Enroll today. Enjoy tomorrow. University System of Georgia Benefits 403(b) and 457(b) Retirement Plans SAVING : INVESTING : PLANNING

|

|

|

- Hubert Washington

- 5 years ago

- Views:

Transcription

1 Enroll today. Enjoy tomorrow. University System of Georgia Benefits 403(b) and 457(b) Retirement Plans SAVING : INVESTING : PLANNING

2 Plan Highlights 2

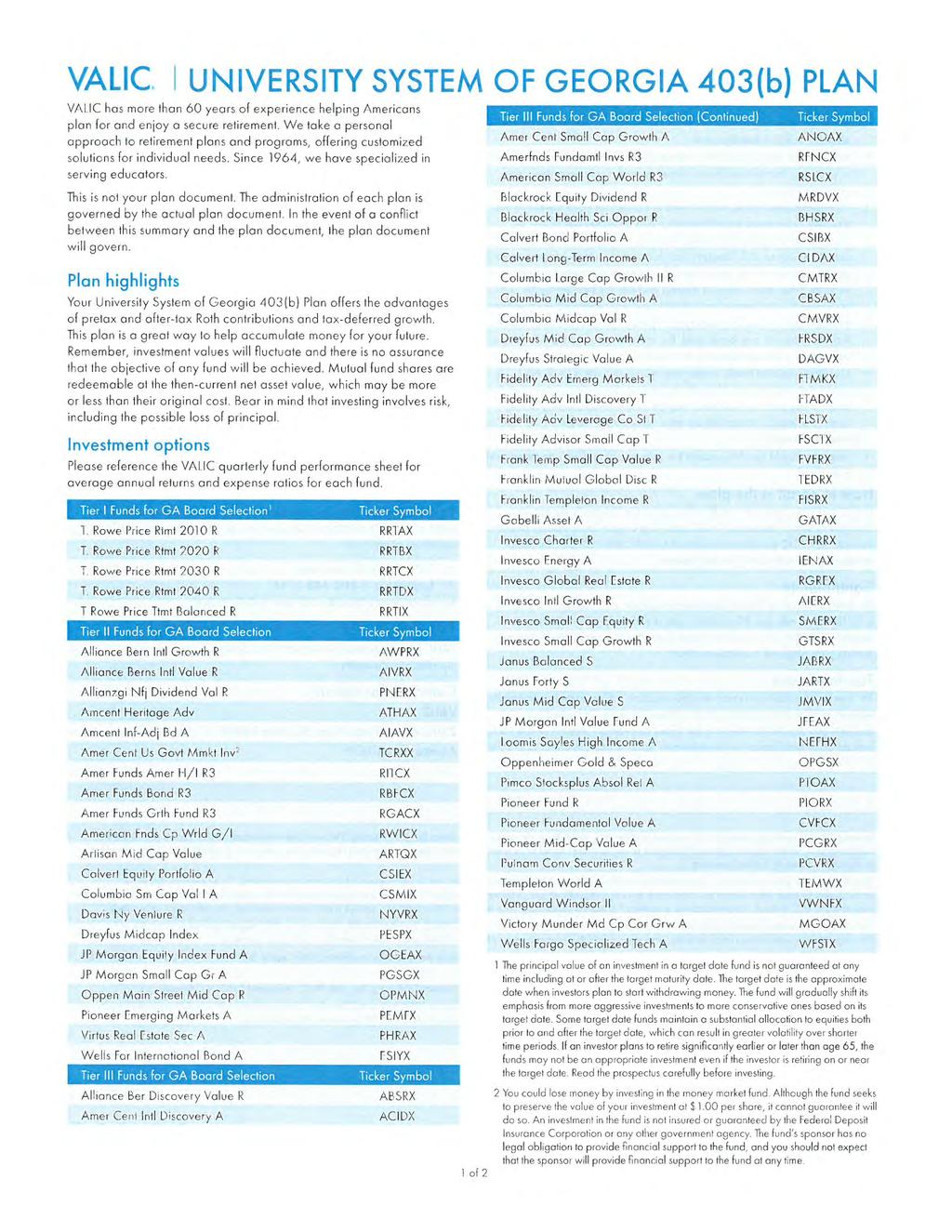

3 Plan Highlights It s your future. Make it the one you envision. As an employee of the University System of Georgia, you have a special opportunity to save for your future. Depending on which institution you work for, you can contribute to a 403(b) plan, a 457(b) plan, or both. You set aside money through payroll reduction contributions that lower your taxable income and may reduce your current income taxes. You may also make after-tax contributions to a Roth account in the plan by convenient payroll reduction. Either way, taxes on your earnings from your account are deferred until withdrawal. Withdrawals from a Roth account are potentially tax free if certain conditions are met. Pay yourself first. Decide how much, then save automatically by convenient payroll reduction. It doesn t get much simpler. This is not your plan document. The administration of each plan is governed by the actual plan document. If discrepancies arise between this summary and the plan document, the plan document will govern. Click VALIC.com/usg 1

4 Plan Highlights Enroll in the University System of Georgia 403(b) and 457(b) Retirement Plans Here are a few reasons your plan may be your most valuable opportunity to save for retirement: You contribute automatically by convenient payroll reduction. You can contribute pretax dollars, which may reduce your current income taxes. You decide how to invest your contributions. You defer taxes on interest and earnings until withdrawal. Taxes must be paid at withdrawal, and federal withdrawal restrictions apply. You may incur a 10% federal early withdrawal tax penalty if you withdraw funds from your 403(b) account or from amounts rolled over to the 457(b) plan from non-457(b) plans before age 59½. Enrolling is easy! Here s how It s easy to join simply decide how much you want to save and how you want to invest your money. By phone Call the Enrollment Center at Online Visit the custom website created just for the University System of Georgia employees at VALIC.com/usg In person Your local VALIC financial advisor will walk through the enrollment process with you Once you enroll, you can change your contribution rate at any time. Use the VALIC.com calculators to determine the appropriate contribution rate to meet your retirement goal, or work with your VALIC financial advisor. Custom website Take advantage of the custom website we provide specially for University System of Georgia employees. For additional information about the plan, including access to fund performance, prospectuses, financial planning tools and more, visit VALIC.com/usg. 42

5 Plan Highlights It s your choice In addition to the 403(b) plan, University System of Georgia also sponsors a 457(b) Deferred Compensation Plan (DCP). You can contribute to either or both plans. Contributing to both plans allows you to save even more for retirement, tax deferred. 403(b) Retirement Savings Plan 457(b) Deferred Compensation Plan Your contributions As much as 100% of your annual includible compensation, up to $18,500 in You can increase or decrease the amount you contribute to the plan as often as the University System of Georgia allows. As much as 100% of your annual includible compensation, up to $18,500 in You can increase or decrease the amount you contribute to the plan as often as the University System of Georgia allows. Catch-up contributions You might be eligible to contribute up to an additional $3,000 in 2018 if you have at least 15 years of service with the employer $6,000 in 2018 if you are age 50 or older If you are eligible for both catch-up provisions, you must exhaust the 15-year catch-up first. You may be eligible to contribute up to an additional $18,500 in 2018 if you are within the last three taxable years ending the year before you reach normal retirement age (as specified in the plan) and have undercontributed in prior years, or $6,000 in 2018 if you are age 50 or older If you are eligible for both, you cannot combine the two catch-up amounts, but you can contribute up to the higher amount. Please check with your employer or human resources department to determine whether your institution offers both plans. Pretax or Roth contributions You have a choice regarding your contributions to your 403(b) plan. You can direct all of your contributions to a traditional pretax account, to a Roth account or to a combination of the two. Contributions to a Roth account are after-tax. Regardless of your election, you are subject to the annual contribution limits detailed previously. Qualified distributions from a Roth account are tax-free. Generally, a qualified Roth distribution is a distribution that (1) is withdrawn after the end of the five-year period beginning with the first year in which a Roth contribution was made to the plan, and (2) is after age 59½, death or disability. Click VALIC.com/usg 3

6 Plan Highlights A plan for the long term Vesting Vesting refers to your ownership of money in your retirement plan account. You are always100% vested in your own contributions, plus rollover contributions, and any earnings they generate. Account statement We send all active participants a comprehensive account statement every calendar quarter. This account statement documents all activity for the preceding period, including total contributions and transfers among investment options. You can choose to go paperless if you wish. Receive secure, paperless, electronic notification when your retirement account statements, transaction confirmations and certain regulatory documents are available online through our secure connection, PersonalDeliver-e. Managing these items electronically is faster and more secure than paper mail. Simply log in to your account at VALIC.com/usg to sign up for this free service. Account consolidation You might be able to transfer your vested retirement account balance from a prior employer s plan to your retirement plan with University System of Georgia. This may be a way to simplify your financial profile and to ensure your overall investments are suitably diversified and consistent with your investment preferences. However, before moving funds, check with your other provider to determine if your account has any restrictions, imposes a withdrawal penalty or provides favorable terms. 4 64

Deferred Compensation Plan Turning age 70K Your death Severance from employment Unforeseeable emergencies You must begin taking distributions when you")

