Testing the Stickiness of Macroeconomic Indicators and Disaggregated Prices in Japan: A FAVAR Approach

|

|

|

- Bennett Bridges

- 5 years ago

- Views:

Transcription

1 International Journal of Economics and Finance; Vol. 6, No. 7; 24 ISSN 96-97X E-ISSN Published by Canadian Center of Science and Education Testing the Stickiness of Macroeconomic Indicators and Disaggregated Prices in Japan: A FAVAR Approach Faculty of Economics, Meikai University, Japan Tao Gu Correspondence: Tao Gu, Faculty of Economics, Meikai University, Akemi, Urayasu, Chiba, , Japan. Tel: tgu@meikai.ac.jp Received: April 5, 24 Accepted: May, 24 Online Published: June 25, 24 doi:.5539/ijef.v6n7p85 URL: Abstract This paper compares the stickiness of macroeconomic indicators and disaggregated prices in Japan using a factor-augmented vector autoregressive (FAVAR) approach. We present three main findings. First, fluctuations in common components are the main source of the volatility in disaggregated inflation rates, and generate most of the fluctuations in aggregate inflation. Second, disaggregated prices appear sticky in response to macroeconomic disturbances, but flexible in response to sector-specific shocks. Third, unexpected tight monetary policy shocks have a gradual negative effect on producer prices; however, only a minor effect was observed on consumer prices. Keywords: sticky prices, monetary policy, macroeconomic models, VAR models. Introduction Nominal price rigidities and monopolistic competition are the two core assumptions in New Keynesian models. In the absence of a commitment device or reputational considerations, these assumptions generate a time-consistency problem for monetary policy (Kydland & Prescott, 977; Barro & Gordon, 983). Therefore, the degree to which prices are sticky is a key parameter when evaluating the effects of monetary policy in the latest macroeconomic models. Recently, evidence of the behavior of disaggregated prices suggests that prices are much more volatile than conventionally assumed in studies based on aggregate data, throwing suspicion on the hypothesis of price rigidity used in New Keynesian models. For instance, in the US case, Bils and Klenow (24), examining the frequency of price changes for 35 categories of goods and services covering about 7% of consumer spending, based on unpublished data from the BLS for 995 to 997, report much more frequent price changes, with half of prices lasting 4.3 months or shorter. They conclude that actual inflation rates are far more volatile and transient than implied by the popular Calvo and Taylor versions of sticky-price models, thereby casting doubt on the validity of such models. In addition, Klenow and Kryvtsov (28) report that price changes are frequent and typically large in absolute value using the CPI Research Database maintained by the US Bureau of Labor Statistics from 988 to 25. In the Japanese case, Abe and Tonogi (2) use Japanese daily scanner data with three billion observations of prices and quantities from 988 to 25, investigating micro and macro price dynamics. They find that the frequency of price changes is much larger than that found in standard monthly datasets, casting doubt on standard New Keynesian assumptions. However, Boivin et al. (29) estimate a factor-augmented vector autoregression (FAVAR) model that augments the standard VAR with a small number of estimated factors summarizing large amounts of information about the economy, thus solving the degrees of freedom problem. This method can properly evaluate the relative importance of the sector-specific and macroeconomic shocks in the individual price series or macroeconomic price indices. The main finding of their study is that disaggregated prices appear sticky in response to macroeconomic and monetary disturbances, but flexible in response to sector-specific shocks, therefore suggesting that the flexibility of disaggregated prices is not in conflict with stickiness of aggregate inflation. The purpose of this paper is to compare the stickiness of macroeconomic indicators and disaggregated prices in Japan using the FAVAR approach of Boivin et al. (29). We find that fluctuations in the common factors are the main source of the volatility of disaggregated inflation rates, and generate most of the fluctuations in aggregate 85

2 International Journal of Economics and Finance Vol. 6, No. 7; 24 inflation. Furthermore, disaggregated prices appear sticky in response to macroeconomic disturbances, but flexible in response to sector-specific shocks, implying the validity of the standard New Keynesian assumptions as discussed by Boivin et al. (29). Third, we find that unexpected tight monetary policy shocks have a gradual negative effect on producer prices; however, only a minor effect was observed on consumer prices. The remainder of the paper is organized as follows. Section 2 reviews the econometric framework of FAVAR, Section 3 discusses the various datasets used in our estimation, Section 4 presents the estimation results, and Section 5 concludes. 2. FAVAR Model The empirical framework that we apply is based on the FAVAR model proposed in Bernanke et al. (25). FAVAR augments the standard VAR with a small number of estimated factors summarizing large amounts of information about the economy and thus can solve the degrees of freedom problem, and reduces the chance of misspecifying the econometric model. In this paper, we follow the empirical strategy provided by Boivin et al. (29) in which the FAVAR framework is used to decompose the volatilities of each variable into a common and an idiosyncratic component, and also macroeconomic disturbances, such as monetary policy shocks. We explain the FAVAR framework developed by Bernanke et al. (25) briefly below; please refer to the original paper for a full discussion. To analyze the effects of monetary policy, we assume that the collateralized overnight call rate,, is the policy instrument. The rest of the common dynamics are captured by a vector of important unobserved factors, where is relatively small. Assume that the joint dynamics of and are given by () where, and is a matrix of polynomials of finite order that may contain a priori restrictions, as in standard structural VARs. The error term is i.i.d. with zero mean. The system () is a VAR in. We assume that the unobservable factors summarize the information contained in a large panel of economic time series. Let be a vector of a wide range of economic variables, where is assumed to be large, i.e.,. Furthermore, we assume that the large set of observable series is related to the common factors according to (2) where is an matrix of factor loadings, and the vector contains series-specific components that are uncorrelated with the common components. These series-specific components are allowed to be serially correlated and weakly correlated across indicators. Following Boivin et al. (29), we estimate this empirical model in two steps. In the first step, we extract principal components from the large dataset to obtain consistent estimates of the common factors. In the second step, the FAVAR model is estimated by standard VAR methods with replaced by. 3. Datasets The dataset used in the estimation of our FAVAR consists of 678 monthly series, and the data span the period from 98: to 998:8. (Note ) In this paper, all data series are transformed using the first difference of the logs of series seasonally adjusted by Census X2 ARIMA software, except for interest rates, where the series are in levels, and the unemployment rate, which is only transformed using the first difference of the seasonally adjusted series. Our dataset includes 34 monthly macroeconomic time series from the Nikkei NEEDS database. In the dataset, we appended 343 series of disaggregated consumer prices from the Ministry of Internal Affairs and Communications, and 2 series of disaggregated producer prices from the Bank of Japan. (Note 2) For brevity, we include the details of our data as well as the transformations applied to each particular series in an appendix, which is available from the author upon request. 4. Main Results We used the two-step estimation system () (2) for the FAVAR model using Matlab for the period 98: to 998:8, with the balanced panel data described in Section 3, and including five common factors in the vector. The lag length used in estimating () is Sources of Fluctuations and Persistence We can analyze the sources of fluctuations in disaggregated (aggregated) inflation rates and the persistence in 86

3 International Journal of Economics and Finance Vol. 6, No. 7; 24 disaggregated (aggregated) inflation rates by estimating the system () (2). Some summary statistics of the volatility and the persistence of monthly inflation at both the macro and sectoral levels are reported in the following subsection. 4.. Inflation Volatility To investigate the sources of fluctuations in disaggregated inflation rates derived from (2), we use (3) where is the monthly log change in the respective price series, and is a vector of factor loadings. From this formulation, it is easy to decompose the fluctuations in disaggregated inflation rates due to the macroeconomic factors, and sector-specific conditions represented by the term. As shown in the first column of Table, the standard deviation of monthly aggregate inflation for the consumer price index (CPI, without fresh food) is.2 percent, and ranges between.8 percent and.67 percent for the inflation rates of durable goods, nondurable goods, and services. The statistic, which measures the fraction of the variance in inflation explained by the common component, lies above.5 for all of the aggregate measures except for nondurable goods, indicating that the main source of the volatility in aggregate inflation is shocks in common factors. However, the situation is considerably distinct for more disaggregated consumer prices and disaggregated producer prices. For example, the standard deviation is.38 percent on average (across sectors) for disaggregated inflation rates, which are more volatile than aggregate ones. In addition, the main source of this volatility is idiosyncratic shocks. As the empirical results shown in Table show, the mean volatility of the common component of inflation is only.5 percent, whereas the idiosyncratic one is.26, more than twice as large. Furthermore, the average statistic for both disaggregated consumer prices and disaggregated producer prices is.26, implying that 74 percent of the fluctuations for the monthly disaggregated inflation are due to idiosyncratic shocks. We find a similar pattern for disaggregated consumer inflation rates and disaggregated producer inflation rates. Furthermore, the inflation volatilities are considerably different across sectors, and are dependent on sector-specific conditions. Table shows that our results are close to those of Boivin et al. (29) Inflation Persistence Next, we discuss aggregate and disaggregated inflation persistence. To evaluate the extent of persistence, we also follow Boivin et al. (29) by estimating for each inflation series and each of its components, and, an autoregressive process with 3 lags of the form (4) and measuring the degree of persistence by the sum of the coefficients on all lags,. As reported in Table, fluctuations in aggregate inflation are persistent with a value of.56 for the CPI (without fresh food) inflation rate, and range between.6 and.55 for the inflation rates of durable goods, nondurable goods, and services. On the other hand, the disaggregated inflation series exhibit different characteristics to the aggregated indicators. (Note 3) As illustrated in Table, the average level of persistence for all sectors is only., and varies significantly across sectors. In addition, the inflation persistence is attributable to fluctuations in common macroeconomic factors in most cases; however, the individual components exhibit, on average, nearly no persistence. These phenomena are also found in the US economy, as Boivin et al. (29) noted. Table. Volatility and persistence of monthly aggregated and disaggregated inflation series Aggregated series CPI Disaggregated series ALL Inflation Standard deviation (in percent) Common Sector components specific R2 Inflation Persistence Common components Sector specific All items, less fresh food Durables Nondurables Services Average Median Min Max

