Federal Reserve Monetary Policy Since the Financial Crisis

|

|

|

- Gerard Jordan

- 6 years ago

- Views:

Transcription

1 Federal Reserve Monetary Policy Since the Financial Crisis Hitotsubashi-IMF Seminar 23 January 2014 Ellen E. Meade Senior Adviser Division of Monetary Affairs Federal Reserve Board

2 Overview 1. Central bank mandate and progress toward objectives 2. Nontraditional monetary policy 3. Flow-based asset purchase program 4. Recent developments 5. The road ahead 1 P age

3 Federal Reserve s Mandate The goals of monetary policy spelled out in the Federal Reserve Act Board of Governors and the Federal Open Market Committee (FOMC) "to promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates" 2 P age

4 Progress toward Objectives 3 P age

5 4 P age

6 5 P age

7 6 P age

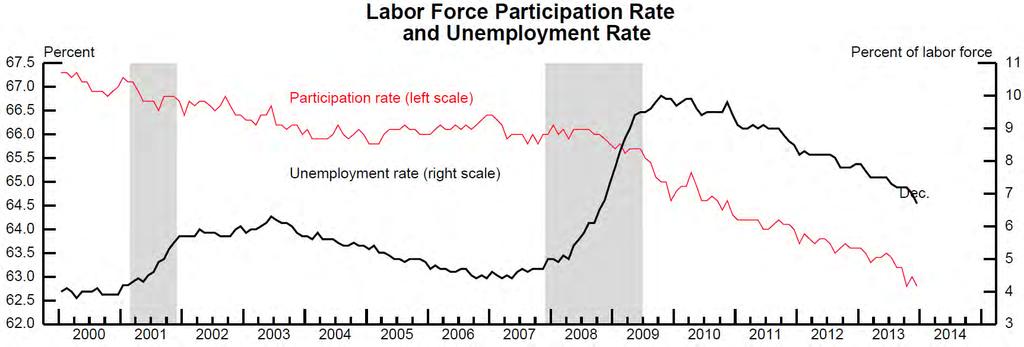

8 Points to Note Does GDP growth understate progress? o GDP vs. GDI Divergence between labor market and goods market Different signals from the labor market o Unemployment rate vs. labor force participation rate Softness in inflation o Oil prices o Administered prices for medical care o Imputed banking services 7 P age

9 Nontraditional Monetary Policy 8 P age

10 9 P age

11 Policy at the Zero Lower Bound (ZLB) Approach to providing additional accommodation since late 2008 Asset purchase programs (LSAPs) Depress term premiums and put downward pressure on longer-term rates Ease financial conditions more broadly Signal commitment to accommodative policy stance Uncharted waters Forward guidance about path of policy Shapes expectations regarding future short-term rates Reduces uncertainty regarding interest rates Feasibility of commitment over long horizons 10 P age

12 Asset Purchase Programs LSAP #1 Announced November 2008, increased March 2009, completed March 2010 Total $1.25 trillion agency MBS, $175 billion agency debt securities, $300 billion Treasury securities Reduced yield on 10-year Treasury securities 40 to 110 basis points LSAP #2 Announced November 2010, completed June 2011 Total $600 billion Treasury securities Reduced yield on 10-year Treasury securities 15 to 45 basis points 11 P age

13 Asset Purchase Programs (continued) Maturity Extension Program Announced September 2011, extended June 2012, completed December 2012 Buy 6-30 years, sell 1-3 years; did not increase balance sheet Total nearly $700 billion Treasury securities Total effect of 2 LSAPs + MEP = 80 to 120 basis points Flow-based purchase program $40 billion agency MBS per month since September 2012 $45 billion Treasury securities per month since December 2012 Taper to $35 billion agency MBS, $40 billion Treasuries starting January P age

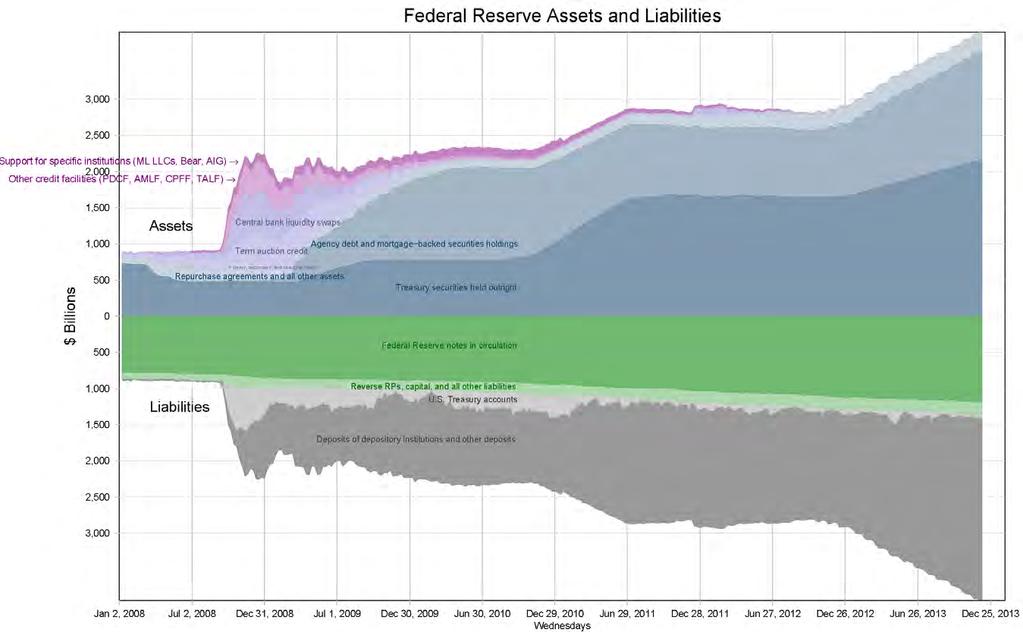

14 Federal Reserve Balance Sheet Flow-based purchases from September 2012 through January 2014 total more than $1.2 trillion Reinvestment policy Maturing Treasury securities rolled over at auction Maturing agency debt and MBS securities reinvested in agency MBS Asset purchases have expanded reserve balances held at Federal Reserve Banks from $870 billion in August 2007 to $2.5 trillion 13 P age

15 14 P age

16 Forward Guidance Defines the period over which rates will remain low Unspecified length o exceptionally low levels of the federal funds rate for some time (December 2008) o for an extended period (March 2009) Calendar dates o at least through mid-2013 (August 2011) o at least through late-2014 (January 2012) o at least through mid-2015 (September 2012) Thresholds provide economic conditionality (December 2012) o exceptionally low range for the federal funds rate will be appropriate at least as long as the unemployment rate remains above 6-1/2 percent, inflation between one and two years ahead is projected to be no more than a half percentage point above the Committee s 2 percent longer-run goal and inflation expectations well anchored 15 P age

17 Forward Guidance (continued) Describes what happens after crossing threshold consider other information, including additional measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial developments (December 2012) based on assessment of these factors... it likely will be appropriate to maintain the current target range for the federal funds rate well past the time that the unemployment rate declines below 6½ percent, especially if projected inflation continues to run below the Committee's 2 percent longerrun goal (December 2013) Describes the path after funds rate liftoff Take a balanced approach 16 P age

