Getting Retirement-Ready: Have your cake and eat it too!

|

|

|

- Wilfrid Burke

- 6 years ago

- Views:

Transcription

1 This firm is not a CPA firm. Getting Retirement-Ready: Have your cake and eat it too! The 2017 Spring Accounting Expo May 22, 2017 Steven R. Goodman, CPA, CFP

2 Have your cake and eat it too! 2

3 Common Retirement Planning Mistakes/Challenges 1. Starting too late (better late than never) 2. Not taking advantage of time / Underestimating investment horizon 3. Not having a retirement plan 4. Not investing regularly / Ignoring your plan 5. Not taking full advantage of tax-deferred retirement accounts 3

4 Common Retirement Planning Mistakes/Challenges 6. Not properly managing financial / investment risks 7. Poor asset allocation 8. Relying too heavily on your company s stock 9. Falling for the sales pitch 10. Underestimating the importance & need for diversification 11. Exiting in a downturn / Emotional investing 4

5 Common Retirement Planning 12. Cashing out or borrowing heavily against your retirement accounts 13. Underestimating cash needs 14. Failing to consider taxes and inflation 15. Misunderstanding effective tax rate 16. Not providing for a spouse Mistakes/Challenges 17. Overestimating ability to continue working 5

6 Common Retirement Planning 18. Retiring based on your birthday instead of your bank account 19. Taking Social Security at too early an age 20. Taking withdrawals from the wrong location 21. Outspending means Mistakes/Challenges 6

7 The Facts of Life And Don t Forget About Taxes! 7

8 Retirement Planning Phases Accumulation Phase (30-40 years) Distribution Phase (30+ years) 20s 30s 40s 50s 60s 70s 80s 90s 8

9 Benefit of Investing Early Annual Salary $65,000: Assumes a 3% per year increase and 10% per month contribution in a tax-deferred account Assumed Rate of Return 7.59% blended return calculated using historical average annualized benchmark index returns for the period 1926 through February 28, 2017 for a 70% Stocks/30% Bonds/0% Cash portfolio allocation less 1% hypothetical portfolio management fee. Cash is represented by the U.S. T-Bill, bonds are represented by the Bloomberg Barclays Intermediate Government/Credit Index, and stocks are represented by the S&P 500 Index. 9

,")

10 Your 20s and 30s (Early Career) Retirement Strategies: A To-Do List Determine risk profile / asset allocation Contribute as much as you can to tax-deferred plans i.e. IRAs, 401(k), 403(b), 457 Consider Roth contributions Monitor investments / re-balance Manage your spending and debt Consider life insurance and disability insurance Consult on estate planning

11 Retirement Strategies: A To-Do List Your 40s and 50s (Mid-Career) Continue contributing as much as you can to tax-deferred plans Contribute to non-qualified asset sources Monitor investments / re-balance Review asset allocation / adjust target as appropriate Assess after-tax retirement cash needs Consider health, life, disability, and long-term care insurance Review/Consult on estate planning

12 Special Considerations For the corporate employees: Plan for the possibility of a forced early retirement Consider carrying insurance other than that provided by your current company Develop a plan for exercising your stock options that will minimize the tax cost Review company benefits to take full advantage of those that apply to pre-retirees and retirees Optimize the use of your 401(k) plan For business owners: Possible strategies for customized Defined Benefit Plan Strategies to monetize business for retirement cash needs 12

13 Your Early 60s (Late Career) Review asset allocation / adjust target as appropriate Determine your Social Security and pension income Monitor investments / re-balance Review estate plan Retirement Strategies: A To-Do List Reduce debt as much as possible

Arrange to have your periodic payments directly deposited into your checking account ENJOY IT!")

14 Your Retirement Review asset allocation / adjust target as appropriate Decide a retirement date and apply for your Social Security Benefits when appropriate Evaluate when and from what sources to start withdrawing money for retirement (cash flow analysis) Arrange to have your periodic payments directly deposited into your checking account ENJOY IT! Retirement Strategies: A To-Do List 60 Retirement 14

15 Some Factors Investors Need to Consider Risk Return Profile Goals & Objectives Family Analysis: Market / Sector Industry & Company Investor Fiscal & Monetary Policy Political Environment (U.S. & Foreign) Economic Environment (U.S. & Foreign) Time 15

16 Other Risks Reality vs Goals Perception vs Reality Zero I want to double my money in 3 years and retire This is different, equities will not go back up This does not exist Timing Markets Day trader and success? 16

17 Emotional Other Risks (Continued) I feel it will come back Taxes Family Gain / loss (should not drive investment decisions) Decision blockers / influencers Regulatory/Political SEC, Feds, State, Agency rules always changing 17

18 Industry Other Risks (Continued) Obsolescence, alternatives, declining Management Good business, bad managers Known, Unknown Ike, Oil Spill Unknown Diversification 18

19 Guarantee Other Risks (Continued) What does this actually mean? Exit Fraud Time Risk Benchmark Limited Partnerships / ARS Madoff / Stanford vet your advisors To achieve goal, health Returns measured against inappropriate parameter 19

20 Ratings Other Risks (Continued) Any highly rated bonds ever default? Understanding of Metrics Tips /Rumors Not-Rebalancing P/E, EPS, Beta, Projections, Forecasts, etc Really, you want to invest using tips? Ignoring asset allocation Bottom Line: Do you understand and accept the risks relevant to your circumstances and investments? 20

21 Effect of Investor Behavior 10% 9% 8% 7% 6% 5% 4% 3% 2% 1% 0% 8.19% 20-Year Annualized Returns ( ) 5.34% 4.83% US Stocks US Bonds International Stocks 3.14% 2.20% 2.11% Homes Inflation Average Investor US Stocks: S&P 500 Total Return Index; US Bonds: Barclays US Aggregate Bond Total Return Index; International Stocks: MSCI EAFE Total Return Index; Homes: U.S. existing home sales median price; Inflation: CPI-U; Average Investor: Average Asset Allocation Investor from "Quantitative Analysis of Investor Behavior, 2016," Dalbar, Inc., 21

22 Sources: Standard & Poor s, Barclays Capital and Ibbotson Associates Returns are through 3/31/

23 S&P 500 Index Historical Calendar Year Returns Source: Ibbotson Associates 23

24 Federal Reserve Interest Rate Expectations 24

25 Impact of Rising Interest Rates on Bond Values Note: Calculations are based on a hypothetical $10,000 par value bond with a 3.5% coupon rate and a base yield of 3.5%. 25

26 Passive Bond Investing Vanguard Total Bond Market Index Fund (VBTLX) Source: Morningstar, accessed April

27 Effect of Rising Interest Rates on Bond Funds 4 th Quarter st Quarter 2017 Vanguard Long-Term Bond Index Fund (VBLTX) Fidelity Long-Term Treasury Bond Index Fund (FLBAX) Vanguard Total Bond Market Index Fund (VBTLX) Fidelity Total Bond Index Fund (FTBFX) 27

28 Determine Risk Tolerance Risk Tolerance = A level of volatility (risk) that an investor accepts plus An understanding that achieving a financial goal is not a certainty. 28

29 Determine Asset Allocation Asset Class Cash & Equivalents Bonds Stocks Real Estate Other Example Savings account, money market funds, short term treasuries and certificates of deposit (mature in less than 1 year) Short-term (1-5 Years), intermediate-term (5-10 years), long-term (10+ years), investment grade, high yield Small-cap, mid-cap, large-cap, growth, growth and income, value, international, emerging markets, indexes Home, residential rental property, apartments / condos, office buildings, shopping centers, REITs Art, coins, precious metals, collectibles, natural resources, commodities, intangibles 29

30 Asset Allocation: Which spices & how much in Your Portfolio? Cash Bonds Stocks?%?%?% Portfolio 30

31 FIDELITY FREEDOM 2020 FUND [CA TE GO R [CATE GORY NAME ] [PERC ENTA GE] [CA TE GO R Target Date Funds (a sampling) VANGUARD TARGET RETIREMENT FUND 2020 [CA TEG OR Y [CATE GORY NAME] [PERC ENTAG E] [CA TEG OR Y WELLS FARGO DOW JONES TARGET 2020 FUND Cash & Other, 9% Bon d, 62% Sto ck, 29% Source: Morningstar, 02/28/

32 [CA TEG ORY NA [CAT EGOR Y NAM E] [CAT EGOR Y NAM E] [PER Aggressive [CA TE GO RY N [CA TEG ORY NA ME] [V [CA TEG ORY NA ME] Moderate [CA TE GO RY N [CA TE GO RY N [CA TEG ORY NA ME] [V Conservative 32 Consider Your Asset Allocation Sample Allocations

33 Asset Allocation Sample Return Conservative Portfolio Sample Return Asset Class Allocation Asset Class Portfolio Cash 10.0% 3.4% 0.3% Bonds 60.0% 5.1% 3.1% Stocks 30.0% 10.1% 3.0% Total Sample Return 6.4% NOTE: Sample asset class returns are calculated using historical average annualized benchmark index returns gross of fees for the period 1926 through March 31, Cash is represented by the U.S. T-Bill, bonds are represented by the Bloomberg Barclays Intermediate Government/Credit Index, and stocks are represented by the S&P 500 Index. 33

