LIVING IN RETIREMENT: A TIAA FINANCIAL ESSENTIALS WORKSHOP. Paying Yourself: Income options in retirement Kyle Andrews February 23, 2017

|

|

|

- Aron Wilcox

- 6 years ago

- Views:

Transcription

1 LIVING IN RETIREMENT: A TIAA FINANCIAL ESSENTIALS WORKSHOP Paying Yourself: Income options in retirement Kyle Andrews February 23, 2017

2 Retirement overview Retirement confidence is rebounding after recent years hitting record lows 1 The majority of workers (54%) plan to work past age 65 or do not plan to retire. 2 Retirement may last 30 years or more; average time spent in retirement is 19 years for men, 21 years for women 3 Median income for those age 65 or older was $22,177 as of Only 31% of Americans sought advice on translating their retirement savings into lifetime income. 5

3 Today s agenda Wants and needs in retirement: The income floor Retirement investments: What to consider Retirement account options: The basics Other investments & savings Action steps

4 Having enough starts with having a plan: The income floor Retirement needs Home & home-related Healthcare Food & clothing Transportation Insurance Taxes and debt payments

5 Once you establish your income floor, you can establish your lifestyle Retirement wants Vacation/second home Hobbies Travel Time with family and friends Volunteerism Legacy assets

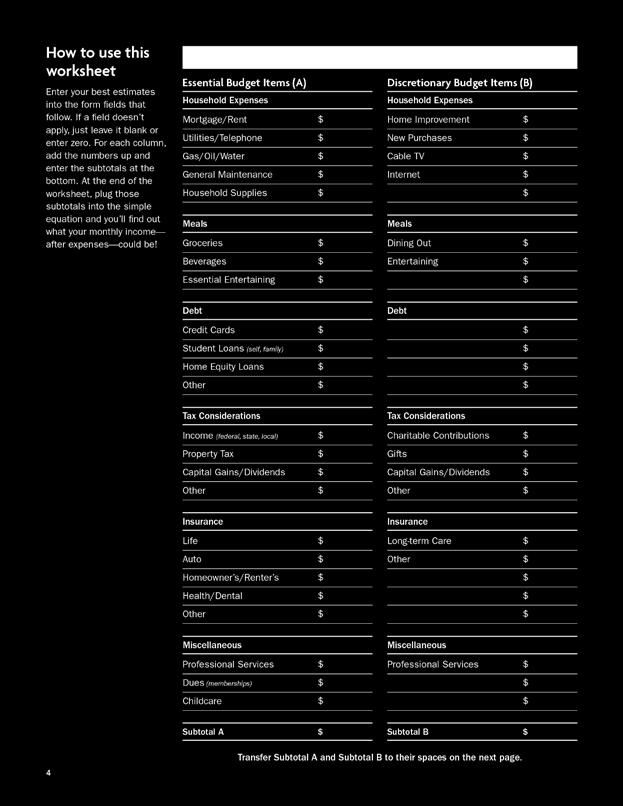

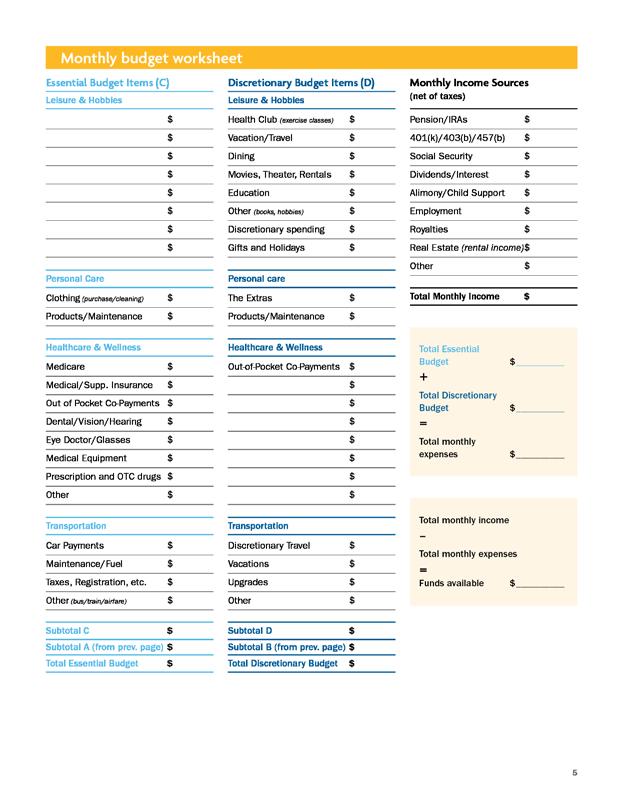

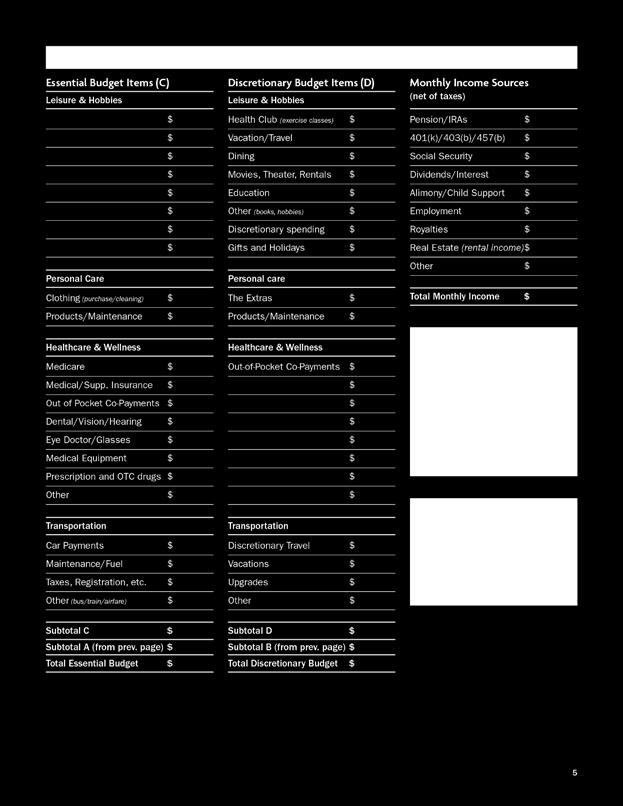

6 The budget worksheet

Annuities Other investment and savings")

7 The most common sources of retirement income Social Security Defined Contribution plans (401(k), 403(b)) Defined Benefit plans Individual Retirement Accounts (IRAs) Annuities Other investment and savings accounts

8 Social Security still viable, still reliable Income traits: Taxable, fixed monthly income from the government Income options: Fixed benefit Other traits: Reduced benefits can be taken as early as age 62 Full benefits available if you wait to full retirement age Full retirement age depends on when you were born. Spouse gets a benefit, too How and when you and your spouse elect to receive Social Security benefit can make a big difference in your monthly payment. Sources: 1) ssa.gov 2) TIAA-CREF collateral

9 Employer-sponsored retirement accounts: Defined Contribution plans (401(k) and 403(b)) Income traits: Taxable, variable monthly income from your employer-sponsored account Income options: Roll it into an IRA Leave it alone Take periodic distributions Annuity (lifetime income) Lump-sum withdrawal Other traits: May borrow money from it (if plan permits), but must pay it back Minimum withdrawal age of 59½ (or be subject to IRS penalty) Mandatory withdrawals beginning at age 70½

10 Employer-sponsored retirement accounts: Defined Benefit plans Income traits: Taxable, fixed monthly income from an employer-sponsored and managed account Income options: Fixed benefit based on company s formula very often at termination Typically funded entirely by the company (although government plans often require employees to contribute) Benefits determined by personalized factors, not investment performance Length of service with company Earnings history (so-called terminal income) NOT an individual account 1 Benefits may come out of company income if investments underperform Maximum benefit is $215,000, no contribution limit* * IRS, Defined Benefit Plan Benefit Limits irs.gov/retirement-plans/plan-participant-employee/retirement-topics-defined-benefit-plan-benefit-limits

