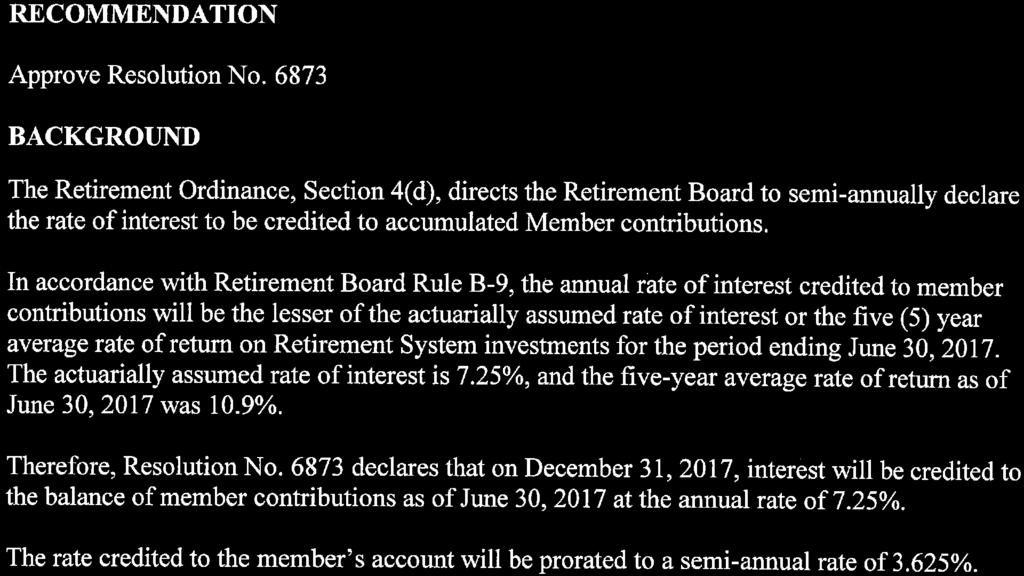

The next regular meeting of the Retirement Board will be held at 8:30 a.m. on Thursday, March 15, 2018.

|

|

|

- Ferdinand Craig

- 6 years ago

- Views:

Transcription

1

2

3 11. Working Capital Management Strategy S. Skoda 12. Annual Retirement Board Training Report E. Grassetti REPORTS FROM THE RETIREMENT BOARD: 13. Brief report on any course, workshop, or conference attended since the last Retirement Board Meeting ITEMS TO BE CALENDARED: MEETING ADJOURNMENT: The next regular meeting of the Retirement Board will be held at 8:30 a.m. on Thursday, March 15, Retirement Board Meetings March 15, 2018 May17, 2018 July 19, 2018 September 20, 2018 November 15, 2018

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21 East Bay Municipal Utility District Retirement System Actuarial Valuation and Review of Pension Plan and Health Insurance Benefit Plan as of June 30, 2017 Supplemental Exhibits This report has been prepared at the request of the Retirement Board to assist in administering the Fund. This valuation report may not otherwise be copied or reproduced in any form without the consent of the Retirement Board and may only be provided to other parties in its entirety. The measurements shown in this actuarial valuation may not be applicable for other purposes. Copyright 2018 by The Segal Group, Inc. All rights reserved.

22 100 MONTGOMERY STREET, SUITE 500 SAN FRANCISCO, CA T January 12, 2018 Ms. Sophia Skoda Director of Finance East Bay Municipal Utility District 375 Eleventh Street Oakland, CA Re: June 30, 2017 Actuarial Valuations Supplemental Exhibits Dear Sophia: Enclosed please find two exhibits that provide supplemental information to the June 30, 2017 actuarial valuations for the pension and health insurance benefit (HIB) plans. Exhibit A provides a summary of the funding valuation results for both the pension plan and HIB plan. In particular, for the HIB plan, this information is based on our HIB funding valuation report dated January 12, 2018 that includes a maximum monthly benefit of $450 ($550 benefit for a retiree with a spouse or EBMUD domestic partner). It does not include the accounting liability for the implicit subsidy associated with the pooling of the health care premium rate for actives and retirees under age 65. In Exhibit B, we have included a comparison of the historical Projected Benefit Obligations with the market value of assets for both plans. We look forward to discussing this information with you and the Board. Sincerely, Andy Yeung, ASA, MAAA, FCA, EA Vice President and Actuary DNA/bqb Enclosures v3/

23 I. Total Membership Exhibit A East Bay Municipal Utility District Retirement System Summary of Significant Valuation Results for the Funding Valuations June 30, 2017 June 30, 2016 Change From Prior Year A. Active Members 1,802 1, % B. Pensioners and Beneficiaries 1,713 1, % II. Valuation Salary (1) III. A. Total Annual Payroll $184,858,798 $183,970, % B. Average Yearly Salary 102, , % Total System Assets A. Valuation Value of Pension Plan Assets $1,549,213,319 $1,425,784, % B. Valuation Value of HIB Plan Assets 31,451,690 27,002, % C. Total Valuation Value (Actuarial Value) $1,580,665,009 $1,452,786, % D. Market Value of Pension Plan Assets $1,580,556,000 $1,391,771, % E. Market Value of HIB Plan Assets 32,088,000 26,358, % F. Total Market Value $1,612,644,000 $1,418,129, % IV. Unfunded Actuarial Accrued Liability (UAAL) and Funded Ratio (2) A. Pension Plan $518,801,626 $570,078, % B. Funded Ratio 74.9% 71.4% 3.5% C. HIB Plan $86,207,371 $88,652, % D. Funded Ratio 26.7% 23.3% 3.4% E. Pension Plan and HIB Plan $605,008,997 $658,731, % F. Funded Ratio 72.3% 68.8% 3.5% (1) Projected payroll. (2) Based on valuation value of assets. Note: The HIB information is based on our HIB funding valuation report that includes a maximum monthly benefit of $450 ($550 for a retiree with a spouse or EBMUD domestic partner). It does not include the accounting liability for the implicit subsidy associated with the pooling of the health care premium rate for actives and retirees under age 65. 1

