Testing for Bubbles in Asset prices: Evidence from QE and other applications

|

|

|

- Rolf Jordan

- 6 years ago

- Views:

Transcription

1 Testing for Bubbles in Asset prices: Evidence from QE and other applications Views expressed are those of the presenter and do not necessarily reflect official positions of De Nederlandsche Bank.

2 Outline Introduction Asset Bubble indicator Theoretical framework GSADF Alternative Unit Root test: Phillips-Perron Effects of QE on equity and government bond markets MSCI Europe Government bond yields Other applications Limitations, conclusions and future research 2

3 Introduction An asset price bubble is characterized by periods of sustained increases in the price of an asset which is not justified by the value based on fundamental drivers. Bubbles in asset prices often precede a crash of a specific market (Tulip Mania, Asian financial crisis, Dot.com, GFC). Motivation 1. Monetary policy conventional and unconventional 2. Fragile economic recovery Asset price bubbles, where prices may diverge from fundamental values Goal Tool to monitor existence of bubbles in different asset classes (equities, bond market, commodities, housing prices) 3

4 Asset Bubble Indicator: Theoretical framework Prices of an asset are based on discounted expected cashflows, fundamental drivers and a bubble component: P t = i= r f i E t D t+i + U t+i + B t E t B t+1 = 1 + r f B t P is the price of an asset, r is the risk free rate, D are the cash flows of an asset, U the unobserved fundamental drivers and B a bubble component. If B=0 there is no bubble. If B>0 a bubble is present (i.c.w. r>0). 4

A unit root (H0) vs. explosive price behavior (H1), π r1,r2 =0 vs π r1,r2 >0.")

, the great crash episode (1928M11-1929M10), the postwar boom in 1954 (1955M01-1956M04), black Monday in October 1987")

5 Asset Bubbles Indicator: The GSADF test The procedure is developed by Phillips et al. (2015) (Generalized Sup Augmented Dickey Fuller (GSADF)). Δy t = α r1,r2 + π r1,r2 y t 1 + k i ψ r1,r2 Δy t i i=1 + γt + u t ADF test (1) A unit root (H0) vs. explosive price behavior (H1), π r1,r2 =0 vs π r1,r2 >0. ADF r2 r1 = π r1,r2 (ADF statistic) s.e.(π r1,r2 ) The test is based on varying starting points and ending points in time. Post long-depression period (1879M M04), the great crash episode (1928M M10), the postwar boom in 1954 (1955M M04), black Monday in October 1987 (1986M M09), and the dot-com bubble (1995M M08). 5

6 Asset Bubbles Indicator: GSADF test 6

7 GSADF test summary of procedure 1) Determine the model specification, minimum observations, nr. of simulations etc. 2) Compute the critical values (GSADF/BSADF) with Monte carlo simulations. 3) Perform ADF regressions for the subperiods and calculate ADF statistics. 4) Take the maximum value of the ADF statistics to examine bubbles at each point in time (BSADF statistics). Take the maximum of the BSADF statistics (GSADF). 5) Choose a confidence level and compare GSADF statistic with the critical value. 6) Determine the starting and ending point of a bubble (BS)ADF statistic > critical value (starting point), (BS)ADF statistic < critical value (ending point). 7

8 Phillips-Perron Unit root test Δy t = α r1,r2 + π r1,r2 y t 1 + +γt + u t PP test (2) Unit root test to examine a unit root (H0) vs stationary process (H1). Newey-West standard errors robust against autocorrelation of unknown form. Same hypothesis formulation as GSADF: H0 unit root, H1 explosive process. Advantages/ drawbacks: + Robust against unknown form of autocorrelation. + Procedure with Phillips-Perron allows more datapoints to be used Performance ADF test is more efficient if the lag structure is known More complex than the ADF test (Newey-West standard errors) 8

9 Monetary policy & Quantitative Easing Low interest rate environment Key interest rate December 2008 October 2015 Deposit facility 2% -0.20% Main refinancing operations 2.5% 0.05% Marginal lending facility 3% 0.3% Extended Asset Purchasing Program (EAP) CBPP3: Covered Bonds since 20 October, ~EUR 131 bln (October 2015 holdings) ABSPP: Asset Backed Securities since 21 November 2014, ~EUR 14 bln (October 2015 holdings) PSPP: Public sector securities since 9 March 2015, ~EUR 393 bln. (October 2015 holdings) 9

10 During the crisis central banks took all kinds of unconventional measures 10

11 Effect on MSCI Europe Equity market Shiller Price/earnings ratio: Current market price index is divided by a 7 year average of the earnings in real terms. This measure is often used to examine overvaluation of a specific stock or index. Monthly data from until Monte Carlo is based on 2000 simulations and 3 lags in GSADF according to SBIC criterion. In the Phillips-Perron procedure 10 Newey-West lags are specified to calculate the standard errors. 11

12 12

13 Government Bonds Examine the yield of the 10 yr Government Bond for the Netherlands and Italy. ( until ) In the academic literature several determinants of yields are often used (debt to GDP, inflation, GDP growth, fiscal deficit to GDP, bid-ask spread, EONIA rate, VIX index, current account balance etc). Debt to GDP seems to be an often used important long-term determinant. Monte Carlo is based on 2000 simulations and 4 lags in GSADF. In the Phillips-Perron procedure 10 Newey-West lags are specified to calculate the standard errors. 13

14 14

15 15

16 16

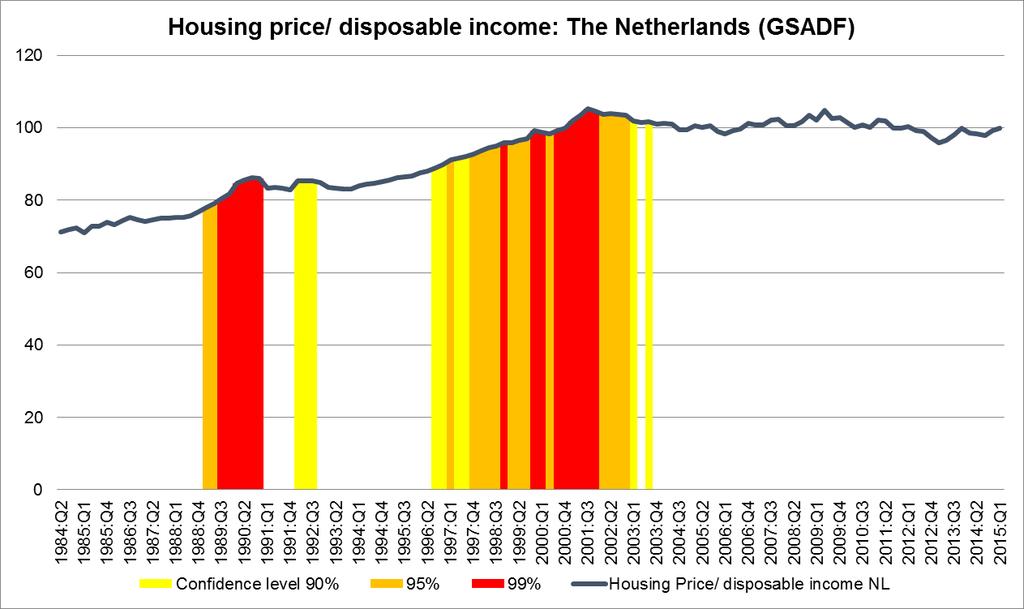

17 Other applications Energy stock prices: Bohl et al. (2015) International Review of Financial Analysis. Oil prices: Caspi et al. (2015) Energy Economics Residential Property: Yiu et al. (2013) Journal of Asian Economics Food commodity prices: Etienne et al. (2014) Journal of International Money and Finance Sterling-Dollar FX rate: Bettendorf & Chen (2013) Economics Letters Chinese RMB-Dollar FX rate: Jiang et al. (2015) Applied Economics International housing prices: (2013) Federal Reserve Dallas Working Paper Our results with housing prices: For Real Housing Prices NL: strongest signal between Q Q3 For Housing price/disposable income: weaker post 80s signals, but still signals between 1996Q3-2003Q3 17

