BNM-AFI Training Programme

|

|

|

- Felix Lawrence

- 6 years ago

- Views:

Transcription

Sasana Kijang, Bank Negara Malaysia Presentation by: Mr. N. R. Lamare Mr. Dilavar K.")

1 Sequencing of Financial Education Integrated with Financial Inclusion Agenda and Consumer Protection Strategy - India Experience BNM-AFI Training Programme Financial Inclusion Strategy & Data (25-28 November 2014) Sasana Kijang, Bank Negara Malaysia Presentation by: Mr. N. R. Lamare Mr. Dilavar K. Nalband 1

2 Structure of presentation India: some facts Historical perspective of FI efforts Earlier Approach and New Approach Definition of FI Our Strategy to Financial Inclusion Initiatives taken, FIPs- Performance highlights Financial Literacy- Initiative taken by RBI PMJDY Performance of PMJDY Way forward 2

3 Structure of presentation Geographical area 7 th in the world - Widely dispersed terrain Population 2 nd in the world 1.25 billion By nominal GDP 10 th largest economy in the world 31 States and 6 Union Territories, 673 districts, 600 thousand plus Villages Multilingual and multiethnic society Low level of General Literacy (74% in 2011; FEMALE-65%), Large no. of Financially excluded people (more than 50%) 3

4 Historical perspective towards F.I. Cooperative movement (1904) All India Rural Credit Survey Creation of all India banks like SBI Cooperatives brought under -Banking Regulation (1966) Nationalisation of banks (1969) Lead Bank Scheme (SLBC-DLCC-BLCC structure) Priority Sector Guidelines, revised in 2012 Regional Rural Banks (1976) Service Area Approach NABARD (1982) SHG-Bank Linkage ( ) 4

5 Why then F I has not happened Subsidy Based Approach- Interest rate relaxations Target oriented Policy intent- Simply help the poor - not directed towards making them self sufficient Never treated banking for poor as a viable commercial business - A social obligation Lack of integration with business plans of banks Branches as only delivery mode- Focus shifted on profitability during reforms era ( ) - Unbanked areas neglected Absence of suitable technology to reach large geography economically Lack of MIS-data Driven only through public sector banks Cooperatives - poor performance (large were unlicensed) 5

6 Why then F I has not happened- Definition of F.I. Technology is now available Branchless modes of delivery innovated Focus shifted from growth to inclusive growth Realised that poor is bankable Importance given to sustainability, viability & scalability Financial Inclusion has been comprehensively defined Financial Inclusion is the process of ensuring access to appropriate financial products and services needed by all sections of the society in general and vulnerable groups such as weaker sections and low income groups in particular at an affordable cost in a fair and transparent manner by mainstream institutional players. 6

7 Financial Inclusion Strategy FINNANCIAL INCLUSION STRATEGY Planned and Structured approach Roadmap for providing banking services in all unbanked villages Adopted Bank-led model Other intermediaries to partner with banks Coverage of remote locations Through B & M Branches and through Branchless modes Emphasis on Financial Education Integrating awareness and access of banking services

8 Our Strategy to Financial inclusion A Planned and Structured approach-to connect masses to mainstream financial institutions Adopted Bank-led model for financial inclusion BC/BF models - Other intermediaries to partner with banks Leveraging on technology- ICT based delivery model- User friendly-cost effective- Cover remote locations Emphasis on doing it as a normal business Delivery Model Combination of Brick & Mortar Branches and ICT based BC outlets Financial Literacy as an integral part of FI A bouquet of Financial services- Minimum four products A savings cum overdraft account A pure savings account, ideally a recurring or variable recurring deposit A remittance product to facilitate EBT and other remittances Entrepreneurial credit products like a General Purpose Credit Card (GCC) or a Kisan Credit Card(KCC) Branch authorisation simplified Banks mandated to open 25 % of all new branches in unbanked rural centers 8

9 Our Strategy to Financial inclusion Objective Focus Approach Improve financial access through financial education Villages and unbanked pockets in urban locations Multi Agency-Partnership with Government & other stakeholders Guidance FSDC - Technical Group on FI&FL - Financial Sector Regulators, Government, Education Boards, Curriculum Developers as members 9

10 Financial Inclusion Institutional Framework Government of India and Reserve Bank of India Financial Stability Development Council (FSDC) FSDC Technical Group on Financial Inclusion and Financial Literacy Remarks Headed by Union Finance Minister Headed by Deputy Governor of RBI Financial Inclusion Advisory Committee of RBI Scheduled Commercial Banks & RRBs State/ UT Level Bankers Committees Lead District Managers Financial Literacy Centres Partnership with other stakeholders Headed by DG of RBI 1,20,344 branches (Sep 2014) 29 States and 7 UTs All 673 Districts (Mar 2014) 942 FLCs (Mar 2014) Other regulators, Govt. organisations / agencies, NGOs, etc.

11 Technical Group on Financial Inclusion and Financial Literacy under FSDC Group formed in August 2011 under the aegis of FSDCquarterly review meetings are held To coordinate efforts of all the financial sector regulators. DG in charge of FSU as Chairman, Secretary- DFS, DEA(FSDC office), senior executives of SEBI, IRDA, PFRDA,FMC, NCFE as members National Strategy on Financial Education prepared, National Centre for Financial Education formed with representation from all regulators, MOF, CBSE, NCERT- to implement National Strategy Financial Education to be included in the School Curriculum to be integrated into existing subject of Class VI to Class X 11

12 National Strategy for Financial Education National Strategy for Financial Education ( ) prepared by FSDC Technical Group on FI and FL Timeframe for implementation is 5 years Co-existence of financially excluded population with the financially included who use sophisticated financial products called for tiered approach as under: Level 1: Financially excluded population on basic financial education in order to link them to the formal financial sector Level 2: Financially included consumers with sector-focused approach on various financial products and services to enable them to make informed choices Level 3: To ensure consumer protection for all users 12

13 National Strategy for Financial Education National Strategy for Financial Education is now integrated in the Financial Inclusion Agenda Key component of the National Strategy is a continuum of financial literacy, financial education and consumer protection NSFE to create dedicated institutional structure to create standard financial education material and maintain website on finance which will be a one-stop repository for all financial activities Coordination with regulators such as the Reserve Bank of India, the Securities and Exchange Board of India, the Insurance Regulatory and Development Authority, the Pension Fund Regulatory and Development Authority, Forward Markets Commission, etc. and NGOs, MFIs, etc. 13

of banks. Enabling Financial Literacy initiatives through policy intervention.")

14 Adoption of Financial Inclusion as Policy of RBI (Recap) Annual Policy Statement of RBI Adoption of Financial Inclusion as a policy by Reserve Bank of India Facilitating Financial Inclusion and monitoring Financial Inclusion Plans (FIPs) of banks. Enabling Financial Literacy initiatives through policy intervention. Taking banking services to the masses and making them participate in the developmental process of the economy 14

15 National Strategy for Financial Education National Strategy for Financial Education is now integrated in the Financial Inclusion Agenda Key component of the National Strategy is a continuum of financial literacy, financial education and consumer protection NSFE to create dedicated institutional structure to create standard financial education material and maintain website on finance which will be a one-stop repository for all financial activities Coordination with regulators such as the Reserve Bank of India, the Securities and Exchange Board of India, the Insurance Regulatory and Development Authority, the Pension Fund Regulatory and Development Authority, Forward Markets Commission, etc. and NGOs, MFIs, etc. 15

16 Initiatives of RBI Project Financial Literacy (Recap) Reserve Bank of India has undertaken a project entitle Project Financial Literacy Trilingual Forms / Brochures / Pamphlets to be used by banks (Dec 2005) Banking Services by Business Facilitators and Business Correspondents (Jan 2006) Financial Literacy and Credit Counselling Centres (FLCC) Model Scheme (Feb 2009) FLCC support to Lead Bank from Financial Inclusion Fund (FIF) (Dec 2010) FLCCs at all levels Block, District, Town and City levels (Mar 2011) 16

17 National Strategy for Financial Education National Strategy for Financial Education is now integrated in the Financial Inclusion Agenda Key component of the National Strategy is a continuum of financial literacy, financial education and consumer protection NSFE to create dedicated institutional structure to create standard financial education material and maintain website on finance which will be a one-stop repository for all financial activities Coordination with regulators such as the Reserve Bank of India, the Securities and Exchange Board of India, the Insurance Regulatory and Development Authority, the Pension Fund Regulatory and Development Authority, Forward Markets Commission, etc. and NGOs, MFIs, etc. 17

18 Initiatives of RBI Project Financial Literacy Roadmap Phase-I ( ) - Provision of Banking Services in villages having population over 2000 by March 2013 (Nov 2009) Sub-Committee of DCC to draw Roadmap by March 2010 Reporting Format Roadmap Phase-II ( ) - Provision of banking services in villages with population below 2000 by March 2016 (June 2012) To cover about 4,90,000 unbanked villages by March 2016 A total of 383,804 villages covered by March 2014 Financial Inclusion Plan (FIP) : Disaggregation Statewise upto HO/CO and Branch Level from April 2013 (May 2013) Roadmap and FIP go hand in hand with Financial Literacy campaigns 18

19 National Strategy for Financial Education National Strategy for Financial Education is now integrated in the Financial Inclusion Agenda Key component of the National Strategy is a continuum of financial literacy, financial education and consumer protection NSFE to create dedicated institutional structure to create standard financial education material and maintain website on finance which will be a one-stop repository for all financial activities Coordination with regulators such as the Reserve Bank of India, the Securities and Exchange Board of India, the Insurance Regulatory and Development Authority, the Pension Fund Regulatory and Development Authority, Forward Markets Commission, etc. and NGOs, MFIs, etc. 19

20 RBI Guidelines and Materials on Financial Literacy Financial Literacy Centres (FLC) Guidelines Quarterly Reporting Format (June 2012) for Two essentials 'Financial Literacy' and easy 'Financial Access'. FLCs and rural branches of banks are required to conduct at least one Financial Literacy Camps every month. Comic books, pamphlets, brochures and posters published and made available in RBI website Standardized Financial Literacy Materials (Jan 2013) published for use in Financial Literacy Camps. 20

21 National Strategy for Financial Education National Strategy for Financial Education is now integrated in the Financial Inclusion Agenda Key component of the National Strategy is a continuum of financial literacy, financial education and consumer protection NSFE to create dedicated institutional structure to create standard financial education material and maintain website on finance which will be a one-stop repository for all financial activities Coordination with regulators such as the Reserve Bank of India, the Securities and Exchange Board of India, the Insurance Regulatory and Development Authority, the Pension Fund Regulatory and Development Authority, Forward Markets Commission, etc. and NGOs, MFIs, etc. 21