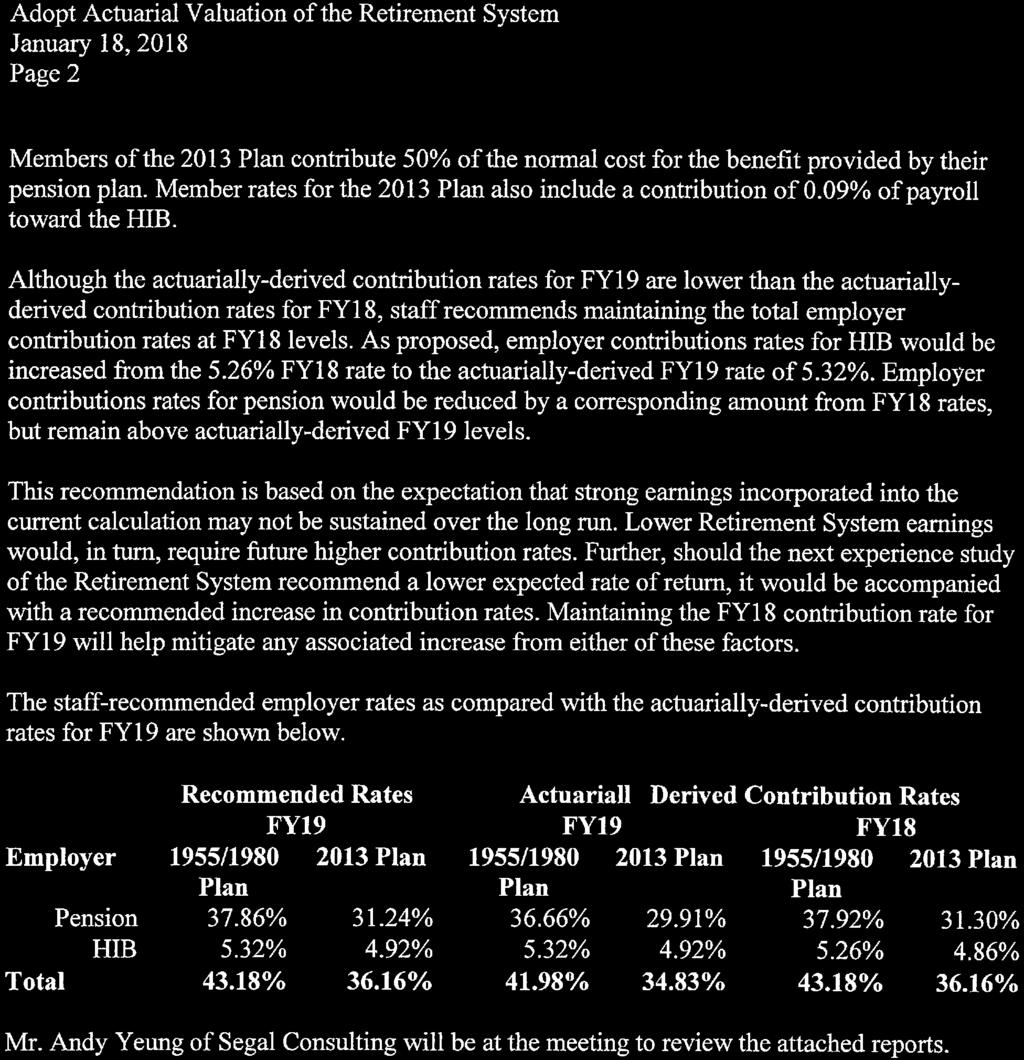

24 Exhibit A (continued) East Bay Municipal Utility District Retirement System Summary of Significant Valuation Results for the Funding Valuations June 30, 2017 June 30, 2016 Change From Prior Year V. Projected Benefit Obligation (3) A. Pension Plan $2,013,986, 000 $1,939,458, % B. Funded Ratio 78.5% 71.8% 6.7% C. HIB Plan $123,497,000 $121,744, % D. Funded Ratio 26.0% 21.7% 4.3% E. Pension Plan and HIB Plan $2,137,483,000 $2,061,202, % F. Funded Ratio 75.4% 68.8% 6.6% VI. Budget Items (4) FY FY Difference 1955/1980 Plan 2013 Tier Combined (5) 1955/1980 Plan 2013 Tier Combined (5) 1955/1980 Plan 2013 Tier Combined (5) A. Pension Plan 1. Total Normal Cost 24.22% 17.56% 22.76% 24.23% 17.70% 22.80% -0.01% -0.14% -0.04% 2. Employee Contributions -8.66% (6) -8.75% -8.68% -8.66% (6) -8.75% -8.68% 0.00% 0.00% 0.00% 3. Employer Normal Cost 15.56% 8.81% 14.08% 15.57% 8.95% 14.12% -0.01% -0.14% -0.04% 4. UAAL (paid by Employer) 21.10% 21.10% 21.10% 22.35% 22.35% 22.35% -1.25% -1.25% -1.25% 5. Total Employer Contribution 36.66% 29.91% 35.18% 37.92% 31.30% 36.47% -1.26% -1.39% -1.29% B. HIB Plan 1. Total Normal Cost 1.23% 0.83% 1.14% 1.25% 0.85% 1.16% -0.02% -0.02% -0.02% 2. Employee Contributions -0.09% -0.09% -0.09% -0.09% -0.09% -0.09% 0.00% 0.00% 0.00% 3. Employer Normal Cost 1.14% 0.74% 1.05% 1.16% 0.76% 1.07% -0.02% -0.02% -0.02% 4. UAAL (paid by Employer) 4.18% 4.18% 4.18% 4.10% 4.10% 4.10% 0.08% 0.08% 0.08% 5. Total Employer Contribution 5.32% 4.92% 5.23% 5.26% 4.86% 5.17% 0.06% 0.06% 0.06% C. Total Contribution 1. Employee Contribution (A2 + B2) 8.75% 8.84% 8.77% 8.75% 8.84% 8.77% 0.00% 0.00% 0.00% 2. Employer Contribution (A5 + B5) 41.98% 34.83% 40.41% 43.18% 36.16% 41.64% -1.20% -1.33% -1.23% (3) Based on market value of assets. (4) (5) (6) Contribution rates, payable at the end of each pay period, are expressed as a percentage of projected pay. Aggregated based on June 30, 2017 projected annual payroll. The rate of 8.66% payable during fiscal years 2017/2018 and 2018/2019 is calculated by taking the total employee rate payable beginning April 18, 2016 (i.e., 8.75%), less the HIB employee contribution rate of 0.09%. 2

25 Exhibit B East Bay Municipal Utility District Retirement System Comparison of Projected Benefit Obligation with the Market Value of Assets (Dollar Amounts in Thousands) Actuarial Valuation Date Projected Benefit Obligation Market Value of Assets Funded Ratio 06/30/2002 $749,113 $536, % 06/30/ , , % 06/30/ , , % 06/30/ , , % 06/30/2006 1,068, , % 06/30/2007 1,160, , % 06/30/2008 1,289, , % 06/30/2009 1,366, , % 06/30/2010 1,444, , % 06/30/2011 1,498, , % 06/30/2012 1,606, , % 06/30/2013 1,699,340 1,124, % 06/30/2014 1,815,349 1,346, % 06/30/2015 1,907,462 1,407, % 06/30/2016 2,061,202 1,418, % 06/30/2017 2,137,483 1,612, % v3/

26 East Bay Municipal Utility District Retirement System Actuarial Valuation and Review of Pension Plan as of June 30, 2017 This report has been prepared at the request of the Retirement Board to assist in administering the Fund. This valuation report may not otherwise be copied or reproduced in any form without the consent of the Retirement Board and may only be provided to other parties in its entirety. The measurements shown in this actuarial valuation may not be applicable for other purposes. Copyright 2018 by The Segal Group, Inc., parent of The Segal Company. All rights reserved.

27 100 MONTGOMERY STREET, SUITE 500 SAN FRANCISCO, CA T January 12, 2018 Ms. Sophia Skoda Director of Finance East Bay Municipal Utility District 375 Eleventh Street Oakland, CA Dear Sophia: We are pleased to submit this Actuarial Valuation and Review as of June 30, 2017 for only the pension plan. The Review of Contribution Rates and Funding Status for the health insurance benefit (HIB) plan is provided in a separate report. This report summarizes the actuarial data used in the valuation, establishes the funding requirements for fiscal 2018/2019 and analyzes the preceding year s experience. This report was prepared in accordance with generally accepted actuarial principles and practices, at the request of the Board to assist in administering the Plan. The census and financial information on which our calculations were based were prepared by EBMUD. That assistance is gratefully acknowledged. The measurements shown in this actuarial valuation may not be applicable for other purposes. Future actuarial measurements may differ significantly from the current measurements presented in this report due to such factors as the following: plan experience differing from that anticipated by the economic or demographic assumptions; changes in economic or demographic assumptions; increases or decreases expected as part of the natural operation of the methodology used for these measurements (such as the end of an amortization period); and changes in plan provisions or applicable law. The actuarial calculations were directed under my supervision. I am a member of the American Academy of Actuaries and I meet the Qualification Standards of the American Academy of Actuaries to render the actuarial opinion herein. To the best of our knowledge, the information supplied in this actuarial valuation is complete and accurate. Further, in our opinion, the assumptions as approved by the Board are reasonably related to the experience of and the expectations for the Plan. We look forward to reviewing this report at your next meeting and to answering any questions. Sincerely, Segal Consulting, a Member of the Segal Group, Inc. By: JRC/hy Andy Yeung, ASA, MAAA, FCA, EA Vice President and Actuary

28 SECTION 1 SECTION 2 SECTION 3 SECTION 4 VALUATION SUMMARY VALUATION RESULTS SUPPLEMENTAL INFORMATION REPORTING INFORMATION Purpose... i Significant Issues in Valuation Year... ii Summary of Key Valuation Results... iv Important Information about Actuarial Valuations... vi A. Participant Data... 1 B. Financial Information... 4 C. Actuarial Experience... 7 D. Employer and Member Contributions E. Funded Ratio F. Volatility Ratios EXHIBIT A Table of Plan Coverage EXHIBIT B Participants in Active Service as of June 30, EXHIBIT C Reconciliation of Participant Data EXHIBIT D Summary Statement of Income and Expenses on an Actuarial Value Basis for All Pension Plan and HIB Plan Assets EXHIBIT I Summary of Actuarial Valuation Results EXHIBIT II Actuarial Assumptions and Actuarial Cost Method EXHIBIT III Summary of Plan Provisions EXHIBIT E Summary Statement of Assets for Pension and HIB Plans EXHIBIT F Development of the Fund Through June 30, 2017 for All Pension Plan and HIB Plan Assets EXHIBIT G Actuarial Balance Sheet EXHIBIT H Development of Unfunded Actuarial Accrued Liability for Year Ended June 30, EXHIBIT I Table of Amortization Bases EXHIBIT J Section 415 Limitations EXHIBIT K Definitions of Pension Terms.. 33

29 SECTION 1: Valuation Summary for the East Bay Municipal Utility District Retirement System Purpose This report has been prepared by Segal Consulting ( Segal ) to present a valuation of the East Bay Municipal Utility District Retirement System as of June 30, The valuation was performed to determine whether the assets and contributions are sufficient to provide the prescribed benefits. The contribution requirements presented in this report are based on: Ref: Pg. 31 The benefit provisions of the pension plan, as administered by the Board; The characteristics of covered active participants, inactive vested participants, and retired participants and beneficiaries as of June 30, 2017, provided by EBMUD; The assets of the plan as of June 30, 2017, provided by EBMUD; Economic assumptions regarding future salary increases and investment earnings adopted by the Board for the June 30, 2017 valuation; and Other actuarial assumptions, regarding employee terminations, retirement, death, etc., adopted by the Board for the June 30, 2017 valuation. One of the general goals of an actuarial valuation is to establish contributions which fully fund the System s liabilities, and which, as a percentage of payroll, remain as level as possible for each generation of active members. Annual actuarial valuations measure the progress toward this goal, as well as test the adequacy of the contribution rates. In preparing this valuation, we have employed generally accepted actuarial methods and assumptions to evaluate the System s assets, liabilities and future contribution requirements. Our calculations are based upon member data and financial information provided to us by the System s staff. This information has not been audited by us, but it has been reviewed and found to be consistent, both internally and with prior year s information. The contribution requirements are determined as a percentage of payroll. The System s employer rates provide for both normal cost and a payment or credit to amortize any unfunded or overfunded actuarial accrued liabilities. In the valuation, new unfunded actuarial accrued liabilities (UAAL) established on or after July 1, 2011 as a result of actuarial gains or losses and change in actuarial assumptions/methods has been amortized over separate declining 20-year and 25-year periods, respectively. The balance of the UAAL established prior to July 1, 2011 continues to be amortized in layers over the current respective remaining fixed periods. Based on the total UAAL contribution rate recommended in the June 30, 2017 valuation, the equivalent single amortization period is about 18 years. The rates calculated in this report may be adopted by the Board for the fiscal year that extends from July 1, 2018 through June 30, i

