Preparing for Your Retirement: An IRA Review

|

|

|

- Erika Robbins

- 5 years ago

- Views:

Transcription

1 Preparing for Your Retirement: An IRA Review How much of your earning power will be available for your use when you retire? What will happen to your standard of living when your income ceases at retirement? Are you currently saving for retirement on a tax-advantaged basis? Table of Contents Your Earning Power Sources of Retirement Income Important Facts About Social Security Retirement Benefits If You Wait You Lose! A Potential Solution Using an IRA Traditional IRA vs. Roth IRA A 2008 Comparison Which Is Beter the Traditional IRA or the Roth IRA? Understanding Traditional IRAs Traditional IRA Taxation Understanding Roth IRAs Roth IRA Taxation IRA-to-IRA Rollovers Important Information Page IRA Review 1

2 Your Earning Power Earning Power: Your earning power - your ability to earn an income - is your most valuable asset. Your Income Investment Income Other Income Spouse s Income Few people realize that a 30-year-old couple will earn 3.5 million dollars by age 65 if their total family income averages $100,000 for their entire careers, without any raises. How Much Will You Earn in a Lifetime? Years to Your Future Earning Power If Your Family Income Averages: Age 65 $50,000 $100,000 $250,000 $500, $2,000,000 $4,000,000 $10,000,000 $20,000, ,750,000 3,500,000 8,750,000 17,500, ,500,000 3,000,000 7,500,000 15,000, ,250,000 2,500,000 6,250,000 12,500, ,000,000 2,000,000 5,000,000 10,000, ,000 1,500,000 3,750,000 7,500, ,000 1,000,000 2,500,000 5,000, , ,000 1,250,000 2,500,000 How much of your earning power do you pay in taxes? What will happen to your standard of living when your income ceases at retirement? IRA Review 2

3 Sources of Retirement Income When you retire and your earning power ceases, you will have to depend on three primary sources for your retirement income: Social Security According to the Social Security Administration, the average retired worker in 2008 receives an estimated $1,079 monthly benefit, about 40% of average pre-retirement income. As pre-retirement income increases, however, the percentage replaced by Social Security declines. Employer-Provided Plans You may be eligible to participate in a retirement plan established by your employer and receive pension income at your retirement. Personal Retirement Savings For many people, there is a gap between the retirement income they can expect from Social Security and employer-provided plans and their retirement income objectives. Personal retirement savings represent the only way to bridge that gap! If sufficient retirement income is not available, will you defer your retirement age, or will you choose to reduce your standard of living? IRA Review 3

4 Important Facts About Social Security Retirement Benefits The Social Security Normal Retirement Age, currently age 66 for those people born between 1943 and 1954, is gradually increasing to age 67 for persons born after Early retirement results in a permanent reduction in the Social Security retirement benefit. For example, the Social Security retirement benefit of a worker born in 1946 who retires early at age 62 in 2008 will be reduced by 30%. According to the Social Security Administration: The maximum Social Security retirement benefit for a worker retiring at full retirement age in 2008 is $2,185 monthly. The average Social Security benefit for all retired workers in 2008 is $1,079. The Social Security spousal retirement benefit is limited to a maximum of 50% of the retired worker s benefit. The spousal retirement benefit is reduced if the worker retires before his or her full retirement age. How much do you want to rely on a source of retirement income over which you have no control? Consider this quote from a Time magazine article titled "Social Insecurity": For government to pay pensions to the advancing tide of baby boomers will almost certainly require stunning benefit reductions or huge tax increases. Most likely both. After years of fiscal and political fecklessness, an explosive conclusion. Question: Answer: When was this article published? March 12, 1995, although the same statement could easily apply today, in the absence of any reform to the Social Security system. IRA Review 4

5 If You Wait You Lose! The eighth wonder of the world is compound interest. -- Albert Einstein Delaying retirement savings can keep you from realizing your retirement dreams! If $100 a month is saved, what will the savings be worth at age 65, assuming a hypothetical 10% rate of return*? $908,734 $559,461 $207,929 $72,399 $20, Age When You Begin to Save $100 a Month * This is a hypothetical illustration only and is not indicative of any particular investment or investment performance. It does not reflect the fees and expenses associated with any particular investment, which would reduce the performance shown in this hypothetical illustration if they were included. In addition, rates of return will vary over time, particularly for long-term investments. IRA Review 5

6 A Potential Solution Using an IRA Those who qualify for a traditional tax-deductible IRA can use money that would otherwise be paid in taxes to establish a retirement fund that accumulates tax deferred. Taxes, however, must be paid as distributions are received from a taxdeductible IRA. A second alternative for those who qualify is the Roth IRA. While contributions to a Roth IRA are not tax deductible, the retirement fund accumulates tax deferred and distributions are received free of income tax. Either a traditional tax-deductible IRA or a non-deductible Roth IRA can produce results superior to a savings plan whose growth is taxed. 20 Year Results (1) 8% Hypothetical Annual Rate of Return/$5,000 Annual Contribution/25% Income Tax Bracket $48,741 $247,115 $247,115 $194,964 Traditional Tax-Deductible IRA (2) Non-Deductible Roth IRA (3) Non-Deductible Savings (4) (1) This is a hypothetical illustration only and is not indicative of any particular investment or performance. It does not reflect the fees and expenses associated with any particular investment, which would reduce the performance shown in this hypothetical illustration if they were included. In addition, rates of return will vary over time, particularly for longer-term investments. Depending on the performance of your IRA investment, it is also possible to lose money. (2) Traditional Tax-Deductible IRA: Assumes the $1,250 annual tax savings are invested in an account whose growth is taxed each year. If the $247,115 value of the tax-deductible IRA is surrendered at the end of the 20th year, the principal amount remaining after payment of income tax is $185,336 at a 25% rate (assumes no penalty tax is assessed). When added to the future value of the tax savings ($48,741), on which income tax has already been paid, the after-tax value of the IRA plus the future value of the tax savings results in total cash available of $234,077. (3) Non-Deductible Roth IRA: If surrendered at the end of the 20th year, the full principal amount of $247,115 is available free of income tax (assumes no penalty tax is assessed). (4) Non-Deductible Savings: Assumes the income tax is paid out of investment earnings each year, meaning that the full principal amount of $194,964 is available free of income tax at the end of the 20th year. IRA Review 6

7 Traditional IRA vs. Roth IRA A 2008 Comparison Eligible individuals can contribute to a tax-deductible traditional IRA, to a nondeductible Roth IRA or to a combination of the two. However, no more than a combined total of $5,000/$6,000 if age 50 or older in 2008 (or 100% of earned income if less) may be contributed to these accounts each year. Individuals who are not eligible for deductible contributions to a traditional IRA or to make contributions to a Roth IRA may still make non-deductible contributions to a traditional IRA and receive the benefits of tax-deferred growth. Which type of IRA is best for you depends on your situation, needs and objectives. The comparison that follows is designed to help you make an informed decision. Deductible Contributions Limit on Contributions Tax-Deferred Growth Tax-Free Distributions Age Limits Income Limits Minimum Distribution Requirement Bankruptcy Protection Traditional IRA (tax deductible) Roth IRA Traditional IRA (non-deductible) Yes No No Yes (lesser of $5,000; $6,000 if age 50 or older; or 100% of earned income) Yes (lesser of $5,000; $6,000 if age 50 or older; or 100% of earned income) Yes (lesser of $5,000; $6,000 if age 50 or older; or 100% of earned income) Yes Yes Yes No (fully taxable) Yes (contributions cannot be made after age 70-1/2) No Yes (distributions must begin by age 70-1/2) Yes, up to $1 million for all IRAs Yes (if qualified distributions) No Yes (contribution phased out if adjusted gross income exceeds specified limits) No Yes, up to $1 million for all IRAs No (partially taxable) Yes (contributions cannot be made after age 70-1/2) No Yes (distributions must begin by age 70-1/2) Yes, up to $1 million for all IRAs IRA Review 7

8 Which Is Beter the Traditional IRA or the Roth IRA? Depending on your situation and objectives, the tax-free distribution feature of the Roth IRA may produce superior overall results when compared to a traditional IRA, which may provide for tax-deductible contributions, but taxable distributions. In choosing between a traditional IRA and a Roth IRA, you may find it helpful to evaluate both the accumulation period and the distribution period results of the respective plans. Traditional vs. Roth IRA Accumulation Period: $5,000 Annual Contribution Each Year for 20 Years Values in 20 Years (1) 8% Hypothetical Annual Rate of Return 25% Income Tax Bracket Total IRA Value Deductible IRA Tax Savings (2) Total Cash Available Traditional IRA (deductible contributions) $247,115 $48,741 $295,856 Traditional IRA (non-deductible contributions) $247, $247,115 Roth IRA (non-deductible contributions) $247, $247,115 Distribution Period: Total Cash Available Distributed in Equal Amounts Over 20 Years (3) 8% Hypothetical Annual Rate of Return 25% Income Tax Bracket Total Cash Available Annual After-Tax Distribution Total Distributions Traditional IRA (deductible contributions; fully taxable IRA distributions) Traditional IRA (non-deductible contributions; partially taxable distributions) Roth IRA (non-deductible contributions; tax-free distributions) $295,856 $21,535 $430,707 $247,115 $18,729 $374,581 $247,115 $23,305 $466,097 (1) This is a hypothetical illustration only and is not indicative of any particular investment or performance. It does not reflect the fees and expenses associated with any particular investment, which would reduce the performance shown in this hypothetical illustration if they were included. In addition, rates of return will vary over time, particularly for longer-term investments. Depending on the performance of your IRA investment, it is also possible to lose money. (2) Assumes that the $1,250 annual tax savings on the $5,000 traditional deductible IRA contribution (25% tax bracket) are invested in a taxable account. (3) Assumes that principal and interest are distributed in equal annual installments over 20 years. IRA Review 8