22 Financial Literacy Materials of RBI RBI prepared Standardized FL Materials consisting of: 1. Financial Literacy Guide - Ready reckoner for trainers - Contains 5 Sections - 50 Questions - Money Management, Savings, Saving with banks, Borrowings, Borrowing from banks 2. Financial Diary - For distribution to target audience - Financial planning - Record income and expenses - on Weekly / Monthly / Yearly basis 3. A set of 16 Financial Literacy Posters - Pictorial Communication Appealing slogans for display Available in 13 regional languages on RBI Website ( 22

23 National Strategy for Financial Education National Strategy for Financial Education is now integrated in the Financial Inclusion Agenda Key component of the National Strategy is a continuum of financial literacy, financial education and consumer protection NSFE to create dedicated institutional structure to create standard financial education material and maintain website on finance which will be a one-stop repository for all financial activities Coordination with regulators such as the Reserve Bank of India, the Securities and Exchange Board of India, the Insurance Regulatory and Development Authority, the Pension Fund Regulatory and Development Authority, Forward Markets Commission, etc. and NGOs, MFIs, etc. 23

24 Financial Literacy-Material Basic Concepts for unbanked Audience- Hindi and English and 13 regional languages. Available on RBI Website Financial Literacy Guide-Trainer s Guide 5 Sections- 50 Questions Financial Diary- Facilitate Financial Planning to record income and expenses- Weekly/Monthly/ Yearly Set of 16 posters-basic Messages Pictorial Communication- Appealing Slogans 24

25 Financial Literacy Messages 1. Why save? 11. What is the difference between saving and investment? 2. Why invest? 12. Why borrow for income-generating purposes? 3. Why insure? 13. Why repay loans? 4. Why financial planning? 14. Why repay loans on time? 5. Why will you need a regular stream of income post-working life why pensions? 6. Why save or invest regularly and consistently? 15. Why do you need insurance? 16. What is interest? How do moneylenders charge very high interest rates? 7. Why insure fully? 17. Why and how can you evaluate the various products available? 8. Why save with banks? 18. What are the dos and don ts of investment? 9. Why borrow within limits? 19. What are investors rights and responsibilities? 10. Why borrow from banks? 20. What mechanisms are available to redress grievances? 25

26 Literacy Camps Guidelines 3 sessions- 2 hrs each- Spread over three months Annual calendar- Advance publicity-involvement of Local Government, prominent persons, NGOs etc, Data base of participants First Session Second Session-Fortnight after first session Visit - 15 days after second session-to ensure Third Session-2 months after second session Understanding of Basic financial concepts Financial Planning How to use financial diary Concept of door step banking ( Branchless) Introduction -Business Correspondent (BC) Services available through BC Demo of ICT device - Modus operandi Account Opening Timely delivery of smart cards Start of BC operations Feedback from villagers & BC Review usage of accounts Solve operational issues at site Follow up transaction levels- Regular Reporting system 26

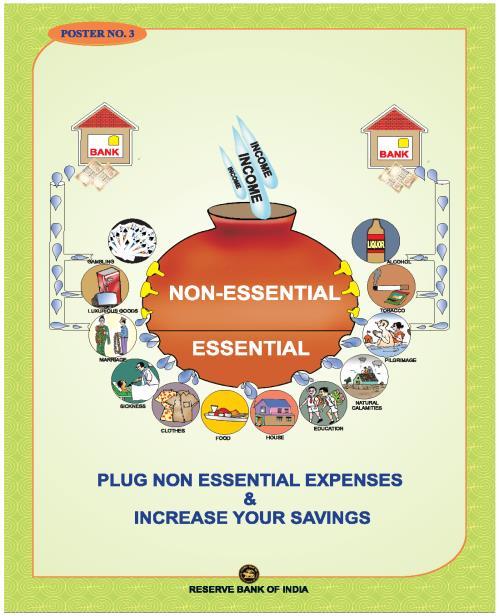

27 Manage Your Finance 1. UNDERSTAND YOUR EXPENSES 2. DO NOT SPEND MORE THAN YOUR INCOME 3. PLUG NON ESSENTIAL EXPENSES & INCREASE YOUR SAVINGS 4. ACHIEVE YOUR GOAL WITH FINANCIAL PLANNING 5. THINK TWICE BEFORE SPENDING 6. THE LESS YOU SPEND, THE MORE YOU CAN SAVE 27

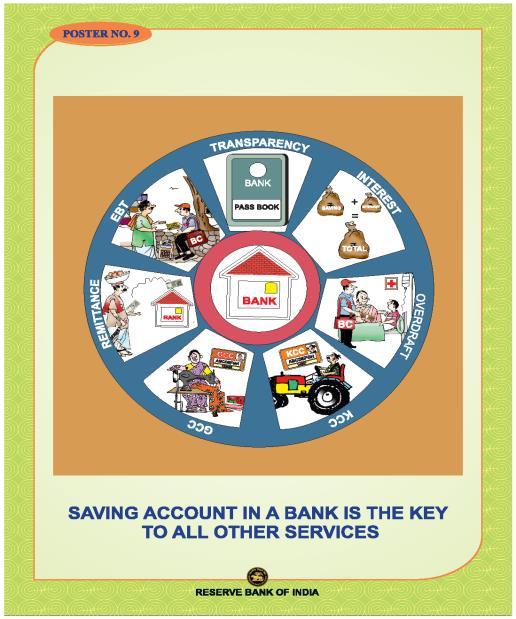

28 SAVINGS 7. SAVE MONEY FOR LIFE CYCLE NEEDS 8. DO NOT LOOSE YOUR HARD EARNED MONEY, ALWAYS SAVE IN A BANK ACCOUNT 9. SAVING ACCOUNT IN A BANK IS THE KEY TO ALL OTHER SERVICES 10. BANK IS NOW AVAILABLE AT YOUR DOOR STEP 28

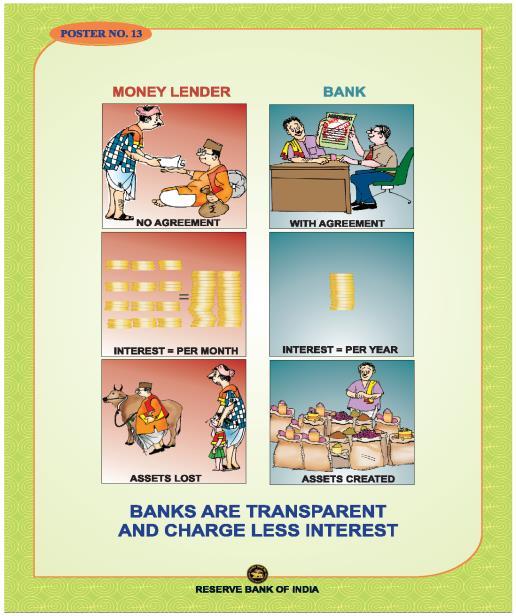

29 Borrowings 11. MANAGE YOUR DEBT OTHERWISE DEBT WILL DAMAGE YOU 12. BORROW TO UNDERTAKE AN ACTIVITY WHICH ENHANCES YOUR INCOME 13. BANKS ARE TRANSPARENT AND CHARGE LESS INTEREST 14. A BANK MEETS ALL YOUR REQUIREMENTS 29

30 Activities of Financial Literacy Centres SR Particulars of activities (as on 31 March each year) No. of Outdoor Activities conducted Outdoor activities- No. of persons participated Indoor activities- No. of persons participated Total No. of Persons participated - Outdoor & Indoor activities In the year 2013 In the year 2014 Progress in 2 years bn bn bn bn bn bn 30

31 Modes to Reach the un-banked Mobile Van banking BC visiting remote locations BC outlet located in a village A low cost rural bank branch 31

32 Technology for the un-banked Customer s enrollment Switch to connect all banks Issue of Smart Card Operating through Smart Card on Hand Held Machine Bank Server

33 How does it work ICT Device - Components Customer Authentication at BC Customer receiving Money BC initiating a transaction 33

34 Financial Literacy for un-banked Financial Literacy Centre - Awareness camp Literacy drive by RBI Accounts opened in camps Women getting linked to banks 34

35 Catching them young Financial Literacy in a school Curious to know more about banks Opening accounts for children Children learning to operate 35

36 Educating for inclusion At a busy suburban station in Mumbai 36

37 Impact of Activities of Financial Literacy Centres Banking connectivity available to more than 408,000 Villages, 47,000 through Branches, others through Branchless modes 65,000 urban unbanked locations connected through Branchless modes 250 Million Basic Saving Bank Deposit(BSBD) accounts 122 million accounts through BC based Branchless modes 48 Million people provided small revolving credit Business purpose Farm sector and Non Farm Sector 37

is the most used banking product 44% of the participants had availed of credit product Remittances and Direct Benefit")

38 Impact of Activities of Financial Literacy Centres Findings of Impact Study in October 2013 across 46 Districts in 23 States with 730 participants who had attended the Financial Literacy Camps: 99% of the participants had got linked to formal banking system Saving account (89%) is the most used banking product 44% of the participants had availed of credit product Remittances and Direct Benefit Transfer (DBT) were the least used product (20%) Financial Literacy activities of rural branches of banks have been placed under structured monitoring mechanism from the quarter ended June

39 Funds for Financial Education Financial Inclusion Fund (FIF) managed by National Bank for Agriculture and Rural Development (NABARD) -Rs. 5 billon each Prioritized activities / institutions for support from FIF: Training and Capacity Building of the staff of cooperatives including Primary Agricultural Cooperative Society (PACS) Training and Capacity Building of the staff of Regional Rural Banks (RRBs)/ Business Correspondents (BC)/ Business Facilitators (BF) Financial Literacy Campaign/ Programmes Projects involving awareness at field level and support in opening of accounts for micro insurance / pension Generic content to be developed on Financial Literacy National Skill development Fund- Rs 10 Billion- Creating a pool of 15o Million skilled workers by 2022 Set up National Level Infrastructure- Unique Identification Number (UID) Biometric Authentication 39

40 Funds for Financial Education and Other Developments in FI Creation of Depositors Education and Awareness Fund Scheme, (DEAF) 2014 (Mar 2014) Unclaimed deposit for 10 yrs in banks to go to the Fund Part of the fund to be utilised to promote financial literacy awareness Further simplification of KYC Norms One documentary proof of address for opening of bank account (June 9, 2014) NBFC-NDs as BCs subject to conditions and Distance Criteria (June 24, 2014) 40

41 ACCESS Strategy planned All 6 lakh villages to be covered Focus on increasing rural branches Opening accounts of all eligible individual BC MODEL TRANSACTIO N FINANCIAL EDUCATIO N Financial Inclusion Centers-Service branch for BCs Grievance Redressal,Cash Management, BC Supervision LPG Distributors as BC/BFs Leverage on DBT implementation Experiment innovations Remittance for Migrants Hassle free Emergency credit (In built OD) Entrepreneur Credit- KCCs & GCCs National Strategy on Financial Education Dedicated Website- Inclusion in School Curriculum Financial Literacy Camps 41

