Anesu Daka CA(SA)- CAA

|

|

|

- Leon Richards

- 5 years ago

- Views:

Transcription

1

2 FAC August 2015

3 Tut 105/ IAS32/39/IFRS9&7-Financial instruments 2. IAS 33-Earnings per share 3. IAS 17- Leases

4 Forex Transactions: IAS 21

5 Effects in foreign exchange rates transactions IAS 21

6 KEY CONCEPTS The following key concepts are fundamental to this study unit: 1. The determination of the date of the foreign currency transaction and recording thereof at the spot exchange rate on that date. 2. Translating monetary items at reporting date and on settlement at the appropriate exchange rate. 3. The recognition of exchange differences in profit or loss for the period, other comprehensive income or the carrying amount of an asset or liability. 4. The presentation and disclosure of the effects of changes in foreign exchange rates.

7 Schematic Picture of IAS 21 Foreign Exchange Activities Foreign currency transactions IAS Foreign Operations IAS Hedging foreign currency transactions IAS Hedge of a net investment in a foreign operation IAS

8 Exchange rate the ratio at which the currencies of two countries are exchanged. Either: $1= R7 or R1=$ (watch-out for this) Naming rates:- selling/offer/ask rate is the rate at which the intermediary/bank is willing to sell foreign currency to the buyer (importer). - buying/bid rate is the rate at which the intermediary/bank is willing to buy forex from a seller (exporter). NB: the bid rate is always lower than the offer rate. Use IAS 39.AG 72- bid rate to value asset held or liability issued and ask rate for assets to be acquired and liability held

9 Types of Exchange rates Spot rate- is the exchange rate for immediate delivery of currencies to be exchanged at a particular time. Closing rate- is the spot rate at the reporting date. Forward rate- is the exchange rate for the exchange of two currencies at a future agreed date.

10 Identification of transaction date In the context of the movement of assets between countries, certain generally accepted shipping and trade terms are used. f.o.b ( free on board *named port of shipping+ ) (most used) the seller accepts responsibility only for getting the asset safely on board the ship which will deliver the asset from the source country to the destination country. The buyer is responsible for the goods from the moment that the asset passes over the ship s rail, and in addition bears all further costs of delivery. Therefore, the risks and rewards of ownership are transferred from the seller to the buyer at that point. Transaction date is therefore shipping date. c.i.f ( cost,insurance and freight *named port of destination+ ) the seller is responsible for paying the costs of delivering the asset to the named port of destination. These costs include the costs of insuring the asset while it is in transit. Transaction date for c.i.f. sales is therefore also delivery date. NB: if question says CIF without any further information use delivery date However, it is internationally accepted practice that the risks and rewards of ownership are, as is the case with f.o.b. contracts, still transferred from the seller to the buyer at the moment that the asset passes over the ship s rail. Transaction date for c.i.f. sales is therefore also shipping date, in this case.

11

12 Initial Recognition Recognise (record an asset or liability) when the risk and reward of ownership has passed. Risk and rewards of ownership passes on TRANSACTION DATE date of shipment of F.O.B (free on board) Dr Inventory/PPE, Bank e.t.c Cr Foreign payable/loan, e.t.c

13 Monetary VS Non-Monetary Monetary items Money held and assets and liabilities to be received of paid in fixed or determinable amounts of money, e.g.: all current assets except inventory, current liabilities (e.g. payables), long-term loans, debentures, deferred tax, dividends payable, convertible debentures into redeemable preference shares or convertible preference share into debenture Non-monetary items Assets and liabilities to be received of paid NOT in fixed or determinable amounts of money, e.g: Inventories, PPE, Investment in ordinary shares, ordinary share capital, payments in advance, goodwill, intangible assets, reserves, Convertible preference share or debentures into ordinary or nonredeemable preference shares.

14 Measurement Initial Measurement A foreign currency transaction should be recorded initially at the rate of exchange at the date of the transaction (use of averages is permitted if they are a reasonable approximation of actual). [IAS ] Subsequent Measurement: [IAS 21.23] foreign currency monetary amounts (foreign payables, debtors, e.g.) should be reported using the closing rate non-monetary items (inventory, PPE, e.g.) carried at historical cost should be reported using the exchange rate at the date of the transaction non-monetary items carried at fair value should be reported at the rate that existed when the fair values were determined (closing rate) e.g. use closing rate to determine NRV, Recoverable amount, FV, e.t.c

15 Item Description Recognition of exchange Recognition of Exchange differences Monetary IAS Foreign payable, foreign loan, foreign debtor, e.t.c Separate and recognise in P/L Monetary item in a foreign operation IAS and 48 and 48C Line items in SofP of a foreign operation- payables e.t.c Translate the total Net Asset Value and recognise FCTR in OCI -Reclassify to P/L trhough OCI on disposal with loss of control of the foreign op. -Reattribute to NCI directly in SOCIE if control is not lost (partial disposal) Non-monetary item: PPE, inventory, investment in shares, investment property, e.t.c Do not recognise the exchange different separately. Recognise in P/L or OCI wherever appropriate for the item Other Gains & losses Revaluation surplus Measure at spot rate at revaluation date & recognise in OCI

16

17

18 Calculation of Exchange Gains and Losses on Debt Instruments US$ Rate ZAR Principal-Fair Value 1,000, ,000,000 Interest Expense 10% at avg rate 50, ,500 Pmt- coupon 10% at spot AmortisedCarrying Amt at 31 Dec ,050,000 8,402,500 Exchange loss (Balancing figure) 102,500 Carrying amount at 31 Dec ,050, ,505,000 Interest Expense 10% at avg rate 50, ,500 Pmt- coupon 10% at spot (100,000) 8.15 (815,000) AmortisedCarrying Amt at 31 Dec ,000,000 8,095,500 Exchange loss (Balancing figure) 54,500 Carrying amount at 30 June ,000, ,150,000 Pmt- of Capital (1,000,000) 8.15 (8,150,000) Carrying amount at 31 Dec

19

20

21 Disclosure IAS An entity shall disclose: the amount of exchange differences recognised in profit or loss except for those arising on financial instruments measured at fair value through profit or loss in accordance with IFRS 9; and net exchange differences recognised in other comprehensive income and accumulated in a separate component of equity, and a reconciliation of the amount of such exchange differences at the beginning and end of the period. 53 When the presentation currency is different from the functional currency, that fact shall be stated, together with disclosure of the functional currency and the reason for using a different presentation currency. 54 When there is a change in the functional currency of either the reporting entity or a significant foreign operation, that fact and the reason for the change in functional currency shall be disclosed.

22 Apply IAS 21 Q21.1 and Q21.3

23

24 Financial Instruments IAS 32 - Presentation IFRS 9 - Recognition & Measurement IFRIC 19 Extinguishing Liabilities with Equity Instruments IFRS 7 - Financial Instruments: Disclosures

25

26 Past CTA/FQE Exams: Examinability - All most in all past exams (both FinAcc 1 and FinAcc 2 Questions)

27 Examinability 2015 Possible areas of focus: New areas: Classification- financial assets (amortised cost vs Fair Value (FVTPL vs FVOCI) Reclassifications Hedging Impairment Compound financial Instruments + deferred tax is always important

28 Financial Instrument Framework IAS 32 Presentation: Classification into: o Financial Instrument o Financial Asset o Financial liabilities o Equity Instruments o Fair value IFRS 13 Classification as equity or liability Compound financial instruments Treasury shares

29 Financial Instruments Introduction and Classification

30 Financial instrument A financial instrument is any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity. IAS 32, Para 11

31 Financial Instrument a contract Share Certificate 10 m shares Bond US$10 m that gives rise to a financial asset of one entity (Holder) and a financial liability or equity instrument of another entity (Issuer).

32 Financial Instrument Diagram Financial Asset (inv in shares or bonds) HOLDER Of Contract Contract- e.g. share certificate or Bond Financial Liability ISSUER of contract Equity

33 Financial asset A financial asset is any asset that is: Cash An Equity instrument of another entity A contractual right: To receive cash or another financial asset from another entity, or To exchange financial assets or financial liabilities with another entity under conditions that are potentially favourable to the entity; or A contract that will or may be settled in the entity s own equity instruments and is: A non-derivative for which the entity is or may be obliged to receive a variable number of the entity s own equity instruments; or A derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of the entity s own equity instruments IAS 32, Para 11

34 Financial liability A financial liability is any liability that is: A contractual obligation: To deliver cash or another financial asset to another entity, or To exchange financial assets or financial liabilities with another entity under conditions that are potentially unfavourable to the entity, or A contract that will or may be settled in the entity s own equity instruments and is: A non-derivative for which the entity is or may be obliged to deliver a variable number of the entity s own equity instruments, or A derivative that will or may be settled other than by the exchange of a fixed amount of cash or another financial asset for a fixed number of the entity s own equity instuments IAS 32, Para 11

35 Equity instrument An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities. IAS 32, Para 11

36 Types of Financial Instruments 1. Equity Instruments: shares 2. Debt Instruments Loan Receivable Payable Debentures Preference shares 3. Derivatives: forwards, futures, options, swaps

37

38

39

40

41 Financial Instrument Issuer Holder Liability Equity Financial Asset

42 Classification as Liability or Equity The FUNDAMENTAL PRINCIPLE of IAS 32 is that a financial instrument should be classified as either a financial liability or an equity instrument according to the : substance of the contract, not its legal form, and the definitions of financial liability or equity instrument. [IAS 32.15]

43 Classification as Liability or Equity A financial instrument is an equity instrument only if: (a) the instrument includes NO contractual obligation to deliver cash or another financial asset to another entity and (b) (b) if the instrument will or may be settled in the issuer's own equity instruments, it is either: a non-derivative that includes NO contractual obligation for the issuer to deliver a VARIABLE number of its own equity instruments (for fixed number of its own shares); or a derivative that will be settled only by the issuer exchanging a fixed amount of cash or another financial asset for a fixed number of its own equity instruments. [IAS 32.16]

44 Classification as Liability or Equity Illustration preference shares If an entity issues preference (preferred) shares that pay a fixed rate of dividend and that have a mandatory redemption feature at a future date, the substance is that they are a contractual obligation to deliver cash and, therefore, should be recognised as a liability. [IAS 32.18(a)] In contrast, preference shares that do not have a fixed maturity, and where the issuer does not have a contractual obligation to make any payment are equity. In this example even though both instruments are legally termed preference shares they have different contractual terms and one is a financial liability while the other is equity.

