Output Growth Volatility and Inflation Uncertainty in East Asian Countries. Dilshod N. Murodov

|

|

|

- Beverly Underwood

- 5 years ago

- Views:

Transcription

1 Output Growth Volatility and Inflation Uncertainty in East Asian Countries Dilshod N. Murodov Lecturer, Department of Finance, Banking and Finance Academy of Uzbekistan Visiting Scholar, Policy Research Institute Ministry of Finance, Japan

2 Contents Part 1: Part 2: Part 3: Part 4: Part 5: Introduction Literature Review Data and Analysis Econometric Approach Results and Concluding Remarks

3 Introduction

4 Overview of the study Almost a decade after the GFC of 2008, the nexus between volatile output growth and inflation uncertainty performance is still a critical subject to policymaking. The increase in output volatility, especially in developing countries, owes to relatively recent reductions in government spending, a fall in inflation and several structural reforms. The outward oriented economy and strong performance in the financial markets tends to cause more external shock spillover and output volatility (Bloom, 2009). The foremost impetus is the cognate economic structure and the rapid industrialization after WWII, which suffer different degrees of setback, especially during recessions (Li and Kwok, 2009).

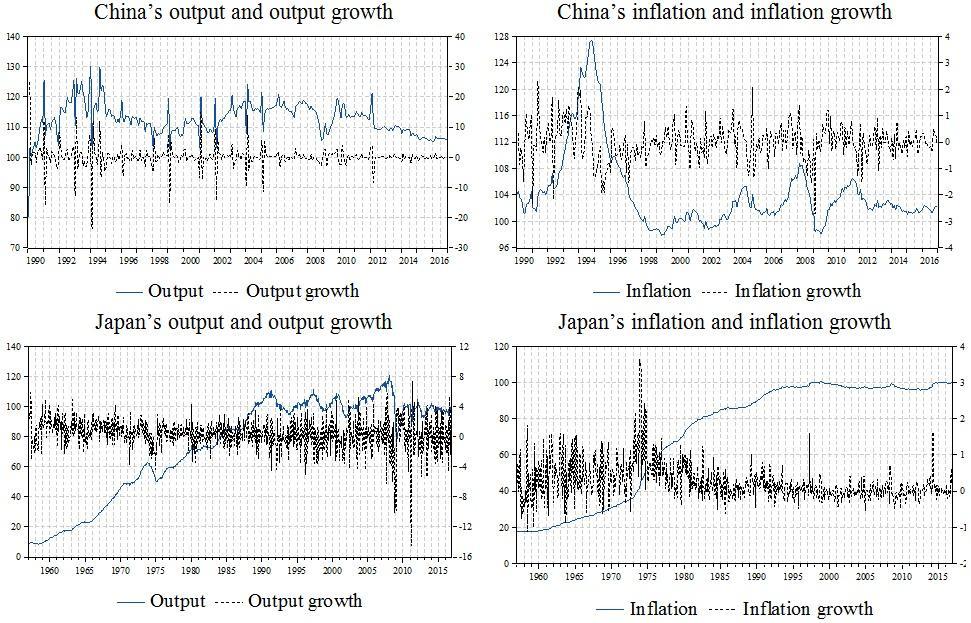

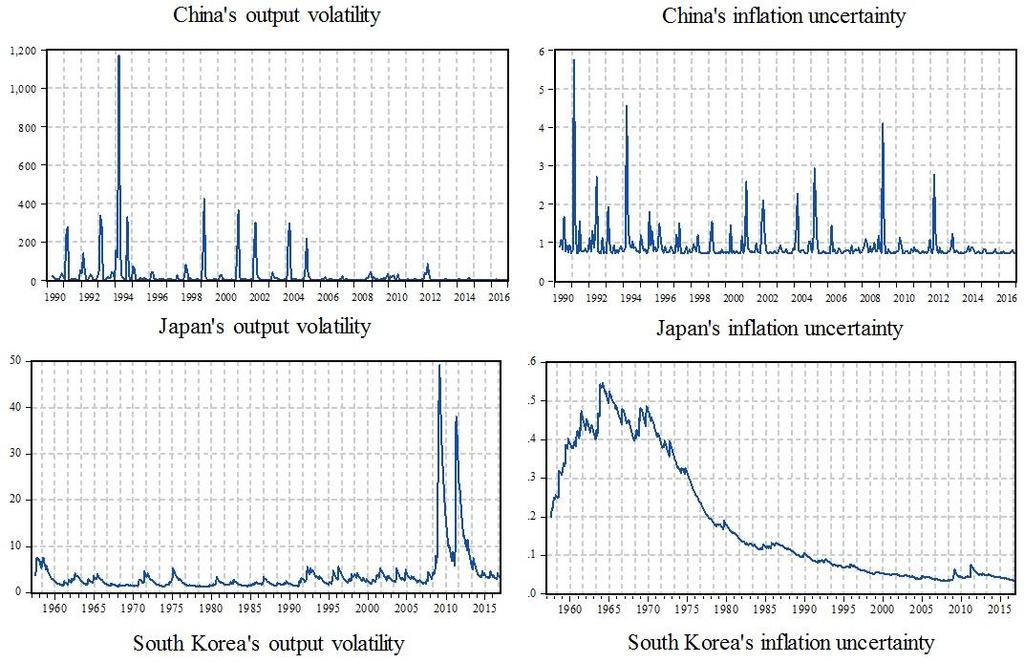

5 Mainland China Since 1979, market economic reforms and opening up policy adaptation. In the 1990s, FDI massively oriented towards agriculture and industrial output, from service sectors in coastal areas to the establishment of the modern enterprise system. Prior to the 1990s, the government took advantage of the relative stability of the overall price level to undertake major price reforms. Since the 1990s, the government has liberalized industrial output prices from the state determined methodology. Consequently, two double digit inflationary spells appeared and inflation rates exhibited conspicuous patterns.

6 Japan Has unique originality of growth in that so far it is the only nation among the G7 not from Western Europe or North America. Growth stages are split into catch up ( s), bubble economy (1970s 1980s) and long stagnation (1990s<) periods. Common shared purpose was to catch up with North America and Western European nations experience in the government, household and business sectors. The government created a system that was able to mobilize and direct funds to key industries; After achieving common goals, business and households should have changed their behavior from collective to autonomous with greater competition.

7 Japan cont. Lacking innovative investment opportunities and poor corporate governance, business entities and financial institutions rushed into speculation in financial and real estate markets, creating a bubble. In the 1990s, the adaptation of restrictive monetary policies caused the bubble to burst in stock and property markets. Struggling with the aftermath of the burst, the pile up due to excessive investment and lending and over borrowing resulted in excess capacity and setting non performing loans. It caused long lasting stagnation, persistent deflation, and financial crashes, despite the expansion of government expenditures and the money supply, and it shaped a public domestic debt overhang as well. On solvation, the economy was confronted with a multi pronged fight to cease deflation, introduce a new policy on budget, adopt regular reforms on business by giving tax reforms, resolve non performing loans, and stabilize the financial system.

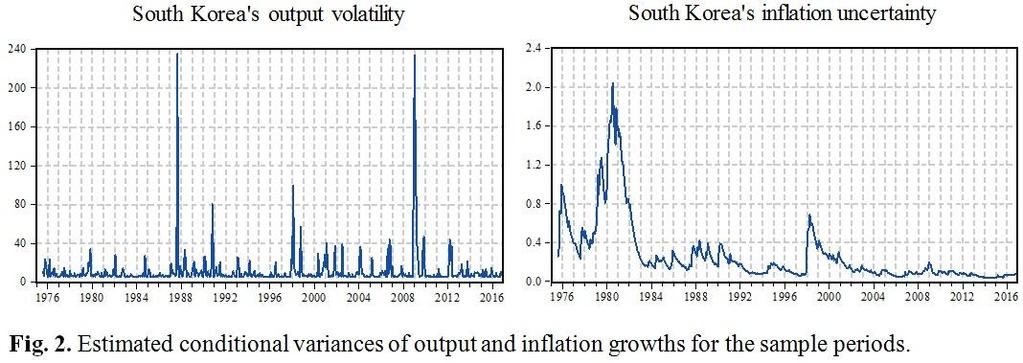

8 South Korea Since the 1960s, catching up, maintenance of good institutions, high investment, financial openness and human capital in technology have contributed to strong growth. Until the 1980s, government intervened DDI along the lines of comparative advantage in industrial output. Tax exemptions were provided to labor intensive manufacturing to enhance exports, and high tariffs were imposed to preserve local products. Due to the shocks of AFC in 1998, inflation targeted policy geared towards setting more stability in internal price. Notwithstanding, the persistence of inflation remained relatively high while that of output measures has declined considerably.

9

10

11 Objectives of the study The underlying issue of the current work proposes three main objectives: First, the impact of output growth volatility on performance of inflation growth uncertainty for the respective East Asian economies will be examined. Next, the Granger causality in variance test will be conducted on any shock or volatility spillover effects between the variables to see how the estimated growth series react to each other s on cross variance correlation analysis. Lastly, we carry out generalized impulse response function analysis to inspect the effects of historical innovations on the conditional standard deviations and covariances.

12 Authors Keynes (1936) Cukierman and Meltzer (1986) Devereux (1989) Grier and Perry (2000) Cukierman and Gerlach (2003) Korap (2009) Türkyılmaz and Özer (2010) Literature Review Results no permanent trade off between output and inflation, except for short periods. more output growth reduces inflation, higher output volatility reduces inflation uncertainty. more real output growth reduces the optimal amount of wage indexation and pushes the policymaker to engineer more inflation surprises to obtain favorable real effects. higher output growth volatility raised the average inflation rate in the US from positive causal effect of output growth volatility and inflation uncertainty. an increase in output growth volatility leads to more inflation for Turkey (1987:M1-2008:M9). a causal relation between output growth volatility and inflation in agreement with Devereux (1989). Note: In literature, negative relations between inflation uncertainty and output growth volatility is known as the Taylor effect.

