BOOTSTRAPPING A ZERO-SWAP CURVE FOR TENOR 3M USING PYTHON

|

|

|

- Jonah Webb

- 6 years ago

- Views:

Transcription

1 Division of Applied Mathematics School of Education, Culture & Communication Mälardalen University Box 883, Västerås, Sweden Date: 16 th December, 2014 BOOTSTRAPPING A ZERO-SWAP CURVE FOR TENOR 3M USING PYTHON Seminar Report MMA708- ANALYTICAL FINANCE I LECTURER: JAN RÖMAN AUTHORS: FYNN-AIKINS EKOW ADOBAH-OTCHEY DANIEL

2 Table of Contents 1. Introduction The Yield Curve Valuation Discount Curve The Par, Spot curve and the Forward Rate curve Discount factors Bootstrapping a swap curve Extracting discount factors from deposit rates Extracting discount factors from futures contract Extracting discount factors from swap rates Applications and Results Data Used in Zero Swap-Curve Tenor 3M Python Programming Illustration for the Zero Swap-Curve Tenor 3M Conclusions Comments Appendix Zero swap curve for tenor 3M Discount Curve References... 9

3 1. Introduction Fundamental to any trading and risk management activity is the ability to value future cash flows of an asset. In modern finance the accepted approach to valuation is the discounted cash flows (DCF) methodology. If C(t) is a cash flow occurring t years from today, according to the DCF model, the value of this cash flow today is V0=C(t)Z(t) where Z(t) is the present value (PV) factor or discount factor. This report is based on the usage of the Python Programming Language to bootstrap such scenarios.

4 2. The Yield Curve 2.1. Valuation To value any asset, the necessary information is the cash flows, their payment dates, and the corresponding discount factors to PV these cash flows. The cash flows and their payment dates can be directly obtained from the contract specification but the discount factor requires the knowledge of the yield curve. All investors will have a specific risk/reward profile that they are comfortable with, and a bond s yield relative to its perceived risk will influence the decision to buy (or sell) it. Much of the analysis and pricing activity that takes place in the bond markets revolves around the yield curve. The yield curve plays a central role in the pricing, trading and risk management activities of all financial products ranging from cash instruments to exotic structured derivative products. The yield curve describes the relationship between a particular yield-to-maturity and a bond s maturity. Plotting the yields of bonds along the term structure will give us our yield curve. Strictly speaking, the yield curve describes the term structure of interest rates in any market, i.e. the relationship between the market yield and maturity of instruments with similar credit risk. The market yield curve can be described by a number of alternative but equivalent ways: discount curve, par-coupon curve, zero-coupon or spot curve and forward rate curve Discount Curve The discount curve reflects the discount factor applicable at different dates in the future and represents the information about the market in the most primitive fashion. This is the most primitive way to represent the yield curve and is primarily used for valuation of cash flows. An example of discount curve for the German bond market based on the closing prices on 29 October 1998 is shown in Figure 2.1

5 Figure 2.1 Discount curve 2.3. The Par, Spot curve and the Forward Rate curve The par, spot, and forward curves that can be derived from the discount curve is useful for developing yield curve trading ideas. Par, spot and forward rates have a close mathematical relationship. The spot interest rates are also called zero-coupon rates, because they are the interest rates that would be applicable to a zero-coupon bond. It indicates the yield of a zero coupon bond for different maturity. A par yield is the yield-to-maturity on a bond that is trading at par. This means that the yield is equal to the bond s coupon level. A zero-coupon bond is a bond which has no coupons, and therefore only one cash flow, the redemption payment on maturity. It is therefore a discount instrument, as it is issued at a discount to par and redeemed at par. The yield on a zero-coupon bond can be viewed as a true yield, at the time that is it purchased, if the paper is held to maturity. This is because no reinvestment of coupons is involved and so there are no interim cash flows vulnerable to a change in interest rates. Zero-coupon yields are the key determinant of value in the capital markets, and they are calculated and quoted for every major currency. Zero-coupon rates can be used to value any cash flow that occurs at a future date. The forward par curve or the forward rate curve can also be constructed. Both these curves show the future evolution of the interest rates as seen from today s market yield curve.

6 The forward rate curve shows the anticipated market interest rate for a specific tenor at different points in the future while the forward curve presents the evolution of the entire par curve at a future date. Figure 2.2 shows the par, spot, forward curves German government market on 29 October Figure 2.2 Par-, zero-, and forward yield curves.

7 2.4. Discount factors Since discount factor curve forms the fundamental building block for pricing and trading in both the cash and derivative markets we will begin by focusing on the methodology for constructing the discount curve from market data. Armed with the knowledge of discount curve we will then devote our attention to developing other representation of market yield curve. The process for building the yield curve can be summarized in Figure 2.3 Figure 2.3 Yield curve modeling process.

8 3. Bootstrapping a swap curve Market participant also refers to the swap curve as the LIBOR curve. The swap market yield curve is built by splicing together the rates from market instruments that represent the most liquid instruments or dominant instruments in their tenors. At the very short end, the yield curve uses the cash deposit rates, where available the International Money Market (IMM) futures contracts are used for intermediate tenors and finally par swap rates are used for longer tenors. A methodology for building the yield curve from these market rates, is referred to as bootstrapping or zero coupon stripping. The LIBOR curve can be built using the following combinations of market rates: Cash deposit, futures and swaps Cash deposit and swaps The reason for the popularity of the bootstrapping approach is its ability to produce a no-arbitrage yield curve, meaning that the discount factor obtained from bootstrapping can recover market rates that has been used in their construction. The downside to this approach is the fact that the forward rate curve obtained from this process is not a smooth curve. While there exists methodologies to obtain smooth forward curves with the help of various fitting algorithms they are not always preferred as they may violate the no-arbitrage constraint or have unacceptable behavior in risk calculations Extracting discount factors from deposit rates The first part of the yield curve is built using the cash deposit rates quoted in the market. The interest on the deposit rate accrue on a simple interest rate basis and as such is the simplest instrument to use in generating discount curve. It is calculated using the following fundamental relationship in finance: Present value = Future value discount factor To find the discount factors, first, we can calculate the overnight discount factor. i.e. D O/ N 1 d par O/ N 1 ro / N. 360

9 This will enable derive the spot or zero rate for the overnight i.e. Z O/ N ln D 100 do/ N 365 O/ N Next, we use the tomorrow next rate to calculate the discount factor for the spot date. The tomorrow next rate is a forward rate between trade day plus one business day to trade date plus two business day. Therefore, the discount factor for the spot date is given by the following functions: Discont factor the tomorrow next, D T/ N D O/ N d par T/ N 1 rt/ N. 360 The zero rateis Z T/ N ln 100 D d T/ N T/ N 1 360

10 3.2. Extracting discount factors from futures contract Next we consider the method for extracting the discount factor from the futures contract. The prices for IMM futures contract reflect the effective interest rate for lending or borrowing 3-month LIBOR for a specific time period in the future. The contracts are quoted on a price basis and are available for the months March, June, September and December. The settlement dates for the contracts vary from exchange to exchange. Typically these contracts settle on the third Wednesday of the month and their prices reflect the effective future interest rate for a 3-month period from the settlement date Extracting discount factors from swap rates As we go further away from the spot date we either run out of the futures contract or, as is more often the case, the futures contract become unsuitable due to lack of liquidity. Therefore to generate the yield curve we need to use the next most liquid instrument, i.e. the swap rate. We need to know the swap rate and discount factor. If a swap rate is not available then it has to be interpolated. Similarly, if the discount factors on the swap payment dates are not available then they also have to be interpolated. 1