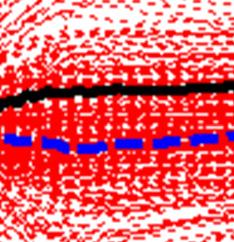

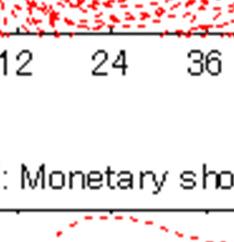

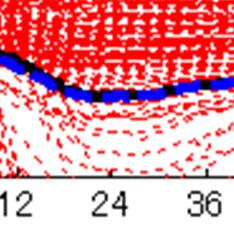

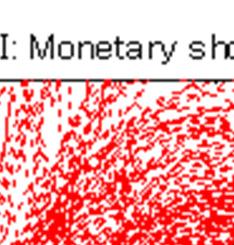

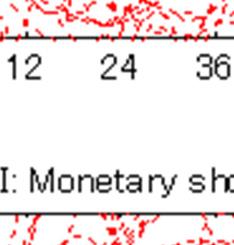

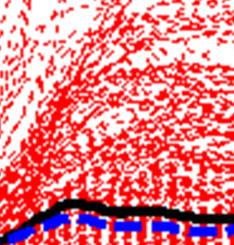

4 International Journal of Economics and Finance Vol. 6, No. 7; 24 Std CPI Average Median Min Max Std PPI Average Median Min Max Std Note. Sample is 98: 998:8. Inflation is measured as the log difference of the price series. Common components are and sector-specific components are in (3), respectively. statistics are the fraction of the variance of inflation explained by. Persistence is calculated using the estimated AR processes with 3 lags. 4.2 Effects of Macroeconomic Shocks and Sector-Specific Shocks In this subsection, we discuss the effects of sector-specific and macroeconomic shocks to the disaggregated price series. First, we confirm the response of each of the sectoral (log) price levels to its own sector-specific shock. As shown in the left panels of Figure A, sectoral price levels respond immediately after a reduction in of one standard deviation, and tend to reach their new equilibrium level quickly (black solid lines display the (unweighted) average responses). Therefore, there is no persistence in the responses to the sector-specific disturbances for the disaggregated price series. Next, we examine the responses of prices to macroeconomic disturbances. The middle panels of Figure A show the responses of each sectoral price to a macroeconomic shock. The degree of the shock is a reduction in the common component by one standard deviation. In contrast to the responses to sector-specific disturbances, macroeconomic shocks produce relatively moderate price falls in the first few months after the shock, then reach their new equilibrium level in about 2 months on average. This is very different from the situation for sector-specific shocks, implying that the responses of prices to macroeconomic shocks are small, implying persistence in inflation rates. Overall, the results above suggest that disaggregated prices appear sticky in response to macroeconomic disturbances, but flexible in response to sector-specific shocks. 4.3 Impulse Response to Monetary Policy Shocks To analyze the responses of the price series to monetary policy shocks, we consider an unexpected contractionary monetary policy shock, i.e., a 25-basis-point innovation in the collateralized overnight call rate. The results of the FAVAR estimation are presented in the right panels of Figure A. They contain the disaggregated price responses of CPI and PPI, the unweighted average responses (thick black solid line) of the disaggregated CPI and PPI, respectively, and the impulse responses of the aggregated CPI (without fresh food) and aggregated PPI (thick blue dashed line) to the same identified monetary policy shock. The unweighted average response of the CPI (without fresh food) shows a gradual increase; however, the response of the CPI (without fresh food) shows a minor decrease. In the PPI case, the unweighted average price response and the response of the aggregate price index to a monetary shock are very similar. They continue to decline after the monetary policy shock for nearly two years, and the size of the decline is greater than that of the CPI (without fresh food). Therefore, we conclude that the unexpected tight monetary policy shock has a gradual negative effect on producer prices; however, only a minor effect was observed on consumer prices. Next, we examine the differences in the traditional VAR and the FAVAR frameworks. Figure B shows the result of a three-variable structural VAR model (PPI, IIP and Call Rate), (Note 4) the same VAR augmented with first principal component that summarize the information contained in a large number of economic variables and the FAVAR model. The thick blue solid line displays the impulse responses generated by the FAVAR, the thick green dashed line shows the impulse responses obtained from the three-variable structural VAR and the red solid line represents the responses of the same VAR augmented with one factor. Unlike the results of the estimation above, the PPI deflator is replaced by the CPI (without fresh food) in the structural VAR model. The impulse responses are displayed in Figure C. As illustrated, a price puzzle exists in the VAR models. Furthermore, the impulse response of IIP in the VAR is also inconsistent with standard economic theory. (Note 5) In contrast to the results estimated by structural VAR models, the FAVAR shows a more instinctive response of IIP, and more importantly, there is no positive response of the price index to the monetary policy tightening shock. The information set included in the FAVAR model is comparatively close to the information set of the actual monetary policy maker; therefore, this suggests that the FAVAR is more appropriate than the standard VAR approach. 88

, and to an")

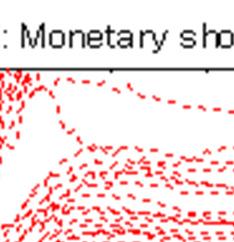

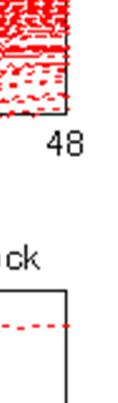

5 International Journal of Economics and Finance Vol. 6, No. 7; 24 Figure A. Sectoral price impulse responses to various shocks Note. Estimated impulse responses of sectoral prices (in percent) to a sector-specific shock of one standard deviation (left panels), to a shock to the common component of one standard deviation (middle panels), and to an identified monetary policy shock (right panels). The monetary shock is a surprise increase of 25 basis points in the collateralized overnight call rate. Thick black solid lines represent unweighted average responses. Thick blue dashed lines represent the response of the aggregate CPI (without fresh food) and PPII price indices to a monetary policy shock..4 Price Level (log): PPI IIP Baseline Favar (5 factors) VAR (IIP, PPI, Call Rate) VAR & factor Figure B. Estimated impulse responses to an identified monetary policy shock (PPI) Note. Sample is 98: 998:8. Monetary shock is an unexpected increase of 25 basis points in the collateralized overnight call rate. Responses reported are estimated using the baseline FAVAR (thick blue solid line), the three-variable VAR (thick green dashed line), and the same VAR augmented with the first principal component of the large dataset (red solid line). 89

6 International Journal of Economics and Finance Vol. 6, No. 7; 24.6 Price Level (log): CPI IIP Figure C. Estimated impulse responses to an identified monetary policy shock (CPI, without fresh food) Note. See Figure B notes. Baseline Favar (5 factors) VAR (IIP, CPI, Call Rate) VAR & factor Factor Factor2 Factor3 Factor4 Factor Figure 2A. Time series of the five factors before removing the consumption tax effect Note. The five lines are extracted factors from the balanced panel dataset. The outliers in April 989 and April 997 indicate the consumption tax effects Factor Factor2 Factor3 Factor4 Factor5 Figure 2B. Time series of the five factors after removing the consumption tax effect Note. The five lines are extracted factors from the balanced panel data set after removing the consumption tax effect. We introduce dummy variables that equal for the consumption tax months (April 997 and April 989) and otherwise for the macroeconomic indicators and all disaggregated prices. 9

).")

