends 17.4 Dividend Capture and Tax Clienteles

Copyright 2009 Pearson Education Canada

CHAPTER FIVE Qualitative Questions Question 1 Shareholders prefer to have cash dividends paid to them now rather than waiting for potential payments in the future. Future cash flows from retained earnings

CHAPTER FIVE Qualitative Questions Question 1 Shareholders prefer to have cash dividends paid to them now rather than waiting for potential payments in the future. Future cash flows from retained earnings

AFM 371 Winter 2008 Chapter 19 - Dividends And Other Payouts

AFM 371 Winter 2008 Chapter 19 - Dividends And Other Payouts 1 / 29 Outline Background Dividend Policy In Perfect Capital Markets Share Repurchases Dividend Policy In Imperfect Markets 2 / 29 Introduction

AFM 371 Winter 2008 Chapter 19 - Dividends And Other Payouts 1 / 29 Outline Background Dividend Policy In Perfect Capital Markets Share Repurchases Dividend Policy In Imperfect Markets 2 / 29 Introduction

Dividend Policy. Supplement to Chapter 17 FIL 341 Prepared by Keldon Bauer

Dividend Policy Supplement to Chapter 17 FIL 341 Prepared by Keldon Bauer Dividends or Capital Gains? The ultimate goal of financial managers should be the maximization of shareholder wealth. Shareholder

Dividend Policy Supplement to Chapter 17 FIL 341 Prepared by Keldon Bauer Dividends or Capital Gains? The ultimate goal of financial managers should be the maximization of shareholder wealth. Shareholder

Gatton College of Business and Economics Department of Finance & Quantitative Methods. Chapter 17. Finance 300 David Moore

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 17 Finance 300 David Moore Payout Policy Discuss dividends and repurchases Methods Costs and benefits 14-2

Gatton College of Business and Economics Department of Finance & Quantitative Methods Chapter 17 Finance 300 David Moore Payout Policy Discuss dividends and repurchases Methods Costs and benefits 14-2

CHAPTER 19 DIVIDENDS AND OTHER PAYOUTS

CHAPTER 19 DIVIDENDS AND OTHER PAYOUTS Answers to Concepts Review and Critical Thinking Questions 1. Dividend policy deals with the timing of dividend payments, not the amounts ultimately paid. Dividend

CHAPTER 19 DIVIDENDS AND OTHER PAYOUTS Answers to Concepts Review and Critical Thinking Questions 1. Dividend policy deals with the timing of dividend payments, not the amounts ultimately paid. Dividend

Capital Structure Management

MBA III Semester Capital Structure Management POST RAJ POKHAREL M.Phil. (TU) 01/2010) 1 What is Capital Structure? Definition The capital structure of a firm is the mix of different securities issued

MBA III Semester Capital Structure Management POST RAJ POKHAREL M.Phil. (TU) 01/2010) 1 What is Capital Structure? Definition The capital structure of a firm is the mix of different securities issued

Chapter 6. Stock Valuation

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Key Concepts and Skills

Chapter 14 Dividends and Dividend Policy Key Concepts and Skills Understand dividend types and how they are paid Understand the issues surrounding dividend policy decisions Understand the difference between

Chapter 14 Dividends and Dividend Policy Key Concepts and Skills Understand dividend types and how they are paid Understand the issues surrounding dividend policy decisions Understand the difference between

Chapter 6. Stock Valuation

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

TABLE OF CONTENTS General Admission Criteria Ongoing Obligations

Rules prime market TABLE OF CONTENTS General 4 1. Scope of Application 4 2. Participation Bid and Decision on Participation 4 Participation Bid 4 Competence for Stating the Grounds for Acceptance or Rejection

Rules prime market TABLE OF CONTENTS General 4 1. Scope of Application 4 2. Participation Bid and Decision on Participation 4 Participation Bid 4 Competence for Stating the Grounds for Acceptance or Rejection

Dividend irrelevance in a world without taxes. The effect of taxes. The information contents of dividends. Dividend policy in practice.

Dividends - lecture Dividend irrelevance in a world without taxes. The effect of taxes. Tax disadvantage of dividends. The information contents of dividends. Dividend policy in practice. Factors influencing

Dividends - lecture Dividend irrelevance in a world without taxes. The effect of taxes. Tax disadvantage of dividends. The information contents of dividends. Dividend policy in practice. Factors influencing

CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION 1 CONDENSED CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

CONTENTS CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION 1 CONDENSED CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME 2 CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

CONTENTS CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION 1 CONDENSED CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME 2 CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

FN428 : Investment Banking. Lecture : Dividend Policy

FN428 : Investment Banking Lecture : Dividend Policy Dividend Policy : The Questions Profitable companies regularly face three important questions: (1) How much of our free cash flow should we pass on

FN428 : Investment Banking Lecture : Dividend Policy Dividend Policy : The Questions Profitable companies regularly face three important questions: (1) How much of our free cash flow should we pass on

CHAPTER 16 The Dividend Controversy. 1. Newspaper exercise; answers will vary depending on the stocks chosen.

