FINANCIAL MARKETS cont d

|

|

|

- Catherine Day

- 6 years ago

- Views:

Transcription

1 FINANCIAL MARKETS cont d The Stock Market, the Theory of Rational Expectations, and the Efficient Market Hypothesis

2 Stocks or Company Shares Common stock is the principal way that corporations or companies raise equity capital. Holders of common stock own an interest in the corporation consistent with the percentage of outstanding shares owned. This ownership interest gives stockholders those who hold stock in a corporation a bundle of rights. The most important are the right to vote and to be the residual claimant of all funds flowing into the firm (known as cash flows), meaning that the stockholder receives whatever remains after all other claims against the firm s assets have been satisfied.

3 Stocks Stockholders are paid dividends from the net earnings of the corporation. Dividends are payments made periodically, usually every quarter, to stockholders (in Ghana annually) The board of directors of the firm sets the level of the dividend, usually upon the recommendation of management. In addition, the stockholder has the right to sell the stock.

4 Common Stock - Rights Share of firm s ownership: Ownership interest- a bundle of rights -right to vote- right to sell stocks A residual claimant Paid after all other creditors last in line Limited liability Shareholders cannot be liable beyond stock investment

5

6 All-share Index Figure 5: Performance of GSE All-share index All-share index Years

7 Issues Stocks and How are stocks priced How to incorporate peoples expectations about the market Market Efficiency and Efficient Market Hypothesis rational expectations theory and adaptive expectation Explain the implications of the rational expectations theory efficient market hypothesis State and explain the three types of efficient market hypothesis

8 Measuring the Stock Market Stock market indexes-a stock index or stock market index is a measurement of the value of a section of the stock market. It is computed from the prices of selected stocks (typically a weighted average). It is a tool used by investors and financial managers to describe the market, and to compare the return on specific investments. Market capitalization is commonly utilized for benchmarking stock markets across countries or across time. As a measure of the value of all stocks listed on an exchange, it intends to summarize the development of a stock market

9 The Value of a security or Asset in Finance One basic principle of finance is that the value of any investment is found by computing the value today of all cash flows the investment will generate over its life. For example, a commercial building will sell for a price that reflects the net cash flows (rents expenses) it is projected to have over its useful life. Similarly, we value common stock as the value in today s dollars (or cedis) of all future cash flows. The cash flows a stockholder might earn from stock are dividends, the sales price of the stock, or both.

10 Stock Valuation Recall: We value an asset based on the present value of the expected future cash flows For stocks there are dividend payments which affect the resale price

11 STOCK VALUATION If stock is bought and held for one period to get a dividend, then sold. We call this valuation - the one-period valuation model

12 One-period valuation model The cash flows consist of one dividend payment plus a final sales price. When these cash flows are discounted back to the present, the following equation computes the current price of the stock: where P 0 =the current price of the stock. The zero subscript refers to time period zero, or the present. Div 1 =the dividend paid at the end of year 1. k e =the required return on investments in equity. P 1 =the price at the end of the first period; the assumed sales price of the stock.

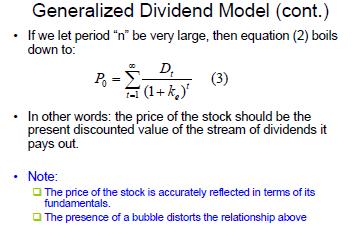

13 The Generalized Dividend Valuation Model Using the same concept, the one-period dividend valuation model can be extended to any number of periods: The value of stock is the present value of all future cash flows. The only cash flows that an investor will receive are dividends and a final sales price when the stock is ultimately sold in period n. The generalized multi-period formula for stock valuation can be written as:

14

15

16 General Dividend Valuation Model The generalized dividend valuation model requires that we compute the present value of an infinite stream of dividends, a process that could be difficult, to say the least. Simplified models have been developed to make the calculations easier. One such model is the Gordon growth model, which assumes constant dividend growth.

17 General Dividend Valuation Model This reasoning implies that the current value of a share of stock can be calculated as simply the present value of the future dividend stream. This says that the price of stock is determined only by the present value of dividends and that nothing else matters. As n tends to infinity n the last term P ne /(1+k e ) 0

18

19 The generalized dividend model is rewritten in Equation 3 without the final sales price:- as the fundamental only -P 0 =the current price of the stock

20

21 The Gordon Growth Model Many firms strive to increase their dividends at a constant rate each year. Equation 4 rewrites Equation 3 to reflect this constant growth in dividends: Where D 0 =the most recent dividend paid g =the expected constant growth rate in dividends k e =the required return on an investment in equity P 0 =the current price of the stock

22

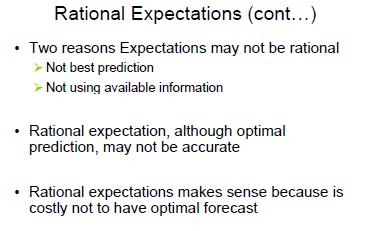

23

24 EXPECTATIONS The analysis of stock price evaluation we have outlined in the previous section depends on people s expectations especially of cash flows. Indeed, it is difficult to think of any sector in the economy in which expectations are not crucial; this is why it is important to examine how expectations are formed. We do so by outlining the theory of rational expectations

25

26 Adaptive expectations is an economic theory which gives importance to past events in predicting future outcomes. A common example is for predicting inflation. Adaptive expectations states that if inflation increased in the past year, people will expect a higher rate of inflation in the next year.

27 DEFINITION of 'Adaptive Expectations Hypothesis' A hypothesis stating that individuals make investment decisions based on the direction of recent historical data, such as past inflation rates, and adjust the data (based on their expectations) to predict future rates. For example, if inflation over the last 10 years has been running in the 2-3% range, investors would use an inflation expectation of that range when making investment decisions. Consequently, if a temporary extreme fluctuation in inflation occurred recently, such as a cost-push inflation phenomenon, investors will overestimate the movement of inflation rates in the future.

28

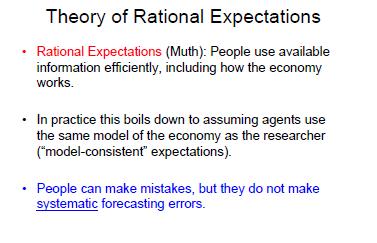

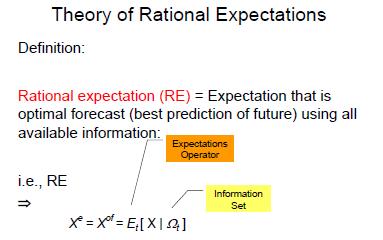

29 What is the 'Rational Expectations Theory' The rational expectations theory is an economic idea that the people make choices based on their rational outlook, available information and past experiences. The theory suggests that the current expectations in the economy are equivalent to what people think the future state of the economy will become. This contrasts with the idea that government policy influences people's decisions. Rational expectations (RE) was propounded Lucas Read more: Rational Expectations Theory Definition Investopedia

30 Rational Expectations Is economic-behavior according to which: (1) On average, people can quite correctly predict future conditions and take actions accordingly, even if they do not fully understand the cause-and-effect (causal) relationships underlying the events and their own thinking. Thus, while they do not have perfect foresights, they construct their expectations in a rational manner that, more often than not, turn out to be correct. Any error that creeps in is usually due to random (non-systemic) and unforeseeable causes. (2) In efficient markets with perfect or near perfect information (such as in modern open-market economies) people will anticipate government's actions to stimulate or restrain the economy, and will adjust their response accordingly. Read more: TRE.html

31 For example, if the government attempts to increase the money supply, people will raise their prices and wage demands to compensate for the inflationary impact of the increase. Similarly, during periods of accelerating inflation, they will anticipate stricter credit controls accompanied by high interest rates. Therefore they will attempt to borrow up to their credit capability, thus largely nullifying the controls. This theory was proposed not as a plausible explanation of human behavior, but to serve as a model against which extreme forms of behavior could be compared. Read more:

32 Rational Expectations The rational expectations theory is often used to explain expected rates of inflation. For example, if inflation rates within an economy were higher than expected in the past, people take that into account along with other indicators to assume that inflation may further increase in the future. The rational expectations theory also explains how producers and suppliers use past events to predict future business operations. If a company believes that the price for its product will be higher in the future, for example, it will stop or slow production until the price rises. Since the company weakens supply while demand stays the same, the price will increase.