NBFC-NDs as BCs")

42 Funds for Financial Education and Other Developments in FI Creation of Depositors Education and Awareness Fund Scheme, (DEAF) 2014 (Mar 2014) Unclaimed deposit for 10 yrs in banks to go to the Fund Part of the fund to be utilised to promote financial literacy awareness Further simplification of KYC Norms One documentary proof of address for opening of bank account (June 9, 2014) NBFC-NDs as BCs subject to conditions and Distance Criteria (June 24, 2014) 42

Phase II (15 August 2015-14 August")

43 Pradhan Mantri Jan Dhan Yojana PMJDY Phase I (15 August August 2015) Phase II (15 August August 2018) 43

44 Prime Minister Jan Dhan Yojana (PMJDY) Pradhan Mantri Jan-Dhan Yojana Objective Objective of "Pradhan Mantri Jan-Dhan Yojana (PMJDY)" is ensuring access to various financial services like availability of basic savings bank account, access to need based credit, remittances facility, insurance and pension to the excluded sections i.e. weaker sections & low income groups. This deep penetration at affordable cost is possible only with effective use of technology. PMJDY is a National Mission on Financial Inclusion encompassing an integrated approach to bring about comprehensive financial inclusion of all the households in the country. The plan envisages universal access to banking facilities with at least one basic banking account for every household, financial literacy, access to credit, insurance and pension facility. 44

45 Pradhan Mantri Jan-Dhan Yojana Objective of "Pradhan Mantri Jan-Dhan Yojana (PMJDY)" is ensuring access to various financial services like availability of basic savings bank account, access to need based credit, remittances facility, insurance and pension to the excluded sections i.e. weaker sections & low income groups. This deep penetration at affordable cost is possible only with effective use of technology. PMJDY is a National Mission on Financial Inclusion encompassing an integrated approach to bring about comprehensive financial inclusion of all the households in the country. The plan envisages universal access to banking facilities with at least one basic banking account for every household, financial literacy, access to credit, insurance and pension facility. 45

46 Prime Minister Jan Dhan Yojana (PMJDY) Financial Inclusion on a Mission Mode Under the Department of Financial Services, Ministry of Finance, Government of India Announced by the Prime Minister of India on August 15, 2014 Formally launched on August 28, 2014 Focus shift from Villages to Households and coverage of full geography Focus on use of Technology Renewed focus on financial literacy campaign Facility of call centre & toll free number by Indian Banks Association Aggressive media campaign to increase citizens awareness Strengthened monitoring mechanism 46

47 Prime Minister Jan Dhan Yojana (PMJDY) (PMJDY) contd.. Financial Inclusion -6 Pillers Universal Access to banking facilities Unorganized sector pension schemes Micro Insurance 6 pillars Creation of Credit Guarantee Fund Basic Accounts with O/D facility and RuPay Debit card Financial Literacy Programmes 47

48 Prime Minister Jan Dhan Yojana (PMJDY) 6 Pillars under FI on a Mission Mode Mission Mode Objectives under PMJDY rests on 6 Pillars : 1. Universal access to banking facilities: Mapping of every district of the country into Sub Service area (SSA) catering to households in a manner that every habitation has access to banking services within 5 km by March Financial Literary Programme: To be extended to the block level from district level at present by March Providing Basic Banking Accounts: to all families and to all beneficiaries of Government Scheme by March 2016 and then on an ongoing basis 48

49 Prime Minister Jan Dhan Yojana (PMJDY) 6 Pillars under FI on a Mission Mode 4. Micro Credit Availability & Creation of Credit Guarantee Fund for coverage of defaults in such accounts : Facility of an overdraft of Rs 5000/-through debit card to every basic banking account holder on completion of financial literary training by March Micro Insurance: By March 2017 and then on an ongoing basis. 6. Unorganized sector Micro Pension schemes like Swavlambam: By March 2017 and then on an ongoing basis 49

![Minister] Steering Committee [Secretary (FS)]](/docs-images/77/75986190/images/50-4.jpg "Ministers of Communications, Rural")

, Governor RBI, Chairman")

![IBA Mission Director [Joint Secretary (FS) ]](/docs-images/77/75986190/images/50-6.jpg "State Level Implementation Committee District")

50 Prime Minister Jan Dhan Yojana (PMJDY) Monitoring Mechanism Mission Head [Finance Minister] Steering Committee [Secretary (FS)] Ministers of Communications, Rural Development, Secretary (FS), Secretary (RD), Secretary (Telecom), Governor RBI, Chairman IBA Mission Director [Joint Secretary (FS) ] State Level Implementation Committee District Level Implementation Committee 50

51 Prime Minister Jan Dhan Yojana (PMJDY) Financial Inclusion on a Mission Mode Target to open 75,000,000 bank accounts for the financially excluded population under PMJDY by August 15, 2015, but revised to January 26, Banks achieved opening of more than 78.1 million PMJDY accounts as on November 20, 2014, well ahead of date. Financial Literacy Centres to be set up at the block levels in rural areas Financial Literacy Cell to be set up in rural branches of banks 51

Rural Urban Total No Of Rupay Debit Cards (In Lacs) Balance In Accounts (In Lacs) No Of Accounts With Zero Balance (In Lacs) 1 Public Sector Banks 343.71 288.89 632.6 442.")

52 PMJDY- PMJDY- Progress as on November 20, 2014 Progress as on November 20, 2014 S. No No Of Accounts (In Lacs) Rural Urban Total No Of Rupay Debit Cards (In Lacs) Balance In Accounts (In Lacs) No Of Accounts With Zero Balance (In Lacs) 1 Public Sector Banks Regional Rural Banks Private Banks Total (78.7 m) (47.1 m) (62.13 b) (59.0 m) 52

53 Financial Inclusion and Financial Literacy Initiatives in a Nutshell Financial Literacy & Financial Inclusion to go together - Financial Stability Development Council (FSDC) - Mandated to focus on Financial Inclusion and Financial Literacy A technical group on Financial Inclusion and Financial Literacy under aegis of FSDC Coordinating the efforts of all Financial Sector Regulators National Strategy on Financial Education prepared Financial Literacy Centres set up in most of the districts (650+) FLCs and rural bank branches (35000+) - To conduct awareness camps every month Comprehensive Operational Guidelines for conduct of camps - Standardised Financial Literacy Material (FL Guide, Diary and Posters) Mass scale awareness- Outreach Visits, Camps, Quiz, Essay Competition, Role Play, Comic Books, Fairs and Exhibitions, etc. Financial Education website (RBI Website > Financial Literacy - To be included in School Curriculum at National Level PMJDY for Financial Inclusion on a Mission Mode 53

54 A Thought FINANCIAL LITERACY: a step to FINANCIAL INCLUSION FINANCIAL INCLUSION: TREE OF PROSPERITY HAVE COMPASSION FOR THE POOR 54

55 THANK YOU

56 Use of Technology - BC Models Smart Card Biometric -Using Handheld Machine Online & offline Kiosk Model Bio-metrically enabled, Internet based Online, Real time banking transactions Mobile Phone Uses low end mobile with PIN & signature booklet, avoids cost of Handheld machine and smart cards etc. 3 level security check - Mobile number, Booklet & Security PIN. 56

57 Smart Card Based Model Customer s enrollment Bank s CBS Transactions with Hand Held Machine Issue of Smart Card FI Server 57

58 Mobile based Model Customer sends money from BC(Retail shop) Mobile service provider Transfer of funds Beneficiary gets money 3 Level security check- Mobile number, Booklet & Security PIN Bank server 58

59 CUSTOMERS ICT Model- General Overview CORE BANKING SMART CARD Based 1 SMART CARD Based 2 MOBILE PHONE Based 1 MOBILE PHONE Based 2 SMART CARD TSP MOBILE SERVICE PROVIDER Standardised message /data SWITCH CBS format KIOSK Based 1 KIOSK Based 2 KIOSK BANKING SERVER 59

60 UIDAI Model- Enabling Inclusion Basic Saving account Business Correspondents Mobile Phone banking Settlement Authority Any account, anywhere technology POS machine Banking 60

61 UID Enabled Direct Transfer Transfer money Block NREGA To UID Amount Rs546 GP NREGA Government bank a/c Central switch at NPCI ID mapper Resident - Ram UID Debit Government a/c Credit Ram s a/c Muster roll with Ram s UID Info IVRS/ SMS UID enabled Resident no -frills bank a/c existing or new 61

62 UIDAI based Transactions ID mapper 8. Info- IVRS/ SMS Resident - Ram UID Debit 4. Authenticate and execute Ram s bank a/c 5. Authenticate NPCI switch 1. Withdrawal request 9. Cash 3.NPCI request 7. Credit TransferMoney From UID To UID Amount Money transfer instruction + biometrics BC s bank a/c BC (Kirana, SHG, PO etc)) With Micro-ATM UID:

Deepali Pant Joshi: Financial intermediation for all economic growth with equity

Deepali Pant Joshi: Financial intermediation for all economic growth with equity Speech by Dr Deepali Pant Joshi, Executive Director of the Reserve Bank of India, at the Financial Inclusion Conclave of

Deepali Pant Joshi: Financial intermediation for all economic growth with equity Speech by Dr Deepali Pant Joshi, Executive Director of the Reserve Bank of India, at the Financial Inclusion Conclave of

Financial Inclusion & Postal Banking The India Story

Financial Inclusion & Postal Banking The India Story A Presentation by Sandip Ghose Reserve Bank of India at the UPU-AFI Workshop, Berne, Switzerland 9 th & 10 th November, 2009 Financial Inclusion : Definition

Financial Inclusion & Postal Banking The India Story A Presentation by Sandip Ghose Reserve Bank of India at the UPU-AFI Workshop, Berne, Switzerland 9 th & 10 th November, 2009 Financial Inclusion : Definition

Financial Literacy and Consumer Protection Necessary Foundation for Financial Inclusion

Financial Literacy and Consumer Protection Necessary Foundation for Financial Inclusion Trinity to make Financial Stability Possible Financial Inclusion Consumer Protection Financial Literacy Globally,

Financial Literacy and Consumer Protection Necessary Foundation for Financial Inclusion Trinity to make Financial Stability Possible Financial Inclusion Consumer Protection Financial Literacy Globally,

Chapter V Financial Inclusion: Policy and Progress

Report on Trend and Progress of Banking in India 2015-16 Chapter V Financial Inclusion: Policy and Progress 5.1 Providing universal access to banking services and improving the forms of credit delivery,

Report on Trend and Progress of Banking in India 2015-16 Chapter V Financial Inclusion: Policy and Progress 5.1 Providing universal access to banking services and improving the forms of credit delivery,

