Agricultural Markets Task Force. Futures Markets

|

|

|

- Peregrine Johns

- 5 years ago

- Views:

Transcription

1 Agricultural Markets Task Force Futures Markets

2 pig meat - risk management market information DLV Market Advisory Services Ir. Bart Teuwen April 2016

3 Content What to remember? Futures Market(s) on Hogs Context Change of Context Hog futures Use by farmers Intermezzo: MAS-Index Intermezzo: Risk management in the USA pork meat chain Policy recommendations Questions?

4 What to remember? Risk management is the execution of a decision based upon a certain insight derived from information Without information you don t have a clue about which position you should take on the market With information you develop an insight and a view. Through executing a risk management strategy you try to manage your cash flow in the future INFORMATION IS KEY

5 What to remember? Market information is the alfa and omega of risk management INFORMATION IS KEY

6 What to remember? Transparency and futures market are two sides of the same coin You need market information to get a futuresmarket liquid But you also need a futuresmarket to get an incentive for commercial players (companies active within the chain) to disclose marketinformation (<=> biconditional logical connective). INFORMATION FUTURES MARKET

7 Futures Market on Hogs

8 Futures Market on Hogs There are 2 Futures Markets on hogs CME, Chicago very liquid Eurex / EEX not liquid at all Correlation VEZG with CME is very weak Period to : 38,41% So basically we only have 1 futures market on hogs, that is very illiquide

9 FAHG: Contract specifications Contract size= kg (slaughtered weight) The convergence between the futures-quote (FCF) is very good with spot prices. Cash settlement upon the Hog Index

10 FAHG: Contract specifications Settlement: Cash settlement upon Hog-Index

11 FAHG: Convergence spot - futures Correlations Westvlees - Eurex/EEX Vion - Eurex/EEX VEZG - Eurex/EEX 95,303% 94,600% 96,884%

12 FAHG: Contract specifications Cash Settlement is a very elegant way to force the futures-price to converge with the spot price Question is: where do we settle against? Are these prices reflecting the real market? Preferably derived from a real negtotiation? Are these prices subject to manipulation? Some will identify the Eurex/EEX-contract as too German The other possibility to settle a futures contract is through physical delivery

13 FAHG: Contract specifications Cost of transaction in USA is 10 times lower then Eurex/EEX USA: 3 cents per pig Eurex/EEX: 26,6 cents per pig Cost of transaction may be acceptable to farmers and speculators. It isn t for packers, nor processors!

14 So, we have a very good correlating futurescontract, that is too expensive and very illiquid In a context where the whole industry is facing a lot of risk, with barely no tools to manage that risk

15 Context Change of Context Marketplace = Spot + Forward + Futures During recent years the forward market on the sales side of packers has increased, mainly on the export. But also on domestic markets the interest to contract forward increases. However, there is barely no forward contracting between farmers and slaughterhouses

However, we do see different reactions on offering (or not) forward contracts in the feed")

16 Context Change of Context In a context of price volatility competing companies tend to show herd behaviour Price volatility didn t bring any distinctive pricing policy between competing companies (although price volatility is an opportunity to differentiate) However, we do see different reactions on offering (or not) forward contracts in the feed sector

17 Hog futures - Use by farmers

18 Hog futures - Use by farmers 2012: Pig Trading Company cooperative initiative Hedging the crush margin Elaboration of a hedge protocol Gaining more insights on how pig and pork markets function

19 Hog futures - Use by farmers Hedge Protocol

20 Hog futures - Use by farmers Conclusions Hedge Protocol gives a handhold/grip to evaluate quotes on the futures markets By simultaneous taking position on feed and meat it s possible to hedge the crush margin Although hedging feed requires cooperation (because of magnitude feed lots contract size) Liquidity on hog futures is very, very poor (not existing!) Overall financial result is positive Besides the financial result farmers are VERY enthousiastic about the gained insights in the market Farmers are also VERY convinced of the importance of objective, accurate and up-to-date market information...

21 Hog futures - Use by farmers Conclusions... Farmers are aware of the fact that hedging is not a binary decision. There is a lot of space between 0% and 100% Farmers do evaluate the cooperative way of hedging as positive Forward contracts have 3 big disadvantages compared to futures markets futures market is anonymous: it s possible to execute your risk management strategy without exposing your position or strategy Futures market eliminate counter party risk Futures markets are flexible (on quantity and time)

22 Intermezzo MAS-Index

23 MAS-Index (0,3716xMW)+(0,2688xCo)+(0,2160xSB)+64,0328 MW = Milling Wheat-futures FCF, Euronext Co = Corn-futures FCF, CME SB = Soybean-futures FCF, CME Hedging-effectiveness of 95,10%

24 MAS-Index

25 MAS-Index

26 MAS-Index

27 MAS-Index

28 MAS-Index

29 Intermezzo Risk management in the USA pork meat chain

30 USA-farmers Use of futures Market

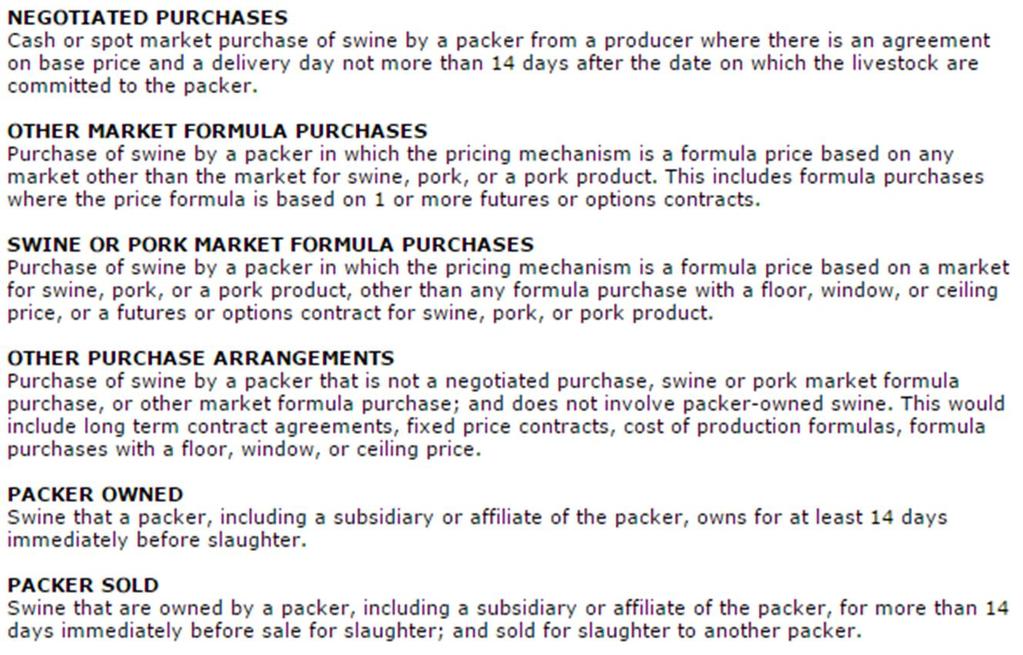

31 USA-farmers Negotiated purchase (spot): 2,6% Swine or Pork Market Formula Purchase: 38,9% Based on a major market price Based on Carcass Cutout Value Other Market Formula Purchase: 10,0% Based upon CME-futures Other Purchase arrangement: 12,5% Cost-Plus (based on corn + soybean meal) Window contract Floor contract Packer owned (27,2%) & Packer sold (4,0%)

32 USA-farmers

33 USA-farmers Hog contracting in the US developed out of the desire of large producers to manage price risk (Producer Motivations). While most of the research around AMA s has centered on the risk management area, it appears that a significant component of the rise of AMA s was the result of a desire to standardize a competitive product (Jang et al, 2009). Because large producers produced a large number of consistently high quality hogs, packers had the incentive to lock up the supply (Packer Motivations).

