1. Social Security benefits are modest; yet they are the main income for most seniors and other beneficiaries. (Page 2)

|

|

|

- Daniel Leonard Nelson

- 5 years ago

- Views:

Transcription

2. Social Security is efficient. It spends less than 1% for administration.")

1 What s Next for Social Security? Essential Facts for Action Virginia P. Reno, National Academy of Social Insurance vreno@nasi.org, October Social Security benefits are modest; yet they are the main income for most seniors and other beneficiaries. (Page 2) 2. Social Security is efficient. It spends less than 1% for administration. The rest is benefits paid to the people who rely on it. 3. Social Security is affordable. It flattens out at 6% of the economy even as more people will rely on it. (Page 3) 4. Benefits are already being cut by more than most people realize. Cuts enacted in 1983 and 1993 are phasing in slowly. By 2050, retirement benefits will be 24% lower than they would have been without the cuts. (Page 4) 5. Americans are willing to pay more to preserve Social Security. Republicans, Democrats, and independents agree that it is critical to preserve Social Security, even if it means that working Americans pay more. (Page 6) 6. Americans favor a Social Security package that increases taxes in two ways, raises benefits in two ways, and does not cut benefits. The package would: (Page 7) Gradually, over 10 years, eliminate the cap on earnings that are taxed for Social Security benefits; Gradually, over 20 years, raise the Social Security tax rate that workers and employers each pay from 6.2% to 7.2%; Increase the COLA to reflect inflation that seniors actually face; and Increase the special minimum benefit so that someone who paid into Social Security for 30 years could retire at 62 or later and not be poor.

2 Social Security Benefits are Modest: Yet They Are the Main Income for Most Seniors Monthly Social Security benefits are modest an average of $1,264 in January Yet they are the main income for most seniors. Social Security also provides life insurance and disability income protection to workers and their families. The benefits keep more than 21 million Americans out of poverty, including 1 million children, 6 million adults under age 65, and 14 million seniors. When seniors are divided into five groups based on their total income, the following charts show: Seniors in the lowest two income quintiles with less than about $20,150 in total annual income get more than 8 of their income from Social Security. Seniors in the middle group, with incomes up to $32,600, get two thirds of their income from Social Security. Seniors in the upper middle income group get almost half (44%) of their income from Social Security, while pensions and annuities take on a larger role. Only in the top group (with total annual incomes over $58,000) is Social Security not the largest single income source. Most seniors in this group are still working, and earnings are their largest single income source. 2

3 Social Security Is Affordable: It Flattens Out at 6% of the Economy The affordability of Social Security or spending for other national needs, such as health care, education, or defense is often evaluated relative to the size of the entire economy, or gross domestic product (GDP). Social Security was 5. of GDP in 2012 and is projected to rise to 6.2% of the economy by 2035 after all baby boomers are retired. It is projected to then flatten out at 6. to 6.2% of the economy for the rest of the next 75 years. Social Security Outgo as a Percent of the Economy (GDP), Percent of GDP 45% 35% 25% 15% 5% % 6.2% Source: 2013 Trustees Report, Table VI.F4. Can we afford that increase in spending for Social Security as boomers retire? The 1.2 percentage point increase as baby boomers retire is considerably smaller than the increase in national spending for public education when boomers were children. In the 1950s and 1960s spending for public education rose rapidly with little or no advance warning. From 1950 to 1975 education spending grew by 2.8 percentage points (from 2.5% to 5.3% of GDP). 1 Local governments responded quickly to add classrooms and teachers as boomers showed up in record numbers to enroll in kindergarten. The retirement of the baby boom, in contrast, is not a surprise. It has long been reflected in Social Security projections. While Social Security remains a stable share of the economy, more people will rely on it. Those over age 65 are projected to increase from about 14% to 21% of the population by 2035 and then gradually increase further to 23% by Beneficiaries (including those under age 65) are projected to increase from 18% of the population in 2012 to 26% by Social Security will remain affordable even as more Americans rely on it because benefit cuts already in law are phasing in now. 1 Reno, Virginia P. (2008) Building on Social Security s Success, EPI Briefing Paper #208, Economic Policy Institute, Washington, DC. Page 7. 3