9 Understanding Traditional IRAs Eligibility: Single Person: Married Couple: Older Workers: Deductibility: A single person who is under age 70-1/2 and has earned income may establish and contribute up to the lesser of $5,000 or 100% of earned income to an IRA. Up to $5,000 can be contributed to an IRA for each spouse, even if one spouse has no earned income, provided that the combined compensation of both spouses is at least equal to the combined IRA contribution (maximum of $10,000). Workers who are age 50 or older may contribute an additional $1,000 to an IRA in 2008, for a total of $6,000, provided that earned income is at least equal to the IRA contribution. IRA contributions are fully deducted from income, unless you and your spouse are active participants in an employersponsored retirement plan, including a tax-deferred annuity (TDA). In that event, the IRA deduction is gradually phased out as follows: Adjusted Gross Income Maximum IRA Deductions (2008 Tax Year) One IRA Joint Taxpayers Two IRAs Age 50 or Older Single Taxpayers One IRA Age 50 or Older $53,000 & under $5,000 $10,000 $6,000 $5,000 $6,000 $58,000 $5,000 $10,000 $6,000 $2,500 $3,000 $63,000 $5,000 $10,000 $6,000 $ 0 $ 0 $85,000 $5,000 $10,000 $6,000 $ 0 $ 0 $95,000 $2,500 $5,000 $3,000 $ 0 $ 0 $105,000 & above $ 0 $ 0 $ 0 $ 0 $ 0 The spouse of an active participant in an employer-sponsored retirement plan who is not covered by his or her own plan can make fully-deductible IRA contributions, if the couple s adjusted gross income is below $159,000 in 2008 and partially-deductible IRA contributions if between $159,000 and $169,000 in Contribution Deadline: An IRA can be established and contributions made between January 1 of the current tax year and the date the income tax return for the current year is filed (no later than April 15th of the following year). IRA Review 9

10 Traditional IRA Taxation During Life: Contributions (2008): Deductible up to $5,000 (up to $10,000 for a married couple; additional $1,000 contribution available to workers age 50 and older in 2008) unless the individual is an active participant in an employer-sponsored qualified retirement plan, in which case the tax deduction is gradually phased out. In 2008, this phase-out begins at adjusted gross incomes in excess of $85,000 for married couples filing jointly ($53,000 for single taxpayers) and ends at $105,000 for married couples ($63,000 for single taxpayers), at which point there is no IRA deduction. The spouse of an active participant in an employer-sponsored retirement plan who is not covered by his or her own plan can make fully-deductible IRA contributions, if the couple s adjusted gross income is below $159,000 and partialy-deductible IRA contributions if between $159,000 and $169,000 in Growth: The earnings on IRA contributions (whether deductible or non-deductible) accumulate tax-free until distributed. Distributions: IRA distributions are taxed under the rules of IRC Sec. 72. This means that the taxpayer is entitled to recover any non-deductible IRA contributions tax-free when distributions begin. Other than this tax-free return of the investment in the contract, al IRA distributions are includable in gross income in the year received. In addition: Premature distributions made prior to age 59-1/2 are subject to a 10% excise or penalty tax in addition to the regular income tax on the amount of the distribution. (Exceptions to the penalty tax include payments made on account of death, disability, to cover certain medical expenses, to pay qualified higher education expenses, for the purchase of a first home ($10,000 lifetime limit), or in a series of substantially equal periodic payments over the taxpayer s life expectancy.) Minimum distributions from an IRA must begin by April 1 of the year after the year in which the taxpayer attains age 70-1/2, or a 50% excise tax is levied on the difference between what was paid out and what should have been paid out under IRA minimum distribution rules. At Death: Estate Taxation: deceased owner. The value of the IRA is included in the gross estate of the Income Taxation: Regular IRA distributions received by a beneficiary after the regular IRA owner s death are taxed in the same manner as if received by the owner. IRA Review 10

11 Understanding Roth IRAs Eligibility: (2008) Single taxpayers with adjusted gross income of up to $101,000 or married couples filing jointly with adjusted gross income of up to $159,000 are eligible to contribute the full $5,000 annually to a Roth IRA. Workers who are age 50 or older may contribute an additional $1,000 to a Roth IRA in 2008, for a total of $6,000. The contribution amount is gradually reduced to zero for adjusted gross income levels between $101,000 and $116,000 for single taxpayers, and between $159,000 and $169,000 for couples. Unlike regular IRAs, contributions to a Roth IRA can be made even after age 70-1/2. Deductibility: Contributions to a Roth IRA are non-deductible. Instead, the tax advantages of a Roth IRA are backloaded. Earnings on Roth IRA contributions accumulate without tax and distributions may be received tax free. Qualified Distributions: Qualified distributions from a Roth IRA are not included in gross income and are not subject to the additional 10% penalty tax for premature distributions. To be a tax-free qualified distribution: The distribution must occur more than five years after the individual first contributed to the Roth IRA; and The individual must be at least 59-1/2 years old, disabled, deceased or the funds must be used to purchase a first home ($10,000 lifetime limit). Converting from a Traditional IRA to a Roth IRA: Taxpayers with adjusted gross incomes not exceeding $100,000 can convert a traditional IRA into a Roth IRA, where IRA assets will continue to accumulate tax-deferred, but be eligible to receive tax-free Roth IRA taxation when distributed. Income taxes must be paid on the amount that is converted, but there is no premature distribution penalty tax. Beginning in 2010, the $100,000 adjusted gross income ceiling for converting a traditional IRA to a Roth IRA will be eliminated. IRA Review 11

12 Roth IRA Taxation During Life: Contributions: Not deductible. Growth: The earnings on Roth IRA contributions accumulate tax-free until distributed. Distributions: Qualified distributions from a Roth IRA are received free of income tax and are not subject to the 10% premature withdrawal penalty tax. Roth IRA distributions that do not meet the qualified distribution requirements will be included in income to the extent that the distribution represents earnings on Roth IRA contributions and may be subject to a 10% premature withdrawal penalty tax. Distribution Made Within 5 Years of First Roth IRA Contribution Distribution Made More Than 5 Years After First Roth IRA Contribution Reason for Distribution: Earnings Taxable Subject to 10% Penalty Earnings Taxable Subject to 10% Penalty On or after age 59-1/2 Yes No No No Before age 59-1/2 (exceptions follow): Yes Yes Yes Yes Death Yes No No No Disability Yes No No No First-time homebuyer ($10,000 limit) Substantially equal periodic payments Medical expenses above 7.5% of adjusted gross income Health insurance premiums paid by the unemployed Yes No No No Yes No Yes No Yes No Yes No Yes No Yes No Higher education expenses Yes No Yes No There is no requirement that distributions from a Roth IRA begin by age 70-1/2. At Death: Estate Taxation: deceased owner. The value of a Roth IRA is included in the gross estate of the Income Taxation: Roth IRA distributions received by a beneficiary after the Roth IRA owner s death are taxed inthe same manner as if received by the owner. IRA Review 12

13 IRA-to-IRA Rollovers Can Funds Be Transferred Between Traditional IRAs and Between Roth IRAs? Yes, funds can be moved from a traditional IRA to another traditional IRA or from a Roth IRA to another Roth IRA without any taxes or penalty, assuming certain requirements are met: The trustee of the existing IRA either transfers the funds directly to the trustee of the receiving IRA; or The funds in the existing IRA are distributed to you and you roll them over to the receiving IRA within 60 days of receiving the distribution. Only one rollover from a traditional IRA to another traditional IRA, or from a Roth IRA to another Roth IRA can be made in any one-year period. Can Funds Be Transferred From a Roth IRA to a Traditional IRA? No, funds cannot be moved from a Roth IRA to a traditional IRA. IRA Review 13

14 IRA-to-IRA Rollovers Can Funds Be Transferred From a Traditional IRA to a Roth IRA? Yes, if modified adjusted gross income does not exceed $100,000 in the year of the conversion or rollover, whether you are single or married and filing a joint return. Taxpayers who are married and file separately cannot convert or roll over funds from a traditional IRA to a Roth IRA. Beginning in 2010, the $100,000 adjusted gross income ceiling will be eliminated. After careful review, you may decide that a Roth IRA is a better retirement savings option for you than a traditional IRA. In this event, if you already have funds in a traditional IRA, you may want to consider moving those funds into a Roth IRA. Advantages: Qualified distributions from a Roth IRA are received free of income tax. If non-qualified distributions are taken, the portion of the distribution represented by traditional IRA contributions is not taxable. There is no minimum age by which you must begin receiving distributions from a Roth IRA. The premature distribution penalty tax does not apply to amounts converted or rolled over from a traditional IRA to a Roth IRA. Qualified distributions from a Roth IRA are not included in determining the taxable portion of any Social Security benefits being received. Disadvantages: The amount that is converted or rolled over to the Roth IRA is subject to federal income tax in the year of the conversion or roll over, to the extent that the funds consist of earnings and tax-deductible contributions to the traditional IRA. For conversions made in 2010, taxpayers will be able to recognize the conversion income in 2010 or average it over the next two years. In the year of the conversion or roll over, this taxable income can serve to increase the taxable portion of any Social Security benefits being received. The premature distribution penalty tax applies to any converted or rolled over amounts distributed from the Roth IRA during the five-year period following the conversion or roll over. You should seek professional tax advice before converting or rolling over funds from a traditional IRA to a Roth IRA in order to avoid unforeseen and/or negative tax and, possibly, creditor protection consequences. IRA Review 14

