Impact of President Bush Plan for Social Security Reform. Gerald Schillaci ACSW June10, 2005 Houston

|

|

|

- Neal Rose

- 5 years ago

- Views:

Transcription

1 Impact of President Bush Plan for Social Security Reform Gerald Schillaci ACSW June10, 2005 Houston

2 President s Commission Reform Model 2 Model 2 Basic : Gradual reduction in replacement ratio for new retirees based on change in the wage indexing to CPI indexing. Estimated reduction is a 1.1% reduction compounded for the number of years birth-year exceeds It is this reduction in benefits that re-aligns the system costs with tax revenue. The reduction is not specified but theoretical. Model 2 Optional : Personal Accounts(so-called privatization) Up to 4% of pay or $1,000 if lessor could be diverted from the traditional program to a 401K type account the participant would control and invest.

3 Social Security in Crisis 4 trillion actuarial deficit? 11.1 trillion? 12.7 trillion? How much is 4 trillion dollars, anyway? No. workers Aggregate Annual (2003) Wages Avg Wage 147,782, trillion 34,065 If 4 trillion is the official deficit of the system, what would it take to fix it? Immediate increase in FICA tax of 1.9% from 12.4% to 14.3%(not going to happen), or Immediate decrease in all benefits of 13%(not going to happen)

4 Pension Funding terminology Pay as you go funding ( income required to equal outgo for one year) No build up of assets except perhaps a short term liquidity requirement. No assets reserved to insure payment of benefits accrued Modified Pay as you go funding (income required to equal outgo for an extended period, 75 years), 4 trillion deficit (official social security basis) Solvency is required for 75 years on a cash flow basis Solvency is defined as having cash to pay cash benefits No reserve to insure payment of accrued benefits required A liquidity reserve of one year s benefits is required at the end of the 75 year period Full Reserve Funding(prefunded), 12.7 trillion deficit Asset buildup targeted to equal or exceed accrued liability To protect the pensions of workers in private enterprise

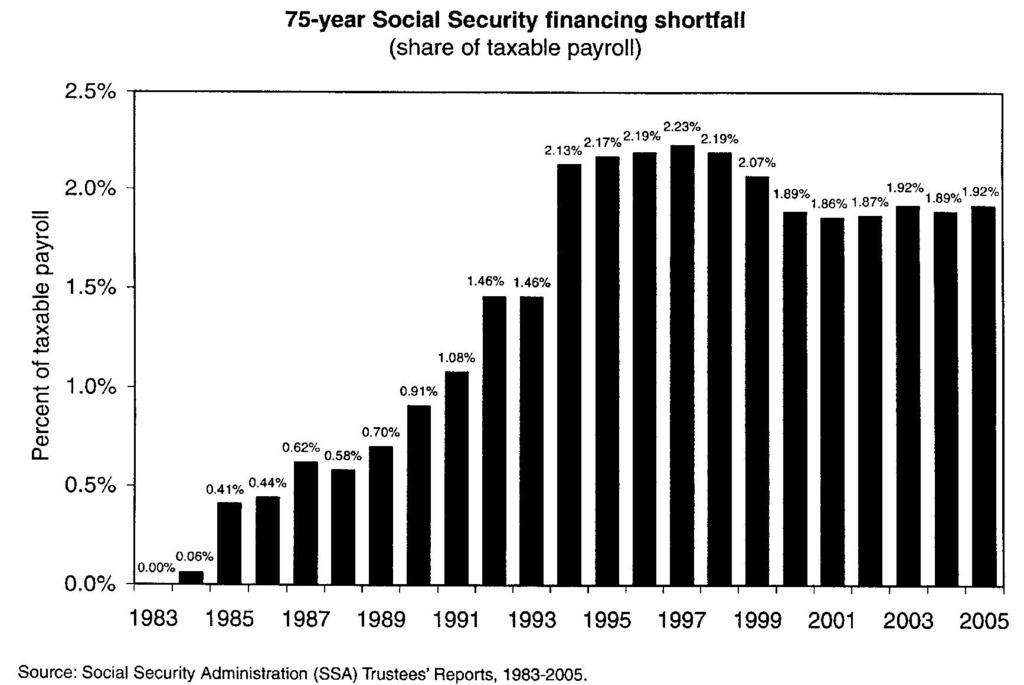

5 Social Security Basics Payroll Tax is 12.4% (combined ER and EE) up to 90,000 annual max No scheduled future increases in the tax rate, and no political will to increase tax rate, in either political party. The 90,000 annual max is indexed automatically to increases in average national wage. The 12.4% tax rate is actuarially deficient by a little less than 1.92% of payroll based on the 75 year valuation period (2005 Trustees Report). That is, about 14.32% is indicated as the correct tax actuarially.

6 Social Security Basics (cont) The social security program is a defined benefit plan that provides a benefit based on a formula that takes into account career average (indexed) earnings, years of service, age at retirement,etc. the formula is progressive, meaning it is biased in favor of lower paid. The formula is indexed in a way that provides stable replacement ratios for new retirees with average earnings, no matter what year he retires.

7 Social Security Basics (cont) Replacement Ratios for new retirees Low Wage Average Maximum Earner Earner Earner $11,200 $34,065 $90,000 72% 42% 26% These replacement ratios will be extremely stable under the current formula because everything in the benefit formula is indexed to average wage. Keeps benefits for new retirees in line with increasing standard of living, not just inflation. After retirement, benefits are indexed to CPI, not wages.

8

9 Actuarial Balance (from 2005 Trustees Report) (Official Criteria for actuarial condition) PV of cash paid benefits 75 years trill. + PV liquidity reserve time PV of FIT paid on SS benefits Beginning trust fund assets =Total funded by 12.4% payroll tax Divide by PV 12.4% tax for 75 years trill. Levelized Cost 75 years 14.31% Subtract from actual tax rate 12.40% Difference is actuarial balance -1.92%

10 Beyond 75 years The 75 year actuarial balance calculation basically ignores the period beyond the 75 th projection year, except for the liquidity reserve Every year the valuation period moves up one year and captures the 76 th year from the previous valuation If projected cash flow is negative for that year (benefits exceed the 12.4% tax), there will be creeping actuarial imbalance simply from the change in actuarial period

11 Projected Cash Flows by Year (as a % of payroll) (2005 Trustees Report) Year cash flow / payroll %

12

13

14

15

16

17

18 Infinite Valuation Period Actuarial Balance-Infinite (3.50%) -75 year (1.92%) PV of Unfunded Liability -Infinite 11.1 trillion -75 year 4.3 trillion Given the uncertainty of projections 75 years into the future, extending these projections into the infinite future can only increase the uncertainty, so that the results can have only limited value for policymakers. This is largely due to anomalies and incongruities that inevitably arise from extending any set of long-range actuarial assumptions to infinity. American Academy of Actuaries Issue Brief

19 Presidents 2001 Commission Recognized that solving the so-called actuarial balance for 75 years was not addressing the long term problem permanently. Rejected the infinite valuation approach Instead came up with the concept of sustainablity of solvency in addition to the standard 75 year balance requirement Translation: In the absence of scheduled tax rate increases, benefits must be gradually reduced to eliminate negative projected cash flows in future periods

20 President s Commission Model 2 Reform Proposal Model 2 Basic : Gradual reduction in replacement ratio for new retirees based on change in the wage indexing to CPI indexing. Estimated reduction is a 1.1% reduction compounded for the number of years birth-year exceeds It is this reduction in benefits that re-aligns the system costs with tax revenue. The reduction is not specified but theoretical. Model 2 Optional : Personal Accounts(so-called privatization) Up to 4% of pay or $1,000 if lessor could be diverted from the traditional program to a 401K type account the participant would control and invest.

