New & Improved Redefining the Preretiree Experience

|

|

|

- Archibald Blair

- 5 years ago

- Views:

Transcription

1 New & Improved Redefining the Preretiree Experience Marty Allenbaugh Product Manager Rachel Weker Product Development Manager

2 Who Is a Preretiree? Active Retirement Plan Participants Born before 1960 (age 50+) 2

3 Preretiree Pop Quiz

4 True or False Most U.S. workers plan to retire prior to age 65 4

5 False 74% Plan to Retire at Age 65 or Later Only 26% of U.S. workers plan to retire before age 65 Retirement Prior to Age 65 26% Planned Retirement 5 Source: EBRI 2009 Retirement Confidence Survey

6 True or False Due to their low savings rates, most U.S. workers are forced to retire at age 65 or later 6

7 False They Are Retiring Earlier Than Expected 72% of retirees actually retired before age 65 Retirement Prior to Age 65 72% 26% Planned Retirement Actual Retirement 7 Source: EBRI 2009 Retirement Confidence Survey

8 True or False Retirees confidence levels about having a financially secure retirement have dropped to levels not seen since the last bear market in 2001 and

9 False The Percentage of Very Confident Retirees Has Dropped 50% During This Time Period 9

10 True or False The life expectancy for a couple in their 70s is greater than a couple in their 50s 10

11 True Life Expectancy Increases as You Reach Age Milestones Individual Couple Life Expectancy Age Age 50 Age 60 Age 65 Age Source: 2008 IRS Publication 590

12 True or False The number of preretirees will start to decline over the next few years as baby boomers start to retire 12

13 False Preretiree Base Should Increase Another 25% Over the Next Few Years 97,000 of our preretirees are age 60+, while another 190,000 participants will be celebrating their 50th birthday over the next five years 13 *These numbers are based only on the T. Rowe Price Retirement Plan Services universe.

14 True or False With the expansion of available online planning tools, a growing percentage of workers are calculating how much money they need to save for a comfortable retirement 14

simply guess at how much they will need for a comfortable")

15 False Planning Percentage Reached an All-Time High Nine Years Ago 15 An equal proportion (44%) simply guess at how much they will need for a comfortable retirement.

16 New Preretiree Program Retirement Income Consultations

17 Preretiree 1-on-1 Retirement Income Consultations Target audience is preretirees (age 50+ plan participants) We help the participant review their retirement income strategy with the help of our online tool 30-minute individual conferences Use our meeting registration service for participants to set appointments One-on-one meetings include: Personalized total retirement outlook statements Retirement Income Calculator Conducted these sessions on site and online 17

18

19

20

21

22

23

24

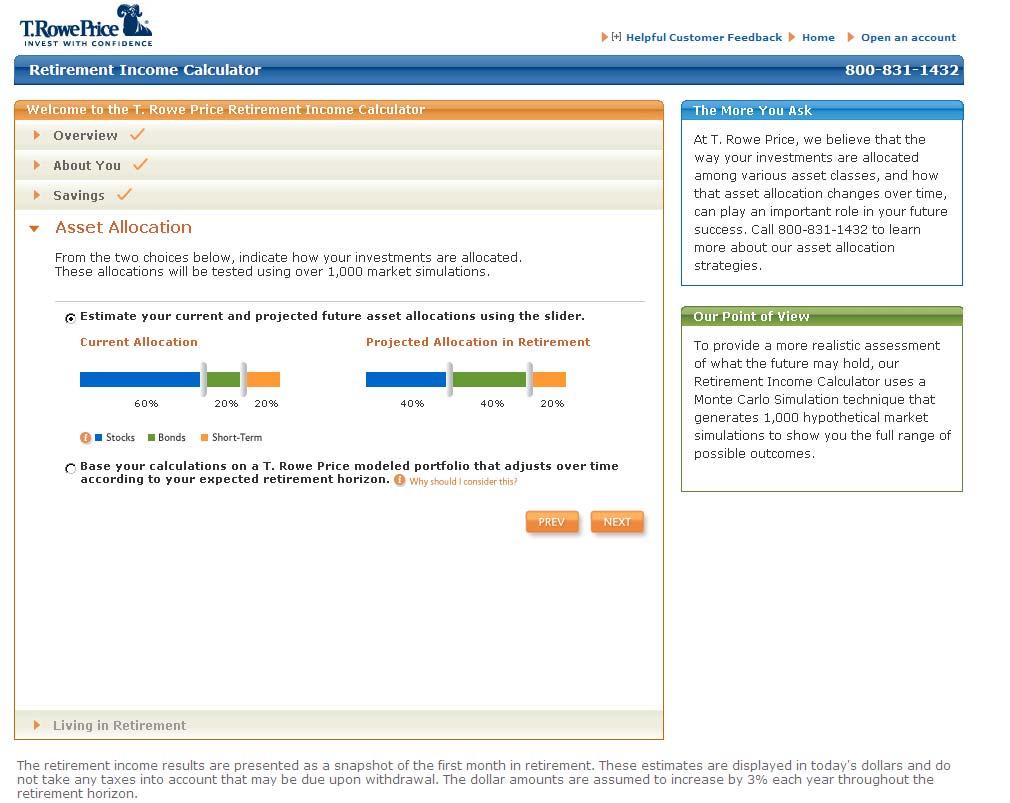

25 Monte Carlo Simulation Monte Carlo Simulation Monte Carlo simulations model future uncertainty. In contrast to tools generating average outcomes, Monte Carlo analyses produce outcome ranges based on probability, thus incorporating future uncertainty. Material Assumptions Include: Underlying long-term expected annual returns for the asset classes are not based on historical returns, but estimates, which include reinvested dividends and capital gains. Expected returns, plus assumptions about asset class volatility and correlations with other classes, are used to generate random monthly returns for each class over specific time periods. These monthly returns are then used to generate hundreds of scenarios, representing a spectrum of possible performance for the modeled asset classes. Success rates are based on these scenarios. Success rate is defined as the percent of market simulations that result in a positive balance at the end of the time horizon. Taxes on withdrawals are not taken into account, nor are early withdrawal penalties. However, fees (average expense ratios for typical actively managed funds within each asset class) are subtracted from the expected annual returns. Required minimum distributions (RMDs) are included. In the simulations, if the RMD is greater than the planned withdrawal, the excess amount is reinvested in a taxable account. Material Limitations Include: Extreme market movements may occur more often than in the model. Some asset classes have relatively short histories. Expected results for each asset class may differ from our assumptions, with those for classes with limited histories potentially diverging more. Market crises can cause asset classes to perform similarly, lowering the accuracy of projected portfolio volatility and returns. Correlation assumptions are less reliable for short periods. The model assumes correlations among asset class returns. It does not reflect the average periods of bull and bear markets, which can be longer than those modeled. 25

26 Monte Carlo Simulation, continued Inflation is assumed to be constant, so variations are not reflected in our calculations. The analysis assumes a diversified portfolio, which is rebalanced monthly. Not all asset classes are represented, and other asset classes may be similar or superior to those used. Portfolio and Initial Withdrawal Amount The underlying long-term expected annual return assumptions (without fees) are 10% for stocks, 6.5% for bonds, and 4.75% for short-term bonds. Net-of-fee expected returns use these expense ratios: 1.211% for stocks, 0.762% for bonds, and 0.648% for short-term bonds. The portfolio is either determined by the user or based on preconstructed allocations that shift in 5% increments throughout the retirement horizon (as displayed in the graphic "Why should I consider this?" in the Asset Allocation section). The initial withdrawal amount is the percentage of the initial value of the investments withdrawn on the first day of the first year. In subsequent years, the amount withdrawn grows by a 3% annual rate of inflation. Success rates are based on simulating 1,000 market scenarios and various asset-allocation strategies. IMPORTANT: The projections or other information generated by the T. Rowe Price Retirement Income Calculator regarding the likelihood of various investment outcomes are hypothetical in nature, do not reflect actual investment results, and are not guarantees of future results. The simulations are based on assumptions. There can be no assurance that the projected or simulated results will be achieved or sustained. The results present only a range of possible outcomes. Actual results will vary with each use and over time, and such results may be better or worse than the simulated scenarios. Clients should be aware that the potential for loss (or gain) may be greater than demonstrated in the simulations. The results are not predictions, but they should be viewed as reasonable estimates. Source: T. Rowe Price Associates, Inc. 26

27 Online 1-on-1 Benefits 27 More robust experience Guaranteed Internet access allows us to demo our online planning tools (Web access not always available with on-site one-on-ones) We can display this information on the participant s desktop as compared to sharing a laptop with an on-site attendee More interactive experience Attendees enter their retirement data into our planning tools More convenient experience Can conduct evening sessions Preferred channel with our Investor Center pilot group 100% of participants scheduled an online consultation vs. conducting this same session face to face at one of our Investor Centers More cost-efficient strategy Four times less expensive for our clients

were interested in attending an online retirement")

