New Generation Grain Contracts Decision Contracts

|

|

|

- Logan Harrison

- 5 years ago

- Views:

Transcription

1 New Generation Grain Contracts Decision Contracts MARKET BASED RISK MANAGEMENT FOR AGRICULTURE September 2006 Iowa State University Regis Lefaucheur Decision Commodities, LLC 614 Billy Sunday Rd., Suite 600 Ames, Iowa

2 Decision Commodities Based in Ames, IA Provides innovative forward contracts to grain producers to help them take the emotion, stress and guesswork out of grain pricing Customer base: Iowa, Illinois, Minnesota, North Dakota, Wisconsin, Missouri Decision Contracts enable producers to put discipline into grain marketing 2

3 Decision Commodities What does Decision Commodities do? Take the EMOTION out of selling Take the GUESSWORK out of selling Consistently outguessing or outperforming the market is impossible. 3

4 Grain Industry Vocabulary Definitions: Futures price Basis Cash Price Spread Relationships 4

5 Producer Hedging 01 Feb 2006 Harvest Price Decrease Scenario $2.50 Lower $2.10 -$0.40 Futures $2.50 $2.10 +$0.40 Producer Goal: Lock in an attractive price (higher is better) Protection against lower prices 01 Feb 2006 Harvest Price Increase Scenario $2.50 Higher $2.90 +$0.40 Futures $2.50 $2.90 -$0.40 5

6 Elevator Hedging Harvest January 15 sale Price Decrease Scenario $2.90 Lower $2.70 -$0.20 Futures $2.90 $2.70 +$0.20 Elevator Goal: Lock in the price of the grain he bought to protect his margins (storage, drying, basis, hedging) Harvest January 15 Sale Price Increase Scenario $2.90 Higher $3.10 +$0.20 Futures $2.90 $3.10 -$0.20 6

7 End User: feed mill, ethanol 01 Feb 2005 Harvest Price Decrease Scenario $2.50 Lower $2.10 +$0.40 Futures -$0.40 End User Goal: Lock in an attractive price (lower is better) Protection against higher prices 01 Feb 2005 Harvest Price Increase Scenario $2.50 Higher $2.90 -$0.40 Futures $2.50 $2.90 +$0.40 7

8 Decision Contracts Insurance against low prices Put Option Contract Risk Management Continuum Futures Contract Insurance against high prices Call Option Contract Farmers Price Sensitive Elevator Margin Dependent End-User Price Sensitive 8

9 Relationship Between Basis And Cash Price Futures Price -Basis = Cash Price (paid to the producer) $ (Dec 2006) - $0.40 = $ See: 9

10 10 Example

11 11 Example

12 BASIS What is BASIS? Chicago Board of Trade - Corn Futures Price = $2.75 Processor Bid - $2.70 BASIS = 0.05 under Warehouse Bid - $2.60 BASIS = 0.10 under Producer Bid - $2.50 BASIS = 0.25 under How can a user increase or decrease the movement of grain locally if they can t change the price on the Chicago Board of Trade? 12

13 What factors contribute to determining the BASIS? BASIS Feed Ethanol River Processing Processing 13

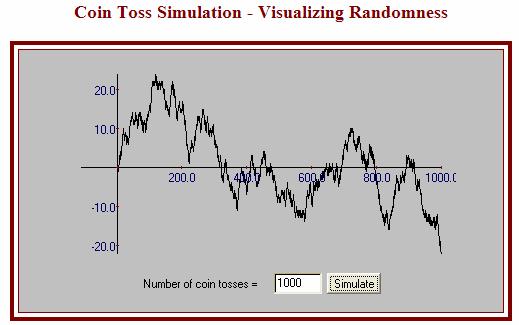

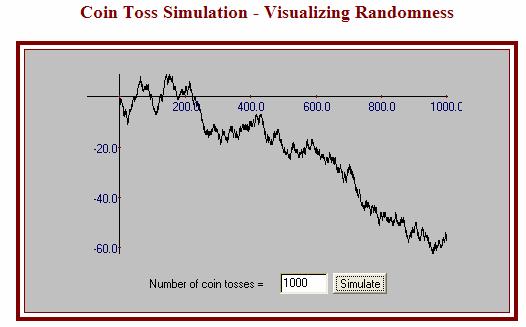

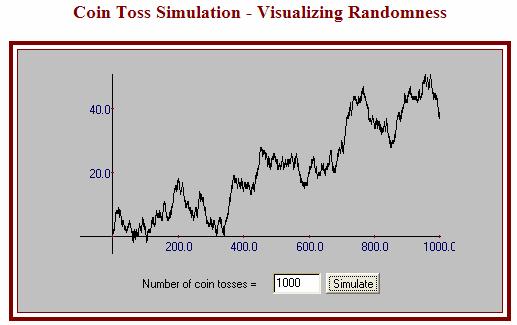

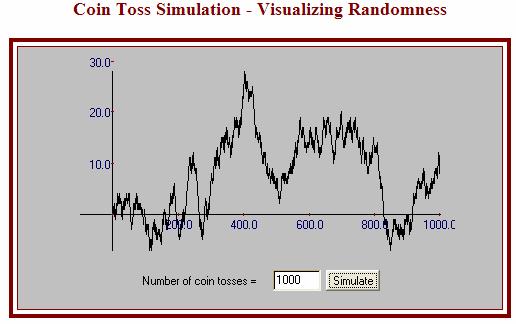

14 14

15 BASIS Industrial Export Ethanol Dairy Feed Poultry Export 15 What impact does a BASIS change in one area have on other areas? Which markets have the greatest influence on basis, spreads and the futures market?

16 SPREAD Spread = price difference between various futures reference months The Spread can be Carry or Inverted Spread= + $ / Carry Spread= - $ / Inverted 16

17 STORE or SELL? What decision should a producer make? STORE Wide Carry Basis Spread SELL Narrow Inverted Low Futures price High Result: Decrease in the movement of grain Result: Increase in the movement of grain 17

18 EFFICIENT MARKET HYPOTHESIS RANDOMNESS 18

19 Efficient Market Hypothesis According to Fama, an efficient market is one that accurately incorporates all known information in determining price. This is know as the efficient market hypothesis. Although there is considerable disagreement about the degree to which EMH holds, it has become the dominant paradigm used by economists to understand and investigate the behavior of financial and commodity markets. Markets for commodities and products that are widely traded in agriculture and the food industry are a model of efficiency. The compile all the information and knowledge of traders, businesses and producers, and express this data in the form of a price. 19

20 Efficient Market Hypothesis The daily pricing process in the market is usually referred to as a random walk. A commonly used analogy of a random walk is the flipping of a fair coin. Overtime, the expected change is price is zero. The market is all-knowing. Consistently outguessing or outperforming it is very difficult (if not impossible) 20

21 Randomness What does randomness looks like? 21

22 Randomness and Unpredictability Randomness CBOT Corn December Futures 2005 It is easy to see patterns in random events 22

23 SOYBEAN Up/Down days Number of trading days up/down Nov 01 to Oct NOV Soybean CBOT ($0.50) ($0.35) ($0.25) ($0.22) ($0.20) ($0.18) ($0.16) ($0.14) ($0.12) ($0.10) ($0.08) ($0.06) ($0.04) ($0.02) $0.00 $0.02 $0.04 $0.06 $0.08 $0.10 $0.12 $0.14 $0.16 $0.18 $0.20 $0.22 $0.25 $0.35 $0.50 Decision Commodities LLC

24 SOYBEAN Up/Down days By year (days) 1997 Up 126 Down 126 Total 252 SOYBEAN TOTALS Average of up/down Standard deviation $0.00 $ Minimum Maximum $-0.49 $ Total Days Up Days Down Days Nov 01 to Oct NOV Soybean CBOT 24

25 Randomness and Unpredictability Another way to view markets is that while prices can t be predicted, prices aren t all that random either. While we can t guarantee that the pattern depicted below will be repeated in the future, this 25 year frequency histogram tends to suggest that there is some central tendency around $2.15 to $2.95 range. Frequency of Closing Prices in CBOT December Corn $1.60 $1.75 $1.90 $2.05 $2.20 $2.35 $2.50 $2.65 $2.80 $2.95 $3.10 $3.25 $3.40 $3.55 $3.70 $3.85 $

26 BEHAVIORAL FINANCE AND EMOTIONS 26

27 Behavioral Finance and Emotions 2004 December Corn Futures to

28 Behavioral Finance Regret: Regret management is probably a more accurate term for risk management. There is a very natural tendency to avoid regret. In grain marketing, this is often embodied into a decision not to decide. Regret is the more powerful behavioral issue. Obviously, regret can significantly impair our ability to make rational choices. Risk aversion: Most people are risk averse and seek to avoid risk. However, there tends to be identifiable biases in human behavior that lead to irrational decision making. One of these biases is the tendency to accept increases risk over a guaranteed loss. It reflects a tendency to underestimate the chances of extreme market situation occurring. In grain marketing, this tendency leads some to accept price risk rather than pay for insurance such as a put option purchase or guaranteed minimum price contract. Why don t producers want to pay 5 cents to protect 50 cents? 28

29 Long Term Corn Prices 2004 December Corn Futures to Reference price anchoring: It is the tendency for a person to fix a specific figure in their mind as the perceived value. An example of driving with eyes fixed on the rear view mirror is establishing a target price based on last year s market price. Bull or bear forecasts coming from newsletters, magazines, market advisors, radio shows Reality takes a long time to soak in, and when it does, it is usually too late as opportunities are long gone.