11 4. Applications and Results 4.1. Data Used in Zero Swap-Curve Tenor 3M Start date Deposits Tenor Bid Ask mid start date maturity period days O/N T/N W M M M M FRA Tenor Bid Ask mid start date maturity period days 3M-6M M-9M M-12M M-15M M-18M M-21M M-24M Swap 3M Tenor Bid Ask mid start date maturity period days 2Y Y Y Y Y Y Y Y Y Y Y Y Y Y

12 4.2. Python Programming Illustration for the Zero Swap-Curve Tenor 3M For the above data, the following was the output using Python: 3

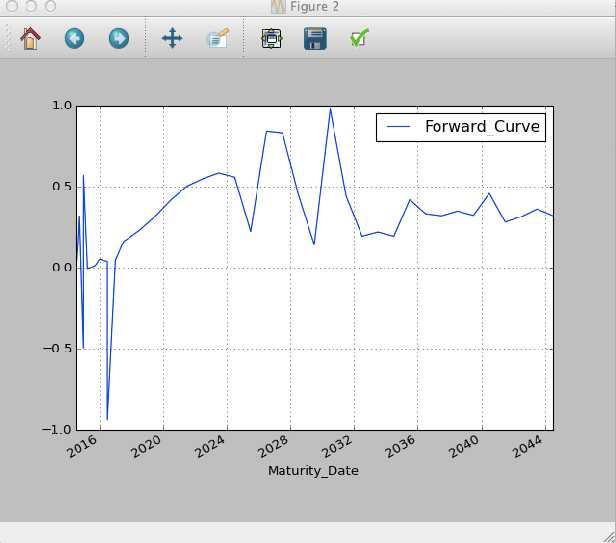

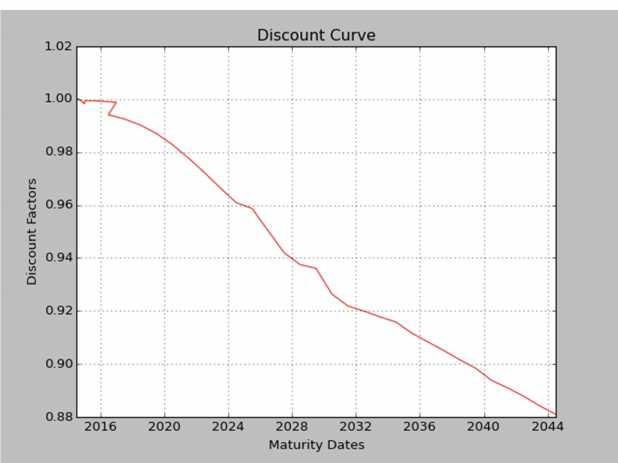

13 The discount, zero and forward rate curve output is also as follows: 4

14 5

15 6

16 5. Conclusions 5.1 Comments Bootstrapping a yield curve is important when valuing a variety of interest rate products. One of the main purposes of a yield curve is to value and price a portfolio of instruments and financial contracts. Bootstrapping a yield curve can be used to price a whole series of different interest rate instruments. Thus the yield curve can also be used to derive forward rates which are necessary to price instruments like interest rate swaps correctly. 5.2 Appendix Zero swap curve for tenor 3M import math import pandas as pd for (x,w) in zip(c1,m1): dc1 = 1 / ((1 + (float(w)/100) * ((float(x) / 360)))) dc2 = dc1 / ((1 + (float(w)/100) * ((float(x) / 360)))) dc3 = dc2 / ((1 + (float(w)/100) * ((float(x) / 360)))) Z1 = -100 * math.log(float(dc1))/ (float(x) / 365) print "Zero Cash :",Z1 for (a,b) in zip(f1,m2): fr1 = b + ((b/100)/a)* a fr2 = math.exp(- float(fr1) * (a / 365)) fr3 = float(fr2) * (1 / (1 + (b/100) * a/360)) Z2 = -100 * math.log(float(fr3))/ (float(a) / 365) print "Zero Forward :",Z2 for (g,h) in zip(s1,m3): Sr = (dc2 - (h/100) * (math.exp((- h/100 + ((h/100)/g) * g * (g/ 365))))) / (1 + (h/100)) Z3 = -100 * math.log(float(sr))/ (float(g) / 365) print "Zero Swap :",Z3 for (j,k) in zip(m4,n1): F1 =( * k) / j print "Forward Cash :",F1 for l,o in zip(m5,n2): F2 =( * o )/ l print "Forward ForwardRate :",F2 for s,t in zip(m6,n3): F3 =( * t )/ s print "Forward Swap :",F3 df = pd.dataframe.from_csv('zeroforward.csv', parse_dates=true) 7

17 df.zero_curve.plot(color='g') df.forward_curve.plot(color='r') df.plot(legend=true) Discount Curve import numpy as np import matplotlib.pyplot as plt import matplotlib.dates as mdates def graph(): date, value = np.loadtxt('discount.csv', delimiter =',', unpack=true, converters = {0:mdates.strpdate2num('%d-%m-%Y')}) plt.plot_date(x=date, y=value, linestyle='-', marker="", color='r') plt.xlabel("maturity Dates") plt.ylabel("discount Factors") plt.title("discount Curve") plt.grid(true) plt.show() graph() ): 8

18 6. References [1] Röman, Jan, Lecture Notes For Analytical Finance 2 (2014) [2] Lore Marc and Borodovsky Lev, The Professional s Handbook of Financial Risk Management, Butterworth-Heinemann (2000) 9

Mathematics of Financial Derivatives. Zero-coupon rates and bond pricing. Lecture 9. Zero-coupons. Notes. Notes

Mathematics of Financial Derivatives Lecture 9 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Zero-coupon rates and bond pricing Zero-coupons Definition:

Mathematics of Financial Derivatives Lecture 9 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Zero-coupon rates and bond pricing Zero-coupons Definition:

Mathematics of Financial Derivatives

Mathematics of Financial Derivatives Lecture 9 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Zero-coupon rates and bond pricing 2.

Mathematics of Financial Derivatives Lecture 9 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Zero-coupon rates and bond pricing 2.

Lecture 9. Basics on Swaps

Lecture 9 Basics on Swaps Agenda: 1. Introduction to Swaps ~ Definition: ~ Basic functions ~ Comparative advantage: 2. Swap quotes and LIBOR zero rate ~ Interest rate swap is combination of two bonds:

Lecture 9 Basics on Swaps Agenda: 1. Introduction to Swaps ~ Definition: ~ Basic functions ~ Comparative advantage: 2. Swap quotes and LIBOR zero rate ~ Interest rate swap is combination of two bonds:

Problems and Solutions

1 CHAPTER 1 Problems 1.1 Problems on Bonds Exercise 1.1 On 12/04/01, consider a fixed-coupon bond whose features are the following: face value: $1,000 coupon rate: 8% coupon frequency: semiannual maturity:

1 CHAPTER 1 Problems 1.1 Problems on Bonds Exercise 1.1 On 12/04/01, consider a fixed-coupon bond whose features are the following: face value: $1,000 coupon rate: 8% coupon frequency: semiannual maturity:

Building a Zero Coupon Yield Curve

Building a Zero Coupon Yield Curve Clive Bastow, CFA, CAIA ABSTRACT Create and use a zero- coupon yield curve from quoted LIBOR, Eurodollar Futures, PAR Swap and OIS rates. www.elpitcafinancial.com Risk-

Building a Zero Coupon Yield Curve Clive Bastow, CFA, CAIA ABSTRACT Create and use a zero- coupon yield curve from quoted LIBOR, Eurodollar Futures, PAR Swap and OIS rates. www.elpitcafinancial.com Risk-

