ANNUAL GENERAL REPORT OF THE CONTROLLER AND AUDITOR GENERAL

|

|

|

- Dinah Stevens

- 5 years ago

- Views:

Transcription

1 ANNUAL GENERAL REPORT OF THE CONTROLLER AND AUDITOR GENERAL On the Audit of the Financial Statements of Donor Funded Projects for the year ended 30 th June, 2012

2115157/8, Fax: 255(022)2117527, E-mail: ocag@nao.go.tz, Website: www.nao.go.tz Your Excellency Dr. Jakaya M.")

2 THE UNITED REPUBLIC OF TANZANIA NATIONAL AUDIT OFFICE Office of the Controller and Auditor General, Samora Avenue, P.O. Box 9080, DAR ES SALAAM. Telegram: Ukaguzi", Telephone: 255(022) /8, Fax: 255(022) , Website: Your Excellency Dr. Jakaya M. Kikwete, The President of the United Republic of Tanzania, State House, P.O. Box 9120, Dar es Salaam. Re: Submission of Annual General Report of the Controller and Auditor General on the Financial Statements of Donor Funded Projects for the year ended 30th June, 2012 Pursuant to Article 143(4) of the Constitution of the United Republic of Tanzania of 1977 (revised 2005), and Sec.34 (1) (c) of the Public Audit Act No. 11 of 2008, I hereby submit to you my second General Report on Donor Funded Projects for the year ended 30 th June, I submit. Ludovick S.L. Utouh CONTROLLER AND AUDITOR GENERAL ii

3 List of abbreviations A/C ACGEN ASDP ASDS ASLMs ASP BHSP BoQ BWOs CAATs CAG CCTTFA CDTI CFS CMC CPO DADPs DANIDA DASIP DDPs DHIR PMO- RALG DRTA DSS EAPHLNP ES-FEAT EU HBF HSPS IA IDA IFAD ISA ISSAIs JICA LAFM LART LGAs Account Accountant General Agriculture Sector Development Programme Agricultural Sector Development Strategy Agricultural Sector Lead Ministries African Stockpiles Program Basic Heath Services Project Bills of Quantity Basin Water Offices Computer Assisted Audit Techniques Controller and Auditor General Central Corridor Transit Transport Facilitation Agency Community Development Training Institute Consolidated Financial Statements Community Managment Committee Central Payment Office District Agricultural Development Plans Danish International Development Agency District Agriculture Sector Project District Deveopment Plans District Health Insfrastructure Rehabilitation Dar es Salaam Rapid Transport Agency Diagnostic Service Section East Africa Pblic Health Labortory Networking Project Ethics Secretariat FEAT European Union Health Basket Fund Health Sector Project Support Irish Aid International Development Association International Fund for Agricultural Development International Standards on Auditing International Standards of Supreme Audit Institutions Japan International Cooperation Agency Local Authority Financial Memorandum Loans and Realization Trust Local Government Authorities iii

4 LGSP Local Government Support Project LGTP Local Government Transport Program LSRP Legal Sector Reform Program MDAs Ministries, Departments and Agencies, MDG Milenium Development Goals Marketing Insfrastructure, Value Addtion and Rural MIVARF Finaue Support Progrm MoU Memorandum of Understanding MoW Ministry of Water NAO National Audit Office NBAA National Board of Accountants and Auditors NVF National Village Fund NWSDS National Water Sector Development Strategy OC Other Charges OPD Output Patient Department PAC Public Accounts Committee PE Procuring Entities PFA Public Finance Act (No. 6 of 2001 revised 2004) PFGAs Participatory Farmers Groups Associations PFMRP Public Financial Management Reform Programme PFR Public Finance Regulations PLHIV People Living with HIV PMG Paymaster General PPA Public Procurement Act (No. 21 of 2004) PPRA Public Procurement Regulatory Authority PSCP Private Sector Competitive Project PSRP Public Service Reform Program RAS Regional Administrative Secretariat RCIP Regional Communication Infrastucture Project REA-WBFP Rural Energy Agency World Bank Financed Projects Reg. Regulation RSSP1 Road Sector Support Project RWBO Rufiji Water Basin Organisation RWSSP Rural Water Supply Sanitation Program Sect. Section SIDA Swedish International Development Agency SNAO Swedish National Audit Office TASAF Tanzania Social Action Fund TMU TASAF Management Unit TPRS Tanzania Poverty Reduction Strategy iv

5 TRA URT USD VFC VFJA WSDP Tanzania Revenue Authority United Republic of Tanzania United States Dollars Village Fund Coordinator Village Fund Justification Assistant Water Sector Development Programmme v

6 TABLE OF CONTENTS List of abbreviations... iii Foreword... ix Acknowledgement... xii Executive Summary... 1 CHAPTER ONE BACKGROUND INFORMATION Audit of Donor Funded Projects Functions and Responsibilities of the CAG on the Donor Funded Projects Organisation of audit work at the National Audit Office Scope and Applicable Audit Standards Accounting Policies... 8 CHAPTER TWO.. 11 BASIS OF AUDIT OPINION Introduction Types of Audit Opinion Audit Opinions Issued on Donor Funded Projects CHAPTER THREE FINANCIAL PERFOMANCE OF THE PROJECTS Introduction Water Sector Development Programme Tanzania Social Action Fund (TASAF II) Agriculture Sector Development Programme (ASDP) Health Basket Fund Programme Financing Other Projects CHAPTER FOUR PRESENTATION AND ANALYSIS OF AUDIT RESULTS Introduction Major Donor Funded Projects OTHER DONOR FUNDED PROJECTS CHAPTER FIVE REVIEW OF PROCUREMENT PROCESSES Introduction Agricultural Sector Development Programme (ASDP) Health Basket Fund (HBF) Tanzania Social Action Fund (TASAF) Water Sector Development Programme Other Projects vi

7 CHAPTER SIX WEAKNESSES IN FINANCIAL MANAGEMENT Introduction AGRICULTURE SECTOR DEVELOPMENT PROGRAMME (ASDP) WATER SECTOR DEVELOPMENT PROGRAMME (WSDP) HEALTH BASKET FUNDS (HBF) TANZANIA SOCIAL ACTION FUND (TASAF) GLOBAL FUND AND OTHER PROJECTS CHAPTER SEVEN CONCLUSION AND RECOMMENDATIONS Conclusion Recommendations ANNEXTURES vii

8 Office of the Controller and Auditor General, The National Audit Office, United Republic of Tanzania. (Established under Article 143 of the Constitution of the URT The statutory duties and responsibilities of the Controller and Auditor General are given under Article 143 of the Constitution of the URT of 1977 (revised 2005) and further elaborated in Sect 10(1) of the Public Audit Act No. 11 of Vision To be a centre of excellence in public sector auditing. Mission To provide efficient audit services in order to enhance accountability and value for money in the collection and use of public resources. Core Values In providing quality services, NAO is guided by the following Core Values: Objectivity: We are an impartial organization, offering services to our clients in an objective and unbiased manner; Excellence: We are professionals providing high quality audit services based on best practices; Integrity: We observe and maintain high standards of ethical behaviour and the rule of law; People focus: We focus on stakeholders needs by building a culture of good customer care and having competent and motivated work force; Innovation: We are a creative organization that constantly promotes a culture of developing and accepting new ideas from inside and outside the organization; and Best resource utilisation: We are an organisation that values and uses public resources entrusted to it in efficient, economic and effective manner. We do this by:- Contributing to better stewardship of public funds by ensuring that our clients are accountable for the resources entrusted to them; Helping to improve the quality of public services by supporting innovation on the use of public resources; Providing technical advice to our clients on operational gaps in their operating systems; Systematically involving our clients in the audit process and audit cycles; and Providing audit staff with adequate working tools and facilities that promote independence. This audit report is intended to be used by Government Authorities. However, upon receipt of the report by the Speaker and once tabled in Parliament, the report becomes a matter of public record and its distribution may not be limited. viii

9 Foreword This general report is a summary of results on the audit of Donor Funded Projects financed by Development Partners and The United Republic of Tanzania. The projects are categorized in two categories i.e major four projects and the other projects as listed below: First category of major projects funded through Basket Funding arrangement are as follows:- Tanzania Social Action Fund (TASAF), Agricultural Sector Development Programme (ASDP), Water Sector Development Programme (WSDP) Health Basket Fund (HBF). Second category of other projects funded through bilateral funding arrangements Apart from the audit of projects which are funded through Basket funding arrangement, I also covered other projects which are financed through bilateral arrangements. The general report for Donor Funded Projects is being prepared and submitted to the President of the URT in accordance with Article 143 of the Constitution of the United Republic of Tanzania of 1977 (revised 2005) and Section 34(1) & (2) of the Public Audit Act No. 11 of Pursuant to Article 143(2) (c) of the Constitution of the URT of 1977 (revised 2005), the Controller and Auditor General, shall at least once every year audit and give an audit report in respect of the accounts of the Government of the United Republic, the accounts managed by all officers of the Government of the United Republic, the accounts of all Courts of the United Republic and the accounts managed by the Clerk of the National Assembly. Under Article 143(4) of the Constitution of the URT, the Controller and Auditor General is required to submit to the President of the URT every report he makes pursuant to the provisions of sub Article (2) of the same Article. Upon receipt of such reports, the President shall direct the persons concerned to submit these reports before the first sitting of the National Assembly preferably ix

