Medicare Made Easy Know the facts

|

|

|

- Suzan Dorsey

- 5 years ago

- Views:

Transcription

1 Who Why Medicare Made Easy Know the facts How Where When What Securities offered through Centaurus Financial Inc., a registered broker/dealer. Member FINRA and SIPC Centaurus Financial, Inc., and Herbert Financial Group are not affiliated companies

2 Welcome & Introductions We Provide Full Service Holistic Planning NOT just Investment Management Budgeting Organizing and Goal Setting Comprehensive Financial Plan Retirement Income Analysis Tax Advantaged Investing Life Insurance Analysis Long Term Care Insurance Coordination with Tax, Legal & now Health Professionals LIFE HEALTH WEALTH TAXES ESTATE

3 Health Care Cost in Retirement November 2015 Harris Poll of U.S. adults age 50 and older found that: 69% of affluent pre-retirees listed soaring retirement health care costs as their #1 fear 59% worry they will become a burden on their families as they get older 38% expect healthcare costs to be their biggest expense in retirement 55% fear healthcare costs will use up the money they planned to leave to their children 78% don t have a plan to pay for medical and long term care expenses 69% are concerned they will run out of money in retirement 65% wish they understood Medicare better Changing Environment and our Clients Need Help

4 Introducing Associated Health Options, LLC Evelyn Herbert Evy is a licensed independent Health Insurance Agent and the sole proprietor of Associated Health Options, LLC She specializes in senior health care, assisting her clients with their Medicare options There are no fees or additional costs to work with Evy. The appointment is completely no-cost and no-obligation. Whether you choose to work with her, call a number or go online and do the research and enrollment yourself, the cost is always the same. Evy is licensed to offer: Medicare Supplement Insurance Medicare Advantage Plans Part D Prescription Drug Plans

5 Big Problem: Gaps In Advice 70% 60% 50% 40% 30% 20% Expects Advice Offered Advice 10% 0% Health Care Advice Social Security Benefits 2015 The New Foundation of Retirement Planning : Social Security and Medicare by Senior Market Sales

Hospital Insurance Medicare (Part B) Medical Insurance Medicare (Part")

6 What Makes up Medicare? Medicare (Part A) Hospital Insurance Medicare (Part B) Medical Insurance Medicare (Part C) Medicare Advantage Medicare (Part D) Prescription Drug Coverage

7 Original Medicare (Part A) Hospital

8 Original Medicare (Part A) Hospital You receive up to 60 days in the hospital for each admission as an in-patient, each year, for each separate medical issue. There is a deductible for each stay ($1316 in 2017), for each separate issue. If returning for the same issue then there is no additional deductible. You also receive 20 days in-home visits or rehabilitation at no charge. Hospice is also covered under (Part A) at no charge to you during that period, after a three day minimum, medically necessary, inpatient hospital stay. Medicare (Part A) is a zero premium plan if you, or your spouse paid into Social Security for a minimum of 40 quarters (10 years). Everyone should begin (Part A) when they are first eligible, even if you are still employed and have other coverage. (Part A) is a zero premium plan and there is no penalty for having additional coverage.

Skilled Nursing Facility")

9 Hospital Stay Medicare pays all covered costs for the first 60 days, except the first $1,316 (in 2017) In 2017, you pay $1,316 deductible per benefit period $0 for the first 60 days of each benefit period $329 per day for days of each benefit period $658 per ** lifetime reserve after day 90 of each benefit period **(Up to a maximum of 60 days over your lifetime) Skilled Nursing Facility Stay In 2017, you pay $0 for the first 20 days of each benefit period $ per day for days of each benefit period (Out of pocket for each day after 100 th day)

10 Medicare (Part B): Medical Insurance Covers 80% of your medical bills Covers medical needs i.e.: x-rays, lab, doctors, wheel chairs, etc. Average cost in 2017 is $134 +/- a month depending on your income level You can begin Part B when you turn 65, or when you retire if working past 65 Penalty can be imposed for failure to enroll

11

12 What s the Part B late enrollment penalty? If you don t sign up for Part B when you re first eligible, you may have to pay a late enrollment penalty for as long as you have Part B. Your monthly premium for Part B may go up 10% for each full 12-month period that you could ve had Part B, but didn t sign up for it. If you re allowed to sign up for Part B during a Special Enrollment Period, you usually don t pay a late enrollment penalty.

13 Original Medicare Can Leave You With: NO Maximum out of Your Pocket NO Prescription Drug Coverage NO Foreign Travel NO Dental, Vision, Hearing, Fitness Ways to Protect Yourself Where Original Medicare Doesn t Replace with a Medicare Advantage Plan, (Part C) Add a Medicare Supplement and Stand Alone Prescription Drug Plan

14 Medicare (Part C) Medicare Advantage Alternative to Original Medicare You still get complete Part A and Part B coverage through the plan. Note: You must continue to pay for your Part B premium. You still have Medicare rights and protections Medicare Advantage Plans have a yearly limit on your out-of-pocket costs for medical services. Once you reach this limit, you ll pay nothing for covered services. This limit may be different between Medicare Advantage Plans and can change each year.

15 Medicare - (Part C) Continued.. Types of Advantage Plans HMO: You have a network of doctors and ancillary medical professionals who take care of your medical needs You must get referral from your Primary Care Physician before you see a specialist HMO-POS: You have a network of medical professionals, but you may go out of network and you do not need a referral PPO: You have a Primary Provider. You do not have a network and you do not need a referral to see a specialist PFFS: You may see any doctor or medical professional as long as he/she accepts the terms and conditions of your insurance

16 Advantages You may receive additional, value-added benefits (i.e., dental, hearing, fitness, World Travel, etc.) You could save money if you stay reasonably healthy You can check with the plan before you get a service to find out if it's covered and what your costs may be You can join a Medicare Advantage Plan even if you have a pre- existing condition, except for End-Stage Renal Disease (ESRD) Disadvantages You may be limited to in network medical professionals If the plan decides to stop participating in Medicare, you'll have to join another Medicare Health Plan or return to Original Medicare You may pay higher amounts if you have medical issues If you receive care outside the network, services may not be covered You can only join a plan at certain times during the year. In most cases, you're enrolled in a plan for a year

17 Medicare Supplements or Medigap Plans

18 Medicare Supplements or Medigap Plans Medicare Supplement Plans supplement Original Medicare You are still enrolled in Original Medicare Part A & B Covers the 20% medical expense that Original Medicare doesn t Covers world travel for emergencies You must also have a Medicare Part D plan to provide appropriate prescription drug coverage (not provided by Medicare Supplements) Does not require open enrollment window to purchase Covers certain cost-sharing expenses required by Medicare, such as co-insurance and deductibles There are NO networks in a Med. Sup. Plan. You can see any doctor anywhere as long as he/she accepts Medicare.

19 Medicare Supplements or Medigap Plans The best time to buy a Medigap policy is during your Medigap Open Enrollment Period. This period lasts for 6 months and begins on the first day of the month in which you re 65 or older and enrolled in Medicare Part B. During this period, an insurance company can t use medical underwriting. This means the insurance company can t do any of these because of your health problems: Refuse to sell you any Medigap policy it offers Charge you more for Medigap policy than they charge someone with no health problems Make you wait for coverage to start

20 Medicare Supplements or Medigap Plans There are 10 Medicare Supplement plans (designated by letter) available in most states. Coverage is standardized across each plan letter, meaning you ll get the exact same benefits for Medicare Supplement Coverage within same letter. Even if benefits are the same across plans of the same letter category, premiums may vary by insurance company/location.

21 Medicare Supplemental Insurance AKA Medigap Benefits A B C D F G K L M N Part A coinsurance and hospital costs up to an additional 365 days after Medicare benefits are used up Part B coinsurance or copayment 50% 75% *** Blood (First 3 pints) 50% 75% Part A hospice care coinsurance or copayment 50% 75% Skilled nursing facility care coinsurance No No 50% 75% Part A deductible No 50% 75% 50% Part B deductible No No No No No No No No Part B excess charge No No No No No No No No Foreign travel exchange (up to plan limits) No No 80% 80% 80% 80% No No 80% 80% Out-of-pocket limit** N/A N/A N/A N/A N/A N/A $4960 $2480 N/A N/A

22 Medicare (Part D) Prescription Drug Coverage All prescription plans must have a minimum of 2 drugs in each area of need. Prescription drugs not on a plan s formulary may be approved by the plan with a request for exception by your physician. All plans follow Federal guidelines. All plans must provide a therapeutic equivalent to all medications in the standard Medicare formulary.