MÄLARDALENS HÖGSKOLA

MÄLARDALENS HÖGSKOLA A Monte-Carlo calculation for Barrier options Using Python Mwangota Lutufyo and Omotesho Latifat oyinkansola 2016-10-19 MMA707 Analytical Finance I: Lecturer: Jan Roman Division of

MÄLARDALENS HÖGSKOLA A Monte-Carlo calculation for Barrier options Using Python Mwangota Lutufyo and Omotesho Latifat oyinkansola 2016-10-19 MMA707 Analytical Finance I: Lecturer: Jan Roman Division of

Vanilla interest rate options

Vanilla interest rate options Marco Marchioro derivati2@marchioro.org October 26, 2011 Vanilla interest rate options 1 Summary Probability evolution at information arrival Brownian motion and option pricing

Vanilla interest rate options Marco Marchioro derivati2@marchioro.org October 26, 2011 Vanilla interest rate options 1 Summary Probability evolution at information arrival Brownian motion and option pricing

Term Par Swap Rate Term Par Swap Rate 2Y 2.70% 15Y 4.80% 5Y 3.60% 20Y 4.80% 10Y 4.60% 25Y 4.75%

Revisiting The Art and Science of Curve Building FINCAD has added curve building features (enhanced linear forward rates and quadratic forward rates) in Version 9 that further enable you to fine tune the

Revisiting The Art and Science of Curve Building FINCAD has added curve building features (enhanced linear forward rates and quadratic forward rates) in Version 9 that further enable you to fine tune the

Interest Rate Markets

Interest Rate Markets 5. Chapter 5 5. Types of Rates Treasury rates LIBOR rates Repo rates 5.3 Zero Rates A zero rate (or spot rate) for maturity T is the rate of interest earned on an investment with

Interest Rate Markets 5. Chapter 5 5. Types of Rates Treasury rates LIBOR rates Repo rates 5.3 Zero Rates A zero rate (or spot rate) for maturity T is the rate of interest earned on an investment with

Mathematics of Financial Derivatives

Mathematics of Financial Derivatives Lecture 11 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Mechanics of interest rate swaps (continued)

Mathematics of Financial Derivatives Lecture 11 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. Mechanics of interest rate swaps (continued)

Appendix A Financial Calculations

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

We consider three zero-coupon bonds (strips) with the following features: Bond Maturity (years) Price Bond Bond Bond

with the following features: Bond Maturity (years) Price Bond Bond Bond") 15 3 CHAPTER 3 Problems Exercise 3.1 We consider three zero-coupon bonds (strips) with the following features: Each strip delivers $100 at maturity. Bond Maturity (years) Price Bond 1 1 96.43 Bond 2 2

15 3 CHAPTER 3 Problems Exercise 3.1 We consider three zero-coupon bonds (strips) with the following features: Each strip delivers $100 at maturity. Bond Maturity (years) Price Bond 1 1 96.43 Bond 2 2

ACI Dealing Certificate (008) Sample Questions

Sample Questions") ACI Dealing Certificate (008) Sample Questions Setting the benchmark in certifying the financial industry globally 8 Rue du Mail, 75002 Paris - France T: +33 1 42975115 - F: +33 1 42975116 - www.aciforex.org

ACI Dealing Certificate (008) Sample Questions Setting the benchmark in certifying the financial industry globally 8 Rue du Mail, 75002 Paris - France T: +33 1 42975115 - F: +33 1 42975116 - www.aciforex.org

MFE8812 Bond Portfolio Management

MFE8812 Bond Portfolio Management William C. H. Leon Nanyang Business School January 16, 2018 1 / 63 William C. H. Leon MFE8812 Bond Portfolio Management 1 Overview Value of Cash Flows Value of a Bond

MFE8812 Bond Portfolio Management William C. H. Leon Nanyang Business School January 16, 2018 1 / 63 William C. H. Leon MFE8812 Bond Portfolio Management 1 Overview Value of Cash Flows Value of a Bond

FINCAD XL and Analytics v10.1 Release Notes

FINCAD XL and Analytics v10.1 Release Notes FINCAD XL and Analytics v10.1 Release Notes Software Version: FINCAD XL 10.1 Release Date: May 15, 2007 Document Revision Number: 1.0 Disclaimer FinancialCAD

FINCAD XL and Analytics v10.1 Release Notes FINCAD XL and Analytics v10.1 Release Notes Software Version: FINCAD XL 10.1 Release Date: May 15, 2007 Document Revision Number: 1.0 Disclaimer FinancialCAD

Introduction to Bonds. Part One describes fixed-income market analysis and the basic. techniques and assumptions are required.

PART ONE Introduction to Bonds Part One describes fixed-income market analysis and the basic concepts relating to bond instruments. The analytic building blocks are generic and thus applicable to any market.

PART ONE Introduction to Bonds Part One describes fixed-income market analysis and the basic concepts relating to bond instruments. The analytic building blocks are generic and thus applicable to any market.

Fin 5633: Investment Theory and Problems: Chapter#15 Solutions

Fin 5633: Investment Theory and Problems: Chapter#15 Solutions 1. Expectations hypothesis: The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping

Fin 5633: Investment Theory and Problems: Chapter#15 Solutions 1. Expectations hypothesis: The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping

The Bloomberg CDS Model

1 The Bloomberg CDS Model Bjorn Flesaker Madhu Nayakkankuppam Igor Shkurko May 1, 2009 1 Introduction The Bloomberg CDS model values single name and index credit default swaps as a function of their schedule,

1 The Bloomberg CDS Model Bjorn Flesaker Madhu Nayakkankuppam Igor Shkurko May 1, 2009 1 Introduction The Bloomberg CDS model values single name and index credit default swaps as a function of their schedule,

Chapter 2: BASICS OF FIXED INCOME SECURITIES

Chapter 2: BASICS OF FIXED INCOME SECURITIES 2.1 DISCOUNT FACTORS 2.1.1 Discount Factors across Maturities 2.1.2 Discount Factors over Time 2.1 DISCOUNT FACTORS The discount factor between two dates, t

Chapter 2: BASICS OF FIXED INCOME SECURITIES 2.1 DISCOUNT FACTORS 2.1.1 Discount Factors across Maturities 2.1.2 Discount Factors over Time 2.1 DISCOUNT FACTORS The discount factor between two dates, t

ANALYTICAL FINANCE II Floating Rate Notes, fixed coupon bonds and swaps

ANALYTICAL FINANCE II Floating Rate Notes, fixed coupon bonds and swaps Ali Salih & Vadim Suvorin Division of Applied Mathematics Mälardalen University, Box 883, 72132 Västerȧs, SWEDEN December 15, 2010

ANALYTICAL FINANCE II Floating Rate Notes, fixed coupon bonds and swaps Ali Salih & Vadim Suvorin Division of Applied Mathematics Mälardalen University, Box 883, 72132 Västerȧs, SWEDEN December 15, 2010

Chapter 8. Swaps. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 8 Swaps Introduction to Swaps A swap is a contract calling for an exchange of payments, on one or more dates, determined by the difference in two prices A swap provides a means to hedge a stream

Chapter 8 Swaps Introduction to Swaps A swap is a contract calling for an exchange of payments, on one or more dates, determined by the difference in two prices A swap provides a means to hedge a stream

Measuring Interest Rates. Interest Rates Chapter 4. Continuous Compounding (Page 77) Types of Rates

Types of Rates") Interest Rates Chapter 4 Measuring Interest Rates The compounding frequency used for an interest rate is the unit of measurement The difference between quarterly and annual compounding is analogous to

Interest Rates Chapter 4 Measuring Interest Rates The compounding frequency used for an interest rate is the unit of measurement The difference between quarterly and annual compounding is analogous to