18 Data & Model limitations For each asset or asset class it is difficult to choose appropriate fundamentals. The methodology focuses on strong price movements rather than price levels. With both procedures it is difficult to choose the correct model specification (lag structure, constant, trend). Also may flag explosive behavior in strong declining markets. Procedure is less applicable in short time series. Monte carlo simulations may take a considerable amount of computational time. 18

19 Conclusions The GSADF and GSPP are statistical procedures to examine the existence of explosive price behavior. The GSPP is less efficient in small samples but more robust against unknown form of autocorrelation. The anticipation and implementation of QE has an effect on equity and government bond markets in Europe. Exogenous shocks like the political uncertainty in Greece and China mitigate effects of QE. 19

20 Appendix 20

GDP, Share Prices, and Share Returns: Australian and New Zealand Evidence

Journal of Money, Investment and Banking ISSN 1450-288X Issue 5 (2008) EuroJournals Publishing, Inc. 2008 http://www.eurojournals.com/finance.htm GDP, Share Prices, and Share Returns: Australian and New

Journal of Money, Investment and Banking ISSN 1450-288X Issue 5 (2008) EuroJournals Publishing, Inc. 2008 http://www.eurojournals.com/finance.htm GDP, Share Prices, and Share Returns: Australian and New

Testing for Bubbles in Stock Markets with Irregular Dividend Distribution

MPRA Munich Personal RePEc Archive Testing for Bubbles in Stock Markets with Irregular Dividend Distribution Itamar Caspi and Meital Graham Bank of Israel, Bar-Ilan University, Hebrew University of Jerusalem

MPRA Munich Personal RePEc Archive Testing for Bubbles in Stock Markets with Irregular Dividend Distribution Itamar Caspi and Meital Graham Bank of Israel, Bar-Ilan University, Hebrew University of Jerusalem

The Economic Consequences of Dollar Appreciation for US Manufacturing Investment: A Time-Series Analysis

The Economic Consequences of Dollar Appreciation for US Manufacturing Investment: A Time-Series Analysis Robert A. Blecker Unpublished Appendix to Paper Forthcoming in the International Review of Applied

The Economic Consequences of Dollar Appreciation for US Manufacturing Investment: A Time-Series Analysis Robert A. Blecker Unpublished Appendix to Paper Forthcoming in the International Review of Applied

Identifying a housing bubble in South Africa

Identifying a housing bubble in South Africa Christine Patterson a, Shane Steenkamp a a Department of Economics, Stellenbosch University, South Africa Abstract Emerging market economies are high sources

Identifying a housing bubble in South Africa Christine Patterson a, Shane Steenkamp a a Department of Economics, Stellenbosch University, South Africa Abstract Emerging market economies are high sources

TESTING FOR STOCK PRICE BUBBLES: A REVIEW OF ECONOMETRIC TOOLS

The International Journal of Business and Finance Research Vol. 10, No. 4, 2016, pp. 29-42 ISSN: 1931-0269 (print) ISSN: 2157-0698 (online) www.theibfr.com TESTING FOR STOCK PRICE BUBBLES: A REVIEW OF

The International Journal of Business and Finance Research Vol. 10, No. 4, 2016, pp. 29-42 ISSN: 1931-0269 (print) ISSN: 2157-0698 (online) www.theibfr.com TESTING FOR STOCK PRICE BUBBLES: A REVIEW OF

Discussion Paper Series No.196. An Empirical Test of the Efficiency Hypothesis on the Renminbi NDF in Hong Kong Market.

Discussion Paper Series No.196 An Empirical Test of the Efficiency Hypothesis on the Renminbi NDF in Hong Kong Market IZAWA Hideki Kobe University November 2006 The Discussion Papers are a series of research

Discussion Paper Series No.196 An Empirical Test of the Efficiency Hypothesis on the Renminbi NDF in Hong Kong Market IZAWA Hideki Kobe University November 2006 The Discussion Papers are a series of research

Asset Price Bubbles and Systemic Risk

Asset Price Bubbles and Systemic Risk Markus Brunnermeier, Simon Rother, Isabel Schnabel AFA 2018 Annual Meeting Philadelphia; January 7, 2018 Simon Rother (University of Bonn) Asset Price Bubbles and

Asset Price Bubbles and Systemic Risk Markus Brunnermeier, Simon Rother, Isabel Schnabel AFA 2018 Annual Meeting Philadelphia; January 7, 2018 Simon Rother (University of Bonn) Asset Price Bubbles and

Are There Bubbles in the Sterling-dollar Exchange Rate? New Evidence from Sequential ADF Tests. April 9, 2013

Are There Bubbles in the Sterling-dollar Exchange Rate? New Evidence from Sequential ADF Tests Timo Bettendorf University of Kent Wenjuan Chen Freie Universität Berlin April 9, 213 Abstract There has been

Are There Bubbles in the Sterling-dollar Exchange Rate? New Evidence from Sequential ADF Tests Timo Bettendorf University of Kent Wenjuan Chen Freie Universität Berlin April 9, 213 Abstract There has been

Scarcity effects of QE: A transaction-level analysis in the Bund market

Scarcity effects of QE: A transaction-level analysis in the Bund market Kathi Schlepper Heiko Hofer Ryan Riordan Andreas Schrimpf Deutsche Bundesbank Deutsche Bundesbank Queen s University Bank for International

Scarcity effects of QE: A transaction-level analysis in the Bund market Kathi Schlepper Heiko Hofer Ryan Riordan Andreas Schrimpf Deutsche Bundesbank Deutsche Bundesbank Queen s University Bank for International

Travel Hysteresis in the Brazilian Current Account

Universidade Federal de Santa Catarina From the SelectedWorks of Sergio Da Silva December, 25 Travel Hysteresis in the Brazilian Current Account Roberto Meurer, Federal University of Santa Catarina Guilherme

Universidade Federal de Santa Catarina From the SelectedWorks of Sergio Da Silva December, 25 Travel Hysteresis in the Brazilian Current Account Roberto Meurer, Federal University of Santa Catarina Guilherme

Testing for bubbles in EU and US property markets

Department of Banking & Financial Management Testing for bubbles in EU and US property markets By Panagiota Diakoumi Supervisor: Prof. Christina Christou University of Piraeus 30/6/2015 Testing for bubbles

Department of Banking & Financial Management Testing for bubbles in EU and US property markets By Panagiota Diakoumi Supervisor: Prof. Christina Christou University of Piraeus 30/6/2015 Testing for bubbles

Date Stamping Bubbles in Real Estate Investment Trusts

MPRA Munich Personal RePEc Archive Date Stamping Bubbles in Real Estate Investment Trusts Diego Escobari and Mohammad Jafarinejad The University of Texas Rio Grande Valley 19. October 2015 Online at https://mpra.ub.uni-muenchen.de/67372/

MPRA Munich Personal RePEc Archive Date Stamping Bubbles in Real Estate Investment Trusts Diego Escobari and Mohammad Jafarinejad The University of Texas Rio Grande Valley 19. October 2015 Online at https://mpra.ub.uni-muenchen.de/67372/

Effects of the U.S. Quantitative Easing on the Peruvian Economy

Effects of the U.S. Quantitative Easing on the Peruvian Economy Discussion by Lamont Black DePaul University 1 Summary The effect of QE on small open economies. Effects on key macroeconomic variables for