18 December 2013 Summary of Economic Projections 17 P age

19 Effects of Forward Guidance Pushed back the anticipated date of the onset of tightening Flattened the expected pace of tightening once it is underway Reduced uncertainty about the path of future policy Helped to keep market expectations reasonably aligned with those of the Committee and pushed back against expectations that the Committee would begin raising the federal funds rate prematurely 18 P age

20 Adoption of for some time in mid-december 2008 Consensus of professional forecasters (from the Blue Chip Financial Indicators) regarding the quarterly average value of the federal funds rate at forecast horizons from 0 to 6 quarters ahead as of December 1, 2008 (dashed line) and February 1, 2009 (solid line), from Unconventional Monetary Policy and Central Bank Communications, speech by Janet Yellen at the U.S. Monetary Policy Forum, February 25, P age

21 Computed from rates on overnight interest rate swaps, assuming a monthly term premium of zero 20 P age

22 Implied volatility of short-term rates has fallen to low levels 21 P age

23 Flow-based Asset Purchase Program 22 P age

24 Conditions for Ending Program With earlier programs, total quantity of asset purchases and time frame for program completion was announced when program commenced Flow-based program different Stopping conditions state-contingent and depend on economic outcomes FOMC indicated it was looking for substantial improvement in the outlook for the labor market in a context of price stability Would take appropriate account of likely efficacy and costs of purchases 23 P age

25 Efficacy and Costs Efficacy = Benefits Downward pressure on longer-term rates Foster stronger economic recovery Provide signal about policy intentions Guard against downside risks to economy Possible that effects diminish as purchases grow Potential Costs Impair market functioning Implications for financial stability and inflation expectations Complications for exit from unconventional policy Federal Reserve income and remittances to Treasury 24 P age

26 Recent Developments 25 P age

27 Spring/Summer 2013 Nominal yield on 10-year Treasury below 1.7 percent in late April Between April 30/May 1 FOMC and June meeting, tightening of financial conditions Chairman s JEC testimony in May 10-year Treasury rose 53 basis points over intermeeting period Expected path of federal funds rate shifted in At press conference following June meeting, Chairman sought to provide clarity Improvement in economy since start of flow-based purchase program Policy is data dependent purchases vary with economic conditions If conditions evolve as expected, reduce pace of purchases later in 2013 o End around mid-2014 when unemployment rate about 7 percent Forward guidance thresholds for the funds rate are not triggers Distinction between tapering of asset purchases and liftoff of funds rate 26 P age

28 Market Reaction Longer-term yields continued to rise after the June FOMC meeting Between June and July meetings, 10-year Treasury yield up 44 basis points and another 23 basis points between July and September meetings Financial market movements often difficult to account for, even ex post Improvements in the economic outlook Reported unwinding of levered positions together with liquidations of other positions in response to investor losses and rise in volatility o May have reduced future risks to financial stability o May have lowered probability of sharper market correction later on Market participants may have seen June communication as indicating lessening of commitment to highly accommodative stance of policy o Appeared that forward guidance for the federal funds rate became less effective after June o Markets did not view two nontraditional policy tools as distinct 27 P age

29 No Taper in September FOMC applied the framework announced at the June meeting and decided not to begin the taper Outlook similar to June but not sufficient confirmation to warrant taper Labor market conditions still far from what all of us would like to see Meaningful progress made since program began Purchases not on a preset course Restrictive fiscal policy and debate over debt ceiling Concerns about tightening of financial conditions both long-term and shortterm yields Tightening over intermeeting period was not welcome or warranted 28 P age

30 Median funds rate in 2016 = 2 percent, below longer-run equilibrium value of 4 percent Gradual increase after liftoff, more gradual than in previous episodes of tightening Headwinds to economic recovery 29 P age

31 Market Reaction Investors had priced in significant odds that the FOMC would reduce the pace of purchases at the September meeting Interest rates moved lower following the decision to maintain the current pace of purchases o 10-year Treasury moved down 15+ basis points on announcement o Dropped 33 basis points over intermeeting period leading up to October FOMC meeting Decision in September led to some criticism that the Federal Reserve had not communicated well in advance o Current environment is very complex o A number of FOMC participants noted that decision was a close call 30 P age

32 December Tapering Positive tone of incoming data and strong November employment report Cumulative progress in labor market since September 2012 along with substantial improvement in labor market outlook o Unemployment rate fallen from 8.1 percent to 7 percent in November Taper of $5 billion each in Treasury and MBS purchases o Purchasing $75 per month from January 2014 o Still adding to accommodation but at a slower pace o Committee will likely reduce the pace of asset purchases in further measured steps at future meetings o purchases not on preset course but are dependent on data Qualitative forward guidance for post-threshold period o Appropriate to maintain range for funds rate well past the time threshold is crossed, especially if inflation below 2 percent 31 P age

33 The Road Ahead 32 P age

34 December FOMC statement pointed to further measured steps at future meetings o If taper $10 billion per meeting program ends in 2014:Q4 o Could be adjusted up or down as necessary depending upon economy SEP gives indication of time between crossing unemployment threshold and liftoff of federal funds rate as well as gradual tightening after liftoff Exit strategy principles discussed in minutes of June 2011 FOMC meeting Broad principles remain applicable Cease reinvestments and allow maturing securities to roll off balance sheet Use reserve draining operations to reduce the size of reserve balances o Term deposits, term and overnight reverse repos Large majority of participants expect no sales of agency mortgage-backed securities during the process of normalizing monetary policy 33 P age

35 Thank you 34 P age

Responses to Survey of Primary Dealers Markets Group, Federal Reserve Bank of New York April 2012

Responses to Survey of Primary Dealers Markets Group, Federal Reserve Bank of New York April Responses to the Primary Dealer Policy Expectations Survey Distributed: 4/12/ Received by: 4/16/ For most questions,

Responses to Survey of Primary Dealers Markets Group, Federal Reserve Bank of New York April Responses to the Primary Dealer Policy Expectations Survey Distributed: 4/12/ Received by: 4/16/ For most questions,

Responses to Survey of Market Participants

Responses to Survey of Market Participants Markets Group, Reserve Bank of New York December 2015 Page 1 of 15 Responses to Survey of Market Participants Distributed: 12/03/2015 Received by: 12/07/2015

Responses to Survey of Market Participants Markets Group, Reserve Bank of New York December 2015 Page 1 of 15 Responses to Survey of Market Participants Distributed: 12/03/2015 Received by: 12/07/2015

Brian P Sack: Managing the Federal Reserve s balance sheet

Brian P Sack: Managing the Federal Reserve s balance sheet Remarks by Mr Brian P Sack, Executive Vice President of the Markets Group of the Federal Reserve Bank of New York, at the 2010 Chartered Financial

Brian P Sack: Managing the Federal Reserve s balance sheet Remarks by Mr Brian P Sack, Executive Vice President of the Markets Group of the Federal Reserve Bank of New York, at the 2010 Chartered Financial

US Federal Reserve: Feels like the first time

US Federal Reserve: Feels like the first time Economic research note December 17, 2015 The US Federal Reserve (the Fed) has, finally and unanimously, started the monetary policy normalization process by

US Federal Reserve: Feels like the first time Economic research note December 17, 2015 The US Federal Reserve (the Fed) has, finally and unanimously, started the monetary policy normalization process by