28 April 15 Ready, Set, Retire Cross-Plan Webinar Special preretiree Webinar conducted by Chris Fahlund a Certified Financial Planner with T. Rowe Price 1,876 preretirees from 200 different RPS clients attended this event 520 attendees completed the end of program survey 364 (70%) were interested in attending an online retirement income consultation 112 online consultations were completed 28

29 Participant Promoting the Program 29

30 One-on-One Registration Web site 30

31 One-on-One Attendee Survey Results Did the Information Provided in This Session Meet Your Needs? 98.3%, (116) 1.7%, (2) 2 No (please specify) Yes 31

32 96.7% Satisfaction Scores Across All Questions Please Show How Much You Agree With Each Statement I understood the information that w as presented 0.8% 24.2% 75.0% Strongly Agree Agree The T. Row e Price Representative w as know ledgeable and w ell prepared 1.7% 0.8% 15.1% 82.4% Uncertain Disagree Based on today's session, I feel more confident making retirement planning decisions 1.7% 0.8% 0.8% 30.0% 66.7% Strongly Disagree I w ould attend a similar event in the future 1.7% 0.8% 0.8% 19.0% 77.7%

33 Average Account Balance of $203, on-1 Attendee Profile vs. RPS Active Preretiree Plan Average RPS Plan Average 1-on-1 Attendee Data % % 22.6% 0 6.4% 100K+ 250K+ 500K+ 1.1% 6.6% Account Balance 33

34 2010 Preretiree Consultation Goals Two preretiree cross plan Webinar events in 2010 June and October events 4,000 attendees expected Survey our audience and recording viewers to gauge their interest in attending an online consultation We want to complete 1,200+ preretiree consultations in 2010 Roll out new online tool for our pre-term consultation attendees 34

35 Retirement Income Solutions

36 Industry Activity Around Retirement Income Exploration of different investment solutions Payout funds Target-date funds Annuities fixed and variable Living benefits Evaluation of regulatory changes Default annuitization? Press focus on inadequacy of 401(k) Need for retirement insurance? 36

37 Significant Considerations Around Different Solutions Financial stability Regulatory framework Fiduciary obligations Cost/benefit trade-offs Portability 37

38 Retirement Income Solutions Participant Concerns Flexibility Control Reliability Complexity Cost 38

39 Product Awareness Hasn t Translated Into Usage Levels of Product Interest and Usage Variable Immediate Life Annuities Variable Deferred Annuities w ith Living Benefits Fixed Deferred Annuities - Periodic Contributions Diversified Managed Payout Funds Guaranteed Fixed Immediate Life Annuities Systematic Withdraw al Programs Not at all interested Used or interested 0% 10% 20% 30% 40% 50% 60% 70% 39 Source: FRC 2009 Consumer Retirement Income and Planning Survey, May 2009

40 Participant Needs Certainly Exist Participants want to get their financial house in order during transitional phase to full retirement from partial Saving is highest priority for yr old; college and paying down debt is highest for yr old 401(k) is 2nd most important source of income in retirement 56% of households make investment decisions on own; 31% consult with advisor; 13% grant authority to advisor 46% of respondents don t have a formal plan Participant behavior may not optimize retirement decisions 40 Source: FRC 2009 Consumer Retirement Income and Planning Survey, May 2009

41 TRP Solution Name TBD Develop a program to help participants model, create, and manage a flexible source of income from their plan account throughout a potentially lengthy retirement Delivers educational value Offers planning functionality Provides transactional capabilities Participant research completed in September confirming value and approach 41

42 PROTOTYPE: CONCEPT IN DEVELOPMENT Step 1: Receive suggested approach for income program designed to generate payments throughout age 95 42

43 PROTOTYPE: CONCEPT IN DEVELOPMENT Step 2: Model impact of different changes to income program 43

44 PROTOTYPE: CONCEPT IN DEVELOPMENT Step 3: Implement income program 44

45 PROTOTYPE: CONCEPT IN DEVELOPMENT Step 4: Initiate Payments 45

46 Well Received After Extensive Research Met the needs of a diverse population From more sophisticated to not From those just starting to plan to those ready to implement payments Seen as providing ongoing value Engages participants, provides initial education and modeling Facilitates implementation of income stream Provides ongoing monitoring and management Allows complete flexibility and control Participants indicated likelihood to use 46

47 Specific Reactions Participants rated application as an average score: 87 (scale of 1 100) Described as good, flexible, complete/well thought out, educational Functionality/Aspect Liked Best Modeling (21 references as best ) Ease of use (16) Flexibility (6) Functionality/Aspect Liked Least On my own/need help making decisions (6 references as least ) Identity verification question (4) Can t add other investments (3) 47 Avg. Score: 87 (scale of 1-100)

48 In Their Words Like the modeling 48

49 In Their Words Still want high touch 49

50 In Their Words It s a great tool 50

51 Aha Moments How Will They Use It Retirement is not a single account strategy Participants want to consolidate additional assets in retirement, even if 401(k) is primary source. Interested in consolidating assets with this tool, but not an issue that would preclude use. Planning & implementation is not a one-stop deal Participants indicated likelihood to play with modeling component And then come back to set up payments 51

52 Aha Moments How They Want To Use It A good tool doesn t preclude the need for assistance Some would want to talk to someone to validate their strategy Some would need to talk to someone to walk them through the process (really get it) Some would prefer to talk to someone Existence of advisor didn t preclude desire/need for tool Felt it would help educate them in advance of their meetings Felt it would be good to use as part of advisor experience Felt it would provide validation of advisor approach 52

53 Plan Adoption Requirements Preretiree modeling calculator available for all plans Requirements for use of full application No QJSA Paperless withdrawals Allow installments and partial withdrawals Allow all products/all sources exchanges Offer TRP RDFs 53

54 What to do in 2010 Review your communications plan with your communication consultant Take advantage of the two free preretiree crossplan Webinars scheduled to take place in 2010 Your attendees will be automatically invited to sign-up for a retirement income consultation Talk to your T. Rowe Price Associate about retirement income solutions implementation 54 T. Rowe Price Investment Services, Inc.

Determining a Realistic Withdrawal Amount and Asset Allocation in Retirement

Determining a Realistic Withdrawal Amount and Asset Allocation in Retirement >> Many people look forward to retirement, but it can be one of the most complicated stages of life from a financial planning

Determining a Realistic Withdrawal Amount and Asset Allocation in Retirement >> Many people look forward to retirement, but it can be one of the most complicated stages of life from a financial planning

Revisiting T. Rowe Price s Asset Allocation Glide-Path Strategy

T. Rowe Price Revisiting T. Rowe Price s Asset Allocation Glide-Path Strategy Retirement Insights i ntroduction Given 2008 s severe stock market losses, many investors approaching or already in retirement

T. Rowe Price Revisiting T. Rowe Price s Asset Allocation Glide-Path Strategy Retirement Insights i ntroduction Given 2008 s severe stock market losses, many investors approaching or already in retirement

Measuring Retirement Plan Effectiveness

T. Rowe Price Measuring Retirement Plan Effectiveness T. Rowe Price Plan Meter helps sponsors assess and improve plan performance Retirement Insights Once considered ancillary to defined benefit (DB) pension

T. Rowe Price Measuring Retirement Plan Effectiveness T. Rowe Price Plan Meter helps sponsors assess and improve plan performance Retirement Insights Once considered ancillary to defined benefit (DB) pension

Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS

PRICE PERSPECTIVE June 2015 In-depth analysis and insights to inform your decision-making. Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS EXECUTIVE SUMMARY Plan sponsors today are faced

PRICE PERSPECTIVE June 2015 In-depth analysis and insights to inform your decision-making. Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS EXECUTIVE SUMMARY Plan sponsors today are faced

Retirement Income: Recovering From Market Devastation

Retirement Income: Recovering From Market Devastation Certainly, many investors experienced losses in the value of their retirement account balances last year. Having suffered devastating losses in their

Retirement Income: Recovering From Market Devastation Certainly, many investors experienced losses in the value of their retirement account balances last year. Having suffered devastating losses in their

Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS

PRICE PERSPECTIVE In-depth analysis and insights to inform your decision-making. Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS EXECUTIVE SUMMARY Plan sponsors today are faced with unprecedented

PRICE PERSPECTIVE In-depth analysis and insights to inform your decision-making. Getting Beyond Ordinary MANAGING PLAN COSTS IN AUTOMATIC PROGRAMS EXECUTIVE SUMMARY Plan sponsors today are faced with unprecedented