CHAPTER 16 The Dividend Controversy Answers to Practice Questions 1. Newspaper exercise; answers will vary depending on the stocks chosen. 2. a. Distributes a relatively low proportion of current earnings

CHAPTER 16 The Dividend Controversy Answers to Practice Questions 1. Newspaper exercise; answers will vary depending on the stocks chosen. 2. a. Distributes a relatively low proportion of current earnings

DIVIDEND POLICY

DIVIDEND POLICY 2017 1 General Thoughts on Dividends 2 Dividend Policy Russki Stil 28 April 2017 - Russia demands big dividend payouts from state-owned companies Putin-backed move sparks rise in shares

DIVIDEND POLICY 2017 1 General Thoughts on Dividends 2 Dividend Policy Russki Stil 28 April 2017 - Russia demands big dividend payouts from state-owned companies Putin-backed move sparks rise in shares

Module 4: Capital Structure and Dividend Policy

Module 4: Capital Structure and Dividend Policy Reading 4.1 Capital structure theory Reading 4.2 Capital structure theory in perfect markets Reading 4.3 Impact of corporate taxes on capital structure Reading

Module 4: Capital Structure and Dividend Policy Reading 4.1 Capital structure theory Reading 4.2 Capital structure theory in perfect markets Reading 4.3 Impact of corporate taxes on capital structure Reading

UOA DEVELOPMENT BHD Interim Financial Report 30 September 2017 CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION 1

CONTENTS CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION 1 CONDENSED CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME 2 CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

CONTENTS CONDENSED CONSOLIDATED STATEMENT OF FINANCIAL POSITION 1 CONDENSED CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME 2 CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

Linear Technologies Dividend Policy Dr. C. Bülent Aybar

Linear Technologies Dividend Policy Dr. C. Bülent Aybar Professor of International Finance Review of Dividend Policy The firm initiated a dividend in 1992. Since then it has raised the dividend by $0.01

Linear Technologies Dividend Policy Dr. C. Bülent Aybar Professor of International Finance Review of Dividend Policy The firm initiated a dividend in 1992. Since then it has raised the dividend by $0.01

F3 Financial Strategy

Strategic Level Paper F3 Financial Strategy Senior Examiner s Answers SECTION A Answer to Question One (a)(i) Valuation of Company NN (excluding potential synergistic benefits and integration costs) NN:

Strategic Level Paper F3 Financial Strategy Senior Examiner s Answers SECTION A Answer to Question One (a)(i) Valuation of Company NN (excluding potential synergistic benefits and integration costs) NN:

Returning Cash to the Owners: Dividend Policy

Returning Cash to the Owners: Dividend Policy Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate

Returning Cash to the Owners: Dividend Policy Aswath Damodaran Aswath Damodaran 1 First Principles Invest in projects that yield a return greater than the minimum acceptable hurdle rate. The hurdle rate

Investments 5: Stock Basics

Personal Finance: Another Perspective Investments 5: Stock Basics Updated 2017-07-07 1 Objectives A. Understand risk and return for stocks B. Understand stock terminology C. Understand how stocks are valued

Personal Finance: Another Perspective Investments 5: Stock Basics Updated 2017-07-07 1 Objectives A. Understand risk and return for stocks B. Understand stock terminology C. Understand how stocks are valued

Stock Split Frequently Asked Questions

Stock Split Frequently Asked Questions Q: What is a two-for-one stock split? A: All stockholders at the close of business on January 4, 2012 (RECORD DATE) will receive one (1) additional share, in the

Stock Split Frequently Asked Questions Q: What is a two-for-one stock split? A: All stockholders at the close of business on January 4, 2012 (RECORD DATE) will receive one (1) additional share, in the

BBK3413 Investment Analysis Prepared by Khairul Anuar. L3 - Initial Public Offering & Rights Issue

BBK3413 Investment Analysis Prepared by Khairul Anuar L3 - Initial Public Offering & Rights Issue 1 Content Content 1. Sources of Funds for Private Companies 2. Initial Public Offering 3. Advantages and

BBK3413 Investment Analysis Prepared by Khairul Anuar L3 - Initial Public Offering & Rights Issue 1 Content Content 1. Sources of Funds for Private Companies 2. Initial Public Offering 3. Advantages and

Module 1: Accounting Information in Capital Markets

Module 1: Accounting Information in Capital Markets INFORMATION THEORY - What is it? Theory on the usefulness of accounting information in investment decisions [Previously there was dissatisfaction with

Module 1: Accounting Information in Capital Markets INFORMATION THEORY - What is it? Theory on the usefulness of accounting information in investment decisions [Previously there was dissatisfaction with

VALUATION OF DEBT AND EQUITY

15 VALUATION OF DEBT AND EQUITY Introduction Debt Valuation - Par Value - Long Term versus Short Term - Zero Coupon Bonds - Yield to Maturity - Investment Strategies Equity Valuation - Growth Stocks -

15 VALUATION OF DEBT AND EQUITY Introduction Debt Valuation - Par Value - Long Term versus Short Term - Zero Coupon Bonds - Yield to Maturity - Investment Strategies Equity Valuation - Growth Stocks -

The Pinnacle Fund Simplified Prospectus

The Pinnacle Fund Simplified Prospectus September 10, 2010 Class A, Class I and Manager Class units Pinnacle Emerging Markets Equity Fund No securities regulatory authority has expressed an opinion about

The Pinnacle Fund Simplified Prospectus September 10, 2010 Class A, Class I and Manager Class units Pinnacle Emerging Markets Equity Fund No securities regulatory authority has expressed an opinion about

DIVIDENDS & SHARE REPURCHASE

DIVIDENDS & SHARE REPURCHASE 1 EY = Earning Yield ATCF = After Tax Cost of Financing CFO = Chief Financial Officer DRPs = Dividend Reinvestment Plans 1. INTRODUCTION Dividend payout to shareholders based

DIVIDENDS & SHARE REPURCHASE 1 EY = Earning Yield ATCF = After Tax Cost of Financing CFO = Chief Financial Officer DRPs = Dividend Reinvestment Plans 1. INTRODUCTION Dividend payout to shareholders based

DIVIDEND CONTROVERSY: A THEORETICAL APPROACH

DIVIDEND CONTROVERSY: A THEORETICAL APPROACH ILIE Livia Lucian Blaga University of Sibiu, Romania Abstract: One of the major financial decisions for a public company is the dividend policy - the proportion

DIVIDEND CONTROVERSY: A THEORETICAL APPROACH ILIE Livia Lucian Blaga University of Sibiu, Romania Abstract: One of the major financial decisions for a public company is the dividend policy - the proportion

