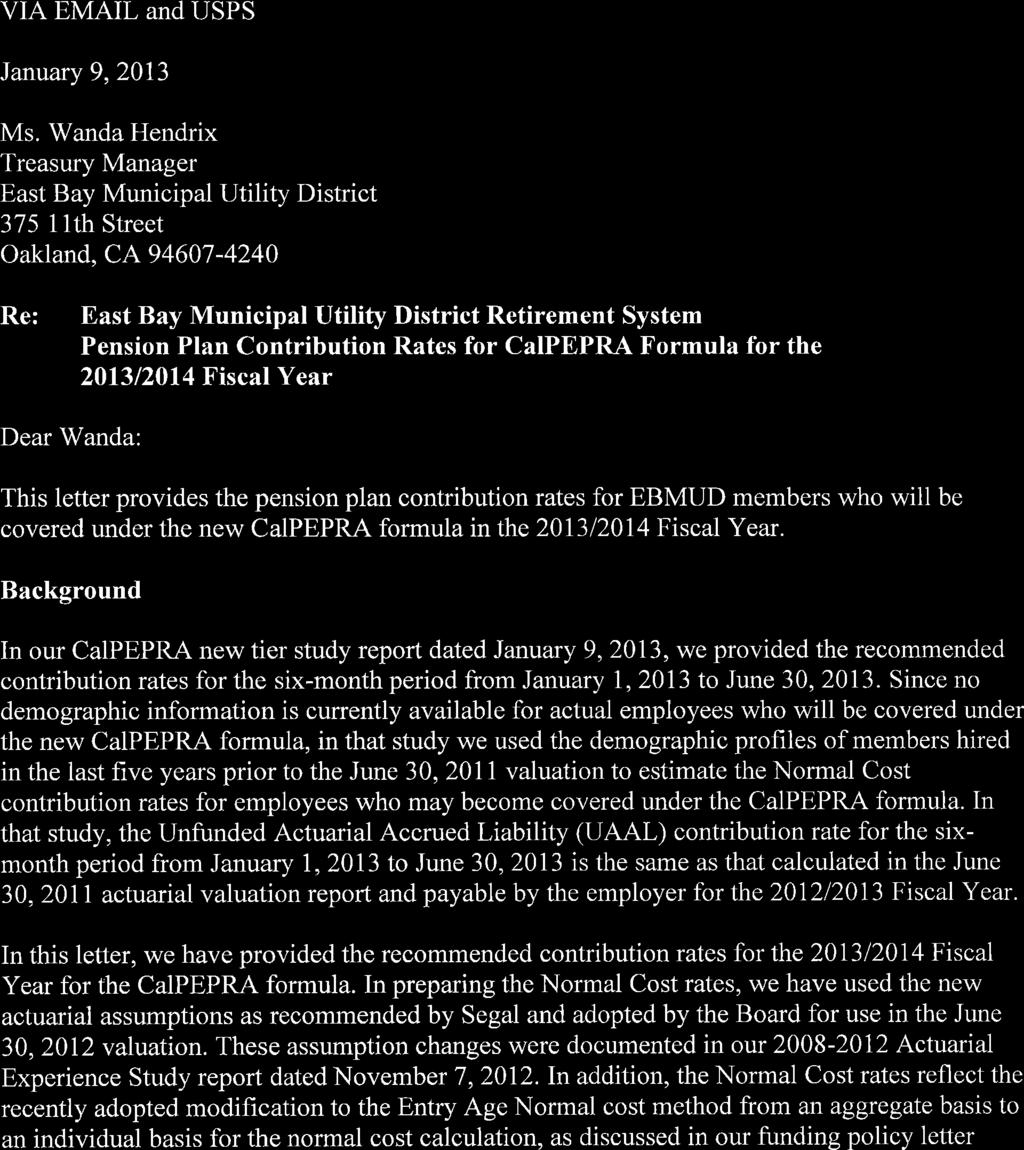

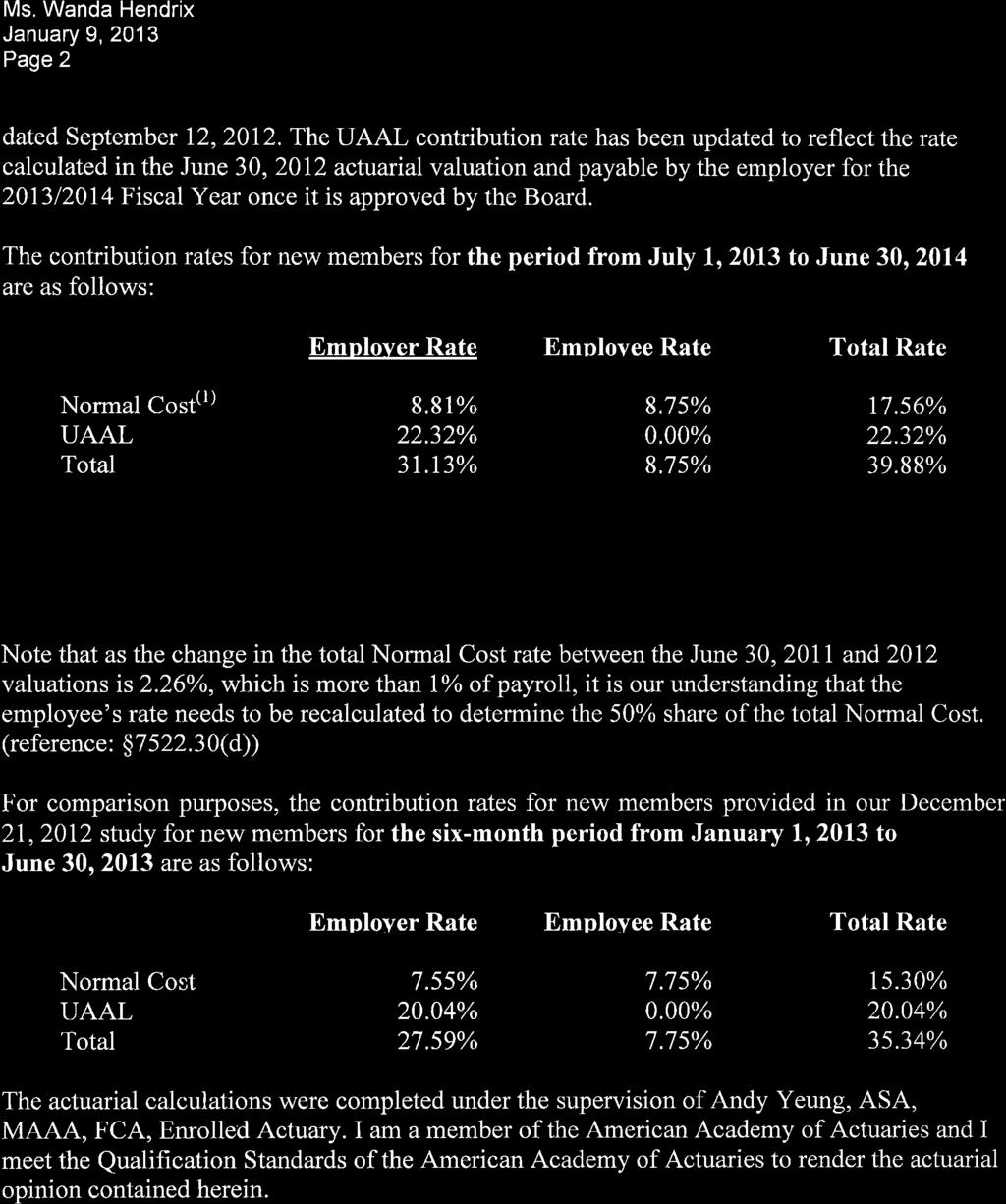

AGENDA EBMUD EMPLOYEES RETIREMENT SYSTEM January 17, 2013 Training Resource Center (TRC1) 8:30 a.m.

|

|

|

- Mark Fleming

- 5 years ago

- Views:

Transcription

1

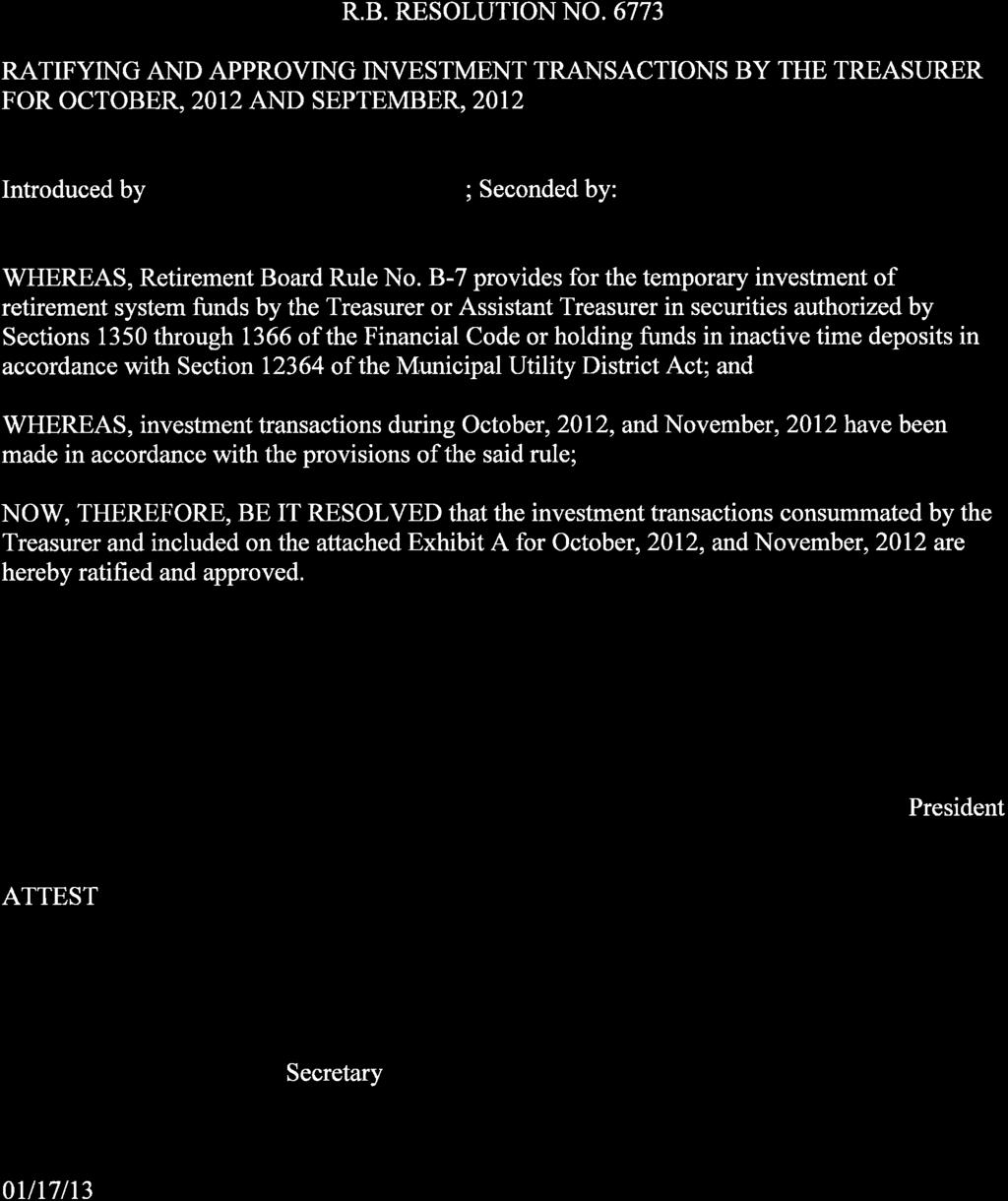

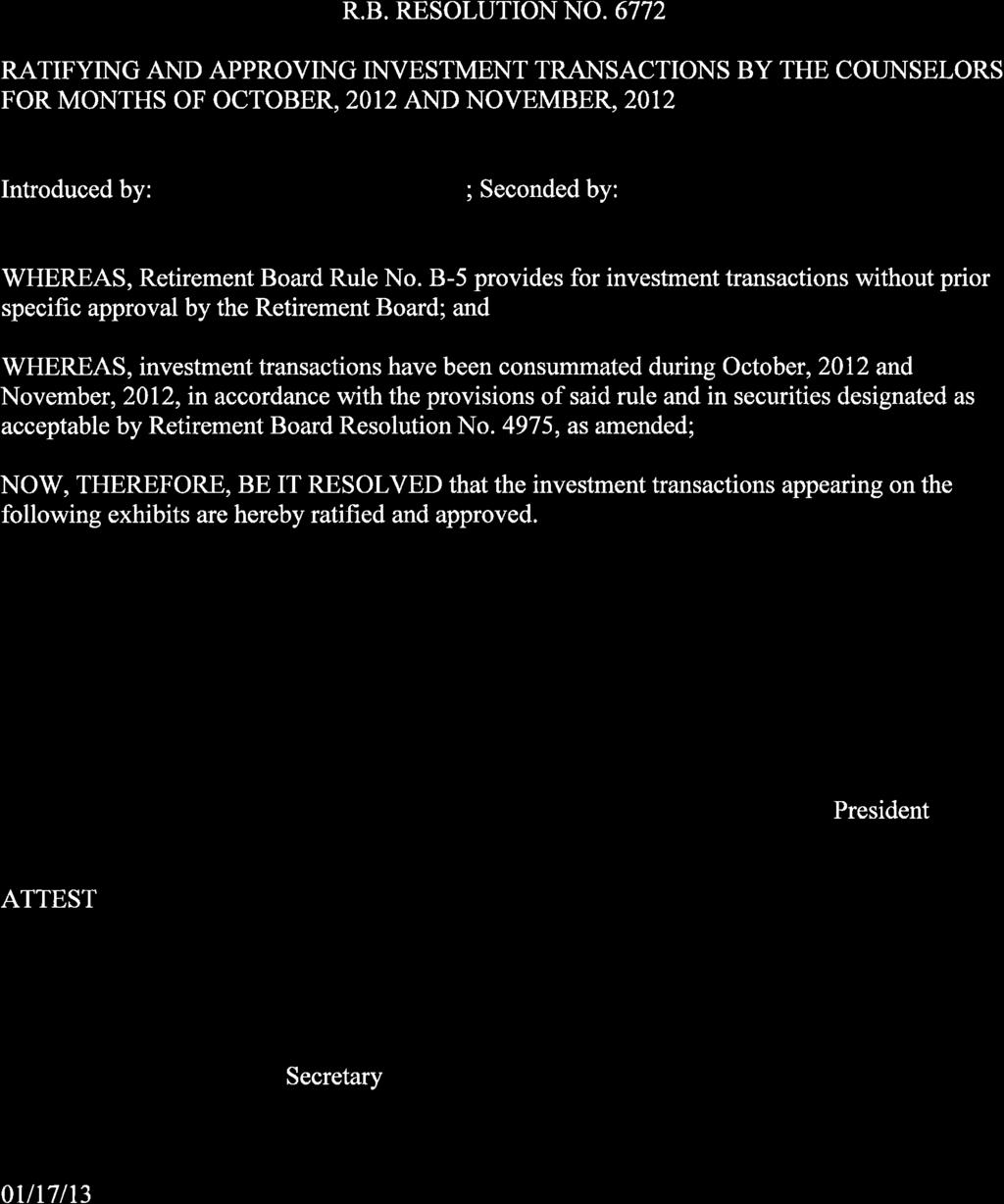

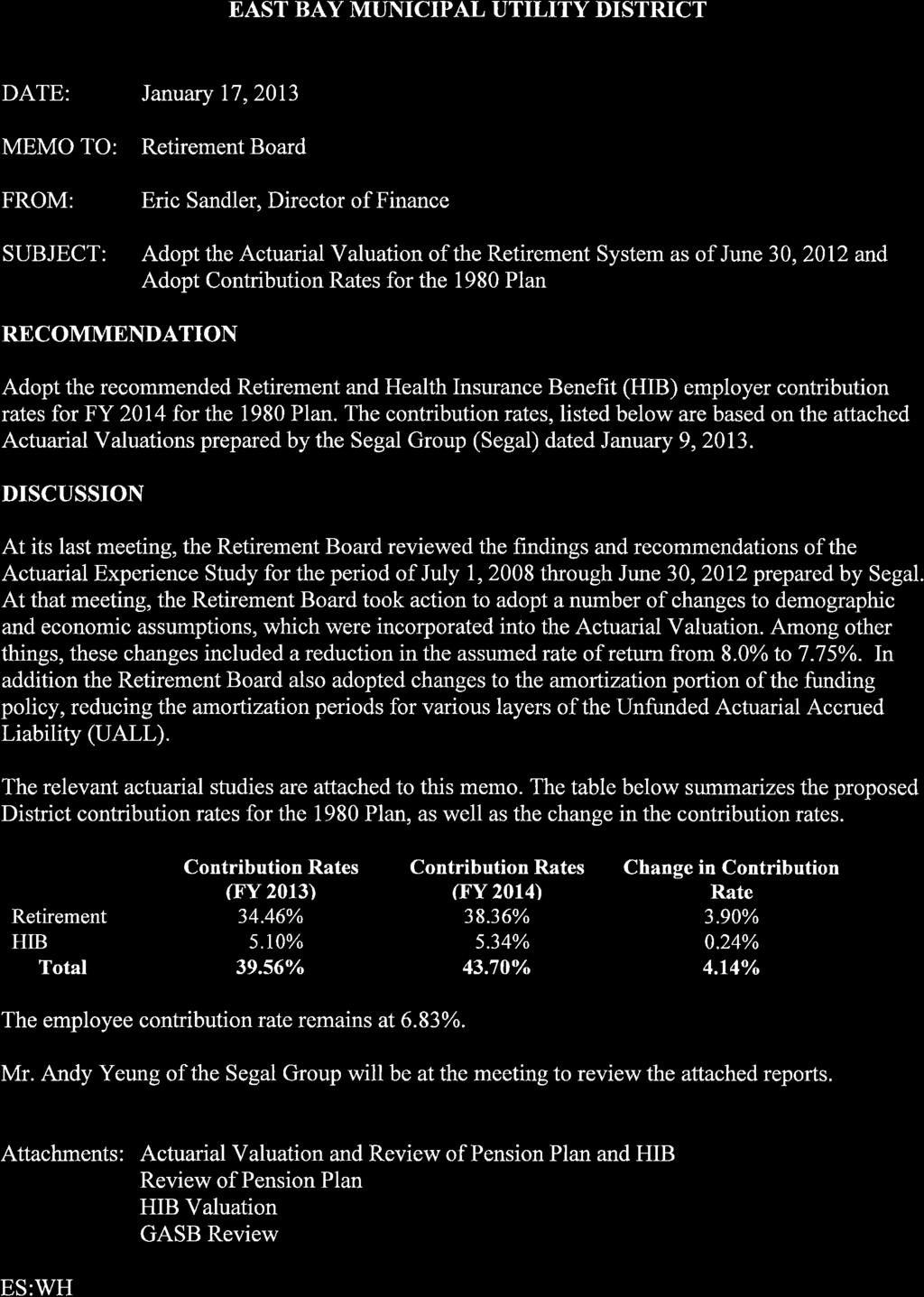

2 AGENDA EBMUD EMPLOYEES RETIREMENT SYSTEM January 17, 2013 Training Resource Center (TRC1) 8:30 a.m. ROLL CALL: PUBLIC COMMENT: The Retirement Board is limited by State Law to providing a brief response, asking questions for clarification, or referring a matter to staff when responding to items that are not listed on the agenda. ANNOUNCEMENT OF CLOSED SESSION AGENDA: 1. Existing Litigation Pursuant to Government Code Section (a): EBMUD Employees Retirement System v. Arceneaux Alameda County Superior Court, Small Claims Division Case No. RS ROLL CALL: REGULAR BUSINESS MEETING: Upon completion of Closed Session PUBLIC COMMENT: The Retirement Board is limited by State Law to providing a brief response, asking questions for clarification, or referring a matter to staff when responding to items that are not listed on the agenda. CONSENT CALENDAR: 1. Approval of Minutes Regular Meeting of November 15, Treasurer s Statement of Receipts and Disbursements for October 2012 and November Ratifying and Approving Investment Transactions by Counselors for October 2012 and November 2012 (R.B. Resolution No. 6772) 4. Ratifying and Approving Investment Transactions by Treasurer for October and November 2012 (R.B. Resolution No. 6773) ACTION: 5. Adopt the Actuarial Valuation of the Retirement System as of June 30, 2012 E. Sandler a) Adopt the contribution rates for the 1980 Plan and the Health Insurance Benefit b) Adopt the contribution rates for the 2013 Plan 6. Declaring the Rate of Interest Credited to Members (R. B. Resolution No. 6774) E. Grassetti