K C Chakrabarty: Financial literacy and consumer protection

K C Chakrabarty: Financial literacy and consumer protection Remarks by Dr K C Chakrabarty, Deputy Governor of the Reserve Bank of India, in a panel discussion on Financial literacy and consumer protection,

K C Chakrabarty: Financial literacy and consumer protection Remarks by Dr K C Chakrabarty, Deputy Governor of the Reserve Bank of India, in a panel discussion on Financial literacy and consumer protection,

A STUDY ON EVALUATION OF THE PERFORMANCE OF FINANCIAL INCLUSION PLANS (FIP) OF BANKS, IN INDIA FOR THE PERIOD ( )

OF BANKS, IN INDIA FOR THE PERIOD ( )") A STUDY ON EVALUATION OF THE PERFORMANCE OF FINANCIAL INCLUSION PLANS (FIP) OF BANKS, IN INDIA FOR THE PERIOD (2010-16) Dr. Rajeev K. Saxena Associate Professor Department of EAFM University of Rajasthan,

A STUDY ON EVALUATION OF THE PERFORMANCE OF FINANCIAL INCLUSION PLANS (FIP) OF BANKS, IN INDIA FOR THE PERIOD (2010-16) Dr. Rajeev K. Saxena Associate Professor Department of EAFM University of Rajasthan,

IDBI Bank Ltd. Financial Inclusion : Achievements

Background IDBI Bank Ltd. Financial Inclusion : Achievements 2013-14 The Government of India, in concert with the Reserve Bank of India, has embarked upon the mission of fostering inclusive growth in the

Background IDBI Bank Ltd. Financial Inclusion : Achievements 2013-14 The Government of India, in concert with the Reserve Bank of India, has embarked upon the mission of fostering inclusive growth in the

FINANCIAL INCLUSION AND ECONOMIC GROWTH

FINANCIAL INCLUSION AND ECONOMIC GROWTH Associate Professor & HOD, Banking & Finance Poona College of Arts, Science & Commerce, Camp, Pune-1 Savitribai Phule Pune University. (MS) INDIA Economic growth

FINANCIAL INCLUSION AND ECONOMIC GROWTH Associate Professor & HOD, Banking & Finance Poona College of Arts, Science & Commerce, Camp, Pune-1 Savitribai Phule Pune University. (MS) INDIA Economic growth

PRADHAN MANTRI J AN-DHAN YOJANA (PMJDY) - Frequently Asked Questions (FAQs)

- Frequently Asked Questions (FAQs)") PRADHAN MANTRI J AN-DHAN YOJANA (PMJDY) - Frequently Asked Questions (FAQs) Q. 1. What is Pradhan Mantri Jan-Dhan Yojana? Ans. Pradhan Mantri Jan-Dhan Yojana (PMJDY) is National Mission for Financial Inclusion

PRADHAN MANTRI J AN-DHAN YOJANA (PMJDY) - Frequently Asked Questions (FAQs) Q. 1. What is Pradhan Mantri Jan-Dhan Yojana? Ans. Pradhan Mantri Jan-Dhan Yojana (PMJDY) is National Mission for Financial Inclusion

Frequently Asked Questions (FAQs) on Pradhan Mantri Jan Dhan Yojana (PMJDY)

on Pradhan Mantri Jan Dhan Yojana (PMJDY)") Frequently Asked Questions (FAQs) on Pradhan Mantri Jan Dhan Yojana (PMJDY) Q. 1. What is Pradhan Mantri Jan-Dhan Yojana? Ans. Pradhan Mantri Jan-Dhan Yojana (PMJDY) is National Mission for Financial Inclusion

Frequently Asked Questions (FAQs) on Pradhan Mantri Jan Dhan Yojana (PMJDY) Q. 1. What is Pradhan Mantri Jan-Dhan Yojana? Ans. Pradhan Mantri Jan-Dhan Yojana (PMJDY) is National Mission for Financial Inclusion

ROLE OF GOVERNMENT IN FINANCIAL INCLUSION

Continuous issue-14 May - August 2015 ROLE OF GOVERNMENT IN FINANCIAL INCLUSION INTRODUCTION: Providing financial access to the poor by connecting them with banks has always been an important priority

Continuous issue-14 May - August 2015 ROLE OF GOVERNMENT IN FINANCIAL INCLUSION INTRODUCTION: Providing financial access to the poor by connecting them with banks has always been an important priority

PRADHAN MANTRI JAN-DHAN YOJANA (PMJDY) - Frequently Asked Questions (FAQs)

- Frequently Asked Questions (FAQs)") PRADHAN MANTRI JAN-DHAN YOJANA (PMJDY) - Frequently Asked Questions (FAQs) Q. 1. What is Pradhan Mantri Jan-Dhan Yojana? Ans. Pradhan Mantri Jan-Dhan Yojana (PMJDY) is National Mission for Financial Inclusion

PRADHAN MANTRI JAN-DHAN YOJANA (PMJDY) - Frequently Asked Questions (FAQs) Q. 1. What is Pradhan Mantri Jan-Dhan Yojana? Ans. Pradhan Mantri Jan-Dhan Yojana (PMJDY) is National Mission for Financial Inclusion

Financial Inclusion Policy. Bank has Board approved FI Policy and salient features of the Policy are as below:

Financial Inclusion Policy Bank has Board approved FI Policy and salient features of the Policy are as below: Purpose of the Financial Inclusion Policy: Financial Inclusion Policy is required (a) To give

Financial Inclusion Policy Bank has Board approved FI Policy and salient features of the Policy are as below: Purpose of the Financial Inclusion Policy: Financial Inclusion Policy is required (a) To give

Role Of Private Sector Banks In Financial Inclusion: A Case Study On West-Bengal

ISSN (Online): 232-9364, ISSN (Print): 232-9356 Volume 2 Issue 3 ǁ. 2 ǁ PP.38-45 Role Of Private Sector Banks In Inclusion: A Case Study On West-Bengal *Mr. SOURAV DUTTA MUSTAFI, **Mr. JOYDEEP CHAKRABORTY

ISSN (Online): 232-9364, ISSN (Print): 232-9356 Volume 2 Issue 3 ǁ. 2 ǁ PP.38-45 Role Of Private Sector Banks In Inclusion: A Case Study On West-Bengal *Mr. SOURAV DUTTA MUSTAFI, **Mr. JOYDEEP CHAKRABORTY

Progress of financial inclusion through Pradhan Mantri Jan Dhan Yojana

Progress of financial inclusion through Pradhan Mantri Jan Dhan Yojana Irrinki Mohana Krishna, Research Scholar, JNTUK, KAKINADA & Associate Professor, MBA Dept, Kakinada Institute of Engineering & Technology,

Progress of financial inclusion through Pradhan Mantri Jan Dhan Yojana Irrinki Mohana Krishna, Research Scholar, JNTUK, KAKINADA & Associate Professor, MBA Dept, Kakinada Institute of Engineering & Technology,

Deepali Pant Joshi: Financial inclusion

Deepali Pant Joshi: Financial inclusion Speech by Dr Deepali Pant Joshi, Executive Director of the Reserve Bank of India, at the Vth Dun & Bradstreet Conclave on Financial Inclusion, Kolkatta, 28 October

Deepali Pant Joshi: Financial inclusion Speech by Dr Deepali Pant Joshi, Executive Director of the Reserve Bank of India, at the Vth Dun & Bradstreet Conclave on Financial Inclusion, Kolkatta, 28 October

Deepali Pant Joshi: Consumer protection agenda for inclusive growth

Deepali Pant Joshi: Consumer protection agenda for inclusive growth Address by Dr Deepali Pant Joshi, Executive Director of the Reserve Bank of India, at the National Seminar on Consumer protection agenda

Deepali Pant Joshi: Consumer protection agenda for inclusive growth Address by Dr Deepali Pant Joshi, Executive Director of the Reserve Bank of India, at the National Seminar on Consumer protection agenda

Study Report on. Impact of Pradhan Mantri Jan DhanYojana (PMJDY)

") Study Report on Impact of Pradhan Mantri Jan DhanYojana (PMJDY) March 2016 Bankers Institute of Rural Development, Lucknow & College of Agricultural Banking, Pune Caveat The study was carried out to observe

Study Report on Impact of Pradhan Mantri Jan DhanYojana (PMJDY) March 2016 Bankers Institute of Rural Development, Lucknow & College of Agricultural Banking, Pune Caveat The study was carried out to observe

FINANCIAL INCLUSION - INDIAN EXPERIENCE

FINANCIAL INCLUSION - INDIAN EXPERIENCE Financial Inclusion (FI) Simplicity and reliability in financial inclusion in India, though not a cure all, can be a way of liberating the poor from dependence on

FINANCIAL INCLUSION - INDIAN EXPERIENCE Financial Inclusion (FI) Simplicity and reliability in financial inclusion in India, though not a cure all, can be a way of liberating the poor from dependence on

Financial Inclusion and India-Challenges, Opportunities

Financial Inclusion and India-Challenges, Opportunities New Horizon College, 3 RD A Cross, 2 nd A main, Kasturinagar, Bangalore-560003. Abstract In recent times Financial Inclusion and Inclusive Growth

Financial Inclusion and India-Challenges, Opportunities New Horizon College, 3 RD A Cross, 2 nd A main, Kasturinagar, Bangalore-560003. Abstract In recent times Financial Inclusion and Inclusive Growth

(I) Provision of banking services to villages with population below 2000:

Provision of banking services to villages with population below 2000:") AGENDA ITEM NO: 01 FINANCIAL INCLUSION PLAN (FIP) OF J&K STATE: (I) Provision of banking services to villages with population below 2000: The FIP-II target for coverage of 5,582 identified unbanked villages

AGENDA ITEM NO: 01 FINANCIAL INCLUSION PLAN (FIP) OF J&K STATE: (I) Provision of banking services to villages with population below 2000: The FIP-II target for coverage of 5,582 identified unbanked villages

PRADHAN MANTRI JAN DHAN YOJANA

LOK SABHA SECRETARIAT PARLIAMENT LIBRARY AND REFERENCE, RESEARCH, DOCUMENTATION AND INFORMATION SERVICE (LARRDIS) MEMBERS REFERENCE SERVICE REFERENCE NOTE. No. 7 /RN/Ref./November /2014 For the use of

LOK SABHA SECRETARIAT PARLIAMENT LIBRARY AND REFERENCE, RESEARCH, DOCUMENTATION AND INFORMATION SERVICE (LARRDIS) MEMBERS REFERENCE SERVICE REFERENCE NOTE. No. 7 /RN/Ref./November /2014 For the use of

Financial Inclusion Initiatives in India

International Journal of Trade & Commerce-IIARTC July-December 2017, Volume 6, No. 2 pp. 492-500 SGSR. (www.sgsrjournals.co.in) All rights reserved UGC COSMOS (Germany) JIF: 5.135; ISRA JIF: 4.816; NAAS