34 Asset Allocation Sample Return Moderate Portfolio Sample Return Asset Class Allocation Asset Class Portfolio Cash 5.0% 3.4% 0.2% Bonds 45.0% 5.1% 2.3% Stocks 50.0% 10.1% 5.0% Total Sample Return 7.5% NOTE: Sample asset class returns are calculated using historical average annualized benchmark index returns gross of fees for the period 1926 through March 31, Cash is represented by the U.S. T-Bill, bonds are represented by the Bloomberg Barclays Intermediate Government/Credit Index, and stocks are represented by the S&P 500 Index. 34

35 Asset Allocation Sample Return Aggressive Portfolio Sample Return Asset Class Allocation Asset Class Portfolio Cash 1.0% 3.4% 0.0% Bonds 9.0% 5.1% 0.5% Stocks 90.0% 10.1% 9.1% Total Sample Return 9.6% NOTE: Sample asset class returns are calculated using historical average annualized benchmark index returns gross of fees for the period 1926 through March 31, Cash is represented by the U.S. T-Bill, bonds are represented by the Bloomberg Barclays Intermediate Government/Credit Index, and stocks are represented by the S&P 500 Index. 35

36 Sample Asset Allocation Transition Pre-Retirement Post-Retirement 36

37 Consider Tax Efficiency Now 37

38 Effective Tax Rates 2017 Tax Brackets - Married Filing Joint Taxpayers But Not Over Pay + Of Excess Over 2017 Effective Tax Rate - MFJ Taxable Income Effective Tax Rate If Over Pay $0 $18,650 $0 10% $0 $18,650 $1, % $18,650 $75,900 $1,865 15% $18,650 $75,900 $10, % $75,900 $153,100 $10,453 25% $75,900 $153,100 $29, % $153,100 $233,350 $29,753 28% $153,100 $233,350 $52, % $233,350 $416,700 $52,223 33% $233,350 $416,700 $112, % $416,700 $470,700 $112,728 35% $416,700 $470,700 $131, % $470,700 $131, % $470, Tax Brackets - Single 2017 Effective Tax Rate - Single But Not Over Pay + Of Excess Over Taxable Income Effective Tax Rate If Over Pay $0 $9,325 $0 10% $0 $9,325 $ % $9,325 $37,950 $933 15% $9,325 $37,950 $5, % $37,950 $91,900 $5,226 25% $37,950 $91,900 $18, % $91,900 $191,650 $18,714 28% $91,900 $191,650 $46, % $191,650 $416,700 $46,644 33% $191,650 $416,700 $120, % $416,700 $418,400 $120,910 35% $416,700 $418,400 $121, % $418,400 $121, % $418,400 38

39 Tax-Efficient Planning Bracket Management & Preferential Rate Opportunities 39

40 Sample Tax-Efficient Allocation by Account Portfolio Target Account Targets Non-Qualified $900,000 4% Cash 36% Fixed Income 60% Equities IRAs & 401(k) $800,000 2% Cash 73% Fixed Income 25% Equities Roth IRAs $100,000 0% Cash 20% Fixed Income 80% Equities 40

41 Qualified Cash, 2% Construct Diversified Portfolio Sample Tax-Efficient Portfolio Structure Non-Qualified Cash, 4% Taxable Bonds, 67% High Dividen d Equities, 31% [CATEGO RY NAME], [VALUE] No/Low Dividend Equities, 60% 41

42 Types of Retirement Vehicles Individual Retirement Arrangements (IRAs) Roth IRAs 401(k) Plans 403(b) Plans SIMPLE IRA & 401(k) Plans SEP Plans SARSEP Plans Payroll Deduction IRAs Profit Sharing Plans Defined Benefit Plans Money Purchase Plans Employee Stock Ownership Plans 457 Plans HSA Accounts? 42

Hypothetical Example 43")

43 Net Unrealized Appreciation (NUA) Hypothetical Example 43 43

44 Potential Tax Savings NUA vs. IRA NOTE: Assumed ordinary marginal tax rate of 25% and capital gains rate of 15%. 44

45 Retirement Distribution Rules of Thumb Save 8-10 times your ending salary Safe withdrawal rate Detailed retirement analysis 45

Plus: Future")

46 Net Cash flow from current budget Retirement After-Tax Cash Needs Less: Expenses reduced or eliminated in retirement (Education costs, mortgage, commuting, etc.) Plus: Future retirement expenses (Additional travel, health care, etc.) = After-Tax Retirement Cash Needs 46

47 Income Needed During Working Years vs. Cash Needed in Retirement 47

48 $100,000 $80,000 $60,000 $40,000 $100,000 Impact of Inflation on Fixed Annual Income $86,261 $74,409 $64,186 Fixed Annual Amount: $100,000 Inflation Rate: 3% $55,368 $47,761 $41,199 $20,000 $0 Now Years Inflation-adjusted amount needed in 30 years to equal $100,000 in today s dollars is $242,

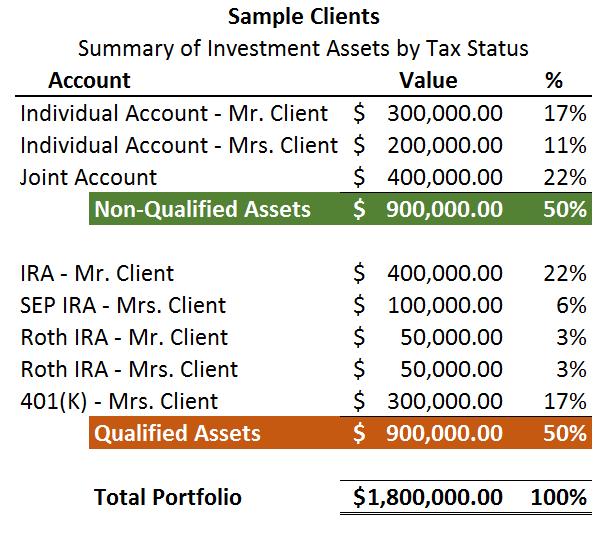

49 Retirement Distribution Tax Efficiency Non-Qualified Assets $900,000 Monthly Distributions $9,000 Qualified Assets $900,000 Annual Distributions $108,000 Total Portfolio $1,800,000 0 Monthly Distributions $9,000 0 Annual Distributions $108,000 0 Distributions From: 2017 Non-Qualified Qualified Qualified January $9,000 $9,000 February $9,000 $9,000 March $9,000 $9,000 April $9,000 $9,000 May $9,000 $9,000 June $9,000 $9,000 July $9,000 $9,000 August $9,000 $9,000 September $9,000 $9,000 October $9,000 $9,000 November $9,000 $9,000 December $9,000 $9,000 $54,000 $54,000 $108,000 Est. Taxable Interest (5% Coupon)* $22,500 $22,500 Est. Taxable Dividends (2% Yield)* $9,000 $9,000 Estimated Capital Gain** $27,000 $27,000 IRA Distribution $54,000 $108,000 Adusted Gross Income $112,500 $166,500 Less: Standard Deduction (2017) ($12,700) ($12,700) Less: Two Exemptions (2017) ($8,100) ($8,100) Taxable Income $91,700 $145,700 Tax Bill $9,793 $24,303 Tax as % of Taxable Income (Effective Tax Rate) 10.68% 16.68% *Income items based on 50/50 Asset Allocation Tax as % of Total Distribution 9.07% 22.50% **Capital Gain assumes 20% turnover of taxable account with 15% of proceeds being capital gain ($900,000 x 20% x 15%). Note, when 6 months of distributions are taken from the taxable joint account, taxable income drops into the 15% tax bracket. Under current law, qualified dividends and long-term capital gains for taxpayers in the 15% tax bracket are taxed at 0%. 49