13 Data and Analysis

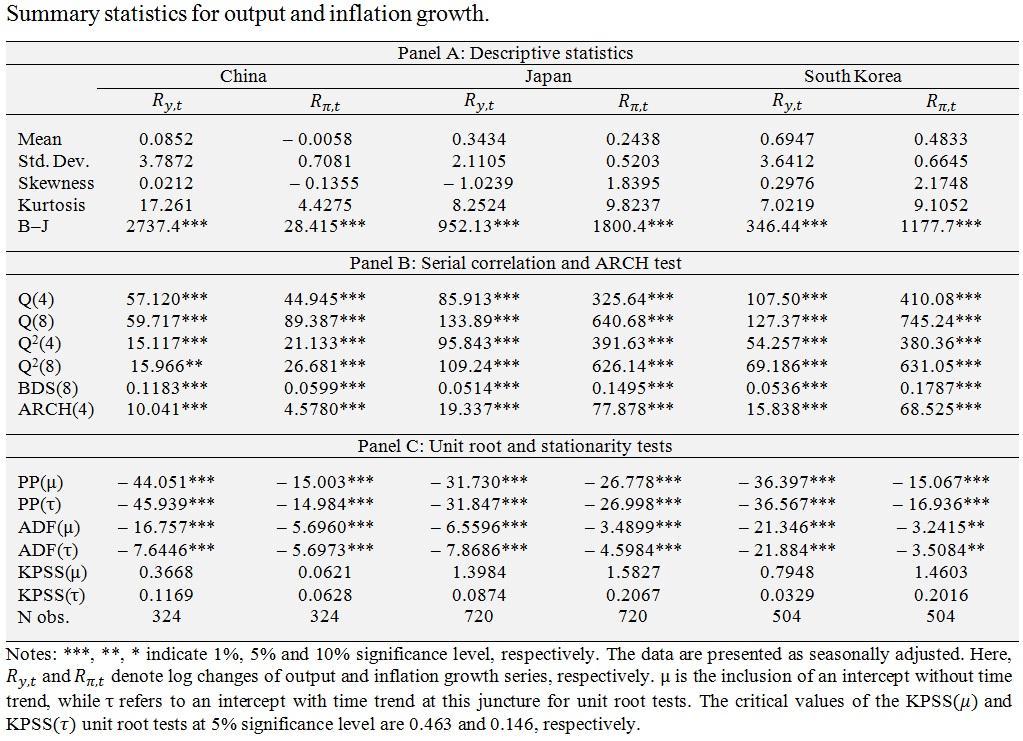

14 Data source & description Country China Japan South Korea Source National Bureau of Statistics of China Statistics Bureau of Japan Statistics Korea Timespan 1990:1-2016:12, monthly 1957:1-2016:12, monthly 1970:1-2016:12, monthly Scale Corresponding Period of the Previous Year (index, CPPY=100) (Index, 2015=100) (Index, 2015=100) Adjustment Price index, not seasonally adjusted Price index, not seasonally adjusted Price index, not seasonally adjusted Notes: Index of real industrial production (IIP) and consumer price index (CPI) are proxies of output and inflation growth for the respective economies. The data are retrieved through DataStream online services.

15

16 Econometric Approach

17 Methodology A general multivariate GARCH in mean process: highly functional in financial issues related works owing to volatility on them. conventionally applied to describe and forecast the correlations between the volatilities and co volatilities as well as spillover effects directly (through conditional standard deviations) or indirectly (through covariances) (Bauwens et al., 2006).

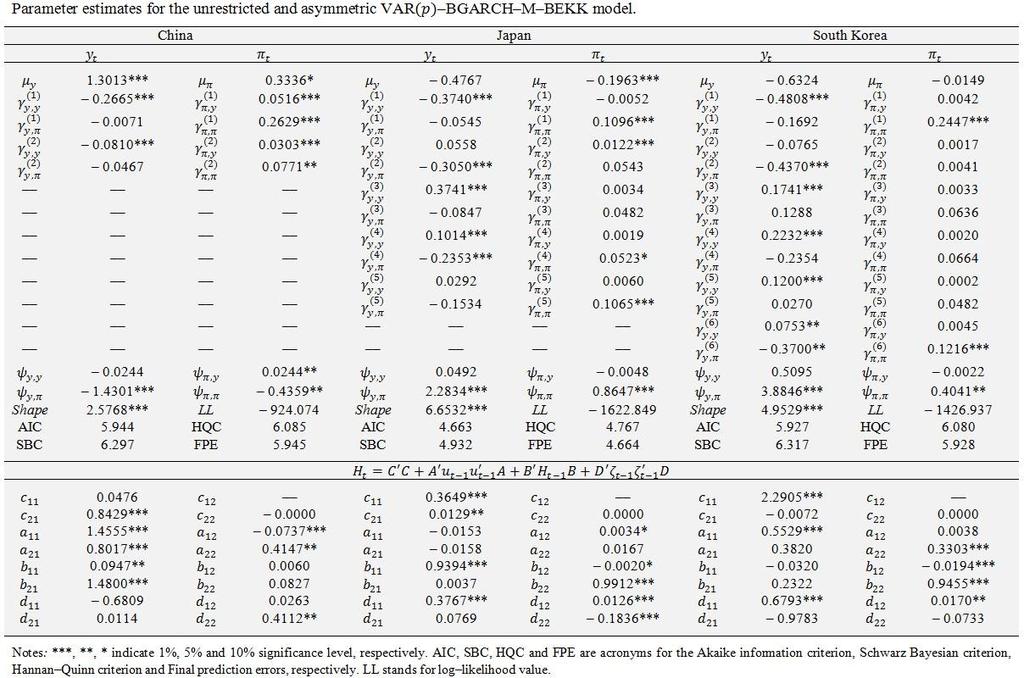

18 Main equation of the study Y t = M + p Γ i i=1 Y t i + Ψ H t + U t ; U t Ω t 1 ~ 0, H t, H t = h y,t h y,π,t h π,y,t h π,t Y t is an exogenous variable that captures y t output growth and π t inflation growth. M is the intercept while Γ i is the coefficient of lagged Y t. Ψ (Psi) is the coefficient of captured heteroscedasticity, H t, and as usual U t represents the residual terms. Also, Ω t 1 is available information set at the time t 1, and zero is the null vector. Y t = y t π t (i) ; M = μ y μ ; Γ i = γ 11 π (i) γ 21 (i) γ 12 ; Y (i) t i = y t i γ π t i 22 Ψ = ψ 11 ψ 12 ψ 21 ψ 22 ; U t = u y,t u π,t ;

19 Methodology cont. y t π t (i) = μ y μ + γ 11 π + u y,t u π,t ; (i) γ 21 (i) γ 12 (i) γ 22 y t i π t i + ψ 11 ψ 12 ψ 21 ψ 22 h y,t h π,t where the discrete equations can be drawn as follows (i) (i) y t = μ y + γ 11 yt 1 + γ 12 πt 1 + ψ 11 h y,t + ψ 12 h π,t + u y,t (i) (i) π t = μ π + γ 21 yt 1 + γ 22 πt 1 + ψ 21 h y,t + ψ 22 h π,t + u π,t

20 Methodology cont. Second moment equation to ensure positive definiteness (BEKK variance covariance specification) H t = C C + A u t 1 u t 1 A + B H t 1 B + D ζ t 1 ζ t 1 D C = c 11 0 c 21 c 22 ; A = a 11 a 12 a 21 a 22 ; B = b 11 b 12 b 21 b 22 ; D = d 11 d 12 d 21 d 22 ; ζ t 1 = ζ y,t 1 ζ π,t 1 ; C is an upper triangular matrix to ensure for the positive definiteness of H t ; A, B and D are 2 2 dimensional matrices to capture the lagged conditional standard deviations and covariances; H t 1 as well as the past values of u t 1 u t 1 and ζ t 1 ζ t 1, are joint estimations of contemporaneous volatility of output growth and inflation uncertainty. This parametrization further contains a possible asymmetry, which is captured by the matrix D. As proposed by Grier et al., (2004), a term, ζ t 1 ζ t 1, accounts for the potential asymmetric responses. More specifically, if the output growth volatility and inflation uncertainty are lower than their expected levels, it is generally treated as negative innovations or bad news regarding the changes of the growth. Hence, the variables ζ y,t, and ζ π,t are defined as min {u y,t, 0} and min {u π,t, 0}, which are negative residuals or bad news about the output and inflation growth, respectively. The acronym BEKK was named after the scholars Yoshi Baba, Robert Engle, Dennis Kraft, and Ken Kroner.