International Journal of Trade & Commerce-IIARTC July-December 2017, Volume 6, No. 2 pp. 492-500 SGSR. (www.sgsrjournals.co.in) All rights reserved UGC COSMOS (Germany) JIF: 5.135; ISRA JIF: 4.816; NAAS

E- ISSN X ISSN MICRO FINANCE-AN IMPERATIVE FOR FINANCIAL INCLUSION IN INDIA

MICRO FINANCE-AN IMPERATIVE FOR FINANCIAL INCLUSION IN INDIA Dr.K.Jayalakshmi PDF(ICSSR),Dept. of Commerce,S.K.University, Anantapur. Andhra Pradesh. Abstract Financial inclusion is a flagship programme

MICRO FINANCE-AN IMPERATIVE FOR FINANCIAL INCLUSION IN INDIA Dr.K.Jayalakshmi PDF(ICSSR),Dept. of Commerce,S.K.University, Anantapur. Andhra Pradesh. Abstract Financial inclusion is a flagship programme

PRADHAN MANTRI JAN-DHAN YOJANA (PMJDY) Frequently Asked Questions (FAQs)

Frequently Asked Questions (FAQs)") PRADHAN MANTRI JAN-DHAN YOJANA (PMJDY) Frequently Asked Questions (FAQs) Q.1. What is Pradhan Mantri Jan-Dhan Yojana? Ans. Pradhan Mantri Jan-Dhan Yojana (PMJDY) is National Mission for Financial Inclusion

PRADHAN MANTRI JAN-DHAN YOJANA (PMJDY) Frequently Asked Questions (FAQs) Q.1. What is Pradhan Mantri Jan-Dhan Yojana? Ans. Pradhan Mantri Jan-Dhan Yojana (PMJDY) is National Mission for Financial Inclusion

6 Pillars. Creation of Credit Guarantee Fund. Micro - Insurance. Universal access to banking facilities. Financial Literacy Programme

Vision To ensure universal access to banking & other financial services at reasonable distance and affordable cost. Make financial inclusion an enabler for inclusive growth. Universal access to banking

Vision To ensure universal access to banking & other financial services at reasonable distance and affordable cost. Make financial inclusion an enabler for inclusive growth. Universal access to banking

Role of Banks in Financial Inclusion

60 Role of Banks in Financial Inclusion Neha Garg, Student of M. Com., Department of Commerce, Kurukshetra University, Kurukshetra ABSTRACT Financial inclusion is the buzz word in the current economy in

60 Role of Banks in Financial Inclusion Neha Garg, Student of M. Com., Department of Commerce, Kurukshetra University, Kurukshetra ABSTRACT Financial inclusion is the buzz word in the current economy in

Analysis of Financial Inclusion Opportunities and Challenges for India

18 Analysis of Financial Inclusion Opportunities and Challenges for India ABSTRACT: Dr. G. Gangaiah Lecturers in Commerce Govt. Degree College, Nagari. ggyadav2010@gmail.com Cell:9290293399 The banking

18 Analysis of Financial Inclusion Opportunities and Challenges for India ABSTRACT: Dr. G. Gangaiah Lecturers in Commerce Govt. Degree College, Nagari. ggyadav2010@gmail.com Cell:9290293399 The banking

PRESS RELEASE. Performance driven Progress

CORPORATE OFFICE: GANDHINAGAR BANGALORE PRESS RELEASE 30.07.2012 SyndicateBank Announces its Financial Results for the quarter ended 30 th June 2012 Performance driven Progress (Q 1 of 2012 vis a vis Q

CORPORATE OFFICE: GANDHINAGAR BANGALORE PRESS RELEASE 30.07.2012 SyndicateBank Announces its Financial Results for the quarter ended 30 th June 2012 Performance driven Progress (Q 1 of 2012 vis a vis Q

PRADHAN MANTRI JAN DHAN YOJNA AN APPROACH TO TAKE IT AHEAD

PRADHAN MANTRI JAN DHAN YOJNA AN APPROACH TO TAKE IT AHEAD Contents PMJDY - Pradhan Mantri Jan Dhan Yojna... Achievements of PJMJDY... Issues faced by PJMJDY... Threats... Way ahead... The Current and

PRADHAN MANTRI JAN DHAN YOJNA AN APPROACH TO TAKE IT AHEAD Contents PMJDY - Pradhan Mantri Jan Dhan Yojna... Achievements of PJMJDY... Issues faced by PJMJDY... Threats... Way ahead... The Current and

Access to Financial Services to the Rural Household Enterprises A Study of Srikakulam District, Andhra Pradesh

Access to Financial Services to the Rural Household Enterprises A Study of Srikakulam District, Andhra Pradesh Ch. Ganga Bhavani *, Prof.P. Veni** * Research Scholar, Department of Commerce and Management

Access to Financial Services to the Rural Household Enterprises A Study of Srikakulam District, Andhra Pradesh Ch. Ganga Bhavani *, Prof.P. Veni** * Research Scholar, Department of Commerce and Management

International Journal of Business and Administration Research Review, Vol. 2 Issue.10, April- June, Page 126

PMJDY: A BOLD PATH WAY FOR FINANACIAL INCLUSION Aswathy V K * Shiny V N** *Research scholar in commerce, Kerala University Library Research Centre, University of Kerala. **Research scholar in commerce,

PMJDY: A BOLD PATH WAY FOR FINANACIAL INCLUSION Aswathy V K * Shiny V N** *Research scholar in commerce, Kerala University Library Research Centre, University of Kerala. **Research scholar in commerce,

Structure of the presentation

Structure of the presentation Issues in Financial Literacy in India Financial Access-itself an important Communication Channel A different mix of content of Financial Literacy material for financially

Structure of the presentation Issues in Financial Literacy in India Financial Access-itself an important Communication Channel A different mix of content of Financial Literacy material for financially

PMJDY : A CONCEPTUAL ANALYSIS AND INCLUSIVE FINANCING Dr. Vinit Kumar*, Dolly Singh**

PMJDY : A CONCEPTUAL ANALYSIS AND INCLUSIVE FINANCING Dr. Vinit Kumar*, Dolly Singh** *Deptt. of Human Rights, School for Legal Studies, B. B. Ambedkar University, Lucknow-25 **M.Phil Scholar, Deptt. of

PMJDY : A CONCEPTUAL ANALYSIS AND INCLUSIVE FINANCING Dr. Vinit Kumar*, Dolly Singh** *Deptt. of Human Rights, School for Legal Studies, B. B. Ambedkar University, Lucknow-25 **M.Phil Scholar, Deptt. of

Segment -1 (Background)

") Segment -1 (Background) Pradhan Mantra Jan Dhan Yojana (PMJDY) Commencement of Financial Inclusion Plan in India-Background Financial Inclusion has always remained the focused area of the Government of

Segment -1 (Background) Pradhan Mantra Jan Dhan Yojana (PMJDY) Commencement of Financial Inclusion Plan in India-Background Financial Inclusion has always remained the focused area of the Government of

1 Assistant Professor, Govt. P.G. College, Bhiwani, Haryana

Financial Inclusion - Role of Indian Banks in Reaching Out to the Unbanked and Backward Areas Preeti 1 Abstract A nation can grow economically and socially if it s weaker section can turn out to be financial

Financial Inclusion - Role of Indian Banks in Reaching Out to the Unbanked and Backward Areas Preeti 1 Abstract A nation can grow economically and socially if it s weaker section can turn out to be financial

A STUDY OF PRADHAN MANTRI JAN-DHAN YOJANA IN INDIA

A STUDY OF PRADHAN MANTRI JAN-DHAN YOJANA IN INDIA Mahendra K Sonawane IBM&R, Wakad, Pune-57 Email Id- mksona56@gmail.com Abstract: Pradhan Mantri Jan Dhan Yojana is an ambitious scheme for comprehensive

A STUDY OF PRADHAN MANTRI JAN-DHAN YOJANA IN INDIA Mahendra K Sonawane IBM&R, Wakad, Pune-57 Email Id- mksona56@gmail.com Abstract: Pradhan Mantri Jan Dhan Yojana is an ambitious scheme for comprehensive

FINANCIAL INCLUSION USING PRADHAN MANTRI JAN-DHAN YOJANA A CONCEPTUAL STUDY

FINANCIAL INCLUSION USING PRADHAN MANTRI JAN-DHAN YOJANA A CONCEPTUAL STUDY Mr. Divyesh Kumar, Research Scholar, Assistant Professor, Dayananda Sagar Academy of Technology and Management, Udayapura, Kanakapura

FINANCIAL INCLUSION USING PRADHAN MANTRI JAN-DHAN YOJANA A CONCEPTUAL STUDY Mr. Divyesh Kumar, Research Scholar, Assistant Professor, Dayananda Sagar Academy of Technology and Management, Udayapura, Kanakapura

A STUDY ON PRADHAN MANTRI JAN DHAN YOJANA WITH REFERENCE TO NATIONALIZED BANK (BANK OF BARODA)

") A STUDY ON PRADHAN MANTRI JAN DHAN YOJANA WITH REFERENCE TO NATIONALIZED BANK (BANK OF BARODA) Abstract Sri Lakshmi & DMamatha Final year MBA & DrPonniah V M, Professor, Faculty of Management, SRM University,

A STUDY ON PRADHAN MANTRI JAN DHAN YOJANA WITH REFERENCE TO NATIONALIZED BANK (BANK OF BARODA) Abstract Sri Lakshmi & DMamatha Final year MBA & DrPonniah V M, Professor, Faculty of Management, SRM University,

Airo International Research Journal ISSN: March, 2017 Volume IX

1 Impact of Demonetization on Financial inclusion D. VENKAIAH M.Com;M.B.A;M.Phil; (PhD) Research Scholar G.Pulla Reddy Degree & P.G College Abstract Demonetization causes inconvenience for initial few

1 Impact of Demonetization on Financial inclusion D. VENKAIAH M.Com;M.B.A;M.Phil; (PhD) Research Scholar G.Pulla Reddy Degree & P.G College Abstract Demonetization causes inconvenience for initial few

Financial Inclusion in India: Challenges and Opportunities Ms. Richa Aggarwal 1

Financial Inclusion in India: Challenges and Opportunities Ms. Richa Aggarwal 1 ABSTRACT A robust and strong financial system is an essential pillar of sustainable development, economic growth, and progress

Financial Inclusion in India: Challenges and Opportunities Ms. Richa Aggarwal 1 ABSTRACT A robust and strong financial system is an essential pillar of sustainable development, economic growth, and progress

Financial Inclusion for Inclusive Growth in India

Financial Inclusion for Inclusive Growth in India Ms. Chitra Saruparia Assistant Professor, Faculty of Policy Science National Law University, Jodhpur chitrasnlu@gmail.com Introduction The term inclusive