11 Individual Retirement Accounts: The Traditional IRA Income traits: Taxable, variable income from a personal retirement investment account Income options: Take it in a lump sum Periodic disbursements Rollover into another Traditional IRA Annuity (Investment Solutions IRA) Other traits: 10% penalty for early withdrawal, plus taxes Minimum withdrawal age of 59½; mandatory distributions begin at age 70½ Penalties for not taking minimum distributions! Special rules may impact taxes Special rules for spouses

12 Individual Retirement Accounts: The Roth IRA Income traits: Tax-free, variable income from a personal retirement investment account Income options: Take it in a lump sum Periodic disbursements Rollover into another Roth IRA Annuity payout Other traits: 10% penalty for early withdrawal, plus taxes on earnings Minimum withdrawal age of 59½ NOTE: Special disbursement rules can apply No mandatory distributions No penalties for not withdrawing Account must be disbursed if accountholder dies Roth account must be five years old before you can take a distribution without tax penalty Contributions (but not gains) are always available for withdrawal without tax or penalty

13 Lifetime annuities: Flexibility, choice and lifetime income Income traits: Income guaranteed for life Income options: Fixed annuities guaranteed principal and specified interest rate Variable annuities fluctuating payments with potential for upside as well as losses. Other traits: LOTS of options to help meet your needs for lifetime income Money can sometimes be transferred between annuities Surrender charges may apply Fees vary look for a low-cost provider

14 TIAA income options: Flexible retirement income Life Annuity: Guaranteed income for life, fixed or variable TIAA Interest Only: Income from a TIAA Traditional Annuity that leaves principal unchanged Transfer Payout Annuity: Allows you to access and reallocate TIAA Traditional Annuity over a set number of years Cash withdrawals: Lump sum or systematic Minimum Distribution Option: Automatically withdraws the minimum required amount from your account once you ve reached the minimum age

15 Lifetime income payout options Some common payout options*: Life only Life with a guarantee period Joint life and last survivor * Not all options available and some providers may offer different payouts.

16 Other investments and savings Income traits: Variable income from personal investments, bonds and savings Income options: Periodic disbursements Take it in a lump sum Other traits: Can incur capital gains taxes No minimum withdrawal age No mandatory disbursements

17 Group activity: Who am I? OPTIONAL Each group will have a chance to identify the investment I m portraying. If you look in your workshop guide, this activity is included, and there is an answer key at the bottom. Discuss these in your groups. I will read a description of an investment, and each group will have a few moments to come to a consensus answer before we move on to the next question. The Who am I? interactive game. INCOME OPTION 1 Sure, the income I offer in retirement is taxable. You can even use it to buy other stuff, like IRAs and annuities if you want to. I don t know why you d do that. I already offer a fixed benefit regardless of what the markets are doing. The good news is that almost everyone has access to me no matter who the employer is. INCOME OPTION 2 You can t rely on Social Security for everything, you know. You should invest in me up to the maximum amount allowed. If you re lucky, there may even be what some people call free money on had to add to the mix. I ll keep growing until you re ready to hit the retirement trail. After that, what you do with me is up to you. INCOME OPTION 3 I was created to help people who didn t get any help creating retirement saving. The government was kind enough to bring me into being many years ago, though they ve been messing with me ever since. The IRS keeps a close eye on the money I generate. Don t like it? You ll want to talk to my little brother. INCOME OPTION 4 I guarantee you an amount of income in retirement. My issuer s ability to pay may be called into question from time to time, but I wouldn t worry about that. Once you decide when you want to get started, I ll start sending checks. Don t start too early or the benefit gets shaved. Don t thank me. It s my job. INCOME OPTION 5 So you want a certain amount of money for the rest of your life? I think we can make that happen. We can play the market if you want, or I can insulate you from it. That s your call. Tired of tracking down your other retirement investments? Bring them to me. No, no, don t worry about minimum ages and required disbursements. Those are just between me and you. ANSWER CHOICES A. 401(k)/403(b) B. Social Security C. Defined Benefit plan D. IRA E. Annuities

18 Income option 1: Who am I? OPTIONAL Sure, the income I offer in retirement is taxable. I already offer a fixed benefit regardless of what the markets are doing. The good news is that almost everyone has access to me, no matter who the employer is.

19 Income option 2: Who am I? OPTIONAL You can t rely on Social Security for everything, you know. You should invest in me up to the maximum amount allowed. If you re lucky, there may even be what some people call free money on hand to add to the mix. I have the potential for growth until you re ready to hit the retirement trail. After that, what you do with me is up to you.

20 Income option 3: Who am I? OPTIONAL I was created to help people who didn t get any help creating retirement saving. The government was kind enough to bring me into being many years ago, although they ve been messing with me ever since. The IRS keeps a close eye on the money I generate. Don t like it? You ll want to talk to my little brother.

21 Income option 4: Who am I? OPTIONAL I guarantee you an amount of income in retirement. My issuer s ability to pay may be called into question from time to time. Once you decide when you want to get started, I ll start sending checks. Don t start too early or the benefit gets shaved. Don t thank me. It s my job.

22 Income option 5: Who am I? OPTIONAL So you want a certain amount of money for the rest of your life? I think we can make that happen. We can play the market if you want, or I can insulate you from it. That s your call. I m a lot more versatile than most people think. The bottom line is than I can help make sure you get paid for as long as you want.

23 The Answers OPTIONAL Question 1: Social Security Question 2: 401(k)/403(b) or Defined Contribution plan Question 3: Traditional IRA Question 4: Social Security (again!) Question 5: Annuities Annuities guarantees are based on the claims-paying ability of the issuer. Payments from the variable annuity accounts are not guaranteed and will rise or fall based on investment performance.

24 Tally the scores! OPTIONAL Question 1: Social Security 20 Question 2: 401(k)/403(b) or Defined Contribution plan 20 Question 3: Traditional IRA 20 Question 4: Social Security (again!) 20 Question 5: Annuities 20 Bonus question: Closest answer wins! What percentage of Americans 65 and older held a paying job in 2016?

25 Recap: What to consider in retirement investments What will the investment/asset be used for? How liquid or easy to withdraw is it? How is each investment/asset taxed on withdrawal? What is it invested in what is the risk?

26 Putting it all together: Action steps Estimate your required expenses and secure them with guaranteed income Estimate the cost to do what you want in retirement and invest accordingly Plan your income carefully and know which assets will pay what amount and when Taxes, taxes, taxes Consider consolidation

27 Additional tools TIAA.org/tools Retirement Advisor Retirement Goal Evaluator Budget Worksheet

28 Questions?

29 Thank You! Call to schedule a one-on-one counseling session for advice with a TIAA Financial Consultant. Schedule online at TIAA.org/schedulenow

30 Sources Retirement confidence remains at a consistent high after recent years hitting record lows. 1 Employee Benefit Research Institute, The 2016 Retirement Confidence Survey, March 2016 The majority of workers (54%) plan to work past age 65 or do not plan to retire. 2 Transamerica Center for Retirement Studies, Perspectives on Retirement: Baby Boomers, Generation X, and Millennials 17th Annual Transamerica Retirement Survey of Workers, August 2016 Average time spent in retirement is 19 years for men, 21 years for women 3 Social Security Administration, Calculators: Life Expectancy, accessed online September 2016 Median income for those age 65 or older was $22,177 as of Social Security Administration, Facts and Figures about Social Security, 2015, accessed online September 2016 Only 31% of Americans sought advice on translating their retirement savings into lifetime income. 5 TIAA, TIAA-CREF Lifetime Income Survey, accessed online September % of retirees are still paying off their mortgages. 6 Transamerica Center for Retirement Studies, The Current State of Retirement: Pre-Retiree Expectations and Retiree Realities, accessed online September 2016 Average annual healthcare spending can reach nearly $4,400 for households over 65 and can jump to more than $6,600 for those 85 and older. 7 Employee Benefit Research Institute, Utilization Patterns and Out-of-Pocket Expenses for Different Health Care Services Among American Retirees, accessed online September 2016