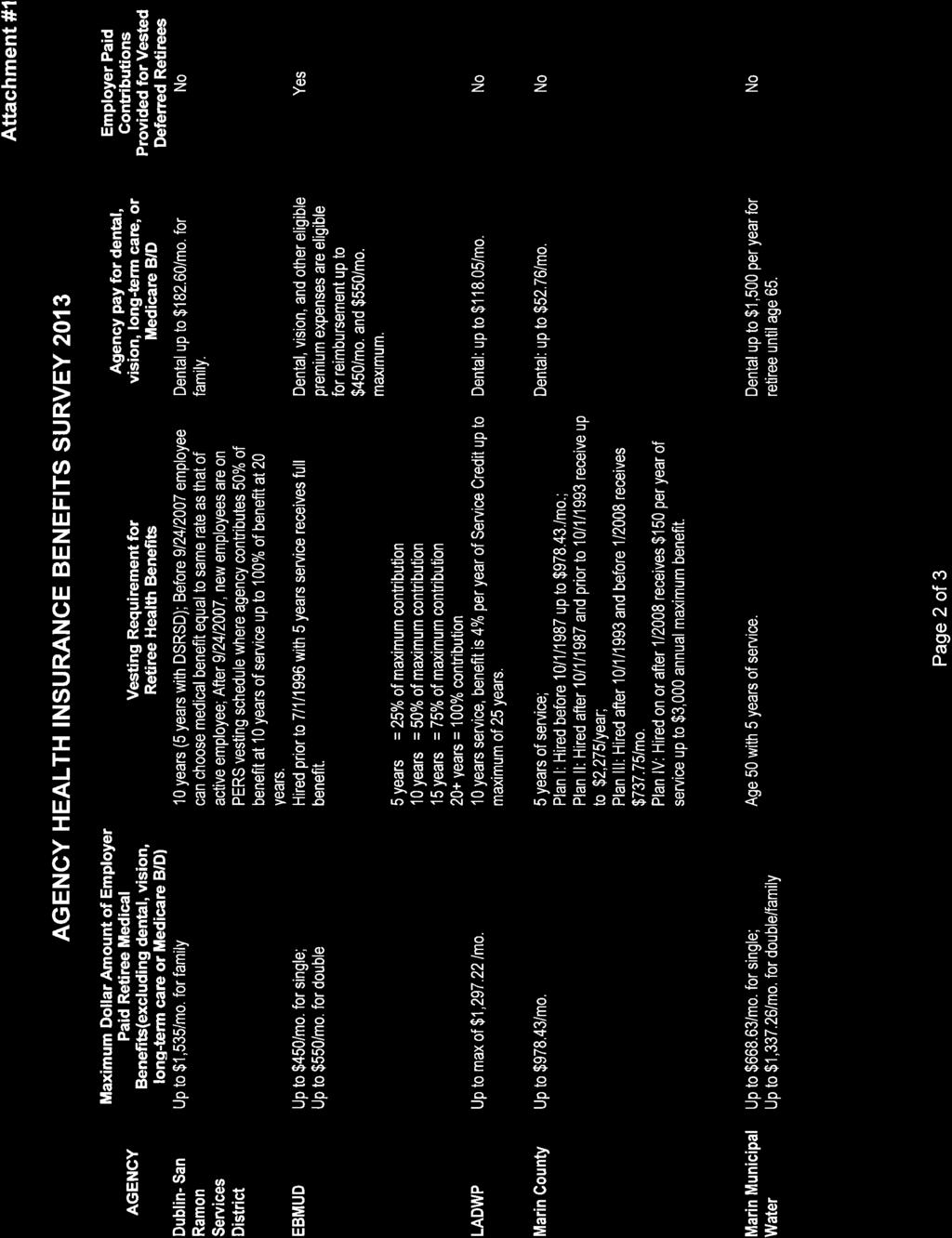

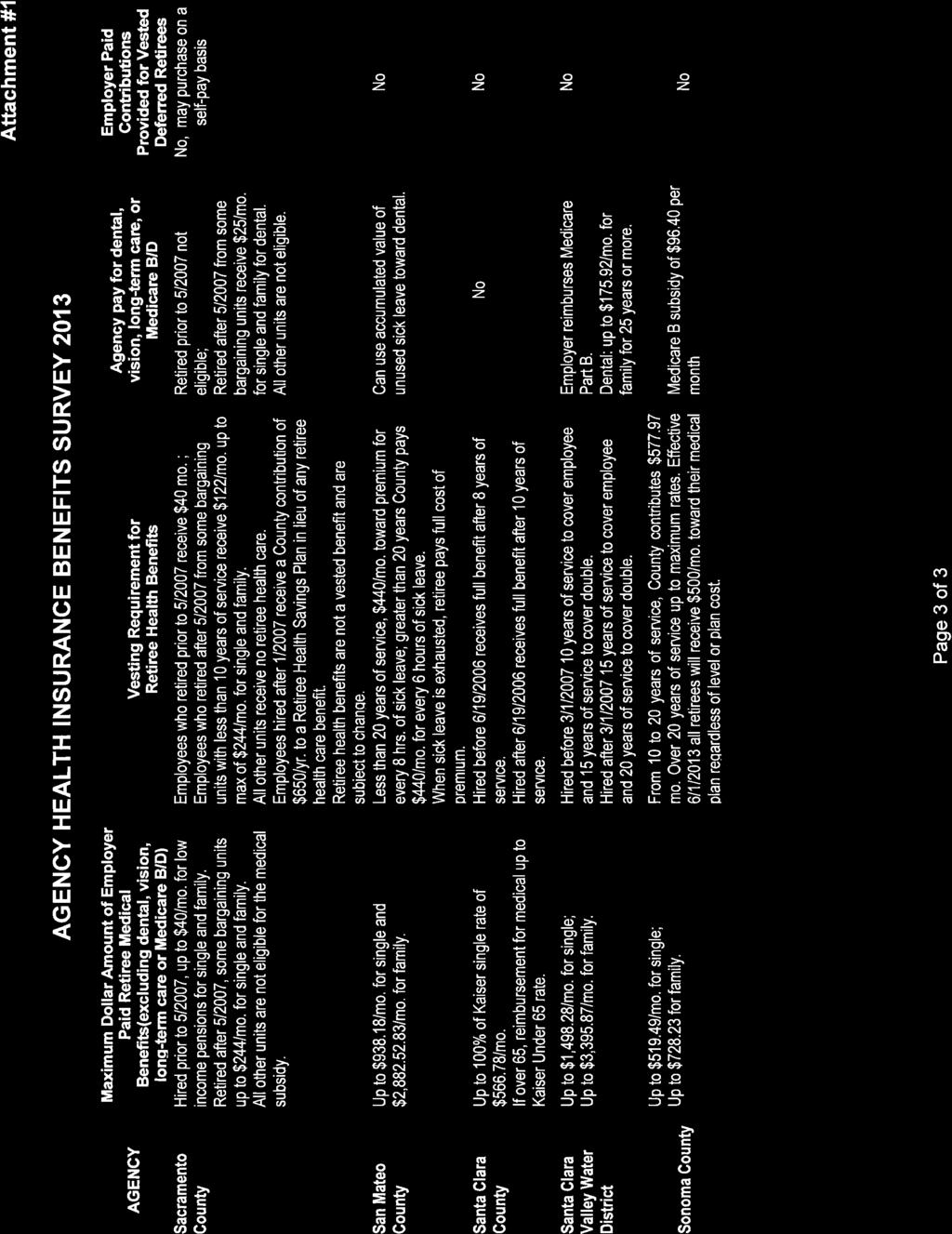

3 EBMUD Employees Retirement System Meeting of January 17, 2013 Page 2 INFORMATION: 7. Annual Health Insurance Benefit Survey E. Grassetti 8. Investment Fund Managers Fees E. Sandler REPORTS FROM THE RETIREMENT BOARD: 9. Brief report on any course, workshop, or conference attended since the last Retirement Board meeting. ITEMS TO BE CALENDARED: MEETING ADJOURNMENT: The next regular meeting of the Retirement Board will be held at 8:30 a.m. on Thursday, March 21, 2013.

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

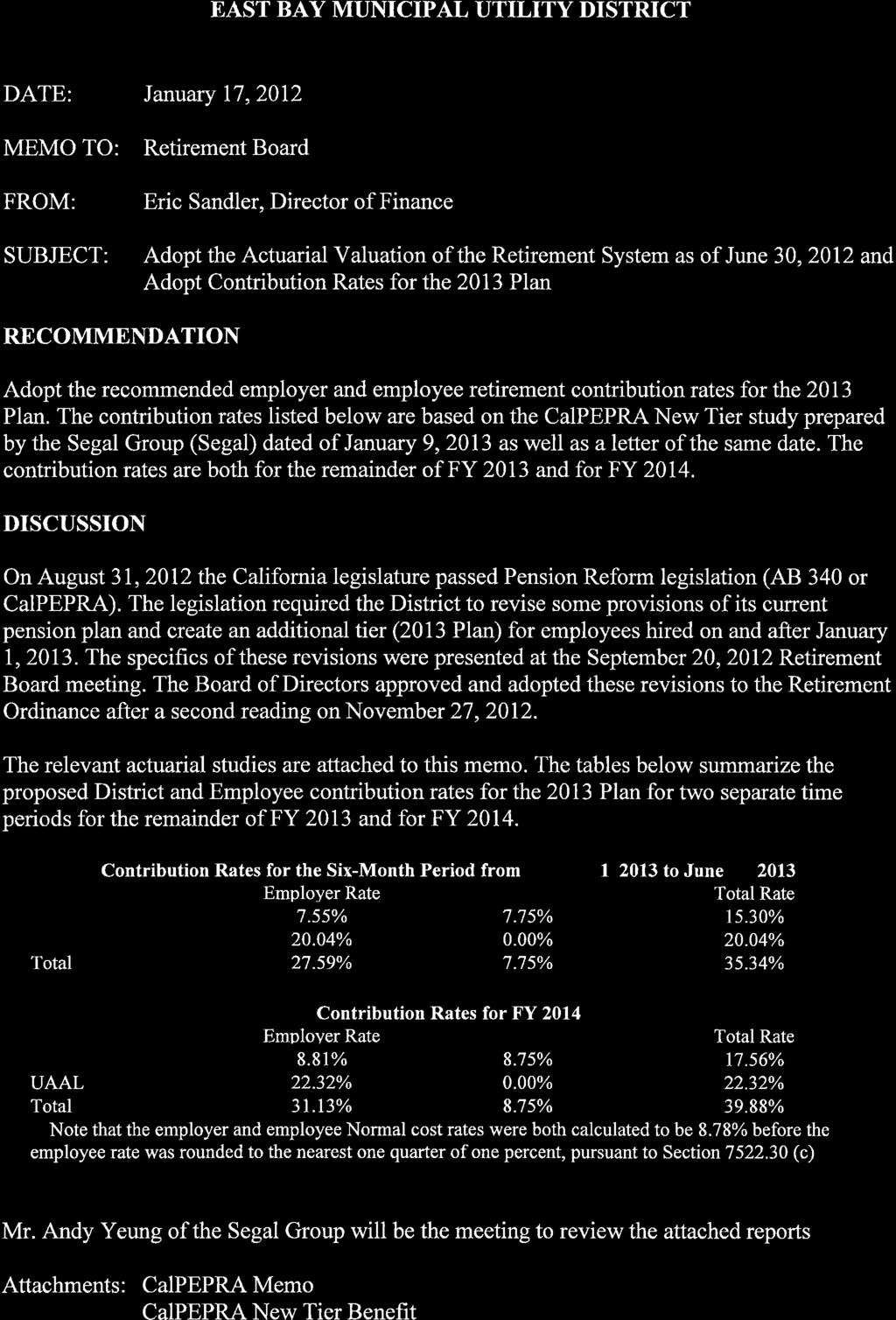

20 East Bay Municipal Utility District Retirement System Actuarial Valuation and Review of Pension Plan and Health Insurance Benefit Plan as of June 30, 2012 Supplemental Exhibits This report has been prepared at the request of the Retirement Board to assist in administering the Fund. This valuation report may not otherwise be copied or reproduced in any form without the consent of the Retirement Board and may only be provided to other parties in its entirety. The measurements shown in this actuarial valuation may not be applicable for other purposes. Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

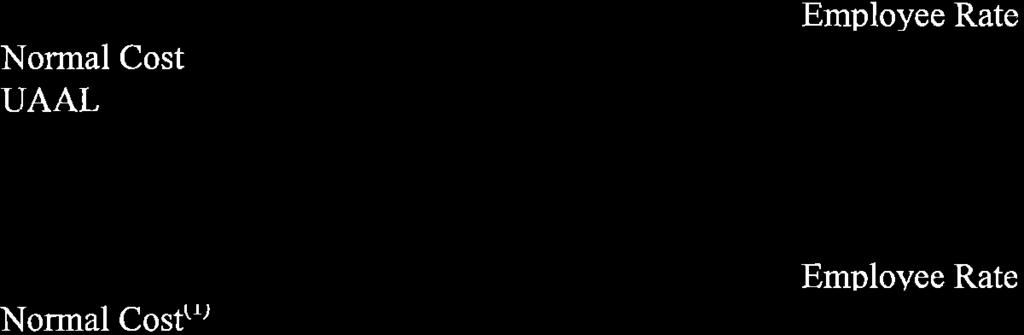

21 THE SEGAL COMPANY 100 Montgomery Street, Suite 500 San Francisco, CA T F January 9, 2013 Ms. Wanda Hendrix Treasury Manager East Bay Municipal Utility District 375 Eleventh Street Oakland, CA Re: June 30, 2012 Actuarial Valuations Supplemental Exhibits Dear Wanda: Enclosed please find two exhibits that provide supplemental information to the June 30, 2012 actuarial valuations for the pension and health insurance benefit (HIB) plans. For the HIB plan, this information is based on our HIB funding valuation report dated January 9, 2013 that includes a monthly benefit of $450 ($550 benefit for a retiree with a spouse or qualified domestic partner). It does not include the accounting liability for the implicit subsidy associated with the pooling of the health care premium rate for actives and retirees under age 65. Exhibit A provides a summary of results for both the pension plan and HIB plan valuations. In Exhibit B, we have included a comparison of the historical Pension Benefit Obligations with the market value of assets for both plans. We look forward to discussing this information with you and the Board. Sincerely, Andy Yeung, ASA, MAAA, FCA, EA Vice President and Associate Actuary DNA/bqb Enclosures v3/ Benefits, Compensation and HR Consulting Offices throughout the United States and Canada Founding Member of the Multinational Group of Actuaries and Consultants, a global affiliation of independent firms

22 I. Total Membership Exhibit A East Bay Municipal Utility District Retirement System Summary of Significant Valuation Results June 30, 2012 June 30, 2011 Percent Change A. Active Members 1,703 1, % B. Pensioners and Beneficiaries 1,361 1, % II. Valuation Salary* A. Total Annual Payroll $158,847,491 $159,504, % B. Average Monthly Salary 93,275 93, % III. Total System Assets A. Valuation Value of Pension Plan Assets $1,021,546,227 $954,718, % B. Valuation Value of HIB Plan Assets 14,240,105 12,047, % C. Total Valuation Value (Actuarial Value) $1,035,786,332 $966,766, % D. Market Value of Pension Plan Assets $973,403,000 $956,173, % E. Market Value of HIB Plan Assets 13,569,000 12,066, % F. Total Market Value $986,972,000 $968,239, % IV. Unfunded Actuarial Accrued Liability (UAAL) and Funded Ratio A. Pension Plan $535,150,038 $491,319, % B. Funded Ratio** 65.6% 66.0% N/A C. HIB Plan $88,961,173 $86,398, % D. Funded Ratio** 13.8% 12.2% N/A E. Pension Plan and HIB Plan $624,111,211 $577,718, % F. Funded Ratio** 62.4% 62.6% N/A * Projected payroll. ** Based on valuation value of assets. Note: The health insurance benefits (HIB) information is based on our HIB funding valuation report that includes a monthly benefit of $450 ($550 for a retiree with a spouse or qualified domestic partner). It does not include the accounting liability for the implicit subsidy associated with the pooling of the health care premium rate for actives and retirees under age 65.