15 Important Information The information, general principles and conclusions presented in this report are subject to local, state and federal laws and regulations, court cases and any revisions of same. While every care has been taken in the preparation of this report, neither VSA, L.P. nor The National Underwriter Company is engaged in providing legal, accounting, financial or other professional services. This report should not be used as a substitute for the professional advice of an attorney, accountant, or other qualified professional. U.S. Treasury Circular 230 may require us to advise you that "any tax information provided in this document is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer. The tax information was written to support the promotion or marketing of the transaction(s) or matter(s) addressed and you should seek advice based on your particular circumstances from an independent tax advisor." VSA, LP All rights reserved (VSA 1a2-06 ed ) IRA Review 15

16 R E T I R E M E N T P L A N COMPARISON No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency For broker/dealer use only. Not for use with the public.

17 RETIREMENT PLAN CONTRIBUTION LIMITS Pursuant to the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA) 2008 Limit: Indexed in Increments of: IRA & Roth IRA & Roth Catch-up Contribution For Ages 50+ SIMPLE IRA SIMPLE IRA Catch-up Contribution For Ages 50+ SEP-IRA Elective Employee Deferral Limit TSA/403(b) and 401(k) $5,000 $500 $1,000 Not indexed for inflation $10,500 $500 $2,500 $500 Lesser of 25% of compensation or $46,000 $1,000 $15,500 $500 Under IRC 402(g)(8), an eligible employee in a TSA/403(b) with 15 years or more of service with the current eligible employer can increase the elective employee deferral limit up to an additional $3,000 per year. TSA/403(b) and 401(k) Catch-up Contribution for Ages 50+ Defined Benefit Defined Contribution Plans 1 Compensation for Benefit Purposes $5,000 $500 Lesser of 100% of compensation or $185,000 $5,000 Lesser of 100% of compensation or $46,000 $1,000 $230,000 $5,000 1 Defined contribution plans include but are not limited to: 401(k), profit sharing, and money purchase pension. The above chart represents maximum contribution limits and makes no reference to deduction limits.