Student Learning Outcomes

Chapter 18 Shareholders Equity Part 2: Additional Issues Intermediate Accounting II Dr. Chula King Student Learning Outcomes Distinguish between accounting for retired shares and for treasury shares Describe

Chapter 18 Shareholders Equity Part 2: Additional Issues Intermediate Accounting II Dr. Chula King Student Learning Outcomes Distinguish between accounting for retired shares and for treasury shares Describe

An Analysis of Microsoft. October 7, 2011

An Analysis of Microsoft October 7, 2011 T2 Partners Management L.P. Manages Hedge Funds and Mutual Funds and is a Registered Investment Advisor The General Motors Building 767 Fifth Avenue, 18 th Floor

An Analysis of Microsoft October 7, 2011 T2 Partners Management L.P. Manages Hedge Funds and Mutual Funds and is a Registered Investment Advisor The General Motors Building 767 Fifth Avenue, 18 th Floor

Ch. 11.3: The Stock Market

Ch. 11.3: The Stock Market How does the stock market work? http://www.youtube.com/watch?v=f3qpgxbtdeo Corporations raise funds by issuing stock, which represents ownership in the corporation. Sept. 12,

Ch. 11.3: The Stock Market How does the stock market work? http://www.youtube.com/watch?v=f3qpgxbtdeo Corporations raise funds by issuing stock, which represents ownership in the corporation. Sept. 12,

RHB ISLAMIC BOND FUND

Date: 7 February 2018 RHB ISLAMIC BOND FUND RESPONSIBILITY STATEMENT This Product Highlights Sheet has been reviewed and approved by the directors of RHB Asset Management Sdn Bhd ( RHBAM ) and they have

Date: 7 February 2018 RHB ISLAMIC BOND FUND RESPONSIBILITY STATEMENT This Product Highlights Sheet has been reviewed and approved by the directors of RHB Asset Management Sdn Bhd ( RHBAM ) and they have

CA - FINAL SECURITY VALUATION. FCA, CFA L3 Candidate

CA - FINAL SECURITY VALUATION FCA, CFA L3 Candidate 2.1 Security Valuation Study Session 2 LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement

CA - FINAL SECURITY VALUATION FCA, CFA L3 Candidate 2.1 Security Valuation Study Session 2 LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement

about your personal pension Single price, series 6 member s guide We ll help you get there

about your personal pension Single price, series 6 member s guide investments pensions PROTECTION We ll help you get there contents Your Personal Pension 4 The contract 4 Eligibility 4 Contributions 5

about your personal pension Single price, series 6 member s guide investments pensions PROTECTION We ll help you get there contents Your Personal Pension 4 The contract 4 Eligibility 4 Contributions 5

Genworth MI Canada Inc. Management s Discussion and Analysis For the first quarter ended March 31, 2011

Management s Discussion and Analysis For the first quarter ended March 31, 2011 May 2, 2011 ( Genworth Canada or the Company ) completed its initial public offering ( IPO ) on July 7, 2009. The full three-month

Management s Discussion and Analysis For the first quarter ended March 31, 2011 May 2, 2011 ( Genworth Canada or the Company ) completed its initial public offering ( IPO ) on July 7, 2009. The full three-month

Corporate Finance. Dr Cesario MATEUS Session

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 3 20.02.2014 Selecting the Right Investment Projects Capital Budgeting Tools 2 The Capital Budgeting Process Generation

Corporate Finance Dr Cesario MATEUS cesariomateus@gmail.com www.cesariomateus.com Session 3 20.02.2014 Selecting the Right Investment Projects Capital Budgeting Tools 2 The Capital Budgeting Process Generation

ACM GOVERNMENT OPPORTUNITY FUND, INC Avenue of the Americas New York, New York October 27, 2006

Investments ACM GOVERNMENT OPPORTUNITY FUND, INC. 1345 Avenue of the Americas New York, New York 10105 October 27, 2006 Dear Stockholders: The Board of Directors (the Directors ) of ACM Government Opportunity

Investments ACM GOVERNMENT OPPORTUNITY FUND, INC. 1345 Avenue of the Americas New York, New York 10105 October 27, 2006 Dear Stockholders: The Board of Directors (the Directors ) of ACM Government Opportunity

Chapter 16: Payout Policy

FIN 302 Class Notes Chapter 16: Payout Policy Companies can pay out cash to their shareholders in two ways: cash dividends or stock repurchases. Cash dividends: Regular cash dividends (quarterly) Extra

FIN 302 Class Notes Chapter 16: Payout Policy Companies can pay out cash to their shareholders in two ways: cash dividends or stock repurchases. Cash dividends: Regular cash dividends (quarterly) Extra

Cost of Capital, Capital Structure, and Dividend Policy

Cost of Capital, Capital Structure, and Dividend Policy 1. A relatively young firm has capital components valued at book and market and market component costs as follows. No new securities have been issued

Cost of Capital, Capital Structure, and Dividend Policy 1. A relatively young firm has capital components valued at book and market and market component costs as follows. No new securities have been issued

DIVIDENDS AND PAYOUT POLICY

LEARNING OBJECTIVES 17 DIVIDENDS AND PAYOUT POLICY After studying this chapter, you should understand: LO1 Dividend types and how dividends are paid. LO2 The issues surrounding dividend policy decisions.