31 Sources A 65-year-old couple can now expect to spend an estimated $260,000 on health care throughout retirement, including costs for Medicare premiums, co-payments, deductibles and prescription drugs. 8 US News & World Report, How a Health Savings Account Can Help You Save for Retirement, September 2016 The cost of eating at home increased to 1.1% while eating out increased by 7.9% in Bureau of Labor Statistics, Consumer Expenditures 2015, August 2016 Social Security can be expected to replace about 40% of preretirement income 10 The Motley Fool, How Much of My Income Will Social Security Replace in Retirement?, February 2016 A spouse s benefit may be up to 50% of yours. 11 Social Security Administration, Retirement Planner: Benefits For Your Spouse, accessed online September 2016 A man age 65 will likely live to just over 84 years old. Likewise, 65-year-old woman today may expect to live until just over 86 and a half. That can mean about 20 years in retirement. 12 Social Security Administration, Calculators: Life Expectancy, accessed online September 2016 What percentage of Americans 65 and older held a paying job in 2015? Nearly 9 million, or 19% 13 AARP, Older Workers: More Likely to Work Part Time, accessed online September 2016

32 You should consider the investment objectives, risks, charges and expenses carefully before investing. Please call or log on to TIAA.org for underlying product and fund prospectuses that contain this and other information. Read the prospectuses carefully before investing. Investment, insurance and annuity products are not FDIC insured, are not bank guaranteed, are not deposits, are not insured by any federal government agency, are not a condition to any banking service or activity, and may lose value. Investment products may be subject to market and other risk factors. See the applicable product literature, or visit TIAA.org for details. TIAA-CREF Individual & Institutional Services, LLC and Teachers Personal Investors Services, Inc., Nuveen Securities, LLC, members FINRA and SIPC, distribute securities products. Annuity contracts and certificates are issued by Teachers Insurance and Annuity Association of America (TIAA) and College Retirement Equities Fund (CREF), New York, NY. Each is solely responsible for its own financial condition and contractual obligations. Annuities guarantees are based on the claims-paying ability of the issuer. Payments from the variable annuity accounts are not guaranteed and will rise or fall based on investment performance.

33 Before consolidating assets, be sure to carefully consider the benefits of both the existing and new product. There will likely be differences in features, costs, surrender charges, services, company strength and other important aspects. There may also be tax consequences or other penalties associated with the transfer of assets. Indirect transfers may be subject to taxation and penalties. Consult with your own advisors regarding your particular situation. The TIAA-CREF Retirement Advisor is a brokerage service provided by TIAA-CREF Individual & Institutional Services, LLC, a registered broker/dealer and member of FINRA. After-tax annuities are issued by TIAA-CREF Life Insurance Company, New York, NY. Each of the foregoing is solely responsible for its own financial condition and contractual obligations. The tax information in this guide is not intended to be used, and cannot be used, to avoid possible tax penalties. The TIAA group of companies does not provide legal or tax advice. Please consult with your legal or tax advisor. For its stability, claims-paying ability and overall financial strength, Teachers Insurance and Annuity Association of America (TIAA) is a member of one of only three insurance groups in the United States to currently hold the highest rating available to U.S. insurers from three of the four leading insurance company rating agencies: A.M. Best (A++ as of 6/16), Fitch (AAA as of 5/16) and Standard & Poor's (AA+ as of 7/15), and the second highest possible rating from Moody s Investors Service (Aa1 as of 8/15). There is no guarantee that current ratings will be maintained. The financial strength ratings represent a company s ability to meet policyholders obligations and do not apply to variable annuities or any other product or service not fully backed by TIAA s claims-paying ability. The ratings also do not apply to the safety or the performance of the variable accounts, which will fluctuate in value. TIAA.org 2016 Teachers Insurance and Annuity Association of America-College Retirement Equities Fund, 730 Third Avenue, New York, NY C

Paying Yourself: Income options in retirement. Laura Maxwell November 1, 2017 TIAA PUBLIC

LIVING IN RETIREMENT: A TIAA FINANCIAL ESSENTIALS WORKSHOP Paying Yourself: Income options in retirement Laura Maxwell November 1, 2017 Retirement overview Retirement confidence declined to 60% in 2017,

LIVING IN RETIREMENT: A TIAA FINANCIAL ESSENTIALS WORKSHOP Paying Yourself: Income options in retirement Laura Maxwell November 1, 2017 Retirement overview Retirement confidence declined to 60% in 2017,

Halfway There: A retirement checkup Hank Conway 10/30/2018 PLANNING FOR TODAY AND TOMORROW: A TIAA FINANCIAL ESSENTIALS WORKSHOP

PLANNING FOR TODAY AND TOMORROW: A TIAA FINANCIAL ESSENTIALS WORKSHOP Halfway There: A retirement checkup Hank Conway 10/30/2018 Institution logo Scale to achieve visual balance with the TIAA logo. Align

PLANNING FOR TODAY AND TOMORROW: A TIAA FINANCIAL ESSENTIALS WORKSHOP Halfway There: A retirement checkup Hank Conway 10/30/2018 Institution logo Scale to achieve visual balance with the TIAA logo. Align

INVESTING IN YOUR FUTURE: A TIAA FINANCIAL ESSENTIALS WORKSHOP. Money at Work 1: Foundations of investing

INVESTING IN YOUR FUTURE: A TIAA FINANCIAL ESSENTIALS WORKSHOP Money at Work 1: Foundations of investing Staying on course: Today s agenda Retirement Advisor Understanding saving Risk tolerance Asset classes

INVESTING IN YOUR FUTURE: A TIAA FINANCIAL ESSENTIALS WORKSHOP Money at Work 1: Foundations of investing Staying on course: Today s agenda Retirement Advisor Understanding saving Risk tolerance Asset classes

Replacing your salary in retirement

Replacing your salary in retirement We can help Wondering how you ll replace your salary when you retire? Will you have enough income to last your lifetime? Fortunately, you still have time and options

Replacing your salary in retirement We can help Wondering how you ll replace your salary when you retire? Will you have enough income to last your lifetime? Fortunately, you still have time and options

Within Reach: Transitioning from career to retirement

Within Reach: Transitioning from career to retirement Get ready for a new journey LIVING IN RETIREMENT: A TIAA FINANCIAL ESSENTIALS WORKSHOP In every journey, there are choices Preservation is important

Within Reach: Transitioning from career to retirement Get ready for a new journey LIVING IN RETIREMENT: A TIAA FINANCIAL ESSENTIALS WORKSHOP In every journey, there are choices Preservation is important

Lifetime Income: Help secure your retirement. Presented by: Laura Sines March 1, 2018 LIFETIME INCOME: HELP SECURE YOUR RETIREMENT

LIFETIME INCOME: HELP SECURE YOUR RETIREMENT Lifetime Income: Help secure your retirement Presented by: Laura Sines March 1, 2018 Annuitants: Lifetime income summary as of 12/31/17 289 Total annuitants

LIFETIME INCOME: HELP SECURE YOUR RETIREMENT Lifetime Income: Help secure your retirement Presented by: Laura Sines March 1, 2018 Annuitants: Lifetime income summary as of 12/31/17 289 Total annuitants

4/3/2017. Charting Your Course: A financial guide for women. Today s agenda. Savings challenges women may face. Alicia Brady April 11, 2107

SAVING FOR LIFE S MILESTONES: A TIAA FINANCIAL ESSENTIALS WORKSHOP Charting Your Course: A financial guide for women Alicia Brady April 11, 2107 Today s agenda Evaluate your financial health Set financial

SAVING FOR LIFE S MILESTONES: A TIAA FINANCIAL ESSENTIALS WORKSHOP Charting Your Course: A financial guide for women Alicia Brady April 11, 2107 Today s agenda Evaluate your financial health Set financial

Transfers and withdrawals from the TIAA Traditional Annuity. TIAA s Transfer Payout Annuity

Transfers and withdrawals from the TIAA Traditional Annuity TIAA s Transfer Payout Annuity You may have the opportunity to move funds out of the TIAA Traditional Annuity, issued by Teachers Insurance and

Transfers and withdrawals from the TIAA Traditional Annuity TIAA s Transfer Payout Annuity You may have the opportunity to move funds out of the TIAA Traditional Annuity, issued by Teachers Insurance and

FOR WOMEN: A TIAA FINANCIAL ESSENTIALS WORKSHOP. She s Got It: A woman s guide to savings and investing