45 Classification of preference Share Capital Capital amount of preference shares Preference dividend payments Classification as liability or equity Non-redeemable Discretionary Equity instrument Non-redeemable Compulsory Compound instrument Compulsory redemption Discretionary Compound instrument Compulsory redemption Compulsory Financial Liability Redeemable at option of holder Redeemable at option of issuer Compulsory Discretionary Compulsory Discretionary Financial Liability Compound instrument Compound instrument Equity instrument

46 Classification as Liability or Equity Illustration issuance of fixed monetary amount of equity instruments A contractual right or obligation to receive or deliver a number of its own shares or other equity instruments that varies so that the fair value of the entity's own equity instruments to be received or delivered equals the fixed monetary amount of the contractual right or obligation is a financial liability. [IAS 32.20] Such instruments are financial liabilities. EG:A $1million convertible debenture, convertible into ordinary shares at the market price at date of conversion.

47 Classification as Liability or Equity Illustration issuance of fixed monetary amount of equity instruments If number shares are variable- financial liability If number shares are fixed Equity instrument

48 Classification as Liability or Equity Illustration - one party has a choice over how an instrument is settled (para 21-24) When a derivative financial instrument gives one party a choice over how it is settled (for instance, the issuer or the holder can choose settlement net in cash or by exchanging shares for cash), it is a financial asset or a financial liability unless all of the settlement alternatives would result in it being an equity instrument. [IAS 32.26]

49

50 Financial Liability vs Equity Instrument

51 Try the following Examples

52

53

54

55 Contingent Settlement Provisions- par 25 An entity may issue a financial instrument where the way it is settled depends on: The occurrence or non-occurrence of uncertain future events, or The outcome of uncertain circumstances, that are beyond the control of both the issuer and the holder of the instrument, such as a change in a stock market index, consumer price index, interest rate or taxation requirements, or the issuer s future revenues, net income or debtto-equity ratio.

56 Contingent Settlement Provisions. Conclusion The issuer of such an instrument does not have the unconditional right to avoid delivering cash or another financial asset (or otherwise to settle it in such a way that it would be a financial liability). Therefore, it is a financial liability of the issuer unless the possibility of settlement is remote.

57

58

59 Compound Financial Instruments Some financial instruments - sometimes called compound instruments - have both a liability and an equity component from the issuer's perspective. In that case, IAS 32 requires that the component parts be accounted for and presented separately according to their substance based on the definitions of liability and equity. The split is made at issuance and not revised for subsequent changes in market interest rates, share prices, or other event that changes the likelihood that the conversion option will be exercised. [IAS ]

60

61

62

63

64

65

66

67

68 Interest, Dividends, and losses Interest, dividends, gains, and losses relating to an instrument classified as a liability should be reported in profit or loss. This means that dividend payments on preferred shares classified as liabilities are treated as expenses (finance cost). On the other hand, distributions (such as dividends) to holders of a financial instrument classified as equity should be charged directly against equity (Retained Earnings), not against earnings. [IAS 32.35] Transaction costs of an equity transaction are deducted from equity. Transaction costs related to an issue of a compound financial instrument are allocated to the liability and equity components in proportion to the allocation of proceeds and deducted as such.

69 Cost of issuing or re-acquiring equity Costs of issuing or reacquiring equity instruments (other than in a business combination) are accounted for as a deduction from equity, net of any related income tax benefit. [IAS 32.35] Dr Equity Dr Financial liability (Amortised Cost) Cr Bank/payables NB: if it s a compound fin instrument the issue cost should be split in proportion to the components

70 Treasury Shares Identify: Treasury shares- arises when an entity reacquires (buy-back) its own equity instruments. Such buy-backs happen in two ways: 1) by the entity when it buys back its own shares from shareholders or 2) when other members of the consolidated group hold shares in other group companies, especially shares of the parent. Recognition: those instruments ( treasury shares ) shall be deducted from equity. Gains/Losses on buy back: No gain or loss shall be recognised in profit or loss on the purchase, sale, issue or cancellation of an entity s own equity instruments. Consideration paid or received shall be recognised directly in equity.

71 Example: Share buy-back A Ltd issued shares on 1Jan 2010 at $1.20. On 31 December shares were bought back at $1.30 per share, where after the shares were cancelled. The transaction cost associated with the share buy-back is $2000. What are the Jes necessary to account for the share-buy back?

72 Example: Share buy-back 31 December 2011 Dr Share Capital (25000*1.2) Dr Share Premium/capital/RE (25000*( ) 2500 Cr Bank (25000*1.30) Dr Share Premium/capital/RE 2000 Cr Bank 2000

73 Offsetting IAS 32 also prescribes rules for the offsetting of financial assets and financial liabilities. It specifies that a financial asset and a financial liability should be offset and the net amount reported when, and only when, an entity: [IAS 32.42] has a legally enforceable right to set off the amounts; and intends either to settle on a net basis, or to realise the asset and settle the liability simultaneously. [IAS 32.48]

74 Summary Financial instruments issued to raise capital must be classified as liabilities or equity by the issuer; Classification of a financial instrument as a liability or equity depends on the following: Substance of the contractual arrangement on initial recognition NOT the legal form Definition of financial liability and an equity instrument Critical feature of a financial liability: - is the obligation to deliver cash or another financial instrument. Compound financial instruments are split into equity and liability components and presented separately. Interest, dividends, losses and gains are treated according to whether they relate to equity or financial liability

75 IFRS9: Financial Instruments Recognition and Measurement

76

77 FINANCIAL ASSETS 1. Initial Recognition 2. Classification 3. Initial Measurement 4. Subsequent Measurement 5. Impairment of Amortised Cost Financial Asset 6. Derecognition 7. Hedging

78 Financial assets are classified in IFRS 9 as amortised cost or Fair value thru P&L or OCI Financial Asset (inv in shares or bonds) HOLDER Of Contract Classification Classification as financial liabiltiy or equity is done in IAS 32 Contract- e.g. share certificate or Bond Financial Liabilities are classified as Fv thru P&L or other under IFRS 9 Financial Liability ISSUER of contract Equity

79 Initial recognition An entity shall recognise a financial instrument in its statement of financial position when it becomes party to the contractual provisions of the instrument. IFRS 9, Para 3.1.1

80 Initial measurement At initial recognition, an entity shall measure a financial asset at its fair value, (with the exception of Trade Receivables in terms of IFRS 15, which are measured at their transaction price) plus, in the case of a financial asset not at fair value through P&L, transaction costs that are directly attributable to the acquisition or issue of the financial asset. IFRS 9, Para 5.1.1

81 Initial recognition Fair Value Price paid to acquire the asset Entry price Price received to assume the liability IFRS 13, Para 57

82 Initial recognition Fair Value Definition of fair value: Price that would be received to sell an asset Price that would be paid to transfer a liability In an orderly transaction Between market participants Exit price At the measurement date IFRS 13, Para 9

83 Initial recognition Fair Value Entry price Exit price The entry price will typically equal the exit price when the transaction to buy an asset takes place in the market in which the asset would be sold.

84 Initial recognition Fair Value Transaction price Fair Value The best evidence of the fair value of a financial instrument at initial recognition is normally the transaction price (ie the fair value of the consideration given or received, see also IFRS 13). IFRS 9, Para B5.1.2 A

85 Initial recognition Fair Value Transaction price Fair Value a) If that fair value is evidenced by a quoted price in an active market for an identical asset or liability (ie a Level 1 input) or based on a valuation technique that uses only data from observable markets. An entity shall recognise the difference between the fair value at initial recognition and the transaction price as a gain or loss. IFRS 9, Para B5.1.2 A (a)

86 Initial recognition Fair Value Transaction price Fair Value b) In all other cases, the difference between the fair value at initial recognition and the transaction price shall be deferred. IFRS 9, Para B5.1.2 A (a)

87 Classification of Financial Assets on initial recognition Amortised Cost Fair value Collect only principal and cash on specified dates All other financial assets IFRS 9, Para

88 Classification: Amortised Cost Financial assets may be measured at amortised cost: Business model is to hold assets in order to collect contractual cash flows; AND Cash flows arise on specified dates and are solely payments of principal and interest Interest should only be made up of time value of money, credit risk and other basic lending risks and costs Still, the entity may choose to irrevocably designate such a financial asset as measured at fair value (profit and loss) Eliminates or significantly reduces accounting mismatch IFRS 9, Para and Debt Instruments!