Financial Inclusion for Inclusive Growth in India Ms. Chitra Saruparia Assistant Professor, Faculty of Policy Science National Law University, Jodhpur chitrasnlu@gmail.com Introduction The term inclusive

FINANCIAL INCLUSION IN INDIA: A STUDY OF MEASURES AND PROGRESS

FINANCIAL INCLUSION IN INDIA: A STUDY OF MEASURES AND PROGRESS 1 SMRITI, 2 SAHIL KAPOOR ( 1 Assistant Professor, Dayanand Mahila Mahavidyalya, Kurukshetra, 2 Research Scholar, University School Of Management,

FINANCIAL INCLUSION IN INDIA: A STUDY OF MEASURES AND PROGRESS 1 SMRITI, 2 SAHIL KAPOOR ( 1 Assistant Professor, Dayanand Mahila Mahavidyalya, Kurukshetra, 2 Research Scholar, University School Of Management,

A Peer Reviewed International Journal of Asian Research Consortium AJRBF:

ABSTRACT A Peer Reviewed International Journal of Asian Research Consortium : ASIAN JOURNAL OF RESEARCH IN BANKING AND FINANCE FINANCIAL INCLUSION AND ROLE OF MICROFINANCE DR. MUKUND CHANDRA MEHTA* *Assistant

ABSTRACT A Peer Reviewed International Journal of Asian Research Consortium : ASIAN JOURNAL OF RESEARCH IN BANKING AND FINANCE FINANCIAL INCLUSION AND ROLE OF MICROFINANCE DR. MUKUND CHANDRA MEHTA* *Assistant

FINANCIAL INCLUSION AND SOCIAL CHANGES

FINANCIAL INCLUSION AND SOCIAL CHANGES Asst. Professor Poona College, Pune (MS) INDIA The concept of Inclusive growth was first envisaged in the Eleventh five year plan document which intended to achieve

FINANCIAL INCLUSION AND SOCIAL CHANGES Asst. Professor Poona College, Pune (MS) INDIA The concept of Inclusive growth was first envisaged in the Eleventh five year plan document which intended to achieve

UNITED BANK OF INDIA FINANCIAL RESULTS FY

29 th April, 2011 UNITED BANK OF INDIA FINANCIAL RESULTS FY 2010-11 PRESS RELEASE 1. Table of Contents Highlights for Q4 ended March 31, 2011 (Q4 FY11) Highlights for FY ended March 31, 2011 (FY11) Other

29 th April, 2011 UNITED BANK OF INDIA FINANCIAL RESULTS FY 2010-11 PRESS RELEASE 1. Table of Contents Highlights for Q4 ended March 31, 2011 (Q4 FY11) Highlights for FY ended March 31, 2011 (FY11) Other

Usha Thorat: Financial regulation and financial inclusion working together or at cross-purposes

Usha Thorat: Financial regulation and financial inclusion working together or at cross-purposes Speech by Ms Usha Thorat, Deputy Governor of the Bank of India, at the Tenth Annual International Seminar

Usha Thorat: Financial regulation and financial inclusion working together or at cross-purposes Speech by Ms Usha Thorat, Deputy Governor of the Bank of India, at the Tenth Annual International Seminar

PROGRESS OF FINANCIAL INCLUSION THROUGH FIPs OF SCHEDULED COMMERCIAL BANKS

Management PROGRESS OF FINANCIAL INCLUSION THROUGH FIPs OF SCHEDULED COMMERCIAL BANKS Mohana Krishna Irrinki *1, Kuberudu Burlakanti 2 *1 Research Scholar, JNTUK, Kakinada, Andhra Pradesh, India 2 Professor

Management PROGRESS OF FINANCIAL INCLUSION THROUGH FIPs OF SCHEDULED COMMERCIAL BANKS Mohana Krishna Irrinki *1, Kuberudu Burlakanti 2 *1 Research Scholar, JNTUK, Kakinada, Andhra Pradesh, India 2 Professor

Financial Inclusion in India through SHG-Bank Linkage Programme and other finance Initiatives of NABARD

Financial Inclusion in India through SHG-Bank Linkage Programme and other finance Initiatives of NABARD By A Ramanathan, Chief General Manager Micro Finance Innovations Department NABARD Mumbai What is

Financial Inclusion in India through SHG-Bank Linkage Programme and other finance Initiatives of NABARD By A Ramanathan, Chief General Manager Micro Finance Innovations Department NABARD Mumbai What is

How Comprehensive is Financial Inclusion in India?

How Comprehensive is Financial Inclusion in India? Mr. A.P. Hota is Managing Director & CEO of National Payments Corporation of India since February 2009. A significant part of his career has been in the

How Comprehensive is Financial Inclusion in India? Mr. A.P. Hota is Managing Director & CEO of National Payments Corporation of India since February 2009. A significant part of his career has been in the

United Bank of India Lead Bank Division Head Office: Kolkata

United Bank of India Lead Bank Division Head Office: Kolkata Proceedings of the Special SLBC Meeting on Implementation of Comprehensive Financial Inclusion (CFI) Plan held at SUCHINTAN, United Bank of

United Bank of India Lead Bank Division Head Office: Kolkata Proceedings of the Special SLBC Meeting on Implementation of Comprehensive Financial Inclusion (CFI) Plan held at SUCHINTAN, United Bank of

PRADHAN MANTRI JAN DHAN YOJANA (PMJDY): A RIGHT PATH TOWARDS POVERTY ALLEVIATION IN INDIA Dr. Amit Kumar

: A RIGHT PATH TOWARDS POVERTY ALLEVIATION IN INDIA Dr. Amit Kumar") PRADHAN MANTRI JAN DHAN YOJANA (PMJDY): A RIGHT PATH TOWARDS POVERTY ALLEVIATION IN INDIA Dr. Amit Kumar Assistant Professor, Department of Commerce, Sunbeam College for Women, Varanasi, U.P. (INDIA) E-mail:

PRADHAN MANTRI JAN DHAN YOJANA (PMJDY): A RIGHT PATH TOWARDS POVERTY ALLEVIATION IN INDIA Dr. Amit Kumar Assistant Professor, Department of Commerce, Sunbeam College for Women, Varanasi, U.P. (INDIA) E-mail:

A STUDY ON FINANCIAL INCLUSION PLANS OF SCHEDULED COMMERCIAL BANKS IN INDIA

A STUDY ON FINANCIAL INCLUSION PLANS OF SCHEDULED COMMERCIAL BANKS IN INDIA Dr. M. Anbalagan, M.Com, M. Phil, B.Ed. Ph.D. Assistant Professor in Commerce Kalasalingam University, Krishnankoil & Prof. M.

A STUDY ON FINANCIAL INCLUSION PLANS OF SCHEDULED COMMERCIAL BANKS IN INDIA Dr. M. Anbalagan, M.Com, M. Phil, B.Ed. Ph.D. Assistant Professor in Commerce Kalasalingam University, Krishnankoil & Prof. M.

Financial Inclusion in India: An Emerging issue in Indian Economy

Financial Inclusion in India: An Emerging issue in Indian Economy Mr.Anuj Jatav Assistant Professor, Department of Commerce, College of Vocational Studies, University of Delhi. Abstract: Financial Inclusion

Financial Inclusion in India: An Emerging issue in Indian Economy Mr.Anuj Jatav Assistant Professor, Department of Commerce, College of Vocational Studies, University of Delhi. Abstract: Financial Inclusion

Pradhan Mantri Jan Dhan Yojana (PMJDY): An Innovative Scheme for Financial Inclusion in India

: An Innovative Scheme for Financial Inclusion in India") 1. Introduction Pradhan Mantri Jan Dhan Yojana (PMJDY): An Innovative Scheme for Financial Inclusion in India Jitender Goel Assistant Professor, Department of Commerce, Acharya Narendra Dev College University

1. Introduction Pradhan Mantri Jan Dhan Yojana (PMJDY): An Innovative Scheme for Financial Inclusion in India Jitender Goel Assistant Professor, Department of Commerce, Acharya Narendra Dev College University

Financial Inclusion An Indian Outlook

Financial Inclusion An Indian Outlook Dr. A. G. Jayakumari Director, SSR IMR, Silvassa Abstract The Indian economy is the second fastest growing economy in the world. Majority of the population in India

Financial Inclusion An Indian Outlook Dr. A. G. Jayakumari Director, SSR IMR, Silvassa Abstract The Indian economy is the second fastest growing economy in the world. Majority of the population in India

Airo International Research Journal February, 2017 Volume IX, ISSN:

1 A STUDY ON FINANCIAL INCLUSION THROUGH PMJDY Rashmi Joshi Assistant Professor, Department of Commerce, DM College, Moga, Punjab, India Declaration of Author: I hereby declare that the content of this

1 A STUDY ON FINANCIAL INCLUSION THROUGH PMJDY Rashmi Joshi Assistant Professor, Department of Commerce, DM College, Moga, Punjab, India Declaration of Author: I hereby declare that the content of this

Cost of social banking

Cost of social banking The traditional self-centered, profit-oriented banking concept is fading, and a modern socio-economic role is emerging for the. The social control imposed over for the first time

Cost of social banking The traditional self-centered, profit-oriented banking concept is fading, and a modern socio-economic role is emerging for the. The social control imposed over for the first time

I, ROLE OF BANKING SECTOR IN FINANCIAL INCLUSION M.