US Federal Reserve: Feels like the first time

US Federal Reserve: Feels like the first time Economic research note 17 December 2015 The US Federal Reserve (the Fed) has, finally and unanimously, started the monetary policy normalisation process by

US Federal Reserve: Feels like the first time Economic research note 17 December 2015 The US Federal Reserve (the Fed) has, finally and unanimously, started the monetary policy normalisation process by

How Will the Federal Reserve Adjust Its Balance Sheet During Policy Normalization? 12/10/2015

FOR PROFESSIONAL INVESTORS How Will the Federal Reserve Adjust Its Balance Sheet During Policy Normalization? 12/10/2015 INTRODUCTION Market participants remain highly focused on prospects for the Federal

FOR PROFESSIONAL INVESTORS How Will the Federal Reserve Adjust Its Balance Sheet During Policy Normalization? 12/10/2015 INTRODUCTION Market participants remain highly focused on prospects for the Federal

Brian P Sack: The SOMA portfolio at $2.654 trillion

Brian P Sack: The SOMA portfolio at $2.654 trillion Remarks by Mr Brian P Sack, Executive Vice President of the Federal Reserve Bank of New York, before the Money Marketeers of New York University, New

Brian P Sack: The SOMA portfolio at $2.654 trillion Remarks by Mr Brian P Sack, Executive Vice President of the Federal Reserve Bank of New York, before the Money Marketeers of New York University, New

Implementation and Transmission of Monetary Policy

The Federal Reserve in the 21 st Century Implementation and Transmission of Monetary Policy Argia M. Sbordone, Vice President Research and Statistics Group March 27, 2017 The views expressed in this presentation

The Federal Reserve in the 21 st Century Implementation and Transmission of Monetary Policy Argia M. Sbordone, Vice President Research and Statistics Group March 27, 2017 The views expressed in this presentation

Communications Challenges and Quantitative Easing. Remarks by. Jerome H. Powell. Member. Board of Governors of the Federal Reserve System.

For release on delivery 11:00 a.m. EDT October 11, 2013 Communications Challenges and Quantitative Easing Remarks by Jerome H. Powell Member Board of Governors of the Federal Reserve System at the 2013

For release on delivery 11:00 a.m. EDT October 11, 2013 Communications Challenges and Quantitative Easing Remarks by Jerome H. Powell Member Board of Governors of the Federal Reserve System at the 2013

Implementation and Transmission of Monetary Policy

The Federal Reserve in the 21 st Century Implementation and Transmission of Monetary Policy Argia M. Sbordone, Vice President Research and Statistics Group March 21, 2016 The views expressed in this presentation

The Federal Reserve in the 21 st Century Implementation and Transmission of Monetary Policy Argia M. Sbordone, Vice President Research and Statistics Group March 21, 2016 The views expressed in this presentation

January minutes: key signaling language

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: FOMC Minutes Wednesday, February 20, 2019 January minutes:

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: FOMC Minutes Wednesday, February 20, 2019 January minutes:

An Update on the Tapering Debate

An Update on the Tapering Debate James Bullard President and CEO, FRB-St. Louis 14 August 2013 Paducah, Kentucky Any opinions expressed here are my own and do not necessarily reflect those of others on

An Update on the Tapering Debate James Bullard President and CEO, FRB-St. Louis 14 August 2013 Paducah, Kentucky Any opinions expressed here are my own and do not necessarily reflect those of others on

RESPONSES TO SURVEY OF

RESPONSES TO SURVEY OF MARKET PARTICIPANTS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v November 2016 JANUARY Distributed: 1/17/ Received by: 1/22/ The Survey of Market Participants

RESPONSES TO SURVEY OF MARKET PARTICIPANTS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v November 2016 JANUARY Distributed: 1/17/ Received by: 1/22/ The Survey of Market Participants

Fed signals mid-2015 rate hike, but it all depends on the data

Research Department Fed signals mid-2015 rate hike, but it all depends on the data December 18, 2014 The Federal Open Market Committee sent a strong signal that it expects to tighten monetary policy in

Research Department Fed signals mid-2015 rate hike, but it all depends on the data December 18, 2014 The Federal Open Market Committee sent a strong signal that it expects to tighten monetary policy in

FOMC Statement: December th

Central Banks FOMC Statement: December 15-16 th Kim Chase / Nathaniel Karp / Boyd Nash-Stacey The Force Awakens: Yellen and Fellow FOMC Jedis Announce Rate Hike 25 basis points increase we have FOMC reasonably

Central Banks FOMC Statement: December 15-16 th Kim Chase / Nathaniel Karp / Boyd Nash-Stacey The Force Awakens: Yellen and Fellow FOMC Jedis Announce Rate Hike 25 basis points increase we have FOMC reasonably

RESPONSES TO SURVEY OF

RESPONSES TO SURVEY OF MARKET PARTICIPANTS Markets Group, Federal Reserve Bank of New York 0 RESPONSES TO SURVEY OF a v MARCH Distributed: 3/8/ Received by: 3/12/ The Survey of Market Participants is formulated

RESPONSES TO SURVEY OF MARKET PARTICIPANTS Markets Group, Federal Reserve Bank of New York 0 RESPONSES TO SURVEY OF a v MARCH Distributed: 3/8/ Received by: 3/12/ The Survey of Market Participants is formulated

Responses to Survey of Primary Dealers

Responses to Survey of Primary Dealers Markets Group, Federal Reserve Bank of New York September 2013 Page 1 of 14 Responses to the Primary Dealer Policy Expectations Survey Distributed: 9/5/2013 Received

Responses to Survey of Primary Dealers Markets Group, Federal Reserve Bank of New York September 2013 Page 1 of 14 Responses to the Primary Dealer Policy Expectations Survey Distributed: 9/5/2013 Received

Reconciling FOMC Forecasts and Forward Guidance. Mickey D. Levy Blenheim Capital Management

Reconciling FOMC Forecasts and Forward Guidance Mickey D. Levy Blenheim Capital Management Prepared for Shadow Open Market Committee September 20, 2013 Reconciling FOMC Forecasts and Forward Guidance Mickey

Reconciling FOMC Forecasts and Forward Guidance Mickey D. Levy Blenheim Capital Management Prepared for Shadow Open Market Committee September 20, 2013 Reconciling FOMC Forecasts and Forward Guidance Mickey

ECON 4325 Wednesday seminar 2016 The presentation package is complete

ECON 4325 Wednesday seminar 2016 The presentation package is complete 1 2 WHAT ARE THE CURRENT STANCE OF MONETARY POLICY? Norges Bank: ECB: Fed: BoE: 0,5 % 0,00 % (0.25% and -0.4 %) 0.25-0.5 % 0,5 % 3

ECON 4325 Wednesday seminar 2016 The presentation package is complete 1 2 WHAT ARE THE CURRENT STANCE OF MONETARY POLICY? Norges Bank: ECB: Fed: BoE: 0,5 % 0,00 % (0.25% and -0.4 %) 0.25-0.5 % 0,5 % 3

RESPONSES TO SURVEY OF

RESPONSES TO SURVEY OF PRIMARY DEALERS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v November 2016 SEPTEMBER 2017 Distributed: 9/7/2017 Received by: 9/11/2017 The Survey of

RESPONSES TO SURVEY OF PRIMARY DEALERS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v November 2016 SEPTEMBER 2017 Distributed: 9/7/2017 Received by: 9/11/2017 The Survey of

For almost a decade, the Federal Reserve Bank of New York has produced the

current FEDERAL RESERVE BANK OF NEW YORK issues in Economics and Finance Volume 19, Number 6 www.newyorkfed.org/research/current_issues Understanding the New York Fed s Survey of Primary Dealers Ellen

current FEDERAL RESERVE BANK OF NEW YORK issues in Economics and Finance Volume 19, Number 6 www.newyorkfed.org/research/current_issues Understanding the New York Fed s Survey of Primary Dealers Ellen

Let s Talk About It: What Policy Tools Should the Fed Normally Use?