30 Behavioral Finance Escalation: too much invested to quit. A situation where a person enters a transaction hoping for a favorable outcome but after circumstances change to unfavorable, the person finds it difficult to escape or even adds to it. Endowment: Associated with the fear of giving up something. It is more painful to give up an asset than it is pleasurable to obtain. Ownership as a positive feeling. Producers have a tendency to store grain beyond economic justification, because when it is sold, there is no opportunity to gain anymore. For grain under storage, the perceived value increases with the duration of ownership. 30

31 Behavioral Finance Which one of the following would you choose? A. Winning a guaranteed $3,000 B. Taking an 80% chance of winning $4,000 Now consider this option A. Lose $3,000 B. Take an 80% chance of losing $4,000 31

32 Behavioral Finance Results: You are not alone if you said you would take the $3,000 but roll the dice and risk losing the $4,000 As human being, we don t deal with losses the same way we do with gains We will ride a loss to the bitter end while cutting a gain short Contributing to this mindset is a condition known as the Gambler s fallacy, which is the belief that a successful outcome is due after a run of back luck. But chance or the randomness of an efficient market is not self-correcting. Flipping 10 consecutive heads does not increase the chance that the eleventh toss will yield a tails, any more than a trend of lower grain prices ensures an up- or downswing in tomorrow s market. 32

33 33

34 Agricultural Market Advisory Services AGMAS Agmas study (U of I Urbana): provide a neutral evaluation of the performance of market advisory services for corn, soybean and wheat. Tracking about advisory programs per year since 1994 Paid subscriptions obtained for each services Recommendations recorded in real-time Two important issues:. Market advisory service performance relative to appropriate benchmarks. Predictability of market advisory service from yearto-year Result data available for the period

35 Agricultural Market Advisory Services Benchmarks: average of two-year marketing window (24 months) : price offered by the market USDA producer average : an indicator of marketing performance of farmers 35

36 Performance relative to Benchmark Performance of Market Advisory Services Corn - Average of AgResource Utterback Marketing Services Brock (hedge) Ag Review AgriVisor (aggressive cash) Allendale (futures only) AgLine by Doane (hedge) Progressive Ag AgriVisor (basic cash) AgLine by Doane (cash only) AgriVisor (aggressive hedge) AgriVisor (basic hedge) Top Farmer Intelligence Brock (cash only) Risk Mgmt Group (futures & options) Risk Mgmt Group (cash only) Risk Mgmt Group (options only) Co-Mark Northstar Commodity Allendale (futures & options) Freese-Notis Steward-Peterson Advisory Reports Pro Farmer (cash only) Pro Farmer (hedge) Ag Financial Strategies $1.85 $2.30 $2.28 $2.27 $2.27 $2.22 $2.21 $2.20 $2.19 $2.19 $2.18 $2.17 $2.16 $2.16 $2.16 $2.14 $2.13 $2.11 $2.10 $2.09 $2.09 $2.07 $2.02 $1.99 $ Month Average: $2.15 USDA Producer Average: $2.05 $1.70 $1.80 $1.90 $2.00 $2.10 $2.20 $2.30 $2.40 $

37 Predictability from year-to-year Ranking of Market Advisory Services - Corn Rank AgResource AgResource Progressive Ag Brock (hedge) AgResource 2 Allendale (futures only) Utterback Marketing Services Top Farmer Intelligence Brock (cash only) Progressive Ag 3 AgLine by Doane (hedge) Top Farmer Intelligence Ag Review Ag Review AgLine by Doane (cash only) 4 AgriVisor (aggressive cash) Brock (hedge) Utterback Marketing Services Risk Mgmt Group (futures & options) AgLine by Doane (hedge) 5 Ag Review AgLine by Doane (hedge) Co-Mark AgriVisor (basic hedge) Ag Review 6 Top Farmer Intelligence AgriVisor (aggressive cash) Steward-Peterson Advisory Reports AgriVisor (aggressive hedge) Freese-Notis 7 AgriVisor (basic cash) AgriVisor (aggressive hedge) Risk Mgmt Group (cash only) AgriVisor (basic cash) Northstar Commodity 8 Risk Mgmt Group (cash only) AgriVisor (basic cash) Allendale (futures only) AgriVisor (aggressive cash) Brock (cash only) 9 Allendale (futures & options) AgriVisor (basic hedge) Risk Mgmt Group (options only) AgResource AgriVisor (basic hedge) 10 Brock (cash only) Risk Mgmt Group (cash only) Risk Mgmt Group (futures & options) Progressive Ag AgriVisor (aggressive hedge) 11 Utterback Marketing Services Risk Mgmt Group (futures & options) Allendale (futures & options) Risk Mgmt Group (options only) AgriVisor (basic cash) 12 AgLine by Doane (cash only) AgLine by Doane (cash only) AgriVisor (aggressive cash) Risk Mgmt Group (cash only) AgriVisor (aggressive cash) 13 AgriVisor (basic hedge) Allendale (futures only) AgriVisor (aggressive hedge) Freese-Notis Brock (hedge) 14 Brock (hedge) Risk Mgmt Group (options only) AgLine by Doane (cash only) Co-Mark Allendale (futures & options) 15 AgriVisor (aggressive hedge) Progressive Ag AgLine by Doane (hedge) Steward-Peterson Advisory Reports Co-Mark 16 Risk Mgmt Group (options only) Freese-Notis AgriVisor (basic cash) Utterback Marketing Services Risk Mgmt Group (futures & options) 17 Risk Mgmt Group (futures & options) Co-Mark Pro Farmer (cash only) AgLine by Doane (hedge) Risk Mgmt Group (options only) 18 Progressive Ag Ag Review Northstar Commodity Northstar Commodity Steward-Peterson Advisory Reports 19 Steward-Peterson Advisory Reports Brock (cash only) AgriVisor (basic hedge) AgLine by Doane (cash only) Allendale (futures only) 20 Freese-Notis Allendale (futures & options) Pro Farmer (hedge) Top Farmer Intelligence Pro Farmer (cash only) 21 Pro Farmer (hedge) Pro Farmer (cash only) Brock (cash only) Allendale (futures only) Risk Mgmt Group (cash only) 22 Pro Farmer (cash only) Pro Farmer (hedge) Brock (hedge) Pro Farmer (cash only) Top Farmer Intelligence 23 Steward-Peterson Advisory Reports Freese-Notis Allendale (futures & options) Pro Farmer (hedge) 24 Ag Financial Strategies Pro Farmer (hedge) Utterback Marketing Services 25 AgResource Ag Financial Strategies Ag Financial Strategies Agmas Study released on 03/

38 Agricultural Market Advisory Services Limited evidence that advisory services outperform market benchmarks, particularly after taking risk into account Substantial evidence that advisory services outperform farmer benchmarks, even after taking risk into account Little evidence that past performance can be used to predict future performance 38

39 Decision Contracts Farmers continue to identify price and income risk as their greatest management challenge 39

40 Setting goals Corn Prices (Dec CBOT) $3.50 $3.40 $3.30 $3.20 $3.10 $3.00 Upper Third $2.90 $2.80 $2.70 $2.60 Average Price $2.50 $2.40 $2.30 $2.20 Lower Third $2.10 $2.00 $1.90 $ $1.70 Decision Commodities LLC 40 Price series for CZ contract : Average Price = $2.37 Upper Third = $ 2.44 and above Lower Third = $ 2.27 and below

41 Daily Average Corn Prices Based on December Corn (CZ) In the last 22 years for corn: Marketing at harvest was high price point = 3 years (93, 95, 02) High price point was spring/summer = 7 years (84, 87, 88, 90, 94, 96,04) High price point was before spring = 12 years (85,86,89,92,94,97,98,99,00,01,03,05) $2.70 December CBOT Corn Average Prices (Jan 1 to November months) $ $2.50 $2.40 $2.30 HARVEST $2.20 $2.10 PLANTING $ Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