21 Change from wage indexing to CPI indexing National Average Wage , , Compounded Increase for 50 years 5.05% CPI-W(urban workers) Compounded Increase for 50 years 3.82% 50 year average differential 1.23% Assumed future differential 1.10% Driver of differential is productivity increase (increases standard of living; wage grows faster than CPI) Assumed productivity increase in future 1.60%

22

23 Illustration of Benefit reduction under Model 2 Retiree in 2032 Pension Reform Reform Current Law Pension w/pa Average earner 16,116 12,917 14,772 Max earner 21,288 17,062 19,008 Retiree in 2052 Average earner 19,541 12,554 18,300 Max earner 25,823 16,590 22,884

24 Rationale for Reform Model 2 Reform Model 2 achieves actuarial balance by reducing the replacement ratios (benefits) of our young people, children and grandchildren Is it fair? Although it may seem the solution is unbalanced, the following rationalizations are offered: Younger participants will benefit from PA accounts and social security actuaries estimate that average investment results will be 1.6% greater than the break even rate(break even rate is 3% plus inflation). Younger participants will have more time to adjust to program changes. Guaranteed benefits, even with the reductions, will be as good as today s benefit s after adjusting for inflation, (but not as good on a replacement ratio basis). Congress may do ad-hoc increases in the future to restore benefits, if affordable. This is how the system operated before automatic indexing.

25 Personalized Accounts(PA s) with Carve-out Assume a private pension plan with a lump sum option based on 5% interest Suppose the plan allowed lump sum not just at retirement but every year based on the benefit earned that year Suppose you took all the lump sums and accumulated them and were able to earn 6% At retirement you were allowed to buy back in to a guaranteed pension by taking your cumulative lump sums with interest and do a reverse lump sum(annuitization) at the same 5% basis Your benefit is enhanced by the increased interest earnings of 6% over the assumed 5%

26 Personalized Accounts(PA s) with carve-out This example is very analogous to what happens with the personalized accounts with carve-out except that only a portion of the guaranteed social security benefit could be lump-summed out, as defined by the 4% of pay or $1000 limits Net effect will be a wash on the guaranteed benefit if the cumulative investment return is same as the assumed rate, eg 3% plus inflation. Very similar to variable annuity concept Social security estimates that on average, participants could outperform the break-even rate by 1.6% over the long term with 50/50 mix of stocks/bonds(breakeven rate is 3% plus inflation)

27 Personalized Accounts Investment Options Two Tier System Tier 1 for accounts up to $5000: Centralized approach with limited choices Choice of 5 indexed funds similar to the Federal Employee TSP(Thrift Savings Plan) Plus 3 balanced funds Tier 2 for accounts greater than $5,000: De-centralized approach with private providers No sales loads, only clearly identified annual fee for management Must be very diversified

28 Actuarial Balance and Projected Cash Flows by Year (as a % of payroll) (2001 Commission Report-Actuarial Memo) with Reform Model 2 Actuarial Balance is positive for 75 years at +.13% The trend of increasingly negative annual cash flow is removed. The effects of transition cost is included. Year cash flow / payroll %

29 Reasons for considering personal accounts Studies show that asset-holding has substantial positive long-term effect on health and marital stability Personal accounts would give workers a legal right to their assets and thus provide a substantially stronger guarantee than the current unsustainable program Personal accounts would permit individuals to seek a higher rate of return on their social security contributions and enhance their ultimate benefit

30 Personal Accounts vs the Trust Fund One of the biggest objections to pre-funding social security (as opposed to pay as you go funding) is that any accumulating assets is by law only invested in federal treasury debt(bonds). There has always been ambiguity as to whether this represents real savings, or a squandering of taxpayer money on additional government spending, which the debt finances. The personal accounts provide a mechanism to do pre-funding of social security in a way that removes this ambiguity.

31 Trust fund In my travels around the country I hear people say, why don't you just give us the money back we put in. But that's not the way Social Security works. It's a pay-as-you-go system. You pay; we go ahead and spend. (Laughter.) You pay through payroll taxes; we spend on paying for the beneficiaries, the retirees for that year. But if we've got any money left over, we didn't save it for you, we spent it on government. That's the way it works. It's a pay-as-you-go. And then there's -- all that's left over is a file cabinet full of IOUs. I have seen the file cabinet in West Virginia firsthand, and I saw all the IOUs. But the system is not the kind of system where we're holding the money for you. That's not the way it works. We're spending your money and left behind some paper that can only be good if the government decides to redeem the paper. That's a pay-as-you-go system.

32 Raiding the Trust Fund What is referred to as "raiding the Social Security Trust Fund" has no effect on the Social Security Trust Fund. Its real effect is to raise the national debt. In 1969, President Johnson started combining the financial data of the Social Security program with the financial data of the federal government for the purpose of reporting the budget. In 1969, the federal government was running a deficit and the Social Security program was running a surplus. By adding the two together, Johnson was able to tell the American people that the federal budget had a surplus, while in reality, it had a deficit. So what does "raiding the Trust Fund" mean? When Social Security loans money to the federal government, the government can either spend the money or use it to pay off someone else that the federal government owes money to. If the federal government spends the money, this action is what some people refer to as, "raiding the Social Security Trust Fund." The point to realize here is that it is not Social Security or senior citizens who get a raw deal in this situation, but younger people who will be stuck paying the debt in the future.

33 Lockbox What is referred to as "putting Social Security into a lockbox" has no effect on Social Security. "I will put Social Security into a lockbox." This is one of the most common campaign promises. What does it mean? It means that Social Security loans its surplus money to the federal government, and the federal government uses the money to pay off someone else it owes money to. Although the effect on Social Security and the national debt is neutral, it would be great if this always happened, because the alternative is that the federal government borrows the money from Social Security and spends it, which increases the national debt. Again, the key point to realize is that there is no effect on Social Security. Privatization would put Social Security surpluses into the accounts of individual citizens. This money would be their personal property that no one could touch (including the individuals who own it) until they are eligible to receive Social Security benefits. The concept is simple: Get the money out of the reach of politicians. If they don't have it, there is no way they can spend it or take advantage of a confusing situation to make people believe that they are saving it.

34 Transition financing needed to finance personal accounts while maintaining the liquidity requirement in the traditional Trust Fund This financing would be in the form of transfers from general tax revenues to the Trust fund as needed to maintain liquidity Year % payroll Year % payroll %

35 Transition Financing (cont) Year % payroll % These costs can be considered an investment in a lower cost, better funded system for the future. The amounts in the personal accounts are a form of pre-funding of benefit cost, which (as in the private pension system) reduces future average payroll costs by earning interest to partially defray costs.

36 Personalized Accounts The moneys diverted to the personal accounts result in a reduction in guaranteed benefits on a cost neutral basis to the system In the short term however, the liquidity needs of the system are increased The transition costs can be interpreted as a loan from the Treasury to the SS Trust Fund to cover the short term liquidity problem (which will be paid back) In the long term system costs are lower due to the partial pre-funding that the personal accounts represent (interest defrays part of the cost) By the end of the 75 year projection period, it is estimated 12.3 trillion of pre-funding in the personal accounts would contribute interest offset to costs

37 Personalized Accounts On a present value basis, the total transition costs would be.4 trillion, are 1/3 of 1% of Gross Domestic Product for 1 year.

38 Impact of Reform Every private pension plan,whether defined benefit are not, will likely need to be re-evaluated for benefit adequacy in light of social security reductions. Private plans integrated with social security may need to be adjusted Tier II funds will create new opportunities similar to the current 401K marketplace.

39 Alternative Fixes Gradually increase the taxable wage base to restore the 90% of all wages targeted by Congress per the 1983 amendments +.6% invest 20% of Trust funds in equities +.4% improve the accuracy of the post retirement COLA increase(use CPI-chained) +.4% cover all state and local government EEs +.2% Dedicate residual estate tax in Total improvement to actuarial balance +2.1%

40 Alternative Fixes The estate tax that applies in 2009 to estates in excess of 3.5 million(7 million for a married couple) at tax rate of 45% will be phased out entirely in The chief actuary of Social Security, among other, has suggested instead dedicating this tax to fix the SS deficit. The CPI index currently used to increase retirees benefits in the annual COLA overstates the increase in the cost of living by not taking into account the substitution phenomenon in consumers behavior. The chained CPI index solves this and lowers annual CPI increase by approx. 3/10 of a % annually.