LEARNING OBJECTIVES 17 DIVIDENDS AND PAYOUT POLICY After studying this chapter, you should understand: LO1 Dividend types and how dividends are paid. LO2 The issues surrounding dividend policy decisions.

proposed subdivision of every one (1) GDEX Shares into two (2) Subdivided Shares in GDEX ( Proposed Share Split );

GDEX Shares into two (2) Subdivided Shares in GDEX ( Proposed Share Split );") GD EXPRESS CARRIER BHD ( GDEX OR THE COMPANY ) (I) (II) (III) PROPOSED SUBDIVISION OF EVERY ONE (1) EXISTING ORDINARY SHARE OF RM0.10 EACH IN GDEX ( GDEX SHARES ) INTO TWO (2) ORDINARY SHARES OF RM0.05

GD EXPRESS CARRIER BHD ( GDEX OR THE COMPANY ) (I) (II) (III) PROPOSED SUBDIVISION OF EVERY ONE (1) EXISTING ORDINARY SHARE OF RM0.10 EACH IN GDEX ( GDEX SHARES ) INTO TWO (2) ORDINARY SHARES OF RM0.05

BUS512M Session 9. Accounting for Financing Decisions: Long-Term Liabilities and Stockholders Equity

BUS512M Session 9 Accounting for Financing Decisions: Long-Term Liabilities and Stockholders Equity Liabilities Current or Short-term Liabilities Long-term Debt (borrowed funds) Lease Liabilities Deferred

BUS512M Session 9 Accounting for Financing Decisions: Long-Term Liabilities and Stockholders Equity Liabilities Current or Short-term Liabilities Long-term Debt (borrowed funds) Lease Liabilities Deferred

General comments This question had easily the highest percentage mark on the paper. Overall, the candidates performance was very good indeed.

MARK PLAN AND EXAMINER S COMMENTARY The marking plan set out below was that used to mark this question. Markers were encouraged to use discretion and to award partial marks where a point was either not

MARK PLAN AND EXAMINER S COMMENTARY The marking plan set out below was that used to mark this question. Markers were encouraged to use discretion and to award partial marks where a point was either not

PUBLIC INVESTMENT BANK

PUBLIC INVESTMENT BANK PublicInvest Research Results Review Thursday, November 26, 2015 KDN PP17686/03/2013(032117) PRESTARIANG Outperform DESCRIPTION An ICT service provider focusing on ICT training and

PUBLIC INVESTMENT BANK PublicInvest Research Results Review Thursday, November 26, 2015 KDN PP17686/03/2013(032117) PRESTARIANG Outperform DESCRIPTION An ICT service provider focusing on ICT training and

Arbuthnot Banking Group Acquisition of Everyday Loans

Arbuthnot Banking Group Acquisition of Everyday Loans Capitalising opportunities Financials In line with its stated strategy, Arbuthnot Banking Group s (ABG) 75.5% subsidiary Secure Trust Bank (STB) has

Arbuthnot Banking Group Acquisition of Everyday Loans Capitalising opportunities Financials In line with its stated strategy, Arbuthnot Banking Group s (ABG) 75.5% subsidiary Secure Trust Bank (STB) has

CHAPTER17 DIVIDENDS AND DIVIDEND POLICY

CHAPTER17 DIVIDENDS AND DIVIDEND POLICY Learning Objectives LO1 Dividend types and how dividends are paid. LO2 The issues surrounding dividend policy decisions. LO3 The difference between cash and stock

CHAPTER17 DIVIDENDS AND DIVIDEND POLICY Learning Objectives LO1 Dividend types and how dividends are paid. LO2 The issues surrounding dividend policy decisions. LO3 The difference between cash and stock

DIVIDENDS DIVIDEND POLICY

DIVIDENDS ANE) - DIVIDEND POLICY H. Kent Baker The Robert W. Kolb Series in Finance WILEY John Wiley & Sons, Inc. Contents Acknowledgments XV1 PART I Dividends and Dividend Policy: History, Trends, and

DIVIDENDS ANE) - DIVIDEND POLICY H. Kent Baker The Robert W. Kolb Series in Finance WILEY John Wiley & Sons, Inc. Contents Acknowledgments XV1 PART I Dividends and Dividend Policy: History, Trends, and

Digital River, Inc. Fourth Quarter Results (In thousands, except share data) Subject to reclassification

Subject to reclassification") (In thousands, except share data) Consolidated Balance Sheets (Unaudited) 2012 2011 Assets Current assets Cash and cash equivalents $ 542,851 $ 497,193 Short-term investments 162,794 223,349 Accounts receivable,

(In thousands, except share data) Consolidated Balance Sheets (Unaudited) 2012 2011 Assets Current assets Cash and cash equivalents $ 542,851 $ 497,193 Short-term investments 162,794 223,349 Accounts receivable,

JEM034 Corporate Finance Winter Semester 2017/2018

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #8 Olga Bychkova Topics Covered Today Overview of corporate financing (chapter 14 in BMA) How corporations issue securities (chapter 15 in BMA)

JEM034 Corporate Finance Winter Semester 2017/2018 Lecture #8 Olga Bychkova Topics Covered Today Overview of corporate financing (chapter 14 in BMA) How corporations issue securities (chapter 15 in BMA)

Chapter 20: Solutions. Page 1

Chapter 20: Solutions Problem 1 a. True b. True c. False Problem 2 Firms usually do not change their dividends very frequently. This is what is meant by "sticky" dividends. Part of the reason for "sticky"

Chapter 20: Solutions Problem 1 a. True b. True c. False Problem 2 Firms usually do not change their dividends very frequently. This is what is meant by "sticky" dividends. Part of the reason for "sticky"

RHB GOLDENLIFE TODAY

Date: 15 July 2017 RHB GOLDENLIFE TODAY RESPONSIBILITY STATEMENT This Product Highlights Sheet has been reviewed and approved by the directors of RHB Asset Management Sdn Bhd and they have collectively

Date: 15 July 2017 RHB GOLDENLIFE TODAY RESPONSIBILITY STATEMENT This Product Highlights Sheet has been reviewed and approved by the directors of RHB Asset Management Sdn Bhd and they have collectively

Dividend Decisions. LOS 1 : Introduction 1.1

1.1 Dividend Decisions LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement Sales Less: Variable cost Contribution Less: Fixed cost excluding Dep.

1.1 Dividend Decisions LOS 1 : Introduction Note: Total Earnings mean Earnings available to equity share holders Income Statement Sales Less: Variable cost Contribution Less: Fixed cost excluding Dep.