42 Corn - High Low Average Historical Prices DEC Corn Historical Price ranges (Full length of contract) High Top third Average Bottom third Low $4.00 $3.80 $3.84 $3.60 $3.40 $3.37 $3.37 $3.20 $3.00 $2.80 $2.60 $3.08 $2.99 $2.91 $2.83 $2.73 $2.93 $2.69 $2.87 $2.87 $3.17 $2.47 $2.40 $2.39 $2.36 $2.38 $2.29 $2.20 $2.04 $2.11 $2.00 $2.00 $1.99 $1.88 $1.93 $1.87 $1.86 $ Last Update: 08/24/2006 Decision Commodities LLC 42

43 Decision Contracts Decision Commodities automated pricing models : Index Rally Accelerator Topper 43

44 Decision Contracts...a tool that delivers execution discipline without major time requirements Example You want to pre-harvest market 20,000 bushels of corn for Fall delivery, starting in January. The Index pricing model can, for example, price an even increment of bushels every day between January and September, achieving an average price for that time period. Assuming 100 (market) days between January and September, 200 bushels will be priced every day at the price of the underlying futures contract. You sign a forward contract with local grain elevator (specifying Decision Contracts as pricing mechanism), and deliver grain in same manner as usual. 44

45 Decision Contracts Producer Cash Contract Grain Elevator Ethanol Plant Basis Forward futures price Decision Contracts provides pricing mechanism for the futures price 45

46 Decision Contracts Index Pricing Model Index: Average Price Contract Prices an even increment of bushels each day for a given pricing period. Producer settings: Pricing period beginning Pricing Period end Delivery Period Bushels Example: 10,000 bu 100 days 100 bu would be priced each day 2006 The Index price model will result in the average price for the specified time pricing period. 46

47 Decision Contracts Rally Pricing Model Rally: Bushels price on days during the pricing period when: 1) the day s closing price is above the floor price and 2) the one day price change is less than the sensitivity level. Producer Settings: Pricing period beginning Pricing period end Bushels Bushels price if one Price Floor day price change UpPoint less than UpPoint Throttle $ $2.35 $2.34 $2.33 $2.32 $2.31 $2.30 $2.29 $2.28 Floor Bushels Bushels to Price = Remaining Bu Remaining Days If UpPoint = 0 pricing occurs when price goes down. X Throttle $2.27 Day

48 Rally Example 10,000 bu = 100 X 5 (Throttle) = 500 bu 100 days 500 bu on the first day 48

49 Decision Contracts Accelerator Pricing Model Accelerator: The daily amount of bushels priced accelerates as the futures prices increase, and vice versa Bushels price on days during the pricing period when: 1) the day s closing price is above the floor price 2) pricing factor increases (decreases) as futures prices go up (or go down) Producer Settings: Pricing period beginning Pricing period end Bushels Floor and Pivot Bu priced = (remaining bushels) X Throttle remaining days 49

50 Decision Contracts Accelerator Pricing Model December Corn Range (CZ) Min Max Throttle Pivot $2.60 $2.50 $2.40 $2.30 > $2.59 $2.49 $ Very Aggressive Aggressive Moderate Slow Throttle acts as a multiplier of daily bushels priced PF =10 Floor PF =6 PF = 4 PF = Daily bushels priced 50

= $2.")

51 Decision Contracts Accelerator Pricing Model December Corn 2003 Accelerator (red) = $2.41 Bu priced = % Floor price (purple) = $2.30 Daily bushels sold increase when futures prices move into upper ranges, and vice versa 51

52 Decision Contracts Topper Pricing Model Topper: Bushels will price on days when grain prices close up sharply from the previous day, during the pricing period. Producer Settings: Pricing period beginning Pricing period end Bushels Price Floor Trigger Throttle Number of trading days up/down Dec 01 to Nov DEC Corn CBOT ($0.20) ($0.15) ($0.10) ($0.09) ($0.08) ($0.07) ($0.06) ($0.05) ($0.04) ($0.03) ($0.02) ($0.01) $0.00 $0.01 $0.02 $0.03 $0.04 $0.05 $0.06 $0.07 $0.08 $0.09 $0.10 $0.15 $ Decision Commodities LLC

53 What are producers saying? I only sell one time per year, that way the check is bigger I only sell grain when prices are in the top third of the market 53

54 What are producers saying? forward contracts are always terrible ways to market 20% of the time I sold too soon, and 80% of the time I didn t market enough 54

55 What are producers saying? I hope I made the right hum Well I guess I should have bought more decision 55

56 Thank you. Decision Commodities, LLC 614 Billy Sunday Rd., Suite 600 Ames, Iowa

The Pricing Performance of Market Advisory Services in Corn and Soybeans Over : A Non-Technical Summary

The Pricing Performance of Market Advisory Services in Corn and Soybeans Over 1995-2001: A Non-Technical Summary by Scott H. Irwin, Joao Martines-Filho and Darrel L. Good The Pricing Performance of Market

The Pricing Performance of Market Advisory Services in Corn and Soybeans Over 1995-2001: A Non-Technical Summary by Scott H. Irwin, Joao Martines-Filho and Darrel L. Good The Pricing Performance of Market

ACE 427 Spring Lecture 6. by Professor Scott H. Irwin

ACE 427 Spring 2013 Lecture 6 Forecasting Crop Prices with Futures Prices by Professor Scott H. Irwin Required Reading: Schwager, J.D. Ch. 2: For Beginners Only. Schwager on Futures: Fundamental Analysis,

ACE 427 Spring 2013 Lecture 6 Forecasting Crop Prices with Futures Prices by Professor Scott H. Irwin Required Reading: Schwager, J.D. Ch. 2: For Beginners Only. Schwager on Futures: Fundamental Analysis,

UK Grain Marketing Series January 19, Todd D. Davis Assistant Extension Professor. Economics

Introduction to Basis, Cash Forward Contracts, HTA Contracts and Basis Contracts UK Grain Marketing Series January 19, 2016 Todd D. Davis Assistant Extension Professor Outline What is basis and how can

Introduction to Basis, Cash Forward Contracts, HTA Contracts and Basis Contracts UK Grain Marketing Series January 19, 2016 Todd D. Davis Assistant Extension Professor Outline What is basis and how can

Econ 338c. April 12, 2007

60 Econ 338c April 12, 2007 10 Traits of a Successful Grain Marketer Starts Early (before planting) Knows production, storage costs & risk bearing ability Understands basis & mkt. carry Follows several

60 Econ 338c April 12, 2007 10 Traits of a Successful Grain Marketer Starts Early (before planting) Knows production, storage costs & risk bearing ability Understands basis & mkt. carry Follows several

Basis: The price difference between the cash price at a specific location and the price of a specific futures contract.

Section I Chapter 8: Basis Learning objectives The relationship between cash and futures prices Basis patterns Basis in different regions Speculators trade price, hedgers trade basis Key terms Basis: The

Section I Chapter 8: Basis Learning objectives The relationship between cash and futures prices Basis patterns Basis in different regions Speculators trade price, hedgers trade basis Key terms Basis: The

Fall 2017 Crop Outlook Webinar

Fall 2017 Crop Outlook Webinar Chris Hurt, Professor & Extension Ag. Economist James Mintert, Professor & Director, Center for Commercial Agriculture Fall 2017 Crop Outlook Webinar October 13, 2017 50%

Fall 2017 Crop Outlook Webinar Chris Hurt, Professor & Extension Ag. Economist James Mintert, Professor & Director, Center for Commercial Agriculture Fall 2017 Crop Outlook Webinar October 13, 2017 50%

HEDGING WITH FUTURES AND BASIS

Futures & Options 1 Introduction The more producer know about the markets, the better equipped producer will be, based on current market conditions and your specific objectives, to decide whether to use

Futures & Options 1 Introduction The more producer know about the markets, the better equipped producer will be, based on current market conditions and your specific objectives, to decide whether to use

The Margin Protection Program for Dairy in the 2014 Farm Bill (AEC ) September 2014

September 2014") The Margin Protection Program for Dairy in the 2014 Farm Bill (AEC 2014-15) September 2014 Kenny Burdine 1 Introduction: The Margin Protection Program for Dairy (MPP-Dairy) was authorized in the Food,

The Margin Protection Program for Dairy in the 2014 Farm Bill (AEC 2014-15) September 2014 Kenny Burdine 1 Introduction: The Margin Protection Program for Dairy (MPP-Dairy) was authorized in the Food,

Crops Marketing and Management Update

Crops Marketing and Management Update Grains and Forage Center of Excellence Dr. Todd D. Davis Assistant Extension Professor Department of Agricultural Economics Vol. 2018 (3) March 11, 2018 Topics in

