This page intentionally left blank.

|

|

|

- Adelia Flowers

- 6 years ago

- Views:

Transcription

1

2 This page intentionally left blank.

3 Table of Contents Introductory Section Page Letter of Transmittal 1 GFOA Certificate of Achievement 5 Organizational Chart 6 List of Principal City Officials 7 Financial Section Independent Auditors Report 11 Management s Discussion and Analysis 16 Basic Financial Statements: Government-wide Financial Statements: Statement of Net Position 25 Statement of Activities 26 Fund Financial Statements: Balance Sheet Governmental Funds 30 Reconciliation of Fund Balances of Governmental Funds to Net Position of Governmental Funds 31 Statement of Revenues, Expenditures and Changes in Fund Balances Governmental Funds 32 Reconciliation of Net Changes in Fund Balances of Governmental Funds to Change in Net Position of Governmental Activities 33 Statement of Revenues, Expenditures and Change in Fund Balance Budget and Actual - General Fund 34 Statement of Revenues, Expenditures and Change in Fund Balance Budget and Actual - Community Development Special Revenue Fund 39 Statement of Net Position Proprietary Funds 40 Reconciliation of Net Position of Enterprise Funds to Net Position of Business-type Activities 43 Statement of Revenues, Expenses and Changes in Fund Net Position Proprietary Funds 44 Reconciliation of Change in Net Position of Enterprise Funds to Change in Net Position of Business-type Activities 47 Statement of Cash Flows Proprietary Funds 48 Statement of Fiduciary Assets and Liabilities - Fiduciary Funds 52 Statement of Changes in Fiduciary Net Position - Pension and Other Employee Benefit Trust Funds 53 Combining Statement of Net Position Component Units 56 Combining Statement of Activities Component Units 58 Notes to Financial Statements 62

4 Table of Contents Required Supplementary Information: Schedules of Funding Progress and Employer Contributions - Police and Fire Retirement System 100 Schedule of Changes in Net Pension Liability and Related Ratios 101 Schedule of the Net Pension Liability 102 Schedule of City Contributions 103 Schedules of Funding Progress and Employer Contributions: Municipal Employees Retirement System of Michigan 104 Other Postemployment Benefits 105 Combining and Individual Fund Financial Statements and Schedules: Combining Balance Sheet Nonmajor Governmental Funds 108 Combining Statement of Revenues, Expenditures and Changes in Fund Balance Nonmajor Governmental Funds 109 Combining Balance Sheet Nonmajor Special Revenue Funds 110 Combining Statement of Revenues, Expenditures and Changes in Fund Balance Nonmajor Special Revenue Funds 114 Schedule of Revenues, Expenditures and Changes in Fund Balance Final Budget and Actual Nonmajor Special Revenue Funds 118 Combining Balance Sheet Nonmajor Debt Service Funds 128 Combining Statement of Revenues, Expenditures and Changes in Fund Balance Nonmajor Debt Service Funds 130 Combining Balance Sheet Nonmajor Capital Projects Funds 132 Combining Statement of Revenues, Expenditures and Changes in Fund Balance Nonmajor Capital Projects Funds 134 Combining Balance Sheet Nonmajor Permanent Funds 136 Combining Statement of Revenues, Expenditures and Changes in Fund Balance Nonmajor Permanent Funds 137 Combining Statement of Net Position - Nonmajor Enterprise Funds 138 Combining Statement of Revenues, Expenses and Changes in Fund Net Position Nonmajor Enterprise Funds 139 Combining Statement of Cash Flows Nonmajor Enterprise Funds 140 Combining Statement of Net Position Internal Service Funds 142 Combining Statement of Revenues, Expenses and Changes in Fund Net Position Internal Service Funds 143 Combining Statement of Cash Flows Internal Service Funds 144 Combining Statement of Fiduciary Net Position - Pension and Other Employee Benefits Trust Funds 147 Combining Statement of Changes in Assets and Liabilities - Pension and Other Employee Benefits Trust Funds 148 Combining Statement of Fiduciary Net Position - Agency Funds 151 Combining Statement of Changes in Assets and Liabilities - Agency Funds 152 Page

5 Table of Contents Statistical Section (Unaudited) Page Net Position by Component 158 Changes in Net Position 160 Fund Balances - Governmental Funds 164 Changes in Fund Balances - Governmental Funds 166 Changes in Fund Balances - General Fund 168 Assessed and Taxable Value of Property 170 Direct and Overlapping Property Tax Rates 172 Principal Property Taxpayers 174 Property Tax Levies and Collections 177 Number of Water System Customers by User Class 178 Number of Water System Customers by User Class as a Percent of Total 180 Water System Revenues by User Class 182 Water System Revenues by User Class as a Percent of Total Revenue 184 Water System Sales Volume by User Class (Cubic Feet) 186 Water System Sales Volume by User Class as a Percent of Total Sales (Cubic Feet) 188 Water Pumped and Sold (Cubic Feet) 190 Water Revenues and Usage Major Customers 191 Current Water Rates (Beginning as of July 1, 2008) 193 Number of Wastewater System Customers by User Class 194 Wastewater System Customers by User Class as a Percent of Total 196 Wastewater System Revenues by User Class 198 Wastewater System Revenues by User Class as a Percent of Total Revenue 200 Wastewater System Ten Year History of Volumes 203 Wastewater System Sales Volume by User Class (Cubic Feet) 204 Wastewater System Sales Volume by User Class as a Percent of Total Sales (Cubic Feet) 206 Wastewater Revenue and Usage Major Customers 208 Largest Wastewater Customers 209 Current Wastewater Rates 210 Ratios of General Bonded Debt Outstanding 214 Computation of Net Direct and Overlapping Debt 216 Legal Debt Margin 217 Water and Wastewater System Revenue Bond Coverage 218 Demographic and Economic Statistics 219 Principal Employers 220 Full-time Equivalent Employees by Function/Program 222 Operating Indicators by Function/Program 224 Capital Asset Statistics by Function/Program 226 Schedule of Insurance 228

6 This page intentionally left blank.

7 INTRODUCTORY SECTION

8 This page intentionally left blank.

9 December 18, 2014 To the Honorable Mayor, Members of the City Commission and Citizens of the City of Battle Creek: State law requires that all local governments, subject to certain size criteria, publish within six months of the close of each fiscal year a complete set of financial statements presented in conformity with generally accepted accounting principles (GAAP) and audited in accordance with generally accepted auditing standards by a firm of licensed certified public accountants. Pursuant to that requirement, we hereby issue the comprehensive annual financial report of the City of Battle Creek for the fiscal year ended June 30, This report consists of management s representations concerning the finances of the City of Battle Creek. Consequently, management assumes full responsibility for the completeness and reliability of all of the information presented in this report. To provide a reasonable basis for making these representations, City management has established a comprehensive internal control framework that is designed both to protect the government s assets from loss, theft, or misuse and to compile sufficient reliable information for the preparation of the City s financial statements in conformity with GAAP. Because the cost of internal controls should not outweigh their benefits, the City s comprehensive framework of internal controls has been designed to provide reasonable rather than absolute assurance that the financial statements will be free from material misstatement. As management, we assert that, to the best of our knowledge and belief, this financial report is complete and reliable in all material respects. The City s financial statements have been audited by Rehmann Robson, a firm of licensed certified public accountants. The goal of the independent audit was to provide reasonable assurance that the financial statements of the City for the fiscal year ended June 30, 2014 are free of material misstatement. The independent audit involved examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements; assessing the accounting principles used and significant estimates made by management; and evaluating the overall financial statement presentation. The independent auditor concluded, based upon the audit, that there was a reasonable basis for rendering an unmodified opinion that the City s financial statements for the fiscal year ended June 30, 2014 are fairly presented in conformity with GAAP. The independent auditor s report is presented as the first component of the financial section of this report. GAAP require that management provide a narrative introduction, overview, and analysis to accompany the basic financial statements in the form of Management s Discussion and Analysis (MD&A). This letter of transmittal is designed to complement MD&A and should be read in conjunction with it. The City s MD&A can be found immediately following the report of the independent auditors. 1

