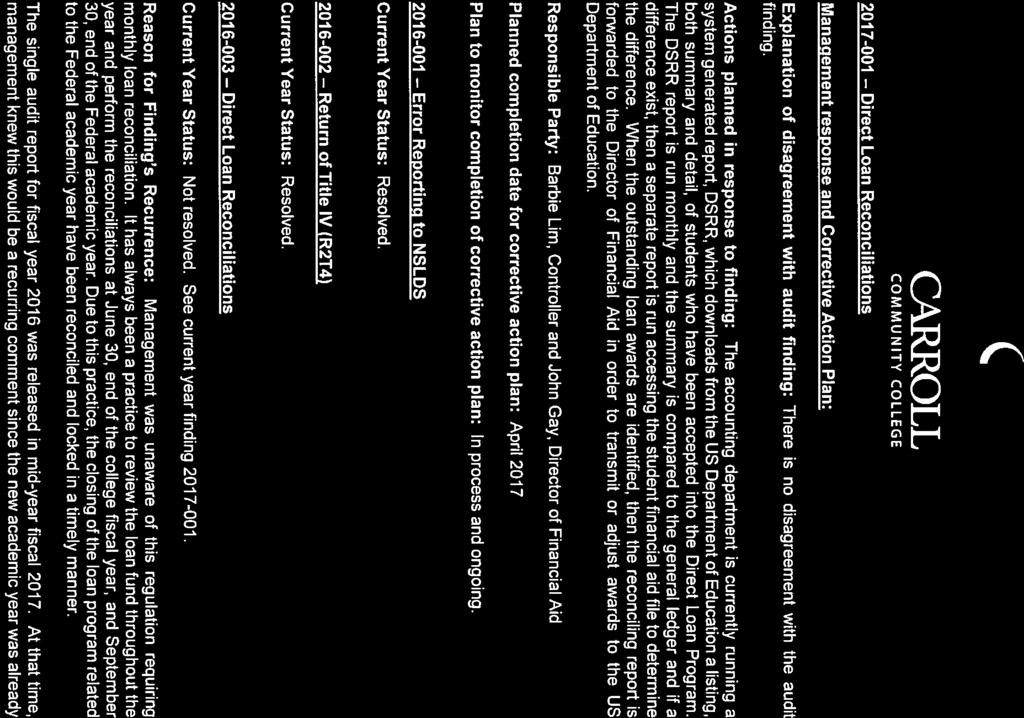

CARROLL COMMUNITY COLLEGE FINANCIAL STATEMENTS YEARS ENDED JUNE 30, 2017 AND 2016

|

|

|

- Jocelyn Shaw

- 5 years ago

- Views:

Transcription

1 FINANCIAL STATEMENTS YEARS ENDED

2 TABLE OF CONTENTS YEARS ENDED INDEPENDENT AUDITORS REPORT 1 MANAGEMENT S DISCUSSION AND ANALYSIS 3 FINANCIAL STATEMENTS STATEMENTS OF NET POSITION (DEFICIT) 13 STATEMENTS OF REVENUES, EXPENSES AND CHANGES IN NET POSITION (DEFICIT) 14 STATEMENTS OF CASH FLOWS 15 STATEMENTS OF FINANCIAL POSITION COMPONENT UNIT 16 STATEMENT OF ACTIVITIES COMPONENT UNIT- YEAR ENDED JUNE 30, STATEMENT OF ACTIVITIES COMPONENT UNIT- YEAR ENDED JUNE 30, NOTES TO FINANCIAL STATEMENTS 19 REQUIRED SUPPLEMENTARY INFORMATION SCHEDULE OF FUNDING PROGRESS AND EMPLOYER CONTRIBUTIONS FOR OTHER POSTEMPLOYMENT BENEFITS 47 SCHEDULE OF COLLEGE S PROPORTIONATE SHARE OF THE NET PENSION LIABILITY 48 NOTES TO THE REQUIRED SUPPLEMENTARY INFORMATION 49 REPORT REQUIRED BY GOVERNMENT AUDITING STANDARDS INDEPENDENT AUDITORS REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS 50

3 Board of Trustees Carroll Community College CliftonLarsonAllen LLP CLAconnect.com INDEPENDENT AUDITORS REPORT Board of Trustees Carroll Community College Westminster, Maryland Report on the Financial Statements We have audited the accompanying financial statements of the business-type activities and the discretely presented component unit of Carroll Community College (the College), a component unit of Carroll County, Maryland, as of and for the years ended June 30, 2017 and 2016, and the related notes to the financial statements, which collectively comprise the College s basic financial statements as listed in the table of contents. Management s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditors Responsibility Our responsibility is to express opinions on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. The financial statements of Carroll Community College Foundation, Inc. were not audited in accordance with Government Auditing Standards. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditors judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. (1)

4 Board of Trustees Carroll Community College We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions. Opinions In our opinion, the basic financial statements referred to above present fairly, in all material respects, the financial position of the business-type activities and the discretely presented component unit of Carroll Community College as of June 30, 2017 and 2016, and the respective changes in financial position and, where applicable, cash flows thereof for the years then ended in accordance with accounting principles generally accepted in the United States of America. Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that the management s discussion and analysis, schedule of funding progress and employer contributions for the other post-employment benefits, and the schedule of the College s proportionate share of the net pension liability, as listed in the table of contents, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated October 6, 2017, on our consideration of the College s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts and grant agreements, and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting and compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in consideration of the College s internal control over financial reporting and compliance. a CliftonLarsonAllen LLP Baltimore, Maryland October 6, 2017 (2)

5 MANAGEMENT S DISCUSSION AND ANALYSIS The following discussion and analysis provides an overview of the financial activities of Carroll Community College (the College). The Financial Statements and Management s Discussion and Analysis include a comparative analysis to the prior two years financial statements. As required by GASB 35, the annual financial statement consists of three basic financial statements that provide financial information on the College as a whole. Statements of Net Position Statements of Revenues, Expenses and Changes in Net Position Statements of Cash Flows Management s Discussion and Analysis includes comments on each of the three statements. In addition, the College has implemented Governmental Accounting Standards Board (GASB) Statement No. 39, Determining Whether Certain Organizations are Component Units and GASB Statement No. 61, The Financial Reporting Entity Omnibus, an amendment of GASB Statements No. 14 and No. 34. It has been determined that the Carroll Community College Foundation (the Foundation) is a component unit, whose sole purpose is to serve the institution by providing resources for scholarships and other College projects. The Foundation statements for June 30, 2017 and 2016 are displayed in the financial statements section of the report. Financial and Enrollment Highlights The college contributed $200,000 towards its Other Post-Employment Benefits (OPEB) obligation to the Carroll County Master Retiree Benefit Trust. The college in past years has operated on a pay as you go basis for retiree health care. It is the college s intent to continue its contributing to the Trust. Federal Direct Loans issued to students totaled $2.167 million in fiscal year This amount represents a decrease of 7% when compared to awards issued in fiscal year 2016 which totaled $2.33 million. The Federal Direct Lending Program was initiated in fiscal year Self-insured healthcare has resulted in a cost deficit of approximately $104,726 for fiscal year State appropriations for fiscal year 2017 increased 3.55% when compared to fiscal year 2016 with total appropriations for operations of $8,020,376 and $7,745,631 respectively. Fiscal year 2016 when compared to fiscal year 2015 reflected an increase of approximately 3.2%. County appropriations for operations and capital improvements increased 7.63% in fiscal year 2017 when compared to fiscal year Total appropriations for fiscal years 2017 and 2016 were $10,019,006 and $9,309,140 respectively. Federal financial aid, Title IV, for fiscal year 2017 was approximately $2.618 million, which represents a decrease of 8.5% when compared to fiscal year The funding levels of federal financial aid for fiscal years 2016 and 2015 were $2.861 and $3.239 million respectively. Title IV programs for the College includes College Work Study, Supplemental Education Opportunity Grant, and Pell Grant. The decreases in aid for the prior periods was attributable to declining enrollment and less students applying and being accepted into the Pell Program. (3)