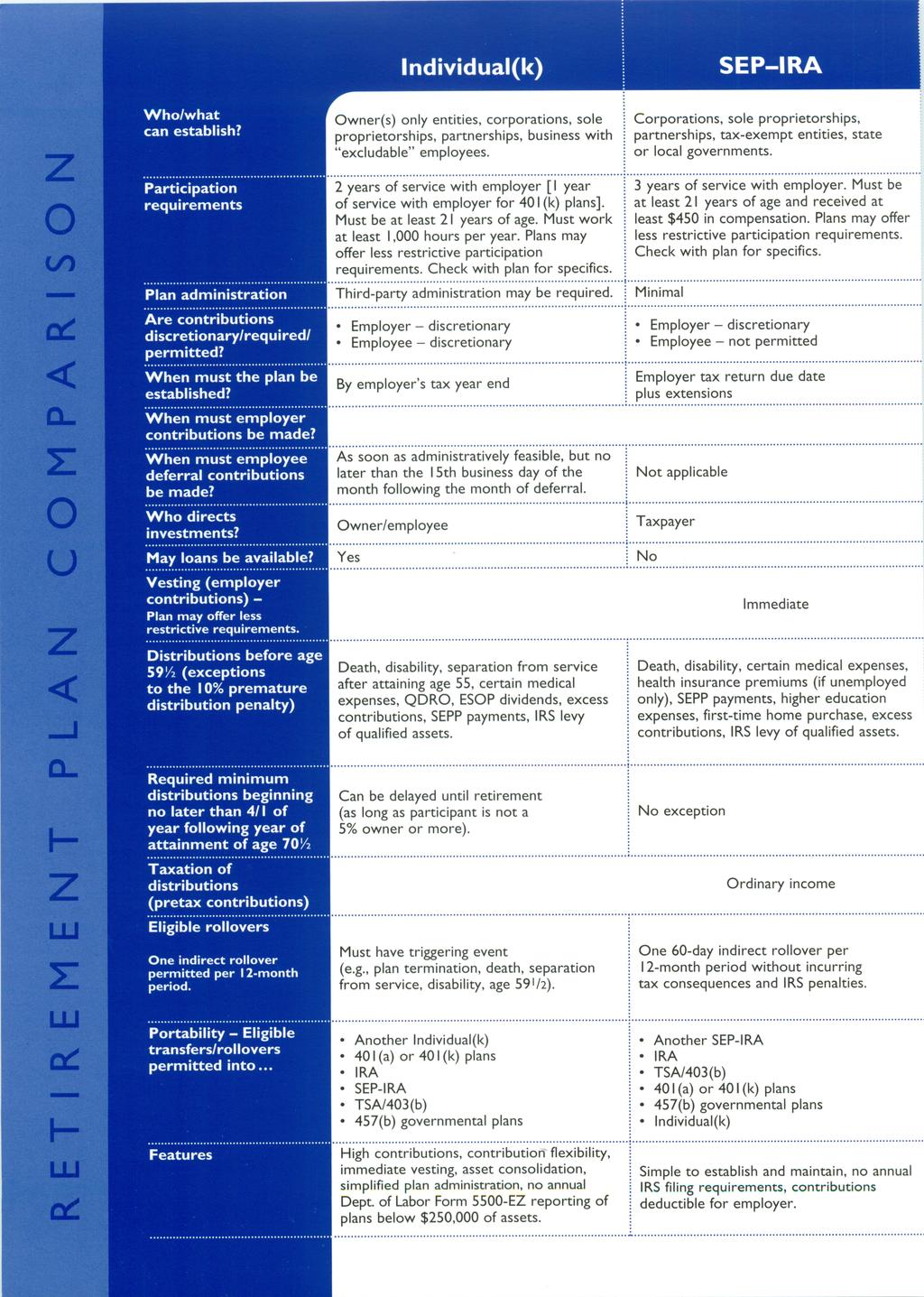

18 Individual(k) SEP IRA SIMPLE IRA Profit-sharing Plan 401(k) Plan Defined Benefit 403(b) Non-ERISA Pension Plan Traditional IRA Roth IRA (Employee Deferrals Only) R E T I R E M E N T P L A N C O M P A R I S O N Who/what can establish? Participation requirements Plan administration Are contributions discretionary/required/ permitted? When must the plan be established? When must employer contributions be made? When must employee deferral contributions be made? Who directs investments? May loans be available? Vesting (employer contributions) Plan may offer less restrictive requirements. Distributions before age 59½ (exceptions to the 10% premature distribution penalty) Required minimum distributions beginning no later than 4/1 of year following year of attainment of age 70½ Taxation of distributions (pretax contributions) Eligible rollovers One indirect rollover permitted per 12-month period. Portability Eligible transfers/rollovers permitted into Features Owner(s) only entities, corporations, sole proprietorships, partnerships, business with excludable employees. 2 years of service with employer [1 year of service with employer for 401(k) plans]. Must be at least 21 years of age. Must work at least 1,000 hours per year. Plans may offer less restrictive participation requirements. Check with plan for specifics. Third-party administration may be required. Employer discretionary Employee discretionary By employer s tax year end As soon as administratively feasible, but no later than the 15th business day of the month following the month of deferral. Owner/employee Yes Death, disability, separation from service after attaining age 55, certain medical expenses, QDRO, ESOP dividends, excess contributions, SEPP payments, IRS levy of qualified assets. Can be delayed until retirement (as long as participant is not a 5% owner or more). Must have triggering event (e.g., plan termination, death, separation from service, disability, age 59 1 /2). Another Individual(k) 401(a) or 401(k) plans IRA SEP-IRA TSA/403(b) 457(b) governmental plans High contributions, contribution flexibility, immediate vesting, asset consolidation, simplified plan administration, no annual Dept. of Labor Form 5500-EZ reporting of plans below $250,000 of assets. Corporations, sole proprietorships, partnerships, tax-exempt entities, state or local governments. 3 years of service with employer. Must be at least 21 years of age and received at least $450 in compensation. Plans may offer less restrictive participation requirements. Check with plan for specifics. Minimal Employer discretionary Employee not permitted Employer tax return due date plus extensions Not applicable Taxpayer No Death, disability, certain medical expenses, health insurance premiums (if unemployed only), SEPP payments, higher education expenses, first-time home purchase, excess contributions, IRS levy of qualified assets. No exception Immediate Ordinary income One 60-day indirect rollover per 12-month period without incurring tax consequences and IRS penalties. Another SEP-IRA IRA TSA/403(b) 401(a) or 401(k) plans 457(b) governmental plans Individual(k) Simple to establish and maintain, no annual IRS filing requirements, contributions deductible for employer. Corporations, sole proprietorships, partnerships, tax-exempt entities, state or local governments (without another retirement program). Must have 100 employees or less. Employees must receive at least $5,000 in compensation during any 2 previous years. Plan may be established between 1/1 and 10/1. Plans may offer less restrictive participation requirements. Minimal Employer required Employee discretionary Between 1/1 and 10/1 of calendar year Employer tax return due date plus extensions No later than 30 days after the last day of the month to which the salary deferral Not applicable amounts relate. Employer/taxpayer No 10% penalty is increased to 25% for distribution within 2 years of first contribution (unless exception applies). Death, disability, certain medical expenses, health insurance premiums (if unemployed only), SEPP payments, higher education expenses, first-time home purchase, excess contributions, IRS levy of qualified assets. No exception Must wait 2 years from the date of the first SIMPLE IRA contribution and roll within 60 days to avoid tax consequences and IRS penalties. During the 2-year period, can only roll or transfer into another SIMPLE IRA. Another SIMPLE IRA IRA SEP-IRA TSA/403(b) 401(a) or 401(k) plans 457(b) governmental plans Individual(k) Contributions deductible for employer, no discrimination testing, not subject to topheavy rules, some funding responsibility with employees, deferral reduces taxable income to employee. Employer discretionary Employee not permitted Trustees or participant check with plan Yes 5-year cliff or 7-year graded schedule Can be delayed until retirement (as long as participant is not a 5% owner or more). Contributions discretionary, flexibility in plan design, contributions and plan expenses may be deductible by employer, vesting schedule. Corporations Partnerships Employer may be required Employee discretionary As soon as administratively feasible, but no later than the 15th business day of the month following the month of deferral. Trustees or participant check with plan Yes Sole proprietorships Tax-exempt entities 2 years of service with employer [1 year of service with employer for 401(k) plans]. Must be at least 21 years of age. Must work at least 1,000 hours per year. Plans may offer less restrictive participation requirements. Check with plan for specifics. 3-year cliff or 6-year graded schedule Can be delayed until retirement (as long as participant is not a 5% owner or more). Flexibility in plan design, contributions and plan expenses may be deductible by employer, funding responsibility with participants, deferred amount reduces employee's taxable income, vesting schedule. Employer required Employee not permitted Not applicable Trustees Yes 5-year cliff or 7-year graded schedule Death, disability, separation from service after attaining age 55, certain medical expenses, QDRO, ESOP dividends, excess contributions, SEPP payments, IRS levy of qualified assets. Ordinary income and/or net-unrealized appreciation By employer s tax year end Another 401(a) or 401(k) plan SEP-IRA 457(b) governmental plans Third-party administration may be required. Can be delayed until retirement (as long as participant is not a 5% owner or more). Must have triggering event (e.g., plan termination, death, separation from service, disability, age 59½). IRA TSA/403(b) Individual(k) Contribution levels may be substantially higher than other types of retirement plans, favors older, highly compensated employees, vesting schedule. Tax-exempt entities qualifying under 501(c)(3). No requirements Employer not permitted Employee discretionary As soon as administratively feasible. Participant Yes Not applicable employer contributions not permitted Death, disability, separation from service after attaining age 55, certain medical expenses, QDRO, excess contributions, SEPP payments, IRS levy of qualified assets. Distribution of pre-1987 assets may be delayed until age 75. Ordinary income Must have triggering event (e.g., death, separation from service, disability, age 59 1 /2). Another TSA/403(b) 401(a) or 401(k) plans IRA SEP-IRA 457(b) governmental plans Individual(k) Deferred amount reduces employee s taxable income, special elections may further increase the amounts an employee can defer, earnings are tax-deferred, contribution limits are greater than IRAs. Must have earned income and must be under age 70½. Individuals with certain modified adjusted gross income levels may not be able to fully deduct contributions. No No exception Another IRA SEP-IRA TSA/403(b) 401(a) or 401(k) plans 457(b) governmental plans Individual(k) Tax-deferred growth Not applicable Not applicable Individual taxpayers Not applicable Discretionary Not applicable Taxpayer Must have earned income. No maximum age restrictions. Individuals with certain modified adjusted gross income levels may not be able to contribute. Death, disability, certain medical expenses, health insurance premiums (if unemployed only), SEPP payments, higher education expenses, first-time home purchase, excess contributions, IRS levy of qualified assets. No Not applicable Not applicable Qualified distribution no income tax One 60-day indirect rollover per 12-month period without incurring tax consequences and IRS penalties. Another Roth IRA Tax-free growth For broker/dealer use only. Not for use with the public.

19

20

21

22

23 A FINAL WORD Keep in mind that qualified plans, as well as IRAs, are already tax-deferred. A variable annuity should be chosen to fund a qualified plan or IRA in order to benefit from features other than tax deferral. These features include lifetime income, living and death benefit options, and the ability to transfer among investment options without sales or withdrawal charges. This material is not intended to be used, nor can it be used by any taxpayer, for the purpose of avoiding U.S. federal, state, or local tax penalties. This material is written to support the promotion or marketing of the transaction(s) or matter(s) addressed by this material. Pacific Life, Pacific Life & Annuity, Pacific Life Funds, their affiliates, distributor, and respective representatives do not provide tax, accounting, or legal advice. Any taxpayer should seek advice based on the taxpayer s particular circumstances from an independent tax advisor. Representations made herein are neither complete nor necessarily up to date. Pacific Life Insurance Company is licensed to issue individual life insurance and annuity products in all states except New York. Product availability and features vary by state. Individual life insurance and annuity products are available in New York through Pacific Life & Annuity Company. Product and rider guarantees are backed by the financial strength and claims-paying ability of either Pacific Life or Pacific Life & Annuity. Each company is solely responsible for the financial obligations accruing under the policies it issues. (800) Mailing address: P.O. Box 2378, Omaha, NE (800) Mailing address: P.O. Box 9768, Providence, RI (800) Mailing address: P.O. Box 2829, Omaha, NE /08 For broker/dealer use only. Not for use with the public. D642708A

24 Preparing for Your Retirement: The Role of Life Insurance in Retirement Planning Did you know that cash value life insurance is the only financial product with the flexibility to provide benefits if you die, if you become disabled or if you live to retirement? Table of Contents Your Earning Power Sources of Retirement Income Important Facts About Social Security Retirement Benefits Potential Solution for a Lifetime Cash Value Life Insurance Cash Value Life Insurance and Retirement Planning Advantages of Cash Value Life Insurance Tax Issues Types of Cash Value Life Insurance Important Information Page Role of Life Insurance in Retirement Planning 1

25 Your Earning Power Earning Power: Your earning power - your ability to earn an income - is your most valuable asset. Your Income Investment Income Other Income Spouse s Income Few people realize that a 30-year-old couple will earn 3.5 million dollars by age 65 if their total family income averages $100,000 for their entire careers, without any raises. How Much Will You Earn in a Lifetime? Years to Your Future Earning Power If Your Family Income Averages: Age 65 $50,000 $100,000 $250,000 $500, $2,000,000 $4,000,000 $10,000,000 $20,000, ,750,000 3,500,000 8,750,000 17,500, ,500,000 3,000,000 7,500,000 15,000, ,250,000 2,500,000 6,250,000 12,500, ,000,000 2,000,000 5,000,000 10,000, ,000 1,500,000 3,750,000 7,500, ,000 1,000,000 2,500,000 5,000, , ,000 1,250,000 2,500,000 If something happens to you during your working years, how will your family replace your earning power? If, as is likely, you live to retirement, will you have sufficient retirement income to replace your earning power? Role of Life Insurance in Retirement Planning 2

26 Sources of Retirement Income When you retire and your earning power ceases, you will have to depend on three primary sources for your retirement income: Social Security According to the Social Security Administration, the average retired worker in 2009 receives an estimated $1,153 monthly benefit, about 40% of average pre-retirement income. As pre-retirement income increases, however, the percentage replaced by Social Security declines. Employer-Provided Plans You may be eligible to participate in a retirement plan established by your employer and receive pension income at your retirement. Personal Retirement Savings For many people, there is a gap between the retirement income they can expect from Social Security and employer-provided plans and their retirement income objectives. Personal retirement savings represent the only way to bridge that gap! Of these three primary sources of retirement income, personal retirement savings is the one over which we exercise the most control! Role of Life Insurance in Retirement Planning 3

27 Important Facts About Social Security Retirement Benefits The Social Security Normal Retirement Age, currently age 66 for those people born between 1943 and 1954, is gradually increasing to age 67 for persons born after Early retirement results in a permanent reduction in the Social Security retirement benefit. For example, the Social Security retirement benefit of a worker born between 1943 and 1954 who retires early at age 62 will be reduced by 25%. According to the Social Security Administration: The maximum Social Security retirement benefit for a worker retiring at full retirement age in 2009 is $2,323 monthly. The average Social Security benefit for all retired workers in 2009 is $1,153. The Social Security spousal retirement benefit is limited to a maximum of 50% of the retired worker s benefit. The spousal retirement benefit is reduced if the worker retires before his or her full retirement age. How much do you want to rely on a source of retirement income over which you have no control? Consider this quote from a Time magazine article titled "Social Insecurity": For government to pay pensions to the advancing tide of baby boomerswill almost certainly require stunning benefit reductions or huge tax increases. Most likely both. After years of fiscal and political fecklessness, an explosive conclusion. Question: Answer: When was this article published? March 12, 1995, although the same statement could easily apply today, in the absence of any reform to the Social Security system. Role of Life Insurance in Retirement Planning 4