FOR WOMEN: A TIAA FINANCIAL ESSENTIALS WORKSHOP She s Got It: A woman s guide to savings and investing Agenda She s got it: A woman s guide to saving and investing Financial goals and strategies Basics

FOR WOMEN: A TIAA FINANCIAL ESSENTIALS WORKSHOP She s Got It: A woman s guide to savings and investing Agenda She s got it: A woman s guide to saving and investing Financial goals and strategies Basics

Guide to online withdrawals

Less time, paper and phone calls Many types of withdrawal requests can be completed online through your account on TIAA.org, 1 which saves time and reduces the need for paper forms. This guide includes

Less time, paper and phone calls Many types of withdrawal requests can be completed online through your account on TIAA.org, 1 which saves time and reduces the need for paper forms. This guide includes

Introducing the after-tax contribution option Roth

Introducing the after-tax contribution option Roth Today s agenda The after-tax Roth contribution option Why the after-tax Roth contribution option may be right for you Comparing after-tax Roth contributions

Introducing the after-tax contribution option Roth Today s agenda The after-tax Roth contribution option Why the after-tax Roth contribution option may be right for you Comparing after-tax Roth contributions

Innovative, flexible, low-cost retirement solution

TIAA-CREF Life Insurance Company Innovative, flexible, low-cost retirement solution The Intelligent Variable Annuity What s inside 1 Innovating to better meet your retirement needs 2 The reality of retirement

TIAA-CREF Life Insurance Company Innovative, flexible, low-cost retirement solution The Intelligent Variable Annuity What s inside 1 Innovating to better meet your retirement needs 2 The reality of retirement

A guide to your retirement income options with TIAA-CREF

A guide to your retirement income options with TIAA-CREF Helping you make important decisions about your retirement How will I know when the time is right to retire? Making the decision to retire is no

A guide to your retirement income options with TIAA-CREF Helping you make important decisions about your retirement How will I know when the time is right to retire? Making the decision to retire is no

Receiving Required Minimum Distributions. Making it simple with TIAA

Receiving Required Minimum Distributions Making it simple with TIAA Required Minimum Distributions what you need to know What are Required Minimum Distributions? 1 How can you receive minimum distributions

Receiving Required Minimum Distributions Making it simple with TIAA Required Minimum Distributions what you need to know What are Required Minimum Distributions? 1 How can you receive minimum distributions

SPENDING WITHIN YOUR MEANS: A TIAA FINANCIAL ESSENTIALS WORKSHOP. Inside Money: Managing income and debt Dave Croce March 20, 2018

SPENDING WITHIN YOUR MEANS: A TIAA FINANCIAL ESSENTIALS WORKSHOP Inside Money: Managing income and debt Dave Croce March 20, 2018 Agenda Why budgeting is important Budgeting basics What cash flow is and

SPENDING WITHIN YOUR MEANS: A TIAA FINANCIAL ESSENTIALS WORKSHOP Inside Money: Managing income and debt Dave Croce March 20, 2018 Agenda Why budgeting is important Budgeting basics What cash flow is and

Retirement Income Planner

Retirement Income Planner Overview and map TIAA is committed to delivering the most innovative retirement income planning solutions to help you to feel confident about your decision on when to retire and

Retirement Income Planner Overview and map TIAA is committed to delivering the most innovative retirement income planning solutions to help you to feel confident about your decision on when to retire and

FOR WOMEN: A TIAA FINANCIAL ESSENTIALS WORKSHOP. Postcards from the Future: A woman s guide to financially ever after ShaShanna Crumpler May 26, 2016

FOR WOMEN: A TIAA FINANCIAL ESSENTIALS WORKSHOP Postcards from the Future: A woman s guide to financially ever after ShaShanna Crumpler May 26, 2016 Today s agenda Challenges most women face in planning

FOR WOMEN: A TIAA FINANCIAL ESSENTIALS WORKSHOP Postcards from the Future: A woman s guide to financially ever after ShaShanna Crumpler May 26, 2016 Today s agenda Challenges most women face in planning

Demystifying Annuities

Demystifying Annuities Agenda Lessons from Mt. Everest Retirement Planning Considerations How do you know what s right for you All About Annuities Tools and Resources Questions The Perils of Descent What

Demystifying Annuities Agenda Lessons from Mt. Everest Retirement Planning Considerations How do you know what s right for you All About Annuities Tools and Resources Questions The Perils of Descent What

Help for pursuing your financial goals

Help for pursuing your financial goals Pursuing financial well-being TIAA can help hat does success look like for you? On the following pages, you can learn about some of TIAA s products and services,

Help for pursuing your financial goals Pursuing financial well-being TIAA can help hat does success look like for you? On the following pages, you can learn about some of TIAA s products and services,

TIAA 2017 Lifetime Income Survey executive summary

TIAA 2017 Lifetime Income Survey executive summary Americans recognize the importance of having a source of monthly income they can t outlive to cover their essential living expenses during retirement,

TIAA 2017 Lifetime Income Survey executive summary Americans recognize the importance of having a source of monthly income they can t outlive to cover their essential living expenses during retirement,

The Roth contribution option. For retirement plans

The Roth contribution option For retirement plans Contents 2 The Roth contribution option savings choice Learn about the differences between pretax and after-tax contributions 4 Comparing Roth after-tax

The Roth contribution option For retirement plans Contents 2 The Roth contribution option savings choice Learn about the differences between pretax and after-tax contributions 4 Comparing Roth after-tax

Introducing the AfterTax Roth Contribution. Option. October 2017

Introducing the AfterTax Roth Contribution Option October 2017 Today s Agenda The after-tax Roth contribution option Why the after-tax Roth contribution option may be right for you Comparing after-tax

Introducing the AfterTax Roth Contribution Option October 2017 Today s Agenda The after-tax Roth contribution option Why the after-tax Roth contribution option may be right for you Comparing after-tax

TIAA Individual Advisory Services. Personalized financial advice for every stage of life

TIAA Individual Advisory Services Personalized financial advice for every stage of life Personalized solutions for your financial independence Find an advisor today. Go to TIAA.org/ individualadvisoryservices

TIAA Individual Advisory Services Personalized financial advice for every stage of life Personalized solutions for your financial independence Find an advisor today. Go to TIAA.org/ individualadvisoryservices

Strategies for staying on track. Prepare yourself for the journey ahead

Strategies for staying on track Prepare yourself for the journey ahead TIAA and you: Working together to pursue a financially secure future At TIAA, our mission is simple: We re here to help our customers

Strategies for staying on track Prepare yourself for the journey ahead TIAA and you: Working together to pursue a financially secure future At TIAA, our mission is simple: We re here to help our customers

RETIREMENT GUIDE. Wise Options For Retirement

RETIREMENT GUIDE Wise Options For Retirement Table of Contents Retirement Phases and Income Needs 3 Retirement Planning Considerations 4 How Much Will You Need To Save? 5 How Long Will Your Savings Last?

RETIREMENT GUIDE Wise Options For Retirement Table of Contents Retirement Phases and Income Needs 3 Retirement Planning Considerations 4 How Much Will You Need To Save? 5 How Long Will Your Savings Last?