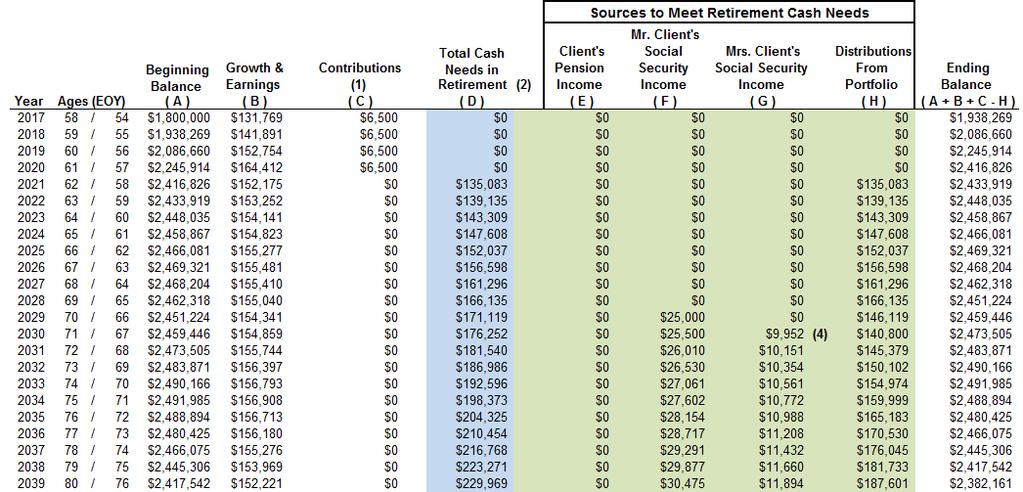

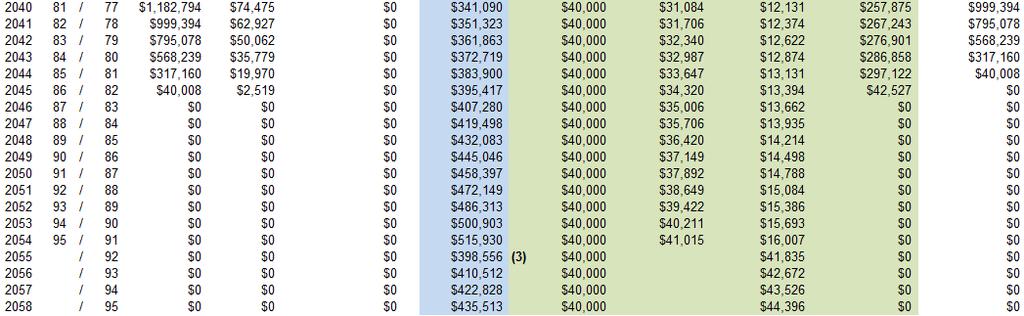

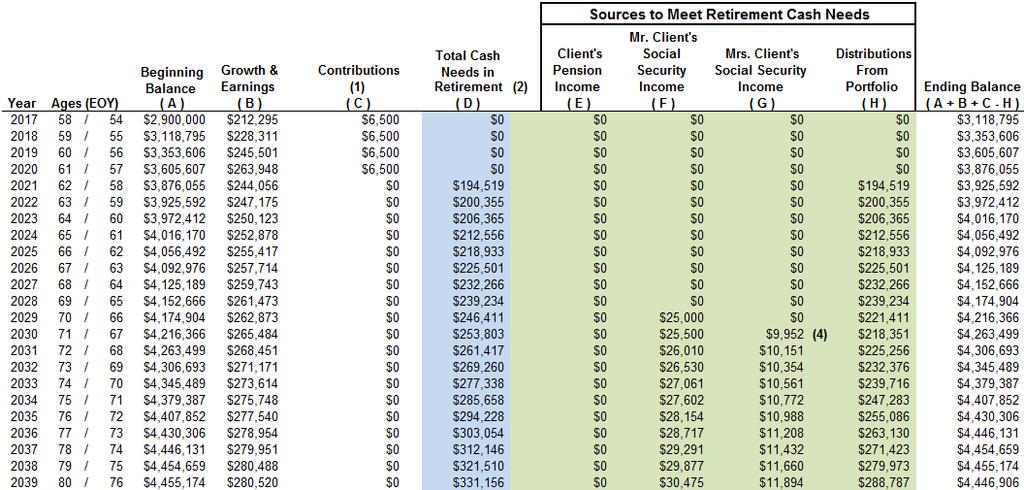

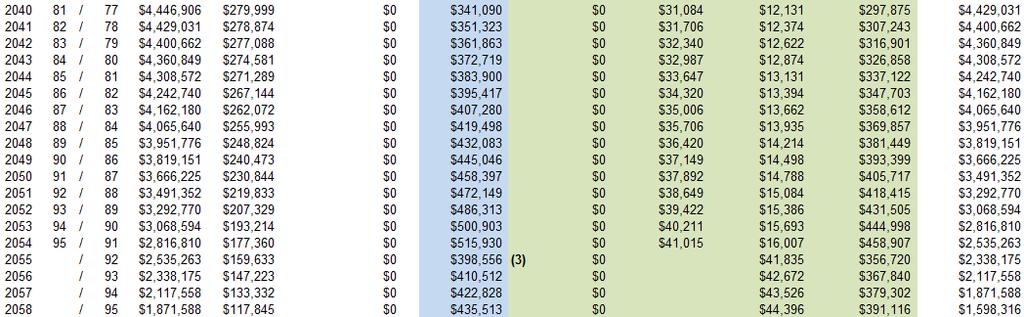

50 Example Retirement Analysis No. 1 (1) This amount reflects spousal benefits, which is based on half of Mr. Client's FRA Social Security Benefits. This is higher than her own benefit of $417/month. 50

51 Retirement Analysis Return Assumptions 51

52 52

53 53 53

This amount reflects spousal benefits, which is based on half of Mr.")

54 Example Retirement Analysis No. 2 (1) This amount reflects spousal benefits, which is based on half of Mr. Client's FRA Social Security Benefits. This is higher than her own benefit of $417/month. 54

55 . 55

56

This amount reflects spousal benefits, which is based on half of Mr.")

57 Example Retirement Analysis No. 3 (1) This amount reflects spousal benefits, which is based on half of Mr. Client's FRA Social Security Benefits. This is higher than her own benefit of $417/month. 57

58 58

59 59

This amount reflects spousal benefits, which is based on half of Mr.")

60 Example Retirement Analysis No. 4 (1) This amount reflects spousal benefits, which is based on half of Mr. Client's FRA Social Security Benefits. This is higher than her own benefit of $417/month

61 61

62 62

63 Thank you Additional information or answers to questions can be obtained by contacting: Steven R. Goodman, CPA, CFP Goodman Financial contributors to this Presentation Ed Roth, CFA, CPA, CFP, CEBS Wade D. Egmon, CPA, CFP Charlotte M. Jungen, CPA, CFP Morgann Ellis, CFP Chelsea Bailey Anna Ceker Dana Woodruff Quinten Womack Goodman Financial Corporation 5177 Richmond Ave, Suite 700 Houston, TX (713) Toll Free: (877) This firm is not a CPA firm. 63

JOURNEY. Planning for Financial Security SAVING : INVESTING : PLANNING

JOURNEY Planning for Financial Security SAVING : INVESTING : PLANNING Agenda 1 Cash management 2 Investment planning 3 Tax planning 4 Risk management 5 Retirement planning 6 Estate planning SAVING : INVESTING

JOURNEY Planning for Financial Security SAVING : INVESTING : PLANNING Agenda 1 Cash management 2 Investment planning 3 Tax planning 4 Risk management 5 Retirement planning 6 Estate planning SAVING : INVESTING

THE FREEDOM UMA. Unified Managed Account Strategies

THE FREEDOM UMA Unified Managed Account Strategies Freedom UMA Effective investment planning cannot be left to chance. It requires research, consultation, planning, execution and constant monitoring. When

THE FREEDOM UMA Unified Managed Account Strategies Freedom UMA Effective investment planning cannot be left to chance. It requires research, consultation, planning, execution and constant monitoring. When

The case for professional financial advice

The case for professional financial advice Professional financial advisors provide several services that may help the performance of a long-term financial program, and offer value to investors who might

The case for professional financial advice Professional financial advisors provide several services that may help the performance of a long-term financial program, and offer value to investors who might

Portfolio Management & Analysis

Index Portfolio Monitor, Analysis and Maintenance Page 2 Portfolio Rebalancing Emotional Control Annual Performance Page 3 Detailed Analysis Page 4 Portfolio Risk Level Portfolio Management & Analysis

Index Portfolio Monitor, Analysis and Maintenance Page 2 Portfolio Rebalancing Emotional Control Annual Performance Page 3 Detailed Analysis Page 4 Portfolio Risk Level Portfolio Management & Analysis

Vanguard Funds. Supplement to the Prospectus. Important Information Regarding Wire Redemptions

Vanguard Funds Supplement to the Prospectus Important Information Regarding Wire Redemptions Effective February 15, 2018, Vanguard will impose a $10 wire fee on outgoing wire redemptions from retirement

Vanguard Funds Supplement to the Prospectus Important Information Regarding Wire Redemptions Effective February 15, 2018, Vanguard will impose a $10 wire fee on outgoing wire redemptions from retirement

Building and Managing a Diversified Portfolio

Building and Managing a Diversified Portfolio Craig L. Israelsen, Ph.D. Designer of the Portfolio Presentation AAII Silicon Valley Chapter April 14, 2018 Based on research by Craig L. Israelsen, Ph.D.

Building and Managing a Diversified Portfolio Craig L. Israelsen, Ph.D. Designer of the Portfolio Presentation AAII Silicon Valley Chapter April 14, 2018 Based on research by Craig L. Israelsen, Ph.D.