Crops Marketing and Management Update Grains and Forage Center of Excellence Dr. Todd D. Davis Assistant Extension Professor Department of Agricultural Economics Vol. 2018 (3) March 11, 2018 Topics in

Improving Your Crop Marketing Skills: Basis, Cost of Ownership, and Market Carry

Improving Your Crop Marketing Skills: Basis, Cost of Ownership, and Market Carry Nathan Thompson & James Mintert Purdue Center for Commercial Agriculture Many Different Ways to Price Grain Today 1) Spot

Improving Your Crop Marketing Skills: Basis, Cost of Ownership, and Market Carry Nathan Thompson & James Mintert Purdue Center for Commercial Agriculture Many Different Ways to Price Grain Today 1) Spot

Soybeans face make or break moment Futures need a two-fer to avoid losses By Bryce Knorr, senior grain market analyst

Soybeans face make or break moment Futures need a two-fer to avoid losses By Bryce Knorr, senior grain market analyst A year ago USDA shocked the market by cutting its forecast of soybean production, helping

Soybeans face make or break moment Futures need a two-fer to avoid losses By Bryce Knorr, senior grain market analyst A year ago USDA shocked the market by cutting its forecast of soybean production, helping

Hedging Potential for MGEX Soft Red Winter Wheat Index (SRWI) Futures

Futures") Hedging Potential for MGEX Soft Red Winter Wheat Index (SRWI) Futures Introduction In December 2003, MGEX launched futures and options that will settle financially to the Soft Red Winter Wheat Index (SRWI),

Hedging Potential for MGEX Soft Red Winter Wheat Index (SRWI) Futures Introduction In December 2003, MGEX launched futures and options that will settle financially to the Soft Red Winter Wheat Index (SRWI),

Crops Marketing and Management Update

Crops Marketing and Management Update Grains and Forage Center of Excellence Dr. Todd D. Davis Assistant Extension Professor Department of Agricultural Economics Vol. 2018 (2) February 14, 2018 Topics

Crops Marketing and Management Update Grains and Forage Center of Excellence Dr. Todd D. Davis Assistant Extension Professor Department of Agricultural Economics Vol. 2018 (2) February 14, 2018 Topics

Futures markets allow the possibility of forward pricing. Forward pricing or hedging allows decision makers pricing flexibility.

II) Forward Pricing and Risk Transfer Cash market participants are price takers. Futures markets allow the possibility of forward pricing. Forward pricing or hedging allows decision makers pricing flexibility.

II) Forward Pricing and Risk Transfer Cash market participants are price takers. Futures markets allow the possibility of forward pricing. Forward pricing or hedging allows decision makers pricing flexibility.

Crops Marketing and Management Update

Crops Marketing and Management Update Grains and Forage Center of Excellence Dr. Todd D. Davis Assistant Extension Professor Department of Agricultural Economics Vol. 2017 (2) February 16, 2017 Topics

Crops Marketing and Management Update Grains and Forage Center of Excellence Dr. Todd D. Davis Assistant Extension Professor Department of Agricultural Economics Vol. 2017 (2) February 16, 2017 Topics

HEDGING WITH FUTURES. Understanding Price Risk

HEDGING WITH FUTURES Think about a sport you enjoy playing. In many sports, such as football, volleyball, or basketball, there are two general components to the game: offense and defense. What would happen

HEDGING WITH FUTURES Think about a sport you enjoy playing. In many sports, such as football, volleyball, or basketball, there are two general components to the game: offense and defense. What would happen

Managing Hog Price Risk: Futures, Options, and Packer Contracts

Managing Hog Price Risk: Futures, Options, and Packer Contracts John D. Lawrence, Extension Livestock Economist and Director, Iowa Beef Center, and Alan Vontalge, Extension Economist, Iowa State University

Managing Hog Price Risk: Futures, Options, and Packer Contracts John D. Lawrence, Extension Livestock Economist and Director, Iowa Beef Center, and Alan Vontalge, Extension Economist, Iowa State University

New Generation Grain Contracts

New Generation Grain Contracts Econ 338c April 19, 2007 Steven D. Johnson Farm Management Field Specialist Presentation Objectives Highlight 7 Megatrends in the Grain Industry Identify Producer Challenges

New Generation Grain Contracts Econ 338c April 19, 2007 Steven D. Johnson Farm Management Field Specialist Presentation Objectives Highlight 7 Megatrends in the Grain Industry Identify Producer Challenges

Informed Storage: Understanding the Risks and Opportunities

Art Informed Storage: Understanding the Risks and Opportunities Randy Fortenbery School of Economic Sciences College of Agricultural, Human, and Natural Resource Sciences Washington State University The

Art Informed Storage: Understanding the Risks and Opportunities Randy Fortenbery School of Economic Sciences College of Agricultural, Human, and Natural Resource Sciences Washington State University The

Commodity Risk Through the Eyes of an Ag Lender

Commodity Risk Through the Eyes of an Ag Lender Wisconsin Banker s Association April 5 th, 2017 Michael Irgang, Executive Vice President 1 Michael Irgang: Bio Michael Irgang is currently Executive Vice

Commodity Risk Through the Eyes of an Ag Lender Wisconsin Banker s Association April 5 th, 2017 Michael Irgang, Executive Vice President 1 Michael Irgang: Bio Michael Irgang is currently Executive Vice

DEVELOP THE RIGHT PLAN FOR YOU.

DEVELOP THE RIGHT PLAN FOR YOU. The Agricultural Risk Consulting Group LLC Developing and Implementing Sound Risk Management Solutions (866) 574-2724 agriskconsulting.net What should you look for in a

DEVELOP THE RIGHT PLAN FOR YOU. The Agricultural Risk Consulting Group LLC Developing and Implementing Sound Risk Management Solutions (866) 574-2724 agriskconsulting.net What should you look for in a

A BULLISH CASE FOR CORN AND SOYBEANS IN 2016

A BULLISH CASE FOR CORN AND SOYBEANS IN 2016 Probabilities for higher prices, and the factors that could spur price rallies. Commodity markets tend to move on three variables: perception, momentum and

A BULLISH CASE FOR CORN AND SOYBEANS IN 2016 Probabilities for higher prices, and the factors that could spur price rallies. Commodity markets tend to move on three variables: perception, momentum and

Dairy Programs in the 2012 Farm Bill. Who should sign up for subsidized margin insurance with supply management?

Dairy Programs in the 2012 Farm Bill Who should sign up for subsidized margin insurance with supply management? Dr. Marin Bozic University of Minnesota Introduction Substantial increases in milk production

Dairy Programs in the 2012 Farm Bill Who should sign up for subsidized margin insurance with supply management? Dr. Marin Bozic University of Minnesota Introduction Substantial increases in milk production

Managing Class IV Opportunities

Managing Class IV Opportunities Dairy producers focus most of their hedging efforts on mitigating collapses in milk prices or collapses in margins. At more fortunate times they can turn their attention

Managing Class IV Opportunities Dairy producers focus most of their hedging efforts on mitigating collapses in milk prices or collapses in margins. At more fortunate times they can turn their attention

GRAIN HEDGE POSITION REPORT

GRAIN HEDGE POSITION REPORT CROP: Corn DATE: April 16, 2006 LONG POSITION SHORT POSITION Total Grain on Hand 753896 Grain in Transit Total Offsite Grain Total Stocks 753896 Unpriced Grain Storage 106375

GRAIN HEDGE POSITION REPORT CROP: Corn DATE: April 16, 2006 LONG POSITION SHORT POSITION Total Grain on Hand 753896 Grain in Transit Total Offsite Grain Total Stocks 753896 Unpriced Grain Storage 106375

Marketing Plans Development & Maintenance

Marketing Plans Development & Maintenance Kevin McNew MSU-Bozeman A Marketing Plan Should Remove emotion from the marketing decision and incorporate financial goals Be consistent with your approach to

Marketing Plans Development & Maintenance Kevin McNew MSU-Bozeman A Marketing Plan Should Remove emotion from the marketing decision and incorporate financial goals Be consistent with your approach to

2013 Risk and Profit Conference Breakout Session Presenters. 4. Basics of Futures and Options: Part 1

2013 Risk and Profit Conference Breakout Session Presenters Sean Fox 4. Basics of Futures and Options: Part 1 John A. (Sean) Fox is a native of Ireland and has been on the faculty

2013 Risk and Profit Conference Breakout Session Presenters Sean Fox 4. Basics of Futures and Options: Part 1 John A. (Sean) Fox is a native of Ireland and has been on the faculty

Grain Marketing. Innovative. Responsive. Trusted.

Grain Marketing Extension is a Division of the Institute of Agriculture and Natural Resources at the University of Nebraska Lincoln cooperating with the Counties and the United States Department of Agriculture.