23 Medicare (Part D) Gap and Penalties: The Part D GAP in coverage is when the cost of your prescription for that year (both the cost you paid and the cost the health plan paid, combined) exceeds a certain amount $3,700 in You may fall into the gap and pay much higher drug costs until you reach $4,950 in (This only applies to small percentages of people). There are ways to avoid this gap, including buying inexpensive prescriptions without using your insurance card, or supplementing an expensive drug for another identical less expensive generic drug. Individuals who delay joining a Medicare prescription drug plan after their initial eligibility face a monthly premium that will increase by 1% per month for each month of delay Part D penalty: This is a 1% per month penalty that is applied to the cost of the Part D Plan for the rest of your life! This is imposed if you don t have other credible prescription coverage such as VA, TriCare, or credible drug coverage from your employer when you apply for Part B. The penalty is 1% of the average cost of a Medicare prescription plan (currently $34/month). 1% X $34 = $0.34

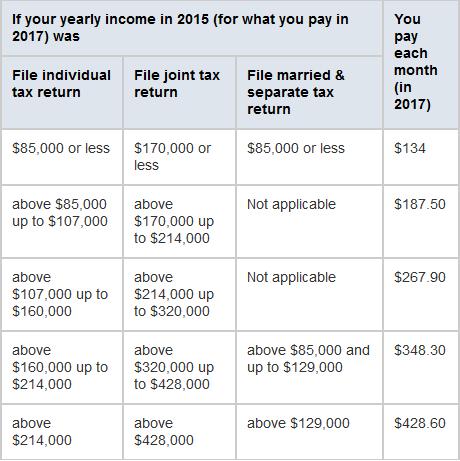

24 Part D - Premiums By Income The chart shows your estimated prescription drug plan monthly premium based on your income as reported to your IRS tax return from 2 years ago and most recent year. If your income is above a certain limit, you ll pay an income-related monthly adjustment amount in addition to your plan premium. If your filing status and year income in 2015 was: File Individual Tax Return File Joint Tax Return File Married & Separate Tax Return You Pay (in 2016) $85,000 or less $170,000 or less $85,000 or less your plan premium above $85,000 up to $107,000 above $107,000 up to $160,000 above $160,000 up to $214,000 above $170,000 up to $214,000 above $214,000 up to $320,000 above $20,000 up to $428,000 not applicable not applicable above $85,000 up to $129,000 $ your plan premium $ your plan premium $ your plan premium above $214,000 above $428,000 above $129,000 $ your plan premium

25 Annual Enrollment Period: Oct 15 Dec 7 Each year, you have a chance to make changes to your Medicare Advantage or Medicare prescription drug coverage for the following year.

26 Insurance Agents: What does my insurance agent do? An insurance agent explains all of your policy choices and benefits every year. The agent will ask probing questions to help guide you through the process of choosing the right plan for you. Clients choose the policy. It is the agents job to tell them the positives and negatives to each policy they consider. He/she will help you with billing problems & concerns throughout the year.

27 How Are Agents Compensated? Insurance companies pay the agents. Clients pay nothing to the agent. Generally, agents/brokers receive an initial payment in the first year of the policy and half as much for years two (2) and beyond if the member remains enrolled in the plan. You pay nothing extra for an agent s services. Whether you use an agent or not, your premiums will stay the same.

28 My Contact Information Phone Number: (248)

29 1 Social Security Key 1: Social Security basics

30 Facts to know Basic facts 1 Expected (workers expecting to retire) and actual (retirees) sources of income in retirement Social Security Employment Employer-sponsored retirement savings plan Individual retirement account or IRA Other personal savings and investments Employer-provided traditional pension or cash balance plan Workers Retirees Workers Retirees Workers Retirees Workers Retirees Workers Retirees Workers Retirees 35% 49% 19% 57% 8% 17% 62% 29% 46% 31% 19% 18% 29% 40% 18% 24% 23% 42% 20% 30% 27% 29% 30% 17% Major source Minor source 84% 91% 76% 25% 77% 37% 69% 42% 65% 50% 56% 47% Employer Benefit Research Institute, The 2016 Retirement Confidence Survey: Worker Confidence Stable, Retiree Confidence Continues to Increase, Issue Brief No. 422, March 2016.

31 Basic facts 1 Social Security is more than just retirement Nearly 61 million Americans were estimated to receive approximately $918 billion in Social Security benefits in Average monthly benefit using June 2016 beneficiary data Survivors 10% Retired workers and their dependents Disabled and their dependents $1,166 18% 72% $1,348 Social Security Administration, Fact Sheet, Social Security, 2016.

and DI (disability income) trust fund is expected to be depleted 1 Revenue coming into the OASI and DI trust funds will be adequate to pay")

32 Social Security basics 1 Will it be there? By 2034, the combined OASI (old age and survivor income) and DI (disability income) trust fund is expected to be depleted 1 Revenue coming into the OASI and DI trust funds will be adequate to pay about 79% of scheduled benefits in The 2016 Annual Report of the Board of Trustees of the Federal Old-Age and Survivors Insurance and Federal Disability Insurance Trust Funds, June 22, 2016.

33 Statements now online Social Security basics 1

34 2 Social Security Key 2: Income benefits

35 Income benefits 3 How to qualify for benefits Must be fully insured (earned required number of Social Security credits to qualify) Most workers need 40 credits or about 10 years of work 1 Through 1977, you earned one credit for each calendar quarter in which you had wages or salary of at least $50 in covered employment 1 Since 1978, you earn credits on the basis of your annual earnings up to four credits in any year In 2017, one credit is recorded for every $1,300 you earn in a year, with four credits if you earn $5,200 or more 2 1 Social Security Administration, Benefits Planner: Social Security Credits 2 Social Security Administration, 2017 Social Security Changes, Fact Sheet

36 How benefits are calculated Income benefits 3 PIA (primary insurance amount) $ FRA (full retirement age) Benefit is reduced if taken prior to FRA Monthly benefit is adjusted up if your start is delayed Social Security Administration, Primary Insurance Amount.

37 3 Social Security Key 3: Taxation of benefits

38 Benefits are subject to income tax Taxation of benefits 4 Sum of your adjusted gross income + nontaxable interest + ½ of your Social Security benefits = Your combined income Combined income: single or head of household 0% $25,000 $34,000 up to 50% up to 85% Combined income: married, filing jointly $32,000 $44,000 0% up to 50% up to 85% Note: These percentages are the amount of Social Security benefit included in income, not the tax rate on the Social Security benefit. Social Security Administration, Benefits Planner: Income Taxes And Your Social Security Benefits..

39 4 Social Security Key 4: When to start benefits

40 When to start your benefits When to start benefits 5 Full retirement age (FRA) Can start benefits as early as age 62 If age 62, receive less than at full retirement age Maximum benefits can be attained at age 70 Year of birth Full retirement age (FRA) Age 62 benefit reduction 1937 or earlier % and 2 months 20.83% and 4 months 21.67% and 6 months 22.50% and 8 months 23.33% and 10 months 24.17% % and 2 months 25.83% and 4 months 26.67% and 6 months 27.50% and 8 months 28.33% and 10 months 29.17%% 1960 and later % Social Security Administration, Retirement Planner: Benefits By Year Of Birth.

41 Enhancing benefits by delaying start date When to start benefits Starting benefits at various ages and living to different ages Delaying your start past FRA will result in delayed retirement credits (DRC) Accumulated benefits age Start age $144,000 $234,000 $324,000 $414,000 $504, $124,776 $228,756 $332,736 $436,716 $540, $96,000 $216,000 $336,000 $456,000 $576, $55,680 $194,880 $334,080 $473,280 $612, $0 $158,400 $316,800 $475,200 $633,600 Full retirement age of 66, full retirement benefit $2,000/month, no cost-of-living adjustment (COLA), no discounting. For illustration purposes only, not an actual client. Social Security benefits are first received the month following the month they are due. However, this table reflects 12 monthly payments in the first year and all subsequent years. Social Security Administration, Retirement Planner: Delayed Retirement Credits.