No. 14-12 Let s Talk About It: What Policy Tools Should the Fed Normally Use? Abstract: Michelle L. Barnes The use of a wide variety of monetary and credit policy instruments during the most recent crisis

No. 14-12 Let s Talk About It: What Policy Tools Should the Fed Normally Use? Abstract: Michelle L. Barnes The use of a wide variety of monetary and credit policy instruments during the most recent crisis

Responses to Survey of Market Participants

Responses to Survey of Market Participants Markets Group, Federal Reserve Bank of New York April 2015 Page 1 of 10 Responses to Survey of Market Participants Distributed: 04/16/2015 Received by: 04/20/2015

Responses to Survey of Market Participants Markets Group, Federal Reserve Bank of New York April 2015 Page 1 of 10 Responses to Survey of Market Participants Distributed: 04/16/2015 Received by: 04/20/2015

FRBSF Economic Letter

FRBSF Economic Letter 217-34 November 2, 217 Research from Federal Reserve Bank of San Francisco A New Conundrum in the Bond Market? Michael D. Bauer When the Federal Reserve raises short-term interest

FRBSF Economic Letter 217-34 November 2, 217 Research from Federal Reserve Bank of San Francisco A New Conundrum in the Bond Market? Michael D. Bauer When the Federal Reserve raises short-term interest

Diffusion indices of forecast risks in Summary of Economic Projections From September 2016 FOMC to December 2018 FOMC.

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas

U.S. Monetary Policy Since Late Structure of the Federal Reserve System

U.S. Monetary Policy Since Late 2007 Winthrop P. Hambley Senior Adviser February 28, 2014 1 Structure of the Federal Reserve System Board of Governors, Washington D.C. 7 members nominated by the President,

U.S. Monetary Policy Since Late 2007 Winthrop P. Hambley Senior Adviser February 28, 2014 1 Structure of the Federal Reserve System Board of Governors, Washington D.C. 7 members nominated by the President,

Economic Outlook and Monetary Policy

Economic Outlook and Monetary Policy Enterprise Risk Management Symposium Chicago, IL September 3, 214 Spencer Krane Senior Vice President Federal Reserve Bank of Chicago The views expressed here are my

Economic Outlook and Monetary Policy Enterprise Risk Management Symposium Chicago, IL September 3, 214 Spencer Krane Senior Vice President Federal Reserve Bank of Chicago The views expressed here are my

The Fed and The U.S. Economic Outlook

The Fed and The U.S. Economic Outlook Maria Luengo-Prado Senior Economist and Policy Advisor Federal Reserve Bank of Boston May 13, 2016 Presentation prepared for the Telergee Alliance CFO & Controllers

The Fed and The U.S. Economic Outlook Maria Luengo-Prado Senior Economist and Policy Advisor Federal Reserve Bank of Boston May 13, 2016 Presentation prepared for the Telergee Alliance CFO & Controllers

November minutes: key signaling language

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: FOMC Minutes Thursday, November 29, 2018 November minutes:

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer Thomas Demas, Managing Director Michael Warren, Energy Strategist Data Insights: FOMC Minutes Thursday, November 29, 2018 November minutes:

US Fed raised rates by 25 basis points

Dr. Mohd Afzanizam Abdul Rashid Chief Economist 03-2088 8075 afzanizam@bankislam.com.my US Fed raised rates by 25 basis points Facts The US Federal Open Market Committee (FOMC) meeting last night concluded

Dr. Mohd Afzanizam Abdul Rashid Chief Economist 03-2088 8075 afzanizam@bankislam.com.my US Fed raised rates by 25 basis points Facts The US Federal Open Market Committee (FOMC) meeting last night concluded

Responses to Survey of Primary Dealers Markets Group, Federal Reserve Bank of New York October 2012

Responses to Survey of Primary Dealers Markets Group, Federal Reserve Bank of New York October 2012 Responses to the Primary Dealer Policy Expectations Survey Distributed: 10/11/2012 Received by: 10/15/2012

Responses to Survey of Primary Dealers Markets Group, Federal Reserve Bank of New York October 2012 Responses to the Primary Dealer Policy Expectations Survey Distributed: 10/11/2012 Received by: 10/15/2012

RESPONSES TO SURVEY OF

RESPONSES TO SURVEY OF PRIMARY DEALERS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v November 2016 JANUARY Distributed: 1/17/ Received by: 1/22/ The Survey of Primary Dealers

RESPONSES TO SURVEY OF PRIMARY DEALERS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v November 2016 JANUARY Distributed: 1/17/ Received by: 1/22/ The Survey of Primary Dealers

Janet L Yellen: Unconventional monetary policy and central bank communications

Janet L Yellen: Unconventional monetary policy and central bank communications Speech by Ms Janet L Yellen, Vice Chair of the Board of Governors of the Federal Reserve System, at the University of Chicago

Janet L Yellen: Unconventional monetary policy and central bank communications Speech by Ms Janet L Yellen, Vice Chair of the Board of Governors of the Federal Reserve System, at the University of Chicago

On Principles: Fed does about-face on operational framework and balance sheet strategy

Economic Analysis On Principles: Fed does about-face on operational framework and balance sheet strategy Boyd Nash-Stacey / Nathaniel Karp After the January meeting, the Federal Reserve Open Market Committee

Economic Analysis On Principles: Fed does about-face on operational framework and balance sheet strategy Boyd Nash-Stacey / Nathaniel Karp After the January meeting, the Federal Reserve Open Market Committee

Janet L Yellen: The outlook for the US economy and economic policy

Janet L Yellen: The outlook for the US economy and economic policy Speech by Ms Janet L Yellen, Vice Chair of the Board of Governors of the Federal Reserve System, at the 2011 Annual Meeting of the Financial

Janet L Yellen: The outlook for the US economy and economic policy Speech by Ms Janet L Yellen, Vice Chair of the Board of Governors of the Federal Reserve System, at the 2011 Annual Meeting of the Financial

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 2012-38 December 24, 2012 Monetary Policy and Interest Rate Uncertainty BY MICHAEL D. BAUER Market expectations about the Federal Reserve s policy rate involve both the future path

FRBSF ECONOMIC LETTER 2012-38 December 24, 2012 Monetary Policy and Interest Rate Uncertainty BY MICHAEL D. BAUER Market expectations about the Federal Reserve s policy rate involve both the future path

The Economic Outlook and Unconventional Monetary Policy

The Economic Outlook and Unconventional Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Babson College s Stephen D. Cutler Center for Investments and

The Economic Outlook and Unconventional Monetary Policy Eric S. Rosengren President & Chief Executive Officer Federal Reserve Bank of Boston Babson College s Stephen D. Cutler Center for Investments and