How to Use JIBAR Futures to Hedge Against Interest Rate Risk

How to Use JIBAR Futures to Hedge Against Interest Rate Risk Introduction A JIBAR future carries information regarding the market s consensus of the level of the 3-month JIBAR rate, at a future point in

How to Use JIBAR Futures to Hedge Against Interest Rate Risk Introduction A JIBAR future carries information regarding the market s consensus of the level of the 3-month JIBAR rate, at a future point in

Stat 274 Theory of Interest. Chapters 8 and 9: Term Structure and Interest Rate Sensitivity. Brian Hartman Brigham Young University

Stat 274 Theory of Interest Chapters 8 and 9: Term Structure and Interest Rate Sensitivity Brian Hartman Brigham Young University Yield Curves ν(t) is the current market price for a t-year zero-coupon

Stat 274 Theory of Interest Chapters 8 and 9: Term Structure and Interest Rate Sensitivity Brian Hartman Brigham Young University Yield Curves ν(t) is the current market price for a t-year zero-coupon

Interest Rate Forwards and Swaps

Interest Rate Forwards and Swaps 1 Outline PART ONE Chapter 1: interest rate forward contracts and their pricing and mechanics 2 Outline PART TWO Chapter 2: basic and customized swaps and their pricing

Interest Rate Forwards and Swaps 1 Outline PART ONE Chapter 1: interest rate forward contracts and their pricing and mechanics 2 Outline PART TWO Chapter 2: basic and customized swaps and their pricing

Contents. 1. Introduction Workbook Access Copyright and Disclaimer Password Access and Worksheet Protection...

Contents 1. Introduction... 3 2. Workbook Access... 3 3. Copyright and Disclaimer... 3 4. Password Access and Worksheet Protection... 4 5. Macros... 4 6. Colour Coding... 4 7. Recalculation... 4 8. Explanation

Contents 1. Introduction... 3 2. Workbook Access... 3 3. Copyright and Disclaimer... 3 4. Password Access and Worksheet Protection... 4 5. Macros... 4 6. Colour Coding... 4 7. Recalculation... 4 8. Explanation

Pricing Barrier Options Using Monte Carlo Simulation Pricing Options with Python

Pricing Barrier Options Using Monte Carlo Simulation Pricing Options with Python Submitted by: Augustine Y. D. Farley Ahmad Ahmad Programme: Financial Engineering Submitted to: Jan Roman Lecturer (Analytical

Pricing Barrier Options Using Monte Carlo Simulation Pricing Options with Python Submitted by: Augustine Y. D. Farley Ahmad Ahmad Programme: Financial Engineering Submitted to: Jan Roman Lecturer (Analytical

Fixed-Income Analysis. Solutions 5

FIN 684 Professor Robert B.H. Hauswald Fixed-Income Analysis Kogod School of Business, AU Solutions 5 1. Forward Rate Curve. (a) Discount factors and discount yield curve: in fact, P t = 100 1 = 100 =

FIN 684 Professor Robert B.H. Hauswald Fixed-Income Analysis Kogod School of Business, AU Solutions 5 1. Forward Rate Curve. (a) Discount factors and discount yield curve: in fact, P t = 100 1 = 100 =

Calculating VaR. There are several approaches for calculating the Value at Risk figure. The most popular are the

VaR Pro and Contra Pro: Easy to calculate and to understand. It is a common language of communication within the organizations as well as outside (e.g. regulators, auditors, shareholders). It is not really

VaR Pro and Contra Pro: Easy to calculate and to understand. It is a common language of communication within the organizations as well as outside (e.g. regulators, auditors, shareholders). It is not really

Asset-or-nothing digitals

School of Education, Culture and Communication Division of Applied Mathematics MMA707 Analytical Finance I Asset-or-nothing digitals 202-0-9 Mahamadi Ouoba Amina El Gaabiiy David Johansson Examinator:

School of Education, Culture and Communication Division of Applied Mathematics MMA707 Analytical Finance I Asset-or-nothing digitals 202-0-9 Mahamadi Ouoba Amina El Gaabiiy David Johansson Examinator:

Financial Market Introduction

Financial Market Introduction Alex Yang FinPricing http://www.finpricing.com Summary Financial Market Definition Financial Return Price Determination No Arbitrage and Risk Neutral Measure Fixed Income

Financial Market Introduction Alex Yang FinPricing http://www.finpricing.com Summary Financial Market Definition Financial Return Price Determination No Arbitrage and Risk Neutral Measure Fixed Income

Solutions to Practice Problems

Solutions to Practice Problems CHAPTER 1 1.1 Original exchange rate Reciprocal rate Answer (a) 1 = US$0.8420 US$1 =? 1.1876 (b) 1 = US$1.4565 US$1 =? 0.6866 (c) NZ$1 = US$0.4250 US$1 = NZ$? 2.3529 1.2

Solutions to Practice Problems CHAPTER 1 1.1 Original exchange rate Reciprocal rate Answer (a) 1 = US$0.8420 US$1 =? 1.1876 (b) 1 = US$1.4565 US$1 =? 0.6866 (c) NZ$1 = US$0.4250 US$1 = NZ$? 2.3529 1.2

1. Parallel and nonparallel shifts in the yield curve. 2. Factors that drive U.S. Treasury security returns.

LEARNING OUTCOMES 1. Parallel and nonparallel shifts in the yield curve. 2. Factors that drive U.S. Treasury security returns. 3. Construct the theoretical spot rate curve. 4. The swap rate curve (LIBOR

LEARNING OUTCOMES 1. Parallel and nonparallel shifts in the yield curve. 2. Factors that drive U.S. Treasury security returns. 3. Construct the theoretical spot rate curve. 4. The swap rate curve (LIBOR

Chapter 7. Interest Rate Forwards and Futures. Copyright 2009 Pearson Prentice Hall. All rights reserved.

Chapter 7 Interest Rate Forwards and Futures Bond Basics U.S. Treasury Bills (

Chapter 7 Interest Rate Forwards and Futures Bond Basics U.S. Treasury Bills (

Swaps 7.1 MECHANICS OF INTEREST RATE SWAPS LIBOR

7C H A P T E R Swaps The first swap contracts were negotiated in the early 1980s. Since then the market has seen phenomenal growth. Swaps now occupy a position of central importance in derivatives markets.

7C H A P T E R Swaps The first swap contracts were negotiated in the early 1980s. Since then the market has seen phenomenal growth. Swaps now occupy a position of central importance in derivatives markets.

Concepts in Best Practice: Transfer Pricing Customer Accounts

This white paper discusses the fundamental concepts of transfer pricing and outlines industry best practices, applicable to any firm attempting to quantify a cost or worth of customer funds. The content

This white paper discusses the fundamental concepts of transfer pricing and outlines industry best practices, applicable to any firm attempting to quantify a cost or worth of customer funds. The content

Actuarial Society of India EXAMINATIONS

Actuarial Society of India EXAMINATIONS 20 th June 2005 Subject CT1 Financial Mathematics Time allowed: Three Hours (10.30 am - 13.30 pm) INSTRUCTIONS TO THE CANDIDATES 1. Do not write your name anywhere

Actuarial Society of India EXAMINATIONS 20 th June 2005 Subject CT1 Financial Mathematics Time allowed: Three Hours (10.30 am - 13.30 pm) INSTRUCTIONS TO THE CANDIDATES 1. Do not write your name anywhere

Financial Returns. Dakota Wixom Quantitative Analyst QuantCourse.com INTRO TO PORTFOLIO RISK MANAGEMENT IN PYTHON

INTRO TO PORTFOLIO RISK MANAGEMENT IN PYTHON Financial Returns Dakota Wixom Quantitative Analyst QuantCourse.com Course Overview Learn how to analyze investment return distributions, build portfolios and

