Demography, Capital Flows and International Portfolio Choice over the Life-cycle

|

|

|

- Meagan Page

- 5 years ago

- Views:

Transcription

1 Demography, Capital Flows and International Portfolio Choice over the Life-cycle Margaret Davenport (University of Lausanne) Katja Mann (University of Bonn) EEA-ESEM Annual Congress 23 August 2017

2 Imbalances in debt and equity position of US vis-à-vis EU 6 Bilateral Positions: US vs EU 4 Net External Positions (ratio to GDP) Net Bilateral Position (portfolio + other investment) Net Risky Position (portfolio equity) Net Safe Position (portfolio debt + net claims banking sector) Year sources: IMF Coordinated Portfolio Investment Survey, Treasury International Capital System. EU refers to the 15 EU countries of pre shares importance 2 / 22

3 Faster population aging in EU than US Old-age dependency Life expectancy at age old age dependency ratio year life expectancy at age year EU US EU US source: United Nations Population Division. EU refers to the 15 EU countries of pre / 22

4 Research Question What is the effect of population aging on international portfolio choice? Facts on Savings and Portfolio Choice details definitions hump-shaped savings pattern over the life-cycle portfolio share of risky assets declines with age Implications: Demography and Capital Flows aggregate safe and risky asset demands reflect population s age structure autarky: demographics should affect asset prices and returns financial integration of regions with different demographics: asset trades world market-clearing asset returns reflect world demographics 4 / 22

5 Research Question What is the effect of population aging on international portfolio choice? Facts on Savings and Portfolio Choice details definitions hump-shaped savings pattern over the life-cycle portfolio share of risky assets declines with age Implications: Demography and Capital Flows aggregate safe and risky asset demands reflect population s age structure autarky: demographics should affect asset prices and returns financial integration of regions with different demographics: asset trades world market-clearing asset returns reflect world demographics 4 / 22

6 Research Question What is the effect of population aging on international portfolio choice? Facts on Savings and Portfolio Choice details definitions hump-shaped savings pattern over the life-cycle portfolio share of risky assets declines with age Implications: Demography and Capital Flows aggregate safe and risky asset demands reflect population s age structure autarky: demographics should affect asset prices and returns financial integration of regions with different demographics: asset trades world market-clearing asset returns reflect world demographics 4 / 22

7 Methodology 1 Structural general equilibrium model with multi-period overlapping generations with stochastic survival portfolio choice between a safe and a risky asset two fully integrated world regions with different demography asset supply modeled through Lucas trees 2 Calibration and simulation demographic transitions for US and EU between 1950 and 2095 full financial integration from 1990 details 5 / 22

8 Findings and contribution Findings: demographics can explain a large share of bilateral asset positions and return rate movements in we predict asset returns to decrease persistently while external positions fluctuate, continuing to be sizable Contribution: imbalances and high risk-content of US position arise naturally from demographic differences and likely represent a long-run phenomenon demography as novel demand-side explanation for low interest rates and safe asset shortage, complementing e.g. Bernanke (2005), Gourinchas and Jeanne (2012), Eggertson and Mehrotra (2014), Caballero and Fahri (2017) literature 6 / 22

9 Demographics New cohorts born at N b start working immediately, and retire at age N r (fixed). Maximum lifetime is N d. Cohort size L n,t and population size L t = N d n=n L b n,t are determined by two demographic parameters: Birth rate γ t : L N b,t+1 = (1 + γ t+1 ) L N b,t Survival probability δ n,t L n,t = ( n 1 l=n b δ l,t n+l ) L N b,t n Regions e, u differ in terms of demographics - region e ages faster than u: δ e t > δ u t, γ e t < γ u t 7 / 22

10 Financial assets Two types of assets: safe bonds B t and risky stocks S t. asset prices are normalized to 1 bond pays return R t = 1 + d t, where d t is the dividend stock pays return R t = 1 + d t + risk premium t + ε t, where ε t N (0, σ ε ) asset returns are perfectly correlated internationally and the exchange rate is fixed domestic and foreign assets are identical to agents demographics affect net flows in debt and equity 8 / 22

11 Financial assets Supply: Lucas tree endowment economy with two types of trees. Aggregate supply of each asset is a linear function of the total population: B t = λl t S t = λl t with λ, λ scaling parameters. simple supply side allows focus on demand side constant risky share in line with empirical evidence (Gorton, Lewellen and Metrick, 2012) 9 / 22

12 Labor and pension income Labor income (ages n N r ) follows a stochastic iid process y i,n,t = P i,n,t ζ i,n,t θ i,n,t P i,n,t = G n P i,n,t 1 η i,n,t G n, age-specific component (hump shape over life-cycle) θ i,n,t, η i,n,t log-normally distributed shocks ζ i,n,t iid zero income shock Pension income (n > N r ) is a fixed share φ of last working period s deterministic income ỹ i,n,t = φp i,nr,tζ i,n,t Alternative: PAYGo details 10 / 22

13 Optimization problem Preferences are CRRA. Households maximize expected lifetime utility of consumption at each age n, ( N d n 1 ) U i,n,t = E β n u(c i,n,t+n ), n=t l=n b δ l,t+l subject to with x i,n,t = R tb i,n 1,t 1 + R ts i,n 1,t 1 + y i,n,t x i,n,t = R tb i,n 1,t 1 + R ts i,n 1,t 1 + ỹ i,n,t x i,n,t = c i,n,t + b i,n,t + s i,n,t }{{} a i,n,t if n N r if n > N r Natural borrowing constraint due to zero income shock: a i,n,t 0. Additional assumption: no short-sales in either asset. FOCs 11 / 22

14 Open economy: Market clearing and external positions Aggregate demand B t = N d Market clearing conditions: Bond market: Stock market: n=n b L n,tb n,t, S t = N d n=n b L n,ts n,t. B e t + B u t = B e t + B u t S e t + S u t = S e t + S u t Consumption aggregate clearing: C t + B e t + B u t + S e t + S u t = Y t + R t(b e t 1 + B u t 1) + R t(s e t 1 + S u t 1) Resulting external positions: NFB u t = B u t B u t = B e t B e t = NFB e t NFS u t = S u t S u t = S e t S e t = NFS e t, 12 / 22

15 Numerical Solution - Main parameters Demographics: Data and projections on birth rate γ t and survival probabilities δ n,t from UN Population Prospects spanning 1950 to 2095 Supply side parameters: Derive λ, λ in a partial equilibrium set-up for the US as a closed economy (1950 to 1989), using data on US 3-month government bond return and historical risk premium (Damodaran, 2016) λ = B t 1 S t λ = L t 40 L 1950 t where B t, S t are model-generated demands resulting from observed return rates, L t is population. 13 / 22

16 Numerical Solution - Additional parameters Age at birth N b 20 Maximum Age N d 100 Retirement Age N r 65 Subjective discount factor β 0.96 (Cocco et al, 2005) CRRA parameter ϑ 8 (Mehra & Prescott, 1985) Variance return shock σɛ (Fama and French, 2002) Var. transitory income shock σθ (Cocco et al, 2005) Var. permanent income shock ση (Cocco et al, 2005) Probability of zero income p 0.01 (Carroll, 1992) Age-dependent income growth G n, P n (Cocco et al, 2005) Pension replacement rate φ 0.68 (Cocco et al, 2005) Safe asset supply parameter λ estimated Risky asset supply parameter λ 77.3 estimated 14 / 22

17 Results (1): Return rates 0.04 Bond Returns Bond Returns Risk Premium Risk Premium bond return, model real return 3-month T-bill, data model data 15 / 22

18 Results (2): US external positions 5 Net Safe Position over Endowment 0 percent of GDP Net Risky Position over Endowment 4 percent of GDP model data life-cycle US aggregates 16 / 22

19 Decomposing the effect Demographic change can affect aggregate asset demand in three ways: distribution channel: changes in relative size of age groups due to decreased fertility and increased longevity life-cycle channel: changes in agents savings and portfolio choice due to increased life expectancy valuation channel: changes in market-clearing return rates Decompose these in counterfactual exercise: holding either or both of returns and life-cycle responses of individuals fixed 17 / 22