Grain Marketing Extension is a Division of the Institute of Agriculture and Natural Resources at the University of Nebraska Lincoln cooperating with the Counties and the United States Department of Agriculture.

factors that affect marketing

Grain Marketing / no. 26 factors that affect marketing Crop Insurance Coverage Producers who buy at least 80 percent Revenue Protection for corn are more likely to indicate that crop insurance is an important

Grain Marketing / no. 26 factors that affect marketing Crop Insurance Coverage Producers who buy at least 80 percent Revenue Protection for corn are more likely to indicate that crop insurance is an important

MGEX CBOT Wheat Spread Options. Product Overview

MGEX CBOT Wheat Spread Options Product Overview May 7, 2012 MGEX-CBOT Wheat Spread Options Overview - MGEX: Hard Red Spring Wheat futures listed on the Minneapolis Grain Exchange, Inc. - CBOT: Soft Red

MGEX CBOT Wheat Spread Options Product Overview May 7, 2012 MGEX-CBOT Wheat Spread Options Overview - MGEX: Hard Red Spring Wheat futures listed on the Minneapolis Grain Exchange, Inc. - CBOT: Soft Red

Program on Dairy Markets and Policy Information Letter Series

Program on Dairy Markets and Policy Information Letter Series MILC Sign-up, LGM-Dairy, and Planning for the October 2011 to September 2012 Fiscal Year Information Letter Number 11-01 September 2011 Andrew

Program on Dairy Markets and Policy Information Letter Series MILC Sign-up, LGM-Dairy, and Planning for the October 2011 to September 2012 Fiscal Year Information Letter Number 11-01 September 2011 Andrew

December 6-7, Steven D. Johnson. Farm & Ag Business Management Specialist

December 6-7, 2018 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management 1 Learning Objectives Highlight Current Corn

December 6-7, 2018 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management 1 Learning Objectives Highlight Current Corn

New Generation Grain Marketing Contracts

New Generation Grain Marketing Contracts by Lewis A. Hagedorn, Scott H. Irwin, Darrel L. Good, Joao Martines-Filho, Bruce J. Sherrick, and Gary D. Schnitkey New Generation Grain Marketing Contracts by

New Generation Grain Marketing Contracts by Lewis A. Hagedorn, Scott H. Irwin, Darrel L. Good, Joao Martines-Filho, Bruce J. Sherrick, and Gary D. Schnitkey New Generation Grain Marketing Contracts by

Post Harvest Marketing Tips

Post Harvest Marketing Tips (from my best friends) Edward Usset Grain Marketing Economist, University of Minnesota usset001@umn.edu Corn & Soybean Digest columnist Center for Farm Financial Management

Post Harvest Marketing Tips (from my best friends) Edward Usset Grain Marketing Economist, University of Minnesota usset001@umn.edu Corn & Soybean Digest columnist Center for Farm Financial Management

Development of a Market Benchmark Price for AgMAS Performance Evaluations. Darrel L. Good, Scott H. Irwin, and Thomas E. Jackson

Development of a Market Benchmark Price for AgMAS Performance Evaluations by Darrel L. Good, Scott H. Irwin, and Thomas E. Jackson Development of a Market Benchmark Price for AgMAS Performance Evaluations

Development of a Market Benchmark Price for AgMAS Performance Evaluations by Darrel L. Good, Scott H. Irwin, and Thomas E. Jackson Development of a Market Benchmark Price for AgMAS Performance Evaluations

Hedging in 2014 "" Wisconsin Crop Management Conference & Agri-Industry Showcase 01/16/2014" Fred Seamon Senior Director CME Group"

Hedging in 2014 Wisconsin Crop Management Conference & Agri-Industry Showcase 01/16/2014 Fred Seamon Senior Director CME Group Disclaimer Futures trading is not suitable for all investors, and involves

Hedging in 2014 Wisconsin Crop Management Conference & Agri-Industry Showcase 01/16/2014 Fred Seamon Senior Director CME Group Disclaimer Futures trading is not suitable for all investors, and involves

Soybeans face long road End to tariffs wouldn t help 2018 exports much By Bryce Knorr, senior grain market analyst

Soybeans face long road End to tariffs wouldn t help 2018 exports much By Bryce Knorr, senior grain market analyst Forecasting grain prices is relatively easy in normal times. Most models assume the future

Soybeans face long road End to tariffs wouldn t help 2018 exports much By Bryce Knorr, senior grain market analyst Forecasting grain prices is relatively easy in normal times. Most models assume the future

HEDGING. dairy. There Are Many Options. Dairy Economist and Policy Analysts Workshop May 2017

HEDGING dairy Dairy Economist and Policy Analysts Workshop May 2017 5201 East Terrace Drive, Suite 280 l Madison, WI 53718 l800-726-9928 l info@blimling.com 2017 Blimling and Associates, Inc. This report

HEDGING dairy Dairy Economist and Policy Analysts Workshop May 2017 5201 East Terrace Drive, Suite 280 l Madison, WI 53718 l800-726-9928 l info@blimling.com 2017 Blimling and Associates, Inc. This report

Schindler Capital Management, LLC / Dairy Advantage Program. Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Schindler Capital Management, LLC / Dairy Advantage Program Fundamental / Ag & Livestock Performance Since August 2005 Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2005-11.20% 3.20% -6.67% -13.73%

Schindler Capital Management, LLC / Dairy Advantage Program Fundamental / Ag & Livestock Performance Since August 2005 Year Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 2005-11.20% 3.20% -6.67% -13.73%

AGRICULTURAL PRODUCTS. Soybean Crush Reference Guide

AGRICULTURAL PRODUCTS Soybean Crush Reference Guide As the world s largest and most diverse derivatives marketplace, CME Group (cmegroup.com) is where the world comes to manage risk. CME Group exchanges

AGRICULTURAL PRODUCTS Soybean Crush Reference Guide As the world s largest and most diverse derivatives marketplace, CME Group (cmegroup.com) is where the world comes to manage risk. CME Group exchanges

Recent Convergence Performance of CBOT Corn, Soybean, and Wheat Futures Contracts

The magazine of food, farm, and resource issues A publication of the American Agricultural Economics Association Recent Convergence Performance of CBOT Corn, Soybean, and Wheat Futures Contracts Scott

The magazine of food, farm, and resource issues A publication of the American Agricultural Economics Association Recent Convergence Performance of CBOT Corn, Soybean, and Wheat Futures Contracts Scott

Commodity products. Grain and Oilseed Hedger's Guide

Commodity products Grain and Oilseed Hedger's Guide In a world of increasing volatility, customers around the globe rely on CME Group as their premier source for price discovery and managing risk. Formed

Commodity products Grain and Oilseed Hedger's Guide In a world of increasing volatility, customers around the globe rely on CME Group as their premier source for price discovery and managing risk. Formed

1997 Pricing Performance of Market Advisory Services for Corn and Soybeans. Thomas E. Jackson, Scott H. Irwin, and Darrel L. Good

1997 Pricing Performance of Market Advisory Services for Corn and Soybeans by Thomas E. Jackson, Scott H. Irwin, and Darrel L. Good 1997 Pricing Performance of Market Advisory Services for Corn and Soybeans

1997 Pricing Performance of Market Advisory Services for Corn and Soybeans by Thomas E. Jackson, Scott H. Irwin, and Darrel L. Good 1997 Pricing Performance of Market Advisory Services for Corn and Soybeans

Advisory Service Marketing Profiles for Corn Over

Advisory Service Marketing Profiles for Corn Over 1995-2 by Joao Martines-Filho, Scott H. Irwin, Darrel L. Good, Silvina M. Cabrini, Brain G. Stark, Wei Shi, Ricky L. Webber, Lewis A. Hagedorn, and Steven

Advisory Service Marketing Profiles for Corn Over 1995-2 by Joao Martines-Filho, Scott H. Irwin, Darrel L. Good, Silvina M. Cabrini, Brain G. Stark, Wei Shi, Ricky L. Webber, Lewis A. Hagedorn, and Steven

Turner s Take WASDE Expectations vs. Sept WASDE report:

Published by: Craig Turner 11/4/2013 4:02:09 PM In this issue 1) CORN: USDA Friday exected to be bearish. Looking to short Corn ahead of WASDE 2) SOYBEANS: Short Bean Ideas with Long Call Protection 3)

Published by: Craig Turner 11/4/2013 4:02:09 PM In this issue 1) CORN: USDA Friday exected to be bearish. Looking to short Corn ahead of WASDE 2) SOYBEANS: Short Bean Ideas with Long Call Protection 3)

How to Write a Pre-Harvest Marketing Plan

How to Write a Pre-Harvest Marketing Plan Edward Usset, Grain Marketing Economist University of Minnesota Columnist, Corn & Soybean Digest usset001@umn.edu www.cffm.umn.edu Three slides that explain the