10 before the expiration of seven days from the day the sitting of the National Assembly began. The enactment of the Public Audit Act No. 11 of 2008 enhanced the operational independence of my office in the fulfillment of my Constitutional mandate. This was a result of the efforts of his Excellency the President of the United Republic of Tanzania Dk. Jakaya Mrisho Kikwete. The operational independence of my office is expected to enable me acquire the necessary control over all the resources available for the office including human and financial resources, which will enable my office to perform its tasks without being under any undue influence and control of any person or authority. It is worth noting that while my office reports on non compliance with various laws, rules and regulations and on weaknesses in internal control systems across the public sector entities and in particular the Donor Funded Projects, the ultimate responsibility for the maintenance of an effective and adequate system of internal control and a compliant framework lies with each Accounting Officer. Parliament and the Tanzanian public looks upon the Controller and Auditor General and the National Audit Office (NAO) for assurance in regard to financial reporting and public resources management in the Public Sector and in relation to the efficiency and effectiveness of programs administration. My office contributes through recommendations given towards improvements in the public sector performance. In this regard, the Government, Development Partners and my office each have a role to play in contributing to Parliamentary and public confidence building in public resources management. However, while the roles of public sector entities and NAO may differ, the desire for efficient utilization of public resources remains a common ground. In order to meet the Parliamentarian and the public s expectations, NAO continually reviews its audit approaches to ensure that the audit coverage provides an effective and independent review of the performance and accountability of x

11 public sector entities which are recipients of funds from Development Partners. Moreover, we wish to ensure that our audit coverage is well targeted and addresses priority areas so as to maximize our contribution in improving public financial management. Since our work acts as a catalyst in improving financial management, we continue discussing with our auditees on contemporary issues and developments that impact on public sector management, particularly financial reporting and good governance. I hope that the National Assembly, the Development Partners and the public in general will find the information in this report useful in holding the Accounting Officers to account for their stewardship role of Donor funds and their delivery of improved public services to Tanzanians which they are serving. In this regard, I will appreciate to receive feedback from the users of this report on how to further improve it in the future. Ludovick S.L. Utouh CONTROLLER AND AUDITOR GENERAL National Audit Office, Dar es Salaam. March, 2013 xi

12 Acknowledgement I would like to express my gratitude to those who created an enabling environment for me to discharge my Constitutional obligations. My sincere appreciation is extended to all our stakeholders including the Paymaster General, the Treasury and all Accounting Officers in the respective MDAS and LGAs who are managing and supervising the Donor Funded Projects financed in MDAs and LGAs for the much needed support, cooperation and for providing vital information needed for the preparation of this Annual General Report. Also, I would like to thank all the public servants throughout Tanzania mainland, whether in Central or Local Governments without forgetting the role of taxpayers and Development Partners to whom this report is dedicated. Their invaluable contributions in building the nation cannot be underestimated. I would like to acknowledge the professionalism and commitment of my staff in achieving our goals and undertaking the work associated with meeting our ambitious audit programs despite the fact that they have been working in very difficult conditions marked with insufficient funding, working tools, low salaries and sometimes working in very remote locations which are not easily accessible. Furthermore, I would like to express my thanks to members of my staff for their endeavors to once again enable me discharge my statutory responsibilities. With lots of appreciation, I am obliged to pay tribute to my family and the families of my staff members for their tolerance during our long absence from them in fulfilling these Constitutional obligations. Lastly, I would also like to thank the Printer for expediting the printing of this report for its timely submission on the statutory due date. May the almighty God bless you all as we commit ourselves to promote accountability and good governance on the use of the public resources of the country. xii

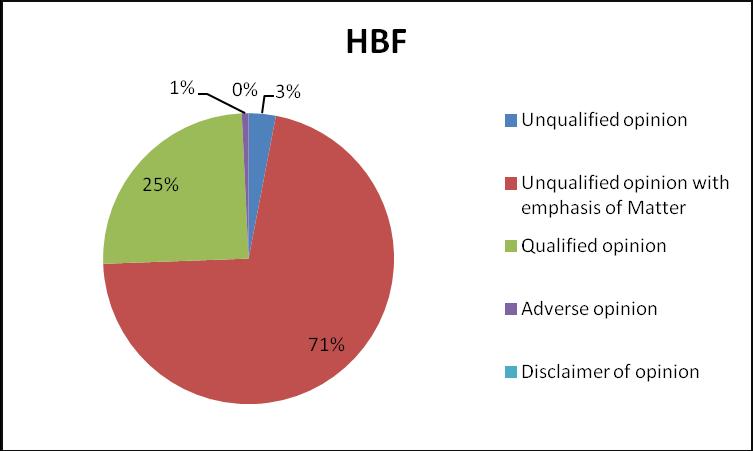

13 Executive Summary This year s Annual General Report for Donor Funded Projects is the second report and dwells on the following:- A. Background and General Information B. Basis of Audit Opinion C. Financial Performance of the projects D. Presentations and Analysis of Audit results E. Procurement Irregularities F. Financial Management G. Conclusion and Recommendations A: Background and General Information This part of the report gives a summary of the final results of the audit of the financial statements of Donor Funded Projects for the year ended 30 th June, The scope of audit in the Donor Funded Projects comprises: Water Sector Development Programme (WSDP), Agricultural Sector Development Programme (ASDP), Tanzania Social Action Fund (TASAF), Health Basket Fund (HBF) and other Donor Funded Projects. B: Basis of Audit Opinion The outcome of the audits of Donor Funded Projects for the year under review is as shown in the Table I below:- Table 1: Audit Opinion Summary Project Unqualifie d without emphasis of matter Unqualifi ed With Emphasis of Matter Qualifi ed Adver se Disclai mer Tota l TASAF ASDP WSDP HBF Sub total Other project Grand Total

14 C: Performance Report on Major Projects and Others This section gives highlights of performance report of major projects and others including sources of financing, expenditure details and unspent balances at the end of the year. There is a chapter on performance of major Donor Funded Projects in order to evaluate whether funds appropriated to the projects were exclusively spent for the intended purposes; their contribution to the economy and social development of this country, including challenges encountered; and whether value for money was realized. D: Presentations and Analysis of Audit Results This chapter gives analysis of the reasons which gave rise to issuance of a particular type of opinion to a Donor Funded Project. The analysis is aimed at amplifying the basic criteria used in forming the opinions as discussed in the preceding chapter. A total of 4 major Donor Funded Projects were audited in the financial year 2011/2012 constituting a total of 523 audit reports whereas 93 other Donor Funded Projects were also audited making a total of 616 Donor Funded Projects audit reports. E: Procurement Irregularities In the individual management letters submitted to each Accounting Officer, I have made a statement that almost all major Donor Funded Projects did not fully comply with the procurement laws as required by the Public Procurement Act No. 21 of 2004 and its related Regulations of My concern is on the level of understanding of the requirements of the country s procurement laws and regulations. F: Financial Management This chapter aims at providing information on the matters from the previous audit recommendations which had been issued separately to each individual accounting officer, funding analysis and current key audit findings. 2

15 G: Conclusion and Recommendations Finally, as per the mandate vested in me under Sect.10 of the Public Audit Act No. 11 of 2008, I have made a number of recommendations in Chapter Seven of this report, of which if implemented I believe will contribute in improving the management of Donor Funded Projects in our country. The conclusion and recommendations include the following among others: Accounting Officers do not adequately manage or supervise projects and in particular, address and implement audit recommendations. There are previous year s recommendations which remained unattended amounting to Shs. 20,289,040,011 as at the report date. There is a serious problem of non compliance with the requirements of MoUs which insists on adherence with the financial and procurement laws of Tanzania. During the year under review, we observed anomalies amounting to Shs.39,461,168,319 and Shs.5,036,540,269 in respect of procurement and financial management respectively. The Ministry of Finance should be strengthened and imposed stricter financial control on Accounting Officers and improve accounting of Government expenditures including Donor Funded projects. In addition, the Ministry has to ensure that all Accounting Officers prepare financial statements of the Donor funded projects under them and submit them for audit on time. There has been remarkable delay in release of funds from Development Partners and Treasury to project implementing partners. This has contributed in delay or non implementation of earmarked projects and also resulting in huge amounts of unspent balances at the end of the financial year amounting to Shs. 299,852,509,319, and USD 213,520,573 as at 30 th June,

16 Development Partners, the Ministry of Finance (Treasury) and PMO RALG should ensure timely release of funds earmarked for implementation of project activities to avoid delays in the fulfillment of projects objectives which in most cases results to have huge unspent project fund at year end and higher costs due to inflation. 4