6 MANAGEMENT S DISCUSSION AND ANALYSIS The chart below reflects credit and non-credit student FTE for the last five years. Statements of Net Position The Statements of Net Position include all assets and liabilities of the College using the accrual basis of accounting, which is similar to the accounting methods used by most private-sector institutions. Net position measures the difference between assets and liabilities and is one way to measure the financial health of the College. Net position is divided into three major categories, as follows: Investment in Capital Assets represents property, plant and equipment owned by the College net of accumulated depreciation and related debt. The College had no capital asset related debt as of June 30, 2017 and Restricted Net Position represents assets available to the College but, reserved for a specific purpose. The College has no restricted net position. Unrestricted Net Position represents assets available to the College with no restrictions. For fiscal year 2017, the College experienced a decrease in total net position of $2,242,511. Decreases in net position for fiscal years 2016 and 2015 were $1,962,494 and $2,394,739, respectively. These continued decreases are primarily due to the College s Other Postemployment Benefits (OPEB), which remains unfunded and is presented as a liability on the Statements of Net Position in accordance with General Accounting Standards Board pronouncement 45. Increases in the OPEB liability for these periods were $2,640,880, $2,625,439 and $2,481,513, respectively. (4)

7 MANAGEMENT S DISCUSSION AND ANALYSIS The College experienced decreases in both current assets and current liabilities in the amounts of $923,422 and $1,060,659, respectively, for the fiscal year. The decreases in current assets is primarily attributable to prepaid expenses which includes the release of one month s escrow held by Carefirst and less prepayment for subsequent fiscal year services. The prepayment of self-funded health care required an estimated two months of benefits and a prepayment for a hospital deposit. Capital assets for the period represent a net increase of $198,219 when compared to an increase of $462,484 and an increase of $216,380 for fiscal years 2016 and 2015, respectively. This category consists of renovations, equipment in excess of $2,500, and library books. These items are depreciated over periods ranging from 3-15 years using the straight-line depreciation method of accounting. The College by law is not authorized to issue debt to support capital expansion, therefore long-term debt related to capital assets remains at $0. Net Position at June 30: Assets Current Assets $ 8,584,980 $ 9,508,402 $ 9,202,547 Capital Assets 2,221,908 2,023,689 1,561,205 Total Assets 10,806,888 11,532,091 10,763,752 Liabilities Current Liabilities 3,965,775 5,026,434 4,932,253 Noncurrent Liabilities 22,925,700 20,347,733 17,711,081 Total Liabilities 26,891,475 25,374,167 22,643,334 Net Position (Deficit) Net Investment in Capital Assets 2,221,908 2,023,689 1,561,205 Unrestricted (18,306,495) (15,865,765) (13,440,787) Total Net Position (Deficit) $ (16,084,587) $ (13,842,076) $ (11,879,582) (5)

8 MANAGEMENT S DISCUSSION AND ANALYSIS Statement of Revenues, Expenses, and Changes in Net Assets The purpose of the statement is to present the revenues earned and expenses incurred by the College, both operating and non-operating, as well as any other revenues, expenses, gains and losses incurred or spent by the institution. Tuition and Fees, net of scholarships allowances, make up 28.8% of the total revenue for the College, a, increase of 0.2% over the prior year. In the previous fiscal year, tuition and fees made up 28.6% of total revenue for the College, which represents a decrease of.3% when compared to fiscal year State and Local Appropriations represent 51.2% of the total revenue for the institution, compared to 47.9% for fiscal year 2016 and 49.0% for fiscal year Other sources make up 9.2% of all revenues, which include certain fringe benefits paid by the State of Maryland, investment revenues, and auxiliaries. In fiscal year 2016, other sources comprised of 10.8% for total college revenue. Federal, State, local and other grants make up approximately 10.8% of total revenues, a decrease of 1.9% when compared to fiscal year The same revenues in fiscal year 2016 represented 12.7% of total revenues, an increase of.6% over Statements of Revenues, Expenses and Changes in Net Position Operating Revenues Tuition and Fees, Net $ 10,171,230 $ 10,184,544 $ 10,059,850 Auxiliary Enterprises 409, , ,752 Grants and Contracts 1,454,632 1,429,898 1,209,542 Other 214, , ,338 Total 12,250,036 12,504,466 12,046,482 Operating Expenses 37,506,658 37,597,418 37,228,805 Operating Loss (25,256,622) (25,092,952) (25,182,323) Non-Operating Revenues County Appropriation 10,019,006 9,309,140 9,327,614 State Appropriation 8,020,376 7,745,631 7,705,441 Pell Grants 2,358,964 2,613,901 2,992,344 Investment Income 29,629 11,579 5,892 Other Grants and Gifts 485, , ,585 Certain Fringe Benefits Paid Directly by the State of Maryland 1,411,806 1,434,081 1,452,244 Other Sources 689,245 1,522, ,464 Total 23,014,111 23,130,458 22,787,584 Decrease in Net Position (2,242,511) (1,962,494) (2,394,739) Net Position - Beginning of Year (13,842,076) (11,879,582) (9,484,843) Net Position - End of Year $ (16,084,587) $ (13,842,076) $ (11,879,582) (6)

9 MANAGEMENT S DISCUSSION AND ANALYSIS Operating Expenses by Functional Category Expenses for all functional categories represent the following for the years ended June 30: Instruction $ 15,105,681 $ 15,784,709 $ 15,609,094 Grants 61,825 58,823 64,052 Academic Support 5,282,156 4,882,766 4,581,112 Student Services 4,005,510 4,087,071 4,152,166 Plant Operations and Maintenance 3,473,840 3,399,843 3,686,364 Institutional Support 6,967,946 6,350,349 6,436,569 Auxiliary Enterprises 273, , ,436 Other 531, , ,294 Depreciation 392, , ,474 Certain Fringe Benefits Paid Directly by the State of Maryland 1,411,806 1,434,081 1,452,244 Total Operating Expenses $ 37,506,658 $ 37,597,418 $ 37,228,805 (7)

10 MANAGEMENT S DISCUSSION AND ANALYSIS Operating Expenses by Object Classification Expenses by Object Classification represent the following for the years ended June 30: Salaries and Fringe Benefits $ 27,618,715 $ 26,934,293 $ 26,739,945 Contracted Services 3,752,809 4,488,950 3,997,368 Depreciation 392, , ,474 Supplies and Materials 1,614,856 1,568,981 1,501,817 Utilities 1,005, ,226 1,097,932 Communications 209, , ,240 Conferences and Meetings 407, , ,275 Scholarships (Net) 891,801 1,076,622 1,251,334 Fixed Charges 202, , ,176 Certain Fringe Benefits Paid Directly by the State of Maryland 1,411,806 1,434,081 1,452,244 Total Expenses $ 37,506,658 $ 37,597,418 $ 37,228,805 (8)

11 MANAGEMENT S DISCUSSION AND ANALYSIS Operating Expenses by Object Category Salaries and fringe benefits clearly represent the largest operating expense at 74%, 72% and 72% for fiscal years 2017, 2016 and 2015, respectively. This line includes Other Post-Employment Benefits and does not include certain fringe benefits paid by the State of Maryland. Utility costs are paid by the county government and are recorded by the College as in-kind costs for both budgetary and accounting purposes. Utility costs increased 5.9% in fiscal year 2017 compared to a decrease of 13.4% in fiscal year Scholarships represent financial aid expense less institutional scholarships, which has been deducted from tuition revenue. Scholarship allowances for the fiscal years 2017, 2016 and 2015 are $2,221,849, $2,319,127, and $2,482,453, respectively. Depreciation reflects no changes in the useful life of the College s fixed assets definitions from the previous fiscal year. (9)