How to Write a Pre-Harvest Marketing Plan Edward Usset, Grain Marketing Economist University of Minnesota Columnist, Corn & Soybean Digest usset001@umn.edu www.cffm.umn.edu Three slides that explain the

Performance of market advisory firms

Price risk management: What to expect? #3 out of 5 articles Performance of market advisory firms Kim B. Anderson & B. Wade Brorsen This is the third of a five part series on managing price (marketing)

Price risk management: What to expect? #3 out of 5 articles Performance of market advisory firms Kim B. Anderson & B. Wade Brorsen This is the third of a five part series on managing price (marketing)

Crop Risk Management

Crop Risk Management January 28 th, 2010 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957 5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farmmanagement.htm Source: Johnson,

Crop Risk Management January 28 th, 2010 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957 5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farmmanagement.htm Source: Johnson,

Storing Unpriced Grain: Strategies & Tools

Storing Unpriced Grain: Strategies & Tools December 2013 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management Crop

Storing Unpriced Grain: Strategies & Tools December 2013 Steven D. Johnson Farm & Ag Business Management Specialist (515) 957-5790 sdjohns@iastate.edu www.extension.iastate.edu/polk/farm-management Crop

New Paradigms in Marketing: Are Speculators or the Fundamentals Driving Prices? Scott H. Irwin

New Paradigms in Marketing: Are Speculators or the Fundamentals Driving Prices? Scott H. Irwin Outline of Presentation Role of speculation in the recent commodity price boom Changing fundamentals Convergence

New Paradigms in Marketing: Are Speculators or the Fundamentals Driving Prices? Scott H. Irwin Outline of Presentation Role of speculation in the recent commodity price boom Changing fundamentals Convergence

Wheat market may take patience Exports, seasonal weakness weigh on prices for now. By Bryce Knorr, Senior Grain Market Analyst

Wheat market may take patience Exports, seasonal weakness weigh on prices for now By Bryce Knorr, Senior Grain Market Analyst The best days of the wheat rally may still be ahead. But first the market may

Wheat market may take patience Exports, seasonal weakness weigh on prices for now By Bryce Knorr, Senior Grain Market Analyst The best days of the wheat rally may still be ahead. But first the market may

AGRICULTURAL RISK MANAGEMENT. Global Grain Geneva November 12, 2013

AGRICULTURAL RISK MANAGEMENT Global Grain Geneva November 12, 2013 Managing Price Risk is Easier to Swallow Than THE ALTERNATIVE Is Your Business Protected Is Your Business Protected Is Your Business Protected

AGRICULTURAL RISK MANAGEMENT Global Grain Geneva November 12, 2013 Managing Price Risk is Easier to Swallow Than THE ALTERNATIVE Is Your Business Protected Is Your Business Protected Is Your Business Protected

Merricks Capital Wheat Basis and Carry Trade

Merricks Capital Wheat Basis and Carry Trade Executive Summary Regulatory changes post the Global Financial Crisis (GFC) has reduced the level of financing available to a wide range of markets. Merricks

Merricks Capital Wheat Basis and Carry Trade Executive Summary Regulatory changes post the Global Financial Crisis (GFC) has reduced the level of financing available to a wide range of markets. Merricks

Corn and Soybeans Basis Patterns for Selected Locations in South Dakota: 1999

South Dakota State University Open PRAIRIE: Open Public Research Access Institutional Repository and Information Exchange Department of Economics Research Reports Economics 5-15-2000 Corn and Soybeans

South Dakota State University Open PRAIRIE: Open Public Research Access Institutional Repository and Information Exchange Department of Economics Research Reports Economics 5-15-2000 Corn and Soybeans

Macroeconomic Outlook: Implications for Agriculture. It has been 26 years since we have experienced a significant recession

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

Macroeconomic Outlook: Implications for Agriculture John B. Penson, Jr. Regents Professor and Stiles Professor of Agriculture Texas A&M University Our Recession History September 1902 August1904 23 May

Third Quarter Earnings Call. November 8, 2016

Third Quarter Earnings Call November 8, 2016 Forward Looking Statements & Non-GAAP Measures Certain information discussed today constitutes forward-looking statements. Actual results could differ materially

Third Quarter Earnings Call November 8, 2016 Forward Looking Statements & Non-GAAP Measures Certain information discussed today constitutes forward-looking statements. Actual results could differ materially

Provide a brief review of futures. Carefully review alternative market

Provide a brief review of futures markets. Carefully review alternative market conditions i and which h marketing strategies work best under alternative conditions. Have an open and interactive discussion!!

Provide a brief review of futures markets. Carefully review alternative market conditions i and which h marketing strategies work best under alternative conditions. Have an open and interactive discussion!!

Considerations When Using Grain Contracts

Considerations When Using Grain Contracts Overview The grain industry has developed several new tools to help farmers manage increasing risks and price volatility. Elevators can use grain options markets

Considerations When Using Grain Contracts Overview The grain industry has developed several new tools to help farmers manage increasing risks and price volatility. Elevators can use grain options markets

Recent Delivery Performance of CBOT Corn, Soybean, and Wheat Futures Contracts

Recent Delivery Performance of CBOT Corn, Soybean, and Wheat Futures Contracts Statement to the CFTC Agricultural Forum, April 22, 28 Scott H. Irwin, Philip Garcia, Darrel L. Good, and Eugene L. Kunda

Recent Delivery Performance of CBOT Corn, Soybean, and Wheat Futures Contracts Statement to the CFTC Agricultural Forum, April 22, 28 Scott H. Irwin, Philip Garcia, Darrel L. Good, and Eugene L. Kunda

Econ 337 Spring 2015 Due 10am 100 points possible

Econ 337 Spring 2015 Final Due 5/4/2015 @ 10am 100 points possible Fill in the blanks (2 points each) 1. Basis = price price 2. A bear thinks prices will. 3. A bull thinks prices will. 4. are willing to

Econ 337 Spring 2015 Final Due 5/4/2015 @ 10am 100 points possible Fill in the blanks (2 points each) 1. Basis = price price 2. A bear thinks prices will. 3. A bull thinks prices will. 4. are willing to

Portfolios of Agricultural Market Advisory Services: How Much Diversification is Enough?

Portfolios of Agricultural Market Advisory Services: How Much Diversification is Enough? Silvina M. Cabrini, Brian G. Stark, Scott H. Irwin, Darrel L. Good and Joao Martines-Filho* Paper presented at the

Portfolios of Agricultural Market Advisory Services: How Much Diversification is Enough? Silvina M. Cabrini, Brian G. Stark, Scott H. Irwin, Darrel L. Good and Joao Martines-Filho* Paper presented at the

Knowing and Managing Grain Basis

Curriculum Guide I. Goals and Objectives A. To learn the definition of basis and gain an understanding of the factors that determine basis. B. To gain an understanding of the seasonal trends in basis.

Curriculum Guide I. Goals and Objectives A. To learn the definition of basis and gain an understanding of the factors that determine basis. B. To gain an understanding of the seasonal trends in basis.

Crops Marketing and Management Update

Crops Marketing and Management Update Department of Agricultural Economics Princeton REC Dr. Todd D. Davis Assistant Extension Professor -- Crop Economics Marketing & Management Vol. 2016 (2) February

Crops Marketing and Management Update Department of Agricultural Economics Princeton REC Dr. Todd D. Davis Assistant Extension Professor -- Crop Economics Marketing & Management Vol. 2016 (2) February

Price Risk. Management in December Corn Futures. Wayne D. Purcell Alumni Distinguished Professor Department of Agricultural and Applied Economics

Price Risk Management in December Corn Futures Wayne D. Purcell Alumni Distinguished Professor Department of Agricultural and Applied Economics Agricultural Competitiveness Virginia s Rural Economic Analysis

Price Risk Management in December Corn Futures Wayne D. Purcell Alumni Distinguished Professor Department of Agricultural and Applied Economics Agricultural Competitiveness Virginia s Rural Economic Analysis

Futures and Options Markets, Basis, and the Timing of Grain Sales in Montana

Futures and Options Markets, Basis, and the Timing of Grain Sales in Montana Mike Mastel and David Buschena Montana State University Bozeman Special Report No. 4 March S U M M A R Y Futures and Options

Futures and Options Markets, Basis, and the Timing of Grain Sales in Montana Mike Mastel and David Buschena Montana State University Bozeman Special Report No. 4 March S U M M A R Y Futures and Options

Dairy Outlook and Utilizing MPP- and LGM-Dairy: Kenny Burdine University of Kentucky Agricultural Economics

Dairy Outlook and Utilizing MPP- and LGM-Dairy: 2015 Kenny Burdine University of Kentucky Agricultural Economics Outline for Discussion Review of Current Market Conditions Cow numbers, production expectations,