17 CHAPTER ONE 1.0 BACKGROUND INFORMATION This report is issued following the comprehensive audit of the accounts and underlying documents of Donor Funded Projects pursuant to Article 143 (4) of the Constitution of the United Republic of Tanzania of 1977 (revised 2005) for the financial year 2011/2012. In 2010/2011, I issued the first general report on Donor Funded Projects together with the management letters and audit reports to each Accounting Officer separately. Therefore, outstanding matters in this report refer to the audited reports that were issued to the individual project Accounting Officers. 1.1 Audit of Donor Funded Projects I am required by Article 143 of the Constitution of the URT to audit the Public Accounts and all offices, Courts and authorities of the Government of Tanzania and Donor Funded Projects and submit my reports thereon to the President who shall cause them to be laid before Parliament. In discharging these duties, I am required in terms of Section 10 of the Public Audit Act No. 11 of 2008, to satisfy myself that:- All reasonable precautions have been taken to safeguard the collection of public money and that the law, directives or instructions relating thereto have been duly observed. All money disbursed have been expended and applied under proper authority and for the purpose intended by such authority and, adequate regulations exist for the guidance of storekeepers and stores accounts and that they have been duly observed. In addition, I have the duty, by virtue of the same Section to draw the attention of the Parliament to any apparent lack of economy in the expenditure or use of public money or stores. 5

18 1.2 Functions and Responsibilities of the CAG on the Donor Funded Projects My responsibility as an Auditor is to express an opinion on the financial Statements of Donor Funded projects based on my audit. I conducted my audit in accordance with the International Standards of Supreme Audit Institutions (ISSAIs) and such other procedures I considered necessary in the circumstances. In addition, Sect. 10 (2) of the PAA No. 11 of 2008 requires me to satisfy myself that the accounts have been prepared in accordance with the appropriate accounting standards and that reasonable precautions have been taken to safeguard the collection of revenue, receipt, custody, disposal, issue and proper use of public property, and that the law, directions and instructions applicable thereto have been duly observed and expenditures of public money have been properly authorized. Further, Sect 44(2) of the Public Procurement Act No.21 of 2004 and Reg. No. 31 of the Public Procurement (Goods, Works, Non-consultant services and Disposal of Public Assets by Tender) Regulations of 2005 requires me to state in my annual audit report whether or not the auditee has complied with the provisions of the Law and its Regulations. 1.3 Organisation of audit work at the National Audit Office The report provides a summary of the final results of the audit exercise, which was carried out by my office throughout the country in the course of the year under review. In order for my office to effectively handle this enormous task of auditing all the Donor Funded Projects in the country, it has established offices in the regions in Tanzania mainland for administrative purposes. Audit Staff It is worth noting the Government s efforts in improving the welfare of my staff, although there is a need for further improvement. A new organization structure for my office was recently approved by His Excellency Dr. Jakaya 6

19 Mrisho Kikwete the President of the United Republic of Tanzania. I have also submitted a proposal of enhanced salary package for my office to the President s Office Public Service Management. In the meantime, the audit scope has expanded considerably. There is an intention of expanding our coverage up to the district level. These efforts would require the approval of the Government and for it to set aside a budgetary provision to cater for this expansion. In keeping with current trends, the audit work is no longer confined to financial and compliance auditing. It is my intention to ensure that my audit staff are trained in performance, forensic, environmental,contract auditing, gender based auditing, management auditing, risk based auditing and Information Technology (Computer Assisted Audit Techniques CAATs) in order to be able to perform what is commonly referred to as comprehensive audit which encompasses the audit of every aspect in an organization.with the recent discovery of gas reserves and the possibility of discovery of oil reserves,it is the intension of my office to build the capacity of my auditors to audit on this area. 1.4 Scope and Applicable Audit Standards Scope of Audit The scope of audit covered on risk and materiality basis, proper expenditure and authorization, performance of Donor Funded Projects and physical verification. Audits were performed to satisfy myself as to the compliance with established Regulations, the exercise of economy, efficiency and effectiveness in the utilization of public resources. In addition, audit was performed to highlight irregularities, although not exhaustively, that have been reported on in some detail not only through regular inspection reports, but more emphatically through reference sheets to spotlight areas of serious concerns on proper accountability and need for stringent administration of public resources. 7

20 In the course of the audit, the findings are brought to the attention of the Accounting Officers of Donor Funded Projects being audited through an exit meeting. Accounting Officers are given an opportunity to respond to my observations, recommendations and related commentary, after which the Accounting Officers are issued with the audit report, signed by the Controller and Auditor General containing the audit opinion. A management letter signed by the Assistant Auditor General is also issued separately Applicable Auditing Standards I conducted my audit in accordance with the International Standards of Supreme Audit Institutions (ISSAIs) issued by the International Federation of Accountants (IFAC) in which Tanzania is a member through the National Board of Accountants and Auditors (NBAA) and such other procedures I considered necessary in the circumstances. These standards require that I comply with ethical requirements of planning and performing of the audit to obtain reasonable assurance of whether the financial statements are free from material misstatements. 1.5 Accounting Policies Financial statements of the DFPs are prepared according to the MoU requirements; although they all observe the Public Financial Management Systems of this country. Reg.53 of the Public Finance Regulations of 2001 (revised 2004) states that the accounting policies of the Government are so framed to ensure that the resources appropriated by Parliament are properly accounted for. In terms of the Public Finance Act No. 6 of 2001 (revised 2004) all revenues received by the Government shall be deposited into the Consolidated Fund. Payments out of the Consolidated Fund will be made through appropriations by Parliament. 8

21 1.6 Preparation and Submission of Financial Statements for Audit Responsibilities of the Accounting Officer - Central Government Sect. 25(4) of the Public Finance Act (PFA) No. 6 of 2001 (revised 2004), places responsibility on the Accounting Officer to prepare financial statements for each financial year which give a true and fair view of the receipts and payments made under the project as at the end of the financial year. It also requires management to ensure that the project management keeps proper accounting records which will disclose with reasonable accuracy its financial position and its responsibility in safeguarding the assets of the reporting entity Management Responsibilities to the Financial Statement - Local Government Financed Projects Where the Local Government Authority receives funds from the Development Partners, preparation of the financial statements is the responsibility of the Council s management as per Order No. 25(1) of the Local Authorities Financial Memorandum of 2009 and as per the signed Memorandum of Understanding between the Local Government Authorities and Development Partners. Order Nos.11 to 14 of the Local Authorities Financial Memorandum (LAFM) of 2009 requires the management to establish and support a sound system of internal control within the Council. In addition, Order No. 25(1) places responsibility on the Council s management to prepare the financial statements of Donor Funded Projects in accordance with the laws, regulations, directives issued by the Minister responsible for Local Governments, the Local Government Financial Memorandum; the International Public Sector Accounting Standards (IPSASs) and the MOU. 1.7 Internal Control Systems Internal Control System refers to all means by which Government resources are directed, monitored, and measured. Internal controls play an important role in 9

22 preventing and detecting frauds/misappropriations and protecting the public resources, both tangible and intangible. Implementing an effective internal control structure is an essential responsibility of the management of the entity. 10

23 CHAPTER TWO BASIS OF AUDIT OPINION 2.0 Introduction The auditor's opinion is a formal opinion, or disclaimer thereof, issued by an independent external auditor as a result of an audit on the financial statements or evaluation performed on an entity or subdivision thereof (called an auditee ). The opinion is provided to the user of these financial statements as an assurance service in order for the user to make decisions based on the results of the audit. An auditor s opinion is considered an essential tool when reporting financial information to users. In the public sector, it is intended to advise Parliament and other users on whether Donor Funded Project s financial statements have been prepared in conformity with the International Public Sector Accounting Standards (IPSAS) and in the manner required by Sect. 25(4) of the Public Finance Act, 2001 (revised 2004) and Order Nos. 11 to 14 of the Local Authorities Financial Memorandum (LAFM) of 2009 including the Donor Funded Project s MoUs compliance with laws and regulations. In ordinary language, the opinion is an assurance on whether the financial information presented by the auditee is materially correct and trustworthy for making various decisions such as the Government s decision on whether the allocations made to Donor Funded Projects have been spent for the benefit of the citizens. It is important to note that the auditor s opinion on the financial statements is on whether the information presented is correct and free of material misstatements, whereas all other determinations are left for the user to decide. 11