7 International Journal of Economics and Finance Vol. 6, No. 7; Controlling the Consumption Tax Effect As a robustness check, we reestimate the model by controlling the consumption tax effect. The Japanese government imposed a consumption tax of 3% in April 989 and raised it to 5% in April 997. These events may affect the estimation results. To remove the consumption tax effect for the macroeconomicc indicators and all disaggregated prices, we introduce dummy variables that equal for consumption tax months (April 9977 and April 989) and otherwise (we do this using Stata) ). The differences in the time series of the five factors before and after removing the consumption tax effect are presented in Figures 2A and 2B, respectively. The estimated impulse responses of the sectoral price shocks are illustrated in Figure 3A. The cases of a sector-specific shock s and a shock to the common component are similar to Figure A, supporting the robustnesss of our results. In Figures 3B and 3C, we again examinee the differences in the three-variable However, for the monetary policy shock, the results are structural VAR model, the same VAR augmented with one factor, and the FAVAR model. counterintuitive, even in the FAVAR case. The reason for these phenomena may be that we didd not consider all of the effects of the consumption tax when extracting principal components from the large dataset. For example, before imposing a consumption tax, consumers may stock up on goods. Introducing dummy variables, such as the indicator of Department Store Sales in our database, that equal for consumption tax months only, may not be adequate for removing this effect. This is a type of information loss that may affect the empirical results. Figure 3A. Sectoral price impulse responses to various shockss after removing the consumption tax effect Note. The consumption tax effect of macroeconomic indicators and all disaggregated prices are removed. See also Figure A notes. 9

8 International Journal of Economics and Finance Vol. 6, No. 7; 24.3 Price Level (log): PPI IIP Baseline Favar (5 factors) VAR (IIP, PPI, Call Rate) VAR & factor Figure 3B. Estimated impulse responses to an identified monetary policy shock after removing the consumption tax effect (PPI) Note. The consumption tax effect of the macroeconomic indicators and all disaggregated prices are removed. See also Figure B notes..5 Price Level (log): CPI IIP Baseline Favar (5 factors) VAR (IIP, CPI, Call Rate) VAR & factor Figure 3C. Estimated impulse responses to an identified monetary policy shock after removing the consumption tax effect (CPI, without fresh food) Note. The consumption tax effect of the macroeconomic indicators and all disaggregated prices are removed. See also Figure B notes. 5. Conclusion The purpose of this paper is to compare the stickiness of macroeconomic indicators and disaggregated prices in Japan using a FAVAR approach. There are three main findings. First, fluctuations in the common factors are the main source of volatility in disaggregated inflation rates and generate most of the fluctuations in aggregate inflation. Second, disaggregated prices appear sticky in response to macroeconomic disturbances, but flexible in response to sector-specific shocks, implying the validity of the standard New Keynesian assumption as discussed by Boivin et al. (29). Third, unexpected tight monetary policy shocks have a gradual negative effect on producer prices; however, only a minor effect was observed on consumer prices. In future research, an estimation that considers the period of zero interest rate policy since 999 in Japan is required. A Markov-switching dynamic factor model may be a suitable method for this exercise. Acknowledgements I would like to express my sincere gratitude to Etsuro Shioji, Tsutomu Watanabe, and an anonymous referee for their helpful comments and encouragement. This research is financially supported by the Suntory Foundation. Of course, all errors remain my responsibility. References Abe, N., & Tonogi, A. (2). Micro and Macro Price Dynamics in Daily Data. Journal of Monetary Economics, 57, Altissimo, F., Mojon, B., & Zaffaroni, P. (27). Fast Micro and Slow Macro: Can Aggregation Explain the 92

9 International Journal of Economics and Finance Vol. 6, No. 7; 24 Persistence of Inflation? FRB of Chicago Working Paper No Barro, R. J., & Gordon, D. B. (983). A Positive Theory of Monetary Policy in a Natural Rate Model. Journal of Political Economy, 9, Bernanke, B. S., & Blinder, A. S. (992). The Federal Funds Rate and the Channels of Monetary Transmission. American Economic Review, 82, Bernanke, B. S., Blinder, & Eliasz, P. S. (25). Measuring MonetaryPolicy: A Factor Augmented Vector Autoregressive (FAVAR) Approach. Quarterly Journal of Economics, 2, Bils, M., & Klenow, P. J. (24). Some Evidence on the Importance of Sticky Prices. Journal of Political Economy, 2, Boivin, J., Giannoni, M. P., & Mihov, I. (29). Sticky Prices and Monetary Policy: Evidence from Disaggregated US Data. American Economic Review, 99, Clark, T. E. (26). Disaggregate Evidence on the Persistence of Consumer Price Inflation. Journal of Applied Econometrics, 2, Klenow, P. J., & Kryvtsov, O. (28). State-Dependent or Time-Dependent Pricing: Does It Matter for Recent U.S. Inflation? Quarterly Journal of Economics, 23, Kydland, F. E., & Prescott, E. C. (977). Rules Rather than Discretion: The Inconsistency of Optimal Plans. Journal of Political Economy, 85, Shibamoto, M. (27). An Analysis of Monetary Policy Shocks in Japan: a Factor Augmented Vector Autoregressive Approach. Japanese Economic Review, 58, x Sims, C. A. (992). Interpreting the Macroeconomic Time Series Facts: The Effects of Monetary Policy. European Economic Review, 36, Notes Note. We choose this period to avoid the effects of the second oil price shock and the zero interest rate monetary policy regime. Note 2. Disaggregated producer prices are available from 98:. In this paper, we normalized them to the base year of 25 following a suggestion made by the Bank of Japan. Note 3. See also Clark (26) and Altissimo et al. (27). Note 4. IIP is the abbreviation for Index of Industrial Production (Mining and Manufacturing). Note 5. Shibamono (27) obtains the same result for Japan. Copyrights Copyright for this article is retained by the author(s), with first publication rights granted to the journal. This is an open-access article distributed under the terms and conditions of the Creative Commons Attribution license ( 93

Measuring the Channels of Monetary Policy Transmission: A Factor-Augmented Vector Autoregressive (Favar) Approach

Approach") Measuring the Channels of Monetary Policy Transmission: A Factor-Augmented Vector Autoregressive (Favar) Approach 5 UDK: 338.23:336.74(73) DOI: 10.1515/jcbtp-2016-0009 Journal of Central Banking Theory

Measuring the Channels of Monetary Policy Transmission: A Factor-Augmented Vector Autoregressive (Favar) Approach 5 UDK: 338.23:336.74(73) DOI: 10.1515/jcbtp-2016-0009 Journal of Central Banking Theory

Missing Aggregate Dynamics:

Discussion of Missing Aggregate Dynamics: On the Slow Convergence of Lumpy Adjustment Models by D. Berger, R. Caballero and E. Engel Marc Giannoni Federal Reserve Bank of New York Workshop on Price Dynamics,

Discussion of Missing Aggregate Dynamics: On the Slow Convergence of Lumpy Adjustment Models by D. Berger, R. Caballero and E. Engel Marc Giannoni Federal Reserve Bank of New York Workshop on Price Dynamics,

A Granular Interpretation to Inflation Variations

A Granular Interpretation to Inflation Variations José Miguel Alvarado a Ernesto Pasten b Lucciano Villacorta c a Central Bank of Chile b Central Bank of Chile b Central Bank of Chile May 30, 2017 Abstract

A Granular Interpretation to Inflation Variations José Miguel Alvarado a Ernesto Pasten b Lucciano Villacorta c a Central Bank of Chile b Central Bank of Chile b Central Bank of Chile May 30, 2017 Abstract

Inflation Regimes and Monetary Policy Surprises in the EU

Inflation Regimes and Monetary Policy Surprises in the EU Tatjana Dahlhaus Danilo Leiva-Leon November 7, VERY PRELIMINARY AND INCOMPLETE Abstract This paper assesses the effect of monetary policy during

Inflation Regimes and Monetary Policy Surprises in the EU Tatjana Dahlhaus Danilo Leiva-Leon November 7, VERY PRELIMINARY AND INCOMPLETE Abstract This paper assesses the effect of monetary policy during

Zhenyu Wu 1 & Maoguo Wu 1

International Journal of Economics and Finance; Vol. 10, No. 5; 2018 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education The Impact of Financial Liquidity on the Exchange

International Journal of Economics and Finance; Vol. 10, No. 5; 2018 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education The Impact of Financial Liquidity on the Exchange

Core Inflation and the Business Cycle

Bank of Japan Review 1-E- Core Inflation and the Business Cycle Research and Statistics Department Yoshihiko Hogen, Takuji Kawamoto, Moe Nakahama November 1 We estimate various measures of core inflation

Bank of Japan Review 1-E- Core Inflation and the Business Cycle Research and Statistics Department Yoshihiko Hogen, Takuji Kawamoto, Moe Nakahama November 1 We estimate various measures of core inflation

Corporate Investment and Portfolio Returns in Japan: A Markov Switching Approach

Corporate Investment and Portfolio Returns in Japan: A Markov Switching Approach 1 Faculty of Economics, Chuo University, Tokyo, Japan Chikashi Tsuji 1 Correspondence: Chikashi Tsuji, Professor, Faculty