89 Classification: Fair value through OCI Financial assets may be measured at fair value through OCI: Business model whose objective is achieved by both collecting contractual cash flows and selling financial assets and; AND The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding Interest should only be made up of time value of money, credit risk and other basic lending risks and costs Still, the entity may choose to irrevocably designate such a financial asset as measured at fair value through profit and loss Eliminates or significantly reduces accounting mismatch Debt Instruments! IFRS 9, Para A and 4.1.3

90 Classification: Fair value through OCI continued An entity may make an irrevocable designation on initial recognition to classify a financial asset as subsequently measured at fair value through OCI of an investment in an equity instrument that is neither held for trading nor represents contingent consideration (in terms of IFRS 3) IFRS 9, Para and Equity Instruments!

91 IFRS 9 s debt instrument model Is the objective of the entity s business model to hold the financial asset to collect contractual cash flows? NO Is the financial asset held to achieve an objective by both collecting contractual cash flows and selling financial assets? NO YES YES Do contractual cash flows represent solely payments of principal and interest YES YES NO FVPL Does the company apply the fair value option to eliminate an accounting mismatch? YES NO NO Amortised Cost FVOCI

92 Classification: Fair value through P&L If these requirements are not met (i.e. the financial asset cannot be classified as either subsequently measured at amortised cost, or fair value through other comprehensive income), the financial asset is classified as subsequently measured at fair value IFRS 9, Para 4.1.4

93 Classification of financial assets on initial recognition Amortised Cost Fair value (OCI) Fair value (P+L) IFRS 9, para and IFRS 9, para 4.1.2A, and para IFRS 9, Para and para 4.1.5

94 Initial recognition - Transaction costs Amortised Cost Fair value (OCI) Fair value (P+L) Include transaction costs in the value of the asset Include transaction costs in the value of the asset Transaction costs are expensed in profit or loss IFRS 9, Para 5.1.1

95 Subsequent measurement Fair value (P+L) Fair value (OCI) Amortised Cost Fair value Amortised cost IFRS 9, Para 5.2.1

96

97

98

99

100 Impairment of Financial Assets Expected Credit Losses

101 IASB s intention Incurred Loss Model (IAS 39) Expected Loss Model (IFRS 9) Under the impairment approach in IFRS 9 it is no longer necessary for a credit event to have occurred before credit losses are recognised. Instead, an entity always accounts for expected credit losses, and changes in those expected credit losses. The amount of expected credit losses is updated at each reporting date to reflect changes in credit risk since initial recognition and, consequently, more timely information is provided about expected credit losses. IFRS 9, IN 9

102 IASB s intention - previously Initial recognition of a financial asset! T1 T2 T3 T4 T5 IAS 39: recognise loss only on the occurrence of the trigger loss event Dr Impairment Expense (P&L) Cr Financial Asset

103 IASB s intention currently Initial recognition of a financial asset! T1 T2 T3 T4 T5 IFRS 9: assess credit risk constantly and start recognising losses earlier Dr Impairment Expense (P&L) Cr Expected Credit Loss Allowance

104 Scope: which assets are subject to the ECL model? Financial assets measured at amortised cost; Exception: Purchased / originated credit impaired financial assets Financial assets measured at FV through OCI; Trade receivables, contract assets and lease receivables; IFRS 9 para

105 Overview of requirements Stage 1 Stage 2 Stage 3 No significant increase in credit risk Significant increase in credit risk Credit impaired Performing Under-performing Non-performing ECL Allowance 12 month expected credit losses Interest revenue Lifetime expected credit losses Lifetime expected credit losses Gross basis Gross basis Net basis

106 Overview of requirements Stage 1 Stage 2 Stage 3 No significant increase in credit risk Significant increase in credit risk Credit impaired Performing Under-performing Non-performing ECL Allowance 12 month expected credit losses Lifetime expected credit losses Interest revenue Lifetime expected credit losses Gross basis Gross basis Net basis

107 Overview of requirements Stage 1 Stage 2 Stage 3 No significant increase in credit risk Significant increase in credit risk Credit impaired Performing Under-performing Non-performing ECL Allowance 12 month expected credit losses Lifetime expected credit losses Interest revenue Lifetime expected credit losses Gross basis Gross basis Net basis IFRS 9 Appendix A

108 Overview of requirements Stage 1 Stage 2 Stage 3 No significant increase in credit risk Significant increase in credit risk Credit impaired Performing Under-performing Non-performing ECL Allowance 12 month expected credit losses Lifetime expected credit losses Interest revenue Lifetime expected credit losses Gross basis Gross basis Net basis IFRS 9 Appendix A

109 Overview of requirements IFRS Change in credit quality since initial recognition of financial asset Stage 1 (IFRS 9 par 5.5.5) No significant increase in credit risk Stage 2 (IFRS 9 par 5.5.3) Significant increase in credit risk Stage 3 Credit impaired Performing Under-performing Non-performing Expected Credit Losses Recognised (ECL Allowance) 12 month expected credit losses Lifetime expected credit losses Interest revenue Lifetime expected credit losses Gross basis Gross basis Net basis General deterioration of the credit quality of the financial asset

110 General approach Recognise a loss allowance for expected credit losses on all financial assets within the scope; If: Credit risk has increased significantly since initial recognition, the loss allowance will be at an amount equal to lifetime expected credit losses Credit risk has NOT increased significantly since initial recognition, the loss allowance will be at an amount equal to 12month expected credit losses

111 More useful terms Credit risk.the risk that one party to a financial instrument will cause a financial loss for the other party by failing to discharge an obligation. IFRS 7 Appendix A

112 More useful terms Expected Credit Losses IFRS 9 Appendix A

113 General approach Expected Credit Losses IFRS 9 par

114 General approach continued Lifetime expected losses IFRS 9 Appendix A i.e. the loss which will arise should default take place!

115 General approach continued 12-month expected losses IFRS 9 Appendix A

116 General approach continued Loss allowance: R Dr Expected credit losses XXX Cr Impairment allowance XXX Recognition of an impairment in a financial asset The expected credit loss / impairment is presented separately on the face of the Statement of P&L. The allowance is presented separately on the face of the Statement of Financial Position.

117 Measurement of Expected Credit Losses PV of expected cash flows (discounted at original EIR) PV of contractual cash flows (discounted at original EIR) Credit losses

118 Measurement of Expected Credit Losses Credit losses Probability of default event taking place in the next 12 months 12-month expected credit losses

119 When are 12-month ECL recognised? The ECL allowance will reflect 12-month ECL : On initial recognition; or When the credit risk presented by the financial instrument is low ; or When the credit risk presented by the financial instrument has not significantly increased since initial recognition / previous reporting date.

120 Measurement of Expected Credit Losses Credit losses Probability of default event taking place in lifetime of the instrument Lifetime expected credit losses

121 When are lifetime ECL recognised? The ECL allowance will reflect lifetime ECL when: The credit risk presented by the financial instrument is no longer low ; or The credit risk presented by the financial instrument has significantly increased since initial recognition / previous reporting date.

122 Exceptions to the general approach Trade receivables, contract assets and lease receivables; and IFRS Purchased / Originated Credit-impaired Financial Assets IFRS

123 Amortised Cost

124

125

126

127 FVOCI Debentures

128

129

130 Reclassification adjustments from OCI IFRS 9 FV OCI- Equity Instruments IFRS9.B5.7.1 does NOT require reclassification to P/L of cumulative gains & losses recognised in OCI upon sale or impairment of AFS asset. An entity can chose transfer within equity to RE or to leave the reserve as is. Dr Mark-to Mkt reserve (SOCIE) Cr Retained Earnings (SOCIE) IFRS 9- FVOCI Debt Instruments Reclassification to P/L of cumulative gains & losses recognised in OCI upon sale or impairment of AFS asset. Dr Loss allowance (OCI) Dr Fv adjustments (OCI) Cr Reclassification adjustment (P/L) Dr Tax Expense Cr fv adjustment reserve (OCI) NB: the reclassification was done before tax

131 Financial instruments Reclassification (FA) Reclassification allowed when business model for the managing of financial assets changes. But should be: Significant Infrequent Demonstrable to external parties The following are not changes to a business model: A change in intention related to the financial assets Temporary disappearance of a market Transfer of financial assets between parts of the entity with different business models Reclassification shall apply prospectively from reclassification date (first day from next reporting period)

132 Financial instruments Reclassification (FA) Amortised cost reclassified to Fair value Determine the fair value at reclassification date Difference between previous carrying amount and fair value P/L Fair value reclassified to Amortised cost Determine fair value at reclassification date FV at the reclassification date becomes the new carrying amount

133 Only financial assets Only when an entity changes its business model Change is demonstrable and significant to the entity s operations Apply prospectively 1 st day of the reporting period (no restatement of previous gains / losses / interest) Reallocate CA before FV adjustment from one category to another Determine FV at reclassification date Restate previous CA to the FV on reclassification date Gains / losses recognised in P/L