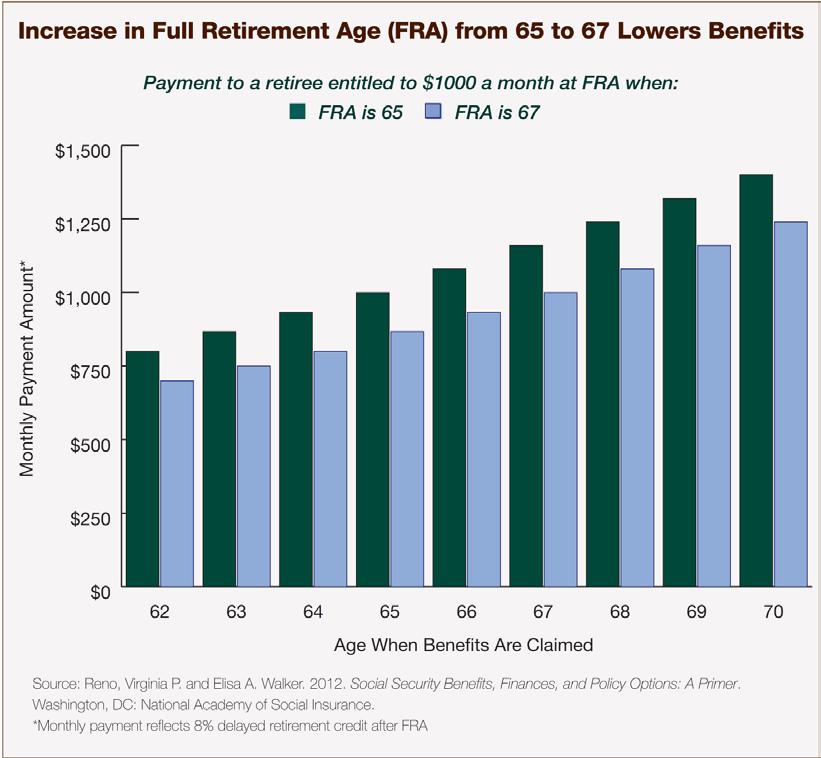

4 Social Security Benefits Are Already Being Cut By More than Many Americans Realize Reductions in Social Security benefits enacted in 1983 and 1993 are phasing in slowly. By 2050, net retirement benefits will be about 24% lower than they would have been in the absence of cuts already enacted that: (a) increase the full benefit retirement age; (b) tax a growing share of Social Security benefits; and (c) permanently delay the cost-of-living adjustment (COLA) from July to January. Increase Retirement Age: The age of eligibility for full retirement benefits is gradually increasing from 65 to 67; it is 66 now and will be 67 for workers born after The increase reduces benefits at any age they are claimed. As shown in the figure on the following page, when the full retirement age (FRA) was 65, a retiree entitled to a monthly benefit of $1,000 would receive that amount at 65. When the FRA is 67, a worker entitled to $1,000 will receive $867 a month at age 65. The reduction occurs at any age benefits are claimed. 13.3% cut Tax a Growing Share of Benefits and Send Funds to Social Security and Medicare. The Social Security amendments of 1983 called for taxing up to of Social Security benefits for couples with more than $32,000 in countable income and singles with more than $25, The tax revenues go to the Social Security fund. In 1993 Congress called for taxing up to 85% of Social Security benefits for couples with more than $44,000 in countable income and singles with more than $34,000. These additional revenues go to Medicare s hospital insurance fund. More people will pay taxes on their Social Security benefits in the future because the thresholds do not rise as incomes rise. The reduction in net Social Security income is projected to increase to 9.5% in % cut Percent Reduction in Net Social Security Income Due to Taxing Benefits Year Total To SS fund To HI fund Source: Social Security and Medicare Trustees Reports, 2012 Permanently Delay the COLA: Prior to 1983, retirees received their first COLA in July of the year they reached age 62. After 1983, they receive their first COLA in January of the year after they turn 62. This is a permanent half-year delay. With future COLAs assumed to be 2.8% per year on average, this change lowers annual Social Security income by 1.4% per year for all current and future beneficiaries. 1.4% cut Three changes together: 24.2% total cut No Payroll Tax Increase Balances These Cuts: No legislation has balanced these long-term benefit cuts with any increase in payroll tax contributions from workers and employers. The Social Security rate remains 6.2% for workers and employers each. It was set in 1977 to take effect in 1990 and has not been updated since. 2 Countable income for the taxation of benefits is defined as adjusted gross income plus part of Social Security benefits and certain nontaxable interest. Social Security Administration, Benefits Planner: Taxes and Your Social Security Benefit. 4

5 5

finds that Americans don t mind paying for Social Security because they value it for themselves, for their families and for security and stability it provides to the millions of retirees, disabled")

6 Americans Are Willing to Pay More to Preserve Social Security: Republicans, Democrats and Independents Agree NASI s recent survey (Strengthening Social Security: What Do Americans Want? ) finds that Americans don t mind paying for Social Security because they value it for themselves, for their families and for security and stability it provides to the millions of retirees, disabled persons, and children and widowed spouses of deceased workers. Percent Agreeing: I don't mind paying Social Security taxes because it provides security and stability to millions of retired Americans, the disabled, and children and widowed spouses of deceased workers % 84% 86% 74% Total Republican Democrat Independent Strikingly, large majorities of Republicans, Democrats and independents agree it is important to preserve Social Security for future generations even if it means increasing working Americans contributions to Social Security taxes. Majorities of Republicans, Democrats and independents also agree it is important to preserve Social Security for future generations if it if means increasing wealthy Americans Social Security taxes Percent Agreeing: It is critical that we preserve Social Security for future generations, even if it means increasing working Americans' contributions to Social Security taxes. 82% 74% 88% 83% Total Republican Democrat Independent Percent Agreeing: It is critical that we preserve Social Security for future generations, even if it means increasing wealthy Americans' contributions to Social Security taxes. 87% 71% 97% 86% Total Republican Democrat Independent Source: Jasmine V. Tucker, Virginia P. Reno, and Thomas N. Bethell. Strengthening Social Security: What Do Americans Want? National Academy of Social Insurance,

7 Americans Favor a Social Security Package that Increases Taxes in Two Ways, Raises Benefits in Two Ways, And Does Not Cut Benefits The same NASI survey used a new approach to measuring public opinion about Social Security. In addition to asking participants whether they would favor a particular change, the survey allowed participants to craft a preferred package of changes, much as lawmakers might do. Participants considered various combinations of 12 possible changes, including four ways to raise taxes; four ways to lower benefits (by raising the retirement age, reducing the COLA, or means-testing benefits); and four ways to increase benefits. The most favored package of changes would: Gradually, over 10 years, eliminate the cap on earnings taxed for Social Security. The 5% of workers who earn more than the cap would then pay into Social Security all year, as other workers do. Gradually, over 20 years, raise the Social Security tax that workers and employers each pay from 6.2% of earnings to 7.2%. The change would be so gradual that someone making $50,000 a year would pay 50 cents a week more each year, and their employers would too. Increase the COLA to more accurately reflect the inflation experienced by seniors, who typically pay more out-of-pocket for medical care than other Americans. Raise Social Security s minimum benefit so that a worker who pays into Social Security for 30 years can retire at 62 or later with benefits above the federal poverty line ($10,788 in 2011). Lifetime low-wage workers are now at risk of falling into poverty in their old age, even after paying Social Security taxes throughout their work lives. Seven in ten Americans, across age and income groups, favored this package. Conclusion Over the next 75 years, Social Security s average cost is about 6% of GDP (as shown on page 3), while taxes Congress has thus far scheduled to pay for Social Security amount to about 5% of GDP, leaving a shortfall of 1% of GDP. The two gradual tax increases favored by 7 in 10 Americans would close the entire shortfall and pay for the two modest benefit increases also favored by 7 in 10 Americans. 7

Americans Make Hard Choices on Social Security:

Americans Make Hard Choices on Social Security: Report Highlights Elisa A. Walker, Virginia P. Reno, and Thomas N. Bethell October 2014 In brief: The National Academy of Social Insurance conducted a multigenerational

Americans Make Hard Choices on Social Security: Report Highlights Elisa A. Walker, Virginia P. Reno, and Thomas N. Bethell October 2014 In brief: The National Academy of Social Insurance conducted a multigenerational

Strengthening. Social Security: What Do Americans Want? Jasmine V. Tucker, Virginia P. Reno, and Thomas N. Bethell

Strengthening Social Security: What Do Americans Want? Jasmine V. Tucker, Virginia P. Reno, and Thomas N. Bethell Board of Directors Lisa Mensah Chair G. Lawrence Atkins President Jacob Hacker Vice President

Strengthening Social Security: What Do Americans Want? Jasmine V. Tucker, Virginia P. Reno, and Thomas N. Bethell Board of Directors Lisa Mensah Chair G. Lawrence Atkins President Jacob Hacker Vice President

59 million people receive Social Security each month, in one of three categories: Nearly 1 in 5 Americans gets Social Security benefits.

National Academy of Social Insurance www.nasi.org October 2015 59 million people receive Social Security each month, in one of three categories: Retirement insurance Survivor insurance Disability insurance

National Academy of Social Insurance www.nasi.org October 2015 59 million people receive Social Security each month, in one of three categories: Retirement insurance Survivor insurance Disability insurance

The primer is updated to reflect estimates from the 2016 Social Security Trustees Report.

The purpose of this primer is to provide basic information and charts about Social Security: its benefits, financing, affordability, and policy options to strengthen it. The primer is formatted as a slide

The purpose of this primer is to provide basic information and charts about Social Security: its benefits, financing, affordability, and policy options to strengthen it. The primer is formatted as a slide

More than 62 million people receive Social Security each month, in one of three categories: Nearly 1 in 5 Americans gets Social Security benefits.