30 SECTION 1: Valuation Summary for the East Bay Municipal Utility District Retirement System Significant Issues in Valuation Year The following key findings were the result of this actuarial valuation: Ref: Pgs. 18 and 30 Ref: Pg. 15 Ref: Pg. 16 Ref: Pg. 5 The funded ratio measured on a valuation value of assets basis increased from 71.4% at June 30, 2016 to 74.9% at June 30, The funded ratio if measured on a market value of assets basis increased from 69.7% to 76.4%. The UAAL decreased from $570.1 million as of June 30, 2016 to $518.8 million as of June 30, The decrease in the UAAL is primarily due to (a) the higher than expected return on the valuation value of assets (after smoothing) and (b) lower than expected salary increases for actives, 1 offset somewhat by (c) the normal one-year lag in implementing the contribution rates in the June 30, 2016 valuation and (d) other actuarial losses. A complete reconciliation of the System s unfunded actuarial accrued liability is provided in Section 3, Exhibit H. The aggregate employer rate calculated in this valuation has decreased from 36.47% of payroll to 35.18% of payroll. The decrease in the employer rate was primarily due to (a) a decrease in the normal cost rate mostly due to the enrollment of new employees in the 2013 Tier, (b) the higher than expected return on the valuation value of assets (after smoothing), and (c) lower than expected salary increases for actives, 1 offset somewhat by (d) lower than expected growth in total payroll, (e) the normal one-year lag in implementing the contribution rates in the June 30, 2016 valuation, and (f) other actuarial losses. The aggregate member rate calculated in this valuation has remained unchanged at 8.68% of payroll. A reconciliation of the System s aggregate member rate is provided in Section 2, Subsection D (see Chart 15). As indicated in Section 2, Subsection B (see Chart 7) of this report, the total unrecognized investment gain as of June 30, 2017 is $32.0 million for the assets for the pension and HIB plans (note that in the previous valuation, this amount was a deferred loss of $34.7 million). This investment gain will be recognized in the determination of the actuarial value of assets for funding purposes in the next few years. This implies that earning the assumed rate of investment return of 7.25% per year (net of expenses) on a market value basis will produce investment gains on the actuarial value of assets after June 30, We understand that, as a result of ongoing negotiations, there have been no general salary increases other than individual merit and promotional increases since April 2016, if applicable. As a result, the liabilities and the employer contribution rates measured in this report do not reflect any pay increases that might be agreed to by the District and the bargaining parties subsequent to the date of this valuation as of June 30, ii

31 SECTION 1: Valuation Summary for the East Bay Municipal Utility District Retirement System The deferred gains of $32.0 million represent 2.0% of the market value of assets as of June 30, Unless offset by future investment losses or other unfavorable experience, the recognition of the net $32.0 million market gain is expected to have an impact on the System s future funded percentage and contribution rate requirements. This potential impact may be illustrated as follows: If the pension plan portion of the net deferred gains were recognized immediately and entirely in the valuation value of assets, the funded percentage would increase from 74.9% to 76.4%. If the pension plan portion of the net deferred gains were recognized immediately and entirely in the valuation value of assets, the aggregate employer rate (payable at the end of each pay period) would decrease from 35.18% to about 34.0% of payroll. The actuarial valuation report as of June 30, 2017 is based on financial information as of that date. Changes in the value of assets subsequent to that date are not reflected. Declines in asset values will increase the actuarial cost of the plan, while increases will decrease the actuarial cost of the plan. Impact of Future Experience on Contribution Rates Future contribution requirements may differ from those determined in the valuation because of: Differences between actual experience and anticipated experience; Changes in actuarial assumptions or methods; Changes in statutory provisions; and Difference between the contribution rates determined by the valuation and those adopted by the Board. iii

32 SECTION 1: Valuation Summary for the East Bay Municipal Utility District Retirement System Summary of Key Valuation Results June 30, 2017 June 30, 2016 Employer Contribution Rates: Estimated Estimated (payable at the end of each pay period) Total Rate Annual Amount (1) Total Rate Annual Amount (1) 1955/1980 Plan 36.66% $52,931, % $54,750, Tier 29.91% 12,105, % 12,668,524 Combined 35.18% 65,037, % 67,419,042 Average Member Contribution Rates: Estimated Estimated (payable at the end of each pay period) Total Rate Annual Amount (1) Total Rate Annual Amount (1) 1955/1980 Plan 8.66% (2) $12,503, % (2) $12,503, Tier 8.75% 3,541, % 3,541,521 Combined 8.68% 16,045, % 16,045,199 Funded Status: Actuarial accrued liability (AAL) $2,068,014,945 $1,995,863,155 Valuation value of pension plan assets (3) (VVA) 1,549,213,319 1,425,784,553 Market value of pension plan assets (3) (MVA) 1,580,556,000 1,391,771,000 Actuarial value of pension plan and HIB plan assets 1,580,665,009 1,452,786,717 Market value of pension plan and HIB plan assets 1,612,644,000 1,418,129,000 Funded ratio on VVA basis 74.9% 71.4% Funded ratio on pension plan MVA basis 76.4% 69.7% Unfunded actuarial accrued liability (UAAL) on VVA basis $518,801,626 $570,078,602 Unfunded actuarial accrued liability (UAAL) on pension plan MVA basis 487,458, ,092,155 (1) Estimated based on June 30, 2017 projected payroll of $184,858,798. (2) The rate of 8.66% payable during fiscal years 2017/2018 and 2018/2019 is calculated by taking the total employee rate payable beginning April 18, 2016 (i.e., 8.75%), less the HIB employee contribution rate of 0.09%. (3) Net of HIB plan assets. iv

33 SECTION 1: Valuation Summary for the East Bay Municipal Utility District Retirement System Summary of Key Valuation Results (continued) June 30, 2017 June 30, 2016 Demographic Data: Number of retired participants and beneficiaries 1,713 1,630 Number of vested participants Number of active participants 1,802 1,789 Projected total payroll $184,858,798 $183,970,858 Projected average payroll 102, ,834 Key Economic Assumptions: Interest rate 7.25% 7.25% Inflation rate 3.00% 3.00% Across the board salary increase 0.50% 0.50% Cost of living adjustments 3.00% 3.00% v

34 SECTION 1: Valuation Summary for the East Bay Municipal Utility District Retirement System Important Information about Actuarial Valuations An actuarial valuation is a budgeting tool with respect to the financing of future projected obligations of a pension plan. It is an estimated forecast the actual long-term cost of the plan will be determined by the actual benefits and expenses paid and the actual investment experience of the plan. In order to prepare an actuarial valuation, Segal relies on a number of input items. These include: Plan of benefits Plan provisions define the rules that will be used to determine benefit payments, and those rules, or the interpretation of them, may change over time. Even where they appear precise, outside factors may change how they operate. It is important to keep Segal informed with respect to plan provisions and administrative procedures, and to review the plan summary included in our report to confirm that Segal has correctly interpreted the plan of benefits. Participant data An actuarial valuation for a plan is based on data provided to the actuary by the System. Segal does not audit such data for completeness or accuracy, other than reviewing it for obvious inconsistencies compared to prior data and other information that appears unreasonable. It is important for Segal to receive the best possible data and to be informed about any known incomplete or inaccurate data. Assets This valuation is based on the market value of assets as of the valuation date, as provided by the System. The System uses an actuarial value of assets that differs from market value to gradually reflect year-to-year changes in the market value of assets in determining the contribution requirements. Actuarial assumptions In preparing an actuarial valuation, Segal projects the benefits to be paid to existing plan participants for the rest of their lives and the lives of their beneficiaries. This projection requires actuarial assumptions as to the probability of death, disability, termination, and retirement of each participant for each year. In addition, the benefits projected to be paid for each of those events in each future year reflect actuarial assumptions as to salary increases and cost-of-living adjustments. The projected benefits are then discounted to a present value, based on the assumed rate of return that is expected to be achieved on the plan s assets. There is a reasonable range for each assumption used in the projection and the results may vary materially based on which assumptions are selected. It is important for any user of an actuarial valuation to understand this concept. Actuarial assumptions are periodically reviewed to ensure that future valuations reflect emerging plan experience. While future changes in actuarial assumptions may have a significant impact on the reported results, that does not mean that the previous assumptions were unreasonable. The user of Segal s actuarial valuation (or other actuarial calculations) should keep the following in mind: vi

35 SECTION 1: Valuation Summary for the East Bay Municipal Utility District Retirement System The valuation is prepared at the request of the Board to assist the sponsors of the Fund in preparing items related to the pension plan in their financial reports. Segal is not responsible for the use or misuse of its report, particularly by any other party. An actuarial valuation is a measurement of the plan s assets and liabilities at a specific date. Accordingly, except where otherwise noted, Segal did not perform an analysis of the potential range of future financial measures. The actual long-term cost of the plan will be determined by the actual benefits and expenses paid and the actual investment experience of the plan. If the System is aware of any event or trend that was not considered in this valuation that may materially change the results of the valuation, Segal should be advised, so that we can evaluate it. Segal does not provide investment, legal, accounting, or tax advice. Segal s valuation is based on our understanding of applicable guidance in these areas and of the plan s provisions, but they may be subject to alternative interpretations. The Board should look to their other advisors for expertise in these areas. As Segal Consulting has no discretionary authority with respect to the management or assets of the Retirement System, it is not a fiduciary in its capacity as actuaries and consultants with respect to the Retirement System. vii