Retirement Income Analysis Executive Summary

Plan Meter Retirement Income Analysis Executive Summary T. Rowe Price Prepared for: RockTenn Measuring and improving retirement preparedness T. Rowe Price s proprietary Plan Meter report is an analytical

Plan Meter Retirement Income Analysis Executive Summary T. Rowe Price Prepared for: RockTenn Measuring and improving retirement preparedness T. Rowe Price s proprietary Plan Meter report is an analytical

Retirement Investing RETIRING IN A VOLATILE MARKET

PRICE PERSPECTIVE February 218 Retirement Investing RETIRING IN A VOLATILE MARKET In-depth analysis and insights to inform your decision-making. EXECUTIVE SUMMARY After enjoying a prolonged period of positive

PRICE PERSPECTIVE February 218 Retirement Investing RETIRING IN A VOLATILE MARKET In-depth analysis and insights to inform your decision-making. EXECUTIVE SUMMARY After enjoying a prolonged period of positive

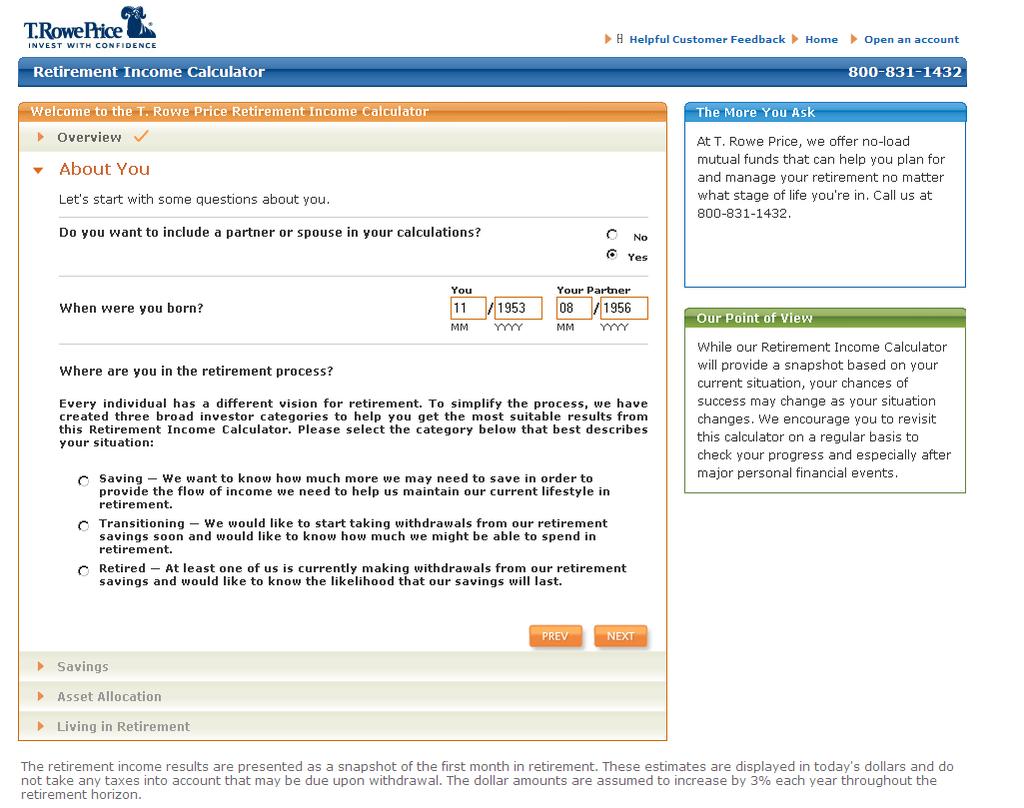

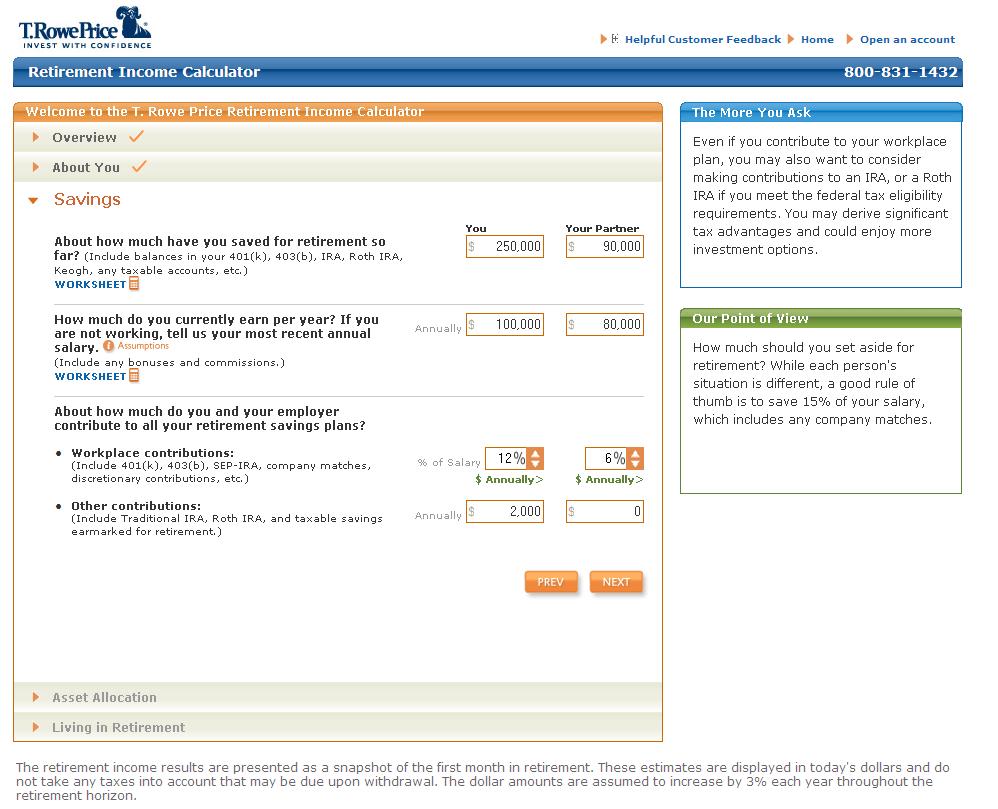

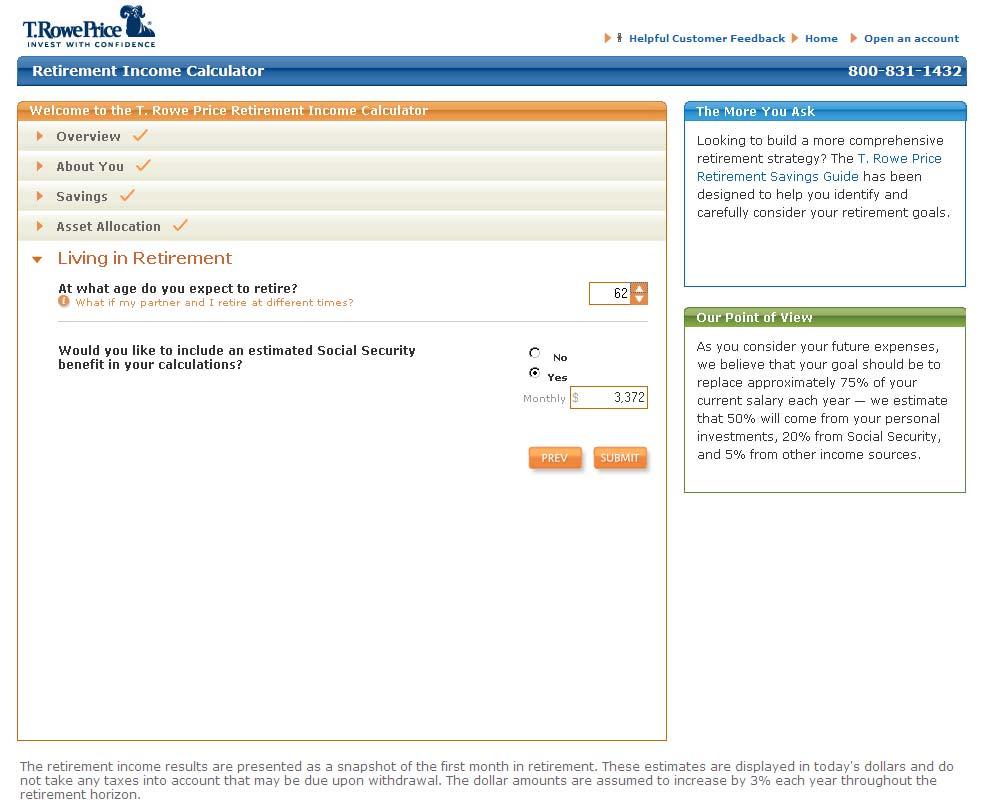

Retirement Income Calculator Methodology and Assumptions

Retirement Income Calculator Methodology and Assumptions OVERVIEW The T. Rowe Price Retirement Income Calculator allows retirement savers to estimate the durability of their current savings across 1,000