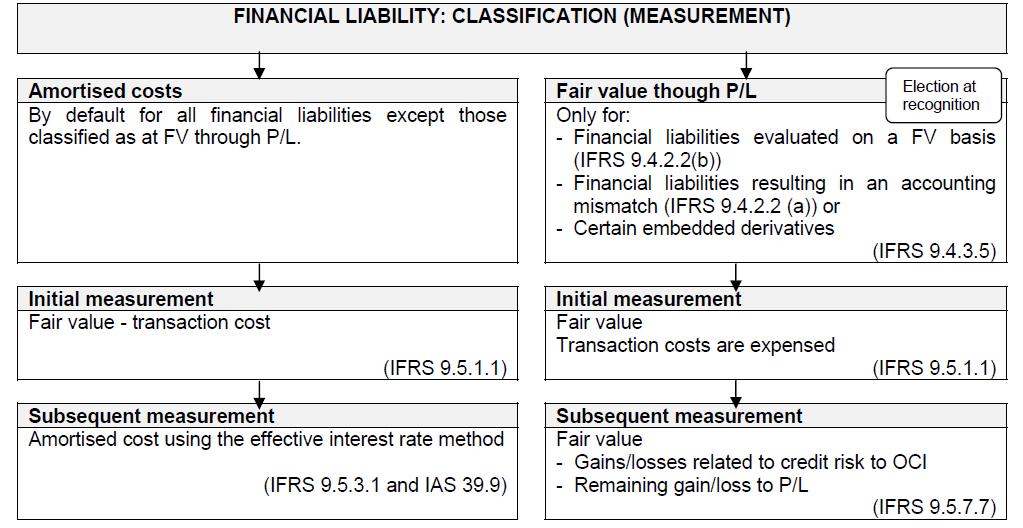

134 RECLASSIFICATION FROM : AMORTISED COST TO A FAIR VALUE THROUGH PROFIT OR LOSS A Ltd owns an investment in unlisted bonds. As the objective of the applicable business model was to hold assets to collect contractual cash flows, the bonds were accounted for at amortised cost. The bonds were acquired at the beginning of year 1 at fair value and mature at the end of year 4, when the principal amount will be R1 mil. The coupon rate is 10% per annum while the fair interest rate amounted to 11% at the beginning of year 1, 15% at the end of year 1/beginning of year 2 and 12% at the end of year 2. During year 1, A ltd purchased a large investment banking operation. As a result, A Ltd combined all the debt investments it holds in the banking portfolio. The investment banking operation's portfolio is actively managed and accordingly its business model had the objective of realising fair value gains through sale, which is now the objective of the combined portfolio. A Ltd distinguishes between interest income and other fair value adjustments for disclosure and recording purposes. (method 1) REQUIRED: JOURNAL ENTRIES YEAR 1 AND YEAR 2

135 SUGGESTED SOLUTION YEAR 1 DR CR J1 Financial asset at amortised cost (SFP) Bank (SFP) (FV=1mil; pmt = , n =4; i=11%) Initial recognition of investment J2 Bank (SFP) Financial asset at amortised cost (SFP Interest income (P/L) ( X 11%) NO ADJUSTMENT TO FAIR VALUE -CARRIED AT AMORTISED COST

136 SUGGESTED SOLUTION YEAR 2 DR CR J1 Financial asset at FVTPL (SFP) (1 st day of reporting period) Financial asset at amortised cost (SFP) RECLASSIFICATION ( ) J2 Fair Value adjustment (P/L) Financial asset at FVTPL (SFP) (FV=1mil; pmt = , n =3; i=15%) = R J3 Bank (SFP) Financial asset at FVTPL (SFP) Interest income (P/L) ( X 11%) J4 Financial asset at FVTPL (SFP) Fair Value adjustment (P/L) (FV=1mil; pmt = , n =2; i=12%) = R ( ) ORIGINAL EIR CALCULATE NEW FAIR VALUE

137 IFRS 7.12B: DICLOSURE Financial assets measured at amortised cost reclassified to be measured at fair value On 1 January 2011, after a change in the applicable business model the entity reclassified financial assets, with a carrying amount of R at this date, previously measured at amortised cost, to be measured at fair value. The entity no longer holds the financial asset to collect contractual cash flows, however this is now actively managed to realise fair value gains through sale by the entity's investment banking division. The reclassification has lead to a decrease in financial assets at amortised cost and an increase in financial assets mandatorily held at fair value through profit or loss with a resulting fair value gain, both upon reclassification and through subsequent measurement, being recorded. NB: ALSO NOTE DISCLOSURE FOR RECLASSICATION FROM FAIR VALUE TO AMORTISED COST

138 Disclosures Financial instruments disclosures are in IFRS 7 Financial Instruments: Disclosures, and no longer in IAS 32. The disclosures relating to treasury shares are in IAS 1 Presentation of Financial Statements and IAS 24 Related Parties for share repurchases from related parties. [IAS and 39]

139 FINANCIAL LIABILITY 1. Classification 2. Initial Measurement 3. Subsequent Measurement 4. Impairment of Amortised Cost Financial Asset 5. Derecognition

140 FINANCIAL LIABILITY 1. Classification

141 Classification Of Financial Liability Financial Liabilities shall be classified at either: At FVTPL, or Financial Liabilities at Amortised Cost A financial liability is classified as FVTPL if: It is held for trading Upon initial recognition it is designated at FVTPL

142 Measurement of Financial Assets [para ] Initial Measurement Measure the following liabilities at FV less transaction costs: Amortised Cost Measure the FVTPL: at FV only, exclude the transaction costs Transaction cost must expensed in P/L Subsequent measurement: Use FV- if classified as FVTPL Use Amortised Cost- if not classified as FVTPL

143 Initial recognition Measurement bases Amortised Cost Fair value (P+L) NOTE Other exceptions (IFRS 9, para 4.2.1) IFRS 9, Para a ALL financial liabilities IFRS 9, Para IRREVOCABLE designation IFRS 9, Para Derivative liabilities OR Avoiding inconsistent measurement OR Asset management purposes

144 Initial recognition Hybrid contracts Embedded derivative Fair value (P+L) ONLY if: Economic characteristics and risks of the two items are NOT closely related Embedded derivative meets the definition of a derivative Hybrid contract is NOT measured at fair value (P+L) Amortised cost Non-derivative host (NOT a financial asset) IFRS 9, Para 4.3

145 Initial recognition Transaction costs Fair value (P+L) Amortised Cost If transaction price does not equal fair value, recognise a day one gain / loss (in profit and loss) Include transaction costs in the value of the asset IFRS 9, Para IFRS 9, Para 5.1.1A

146 Subsequent measurement Amortised Cost Fair value (P+L) Amortised cost Fair value IFRS 9, Para 5.3

147 Subsequent measurement Change in credit risk Issuer s own discount rate: Credit risk Credit risk 2% 2.8% Risk-free interest rate Risk-free interest rate 7% 8.2% 31 December March 2013

148 Subsequent measurement Change in credit risk Fair value of loan has decreased by 2% (11-9) Market interest rates have increased (7% to 8.2%) G Mac s credit rating has worsened Portion relating to market movements P+L Portion relating to credit risk movements IFRS 9, Para Credit risk movements will ONLY be included in P+L Another corresponding financial instrument exists Equal and opposite movement in P+L OCI IFRS 9, Para 5.7.8

149 Subsequent measurement Change in credit risk To isolate the credit rating effect: Calculate the PV (fair value) of the loan assuming that market interest rates had NOT changed

150 Classification and measurement of financial liabilities Held for trading? YES NO FVO used? 1. Managed on FV basis? 2. Accounting mismatch? 3. Embedded derivative? YES Changes due to own credit? Other fair value changes? Fair value through OCI Fair value through profit or loss NO Includes embedded derivatives? YES Separate embedded derivative using IAS 39 YES NO Host debt Embedded derivative Amortised cost Fair value through profit or loss

151

152 Extinguishing Financial Liabilities with Equity Instruments IFRIC 19

153 Background A debtor and creditor might renegotiate the terms of a financial liability, with the result that the debtor extinguishes the liability fully or partially by issuing equity instruments to the creditor. These transactions are sometimes referred to as debt for equity swaps.

154 Scope IFRIC 19 applies to: the accounting by an entity (debtor) when the terms of a financial liability are renegotiated and result in the entity issuing equity instruments to a creditor of the entity to extinguish all or part of the financial liability. It does not address the accounting by the creditor. An entity shall NOT apply this Interpretation to transactions in situations where: the creditor is also a direct or indirect shareholder and is acting in its capacity as a direct or indirect existing shareholder. the creditor and the entity are controlled by the same party or parties before and after the transaction and the substance of the transaction includes an equity distribution by, or contribution to, the entity. extinguishing the financial liability by issuing equity shares is in accordance with the original terms of the financial liability.

155 Issue(s) 4 This Interpretation addresses the following issues: 1. Are an entity s equity instruments issued to extinguish all or part of a financial liability consideration paid in accordance with paragraph of IFRS 9? (recognition of equity issued) 2. How should an entity initially measure the equity instruments issued to extinguish such a financial liability? (measurement of equity issued) 3. How should an entity account for any difference between the carrying amount of the financial liability extinguished and the initial measurement amount of the equity instruments issued? (recognition of the diff between the CA of financial liability and the value of the equity issued to extinguish it- in P/L or OCI or directly in Equity)

156 Recognition If a debtor issues equity instruments to a creditor to extinguish all or part of a financial liability, those equity instruments are 'consideration paid' in accordance with paragraph of IFRS 9. Accordingly, the debtor should derecognise the financial liability fully or partly. Dr Financial Liability- CA Dr Loss on settlement Cr Share Capital-equity Cr Gain on settlement

157 Measurement The debtor should measure the equity instruments issued to the creditor at fair value of equity issued, unless fair value is not reliably determinable, in which case the equity instruments issued are measured at the fair value of the liability extinguished. Dr Financial Liability- CA Dr Loss on settlement Cr Share Capital-equity Cr Gain on settlement NB: the loss or gain on settlement arises when the equity is measured at the fair value of the equity issued, which is either greater or lesser than the CA of liability.