36 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System A. PARTICIPANT DATA The Actuarial Valuation and Review considers the number and demographic characteristics of covered participants, including active participants, vested terminated participants, retired participants and beneficiaries. This section presents a summary of significant statistical data on these participant groups. More detailed information for this valuation year and the preceding valuation can be found in Section 3, Exhibits A, B, and C. A historical perspective of how the participant population has changed over the past ten valuations can be seen in this chart. CHART 1 Participant Population: Year Ended June 30 Active Participants Vested Terminated Participants Retired Participants and Beneficiaries Ratio of Non-Actives to Actives , , , , , , , , , , , , , , , , , , , ,

37 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Active Participants Plan costs are affected by the age, years of service and payroll of active participants. In this year s valuation, there were 1,802 active participants with an average age of 48.0, average service of 12.8 years and average payroll of $102,585. The 1,789 active participants in the prior valuation had an average age of 48.5, average service of 13.3 years and average payroll of $102,834. Inactive Participants In this year s valuation, there were 267 participants with a vested right to a deferred or immediate vested benefit compared to 248 in the prior valuation. These graphs show a distribution of active participants by age and by years of service. CHART 2 Distribution of Active Participants by Age as of June 30, 2017 CHART 3 Distribution of Active Participants by Years of Service as of June 30,

38 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Retired Participants and Beneficiaries As of June 30, 2017, 1,428 retired participants and 285 beneficiaries were receiving total monthly benefits of $7,963,078. For comparison, in the previous valuation, there were 1,346 retired participants and 284 beneficiaries receiving monthly benefits of $7,333,672. These graphs show a distribution of the current retired participants and beneficiaries based on their monthly amount and age, by type of pension. Beneficiary Disability Regular CHART 4 Distribution of Retired Participants and Beneficiaries by Type and by Monthly Amount as of June 30, CHART 5 Distribution of Retired Participants and Beneficiaries by Type and by Age as of June 30,

39 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System B. FINANCIAL INFORMATION Pension plan funding anticipates that, over the long term, both contributions and net investment earnings (less investment fees and administrative expenses) will be needed to cover benefit payments. Pension plan assets change as a result of the net impact of these income and expense components. Additional financial information, including a summary of these transactions for the valuation year, is presented in Section 3, Exhibits D, E and F. The chart depicts the components of changes in the actuarial value of assets over the last ten years. Note: The first bar represents increases in assets during each year while the second bar details the decreases. CHART 6 Comparison of Increases and Decreases in the Actuarial Value of Assets for Years Ended June 30, (for Pension and HIB benefits) $ Millions Adjustment toward market value Benefits paid Net interest and dividends Contributions

40 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System It is desirable to have level and predictable plan costs from one year to the next. For this reason, the Board has approved an asset valuation method that gradually adjusts to market value. Under this valuation method, the full value of market fluctuations is not recognized in a single year and, as a result, the asset value and the plan costs are more stable. The amount of the adjustment to recognize market value is treated as income, which may be positive or negative. Realized and unrealized gains and losses are treated equally and, therefore, the sale of assets has no immediate effect on the actuarial value. The chart shows the determination of the actuarial value of assets as of the valuation date. CHART 7 Determination of Actuarial Value of Assets for Year Ended June 30, 2017 (for Pension and HIB plans) 1. Market value of assets: (a) Pension plan $1,580,556,000 (b) HIB plan 32,088,000 (c) Total $1,612,644,000 Actual Market Expected Market Investment Deferred Deferred 2. Calculation of deferred return: Return (net) Return (net) Gain / (Loss) Factor Return (a) Year ended June 30, 2013 $137,318,000 $76,491,803 $60,826,197 0% $0 (b) Year ended June 30, ,575,000 87,289, ,285,161 20% 26,257,032 (c) Year ended June 30, ,937, ,068,500 (42,131,500) 40% (16,852,600) (d) Year ended June 30, ,894, ,466,650 (92,572,650) 60% (55,543,590) (e) Year ended June 30, ,254, ,606,314 97,647,686 80% 78,118,149 (f) Total unrecognized return* $31,978, Preliminary actuarial value: (1c) - (2f) $1,580,665, Adjustment to be within 30% corridor of market value 0 5. Final actuarial value of assets for pension and HIB plans: (3) + (4) $1,580,665, Actuarial value as a percentage of market value: (5) (1c) 98.0% 7. Valuation value of pension plan assets: (1a) (1c) x (5) $1,549,213,319 * The amount of deferred return that will be recognized in each subsequent valuation is as follows (amounts may not total exactly due to rounding): 6/30/2018 $18,845,739 6/30/2019 (7,411,293) 6/30/2020 1,015,007 6/30/ ,529,537 Total $31,978,991 5

41 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System The market value, actuarial value, and valuation value of assets are representations of EBMUD s financial status. As investment gains and losses are gradually taken into account, the actuarial value of assets tracks the market value of assets. The valuation value of assets is the actuarial value, excluding HIB assets. The valuation value of assets is significant because EBMUD s liabilities are compared to these assets to determine what portion, if any, remains unfunded. Amortization of the unfunded actuarial accrued liability is an important element in determining the contribution requirement. This chart shows the change in the actuarial value of assets versus the market value over the past eleven years. CHART 8 Market Value, Actuarial Value, and Valuation Value of Assets as of June 30, * 1.60 Market Value Actuarial Value $ Billions Valuation Value * Market Value and Actuarial Value of Assets are for pension and HIB benefits. Valuation Value of Assets are for pension benefits only. 6

42 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System C. ACTUARIAL EXPERIENCE To calculate the required contribution, assumptions are made about future events that affect the amount and timing of benefits to be paid and assets to be accumulated. Each year actual experience is measured against the assumptions. If overall experience is more favorable than anticipated (an actuarial gain), the contribution requirement will decrease from the previous year. On the other hand, the contribution requirement will increase if overall actuarial experience is less favorable than expected (an actuarial loss). Taking account of experience gains or losses in one year without making a change in assumptions reflects the belief that the single year s experience was a short-term development and that, over the long term, experience will return to the original assumptions. For contribution requirements to remain stable, assumptions should approximate experience. If assumptions are changed, the contribution requirement is adjusted to take into account a change in experience anticipated for all future years. The total gain is $50,022,788, a $28,130,737 gain from investments and a $21,892,051 gain from all other sources. The net experience variation from individual sources other than investments was 1.06% of the actuarial accrued liability. A discussion of the major components of the actuarial experience is provided on the following pages. This chart provides a summary of the actuarial experience during the past year. CHART 9 Actuarial Experience for Year Ended June 30, Net gain from investments* $28,130, Net gain from other experience** 22,641, Net loss from one-year lag in implementing the contribution rate calculated in the June 30, 2016 valuation until fiscal year 2017/2018 (749,018) 4. Net experience gain: (1) + (2) + (3) $50,022,788 * Details in Chart 10. ** Details in Section 3, Exhibit H. 7

43 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Investment Rate of Return A major component of projected asset growth is the assumed rate of return. The assumed return should represent the expected long-term rate of return, based on EBMUD s investment policy. For valuation purposes, the assumed rate of return on the valuation value of assets is 7.25% (for the June 30, 2016 valuation). The actual rate of return on a valuation value basis (after smoothing) for the 2016/2017 plan year was 9.23%. Since the actual return for the year was greater than the assumed return, EBMUD experienced an actuarial gain during the year ended June 30, 2017 with regard to its investments. This chart shows the gain/(loss) due to investment experience. CHART 10 Investment Experience for Year Ended June 30, 2017 Valuation Value, Actuarial Value, and Market Value of Assets Valuation Value (includes pension plan assets only) Actuarial Value Market Value (includes pension (includes pension and HIB plan assets) and HIB plan assets) 1. Actual return $131,217,766 $133,617,292 $200,254, Average value of assets $1,421,890,053 $1,449,917,217 $1,415,259, Actual rate of return: (1) (2) 9.23% 9.22% 14.15% 4. Assumed rate of return 7.25% 7.25% 7.25% 5. Expected return: (2) x (4) $103,087,029 $105,118,998 $102,606, Actuarial gain/(loss): (1) (5) $28,130,737 $28,498,294 $97,647,686 8

44 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Because actuarial planning is long term, it is useful to see how the assumed investment rate of return has followed actual experience over time. The chart below shows the rate of return on a valuation value, actuarial value, and market value basis for the last ten years. CHART 11 Investment Return Valuation Value, Actuarial Value, and Market Value: * Valuation Value Investment Return Actuarial Value Investment Return Market Value Investment Return Year Ended June 30 Amount Percent Amount Percent Amount Percent 2008 $71,124, % $72,404, % $(76,707,000) (8.40)% 2009 (40,442,084) (4.49)% (40,593,156) (4.47)% (171,905,000) (20.47)% ,167, % 51,966, % 95,737, % ,223, % 33,642, % 191,970, % ,558, % 65,488, % 15,202, % ,506, % 76,545, % 137,318, % ,077, % 113,600, % 218,575, % ,145, % 118,952, % 58,937, % ,598, % 104,468, % 12,894, % ,217, % 133,617, % 200,254, % Five-Year Average Return 8.85% 8.84% 10.34% Ten-Year Average Return 6.38% 6.39% 5.61% * Market Value and Actuarial Value of Assets are for the pension plan and the HIB plan. Valuation Value of Assets are for the pension plan only. 9