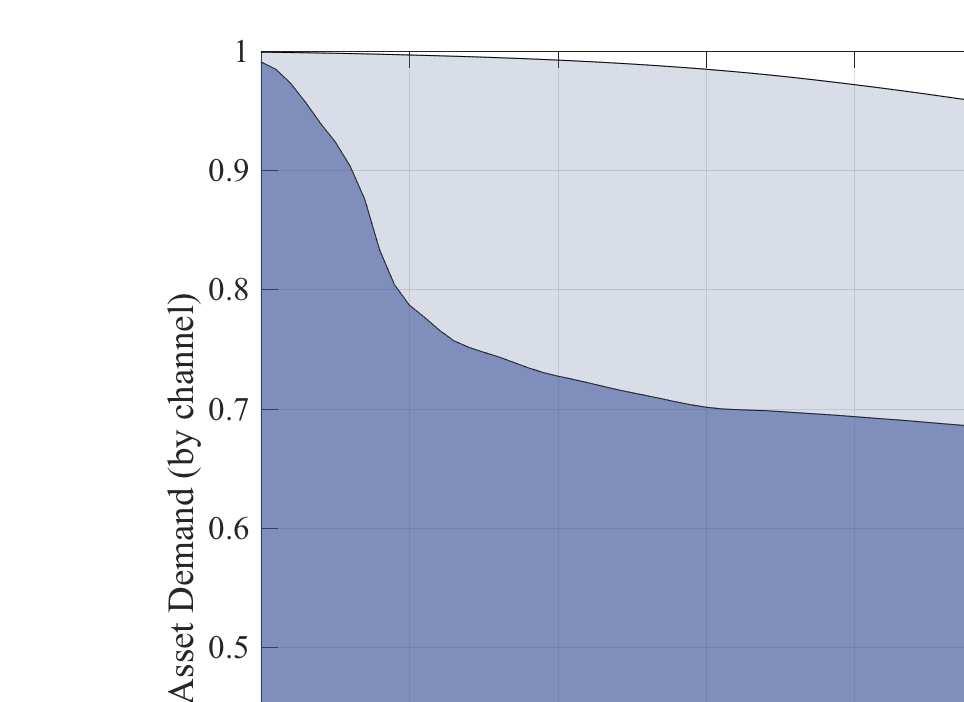

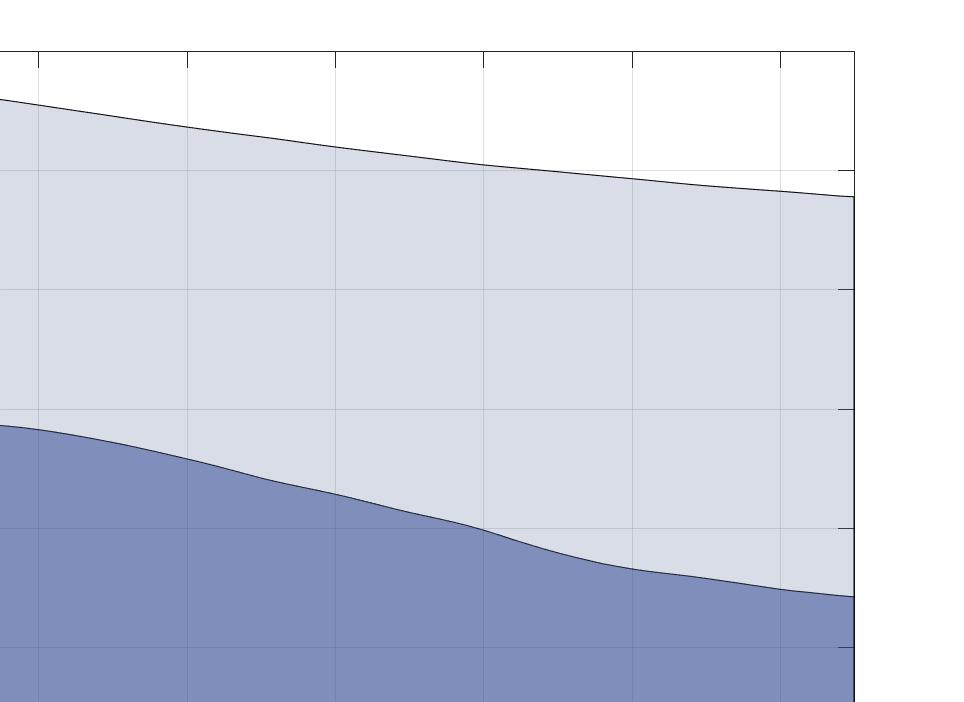

20 Channels over time age groups 18 / 22

21 Conclusion In a structural general equilibrium model with life-cycle portfolio choice, we show that demographic change in the EU and US increases the demand for financial assets, evidenced by a decrease in return rates the faster-aging EU will export risky and import safe assets, explaining the observed bilateral external positions effects result from a shift in population structure towards the elderly rather than from change in life-cycle behavior or return rate responses 19 / 22

22 Appendix 20 / 22

23 Robustness checks and extensions EU is poorer than US (70 percent of US labor income) US position slightly more negative, but similar variation retirement at age 62 similar external positions more more PAYGo pension system with constant and common tax rate of 12.4 percent, varying replacement rate (US data, OECD 2016) more similar external positions until around 2030 once most US baby boomers are dead (but those in EU still alive), extreme external positions emerge implausibly low equilibrium safe return rates from 2040 PAYGo pension system with different tax rates, in line with US and EU data (OECD 2016) more implausibly high positive US external positions 20 / 22

24 Related Literature Demographic change and portfolio choice in a closed economy: Auerbach & Kotlikoff (1987), Abel (2001, 2003), Brooks (2000, 2006), Kuhle, Ludwig & Börsch-Supan (2007) Demographic change and portfolio choice in an open economy: De Santis & Lührmann (2009) Demographic change and (aggregate) international capital flows: Börsch-Supan, Ludwig & Winter (2006), Krueger & Ludwig (2007), Backus, Cooley & Henriksen (2014), Bárány, Coeurdacier & Guibaud (2015) Asymmetries in international positions: Gourinchas and Rey (2007), Gourinchas, Rey and Govillot (2010); Caballero, Farhi and Gourinchas (2008), Mendoza, Quadrini and Rios-Rull (2009) back 21 / 22

25 Estimated Life-cycle Savings and Portfolio Shares financial assets (thsd $) conditional risky share Total financial assets, US Conditional risky share of financial assets, US estimation based on Survey of Consumer Finances, 1989 to 2013; following Deaton & Paxson (1994): controlling for time- and cohort-fixed effects and for endogenous participation details declining risky share with age is also found by Poterba and Samwick (2001), Guiso, Haliassos & Japelli (2002), Fagereng, Gottlieb & Guiso (2017), among others back 21 / 22

26 Estimation of Life-cycle Asset Holdings and Risky Share Deaton & Paxson (1994) method to estimate cohort-, time- and age-fixed effects simultaneously Heckman estimation of risky share first stage: probit estimation of participation in stockmarket P iact prob(p iact = 1 x) = prob(δ aa a + δ cc c + δ td t + δ 0Trend+ υz iact + υ 2L iact + η iact > 0) second stage: estimation of the risky share conditional on participation; Deaton & Paxson (1994) method: ω iact = β aa a + β cc c + β td t + β 0Trend + δz iact + δ 2λ iact + ε iact. estimation of life-cycle financial asset holdings: z iact = γ a A a + γg c + γ t D t + ψz iact + ν iact back 21 / 22

27 Definition of safe and risky assets Source Risky assets Safe assets SCF stocks; stock mutual funds; IRAs/Keoghs invested in stock; other managed assets with equity interest (annuities, trusts, managed investment accounts) if invested in stocks; thrift-type retirement accounts invested in stocks; savings accounts classified as 529 or other accounts that may be invested in stocks CPIS and TIC short- and long-term debt instruments, e.g. bonds, debentures, treasury bills, negotiable certificates of deposit, commercial papers, bankers acceptances transaction accounts; certificates of deposit; bonds (except mortgagebacked); mutual funds invested in bonds; quasi-liquid retirement accounts (IRAs and thrift-type accounts) and individual retirement accounts/keoghs if invested in bonds; savings bonds; cash value of life insurance; other managed assets (trusts, annuities, managed investment accounts) if invested in bonds equity and investment fund shares, e.g. shares, stocks, participations or similar documents back 21 / 22