10 Profile of the Government The City of Battle Creek, incorporated as a City in 1859 and as a Home Rule City in 1913, is located in southwest Michigan, approximately 115 miles west of Detroit and 160 miles northeast of Chicago. It is the largest city in Calhoun County, encompassing an area of 44 square miles, with a current estimated population of 51,848. The City is well known as the breakfast food capital of the world. The government has operated under the commission-manager form of government since Policymaking and legislative authorities are vested in the City Commission, which is comprised of nine members including the mayor. The governing council is responsible, among other things, for passing ordinances and resolutions, making public policy decisions, adopting the budget, appointing boards, commissions, and committees, approving contracts, authorizing real estate transactions, awarding bids, selling property, and hiring the government s manager and attorney. Four commissioners are elected at-large for two-year terms and five commissioners are elected from the five wards in the city, also serving two-year terms. The City Commission elects a Mayor and Vice-Mayor from among its members. The City Manager is the chief administrative officer of the City and is appointed by and serves at the pleasure of the City Commission. The City Manager is responsible for carrying out the policies and ordinances of the City Commission, for overseeing the day-to-day operations of the government, and appointing government s department heads. The City of Battle Creek provides a full range of services including: police and fire protection; the construction and maintenance of highways, streets and other infrastructure; wastewater treatment and disposal; water treatment and distribution; economic development; recreational activities; public transportation services and cultural events. Factors Affecting Financial Condition The information presented in the financial statements is perhaps best understood when it is considered from the broader perspective of the specific environment within which the City of Battle Creek operates. Local economy. The City s economy is diverse with industrial and commercial categories accounting for over 50% of the 2014 taxable valuation. The remainder, primarily residential, provides area residents with convenient and affordable housing to take advantage of the City s industrial, commercial, cultural, educational and recreational opportunities. The City is home to Kellogg Company s world headquarters, the W.K. Kellogg Foundation, and the International Food Protection Training Institute. Battle Creek has many other major corporate community members including Post Cereals, ConAgra Foods, Denso, II Stanley, and Duncan Aviation. The City is revitalizing its downtown to accommodate food science and other innovation industries. Battle Creek s commercial airport and industrial park are diversifying the economy and attracting worldwide business for military, aviation, aerospace and alternative energy. Long term financial planning. The City of Battle Creek believes long-term financial planning has been and will continue to be an important component to ensure the City s fiscal health. Economic development and downtown development continue to be high priorities for the City. Battle Creek Unlimited, a non-profit organization partnering with the City to perform economic development, continues to promote and develop the City s Fort Custer Industrial Park (FCIP) and the downtown in an effort to maintain and enhance the City s tax base. 2

11 Along with efforts to ensure a future growth in tax revenue, the City has developed a Capital Improvement Program (CIP) to identify its long-term capital needs and ability to fund the program. Over the next six years, the City has identified over $131.6 million in capital needs. In September, 2013 the City issued $15,370,000 in general obligation limited tax bonds to fund a number of the capital improvements identified in the CIP including $3.5 million for Downtown Quiet Zone, $3 million for Kellogg Arena Improvements and $1.2 million for a public safety records management system. From an operational perspective, the City s revenue profile is diverse and has shown improvement over the prior year. Income tax revenue accounts for 37.6% of general fund revenues for the year ending June 30, 2014 and has shown growth two of the last three years. Property tax revenue makes up another 32.4% of general fund revenues for the year ending June 30, 2014, and the City has a mill (6.7%) margin available under the Headlee roll-back limit for operation. This could generate approximately $700,000 in additional property tax revenue. June 30, 2014 is the second year in a row the City has shown positive operations in the general fund and added to fund balance. The implementation of a high deductible health care plan and negotiation of lower cost pension benefits for new employees has had positive financial results across all city funds and has allowed flexibility for negotiation of pay raises and contributions to employees health savings accounts. The City will continue to pursue ways to keep costs in line with revenues. Awards and Acknowledgements The Government Finance Officers Association of the United States and Canada (GFOA) awarded a Certificate of Achievement for Excellence in Financial Reporting to the City of Battle Creek for its comprehensive annual financial report (CAFR) for the fiscal year ended June 30, This was the fifteenth consecutive year that the City has received this prestigious award. In order to be awarded a Certificate of Achievement, the government published an easily readable and efficiently organized CAFR. This report satisfied both generally accepted accounting principles and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only. We believe that our current CAFR continues to meet the Certificate of Achievement Program s requirements and we are submitting it to the GFOA to determine its eligibility for another certificate. The preparation of this report would not have been possible without the efficient and dedicated services of the entire staff of the City of Battle Creek. We would like to express our appreciation to all members of the departments who assisted and contributed to the preparation of this report. Credit also must be given to the Mayor and City Commission for their support for maintaining the highest standards of professionalism in the management of the City of Battle Creek s finances. Susan E. Bedsole Interim City Manager / Community Services Director Linda A. Morrison Interim Assistant City Manager / Finance Director [Signatures omitted for security purposes.] 3

12 This page intentionally left blank. 4

13 GFOA Certificate of Achievement 5

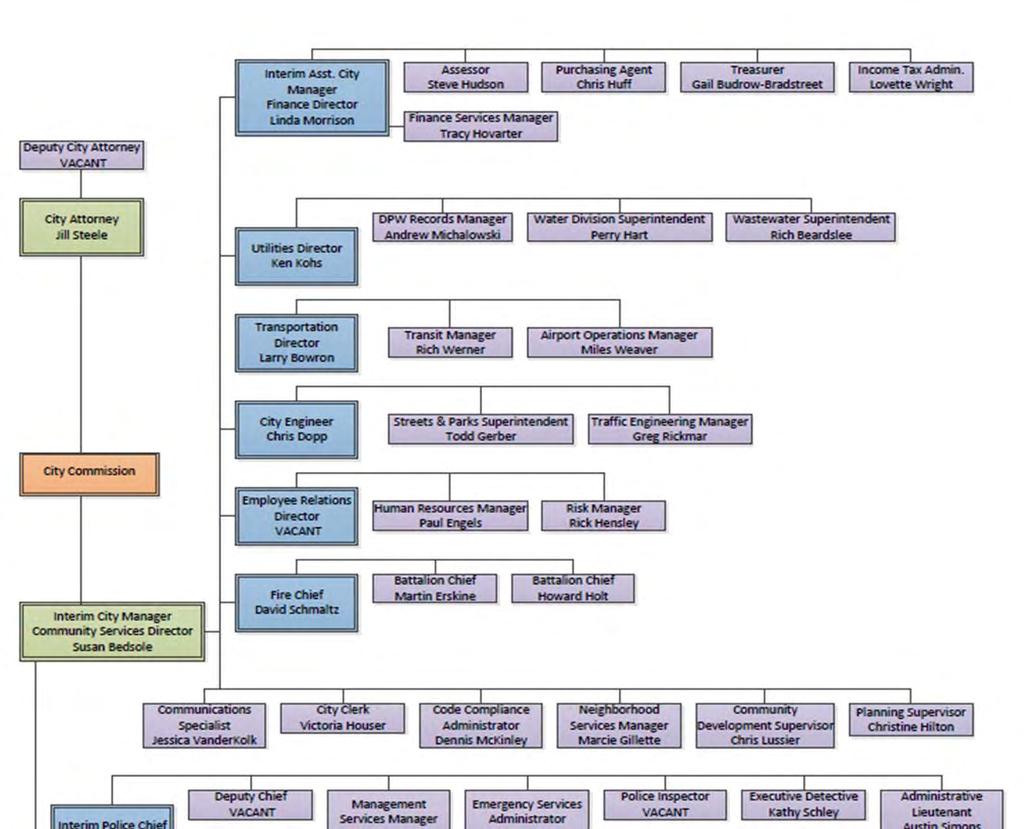

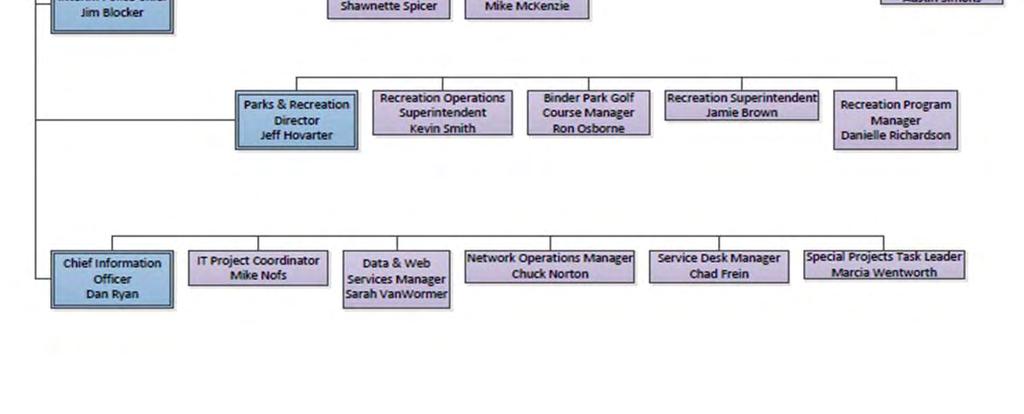

14 Organizational Chart 6

15 List of Principal City Officials CITY COMMISSION: David Walters Mayor Deborah Owens Vice Mayor Susan Baldwin Mark Behnke Jeffrey Domenico Lynn Ward Gray Andy Helmboldt Dean Newsome Mike Sherzer Administration Susan E. Bedsole Interim City Manager/ Community Services Director Jill Humphreys Steele City Attorney Linda A. Morrison Interim Assistant City Manager / Finance Director 7