Retirement Income Calculator Methodology and Assumptions OVERVIEW The T. Rowe Price Retirement Income Calculator allows retirement savers to estimate the durability of their current savings across 1,000

INCOME PAY OPTIONAL GUARANTEED LIVING BENEFIT RIDER 14192Z PRT 08-10

INCOME PAY OPTIONAL GUARANTEED LIVING BENEFIT RIDER 14192Z PRT 08-10 DRIVE YOUR RETIREMENT DECISIONS For people age 40 and above interested in guaranteed income during their retirement, the Income Pay

INCOME PAY OPTIONAL GUARANTEED LIVING BENEFIT RIDER 14192Z PRT 08-10 DRIVE YOUR RETIREMENT DECISIONS For people age 40 and above interested in guaranteed income during their retirement, the Income Pay

Investment Progress Toward Goals. Prepared for: Bob and Mary Smith January 19, 2011

Prepared for: Bob and Mary Smith January 19, 2011 Investment Progress Toward Goals Understanding Your Results Introduction I am pleased to present you with this report that will help you answer what may

Prepared for: Bob and Mary Smith January 19, 2011 Investment Progress Toward Goals Understanding Your Results Introduction I am pleased to present you with this report that will help you answer what may

Personalized Investment Plan

Personalized Investment Plan October 27, 2014 PREPARED FOR John Sampler and Jane Client PREPARED BY: Randy Schaller Senior Investment Advisor Table Of Contents Personal Information and Summary of Financial

Personalized Investment Plan October 27, 2014 PREPARED FOR John Sampler and Jane Client PREPARED BY: Randy Schaller Senior Investment Advisor Table Of Contents Personal Information and Summary of Financial

A New Generation Retirement Strategy

A New Generation Retirement Strategy Today, Optimizing Retirement Income Requires an Increased Focus on Efficiency 8/13 80060-13A No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not

A New Generation Retirement Strategy Today, Optimizing Retirement Income Requires an Increased Focus on Efficiency 8/13 80060-13A No bank guarantee Not a deposit May lose value Not FDIC/NCUA insured Not

The Voya Retire Ready Index TM

The Voya Retire Ready Index TM Measuring the retirement readiness of Americans Table of contents Introduction...2 Methodology and framework... 3 Index factors... 4 Index results...6 Key findings... 7 Role

The Voya Retire Ready Index TM Measuring the retirement readiness of Americans Table of contents Introduction...2 Methodology and framework... 3 Index factors... 4 Index results...6 Key findings... 7 Role

Income Pay. Optional Guaranteed Lifetime Benefit Rider. Consumer Brochure Z REV Z REV 12-16

Income Pay Optional Guaranteed Lifetime Benefit Rider Consumer Brochure 1 23047Z REV 12-16 23047Z REV 12-16 Drive Your Retirement Decisions For people age 40 and above interested in guaranteed income during

Income Pay Optional Guaranteed Lifetime Benefit Rider Consumer Brochure 1 23047Z REV 12-16 23047Z REV 12-16 Drive Your Retirement Decisions For people age 40 and above interested in guaranteed income during

Optional Income Protection Rider

Optional Income Protection Rider Prepare for the unpredictable. part I am going to work full-time. Issued by Genworth Life and Annuity Insurance Company 124768 11/01/11 Life s circumstances and the financial

Optional Income Protection Rider Prepare for the unpredictable. part I am going to work full-time. Issued by Genworth Life and Annuity Insurance Company 124768 11/01/11 Life s circumstances and the financial

DETAILED METHODOLOGY. Fidelity Income Strategy Evaluator

DETAILED METHODOLOGY Fidelity Income Strategy Evaluator Updated March 2017 FIDELITY INCOME STRATEGY EVALUATOR METHODOLOGY OVERVIEW The Fidelity Income Strategy Evaluator (ISE, the Tool ) is an educational

DETAILED METHODOLOGY Fidelity Income Strategy Evaluator Updated March 2017 FIDELITY INCOME STRATEGY EVALUATOR METHODOLOGY OVERVIEW The Fidelity Income Strategy Evaluator (ISE, the Tool ) is an educational

Luke and Jen Smith. MONTE CARLO ANALYSIS November 24, 2014

Luke and Jen Smith MONTE CARLO ANALYSIS November 24, 2014 PREPARED BY: John Davidson, CFP, ChFC 1001 E. Hector St., Ste. 401 Conshohocken, PA 19428 (610) 684-1100 Table Of Contents Table Of Contents...

Luke and Jen Smith MONTE CARLO ANALYSIS November 24, 2014 PREPARED BY: John Davidson, CFP, ChFC 1001 E. Hector St., Ste. 401 Conshohocken, PA 19428 (610) 684-1100 Table Of Contents Table Of Contents...

Target Date Glide Paths: BALANCING PLAN SPONSOR GOALS 1

PRICE PERSPECTIVE In-depth analysis and insights to inform your decision-making. Target Date Glide Paths: BALANCING PLAN SPONSOR GOALS 1 EXECUTIVE SUMMARY We believe that target date portfolios are well

PRICE PERSPECTIVE In-depth analysis and insights to inform your decision-making. Target Date Glide Paths: BALANCING PLAN SPONSOR GOALS 1 EXECUTIVE SUMMARY We believe that target date portfolios are well

Optional Income Protection Rider

Optional Income Protection Rider Prepare for the unpredictable. part I am going to work full-time. Issued by Genworth Life and Annuity Insurance Company 124768 11/12/12 Life s circumstances and the financial

Optional Income Protection Rider Prepare for the unpredictable. part I am going to work full-time. Issued by Genworth Life and Annuity Insurance Company 124768 11/12/12 Life s circumstances and the financial

North American. CharterSM. Plus Fixed Index Annuity 22482Z PRT 8-15

22482Z PRT 8-15 North American CharterSM Plus Fixed Index Annuity Retirement. many people, retirement is viewed as a time of rest and reflection. They have worked hard and planned diligently to ensure

22482Z PRT 8-15 North American CharterSM Plus Fixed Index Annuity Retirement. many people, retirement is viewed as a time of rest and reflection. They have worked hard and planned diligently to ensure

MetLife Retirement Income. A Survey of Pre-Retiree Knowledge of Financial Retirement Issues

MetLife Retirement Income IQ Study A Survey of Pre-Retiree Knowledge of Financial Retirement Issues June, 2008 The MetLife Mature Market Institute Established in 1997, the Mature Market Institute (MMI)

MetLife Retirement Income IQ Study A Survey of Pre-Retiree Knowledge of Financial Retirement Issues June, 2008 The MetLife Mature Market Institute Established in 1997, the Mature Market Institute (MMI)

Enroll today. Enjoy tomorrow. University System of Georgia Benefits 403(b) and 457(b) Retirement Plans SAVING : INVESTING : PLANNING

and 457(b) Retirement Plans SAVING : INVESTING : PLANNING") Enroll today. Enjoy tomorrow. University System of Georgia Benefits 403(b) and 457(b) Retirement Plans SAVING : INVESTING : PLANNING 2 It s your future. Make it the one you envision. As an employee of

Enroll today. Enjoy tomorrow. University System of Georgia Benefits 403(b) and 457(b) Retirement Plans SAVING : INVESTING : PLANNING 2 It s your future. Make it the one you envision. As an employee of

North American Guarantee Choice SM

North American Guarantee Choice SM Multi-Year Guarantee Annuity Consumer Brochure 1 19734Z PRT 12-14 19734Z PRT 12-14 North American Guarantee Choice Are you looking for ways to manage your future retirement

North American Guarantee Choice SM Multi-Year Guarantee Annuity Consumer Brochure 1 19734Z PRT 12-14 19734Z PRT 12-14 North American Guarantee Choice Are you looking for ways to manage your future retirement

Optional Income Protection Rider

Optional Income Protection Rider Prepare for the unpredictable. part I am going to work full-time. Issued by Genworth Life and Annuity Insurance Company 124768 08/18/14 Can you predict how long you ll

Optional Income Protection Rider Prepare for the unpredictable. part I am going to work full-time. Issued by Genworth Life and Annuity Insurance Company 124768 08/18/14 Can you predict how long you ll

Financial Goal Plan. John and Jane Doe. Prepared by: William LaChance Financial Advisor

Financial Goal Plan John and Jane Doe Prepared by: William LaChance Financial Advisor December 15, 215 Table Of Contents Summary of Goals and Resources Personal Information and Summary of Financial Goals

Financial Goal Plan John and Jane Doe Prepared by: William LaChance Financial Advisor December 15, 215 Table Of Contents Summary of Goals and Resources Personal Information and Summary of Financial Goals

Make your money work as hard as you do.