41 Alternative Fixes Raising retirement age gradually. This solution has already been used to solve past imbalances, but could be extended. The effect would be very similar to the reduction of benefits under the President s Model 2, although it would probably result in a less powerful decrease rate. Most likely the increase in retirement age would be based on increase in life expectancy, and counterbalance the increase in cost from improving mortality.

42 Alternative Fixes Means Testing would reduce or eliminate benefits for higher income or wealthier Americans. This is different from the so-called earnings test which simply delayed the start date of Social security until a person actually retired, based on the evidence of his paid wages. There are a number of philosophical and practical problems with means testing It is a violation of the earned right principle of the system, and could erode public support It would be a disincentive for savings and administratively burdensome and expensive Does not appear to have widespread public support

43

44

45 Medicare and Social Security as % of GDP Year Medicare Social Security Both % 4.3% 6.9%

46 Expert opinion cited in conclusion section of AAA Issue Brief on Social Security Actuarial Assumptions Predictions are always difficult. Especially when they re about the future. Yogi Berra

Social Security. Current Reform Proposals: How They Would Affect People With Disabilities. Consortium for Citizens with Disabilities June 1, 2011

Social Security Current Reform Proposals: How They Would Affect People With June 1, 2011 Social Security Background on the Social Security Programs 2 Social Security 54.2 million people receive Social

Social Security Current Reform Proposals: How They Would Affect People With June 1, 2011 Social Security Background on the Social Security Programs 2 Social Security 54.2 million people receive Social

17. Social Security. Congress should allow workers to privately invest at least half their Social Security payroll taxes through individual accounts.

17. Social Security Congress should allow workers to privately invest at least half their Social Security payroll taxes through individual accounts. Although President Bush failed in his efforts to reform

17. Social Security Congress should allow workers to privately invest at least half their Social Security payroll taxes through individual accounts. Although President Bush failed in his efforts to reform

Social Security: Is a Key Foundation of Economic Security Working for Women?

Committee on Finance United States Senate Hearing on Social Security: Is a Key Foundation of Economic Security Working for Women? Statement of Janet Barr, MAAA, ASA, EA on behalf of the American Academy

Committee on Finance United States Senate Hearing on Social Security: Is a Key Foundation of Economic Security Working for Women? Statement of Janet Barr, MAAA, ASA, EA on behalf of the American Academy

59 million people receive Social Security each month, in one of three categories: Nearly 1 in 5 Americans gets Social Security benefits.

National Academy of Social Insurance www.nasi.org October 2015 59 million people receive Social Security each month, in one of three categories: Retirement insurance Survivor insurance Disability insurance

National Academy of Social Insurance www.nasi.org October 2015 59 million people receive Social Security each month, in one of three categories: Retirement insurance Survivor insurance Disability insurance

The Trustees Report for the Old-Age, Survivors, and Disability

American Academy of Actuaries MARCH 2009 May 2009 Looming Financial Challenges Social Security will face financial challenges sooner than was expected. New actuarial projections show income from taxes

American Academy of Actuaries MARCH 2009 May 2009 Looming Financial Challenges Social Security will face financial challenges sooner than was expected. New actuarial projections show income from taxes

Social Security and Medicare Lifetime Benefits and Taxes

E X E C U T I V E O F F I C E R E S E A R C H Social Security and Lifetime Benefits and Taxes 2018 Update C. Eugene Steuerle and Caleb Quakenbush October 2018 Since 2003, we and our colleagues have released

E X E C U T I V E O F F I C E R E S E A R C H Social Security and Lifetime Benefits and Taxes 2018 Update C. Eugene Steuerle and Caleb Quakenbush October 2018 Since 2003, we and our colleagues have released

shortfalls in perpetuity. 3 The 2003 Trustees report, for example, pushes the insolvency date back by assuming that older

Dr. Dave. I ve read that the President s proposal to create personal savings accounts within the Social Security system will do nothing to reduce the system s projected revenue shortfall. Is that true?

Dr. Dave. I ve read that the President s proposal to create personal savings accounts within the Social Security system will do nothing to reduce the system s projected revenue shortfall. Is that true?

The primer is updated to reflect estimates from the 2016 Social Security Trustees Report.

The purpose of this primer is to provide basic information and charts about Social Security: its benefits, financing, affordability, and policy options to strengthen it. The primer is formatted as a slide

The purpose of this primer is to provide basic information and charts about Social Security: its benefits, financing, affordability, and policy options to strengthen it. The primer is formatted as a slide

Lecture 8. Chapter 8 Social Security

Lecture 8 Chapter 8 Social Security Social Security Why we should care Social Security The Future of Social Security Will the federal government be able to keep the promises made by the Social Security

Lecture 8 Chapter 8 Social Security Social Security Why we should care Social Security The Future of Social Security Will the federal government be able to keep the promises made by the Social Security

How Today s Social Security Works

How Today s Social Security Works DAVID C. JOHN What Is Social Security? Social Security is probably the most popular federal program, yet most people know almost nothing about it. In practice, Social

How Today s Social Security Works DAVID C. JOHN What Is Social Security? Social Security is probably the most popular federal program, yet most people know almost nothing about it. In practice, Social

2010 Social Security Trustees Report: Reform Needed Now

2010 Social Security Trustees Report: Reform Needed Now David C. John Abstract: The 2010 annual report by the Social Security trustees has been released. It comes as no surprise that the Trustees Report

2010 Social Security Trustees Report: Reform Needed Now David C. John Abstract: The 2010 annual report by the Social Security trustees has been released. It comes as no surprise that the Trustees Report

More than 62 million people receive Social Security each month, in one of three categories: Nearly 1 in 5 Americans gets Social Security benefits.

National Academy of Social Insurance www.nasi.org August 2018 More than 62 million people receive Social Security each month, in one of three categories: Retirement insurance Survivors insurance Disability

National Academy of Social Insurance www.nasi.org August 2018 More than 62 million people receive Social Security each month, in one of three categories: Retirement insurance Survivors insurance Disability

Congressional Research Service Report for Congress Social Security Primer, April 30, 2012

Congressional Research Service Report for Congress Social Security Primer, April 30, 2012 Click to open document in a browser 2012ARD 094-204 112th Congress Social Security Primer Dawn Nuschler Specialist

Congressional Research Service Report for Congress Social Security Primer, April 30, 2012 Click to open document in a browser 2012ARD 094-204 112th Congress Social Security Primer Dawn Nuschler Specialist

Social Security: and Sustainability. Presented by Stephen C. Goss, Chief Actuary

Social Security: Part I. The System, Solvency, and Sustainability Presented by Stephen C. Goss, Chief Actuary Social Security Administration, May 12, 2010 What We Need to Know (1) System What it is, what

Social Security: Part I. The System, Solvency, and Sustainability Presented by Stephen C. Goss, Chief Actuary Social Security Administration, May 12, 2010 What We Need to Know (1) System What it is, what

BACKGROUNDER. A lthough often brushed aside as the lesser of our nation s. Raising the Social Security Payroll Tax Cap: Solving Nothing, Harming Much

BACKGROUNDER No. 2923 Raising the Social Security Payroll Tax Cap: Solving Nothing, Harming Much Rachel Greszler Abstract Social Security is an insolvent program that demands immediate reform but raising

BACKGROUNDER No. 2923 Raising the Social Security Payroll Tax Cap: Solving Nothing, Harming Much Rachel Greszler Abstract Social Security is an insolvent program that demands immediate reform but raising

Social Security Its Problems and How to Solve Them

Social Security Its Problems and How to Solve Them Currently social security is running a cash surplus. The surplus will grow smaller when the baby boomers begin to retire, and it will turn into a cash

Social Security Its Problems and How to Solve Them Currently social security is running a cash surplus. The surplus will grow smaller when the baby boomers begin to retire, and it will turn into a cash