Digital River, Inc. First Quarter Results (In thousands, except share data) Subject to reclassification

Subject to reclassification") (In thousands, except share data) Consolidated Balance Sheets (Unaudited) December 31, Assets Current assets Cash and cash equivalents $ 500,742 $ 542,851 Short-term investments 144,615 162,794 Accounts

(In thousands, except share data) Consolidated Balance Sheets (Unaudited) December 31, Assets Current assets Cash and cash equivalents $ 500,742 $ 542,851 Short-term investments 144,615 162,794 Accounts

DIVIDENDS AND DIVIDEND POLICY

590 PART 6 Cost of Capital and Long-Term Financial Policy 18 DIVIDENDS AND DIVIDEND POLICY Cost of Capital and Long-Term Financial Policy PART 6 On February 16, 2006, Halliburton announced a broad plan

590 PART 6 Cost of Capital and Long-Term Financial Policy 18 DIVIDENDS AND DIVIDEND POLICY Cost of Capital and Long-Term Financial Policy PART 6 On February 16, 2006, Halliburton announced a broad plan

Applied Corporate Finance. Unit 5

Applied Corporate Finance Unit 5 Dividend Policy Measures Yield, Payout and Dividend Rate Determinants of Dividend Policy Various schools of though on Dividend Policy Managing Changes in Dividend Policy

Applied Corporate Finance Unit 5 Dividend Policy Measures Yield, Payout and Dividend Rate Determinants of Dividend Policy Various schools of though on Dividend Policy Managing Changes in Dividend Policy

Handout for week 2 Understanding Balance sheet

Handout for week 2 Understanding Balance sheet The purpose of financial accounting is generating status and performance reports in the form of Balance Sheet and Statement of Profit & Loss (Income Statement).

Handout for week 2 Understanding Balance sheet The purpose of financial accounting is generating status and performance reports in the form of Balance Sheet and Statement of Profit & Loss (Income Statement).

MY EG Services Berhad

1Q FY June 2013 results MY EG Services Berhad 30 November 2012 Results in line with our forecasts New JPJ, immigration services to drive growth Customs tax service to start mid-2013, after elections Strong

1Q FY June 2013 results MY EG Services Berhad 30 November 2012 Results in line with our forecasts New JPJ, immigration services to drive growth Customs tax service to start mid-2013, after elections Strong

SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment Plan The NFU Mutual Select Individual Savings Account (ISA) INVESTMENTS

INVESTMENTS") SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment Plan The NFU Mutual Select Individual Savings Account (ISA) INVESTMENTS SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment

SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment Plan The NFU Mutual Select Individual Savings Account (ISA) INVESTMENTS SUPPLEMENTARY INFORMATION DOCUMENT The NFU Mutual Select Investment

AFFIN HOLDINGS BHD (AFFIN)

") AFFIN HOLDINGS BHD (AFFIN) All figures in millions of Ringgit Malaysia except per share values and ratios Analysis Date: 21/06/2013 Financial Year: 2012 31/12/2012 Latest Quarter: 31/12/2012 Price: 4.15

AFFIN HOLDINGS BHD (AFFIN) All figures in millions of Ringgit Malaysia except per share values and ratios Analysis Date: 21/06/2013 Financial Year: 2012 31/12/2012 Latest Quarter: 31/12/2012 Price: 4.15

For personal use only SECOND QUARTER ENDED 30 JUNE 2015

SECOND QUARTER ENDED 30 JUNE 2015 SECOND QUARTER ENDED 30 JUNE 2015 (Cover) The Setapak land development is a strategically located new mixed-use project that features the perfect lifestyle combination

SECOND QUARTER ENDED 30 JUNE 2015 SECOND QUARTER ENDED 30 JUNE 2015 (Cover) The Setapak land development is a strategically located new mixed-use project that features the perfect lifestyle combination

The Incidence of Financial Transactions Taxes

December 2015 The Incidence of Financial Transactions Taxes By Dean Baker and Nicole Woo* Center for Economic and Policy Research 1611 Connecticut Ave. NW Suite 400 Washington, DC 20009 tel: 202-293-5380

December 2015 The Incidence of Financial Transactions Taxes By Dean Baker and Nicole Woo* Center for Economic and Policy Research 1611 Connecticut Ave. NW Suite 400 Washington, DC 20009 tel: 202-293-5380

SHARES 101. Differences Between Stocks And Shares. What Is A Stock? Five Things To Know About Shares. What Is A Stock Market?

SHARES 101 Differences Between Stocks And Shares None. There are always questions being asked about the differences between stocks and shares. The bottom line is that stocks and shares are the same thing,

SHARES 101 Differences Between Stocks And Shares None. There are always questions being asked about the differences between stocks and shares. The bottom line is that stocks and shares are the same thing,

Security Analysis. macroeconomic factors and industry level analysis

Security Analysis (Text reference: Chapter 14) discounted cash flow techniques price-earnings ratios other multiples example #1: U.S. retail stores more on price to book value multiples more on price to

Security Analysis (Text reference: Chapter 14) discounted cash flow techniques price-earnings ratios other multiples example #1: U.S. retail stores more on price to book value multiples more on price to

THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613. Business Finance Final Exam

Student Name: Student ID Number: THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613 Business Finance Final Exam (1) TIME ALLOWED - 2 hours (2) TOTAL NUMBER OF QUESTIONS - 50 (3) ANSWER ALL QUESTIONS

Student Name: Student ID Number: THE UNIVERSITY OF NEW SOUTH WALES JUNE / JULY 2006 FINS1613 Business Finance Final Exam (1) TIME ALLOWED - 2 hours (2) TOTAL NUMBER OF QUESTIONS - 50 (3) ANSWER ALL QUESTIONS