Effects of the U.S. Quantitative Easing on the Peruvian Economy Discussion by Lamont Black DePaul University 1 Summary The effect of QE on small open economies. Effects on key macroeconomic variables for

Impact of Economic Regulation through Monetary Policy: Impact Analysis of Monetary Policy Tools on Economic Stability in Uzbekistan

International Journal of Innovation and Economic Development ISSN 1849-7020 (Print) ISSN 1849-7551 (Online) URL: http://dx.doi.org/10.18775/ijied.1849-7551-7020.2015.35.2005 DOI: 10.18775/ijied.1849-7551-7020.2015.35.2005

International Journal of Innovation and Economic Development ISSN 1849-7020 (Print) ISSN 1849-7551 (Online) URL: http://dx.doi.org/10.18775/ijied.1849-7551-7020.2015.35.2005 DOI: 10.18775/ijied.1849-7551-7020.2015.35.2005

Commodity Price Bubbles and Macroeconomics: Evidence from Chinese Agricultural Markets

Commodity Price Bubbles and Macroeconomics: Evidence from Chinese Agricultural Markets Jian Li a Jean-Paul Chavas b Xiaoli L. Etienne c Chongguang Li a a. College of Economics and Management, Huazhong

Commodity Price Bubbles and Macroeconomics: Evidence from Chinese Agricultural Markets Jian Li a Jean-Paul Chavas b Xiaoli L. Etienne c Chongguang Li a a. College of Economics and Management, Huazhong

INVESTIGATION OF THE RELATIONSHIP BETWEEN CURRENT ACCOUNT DEFICIT AND SAVINGS IN MENA ECONOMIES: AN EMPIRICAL APPROACH

INVESTIGATION OF THE RELATIONSHIP BETWEEN CURRENT ACCOUNT DEFICIT AND SAVINGS IN MENA ECONOMIES: AN EMPIRICAL APPROACH Dr. Gülgün Çiğdem, Kadir Has University, Vocational School, Banking and Insurance,

INVESTIGATION OF THE RELATIONSHIP BETWEEN CURRENT ACCOUNT DEFICIT AND SAVINGS IN MENA ECONOMIES: AN EMPIRICAL APPROACH Dr. Gülgün Çiğdem, Kadir Has University, Vocational School, Banking and Insurance,

Estimating a Monetary Policy Rule for India

MPRA Munich Personal RePEc Archive Estimating a Monetary Policy Rule for India Michael Hutchison and Rajeswari Sengupta and Nirvikar Singh University of California Santa Cruz 3. March 2010 Online at http://mpra.ub.uni-muenchen.de/21106/

MPRA Munich Personal RePEc Archive Estimating a Monetary Policy Rule for India Michael Hutchison and Rajeswari Sengupta and Nirvikar Singh University of California Santa Cruz 3. March 2010 Online at http://mpra.ub.uni-muenchen.de/21106/

Application of Structural Breakpoint Test to the Correlation Analysis between Crude Oil Price and U.S. Weekly Leading Index

Open Journal of Business and Management, 2016, 4, 322-328 Published Online April 2016 in SciRes. http://www.scirp.org/journal/ojbm http://dx.doi.org/10.4236/ojbm.2016.42034 Application of Structural Breakpoint

Open Journal of Business and Management, 2016, 4, 322-328 Published Online April 2016 in SciRes. http://www.scirp.org/journal/ojbm http://dx.doi.org/10.4236/ojbm.2016.42034 Application of Structural Breakpoint

Composition of Foreign Capital Inflows and Growth in India: An Empirical Analysis.

Composition of Foreign Capital Inflows and Growth in India: An Empirical Analysis. Author Details: Narender,Research Scholar, Faculty of Management Studies, University of Delhi. Abstract The role of foreign

Composition of Foreign Capital Inflows and Growth in India: An Empirical Analysis. Author Details: Narender,Research Scholar, Faculty of Management Studies, University of Delhi. Abstract The role of foreign

The Dynamics between Government Debt and Economic Growth in South Asia: A Time Series Approach

The Empirical Economics Letters, 15(9): (September 16) ISSN 1681 8997 The Dynamics between Government Debt and Economic Growth in South Asia: A Time Series Approach Nimantha Manamperi * Department of Economics,

The Empirical Economics Letters, 15(9): (September 16) ISSN 1681 8997 The Dynamics between Government Debt and Economic Growth in South Asia: A Time Series Approach Nimantha Manamperi * Department of Economics,

11. Testing Bubbles: Exuberance and collapse in the Shanghai A-share stock market

11. Testing Bubbles: Exuberance and collapse in the Shanghai A-share stock market Zhenya Liu, Danyuanni Han and Shixuan Wang Introduction When a stock market bubble bursts, it can trigger financial crises

11. Testing Bubbles: Exuberance and collapse in the Shanghai A-share stock market Zhenya Liu, Danyuanni Han and Shixuan Wang Introduction When a stock market bubble bursts, it can trigger financial crises

The QE Placebo. Daniel Gros. The ECB and its Watchers, XIX March 14, 2018

The QE Placebo Daniel Gros The ECB and its Watchers, XIX March 14, 2018 Debate 1: Assessment of Quantitative Easing and Challenges of Policy Normalization Frankfurt, 14 March, 2018 Bernanke: the problem

The QE Placebo Daniel Gros The ECB and its Watchers, XIX March 14, 2018 Debate 1: Assessment of Quantitative Easing and Challenges of Policy Normalization Frankfurt, 14 March, 2018 Bernanke: the problem

A Note on the Oil Price Trend and GARCH Shocks

MPRA Munich Personal RePEc Archive A Note on the Oil Price Trend and GARCH Shocks Li Jing and Henry Thompson 2010 Online at http://mpra.ub.uni-muenchen.de/20654/ MPRA Paper No. 20654, posted 13. February

MPRA Munich Personal RePEc Archive A Note on the Oil Price Trend and GARCH Shocks Li Jing and Henry Thompson 2010 Online at http://mpra.ub.uni-muenchen.de/20654/ MPRA Paper No. 20654, posted 13. February

A Note on the Oil Price Trend and GARCH Shocks

A Note on the Oil Price Trend and GARCH Shocks Jing Li* and Henry Thompson** This paper investigates the trend in the monthly real price of oil between 1990 and 2008 with a generalized autoregressive conditional

A Note on the Oil Price Trend and GARCH Shocks Jing Li* and Henry Thompson** This paper investigates the trend in the monthly real price of oil between 1990 and 2008 with a generalized autoregressive conditional

Long Run Money Neutrality: The Case of Guatemala

Long Run Money Neutrality: The Case of Guatemala Frederick H. Wallace Department of Management and Marketing College of Business Prairie View A&M University P.O. Box 638 Prairie View, Texas 77446-0638

Long Run Money Neutrality: The Case of Guatemala Frederick H. Wallace Department of Management and Marketing College of Business Prairie View A&M University P.O. Box 638 Prairie View, Texas 77446-0638

Exchange Rate Pass-Through to Domestic Prices: The Turkish Case ( )

") Exchange Rate Pass-Through to Domestic Prices: The Turkish Case (2002-2014) İlyas Şıklar Anadolu University, Eskisehir, Turkey E-mail: isiklar@anadolu.edu.tr Merve Kocaman Anadolu University, Eskisehir,

Exchange Rate Pass-Through to Domestic Prices: The Turkish Case (2002-2014) İlyas Şıklar Anadolu University, Eskisehir, Turkey E-mail: isiklar@anadolu.edu.tr Merve Kocaman Anadolu University, Eskisehir,

Discussion of Jeffrey Frankel s Systematic Managed Floating. by Assaf Razin. The 4th Asian Monetary Policy Forum, Singapore, 26 May, 2017