National Academy of Social Insurance www.nasi.org August 2018 More than 62 million people receive Social Security each month, in one of three categories: Retirement insurance Survivors insurance Disability

National Academy of Social Insurance www.nasi.org August 2018 More than 62 million people receive Social Security each month, in one of three categories: Retirement insurance Survivors insurance Disability

When Should I Take Social Security?

When Should I Take Social Security? Presentations By: Virginia Reno National Academy of Social Insurance May 14, 2014 Joan Entmacher National Women s Law Center Leticia Miranda National Council of La Raza

When Should I Take Social Security? Presentations By: Virginia Reno National Academy of Social Insurance May 14, 2014 Joan Entmacher National Women s Law Center Leticia Miranda National Council of La Raza

Strengthening Social Security for the Long Run. By Janice M. Gregory, Thomas N. Bethell, Virginia P. Reno, and Benjamin W. Veghte

Social Security November 2010 No. 35 Brief Strengthening Social Security for the Long Run By Janice M. Gregory, Thomas N. Bethell, Virginia P. Reno, and Benjamin W. Veghte Summary In policy discussions

Social Security November 2010 No. 35 Brief Strengthening Social Security for the Long Run By Janice M. Gregory, Thomas N. Bethell, Virginia P. Reno, and Benjamin W. Veghte Summary In policy discussions

Social Security. Current Reform Proposals: How They Would Affect People With Disabilities. Consortium for Citizens with Disabilities June 1, 2011

Social Security Current Reform Proposals: How They Would Affect People With June 1, 2011 Social Security Background on the Social Security Programs 2 Social Security 54.2 million people receive Social

Social Security Current Reform Proposals: How They Would Affect People With June 1, 2011 Social Security Background on the Social Security Programs 2 Social Security 54.2 million people receive Social

S o c i a l S e c u r i t y

S o c i a l S e c u r i t y Brief June 2013 No. 41 Social Security Disability Insurance: Action Needed to Address Finances By Virginia P. Reno, Elisa A. Walker, and Thomas N. Bethell Summary Currently,

S o c i a l S e c u r i t y Brief June 2013 No. 41 Social Security Disability Insurance: Action Needed to Address Finances By Virginia P. Reno, Elisa A. Walker, and Thomas N. Bethell Summary Currently,

Fast Facts & Figures About Social Security, 2005

Fast Facts & Figures About Social Security, 2005 Social Security Administration Office of Policy Office of Research, Evaluation, and Statistics 500 E Street, SW, 8th Floor Washington, DC 20254 SSA Publication

Fast Facts & Figures About Social Security, 2005 Social Security Administration Office of Policy Office of Research, Evaluation, and Statistics 500 E Street, SW, 8th Floor Washington, DC 20254 SSA Publication

How Would Seniors Fare by Age, Gender, Race and Ethnicity, and Income Under the Bowles-Simpson Social Security Proposals by 2070?

S o c i a l September 2011 No. 38 S e c u r i t y Brief How Would Seniors Fare by Age, Gender, Race and Ethnicity, and Income Under the Bowles-Simpson Social Security Proposals by 2070? By Virginia P.

S o c i a l September 2011 No. 38 S e c u r i t y Brief How Would Seniors Fare by Age, Gender, Race and Ethnicity, and Income Under the Bowles-Simpson Social Security Proposals by 2070? By Virginia P.

Fixing Social Security Conducted by the Program for Public Consultation, School of Public Policy, University of Maryland.

Fixing Social Security Conducted by the Program for Public Consultation, School of Public Policy, University of Maryland Questionnaire National Sample, California, Florida, New York, Ohio, Texas Field

Fixing Social Security Conducted by the Program for Public Consultation, School of Public Policy, University of Maryland Questionnaire National Sample, California, Florida, New York, Ohio, Texas Field

Understanding Social Security Retirement Benefits

Understanding Social Security Retirement Brian Ellenbecker, CFP, CPWA, CIMA Vice President Senior Financial Planner Robert W. Baird & Co. February, 2016 Follow us on Twitter: @rwbaird Agenda What s new

Understanding Social Security Retirement Brian Ellenbecker, CFP, CPWA, CIMA Vice President Senior Financial Planner Robert W. Baird & Co. February, 2016 Follow us on Twitter: @rwbaird Agenda What s new

The Fair Tax Benefits Seniors

TP PT U.S. A FairTax Whitepaper The Fair Tax Benefits Seniors The FairTax benefits seniors. Let s count the ways: 1) The FairTax repeals the taxation of Social Security benefits and adjusts Social Security

TP PT U.S. A FairTax Whitepaper The Fair Tax Benefits Seniors The FairTax benefits seniors. Let s count the ways: 1) The FairTax repeals the taxation of Social Security benefits and adjusts Social Security

shortfalls in perpetuity. 3 The 2003 Trustees report, for example, pushes the insolvency date back by assuming that older

Dr. Dave. I ve read that the President s proposal to create personal savings accounts within the Social Security system will do nothing to reduce the system s projected revenue shortfall. Is that true?

Dr. Dave. I ve read that the President s proposal to create personal savings accounts within the Social Security system will do nothing to reduce the system s projected revenue shortfall. Is that true?

Social Security and Retirement Planning

Social Security and Welcome Each course in the series covers an investment topic or strategy that can provide you with: Timely Information Keys to Success Prospects & Prosperity Today s Presentation The

Social Security and Welcome Each course in the series covers an investment topic or strategy that can provide you with: Timely Information Keys to Success Prospects & Prosperity Today s Presentation The

Social Security fundamentals

Page 1 of 12 Guidelines for making well-informed decisions Table of contents 2 Key concept #1: Social Security will be around into the foreseeable future 3 Key concept #2: How benefits are calculated 4

Page 1 of 12 Guidelines for making well-informed decisions Table of contents 2 Key concept #1: Social Security will be around into the foreseeable future 3 Key concept #2: How benefits are calculated 4

Social Security and Your Retirement

Social Security and Your Retirement January 2013 ACI-1111-3702 American Century Investment Services, Inc. Distributor 2013 American Century Investments Proprietary Holdings, Inc. All rights reserved. Social

Social Security and Your Retirement January 2013 ACI-1111-3702 American Century Investment Services, Inc. Distributor 2013 American Century Investments Proprietary Holdings, Inc. All rights reserved. Social

SOCIAL SECURITY? WHAT CAN YOU EXPECT FROM. Retirement. Safety Net. Security. Future Shortfalls. Retirement. Income. The Story Behind America s

WHAT CAN YOU EXPECT FROM SOCIAL SECURITY? The Story Behind America s Retirement Safety Net How Social Security Works Today Future Shortfalls Are Easy to Foresee Time to Get Serious About Your Own Retirement

WHAT CAN YOU EXPECT FROM SOCIAL SECURITY? The Story Behind America s Retirement Safety Net How Social Security Works Today Future Shortfalls Are Easy to Foresee Time to Get Serious About Your Own Retirement

What to Expect A new President and His Congress

2017 - What to Expect A new President and His Congress The 1 st 100 days Executive Branch Regulatory Changes and Federal Agency Staffing - Execute as Promised. Then Conflict and Confusion as Legislative