45 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Subsection B described the actuarial asset valuation method that gradually takes into account fluctuations in the market value rate of return. The effect of this is to stabilize the actuarial rate of return, which contributes to leveling pension plan (and HIB plan) costs. This chart illustrates how this leveling effect has actually worked over the years CHART 12 Market Value, Actuarial Value, and Valuation Value of Assets: Rates of Return for Years Ended June 30, * Market Value Actuarial Value Valuation Value 30% 25% 20% 15% 10% 5% 0% -5% -10% -15% -20% -25% * Market Value and Actuarial Value of Assets are for pension and HIB benefits. Valuation Value of Assets are for pension benefits only. 10

46 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Other Experience There are other differences between the expected and the actual experience that appear when the new valuation is compared with the projections from the previous valuation. These include: the extent of turnover among the participants, retirement experience (earlier or later than expected), mortality (more or fewer deaths than expected), the number of disability retirements, and salary increases different than assumed. The net gain from this other experience for the year ended June 30, 2017 amounted to $21,892,051, which is 1.06% of the actuarial accrued liability. 11

47 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System D. EMPLOYER AND MEMBER CONTRIBUTIONS Employer contributions consist of two components: Normal Cost Contribution to the Unfunded Actuarial Accrued Liability (UAAL) Member contributions: The annual contribution rate that, if paid annually from a member s first year of membership through the year of retirement, would accumulate to the amount necessary to fully fund the member's retirement-related benefits. Accumulation includes annual crediting of interest at the assumed investment earnings rate. The contribution rate is expressed as a level percentage of the member s compensation. The annual contribution rate that, if paid annually over the UAAL amortization period, would accumulate to the amount necessary to fully fund the UAAL. Accumulation includes annual crediting of interest at the assumed investment earning rate. The contribution (or rate credit in the case of a negative UAAL) is calculated to remain as a level percentage of future active member payroll (including payroll for new members as they enter the System) assuming a constant number of active members. In order to remain as a level percentage of payroll, amortization payments (credits) are scheduled to increase at the annual rate of 3.50% (i.e., 3.00% inflation plus 0.50% across-the-board salary increase). Plan changes, assumption changes, and experience gains/losses prior to July 1, 2011 are amortized over separate decreasing 30-year amortization periods. On or after July 1, 2011, plan changes are amortized over separate decreasing 15-year periods; assumption or method changes are amortized over separate decreasing 25-year periods; and experience gains/losses are amortized over separate decreasing 20-year periods. The recommended employer contribution rates are provided on Chart /1980 Plan Members Employee contribution rates for 1955/1980 Plan members are prescribed in the Ordinance. Effective April 17, 2006, the rate of member retirement contributions is 6.83%, and 6.74% of that rate is allocated to pay pension benefits. The rest, or 0.09%, is used to pay HIB benefits. The Board of Directors may adjust the employee rates solely pursuant to the terms of a negotiated collective bargaining agreement or memorandum of understanding with employee bargaining units. 12

48 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System Based on bargaining unit contract negotiations in 2013, members are contracted to pay the following employee rates (as a percentage of pay) beginning April 22, 2013: Member Rate Effective Date (a) Total (b) HIB Plan (c) = (a) (b) Pension Plan April 17, 2006* 6.83%* 0.09% 6.74% April 22, % 0.09% 7.24% April 21, % 0.09% 7.74% April 20, % 0.09% 8.24% April 18, % 0.09% 8.66% * Pursuant to the Ordinance Tier Members Pursuant to Section (a) of the Government Code, 2013 Tier members are required to contribute at least 50% of the Normal Cost rate. In addition, there are certain additional requirements that would have to be met such as requiring the employee rates be rounded to the nearest one quarter of one percent and requiring the new employees to pay the contribution rate of similarly situated employees, if it is greater. (reference: Section (c)). We further understand that different rules may have to be applied for collectively bargained employees, non-represented, managerial or other supervisory employees. (reference: Section (e)). In preparing the Normal Cost rates in this report, we have assumed that exactly 50% of the Normal Cost would be paid by the new members and we have taken into account in this valuation only the requirements of Section (c), but not requirements of Section (e). We have also compared the total Normal Cost rates between the current valuation and the initial CalPEPRA valuation so that a rate increase (or decrease) of less than 1% of payroll would result in no change to the member s rate (reference: Section (d)). In particular, the total Normal Cost rate of 17.56% was determined in the first CalPEPRA valuation and has been used since then to determine the 50% of the Normal Cost paid by the employees because the change in the total Normal Cost has been less than 1% of payroll. Accumulation for all members includes crediting of interest at the assumed investment earnings rate. The member contribution rates are provided on Chart

49 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System CHART 13 Recommended Contribution Rates (% of payroll; payable at the end of each pay period) June 30, 2017 Valuation Rate Estimated Annual Amount (1) June 30, 2016 Valuation Rate Estimated Annual Amount (1) 1955/1980 Plan Total Normal Cost 24.22% $34,969, % $34,984,310 Expected Employee Contributions -8.66% (2) -12,503, % (2) -12,503,678 Employer Normal Cost 15.56% $22,466, % $22,480,632 UAAL 21.10% 30,465, % 32,269,886 Total Employer Contribution 36.66% $52,931, % $54,750, Tier Total Normal Cost 17.56% (3) $7,107, % $7,163,990 Expected Employee Contributions -8.75% -3,541, % -3,541,521 Employer Normal Cost 8.81% $3,565, % $3,622,469 UAAL 21.10% 8,540, % 9,046,055 Total Employer Contribution 29.91% $12,105, % $12,668,524 Combined Total Normal Cost 22.76% $42,077, % $42,148,300 Expected Employee Contributions -8.68% -16,045, % -16,045,199 Employer Normal Cost 14.08% $26,031, % $26,103,101 UAAL 21.10% 39,005, % 41,315,941 Total Employer Contribution 35.18% $65,037, % $67,419,042 (1) Amounts are based on the following June 30, 2017 projected annual payroll: 1955/1980 Plan $144,384, Tier 40,474,521 Combined $184,858,798 (2) The rate of 8.66% payable during fiscal years 2017/2018 and 2018/2019 is calculated by taking the total employee rate payable beginning April 18, 2016 (i.e., 8.75%), less the HIB employee contribution rate of 0.09%. (3) 17.56% has been calculated using membership data and actuarial assumptions as of June 30, It is a pure coincidence that this rate is the same as the rate we calculated in the first CalPEPRA valuation. 14

50 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System The employer contribution rates as of June 30, 2017 are based on all of the data described in the previous sections, the actuarial assumptions described in Section 4, and the Plan provisions adopted at the time of preparation of the Actuarial Valuation. They include all changes affecting future costs, adopted benefit changes, actuarial gains and losses, and changes in the actuarial assumptions. Reconciliation of Recommended Employer Contribution The chart below details the changes in the recommended employer contribution from the prior valuation to the current year s valuation. The chart reconciles the employer contribution from the prior valuation to the amount determined in this valuation. CHART 14 Reconciliation of Recommended Employer Contribution Rate from June 30, 2016 to June 30, 2017 Contribution Rate Estimated Amount* Recommended Contribution Rate as of June 30, % $67,419,042 Effect of actuarial experience during fiscal 2016/ Effect of decrease in employer normal cost due to payroll and demographic changes (0.04)% $(73,944) 2. Effect of investment gain (after smoothing) (1.08)% (1,996,475) 3. Effect of lower than expected salary increases (0.91)% (1,682,215) 4. Effect of lower than expected growth in total payroll 0.67% 1,238, Effect of one-year lag in implementing rates 0.03% 55, Effect of other experience losses 0.04% 76,785 Subtotal (1.29)% $(2,381,837) Recommended Contribution Rate as of June 30, % $65,037,205 * Based on June 30, 2017 projected annual payroll of $184,858,

51 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System The member contribution rates as of June 30, 2017 are based on all of the data described in the previous sections, the actuarial assumptions described in Section 4, and the Plan provisions adopted at the time of preparation of the Actuarial Valuation. They include all changes affecting future costs, adopted benefit changes, actuarial gains and losses, and changes in the actuarial assumptions. Reconciliation of Recommended Employee Contribution The chart below details the changes in the recommended member contribution rate from the prior valuation to the current year s valuation. The chart reconciles the employee contribution from the prior valuation to the amount determined in this valuation. CHART 15 Reconciliation of Recommended Employee Contribution Rate from June 30, 2016 to June 30, 2017 Contribution Rate Estimated Amount* Average Contribution Rate as of June 30, % $16,045, Effect of change in member demographics 0.00% 0 Average Contribution Rate as of June 30, % $16,045,199 * Based on June 30, 2017 projected annual payroll of $184,858,