28 Table: Share of bilateral positions in total external asset positions EU US debt equity debt equity OFCs as RoW OFCs as bilateral Source: CPIS, using a definition of offshore financial centers (OFCs) by the IMF. Numbers are averaged over back 21 / 22

29 First order conditions The first order conditions with respect to consumption and assets result in the Euler equation (ω = risky share) [ )] c ϑ i,n,t = β δ n,t E t c ϑ i,n+1,t+1 ((1 ω i,n,t )R t+1 + ω i,n,t R t+1 and the portfolio share optimality condition: β δ n,t E t [c i,n+1,t+1 a n,t ( R ] t+1 R t+1 ) = 0 Effect of demographic change (increase in δ n,t ): savings: reduce current consumption in Euler eq.s portfolio choice (through savings): increase the share of risky assets back 21 / 22

30 Simulation results: Life-cycle asset holdings 600 Life-cycle Financial Assets 1 Life-cycle Risky Share thousands of 2010 US dollars thousands of 2010 US dollars age age Total, 1950 Total, 2010 Total, 2095 Risky Assets, 1950 Risky Assets, 2010 Risky Assets, 2095 back 21 / 22

31 Simulation results: US aggregates 0.12 Consumption over Total Financial Assets, Household Sector Total Financial Assets, Household Sector trillions of US dollars Total Risky Assets over GDP, Household Sector Aggregate Endowment (GDP) trillions of US dollars model data (right axis) back 21 / 22

32 Channels across age groups back 21 / 22

33 US and EU share of of world external assets assets Year equity debt source: Lane and Milesi-Ferretti (2007) back 21 / 22

34 PAYGo pension system working-age individuals pay a constant tax rate τ on their labor income retirees of any age n earn a period t income Ỹ t = N r 1 n=n τy n,tl b n,t N d n=n L ; r n,t pension income is larger when the working-age population is larger or more concentrated at high-earning age groups, when the tax rate is higher, or the number of retirees smaller for now we assume that retirement age is held constant and that the government budget always balances back 22 / 22

35 0.05 Safe Assets Risky Assets Year back 22 / 22

36 0 Safe Assets Risky Assets Year back 22 / 22

37 1.5 Safe Assets Risky Assets Year back 22 / 22

38 0.2 Safe Assets Risky Assets Year back 22 / 22

39 de jure financial openness year EU US source: Chinn and Ito (2008) back 22 / 22

Demography, Capital Flows and International Portfolio Choice over the Life-cycle

Demography, Capital Flows and International Portfolio Choice over the Life-cycle Margaret Davenport Katja Mann December 31, 2016 Preliminary and incomplete Abstract In an aging world, how does a country

Demography, Capital Flows and International Portfolio Choice over the Life-cycle Margaret Davenport Katja Mann December 31, 2016 Preliminary and incomplete Abstract In an aging world, how does a country

Household Saving, Financial Constraints, and the Current Account Balance in China

Household Saving, Financial Constraints, and the Current Account Balance in China Ayşe İmrohoroğlu USC Marshall Kai Zhao Univ. of Connecticut Facing Demographic Change in a Challenging Economic Environment-

Household Saving, Financial Constraints, and the Current Account Balance in China Ayşe İmrohoroğlu USC Marshall Kai Zhao Univ. of Connecticut Facing Demographic Change in a Challenging Economic Environment-

Financial Integration and Growth in a Risky World

Financial Integration and Growth in a Risky World Nicolas Coeurdacier (SciencesPo & CEPR) Helene Rey (LBS & NBER & CEPR) Pablo Winant (PSE) Barcelona June 2013 Coeurdacier, Rey, Winant Financial Integration...

Financial Integration and Growth in a Risky World Nicolas Coeurdacier (SciencesPo & CEPR) Helene Rey (LBS & NBER & CEPR) Pablo Winant (PSE) Barcelona June 2013 Coeurdacier, Rey, Winant Financial Integration...

Financial Integration, Financial Deepness and Global Imbalances

Financial Integration, Financial Deepness and Global Imbalances Enrique G. Mendoza University of Maryland, IMF & NBER Vincenzo Quadrini University of Southern California, CEPR & NBER José-Víctor Ríos-Rull

Financial Integration, Financial Deepness and Global Imbalances Enrique G. Mendoza University of Maryland, IMF & NBER Vincenzo Quadrini University of Southern California, CEPR & NBER José-Víctor Ríos-Rull

Exorbitant Duty. Hélène Rey London Business School CEPR & NBER Nicolas Govillot Mines de Paris

Exorbitant Privilege and Exorbitant Duty PO P.O. Gourinchas UC Berkeley, CEPR & NBER Hélène Rey London Business School CEPR & NBER Nicolas Govillot Mines de Paris Research Agenda on balance sheet of countries

Exorbitant Privilege and Exorbitant Duty PO P.O. Gourinchas UC Berkeley, CEPR & NBER Hélène Rey London Business School CEPR & NBER Nicolas Govillot Mines de Paris Research Agenda on balance sheet of countries

Advanced International Finance Part 3

Advanced International Finance Part 3 Nicolas Coeurdacier - nicolas.coeurdacier@sciences-po.fr Spring 2011 Global Imbalances and Valuation Effects (2) - Models of Global Imbalances Caballerro, Fahri and

Advanced International Finance Part 3 Nicolas Coeurdacier - nicolas.coeurdacier@sciences-po.fr Spring 2011 Global Imbalances and Valuation Effects (2) - Models of Global Imbalances Caballerro, Fahri and

Demographic Trends and the Real Interest Rate

Demographic Trends and the Real Interest Rate Noëmie Lisack Rana Sajedi Gregory Thwaites Bank of England November 2017 This does not represent the views of the Bank of England 1 / 43 Disclaimer This does

Demographic Trends and the Real Interest Rate Noëmie Lisack Rana Sajedi Gregory Thwaites Bank of England November 2017 This does not represent the views of the Bank of England 1 / 43 Disclaimer This does

Currency Risk Factors in a Recursive Multi-Country Economy

Currency Risk Factors in a Recursive Multi-Country Economy R. Colacito M.M. Croce F. Gavazzoni R. Ready NBER SI - International Asset Pricing Boston July 8, 2015 Motivation The literature has identified

Currency Risk Factors in a Recursive Multi-Country Economy R. Colacito M.M. Croce F. Gavazzoni R. Ready NBER SI - International Asset Pricing Boston July 8, 2015 Motivation The literature has identified

Home Production and Social Security Reform

Home Production and Social Security Reform Michael Dotsey Wenli Li Fang Yang Federal Reserve Bank of Philadelphia SUNY-Albany October 17, 2012 Dotsey, Li, Yang () Home Production October 17, 2012 1 / 29

Home Production and Social Security Reform Michael Dotsey Wenli Li Fang Yang Federal Reserve Bank of Philadelphia SUNY-Albany October 17, 2012 Dotsey, Li, Yang () Home Production October 17, 2012 1 / 29

Topic 3: Global Imbalances Econ 2530b, Gita Gopinath

Topic 3: Global Imbalances Econ 2530b, Gita Gopinath Facts Mendoza, Quadrini, Rios-Rull (2009 JPE) Precautionary Savings (Demand for assets) Caballero, Farhi, Gourinchas (2008 AER) Quality of financial

Topic 3: Global Imbalances Econ 2530b, Gita Gopinath Facts Mendoza, Quadrini, Rios-Rull (2009 JPE) Precautionary Savings (Demand for assets) Caballero, Farhi, Gourinchas (2008 AER) Quality of financial

NBER WORKING PAPER SERIES THE "GREAT MODERATION" AND THE US EXTERNAL IMBALANCE. Alessandra Fogli Fabrizio Perri

NBER WORKING PAPER SERIES THE "GREAT MODERATION" AND THE US EXTERNAL IMBALANCE Alessandra Fogli Fabrizio Perri Working Paper 12708 http://www.nber.org/papers/w12708 NATIONAL BUREAU OF ECONOMIC RESEARCH

NBER WORKING PAPER SERIES THE "GREAT MODERATION" AND THE US EXTERNAL IMBALANCE Alessandra Fogli Fabrizio Perri Working Paper 12708 http://www.nber.org/papers/w12708 NATIONAL BUREAU OF ECONOMIC RESEARCH