2017 - What to Expect A new President and His Congress The 1 st 100 days Executive Branch Regulatory Changes and Federal Agency Staffing - Execute as Promised. Then Conflict and Confusion as Legislative

Lawrence H. Thompson DISTRIBUTING THE GAINS FROM ECONOMIC GROWTH. Brief Series No. 11 August 2000

URBAN INSTITUTE Brief Series No. 11 August 2000 Sharing the Pain of Social Security and Medicare Reform Lawrence H. Thompson AS THE BABY BOOMERS LEAVE THE WORKforce, additional stress on programs designed

URBAN INSTITUTE Brief Series No. 11 August 2000 Sharing the Pain of Social Security and Medicare Reform Lawrence H. Thompson AS THE BABY BOOMERS LEAVE THE WORKforce, additional stress on programs designed

Medicare at Risk. Alyene Senger John W. Fleming. March 2013 VISUALIZING THE NEED FOR REFORM 2010: $4,136 $128,000 $188,000 $60,000 $6,000

Medicare at Risk VISUALIZING THE NEED FOR REFORM Federal Deficit Medicare Shortfall $6,000 2010: $4,136 $188,000 $128,000 $60,000 Single Female March 2013 Alyene Senger John W. Fleming Medicare spending

Medicare at Risk VISUALIZING THE NEED FOR REFORM Federal Deficit Medicare Shortfall $6,000 2010: $4,136 $188,000 $128,000 $60,000 Single Female March 2013 Alyene Senger John W. Fleming Medicare spending

5/15/2018. Myra O Dell, CFP Financial Advisor. Philip Bachman Financial Advisor

Myra O Dell, CFP Financial Advisor Philip Bachman Financial Advisor Anti-poverty program providing retirement, disability, and survivors benefits Social insurance (not social welfare) Self-funding Posters

Myra O Dell, CFP Financial Advisor Philip Bachman Financial Advisor Anti-poverty program providing retirement, disability, and survivors benefits Social insurance (not social welfare) Self-funding Posters

Social Security. Yolanda York Public Affairs Specialist.

Social Security Yolanda York Public Affairs Specialist www.socialsecurity.gov The Real Beginning... Bismarck introduced first Social Security old-age benefits in Germany in 1889 2 2 3 Who Gets Benefits

Social Security Yolanda York Public Affairs Specialist www.socialsecurity.gov The Real Beginning... Bismarck introduced first Social Security old-age benefits in Germany in 1889 2 2 3 Who Gets Benefits

Social Security Reform Options

A Public Policy MONOGRAPH Social Security Reform Options March 2014 Social Security Committee A Public Policy Monograph Social Security Reform Options March 2014 Social Security Committee The is an 18,000-member

A Public Policy MONOGRAPH Social Security Reform Options March 2014 Social Security Committee A Public Policy Monograph Social Security Reform Options March 2014 Social Security Committee The is an 18,000-member

SOCIAL SECURITY INFORMATION Annual Delegates Meeting

SOCIAL SECURITY INFORMATION 2017 Annual Delegates Meeting IN THE BEGINNING The Social Security Act was signed into law on August 14, 1935. Taxes were collected for the first time in January 1937 and the

SOCIAL SECURITY INFORMATION 2017 Annual Delegates Meeting IN THE BEGINNING The Social Security Act was signed into law on August 14, 1935. Taxes were collected for the first time in January 1937 and the

Planning for the Future: What Women Need to Know About Social Security September 7, 2011

Planning for the Future: What Women Need to Know About Social Security September 7, 2011 Speakers for this Session Maria Freese Director of Government Relations and Policy, National Committee to Preserve

Planning for the Future: What Women Need to Know About Social Security September 7, 2011 Speakers for this Session Maria Freese Director of Government Relations and Policy, National Committee to Preserve

SOCIAL SECURITY. Office of the Chief Actuary. June 9, 2016

Office of the Chief Actuary June 9, 2016 Mr. Kent Conrad, Co-Chair Mr. James B. Lockhart, III, Co-Chair Commission on Retirement Security and Personal Savings Bipartisan Policy Center 1225 Eye Street NW,

Office of the Chief Actuary June 9, 2016 Mr. Kent Conrad, Co-Chair Mr. James B. Lockhart, III, Co-Chair Commission on Retirement Security and Personal Savings Bipartisan Policy Center 1225 Eye Street NW,

Congressional Research Service Report for Congress Social Security Primer, April 30, 2012

Congressional Research Service Report for Congress Social Security Primer, April 30, 2012 Click to open document in a browser 2012ARD 094-204 112th Congress Social Security Primer Dawn Nuschler Specialist

Congressional Research Service Report for Congress Social Security Primer, April 30, 2012 Click to open document in a browser 2012ARD 094-204 112th Congress Social Security Primer Dawn Nuschler Specialist

What You Need to Know About Social Security

What You Need to Know About Social Security Social Security is an important piece of many American s retirement income and it was only designed to replace a portion of your income and survivor needs. Your

What You Need to Know About Social Security Social Security is an important piece of many American s retirement income and it was only designed to replace a portion of your income and survivor needs. Your

Railroad Retirement Board: Retirement, Survivor, Disability, Unemployment, and Sickness Benefits

Railroad Retirement Board: Retirement, Survivor, Disability, Unemployment, and Sickness Benefits Alison M. Shelton Analyst in Income Security July 17, 2012 The House Ways and Means Committee is making

Railroad Retirement Board: Retirement, Survivor, Disability, Unemployment, and Sickness Benefits Alison M. Shelton Analyst in Income Security July 17, 2012 The House Ways and Means Committee is making

A Social Security Plan For All by Robert C. Pozen

A Social Security Plan For All by Robert C. Pozen I. Multiple Goals The goals for reform of Social Security (SS) are different for Republicans and Democrats, but they can be reconciled to a significant

A Social Security Plan For All by Robert C. Pozen I. Multiple Goals The goals for reform of Social Security (SS) are different for Republicans and Democrats, but they can be reconciled to a significant

The New Health Care Law and You

The New Health Care Law and You Congress enacted a new health care law that brings a number of benefits to all Americans, including people over 50. Some of these changes you will see right now. Others

The New Health Care Law and You Congress enacted a new health care law that brings a number of benefits to all Americans, including people over 50. Some of these changes you will see right now. Others

Savvy Social Security Planning for Boomers. By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC

Savvy Social Security Planning for Boomers By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Two ways Social Security planning can help your business Reach out to new clients

Savvy Social Security Planning for Boomers By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Two ways Social Security planning can help your business Reach out to new clients

The Trustees Report for the Old-Age, Survivors, and Disability

American Academy of Actuaries MARCH 2009 May 2009 Looming Financial Challenges Social Security will face financial challenges sooner than was expected. New actuarial projections show income from taxes

American Academy of Actuaries MARCH 2009 May 2009 Looming Financial Challenges Social Security will face financial challenges sooner than was expected. New actuarial projections show income from taxes

Medicare and Social Security: Weighing Solvency

Medicare and Social Security: Weighing Solvency Cori E. Uccello, MAAA, FSA, FCA, MPP Senior Health Fellow, Ron Gebhardtsbauer, MAAA, FSA, FCA Senior Pension Fellow, April 1, 2005 Noon 1:00 pm B-339 Rayburn

