Proving the Relation between Stock and Interbank Markets: The Bahrain Stock Exchange

|

|

|

- Constance Horn

- 5 years ago

- Views:

Transcription

1 MPRA Munich Personal RePEc Archive Proving the Relation between Stock and Interbank Markets: The Bahrain Stock Exchange Aleksandr Matveev Universidad Pontificia Comillas, Madrid, Spain, Universite Paris-Sud XI, Paris, France, Moscow State University, Moscow, Russia, Central bank of the Russian Federation 2014 Online at MPRA Paper No , posted 30 March :54 UTC

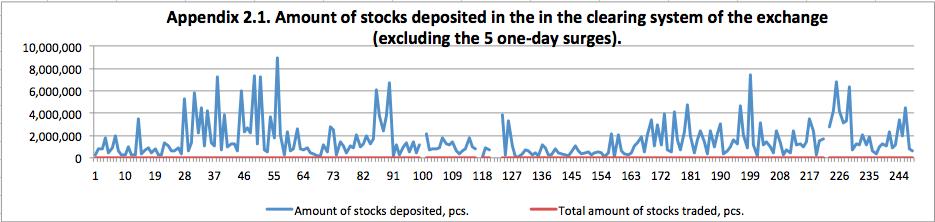

2 Proving The Association Between Stock Market And Interbank Lending Market Parameters: The Bahrain Stock Exchange By AleksandrMatveev 1 Lomonosov Moscow State University, Economics Faculty sasha matveev@mail.ru Abstract The present paper deals with further analysis of the relationship between the interbank loan rateon the one hand and the volume of investment and the amount of stocks tradable on the stock exchange on the other hand, as corroborated by calculations performed on Bahrain Stock Exchange data 2. Keywords: interbank credit market, equity market, stock market, speculations, trading volumes, BSE JEL Classification: G12, G14, G17, G21 1. Introduction There has been a number of studies into the association between interbank loan rates and stock market parameters(m.yandiev, 2011; M.Yandiev, A.Pakhalov, 2013), providing both the detailed theoretical rationalisation for such an association and its practical corroboration based on calculations performed on the data provided by the Moscow Stock Exchange. The present paper crosschecks M. Yandiev s formula explicating the association by applying it to the Bahrain Stock Exchange. The formula itself is as follows: u I * R * * U where I is the volume of speculative investments; R is the interest rate on overnight interbank loans, in fractions; U isthe total amount of stocks involved in deals; u isthe mean loss per deal a trader can allow aiming to close the trading day in the black (logically a constant) The formulacan be regarded as adequate as long as ushows little volatility over a significant length of time. 1 Academic advisor: MagometYandiyev, Associate Professor, Faculty of Economics, Moscow State University 2 The paper s author and academic advisor express their deepest gratitude to MrAbdulrahmanShehab (Executive Manager of Al-Baraka Banking Group), Mr Ahmed M. AbdulGhaffar (Vice President of Al-Baraka Banking Group), Mr Khalid AlHajri (Bahrain Bourse) for their valuable help in collecting the input data for this study Electronic copy available at:

3 Compared to the prior research, the present study goes on to calculate u through a number of different approaches. This was done to check the practicability of using each approach and find the one producing more accurate results. Also it should be noted that the data series included isolated instances of excessive surges in trading volumes, possibly distorting the theoretical model s resulting figures. This called for crosschecking the two approaches results, the one including the irregularities and the one excluding them. 2. Description of the data The raw data, as indicated above, came from the figures provided by the Bahrain Stock Exchange and the Reuters news agency: Total amount of funds deposited in BSE, in MM (I, see Appendix 1); Amount of stocks deposited in BSE, pcs (U, see Appendix 2); Fraction of stocks in the total volume of stock trading (alternative calculation of U, see Appendix 6); BSE overnight interbank loan rate (R, see Appendix 3). 3. First approach:proving the hypothesis through calculating standard deviation of u The projected characteristics of u were proved through calculating its standard deviation. A number of methods of calculating it was employed for greater precision: with absolute and relative u deviations, as well as using a logarithmic function (see Appendix 11). Moreover, given the surges in daily trading observed throughout the year (on 22.05, 14.06, 20.06, 24.06, and 19.11) (see Appendix 1), their impact on the resulting figures had to be assessed. To that end a second calculation of standard deviation of u was carried out excluding these anomalies. The results were: 1) Calculating the standard deviation of u usingitsabsolutevalues (in both total volume of deposited assets and volume of trading) proved the formula s applicability: u stayed within a narrow range of low values. Allowing for an accidental nature of the aforementioned surges in trading, the standard deviation of u falls significantly, not exceeding 1% of a security s average value. This agrees with the parameter s low volatility, observed by a narrow range of values on the relevant diagram (see Appendices 5 and 6). Therefore the value of u was assumed to be constant (see Appendix 4). 2) Calculating the standard deviation of u usingitsrelativevalues (in both total amount of deposited stocks and volume of trading) proved unusable. This was due to the fact that, even with a small spread in initial values, however small they themselves may be, their ratio is significantly larger, around 1. This, in turn, far increases their average value and, as a consequence, its standard deviation. 3) Relatively large values of u in cases of surges in speculation can be attributed to the accompanying rise in acceptable levels of speculator risk due to an increase in the total value of deposited assets. By the same logic, it can be assumed that increases in u before holidays (when there is no trade at the exchange) are due to greater uncertainties and a dulling of risk awareness, or its underestimation. Electronic copy available at:

4 4) Also noteworthy is the excessive volume of deposited assets, of which only an insignificant number was actively traded. In 100 deposited securities only an average of 4.3 were actively traded, with only 20% of a security s trading value backed by the funds deposited in the exchange (see Appendix 7). This shows an exchange s balanced risk policy: having the securities on offer exceed the demand by several times the number, while zealously attracting the clients funds. 4. Second approach:proving the hypothesis through regression analysis The second method of proving the formula s applicability required regression analysis of time series. This enabled ascertaining the relation between the theoretical model s variables, assessing its extent, and also its conformity to the criterion used for evaluating the formula. The time series input used for the model s 5 variables consisted of 255 observations (one for each working day of 2012, see Appendix 8). The analysis was done for each of the 4 methods of calculating standard deviation. All calculations were made using the Gretl econometrics package. As regression analysis of time series requires all of the variables to be stationary (Verbeek, 2004, p ), the first stage of the analysis included an augmented Dickey Fuller test (ADF) for each of the variables. Lag length in each case was established based on the Schwarz information criterion (SIC). All the tests were done after de-trending the time series.the results are presented in Appendix 9. ADF test shown all the variables except Rto be stationary, enabling using them for regression analysis, while using variable R needed it first to be confirmed to be cointegrated.according to Verbeek (MarnoVerbeek, 2004, p ), in case of cointegrated variables (with first differences ofr being stationary), the theoretical model can yield super consistent estimates, providing for meaningful conclusions. In this case, in both u for the total amount of stocks and u for the volume of trading the first differences of Rare stationary at the 1% level of significance (see Appendix 10). This means that R is cointegrated and can be used in the theoretical model. The results of using regression analysis were: 1) Different methods of calculating standard deviation as one of the variables did not have an impact on the result; 2) Linear regressions using the dependent u_small_volwere generallysignificant, with R being significant at the 1% level of significance, and I being not significant. Therefore u for the volume of trading is heavily dependent on the volume of assets deposited in the exchange, but independent of the interbank loan rate. 3) Linear regressions using the dependent u_small_depweregenerallynot significant, with R being significant at the 1% level of significance, and I being not significant. Therefore u for the volume of trading is heavily dependent on the interbank loan rate, but independent of the volume of assets deposited in the exchange. 4) Coefficients of Rand I were never negative in all of the cases, pointing to their direct relationship with the dependent variables. Electronic copy available at:

5 5. Conclusions The result of calculations made in the several approaches have proven that value of u remained relatively stable and low throughout the whole of Moreover, the resulting theoretic econometric model revealed the conjectured relationship between the variables. Therefore, it can be claimed that the formula was able to adequately describe the situation at the Bahrain stock market in Sources 1. Verbeek, Marno. A guide to modern econometrics. 2 nd edition. Chichester^ John Wiley & Sons Ltd, ISBN Yandiev, Magomet. The Damped Fluctuations as a Base of Market Quotations. Economics and management, 16, ISSN URL: 3. Yandiev, Magomet, Pakhalov, Alexander. The Relationship between Stock Market Parameters and Interbank Lending Market: An Empirical Evidence. URL:

6 7. Appendices

7

8 Appendix 4. u parameter calculations u, cents, 2012 г. WithUas volume of stocks traded WithUas total amount of deposited stocks Average, cents , Volatility, cents , Average security cost, BHD