158 Accounting for the difference The difference between the carrying amount of the financial liability (or part of a financial liability) extinguished, and the consideration paid, shall be recognised in profit or loss, in accordance with paragraph of IFRS 9. Dr Financial Liability- CA Dr Loss on settlement (P/L) Cr Share Capital-equity Cr Gain on settlement (P/L) An entity shall disclose a gain or loss recognised in accordance with paragraphs 9 and 10 as a separate line item in profit or loss or in the notes.

159 Partial extinguishment If only part of a liability is extinguished, the debtor must determine whether any part of the consideration paid relates to modification of the terms of the remaining liability. If it does, the debtor must allocate the fair value of the consideration paid between the liability extinguished and the liability retained. If the remaining liability has been substantially modified, the entity shall account for the modification as the extinguishment of the original liability and the recognition of a new liability as required by paragraph of IFRS 9.

160 EXAMPLE 1: Question Friendly Ltd has authorised ordinary shares and an outstanding creditor with a fair value of R owing to Happy Ltd. Of the ordinary shares, have been issued. Since the company is growing rapidly and is experiencing some cash flow challenges, it was decided to approach Happy Ltd with the proposal of issuing ordinary shares in Friendly Ltd to Happy Ltd in full and final settlement of the R owing to Happy Ltd. Happy Ltd agreed to the proposal and shares in Friendly Ltd were issued at their fair value of R5,00 per share to Happy Ltd on the date on which the creditor was supposed to be settled (1 July 20.12). Q- Record the above transaction in Friendly Ltd s books

161 EXAMPLE 1: Solution The journal entry illustrating how to account for the transaction will as follows: 1 July Dr Financial liability: Happy Ltd Cr Share capital ( x R5,00) Extinguishing the financial liability owing to Happy Ltd by issuing shares in Friendly Ltd in full and final settlement.

162 EXAMPLE 2: Question Friendly Ltd has authorised ordinary shares and an outstanding creditor with a fair value of R owing to Happy Ltd. Of the ordinary shares, have been issued. Since the company is growing rapidly and is experiencing some cash flow challenges, it was decided to approach Happy Ltd with the proposal of issuing ordinary shares in Friendly Ltd to Happy Ltd in full and final settlement of the R owing to Happy Ltd. Happy Ltd agreed to the proposal and shares in Friendly Ltd were issued at their fair value of R5,00 per share to Happy Ltd on the date on which the creditor was supposed to be settled (1 July 20.12). Q- Record the above transaction in Friendly Ltd s books

163 EXAMPLE 2: Solution The journal entry illustrating how to account for the transaction will as follows: 1 July Dr Financial liability: Happy Ltd Dr Loss on settlement (P/L) Cr Share capital ( x R5,00) Extinguishing the financial liability owing to Happy Ltd by issuing shares in Friendly Ltd in full and final settlement.

164

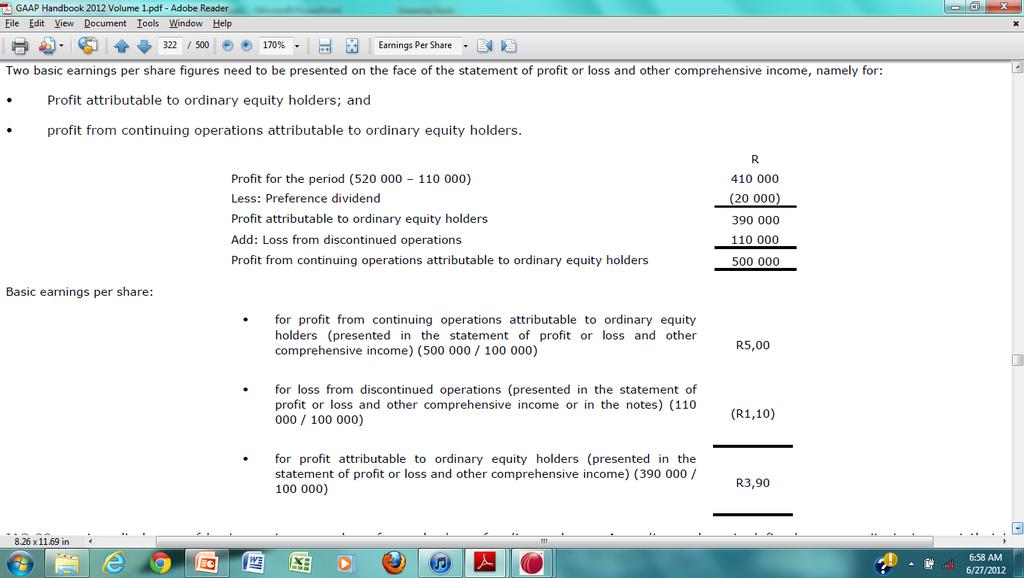

165 Earnings Per Share IAS 33

166 Background Required for quoted/listed entities Earnings per share (EPS) is a ratio widely used by most user groups, in particular financial analysts and the financial press. The users of financial statements use EPS and dividends per share (DPS) to evaluate the current performance and the performance over time of an entity and to compare it with the performance of other entities. Diluted earnings per share assist the users of financial statements to evaluate the sensitivity of EPS with regard to future changes in the capital structure of the enterprise.

167 Earnings Per Share Earnings per share includes: Basic Earnings Per Share (BEPS) Diluted Earnings Per Share (DEPS) Head-line Earnings Per Share (HEPS) Dividend Per Share (DPS)

168 KEY CONCEPTS The following key concepts are fundamental to this study unit: The calculation of basic earnings per share for: Profit attributable to ordinary equity holders of the parent entity. Profit from continuing operations attributable to ordinary equity holders of the parent entity. The calculation of diluted earnings per share for: Profit attributable to ordinary equity holders of the parent entity. Profit from continuing operations attributable to ordinary equity holders of the parent entity. Calculation of headline earnings per share (level 1) The calculation of dividend per share. The presentation and disclosure of earnings, head-line earnings and dividends per share amounts.

169 Basic Earnings Per Share (BEPS) ( ) Objective - to provide a measure of the interests of each ordinary share of a parent entity in the performance of the entity over the reporting period. Calculate BEPS for continuing operations if so required. See formula in next slide

170 Basic Earnings Per Share (BEPS) ( ) BEPS = Basic Earnings WANOS* *Weighted Average Number of Ord Shares Approach: - Always put the formula down first and calculate each component one-by-one. - NB: most marks are on the WANOS

171 Basic Earnings Per Share (BEPS) ( ) Basic Earnings (33.12) For the purpose of calculating basic earnings per share, the amounts attributable to ordinary equity holders of the parent entity in respect of: (a) profit or loss from continuing operations attributable to the parent entity; and (b) profit or loss attributable to the parent entity shall be the amounts in (a) and (b) adjusted for the after-tax amounts of preference dividends, differences arising on the settlement of preference shares, and other similar effects of preference shares classified as equity.

172 BEPS- Continuing Example A company has a profit from continuing operations amounting to R and a loss from discontinued operations amounting to R A non-cumulative preference dividend of R was declared during the year ordinary shares were in issue throughout the year.

173

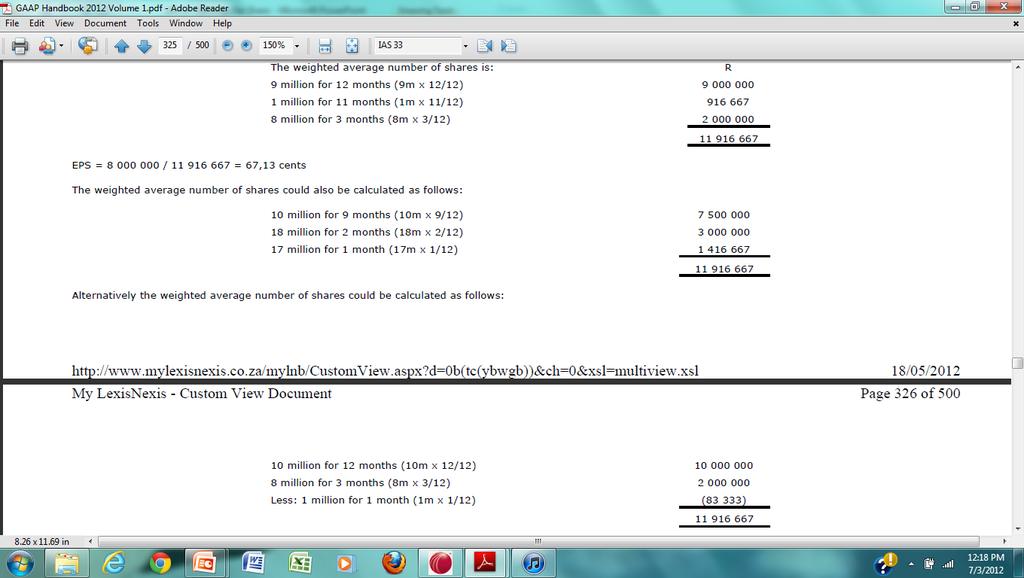

174 Impact of pref share on Basic Earnings If Pref share are classified as financial liabilitiespref dividend is a finance cost no impact on earnings as already deducted as a finance cost in the P/L; If preference shares classified as equity- deduct from profit for the period as follows: After tax Cumulative dividend- deduct even if dividend not declared & paid After Tax-Non-cumulative dividend- deduct only if dividend has been declared

175 Weighted Average Number of Ordinary Shares (WANOS) Use WANOS for BEPS The rationale behind using a weighted average number of ordinary shares outstanding is to reflect the proportionate change in earnings in comparison with the capital (resources) that was available to generate it. For example, if an entity had shares in issue throughout year 1 and at the start of year 2 issued a further shares for cash, the company had more capital (resources) available with which earnings could be generated in year 2 compared to year 1. By using as the denominator in year 1 and as the denominator in year 2, this relative change in the resources available to generate earnings is reflected in the EPS figures. This method improves the comparability of EPS figures from year to year.