Investment Policies and Objectives. of the

Investment Policies and Objectives of the Lower Colorado River Authority 401(k) Plan And the Lower Colorado River Authority Deferred Compensation Plan Effective as of August 17, 2015 The Lower Colorado

Investment Policies and Objectives of the Lower Colorado River Authority 401(k) Plan And the Lower Colorado River Authority Deferred Compensation Plan Effective as of August 17, 2015 The Lower Colorado

LIFETIME INCOME CASE STUDY

Retirement Preparedness: Why 401(k) s Are Essential LIFETIME INCOME CASE STUDY Presented by Financial Sense Advisors, Inc. Registered Investment Advisor Austin & Gloria Kaiser Important Notice: This is

Retirement Preparedness: Why 401(k) s Are Essential LIFETIME INCOME CASE STUDY Presented by Financial Sense Advisors, Inc. Registered Investment Advisor Austin & Gloria Kaiser Important Notice: This is

Investment Strategy. Interpreting key concepts and choosing appropriate strategies

Investment Strategy Interpreting key concepts and choosing appropriate strategies STANDARDS Contents Asset Allocation 2 Strategic asset allocation 6 Tactical allocation 8 Choosing the appropriate mix 9

Investment Strategy Interpreting key concepts and choosing appropriate strategies STANDARDS Contents Asset Allocation 2 Strategic asset allocation 6 Tactical allocation 8 Choosing the appropriate mix 9

Vanguard Funds. Supplement to the Prospectus. Frequent-Trading Limitations

Vanguard Funds Supplement to the Prospectus Effective February 15, 2018, the text under the heading Frequent-Trading Limitations within the Investing With Vanguard section is amended to read as follows:

Vanguard Funds Supplement to the Prospectus Effective February 15, 2018, the text under the heading Frequent-Trading Limitations within the Investing With Vanguard section is amended to read as follows:

Drexel University Retirement Plan

Drexel University Retirement Plan 23A 7% is the average saving rate at Vanguard. Source: Vanguard, How America Saves 2016. Vanguard recommends saving 12% 15%. Retirement Income Calculator How much

Drexel University Retirement Plan 23A 7% is the average saving rate at Vanguard. Source: Vanguard, How America Saves 2016. Vanguard recommends saving 12% 15%. Retirement Income Calculator How much

YOUR GUIDE TO GETTING STARTED

University of Colorado Hospital Authority 401(a) Investment Account, 403(b) Matching Account, and the 457(b) Deferred Compensation Plan Invest in your retirement and yourself today, with help from the

University of Colorado Hospital Authority 401(a) Investment Account, 403(b) Matching Account, and the 457(b) Deferred Compensation Plan Invest in your retirement and yourself today, with help from the

Schwab Indexed Retirement Trust Fund 2040

Fund Facts Trustee Fund Type Charles Schwab Bank Collective Trust Fund Category Target Date 2036-2040 Benchmark 2040 Custom Index 1 Unit Class Inception Date Fund Inception Date 1/5/2009 Net Asset Value

Fund Facts Trustee Fund Type Charles Schwab Bank Collective Trust Fund Category Target Date 2036-2040 Benchmark 2040 Custom Index 1 Unit Class Inception Date Fund Inception Date 1/5/2009 Net Asset Value

Exchange Traded Fund Strategies

Exchange Traded Fund Strategies 221 W. 6 th Street, Suite 1210 Austin, Texas 78701 Phone 512.477.3110 Fax 512.472.1046 Teresa Finney Senior Vice President, Investments Richard A. Funk, CFP First Vice President,

Exchange Traded Fund Strategies 221 W. 6 th Street, Suite 1210 Austin, Texas 78701 Phone 512.477.3110 Fax 512.472.1046 Teresa Finney Senior Vice President, Investments Richard A. Funk, CFP First Vice President,

Vanguard Funds. Supplement to the Prospectus. Frequent-Trading Limitations

Vanguard Funds Supplement to the Prospectus Effective February 15, 2018, the text under the heading Frequent-Trading Limitations within the Investing With Vanguard section is amended to read as follows:

Vanguard Funds Supplement to the Prospectus Effective February 15, 2018, the text under the heading Frequent-Trading Limitations within the Investing With Vanguard section is amended to read as follows:

Schwab Intelligent Portfolios. Investing has changed forever.

Schwab Intelligent Portfolios. Investing has changed forever. Technology that will change the way you invest. Schwab Intelligent Portfolios is an automated investment advisory service that builds, monitors,

Schwab Intelligent Portfolios. Investing has changed forever. Technology that will change the way you invest. Schwab Intelligent Portfolios is an automated investment advisory service that builds, monitors,

Liberty Mutual 401(k) Plan Annual Fee Disclosure Statement

Plan Annual Fee Disclosure Statement") Liberty Mutual 401(k) Plan Annual Fee Disclosure Statement Important information about Your Options, Fees and Other Expenses The Liberty Mutual 401(k) Plan (the Plan ) is a great way to build savings for

Liberty Mutual 401(k) Plan Annual Fee Disclosure Statement Important information about Your Options, Fees and Other Expenses The Liberty Mutual 401(k) Plan (the Plan ) is a great way to build savings for

Investment Advisor(s)

") Vanguard Funds Supplement to the Prospectus At a special meeting held on November 15, 2017, shareholders of the Vanguard funds voted on several proposed changes to the funds. As a result, the following

Vanguard Funds Supplement to the Prospectus At a special meeting held on November 15, 2017, shareholders of the Vanguard funds voted on several proposed changes to the funds. As a result, the following

Investments 7: Building Your Portfolio

Personal Finance: Another Perspective Investments 7: Building Your Portfolio Updated 2017/06/07 1 1 Objectives A. Understand Which Factors Control Investment Returns B. Understand the Priority of Money

Personal Finance: Another Perspective Investments 7: Building Your Portfolio Updated 2017/06/07 1 1 Objectives A. Understand Which Factors Control Investment Returns B. Understand the Priority of Money

Strategies for staying on track to your retirement

Strategies for staying on track to your retirement TIAA-CREF and you: Planning an income for life For more than 90 years, we at TIAA-CREF have dedicated ourselves to helping those who serve the greater

Strategies for staying on track to your retirement TIAA-CREF and you: Planning an income for life For more than 90 years, we at TIAA-CREF have dedicated ourselves to helping those who serve the greater

John Client & Jane Client

REPORT PREPARED FOR John Client & Jane Client by Patrick Brewer, CFA, CPA SurePath Wealth Management T his report is not complete without the a ccompa ny ing disclosure pa ge. Important Information This

REPORT PREPARED FOR John Client & Jane Client by Patrick Brewer, CFA, CPA SurePath Wealth Management T his report is not complete without the a ccompa ny ing disclosure pa ge. Important Information This

ASSET ALLOCATION & INVESTMENT PLANNING. CHITRA IYER COO MFA Consulting Pvt. Ltd.

ASSET ALLOCATION & INVESTMENT PLANNING CHITRA IYER COO MFA Consulting Pvt. Ltd. Asset Allocation Investor s dilemma What is Asset Allocation? Asset allocation - Why does it matter? Asset allocation - How

ASSET ALLOCATION & INVESTMENT PLANNING CHITRA IYER COO MFA Consulting Pvt. Ltd. Asset Allocation Investor s dilemma What is Asset Allocation? Asset allocation - Why does it matter? Asset allocation - How

FundSource. Professionally managed, diversified mutual fund portfolios. A sophisticated approach to mutual fund investing

FundSource Professionally managed, diversified mutual fund portfolios Is this program right for you? FundSource is designed for investors who: Want a diversified portfolio of mutual funds that fits their

FundSource Professionally managed, diversified mutual fund portfolios Is this program right for you? FundSource is designed for investors who: Want a diversified portfolio of mutual funds that fits their

GUIDANCE. Retirement Income Strategies SAVING : INVESTING : PLANNING

GUIDANCE Retirement Income Strategies About this seminar Objectives > To explore the major risks to retirement > To introduce the benefits of sound financial planning > To provide simple action steps to

GUIDANCE Retirement Income Strategies About this seminar Objectives > To explore the major risks to retirement > To introduce the benefits of sound financial planning > To provide simple action steps to

IBM 401(k) Plus Plan. Individual Fund Flyer Conservative Fund

Plus Plan. Individual Fund Flyer Conservative Fund") IBM 401(k) Plus Plan Individual Fund Flyer Conservative Fund This investment option is a unitized fund and not a mutual fund and as such is not registered with the Securities Exchange Commission (SEC).

IBM 401(k) Plus Plan Individual Fund Flyer Conservative Fund This investment option is a unitized fund and not a mutual fund and as such is not registered with the Securities Exchange Commission (SEC).