16 This page intentionally left blank. 8

17 FINANCIAL SECTION 9

18 This page intentionally left blank. 10

19 Rehmann Robson INDEPENDENT AUDITORS' REPORT 675 Robinson Rd. Jackson, MI Ph: Fx: rehmann.com December 18, 2014 Honorable Mayor and Members of the City Commission City of Battle Creek, Michigan Report on the Financial Statements We have audited the accompanying financial statements of the governmental activities, the businesstype activities, the aggregate discretely presented component units, each major fund and the aggregate remaining fund information of the City of Battle Creek, Michigan (the "City") as of and for the year ended June 30, 2014, and the related notes to the financial statements, which collectively comprise the City's basic financial statements as listed in the table of contents. Management's Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Independent Auditors' Responsibility Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the City s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions. Rehmann is an independent member of Nexia International. CPAs & Consultants Wealth Advisors Corporate Investigators 11

20 Opinions In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, the aggregate discretely presented component units, each major fund and the aggregate remaining fund information of the City of Battle Creek, Michigan, as of June 30, 2014, and the respective changes in financial position and the respective budgetary comparison for the general fund and community development special revenue fund for the year then ended in accordance with accounting principles generally accepted in the United States of America. Implementation of GASB Statement No. 67 The City implemented the provisions of GASB Statement No. 67, Financial Reporting for Pension Plans, in the current year. While there was no effect on the amounts reported in the financial statements themselves, there were substantial changes to the disclosures found in Note 17 to the financial statements, including the calculation of the City's net pension liability, which will be required to be recorded by the City in its next fiscal year. Our opinion is not modified with respect to this matter. Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that management's discussion and analysis and the schedules of funding progress and employer contributions listed in the table of contents be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information Our audit was conducted for the purpose of forming opinions of the financial statements that collectively comprise the City's basic financial statements. The introductory section, combining and individual fund financial statements and schedules, and statistical section are presented for purposes of additional analysis and are not a required part of the basic financial statements. The combining and individual fund financial statements and schedules are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the combining and individual fund financial statements and schedules are fairly stated, in all material respects, in relation to the basic financial statements as a whole. 12

21 The introductory section and statistical tables have not been subjected to the auditing procedures applied in the audit of the basic financial statements, and accordingly, we do not express an opinion or provide any assurance on them. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued, under separate cover, our report dated December 18, 2014 on our consideration of the City of Battle Creek, Michigan's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the City's internal control over financial reporting and compliance. 13

22 This page intentionally left blank. 14

23 MANAGEMENT'S DISCUSSION AND ANALYSIS 15

24 Management's Discussion and Analysis As management of the City of Battle Creek, Michigan, we offer readers of the City s financial statements this narrative overview and analysis of the financial activities of the City for the fiscal year ended June 30, We encourage readers to consider the information presented here in conjunction with additional information that we have furnished in our letter of transmittal, as noted in the table of contents. Financial Highlights The assets and deferred outflows of resources of the City exceeded its liabilities and deferred inflows of resources at the close of the most recent fiscal year by $343,031,820 (net position). Of this amount, $34,456,702 (unrestricted net position) may be used to meet the government s ongoing obligations to citizens and creditors. The government s total net position decreased by $5,461,329. As of the close of the current fiscal year, the City s governmental funds reported combined ending fund balances of $23,688,184, an increase of $10,710,919 in comparison with the prior year. Approximately 27% of the combined fund balance, or $6,449,504 was available for spending at the City's discretion ('unassigned fund balance"). At the end of the current fiscal year, unassigned fund balance for the general fund was $6,580,891 or 15.3% of total budgeted general fund operating revenues. The City s total bonded debt increased by $11,925,000 during the current fiscal year. The City issued a new bond and also advance refunded a bond. Combined enterprise funds net position increased $333,682. This included an increase of $1,484,868 in net position of the water and wastewater system fund. Overview of the Financial Statements This discussion and analysis is intended to serve as an introduction to the City s basic financial statements. The City s basic financial statements are comprised of three components: 1) government-wide financial statements, 2) fund financial statements, and 3) notes to the financial statements. This report also contains other supplementary information in addition to the basic financial statements themselves. Government-wide financial statements. The government-wide financial statements are designed to provide readers with a broad overview of the City s finances, in a manner similar to a private sector business. The statement of net position presents information on all of the City s assets, deferred outflows of resources, and liabilities, with the difference between the three reported as net position. Over time, increases or decreases in net position may serve as a useful indicator of whether the financial position of the City is improving or deteriorating. The statement of activities presents information shows how the government s net position changed during the most recent fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. Thus, revenues and expenses are reported in this statement for some items that will only result in cash flows in future fiscal periods (e.g., earned but unused vacation leave). Both of the government-wide financial statements distinguish functions of the City that are principally supported by taxes and intergovernmental revenues (governmental activities) from other functions that are intended to recover all or a significant portion of their costs through user fees and charges (business-type activities). The governmental activities of the City include general government, public safety, public works, highways and streets, parks and recreation and community development. The business-type activities of the City include wastewater, water, public transit, solid waste collection and other enterprise operations. 16

25 Management's Discussion and Analysis The government-wide financial statements include not only the City itself (known as the primary government), but also legally separate entities for which the City is financially accountable. Financial information for these component units are reported separately from the financial information presented for the primary government itself. These component units include the Downtown Development Authority, the Lakeview Downtown Development Authority, the Tax Incremental Financing Authority, the Brownfield Redevelopment Authority and the Local Development Finance Authority. The Building Authority, although also legally separate, functions for all practical purposes as a department of the City, and therefore has been included as an integral part of the primary government. Fund financial statements. A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. The City, like other state and local governments, uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. All of the funds of the City can be divided into three categories: governmental funds, proprietary funds, and fiduciary funds. Governmental funds. Governmental funds are used to account for essentially the same functions reported as governmental activities in the government-wide financial statements. However, unlike the government-wide financial statements, governmental fund financial statements focus on near-term inflows and outflows of spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such information may be useful in evaluating a government s near-term financing requirements. Because the focus of governmental funds is narrower than that of the government-wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of the government s near-term financing decisions. Both the governmental fund balance sheet and the governmental fund statement of revenues, expenditures, and changes in fund balances provide a reconciliation to facilitate this comparison between governmental funds and governmental activities. The City maintains 24 individual governmental funds. Information is presented separately in the governmental fund balance sheet and in the governmental fund statement of revenues, expenditures, and changes in fund balances for the general fund, community development special revenue fund and capital improvements capital projects fund, which are considered to be major funds. Data from the other 21 governmental funds are combined into a single, aggregated presentation. Individual fund data for each of these nonmajor governmental funds is provided in the form of combining statements elsewhere in this report. The City adopts an annual appropriated budget for its general and special revenue funds. Budgetary comparison statements or schedules have been provided herein to demonstrate compliance with those budgets. Proprietary funds. The City maintains two different types of proprietary funds. Enterprise funds are used to report the same functions presented as business-type activities in the government-wide financial statements. The City uses enterprise funds to account for its wastewater, water, public transit, solid waste collection and other operations. Internal service funds are an accounting device used to accumulate and allocate costs internally among the City s various functions. The City uses internal service funds to account for its equipment maintenance, self-insurance, information management services and printing/reproduction services. Because these services predominantly benefit governmental rather than business-type functions, they have been included within governmental activities in the government-wide financial statements. Proprietary funds provide the same type of information as the government-wide financial statements, only in more detail. The proprietary fund financial statements provide separate information for the wastewater and water system fund, economic development fund and W.K. Kellogg Airport fund, which are considered to be major funds of the City. Conversely, all of the internal service funds are combined into a single, aggregated presentation in the proprietary fund financial statements. Individual fund data for the internal service funds is provided in the form of combining statements elsewhere in this report. Fiduciary funds. Fiduciary funds are used to account for resources held for the benefit of parties outside the government. Fiduciary funds are not reflected in the government-wide financial statements because the resources of those funds are not available to support the City s own programs. The accounting used for fiduciary funds is much like that used for proprietary funds. 17