21 Results

22

23

24

25

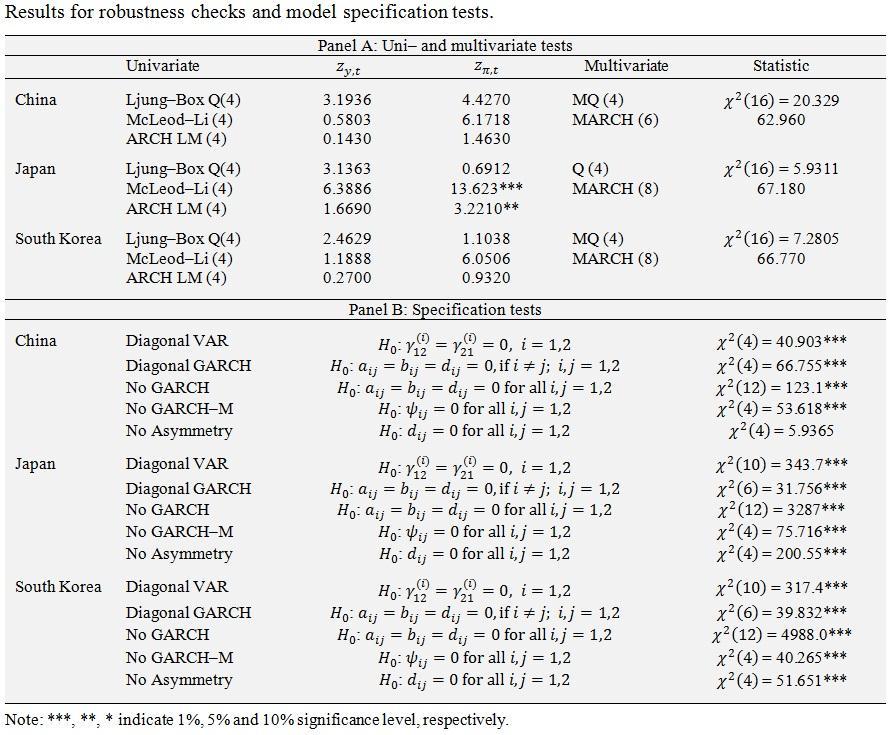

26 Granger causality in variance Based on Hafner and Herwartz (2008), we demonstrate two conditionally heteroscedastic and stationary series y t and π t. π t does not Granger cause y t in variance, designated by π t y t if, Var y t F t 1 = Var y t F t 1 t Z. Here, there is no causality relationship if y t does Granger cause π t in variance, and the conditional variance of π t can be prophesied more precisely by fitting the information set of y t.

27 Generalized Impulse Response Function To inspect an innovation in output volatility (often measured by one standard deviation), a shock may affect inflation uncertainty through dynamic interactions. Allowing for composition dependence in multivariate models of GIRFs is their main advantage compared to other customary IRFs. The effects of a shock to output volatility is not isolated from having a contemporaneous impact on inflation uncertainty. GIRF K n, ρ t, ω t 1 = E K t+n ρ t, ω t 1 E K t+n ω t 1 where, n = 0,1,2,3, GIRF is conditional on ρ t and ω t 1 and constructs the response by averaging out future shocks given the past and present. A natural reference point for the GIRF is the conditional expectation of K t+n given only the history ω t 1, and in this benchmark response, the current shock is also averaged out.

28

29

30 Concluding Remarks Real output growth volatility has a significant positive effect in China, whereas in Japan and South Korea it has an adverse impact on inflation uncertainty. Strong evidence of bi directional causal relations in China and uni directional relations in South Korea. No causality relations are detected for Japan. Significant influences in response to the shocks in China and South Korea s inflation uncertainty, while insignificant influence in Japan.

31 References Bauwens, L., Laurent, S., Jeroen, V., Rombouts, K Multivariate GARCH models: A survey. Journal of Applied Econometrics, 21, Blackburn, K Can stabilization policy reduce long run growth? Economic Journal, 109(1), Bollerslev, T., Wooldridge, J. M Quasi maximum likelihood estimation and inference in dynamic models with varying covariances. Econometric Reviews, 11, Bredin, D., Fountas, S Macroeconomic uncertainty and performance in the European Union. Journal of International Money and Finance, 28(6), Caporale, G. M., Sova, A., Sova, R Trade flows and trade specialization: The case of China. China Economic Review, 34, Cheung, Y. W., Ng, N. K A causality in variance test and its application to financial market prices. Journal of Econometrics, 72, Cuikerman, A., Gerlach, S The inflation bias revisited. Theory and some international evidence. The Manchester School, 71(5), Engle, R Autoregressive conditional heteroscedasticity with estimates of the variance of UK inflation. Econometrica, 50, Fountas, S., Karnasos, M., Kim, J. (2002). Inflation and output growth uncertainty and their relationship with inflation and output growth. Economics Letters, 75, Friedman, M. (1977). Nobel lecture: Inflation and unemployment. Journal of Political Economy, 85, Grier, K. B., Henry, O. T., Olekalns, N., Shields, K The asymmetric effects of uncertainty on inflation and output growth. Journal of Applied Econometrics, 19(5), Hafner, C. M., Herwartz, H Testing for causality in variance using multivariate GARCH models. Annales d Economie et de Statistique, 89, He, Q., Chen, H Recent macroeconomic stability in China. China Economic Review, 30, Koop, G., Pesaran M. H., Potter S. M Impulse response analysis in non linear multivariate models. Journal of Econometrics, 74, Laurenceson, J., Rodgers, R China s macroeconomic volatility How important is the business cycle? China Economic Review, 21, Li, K. W., Kwok, M. L., Output growth of five crisis affected East Asia economies. Japan and the World Economy, 21, Mahadevan, R., Suardi, S., The effects of uncertainty dynamics on exports, imports and productivity growth. Journal of Asian Economies, 22, Tseng, W., Zebregs, H., Foreign direct investment in China: Some lessons for other countries. International Monetary Fund Discussion Paper PDP/02/3, 90,

32 Thanks for your attention

33 Q&A session

DEPARTMENT OF ECONOMICS DISCUSSION PAPER SERIES. Macroeconomic Uncertainty and Performance in Asian countries

ISSN 1791-3144 DEPARTMENT OF ECONOMICS DISCUSSION PAPER SERIES Macroeconomic Uncertainty and Performance in Asian countries Don Bredin, John Elder and Stilianos Fountas WP 2008-10 Department of Economics

ISSN 1791-3144 DEPARTMENT OF ECONOMICS DISCUSSION PAPER SERIES Macroeconomic Uncertainty and Performance in Asian countries Don Bredin, John Elder and Stilianos Fountas WP 2008-10 Department of Economics

Macroeconomic Uncertainty and Performance in the European Union and Implications for the Objectives of Monetary Policy

Macroeconomic Uncertainty and Performance in the European Union and Implications for the Objectives of Monetary Policy Don Bredin University College Dublin Stilianos Fountas University of Macedonia May

Macroeconomic Uncertainty and Performance in the European Union and Implications for the Objectives of Monetary Policy Don Bredin University College Dublin Stilianos Fountas University of Macedonia May

Volatility Spillovers and Causality of Carbon Emissions, Oil and Coal Spot and Futures for the EU and USA

22nd International Congress on Modelling and Simulation, Hobart, Tasmania, Australia, 3 to 8 December 2017 mssanz.org.au/modsim2017 Volatility Spillovers and Causality of Carbon Emissions, Oil and Coal

22nd International Congress on Modelling and Simulation, Hobart, Tasmania, Australia, 3 to 8 December 2017 mssanz.org.au/modsim2017 Volatility Spillovers and Causality of Carbon Emissions, Oil and Coal

The Relationship between Inflation, Inflation Uncertainty and Output Growth in India

Economic Affairs 2014, 59(3) : 465-477 9 New Delhi Publishers WORKING PAPER 59(3): 2014: DOI 10.5958/0976-4666.2014.00014.X The Relationship between Inflation, Inflation Uncertainty and Output Growth in

Economic Affairs 2014, 59(3) : 465-477 9 New Delhi Publishers WORKING PAPER 59(3): 2014: DOI 10.5958/0976-4666.2014.00014.X The Relationship between Inflation, Inflation Uncertainty and Output Growth in

Macro News and Exchange Rates in the BRICS. Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo. February 2016

Economics and Finance Working Paper Series Department of Economics and Finance Working Paper No. 16-04 Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo Macro News and Exchange Rates in the

Economics and Finance Working Paper Series Department of Economics and Finance Working Paper No. 16-04 Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo Macro News and Exchange Rates in the

THE INFLATION - INFLATION UNCERTAINTY NEXUS IN ROMANIA

THE INFLATION - INFLATION UNCERTAINTY NEXUS IN ROMANIA Daniela ZAPODEANU University of Oradea, Faculty of Economic Science Oradea, Romania Mihail Ioan COCIUBA University of Oradea, Faculty of Economic

THE INFLATION - INFLATION UNCERTAINTY NEXUS IN ROMANIA Daniela ZAPODEANU University of Oradea, Faculty of Economic Science Oradea, Romania Mihail Ioan COCIUBA University of Oradea, Faculty of Economic

Analysis of Volatility Spillover Effects. Using Trivariate GARCH Model

Reports on Economics and Finance, Vol. 2, 2016, no. 1, 61-68 HIKARI Ltd, www.m-hikari.com http://dx.doi.org/10.12988/ref.2016.612 Analysis of Volatility Spillover Effects Using Trivariate GARCH Model Pung

Reports on Economics and Finance, Vol. 2, 2016, no. 1, 61-68 HIKARI Ltd, www.m-hikari.com http://dx.doi.org/10.12988/ref.2016.612 Analysis of Volatility Spillover Effects Using Trivariate GARCH Model Pung

University of Macedonia Department of Economics. Discussion Paper Series. Inflation, inflation uncertainty and growth: are they related?