Making the most of your retirement. Your income options

Making the most of your retirement Your income options This brochure is for people within 10 years of retiring and starting to explore the options for withdrawing funds from their retirement plans. You

Making the most of your retirement Your income options This brochure is for people within 10 years of retiring and starting to explore the options for withdrawing funds from their retirement plans. You

A guide for the road to retirement. Announcing changes to Wesleyan University s 403(b)(7) Retirement Plan

(7) Retirement Plan") A guide for the road to retirement Announcing changes to Wesleyan University s 403(b)(7) Retirement Plan 1 Overview of topics we ll be covering today Why the changes What is staying the same and what is

A guide for the road to retirement Announcing changes to Wesleyan University s 403(b)(7) Retirement Plan 1 Overview of topics we ll be covering today Why the changes What is staying the same and what is

THE SUNY OPTIONAL RETIREMENT PROGRAM (ORP) PROVIDED THROUGH TIAA

PROVIDED THROUGH TIAA") THE SUNY OPTIONAL RETIREMENT PROGRAM (ORP) PROVIDED THROUGH TIAA Making the Most of Your Retirement Pre-Retirement Questions and Answers THE SUNY OPTIONAL RETIREMENT PLAN (ORP) PROVIDED THROUGH TIAA Pre-Retirement

THE SUNY OPTIONAL RETIREMENT PROGRAM (ORP) PROVIDED THROUGH TIAA Making the Most of Your Retirement Pre-Retirement Questions and Answers THE SUNY OPTIONAL RETIREMENT PLAN (ORP) PROVIDED THROUGH TIAA Pre-Retirement

TIAA-CREF Investment Horizon Annuity

TIAA-CREF Life Insurance Company TIAA-CREF Investment Horizon Annuity Save tax deferred with guaranteed rates. TIAA: Financial services Almost 100 years ago, Teachers Insurance and Annuity Association

TIAA-CREF Life Insurance Company TIAA-CREF Investment Horizon Annuity Save tax deferred with guaranteed rates. TIAA: Financial services Almost 100 years ago, Teachers Insurance and Annuity Association

Flexible protection with the added value of wealth accumulation potential

TIAA-CREF Life Insurance Company Flexible protection with the added value of wealth accumulation potential Intelligent Life Variable Universal Life Insurance Intelligent Life Survivorship Variable Universal

TIAA-CREF Life Insurance Company Flexible protection with the added value of wealth accumulation potential Intelligent Life Variable Universal Life Insurance Intelligent Life Survivorship Variable Universal

Getting to know TIAA s individual financial solutions and its financial professionals

Getting to know TIAA s individual financial solutions and its financial professionals For nearly 100 years, TIAA has served the retirement needs of plan participants who work in the academic, medical,

Getting to know TIAA s individual financial solutions and its financial professionals For nearly 100 years, TIAA has served the retirement needs of plan participants who work in the academic, medical,

Guide to online withdrawals

Streamlined withdrawal processing The online withdrawal process on the secure My TIAA-CREF website has the same easy-to-use navigation and functionality as other websites that you visit regularly to shop,

Streamlined withdrawal processing The online withdrawal process on the secure My TIAA-CREF website has the same easy-to-use navigation and functionality as other websites that you visit regularly to shop,

TIAA-CREF Ready to Retire Survey Executive Summary. November 19, 2014

TIAA-CREF Ready to Retire Survey Executive Summary November 19, 2014 1 TIAA-CREF Survey: Half of Employees Approaching Retirement Wish They Had Started Saving Sooner Despite regrets, Americans can take

TIAA-CREF Ready to Retire Survey Executive Summary November 19, 2014 1 TIAA-CREF Survey: Half of Employees Approaching Retirement Wish They Had Started Saving Sooner Despite regrets, Americans can take

Your guide to 403(b) tax-deferred annuity or voluntary savings plans. How much can you contribute in 2018?

tax-deferred annuity or voluntary savings plans. How much can you contribute in 2018?") Your guide to 403(b) tax-deferred annuity or voluntary savings plans How much can you contribute in 2018? Tax-deferred annuity plans ( TDA Plans ) are voluntary savings plans that help you build the extra

Your guide to 403(b) tax-deferred annuity or voluntary savings plans How much can you contribute in 2018? Tax-deferred annuity plans ( TDA Plans ) are voluntary savings plans that help you build the extra

Table of contents. 2 Federal income tax rates 12 Required minimum distributions. 4 Child credits 13 Roth IRAs

2017 tax guide Table of contents 2 Federal income tax rates 12 Required minimum distributions 4 Child credits 13 Roth IRAs 5 Taxes: estates, gifts, Social Security 15 SEPs, Keoghs 6 Rules on retirement

2017 tax guide Table of contents 2 Federal income tax rates 12 Required minimum distributions 4 Child credits 13 Roth IRAs 5 Taxes: estates, gifts, Social Security 15 SEPs, Keoghs 6 Rules on retirement

TIAA-CREF Investing in You Survey Executive Summary. August 12, 2014

{ TIAA-CREF Investing in You Survey Executive Summary August 12, 2014 TIAA-CREF Survey Finds One-Third of Americans Have Never Increased Their Retirement Plan Contribution Rate Millennials are most likely

{ TIAA-CREF Investing in You Survey Executive Summary August 12, 2014 TIAA-CREF Survey Finds One-Third of Americans Have Never Increased Their Retirement Plan Contribution Rate Millennials are most likely

Focus on income: Help shape your participants retirement

Focus on income: Help shape your participants retirement Target Date Plus Models offered as part of the TIAA Custom Portfolios Model Service FPO For institutional investor use only. Not for use with or

Focus on income: Help shape your participants retirement Target Date Plus Models offered as part of the TIAA Custom Portfolios Model Service FPO For institutional investor use only. Not for use with or

Complete your retirement picture with guaranteed income

Complete your retirement picture with guaranteed income ANNUITIES INCOME Brighthouse Income Annuity SM Add immediate income for more certainty. All guarantees are subject to the claims-paying ability and

Complete your retirement picture with guaranteed income ANNUITIES INCOME Brighthouse Income Annuity SM Add immediate income for more certainty. All guarantees are subject to the claims-paying ability and

Strategies for staying on track to your retirement

Strategies for staying on track to your retirement TIAA-CREF and you: Planning an income for life For more than 90 years, we at TIAA-CREF have dedicated ourselves to helping those who serve the greater

Strategies for staying on track to your retirement TIAA-CREF and you: Planning an income for life For more than 90 years, we at TIAA-CREF have dedicated ourselves to helping those who serve the greater

A new chapter for the Grand Valley State University retirement program

A new chapter for the Grand Valley State University retirement program Transition seminar topics Why we re here today Transition experience Updates to the new investment menu Retirement program features

A new chapter for the Grand Valley State University retirement program Transition seminar topics Why we re here today Transition experience Updates to the new investment menu Retirement program features

A guide for the road to retirement. Announcing updates to the Eastern Michigan University Retirement Plan

A guide for the road to retirement Announcing updates to the Eastern Michigan University Retirement Plan 1 Overview of topics we ll be covering today Why changes are being made What stays the same Plan

A guide for the road to retirement Announcing updates to the Eastern Michigan University Retirement Plan 1 Overview of topics we ll be covering today Why changes are being made What stays the same Plan

TIAA-CREF Investment Options Survey Executive Summary February 26, 2015

TIAA-CREF Investment Options Survey Executive Summary February 26, 2015 1 . TIAA-CREF Survey: More Americans Are Unfamiliar with Investment Options in Their Retirement Plans These findings come from TIAA-CREF

TIAA-CREF Investment Options Survey Executive Summary February 26, 2015 1 . TIAA-CREF Survey: More Americans Are Unfamiliar with Investment Options in Their Retirement Plans These findings come from TIAA-CREF

Distributions from your employersponsored. retirement plan. Allianz Life Insurance Company of North America Allianz Life Insurance Company of New York

Distributions from your employersponsored retirement plan Understanding your options Allianz Life Insurance Company of North America Allianz Life Insurance Company of New York AMK-068-N Page 1 of 12 Your

Distributions from your employersponsored retirement plan Understanding your options Allianz Life Insurance Company of North America Allianz Life Insurance Company of New York AMK-068-N Page 1 of 12 Your

Your Guide to the Retiree Medical Account Plan

Your Guide to the Retiree Medical Account Plan What you need to know A benefit for NYU Lutheran employees Table of Contents The Retiree Medical Account Plan At-A-Glance...1 Creating Your Own Portfolio...3

Your Guide to the Retiree Medical Account Plan What you need to know A benefit for NYU Lutheran employees Table of Contents The Retiree Medical Account Plan At-A-Glance...1 Creating Your Own Portfolio...3

4-step guide to life insurance

TIAA-CREF Life Insurance Company 4-step guide to life insurance Our promise to help you protect what matters most At TIAA, we understand the need for life insurance our promise is to help you make the

TIAA-CREF Life Insurance Company 4-step guide to life insurance Our promise to help you protect what matters most At TIAA, we understand the need for life insurance our promise is to help you make the