Wells Fargo Target Today Fund (formerly Wells Fargo Dow Jones Target Today Fund)

") Prospectus July 14, 2017 Target Date Funds Wells Fargo Fund Wells Fargo Target Today Fund (formerly Wells Fargo Dow Jones Target Today Fund) Wells Fargo Target 2010 Fund (formerly Wells Fargo Dow Jones

Prospectus July 14, 2017 Target Date Funds Wells Fargo Fund Wells Fargo Target Today Fund (formerly Wells Fargo Dow Jones Target Today Fund) Wells Fargo Target 2010 Fund (formerly Wells Fargo Dow Jones

PLAN YOUR FINANCIAL FUTURE PREPARING FOR RETIREMENT

This program is made possible by a grant from the FINRA Investor Education Foundation through Smart Investing@your library, a partnership with the American Library Association. PLAN YOUR FINANCIAL FUTURE

This program is made possible by a grant from the FINRA Investor Education Foundation through Smart Investing@your library, a partnership with the American Library Association. PLAN YOUR FINANCIAL FUTURE

Navigating the ETF Landscape

Navigating the ETF Landscape Daniel Prince, CFA Director, Head of ishares Product Consulting May 3, 2017 Agenda What are Exchange Traded Funds (ETFs) What is driving ETF usage ETF trends and innovation

Navigating the ETF Landscape Daniel Prince, CFA Director, Head of ishares Product Consulting May 3, 2017 Agenda What are Exchange Traded Funds (ETFs) What is driving ETF usage ETF trends and innovation

INSURANCE PRODUCTS offered through: Page 1 of 16. Presented by: Judson D. MallardCFP, ChFC, CFS

Disclosure Notice The information that follows is intended to serve as a basis for further discussion with your financial, legal, tax and/or accounting advisors. It is not a substitute for competent advice

Disclosure Notice The information that follows is intended to serve as a basis for further discussion with your financial, legal, tax and/or accounting advisors. It is not a substitute for competent advice

Wells Fargo Target 2020 Fund

Summary Prospectus July 14, 2017 Wells Fargo Target 2020 Fund Class/Ticker: Class A - STTRX; Class C - WFLAX Link to Prospectus Link to SAI Before you invest, you may want to review the Fund's prospectus,

Summary Prospectus July 14, 2017 Wells Fargo Target 2020 Fund Class/Ticker: Class A - STTRX; Class C - WFLAX Link to Prospectus Link to SAI Before you invest, you may want to review the Fund's prospectus,

Vanguard Funds. Supplement to the Prospectus. Important Information Regarding Wire Redemptions

Vanguard Funds Supplement to the Prospectus Important Information Regarding Wire Redemptions Effective February 15, 2018, Vanguard will impose a $10 wire fee on outgoing wire redemptions from retirement

Vanguard Funds Supplement to the Prospectus Important Information Regarding Wire Redemptions Effective February 15, 2018, Vanguard will impose a $10 wire fee on outgoing wire redemptions from retirement

Santé Operations LLC 401(k) Profit Sharing Plan and Trust Summary Guide September 30, Tim Wood, Principal David Foster, CFP, Principal

Profit Sharing Plan and Trust Summary Guide September 30, Tim Wood, Principal David Foster, CFP, Principal") Santé Operations LLC 401(k) Profit Sharing Plan and Trust Summary Guide September 30, 2018 Tim Wood, Principal David Foster, CFP, Principal Foster Wealth, Inc. is a Registered Investment Advisor Welcome

Santé Operations LLC 401(k) Profit Sharing Plan and Trust Summary Guide September 30, 2018 Tim Wood, Principal David Foster, CFP, Principal Foster Wealth, Inc. is a Registered Investment Advisor Welcome

YOUR GUIDE TO GETTING STARTED

Rochester Regional Health 401(k) Defined Contribution Plan Invest in your retirement and yourself today, with help from the Rochester Regional Health 401(k) Defined Contribution Plan and Fidelity. YOUR

Rochester Regional Health 401(k) Defined Contribution Plan Invest in your retirement and yourself today, with help from the Rochester Regional Health 401(k) Defined Contribution Plan and Fidelity. YOUR

SUPPLEMENT DATED APRIL 2018 TO NEW YORK S 529 COLLEGE SAVINGS PROGRAM DIRECT PLAN

SUPPLEMENT DATED APRIL 2018 TO NEW YORK S 529 COLLEGE SAVINGS PROGRAM DIRECT PLAN DISCLOSURE BOOKLET AND TUITION SAVINGS AGREEMENT DATED AUGUST 31, 2016 This Supplement describes important changes and

SUPPLEMENT DATED APRIL 2018 TO NEW YORK S 529 COLLEGE SAVINGS PROGRAM DIRECT PLAN DISCLOSURE BOOKLET AND TUITION SAVINGS AGREEMENT DATED AUGUST 31, 2016 This Supplement describes important changes and

401(k) Plan Highlights

Plan Highlights") 401(k) Plan Highlights RETIREMENT & BENEFIT PLAN SERVICES HomeServices Retirement Savings Plan Congratulations! You are eligible to join the HomeServices Retirement Savings Plan (the Plan ). The Plan offers

401(k) Plan Highlights RETIREMENT & BENEFIT PLAN SERVICES HomeServices Retirement Savings Plan Congratulations! You are eligible to join the HomeServices Retirement Savings Plan (the Plan ). The Plan offers

An Introduction to Bonds

An Introduction to Bonds Agenda Bond basics Different types of bonds Bond features Yield and tax considerations Bond risks Credit quality Bond investing strategies and client suitability Defining Characteristics

An Introduction to Bonds Agenda Bond basics Different types of bonds Bond features Yield and tax considerations Bond risks Credit quality Bond investing strategies and client suitability Defining Characteristics

Vanguard Funds. Supplement to the Prospectus. Frequent-Trading Limitations

Vanguard Funds Supplement to the Prospectus Effective February 15, 2018, the text under the heading Frequent-Trading Limitations within the Investing With Vanguard section is amended to read as follows:

Vanguard Funds Supplement to the Prospectus Effective February 15, 2018, the text under the heading Frequent-Trading Limitations within the Investing With Vanguard section is amended to read as follows:

MoneyWise Module 3 Saving and Investing: The Road to Financial Independence

Personal Finance Essentials: 8 Financial Priorities III MoneyWise Workshop Saving and Investing: The Road to Financial Independence Module 3 Discussion Topics 1. Perspectives: Spiritual matters 5. Investing

Personal Finance Essentials: 8 Financial Priorities III MoneyWise Workshop Saving and Investing: The Road to Financial Independence Module 3 Discussion Topics 1. Perspectives: Spiritual matters 5. Investing

RBC Strategic Asset Allocation Models

Page 1 of 7 United States Traditional Fixed Income Only Last updated: March 218 Fixed Income Only The focus is capital preservation. The portfolio is only invested in fixed income asset classes. The investor

Page 1 of 7 United States Traditional Fixed Income Only Last updated: March 218 Fixed Income Only The focus is capital preservation. The portfolio is only invested in fixed income asset classes. The investor

Supplement to the Prospectus Dated January 26, Prospectus Changes. All references to the Dow Jones U.S. Total Stock Market Index are deleted.

Vanguard Target Retirement Income Fund Vanguard Target Retirement 2015 Fund Vanguard Target Retirement 2025 Fund Vanguard Target Retirement 2035 Fund Vanguard Target Retirement 2045 Fund Supplement to

Vanguard Target Retirement Income Fund Vanguard Target Retirement 2015 Fund Vanguard Target Retirement 2025 Fund Vanguard Target Retirement 2035 Fund Vanguard Target Retirement 2045 Fund Supplement to

Investment Advisor(s)

") Vanguard Funds Supplement to the Prospectus At a special meeting held on November 15, 2017, shareholders of the Vanguard funds voted on several proposed changes to the funds. As a result, the following

Vanguard Funds Supplement to the Prospectus At a special meeting held on November 15, 2017, shareholders of the Vanguard funds voted on several proposed changes to the funds. As a result, the following

REPORT PREPARED FOR Client Sample & Co-client Sample

REPORT PREPARED FOR Client Sample & Co-client Sample by Steve Harvey Steve Harvey LLC Generated on 01/30/2019 Steve Harvey 119 Oronoco Street, Suite 102 Alexandria, Virginia 22314 steve@steveharveyllc.com

REPORT PREPARED FOR Client Sample & Co-client Sample by Steve Harvey Steve Harvey LLC Generated on 01/30/2019 Steve Harvey 119 Oronoco Street, Suite 102 Alexandria, Virginia 22314 steve@steveharveyllc.com

Investment Tax Planning

Select Portfolio Management, Inc. David M. Jones, MBA Wealth Advisor 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 dave.jones@selectportfolio.com www.selectportfolio.com Investment Tax Planning

Select Portfolio Management, Inc. David M. Jones, MBA Wealth Advisor 120 Vantis, Suite 430 Aliso Viejo, CA 92656 949-975-7900 dave.jones@selectportfolio.com www.selectportfolio.com Investment Tax Planning

Vanguard Funds. Supplement to the Prospectus. Frequent-Trading Limitations

Vanguard Funds Supplement to the Prospectus Effective February 15, 2018, the text under the heading Frequent-Trading Limitations within the Investing With Vanguard section is amended to read as follows:

Vanguard Funds Supplement to the Prospectus Effective February 15, 2018, the text under the heading Frequent-Trading Limitations within the Investing With Vanguard section is amended to read as follows:

CALM, COOL AND INVESTED

CALM, COOL AND INVESTED Staying on track to live the life you want This brochure provides year-end performance. When data for subsequent quarters are available, the brochure must be accompanied by a performance