Lifetime Income Track Living benefit guide Make your money work as hard as you do. Your key to retirement income potential. A Nationwide Destination SM Series 2.0 variable annuity with the Nationwide Lifetime

Lifetime Income Track Living benefit guide Make your money work as hard as you do. Your key to retirement income potential. A Nationwide Destination SM Series 2.0 variable annuity with the Nationwide Lifetime

ERIE COUNTY. New York. Enrollment Brochure

ERIE COUNTY New York Enrollment Brochure Erie County is dedicated to the health and wellness of our community and your retirement. The Erie County 457(b) Deferred Compensation Plan The future is yours

ERIE COUNTY New York Enrollment Brochure Erie County is dedicated to the health and wellness of our community and your retirement. The Erie County 457(b) Deferred Compensation Plan The future is yours

Establishing Your Retirement Income Stream

1 Establishing Your Retirement Income Stream What is important about retirement planning to you? 2 Building your retirement house 4 Legacy Benefits 3 2 Retirement income planning Accumulation 1 Expenses

1 Establishing Your Retirement Income Stream What is important about retirement planning to you? 2 Building your retirement house 4 Legacy Benefits 3 2 Retirement income planning Accumulation 1 Expenses

JULY s Retirement Readiness Tools & Resources

JULY s Retirement Readiness Tools & Resources JULY Overview Founded 1994 / Privately Owned National Recordkeeping Firm 3,300 Clients 92,000 Participants $2.8 Billion In Plan Assets Plan Sizes $0 to $30

JULY s Retirement Readiness Tools & Resources JULY Overview Founded 1994 / Privately Owned National Recordkeeping Firm 3,300 Clients 92,000 Participants $2.8 Billion In Plan Assets Plan Sizes $0 to $30

John and Margaret Boomer

Retirement Lifestyle Plan Includes Insurance and Estate - Using Projected Returns John and Margaret Boomer Prepared by : Sample Report June 06, 2012 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-9

Retirement Lifestyle Plan Includes Insurance and Estate - Using Projected Returns John and Margaret Boomer Prepared by : Sample Report June 06, 2012 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-9

Optimal Withdrawal Strategy for Retirement Income Portfolios

Optimal Withdrawal Strategy for Retirement Income Portfolios David Blanchett, CFA Head of Retirement Research Maciej Kowara, Ph.D., CFA Senior Research Consultant Peng Chen, Ph.D., CFA President September

Optimal Withdrawal Strategy for Retirement Income Portfolios David Blanchett, CFA Head of Retirement Research Maciej Kowara, Ph.D., CFA Senior Research Consultant Peng Chen, Ph.D., CFA President September

Anthony and Denise Martin

Sample Client Reports Disclosures & Glossary Report Anthony and Denise Martin Prepared by: Advisor Name Advisor Phone Number Advisor Email Address March 08, 2018 Table Of Contents IMPORTANT DISCLOSURE

Sample Client Reports Disclosures & Glossary Report Anthony and Denise Martin Prepared by: Advisor Name Advisor Phone Number Advisor Email Address March 08, 2018 Table Of Contents IMPORTANT DISCLOSURE

My retirement, March 18 April 15, Explore Compare Choose. Retirement Choice Decision Guide For Johns Hopkins University Support Staff

My retirement, Retirement Choice Decision Guide For Johns Hopkins University Support Staff March 18 April 15, 2011 Explore Compare Choose You need to make an important decision regarding your retirement

My retirement, Retirement Choice Decision Guide For Johns Hopkins University Support Staff March 18 April 15, 2011 Explore Compare Choose You need to make an important decision regarding your retirement

SEP-IRA PLAN. Employee Guidebook CONTENTS. Welcome Building retirement savings Options for investing Get started Open your account

SEP-IRA PLAN Employee Guidebook CONTENTS WELCOME. We know your retirement savings will be one of your most valuable assets, so we are committed to managing risk and taking a long-term approach to investing.

SEP-IRA PLAN Employee Guidebook CONTENTS WELCOME. We know your retirement savings will be one of your most valuable assets, so we are committed to managing risk and taking a long-term approach to investing.

A guide to your retirement income options with TIAA-CREF

A guide to your retirement income options with TIAA-CREF Helping you make important decisions about your retirement How will I know when the time is right to retire? Making the decision to retire is no

A guide to your retirement income options with TIAA-CREF Helping you make important decisions about your retirement How will I know when the time is right to retire? Making the decision to retire is no

Financial Goal Plan. Jane and John Doe. Prepared by: Alex Schmitz, CFP Director of Financial Planning

Financial Goal Plan Jane and John Doe Prepared by: Alex Schmitz, CFP Director of Financial Planning March 07, 2018 Table Of Contents Table of Contents Section Title IMPORTANT DISCLOSURE INFORMATION 1-5

Financial Goal Plan Jane and John Doe Prepared by: Alex Schmitz, CFP Director of Financial Planning March 07, 2018 Table Of Contents Table of Contents Section Title IMPORTANT DISCLOSURE INFORMATION 1-5

SanJose.beready2retire.com. City of San José Deferred Compensation. Plan Overview DEFER R ED CO MPENSATION PLAN PLAN SAVE GROW

SanJose.beready2retire.com City of San José Deferred Compensation Plan Overview DEFER R ED CO MPENSATION PLAN PLAN SAVE GROW Having the income you need in your later years may require careful planning

SanJose.beready2retire.com City of San José Deferred Compensation Plan Overview DEFER R ED CO MPENSATION PLAN PLAN SAVE GROW Having the income you need in your later years may require careful planning

MassMutual Odyssey Select SM

MassMutual Odyssey Select SM A Flexible Premium Deferred Fixed Annuity Save for retirement your way MassMutual Odyssey Select (Odyssey Select) is a flexible premium deferred fixed annuity issued by Massachusetts

MassMutual Odyssey Select SM A Flexible Premium Deferred Fixed Annuity Save for retirement your way MassMutual Odyssey Select (Odyssey Select) is a flexible premium deferred fixed annuity issued by Massachusetts

Principia Presentations & Education

Principia Presentations & Education The 2008 Principia Presentations & Education library encompasses a collection of communication resources developed to assist advisors during client interactions. Specialized

Principia Presentations & Education The 2008 Principia Presentations & Education library encompasses a collection of communication resources developed to assist advisors during client interactions. Specialized

INVESTMENT PLAN. Sample Client. For. May 04, Prepared by : Sample Advisor Financial Consultant.

INVESTMENT PLAN For Sample Client May 04, 2012 Prepared by : Sample Advisor Financial Consultant sadvisor@loringward.com Materials provided to approved advisors by LWI Financial Inc., ( Loring Ward ).

INVESTMENT PLAN For Sample Client May 04, 2012 Prepared by : Sample Advisor Financial Consultant sadvisor@loringward.com Materials provided to approved advisors by LWI Financial Inc., ( Loring Ward ).

City of San José Deferred Compensation Plan Overview D EF ER R ED C OMPE NSATION PLAN PLAN SAVE GROW

www.voyaretirementplans.com/custom/sanjose City of San José Deferred Compensation Plan Overview D EF ER R ED C OMPE NSATION PLAN PLAN SAVE GROW You should consider the investment objectives, risks, and

www.voyaretirementplans.com/custom/sanjose City of San José Deferred Compensation Plan Overview D EF ER R ED C OMPE NSATION PLAN PLAN SAVE GROW You should consider the investment objectives, risks, and

John and Margaret Boomer

Retirement Lifestyle Plan Using Projected Returns John and Margaret Boomer Prepared by : Sample Advisor Financial Advisor September 17, 2008 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-7 Presentation

Retirement Lifestyle Plan Using Projected Returns John and Margaret Boomer Prepared by : Sample Advisor Financial Advisor September 17, 2008 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-7 Presentation

Complete your retirement picture with guaranteed income

Complete your retirement picture with guaranteed income ANNUITIES INCOME Brighthouse Income Annuity SM Add immediate income for more certainty. All guarantees are subject to the claims-paying ability and

Complete your retirement picture with guaranteed income ANNUITIES INCOME Brighthouse Income Annuity SM Add immediate income for more certainty. All guarantees are subject to the claims-paying ability and