LIVING WELL IN RETIREMENT MAKING THE MOST OF YOUR RETIREMENT HOW TO CHOOSE THE RIGHT INCOME OPTIONS FOR YOU

LIVING WELL IN RETIREMENT MAKING THE MOST OF YOUR RETIREMENT HOW TO CHOOSE THE RIGHT INCOME OPTIONS FOR YOU TIAA-CREF: Helping to provide you A GUARANTEED income for life For more than 90 years, we at

LIVING WELL IN RETIREMENT MAKING THE MOST OF YOUR RETIREMENT HOW TO CHOOSE THE RIGHT INCOME OPTIONS FOR YOU TIAA-CREF: Helping to provide you A GUARANTEED income for life For more than 90 years, we at

WHAT MATTERS MOST. A woman s guide to an inspired retirement strategy

WHAT MATTERS MOST A woman s guide to an inspired retirement strategy Issued by Pruco Life Insurance Company (in New York, issued by Pruco Life Insurance Company of New Jersey). 0250519-00002-00 Ed. 01/2014

WHAT MATTERS MOST A woman s guide to an inspired retirement strategy Issued by Pruco Life Insurance Company (in New York, issued by Pruco Life Insurance Company of New Jersey). 0250519-00002-00 Ed. 01/2014

IRA Assets and Rollovers. Unlocking Opportunities at Ages 60 to 70. Retirement SOLUTIONS 12/ A

IRA Assets and Rollovers Unlocking Opportunities at Ages 60 to 70 Retirement 12/15 23077-15A SOLUTIONS Using Rollovers as a Retirement Strategy As you reflect on your retirement goals, a few questions

IRA Assets and Rollovers Unlocking Opportunities at Ages 60 to 70 Retirement 12/15 23077-15A SOLUTIONS Using Rollovers as a Retirement Strategy As you reflect on your retirement goals, a few questions

Thinking differently about helping your clients measure retirement success

Thinking differently about helping your clients measure retirement success April 2018 For institutional investor use only. Not for use with or distribution to the public. 100 years of dedicated service

Thinking differently about helping your clients measure retirement success April 2018 For institutional investor use only. Not for use with or distribution to the public. 100 years of dedicated service

Guide to online loans

Less paperwork. Faster service. You can request a loan online through your account on TIAA.org. 1 No paper application is needed, which saves time and helps you receive the funds quickly. This guide includes

Less paperwork. Faster service. You can request a loan online through your account on TIAA.org. 1 No paper application is needed, which saves time and helps you receive the funds quickly. This guide includes

Prudential ANNUITIES ANNUITIES UNDERSTANDING. Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey.

Prudential ANNUITIES UNDERSTANDING ANNUITIES Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey. 0160994-00008-00 Ed. 05/2017 Meeting the challenges of retirement

Prudential ANNUITIES UNDERSTANDING ANNUITIES Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey. 0160994-00008-00 Ed. 05/2017 Meeting the challenges of retirement

Getting Ready for Retirement 2018

Getting Ready for Retirement 2018 Getting Ready for Retirement This presentation summarizes the benefits you may be eligible for in retirement. For more detailed information, please refer to the Research

Getting Ready for Retirement 2018 Getting Ready for Retirement This presentation summarizes the benefits you may be eligible for in retirement. For more detailed information, please refer to the Research

The George Washington University Retirement Plans. How to get started

The George Washington University Retirement Plans How to get started Table of Contents Why Save 3 Plans at a Glance 4 Investment Providers 7 How to Enroll 8 Provider Fact Sheets 9 Investment Education

The George Washington University Retirement Plans How to get started Table of Contents Why Save 3 Plans at a Glance 4 Investment Providers 7 How to Enroll 8 Provider Fact Sheets 9 Investment Education

Ready to invest? Brokerage reference guide

Ready to invest? Brokerage reference guide You ve got goals. You can start investing for them today with a TIAA Brokerage account. Build and adjust your portfolio based on your needs. Choose how to manage

Ready to invest? Brokerage reference guide You ve got goals. You can start investing for them today with a TIAA Brokerage account. Build and adjust your portfolio based on your needs. Choose how to manage

Flexible protection to help meet a lifetime of needs

TIAA-CREF Life Insurance Company Flexible protection to help meet a lifetime of needs Intelligent Life Universal Life Insurance and Intelligent Life Survivorship Universal Life Insurance For the milestones

TIAA-CREF Life Insurance Company Flexible protection to help meet a lifetime of needs Intelligent Life Universal Life Insurance and Intelligent Life Survivorship Universal Life Insurance For the milestones

UPMC RETIREMENT BENEFITS YOUR RETIREMENT GUIDE. A Step-by-Step Checklist

UPMC RETIREMENT BENEFITS YOUR RETIREMENT GUIDE A Step-by-Step Checklist YOU RE RETIRING SOON CONGRATULATIONS! RETIRING IS A BIG STEP You ll be asked to make many important decisions about your UPMC benefits

UPMC RETIREMENT BENEFITS YOUR RETIREMENT GUIDE A Step-by-Step Checklist YOU RE RETIRING SOON CONGRATULATIONS! RETIRING IS A BIG STEP You ll be asked to make many important decisions about your UPMC benefits

Getting Ready to Retire

How to Prepare for Your Retirement A GUIDE TO: Getting Ready to Retire EDUCATION GUIDE Create a plan now for a more comfortable retirement If you re five years or less from retirement, now is the time

How to Prepare for Your Retirement A GUIDE TO: Getting Ready to Retire EDUCATION GUIDE Create a plan now for a more comfortable retirement If you re five years or less from retirement, now is the time

Hartford Lifetime Income Summary booklet

Hartford Lifetime Income Summary booklet A group deferred fixed annuity issued by Hartford Life Insurance Company TABLE OF CONTENTS 2 HLI at a glance 4 Is this investment option right for you? 4 How HLI

Hartford Lifetime Income Summary booklet A group deferred fixed annuity issued by Hartford Life Insurance Company TABLE OF CONTENTS 2 HLI at a glance 4 Is this investment option right for you? 4 How HLI

FOR WOMEN WHY IT S DIFFERENT. What Matters Most for RETIREMENT PLANNING

What Matters Most for RETIREMENT PLANNING WHY IT S DIFFERENT FOR WOMEN Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey. 0250519-00006-00 Ed. 09/2017 YOUR LIFE IS

What Matters Most for RETIREMENT PLANNING WHY IT S DIFFERENT FOR WOMEN Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey. 0250519-00006-00 Ed. 09/2017 YOUR LIFE IS

Frequently asked questions about TIAA Traditional Annuity

about TIAA Traditional Annuity TIAA Traditional Annuity can provide you with certainty, income you can t outlive and peace of mind. Table of contents: Section 1 Overview Section 2 Interest crediting rates

about TIAA Traditional Annuity TIAA Traditional Annuity can provide you with certainty, income you can t outlive and peace of mind. Table of contents: Section 1 Overview Section 2 Interest crediting rates

Learn about distribution options for your employer retirement plan assets. Investor education

Learn about distribution options for your employer retirement plan assets Investor education It s your retirement: Choose wisely As you plan your retirement, you ll need to decide what to do with the

Learn about distribution options for your employer retirement plan assets Investor education It s your retirement: Choose wisely As you plan your retirement, you ll need to decide what to do with the

FOR RETIREMENT. Planning ahead. Understanding the Roth feature of your 401(k) retirement plan. Plan Participant Guide

retirement plan. Plan Participant Guide") FOR RETIREMENT Planning ahead Understanding the Roth feature of your 401(k) retirement plan Plan Participant Guide 2057664 What is a Roth 401(k)? A Roth 401(k) allows you to make after-tax contributions

FOR RETIREMENT Planning ahead Understanding the Roth feature of your 401(k) retirement plan Plan Participant Guide 2057664 What is a Roth 401(k)? A Roth 401(k) allows you to make after-tax contributions

Driving Better Outcomes with the TIAA Plan Outcome Assessment

Driving Better Outcomes with the TIAA Plan Outcome Assessment A guide to measuring employee retirement readiness and optimizing plan effectiveness For institutional investor use only. Not for use with

Driving Better Outcomes with the TIAA Plan Outcome Assessment A guide to measuring employee retirement readiness and optimizing plan effectiveness For institutional investor use only. Not for use with

TIME TO FOCUS ON YOUR FUTURE

TIME TO FOCUS ON YOUR FUTURE Enroll online in the new HMH 401(k) Savings Plan at TIAA Active enrollment in the new 401(k) plan is required because your previous elections will not be provided to TIAA.