12 MANAGEMENT S DISCUSSION AND ANALYSIS Statement of Cash Flows The Statement of Cash Flows provides information about cash receipts and cash payments during the year. This statement also helps users assess the College s ability to generate net cash flow and its ability to meet obligations as they come due. The primary cash receipts from operating activities consist of tuition and fees, auxiliary enterprises, and grants and contracts. Major cash outlays in operating activities consist of salaries and benefits and outsourced services. State and local appropriations and Pell grants are the primary source of non-capital financing activities. Accounting standards require that we reflect this source of revenue as non-operating even though the College s budget depends on this to continue the current level of operations. Cash flows from investment activities represent income earned on cash invested in the Maryland Local Government Pool (MLGIP), which is held by PNC Bank and a checking, public fund savings account held by Branch Bank and Trust Cash Provided (Used) By: Operating Activities $ (20,690,674) $ (21,019,615) $ (20,054,386) Noncapital Financing Activities 20,076,379 20,201,208 19,609,899 Capital Financing Activities 905, ,264 1,150,250 Investing Activities 29,629 11,579 5,892 Net Increase (Decrease) in Cash 321,226 (146,564) 711,655 Cash - Beginning of Year 6,986,661 7,133,225 6,421,570 Cash - End of Year $ 7,307,887 $ 6,986,661 $ 7,133,225 Economic Factors That Will Affect the Future The economic position of the College is closely tied to that of the County and State governments. The County and State governments provide vital resources to the College s operating budget as noted in the Statements of Revenues, Expenses and Changes in Net Position. In addition, enrollment is a major factor in determining revenue. As the College completed this fiscal year, the outlook for fiscal years 2018 and 2019 are closely tied to the revenue stream produced by local income and sales taxes at the state level and property tax and local income tax revenues at the county level. The State budget is also impacted by what the Federal Government does due to the large presence of Federal workforce in the State of Maryland. The County Government has built into its budgeted operating plan a 3% increase in funding to the college in fiscal years 2019 and through fiscal year This plan is evaluated annually. The College has received an increase of 7% of funds from the County government in fiscal year 2018 over what was provided in fiscal year (10)

13 MANAGEMENT S DISCUSSION AND ANALYSIS The State of Maryland s economic climate is stable. The State s revenue stream is heavily influenced by Federal government programs. The combination of what actions the State of Maryland will take as it sets it financial priorities and uncertainly related to the Federal budget situation leads the College to be cautious when predicting future state aid. The amount of State Aid to be received each year is subject to annual evaluation by the State and is expected remain consistent over the next few years. In fiscal year 2018, the State made a modest increase in funding to the community college system overall of approximately.40%. Distribution of State funds is based on a formula with funds not evenly distributed to each college. In addition, the State provided $4 million in a one-time grant to the Community College System if each of the Community Colleges kept any tuition increase at 2% or less. As a result of receiving this incentive grant Carroll Community College will receive an increase of approximately 1.4% in Fiscal Year The college will receive an additional $440,000 in FY 2019 due to an increase in the small college grant, representing a 5% increase in State contribution. Those funds will become part of the base funding level in FY2019 and beyond. The College expects enrollments to decline in FY2018 as it did in FY2017. Fewer high school graduates is the main reason for this expected decline. Fewer enrollments equate to less tuition and fee revenue. The College s annual operating budget and Five-Year Strategic Plan anticipates a small annual decline in enrollment for at least the next five years thus fewer tuition dollars before the impact of a tuition increase is factored into the equation. New programs are being evaluated to determine if enrollment growth can be generated through new offerings while at a minimum covering the cost of implementing these new programs. The College is seeking to limit future tuition increases to no more that 5% per year. The College maintains a contingency plan in the event that there is a reduction to the State or County appropriation in excess of what the annual operating budget is based on. The College does not anticipate the need to take any drastic actions to maintain a balanced budget. The College maintains a financial reserve that when coupled with an active budget review and contingency planning process allows the College to be better prepared for changing fiscal conditions. During the recent budget cycle for fiscal year 2018, the Board of Trustees increased tuition by $2 per credit or 1.5%. The tuition rates for out-of-county and out-of-state residents were increased proportionally. The College will continue to be evaluating future tuition increases against the availability of State and County funding levels. The College is actively working with the Carroll Community College Foundation to identify needs and raise funds to offset some of the College s future financial requirements. In FY2018, the Carroll Community College Foundation plans to provide $166,000 in direct support to the college to offset the cost of equipment needed for a new Digital Fabrication program. In addition, the Foundation has embarked on a campaign to raise between $5 and $8 million in support of the College. As part of this campaign, the Foundation is seeking to raise $1,750,000 to be dedicated to support technology on campus. The County Government has pledged to match this effort dollar for dollar over the next 5 years. Contacting the College s Financial Management The financial report is designed to provide interested parties with a general overview of Carroll Community College s finances. If you have questions about this report or require additional financial information, contact Carroll Community College, Administration Office, 1601 Washington Road, Westminster, Maryland (11)

14 STATEMENTS OF NET POSITION (DEFICIT) ASSETS Current Assets: Cash and Cash Equivalents $ 7,307,887 $ 6,986,661 Accounts Receivable: Carroll County 41, ,856 State of Maryland 63, ,121 Federal Government 40,023 13,131 Student and Other (Net of Allowance of $462,658 and $412,036, Respectively) 177, ,695 Other Receivables 141, ,482 Due from Carroll Community College Foundation 13,151 68,733 Prepaid Expenses 798,651 1,570,723 Total Current Assets 8,584,980 9,508,402 Noncurrent Assets: Capital Assets 2,221,908 2,023,689 Total Assets 10,806,888 11,532,091 LIABILITIES Current Liabilities: Accounts Payable: Carroll County 22, Other Payables 214, ,754 Accrued Salaries and Taxes 451,384 1,071,758 Claims Payable 715, ,072 Compensated Absences - Current 740, ,758 Unearned Revenue 1,821,630 1,736,005 Total Current Liabilities 3,965,775 5,026,434 Noncurrent Liabilities: Compensated Absences, Net of Current Portion 134, ,190 Other Post Employment Benefits 22,791,423 20,150,543 Total Noncurrent Liabilities 22,925,700 20,347,733 Total Liabilities 26,891,475 25,374,167 NET POSITION (DEFICIT) Net Investment in Capital Assets 2,221,908 2,023,689 Unrestricted (Deficit) (18,306,495) (15,865,765) Total Net Position (Deficit) $ (16,084,587) $ (13,842,076) See accompanying Notes to Financial Statements. (12)

15 STATEMENTS OF REVENUES, EXPENSES, AND CHANGES IN NET POSITION (DEFICIT) YEARS ENDED OPERATING REVENUES Tuition and Fees $ 12,393,079 $ 12,503,671 Scholarship Allowances (2,221,849) (2,319,127) 10,171,230 10,184,544 Federal Grants and Contracts 263, ,058 State, Local and Other Grants and Contracts 1,190,747 1,182,840 Auxiliary Enterprises 409, ,794 Other Sources 214, ,230 Total Operating Revenues 12,250,036 12,504,466 OPERATING EXPENSES Instruction 15,105,681 15,784,709 Grants 61,825 58,823 Academic Support 5,282,156 4,882,766 Student Services 4,005,510 4,087,071 Plant Operations and Maintenance 3,473,840 3,399,843 Institutional Support 6,967,946 6,350,349 Auxiliary Enterprises 273, ,398 Other 531, ,535 Depreciation 392, ,843 Certain Fringe Benefits Paid Directly by the State of Maryland 1,411,806 1,434,081 Total Operating Expenses 37,506,658 37,597,418 Operating Loss (25,256,622) (25,092,952) NONOPERATING REVENUES County Appropriation 8,523,370 7,827,680 County Capital Appropriation 1,495,636 1,481,460 State Appropriation 8,020,376 7,745,631 Pell Grants 2,358,964 2,613,901 Investment Income 29,629 11,579 Other Grants and Gifts 485, ,318 Certain Fringe Benefits Paid Directly by the State of Maryland 1,411,806 1,434,081 Other Sources 689,245 1,522,808 Total Nonoperating Revenues 23,014,111 23,130,458 CHANGE IN NET POSITION (DEFICIT) (2,242,511) (1,962,494) Net Position (Deficit) - Beginning of Year (13,842,076) (11,879,582) NET POSITION (DEFICIT) - END OF YEAR $ (16,084,587) $ (13,842,076) See accompanying Notes to Financial Statements. (13)