COMMUNICATION THE BOARD OF TRUSTEES, FEDERAL OLD-AGE AND SURVIVORS INSURANCE AND DISABILITY INSURANCE TRUST FUNDS

109th Congress, 1st Session House Document 109-18 THE 2005 ANNUAL REPORT OF THE BOARD OF TRUSTEES OF THE FEDERAL OLD-AGE AND SURVIVORS INSURANCE AND DISABILITY INSURANCE TRUST FUNDS COMMUNICATION FROM

109th Congress, 1st Session House Document 109-18 THE 2005 ANNUAL REPORT OF THE BOARD OF TRUSTEES OF THE FEDERAL OLD-AGE AND SURVIVORS INSURANCE AND DISABILITY INSURANCE TRUST FUNDS COMMUNICATION FROM

A Social Security Plan For All by Robert C. Pozen

A Social Security Plan For All by Robert C. Pozen I. Multiple Goals The goals for reform of Social Security (SS) are different for Republicans and Democrats, but they can be reconciled to a significant

A Social Security Plan For All by Robert C. Pozen I. Multiple Goals The goals for reform of Social Security (SS) are different for Republicans and Democrats, but they can be reconciled to a significant

Statement of Donald E. Fuerst, MAAA, FSA, FCA, EA Senior Pension Fellow American Academy of Actuaries

Statement of Donald E. Fuerst, MAAA, FSA, FCA, EA Senior Pension Fellow American Academy of Actuaries To the Committee on Ways and Means Subcommittee on Social Security U.S. House of Representatives Hearing

Statement of Donald E. Fuerst, MAAA, FSA, FCA, EA Senior Pension Fellow American Academy of Actuaries To the Committee on Ways and Means Subcommittee on Social Security U.S. House of Representatives Hearing

AARP PRINCIPLES SOCIAL SECURITY

RETIREMENT INCOME 3 Table of Contents INTRODUCTION...3-1 AARP PRINCIPLES...3-4 SOCIAL SECURITY Introduction...3-5 The Long-Term Status of the Trust Funds...3-6 SOCIAL SECURITY REFORM PROPOSALS...3-7 AARP

RETIREMENT INCOME 3 Table of Contents INTRODUCTION...3-1 AARP PRINCIPLES...3-4 SOCIAL SECURITY Introduction...3-5 The Long-Term Status of the Trust Funds...3-6 SOCIAL SECURITY REFORM PROPOSALS...3-7 AARP

THE PENNSYLVANIA STATE UNIVERSITY SCHREYER HONORS COLLEGE DEPARTMENT OF RISK MANAGEMENT THE PROS AND CONS OF PRIVATIZING SOCIAL SECURITY

THE PENNSYLVANIA STATE UNIVERSITY SCHREYER HONORS COLLEGE DEPARTMENT OF RISK MANAGEMENT THE PROS AND CONS OF PRIVATIZING SOCIAL SECURITY ALLISON LAVELLA SPRING 2016 A thesis submitted in partial fulfillment

THE PENNSYLVANIA STATE UNIVERSITY SCHREYER HONORS COLLEGE DEPARTMENT OF RISK MANAGEMENT THE PROS AND CONS OF PRIVATIZING SOCIAL SECURITY ALLISON LAVELLA SPRING 2016 A thesis submitted in partial fulfillment

WHAT THE NEW TRUSTEES REPORT SHOWS ABOUT SOCIAL SECURITY By Jason Furman and Robert Greenstein

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised June 15, 2006 Executive Summary WHAT THE NEW TRUSTEES REPORT SHOWS ABOUT SOCIAL

820 First Street NE, Suite 510 Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org Revised June 15, 2006 Executive Summary WHAT THE NEW TRUSTEES REPORT SHOWS ABOUT SOCIAL

SOCIAL SECURITY: A Background Briefing

UPDATED: May 15, 2006 In reference to the 2006 Report of the OASDI Trustees SOCIAL SECURITY: A Background Briefing Social Security is the most successful program in our country s history. People look upon

UPDATED: May 15, 2006 In reference to the 2006 Report of the OASDI Trustees SOCIAL SECURITY: A Background Briefing Social Security is the most successful program in our country s history. People look upon

REPORT TO THE PEOPLE OF SAN DIEGO REGARDING THE SAN DIEGO CITY EMPLOYEES RETIREMENT SYSTEM

SAN DIEGO CITY ATTORNEY REPORT TO THE PEOPLE OF SAN DIEGO REGARDING THE SAN DIEGO CITY EMPLOYEES RETIREMENT SYSTEM 20 December 2007 I. INTRODUCTION San Diego taxpayers have a right to know about the financial

SAN DIEGO CITY ATTORNEY REPORT TO THE PEOPLE OF SAN DIEGO REGARDING THE SAN DIEGO CITY EMPLOYEES RETIREMENT SYSTEM 20 December 2007 I. INTRODUCTION San Diego taxpayers have a right to know about the financial

State Universities Retirement System of Illinois

State Universities Retirement System of Illinois Pension Reform Studies HB 6258 December 20, 2012 Copyright 2012 GRS All rights reserved. Opening Comments 2 This report contains one scenario for HB 6258

State Universities Retirement System of Illinois Pension Reform Studies HB 6258 December 20, 2012 Copyright 2012 GRS All rights reserved. Opening Comments 2 This report contains one scenario for HB 6258

Medicare and Social Security: Weighing Solvency

Medicare and Social Security: Weighing Solvency Cori E. Uccello, MAAA, FSA, FCA, MPP Senior Health Fellow, Ron Gebhardtsbauer, MAAA, FSA, FCA Senior Pension Fellow, April 1, 2005 Noon 1:00 pm B-339 Rayburn

Medicare and Social Security: Weighing Solvency Cori E. Uccello, MAAA, FSA, FCA, MPP Senior Health Fellow, Ron Gebhardtsbauer, MAAA, FSA, FCA Senior Pension Fellow, April 1, 2005 Noon 1:00 pm B-339 Rayburn

Social Security and the Budget

URBAN INSTITUTE Brief Series No. 28 May 2010 Social Security and the Budget Eugene Steuerle and Stephanie Rennane Almost every investigation of the nation s longterm budget tells a similar story: the nation

URBAN INSTITUTE Brief Series No. 28 May 2010 Social Security and the Budget Eugene Steuerle and Stephanie Rennane Almost every investigation of the nation s longterm budget tells a similar story: the nation

The Social Security Protection Plan

1 of 7 3/8/2006 4:04 PM January 2006 The Social Security Protection Plan How we can cope calmly with the system s long-term shortfall Robert M. Ball All is momentarily quiet on the Social Security front.

1 of 7 3/8/2006 4:04 PM January 2006 The Social Security Protection Plan How we can cope calmly with the system s long-term shortfall Robert M. Ball All is momentarily quiet on the Social Security front.

Social Security and Medicare Lifetime Benefits and Taxes

EXECUTIVE OFFICE RESEARCH Social Security and Lifetime Benefits and Taxes 2017 Update C. Eugene Steuerle and Caleb Quakenbush June 2018 Since 2003, we and our colleagues have been releasing periodic data

EXECUTIVE OFFICE RESEARCH Social Security and Lifetime Benefits and Taxes 2017 Update C. Eugene Steuerle and Caleb Quakenbush June 2018 Since 2003, we and our colleagues have been releasing periodic data

BACKGROUNDER. Social Security touches the life of almost every worker in America, How Social Security Works in Key Points.