176 Weighted Average Number of Ordinary Shares (WANOS)-IAS For BEPS, the number of ordinary shares shall be the WANOS outstanding during the period. When do share issue impact WANOS? Shares are usually included in the WANOS from the date consideration is receivable (which is generally the date of their issue), for example: ordinary shares issued in exchange for cash are included when cash is receivable; (new shares issued X N/12, where N= period in issue) ordinary shares issued on the voluntary reinvestment of dividends on ordinary or preference shares are included when dividends are reinvested; (shares in issue at issue X capitalisation issue ratio) ordinary shares issued as a result of the conversion of a debt instrument to ordinary shares are included from the date that interest ceases to accrue; (new shares issued X N/12, where N= period in issue)

177 Weighted Average Number of Ordinary Shares (WANOS)-IAS ordinary shares issued in place of interest or principal on other financial instruments are included from the date that interest ceases to accrue; ordinary shares issued in exchange for the settlement of a liability of the entity are included from the settlement date; ordinary shares issued as consideration for the acquisition of an asset other than cash are included as of the date on which the acquisition is recognised; and ordinary shares issued for the rendering of services to the entity are included as the services are rendered.

178 Weighted Average Number of Ordinary Shares (WANOS)-IAS Ordinary shares issued as part of the consideration transferred in a business combination are included in the WANOS from the acquisition date. Ordinary shares on conversion of a mandatorily convertible instrument are included in WANOS from the date the contract is entered into. Contingently issuable shares are treated as outstanding and are included in WANOS only from the date when all necessary conditions are satisfied

179 WANOS New share issues (with a change in resources) Impact BEPS Adjust proportionately for the time it was in issue during the year. E.g. if 1200 new shares were issued for cash on 30 September for a December Y/E, BEPS WANOS shall be increased by 300 (1200*3/12)

180 WANOS Share buy back (with a change in resources) Impact BEPS Adjust proportionately for the time it was NOT in issue during the year. E.g. if 1200 new shares were issued for cash on 30 September for a December Y/E, BEPS WANOS shall be decreased by 300 (1200*3/12)

181 WANOS Example: New share issues (with a change in resources) A company earned profit of R8 million during the year and had 10 million ordinary shares in issue at 1 January. On 30 September a further 8 million shares were issued, while 1 million shares were bought back at 30 November. The company s year-end is 31 December.

182

183 WANOS Mandatorily/Compulsory Convertible Instruments IAS33.23 Ordinary shares that will be issued upon the conversion of a mandatorily convertible instrument are included in the calculation of BEPS from the date the contract is entered into. For the purposes of diluted EPS, mandatorily convertible instruments are not potential ordinary shares, as it is not a contract that may entitle its holder to ordinary shares. It is a contract that definitely entitles its holder to ordinary shares.

184 WANOS Example: Mandatorily/Compulsory Convertible Instruments During the year A Ltd earned profit of R , while ordinary shares were in issue throughout the year. Halfway through the year debentures of R10 each were issued by A Ltd, which will be converted into ordinary shares after five years on the basis of three ordinary shares for every debenture held. Conversion is mandatory and there is no option for cash settlement. Assume that the interest expense relating to these debentures amounted to R4 500 (before tax).

185 WANOS Example: Mandatorily/Compulsory Convertible Instruments Earnings 580,000 WANOS: Shares in issue. 200,000 Mandatory Convertible shares 7, ,500 BEPS = /207,500 = 2.80 NB: No adjustment is made for the interest paid on the debentures as basic earnings, per definition, includes all income and expenses recognised in profit or loss.

186 WANOS Capitalisation or bonus issues: In a capitalisation or bonus issue, ordinary shares are issued to existing shareholders for no additional consideration. Therefore, the number of ordinary shares outstanding is increased without an increase in resources. The number of ordinary shares outstanding before the event is adjusted for the proportionate change in the number of ordinary shares outstanding, as if the event had occurred at the beginning of the earliest period presented. (see example) NB: Always adjust the prior year BEPS as capitalisation are regarded as issued at incorporation in proportion to the shares outstanding.

187 WANOS Example: Capitalisation issue A company s issued share capital consisted of 10 million shares at 1 January 20X2. During 20X2 a one for four capitalisation issue took place out of retained earnings. Earnings in 20X2 amounted to R5 million while EPS in 20X1 was 45 cents.

188 WANOS Example: Capitalisation issue EPS for 20X2 would be calculated as R5m/12,5m = 40 cents (2,5m shares were issued by way of the one-for-four capitalisation issue). The comparative EPS (i.e. 20X1) requires restatement in proportion to the revised number of shares in issue, i.e. 45 cents x 10m/12,5m = 36 cents. (This can also be calculated by taking earnings of R4,5m in 20X1 (EPS 45c x 10m shares) and shares of 12,5m, i.e. R4,5m/12,5 = 36 cents.) The comparative figures are adjusted to provide a more meaningful comparison between the current year's EPS which, despite there being no increase in total equity, is based on the increased number of shares in issue. Therefore, the increased number of shares in issue is also taken into account for the comparative period. This is in contrast to an issue for value where the increased shares in issue are expected to generate increased earnings in the current year and as a result, the current year EPS is based on the increased number of shares in issue, but the comparative EPS is not adjusted. Where shares are issued for value prior to a capitalisation issue, the effect of the new issue, which has been weighted for purposes of the EPS calculation, should be taken into account when calculating the effect of the capitalisation issue.

189 WANOS Example: Capitalisation issue after shares issued at fair value A company had issued share capital of 10 million shares at 1 January 20X2. On 1 March 20X2 there was an issue of shares at fair value. On 1 September 20X2 a one for four capitalisation issue took place.

190 WANOS Example: Capitalisation issue after shares issued at fair value WANOS- current year: Outstanding on 1 January New issue-fv on 1/3/12(300k*10/ Cap issue ¼* Note that the comparative basic EPS figure will be recalculated using a weighted average number of shares of [ ( / 4)].

191 WANOS Share Split Where shares are split there is no effect on the company s overall capital. Therefore, the treatment is identical to that applied to capitalisation or bonus issues. Consolidation of shares A consolidation of ordinary shares generally reduces the number of ordinary shares outstanding without a corresponding reduction in resources. Therefore, EPS is based on the decreased number of ordinary shares after the share consolidation and comparatives are proportionately adjusted.

192 WANOS Rights Issue Refer to IE 4 in IAS 33 Rights issues can take place at or below the fair value of the shares. Where a rights issue takes place at fair value, it is treated in the same way as a new share issue for value. Where a rights issue takes place at less than the fair value, it involves two components: an issue of shares for full value and a bonus issue. The number of ordinary shares to be used in calculating basic earnings per share for all periods prior to the rights issue is the number of ordinary shares outstanding prior to the issue, multiplied by the adjusting factor: Adjusting factor = Fair value per share immediately prior to the exercise of rights Theoretical ex-rights fair value per share

193 WANOS Rights Issue The theoretical ex-rights fair value per share is calculated by adding the aggregate fair value of the shares immediately prior to the exercise of the rights to the proceeds from the exercise of the rights, and dividing by the number of shares outstanding after the exercise of the rights. Where the rights themselves are to be publicly traded separately from the shares prior to the exercise date, fair value for the purposes of this calculation is measured at the close of the last day on which the shares are traded together with the rights. Theoretical Ex-rights fair value per share = Fair value of all issued shares prior to the exercise of rights + total proceeds received from exercise of rights Number of shares in issue prior to the exercise + number of shares issued in the exercise

194

195 What does the EPS future look like?

196 Diluted Earnings Per Share para DEPS= Diluted Earnings Diluted WANOS NB: Objective- to estimate possible future reduction in EPS DEPS is calculated for: Profit attributable to parent: Profit/loss from continuing operations if presented Profit/loss from discontinued operations

197 Diluted Earnings- para 33 Diluted earnings= Basic Earnings adjusted by the after-tax effect of: dividends saving on items of dilutive instruments (e.g. dividends on convertible preference shares) Interest saving on conversion of debt instruments Other changes in income that would result from dilutive instruments (transaction costs and discounts on conversion)

198 Diluted WANOS Diluted WANOS = Basic WANOS + effects of dilutive (potential ordinary shares) instruments NB: Only potential ordinary shares are dilutive Dilutive instruments shall be deemed to be issued as: at the beginning of the year (if issued in prior years) or from the issue date if issued in the current year

199 Diluted WANOS Dilutive potential Ord Shares Anti-dilutive potential Ord Shares decrease earnings per share or increase loss per share USE to calculate DEPS increase earnings per share or decrease loss per share IGNORE FOR DEPS calculation