26 Management's Discussion and Analysis Notes to the financial statements. The notes provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements. Other information. In addition to the basic financial statements and accompanying notes, this report also presents certain required supplementary information. This includes three schedules concerning the City s progress in funding its obligation to provide pension and other postemployment benefits to its employees. The combined statements referred to earlier in connection with nonmajor, internal service and fiduciary funds are presented immediately following the required supplementary information. Government-wide Financial Analysis As noted earlier, net position may serve over time as a useful indicator of a government s financial position. In the case of the City of Battle Creek, assets and deferred outflows of resources exceeded liabilities and deferred inflows of resources by $343,031,820 at the close of the most recent fiscal year. By far the largest portion of the City s net position (86 percent) reflects its investment in capital assets (e.g., land, buildings, vehicles, equipment, systems and infrastructure), less any related debt used to acquire those assets that are still outstanding. The City uses these capital assets to provide services to citizens; consequently, these assets are not available for future spending. Although the City s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities. Net Position Governmental activities Business-type activities Total Assets Current and other assets $ 52,781,707 $ 38,416,953 $ 23,359,348 $ 22,157,340 $ 76,141,055 $ 60,574,293 Capital assets 234,890, ,290, ,167, ,075, ,057, ,365,690 Total assets 287,671, ,707, ,527, ,232, ,199, ,939,983 Deferred outflows of resources Deferred charge on refunding 255, , , , , ,510 Liabilities Other liabilities 22,777,465 16,269,048 2,188,811 1,884,690 24,966,276 18,153,738 Long-term liabilities 34,845,929 21,094,961 10,755,193 12,691,334 45,601,122 33,786,295 Total liabilities 57,623,394 37,364,009 12,944,004 14,576,024 70,567,398 51,940,033 Deferred inflows of resources Deferred gain on refunding - 25, ,311 Net position Net investment in capital assets 213,803, ,155,508 92,099,833 92,885, ,903, ,040,706 Restricted 2,671,582 3,326, ,671,582 3,326,396 Unrestricted 13,828,647 16,137,588 20,628,055 19,988,459 34,456,702 36,126,047 Total net position $ 230,303,932 $ 235,619,492 $ 112,727,888 $ 112,873,657 $ 343,031,820 $ 348,493,149 18

27 Management's Discussion and Analysis An additional portion of the City s net position (0.8 percent) represents resources that are subject to external restrictions on how they may be used. The remaining balance of unrestricted net position (10.0 percent or $34,456,702) may be used to meet the government s ongoing obligations to citizens and creditors. At the end of the current fiscal year, the City is able to report positive balances in all three categories of net position, both for the government as a whole, as well as for its governmental and business-type activities; the same held true for the prior fiscal year. The City s net position decreased by $5,461,329 during the current year as compared to a prior year decrease of $3,266,929. The change in the amount of the decrease between the current and prior year was $2,194,400; there are a variety of offsetting increases and decreases in the revenues and expenses and between the governmental and business-type activities, which are discussed in the succeeding sections. Changes in Net Position Governmental activities Business-type activities Total Revenue: Program revenue: Charges for services $ 7,489,959 $ 8,878,555 $ 31,347,774 $ 30,132,800 $ 38,837,733 $ 39,011,355 Grants and contributions - Operating 10,289,625 12,618,453 3,571,072 5,060,638 13,860,697 17,679,091 General revenue: Property taxes 16,258,935 15,809, ,258,935 15,809,783 Income taxes 16,093,707 16,234, ,093,707 16,234,540 Unrestricted grants and contributions 5,336,347 5,271, ,336,347 5,271,399 Other 953, ,196 96,548 (63,487) 1,049, ,709 ` Total revenue 56,421,609 59,183,926 35,015,394 35,129,951 91,437,003 94,313,877 Expenses: General government 12,208,561 10,372, ,208,561 10,372,803 Public safety 27,215,335 26,952, ,215,335 26,952,192 Public works 2,199,624 1,891, ,199,624 1,891,765 Highways and streets 9,731,567 11,585, ,731,567 11,585,808 Parks and recreation 5,759,128 6,323, ,759,128 6,323,529 Community development 3,019,449 4,907, ,019,449 4,907,271 Interest on long-term debt 1,206, , ,206, ,018 Sewer ,642,028 15,247,288 15,642,028 15,247,288 Water - - 7,930,788 7,520,760 7,930,788 7,520,760 Transit system - - 4,814,924 4,924,554 4,814,924 4,924,554 Solid waste collection - - 3,004,407 2,940,000 3,004,407 2,940,000 Airport - - 2,485,677 2,511,613 2,485,677 2,511,613 Parking - - 1,549,455 1,509,283 1,549,455 1,509,283 Economic development , , , ,922 Total expenses 61,340,653 62,778,386 35,557,679 34,802,420 96,898,332 97,580,806 Increase (decrease) in net position before transfers (4,919,044) (3,594,460) (542,285) 327,531 (5,461,329) (3,266,929) Transfers (396,516) (349,082) 396, , Change in net position (5,315,560) (3,943,542) (145,769) 676,613 (5,461,329) (3,266,929) Net position, beginning of year 235,619, ,563, ,873, ,197, ,493, ,760,078 Net position, end of year $ 230,303,932 $ 235,619,492 $ 112,727,888 $ 112,873,657 $ 343,031,820 $ 348,493,149 19

28 Management's Discussion and Analysis Governmental activities. Governmental activities decreased the City s net position by $5,315,560 (as compared to a prior year decrease of $3,943,542). Key elements of this decrease and the change from the prior year include: Total revenue decreased by $2.8 million primarily as a result of decreased federal intergovernmental and other revenue from the neighborhood stabilization program in the Community Development Block Grant fund. This $2.1 million decrease in revenue has a corresponding decrease in expenses. Business type activities. Business type activities decreased the City s net position by $145,769 as compared to an increase of $676,613 the prior year. Key elements of this decrease and the change from the prior year include: Water and wastewater charges for services increased $817,772 over the prior year offset with a corresponding increase in contractual expenses. Revenue increases include a rate increase that was effective 7/1/13. Contractual expenses increased due to two major on-going capital projects in the water and wastewater systems: the Pulver Dryer solids handling project and water meter replacement project. Financial Analysis of the City s Governmental Funds As noted earlier, the City uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. Governmental funds. The focus of the City s governmental funds is to provide information on near-term inflows, outflows, and balances of spendable resources. Such information is useful in assessing the City s financing requirements. In particular, unassigned fund balance may serve as a useful measure of a government s net resources available for spending at the end of the fiscal year. As of the end of the current fiscal year, the City s governmental funds reported combined ending fund balances of $23,688,184 an increase of $10,710,919 in comparison with the prior year. Nonspendable portion of fund balance has increased from $1,460,910 to $1,501,305. Nonspendable fund balance is not available for new spending because it has been set aside for the following purposes: to generate income for the support and maintenance of the youth center and Kellogg Arena ($879,909); and for inventories and prepaid expenditures ($621,396). A new fund was added to the governmental funds for the year ending June 30, 2014 to account for the capital improvement bonds that were sold in September Proceeds of $15,370,000 plus a premium of $383,666 were partially spent in the current fiscal year, with some projects being longer term. These projects include repairs to the City s linear park, parking lot repairs in many of the City s parks, decorative lighting upgrades along a major corridor, culvert replacements and a diversion channel in addition to the projects discussed in the letter of transmittal. The general fund is the chief operating fund of the City. At the end of the current fiscal year, unassigned fund balance (which is only reported in the general fund) was $6,580,891, while total fund balance was $8,149,022. In accordance with the City s adopted fund balance policy, the minimum unassigned fund balance in the general fund of no less than 8 percent of current year budgeted operating revenue has been met. The percent as of June 30, 2014 is 15.3%. The fund balance of the City s general fund increased by $479,877 during the current fiscal year. This was favorable as compared to the final budgeted decrease in fund balance of $180,532. The community development fund has a fund balance of $46 which increased from the previous year of no fund balance. Original budget estimates anticipated a greater level of activity than actually occurred; however, community development grant funds may be carried over to subsequent years. Proprietary funds. The City s proprietary funds provide the same type of information found in the government-wide financial statements, but in more detail. 20