9

10 Appendix 8. Variable name in the theoretical model Variable name ingretl Definition u u_small_vol Mean loss per deal (calculated using the volume of trade) u I u_small_dep I Mean loss per deal (calculated using the amount of stocks deposited) Volume of speculative investment (amount of money in the exchange s authorized bank); R R Overnight interbank loan rate Appendix Unit root test for u_small_vol Results of theadf test Augmented Dickey-Fuller test for u_small_vol including 3 lags of (1-L)u_small_vol (max was 3) sample size 242 unit-root null hypothesis: a = 1 test with constant model: (1-L)y = b0 + (a-1)*y(-1) e 1st-order autocorrelation coeff.for e:

11 lagged differences: F(3, 237) = [0.0000] estimated value of (a - 1): test statistic: tau_c(1) = asymptotic p-value 5.596e Unit root test for u_small_dep Results of the ADF test Augmented Dickey-Fuller test for u_small_dep including 2 lags of (1-L)u_small_dep (max was 4) sample size 243 unit-root null hypothesis: a = 1 test with constant model: (1-L)y = b0 + (a-1)*y(-1) e 1st-order autocorrelation coeff.for e: lagged differences: F(2, 239) = [0.0000] estimated value of (a - 1): test statistic: tau_c(1) = asymptotic p-value 1.58e Unit root test for I

12 Results of the ADF test Augmented Dickey-Fuller test for I including 3 lags of (1-L)I (max was 4) sample size 242 unit-root null hypothesis: a = 1 test with constant model: (1-L)y = b0 + (a-1)*y(-1) e 1st-order autocorrelation coeff.for e: lagged differences: F(3, 237) = [0.0000] estimated value of (a - 1): test statistic: tau_c(1) = asymptotic p-value 2.857e Unit root test for I

13 Results of the ADF test Augmented Dickey-Fuller test for R including one lag of (1-L)R (max was 2) sample size 244 unit-root null hypothesis: a = 1 test with constant model: (1-L)y = b0 + (a-1)*y(-1) e 1st-order autocorrelation coeff.for e: estimated value of (a - 1): test statistic: tau_c(1) = asymptotic p-value Results of the ADF test (first differences of selected variables) Augmented Dickey-Fuller test for d_r including 2 lags of (1-L)d_R (max was 2) sample size 242 unit-root null hypothesis: a = 1

14 test with constant model: (1-L)y = b0 + (a-1)*y(-1) e 1st-order autocorrelation coeff.for e: lagged differences: F(2, 238) = [0.0120] estimated value of (a - 1): test statistic: tau_c(1) = asymptotic p-value 5.159e-026 ADF test results summary Variable name ingretl u_small_vol u_small_dep I R ADF testresult Variable is stationary at the 1% level of significance Variable is stationary at the 1% level of significance Variable is stationary at the 1% level of significance Variable is stationary in first differences at the 1% level of significance Appendix ) Calculation with volume of trade Linear regression of u_small_volusingi andr Model 2: OLS, using observations Dependent variable: u_small_vol Coefficient Std. Error t-ratio p-value const I e e < *** R

15 Meandependentvar S.D. dependentvar Sumsquaredresid S.E. ofregression R-squared Adjusted R-squared F(2, 243) P-value(F) 7.4e-210 Log-likelihood Akaikecriterion Schwarzcriterion Hannan-Quinn rho Durbin-Watson ADF test results for residuals ADF test foru_small_vol_residual Dickey-Fuller test for u_small_vol_residual sample size 245 unit-root null hypothesis: a = 1 test with constant model: (1-L)y = b0 + (a-1)*y(-1) + e 1st-order autocorrelation coeff.for e: estimated value of (a - 1): test statistic: tau_c(1) = p-value 1.916e-024

16 10.2) Calculation with amount of deposited funds Linear regression of u_small_depusingi andr Model 1: OLS, using observations Dependent variable: u_small_dep Coefficient Std. Error t-ratio p-value const e e < *** I R < *** Meandependentvar 2.62e-06 S.D. dependentvar 1.47e-06 Sumsquaredresid 4.74e-10 S.E. ofregression 1.40e-06 R-squared Adjusted R-squared F(2, 243) P-value(F) 8.43e-07 Log-likelihood Akaikecriterion Schwarzcriterion Hannan-Quinn rho Durbin-Watson ADF test results for residuals ADF test foru_small_dep_residual Dickey-Fuller test for u_small_dep_residual

17 sample size 245 unit-root null hypothesis: a = 1 test with constant model: (1-L)y = b0 + (a-1)*y(-1) + e 1st-order autocorrelation coeff.for e: estimated value of (a - 1): test statistic: tau_c(1) = p-value 1.245e-024 Appendix 11. 1) 2) 3) 4)

Brief Sketch of Solutions: Tutorial 2. 2) graphs. 3) unit root tests

graphs. 3) unit root tests") Brief Sketch of Solutions: Tutorial 2 2) graphs LJAPAN DJAPAN 5.2.12 5.0.08 4.8.04 4.6.00 4.4 -.04 4.2 -.08 4.0 01 02 03 04 05 06 07 08 09 -.12 01 02 03 04 05 06 07 08 09 LUSA DUSA 7.4.12 7.3 7.2.08 7.1.04

Brief Sketch of Solutions: Tutorial 2 2) graphs LJAPAN DJAPAN 5.2.12 5.0.08 4.8.04 4.6.00 4.4 -.04 4.2 -.08 4.0 01 02 03 04 05 06 07 08 09 -.12 01 02 03 04 05 06 07 08 09 LUSA DUSA 7.4.12 7.3 7.2.08 7.1.04

Exchange Rate and Economic Growth in Indonesia ( )

") Exchange Rate and Economic Growth in Indonesia (1984-2013) Name: Shanty Tindaon JEL : E47 Keywords: Economic Growth, FDI, Inflation, Indonesia Abstract: This paper examines the impact of FDI, capital stock,

Exchange Rate and Economic Growth in Indonesia (1984-2013) Name: Shanty Tindaon JEL : E47 Keywords: Economic Growth, FDI, Inflation, Indonesia Abstract: This paper examines the impact of FDI, capital stock,

MODELING EXCHANGE RATE VOLATILITY OF UZBEK SUM BY USING ARCH FAMILY MODELS

International Journal of Economics, Commerce and Management United Kingdom Vol. VI, Issue 11, November 2018 http://ijecm.co.uk/ ISSN 2348 0386 MODELING EXCHANGE RATE VOLATILITY OF UZBEK SUM BY USING ARCH

International Journal of Economics, Commerce and Management United Kingdom Vol. VI, Issue 11, November 2018 http://ijecm.co.uk/ ISSN 2348 0386 MODELING EXCHANGE RATE VOLATILITY OF UZBEK SUM BY USING ARCH

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE ECONOMETRICS. Mr.

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE COURSE: COURSE CODE: ECONOMETRICS ECM 312S DATE: NOVEMBER 2014 MARKS: 100 TIME: 3 HOURS NOVEMBER EXAMINATION:

POLYTECHNIC OF NAMIBIA SCHOOL OF MANAGEMENT SCIENCES DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE COURSE: COURSE CODE: ECONOMETRICS ECM 312S DATE: NOVEMBER 2014 MARKS: 100 TIME: 3 HOURS NOVEMBER EXAMINATION:

SUSTAINABILITY PLANNING POLICY COLLECTING THE REVENUES OF THE TAX ADMINISTRATION

2007 2008 2009 2010 Year IX, No.12/2010 127 SUSTAINABILITY PLANNING POLICY COLLECTING THE REVENUES OF THE TAX ADMINISTRATION Prof. Marius HERBEI, PhD Gheorghe MOCAN, PhD West University, Timişoara I. Introduction

2007 2008 2009 2010 Year IX, No.12/2010 127 SUSTAINABILITY PLANNING POLICY COLLECTING THE REVENUES OF THE TAX ADMINISTRATION Prof. Marius HERBEI, PhD Gheorghe MOCAN, PhD West University, Timişoara I. Introduction

Forecasting the Philippine Stock Exchange Index using Time Series Analysis Box-Jenkins

EUROPEAN ACADEMIC RESEARCH Vol. III, Issue 3/ June 2015 ISSN 2286-4822 www.euacademic.org Impact Factor: 3.4546 (UIF) DRJI Value: 5.9 (B+) Forecasting the Philippine Stock Exchange Index using Time HERO

EUROPEAN ACADEMIC RESEARCH Vol. III, Issue 3/ June 2015 ISSN 2286-4822 www.euacademic.org Impact Factor: 3.4546 (UIF) DRJI Value: 5.9 (B+) Forecasting the Philippine Stock Exchange Index using Time HERO