Aging, Social Security Reform and Factor Price in a Transition Economy

Aging, Social Security Reform and Factor Price in a Transition Economy Tomoaki Yamada Rissho University 2, December 2007 Motivation Objectives Introduction: Motivation Rapid aging of the population combined

Aging, Social Security Reform and Factor Price in a Transition Economy Tomoaki Yamada Rissho University 2, December 2007 Motivation Objectives Introduction: Motivation Rapid aging of the population combined

Groupe de Travail: International Risk-Sharing and the Transmission of Productivity Shocks

Groupe de Travail: International Risk-Sharing and the Transmission of Productivity Shocks Giancarlo Corsetti Luca Dedola Sylvain Leduc CREST, May 2008 The International Consumption Correlations Puzzle

Groupe de Travail: International Risk-Sharing and the Transmission of Productivity Shocks Giancarlo Corsetti Luca Dedola Sylvain Leduc CREST, May 2008 The International Consumption Correlations Puzzle

Oil Price Uncertainty in a Small Open Economy

Yusuf Soner Başkaya Timur Hülagü Hande Küçük 6 April 212 Oil price volatility is high and it varies over time... 15 1 5 1985 199 1995 2 25 21 (a) Mean.4.35.3.25.2.15.1.5 1985 199 1995 2 25 21 (b) Coefficient

Yusuf Soner Başkaya Timur Hülagü Hande Küçük 6 April 212 Oil price volatility is high and it varies over time... 15 1 5 1985 199 1995 2 25 21 (a) Mean.4.35.3.25.2.15.1.5 1985 199 1995 2 25 21 (b) Coefficient

Designing the Optimal Social Security Pension System

Designing the Optimal Social Security Pension System Shinichi Nishiyama Department of Risk Management and Insurance Georgia State University November 17, 2008 Abstract We extend a standard overlapping-generations

Designing the Optimal Social Security Pension System Shinichi Nishiyama Department of Risk Management and Insurance Georgia State University November 17, 2008 Abstract We extend a standard overlapping-generations

Retirement in the Shadow (Banking)

") Retirement in the Shadow (Banking) Guillermo Ordoñez 1 Facundo Piguillem 2 1 University of Pennsylvania 2 EIEF October 6, 2015 1/37 Motivation Since 1980 the US has experienced fundamental changes: Large

Retirement in the Shadow (Banking) Guillermo Ordoñez 1 Facundo Piguillem 2 1 University of Pennsylvania 2 EIEF October 6, 2015 1/37 Motivation Since 1980 the US has experienced fundamental changes: Large

Why Are Interest Rates So Low? The Role of Demographic Change

Why Are Interest Rates So Low? The Role of Demographic Change Noëmie Lisack Rana Sajedi Gregory Thwaites Bank of England April 2017 1 / 31 Disclaimer This does not represent the views of the Bank of England

Why Are Interest Rates So Low? The Role of Demographic Change Noëmie Lisack Rana Sajedi Gregory Thwaites Bank of England April 2017 1 / 31 Disclaimer This does not represent the views of the Bank of England

The Japanese saving rate between 1960 and 2000: productivity, policy changes, and demographics

Economic Theory (2007) 32: 87 104 DOI 10.1007/s00199-006-0200-9 SYMPOSIUM Kaiji Chen Ayşe İmrohoroğlu Selahattin İmrohoroğlu The Japanese saving rate between 1960 and 2000: productivity, policy changes,

Economic Theory (2007) 32: 87 104 DOI 10.1007/s00199-006-0200-9 SYMPOSIUM Kaiji Chen Ayşe İmrohoroğlu Selahattin İmrohoroğlu The Japanese saving rate between 1960 and 2000: productivity, policy changes,

Credit and hiring. Vincenzo Quadrini University of Southern California, visiting EIEF Qi Sun University of Southern California.

Credit and hiring Vincenzo Quadrini University of Southern California, visiting EIEF Qi Sun University of Southern California November 14, 2013 CREDIT AND EMPLOYMENT LINKS When credit is tight, employers

Credit and hiring Vincenzo Quadrini University of Southern California, visiting EIEF Qi Sun University of Southern California November 14, 2013 CREDIT AND EMPLOYMENT LINKS When credit is tight, employers

Global Real Rates: A Secular Approach

Global Real Rates: A Secular Approach Pierre-Olivier Gourinchas 1 Hélène Rey 2 1 UC Berkeley & NBER & CEPR 2 London Business School & NBER & CEPR FRBSF Fed, April 2017 Prepared for the conference Do Changes

Global Real Rates: A Secular Approach Pierre-Olivier Gourinchas 1 Hélène Rey 2 1 UC Berkeley & NBER & CEPR 2 London Business School & NBER & CEPR FRBSF Fed, April 2017 Prepared for the conference Do Changes

POPULATION AGING AND INTERNATIONAL CAPITAL FLOWS. Stockholm School of Economics, Sweden; CEPR and Stockholm School of Economics, Sweden

INTERNATIONAL ECONOMIC REVIEW Vol. 47, No. 3, August 2006 POPULATION AGING AND INTERNATIONAL CAPITAL FLOWS BY DAVID DOMEIJ AND MARTIN FLODÉN 1 Stockholm School of Economics, Sweden; CEPR and Stockholm

INTERNATIONAL ECONOMIC REVIEW Vol. 47, No. 3, August 2006 POPULATION AGING AND INTERNATIONAL CAPITAL FLOWS BY DAVID DOMEIJ AND MARTIN FLODÉN 1 Stockholm School of Economics, Sweden; CEPR and Stockholm

Does the Social Safety Net Improve Welfare? A Dynamic General Equilibrium Analysis

Does the Social Safety Net Improve Welfare? A Dynamic General Equilibrium Analysis University of Western Ontario February 2013 Question Main Question: what is the welfare cost/gain of US social safety

Does the Social Safety Net Improve Welfare? A Dynamic General Equilibrium Analysis University of Western Ontario February 2013 Question Main Question: what is the welfare cost/gain of US social safety

Debt Covenants and the Macroeconomy: The Interest Coverage Channel

Debt Covenants and the Macroeconomy: The Interest Coverage Channel Daniel L. Greenwald MIT Sloan EFA Lunch, April 19 Daniel L. Greenwald Debt Covenants and the Macroeconomy EFA Lunch, April 19 1 / 6 Introduction

Debt Covenants and the Macroeconomy: The Interest Coverage Channel Daniel L. Greenwald MIT Sloan EFA Lunch, April 19 Daniel L. Greenwald Debt Covenants and the Macroeconomy EFA Lunch, April 19 1 / 6 Introduction

The Role of Investment Wedges in the Carlstrom-Fuerst Economy and Business Cycle Accounting

MPRA Munich Personal RePEc Archive The Role of Investment Wedges in the Carlstrom-Fuerst Economy and Business Cycle Accounting Masaru Inaba and Kengo Nutahara Research Institute of Economy, Trade, and

MPRA Munich Personal RePEc Archive The Role of Investment Wedges in the Carlstrom-Fuerst Economy and Business Cycle Accounting Masaru Inaba and Kengo Nutahara Research Institute of Economy, Trade, and

The Demand and Supply of Safe Assets (Premilinary)

") The Demand and Supply of Safe Assets (Premilinary) Yunfan Gu August 28, 2017 Abstract It is documented that over the past 60 years, the safe assets as a percentage share of total assets in the U.S. has

The Demand and Supply of Safe Assets (Premilinary) Yunfan Gu August 28, 2017 Abstract It is documented that over the past 60 years, the safe assets as a percentage share of total assets in the U.S. has

Retirement Financing: An Optimal Reform Approach. QSPS Summer Workshop 2016 May 19-21

Retirement Financing: An Optimal Reform Approach Roozbeh Hosseini University of Georgia Ali Shourideh Wharton School QSPS Summer Workshop 2016 May 19-21 Roozbeh Hosseini(UGA) 0 of 34 Background and Motivation

Retirement Financing: An Optimal Reform Approach Roozbeh Hosseini University of Georgia Ali Shourideh Wharton School QSPS Summer Workshop 2016 May 19-21 Roozbeh Hosseini(UGA) 0 of 34 Background and Motivation

Sang-Wook (Stanley) Cho

Cho") Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales March 2009 Motivation & Question Since Becker (1974), several studies analyzing

Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales March 2009 Motivation & Question Since Becker (1974), several studies analyzing

International Trade and Income Differences

International Trade and Income Differences By Michael E. Waugh AER (Dec. 2010) Content 1. Motivation 2. The theoretical model 3. Estimation strategy and data 4. Results 5. Counterfactual simulations 6.