29 Management's Discussion and Analysis Unrestricted net position of the water and wastewater system fund at the end of the year amounted to $7,678,908. The fund had an increase in total net position for the year of $1,484,868. Factors concerning the finances of this fund have already been addressed in the discussion of the City s business type activities. The economic development fund had total net position at the end of the year of $9,860,823, all of which was unrestricted. For the year, the fund had a decrease in net position of $38,829. The W.K. Kellogg Airport fund had total net position of $11,464,500 of which $552,018 was unrestricted; the fund had a decrease in net position of $589,506 for the year. The decrease in net position is due to depreciation. The substantial decrease in W.K. Kellogg Airport intergovernmental subsidies from the prior year is the completion in the prior year of a federal noise mitigation grant used to purchase properties within an identified area around the airport. The Battle Creek Transit System had a total net position of $2,942,362 of which $726,226 was unrestricted; the fund had a decrease in net position of $504,155 for the year primarily as a result of depreciation expense. General Fund Budgetary Highlights Mid-year adjustments were made to the general fund budget to account for minor changes in transfers out and departmental budgeted revenues. Budgeted expenses also increased for any prior year encumbrances carried forward, as they are a use of the prior year fund balance and were reflected in the assigned fund balance at 6/30/13. Net change in fund balance for the general fund was an increase of $479,877 compared to a budgeted decrease of $180,532. This is primarily due to departmental savings from changes in health insurance to a high deductible plan. Capital Assets and Debt Administration Capital Assets. The City s investment in capital assets for its governmental and business-type activities as of June 30, 2014, amounted to $337,057,980 (net of accumulated depreciation). This investment in capital assets includes land, improvements, buildings, systems, vehicles and equipment, park facilities, roads, highways, and bridges. Net capital assets for governmental activities increased by 0.3%, and for business-type activities decreased by 2.8%. Overall, total net capital assets for the City decreased by 1%. City of Battle Creek's Capital Assets (Net of Depreciation) Governmental activities Business-type activities Total Land and land improvements $ 15,106,878 $ 7,603,222 $ 5,436,093 $ 5,226,546 $ 20,542,971 $ 12,829,768 Construction in progress 6,192,398 9,003,623 3,870,017-10,062,415 9,003,623 Buildings 28,748,440 30,084,603 18,134,556 19,928,338 46,882,996 50,012,941 Vehicles 2,024,361 2,072, ,003 1,000,884 2,590,364 3,073,416 Equipment 2,454,457 2,978,149 1,000,854 1,606,489 3,455,311 4,584,638 Systems ,160,304-73,160,304 - Infrastructure 180,363, ,548,296-77,313, ,363, ,861,304 Total $ 234,890,153 $ 234,290,425 $ 102,167,827 $ 105,075,265 $ 337,057,980 $ 339,365,690 Major capital asset events during the current fiscal year included: Fleet operation purchases of vehicles and equipment in the amount of $580,335. The completion of the Downtown Transformation project (a multi-year endeavor) resulted in total additions to capital assets of $8,158,579. Additional information on the City s capital assets can be found in note 8 to the financial statements. 21

30 Management's Discussion and Analysis Long term debt. At the end of the current fiscal year, the City had total bonded debt outstanding of $38,185,000. Of this amount, $28,790,000 is comprised of debt backed by the full faith and credit of the government. The remainder of the City s bonded debt represents bonds secured solely by specified revenue sources. General Obligation and Revenue Bonds Governmental activities Business-type activities Total General obligation bonds $ 28,790,000 $ 15,130,000 $ - $ - $ 28,790,000 $ 15,130,000 Revenue bonds - - 9,395,000 11,130,000 9,395,000 11,130,000 Total $ 28,790,000 $ 15,130,000 $ 9,395,000 $ 11,130,000 $ 38,185,000 $ 26,260,000 The City s total bonded debt increased by $11,925,000 (45.4 percent) during the current fiscal year. During the year the City issued a new bond for capital improvements in the amount of $15,370,000 and also advance refunded a bond. The following chart depicts the City s credit rating for the various outstanding debt and the different rating agencies: Moody's S&P Fitch General obligation limited tax bonds Aa3 AA- AA Water and wastewater revenue bonds Aa3 A AA- State statutes limit the amount of general obligation debt a governmental entity may issue to 10 percent of its total state equalized valuation. The current debt limitation for the City is $160,147,070 which is significantly in excess of the City s outstanding general obligation debt. Additional information on the City s long term debt can be found in note 11 to the financial statements. Economic Factors City Administration, accompanied by a representative from Battle Creek Unlimited, visited bond rating agencies in July 2013 in anticipation of the sale of the $15 million capital improvement bond issue. The City of Detroit had just declared bankruptcy, and there was much speculation within the municipal bond industry. The City of Battle Creek had all three bond ratings affirmed even in light of what was called the Michigan penalty due to management s demonstrated ability to maintain adequate and stable general fund reserves despite revenue pressures and economic and real estate pressures in the area. Next Year s Budgets and Rates Developed the fiscal year ending June 30, 2015 budget with no increase in property taxes. Increased budgeted income tax revenue $100,000 for compliance. Included a 1% increase in general fund expenditures. Included 2-2.5% wage raises in many collective bargaining agreements. Continued the progress of health insurance plan savings due to transition to high deductible plans with City contributions to health savings accounts. Requests for Information This financial report is designed to provide a general overview of the City s finances for all those with an interest in the government s finances. The financial statements are available on the City s web site: Questions concerning any of the information provided in this report or requests for additional financial information should be addressed to the City Finance Director, P.O. Box 1717, Battle Creek, Michigan

31 BASIC FINANCIAL STATEMENTS 23

32 GOVERNMENT-WIDE FINANCIAL STATEMENTS 24

33 Statement of Net Position June 30, 2014 Primary Government Governmental Business-type Component Activities Activities Total Units Assets Pooled cash and investments $ 37,800,375 $ 14,521,290 $ 52,321,665 $ 26,243,859 Receivables 10,147,870 6,583,951 16,731,821 3,298,968 Receivables, long-term portion 4,075, ,372 4,315,372 4,070,718 Internal balances (600,474) 600, Inventories, prepaid items and other assets 1,358,936 1,413,261 2,772,197 16,542 Capital assets not being depreciated 8,243,038 7,322,880 15,565,918 13,107,100 Capital assets being depreciated, net 226,647,115 94,844, ,492,062 1,039,745 Total assets 287,671, ,527, ,199,035 47,776,932 Deferred outflows of resources Deferred charge on refunding 255, , ,183 1,759,939 Liabilities Accounts payable and accrued liabilities 12,160,584 2,076,096 14,236,680 2,647,194 Accrued interest payable 262, , ,827 Unearned revenue 1,041, ,715 1,153,919 - Long-term liabilities: Due within one year 3,839,104 2,700,962 6,540,066 3,907,521 Due in more than one year 31,006,825 8,054,231 39,061,056 47,220,297 Other liability due in more than one year - net other postemployment benefits liability 9,312,938-9,312,938 - Total liabilities 57,623,394 12,944,004 70,567,398 54,126,839 Net position Net investment in capital assets 213,803,703 92,099, ,903,536 14,146,845 Restricted for: Debt service 58,357-58,357 - Capital projects 1,663,316-1,663,316 - Endowment - nonexpendable 879, ,909 - Endowment - expendable 70,000-70,000 - Other purposes ,414,804 Unrestricted (deficit) 13,828,647 20,628,055 34,456,702 (20,151,617) Total net position (deficit) $ 230,303,932 $ 112,727,888 $ 343,031,820 $ (4,589,968) The accompanying notes are an integral part of these financial statements. 25

34 Statement of Activities For the Year Ended June 30, 2014 Program Revenues Operating Capital Charges Grants and Grants and Net (Expense) Functions / Programs Expenses for Services Contributions Contributions Revenues Primary government Governmental activities: General government $ 12,208,561 $ 2,824,535 $ 2,197,872 $ - $ (7,186,154) Public safety 27,215, , ,794 - (25,510,413) Public works 2,199, ,493 92,427 - (1,905,704) Highways and streets 9,731,567 27,929 5,758,357 - (3,945,281) Parks and recreation 5,759,128 3,250, (2,508,178) Community development 3,019, ,924 1,443,175 - (1,298,350) Interest on long-term debt 1,206, (1,206,989) Total governmental activities 61,340,653 7,489,959 10,289,625 - (43,561,069) Business-type activities: Wastewater 15,642,028 15,586,240 18,775 - (37,013) Water 7,930,788 9,465,371 31,852-1,566,435 Public transit 4,814, ,705 2,917,721 - (1,471,498) Solid waste collection 3,004,407 3,082, ,762 Airport 2,485,677 1,365, ,724 - (517,206) Parking 1,549,455 1,330, (218,484) Economic development 130,400 91, (38,829) Total business-type activities 35,557,679 31,347,774 3,571,072 - (638,833) Total primary government $ 96,898,332 $ 38,837,733 $ 13,860,697 $ - $ (44,199,902) Component units Community development $ 11,175,739 $ 186,329 $ - $ 480,301 $ (10,509,109) continued 26

35 Statement of Activities For the Year Ended June 30, 2014 Primary Government Governmental Business-type Component Activities Activities Total Units Changes in net position Net revenues (expense) $ (43,561,069) $ (638,833) $ (44,199,902) $ (10,509,109) General revenues: Property taxes 16,258,935-16,258,935 14,252,945 Income taxes 16,093,707-16,093,707 - Grants and contributions not restricted to specific programs 5,336,347-5,336,347 - Unrestricted investment earnings 953,036 96,548 1,049, ,866 Transfers (396,516) 396, Total general revenues and transfers 38,245, ,064 38,738,573 15,047,811 Change in net position (5,315,560) (145,769) (5,461,329) 4,538,702 Net position (deficit), beginning of year 235,619, ,873, ,493,149 (9,128,670) Net position (deficit), end of year $ 230,303,932 $ 112,727,888 $ 343,031,820 $ (4,589,968) concluded. The accompanying notes are an integral part of these financial statements. 27