John and Margaret Boomer

Insurance Analysis Using Projected Returns John and Margaret Boomer Prepared by : Sample Report June 11, 2012 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-9 Risk Management Personal Information

Insurance Analysis Using Projected Returns John and Margaret Boomer Prepared by : Sample Report June 11, 2012 Table Of Contents IMPORTANT DISCLOSURE INFORMATION 1-9 Risk Management Personal Information

THREE SIMPLE STEPS TO ENROLL

University of Minnesota Retirement Plans Complete the application Match the results Complete the quiz Retirement for U THREE SIMPLE STEPS TO ENROLL Need help? A Securian Plan Specialist can provide information

University of Minnesota Retirement Plans Complete the application Match the results Complete the quiz Retirement for U THREE SIMPLE STEPS TO ENROLL Need help? A Securian Plan Specialist can provide information

Coping with Sequence Risk: How Variable Withdrawal and Annuitization Improve Retirement Outcomes

Coping with Sequence Risk: How Variable Withdrawal and Annuitization Improve Retirement Outcomes September 25, 2017 by Joe Tomlinson Both the level and the sequence of investment returns will have a big

Coping with Sequence Risk: How Variable Withdrawal and Annuitization Improve Retirement Outcomes September 25, 2017 by Joe Tomlinson Both the level and the sequence of investment returns will have a big

Inverted Withdrawal Rates and the Sequence of Returns Bonus

Inverted Withdrawal Rates and the Sequence of Returns Bonus May 17, 2016 by John Walton Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of

Inverted Withdrawal Rates and the Sequence of Returns Bonus May 17, 2016 by John Walton Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of

Navigate your journey to and through retirement

Navigate your journey to and through retirement Voya Quest 7 Index Annuity A flexible premium deferred fixed index annuity with an optional guaranteed lifetime income rider issued by Voya Insurance and

Navigate your journey to and through retirement Voya Quest 7 Index Annuity A flexible premium deferred fixed index annuity with an optional guaranteed lifetime income rider issued by Voya Insurance and

The American College Defined Contribution Rollover Survey

The American College Defined Contribution Rollover Survey January 2016 Table of Contents Methodology 3 Key Findings 5 The Rollover Decision 14 Retirement Financial Planning 33 Investment Management 52

The American College Defined Contribution Rollover Survey January 2016 Table of Contents Methodology 3 Key Findings 5 The Rollover Decision 14 Retirement Financial Planning 33 Investment Management 52

North American Guarantee Choice SM

North American Guarantee Choice SM Multi-Year Guarantee Annuity Consumer Brochure 1 19734Z-CT REV 10-15 19734Z-CT REV 10-15 North American Guarantee Choice SM Are you looking for ways to manage your future

North American Guarantee Choice SM Multi-Year Guarantee Annuity Consumer Brochure 1 19734Z-CT REV 10-15 19734Z-CT REV 10-15 North American Guarantee Choice SM Are you looking for ways to manage your future

Income Mindsets. Why segmentation is key to winning in the Baby Boomer market (1/11/18)

") Income Mindsets Why segmentation is key to winning in the Baby Boomer market 1678298 (1/11/18) 1 Retirement income isn t one-size-fits-all 2 Retirement planning and advice is different, too. Accumulation

Income Mindsets Why segmentation is key to winning in the Baby Boomer market 1678298 (1/11/18) 1 Retirement income isn t one-size-fits-all 2 Retirement planning and advice is different, too. Accumulation

Retirement Lifestyle Solution

ADVISOR SALES GUIDE AND TOOLKIT Retirement Lifestyle Solution INVESTED. TOGETHER. How do we address the retirement income challenge? 61% of Baby Boomers say they re more afraid of running out of money

ADVISOR SALES GUIDE AND TOOLKIT Retirement Lifestyle Solution INVESTED. TOGETHER. How do we address the retirement income challenge? 61% of Baby Boomers say they re more afraid of running out of money

An Insider s Guide to Annuities. The Safe Money Guide. retirement security investment growth

The Safe Money Guide retirement security investment growth An Insider s Guide to Annuities 1 Presented by Joe Brown Brown Advisory Group, LLC http://joebrown.retirevillage.com An Insider s Guide to Annuities

The Safe Money Guide retirement security investment growth An Insider s Guide to Annuities 1 Presented by Joe Brown Brown Advisory Group, LLC http://joebrown.retirevillage.com An Insider s Guide to Annuities

Making Informed Rollover Decisions

Making Informed Rollover Decisions WHAT TO DO WITH YOUR EMPLOYER-SPONSORED RETIREMENT PLAN ASSETS DEFINED CONTRIBUTION PLANS: A defined contribution plan does not promise a specific amount of benefits

Making Informed Rollover Decisions WHAT TO DO WITH YOUR EMPLOYER-SPONSORED RETIREMENT PLAN ASSETS DEFINED CONTRIBUTION PLANS: A defined contribution plan does not promise a specific amount of benefits

403(b) PLAN. Employee Guidebook. Welcome Building retirement savings Options for investing You have control Open your account CONTENTS

PLAN. Employee Guidebook. Welcome Building retirement savings Options for investing You have control Open your account CONTENTS") 403(b) PLAN CONTENTS Employee Guidebook WELCOME. One of the main reasons your employer chose T. Rowe Price as an investment provider for your 403(b) plan is because we ve established a reputation for competitive

403(b) PLAN CONTENTS Employee Guidebook WELCOME. One of the main reasons your employer chose T. Rowe Price as an investment provider for your 403(b) plan is because we ve established a reputation for competitive

North American. Charter Plus 10. Fixed Index Annuity 25304Z-20 PRT 4-17

25304Z-20 PRT 4-17 North American Charter Plus 10 Fixed Index Annuity Retirement. many people, retirement is viewed as a time of rest and reflection. They have worked hard and planned diligently to ensure

25304Z-20 PRT 4-17 North American Charter Plus 10 Fixed Index Annuity Retirement. many people, retirement is viewed as a time of rest and reflection. They have worked hard and planned diligently to ensure

CREATE CUSTOM LOOK. ADD NEW COLORS AND REPLACE FONTS IN STYLE SHEETS THROUGHOUT BROCHURE. Baptist Health. 403(b) and 401(k) Retirement Plans

and 401(k) Retirement Plans") CREATE CUSTOM LOOK. ADD NEW COLORS AND REPLACE FONTS IN STYLE SHEETS THROUGHOUT BROCHURE. Baptist Health 403(b) and 401(k) Retirement Plans 2 Baptist Health 403(b) and 401(k) Retirement Plans The Baptist

CREATE CUSTOM LOOK. ADD NEW COLORS AND REPLACE FONTS IN STYLE SHEETS THROUGHOUT BROCHURE. Baptist Health 403(b) and 401(k) Retirement Plans 2 Baptist Health 403(b) and 401(k) Retirement Plans The Baptist

CHOICE Variable Annuity Fact Sheet

PACIFIC CHOICE Variable Annuity Fact Sheet Why a Variable Annuity A variable annuity, like Pacific Choice, is a long-term contract between you and an insurance company that helps you grow, protect, and

PACIFIC CHOICE Variable Annuity Fact Sheet Why a Variable Annuity A variable annuity, like Pacific Choice, is a long-term contract between you and an insurance company that helps you grow, protect, and

LIVING IN RETIREMENT: A TIAA FINANCIAL ESSENTIALS WORKSHOP. Paying Yourself: Income options in retirement Kyle Andrews February 23, 2017

LIVING IN RETIREMENT: A TIAA FINANCIAL ESSENTIALS WORKSHOP Paying Yourself: Income options in retirement Kyle Andrews February 23, 2017 Retirement overview Retirement confidence is rebounding after recent

LIVING IN RETIREMENT: A TIAA FINANCIAL ESSENTIALS WORKSHOP Paying Yourself: Income options in retirement Kyle Andrews February 23, 2017 Retirement overview Retirement confidence is rebounding after recent

Understanding and Achieving Participant Financial Wellness

Understanding and Achieving Participant Financial Wellness Insights from our research From August 25, 2017 to January 31, 2018, the companies of OneAmerica fielded an online survey to retirement plan participants

Understanding and Achieving Participant Financial Wellness Insights from our research From August 25, 2017 to January 31, 2018, the companies of OneAmerica fielded an online survey to retirement plan participants

The oldest members of the 78 million U.S. baby

A Framework for Managing Retirement Income GWM INVESTMENT MANAGEMENT & GUIDANCE FALL 2009 You ve probably spent most of your life focusing on the accumulation of assets. In retirement, however, you need

A Framework for Managing Retirement Income GWM INVESTMENT MANAGEMENT & GUIDANCE FALL 2009 You ve probably spent most of your life focusing on the accumulation of assets. In retirement, however, you need