Charles I Plosser: Economic outlook and communicating monetary policy

Charles I Plosser: Economic outlook and communicating monetary policy Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve Bank of Philadelphia, at the 2012 Economic

Charles I Plosser: Economic outlook and communicating monetary policy Speech by Mr Charles I Plosser, President and Chief Executive Officer of the Federal Reserve Bank of Philadelphia, at the 2012 Economic

The Economic Recovery and Monetary Policy: Taking the First Step Towards the Long Run

The Economic Recovery and Monetary Policy: Taking the First Step Towards the Long Run Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City Santa Fe, New Mexico June

The Economic Recovery and Monetary Policy: Taking the First Step Towards the Long Run Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City Santa Fe, New Mexico June

Diffusion indices of forecast risks in Summary of Economic Projections From September 2016 FOMC to June 2018 FOMC. Mar '17 FOMC

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer

Trend Macrolytics, LLC Donald Luskin, Chief Investment Officer

SURVEY OF PRIMARY DEALERS

SURVEY OF PRIMARY DEALERS This survey is formulated by the Trading Desk at the Federal Reserve Bank of New York to enhance policymakers' understanding of market expectations on a variety of topics related

SURVEY OF PRIMARY DEALERS This survey is formulated by the Trading Desk at the Federal Reserve Bank of New York to enhance policymakers' understanding of market expectations on a variety of topics related

NET ISSUANCE EXPECTED TO INCREASE

NET ISSUANCE EXPECTED TO INCREASE 900 800 700 600 500 400 300 200 100 0 Summary of Bill, Coupon, and TIPS Issuance by Treasury 2008:Q1 2014:Q1E $ Billions CMBs 13 week Bills 52 week Bills 3 year Notes

NET ISSUANCE EXPECTED TO INCREASE 900 800 700 600 500 400 300 200 100 0 Summary of Bill, Coupon, and TIPS Issuance by Treasury 2008:Q1 2014:Q1E $ Billions CMBs 13 week Bills 52 week Bills 3 year Notes

Thoughts on US Monetary Policy Prepared for Hutchins Center Conference, March 21, 2016

Thoughts on US Monetary Policy Prepared for Hutchins Center Conference, March 21, 2016 Richard H. Clarida Professor of Economics and International Affairs Columbia University Global Strategic Advisor PIMCO

Thoughts on US Monetary Policy Prepared for Hutchins Center Conference, March 21, 2016 Richard H. Clarida Professor of Economics and International Affairs Columbia University Global Strategic Advisor PIMCO

Survey of Primary Dealers

Survey of Primary Dealers Markets Group, Federal Reserve Bank of New York April 2016 Policy Expectations Survey Please respond by Monday, April 18, at 2:00 pm to the questions below. Your time and input

Survey of Primary Dealers Markets Group, Federal Reserve Bank of New York April 2016 Policy Expectations Survey Please respond by Monday, April 18, at 2:00 pm to the questions below. Your time and input

A Perspective on Unconventional Monetary Policy

A Perspective on Unconventional Monetary Policy Macro Workshop 2014 Central Bank of Turkey Istanbul, Turkey June 2, 2014 Charles L. Evans President and CEO Federal Reserve Bank of Chicago The views I express

A Perspective on Unconventional Monetary Policy Macro Workshop 2014 Central Bank of Turkey Istanbul, Turkey June 2, 2014 Charles L. Evans President and CEO Federal Reserve Bank of Chicago The views I express

RESPONSES TO SURVEY OF

RESPONSES TO SURVEY OF PRIMARY DEALERS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v JUNE Distributed: 5/31/ Received by: 6/4/ The Survey of Primary Dealers is formulated by

RESPONSES TO SURVEY OF PRIMARY DEALERS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v JUNE Distributed: 5/31/ Received by: 6/4/ The Survey of Primary Dealers is formulated by

Unconventional Monetary Policy and Central Bank Communications. Remarks by. Janet L. Yellen. Vice Chair

For release on delivery 1:30 p.m. EST February 25, 2011 Unconventional Monetary Policy and Central Bank Communications Remarks by Janet L. Yellen Vice Chair Board of Governors of the Federal Reserve System

For release on delivery 1:30 p.m. EST February 25, 2011 Unconventional Monetary Policy and Central Bank Communications Remarks by Janet L. Yellen Vice Chair Board of Governors of the Federal Reserve System

Economic Outlook and Monetary Policy

Economic Outlook and Monetary Policy Northwestern University Advanced Workshop for Central Bankers September 9, 218 Spencer Krane Senior Vice President Federal Reserve Bank of Chicago The views I express

Economic Outlook and Monetary Policy Northwestern University Advanced Workshop for Central Bankers September 9, 218 Spencer Krane Senior Vice President Federal Reserve Bank of Chicago The views I express

Chapter Eighteen 4/23/2018. Chapter 18 Monetary Policy: Stabilizing the Domestic Economy Part 4. Unconventional Policy Tools

Chapter Eighteen Chapter 18 Monetary Policy: Stabilizing the Domestic Economy Part 4 Unconventional Policy Tools Using non-traditional policy tools for stabilization : When lowering the target interest-rate

Chapter Eighteen Chapter 18 Monetary Policy: Stabilizing the Domestic Economy Part 4 Unconventional Policy Tools Using non-traditional policy tools for stabilization : When lowering the target interest-rate

Normalizing Monetary Policy

Normalizing Monetary Policy Martin Feldstein The current focus of Federal Reserve policy is on normalization of monetary policy that is, on increasing short-term interest rates and shrinking the size of

Normalizing Monetary Policy Martin Feldstein The current focus of Federal Reserve policy is on normalization of monetary policy that is, on increasing short-term interest rates and shrinking the size of

Fed Balance Sheet Normalization

Strategy June 9, 2017 Contacts And Impact on Cash Investment Strategies Abstract Key takeaways: While details are lacking, one can generally expect balance sheet normalization to start at the end of 2017,

Strategy June 9, 2017 Contacts And Impact on Cash Investment Strategies Abstract Key takeaways: While details are lacking, one can generally expect balance sheet normalization to start at the end of 2017,

The Macroeconomic Effects of the Federal Reserve s Unconventional Monetary Policies*

The Macroeconomic Effects of the Federal Reserve s Unconventional Monetary Policies* Eric Engen, Thomas Laubach, and Dave Reifschneider Federal Reserve Board December 27, 2014 Abstract After reaching the

The Macroeconomic Effects of the Federal Reserve s Unconventional Monetary Policies* Eric Engen, Thomas Laubach, and Dave Reifschneider Federal Reserve Board December 27, 2014 Abstract After reaching the

Intermediate Open Economy Macroeconomics

Intermediate Open Economy Macroeconomics Martin Ellison 1 Course preliminaries Lecture notes: I upload them online before class. They are comprehensive and detailed. All material is posted on my webpage:

Intermediate Open Economy Macroeconomics Martin Ellison 1 Course preliminaries Lecture notes: I upload them online before class. They are comprehensive and detailed. All material is posted on my webpage:

Survey of Market Participants

Survey of Market Participants Markets Group, Federal Reserve Bank of New York December 2016 Policy Expectations Survey Please respond by Monday, December 5 at 5:00 pm to the questions below. Your time

Survey of Market Participants Markets Group, Federal Reserve Bank of New York December 2016 Policy Expectations Survey Please respond by Monday, December 5 at 5:00 pm to the questions below. Your time