52 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System E. FUNDED RATIO A critical piece of information regarding the Plan s financial status is the funded ratio. This ratio compares the actuarial value of assets to the actuarial accrued liabilities of the Plan as calculated. High ratios indicate a well-funded plan with assets sufficient to cover the plan s actuarial accrued liabilities. Lower ratios may indicate recent changes to benefit structures, funding of the plan below actuarial requirements, poor asset performance, or a variety of other factors. The chart below depicts a history of the funded ratios for this plan. The funded status measures shown in this valuation are appropriate for assessing the need for or amount of future contributions. However, they are not necessarily appropriate for assessing the sufficiency of Plan assets to cover the estimated cost of setting the Plan s benefit obligations. As the chart below shows, the measures are different depending on whether the valuation value or market value of assets is used. CHART 16 Funded Ratio for Plan Years Ending June 30, % 80% 75% VVA Basis MVA Basis 70% 65% 60% 55% 50% 45%

53 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System CHART 17 Schedule of Funding Progress (Dollar Amounts in Thousands) Actuarial Valuation Date Valuation Value of Assets (a) Actuarial Accrued Liability (AAL) (b) Unfunded/ (Overfunded) AAL (UAAL) (b) - (a) Funded Ratio (a) / (b) Covered Payroll (c) UAAL as a Percentage of Covered Payroll [(b) - (a)] / (c) 06/30/2008 $900,917 $1,244,993 $344, % $158, % 06/30/ ,021 1,323, , % 161, % 06/30/ ,845 1,396, , % 164, % 06/30/ ,719 1,446, , % 159, % 06/30/2012 1,021,546 1,556, , % 158, % 06/30/2013 1,095,847 1,646, , % 159, % 06/30/2014 1,210,321 1,756, , % 167, % 06/30/2015 1,327,113 1,845, , % 174, % 06/30/2016 1,425,785 1,995, , % 183, % 06/30/2017 1,549,213 2,068, , % 184, % 18

54 SECTION 2: Valuation Results for the East Bay Municipal Utility District Retirement System F. VOLATILITY RATIOS Retirement plans are subject to volatility in the level of required contributions. This volatility tends to increase as retirement plans become more mature. The Asset Volatility Ratio (AVR), which is equal to the market value of assets divided by total payroll, provides an indication of the potential contribution volatility for any given level of investment volatility. A higher AVR indicates that the plan is subject to a greater level of contribution volatility. This is a current measure since it is based on the current level of assets. For EBMUD, the current AVR is about 8.6. This means that a 1% asset gain/(loss) (relative to the assumed investment return) translates to about 8.6% of one-year s payroll. Since EBMUD amortizes actuarial gains and losses over a 20-year period, there would be a 0.6% of payroll decrease/(increase) in the required contribution for each 1% asset gain/(loss). The Liability Volatility Ratio (LVR), which is equal to the Actuarial Accrued Liability divided by payroll, provides an indication of the longer-term potential for contribution volatility for any given level of investment volatility. This is because, over an extended period of time, the plan s assets should track the plan s liabilities. For example, if a plan is 50% funded on a market value basis, the liability volatility ratio would be double the asset volatility ratio and the plan sponsor should expect contribution volatility to increase over time as the plan becomes better funded. The LVR also indicates how volatile contributions will be in response to changes in the Actuarial Accrued Liability due to actual experience or to changes in actuarial assumptions. For EBMUD, the current LVR is about This is about 30% higher than the AVR. Therefore, we would expect that contribution volatility will increase over the long-term. This chart shows how the asset and liability volatility ratios have varied over time. CHART 18 Volatility Ratios for Years Ended June 30, Year Ended June 30 Asset Volatility Ratio Liability Volatility Ratio

55 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System This exhibit summarizes the participant data used for the current and prior valuations. EXHIBIT A Table of Plan Coverage i. All Year Ended June 30 Category Change From Prior Year Active participants in valuation: Number 1,802 1, % Average age Average service Projected total payroll $184,858,798 $183,970, % Projected average payroll $102,585 $102, % Account balances $180,582,819 $170,846, % Total active vested participants 1,215 1, % Vested terminated participants: Number % Average age Retired participants: Number in pay status 1,370 1, % Average age Average monthly benefit $5,175 $5, % Disabled participants: Number in pay status % Average age Average monthly benefit $2,209 $2, % Beneficiaries: Number in pay status % Average age Average monthly benefit $2,615 $2, % 20

56 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT A Table of Plan Coverage ii. 1955/1980 Plan Year Ended June 30 Category Change From Prior Year Active participants in valuation: Number 1,334 1, % Average age Average service Projected total payroll $144,384,277 $153,100, % Projected average payroll $108,234 $107, % Account balances $173,283,945 $166,926, % Total active vested participants 1,215 1, % Vested terminated participants: Number % Average age Retired participants: Number in pay status 1,370 1, % Average age Average monthly benefit $5,175 $5, % Disabled participants: Number in pay status % Average age Average monthly benefit $2,209 $2, % Beneficiaries: Number in pay status % Average age Average monthly benefit $2,615 $2, % 21

57 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT A Table of Plan Coverage iii Tier Year Ended June 30 Category Change From Prior Year Active participants in valuation: Number % Average age Average service Projected total payroll $40,474,521 $30,870, % Projected average payroll $86,484 $84, % Account balances $7,298,874 $3,919, % Total active vested participants 0 0 N/A Vested terminated participants: Number % Average age Retired participants: Number in pay status N/A N/A N/A Average age N/A N/A N/A Average monthly benefit N/A N/A N/A Disabled participants: Number in pay status N/A N/A N/A Average age N/A N/A N/A Average monthly benefit N/A N/A N/A Beneficiaries: Number in pay status N/A N/A N/A Average age N/A N/A N/A Average monthly benefit N/A N/A N/A 22

58 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT B Participants in Active Service as of June 30, 2017 By Age, Years of Service, and Average Projected Payroll i. 1955/1980 Plan Years of Service Age Total & over Under $93,848 $88,058 $101, ,146 93,536 99,909 $115, ,608 93, , ,777 $120, , , , , ,474 $108, ,387 98, , , , ,704 $131, , , , , , , ,532 $133,565 $92, ,530 97, , , , , , , ,672 $118, , ,470 99, ,630 92, , , , , , , ,887 95, ,091 99, ,878 84, , , , & over , ,920 87,875 76,635 84,527 97,528 82, Total 1, $108,234 $99,962 $106,106 $107,297 $102,490 $112,776 $112,602 $121,152 $113,275 $120,858 23

59 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT B Participants in Active Service as of June 30, 2017 By Age, Years of Service, and Average Projected Payroll ii Tier Years of Service Age Total & over Under $77,032 $77, ,248 82, ,776 83, ,158 89, ,448 90, ,077 92, ,773 83, ,560 89, ,108 80, ,224 89, & over , , Total $86,484 $86,

60 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT C Reconciliation of Participant Data Active Participants Vested Participants Disableds Retired Participants Beneficiaries Number as of June 30, , , ,667 New participants Terminations with vested rights Refund of contributions Retirements New disabilities Return to work Died with or without beneficiary (1) -29 Data adjustments 0 16 (2) Number as of June 30, , , ,782 (1) This is the net increase in the number of beneficiaries after subtracting the number of beneficiaries who died during the year. (2) Includes 6 members who were hired and terminated employment during fiscal year 2016/2017 and 10 members who were previously indicated by EBMUD as having a refund of contributions in the prior valuation. Total 25

61 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT D Summary Statement of Income and Expenses on an Actuarial Value Basis for All Pension Plan and HIB Plan Assets Year Ended June 30, 2017 Year Ended June 30, 2016 Contribution income: Employer contributions $76,860,000 $74,672,000 Employee contributions 16,018,000 14,925,000 Net contribution income $92,878,000 $89,597,000 Investment income: Interest, dividends and other income $28,865,000 $26,323,000 Recognition of capital appreciation 111,575,292 84,098,421 Less investment and administrative fees (6,823,000) (5,953,000) Net investment income $133,617,292 $104,468,421 Total income available for benefits $226,495,292 $194,065,421 Less benefit payments: Benefits paid $(98,152,000) $(91,152,000) Refund of contributions (465,000) (419,000) Net benefit payments $(98,617,000) $(91,571,000) Change in amount available for future benefits $127,878,292 $102,494,421 26

62 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT E Summary Statement of Assets for Pension and HIB Plans Year Ended June 30, 2017 Year Ended June 30, 2016 Cash equivalents $48,988,000 $40,657,000 Accounts receivable: Brokers, securities sold $4,449,000 $1,444,000 Employer and employee contributions 1,263,000 4,551,000 Interest and dividends 2,341,000 2,237,000 Total accounts receivable $8,053,000 $8,232,000 Investments: Equities $1,227,836,000 $1,038,078,000 Fixed income investments 251,860, ,447,000 Real estate 84,282,000 83,140,000 Securities lending collateral 108,858, ,265,000 Other assets 518, ,000 Total investments at market value $1,673,354,000 $1,497,432,000 Total assets $1,730,395,000 $1,546,321,000 Less accounts payable: Accounts payable and accrued expenses $(2,061,000) $(1,755,000) Payables to brokers, securities purchased (6,832,000) (7,172,000) Securities lending collateral (108,858,000) (119,265,000) Total accounts payable $(117,751,000) $(128,192,000) Net assets at market value $1,612,644,000 $1,418,129,000 Net assets at actuarial value $1,580,665,009 $1,452,786,717 Net assets at valuation value (pension plan only) $1,549,213,319 $1,425,784,553 27