Discussion of Jeffrey Frankel s Systematic Managed Floating by Assaf Razin The 4th Asian Monetary Policy Forum, Singapore, 26 May, 2017 Scope Jeff s paper proposes to define an intermediate arrangement,

Discussion of Jeffrey Frankel s Systematic Managed Floating by Assaf Razin The 4th Asian Monetary Policy Forum, Singapore, 26 May, 2017 Scope Jeff s paper proposes to define an intermediate arrangement,

Identifying Price Bubble Periods in the Energy Sector

MPRA Munich Personal RePEc Archive Identifying Price Bubble Periods in the Energy Sector Shahil Sharma and Diego Escobari The University of Texas Rio Grande Valley November 217 Online at https://mpra.ub.uni-muenchen.de/83355/

MPRA Munich Personal RePEc Archive Identifying Price Bubble Periods in the Energy Sector Shahil Sharma and Diego Escobari The University of Texas Rio Grande Valley November 217 Online at https://mpra.ub.uni-muenchen.de/83355/

Prerequisites for modeling price and return data series for the Bucharest Stock Exchange

Theoretical and Applied Economics Volume XX (2013), No. 11(588), pp. 117-126 Prerequisites for modeling price and return data series for the Bucharest Stock Exchange Andrei TINCA The Bucharest University

Theoretical and Applied Economics Volume XX (2013), No. 11(588), pp. 117-126 Prerequisites for modeling price and return data series for the Bucharest Stock Exchange Andrei TINCA The Bucharest University

Time-varying wage Phillips curves in the euro area with a new measure for labor market slack

Time-varying wage Phillips curves in the euro area with a new measure for labor market slack Dennis Bonam 1, Duncan van Limbergen 1 and Jakob de Haan 1,2,3 1 De Nederlandsche Bank 2 University of Groningen

Time-varying wage Phillips curves in the euro area with a new measure for labor market slack Dennis Bonam 1, Duncan van Limbergen 1 and Jakob de Haan 1,2,3 1 De Nederlandsche Bank 2 University of Groningen

INTERDEPENDENCE OF THE BANKING SECTOR AND THE REAL SECTOR: EVIDENCE FROM OECD COUNTRIES

INTERDEPENDENCE OF THE BANKING SECTOR AND THE REAL SECTOR: EVIDENCE FROM OECD COUNTRIES İlkay Şendeniz-Yüncü * Levent Akdeniz ** Kürşat Aydoğan *** March 2006 Abstract This paper investigates the validity

INTERDEPENDENCE OF THE BANKING SECTOR AND THE REAL SECTOR: EVIDENCE FROM OECD COUNTRIES İlkay Şendeniz-Yüncü * Levent Akdeniz ** Kürşat Aydoğan *** March 2006 Abstract This paper investigates the validity

Current Account Balances and Output Volatility

Current Account Balances and Output Volatility Ceyhun Elgin Bogazici University Tolga Umut Kuzubas Bogazici University Abstract: Using annual data from 185 countries over the period from 1950 to 2009,

Current Account Balances and Output Volatility Ceyhun Elgin Bogazici University Tolga Umut Kuzubas Bogazici University Abstract: Using annual data from 185 countries over the period from 1950 to 2009,

Speculative Bubbles in Real Estate Market : Detection and Cycles

Speculative Bubbles in Real Estate Market : Detection and Cycles Recent trends in the real estate market and its analysis - 2017 edition - National Bank of Poland (NBP) Dr. Firano Zakaria zakaria. rano@um5.ac.ma

Speculative Bubbles in Real Estate Market : Detection and Cycles Recent trends in the real estate market and its analysis - 2017 edition - National Bank of Poland (NBP) Dr. Firano Zakaria zakaria. rano@um5.ac.ma

Volume 31, Issue 2. The profitability of technical analysis in the Taiwan-U.S. forward foreign exchange market

Volume 31, Issue 2 The profitability of technical analysis in the Taiwan-U.S. forward foreign exchange market Yun-Shan Dai Graduate Institute of International Economics, National Chung Cheng University

Volume 31, Issue 2 The profitability of technical analysis in the Taiwan-U.S. forward foreign exchange market Yun-Shan Dai Graduate Institute of International Economics, National Chung Cheng University

How do stock prices respond to fundamental shocks?

Finance Research Letters 1 (2004) 90 99 www.elsevier.com/locate/frl How do stock prices respond to fundamental? Mathias Binswanger University of Applied Sciences of Northwestern Switzerland, Riggenbachstr

Finance Research Letters 1 (2004) 90 99 www.elsevier.com/locate/frl How do stock prices respond to fundamental? Mathias Binswanger University of Applied Sciences of Northwestern Switzerland, Riggenbachstr

Predicting RMB exchange rate out-ofsample: Can offshore markets beat random walk?

Predicting RMB exchange rate out-ofsample: Can offshore markets beat random walk? By Chen Sichong School of Finance, Zhongnan University of Economics and Law Dec 14, 2015 at RIETI, Tokyo, Japan Motivation

Predicting RMB exchange rate out-ofsample: Can offshore markets beat random walk? By Chen Sichong School of Finance, Zhongnan University of Economics and Law Dec 14, 2015 at RIETI, Tokyo, Japan Motivation

Are Greek budget deficits 'too large'? National University of Ireland, Galway

Provided by the author(s) and NUI Galway in accordance with publisher policies. Please cite the published version when available. Title Are Greek budget deficits 'too large'? Author(s) Fountas, Stilianos

Provided by the author(s) and NUI Galway in accordance with publisher policies. Please cite the published version when available. Title Are Greek budget deficits 'too large'? Author(s) Fountas, Stilianos

How can saving deposit rate and Hang Seng Index affect housing prices : an empirical study in Hong Kong market

Lingnan Journal of Banking, Finance and Economics Volume 2 2010/2011 Academic Year Issue Article 3 January 2010 How can saving deposit rate and Hang Seng Index affect housing prices : an empirical study

Lingnan Journal of Banking, Finance and Economics Volume 2 2010/2011 Academic Year Issue Article 3 January 2010 How can saving deposit rate and Hang Seng Index affect housing prices : an empirical study

CHAPTER 2 THEORETICAL FOUNDATION. Bank is one of a well-known financial institution in Indonesia. In general,

CHAPTER 2 THEORETICAL FOUNDATION 2.1 Bank Bank is one of a well-known financial institution in Indonesia. In general, bank is known as a place for people to save their money. It is a safer and better way

CHAPTER 2 THEORETICAL FOUNDATION 2.1 Bank Bank is one of a well-known financial institution in Indonesia. In general, bank is known as a place for people to save their money. It is a safer and better way

Discussion on International Spillovers of Quantitative Easing

Discussion on International Spillovers of Quantitative Easing by M. Kolasa and G. Weso lowski Soňa Benecká First Annual Workshop ESCB Research Cluster 1 on Monetary Economics 10 October 2017 Summary and

Discussion on International Spillovers of Quantitative Easing by M. Kolasa and G. Weso lowski Soňa Benecká First Annual Workshop ESCB Research Cluster 1 on Monetary Economics 10 October 2017 Summary and

Department of Economics Working Paper

Department of Economics Working Paper Rethinking Cointegration and the Expectation Hypothesis of the Term Structure Jing Li Miami University George Davis Miami University August 2014 Working Paper # -

Department of Economics Working Paper Rethinking Cointegration and the Expectation Hypothesis of the Term Structure Jing Li Miami University George Davis Miami University August 2014 Working Paper # -

EMPIRICAL STUDY ON RELATIONS BETWEEN MACROECONOMIC VARIABLES AND THE KOREAN STOCK PRICES: AN APPLICATION OF A VECTOR ERROR CORRECTION MODEL

FULL PAPER PROCEEDING Multidisciplinary Studies Available online at www.academicfora.com Full Paper Proceeding BESSH-2016, Vol. 76- Issue.3, 56-61 ISBN 978-969-670-180-4 BESSH-16 EMPIRICAL STUDY ON RELATIONS

FULL PAPER PROCEEDING Multidisciplinary Studies Available online at www.academicfora.com Full Paper Proceeding BESSH-2016, Vol. 76- Issue.3, 56-61 ISBN 978-969-670-180-4 BESSH-16 EMPIRICAL STUDY ON RELATIONS

Environnmental and Energy and in Europe: are there multiple bubbles?