Medicare and Social Security: Weighing Solvency Cori E. Uccello, MAAA, FSA, FCA, MPP Senior Health Fellow, Ron Gebhardtsbauer, MAAA, FSA, FCA Senior Pension Fellow, April 1, 2005 Noon 1:00 pm B-339 Rayburn

Social Security Reform

Election 2004: A Guide to Analyzing the Issues The Questions Candidates Should Answer about... Social Security Reform Founded in 1965, the Academy is a non-partisan, non-profit professional association

Election 2004: A Guide to Analyzing the Issues The Questions Candidates Should Answer about... Social Security Reform Founded in 1965, the Academy is a non-partisan, non-profit professional association

Notes Unless otherwise indicated, the years referred to in this report are calendar years. Fiscal years run from October to September 3 and are design

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Social Security Policy Options, Percentage of Gross Domestic Product Actual Projected Outlays With Scheduled Benefits 6 Tax Revenues Outlays With

CONGRESS OF THE UNITED STATES CONGRESSIONAL BUDGET OFFICE Social Security Policy Options, Percentage of Gross Domestic Product Actual Projected Outlays With Scheduled Benefits 6 Tax Revenues Outlays With

A Guide to Planning a Financially Secure Retirement

A Guide to Planning a Financially Secure Retirement The information presented here is for general reference only, and may or may not be appropriate for your specific situation. A conversation with a financial

A Guide to Planning a Financially Secure Retirement The information presented here is for general reference only, and may or may not be appropriate for your specific situation. A conversation with a financial

What the 2018 Trustees Report Shows About Social Security

June 29, 2018 What the 2018 Trustees Report Shows About Social Security By Kathleen Romig Social Security can pay full benefits for 16 more years, the trustees latest annual report shows, but will then

June 29, 2018 What the 2018 Trustees Report Shows About Social Security By Kathleen Romig Social Security can pay full benefits for 16 more years, the trustees latest annual report shows, but will then

Nebraska Wealth Management Conference Omaha October 18, Social Security: Long-term Prognosis/Retirement Planning

Nebraska Wealth Management Conference Omaha October 18, 2016 Social Security: Long-term Prognosis/Retirement Planning Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 Social Security:

Nebraska Wealth Management Conference Omaha October 18, 2016 Social Security: Long-term Prognosis/Retirement Planning Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 Social Security:

Defining the problem: the difference between current deficit and long-term deficits

KEY POINTS FOR FEDERAL DEFICIT DISCUSSIONS Overview: Unless our budget policies are changed, the imbalance between spending and revenues will eventually become unsustainable rapidly rising debt will threaten

KEY POINTS FOR FEDERAL DEFICIT DISCUSSIONS Overview: Unless our budget policies are changed, the imbalance between spending and revenues will eventually become unsustainable rapidly rising debt will threaten

PLANNING FOR RETIREMENT:

December 13, 2016 PLANNING FOR RETIREMENT: WHAT WOMEN NEED TO KNOW LATER IN THEIR CAREERS PRESENTERS: BEN VEGHTE NATIONAL ACADEMY OF SOCIAL INSURANCE AMY MATSUI NATIONAL WOMEN S LAW CENTER JASMINE TUCKER

December 13, 2016 PLANNING FOR RETIREMENT: WHAT WOMEN NEED TO KNOW LATER IN THEIR CAREERS PRESENTERS: BEN VEGHTE NATIONAL ACADEMY OF SOCIAL INSURANCE AMY MATSUI NATIONAL WOMEN S LAW CENTER JASMINE TUCKER

BACKGROUNDER. Social Security s main program, also known as Old-Age and Survivors. Social Security: $39 Billion Deficit in 2014, Insolvent by 2035

BACKGROUNDER No. 3043 Social Security: $39 Billion Deficit in 2014, Insolvent by 2035 Romina Boccia Abstract Social Security ran a $39 billion deficit in 2014, closing out five years of consecutive cash-flow

BACKGROUNDER No. 3043 Social Security: $39 Billion Deficit in 2014, Insolvent by 2035 Romina Boccia Abstract Social Security ran a $39 billion deficit in 2014, closing out five years of consecutive cash-flow

Medicare Made Easy Know the facts

Who Why Medicare Made Easy Know the facts How Where When What 248.648.8598 Securities offered through Centaurus Financial Inc., a registered broker/dealer. Member FINRA and SIPC Centaurus Financial, Inc.,

Who Why Medicare Made Easy Know the facts How Where When What 248.648.8598 Securities offered through Centaurus Financial Inc., a registered broker/dealer. Member FINRA and SIPC Centaurus Financial, Inc.,

Prospects for the Social Safety Net for Future Low Income Seniors

Prospects for the Social Safety Net for Future Low Income Seniors Marilyn Moon American Institutes for Research Presented at Forgotten Americans: The Future of Support for Older Low-Income Adults National

Prospects for the Social Safety Net for Future Low Income Seniors Marilyn Moon American Institutes for Research Presented at Forgotten Americans: The Future of Support for Older Low-Income Adults National

The American Academy of Actuaries is a national organization formed in 1965 to bring

American Academy of Actuaries The American Academy of Actuaries is a national organization formed in 1965 to bring together, under a single entity, actuaries of all specialties within the United States.

American Academy of Actuaries The American Academy of Actuaries is a national organization formed in 1965 to bring together, under a single entity, actuaries of all specialties within the United States.

Social Security: America s Most Successful Social Program

Social Security: America s Most Successful Social Program 56% of the aged receiving Social Security are women More than 204 million workers and their families are protected by Social Security Almost every

Social Security: America s Most Successful Social Program 56% of the aged receiving Social Security are women More than 204 million workers and their families are protected by Social Security Almost every

Medicare in Ryan s 2014 Budget By Paul N. Van de Water

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org March 15, 2013 Medicare in Ryan s 2014 Budget By Paul N. Van de Water The Medicare proposals

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org March 15, 2013 Medicare in Ryan s 2014 Budget By Paul N. Van de Water The Medicare proposals

Woska Associates Employment Law Group

Woska Associates Employment Law Group August 2003 Rev. 9/04; 2/05; 6/05; 9/05; 1/06; 4/06; 11/06; 8/07; 11/07; 10/08; 12/09; 11/10; 11/11; 12/12; 12/13; 11/14; 1/17; 11/17; 12/18 Employment Law Forum Social

Woska Associates Employment Law Group August 2003 Rev. 9/04; 2/05; 6/05; 9/05; 1/06; 4/06; 11/06; 8/07; 11/07; 10/08; 12/09; 11/10; 11/11; 12/12; 12/13; 11/14; 1/17; 11/17; 12/18 Employment Law Forum Social

What the 2013 Trustees Report Shows About Social Security

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org June 18, 2013 What the 2013 Trustees Report Shows About Social Security By Kathy A.

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org June 18, 2013 What the 2013 Trustees Report Shows About Social Security By Kathy A.