International Trade and Income Differences By Michael E. Waugh AER (Dec. 2010) Content 1. Motivation 2. The theoretical model 3. Estimation strategy and data 4. Results 5. Counterfactual simulations 6.

Demographic Uncertainty and Generational Consumption Risk with Endogenous Human Capital

DISCUSSION PAPER SERIES IZA DP No. 11358 Demographic Uncertainty and Generational Consumption Risk with Endogenous Human Capital Patrick Emerson Shawn D. Knabb FEBRUARY 2018 DISCUSSION PAPER SERIES IZA

DISCUSSION PAPER SERIES IZA DP No. 11358 Demographic Uncertainty and Generational Consumption Risk with Endogenous Human Capital Patrick Emerson Shawn D. Knabb FEBRUARY 2018 DISCUSSION PAPER SERIES IZA

Atkeson, Chari and Kehoe (1999), Taxing Capital Income: A Bad Idea, QR Fed Mpls

, Taxing Capital Income: A Bad Idea, QR Fed Mpls") Lucas (1990), Supply Side Economics: an Analytical Review, Oxford Economic Papers When I left graduate school, in 1963, I believed that the single most desirable change in the U.S. structure would be the

Lucas (1990), Supply Side Economics: an Analytical Review, Oxford Economic Papers When I left graduate school, in 1963, I believed that the single most desirable change in the U.S. structure would be the

The Eurozone Debt Crisis: A New-Keynesian DSGE model with default risk

The Eurozone Debt Crisis: A New-Keynesian DSGE model with default risk Daniel Cohen 1,2 Mathilde Viennot 1 Sébastien Villemot 3 1 Paris School of Economics 2 CEPR 3 OFCE Sciences Po PANORisk workshop 7

The Eurozone Debt Crisis: A New-Keynesian DSGE model with default risk Daniel Cohen 1,2 Mathilde Viennot 1 Sébastien Villemot 3 1 Paris School of Economics 2 CEPR 3 OFCE Sciences Po PANORisk workshop 7

Macroeconomics Sequence, Block I. Introduction to Consumption Asset Pricing

Macroeconomics Sequence, Block I Introduction to Consumption Asset Pricing Nicola Pavoni October 21, 2016 The Lucas Tree Model This is a general equilibrium model where instead of deriving properties of

Macroeconomics Sequence, Block I Introduction to Consumption Asset Pricing Nicola Pavoni October 21, 2016 The Lucas Tree Model This is a general equilibrium model where instead of deriving properties of

Asset Pricing and Equity Premium Puzzle. E. Young Lecture Notes Chapter 13

Asset Pricing and Equity Premium Puzzle 1 E. Young Lecture Notes Chapter 13 1 A Lucas Tree Model Consider a pure exchange, representative household economy. Suppose there exists an asset called a tree.

Asset Pricing and Equity Premium Puzzle 1 E. Young Lecture Notes Chapter 13 1 A Lucas Tree Model Consider a pure exchange, representative household economy. Suppose there exists an asset called a tree.

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Fall, 2016

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2016 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2016 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Fall, 2010 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements, state

A Life-Cycle Overlapping-Generations Model of the Small Open Economy Ben J. Heijdra & Ward E. Romp

Mortality and Macroeconomics: Tilburg University 1 A Life-Cycle Overlapping-Generations Model of the Small Open Economy & Ward E. Romp Mortality and Macroeconomics Tilburg University Version 1. 7 December

Mortality and Macroeconomics: Tilburg University 1 A Life-Cycle Overlapping-Generations Model of the Small Open Economy & Ward E. Romp Mortality and Macroeconomics Tilburg University Version 1. 7 December

Not All Oil Price Shocks Are Alike: A Neoclassical Perspective

Not All Oil Price Shocks Are Alike: A Neoclassical Perspective Vipin Arora Pedro Gomis-Porqueras Junsang Lee U.S. EIA Deakin Univ. SKKU December 16, 2013 GRIPS Junsang Lee (SKKU) Oil Price Dynamics in

Not All Oil Price Shocks Are Alike: A Neoclassical Perspective Vipin Arora Pedro Gomis-Porqueras Junsang Lee U.S. EIA Deakin Univ. SKKU December 16, 2013 GRIPS Junsang Lee (SKKU) Oil Price Dynamics in

Heterogeneous Firm, Financial Market Integration and International Risk Sharing

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Why are real interest rates so low?

Why are real interest rates so low? M. Marx, B. Mojon, F. Velde Warsaw 17 December, 2015 Motivation (1/2) Why are interest rates so low? What can we do about it? Motivation (2/2) The debate on the level

Why are real interest rates so low? M. Marx, B. Mojon, F. Velde Warsaw 17 December, 2015 Motivation (1/2) Why are interest rates so low? What can we do about it? Motivation (2/2) The debate on the level

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Preliminary Examination: Macroeconomics Spring, 2007

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Spring, 2007 Instructions: Read the questions carefully and make sure to show your work. You

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Preliminary Examination: Macroeconomics Spring, 2007 Instructions: Read the questions carefully and make sure to show your work. You

The Saving Rate in Japan: Why It Has Fallen and Why It Will Remain Low

CIRJE-F-535 The Saving Rate in Japan: Why It Has Fallen and Why It Will Remain Low R.Anton Braun University of Tokyo Daisuke Ikeda Northwestern University and Bank of Japan Douglas H. Joines University

CIRJE-F-535 The Saving Rate in Japan: Why It Has Fallen and Why It Will Remain Low R.Anton Braun University of Tokyo Daisuke Ikeda Northwestern University and Bank of Japan Douglas H. Joines University

Credit Constraints and Growth in a Global Economy

Credit Constraints and Growth in a Global Economy Nicolas Coeurdacier (Sciences-Po Paris and CEPR) Stephane Guibaud (LSE) Keyu Jin (LSE) March 16, 211 Abstract In a period of rapid integration and accelerated

Credit Constraints and Growth in a Global Economy Nicolas Coeurdacier (Sciences-Po Paris and CEPR) Stephane Guibaud (LSE) Keyu Jin (LSE) March 16, 211 Abstract In a period of rapid integration and accelerated

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics. Ph. D. Comprehensive Examination: Macroeconomics Spring, 2009

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2009 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements,

STATE UNIVERSITY OF NEW YORK AT ALBANY Department of Economics Ph. D. Comprehensive Examination: Macroeconomics Spring, 2009 Section 1. (Suggested Time: 45 Minutes) For 3 of the following 6 statements,

Fiscal Cost of Demographic Transition in Japan

RIETI Discussion Paper Series 15-E-013 Fiscal Cost of Demographic Transition in Japan KITAO Sagiri RIETI The Research Institute of Economy, Trade and Industry http://www.rieti.go.jp/en/ RIETI Discussion

RIETI Discussion Paper Series 15-E-013 Fiscal Cost of Demographic Transition in Japan KITAO Sagiri RIETI The Research Institute of Economy, Trade and Industry http://www.rieti.go.jp/en/ RIETI Discussion

Homework 3: Asset Pricing

Homework 3: Asset Pricing Mohammad Hossein Rahmati November 1, 2018 1. Consider an economy with a single representative consumer who maximize E β t u(c t ) 0 < β < 1, u(c t ) = ln(c t + α) t= The sole

Homework 3: Asset Pricing Mohammad Hossein Rahmati November 1, 2018 1. Consider an economy with a single representative consumer who maximize E β t u(c t ) 0 < β < 1, u(c t ) = ln(c t + α) t= The sole

Why Have Interest Rates Fallen Far Below the Return on Capital

Why Have Interest Rates Fallen Far Below the Return on Capital Magali Marx Banque de France Benoît Mojon Banque de France François R. Velde Federal Reserve Bank of Chicago Macroeconomic and Financial Imbalances

Why Have Interest Rates Fallen Far Below the Return on Capital Magali Marx Banque de France Benoît Mojon Banque de France François R. Velde Federal Reserve Bank of Chicago Macroeconomic and Financial Imbalances

Will Bequests Attenuate the Predicted Meltdown in Stock Prices When Baby Boomers Retire?