BACKGROUNDER No. 2906 How Social Security Works in 2014 Romina Boccia Abstract Social Security affects the lives of almost all Americans, yet most people do not have a firm understanding of how the nearly

BACKGROUNDER No. 2906 How Social Security Works in 2014 Romina Boccia Abstract Social Security affects the lives of almost all Americans, yet most people do not have a firm understanding of how the nearly

New Report Shows Modest Improvement. Social Security s Financial Soundness Should Be Addressed Now

American Academy of Actuaries Issue Brief JUNE 2016 An Actuarial Perspective on the 2016 Social Security Trustees Report 1850 M Street NW, Suite 300 Washington, DC 20036 202-223-8196 www.actuary.org Craig

American Academy of Actuaries Issue Brief JUNE 2016 An Actuarial Perspective on the 2016 Social Security Trustees Report 1850 M Street NW, Suite 300 Washington, DC 20036 202-223-8196 www.actuary.org Craig

Federal Employees Retirement System: Benefits and Financing

Federal Employees Retirement System: Benefits and Financing Katelin P. Isaacs Analyst in Income Security January 5, 2011 Congressional Research Service CRS Report for Congress Prepared for Members and

Federal Employees Retirement System: Benefits and Financing Katelin P. Isaacs Analyst in Income Security January 5, 2011 Congressional Research Service CRS Report for Congress Prepared for Members and

Federal Employees Retirement System: Benefits and Financing

Federal Employees Retirement System: Benefits and Financing Katelin P. Isaacs Analyst in Income Security February 21, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional

Federal Employees Retirement System: Benefits and Financing Katelin P. Isaacs Analyst in Income Security February 21, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional

City of Madison Heights Police and Fire Retirement System Actuarial Valuation Report June 30, 2017

City of Madison Heights Police and Fire Retirement System Actuarial Valuation Report June 30, 2017 Table of Contents Page Items -- Cover Letter Basic Financial Objective and Operation of the Retirement

City of Madison Heights Police and Fire Retirement System Actuarial Valuation Report June 30, 2017 Table of Contents Page Items -- Cover Letter Basic Financial Objective and Operation of the Retirement

Social Security and Your Retirement

Social Security and Your Retirement January 2013 ACI-1111-3702 American Century Investment Services, Inc. Distributor 2013 American Century Investments Proprietary Holdings, Inc. All rights reserved. Social

Social Security and Your Retirement January 2013 ACI-1111-3702 American Century Investment Services, Inc. Distributor 2013 American Century Investments Proprietary Holdings, Inc. All rights reserved. Social

WikiLeaks Document Release

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RL32879 Social Security Reform: President Bush s Individual Account Proposal Laura Haltzel, Domestic Social Policy Division

WikiLeaks Document Release February 2, 2009 Congressional Research Service Report RL32879 Social Security Reform: President Bush s Individual Account Proposal Laura Haltzel, Domestic Social Policy Division

Testimony for the Senate Finance Committee on February 2, 2005 Stephen C. Goss, Chief Actuary Social Security Administration

Testimony for the Senate Finance Committee on February 2, 25 Stephen C. Goss, Chief Actuary Mr. Chairman, ranking member, and members of the committee, thank you very much for the opportunity to talk with

Testimony for the Senate Finance Committee on February 2, 25 Stephen C. Goss, Chief Actuary Mr. Chairman, ranking member, and members of the committee, thank you very much for the opportunity to talk with

The Future of Social Security

The Future of Social Security Andrew B. Abel October 4, 2000 OASDI Operations Estimates for 2000 (billions of dollars, except Trust fund ratio) Trust fund at beginning of year 896.1 Income excluding interest

The Future of Social Security Andrew B. Abel October 4, 2000 OASDI Operations Estimates for 2000 (billions of dollars, except Trust fund ratio) Trust fund at beginning of year 896.1 Income excluding interest

REPLACING WAGE INDEXING WITH PRICE INDEXING WOULD RESULT IN DEEP REDUCTIONS OVER TIME IN SOCIAL SECURITY BENEFITS

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org http://www.cbpp.org Revised December 14, 2001 REPLACING WAGE INDEXING WITH PRICE INDEXING WOULD

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org http://www.cbpp.org Revised December 14, 2001 REPLACING WAGE INDEXING WITH PRICE INDEXING WOULD

At the end of Class 20, you will be able to answer the following:

1 Objectives for Class 20: The Tax System At the end of Class 20, you will be able to answer the following: 1. What are the main taxes collected at each level of government? 2. How do American taxes as

1 Objectives for Class 20: The Tax System At the end of Class 20, you will be able to answer the following: 1. What are the main taxes collected at each level of government? 2. How do American taxes as

Ch In other countries the replacement rate is often higher. In the Netherlands it is over 90%. This means that after taxes Dutch workers receive

Ch. 13 1 About Social Security o Social Security is formally called the Federal Old-Age, Survivors, Disability Insurance Trust Fund (OASDI). o It was created as part of the New Deal and was designed in

Ch. 13 1 About Social Security o Social Security is formally called the Federal Old-Age, Survivors, Disability Insurance Trust Fund (OASDI). o It was created as part of the New Deal and was designed in

Options to Address Unfunded Pension Liability

Options to Address Unfunded Pension Liability Presentation to City Council September 14, 2010 Karen Montgomery, Assistant City Manager Actuarial Information Prepared by Doug Anderson, EA,ASA, MAAA Gallagher

Options to Address Unfunded Pension Liability Presentation to City Council September 14, 2010 Karen Montgomery, Assistant City Manager Actuarial Information Prepared by Doug Anderson, EA,ASA, MAAA Gallagher

Retirement and Social Security

Life Guide The Social Security Administration estimates that 96% of American workers are covered by Social Security. For most of them, their monthly Social Security check will form an important part of

Life Guide The Social Security Administration estimates that 96% of American workers are covered by Social Security. For most of them, their monthly Social Security check will form an important part of

Issue Brief. Amer ican Academy of Actuar ies. An Actuarial Perspective on the 2006 Social Security Trustees Report

AMay 2006 Issue Brief A m e r i c a n Ac a d e my o f Ac t ua r i e s An Actuarial Perspective on the 2006 Social Security Trustees Report Each year, the Board of Trustees of the Old-Age, Survivors, and

AMay 2006 Issue Brief A m e r i c a n Ac a d e my o f Ac t ua r i e s An Actuarial Perspective on the 2006 Social Security Trustees Report Each year, the Board of Trustees of the Old-Age, Survivors, and

Since the publication of the first edition of this book in

Saving Social Security: An Update Since the publication of the first edition of this book in early 2004, the Social Security debate has moved to the top of the domestic policy agenda. In his February 2005

Saving Social Security: An Update Since the publication of the first edition of this book in early 2004, the Social Security debate has moved to the top of the domestic policy agenda. In his February 2005

Risk Management - Managing Life Cycle Risks. Table of Contents. Case Study 01: Does Privatization Provide a More Equitable Solution?...

Risk Management - Managing Life Cycle Risks Module 10: Social Security Table of Contents Case Study 01: Does Privatization Provide a More Equitable Solution?..... Page 2 Case Study 02:The Future of Social

Risk Management - Managing Life Cycle Risks Module 10: Social Security Table of Contents Case Study 01: Does Privatization Provide a More Equitable Solution?..... Page 2 Case Study 02:The Future of Social

How The Chained Consumer Price Index Would Affect Social Security Benefits

How The Chained Consumer Price Index Would Affect Social Security Benefits By Mary Johnson February 2018 How The Chained Consumer Price Index Would Affect Social Security Benefits By Mary Johnson, Social

How The Chained Consumer Price Index Would Affect Social Security Benefits By Mary Johnson February 2018 How The Chained Consumer Price Index Would Affect Social Security Benefits By Mary Johnson, Social

National Committee to Preserve Social Security and Medicare PAC 2018 CONGRESSIONAL CANDIDATE QUESTIONNAIRE

National Committee to Preserve Social Security and Medicare PAC 2018 CONGRESSIONAL CANDIDATE QUESTIONNAIRE Candidate Name: State: District: Affordable Care Act The Affordable Care Act (ACA) is a highly

National Committee to Preserve Social Security and Medicare PAC 2018 CONGRESSIONAL CANDIDATE QUESTIONNAIRE Candidate Name: State: District: Affordable Care Act The Affordable Care Act (ACA) is a highly

Savvy Social Security Planning for Boomers. By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC

Savvy Social Security Planning for Boomers By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Two ways Social Security planning can help your business Reach out to new clients

Savvy Social Security Planning for Boomers By Elaine Floyd, CFP Director of Retirement and Life Planning, Horsesmouth, LLC 1 Two ways Social Security planning can help your business Reach out to new clients

75-YEAR PAY-AS-YOU-GO PROPOSAL COULD ADVERSELY AFFECT SOCIAL SECURITY, MEDICARE, SSI, VETERANS DISABILITY, AND OTHER PROGRAMS