42 5 Social Security Key 5: Working in retirement

43 In 2017, if you work Working in retirement 6 Age 62 FRA FRA up to birthday month After FRA Reduced $1 for every $2 above $16,920 Reduced $1 for every $3 above $44,880 No reduction Any reduction in Social Security income in early retirement (due to working) will result in positive adjustment to your monthly benefit when you reach your full retirement age Social Security Administration, 2017 Social Security Changes, Fact Sheet.

Current year earnings $40,000 Social Security earning limit $16,920 Excess earnings $23,080 Reduction in Social Security benefits $11,540 Net Social")

44 Hypothetical example Working in retirement 6 Susan, born 1955 Eligible for maximum benefits My benefits Retire in 2017 on 62 nd birthday and returned Annual Social to work Security less benefit than one year $16,800 later (75% of FRA benefits) Current year earnings $40,000 Social Security earning limit $16,920 Excess earnings $23,080 Reduction in Social Security benefits $11,540 Net Social Security benefits $ 5,260 This hypothetical example is for illustrative purposes only and does not represent an actual client.

45 6 Social Security Key 6: Spouse and survivor benefits

46 Benefits available for spouses Spouse and survivor 7 When a spouse does not qualify for his or her own retirement benefits: Nonqualifying spouse can collect on the record of the spouse who is qualified to receive benefits - To qualify, the nonqualifying spouse must have been married at least one year to the qualifying spouse or be the parent of their child - If nonqualifying spouse is at FRA or later, receives an amount equal to 50% of the PIA of the qualifying spouse (not necessarily their benefit amount) - If nonqualifying spouse is age 62, they may receive permanently reduced benefits The rules are complicated and vary depending on your situation, so talk to a Social Security representative about the options available to you. Social Security Administration, Retirement Planner: Benefits For Your Spouse.

47 Benefits available for spouses Spouse and survivor 7 When both spouses qualify for their own benefits, generally the spouse with the lower benefit would: 1. Take benefits generated by own earnings history OR 2. Take half of the other spouse s retirement benefit if greater (made up of personal benefit plus the difference to make up half of the primary wage earners benefit) The rules are complicated and vary depending on your situation, so talk to a Social Security representative about the options available to you. Social Security Administration, Retirement Planner: Benefits For Your Spouse.

48 Benefits available for spouses Spouse and survivor 7 When both spouses qualify for benefits Advanced option for spouse A who was age 62 or older in 2015: At full retirement age, spouse A could delay receiving their own retirement benefit and start a spousal benefit which is half of spouse B s benefit. - To do so either spouse B is receiving own benefits OR spouse B filed and suspended prior to April 30, If spouse A s retirement benefits are delayed, a higher benefit may be received at a later date based on the effect of delayed retirement credits. The rules are complicated and vary depending on your situation, so talk to a Social Security representative about the options available to you. Social Security Administration, Retirement Planner: Benefits For Your Spouse.

49 Benefits available for survivors Spouse and survivor 7 The earliest a widow(er) can start receiving Social Security benefits is age 60 If you receive survivor benefits early: Benefits based on your age can begin any time between age 60 and your FRA. Starting early, however, your survivor benefits are reduced a fraction of a percentage for each month before your FRA If you receive benefits AND you qualify for retirement benefits that are more than your survivor benefits you can switch to your own benefit as early as age 62 Social Security Administration, Survivors Planner: If You Are The Worker s Widow or Widower. The rules are complicated and vary depending on your situation, so talk to a Social Security representative about the options available to you.

Social Security Administration, Retirement Planner: Benefits For Your Divorced Spouse.")

50 Benefits available for divorced spouse Spouse and survivor 7 If married for at least 10 years, ex-spouse can get Social Security benefits based on other ex-spouse s record The person receiving benefits must be age 62 or older and unmarried The benefit that the receiving person is entitled to receive based on his or her own work is less than the benefit based on the divorce The amount of benefit has no effect on the other ex-spouse or their current spouse If divorced for at least two years, and if both ex-spouses are at least age 62, divorced spouse can get benefits even if other ex-spouse is not retired (has not started Social Security benefits) Social Security Administration, Retirement Planner: Benefits For Your Divorced Spouse. The rules are complicated and vary depending on your situation,so talk to a Social Security representative about the options available to you.

Social Security: Allianz Life Insurance Company of North America Allianz Life Insurance Company of New York. Change Creates Opportunities

Allianz Life Insurance Company of North America Allianz Life Insurance Company of New York Social Security: Change Creates Opportunities Presented by Randy Kitzmiller RVP, Annuities Ash Brokerage ENT-843-N

Allianz Life Insurance Company of North America Allianz Life Insurance Company of New York Social Security: Change Creates Opportunities Presented by Randy Kitzmiller RVP, Annuities Ash Brokerage ENT-843-N

Medicare Educational Video. Presented by: Medicare Simplified Medicare Simplified. All rights reserved.

Medicare Educational Video Presented by: Medicare Simplified Copyright 2014 Medicare Simplified. All rights reserved. TABLE OF CONTENTS SUBJECT TIME ON CLOCK(HR/MIN/SEC) INTRODUCTION 00:00:00 YOUR MEDICARE

Medicare Educational Video Presented by: Medicare Simplified Copyright 2014 Medicare Simplified. All rights reserved. TABLE OF CONTENTS SUBJECT TIME ON CLOCK(HR/MIN/SEC) INTRODUCTION 00:00:00 YOUR MEDICARE

Understanding Your Medicare Options. Medicare Made Clear

Understanding Your Medicare Options Medicare Made Clear Top Medicare questions 1 Who is eligible for Medicare? 2 What are my coverage options? 3 When can I enroll? 4 What are my next steps? 5 Once I am

Understanding Your Medicare Options Medicare Made Clear Top Medicare questions 1 Who is eligible for Medicare? 2 What are my coverage options? 3 When can I enroll? 4 What are my next steps? 5 Once I am

CENTERS FOR MEDICARE & MEDICAID SERVICES

CENTERS FOR MEDICARE & MEDICAID SERVICES 2015 Medicare checklist Read the information in this booklet carefully. It has important information about the decisions you need to make. Watch the mail for your

CENTERS FOR MEDICARE & MEDICAID SERVICES 2015 Medicare checklist Read the information in this booklet carefully. It has important information about the decisions you need to make. Watch the mail for your

Understanding Social Security and Medicare

Understanding Social Security and Medicare How these programs fit into your retirement strategies Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America ENT-1520-N Social

Understanding Social Security and Medicare How these programs fit into your retirement strategies Allianz Life Insurance Company of New York Allianz Life Insurance Company of North America ENT-1520-N Social

MEDICARE 101 PRESENTED BY WESTERN MARKETING

MEDICARE 101 PRESENTED BY WESTERN MARKETING WHAT IS MEDICARE? A health insurance program for: People 65 years of age and older People under age 65 with certain disabilities People with End-State Renal

MEDICARE 101 PRESENTED BY WESTERN MARKETING WHAT IS MEDICARE? A health insurance program for: People 65 years of age and older People under age 65 with certain disabilities People with End-State Renal

Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare

CENTERS FOR MEDICARE & MEDICAID SERVICES 2013 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information about: What is a Medicare

CENTERS FOR MEDICARE & MEDICAID SERVICES 2013 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information about: What is a Medicare

Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare

CENTERS FOR MEDICARE & MEDICAID SERVICES 2014 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information about: Medicare Supplement

CENTERS FOR MEDICARE & MEDICAID SERVICES 2014 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information about: Medicare Supplement

Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare

CENTERS FOR MEDICARE & MEDICAID SERVICES 2011 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information about the following:

CENTERS FOR MEDICARE & MEDICAID SERVICES 2011 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information about the following:

Choosing a Medigap Policy:

C E N T E R S F O R M E D I C A R E & M E D I C A I D S E R V I C E S 2016 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information

C E N T E R S F O R M E D I C A R E & M E D I C A I D S E R V I C E S 2016 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information

MEDICARE MADE SIMPLE. It s as easy as A, B, C, D

MEDICARE MADE SIMPLE It s as easy as A, B, C, D PINNACLE FINANCIAL SERVICES 65 W STREET RD, SUITE A-101 WARMINSTER, PA 18974 1-(800)-772-6881 WWW.PFSINSURANCE.COM LAST UPDATED JANUARY 2, 2019 WHAT IS MEDICARE?