23 Exhibit A (continued) East Bay Municipal Utility District Retirement System Summary of Significant Valuation Results V. Projected Benefit Obligation June 30, 2012 June 30, 2011 Percent Change A. Pension Plan $1,498,136,000 $1,395,484, % B. Funded Ratio*** 65.0% 68.5% N/A C. HIB Plan $108,837,000 $103,395, % D. Funded Ratio*** 12.5% 11.7% N/A E. Pension Plan and HIB Plan $1,606,973,000 $1,498,879, % F. Funded Ratio*** 61.4% 64.6% N/A VI. Budget Items**** FY FY Change Beginning of Year End of Pay Periods Beginning of Year End of Pay Periods Beginning of Year End of Pay Periods A. Pension Plan 1. Normal Cost as a Percent of Pay 15.45% 16.04% 13.88% 14.42% 1.57% 1.62% 2. Amortization of UAAL 21.50% 22.32% 19.28% 20.04% 2.22% 2.28% 3. Total Pension Plan Contribution 36.95% 38.36% 33.16% 34.46% 3.79% 3.90% B. HIB Plan 1. Normal Cost as a Percent of Pay 1.15% 1.19% 1.15% 1.19% 0.00% 0.00% 2. Amortization of UAAL 4.00% 4.15% 3.76% 3.91% 0.24% 0.24% 3. Total HIB Plan Contribution 5.15% 5.34% 4.91% 5.10% 0.24% 0.24% C. Total Contribution (Item A3 + Item B3) 42.10% 43.70% 38.07% 39.56% 4.03% 4.14% *** Based on market value of assets. **** Employer rates only (i.e., excludes the employee contribution rates of 6.74% for the pension plan and 0.09% for the HIB plan, payable at the end of each pay period). Note: The health insurance benefits (HIB) information is based on our HIB funding valuation report that includes a monthly benefit of $450 ($550 for a retiree with a spouse or qualified domestic partner). It does not include the accounting liability for the implicit subsidy associated with the pooling of the health care premium rate for actives and retirees under age 65.

24 Exhibit B East Bay Municipal Utility District Retirement System Comparison of Projected Benefit Obligation with the Market Value of Assets (Dollar Amounts in Thousands) Actuarial Valuation Date Projected Benefit Obligation Market Value of Assets Funded Ratio 06/30/2002 $749,113 $536, % 06/30/ , , % 06/30/ , , % 06/30/ , , % 06/30/2006 1,068, , % 06/30/2007 1,160, , % 06/30/2008 1,289, , % 06/30/2009 1,366, , % 06/30/2010 1,444, , % 06/30/2011 1,498, , % 06/30/2012 1,606, , % v3/

25 East Bay Municipal Utility District Retirement System Actuarial Valuation and Review of Pension Plan as of June 30, 2012 This report has been prepared at the request of the Retirement Board to assist in administering the Fund. This valuation report may not otherwise be copied or reproduced in any form without the consent of the Retirement Board and may only be provided to other parties in its entirety. The measurements shown in this actuarial valuation may not be applicable for other purposes. Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

26 The Segal Company 100 Montgomery Street Suite 500 San Francisco, CA T F January 9, 2013 Ms. Wanda Hendrix Treasury Manager East Bay Municipal Utility District 375 Eleventh Street Oakland, CA Dear Wanda: We are pleased to submit this Actuarial Valuation and Review as of June 30, 2012 for only the pension plan. The Actuarial Valuation and Review for the health insurance benefit (HIB) plan is provided in a separate report. This report summarizes the actuarial data used in the valuation, establishes the funding requirements for fiscal 2013/2014 and analyzes the preceding year s experience. This report was prepared in accordance with generally accepted actuarial principles and practices, at the request of the Board to assist in administering the Plan. The census and financial information on which our calculations were based were prepared by EBMUD. That assistance is gratefully acknowledged. The actuarial calculations were completed under the supervision of Andy Yeung, ASA, MAAA, FCA, Enrolled Actuary. The measurements shown in this actuarial valuation may not be applicable for other purposes. Future actuarial measurements may differ significantly from the current measurements presented in this report due to such factors as the following: plan experience differing from that anticipated by the economic or demographic assumptions; increases or decreases expected as part of the natural operation of the methodology used for these measurements (such as the end of an amortization period); and changes in plan provisions or applicable law. I am a Member of the American Academy of Actuaries and I meet the Qualification Standards of the American Academy of Actuaries to render the actuarial opinion herein. To the best of our knowledge, the information supplied in this actuarial valuation is complete and accurate. Further, in our opinion, the assumptions as approved by the Board are reasonably related to the experience of and the expectations for the Plan. We look forward to reviewing this report at your next meeting and to answering any questions. Sincerely, THE SEGAL COMPANY By: Andy Yeung, ASA, MAAA, EA, FCA Vice President and Associate Actuary

27 SECTION 1 SECTION 2 SECTION 3 SECTION 4 VALUATION SUMMARY VALUATION RESULTS Purpose... i Significant Issues in Valuation Year... ii Summary of Key Valuation Results... v A. Participant Data... 1 B. Financial Information... 4 C. Actuarial Experience... 7 D. Recommended Contribution. 12 E. Information Required by GASB F. Volatility Ratios SUPPLEMENTAL INFORMATION REPORTING INFORMATION EXHIBIT A Table of Plan Coverage EXHIBIT B Participants in Active Service as of June 30, EXHIBIT C Reconciliation of Participant Data EXHIBIT D Summary Statement of Income and Expenses on an Actuarial Value Basis for All Pension Plan and HIB Plan Assets EXHIBIT E Summary Statement of Assets for Pension and HIB Plans EXHIBIT F Development of the Fund Through June 30, 2012 for All Pension Plan and HIB Plan Assets EXHIBIT G Development of Unfunded/(Overfunded) Actuarial Accrued Liability for Year Ended June 30, EXHIBIT H Table of Amortization Bases EXHIBIT I Section 415 Limitations EXHIBIT J Definitions of Pension Terms EXHIBIT I Summary of Actuarial Valuation Results EXHIBIT II Supplementary Information Required by GASB Schedule of Employer Contributions EXHIBIT III Supplementary Information Required by GASB Schedule of Funding Progress EXHIBIT IV Supplementary Information Required by GASB EXHIBIT V Actuarial Assumptions and Actuarial Cost Method EXHIBIT VI Summary of Plan Provisions... 43

28 SECTION 1: Valuation Summary for the East Bay Municipal Utility District Retirement System Purpose This report has been prepared by The Segal Company to present a valuation of the East Bay Municipal Utility District Retirement System as of June 30, The valuation was performed to determine whether the assets and contributions are sufficient to provide the prescribed benefits. The contribution requirements presented in this report are based on: The benefit provisions of the pension plan, as administered by the Board; The characteristics of covered active participants, inactive vested participants, and retired participants and beneficiaries as of June 30, 2012, provided by EBMUD; The assets of the plan as of June 30, 2012, provided by EBMUD; Economic assumptions regarding future salary increases and investment earnings adopted by the Board for the June 30, 2012 valuation; and Other actuarial assumptions, regarding employee terminations, retirement, death, etc., adopted by the Board for the June 30, 2012 valuation. One of the general goals of an actuarial valuation is to establish contributions which fully fund the System s liabilities, and which, as a percentage of payroll, remain as level as possible for each generation of active members. Annual actuarial valuations measure the progress toward this goal, as well as test the adequacy of the contribution rates. In preparing this valuation, we have employed generally accepted actuarial methods and assumptions to evaluate the System s assets, liabilities and future contribution requirements. Our calculations are based upon member data and financial information provided to us by the System s staff. This information has not been audited by us, but it has been reviewed and found to be consistent, both internally and with prior year s information. The contribution requirements are determined as a percentage of payroll. The System s employer rates provide for both normal cost and a payment or credit to amortize any unfunded or overfunded actuarial accrued liabilities. In the valuation, new UAAL established on or after July 1, 2011 as a result of actuarial gains or losses and change in actuarial assumptions has been amortized over separate declining 20-year and 25-year periods, respectively. The balance of the UAAL established prior to July 1, 2011 continues to be amortized in layers over the current respective remaining fixed periods. The rates calculated in this report may be adopted by the Board for the fiscal year that extends from July 1, 2013 through June 30, i

29 SECTION 1: Valuation Summary for the East Bay Municipal Utility District Retirement System Significant Issues in Valuation Year The following key findings were the result of this actuarial valuation: Ref: Pg. 33 Ref: Pg. 13 Ref: Pg. 13 Ref: Pgs. 23 and 31 The results of this valuation reflect changes in the actuarial assumptions as recommended by Segal and adopted by the Board for the June 30, 2012 valuation. These changes were documented in our Actuarial Experience Study and are also outlined in Section 4, Exhibit V of this report. These assumption changes resulted in an increase in the employer contribution rate of 2.79% of payroll. The assumption changes that had the largest impact on the contribution rate increase include the changes in the economic assumptions, the mortality assumption, and the introduction of the sick leave conversion assumption. In our review of the Board s actuarial funding policy (reference: letter dated September 12, 2012), we recommended a modification to the Entry Age Normal cost method that is currently used by EBMUD. The modification we recommended was a change in the normal cost calculation from an aggregate basis to an individual basis, and this change was adopted by the Board for use in the June 30, 2012 valuation. The results of this valuation reflect the change in the normal cost calculation, and this change resulted in an increase in the employer contribution rate of 0.72% of payroll. In the review of the Board s actuarial funding policy mentioned above, we also recommended alternative amortization periods for use in amortizing new unfunded actuarial accrued liability (UAAL) on or after July 1, 2011, with separate amortization periods depending on the source of the UAAL change. The Board adopted alternative #3 from that letter, which utilizes the following amortization periods by source: 20 years for actuarial gains or losses; 25 years for assumption or method changes, 15 years for plan amendments; 5 years for Early Retirement Incentive Programs; and 30 years for actuarial surplus. The results of this valuation reflect the changes in the amortization periods, and these changes resulted in an increase in the employer contribution rate of 0.06% of payroll. The funded ratio measured on a valuation value of assets basis decreased from 66.0% at June 30, 2011 to 65.6% at June 30, The funded ratio if measured on a market value of assets basis decreased from 66.1% to 62.5%. The UAAL increased from $491.3 million as of June 30, 2011 to $535.2 million as of June 30, The increase in the UAAL is primarily due to (a) the lower than expected return on the valuation value of assets (after smoothing), (b) the change in the actuarial assumptions, and (c) other actuarial losses, offset somewhat by actuarial gains from (d) less than expected salary increases for actives, and (e) less than expected COLA increases for retirees and beneficiaries. A complete reconciliation of the System s unfunded actuarial accrued liability is provided in Section 3, Exhibit G. ii

30 SECTION 1: Valuation Summary for the East Bay Municipal Utility District Retirement System Ref: Pg. 13 Ref: Pg. 5 Ref: Pg. 5 The aggregate employer rate calculated in this valuation has increased from 34.46% of payroll to 38.36% of payroll. The increase in the employer rate was primarily due to (a) lower than expected return on the valuation value of assets (after smoothing), (b) normal one-year lag in implementing the higher contribution rate calculated in the June 30, 2011 valuation for fiscal year , (c) less than expected growth in total payroll base to amortize the System s UAAL, (d) increase in normal cost rate due to a change in demographic profile for active members, (e) other actuarial losses, (f) the change in the actuarial assumptions, (g) the change to the individual Entry Age Normal cost method, and (h) the change in the amortization periods for actuarial (gains)/losses and assumption/method changes, offset somewhat by (i) less than expected salary increases for individual active members, and (j) less than expected COLA increases for retirees and beneficiaries. Based on action taken by the Board in 2012, the total unrecognized deferred gain of $1.5 million through June 30, 2011 as of that valuation has been recognized in four level amounts with three years of recognition remaining after the June 30, 2012 valuation. As indicated in Section 2, Subsection B (see Chart 7) of this report, the total unrecognized investment loss as of June 30, 2012 is $48.8 million for the assets for the pension and HIB plans. This investment loss will be recognized in the determination of the actuarial value of assets for funding purposes in the next few years. This implies that earning the assumed rate of investment return of 7.75% per year (net of expenses) on a market value basis will produce investment losses on the actuarial value of assets after June 30, The deferred losses of $48.8 million represent 4.9% of the market value of assets as of June 30, Unless offset by future investment gains or other favorable experience, the recognition of the $48.8 million market loss is expected to have a significant impact on the System s future funded percentage and contribution rate requirements. This potential impact may be illustrated as follows: If the pension plan portion of the deferred losses were recognized immediately and entirely in the valuation value of assets, the funded percentage would decrease from 65.6% to 62.5%. If the pension plan portion of the deferred losses were recognized immediately and entirely in the valuation value of assets, the aggregate employer rate would increase from 38.36% to about 40.6% of payroll. The actuarial valuation report as of June 30, 2012 is based on financial information as of that date. Changes in the value of assets subsequent to that date are not reflected. Declines in asset values will increase the actuarial cost of the plan, while increases will decrease the actuarial cost of the plan. iii