ISSN 1791-3144 University of Macedonia Department of Economics Discussion Paper Series Inflation, inflation uncertainty and growth: are they related? Stilianos Fountas Discussion Paper No. 12/2010 Department

ISSN 1791-3144 University of Macedonia Department of Economics Discussion Paper Series Inflation, inflation uncertainty and growth: are they related? Stilianos Fountas Discussion Paper No. 12/2010 Department

Macro News and Stock Returns in the Euro Area: A VAR-GARCH-in-Mean Analysis

Department of Economics and Finance Working Paper No. 14-16 Economics and Finance Working Paper Series Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo Macro News and Stock Returns in the Euro

Department of Economics and Finance Working Paper No. 14-16 Economics and Finance Working Paper Series Guglielmo Maria Caporale, Fabio Spagnolo and Nicola Spagnolo Macro News and Stock Returns in the Euro

Provided by the author(s) and NUI Galway in accordance with publisher policies. Please cite the published version when available.

and NUI Galway in accordance with publisher policies. Please cite the published version when available.") Provided by the author(s) and NUI Galway in accordance with publisher policies. Please cite the published version when available. Title Are Economic Growth and the Variability of the Business Cycle Related?

Provided by the author(s) and NUI Galway in accordance with publisher policies. Please cite the published version when available. Title Are Economic Growth and the Variability of the Business Cycle Related?

Oil Price Effects on Exchange Rate and Price Level: The Case of South Korea

Oil Price Effects on Exchange Rate and Price Level: The Case of South Korea Mirzosaid SULTONOV 東北公益文科大学総合研究論集第 34 号抜刷 2018 年 7 月 30 日発行 研究論文 Oil Price Effects on Exchange Rate and Price Level: The Case

Oil Price Effects on Exchange Rate and Price Level: The Case of South Korea Mirzosaid SULTONOV 東北公益文科大学総合研究論集第 34 号抜刷 2018 年 7 月 30 日発行 研究論文 Oil Price Effects on Exchange Rate and Price Level: The Case

Modelling Inflation Uncertainty Using EGARCH: An Application to Turkey

Modelling Inflation Uncertainty Using EGARCH: An Application to Turkey By Hakan Berument, Kivilcim Metin-Ozcan and Bilin Neyapti * Bilkent University, Department of Economics 06533 Bilkent Ankara, Turkey

Modelling Inflation Uncertainty Using EGARCH: An Application to Turkey By Hakan Berument, Kivilcim Metin-Ozcan and Bilin Neyapti * Bilkent University, Department of Economics 06533 Bilkent Ankara, Turkey

STOCK RETURNS AND INFLATION: THE IMPACT OF INFLATION TARGETING

STOCK RETURNS AND INFLATION: THE IMPACT OF INFLATION TARGETING Alexandros Kontonikas a, Alberto Montagnoli b and Nicola Spagnolo c a Department of Economics, University of Glasgow, Glasgow, UK b Department

STOCK RETURNS AND INFLATION: THE IMPACT OF INFLATION TARGETING Alexandros Kontonikas a, Alberto Montagnoli b and Nicola Spagnolo c a Department of Economics, University of Glasgow, Glasgow, UK b Department

RISK SPILLOVER EFFECTS IN THE CZECH FINANCIAL MARKET

RISK SPILLOVER EFFECTS IN THE CZECH FINANCIAL MARKET Vít Pošta Abstract The paper focuses on the assessment of the evolution of risk in three segments of the Czech financial market: capital market, money/debt

RISK SPILLOVER EFFECTS IN THE CZECH FINANCIAL MARKET Vít Pošta Abstract The paper focuses on the assessment of the evolution of risk in three segments of the Czech financial market: capital market, money/debt

Inflation, Inflation Uncertainty and Output Growth, Are They Related? A Study on South East Asian Economies,

2012, TextRoad Publication ISSN 2090-4304 Journal of Basic and Applied Scientific Research www.textroad.com Inflation, Inflation Uncertainty and Output Growth, Are They Related? A Study on South East Asian

2012, TextRoad Publication ISSN 2090-4304 Journal of Basic and Applied Scientific Research www.textroad.com Inflation, Inflation Uncertainty and Output Growth, Are They Related? A Study on South East Asian

The Relationship between Inflation and Inflation Uncertainty: Evidence from the Turkish Economy

Available online at www.sciencedirect.com Procedia Economics and Finance 1 ( 2012 ) 219 228 International Conference of Applied Economics The Relationship between Inflation and Inflation Uncertainty: Evidence

Available online at www.sciencedirect.com Procedia Economics and Finance 1 ( 2012 ) 219 228 International Conference of Applied Economics The Relationship between Inflation and Inflation Uncertainty: Evidence

Equity Price Dynamics Before and After the Introduction of the Euro: A Note*

Equity Price Dynamics Before and After the Introduction of the Euro: A Note* Yin-Wong Cheung University of California, U.S.A. Frank Westermann University of Munich, Germany Daily data from the German and

Equity Price Dynamics Before and After the Introduction of the Euro: A Note* Yin-Wong Cheung University of California, U.S.A. Frank Westermann University of Munich, Germany Daily data from the German and

Volume 35, Issue 1. Thai-Ha Le RMIT University (Vietnam Campus)

") Volume 35, Issue 1 Exchange rate determination in Vietnam Thai-Ha Le RMIT University (Vietnam Campus) Abstract This study investigates the determinants of the exchange rate in Vietnam and suggests policy

Volume 35, Issue 1 Exchange rate determination in Vietnam Thai-Ha Le RMIT University (Vietnam Campus) Abstract This study investigates the determinants of the exchange rate in Vietnam and suggests policy

Structural Cointegration Analysis of Private and Public Investment

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

International Journal of Business and Economics, 2002, Vol. 1, No. 1, 59-67 Structural Cointegration Analysis of Private and Public Investment Rosemary Rossiter * Department of Economics, Ohio University,

Does Commodity Price Index predict Canadian Inflation?

2011 年 2 月第十四卷一期 Vol. 14, No. 1, February 2011 Does Commodity Price Index predict Canadian Inflation? Tao Chen http://cmr.ba.ouhk.edu.hk Web Journal of Chinese Management Review Vol. 14 No 1 1 Does Commodity

2011 年 2 月第十四卷一期 Vol. 14, No. 1, February 2011 Does Commodity Price Index predict Canadian Inflation? Tao Chen http://cmr.ba.ouhk.edu.hk Web Journal of Chinese Management Review Vol. 14 No 1 1 Does Commodity

Introductory Econometrics for Finance

Introductory Econometrics for Finance SECOND EDITION Chris Brooks The ICMA Centre, University of Reading CAMBRIDGE UNIVERSITY PRESS List of figures List of tables List of boxes List of screenshots Preface

Introductory Econometrics for Finance SECOND EDITION Chris Brooks The ICMA Centre, University of Reading CAMBRIDGE UNIVERSITY PRESS List of figures List of tables List of boxes List of screenshots Preface

An Empirical Study on the Determinants of Dollarization in Cambodia *

An Empirical Study on the Determinants of Dollarization in Cambodia * Socheat CHIM Graduate School of Economics, Osaka University 1-7 Machikaneyama, Toyonaka, Osaka, 560-0043, Japan E-mail: chimsocheat3@yahoo.com

An Empirical Study on the Determinants of Dollarization in Cambodia * Socheat CHIM Graduate School of Economics, Osaka University 1-7 Machikaneyama, Toyonaka, Osaka, 560-0043, Japan E-mail: chimsocheat3@yahoo.com

List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements

Table of List of figures List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements page xii xv xvii xix xxi xxv 1 Introduction 1 1.1 What is econometrics? 2 1.2 Is

Table of List of figures List of tables List of boxes List of screenshots Preface to the third edition Acknowledgements page xii xv xvii xix xxi xxv 1 Introduction 1 1.1 What is econometrics? 2 1.2 Is

VOLATILITY COMPONENT OF DERIVATIVE MARKET: EVIDENCE FROM FBMKLCI BASED ON CGARCH

VOLATILITY COMPONENT OF DERIVATIVE MARKET: EVIDENCE FROM BASED ON CGARCH Razali Haron 1 Salami Monsurat Ayojimi 2 Abstract This study examines the volatility component of Malaysian stock index. Despite

VOLATILITY COMPONENT OF DERIVATIVE MARKET: EVIDENCE FROM BASED ON CGARCH Razali Haron 1 Salami Monsurat Ayojimi 2 Abstract This study examines the volatility component of Malaysian stock index. Despite

Volatility spillovers among the Gulf Arab emerging markets

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2010 Volatility spillovers among the Gulf Arab emerging markets Ramzi Nekhili University

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2010 Volatility spillovers among the Gulf Arab emerging markets Ramzi Nekhili University

FIW Working Paper N 58 November International Spillovers of Output Growth and Output Growth Volatility: Evidence from the G7.