MEDICARE MADE SIMPLE It s as easy as A, B, C, D PINNACLE FINANCIAL SERVICES 65 W STREET RD, SUITE A-101 WARMINSTER, PA 18974 1-(800)-772-6881 WWW.PFSINSURANCE.COM LAST UPDATED JANUARY 2, 2019 WHAT IS MEDICARE?

2009 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare

CENTERS FOR MEDICARE & MEDICAID SER VICES 2009 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare cial government guide has important information about the following: What

CENTERS FOR MEDICARE & MEDICAID SER VICES 2009 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare cial government guide has important information about the following: What

Your complimentary Medicare Guidebook

Learn Protect Assess Enroll Your complimentary Medicare Guidebook Learn Original Medicare... 4 Medicare Prescription Drug Coverage.............. 6 Medicare Supplement Insurance... 8 Medicare Advantage...

Learn Protect Assess Enroll Your complimentary Medicare Guidebook Learn Original Medicare... 4 Medicare Prescription Drug Coverage.............. 6 Medicare Supplement Insurance... 8 Medicare Advantage...

Get started with the basics of Medicare

Get started with the basics of Medicare innovationhealthmedicare.com 71.02.315.1 (3/18) You have a lot of choices for Medicare coverage. And you probably have a lot of questions, too. A C B D So let s

Get started with the basics of Medicare innovationhealthmedicare.com 71.02.315.1 (3/18) You have a lot of choices for Medicare coverage. And you probably have a lot of questions, too. A C B D So let s

It s Time for Medicare

It s Time for Medicare med-ageinbook-1214 Medicare What you need to know. You re turning 65. Or you re already 65 and getting ready to retire and lose your healthcare coverage. You re almost ready for

It s Time for Medicare med-ageinbook-1214 Medicare What you need to know. You re turning 65. Or you re already 65 and getting ready to retire and lose your healthcare coverage. You re almost ready for

Choosing a Medigap Policy:

CENTERS FOR MEDICARE & MEDICAID SERVICES 2018 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information about: Medicare Supplement

CENTERS FOR MEDICARE & MEDICAID SERVICES 2018 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information about: Medicare Supplement

Medicare Supplement Insurance (Medigap) Review

Review") Medicare Supplement Insurance (Medigap) Review 1 Medicare Part A (Hospital Insurance) Part A Covers: Inpatient hospital care Care in a skilled nursing facility (SNF) Home health care Hospice care Blood

Medicare Supplement Insurance (Medigap) Review 1 Medicare Part A (Hospital Insurance) Part A Covers: Inpatient hospital care Care in a skilled nursing facility (SNF) Home health care Hospice care Blood

2008 Choosing a Medigap Policy:

CENTERS FOR MEDICARE & MEDICAID SERVICES 2008 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This is the official government guide with important information about what

CENTERS FOR MEDICARE & MEDICAID SERVICES 2008 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This is the official government guide with important information about what

Choosing a Medigap Policy:

CENTERS FOR MEDICARE & MEDICAID SERVICES 2019 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information about: Medicare Supplement

CENTERS FOR MEDICARE & MEDICAID SERVICES 2019 Choosing a Medigap Policy: A Guide to Health Insurance for People with Medicare This official government guide has important information about: Medicare Supplement

Understanding Your Medicare Options. Medicare Made Clear

Understanding Your Medicare Options Medicare Made Clear 1. Eligibility 2. Coverage Options 3. Enrollment 4. Next Steps 5. Resources Agenda 2 ELIGIBILITY Medicare Made Clear ELIGIBILITY Original Medicare

Understanding Your Medicare Options Medicare Made Clear 1. Eligibility 2. Coverage Options 3. Enrollment 4. Next Steps 5. Resources Agenda 2 ELIGIBILITY Medicare Made Clear ELIGIBILITY Original Medicare

Guide to Medicare. Helping You Navigate the Medicare Maze

G U I D E T O M E D I C A R E Guide to Medicare Helping You Navigate the Medicare Maze 7807 E. Peakview Ave., S ui te 410 Cen t enn ial, CO 80 111 303-741- 9772 www.de chtmanweal t h.com Not connected

G U I D E T O M E D I C A R E Guide to Medicare Helping You Navigate the Medicare Maze 7807 E. Peakview Ave., S ui te 410 Cen t enn ial, CO 80 111 303-741- 9772 www.de chtmanweal t h.com Not connected

Tribal Basic Training. March 2, 2016

Tribal Basic Training March 2, 2016 Welcome to Basic Medicare introduction: Part A Part B Part D Medigaps Part C Help paying Medicare costs: Medicare Savings Program Extra Help / Low Income Subsidy (LIS)

Tribal Basic Training March 2, 2016 Welcome to Basic Medicare introduction: Part A Part B Part D Medigaps Part C Help paying Medicare costs: Medicare Savings Program Extra Help / Low Income Subsidy (LIS)

(Talk about years of experience Premera has and the years of training and experience we have as Medicare Representatives.)

") Facilitator: Thank you for joining us! We are going to be together for about 45 minutes this morning / afternoon. During that time I m going to give you an overview of Medicare so you have a better understanding

Facilitator: Thank you for joining us! We are going to be together for about 45 minutes this morning / afternoon. During that time I m going to give you an overview of Medicare so you have a better understanding

Celebrating 65 (SM) And the Possibilities it Brings...

And the Possibilities it Brings...") Celebrating 65 (SM) And the Possibilities it Brings... TABLE OF CONTENTS What is........................ 2 In this Brochure................................. 3 Making Sense of Social Security....................

Celebrating 65 (SM) And the Possibilities it Brings... TABLE OF CONTENTS What is........................ 2 In this Brochure................................. 3 Making Sense of Social Security....................

NEW PSALMIST BAPTIST CHURCH 2018 SPRING INSTITUTE Releasing Your Dreams Bishop Walter S. Thomas, Sr., Pastor. Medicare & You 2018

NEW PSALMIST BAPTIST CHURCH 2018 SPRING INSTITUTE Releasing Your Dreams Bishop Walter S. Thomas, Sr., Pastor Medicare & You 2018 BLESSING US INDEED SENIOR SERVICES Mary Dent, LCB 443-850-8410 For informational

NEW PSALMIST BAPTIST CHURCH 2018 SPRING INSTITUTE Releasing Your Dreams Bishop Walter S. Thomas, Sr., Pastor Medicare & You 2018 BLESSING US INDEED SENIOR SERVICES Mary Dent, LCB 443-850-8410 For informational

A Simplified Guide to Medicare Options

A Simplified Guide to Medicare Options Brought to You by 5-out-of-5-Star Medicare Advantage Plans A Simplified Guide to Medicare Options Table of Contents What is Medicare?... 3 Seven Things to Know About

A Simplified Guide to Medicare Options Brought to You by 5-out-of-5-Star Medicare Advantage Plans A Simplified Guide to Medicare Options Table of Contents What is Medicare?... 3 Seven Things to Know About

Medicare in Maryland Navigating Medicare and Understanding Your Options

Medicare in Maryland Navigating Medicare and Understanding Your Options H8854_17_4041-07_003_OE CMS Accepted 6/13/2017 Table of Contents Introduction... 1 Medicare: A Brief History... 2 The Four Parts

Medicare in Maryland Navigating Medicare and Understanding Your Options H8854_17_4041-07_003_OE CMS Accepted 6/13/2017 Table of Contents Introduction... 1 Medicare: A Brief History... 2 The Four Parts

Guide to Medicare. Provided by: Medicare MarketPlace. Helping You Navigate the Medicare Maze

Guide to Medicare Helping You Navigate the Medicare Maze Provided by: Medicare MarketPlace Not connected with or endorsed by the United States government or the federal Medicare program. Medicare is complicated.

Guide to Medicare Helping You Navigate the Medicare Maze Provided by: Medicare MarketPlace Not connected with or endorsed by the United States government or the federal Medicare program. Medicare is complicated.