Corporate Investment and Portfolio Returns in Japan: A Markov Switching Approach 1 Faculty of Economics, Chuo University, Tokyo, Japan Chikashi Tsuji 1 Correspondence: Chikashi Tsuji, Professor, Faculty

For Online Publication. The macroeconomic effects of monetary policy: A new measure for the United Kingdom: Online Appendix

VOL. VOL NO. ISSUE THE MACROECONOMIC EFFECTS OF MONETARY POLICY For Online Publication The macroeconomic effects of monetary policy: A new measure for the United Kingdom: Online Appendix James Cloyne and

VOL. VOL NO. ISSUE THE MACROECONOMIC EFFECTS OF MONETARY POLICY For Online Publication The macroeconomic effects of monetary policy: A new measure for the United Kingdom: Online Appendix James Cloyne and

The Transmission of International Shocks: A Factor Augmented VAR Approach

Discussion of The Transmission of International Shocks: A Factor Augmented VAR Approach by H. Mumtaz and P. Surico Marc Giannoni Columbia University, NBER and CEPR Conference on Domestic Prices in an Integrated

Discussion of The Transmission of International Shocks: A Factor Augmented VAR Approach by H. Mumtaz and P. Surico Marc Giannoni Columbia University, NBER and CEPR Conference on Domestic Prices in an Integrated

Swiss National Bank Working Papers

211-7 Swiss National Bank Working Papers Sectoral Inflation Dynamics, Idiosyncratic Shocks and Monetary Policy Daniel Kaufmann and Sarah Lein The views expressed in this paper are those of the author(s)

211-7 Swiss National Bank Working Papers Sectoral Inflation Dynamics, Idiosyncratic Shocks and Monetary Policy Daniel Kaufmann and Sarah Lein The views expressed in this paper are those of the author(s)

Sustainability of Current Account Deficits in Turkey: Markov Switching Approach

Sustainability of Current Account Deficits in Turkey: Markov Switching Approach Melike Elif Bildirici Department of Economics, Yıldız Technical University Barbaros Bulvarı 34349, İstanbul Turkey Tel: 90-212-383-2527

Sustainability of Current Account Deficits in Turkey: Markov Switching Approach Melike Elif Bildirici Department of Economics, Yıldız Technical University Barbaros Bulvarı 34349, İstanbul Turkey Tel: 90-212-383-2527

Monetary Policy and Investment Dynamics: Evidence from Disaggregate Data

Monetary Policy and Investment Dynamics: Evidence from Disaggregate Data Gregory E. Givens a,, Robert R. Reed a a Department of Economics, Finance, and Legal Studies, University of Alabama, Tuscaloosa,

Monetary Policy and Investment Dynamics: Evidence from Disaggregate Data Gregory E. Givens a,, Robert R. Reed a a Department of Economics, Finance, and Legal Studies, University of Alabama, Tuscaloosa,

The Effects of Japanese Monetary Policy Shocks on Exchange Rates: A Structural Vector Error Correction Model Approach

MONETARY AND ECONOMIC STUDIES/FEBRUARY 2003 The Effects of Japanese Monetary Policy Shocks on Exchange Rates: A Structural Vector Error Correction Model Approach Kyungho Jang and Masao Ogaki This paper

MONETARY AND ECONOMIC STUDIES/FEBRUARY 2003 The Effects of Japanese Monetary Policy Shocks on Exchange Rates: A Structural Vector Error Correction Model Approach Kyungho Jang and Masao Ogaki This paper

Regional Business Cycles In the United States

Regional Business Cycles In the United States By Gary L. Shelley Peer Reviewed Dr. Gary L. Shelley (shelley@etsu.edu) is an Associate Professor of Economics, Department of Economics and Finance, East Tennessee

Regional Business Cycles In the United States By Gary L. Shelley Peer Reviewed Dr. Gary L. Shelley (shelley@etsu.edu) is an Associate Professor of Economics, Department of Economics and Finance, East Tennessee

Fractional Integration and the Persistence Of UK Inflation, Guglielmo Maria Caporale, Luis Alberiko Gil-Alana.

Department of Economics and Finance Working Paper No. 18-13 Economics and Finance Working Paper Series Guglielmo Maria Caporale, Luis Alberiko Gil-Alana Fractional Integration and the Persistence Of UK

Department of Economics and Finance Working Paper No. 18-13 Economics and Finance Working Paper Series Guglielmo Maria Caporale, Luis Alberiko Gil-Alana Fractional Integration and the Persistence Of UK

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg *

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg * Eric Sims University of Notre Dame & NBER Jonathan Wolff Miami University May 31, 2017 Abstract This paper studies the properties of the fiscal

State-Dependent Fiscal Multipliers: Calvo vs. Rotemberg * Eric Sims University of Notre Dame & NBER Jonathan Wolff Miami University May 31, 2017 Abstract This paper studies the properties of the fiscal

Recent Comovements of the Yen-US Dollar Exchange Rate and Stock Prices in Japan

15, Vol. 1, No. Recent Comovements of the Yen-US Dollar Exchange Rate and Stock Prices in Japan Chikashi Tsuji Professor, Faculty of Economics, Chuo University 7-1 Higashinakano Hachioji-shi, Tokyo 19-393,

15, Vol. 1, No. Recent Comovements of the Yen-US Dollar Exchange Rate and Stock Prices in Japan Chikashi Tsuji Professor, Faculty of Economics, Chuo University 7-1 Higashinakano Hachioji-shi, Tokyo 19-393,

Spillovers of US Conventional and Unconventional Monetary Policies to Russian Financial Markets

International Journal of Economics and Finance; Vol. 10, No. 2; 2018 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Spillovers of US Conventional and Unconventional

International Journal of Economics and Finance; Vol. 10, No. 2; 2018 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Spillovers of US Conventional and Unconventional

Demographics and the behavior of interest rates

Demographics and the behavior of interest rates (C. Favero, A. Gozluklu and H. Yang) Discussion by Michele Lenza European Central Bank and ECARES-ULB Firenze 18-19 June 2015 Rubric Persistence in interest

Demographics and the behavior of interest rates (C. Favero, A. Gozluklu and H. Yang) Discussion by Michele Lenza European Central Bank and ECARES-ULB Firenze 18-19 June 2015 Rubric Persistence in interest

Available online at ScienceDirect. Procedia Economics and Finance 32 ( 2015 ) Andreea Ro oiu a, *

Andreea Ro oiu a, *") Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 32 ( 2015 ) 496 502 Emerging Markets Queries in Finance and Business Monetary policy and time varying parameter vector

Available online at www.sciencedirect.com ScienceDirect Procedia Economics and Finance 32 ( 2015 ) 496 502 Emerging Markets Queries in Finance and Business Monetary policy and time varying parameter vector

How do stock prices respond to fundamental shocks?

Finance Research Letters 1 (2004) 90 99 www.elsevier.com/locate/frl How do stock prices respond to fundamental? Mathias Binswanger University of Applied Sciences of Northwestern Switzerland, Riggenbachstr

Finance Research Letters 1 (2004) 90 99 www.elsevier.com/locate/frl How do stock prices respond to fundamental? Mathias Binswanger University of Applied Sciences of Northwestern Switzerland, Riggenbachstr

Did the Stock Market Regime Change after the Inauguration of the New Cabinet in Japan?

Did the Stock Market Regime Change after the Inauguration of the New Cabinet in Japan? Chikashi Tsuji Faculty of Economics, Chuo University 742-1 Higashinakano Hachioji-shi, Tokyo 192-0393, Japan E-mail:

Did the Stock Market Regime Change after the Inauguration of the New Cabinet in Japan? Chikashi Tsuji Faculty of Economics, Chuo University 742-1 Higashinakano Hachioji-shi, Tokyo 192-0393, Japan E-mail:

Global and National Macroeconometric Modelling: A Long-run Structural Approach Overview on Macroeconometric Modelling Yongcheol Shin Leeds University

Global and National Macroeconometric Modelling: A Long-run Structural Approach Overview on Macroeconometric Modelling Yongcheol Shin Leeds University Business School Seminars at University of Cape Town

Global and National Macroeconometric Modelling: A Long-run Structural Approach Overview on Macroeconometric Modelling Yongcheol Shin Leeds University Business School Seminars at University of Cape Town

Converting TSX 300 Index to S&P/TSX Composite Index: Effects on the Index s Capitalization and Performance

International Journal of Economics and Finance; Vol. 8, No. 6; 2016 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Converting TSX 300 Index to S&P/TSX Composite Index:

International Journal of Economics and Finance; Vol. 8, No. 6; 2016 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Converting TSX 300 Index to S&P/TSX Composite Index:

Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison

DEPARTMENT OF ECONOMICS JOHANNES KEPLER UNIVERSITY LINZ Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison by Burkhard Raunig and Johann Scharler* Working Paper