33 The producer believes that the price will rise in the future and makes a rational decision to slow production, and this decision partially affects what happens in the future. By relying on the rational expectations theory, companies can inadvertently effect future inflation in an economy. An Example of Rational Expectations Theory

34 Rational expectations theory, while valid, can sometimes have adverse effects on the global economy. For example, Former Bank of England governor Mervyn King has pointed out that central banks can easily become a prisoner of the economy's rational expectations theory. (The End of Alchemy: Money, Banking and the Future of the Global Economy, by Mervyn King, 2016) Since the theory stipulates that people in an economy make assumptions based largely on past experiences, specific monetary policies enacted by central banks can actually cause disequilibrium in an economy. When the Federal Reserve decided on a quantitative easing program to help the economy through the 2008 financial crisis, it set unattainable expectations for the country, as outlined by the theory. The quantitative easing program reduced interest rates for more than seven years, and people began to believe that interest rates would remain low. In 2015, when Janet Yellen announced that the Federal Reserve would increase interest rates starting in 2016, the markets reacted negatively. This rational expectations theory subsequently trapped the Federal Reserve into making decisions that would take expectations of the economy into account, and Yellen soon backed off her initial decision to increase rates as many as four times in the coming years.

35

36

37

38

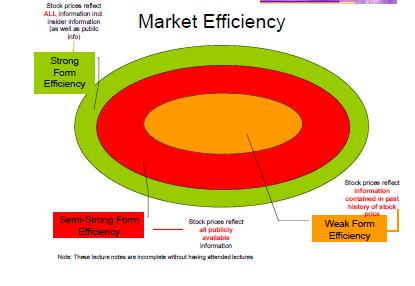

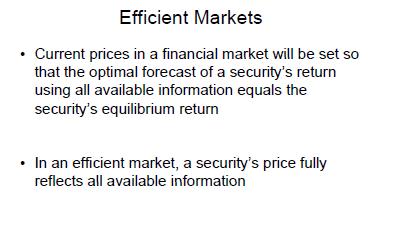

39 Some definitions The price-earnings ratio (PE Ratio) is the ratio for valuing a company that measures its current share price relative to its pershare earnings. The price-earnings ratio can be calculated as: Market Value per Share / Earnings per Share. What is an efficient market? Efficient market is one where the market price is an unbiased estimate of the true value of the investment.

40 MARKET EFFICIENCY IN FINANCIAL MARKETS Implicit in this definition of an efficient market are several key concepts - (a) Market efficiency does not require that the market price be equal to true value at every point in time. All it requires is that errors in the market price be unbiased, i.e., that prices can be greater than or less than true value, as long as these deviations are random. (b) The fact that the deviations from true value are random implies, in a rough sense, that there is an equal chance that stocks are under or over valued at any point in time, and that these deviations are uncorrelated with any observable variable. For instance, in an efficient market, stocks with lower PE ratios should be no more or less likely to undervalued than stocks with high PE ratios. (c) If the deviations of market price from true value are random, it follows that no group of investors should be able to consistently find under or overvalued stocks using any investment strategy.

41 Market Efficiency for Investor Groups Definitions of market efficiency have to be specific not only about the market that is being considered but also the investor group that is covered. It is extremely unlikely that all markets are efficient to all investors, but it is entirely possible that a particular market (for instance, the New York Stock Exchange) is efficient with respect to the average investor. It is also possible that some markets are efficient while others are not, and that a market is efficient with respect to some investors and not to others. This is a direct consequence of differential tax rates and transactions costs, which confer advantages on some investors relative to others.

42 Market Efficiency for Investor Groups Definitions of market efficiency are also linked up with assumptions about what information is available to investors and reflected in the price. For instance, a strict definition of market efficiency that assumes that all information, public as well as private, is reflected in market prices would imply that even investors with precise inside information will be unable to beat the market.

43 EFFICIENCY OF FINANCIAL MARKETS- the concept of financial efficiency is closely related to the rational expectations hypothesis A financial market is efficient when security prices fully reflect all available information. An efficient financial market is in equilibrium when the demand for and supply of Secutities is equal. Characteristics of an efficient financial market are :- 1. Information is available to all buyers and sellers of financial securities 2. Transactions must be executed without significant price changes 3. Security prices are independent of individual buyers and sellers 4. There are no transaction costs. In other words there are no brokerage fees, transfer charges or taxes etc when securities are bought and sold 5. Prices of securities are promptly adjusted to equalise their yields. i.e. risk adjusted expected returns on all investments are equalised 6. The efficient-market resources are used in a non-wasteful manner 7. The resources are allocated to the socially most productive uses

44 MARKET EFFICIENCY ISSUES Market efficiency refers to the degree to which stock prices and other securities prices reflect all available, relevant information. The efficient market hypothesis (EMH) is an investment theory that states it is impossible to "beat the market" because stock market efficiency causes existing share prices to always incorporate and reflect all relevant information. Notice that the level/degree/form of efficiency in a market depends on two dimensions: 1. The type of information incorporated into price (which information is available?). 2. The speed with which new information is incorporated into price ( how fast information is reflected?). Efficient Capital Market. Efficient capital market is a market where the share prices reflect new information accurately and in real time. Capital market efficiency is judged by its success in incorporating and inducting information, generally about the basic value of securities, into the price of securities. Definitions from Investopedia

45 The efficiency of a financial market can be judged from the following:- 1. Proper Valuation This requires that the market price of a financial security must equal its intrinsic value, which is the present value of its future stream of cash flows from investment made in it. PV/(1+r) t 2. Operationally Efficient This means a) minimisation of administrative and transaction costs b) providing maximum convenience to lenders and borrowers while transmitting resources, c) providing a fair return to financial intermediaries for these services 3. Allocationally Efficient For this a0 It should channel its financial resources into such investment projects and uses where, the marginal efficiency of capital after adjusting for risk differences is the highest 4. Insurance against Risk- A market to be efficient must hedge and reduce risks such as possible future contingencies. 5. Information Arbitrage If a person gains much on the basis of commonly available information the financial market is not efficient. It is only under perfect competition that a market is efficient.

46 Classification or Types of Efficient Markets- 3 types Weak Form of Efficient Market- In this market, the best forecasting of a bond price of the next period is the price of the current period. Any past information on bond price cannot improve its forecasting. It is very difficult to forecast returns to bonds on the basis of past data on bond prices Semi-strong Form of Efficient Market the current of bonds does better forecasting of future prices. However any available information of will not be helpful in forecasting of future prices or returns to bonds or assets. Such information consists of past prices of assets, rates of interest, profit, etc. But a broker of any stock may earn profit in future by selling or purchasing bonds on the basis of internal information of the company. Strong Form of Efficient market In this, any available current information cannot improve forecasting of future values of the asset by using the recently known values of that asset price. Any available information may not be helpful in forecasting stock price movements. In reality, the strong form of efficient market is not possible because nobody can forecast future stock prices according to internal information.

47

48

49 Implications of market efficiency An immediate and direct implication of an efficient market is that no group of investors should be able to consistently beat the market using a common investment strategy An efficient market would also carry very negative implications for many (at least three) investment strategies and actions that are taken for granted:- (a) In an efficient market, equity research and valuation would be a costly task that provided no benefits. The odds of finding an undervalued stock should be random (50/50). At best, the benefits from information collection and equity research would cover the costs of doing the research.

50 Implications of Market Efficiency (b) In an efficient market, a strategy of randomly diversifying across stocks or indexing to the market, carrying little or no information cost and minimal execution costs, would be superior to any other strategy, that created larger information and execution costs. There would be no value added by portfolio managers and investment strategists. (c) In an efficient market, a strategy of minimizing trading, i.e., creating a portfolio and not trading unless cash was needed, would be superior to a strategy that required frequent trading.

51 What market efficiency does not imply: An efficient market does not imply that - (a) stock prices cannot deviate from true value; in fact, there can be large deviations from true value. The only requirement is that the deviations be random. (b) no investor will 'beat' the market in any time period. To the contrary, approximately half of all investors, prior to transactions costs, should beat the market in any period.

52 What market efficiency does not imply: (c) No group of investors will beat the market in the long term. Given the number of investors in financial markets, the laws of probability would suggest that a fairly large number are going to beat the market consistently over long periods, not because of their investment strategies but because they are lucky. It would not, however, be consistent if a disproportionately large number of these investors used the same investment strategy. In an efficient market, the expected returns from any investment will be consistent with the risk of that investment over the long term, though there may be deviations from these expected returns in the short term.