16 STATEMENTS OF CASH FLOWS YEARS ENDED CASH FLOWS FROM OPERATING ACTIVITIES Tuition and Fees $ 10,185,419 $ 10,108,749 Operating Grants and Contracts 1,648,275 1,606,954 Other Sources 578, ,354 Payments to Suppliers (8,469,519) (8,623,010) Payments for Salaries and Benefits (25,031,271) (25,240,652) Auxiliary Enterprises Charges 397, ,990 Net Cash Used by Operating Activities (20,690,674) (21,019,615) CASH FLOWS FROM NONCAPITAL FINANCING ACTIVITIES County Appropriations 8,523,370 7,827,680 State Appropriations 8,020,376 7,745,631 Pell Grants 2,358,964 2,613,901 Direct Loan Receipts 2,166,715 2,331,408 Direct Loan Disbursements (2,166,715) (2,331,408) Other Grants and Gifts 485, ,318 Other Sources 688,584 1,520,678 Net Cash Provided by Noncapital Financing Activities 20,076,379 20,201,208 CASH FLOWS FROM CAPITAL FINANCING ACTIVITIES County Capital Appropriation 1,495,636 1,481,460 Purchases of Capital Assets (589,744) (821,196) Net Cash Provided by Capital Financing Activities 905, ,264 CASH FLOWS FROM INVESTING ACTIVITIES Investment Income 29,629 11,579 NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS 321,226 (146,564) Cash and Cash Equivalents - Beginning of Year 6,986,661 7,133,225 CASH AND CASH EQUIVALENTS - END OF YEAR $ 7,307,887 $ 6,986,661 RECONCILIATION OF OPERATING LOSS TO NET CASH USED BY OPERATING ACTIVITIES Operating Loss $ (25,256,622) $ (25,092,952) Adjustments to Reconcile Operating Loss to Net Cash Used by Operating Activities: Depreciation 392, ,843 Certain Fringe Benefits Paid by the State of Maryland 1,411,806 1,434,081 Effects of Changes in Operating Assets and Liabilities: Accounts Receivable - State of Maryland 136,247 58,709 Accounts Receivable - Federal government (26,891) (11,301) Accounts Receivable - Student and Other 309, ,041 Due from Carroll Community College Foundation 55,622 3,556 Prepaid Expenses 772,072 (1,292,199) Accounts Payable (385,568) 245,192 Accrued Salaries and Taxes (622,252) 145,720 Claims Payable (187,736) 202,510 Compensated Absences (15,520) 12,170 Unearned Revenue 85, ,576 Other Post Retirement Benefits 2,640,880 2,625,439 Net Cash Used by Operating Activities $ (20,690,674) $ (21,019,615) See accompanying Notes to Financial Statements. (14)

17 STATEMENTS OF FINANCIAL POSITION COMPONENT UNIT ASSETS Cash and Cash Equivalents $ 292,118 $ 254,658 Investments 9,765,304 8,590,883 Contributions Receivable, Net 1,852, ,315 Accounts and Interest Receivable 30,920 23,403 Art Collections 384, ,525 Total Assets $ 12,325,780 $ 9,529,784 LIABILITIES AND NET ASSETS ACCOUNTS PAYABLE Carroll Community College $ 13,151 $ 68,733 NET ASSETS Unrestricted 2,473,630 2,296,641 Temporarily Restricted 3,504,949 2,058,004 Permanently Restricted 6,334,050 5,106,406 Total Net Assets 12,312,629 9,461,051 Total Liabilities and Net Assets $ 12,325,780 $ 9,529,784 See accompanying Notes to Financial Statements. (15)

18 STATEMENT OF ACTIVITIES COMPONENT UNIT YEAR ENDED JUNE 30, 2017 REVENUES, GAINS AND OTHER SUPPORT Contributions 209,679 Temporarily Permanently Unrestricted Restricted Restricted Total $ $ 950,501 $ 1,227,644 $ 2,387,824 In-kind Contributions 419,758 2, ,358 Fundraising Activities 331, ,822 Net Investment Income 29, , ,966 Net Unrealized and Realized Gain on Investments 177, , ,983 Unrealized Gain on Artwork 2, ,425 Net Assets Released from Restrictions: Satisfaction of Restrictions 322,085 (322,085) - - Total Revenues, Gains and Other Support 1,492,789 1,446,945 1,227,644 4,167,378 EXPENSES Scholarships and Grants Awarded 510, ,485 Management and General - Noncash Expenses of $422, , ,682 Fundraising - Noncash Expenses of $55, , ,633 Total Expenses 1,315, ,315,800 CHANGE IN NET ASSETS 176,989 1,446,945 1,227,644 2,851,578 Net Assets - Beginning of Year 2,296,641 2,058,004 5,106,406 9,461,051 NET ASSETS - END OF YEAR $ 2,473,630 $ 3,504,949 $ 6,334,050 $ 12,312,629 See accompanying Notes to Financial Statements. (16)

19 STATEMENT OF ACTIVITIES COMPONENT UNIT YEAR ENDED JUNE 30, 2016 REVENUES, GAINS AND OTHER SUPPORT Contributions 56,367 Temporarily Permanently Unrestricted Restricted Restricted Total $ $ 254,467 $ 179,082 $ 489,916 In-kind Contributions 396,833 2, ,443 Fundraising Activities 349, ,988 Net Investment Income 29, , ,220 Net Unrealized and Realized Gain on Investments 9,311 42,235-51,546 Realized Loss on Real Estate (5,000) - - (5,000) Net Assets Released from Restrictions: Satisfaction of Restrictions 382,788 (382,788) - Total Revenues, Gains and Other Support 1,219,708 29, ,082 1,428,113 EXPENSES Scholarships and Grants Awarded 515, ,040 Management and General - Noncash Expenses of $399, , ,471 Fundraising - Noncash Expenses of $65, , ,522 Total Expenses 1,143, ,143,033 CHANGE IN NET ASSETS 76,675 29, , ,080 Net Assets - Beginning of Year 2,219,966 2,028,681 4,927,324 9,175,971 NET ASSETS - END OF YEAR $ 2,296,641 $ 2,058,004 $ 5,106,406 $ 9,461,051 See accompanying Notes to Financial Statements. (17)

20 NOTES TO FINANCIAL STATEMENTS NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Carroll Community College (the College) is considered a body politic under Maryland State law as an instrumentality of the State of Maryland (the State). The College is governed by the Board of Trustees of Carroll Community College, a seven-member board, who are appointed for six-year terms by the governor of the State with the advice and consent of the State Senate. The significant accounting policies followed by the College are described below. Funding is received from the State based on full-time-equivalent students enrolled as reported two years earlier. Although the College is not a Carroll County, Maryland (the County) agency, the County approves the College s operating budget and provides a substantial amount of funding. As a result of this relationship with the County, the College s financial statements are considered component unit financial statements and are properly included in the Comprehensive Annual Financial Report of the County in accordance with generally accepted accounting principles in the United States of America. The Carroll Community College Foundation, Inc. (the Foundation) is a separate legal entity. It has a separate Board of Directors that works closely with the College. The College President, Vice-President of Administration and a College Trustee are ex-officio members of the Foundation Board. Although the College does not control the timing or amount of receipts from the Foundation, all of the resources or income thereon that the Foundation holds and invests are restricted to the activities of the College by the donors. Because these restricted resources held by the Foundation can only be used by, or for the benefit of the College, the Foundation is considered a component unit of the College and is discretely presented in the College s financial statements in accordance with the Government Accounting Standards Board Statement No. 39, Determining Whether Certain Organizations are Component Units, as amended. The Foundation is a private nonprofit organization that reports under FASB standards. As such, certain revenue recognition criteria and presentation features are different from GASB revenue recognition criteria and presentation features. No modifications have been made to the Foundation s financial information in the College s financial reporting entity for these differences. Significant accounting policies followed by the College are described below. Basis of Presentation The College presents its financial statements in accordance with Governmental Accounting Standards Board (GASB) Statement No. 34 Basic Financial Statements and Management Discussion and Analysis for State and Local Governments and No. 35 Basic Financial Statements and Management s Discussion and Analysis for Public Colleges and Universities. (18)