Will Bequests Attenuate the Predicted Meltdown in Stock Prices When Baby Boomers Retire? Andrew B. Abel The Wharton School of the University of Pennsylvania and National Bureau of Economic Research June

Will Bequests Attenuate the Predicted Meltdown in Stock Prices When Baby Boomers Retire? Andrew B. Abel The Wharton School of the University of Pennsylvania and National Bureau of Economic Research June

The Impact of Personal Bankruptcy Law on Entrepreneurship

The Impact of Personal Bankruptcy Law on Entrepreneurship Ye (George) Jia University of Prince Edward Island Small Business, Entrepreneurship and Economic Recovery Conference at Federal Reserve Bank of

The Impact of Personal Bankruptcy Law on Entrepreneurship Ye (George) Jia University of Prince Edward Island Small Business, Entrepreneurship and Economic Recovery Conference at Federal Reserve Bank of

General Examination in Macroeconomic Theory SPRING 2016

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 2016 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 60 minutes Part B (Prof. Barro): 60

HARVARD UNIVERSITY DEPARTMENT OF ECONOMICS General Examination in Macroeconomic Theory SPRING 2016 You have FOUR hours. Answer all questions Part A (Prof. Laibson): 60 minutes Part B (Prof. Barro): 60

Adjustment Costs, Agency Costs and Terms of Trade Disturbances in a Small Open Economy

Adjustment Costs, Agency Costs and Terms of Trade Disturbances in a Small Open Economy This version: April 2004 Benoît Carmichæl Lucie Samson Département d économique Université Laval, Ste-Foy, Québec

Adjustment Costs, Agency Costs and Terms of Trade Disturbances in a Small Open Economy This version: April 2004 Benoît Carmichæl Lucie Samson Département d économique Université Laval, Ste-Foy, Québec

Consumption and Labor Supply with Partial Insurance: An Analytical Framework

Consumption and Labor Supply with Partial Insurance: An Analytical Framework Jonathan Heathcote Federal Reserve Bank of Minneapolis, CEPR Kjetil Storesletten Federal Reserve Bank of Minneapolis, CEPR Gianluca

Consumption and Labor Supply with Partial Insurance: An Analytical Framework Jonathan Heathcote Federal Reserve Bank of Minneapolis, CEPR Kjetil Storesletten Federal Reserve Bank of Minneapolis, CEPR Gianluca

Convergence of Life Expectancy and Living Standards in the World

Convergence of Life Expectancy and Living Standards in the World Kenichi Ueda* *The University of Tokyo PRI-ADBI Joint Workshop January 13, 2017 The views are those of the author and should not be attributed

Convergence of Life Expectancy and Living Standards in the World Kenichi Ueda* *The University of Tokyo PRI-ADBI Joint Workshop January 13, 2017 The views are those of the author and should not be attributed

Foreign Competition and Banking Industry Dynamics: An Application to Mexico

Foreign Competition and Banking Industry Dynamics: An Application to Mexico Dean Corbae Pablo D Erasmo 1 Univ. of Wisconsin FRB Philadelphia June 12, 2014 1 The views expressed here do not necessarily

Foreign Competition and Banking Industry Dynamics: An Application to Mexico Dean Corbae Pablo D Erasmo 1 Univ. of Wisconsin FRB Philadelphia June 12, 2014 1 The views expressed here do not necessarily

International Capital Flows: A Role for Demography?

International Capital Flows: A Role for Demography? David Backus, Thomas Cooley, and Espen Henriksen NUS October 12, 2010 This version: October 11, 2010 Backus, Cooley, and Henriksen (NYU) International

International Capital Flows: A Role for Demography? David Backus, Thomas Cooley, and Espen Henriksen NUS October 12, 2010 This version: October 11, 2010 Backus, Cooley, and Henriksen (NYU) International

Taxing Firms Facing Financial Frictions

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

Taxing Firms Facing Financial Frictions Daniel Wills 1 Gustavo Camilo 2 1 Universidad de los Andes 2 Cornerstone November 11, 2017 NTA 2017 Conference Corporate income is often taxed at different sources

Volume Title: Social Security Policy in a Changing Environment. Volume Author/Editor: Jeffrey Brown, Jeffrey Liebman and David A.

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Social Security Policy in a Changing Environment Volume Author/Editor: Jeffrey Brown, Jeffrey

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Social Security Policy in a Changing Environment Volume Author/Editor: Jeffrey Brown, Jeffrey

Financial integration: Patterns, effects and challenges.

Financial integration: Patterns, effects and challenges. Viktoria Hnatkovska UBC and Wharton School BREAD-IGC-ISI Summer School, Delhi July 23 2012 Introduction New Delhi, March 2012: Mr Kaushik Basu,

Financial integration: Patterns, effects and challenges. Viktoria Hnatkovska UBC and Wharton School BREAD-IGC-ISI Summer School, Delhi July 23 2012 Introduction New Delhi, March 2012: Mr Kaushik Basu,

Business Cycles and Household Formation: The Micro versus the Macro Labor Elasticity

Business Cycles and Household Formation: The Micro versus the Macro Labor Elasticity Greg Kaplan José-Víctor Ríos-Rull University of Pennsylvania University of Minnesota, Mpls Fed, and CAERP EFACR Consumption

Business Cycles and Household Formation: The Micro versus the Macro Labor Elasticity Greg Kaplan José-Víctor Ríos-Rull University of Pennsylvania University of Minnesota, Mpls Fed, and CAERP EFACR Consumption

Temi di Discussione. Medium and long term implications of financial integration without financial development. (Working Papers) June 2017

June 2017") Temi di Discussione (Working Papers) Medium and long term implications of financial integration without financial development by Flavia Corneli June 2017 Number 1120 Temi di discussione (Working papers)

Temi di Discussione (Working Papers) Medium and long term implications of financial integration without financial development by Flavia Corneli June 2017 Number 1120 Temi di discussione (Working papers)

International Macroeconomics and Finance Session 4-6

International Macroeconomics and Finance Session 4-6 Nicolas Coeurdacier - nicolas.coeurdacier@sciences-po.fr Master EPP - Fall 2012 International real business cycles - Workhorse models of international

International Macroeconomics and Finance Session 4-6 Nicolas Coeurdacier - nicolas.coeurdacier@sciences-po.fr Master EPP - Fall 2012 International real business cycles - Workhorse models of international

Aging and Pensions in General Equilibrium: Labor Market Imperfections Matter

DISCUSSION PAPER SERIES IZA DP No. 5276 Aging and Pensions in General Equilibrium: Labor Market Imperfections Matter David de la Croix Olivier Pierrard Henri R. Sneessens October 2010 Forschungsinstitut

DISCUSSION PAPER SERIES IZA DP No. 5276 Aging and Pensions in General Equilibrium: Labor Market Imperfections Matter David de la Croix Olivier Pierrard Henri R. Sneessens October 2010 Forschungsinstitut

Question 1 Consider an economy populated by a continuum of measure one of consumers whose preferences are defined by the utility function:

Question 1 Consider an economy populated by a continuum of measure one of consumers whose preferences are defined by the utility function: β t log(c t ), where C t is consumption and the parameter β satisfies

Question 1 Consider an economy populated by a continuum of measure one of consumers whose preferences are defined by the utility function: β t log(c t ), where C t is consumption and the parameter β satisfies

Labor Economics Field Exam Spring 2011

Labor Economics Field Exam Spring 2011 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

Labor Economics Field Exam Spring 2011 Instructions You have 4 hours to complete this exam. This is a closed book examination. No written materials are allowed. You can use a calculator. THE EXAM IS COMPOSED

Capital Goods Trade and Economic Development

Capital Goods Trade and Economic Development Piyusha Mutreja B. Ravikumar Michael Sposi Syracuse U. FRB St. Louis FRB Dallas December 2014 NYU-FRBATL Conference Disclaimer: The following views are those

Capital Goods Trade and Economic Development Piyusha Mutreja B. Ravikumar Michael Sposi Syracuse U. FRB St. Louis FRB Dallas December 2014 NYU-FRBATL Conference Disclaimer: The following views are those

Wealth Accumulation in the US: Do Inheritances and Bequests Play a Significant Role

Wealth Accumulation in the US: Do Inheritances and Bequests Play a Significant Role John Laitner January 26, 2015 The author gratefully acknowledges support from the U.S. Social Security Administration

Wealth Accumulation in the US: Do Inheritances and Bequests Play a Significant Role John Laitner January 26, 2015 The author gratefully acknowledges support from the U.S. Social Security Administration

Capital Inflows: A Threat to Growth?