31 SECTION 1: Valuation Summary for the East Bay Municipal Utility District Retirement System Ref: Pg. 16 The California Actuarial Advisory Panel (CAAP) has recently adopted a set of model disclosure elements recommended for actuarial valuation reports for public retirement systems in California. Information has been added to this valuation report consistent with the recommendations regarding basic disclosure elements. In particular, we are now including new information regarding measures of plan volatility. The Governmental Accounting Standards Board (GASB) recently approved two new Statements affecting the reporting of pension liabilities for accounting purposes. Statement 67 replaces Statement 25 and is for plan reporting. Statement 68 replaces Statement 27 and is for employer reporting. It is important to note that the new GASB rules only redefine pension expense for financial reporting purposes, and do not apply to contribution amounts for actual pension funding purposes. Employers and plans can still develop and adopt funding policies under current practices. Because these new Statements are not effective until the fiscal year ending June 30, 2014 for Plan reporting and the fiscal year ending June 30, 2015 for employer reporting, the financial reporting information in this report continues to be in accordance with Statements 25 and 27. The California Public Employees Pension Reform Act of 2013 (AB340) was passed on September 12, AB340 will become effective on January 1, In general, it affects new members who enter the plan on or after January 1, There will be new plan provisions that include new benefit formulas, cap on pensionable income, 3-year final average salary, and new cost sharing by members. There are also changes that may affect current members including the normal cost sharing by members. We have not reflected any of the AB340 provisions in this report. The impact of AB340 will be addressed in a later report. Impact of Future Experience on Contribution Rates Future contribution requirements may differ from those determined in the valuation because of: Differences between actual experience and anticipated experience; Changes in actuarial assumptions or methods; Changes in statutory provisions; and Difference between the contribution rates determined by the valuation and those adopted by the Board. iv

32 SECTION 1: Valuation Summary for the East Bay Municipal Utility District Retirement System Summary of Key Valuation Results Contributions calculated as of June 30: Employer rate (payable at the end of each pay period) 38.36% 34.46% Employer annual amount (1) $60,933,898 $54,738,845 Employee rate (aggregate) 6.74% 6.74% Employee annual amount (1) $10,706,321 $10,706,321 Funding elements for plan year beginning July 1: Normal cost (beginning of year) (1) $34,856,820 $32,357,234 Market value of pension plan and HIB plan assets (MVA) 986,972, ,239,000 Actuarial value of pension plan and HIB plan assets (AVA) 1,035,786, ,766,525 Valuation value of pension plan assets (2) (VVA) 1,021,546, ,718,875 Actuarial accrued liability (AAL) 1,556,696,265 1,446,038,834 Unfunded/(overfunded) actuarial accrued liability (UAAL) 535,150, ,319,959 Funded ratio on VVA basis 65.6% 66.0% Market value of pension plan assets 973,403, ,173,000 Funded ratio on pension plan MVA basis 62.5% 66.1% GASB 25/27 for fiscal year ended June 30: Annual required contributions $52,156,000 $50,987,000 Actual contributions 52,156,000 50,987,000 Percentage contributed 100.0% 100.0% Demographic data for plan year ended June 30: Number of retired participants and beneficiaries 1,361 1,325 Number of vested former participants Number of active participants 1,703 1,702 Projected total payroll $158,847,491 $159,504,853 Projected average payroll 93,275 93,716 (1) Estimated based on June 30, 2012 projected payroll of $158,847,491. (2) Net of HIB plan assets. v

33 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System A. PARTICIPANT DATA The Actuarial Valuation and Review considers the number and demographic characteristics of covered participants, including active participants, vested terminated participants, retired participants and beneficiaries. This section presents a summary of significant statistical data on these participant groups. More detailed information for this valuation year and the preceding valuation can be found in Section 3, Exhibits A, B, and C. A historical perspective of how the participant population has changed over the past eight valuations can be seen in this chart. CHART 1 Participant Population: Year Ended June 30 Active Participants Vested Terminated Participants* Retired Participants and Beneficiaries Ratio of Non-Actives to Actives , , , , , , , , , , , , , , , , * Includes terminated participants due a refund of employee contributions. 1

34 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Active Participants Plan costs are affected by the age, years of service and payroll of active participants. In this year s valuation, there were 1,703 active participants with an average age of 49.9, average service of 15.1 years and average payroll of $93,275. The 1,702 active participants in the prior valuation had an average age of 49.6, average service of 14.9 years and average payroll of $93,716. Inactive Participants In this year s valuation, there were 224 participants with a vested right to a deferred or immediate vested benefit compared to 226 in the prior valuation. These graphs show a distribution of active participants by age and by years of service. CHART 2 Distribution of Active Participants by Age as of June 30, 2012 CHART 3 Distribution of Active Participants by Years of Service as of June 30,

35 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Retired Participants and Beneficiaries As of June 30, 2012, 1,117 retired participants and 244 beneficiaries were receiving total monthly benefits of $5,216,008. For comparison, in the previous valuation, there were 1,086 retired participants and 239 beneficiaries receiving monthly benefits of $4,880,792. These graphs show a distribution of the current retired participants and beneficiaries based on their monthly amount and age, by type of pension. Beneficiary Disability Regular CHART 4 Distribution of Retired Participants and Beneficiaries by Type and by Monthly Amount as of June 30, CHART 5 Distribution of Retired Participants and Beneficiaries by Type and by Age as of June 30,

36 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System B. FINANCIAL INFORMATION Pension plan funding anticipates that, over the long term, both contributions and net investment earnings (less investment fees and administrative expenses) will be needed to cover benefit payments. Pension plan assets change as a result of the net impact of these income and expense components. Additional financial information, including a summary of these transactions for the valuation year, is presented in Section 3, Exhibits D, E and F. The chart depicts the components of changes in the actuarial value of assets over the last seven years. Note: The first bar represents increases in assets during each year while the second bar details the decreases. CHART 6 Comparison of Increases and Decreases in the Actuarial Value of Assets for Years Ended June 30, (for pension and HIB benefits) Adjustment toward market value Benefits paid Net interest and dividends Contributions $ Millions

37 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System It is desirable to have level and predictable plan costs from one year to the next. For this reason, the Board has approved an asset valuation method that gradually adjusts to market value. Under this valuation method, the full value of market fluctuations is not recognized in a single year and, as a result, the asset value and the plan costs are more stable. The amount of the adjustment to recognize market value is treated as income, which may be positive or negative. Realized and unrealized gains and losses are treated equally and, therefore, the sale of assets has no immediate effect on the actuarial value. The chart shows the determination of the actuarial value of assets as of the valuation date. CHART 7 Determination of Actuarial Value of Assets for Year Ended June 30, 2012 (for pension and HIB plans) 1. Market value of assets: (a) Pension plan $973,403,000 (b) HIB plan 13,569,000 (c) Total $986,972,000 Actual Market Expected Market Investment Deferred Deferred 2. Calculation of deferred return: Return (net) Return (net) Gain / (Loss) Factor Return (a) Year ended June 30, $76,707,000 $75,340,031 -$152,047,031 (b) Year ended June 30, ,905,000 69,269, ,174,846 see footnote (1) below (c) Year ended June 30, ,737,000 55,360,181 40,376,819 (d) Year ended June 30, ,970,000 61,812, ,157,160 75% $1,104,356 (e) Year ended June 30, ,202,000 77,600,360-62,398,360 80% -49,918,688 (f) Total unrecognized return* -$48,814, Preliminary actuarial value: (1c) - (2f) $1,035,786, Adjustment to be within 30% corridor of market value $0 5. Final actuarial value of assets for pension and HIB plans: (3) + (4) $1,035,786, Actuarial value as a percentage of market value: (5) (1c) 104.9% 7. Valuation value of pension plan assets: (1a) (1c) x (5) $1,021,546,227 (1) Based on action taken by the Board in 2012, the total deferred gain of $1,472,475 through June 30, 2011 as of that valuation has been recognized in four level amounts, with three years of recognition remaining after the June 30, 2012 valuation. * The amount of deferred return that will be recognized in each subsequent valuation is as follows (amounts may not total exactly due to rounding): 6/30/2013 -$12,111,553 6/30/ ,111,553 6/30/ ,111,553 6/30/ ,479,672 Total -$48,814,332 5

38 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System The market value, actuarial value, and valuation value of assets are representations of EBMUD s financial status. As investment gains and losses are gradually taken into account, the actuarial value of assets tracks the market value of assets. The valuation value of assets is the actuarial value, excluding HIB assets. The valuation value of assets is significant because EBMUD s liabilities are compared to these assets to determine what portion, if any, remains unfunded. Amortization of the unfunded actuarial accrued liability is an important element in determining the contribution requirement. This chart shows the change in the actuarial value of assets versus the market value over the past eight years. CHART 8 Market Value, Actuarial Value, and Valuation Value of Assets as of June 30, * 1,100 1,000 $ Millions Actuarial Value Market Value Valuation Value * Market Value and Actuarial Value of Assets are for pension and HIB benefits. Valuation Value of Assets are for pension benefits only. 6

39 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System C. ACTUARIAL EXPERIENCE To calculate the required contribution, assumptions are made about future events that affect the amount and timing of benefits to be paid and assets to be accumulated. Each year actual experience is measured against the assumptions. If overall experience is more favorable than anticipated (an actuarial gain), the contribution requirement will decrease from the previous year. On the other hand, the contribution requirement will increase if overall actuarial experience is less favorable than expected (an actuarial loss). Taking account of experience gains or losses in one year without making a change in assumptions reflects the belief that the single year s experience was a short-term development and that, over the long term, experience will return to the original assumptions. For contribution requirements to remain stable, assumptions should approximate experience. If assumptions are changed, the contribution requirement is adjusted to take into account a change in experience anticipated for all future years. The total gain is $15,668,764, a $11,909,918 loss from investments and a $27,578,682 gain from all other sources. The net experience variation from individual sources other than investments was 1.77% of the actuarial accrued liability. A discussion of the major components of the actuarial experience is provided on the following pages. This chart provides a summary of the actuarial experience during the past year. CHART 9 Actuarial Experience for Year Ended June 30, Net gain/(loss) from investments* -$11,909, Net gain/(loss) from other experience** 30,628, Net gain/(loss) from one year delay in implementing the higher contribution rate calculated in the June 30, 2011 valuation until fiscal year 2012/2013-3,050, Net experience gain/(loss): (1) + (2) + (3) $15,668,764 * Details in Chart 10. ** Details in Section 3, Exhibit G. 7

40 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Investment Rate of Return A major component of projected asset growth is the assumed rate of return. The assumed return should represent the expected long-term rate of return, based on EBMUD s investment policy. For valuation purposes, the assumed rate of return on the valuation value of assets is 8.00% (for the June 30, 2011 valuation). The actual rate of return on a valuation value basis (after smoothing) for the 2012 plan year was 6.75%. Since the actual return for the year was less than the assumed return, EBMUD experienced an actuarial loss during the year ended June 30, 2012 with regard to its investments. This chart shows the gain/(loss) due to investment experience. CHART 10 Investment Experience for Year Ended June 30, 2012 Valuation Value, Actuarial Value, and Market Value of Assets Valuation Value (includes pension Actuarial Value (includes pension Market Value (includes pension plan assets only) and HIB plan assets) and HIB plan assets) 1. Actual return $64,558,352 $65,488,807 $15,202, Average value of assets $955,853,375 $968,532,025 $970,004, Actual rate of return: (1) (2) 6.75% 6.76% 1.57% 4. Assumed rate of return 8.00% 8.00% 8.00% 5. Expected return: (2) x (4) $76,468,270 $77,482,562 $77,600, Actuarial gain/(loss): (1) (5) -$11,909,918 -$11,993,755 -$62,398,360 8