My Medicare Options Workbook

My Medicare Options Workbook This workbook will walk you through the process of deciding what steps you need to take now that you are eligible for Medicare. Table of Contents Introduction... 3 Where do

My Medicare Options Workbook This workbook will walk you through the process of deciding what steps you need to take now that you are eligible for Medicare. Table of Contents Introduction... 3 Where do

Medicare Enrollment and Coverage Decisions. Transitioning from Employer-Sponsored Group Health Plans to Medicare

Medicare Enrollment and Coverage Decisions Transitioning from Employer-Sponsored Group Health Plans to Medicare City of Roswell July 9, 2014 Introduction Kris Alderman Lewis Brisbois Bisgaard & Smith ERISA

Medicare Enrollment and Coverage Decisions Transitioning from Employer-Sponsored Group Health Plans to Medicare City of Roswell July 9, 2014 Introduction Kris Alderman Lewis Brisbois Bisgaard & Smith ERISA

Medicare. has 4 Parts. Medicare is Health Insurance. Medigap. Part A Hospital Insurance. Part D Prescription Drug Plan. Part B Medical Insurance

Basics is Health Insurance Parts A and B is called Original administered by the federal government Part A Hospital Insurance Medigap Parts C and D can be individual plans purchased through private insurance

Basics is Health Insurance Parts A and B is called Original administered by the federal government Part A Hospital Insurance Medigap Parts C and D can be individual plans purchased through private insurance

MEDICARE PLANNING WORKBOOK

Make the most of Medicare. To learn more about Transamerica s Field Guide to Medicare series and to get support materials: Contact: Your Financial Professional MEDICARE PLANNING WORKBOOK A FIELD GUIDE

Make the most of Medicare. To learn more about Transamerica s Field Guide to Medicare series and to get support materials: Contact: Your Financial Professional MEDICARE PLANNING WORKBOOK A FIELD GUIDE

Welcome to Medicare 2013

Welcome to Medicare 2013 1 Agenda Basics of Original Medicare Obtaining coverage What is covered (Part A, B) Prescription drug coverage (Part D) Supplementing Original Medicare Medigap plans Alternatives

Welcome to Medicare 2013 1 Agenda Basics of Original Medicare Obtaining coverage What is covered (Part A, B) Prescription drug coverage (Part D) Supplementing Original Medicare Medigap plans Alternatives

AC: MEDICARE CHOICES HOW TO NAVIGATE

AC: 26997-0516-8318 MEDICARE CHOICES HOW TO NAVIGATE MEDICARE HEALTH INSURANCE AT A GLANCE AGE 65 ELIGIBILITY Part A Part B Part D Medigap Part C WHAT IT COVERS Hospital Insurance (Inpatient services)

AC: 26997-0516-8318 MEDICARE CHOICES HOW TO NAVIGATE MEDICARE HEALTH INSURANCE AT A GLANCE AGE 65 ELIGIBILITY Part A Part B Part D Medigap Part C WHAT IT COVERS Hospital Insurance (Inpatient services)

Getting started with Medicare

Getting started with Medicare Look inside to: Learn about Medicare Find out about coverage and costs Discover when to enroll Medicare Made Clear Learning about Medicare can be like learning a new language.

Getting started with Medicare Look inside to: Learn about Medicare Find out about coverage and costs Discover when to enroll Medicare Made Clear Learning about Medicare can be like learning a new language.

MedicAre: don t delay. apply for Medicare as soon as you become eligible. You ve earned it. Make the most of it.

2015 don t delay. apply for Medicare as soon as you become eligible. MedicAre: You ve earned it. Make the most of it. You can enroll in Medicare the three months before, during and the three months after

2015 don t delay. apply for Medicare as soon as you become eligible. MedicAre: You ve earned it. Make the most of it. You can enroll in Medicare the three months before, during and the three months after

Important things to keep in mind

Important things to keep in mind Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution Not insured by any federal government agency May lose value The content of this presentation

Important things to keep in mind Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution Not insured by any federal government agency May lose value The content of this presentation

RETIREMENT PLANNING PROGRAMS: THE ESSENTIAL ELEMENTS

RETIREMENT PLANNING PROGRAMS: THE ESSENTIAL ELEMENTS By: Marcia S. Wagner, Esq. The Wagner Law Group A Professional Corporation 99 Summer Street, 13 th Floor Boston, MA 02110 Tel: (617) 357-5200 Fax: (617)

RETIREMENT PLANNING PROGRAMS: THE ESSENTIAL ELEMENTS By: Marcia S. Wagner, Esq. The Wagner Law Group A Professional Corporation 99 Summer Street, 13 th Floor Boston, MA 02110 Tel: (617) 357-5200 Fax: (617)

& Medicare. You This is the official U.S. government Medicare handbook. What s important in 2016 (page 12) What Medicare covers (page 37)

What Medicare covers (page 37)") & Medicare You 2016 This is the official U.S. government Medicare handbook. What s important in 2016 (page 12) What Medicare covers (page 37) CENTERS for MEDICARE & MEDICAID SERVICES Section 6 What are

& Medicare You 2016 This is the official U.S. government Medicare handbook. What s important in 2016 (page 12) What Medicare covers (page 37) CENTERS for MEDICARE & MEDICAID SERVICES Section 6 What are

Welcome to Medicare CENTERS FOR MEDICARE & MEDICAID SERVICES

Welcome to Medicare CENTERS FOR MEDICARE & MEDICAID SERVICES Your Personalized Medicare Manager Is Waiting for You Online. Register at www.mymedicare.gov Medicare s secure online service for accessing

Welcome to Medicare CENTERS FOR MEDICARE & MEDICAID SERVICES Your Personalized Medicare Manager Is Waiting for You Online. Register at www.mymedicare.gov Medicare s secure online service for accessing

Welcome. to Medicare. An educational Medicare guide compliments of the Medicare Welcome Team. Y0041_H3156_AH_15_28071 Accepted (1/7/2015)

") Welcome to Medicare An educational Medicare guide compliments of the Medicare Welcome Team Y0041_3156_A_15_28071 Accepted (1/7/2015) qualifies? WO You are almost ready to enroll in Medicare, and we would

Welcome to Medicare An educational Medicare guide compliments of the Medicare Welcome Team Y0041_3156_A_15_28071 Accepted (1/7/2015) qualifies? WO You are almost ready to enroll in Medicare, and we would

How Medicare Works. Helping you make the most of Medicare. MedicareBlue SM Rx (PDP) S5743_ mmddyy_xxx

S5743_ mmddyy_xxx") How Medicare Works Helping you make the most of Medicare 2018 MedicareBlue SM Rx (PDP) S5743_ mmddyy_xxx About Medicare Whether you re new to Medicare or want a refresher, this guide can help you understand

How Medicare Works Helping you make the most of Medicare 2018 MedicareBlue SM Rx (PDP) S5743_ mmddyy_xxx About Medicare Whether you re new to Medicare or want a refresher, this guide can help you understand

Health Care and Long-Term Care Study, a consumer study of U.S. adults ages 50 and up, Nationwide/Harris Poll Survey (November 2016).

.") 1 Health Care and Long-Term Care Study, a consumer study of U.S. adults ages 50 and up, Nationwide/Harris Poll Survey (November 2016). 1 Important things to keep in mind Not a deposit Not FDIC or NCUSIF

1 Health Care and Long-Term Care Study, a consumer study of U.S. adults ages 50 and up, Nationwide/Harris Poll Survey (November 2016). 1 Important things to keep in mind Not a deposit Not FDIC or NCUSIF

Welcome. Medicare 101 Educational Seminar

Welcome Medicare 101 Educational Seminar 2 Basics of Medicare What Is Medicare? Medicare is a federally funded health insurance program. It includes Part A and Part B (known as Original Medicare). Medicare

Welcome Medicare 101 Educational Seminar 2 Basics of Medicare What Is Medicare? Medicare is a federally funded health insurance program. It includes Part A and Part B (known as Original Medicare). Medicare

Medicare Advantage (Part C) Review

Review") Medicare Advantage (Part C) Review 1 Medicare For people 65+ and under 65 with a disability 4 parts of Medicare Part A: Hospital Insurance Part B: Medical Insurance Part C: Medicare Advantage Plans Part

Medicare Advantage (Part C) Review 1 Medicare For people 65+ and under 65 with a disability 4 parts of Medicare Part A: Hospital Insurance Part B: Medical Insurance Part C: Medicare Advantage Plans Part

Welcome to Kaiser Permanente Presenting Medicare 101 and Kaiser Permanente Senior Advantage (HMO)

") Welcome to Kaiser Permanente Presenting Medicare 101 and Kaiser Permanente Senior Advantage (HMO) San Diego City Employees Retirement System Nancy Voltero Retiree Consultant October 12, 2016 2 Basics of

