Chapter 9 Debt Valuation and Interest Rates

|

|

|

- Lester Bryan

- 6 years ago

- Views:

Transcription

1 Chapter 9 Debt Valuation and Interest Rates

2 Slide Contents Learning Objectives Principles Used in This Chapter 1.Overview of Corporate Debt 2.Valuing Corporate Debt 3.Bond Valuation: Four Key Relationships 4.Types of Bonds 5.Determinants of Interest Rates 9-2

3 Learning Objectives 1. Identify the key features of bonds and describe the difference between private and public debt markets. 2. Calculate the value of a bond and relate it to the yield to maturity on the bond. 3. Describe the four key bond valuation relationships. 4. Identify the major types of corporate bonds. 5. Explain the effects of inflation on interest rates and describe the term structure of interest rates. 9-3

4 9.1 Overview of Corporate Debt

5 Corporate Borrowings There are two main sources of borrowing for a corporation: 1. Loan from a financial institution (known as private debt) 2. Bonds (known as public debt since they can be traded in public financial markets) 9-5

6 Corporate Borrowings (cont.) Smaller firms choose to raise money from banks in the form of loans because of the high costs associated with issuing bonds. Larger firms generally raise money from banks for short-term needs and depend on the bond market for long-term financing needs. 9-6

7 Borrowing Money in the Private Financial Market (cont.) In the private financial market, loans are typically floating rate loans i.e. the interest rate is periodically adjusted based on a specific benchmark rate. The most popular benchmark rate is the London Interbank Offered Rate (LIBOR) LIBOR is the daily interest rate that is based on the interest rates at which banks offer to lend in the London wholesale or interbank market. 9-7

8 Borrowing Money in the Public Financial Market Firms also raise money by selling debt securities to individual investors and financial institutions such as mutual funds. In order to sell debt securities to the public, the issuing firm must meet the legal requirements as specified by the securities laws. 9-8

9 Borrowing Money in the Public Financial Market Corporate bond is a debt security issued by corporation that has promised future payments and a maturity date. If the firm fails to pay the promised future payments of interest and principal, the bond trustee can classify the firm as insolvent and force the firm into bankruptcy. 9-9

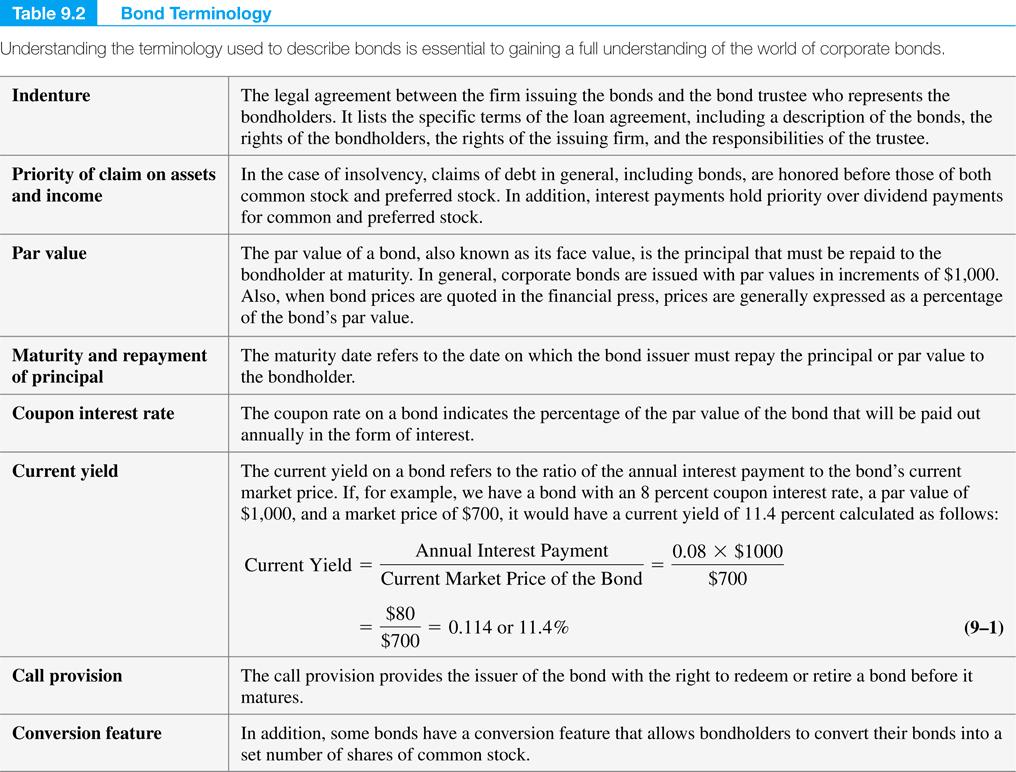

10 Basic Bond Features The basic features of a bond include the following: Bond Indenture Claims on Assets and Income Par or Face Value Coupon Interest Rate Maturity and Repayment of Principal Call Provision and Conversion Features 9-10