34 USA-packers Their Risk management can be divided into 4 categories 1. Hedging the purchase price risk deriving from marketing contracts with their suppliers 2. Hedging the purchase price risk deriving from their forward sales 3. Hedging as a service 1. to their suppliers 2. to their customers 4. Hedging their own production

35 Policy Recommendations

36 Policy Recommendations Transparency and futures market are two sides of the same coin You need market information to get a futuresmarket liquid. But you also need a futuresmarket to get an incentive for commercial players (companies active within the chain) to disclose marketinformation (<=> biconditional logical connective). European Union needs to embrace a (good functioning) futures market, including speculation (with food) A futures market is very important to lubricate the food chain, to help the commodity to move through the chain A futures market mitigates risk inside the food chain towards speculators

37 Policy Recommendations A clear and persistent policy Risk management requires attitude, education, guidance and experience (and hence time) And not only for farmers! Risk management will never be practiced by all companies - some companies will, others won t use risk management instruments No policy that impacts the market Every measure that impacts the market is distorting the futures market and destroying the faith of those who are not involved in the physical product

38 Questions? More information: DLV Market Advisory Services Rijkelstraat 28, 3550 Heusden-Zolder (Belgium) Bart Teuwen

Answer each of the following questions by circling True or False (2 points each).

.") Name: Econ 337 Agricultural Marketing, Spring 2019 Exam I; March 28, 2019 Answer each of the following questions by circling True or False (2 points each). 1. True False Some risk transfer premium is appropriate

Name: Econ 337 Agricultural Marketing, Spring 2019 Exam I; March 28, 2019 Answer each of the following questions by circling True or False (2 points each). 1. True False Some risk transfer premium is appropriate

ECON 337 Agricultural Marketing. Spring Exam I. Due April 16, Start of Lab (or before)

") Name: KEY ECON 337 Agricultural Marketing Spring 2013 Exam I Due April 16, 2013 @ Start of Lab (or before) Answer each of the following questions by circling True or False (2 points each). 1. True False

Name: KEY ECON 337 Agricultural Marketing Spring 2013 Exam I Due April 16, 2013 @ Start of Lab (or before) Answer each of the following questions by circling True or False (2 points each). 1. True False

More information on other ways of forward contracting hogs is available in the module Hog Market Contracting.

Hedging Hogs by the Farm Manager Introduction Hog prices can vary significantly from year to year and even day to day. With this volatility in the hog market, forward pricing opportunities arise worthy

Hedging Hogs by the Farm Manager Introduction Hog prices can vary significantly from year to year and even day to day. With this volatility in the hog market, forward pricing opportunities arise worthy

Buying Hedge with Futures

Buying Hedge with Futures What is a Hedge? A buying hedge involves taking a position in the futures market that is equal and opposite to the position one expects to take later in the cash market. The hedger

Buying Hedge with Futures What is a Hedge? A buying hedge involves taking a position in the futures market that is equal and opposite to the position one expects to take later in the cash market. The hedger

HEDGING WITH FUTURES AND BASIS

Futures & Options 1 Introduction The more producer know about the markets, the better equipped producer will be, based on current market conditions and your specific objectives, to decide whether to use

Futures & Options 1 Introduction The more producer know about the markets, the better equipped producer will be, based on current market conditions and your specific objectives, to decide whether to use

TRADING THE CATTLE AND HOG CRUSH SPREADS

TRADING THE CATTLE AND HOG CRUSH SPREADS Chicago Mercantile Exchange Inc. (CME) and the Chicago Board of Trade (CBOT) have signed a definitive agreement for CME to provide clearing and related services

TRADING THE CATTLE AND HOG CRUSH SPREADS Chicago Mercantile Exchange Inc. (CME) and the Chicago Board of Trade (CBOT) have signed a definitive agreement for CME to provide clearing and related services

Using the Futures Market in Response to Low Market Prices By Gary Schnitkey

Monday, Aug 2, 1999 Using the Futures Market in Response to Low Market Prices By Gary Schnitkey Cash market hog prices have been below $20 per cwt. during late October and November, their lowest levels

Monday, Aug 2, 1999 Using the Futures Market in Response to Low Market Prices By Gary Schnitkey Cash market hog prices have been below $20 per cwt. during late October and November, their lowest levels

Financing hog operations

Financing hog operations Introduction Author Mark Greenwood, Ag Star Reviewers Gary Thome, Riverland College John Murray, MN State Colleges and Universities To look at financing swine operations, I think

Financing hog operations Introduction Author Mark Greenwood, Ag Star Reviewers Gary Thome, Riverland College John Murray, MN State Colleges and Universities To look at financing swine operations, I think

HEDGING WITH FUTURES. Understanding Price Risk

HEDGING WITH FUTURES Think about a sport you enjoy playing. In many sports, such as football, volleyball, or basketball, there are two general components to the game: offense and defense. What would happen

HEDGING WITH FUTURES Think about a sport you enjoy playing. In many sports, such as football, volleyball, or basketball, there are two general components to the game: offense and defense. What would happen

Figure1: Alberta Index 100 Weekly Average Hog Price

Hog Market Contracting in Western Canada Introduction Hog prices vary significantly over time as shown in Figure 1. The chart shows that producers face significant price risk. Sometimes producers have

Hog Market Contracting in Western Canada Introduction Hog prices vary significantly over time as shown in Figure 1. The chart shows that producers face significant price risk. Sometimes producers have

WEEK 1: INTRODUCTION TO FUTURES

WEEK 1: INTRODUCTION TO FUTURES Futures: A contract between two parties where one party buys something from the other at a later date, at a price agreed today. The parties are subject to daily settlement

WEEK 1: INTRODUCTION TO FUTURES Futures: A contract between two parties where one party buys something from the other at a later date, at a price agreed today. The parties are subject to daily settlement

AGRICULTURAL DERIVATIVES

AGRICULTURAL DERIVATIVES Key Information Document (KID) 2018 JSE Limited Reg No: 2005/022939/06 Member of the World Federation of Exchanges Page 1 of 6 PURPOSE This document provides you with key information

AGRICULTURAL DERIVATIVES Key Information Document (KID) 2018 JSE Limited Reg No: 2005/022939/06 Member of the World Federation of Exchanges Page 1 of 6 PURPOSE This document provides you with key information

Commodity products. Grain and Oilseed Hedger's Guide

Commodity products Grain and Oilseed Hedger's Guide In a world of increasing volatility, customers around the globe rely on CME Group as their premier source for price discovery and managing risk. Formed

Commodity products Grain and Oilseed Hedger's Guide In a world of increasing volatility, customers around the globe rely on CME Group as their premier source for price discovery and managing risk. Formed