36 This page intentionally left blank. 28

37 FUND FINANCIAL STATEMENTS 29

38 Balance Sheet Governmental Funds June 30, 2014 Capital Nonmajor Total Community Improvements Governmental Governmental General Development Bond Funds Funds Assets Pooled cash and investments $ 7,489,947 $ - $ 12,309,291 $ 5,690,982 $ 25,490,220 Receivables: Interest 133, , ,033 Accounts 2,118,190 48,122-1,223,312 3,389,624 Special assessments 204, ,818 Grants 39, , , ,346 Loans 1,866,805 2,771, ,000-4,888,242 Inventories 9, , ,855 Prepaid items 475, , ,541 Interfund receivable 930, ,157 Total assets $ 13,267,790 $ 2,933,260 $ 12,559,314 $ 7,280,472 $ 36,040,836 Liabilities Accounts payable $ 1,276,961 $ 20,404 $ 1,904,815 $ 966,529 $ 4,168,709 Accrued payroll 1,749, ,749,122 Retentions, deposits and other liabilities , ,364 Interfund payable - 141, , ,761 Unearned revenue 70, , ,924 Total liabilities 3,096, ,777 1,904,815 2,395,476 7,558,880 Deferred inflows of resources Unavailable revenue: Loans receivable 1,866,805 2,771, ,638,242 Special assessments 155, ,530 Total deferred inflows of resources 2,021,956 2,771, ,793,772 Fund balances Nonspendable 484, ,016,652 1,501,305 Restricted 147, ,654, ,880 11,624,559 Committed 844, ,436,895 3,281,519 Assigned 91, , ,297 Unassigned (deficit) 6,580, (131,387) 6,449,504 Total fund balances 8,149, ,654,499 4,884,617 23,688,184 Total liabilities, deferred inflows of resources and fund balances $ 13,267,790 $ 2,933,260 $ 12,559,314 $ 7,280,472 $ 36,040,836 The accompanying notes are an integral part of these financial statements. 30

39 Reconciliation Fund Balances of Governmental Funds to Net Position of Governmental Activities June 30, 2014 Fund balances - total governmental funds $ 23,688,184 Amounts reported for governmental activities in the statement of net position are different because: Capital assets used in governmental activities are not financial resources and therefore are not reported in the funds. Capital assets 385,428,022 Accumulated depreciation (153,490,857) Internal service funds are used by management to charge the costs of certain equipment usage to individual governmental funds. The assets and liabilities of the internal service funds are included in governmental activities in the statement of net position. Net position of governmental internal service funds 10,000,305 Portion of internal service funds net operating income attributed to business-type funds (600,474) Because the focus of governmental funds is on short-term financing, some assets will not be available to pay for current expenditures. Those assets (i.e., receivables) are offset by deferred outflows of resources in the governmental funds and, therefore, not included in fund balance. Unavailable special assessments 155,530 Loans receivable related to the sale of capital assets and other loans 4,638,242 Gains and losses on refunding are not reported in the governmental funds, whereas they are capitalized and amortized for net position. Deferred charge on refunding 255,466 Certain liabilities, such as bonds payable, are not due and payable in the current period and therefore are not reported in the funds. Bonds and installment contracts payable (31,996,415) Receivables from other entities for their share of debt 4,515,000 Accrued interest on bonds and installment contracts payable (262,739) Net other postemployment benefits liability (9,312,938) Compensated absences (2,713,394) Net position of governmental activities $ 230,303,932 The accompanying notes are an integral part of these financial statements. 31

40 Statement of Revenues, Expenditures and Changes in Fund Balances Governmental Funds For the Year Ended June 30, 2014 Capital Nonmajor Total Community Improvements Governmental Governmental General Development Bond Funds Funds Revenues Taxes $ 30,777,650 $ - $ - $ 1,574,992 $ 32,352,642 Licenses and permits 744, , ,738 Intergovernmental 6,659,514 1,088,562-7,695,029 15,443,105 Charges for services 1,981, ,538,976 4,520,247 Fines and forfeitures 134, ,497 Investment earnings 511, ,894 35, ,839 Contributions , ,742 Other 1,965,686 99, ,600 2,823,774 Total revenues 42,774,315 1,366,726 12,894 12,747,649 56,901,584 Expenditures Current expenditures: General government 7,225,082-4,799,722 1,193,236 13,218,040 Public safety 25,303, ,036 25,587,422 Public works 2,152, ,152,726 Highway and streets ,261,973 9,261,973 Parks and recreation 2,708, ,076,524 4,784,815 Community development - 1,364, ,984 1,725,369 Inspections , ,325 Unallocated 1,272, ,272,866 Debt service: Principal retirement ,960,721 1,960,721 Interest ,183,898 1,183,898 Bond issuance costs , ,339 Total expenditures 38,662,351 1,364,385 5,112,061 16,759,697 61,898,494 Revenue over (under) expenditures 4,111,964 2,341 (5,099,167) (4,012,048) (4,996,910) Other financing sources (uses) Issuance of bonds ,370,000-15,370,000 Premium on issuance of bonds , ,666 Transfers in 16, ,383,517 5,400,117 Transfers out (3,648,687) (2,295) - (1,794,972) (5,445,954) Total other financing sources (uses) (3,632,087) (2,295) 15,753,666 3,588,545 15,707,829 Net change in fund balances 479, ,654,499 (423,503) 10,710,919 Fund balances, beginning of year 7,669, ,308,120 12,977,265 Fund balances, end of year $ 8,149,022 $ 46 $ 10,654,499 $ 4,884,617 $ 23,688,184 The accompanying notes are an integral part of these financial statements. 32

41 Reconciliation Net Changes in Fund Balances of Governmental Funds to Change in Net Position of Governmental Activities For the Year Ended June 30, 2014 Net change in fund balances - total governmental funds $ 10,710,919 Amounts reported for governmental activities in the statement of activities are different because: Governmental funds report capital outlays as expenditures. However, in the statement of activities, the cost of those assets is allocated over their estimated useful lives and reported as depreciation expense. Capital outlay 9,205,954 Depreciation expense (8,454,644) Revenues in the statement of activities that do not provide resources are not reported as revenues in the funds, but rather deferred to subsequent fiscal years. Change in special assessments (87,692) Change in assets held for resale (175,099) Change in unearned revenues related to loans receivable (313,787) Bond proceeds provide current financial resources to governmental funds in the period issued, but issuing bonds increases long-term liabilities in the statement of net position. Repayment of bond principal is an expenditure in the governmental funds, but the repayment reduces long-term liabilities in the statement of net position. Principal payments on long-term liabilities 1,960,721 Amount received from other entities for their share of debt principal (425,000) Proceeds from issuance of long-term debt (15,370,000) Premium from issuance of long-term debt (383,666) Internal service funds are used by management to charge the costs of certain equipment usage to individual governmental funds. The net revenues (expense) attributable to those funds is reported with governmental activities. Net operating loss from governmental activities in internal service funds (954,031) Interest earnings from governmental internal service funds 207,816 Interest paid from governmental activities in internal service funds (1,574) Gain on disposal of capital assets 33,504 Transfers received in governmental internal service funds 689,760 Transfers made from governmental internal services funds (1,040,439) Some expenses reported in the statement of activities do not require the use of current financial resources and therefore are not reported as expenditures in the funds. Change in accrued interest payable on bonds (21,517) Change in net other postemployment benefits liability (722,258) Change in the accrual for compensated absences (174,527) Change in net position of governmental activities $ (5,315,560) The accompanying notes are an integral part of these financial statements. 33

42 Statement of Revenues, Expenditures and Change in Fund Balance Budget and Actual - General Fund For the Year Ended June 30, 2014 Actual Original Final Over (Under) Budget Budget Actual Final Budget Revenues Taxes: City income $ 16,350,000 $ 16,350,000 $ 16,093,707 $ (256,293) Real estate 12,514,734 12,514,734 11,874,167 (640,567) Personal property 1,400,000 1,400,000 1,963, ,780 Administration fees 727, , ,054 3,554 Other 2,000 2, , ,942 Total taxes 30,994,234 30,994,234 30,777,650 (216,584) Licenses and permits 718, , ,302 26,004 Intergovernmental: State shared - statutory 1,329,768 1,329,768 1,393,833 64,065 State shared - constitutional 3,923,648 3,923,648 3,905,356 (18,292) Other 1,322,363 1,322,363 1,360,325 37,962 Total intergovernmental 6,575,779 6,575,779 6,659,514 83,735 Charges for services: Parks and recreation 1,082,445 1,274,496 1,180,827 (93,669) Police services 871, , ,444 (71,300) Total charges for services 1,954,189 2,146,240 1,981,271 (164,969) Fines and forfeitures 181, , ,497 (47,003) Investment income 594, , ,395 (83,371) Other: Rent and leases 239, , ,354 (11,064) Contributions and donations 192, Miscellaneous and other 434, , , ,663 Administrative reimbursements 1,067,434 1,067,434 1,075,328 7,894 Total other 1,933,378 1,757,409 1,965, ,277 Total revenues 42,952,144 42,968,226 42,774,315 (193,911) continued 34