7 Plan Highlights Withdrawals Generally, you can withdraw your account balance if any of these events apply: 403(b) Retirement Savings Plan Turning age 59½ Your death Your disability Severance from employment Immediate financial hardship 457(b) Deferred Compensation Plan Turning age 70K Your death Severance from employment Unforeseeable emergencies You must begin taking distributions when you reach age 70½ or retire from the University System of Georgia, whichever occurs later. Remember that income tax is due upon withdrawal, and withdrawals from your 403(b) account before age 59½ are subject to federal restrictions and may be subject to a 10% federal early withdrawal tax penalty. The 10% penalty also applies to the amounts rolled over to the 457(b) plan from non-457(b) eligible retirement plans. Qualified distributions from a Roth account are tax-free. Generally, a qualified Roth distribution is a distribution that (1) is withdrawn after the end of the five-year period beginning with the first year in which a Roth contribution was made to the plan, and (2) is after age 59½, death or disability. Click VALIC.com/usg 5

8 Plan Highlights 86

9 With more people approaching retirement, stand out from the crowd The simple truth is that most people haven t invested the time or money to build a secure financial future. Recent studies show that: 16% of workers say they are not at all confident about having enough money for a comfortable retirement* 26% of workers have less than $1,000 in savings, and 54% say their savings and investments total less than $25,000* Only 26% of workers are very confident about having enough money to pay basic living expenses in retirement* The good news is The good news is that wherever you may be in your working career, you have several sources to access for retirement income, including: Pension plans 403(b) and 457(b) retirement savings plans Social Security Savings/investments IRAs Some of these sources offer a built-in safety net for a small portion of the population. For everyone else, options need to be weighed and decisions made. *Source: Lisa Greenwald, Craig Copeland and Jack VanDerhei, The 2017 Retirement Confidence Survey -- Many Workers Lack Retirement Confidence and Feel Stressed About Retirement Preparations, EBRI Issue Brief, no. 431 (Employee Benefits Research Institute), March 21, Click VALIC.com/usg 7

10 Plan Highlights 5 Reasons to save more 1 We re living longer Life expectancy has increased dramatically and continues to rise. You could spend decades enjoying retirement. Average Life Expectancy 85.5 Years 83 Years Source: National Center for Health Statistics from birth, Retirement lifestyles are changing People today are reinventing retirement and staying active longer. That takes more money. For example, generally, a worker will need 11 times their final pay at age 65 to maintain the same standard of living with an average life expectancy. Source: Aon Consulting, The Real Deal 2015 Retirement Adequacy at Large Companies. 10 8

11 3 Inflation isn t going away Inflation diminishes the real annual rate of return on your investment. It also reduces your purchasing power over time. Either way, inflation erodes the value of your money. That means you need a retirement plan that factors inflation into its calculations. Inflation has averaged around 3% annually for the past 20 years, Today In 20 years In 40 years which may not sound like much, but it can take a big bite. For example, in 40 years you ll need $130,482 to equal $40,000 today. $40,000 $72,244 $130,482 Source: InflationData.com, Average Annual Inflation Data by Decade, Social Security outlook Social Security was never designed to do more than supplement retirement income. Estimated average annual benefit payable to retired worker in 2017* $16,320 Estimated average annual benefit payable to couple in 2017* $27,120 Maximum annual benefit for a worker at full retirement in 2017* $32,244 * After 0.3% COLA Social Security is also under increasing stress as baby boomers retire and fewer workers remain to support the system. With less money coming in and more retirees collecting benefits, current projections indicate a potential reduction in future benefits. Fact Sheet: 2017 Social Security Changes. 5 Rising healthcare expenses As we age, more of our money is likely to be needed for healthcare and related medical expenses. And according to many studies, the rate of inflation for healthcare is likely to continue for years to come. Source: Willis Towers Watson 2016 Emerging Trends in Health Care Survey. Click VALIC.com/usg 9

12 Plan Highlights 10 12

13 Make time your ally Every day you postpone saving means less time to benefit from compound interest. The only way to make up for lost time is to save more in the years remaining until retirement. Consider a hypothetical 25-year-old who saved $300 a month through pretax salary reduction contributions to a tax-qualified retirement plan. She saved for 10 years, then left the money invested. Assuming a 5% annual rate of return on investment, our young investor would have accumulated more than $200,000 by the time she was 65. And her out-of-pocket cash outlay was just $36,000! Remember, investing involves risk, including possible loss of principal. However, a 35-year-old in the same plan would have to save at the same rate for 21 years to accumulate $200,000 by age 65, and would have to contribute about $75,600 out of pocket. A 45-year-old contributing the same amount would have to save for 27 years to reach $200,000. His out-of-pocket cash outlay? $97,200. And he wouldn t reach his goal until age 72! (See chart.) Your out-of-pocket cost to accumulate $200,000 Deposits $36, years old $300 per month for 10 years $75, years old $300 per month for 21 years $97, years old $300 per month for 27 years NOTE: $300 in pretax contributions would equal about $400 out of pocket if paid with after-tax dollars. This chart compares the total out-of-pocket costs required to fund the retirement goals of three taxqualified plan investors who began contributing $300 a month at different ages. The example assumes a 5% annual rate of return. Tax-qualified plan accumulations are taxed as ordinary income when withdrawn. Federal restrictions and a 10% federal early withdrawal tax penalty can apply to early withdrawals. This chart is hypothetical and should only be viewed as an example. It does not reflect the return of any specific investment and is not a guarantee of future income. Remember, investing involves risk, including the possible loss of principal. Click VALIC.com/usg 11

14 Why enroll? It s a simple, effective way to build your future A tax-deferred retirement plan is an easy way to set aside money for your future. You contribute to the plan through convenient payroll reduction before withholding tax is calculated. This reduces your taxable income while you save for retirement. Taxes on all interest and earnings from your account are deferred until withdrawal, usually at retirement. (Remember that income taxes are payable upon withdrawal, and federal restrictions and tax penalties can apply to early withdrawals, depending on your contract.) You re in control You decide how to invest the money in your retirement account from among the investment options available in your plan. Your retirement plan offers access to investment options covering a broad spectrum of asset categories and classes. This gives you the flexibility to create a diversified investment mix to suit your individual needs and goals. Keep in mind that investments in variable annuities and mutual funds fluctuate in value, so they could, when redeemed, be worth more or less than the original cost. Bear in mind that investing involves risk, including possible loss of principal. The advantages of a tax-deferred plan Taxable account Tax-deferred account $81,500 $65,700 $35,400 $40,600 $14,500 $15, years 20 years 30 years This chart compares the hypothetical results of contributing $100 each month to (1) a taxable account and (2) a tax-qualified retirement account. Bear in mind that a $100 pretax contribution to a tax-qualified account has a current cost of $75 (assuming a 25% income tax bracket) and also reduces current taxable income. The chart assumes a 5% annual rate of return. Remember investing involves risk, including possible loss of principal. Fees and charges, if applicable, are not reflected in this example and would reduce the amount shown. Income taxes on tax-deferred accounts are payable upon withdrawal. Federal restrictions and a 10% federal early withdrawal tax penalty may apply to withdrawals prior to age 59½. This information is hypothetical and only an example. It does not reflect the return of any investment and is not a guarantee of future income. Lower maximum capital gains rates may apply to certain investments in a taxable account (subject to IRS limitations, capital losses may also be deducted against capital gains), which would reduce the differences between the changes of the accounts shown in the chart. You should consider your personal investment horizon and current and anticipated income tax brackets when making investment decisions, as they may further affect the results of the comparison

15 University System of Georgia 403(b) Plan & 457(b) Plan TIAA plan highlights We re here to help If you need assistance with enrolling online, call TIAA at , weekdays, 8 a.m. to 10 p.m. or Saturday, 9 a.m. to 6 p.m. (ET). Get the TIAA app.* What sets TIAA apart TIAA is the financial services company that as of December 31, 2017, serves five million of your colleagues in the academic, medical, cultural and research fields. We were founded nearly a century ago as the vision of one of history s greatest philanthropists, Andrew Carnegie, to make a difference in the lives of teachers. Today, we are a global asset manager with award-winning performance. For six years ( ), TIAA has received the Thomson Reuters Lipper Fund Award for Best Overall Large Fund Company. 1 TIAA investment options The plan offers choices like TIAA Traditional, a guaranteed annuity that is designed to be a core component of a diversified retirement savings portfolio. Contributing to TIAA Traditional gives you the peace of mind and certainty that you will have an income in retirement that can help cover your essential living expenses without worrying about outliving it. Even in the most volatile markets, the principal you contribute is protected. In fact, your principal and earnings will grow every day guaranteed. Guarantees are backed by the financial strength and claims-paying ability of Teachers Insurance and Annuity Association of America, which issues the product. 2 The plan offers the TIAA Real Estate Account a variable annuity account that invests primarily in income-producing commercial real estate. Investment performance for commercial real estate generally has a low correlation with either stock or bond market performance. However, there are risks associated with real-estate ownership and you should read the Account s prospectus carefully before you invest. 3 Personalized retirement plan advice TIAA can provide you with personalized retirement planning and advice on your retirement plan portfolio, at no additional cost.