How Exchange Rates Affect Agricultural Markets

How Exchange Rates Affect Agricultural Markets Introduction The exchange rate between two currencies specifies how much one currency is worth in terms of the other. The Canadian exchange rate impacts the

How Exchange Rates Affect Agricultural Markets Introduction The exchange rate between two currencies specifies how much one currency is worth in terms of the other. The Canadian exchange rate impacts the

The Role of Market Prices by

The Role of Market Prices by Rollo L. Ehrich University of Wyoming The primary function of both cash and futures prices is the coordination of economic activity. Prices are the signals that guide business

The Role of Market Prices by Rollo L. Ehrich University of Wyoming The primary function of both cash and futures prices is the coordination of economic activity. Prices are the signals that guide business

Introduction. This module examines:

Introduction Financial Instruments - Futures and Options Price risk management requires identifying risk through a risk assessment process, and managing risk exposure through physical or financial hedging

Introduction Financial Instruments - Futures and Options Price risk management requires identifying risk through a risk assessment process, and managing risk exposure through physical or financial hedging

Thanks also to Daniels Trading who provided some of the data and technical assistance.

GUY BOWER Contents 1. Introduction 3 2. Mini Glossary 4 3. Strategy #1: The Bull Spread 6 4. Strategy #2: The Bear Spread 8 5. Strategy #3: The Inter Commodity Spread 10 6. Summation 12 7. About the Author

GUY BOWER Contents 1. Introduction 3 2. Mini Glossary 4 3. Strategy #1: The Bull Spread 6 4. Strategy #2: The Bear Spread 8 5. Strategy #3: The Inter Commodity Spread 10 6. Summation 12 7. About the Author

NAVIGATING. a BriEF guide to the DErivativEs MarkEtPLaCE and its role in EnaBLing ECOnOMiC growth

NAVIGATING a BriEF guide to the DErivativEs MarkEtPLaCE and its role in EnaBLing ECOnOMiC growth p 1 OVERVIEW What does risk look like p 14 THE BIG ECONOMIC PICTURE A quick lesson in supply and demand

NAVIGATING a BriEF guide to the DErivativEs MarkEtPLaCE and its role in EnaBLing ECOnOMiC growth p 1 OVERVIEW What does risk look like p 14 THE BIG ECONOMIC PICTURE A quick lesson in supply and demand

U.S. Market Hog Sales, *

U.S. Market Hog Sales, 2002-2012* May 2013 Ron Plain, Professor, University of Missouri Dept. of Agricultural & Applied Economics * This is an updated version of a study done by Glenn Grimes which was

U.S. Market Hog Sales, 2002-2012* May 2013 Ron Plain, Professor, University of Missouri Dept. of Agricultural & Applied Economics * This is an updated version of a study done by Glenn Grimes which was

Web Resources. Acknowledgements

GUY BOWER Web Resources Daniels Trading offer comprehensive, reliable and customer-focused commodity futures brokerage services to address all trading preferences. Their website is also a great place for

GUY BOWER Web Resources Daniels Trading offer comprehensive, reliable and customer-focused commodity futures brokerage services to address all trading preferences. Their website is also a great place for

Livestock Market Terms, Part II

G84-709-A Livestock Market Terms, Part II The second in a series of three*, this NebGuide defines terminology used in general market and futures market reports. Allen C. Wellman, Extension Marketing Specialist

G84-709-A Livestock Market Terms, Part II The second in a series of three*, this NebGuide defines terminology used in general market and futures market reports. Allen C. Wellman, Extension Marketing Specialist

Futures have Infrequent Expiry Dates

Futures have Infrequent Expiry Dates CME Futures on lean hogs mature on only 8 months of the year, and only on the 10th business day of the contract month at 12:00pm. It would be a coincidence if the pig

Futures have Infrequent Expiry Dates CME Futures on lean hogs mature on only 8 months of the year, and only on the 10th business day of the contract month at 12:00pm. It would be a coincidence if the pig

UK Grain Marketing Series January 19, Todd D. Davis Assistant Extension Professor. Economics

Introduction to Basis, Cash Forward Contracts, HTA Contracts and Basis Contracts UK Grain Marketing Series January 19, 2016 Todd D. Davis Assistant Extension Professor Outline What is basis and how can

Introduction to Basis, Cash Forward Contracts, HTA Contracts and Basis Contracts UK Grain Marketing Series January 19, 2016 Todd D. Davis Assistant Extension Professor Outline What is basis and how can

Futures & Options for Farm Risk Management. Torbjörn Iwarson, ,

Futures & Options for Farm Risk Management Torbjörn Iwarson, +46-76-050 83 65, torbjorn.iwarson@svenskacommodities.se twitter: @TorbjornIwarson Forward contracts are not a recent invention Confirmation

Futures & Options for Farm Risk Management Torbjörn Iwarson, +46-76-050 83 65, torbjorn.iwarson@svenskacommodities.se twitter: @TorbjornIwarson Forward contracts are not a recent invention Confirmation

The impacts of cereal, soybean and rapeseed meal price shocks on pig and poultry feed prices

The impacts of cereal, soybean and rapeseed meal price shocks on pig and poultry feed prices Abstract The goal of this paper was to estimate how changes in the market prices of protein-rich and energy-rich

The impacts of cereal, soybean and rapeseed meal price shocks on pig and poultry feed prices Abstract The goal of this paper was to estimate how changes in the market prices of protein-rich and energy-rich

Influences on the Market. Common Marketing Terms. Types of Contracts. Terms of Contracts

Jackie Reichter DeBruce Grain, Nebraska City Grain Marketing Commodity od Exchanges/Futures Symbols Influences on the Market Common Marketing Terms Types of Contracts Terms of Contracts Commodity Exchanges

Jackie Reichter DeBruce Grain, Nebraska City Grain Marketing Commodity od Exchanges/Futures Symbols Influences on the Market Common Marketing Terms Types of Contracts Terms of Contracts Commodity Exchanges

MIFID2 IMPLEMENTATION THE AMF S POSITION LIMITS ON AGRICULTURAL DERIVATIVES. Antonio OCANA ALVAREZ September 20th, 2017

MIFID2 IMPLEMENTATION THE AMF S POSITION LIMITS ON AGRICULTURAL DERIVATIVES Antonio OCANA ALVAREZ September 20th, 2017 Outline 1 Legislative and regulatory framework 2 The AMF s position limits on agricultural

MIFID2 IMPLEMENTATION THE AMF S POSITION LIMITS ON AGRICULTURAL DERIVATIVES Antonio OCANA ALVAREZ September 20th, 2017 Outline 1 Legislative and regulatory framework 2 The AMF s position limits on agricultural

Managing Hog Price Risk: Futures, Options, and Packer Contracts

Managing Hog Price Risk: Futures, Options, and Packer Contracts John D. Lawrence, Extension Livestock Economist and Director, Iowa Beef Center, and Alan Vontalge, Extension Economist, Iowa State University

Managing Hog Price Risk: Futures, Options, and Packer Contracts John D. Lawrence, Extension Livestock Economist and Director, Iowa Beef Center, and Alan Vontalge, Extension Economist, Iowa State University

Managing Agricultural Risk July 2011

Managing Agricultural Risk July 2011 Michael Swanson Ph.D. Wells Fargo Ag Industries Easy to confuse Dangerous when confused Wells Fargo Ag Industries - 2 Is Agricultural Risk Rising? Yes Quantifiably

Managing Agricultural Risk July 2011 Michael Swanson Ph.D. Wells Fargo Ag Industries Easy to confuse Dangerous when confused Wells Fargo Ag Industries - 2 Is Agricultural Risk Rising? Yes Quantifiably

Basis: The price difference between the cash price at a specific location and the price of a specific futures contract.