FIW Working Paper FIW Working Paper N 58 November 2010 International Spillovers of Output Growth and Output Growth Volatility: Evidence from the G7 Nikolaos Antonakakis 1 Harald Badinger 2 Abstract This

FIW Working Paper FIW Working Paper N 58 November 2010 International Spillovers of Output Growth and Output Growth Volatility: Evidence from the G7 Nikolaos Antonakakis 1 Harald Badinger 2 Abstract This

Comovement of Asian Stock Markets and the U.S. Influence *

Global Economy and Finance Journal Volume 3. Number 2. September 2010. Pp. 76-88 Comovement of Asian Stock Markets and the U.S. Influence * Jin Woo Park Using correlation analysis and the extended GARCH

Global Economy and Finance Journal Volume 3. Number 2. September 2010. Pp. 76-88 Comovement of Asian Stock Markets and the U.S. Influence * Jin Woo Park Using correlation analysis and the extended GARCH

Information Technology, Productivity, Value Added, and Inflation: An Empirical Study on the U.S. Economy,

Information Technology, Productivity, Value Added, and Inflation: An Empirical Study on the U.S. Economy, 1959-2008 Ashraf Galal Eid King Fahd University of Petroleum and Minerals This paper is a macro

Information Technology, Productivity, Value Added, and Inflation: An Empirical Study on the U.S. Economy, 1959-2008 Ashraf Galal Eid King Fahd University of Petroleum and Minerals This paper is a macro

BESSH-16. FULL PAPER PROCEEDING Multidisciplinary Studies Available online at

FULL PAPER PROEEDING Multidisciplinary Studies Available online at www.academicfora.com Full Paper Proceeding BESSH-2016, Vol. 76- Issue.3, 15-23 ISBN 978-969-670-180-4 BESSH-16 A STUDY ON THE OMPARATIVE

FULL PAPER PROEEDING Multidisciplinary Studies Available online at www.academicfora.com Full Paper Proceeding BESSH-2016, Vol. 76- Issue.3, 15-23 ISBN 978-969-670-180-4 BESSH-16 A STUDY ON THE OMPARATIVE

A joint Initiative of Ludwig-Maximilians-Universität and Ifo Institute for Economic Research

A joint Initiative of Ludwig-Maximilians-Universität and Ifo Institute for Economic Research Working Papers EQUITY PRICE DYNAMICS BEFORE AND AFTER THE INTRODUCTION OF THE EURO: A NOTE Yin-Wong Cheung Frank

A joint Initiative of Ludwig-Maximilians-Universität and Ifo Institute for Economic Research Working Papers EQUITY PRICE DYNAMICS BEFORE AND AFTER THE INTRODUCTION OF THE EURO: A NOTE Yin-Wong Cheung Frank

Estimating time-varying risk prices with a multivariate GARCH model

Estimating time-varying risk prices with a multivariate GARCH model Chikashi TSUJI December 30, 2007 Abstract This paper examines the pricing of month-by-month time-varying risks on the Japanese stock

Estimating time-varying risk prices with a multivariate GARCH model Chikashi TSUJI December 30, 2007 Abstract This paper examines the pricing of month-by-month time-varying risks on the Japanese stock

Corresponding author: Gregory C Chow,

Co-movements of Shanghai and New York stock prices by time-varying regressions Gregory C Chow a, Changjiang Liu b, Linlin Niu b,c a Department of Economics, Fisher Hall Princeton University, Princeton,

Co-movements of Shanghai and New York stock prices by time-varying regressions Gregory C Chow a, Changjiang Liu b, Linlin Niu b,c a Department of Economics, Fisher Hall Princeton University, Princeton,

The Effects of Oil Shocks on Turkish Macroeconomic Aggregates

International Journal of Energy Economics and Policy ISSN: 2146-4553 available at http: www.econjournals.com International Journal of Energy Economics and Policy, 2016, 6(3), 471-476. The Effects of Oil

International Journal of Energy Economics and Policy ISSN: 2146-4553 available at http: www.econjournals.com International Journal of Energy Economics and Policy, 2016, 6(3), 471-476. The Effects of Oil

FORECASTING PAKISTANI STOCK MARKET VOLATILITY WITH MACROECONOMIC VARIABLES: EVIDENCE FROM THE MULTIVARIATE GARCH MODEL

FORECASTING PAKISTANI STOCK MARKET VOLATILITY WITH MACROECONOMIC VARIABLES: EVIDENCE FROM THE MULTIVARIATE GARCH MODEL ZOHAIB AZIZ LECTURER DEPARTMENT OF STATISTICS, FEDERAL URDU UNIVERSITY OF ARTS, SCIENCES

FORECASTING PAKISTANI STOCK MARKET VOLATILITY WITH MACROECONOMIC VARIABLES: EVIDENCE FROM THE MULTIVARIATE GARCH MODEL ZOHAIB AZIZ LECTURER DEPARTMENT OF STATISTICS, FEDERAL URDU UNIVERSITY OF ARTS, SCIENCES

GARCH Models for Inflation Volatility in Oman

Rev. Integr. Bus. Econ. Res. Vol 2(2) 1 GARCH Models for Inflation Volatility in Oman Muhammad Idrees Ahmad Department of Mathematics and Statistics, College of Science, Sultan Qaboos Universty, Alkhod,

Rev. Integr. Bus. Econ. Res. Vol 2(2) 1 GARCH Models for Inflation Volatility in Oman Muhammad Idrees Ahmad Department of Mathematics and Statistics, College of Science, Sultan Qaboos Universty, Alkhod,

The Relationship between Macroeconomic Volatility and Growth: Dynamics, Country Interactions and Nonlinearities

The Relationship between Macroeconomic Volatility and Growth: Dynamics, Country Interactions and Nonlinearities STEVEN TRYPSTEEN University of Nottingham This paper investigates the relationship between

The Relationship between Macroeconomic Volatility and Growth: Dynamics, Country Interactions and Nonlinearities STEVEN TRYPSTEEN University of Nottingham This paper investigates the relationship between

Testing the Dynamic Linkages of the Pakistani Stock Market with Regional and Global Markets

The Lahore Journal of Economics 22 : 2 (Winter 2017): pp. 89 116 Testing the Dynamic Linkages of the Pakistani Stock Market with Regional and Global Markets Zohaib Aziz * and Javed Iqbal ** Abstract This

The Lahore Journal of Economics 22 : 2 (Winter 2017): pp. 89 116 Testing the Dynamic Linkages of the Pakistani Stock Market with Regional and Global Markets Zohaib Aziz * and Javed Iqbal ** Abstract This

Volume 30, Issue 4. Non-stationary Variance and Volatility Causality. Kamel malik Bensafta GERCIE, University François Rabelais de Tours, France

Volume 3, Issue 4 Non-stationary Variance and Volatility Causality Kamel malik Bensafta GERCIE, University François Rabelais de Tours, France Abstract This paper aims to describe bias estimates when non-stationary

Volume 3, Issue 4 Non-stationary Variance and Volatility Causality Kamel malik Bensafta GERCIE, University François Rabelais de Tours, France Abstract This paper aims to describe bias estimates when non-stationary

Does High Inflation Lead to Increased Inflation Uncertainty? Evidence from Nine African Countries

Does High Inflation Lead to Increased Inflation Uncertainty? Evidence from Nine African Countries Scott W. Hegerty Northeastern Illinois University ABSTRACT The connection between inflation and its volatility

Does High Inflation Lead to Increased Inflation Uncertainty? Evidence from Nine African Countries Scott W. Hegerty Northeastern Illinois University ABSTRACT The connection between inflation and its volatility

UNCERTAINTY OF THE INFLATION AND ECONOMIC GROWTH: THE CASE OF EAST AFRICAN COUNTRIES 1

Vol. 7, No.1, Summer 2018 2012 Published by JSES. UNCERTAINTY OF THE INFLATION AND ECONOMIC GROWTH: THE CASE OF EAST AFRICAN COUNTRIES 1 Muhia John GACHUNGA a Abstract Based on a VAR-GARCH model this paper

Vol. 7, No.1, Summer 2018 2012 Published by JSES. UNCERTAINTY OF THE INFLATION AND ECONOMIC GROWTH: THE CASE OF EAST AFRICAN COUNTRIES 1 Muhia John GACHUNGA a Abstract Based on a VAR-GARCH model this paper

Uncertainty and Economic Activity: A Global Perspective

Uncertainty and Economic Activity: A Global Perspective Ambrogio Cesa-Bianchi 1 M. Hashem Pesaran 2 Alessandro Rebucci 3 IV International Conference in memory of Carlo Giannini 26 March 2014 1 Bank of

Uncertainty and Economic Activity: A Global Perspective Ambrogio Cesa-Bianchi 1 M. Hashem Pesaran 2 Alessandro Rebucci 3 IV International Conference in memory of Carlo Giannini 26 March 2014 1 Bank of

Credit Shocks and the U.S. Business Cycle. Is This Time Different? Raju Huidrom University of Virginia. Midwest Macro Conference

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

Credit Shocks and the U.S. Business Cycle: Is This Time Different? Raju Huidrom University of Virginia May 31, 214 Midwest Macro Conference Raju Huidrom Credit Shocks and the U.S. Business Cycle Background

The Fall of Oil Prices and Changes in the Dynamic Relationship between the Stock Markets of Russia and Kazakhstan

Journal of Reviews on Global Economics, 2015, 4, 147-151 147 The Fall of Oil Prices and Changes in the Dynamic Relationship between the Stock Markets of Russia and Kazakhstan Mirzosaid Sultonov * Tohoku

Journal of Reviews on Global Economics, 2015, 4, 147-151 147 The Fall of Oil Prices and Changes in the Dynamic Relationship between the Stock Markets of Russia and Kazakhstan Mirzosaid Sultonov * Tohoku

Time Variation in Asset Return Correlations: Econometric Game solutions submitted by Oxford University

Time Variation in Asset Return Correlations: Econometric Game solutions submitted by Oxford University June 21, 2006 Abstract Oxford University was invited to participate in the Econometric Game organised

Time Variation in Asset Return Correlations: Econometric Game solutions submitted by Oxford University June 21, 2006 Abstract Oxford University was invited to participate in the Econometric Game organised

Application of Conditional Autoregressive Value at Risk Model to Kenyan Stocks: A Comparative Study

American Journal of Theoretical and Applied Statistics 2017; 6(3): 150-155 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20170603.13 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