TIME TO FOCUS ON YOUR FUTURE Enroll online in the new HMH 401(k) Savings Plan at TIAA Active enrollment in the new 401(k) plan is required because your previous elections will not be provided to TIAA.

What s Your Strategy? Design a Personal Income Strategy to help you navigate your way to a secure retirement

What s Your Strategy? Design a Personal Income Strategy to help you navigate your way to a secure retirement Is your Income Strategy designed to guide you through changing markets? One of the most important

What s Your Strategy? Design a Personal Income Strategy to help you navigate your way to a secure retirement Is your Income Strategy designed to guide you through changing markets? One of the most important

Your financial goal planner. A roadmap for planning your financial journey

Your financial goal planner A roadmap for planning your financial journey Planning for your financial well-being is why we re here Wherever you are on your financial journey, you can ask a TIAA financial

Your financial goal planner A roadmap for planning your financial journey Planning for your financial well-being is why we re here Wherever you are on your financial journey, you can ask a TIAA financial

Moving with focus. A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan for Health Ventures

Savings Plan for Health Ventures") Moving with focus A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan for Health Ventures Table of contents A new chapter is about to start... 1 What you need to know about

Moving with focus A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan for Health Ventures Table of contents A new chapter is about to start... 1 What you need to know about

Are you ready to roll?

Are you ready to roll? Is an IRA Rollover right for you? Variable Annuities: Are Not a Deposit of Any Bank Are Not FDIC Insured Are Not Insured by Any Federal Government Agency Are Not Guaranteed by Any

Are you ready to roll? Is an IRA Rollover right for you? Variable Annuities: Are Not a Deposit of Any Bank Are Not FDIC Insured Are Not Insured by Any Federal Government Agency Are Not Guaranteed by Any

SUMMARY PLAN DESCRIPTION FOR THE. ST. OLAF COLLEGE 403(b) RETIREMENT PLAN

RETIREMENT PLAN") SUMMARY PLAN DESCRIPTION FOR THE ST. OLAF COLLEGE 403(b) RETIREMENT PLAN January 1, 2018 TABLE OF CONTENTS INTRODUCTION: YOUR RETIREMENT SAVINGS PROGRAM...1 GENERAL INFORMATION CONCERNING YOUR PLAN...2

SUMMARY PLAN DESCRIPTION FOR THE ST. OLAF COLLEGE 403(b) RETIREMENT PLAN January 1, 2018 TABLE OF CONTENTS INTRODUCTION: YOUR RETIREMENT SAVINGS PROGRAM...1 GENERAL INFORMATION CONCERNING YOUR PLAN...2

Countdown to Retirement Presented by Timothy Weller

Countdown to Retirement Presented by Timothy Weller There s a lot to consider as you prepare for retirement, so it s wise to begin planning well ahead of time. The checklists below are designed to help

Countdown to Retirement Presented by Timothy Weller There s a lot to consider as you prepare for retirement, so it s wise to begin planning well ahead of time. The checklists below are designed to help

LIFETIME INCOME. * CREATED TO SERVE.

LIFETIME INCOME. * *SERIOUSLY. Creating lifetime income in retirement can be done. It just takes teamwork. It takes focus from our plan sponsor clients and their trusted advisors. Proven income-producing

LIFETIME INCOME. * *SERIOUSLY. Creating lifetime income in retirement can be done. It just takes teamwork. It takes focus from our plan sponsor clients and their trusted advisors. Proven income-producing

Annuities in Retirement Income Planning

For much of the recent past, individuals entering retirement could look to a number of potential sources for the steady income needed to maintain a decent standard of living: Defined benefit (DB) employer

For much of the recent past, individuals entering retirement could look to a number of potential sources for the steady income needed to maintain a decent standard of living: Defined benefit (DB) employer

Making Informed Rollover Decisions

Making Informed Rollover Decisions WHAT TO DO WITH YOUR EMPLOYER-SPONSORED RETIREMENT PLAN ASSETS DEFINED CONTRIBUTION PLANS: A defined contribution plan does not promise a specific amount of benefits

Making Informed Rollover Decisions WHAT TO DO WITH YOUR EMPLOYER-SPONSORED RETIREMENT PLAN ASSETS DEFINED CONTRIBUTION PLANS: A defined contribution plan does not promise a specific amount of benefits

I highly recommend all of our actively assigned diocesan priests to join this new savings plan and begin saving now for their future retirement.

PASTORAL CENTER: HUMAN RESOURCES DEPARTMENT 13280 CHAPMAN AVENUE, GARDEN GROVE, CA 92840 NEW RETIREMENT SAVINGS PLANS FOR DIOCESAN PRIESTS Dear Presbyterate, The Diocese of Orange is pleased to announce

PASTORAL CENTER: HUMAN RESOURCES DEPARTMENT 13280 CHAPMAN AVENUE, GARDEN GROVE, CA 92840 NEW RETIREMENT SAVINGS PLANS FOR DIOCESAN PRIESTS Dear Presbyterate, The Diocese of Orange is pleased to announce

Moving with focus. A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan

Savings Plan") Moving with focus A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan Table of contents A new chapter is about to start... 1 What you need to know about your new Hackensack

Moving with focus A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan Table of contents A new chapter is about to start... 1 What you need to know about your new Hackensack

SEVEN LIFE-DEFINING FINANCIAL DECISIONS

SEVEN LIFE-DEFINING FINANCIAL DECISIONS A Joint Project of The Actuarial Foundation and WISER, the Women's Institute for a Secure Retirement 5 PLANNING FOR RETIREMENT The money that you have to support

SEVEN LIFE-DEFINING FINANCIAL DECISIONS A Joint Project of The Actuarial Foundation and WISER, the Women's Institute for a Secure Retirement 5 PLANNING FOR RETIREMENT The money that you have to support

Where to save your money for the long term. How to make the most of your 401(k) and HSA

and HSA") Where to save your money for the long term How to make the most of your 401(k) and GETTING STARTED Two great choices for long-term saving Having access to both a workplace retirement savings plan like

Where to save your money for the long term How to make the most of your 401(k) and GETTING STARTED Two great choices for long-term saving Having access to both a workplace retirement savings plan like

Retiree health savings

Addressing workforce challenges and employee concerns Healthcare costs in retirement are a top concern for Americans. Unfortunately, overall employer benefit offerings haven t kept pace with employee and

Addressing workforce challenges and employee concerns Healthcare costs in retirement are a top concern for Americans. Unfortunately, overall employer benefit offerings haven t kept pace with employee and

Building the right investment approach to help employees become retirement ready

to help employees become retirement ready Does your plan meet today s higher standards for generating favorable retirement outcomes? As a plan fiduciary, it s critical to work with the right retirement

to help employees become retirement ready Does your plan meet today s higher standards for generating favorable retirement outcomes? As a plan fiduciary, it s critical to work with the right retirement

PLANNING FOR TODAY AND TOMORROW:

PLANNING FOR TODAY AND TOMORROW: A TIAA FINANCIAL ESSENTIALS WORKSHOP Equally Prepared: Financial planning for the LGBT community Chandler Mercer Janet Bandera May 22, 2017 Staying on course: Today s agenda

PLANNING FOR TODAY AND TOMORROW: A TIAA FINANCIAL ESSENTIALS WORKSHOP Equally Prepared: Financial planning for the LGBT community Chandler Mercer Janet Bandera May 22, 2017 Staying on course: Today s agenda

Moving with focus. A retirement plan as focused as you.

Moving with focus A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan for Shrewsbury Collectively Bargained Team Members Table of contents A new chapter is about to start...

Moving with focus A retirement plan as focused as you. Hackensack Meridian Health 401(k) Savings Plan for Shrewsbury Collectively Bargained Team Members Table of contents A new chapter is about to start...