401(k) IQ in the Workplace Survey Report

IQ in the Workplace Survey Report") 401(k) IQ in the Workplace Survey Report 2017 Fisher Investments. Investing in securities involves the risk of loss. Intended for use by employers considering or sponsoring retirement plans; not for personal

401(k) IQ in the Workplace Survey Report 2017 Fisher Investments. Investing in securities involves the risk of loss. Intended for use by employers considering or sponsoring retirement plans; not for personal

ODYSSEY Variable Annuity Fact Sheet

PACIFIC ODYSSEY Variable Annuity Fact Sheet Why a Variable Annuity A variable annuity, like Pacific Odyssey, is a long-term contract between you and an insurance company that helps you grow, protect, and

PACIFIC ODYSSEY Variable Annuity Fact Sheet Why a Variable Annuity A variable annuity, like Pacific Odyssey, is a long-term contract between you and an insurance company that helps you grow, protect, and

BETTER PARTICIPANT OUTCOMES

BETTER PARTICIPANT OUTCOMES through in-plan guaranteed retirement income Christine C. Marcks John J. Kalamarides President Senior Vice President Full Service Solutions Prudential Retirement Prudential

BETTER PARTICIPANT OUTCOMES through in-plan guaranteed retirement income Christine C. Marcks John J. Kalamarides President Senior Vice President Full Service Solutions Prudential Retirement Prudential

taking control of my future

variable annuity taking control of my future Retirement Cornerstone variable annuity Variable Annuities: Are Not a Deposit of Any Bank Are Not FDIC Insured Are Not Insured by Any Federal Government Agency

variable annuity taking control of my future Retirement Cornerstone variable annuity Variable Annuities: Are Not a Deposit of Any Bank Are Not FDIC Insured Are Not Insured by Any Federal Government Agency

The How Do I Save For Retirement Challenge

0278470-00003-00 Exp 12/12/2018 RSPP487 The How Do I Save For Retirement Challenge Presented by Dallas Chastain Place client logo here Magellan Health, Inc. Retirement Savings Plan This presentation is

0278470-00003-00 Exp 12/12/2018 RSPP487 The How Do I Save For Retirement Challenge Presented by Dallas Chastain Place client logo here Magellan Health, Inc. Retirement Savings Plan This presentation is

Target-Date Glide Paths: Balancing Plan Sponsor Goals 1

Target-Date Glide Paths: Balancing Plan Sponsor Goals 1 T. Rowe Price Investment Dialogue November 2014 Authored by: Richard K. Fullmer, CFA James A Tzitzouris, Ph.D. Executive Summary We believe that

Target-Date Glide Paths: Balancing Plan Sponsor Goals 1 T. Rowe Price Investment Dialogue November 2014 Authored by: Richard K. Fullmer, CFA James A Tzitzouris, Ph.D. Executive Summary We believe that

Millennial, Gen X, and Baby Boomer Workers and Retirees RETIREMENT SAVING & SPENDING STUDY

Millennial, Gen X, and Baby Boomer Workers and Retirees RETIREMENT SAVING & SPENDING STUDY Table of Contents Methodology Workers with 401(k)s: Millennials, Gen X, and Baby boomers Workers 401(k) Accounts

Millennial, Gen X, and Baby Boomer Workers and Retirees RETIREMENT SAVING & SPENDING STUDY Table of Contents Methodology Workers with 401(k)s: Millennials, Gen X, and Baby boomers Workers 401(k) Accounts

Build your retirement plan to last a lifetime.

Build your retirement plan to last a lifetime. PHOENIX PERSONAL INCOME ANNUITY A single-premium fixed indexed annuity with lifetime income options For use by financial professionals with the general public.

Build your retirement plan to last a lifetime. PHOENIX PERSONAL INCOME ANNUITY A single-premium fixed indexed annuity with lifetime income options For use by financial professionals with the general public.

Building Your. Retirement Roadmap

Building Your Retirement Roadmap Today s Agenda Discuss a roadmap for saving to help you meet your retirement goals Look at key financial principles to follow Review action steps to consider How Fidelity

Building Your Retirement Roadmap Today s Agenda Discuss a roadmap for saving to help you meet your retirement goals Look at key financial principles to follow Review action steps to consider How Fidelity

MNL IndexBuilder SM. Fixed Index Annuity

MNL IndexBuilder SM Fixed Index Annuity Z 22481Y PRT 8-15 PRT 8-15 Retirement. For many people, retirement is viewed as a time of rest and reflection. They have worked hard and planned diligently to ensure

MNL IndexBuilder SM Fixed Index Annuity Z 22481Y PRT 8-15 PRT 8-15 Retirement. For many people, retirement is viewed as a time of rest and reflection. They have worked hard and planned diligently to ensure

NAC IncomeChoice. Fixed Index Annuity. Consumer Brochure Z REV Z REV 2-17

NAC IncomeChoice Fixed Index Annuity Consumer Brochure 1 23713Z REV 2-17 23713Z REV 2-17 The Income You Need The Potential You Want Like many individuals, you ve probably spent years saving for retirement

NAC IncomeChoice Fixed Index Annuity Consumer Brochure 1 23713Z REV 2-17 23713Z REV 2-17 The Income You Need The Potential You Want Like many individuals, you ve probably spent years saving for retirement

Guaranteed Income for Life. Voya IncomeProtector Withdrawal Benefit. Available with a Fixed Index Annuity from Voya Insurance and Annuity Company

Guaranteed Income for Life Voya IncomeProtector Withdrawal Benefit Available with a Fixed Index Annuity from Voya Insurance and Annuity Company Guaranteed Income for Life The median income for retired

Guaranteed Income for Life Voya IncomeProtector Withdrawal Benefit Available with a Fixed Index Annuity from Voya Insurance and Annuity Company Guaranteed Income for Life The median income for retired

Mapping the Road to Retirement

Mapping the Road to Retirement A Fidelity Perspective Steps You Can Take to Improve Your Retirement Readiness. Every one of us wants to look forward to a secure financial future. Many are taking steps

Mapping the Road to Retirement A Fidelity Perspective Steps You Can Take to Improve Your Retirement Readiness. Every one of us wants to look forward to a secure financial future. Many are taking steps

Joe and Jane Coastal Member

Retirement Plan Joe and Jane Coastal Member Prepared by: Catherine Bryant Financial Advisor Coastal Wealth Management/CUSO FS January 31, 2018 Table Of Contents Personal Information and Summary of Financial

Retirement Plan Joe and Jane Coastal Member Prepared by: Catherine Bryant Financial Advisor Coastal Wealth Management/CUSO FS January 31, 2018 Table Of Contents Personal Information and Summary of Financial

David M. Jones, MBA, CFP

White Paper: How Traditional Investing Can Fail Baby Boomers David M. Jones, MBA, CFP www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities

White Paper: How Traditional Investing Can Fail Baby Boomers David M. Jones, MBA, CFP www.selectportfolio.com Toll Free 800.445.9822 Tel 949.975.7900 Fax 949.900.8181 Securities offered through Securities

Charter Plus 10 Fixed Index Annuity

25304Z REV 7-17 North American Charter Plus 10 Fixed Index Annuity Retirement. many people, retirement is viewed as a time of rest and reflection. They have worked hard and planned diligently to ensure

25304Z REV 7-17 North American Charter Plus 10 Fixed Index Annuity Retirement. many people, retirement is viewed as a time of rest and reflection. They have worked hard and planned diligently to ensure

Prudential ANNUITIES ANNUITIES UNDERSTANDING. Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey.

Prudential ANNUITIES UNDERSTANDING ANNUITIES Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey. 0160994-00008-00 Ed. 05/2017 Meeting the challenges of retirement

Prudential ANNUITIES UNDERSTANDING ANNUITIES Issued by Pruco Life Insurance Company and by Pruco Life Insurance Company of New Jersey. 0160994-00008-00 Ed. 05/2017 Meeting the challenges of retirement

Rev Up Your Readiness to Retire

Rev Up Your Readiness to Retire Posted: 12/6/2013 by Fidelity Viewpoints Fidelity study finds more than half of Americans at risk. Consider six steps to get on track. Despite improvements in the economy,

Rev Up Your Readiness to Retire Posted: 12/6/2013 by Fidelity Viewpoints Fidelity study finds more than half of Americans at risk. Consider six steps to get on track. Despite improvements in the economy,

Lewis Coopersmith, Ph. D.