COMMONWEALTH JOURNAL OF COMMERCE & MANAGEMENT RESEARCH AN ANALYSIS OF RELATIONSHIP BETWEEN GOLD & CRUDEOIL PRICES WITH SENSEX AND NIFTY

AN ANALYSIS OF RELATIONSHIP BETWEEN GOLD & CRUDEOIL PRICES WITH SENSEX AND NIFTY Dr. S. Nirmala Research Supervisor, Associate Professor- Department of Business Administration & Principal, PSGR Krishnammal

AN ANALYSIS OF RELATIONSHIP BETWEEN GOLD & CRUDEOIL PRICES WITH SENSEX AND NIFTY Dr. S. Nirmala Research Supervisor, Associate Professor- Department of Business Administration & Principal, PSGR Krishnammal

Brief Sketch of Solutions: Tutorial 1. 2) descriptive statistics and correlogram. Series: LGCSI Sample 12/31/ /11/2009 Observations 2596

descriptive statistics and correlogram. Series: LGCSI Sample 12/31/ /11/2009 Observations 2596") Brief Sketch of Solutions: Tutorial 1 2) descriptive statistics and correlogram 240 200 160 120 80 40 0 4.8 5.0 5.2 5.4 5.6 5.8 6.0 6.2 Series: LGCSI Sample 12/31/1999 12/11/2009 Observations 2596 Mean

Brief Sketch of Solutions: Tutorial 1 2) descriptive statistics and correlogram 240 200 160 120 80 40 0 4.8 5.0 5.2 5.4 5.6 5.8 6.0 6.2 Series: LGCSI Sample 12/31/1999 12/11/2009 Observations 2596 Mean

Foreign and Public Investment and Economic Growth: The Case of Romania

MPRA Munich Personal RePEc Archive Foreign and Public Investment and Economic Growth: The Case of Romania Cristian Valeriu Stanciu and Narcis Eduard Mitu University of Craiova, Faculty of Economics and

MPRA Munich Personal RePEc Archive Foreign and Public Investment and Economic Growth: The Case of Romania Cristian Valeriu Stanciu and Narcis Eduard Mitu University of Craiova, Faculty of Economics and

ANALYSIS OF CORRELATION BETWEEN THE EXPENSES OF SOCIAL PROTECTION AND THE ANTICIPATED OLD AGE PENSION

ANALYSIS OF CORRELATION BETWEEN THE EXPENSES OF SOCIAL PROTECTION AND THE ANTICIPATED OLD AGE PENSION Nicolae Daniel Militaru Ph. D Abstract: In this article, I have analysed two components of our social

ANALYSIS OF CORRELATION BETWEEN THE EXPENSES OF SOCIAL PROTECTION AND THE ANTICIPATED OLD AGE PENSION Nicolae Daniel Militaru Ph. D Abstract: In this article, I have analysed two components of our social

Conflict of Exchange Rates

MPRA Munich Personal RePEc Archive Conflict of Exchange Rates Rituparna Das and U R Daga 2004 Online at http://mpra.ub.uni-muenchen.de/22702/ MPRA Paper No. 22702, posted 17. May 2010 13:37 UTC Econometrics

MPRA Munich Personal RePEc Archive Conflict of Exchange Rates Rituparna Das and U R Daga 2004 Online at http://mpra.ub.uni-muenchen.de/22702/ MPRA Paper No. 22702, posted 17. May 2010 13:37 UTC Econometrics

AN EMPIRICAL ANALYSIS OF THE PUBLIC DEBT RELEVANCE TO THE ECONOMIC GROWTH OF THE USA

AN EMPIRICAL ANALYSIS OF THE PUBLIC DEBT RELEVANCE TO THE ECONOMIC GROWTH OF THE USA Petar Kurečić University North, Koprivnica, Trg Žarka Dolinara 1, Croatia petar.kurecic@unin.hr Marin Milković University

AN EMPIRICAL ANALYSIS OF THE PUBLIC DEBT RELEVANCE TO THE ECONOMIC GROWTH OF THE USA Petar Kurečić University North, Koprivnica, Trg Žarka Dolinara 1, Croatia petar.kurecic@unin.hr Marin Milković University

Balance of payments and policies that affects its positioning in Nigeria

MPRA Munich Personal RePEc Archive Balance of payments and policies that affects its positioning in Nigeria Anulika Azubike Nnamdi Azikiwe University, Awka, Anambra State, Nigeria. 1 November 2016 Online

MPRA Munich Personal RePEc Archive Balance of payments and policies that affects its positioning in Nigeria Anulika Azubike Nnamdi Azikiwe University, Awka, Anambra State, Nigeria. 1 November 2016 Online

Unemployment and Labour Force Participation in Italy

MPRA Munich Personal RePEc Archive Unemployment and Labour Force Participation in Italy Francesco Nemore Università degli studi di Bari Aldo Moro 8 March 2018 Online at https://mpra.ub.uni-muenchen.de/85067/

MPRA Munich Personal RePEc Archive Unemployment and Labour Force Participation in Italy Francesco Nemore Università degli studi di Bari Aldo Moro 8 March 2018 Online at https://mpra.ub.uni-muenchen.de/85067/

Estimating Egypt s Potential Output: A Production Function Approach

MPRA Munich Personal RePEc Archive Estimating Egypt s Potential Output: A Production Function Approach Osama El-Baz Economist, osamaeces@gmail.com 20 May 2016 Online at https://mpra.ub.uni-muenchen.de/71652/

MPRA Munich Personal RePEc Archive Estimating Egypt s Potential Output: A Production Function Approach Osama El-Baz Economist, osamaeces@gmail.com 20 May 2016 Online at https://mpra.ub.uni-muenchen.de/71652/

The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock

MPRA Munich Personal RePEc Archive The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock Binh Le Thanh International University of Japan 15. August 2015 Online

MPRA Munich Personal RePEc Archive The source of real and nominal exchange rate fluctuations in Thailand: Real shock or nominal shock Binh Le Thanh International University of Japan 15. August 2015 Online

An Examination of Seasonality in Indian Stock Markets With Reference to NSE

SUMEDHA JOURNAL OF MANAGEMENT, Vol.3 No.3 July-September, 2014 ISSN: 2277-6753, Impact Factor:0.305, Index Copernicus Value: 5.20 An Examination of Seasonality in Indian Stock Markets With Reference to

SUMEDHA JOURNAL OF MANAGEMENT, Vol.3 No.3 July-September, 2014 ISSN: 2277-6753, Impact Factor:0.305, Index Copernicus Value: 5.20 An Examination of Seasonality in Indian Stock Markets With Reference to

Empirical Analysis of Private Investments: The Case of Pakistan

2011 International Conference on Sociality and Economics Development IPEDR vol.10 (2011) (2011) IACSIT Press, Singapore Empirical Analysis of Private Investments: The Case of Pakistan Dr. Asma Salman 1

2011 International Conference on Sociality and Economics Development IPEDR vol.10 (2011) (2011) IACSIT Press, Singapore Empirical Analysis of Private Investments: The Case of Pakistan Dr. Asma Salman 1

Econometric Models for the Analysis of Financial Portfolios

Econometric Models for the Analysis of Financial Portfolios Professor Gabriela Victoria ANGHELACHE, Ph.D. Academy of Economic Studies Bucharest Professor Constantin ANGHELACHE, Ph.D. Artifex University

Econometric Models for the Analysis of Financial Portfolios Professor Gabriela Victoria ANGHELACHE, Ph.D. Academy of Economic Studies Bucharest Professor Constantin ANGHELACHE, Ph.D. Artifex University

CAN MONEY SUPPLY PREDICT STOCK PRICES?

54 JOURNAL FOR ECONOMIC EDUCATORS, 8(2), FALL 2008 CAN MONEY SUPPLY PREDICT STOCK PRICES? Sara Alatiqi and Shokoofeh Fazel 1 ABSTRACT A positive causal relation from money supply to stock prices is frequently

54 JOURNAL FOR ECONOMIC EDUCATORS, 8(2), FALL 2008 CAN MONEY SUPPLY PREDICT STOCK PRICES? Sara Alatiqi and Shokoofeh Fazel 1 ABSTRACT A positive causal relation from money supply to stock prices is frequently

Estimation, Analysis and Projection of India s GDP

MPRA Munich Personal RePEc Archive Estimation, Analysis and Projection of India s GDP Ugam Raj Daga and Rituparna Das and Bhishma Maheshwari 2004 Online at https://mpra.ub.uni-muenchen.de/22830/ MPRA Paper

MPRA Munich Personal RePEc Archive Estimation, Analysis and Projection of India s GDP Ugam Raj Daga and Rituparna Das and Bhishma Maheshwari 2004 Online at https://mpra.ub.uni-muenchen.de/22830/ MPRA Paper

Trade Openness, Economic Growth and Unemployment Reduction in Arab Region

International Journal of Economics and Financial Issues ISSN: 2146-4138 available at http: www.econjournals.com International Journal of Economics and Financial Issues, 2018, 8(1), 179-183. Trade Openness,

International Journal of Economics and Financial Issues ISSN: 2146-4138 available at http: www.econjournals.com International Journal of Economics and Financial Issues, 2018, 8(1), 179-183. Trade Openness,

Factor Affecting Yields for Treasury Bills In Pakistan?