Environnmental and Energy and in Europe: are there multiple bubbles? Anna Creti 1 Marc Joëts 2 1 U. Paris Dauphine, LeDA-CGMP & Ecole Polytechnique 2 Banque de France FIME June 2018 (U. Paris Bubbles Dauphine,

Environnmental and Energy and in Europe: are there multiple bubbles? Anna Creti 1 Marc Joëts 2 1 U. Paris Dauphine, LeDA-CGMP & Ecole Polytechnique 2 Banque de France FIME June 2018 (U. Paris Bubbles Dauphine,

Explaining Interest Rates in the Dutch Mortgage Market: A Time Series Analysis

Explaining Interest Rates in the Dutch Mortgage Market: A Time Series Analysis by: Machiel Mulder and Mark Lengton In order to explain the development in mortgage interest rates in the Dutch market, we

Explaining Interest Rates in the Dutch Mortgage Market: A Time Series Analysis by: Machiel Mulder and Mark Lengton In order to explain the development in mortgage interest rates in the Dutch market, we

REIT ETFs performance during the financial crisis

ABSTRACT REIT ETFs performance during the financial crisis Stoyu I. Ivanov San José State University In this study the disintegration hypothesis is tested. It is examined whether the Vanguard Real Estate

ABSTRACT REIT ETFs performance during the financial crisis Stoyu I. Ivanov San José State University In this study the disintegration hypothesis is tested. It is examined whether the Vanguard Real Estate

Impact of Exchange Rate on Exports in Case of Pakistan

Impact of Exchange Rate on Exports in Case of Pakistan Khalil Ahmed Govt Civil Lines, Islamia College, Lahore, Pakistan. National College of Business Administration and Economics, Lahore, Pakistan. Muhammad

Impact of Exchange Rate on Exports in Case of Pakistan Khalil Ahmed Govt Civil Lines, Islamia College, Lahore, Pakistan. National College of Business Administration and Economics, Lahore, Pakistan. Muhammad

Web Appendix for The Political Sources of Systematic Investment Risk: Lessons from a Consensus Democracy

Web Appendix for The Political Sources of Systematic Investment Risk: Lessons from a Consensus Democracy Published in Journal of Politics 71 (2) 2009, 661-677 Michael M. Bechtel 2nd October 2009 This appendix

Web Appendix for The Political Sources of Systematic Investment Risk: Lessons from a Consensus Democracy Published in Journal of Politics 71 (2) 2009, 661-677 Michael M. Bechtel 2nd October 2009 This appendix

Are Bitcoin Prices Rational Bubbles *

The Empirical Economics Letters, 15(9): (September 2016) ISSN 1681 8997 Are Bitcoin Prices Rational Bubbles * Hiroshi Gunji Faculty of Economics, Daito Bunka University Takashimadaira, Itabashi, Tokyo,

The Empirical Economics Letters, 15(9): (September 2016) ISSN 1681 8997 Are Bitcoin Prices Rational Bubbles * Hiroshi Gunji Faculty of Economics, Daito Bunka University Takashimadaira, Itabashi, Tokyo,

Personal income, stock market, and investor psychology

ABSTRACT Personal income, stock market, and investor psychology Chung Baek Troy University Minjung Song Thomas University This paper examines how disposable personal income is related to investor psychology

ABSTRACT Personal income, stock market, and investor psychology Chung Baek Troy University Minjung Song Thomas University This paper examines how disposable personal income is related to investor psychology

The Influence of Monetary Policy on Equity and Volatility Indices in the U.S. and Canada

International Journal of Economics and Finance; Vol. 8, No. 4; 2016 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education The Influence of Monetary Policy on Equity and

International Journal of Economics and Finance; Vol. 8, No. 4; 2016 ISSN 1916-971X E-ISSN 1916-9728 Published by Canadian Center of Science and Education The Influence of Monetary Policy on Equity and

Behavioural Equilibrium Exchange Rate (BEER)

") Behavioural Equilibrium Exchange Rate (BEER) Abstract: In this article, we will introduce another method for evaluating the fair value of a currency: the Behavioural Equilibrium Exchange Rate (BEER), a

Behavioural Equilibrium Exchange Rate (BEER) Abstract: In this article, we will introduce another method for evaluating the fair value of a currency: the Behavioural Equilibrium Exchange Rate (BEER), a

Determinants of Cyclical Aggregate Dividend Behavior

Review of Economics & Finance Submitted on 01/Apr./2012 Article ID: 1923-7529-2012-03-71-08 Samih Antoine Azar Determinants of Cyclical Aggregate Dividend Behavior Dr. Samih Antoine Azar Faculty of Business

Review of Economics & Finance Submitted on 01/Apr./2012 Article ID: 1923-7529-2012-03-71-08 Samih Antoine Azar Determinants of Cyclical Aggregate Dividend Behavior Dr. Samih Antoine Azar Faculty of Business

GRANGER CAUSALITY RELATION BETWEEN INTEREST RATES AND STOCK MARKETS: EVIDENCE FROM EMERGING MARKETS

GRANGER CAUSALITY RELATION BETWEEN INTEREST RATES AND STOCK MARKETS: EVIDENCE FROM EMERGING MARKETS Assoc. Prof. Dilek Leblebici Teker Assoc. Prof. Elcin (Corresponding Author) Isık University Istanbul

GRANGER CAUSALITY RELATION BETWEEN INTEREST RATES AND STOCK MARKETS: EVIDENCE FROM EMERGING MARKETS Assoc. Prof. Dilek Leblebici Teker Assoc. Prof. Elcin (Corresponding Author) Isık University Istanbul

Integration of Foreign Exchange Markets: A Short Term Dynamics Analysis

Global Journal of Management and Business Studies. ISSN 2248-9878 Volume 3, Number 4 (2013), pp. 383-388 Research India Publications http://www.ripublication.com/gjmbs.htm Integration of Foreign Exchange

Global Journal of Management and Business Studies. ISSN 2248-9878 Volume 3, Number 4 (2013), pp. 383-388 Research India Publications http://www.ripublication.com/gjmbs.htm Integration of Foreign Exchange

The Impact of Government Expenditures on Imports within the Euro Area

The Impact of Government Expenditures on Imports within the Euro Area An Analysis of Germany and the Peripheral Countries By Marion C.G. Mulder 363424 Abstract Southern European countries emphasize the

The Impact of Government Expenditures on Imports within the Euro Area An Analysis of Germany and the Peripheral Countries By Marion C.G. Mulder 363424 Abstract Southern European countries emphasize the

THE IMPACT OF IMPORT ON INFLATION IN NAMIBIA

European Journal of Business, Economics and Accountancy Vol. 5, No. 2, 207 ISSN 2056-608 THE IMPACT OF IMPORT ON INFLATION IN NAMIBIA Mika Munepapa Namibia University of Science and Technology NAMIBIA

European Journal of Business, Economics and Accountancy Vol. 5, No. 2, 207 ISSN 2056-608 THE IMPACT OF IMPORT ON INFLATION IN NAMIBIA Mika Munepapa Namibia University of Science and Technology NAMIBIA