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org June 11, 2004 75-YEAR PAY-AS-YOU-GO PROPOSAL COULD ADVERSELY AFFECT SOCIAL SECURITY,

820 First Street, NE, Suite 510, Washington, DC 20002 Tel: 202-408-1080 Fax: 202-408-1056 center@cbpp.org www.cbpp.org June 11, 2004 75-YEAR PAY-AS-YOU-GO PROPOSAL COULD ADVERSELY AFFECT SOCIAL SECURITY,

Comparing the benefits you will get from your federal DB and DC plans

Comparing the benefits you will get from your federal DB and DC plans RON GEBHARDTSBAUER Senior Pension Fellow American Academy of Actuaries A Briefing Sponsored by the American Academy of Actuaries Tuesday,

Comparing the benefits you will get from your federal DB and DC plans RON GEBHARDTSBAUER Senior Pension Fellow American Academy of Actuaries A Briefing Sponsored by the American Academy of Actuaries Tuesday,

SOCIAL SECURITY ADMINISTRATION

SOCIAL SECURITY ADMINISTRATION Since 2001, the Administration: Improved productivity by 13.1 percent, enabling the agency to provide more accurate and a wider variety of services with fewer resources than

SOCIAL SECURITY ADMINISTRATION Since 2001, the Administration: Improved productivity by 13.1 percent, enabling the agency to provide more accurate and a wider variety of services with fewer resources than

POLICY BRIEF Social Security: Experts Discuss Funding Issues and Options

Social Security: Experts Discuss Funding Issues and Options By Mimi Lord, TIAA-CREF Institute April 2005 EXECUTIVE SUMMARY Due to the aging of Baby Boomers, longer life expectancies and other demographic

Social Security: Experts Discuss Funding Issues and Options By Mimi Lord, TIAA-CREF Institute April 2005 EXECUTIVE SUMMARY Due to the aging of Baby Boomers, longer life expectancies and other demographic

MODERNIZING SOCIAL SECURITY: HELPING THE OLDEST OLD

October 2018, Number 18-18 RETIREMENT RESEARCH MODERNIZING SOCIAL SECURITY: HELPING THE OLDEST OLD By Alicia H. Munnell and Andrew D. Eschtruth* Introduction People become more financially vulnerable the

October 2018, Number 18-18 RETIREMENT RESEARCH MODERNIZING SOCIAL SECURITY: HELPING THE OLDEST OLD By Alicia H. Munnell and Andrew D. Eschtruth* Introduction People become more financially vulnerable the

Social Security The Choice of a Lifetime. Timothy O Mara, Vice President, Nationwide Retirement Institute

Social Security The Choice of a Lifetime Timothy O Mara, Vice President, Nationwide Retirement Institute FOR BROKER/DEALER USE ONLY NOT FOR USE WITH THE GENERAL PUBLIC Important things to keep in mind

Social Security The Choice of a Lifetime Timothy O Mara, Vice President, Nationwide Retirement Institute FOR BROKER/DEALER USE ONLY NOT FOR USE WITH THE GENERAL PUBLIC Important things to keep in mind

Social Security. Social Security Basics *Facts Continued. Social Security Basics. Social Security Basics *Facts Continued. Social Security Basics

Social Security Presented by: Jessica Carey Mike Priskos Tim Drisdom Social Security Basics *Facts Continued To become eligible for his or her benefit and benefits for family members or survivors, a worker

Social Security Presented by: Jessica Carey Mike Priskos Tim Drisdom Social Security Basics *Facts Continued To become eligible for his or her benefit and benefits for family members or survivors, a worker

President Obama Releases 2014 Federal Budget Proposal

Private Wealth Management Products & Services April 2013 President Obama Releases 2014 Federal Budget Proposal 2014 proposal consistent with prior budgets, but enactment is uncertain After more than two

Private Wealth Management Products & Services April 2013 President Obama Releases 2014 Federal Budget Proposal 2014 proposal consistent with prior budgets, but enactment is uncertain After more than two

Social Security: What Would Happen If the Trust Funds Ran Out?

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 8-28-2014 Social Security: What Would Happen If the Trust Funds Ran Out? Noah P. Meyerson Congressional Research

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 8-28-2014 Social Security: What Would Happen If the Trust Funds Ran Out? Noah P. Meyerson Congressional Research

Checks and Balances TV: America s #1 Source for Balanced Financial Advice

The TruTh about SOCIAL SECURITY Social Security: a simple idea that s grown out of control. Social Security is the widely known retirement safety net for the American Workforce. When it began in 1935,

The TruTh about SOCIAL SECURITY Social Security: a simple idea that s grown out of control. Social Security is the widely known retirement safety net for the American Workforce. When it began in 1935,

VILLAGE OF CARPENTERSVILLE CARPENTERSVILLE POLICE PENSION FUND. Actuarial Valuation Report. For the Year. Beginning January 1, 2016

T W S Actuary VILLAGE OF CARPENTERSVILLE CARPENTERSVILLE POLICE PENSION FUND Actuarial Valuation Report For the Year Beginning January 1, 2016 And Ending December 31, 2016 Timothy W. Sharpe, Actuary, Geneva,

T W S Actuary VILLAGE OF CARPENTERSVILLE CARPENTERSVILLE POLICE PENSION FUND Actuarial Valuation Report For the Year Beginning January 1, 2016 And Ending December 31, 2016 Timothy W. Sharpe, Actuary, Geneva,

SOCIAL SECURITY. Office of the Chief Actuary. June 9, 2016

Office of the Chief Actuary June 9, 2016 Mr. Kent Conrad, Co-Chair Mr. James B. Lockhart, III, Co-Chair Commission on Retirement Security and Personal Savings Bipartisan Policy Center 1225 Eye Street NW,

Office of the Chief Actuary June 9, 2016 Mr. Kent Conrad, Co-Chair Mr. James B. Lockhart, III, Co-Chair Commission on Retirement Security and Personal Savings Bipartisan Policy Center 1225 Eye Street NW,

Federal Employees Retirement System: Benefits and Financing

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 2-14-2012 Federal Employees Retirement System: Benefits and Financing Katelin P. Isaacs Congressional Research

Cornell University ILR School DigitalCommons@ILR Federal Publications Key Workplace Documents 2-14-2012 Federal Employees Retirement System: Benefits and Financing Katelin P. Isaacs Congressional Research

1. Social Security benefits are modest; yet they are the main income for most seniors and other beneficiaries. (Page 2)

") What s Next for Social Security? Essential Facts for Action Virginia P. Reno, National Academy of Social Insurance vreno@nasi.org, 202-243-7282 October 2013 1. Social Security benefits are modest; yet

What s Next for Social Security? Essential Facts for Action Virginia P. Reno, National Academy of Social Insurance vreno@nasi.org, 202-243-7282 October 2013 1. Social Security benefits are modest; yet

Note: The material in this publication is based on the law in effect at the time it went to publication.