Section I Chapter 8: Basis Learning objectives The relationship between cash and futures prices Basis patterns Basis in different regions Speculators trade price, hedgers trade basis Key terms Basis: The

Section I Chapter 8: Basis Learning objectives The relationship between cash and futures prices Basis patterns Basis in different regions Speculators trade price, hedgers trade basis Key terms Basis: The

Feb 2005 Iowa Pork Regional Conferences 1. Optimal Selling Strategies & Comparing Packer Matrices IPPA-IPIC Regional Meetings

IPPA-IPIC Regional Meetings Percent of Hogs Sold on Carcass Merit Basis Optimal Selling Strategies & Comparing Packer Matrices Steve R. Meyer, Ph.D. President Paragon Economics, Inc. Percent - - - - -

IPPA-IPIC Regional Meetings Percent of Hogs Sold on Carcass Merit Basis Optimal Selling Strategies & Comparing Packer Matrices Steve R. Meyer, Ph.D. President Paragon Economics, Inc. Percent - - - - -

ROLE OF CLEARING HOUSES AND FINANCIAL SERVICE PROVIDERS

ROLE OF CLEARING HOUSES AND FINANCIAL SERVICE PROVIDERS DISCLAIMER INTL FCStone Ltd Registered in England and Wales Company No. 5616586 Authorised and regulated by the UK Financial Conduct Authority [FRN:

ROLE OF CLEARING HOUSES AND FINANCIAL SERVICE PROVIDERS DISCLAIMER INTL FCStone Ltd Registered in England and Wales Company No. 5616586 Authorised and regulated by the UK Financial Conduct Authority [FRN:

Ingredient and commodity prices are at all-time highs! That was the news

Optimize Your Buy Side Stabilizing Margins with Better Procurement Practices By Dennis Collins, Director, Trilateral, Inc. Ingredient and commodity prices are at all-time highs! That was the news just

Optimize Your Buy Side Stabilizing Margins with Better Procurement Practices By Dennis Collins, Director, Trilateral, Inc. Ingredient and commodity prices are at all-time highs! That was the news just

The Benefits for Canada from Pork Exports

The Benefits for Canada from Pork Exports October 16, 2006 By Kevin Grier George Morris Centre Purpose and Objectives The purpose of this project is to illustrate and describe the benefits to Canada from

The Benefits for Canada from Pork Exports October 16, 2006 By Kevin Grier George Morris Centre Purpose and Objectives The purpose of this project is to illustrate and describe the benefits to Canada from

Examples of Derivative Securities: Futures Contracts

Finance Derivative Securities Lecture 1 Introduction to Derivatives Examples of Derivative Securities: Futures Contracts Agreement made today to: Buy 5000 bushels of wheat @ US$4.50/bushel on December

Finance Derivative Securities Lecture 1 Introduction to Derivatives Examples of Derivative Securities: Futures Contracts Agreement made today to: Buy 5000 bushels of wheat @ US$4.50/bushel on December

Hedging techniques in commodity risk management

Hedging techniques in commodity risk management Josef TAUŠER, Radek ČAJKA Faculty of International Relations, University of Economics, Prague Abstract: The article focuses on selected aspects of risk management

Hedging techniques in commodity risk management Josef TAUŠER, Radek ČAJKA Faculty of International Relations, University of Economics, Prague Abstract: The article focuses on selected aspects of risk management

Tim Petry Livestock Economist Agribusiness and Applied Economics.

Tim Petry Livestock Economist Agribusiness and Applied Economics www.ag.ndsu.edu/aginfo/lsmkt/livestock.htm Lean Hogs.ppt 2-19-08 www.ers.usda.gov Livestock, Dairy, Poultry Outlook www.nass.usda.gov Hog

Tim Petry Livestock Economist Agribusiness and Applied Economics www.ag.ndsu.edu/aginfo/lsmkt/livestock.htm Lean Hogs.ppt 2-19-08 www.ers.usda.gov Livestock, Dairy, Poultry Outlook www.nass.usda.gov Hog

Jake Bernstein Advanced Trader Sessions (ATS)

") Jake Bernstein Advanced Trader Sessions (ATS) http://www.jakebernstein.com 800-678-5253 831-430-0600 ATS 1 Session 4 16 February 2012 January Effect Weekly Trigger: Status Big Moves and COT: A Much Closer

Jake Bernstein Advanced Trader Sessions (ATS) http://www.jakebernstein.com 800-678-5253 831-430-0600 ATS 1 Session 4 16 February 2012 January Effect Weekly Trigger: Status Big Moves and COT: A Much Closer

Commodities: A Strategic Asset Allocation?

FINANCE, INVESTMENT & RISK MANAGEMENT CONFERENCE 15-17 JUNE 2008 HILTON DEANSGATE, MANCHESTER Commodities: A Strategic Asset Allocation? John.McManus@union-investment.de Commodities: A Distinct Asset Class

FINANCE, INVESTMENT & RISK MANAGEMENT CONFERENCE 15-17 JUNE 2008 HILTON DEANSGATE, MANCHESTER Commodities: A Strategic Asset Allocation? John.McManus@union-investment.de Commodities: A Distinct Asset Class

Turner s Take WASDE Expectations vs. Sept WASDE report:

Published by: Craig Turner 11/4/2013 4:02:09 PM In this issue 1) CORN: USDA Friday exected to be bearish. Looking to short Corn ahead of WASDE 2) SOYBEANS: Short Bean Ideas with Long Call Protection 3)

Published by: Craig Turner 11/4/2013 4:02:09 PM In this issue 1) CORN: USDA Friday exected to be bearish. Looking to short Corn ahead of WASDE 2) SOYBEANS: Short Bean Ideas with Long Call Protection 3)

2013 Risk and Profit Conference Breakout Session Presenters. 4. Basics of Futures and Options: Part 1

2013 Risk and Profit Conference Breakout Session Presenters Sean Fox 4. Basics of Futures and Options: Part 1 John A. (Sean) Fox is a native of Ireland and has been on the faculty

2013 Risk and Profit Conference Breakout Session Presenters Sean Fox 4. Basics of Futures and Options: Part 1 John A. (Sean) Fox is a native of Ireland and has been on the faculty

BUSM 411: Derivatives and Fixed Income

BUSM 411: Derivatives and Fixed Income 1. Introduction to derivatives In the last 30 years, derivatives have become increasingly important in finance. Futures and options are actively traded on many exchanges

BUSM 411: Derivatives and Fixed Income 1. Introduction to derivatives In the last 30 years, derivatives have become increasingly important in finance. Futures and options are actively traded on many exchanges