Capital Inflows: A Threat to Growth? David Backus, Thomas Cooley, and Espen Henriksen Restoring Growth in Advanced Economies NCAER, World Bank, & NYU October 7, 2010 This version: October 9, 2010 Backus,

Capital Inflows: A Threat to Growth? David Backus, Thomas Cooley, and Espen Henriksen Restoring Growth in Advanced Economies NCAER, World Bank, & NYU October 7, 2010 This version: October 9, 2010 Backus,

Aging and Deflation from a Fiscal Perspective

Aging and Deflation from a Fiscal Perspective Mitsuru Katagiri, Hideki Konishi, and Kozo Ueda Bank of Japan and Waseda Univ December 2014 @ CIGS FTPL December 2014 @ CIGS 1 / 35 Negative Correlation bw

Aging and Deflation from a Fiscal Perspective Mitsuru Katagiri, Hideki Konishi, and Kozo Ueda Bank of Japan and Waseda Univ December 2014 @ CIGS FTPL December 2014 @ CIGS 1 / 35 Negative Correlation bw

Household Saving, Financial Constraints, and the Current Account in China

Household Saving, Financial Constraints, and the Current Account in China Ayşe İmrohoroğlu Kai Zhao November 2017 Abstract In this paper, we present a model economy that can account for the changes in

Household Saving, Financial Constraints, and the Current Account in China Ayşe İmrohoroğlu Kai Zhao November 2017 Abstract In this paper, we present a model economy that can account for the changes in

Chapter 5 Macroeconomics and Finance

Macro II Chapter 5 Macro and Finance 1 Chapter 5 Macroeconomics and Finance Main references : - L. Ljundqvist and T. Sargent, Chapter 7 - Mehra and Prescott 1985 JME paper - Jerman 1998 JME paper - J.

Macro II Chapter 5 Macro and Finance 1 Chapter 5 Macroeconomics and Finance Main references : - L. Ljundqvist and T. Sargent, Chapter 7 - Mehra and Prescott 1985 JME paper - Jerman 1998 JME paper - J.

Portability, salary and asset price risk: a continuous-time expected utility comparison of DB and DC pension plans

Portability, salary and asset price risk: a continuous-time expected utility comparison of DB and DC pension plans An Chen University of Ulm joint with Filip Uzelac (University of Bonn) Seminar at SWUFE,

Portability, salary and asset price risk: a continuous-time expected utility comparison of DB and DC pension plans An Chen University of Ulm joint with Filip Uzelac (University of Bonn) Seminar at SWUFE,

Imperfect Information and Market Segmentation Walsh Chapter 5

Imperfect Information and Market Segmentation Walsh Chapter 5 1 Why Does Money Have Real Effects? Add market imperfections to eliminate short-run neutrality of money Imperfect information keeps price from

Imperfect Information and Market Segmentation Walsh Chapter 5 1 Why Does Money Have Real Effects? Add market imperfections to eliminate short-run neutrality of money Imperfect information keeps price from

Demographic Change, Relative Factor Prices, International Capital Flows, and Their Differential Effects on the Welfare of Generations 1

Demographic Change, Relative Factor Prices, International Capital Flows, and Their Differential Effects on the Welfare of Generations 1 Alexander Ludwig *, Dirk Krüger *,**,***, and Axel Börsch-Supan *,**

Demographic Change, Relative Factor Prices, International Capital Flows, and Their Differential Effects on the Welfare of Generations 1 Alexander Ludwig *, Dirk Krüger *,**,***, and Axel Börsch-Supan *,**

Exchange Rates and Fundamentals: A General Equilibrium Exploration

Exchange Rates and Fundamentals: A General Equilibrium Exploration Takashi Kano Hitotsubashi University @HIAS, IER, AJRC Joint Workshop Frontiers in Macroeconomics and Macroeconometrics November 3-4, 2017

Exchange Rates and Fundamentals: A General Equilibrium Exploration Takashi Kano Hitotsubashi University @HIAS, IER, AJRC Joint Workshop Frontiers in Macroeconomics and Macroeconometrics November 3-4, 2017

Household income risk, nominal frictions, and incomplete markets 1

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

How Much Insurance in Bewley Models?

How Much Insurance in Bewley Models? Greg Kaplan New York University Gianluca Violante New York University, CEPR, IFS and NBER Boston University Macroeconomics Seminar Lunch Kaplan-Violante, Insurance

How Much Insurance in Bewley Models? Greg Kaplan New York University Gianluca Violante New York University, CEPR, IFS and NBER Boston University Macroeconomics Seminar Lunch Kaplan-Violante, Insurance

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Retirement Saving, Annuity Markets, and Lifecycle Modeling. James Poterba 10 July 2008

Retirement Saving, Annuity Markets, and Lifecycle Modeling James Poterba 10 July 2008 Outline Shifting Composition of Retirement Saving: Rise of Defined Contribution Plans Mortality Risks in Retirement

Retirement Saving, Annuity Markets, and Lifecycle Modeling James Poterba 10 July 2008 Outline Shifting Composition of Retirement Saving: Rise of Defined Contribution Plans Mortality Risks in Retirement

Household Finance in China

Household Finance in China Russell Cooper 1 and Guozhong Zhu 2 October 22, 2016 1 Department of Economics, the Pennsylvania State University and NBER, russellcoop@gmail.com 2 School of Business, University

Household Finance in China Russell Cooper 1 and Guozhong Zhu 2 October 22, 2016 1 Department of Economics, the Pennsylvania State University and NBER, russellcoop@gmail.com 2 School of Business, University

Life Cycle Uncertainty and Portfolio Choice Puzzles

Life Cycle Uncertainty and Portfolio Choice Puzzles Yongsung Chang University of Rochester Yonsei University Jay H. Hong University of Rochester Marios Karabarbounis Federal Reserve Bank of Richmond December

Life Cycle Uncertainty and Portfolio Choice Puzzles Yongsung Chang University of Rochester Yonsei University Jay H. Hong University of Rochester Marios Karabarbounis Federal Reserve Bank of Richmond December

Country Spreads and Emerging Countries: Who Drives Whom? Martin Uribe and Vivian Yue (JIE, 2006)

") Country Spreads and Emerging Countries: Who Drives Whom? Martin Uribe and Vivian Yue (JIE, 26) Country Interest Rates and Output in Seven Emerging Countries Argentina Brazil.5.5...5.5.5. 94 95 96 97 98

Country Spreads and Emerging Countries: Who Drives Whom? Martin Uribe and Vivian Yue (JIE, 26) Country Interest Rates and Output in Seven Emerging Countries Argentina Brazil.5.5...5.5.5. 94 95 96 97 98

MACROECONOMICS. Prelim Exam

MACROECONOMICS Prelim Exam Austin, June 1, 2012 Instructions This is a closed book exam. If you get stuck in one section move to the next one. Do not waste time on sections that you find hard to solve.

MACROECONOMICS Prelim Exam Austin, June 1, 2012 Instructions This is a closed book exam. If you get stuck in one section move to the next one. Do not waste time on sections that you find hard to solve.