Note: The material in this publication is based on the law in effect at the time it went to publication. Under the Balanced Budget Act of 1997, Public Law 105-33, for fiscal year 1998, employee retirement

Note: The material in this publication is based on the law in effect at the time it went to publication. Under the Balanced Budget Act of 1997, Public Law 105-33, for fiscal year 1998, employee retirement

UGBC Social Security Forum

UGBC Social Security Forum April 27, 2005 Prof. Bob Murphy Department of Economics Boston College The First Social Security Recipient: Ernest Ackerman Retired as a railroad motorman 1 day after Social

UGBC Social Security Forum April 27, 2005 Prof. Bob Murphy Department of Economics Boston College The First Social Security Recipient: Ernest Ackerman Retired as a railroad motorman 1 day after Social

BACKGROUNDER. Social Security s main program, also known as Old-Age and Survivors. Social Security: $39 Billion Deficit in 2014, Insolvent by 2035

BACKGROUNDER No. 3043 Social Security: $39 Billion Deficit in 2014, Insolvent by 2035 Romina Boccia Abstract Social Security ran a $39 billion deficit in 2014, closing out five years of consecutive cash-flow

BACKGROUNDER No. 3043 Social Security: $39 Billion Deficit in 2014, Insolvent by 2035 Romina Boccia Abstract Social Security ran a $39 billion deficit in 2014, closing out five years of consecutive cash-flow

D A T A D I G E S T PUBLIC POLICY INSTITUTE PPI

PPI PUBLIC POLICY INSIUE HE EFFEC OF USING PRICE INDEXAION INSEAD OF WAGE INDEXAION IN CALCULAING HE INIIAL SOCIAL SECURIY BENEFI D A A D I G E S Introduction Social Security today is facing a longterm

PPI PUBLIC POLICY INSIUE HE EFFEC OF USING PRICE INDEXAION INSEAD OF WAGE INDEXAION IN CALCULAING HE INIIAL SOCIAL SECURIY BENEFI D A A D I G E S Introduction Social Security today is facing a longterm

Social Security and the Aging of America

Social Security and the Aging of America 1 Richard Jackson President Global Aging Institute CCA Webinar January 11, 2017 Social Security consists of two separate programs: Old-age and Survivors Insurance

Social Security and the Aging of America 1 Richard Jackson President Global Aging Institute CCA Webinar January 11, 2017 Social Security consists of two separate programs: Old-age and Survivors Insurance

SOCIAL SECURITY S $20 TRILLION SHORTFALL: WHY REFORM IS NEEDED

SOCIAL SECURITY S $20 TRILLION SHORTFALL: WHY REFORM IS NEEDED DANIEL J. MITCHELL Reforming Social Security has become a frontburner issue in Washington, D.C., due in large part to growing recognition

SOCIAL SECURITY S $20 TRILLION SHORTFALL: WHY REFORM IS NEEDED DANIEL J. MITCHELL Reforming Social Security has become a frontburner issue in Washington, D.C., due in large part to growing recognition

A Guide to Medicare s s Financial Challenges and Options for Improvement

A Guide to Medicare s s Financial Challenges and Options for Improvement December 12, 2011 December 2011 Notes for speakers: Presentation of the full slide deck will take approximately 25 to 30 minutes,

A Guide to Medicare s s Financial Challenges and Options for Improvement December 12, 2011 December 2011 Notes for speakers: Presentation of the full slide deck will take approximately 25 to 30 minutes,

What Every Actuary Should Know About Medicare From Structure to Reform

What Every Actuary Should Know About Medicare From Structure to Reform Cori E. Uccello, FSA, MAAA, MPP Senior Health Fellow, American Academy of Actuaries Thomas F. Wildsmith, FSA, MAAA Vice President

What Every Actuary Should Know About Medicare From Structure to Reform Cori E. Uccello, FSA, MAAA, MPP Senior Health Fellow, American Academy of Actuaries Thomas F. Wildsmith, FSA, MAAA Vice President

Fixing Social Security Conducted by the Program for Public Consultation, School of Public Policy, University of Maryland.

Fixing Social Security Conducted by the Program for Public Consultation, School of Public Policy, University of Maryland Questionnaire National Sample, California, Florida, New York, Ohio, Texas Field

Fixing Social Security Conducted by the Program for Public Consultation, School of Public Policy, University of Maryland Questionnaire National Sample, California, Florida, New York, Ohio, Texas Field

Federal Employees Retirement System: Budget and Trust Fund Issues

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security June 13, 2013 CRS Report for Congress Prepared for Members and Committees of Congress Congressional

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security June 13, 2013 CRS Report for Congress Prepared for Members and Committees of Congress Congressional

Social Security: Actuarial Status and Assumptions

Social Security: Actuarial Status and Assumptions Webinar November 27, 2012 Social Security Webinar, Nov. 27, 2012 All Rights Reserved. PANELISTS: Moderator: Mark Shemtob, MAAA, ASA, EA; Member, Social

Social Security: Actuarial Status and Assumptions Webinar November 27, 2012 Social Security Webinar, Nov. 27, 2012 All Rights Reserved. PANELISTS: Moderator: Mark Shemtob, MAAA, ASA, EA; Member, Social

Federal Employees Retirement System: Budget and Trust Fund Issues

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security August 24, 2015 Congressional Research Service 7-5700 www.crs.gov RL30023 Summary Most of

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security August 24, 2015 Congressional Research Service 7-5700 www.crs.gov RL30023 Summary Most of

Social Security: The Trust Fund

Dawn Nuschler Specialist in Income Security Gary Sidor Information Research Specialist July 31, 2014 Congressional Research Service 7-5700 www.crs.gov RL33028 Summary The Social Security program pays benefits

Dawn Nuschler Specialist in Income Security Gary Sidor Information Research Specialist July 31, 2014 Congressional Research Service 7-5700 www.crs.gov RL33028 Summary The Social Security program pays benefits

SOCIAL SECURITY S FINANCIAL OUTLOOK: THE 2007 REPORT IN PERSPECTIVE

April 2007, Number 7-6 SOCIAL SECURITY S FINANCIAL OUTLOOK: THE 2007 REPORT IN PERSPECTIVE By Alicia H. Munnell* Introduction The Trustees of the Social Security system have just issued the 2007 report.

April 2007, Number 7-6 SOCIAL SECURITY S FINANCIAL OUTLOOK: THE 2007 REPORT IN PERSPECTIVE By Alicia H. Munnell* Introduction The Trustees of the Social Security system have just issued the 2007 report.

SUMMARY PLAN DESCRIPTION

CITY OF FRESNO FIRE & POLICE RETIREMENT SYSTEM SUMMARY PLAN DESCRIPTION REVISED JUNE 2006 CITY OF FRESNO FIRE & POLICE RETIREMENT SYSTEM SUMMARY PLAN DESCRIPTION REVISED JUNE 2006 City of Fresno Retirement

CITY OF FRESNO FIRE & POLICE RETIREMENT SYSTEM SUMMARY PLAN DESCRIPTION REVISED JUNE 2006 CITY OF FRESNO FIRE & POLICE RETIREMENT SYSTEM SUMMARY PLAN DESCRIPTION REVISED JUNE 2006 City of Fresno Retirement

TO: Interested Parties FROM: David Brown, Policy Advisor for the Economic Program RE: The Context and the Case for Chained CPI

The Economic Program April 2013 TO: Interested Parties FROM: David Brown, Policy Advisor for the Economic Program RE: The Context and the Case for Chained CPI When the president included a previously obscure

The Economic Program April 2013 TO: Interested Parties FROM: David Brown, Policy Advisor for the Economic Program RE: The Context and the Case for Chained CPI When the president included a previously obscure

Challenge. If you have any questions on the book or on planning your retirement please contact the author Marc Bautis.

Retirement Fitness Challenge The Retirement Fitness Challenge, while simple in concept, is an evolving program that presents different layers of complexity based on each retiree s unique needs. The following

Retirement Fitness Challenge The Retirement Fitness Challenge, while simple in concept, is an evolving program that presents different layers of complexity based on each retiree s unique needs. The following

University of Puerto Rico Retirement System. Actuarial Valuation Valuation Report

University of Puerto Rico Retirement System Actuarial Valuation Valuation Report As of June 30, 2015 Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve April 11, 2016

University of Puerto Rico Retirement System Actuarial Valuation Valuation Report As of June 30, 2015 Cavanaugh Macdonald C O N S U L T I N G, L L C The experience and dedication you deserve April 11, 2016

CHARTS MAY 7, 2013 WASHINGTON, D.C.