16 University System of Georgia 403(b) Plan & 457(b) Plan Investment choices that match your goals We provide a wide range of financial services to help meet your needs. From retirement savings accounts and brokerage services, to life insurance, to education savings and mutual funds, we can help you understand the choices that suit your personal situation. These products and services are offered by various entities within the TIAA group of companies. Low costs TIAA is committed to keeping costs low, which is why our expenses are generally among the lowest in the variable annuity and mutual funds industry according to Morningstar Direct (March 31, 2018) based on Morningstar expense comparisons by category. 4 Our low costs can help put more of your money working toward your retirement and other goals. Lower costs do not necessarily result in higher returns. Prepare to enroll online TIAA makes it easy for you to enroll online in the University System of Georgia 403(b) Plan & 457(b) Plan. Online enrollment is the fastest and easiest way to enroll. Before you enroll, have the following information available: WW WW WW Your investment choices and allocations: Go to TIAA.org/usg to review your investment choices. Your Social Security Number Your beneficiary s Social Security Number, birth date and address To enroll online Go to TIAA.org/usg and click on Enroll Now. Use the drop-down menus to select your school and the plan in which you wish to enroll. You will come to the Welcome page. Once on this page: WW WW WW If you are a first-time user: Click Register with TIAA to set up your user ID and password. If you are a returning user: Enter your established TIAA user ID and click Log In. Follow the on-screen directions to complete your enrollment application. Note: At the allocation screen, click on any investment choice to view its fact sheet. Print a confirmation page from the Thank You screen. Important In addition to enrolling with TIAA as your provider for this plan, you must complete a Salary Reduction Agreement. Obtain a copy of the form by contacting your Campus HR/Benefits Office and then return the completed and signed form back to that office as well.

17 UNIVERSITY SYSTEM OF GEORGIA 403(B) PLAN Plan Highlights Summary Investments About Investments As one of America's largest privately held investment companies, chances are you already know Investments by reputation. Founded in 1946, has always been committed to providing exceptional money management, outstanding customer service, and state-ofthe-art technology. is committed to providing a range of investment options, proven long-term performance, educational resources, and superior customer service to all employees to help you plan for retirement. With, you can count on: More than 70 years of investment experience More than 20 years of experience helping people plan for retirement Powerful online tools, experienced professional support, and easy access that can help make you a wiser investor Categories to the left have potentially more inflation risk and less investment risk Plan highlights Your retirement plan with Investments offers the advantage of pretax contributions and tax-deferred growth. Many of the plan s benefits are designed to help you improve your ability to reach your financial goals. Keep in mind that investing involves risk. The value of your investment will fluctuate over time and you may gain or lose money. Investment options When it comes to mutual funds, has a long-standing commitment to research and performance. By investing your contributions at, you have access to hundreds of investment options, all categorized in an easy-to-understand format. Shown below is a look at the categories of investment options offered by your plan. A complete description of the plan s investment options and their performance, as well as planning tools to help you choose an appropriate mix, are available online at NetBenefits at Categories to the right have potentially more investment risk and less inflation risk Money Market (or Short Term) Bond Balanced/ Hybrid Domestic Equity International/ Global Equity Specialty Large Value Mid Value Small Value Large Blend Mid Blend Small Blend Large Growth Mid Growth Small Growth This spectrum, with the exception of the Domestic Equity category, is based on s analysis of the characteristics of the general investment categories and not on the actual investment options and their holdings, which can change frequently. Investment options in the Domestic Equity category are based on the options Morningstar categories as of 4/30/18. Morningstar categories are based on a fund s style as measured by its underlying portfolio holdings over the past three years and may change at any time. These style calculations do not represent the investment options objectives and do not predict the investment options future styles. Investment options are listed in alphabetical order within each investment category. Risk associated with the investment options can vary significantly within each particular investment category and the relative risk of categories may change under certain economic conditions. For a more complete discussion of risk associated with the mutual fund options, please read the prospectuses before making your investment decisions. The spectrum does not represent actual or implied performance. Target Date Funds offer a blend of stocks, bonds, and short-term investments within a single fund. They are designed for investors who don t want to go through the process of picking several funds from the three asset classes but who still want to diversify among stocks, bonds, and short-term investments. The plan's designated default funds are the Freedom Funds -. Investment options to the left have potentially more inflation risk and less investment risk Investment options to the right have potentially more investment risk and less inflation risk Income Target date investments are represented on a separate spectrum because they are generally designed for investors expecting to retire around the year indicated in each investment s name. The investments are managed to gradually become more conservative over time. The investment risk of each target date investment changes over time as its asset allocation changes. The investments are subject to the volatility of the financial markets, including that of equity and fixed income investments in the U.S. and abroad, and may be subject to risks associated with investing in high-yield, small-cap, and foreign securities. Principal invested is not guaranteed at any time, including at or after the investments target dates.

18 Customer service At, we do more than just provide investment opportunities. We also offer the types of tools and resources that can help you become a better investor. Our commitment to investor education means you have easy access to the people and information you need to help you make informed investment decisions. Online Simply log on to NetBenefits, at virtually anywhere, any time, for immediate access to your account. You can view your account balances, request exchanges between investment options, track your contributions, access fund information, and more. By phone Call us toll free at , virtually 24 hours a day, seven days a week, for account balance transactions and more. And with our phone system s natural language capabilities, you can quickly and easily monitor and manage your account by using simple phrases and voice commands. Knowledgeable representatives Call a Retirement Services Representative at , Monday through Friday, 8 a.m. to midnight Eastern time, for account information and assistance. s representatives are knowledgeable, dedicated, professional, and committed to helping you take full advantage of your retirement plans. One-on-one help from Tap into s support and experience and feel more confident about your financial future. A Retirement Planner is ready to help you: Manage your retirement savings goals Choose from a wide range of investments Build a plan that s easy to put into action Schedule a complimentary one-on-one appointment by calling or by registering online at fidelity.com/reserve. Education how and when you need it To help you make knowledgeable and confident decisions about your money, offers flexible learning opportunities, including: Online workshops, tools, and resources On-site learning opportunities Regular and print messages Experienced representatives Withdrawal restrictions Withdrawals from the plan are generally permitted when you terminate your employment or retire, as defined by your plan. Keep in mind that withdrawals are subject to income taxes and possibly to early withdrawal penalties. To enroll in the plan Contact a Retirement Services Representative to begin enrollment today. To schedule an appointment, call Investments toll free at , Monday through Friday, 8 a.m. to midnight Eastern time. Before investing in any mutual fund, consider the investment objectives, risks, charges, and expenses. Contact for a prospectus or, if available, a summary prospectus containing this information. Read it carefully. Investing involves risk, including risk of loss. The trademarks and/or service marks appearing above are the property of FMR LLC and may be registered. Brokerage Services LLC, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI FMR LLC. All rights reserved EPC

19

20

21 * Not all features are available on all devices. 1 The Lipper Large Fund Award is given to the group with the lowest average decile ranking of three years Consistent Return for eligible funds over the three-year period ended 11/30/12 (36 fund companies), 11/30/13 (48), 11/30/14 (48), 11/30/15 (37), 11/30/16 (34) and 11/30/17 (34) with at least five equity, five bond, or three mixed-asset portfolios. Note this award pertains to mutual funds within the TIAA-CREF group of mutual funds; other funds distributed by Nuveen Securities were not included. From Thomson Reuters Lipper Awards, 2018 Thomson Reuters. All rights reserved. Used by permission and protected by the Copyright Laws of the United States. The printing, copying, redistribution, or retransmission of this Content without express written permission is prohibited. Past performance does not guarantee future results. Certain funds have fee waivers in effect. Without such waivers ratings could be lower. For current performance, rankings and prospectuses, please visit the Research and Performance section on TIAA.org. Securities offered through Nuveen, LLC, and TIAA-CREF Individual & Institutional Services, LLC, members FINRA and SIPC. 2 TIAA Traditional is a guaranteed insurance contract and not an investment for federal securities law purposes. All guarantees are based on TIAA s claims-paying ability. Interest credited to TIAA Traditional Annuity accumulations includes a guaranteed rate, plus additional amounts as may be established on a year-by-year basis by the TIAA Board of Trustees. The additional amounts, when declared, remain in effect through the declaration year, which begins each March 1 for accumulating annuities and January 1 for payout annuities. Interest in excess of the guaranteed amount is not guaranteed for periods other than the period for which it is declared. Withdrawals and transfers out will reduce account balances. Past performance is no guarantee of future results. 3 The real estate industry is subject to various risks including fluctuations in underlying property values, expenses and income, and potential environmental liabilities. 4 Morningstar ratings are based on each mutual fund (institutional share class) or variable annuity account s (lowest cost) share class and include U.S. open-end mutual funds, CREF Variable Accounts and the Life Funds. The Morningstar Rating or star rating is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. The rating is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product s monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. Morningstar ratings may be higher or lower on a monthly basis. The top 10% of funds or accounts in each product category receive five stars, the next 22.5% receive four stars and the next 35% receive three stars. The overall star ratings are Morningstar s published ratings, which are derived from weighted averages of the performance figures associated with the three-, five-, and 10-year (if applicable) Morningstar rating metrics for the period ended March 31, Morningstar is an independent service that rates mutual funds. Past performance cannot guarantee future results. For current performance and ratings, please visit TIAA.org/public/investmentperformance. Investment, insurance and annuity products are not FDIC insured, are not bank guaranteed, are not bank deposits, are not insured by any federal government agency, are not a condition to any banking service or activity, and may lose value. Investment products may be subject to market and other risk factors. See the applicable product literature, or visit TIAA.org/usg for details. You should consider the investment objectives, risks, charges and expenses carefully before investing. Please call or go to TIAA.org/usg for current fund and product prospectuses that contain this and other information. Please read the prospectuses carefully before investing. TIAA-CREF Individual & Institutional Services, LLC, Teachers Personal Investors Services, Inc., and Nuveen Securities, LLC, Members FINRA and SIPC, distribute securities products. Annuity contracts and certificates are issued by Teachers Insurance and Annuity Association of America (TIAA) and College Retirement Equities Fund (CREF), New York, NY. Each is solely responsible for its own financial condition and contractual obligations Teachers Insurance and Annuity Association of America-College Retirement Equities Fund, 730 Third Avenue, New York, NY _ (05/18)