The Demand for Money in China: Evidence from Half a Century

International Journal of Business and Social Science Vol. 5, No. 1; September 214 The Demand for Money in China: Evidence from Half a Century Dr. Liaoliao Li Associate Professor Department of Business

International Journal of Business and Social Science Vol. 5, No. 1; September 214 The Demand for Money in China: Evidence from Half a Century Dr. Liaoliao Li Associate Professor Department of Business

A COMPARATIVE ANALYSIS OF REAL AND PREDICTED INFLATION CONVERGENCE IN CEE COUNTRIES DURING THE ECONOMIC CRISIS

A COMPARATIVE ANALYSIS OF REAL AND PREDICTED INFLATION CONVERGENCE IN CEE COUNTRIES DURING THE ECONOMIC CRISIS Mihaela Simionescu * Abstract: The main objective of this study is to make a comparative analysis

A COMPARATIVE ANALYSIS OF REAL AND PREDICTED INFLATION CONVERGENCE IN CEE COUNTRIES DURING THE ECONOMIC CRISIS Mihaela Simionescu * Abstract: The main objective of this study is to make a comparative analysis

SUSTAINABILITY PLANNING POLICY COLLECTING THE REVENUES OF THE TAX ADMINISTRATION

2007 2008 2009 2010 Year IX, No.12/2010 127 SUSTAINABILITY PLANNING POLICY COLLECTING THE REVENUES OF THE TAX ADMINISTRATION Prof. Marius HERBEI, PhD Gheorghe MOCAN, PhD West University, Timişoara I. Introduction

2007 2008 2009 2010 Year IX, No.12/2010 127 SUSTAINABILITY PLANNING POLICY COLLECTING THE REVENUES OF THE TAX ADMINISTRATION Prof. Marius HERBEI, PhD Gheorghe MOCAN, PhD West University, Timişoara I. Introduction

Testing Random Walk Hypothesis for Bombay Stock Exchange Listed Stocks

International Journal of Management, IT & Engineering Vol. 8 Issue 2, February 2018, ISSN: 2249-0558 Impact Factor: 7.119 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International

International Journal of Management, IT & Engineering Vol. 8 Issue 2, February 2018, ISSN: 2249-0558 Impact Factor: 7.119 Journal Homepage: Double-Blind Peer Reviewed Refereed Open Access International

Informed Trading of Futures Markets During the Financial Crisis: Evidence from the VPIN

International Journal of Economics and Finance; Vol. 9, No. 9; 07 ISSN 96-97X E-ISSN 96-978 Published by Canadian Center of Science and Education Informed Trading of Futures Markets During the Financial

International Journal of Economics and Finance; Vol. 9, No. 9; 07 ISSN 96-97X E-ISSN 96-978 Published by Canadian Center of Science and Education Informed Trading of Futures Markets During the Financial

RETURNS AND VOLATILITY SPILLOVERS IN BRIC (BRAZIL, RUSSIA, INDIA, CHINA), EUROPE AND USA

, EUROPE AND USA") RETURNS AND VOLATILITY SPILLOVERS IN BRIC (BRAZIL, RUSSIA, INDIA, CHINA), EUROPE AND USA Burhan F. Yavas, College of Business Administrations and Public Policy California State University Dominguez Hills

RETURNS AND VOLATILITY SPILLOVERS IN BRIC (BRAZIL, RUSSIA, INDIA, CHINA), EUROPE AND USA Burhan F. Yavas, College of Business Administrations and Public Policy California State University Dominguez Hills

Study of Relationship Between USD/INR Exchange Rate and BSE Sensex from

DOI : 10.18843/ijms/v5i3(1)/13 DOIURL :http://dx.doi.org/10.18843/ijms/v5i3(1)/13 Study of Relationship Between USD/INR Exchange Rate and BSE Sensex from 2008-2017 Hardeepika Singh Ahluwalia, Assistant

DOI : 10.18843/ijms/v5i3(1)/13 DOIURL :http://dx.doi.org/10.18843/ijms/v5i3(1)/13 Study of Relationship Between USD/INR Exchange Rate and BSE Sensex from 2008-2017 Hardeepika Singh Ahluwalia, Assistant

Economic and Monetary Policy Perspectives for Europe and the Euro Area

Economic and Monetary Policy Perspectives for Europe and the Euro Area Peter Mooslechner Executive Director and Member of the Governing Board Oesterreichische Nationalbank Roundtable Discussion, Austrian

Economic and Monetary Policy Perspectives for Europe and the Euro Area Peter Mooslechner Executive Director and Member of the Governing Board Oesterreichische Nationalbank Roundtable Discussion, Austrian

RATIONAL BUBBLES AND LEARNING

RATIONAL BUBBLES AND LEARNING Rational bubbles arise because of the indeterminate aspect of solutions to rational expectations models, where the process governing stock prices is encapsulated in the Euler

RATIONAL BUBBLES AND LEARNING Rational bubbles arise because of the indeterminate aspect of solutions to rational expectations models, where the process governing stock prices is encapsulated in the Euler

VOLATILITY COMPONENT OF DERIVATIVE MARKET: EVIDENCE FROM FBMKLCI BASED ON CGARCH

VOLATILITY COMPONENT OF DERIVATIVE MARKET: EVIDENCE FROM BASED ON CGARCH Razali Haron 1 Salami Monsurat Ayojimi 2 Abstract This study examines the volatility component of Malaysian stock index. Despite

VOLATILITY COMPONENT OF DERIVATIVE MARKET: EVIDENCE FROM BASED ON CGARCH Razali Haron 1 Salami Monsurat Ayojimi 2 Abstract This study examines the volatility component of Malaysian stock index. Despite

Financial crisis, unconventional monetary policy and international spillovers

Financial crisis, unconventional monetary policy and international spillovers Qianying Chen, IMF Andrew Filardo, BIS Dong He, HKIMR Feng Zhu, BIS ECB-IMF Conference on International dimensions of conventional

Financial crisis, unconventional monetary policy and international spillovers Qianying Chen, IMF Andrew Filardo, BIS Dong He, HKIMR Feng Zhu, BIS ECB-IMF Conference on International dimensions of conventional

Does External Debt Increase Net Private Wealth? The Relative Impact of Domestic versus External Debt on the US Demand for Money

Journal of Applied Finance & Banking, vol. 3, no. 5, 2013, 85-91 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2013 Does External Debt Increase Net Private Wealth? The Relative Impact

Journal of Applied Finance & Banking, vol. 3, no. 5, 2013, 85-91 ISSN: 1792-6580 (print version), 1792-6599 (online) Scienpress Ltd, 2013 Does External Debt Increase Net Private Wealth? The Relative Impact

Episodes of Exuberance in Housing Markets: In Search of the Smoking Gun *

Federal Reserve Bank of Dallas Globalization and Monetary Policy Institute Working Paper No. 165 http://www.dallasfed.org/assets/documents/institute/wpapers/2013/0165.pdf Episodes of Exuberance in Housing

Federal Reserve Bank of Dallas Globalization and Monetary Policy Institute Working Paper No. 165 http://www.dallasfed.org/assets/documents/institute/wpapers/2013/0165.pdf Episodes of Exuberance in Housing

Global Economic and Market Outlook for Gavyn Davies, Chairman, Fulcrum Asset Management

Global Economic and Market Outlook for 2018 Gavyn Davies, Chairman, Fulcrum Asset Management After many years of persistent downgrades to consensus GDP forecasts, 2017 has seen the first upgrades since

Global Economic and Market Outlook for 2018 Gavyn Davies, Chairman, Fulcrum Asset Management After many years of persistent downgrades to consensus GDP forecasts, 2017 has seen the first upgrades since

Graduated from Glasgow University in 2009: BSc with Honours in Mathematics and Statistics.