DEPARTMENT OF ECONOMICS JOHANNES KEPLER UNIVERSITY LINZ Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison by Burkhard Raunig and Johann Scharler* Working Paper

A Brief Report on Norwegian Business Cycles Statistics, Preliminary draft

A Brief Report on Norwegian Business Cycles Statistics, 198-26. 1 - Preliminary draft Hege Marie Gjefsen - hegemgj@student.sv.uio.no Tord Krogh - tskrogh@gmail.com Marie Norum Lerbak lerbak@gmail.com 28.2.28

A Brief Report on Norwegian Business Cycles Statistics, 198-26. 1 - Preliminary draft Hege Marie Gjefsen - hegemgj@student.sv.uio.no Tord Krogh - tskrogh@gmail.com Marie Norum Lerbak lerbak@gmail.com 28.2.28

The Price Puzzle and Monetary Policy Transmission Mechanism in Pakistan: Structural Vector Autoregressive Approach

The Price Puzzle and Monetary Policy Transmission Mechanism in Pakistan: Structural Vector Autoregressive Approach Muhammad Javid 1 Staff Economist Pakistan Institute of Development Economics Kashif Munir

The Price Puzzle and Monetary Policy Transmission Mechanism in Pakistan: Structural Vector Autoregressive Approach Muhammad Javid 1 Staff Economist Pakistan Institute of Development Economics Kashif Munir

Sectoral price data and models of price setting

Sectoral price data and models of price setting Bartosz Maćkowiak European Central Bank and CEPR Emanuel Moench Federal Reserve Bank of New York Mirko Wiederholt Northwestern University December 2008 Abstract

Sectoral price data and models of price setting Bartosz Maćkowiak European Central Bank and CEPR Emanuel Moench Federal Reserve Bank of New York Mirko Wiederholt Northwestern University December 2008 Abstract

News and Monetary Shocks at a High Frequency: A Simple Approach

WP/14/167 News and Monetary Shocks at a High Frequency: A Simple Approach Troy Matheson and Emil Stavrev 2014 International Monetary Fund WP/14/167 IMF Working Paper Research Department News and Monetary

WP/14/167 News and Monetary Shocks at a High Frequency: A Simple Approach Troy Matheson and Emil Stavrev 2014 International Monetary Fund WP/14/167 IMF Working Paper Research Department News and Monetary

Empirical Analysis of the US Swap Curve Gough, O., Juneja, J.A., Nowman, K.B. and Van Dellen, S.

WestminsterResearch http://www.westminster.ac.uk/westminsterresearch Empirical Analysis of the US Swap Curve Gough, O., Juneja, J.A., Nowman, K.B. and Van Dellen, S. This is a copy of the final version

WestminsterResearch http://www.westminster.ac.uk/westminsterresearch Empirical Analysis of the US Swap Curve Gough, O., Juneja, J.A., Nowman, K.B. and Van Dellen, S. This is a copy of the final version

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities - The models we studied earlier include only real variables and relative prices. We now extend these models to have

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities - The models we studied earlier include only real variables and relative prices. We now extend these models to have

New evidence on the effects of US monetary policy on exchange rates

Economics Letters 71 (2001) 255 263 www.elsevier.com/ locate/ econbase New evidence on the effects of US monetary policy on exchange rates a b, * Sarantis Kalyvitis, Alexander Michaelides a University

Economics Letters 71 (2001) 255 263 www.elsevier.com/ locate/ econbase New evidence on the effects of US monetary policy on exchange rates a b, * Sarantis Kalyvitis, Alexander Michaelides a University

Monetary policy transmission in Switzerland: Headline inflation and asset prices

Monetary policy transmission in Switzerland: Headline inflation and asset prices Master s Thesis Supervisor Prof. Dr. Kjell G. Nyborg Chair Corporate Finance University of Zurich Department of Banking

Monetary policy transmission in Switzerland: Headline inflation and asset prices Master s Thesis Supervisor Prof. Dr. Kjell G. Nyborg Chair Corporate Finance University of Zurich Department of Banking

Chapter 9, section 3 from the 3rd edition: Policy Coordination

Chapter 9, section 3 from the 3rd edition: Policy Coordination Carl E. Walsh March 8, 017 Contents 1 Policy Coordination 1 1.1 The Basic Model..................................... 1. Equilibrium with Coordination.............................

Chapter 9, section 3 from the 3rd edition: Policy Coordination Carl E. Walsh March 8, 017 Contents 1 Policy Coordination 1 1.1 The Basic Model..................................... 1. Equilibrium with Coordination.............................

Using Exogenous Changes in Government Spending to estimate Fiscal Multiplier for Canada: Do we get more than we bargain for?

Using Exogenous Changes in Government Spending to estimate Fiscal Multiplier for Canada: Do we get more than we bargain for? Syed M. Hussain Lin Liu August 5, 26 Abstract In this paper, we estimate the

Using Exogenous Changes in Government Spending to estimate Fiscal Multiplier for Canada: Do we get more than we bargain for? Syed M. Hussain Lin Liu August 5, 26 Abstract In this paper, we estimate the

Growth Rate of Domestic Credit and Output: Evidence of the Asymmetric Relationship between Japan and the United States

Bhar and Hamori, International Journal of Applied Economics, 6(1), March 2009, 77-89 77 Growth Rate of Domestic Credit and Output: Evidence of the Asymmetric Relationship between Japan and the United States

Bhar and Hamori, International Journal of Applied Economics, 6(1), March 2009, 77-89 77 Growth Rate of Domestic Credit and Output: Evidence of the Asymmetric Relationship between Japan and the United States

The relationship between output and unemployment in France and United Kingdom

The relationship between output and unemployment in France and United Kingdom Gaétan Stephan 1 University of Rennes 1, CREM April 2012 (Preliminary draft) Abstract We model the relation between output

The relationship between output and unemployment in France and United Kingdom Gaétan Stephan 1 University of Rennes 1, CREM April 2012 (Preliminary draft) Abstract We model the relation between output

The Transmission of International Shocks: A Factor-Augmented VAR Approach

HAROON MUMTAZ PAOLO SURICO The Transmission of International Shocks: A Factor-Augmented VAR Approach The empirical literature on the transmission of international shocks is based on small-scale VARs. In

HAROON MUMTAZ PAOLO SURICO The Transmission of International Shocks: A Factor-Augmented VAR Approach The empirical literature on the transmission of international shocks is based on small-scale VARs. In

The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock

MPRA Munich Personal RePEc Archive The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock Binh Le Thanh International University of Japan 15. August 2015 Online

MPRA Munich Personal RePEc Archive The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock Binh Le Thanh International University of Japan 15. August 2015 Online

Test of the Bank Lending Channel: The Case of Poland

Eurasian Journal of Business and Economics 2013, 6 (12), 143-149. Test of the Bank Lending Channel: The Case of Poland Yu HSING* Abstract This paper tests the bank lending channel for Poland based on a

Eurasian Journal of Business and Economics 2013, 6 (12), 143-149. Test of the Bank Lending Channel: The Case of Poland Yu HSING* Abstract This paper tests the bank lending channel for Poland based on a

Asian Economic and Financial Review SOURCES OF EXCHANGE RATE FLUCTUATION IN VIETNAM: AN APPLICATION OF THE SVAR MODEL

Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 journal homepage: http://www.aessweb.com/journals/5002 SOURCES OF EXCHANGE RATE FLUCTUATION IN VIETNAM: AN APPLICATION OF THE SVAR

Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 journal homepage: http://www.aessweb.com/journals/5002 SOURCES OF EXCHANGE RATE FLUCTUATION IN VIETNAM: AN APPLICATION OF THE SVAR

Volatility Risk and January Effect: Evidence from Japan

International Journal of Economics and Finance; Vol. 7, No. 6; 2015 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Volatility Risk and January Effect: Evidence from

International Journal of Economics and Finance; Vol. 7, No. 6; 2015 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education Volatility Risk and January Effect: Evidence from

The Stance of Monetary Policy

The Stance of Monetary Policy Ben S. C. Fung and Mingwei Yuan* Department of Monetary and Financial Analysis Bank of Canada Ottawa, Ontario Canada K1A 0G9 Tel: (613) 782-7582 (Fung) 782-7072 (Yuan) Fax:

The Stance of Monetary Policy Ben S. C. Fung and Mingwei Yuan* Department of Monetary and Financial Analysis Bank of Canada Ottawa, Ontario Canada K1A 0G9 Tel: (613) 782-7582 (Fung) 782-7072 (Yuan) Fax:

Economics Letters 108 (2010) Contents lists available at ScienceDirect. Economics Letters. journal homepage:

Contents lists available at ScienceDirect. Economics Letters. journal homepage:") Economics Letters 108 (2010) 167 171 Contents lists available at ScienceDirect Economics Letters journal homepage: www.elsevier.com/locate/ecolet Is there a financial accelerator in US banking? Evidence