41 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Because actuarial planning is long term, it is useful to see how the assumed investment rate of return has followed actual experience over time. The chart below shows the rate of return on a valuation value, actuarial value, and market value basis for the last eight years. CHART 11 Investment Return Valuation Value, Actuarial Value, and Market Value: * Valuation Value Investment Return Actuarial Value Investment Return Market Value Investment Return Year Ended June 30 Amount Percent Amount Percent Amount Percent 2005 $28,180, % $28,310, % $51,008, % ,252, % 45,449, % 66,439, % ,055, % 84,360, % 144,934, % ,124, % 72,404, % -76,707, % ,442, % -40,593, % -171,905, % ,167, % 51,966, % 95,737, % ,223, % 33,642, % 191,970, % ,558, % 65,488, % 15,202, % Eight-Year Average Return 5.22% 5.24% 5.07% * Market Value and Actuarial Value of Assets are for the pension plan and the HIB plan. Valuation Value of Assets are for the pension plan only. 9

42 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Subsection B described the actuarial asset valuation method that gradually takes into account fluctuations in the market value rate of return. The effect of this is to stabilize the actuarial rate of return, which contributes to leveling pension plan costs. This chart illustrates how this leveling effect has actually worked over the years CHART 12 Market Value, Actuarial Value, and Valuation Value of Assets: Rates of Return for Years Ended June 30, * Actuarial Value Market Value Valuation Value 30% 25% 20% 15% 10% 5% 0% -5% -10% -15% -20% -25% * Market Value and Actuarial Value of Assets are for pension and HIB benefits. Valuation Value of Assets are for pension benefits only. 10

43 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Other Experience There are other differences between the expected and the actual experience that appear when the new valuation is compared with the projections from the previous valuation. These include: the extent of turnover among the participants, retirement experience (earlier or later than expected), mortality (more or fewer deaths than expected), the number of disability retirements, and salary increases different than assumed. The net gain from this other experience for the year ended June 30, 2012 amounted to $27,578,682, which is 1.77% of the actuarial accrued liability. 11

44 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System D. RECOMMENDED CONTRIBUTION The amount of annual contribution required to fund the Plan is comprised of an employer normal cost payment and a payment on the unfunded actuarial accrued liability. This total amount is then divided by the projected payroll for active members to determine the funding rate of 38.36% of payroll. The chart compares this valuation s recommended contribution with the prior valuation. CHART 13 Recommended Contribution (% of payroll) 6/30/12 6/30/11 1. Total normal cost 21.94% 20.37% 2. Expected employee contributions (1) -6.49% -6.49% 3. Employer normal cost: (1) + (2) 15.45% 13.88% 4. Unfunded/(overfunded) actuarial accrued liability 21.50% 19.28% 5. Total recommended contribution, beginning of year: (3) + (4) 36.95% 33.16% 6. Total recommended contribution, end of each pay period 38.36% 34.46% (1) Discounted to beginning of year. The employee contribution rate for contributions made at the end of each pay period would be 6.74%. 12

45 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System The contribution rates as of June 30, 2012 are based on all of the data described in the previous sections, the actuarial assumptions described in Section 4, and the Plan provisions adopted at the time of preparation of the Actuarial Valuation. They include all changes affecting future costs, adopted benefit changes, actuarial gains and losses and changes in the actuarial assumptions. Reconciliation of Recommended Contribution The chart below details the changes in the recommended contribution from the prior valuation to the current year s valuation. The chart reconciles the contribution from the prior valuation to the amount determined in this valuation. CHART 14 Reconciliation of Recommended Contribution Rate from June 30, 2011 to June 30, 2012 Contribution Rate Estimated Annual Amount (1) Recommended Contribution as of June 30, % $54,738,845 Effect of investment loss 0.42% 667,159 Effect of one-year lag in implementing rates 0.11% 174,732 Effect of lower than expected salary increases -1.08% -1,715,553 Effect of lower than expected growth in total payroll 0.84% 1,334,319 Effect of lower than expected retiree COLA increases -0.16% -254,156 Effect of increase in employer normal cost due to demographic changes 0.05% 79,424 Effect of other experience losses 0.15% 238,273 Effect of change to individual Entry Age Normal method 0.72% 1,143,702 Effect of change in amortization periods for actuarial (gains)/losses and assumption/method changes 0.06% (2) 95,308 Effect of change in actuarial assumptions 2.79% 4,431,845 Total Change 3.90% $6,195,053 Recommended Contribution as of June 30, % $60,933,898 (1) (2) Based on projected payroll as of June 30, 2012 of $158,847,491. Combined effect of change in amortization periods for actuarial gains (-0.15% of payroll) and for assumption changes (0.21% of payroll). 13

46 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Employee contribution rates are prescribed in the Ordinance. Effective April 17, 2006, the rate of member retirement contributions is 6.83% and 6.74% of that rate is allocated to pay pension benefits. The rest, or 0.09%, is used to pay HIB benefits. The Board of Directors may adjust the employee rates solely pursuant to the terms of a negotiated collective bargaining agreement or memorandum of understanding with employer bargaining units. 14

47 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System E. INFORMATION REQUIRED BY GASB Governmental Accounting Standards Board (GASB) reporting information provides standardized information for comparative purposes of governmental pension plans. This information allows a reader of the financial statements to compare the funding status of one governmental plan to another on relatively equal terms. Critical information to GASB is the historical comparison of the GASB required contribution to the actual contributions. This comparison demonstrates whether a plan is being funded within the range of the GASB reporting requirements. Chart 15 below presents a graphical representation of this information for the Plan. actuarial value of assets to the actuarial accrued liabilities of the plan as calculated under GASB. High ratios indicate a well-funded plan with assets sufficient to pay most benefits. Lower ratios may indicate recent changes to benefit structures, funding of the plan below actuarial requirements, poor asset performance, or a variety of other factors. The details regarding the calculations of these values and other GASB numbers may be found in Section 4, Exhibits II, III, and IV. The other critical piece of information regarding the Plan s financial status is the funded ratio. This ratio compares the These graphs show key GASB factors. CHART 15 Required Versus Actual Contributions CHART 16 Funded Ratio $ Millions % 80% 60% 40% 20% 0% Required Actual 15

48 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System F. VOLATILITY RATIOS Retirement plans are subject to volatility in the level of required contributions. This volatility tends to increase as retirement plans become more mature. The Asset Volatility Ratio (AVR), which is equal to the market value of assets divided by total payroll, provides an indication of the potential contribution volatility for any given level of investment volatility. A higher AVR indicates that the plan is subject to a greater level of contribution volatility. This is a current measure since it is based on the current level of assets. For EBMUD, the current AVR is about 6.1. This means that a 1% asset gain/(loss) (relative to the assumed investment return) translates to about 6.1% of one-year s payroll. Since EBMUD amortizes actuarial gains and losses over a 20-year period, there would be a 0.4% of payroll decrease/(increase) in the required contribution for each 1% asset gain/(loss). The Liability Volatility Ratio (LVR), which is equal to the Actuarial Accrued Liability divided by payroll, provides an indication of the longer-term potential for contribution volatility for any given level of investment volatility. This is because, over an extended period of time, the plan s assets should track the plan s liabilities. For example, if a plan is 50% funded on a market value basis, the liability volatility ratio would be double the asset volatility ratio and the plan sponsor should expect contribution volatility to increase over time as the plan becomes better funded. The LVR also indicates how volatile contributions will be in response to changes in the Actuarial Accrued Liability due to actual experience or to changes in actuarial assumptions. For EBMUD, the current LVR is about 9.8. This is about 61% higher than the AVR. Therefore, we would expect that contribution volatility will increase over the long-term. This chart shows how the asset and liability volatility ratios have varied over time. CHART 17 Volatility Ratios for Years Ended June 30, Year Ended June 30 Asset Volatility Ratio Liability Volatility Ratio

49 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT A Table of Plan Coverage Year Ended June 30 Category Change From Prior Year Active participants in valuation: Number 1,703 1, % Average age N/A Average service N/A Projected total payroll $158,847,491 $159,504, % Projected average payroll $93,275 $93, % Account balances $145,556,365 $140,440, % Total active vested participants 1,415 1, % Vested terminated participants: Number % Average age N/A Retired participants: Number in pay status 1,054 1, % Average age N/A Average monthly benefit $4,326 $4, % Disabled participants: Number in pay status % Average age N/A Average monthly benefit $1,941 $1, % Beneficiaries: Number in pay status % Average age N/A Average monthly benefit $2,190 $2, % 17

50 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT B Participants in Active Service as of June 30, 2012 By Age, Years of Service, and Average Projected Payroll Years of Service Age Total & over Under $68,094 $68, ,589 73,626 $100, ,288 83,153 88,290 $97, ,327 82,435 89,640 85,750 $90, ,094 88,957 91,776 92,976 94,905 $112, ,677 87,602 95,929 91,009 92, ,012 $111,489 $82, ,476 95,256 92,712 90,259 94,525 94, ,862 99,423 $105, ,412 84,593 93,812 79, ,461 96,695 98, , , ,449 79,698 96,506 86,964 96, , , ,265 95,844 $86, ,552 79,680 72,656 93, ,422 76,234 82, ,336 84, & over , ,726 42,305 69, , ,831 Total 1, $93,275 $84,223 $92,326 $88,106 $95,462 $98,246 $101,366 $100,793 $101,086 $82,006 18

51 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT C Reconciliation of Participant Data Active Participants Vested Former Participants Disableds Retired Participants Beneficiaries Total Number as of June 30, , , ,253 New participants 75 N/A N/A N/A N/A 75 Terminations with vested rights (16) Terminations without vested rights (1) N/A N/A N/A N/A (1) Retirements (54) (11) N/A 65 N/A 0 New disabilities (2) 0 2 N/A N/A 0 Return to work 2 (2) 0 0 N/A 0 Died with or without beneficiary (3) 0 (2) (34) 5 (1) (34) Refund of contributions 0 (5) (5) Data adjustments Number as of June 30, , , ,288 (1) This is the net increase in the number of beneficiaries after subtracting the number of beneficiaries who died during the year. 19

52 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT D Summary Statement of Income and Expenses on an Actuarial Value Basis for All Pension Plan and HIB Plan Assets Year Ended June 30, 2012 Year Ended June 30, 2011 Contribution income: Employer contributions $59,651,000 $58,481,000 Employee contributions 10,723,000 10,850,000 Net contribution income $70,374,000 $69,331,000 Investment income: Interest, dividends and other income $21,117,000 $19,674,000 Recognition of capital appreciation 48,899,807 18,018,654 Less investment and administrative fees -4,528,000-4,050,000 Net investment income $65,488,807 $33,642,654 Total income available for benefits $135,862,807 $102,973,654 Less benefit payments: Benefits paid -$66,254,000 -$61,862,000 Refund of contributions -589, ,000 Net benefit payments -$66,843,000 -$62,114,000 Change in amount available for future benefits $69,019,807 $40,859,654 20

53 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT E Summary Statement of Assets for Pension and HIB Plans Year Ended June 30, 2012 Year Ended June 30, 2011 Cash equivalents $33,068,000 $48,462,000 Accounts receivable: Brokers, securities sold $8,036,000 $23,333,000 Employer and employee contributions 2,602,000 2,132,000 Interest and dividends 2,276,000 2,079,000 Total accounts receivable $12,914,000 $27,544,000 Investments: Equities $693,123,000 $688,601,000 Fixed income investments 216,206, ,597,000 Real estate 48,876,000 17,730,000 Securities lending collateral 100,577, ,553,000 Other assets 434, ,000 Total investments at market value $1,059,216,000 $1,060,911,000 Total assets $1,105,198,000 $1,136,917,000 Less accounts payable: Accounts payable and accrued expenses -$1,365,000 -$1,362,000 Payables to brokers, securities purchased -16,284,000-37,763,000 Securities lending collateral -100,577, ,553,000 Total accounts payable -$118,226,000 -$168,678,000 Net assets at market value $986,972,000 $968,239,000 Net assets at actuarial value $1,035,786,332 $966,766,525 Net assets at valuation value (pension plan only) $1,021,546,227 $954,718,875 21