22

23 VALIC has more than half a century of experience helping Americans plan for and enjoy a secure retirement. We provide real solutions for real lives by consistently offering products and services that are innovative, simple to understand and easy to use. We take a personal approach to retirement plans and programs, offering customized solutions for individual needs. We are committed to the same unchanging standard of one-on-one service we have delivered since our founding. Our goal is to help you live retirement on your terms. Investors should carefully consider the investment objectives, risks, fees, charges and expenses before investing. This and other important information is contained in the prospectus, which can be obtained from your financial professional or at You can also request a copy by calling Read the prospectuses carefully before investing. This information is general in nature, may be subject to change, and does not constitute legal, tax or accounting advice from any company, its employees, financial professionals or other representatives. Applicable laws and regulations are complex and subject to change. Any tax statements in this material are not intended to suggest the avoidance of U.S. federal, state or local tax penalties. For advice concerning your individual circumstances, consult a professional attorney, tax advisor or accountant. Your Future is Calling. Meet It with Confidence. CLICK VALIC.com/usg CALL VISIT your financial advisor Securities and investment advisory services offered through VALIC Financial Advisors, Inc. ( VFA ), member FINRA, SIPC and an SEC-registered investment advisor. VFA registered representatives offer securities and other products under retirement plans and IRAs, and to clients outside of such arrangements. Annuities issued by The Variable Annuity Life Insurance Company ( VALIC ). Variable annuities distributed by its affiliate, AIG Capital Services, Inc. ( ACS ), member FINRA. VALIC, VFA and ACS are members of American International Group, Inc. ( AIG ). VALIC represents The Variable Annuity Life Insurance Company and its subsidiaries, VALIC Financial Advisors, Inc. and VALIC Retirement Services Company. American International Group, Inc. (AIG) is a leading global insurance organization. Founded in 1919, today AIG member companies provide a wide range of property casualty insurance, life insurance, retirement products and other financial services to customers in more than 80 countries and jurisdictions. Copyright The Variable Annuity Life Insurance Company. All rights reserved. VC (02/2018) J22801 EE

Enroll today. Enjoy tomorrow. University System of Georgia Benefits 403(b) and 457(b) Retirement Plans SAVING : INVESTING : PLANNING

and 457(b) Retirement Plans SAVING : INVESTING : PLANNING") Enroll today. Enjoy tomorrow. University System of Georgia Benefits 403(b) and 457(b) Retirement Plans SAVING : INVESTING : PLANNING 2 It s your future. Make it the one you envision. As an employee of

Enroll today. Enjoy tomorrow. University System of Georgia Benefits 403(b) and 457(b) Retirement Plans SAVING : INVESTING : PLANNING 2 It s your future. Make it the one you envision. As an employee of

CREATE CUSTOM LOOK. ADD NEW COLORS AND REPLACE FONTS IN STYLE SHEETS THROUGHOUT BROCHURE. Baptist Health. 403(b) and 401(k) Retirement Plans

and 401(k) Retirement Plans") CREATE CUSTOM LOOK. ADD NEW COLORS AND REPLACE FONTS IN STYLE SHEETS THROUGHOUT BROCHURE. Baptist Health 403(b) and 401(k) Retirement Plans 2 Baptist Health 403(b) and 401(k) Retirement Plans The Baptist

CREATE CUSTOM LOOK. ADD NEW COLORS AND REPLACE FONTS IN STYLE SHEETS THROUGHOUT BROCHURE. Baptist Health 403(b) and 401(k) Retirement Plans 2 Baptist Health 403(b) and 401(k) Retirement Plans The Baptist

ERIE COUNTY. New York. Enrollment Brochure

ERIE COUNTY New York Enrollment Brochure Erie County is dedicated to the health and wellness of our community and your retirement. The Erie County 457(b) Deferred Compensation Plan The future is yours

ERIE COUNTY New York Enrollment Brochure Erie County is dedicated to the health and wellness of our community and your retirement. The Erie County 457(b) Deferred Compensation Plan The future is yours

Gwinnett County Public Schools. Retirement Savings Plans

Gwinnett County Public Schools Retirement Savings Plans Agenda 1 Plan highlights 2 Five reasons to save for retirement 3 Enrolling in the plan 4 Questions and answers 2 1. Plan highlights Plan highlights

Gwinnett County Public Schools Retirement Savings Plans Agenda 1 Plan highlights 2 Five reasons to save for retirement 3 Enrolling in the plan 4 Questions and answers 2 1. Plan highlights Plan highlights

The State University of New York. Optional Retirement Plan SAVING : INVESTING : PLANNING

The State University of New York Optional Retirement Plan SAVING : INVESTING : PLANNING An optional retirement plan (ORP) is an alternative to the State s defined benefit plan, and provides you with greater

The State University of New York Optional Retirement Plan SAVING : INVESTING : PLANNING An optional retirement plan (ORP) is an alternative to the State s defined benefit plan, and provides you with greater

Helping You Maximize. Your Retirement. 403(b) Program Overview Guide The University of North Carolina System

Program Overview Guide The University of North Carolina System") Helping You Maximize Your Retirement 403(b) Program Overview Guide The System Appalachian State University East Carolina University Elizabeth City State University Fayetteville State University Agricultural

Helping You Maximize Your Retirement 403(b) Program Overview Guide The System Appalachian State University East Carolina University Elizabeth City State University Fayetteville State University Agricultural

Introducing the after-tax contribution option Roth

Introducing the after-tax contribution option Roth Today s agenda The after-tax Roth contribution option Why the after-tax Roth contribution option may be right for you Comparing after-tax Roth contributions

Introducing the after-tax contribution option Roth Today s agenda The after-tax Roth contribution option Why the after-tax Roth contribution option may be right for you Comparing after-tax Roth contributions

TIAA Brokerage: For non-retirement accounts Investing as you like it

TIAA Brokerage: For non-retirement accounts Investing as you like it From our retirement roots, TIAA has continued to evolve and grow our financial services organization. We remain true to our not-for-profit

TIAA Brokerage: For non-retirement accounts Investing as you like it From our retirement roots, TIAA has continued to evolve and grow our financial services organization. We remain true to our not-for-profit

The Churchill Benefit Corporation 401(k) Savings Plan

Savings Plan") The Churchill Benefit Corporation 401(k) Savings Plan There are many great benefits to being part of the The Churchill Benefit Corporation 401(k) Savings Plan. Among those benefits is exceptional customer

The Churchill Benefit Corporation 401(k) Savings Plan There are many great benefits to being part of the The Churchill Benefit Corporation 401(k) Savings Plan. Among those benefits is exceptional customer

Strategies for staying on track. Prepare yourself for the journey ahead

Strategies for staying on track Prepare yourself for the journey ahead TIAA and you: Working together to pursue a financially secure future At TIAA, our mission is simple: We re here to help our customers

Strategies for staying on track Prepare yourself for the journey ahead TIAA and you: Working together to pursue a financially secure future At TIAA, our mission is simple: We re here to help our customers

The Roth contribution option. For retirement plans

The Roth contribution option For retirement plans Contents 2 The Roth contribution option savings choice Learn about the differences between pretax and after-tax contributions 4 Comparing Roth after-tax

The Roth contribution option For retirement plans Contents 2 The Roth contribution option savings choice Learn about the differences between pretax and after-tax contributions 4 Comparing Roth after-tax

Help for pursuing your financial goals

Help for pursuing your financial goals Pursuing financial well-being TIAA can help hat does success look like for you? On the following pages, you can learn about some of TIAA s products and services,