Dairy Outlook and Utilizing MPP- and LGM-Dairy: 2015 Kenny Burdine University of Kentucky Agricultural Economics Outline for Discussion Review of Current Market Conditions Cow numbers, production expectations,

Winter fertilizer bargains could be rare Global market shows signs of stability By Bryce Knorr, grain market analyst

Winter fertilizer bargains could be rare Global market shows signs of stability By Bryce Knorr, grain market analyst While fertilizer costs continued to edge mostly higher this week, the strong summer

Winter fertilizer bargains could be rare Global market shows signs of stability By Bryce Knorr, grain market analyst While fertilizer costs continued to edge mostly higher this week, the strong summer

ARE DAIRY FUTURES IN YOUR FUTURE? GEOFF BENSON

ARE DAIRY FUTURES IN YOUR FUTURE? GEOFF BENSON Ag. & Resource Economics North Carolina State University US All Milk Price and Trend, 1989-2003 19.00 18.00 17.00 US All Milk Price Linear Trend $/100 lb

ARE DAIRY FUTURES IN YOUR FUTURE? GEOFF BENSON Ag. & Resource Economics North Carolina State University US All Milk Price and Trend, 1989-2003 19.00 18.00 17.00 US All Milk Price Linear Trend $/100 lb

Introduction to Futures & Options Markets

Introduction to Futures & Options Markets Kevin McNew Montana State University Marketing Your Crop Marketing: knowing when and how to price your crop. When Planting Pre-Harvest Harvest Post-Harvest How

Introduction to Futures & Options Markets Kevin McNew Montana State University Marketing Your Crop Marketing: knowing when and how to price your crop. When Planting Pre-Harvest Harvest Post-Harvest How

Optimal Grain Marketing: Balancing Risks and Revenue -- Producer s Booklet

National Grain and Feed Foundation 1201 New York Ave., N.W., Suite 830, Washington, D.C., 20005-3917 Copyright 1999. National Grain and Feed Foundation. All Rights Reserved. Please contact the National

National Grain and Feed Foundation 1201 New York Ave., N.W., Suite 830, Washington, D.C., 20005-3917 Copyright 1999. National Grain and Feed Foundation. All Rights Reserved. Please contact the National

MARGIN M ANAGER The Leading Resource for Margin Management Education

Margin Management Since 1999 MARGIN M ANAGER The Leading Resource for Margin Management Education Learn more at MarginManager.Com March INSIDE THIS ISSUE Dear Ag Industry Associate, The USDA released several

Margin Management Since 1999 MARGIN M ANAGER The Leading Resource for Margin Management Education Learn more at MarginManager.Com March INSIDE THIS ISSUE Dear Ag Industry Associate, The USDA released several

2/20/2012. Goal: Use price management tools to secure a profit for the farm.

Katie Behnke Agriculture Agent Shawano County Futures, options, contracts, and the cash market are all tools we can use to manage our business. Important to remember - we are not speculators Goal: Use

Katie Behnke Agriculture Agent Shawano County Futures, options, contracts, and the cash market are all tools we can use to manage our business. Important to remember - we are not speculators Goal: Use

Pulling the Marketing Trigger

Pulling the Marketing Trigger Robert Wisner Iowa State University Why Marketing is Critical Typical Corn Net Profit Margin, Past Years: $.30/ bu. $.10 increase in Price = 33% increase in Net Returns Also

Pulling the Marketing Trigger Robert Wisner Iowa State University Why Marketing is Critical Typical Corn Net Profit Margin, Past Years: $.30/ bu. $.10 increase in Price = 33% increase in Net Returns Also

Weather targets fertilizer market too Heavy rains stall shipments, delay fall applications By Bryce Knorr, grain market analyst

Weather targets fertilizer market too Heavy rains stall shipments, delay fall applications By Bryce Knorr, grain market analyst The Midwest is finally starting to dry out from heavy rains in the first

Weather targets fertilizer market too Heavy rains stall shipments, delay fall applications By Bryce Knorr, grain market analyst The Midwest is finally starting to dry out from heavy rains in the first

Price Trend Effects On Cash Sales & Forward Contracts. Grain Marketing Principles & Tools Cash Grain Basis, Forward Contracts, Futures & Options

Grain Marketing Principles & Tools Cash Grain Basis, Forward Contracts, Futures & Options Dr. Daniel M. O Brien Extension Agricultural Economist K-State Research and Extension Price Trend Effects On Cash

Grain Marketing Principles & Tools Cash Grain Basis, Forward Contracts, Futures & Options Dr. Daniel M. O Brien Extension Agricultural Economist K-State Research and Extension Price Trend Effects On Cash

Understanding Markets and Marketing

Art Understanding Markets and Marketing Randy Fortenbery School of Economic Sciences College of Agricultural, Human, and Natural Resource Sciences Washington State University The objective of marketing

Art Understanding Markets and Marketing Randy Fortenbery School of Economic Sciences College of Agricultural, Human, and Natural Resource Sciences Washington State University The objective of marketing

DIGGING DEEPER INTO THE VOLATILITY ASPECTS OF AGRICULTURAL OPTIONS

R.J. O'BRIEN ESTABLISHED IN 1914 DIGGING DEEPER INTO THE VOLATILITY ASPECTS OF AGRICULTURAL OPTIONS This article is a part of a series published by R.J. O Brien & Associates Inc. on risk management topics

R.J. O'BRIEN ESTABLISHED IN 1914 DIGGING DEEPER INTO THE VOLATILITY ASPECTS OF AGRICULTURAL OPTIONS This article is a part of a series published by R.J. O Brien & Associates Inc. on risk management topics

Montana MarketManager A PRIMER ON UNDERSTANDING FUTURES AND OPTIONS MARKETS. Workshop 5 - Part 1 Winter 2000 Marketing Workshops January 6 & 7, 2000

Montana MarketManager A PRIMER ON UNDERSTANDING FUTURES AND OPTIONS MARKETS Workshop 5 - Part 1 Winter 2000 Marketing Workshops January 6 & 7, 2000 Larry D. Makus College of Agriculture University of Idaho

Montana MarketManager A PRIMER ON UNDERSTANDING FUTURES AND OPTIONS MARKETS Workshop 5 - Part 1 Winter 2000 Marketing Workshops January 6 & 7, 2000 Larry D. Makus College of Agriculture University of Idaho

MARGIN M ANAGER The Leading Resource for Margin Management Education

Margin Management Since 1999 MARGIN M ANAGER The Leading Resource for Margin Management Education March 2015 Learn more at MarginManager.Com INSIDE THIS ISSUE Dear Ag Industry Associate, Margin Watch Reports

Margin Management Since 1999 MARGIN M ANAGER The Leading Resource for Margin Management Education March 2015 Learn more at MarginManager.Com INSIDE THIS ISSUE Dear Ag Industry Associate, Margin Watch Reports

VOLATILITY TRADING IN AGRICULTURAL OPTIONS

R.J. O'BRIEN ESTABLISHED IN 1914 VOLATILITY TRADING IN AGRICULTURAL OPTIONS This article is a part of a series published by R.J. O Brien on risk management topics for commercial agri-business clients.

R.J. O'BRIEN ESTABLISHED IN 1914 VOLATILITY TRADING IN AGRICULTURAL OPTIONS This article is a part of a series published by R.J. O Brien on risk management topics for commercial agri-business clients.

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives Dillon M. Feuz Department of Applied Economics Utah State University 3530 Old Main Hill Logan, UT 84322-3530 435-797-2296 dillon.feuz@usu.edu

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives Dillon M. Feuz Department of Applied Economics Utah State University 3530 Old Main Hill Logan, UT 84322-3530 435-797-2296 dillon.feuz@usu.edu

Advisory Service Marketing Profiles for Corn over

Advisory Service Marketing Profiles for Corn over 22-24 by Evelyn V. Colino, Silvina M. Cabrini, Nicole M. Aulerich, Tracy L. Brandenberger, Robert P. Merrin, Wei Shi, Scott H. Irwin, Darrel L. Good, and

Advisory Service Marketing Profiles for Corn over 22-24 by Evelyn V. Colino, Silvina M. Cabrini, Nicole M. Aulerich, Tracy L. Brandenberger, Robert P. Merrin, Wei Shi, Scott H. Irwin, Darrel L. Good, and

Fourth Quarter 2014 Earnings Conference Call. 26 November 2014

Fourth Quarter 2014 Earnings Conference Call 26 November 2014 Safe Harbor Statement & Disclosures The earnings call and accompanying material include forward-looking comments and information concerning

Fourth Quarter 2014 Earnings Conference Call 26 November 2014 Safe Harbor Statement & Disclosures The earnings call and accompanying material include forward-looking comments and information concerning