24 2.1 Types of Audit Opinion There are five common types of auditor s opinions, each one presenting a different situation encountered during the auditor s work. The five opinions are as follows: (i) Unqualified Opinion Unqualified Opinion is sometimes regarded by many as equivalent to Clean audit opinion. This type of opinion is issued when the financial statements presented are free of material misstatements and are in conformity with the International Public Sector Accounting Standards (IPSAS) including compliance with laws and regulations. It is the best type of an audit opinion an auditee may receive from an external auditor. (ii) Unqualified Opinion with Emphasis of Matter In certain circumstances, the audit opinion may be modified by adding an emphasis of matter paragraph to highlight a matter(s) affecting the financial statements. The addition of such an emphasis of matter paragraph does not affect the audit opinion.fthe main objective of the emphasis of matter paragraph is to bring closer understanding of the situation obtained in the audited entity, despite the unqualified opinion given. (iii) Qualified Opinion The nature of the circumstances giving rise to qualification will generally fall into one or two categories. Where there is an uncertainty which prevents the auditor from forming an opinion on a matter (Uncertainty). Where the auditor is able to form an opinion on a matter but this opinion conflicts with the view given by the financial statements (Disagreement in best practice or records keeping and non compliance with Laws and Regulations). 12

25 (iv) Adverse Opinion An Adverse Opinion is issued when it is determined that the financial statements are materially misstated and, when considered as a whole, do not conform to the International Public Sector Accounting Standards (IPSAS), cash and accrual basis of accounting, essentially stating that the information contained is materially incorrect, unreliable, and inaccurate in order to assess the results of operations. The wording of the adverse opinion is clear in which I state that the financial statements are not in accordance with the International Public Sector Accounting Standards (IPSAS). (v) Disclaimer of Opinion A Disclaimer of Opinion, commonly referred to simply as a Disclaimer, is issued when I could not form, and consequently refuses to present, an opinion on the financial statements. This type of opinion is expressed when I tried to audit but could not complete the work due to various reasons and therefore I do not issue an opinion. Certain situations where a disclaimer of opinion may be appropriate includes: a lack of independence, or, when there are significant scope limitations, whether intentional or not, or when the auditee refuses to provide evidence and information to me in significant areas of the financial statements and when there are significant uncertainties within the auditee. 2.2 Audit Opinions Issued on Donor Funded Projects The following table presents the types of audit opinions issued to Donor Funded Projects for the financial year 2011/2012: 13

26 Project Table 2: Audit Opinions Issued Unquali fied without emphas is of matter Unqualifi ed With Emphasis of Matter Quali fied Adver se Disclai mer Total TASAF ASDP WSDP HBF Sub total Other project Grand Total Opinion 2011/ % 2010/ % Unqualified without emphasis of matter Unqualified with emphasis of matter Qualified Adverse Disclaimer Total From the table above, it can be analysed in a pie chart as follows: 14

27 15

28 16

29 17

30 3.0 Introduction CHAPTER THREE FINANCIAL PERFOMANCE OF THE PROJECTS This chapter gives a detailed analysis of the portfolio of financial performance of WSDP, TASAF, ASDP, HBF and other audited Donor Funded Projects for the financial year 2011/2012. These projects have been financed by the Government of Tanzania and various Development Partners whose financial contribution and implementation status are presented below: 3.1 Water Sector Development Programme Financial Performance of the Water Sector Basket Fund (a) Holding Account The Government of the United Republic of Tanzania and the Development Partners committed to contribute to the Water Sector Basket Fund Holding Account. During the financial year 2011/2012, there was a total sum of USD. 67,279, in which USD.52,571, was received during the year while USD.14,707, was in respect of the opening balance. Funds transferred during the year was USD.37,544, in which USD.36,581, was transferred to the Ministry of Water and Irrigation and USD.963, was transferred to the Ministry of Health and Social Welfare leaving unspent balance of USD.29,734,919 as at 30 th June, 2012 as shown in Table 3 below: Table 3: Financial performance Details Amount (USD) 2011/2012 Opening balance 14,707, KFW 10,822, IDA 31,510, DFID 9,702, Ministry of Water 536, Total funds Available 67,279,

31 Less Transfers Ministry of Water and Irrigation 36,581, Ministry of Health and Social 963, Welfare Total transfers 37,544, Closing Balance 29,734, (b) Financing of the Water Sector Development Programme During the year under review the Government of Tanzania and Development Partners released Shs. 235,655,721,544 for WSDP projects. In addition, there was an opening balance of Shs. 24,578,395, together with outstanding advances of Sh.47,329,118,931 which in total made Shs. 307,563,235,875 available for use in implementing various WSDP activities in the country. The WSDP financing for the financial year 2011/2012 is as shown in Table 4 and 5 below: Table 4: Source of Funds for WSDP 2011/2012 Donor/Government Amount (Shs) GoT Contributions 26,082,467,232 DPs Contribution to Basket F und 181,264,362,674 DPs Contribution to Earmarked 28,495,778,731 Projects Other sources-community Contribution 2,152,981,712 Adjustment: Gain/(Loss) due to Exchange rate fluctuations (2,339,868,805) Total Contribution/released 235,655,721,544 Add: 24,578,395,401 Opening balance as on 1/7/2011 Outstanding Advances 47,329,118,931 Total fund available during the year 307,563,235,875 19

32 Table 5: Funds Contributed by DPs to WSDP under Basket arrangement 2011/2012 Name of Development Amount ( Shs.) Partner IDA 49,169,068, Germany (KfW) 20,782,467, AfDB 79,123,840, Royal Netherland Embassy 17,150,886, DFID 15,038,100, TOTAL 181,264,362, Funds Utilization Review of the Statement of Receipts and Payments noted that during the year under review, the WSDP had total funds available of Shs. 307,563,235,875 while total expenditure was Shs. 148,926,145,182 resulting to a closing balance of Shs. 158,637,090,693 as reflected in Table 6 below: 20

33 Table 6: Receipts and Payments 2011/2012 Description Amount (Shs.) Amount (Shs.) Amount of Funds Available 307,563,235,875 Expenditure Components wise Water Resources 5,674,821,444 Management Rural Water and 33,607,138,606 Sanitation Services Urban Water and Sanitation Services 100,625,494,220 Water Sector Institutional Strengthening and Capacity Building 9,018,693, ,926,145,182 Closing balance as at 30 th June, ,637,090,693 Further, it was noted that during the financial year 2011/2012, 131 Councils had total funds available amounting to Shs 88,303,090,628 to implement WSDP activities in the Councils. However, as at 30 th June, 2012 the Councils closed accounts with an unspent amount of Shs.64,556,055,033 equal to 73% of the amount available. Details are as shown in Annexure I. 3.2 Tanzania Social Action Fund (TASAF II) Project Financing The TASAF II project life span is four (4) years starting from the year 2005/2006 and is financed by the World Bank through the International Development Association (IDA) and the Government of the United Republic of Tanzania (GoT). The DFA was signed between the GoT and IDA on 19 th January, The total TASAF II IDA funding is USD million comprising of USD million credit and USD 21.0 million grant. A total sum of Shs 55,701,277, which includes Shs. 14,848,919, being opening balance from previous year was received from various sources during the year under review. However, up to 30 th June 2012 there was unspent balance of Shs. 12,815,934,

34 indicating that Shs 42,885,343, was spent as shown in Table 7 below: Table 7: Source and Utilization of Funds for TASAF Receipts from Amount (Shs) 2011/2012 Amount (Shs) 2010/2011 Opening balance 14,848,919, ,471,221, IDA 39, ,648,178, Government 0 Contribution 0 Others 1,564,073, ,981,100, Total receipts for the 83,100,501, year 55,701,277, Total expenditure 42,885,343, ,251,581, Closing balance 1/7/ ,815,934, ,848,919, Funds Released to LGAs Total funds available in the LGAs during the year amounted to Shs. 39,915,181,983 which included an opening balance of Shs.6,376,697,957 being unspent monies during the year 2011/2012. However as at 30 th June, 2012 the Councils closed accounts with unspent amount of Shs.5,807,528,697 equal to 14% of the amount available. The huge closing balance was caused by various Councils failing to implement projects as planned. (Refer Annexure II). Table 8: Source of Funds for TASAF Details Amount (Shs.) 2010/2011 Opening balance 6,376,697,957 Amount received 33,538,484,026 Funds available during the year 39,915,181,983 Amount spent 34,107,653,286 Balance as at 30 th June,2012 5,807,528,697 In addition, a sum of TZS 39,288,285, (equivalent to USD 24,252,028.16) was requested during the year as part of the Additional Financing I and II (USD 30.0 million and USD 35.0 million respectively) for addressing food insecurity in selected 22