Brian P Sack: Implementing the Federal Reserve s asset purchase program

Brian P Sack: Implementing the Federal Reserve s asset purchase program Remarks by Mr Brian P Sack, Executive Vice President of the Federal Reserve Bank of New York, at the Global Interdependence Center

Brian P Sack: Implementing the Federal Reserve s asset purchase program Remarks by Mr Brian P Sack, Executive Vice President of the Federal Reserve Bank of New York, at the Global Interdependence Center

Monetary Policy Implementation with a Large Central Bank Balance Sheet

Monetary Policy Implementation with a Large Central Bank Balance Sheet Antoine Martin Fed 21, March 28, 2017 The views expressed herein are our own and may not reflect the views of the Federal Reserve

Monetary Policy Implementation with a Large Central Bank Balance Sheet Antoine Martin Fed 21, March 28, 2017 The views expressed herein are our own and may not reflect the views of the Federal Reserve

In This Issue: September 2013 (August 16, 2013-October 3, 2013)

") September (August 16, -October 3, ) In This Issue: Banking and Financial Markets Banks Planning for a Stronger Economy Tracking Recent Levels of Financial Stress Inflation and Prices Expected Inflation

September (August 16, -October 3, ) In This Issue: Banking and Financial Markets Banks Planning for a Stronger Economy Tracking Recent Levels of Financial Stress Inflation and Prices Expected Inflation

FOMC Preview: When, How Often, and How Much

FOMC Preview: When, How Often, and How Much March 17, 2015 by John Canally of LPL Financial The policymaking arm of the Federal Reserve (Fed), the Federal Open Market Committee (FOMC), will hold its second

FOMC Preview: When, How Often, and How Much March 17, 2015 by John Canally of LPL Financial The policymaking arm of the Federal Reserve (Fed), the Federal Open Market Committee (FOMC), will hold its second

The Yield Curve and Monetary Policy in 2018

The Yield Curve and Monetary Policy in 2018 Christopher Waller Executive Vice President and Director of Research Federal Reserve Bank of St. Louis May 22, 2018 The views expressed here are those of the

The Yield Curve and Monetary Policy in 2018 Christopher Waller Executive Vice President and Director of Research Federal Reserve Bank of St. Louis May 22, 2018 The views expressed here are those of the

RESPONSES TO SURVEY OF

RESPONSES TO SURVEY OF a v MARCH Distributed: 3/2/ Received by: 3/6/ The Survey of Primary Dealers is formulated by the Trading Desk at the Federal Reserve Bank of New York to enhance policymakers' understanding

RESPONSES TO SURVEY OF a v MARCH Distributed: 3/2/ Received by: 3/6/ The Survey of Primary Dealers is formulated by the Trading Desk at the Federal Reserve Bank of New York to enhance policymakers' understanding

National Economic Indicators. December 11, 2017

National Economic Indicators December 11, 17 Table of Contents GDP Release Date Latest Period Page Table: Real Gross Domestic Product Nov-9-17 8:3 Q3-17 Real Gross Domestic Product Nov-9-17 8:3 Q3-17 5

National Economic Indicators December 11, 17 Table of Contents GDP Release Date Latest Period Page Table: Real Gross Domestic Product Nov-9-17 8:3 Q3-17 Real Gross Domestic Product Nov-9-17 8:3 Q3-17 5

Monetary Policy in a Lower Interest Rate Environment

Monetary Policy in a Lower Interest Rate Environment Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago CFA Society Auckland, New Zealand October 5, 2016 FEDERAL RESERVE

Monetary Policy in a Lower Interest Rate Environment Charles L. Evans President and Chief Executive Officer Federal Reserve Bank of Chicago CFA Society Auckland, New Zealand October 5, 2016 FEDERAL RESERVE

US FOMC Tampering the speed of FFR hike

Dr. Mohd Afzanizam Abdul Rashid Chief Economist 03-2088 8075 afzanizam@bankislam.com.my US FOMC Tampering the speed of FFR hike Facts The US Federal Open Market Committee (FOMC) meeting last night decided

Dr. Mohd Afzanizam Abdul Rashid Chief Economist 03-2088 8075 afzanizam@bankislam.com.my US FOMC Tampering the speed of FFR hike Facts The US Federal Open Market Committee (FOMC) meeting last night decided

Making Monetary Policy: Rules, Benchmarks, Guidelines, and Discretion

EMBARGOED UNTIL 8:35 AM U.S. Eastern Time on Friday, October 13, 2017 OR UPON DELIVERY Making Monetary Policy: Rules, Benchmarks, Guidelines, and Discretion Eric S. Rosengren President & Chief Executive

EMBARGOED UNTIL 8:35 AM U.S. Eastern Time on Friday, October 13, 2017 OR UPON DELIVERY Making Monetary Policy: Rules, Benchmarks, Guidelines, and Discretion Eric S. Rosengren President & Chief Executive

Joseph S Tracy: A strategy for the 2011 economic recovery

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

Joseph S Tracy: A strategy for the 2011 economic recovery Remarks by Mr Joseph S Tracy, Executive Vice President of the Federal Reserve Bank of New York, at Dominican College, Orangeburg, New York, 28

Threading the Needle. Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City

Threading the Needle Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City July 17, 2018 Federal Reserve Bank of Kansas City Agricultural Symposium Kansas City, Mo.

Threading the Needle Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City July 17, 2018 Federal Reserve Bank of Kansas City Agricultural Symposium Kansas City, Mo.

Evolution of Unconventional Monetary Policy: Japan s Experiences

Evolution of Unconventional Monetary Policy: Japan s Experiences CIGS Conference on Macroeconomic Theory and Policy May 29, 2017 Institute for Monetary and Economic Studies Bank of Japan Shigenori SHIRATSUKA

Evolution of Unconventional Monetary Policy: Japan s Experiences CIGS Conference on Macroeconomic Theory and Policy May 29, 2017 Institute for Monetary and Economic Studies Bank of Japan Shigenori SHIRATSUKA

2014 Annual Review & Outlook

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

2014 Annual Review & Outlook As we enter 2014, the current economic expansion is 4.5 years in duration, roughly the average life of U.S. economic expansions. There is every reason to believe it will continue,

Effects Of Monetary Policies On Asset Prices In India

Effects Of Monetary Policies On Asset Prices In India Akash Joshi 1 Assistant Manager, Citibank, Mumbai, India Abstract: The saying goes, when United States (US) sneeze, the rest of the world catches a

Effects Of Monetary Policies On Asset Prices In India Akash Joshi 1 Assistant Manager, Citibank, Mumbai, India Abstract: The saying goes, when United States (US) sneeze, the rest of the world catches a

Thoughts on the Normalization of Monetary Policy. Remarks by. Jerome H. Powell. Member. Board of Governors of the Federal Reserve System

For release on delivery 8:00 a.m. EDT June 1, 2017 Thoughts on the Normalization of Monetary Policy Remarks by Jerome H. Powell Member Board of Governors of the Federal Reserve System at The Economic Club

For release on delivery 8:00 a.m. EDT June 1, 2017 Thoughts on the Normalization of Monetary Policy Remarks by Jerome H. Powell Member Board of Governors of the Federal Reserve System at The Economic Club

RESPONSES TO SURVEY OF

RESPONSES TO SURVEY OF PRIMARY DEALERS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v November 2016 DECEMBER 2017 Distributed: 11/30/2017 Received by: 12/4/2017 The Survey of

RESPONSES TO SURVEY OF PRIMARY DEALERS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v November 2016 DECEMBER 2017 Distributed: 11/30/2017 Received by: 12/4/2017 The Survey of

Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.C.

Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.C. The Macroeconomic Effects of the Federal Reserve s Unconventional

Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.C. The Macroeconomic Effects of the Federal Reserve s Unconventional

Slow recovery from worst downturn since Great Depression. Monetary policy at the zero lower bound: Empirical evidence

Monetary policy at the zero lower bound: Empirical evidence A. Brief summary of 27-214 1. Emergency lending 2. Large-scale asset purchases 3. Forward guidance Slow recovery from worst downturn since Great

Monetary policy at the zero lower bound: Empirical evidence A. Brief summary of 27-214 1. Emergency lending 2. Large-scale asset purchases 3. Forward guidance Slow recovery from worst downturn since Great

The Federal Reserve System and Central Banking in the US

The Federal Reserve System and Central Banking in the US Christ University, Bangalore, India March 10, 2014 Sonya Ravindranath Waddell Regional Economist Overview A Little History of the Federal Reserve

The Federal Reserve System and Central Banking in the US Christ University, Bangalore, India March 10, 2014 Sonya Ravindranath Waddell Regional Economist Overview A Little History of the Federal Reserve

ECON 4325 Wednesday seminar 2016

ECON 4325 Wednesday seminar 2016 1 2 WHAT ARE THE CURRENT STANCE OF MONETARY POLICY? Norges Bank: ECB: Fed: BoE: 0,75 % 0,00 % (0.25% and -0.4 %) 0.25-0.5 % 0,5 % 3 WHAT ARE THE DIFFERENT INFLATION TARGETS?

ECON 4325 Wednesday seminar 2016 1 2 WHAT ARE THE CURRENT STANCE OF MONETARY POLICY? Norges Bank: ECB: Fed: BoE: 0,75 % 0,00 % (0.25% and -0.4 %) 0.25-0.5 % 0,5 % 3 WHAT ARE THE DIFFERENT INFLATION TARGETS?

Expectations for U.S. Monetary Policy

US Economic Analysis US Kim Fraser kim.fraser@bbvacompass.com Shushanik Papanyan shushanik.papanyan@bbvacompass.com Expectations for U.S. Monetary Policy A Review of the FOMC and Plans for an Exit Strategy

US Economic Analysis US Kim Fraser kim.fraser@bbvacompass.com Shushanik Papanyan shushanik.papanyan@bbvacompass.com Expectations for U.S. Monetary Policy A Review of the FOMC and Plans for an Exit Strategy

Is the Flattening Yield Curve Sending a Message?

Is the Flattening Yield Curve Sending a Message? FEBRUARY 2018 Sean Simko, ChFC Managing Director SEI Fixed Income Portfolio Management SEI Fixed Income Portfolio Management (SFIPM) manages fixed-income

Is the Flattening Yield Curve Sending a Message? FEBRUARY 2018 Sean Simko, ChFC Managing Director SEI Fixed Income Portfolio Management SEI Fixed Income Portfolio Management (SFIPM) manages fixed-income

Why are bond yields and volatility so low?

Why are bond yields and volatility so low? June 9, 2014 by Carl Tannenbaum and Asha Bangalore of Northern Trust I never liked mid-year report cards. They were just another opportunity for my parents and

Why are bond yields and volatility so low? June 9, 2014 by Carl Tannenbaum and Asha Bangalore of Northern Trust I never liked mid-year report cards. They were just another opportunity for my parents and

Monetary Policy as the Economy Approaches the Fed s Dual Mandate

EMBARGOED UNTIL Wednesday, February 15, 2017 at 1:10 P.M., U.S. Eastern Time OR UPON DELIVERY Monetary Policy as the Economy Approaches the Fed s Dual Mandate Eric S. Rosengren President & Chief Executive

EMBARGOED UNTIL Wednesday, February 15, 2017 at 1:10 P.M., U.S. Eastern Time OR UPON DELIVERY Monetary Policy as the Economy Approaches the Fed s Dual Mandate Eric S. Rosengren President & Chief Executive

NET ISSUANCE EXPECTED TO INCREASE

NET ISSUANCE EXPECTED TO INCREASE 600 Summary of Bill, Coupon, and TIPS Issuance by Treasury 2009:Q1 2014:Q1E $ Billions 500 400 300 200 100 0 1Q'09 3Q'09 1Q'10 3Q'10 1Q'11 3Q'11 1Q'12 3Q'12 1Q'13 3Q'13

NET ISSUANCE EXPECTED TO INCREASE 600 Summary of Bill, Coupon, and TIPS Issuance by Treasury 2009:Q1 2014:Q1E $ Billions 500 400 300 200 100 0 1Q'09 3Q'09 1Q'10 3Q'10 1Q'11 3Q'11 1Q'12 3Q'12 1Q'13 3Q'13

Economic Outlook, January 2016 Jeffrey M. Lacker President, Federal Reserve Bank of Richmond

Economic Outlook, January 2016 Jeffrey M. Lacker President, Federal Reserve Bank of Richmond Annual Meeting of the South Carolina Business & Industry Political Education Committee Columbia, South Carolina

Economic Outlook, January 2016 Jeffrey M. Lacker President, Federal Reserve Bank of Richmond Annual Meeting of the South Carolina Business & Industry Political Education Committee Columbia, South Carolina

Perry Warjiyo: US monetary policy normalization and EME policy mix the Indonesian experience

Perry Warjiyo: US monetary policy normalization and EME policy mix the Indonesian experience Speech by Mr Perry Warjiyo, Deputy Governor of Bank Indonesia, at the NBER 25th Annual East Asian Seminar on

Perry Warjiyo: US monetary policy normalization and EME policy mix the Indonesian experience Speech by Mr Perry Warjiyo, Deputy Governor of Bank Indonesia, at the NBER 25th Annual East Asian Seminar on

INVESTMENT OUTLOOK. August 2017

INVESTMENT OUTLOOK August 2017 INVESTMENT OUTLOOK AUGUST 2017 MACRO-ECONOMICS AND CURRENCIES Developed and Emerging Markets A series of comments from major central banks during the month, reminded investors

INVESTMENT OUTLOOK August 2017 INVESTMENT OUTLOOK AUGUST 2017 MACRO-ECONOMICS AND CURRENCIES Developed and Emerging Markets A series of comments from major central banks during the month, reminded investors

The Economic Outlook and The Fed s Roles in Monetary Policy and Financial Stability

1 The Economic Outlook and The Fed s Roles in Monetary Policy and Financial Stability Main Line Chamber of Commerce Economic Forecast Breakfast Philadelphia Country Club, Gladwyne, PA January 8, 2008 Charles

1 The Economic Outlook and The Fed s Roles in Monetary Policy and Financial Stability Main Line Chamber of Commerce Economic Forecast Breakfast Philadelphia Country Club, Gladwyne, PA January 8, 2008 Charles

Are We There Yet? The U.S. Economy and Monetary Policy. Remarks by

Are We There Yet? The U.S. Economy and Monetary Policy Remarks by Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City January 15, 2019 Central Exchange Kansas City,