Crops Marketing and Management Update

Crops Marketing and Management Update Department of Agricultural Economics Princeton REC Dr. Todd D. Davis Assistant Extension Professor -- Crop Economics Marketing & Management Vol. 2016 (2) February

Crops Marketing and Management Update Department of Agricultural Economics Princeton REC Dr. Todd D. Davis Assistant Extension Professor -- Crop Economics Marketing & Management Vol. 2016 (2) February

Determining Exchange Rates. Determining Exchange Rates

Determining Exchange Rates Determining Exchange Rates Chapter Objectives To explain how exchange rate movements are measured; To explain how the equilibrium exchange rate is determined; and To examine

Determining Exchange Rates Determining Exchange Rates Chapter Objectives To explain how exchange rate movements are measured; To explain how the equilibrium exchange rate is determined; and To examine

Derivative Instruments

Derivative Instruments Paris Dauphine University - Master I.E.F. (272) Autumn 2016 Jérôme MATHIS jerome.mathis@dauphine.fr (object: IEF272) http://jerome.mathis.free.fr/ief272 Slides on book: John C. Hull,

Derivative Instruments Paris Dauphine University - Master I.E.F. (272) Autumn 2016 Jérôme MATHIS jerome.mathis@dauphine.fr (object: IEF272) http://jerome.mathis.free.fr/ief272 Slides on book: John C. Hull,

Forwards, Futures, Options and Swaps

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

Forwards, Futures, Options and Swaps A derivative asset is any asset whose payoff, price or value depends on the payoff, price or value of another asset. The underlying or primitive asset may be almost

June 2018 Monthly Commodity Market Overview Newsletter. Stock Index Futures. By the ADMIS Research Team

June 2018 Monthly Commodity Market Overview Newsletter By the ADMIS Research Team Stock Index Futures Stock index futures performed well in spite of increased global trade tensions. In fact NASDAQ and

June 2018 Monthly Commodity Market Overview Newsletter By the ADMIS Research Team Stock Index Futures Stock index futures performed well in spite of increased global trade tensions. In fact NASDAQ and

Futures Market in Grain sector Hedging process for farmers and french cooperatives. Agricultural Market Task Force 12 Avril 2016

Futures Market in Grain sector Hedging process for farmers and french cooperatives Agricultural Market Task Force 12 Avril 2016 High volatil market conducts stakeholders to hedge their risks Example :

Futures Market in Grain sector Hedging process for farmers and french cooperatives Agricultural Market Task Force 12 Avril 2016 High volatil market conducts stakeholders to hedge their risks Example :

MARGIN M ANAGER The Leading Resource for Margin Management Education

Margin Management Since 1999 MARGIN M ANAGER The Leading Resource for Margin Management Education August 2014 Learn more at MarginManager.Com INSIDE THIS ISSUE Margin Watch Reports Hog... Pg 4 Dairy...

Margin Management Since 1999 MARGIN M ANAGER The Leading Resource for Margin Management Education August 2014 Learn more at MarginManager.Com INSIDE THIS ISSUE Margin Watch Reports Hog... Pg 4 Dairy...

Cattle: Dollar: Energies:

j 3/11/2015 CONTACTS: Chuck Shelby O: (866) 837-9027 C: (765) 426-7535 Bryan Shelby O: (866) 837-9027 Bill Gentry O: (877) 433-4348 or O: (866) 837-9027 C: (219) 863-0055 Sherman Newlin O: (866) 314-5765

j 3/11/2015 CONTACTS: Chuck Shelby O: (866) 837-9027 C: (765) 426-7535 Bryan Shelby O: (866) 837-9027 Bill Gentry O: (877) 433-4348 or O: (866) 837-9027 C: (219) 863-0055 Sherman Newlin O: (866) 314-5765

Using Futures and Options to Manage Hog Price Volatility

Using Futures and Options to Manage Hog Price Volatility Larry Martin, Ph. D. Agrifood Management Excellence and Dr. Larry Martin &Associates, Inc. Ph: 519 623 8622, dlm@xplornet.com Introduction and Objectives

Using Futures and Options to Manage Hog Price Volatility Larry Martin, Ph. D. Agrifood Management Excellence and Dr. Larry Martin &Associates, Inc. Ph: 519 623 8622, dlm@xplornet.com Introduction and Objectives

FNCE4040 Derivatives Chapter 1

FNCE4040 Derivatives Chapter 1 Introduction The Landscape Forwards and Option Contracts What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another

FNCE4040 Derivatives Chapter 1 Introduction The Landscape Forwards and Option Contracts What is a Derivative? A derivative is an instrument whose value depends on, or is derived from, the value of another

FUTURES CONTRACTS FOR MILK: HOW WILL THEY WORK? Bob Cropp 1

Dairy Day 1996 FUTURES CONTRACTS FOR MILK: HOW WILL THEY WORK? Bob Cropp 1 Summary The two new milk futures contracts offer dairy farmers and other buyers and sellers of milk and dairy products additional

Dairy Day 1996 FUTURES CONTRACTS FOR MILK: HOW WILL THEY WORK? Bob Cropp 1 Summary The two new milk futures contracts offer dairy farmers and other buyers and sellers of milk and dairy products additional

11 06 Class 12 Forwards and Futures

11 06 Class 12 Forwards and Futures From banks to futures markets Financial i l markets as insurance markets Instruments and exchanges; The counterparty risk problem 1 From last time Banks face bank runs

11 06 Class 12 Forwards and Futures From banks to futures markets Financial i l markets as insurance markets Instruments and exchanges; The counterparty risk problem 1 From last time Banks face bank runs

Considerations When Using Grain Contracts

Considerations When Using Grain Contracts Overview The grain industry has developed several new tools to help farmers manage increasing risks and price volatility. Elevators can use grain options markets

Considerations When Using Grain Contracts Overview The grain industry has developed several new tools to help farmers manage increasing risks and price volatility. Elevators can use grain options markets

AGRICULTURAL TRADE OPTIONS WHAT AGRICULTURAL PRODUCERS NEED TO KNOW. Prepared by. Commodity Futures Trading Commission Division of Economic Analysis

AGRICULTURAL TRADE OPTIONS WHAT AGRICULTURAL PRODUCERS NEED TO KNOW Prepared by Commodity Futures Trading Commission Division of Economic Analysis December 1998 AGRICULTURAL TRADE OPTIONS WHAT AGRICULTURAL

AGRICULTURAL TRADE OPTIONS WHAT AGRICULTURAL PRODUCERS NEED TO KNOW Prepared by Commodity Futures Trading Commission Division of Economic Analysis December 1998 AGRICULTURAL TRADE OPTIONS WHAT AGRICULTURAL

Table of Contents. Introduction

Table of Contents Option Terminology 2 The Concept of Options 4 How Do I Incorporate Options into My Marketing Plan? 7 Establishing a Minimum Sale Price for Your Livestock Buying Put Options 11 Establishing

Table of Contents Option Terminology 2 The Concept of Options 4 How Do I Incorporate Options into My Marketing Plan? 7 Establishing a Minimum Sale Price for Your Livestock Buying Put Options 11 Establishing

Introduction to Futures Hedging for Grain Producers

COOPERATIVE EXTENSION SERVICE UNIVERSITY OF KENTUCKY COLLEGE OF AGRICULTURE, LEXINGTON, KY, 40546 AEC-96 Introduction to Futures Hedging for Grain Producers Collin Allgood, Leigh Maynard, and Cory Walters,

COOPERATIVE EXTENSION SERVICE UNIVERSITY OF KENTUCKY COLLEGE OF AGRICULTURE, LEXINGTON, KY, 40546 AEC-96 Introduction to Futures Hedging for Grain Producers Collin Allgood, Leigh Maynard, and Cory Walters,

VOLATILITY: FRIEND OR ENEMY? YOU DECIDE!