Factor Affecting Yields for Treasury Bills In Pakistan? Masood Urahman* Department of Applied Economics, Institute of Management Sciences 1-A, Sector E-5, Phase VII, Hayatabad, Peshawar, Pakistan Muhammad

Factor Affecting Yields for Treasury Bills In Pakistan? Masood Urahman* Department of Applied Economics, Institute of Management Sciences 1-A, Sector E-5, Phase VII, Hayatabad, Peshawar, Pakistan Muhammad

The Credit Cycle and the Business Cycle in the Economy of Turkey

Chinese Business Review, March 2016, Vol. 15, No. 3, 123-131 doi: 10.17265/1537-1506/2016.03.003 D DAVID PUBLISHING The Credit Cycle and the Business Cycle in the Economy of Turkey Şehnaz Bakır Yiğitbaş

Chinese Business Review, March 2016, Vol. 15, No. 3, 123-131 doi: 10.17265/1537-1506/2016.03.003 D DAVID PUBLISHING The Credit Cycle and the Business Cycle in the Economy of Turkey Şehnaz Bakır Yiğitbaş

Determinants of Stock Prices in Ghana

Current Research Journal of Economic Theory 5(4): 66-7, 213 ISSN: 242-4841, e-issn: 242-485X Maxwell Scientific Organization, 213 Submitted: November 8, 212 Accepted: December 21, 212 Published: December

Current Research Journal of Economic Theory 5(4): 66-7, 213 ISSN: 242-4841, e-issn: 242-485X Maxwell Scientific Organization, 213 Submitted: November 8, 212 Accepted: December 21, 212 Published: December

Asian Economic and Financial Review SOURCES OF EXCHANGE RATE FLUCTUATION IN VIETNAM: AN APPLICATION OF THE SVAR MODEL

Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 journal homepage: http://www.aessweb.com/journals/5002 SOURCES OF EXCHANGE RATE FLUCTUATION IN VIETNAM: AN APPLICATION OF THE SVAR

Asian Economic and Financial Review ISSN(e): 2222-6737/ISSN(p): 2305-2147 journal homepage: http://www.aessweb.com/journals/5002 SOURCES OF EXCHANGE RATE FLUCTUATION IN VIETNAM: AN APPLICATION OF THE SVAR

LAMPIRAN. Null Hypothesis: LO has a unit root Exogenous: Constant Lag Length: 1 (Automatic based on SIC, MAXLAG=13)

") 74 LAMPIRAN Lampiran 1 Analisis ARIMA 1.1. Uji Stasioneritas Variabel 1. Data Harga Minyak Riil Level Null Hypothesis: LO has a unit root Lag Length: 1 (Automatic based on SIC, MAXLAG=13) Augmented Dickey-Fuller

74 LAMPIRAN Lampiran 1 Analisis ARIMA 1.1. Uji Stasioneritas Variabel 1. Data Harga Minyak Riil Level Null Hypothesis: LO has a unit root Lag Length: 1 (Automatic based on SIC, MAXLAG=13) Augmented Dickey-Fuller

Kabupaten Langkat Suku Bunga Kredit. PDRB harga berlaku

Lampiran 1. Data Penelitian Tahun Konsumsi Masyarakat PDRB harga berlaku Kabupaten Langkat Suku Bunga Kredit Kredit Konsumsi Tabungan Masyarkat Milyar Rp. Milyar Rp. % Milyar Rp. Milyar Rp. 1990 559,61

Lampiran 1. Data Penelitian Tahun Konsumsi Masyarakat PDRB harga berlaku Kabupaten Langkat Suku Bunga Kredit Kredit Konsumsi Tabungan Masyarkat Milyar Rp. Milyar Rp. % Milyar Rp. Milyar Rp. 1990 559,61

Appendices. Appendix 1 Buy ranges for each portfolio

Appendices Appendix 1 Buy ranges for each portfolio 67 Appendix 2 Every recession declared by the NBER Source: The National Bureau of Economic Research 68 Appendix 3 Multifactor portfolio mathematics Mathematics

Appendices Appendix 1 Buy ranges for each portfolio 67 Appendix 2 Every recession declared by the NBER Source: The National Bureau of Economic Research 68 Appendix 3 Multifactor portfolio mathematics Mathematics

A causal relationship between foreign direct investment, economic growth and export for Central and Eastern Europe Zuzana Gallová 1

A causal relationship between foreign direct investment, economic growth and export for Central and Eastern Europe Zuzana Gallová 1 1 Introduction Abstract. Foreign direct investment is generally considered

A causal relationship between foreign direct investment, economic growth and export for Central and Eastern Europe Zuzana Gallová 1 1 Introduction Abstract. Foreign direct investment is generally considered

What is the effect of inflation on consumer spending behaviour in Ghana?

MPRA Munich Personal RePEc Archive What is the effect of inflation on consumer spending behaviour in Ghana? Gabriel Effah Nyamekye and Eugene Adusei Poku Sunyani Technical University 31 March 217 Online

MPRA Munich Personal RePEc Archive What is the effect of inflation on consumer spending behaviour in Ghana? Gabriel Effah Nyamekye and Eugene Adusei Poku Sunyani Technical University 31 March 217 Online

International capital flows and GDP growth

Volume: 2, Issue: 5, 315-319 May 2015 www.allsubjectjournal.com e-issn: 2349-4182 p-issn: 2349-5979 Impact Factor: 3.762 Department of Economics, Rajeev Gandhi Tribal University, Udaipur, Rajasthan, India

Volume: 2, Issue: 5, 315-319 May 2015 www.allsubjectjournal.com e-issn: 2349-4182 p-issn: 2349-5979 Impact Factor: 3.762 Department of Economics, Rajeev Gandhi Tribal University, Udaipur, Rajasthan, India

An empirical study on the dynamic relationship between crude oil prices and Nigeria stock market

An empirical study on the dynamic relationship between crude oil prices and Nigeria stock market Abstract In this paper, we have examined the crude oil price on the performance of Nigerian stock exchange

An empirical study on the dynamic relationship between crude oil prices and Nigeria stock market Abstract In this paper, we have examined the crude oil price on the performance of Nigerian stock exchange

Prerequisites for modeling price and return data series for the Bucharest Stock Exchange

Theoretical and Applied Economics Volume XX (2013), No. 11(588), pp. 117-126 Prerequisites for modeling price and return data series for the Bucharest Stock Exchange Andrei TINCA The Bucharest University

Theoretical and Applied Economics Volume XX (2013), No. 11(588), pp. 117-126 Prerequisites for modeling price and return data series for the Bucharest Stock Exchange Andrei TINCA The Bucharest University

IMPLICATIONS OF FINANCIAL INTERMEDIATION COST ON ECONOMIC GROWTH IN NIGERIA.

IMPLICATIONS OF FINANCIAL INTERMEDIATION COST ON ECONOMIC GROWTH IN NIGERIA. Dr. Nwanne, T. F. I. Ph.D, HCIB Department of Accounting/Finance, Faculty of Management and Social Sciences Godfrey Okoye University,

IMPLICATIONS OF FINANCIAL INTERMEDIATION COST ON ECONOMIC GROWTH IN NIGERIA. Dr. Nwanne, T. F. I. Ph.D, HCIB Department of Accounting/Finance, Faculty of Management and Social Sciences Godfrey Okoye University,

A case study of Cointegration relationship between Tax Revenue and Foreign Direct Investment: Evidence from Sri Lanka

Abstract A case study of Cointegration relationship between Tax Revenue and Foreign Direct Investment: Evidence from Sri Lanka Mr. AL. Mohamed Aslam Ministry of Finance and Planning, Colombo. (mohamedaslamalm@gmail.com)

Abstract A case study of Cointegration relationship between Tax Revenue and Foreign Direct Investment: Evidence from Sri Lanka Mr. AL. Mohamed Aslam Ministry of Finance and Planning, Colombo. (mohamedaslamalm@gmail.com)

Comparative analysis of monetary and fiscal Policy: a case study of Pakistan

MPRA Munich Personal RePEc Archive Comparative analysis of monetary and fiscal Policy: a case study of Pakistan Syed Tehseen Jawaid and Imtiaz Arif and Syed Muhammad Naeemullah December 2010 Online at

MPRA Munich Personal RePEc Archive Comparative analysis of monetary and fiscal Policy: a case study of Pakistan Syed Tehseen Jawaid and Imtiaz Arif and Syed Muhammad Naeemullah December 2010 Online at

ijcrb.webs.com INTERDISCIPLINARY JOURNAL OF CONTEMPORARY RESEARCH IN BUSINESS AUGUST 2012 VOL 4, NO 4

IMPORTANCE OF INVESTMENT FOR ECONOMIC GROWTH: EVIDENCE FROM PAKISTAN Najid Ahmad*, Muhammad luqman**, Muhammad Farhat Hayat* *Bahauddin Zakariya University, Multan, Sub-Campus Dera Ghazi Khan, Pakistan

IMPORTANCE OF INVESTMENT FOR ECONOMIC GROWTH: EVIDENCE FROM PAKISTAN Najid Ahmad*, Muhammad luqman**, Muhammad Farhat Hayat* *Bahauddin Zakariya University, Multan, Sub-Campus Dera Ghazi Khan, Pakistan

Discussion Paper Series No.196. An Empirical Test of the Efficiency Hypothesis on the Renminbi NDF in Hong Kong Market.