200 Options, warrants and their equivalents The dilutive potential ordinary shares are those that arise from no value/free shares. Free shares are calculated as follows = Average Market Price for the yr less Exercise PriceX # of shares on optionsxn/12 Average market price The free share can therefore be added on the Diluted WANOS NB: Options and Warrants usually do not have impact on Earnings Do Example 5 in IAS 33B

201 Options, warrants and their equivalents Average Market Price for the yr less Exercise Price X # of shares on options X n/12 Average market price = (20-15)/20 X X 12/12 = Diluted WANOS = =

202 Share-based payment- Options In a share based payment arrangement employees are usually required either to: 1 st to work fore the share and then pay an exercise price on exercise date. Which means the consideration arises from work and exercise price. The free shares on share based payment are therefore calculated as follows: AVP less (EP+ SBPFV*n/N) X # of shares on options X n/12 AVP AVP= annual average market price of the share EP = exercise price SBPFV = share based payment fair value still to be worked for n= remaining vesting period N= total vesting period

203 E.G-Share-based payment- Options Vesting Condition-Service Condition At the beginning of year 1 X Ltd grants options to an employee, conditional upon the employee remaining in X Ltd s employment until the end of year 3. These options entitle the employee to acquire one X Ltd share for each option at R1,50 per share. The average market price of X Ltd s shares during year 1 was R2 per share. The fair value per option at the beginning of year 1 was R0,30.

204 Answer The free shares at end of year 1 are: AVP less (EP+ SBPFV*n/N) X # of shares on options Xn/12 AVP = 2- ( *2/3) X 1000 X 12/12 2 = 150 shares

205 Share-based payment- Options Vesting Condition-Service + Performance Condition If the vesting condition includes a performance (market or non-market) condition it is regarded as a contingently issuable share. It shall only included in diluted earnings per share if the contingent event has occurred, with no consideration whether it is a market or non-market condition. E.G if the share price has to increase to 20c per share: -if share price not achieved at year end do not include in WANOS - if share price achieved at yr end include in WANOS

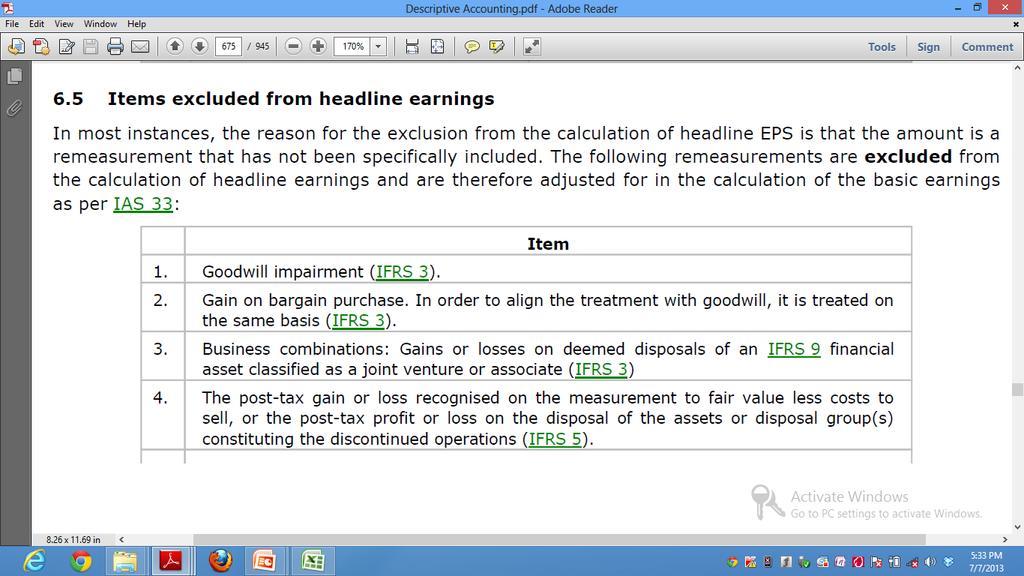

206 E.G-Share-based payment- Options Vesting Condition-Service + Performance Condition At the beginning of year 1 X Ltd grants options to an employee, conditional upon the employee remaining in X Ltd s employment until the end of year 3 and that the share price should increase to 20 cents per share.. These options entitle the employee to acquire one X Ltd share for each option at R1,50 per share. The average market price of X Ltd s shares during year 1 was R2 per share. The fair value per option at the beginning of year 1 was R0,30. The share price is 18 cents at year end. Q how many shares are dilutive a) if share price is 18 cents, (b) if share price is 21 cents

207 Answer a) the performance condition (growth of share price to 20 cents) is a contingent event and the share is therefore contingently issuable. Contingent issuable can only be included in WANOS when the contingent event has been achieved. Since 18c is less than 20c then therefore NOT included in EPS. b) The free shares at end of year 1 are: AVP less (EP+ SBPFV*n/N) X # of shares on options Xn/12 AVP = 2- ( *2/3) X 1000 X 12/12 2 = 150 shares

208 Contingently issuable shares contingently issuable ordinary shares are treated as outstanding and included in the calculation of diluted earnings per share if the conditions are satisfied (ie the events have occurred). included from the beginning of the period (or from the date of the contingent share agreement, if later).

209 Convertible instruments Examples include Convertible debenture and preference shares. Convertible dilutive instruments may affect earnings through interest and dividends. Impact: Increase the earnings with the after-tax effect of interest or dividends that will be saved in future when the debentures or shares are converted. Increase the weighted average number of shares with the expected future increase in ordinary shares resulting from the conversion. Interest is calculated on the liability component using the effective rate after taking transaction costs. Do Example 6 in IAS 33B

210 Ranking dilutive instruments Perform a ranking order with the most dilutive first. Options are usually the most dilutive instruments After ranking start by including the most dilutive instrument Do Example 9 in IAS 33B

211 Dividend per share (DPS) DPS is not covered under IAS 33. IAS requires that the DPS be presented together with EPS. Dividend per share = Shares Dividend for the year Total actual Issued

212 Looking for maintainable growth

213 Headline Earnings Per Share (HEPS) Not covered by IAS 33 Rather calculated in terms of Circular 03/09, Headline Earnings issued by SAICA Request of the JSE Limited. Section 8.63(c) of the JSE Listing Requirements States that listed entities must disclose headline HEPS for the current financial year and the immediately preceding financial year and that the headline earnings must be disclosed with a detailed reconciliation to the IAS 33 basic EPS number. NB: The ZSE listing rules also requires disclosure of HEPS, hence, it is applicable in Zimbabwe.

214 Why HEPS Basic earnings per share is EPS based on earnings for the year. Basic earnings include both maintainable earnings and earnings from extra-ordinary non-maintainable items. HEPS presents only EPS based on maintainable earnings of an entity which is more useful to the user than the basic earnings.

215 HEPS HEPS = Headline Earnings Basic WANOS NB: Headline Earnings= Basic WANOS +/- nonmaintainable earnings effects Approach:- focus on what should not be included in headline earnings and exclude these from the basic earnings. See next slide for excluded items. These are found in Circular 03/09 which is taken to the exam.

216

217

218

219 Example

220

221 Answer

222

223 Leases: IAS 17

224 Examinability 2015 Possible areas of focus: Finance lease- Lessor + Lessee Sale and lease back Deferred tax implications Presentation and Disclosure

225 Determining Whether an Arrangement IFRIC 4 Contains a Lease

226 Exam Approach- IFRIC 4 Approach: Issue Is the arrangement a lease agreement Application: Comment that an assessment is required of whether the arrangements has the substance of a lease as defined by IAS 17. (copy and paste IFRIC 4.6) Define a lease Apply the scenario to prove existence of the following indicators: fulfilment of the arrangement is dependent on the use of a specific asset or assets (IFRIC 4.7-8); and the arrangement conveys a right to use the asset (IFRIC 4.9a-c).

227 Exam Approach Conclude whether the arrangement is a lease arrangement or not Apply the classification criteria as per IAS to determine whether the lease is a finance or operating lease. Conclude on the lease classification

228

229

230

Anesu Daka CA(SA) - CAA

- CAA") FAC4863 4 August 2015 Tut 105/106 1. IAS 21- The effects of changes in foreign exchange rates 2. IAS32/39/IFRS9&7-Financial instruments 3. IAS 39-Hedging 4. IAS 33-Earnings per share 5. IAS 17- Leases

FAC4863 4 August 2015 Tut 105/106 1. IAS 21- The effects of changes in foreign exchange rates 2. IAS32/39/IFRS9&7-Financial instruments 3. IAS 39-Hedging 4. IAS 33-Earnings per share 5. IAS 17- Leases

IAS 32 & IFRS 9 Financial Instruments

Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 & IFRS 9 Financial Instruments Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 Financial

Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 & IFRS 9 Financial Instruments Baker Tilly in South East Europe Cyprus, Greece, Romania, Bulgaria, Moldova IAS 32 Financial

IFRS pocket guide inform.pwc.com

IFRS pocket guide 2016 inform.pwc.com Introduction 1 Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting Standards (IFRS)

IFRS pocket guide 2016 inform.pwc.com Introduction 1 Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting Standards (IFRS)

Financial Instruments: Presentation INTRODUCTION

IAS 32 Financial Instruments: Presentation INTRODUCTION Objective Scope Application The stated objective of IAS 32 is to establish principles for presenting financial instruments as liabilities or equity