43 Statement of Revenues, Expenditures and Changes in Fund Balance Budget and Actual - General Fund For the Year Ended June 30, 2014 Actual Original Final Over (Under) Budget Budget Actual Final Budget Expenditures General government: Administration: Mayor and city commission $ 99,793 $ 99,793 $ 99,106 $ (687) City clerk 225, , ,385 (6,626) City manager 706, , ,244 (177,729) City hall 361, , ,994 (10,414) Neighborhood code compliance 199, , ,946 (6,364) Employee relations 239, , , Human resources 366, , ,157 (30,013) Labor attorney 21,012 21,012 15,304 (5,708) Legal department 836, , ,274 (149,413) Elections 76,439 76,439 74,162 (2,277) Civil service 74,553 74,553 90,515 15,962 Data processing 980, , ,252 - Total administration 4,188,284 4,269,335 3,896,498 (372,837) Community development: City planning 707, , ,735 (17,506) Housing board of appeals 4,100 4,100 2,842 (1,258) Intermodal facility 94,456 94, ,561 17,105 Total community development 806, , ,138 (1,659) Finance: Accounting 765, , ,931 (35,074) Purchasing 257, , ,361 (17,957) Treasurer's office 333, , ,533 (50,357) Assessing 737, , ,991 (32,042) Income tax division 561, , ,630 (4,368) Total finance 2,654,192 2,663,244 2,523,446 (139,798) Total general government 7,648,696 7,739,376 7,225,082 (514,294) continued 35

44 Statement of Revenues, Expenditures and Changes in Fund Balance Budget and Actual - General Fund For the Year Ended June 30, 2014 Actual Original Final Over (Under) Budget Budget Actual Final Budget Expenditures (continued) Public safety: Police department: Administration $ 906,381 $ 897,340 $ 873,506 $ (23,834) Crime lab 697, , ,418 (49,337) Investigation 1,398,102 1,398,102 1,396,140 (1,962) Fleet management 139, , ,398 7,907 Special investigative unit 668, , ,360 13,873 Management service 899, , ,490 (48,721) Patrol 8,864,195 9,205,765 8,942,387 (263,378) Community service 995, , ,342 (1,629) Officer training 227, , ,108 (8,201) Detention center 117, , , Gang task force 526, , ,787 (827) Total police department 15,440,831 15,443,105 15,067,421 (375,684) Fire department: Administration 780, , ,558 (79,667) Fire fighting 7,748,470 7,754,296 7,693,532 (60,764) Total fire department 8,528,695 8,534,521 8,394,090 (140,431) Dispatch 1,660,750 1,660,750 1,681,010 20,260 Civil defense 146, , ,865 (13) Total public safety 25,776,621 25,799,254 25,303,386 (495,868) Public works: Street and storm sewers 397, , ,981 (15,685) Engineering 89,207 89, ,088 71,881 Street lighting 1,310,890 1,310,890 1,367,210 56,320 Outside service 136, , , ,057 Total public works 1,934,153 1,934,153 2,152, ,573 continued 36

45 Statement of Revenues, Expenditures and Changes in Fund Balance Budget and Actual - General Fund For the Year Ended June 30, 2014 Actual Original Final Over (Under) Budget Budget Actual Final Budget Expenditures (concluded) Parks and recreation: Administration $ 839,219 $ 822,171 $ 827,970 $ 5,799 Sports 1,314,924 1,256,174 1,085,813 (170,361) Youth center and water park 841, , ,508 (46,697) Total parks and recreation 2,995,348 2,919,550 2,708,291 (211,259) Unallocated: Special projects 129, , ,550 (18,357) Other 1,064,911 1,092,001 1,148,316 56,315 Total unallocated 1,193,911 1,234,908 1,272,866 37,958 Total expenditures 39,548,729 39,627,241 38,662,351 (964,890) Revenue over expenditures 3,403,415 3,340,985 4,111, ,979 Other financing sources (uses) Transfers in - 44,400 16,600 (27,800) Transfers out (3,450,215) (3,565,917) (3,648,687) (82,770) Total other financing sources (uses) (3,450,215) (3,521,517) (3,632,087) (110,570) Net change in fund balance (46,800) (180,532) 479, ,409 Fund balance, beginning of year 7,669,145 7,669,145 7,669,145 - Fund balance, end of year $ 7,622,345 $ 7,488,613 $ 8,149,022 $ 660,409 concluded. The accompanying notes are an integral part of these financial statements. 37

46 This page intentionally left blank. 38

47 Statement of Revenues, Expenditures and Change in Fund Balance Budget and Actual - Community Development Special Revenue Fund For the Year Ended June 30, 2014 Actual Original Final Over (Under) Budget Budget Actual Final Budget Revenues Licenses and permits $ - $ 177,716 $ 178,436 $ 720 Intergovernmental 1,583,018 1,583,018 1,088,562 (494,456) Investment income Loan collection and other - 94,441 99,488 5,047 - Total revenues 1,583,018 1,855,414 1,366,726 (488,688) Expenditures Community development 1,580,723 1,853,119 1,364,385 (488,734) Revenues over expenditures 2,295 2,295 2, Other financing uses Transfers out (2,295) (2,295) (2,295) - Net change in fund balance Fund balance, beginning of year Fund balance, end of year $ - $ - $ 46 $ 46 The accompanying notes are an integral part of these financial statements. 39

48 Statement of Net Position Proprietary Funds June 30, 2014 Business-type Activities - Enterprise Funds Water and Nonmajor Wastewater Economic W.K. Kellogg Battle Creek Enterprise System Development Airport Transit System Funds Assets Current assets: Pooled cash and investments $ 4,767,178 $ 8,070,622 $ 686,421 $ - $ 1,492,465 Receivables: Interest 4,390 61,458 14, Accounts 2,998,143 2,270 44, ,970 Special assessments 103, Grants 24, ,231,703 - Loans, current portion - 1,486, Other assets ,145 Inventories 1,327, ,400 - Prepaid items Total current assets 9,225,259 9,620, ,203 1,317,248 2,105,840 Noncurrent assets: Loans receivable, net - 240, Capital assets, net 82,735,106-11,406,612 2,216,136 5,809,973 Total noncurrent assets 82,735, ,372 11,406,612 2,216,136 5,809,973 Total assets 91,960,365 9,860,823 12,151,815 3,533,384 7,915,813 Deferred outflows of resources Deferred charge on refunding 144, Liabilities Current liabilities: Accounts payable and accrued liabilities 896,618-73,688 56, ,374 Compensated absences 363,720-56, ,994 7,660 Retentions, deposits and other liabilities 180, ,812 Accrued interest payable 79,482-10, Claims payable, current portion Interfund payable ,248 76,148 Unearned revenue 26,119-52,896-33,700 Lease payable, current portion , Bonds payable, current portion 1,988, Total current liabilities 3,534, , , ,694 Noncurrent liabilities: Advances from other government ,540 Claims payable Lease payable , Bonds payable 7,730, Total noncurrent liabilities 7,730, , ,540 Total liabilities 11,264, , , ,234 Net position Net investment in capital assets 73,161,242-10,912,482 2,216,136 5,809,973 Unrestricted 7,678,908 9,860, , ,226 1,209,606 Total net position $ 80,840,150 $ 9,860,823 $ 11,464,500 $ 2,942,362 $ 7,019,579 continued The accompanying notes are an integral part of these financial statements. 40

49 Statement of Net Position Proprietary Funds June 30, 2014 Governmental Activities Total Assets Current assets: Pooled cash and investments 15,016,686 Internal Service Funds $ $ 11,783,329 Receivables: Interest 80, ,671 Accounts 3,657, ,340 Special assessments 103,407 - Grants 1,256,128 - Loans, current portion 1,486,101 - Other assets 30,145 - Inventories 1,383, ,680 Prepaid items - 142,860 Total current assets 23,014,001 13,229,880 Noncurrent assets: Loans receivable, net 240,372 - Capital assets, net 102,167,827 2,952,988 Total noncurrent assets 102,408,199 2,952,988 Total assets 125,422,200 16,182,868 Deferred outflows of resources Deferred charge on refunding 144,717 - Liabilities Current liabilities: Accounts payable and accrued liabilities 1,340,460 1,941,570 Compensated absences 542, ,120 Retentions, deposits and other liabilities 248,224 - Accrued interest payable 89,975 - Claims payable, current portion - 2,324,796 Interfund payable 495,396 - Unearned revenue 112,715 70,280 Lease payable, current portion 170,480 - Bonds payable, current portion 1,988,000 - Total current liabilities 4,987,732 4,472,766 Noncurrent liabilities: Advances from other government 397,540 - Claims payable - 1,709,797 Lease payable 323,650 - Bonds payable 7,730,581 - Total noncurrent liabilities 8,451,771 1,709,797 Total liabilities 13,439,503 6,182,563 Net position Net investment in capital assets 92,099,833 2,952,988 Unrestricted 20,027,581 7,047,317 Total net position $ 112,127,414 $ 10,000,305 concluded. 41