CHARTS MAY 7, 2013 WASHINGTON, D.C. America s long-term debt outlook is unsustainable. Unless we change course, in coming decades rising debt and interest payments will weigh down our economy and divert

CHARTS MAY 7, 2013 WASHINGTON, D.C. America s long-term debt outlook is unsustainable. Unless we change course, in coming decades rising debt and interest payments will weigh down our economy and divert

Pension Plan 1. Offers Financial Security to Your Family in Case of Your Death

Pension Plan 1 PLAN HIGHLIGHTS The Employees Retirement Plan of USEC Inc. (the Pension Plan ) helps build financial security and provide you with a dependable source of income throughout your retirement

Pension Plan 1 PLAN HIGHLIGHTS The Employees Retirement Plan of USEC Inc. (the Pension Plan ) helps build financial security and provide you with a dependable source of income throughout your retirement

Current Event: Social Security and Medicare 1

Current Event: Social Security and Medicare 1 One of the most worrisome aspects of the long term U.S. fiscal situation is the obligations to entitlement programs such as Social Security and Medicare. These

Current Event: Social Security and Medicare 1 One of the most worrisome aspects of the long term U.S. fiscal situation is the obligations to entitlement programs such as Social Security and Medicare. These

I S S U E B R I E F PUBLIC POLICY INSTITUTE PPI PRESIDENT BUSH S TAX PLAN: IMPACTS ON AGE AND INCOME GROUPS

PPI PUBLIC POLICY INSTITUTE PRESIDENT BUSH S TAX PLAN: IMPACTS ON AGE AND INCOME GROUPS I S S U E B R I E F Introduction President George W. Bush fulfilled a 2000 campaign promise by signing the $1.35

PPI PUBLIC POLICY INSTITUTE PRESIDENT BUSH S TAX PLAN: IMPACTS ON AGE AND INCOME GROUPS I S S U E B R I E F Introduction President George W. Bush fulfilled a 2000 campaign promise by signing the $1.35

The Wrong Way to Fix Social Security. Peter R. Orszag 1 Joseph A. Pechman Senior Fellow The Brookings Institution

The Wrong Way to Fix Social Security Peter R. Orszag 1 Joseph A. Pechman Senior Fellow The Brookings Institution Hearing before the Democratic Policy Committee January 28, 2005 The Bush Administration

The Wrong Way to Fix Social Security Peter R. Orszag 1 Joseph A. Pechman Senior Fellow The Brookings Institution Hearing before the Democratic Policy Committee January 28, 2005 The Bush Administration

Federal Employees Retirement System: Budget and Trust Fund Issues

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security September 27, 2012 CRS Report for Congress Prepared for Members and Committees of Congress

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security September 27, 2012 CRS Report for Congress Prepared for Members and Committees of Congress

Social Security 76% 1. The choice of a lifetime. Your choice on when to file could increase your annual benefit by as much as

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

Social Security Guide NATIONWIDE RETIREMENT INSTITUTE Social Security The choice of a lifetime Your choice on when to file could increase your annual benefit by as much as 76% 1 1 Nationwide as of May

Social Security: The Notch Issue

Order Code RS22678 June 13, 2007 Summary Social Security: The Notch Issue Kathleen Romig Analyst in Social Security Domestic Social Policy Division Some Social Security beneficiaries who were born from

Order Code RS22678 June 13, 2007 Summary Social Security: The Notch Issue Kathleen Romig Analyst in Social Security Domestic Social Policy Division Some Social Security beneficiaries who were born from

Federal Employees Retirement System: Budget and Trust Fund Issues

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security March 24, 2014 Congressional Research Service 7-5700 www.crs.gov RL30023 Summary Most of the

Federal Employees Retirement System: Budget and Trust Fund Issues Katelin P. Isaacs Analyst in Income Security March 24, 2014 Congressional Research Service 7-5700 www.crs.gov RL30023 Summary Most of the

SOCIAL SECURITY S FINANCIAL OUTLOOK: THE 2006 UPDATE IN PERSPECTIVE

April 2006, Number 46 SOCIAL SECURITY S FINANCIAL OUTLOOK: THE 2006 UPDATE IN PERSPECTIVE By Alicia H. Munnell* Introduction The Social Security Trustees have just issued their 2006 Report on the financial

April 2006, Number 46 SOCIAL SECURITY S FINANCIAL OUTLOOK: THE 2006 UPDATE IN PERSPECTIVE By Alicia H. Munnell* Introduction The Social Security Trustees have just issued their 2006 Report on the financial

Introduction.

Testimony of Ed Lorenzen Executive Director, The Moment of Truth Project Senior Advisor, Committee for a Responsible Federal Budget Before the Subcommittee on Social Security Committee on Ways and Means

Testimony of Ed Lorenzen Executive Director, The Moment of Truth Project Senior Advisor, Committee for a Responsible Federal Budget Before the Subcommittee on Social Security Committee on Ways and Means

What the 2018 Trustees Report Shows About Social Security

June 29, 2018 What the 2018 Trustees Report Shows About Social Security By Kathleen Romig Social Security can pay full benefits for 16 more years, the trustees latest annual report shows, but will then

June 29, 2018 What the 2018 Trustees Report Shows About Social Security By Kathleen Romig Social Security can pay full benefits for 16 more years, the trustees latest annual report shows, but will then

Important things to keep in mind

Important things to keep in mind Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution Not insured by any federal government agency May lose value The content of this presentation

Important things to keep in mind Not a deposit Not FDIC or NCUSIF insured Not guaranteed by the institution Not insured by any federal government agency May lose value The content of this presentation

House Bill COLA provisions in the 5 Ohio Retirement Systems

259 N. Radnor-Chester Road, Suite 300 Radnor, PA 19087-5260 Tel + 1 610 687.5644 Fax + 1 610 687.4236 www.milliman.com Director Ohio Retirement Study Council 88 East Broad Street, Suite 1175 Columbus,

259 N. Radnor-Chester Road, Suite 300 Radnor, PA 19087-5260 Tel + 1 610 687.5644 Fax + 1 610 687.4236 www.milliman.com Director Ohio Retirement Study Council 88 East Broad Street, Suite 1175 Columbus,

The Impact of Recent Pension Reforms on Teacher Benefits: A Case Study of California Teachers

P R O G R A M O N R E T I R E M E N T P O L I C Y RESEARCH REPORT The Impact of Recent Pension Reforms on Teacher Benefits: A Case Study of California Teachers Richard W. Johnson November 2017 Contents

P R O G R A M O N R E T I R E M E N T P O L I C Y RESEARCH REPORT The Impact of Recent Pension Reforms on Teacher Benefits: A Case Study of California Teachers Richard W. Johnson November 2017 Contents

Social Security Reform: Current Issues and Legislation

Social Security Reform: Current Issues and Legislation Dawn Nuschler Specialist in Income Security November 28, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional

Social Security Reform: Current Issues and Legislation Dawn Nuschler Specialist in Income Security November 28, 2012 CRS Report for Congress Prepared for Members and Committees of Congress Congressional

William (Larry) Minnix, Jr., Chair

Minnix, Jr., Chair") William (Larry) Minnix, Jr., Chair The Honorable Barack Obama The White House Washington, DC 20500 Dear Mr. President: On behalf of the Leadership Council of Aging Organizations (LCAO), a coalition of

William (Larry) Minnix, Jr., Chair The Honorable Barack Obama The White House Washington, DC 20500 Dear Mr. President: On behalf of the Leadership Council of Aging Organizations (LCAO), a coalition of

Teachers Retirement System of the State of Illinois

Teachers Retirement System of the State of Illinois Preliminary Actuarial Valuation and Review of Pension Benefits as of June 30, 2018 October 16, 2018 Copyright 2018 by The Segal Group, Inc. All rights

Teachers Retirement System of the State of Illinois Preliminary Actuarial Valuation and Review of Pension Benefits as of June 30, 2018 October 16, 2018 Copyright 2018 by The Segal Group, Inc. All rights

NONPARTISAN SOCIAL SECURITY REFORM PLAN Jeffrey Liebman, Maya MacGuineas, and Andrew Samwick 1 December 14, 2005

NONPARTISAN SOCIAL SECURITY REFORM PLAN Jeffrey Liebman, Maya MacGuineas, and Andrew Samwick 1 December 14, 2005 OVERVIEW The three of us former aides to President Clinton, Senator McCain, and President

NONPARTISAN SOCIAL SECURITY REFORM PLAN Jeffrey Liebman, Maya MacGuineas, and Andrew Samwick 1 December 14, 2005 OVERVIEW The three of us former aides to President Clinton, Senator McCain, and President