Help for pursuing your financial goals Pursuing financial well-being TIAA can help hat does success look like for you? On the following pages, you can learn about some of TIAA s products and services,

Life is a Journey. The University System of Maryland Retirement Plans

Life is a Journey R E T I R E M E N T A D E S T I N AT I O N The University System of Maryland Retirement Plans Fidelity Can Help Your Every Step of the Way. Online Log on to netbenefits.com/usm the home

Life is a Journey R E T I R E M E N T A D E S T I N AT I O N The University System of Maryland Retirement Plans Fidelity Can Help Your Every Step of the Way. Online Log on to netbenefits.com/usm the home

Introducing the AfterTax Roth Contribution. Option. October 2017

Introducing the AfterTax Roth Contribution Option October 2017 Today s Agenda The after-tax Roth contribution option Why the after-tax Roth contribution option may be right for you Comparing after-tax

Introducing the AfterTax Roth Contribution Option October 2017 Today s Agenda The after-tax Roth contribution option Why the after-tax Roth contribution option may be right for you Comparing after-tax

Precision Strip Retirement and Savings Plan

Precision Strip Retirement and Savings Plan There are many great benefits to being a participant in the Precision Strip Retirement and Savings Plan. Among those benefits is exceptional customer service

Precision Strip Retirement and Savings Plan There are many great benefits to being a participant in the Precision Strip Retirement and Savings Plan. Among those benefits is exceptional customer service

VALIC Financial Advisors, Inc. An array of financial planning and investment services SAVING : INVESTING : PLANNING

VALIC Financial Advisors, Inc. An array of financial planning and investment services SAVING : INVESTING : PLANNING Your financial advisor will work with you to help make sure your financial plan fits

VALIC Financial Advisors, Inc. An array of financial planning and investment services SAVING : INVESTING : PLANNING Your financial advisor will work with you to help make sure your financial plan fits

TIAA 2017 Lifetime Income Survey executive summary

TIAA 2017 Lifetime Income Survey executive summary Americans recognize the importance of having a source of monthly income they can t outlive to cover their essential living expenses during retirement,

TIAA 2017 Lifetime Income Survey executive summary Americans recognize the importance of having a source of monthly income they can t outlive to cover their essential living expenses during retirement,

INVESTING IN YOUR FUTURE: A TIAA FINANCIAL ESSENTIALS WORKSHOP. Money at Work 1: Foundations of investing

INVESTING IN YOUR FUTURE: A TIAA FINANCIAL ESSENTIALS WORKSHOP Money at Work 1: Foundations of investing Staying on course: Today s agenda Retirement Advisor Understanding saving Risk tolerance Asset classes

INVESTING IN YOUR FUTURE: A TIAA FINANCIAL ESSENTIALS WORKSHOP Money at Work 1: Foundations of investing Staying on course: Today s agenda Retirement Advisor Understanding saving Risk tolerance Asset classes

We help those who do good, do well. Discover what makes TIAA a different kind of financial partner

We help those who do good, do well Discover what makes TIAA a different kind of financial partner Joennis Almeida Social worker 30 years old Participant since 2013 Kristin Austin University Administrator

We help those who do good, do well Discover what makes TIAA a different kind of financial partner Joennis Almeida Social worker 30 years old Participant since 2013 Kristin Austin University Administrator

Enrollment Overview. for SoutheastHEALTH Retirement Plan. Prepare for the next chapter in life

Prepare for the next chapter in life The Difference is How You re Treated More information available at www.sehealthretirement.com Enrollment Overview for SoutheastHEALTH Retirement Plan Products and financial

Prepare for the next chapter in life The Difference is How You re Treated More information available at www.sehealthretirement.com Enrollment Overview for SoutheastHEALTH Retirement Plan Products and financial

The George Washington University Retirement Plans. How to get started

The George Washington University Retirement Plans How to get started Table of Contents Why Save 3 Plans at a Glance 4 Investment Providers 7 How to Enroll 8 Provider Fact Sheets 9 Investment Education

The George Washington University Retirement Plans How to get started Table of Contents Why Save 3 Plans at a Glance 4 Investment Providers 7 How to Enroll 8 Provider Fact Sheets 9 Investment Education

Diocese of Lafayette. Believe. in your future. The Diocese of Lafayette 403(b) Plan Enrollment Overview

Plan Enrollment Overview") Diocese of Lafayette Believe in your future The Diocese of Lafayette 403(b) Plan Enrollment Overview Believe in your future Reaching your retirement goals can take a lot of preparation. Some investment

Diocese of Lafayette Believe in your future The Diocese of Lafayette 403(b) Plan Enrollment Overview Believe in your future Reaching your retirement goals can take a lot of preparation. Some investment

Standard Motor Products, Inc. Profit Sharing 401(k) Capital Accumulation Plan Plan Highlights

Capital Accumulation Plan Plan Highlights") Standard Motor Products, Inc. Profit Sharing 401(k) Capital Accumulation Plan Plan Highlights The Standard Motor Products, Inc. Profit Sharing 401(k) Capital Accumulation Plan (the Plan or SMP 401(k) Plan

Standard Motor Products, Inc. Profit Sharing 401(k) Capital Accumulation Plan Plan Highlights The Standard Motor Products, Inc. Profit Sharing 401(k) Capital Accumulation Plan (the Plan or SMP 401(k) Plan

A guide for the road to retirement. Announcing updates to the Eastern Michigan University Retirement Plan

A guide for the road to retirement Announcing updates to the Eastern Michigan University Retirement Plan 1 Overview of topics we ll be covering today Why changes are being made What stays the same Plan

A guide for the road to retirement Announcing updates to the Eastern Michigan University Retirement Plan 1 Overview of topics we ll be covering today Why changes are being made What stays the same Plan

Getting Started Retirement Plan Details Retirement Plan Details Quick Guide Emory University 403(b) Retirement Plan...

Retirement Plan...") Discover Your Retirement Options - 2018 1 Table of Contents... Getting Started... 4 Retirement Plan Details... 7 Retirement Plan Details Quick Guide.... 7 Emory University 403(b) Retirement Plan.... 8

Discover Your Retirement Options - 2018 1 Table of Contents... Getting Started... 4 Retirement Plan Details... 7 Retirement Plan Details Quick Guide.... 7 Emory University 403(b) Retirement Plan.... 8

Your Plan Features Guide

Move your future forward with your workplace savings plan egain Corporation 401(k) Your Plan Features Guide Invest some of what you earn today for what you plan to accomplish tomorrow. Take a look and

Move your future forward with your workplace savings plan egain Corporation 401(k) Your Plan Features Guide Invest some of what you earn today for what you plan to accomplish tomorrow. Take a look and

Getting Started: Your UM Voluntary Retirement Plans 1/23/2018

Getting Started: Your UM Voluntary Retirement Plans 1/23/2018 Getting Started: University Of Missouri Voluntary Retirement Plans Take advantage of great savings and investment opportunities available for

Getting Started: Your UM Voluntary Retirement Plans 1/23/2018 Getting Started: University Of Missouri Voluntary Retirement Plans Take advantage of great savings and investment opportunities available for

YOUR GUIDE TO GETTING STARTED

The Retirement Savings Plan of the Presbyterian Church (U.S.A.) Plan No. 57887 Invest in your retirement and yourself today, with help from The Retirement Savings Plan of the Presbyterian Church (U.S.A.)

The Retirement Savings Plan of the Presbyterian Church (U.S.A.) Plan No. 57887 Invest in your retirement and yourself today, with help from The Retirement Savings Plan of the Presbyterian Church (U.S.A.)

TO FOCUS ON RETIREMENT

The Right Time TO FOCUS ON RETIREMENT Equian LLC Retirement Savings Plan Enrollment Overview REVERSED HEADLINE PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED LIFE INSURANCE COMPANY, A ONEAMERICA

The Right Time TO FOCUS ON RETIREMENT Equian LLC Retirement Savings Plan Enrollment Overview REVERSED HEADLINE PRODUCTS AND FINANCIAL SERVICES PROVIDED BY AMERICAN UNITED LIFE INSURANCE COMPANY, A ONEAMERICA

YOUR GUIDE TO GETTING STARTED

The Retirement Savings Plan of the Presbyterian Church (U.S.A.) Plan No. 57887 Invest in your retirement and yourself today, with help from The Retirement Savings Plan of the Presbyterian Church (U.S.A.)

The Retirement Savings Plan of the Presbyterian Church (U.S.A.) Plan No. 57887 Invest in your retirement and yourself today, with help from The Retirement Savings Plan of the Presbyterian Church (U.S.A.)

Receiving Required Minimum Distributions. Making it simple with TIAA

Receiving Required Minimum Distributions Making it simple with TIAA Required Minimum Distributions what you need to know What are Required Minimum Distributions? 1 How can you receive minimum distributions

Receiving Required Minimum Distributions Making it simple with TIAA Required Minimum Distributions what you need to know What are Required Minimum Distributions? 1 How can you receive minimum distributions

Your DePaul University 403(b) Retirement Plan ENROLLMENT GUIDE

Retirement Plan ENROLLMENT GUIDE") Your DePaul University 403(b) Retirement Plan ENROLLMENT GUIDE Invest some of what you earn today for what you plan to accomplish tomorrow. Dear DePaul University 403(b) Retirement Plan employee: It s

Your DePaul University 403(b) Retirement Plan ENROLLMENT GUIDE Invest some of what you earn today for what you plan to accomplish tomorrow. Dear DePaul University 403(b) Retirement Plan employee: It s

Your life. Your future. Your options.