ROLE OF BANKING SECTOR IN FINANCIAL INCLUSION M. Mala* & Dr. G. Vasanthi** * Ph.D Research Scholar Cum Special Officer, Department of Commerce, Annamalai University, Chidambaram, Tamilnadu ** Professor

ROLE OF BANKING SECTOR IN FINANCIAL INCLUSION M. Mala* & Dr. G. Vasanthi** * Ph.D Research Scholar Cum Special Officer, Department of Commerce, Annamalai University, Chidambaram, Tamilnadu ** Professor

Financial Inclusion: An Overview

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 18, Issue 2.Ver. I (Feb. 2016), PP 37-44 www.iosrjournals.org Financial Inclusion: An Overview Dr. Rajeshwari

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 18, Issue 2.Ver. I (Feb. 2016), PP 37-44 www.iosrjournals.org Financial Inclusion: An Overview Dr. Rajeshwari

Aadhaar Enabled Administration of Health Insurance in Sikkim, India. Pompy Sridhar 12 th International Microinsurance Conference 2016

Aadhaar Enabled Administration of Health Insurance in Sikkim, India Pompy Sridhar 12 th International Microinsurance Conference 2016 Agenda The following will be discussed What is Aadhaar Rationale for

Aadhaar Enabled Administration of Health Insurance in Sikkim, India Pompy Sridhar 12 th International Microinsurance Conference 2016 Agenda The following will be discussed What is Aadhaar Rationale for

~ pt ~ ~ fctcmr ~ ~ Qi'lIClill"l ~ 'fttr snmlilc6l F.Nm

~ pt ~ ~ fctcmr ~ ~ Qi'lIClill"l ~ 'fttr snmlilc6l F.Nm ~~ :~, iww ('i), ~ - 400 051 ~: +912226530024 ~: +912226530150 t-m-r : dfibt@nabard.org ~ : www.nabard.org No.NB.DFIBT.HO/ 12 January 2015 4-15~-

~ pt ~ ~ fctcmr ~ ~ Qi'lIClill"l ~ 'fttr snmlilc6l F.Nm ~~ :~, iww ('i), ~ - 400 051 ~: +912226530024 ~: +912226530150 t-m-r : dfibt@nabard.org ~ : www.nabard.org No.NB.DFIBT.HO/ 12 January 2015 4-15~-

EFFECT OF FINANCIAL INCLUSION THROUGH JAN-DHAN- YOJNA ON LIVING STANDARD OF RURAL POPULATION OF INDIA

Volume 6, Issue 6 (June, 2017) UGC APPROVED Online ISSN-2320-0073 Published by: Abhinav Publication Abhinav International Monthly Refereed Journal of Research in EFFECT OF FINANCIAL INCLUSION THROUGH JAN-DHAN-

Volume 6, Issue 6 (June, 2017) UGC APPROVED Online ISSN-2320-0073 Published by: Abhinav Publication Abhinav International Monthly Refereed Journal of Research in EFFECT OF FINANCIAL INCLUSION THROUGH JAN-DHAN-

Financial Inclusion: Issues and Prospects

Pacific Business Review International 84 Pacific Volume Business 5 Issue Review 3 (September International 2012) Financial Inclusion: Issues and Prospects PROF. N.S RAO*, MRS. HARSHITA BHATNAGAR** Strong

Pacific Business Review International 84 Pacific Volume Business 5 Issue Review 3 (September International 2012) Financial Inclusion: Issues and Prospects PROF. N.S RAO*, MRS. HARSHITA BHATNAGAR** Strong

PMJDY: A gateway to Financial Inclusion

ABSTRACT PMJDY: A gateway to Financial Inclusion Assistant Professor, Shaheed Bhagat Singh College, Delhi University, New Delhi, India. PMJDY initiated on the principle of Sab ka sath, sab ka Vikas clearly

ABSTRACT PMJDY: A gateway to Financial Inclusion Assistant Professor, Shaheed Bhagat Singh College, Delhi University, New Delhi, India. PMJDY initiated on the principle of Sab ka sath, sab ka Vikas clearly

Pradhan Mantri Jan Dhan Yojana The National Mission on Financial Inclusion

Pradhan Mantri Jan Dhan Yojana (PMJDY) Ministry of Finance www.swaniti.in Pradhan Mantri Jan Dhan Yojana The National Mission on Financial Inclusion Key Features of PMJDY The Pradhan Mantri Jan Dhan Yojana

Pradhan Mantri Jan Dhan Yojana (PMJDY) Ministry of Finance www.swaniti.in Pradhan Mantri Jan Dhan Yojana The National Mission on Financial Inclusion Key Features of PMJDY The Pradhan Mantri Jan Dhan Yojana

ROLE OF RRB IN RURAL DEVELOPMENT. G.K.Lavanya, Assistant Professor, St.Joseph scollege

ROLE OF RRB IN RURAL DEVELOPMENT G.K.Lavanya, Assistant Professor, St.Joseph scollege ABSTRACT: The importance of the rural banking in the economic development of a country cannot be overlooked. The objective

ROLE OF RRB IN RURAL DEVELOPMENT G.K.Lavanya, Assistant Professor, St.Joseph scollege ABSTRACT: The importance of the rural banking in the economic development of a country cannot be overlooked. The objective

FINANCIAL INCLUSION IN INDIA AN OVERVIEW

Volume 6, Issue 7 (July, 2017) UGC APPROVED Online ISSN-2277-1166 Published by: Abhinav Publication Abhinav National Monthly Refereed Journal of Research in FINANCIAL INCLUSION IN INDIA AN OVERVIEW Suman

Volume 6, Issue 7 (July, 2017) UGC APPROVED Online ISSN-2277-1166 Published by: Abhinav Publication Abhinav National Monthly Refereed Journal of Research in FINANCIAL INCLUSION IN INDIA AN OVERVIEW Suman

Catalyzing Financial Inclusion

Catalyzing Financial Inclusion Through the CSCs An Implementation Handbook Contents Introduction 2 Salient Features of India s Financial Inclusion Strategy 3 Understanding the Business Correspondent Model

Catalyzing Financial Inclusion Through the CSCs An Implementation Handbook Contents Introduction 2 Salient Features of India s Financial Inclusion Strategy 3 Understanding the Business Correspondent Model

Financial Inclusion - A study of various Initiatives and suggestions for the Future

Financial Inclusion - A study of various Initiatives and suggestions for the Future Mr. Adusupalle Muniraju Assistant Professor Balaji Institute of International Business (BIIB), Pune-411033 Email: muni.raju@biibpune.com

Financial Inclusion - A study of various Initiatives and suggestions for the Future Mr. Adusupalle Muniraju Assistant Professor Balaji Institute of International Business (BIIB), Pune-411033 Email: muni.raju@biibpune.com

भ रत य रज़व ब क RESERVE BANK OF INDIA RPCD.CO.BC.FID.No. 16 / / August 12, 2011

RBI/2011 12/153 भ रत य रज़व ब क RESERVE BANK OF INDIA www.rbi.org.in RPCD.CO.BC.FID.No. 16 /12.01.019/2011 12 August 12, 2011 The Chairman/CMD/CEO of all scheduled commercial banks Dear Sir/Madam, Operational

RBI/2011 12/153 भ रत य रज़व ब क RESERVE BANK OF INDIA www.rbi.org.in RPCD.CO.BC.FID.No. 16 /12.01.019/2011 12 August 12, 2011 The Chairman/CMD/CEO of all scheduled commercial banks Dear Sir/Madam, Operational

Financial Inclusion through Pradhan Mantri Jan-Dhan Yojana (PMJDY) Scheme

Scheme") Asian Journal of Managerial Science ISSN: 2249-6300 Vol. 6 No. 1, 2017, pp.10-14 The Research Publication, www.trp.org.in Financial Inclusion through Pradhan Mantri Jan-Dhan Yojana (PMJDY) Scheme M. Rifaya

Asian Journal of Managerial Science ISSN: 2249-6300 Vol. 6 No. 1, 2017, pp.10-14 The Research Publication, www.trp.org.in Financial Inclusion through Pradhan Mantri Jan-Dhan Yojana (PMJDY) Scheme M. Rifaya

MUDRA s delivery channel is conceived to be through the route of refinance primarily to Banks/NBFCs/MFIs.

1. What is MUDRA? MUDRA, which stands for Micro Units Development & Refinance Agency Ltd, is a financial institution beingset up by Government of India for development and refinancing micro units enterprises.

1. What is MUDRA? MUDRA, which stands for Micro Units Development & Refinance Agency Ltd, is a financial institution beingset up by Government of India for development and refinancing micro units enterprises.

Delivering Financial Inclusion Services to Rural Citizens through the Common Service Centers. An Evaluation of State Implementation Models

Delivering Financial Inclusion Services to Rural Citizens through the Common Service Centers An Evaluation of State Implementation Models March 2011 Table of Contents I. Introduction... 3 II. Financial

Delivering Financial Inclusion Services to Rural Citizens through the Common Service Centers An Evaluation of State Implementation Models March 2011 Table of Contents I. Introduction... 3 II. Financial

CHAPTER 3. Financial Inclusion in India

CHAPTER 3 Financial Inclusion in India 3.1 Introduction: Bank nationalization in India marked a paradigm shift in the focus of banking. The importance of financial inclusion, based on the principle of

CHAPTER 3 Financial Inclusion in India 3.1 Introduction: Bank nationalization in India marked a paradigm shift in the focus of banking. The importance of financial inclusion, based on the principle of

Financial Inclusion: Role of Banks

Financial Inclusion: Role of s 1 Love Gogia Abstract The issue of financial inclusion is a development policy priority in many countries. Around 50% of the Indian population suffers from chronic poverty

Financial Inclusion: Role of s 1 Love Gogia Abstract The issue of financial inclusion is a development policy priority in many countries. Around 50% of the Indian population suffers from chronic poverty

EMPOWERING FINANCIAL INCLUSION THROUGH FINANCIAL LITERACY

Abstract EMPOWERING FINANCIAL INCLUSION THROUGH FINANCIAL LITERACY The term financial inclusion means availability of banking services at an affordable cost to disadvantaged and low-income groups. The

Abstract EMPOWERING FINANCIAL INCLUSION THROUGH FINANCIAL LITERACY The term financial inclusion means availability of banking services at an affordable cost to disadvantaged and low-income groups. The

GENERAL AWARENESS CHANGING ROLE OF BANKS IN INDIA

SBI PROBATIONARY OFFICERS GENERAL AWARENESS CHANGING ROLE OF BANKS IN INDIA Role of banks in India has changed a lot since economic reforms of 1991. These changes came due to liberalization, privatization

SBI PROBATIONARY OFFICERS GENERAL AWARENESS CHANGING ROLE OF BANKS IN INDIA Role of banks in India has changed a lot since economic reforms of 1991. These changes came due to liberalization, privatization

Analyzing Data of Pradhan Mantri Jan Dhan Yojana

Technical Report 217 Analyzing Data of Pradhan Mantri Jan Dhan Yojana Tulika Dutta and Ashish Das Department of Mathematics Indian Institute of Technology Bombay Mumbai-476, India May 217 Indian Institute

Technical Report 217 Analyzing Data of Pradhan Mantri Jan Dhan Yojana Tulika Dutta and Ashish Das Department of Mathematics Indian Institute of Technology Bombay Mumbai-476, India May 217 Indian Institute

ROLE OF BUSINESS CORRESPONDENTS IN BANKING SECTOR ACTIVITIES

ROLE OF BUSINESS CORRESPONDENTS IN BANKING SECTOR ACTIVITIES K.Subha, Research Scholar, Alagappa Institute of Management, Alagappa University Karaikudi Abstract The RBI has permitted banks to use the services

ROLE OF BUSINESS CORRESPONDENTS IN BANKING SECTOR ACTIVITIES K.Subha, Research Scholar, Alagappa Institute of Management, Alagappa University Karaikudi Abstract The RBI has permitted banks to use the services

INDIA. QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork Conducted September 2016 through January January 2016

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork Conducted September 2016 through January 2017 January 2016 Key definitions Access Access to a bank account or mobile money account means an