INTRO TO PORTFOLIO RISK MANAGEMENT IN PYTHON Financial Returns Dakota Wixom Quantitative Analyst QuantCourse.com Course Overview Learn how to analyze investment return distributions, build portfolios and

Financial Mathematics Principles

1 Financial Mathematics Principles 1.1 Financial Derivatives and Derivatives Markets A financial derivative is a special type of financial contract whose value and payouts depend on the performance of

1 Financial Mathematics Principles 1.1 Financial Derivatives and Derivatives Markets A financial derivative is a special type of financial contract whose value and payouts depend on the performance of

Interest Rate Basis Curve Construction and Bootstrapping Guide

Interest Rate Basis Curve Construction and Bootstrapping Guide Michael Taylor FinPricing The term structure of an interest rate basis curve is defined as the relationship between the basis zero rate and

Interest Rate Basis Curve Construction and Bootstrapping Guide Michael Taylor FinPricing The term structure of an interest rate basis curve is defined as the relationship between the basis zero rate and

P1.T4.Valuation Tuckman, Chapter 5. Bionic Turtle FRM Video Tutorials

P1.T4.Valuation Tuckman, Chapter 5 Bionic Turtle FRM Video Tutorials By: David Harper CFA, FRM, CIPM Note: This tutorial is for paid members only. You know who you are. Anybody else is using an illegal

P1.T4.Valuation Tuckman, Chapter 5 Bionic Turtle FRM Video Tutorials By: David Harper CFA, FRM, CIPM Note: This tutorial is for paid members only. You know who you are. Anybody else is using an illegal

Alan Brazil. Goldman, Sachs & Co.

Alan Brazil Goldman, Sachs & Co. Assumptions: Coupon paid every 6 months, $100 of principal paid at maturity, government guaranteed 1 Debt is a claim on a fixed amount of cashflows in the future A mortgage

Alan Brazil Goldman, Sachs & Co. Assumptions: Coupon paid every 6 months, $100 of principal paid at maturity, government guaranteed 1 Debt is a claim on a fixed amount of cashflows in the future A mortgage

An Introduction to Modern Pricing of Interest Rate Derivatives

School of Education, Culture and Communication Division of Applied Mathematics MASTER THESIS IN MATHEMATICS / APPLIED MATHEMATICS An Introduction to Modern Pricing of Interest Rate Derivatives by Hossein

School of Education, Culture and Communication Division of Applied Mathematics MASTER THESIS IN MATHEMATICS / APPLIED MATHEMATICS An Introduction to Modern Pricing of Interest Rate Derivatives by Hossein

Introduction. Practitioner Course: Interest Rate Models. John Dodson. February 18, 2009

Practitioner Course: Interest Rate Models February 18, 2009 syllabus text sessions office hours date subject reading 18 Feb introduction BM 1 25 Feb affine models BM 3 4 Mar Gaussian models BM 4 11 Mar

Practitioner Course: Interest Rate Models February 18, 2009 syllabus text sessions office hours date subject reading 18 Feb introduction BM 1 25 Feb affine models BM 3 4 Mar Gaussian models BM 4 11 Mar

FIXED INCOME I EXERCISES

FIXED INCOME I EXERCISES This version: 25.09.2011 Interplay between macro and financial variables 1. Read the paper: The Bond Yield Conundrum from a Macro-Finance Perspective, Glenn D. Rudebusch, Eric

FIXED INCOME I EXERCISES This version: 25.09.2011 Interplay between macro and financial variables 1. Read the paper: The Bond Yield Conundrum from a Macro-Finance Perspective, Glenn D. Rudebusch, Eric

INTERPOLATING YIELD CURVE DATA IN A MANNER THAT ENSURES POSITIVE AND CONTINUOUS FORWARD CURVES

SAJEMS NS 16 (2013) No 4:395-406 395 INTERPOLATING YIELD CURVE DATA IN A MANNER THAT ENSURES POSITIVE AND CONTINUOUS FORWARD CURVES Paul F du Preez Johannesburg Stock Exchange Eben Maré Department of Mathematics

SAJEMS NS 16 (2013) No 4:395-406 395 INTERPOLATING YIELD CURVE DATA IN A MANNER THAT ENSURES POSITIVE AND CONTINUOUS FORWARD CURVES Paul F du Preez Johannesburg Stock Exchange Eben Maré Department of Mathematics

Fixed Income Investment

Fixed Income Investment Session 1 April, 24 th, 2013 (Morning) Dr. Cesario Mateus www.cesariomateus.com c.mateus@greenwich.ac.uk cesariomateus@gmail.com 1 Lecture 1 1. A closer look at the different asset

Fixed Income Investment Session 1 April, 24 th, 2013 (Morning) Dr. Cesario Mateus www.cesariomateus.com c.mateus@greenwich.ac.uk cesariomateus@gmail.com 1 Lecture 1 1. A closer look at the different asset

Derivatives Pricing This course can also be presented in-house for your company or via live on-line webinar

Derivatives Pricing This course can also be presented in-house for your company or via live on-line webinar The Banking and Corporate Finance Training Specialist Course Overview This course has been available

Derivatives Pricing This course can also be presented in-house for your company or via live on-line webinar The Banking and Corporate Finance Training Specialist Course Overview This course has been available

PASS4TEST. IT Certification Guaranteed, The Easy Way! We offer free update service for one year

PASS4TEST \ http://www.pass4test.com We offer free update service for one year Exam : 3I0-012 Title : ACI Dealing Certificate Vendor : ACI Version : DEMO 1 / 7 Get Latest & Valid 3I0-012 Exam's Question

PASS4TEST \ http://www.pass4test.com We offer free update service for one year Exam : 3I0-012 Title : ACI Dealing Certificate Vendor : ACI Version : DEMO 1 / 7 Get Latest & Valid 3I0-012 Exam's Question

Zero Coupon Yield Curves Technical Documentation Bis

ZERO COUPON YIELD CURVES TECHNICAL DOCUMENTATION BIS PDF - Are you looking for zero coupon yield curves technical documentation bis Books? Now, you will be happy that at this time zero coupon yield curves

ZERO COUPON YIELD CURVES TECHNICAL DOCUMENTATION BIS PDF - Are you looking for zero coupon yield curves technical documentation bis Books? Now, you will be happy that at this time zero coupon yield curves

Convenience Yield Calculator Version 1.0

Convenience Yield Calculator Version 1.0 1 Introduction This plug-in implements the capability of calculating instantaneous forward price for commodities like Natural Gas, Fuel Oil and Gasoil. The deterministic

Convenience Yield Calculator Version 1.0 1 Introduction This plug-in implements the capability of calculating instantaneous forward price for commodities like Natural Gas, Fuel Oil and Gasoil. The deterministic

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 6. Variable interest rates and portfolio insurance. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam

Manual for SOA Exam FM/CAS Exam 2. Chapter 6. Variable interest rates and portfolio insurance. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam

Introduction, Forwards and Futures

Introduction, Forwards and Futures Liuren Wu Options Markets Liuren Wu ( ) Introduction, Forwards & Futures Options Markets 1 / 31 Derivatives Derivative securities are financial instruments whose returns

Introduction, Forwards and Futures Liuren Wu Options Markets Liuren Wu ( ) Introduction, Forwards & Futures Options Markets 1 / 31 Derivatives Derivative securities are financial instruments whose returns

Fixed-Income Analysis. Assignment 5

FIN 684 Professor Robert B.H. Hauswald Fixed-Income Analysis Kogod School of Business, AU Assignment 5 Please be reminded that you are expected to use contemporary computer software to solve the following

FIN 684 Professor Robert B.H. Hauswald Fixed-Income Analysis Kogod School of Business, AU Assignment 5 Please be reminded that you are expected to use contemporary computer software to solve the following