63 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT F Development of the Fund Through June 30, 2017 for All Pension Plan and HIB Plan Assets Year Ended June 30 Employer Contributions Employee Contributions Net Actuarial Value Investment Return* Benefit Payments Actuarial Value of Assets at End of Year 2008 $44,603,000 $10,394,000 $72,404,538 $50,780,000 $907,927, ,803,000 10,740,000 (40,593,156) 54,502, ,375, ,756,000 10,918,000 51,966,871 58,109, ,906, ,481,000 10,850,000 33,642,654 62,114, ,766, ,651,000 10,723,000 65,488,807 66,843,000 1,035,786, ,567,000 10,566,000 76,545,489 72,095,000 1,112,369, ,117,000 12,133, ,600,558 78,265,000 1,229,955, ,141,000 13,427, ,952,917 85,184,000 1,350,292, ,672,000 14,925, ,468,421 91,571,000 1,452,786, ,860,000 16,018, ,617,292 98,617,000 1,580,665,009 * Net of investment fees and administrative expenses. 28

64 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT G Actuarial Balance Sheet An overview of the Plan s funding is given by an Actuarial Balance Sheet. In this approach, we first determine the amount and timing of all future payments that will be made by the Plan for current participants. We then discount these payments at the valuation interest rate to the date of the valuation, thereby determining their present value. We refer to this present value as the liability of the Plan. Second, we determine how this liability will be met. These actuarial assets include the net amount of assets already accumulated by the Plan, the present value of future member contributions, the present value of future employer normal cost contributions, and the present value of future employer amortization payments. Actuarial Balance Sheet Assets June 30, 2017 June 30, Total valuation assets $1,549,213,319 $1,425,784, Present value of future contribution by members 138,093, ,921, Present value of future employer contributions for: (a) entry age normal cost 187,172, ,681,065 (b) unfunded actuarial accrued liability 518,801, ,078, Total current and future assets $2,393,280,373 $2,321,466,086 Liabilities June 30, 2017 June 30, Present value of benefits for retirees and beneficiaries $1,259,012,986 $1,163,750, Present value of benefits for terminated vested members 43,660,442 43,969, Present value of benefits for active members 1,090,606,945 1,113,746, Total liabilities $2,393,280,373 $2,321,466,086 29

65 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT H Development of Unfunded Actuarial Accrued Liability for Year Ended June 30, Unfunded actuarial accrued liability at beginning of year $570,078, Normal cost at beginning of year 41,105, Expected employer and member contributions at beginning of year (80,811,863) 4. Interest 38,451, Expected unfunded actuarial accrued liability $568,824, Changes due to: (a) Gain from investments (after smoothing) $(28,130,737) (b) Gain on salaries lower than expected (23,702,193) (c) Loss due to one-year lag in implementing contribution rates in June 30, 2016 valuation (with interest to end of year) 749,018 (d) Loss from all other sources 1,061,124 (e) Total changes $(50,022,788) 7. Unfunded actuarial accrued liability at end of year $518,801,626 Note: The net gain from other experience of $22,641,069 from Section 2, Chart 9 is equal to the sum of items 6(b) and 6(d). 30

66 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT I Table of Amortization Bases Type Date Established Initial Years Initial Amount Outstanding Balance Years Remaining Annual Payment* Experience Gain 6/30/ $(10,871,830) $(11,972,424) 13 $(1,130,151) Change in Assumptions 6/30/ ,629,891 9,503, ,097 Plan Amendments 6/30/ ,607,265 14,984, ,414, % COLA Assumption 6/30/ ,057,441 29,796, ,812,681 Experience Loss 6/30/ ,292,281 2,567, ,723 Experience Loss 6/30/ ,232,251 29,724, ,512,460 Plan Amendments 6/30/ ,111,914 5,792, ,606 Experience Loss 6/30/ ,692,270 49,879, ,016,987 Plan Amendments 6/30/ ,138,578 76,646, ,172,597 Experience Loss 6/30/ ,731,232 37,503, ,888,697 New Assumption / Domestic Partners 6/30/ (9,812,646) (11,243,474) 17 (866,016) Experience Loss 6/30/ ,910,233 30,844, ,279,881 Remove Limit Pension Base 6/30/ ,315,928 31,167, ,303,734 Experience Loss 6/30/ ,160,133 16,187, ,151,672 Experience Gain 6/30/ (3,098,126) (3,523,178) 20 (241,901) Experience Gain 6/30/ (7,800,585) (8,803,274) 21 (584,730) Change in Assumptions 6/30/ ,413,374 58,022, ,853,935 Experience Loss 6/30/ ,894, ,400, ,268,517 Experience Loss 6/30/ ,039,098 3,356, ,983 Change in Assumptions 6/30/ ,098,499 8,945, ,557 Experience Loss 6/30/ ,428,038 4,828, ,958 Experience Gain 6/30/ (15,668,764) (15,244,163) 15 (1,288,513) Change in Assumptions 6/30/ ,400,521 55,260, ,794,150 Experience Loss 6/30/ ,858,322 10,677, ,882 Experience Gain 6/30/ (26,406,581) (26,145,148) 17 (2,013,800) Change in Assumptions 6/30/ ,421,049 18,850, ,213,920 Experience Gain 6/30/ (28,955,525) (28,838,293) 18 (2,131,585) Experience Gain 6/30/ (1,408,751) (1,407,148) 19 (100,110) Change in Assumptions 6/30/ ,595,760 53,061, ,230,164 Experience Gain 6/30/ (50,022,788) (50,022,788) 20 (3,434,563) Total $518,801,626 $37,661,337 * Beginning of year payment, reflecting level percentage of payroll. Note: The equivalent single amortization period is about 18 years. 31

67 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT J Section 415 Limitations Section 415 of the Internal Revenue Code (IRC) specifies the maximum benefits that may be paid to an individual from a defined benefit plan and the maximum amounts that may be allocated each year to an individual s account in a defined contribution plan. Contribution rates determined in this valuation have not been reduced for the Section 415 limitations. Actual limitations will result in actuarial gains as they occur. A qualified pension plan may not pay benefits in excess of the Section 415 limits. The ultimate penalty for noncompliance is disqualification: active participants could be taxed on their vested benefits and the IRS may seek to tax the income earned on the plan s assets. In particular, Section 415(b) of the IRC limits the maximum annual benefit payable at the Normal Retirement Age to a dollar limit of $160,000 indexed for inflation. That limit is $215,000 for 2017 and $220,000 for Normal Retirement Age for these purposes is age 62. These are the limits in simplified terms. They must be adjusted based on each participant s circumstances, for such things as age at retirement, form of benefits chosen and after tax contributions. Benefits for members in the non-calpepra plan in excess of the limits may be paid through a qualified governmental excess plan that meets the requirements of Section 415(m). Legal Counsel s review and interpretation of the law and regulations should be sought on any questions in this regard. 32

68 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System EXHIBIT K Definitions of Pension Terms The following list defines certain technical terms for the convenience of the reader: Assumptions or Actuarial Assumptions: Normal Cost: Actuarial Accrued Liability For Actives: Actuarial Accrued Liability For Pensioners: Unfunded Actuarial Accrued Liability: Amortization of the Unfunded Actuarial Accrued Liability: The estimates on which the cost of the Plan is calculated including: (a) (b) (c) (d) Investment return the rate of investment yield that the Plan will earn over the long-term future; Mortality rates the death rates of employees and pensioners; life expectancy is based on these rates; Retirement rates the rate or probability of retirement at a given age; and Turnover rates the rates at which employees of various ages are expected to leave employment for reasons other than death, disability, or retirement. The amount of contributions required to fund the benefit allocated to the current year of service. The equivalent of the accumulated normal costs allocated to the years before the valuation date. The single sum value of lifetime benefits to existing pensioners. This sum takes account of life expectancies appropriate to the ages of the pensioners and the interest that the sum is expected to earn before it is entirely paid out in benefits. The extent to which the actuarial accrued liability of the Plan exceeds the assets of the Plan. There is a wide range of approaches to paying off the unfunded actuarial accrued liability, from meeting the interest accrual only to amortizing it over a specific period of time. Payments made over a period of years equal in value to the Plan s unfunded actuarial accrued liability. 33

69 SECTION 3: Supplemental Information for the East Bay Municipal Utility District Retirement System Investment Return: The rate of earnings of the Plan from its investments, including interest, dividends and capital gain and loss adjustments, computed as a percentage of the average value of the fund. For actuarial purposes, the investment return often reflects a smoothing of the capital gains and losses to avoid significant swings in the value of assets from one year to the next. 34

70 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System EXHIBIT I Summary of Actuarial Valuation Results The valuation was made with respect to the following data supplied to us: 1. Retired participants as of the valuation date (including 285 beneficiaries in pay status) 1, Participants inactive during year ended June 30, 2017 with vested rights Participants active during the year ended June 30, ,802 Fully vested 1,215 Not vested 587 The actuarial factors as of the valuation date are as follows: 1. Normal cost, beginning of year $40,636, Present value of future benefits 2,393,280, Present value of future normal costs 325,265, Actuarial accrued liability Retired participants and beneficiaries $1,259,012,986 Inactive participants with vested rights 43,660,442 Active participants 765,341,517 Subtotal $2,068,014, Valuation value of assets ($1,612,644,000 at market value for pension and HIB plans, as reported by the auditor, and $1,580,665,009 at actuarial value for pension and HIB plans) $1,549,213,319 (1) 6. Unfunded actuarial accrued liability $518,801,626 (1) Net of HIB assets. 35