CALM, COOL AND INVESTED Staying on track to live the life you want This brochure provides year-end performance. When data for subsequent quarters are available, the brochure must be accompanied by a performance

Creating Retirement Income to Last In this brochure, you ll find:

Creating Retirement Income to Last In this brochure, you ll find: An overview of the five key risks How to maximize income sources Your action plan Fidelity contact information Creating Retirement Income

Creating Retirement Income to Last In this brochure, you ll find: An overview of the five key risks How to maximize income sources Your action plan Fidelity contact information Creating Retirement Income

Vanguard Funds. Supplement to the Prospectus. Important Information Regarding Wire Redemptions

Vanguard Funds Supplement to the Prospectus Important Information Regarding Wire Redemptions Effective February 15, 2018, Vanguard will impose a $10 wire fee on outgoing wire redemptions from retirement

Vanguard Funds Supplement to the Prospectus Important Information Regarding Wire Redemptions Effective February 15, 2018, Vanguard will impose a $10 wire fee on outgoing wire redemptions from retirement

Quarterly Newsletter - Q1 2018

Quarterly Newsletter - Q1 2018 2018 Contribution Limit Changes The IRS increased the 402(g) contribution rates for 401(k), 403(b) and 457(b) plans this year, as well as increasing the maximum 415(c) limit

Quarterly Newsletter - Q1 2018 2018 Contribution Limit Changes The IRS increased the 402(g) contribution rates for 401(k), 403(b) and 457(b) plans this year, as well as increasing the maximum 415(c) limit

FINANCIAL FITNESS CENTER COURSES

Primary Subject Accounting Accounting Accounting Estate Planning Estate Planning Estate Planning ETFs ETFs Financial Institutions Tutorial Understanding the Balance Sheet Understanding the Income Statement

Primary Subject Accounting Accounting Accounting Estate Planning Estate Planning Estate Planning ETFs ETFs Financial Institutions Tutorial Understanding the Balance Sheet Understanding the Income Statement

Learn about asset allocation. Investor education

Learn about asset allocation Investor education Building a strong foundation Asset allocation is one of the key ingredients of a successful investment strategy. Use this brief guide to gain a more complete

Learn about asset allocation Investor education Building a strong foundation Asset allocation is one of the key ingredients of a successful investment strategy. Use this brief guide to gain a more complete

PORTFOLIO OPTIMIZATION FUNDS

PORTFOLIO OPTIMIZATION FUNDS DIVERSIFIED ASSET ALLOCATION SOLUTIONS UPDATED AS OF 3/31/18 MFC0639-0318 PORTFOLIO OPTIMIZATION FUNDS With thousands of mutual funds on the market today, creating a portfolio

PORTFOLIO OPTIMIZATION FUNDS DIVERSIFIED ASSET ALLOCATION SOLUTIONS UPDATED AS OF 3/31/18 MFC0639-0318 PORTFOLIO OPTIMIZATION FUNDS With thousands of mutual funds on the market today, creating a portfolio

Preparing to Reach Your Retirement Destination ANNUITIES VARIABLE. Gold Track Select

Preparing to Reach Your Retirement Destination ANNUITIES VARIABLE Gold Track Select WHY AN ANNUITY? The tool you need to be prepared for a long life. Retirement should be everything you hoped it would

Preparing to Reach Your Retirement Destination ANNUITIES VARIABLE Gold Track Select WHY AN ANNUITY? The tool you need to be prepared for a long life. Retirement should be everything you hoped it would

Forum Portfolio Investment Policy Statement

Forum Portfolio Investment Policy Statement Prepared for John Smith and Mary Smith Sunday February 12, 2017 60% Equities / 40% Fixed Income Growth Portfolio I. Purpose This Investment Policy Statement

Forum Portfolio Investment Policy Statement Prepared for John Smith and Mary Smith Sunday February 12, 2017 60% Equities / 40% Fixed Income Growth Portfolio I. Purpose This Investment Policy Statement

Diversified Managed Allocations

Diversified Managed Allocations Multi-strategy portfolios with a focus on flexibility Is this program right for you? DMA is designed for investors who: Want experienced, professional money managers to

Diversified Managed Allocations Multi-strategy portfolios with a focus on flexibility Is this program right for you? DMA is designed for investors who: Want experienced, professional money managers to

Vanguard Variable Insurance Fund Moderate Allocation Portfolio Summary Prospectus

Vanguard Variable Insurance Fund Moderate Allocation Portfolio Summary Prospectus April 28, 2017 The Fund s statutory Prospectus and Statement of Additional Information dated April 28, 2017, as may be

Vanguard Variable Insurance Fund Moderate Allocation Portfolio Summary Prospectus April 28, 2017 The Fund s statutory Prospectus and Statement of Additional Information dated April 28, 2017, as may be

Vanguard Bond ETFs Prospectus

Vanguard Bond ETFs Prospectus April 26, 2018 Exchange-traded fund shares that are not individually redeemable and are listed on NYSE Arca Vanguard Total Bond Market Index Fund ETF Shares (BND) Vanguard

Vanguard Bond ETFs Prospectus April 26, 2018 Exchange-traded fund shares that are not individually redeemable and are listed on NYSE Arca Vanguard Total Bond Market Index Fund ETF Shares (BND) Vanguard

Ben E. Keith Company Retirement Plans. Welcome to Empower Retirement!

Ben E. Keith Company Retirement Plans Welcome to Empower Retirement! Agenda Who is Empower Retirement? Your new 401(k) plan at Empower Investment options Transfer of your Ben E. Keith Profit Sharing Plan

Ben E. Keith Company Retirement Plans Welcome to Empower Retirement! Agenda Who is Empower Retirement? Your new 401(k) plan at Empower Investment options Transfer of your Ben E. Keith Profit Sharing Plan

Taxes and Investing. David Grabiner Bogleheads 2016 September 29, 2016

Taxes and Investing David Grabiner Bogleheads 2016 September 29, 2016 First things first Do not treat this as tax advice Not just a legal disclaimer; only your tax advisor knows the details of your tax

Taxes and Investing David Grabiner Bogleheads 2016 September 29, 2016 First things first Do not treat this as tax advice Not just a legal disclaimer; only your tax advisor knows the details of your tax

INVESTING FOR YOUR FINANCIAL FUTURE

INVESTING FOR YOUR FINANCIAL FUTURE Saving now, while time is on your side, can help provide you with freedom to do what you want later in life. B B INVESTING FOR YOUR FINANCIAL FUTURE YOUR FINANCIAL FUTURE

INVESTING FOR YOUR FINANCIAL FUTURE Saving now, while time is on your side, can help provide you with freedom to do what you want later in life. B B INVESTING FOR YOUR FINANCIAL FUTURE YOUR FINANCIAL FUTURE

Get retirement ready. Schwab Moneywise Workshop Series Month Day, Year

Get retirement ready. Schwab Moneywise Workshop Series Month Day, Year Debunking common assumptions Today we ll talk about Putting your plan together Managing your portfolio while you are waiting Taking

Get retirement ready. Schwab Moneywise Workshop Series Month Day, Year Debunking common assumptions Today we ll talk about Putting your plan together Managing your portfolio while you are waiting Taking

Understanding IRA and SIMPLE Plans

This Document Will Help You Prepare To Take The Online Examination A Center for Continuing Education 707 Whitlock Ave, SW, Suite C-27 Marietta, GA 30064 770-702-7917 800-344-1921 Fax: 770-702-7914 www.acceducation.com

This Document Will Help You Prepare To Take The Online Examination A Center for Continuing Education 707 Whitlock Ave, SW, Suite C-27 Marietta, GA 30064 770-702-7917 800-344-1921 Fax: 770-702-7914 www.acceducation.com

Advice and Planning. The Value of Working with a PNC Investments Financial Advisor

Advice and Planning The Value of Working with a PNC Investments Financial Advisor Financial Planning The Strong Foundation From Which We Work Just as you wouldn t contemplate starting a trip without a

Advice and Planning The Value of Working with a PNC Investments Financial Advisor Financial Planning The Strong Foundation From Which We Work Just as you wouldn t contemplate starting a trip without a

Beyond the Basics: Investing 201 March Presented by: Janet Gray, CFP Money Coaches Canada

Beyond the Basics: Investing 201 March 2016 Presented by: Janet Gray, CFP Money Coaches Canada Objectives: Review factors to consider when designing your investment portfolio: Risk tolerance Diversification

Beyond the Basics: Investing 201 March 2016 Presented by: Janet Gray, CFP Money Coaches Canada Objectives: Review factors to consider when designing your investment portfolio: Risk tolerance Diversification

ASSET ALLOCATION MADE EASY

ASSET ALLOCATION MADE EASY REACHING YOUR GOALS AT YOUR PACE Most people can rattle off their investment goals: retirement, college tuition, a new house. That s easy. What s harder is successfully reaching