Welcome to Kaiser Permanente Presenting Medicare 101 and Kaiser Permanente Senior Advantage (HMO) San Diego City Employees Retirement System Nancy Voltero Retiree Consultant October 12, 2016 2 Basics of

Advocate Medicare Resource

Advocate Medicare Resource Understanding Medicare Options About this Guidebook This guidebook has been designed to assist Medicare beneficiary patients in understanding the basics of Medicare and Medicare

Advocate Medicare Resource Understanding Medicare Options About this Guidebook This guidebook has been designed to assist Medicare beneficiary patients in understanding the basics of Medicare and Medicare

Medicare and Social Security Understanding the A-B-Cs and 1-2-3s for Your Clients INSIGHTS PERSPECTIVES ON WEALTH MANAGEMENT

INSIGHTS PERSPECTIVES ON WEALTH MANAGEMENT Medicare and Social Security Understanding the A-B-Cs and 1-2-3s for Your Clients INSIGHTS PERSPECTIVES ON WEALTH MANAGEMENT MEDICARE AND SOCIAL SECURITY 1 INSIGHTS

INSIGHTS PERSPECTIVES ON WEALTH MANAGEMENT Medicare and Social Security Understanding the A-B-Cs and 1-2-3s for Your Clients INSIGHTS PERSPECTIVES ON WEALTH MANAGEMENT MEDICARE AND SOCIAL SECURITY 1 INSIGHTS

Understanding Medicare and Coverage Expansion Options. Rick Seely Account Executive MDA Insurance

Understanding Medicare and Coverage Expansion Options Rick Seely Account Executive MDA Insurance 1 Rick s Goals Today Help you determine if and when you should enroll in Medicare Parts A & B ---------------------------------------------RECOMMEND

Understanding Medicare and Coverage Expansion Options Rick Seely Account Executive MDA Insurance 1 Rick s Goals Today Help you determine if and when you should enroll in Medicare Parts A & B ---------------------------------------------RECOMMEND

2011 Guide to Social Security

2011 Guide to Social Security 39th Edition A simple explanation with easy-reference benefit tables. Contents Page 1 Introduction... 3 Are You Missing Out?.... 3 Major Changes in 2011... 4 2Who Is Covered

2011 Guide to Social Security 39th Edition A simple explanation with easy-reference benefit tables. Contents Page 1 Introduction... 3 Are You Missing Out?.... 3 Major Changes in 2011... 4 2Who Is Covered

An Introduction to Medicare

An Introduction to Medicare Medicare can be confusing, but we re here to help you and your employees make sense of it all. This Medicare overview is a great place to start. It goes over the Medicare basics

An Introduction to Medicare Medicare can be confusing, but we re here to help you and your employees make sense of it all. This Medicare overview is a great place to start. It goes over the Medicare basics

Get started with the basics of Medicare

Get started with the basics of Medicare 72.02.354.1 (1/18) aetnamedicare.com You have a lot of choices for Medicare coverage. And you probably have a lot of questions, too. A C B D So let s get started

Get started with the basics of Medicare 72.02.354.1 (1/18) aetnamedicare.com You have a lot of choices for Medicare coverage. And you probably have a lot of questions, too. A C B D So let s get started

Welcome to Medicare CENTERS FOR MEDICARE & MEDICAID SERVICES

Welcome to Medicare CENTERS FOR MEDICARE & MEDICAID SERVICES Your Personalized Medicare Manager Is Waiting for You Online. Go to My.Medicare.gov and get the personalized information you need to make better

Welcome to Medicare CENTERS FOR MEDICARE & MEDICAID SERVICES Your Personalized Medicare Manager Is Waiting for You Online. Go to My.Medicare.gov and get the personalized information you need to make better

Your Guide to Understanding Medicare 2017

Your Guide to Understanding Medicare 2017 One of the most important decisions you ll ever make for your health & financial wellbeing This guide is not an insurance solicitation or promotion for any particular

Your Guide to Understanding Medicare 2017 One of the most important decisions you ll ever make for your health & financial wellbeing This guide is not an insurance solicitation or promotion for any particular

Getting Started with Medicare.

Getting Started with Medicare. Look inside to: Learn about Medicare Compare plans and choose the right one for you See if you qualify for financial help Learn how to enroll in Medicare if you plan on working

Getting Started with Medicare. Look inside to: Learn about Medicare Compare plans and choose the right one for you See if you qualify for financial help Learn how to enroll in Medicare if you plan on working

Understanding Social Security

Understanding Social Security Guide for Advisors A Look at the Big Picture For Financial Professional Use Only. Not for Use With Consumers. Is Your Clients Picture of Retirement Incomplete? Building retirement

Understanding Social Security Guide for Advisors A Look at the Big Picture For Financial Professional Use Only. Not for Use With Consumers. Is Your Clients Picture of Retirement Incomplete? Building retirement

The A,B,C, & Ds of Medicare & Medicare Supplement Plans

The A,B,C, & Ds of Medicare & Medicare Supplement Plans WMI Mutual Insurance Company 1 Question: How many baby boomers turn 65 everyday? 2 As the year 2011 began on Jan. 1, the oldest members of the Baby

The A,B,C, & Ds of Medicare & Medicare Supplement Plans WMI Mutual Insurance Company 1 Question: How many baby boomers turn 65 everyday? 2 As the year 2011 began on Jan. 1, the oldest members of the Baby

Supplementing Medicare: Medigap Plans. What are Medigap Policies?

FACT SHEET Supplementing Medicare: Medigap Plans (B-002) p. 1 of 5 Supplementing Medicare: Medigap Plans What are Medigap Policies? Insurance companies sell supplemental insurance to cover part, or all,

FACT SHEET Supplementing Medicare: Medigap Plans (B-002) p. 1 of 5 Supplementing Medicare: Medigap Plans What are Medigap Policies? Insurance companies sell supplemental insurance to cover part, or all,

LIFE FINANCIAL MEDICARE HEALTH

LIFE FINANCIAL MEDICARE HEALTH 4000 Spring Garden St., Suite G Greensboro, NC 27407 Office 336-851-5633 Fax 336-851-5634 LIFE 4000 Spring Garden St., Suite G Greensboro, NC 27407 Office 336-851-5633 Fax

LIFE FINANCIAL MEDICARE HEALTH 4000 Spring Garden St., Suite G Greensboro, NC 27407 Office 336-851-5633 Fax 336-851-5634 LIFE 4000 Spring Garden St., Suite G Greensboro, NC 27407 Office 336-851-5633 Fax

CRACKING THE MEDICARE CODE

CRACKING THE MEDICARE CODE What You Need to Know Before Signing Up for Medical Coverage A publication of Trust Company of Oklahoma 2018 MEDICARE care, nursing home care, hospice, and home health services.

CRACKING THE MEDICARE CODE What You Need to Know Before Signing Up for Medical Coverage A publication of Trust Company of Oklahoma 2018 MEDICARE care, nursing home care, hospice, and home health services.

Your Guide to Medicare Insurance

Presented by: 3609 Lake Avenue Fort Wayne, IN 46805 Phone: (260) 484-7010 Fax: (260) 484-7204 www.buyhealthinsurancehere.com Medicare is health insurance for individuals age 65 or older; certain individuals

Presented by: 3609 Lake Avenue Fort Wayne, IN 46805 Phone: (260) 484-7010 Fax: (260) 484-7204 www.buyhealthinsurancehere.com Medicare is health insurance for individuals age 65 or older; certain individuals

Medicare Overview. Employee Benefits Handout

Employee Benefits Handout Defense Civilian Personnel Advisory Services (DCPAS) Benefits, Wage & Non-Appropriated Funds Line of Business Benefits & Work Life Programs Division 4800 Mark Center Drive, Suite

Employee Benefits Handout Defense Civilian Personnel Advisory Services (DCPAS) Benefits, Wage & Non-Appropriated Funds Line of Business Benefits & Work Life Programs Division 4800 Mark Center Drive, Suite

The Cost of Medicare During Retirement

Private Wealth Management Products & Services The Cost of Medicare During Retirement There are two primary influences on the cost of Medicare for an individual. The first of these is when the retiree applies

Private Wealth Management Products & Services The Cost of Medicare During Retirement There are two primary influences on the cost of Medicare for an individual. The first of these is when the retiree applies