Gallery of equations. 1. Introduction

Gallery of equations. Introduction Exchange-traded markets Over-the-counter markets Forward contracts Definition.. A forward contract is an agreement to buy or sell an asset at a certain future time for

Gallery of equations. Introduction Exchange-traded markets Over-the-counter markets Forward contracts Definition.. A forward contract is an agreement to buy or sell an asset at a certain future time for

Compounding Swap Vaulation Pratical Guide

Vaulation Pratical Guide Alan White FinPricing http://www.finpricing.com Summary Compounding Swap Introduction Compounding Swap or Compounding Swaplet Payoff Valuation Practical Notes A real world example

Vaulation Pratical Guide Alan White FinPricing http://www.finpricing.com Summary Compounding Swap Introduction Compounding Swap or Compounding Swaplet Payoff Valuation Practical Notes A real world example

Solution to Problem Set 2

M.I.T. Spring 1999 Sloan School of Management 15.15 Solution to Problem Set 1. The correct statements are (c) and (d). We have seen in class how to obtain bond prices and forward rates given the current

M.I.T. Spring 1999 Sloan School of Management 15.15 Solution to Problem Set 1. The correct statements are (c) and (d). We have seen in class how to obtain bond prices and forward rates given the current

Challenges In Modelling Inflation For Counterparty Risk

Challenges In Modelling Inflation For Counterparty Risk Vinay Kotecha, Head of Rates/Commodities, Market and Counterparty Risk Analytics Vladimir Chorniy, Head of Market & Counterparty Risk Analytics Quant

Challenges In Modelling Inflation For Counterparty Risk Vinay Kotecha, Head of Rates/Commodities, Market and Counterparty Risk Analytics Vladimir Chorniy, Head of Market & Counterparty Risk Analytics Quant

Glossary of Swap Terminology

Glossary of Swap Terminology Arbitrage: The opportunity to exploit price differentials on tv~otherwise identical sets of cash flows. In arbitrage-free financial markets, any two transactions with the same

Glossary of Swap Terminology Arbitrage: The opportunity to exploit price differentials on tv~otherwise identical sets of cash flows. In arbitrage-free financial markets, any two transactions with the same

CHAPTER 15: THE TERM STRUCTURE OF INTEREST RATES

CHAPTER : THE TERM STRUCTURE OF INTEREST RATES. Expectations hypothesis: The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is explained

CHAPTER : THE TERM STRUCTURE OF INTEREST RATES. Expectations hypothesis: The yields on long-term bonds are geometric averages of present and expected future short rates. An upward sloping curve is explained

Foundations of Finance

Lecture 7: Bond Pricing, Forward Rates and the Yield Curve. I. Reading. II. Discount Bond Yields and Prices. III. Fixed-income Prices and No Arbitrage. IV. The Yield Curve. V. Other Bond Pricing Issues.

Lecture 7: Bond Pricing, Forward Rates and the Yield Curve. I. Reading. II. Discount Bond Yields and Prices. III. Fixed-income Prices and No Arbitrage. IV. The Yield Curve. V. Other Bond Pricing Issues.

Chapter 10: Futures Arbitrage Strategies

Chapter 10: Futures Arbitrage Strategies I. Short-Term Interest Rate Arbitrage 1. Cash and Carry/Implied Repo Cash and carry transaction means to buy asset and sell futures Use repurchase agreement/repo

Chapter 10: Futures Arbitrage Strategies I. Short-Term Interest Rate Arbitrage 1. Cash and Carry/Implied Repo Cash and carry transaction means to buy asset and sell futures Use repurchase agreement/repo

Practice set #3: FRAs, IRFs and Swaps.

International Financial Managment Professor Michel Robe What to do with this practice set? Practice set #3: FRAs, IRFs and Swaps. To help students with the material, seven practice sets with solutions

International Financial Managment Professor Michel Robe What to do with this practice set? Practice set #3: FRAs, IRFs and Swaps. To help students with the material, seven practice sets with solutions

Global Securities & Investment Management Target Audience: Objectives:

Global Securities & Investment Management Target Audience: This course is focused at those who are seeking to acquire an overview of Finance, more specifically a foundation in capital markets, products,

Global Securities & Investment Management Target Audience: This course is focused at those who are seeking to acquire an overview of Finance, more specifically a foundation in capital markets, products,

ISDA. International Swaps and Derivatives Association, Inc. Disclosure Annex for Interest Rate Transactions

Copyright 2012 by International Swaps and Derivatives Association, Inc. This document has been prepared by Mayer Brown LLP for discussion purposes only. It should not be construed as legal advice. Transmission

Copyright 2012 by International Swaps and Derivatives Association, Inc. This document has been prepared by Mayer Brown LLP for discussion purposes only. It should not be construed as legal advice. Transmission

Advanced OIS Discounting:

Advanced OIS Discounting: Building Proxy OIS Curves When OIS Markets are Illiquid or Nonexistent November 6, 2013 About Us Our Presenters: Ion Mihai, Ph.D. Quantitative Analyst imihai@numerix.com Jim Jockle

Advanced OIS Discounting: Building Proxy OIS Curves When OIS Markets are Illiquid or Nonexistent November 6, 2013 About Us Our Presenters: Ion Mihai, Ph.D. Quantitative Analyst imihai@numerix.com Jim Jockle

INTEREST RATES AND FX MODELS

INTEREST RATES AND FX MODELS 1. The Forward Curve Andrew Lesniewsi Courant Institute of Mathematics New Yor University New Yor February 3, 2011 2 Interest Rates & FX Models Contents 1 LIBOR and LIBOR based

INTEREST RATES AND FX MODELS 1. The Forward Curve Andrew Lesniewsi Courant Institute of Mathematics New Yor University New Yor February 3, 2011 2 Interest Rates & FX Models Contents 1 LIBOR and LIBOR based

Understanding the American Federal Reserve

Understanding the American Federal Reserve The Federal Reserve headquarters is in Washington, DC. The basic structure of the Federal Reserve System includes: The Federal Reserve Board of Governors The

Understanding the American Federal Reserve The Federal Reserve headquarters is in Washington, DC. The basic structure of the Federal Reserve System includes: The Federal Reserve Board of Governors The

Lecture 2 Valuation of Fixed Income Securities (a)

") Lecture 2 Valuation of Fixed Income Securities (a) Since we all now have a basic idea of how time value of money works, it is time we put the techniques we learned to some use 1 Fixed Income Securities

Lecture 2 Valuation of Fixed Income Securities (a) Since we all now have a basic idea of how time value of money works, it is time we put the techniques we learned to some use 1 Fixed Income Securities

Global Financial Management. Option Contracts

Global Financial Management Option Contracts Copyright 1997 by Alon Brav, Campbell R. Harvey, Ernst Maug and Stephen Gray. All rights reserved. No part of this lecture may be reproduced without the permission

Global Financial Management Option Contracts Copyright 1997 by Alon Brav, Campbell R. Harvey, Ernst Maug and Stephen Gray. All rights reserved. No part of this lecture may be reproduced without the permission

Vasicek. Ngami Valery Ogunniyi Oluwayinka Maarse Bauke Date: Mälardalen University. Find the term structure of interest rate

Mälardalen University Vasicek Find the term structure of interest rate Analytical Finance II Teacher: Jan Röman Authors: Ngami Valery Ogunniyi Oluwayinka Maarse Bauke Date:2011-12-12 Table of Contents

Mälardalen University Vasicek Find the term structure of interest rate Analytical Finance II Teacher: Jan Röman Authors: Ngami Valery Ogunniyi Oluwayinka Maarse Bauke Date:2011-12-12 Table of Contents