28 A Potential Solution for a Lifetime Cash Value Life Insurance Cash value life insurance is the only financial product with the flexibility to provide benefits: If You Die... Should you die prematurely, the death benefit is available to help replace your earning power. This means that funds are available to provide your family with an income, enable them to remain in their home, help pay for an education for your children...whatever the financial needs that arise at your death, funds will be available to help meet those needs. If You Become Disabled... With the waiver of premium benefit, your plan can become self-completing in the event of your disability. This means that if you are sick or hurt and unable to work, policy benefits will remain available just as though you were paying the premiums. If You Live to Retirement... Most of us can expect to live to retirement age, at which time cash value life insurance can serve as a source of retirement income, while still maintaining needed life insurance protection.* This means that the same life insurance that protected your family s financial security during your working years can continue to play an important role in helping to provide retirement security. * Withdrawals and loans wil reduce the policy s death benefit and cash value available for use. Role of Life Insurance in Retirement Planning 5

29 Cash Value Life Insurance and Retirement Planning Cash value life insurance brightens your financial picture with flexibility, accessibility to cash values, tax-deferred growth and an immediate death benefit. In addition, there are a number of roles that cash value life insurance can play in your retirement planning: Source of Retirement Income At retirement, the cash value available in the policy can be: taken in a lump sum by surrendering the policy; converted into a guaranteed lifetime income; or periodically withdrawn and/or borrowed to supplement your retirement income (withdrawals and loans will reduce the policy s death benefit and cash value available for use). Retirement Income Protection At retirement, you can elect the maximum life annuity pension option from your pension plan and use life insurance death benefits to help replace your pension income for your spouse, if you should die first. You and your spouse then enjoy a higher pension income while both of you are alive, with the knowledge that if something should happen to you, your spouse will have a continuing source of retirement income. Accelerated Death Benefits Many life insurance companies make it possible for policyholders to colect a portion of a policy s death benefit early, if the policyholder is terminally ill, stricken with a specific catastrophic illness or requires long-term care in a nursing home. Role of Life Insurance in Retirement Planning 6

30 Advantages of Cash Value Life Insurance Immediate Death Benefit During your working years, your family is protected by the life insurance. In the event of your premature death, income-tax-free benefits are paid to your family. Tax-Deferred Growth Under current law, the annual growth of the cash value in a cash value life insurance contract is not subject to current income tax. Flexibility Certain types of cash value life insurance allow you to increase or decrease your premium payments, or make large, single premium payments. Access to Cash Values You can borrow or withdraw life insurance cash values prior to age 59-1/2 without tax penalty.* Ownership Since you own the policy, benefits are not affected by changes in employment or by changes in Social Security or employer-provided pensions. Disability Protection If you become disabled, the waiver of premium benefit can take over your premium payments for you. Tax-Advantaged Retirement Income The cash value in the policy can be converted to a retirement income that is partially or fully free from federal income tax.* * Withdrawals and loans wil reduce the policy s death benefit and cash value available for use. Role of Life Insurance in Retirement Planning 7

31 Tax Issues Affecting the Role of Cash Value Life Insurance in Retirement Planning Tax-Deferred Growth The Tax Court has held that cash values are not constructively received by a taxpayer when he or she could not reach them without surrendering the policy. The necessity of surrendering the policy constituted a substantial limitation or restriction on their receipt (Theodore H. Cohen, 39 TC 1055, acq CB-4). FIFO Taxation of Withdrawals Assuming a single premium or periodic premium life insurance contract satisfies the conditions of the seven-pay test of IRC Sec. 7702A(b) (i.e., not a modified endowment contract), living benefits received from the contract are taxed under the cost recovery rule, regardless of when the contract was entered into or when premiums were paid. This means that such amounts received from the contract are included in gross income only to the extent they exceed the investment in the contract (IRC Sec. 7702). Policy Loans Are Income Tax Free Policy loans from life insurance contracts are not treated as distributions, assuming the policy qualifies as life insurance under IRC Sec and is not considered a modified endowment contract. Upon policy lapse or surrender, the outstanding loan balance is automatically repaid from policy cash values. This may, however, cause the recognition of taxable income. At death, the death benefit will automatically be reduced by the amount of the outstanding loan, an action that does not cause the recognition of taxable income. Income-Tax-Free Death Benefit As a general rule, death benefits are excludable from the beneficiary s gross income (IRC Sec. 101(a)(1)). Income-Tax-Free Accelerated Death Benefits Depending on current tax law, receiving an accelerated death benefit disbursement may trigger a "taxable event" for the insured. Consult a tax professional about the possible tax implications of accepting a disbursement of accelerated death benefit funds. Role of Life Insurance in Retirement Planning 8

32 Types of Cash Value Life Insurance There are four types of cash value life insurance from which you can select a policy that best satisfies your needs and objectives. The primary differences in the types of cash value life insurance fall into three categories: fixed or flexible premiums; responsibility for investment decisions; and benefit guarantees or benefits based on actual investment returns. Whole Life Insurance Universal Life Insurance Variable Life Insurance Variable Universal Life Insurance The policyowner pays a fixed, level premium and cash values accumulate at a guaranteed* rate of return. The insurance company promises to pay a guaranteed* death benefit. Policy dividends may be payable. The policyowner can increase or decrease premium payments and select from a level or increasing death benefit. Cash value accumulations reflect current interest rates or are tied to a stock market index, such as the S&P 500 Index. The policyowner pays a fixed, level premium and selects from a variety of investment options for cash value accumulations. There is generally a minimum guaranteed* death benefit and the potential for higher death benefits, depending on the performance of the investment options selected. There is no minimum guaranteed cash value. Instead, the cash value available depends on the performance of the investment options selected. The policyowner can increase or decrease premium payments and select from a variety of investment options for cash value accumulations. If a minimum premium payment schedule is maintained, there may be a minimum guaranteed* death benefit. Cash values are not guaranteed. Instead, the cash value available, as well as the potential for a higher death benefit, depend on the performance of the investment options selected. Guarantees are subject to the claims-paying ability of the issuing insurance company. NOTE: Your licensed financial adviser will discuss with you how specific cash value life insurance products may work for you in your particular situation, including the product's features, benefits, risks, charges and expenses. Role of Life Insurance in Retirement Planning 9

33 Important Information The information, general principles and conclusions presented in this report are subject to local, state and federal laws and regulations, court cases and any revisions of same. While every care has been taken in the preparation of this report, neither VSA, L.P. nor The National Underwriter Company is engaged in providing legal, accounting, financial or other professional services. This report should not be used as a substitute for the professional advice of an attorney, accountant, or other qualified professional. Life insurance contracts contain exclusions, limitations, reductions of benefits and terms for keeping them in force. All contract guarantees are based on the claimspaying ability of the issuing insurance company. Consult with your licensed financial representative on how specific life insurance contracts may work for you in your particular situation. Your licensed financial representative will also provide you with costs and complete details about specific life insurance contracts recommended to meet your specific needs and financial objectives. Before purchasing a variable life insurance policy, carefully consider the contract and the underlying funds' investment objectives, risks, charges and expenses. Both the contract prospectus and the underlying fund prospectuses contain information relating to investment objectives, risks, charges and expenses, as well as other important information. The prospectuses are available from your licensed financial representative or the insurance company. You should read them carefully before purchasing a variable life insurance policy. U.S. Treasury Circular 230 may require us to advise you that "any tax information provided in this document is not intended or written to be used, and cannot be used, by any taxpayer for the purpose of avoiding penalties that may be imposed on the taxpayer. The tax information was written to support the promotion or marketing of the transaction(s) or matter(s) addressed and you should seek advice based on your particular circumstances from an independent tax advisor." VSA, LP All rights reserved (VSA 1a2-02 ed ) Role of Life Insurance in Retirement Planning 10

34 Seminar Survey Date: / / Guest: Spouse: Address: Work Phone: City, State, Zip: Home Phone: Who invited you: Current Employer: THE NEXT STEP THE BUSINESS I want to discuss the business opportunity. I know of someone who might be interested in the business. THE CONCEPTS AND PRODUCTS I am interested in learning more about your products & services. I am interested in no-obligation review of my financial situation. APPOINTMENT Office Home Mon Tue Wed Thu Fri Date: / / Time: Sat FEEDBACK:

Epiphany Click")

35 Professional Development System (PDS) Epiphany Click to here go back to PDS menu Paradigm Epi Digm Rev

Preparing for Your Retirement: The Role of Life Insurance in Retirement Planning

Preparing for Your Retirement: The Role of Life Insurance in Retirement Planning Did you know that cash value life insurance is the only financial product with the flexibility to provide benefits if you

Preparing for Your Retirement: The Role of Life Insurance in Retirement Planning Did you know that cash value life insurance is the only financial product with the flexibility to provide benefits if you

Preparing for Your Retirement: An IRA Review Prepared for: Great Southern Bank

Preparing for Your Retirement: An IRA Review Prepared for: Great Southern Bank Presented by: Marketing Financial Advanced Case Design 2960 E. Battlefield Springfield, MO 65804 Office: (800) 677-1087 Dennis@marketingfinancial.com

Preparing for Your Retirement: An IRA Review Prepared for: Great Southern Bank Presented by: Marketing Financial Advanced Case Design 2960 E. Battlefield Springfield, MO 65804 Office: (800) 677-1087 Dennis@marketingfinancial.com

Preparing for Your Retirement: An IRA Review

Preparing for Your Retirement: An IRA Review How much of your earning power will be available for your use when you retire? What will happen to your standard of living when your income ceases at retirement?