QUICKSIGHTS REPORT FOURTH ANNUAL FII TRACKER SURVEY Fieldwork Conducted September 2016 through January 2017 January 2016 Key definitions Access Access to a bank account or mobile money account means an

F.No.6/41/2012-FI( Vol.III) Government of India Ministry of Finance Department of Financial Services

Government of India Ministry of Finance Department of Financial Services") To: 1. Shri Ajit Seth, Cabinet Secretary, Rashtrapati Bhawan, New Delhi. 2. Shri Pulok Chatterji, Pr. Secretary to PM, South Block, New Delhi. 3. Shri R.S. Gujral, Secretary, D/o Expenditure, North Block,

To: 1. Shri Ajit Seth, Cabinet Secretary, Rashtrapati Bhawan, New Delhi. 2. Shri Pulok Chatterji, Pr. Secretary to PM, South Block, New Delhi. 3. Shri R.S. Gujral, Secretary, D/o Expenditure, North Block,

The Chairman/ Managing Director of All Public Sector Banks Chairman of All Regional Rural Banks ( through Sponsored Banks)

") To F. No. 21/13/2009-FI (Vol II-Pt.) Government of India Ministry of Finance Department of Financial Services ***** Jeevan Deep Building, Sansad Marg, New Delhi, dated the 4 th April, 2012 The Chairman/

To F. No. 21/13/2009-FI (Vol II-Pt.) Government of India Ministry of Finance Department of Financial Services ***** Jeevan Deep Building, Sansad Marg, New Delhi, dated the 4 th April, 2012 The Chairman/

RBI/ /40 RPCD. MFFI. BC.No.09 / / July 1, Master Circular on Micro Credit

RBI/ 2009-10/40 RPCD. MFFI. BC.No.09 / 12.01.001/ 2009-10 July 1, 2009 The Chairman/ Managing Director/ Chief Executive Officer All Scheduled Commercial Banks Dear Sir, Master Circular on Micro Credit

RBI/ 2009-10/40 RPCD. MFFI. BC.No.09 / 12.01.001/ 2009-10 July 1, 2009 The Chairman/ Managing Director/ Chief Executive Officer All Scheduled Commercial Banks Dear Sir, Master Circular on Micro Credit

Banking Development in U.T. of Puducherry

State Level Bankers Committee, Puducherry Convenor: Indian Bank Banking Development in U.T. of Puducherry (As of Dec 2016) (Rs. in Crores) S. No Details/Sector March 2013 March 2014 March 2015 March 2016

State Level Bankers Committee, Puducherry Convenor: Indian Bank Banking Development in U.T. of Puducherry (As of Dec 2016) (Rs. in Crores) S. No Details/Sector March 2013 March 2014 March 2015 March 2016

Gram Swaraj Abhiyan 2018 (14 th April to 5 th May 18)

") Gram Swaraj Abhiyan 2018 (14 th April to 5 th May 18) Saturation of Financial Inclusion Schemes in select villages - PM Jan-Dhan Yojana - PM Suraksha Bima Yojana - PM Jeevan-Jyoti Bima Yojana PM Jan-Dhan

Gram Swaraj Abhiyan 2018 (14 th April to 5 th May 18) Saturation of Financial Inclusion Schemes in select villages - PM Jan-Dhan Yojana - PM Suraksha Bima Yojana - PM Jeevan-Jyoti Bima Yojana PM Jan-Dhan

International Journal of Scientific & Innovative Research Studies ISSN :

Pradhan Mantri Jan Dhan Yojana (PMJDY): Financial Inclusion and Inclusive Growth in India Dr. Vinit Kumar, Deptt. of Human Rights, School for Legal Studies, B. B. Ambedkar University, Lucknow-226025 ABSTRACT

Pradhan Mantri Jan Dhan Yojana (PMJDY): Financial Inclusion and Inclusive Growth in India Dr. Vinit Kumar, Deptt. of Human Rights, School for Legal Studies, B. B. Ambedkar University, Lucknow-226025 ABSTRACT

Banking Development in U.T. of Puducherry

State Level Bankers Committee, Puducherry Convenor: Indian Bank Banking Development in U.T. of Puducherry (As of Sep 2016) (Rs. in Crores) S. No Details/Sector March 2013 March 2014 March 2015 March 2016

State Level Bankers Committee, Puducherry Convenor: Indian Bank Banking Development in U.T. of Puducherry (As of Sep 2016) (Rs. in Crores) S. No Details/Sector March 2013 March 2014 March 2015 March 2016

SHPI-Bank Consultation Meet Taking SHG Bank Linkage to the Next Level 3 rd May, 2013, Patna. Organized by: ACCESS ASSIST.

SHPI-Bank Consultation Meet Taking SHG Bank Linkage to the Next Level 3 rd May, 2013, Patna Organized by: ACCESS ASSIST Summary Paper SAMRIDHI (Poorest State Inclusive Growth Programme)is being implemented

SHPI-Bank Consultation Meet Taking SHG Bank Linkage to the Next Level 3 rd May, 2013, Patna Organized by: ACCESS ASSIST Summary Paper SAMRIDHI (Poorest State Inclusive Growth Programme)is being implemented

Financial Inclusion in India

Navajyoti, International Journal of Multi-Disciplinary Research Volume 2, Issue 2, February 2018 Financial Inclusion in India Namita P Konnur 1 Assistant Professor, Jyoti Nivas College, Bangalore Dr. N.Babitha

Navajyoti, International Journal of Multi-Disciplinary Research Volume 2, Issue 2, February 2018 Financial Inclusion in India Namita P Konnur 1 Assistant Professor, Jyoti Nivas College, Bangalore Dr. N.Babitha

Including the Excluded: The Scenario of Financial Inclusion in India

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 20, Issue 2. Ver. VII (February. 2018), PP 64-69 www.iosrjournals.org Including the Excluded: The Scenario

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 20, Issue 2. Ver. VII (February. 2018), PP 64-69 www.iosrjournals.org Including the Excluded: The Scenario

Minutes of the 156 th Meeting of State Level Bankers Committee, Madhya Pradesh

1 Minutes of the 156 th Meeting of State Level Bankers Committee, Madhya Pradesh - 20.02.2015 The 156 th meeting of State Level Bankers Committee in Madhya Pradesh was held on 20.02.2015, in the Conference

1 Minutes of the 156 th Meeting of State Level Bankers Committee, Madhya Pradesh - 20.02.2015 The 156 th meeting of State Level Bankers Committee in Madhya Pradesh was held on 20.02.2015, in the Conference

Review of performance of Pradhan Mantri Mudra Yojana

Review of performance of Pradhan Mantri Mudra Yojana (An analysis on the performance of PMMY during FY 2015-16) hetbpeer meheàuelee keàer kegbàpeer 2 MUDRA/PMMY Micro Units Development & Refinance Agency

Review of performance of Pradhan Mantri Mudra Yojana (An analysis on the performance of PMMY during FY 2015-16) hetbpeer meheàuelee keàer kegbàpeer 2 MUDRA/PMMY Micro Units Development & Refinance Agency

DateDdddd. UNITED BANK OF INDIA (The Bank that begins with U) Financial Results for Q-3 (FY ) PRESS RELEASE

Financial Results for Q-3 (FY ) PRESS RELEASE") DateDdddd Date: 20 th January, 2011 UNITED BANK OF INDIA (The Bank that begins with U) Financial Results for Q-3 (FY 2010-11) PRESS RELEASE 1. Table of Contents Highlights for Q3 ended, December, 2010

DateDdddd Date: 20 th January, 2011 UNITED BANK OF INDIA (The Bank that begins with U) Financial Results for Q-3 (FY 2010-11) PRESS RELEASE 1. Table of Contents Highlights for Q3 ended, December, 2010

Performance highlights for the Quarter ended 30 th June 2016 Performance highlights of the Bank -June 16 [Q1] over June 15 [Q1]:

![Performance highlights for the Quarter ended 30 th June 2016 Performance highlights of the Bank -June 16 [Q1] over June 15 [Q1]:](/thumbs/92/109840252.jpg "Performance highlights for the Quarter ended 30 th June 2016 Performance highlights of the Bank -June 16 [Q1] over June 15 [Q1]:") Sector Bank Performance highlights for the Quarter ended 30 th June 2016 Performance highlights of the Bank -June 16 [Q1] over June 15 [Q1]: Parameter A Premier Public Sector Bank As at 30 June 15[Q1]

Sector Bank Performance highlights for the Quarter ended 30 th June 2016 Performance highlights of the Bank -June 16 [Q1] over June 15 [Q1]: Parameter A Premier Public Sector Bank As at 30 June 15[Q1]

Performance Appraisal of Andhra Bank and its role in Financial Inclusion

WWW..COM ISSN: 2278-3970 Performance Appraisal of Andhra Bank and its role in Financial Inclusion Dr. K.V.S.Prasad 1, Prof. G. Sudarsana Rao 2 1 Assistant Professor, Department of Basic Science and Humanities,

WWW..COM ISSN: 2278-3970 Performance Appraisal of Andhra Bank and its role in Financial Inclusion Dr. K.V.S.Prasad 1, Prof. G. Sudarsana Rao 2 1 Assistant Professor, Department of Basic Science and Humanities,

Sai Om Journal of Commerce & Management A Peer Reviewed National Journal

Volume 3, Issue 3 (March, 2016) Online ISSN-2347-7563 Published by: Sai Om Publications HOW TO BRING PMJDY ACCOUNT FOR TRANSACTIONS AND REDUCE ZERO BALANCE ACCOUNTS- A STUDY Dhanasekaran Perumalsamy Chief

Volume 3, Issue 3 (March, 2016) Online ISSN-2347-7563 Published by: Sai Om Publications HOW TO BRING PMJDY ACCOUNT FOR TRANSACTIONS AND REDUCE ZERO BALANCE ACCOUNTS- A STUDY Dhanasekaran Perumalsamy Chief

Financial Literacy An overview of growing efforts

85 Financial Literacy An overview of growing efforts Sweta kumari Research scholar, Dr. B.R.Ambedkar University, Muzzufurpur Priya Viz Research Scholar, Sainath University, Ranchi Jharkhand Abstract: In

85 Financial Literacy An overview of growing efforts Sweta kumari Research scholar, Dr. B.R.Ambedkar University, Muzzufurpur Priya Viz Research Scholar, Sainath University, Ranchi Jharkhand Abstract: In

M2i s Experience in Microfinance

M2i s Experience in Microfinance Title Duration Client Page Implementation of Risk Management International Finance June 2012-May 2015 Framework in 5 MFIs Corporation 3 Adaptation of Global Risk International

M2i s Experience in Microfinance Title Duration Client Page Implementation of Risk Management International Finance June 2012-May 2015 Framework in 5 MFIs Corporation 3 Adaptation of Global Risk International

FINANCIAL LITERACY: AN INDIAN SCENARIO