Economics Letters 108 (2010) 167 171 Contents lists available at ScienceDirect Economics Letters journal homepage: www.elsevier.com/locate/ecolet Is there a financial accelerator in US banking? Evidence

Effects of monetary policy shocks on the trade balance in small open European countries

Economics Letters 71 (2001) 197 203 www.elsevier.com/ locate/ econbase Effects of monetary policy shocks on the trade balance in small open European countries Soyoung Kim* Department of Economics, 225b

Economics Letters 71 (2001) 197 203 www.elsevier.com/ locate/ econbase Effects of monetary policy shocks on the trade balance in small open European countries Soyoung Kim* Department of Economics, 225b

Journal of Central Banking Theory and Practice, 2017, 1, pp Received: 6 August 2016; accepted: 10 October 2016

BOOK REVIEW: Monetary Policy, Inflation, and the Business Cycle: An Introduction to the New Keynesian... 167 UDK: 338.23:336.74 DOI: 10.1515/jcbtp-2017-0009 Journal of Central Banking Theory and Practice,

BOOK REVIEW: Monetary Policy, Inflation, and the Business Cycle: An Introduction to the New Keynesian... 167 UDK: 338.23:336.74 DOI: 10.1515/jcbtp-2017-0009 Journal of Central Banking Theory and Practice,

Structural Cointegration Analysis of Private and Public Investment

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

Does Commodity Price Index predict Canadian Inflation?

2011 年 2 月第十四卷一期 Vol. 14, No. 1, February 2011 Does Commodity Price Index predict Canadian Inflation? Tao Chen http://cmr.ba.ouhk.edu.hk Web Journal of Chinese Management Review Vol. 14 No 1 1 Does Commodity

2011 年 2 月第十四卷一期 Vol. 14, No. 1, February 2011 Does Commodity Price Index predict Canadian Inflation? Tao Chen http://cmr.ba.ouhk.edu.hk Web Journal of Chinese Management Review Vol. 14 No 1 1 Does Commodity

A Reply to Roberto Perotti s "Expectations and Fiscal Policy: An Empirical Investigation"

A Reply to Roberto Perotti s "Expectations and Fiscal Policy: An Empirical Investigation" Valerie A. Ramey University of California, San Diego and NBER June 30, 2011 Abstract This brief note challenges

A Reply to Roberto Perotti s "Expectations and Fiscal Policy: An Empirical Investigation" Valerie A. Ramey University of California, San Diego and NBER June 30, 2011 Abstract This brief note challenges

Is the New Keynesian Phillips Curve Flat?

Is the New Keynesian Phillips Curve Flat? Keith Kuester Federal Reserve Bank of Philadelphia Gernot J. Müller University of Bonn Sarah Stölting European University Institute, Florence January 14, 2009

Is the New Keynesian Phillips Curve Flat? Keith Kuester Federal Reserve Bank of Philadelphia Gernot J. Müller University of Bonn Sarah Stölting European University Institute, Florence January 14, 2009

Business Cycles in Pakistan

International Journal of Business and Social Science Vol. 3 No. 4 [Special Issue - February 212] Abstract Business Cycles in Pakistan Tahir Mahmood Assistant Professor of Economics University of Veterinary

International Journal of Business and Social Science Vol. 3 No. 4 [Special Issue - February 212] Abstract Business Cycles in Pakistan Tahir Mahmood Assistant Professor of Economics University of Veterinary

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

BESSH-16. FULL PAPER PROCEEDING Multidisciplinary Studies Available online at

FULL PAPER PROEEDING Multidisciplinary Studies Available online at www.academicfora.com Full Paper Proceeding BESSH-2016, Vol. 76- Issue.3, 15-23 ISBN 978-969-670-180-4 BESSH-16 A STUDY ON THE OMPARATIVE

FULL PAPER PROEEDING Multidisciplinary Studies Available online at www.academicfora.com Full Paper Proceeding BESSH-2016, Vol. 76- Issue.3, 15-23 ISBN 978-969-670-180-4 BESSH-16 A STUDY ON THE OMPARATIVE

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE Abstract Petr Makovský If there is any market which is said to be effective, this is the the FOREX market. Here we

INFORMATION EFFICIENCY HYPOTHESIS THE FINANCIAL VOLATILITY IN THE CZECH REPUBLIC CASE Abstract Petr Makovský If there is any market which is said to be effective, this is the the FOREX market. Here we

Volume 29, Issue 3. Application of the monetary policy function to output fluctuations in Bangladesh

Volume 29, Issue 3 Application of the monetary policy function to output fluctuations in Bangladesh Yu Hsing Southeastern Louisiana University A. M. M. Jamal Southeastern Louisiana University Wen-jen Hsieh

Volume 29, Issue 3 Application of the monetary policy function to output fluctuations in Bangladesh Yu Hsing Southeastern Louisiana University A. M. M. Jamal Southeastern Louisiana University Wen-jen Hsieh

Unemployment Fluctuations and Nominal GDP Targeting

Unemployment Fluctuations and Nominal GDP Targeting Roberto M. Billi Sveriges Riksbank 3 January 219 Abstract I evaluate the welfare performance of a target for the level of nominal GDP in the context

Unemployment Fluctuations and Nominal GDP Targeting Roberto M. Billi Sveriges Riksbank 3 January 219 Abstract I evaluate the welfare performance of a target for the level of nominal GDP in the context

Understanding the Relative Price Puzzle

Understanding the Relative Price Puzzle Lin Liu University of Rochester April 213 Abstract This paper examines the impact of unpredictable monetary policy movements in an economy with both durables and

Understanding the Relative Price Puzzle Lin Liu University of Rochester April 213 Abstract This paper examines the impact of unpredictable monetary policy movements in an economy with both durables and

Misspecification, Identification or Measurement? Another Look at the Price Puzzle

Department of Economics Working Paper Series Misspecification, Identification or Measurement? Another Look at the Price Puzzle Shuyun May Li, Roshan Perera and Kalvinder Shields JAN 2013 Research Paper

Department of Economics Working Paper Series Misspecification, Identification or Measurement? Another Look at the Price Puzzle Shuyun May Li, Roshan Perera and Kalvinder Shields JAN 2013 Research Paper

Inflation Dynamics in FYR Macedonia

WP/11/287 Inflation Dynamics in FYR Macedonia Maral Shamloo 211 International Monetary Fund WP/11/287 IMF Working Paper European Department Inflation Dynamics in FYR Macedonia 1 Prepared by Maral Shamloo

WP/11/287 Inflation Dynamics in FYR Macedonia Maral Shamloo 211 International Monetary Fund WP/11/287 IMF Working Paper European Department Inflation Dynamics in FYR Macedonia 1 Prepared by Maral Shamloo

Shocked by the world! Introducing the three block open economy FAVAR

Shocked by the world! Introducing the three block open economy FAVAR Özer Karagedikli Leif Anders Thorsrud November 5, 2 Abstract We estimate a three block FAVAR with separate world, regional and domestic

Shocked by the world! Introducing the three block open economy FAVAR Özer Karagedikli Leif Anders Thorsrud November 5, 2 Abstract We estimate a three block FAVAR with separate world, regional and domestic

Was The New Deal Contractionary? Appendix C:Proofs of Propositions (not intended for publication)

") Was The New Deal Contractionary? Gauti B. Eggertsson Web Appendix VIII. Appendix C:Proofs of Propositions (not intended for publication) ProofofProposition3:The social planner s problem at date is X min

Was The New Deal Contractionary? Gauti B. Eggertsson Web Appendix VIII. Appendix C:Proofs of Propositions (not intended for publication) ProofofProposition3:The social planner s problem at date is X min

The Effect of Economic Policy Uncertainty in the US on the Stock Market Performance in Canada and Mexico

International Journal of Economics and Finance; Vol. 4, No. 11; 2012 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education The Effect of Economic Policy Uncertainty in the

International Journal of Economics and Finance; Vol. 4, No. 11; 2012 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education The Effect of Economic Policy Uncertainty in the

The Dynamics of the Term Structure of Interest Rates in the United States in Light of the Financial Crisis of

WPWWW WP/11/84 The Dynamics of the Term Structure of Interest Rates in the United States in Light of the Financial Crisis of 2007 10 Carlos Medeiros and Marco Rodríguez 2011 International Monetary Fund

WPWWW WP/11/84 The Dynamics of the Term Structure of Interest Rates in the United States in Light of the Financial Crisis of 2007 10 Carlos Medeiros and Marco Rodríguez 2011 International Monetary Fund

Forecasting Real Estate Prices

Forecasting Real Estate Prices Stefano Pastore Advanced Financial Econometrics III Winter/Spring 2018 Overview Peculiarities of Forecasting Real Estate Prices Real Estate Indices Serial Dependence in Real