American Journal of Theoretical and Applied Statistics 2017; 6(3): 150-155 http://www.sciencepublishinggroup.com/j/ajtas doi: 10.11648/j.ajtas.20170603.13 ISSN: 2326-8999 (Print); ISSN: 2326-9006 (Online)

How can saving deposit rate and Hang Seng Index affect housing prices : an empirical study in Hong Kong market

Lingnan Journal of Banking, Finance and Economics Volume 2 2010/2011 Academic Year Issue Article 3 January 2010 How can saving deposit rate and Hang Seng Index affect housing prices : an empirical study

Lingnan Journal of Banking, Finance and Economics Volume 2 2010/2011 Academic Year Issue Article 3 January 2010 How can saving deposit rate and Hang Seng Index affect housing prices : an empirical study

A Study on the Relationship between Monetary Policy Variables and Stock Market

International Journal of Business and Management; Vol. 13, No. 1; 2018 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education A Study on the Relationship between Monetary

International Journal of Business and Management; Vol. 13, No. 1; 2018 ISSN 1833-3850 E-ISSN 1833-8119 Published by Canadian Center of Science and Education A Study on the Relationship between Monetary

The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock

MPRA Munich Personal RePEc Archive The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock Binh Le Thanh International University of Japan 15. August 2015 Online

MPRA Munich Personal RePEc Archive The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock Binh Le Thanh International University of Japan 15. August 2015 Online

MA Advanced Macroeconomics 3. Examples of VAR Studies

MA Advanced Macroeconomics 3. Examples of VAR Studies Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) VAR Studies Spring 2016 1 / 23 Examples of VAR Studies We will look at four different

MA Advanced Macroeconomics 3. Examples of VAR Studies Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) VAR Studies Spring 2016 1 / 23 Examples of VAR Studies We will look at four different

REAL EXCHANGE RATES AND BILATERAL TRADE BALANCES: SOME EMPIRICAL EVIDENCE OF MALAYSIA

REAL EXCHANGE RATES AND BILATERAL TRADE BALANCES: SOME EMPIRICAL EVIDENCE OF MALAYSIA Risalshah Latif Zulkarnain Hatta ABSTRACT This study examines the impact of real exchange rates on the bilateral trade

REAL EXCHANGE RATES AND BILATERAL TRADE BALANCES: SOME EMPIRICAL EVIDENCE OF MALAYSIA Risalshah Latif Zulkarnain Hatta ABSTRACT This study examines the impact of real exchange rates on the bilateral trade

Working Paper IIMK/WPS/252/EA/2017/36. June 2017

Working Paper IIMK/WPS/252/EA/2017/36 June 2017 Sources of Uncertainty and the Indian Economy Shubhasis Dey 1 1 Associate Professor, Economics Area, Indian Institute of Management Kozhikode, Kozhikode,

Working Paper IIMK/WPS/252/EA/2017/36 June 2017 Sources of Uncertainty and the Indian Economy Shubhasis Dey 1 1 Associate Professor, Economics Area, Indian Institute of Management Kozhikode, Kozhikode,

The Relationship between Foreign Direct Investment and Economic Development An Empirical Analysis of Shanghai 's Data Based on

The Relationship between Foreign Direct Investment and Economic Development An Empirical Analysis of Shanghai 's Data Based on 2004-2015 Jiaqi Wang School of Shanghai University, Shanghai 200444, China

The Relationship between Foreign Direct Investment and Economic Development An Empirical Analysis of Shanghai 's Data Based on 2004-2015 Jiaqi Wang School of Shanghai University, Shanghai 200444, China

ECONOMIC POLICY UNCERTAINTY AND SMALL BUSINESS DECISIONS

Recto rh: ECONOMIC POLICY UNCERTAINTY CJ 37 (1)/Krol (Final 2) ECONOMIC POLICY UNCERTAINTY AND SMALL BUSINESS DECISIONS Robert Krol The U.S. economy has experienced a slow recovery from the 2007 09 recession.

Recto rh: ECONOMIC POLICY UNCERTAINTY CJ 37 (1)/Krol (Final 2) ECONOMIC POLICY UNCERTAINTY AND SMALL BUSINESS DECISIONS Robert Krol The U.S. economy has experienced a slow recovery from the 2007 09 recession.

Integration of Foreign Exchange Markets: A Short Term Dynamics Analysis

Global Journal of Management and Business Studies. ISSN 2248-9878 Volume 3, Number 4 (2013), pp. 383-388 Research India Publications http://www.ripublication.com/gjmbs.htm Integration of Foreign Exchange

Global Journal of Management and Business Studies. ISSN 2248-9878 Volume 3, Number 4 (2013), pp. 383-388 Research India Publications http://www.ripublication.com/gjmbs.htm Integration of Foreign Exchange

Volatility Clustering in High-Frequency Data: A self-fulfilling prophecy? Abstract

Volatility Clustering in High-Frequency Data: A self-fulfilling prophecy? Matei Demetrescu Goethe University Frankfurt Abstract Clustering volatility is shown to appear in a simple market model with noise

Volatility Clustering in High-Frequency Data: A self-fulfilling prophecy? Matei Demetrescu Goethe University Frankfurt Abstract Clustering volatility is shown to appear in a simple market model with noise

Volatility Clustering of Fine Wine Prices assuming Different Distributions

Volatility Clustering of Fine Wine Prices assuming Different Distributions Cynthia Royal Tori, PhD Valdosta State University Langdale College of Business 1500 N. Patterson Street, Valdosta, GA USA 31698

Volatility Clustering of Fine Wine Prices assuming Different Distributions Cynthia Royal Tori, PhD Valdosta State University Langdale College of Business 1500 N. Patterson Street, Valdosta, GA USA 31698

Lecture Note 9 of Bus 41914, Spring Multivariate Volatility Models ChicagoBooth

Lecture Note 9 of Bus 41914, Spring 2017. Multivariate Volatility Models ChicagoBooth Reference: Chapter 7 of the textbook Estimation: use the MTS package with commands: EWMAvol, marchtest, BEKK11, dccpre,

Lecture Note 9 of Bus 41914, Spring 2017. Multivariate Volatility Models ChicagoBooth Reference: Chapter 7 of the textbook Estimation: use the MTS package with commands: EWMAvol, marchtest, BEKK11, dccpre,

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis WenShwo Fang Department of Economics Feng Chia University 100 WenHwa Road, Taichung, TAIWAN Stephen M. Miller* College of Business University

The Great Moderation Flattens Fat Tails: Disappearing Leptokurtosis WenShwo Fang Department of Economics Feng Chia University 100 WenHwa Road, Taichung, TAIWAN Stephen M. Miller* College of Business University

How Far do Shocks Move Across Borders? Examining Volatility Transmission in Major Agricultural Futures Markets

How Far do Shocks Move Across Borders? Examining Volatility Transmission in Major Agricultural Futures Markets Manuel A. Hernandez Raul Ibarra Danilo R. Trupkin ABSTRACT This paper examines the level of

How Far do Shocks Move Across Borders? Examining Volatility Transmission in Major Agricultural Futures Markets Manuel A. Hernandez Raul Ibarra Danilo R. Trupkin ABSTRACT This paper examines the level of

PRICE VOLATILITY IN ETHANOL MARKETS

PRICE VOLATILITY IN ETHANOL MARKETS Teresa Serra CREDA-UPC-IRTA, Parc Mediterrani de la Tecnologia, Edifici ESAB, Avinguda del Canal Olímpic s/n, 08860 Castelldefels, Spain, Phone: 34-93-55-09, Fax: 34-93-55-00,

PRICE VOLATILITY IN ETHANOL MARKETS Teresa Serra CREDA-UPC-IRTA, Parc Mediterrani de la Tecnologia, Edifici ESAB, Avinguda del Canal Olímpic s/n, 08860 Castelldefels, Spain, Phone: 34-93-55-09, Fax: 34-93-55-00,

Volatility spillover and volatility impulse response functions in crude oil, gold and exchange markets

Volatility spillover and volatility impulse response functions in crude oil, gold and exchange markets Preliminary and uncompleted version Nasser Khiabani Department of economics, niversity of Alameh Tabatabai

Volatility spillover and volatility impulse response functions in crude oil, gold and exchange markets Preliminary and uncompleted version Nasser Khiabani Department of economics, niversity of Alameh Tabatabai

SHORT-RUN DEVIATIONS AND TIME-VARYING HEDGE RATIOS: EVIDENCE FROM AGRICULTURAL FUTURES MARKETS TAUFIQ CHOUDHRY

SHORT-RUN DEVIATIONS AND TIME-VARYING HEDGE RATIOS: EVIDENCE FROM AGRICULTURAL FUTURES MARKETS By TAUFIQ CHOUDHRY School of Management University of Bradford Emm Lane Bradford BD9 4JL UK Phone: (44) 1274-234363

SHORT-RUN DEVIATIONS AND TIME-VARYING HEDGE RATIOS: EVIDENCE FROM AGRICULTURAL FUTURES MARKETS By TAUFIQ CHOUDHRY School of Management University of Bradford Emm Lane Bradford BD9 4JL UK Phone: (44) 1274-234363

INFLATION, INFLATION UNCERTAINTY AND A COMMON EUROPEAN MONETARY POLICY*

The Manchester School Vol 72 No. 2 March 2004 1463 6786 221 242 INFLATION, INFLATION UNCERTAINTY AND A COMMON EUROPEAN MONETARY POLICY* by S. FOUNTAS University of Macedonia A. IOANNIDIS University of

The Manchester School Vol 72 No. 2 March 2004 1463 6786 221 242 INFLATION, INFLATION UNCERTAINTY AND A COMMON EUROPEAN MONETARY POLICY* by S. FOUNTAS University of Macedonia A. IOANNIDIS University of

Portfolio construction by volatility forecasts: Does the covariance structure matter?