Understanding the New Normal: The Role of Demographics

Understanding the New Normal: The Role of Demographics Etienne Gagnon, Benjamin K. Johannsen, David Lopez-Salido 1 October, 2017 1 The analysis and conclusions set forth are those of the authors and do

Understanding the New Normal: The Role of Demographics Etienne Gagnon, Benjamin K. Johannsen, David Lopez-Salido 1 October, 2017 1 The analysis and conclusions set forth are those of the authors and do

Sang-Wook (Stanley) Cho

Cho") Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales, Sydney July 2009, CEF Conference Motivation & Question Since Becker (1974), several

Beggar-thy-parents? A Lifecycle Model of Intergenerational Altruism Sang-Wook (Stanley) Cho University of New South Wales, Sydney July 2009, CEF Conference Motivation & Question Since Becker (1974), several

Microeconomic Foundations of Incomplete Price Adjustment

Chapter 6 Microeconomic Foundations of Incomplete Price Adjustment In Romer s IS/MP/IA model, we assume prices/inflation adjust imperfectly when output changes. Empirically, there is a negative relationship

Chapter 6 Microeconomic Foundations of Incomplete Price Adjustment In Romer s IS/MP/IA model, we assume prices/inflation adjust imperfectly when output changes. Empirically, there is a negative relationship

Capital markets liberalization and global imbalances

Capital markets liberalization and global imbalances Vincenzo Quadrini University of Southern California, CEPR and NBER February 11, 2006 VERY PRELIMINARY AND INCOMPLETE Abstract This paper studies the

Capital markets liberalization and global imbalances Vincenzo Quadrini University of Southern California, CEPR and NBER February 11, 2006 VERY PRELIMINARY AND INCOMPLETE Abstract This paper studies the

Can Financial Frictions Explain China s Current Account Puzzle: A Firm Level Analysis (Preliminary)

") Can Financial Frictions Explain China s Current Account Puzzle: A Firm Level Analysis (Preliminary) Yan Bai University of Rochester NBER Dan Lu University of Rochester Xu Tian University of Rochester February

Can Financial Frictions Explain China s Current Account Puzzle: A Firm Level Analysis (Preliminary) Yan Bai University of Rochester NBER Dan Lu University of Rochester Xu Tian University of Rochester February

Online Appendix. Revisiting the Effect of Household Size on Consumption Over the Life-Cycle. Not intended for publication.

Online Appendix Revisiting the Effect of Household Size on Consumption Over the Life-Cycle Not intended for publication Alexander Bick Arizona State University Sekyu Choi Universitat Autònoma de Barcelona,

Online Appendix Revisiting the Effect of Household Size on Consumption Over the Life-Cycle Not intended for publication Alexander Bick Arizona State University Sekyu Choi Universitat Autònoma de Barcelona,

NBER WORKING PAPER SERIES

NBER WORKING PAPER SERIES DEMOGRAPHIC CHANGE, RELATIVE FACTOR PRICES, INTERNATIONAL CAPITAL FLOWS, AND THEIR DIFFERENTIAL EFFECTS ON THE WELFARE OF GENERATIONS Alexander Ludwig Dirk Krueger Axel H. Boersch-Supan

NBER WORKING PAPER SERIES DEMOGRAPHIC CHANGE, RELATIVE FACTOR PRICES, INTERNATIONAL CAPITAL FLOWS, AND THEIR DIFFERENTIAL EFFECTS ON THE WELFARE OF GENERATIONS Alexander Ludwig Dirk Krueger Axel H. Boersch-Supan

Population Aging and International Capital Flows

Population Aging and International Capital Flows David Domeij and Martin Flodén 1 Department of Economics, Stockholm School of Economics Department of Economics, Stockholm School of Economics and CEPR

Population Aging and International Capital Flows David Domeij and Martin Flodén 1 Department of Economics, Stockholm School of Economics Department of Economics, Stockholm School of Economics and CEPR

Real Business Cycles (Solution)

") Real Business Cycles (Solution) Exercise: A two-period real business cycle model Consider a representative household of a closed economy. The household has a planning horizon of two periods and is endowed

Real Business Cycles (Solution) Exercise: A two-period real business cycle model Consider a representative household of a closed economy. The household has a planning horizon of two periods and is endowed

Demographic Change and the Equity Premium

Demographic Change and the Equity Premium Wolfgang Kuhle MEA, Universität Mannheim Alexander Ludwig MEA, Universität Mannheim Axel Börsch-Supan MEA, Universität Mannheim and NBER This Version: December

Demographic Change and the Equity Premium Wolfgang Kuhle MEA, Universität Mannheim Alexander Ludwig MEA, Universität Mannheim Axel Börsch-Supan MEA, Universität Mannheim and NBER This Version: December

The Excess Burden of Government Indecision

The Excess Burden of Government Indecision Francisco J. Gomes, Laurence J. Kotlikoff and Luis M. Viceira 1 First draft: March 26, 2006 This draft: June 20, 2008 1 Gomes: London Business School and CEPR.

The Excess Burden of Government Indecision Francisco J. Gomes, Laurence J. Kotlikoff and Luis M. Viceira 1 First draft: March 26, 2006 This draft: June 20, 2008 1 Gomes: London Business School and CEPR.

Topic 8: Financial Frictions and Shocks Part1: Asset holding developments

Topic 8: Financial Frictions and Shocks Part1: Asset holding developments - The relaxation of capital account restrictions in many countries over the last two decades has produced dramatic increases in

Topic 8: Financial Frictions and Shocks Part1: Asset holding developments - The relaxation of capital account restrictions in many countries over the last two decades has produced dramatic increases in

The Lost Generation of the Great Recession

The Lost Generation of the Great Recession Sewon Hur University of Pittsburgh January 21, 2016 Introduction What are the distributional consequences of the Great Recession? Introduction What are the distributional

The Lost Generation of the Great Recession Sewon Hur University of Pittsburgh January 21, 2016 Introduction What are the distributional consequences of the Great Recession? Introduction What are the distributional

A Structural Model of Continuous Workout Mortgages (Preliminary Do not cite)

") A Structural Model of Continuous Workout Mortgages (Preliminary Do not cite) Edward Kung UCLA March 1, 2013 OBJECTIVES The goal of this paper is to assess the potential impact of introducing alternative

A Structural Model of Continuous Workout Mortgages (Preliminary Do not cite) Edward Kung UCLA March 1, 2013 OBJECTIVES The goal of this paper is to assess the potential impact of introducing alternative

NBER WORKING PAPER SERIES ON THE CONSEQUENCES OF DEMOGRAPHIC CHANGE FOR RATES OF RETURNS TO CAPITAL, AND THE DISTRIBUTION OF WEALTH AND WELFARE

NBER WORKING PAPER SERIES ON THE CONSEQUENCES OF DEMOGRAPHIC CHANGE FOR RATES OF RETURNS TO CAPITAL, AND THE DISTRIBUTION OF WEALTH AND WELFARE Dirk Krueger Alexander Ludwig Working Paper 12453 http://www.nber.org/papers/w12453

NBER WORKING PAPER SERIES ON THE CONSEQUENCES OF DEMOGRAPHIC CHANGE FOR RATES OF RETURNS TO CAPITAL, AND THE DISTRIBUTION OF WEALTH AND WELFARE Dirk Krueger Alexander Ludwig Working Paper 12453 http://www.nber.org/papers/w12453

Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles

: A Potential Resolution of Asset Pricing Puzzles, JF (2004) Presented by: Esben Hedegaard NYUStern October 12, 2009 Outline 1 Introduction 2 The Long-Run Risk Solving the 3 Data and Calibration Results

: A Potential Resolution of Asset Pricing Puzzles, JF (2004) Presented by: Esben Hedegaard NYUStern October 12, 2009 Outline 1 Introduction 2 The Long-Run Risk Solving the 3 Data and Calibration Results

Capital Income Tax Reform and the Japanese Economy (Very Preliminary and Incomplete)

") Capital Income Tax Reform and the Japanese Economy (Very Preliminary and Incomplete) Gary Hansen (UCLA), Selo İmrohoroğlu (USC), Nao Sudo (BoJ) December 22, 2015 Keio University December 22, 2015 Keio

Capital Income Tax Reform and the Japanese Economy (Very Preliminary and Incomplete) Gary Hansen (UCLA), Selo İmrohoroğlu (USC), Nao Sudo (BoJ) December 22, 2015 Keio University December 22, 2015 Keio

A Macroeconomic Model with Financial Panics

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

A Macroeconomic Model with Financial Panics Mark Gertler, Nobuhiro Kiyotaki, Andrea Prestipino NYU, Princeton, Federal Reserve Board 1 March 218 1 The views expressed in this paper are those of the authors

Comments on: A. Armstrong, N. Draper, and E. Westerhout, The impact of demographic uncertainty on public finances in the Netherlands

Comments on: A. Armstrong, N. Draper, and E. Westerhout, The impact of demographic uncertainty on public finances in the Netherlands 1 1 University of Groningen; Institute for Advanced Studies (Vienna);

Comments on: A. Armstrong, N. Draper, and E. Westerhout, The impact of demographic uncertainty on public finances in the Netherlands 1 1 University of Groningen; Institute for Advanced Studies (Vienna);