11 9-11

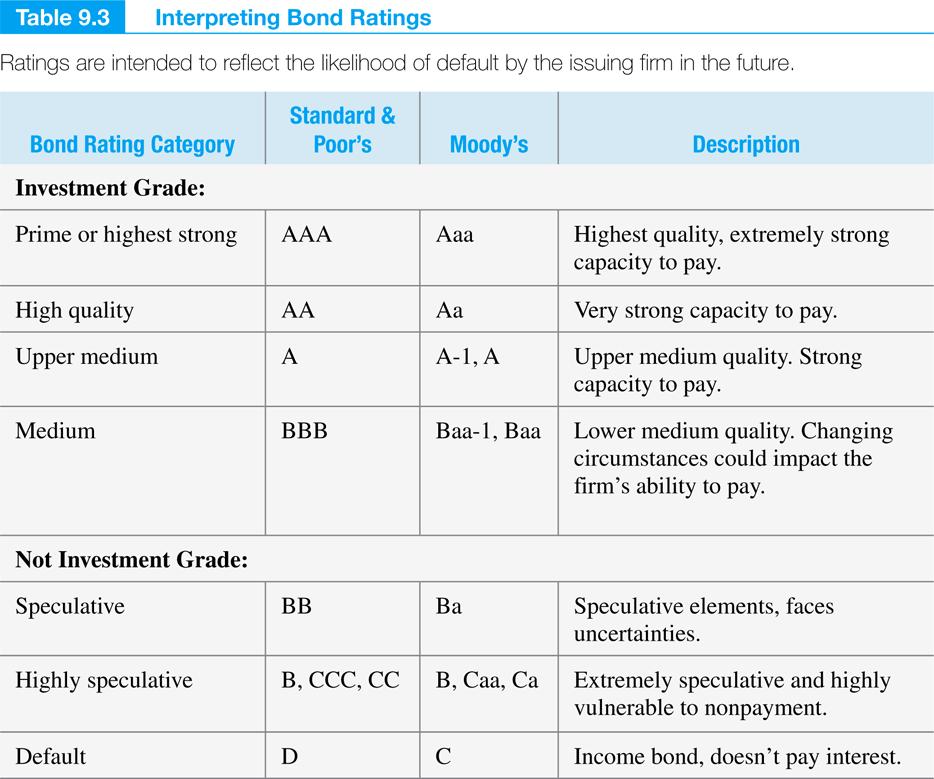

12 Bond Ratings and Default Risk Bond ratings indicate the default risk i.e. the probability that the firm will make the promised payments. Bond ratings affect the rate of return that lenders require of the firm and the firm s cost of borrowing. 9-12

13 9-13

14 9.2 Valuing Corporate Debt

15 Valuing Corporate Debt The value of corporate debt is equal to the present value of the contractually promised principal and interest payments (the cash flows), which discounted back to the present using the market s required yield. 9-15

16 Step-by-Step: Valuing Bonds by Discounting Future Cash Flows Step 1: Determine the amount and timing of bondholder cash flows. The total cash flows equal the promised interest payments and principal payment. Annual Interest = Par value coupon rate Example 9.1: The annual interest for a bond with coupon interest rate of 7% and a par value of $1,000 is equal to $70, (.07 $1,000 = $70). 9-16

17 Step-by-Step: Valuing Bonds by Discounting Future Cash Flows (cont.) Step 2: Estimate the appropriate discount rate on a similar risk bond. Discount rate is the return the bond will yield if it is held to maturity and all bond payments are made. Discount rate can be either calculated or obtained from various sources (such as Yahoo! Finance). 9-17

18 Step-by-Step: Valuing Bonds by Discounting Future Cash Flows (cont.) Step 3: Calculate the present value of the bond s interest and principal payments from Step 1 using the discount rate estimated in step

19 Calculating a Bond s Yield to Maturity (YTM) We can think of YTM as the discount rate that makes the present value of the bond s promised interest and principal equal to the bond s observed market price. 9-19

20 Checkpoint 9.3: Check Yourself Consider a $1,000 par value bond issued by AT&T (T) with a maturity date of 2026 and a stated coupon rate of 8.5%. On January 1, 2007, the bond had 20 years left to maturity. If the market s required yield to maturity on a comparable risk bond is 9%, what is the value of the bond? 9-20