MONTHLY MILK & FEED MARKET UPDATE

MONTHLY MILK & FEED MARKET UPDATE Provided By: Curtis Bosma - (312) 870-1185 - curtisb@highgroundtrading.com December 2014 A Sinking Ship? As the leaves began to fall, so did milk futures. Cheese sellers

MONTHLY MILK & FEED MARKET UPDATE Provided By: Curtis Bosma - (312) 870-1185 - curtisb@highgroundtrading.com December 2014 A Sinking Ship? As the leaves began to fall, so did milk futures. Cheese sellers

Section III Advanced Pricing Tools. Chapter 17: Selling grain and buying call options to establish a minimum price

Section III Chapter 17: Selling grain and buying call options to establish a minimum price Learning objectives Selling grain and buying call options to establish a minimum price Key terms Paper farming:

Section III Chapter 17: Selling grain and buying call options to establish a minimum price Learning objectives Selling grain and buying call options to establish a minimum price Key terms Paper farming:

UK Grain Marketing Series November 5, Todd D. Davis Assistant Extension Professor. Economics

Grain Marketing & Risk Management Overview UK Grain Marketing Series November 5, 2015 Todd D. Davis Assistant Extension Professor Risk vs. Uncertainty Most use these words interchangeably in conversation

Grain Marketing & Risk Management Overview UK Grain Marketing Series November 5, 2015 Todd D. Davis Assistant Extension Professor Risk vs. Uncertainty Most use these words interchangeably in conversation

TITLE: EVALUATION OF OPTIMUM REGRET DECISIONS IN CROP SELLING 1

TITLE: EVALUATION OF OPTIMUM REGRET DECISIONS IN CROP SELLING 1 AUTHORS: Lynn Lutgen 2, Univ. of Nebraska, 217 Filley Hall, Lincoln, NE 68583-0922 Glenn A. Helmers 2, Univ. of Nebraska, 205B Filley Hall,

TITLE: EVALUATION OF OPTIMUM REGRET DECISIONS IN CROP SELLING 1 AUTHORS: Lynn Lutgen 2, Univ. of Nebraska, 217 Filley Hall, Lincoln, NE 68583-0922 Glenn A. Helmers 2, Univ. of Nebraska, 205B Filley Hall,

Non-Convergence of CME Hard Red Winter Wheat Futures and the Impact of Excessive Grain Inventories in Kansas

Non-Convergence of CME Hard Red Winter Wheat Futures and the Impact of Excessive Grain Inventories in Kansas Daniel O Brien, Extension Agricultural Economist Kansas State University August 10, 2016 Summary

Non-Convergence of CME Hard Red Winter Wheat Futures and the Impact of Excessive Grain Inventories in Kansas Daniel O Brien, Extension Agricultural Economist Kansas State University August 10, 2016 Summary

Creating Your Marketing Plan

Creating Your Marketing Plan Jeff Peterson Heartland Farm Partners 402 366 4694 jeffpeterson@heartlandfarmpartners.com www.heartlandfarmpartners.com Topics Developing a marketing plan Answering the essential

Creating Your Marketing Plan Jeff Peterson Heartland Farm Partners 402 366 4694 jeffpeterson@heartlandfarmpartners.com www.heartlandfarmpartners.com Topics Developing a marketing plan Answering the essential

Cary L. Sandell. Wells Fargo Food and Agribusiness Group

Degree of Belief Cary L. Sandell Wells Fargo Food and Agribusiness Group November 2009 Everything is connected. We just can t see it. Every new economic action comes from some other economic action s end

Degree of Belief Cary L. Sandell Wells Fargo Food and Agribusiness Group November 2009 Everything is connected. We just can t see it. Every new economic action comes from some other economic action s end

Managed Futures: A Real Alternative

Managed Futures: A Real Alternative By Gildo Lungarella Harcourt AG Managed Futures investments performed well during the global liquidity crisis of August 1998. In contrast to other alternative investment

Managed Futures: A Real Alternative By Gildo Lungarella Harcourt AG Managed Futures investments performed well during the global liquidity crisis of August 1998. In contrast to other alternative investment

Wade Johannes. Commodity Risk Manager ProEdge Marketing Central Valley Ag

Wade Johannes Commodity Risk Manager ProEdge Marketing Central Valley Ag Farm and cattle feedlot Columbus, NE Graduated from UNL May 1999 Johannes Farms, Inc 1999 to 2005 Cargill in Albion, NE 2005 to

Wade Johannes Commodity Risk Manager ProEdge Marketing Central Valley Ag Farm and cattle feedlot Columbus, NE Graduated from UNL May 1999 Johannes Farms, Inc 1999 to 2005 Cargill in Albion, NE 2005 to

Evaluating the Use of Futures Prices to Forecast the Farm Level U.S. Corn Price

Evaluating the Use of Futures Prices to Forecast the Farm Level U.S. Corn Price By Linwood Hoffman and Michael Beachler 1 U.S. Department of Agriculture Economic Research Service Market and Trade Economics

Evaluating the Use of Futures Prices to Forecast the Farm Level U.S. Corn Price By Linwood Hoffman and Michael Beachler 1 U.S. Department of Agriculture Economic Research Service Market and Trade Economics

Risk Management Tools You Can Use

Management Tools You Can Use Categories of Management Tools Financial Production Price Others Rodney Jones OSU NW Area Extension Economist Overall Financial 1) Know costs of production Your number one

Management Tools You Can Use Categories of Management Tools Financial Production Price Others Rodney Jones OSU NW Area Extension Economist Overall Financial 1) Know costs of production Your number one

4.25 ¾ 4.19 FG March 2018 Wheat ¾ Pivotal new Contract Low 4.02 ½ 5 day chart. Down from last week same day Daily chart... Down Weekly

s 9:50 pm Chicago time 12/11/17 December 12, 2017 March 2018 Corn 3.56 3.52 ¾ FG --------------3.48 ¼ Pivotal new Contract Low 3.43 ¾ 5 day chart. Down from last week same day Daily chart. Down Weekly

s 9:50 pm Chicago time 12/11/17 December 12, 2017 March 2018 Corn 3.56 3.52 ¾ FG --------------3.48 ¼ Pivotal new Contract Low 3.43 ¾ 5 day chart. Down from last week same day Daily chart. Down Weekly

Hedge Strategies Using Options Ahead of USDA June 30 th Reports

Hedge Strategies Using Options Ahead of USDA June 30 th Reports David Hightower June 23, 2014 2014 CME Group. All rights reserved. Options of Options A diverse set of tools to trade around short-term events

Hedge Strategies Using Options Ahead of USDA June 30 th Reports David Hightower June 23, 2014 2014 CME Group. All rights reserved. Options of Options A diverse set of tools to trade around short-term events

Commodity Futures and Options

Commodity Futures and Options ACE 428 Fall 2010 Dr. Mindy Mallory Mindy L. Mallory 2010 Rolling a hedge Definition To continue to hedge for additional months beyond the expiration of the original contract

Commodity Futures and Options ACE 428 Fall 2010 Dr. Mindy Mallory Mindy L. Mallory 2010 Rolling a hedge Definition To continue to hedge for additional months beyond the expiration of the original contract

Saturday, January 5, Notes from Al

Get This Newsletter Every Saturday from Al Kluis Commodities..."Your Markets, Right Now"...AlKluis.com Saturday, January 5, 2013 Notes from Al Happy New Year and welcome to a volatile 2013. It has been

Get This Newsletter Every Saturday from Al Kluis Commodities..."Your Markets, Right Now"...AlKluis.com Saturday, January 5, 2013 Notes from Al Happy New Year and welcome to a volatile 2013. It has been

COMMODITY PRODUCTS Moore Research Report. Seasonals Charts Strategies GRAINS

COMMODITY PRODUCTS 28 Moore Research Report Seasonals Charts Strategies GRAINS Welcome to the 28 Moore Historical GRAINS Report This comprehensive report provides historical daily charts, cash and basis

COMMODITY PRODUCTS 28 Moore Research Report Seasonals Charts Strategies GRAINS Welcome to the 28 Moore Historical GRAINS Report This comprehensive report provides historical daily charts, cash and basis

Risk Management for Stocker Cattle. R. Curt Lacy, Ph.D. Extension Economist-Livestock University of Georgia

Risk Management for Stocker Cattle R. Curt Lacy, Ph.D. Extension Economist-Livestock University of Georgia Risk Management for Stocker Cattle It is NOT uncertainty! It is the negative outcome associated

Risk Management for Stocker Cattle R. Curt Lacy, Ph.D. Extension Economist-Livestock University of Georgia Risk Management for Stocker Cattle It is NOT uncertainty! It is the negative outcome associated