Preparing for Your Retirement: An IRA Review How much of your earning power will be available for your use when you retire? What will happen to your standard of living when your income ceases at retirement?

No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency

Understanding iras A Summary of Individual Retirement Accounts No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency 1/15 23038-15A Contents

Understanding iras A Summary of Individual Retirement Accounts No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency 1/15 23038-15A Contents

No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency

Understanding iras A Summary of Individual Retirement Accounts No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency 11/13 23038-13B Contents

Understanding iras A Summary of Individual Retirement Accounts No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency 11/13 23038-13B Contents

Understanding IRAs. A Summary of Individual Retirement Accounts VLC

Understanding IRAs A Summary of Individual Retirement Accounts VLC0015-0318 TABLE OF CONTENTS Get Ready for Retirement.... 1 What Is an IRA?.... 1 Types of IRAs.... 2 Traditional IRA.... 2 Roth IRA....

Understanding IRAs A Summary of Individual Retirement Accounts VLC0015-0318 TABLE OF CONTENTS Get Ready for Retirement.... 1 What Is an IRA?.... 1 Types of IRAs.... 2 Traditional IRA.... 2 Roth IRA....

Exploring Your IRA Options

Exploring Your IRA Options Traditional IRA Q & A.................. Page 2 Roth IRA Q & A...................... Page 5 Traditional vs. Roth IRAs............... Page 8 How does a Traditional IRA differ from

Exploring Your IRA Options Traditional IRA Q & A.................. Page 2 Roth IRA Q & A...................... Page 5 Traditional vs. Roth IRAs............... Page 8 How does a Traditional IRA differ from

Extending Retirement Assets: A Stretch IRA Review

Extending Retirement Assets: A Stretch IRA Review Are you interested in the possibility of using the funds in your traditional IRA to provide income to one or more generations of family members? Table

Extending Retirement Assets: A Stretch IRA Review Are you interested in the possibility of using the funds in your traditional IRA to provide income to one or more generations of family members? Table

Accumulating Funds in an Annuity: A Deferred Fixed Interest and Indexed Annuity Review

Accumulating Funds in an Annuity: A Deferred Fixed Interest and Indexed Annuity Review Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to

Accumulating Funds in an Annuity: A Deferred Fixed Interest and Indexed Annuity Review Did you know that an annuity can be used to systematically accumulate money for retirement purposes, as well as to

In this chapter we will discuss federal income taxation of life insurance, annuities, and retirement plans.

Chapter Seven FEDERAL TAX CONSIDERATIONS AND RETIREMENT PLANS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Identify taxation of premiums, cash values, policy loans and

Chapter Seven FEDERAL TAX CONSIDERATIONS AND RETIREMENT PLANS LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Identify taxation of premiums, cash values, policy loans and

Understanding FIXED ANNUITIES

Understanding FIXED ANNUITIES An Overview for Your Retirement VLC0440-0917 TABLE OF CONTENTS Get Ready for Retirement.... 1 What Is an Annuity?.... 1 What Is a Fixed Annuity?.... 1 Who s Who in an Annuity?....

Understanding FIXED ANNUITIES An Overview for Your Retirement VLC0440-0917 TABLE OF CONTENTS Get Ready for Retirement.... 1 What Is an Annuity?.... 1 What Is a Fixed Annuity?.... 1 Who s Who in an Annuity?....

Retirement plans guide Facts at a glance

Retirement plans guide Facts at a glance Contents 1 What s your plan? 2 Small business/employer retirement plans 4 IRAs 5 Retirement plan distributions 7 Rollovers and transfers 9 Federal tax rates and

Retirement plans guide Facts at a glance Contents 1 What s your plan? 2 Small business/employer retirement plans 4 IRAs 5 Retirement plan distributions 7 Rollovers and transfers 9 Federal tax rates and

Retirement Planning Guide

Retirement Planning Guide 2012 Edition Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company Western-Southern Life Assurance Company CF-74-0001-1202 FINANCIAL PROFESSIONAL

Retirement Planning Guide 2012 Edition Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company Western-Southern Life Assurance Company CF-74-0001-1202 FINANCIAL PROFESSIONAL

STRATEGIES TO HELP YOU KEEP MORE OF YOUR INVESTMENT EARNINGS

STRATEGIES TO HELP YOU KEEP MORE OF YOUR INVESTMENT EARNINGS VLC0774-0118 CONSIDER TAX-EFFICIENT STRATEGIES THAT HELP INCREASE YOUR INVESTMENT EARNINGS The income we keep after taxes are paid is referred

STRATEGIES TO HELP YOU KEEP MORE OF YOUR INVESTMENT EARNINGS VLC0774-0118 CONSIDER TAX-EFFICIENT STRATEGIES THAT HELP INCREASE YOUR INVESTMENT EARNINGS The income we keep after taxes are paid is referred

ENHANCE YOUR FINANCIAL LEGACY

ENHANCE YOUR FINANCIAL LEGACY Variable Annuities with Death Benefits For California VAC0225CA-0517 AS YOU PLAN FOR RETIREMENT, PROTECT YOUR LOVED ONES A Pacific Life variable annuity can offer three death

ENHANCE YOUR FINANCIAL LEGACY Variable Annuities with Death Benefits For California VAC0225CA-0517 AS YOU PLAN FOR RETIREMENT, PROTECT YOUR LOVED ONES A Pacific Life variable annuity can offer three death

IRA Assets and Rollovers. Unlocking Opportunities at Ages 60 to 70. Retirement SOLUTIONS 12/ A

IRA Assets and Rollovers Unlocking Opportunities at Ages 60 to 70 Retirement 12/15 23077-15A SOLUTIONS Using Rollovers as a Retirement Strategy As you reflect on your retirement goals, a few questions

IRA Assets and Rollovers Unlocking Opportunities at Ages 60 to 70 Retirement 12/15 23077-15A SOLUTIONS Using Rollovers as a Retirement Strategy As you reflect on your retirement goals, a few questions

No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency

Understanding annuities An Overview for Your Retirement No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency 2/15 13096-15A Contents Get Ready

Understanding annuities An Overview for Your Retirement No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not insured by any federal government agency 2/15 13096-15A Contents Get Ready

Chapter Seven LEARNING OBJECTIVES OVERVIEW. 7.1 Taxation of Personal Life Insurance Premiums. Cash Values

Chapter Seven Federal Tax Considerations and Retirement Plans LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Identify taxation of premiums, cash values, policy loans and

Chapter Seven Federal Tax Considerations and Retirement Plans LEARNING OBJECTIVES Upon the completion of this chapter, you will be able to: 1. Identify taxation of premiums, cash values, policy loans and

AN OPPORTUNITY TO FUND RETIREMENT WITH A ROTH IRA

AN OPPORTUNITY TO FUND RETIREMENT WITH A ROTH IRA Consider Doing Business with Pacific Life VLC0707-0318W AN OPPORTUNITY FOR RETIREMENT SAVINGS If you have funds in an Individual Retirement Account (IRA),

AN OPPORTUNITY TO FUND RETIREMENT WITH A ROTH IRA Consider Doing Business with Pacific Life VLC0707-0318W AN OPPORTUNITY FOR RETIREMENT SAVINGS If you have funds in an Individual Retirement Account (IRA),

IN-SERVICE WITHDRAWALS

IN-SERVICE WITHDRAWALS from Your Employer-Sponsored Plan VAC0581-1117 STRATEGIES TO DIVERSIFY YOUR RETIREMENT PORTFOLIO If you and your financial advisor determine that an in-service withdrawal is right

IN-SERVICE WITHDRAWALS from Your Employer-Sponsored Plan VAC0581-1117 STRATEGIES TO DIVERSIFY YOUR RETIREMENT PORTFOLIO If you and your financial advisor determine that an in-service withdrawal is right

UMB Bank, n.a. Universal IRA Information Kit

UMB Bank, n.a. Universal IRA Information Kit INTRODUCTION: What is the Difference between a Traditional IRA and a Roth IRA? With a traditional IRA, an individual may be able to deduct the contribution

UMB Bank, n.a. Universal IRA Information Kit INTRODUCTION: What is the Difference between a Traditional IRA and a Roth IRA? With a traditional IRA, an individual may be able to deduct the contribution

Individual Retirement Account (IRA) Information Kit

Information Kit") Individual Retirement Account (IRA) Information Kit (Effective January 1, 2013) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 1117-03-0713 PEAR TREE FUNDS Individual Retirement