No arbitrage conditions in HJM multiple curve term structure models

No arbitrage conditions in HJM multiple curve term structure models Zorana Grbac LPMA, Université Paris Diderot Joint work with W. Runggaldier 7th General AMaMeF and Swissquote Conference Lausanne, 7-10

No arbitrage conditions in HJM multiple curve term structure models Zorana Grbac LPMA, Université Paris Diderot Joint work with W. Runggaldier 7th General AMaMeF and Swissquote Conference Lausanne, 7-10

Introduction to Forwards and Futures

Introduction to Forwards and Futures Liuren Wu Options Pricing Liuren Wu ( c ) Introduction, Forwards & Futures Options Pricing 1 / 27 Outline 1 Derivatives 2 Forwards 3 Futures 4 Forward pricing 5 Interest

Introduction to Forwards and Futures Liuren Wu Options Pricing Liuren Wu ( c ) Introduction, Forwards & Futures Options Pricing 1 / 27 Outline 1 Derivatives 2 Forwards 3 Futures 4 Forward pricing 5 Interest

UNIVERSITY OF TORONTO Joseph L. Rotman School of Management SOLUTIONS. C (1 + r 2. 1 (1 + r. PV = C r. we have that C = PV r = $40,000(0.10) = $4,000.

= $4,000.") UNIVERSITY OF TORONTO Joseph L. Rotman School of Management RSM332 PROBLEM SET #2 SOLUTIONS 1. (a) The present value of a single cash flow: PV = C (1 + r 2 $60,000 = = $25,474.86. )2T (1.055) 16 (b) The

UNIVERSITY OF TORONTO Joseph L. Rotman School of Management RSM332 PROBLEM SET #2 SOLUTIONS 1. (a) The present value of a single cash flow: PV = C (1 + r 2 $60,000 = = $25,474.86. )2T (1.055) 16 (b) The

Course Outline: Treasury & Capital s Equity s Trading & Operations Equity s - Types of s Classification - Primary and Secondary markets. Cycle A brief outline of the life cycle of an equity share - from

Course Outline: Treasury & Capital s Equity s Trading & Operations Equity s - Types of s Classification - Primary and Secondary markets. Cycle A brief outline of the life cycle of an equity share - from

22 Swaps: Applications. Answers to Questions and Problems

22 Swaps: Applications Answers to Questions and Problems 1. At present, you observe the following rates: FRA 0,1 5.25 percent and FRA 1,2 5.70 percent, where the subscripts refer to years. You also observe

22 Swaps: Applications Answers to Questions and Problems 1. At present, you observe the following rates: FRA 0,1 5.25 percent and FRA 1,2 5.70 percent, where the subscripts refer to years. You also observe

Math 373 Test 4 Fall 2012

Math 373 Test 4 Fall 2012 December 10, 2012 1. ( 3 points) List the three conditions that must be present for arbitrage to exist. 1) No investment 2) No risk 3) Guaranteed positive cash flow 2. (5 points)

Math 373 Test 4 Fall 2012 December 10, 2012 1. ( 3 points) List the three conditions that must be present for arbitrage to exist. 1) No investment 2) No risk 3) Guaranteed positive cash flow 2. (5 points)

Basis Swap Vaulation Pratical Guide

Vaulation Pratical Guide Alan White FinPricing http://www.finpricing.com Summary Interest Rate Basis Swap Introduction The Use of Interest Rate Basis Swap Basis Swap or Basis Swaplet Payoff Valuation Practical

Vaulation Pratical Guide Alan White FinPricing http://www.finpricing.com Summary Interest Rate Basis Swap Introduction The Use of Interest Rate Basis Swap Basis Swap or Basis Swaplet Payoff Valuation Practical

MAY 2017 PROFESSIONAL EXAMINATIONS ADVANCED FINANCIAL MANAGEMENT (PAPER 3.3) QUESTIONS & MARKING SCHEME

QUESTIONS & MARKING SCHEME") MAY 2017 PROFESSIONAL EXAMINATIONS ADVANCED FINANCIAL MANAGEMENT (PAPER 3.3) QUESTIONS & MARKING SCHEME QUESTION ONE a) In the last couple of years, the Cedi has depreciated substantially against the US

MAY 2017 PROFESSIONAL EXAMINATIONS ADVANCED FINANCIAL MANAGEMENT (PAPER 3.3) QUESTIONS & MARKING SCHEME QUESTION ONE a) In the last couple of years, the Cedi has depreciated substantially against the US

E120 MIDTERM Spring Name: (3pts)

") E20 MIDTERM Spring 207 Name: (3pts) SID: (2pts) Any communication with other students during the exam (including showing, viewing or sharing any writing) is strictly prohibited. Any violation will result

E20 MIDTERM Spring 207 Name: (3pts) SID: (2pts) Any communication with other students during the exam (including showing, viewing or sharing any writing) is strictly prohibited. Any violation will result

MATH FOR CREDIT. Purdue University, Feb 6 th, SHIKHAR RANJAN Credit Products Group, Morgan Stanley

MATH FOR CREDIT Purdue University, Feb 6 th, 2004 SHIKHAR RANJAN Credit Products Group, Morgan Stanley Outline The space of credit products Key drivers of value Mathematical models Pricing Trading strategies

MATH FOR CREDIT Purdue University, Feb 6 th, 2004 SHIKHAR RANJAN Credit Products Group, Morgan Stanley Outline The space of credit products Key drivers of value Mathematical models Pricing Trading strategies

Bond Market Development in Emerging East Asia

Bond Market Development in Emerging East Asia Fixed Income Valuation Russ Jason Lo AsianBondsOnline Consultant Valuation of an Asset There are many different ways of valuing an asset. In finance, the gold

Bond Market Development in Emerging East Asia Fixed Income Valuation Russ Jason Lo AsianBondsOnline Consultant Valuation of an Asset There are many different ways of valuing an asset. In finance, the gold

Chapter 10 - Term Structure of Interest Rates

10-1 Chapter 10 - Term Structure of Interest Rates Section 10.2 - Yield Curves In our analysis of bond coupon payments, for example, we assumed a constant interest rate, i, when assessing the present value

10-1 Chapter 10 - Term Structure of Interest Rates Section 10.2 - Yield Curves In our analysis of bond coupon payments, for example, we assumed a constant interest rate, i, when assessing the present value

Sources & Uses 1. Pricing Summary 2. Debt Service Schedule 3. Derivation Of Form 8038 Yield Statistics 6. Proof of D/S for Arbitrage Purposes 7

Table of Contents Report Sources & Uses 1 Pricing Summary 2 Debt Service Schedule 3 Derivation Of Form 8038 Yield Statistics 6 Proof of D/S for Arbitrage Purposes 7 Proof Of Bond Yield @ 3.2996794% 8 Derivation

Table of Contents Report Sources & Uses 1 Pricing Summary 2 Debt Service Schedule 3 Derivation Of Form 8038 Yield Statistics 6 Proof of D/S for Arbitrage Purposes 7 Proof Of Bond Yield @ 3.2996794% 8 Derivation

Lecture 8. Treasury bond futures

Lecture 8 Agenda: Treasury bond futures 1. Treasury bond futures ~ Definition: ~ Cheapest-to-Deliver (CTD) Bond: ~ The wild card play: ~ Interest rate futures pricing: ~ 3-month Eurodollar futures: ~ The

Lecture 8 Agenda: Treasury bond futures 1. Treasury bond futures ~ Definition: ~ Cheapest-to-Deliver (CTD) Bond: ~ The wild card play: ~ Interest rate futures pricing: ~ 3-month Eurodollar futures: ~ The