COMMUNICATION THE BOARD OF TRUSTEES, FEDERAL OLD-AGE AND SURVIVORS INSURANCE AND DISABILITY INSURANCE TRUST FUNDS

109th Congress, 1st Session House Document 109-18 THE 2005 ANNUAL REPORT OF THE BOARD OF TRUSTEES OF THE FEDERAL OLD-AGE AND SURVIVORS INSURANCE AND DISABILITY INSURANCE TRUST FUNDS COMMUNICATION FROM

109th Congress, 1st Session House Document 109-18 THE 2005 ANNUAL REPORT OF THE BOARD OF TRUSTEES OF THE FEDERAL OLD-AGE AND SURVIVORS INSURANCE AND DISABILITY INSURANCE TRUST FUNDS COMMUNICATION FROM

How to Maximize Social Security Benefits Now

MERS of Michigan 2018 Retirement Conference October 5, 2018 How to Maximize Social Security Benefits Now Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 For most retirees, Social Security

MERS of Michigan 2018 Retirement Conference October 5, 2018 How to Maximize Social Security Benefits Now Mary Beth Franklin, CFP Contributing Editor Investment News MBF01 For most retirees, Social Security

Social Security: With You Through Life s Journey

Social Security: With You Through Life s Journey Produced at U.S. taxpayer expense We re With You From Day One We re With You When You Start Work We re There For Your Wedding We re With You If The Unexpected

Social Security: With You Through Life s Journey Produced at U.S. taxpayer expense We re With You From Day One We re With You When You Start Work We re There For Your Wedding We re With You If The Unexpected

Social Security and Medicare: A Survey of Benefits

Social Security and Medicare: A Survey of Benefits #5485L COURSE MATERIAL TABLE OF CONTENTS Chapter 1: Introduction and Overview 1 I. Social Security: The Numbers Game 1 II. Social Security: A Snapshot

Social Security and Medicare: A Survey of Benefits #5485L COURSE MATERIAL TABLE OF CONTENTS Chapter 1: Introduction and Overview 1 I. Social Security: The Numbers Game 1 II. Social Security: A Snapshot

SOCIAL SECURITY YOU R OV E RV I EW OF ADR

YOU R 2 0 1 8 OV E RV I EW OF This booklet is being provided as a supplement to the Social Security and insurance sales presentation titled Strategies to Potentially Increase Your Social Security Benefits.

YOU R 2 0 1 8 OV E RV I EW OF This booklet is being provided as a supplement to the Social Security and insurance sales presentation titled Strategies to Potentially Increase Your Social Security Benefits.

Health Care and Long-Term Care Study, a consumer study of U.S. adults ages 50 and up, Nationwide/Harris Poll Survey (November 2016).

.") 1 Health Care and Long-Term Care Study, a consumer study of U.S. adults ages 50 and up, Nationwide/Harris Poll Survey (November 2016). 1 Important things to keep in mind Not a deposit Not FDIC or NCUSIF

1 Health Care and Long-Term Care Study, a consumer study of U.S. adults ages 50 and up, Nationwide/Harris Poll Survey (November 2016). 1 Important things to keep in mind Not a deposit Not FDIC or NCUSIF

Note: The material in this publication is based on the law in effect at the time it went to publication.

Note: The material in this publication is based on the law in effect at the time it went to publication. Under the Balanced Budget Act of 1997, Public Law 105-33, for fiscal year 1998, employee retirement

Note: The material in this publication is based on the law in effect at the time it went to publication. Under the Balanced Budget Act of 1997, Public Law 105-33, for fiscal year 1998, employee retirement

WHAT YOU NEED TO KNOW ABOUT PREMIUM SUPPORT By Paul N. Van de Water

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org March 19, 2012 WHAT YOU NEED TO KNOW ABOUT PREMIUM SUPPORT By Paul N. Van de Water The

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org March 19, 2012 WHAT YOU NEED TO KNOW ABOUT PREMIUM SUPPORT By Paul N. Van de Water The

NASI Event, Chicago 5 September 2018 Henry J. Aaron

NASI Event, Chicago 5 September 2018 Henry J. Aaron What is the most popular thing the U.S. government does? The easy answer is that it runs the Social Security system. Social Security is the principal

NASI Event, Chicago 5 September 2018 Henry J. Aaron What is the most popular thing the U.S. government does? The easy answer is that it runs the Social Security system. Social Security is the principal

Social Security The Choice of a Lifetime. Timothy O Mara, Vice President, Nationwide Retirement Institute

Social Security The Choice of a Lifetime Timothy O Mara, Vice President, Nationwide Retirement Institute FOR BROKER/DEALER USE ONLY NOT FOR USE WITH THE GENERAL PUBLIC Important things to keep in mind

Social Security The Choice of a Lifetime Timothy O Mara, Vice President, Nationwide Retirement Institute FOR BROKER/DEALER USE ONLY NOT FOR USE WITH THE GENERAL PUBLIC Important things to keep in mind

Account-based pensions: making your super go further in retirement

Booklet 3 Account-based pensions: making your super go further in retirement MAStech Smart technical solutions made simple Contents Introduction 01 Introduction 03 What are account-based pensions? 05 Investing

Booklet 3 Account-based pensions: making your super go further in retirement MAStech Smart technical solutions made simple Contents Introduction 01 Introduction 03 What are account-based pensions? 05 Investing

Important things to keep in mind

Important things to keep in mind Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution Not insured by any federal government agency May lose value The content of this presentation

Important things to keep in mind Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution Not insured by any federal government agency May lose value The content of this presentation

2011 Guide to Social Security

2011 Guide to Social Security 39th Edition A simple explanation with easy-reference benefit tables. Contents Page 1 Introduction... 3 Are You Missing Out?.... 3 Major Changes in 2011... 4 2Who Is Covered

2011 Guide to Social Security 39th Edition A simple explanation with easy-reference benefit tables. Contents Page 1 Introduction... 3 Are You Missing Out?.... 3 Major Changes in 2011... 4 2Who Is Covered

Economic Crisis Fuels Support for Social Security. Americans Views on Social Security

Economic Crisis Fuels Support for Social Security Americans Views on Social Security August 2009 Board of Directors Kenneth S. Apfel, Chair Janice Gregory, President Jacob Hacker, Vice President Jennie

Economic Crisis Fuels Support for Social Security Americans Views on Social Security August 2009 Board of Directors Kenneth S. Apfel, Chair Janice Gregory, President Jacob Hacker, Vice President Jennie

1102 Longworth House Office Building 1106 Longworth House Office Building Washington, DC Washington, DC 20515

February 23, 2017 The Honorable Kevin Brady The Honorable Richard Neal Chairman Ranking Member Committee on Ways and Means Committee on Ways and Means U.S. House of Representatives U.S. House of Representatives

February 23, 2017 The Honorable Kevin Brady The Honorable Richard Neal Chairman Ranking Member Committee on Ways and Means Committee on Ways and Means U.S. House of Representatives U.S. House of Representatives

Status of the Social Security and Medicare Programs

Social Security Online Actuarial Publications Status of the Social Security and Medicare Programs A SUMMARY OF THE 2011 ANNUAL REPORTS Social Security and Medicare Boards of Trustees A MESSAGE TO THE PUBLIC:

Social Security Online Actuarial Publications Status of the Social Security and Medicare Programs A SUMMARY OF THE 2011 ANNUAL REPORTS Social Security and Medicare Boards of Trustees A MESSAGE TO THE PUBLIC:

Social Security: Allianz Life Insurance Company of North America Allianz Life Insurance Company of New York. Change Creates Opportunities

Allianz Life Insurance Company of North America Allianz Life Insurance Company of New York Social Security: Change Creates Opportunities Presented by Randy Kitzmiller RVP, Annuities Ash Brokerage ENT-843-N

Allianz Life Insurance Company of North America Allianz Life Insurance Company of New York Social Security: Change Creates Opportunities Presented by Randy Kitzmiller RVP, Annuities Ash Brokerage ENT-843-N

Social Security and Medicare Lifetime Benefits and Taxes

E X E C U T I V E O F F I C E R E S E A R C H Social Security and Lifetime Benefits and Taxes 2018 Update C. Eugene Steuerle and Caleb Quakenbush October 2018 Since 2003, we and our colleagues have released

E X E C U T I V E O F F I C E R E S E A R C H Social Security and Lifetime Benefits and Taxes 2018 Update C. Eugene Steuerle and Caleb Quakenbush October 2018 Since 2003, we and our colleagues have released

Social Security and Medicare Changes for 2019: What Clients Need to Know

Social Security and Medicare Changes for 2019: What Clients Need to Know By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 The Opportunities for Education and Advice 2 Education

Social Security and Medicare Changes for 2019: What Clients Need to Know By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 The Opportunities for Education and Advice 2 Education

Social Security Information NYSTRS Delegate Meeting November 4, 2018

Social Security Information 2018 NYSTRS Delegate Meeting November 4, 2018 A Brief History of Social Security Funding Benefit Calculation Retirement Age Reduced Benefits Spousal Benefits Survivor Benefits

Social Security Information 2018 NYSTRS Delegate Meeting November 4, 2018 A Brief History of Social Security Funding Benefit Calculation Retirement Age Reduced Benefits Spousal Benefits Survivor Benefits

Social Security Simplified

Social Security Simplified A NARFE Federal Benefits Institute Webinar Presented by Tammy Flanagan 1 Sponsored by Audience Poll What do you think is the most complicated part of Social Security? A. Understanding

Social Security Simplified A NARFE Federal Benefits Institute Webinar Presented by Tammy Flanagan 1 Sponsored by Audience Poll What do you think is the most complicated part of Social Security? A. Understanding

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2017 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2017 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

GUIDE YOUR CLIENTS TO PLAN FOR RETIREMENT HEALTH CARE COSTS

GUIDE YOUR CLIENTS TO PLAN FOR RETIREMENT HEALTH CARE COSTS How the Health Care Dollar Is Spent 4% Dental Services 5% Nursing Home 10% Prescription Drugs 32% Hospital Care 29% Other 20% Doctor Visits and

GUIDE YOUR CLIENTS TO PLAN FOR RETIREMENT HEALTH CARE COSTS How the Health Care Dollar Is Spent 4% Dental Services 5% Nursing Home 10% Prescription Drugs 32% Hospital Care 29% Other 20% Doctor Visits and

African Americans. Have Their Say about Medicare and Social Security

African Americans Have Their Say about Medicare and Social Security African Americans Have Their Say In March, AARP launched You ve Earned a Say a national conversation about how to protect Medicare and

African Americans Have Their Say about Medicare and Social Security African Americans Have Their Say In March, AARP launched You ve Earned a Say a national conversation about how to protect Medicare and

Social Security: With You Through Life s Journey. Produced at U.S. taxpayer expense

Social Security: With You Through Life s Journey Produced at U.S. taxpayer expense We re With You Through Life s Journey We re With You From Day One Most Popular Baby Names A fun by-product of assigning

Social Security: With You Through Life s Journey Produced at U.S. taxpayer expense We re With You Through Life s Journey We re With You From Day One Most Popular Baby Names A fun by-product of assigning

Savvy Social Security Planning:

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2015 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2015 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

What is the status of Social Security? When should you draw benefits? How a Job Impacts Benefits... 8

TABLE OF CONTENTS Executive Summary... 2 What is the status of Social Security?... 3 When should you draw benefits?... 4 How do spousal benefits work? Plan for Surviving Spouse... 5 File and Suspend...

TABLE OF CONTENTS Executive Summary... 2 What is the status of Social Security?... 3 When should you draw benefits?... 4 How do spousal benefits work? Plan for Surviving Spouse... 5 File and Suspend...

Thinking of Retiring?

Understanding Social Security 2017 Presented by: Charo Boyd Public Affairs Specialist Social Security Making the Right Decision Thinking of Retiring? Deciding what is the right age to retire Early vs.

Understanding Social Security 2017 Presented by: Charo Boyd Public Affairs Specialist Social Security Making the Right Decision Thinking of Retiring? Deciding what is the right age to retire Early vs.

Social Security : A Primer

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents September 2001 Social Security : A Primer U.S. Congressional Budget Office, CBO Follow this and additional

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents September 2001 Social Security : A Primer U.S. Congressional Budget Office, CBO Follow this and additional

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS Take the first step toward understanding when and how to apply. KEY TAKEAWAYS Deciding when and how to start drawing Social Security retirement benefits

MAXIMIZING YOUR SOCIAL SECURITY RETIREMENT BENEFITS Take the first step toward understanding when and how to apply. KEY TAKEAWAYS Deciding when and how to start drawing Social Security retirement benefits

HEALTH CARE COSTS ARE THE PRIMARY DRIVER OF THE DEBT

% of GDP Domenici-Rivlin Protect Medicare Act (Released November 1, 2011) The principal driver of future federal deficits is the rapidly mounting cost of Medicare. The huge growth in the number of eligible

% of GDP Domenici-Rivlin Protect Medicare Act (Released November 1, 2011) The principal driver of future federal deficits is the rapidly mounting cost of Medicare. The huge growth in the number of eligible

Understanding Social Security and Medicare

Understanding Social Security and Medicare How these programs fit into your retirement strategies Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America ENT-1520-N Social

Understanding Social Security and Medicare How these programs fit into your retirement strategies Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America ENT-1520-N Social

Savvy Social Security Planning:

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2017 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Savvy Social Security Planning: What Baby Boomers Need to Know to Maximize Retirement Income Copyright 2017 Horsesmouth, LLC. All Rights Reserved. 1 Baby boomers want to know: Will Social Security be there

Medicaid 101. Medicaid 101. Medicare or Medicaid what s the difference

Medicaid 101 Medicaid 101 Medicaid is available only to certain low-income individuals and families who fit into an eligibility group that is recognized by federal and state law. Medicaid does not pay

Medicaid 101 Medicaid 101 Medicaid is available only to certain low-income individuals and families who fit into an eligibility group that is recognized by federal and state law. Medicaid does not pay