35 LGAs that were experiencing severe food insecurity due to persistent drought and to supplement efforts of completing uncompleted subprojects and making them functional. Further funding of TZS 1,564,073, (Equivalent to USD 965,477.26) from OPEC II was requested and received for Mtwara and Lindi regions to finance various projects. 3.3 Agriculture Sector Development Programme (ASDP) Introduction The programme presents an integration of the ASDP National and Local components into one consolidated set of interventions to be financed through the ASDP Basket Fund. This program supersedes the ASSP and DADP. The Government of Tanzania has adopted an Agricultural Sector Development Strategy (ASDS) which sets the framework for achieving the sector s objectives and targets. An Agricultural Sector Development Programme (ASDP) Framework and Process Document, developed jointly by the five Agricultural Sector Lead Ministries (ASLMs), provides the overall framework and processes for implementing the ASDS. Development activities at national level are to be based on the strategic plans of the line Ministries while activities at District level are to be implemented by Local Government Authorities (LGAs), based on District Agricultural Development Plans (DADPs). The DADPs are part of the broader District Agriculture Development Plans (DADPs) ASDP Basket Fund Holding Account Maintained at the Treasury The Agricultural Sector Development Programme Basket Fund (ASDP) is financed by contributions and loans from Development Partners through the embassy of Ireland, Japan, the European Union, International Development Association, and IFAD. During the year under review, the Programme received a total of USD. 60,487, from the development partners and there was an opening balance of USD 12,095, from the previous year, resulting into total funds available for the year USD. 72,583, On the other hand, the transfers from programme holding account amounted to USD.57,780,498.22, leaving USD 23

36 14,803, as closing balance at the end of the year as detailed in the Table 8 below: I am highly concerned with unspent balance from implementing agencies USD 1,011, and funds not transferred to project at the end of the year USD. 14,803, which in our view has caused project planned activities not implemented. Table 9: Holding Account financing Description 2011/12 Account No : Amount (USD) Opening Balance 12,095, IDA World Bank 41,222, IFAD Loan 18,253, Embassy of Ireland - Embassy of Japan - Unspent balance from Project 1,011, Fund available 72,583, Transfers Ministry of AFS&C 9,819, Local Government Authorities 44,652, Min. of Livestock and Fisheries 2,675, Prime Ministers Office RALG 184, Min. of Industries Trade and Marketing 447, Ministry of Water and Irrigation Bagamoyo Total transfers 57,780, Closing balance 14,803, Funds transferred to the ministries listed above were mainstreamed in the Development Vote of the respective ministries and audited accordingly Fund transferred close to the end of the financial year USD 863, I noted that on 25 th June 2012 five days before closing date of the financial year, the Ministry of Finance transferred a total amount of USD 863, equivalent to Shs 1,367,983, to the implementing agencies vide letter with reference number 24

37 EB/AG/20/03/VOL.V/70 for implementation of approved activities under the Agriculture Sector Development Programme (ASDP). However, there were no justifications to substantiate delays in releasing funds to respective implementers keeping into consideration that all unspent balances at the end of the financial year are supposed to be surrendered to the holding account. Overall transfer of funds for the year 2011/2012 was USD.57,780, being 20 per cent lower ( a decrease of USD14,375,699.85) compared with total transfer of USD.72,156, in financial year 2010/2011. This decrease has negative impact on implementation of the earmarked activities in the year Agriculture Sector Development Programme (ASDP) Local Government Authorities Financing The Agriculture Sector Development Programme in LGAs for the financial year 2011/2012 had total funds available of Shs106,781,540, which included Shs. 27,326,841, being the balance brought forward from the previous year for ASDP activities. Detailed analysis for each Council is explained in annexure III. As at 30 th June, 2012, there was an unspent balance of Shs.32,237,919, indicating that Councils managed to spend Shs.74,543,621, equivalent to per cent of the total funds available as shown in Table 10 below: Table 10: Source of Funds for ASDP 2011/2012 Details Amount (Shs.) Opening balance 27,326,841, Amount received 79,454,699, Funds available during the year 106,781,540, Amount spent 74,543,621, Balance as at 30 th June, ,237,919,

38 3.3.5 Agriculture Sector Development Programme (ASDP) Prime Minister s Office Local Government Authorities Financing PMO RALG had total funds available for ASDP during the financial year of Shs 300,000,000. As at 30 th, June, 2012 there was an unspent balance of Shs. 4, indicating that the project spent Shs. 299,995, equivalent to 100% of available funds as can be elaborated in Table 11 below: Table 11: PMO-RALG Financing in 2011/2012 Details Amount (Shs) Opening balance as at 01/07/ Add: Funds received during the year: 300,000, Total funds available during the 300,000, financial year Less: Total Expenditure for 299,995, /2012 Balance carried down as at 4, /06/ Health Basket Fund Programme Financing Introduction Donors finance the Health Basket funds into a Holding Account at the Bank of Tanzania and thereafter channel these funds to the Ministry of Health and Social Welfare (MoH&SW), PMO RALG and LGAs on a quarterly basis through the Exchequer Account. The funding follows the normal GoT system whereby donors financial commitments are included as part of the annual budget of the respective entity. Accordingly, Health Basket Funds are not maintained in a separate account but commingled in Development Account for ministries and Account Number 6 in the Councils, which is also used for health funds from other sources Financing of Health Basket Financing Fund (HBFF) The source of funds for the Health Basket Financing is contributions from Development Partners. During the year under review, the Programme received a sum of USD 104,121, from the Development Partners as shown in the table below and USD 386, was surrendered by MH&SW. There was an opening balance of USD 3,806, thus making total funds 26

39 available for the year to be USD 108,314, Funds for the Programme are deposited in the HBFF deposit Dollar Account maintained at the Bank of Tanzania under the supervision of the Accountant General as shown in Table 12 below: Table 12: Source of Funds for HBF 2011/2012 Amount ( USD) Development Partners UNDP 600, Danish Embassy 17,942, Ireland 8,810, Nertherlands 20,694, CIDA 24,492, KFW 9,430, Switzerland 3,244, UNICEF 1,000, Norway 5,216, IDA 10,000, Sub-total from development partners 104,121, Unspent Balance for Financial year 2010/ , Opening balance 01 July ,806, Grand total 108,314, Transfer of Funds to Beneficiaries amounting to - USD 106,152, During the year under review, a sum of USD 106,152, was transferred to various beneficiaries leaving a closing balance of USD 2,161,094.9 as at 30 th June 2012 as shown in Table 13 below: Table 13: Transfers of Funds to Beneficiaries Receipts Amount (USD) 2011/2012 Amount (USD) 2010/2011 Unspent Balance for Financial 3,227, year 2010/ , Opening balance 01 July ,806, ,228, UNDP 600,000,00 1,450,

40 Danish Embassy 17,942, ,189, Ireland 8,810, Nertherlands 23,384, ,879, CIDA 24,492, ,506, KFW 9,430, Switzerland 3,244, ,051, UNICEF 1,000, ,500, Norway 5,216, ,333, IDA 10,000, ,000, Total receipts 108,314, ,382, TRANSFERS Ministry of Health & Social 38,708, Welfare 52,414, Local Government Authorities 53,297, ,630, PMO-RALG 441, , Total transfers 106,152, ,804, Closing balance 2,610, , Ministry of Health and Social Welfare Programme Financing Donors are depositing funds into Basket funds holding account at the Bank of Tanzania and thereafter the financing is channeled to the Ministry of Health and Social Welfare (MOHSW) on a quarterly basis through the Exchequer system. The funding to the Ministry follows the normal GoT financial management system whereby donors financial commitments are included as part of the Ministry s annual budget. Funds from the Basket are released to MOHSW on a quarterly basis in the normal Government Exchequer Issues System after obtaining approval from the Basket Financing Committee. Basket Funds are therefore managed as part of GOT resources and accounted for as part of MOHSW voted expenditure. Accordingly, Basket Funds are not maintained in a separate account but commingled in the Development Account, which is also used for funds from other Development sources. 28

41 During the year ended 30 th June, 2012 the Ministry received a total sum of Shs 71,043,000,000. Actual Expenditure incurred during the year amounted to Shs.70,081,984,500 Leaving a unspent balance of Shs.1,024,015, 500 as at 30 th June, 2012 of which Shs.700,000,000 was transferred to Deposit Account and Shs.324,015,500 was transferred to Holding Account at BOT as shown in Table 14 below: Table 14: Source of Funds for HBF MoHSW -2011/2012 Details Amount (Shs.) Received during the year 71,043,000,000 Expenditure 70,081,984,500 Unspent balance 1,024,015, 500 transferred to deposit Account 700,000,000 Transferred to the Holding Account 324,015, PMO-RALG The Health Sector Program Support (HSPS) is financed by Ireland, Netherland, Norway, Germany and World Bank, Swiss Agency for Development and Cooperation. During the year under review, the programme received a total of Shs. 687,000,000. According to the statement of receipts and payments the PMO RALG had total funds available for HSPS during the financial year of Shs 913,514, including opening balance of Shs 226,514, However, as at 30 th, June, 2012 there was an unspent balance of Shs.512,637, equivalent to 56% indicating that the project spent only Shs 400,877, equivalent to 44% as per details shown in Table 15 below: 29