Individual Retirement Account (IRA) Information Kit (Effective January 1, 2013) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 1117-03-0713 PEAR TREE FUNDS Individual Retirement

Understanding ANNUITIES

Understanding ANNUITIES An Overview for Your Retirement VLC0441-0917 TABLE OF CONTENTS Get Ready for Retirement.... 1 What Is an Annuity?.... 1 Who s Who in an Annuity?.... 2 Types of Annuities.... 3 Single

Understanding ANNUITIES An Overview for Your Retirement VLC0441-0917 TABLE OF CONTENTS Get Ready for Retirement.... 1 What Is an Annuity?.... 1 Who s Who in an Annuity?.... 2 Types of Annuities.... 3 Single

TRANSAMERICA PREMIER FUNDS. Disclosure Statement and Custodial Agreement for IRAs. Table of Contents

TRANSAMERICA PREMIER FUNDS Disclosure Statement and Custodial Agreement for IRAs Table of Contents IRA DISCLOSURE STATEMENT Part One: Description of Traditional IRAs 1 Special Note 1 Your Traditional IRA

TRANSAMERICA PREMIER FUNDS Disclosure Statement and Custodial Agreement for IRAs Table of Contents IRA DISCLOSURE STATEMENT Part One: Description of Traditional IRAs 1 Special Note 1 Your Traditional IRA

IRA Assets and Rollovers. Unlocking Opportunities before Age 59½. Retirement SOLUTIONS 12/ B

IRA Assets and Rollovers Unlocking Opportunities before Age 59½ Retirement 12/15 23060-15B SOLUTIONS Using Rollovers as a Retirement Strategy As you reflect on your retirement goals, a few questions may

IRA Assets and Rollovers Unlocking Opportunities before Age 59½ Retirement 12/15 23060-15B SOLUTIONS Using Rollovers as a Retirement Strategy As you reflect on your retirement goals, a few questions may

Retirement Plans Guide Facts at a glance

Retirement Plans Guide Facts at a glance Retirement Plan Limits for 2013 and 2014 The Internal Revenue Service has released cost-of-living adjustments applicable to dollar limits for retirement plans.

Retirement Plans Guide Facts at a glance Retirement Plan Limits for 2013 and 2014 The Internal Revenue Service has released cost-of-living adjustments applicable to dollar limits for retirement plans.

Understanding Life Insurance: A Lesson in Life Insurance

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Your Earning Power Life Questions Types of Term Term Variations Types

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Your Earning Power Life Questions Types of Term Term Variations Types

TRADITIONAL IRA DISCLOSURE STATMENT

TRADITIONAL IRA DISCLOSURE STATMENT The Traditional Individual Retirement Account ( Traditional IRA ) presented with this Disclosure Statement is a retirement plan made available to individuals. An individual

TRADITIONAL IRA DISCLOSURE STATMENT The Traditional Individual Retirement Account ( Traditional IRA ) presented with this Disclosure Statement is a retirement plan made available to individuals. An individual

Understanding Life Insurance: A Lesson in Life Insurance

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

Understanding Life : A Lesson in Life If something happens to you, how will your family replace your earning power? Table of Contents Page Your Earning Power 2 Life Questions 3 Types of Term 4 Term Variations

Savings Banks Employees Retirement Association

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL AT AGE 59 1/2 Participant Name: (Please Print) Certificate No. Current Address (required) (Street) (City, State Zip)

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL AT AGE 59 1/2 Participant Name: (Please Print) Certificate No. Current Address (required) (Street) (City, State Zip)

Rollovers from Employer-Sponsored Retirement Plans

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Rollovers from Employer-Sponsored

Law Office Of Keith R. Miles, LLC Keith Miles Attorney-at-Law 2250 Oak Road PO Box 430 Snellville, GA 30078 678-666-0618 keithmiles@timetoestateplan.com www.timetoestateplan.com Rollovers from Employer-Sponsored

Understanding SEP-IRAs

Understanding SEP-IRAs An Option to Consider when Saving for Retirement VLC0014-0318 TABLE OF CONTENTS What Is a SEP-IRA?.... 1 Who Can Set Up a SEP-IRA?.... 1 How a SEP-IRA Plan Works.... 2 Key Features....

Understanding SEP-IRAs An Option to Consider when Saving for Retirement VLC0014-0318 TABLE OF CONTENTS What Is a SEP-IRA?.... 1 Who Can Set Up a SEP-IRA?.... 1 How a SEP-IRA Plan Works.... 2 Key Features....

Help Preserve Wealth for Your Beneficiaries

Help Preserve Wealth for Your Beneficiaries Using a Stretch Variable Annuity Strategy 6/15 23187-15B Consider a Pacific Life Variable Annuity A variable annuity is a long-term contract between you and

Help Preserve Wealth for Your Beneficiaries Using a Stretch Variable Annuity Strategy 6/15 23187-15B Consider a Pacific Life Variable Annuity A variable annuity is a long-term contract between you and

Caution: Special rules apply to certain distributions to reservists and national guardsmen called to active duty after September 11, 2001.

LPL Financial Sims & Karr Financial Solutions Roger C. Sims Jason R Karr, Alex M. Means 304 North Main Street Greer, SC 29650 864-879-0337 simsandkarr@lpl.com www.simskarr.com Roth IRAs Page 1 of 13, see

LPL Financial Sims & Karr Financial Solutions Roger C. Sims Jason R Karr, Alex M. Means 304 North Main Street Greer, SC 29650 864-879-0337 simsandkarr@lpl.com www.simskarr.com Roth IRAs Page 1 of 13, see

Retirement Planning Guide

2017 Retirement Planning Guide IRA Roth SEP SIMPLE DB 401(a) 401(k) 403(b) Life Insurance Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company Western-Southern Life Assurance

2017 Retirement Planning Guide IRA Roth SEP SIMPLE DB 401(a) 401(k) 403(b) Life Insurance Issuers: Integrity Life Insurance Company National Integrity Life Insurance Company Western-Southern Life Assurance

UMB BANK, N.A INFORMATION KIT

UMB BANK, N.A UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT (EFFECTIVE DECEMBER 1, 2016) 600 University Street, Suite 2412 Seattle, WA 98101 Main: 206.838.9850 Toll Free: 877.701.2883 Fax: 206.838.9851

UMB BANK, N.A UNIVERSAL INDIVIDUAL RETIREMENT ACCOUNT INFORMATION KIT (EFFECTIVE DECEMBER 1, 2016) 600 University Street, Suite 2412 Seattle, WA 98101 Main: 206.838.9850 Toll Free: 877.701.2883 Fax: 206.838.9851

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy March 2018 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I Revocation 3

Plan Comparison for Governmental Plan Sponsors

Comparison for Governmental Sponsors + [Note that enabling legislation is required in order for a governmental employer to sponsor any type of retirement ] Category 457(b) Deferred Compensation 415(m)

Comparison for Governmental Sponsors + [Note that enabling legislation is required in order for a governmental employer to sponsor any type of retirement ] Category 457(b) Deferred Compensation 415(m)

VOLT TECHNICAL SERVICES SAVINGS PLAN SUMMARY PLAN DESCRIPTION. VOLT INFORMATION SCIENCES, INC. (the Sponsor )

") VOLT TECHNICAL SERVICES SAVINGS PLAN SUMMARY PLAN DESCRIPTION VOLT INFORMATION SCIENCES, INC. (the Sponsor ) Effective as of July, 2014 SUMMARY PLAN DESCRIPTION PLAN HIGHLIGHTS Saving for your future is

VOLT TECHNICAL SERVICES SAVINGS PLAN SUMMARY PLAN DESCRIPTION VOLT INFORMATION SCIENCES, INC. (the Sponsor ) Effective as of July, 2014 SUMMARY PLAN DESCRIPTION PLAN HIGHLIGHTS Saving for your future is

Pacific. ExpeditionSM. A Deferred Fixed Annuity for a Confident Retirement. Client Guide A 5/12

Pacific ExpeditionSM A Deferred Fixed Annuity for a Confident Retirement Client Guide 85000-12A 5/12 The Power to Help You Succeed Pacific Life has more than 140 years of experience, and we remain committed

Pacific ExpeditionSM A Deferred Fixed Annuity for a Confident Retirement Client Guide 85000-12A 5/12 The Power to Help You Succeed Pacific Life has more than 140 years of experience, and we remain committed

Mailing Address: P.O. Box 9394 Des Moines, IA FAX (866)

") Mailing Address: P.O. Box 9394 Des Moines, IA 50306-9394 FAX (866) 704-3481 Principal Life Insurance Company Complete this form to withdraw part of your retirement funds while still employed. Participant

Mailing Address: P.O. Box 9394 Des Moines, IA 50306-9394 FAX (866) 704-3481 Principal Life Insurance Company Complete this form to withdraw part of your retirement funds while still employed. Participant

Understanding ROLLOVER OPTIONS

Understanding ROLLOVER OPTIONS Outlining Options for Your Qualified Retirement Plan or IRA VLC0442-0917 TABLE OF CONTENTS Get Ready for Retirement.... 1 What Are Your Options?.... 1 What Happens if You