Your life. Your future. Your options. Whether by chance or by choice, you have options. Explore them with Empower Retirement. Corporate Retirement Plan Participant Brochure You want to retire someday or

Your life. Your future. Your options. Whether by chance or by choice, you have options. Explore them with Empower Retirement. Corporate Retirement Plan Participant Brochure You want to retire someday or

A distinctive solution for your plan and employees. TIAA-CREF Lifecycle Funds

A distinctive solution for your plan and employees TIAA-CREF Lifecycle Funds TIAA has nearly 100 years of experience managing money for retirement and nearly 60 years of asset allocation experience. Our

A distinctive solution for your plan and employees TIAA-CREF Lifecycle Funds TIAA has nearly 100 years of experience managing money for retirement and nearly 60 years of asset allocation experience. Our

Savings & Matching Retirement Plan Quick Guide Fidelity Investments... TIAA Contact Information... Glossary of Terms...

EMORY HEALTHCARE Table of Contents Getting Started... 4 Retirement Plan Details Savings & Matching Retirement Plan Quick Guide.... Emory Healthcare 403(b) Retirement Plan.... Emory Healthcare Roth 403(b)

EMORY HEALTHCARE Table of Contents Getting Started... 4 Retirement Plan Details Savings & Matching Retirement Plan Quick Guide.... Emory Healthcare 403(b) Retirement Plan.... Emory Healthcare Roth 403(b)

The George Washington University Retirement Plans. How to get started

The George Washington University Retirement Plans How to get started Table of Contents Why Save 3 Plans at a Glance 4 Approved Investment Providers 7 How to Enroll 8 Provider Fact Sheets 9 Investment Education

The George Washington University Retirement Plans How to get started Table of Contents Why Save 3 Plans at a Glance 4 Approved Investment Providers 7 How to Enroll 8 Provider Fact Sheets 9 Investment Education

How to make changes to your annuity income

How to make changes to your annuity income What s inside Is it time to make a change? 2 Your annuity income 3 TIAA Traditional income 5 TIAA and CREF variable annuity income 7 How you can adjust your annuity

How to make changes to your annuity income What s inside Is it time to make a change? 2 Your annuity income 3 TIAA Traditional income 5 TIAA and CREF variable annuity income 7 How you can adjust your annuity

Retirement Income Planner

Retirement Income Planner Overview and map TIAA is committed to delivering the most innovative retirement income planning solutions to help you to feel confident about your decision on when to retire and

Retirement Income Planner Overview and map TIAA is committed to delivering the most innovative retirement income planning solutions to help you to feel confident about your decision on when to retire and

Your Opportunity to Enroll in the Laboratory Corporation of America Holdings Deferred Compensation Plan for 2017

Your Opportunity to Enroll in the Laboratory Corporation of America Holdings Deferred Compensation Plan for 2017 As part of LabCorp s comprehensive compensation and benefit programs, we are pleased to

Your Opportunity to Enroll in the Laboratory Corporation of America Holdings Deferred Compensation Plan for 2017 As part of LabCorp s comprehensive compensation and benefit programs, we are pleased to

Your guide to 403(b) tax-deferred annuity or voluntary savings plans. How much can you contribute in 2018?

tax-deferred annuity or voluntary savings plans. How much can you contribute in 2018?") Your guide to 403(b) tax-deferred annuity or voluntary savings plans How much can you contribute in 2018? Tax-deferred annuity plans ( TDA Plans ) are voluntary savings plans that help you build the extra

Your guide to 403(b) tax-deferred annuity or voluntary savings plans How much can you contribute in 2018? Tax-deferred annuity plans ( TDA Plans ) are voluntary savings plans that help you build the extra

The George Washington University Retirement Plans. How to get started

The George Washington University Retirement Plans How to get started 11602_01_BRO_GWU_AllPlans.indd 1 Table of Contents Why Save 3 Plans at a Glance 4 Approved Investment Providers 7 How to Enroll 8 Provider

The George Washington University Retirement Plans How to get started 11602_01_BRO_GWU_AllPlans.indd 1 Table of Contents Why Save 3 Plans at a Glance 4 Approved Investment Providers 7 How to Enroll 8 Provider

A new chapter for the Grand Valley State University retirement program

A new chapter for the Grand Valley State University retirement program Transition seminar topics Why we re here today Transition experience Updates to the new investment menu Retirement program features

A new chapter for the Grand Valley State University retirement program Transition seminar topics Why we re here today Transition experience Updates to the new investment menu Retirement program features

Guide to online withdrawals

Less time, paper and phone calls Many types of withdrawal requests can be completed online through your account on TIAA.org, 1 which saves time and reduces the need for paper forms. This guide includes

Less time, paper and phone calls Many types of withdrawal requests can be completed online through your account on TIAA.org, 1 which saves time and reduces the need for paper forms. This guide includes

I highly recommend all of our actively assigned diocesan priests to join this new savings plan and begin saving now for their future retirement.

PASTORAL CENTER: HUMAN RESOURCES DEPARTMENT 13280 CHAPMAN AVENUE, GARDEN GROVE, CA 92840 NEW RETIREMENT SAVINGS PLANS FOR DIOCESAN PRIESTS Dear Presbyterate, The Diocese of Orange is pleased to announce

PASTORAL CENTER: HUMAN RESOURCES DEPARTMENT 13280 CHAPMAN AVENUE, GARDEN GROVE, CA 92840 NEW RETIREMENT SAVINGS PLANS FOR DIOCESAN PRIESTS Dear Presbyterate, The Diocese of Orange is pleased to announce

YOUR GUIDE TO GETTING STARTED

Virginia Mason Medical Center 401(a) Retirement Plan and VMMC 403(b) Retirement Savings Plan Pursue your retirement goals today, with help from the Virginia Mason Medical Center 401(a) Retirement Plan

Virginia Mason Medical Center 401(a) Retirement Plan and VMMC 403(b) Retirement Savings Plan Pursue your retirement goals today, with help from the Virginia Mason Medical Center 401(a) Retirement Plan

The University of Texas UTSaver 403(b) Program

Program") Program saving : investing : planning For more than half a century, VALIC has specialized in providing tax-qualified retirement programs, and today is the third-largest retirement plan provider to employees

Program saving : investing : planning For more than half a century, VALIC has specialized in providing tax-qualified retirement programs, and today is the third-largest retirement plan provider to employees

Working for Your Future

Working for Your Future Valero Energy Corporation Thrift Plan Highlights Enroll Today Congratulations! You are now eligible to participate in the Valero Energy Corporation Thrift Plan (the Thrift Plan

Working for Your Future Valero Energy Corporation Thrift Plan Highlights Enroll Today Congratulations! You are now eligible to participate in the Valero Energy Corporation Thrift Plan (the Thrift Plan

Get the Most From Your 401(k) Plan

Plan") 401(k) Guide Get the Most From Your 401(k) Plan The Larry H. Miller Associates Retirement Plan and Trust (the Plan ) is a great benefit offered by your company. It s an excellent way to prepare for your

401(k) Guide Get the Most From Your 401(k) Plan The Larry H. Miller Associates Retirement Plan and Trust (the Plan ) is a great benefit offered by your company. It s an excellent way to prepare for your

getting started in your University of Missouri

getting started in your University of Missouri CORE RETIREMENT AND VOLUNTARY Retirement Plans University of Missouri myretirement PROGRAM Welcome to the University of Missouri myretirement Program. Welcome!

getting started in your University of Missouri CORE RETIREMENT AND VOLUNTARY Retirement Plans University of Missouri myretirement PROGRAM Welcome to the University of Missouri myretirement Program. Welcome!

YOUR GUIDE TO GETTING STARTED

Engility Master Savings Plan Invest in your retirement and yourself today, with help from Engility Master Savings Plan and Fidelity. YOUR GUIDE TO GETTING STARTED Invest some of what you earn today for

Engility Master Savings Plan Invest in your retirement and yourself today, with help from Engility Master Savings Plan and Fidelity. YOUR GUIDE TO GETTING STARTED Invest some of what you earn today for

401(k) ANNUAL UPDATE. What s Inside. Need to Enroll in the 401(k)?

ANNUAL UPDATE. What s Inside. Need to Enroll in the 401(k)?") Engility MASTER SAVINGS PLAN 401(k) ANNUAL UPDATE Timely information to Help You take control of your future What s Inside How to enroll 2016 Contribution Limits Make Sure Your 401(k) Account Is On Track

Engility MASTER SAVINGS PLAN 401(k) ANNUAL UPDATE Timely information to Help You take control of your future What s Inside How to enroll 2016 Contribution Limits Make Sure Your 401(k) Account Is On Track

TIME TO FOCUS ON YOUR FUTURE

TIME TO FOCUS ON YOUR FUTURE Enroll online in the new HMH 401(k) Savings Plan at TIAA Active enrollment in the new 401(k) plan is required because your previous elections will not be provided to TIAA.