Discussion Paper Series No.196 An Empirical Test of the Efficiency Hypothesis on the Renminbi NDF in Hong Kong Market IZAWA Hideki Kobe University November 2006 The Discussion Papers are a series of research

Discussion Paper Series No.196 An Empirical Test of the Efficiency Hypothesis on the Renminbi NDF in Hong Kong Market IZAWA Hideki Kobe University November 2006 The Discussion Papers are a series of research

LAMPIRAN. Lampiran I

67 LAMPIRAN Lampiran I Data Volume Impor Jagung Indonesia, Harga Impor Jagung, Produksi Jagung Nasional, Nilai Tukar Rupiah/USD, Produk Domestik Bruto (PDB) per kapita Tahun Y X1 X2 X3 X4 1995 969193.394

67 LAMPIRAN Lampiran I Data Volume Impor Jagung Indonesia, Harga Impor Jagung, Produksi Jagung Nasional, Nilai Tukar Rupiah/USD, Produk Domestik Bruto (PDB) per kapita Tahun Y X1 X2 X3 X4 1995 969193.394

Fiscal Policy and Economic Growth Relationship in Nigeria

International Journal of Business and Social Science Vol. 2 No. 17 www.ijbssnet.com 244 Fiscal Policy and Economic Growth Relationship in Nigeria Sikiru Jimoh Babalola (Corresponding Author) Lecturer Department

International Journal of Business and Social Science Vol. 2 No. 17 www.ijbssnet.com 244 Fiscal Policy and Economic Growth Relationship in Nigeria Sikiru Jimoh Babalola (Corresponding Author) Lecturer Department

Economic Determinants of Unemployment: Empirical Result from Pakistan

Economic Determinants of Unemployment: Empirical Result from Pakistan Gul mina sabir Institute of Management Sciences Peshawar, Pakistan House no 38 A/B civil Quarters Kohat Road Peshawar Mahadalidurrani@gmail.cm

Economic Determinants of Unemployment: Empirical Result from Pakistan Gul mina sabir Institute of Management Sciences Peshawar, Pakistan House no 38 A/B civil Quarters Kohat Road Peshawar Mahadalidurrani@gmail.cm

Donald Trump's Random Walk Up Wall Street

Donald Trump's Random Walk Up Wall Street Research Question: Did upward stock market trend since beginning of Obama era in January 2009 increase after Donald Trump was elected President? Data: Daily data

Donald Trump's Random Walk Up Wall Street Research Question: Did upward stock market trend since beginning of Obama era in January 2009 increase after Donald Trump was elected President? Data: Daily data

Exchange Rate and Economic Performance - A Comparative Study of Developed and Developing Countries

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X. Volume 8, Issue 1 (Jan. - Feb. 2013), PP 116-121 Exchange Rate and Economic Performance - A Comparative Study of Developed and Developing

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X. Volume 8, Issue 1 (Jan. - Feb. 2013), PP 116-121 Exchange Rate and Economic Performance - A Comparative Study of Developed and Developing

Would Central Banks Intervention Cause Uncertainty in the Foreign Exchange Market?

International Business Research; Vol. 8, No. 9; 2015 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education Would Central Banks Intervention Cause Uncertainty in the Foreign

International Business Research; Vol. 8, No. 9; 2015 ISSN 1913-9004 E-ISSN 1913-9012 Published by Canadian Center of Science and Education Would Central Banks Intervention Cause Uncertainty in the Foreign

Testing the Stability of Demand for Money in Tonga

MPRA Munich Personal RePEc Archive Testing the Stability of Demand for Money in Tonga Saten Kumar and Billy Manoka University of the South Pacific, University of Papua New Guinea 12. June 2008 Online at

MPRA Munich Personal RePEc Archive Testing the Stability of Demand for Money in Tonga Saten Kumar and Billy Manoka University of the South Pacific, University of Papua New Guinea 12. June 2008 Online at

THE CREDIT CYCLE and the BUSINESS CYCLE in the ECONOMY of TURKEY

810 September 2014 Istanbul, Turkey 442 THE CYCLE and the BUSINESS CYCLE in the ECONOMY of TURKEY Şehnaz Bakır Yiğitbaş 1 1 Dr. Lecturer, Çanakkale Onsekiz Mart University, TURKEY, sehnazbakir@comu.edu.tr

810 September 2014 Istanbul, Turkey 442 THE CYCLE and the BUSINESS CYCLE in the ECONOMY of TURKEY Şehnaz Bakır Yiğitbaş 1 1 Dr. Lecturer, Çanakkale Onsekiz Mart University, TURKEY, sehnazbakir@comu.edu.tr

Back from the Dead: the GFC and the Resurrection of Long Term Unemployment

Back from the Dead: the GFC and the Resurrection of Long Term Unemployment Bruce Chapman* Crawford School of Economics and Government School Seminar Australian National University September 22 2009 * With

Back from the Dead: the GFC and the Resurrection of Long Term Unemployment Bruce Chapman* Crawford School of Economics and Government School Seminar Australian National University September 22 2009 * With

LAMPIRAN. Tahun Bulan NPF (Milyar Rupiah)

") LAMPIRAN Lampiran 1 Data Penelitian Non Performing Financing (NPF), Capital Adequacy Ratio (CAR), Financing to Deposit Ratio (FDR), Biaya Operasional Pendapatan Operasional (BOPO), Ukuran Bank (Size) Tahun

LAMPIRAN Lampiran 1 Data Penelitian Non Performing Financing (NPF), Capital Adequacy Ratio (CAR), Financing to Deposit Ratio (FDR), Biaya Operasional Pendapatan Operasional (BOPO), Ukuran Bank (Size) Tahun

Empirical Study on Short-Term Prediction of Shanghai Composite Index Based on ARMA Model

Empirical Study on Short-Term Prediction of Shanghai Composite Index Based on ARMA Model Cai-xia Xiang 1, Ping Xiao 2* 1 (School of Hunan University of Humanities, Science and Technology, Hunan417000,

Empirical Study on Short-Term Prediction of Shanghai Composite Index Based on ARMA Model Cai-xia Xiang 1, Ping Xiao 2* 1 (School of Hunan University of Humanities, Science and Technology, Hunan417000,

Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and Its Extended Forms

Discrete Dynamics in Nature and Society Volume 2009, Article ID 743685, 9 pages doi:10.1155/2009/743685 Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and

Discrete Dynamics in Nature and Society Volume 2009, Article ID 743685, 9 pages doi:10.1155/2009/743685 Research Article The Volatility of the Index of Shanghai Stock Market Research Based on ARCH and

IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY

7 IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY 7.1 Introduction: In the recent past, worldwide there have been certain changes in the economic policies of a no. of countries.

7 IMPACT OF MACROECONOMIC VARIABLE ON STOCK MARKET RETURN AND ITS VOLATILITY 7.1 Introduction: In the recent past, worldwide there have been certain changes in the economic policies of a no. of countries.