21 NOTES TO FINANCIAL STATEMENTS NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) Basis of Presentation (Continued) GASB Statement 34 identified three types of special-purpose governments (SPG): (1) those engaged only in governmental activities, (2) those engaged only in business-type activities, and (3) those engaged in both governmental and business-type activities. Business-type activities are financed in whole or in part by fees charged to external parties for goods and services. Given the importance of tuition, fees and other exchange-type transactions in financing higher education, the College adopted the financial reporting model required of SPG s engaged in business-type activities (BTA). Colleges reporting as BTA s follow GASB standards applicable to proprietary (enterprise) funds. The BTA model requires the following component unit financial statement components. Management s Discussion and Analysis Statement of Net Position Statement of Revenues, Expenses and Changes in Net Position Statement of Cash Flow Notes to the Financial Statements The College s component unit financial statements are prepared using the format of a special-purpose government engaged only in business-type activities with an economic resources measurement focus and the accrual basis of accounting. Under the accrual basis of accounting, revenues are recorded when earned and expenses are recorded when they have been reduced to a legal contractual obligation to pay. The statements are intended to report the public institution as an economic unit that includes all measurable assets and liabilities, intangible, financial and capital, of the institution. The Statements of Revenues, Expenses, and Changes in Net Position for special-purpose governments engaged in business-type activities (BTA) require an operating/non-operating format to be used. The College has elected to report its operating expenses by functional classification. The Statements of Cash Flows is presented as the direct method, which depicts cash flows from operating activities and a reconciliation of operating cash flows to operating income. The College s tuition and fees revenue is reported net of any scholarship allowance. The scholarship allowance represents monies received as tuition from outside resources such as the Title IV Federal Grant Program, restricted grants, Board of Trustee Scholarships, as well as waivers. The total scholarship allowance for the years ended June 30, 2017 and 2016 was $2,221,849 and $2,319,127, respectively. Federal Financial Assistance Programs The College participates in federally funded Pell, SEOG, and Federal Work-Study Grants. A separate audit of federal programs is performed in accordance with Title 2 U.S. Code of Federal Regulations Part 200, Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (Uniform Guidance). (19)

22 NOTES TO FINANCIAL STATEMENTS NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) Federal Financial Assistance Programs (Continued) The College participates in the federal direct lending program, which makes it easier for students to secure loan funding for their education. For the years ended June 30, 2017 and 2016, the total amount loaned to students through direct lending was $2,166,715 and $2,331,408, respectively. Operating and Non-Operating Components Financial statement operating components include all transactions and other events that are not defined as capital and related financing, noncapital financing or investing activities. The College s principal ongoing operations determine operating flow activities. Ongoing operations of the College include, but are not limited to, providing intellectual, cultural and social services through two-year associate degree programs, continuing education programs and continuous learning programs. Operating revenues of the College consist of tuition and fees, grants and contracts (except Federal Pell grants), and auxiliary enterprise revenues. The College maintains an encumbrance system for tracking outstanding purchase orders and other commitments for materials or services not received during the year. Encumbrances were $389,368 and $242,039 at June 30, 2017 and 2016, respectively, which represent the estimated amount of expenses ultimately to result when unperformed contracts in process are completed. Encumbrances outstanding do not constitute expenses or liabilities and are not reflected in these financial statements. Unencumbered appropriations expire at year-end, but are typically renewed in the next fiscal year. Cash and Cash Equivalents For purposes of the Statements of Cash Flows for the College, cash and cash equivalents include demand deposits, Maryland Local Government Investment Pool (MLGIP), and shortterm investments held at financial institutions with a maturity date of three months or less at time of purchase. Revenue Recognition and Unearned Revenue Tuition revenue is recognized when instruction is provided. Grant and appropriation revenue is recognized when all of the conditions are met. Unearned revenue is primarily tuition received prior to year-end for semesters beginning after June 30 of the year presented. Grant revenue received during the year that has restrictions on spending are considered unearned until those restrictions are met. Deferred Outflows/Inflows of Resources In addition to assets, the Statements of Net Position (Deficit) will sometimes report a separate section for deferred outflows of resources. This separate financial statement element, deferred outflows of resources, represents a consumption of net position that applies to a future period and so will not be recognized as an outflow of resources (expenses/expenditures) until then. The College has no items that qualify for reporting in this category. (20)

23 NOTES TO FINANCIAL STATEMENTS NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) Deferred Outflows/Inflows of Resources (Continued) In addition to liabilities, the Statements of Net Position (Deficit) will sometimes report a separate section for deferred inflows of resources. This separate financial statement element, deferred inflows of resources, represents an acquisition of net position that applies to a future period and so will not be recognized as an inflow of resources (revenue) until that time. The College has no items that qualify for reporting in this category. Tuition Receivable Tuition receivables are uncollateralized obligations of students resulting from course registration and for which the earnings process is complete. The receivable is due before the end of the semester in which it was incurred. Amounts that remain uncollected ninety (90) days from the date of invoice are considered delinquent and are referred to the collections department. The allowance method for accounts receivable is used to measure bad debts, which include account charge-offs. The allowance for doubtful accounts is determined based upon aging analysis and management s estimation of collectability of such accounts. Compensated Absences It is the College s policy to allow employees to carry over unused annual leave, payable upon termination. There are limits on the amount of carry over based on employee classification. Leave is earned at the following rates: Full-time 12 month support staff: Less than 5 years of service: 10 days per year 5 10 years of service 15 days per year More than 10 years of service 20 days per year Full-time 12 month professional employees: 20 days per year Capital Assets Capital assets are recorded at cost at the time of purchase or fair value at the date of donation in case of gifts. The College s policy is to include only those capital assets with an individual item purchase price or fair value at donation of at least $2,500. The entire library collection is recorded and valued at cost or estimated cost as a unit without regard to individual item cost. Depreciation is provided over the estimated economic life of the item on a straight-line basis as follows: Fiscal Years Number of Years Number of Years Library Books 3 3 Furniture and Equipment 5 5 Building Improvements Vehicles 7 7 (21)

24 NOTES TO FINANCIAL STATEMENTS NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) Postemployment Benefits The College s employees participate in retirement plans as more fully discussed in Note 5. Additionally, the College sponsors postemployment benefits other than the retirement plans as described in Note 6. Federal and State Income Tax Status The College is exempt from federal and state income taxes as it is essentially a political subdivision of the State. Use of Estimates in Preparing Financial Statements The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the component unit financial statements and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates. Net Position Flow Assumptions Sometimes the College will fund outlays for a particular purpose from both restricted and unrestricted resources. In order to calculate the amounts to be reported as restricted and unrestricted net position in the financial statements, a flow assumption must be made about the order in which the resources are considered to be applied. It is the College s policy to consider restricted net position to have been depleted before unrestricted net position is applied. The College had no restricted net position as of June 30, 2017 and Net Position (Deficit) Net Position (Deficit) comprises the various earnings from operating income, non-operating revenues, expenses and capital contributions. Net Position (Deficit) is classified in the following components: Net Investment in Capital Assets This component of Net Position consists of capital assets, net of accumulated depreciation reduced by outstanding debt used to acquire the assets. The College had no outstanding debt as of June 30, 2017 and Restricted This component of Net Position consists of amounts that are restricted to specific purposes when constraints are placed on the use of resources by constitution, external resource providers, or through enabling legislation. The College has no restricted Net Position as of June 30, 2017 and Unrestricted This component of Net Position consists of Net Position (Deficit) that do not meet the definition of restricted or net investment in capital assets. This component includes Net Position (Deficit) that may be allocated for specific purposes by the Board. (22)

25 NOTES TO FINANCIAL STATEMENTS NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) Carroll Community College Foundation, Inc. A separate board governs the discretely presented component unit. The Foundation is a separate entity that has been recognized as a tax-exempt organization as defined by Section 501(c)(3) of the Internal Revenue Code. Complete financial statements for the Foundation can be obtained from the respective administrative offices listed below: Carroll Community College Foundation, Inc Washington Road Westminster, MD Nature of Activities The Foundation is a not-for-profit organization operated for the benefit of Carroll Community College. The Foundation provides scholarships to students, administers funds restricted for special college programs, and provides special awards and grants to students attending Carroll Community College, located in Carroll County, Maryland. The Foundation s primary funding sources are donor contributions and fundraising events. Accrual Basis The financial statements of the Foundation, Inc. have been prepared on the accrual basis of accounting. Net assets and revenues, expenses, gains, and losses are classified based on the existence or absence of donor-imposed restrictions. Accordingly, net assets of the Foundation and changes therein are classified and reported as follows: Unrestricted net assets Net assets that are not subject to donor-imposed stipulations. Temporarily restricted net assets Net assets subject to donor-imposed stipulations that may or will be met, either by actions of the Foundation and/or the passage of time. When a restriction expires, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the Statements of Activities as net assets released from restrictions. Permanently restricted net assets Net assets subject to donor-imposed stipulations that they be maintained permanently by the Foundation. Generally, the donors of these assets permit the Foundation to use all or part of the income earned on any related investments for general or specific purposes. (23)