VOLATILITY: FRIEND OR ENEMY? YOU DECIDE! Jared Morgan INTL FCStone Financial Inc. FCM Division Kansas Farm Bureau -- Young Farmers & Ranchers Conference January 25-27, 2019 Manhattan, KS Part 1 DISCLOSURES

VOLATILITY: FRIEND OR ENEMY? YOU DECIDE! Jared Morgan INTL FCStone Financial Inc. FCM Division Kansas Farm Bureau -- Young Farmers & Ranchers Conference January 25-27, 2019 Manhattan, KS Part 1 DISCLOSURES

Market incompleteness. The benefits of OTC contracts derived or not from futures markets

Market incompleteness. The benefits of OTC contracts derived or not from futures markets By Jean Cordier Professeur Agrocampus Ouest, France Meeting of the expert group on agricultural commodity derivatives

Market incompleteness. The benefits of OTC contracts derived or not from futures markets By Jean Cordier Professeur Agrocampus Ouest, France Meeting of the expert group on agricultural commodity derivatives

Grain Futures: Questions and Answers

1 Fact Sheet 491 Grain Futures: Questions and Answers Introduction Misinformation about the futures markets is commonplace. Some grain farmers are convinced that low prices are the inevitable result of

1 Fact Sheet 491 Grain Futures: Questions and Answers Introduction Misinformation about the futures markets is commonplace. Some grain farmers are convinced that low prices are the inevitable result of

Issue Report 6-9 Emerging Commodity Markets: Current Status and Utilization

Issue Report 6-9 Emerging Commodity Markets: Current Status and Utilization PARK Hwan-Il June 2011 Abstract The continued uptrend in the prices of crude oil, gold, corn, raw cotton, etc. has rekindled

Issue Report 6-9 Emerging Commodity Markets: Current Status and Utilization PARK Hwan-Il June 2011 Abstract The continued uptrend in the prices of crude oil, gold, corn, raw cotton, etc. has rekindled

HOG RISK MANAGEMENT SURVEY: SUMMARY AND PRELIMINARY ANALYSIS

HOG RISK MANAGEMENT SURVEY: SUMMARY AND PRELIMINARY ANALYSIS by George F. Patrick, Purdue University Alan E. Baquet, University of Nebraska Keith H. Coble, Mississippi State University, Thomas O. Knight,

HOG RISK MANAGEMENT SURVEY: SUMMARY AND PRELIMINARY ANALYSIS by George F. Patrick, Purdue University Alan E. Baquet, University of Nebraska Keith H. Coble, Mississippi State University, Thomas O. Knight,

FORWARDS FUTURES Traded between private parties (OTC) Traded on exchange

Traded on exchange") 1 E&G, Ch. 23. I. Introducing Forwards and Futures A. Mechanics of Forwards and Futures. 1. Definitions: Forward Contract - commitment by 2 parties to exchange a certain good for a specific price at a

1 E&G, Ch. 23. I. Introducing Forwards and Futures A. Mechanics of Forwards and Futures. 1. Definitions: Forward Contract - commitment by 2 parties to exchange a certain good for a specific price at a

AGRICULTURAL PRODUCTS. Soybean Crush Reference Guide

AGRICULTURAL PRODUCTS Soybean Crush Reference Guide As the world s largest and most diverse derivatives marketplace, CME Group (cmegroup.com) is where the world comes to manage risk. CME Group exchanges

AGRICULTURAL PRODUCTS Soybean Crush Reference Guide As the world s largest and most diverse derivatives marketplace, CME Group (cmegroup.com) is where the world comes to manage risk. CME Group exchanges

AGRICULTURAL PRODUCTS. Self-Study Guide to Hedging with Livestock Futures and Options

AGRICULTURAL PRODUCTS Self-Study Guide to Hedging with Livestock Futures and Options TABLE OF CONTENTS INTRODUCTION TO THE GUIDE 4 CHAPTER 1: OVERVIEW OF THE LIVESTOCK FUTURES MARKET 5 CHAPTER 2: FINANCIAL

AGRICULTURAL PRODUCTS Self-Study Guide to Hedging with Livestock Futures and Options TABLE OF CONTENTS INTRODUCTION TO THE GUIDE 4 CHAPTER 1: OVERVIEW OF THE LIVESTOCK FUTURES MARKET 5 CHAPTER 2: FINANCIAL

Non-Convergence of CME Hard Red Winter Wheat Futures and the Impact of Excessive Grain Inventories in Kansas

Non-Convergence of CME Hard Red Winter Wheat Futures and the Impact of Excessive Grain Inventories in Kansas Daniel O Brien, Extension Agricultural Economist Kansas State University August 10, 2016 Summary

Non-Convergence of CME Hard Red Winter Wheat Futures and the Impact of Excessive Grain Inventories in Kansas Daniel O Brien, Extension Agricultural Economist Kansas State University August 10, 2016 Summary

Financial Markets & Institutions. forwards.

Financial Markets & Institutions Introduction to derivatives. Futures and forwards. Slides by Emilia Garcia-Appendini The Nature of Derivatives A derivative is an instrument whose value depends on the

Financial Markets & Institutions Introduction to derivatives. Futures and forwards. Slides by Emilia Garcia-Appendini The Nature of Derivatives A derivative is an instrument whose value depends on the

Forward and Futures Contracts

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Forward and Futures Contracts These notes explore forward and futures contracts, what they are and how they are used. We will learn how to price forward contracts

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 Forward and Futures Contracts These notes explore forward and futures contracts, what they are and how they are used. We will learn how to price forward contracts

MEASURING GRAIN MARKET PRICE RISK

MEASURING GRAIN MARKET PRICE RISK Justin Bina and Ted C. Schroeder 1 Kansas State University, Department of Agricultural Economics August 2018 Grain Market Risk Grain production involves considerable risk,

MEASURING GRAIN MARKET PRICE RISK Justin Bina and Ted C. Schroeder 1 Kansas State University, Department of Agricultural Economics August 2018 Grain Market Risk Grain production involves considerable risk,

EC Grain Pricing Alternatives

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Historical Materials from University of Nebraska- Lincoln Extension Extension 1977 EC77-868 Grain Pricing Alternatives Lynn

University of Nebraska - Lincoln DigitalCommons@University of Nebraska - Lincoln Historical Materials from University of Nebraska- Lincoln Extension Extension 1977 EC77-868 Grain Pricing Alternatives Lynn

Issues of and Solutions to Milk Price Volatility in the United States

Issues of and Solutions to Milk Price Volatility in the United States Andrew M. Novakovic, PhD The E.V. Baker Professor of Agricultural Economics Cornell University Ithaca, New York, USA Outline 1. A quick