Forecasting Real Estate Prices Stefano Pastore Advanced Financial Econometrics III Winter/Spring 2018 Overview Peculiarities of Forecasting Real Estate Prices Real Estate Indices Serial Dependence in Real

CONFIDENCE AND ECONOMIC ACTIVITY: THE CASE OF PORTUGAL*

CONFIDENCE AND ECONOMIC ACTIVITY: THE CASE OF PORTUGAL* Caterina Mendicino** Maria Teresa Punzi*** 39 Articles Abstract The idea that aggregate economic activity might be driven in part by confidence and

CONFIDENCE AND ECONOMIC ACTIVITY: THE CASE OF PORTUGAL* Caterina Mendicino** Maria Teresa Punzi*** 39 Articles Abstract The idea that aggregate economic activity might be driven in part by confidence and

Iranian Economic Review, Vol.15, No.28, Winter Business Cycle Features in the Iranian Economy. Asghar Shahmoradi Ali Tayebnia Hossein Kavand

Iranian Economic Review, Vol.15, No.28, Winter 2011 Business Cycle Features in the Iranian Economy Asghar Shahmoradi Ali Tayebnia Hossein Kavand Abstract his paper studies the business cycle characteristics

Iranian Economic Review, Vol.15, No.28, Winter 2011 Business Cycle Features in the Iranian Economy Asghar Shahmoradi Ali Tayebnia Hossein Kavand Abstract his paper studies the business cycle characteristics

Has the Inflation Process Changed?

Has the Inflation Process Changed? by S. Cecchetti and G. Debelle Discussion by I. Angeloni (ECB) * Cecchetti and Debelle (CD) could hardly have chosen a more relevant and timely topic for their paper.

Has the Inflation Process Changed? by S. Cecchetti and G. Debelle Discussion by I. Angeloni (ECB) * Cecchetti and Debelle (CD) could hardly have chosen a more relevant and timely topic for their paper.

E-322 Muhammad Rahman CHAPTER-3

CHAPTER-3 A. OBJECTIVE In this chapter, we will learn the following: 1. We will introduce some new set of macroeconomic definitions which will help us to develop our macroeconomic language 2. We will develop

CHAPTER-3 A. OBJECTIVE In this chapter, we will learn the following: 1. We will introduce some new set of macroeconomic definitions which will help us to develop our macroeconomic language 2. We will develop

Why the saving rate has been falling in Japan

October 2007 Why the saving rate has been falling in Japan Yoshiaki Azuma and Takeo Nakao Doshisha University Faculty of Economics Imadegawa Karasuma Kamigyo Kyoto 602-8580 Japan Doshisha University Working

October 2007 Why the saving rate has been falling in Japan Yoshiaki Azuma and Takeo Nakao Doshisha University Faculty of Economics Imadegawa Karasuma Kamigyo Kyoto 602-8580 Japan Doshisha University Working

A Study on the Relationship between Monetary Policy Variables and Stock Market

International Journal of Business and Management; Vol. 13, No. 1; 2018 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education A Study on the Relationship between Monetary

International Journal of Business and Management; Vol. 13, No. 1; 2018 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education A Study on the Relationship between Monetary

THE CREDIT CYCLE and the BUSINESS CYCLE in the ECONOMY of TURKEY

810 September 2014 Istanbul, Turkey 442 THE CYCLE and the BUSINESS CYCLE in the ECONOMY of TURKEY Şehnaz Bakır Yiğitbaş 1 1 Dr. Lecturer, Çanakkale Onsekiz Mart University, TURKEY, sehnazbakir@comu.edu.tr

810 September 2014 Istanbul, Turkey 442 THE CYCLE and the BUSINESS CYCLE in the ECONOMY of TURKEY Şehnaz Bakır Yiğitbaş 1 1 Dr. Lecturer, Çanakkale Onsekiz Mart University, TURKEY, sehnazbakir@comu.edu.tr

HONG KONG INSTITUTE FOR MONETARY RESEARCH

HONG KONG INSTITUTE FOR MONETARY RESEARCH EFFECTS OF MONETARY POLICY SHOCKS ON EXCHANGE RATE IN EMERGING COUNTRIES Soyoung Kim and Kuntae Lim HKIMR December 2016 香港金融研究中心 (a company incorporated with limited

HONG KONG INSTITUTE FOR MONETARY RESEARCH EFFECTS OF MONETARY POLICY SHOCKS ON EXCHANGE RATE IN EMERGING COUNTRIES Soyoung Kim and Kuntae Lim HKIMR December 2016 香港金融研究中心 (a company incorporated with limited

The Credit Cycle and the Business Cycle in the Economy of Turkey

Chinese Business Review, March 2016, Vol. 15, No. 3, 123-131 doi: 10.17265/1537-1506/2016.03.003 D DAVID PUBLISHING The Credit Cycle and the Business Cycle in the Economy of Turkey Şehnaz Bakır Yiğitbaş

Chinese Business Review, March 2016, Vol. 15, No. 3, 123-131 doi: 10.17265/1537-1506/2016.03.003 D DAVID PUBLISHING The Credit Cycle and the Business Cycle in the Economy of Turkey Şehnaz Bakır Yiğitbaş

Inflation 11/27/2017. A. Phillips Curve. A.W. Phillips (1958) documented relation between unemployment and rate of change of wages in U.K.

documented relation between unemployment and rate of change of wages in U.K.") Inflation A. The Phillips Curve B. Forecasting inflation C. Frequency of price changes D. Microfoundations A. Phillips Curve Irving Fisher (1926) found negative correlation 1903-25 between U.S. unemployment

Inflation A. The Phillips Curve B. Forecasting inflation C. Frequency of price changes D. Microfoundations A. Phillips Curve Irving Fisher (1926) found negative correlation 1903-25 between U.S. unemployment

The Relationship between Inflation, Inflation Uncertainty and Output Growth in India

Economic Affairs 2014, 59(3) : 465-477 9 New Delhi Publishers WORKING PAPER 59(3): 2014: DOI 10.5958/0976-4666.2014.00014.X The Relationship between Inflation, Inflation Uncertainty and Output Growth in

Economic Affairs 2014, 59(3) : 465-477 9 New Delhi Publishers WORKING PAPER 59(3): 2014: DOI 10.5958/0976-4666.2014.00014.X The Relationship between Inflation, Inflation Uncertainty and Output Growth in

The Reaction of Stock Prices to Monetary Policy Shocks in Malaysia: A Structural Vector Autoregressive Model

Available Online at http://ircconferences.com/ Book of Proceedings published by (c) International Organization for Research and Development IORD ISSN: 2410-5465 Book of Proceedings ISBN: 978-969-7544-00-4

Available Online at http://ircconferences.com/ Book of Proceedings published by (c) International Organization for Research and Development IORD ISSN: 2410-5465 Book of Proceedings ISBN: 978-969-7544-00-4

MONETARY POLICY TRANSMISSION MECHANISM IN ROMANIA OVER THE PERIOD 2001 TO 2012: A BVAR ANALYSIS

Scientific Annals of the Alexandru Ioan Cuza University of Iaşi Economic Sciences 60 (2), 2013, 387-398 DOI 10.2478/aicue-2013-0018 MONETARY POLICY TRANSMISSION MECHANISM IN ROMANIA OVER THE PERIOD 2001

Scientific Annals of the Alexandru Ioan Cuza University of Iaşi Economic Sciences 60 (2), 2013, 387-398 DOI 10.2478/aicue-2013-0018 MONETARY POLICY TRANSMISSION MECHANISM IN ROMANIA OVER THE PERIOD 2001

Measuring How Fiscal Shocks Affect Durable Spending in Recessions and Expansions

Measuring How Fiscal Shocks Affect Durable Spending in Recessions and Expansions By DAVID BERGER AND JOSEPH VAVRA How big are government spending multipliers? A recent litererature has argued that while

Measuring How Fiscal Shocks Affect Durable Spending in Recessions and Expansions By DAVID BERGER AND JOSEPH VAVRA How big are government spending multipliers? A recent litererature has argued that while

Conditional versus Unconditional Utility as Welfare Criterion: Two Examples

Conditional versus Unconditional Utility as Welfare Criterion: Two Examples Jinill Kim, Korea University Sunghyun Kim, Sungkyunkwan University March 015 Abstract This paper provides two illustrative examples

Conditional versus Unconditional Utility as Welfare Criterion: Two Examples Jinill Kim, Korea University Sunghyun Kim, Sungkyunkwan University March 015 Abstract This paper provides two illustrative examples

Asian Economic and Financial Review EMPIRICAL TESTING OF EXCHANGE RATE AND INTEREST RATE TRANSMISSION CHANNELS IN CHINA

Asian Economic and Financial Review, 15, 5(1): 15-15 Asian Economic and Financial Review ISSN(e): -737/ISSN(p): 35-17 journal homepage: http://www.aessweb.com/journals/5 EMPIRICAL TESTING OF EXCHANGE RATE