IAS 32 Financial Instruments: Presentation INTRODUCTION Objective Scope Application The stated objective of IAS 32 is to establish principles for presenting financial instruments as liabilities or equity

Financial Instruments Ind AS 32 & 109. CA Chirag Doshi March 18, 2017

Financial Instruments Ind AS 32 & 109 CA Chirag Doshi March 18, 2017 Introduction Ind AS 32, Financial Instruments: Presentation, addresses the presentation of financial instruments as financial liabilities

Financial Instruments Ind AS 32 & 109 CA Chirag Doshi March 18, 2017 Introduction Ind AS 32, Financial Instruments: Presentation, addresses the presentation of financial instruments as financial liabilities

Financial Instruments Standards 11 November Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA Nelson 1

MBA MSc BBA CPA(US) ACA Nelson 1") Instruments Standards 11 November 2006 Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Instruments HKAS 32 Disclosure and presentation HKAS 39 Recognition and measurement

Instruments Standards 11 November 2006 Nelson Lam 林智遠 CFA FCCA FCPA(Practising) MBA MSc BBA CPA(US) ACA 2005-06 Nelson 1 Instruments HKAS 32 Disclosure and presentation HKAS 39 Recognition and measurement

Financial Instruments. October 2015 Slide 2

Presented by: Cost transaction price (in general) Amortised Cost (B/s) EIR - Effective interest method (I/s) OCI - Other Comprehensive Income FVTPL Fair value through profit or loss FVOCI Fair value through

Presented by: Cost transaction price (in general) Amortised Cost (B/s) EIR - Effective interest method (I/s) OCI - Other Comprehensive Income FVTPL Fair value through profit or loss FVOCI Fair value through

What are the common difficulties in studying financial assets and liabilities?

HKICPA Module A Financial Reporting Agenda Financial Assets and Liabilities What are the common difficulties in studying financial assets and liabilities? In today s seminar, we will discuss the following:

HKICPA Module A Financial Reporting Agenda Financial Assets and Liabilities What are the common difficulties in studying financial assets and liabilities? In today s seminar, we will discuss the following:

Stay informed. Visit IFRS pocket guide 2012

Stay informed. Visit www.pwcinform.com IFRS pocket guide 2012 Introduction Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting

Stay informed. Visit www.pwcinform.com IFRS pocket guide 2012 Introduction Introduction This pocket guide provides a summary of the recognition and measurement requirements of International Financial Reporting

PSAK Pocket guide 2018

PSAK Pocket guide 2018 www.pwc.com/id Introduction This pocket guide provides a summary of the recognition, measurement and presentation requirements of Indonesia financial accounting standards (PSAK)

PSAK Pocket guide 2018 www.pwc.com/id Introduction This pocket guide provides a summary of the recognition, measurement and presentation requirements of Indonesia financial accounting standards (PSAK)

Accounting policies. 1. Introduction. 2. Basis of presentation. 3. Consolidation

2 202 FirstRand Group annual financial statements Accounting policies 1. Introduction FirstRand Limited ( the Group ) is an integrated financial services company consisting of banking, insurance and asset

2 202 FirstRand Group annual financial statements Accounting policies 1. Introduction FirstRand Limited ( the Group ) is an integrated financial services company consisting of banking, insurance and asset

Consolidated Financial Statements For the Year Ended 31 December 2018

Consolidated Financial Statements For the Year Ended 31 December 2018 Consolidated Income Statement 2018 2017 Notes QR000 QR000 Interest Income 25 50,744,709 41,958,662 Interest Expense 26 (31,711,804)

Consolidated Financial Statements For the Year Ended 31 December 2018 Consolidated Income Statement 2018 2017 Notes QR000 QR000 Interest Income 25 50,744,709 41,958,662 Interest Expense 26 (31,711,804)

RELEVANT TO ACCA QUALIFICATION PAPERS F7 AND P2 What is a financial instrument? Let us start by looking at the definition of a financial instrument, which is that a financial instrument is a contract that

RELEVANT TO ACCA QUALIFICATION PAPERS F7 AND P2 What is a financial instrument? Let us start by looking at the definition of a financial instrument, which is that a financial instrument is a contract that

FINANCIAL INSTRUMENTS WORKBOOK

FINANCIAL INSTRUMENTS WORKBOOK There are 3 standards we will be referring to in the lectures. They ALL DEAL with FINANCIAL INSTRUMENTS: 1. IFRS 9 (this is the Foundation standard ) as it explains the manner

FINANCIAL INSTRUMENTS WORKBOOK There are 3 standards we will be referring to in the lectures. They ALL DEAL with FINANCIAL INSTRUMENTS: 1. IFRS 9 (this is the Foundation standard ) as it explains the manner

Accounting for Financial Instruments

International Financial Reporting Standards Accounting for Financial Instruments (IAS 39) Executive IFRS workshop for Regulators Diplomatic Academy of Vienna Darrel Scott, IASB member The views expressed

International Financial Reporting Standards Accounting for Financial Instruments (IAS 39) Executive IFRS workshop for Regulators Diplomatic Academy of Vienna Darrel Scott, IASB member The views expressed

IFRS 9 Financial Instruments

A C C O U N T I N G S U M M A R Y IFRS 9 Financial Instruments Objective The objective of this Standard is to establish principles for the financial reporting of financial assets and financial liabilities

A C C O U N T I N G S U M M A R Y IFRS 9 Financial Instruments Objective The objective of this Standard is to establish principles for the financial reporting of financial assets and financial liabilities

BFRS 9 Financial Instruments Overview and Key Changes from Current Standard and Requirements. 28 April 2016

BFRS 9 Financial Instruments Overview and Key Changes from Current Standard and Requirements 28 April 2016 Why is BFRS 9 Important? BFRS 9 will impact all entities, but especially banks, insurers and other

BFRS 9 Financial Instruments Overview and Key Changes from Current Standard and Requirements 28 April 2016 Why is BFRS 9 Important? BFRS 9 will impact all entities, but especially banks, insurers and other

Converse Bank closed joint stock company. Consolidated Financial Statements. 31 December 2017

Converse Bank closed joint stock company Consolidated Financial Statements 31 December 2017 1 Converse Bank CJSC Consolidated financial statements as at 31 December 2017 Contents Consolidated statement

Converse Bank closed joint stock company Consolidated Financial Statements 31 December 2017 1 Converse Bank CJSC Consolidated financial statements as at 31 December 2017 Contents Consolidated statement

EMIRATES NBD BANK PJSC

GROUP CONSOLIDATED FINANCIAL STATEMENTS These Audited Preliminary Financial Statements are subject to Central Bank of UAE Approval and adoption by Shareholders at the Annual General Meeting GROUP CONSOLIDATED

GROUP CONSOLIDATED FINANCIAL STATEMENTS These Audited Preliminary Financial Statements are subject to Central Bank of UAE Approval and adoption by Shareholders at the Annual General Meeting GROUP CONSOLIDATED

IAS 32 & 39 and IFRS 7 Part Two 10 September MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA Nelson 1

CPA(US) FCCA FCPA(Practising) MSCA Nelson 1") IAS 32 & 39 and IFRS 7 Part Two 10 September 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-07 Nelson 1 Today s Agenda Anyone who says they understand IAS 39

IAS 32 & 39 and IFRS 7 Part Two 10 September 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-07 Nelson 1 Today s Agenda Anyone who says they understand IAS 39

IFRS for SMEs IFRS Foundation-World Bank

!International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 11 13 January 2011 Astana, Kazakhstan Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic

!International Financial Reporting Standards 1 IFRS for SMEs IFRS Foundation-World Bank 11 13 January 2011 Astana, Kazakhstan Copyright 2010 IFRS Foundation. All rights reserved. The IFRS for SMEs 2 Topic

Financial Instruments Standards (Part 1) 18 August 2011

18 August 2011") Instruments Standards (Part 1) 18 August 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2006-11 Nelson Consulting Limited 1 HKAS 32, HKAS

Instruments Standards (Part 1) 18 August 2011 Lam Chi Yuen, Nelson 林智遠 MBA MSc BBA ACA ACS CFA CPA(Aust) CPA(US) CTA FCCA FCPA FHKIoD FTIHK MHKSI MSCA 2006-11 Nelson Consulting Limited 1 HKAS 32, HKAS

Regular way purchase or sale of financial assets

International Financial Reporting Standard 9 Financial Instruments Chapter 1 Objective 1.1 The objective of this IFRS is to establish principles for the financial reporting of financial assets and financial

International Financial Reporting Standard 9 Financial Instruments Chapter 1 Objective 1.1 The objective of this IFRS is to establish principles for the financial reporting of financial assets and financial

IAS 32 & 39 and IFRS 7 Part II 18 August MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA Nelson 1

CPA(US) FCCA FCPA(Practising) MSCA Nelson 1") IAS 32 & 39 and IFRS 7 Part II 18 August 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-07 Nelson 1 Today s Agenda Derivatives Derecognition Hedging Afternoon

IAS 32 & 39 and IFRS 7 Part II 18 August 2007 Nelson Lam 林智遠 MBA MSc BBA ACA CFA CPA(Aust) CPA(US) FCCA FCPA(Practising) MSCA 2005-07 Nelson 1 Today s Agenda Derivatives Derecognition Hedging Afternoon

Financial Instruments Standards (Part 1) 21 May 2015