Understanding ROLLOVER OPTIONS Outlining Options for Your Qualified Retirement Plan or IRA VLC0442-0917 TABLE OF CONTENTS Get Ready for Retirement.... 1 What Are Your Options?.... 1 What Happens if You

THE VARIABLE ANNUITY LIFE INSURANCE COMPANY

THE VARIABLE ANNUITY LIFE INSURANCE COMPANY SEPARATE ACCOUNT A UNITS OF INTEREST UNDER GROUP AND INDIVIDUAL FIXED AND VARIABLE DEFERRED ANNUITY CONTRACTS PORTFOLIO DIRECTOR PLUS PORTFOLIO DIRECTOR 2 PORTFOLIO

THE VARIABLE ANNUITY LIFE INSURANCE COMPANY SEPARATE ACCOUNT A UNITS OF INTEREST UNDER GROUP AND INDIVIDUAL FIXED AND VARIABLE DEFERRED ANNUITY CONTRACTS PORTFOLIO DIRECTOR PLUS PORTFOLIO DIRECTOR 2 PORTFOLIO

403(b) Tax Deferred Annuity Plan. Saving for the future you want

Tax Deferred Annuity Plan. Saving for the future you want") 403(b) Tax Deferred Annuity Plan Saving for the future you want Many retirement experts agree...having the money you want in your later years comes from careful planning now. Important information: Variable

403(b) Tax Deferred Annuity Plan Saving for the future you want Many retirement experts agree...having the money you want in your later years comes from careful planning now. Important information: Variable

Janus Universal IRA. Disclosure Statement & Custodial Agreement

Janus Universal IRA Disclosure Statement & Custodial Agreement Janus Universal Individual Retirement Account Disclosure Statement Part One: Description of Traditional IRAs SPECIAL NOTE State Street Bank

Janus Universal IRA Disclosure Statement & Custodial Agreement Janus Universal Individual Retirement Account Disclosure Statement Part One: Description of Traditional IRAs SPECIAL NOTE State Street Bank

INDEPENDENCE PLUS CONTRACT SERIES STATEMENT OF ADDITIONAL INFORMATION. FORM N-4 PART B May 1, 2018 TABLE OF CONTENTS

THE VARIABLE ANNUITY LIFE INSURANCE COMPANY SEPARATE ACCOUNT A UNITS OF INTEREST UNDER GROUP AND INDIVIDUAL FIXED AND VARIABLE DEFERRED ANNUITY CONTRACTS INDEPENDENCE PLUS CONTRACT SERIES STATEMENT OF

THE VARIABLE ANNUITY LIFE INSURANCE COMPANY SEPARATE ACCOUNT A UNITS OF INTEREST UNDER GROUP AND INDIVIDUAL FIXED AND VARIABLE DEFERRED ANNUITY CONTRACTS INDEPENDENCE PLUS CONTRACT SERIES STATEMENT OF

Hardship Withdrawal Form

The Housing Agency Retirement Trust 457 Deferred Compensation Plan Social Security #: Hardship Withdrawal Form Employee Name: Last, First, Middle Your check will be sent to your address of record. Please

The Housing Agency Retirement Trust 457 Deferred Compensation Plan Social Security #: Hardship Withdrawal Form Employee Name: Last, First, Middle Your check will be sent to your address of record. Please

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL OF AFTER TAX/VEC CONTRIBUTIONS AND EARNINGS

PLAN APPLICATION FOR WITHDRAWAL OF AFTER TAX/VEC CONTRIBUTIONS AND EARNINGS") Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL OF AFTER TAX/VEC CONTRIBUTIONS AND EARNINGS Participant Name: (Please Print) Certificate No. Current Address (required)

Savings Banks Employees Retirement Association 401(k) PLAN APPLICATION FOR WITHDRAWAL OF AFTER TAX/VEC CONTRIBUTIONS AND EARNINGS Participant Name: (Please Print) Certificate No. Current Address (required)

Individual Retirement Account (IRA) Information Kit

Information Kit") Individual Retirement Account (IRA) Information Kit (Effective January 1, 2018) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 PEAR TREE FUNDS Individual Retirement Account

Individual Retirement Account (IRA) Information Kit (Effective January 1, 2018) Pear Tree Funds 55 Old Bedford Road Suite 202 Lincoln, MA 01773 1-800-326-2151 PEAR TREE FUNDS Individual Retirement Account

TRADITIONAL IRA DISCLOSURE STATEMENT

TRADITIONAL IRA DISCLOSURE STATEMENT RIGHT TO REVOKE YOUR IRA ACCOUNT The W-2 form will have a check in the "retirement plan" box if you are covered by a retirement plan. You can also obtain IRS Notice

TRADITIONAL IRA DISCLOSURE STATEMENT RIGHT TO REVOKE YOUR IRA ACCOUNT The W-2 form will have a check in the "retirement plan" box if you are covered by a retirement plan. You can also obtain IRS Notice

P A R N A S S U S F U N D S

PARNASSUS FUNDS P A R N A S S U S F U N D S Useful information about IRAs What is a Traditional IRA? A traditional IRA is an Individual Retirement Account that allows you to put away money for your retirement

PARNASSUS FUNDS P A R N A S S U S F U N D S Useful information about IRAs What is a Traditional IRA? A traditional IRA is an Individual Retirement Account that allows you to put away money for your retirement

2017 Retirement Plan Comparison Chart

Employer s Discretionary: not Discretionary: not 100% on the first 3% of employee deferral plus 50% on the next 2% of employee deferral 3% of to all eligible 100% up to 3% of 2% of to eligible Discretionary;

Employer s Discretionary: not Discretionary: not 100% on the first 3% of employee deferral plus 50% on the next 2% of employee deferral 3% of to all eligible 100% up to 3% of 2% of to eligible Discretionary;

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

T. Rowe Price Traditional and Roth IRA Disclosure Statement and Custodial Agreement T. Rowe Price Privacy Policy Effective November 2016 TABLE OF CONTENTS DISCLOSURE STATEMENT Introduction 3 Section I

Traditional and Roth IRAs. Information Kit, Disclosure Statement and Custodial Agreement

Traditional and Roth IRAs Information Kit, Disclosure Statement and Custodial Agreement UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement (EFFECTIVE DECEMBER 1, 2016) Part One:

Traditional and Roth IRAs Information Kit, Disclosure Statement and Custodial Agreement UMB Bank, n.a. Universal Individual Retirement Account Disclosure Statement (EFFECTIVE DECEMBER 1, 2016) Part One:

INTEREST ENHANCED DEATH BENEFIT

INTEREST ENHANCED DEATH BENEFIT Guaranteed Growth for Your Loved Ones, Regardless of Market Performance 9/16 50088-16B Optional Benefit with Pacific Life s Fixed Indexed Annuities GUARANTEED GROWTH, NO

INTEREST ENHANCED DEATH BENEFIT Guaranteed Growth for Your Loved Ones, Regardless of Market Performance 9/16 50088-16B Optional Benefit with Pacific Life s Fixed Indexed Annuities GUARANTEED GROWTH, NO

ENHANCED LIFETIME INCOME BENEFIT 2

ENHANCED LIFETIME INCOME BENEFIT 2 Guaranteed Lifetime Withdrawals, Regardless of Market Performance FAC0107-0517 Optional Benefit Available with Pacific Index Advisory SM Fixed Indexed Annuity ENHANCED

ENHANCED LIFETIME INCOME BENEFIT 2 Guaranteed Lifetime Withdrawals, Regardless of Market Performance FAC0107-0517 Optional Benefit Available with Pacific Index Advisory SM Fixed Indexed Annuity ENHANCED

Table II: Other Key Provisions in HR 1776 of Interest to Governmental Plans

Table II: Other Key Provisions in HR 1776 of Interest to Governmental Plans For a copy of HR 1776, visit http://www.nctr.org/content/pdf/portman_full_bill03.pdf See Table I for Principal Provisions in

Table II: Other Key Provisions in HR 1776 of Interest to Governmental Plans For a copy of HR 1776, visit http://www.nctr.org/content/pdf/portman_full_bill03.pdf See Table I for Principal Provisions in

Frequently asked questions

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

Page 1 of 6 Frequently asked questions Distributions and rollovers from retirement accounts Choosing what to do with your retirement savings is an important decision. Tax implications are just one of several

Savings Banks Employees Retirement Association

Savings Banks Employees Retirement Association IN-PLAN ROTH CONVERSION ELECTION FORM PLEASE NOTE: Your Plan must allow In-Plan Roth Rollovers Participant Name: (Please Print) Certificate No. Current Address

Savings Banks Employees Retirement Association IN-PLAN ROTH CONVERSION ELECTION FORM PLEASE NOTE: Your Plan must allow In-Plan Roth Rollovers Participant Name: (Please Print) Certificate No. Current Address

TERMINATION FORM - 206

INSTRUCTIONS FOR COMPLETING TERMINATION FORM - 206 TERMINATION FORM - 206 Get your money fast! If your Plan Administrator has notified us of your termination, you may be able to easily process this 401(k)

INSTRUCTIONS FOR COMPLETING TERMINATION FORM - 206 TERMINATION FORM - 206 Get your money fast! If your Plan Administrator has notified us of your termination, you may be able to easily process this 401(k)