Issues of and Solutions to Milk Price Volatility in the United States Andrew M. Novakovic, PhD The E.V. Baker Professor of Agricultural Economics Cornell University Ithaca, New York, USA Outline 1. A quick

EXECUTIVE SUMMARY US WHEAT MARKET

MERRICKS CAPITAL SOFT COMMODITIES QUARTERLY THOUGHT PIECE DECEMBER 2016 IN THIS QUARTERLY THOUGHT PIECE WE HIGHLIGHT HOW THE EXIT OF BANK FUNDING AND LARGE GRAIN INVENTORY IS PROVIDING OPPORTUNITIES IN

MERRICKS CAPITAL SOFT COMMODITIES QUARTERLY THOUGHT PIECE DECEMBER 2016 IN THIS QUARTERLY THOUGHT PIECE WE HIGHLIGHT HOW THE EXIT OF BANK FUNDING AND LARGE GRAIN INVENTORY IS PROVIDING OPPORTUNITIES IN

Agricultural Outlook Forum Presented: Thursday, February 19, 2004 IMPLICATIONS OF EXTENDING CROP INSURANCE TO LIVESTOCK

Agricultural Outlook Forum Presented: Thursday, February 19, 2004 IMPLICATIONS OF EXTENDING CROP INSURANCE TO LIVESTOCK Bruce A. Babcock Center for Agricultural and Rural Development Iowa State University

Agricultural Outlook Forum Presented: Thursday, February 19, 2004 IMPLICATIONS OF EXTENDING CROP INSURANCE TO LIVESTOCK Bruce A. Babcock Center for Agricultural and Rural Development Iowa State University

University of Siegen

University of Siegen Faculty of Economic Disciplines, Department of economics Univ. Prof. Dr. Jan Franke-Viebach Seminar Risk and Finance Summer Semester 2008 Topic 4: Hedging with currency futures Name

University of Siegen Faculty of Economic Disciplines, Department of economics Univ. Prof. Dr. Jan Franke-Viebach Seminar Risk and Finance Summer Semester 2008 Topic 4: Hedging with currency futures Name

MARGIN M ANAGER INSIDE THIS ISSUE. Margin Watch Reports. Features DAIRY WHITE PAPER. Dairy... Pg 11 Beef... Corn... Beans... Pg 16 Wheat...

MARGIN M ANAGER Margin Management Since 1999 The Leading Resource for Margin Management Education Learn more at MarginManager.Com Monthly INSIDE THIS ISSUE Margin Watch Reports Dairy... Pg 11 Beef... Pg

MARGIN M ANAGER Margin Management Since 1999 The Leading Resource for Margin Management Education Learn more at MarginManager.Com Monthly INSIDE THIS ISSUE Margin Watch Reports Dairy... Pg 11 Beef... Pg

Fundamental Factors Affecting Agricultural and Other Commodities. Research & Product Development Updated July 11, 2008

Fundamental Factors Affecting Agricultural and Other Commodities Research & Product Development Updated July 11, 2008 Outline Review of key supply and demand factors affecting commodity markets World stocks-to-use

Fundamental Factors Affecting Agricultural and Other Commodities Research & Product Development Updated July 11, 2008 Outline Review of key supply and demand factors affecting commodity markets World stocks-to-use

FULL TIME OPPORTUNITIES

FULL TIME OPPORTUNITIES 2014-2015 BARTLETT & COMPANY WWW.BARTLETTANDCO.COM/CAREERS ABOUT BARTLETT Bartlett and Company is a diverse, growth-oriented agribusiness company. Our principle businesses are grain

FULL TIME OPPORTUNITIES 2014-2015 BARTLETT & COMPANY WWW.BARTLETTANDCO.COM/CAREERS ABOUT BARTLETT Bartlett and Company is a diverse, growth-oriented agribusiness company. Our principle businesses are grain

Improving Your Crop Marketing Skills: Basis, Cost of Ownership, and Market Carry

Improving Your Crop Marketing Skills: Basis, Cost of Ownership, and Market Carry Nathan Thompson & James Mintert Purdue Center for Commercial Agriculture Many Different Ways to Price Grain Today 1) Spot

Improving Your Crop Marketing Skills: Basis, Cost of Ownership, and Market Carry Nathan Thompson & James Mintert Purdue Center for Commercial Agriculture Many Different Ways to Price Grain Today 1) Spot

MARGIN M ANAGER The Leading Resource for Margin Management Education

Margin Management Since 1999 MARGIN M ANAGER The Leading Resource for Margin Management Education February 2015 Learn more at MarginManager.Com INSIDE THIS ISSUE Dear Ag Industry Associate, Margin Watch

Margin Management Since 1999 MARGIN M ANAGER The Leading Resource for Margin Management Education February 2015 Learn more at MarginManager.Com INSIDE THIS ISSUE Dear Ag Industry Associate, Margin Watch

Passive Investors and Managed Money in Commodity Futures. Part 3: Volatility. Prepared for: The CME Group. Prepared by:

Passive Investors and Managed Money in Commodity Futures Part 3: Prepared for: The CME Group Prepared by: October, 2008 Table of Contents Section Slide Number Objective and Approach 3 Graphs 4-13 Correlation

Passive Investors and Managed Money in Commodity Futures Part 3: Prepared for: The CME Group Prepared by: October, 2008 Table of Contents Section Slide Number Objective and Approach 3 Graphs 4-13 Correlation

Evaluating the Hedging Potential of the Lean Hog Futures Contract

Evaluating the Hedging Potential of the Lean Hog Futures Contract Mark W. Ditsch Consolidated Grain and Barge Company Mound City, Illinois Raymond M. Leuthold Department of Agricultural and Consumer Economics

Evaluating the Hedging Potential of the Lean Hog Futures Contract Mark W. Ditsch Consolidated Grain and Barge Company Mound City, Illinois Raymond M. Leuthold Department of Agricultural and Consumer Economics

MARKET REGULATION ADVISORY NOTICE

MARKET REGULATION ADVISORY NOTICE Exchange Subject Rule References Rule 538 CME, CBOT, NYMEX & COMEX Exchange for Related Positions Advisory Date Advisory Number CME Group RA1716-5R Effective Date Effective

MARKET REGULATION ADVISORY NOTICE Exchange Subject Rule References Rule 538 CME, CBOT, NYMEX & COMEX Exchange for Related Positions Advisory Date Advisory Number CME Group RA1716-5R Effective Date Effective

Hog Marketing Practices and Competition Questions

2nd Quarter 2010, 25(2) Hog Marketing Practices and Competition Questions John D. Lawrence JEL Classifications: Q11, Q13 Hog production and marketing practices in the U.S. pork industry have changed dramatically

2nd Quarter 2010, 25(2) Hog Marketing Practices and Competition Questions John D. Lawrence JEL Classifications: Q11, Q13 Hog production and marketing practices in the U.S. pork industry have changed dramatically

Kingdom of Saudi Arabia Capital Market Authority. Investment

Kingdom of Saudi Arabia Capital Market Authority Investment The Definition of Investment Investment is defined as the commitment of current financial resources in order to achieve higher gains in the

Kingdom of Saudi Arabia Capital Market Authority Investment The Definition of Investment Investment is defined as the commitment of current financial resources in order to achieve higher gains in the

Gross margin insurance on Dutch dairy and fattening pig farms

Gross margin insurance on Dutch dairy and fattening pig farms Marcel van Asseldonk and Miranda Meuwissen Gross margin insurance on Dutch dairy and fattening pig farms Marcel van Asseldonk and Miranda

Gross margin insurance on Dutch dairy and fattening pig farms Marcel van Asseldonk and Miranda Meuwissen Gross margin insurance on Dutch dairy and fattening pig farms Marcel van Asseldonk and Miranda

Options Trading in Agricultural Commodities

EC-613 Cooperative Extension Service Purdue University West Lafayette, IN 47907 Options Trading in Agricultural Commodities Steven.P Erickson, Associate Professor Christopher A. Hurt, Assistant Professor

EC-613 Cooperative Extension Service Purdue University West Lafayette, IN 47907 Options Trading in Agricultural Commodities Steven.P Erickson, Associate Professor Christopher A. Hurt, Assistant Professor

2/20/2012. Goal: Use price management tools to secure a profit for the farm.