53 Necessary conditions for market efficiency Markets do not become efficient automatically. It is the actions of investors, sensing bargains and putting into effect schemes to beat the market, that make markets efficient. The necessary conditions for a market inefficiency to be eliminated are as follows - (1) The market inefficiency should provide the basis for a scheme to beat the market and earn excess returns. For this to hold true - (a) The asset (or assets) which is the source of the inefficiency has to be traded. (b) The transactions costs of executing the scheme have to be smaller than the expected profits from the scheme. (2) There should be profit maximizing investors who (a) Recognize the 'potential for excess return' (b) Can replicate the beat the market scheme that earns the excess return (c) Have the resources to trade on the stock until the inefficiency disappears

54 Efficient Markets and Profit-seeking investors: The Internal Contradiction There is an internal contradiction in claiming that there is no possibility of beating the market in an efficient market and then requiring profit-maximizing investors to constantly seek out ways of beating the market and thus making it efficient. If markets were, in fact, efficient, investors would stop looking for inefficiencies, which would lead to markets becoming inefficient again. It makes sense to think about an efficient market as a self-correcting mechanism, where inefficiencies appear at regular intervals but disappear almost instantaneously as investors find them and trade on them.

55 Propositions about market efficiency Proposition 1: The probability of finding inefficiencies in an asset market decreases as the ease of trading on the asset increases. To the extent that investors have difficulty trading on a stock, either because open markets do not exist or there are significant barriers to trading, inefficiencies in pricing can continue for long periods. Example: Stocks versus real estate NYSE vs NASDAQ (a Secondary market)

56 Proposition 2 The probability of finding an inefficiency in an asset market increases as the transactions and information cost of exploiting the inefficiency increases. The cost of collecting information and trading varies widely across markets and even across investments in the same markets. As these costs increase, it pays less and less to try to exploit these inefficiencies.

57 Proposition 2 - example Initial Public Offerings: IPOs supposedly make excess returns, on average. Investing in 'loser' stocks, i.e., stocks that have done very badly in some prior time period should yields excess returns. Transactions costs are likely to be much higher for these stocks since- (a) They then have to be low priced stocks, leading to higher brokerage commissions and expenses (b) The bid-ask becomes a much higher fraction of the total price paid. (c) Trading is often thin on these stocks, and small trades can cause prices to move. [The ask price is what sellers are willing to take for it. If you are selling a stock, you are going to get the bid price, if you are buying a stock you are going to get the ask price. The difference (or "spread") goes to the broker/specialist that handles the transaction.]

58 Corollary 1: Investors who can establish a cost advantage (either in information collection or transactions costs) will be more able to exploit small inefficiencies than other investors who do not possess this advantage. Example: Block trades effect on stock prices & specialists on the Floor of the Exchange Establishing a cost advantage, especially in relation to information, may be able to generate excess returns on the basis of these advantages. Thus a John Templeton, who started investing in Japanese and other Asian markets well before other portfolio managers, might have been able to exploit the informational advantages he had over his peers to make excess returns on his portfolio.

59 Proposition 3: The speed with which an inefficiency is resolved will be directly related to how easily the scheme to exploit the inefficiency can be replicated by other investors. The ease with which a scheme can be replicated itself is inversely related to the time, resources and information needed to execute it. Since very few investors single-handedly possess the resources to eliminate an inefficiency through trading, it is much more likely that an inefficiency will disappear quickly if the scheme used to exploit the inefficiency is transparent and can be copied by other investors.

60

61

62

63

64

65

66

67

68

69

70 D 0 = dividend today g = annual dividend growth rate P n = future resale price in year n P = price today i = discount rate

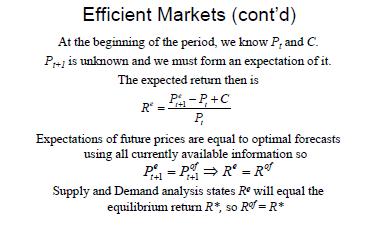

71 value of a stock today n n n n i P i g D i g D i g D P ) (1 ) (1 ) (1... ) (1 ) (1 ) (1 ) 1 (

72 but we do not know the future P. assume stock is held indefinitely, just paying dividends.

73 Dividend-discount model P i D 0 g

74 interest rate = risk free rate + risk premium i = rf + rp then P rf D 0 rp g

75 P rf D 0 rp g higher risk free rate, lower stock price higher risk premium, lower stock price higher dividends, higher stock price higher dividend growth, higher stock price

76 example D = $2, g = 2%, rf = 3%, rp = 5% P= $2/( ) P = $2/.06 = $33.33

77 what if risk premium rises to 7%? P = $2/( ) = $2/.08 = $12.50 what if risk premium falls to 3%? P = $2/( ) = $2/.04 = $50 Dividend discount model shows us why stock prices are volatile

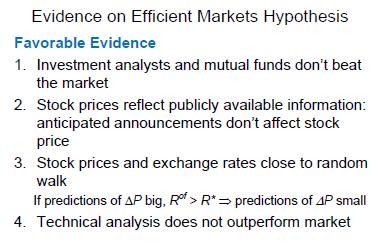

78 Theory of Efficient Markets efficient market hypothesis (EMH) asset prices (stock prices) reflect all available information markets adjust immediately to new information prices incorporate expectations about future

79 example XYZ stock, $25 value of $25 based on --past prices, profits, trading, --forecasts about future profits, market share --relevant economic conditions litigation litigation,

80 not ALL buyers and sellers must act rationally for markets to be efficient just most of them

81 implications IF stock market is efficient, THEN stock prices already reflect all relevant, available information SO, using the same info to predict future prices will not work

82 if future stock prices were predictable Expect price to rise tomorrow, Then you buy it today, Price rises TODAY Stock price today reflects our expectations about future price movements Stock prices are close to a random walk

83 Are markets efficient? a lot of research on efficiency of U.S. stock market to test efficiency, must understand implications of efficiency

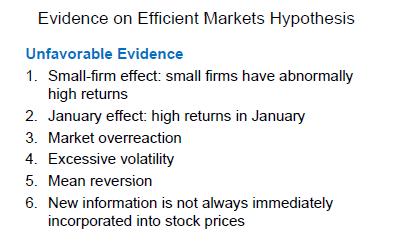

84 it should be almost impossible to beat the market (to earn above-average stock market returns over time) Is this true? -- most evidence says yes -- some evidence suggests that some price inefficiencies do exist

85 Evidence for efficiency do professionally managed mutual funds beat the market? no, on average

86 S&P 500 outperformed 72% of all actively managed large-cap funds in the past 5 years funds that do well in one year do not do well in subsequent year , Wilshire 5000 outperformed 67% of equity funds

87 so if professionals have difficulty earning superior returns then prices likely reflect public information

88 Technical analysis Chartists using past price patterns to predict future price patterns no evidence this technique beats the market

89 Fundamental Analysis Use available data to determine proper value of stock Which may or may not match price Again, we see no evidence that this earns aboveaverage return in the long run

90 WSJ Dartboard contest Over 6-month period 4 professionals pick 1 stock each 4 dartboard stocks Price appreciation of each portfolio Dartboard won about 40% of the time Even the deck stacked in favor of professionals

91 Evidence against efficient markets certain return patterns out there anomalies should not exist if markets are fully efficient

92 small-firm effect risk-adjusted returns of smaller firms higher over time Risk measure? Survivorship bias effect has become smaller over time

93 January effect stocks post larger returns in January (December sell-offs for taxes) should disappear as tax-exempt pension funds attempt to profit, but still exists (but smaller)

94 P/E effect Stocks with low P/E do better over time Not consistent over time Price-to-book value Value investing (Buffet) Not consistent, survivorship

95 Dogs of the Dow Portfolio of 10 DJIA stocks with highest dividend yield (D/P) Once strategy became widespread, it no longer worked.

96 other effects day-of-the-week weather most anomalies are too small to allow a profit after trading costs

97 stock price over-reaction prices fall/rise too much with bad/good news A contrarian strategy might produce superior returns excess volatility stock prices fluctuate more than their fundamentals

98 Bubbles Large gaps between actual asset price and fundamental value Internet stock bubble of late 1990s Housing bubble? Eventually the bubble bursts!