TIME TO FOCUS ON YOUR FUTURE Enroll online in the new HMH 401(k) Savings Plan at TIAA Active enrollment in the new 401(k) plan is required because your previous elections will not be provided to TIAA.

Standard Motor Products, Inc. Profit Sharing 401(k) Capital Accumulation Plan. Plan Highlights 2

Capital Accumulation Plan. Plan Highlights 2") Standard Motor Products, Inc. Profit Sharing 401(k) Capital Accumulation Plan Plan Highlights The Standard Motor Products, Inc. Profit Sharing 401(k) Capital Accumulation Plan (the Plan or SMP 401(k) Plan

Standard Motor Products, Inc. Profit Sharing 401(k) Capital Accumulation Plan Plan Highlights The Standard Motor Products, Inc. Profit Sharing 401(k) Capital Accumulation Plan (the Plan or SMP 401(k) Plan

A guide for the road to retirement. Announcing changes to Wesleyan University s 403(b)(7) Retirement Plan

(7) Retirement Plan") A guide for the road to retirement Announcing changes to Wesleyan University s 403(b)(7) Retirement Plan 1 Overview of topics we ll be covering today Why the changes What is staying the same and what is

A guide for the road to retirement Announcing changes to Wesleyan University s 403(b)(7) Retirement Plan 1 Overview of topics we ll be covering today Why the changes What is staying the same and what is

Innovative, flexible, low-cost retirement solution

TIAA-CREF Life Insurance Company Innovative, flexible, low-cost retirement solution The Intelligent Variable Annuity What s inside 1 Innovating to better meet your retirement needs 2 The reality of retirement

TIAA-CREF Life Insurance Company Innovative, flexible, low-cost retirement solution The Intelligent Variable Annuity What s inside 1 Innovating to better meet your retirement needs 2 The reality of retirement

Helping bring health & well-being to your financial future. Your Bon Secours Retirement Savings Plan Enrollment Guide

Helping bring health & well-being to your financial future Your Bon Secours Retirement Savings Plan Enrollment Guide Invest some of what you earn today for what you plan to accomplish tomorrow. Dear Employee:

Helping bring health & well-being to your financial future Your Bon Secours Retirement Savings Plan Enrollment Guide Invest some of what you earn today for what you plan to accomplish tomorrow. Dear Employee:

YOUR GUIDE TO GETTING STARTED

Albert Einstein College of Medicine, Inc. 403(b) Retirement Income Plan Invest in your retirement and yourself today, with help from the Einstein Retirement Plan and Fidelity. YOUR GUIDE TO GETTING STARTED

Albert Einstein College of Medicine, Inc. 403(b) Retirement Income Plan Invest in your retirement and yourself today, with help from the Einstein Retirement Plan and Fidelity. YOUR GUIDE TO GETTING STARTED

great minds. opportunities. Vanderbilt University 403(b) Retirement Plan Enrollment Guide

Retirement Plan Enrollment Guide") great minds. opportunities. Vanderbilt University 403(b) Retirement Plan Enrollment Guide Invest some of what you earn today for what you plan to accomplish tomorrow. Vanderbilt University and Medical

great minds. opportunities. Vanderbilt University 403(b) Retirement Plan Enrollment Guide Invest some of what you earn today for what you plan to accomplish tomorrow. Vanderbilt University and Medical

TIAA Individual Advisory Services. Personalized financial advice for every stage of life

TIAA Individual Advisory Services Personalized financial advice for every stage of life Personalized solutions for your financial independence Find an advisor today. Go to TIAA.org/ individualadvisoryservices

TIAA Individual Advisory Services Personalized financial advice for every stage of life Personalized solutions for your financial independence Find an advisor today. Go to TIAA.org/ individualadvisoryservices

UNT System ORP and TSA Retirement Program Changes Questions & Answers click to view

click to view The Retirement Redesign 1. Why is UNT System redesigning the retirement plans?...2 2. Who is impacted by the redesign?... 2 3. What was the decision making process?... 2 4. When will these

click to view The Retirement Redesign 1. Why is UNT System redesigning the retirement plans?...2 2. Who is impacted by the redesign?... 2 3. What was the decision making process?... 2 4. When will these

Strategies for staying on track to your retirement

Strategies for staying on track to your retirement TIAA-CREF and you: Planning an income for life For more than 90 years, we at TIAA-CREF have dedicated ourselves to helping those who serve the greater

Strategies for staying on track to your retirement TIAA-CREF and you: Planning an income for life For more than 90 years, we at TIAA-CREF have dedicated ourselves to helping those who serve the greater

Getting on the Right Path with Your Workplace Savings Plan Boyce Brice January 18, 2016

Getting on the Right Path with Your Workplace Savings Plan Boyce Brice January 18, 2016 So, you re starting to think about saving for retirement Today s agenda: Steps to prioritizing your savings Benefits

Getting on the Right Path with Your Workplace Savings Plan Boyce Brice January 18, 2016 So, you re starting to think about saving for retirement Today s agenda: Steps to prioritizing your savings Benefits

Brandeis Retirement Planning Website User Guide

Your Brandeis University Defined Contribution Retirement Plan Brandeis Retirement Planning Website User Guide No matter where you are in your journey, we can help you map out the retirement you envision.

Your Brandeis University Defined Contribution Retirement Plan Brandeis Retirement Planning Website User Guide No matter where you are in your journey, we can help you map out the retirement you envision.

Plan Highlights. Universal Health Services, Inc. Supplemental Deferred Compensation Plan. For Amounts Deferred on or After January 1, 2009 Only*

Universal Health Services, Inc. Supplemental Deferred Compensation Plan Plan Highlights For Amounts Deferred on or After January 1, 2009 Only* *For amounts deferred before January 1, 2009, the terms of

Universal Health Services, Inc. Supplemental Deferred Compensation Plan Plan Highlights For Amounts Deferred on or After January 1, 2009 Only* *For amounts deferred before January 1, 2009, the terms of

401(k) RETIREMENT SAVINGS PLAN

RETIREMENT SAVINGS PLAN") CHI 401(k) RETIREMENT SAVINGS PLAN Helping You Build Financial Security for Retirement CHI Healthy SPIRIT Physical and financial health and wellness SM Invest some of what you earn today for what you plan

CHI 401(k) RETIREMENT SAVINGS PLAN Helping You Build Financial Security for Retirement CHI Healthy SPIRIT Physical and financial health and wellness SM Invest some of what you earn today for what you plan

Roth 401(k) Contributions

Contributions") Roth 401(k) Contributions Another Way to Save in the Hitachi Data Systems 401(k) Retirement and Savings Plan ROTH 401(k) CONTRIBUTIONS ARE AVAILABLE You can sign up to make Roth 401(k) contributions any

Roth 401(k) Contributions Another Way to Save in the Hitachi Data Systems 401(k) Retirement and Savings Plan ROTH 401(k) CONTRIBUTIONS ARE AVAILABLE You can sign up to make Roth 401(k) contributions any

THE SUNY OPTIONAL RETIREMENT PROGRAM (ORP) PROVIDED THROUGH TIAA

PROVIDED THROUGH TIAA") THE SUNY OPTIONAL RETIREMENT PROGRAM (ORP) PROVIDED THROUGH TIAA Making the Most of Your Retirement Pre-Retirement Questions and Answers THE SUNY OPTIONAL RETIREMENT PLAN (ORP) PROVIDED THROUGH TIAA Pre-Retirement

THE SUNY OPTIONAL RETIREMENT PROGRAM (ORP) PROVIDED THROUGH TIAA Making the Most of Your Retirement Pre-Retirement Questions and Answers THE SUNY OPTIONAL RETIREMENT PLAN (ORP) PROVIDED THROUGH TIAA Pre-Retirement

Your Guide to Getting Started

USC Hospital 401(k) Retirement Plan for the employees of USC Verdugo Hills Hospital, part of the Keck Medical Center of USC Invest in your retirement and yourself today, with help from USC Hospital 401(k)

USC Hospital 401(k) Retirement Plan for the employees of USC Verdugo Hills Hospital, part of the Keck Medical Center of USC Invest in your retirement and yourself today, with help from USC Hospital 401(k)

READY 2018 ENROLLMENT GUIDE. Save today. Enjoy tomorrow. ONL

READY 2018 ENROLLMENT GUIDE Save today. Enjoy tomorrow. ONL Table of Contents Plan Details (eligibility, contributions).... 3 Borrowing (loan details).... 8 Withdrawals (in-service, hardship, termination)...

READY 2018 ENROLLMENT GUIDE Save today. Enjoy tomorrow. ONL Table of Contents Plan Details (eligibility, contributions).... 3 Borrowing (loan details).... 8 Withdrawals (in-service, hardship, termination)...