The statistical dilemma: Forecasting future losses for IFRS 9 under a benign economic environment, a trade off between statistical robustness and business need. Katie Cleary Introduction Presenter: Katie

The statistical dilemma: Forecasting future losses for IFRS 9 under a benign economic environment, a trade off between statistical robustness and business need. Katie Cleary Introduction Presenter: Katie

DETECTING BUBBLES IN HONG KONG RESIDENTIAL PROPERTY MARKET

1 DETECTING BUBBLES IN HONG KONG RESIDENTIAL PROPERTY MARKET Matthew S. Yiu ASEAN + 3 Macroeconomic Research Office Jun Yu Singapore Management University Lu Jin Hong Kong Monetary Authority May, 1 Abstract

1 DETECTING BUBBLES IN HONG KONG RESIDENTIAL PROPERTY MARKET Matthew S. Yiu ASEAN + 3 Macroeconomic Research Office Jun Yu Singapore Management University Lu Jin Hong Kong Monetary Authority May, 1 Abstract

PUBLIC DEBT AND DEFICIT IN MEXICO: COMMENT* JohnH. Welch. Federal Reserve Bank of Dallas

PUBLIC DEBT AND DEFICIT IN MEXICO: A COMMENT* JohnH. Welch Federal Reserve Bank of Dallas Resumen: Este comentario muestra que el balance presupuestario intertemporal de México fue mantenido durante el

PUBLIC DEBT AND DEFICIT IN MEXICO: A COMMENT* JohnH. Welch Federal Reserve Bank of Dallas Resumen: Este comentario muestra que el balance presupuestario intertemporal de México fue mantenido durante el

Evaluating the Impact of the Key Factors on Foreign Direct Investment: A Study Based on Bangladesh Economy

Evaluating the Impact of the Key Factors on Foreign Direct Investment: A Study Based on Bangladesh Economy Author s Details: (1) Abu Bakar Seddeke, Senior Officer, South Bangla Agriculture and Commerce

Evaluating the Impact of the Key Factors on Foreign Direct Investment: A Study Based on Bangladesh Economy Author s Details: (1) Abu Bakar Seddeke, Senior Officer, South Bangla Agriculture and Commerce

Empirical Analysis of Private Investments: The Case of Pakistan

2011 International Conference on Sociality and Economics Development IPEDR vol.10 (2011) (2011) IACSIT Press, Singapore Empirical Analysis of Private Investments: The Case of Pakistan Dr. Asma Salman 1

2011 International Conference on Sociality and Economics Development IPEDR vol.10 (2011) (2011) IACSIT Press, Singapore Empirical Analysis of Private Investments: The Case of Pakistan Dr. Asma Salman 1

Lecture 5. Predictability. Traditional Views of Market Efficiency ( )

") Lecture 5 Predictability Traditional Views of Market Efficiency (1960-1970) CAPM is a good measure of risk Returns are close to unpredictable (a) Stock, bond and foreign exchange changes are not predictable

Lecture 5 Predictability Traditional Views of Market Efficiency (1960-1970) CAPM is a good measure of risk Returns are close to unpredictable (a) Stock, bond and foreign exchange changes are not predictable

Testing Regime Non-stationarity of the G-7 Inflation Rates: Evidence from the Markov Switching Unit Root Test

Journal of the Chinese Statistical Association Vol. 47, (2009) 1 18 Testing Regime Non-stationarity of the G-7 Inflation Rates: Evidence from the Markov Switching Unit Root Test Shyh-Wei Chen 1 and Chung-Hua

Journal of the Chinese Statistical Association Vol. 47, (2009) 1 18 Testing Regime Non-stationarity of the G-7 Inflation Rates: Evidence from the Markov Switching Unit Root Test Shyh-Wei Chen 1 and Chung-Hua

RAYMOND JAMES RAYMOND JAMES. -Technical Chart Book -

Technical Strategy Team - Technical Chart Book RAYMOND JAMES -Technical Chart Book - Providing Investors with timely data and technical observations on a broad spectrum of asset classes. Portfolio & Technical

Technical Strategy Team - Technical Chart Book RAYMOND JAMES -Technical Chart Book - Providing Investors with timely data and technical observations on a broad spectrum of asset classes. Portfolio & Technical

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank The views expressed herein are those of the presenter only and do not necessarily reflect those of the ECB or the European

The ECB s Strategy in Good and Bad Times Massimo Rostagno European Central Bank The views expressed herein are those of the presenter only and do not necessarily reflect those of the ECB or the European

An Empirical Research on Chinese Stock Market Volatility Based. on Garch

Volume 04 - Issue 07 July 2018 PP. 15-23 An Empirical Research on Chinese Stock Market Volatility Based on Garch Ya Qian Zhu 1, Wen huili* 1 (Department of Mathematics and Finance, Hunan University of

Volume 04 - Issue 07 July 2018 PP. 15-23 An Empirical Research on Chinese Stock Market Volatility Based on Garch Ya Qian Zhu 1, Wen huili* 1 (Department of Mathematics and Finance, Hunan University of

Does Monetary Policy Affect Stock Prices and Treasury Yields? An Error Correction and Simultaneous Equation Approach

Does Monetary Policy Affect Stock Prices and Treasury Yields? An Error Correction and Simultaneous Equation Approach J. Benson Durham * Division of Monetary Affairs Board of Governors of the Federal Reserve

Does Monetary Policy Affect Stock Prices and Treasury Yields? An Error Correction and Simultaneous Equation Approach J. Benson Durham * Division of Monetary Affairs Board of Governors of the Federal Reserve

Volume 29, Issue 2. Measuring the external risk in the United Kingdom. Estela Sáenz University of Zaragoza

Volume 9, Issue Measuring the external risk in the United Kingdom Estela Sáenz University of Zaragoza María Dolores Gadea University of Zaragoza Marcela Sabaté University of Zaragoza Abstract This paper

Volume 9, Issue Measuring the external risk in the United Kingdom Estela Sáenz University of Zaragoza María Dolores Gadea University of Zaragoza Marcela Sabaté University of Zaragoza Abstract This paper

Chapter 8 A Short Run Keynesian Model of Interdependent Economies

George Alogoskoufis, International Macroeconomics, 2016 Chapter 8 A Short Run Keynesian Model of Interdependent Economies Our analysis up to now was related to small open economies, which took developments

George Alogoskoufis, International Macroeconomics, 2016 Chapter 8 A Short Run Keynesian Model of Interdependent Economies Our analysis up to now was related to small open economies, which took developments

Trading Volume, Volatility and ADR Returns

Trading Volume, Volatility and ADR Returns Priti Verma, College of Business Administration, Texas A&M University, Kingsville, USA ABSTRACT Based on the mixture of distributions hypothesis (MDH), this paper

Trading Volume, Volatility and ADR Returns Priti Verma, College of Business Administration, Texas A&M University, Kingsville, USA ABSTRACT Based on the mixture of distributions hypothesis (MDH), this paper

Hock Ann Lee Labuan School of International Business and Finance, Universiti Malaysia Sabah. Abstract

Income Disparity between Japan and ASEAN 5 Economies: Converge, Catching Up or Diverge? Hock Ann Lee Labuan School of International Business and Finance, Universiti Malaysia Sabah Kian Ping Lim Labuan

Income Disparity between Japan and ASEAN 5 Economies: Converge, Catching Up or Diverge? Hock Ann Lee Labuan School of International Business and Finance, Universiti Malaysia Sabah Kian Ping Lim Labuan