99 weight of evidence so efficiency is not perfect, but earning above-average returns is very difficult

100 Implications of efficiency evidence very difficult for average person to beat the market trying to do so generates trading costs the alternative buy-and-hold diversified portfolio indexing

101 conclusion stock market price behavior combines fundamentals investor psychology markets are not perfectly efficient field of behavioral economics, finance

102 NOTE WELL Questions: Explain the working of the financial market. What do you understand by the efficiency of financial market? Explain the functions of a financial market, Discuss the role of financial markets in the economic development of a country such as Ghana Explain the concept of efficiency of financial markets. What are the various levels of an efficient market? Explain the criteria for judging the efficiency of a financial market Define Money Market and explain its functions Distinguish between Money and Capital Markets and show how they are interrelated Explain the function of financial intermediaries. Discuss their role in a developing country such as Ghana

103 Explain: Equity or common company Stock; mortgage; corporate bond; government treasury bill; government treasury note; government bond; euro bond; Repurchase Agreements (repos); Commercial Paper; Certificates of Deposit; Derivative; Banker s Acceptances Read Mishkin on Models of Asset Pricing (Appendix 1 to Chapter 5 in 7 th edition)

104 What are NBFIs? How do they differ from banks? Explain the functions of NBFIs. What are : Mutual Funds; Finance Companies; Savings and Loans Companies; Credit Unions; Insurance Companies. State the functions of : Bank of Ghana; National Insurance Commission; and Securities and Exchange Commission.

Economics of Money, Banking, and Fin. Markets, 10e

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 7 The Stock Market, the Theory of Rational Expectations, and the Efficient Market Hypothesis 7.1 Computing the Price of Common Stock

Economics of Money, Banking, and Fin. Markets, 10e (Mishkin) Chapter 7 The Stock Market, the Theory of Rational Expectations, and the Efficient Market Hypothesis 7.1 Computing the Price of Common Stock

Types of Stocks. Stock. Common stock. Preferred stock. An equity or an ownership stake in a firm.

Stock Markets Types of Stocks Stock An equity or an ownership stake in a firm. Common stock Common stockholders have the right to vote. Common stockholders receive dividends. Preferred stock Are a hybrid

Stock Markets Types of Stocks Stock An equity or an ownership stake in a firm. Common stock Common stockholders have the right to vote. Common stockholders receive dividends. Preferred stock Are a hybrid

Chapter 7 The Stock Market, the Theory of Rational Expectations, and the Efficient Markets Hypothesis

Chapter 7 The Stock Market, the Theory of Rational Expectations, and the Efficient Markets Hypothesis Multiple Choice 1) Stockholders rights include (a) the right to vote. (b) the right to manage. (c)

Chapter 7 The Stock Market, the Theory of Rational Expectations, and the Efficient Markets Hypothesis Multiple Choice 1) Stockholders rights include (a) the right to vote. (b) the right to manage. (c)

In this model, the value of the stock today is the present value of the expected cash flows (equal to one dividend payment plus a final sales price).

.") Money & Banking Notes Chapter 7 Stock Mkt., Rational Expectations, and Efficient Mkt. Hypothesis Computing the price of common stock: (i) Stockholders (those who hold or own stocks in a corporation) are

Money & Banking Notes Chapter 7 Stock Mkt., Rational Expectations, and Efficient Mkt. Hypothesis Computing the price of common stock: (i) Stockholders (those who hold or own stocks in a corporation) are

Expectations are very important in our financial system.

Chapter 6 Are Financial Markets Efficient? Chapter Preview Expectations are very important in our financial system. Expectations of returns, risk, and liquidity impact asset demand Inflationary expectations

Chapter 6 Are Financial Markets Efficient? Chapter Preview Expectations are very important in our financial system. Expectations of returns, risk, and liquidity impact asset demand Inflationary expectations

CHAPTER 6. Are Financial Markets Efficient? Copyright 2012 Pearson Prentice Hall. All rights reserved.

CHAPTER 6 Are Financial Markets Efficient? Copyright 2012 Pearson Prentice Hall. All rights reserved. Chapter Preview Expectations are very important in our financial system. Expectations of returns, risk,

CHAPTER 6 Are Financial Markets Efficient? Copyright 2012 Pearson Prentice Hall. All rights reserved. Chapter Preview Expectations are very important in our financial system. Expectations of returns, risk,

MBF2253 Modern Security Analysis

MBF2253 Modern Security Analysis Prepared by Dr Khairul Anuar L8: Efficient Capital Market www.notes638.wordpress.com Capital Market Efficiency Capital market history suggests that the market values of

MBF2253 Modern Security Analysis Prepared by Dr Khairul Anuar L8: Efficient Capital Market www.notes638.wordpress.com Capital Market Efficiency Capital market history suggests that the market values of

AFM 371 Winter 2008 Chapter 14 - Efficient Capital Markets

AFM 371 Winter 2008 Chapter 14 - Efficient Capital Markets 1 / 24 Outline Background What Is Market Efficiency? Different Levels Of Efficiency Empirical Evidence Implications Of Market Efficiency For Corporate

AFM 371 Winter 2008 Chapter 14 - Efficient Capital Markets 1 / 24 Outline Background What Is Market Efficiency? Different Levels Of Efficiency Empirical Evidence Implications Of Market Efficiency For Corporate

Monetary Economics Efficient Markets and Alternatives. Gerald P. Dwyer Fall 2015

Monetary Economics Efficient Markets and Alternatives Gerald P. Dwyer Fall 2015 Readings This lecture, Malkiel Part 3 Next lecture, Cuthbertson, Chapter 6 Behavioral Finance Behavioral finance is not a

Monetary Economics Efficient Markets and Alternatives Gerald P. Dwyer Fall 2015 Readings This lecture, Malkiel Part 3 Next lecture, Cuthbertson, Chapter 6 Behavioral Finance Behavioral finance is not a

Market Efficiency: Laying the groundwork

Market Efficiency: Laying the groundwork Why market efficiency ma8ers.. The ques=on of whether markets are efficient, and if not, where the inefficiencies lie, is central to investment valua=on. If markets

Market Efficiency: Laying the groundwork Why market efficiency ma8ers.. The ques=on of whether markets are efficient, and if not, where the inefficiencies lie, is central to investment valua=on. If markets

The Efficient Market Hypothesis

Efficient Market Hypothesis (EMH) 11-2 The Efficient Market Hypothesis Maurice Kendall (1953) found no predictable pattern in stock prices. Prices are as likely to go up as to go down on any particular

Efficient Market Hypothesis (EMH) 11-2 The Efficient Market Hypothesis Maurice Kendall (1953) found no predictable pattern in stock prices. Prices are as likely to go up as to go down on any particular

Introduction to Equity Valuation

Introduction to Equity Valuation FINANCE 352 INVESTMENTS Professor Alon Brav Fuqua School of Business Duke University Alon Brav 2004 Finance 352, Equity Valuation 1 1 Overview Stocks and stock markets

Introduction to Equity Valuation FINANCE 352 INVESTMENTS Professor Alon Brav Fuqua School of Business Duke University Alon Brav 2004 Finance 352, Equity Valuation 1 1 Overview Stocks and stock markets

Efficient Capital Markets

Efficient Capital Markets Why Should Capital Markets Be Efficient? Alternative Efficient Market Hypotheses Tests and Results of the Hypotheses Behavioural Finance Implications of Efficient Capital Markets

Efficient Capital Markets Why Should Capital Markets Be Efficient? Alternative Efficient Market Hypotheses Tests and Results of the Hypotheses Behavioural Finance Implications of Efficient Capital Markets

Chapter 13. Efficient Capital Markets and Behavioral Challenges

Chapter 13 Efficient Capital Markets and Behavioral Challenges Articulate the importance of capital market efficiency Define the three forms of efficiency Know the empirical tests of market efficiency

Chapter 13 Efficient Capital Markets and Behavioral Challenges Articulate the importance of capital market efficiency Define the three forms of efficiency Know the empirical tests of market efficiency

Financial Markets I The Stock, Bond, and Money Markets Every economy must solve the basic problems of production and distribution of goods and

Financial Markets I The Stock, Bond, and Money Markets Every economy must solve the basic problems of production and distribution of goods and services. Financial markets perform an important function

Financial Markets I The Stock, Bond, and Money Markets Every economy must solve the basic problems of production and distribution of goods and services. Financial markets perform an important function

Market efficiency, questions 1 to 10

Market efficiency, questions 1 to 10 1. Is it possible to forecast future prices on an efficient market? 2. Many financial analysts try to predict future prices. Does it imply that markets are inefficient?

Market efficiency, questions 1 to 10 1. Is it possible to forecast future prices on an efficient market? 2. Many financial analysts try to predict future prices. Does it imply that markets are inefficient?