Principal Financial Group 2016 Outlook Call

Principal Financial Group Call December 3, 2015 Use of Non-GAAP Financial Measures A non-gaap financial measure is a numerical measure of performance, financial position, or cash flows that includes adjustments

Principal Financial Group Call December 3, 2015 Use of Non-GAAP Financial Measures A non-gaap financial measure is a numerical measure of performance, financial position, or cash flows that includes adjustments

PRODUCT HIGHLIGHTS SHEET

PRODUCT HIGHLIGHTS SHEET Areca Dividend Income Fund (Date of Constitution: 20 January 2017) RESPONSIBILITY STATEMENT This Product Highlights Sheet has been reviewed and approved by the Board of Directors

PRODUCT HIGHLIGHTS SHEET Areca Dividend Income Fund (Date of Constitution: 20 January 2017) RESPONSIBILITY STATEMENT This Product Highlights Sheet has been reviewed and approved by the Board of Directors

Capital Structure. Katharina Lewellen Finance Theory II February 18 and 19, 2003

Capital Structure Katharina Lewellen Finance Theory II February 18 and 19, 2003 The Key Questions of Corporate Finance Valuation: How do we distinguish between good investment projects and bad ones? Financing:

Capital Structure Katharina Lewellen Finance Theory II February 18 and 19, 2003 The Key Questions of Corporate Finance Valuation: How do we distinguish between good investment projects and bad ones? Financing:

Dividend Decision FINANCE VOL 5

Dividend Decision FINANCE VOL 5 Returning cash to the owner DIVIDEND POLICY Steps to the Dividend Decision 4 I. Dividends are sticky 5 The last quarter of 2008 put stickiness to the test.. Number of S&P

Dividend Decision FINANCE VOL 5 Returning cash to the owner DIVIDEND POLICY Steps to the Dividend Decision 4 I. Dividends are sticky 5 The last quarter of 2008 put stickiness to the test.. Number of S&P

Manulife Financial Corporation

Title: Manulife Financial Corporation - MFC (T) Cdn$13.32 Price: Cdn$13.32 StockRating: Sector Perform TargetPrice: Cdn$14.00 Headline: Title August 7, 2014 The NBF Daily Bulletin MFC (T) Stock Rating:

Title: Manulife Financial Corporation - MFC (T) Cdn$13.32 Price: Cdn$13.32 StockRating: Sector Perform TargetPrice: Cdn$14.00 Headline: Title August 7, 2014 The NBF Daily Bulletin MFC (T) Stock Rating:

RHB MUDHARABAH FUND RESPONSIBILITY STATEMENT

Date: 15 July 2017 RHB MUDHARABAH FUND RESPONSIBILITY STATEMENT This Product Highlights Sheet has been reviewed and approved by the directors of RHB Asset Management Sdn Bhd ( RHBAM ) and they have collectively

Date: 15 July 2017 RHB MUDHARABAH FUND RESPONSIBILITY STATEMENT This Product Highlights Sheet has been reviewed and approved by the directors of RHB Asset Management Sdn Bhd ( RHBAM ) and they have collectively

The Examiner's Answers. Financial Strategy 1

The Examiner's Answers F3 - Financial Strategy Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared candidate. They have been written in this way

The Examiner's Answers F3 - Financial Strategy Some of the answers that follow are fuller and more comprehensive than would be expected from a well-prepared candidate. They have been written in this way

Simplified Prospectus May 23, 2017

Simplified Prospectus May 23, 2017 Class B Units, Class D Units, Class F Units and Class I Units (unless otherwise noted) of: Beutel Goodman Balanced Fund Beutel Goodman Canadian Equity Fund Beutel Goodman

Simplified Prospectus May 23, 2017 Class B Units, Class D Units, Class F Units and Class I Units (unless otherwise noted) of: Beutel Goodman Balanced Fund Beutel Goodman Canadian Equity Fund Beutel Goodman

Since Robo contributes more on a per minute basis, the firm should use additional time in the Assembly Department to produce Robo.

SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) Heli HK$ Robo HK$ Selling price 8,000 24,000 Variable costs (3,240) (9,400) Contribution per unit 4,760 14,600 Answer 1(b) Time required for target

SECTION A CASE QUESTIONS (Total: 50 marks) Answer 1(a) Heli HK$ Robo HK$ Selling price 8,000 24,000 Variable costs (3,240) (9,400) Contribution per unit 4,760 14,600 Answer 1(b) Time required for target

STARHILL REAL ESTATE INVESTMENT TRUST. Interim financial report on result for the financial period ended 31 December 2006.

Interim financial report on result for the financial period ended 31 December 2006. The figures have not been audited. CONDENSED INCOME STATEMENT INDIVIDUAL QUARTER CUMULATIVE QUARTER PRECEDING YEAR CURRENT

Interim financial report on result for the financial period ended 31 December 2006. The figures have not been audited. CONDENSED INCOME STATEMENT INDIVIDUAL QUARTER CUMULATIVE QUARTER PRECEDING YEAR CURRENT

CHAPTER 18: EQUITY VALUATION MODELS

CHAPTER 18: EQUITY VALUATION MODELS PROBLEM SETS 1. Theoretically, dividend discount models can be used to value the stock of rapidly growing companies that do not currently pay dividends; in this scenario,

CHAPTER 18: EQUITY VALUATION MODELS PROBLEM SETS 1. Theoretically, dividend discount models can be used to value the stock of rapidly growing companies that do not currently pay dividends; in this scenario,

Chapter 11 - REPORTING AND ANALYZING STOCKHOLDERS EQUITY

Revised Summer 2018 Chapter 11 Review 1 Chapter 11 - REPORTING AND ANALYZING STOCKHOLDERS EQUITY LO 1: Describe the major characteristics of a corporation. WHAT IS A CORPORATION Corporation: legal entity,