LIVING IN RETIREMENT: A TIAA FINANCIAL ESSENTIALS WORKSHOP. Paying Yourself: Income options in retirement Kyle Andrews February 23, 2017

LIVING IN RETIREMENT: A TIAA FINANCIAL ESSENTIALS WORKSHOP Paying Yourself: Income options in retirement Kyle Andrews February 23, 2017 Retirement overview Retirement confidence is rebounding after recent

LIVING IN RETIREMENT: A TIAA FINANCIAL ESSENTIALS WORKSHOP Paying Yourself: Income options in retirement Kyle Andrews February 23, 2017 Retirement overview Retirement confidence is rebounding after recent

Replacing your salary in retirement

Replacing your salary in retirement We can help Wondering how you ll replace your salary when you retire? Will you have enough income to last your lifetime? Fortunately, you still have time and options

Replacing your salary in retirement We can help Wondering how you ll replace your salary when you retire? Will you have enough income to last your lifetime? Fortunately, you still have time and options

A distinctive solution for your plan and employees. TIAA-CREF Lifecycle Funds

A distinctive solution for your plan and employees TIAA-CREF Lifecycle Funds TIAA-CREF s Lifecycle Funds offer distinct advantages: Asset allocation glidepath designed for longer lifespans Comprehensive

A distinctive solution for your plan and employees TIAA-CREF Lifecycle Funds TIAA-CREF s Lifecycle Funds offer distinct advantages: Asset allocation glidepath designed for longer lifespans Comprehensive

YOUR GUIDE TO GETTING STARTED

CentraCare Health 403(b) Retirement Plan Invest in your retirement and yourself today, with help from the CentraCare Health 403(b) Retirement Plan and Fidelity. YOUR GUIDE TO GETTING STARTED Invest some

CentraCare Health 403(b) Retirement Plan Invest in your retirement and yourself today, with help from the CentraCare Health 403(b) Retirement Plan and Fidelity. YOUR GUIDE TO GETTING STARTED Invest some

MAXIMIZE YOUR SAVINGS

MAXIMIZE YOUR SAVINGS In the Lam Research 401(k) Plan and Other Plans WHAT S INCLUDED Click directly on the section to the right to move to that section. >> Increased Savings and Tax Flexibility Build

MAXIMIZE YOUR SAVINGS In the Lam Research 401(k) Plan and Other Plans WHAT S INCLUDED Click directly on the section to the right to move to that section. >> Increased Savings and Tax Flexibility Build

Moving with focus. A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan for Health Ventures

Savings Plan for Health Ventures") Moving with focus A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan for Health Ventures Table of contents A new chapter is about to start... 1 What you need to know about

Moving with focus A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan for Health Ventures Table of contents A new chapter is about to start... 1 What you need to know about

YOUR GUIDE TO GETTING STARTED

Mohawk Industries Retirement Savings Plan 1 or Plan 2 Invest in your retirement and yourself today, with help from Mohawk Industries Retirement Savings Plan 1 or Plan 2 and Fidelity. YOUR GUIDE TO GETTING

Mohawk Industries Retirement Savings Plan 1 or Plan 2 Invest in your retirement and yourself today, with help from Mohawk Industries Retirement Savings Plan 1 or Plan 2 and Fidelity. YOUR GUIDE TO GETTING

A Guide To Investing In. Your Future. The Texas A&M University System. Retirement Programs

Retirement Programs A Guide To Investing In The Texas A&M University System Your Future Table of Contents Saving For Retirement 4 Plans at a Glance 6 How to Enroll 7 Approved Vendors 9 Selecting a Vendor

Retirement Programs A Guide To Investing In The Texas A&M University System Your Future Table of Contents Saving For Retirement 4 Plans at a Glance 6 How to Enroll 7 Approved Vendors 9 Selecting a Vendor

Maryland Teachers and State Employees Supplemental Retirement Plans. The Basics. 457(b) Roth 457(b) 401(k) Roth 401(k) 403(b)

Roth 457(b) 401(k) Roth 401(k) 403(b)") Maryland Teachers and State Employees Supplemental Retirement Plans The Basics 457(b) Roth 457(b) 401(k) Roth 401(k) 403(b) Maryland Teachers and State Employees Supplemental Retirement Plans Getting started

Maryland Teachers and State Employees Supplemental Retirement Plans The Basics 457(b) Roth 457(b) 401(k) Roth 401(k) 403(b) Maryland Teachers and State Employees Supplemental Retirement Plans Getting started

Quarterly Newsletter - Q1 2018

Quarterly Newsletter - Q1 2018 2018 Contribution Limit Changes The IRS increased the 402(g) contribution rates for 401(k), 403(b) and 457(b) plans this year, as well as increasing the maximum 415(c) limit

Quarterly Newsletter - Q1 2018 2018 Contribution Limit Changes The IRS increased the 402(g) contribution rates for 401(k), 403(b) and 457(b) plans this year, as well as increasing the maximum 415(c) limit

THE MENTAL HEALTH COOPERATIVE RETIREMENT PLAN ENROLLMENT OVERVIEW

SUPPORT YOUR FUTURE T HE M E N T A L H E A L T H CO O P E R A T IVE RETI R EM E N T PL A N E N R O L L M E N T O VE R VIE W TRANSFORM TOMORROW Supporting your future starts with preparation today. Some

SUPPORT YOUR FUTURE T HE M E N T A L H E A L T H CO O P E R A T IVE RETI R EM E N T PL A N E N R O L L M E N T O VE R VIE W TRANSFORM TOMORROW Supporting your future starts with preparation today. Some

Check in to. your future. Enrollment Overview Crestline Hotels & Resorts, LLC Retirement and Savings Plan

Check in to your future Enrollment Overview Crestline Hotels & Resorts, LLC Retirement and Savings Plan Check in to your future! You spend your time every day caring for our guests. But are you taking

Check in to your future Enrollment Overview Crestline Hotels & Resorts, LLC Retirement and Savings Plan Check in to your future! You spend your time every day caring for our guests. But are you taking

YOUR GUIDE TO GETTING STARTED

William Marsh Rice University Supplemental 403(b) Plan, #50190 Invest in your retirement and yourself today, with help from the William Marsh Rice University Supplemental 403(b) Plan and Fidelity. YOUR

William Marsh Rice University Supplemental 403(b) Plan, #50190 Invest in your retirement and yourself today, with help from the William Marsh Rice University Supplemental 403(b) Plan and Fidelity. YOUR

Enrollment Guide for The SUNY ORP Congratulations on your new position. ENROLL TODAY in the SUNY Retirement Program

Enrollment Guide for The SUNY ORP Congratulations on your new position. ENROLL TODAY in the SUNY Retirement Program As a new employee of the State University of New York (SUNY), you can enroll in a retirement

Enrollment Guide for The SUNY ORP Congratulations on your new position. ENROLL TODAY in the SUNY Retirement Program As a new employee of the State University of New York (SUNY), you can enroll in a retirement

Moving with focus. A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan

Savings Plan") Moving with focus A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan Table of contents A new chapter is about to start... 1 What you need to know about your new Hackensack

Moving with focus A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan Table of contents A new chapter is about to start... 1 What you need to know about your new Hackensack

USNH Enrollment Guide for New Hires/First Time Enrollees

USNH Enrollment Guide for New Hires/First Time Enrollees Welcome to the USNH 403(b) and 457(b) Retirement Plans! Start investing in your future and yourself today. The Plans offer Fidelity Investments

USNH Enrollment Guide for New Hires/First Time Enrollees Welcome to the USNH 403(b) and 457(b) Retirement Plans! Start investing in your future and yourself today. The Plans offer Fidelity Investments

Helping educators and staff make future plans a reality. For Plan Sponsor Use Only. Not for Public Distribution.

Helping educators and staff make future plans a reality For Plan Sponsor Use Only. Not for Public Distribution. Navigating one s own financial future is a daunting and difficult task. However, our employees

Helping educators and staff make future plans a reality For Plan Sponsor Use Only. Not for Public Distribution. Navigating one s own financial future is a daunting and difficult task. However, our employees

Moving with focus. A retirement plan as focused as you.

Moving with focus A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan for Shrewsbury Collectively Bargained Team Members Table of contents A new chapter is about to start...

Moving with focus A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan for Shrewsbury Collectively Bargained Team Members Table of contents A new chapter is about to start...

ENHANCEMENTS GUIDE. No matter where you are in your journey, we can help you map out the retirement you envision.

Your Brandeis University Defined Contribution Retirement Plan ENHANCEMENTS GUIDE No matter where you are in your journey, we can help you map out the retirement you envision. It s a great time to take

Your Brandeis University Defined Contribution Retirement Plan ENHANCEMENTS GUIDE No matter where you are in your journey, we can help you map out the retirement you envision. It s a great time to take

TIAA Brokerage Services overview and account setup. Your quick guide to the enhanced brokerage program

TIAA Brokerage Services overview and account setup Your quick guide to the enhanced brokerage program For investors with specialized investing needs, more choice can mean more opportunity to direct retirement