54 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT F Development of the Fund Through June 30, 2012 for All Pension Plan and HIB Plan Assets Year Ended June 30 Employer Contributions Employee Contributions Net Investment Return* Benefit Payments Actuarial Value of Assets at End of Year 2006 $35,635,000 $9,426,000 $45,449,540 $42,634,000 $744,230, ,332,000 9,891,000 84,360,520 46,508, ,305, ,603,000 10,394,000 72,404,538 50,780, ,927, ,803,000 10,740,000-40,593,156 54,502, ,375, ,756,000 10,918,000 51,966,871 58,109, ,906, ,481,000 10,850,000 33,642,654 62,114, ,766, ,651,000 10,723,000 65,488,807 66,843,000 1,035,786,332 * Net of investment fees and administrative expenses. 22

55 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT G Development of Unfunded/(Overfunded) Actuarial Accrued Liability for Year Ended June 30, Unfunded actuarial accrued liability at beginning of year $491,319, Normal cost at beginning of year 32,491, Actual employer and member contributions -62,738, Interest (a) For whole year on (1) + (2) $41,904,888 (b) For half year on (3) -2,509,520 (c) Total interest $39,395, Expected unfunded actuarial accrued liability $500,468, Changes due to:* (a) Loss from investments $11,909,918 (b) Gain on salaries lower than expected -30,332,209 (c) Gain from less COLA benefits granted than anticipated -4,428,575 (d) Loss from all other sources 4,131,917 (e) Loss from change in actuarial assumptions 53,400,521 (f) Total changes $34,681, Unfunded actuarial accrued liability at end of year $535,150,038 *Excludes $3,050,185 loss from contributions less than anticipated due to one-year delay in implementing the higher contribution rate calculated in the June 30, 2011 valuation. That loss is already included in the development of item 5. Note: The net gain/(loss) from other experience of $30,628,867 from Section 2, Chart 9 is equal to the sum of items 6(b) through 6(d). 23

56 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT H Table of Amortization Bases Type* Date Established Initial Years Initial Amount Outstanding Balance Years Remaining Annual Payment* Experience Gain 6/30/ $10,871,830 -$12,764, $959,510 Change in Assumptions 6/30/ ,629,891 10,132, ,644 Plan Amendments 6/30/ ,607,265 15,976, ,200, % COLA Assumption 6/30/ ,057,441 31,768, ,387,996 Experience Loss 6/30/ ,292,281 2,684, ,368 Experience Loss 6/30/ ,232,251 30,552, ,137,021 Plan Amendments 6/30/ ,111,914 5,953, ,444 Experience Loss 6/30/ ,692,270 50,496, ,419,792 Plan Amendments 6/30/ ,138,578 77,594, ,254,933 Experience Loss 6/30/ ,731,232 37,457, ,461,416 New Assumption / Domestic Partners 6/30/ ,812,646-11,229, ,919 Experience Loss 6/30/ ,910,233 30,434, ,944,346 Remove Limit Pension Base 6/30/ ,315,928 30,753, ,964,688 Experience Loss 6/30/ ,160,133 15,798, ,021 Experience Gain 6/30/ ,098,126-3,404, ,652 Experience Gain 6/30/ ,800,585-8,430, ,940 Change in Assumptions 6/30/ ,413,374 55,566, ,295,084 Experience Loss 6/30/ ,894, ,960, ,075,309 Experience Loss 6/30/ ,039,098 3,164, ,826 Change in Assumptions 6/30/ ,098,499 8,432, ,195 Experience Loss 6/30/ ,428,038 4,520, ,941 Experience Gain 6/30/ ,668,764-15,668, ,095,969 Change in Assumptions 6/30/ ,400,521 53,400, ,241,271 Total $535,150,038 $34,149,235 * Level percentage of payroll. Note: The equivalent single amortization period is about 24 years. 24

57 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT I Section 415 Limitations Section 415 of the Internal Revenue Code (IRC) specifies the maximum benefits that may be paid to an individual from a defined benefit plan and the maximum amounts that may be allocated each year to an individual s account in a defined contribution plan. Contribution rates determined in this valuation have not been reduced for the Section 415 limitations. Actual limitations will result in actuarial gains as they occur. A qualified pension plan may not pay benefits in excess of the Section 415 limits. The ultimate penalty for noncompliance is disqualification: active participants could be taxed on their vested benefits and the IRS may seek to tax the income earned on the plan s assets. In particular, Section 415(b) of the IRC limits the maximum annual benefit payable at the Normal Retirement Age to a dollar limit of $160,000 indexed for inflation. That limit is $200,000 for 2012 and $205,000 for Normal Retirement Age for these purposes is age 62. These are the limits in simplified terms. They must be adjusted based on each participant s circumstances, for such things as age at retirement, form of benefits chosen and after tax contributions. Legal Counsel s review and interpretation of the law and regulations should be sought on any questions in this regard. 25

58 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT J Definitions of Pension Terms The following list defines certain technical terms for the convenience of the reader: Assumptions or Actuarial Assumptions: Normal Cost: Actuarial Accrued Liability For Actives: Actuarial Accrued Liability For Pensioners: Unfunded Actuarial Accrued Liability: The estimates on which the cost of the Plan is calculated including: (a) Investment return the rate of investment yield that the Plan will earn over the long-term future; (b) Mortality rates the death rates of employees and pensioners; life expectancy is based on these rates; (c) Retirement rates the rate or probability of retirement at a given age; and (d) Turnover rates the rates at which employees of various ages are expected to leave employment for reasons other than death, disability, or retirement. The amount of contributions required to fund the benefit allocated to the current year of service. The equivalent of the accumulated normal costs allocated to the years before the valuation date. The single sum value of lifetime benefits to existing pensioners. This sum takes account of life expectancies appropriate to the ages of the pensioners and the interest that the sum is expected to earn before it is entirely paid out in benefits. The extent to which the actuarial accrued liability of the Plan exceeds the assets of the Plan. There is a wide range of approaches to paying off the unfunded actuarial accrued liability, from meeting the interest accrual only to amortizing it over a specific period of time. 26

59 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System Amortization of the Unfunded Actuarial Accrued Liability: Payments made over a period of years equal in value to the Plan s unfunded actuarial accrued liability. Investment Return: The rate of earnings of the Plan from its investments, including interest, dividends and capital gain and loss adjustments, computed as a percentage of the average value of the fund. For actuarial purposes, the investment return often reflects a smoothing of the capital gains and losses to avoid significant swings in the value of assets from one year to the next. 27

60 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System EXHIBIT I Summary of Actuarial Valuation Results The valuation was made with respect to the following data supplied to us: 1. Retired participants as of the valuation date (including 244 beneficiaries in pay status) 1, Participants inactive during year ended June 30, 2012 with vested rights Participants active during the year ended June 30, ,703 Fully vested 1,415 Not vested 288 The actuarial factors as of the valuation date are as follows: 1. Normal cost, beginning of year $34,856, Present value of future benefits 1,820,299, Present value of future normal costs 263,603, Actuarial accrued liability Retired participants and beneficiaries $791,344,644 Inactive participants with vested rights 37,669,468 Active participants 727,682,153 Subtotal $1,556,696, Valuation value of assets ($986,972,000 at market value for pension and HIB plans, as reported by the auditor, and $1,035,786,332 at actuarial value for pension and HIB plans) $1,021,546,227 (1) 6. Unfunded actuarial accrued liability $535,150,038 (1) Net of HIB assets. 28

61 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System EXHIBIT I (continued) Summary of Actuarial Valuation Results The determination of the recommended contribution is as follows: 1. Total normal cost $34,856, Expected employee contributions -10,309, Employer normal cost: (1) + (2) $24,547, Payment on unfunded actuarial accrued liability $34,149, Total recommended contribution: beginning of year $58,696, Total recommended contribution: end of pay period $60,933, Projected payroll $158,847, Total recommended contribution as a percentage of projected payroll: (6) (7) 38.36% 29

62 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System EXHIBIT II Supplementary Information Required by GASB Schedule of Employer Contributions Plan Year Ended June 30 Annual Required Actual Contributions (1) Contributions 2007 $33,698,000 $33,698, % Percentage Contributed ,387,000 37,387, % ,485,000 39,485, % ,031,000 44,031, % ,987,000 50,987, % ,156,000 52,156, % (1) Annual required contributions up to the year ended June 30, 2008 were based on adopted contribution rates prepared by the System s prior actuary. 30

63 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System EXHIBIT III Supplementary Information Required by GASB Schedule of Funding Progress (Dollar Amounts in Thousands) Actuarial Valuation Date Valuation Value of Assets (a) Actuarial Accrued Liability (AAL) (b) Unfunded/ (Overfunded) AAL (UAAL) (b) - (a) Funded Ratio (a) / (b) Covered Payroll (c) UAAL as a Percentage of Covered Payroll [(b) - (a)] / (c) 06/30/2007 $827,098 $1,126,106 $299, % $153, % 06/30/ ,917 1,244, , % 158, % 06/30/ ,021 1,323, , % 161, % 06/30/ ,845 1,396, , % 164, % 06/30/ ,719 1,446, , % 159, % 06/30/2012 1,021,546 1,556, , % 158, % 31

64 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System EXHIBIT IV Supplementary Information Required by GASB Valuation date June 30, 2012 Actuarial cost method Amortization method Remaining amortization period Asset valuation method Actuarial assumptions: Entry Age Normal Cost Method Level percent of payroll Plan changes, assumption changes, and experience gains/losses prior to July 1, 2011 are amortized over separate decreasing 30-year amortization periods. On or after July 1, 2011, plan changes are amortized over separate decreasing 15-year periods; assumption changes are amortized over separate decreasing 25-year periods; and experience gains/losses are amortized over separate decreasing 20-year periods. Market value of assets less unrecognized returns in each of the last five years. Unrecognized return is equal to the difference between the actual market return and the expected return on the market value, and is recognized over a five year period, further adjusted, if necessary, to be within 30% of the market value. Investment rate of return 7.75% Inflation rate 3.25% Across the board salary increase 0.50% Projected salary increases* Ranges from 4.25% to 9.75% based on years of service Cost of living adjustments 3.15% Plan membership: Retired participants and beneficiaries receiving 1,361 benefits Terminated participants entitled to, but not yet 224 receiving benefits Active participants 1,703 Total 3,288 * Includes inflation at 3.25% plus across the board salary increase of 0.50% plus merit and promotional increases. See Exhibit V for these increases. 32

65 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System EXHIBIT V Actuarial Assumptions and Actuarial Cost Method Mortality Rates: Pre-retirement, After Service Retirement, and All Beneficiaries Males RP-2000 Combined Healthy Mortality Table projected with scale AA to 2016, set back one year for males Females RP-2000 Combined Healthy Mortality Table projected with scale AA to 2016, set back two years for females After Disability Retirement: Males RP-2000 Combined Healthy Mortality Table projected with scale AA to 2016, set forward six years for males Females RP-2000 Combined Healthy Mortality Table projected with scale AA to 2016, set forward six years for females The tables shown above were determined to contain sufficient provision appropriate to reasonably reflect future mortality improvement, based on a review of mortality experience as of the measurement date. Disability Rates: Rate (%) Rate (%) Age Male Female Age Male Female

66 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Termination Rates: Rate (%) Ordinary Withdrawal* Service Male Female Ordinary Withdrawal** Rate (%) Vested Termination Age Male Female Male Female * Applicable for members with less than five years of service. ** Applicable after five years of service. 34

67 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Retirement Rates: Rate (%) Age Male Female 54* * The rate for members age 54 with 30 or more years of service (i.e., eligible for unreduced benefits) is 50% for males and females. 35

68 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Retirement Age for Inactive Vested Participants: 58 Reciprocity: 30% of members who terminate with a vested benefit are assumed to enter a reciprocal system. For reciprocals, we assume 4.25% compensation increases per annum. Unknown Data for Participants: Same as those exhibited by members with similar known characteristics. If not specified, members are assumed to be male. Percent Married: The Retirement System has indicated the marital status of each member. Age of Spouse: Female spouses are 3 years younger than their male spouses. Same sex domestic partners are assumed to be the same age. Future Benefit Accruals: 1.0 year of service per year of employment plus years of additional service to anticipate conversion of unused sick leave for each year of employment. Net Investment Return: Interest Credited to Employee Accounts: 7.75% Inflation: 3.25% Across the Board Salary Increases: 0.50% 7.75%, net of investment and administrative expenses. Cost of Living Increases: 3.15% per annum. 36