Simple Facts About Medicare

Simple Facts About Medicare What is Medicare? Medicare is a federal system of health insurance for people over 65 years of age and for certain younger people with disabilities. There are two types of Medicare:

Simple Facts About Medicare What is Medicare? Medicare is a federal system of health insurance for people over 65 years of age and for certain younger people with disabilities. There are two types of Medicare:

Medicare 101. Understanding your Medicare options. Brought to you by Wemasol

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Medicare 101 Understanding your Medicare options Brought to you by Wemasol 1. Medicare Parts A - D Medicare

Quality health plans & benefits Healthier living Financial well-being Intelligent solutions Medicare 101 Understanding your Medicare options Brought to you by Wemasol 1. Medicare Parts A - D Medicare

Understanding Medicare Insurance

e m o ry h e a lt h c a r e m e d i c a r e r e s o u r c e Understanding Medicare Insurance a helpful guide medicare insurance helpline * 1-855-256-1501 *Helpline serviced by: Medicare Insurance Helpline

e m o ry h e a lt h c a r e m e d i c a r e r e s o u r c e Understanding Medicare Insurance a helpful guide medicare insurance helpline * 1-855-256-1501 *Helpline serviced by: Medicare Insurance Helpline

2017 Medicare Basics. Module 1

2017 Medicare Basics Module 1 What is Original Medicare? Medicare Overview It is health insurance that is available under Medicare Part A and Part B through the traditional fee-for-service Medicare payment

2017 Medicare Basics Module 1 What is Original Medicare? Medicare Overview It is health insurance that is available under Medicare Part A and Part B through the traditional fee-for-service Medicare payment

MEDICARE PLANNING MEDICARE & SOCIAL SECURITY

MEDICARE PLANNING MEDICARE & SOCIAL SECURITY Presented By: Jerry Snyder CFP Retirement Strategies, Ltd. 5060 Parkcenter Ave. Suite A Dublin, OH 43017 614.799.8668 Jsnyder@retirement-strategies.com www.retirement-strategies.com

MEDICARE PLANNING MEDICARE & SOCIAL SECURITY Presented By: Jerry Snyder CFP Retirement Strategies, Ltd. 5060 Parkcenter Ave. Suite A Dublin, OH 43017 614.799.8668 Jsnyder@retirement-strategies.com www.retirement-strategies.com

Hawaii SHIP (State Health Insurance Assistance Program)/Sage PLUS Program

/Sage PLUS Program") Hawaii SHIP (State Health Insurance Assistance Program)/Sage PLUS Program Federally funded program to assist individuals with questions regarding Medicare benefits Administered by the Department of Health

Hawaii SHIP (State Health Insurance Assistance Program)/Sage PLUS Program Federally funded program to assist individuals with questions regarding Medicare benefits Administered by the Department of Health

ARE & MEDIC AID SERVICES

& Medicare You 2018 This is the official U.S. government Medicare handbook. Learn about your new Medicare card (inside front cover) What Medicare covers (page 29) CENTERS for MEDICARE & MEDICAID SERVICES

& Medicare You 2018 This is the official U.S. government Medicare handbook. Learn about your new Medicare card (inside front cover) What Medicare covers (page 29) CENTERS for MEDICARE & MEDICAID SERVICES

Choosing Between Traditional Medicare and Medicare Advantage

Choosing Between Traditional Medicare and Medicare Advantage If you are eligible for Medicare you can chose between getting Medicare benefits through traditional Medicare (also known as original Medicare

Choosing Between Traditional Medicare and Medicare Advantage If you are eligible for Medicare you can chose between getting Medicare benefits through traditional Medicare (also known as original Medicare

Medicare Advantage Explained 2008

Medicare Advantage Explained 2008 Getting More from Your Medicare Benefits An educational resource from 4 Medicare Basics 7 About Medicare Advantage 9 Medicare Advantage Options 12 Reviewing Your Choices

Medicare Advantage Explained 2008 Getting More from Your Medicare Benefits An educational resource from 4 Medicare Basics 7 About Medicare Advantage 9 Medicare Advantage Options 12 Reviewing Your Choices

A FIELD GUIDE TO MEDICARE

Make the most of Medicare. To learn more about Transamerica s Field Guide to Medicare series and to get support materials: Contact: Your Financial Professional Transamerica Resources, Inc. is an Aegon

Make the most of Medicare. To learn more about Transamerica s Field Guide to Medicare series and to get support materials: Contact: Your Financial Professional Transamerica Resources, Inc. is an Aegon

Medicare 101. Understanding Your Options

Medicare 101 Understanding Your Options Futurity First is an independent, nationwide insurance and investment organization operating a network of community-based offices that specialize in retirement income

Medicare 101 Understanding Your Options Futurity First is an independent, nationwide insurance and investment organization operating a network of community-based offices that specialize in retirement income

Social Security & Medicare: Everything You Didn t Know to Ask

Social Security & Medicare: Everything You Didn t Know to Ask This material is not intended to replace the advice of a qualified attorney, tax advisor, investment professional, or insurance agent. Before

Social Security & Medicare: Everything You Didn t Know to Ask This material is not intended to replace the advice of a qualified attorney, tax advisor, investment professional, or insurance agent. Before

A Guide to Understanding Medicare Benefits

Private Wealth Management Products & Services A Guide to Understanding Medicare Benefits Medicare is a social insurance program created under the Social Security Act of 1965 as signed by President Lyndon

Private Wealth Management Products & Services A Guide to Understanding Medicare Benefits Medicare is a social insurance program created under the Social Security Act of 1965 as signed by President Lyndon

Medicare Made Clear Answer Guide

Medicare Made Clear Answer Guide Y0066_100820_113217 File & Use 08252010 Medicare can be confusing. How do you find the best options to fit your needs? This guide has some answers that may be helpful.

Medicare Made Clear Answer Guide Y0066_100820_113217 File & Use 08252010 Medicare can be confusing. How do you find the best options to fit your needs? This guide has some answers that may be helpful.

Getting Started with Medicare

Getting Started with Medicare TABLE OF CONTENTS 2 What is Medicare? 3 Original Medicare Parts A and B 5 Medicare Part C Medicare Advantage Plans 6 Medicare Part D Prescription Drug Coverage 8 How to Enroll

Getting Started with Medicare TABLE OF CONTENTS 2 What is Medicare? 3 Original Medicare Parts A and B 5 Medicare Part C Medicare Advantage Plans 6 Medicare Part D Prescription Drug Coverage 8 How to Enroll

Medicare Insurance Guide. Help You Can Count On.

Medicare Insurance Guide Help You Can Count On. Help You Can Count On. For many people, Medicare alone does not provide a comprehensive safety net for health care expenses. While Medicare Parts A and B

Medicare Insurance Guide Help You Can Count On. Help You Can Count On. For many people, Medicare alone does not provide a comprehensive safety net for health care expenses. While Medicare Parts A and B

Medicare 101. Understanding Your Options

Medicare 101 Understanding Your Options Futurity First is an independent, nationwide insurance and investment organization operating a network of community-based offices that specialize in retirement income

Medicare 101 Understanding Your Options Futurity First is an independent, nationwide insurance and investment organization operating a network of community-based offices that specialize in retirement income

Health Savings Accounts and Medicare

A Guide to Health Savings Accounts and Medicare Discover how Medicare impacts your HSA, and get answers to frequently asked questions. A Guide to Discover how Medicare impacts your HSA, and get answers

A Guide to Health Savings Accounts and Medicare Discover how Medicare impacts your HSA, and get answers to frequently asked questions. A Guide to Discover how Medicare impacts your HSA, and get answers

Medicare is Health Insurance

Basics is Health Insurance Part A Hospital Insurance Medigap Parts A and B is called Original administered by the federal government Part D Prescriptio n Drug Plan has 4 Parts Part B Medical Insurance

Basics is Health Insurance Part A Hospital Insurance Medigap Parts A and B is called Original administered by the federal government Part D Prescriptio n Drug Plan has 4 Parts Part B Medical Insurance

Social Security, Medicare and Pensions

Social Security, Medicare and Pensions 22 nd Edition Attorney Joseph L. Matthews Introduction... 1 Chapter 1 Social Security: The Basics... 5 Learning Objectives... 5 Introduction... 5 History of Social

Social Security, Medicare and Pensions 22 nd Edition Attorney Joseph L. Matthews Introduction... 1 Chapter 1 Social Security: The Basics... 5 Learning Objectives... 5 Introduction... 5 History of Social

Getting Started with Medicare

Getting Started with Medicare TABLE OF CONTENTS 2 What is Medicare? 3 Original Medicare Parts A and B 5 Medicare Part C Medicare Advantage Plans 6 Medicare Part D Prescription Drug Coverage 8 How to Enroll

Getting Started with Medicare TABLE OF CONTENTS 2 What is Medicare? 3 Original Medicare Parts A and B 5 Medicare Part C Medicare Advantage Plans 6 Medicare Part D Prescription Drug Coverage 8 How to Enroll

Planning for Medicare An Educational Resource from Blue Cross Blue Shield of Massachusetts

Planning for Medicare An Educational Resource from Blue Cross Blue Shield of Massachusetts Blue Cross Blue Shield of Massachusetts is an Independent Licensee of the Blue Cross and Blue Shield Association.