A Note on the Oil Price Trend and GARCH Shocks

MPRA Munich Personal RePEc Archive A Note on the Oil Price Trend and GARCH Shocks Li Jing and Henry Thompson 2010 Online at http://mpra.ub.uni-muenchen.de/20654/ MPRA Paper No. 20654, posted 13. February

MPRA Munich Personal RePEc Archive A Note on the Oil Price Trend and GARCH Shocks Li Jing and Henry Thompson 2010 Online at http://mpra.ub.uni-muenchen.de/20654/ MPRA Paper No. 20654, posted 13. February

Trade Liberalization, Financial Liberalization and Economic Growth: A Case Study of Pakistan

Trade Liberalization, Financial Liberalization and Economic Growth: A Case Study of Pakistan Hina Ali *Fozia Shaheen Abstract: The study emphasis to explore the Trade Liberalization, Financial Liberalization

Trade Liberalization, Financial Liberalization and Economic Growth: A Case Study of Pakistan Hina Ali *Fozia Shaheen Abstract: The study emphasis to explore the Trade Liberalization, Financial Liberalization

Determinants of Merchandise Export Performance in Sri Lanka

Determinants of Merchandise Export Performance in Sri Lanka L.U. Kalpage 1 * and T.M.J.A. Cooray 2 1 Central Environmental Authority, Battaramulla 2 Department of Mathematics, University of Moratuwa *Corresponding

Determinants of Merchandise Export Performance in Sri Lanka L.U. Kalpage 1 * and T.M.J.A. Cooray 2 1 Central Environmental Authority, Battaramulla 2 Department of Mathematics, University of Moratuwa *Corresponding

A SEARCH FOR A STABLE LONG RUN MONEY DEMAND FUNCTION FOR THE US

A. Journal. Bis. Stus. 5(3):01-12, May 2015 An online Journal of G -Science Implementation & Publication, website: www.gscience.net A SEARCH FOR A STABLE LONG RUN MONEY DEMAND FUNCTION FOR THE US H. HUSAIN

A. Journal. Bis. Stus. 5(3):01-12, May 2015 An online Journal of G -Science Implementation & Publication, website: www.gscience.net A SEARCH FOR A STABLE LONG RUN MONEY DEMAND FUNCTION FOR THE US H. HUSAIN

Liquidity Risk Management: A Comparative Study between Domestic and Foreign Banks in Pakistan Asim Abdullah & Abdul Qayyum Khan

A Comparative Study between Domestic and Foreign Banks in Pakistan Asim Abdullah & Abdul Qayyum Khan Abstract The purpose of this study is to establish the firms level aspects which have more influence

A Comparative Study between Domestic and Foreign Banks in Pakistan Asim Abdullah & Abdul Qayyum Khan Abstract The purpose of this study is to establish the firms level aspects which have more influence

Per Capita Housing Starts: Forecasting and the Effects of Interest Rate

1 David I. Goodman The University of Idaho Economics 351 Professor Ismail H. Genc March 13th, 2003 Per Capita Housing Starts: Forecasting and the Effects of Interest Rate Abstract This study examines the

1 David I. Goodman The University of Idaho Economics 351 Professor Ismail H. Genc March 13th, 2003 Per Capita Housing Starts: Forecasting and the Effects of Interest Rate Abstract This study examines the

Lampiran 1. Data Penelitian

LAMPIRAN Lampiran 1. Data Penelitian Tahun Impor PDB KURS DEVISA 1985 5.199,00 2.118.215,40 1.125,00 5.811,00 1986 5.825,00 2.242.661,60 1.641,00 5.841,00 1987 7.209,00 2.353.133,40 1.650,00 5.103,00 1988

LAMPIRAN Lampiran 1. Data Penelitian Tahun Impor PDB KURS DEVISA 1985 5.199,00 2.118.215,40 1.125,00 5.811,00 1986 5.825,00 2.242.661,60 1.641,00 5.841,00 1987 7.209,00 2.353.133,40 1.650,00 5.103,00 1988

ARCH modeling of the returns of first bank of Nigeria

AMERICAN JOURNAL OF SCIENTIFIC AND INDUSTRIAL RESEARCH 015,Science Huβ, http://www.scihub.org/ajsir ISSN: 153-649X, doi:10.551/ajsir.015.6.6.131.140 ARCH modeling of the returns of first bank of Nigeria

AMERICAN JOURNAL OF SCIENTIFIC AND INDUSTRIAL RESEARCH 015,Science Huβ, http://www.scihub.org/ajsir ISSN: 153-649X, doi:10.551/ajsir.015.6.6.131.140 ARCH modeling of the returns of first bank of Nigeria

Interactions between United States (VIX) and United Kingdom (VFTSE) Market Volatility: A Time Series Study

and United Kingdom (VFTSE) Market Volatility: A Time Series Study") Sacred Heart University DigitalCommons@SHU WCOB Student Papers Jack Welch College of Business 4-2017 Interactions between United States (VIX) and United Kingdom (VFTSE) Market Volatility: A Time Series

Sacred Heart University DigitalCommons@SHU WCOB Student Papers Jack Welch College of Business 4-2017 Interactions between United States (VIX) and United Kingdom (VFTSE) Market Volatility: A Time Series

The Impacts of Financial Crisis on Pakistan Economy: An Empirical Approach

International Journal of Empirical Finance Vol. 4, No. 5, 2015, 258-269 The Impacts of Financial Crisis on Pakistan Economy: An Empirical Approach Khalid Mughal 1, Irfan Khan 2, Farhat Usman 3 Abstract

International Journal of Empirical Finance Vol. 4, No. 5, 2015, 258-269 The Impacts of Financial Crisis on Pakistan Economy: An Empirical Approach Khalid Mughal 1, Irfan Khan 2, Farhat Usman 3 Abstract

CHAPTER 5 MARKET LEVEL INDUSTRY LEVEL AND FIRM LEVEL VOLATILITY

CHAPTER 5 MARKET LEVEL INDUSTRY LEVEL AND FIRM LEVEL VOLATILITY In previous chapter focused on aggregate stock market volatility of Indian Stock Exchange and showed that it is not constant but changes

CHAPTER 5 MARKET LEVEL INDUSTRY LEVEL AND FIRM LEVEL VOLATILITY In previous chapter focused on aggregate stock market volatility of Indian Stock Exchange and showed that it is not constant but changes

THE IMPACT OF BANKING RISKS ON THE CAPITAL OF COMMERCIAL BANKS IN LIBYA

THE IMPACT OF BANKING RISKS ON THE CAPITAL OF COMMERCIAL BANKS IN LIBYA Azeddin ARAB Kastamonu University, Turkey, Institute for Social Sciences, Department of Business Abstract: The objective of this

THE IMPACT OF BANKING RISKS ON THE CAPITAL OF COMMERCIAL BANKS IN LIBYA Azeddin ARAB Kastamonu University, Turkey, Institute for Social Sciences, Department of Business Abstract: The objective of this

Chapter 4 Level of Volatility in the Indian Stock Market

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

Chapter 4 Level of Volatility in the Indian Stock Market Measurement of volatility is an important issue in financial econometrics. The main reason for the prominent role that volatility plays in financial

The Frequency of Wars*

The Frequency of Wars* Mark Harrison** Department of Economics and CAGE, University of Warwick Centre for Russian and East European Studies, University of Birmingham Hoover Institution, Stanford University

The Frequency of Wars* Mark Harrison** Department of Economics and CAGE, University of Warwick Centre for Russian and East European Studies, University of Birmingham Hoover Institution, Stanford University

THE IMPACT OF IMPORT ON INFLATION IN NAMIBIA

European Journal of Business, Economics and Accountancy Vol. 5, No. 2, 207 ISSN 2056-608 THE IMPACT OF IMPORT ON INFLATION IN NAMIBIA Mika Munepapa Namibia University of Science and Technology NAMIBIA

European Journal of Business, Economics and Accountancy Vol. 5, No. 2, 207 ISSN 2056-608 THE IMPACT OF IMPORT ON INFLATION IN NAMIBIA Mika Munepapa Namibia University of Science and Technology NAMIBIA

An Empirical Study on the Determinants of Dollarization in Cambodia *

An Empirical Study on the Determinants of Dollarization in Cambodia * Socheat CHIM Graduate School of Economics, Osaka University 1-7 Machikaneyama, Toyonaka, Osaka, 560-0043, Japan E-mail: chimsocheat3@yahoo.com

An Empirical Study on the Determinants of Dollarization in Cambodia * Socheat CHIM Graduate School of Economics, Osaka University 1-7 Machikaneyama, Toyonaka, Osaka, 560-0043, Japan E-mail: chimsocheat3@yahoo.com

Interrelationship between Profitability, Financial Leverage and Capital Structure of Textile Industry in India Dr. Ruchi Malhotra

Interrelationship between Profitability, Financial Leverage and Capital Structure of Textile Industry in India Dr. Ruchi Malhotra Assistant Professor, Department of Commerce, Sri Guru Granth Sahib World

Interrelationship between Profitability, Financial Leverage and Capital Structure of Textile Industry in India Dr. Ruchi Malhotra Assistant Professor, Department of Commerce, Sri Guru Granth Sahib World

An Analysis of Stock Returns and Exchange Rates: Evidence from IT Industry in India

Columbia International Publishing Journal of Advanced Computing doi:10.7726/jac.2016.1001 Research Article An Analysis of Stock Returns and Exchange Rates: Evidence from IT Industry in India Nataraja N.S