Basic Tools of Finance (Chapter 27 in Mankiw & Taylor)

") Basic Tools of Finance (Chapter 27 in Mankiw & Taylor) We have seen that the financial system coordinates saving and investment These are decisions made today that affect us in the future But the future

Basic Tools of Finance (Chapter 27 in Mankiw & Taylor) We have seen that the financial system coordinates saving and investment These are decisions made today that affect us in the future But the future

CHAPTER 17 INVESTMENT MANAGEMENT. by Alistair Byrne, PhD, CFA

CHAPTER 17 INVESTMENT MANAGEMENT by Alistair Byrne, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Describe systematic risk and specific risk; b Describe

CHAPTER 17 INVESTMENT MANAGEMENT by Alistair Byrne, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Describe systematic risk and specific risk; b Describe

A Scholar s Introduction to Stocks, Bonds and Derivatives

A Scholar s Introduction to Stocks, Bonds and Derivatives Martin V. Day June 8, 2004 1 Introduction This course concerns mathematical models of some basic financial assets: stocks, bonds and derivative

A Scholar s Introduction to Stocks, Bonds and Derivatives Martin V. Day June 8, 2004 1 Introduction This course concerns mathematical models of some basic financial assets: stocks, bonds and derivative

The Stock Market, the Theory of Rational Expectations and the Effi cient Market Hypothesis

The Stock Market, the Theory of Rational Expectations and the Effi cient Market Hypothesis Money and Banking Cesar E. Tamayo Department of Economics, Rutgers University July 25, 2011 C.E. Tamayo () Econ

The Stock Market, the Theory of Rational Expectations and the Effi cient Market Hypothesis Money and Banking Cesar E. Tamayo Department of Economics, Rutgers University July 25, 2011 C.E. Tamayo () Econ

Chapter 9. Technical Analysis & Market Efficiency. Technical Analysis. Market Volume Kaplan Financial. Market volume 9-1

Chapter 9 Technical Analysis & Market Efficiency Technical Analysis study of forces at work in the market & their effect on stock prices Implies that price patterns or internal market factors reveal the

Chapter 9 Technical Analysis & Market Efficiency Technical Analysis study of forces at work in the market & their effect on stock prices Implies that price patterns or internal market factors reveal the

CHAPTER 6: ANSWERS TO CONCEPTS IN REVIEW

CHAPTER 6: ANSWERS TO CONCEPTS IN REVIEW 6.1 A common stock is an equity investment that represents ownership in a corporate form of business. Each share represents a fractional ownership interest in the

CHAPTER 6: ANSWERS TO CONCEPTS IN REVIEW 6.1 A common stock is an equity investment that represents ownership in a corporate form of business. Each share represents a fractional ownership interest in the

11th-edition-jeff-madura-test-bank/

Financial Markets And Institutions 11th Edition Madura Test Bank Solutions Completed download Financial Markets And Institutions 11th Edition Jeff Madura Test Bank. Solutions Manual download link is included:

Financial Markets And Institutions 11th Edition Madura Test Bank Solutions Completed download Financial Markets And Institutions 11th Edition Jeff Madura Test Bank. Solutions Manual download link is included:

A Random Walk Down Wall Street

FIN 614 Capital Market Efficiency Professor Robert B.H. Hauswald Kogod School of Business, AU A Random Walk Down Wall Street From theory of return behavior to its practice Capital market efficiency: the

FIN 614 Capital Market Efficiency Professor Robert B.H. Hauswald Kogod School of Business, AU A Random Walk Down Wall Street From theory of return behavior to its practice Capital market efficiency: the

Chapter 6 Investment Analysis and Portfolio Management

Chapter 6 Investment Analysis and Portfolio Management Frank K. Reilly & Keith C. Brown Part 2: INVESTMENT THEORY 6 Pasar Efisien 7 Mnj Portofolio Konsep RETURN, RISIKO, Investasi 9 Model Ret, Risiko 8

Chapter 6 Investment Analysis and Portfolio Management Frank K. Reilly & Keith C. Brown Part 2: INVESTMENT THEORY 6 Pasar Efisien 7 Mnj Portofolio Konsep RETURN, RISIKO, Investasi 9 Model Ret, Risiko 8

Stock Market Basics. Capital Market A market for intermediate or long-term debt or corporate stocks.

Stock Market Basics Capital Market A market for intermediate or long-term debt or corporate stocks. Stock Market and Stock Exchange A stock exchange is the most important component of a stock market. It

Stock Market Basics Capital Market A market for intermediate or long-term debt or corporate stocks. Stock Market and Stock Exchange A stock exchange is the most important component of a stock market. It

CHAPTER 12: MARKET EFFICIENCY AND BEHAVIORAL FINANCE

CHAPTER 12: MARKET EFFICIENCY AND BEHAVIORAL FINANCE 1. The correlation coefficient between stock returns for two non-overlapping periods should be zero. If not, one could use returns from one period to

CHAPTER 12: MARKET EFFICIENCY AND BEHAVIORAL FINANCE 1. The correlation coefficient between stock returns for two non-overlapping periods should be zero. If not, one could use returns from one period to

9 Questions Every ETF Investor Should Ask Before Investing

9 Questions Every ETF Investor Should Ask Before Investing 1. What is an ETF? An exchange-traded fund (ETF) is a pooled investment vehicle with shares that can be bought or sold throughout the day on a

9 Questions Every ETF Investor Should Ask Before Investing 1. What is an ETF? An exchange-traded fund (ETF) is a pooled investment vehicle with shares that can be bought or sold throughout the day on a

CHAPTER 13 EFFICIENT CAPITAL MARKETS AND BEHAVIORAL CHALLENGES

CHAPTER 13 EFFICIENT CAPITAL MARKETS AND BEHAVIORAL CHALLENGES Answers to Concept Questions 1. To create value, firms should accept financing proposals with positive net present values. Firms can create

CHAPTER 13 EFFICIENT CAPITAL MARKETS AND BEHAVIORAL CHALLENGES Answers to Concept Questions 1. To create value, firms should accept financing proposals with positive net present values. Firms can create

Portfolio management strategies:

Portfolio management strategies: Portfolio Management Strategies refer to the approaches that are applied for the efficient portfolio management in order to generate the highest possible returns at lowest

Portfolio management strategies: Portfolio Management Strategies refer to the approaches that are applied for the efficient portfolio management in order to generate the highest possible returns at lowest

1. Primary markets are markets in which users of funds raise cash by selling securities to funds' suppliers.

Test Bank Financial Markets and Institutions 6th Edition Saunders Complete download Financial Markets and Institutions 6th Edition TEST BANK by Saunders, Cornett: https://testbankarea.com/download/financial-markets-institutions-6th-editiontest-bank-saunders-cornett/

Test Bank Financial Markets and Institutions 6th Edition Saunders Complete download Financial Markets and Institutions 6th Edition TEST BANK by Saunders, Cornett: https://testbankarea.com/download/financial-markets-institutions-6th-editiontest-bank-saunders-cornett/

Efficient Market Hypothesis & Behavioral Finance

Efficient Market Hypothesis & Behavioral Finance Supervision: Ing. Luděk Benada Prepared by: Danial Hasan 1 P a g e Contents: 1. Introduction 2. Efficient Market Hypothesis (EMH) 3. Versions of the EMH

Efficient Market Hypothesis & Behavioral Finance Supervision: Ing. Luděk Benada Prepared by: Danial Hasan 1 P a g e Contents: 1. Introduction 2. Efficient Market Hypothesis (EMH) 3. Versions of the EMH

The Federal Reserve System and Open Market Operations

Chapter 15 MODERN PRINCIPLES OF ECONOMICS Third Edition The Federal Reserve System and Open Market Operations Outline What Is the Federal Reserve System? The U.S. Money Supplies Fractional Reserve Banking,

Chapter 15 MODERN PRINCIPLES OF ECONOMICS Third Edition The Federal Reserve System and Open Market Operations Outline What Is the Federal Reserve System? The U.S. Money Supplies Fractional Reserve Banking,

Institutional Finance Financial Crises, Risk Management and Liquidity

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Delwin Olivan Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Delwin Olivan Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

Kingdom of Saudi Arabia Capital Market Authority. Investment

Kingdom of Saudi Arabia Capital Market Authority Investment The Definition of Investment Investment is defined as the commitment of current financial resources in order to achieve higher gains in the

Kingdom of Saudi Arabia Capital Market Authority Investment The Definition of Investment Investment is defined as the commitment of current financial resources in order to achieve higher gains in the

BOND & STOCK VALUATION

Chapter 7 BOND & STOCK VALUATION Bond & Stock Valuation 7-2 1. OBJECTIVE # Use PV to calculate what prices of stocks and bonds should be! Basic bond terminology and valuation! Stock and preferred stock

Chapter 7 BOND & STOCK VALUATION Bond & Stock Valuation 7-2 1. OBJECTIVE # Use PV to calculate what prices of stocks and bonds should be! Basic bond terminology and valuation! Stock and preferred stock