Making the Most of One s Nest Egg: Optimal Tax-wise Planning of Withdrawals from Retirement Accounts* INFORMS New York Metro Wednesday, December 12, 2007 Lewis Coopersmith, Ph. D. Associate Professor,

Making the Most of One s Nest Egg: Optimal Tax-wise Planning of Withdrawals from Retirement Accounts* INFORMS New York Metro Wednesday, December 12, 2007 Lewis Coopersmith, Ph. D. Associate Professor,

Transamerica Small Business Retirement Survey

Transamerica Small Business Retirement Survey Summary of Findings October 16, 2003 Table of Contents Background and Objectives 3 Methodology 4 Key Findings 2003 8 Key Trends - 1998 to 2003 18 Detailed

Transamerica Small Business Retirement Survey Summary of Findings October 16, 2003 Table of Contents Background and Objectives 3 Methodology 4 Key Findings 2003 8 Key Trends - 1998 to 2003 18 Detailed

Secure Your Retirement

4 Creating a Framework 6 Case Study #1: The Dunbars 8 Case Study #2: Professor Harrison 9 Case Study #3: Jane Leahy Advanced Annuity Strategies to Help Secure Your Retirement The Paradigm Has Shifted.

4 Creating a Framework 6 Case Study #1: The Dunbars 8 Case Study #2: Professor Harrison 9 Case Study #3: Jane Leahy Advanced Annuity Strategies to Help Secure Your Retirement The Paradigm Has Shifted.

Opportunities in the state and local government market. Retirement plan support for consultants and advisors

Opportunities in the state and local government market Retirement plan support for consultants and advisors State and local governments have specific needs. Governments generally face decreasing revenues

Opportunities in the state and local government market Retirement plan support for consultants and advisors State and local governments have specific needs. Governments generally face decreasing revenues

RetirementWorks. The input can be made extremely simple and approximate, or it can be more detailed and accurate:

Retirement Income Annuitization The RetirementWorks Retirement Income Annuitization calculator analyzes how much of a retiree s savings should be converted to a monthly annuity stream. It uses a needs-based

Retirement Income Annuitization The RetirementWorks Retirement Income Annuitization calculator analyzes how much of a retiree s savings should be converted to a monthly annuity stream. It uses a needs-based

Let s Talk About: Required Minimum Distributions from Qualified Annuities. Your future. Made easier. SM ANNUITIES

Let s Talk About: Required Minimum Distributions from Qualified Annuities Not FDIC/NCUA Insured May Lose Value Not A Deposit Of A Bank Not Bank Guaranteed Not Insured By Any Federal Government Agency ANNUITIES

Let s Talk About: Required Minimum Distributions from Qualified Annuities Not FDIC/NCUA Insured May Lose Value Not A Deposit Of A Bank Not Bank Guaranteed Not Insured By Any Federal Government Agency ANNUITIES

SOCIAL SECURITY WON T BE ENOUGH:

SOCIAL SECURITY WON T BE ENOUGH: 6 REASONS TO CONSIDER AN INCOME ANNUITY How long before you retire? For some of us it s 20 to 30 years away, and for others it s closer to 5 or 0 years. The key here is

SOCIAL SECURITY WON T BE ENOUGH: 6 REASONS TO CONSIDER AN INCOME ANNUITY How long before you retire? For some of us it s 20 to 30 years away, and for others it s closer to 5 or 0 years. The key here is

RETIREMENT READINESS FOR YOUR EMPLOYEES THE VALUE OF ADVICE AND PLANNING

RETIREMENT READINESS FOR YOUR EMPLOYEES THE VALUE OF ADVICE AND PLANNING Advice and Planning Services is a division of TIAA-CREF Individual & Institutional Services, LLC, a registered investment advisor.

RETIREMENT READINESS FOR YOUR EMPLOYEES THE VALUE OF ADVICE AND PLANNING Advice and Planning Services is a division of TIAA-CREF Individual & Institutional Services, LLC, a registered investment advisor.

An Introduction to Resampled Efficiency

by Richard O. Michaud New Frontier Advisors Newsletter 3 rd quarter, 2002 Abstract Resampled Efficiency provides the solution to using uncertain information in portfolio optimization. 2 The proper purpose

by Richard O. Michaud New Frontier Advisors Newsletter 3 rd quarter, 2002 Abstract Resampled Efficiency provides the solution to using uncertain information in portfolio optimization. 2 The proper purpose

25296Z REV PrimePath 9 Fixed Index Annuity

25296Z REV 3-18 PrimePath 9 Fixed Index Annuity Your PrimePath 9 to Retirement Planning for retirement can be overwhelming will I have enough to retire? How much is enough? How much longer will I need

25296Z REV 3-18 PrimePath 9 Fixed Index Annuity Your PrimePath 9 to Retirement Planning for retirement can be overwhelming will I have enough to retire? How much is enough? How much longer will I need

Your life. Your future. Your options.

Your life. Your future. Your options. Whether by chance or by choice, you have options. Explore them with Empower Retirement. Corporate Retirement Plan Participant Brochure You want to retire someday or

Your life. Your future. Your options. Whether by chance or by choice, you have options. Explore them with Empower Retirement. Corporate Retirement Plan Participant Brochure You want to retire someday or

How Do You Measure Which Retirement Income Strategy Is Best?

How Do You Measure Which Retirement Income Strategy Is Best? April 19, 2016 by Michael Kitces Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those

How Do You Measure Which Retirement Income Strategy Is Best? April 19, 2016 by Michael Kitces Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those

Susan & David Example

Personal Retirement Analysis for Susan & David Example Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com IMPORTANT:

Personal Retirement Analysis for Susan & David Example Asset Advisors Example, LLC A Registered Investment Advisor 2430 NW Professional Drive Corvallis, OR 97330 877-421-9815 www.moneytree.com IMPORTANT:

Lifetime Income Benefit Rider

for a secure Retirement Lifetime Income Benefit Rider (LIBR-2010)* Included automatically on most Fixed Indexed Annuities** for use with Fixed Indexed Annuities *May vary by state. Not available in all

for a secure Retirement Lifetime Income Benefit Rider (LIBR-2010)* Included automatically on most Fixed Indexed Annuities** for use with Fixed Indexed Annuities *May vary by state. Not available in all

Be out living your life, not outliving your savings.

Talk to your financial advisor to learn more about how an annuity can benefit your retirement plan. Discover the value of an annuity. Be out living your life, not outliving your savings. Discover the value

Talk to your financial advisor to learn more about how an annuity can benefit your retirement plan. Discover the value of an annuity. Be out living your life, not outliving your savings. Discover the value

North American Charter 10

North American Charter 10 Annuity Disclosure Statement Thank you for your interest in the North American Charter 10 Annuity from North American Company for Life and Health Insurance. It is important for

North American Charter 10 Annuity Disclosure Statement Thank you for your interest in the North American Charter 10 Annuity from North American Company for Life and Health Insurance. It is important for

Preparing Your Savings for Retirement Miguel Salazar

Preparing Your Savings for Retirement Miguel Salazar The Retirement Income Series Part 1: Preparing Your Savings for Retirement Identify sources of income, including Social Security Assess the impact of

Preparing Your Savings for Retirement Miguel Salazar The Retirement Income Series Part 1: Preparing Your Savings for Retirement Identify sources of income, including Social Security Assess the impact of

Wizard. Retirement Savings. The Wonderful. Featuring a Roth option on the Yellow Brick Road

THE COUNTY OF SAN BERNARDINO IS PLEASED TO PRESENT: The Wonderful Wizard of Retirement Savings Featuring a Roth option on the Yellow Brick Road Retirement planning can seem like a wild don t let your retirement

THE COUNTY OF SAN BERNARDINO IS PLEASED TO PRESENT: The Wonderful Wizard of Retirement Savings Featuring a Roth option on the Yellow Brick Road Retirement planning can seem like a wild don t let your retirement

17 th Annual Transamerica Retirement Survey Influences of Gender on Retirement Readiness

1 th Annual Transamerica Retirement Survey Influences of Gender on Retirement Readiness December 2016 TCRS 1335-1216 Transamerica Institute, 2016 Welcome to the 1 th Annual Transamerica Retirement Survey

1 th Annual Transamerica Retirement Survey Influences of Gender on Retirement Readiness December 2016 TCRS 1335-1216 Transamerica Institute, 2016 Welcome to the 1 th Annual Transamerica Retirement Survey

MFS Retirement Strategies Stretch IRA and distribution options READY, SET, RETIRE. Taking income distributions during retirement

MFS Retirement Strategies Stretch IRA and distribution options READY, SET, RETIRE Taking income distributions during retirement ASSESS YOUR NEEDS INCOME WHEN YOU NEED IT Choosing the right income distribution

MFS Retirement Strategies Stretch IRA and distribution options READY, SET, RETIRE Taking income distributions during retirement ASSESS YOUR NEEDS INCOME WHEN YOU NEED IT Choosing the right income distribution