Asian Economic and Financial Review, 15, 5(1): 15-15 Asian Economic and Financial Review ISSN(e): -737/ISSN(p): 35-17 journal homepage: http://www.aessweb.com/journals/5 EMPIRICAL TESTING OF EXCHANGE RATE

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis Introduction Uthajakumar S.S 1 and Selvamalai. T 2 1 Department of Economics, University of Jaffna. 2

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis Introduction Uthajakumar S.S 1 and Selvamalai. T 2 1 Department of Economics, University of Jaffna. 2

Inflation Targeting, Aggregation, and Inflation Persistence: Evidence from Korean CPI Components 1

Inflation Targeting, Aggregation, and Inflation Persistence: Evidence from Korean CPI Components Peter Tillmann * This paper studies the impact of inflation targeting on the evolution of inflation persistence

Inflation Targeting, Aggregation, and Inflation Persistence: Evidence from Korean CPI Components Peter Tillmann * This paper studies the impact of inflation targeting on the evolution of inflation persistence

VPIN and the China s Circuit-Breaker

International Journal of Economics and Finance; Vol. 9, No. 12; 2017 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education VPIN and the China s Circuit-Breaker Yameng Zheng

International Journal of Economics and Finance; Vol. 9, No. 12; 2017 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education VPIN and the China s Circuit-Breaker Yameng Zheng

Market Timing Does Work: Evidence from the NYSE 1

Market Timing Does Work: Evidence from the NYSE 1 Devraj Basu Alexander Stremme Warwick Business School, University of Warwick November 2005 address for correspondence: Alexander Stremme Warwick Business

Market Timing Does Work: Evidence from the NYSE 1 Devraj Basu Alexander Stremme Warwick Business School, University of Warwick November 2005 address for correspondence: Alexander Stremme Warwick Business

Productivity, monetary policy and financial indicators

Productivity, monetary policy and financial indicators Arturo Estrella Introduction Labour productivity is widely thought to be informative with regard to inflation and it therefore comes up frequently

Productivity, monetary policy and financial indicators Arturo Estrella Introduction Labour productivity is widely thought to be informative with regard to inflation and it therefore comes up frequently

Introduction. Learning Objectives. Chapter 17. Stabilization in an Integrated World Economy

Chapter 17 Stabilization in an Integrated World Economy Introduction For more than 50 years, many economists have used an inverse relationship involving the unemployment rate and real GDP as a guide to

Chapter 17 Stabilization in an Integrated World Economy Introduction For more than 50 years, many economists have used an inverse relationship involving the unemployment rate and real GDP as a guide to

Volume 35, Issue 1. Thai-Ha Le RMIT University (Vietnam Campus)

") Volume 35, Issue 1 Exchange rate determination in Vietnam Thai-Ha Le RMIT University (Vietnam Campus) Abstract This study investigates the determinants of the exchange rate in Vietnam and suggests policy

Volume 35, Issue 1 Exchange rate determination in Vietnam Thai-Ha Le RMIT University (Vietnam Campus) Abstract This study investigates the determinants of the exchange rate in Vietnam and suggests policy

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis WenShwo Fang Department of Economics Feng Chia University 100 WenHwa Road, Taichung, TAIWAN Stephen M. Miller* College of Business University

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis WenShwo Fang Department of Economics Feng Chia University 100 WenHwa Road, Taichung, TAIWAN Stephen M. Miller* College of Business University

Further Test on Stock Liquidity Risk With a Relative Measure

International Journal of Education and Research Vol. 1 No. 3 March 2013 Further Test on Stock Liquidity Risk With a Relative Measure David Oima* David Sande** Benjamin Ombok*** Abstract Negative relationship

International Journal of Education and Research Vol. 1 No. 3 March 2013 Further Test on Stock Liquidity Risk With a Relative Measure David Oima* David Sande** Benjamin Ombok*** Abstract Negative relationship

Long-run Consumption Risks in Assets Returns: Evidence from Economic Divisions

Long-run Consumption Risks in Assets Returns: Evidence from Economic Divisions Abdulrahman Alharbi 1 Abdullah Noman 2 Abstract: Bansal et al (2009) paper focus on measuring risk in consumption especially

Long-run Consumption Risks in Assets Returns: Evidence from Economic Divisions Abdulrahman Alharbi 1 Abdullah Noman 2 Abstract: Bansal et al (2009) paper focus on measuring risk in consumption especially

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Do core inflation measures help forecast inflation? Out-of-sample evidence from French data

Economics Letters 69 (2000) 261 266 www.elsevier.com/ locate/ econbase Do core inflation measures help forecast inflation? Out-of-sample evidence from French data Herve Le Bihan *, Franck Sedillot Banque

Economics Letters 69 (2000) 261 266 www.elsevier.com/ locate/ econbase Do core inflation measures help forecast inflation? Out-of-sample evidence from French data Herve Le Bihan *, Franck Sedillot Banque

Volume 38, Issue 1. The dynamic effects of aggregate supply and demand shocks in the Mexican economy

Volume 38, Issue 1 The dynamic effects of aggregate supply and demand shocks in the Mexican economy Ivan Mendieta-Muñoz Department of Economics, University of Utah Abstract This paper studies if the supply

Volume 38, Issue 1 The dynamic effects of aggregate supply and demand shocks in the Mexican economy Ivan Mendieta-Muñoz Department of Economics, University of Utah Abstract This paper studies if the supply

The Effects of Dollarization on Macroeconomic Stability

The Effects of Dollarization on Macroeconomic Stability Christopher J. Erceg and Andrew T. Levin Division of International Finance Board of Governors of the Federal Reserve System Washington, DC 2551 USA

The Effects of Dollarization on Macroeconomic Stability Christopher J. Erceg and Andrew T. Levin Division of International Finance Board of Governors of the Federal Reserve System Washington, DC 2551 USA

No Matthias Neuenkirch. Monetary Policy Transmission in Vector Autoregressions: A New Approach Using Central Bank Communication

Joint Discussion Paper Series in Economics by the Universities of Aachen Gießen Göttingen Kassel Marburg Siegen ISSN 1867-3678 No. 43-211 Matthias Neuenkirch Monetary Policy Transmission in Vector Autoregressions:

Joint Discussion Paper Series in Economics by the Universities of Aachen Gießen Göttingen Kassel Marburg Siegen ISSN 1867-3678 No. 43-211 Matthias Neuenkirch Monetary Policy Transmission in Vector Autoregressions:

Does the CBOE Volatility Index Predict Downside Risk at the Tokyo Stock Exchange?

International Business Research; Vol. 10, No. 3; 2017 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education Does the CBOE Volatility Index Predict Downside Risk at the Tokyo

International Business Research; Vol. 10, No. 3; 2017 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education Does the CBOE Volatility Index Predict Downside Risk at the Tokyo

Test of the bank lending channel: The case of Hungary

Theoretical and Applied Economics Volume XXI (2014), No. 1(590), pp. 115-120 Test of the bank lending channel: The case of Hungary Yu HSING Southeastern Louisiana University yhsing@selu.edu Abstract. This

Theoretical and Applied Economics Volume XXI (2014), No. 1(590), pp. 115-120 Test of the bank lending channel: The case of Hungary Yu HSING Southeastern Louisiana University yhsing@selu.edu Abstract. This

Quantity versus Price Rationing of Credit: An Empirical Test

Int. J. Financ. Stud. 213, 1, 45 53; doi:1.339/ijfs1345 Article OPEN ACCESS International Journal of Financial Studies ISSN 2227-772 www.mdpi.com/journal/ijfs Quantity versus Price Rationing of Credit:

Int. J. Financ. Stud. 213, 1, 45 53; doi:1.339/ijfs1345 Article OPEN ACCESS International Journal of Financial Studies ISSN 2227-772 www.mdpi.com/journal/ijfs Quantity versus Price Rationing of Credit:

Contrarian Trades and Disposition Effect: Evidence from Online Trade Data. Abstract

Contrarian Trades and Disposition Effect: Evidence from Online Trade Data Hayato Komai a Ryota Koyano b Daisuke Miyakawa c Abstract Using online stock trading records in Japan for 461 individual investors

Contrarian Trades and Disposition Effect: Evidence from Online Trade Data Hayato Komai a Ryota Koyano b Daisuke Miyakawa c Abstract Using online stock trading records in Japan for 461 individual investors

Are Predictable Improvements in TFP Contractionary or Expansionary: Implications from Sectoral TFP? *

Federal Reserve Bank of Dallas Globalization and Monetary Policy Institute Working Paper No. http://www.dallasfed.org/assets/documents/institute/wpapers//.pdf Are Predictable Improvements in TFP Contractionary

Federal Reserve Bank of Dallas Globalization and Monetary Policy Institute Working Paper No. http://www.dallasfed.org/assets/documents/institute/wpapers//.pdf Are Predictable Improvements in TFP Contractionary