42 Table 15: Source of Funds for HBF PMO-RALG Details Amount (Shs) Opening balance as at 01/07/ ,514, Add: Funds received during the year 687,000,000,00 Total funds available during the financial year 913,514, Less: Total Expenditure for 2011/ ,877, Balance carried down as at 30/06/ ,637, Local Government Authorities During the year under review, the LGAs financial performance was as reflected in Table 16 below and detailed analysis as shown in Annexure IV. Table 16: Sources of Funds for HBF LGAs 2011/2012 Details Amount (Shs.) Opening balance at 1/7/2011 8,782,526,242 Add: Funds received during 80,435,231,856 the year Total funds available during 88,805,785,681 the year Less: Total expenditure 76,812,025,208 Balance carried down 30/6/ ,313,520, Other Projects Global Fund Global Fund Accounts Maintained at the Treasury During the financial year under review, the Ministry of Finance received a total of USD 102,798,691 which is equivalent to Shs. 161,933,708, from Global Fund, 30

43 out of this an amount of Shs. 155,925,146, was disbursed to the Ministry of Health and Social Welfare (MoHSW), Shs. 5,438,151, to Tanzania Commission for AIDS (TACAIDS) and Shs. 570,410, to Prime Minister s Office Regional Administration and Local Government as reflected in Table 17 below:- Table 17: 2011/2012 Details Receipts and Disbursement of Global Fund- Amount (Shs) Amount released by Global Fund to Treasury 161,933,708, Transfer To: MoHSW 155,925,146, TACAIDS 5,438,151, PMO - RALG 570,410, National Malaria Control Programme (ACT) During the year 2011/2012 the National Malaria Control Programme (NMCP) had a total of Shs 32,162,839,278 available for implementation of Global Fund activities. However, as at 30 th June, 2012 there was unspent balance of Shs. 2,818,698,100, indicating that NMCP spent Shs. 29,344,141,578 i.e. 91% as analyzed in Table 18 below: Table 18:- Sources of funds for ACT -2011/2012 Details Amount (Shs.) Opening balance at 1/7/ ,175,979 Add: Fund received during the year 32,099,663,699 Total funds available during the year 32,162,839,678 Less: Total expenditure for 2011/ ,344,141,578 Balance carried down 30/6/2012 2,818,698, Diagnostic Service Section (DSS) During the year 2011/2012 the Diagnostic Service Section (DSS) had a total of Shs 3,947,885,860 available for implementation of Global Fund activities. However, as at 30 th June, 2012 there was unspent balance of Shs 31

44 1,596,406,018, indicating that DSS spent only Shs. 1,451,479,842 i.e. 48% as analyzed in Table 19 below: Table 19: Sources of funds for DSS -2011/2012 Details Amount (Shs.) Opening balance at 1/7/2011 2, 939,824,392 Add: Fund received during 108,061,468 the year Total funds available during 3,047,885,860 the year Less: Total expenditure for 1,451,479, /11 Balance carried down 1,596,406,018 30/7/ The Global Fund Round Six Disbursed to the National TB and Leprosy Programme ( NTLP) During the year 2011/2012 the National TB and Leprosy Programme (NTLP) had a total of Shs 9,549,945,620 available for implementation of Global Fund activities. However, as at 30 th June, 2012 there was unspent balance of Shs. 1,360,481,593, indicating that NTLP spent Shs. 7,848,648, i.e. 83% as analyzed in Table 20 below: Table 20: Source of funds for the National TB and Leprosy Programme (NTLP) -2011/2012 Details Amount (Shs.) Opening balance 3, 504,768,943 Add:Fund received during the year 6,045,176,677 Unpresented cheques 340,815,604 Unutilized imprest NIL Intrest earned NIL Total funds available during the year 9,549,945,620 32

45 Less: Total expenditure 7,848,648,423 Balance carried down 1,360,481, Global Fund Round Eight-National Nets Support Programme During the year 2011/2012 the National Nets Support Programme had a total of USD 24,632,497 available for implementation of Global Fund activities. However, as at 30 th June, 2012 there was unspent balance of USD 1,065,380 indicating that NNSP spent USD. 23,567,117 i.e. 96% as analyzed in Table 21 below: Table 21: Sources of funds for Round Eight-National Nets Support Programme -2011/2012 Details Amount (USD) Opening balance at 01/07/ ,704,329 Add: Fund received during the year 3,928,168 Total funds available during the year 24,632,497 Less: Total expenditure for 2011/ ,567,117 Balance carried down 30/06/2012 1,065, National AIDS Control Programme (NACP) During the year 2011/2012 the National AIDS Control Program (NACP) had a total of Shs 6,038,729,953 available for implementation of Global fund activities. However, as at 30 th June, 2012 there was unspent balance of Shs.1,932,144,951, indicating that NACP spent only Shs. 4,106,585,003 i.e. 68% as analyzed in Table 22 below: Table 22: Source of funds for NACP -2011/2012 Details Amount (Shs.) 2011/2012 Opening balance 4,427,030,560 Add: Funds received during the year 1,611,699,394 Other income(stale cheques) 33

46 Total funds available during the year 6,038,729,954 Less: Total expenditure 4,106,585,003 Balance carried down 1,932,144, Monitoring and Evaluation Global Fund Round 8 as Implemented by the Ministry of Health and Social Welfare During the year 2010/2011 the Ministry of Health and Social Welfare had a total of Shs 102,569,551 available for implementation of Global fund activities. However, as at 30 th June, 2012 there was unspent balance of Shs. 58,774,401.14, indicating that the Ministry of Health and Social Welfare spent only Shs. 43,795, i.e. 43% as analyzed in Table 23 below: Table 23: Source of funds for Monitoring and Evaluation Global Fund Round 8 as Implemented by the Ministry of Health and Social Welfare -2011/2012 Details Amount (Shs.) Opening balance at 1/7/ ,826, Add: Fund received during the year 57,742, Total funds available during the year 102,569, Less: Total expenditure for 2011/ ,795, Balance carried down 30/6/ ,774, Global Fund Round 8 BOT USD Account During the year 2011/2012 the Global Fund Round 8 USD Account had a total amount of USD 94,330,124 available for implementing Global Fund activities. However, as at 30 th June, 2012 there was unspent balance of USD 12,764,287, indicating that Global fund Round 8 USD Account spent USD 81,565,837i.e.86% as analyzed in Table 24 below: Table 24: Source of funds for Global Fund Round 8 BOT USD Account -2011/

47 Details Amount (Shs.) Opening balance at 1/7/ ,156,536 Add: Fund received during the year 67,173,588 Total funds available during the year 94,330,124 Less: Total expenditure for 2011/ ,565,837 Balance carried down 30/6/ ,764, Global Fund implemented by Medical Stores Department (MSD) During the year 2011/2012 the Medical Stores Department (MSD) had a total of Shs. 99,996,669,157 available for implementation of Global Fund activities. However, as at 30 th June, 2012 there was unspent balance of Shs. 31,920,182,964, indicating that MSD spent only Shs. 56,878,585,838 i.e. 60% as analyzed in Table 25 below: Table 25: Source of funds for Medical Stores Department (MSD) -2011/2012 Details Amount (Shs.) 2011/2012 Opening balance at 1/7/2011 4,788,172,713 Add: Fund received during the year 95,208,496,444 Total funds available during the year 99,996,669,157 Less: Total expenditure for 2011/12 59,878,585,838 Balance carried down 30/7/ ,118,083, Health System Strengthening- Global Fund Round 9 During the year 2011/2012, the Ministry of Health and Social Welfare had a total of Shs.7,365,984, available for implementation of Global Fund Round 9 activities. However, as at 30 th June, 2012 there was unspent balance of Shs. 2,787,926,698, indicating that the Ministry of Health and Social Welfare spent only Shs.4,578,057,698.8 i.e. 62% as analyzed in Table 26 below: 35

48 Table 26: Source of funds for Health system strengthening- Global Fund Round /2012 Details Amount (Shs.) Opening balance at 1/7/ ,800, Add: Fund received during the year 6,890,184, Total funds available during the year 7,365,984, Less: Total expenditure for 2011/12 4,578,057, Balance carried down 30/7/2012 2,787,926, Global Fund PMO-RALG During the year 2011/2012, the PMO-RALG had a total of Shs 400,432,750 available for implementation of Global Fund Round 9 activities. However, as at 30 th June, 2012 there was unspent balance of Shs. 75,795,340, indicating that PMO-RALG spent Shs. 324,637,410 i.e. 81% as analyzed in Table 27 below: Table 27: Source of funds for Global Fund PMO-RALG /2012 Details Amount (Shs.) Opening balance at 1/7/ ,944,387 Add: Fund received during the year 90,410,575 Add: Fund received from various debtor 246,077,788 Total funds available during the year 400,432,750 Less: Total expenditure for 2011/ ,637,410 Balance carried down 30/6/ ,795, Global Fund (GF) TACAIDS Funds During the year 2011/2012, the Tanzania Commission for AIDS had a total of Shs. 6,193,977,084 available for implementation of Global Fund activities. However, as at 30 th June, 2012 there was unspent balance of Shs. 1,419,815,924 indicating that the TACAIDS spent Shs. 4,774,161,160 i.e. 77 % of the funds available as analysed in Table 28 below: Table 28: Source of funds for Global Fund (GF) TACAIDS Funds 2011/2012 Details Amount (Shs.) 36