Columbia International Publishing Journal of Advanced Computing doi:10.7726/jac.2016.1001 Research Article An Analysis of Stock Returns and Exchange Rates: Evidence from IT Industry in India Nataraja N.S

THE EFFECTIVENESS OF EXCHANGE RATE CHANNEL OF MONETARY POLICY TRANSMISSION MECHANISM IN SRI LANKA

THE EFFECTIVENESS OF EXCHANGE RATE CHANNEL OF MONETARY POLICY TRANSMISSION MECHANISM IN SRI LANKA N.D.V. Sandaroo 1 Sri Lanka Journal of Economic Research Volume 5(1) November 2017 SLJER.05.01.B: pp.31-48

THE EFFECTIVENESS OF EXCHANGE RATE CHANNEL OF MONETARY POLICY TRANSMISSION MECHANISM IN SRI LANKA N.D.V. Sandaroo 1 Sri Lanka Journal of Economic Research Volume 5(1) November 2017 SLJER.05.01.B: pp.31-48

Determinants of Cyclical Aggregate Dividend Behavior

Review of Economics & Finance Submitted on 01/Apr./2012 Article ID: 1923-7529-2012-03-71-08 Samih Antoine Azar Determinants of Cyclical Aggregate Dividend Behavior Dr. Samih Antoine Azar Faculty of Business

Review of Economics & Finance Submitted on 01/Apr./2012 Article ID: 1923-7529-2012-03-71-08 Samih Antoine Azar Determinants of Cyclical Aggregate Dividend Behavior Dr. Samih Antoine Azar Faculty of Business

RESEARCH ON INFLUENCING FACTORS OF RURAL CONSUMPTION IN CHINA-TAKE SHANDONG PROVINCE AS AN EXAMPLE.

335 RESEARCH ON INFLUENCING FACTORS OF RURAL CONSUMPTION IN CHINA-TAKE SHANDONG PROVINCE AS AN EXAMPLE. Yujing Hao, Shuaizhen Wang, guohua Chen * Department of Mathematics and Finance Hunan University

335 RESEARCH ON INFLUENCING FACTORS OF RURAL CONSUMPTION IN CHINA-TAKE SHANDONG PROVINCE AS AN EXAMPLE. Yujing Hao, Shuaizhen Wang, guohua Chen * Department of Mathematics and Finance Hunan University

COINTEGRATION AND MARKET EFFICIENCY: AN APPLICATION TO THE CANADIAN TREASURY BILL MARKET. Soo-Bin Park* Carleton University, Ottawa, Canada K1S 5B6

1 COINTEGRATION AND MARKET EFFICIENCY: AN APPLICATION TO THE CANADIAN TREASURY BILL MARKET Soo-Bin Park* Carleton University, Ottawa, Canada K1S 5B6 Abstract: In this study we examine if the spot and forward

1 COINTEGRATION AND MARKET EFFICIENCY: AN APPLICATION TO THE CANADIAN TREASURY BILL MARKET Soo-Bin Park* Carleton University, Ottawa, Canada K1S 5B6 Abstract: In this study we examine if the spot and forward

Influence of Macroeconomic Indicators on Mutual Funds Market in India

Influence of Macroeconomic Indicators on Mutual Funds Market in India KAVITA Research Scholar, Department of Commerce, Punjabi University, Patiala (India) DR. J.S. PASRICHA Professor, Department of Commerce,

Influence of Macroeconomic Indicators on Mutual Funds Market in India KAVITA Research Scholar, Department of Commerce, Punjabi University, Patiala (India) DR. J.S. PASRICHA Professor, Department of Commerce,

Analysis of the Influence of the Annualized Rate of Rentability on the Unit Value of the Net Assets of the Private Administered Pension Fund NN

Year XVIII No. 20/2018 175 Analysis of the Influence of the Annualized Rate of Rentability on the Unit Value of the Net Assets of the Private Administered Pension Fund NN Constantin DURAC 1 1 University

Year XVIII No. 20/2018 175 Analysis of the Influence of the Annualized Rate of Rentability on the Unit Value of the Net Assets of the Private Administered Pension Fund NN Constantin DURAC 1 1 University

An Empirical Research on the Relationship Between Non-Interest Income Business and Operation Performance of Commercial Banks

Proceedings of the 7th International Conference on Innovation & Management 1477 An Empirical Research on the Relationship Between Non-Interest Income Business and Operation Performance of Commercial Banks

Proceedings of the 7th International Conference on Innovation & Management 1477 An Empirical Research on the Relationship Between Non-Interest Income Business and Operation Performance of Commercial Banks

Openness and Inflation

Openness and Inflation Based on David Romer s Paper Openness and Inflation: Theory and Evidence ECON 5341 Vinko Kaurin Introduction Link between openness and inflation explored Basic OLS model: y = β 0

Openness and Inflation Based on David Romer s Paper Openness and Inflation: Theory and Evidence ECON 5341 Vinko Kaurin Introduction Link between openness and inflation explored Basic OLS model: y = β 0

TRADING VOLUME REACTIONS AND THE ADOPTION OF INTERNATIONAL ACCOUNTING STANDARD (IAS 1): PRESENTATION OF FINANCIAL STATEMENTS IN INDONESIA

: PRESENTATION OF FINANCIAL STATEMENTS IN INDONESIA") TRADING VOLUME REACTIONS AND THE ADOPTION OF INTERNATIONAL ACCOUNTING STANDARD (IAS 1): PRESENTATION OF FINANCIAL STATEMENTS IN INDONESIA Beatrise Sihite, University of Indonesia Aria Farah Mita, University

TRADING VOLUME REACTIONS AND THE ADOPTION OF INTERNATIONAL ACCOUNTING STANDARD (IAS 1): PRESENTATION OF FINANCIAL STATEMENTS IN INDONESIA Beatrise Sihite, University of Indonesia Aria Farah Mita, University

DETERMINANTS OF HERDING BEHAVIOR IN MALAYSIAN STOCK MARKET Abdollah Ah Mand 1, Hawati Janor 1, Ruzita Abdul Rahim 1, Tamat Sarmidi 1

DETERMINANTS OF HERDING BEHAVIOR IN MALAYSIAN STOCK MARKET Abdollah Ah Mand 1, Hawati Janor 1, Ruzita Abdul Rahim 1, Tamat Sarmidi 1 1 Faculty of Economics and Management, University Kebangsaan Malaysia

DETERMINANTS OF HERDING BEHAVIOR IN MALAYSIAN STOCK MARKET Abdollah Ah Mand 1, Hawati Janor 1, Ruzita Abdul Rahim 1, Tamat Sarmidi 1 1 Faculty of Economics and Management, University Kebangsaan Malaysia

CHAPTER V RELATION BETWEEN FINANCIAL DEVELOPMENT AND ECONOMIC GROWTH DURING PRE AND POST LIBERALISATION PERIOD

CHAPTER V RELATION BETWEEN FINANCIAL DEVELOPMENT AND ECONOMIC GROWTH DURING PRE AND POST LIBERALISATION PERIOD V..Introduction As far as India is concerned, financial sector reforms have made tremendous

CHAPTER V RELATION BETWEEN FINANCIAL DEVELOPMENT AND ECONOMIC GROWTH DURING PRE AND POST LIBERALISATION PERIOD V..Introduction As far as India is concerned, financial sector reforms have made tremendous

Notes on the Treasury Yield Curve Forecasts. October Kara Naccarelli

Notes on the Treasury Yield Curve Forecasts October 2017 Kara Naccarelli Moody s Analytics has updated its forecast equations for the Treasury yield curve. The revised equations are the Treasury yields

Notes on the Treasury Yield Curve Forecasts October 2017 Kara Naccarelli Moody s Analytics has updated its forecast equations for the Treasury yield curve. The revised equations are the Treasury yields

International Journal of Informative & Futuristic Research ISSN:

Research Paper Volume 3 Issue 6 February 2016 International Journal of Informative & Futuristic Research A Study Of Cointegration Between Indian, American And Chinese Stock Markets Paper ID IJIFR/ V3/

Research Paper Volume 3 Issue 6 February 2016 International Journal of Informative & Futuristic Research A Study Of Cointegration Between Indian, American And Chinese Stock Markets Paper ID IJIFR/ V3/

Personal income, stock market, and investor psychology

ABSTRACT Personal income, stock market, and investor psychology Chung Baek Troy University Minjung Song Thomas University This paper examines how disposable personal income is related to investor psychology

ABSTRACT Personal income, stock market, and investor psychology Chung Baek Troy University Minjung Song Thomas University This paper examines how disposable personal income is related to investor psychology

The Influence of Leverage and Profitability on Earnings Quality: Jordanian Case

The Influence of Leverage and Profitability on Earnings Quality: Jordanian Case Lina Hani Warrad Accounting Department, Applied Science Private University, Amman, Jordan E-mail: l_warrad@asu.edu.jo DOI:

The Influence of Leverage and Profitability on Earnings Quality: Jordanian Case Lina Hani Warrad Accounting Department, Applied Science Private University, Amman, Jordan E-mail: l_warrad@asu.edu.jo DOI:

An Investigation of Effective Factors on Export in Iran

J. Basic. Appl. Sci. Res., 2(4)4092-4097, 2012 2012, TextRoad Publication ISSN 2090-4304 Journal of Basic and Applied Scientific Research www.textroad.com An Investigation of Effective Factors on Export

J. Basic. Appl. Sci. Res., 2(4)4092-4097, 2012 2012, TextRoad Publication ISSN 2090-4304 Journal of Basic and Applied Scientific Research www.textroad.com An Investigation of Effective Factors on Export

Analysis of the Relation between Treasury Stock and Common Shares Outstanding

Analysis of the Relation between Treasury Stock and Common Shares Outstanding Stoyu I. Nancie Fimbel Investment Fellow Associate Professor San José State University Accounting and Finance Department Lucas

Analysis of the Relation between Treasury Stock and Common Shares Outstanding Stoyu I. Nancie Fimbel Investment Fellow Associate Professor San José State University Accounting and Finance Department Lucas

a good strategy. As risk and return are correlated, every risk you are avoiding possibly deprives you of a

IOSR Journal of Economics and Finance (IOSR-JEF) e-issn: 2321-5933, p-issn: 2321-5925.Volume 8, Issue 4 Ver. I (Jul. Aug.2017), PP 01-07 www.iosrjournals.org An Empirical Study on the Interdependence among

IOSR Journal of Economics and Finance (IOSR-JEF) e-issn: 2321-5933, p-issn: 2321-5925.Volume 8, Issue 4 Ver. I (Jul. Aug.2017), PP 01-07 www.iosrjournals.org An Empirical Study on the Interdependence among

THE USA SHADOW ECONOMY AND THE UNEMPLOYMENT RATE: GRANGER CAUSALITY RESULTS

THE USA SHADOW ECONOMY AND THE UNEMPLOYMENT RATE: GRANGER CAUSALITY RESULTS Ion DOBRE PhD, University Professor, Department of Economic Cybernetics Vice- Dean of Faculty of Cybernetics, Statistics and

THE USA SHADOW ECONOMY AND THE UNEMPLOYMENT RATE: GRANGER CAUSALITY RESULTS Ion DOBRE PhD, University Professor, Department of Economic Cybernetics Vice- Dean of Faculty of Cybernetics, Statistics and

COTTON: PHYSICAL PRICES BECOMING MORE RESPONSIVE TO FUTURES PRICES0F

INTERNATIONAL COTTON ADVISORY COMMITTEE 1629 K Street NW, Suite 702, Washington DC 20006 USA Telephone +1-202-463-6660 Fax +1-202-463-6950 email secretariat@icac.org COTTON: PHYSICAL PRICES BECOMING 1

INTERNATIONAL COTTON ADVISORY COMMITTEE 1629 K Street NW, Suite 702, Washington DC 20006 USA Telephone +1-202-463-6660 Fax +1-202-463-6950 email secretariat@icac.org COTTON: PHYSICAL PRICES BECOMING 1

Impact of Working Capital Management on Profitability: A Case of the Pakistan Textile Industry

Impact of Working Capital Management on Profitability: A Case of the Pakistan Textile Industry Muhammad Aleem* MS Scholar, Iqra National University, Peshawar Dr. Abid Usman Associate Professor, Iqra National

Impact of Working Capital Management on Profitability: A Case of the Pakistan Textile Industry Muhammad Aleem* MS Scholar, Iqra National University, Peshawar Dr. Abid Usman Associate Professor, Iqra National

Relationship between Oil Price, Exchange Rates and Stock Market: An Empirical study of Indian stock market

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 19, Issue 1. Ver. VI (Jan. 2017), PP 28-33 www.iosrjournals.org Relationship between Oil Price, Exchange

IOSR Journal of Business and Management (IOSR-JBM) e-issn: 2278-487X, p-issn: 2319-7668. Volume 19, Issue 1. Ver. VI (Jan. 2017), PP 28-33 www.iosrjournals.org Relationship between Oil Price, Exchange

Appendix. Table A.1 (Part A) The Author(s) 2015 G. Chakrabarti and C. Sen, Green Investing, SpringerBriefs in Finance, DOI /

The Author(s) 2015 G. Chakrabarti and C. Sen, Green Investing, SpringerBriefs in Finance, DOI /") Appendix Table A.1 (Part A) Dependent variable: probability of crisis (own) Method: ML binary probit (quadratic hill climbing) Included observations: 47 after adjustments Convergence achieved after 6 iterations

Appendix Table A.1 (Part A) Dependent variable: probability of crisis (own) Method: ML binary probit (quadratic hill climbing) Included observations: 47 after adjustments Convergence achieved after 6 iterations

Anexos. Pruebas de estacionariedad. Null Hypothesis: TES has a unit root Exogenous: Constant Lag Length: 0 (Automatic - based on SIC, maxlag=9)

") Anexos Pruebas de estacionariedad Null Hypothesis: TES has a unit root Augmented Dickey-Fuller test statistic -1.739333 0.4042 Test critical values: 1% level -3.610453 5% level -2.938987 10% level -2.607932

Anexos Pruebas de estacionariedad Null Hypothesis: TES has a unit root Augmented Dickey-Fuller test statistic -1.739333 0.4042 Test critical values: 1% level -3.610453 5% level -2.938987 10% level -2.607932

A Survey of the Effects of Liberalization of Iran Non-Life Insurance Market by Using the Experiences of WTO Member Countries

A Survey of the Effects of Liberalization of Iran Non-Life Insurance Market by Using the Experiences of WTO Member Countries Marufi Aghdam Jalal 1, Eshgarf Reza 2 Abstract Today, globalization is prevalent

A Survey of the Effects of Liberalization of Iran Non-Life Insurance Market by Using the Experiences of WTO Member Countries Marufi Aghdam Jalal 1, Eshgarf Reza 2 Abstract Today, globalization is prevalent

An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh

Bangladesh Development Studies Vol. XXXIV, December 2011, No. 4 An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh NASRIN AFZAL * SYED SHAHADAT HOSSAIN

Bangladesh Development Studies Vol. XXXIV, December 2011, No. 4 An Empirical Analysis of the Relationship between Macroeconomic Variables and Stock Prices in Bangladesh NASRIN AFZAL * SYED SHAHADAT HOSSAIN

Modeling Exchange Rate Volatility using APARCH Models

96 TUTA/IOE/PCU Journal of the Institute of Engineering, 2018, 14(1): 96-106 TUTA/IOE/PCU Printed in Nepal Carolyn Ogutu 1, Betuel Canhanga 2, Pitos Biganda 3 1 School of Mathematics, University of Nairobi,

96 TUTA/IOE/PCU Journal of the Institute of Engineering, 2018, 14(1): 96-106 TUTA/IOE/PCU Printed in Nepal Carolyn Ogutu 1, Betuel Canhanga 2, Pitos Biganda 3 1 School of Mathematics, University of Nairobi,

BEcon Program, Faculty of Economics, Chulalongkorn University Page 1/7

Mid-term Exam (November 25, 2005, 0900-1200hr) Instructions: a) Textbooks, lecture notes and calculators are allowed. b) Each must work alone. Cheating will not be tolerated. c) Attempt all the tests.

Mid-term Exam (November 25, 2005, 0900-1200hr) Instructions: a) Textbooks, lecture notes and calculators are allowed. b) Each must work alone. Cheating will not be tolerated. c) Attempt all the tests.

How can saving deposit rate and Hang Seng Index affect housing prices : an empirical study in Hong Kong market

Lingnan Journal of Banking, Finance and Economics Volume 2 2010/2011 Academic Year Issue Article 3 January 2010 How can saving deposit rate and Hang Seng Index affect housing prices : an empirical study

Lingnan Journal of Banking, Finance and Economics Volume 2 2010/2011 Academic Year Issue Article 3 January 2010 How can saving deposit rate and Hang Seng Index affect housing prices : an empirical study

Linkage between Gold and Crude Oil Spot Markets in India-A Cointegration and Causality Analysis

Linkage between Gold and Crude Oil Spot Markets in India-A Cointegration and Causality Analysis Narinder Pal Singh Associate Professor Jagan Institute of Management Studies Rohini Sector -5, Delhi Sugandha

Linkage between Gold and Crude Oil Spot Markets in India-A Cointegration and Causality Analysis Narinder Pal Singh Associate Professor Jagan Institute of Management Studies Rohini Sector -5, Delhi Sugandha