Are We There Yet? The U.S. Economy and Monetary Policy Remarks by Esther L. George President and Chief Executive Officer Federal Reserve Bank of Kansas City January 15, 2019 Central Exchange Kansas City,

SURVEY OF PRIMARY DEALERS

SURVEY OF PRIMARY DEALERS This survey is formulated by the Trading Desk at the Federal Reserve Bank of New York to enhance policymakers' understanding of market expectations on a variety of topics related

SURVEY OF PRIMARY DEALERS This survey is formulated by the Trading Desk at the Federal Reserve Bank of New York to enhance policymakers' understanding of market expectations on a variety of topics related

Normalizing Central Banks Balance Sheets: What Is The New Normal? Strategic Issues

FEDERAL RESERVE BANK OF NEW YORK COLUMBIA UNIVERSITY S SCHOOL OF INTERNATIONAL AND PUBLIC AFFAIRS Normalizing Central Banks Balance Sheets: What Is The New Normal? Strategic Issues JULY 11, 2017 Roberto

FEDERAL RESERVE BANK OF NEW YORK COLUMBIA UNIVERSITY S SCHOOL OF INTERNATIONAL AND PUBLIC AFFAIRS Normalizing Central Banks Balance Sheets: What Is The New Normal? Strategic Issues JULY 11, 2017 Roberto

Federal Reserve Communications and Transparency

Federal Reserve Communications and Transparency Celebration in Honor of Michael H. Moskow January 23, 2017 Spencer Krane and Daniel Sullivan Federal Reserve Bank of Chicago The views we express here are

Federal Reserve Communications and Transparency Celebration in Honor of Michael H. Moskow January 23, 2017 Spencer Krane and Daniel Sullivan Federal Reserve Bank of Chicago The views we express here are

William C Dudley: A bit better, but very far from best US economic outlook and the challenges facing the Federal Reserve

William C Dudley: A bit better, but very far from best US economic outlook and the challenges facing the Federal Reserve Remarks by Mr William C Dudley, President and Chief Executive Officer of the Federal

William C Dudley: A bit better, but very far from best US economic outlook and the challenges facing the Federal Reserve Remarks by Mr William C Dudley, President and Chief Executive Officer of the Federal

Four Questions for Current Monetary Policy

Four Questions for Current Monetary Policy James Bullard President and CEO, FRB-St. Louis New York Association for Business Economics 20 September 2013 New York, N.Y. Any opinions expressed here are my

Four Questions for Current Monetary Policy James Bullard President and CEO, FRB-St. Louis New York Association for Business Economics 20 September 2013 New York, N.Y. Any opinions expressed here are my

FINAL EXAM: Macro 302 Winter 2014

FINAL EXAM: Macro 32 Winter 214 Surname: Name: Student Number: State clearly your assumptions when you derive a result. ou must always show your thinking to get full credit. ou have 3 hours to answer all

FINAL EXAM: Macro 32 Winter 214 Surname: Name: Student Number: State clearly your assumptions when you derive a result. ou must always show your thinking to get full credit. ou have 3 hours to answer all

RESPONSES TO SURVEY OF

RESPONSES TO SURVEY OF MARKET PARTICIPANTS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v November 2016 DECEMBER 2017 Distributed: 11/30/2017 Received by: 12/4/2017 The Survey

RESPONSES TO SURVEY OF MARKET PARTICIPANTS Markets Group, Federal Reserve Bank of New York RESPONSES TO SURVEY OF a v November 2016 DECEMBER 2017 Distributed: 11/30/2017 Received by: 12/4/2017 The Survey

Cash Management Portfolios

September 30, 2017 Portfolio Manager Commentary Cash Management Portfolios Chief Investment Officer Jim Palmer What market conditions had a direct impact on the bond market this quarter? During the quarter,

September 30, 2017 Portfolio Manager Commentary Cash Management Portfolios Chief Investment Officer Jim Palmer What market conditions had a direct impact on the bond market this quarter? During the quarter,

Early Observations on Gradual Monetary Policy Normalization

EMBARGOED UNTIL WEDNESDAY, JANUARY 13, 2016 AT 8:20 A.M. EASTERN TIME OR UPON DELIVERY Early Observations on Gradual Monetary Policy Normalization Eric S. Rosengren President & CEO Federal Reserve Bank

EMBARGOED UNTIL WEDNESDAY, JANUARY 13, 2016 AT 8:20 A.M. EASTERN TIME OR UPON DELIVERY Early Observations on Gradual Monetary Policy Normalization Eric S. Rosengren President & CEO Federal Reserve Bank

Responses to Survey of Primary Dealers

Responses to Survey of Primary Dealers Markets Group, Federal Reserve Bank of New York July 2016 Page 1 of 12 Responses to Survey of Primary Dealers Distributed: 07/14/2016 Received by: 07/18/2016 For

Responses to Survey of Primary Dealers Markets Group, Federal Reserve Bank of New York July 2016 Page 1 of 12 Responses to Survey of Primary Dealers Distributed: 07/14/2016 Received by: 07/18/2016 For

INFLATION REPORT PRESS CONFERENCE. Thursday 10 th May Opening Remarks by the Governor

INFLATION REPORT PRESS CONFERENCE Thursday 10 th May 2018 Opening Remarks by the Governor Three months ago, the MPC said that an ongoing tightening of monetary policy over the next few years would be appropriate

INFLATION REPORT PRESS CONFERENCE Thursday 10 th May 2018 Opening Remarks by the Governor Three months ago, the MPC said that an ongoing tightening of monetary policy over the next few years would be appropriate

Views on the Economy and Price-Level Targeting

Views on the Economy and Price-Level Targeting Raphael Bostic President and Chief Executive Officer Federal Reserve Bank of Atlanta Atlanta Economics Club Federal Reserve Bank of Atlanta Atlanta, Georgia

Views on the Economy and Price-Level Targeting Raphael Bostic President and Chief Executive Officer Federal Reserve Bank of Atlanta Atlanta Economics Club Federal Reserve Bank of Atlanta Atlanta, Georgia

The U.S. Economy: An Optimistic Outlook, But With Some Important Risks

EMBARGOED UNTIL 8:10 A.M. Eastern Time on Friday, April 13, 2018 OR UPON DELIVERY The U.S. Economy: An Optimistic Outlook, But With Some Important Risks Eric S. Rosengren President & Chief Executive Officer

EMBARGOED UNTIL 8:10 A.M. Eastern Time on Friday, April 13, 2018 OR UPON DELIVERY The U.S. Economy: An Optimistic Outlook, But With Some Important Risks Eric S. Rosengren President & Chief Executive Officer

Haruhiko Kuroda: How to overcome deflation

Haruhiko Kuroda: How to overcome deflation Speech by Mr Haruhiko Kuroda, Governor of the Bank of Japan, at a conference, held by the London School of Economics and Political Science, London, 21 March 2014.

Haruhiko Kuroda: How to overcome deflation Speech by Mr Haruhiko Kuroda, Governor of the Bank of Japan, at a conference, held by the London School of Economics and Political Science, London, 21 March 2014.

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting ending on 13 December 2017

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting ending on 13 December 2017 Publication date: 14 December 2017 These are the minutes of the Monetary Policy Committee meeting

Monetary Policy Summary and minutes of the Monetary Policy Committee meeting ending on 13 December 2017 Publication date: 14 December 2017 These are the minutes of the Monetary Policy Committee meeting