Institutional Finance Financial Crises, Risk Management and Liquidity

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

Institutional Finance Financial Crises, Risk Management and Liquidity Markus K. Brunnermeier Preceptor: Dong Beom Choi Princeton University 1 Overview Efficiency concepts EMH implies Martingale Property

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L7: The Stock Market www. notes638.wordpress.com 7-1 Chapter Preview In August of 2004, Google went public, auctioning its shares

BBM2153 Financial Markets and Institutions Prepared by Dr Khairul Anuar L7: The Stock Market www. notes638.wordpress.com 7-1 Chapter Preview In August of 2004, Google went public, auctioning its shares

On the 'Lock-In' Effects of Capital Gains Taxation

May 1, 1997 On the 'Lock-In' Effects of Capital Gains Taxation Yoshitsugu Kanemoto 1 Faculty of Economics, University of Tokyo 7-3-1 Hongo, Bunkyo-ku, Tokyo 113 Japan Abstract The most important drawback

May 1, 1997 On the 'Lock-In' Effects of Capital Gains Taxation Yoshitsugu Kanemoto 1 Faculty of Economics, University of Tokyo 7-3-1 Hongo, Bunkyo-ku, Tokyo 113 Japan Abstract The most important drawback

PAPER No.14 : Security Analysis and Portfolio Management MODULE No.24 : Efficient market hypothesis: Weak, semi strong and strong market)

") Subject Paper No and Title Module No and Title Module Tag 14. Security Analysis and Portfolio M24 Efficient market hypothesis: Weak, semi strong and strong market COM_P14_M24 TABLE OF CONTENTS After going

Subject Paper No and Title Module No and Title Module Tag 14. Security Analysis and Portfolio M24 Efficient market hypothesis: Weak, semi strong and strong market COM_P14_M24 TABLE OF CONTENTS After going

FNCE 5610, Personal Finance H Guy Williams, 2009

CH 12: Introduction to Investment Concepts Introduction to Investing Investing is based on the concept that forgoing immediate consumption results in greater future consumption (through compound interest

CH 12: Introduction to Investment Concepts Introduction to Investing Investing is based on the concept that forgoing immediate consumption results in greater future consumption (through compound interest

10. Dealers: Liquid Security Markets

10. Dealers: Liquid Security Markets I said last time that the focus of the next section of the course will be on how different financial institutions make liquid markets that resolve the differences between

10. Dealers: Liquid Security Markets I said last time that the focus of the next section of the course will be on how different financial institutions make liquid markets that resolve the differences between

Personal Finance Unit 3 Chapter Glencoe/McGraw-Hill

Chapter 9 Stocks What You ll Learn Section 9.1 Explain the reasons for investing in common stock. Explain the reasons for investing in preferred stock. Section 9.2 Identify the types of stock investments.

Chapter 9 Stocks What You ll Learn Section 9.1 Explain the reasons for investing in common stock. Explain the reasons for investing in preferred stock. Section 9.2 Identify the types of stock investments.

Capital Budgeting and Business Valuation

Capital Budgeting and Business Valuation Capital budgeting and business valuation concern two subjects near and dear to financial peoples hearts: What should we do with the firm s money and how much is

Capital Budgeting and Business Valuation Capital budgeting and business valuation concern two subjects near and dear to financial peoples hearts: What should we do with the firm s money and how much is

STOCK VALUATION Chapter 8

STOCK VALUATION Chapter 8 OUTLINE 1. Common & Preferred Stock A. Rights B. The Annual Meeting & Voting C. Dividends 2. Stock Valuation A. Zero Growth Dividends B. Constant Growth Dividends C. Non-constant

STOCK VALUATION Chapter 8 OUTLINE 1. Common & Preferred Stock A. Rights B. The Annual Meeting & Voting C. Dividends 2. Stock Valuation A. Zero Growth Dividends B. Constant Growth Dividends C. Non-constant

Equity Portfolio Management Strategies

Equity Portfolio Management Strategies An Overview Passive Equity Portfolio Management Strategies Active Equity Portfolio Management Strategies Investment Styles Asset Allocation Strategies 2 An Overview

Equity Portfolio Management Strategies An Overview Passive Equity Portfolio Management Strategies Active Equity Portfolio Management Strategies Investment Styles Asset Allocation Strategies 2 An Overview

Money and Banking ECON3303. Lecture 7: The Stock Market, Rational Expectations, and the Efficient Market Hypothesis. William J. Crowder Ph.D.

Money and Banking ECON3303 Lecture 7: The Stock Market, Rational Expectations, and the Efficient Market Hypothesis William J. Crowder h.d. Computing the rice of Common Stock The One-eriod Valuation Model:

Money and Banking ECON3303 Lecture 7: The Stock Market, Rational Expectations, and the Efficient Market Hypothesis William J. Crowder h.d. Computing the rice of Common Stock The One-eriod Valuation Model:

Financial Markets and Institutions Midterm study guide Jon Faust Spring 2014

180.266 Financial Markets and Institutions Midterm study guide Jon Faust Spring 2014 The exam will have some questions involving definitions and some involving basic real world quantities. These will be

180.266 Financial Markets and Institutions Midterm study guide Jon Faust Spring 2014 The exam will have some questions involving definitions and some involving basic real world quantities. These will be

Replies to one minute memos, 9/21/03

Replies to one minute memos, 9/21/03 Dear Students, Thank you for asking these great questions. The answer to my question (what is the difference b/n the covered & uncovered interest rate arbitrage? If

Replies to one minute memos, 9/21/03 Dear Students, Thank you for asking these great questions. The answer to my question (what is the difference b/n the covered & uncovered interest rate arbitrage? If

What is an efficient market? What does it imply for investment and valuation

ch06_p111_153.qxp 12/2/11 2:07 PM Page 111 CHAPTER 6 Market Efficiency Definition, Tests, and Evidence What is an efficient market? What does it imply for investment and valuation models? Clearly, market

ch06_p111_153.qxp 12/2/11 2:07 PM Page 111 CHAPTER 6 Market Efficiency Definition, Tests, and Evidence What is an efficient market? What does it imply for investment and valuation models? Clearly, market

Lower prices. Lower costs, esp. wages. Higher productivity. Higher quality/more desirable exports. Greater natural resources. Higher interest rates

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

1 Goods market Reason to Hold Currency To acquire goods and services from that country Important in... Long run (years to decades) Currency Will Appreciate If... Lower prices Lower costs, esp. wages Higher

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

EQUITY RESEARCH AND PORTFOLIO MANAGEMENT By P K AGARWAL IIFT, NEW DELHI 1 MARKOWITZ APPROACH Requires huge number of estimates to fill the covariance matrix (N(N+3))/2 Eg: For a 2 security case: Require

Chapter 10. Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics. Chapter Preview

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

Swap Markets CHAPTER OBJECTIVES. The specific objectives of this chapter are to: describe the types of interest rate swaps that are available,

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

15 Swap Markets CHAPTER OBJECTIVES The specific objectives of this chapter are to: describe the types of interest rate swaps that are available, explain the risks of interest rate swaps, identify other

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM To "finance" something means to pay for it. Since money (or credit) is the means of payment, "financial" basically means "pertaining to money or credit." Financial

Ch. 2 AN OVERVIEW OF THE FINANCIAL SYSTEM To "finance" something means to pay for it. Since money (or credit) is the means of payment, "financial" basically means "pertaining to money or credit." Financial

When to Sell AAII Silicon Valley Chapter Computerized Investing Group

When to Sell AAII Silicon Valley Chapter Computerized Investing Group February 21, 2006 Don Stewart Bob Smithson When to Sell The when to sell topic is of greater concern to most investors than when to

When to Sell AAII Silicon Valley Chapter Computerized Investing Group February 21, 2006 Don Stewart Bob Smithson When to Sell The when to sell topic is of greater concern to most investors than when to

Risk -The most important concept of investment

Investment vs. Saving How is investing different from saving? Investing means putting money to work to earn a rate of, while saving means put the money in a home safe, or a safe deposit box. Investments

Investment vs. Saving How is investing different from saving? Investing means putting money to work to earn a rate of, while saving means put the money in a home safe, or a safe deposit box. Investments

Business Cycles II: Theories

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

The Stock Market Mishkin Chapter 7:Part B (pp )

") The Stock Market Mishkin Chapter 7:Part B (pp. 152-165) Modified Notes from F. Mishkin (Bus. School Edition, 2 nd Ed 2010) L. Tesfatsion (Iowa State University) Last Revised: 1 March 2011 2004 Pearson