26 NOTES TO FINANCIAL STATEMENTS NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) Carroll Community College Foundation, Inc. (Continued) Expenditures which meet the specific purposes of the temporarily restricted net assets are expensed from temporary net assets prior to unrestricted net assets. Cash and Cash Equivalents Amounts in demand deposits or short-term investments with a maturity date of three months or less when purchased are considered cash and cash equivalents. Investments Investment securities are carried at fair value. Accordingly, the change in net unrealized appreciation (depreciation) of marketable securities for the year is reflected in the Statements of Activities. Realized gains and losses on sales of investments are computed on a specific identification basis and are recorded on the settlement date of the transactions in the appropriate net asset category. Certain investments are effectively restricted as to use to the extent of permanently restricted net assets. Investment income and losses on investments of temporarily restricted assets is added to or taken from temporarily restricted net assets when restricted as to use by the donor. Unrealized gains (losses) on the invested corpus of the permanently restricted net assets are recorded in the temporarily restricted net assets. However, realized and unrealized losses on permanently restricted net assets in excess of realized and unrealized gains on previously accumulated permanently restricted net assets are recorded as reductions of unrestricted net assets. Contributions Receivable Pledges are recorded at the fair value pledged by the donor. Pledges deemed to be uncollectible are charged directly against gift and contribution revenue and pledges receivable is reduced. Pledges due in more than one year are discounted to their net present value. The current allowance for uncollectible pledges is 2%. Contributions of temporarily restricted net assets that are received and expended in the same fiscal year are treated as temporarily restricted revenue and net assets released from restriction in that year. Permanently Restricted Contributions Contributions subject to donor-imposed stipulations that must be maintained in perpetuity by the Foundation are included in permanently restricted net assets. Generally, the donors of these assets permit the Foundation to use all or part of the income earned and capital gains on related investments, if any, for general or specific purposes. Temporarily Restricted Contributions Contributions subject to donor-imposed stipulations that may or will be met by actions of the Foundation and/or the passage of time are included in temporarily restricted net assets. Unrestricted Contributions Contributions not subject to donor-imposed stipulations, or whose restrictions have been satisfied, are recorded as unrestricted net assets. (24)

27 NOTES TO FINANCIAL STATEMENTS NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) Carroll Community College Foundation, Inc. (Continued) In-kind Contributions In-kind contributions represent wages and benefits paid by the College on behalf of individuals performing services for the Foundation, as well as other expenses paid by the College for the Foundation. This amount also includes any in-kind gifts made to the Foundation by other parties. A corresponding amount is included in the operating expenses of the Foundation. Real Estate The Foundation was gifted real estate that is being held for sale. The real estate was sold during the year ended June 30, 2016 at a loss of $5,000. Income Tax The Foundation is exempt from taxation under the provisions of Section 501(c)(3) of the Internal Revenue Code. Accordingly, no income tax expense has been provided in the accompanying financial statements. Accounting for Uncertain Tax Positions The Foundation has adopted the guidance in Accounting for Uncertainty in Income Taxes (ASC ); which prescribes a threshold of more-likely-than-not for recognition and derecognition of tax positions taken or expected to be taken in a tax return. It also recognizes related guidance on measurement classification, interest and penalties, and disclosure. The Foundation does not believe that there are any unrecognized tax benefits or costs that should be recognized. Recent Accounting Pronouncements The following GASB pronouncements considered to have an impact on the College have been issued but not yet implemented by the College: In June 2015, GASB issued Statement No. 75, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions. The primary objective of this Statement is to improve accounting and financial reporting by state and local governments for postemployment benefits other than pensions (other postemployment benefits or OPEB). It also improves information provided by state and local governmental employers about financial support for OPEB that is provided by other entities. The scope of this Statement addresses accounting and financial reporting for OPEB that is provided to the employees of state and local governmental employers. This Statement establishes standards for recognizing and measuring liabilities, deferred outflows of resources, deferred inflows of resources, and expense/expenditures. This Statement is effective for fiscal years beginning after June 15, (25)

28 NOTES TO FINANCIAL STATEMENTS NOTE 1 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (CONTINUED) Recent Accounting Pronouncements (Continued) In June 2017, GASB issued Statement No. 87, Leases. The objective of this statement is to better meet the information needs of government financial statement users by improving accounting and financial reporting for leases. This statement will require recognition of certain lease assets and liabilities for leases that previously were classified as operating leases and recognized as inflows or outflows of resources based on the contract s payment provisions. The requirements of this statement are effective for reporting periods beginning after December 15, The College has not yet completed the process of evaluating the impact of GASB Statements Nos. 75 and 87 on its financial statements. NOTE 2 CASH AND CASH EQUIVALENTS AND INVESTMENTS Cash and Cash Equivalents Petty Cash As of June 30, 2017 and 2016, the cash on hand for petty cash and change funds was $3,300. Deposits At June 30, 2017 and 2016, the College s cash and cash equivalents balance by type were as follows: Cash and Cash Equivalents Cash on Hand $ 3,300 $ 3,300 Cash in Bank 1,340,645 2,097,825 Bank Money Market 1,034,221 4,468,038 Maryland Local Government Investment Pool 4,929, ,498 Total Cash and Cash Equivalents $ 7,307,887 $ 6,986,661 As of June 30, 2017 and 2016, the carrying amounts were $1,340,645 and $2,097,825 and the bank balances were $1,883,616 and $2,222,957, respectively. The College also has a public fund savings account with Branch Bank and Trust (BB&T) of $1,034,221 and $4,468,038 at June 30, 2017 and 2016, respectively. Cash and cash equivalents are collateralized by federal agency securities held in the College s name at a rate of 102%. During the year, the College transferred a large portion of the Branch Bank and Trust (BB&T) public funds savings account over to the MLGIP, which is operated by PNC Bank. The balances as of June 30, 2017 and 2016 were $4,929,721 and $417,498 respectively. The reason for the transfer was due to a higher interest rate on investment. (26)

29 NOTES TO FINANCIAL STATEMENTS NOTE 2 CASH AND CASH EQUIVALENTS AND INVESTMENTS (CONTINUED) Cash and Cash Equivalents (Continued) The College s deposit and investment accounts were insured by the Federal Deposit Insurance Corporation (FDIC) or properly collateralized with securities held by the pledging banks agent in the College s name. Article 95, Section 22 and Section of the State Finance and Procurement Article of the Annotated Code of Maryland authorizes, and the College's adopted investment policy authorizes, the College to invest surplus cash in U.S. Treasury obligations, U.S. governmental agencies and instrumentalities securities, collateralized certificates of deposit, repurchase agreements, the Maryland Local Government Investment Pool (MLGIP), commercial paper, and bankers' acceptances. In the opinion of management, the College is in compliance with all provisions of the Annotated Code of Maryland and the College's investment policy. MLGIP Cash and cash equivalents include deposits with the MLGIP. Investments in the MLGIP are available by daily transfer to cover checks issued when paid by the bank. The College is a participant of the MLGIP, which provides all local government units of the state a safe investment vehicle for the short-term investment of funds. The State Legislature created MLGIP with the passage of Article 95 Section 22G, of the Annotated Code of Maryland. The MLGIP, under the administrative control of the State Treasurer, is managed by PNC Bank. An MLGIP Advisory Committee of current participants was formed to review, on a quarterly basis, the activities of the Fund and to provide suggestions to enhance the pool. The pool is rated AAAm by Standard and Poors, their highest rating for money market mutual funds. The fair value of the pool is the same as the value of the pool shares. Interest Rate Risk Fair value fluctuates with interest rates, and increasing interest rates could cause fair value to decline below original cost. To limit the College s exposure to fair value losses arising from increasing interest rates, the College s investment policy limits the term of investment maturities. College management believes the liquidity in the portfolio is adequate to meet cash flow requirements and to preclude the College from having to sell investments below original cost for that purpose. The investments at June 30, 2017 and 2016 met the College s investment policy as of that date. Credit Risk College investment policy does not permit investments in commercial paper or corporate bonds, except as permitted under state law in the state investment pool. The College invests in the MLGIP which is under the administration of the State Treasurer. The MLGIP seeks to maintain a constant value of $1.00 per unit. Unit value is computed using the amortized cost method. In addition, the net asset value of the pool, marked-to-market, is calculated and maintained on a weekly basis to ensure a $1.00 per unit constant value. (27)