ANALYZING THE RELATIONSHIP BETWEEN EONIA AND EONIASWAP RATES. A COINTEGRATION APPROACH

ANALYZING THE RELATIONSHIP BETWEEN EONIA AND EONIASWAP RATES. A COINTEGRATION APPROACH Authors: Codruţa Maria FĂT 1, Simona MUTU 2 A bstract: The aim of this paper is to analyze the behavior of swap rates

ANALYZING THE RELATIONSHIP BETWEEN EONIA AND EONIASWAP RATES. A COINTEGRATION APPROACH Authors: Codruţa Maria FĂT 1, Simona MUTU 2 A bstract: The aim of this paper is to analyze the behavior of swap rates

Unemployment and Labour Force Participation in Italy

MPRA Munich Personal RePEc Archive Unemployment and Labour Force Participation in Italy Francesco Nemore Università degli studi di Bari Aldo Moro 8 March 2018 Online at https://mpra.ub.uni-muenchen.de/85067/

MPRA Munich Personal RePEc Archive Unemployment and Labour Force Participation in Italy Francesco Nemore Università degli studi di Bari Aldo Moro 8 March 2018 Online at https://mpra.ub.uni-muenchen.de/85067/

WHAT DOES THE HOUSE PRICE-TO-

WHAT DOES THE HOUSE PRICE-TO- INCOME RATIO TELL US ABOUT THE HOUSING AFFORDABILITY: A THEORY AND INTERNATIONAL EVIDENCE (THIS VERSION: AUG 2016) Charles Ka Yui LEUNG City University of Hong Kong Edward

WHAT DOES THE HOUSE PRICE-TO- INCOME RATIO TELL US ABOUT THE HOUSING AFFORDABILITY: A THEORY AND INTERNATIONAL EVIDENCE (THIS VERSION: AUG 2016) Charles Ka Yui LEUNG City University of Hong Kong Edward

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis Introduction Uthajakumar S.S 1 and Selvamalai. T 2 1 Department of Economics, University of Jaffna. 2

Government Tax Revenue, Expenditure, and Debt in Sri Lanka : A Vector Autoregressive Model Analysis Introduction Uthajakumar S.S 1 and Selvamalai. T 2 1 Department of Economics, University of Jaffna. 2

Investigating Causal Relationship between Indian and American Stock Markets , Tamilnadu, India

Investigating Causal Relationship between Indian and American Stock Markets M.V.Subha 1, S.Thirupparkadal Nambi 2 1 Associate Professor MBA, Department of Management Studies, Anna University, Regional

Investigating Causal Relationship between Indian and American Stock Markets M.V.Subha 1, S.Thirupparkadal Nambi 2 1 Associate Professor MBA, Department of Management Studies, Anna University, Regional

The impact of international swap lines on stock returns of banks in emerging markets

The impact of international swap lines on stock returns of banks in emerging markets Alin Andries, Andreas Fischer, Pınar Yeşin Conference on Spillovers of Monetary Policy Zurich, July 9, 2015 Disclaimer:

The impact of international swap lines on stock returns of banks in emerging markets Alin Andries, Andreas Fischer, Pınar Yeşin Conference on Spillovers of Monetary Policy Zurich, July 9, 2015 Disclaimer:

Examining the Linkage Dynamics and Diversification Opportunities of Equity and Bond Markets in India

Examining the Linkage Dynamics and Diversification Opportunities of Equity and Bond Markets in India Harip Khanapuri (Assistant Professor, S. S. Dempo College of Commerce and Economics, Cujira, Goa, India)

Examining the Linkage Dynamics and Diversification Opportunities of Equity and Bond Markets in India Harip Khanapuri (Assistant Professor, S. S. Dempo College of Commerce and Economics, Cujira, Goa, India)

JPMorgan Europe High Yield Bond Fund

AVAILABLE FOR PUBLIC CIRCULATION NEW JPMorgan Europe High Yield Bond Fund Asset Management Company of the Year, Asia + Important information 1. The Fund invests at least 7 in European and non-european

AVAILABLE FOR PUBLIC CIRCULATION NEW JPMorgan Europe High Yield Bond Fund Asset Management Company of the Year, Asia + Important information 1. The Fund invests at least 7 in European and non-european

Implied Volatility v/s Realized Volatility: A Forecasting Dimension

4 Implied Volatility v/s Realized Volatility: A Forecasting Dimension 4.1 Introduction Modelling and predicting financial market volatility has played an important role for market participants as it enables

4 Implied Volatility v/s Realized Volatility: A Forecasting Dimension 4.1 Introduction Modelling and predicting financial market volatility has played an important role for market participants as it enables

Effectiveness and Transmission of the ECB s Balance Sheet Policies

Effectiveness and Transmission of the ECB s Balance Sheet Policies Jef Boeckx NBB Maarten Dossche NBB Gert Peersman UGent Motivation There is a large literature that has used SVAR models to examine the

Effectiveness and Transmission of the ECB s Balance Sheet Policies Jef Boeckx NBB Maarten Dossche NBB Gert Peersman UGent Motivation There is a large literature that has used SVAR models to examine the

What triggers stock market jumps?

What triggers stock market jumps? Scott R. Baker (Kellogg, Northwestern) Nick Bloom (Stanford) Steven J. Davis (Chicago Booth) Marco Sammon (Kellogg, Northwestern) January 7 th, 2018 Why does the stock

What triggers stock market jumps? Scott R. Baker (Kellogg, Northwestern) Nick Bloom (Stanford) Steven J. Davis (Chicago Booth) Marco Sammon (Kellogg, Northwestern) January 7 th, 2018 Why does the stock

Inflation and Stock Market Returns in US: An Empirical Study

Inflation and Stock Market Returns in US: An Empirical Study CHETAN YADAV Assistant Professor, Department of Commerce, Delhi School of Economics, University of Delhi Delhi (India) Abstract: This paper

Inflation and Stock Market Returns in US: An Empirical Study CHETAN YADAV Assistant Professor, Department of Commerce, Delhi School of Economics, University of Delhi Delhi (India) Abstract: This paper

The causal link between benchmark crude oil and the U.S. Dollar Value: in rising and falling oil markets

The causal link between benchmark crude oil and the U.S. Dollar Value: in rising and falling oil markets Ahmed, A. Published PDF deposited in Curve March 2016 Original citation: Ahmed, A. (2015) 'The causal

The causal link between benchmark crude oil and the U.S. Dollar Value: in rising and falling oil markets Ahmed, A. Published PDF deposited in Curve March 2016 Original citation: Ahmed, A. (2015) 'The causal

Financial Econometrics Series SWP 2011/13. Did the US Macroeconomic Conditions Affect Asian Stock Markets? S. Narayan and P.K.

Faculty of Business and Law School of Accounting, Economics and Finance Financial Econometrics Series SWP 2011/13 Did the US Macroeconomic Conditions Affect Asian Stock Markets? S. Narayan and P.K. Narayan

Faculty of Business and Law School of Accounting, Economics and Finance Financial Econometrics Series SWP 2011/13 Did the US Macroeconomic Conditions Affect Asian Stock Markets? S. Narayan and P.K. Narayan

U.S. STOCK MARKET P/E RATIOS, STRUCTURAL BREAKS, AND LONG-TERM STOCK RETURNS

Journal of Business Economics and Management ISSN 1611-1699 / eissn 2029-4433 2018 Volume 19 Issue 1: 110 123 https://doi.org/10.3846/16111699.2017.1409263 U.S. STOCK MARKET P/E RATIOS, STRUCTURAL BREAKS,

Journal of Business Economics and Management ISSN 1611-1699 / eissn 2029-4433 2018 Volume 19 Issue 1: 110 123 https://doi.org/10.3846/16111699.2017.1409263 U.S. STOCK MARKET P/E RATIOS, STRUCTURAL BREAKS,