I S S U E B R I E F PUBLIC POLICY INSTITUTE PPI PRESIDENT BUSH S TAX PLAN: IMPACTS ON AGE AND INCOME GROUPS

PPI PUBLIC POLICY INSTITUTE PRESIDENT BUSH S TAX PLAN: IMPACTS ON AGE AND INCOME GROUPS I S S U E B R I E F Introduction President George W. Bush fulfilled a 2000 campaign promise by signing the $1.35

PPI PUBLIC POLICY INSTITUTE PRESIDENT BUSH S TAX PLAN: IMPACTS ON AGE AND INCOME GROUPS I S S U E B R I E F Introduction President George W. Bush fulfilled a 2000 campaign promise by signing the $1.35

New Report Shows Modest Improvement. Social Security s Financial Soundness Should Be Addressed Now

American Academy of Actuaries Issue Brief JUNE 2016 An Actuarial Perspective on the 2016 Social Security Trustees Report 1850 M Street NW, Suite 300 Washington, DC 20036 202-223-8196 www.actuary.org Craig

American Academy of Actuaries Issue Brief JUNE 2016 An Actuarial Perspective on the 2016 Social Security Trustees Report 1850 M Street NW, Suite 300 Washington, DC 20036 202-223-8196 www.actuary.org Craig

How Social Security Benefits Are Computed: In Brief

How Social Security Benefits Are Computed: In Brief Noah P. Meyerson Analyst in Income Security May 12, 2014 Congressional Research Service 7-5700 www.crs.gov R43542 Summary With $812 billion in benefit

How Social Security Benefits Are Computed: In Brief Noah P. Meyerson Analyst in Income Security May 12, 2014 Congressional Research Service 7-5700 www.crs.gov R43542 Summary With $812 billion in benefit

Social Security Planning Strategies

Private Wealth Management Products & Services Social Security Planning Strategies Basic Social Security Planning Strategies One of the biggest decisions a retiree and their family will face is when to

Private Wealth Management Products & Services Social Security Planning Strategies Basic Social Security Planning Strategies One of the biggest decisions a retiree and their family will face is when to

Aging in America: Income and Assets of People on Medicare

Aging in America: Income and Assets of People on Medicare November 6, 2015 National Health Policy Forum Gretchen Jacobson, Ph.D. Associate Director, Program on Medicare Policy Kaiser Family Foundation

Aging in America: Income and Assets of People on Medicare November 6, 2015 National Health Policy Forum Gretchen Jacobson, Ph.D. Associate Director, Program on Medicare Policy Kaiser Family Foundation

CRS Report for Congress Received through the CRS Web

Order Code RL33387 CRS Report for Congress Received through the CRS Web Topics in Aging: Income of Americans Age 65 and Older, 1969 to 2004 April 21, 2006 Patrick Purcell Specialist in Social Legislation

Order Code RL33387 CRS Report for Congress Received through the CRS Web Topics in Aging: Income of Americans Age 65 and Older, 1969 to 2004 April 21, 2006 Patrick Purcell Specialist in Social Legislation

Social Security. Analysis & Strategy. Mulberry Lane Advisors Lawrence Sorace, CFP, NSSA 750 Route 34 Suite #7 Matawan, NJ

Powered by Social Security Solutions Social Security Analysis & Strategy Mulberry Lane Advisors Lawrence Sorace, CFP, NSSA 750 Route 34 Suite #7 Matawan, NJ 07747 215-303-2813 Prepared for Mark Married

Powered by Social Security Solutions Social Security Analysis & Strategy Mulberry Lane Advisors Lawrence Sorace, CFP, NSSA 750 Route 34 Suite #7 Matawan, NJ 07747 215-303-2813 Prepared for Mark Married

The Future of Social Security

The Future of Social Security Andrew B. Abel October 4, 2000 OASDI Operations Estimates for 2000 (billions of dollars, except Trust fund ratio) Trust fund at beginning of year 896.1 Income excluding interest

The Future of Social Security Andrew B. Abel October 4, 2000 OASDI Operations Estimates for 2000 (billions of dollars, except Trust fund ratio) Trust fund at beginning of year 896.1 Income excluding interest

Key Provisions of 2017 Tax Reform

Key Provisions of 2017 Tax Reform The final provisions of the 2017 tax reform bill are finally here. The goal of this publication is to briefly highlight some of the key changes and planning issues of

Key Provisions of 2017 Tax Reform The final provisions of the 2017 tax reform bill are finally here. The goal of this publication is to briefly highlight some of the key changes and planning issues of

Social Security and Medicare Lifetime Benefits and Taxes

EXECUTIVE OFFICE RESEARCH Social Security and Lifetime Benefits and Taxes 2017 Update C. Eugene Steuerle and Caleb Quakenbush June 2018 Since 2003, we and our colleagues have been releasing periodic data

EXECUTIVE OFFICE RESEARCH Social Security and Lifetime Benefits and Taxes 2017 Update C. Eugene Steuerle and Caleb Quakenbush June 2018 Since 2003, we and our colleagues have been releasing periodic data

Medicare and Social Security Understanding the A-B-Cs and 1-2-3s for Your Clients INSIGHTS PERSPECTIVES ON WEALTH MANAGEMENT

INSIGHTS PERSPECTIVES ON WEALTH MANAGEMENT Medicare and Social Security Understanding the A-B-Cs and 1-2-3s for Your Clients INSIGHTS PERSPECTIVES ON WEALTH MANAGEMENT MEDICARE AND SOCIAL SECURITY 1 INSIGHTS

INSIGHTS PERSPECTIVES ON WEALTH MANAGEMENT Medicare and Social Security Understanding the A-B-Cs and 1-2-3s for Your Clients INSIGHTS PERSPECTIVES ON WEALTH MANAGEMENT MEDICARE AND SOCIAL SECURITY 1 INSIGHTS

Retirement and Social Security

Life Guide The Social Security Administration estimates that 96% of American workers are covered by Social Security. For most of them, their monthly Social Security check will form an important part of

Life Guide The Social Security Administration estimates that 96% of American workers are covered by Social Security. For most of them, their monthly Social Security check will form an important part of

ANTICIPATE Social Security and Your Retirement SAVING : INVESTING : PLANNING

ANTICIPATE Social Security and Your Retirement SAVING : INVESTING : PLANNING About this seminar Presentation > Provides comprehensive education > Includes action steps > Provides opportunity to develop

ANTICIPATE Social Security and Your Retirement SAVING : INVESTING : PLANNING About this seminar Presentation > Provides comprehensive education > Includes action steps > Provides opportunity to develop

White Paper Estimating Your Social Security Benefits

White Paper Estimating Your Social Security Benefits www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

White Paper Estimating Your Social Security Benefits www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities Equity Group Member FINRA, SIPC,

Aging Seminar Series:

Aging Seminar Series: Income and Wealth of Older Americans Domestic Social Policy Division Congressional Research Service November 19, 2008 Introduction Aging Seminar Series Focus on important issues regarding

Aging Seminar Series: Income and Wealth of Older Americans Domestic Social Policy Division Congressional Research Service November 19, 2008 Introduction Aging Seminar Series Focus on important issues regarding