30 NOTES TO FINANCIAL STATEMENTS NOTE 2 CASH AND CASH EQUIVALENTS AND INVESTMENTS (CONTINUED) Custodial Credit Risk For an investment, custodial credit risk is the risk that, in the event of failure of the counterparty, the College will not be able to recover all or a portion of the value of its investments or collateral securities that are in the possession of an outside party. At June 30, 2017, all of the College s investments were invested in the MLGIP. Investments Carroll Community College Foundation, Inc. The investments of the Foundation are carried at fair value and summarized at June 30 as follows: Cost Fair Value Cost Fair Value Equity Securities $ 4,980,949 $ 5,810,517 $ 5,153,975 $ 5,198,364 Corporate Bonds 4,047,182 3,954,787 3,388,064 3,392,519 Total $ 9,028,131 $ 9,765,304 $ 8,542,039 $ 8,590,883 The following schedule summarizes the investment return and its classification in the Statements of Activities for the years ended: Temporarily June 30, 2017 Unrestricted Restricted Total Interest and Dividends $ 39,530 $ 158,520 $ 198,050 Investment Advisor's Fees (10,160) (40,924) (51,084) Net Investment Income 29, , ,966 Unrealized Gains 134, , ,329 Realized Gains 43, , ,654 Net Unrealized and Realized Gains 177, , ,983 Total Investment Income $ 207,020 $ 815,929 $ 1,022,949 Temporarily June 30, 2016 Unrestricted Restricted Total Interest and Dividends $ 38,722 $ 148,551 $ 187,273 Investment Advisor's Fees (9,301) (35,752) (45,053) Net Investment Income 29, , ,220 Unrealized Losses (15,515) (59,614) (75,129) Realized Gains 24, , ,675 Net Unrealized and Realized Gains 9,311 42,235 51,546 Total investment income $ 38,732 $ 155,034 $ 193,766 (28)

31 NOTES TO FINANCIAL STATEMENTS NOTE 3 FAIR VALUE MEASUREMENTS Carroll Community College Foundation, Inc. The accounting guidance establishes a framework for measuring fair value. That framework provides a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). The three levels of the fair value hierarchy under the accounting guidance are described as follows: Level 1 Inputs to the valuation methodology are unadjusted quoted prices for identical assets or liabilities in active markets that the Foundation has the ability to access. Level 2 Inputs to the valuation methodology include: Quoted prices for similar assets or liabilities in active markets. Quoted prices for identical or similar assets or liabilities in inactive markets. Inputs other than quoted prices that are observable for the asset or liabilities. Inputs that are derived principally from or corroborated by observable market data by correlation or other means. If the asset or liability has a specified (contractual) term, the Level 2 input must be observable for substantially the full term of the asset or liability. Level 3 Inputs to the valuation methodology are unobservable and significant to the fair value measurement. Carroll Community College Foundation, Inc. The asset or liability s fair value measurement level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement. Valuation techniques used need to maximize the use of observable inputs and minimize the use of unobservable inputs. Following is a description of the valuation methodologies used for instruments measured at fair value and their classification in the valuation hierarchy. Equity securities listed on a national market or exchange are valued at the last sales price or, if there is no sale and the market is still considered active, at the last transaction price before year-end. Such securities are classified within Level 1 of the valuation hierarchy. Debt securities consisting of corporate bonds are generally valued at the most recent price of the equivalent quoted yield for such securities, or those of comparable maturity, quality and type. Debt securities are generally classified within Level 2 of the valuation hierarchy. (29)

32 NOTES TO FINANCIAL STATEMENTS NOTE 3 FAIR VALUE MEASUREMENTS (CONTINUED) Carroll Community College Foundation, Inc. (Continued) The art collection is carried at fair value based on appraised value. The art collection is classified within Level 3 of the valuation hierarchy. The following table presents assets and liabilities measured at fair value by classification within the fair value hierarchy as of June 30, 2017: Fair Value Measurements Using Quoted Prices in Active Significant Markets in Other Significant Identical Observable Unobservable Assets Inputs Inputs (Level 1) (Level 2) (Level 3) Total Recurring basis Equities and Securities $ 5,810,517 $ - $ - $ 5,810,517 Corporate Bonds - 3,954,787-3,954,787 Art Collection , ,950 Total $ 5,810,517 $ 3,954,787 $ 384,950 $ 10,150,254 The following table presents assets and liabilities measured at fair value by classification within the fair value hierarchy as of June 30, 2016: Fair Value Measurements Using Quoted Prices in Active Significant Markets in Other Significant Identical Observable Unobservable Assets Inputs Inputs (Level 1) (Level 2) (Level 3) Total Recurring basis Equities and Securities $ 5,198,364 $ - $ - $ 5,198,364 Corporate Bonds - 3,392,519-3,392,519 Art Collection , ,525 Total $ 5,198,364 $ 3,392,519 $ 382,525 $ 8,973,408 The following table presents the changes in level 3 assets that are measured at fair value on a recurring basis for the years ended June 30, 2017 and 2016: Balance, June 30, 2015 $ 562,525 Proceeds from sale (175,000) Loss on sale (5,000) Balance, June 30, 2016 $ 382,525 Fair Value Adjustment 2,425 Balance, June 30, 2017 $ 384,950 (30)

33 NOTES TO FINANCIAL STATEMENTS NOTE 4 CONTRIBUTIONS RECEIVABLE Carroll Community College Foundation, Inc. Unconditional promises to give at June 30 are as follows: Receivables Due in Less Than One Yyear $ 233,845 $ 177,094 Receivables Due in One to Five Years 1,842, ,952 Total Unconditional Promises to Give 2,076, ,046 Less Discounts to Net Present Value 182,770 8,870 Less Pledges Deemed Uncollectible 41,535 5,861 Net Unconditional Promises to Give $ 1,852,488 $ 278,315 Discount rates used on long-term promises to give were 5% in 2017 and 2016, which approximates the risk free rate as evidenced by the 5-year Treasury bill rate. Pledges deemed uncollectible are 2% of total unconditional promises to give at June 30, 2017 and NOTE 5 PENSION AND RETIREMENT PLANS State of Maryland Pension Plans General Information about the Plan Plan description. The employees of the College are covered by the Maryland State Retirement and Pension System (the System), which is a cost sharing employer public employee retirement system. While there are five retirement and pension systems under the System, employees of the College are a member of either the Teachers Retirement and Pension Systems or the Employees Retirement and Pension Systems. The System was established by the State Personnel and Pensions Article of the Annotated Code of Maryland to provide retirement allowances and other benefits to State employees, teachers, police, judges, legislators, and employees of participating governmental units. The Plans are administered by the State Retirement Agency. Responsibility for the System s administration and operation is vested in a 15-member Board of Trustees. The System issues a publically available financial report that can be obtained at Benefits provided. The System provides retirement allowances and other benefits to State teachers of participating governmental units, among others. For individuals who become members of the Teachers Retirement and Pension Systems on or before June 30, 2011, retirement/pension allowances are computed using both the highest three years Average Final Compensation (AFC) and the actual number of years of accumulated creditable service. For individuals who become members of the Teachers Pension System on or after July 1, 2011, pension allowances are computed using both the highest five years AFC and the actual number of years of accumulated creditable service. Various retirement options are available under each system which ultimately determines how a retirees benefits allowance will be computed. Some of these options require actuarial reductions based on the retirees and/or designated beneficiary s attained age and similar actuarial factors. (31)