Planning for Medicare An Educational Resource from Blue Cross Blue Shield of Massachusetts Blue Cross Blue Shield of Massachusetts is an Independent Licensee of the Blue Cross and Blue Shield Association.

Supplementing Medicare: Medigap Plans

FACT SHEET Supplementing Medicare: Medigap Plans (B-002) p. 1 of 5 Supplementing Medicare: Medigap Plans What are Medigap Policies? Insurance companies sell supplemental insurance to cover part, or all,

FACT SHEET Supplementing Medicare: Medigap Plans (B-002) p. 1 of 5 Supplementing Medicare: Medigap Plans What are Medigap Policies? Insurance companies sell supplemental insurance to cover part, or all,

Medicare consists of: Hospital insurance (Part A) Medical insurance (Part B) Medicare Advantage (Part C) Prescription drug plan (Part D)

Medical insurance (Part B) Medicare Advantage (Part C) Prescription drug plan (Part D)") Medicare Understanding the program s complexities The federal government administers the Medicare insurance program to help seniors afford health care. To fully benefit from the program, you need a grasp

Medicare Understanding the program s complexities The federal government administers the Medicare insurance program to help seniors afford health care. To fully benefit from the program, you need a grasp

Original Medicare with a Medigap vs. Medicare Advantage

Original Medicare with a Medigap vs. Medicare Advantage If you have Original Medicare, the traditional health insurance program run by the federal government, it pays for most of your health care. However,

Original Medicare with a Medigap vs. Medicare Advantage If you have Original Medicare, the traditional health insurance program run by the federal government, it pays for most of your health care. However,

Medicare Made Simple

Medicare Made Simple TABLE OF CONTENTS 2 What is Medicare? 3 Original Medicare Parts A and B 5 Medicare Part C Medicare Advantage Plans 6 Medicare Part D Prescription Drug Coverage 8 How to Enroll 10 Medicare

Medicare Made Simple TABLE OF CONTENTS 2 What is Medicare? 3 Original Medicare Parts A and B 5 Medicare Part C Medicare Advantage Plans 6 Medicare Part D Prescription Drug Coverage 8 How to Enroll 10 Medicare

Understanding Your Healthcare Options in Retirement. Presented by: Tara Tyler

Understanding Your Healthcare Options in Retirement Presented by: Tara Tyler This session has been approved for continuing education credits. You must sign in during the session to receive credit for attending!

Understanding Your Healthcare Options in Retirement Presented by: Tara Tyler This session has been approved for continuing education credits. You must sign in during the session to receive credit for attending!

Understanding Medicare Fundamentals

Understanding Medicare Fundamentals A Healthcare Cost Planning Overview By Mark J. Snodgrass & Pamela K. Edinger JD September 1, 2016 Money Tree Software, Ltd. 2430 NW Professional Dr. Corvallis, OR 98330

Understanding Medicare Fundamentals A Healthcare Cost Planning Overview By Mark J. Snodgrass & Pamela K. Edinger JD September 1, 2016 Money Tree Software, Ltd. 2430 NW Professional Dr. Corvallis, OR 98330

USC Senior Care. A Supplemental Plan to Medicare

USC Senior Care A Supplemental Plan to Medicare Overview What is Senior Care? How much does it cost? How do I enroll? How does Senior Care Interact with Medicare? Frequently Asked Questions USC Senior

USC Senior Care A Supplemental Plan to Medicare Overview What is Senior Care? How much does it cost? How do I enroll? How does Senior Care Interact with Medicare? Frequently Asked Questions USC Senior

Medicare Made Simple

Medicare Made Simple TABLE OF CONTENTS 2 What is Medicare? 3 Original Medicare Parts A and B 5 Medicare Part C Medicare Advantage Plans 6 Medicare Part D Prescription Drug Coverage 8 How to Enroll 10 Medicare

Medicare Made Simple TABLE OF CONTENTS 2 What is Medicare? 3 Original Medicare Parts A and B 5 Medicare Part C Medicare Advantage Plans 6 Medicare Part D Prescription Drug Coverage 8 How to Enroll 10 Medicare

Medicare Overview. It s as easy as A, B, C, D!

1 Medicare Overview It s as easy as A, B, C, D! Original Medicare does not cover care outside the U.S. 2 3 Medicare Eligibility Generally, you are eligible for Medicare coverage at age 65 if you receive

1 Medicare Overview It s as easy as A, B, C, D! Original Medicare does not cover care outside the U.S. 2 3 Medicare Eligibility Generally, you are eligible for Medicare coverage at age 65 if you receive

Click this button to place your order.

Guide to 2018 Social Security 46th Edition A simple explanation with easy-reference benefit tables. Click this button to place your order. 2018 Guide to Social Security Mercer 400 West Market Street, Suite

Guide to 2018 Social Security 46th Edition A simple explanation with easy-reference benefit tables. Click this button to place your order. 2018 Guide to Social Security Mercer 400 West Market Street, Suite

Medicare, Medigap, and Long Term Care Insurance

Medicare, Medigap, and Long Term Care Insurance NYSBA Basics of Elder Law CLE Today s Objectives Medicare eligibility 2015 premiums Deductibles and coinsurance Limitations on coverage Appeals Medigap policies

Medicare, Medigap, and Long Term Care Insurance NYSBA Basics of Elder Law CLE Today s Objectives Medicare eligibility 2015 premiums Deductibles and coinsurance Limitations on coverage Appeals Medigap policies

Medicare at a Glance. Are you Eligible for Medicare?

Medicare at a Glance Medicare is the federal health insurance program for Americans age 65 and older and for younger adults with permanent disabilities, End-Stage Renal Disease (ESRD), or Amyotrophic Lateral

Medicare at a Glance Medicare is the federal health insurance program for Americans age 65 and older and for younger adults with permanent disabilities, End-Stage Renal Disease (ESRD), or Amyotrophic Lateral

THE BEGINNER S GUIDE TO

THE BEGINNER S GUIDE TO MEDICARE Dear Friend, Thanks for requesting a copy of our Beginner s Guide to Medicare. As someone new to Medicare, you may be a little confused about your Medicare coverage options.

THE BEGINNER S GUIDE TO MEDICARE Dear Friend, Thanks for requesting a copy of our Beginner s Guide to Medicare. As someone new to Medicare, you may be a little confused about your Medicare coverage options.

MEDICARE SUPPLEMENT PLANS. Western Marketing Associates Corporation 318 W Huron St. Missouri Valley, IA 51555

MEDICARE SUPPLEMENT PLANS FROM WESTERN MARKETING Western Marketing Associates Corporation 318 W Huron St. Missouri Valley, IA 51555 MEDICARE BASICS WHAT IS MEDICARE? Social insurance program established

MEDICARE SUPPLEMENT PLANS FROM WESTERN MARKETING Western Marketing Associates Corporation 318 W Huron St. Missouri Valley, IA 51555 MEDICARE BASICS WHAT IS MEDICARE? Social insurance program established

Medicare 101 and Senior Advantage Group Offering. Conejo Valley Unified School District November 16, 2009

Medicare 101 and Senior Advantage Group Offering Conejo Valley Unified School District November 16, 2009 What is Medicare? Medicare is a federally funded health insurance program Established in 1965 Administered

Medicare 101 and Senior Advantage Group Offering Conejo Valley Unified School District November 16, 2009 What is Medicare? Medicare is a federally funded health insurance program Established in 1965 Administered