Portfolio construction by volatility forecasts: Does the covariance structure matter? Momtchil Pojarliev and Wolfgang Polasek INVESCO Asset Management, Bleichstrasse 60-62, D-60313 Frankfurt email: momtchil

Portfolio construction by volatility forecasts: Does the covariance structure matter? Momtchil Pojarliev and Wolfgang Polasek INVESCO Asset Management, Bleichstrasse 60-62, D-60313 Frankfurt email: momtchil

University of Pretoria Department of Economics Working Paper Series

University of Pretoria Department of Economics Working Paper Series Dynamic Co-movements between Economic Policy Uncertainty and Housing Market Returns Nikolaos Antonakakis Vienna University of Economics

University of Pretoria Department of Economics Working Paper Series Dynamic Co-movements between Economic Policy Uncertainty and Housing Market Returns Nikolaos Antonakakis Vienna University of Economics

Online Appendix: Asymmetric Effects of Exogenous Tax Changes

Online Appendix: Asymmetric Effects of Exogenous Tax Changes Syed M. Hussain Samreen Malik May 9,. Online Appendix.. Anticipated versus Unanticipated Tax changes Comparing our estimates with the estimates

Online Appendix: Asymmetric Effects of Exogenous Tax Changes Syed M. Hussain Samreen Malik May 9,. Online Appendix.. Anticipated versus Unanticipated Tax changes Comparing our estimates with the estimates

Dynamic Causal Relationships among the Greater China Stock markets

Dynamic Causal Relationships among the Greater China Stock markets Gao Hui Department of Economics and management, HeZe University, HeZe, ShanDong, China Abstract--This study examines the dynamic causal

Dynamic Causal Relationships among the Greater China Stock markets Gao Hui Department of Economics and management, HeZe University, HeZe, ShanDong, China Abstract--This study examines the dynamic causal

Thi-Thanh Phan, Int. Eco. Res, 2016, v7i6, 39 48

INVESTMENT AND ECONOMIC GROWTH IN CHINA AND THE UNITED STATES: AN APPLICATION OF THE ARDL MODEL Thi-Thanh Phan [1], Ph.D Program in Business College of Business, Chung Yuan Christian University Email:

INVESTMENT AND ECONOMIC GROWTH IN CHINA AND THE UNITED STATES: AN APPLICATION OF THE ARDL MODEL Thi-Thanh Phan [1], Ph.D Program in Business College of Business, Chung Yuan Christian University Email:

Financial Econometrics Lecture 5: Modelling Volatility and Correlation

Financial Econometrics Lecture 5: Modelling Volatility and Correlation Dayong Zhang Research Institute of Economics and Management Autumn, 2011 Learning Outcomes Discuss the special features of financial

Financial Econometrics Lecture 5: Modelling Volatility and Correlation Dayong Zhang Research Institute of Economics and Management Autumn, 2011 Learning Outcomes Discuss the special features of financial

Accounting. Oil price shocks and stock market returns. 1. Introduction

Accounting 2 (2016) 103 108 Contents lists available at GrowingScience Accounting homepage: www.growingscience.com/ac/ac.html Oil price shocks and stock market returns Maryam Orouji * Masters in Physics,

Accounting 2 (2016) 103 108 Contents lists available at GrowingScience Accounting homepage: www.growingscience.com/ac/ac.html Oil price shocks and stock market returns Maryam Orouji * Masters in Physics,

Inflation and inflation uncertainty in Argentina,

U.S. Department of the Treasury From the SelectedWorks of John Thornton March, 2008 Inflation and inflation uncertainty in Argentina, 1810 2005 John Thornton Available at: https://works.bepress.com/john_thornton/10/

U.S. Department of the Treasury From the SelectedWorks of John Thornton March, 2008 Inflation and inflation uncertainty in Argentina, 1810 2005 John Thornton Available at: https://works.bepress.com/john_thornton/10/

THE EFFECTS OF FISCAL POLICY ON EMERGING ECONOMIES. A TVP-VAR APPROACH

South-Eastern Europe Journal of Economics 1 (2015) 75-84 THE EFFECTS OF FISCAL POLICY ON EMERGING ECONOMIES. A TVP-VAR APPROACH IOANA BOICIUC * Bucharest University of Economics, Romania Abstract This

South-Eastern Europe Journal of Economics 1 (2015) 75-84 THE EFFECTS OF FISCAL POLICY ON EMERGING ECONOMIES. A TVP-VAR APPROACH IOANA BOICIUC * Bucharest University of Economics, Romania Abstract This

Return, shock and volatility spillovers between the bond markets of Turkey and developed countries

e Theoretical and Applied Economics Volume XXV (2018), No. 3(616), Autumn, pp. 135-144 Return, shock and volatility spillovers between the bond markets of Turkey and developed countries Selçuk BAYRACI

e Theoretical and Applied Economics Volume XXV (2018), No. 3(616), Autumn, pp. 135-144 Return, shock and volatility spillovers between the bond markets of Turkey and developed countries Selçuk BAYRACI

Exchange Rate Pass-through in India

Exchange Rate Pass-through in India Rudrani Bhattacharya, Ila Patnaik and Ajay Shah National Institute of Public Finance and Policy, New Delhi March 27, 2008 udrani Bhattacharya, Ila Patnaik and Ajay Shah

Exchange Rate Pass-through in India Rudrani Bhattacharya, Ila Patnaik and Ajay Shah National Institute of Public Finance and Policy, New Delhi March 27, 2008 udrani Bhattacharya, Ila Patnaik and Ajay Shah

A market risk model for asymmetric distributed series of return

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2012 A market risk model for asymmetric distributed series of return Kostas Giannopoulos

University of Wollongong Research Online University of Wollongong in Dubai - Papers University of Wollongong in Dubai 2012 A market risk model for asymmetric distributed series of return Kostas Giannopoulos

APPLYING MULTIVARIATE

Swiss Society for Financial Market Research (pp. 201 211) MOMTCHIL POJARLIEV AND WOLFGANG POLASEK APPLYING MULTIVARIATE TIME SERIES FORECASTS FOR ACTIVE PORTFOLIO MANAGEMENT Momtchil Pojarliev, INVESCO

Swiss Society for Financial Market Research (pp. 201 211) MOMTCHIL POJARLIEV AND WOLFGANG POLASEK APPLYING MULTIVARIATE TIME SERIES FORECASTS FOR ACTIVE PORTFOLIO MANAGEMENT Momtchil Pojarliev, INVESCO

On the real effects of inflation and inflation uncertainty in Mexico

On the real effects of inflation and inflation uncertainty in Mexico Robin Grier a *, Kevin Grier b a University of Oklahoma, 729 Elm Avenue, Norman, OK 73071 b University of Oklahoma, 729 Elm Avenue,

On the real effects of inflation and inflation uncertainty in Mexico Robin Grier a *, Kevin Grier b a University of Oklahoma, 729 Elm Avenue, Norman, OK 73071 b University of Oklahoma, 729 Elm Avenue,

Volatility spillovers for stock returns and exchange rates of tourism firms in Taiwan

20th International Congress on Modelling and Simulation, Adelaide, Australia, 1 6 December 2013 www.mssanz.org.au/modsim2013 Volatility spillovers for stock returns and exchange rates of tourism firms

20th International Congress on Modelling and Simulation, Adelaide, Australia, 1 6 December 2013 www.mssanz.org.au/modsim2013 Volatility spillovers for stock returns and exchange rates of tourism firms

IS INFLATION VOLATILITY CORRELATED FOR THE US AND CANADA?

IS INFLATION VOLATILITY CORRELATED FOR THE US AND CANADA? C. Barry Pfitzner, Department of Economics/Business, Randolph-Macon College, Ashland, VA, bpfitzne@rmc.edu ABSTRACT This paper investigates the

IS INFLATION VOLATILITY CORRELATED FOR THE US AND CANADA? C. Barry Pfitzner, Department of Economics/Business, Randolph-Macon College, Ashland, VA, bpfitzne@rmc.edu ABSTRACT This paper investigates the

User Guide of GARCH-MIDAS and DCC-MIDAS MATLAB Programs

User Guide of GARCH-MIDAS and DCC-MIDAS MATLAB Programs 1. Introduction The GARCH-MIDAS model decomposes the conditional variance into the short-run and long-run components. The former is a mean-reverting

User Guide of GARCH-MIDAS and DCC-MIDAS MATLAB Programs 1. Introduction The GARCH-MIDAS model decomposes the conditional variance into the short-run and long-run components. The former is a mean-reverting

MEASURING THE OPTIMAL MACROECONOMIC UNCERTAINTY INDEX FOR TURKEY

ECONOMIC ANNALS, Volume LXI, No. 210 / July September 2016 UDC: 3.33 ISSN: 0013-3264 DOI:10.2298/EKA1610007E Havvanur Feyza Erdem* Rahmi Yamak** MEASURING THE OPTIMAL MACROECONOMIC UNCERTAINTY INDEX FOR

ECONOMIC ANNALS, Volume LXI, No. 210 / July September 2016 UDC: 3.33 ISSN: 0013-3264 DOI:10.2298/EKA1610007E Havvanur Feyza Erdem* Rahmi Yamak** MEASURING THE OPTIMAL MACROECONOMIC UNCERTAINTY INDEX FOR