ASSET ALLOCATION MADE EASY REACHING YOUR GOALS AT YOUR PACE Most people can rattle off their investment goals: retirement, college tuition, a new house. That s easy. What s harder is successfully reaching

Performance Supplement. The IBM 401(k) Plus Plan Investment Results

Plus Plan Investment Results") Performance Supplement The IBM 401(k) Plus Plan Investment Results Listed below is the annualized performance of the Primary investment options available through the IBM 401(k) Plus Plan for the period

Performance Supplement The IBM 401(k) Plus Plan Investment Results Listed below is the annualized performance of the Primary investment options available through the IBM 401(k) Plus Plan for the period

Retirement Redefined: Income Planning for the Modern Retiree

Retirement Redefined: Income Planning for the Modern Retiree Challenges and choices facing pre-retiree baby boomers For investors. Not FDIC Insured May Lose Value No Bank Guarantee Retirement Income Planning

Retirement Redefined: Income Planning for the Modern Retiree Challenges and choices facing pre-retiree baby boomers For investors. Not FDIC Insured May Lose Value No Bank Guarantee Retirement Income Planning

Income Investing basics

Income Investing basics investment options that can offer income, growth, and diversification Key questions to consider: What are your income-oriented investment options? What is the role of income in

Income Investing basics investment options that can offer income, growth, and diversification Key questions to consider: What are your income-oriented investment options? What is the role of income in

YOUR GUIDE TO GETTING STARTED

Ensign Services, Inc. 401(k) Retirement Savings Plan Invest in your retirement and yourself today, with help from the Ensign Services, Inc. 401(k) Retirement Savings Plan and Fidelity. YOUR GUIDE TO GETTING

Ensign Services, Inc. 401(k) Retirement Savings Plan Invest in your retirement and yourself today, with help from the Ensign Services, Inc. 401(k) Retirement Savings Plan and Fidelity. YOUR GUIDE TO GETTING

INDEX ADVISORYSM Deferred, Fixed Indexed Annuity

PACIFIC INDEX ADVISORYSM Deferred, Fixed Indexed Annuity FAC0059-0517 o WHY CHOOSE A FIXED INDEXED ANNUITY A fixed indexed annuity is a long-term contract between you and an insurance company that helps:

PACIFIC INDEX ADVISORYSM Deferred, Fixed Indexed Annuity FAC0059-0517 o WHY CHOOSE A FIXED INDEXED ANNUITY A fixed indexed annuity is a long-term contract between you and an insurance company that helps:

Chart your retirement course. It s easier than you think.

Chart your retirement course. It s easier than you think. Page 1 What can you control? Page 2 Today s discussion. 1. Your goals and vision 2. 4. 3. Set contribution Establish an investment strategy Roth

Chart your retirement course. It s easier than you think. Page 1 What can you control? Page 2 Today s discussion. 1. Your goals and vision 2. 4. 3. Set contribution Establish an investment strategy Roth

Six Best and Worst IRA Rollover Decisions

Six Best and Worst IRA Rollover Decisions Provided to you by: Bob Planner CPA Six Best and Worst IRA Rollover Decisions Written by Financial Educators Provided to you by Bob Planner CPA DE 068708 2 2018

Six Best and Worst IRA Rollover Decisions Provided to you by: Bob Planner CPA Six Best and Worst IRA Rollover Decisions Written by Financial Educators Provided to you by Bob Planner CPA DE 068708 2 2018

What Works. Our time-tested approach to investing is very straightforward. And we re ready to make it work for you. Three important steps.

What Works Our time-tested approach to investing is very straightforward. And we re ready to make it work for you. Three important steps. Ten effective principles. Three important steps. Ten effective

What Works Our time-tested approach to investing is very straightforward. And we re ready to make it work for you. Three important steps. Ten effective principles. Three important steps. Ten effective

PROFESSIONALLY MANAGED INVESTMENT SOLUTIONS THROUGH EXCHANGE TRADED FUNDS

PROFESSIONALLY MANAGED INVESTMENT SOLUTIONS THROUGH EXCHANGE TRADED FUNDS SCALING THE HEIGHTS SCALING THE HEIGHTS I WITH EXCHANGE TRADED FUNDS AN ETF-BASED DISCIPLINED PROCESS TO HELP YOU ACHIEVE YOUR

PROFESSIONALLY MANAGED INVESTMENT SOLUTIONS THROUGH EXCHANGE TRADED FUNDS SCALING THE HEIGHTS SCALING THE HEIGHTS I WITH EXCHANGE TRADED FUNDS AN ETF-BASED DISCIPLINED PROCESS TO HELP YOU ACHIEVE YOUR

Spectrum Report Compiled as of: November 30, 2016

Spectrum Report Compiled as of: November 30, 2016 Vanguard Target Retirement 2010 Fund Investor Shares Vanguard Target Retirement 2015 Fund Investor Shares Vanguard Target Retirement Income Fund Investor

Spectrum Report Compiled as of: November 30, 2016 Vanguard Target Retirement 2010 Fund Investor Shares Vanguard Target Retirement 2015 Fund Investor Shares Vanguard Target Retirement Income Fund Investor

MINNESOTA STATE UNIVERSITY MOORHEAD ALUMNI FOUNDATION. Investment Policy. General Overview

MINNESOTA STATE UNIVERSITY MOORHEAD ALUMNI FOUNDATION Policy General Overview The Minnesota State University Moorhead Alumni Foundation, Inc. is a publicly supported corporation that has been determined

MINNESOTA STATE UNIVERSITY MOORHEAD ALUMNI FOUNDATION Policy General Overview The Minnesota State University Moorhead Alumni Foundation, Inc. is a publicly supported corporation that has been determined

Pacific Mutual Door Company Partnership 401k Profit Sharing Plan

Pacific Mutual Door Company Partnership 401k Profit Sharing Plan 1 Plan Highlights 3 Plan Highlights 4 Plan Highlights 5 Plan Highlights 6 Plan Highlights 7 Plan Highlights 8 1.866.909.5148 3400 College

Pacific Mutual Door Company Partnership 401k Profit Sharing Plan 1 Plan Highlights 3 Plan Highlights 4 Plan Highlights 5 Plan Highlights 6 Plan Highlights 7 Plan Highlights 8 1.866.909.5148 3400 College

Deferred Compensation Plan

Deferred Compensation Plan E M P L O Y E E S E R V I C E S A G E N C Y EMPLOYEE BENEFITS A S S E R V I N G I T Y Y O U Y O U S E R V E O U R C O M M U N County of Santa Clara, Employee Services Agency

Deferred Compensation Plan E M P L O Y E E S E R V I C E S A G E N C Y EMPLOYEE BENEFITS A S S E R V I N G I T Y Y O U Y O U S E R V E O U R C O M M U N County of Santa Clara, Employee Services Agency

Target 401(k): Information About Your Investment Options, Fees, and Other Expenses

: Information About Your Investment Options, Fees, and Other Expenses") April 2017 NO ACTION IS REQUIRED Target 401(k): Information About Your Options, Fees, and Other Expenses As required by federal regulations, each year Target sends this notice with information about your

April 2017 NO ACTION IS REQUIRED Target 401(k): Information About Your Options, Fees, and Other Expenses As required by federal regulations, each year Target sends this notice with information about your

A R I S K - B A S E D A S S E T A L L O C A T I O N P R O G R A M TOPS. Pioneers in Strategic ETF Portfolios. 1 of 20

A R I S K - B A S E D A S S E T A L L O C A T I O N P R O G R A M VALMARK ADVISERS, INC. TOPS Pioneers in Strategic ETF Portfolios 1 of 20 TABLE OF CONTENTS 1 2 3 4 Foundational Investment Management Theory

A R I S K - B A S E D A S S E T A L L O C A T I O N P R O G R A M VALMARK ADVISERS, INC. TOPS Pioneers in Strategic ETF Portfolios 1 of 20 TABLE OF CONTENTS 1 2 3 4 Foundational Investment Management Theory

Amended as of January 1, 2018

THE WALLACE FOUNDATION INVESTMENT POLICY Amended as of January 1, 2018 1. INVESTMENT GOAL The investment goal of The Wallace Foundation (the Foundation) is to earn a total return that will provide a steady

THE WALLACE FOUNDATION INVESTMENT POLICY Amended as of January 1, 2018 1. INVESTMENT GOAL The investment goal of The Wallace Foundation (the Foundation) is to earn a total return that will provide a steady

Wells Fargo Target 2060 Fund

Summary Prospectus July 1, 2018 Wells Fargo Target 2060 Fund Class/Ticker: Class A - WFAFX; Class C - WFCFX Link to Prospectus Link to SAI Before you invest, you may want to review the Fund's prospectus,

Summary Prospectus July 1, 2018 Wells Fargo Target 2060 Fund Class/Ticker: Class A - WFAFX; Class C - WFCFX Link to Prospectus Link to SAI Before you invest, you may want to review the Fund's prospectus,

Schwab Diversified Growth Allocation Trust Fund (Closed to new investors) Institutional Unit Class As of June 30, 2017