Revised Summer 2018 Chapter 11 Review 1 Chapter 11 - REPORTING AND ANALYZING STOCKHOLDERS EQUITY LO 1: Describe the major characteristics of a corporation. WHAT IS A CORPORATION Corporation: legal entity,

SUNWAY BUY. FY15 operating earnings within expectations. Company report. (Maintained) CONGLOMERATE

CONGLOMERATE") SUNWAY CONGLOMERATE (SWB MK EQUITY, SWAY.KL) 29 Feb 2016 FY15 operating earnings within expectations Company report Thomas Soon soon-guan-chuan@ambankgroup.com 03-2036 2300 Rationale for report: Company

SUNWAY CONGLOMERATE (SWB MK EQUITY, SWAY.KL) 29 Feb 2016 FY15 operating earnings within expectations Company report Thomas Soon soon-guan-chuan@ambankgroup.com 03-2036 2300 Rationale for report: Company

PHILLIP MASTER ISLAMIC CASH FUND ( the Fund )

") Date of Issuance: 26 March 2018 PHILLIP MASTER ISLAMIC CASH FUND ( the Fund ) RESPONSIBILITY STATEMENT This Product Highlights Sheet ( PHS ) has been reviewed and approved by the directors or authorized

Date of Issuance: 26 March 2018 PHILLIP MASTER ISLAMIC CASH FUND ( the Fund ) RESPONSIBILITY STATEMENT This Product Highlights Sheet ( PHS ) has been reviewed and approved by the directors or authorized

ASEAN EQUITY FUND. ( The Fund ) PRODUCT HIGHLIGHTS SHEET RESPONSIBILITY STATEMENT DISCLAIMER STATEMENTS DATE OF ISSUANCE: 12 FEBRUARY 2018

PRODUCT HIGHLIGHTS SHEET RESPONSIBILITY STATEMENT DISCLAIMER STATEMENTS DATE OF ISSUANCE: 12 FEBRUARY 2018") PRODUCT HIGHLIGHTS SHEET ASEAN EQUITY FUND ( The Fund ) DATE OF ISSUANCE: 12 FEBRUARY 2018 RESPONSIBILITY STATEMENT This Product Highlights Sheet has been reviewed and approved by the directors and/or

PRODUCT HIGHLIGHTS SHEET ASEAN EQUITY FUND ( The Fund ) DATE OF ISSUANCE: 12 FEBRUARY 2018 RESPONSIBILITY STATEMENT This Product Highlights Sheet has been reviewed and approved by the directors and/or

ACCAspace ACCA F9. Provided by ACCA Research Institute. Financial Management (FM) 财务管理 ACCA Lecturer: Sinny Shao. ACCAspace 中国 ACCA 特许公认会计师教育平台

财务管理 ACCA Lecturer: Sinny Shao. ACCAspace 中国 ACCA 特许公认会计师教育平台") ACCAspace Provided by ACCA Research Institute ACCA F9 Financial Management (FM) 财务管理 ACCA Lecturer: Sinny Shao ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright ACCAspace.com Part E:Business Finance Equity Finance

ACCAspace Provided by ACCA Research Institute ACCA F9 Financial Management (FM) 财务管理 ACCA Lecturer: Sinny Shao ACCAspace 中国 ACCA 特许公认会计师教育平台 Copyright ACCAspace.com Part E:Business Finance Equity Finance

LUMP SUM INVESTMENT SOLUTIONS

LUMP SUM INVESTMENT SOLUTIONS VOLUNTARY ANNUITIES METROPOLITAN S INVESTMENT OPTIONS Metropolitan offers solid investment options for you to choose from. Your financial adviser will help you select the

LUMP SUM INVESTMENT SOLUTIONS VOLUNTARY ANNUITIES METROPOLITAN S INVESTMENT OPTIONS Metropolitan offers solid investment options for you to choose from. Your financial adviser will help you select the

Earnings Per Share and Retained Earnings

CHAPTER 17 O BJECTIVES After reading this chapter you will be able to: 1 Compute basic earnings per share (EPS). 2 Understand how to compute the weighted average common shares for EPS. 3 Identify the potential

CHAPTER 17 O BJECTIVES After reading this chapter you will be able to: 1 Compute basic earnings per share (EPS). 2 Understand how to compute the weighted average common shares for EPS. 3 Identify the potential

Statement of Financial Accounting Standards No. 5. Statement of Financial Accounting Standards No.5. Long-Term Investments in Equity Securities

Statement of Financial Accounting Standards No. 5 Statement of Financial Accounting Standards No.5 Long-Term Investments in Equity Securities Revised on 18 June 1998 Translated by Chung-yueh Conrad Chang,

Statement of Financial Accounting Standards No. 5 Statement of Financial Accounting Standards No.5 Long-Term Investments in Equity Securities Revised on 18 June 1998 Translated by Chung-yueh Conrad Chang,

FACULTY ECONOMIC AND MANAGEMENT SCIENCES DEPARTMENT FINANCIAL MANAGEMENT

FACULTY ECONOMIC AND MANAGEMENT SCIENCES DEPARTMENT FINANCIAL MANAGEMENT FINANCIAL MANAGEMENT 300 YEAR TEST 3 Suggested solution 25 September 2012 INTERNAL J E Klopper F Blom L Klopper EXTERNAL G J Plant

FACULTY ECONOMIC AND MANAGEMENT SCIENCES DEPARTMENT FINANCIAL MANAGEMENT FINANCIAL MANAGEMENT 300 YEAR TEST 3 Suggested solution 25 September 2012 INTERNAL J E Klopper F Blom L Klopper EXTERNAL G J Plant

A Measure of How Much a Company Could have Afforded to Pay out: FCFE

189 A Measure of How Much a Company Could have Afforded to Pay out: FCFE The Free Cashflow to Equity (FCFE) is a measure of how much cash is left in the business after non-equity claimholders (debt and