50 This page intentionally left blank. 42

51 Reconciliation Net Position of Enterprise Funds to Net Position of Business-type Activities June 30, 2014 Net position - total enterprise funds $ 112,127,414 Amounts reported for business-type activities in the statement of net position are different because: Internal service funds are used by management to charge the costs of certain services to individual governmental and enterprise funds. The net revenues (expense) of the internal service funds are allocated to governmental and business-type activities. Cumulative portion of internal service funds net operating income attributed to enterprise funds. 600,474 Net position of business-type activities $ 112,727,888 The accompanying notes are an integral part of these financial statements. 43

52 Statement of Revenues, Expenses and Changes in Fund Net Position Proprietary Funds For the Year Ended June 30, 2014 Business-type Activities - Enterprise Funds Water and Wastewater Economic W.K. Kellogg System Development Airport Operating revenues Charges for services $ 24,385,474 $ - $ 935,269 Other 666,137 61,592 26,078 Total operating revenues 25,051,611 61, ,347 Operating expenses Personal services 7,305, ,208 Materials and supplies 2,430, ,654 Contractual and other 6,697, , ,592 Depreciation 6,475, ,669 Total operating expenses 22,908, ,400 2,131,123 Operating income (loss) 2,142,996 (68,808) (1,169,776) Nonoperating revenues (expenses) Intergovernmental subsidies 50, ,724 Interest earnings 71,912 29,979 12,976 Gain on disposal of capital assets Interest expense (280,822) - (29,437) Loss on disposal of capital assets (14,318) - - Total nonoperating revenues (expense) (172,601) 29, ,263 Income (loss) before transfers 1,970,395 (38,829) (583,513) Transfers in Transfers out (485,527) - (5,993) Change in net position 1,484,868 (38,829) (589,506) Net position, beginning of year 79,355,282 9,899,652 12,054,006 Net position, end of year $ 80,840,150 $ 9,860,823 $ 11,464,500 continued The accompanying notes are an integral part of these financial statements. 44

53 Statement of Revenues, Expenses and Changes in Fund Net Position Proprietary Funds - Business-type Activities - Enterprise Funds Governmental Activities Nonmajor Battle Creek Enterprise Internal Transit System Funds Total Service Funds Operating revenues Charges for services $ 419,361 $ 4,755,630 $ 30,495,734 $ 19,055,367 Other 6,344 61, , ,857 Total operating revenues 425,705 4,817,540 31,317,795 19,555,224 Operating expenses Personal services 2,809, ,701 11,154,107 4,004,702 Materials and supplies 807,389 33,074 3,451,702 2,590,767 Contractual and other 547,445 4,117,749 11,910,193 13,609,332 Depreciation 566, ,819 8,237, ,905 Total operating expenses 4,731,170 4,852,343 34,753,651 20,988,706 Operating income (loss) (4,305,465) (34,803) (3,435,856) (1,433,482) Nonoperating revenues (expenses) Intergovernmental subsidies 2,917,721-3,571,072 - Interest earnings - 11, , ,816 Gain on disposal of capital assets ,504 Interest expense - - (310,259) (1,574) Loss on disposal of capital assets - - (14,318) - Total nonoperating revenues (expense) 2,917,721 11,660 3,373, ,746 Income (loss) before transfers (1,387,744) (23,143) (62,834) (1,193,736) Transfers in 888,230 62, , ,760 Transfers out (4,641) (58,409) (554,570) (1,040,439) Change in net position (504,155) (18,696) 333,682 (1,544,415) Net position, beginning of year 3,446,517 7,038, ,793,732 11,544,720 Net position, end of year $ 2,942,362 $ 7,019,579 $ 112,127,414 $ 10,000,305 concluded. 45

54 This page intentionally left blank. 46

55 Reconciliation Change in Net Position of Enterprise Funds to Change in Net Position of Business-type Activities For the Year Ended June 30, 2014 Change in net position - total enterprise funds $ 333,682 Amounts reported for business-type activities in the statement of activities are different because: Internal service funds are used by management to charge the costs of certain services to individual governmental and enterprise funds. The net operating loss of the internal service funds are allocated to governmental and business-type activities. (479,451) Change in net position of business-type activities $ (145,769) The accompanying notes are an integral part of these financial statements. 47

56 Statement of Cash Flows Proprietary Funds For the Year Ended June 30, 2014 Business-type Activities - Enterprise Funds Water and Wastewater Economic W.K. Kellogg System Development Airport Cash flows from operating activities Receipts from customers and users $ 25,548,981 $ 33,476 $ 941,059 Loans collected from borrowers - 117,357 - Receipts from interfund services Payments to suppliers (5,498,842) (157,151) (583,437) Loans made to borrowers - (150,000) - Payments to employees (7,294,282) - (794,147) Payments for interfund services (3,243,526) - - Net cash provided by (used in) operating activities 9,512,331 (156,318) (436,525) Cash flows from noncapital financing activities Transfers in Transfers out (485,527) - (5,993) Intergovernmental subsidies 50, ,724 Net cash provided by (used in) noncapital financing activities (434,900) - 596,731 Cash flows from capital and related financing activities Principal and interest paid on debt (6,480,576) - (192,039) Principal and interest paid on capital lease Issuance of capital bonds 4,385, Purchase of capital assets (5,282,733) - (35,944) Net cash used in capital and related financing activities (7,378,309) - (227,983) Cash flows from investing activities Interest earnings on investments 71,910 29,979 12,976 Net change in pooled cash and investments 1,771,032 (126,339) (54,801) Pooled cash and investments, beginning of year 2,996,146 8,196, ,222 Pooled cash and investments, end of year $ 4,767,178 $ 8,070,622 $ 686,421 continued 48

57 Statement of Cash Flows Proprietary Funds Business-type Activities - Enterprise Funds Governmental Activities Nonmajor Battle Creek Enterprise Internal Transit System Funds Total Service Funds Cash flows from operating activities Receipts from customers and users $ 572,161 $ 4,810,757 $ 31,906,434 $ - Loans collected from borrowers ,357 - Receipts from interfund services ,555,224 Payments to suppliers (612,091) (4,050,130) (10,901,651) (13,802,868) Loans made to borrowers - - (150,000) - Payments to employees (2,999,447) (301,515) (11,389,391) (4,013,636) Payments for interfund services (736,082) (36,160) (4,015,768) - Net cash provided by (used in) operating activities (3,775,459) 422,952 5,566,981 1,738,720 Cash flows from noncapital financing activities Transfers in 888,230 62, , ,760 Transfers out (4,641) (58,409) (554,570) (1,040,439) Intergovernmental subsidies 2,917,721-3,571,072 - Net cash provided by (used in) noncapital financing activities 3,801,310 4,447 3,967,588 (350,679) Cash flows from capital and related financing activities Principal and interest paid on debt - - (6,672,615) - Principal and interest paid on capital lease (176,017) Issuance of capital bonds - - 4,385,000 - Purchase of capital assets (25,851) - (5,344,528) (632,323) Net cash used in capital and related financing activities (25,851) - (7,632,143) (808,340) Cash flows from investing activities Interest earnings on investments - 11, , ,816 Net change in pooled cash and investments - 438,654 2,028, ,517 Pooled cash and investments, beginning of year - 1,053,811 12,988,140 10,995,812 Pooled cash and investments, end of year $ - $ 1,492,465 $ 15,016,686 $ 11,783,329 continued 49

58 Statement of Cash Flows Proprietary Funds For the Year Ended June 30, 2014 Business-type Activities - Enterprise Funds Water and Wastewater Economic W.K Kellogg System Development Airport Cash flows from operating activities Operating income (loss) $ 2,142,996 $ (68,808) $ (1,169,776) Adjustments to reconcile operating income (loss) to net cash from operating activities: Depreciation 6,475, ,669 Amortization 72, Changes in assets and liabilities: Interest receivable 1,355 (28,116) (172) Accounts receivable 423,671 - (20,133) Special assessments receivable 59, Grants receivable 1, Loans receivable - (32,643) - Inventories 60, Prepaid items Accounts payable 342,812 (26,751) 17,762 Retentions, deposits and other liabilities (4,135) - - Compensated absences 11,061-16,061 Accrued interest payable (86,510) - (2,953) Claims payable Interfund payable Unearned revenue 11, Net cash provided by (used in) operating activities $ 9,512,331 $ (156,318) $ (436,525) continued 50