Katie Behnke Agriculture Agent Shawano County Futures, options, contracts, and the cash market are all tools we can use to manage our business. Important to remember - we are not speculators Goal: Use

Katie Behnke Agriculture Agent Shawano County Futures, options, contracts, and the cash market are all tools we can use to manage our business. Important to remember - we are not speculators Goal: Use

MARGIN M ANAGER The Leading Resource for Margin Management Education

Margin Management Since 1999 MARGIN M ANAGER The Leading Resource for Margin Management Education Learn more at MarginManager.Com March INSIDE THIS ISSUE Dear Ag Industry Associate, The USDA released several

Margin Management Since 1999 MARGIN M ANAGER The Leading Resource for Margin Management Education Learn more at MarginManager.Com March INSIDE THIS ISSUE Dear Ag Industry Associate, The USDA released several

Montana MarketManager A PRIMER ON UNDERSTANDING FUTURES AND OPTIONS MARKETS. Workshop 5 - Part 1 Winter 2000 Marketing Workshops January 6 & 7, 2000

Montana MarketManager A PRIMER ON UNDERSTANDING FUTURES AND OPTIONS MARKETS Workshop 5 - Part 1 Winter 2000 Marketing Workshops January 6 & 7, 2000 Larry D. Makus College of Agriculture University of Idaho

Montana MarketManager A PRIMER ON UNDERSTANDING FUTURES AND OPTIONS MARKETS Workshop 5 - Part 1 Winter 2000 Marketing Workshops January 6 & 7, 2000 Larry D. Makus College of Agriculture University of Idaho

Section II Advanced Pricing Tools

Section II Chapter 13: Options Learning objectives The appeal of options Puts vs. calls Understanding premiums Recognizing if an option is in the money, at the money or out of the money Key terms Call

Section II Chapter 13: Options Learning objectives The appeal of options Puts vs. calls Understanding premiums Recognizing if an option is in the money, at the money or out of the money Key terms Call

FOCUSED ON PROFITABLE, CONSISTENT GROWTH

FOCUSED ON PROFITABLE, CONSISTENT GROWTH Investor Presentation August 2013 FORWARD-LOOKING STATEMENTS Certain information contained in this presentation may constitute forward-looking statements, such

FOCUSED ON PROFITABLE, CONSISTENT GROWTH Investor Presentation August 2013 FORWARD-LOOKING STATEMENTS Certain information contained in this presentation may constitute forward-looking statements, such

Functional Training & Basel II Reporting and Methodology Review: Derivatives

Functional Training & Basel II Reporting and Methodology Review: Copyright 2010 ebis. All rights reserved. Page i Table of Contents 1 EXPOSURE DEFINITIONS...2 1.1 DERIVATIVES...2 1.1.1 Introduction...2

Functional Training & Basel II Reporting and Methodology Review: Copyright 2010 ebis. All rights reserved. Page i Table of Contents 1 EXPOSURE DEFINITIONS...2 1.1 DERIVATIVES...2 1.1.1 Introduction...2

December 2018 Monthly Commodity Market Overview Newsletter. Stock Index Futures

December 2018 Monthly Commodity Market Overview Newsletter By the ADMIS Research Team of Steve Freed, Alan Bush, Michael Niemiec & Chris Lehner Stock Index Futures Stock index futures have come under pressure

December 2018 Monthly Commodity Market Overview Newsletter By the ADMIS Research Team of Steve Freed, Alan Bush, Michael Niemiec & Chris Lehner Stock Index Futures Stock index futures have come under pressure

Accounting for Hedging Transactions

CLAconnect.com Accounting for Hedging Transactions Paul Neiffer, CPA Paul Neiffer Bio Paul is an Agribusiness CPA and Principal with CliftonLarsonAllen LLP located in the Kennewick and Yakima, Washington

CLAconnect.com Accounting for Hedging Transactions Paul Neiffer, CPA Paul Neiffer Bio Paul is an Agribusiness CPA and Principal with CliftonLarsonAllen LLP located in the Kennewick and Yakima, Washington

Recent Developments in South Dakota's Hog Market

South Dakota State University Open PRAIRIE: Open Public Research Access Institutional Repository and Information Exchange SDSU Extension Fact Sheets SDSU Extension 2001 Recent Developments in South Dakota's

South Dakota State University Open PRAIRIE: Open Public Research Access Institutional Repository and Information Exchange SDSU Extension Fact Sheets SDSU Extension 2001 Recent Developments in South Dakota's

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives Dillon M. Feuz Department of Applied Economics Utah State University 3530 Old Main Hill Logan, UT 84322-3530 435-797-2296 dillon.feuz@usu.edu

Managing Feed and Milk Price Risk: Futures Markets and Insurance Alternatives Dillon M. Feuz Department of Applied Economics Utah State University 3530 Old Main Hill Logan, UT 84322-3530 435-797-2296 dillon.feuz@usu.edu

Mathematics of Finance II: Derivative securities

Mathematics of Finance II: Derivative securities M HAMED EDDAHBI King Saud University College of Sciences Mathematics Department Riyadh Saudi Arabia Second term 2015 2016 M hamed Eddahbi (KSU-COS) Mathematics

Mathematics of Finance II: Derivative securities M HAMED EDDAHBI King Saud University College of Sciences Mathematics Department Riyadh Saudi Arabia Second term 2015 2016 M hamed Eddahbi (KSU-COS) Mathematics

Monthly Hog Market Update United States Hog Slaughter

This information is provided as a resource by Saskatchewan Agriculture staff All prices are in Canadian dollars unless otherwise noted. Please use this information at your own risk. Monthly Hog Market

This information is provided as a resource by Saskatchewan Agriculture staff All prices are in Canadian dollars unless otherwise noted. Please use this information at your own risk. Monthly Hog Market

Lecture 3. Futures operation

Lecture 3 Futures operation Agenda: 1. Futures contracts: ~ Specification ~ Convergence of futures price to spot price at maturity: 2. Margin trading: ~ Open a margin account and deposit the initial margin

Lecture 3 Futures operation Agenda: 1. Futures contracts: ~ Specification ~ Convergence of futures price to spot price at maturity: 2. Margin trading: ~ Open a margin account and deposit the initial margin