The Stock Market Mishkin Chapter 7:Part B (pp. 152-165) Modified Notes from F. Mishkin (Bus. School Edition, 2 nd Ed 2010) L. Tesfatsion (Iowa State University) Last Revised: 1 March 2011 2004 Pearson

CHAPTER 7 FOREIGN EXCHANGE MARKET EFFICIENCY

CHAPTER 7 FOREIGN EXCHANGE MARKET EFFICIENCY Chapter Overview This chapter has two major parts: the introduction to the principles of market efficiency and a review of the empirical evidence on efficiency

CHAPTER 7 FOREIGN EXCHANGE MARKET EFFICIENCY Chapter Overview This chapter has two major parts: the introduction to the principles of market efficiency and a review of the empirical evidence on efficiency

CHAPTER 3. How Securities are Traded INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 3 How Securities are Traded INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 3-2 How Securities

CHAPTER 3 How Securities are Traded INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 3-2 How Securities

Passive vs. Active Management in Singapore and Beyond

Passive vs. Active Management in Singapore and Beyond Why Exchange Traded Funds (ETFs) provide time-tested advantages over actively managed funds in Singapore and beyond. EXECUTIVE SUMMARY Passive management,

Passive vs. Active Management in Singapore and Beyond Why Exchange Traded Funds (ETFs) provide time-tested advantages over actively managed funds in Singapore and beyond. EXECUTIVE SUMMARY Passive management,

PowerPoint. to accompany. Chapter 9. Valuing Shares

PowerPoint to accompany Chapter 9 Valuing Shares 9.1 Share Basics Ordinary share: a share of ownership in the corporation, which gives its owner rights to vote on the election of directors, mergers or

PowerPoint to accompany Chapter 9 Valuing Shares 9.1 Share Basics Ordinary share: a share of ownership in the corporation, which gives its owner rights to vote on the election of directors, mergers or

Financial Investment

Financial Investment Dagmar Linnertová Dagmar.linnertova@mail.muni.cz Seminars Excercises in a seminars evaluated by lecturer Questions as a preparation for final test (2, 1 or 0 points) maximum points

Financial Investment Dagmar Linnertová Dagmar.linnertova@mail.muni.cz Seminars Excercises in a seminars evaluated by lecturer Questions as a preparation for final test (2, 1 or 0 points) maximum points

Saving, Investment, and the Financial System

7 Saving, Investment, and the Financial System The Financial System The financial system consists of the group of institutions in the economy that help to match one person s saving with another person

7 Saving, Investment, and the Financial System The Financial System The financial system consists of the group of institutions in the economy that help to match one person s saving with another person

The value of investments, and the income from them, may fall or rise and investors may get back less than they invested.

Active Exchange and Traded passive Funds investing (ETFs) What Understanding you need index to know ETFs and how they work This guide has been produced for educational purposes only and should not be regarded

Active Exchange and Traded passive Funds investing (ETFs) What Understanding you need index to know ETFs and how they work This guide has been produced for educational purposes only and should not be regarded

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 10 Raising Funds and Cost of Capital Concept Check 10.1 1. What are the three primary roles

Understanding Financial Management: A Practical Guide Guideline Answers to the Concept Check Questions Chapter 10 Raising Funds and Cost of Capital Concept Check 10.1 1. What are the three primary roles

Columbia Large Cap Growth ETF

Prospectus March 1, 2015 Columbia Large Cap Growth ETF Ticker Symbol RPX This prospectus provides important information about the Columbia Large Cap Growth ETF (the Fund), an exchangetraded fund (ETF)

Prospectus March 1, 2015 Columbia Large Cap Growth ETF Ticker Symbol RPX This prospectus provides important information about the Columbia Large Cap Growth ETF (the Fund), an exchangetraded fund (ETF)

Tactical Gold Allocation Within a Multi-Asset Portfolio

Tactical Gold Allocation Within a Multi-Asset Portfolio Charles Morris Head of Global Asset Management, HSBC Introduction Thank you, John, for that kind introduction. Ladies and gentlemen, my name is Charlie

Tactical Gold Allocation Within a Multi-Asset Portfolio Charles Morris Head of Global Asset Management, HSBC Introduction Thank you, John, for that kind introduction. Ladies and gentlemen, my name is Charlie

Investments 5: Stock Basics

Personal Finance: Another Perspective Investments 5: Stock Basics Updated 2017-07-07 1 Objectives A. Understand risk and return for stocks B. Understand stock terminology C. Understand how stocks are valued

Personal Finance: Another Perspective Investments 5: Stock Basics Updated 2017-07-07 1 Objectives A. Understand risk and return for stocks B. Understand stock terminology C. Understand how stocks are valued

2) Which NYSE member is typically an employee of a brokerage company such as Merrill Lynch?

Which NYSE member is typically an employee of a brokerage company such as Merrill Lynch?") Questions in Chapter 8 concept.qz 1) A is an owner of a seat on the New York Stock Exchange. [A] broker [B] dealer [C] member [D] floor trader [E] specialist [A] :This is an individual who arranges security

Questions in Chapter 8 concept.qz 1) A is an owner of a seat on the New York Stock Exchange. [A] broker [B] dealer [C] member [D] floor trader [E] specialist [A] :This is an individual who arranges security

Unit01. Introduction, Creation of Financial Assets, and Security Markets

FCS 5510 Concept Review Notes: Unit01. Introduction, Creation of Financial Assets, and Security Markets Chapter 01. Definition of investment Portfolio Primary and secondary markets Value and valuation

FCS 5510 Concept Review Notes: Unit01. Introduction, Creation of Financial Assets, and Security Markets Chapter 01. Definition of investment Portfolio Primary and secondary markets Value and valuation

MODERN PORTFOLIO THEORY AND INVESTMENT ANALYSIS 9 TH EDITION

Test Bank to accompany Modern Portfolio Theory and Investment Analysis, 9 th Edition MODERN PORTFOLIO THEORY AND INVESTMENT ANALYSIS 9 TH EDITION ELTON, GRUBER, BROWN, & GOETZMANN The following exam questions

Test Bank to accompany Modern Portfolio Theory and Investment Analysis, 9 th Edition MODERN PORTFOLIO THEORY AND INVESTMENT ANALYSIS 9 TH EDITION ELTON, GRUBER, BROWN, & GOETZMANN The following exam questions

Interest on Reserves, Interbank Lending, and Monetary Policy: Work in Progress

Interest on Reserves, Interbank Lending, and Monetary Policy: Work in Progress Stephen D. Williamson Federal Reserve Bank of St. Louis May 14, 015 1 Introduction When a central bank operates under a floor

Interest on Reserves, Interbank Lending, and Monetary Policy: Work in Progress Stephen D. Williamson Federal Reserve Bank of St. Louis May 14, 015 1 Introduction When a central bank operates under a floor

Dow Theory. Technical Analysis. Support and Resistance Levels. Dow Theory. Stock Price Behavior and Market Efficiency

One of the Funny Things about the Stock Market Stock Price Behavior and Market Chapter 8 One of the funny things about the stock market is that every time one man buys, another sells, and both think they

One of the Funny Things about the Stock Market Stock Price Behavior and Market Chapter 8 One of the funny things about the stock market is that every time one man buys, another sells, and both think they

Test Bank for Essentials of Investments 9th Edition Bodie, Kane, Marcus Complete downloadable file at:

Test Bank for Essentials of Investments 9th Edition Bodie, Kane, Marcus Complete downloadable file at: http://testbankcollection.com/download/essentials-of-investments-9thedition-by-bodie-test-bank/ Chapter

Test Bank for Essentials of Investments 9th Edition Bodie, Kane, Marcus Complete downloadable file at: http://testbankcollection.com/download/essentials-of-investments-9thedition-by-bodie-test-bank/ Chapter

Northern Trust Investments is proud to sponsor this podcast Investing in a World of

INVESTING IN A WORLD OF BUBBLES Northern Trust Investments is proud to sponsor this podcast Investing in a World of Bubbles. This podcast will be of particular interest to advisors looking to help temper

INVESTING IN A WORLD OF BUBBLES Northern Trust Investments is proud to sponsor this podcast Investing in a World of Bubbles. This podcast will be of particular interest to advisors looking to help temper

Guide to Risk and Investment - Novia

www.canaccord.com/uk Guide to Risk and Investment - Novia This document is important. Its purpose is to help with understanding investment in financial markets, the associated risks and the potential returns.

www.canaccord.com/uk Guide to Risk and Investment - Novia This document is important. Its purpose is to help with understanding investment in financial markets, the associated risks and the potential returns.