34 NOTES TO FINANCIAL STATEMENTS NOTE 5 PENSION AND RETIREMENT PLANS (CONTINUED) State of Maryland Pension Plans (Continued) A member of the Teachers Retirement System is generally eligible for full retirement benefits upon the earlier of attaining age 60 or accumulating 30 years of creditable service regardless of age. The annual retirement allowance equals 1/55 (1.81%) of the member s average final compensation (AFC) multiplied by the number of years of accumulated creditable service. A member of the Teachers Pension System on or before June 30, 2011 is eligible for full retirement benefits upon the earlier of attaining age 62, with specified years of eligibility service, or accumulating 30 years of eligibility service regardless of age. An individual who becomes a member of the Teachers Pension System on or after July 1, 2011, is eligible for full retirement benefits if the members combined age and eligibility service equals at least 90 years or if the member is at least age 65 and has accrued at least 10 years of eligibility service. For most individuals who retired from the Teachers Pension System on or before June 30, 2006, the annual pension allowance equals 1.2% of the member s AFC, multiplied by the number of years of credible service accumulated prior to July 1, 1998, plus 1.4% of the member s AFC, multiplied by the number of years of credible service accumulated subsequent to June 30, With certain exceptions, for individuals who are members of the Teachers Pension System on or after July 1, 2006, the annual pension allowance equals 1.2% of the member s AFC, multiplied by the number of years of credible service accumulated prior to July 1, 1998 plus 1.8% of the member s AFC, multiplied by the number of years of credible service accumulated subsequent to June 30, Beginning in July 1, 2011, any new member of the Teachers Pension System shall earn an annual pension allowance equal to 1.5% of the member s AFC multiplied by the number of years of creditable service accumulated as a member of the Teachers Pension System. Contributions. The College and covered members are required by State statute to contribute to the System. Members of the Teachers Pension System are required to contribute 7% annually. Members of the Teachers Retirement System are required to contribute 5-7 % annually, depending on the retirement option selected. The contribution requirements of the System members, as well as the State and participating governmental employers are established and may be amended by the Board of Trustees for the System. The State makes a substantial portion of the College s annual required contribution to the Teachers Retirement and Pension Systems on behalf of the College. The State s contributions on behalf of the College for the years ended June 30, 2017 and 2016 was $864,945 and $885,072, respectively. The fiscal contributions made by the State on behalf of the College have been included as both revenues and expenditures in the in the accompanying Statement of Revenues, Expenses, and Changes in Net Position (Deficit). (32)

35 NOTES TO FINANCIAL STATEMENTS NOTE 5 PENSION AND RETIREMENT PLANS (CONTINUED) State of Maryland Pension Plans (Continued) Pension Liabilities, Pension Expense, and Deferred Outflows of Resources and Deferred Inflows of Resources Related to Pensions At June 30, 2017 and 2016, the College did not report a liability related to the Teachers Retirement and Pension Systems due to a special funding situation. The State of Maryland pays the unfunded liability for the College and the College pays the normal cost related to the Colleges members in the Teachers Retirement and Pension Systems; therefore, the College is not required to record its share of the unfunded pension liability but instead, that liability is recorded by the State of Maryland. The amount recognized by the College as its proportionate share of the net pension liability, the related State support, and the total portion of the net pension liability that was associated with the College were as follows: State's Proportionate Share of the Net Pension Liability $ 10,719,468 $ 8,861,075 College's Proportionate Share of the Net Pension Liability - - Total $ 10,719,468 $ 8,861,075 The net pension liability was measured as of June 30, 2016 and 2015, and the total pension liability used to calculate the net pension liability was determined by an actuarial valuation as of that date. Due to the special funding situation noted above related to the Teachers Retirement and Pension Systems, the College did not report deferred outflows of resources and deferred inflows of resources related to the Teachers Retirement and Pension Systems. Actuarial assumptions. The total pension liability in the following actuarial valuations was determined using the following actuarial assumptions, applied to all periods included in the measurement: Valuation Date June 30, 2016 June 30, 2015 Inflation- general 2.7% 2.7% Inflation- wage 3.2% 3.2% Salary increases 3.3% to 9.2%, including inflation 3.2% to 9.2%, including inflation Investment rate of return 7.55% 7.55% Mortality Rates RP-2014 Mortality Tables with projected generational mortality improvements based on the MP dimensional mortality improvement scale RP-2014 Mortality Tables with projected generational mortality improvements based on the MP dimensional mortality improvement scale (33)

36 NOTES TO FINANCIAL STATEMENTS NOTE 5 PENSION AND RETIREMENT PLANS (CONTINUED) State of Maryland Pension Plans (Continued) Pension Liabilities, Pension Expense, and Deferred Outflows of Resources and Deferred Inflows of Resources Related to Pensions (Continued) The economic and demographic actuarial assumptions used in the June 30, 2016 valuation were adopted by the System s Board of Trustees based upon review of the System s experience study for the period , after completion of the June 30, 2014 valuations. Assumptions from the experience study including investment return, inflation, COLA increases, mortality rates, retirement rates, withdrawal rates, disability rates and rates of salary increase were adopted by the Board for the first use in the actuarial valuation as of June 30, As a result, an investment return assumption of 7.55% and an inflation assumption of 2.70% were used in the June 30, 2016 valuation. The economic and demographic actuarial assumptions used in the June 30, 2015 valuation were adopted by the System s Board of Trustees on May 21, 2015 based upon review of the System s experience study for the period , which was completed during FY2014. Assumptions from the experience study included investment return inflation, COLA increases, mortality rates, retirement rates, withdrawal rates, disability rates and rates of salary increase were adopted by the College for the first use in the actuarial valuation as of June 30, As a result, an investment return assumption of 7.55% and an inflation assumption of 2.70% were used for the June 30, 2015 valuation. The long term expected rate of return on pension plan investments in the June 30, 2016 valuation was determined using a building block method in which best-estimate ranges of expected future real rates of return (expected returns, net of pension plan investment expense and inflation) are developed for each major asset class. These ranges are combined to produce the long-range expected rate of return by weighing the expected future real rates by the target asset allocation percentage and by adding expected inflation. Best estimates of geometric real rates of return were adopted by the Board after considering input from the System s investment consultant(s) and actuary(s). The long term expected rate of return on pension plan investments in the June 30, 2015 valuation was based on the goal of achieving an annualized investment return that over a long-term time frame: (1) meets or exceeds the investment policy benchmark for the system; (2) in nominal terms, equals or exceeds the actuarial rate of return adopted by the Board of Trustees, which was 7.55 percent for fiscal year 2015; and (3) in real terms, exceeds the U.S. inflation rate by at least 3 percent. These ranges are combined to produce the longrange expected rate of return by weighing the expected future real rates by the target asset allocation percentage and by adding expected inflation. Best estimates of geometric real rates of return were adopted by the Board after considering input from the System s investment consultant(s) and actuary(s). (34)

37 NOTES TO FINANCIAL STATEMENTS NOTE 5 PENSION AND RETIREMENT PLANS (CONTINUED) State of Maryland Pension Plans (Continued) Pension Liabilities, Pension Expense, and Deferred Outflows of Resources and Deferred Inflows of Resources Related to Pensions (Continued) For each major asset class that is included in the System s target asset allocation, these best estimates are summarized in the following table: Target Long Term Expected Target Long Term Expected Asset Class Allocation Real Rate of Return Allocation Real Rate of Return Public Equity 35% 5% 35% 6.30% Fixed Income 10% 2% 10% 0.60% Credit Opportunity 10% 3% 10% 3.20% Real Return 14% 3% 14% 1.80% Absolute Return 10% 5% 10% 4.20% Private Equity 10% 6% 10% 7.20% Real Estate 10% 5% 10% 4.40% Cash 1% 1% 1% 0.00% Total 100% 100% The above was the System s Board of Trustees adopted asset allocation policy and best estimate of geometric real rates for each major asset class as of June 30, 2017 and 2016, respectively. For the years ended June 30, 2017 and 2016, the annual money-weighted rate of return on pension plan investments, net of the pension plan expense was 1.10% and 2.71%, respectively. The money-weighted rate of return expresses investment performance, net of investment expense, adjusted for the changing amounts actually invested. Discount rate. The single discount rate used to measure the total pension liability was 7.55% and 7.55% as of June 30, 2017 and 2016, respectively. This single discount rate was based on the expected rate of return on pension plan investments of 7.55% as of June 30, 2017 and The projection of cash flows used to determine this single discount rate assumed that plan member contributions will be made at the current contribution rate and that employer contributions will be made at rates equal to the difference between actuarially determined contribution rates and the member rate. Based on these assumptions, the pension plan s fiduciary net position was projected to be available to make all projected future benefit payments of current plan members. Therefore, the long-term expected rate of return on pension plan investments was applied to all periods of projected benefit payments to determine the total pension liability. (35)