Amortizing and Accreting Swap Vaulation Pratical Guide

Amortizing and Accreting Swap Vaulation Pratical Guide Alan White FinPricing http://www.finpricing.com Summary Interest Rate Amortizing or Accreting Swap Introduction The Use of Amortizing or Accreting

Amortizing and Accreting Swap Vaulation Pratical Guide Alan White FinPricing http://www.finpricing.com Summary Interest Rate Amortizing or Accreting Swap Introduction The Use of Amortizing or Accreting

Option Models for Bonds and Interest Rate Claims

Option Models for Bonds and Interest Rate Claims Peter Ritchken 1 Learning Objectives We want to be able to price any fixed income derivative product using a binomial lattice. When we use the lattice to

Option Models for Bonds and Interest Rate Claims Peter Ritchken 1 Learning Objectives We want to be able to price any fixed income derivative product using a binomial lattice. When we use the lattice to

Modeling Fixed-Income Securities and Interest Rate Options

jarr_fm.qxd 5/16/02 4:49 PM Page iii Modeling Fixed-Income Securities and Interest Rate Options SECOND EDITION Robert A. Jarrow Stanford Economics and Finance An Imprint of Stanford University Press Stanford,

jarr_fm.qxd 5/16/02 4:49 PM Page iii Modeling Fixed-Income Securities and Interest Rate Options SECOND EDITION Robert A. Jarrow Stanford Economics and Finance An Imprint of Stanford University Press Stanford,

Eurocurrency Contracts. Eurocurrency Futures

Eurocurrency Contracts Futures Contracts, FRAs, & Options Eurocurrency Futures Eurocurrency time deposit Euro-zzz: The currency of denomination of the zzz instrument is not the official currency of the

Eurocurrency Contracts Futures Contracts, FRAs, & Options Eurocurrency Futures Eurocurrency time deposit Euro-zzz: The currency of denomination of the zzz instrument is not the official currency of the

EXAMINATION II: Fixed Income Analysis and Valuation. Derivatives Analysis and Valuation. Portfolio Management. Questions.

EXAMINATION II: Fixed Income Analysis and Valuation Derivatives Analysis and Valuation Portfolio Management Questions Final Examination March 2010 Question 1: Fixed Income Analysis and Valuation (56 points)

EXAMINATION II: Fixed Income Analysis and Valuation Derivatives Analysis and Valuation Portfolio Management Questions Final Examination March 2010 Question 1: Fixed Income Analysis and Valuation (56 points)

Introduction to Financial Mathematics

Introduction to Financial Mathematics MTH 210 Fall 2016 Jie Zhong November 30, 2016 Mathematics Department, UR Table of Contents Arbitrage Interest Rates, Discounting, and Basic Assets Forward Contracts

Introduction to Financial Mathematics MTH 210 Fall 2016 Jie Zhong November 30, 2016 Mathematics Department, UR Table of Contents Arbitrage Interest Rates, Discounting, and Basic Assets Forward Contracts

COPYRIGHTED MATERIAL III.1.1. Bonds and Swaps

III.1 Bonds and Swaps III.1.1 INTRODUCTION A financial security is a tradable legal claim on a firm s assets or income that is traded in an organized market, such as an exchange or a broker s market. There

III.1 Bonds and Swaps III.1.1 INTRODUCTION A financial security is a tradable legal claim on a firm s assets or income that is traded in an organized market, such as an exchange or a broker s market. There

Manual for SOA Exam FM/CAS Exam 2.

Manual for SOA Exam FM/CAS Exam 2. Chapter 5. Bonds. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall 2009 Edition,

Manual for SOA Exam FM/CAS Exam 2. Chapter 5. Bonds. c 2009. Miguel A. Arcones. All rights reserved. Extract from: Arcones Manual for the SOA Exam FM/CAS Exam 2, Financial Mathematics. Fall 2009 Edition,

Federated Government Ultrashort Duration Fund

July 31, 2018 Share Class Ticker A FGUAX Institutional FGUSX Service FEUSX R6 FGULX Federated Government Ultrashort Duration Fund Fund Established 1997 A Portfolio of Federated Institutional Trust Dear

July 31, 2018 Share Class Ticker A FGUAX Institutional FGUSX Service FEUSX R6 FGULX Federated Government Ultrashort Duration Fund Fund Established 1997 A Portfolio of Federated Institutional Trust Dear

Essential Learning for CTP Candidates NY Cash Exchange 2018 Session #CTP-08

NY Cash Exchange 2018: CTP Track Cash Forecasting & Risk Management Session #8 (Thur. 4:00 5:00 pm) ETM5-Chapter 14: Cash Flow Forecasting ETM5-Chapter 16: Enterprise Risk Management ETM5-Chapter 17: Financial

NY Cash Exchange 2018: CTP Track Cash Forecasting & Risk Management Session #8 (Thur. 4:00 5:00 pm) ETM5-Chapter 14: Cash Flow Forecasting ETM5-Chapter 16: Enterprise Risk Management ETM5-Chapter 17: Financial

Modeling Fixed-Income Securities and Interest Rate Options

jarr_fm.qxd 5/16/02 4:49 PM Page iii Modeling Fixed-Income Securities and Interest Rate Options SECOND EDITION Robert A. Jarrow Stanford Economics and Finance An Imprint of Stanford University Press Stanford,

jarr_fm.qxd 5/16/02 4:49 PM Page iii Modeling Fixed-Income Securities and Interest Rate Options SECOND EDITION Robert A. Jarrow Stanford Economics and Finance An Imprint of Stanford University Press Stanford,

Derivative Instruments

Derivative Instruments Paris Dauphine University - Master I.E.F. (272) Autumn 2016 Jérôme MATHIS jerome.mathis@dauphine.fr (object: IEF272) http://jerome.mathis.free.fr/ief272 Slides on book: John C. Hull,

Derivative Instruments Paris Dauphine University - Master I.E.F. (272) Autumn 2016 Jérôme MATHIS jerome.mathis@dauphine.fr (object: IEF272) http://jerome.mathis.free.fr/ief272 Slides on book: John C. Hull,

DUKE UNIVERSITY The Fuqua School of Business. Financial Management Spring 1989 TERM STRUCTURE OF INTEREST RATES*

DUKE UNIVERSITY The Fuqua School of Business Business 350 Smith/Whaley Financial Management Spring 989 TERM STRUCTURE OF INTEREST RATES* The yield curve refers to the relation between bonds expected yield

DUKE UNIVERSITY The Fuqua School of Business Business 350 Smith/Whaley Financial Management Spring 989 TERM STRUCTURE OF INTEREST RATES* The yield curve refers to the relation between bonds expected yield

NOTES ON THE BANK OF ENGLAND UK YIELD CURVES

NOTES ON THE BANK OF ENGLAND UK YIELD CURVES The Macro-Financial Analysis Division of the Bank of England estimates yield curves for the United Kingdom on a daily basis. They are of three kinds. One set

NOTES ON THE BANK OF ENGLAND UK YIELD CURVES The Macro-Financial Analysis Division of the Bank of England estimates yield curves for the United Kingdom on a daily basis. They are of three kinds. One set

Fair Forward Price Interest Rate Parity Interest Rate Derivatives Interest Rate Swap Cross-Currency IRS. Net Present Value.

Net Present Value Christopher Ting Christopher Ting http://www.mysmu.edu/faculty/christophert/ : christopherting@smu.edu.sg : 688 0364 : LKCSB 5036 September 16, 016 Christopher Ting QF 101 Week 5 September

Net Present Value Christopher Ting Christopher Ting http://www.mysmu.edu/faculty/christophert/ : christopherting@smu.edu.sg : 688 0364 : LKCSB 5036 September 16, 016 Christopher Ting QF 101 Week 5 September