Institutional Unit Class As of June 30, 2017") Fund Facts Trustee Fund Type Charles Schwab Bank Collective Trust Fund Morningstar Category Allocation - 50-70% Equity Benchmark Global Growth Custom Index 1 Unit Class Inception Date 3/7/2012 Fund Inception

Fund Facts Trustee Fund Type Charles Schwab Bank Collective Trust Fund Morningstar Category Allocation - 50-70% Equity Benchmark Global Growth Custom Index 1 Unit Class Inception Date 3/7/2012 Fund Inception

Saving for the Future MONDELĒZ GLOBAL LLC TIP PLAN. Investment Options Guide

Saving for the Future MONDELĒZ GLOBAL LLC TIP PLAN Investment Options Guide Effective August 31, 2016 TARGET DATE FUNDS The Target Date Funds are designed as an all-in-one approach for participants looking

Saving for the Future MONDELĒZ GLOBAL LLC TIP PLAN Investment Options Guide Effective August 31, 2016 TARGET DATE FUNDS The Target Date Funds are designed as an all-in-one approach for participants looking

Vanguard Total Bond Market Index Fund Summary Prospectus

Click here to view the fund's statutory prospectus or statement of additional information. Vanguard Total Bond Market Index Fund Summary Prospectus August 20, 2013 Institutional Shares & Institutional

Click here to view the fund's statutory prospectus or statement of additional information. Vanguard Total Bond Market Index Fund Summary Prospectus August 20, 2013 Institutional Shares & Institutional

Strategies for staying on track. Prepare yourself for the journey ahead

Strategies for staying on track Prepare yourself for the journey ahead TIAA and you: Working together to pursue a financially secure future At TIAA, our mission is simple: We re here to help our customers

Strategies for staying on track Prepare yourself for the journey ahead TIAA and you: Working together to pursue a financially secure future At TIAA, our mission is simple: We re here to help our customers

NVIT Investor Destinations Funds

NVIT Investor Destinations Funds Nationwide VIT Quarterly Asset class: Allocation Share class Class II Strategy Overview The NVIT Investor Destinations Funds (NVIT ID Funds) consist of seven risk-based

NVIT Investor Destinations Funds Nationwide VIT Quarterly Asset class: Allocation Share class Class II Strategy Overview The NVIT Investor Destinations Funds (NVIT ID Funds) consist of seven risk-based

INDEX FOUNDATIONSM Deferred, Fixed Indexed Annuity

PACIFIC INDEX FOUNDATIONSM Deferred, Fixed Indexed Annuity FAC0265-0418 o WHY CHOOSE A FIXED INDEXED ANNUITY? A fixed indexed annuity is a long-term contract between you and an insurance company that helps:

PACIFIC INDEX FOUNDATIONSM Deferred, Fixed Indexed Annuity FAC0265-0418 o WHY CHOOSE A FIXED INDEXED ANNUITY? A fixed indexed annuity is a long-term contract between you and an insurance company that helps:

INVESTING IN YOUR FUTURE: A TIAA FINANCIAL ESSENTIALS WORKSHOP. Money at Work 1: Foundations of investing

INVESTING IN YOUR FUTURE: A TIAA FINANCIAL ESSENTIALS WORKSHOP Money at Work 1: Foundations of investing Staying on course: Today s agenda Retirement Advisor Understanding saving Risk tolerance Asset classes

INVESTING IN YOUR FUTURE: A TIAA FINANCIAL ESSENTIALS WORKSHOP Money at Work 1: Foundations of investing Staying on course: Today s agenda Retirement Advisor Understanding saving Risk tolerance Asset classes

Your Envision profile. Client name:

Your Envision profile Client name: We ll help you live the life you ve imagined... Personal information Name: Spouse/Partner s name: Mailing address: State of primary residence: Date of birth (mm/dd/yyyy):

Your Envision profile Client name: We ll help you live the life you ve imagined... Personal information Name: Spouse/Partner s name: Mailing address: State of primary residence: Date of birth (mm/dd/yyyy):

CalPERS 457 Plan Target Retirement Date Funds

Asset Allocation CalPERS 457 Plan Target Retirement Date s December 31, 2017 Overview Target Retirement Date s (the "" or "s") are a series of diversified funds, each of which has a predetermined underlying

Asset Allocation CalPERS 457 Plan Target Retirement Date s December 31, 2017 Overview Target Retirement Date s (the "" or "s") are a series of diversified funds, each of which has a predetermined underlying

INDEX FOUNDATIONSM Deferred, Fixed Indexed Annuity

PACIFIC INDEX FOUNDATIONSM Deferred, Fixed Indexed Annuity FAC0265N10-1017 o WHY CHOOSE A FIXED INDEXED ANNUITY A fixed indexed annuity is a long-term contract between you and an insurance company that

PACIFIC INDEX FOUNDATIONSM Deferred, Fixed Indexed Annuity FAC0265N10-1017 o WHY CHOOSE A FIXED INDEXED ANNUITY A fixed indexed annuity is a long-term contract between you and an insurance company that

Using the 1040 to Find Planning Opportunities

Overview Income tax planning is an important aspect of your overall financial picture. The following tables provide a list of some of the items contained in an individual income tax return and a brief

Overview Income tax planning is an important aspect of your overall financial picture. The following tables provide a list of some of the items contained in an individual income tax return and a brief

Benchmarking Target-Date Funds: Art or Science?

Benchmarking Target-Date Funds: Art or Science? Jeremy Stempien Director of Investments Morningstar Investment Management Chicago, Illinois 2013 Morningstar. All Rights Reserved. These materials are for

Benchmarking Target-Date Funds: Art or Science? Jeremy Stempien Director of Investments Morningstar Investment Management Chicago, Illinois 2013 Morningstar. All Rights Reserved. These materials are for

See the following page for important information about your plan investments.

This notice contains important information about changes to the MMC 401(k) Savings and Retirement Plan. Please review it carefully. If you have any questions about the changes to the plan, the plan s investments,

This notice contains important information about changes to the MMC 401(k) Savings and Retirement Plan. Please review it carefully. If you have any questions about the changes to the plan, the plan s investments,

Alpha, Beta, and Now Gamma

Alpha, Beta, and Now Gamma David Blanchett, CFA, CFP Head of Retirement Research Morningstar Investment Management 2012 Morningstar. All Rights Reserved. These materials are for information and/or illustration

Alpha, Beta, and Now Gamma David Blanchett, CFA, CFP Head of Retirement Research Morningstar Investment Management 2012 Morningstar. All Rights Reserved. These materials are for information and/or illustration

Your DePaul University 403(b) Retirement Plan ENROLLMENT GUIDE

Retirement Plan ENROLLMENT GUIDE") Your DePaul University 403(b) Retirement Plan ENROLLMENT GUIDE Invest some of what you earn today for what you plan to accomplish tomorrow. Dear DePaul University 403(b) Retirement Plan employee: It s

Your DePaul University 403(b) Retirement Plan ENROLLMENT GUIDE Invest some of what you earn today for what you plan to accomplish tomorrow. Dear DePaul University 403(b) Retirement Plan employee: It s

The Asset Allocation Decision

The Asset Allocation Decision Individual Investor Life Cycle The Portfolio Management Process The Need for Policy Statement Constructing the Policy Statement The Importance of Asset Allocation 2-2 What

The Asset Allocation Decision Individual Investor Life Cycle The Portfolio Management Process The Need for Policy Statement Constructing the Policy Statement The Importance of Asset Allocation 2-2 What

Behavioral Investment Policy Statement. Coddington Family. Prepared on: 25 January 2013

Behavioral Investment Policy Statement Coddington Family Retirement Account Prepared on: 25 January 2013 Based on completion of the: Natural Behavior Discovery on: 14 March 2012 Financial Personality Discovery

Behavioral Investment Policy Statement Coddington Family Retirement Account Prepared on: 25 January 2013 Based on completion of the: Natural Behavior Discovery on: 14 March 2012 Financial Personality Discovery

Jean M. Lown, Ph.D. Family, Consumer, & Human Development. Thanks to: Barbara O Neill, Ph.D., CFP, Rutgers Cooperative Extension

Ready, Set Retire next year or in 30 years Jean M. Lown, Ph.D. Family, Consumer, & Human Development Thanks to: Barbara O Neill, Ph.D., CFP, Rutgers Cooperative Extension 1 Overview Understanding risk

Ready, Set Retire next year or in 30 years Jean M. Lown, Ph.D. Family, Consumer, & Human Development Thanks to: Barbara O Neill, Ph.D., CFP, Rutgers Cooperative Extension 1 Overview Understanding risk

YOUR GUIDE TO GETTING STARTED

Brandeis University Defined Contribution Retirement Plan Invest in your retirement and yourself today, with help from the Brandeis University 403(b) Plan and Fidelity. YOUR GUIDE TO GETTING STARTED Invest

Brandeis University Defined Contribution Retirement Plan Invest in your retirement and yourself today, with help from the Brandeis University 403(b) Plan and Fidelity. YOUR GUIDE TO GETTING STARTED Invest