49 Opening balance 932,643,027 Add: Fund received during 5,261,334,057 the year Total funds available 6,193,977,084 during the year Less: Total expenditure 4,774,161,160 Balance carried down 1,419,815, Other Projects (excluding Global fund) During audit, the financial performance of other projects which adds to 93 in total were evaluated. Key aspects considered were contributions from Development Partiners, opening balances, amounts received; expenditure incurred during the year and amounts remaining as unspent balances at the year end. See detailed analysis in Annexure V. CHAPTER FOUR PRESENTATION AND ANALYSIS OF AUDIT RESULTS 37

50 4.0 Introduction This chapter analyses the grounds which gave rise to issuance of a particular type of opinion to a Donor Funded Project. The analysis is aimed at amplifying the basic criteria used in forming the opinions as discussed in the preceding chapter. A total of four (4) major Donor Funded Projects were audited in the financial year 2011/2012. Another ninety three (93) other Donor Funded Projects were also audited making a total of ninety seven (97) Donor Funded Projects with a total of 616 audit reports and management letters issued. 4.1 Major Donor Funded Projects TANZANIA SOCIAL ACTION TRUST FUND (TASAF) Introduction The Tanzania Social Action Fund Project Phase II was established on 19 th January, 2005 when the agreement between the Government of the United Republic of Tanzania and the World Bank through the International Development Association (IDA) and the Development Financing Agreement was signed. The Second Tanzania Social Action Fund Project (TASAF II) which forms part of the National Poverty Eradication Strategy was established to empower Communities to access opportunities that contribute to improved livelihood linked to the Millennium Development Goals (MDG), an indicator targets in the Tanzania Poverty Reduction Strategy (TPRS). According to the terms of reference in the TASAF Operational Manual, the objective of conducting the audit is to enable the Controller and Auditor General to express an independent opinion on the TASAF project financial statements for the year under review. 38

51 Operational Objectives The Second Tanzania Social Action Fund Project (TASAF II) was established to empower Communities to access opportunities that contribute to improved livelihood linked to the Millennium Development Goal (MDG) indicator targets in the Tanzania Poverty Reduction Strategy (PRS). TASAF II also aims at:- (i) (ii) (iii) (iv) Promoting formation of voluntary saving groups. Providing support services to communities that will contribute to increased availability and use of basic Social and environment service in line with Specified MDGs targets. Providing employment opportunities to able-bodied individuals in food insecure households, so as to increase their cash income, skills and opportunities of working in VFC financed public work programmes. Providing assistance to households with vulnerable individuals which include ophans, disabled, elderly, and those infected or affected by HIV/AIDS, among others to enable them manage sustainable economic activities Project Management (i) National Level TASAF II Project at the National level is managed by autonomous TASAF Management Unit (TMU) headed by the Executive Director under the President s Office. TMU Coordinates and executes the daily activities of TASAF II. The Executive Director of TASAF reports to the National Steering Committee (NSC) on all the financial and administrative matters connected with the execution of TASAF II programmes. (ii) District Level 39

52 At the District level, the District Executive Directors (DED)/ Municipal Directors (MD) as the head of the District Councils/Municipals for the Local Government team, provide the needed support to TASAF II management team led by the Village Fund Coordinators (VFC). The VFCs are appointed by the District or Local Councils from among qualified existing Council/Municipal Staff in accordance with the terms of references provided by the TMU. The VFC coordinate the activities of TASAF II in the District Council including sensitization and facilitation of the communities on matters pertaining to the implementation/execution of approved community subprojects. VFC is accountable to the TMU on behalf of the Council Directors. According to the terms of reference in the TASAF Operational Manual, the objective of conducting the audit is to enable the Controller and Auditor General to express an independent opinion on the TASAF project financial statements for the year under review. The under listed Councils were audited in the financial year 2011/2012 and the type of audit opinion issued and reasons for giving rise to the issuance of such opinion are as indicated in the respective tables hereunder:- (a) Table 29: Councils issued with unqualified opinion Twenty eight (28) Councils out of a total of 127 Councils audited which is 22% managed to be issued with unqualified audit opinion as listed below: SN Council SN Council 1 Bukombe DC 15 Mtwara MC 2 Korogwe TC 16 Newala DC 3 Moshi MC 17 Mtwara DC 4 Mwanga DC 18 Njombe DC 5 Tanga CC 19 Mvomero DC 6 Lindi MC 20 Ukerewe DC 7 Nachingwea DC 21 Kilosa DC 8 Lindi DC 22 Ilala MC 40

53 9 Mkuranga DC 23 Ulanga DC 10 Kibaha TC 24 Singida DC 11 Bukoba MC 25 Singida MC 12 Iramba DC 26 Tunduru DC 13 Kibondo DC 27 Mbozi DC 14 Temeke DC 28 Morogoro MC (b) Table 30: Councils issued with unqualified opinion with emphasis of matters: A total of seventy five (75) Councils out of a total of 127 Councils audited which is 59 % managed to be issued with unqualified audit opinion with matters of emphasis as listed below: 1 Bunda DC Payments made but not supported by activity reports Shs. 3,917,500 Substandard works on completion of one Staff House at Bulamba Secondary School Shs.29,000,600. Uncompleted works on the construction of Busamba- Namalama road Shs 31,920,000 Uncompleted works on the Administration Block at Kwiramba Secondary School worth Shs.40,237,700 2 Musoma DC Implementation of Auditor s Recommendations Council Management has not responded to the observation raised by Auditors in TASAF Financial Statements for the previous financial year ended 30 th June 2011 and also no response for the issues raised for the year under review. Uncompleted projects worth Shs. 523,844, Unimplemented activities worth Shs.174,123,880 3 Musoma MC Toilet constructed and completed but not in use in Kigera Primary School Shs.9,900,000 Uncompleted works on construction of staff toilet at Mwisenge Secondary School Shs.7,937, Uncompleted works on construction of classrooms, 41

54 staff latrine, and administration block at Baruti Secondary School Shs.17, 752, Serengeti DC Unproduced BOQ and contract on the rehabilitation of Gesarya Dispensary Shs.12,536,900 5 Tarime DC Uncompleted works upon construction of Administration block at Masanga Secondary School Shs.19,453,000 Planned activities worth Shs.133, 382, were partially implemented. 6 Chato DC Non respond to implemention of previous years auditor s recommendations valued Shs. 178,837, Questionable and improper implementation of TASAF project at Kanyindo Primary School Shs. 11,149, Kahama DC Biological Assets, Agricultural assets and Monitoring and supervision expenses worth Shs. 106,872, were included in the figure of Property Plant and Equipment contrary to IPSAS17(6)(a)-(b). Accelerated Food Security Programme Activities not Supported by Certificate of Completion Shs. 401,317, Shinyanga DC Previous year s recommendations raised amounting to Shs. 105,644,027 Nyashimbi Charco dam was not in use with reason behind that the area is dry and has no enough water, hence delay in delivering expected benefits to the Communities of Nyashimbi Village. 9. Bariadi DC Council managed to implement projects worth Shs. 56,149,714 but had not prepared and submitted projects justification reports to the relevant Authorities as at the time of audit. Two construction works worth Shs.461, 254,234 at Nkololo and Mehembe villages have not been completed; hence delay in delivering expected benefits to the intended communities. 42

55 10 Kishapu DC A payment voucher worth Shs. 1,650,000 had been missing from relevant batches. A scrutiny of the Statement of Comparison of Budget and Actual - by nature revealed that Shs. 888,840 was spent over and above the approved budget. Audit review of the project performance and physical verification revealed some project activities worth Shs. 181,240,370 were partly implemented. There were outstanding cheques in the bank reconciliation statements under TASAF account worth Shs 1,350,000 as at 30 th June, Maswa DC Unutilized funds amounting to Shs. 297,035,489 which imply that some planned activities of the same magnitude were partially or not implemented. Five (5) construction works worth Shs. 113,274,450 were in progress though their contractual periods had expired and there were no evidences produced to confirm whether the Council had granted extension of time to the Contractor. Construction of OPD Buildings at Mwadila, Kadaganda and Bugarama Dispensaries worth Shs. 67,337, completed but not in use. 12 Meatu DC There was unutilized funds amounting to Shs. 208,017, which imply that some planned activities of the same magnitude were partially or not implemented Shs.86, 770, was not acknowledged; therefore we were unable to confirm whether the transferred fund was actually received by the bonafide payee. 13 Mwanza CC Planned projects not executed Shs. 42,613,450 Construction of 3 classrooms at Mkuyuni primary School Shs. 25,781,800 Construction of Teacher s house, Kabangaja Shs. 16,831,650 Ten (10) projects worth Shs. 263,462,686 were still in 43