189 A Measure of How Much a Company Could have Afforded to Pay out: FCFE The Free Cashflow to Equity (FCFE) is a measure of how much cash is left in the business after non-equity claimholders (debt and

Using Display Options (Company Information) 2.11 Company Information

2.11 Company Information") 2.11 Company Information Company Information provides the most up-to-date information of each listed company, like major business activities, latest result announcements, historical dividend announcement

2.11 Company Information Company Information provides the most up-to-date information of each listed company, like major business activities, latest result announcements, historical dividend announcement

For personal use only SECOND QUARTER ENDED 30 JUNE 2016

SECOND QUARTER ENDED 30 JUNE 2016 SECOND QUARTER ENDED 30 JUNE 2016 UOA Corporate Tower Lobby A, Avenue 10, The Vertical Bangsar South City No. 8, Jalan Kerinchi 59200 Kuala Lumpur, Malaysia t 1 300 88

SECOND QUARTER ENDED 30 JUNE 2016 SECOND QUARTER ENDED 30 JUNE 2016 UOA Corporate Tower Lobby A, Avenue 10, The Vertical Bangsar South City No. 8, Jalan Kerinchi 59200 Kuala Lumpur, Malaysia t 1 300 88

UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE FINANCIAL PERIOD ENDED 31 MARCH 2018

MALAYSIA STEEL WORKS (KL) BHD (Company No. 7878-V) UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE FINANCIAL PERIOD ENDED 31 MARCH 2018 INDIVIDUAL PERIOD CUMULATIVE PERIOD CURRENT

MALAYSIA STEEL WORKS (KL) BHD (Company No. 7878-V) UNAUDITED CONDENSED CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME FOR THE FINANCIAL PERIOD ENDED 31 MARCH 2018 INDIVIDUAL PERIOD CUMULATIVE PERIOD CURRENT

F2 Revisions. Raising Finance. Long Term Financing. Term loans. Rights issue of shares. New issue of shares. Conventional bonds

F2 Revisions Raising Finance Long Term Financing Equity Debt Rights issue of shares New issue of shares Initial public offering (IPO) or stock market launch Placement (non-public offering) Term loans Conventional

F2 Revisions Raising Finance Long Term Financing Equity Debt Rights issue of shares New issue of shares Initial public offering (IPO) or stock market launch Placement (non-public offering) Term loans Conventional

RHB SMART SERIES FUNDS comprising: RHB SMART TREASURE FUND RHB SMART BALANCED FUND RHB SMART INCOME FUND

Date: 15 June 2017 RHB SMART SERIES FUNDS comprising: RHB SMART TREASURE FUND RHB SMART BALANCED FUND RHB SMART INCOME FUND RESPONSIBILITY STATEMENT This Product Highlights Sheet has been reviewed and

Date: 15 June 2017 RHB SMART SERIES FUNDS comprising: RHB SMART TREASURE FUND RHB SMART BALANCED FUND RHB SMART INCOME FUND RESPONSIBILITY STATEMENT This Product Highlights Sheet has been reviewed and

Excess Cash and Shareholder Payout Strategies A Summary

Excess Cash and Shareholder Payout Strategies A Summary Neeti A++ Dixit This article discusses, unarguably, one of the key principles of finance i.e. extra cash and its treatment by companies. After chalking

Excess Cash and Shareholder Payout Strategies A Summary Neeti A++ Dixit This article discusses, unarguably, one of the key principles of finance i.e. extra cash and its treatment by companies. After chalking

UNIT 5 COST OF CAPITAL

UNIT 5 COST OF CAPITAL UNIT 5 COST OF CAPITAL Cost of Capital Structure 5.0 Introduction 5.1 Unit Objectives 5.2 Concept of Cost of Capital 5.3 Importance of Cost of Capital 5.4 Classification of Cost

UNIT 5 COST OF CAPITAL UNIT 5 COST OF CAPITAL Cost of Capital Structure 5.0 Introduction 5.1 Unit Objectives 5.2 Concept of Cost of Capital 5.3 Importance of Cost of Capital 5.4 Classification of Cost

i2live retirement solutions

PROTECTION i2live i2live retirement solutions A flexible approach to retirement planning Adviser guide - not for use with customers PENSIONS INVESTMENTS About Sun Life Financial of Canada In the UK Sun

PROTECTION i2live i2live retirement solutions A flexible approach to retirement planning Adviser guide - not for use with customers PENSIONS INVESTMENTS About Sun Life Financial of Canada In the UK Sun

FCF t. V = t=1. Topics in Chapter. Chapter 16. How can capital structure affect value? Basic Definitions. (1 + WACC) t

t") Topics in Chapter Chapter 16 Capital Structure Decisions Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Topics in Chapter Chapter 16 Capital Structure Decisions Overview and preview of capital structure effects Business versus financial risk The impact of debt on returns Capital structure theory, evidence,

Employee Stock Purchase Plan

Employee Stock Purchase Plan This document constitutes part of a Prospectus covering securities that have been registered under the Securities Act of 1933. The date of this Prospectus is November 1, 2015.

Employee Stock Purchase Plan This document constitutes part of a Prospectus covering securities that have been registered under the Securities Act of 1933. The date of this Prospectus is November 1, 2015.

BUY. Kiatnakin Bank - KK. Closing Price. Bt30 target price (Upgrade) Bt38 (+26.7%)

Bt38 (+26.7%)") 17 January 2012 Kiatnakin Bank - KK Closing Price BUY Bt30 target price (Upgrade) Bt38 (+26.7%) 4Q11 profit above forecast on lower tax expenses KK posted a 4Q11 net profit of Bt682.78m, down 21.9% QoQ

17 January 2012 Kiatnakin Bank - KK Closing Price BUY Bt30 target price (Upgrade) Bt38 (+26.7%) 4Q11 profit above forecast on lower tax expenses KK posted a 4Q11 net profit of Bt682.78m, down 21.9% QoQ