An Insider s Guide to Annuities. The Safe Money Guide. retirement security investment growth

The Safe Money Guide retirement security investment growth An Insider s Guide to Annuities 1 Presented by Joe Brown Brown Advisory Group, LLC http://joebrown.retirevillage.com An Insider s Guide to Annuities

The Safe Money Guide retirement security investment growth An Insider s Guide to Annuities 1 Presented by Joe Brown Brown Advisory Group, LLC http://joebrown.retirevillage.com An Insider s Guide to Annuities

Save. Plan. Retire. Your Retirement Options

Save. Plan. Retire. Your Retirement Options Table of Contents Retirement Phases & Income Needs... 3 Retirement Planning Considerations... 4 How Much Will You Need To Save?... 5 How Long Will Your Savings

Save. Plan. Retire. Your Retirement Options Table of Contents Retirement Phases & Income Needs... 3 Retirement Planning Considerations... 4 How Much Will You Need To Save?... 5 How Long Will Your Savings

TIAA Brokerage: For non-retirement accounts Investing as you like it

TIAA Brokerage: For non-retirement accounts Investing as you like it From our retirement roots, TIAA has continued to evolve and grow our financial services organization. We remain true to our not-for-profit

TIAA Brokerage: For non-retirement accounts Investing as you like it From our retirement roots, TIAA has continued to evolve and grow our financial services organization. We remain true to our not-for-profit

We re here to help YOU plan for the future

We re here to help YOU plan for the future RETIREMENT PLANNING Annuity Fund of the International Union of Operating Engineers, Local Union 94-94A-94B, AFL-CIO John Hancock Retirement Plan Services LLC

We re here to help YOU plan for the future RETIREMENT PLANNING Annuity Fund of the International Union of Operating Engineers, Local Union 94-94A-94B, AFL-CIO John Hancock Retirement Plan Services LLC

Managing Money in Retirement. A Guide to Retiree Financial Strategies

Managing Money in Retirement A Guide to Retiree Financial Strategies Managing Money in Retirement Managing Money in Retirement QUICK REFERENCE 2 A New Era of Retirement 3 Identifying Your Retirement Needs

Managing Money in Retirement A Guide to Retiree Financial Strategies Managing Money in Retirement Managing Money in Retirement QUICK REFERENCE 2 A New Era of Retirement 3 Identifying Your Retirement Needs

Mindfulness. and investing. Tradeoffs quiz. Weather the year-end tax season. November 2016

Previous issues Are you finding the right balance between today s needs and tomorrow s goals? > Test your knowledge Mindfulness and Weather the year-end tax season These strategies could impact your income

Previous issues Are you finding the right balance between today s needs and tomorrow s goals? > Test your knowledge Mindfulness and Weather the year-end tax season These strategies could impact your income

Planning ahead. Understanding your 403(b) plan. Plan Participant Guide RETIREMENT PLAN SERVICES

plan. Plan Participant Guide RETIREMENT PLAN SERVICES") Planning ahead Understanding your 403(b) plan The Lincoln National Life Insurance Company Lincoln Life & Annuity Company of New York Plan Participant Guide RETIREMENT PLAN SERVICES 2073285 It all starts

Planning ahead Understanding your 403(b) plan The Lincoln National Life Insurance Company Lincoln Life & Annuity Company of New York Plan Participant Guide RETIREMENT PLAN SERVICES 2073285 It all starts

How to make changes to your annuity income

How to make changes to your annuity income What s inside Is it time to make a change? 2 Your annuity income 3 TIAA Traditional income 5 TIAA and CREF variable annuity income 7 How you can adjust your annuity

How to make changes to your annuity income What s inside Is it time to make a change? 2 Your annuity income 3 TIAA Traditional income 5 TIAA and CREF variable annuity income 7 How you can adjust your annuity

Retirement Income Strategies

176984567 Retirement Income Strategies Photo collage Taking steps toward planning a fit retirement FINANCIAL LITERACY EDUCATION PROGRAMS [Name of presenter] [Title of presenter] Agenda 1 The new retirement

176984567 Retirement Income Strategies Photo collage Taking steps toward planning a fit retirement FINANCIAL LITERACY EDUCATION PROGRAMS [Name of presenter] [Title of presenter] Agenda 1 The new retirement

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM. The path to helping participants plan successfully

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM The path to helping participants plan successfully Making a secure retirement a reality. What are your choices? What s the right amount? What s the best

PENTEGRA RETIREMENT SERVICES DISTRIBUTION PATHTM The path to helping participants plan successfully Making a secure retirement a reality. What are your choices? What s the right amount? What s the best

Retirement Plans. Participant education program. Living. in retirement

Retirement Plans Participant education program Living in retirement Lifestyle. Income. Estate planning. 2 Whether or not you ve enrolled in your company s retirement plan, we want you to have access to

Retirement Plans Participant education program Living in retirement Lifestyle. Income. Estate planning. 2 Whether or not you ve enrolled in your company s retirement plan, we want you to have access to

Documeent title on one or two. during the 2013 IRA season

Documeent title on one or two Tax lines savings Gustan opportunities Book 24pt during the 2013 IRA season The IRA season, from January 1 through April 15, may offer you opportunities to cut taxes and enhance

Documeent title on one or two Tax lines savings Gustan opportunities Book 24pt during the 2013 IRA season The IRA season, from January 1 through April 15, may offer you opportunities to cut taxes and enhance

TIAA Brokerage Services overview and account setup. Your quick guide to the enhanced brokerage program

TIAA Brokerage Services overview and account setup Your quick guide to the enhanced brokerage program For investors with specialized investing needs, more choice can mean more opportunity to direct retirement

TIAA Brokerage Services overview and account setup Your quick guide to the enhanced brokerage program For investors with specialized investing needs, more choice can mean more opportunity to direct retirement

The retiree healthcare challenge: Driving better retirement outcomes and enhancing employee well-being

The retiree healthcare challenge: Driving better retirement outcomes and enhancing employee well-being As an employer, you offer a benefits package that supports your core employment goals to recruit,

The retiree healthcare challenge: Driving better retirement outcomes and enhancing employee well-being As an employer, you offer a benefits package that supports your core employment goals to recruit,

Understanding your. What it is, when to take it, and what to do with it.

Understanding your Required Minimum Distribution What it is, when to take it, and what to do with it. MAKE YOUR RMDs STRESS-FREE Once you reach age 70½, the IRS requires you to take money out of your retirement

Understanding your Required Minimum Distribution What it is, when to take it, and what to do with it. MAKE YOUR RMDs STRESS-FREE Once you reach age 70½, the IRS requires you to take money out of your retirement

Loans from your Retirement Accounts

Loans from your Retirement Accounts Table of contents 1 Borrowing limits and collateral 2 Getting your loan: What you need to know 4 Repaying your loan: What you need to know 6 Loans from retirement plans

Loans from your Retirement Accounts Table of contents 1 Borrowing limits and collateral 2 Getting your loan: What you need to know 4 Repaying your loan: What you need to know 6 Loans from retirement plans

Lehigh University Retirement Plan. Important retirement plan updates

Lehigh University Retirement Plan Important retirement plan updates A new chapter for the retirement plan Key dates Week of March 20, 2017 You will be enrolled in new contracts within the plan and receive

Lehigh University Retirement Plan Important retirement plan updates A new chapter for the retirement plan Key dates Week of March 20, 2017 You will be enrolled in new contracts within the plan and receive

ESG: Everyone Says Give Us More Data. Sarah Wilson Responsible Investment TIAA Global Asset Management

ESG: Everyone Says Give Us More Data Sarah Wilson Responsible Investment TIAA Global Asset Management November 10, 2016 Responsible Investment at TIAA: Seeking competitive returns while making a positive

ESG: Everyone Says Give Us More Data Sarah Wilson Responsible Investment TIAA Global Asset Management November 10, 2016 Responsible Investment at TIAA: Seeking competitive returns while making a positive

Don t just wish. Take action.

Retirement Risk Client Guide Don t just wish. Take action. Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution Not insured by any federal government agency May lose value YOUR GUIDE

Retirement Risk Client Guide Don t just wish. Take action. Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution Not insured by any federal government agency May lose value YOUR GUIDE