71 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System EXHIBIT I (continued) Summary of Actuarial Valuation Results The determination of the recommended contribution at the end of each pay period is as follows: 1955/1980 Plan 2013 Tier Combined 1. Total normal cost $34,969,872 $7,107,326 $42,077, Expected employee contributions -12,503,678-3,541,521-16,045, Employer normal cost: (1) + (2) $22,466,194 $3,565,805 $26,031, Payment on unfunded actuarial accrued liability 30,465,082 8,540,124 39,005, Total recommended contribution $52,931,276 $12,105,929 $65,037, Projected payroll $144,384,277 $40,474,521 $184,858, Total recommended contribution as a percentage of projected payroll: (5) (6) 36.66% 29.91% 35.18% Note: The contribution amounts shown above are based on the recommended employer and employee contribution rates payable at the end of each pay period, multiplied by the projected payroll. 36

72 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System EXHIBIT II Actuarial Assumptions and Actuarial Cost Method Rationale for Assumptions: Economic Assumptions: Net Investment Return: Interest Credited to Employee Accounts: 7.25% Inflation: 3.00%* 2 Across the Board Salary Increases: 0.50% The information and analysis used in selecting each assumption that has a significant effect on this actuarial valuation is shown in the July 1, 2012 through June 30, 2016 Actuarial Experience Study report dated November 10, Unless otherwise noted, all actuarial assumptions and methods shown below apply to both tiers. These assumptions were adopted by the Board. 7.25%, net of investment and administrative expenses. Cost of Living Increases: 3.00% per annum. 2 * The maximum amount of pensionable compensation that can be taken into account for 2017 of $118,775 for 2013 Tier members is also assumed to increase by 3.00% per year. 37

73 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Salary Increases: Demographic Assumptions: Mortality Rates: Pre-retirement Males Females Annual Rate of Compensation Increase Inflation: 3.00% per year; plus across the board salary increases of 0.50% per year; plus the following merit and promotional increases based on years of service: Years of Service Merit and Promotional Increases % % % % % % % % Headcount-Weighted RP-2014 Employee Mortality Table projected 20 years with the two-dimensional improvement scale MP-2015, set forward two years for males Headcount-Weighted RP-2014 Employee Mortality Table projected 20 years with the two-dimensional improvement scale MP-2015, set forward one year for females 38

74 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System After Service Retirement and All Beneficiaries Males Females After Disability Retirement: Males Females Headcount-Weighted RP-2014 Healthy Annuitant Mortality Table projected 20 years with the two-dimensional improvement scale MP-2015, set forward two years for males Headcount-Weighted RP-2014 Healthy Annuitant Mortality Table projected 20 years with the two-dimensional improvement scale MP-2015, set forward one year for females Headcount-Weighted RP-2014 Healthy Annuitant Mortality Table projected 20 years with the two-dimensional improvement scale MP-2015, set forward nine years for males Headcount-Weighted RP-2014 Healthy Annuitant Mortality Table projected 20 years with the two-dimensional improvement scale MP-2015, set forward nine years for females The above mortality tables contain a margin slightly less than 20% for males and females combined, based on actual to expected deaths, as a provision to reflect future mortality improvement, based on a review of mortality experience as of the measurement date. Disability Rates: Rate (%) Rate (%) Age Male Female Age Male Female Note: Disability rates applicable after eight years of service. 39

75 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Termination Rates: Rate (%) Ordinary Withdrawal* Service Male Female Rate (%) Ordinary Withdrawal** Vested Termination Age Male Female Male Female * Applicable for members with less than five years of service. ** Applicable after five years of service. 40

76 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Retirement Rates: Rate (%) 1955/1980 Plan 2013 Tier Age Male Female Male Female * * The rate for 1955/1980 Plan members age 54 with 30 or more years of service (i.e., eligible for unreduced benefits) is 50% for males and females. 41

77 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Retirement Age for Inactive Vested Participants: 59 Reciprocity: Unknown Data for Participants: Percent Married/Domestic Partnership: Age of Spouse/Domestic Partner: Future Benefit Accruals: Actuarial Value of Assets: 30% of members who terminate with a vested benefit are assumed to enter a reciprocal system. For reciprocals, we assume 4.00% compensation increases per annum. Same as those exhibited by members with similar known characteristics. If not specified, members are assumed to be male. Spouses/domestic partners of active and inactive members are assumed to be the opposite sex of the member. The percent married/domestic partnership at retirement is assumed to be 80% for male members and 50% for female members. Female (or male) spouses/domestic partners are 3 years younger (or older) than the members. 1.0 year of service per year of employment plus years of additional service to anticipate conversion of unused sick leave for each year of employment. As directed by EBMUD, this assumption has been applied to active members in the 1955/1980 Plan and the 2013 Tier. Market value of assets less unrecognized returns in each of the last five years. Unrecognized return is equal to the difference between the actual market return and the expected return on the market value, and is recognized over a five-year period, further adjusted, if necessary, to be within 30% of the market value. 42

78 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Actuarial Cost Method: Entry Age Cost Method. Entry Age is the age at the member s hire date. Actuarial Accrued Liability is calculated on an individual basis and is based on costs allocated as a level percentage of compensation. The Normal Cost is calculated on an individual basis where the Entry Age Normal Cost is calculated as the sum of the individual Normal Costs. The UAAL from plan changes, assumption changes, and experience gains/losses prior to July 1, 2011 are amortized over separate decreasing 30-year amortization periods. On or after July 1, 2011, any new UAAL resulting from plan changes are amortized over separate decreasing 15-year periods; assumption or method changes are amortized over separate decreasing 25-year periods; and experience gains/losses are amortized over separate decreasing 20-year periods. 43

79 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System EXHIBIT III Summary of Plan Provisions This exhibit summarizes the major provisions of the EBMUD included in the valuation. It is not intended to be, nor should it be interpreted as, a complete statement of all plan provisions. Plan Year: July 1 through June 30 Census Date: June 30 Membership Eligibility: 1955/1980 Plan All employees who first become members before January 1, Tier All employees who first become members on or after January 1, Final Compensation for Benefit Determination: 1955/1980 Plan Highest two consecutive years of compensation earnable (FAS2) Tier Highest thirty-six consecutive months of pensionable compensation (FAS3). Compensation Limit: 1955/1980 Plan None 2013 Tier $118,775 for 2017 Normal or Unreduced Retirement Eligibility: Age and Service Requirement 1955/1980 Plan Age 65; Age 62 with 5 years of service; Age 59 with 20 years of service; Age 54 with 30 years of service; Other combinations of age and service between ages 54 and Tier Age 67 with 5 years of service (for unreduced benefit). 44

80 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Early Retirement Eligibility: Age and Service Requirement 1955/1980 Plan Age 54 with 5 years of service Tier Age 52 with 5 years of service. Benefit Formula: 1955/1980 Plan: 1955 Formula 2.42% (2.82% if member is credited with District Service on or after January 1, 2004) times Final Compensation per year of service including all service extension credit. 1955/80 Formula 2.42% (2.82% if member is credited with District Service on or after January 1, 2004) times Final Compensation per year of service up to August 1, 1980 including all service extension credit, plus 2.20% (2.60% if member is credited with District Service on or after January 1, 2004) times Final Compensation per year of service after August 1, Applies to members who elected to convert to the 1980 Formula in /90 Formula 2.42% (2.82% if member is credited with District Service on or after January 1, 2004) times Final Compensation per year of service up to January 1, 2000 including all service extension credit, plus 2.20% (2.60% if member is credited with District Service on or after January 1, 2004) times Final Compensation per year of service after January 1, Applies to members who elected to convert to the 1980 Formula in Formula 2.20% (2.60% if member is credited with District Service on or after January 1, 2004) times Final Compensation per year of service including all service extension credit. Applies to all members hired on or after January 1, Service Extension Credit 2.42% (2.82% if member is credited with District Service on or after January 1, 2004) for members with any service under the 1955 Formula or 2.20% (2.60% if member is credited with District Service on or after January 1, 2004) for members with service only under the 1980 Formula times Final Compensation per year of Service Extension Credit. Service extension credit is the number of unused sick leave days credited to a member at the time of retirement converted on a 260-day basis. The number of such days is then doubled for the benefit calculation and for service retirements to meet the early retirement provision of the Ordinance. 45

81 SECTION 4: Reporting Information for the East Bay Municipal Utility District Retirement System Benefit Formula: (continued) 1955/1980 Plan: Benefit Adjustments 2013 Tier: Disability: Eligibility Benefit Vesting: Requirements Reduced by 3% per year under the age of eligibility for an unreduced benefit, based on service at retirement, for retirements before age 63 (before age 62 commencing November 1, 2000). Effective July 1, 1999, Service Extension Credit is included in the years of service calculation of service for determining eligibility for unreduced retirement. Retirement Age Benefit Formula % x FAS3 x Years of Service % x FAS3 x Years of Service % x FAS3 x Years of Service % x FAS3 x Years of Service % x FAS3 x Years of Service 67 or later 2.50% x FAS3 x Years of Service Eight years of service (not available for Directors). Greater of: 1.5% times Final Compensation per year of service. One-third of Final Compensation. Five years of service, must leave contributions on deposit, reciprocal service counts for vesting purposes. 46