56 progress, implying delay in service delivery to the respective communities. 14 Misungwi DC There was unspent balance of Shs. 125,293, which implies that some of planned and approved TASAF Activities for the financial year 2011/2012 were either partially implemented or not implemented. Uncompleted works on Construction of Charcoal Dams Shs 86,852, Three (3) Milling Machines subprojects not yet installed Shs 27,681, Money disbursed to three (3) villages for Charcoal Dams but implementation has not started Shs 39,831, Questionable Sustainability of three (3) Fish Farming subproject namely Nyamatala, Mwakalima and Mwaniko amounting to Shs 23,473, Money for Functional activities received but not transferred to the respective subprojects Shs 71,235, Shs. 2,224, paid to various suppliers but these payments were made in the financial year 2011/2012 in respect of previous year claims contrary to Order No. 22(1) of the Local Authority Financial Memorandum (LAFM), Arusha DC 16 Babati TC Payments to the tune of Shs. 4,285,000 were apparently not effected by cheque contrary to Order No. 68 of LAFM, 2009 Non maintenance of Vote book this is contrary to The Local Authority Financial Memorandum (LAFM), 2009 Order No. 23(1) and (2) There was unspent balance of Shs. 77,445,124 which implies that some of planned and approved TASAF Activities for the financial year 2011/2012 were either partially implemented or not implemented. 17 Karatu DC Action plan for the year 2011/2012 was not prepared. 44

57 Hence making it difficult for the audit to know the activities which were planned for implemention. Commitment control over expenditure charge not in place and non maintenance of vote book. 18 Lushoto DC There was unutilized amount of Shs. 112,545,105 due to delay in disbursement of funds this implies that some of planned and approved TASAF activities for the financial year 2011/2012 were either partially implemented or not implemented. 19 Babati DC There was unspent balance of Shs. 31,691,389 which implies that some of planned and approved TASAF Activities for the financial year 2011/2012 were either partially implemented or not implemented. 20 Hai DC Shs 9,792, was disbursed for cultivation of vegetables had not yet started as construction of bore hole to be used for Vegetables irrigation project was at initial stage. Milk goat keeping for elderly at Tindigani village amounted to Shs.10,349,500 Onion cultivation was partially implemented at Mungushi village amounted to Shs.8,816, Handeni DC The charcoal dam was constructed near another charcoal dam constructed by DADPs on the same line of water inlet and therefore, during the rainfall season water can only reach the newly constructed charcoal dam (TASAF) leaving DADPS dam dry. Goat keeping projects at Kidereko and Kweisasu villages worth Shs.21,775,238 are not properly managed. 22 Kilindi DC There was unspent balance of Shs. 139,841,929 which implies that some of planned and approved TASAF Activities for the financial year 2011/2012 were either 45

58 23 Longido DC partially implemented or not implemented. Financial statement prepared report only funds for National village funds and omitted fund for Operational funds of Shs.34,323,003. There was unspent balance of Shs. 356,892,004 which implies that some of planned and approved TASAF Activities for the financial year 2011/2012 were either partially implemented or not implemented at all 24 Meru DC Payment vouchers not stamped and pre audit not effective Shs.3,060,000 Delay in rehabilitation of water system at Poli Ward Shs. 27,668, There was unspent balance of Shs. 27, 226, which implies that some of planned and approved TASAF Activities for the financial year 2011/2012 were either partially implemented or not implemented 25 Mkinga DC Unimplemented activities worth Shs 19,294,81 26 Moshi DC Planned activities worth Shs 88,787,895 were not implemented. 27 Siha DC Unimplemented activities worth Shs 20,139, Pangani DC Activity Performance report not prepared Payments made direct to individual members of groups instead of CMC bank accounts Shs. 236,953,630 Unimplemented activities worth Shs 4,272, Morogoro DC The Council planned to implement 20 sub projects valued at Shs. 159,878,048. However, up to 30 th June, 2012 those activities were not implemented due to non release of funds from TMU. The Council implemented 14 activities worth Shs.215,877,237, however up to 30 th June, 2012 those activities were partially implemented to the tune of Shs. 87,055,819 leaving activities amounting to Shs. 46

59 128,821,419 in progress. 30 Kilombero DC Shs. 33,000,000 was received instead of Shs.13, 636,363 and the project was changed from construction of mikumi-mikoleko road to construction of a bridge. Shortcomings noted in projects quarterly progress report Financial and physical progress reports are not consistent when compared with financial statements figures. Progress reports did not show the status of some of the sub project as a results it is difficult to understand actual implementations status The quarterly progress report did not show approved budget for the year, fund released unrealized, actual expenditure and unspent balance. 31 Rombo DC Activities worth Shs. 91,448, were partially implemented or not implemented. 32 Kilwa DC Activities amounting to Shs. 91, 103,556 were not implemented and completed. Non Disclosure of the Progress Report for the Activities carried during the financial year under Review Shs. 231,795, A sum of Shs.25, 277,838 transferred to various villages could not be confirmed to have reached the respective villages 33 Liwale DC Activities allocated with funds but not yet implemented Shs. 40,351,240 Activities amounting to Shs. 65,194,178 were not implemented. 34 Ruangwa DC Activities amounting to Shs.271,015,787 are still in progress. 7 sub projects allocated Shs.82,438,300 were not 47

60 implemented Acknowledgement receipts to support the amount of Shs.20,785,050 paid to various CMCs were not produced for audit verification. 35 Mafia DC Non sustainability of a poultry farming sub project at Chole Village Shs. 8,790,000 Projects worth Shs. 69,493,600 which had been completed but having some defects. 36 Bagamoyo DC Uncompleted construction of Administration Block at Zinga Secondary School. Payments of operations nature paid from NVF account - Shs.11, 524, Kibaha DC Though the dispensary building have been completed the solar power is not yet installed 38 Kisarawe DC Construction of Mzenga A Market without following the approved drawings Shs. 32,640, Shs. 30,977, was disbursed for construction of teacher s house.the project had not been completed although three years had elapsed.this is contrary to one year standard set for TASAF funded projects. 39 Rufiji DC Substandard completion of three classrooms and Septic tank at Ngorongo - Shs. 8,142,562 Uncompleted construction of laboratory at Ruaruke Secondary School Shs.19,700, Biharamulo DC Undelivered desks worth Shs.270, Muleba DC Non preparation of the Project Budget Irregularities noted on construction of pit latrine holes Shs. 31,508, Shinyanga MC Uncompleted Construction works worth Shs.60,259,500 Two sub projects were totally collapsed, and no action appeared to have been taken by the Municipal 48

61 Management. In this circumstance,the Community has not derived the expected benefits. 43 Bukoba DC Un implemented Previous Years Auditors Matters Shs. 215,783, Three (3) Dispensaries constructed and completed but not giving services to the society Shs. 35,213, Uncompleted construction of Katoma Market Shs. 8,861, Tabora MC Projects worth Shs.346,725,451 equivalent to 27% of the fund received were still in progress. Construction of two in one doctor s house at Lusangi dispensary not completed Shs.37, 373,130 Construction of three (3) classrooms at Tumbi Secondary School not yet completed Shs.49, 929,779 Indigenous seed processing Machine for Hospital Group not yet completed Shs. 10,000, Manyoni DC Procurement made without quotations Shs. 5,340,000 Procurement made without approval of tender board Shs. 3,374, Bahi DC Funds received at the end of financial year for TASAF Activities Shs.186,466,772 Payments made to District Executive Director instead of directly to payee Shs.8,225,000 Non preparation of subproject procurement plans. 47 Nzega DC Activities of TASAF not implemented Shs.4,192, Urambo DC Shs. 39,203,560 issued to two villages for construction of teachers houses but as at the end of the reporting period the activities were not implemented. 49 Chamwino DC Planned activities worth Shs. 181,083, were found to be in initial stages of implementation 50 Igunga DC 49

62 Items not taken on ledger charge Shs.5,648,600 Misstatement of financial statements 51 Kondoa DC TASAF sub projects partly Implemented Shs. 191,885,060 Delay in implementation of TASAF Project activities at Gwandi Village-Shs.23,300, Sikonge DC The Council has not implemented the previous year s audit recommendations which were made on major findings 53 Sengerema DC Financial Statement of NATIONAL VILLAGE FUND for the year ended 30 th June 2012 reported Shs.34,816,000 as payments for facilitation of Development Projects. However, it was not established how the figure reported was derived from thus misleading users of Financial Statements in making decision Payments made to wrong expenditure codes Shs.5, 650,000 Transfer of money to Subprojects accounts without acknowledgement receipts Shs.31,574, % Village Council Money loaned to DED for operational activities, not refunded Shs. 5,090, Council contribution to TASAF accumulated to Shs.23,000, not yet paid 54 Masasi DC Inadequately supported expenditure Shs.3,340,000 Approved CMC projects amounting to Shs.44,925, approved by TMU were changed from original projects without prior approval from TMU The Council paid Shs.5,992,700 for purchase of fuel to be used for supervision of TASAF activities. However, utilization details showing registration number of vehicles utilized the fuel could not be availed for audit verification. 55 Nanyumbu DC Unconfirmed utilization of 396 liters of diesel worth Shs.904,