69 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Salary Increases: Annual Rate of Compensation Increase Inflation: 3.25% per year; plus across the board salary increases of 0.50% per year; plus the following merit and promotional increases based on years of service: Years of Service Merit and Promotional Increases % % % % % % % % Actuarial Value of Assets: Market value of assets less unrecognized returns in each of the last five years. Unrecognized return is equal to the difference between the actual market return and the expected return on the market value, and is recognized over a five-year period, further adjusted, if necessary, to be within 30% of the market value. 37

70 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Actuarial Cost Method: Changes in Actuarial Assumptions: Mortality Rates: Pre-retirement and After Service Retirement: After Disability Retirement: Disability Rates: Entry Age Normal Actuarial Cost Method. Entry Age is the age at the member s hire date. Actuarial Accrued Liability is calculated on an individual basis and is based on costs allocated as a level percentage of compensation. The Normal Cost is calculated on an individual basis where the Entry Age Normal Cost is calculated as the sum of the individual Normal Costs. Based on the July 1, 2008 June 30, 2012 actuarial experience study, the following actuarial assumptions were changed. Previously these assumptions were as follows: RP-2000 Combined Healthy Mortality Table for males, set back two years RP-2000 Combined Healthy Mortality Table for females, unadjusted RP-2000 Combined Healthy Mortality Table for males, set forward four years RP-2000 Combined Healthy Mortality Table for females, set forward four years Rate (%) Age Male Female

71 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Changes in Actuarial Assumptions: (continued) Termination Rates: Rate (%) Ordinary Withdrawal* Service Male Female 0 2.5% 3.0% 1 2.5% 3.0% 2 1.5% 2.5% 3 1.5% 2.0% 4 1.0% 1.5% Ordinary Withdrawal** Rate (%) Vested Termination Age Male Female Male Female * Applicable for members with less than five years of service. ** Applicable after five years of service. 39

72 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Changes in Actuarial Assumptions: (continued) Retirement Rates: Retirement Probability Age Male Female 54* 8.00% 4.00% % 7.00% % 10.00% % 10.00% % 13.00% % 15.00% % 10.00% % 10.00% % 15.00% % 20.00% % 20.00% % 25.00% % 25.00% % 35.00% % 50.00% % 60.00% % % * The rate for members age 54 with 30 or more years of service (i.e., eligible for unreduced benefits) is 70% for males and 45% for females. 40

73 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Changes in Actuarial Assumptions: (continued) Reciprocity: 30% of members who terminate with a vested benefit are assumed to enter a reciprocal system. For reciprocals, we assume 4.70% compensation increases per annum. Age of Spouse: Female spouses are 4 years younger than their male spouses. Same sex domestic partners are assumed to be the same age. Future Benefit Accruals: 1.0 year of service per year. Net Investment Return: Interest Credited to Employee Accounts: 8.00% Inflation: 3.50% 8.00%, net of investment and administrative expenses. Cost of Living Increases: 3.25% per annum. 41

74 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Changes in Actuarial Assumptions: (continued) Salary Increases: Annual Rate of Compensation Increase Inflation: 3.50% per year; plus across the board salary increases of 0.50% per year; plus the following merit and promotional increases based on years of service: Years of Service Merit and Promotional Increases % % % % % % % % % Actuarial Cost Method: Entry Age Normal Actuarial Cost Method. Entry Age is the age at the member s hire date. Actuarial Accrued Liability is calculated on an individual basis and is based on costs allocated as a level percentage of compensation. The Normal Cost is calculated on an aggregate basis by taking the Present Value of Future Normal Costs divided by the Present Value of Future Salaries to obtain a normal cost rate. This normal cost rate is then multiplied by the total current salaries. 42

75 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System EXHIBIT VI Summary of Plan Provisions This exhibit summarizes the major provisions of the EBMUD included in the valuation. It is not intended to be, nor should it be interpreted as, a complete statement of all plan provisions. Plan Year: July 1 through June 30 Census Date: June 30 Final Compensation for Benefit Determination: Highest two consecutive years of compensation earnable. Normal or Unreduced Retirement Eligibility: Age and Service Requirement Age 65; Age 62 with 5 years of service; Age 59 with 20 years of service; Age 54 with 30 years of service; Other combinations of age and service between ages 54 and 59. Early Retirement Eligibility: Age and Service Requirement Age 54 with 5 years of service. 43

76 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Benefit Formula: 1955 Formula 2.42% (2.82% if member is credited with District Service on or after January 1, 2004) times Final Compensation per year of service including all service extension credit. 1955/80 Formula 2.42% (2.82% if member is credited with District Service on or after January 1, 2004) times Final Compensation per year of service up to August 1, 1980 including all service extension credit, plus 2.20% (2.60% if member is credited with District Service on or after January 1, 2004) times Final Compensation per year of service after August 1, Applies to members who elected to convert to the 1980 Formula in /90 Formula 2.42% (2.82% if member is credited with District Service on or after January 1, 2004) times Final Compensation per year of service up to January 1, 2000 including all service extension credit, plus 2.20% (2.60% if member is credited with District Service on or after January 1, 2004) times Final Compensation per year of service after January 1, Applies to members who elected to convert to the 1980 Formula in Formula 2.20% (2.60% if member is credited with District Service on or after January 1, 2004) times Final Compensation per year of service including all service extension credit. Applies to all members hired on or after January 1, Service Extension Credit 2.42% (2.82% if member is credited with District Service on or after January 1, 2004) for members with any service under the 1955 Formula or 2.20% (2.60% if member is credited with District Service on or after January 1, 2004) for members with service only under the 1980 Formula times Final Compensation per year of Service Extension Credit. Service extension credit is the number of unused sick leave days credited to a member at the time of retirement converted on a 260-day basis. The number of such days is then doubled for the benefit calculation and for service retirements to meet the early retirement provision of the Ordinance. Benefit Adjustments Reduced by 3% per year under the age of eligibility for an unreduced benefit, based on service at retirement, for retirements before age 63 (before age 62 commencing November 1, 2000). Effective July 1, 1999, Service Extension Credit is included in the years of service calculation of service for determining eligibility for unreduced retirement. 44

77 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Disability: Eligibility Benefit Eight years of service (not available for Directors). Greater of: 1.5% times Final Compensation per year of service. One-third of Final Compensation. Vesting: Requirements Pre-Retirement Death Benefit: Eligibility Benefit Eligibility Benefit Post-Retirement Death Benefit(s): Member Contributions: Five years of service, must leave contributions on deposit, reciprocal service counts for vesting purposes. Eligible for retirement. 50% of the unmodified service retirement benefit to eligible surviving spouse plus the lump sum payment of accumulated retirement contributions. OR None. Lump sum payment of accumulated retirement contributions. 50% of the unmodified service retirement benefit to surviving spouse or registered domestic partner (tied to the implementation of the AB 205 legislation). Retirement system members currently contribute at a rate of 6.83% of pay, reflecting the allocation of increased costs of the negotiated Plan benefit multiplier enhancement. Member contribution rates, defined in the Ordinance, are scheduled to remain the same. 45

78 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Cost of Living Changes in Plan Provisions: Payable July 1 of each year, the basic minimum COLA benefit is the lesser of 3% and the actual change in the cost of living index. Excess of the actual change of cost of living index over 3% is accumulated in individual retiree COLA banks. Withdrawals from the bank are made in years when the index increases less than 3%. Increases of up to 5% are granted in years when the Retirement Board determines that the System is more than 85% funded on a Projected Benefit Obligation basis. In those years when the System is more than 85% funded and the cost of living index exceeds 5%, any excess cost of living over 5% is accumulated in the COLA bank. Effective October 1, 2000, in those years when the system is more than 85% funded on a Projected Benefit Obligation basis and the cost of living is less than 4%, withdrawals from the bank are made to allow cost of living increases up to 4%. There have been no changes in plan provisions since the last valuation. NOTE: The summary of major plan provisions is designed to outline principal plan benefits as interpreted for purposes of the actuarial valuation. If the System should find the plan summary not in accordance with the actual provisions, the System should alert the actuary so that both can be sure the proper provisions are valued v3/

79 East Bay Municipal Utility District Retirement System Health Insurance Benefit Valuation Review of Contribution Rates and Funding Status June 30, 2012 This report has been prepared at the request of the Retirement Board to assist in administering the Fund. This valuation report may not otherwise be copied or reproduced in any form without the consent of the Retirement Board and may only be provided to other parties in its entirety. The measurements shown in this actuarial valuation may not be applicable for other purposes. Copyright 2013 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

80 THE SEGAL COMPANY 100 Montgomery Street, Suite 500 San Francisco, CA T F January 9, 2013 Ms. Wanda Hendrix Treasury Manager East Bay Municipal Utility District 375 Eleventh Street Oakland, California Dear Wanda: We are pleased to submit our Health Insurance Benefit Valuation as of June 30, 2012 for the prefunded $450 ($550 for a retiree with a spouse or qualified domestic partner) monthly health insurance subsidy. The Governmental Accounting Standards Board (GASB) requires employers, such as EBMUD, that pool health insurance premium rates for actives and retirees under age 65 to also calculate the liability associated with such pooled premiums for retirees under age 65 on an accrual basis. While that liability referred to as the implicit subsidy has to be disclosed, it is not required to be prefunded. The contribution rate developed in this report only includes the prefunding requirement for the $450/$550 benefit. The obligation required for disclosure purposes will be provided in a separate report. This valuation is based on financial statements and census data furnished by EBMUD. The actuarial calculations were completed under the supervision of Thomas Bergman, ASA, MAAA, Enrolled Actuary. The undersigned are Members of the American Academy of Actuaries and meet the qualification requirements to render the actuarial opinion contained herein. Sincerely, THE SEGAL COMPANY By: ER/hy Andy Yeung, FCA, ASA, MAAA, EA Vice President and Associate Actuary Thomas Bergman, ASA, MAAA, EA Assistant Actuary

81 SECTION 1 SECTION 2 SECTION 3 VALUATION SUMMARY Contributing Recommendations and Funding Status... i VALUATION RESULTS A. Introduction... 1 B. Financial Information... 2 C. Funding Ratio... 3 D. Recommended Contribution... 4 SUPPORTING EXHIBITS EXHIBIT I Table of Amortization Bases... 5 EXHIBIT II Actuarial Assumptions/Methods.. 6 EXHIBIT III Summary of Plan... 20

82 SECTION 1: Valuation Summary for EBMUD Health Insurance Benefit Valuation CONTRIBUTION RECOMMENDATIONS AND FUNDING STATUS The contribution rate recommended in the June 30, 2012 valuation has been calculated with the layered amortization approach. In the review of the Board s actuarial funding policy, we recommended alternative amortization periods for use in amortizing new unfunded actuarial accrued liability (UAAL) on or after July 1, 2011, with separate amortization periods depending on the source of the UAAL change. The Board adopted alternative #3 from that letter, which utilizes the following amortization periods by source: 20 years for actuarial gains or losses; 25 years for assumption or method changes, 15 years for plan amendments; 5 years for Early Retirement Incentive Programs; and 30 years for actuarial surplus. The results of this valuation reflect the changes in the amortization periods, but these changes did not have a material impact on the employer contribution rate. In the aggregate, the total payment from all the UAAL layers was about the same as amortizing the entire UAAL over a period of about 19 years. The recommended contribution rate increased to 5.34% of pay. The contribution rate calculated in the prior valuation was 5.10%. This was the result of assumption changes from the experience study and less than expected growth in total payroll base to amortize the System s UAAL. We have maintained the allocation of 0.09% of the member contribution to the HIB plan used in last year s valuation. This report assumes the HIB subsidy limit will remain at the current levels of $450/$550. Future increases in the HIB subsidy will increase the cost of the plan as a percent of pay. Based on prior directions from the District, we have not included the projected excise tax that may be imposed by the Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act. Under these acts, beginning in 2018 health plans that provide a subsidy above certain thresholds (e.g. $11,850 for single or $30,950 for family coverage for non-medicare retirees age and for retirees with careers in high-risk professions) may be subject to a 40% excise tax. Based on action taken by the Board in 2012, the total unrecognized deferred gain of $1.5 million through June 30, 2011 as of that valuation has been recognized in four level amounts with three years of recognition remaining after the June 30, 2012 valuation. i