Oil Price Uncertainty in the Iranian Economy 1

Iran. Econ. Rev. Vol. 21, No.1, 2017. pp. 137-152 Oil Price Uncertainty in the Iranian Economy 1 Elaheh Asadi Mehmandosti* 2 Fatemeh Bazzazan 3 Mirhossein Mousavi 4 Abstract T Received: 2015/12/23 Accepted:

Iran. Econ. Rev. Vol. 21, No.1, 2017. pp. 137-152 Oil Price Uncertainty in the Iranian Economy 1 Elaheh Asadi Mehmandosti* 2 Fatemeh Bazzazan 3 Mirhossein Mousavi 4 Abstract T Received: 2015/12/23 Accepted:

Inflation Expectation Uncertainty, Inflation and the Output Gap

Inflation Expectation Uncertainty, Inflation and the Output Gap Angela Fuest and Torsten Schmidt * This version January 2017 Abstract Uncertainty about the future path of inflation affects consumption,

Inflation Expectation Uncertainty, Inflation and the Output Gap Angela Fuest and Torsten Schmidt * This version January 2017 Abstract Uncertainty about the future path of inflation affects consumption,

Discussion of Trend Inflation in Advanced Economies

Discussion of Trend Inflation in Advanced Economies James Morley University of New South Wales 1. Introduction Garnier, Mertens, and Nelson (this issue, GMN hereafter) conduct model-based trend/cycle decomposition

Discussion of Trend Inflation in Advanced Economies James Morley University of New South Wales 1. Introduction Garnier, Mertens, and Nelson (this issue, GMN hereafter) conduct model-based trend/cycle decomposition

MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES

money 15/10/98 MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES Mehdi S. Monadjemi School of Economics University of New South Wales Sydney 2052 Australia m.monadjemi@unsw.edu.au

money 15/10/98 MONEY, PRICES AND THE EXCHANGE RATE: EVIDENCE FROM FOUR OECD COUNTRIES Mehdi S. Monadjemi School of Economics University of New South Wales Sydney 2052 Australia m.monadjemi@unsw.edu.au

Keywords: China; Globalization; Rate of Return; Stock Markets; Time-varying parameter regression.

Co-movements of Shanghai and New York Stock prices by time-varying regressions Gregory C Chow a, Changjiang Liu b, Linlin Niu b,c a Department of Economics, Fisher Hall Princeton University, Princeton,

Co-movements of Shanghai and New York Stock prices by time-varying regressions Gregory C Chow a, Changjiang Liu b, Linlin Niu b,c a Department of Economics, Fisher Hall Princeton University, Princeton,

Downside Risk: Implications for Financial Management Robert Engle NYU Stern School of Business Carlos III, May 24,2004

Downside Risk: Implications for Financial Management Robert Engle NYU Stern School of Business Carlos III, May 24,2004 WHAT IS ARCH? Autoregressive Conditional Heteroskedasticity Predictive (conditional)

Downside Risk: Implications for Financial Management Robert Engle NYU Stern School of Business Carlos III, May 24,2004 WHAT IS ARCH? Autoregressive Conditional Heteroskedasticity Predictive (conditional)

MFE Macroeconomics Week 3 Exercise

MFE Macroeconomics Week 3 Exercise The first row in the figure below shows monthly data for the Federal Funds Rate and CPI inflation for the period 199m1-18m8. 1 FFR CPI inflation 8 1 6 4 1 199 1995 5

MFE Macroeconomics Week 3 Exercise The first row in the figure below shows monthly data for the Federal Funds Rate and CPI inflation for the period 199m1-18m8. 1 FFR CPI inflation 8 1 6 4 1 199 1995 5

Study of Relationship Between USD/INR Exchange Rate and BSE Sensex from

DOI : 10.18843/ijms/v5i3(1)/13 DOIURL :http://dx.doi.org/10.18843/ijms/v5i3(1)/13 Study of Relationship Between USD/INR Exchange Rate and BSE Sensex from 2008-2017 Hardeepika Singh Ahluwalia, Assistant

DOI : 10.18843/ijms/v5i3(1)/13 DOIURL :http://dx.doi.org/10.18843/ijms/v5i3(1)/13 Study of Relationship Between USD/INR Exchange Rate and BSE Sensex from 2008-2017 Hardeepika Singh Ahluwalia, Assistant

In this chapter we show that, contrary to common beliefs, financial correlations

3GC02 11/25/2013 11:38:51 Page 43 CHAPTER 2 Empirical Properties of Correlation: How Do Correlations Behave in the Real World? Anything that relies on correlation is charlatanism. Nassim Taleb In this

3GC02 11/25/2013 11:38:51 Page 43 CHAPTER 2 Empirical Properties of Correlation: How Do Correlations Behave in the Real World? Anything that relies on correlation is charlatanism. Nassim Taleb In this

Monetary policy transmission in Switzerland: Headline inflation and asset prices

Monetary policy transmission in Switzerland: Headline inflation and asset prices Master s Thesis Supervisor Prof. Dr. Kjell G. Nyborg Chair Corporate Finance University of Zurich Department of Banking

Monetary policy transmission in Switzerland: Headline inflation and asset prices Master s Thesis Supervisor Prof. Dr. Kjell G. Nyborg Chair Corporate Finance University of Zurich Department of Banking

The Analysis of Bidirectional Causality between Stock Market Volatility and Macroeconomic Volatility

The Analysis of Bidirectional Causality between Stock Market Volatility and Macroeconomic Volatility Zeynep Iltuzer 1 Oktay Tas 2 Abstract What underlies the volatility of financial securities has been

The Analysis of Bidirectional Causality between Stock Market Volatility and Macroeconomic Volatility Zeynep Iltuzer 1 Oktay Tas 2 Abstract What underlies the volatility of financial securities has been

Modeling the volatility of FTSE All Share Index Returns

MPRA Munich Personal RePEc Archive Modeling the volatility of FTSE All Share Index Returns Bayraci, Selcuk University of Exeter, Yeditepe University 27. April 2007 Online at http://mpra.ub.uni-muenchen.de/28095/

MPRA Munich Personal RePEc Archive Modeling the volatility of FTSE All Share Index Returns Bayraci, Selcuk University of Exeter, Yeditepe University 27. April 2007 Online at http://mpra.ub.uni-muenchen.de/28095/

Asian Economic and Financial Review EMPIRICAL TESTING OF EXCHANGE RATE AND INTEREST RATE TRANSMISSION CHANNELS IN CHINA

Asian Economic and Financial Review, 15, 5(1): 15-15 Asian Economic and Financial Review ISSN(e): -737/ISSN(p): 35-17 journal homepage: http://www.aessweb.com/journals/5 EMPIRICAL TESTING OF EXCHANGE RATE

Asian Economic and Financial Review, 15, 5(1): 15-15 Asian Economic and Financial Review ISSN(e): -737/ISSN(p): 35-17 journal homepage: http://www.aessweb.com/journals/5 EMPIRICAL TESTING OF EXCHANGE RATE

Asian Economic and Financial Review EXPLORING THE RETURNS AND VOLATILITY SPILLOVER EFFECT IN TAIWAN AND JAPAN STOCK MARKETS

Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 URL: www.aessweb.com EXPLORING THE RETURNS AND VOLATILITY SPILLOVER EFFECT IN TAIWAN AND JAPAN STOCK MARKETS Chi-Lu Peng 1 ---

Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 URL: www.aessweb.com EXPLORING THE RETURNS AND VOLATILITY SPILLOVER EFFECT IN TAIWAN AND JAPAN STOCK MARKETS Chi-Lu Peng 1 ---

An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh

Bangladesh Development Studies Vol. XXXIV, December 2011, No. 4 An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh NASRIN AFZAL * SYED SHAHADAT HOSSAIN

Bangladesh Development Studies Vol. XXXIV, December 2011, No. 4 An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh NASRIN AFZAL * SYED SHAHADAT HOSSAIN

Volume 29, Issue 2. Measuring the external risk in the United Kingdom. Estela Sáenz University of Zaragoza

Volume 9, Issue Measuring the external risk in the United Kingdom Estela Sáenz University of Zaragoza María Dolores Gadea University of Zaragoza Marcela Sabaté University of Zaragoza Abstract This paper

Volume 9, Issue Measuring the external risk in the United Kingdom Estela Sáenz University of Zaragoza María Dolores Gadea University of Zaragoza Marcela Sabaté University of Zaragoza Abstract This paper

Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison

DEPARTMENT OF ECONOMICS JOHANNES KEPLER UNIVERSITY LINZ Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison by Burkhard Raunig and Johann Scharler* Working Paper

DEPARTMENT OF ECONOMICS JOHANNES KEPLER UNIVERSITY LINZ Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison by Burkhard Raunig and Johann Scharler* Working Paper

Volatility Analysis of Nepalese Stock Market

The Journal of Nepalese Business Studies Vol. V No. 1 Dec. 008 Volatility Analysis of Nepalese Stock Market Surya Bahadur G.C. Abstract Modeling and forecasting volatility of capital markets has been important

The Journal of Nepalese Business Studies Vol. V No. 1 Dec. 008 Volatility Analysis of Nepalese Stock Market Surya Bahadur G.C. Abstract Modeling and forecasting volatility of capital markets has been important

Foreign direct investment and profit outflows: a causality analysis for the Brazilian economy. Abstract

Foreign direct investment and profit outflows: a causality analysis for the Brazilian economy Fernando Seabra Federal University of Santa Catarina Lisandra Flach Universität Stuttgart Abstract Most empirical

Foreign direct investment and profit outflows: a causality analysis for the Brazilian economy Fernando Seabra Federal University of Santa Catarina Lisandra Flach Universität Stuttgart Abstract Most empirical