Chapter 9 Valuing Stocks

Chapter 9 Valuing Stocks Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 9.1 The Dividend Discount Model 9.2 Applying the Dividend Discount Model 9.3 Total Payout and Free Cash

Chapter 9 Valuing Stocks Copyright 2011 Pearson Prentice Hall. All rights reserved. Chapter Outline 9.1 The Dividend Discount Model 9.2 Applying the Dividend Discount Model 9.3 Total Payout and Free Cash

Growth and Value Investing: A Complementary Approach

Growth and Value Investing: A Complementary Approach March 14, 2018 by Stephen Dover, Norman Boersma of Franklin Templeton Investments Growth and value investing are often seen as competing styles, with

Growth and Value Investing: A Complementary Approach March 14, 2018 by Stephen Dover, Norman Boersma of Franklin Templeton Investments Growth and value investing are often seen as competing styles, with

Relationship Among a Firm Issuing Securities, the Underwriters and the Public

Investment Companies Relationship Among a Firm Issuing Securities, the Underwriters and the Public Four Phase of IPO The objectives of the chapter are to provide an understanding of: o o o o o o The market

Investment Companies Relationship Among a Firm Issuing Securities, the Underwriters and the Public Four Phase of IPO The objectives of the chapter are to provide an understanding of: o o o o o o The market

Columbia Select Large Cap Value ETF

Prospectus March 1, 2015 Columbia Select Large Cap Value ETF Ticker Symbol GVT This prospectus provides important information about the Columbia Select Large Cap Value ETF (the Fund), an exchange-traded

Prospectus March 1, 2015 Columbia Select Large Cap Value ETF Ticker Symbol GVT This prospectus provides important information about the Columbia Select Large Cap Value ETF (the Fund), an exchange-traded

The Total Cost of ETF Ownership An Important but Complex Calculation

PRACTICE MANAGEMENT INSIGHTS The Total Cost of ETF Ownership An Important but Complex Calculation Christopher Huemmer, CFA Senior Investment Strategist An investor should aim for a full understanding of

PRACTICE MANAGEMENT INSIGHTS The Total Cost of ETF Ownership An Important but Complex Calculation Christopher Huemmer, CFA Senior Investment Strategist An investor should aim for a full understanding of

Derivation of zero-beta CAPM: Efficient portfolios

Derivation of zero-beta CAPM: Efficient portfolios AssumptionsasCAPM,exceptR f does not exist. Argument which leads to Capital Market Line is invalid. (No straight line through R f, tilted up as far as

Derivation of zero-beta CAPM: Efficient portfolios AssumptionsasCAPM,exceptR f does not exist. Argument which leads to Capital Market Line is invalid. (No straight line through R f, tilted up as far as

Factor investing Focus:

Focus: adding value Factoring in the best approach a rose by any other name In association with: Quoniam Asset Management s Thomas Kieselstein explains to European Pensions how best to implement factor

Focus: adding value Factoring in the best approach a rose by any other name In association with: Quoniam Asset Management s Thomas Kieselstein explains to European Pensions how best to implement factor

THE EFFECT OF LIQUIDITY COSTS ON SECURITIES PRICES AND RETURNS

PART I THE EFFECT OF LIQUIDITY COSTS ON SECURITIES PRICES AND RETURNS Introduction and Overview We begin by considering the direct effects of trading costs on the values of financial assets. Investors

PART I THE EFFECT OF LIQUIDITY COSTS ON SECURITIES PRICES AND RETURNS Introduction and Overview We begin by considering the direct effects of trading costs on the values of financial assets. Investors

Unit 9: Money and Banking

Unit 9: Money and Banking Name: Date: / / Functions of Money The first and foremost role of money is that it acts as a medium of exchange. Barter exchanges become extremely difficult in a large economy

Unit 9: Money and Banking Name: Date: / / Functions of Money The first and foremost role of money is that it acts as a medium of exchange. Barter exchanges become extremely difficult in a large economy

Active vs. Passive Money Management

Synopsis Active vs. Passive Money Management April 8, 2016 by Baird s Asset Manager Research of Robert W. Baird Proponents of active and passive investment management styles have made exhaustive and valid

Synopsis Active vs. Passive Money Management April 8, 2016 by Baird s Asset Manager Research of Robert W. Baird Proponents of active and passive investment management styles have made exhaustive and valid

FNCE 317, Economic Markets H Guy Williams, 2006

EFFICIENT MARKETS Chapter Outline Description of Efficient Capital Markets Different Types of Efficiency The Evidence The Behavior Challenge to Market Efficiency Empirical Challenges to Market Efficiency

EFFICIENT MARKETS Chapter Outline Description of Efficient Capital Markets Different Types of Efficiency The Evidence The Behavior Challenge to Market Efficiency Empirical Challenges to Market Efficiency

Evaluating Performance

Evaluating Performance Evaluating Performance Choosing investments is just the beginning of your work as an investor. As time goes by, you ll need to monitor the performance of these investments to see

Evaluating Performance Evaluating Performance Choosing investments is just the beginning of your work as an investor. As time goes by, you ll need to monitor the performance of these investments to see

Chapter 2. Overview of the Financial System. Chapter Preview

Chapter 2 Overview of the Financial System Chapter Preview Suppose you want to start a business manufacturing a household cleaning robot, but you have no funds. At the same time, Walter has money he wishes

Chapter 2 Overview of the Financial System Chapter Preview Suppose you want to start a business manufacturing a household cleaning robot, but you have no funds. At the same time, Walter has money he wishes

Financial Markets Econ 173A: Mgt 183. Capital Markets & Securities

Financial Markets Econ 173A: Mgt 183 Capital Markets & Securities Financial Instruments Money Market Certificates of Deposit U.S. Treasury Bills Money Market Funds Equity Market Common Stock Preferred

Financial Markets Econ 173A: Mgt 183 Capital Markets & Securities Financial Instruments Money Market Certificates of Deposit U.S. Treasury Bills Money Market Funds Equity Market Common Stock Preferred

ECON 3303 Money and Banking Exam 3 Summer MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question.

ECON 3303 Money and Banking Exam 3 Summer 2016 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Sometimes one observes that the price of a

ECON 3303 Money and Banking Exam 3 Summer 2016 Name MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) Sometimes one observes that the price of a

Rents, Profits, and the Financial Environment of Business

21 Rents, Profits, and the Financial Environment of Business Learning Objectives After you have studied this chapter, you should be able to 1. define economic rent, firm, proprietorship, partnership, corporation,

21 Rents, Profits, and the Financial Environment of Business Learning Objectives After you have studied this chapter, you should be able to 1. define economic rent, firm, proprietorship, partnership, corporation,

Chapter 1 - Investments: Background and Issues

Chapter 1 - Investments: Background and Issues Investment vs. investments Real assets vs. financial assets Financial markets and the economy Investment process Competitive markets Players in investment

Chapter 1 - Investments: Background and Issues Investment vs. investments Real assets vs. financial assets Financial markets and the economy Investment process Competitive markets Players in investment

Christiano 362, Winter 2006 Lecture #3: More on Exchange Rates More on the idea that exchange rates move around a lot.

Christiano 362, Winter 2006 Lecture #3: More on Exchange Rates More on the idea that exchange rates move around a lot. 1.Theexampleattheendoflecture#2discussedalargemovementin the US-Japanese exchange

Christiano 362, Winter 2006 Lecture #3: More on Exchange Rates More on the idea that exchange rates move around a lot. 1.Theexampleattheendoflecture#2discussedalargemovementin the US-Japanese exchange

Stock Market Behavior - Investor Biases

Market Tips & Jargons Stock Market Behavior - Investor Biases Random Walk Theory Efficient Market Hypothesis Market Anomaly Investor s Behavioral Biases March 25, 2017 CBMC-RGTC Copyright 2014 Pearson

Market Tips & Jargons Stock Market Behavior - Investor Biases Random Walk Theory Efficient Market Hypothesis Market Anomaly Investor s Behavioral Biases March 25, 2017 CBMC-RGTC Copyright 2014 Pearson

Finance 527: Lecture 35, Psychology of Investing V2

Finance 527: Lecture 35, Psychology of Investing V2 [John Nofsinger]: Welcome to the second video for the psychology of investing. In this one, we re going to talk about overconfidence. Like this little

Finance 527: Lecture 35, Psychology of Investing V2 [John Nofsinger]: Welcome to the second video for the psychology of investing. In this one, we re going to talk about overconfidence. Like this little

Principles of Finance Risk and Return. Instructor: Xiaomeng Lu