21 Step 1: Picture the Problem Years i= 9% Cash flows $85 $85 $85 $1,085 PV of all Cash flows =? $85 annual interest $85 interest + $1,000 Principal 9-21

22 Step 2: Decide on a Solution Strategy Here we know the following: Annual interest payments = $85 Principal amount or par value = $1,000 Time = 20 years YTM or discount rate = 9% We can use the above information to determine the value of the bond by discounting future interest and principal payment to the present. 9-22

23 Step 3: Solve Using Mathematical Equation Bond Value = $ 85{[1-(1/(1.09) 20 ] (.09)} + $1,000/(1.09) 20 = $85 (9.128) + $ = $

24 Step 4: Analyze The value of AT&T bond is $ when the yield to maturity for comparable risk bond is 9%. The bonds are now trading at a discount as the coupon rate on AT&T bonds is lower than the market yield. 9-24

25 9.3 Bond Valuation: Four Key Relationships

26 Bond Valuation: Four Key Relationships First Relationship The value of bond is inversely related to changes in the yield to maturity. YTM = 12% YTM rises to 15% Par value $1,000 $1,000 Coupon rate 12% 12% Maturity date 5 years 5 years Bond Value $1,000 $ Bond Value Drops 9-26

27 Bond Valuation: Four Key Relationships (cont.) 9-27

28 Bond Valuation: Four Key Relationships (cont.) Second Relationship: The market value of a bond will be less than its par value if the yield to maturity is above the coupon interest rate and will be valued above par value if the yield to maturity is below the coupon interest rate. 9-28

29 Bond Valuation: Four Key Relationships (cont.) When a bond can be bought for less than its par value, it is called discount bond. For example, buying a $1,000 par value bond for $950. Bonds will trade at a discount when the yield to maturity on the bond exceeds the coupon rate. 9-29

30 Bond Valuation: Four Key Relationships (cont.) When a bond can be bought for more than its par value, it is called premium bond. For example, buying a $1,000 par value bond for $1,110. Bonds will trade at a premium when the yield to maturity on the bond is less than the coupon rate. 9-30

31 Bond Valuation: Four Key Relationships (cont.) Third Relationship As the maturity date approaches, the market value of a bond approaches its par value. Regardless of whether the bond was trading at a discount or at a premium, the price of bond will converge towards par value as the maturity date approaches. 9-31

32 9-32

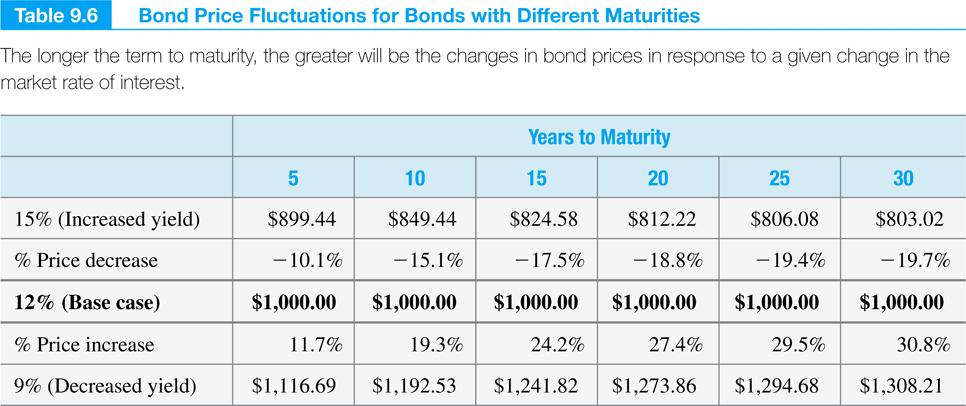

33 Bond Valuation: Four Key Relationships (cont.) Fourth Relationship Long term bonds have greater interest rate risk than short-term bonds. While all bonds are affected by a change in interest rates, long-term bonds are exposed to greater volatility as interest rates change. 9-33

34 9-34

35 9.4 Types of Bonds

36 Types of Bonds The differences among the various types of bond are based on the following bond attributes: 1. Secured versus Unsecured, 2. Priority of claim, 3. Initial offering market, 4. Abnormal risk, 5. Coupon level, 6. Amortizing or non-amortizing, and 7. Convertibility. 9-36

37 Types of Bonds (cont.) Secured versus Unsecured Secured bonds have specific assets pledged to support repayment of the bond. Bonds secured by lien on real property is called a mortgage bond. Unsecured bond are referred to as debentures. 9-37

38 Types of Bonds (cont.) Priority of Claim The priority of claim refers to the order of repayment when the firm s assets are distributed, as in the case of liquidation. Secured bonds are paid first followed by debentures; Among debentures, subordinated debentures have lower priority than secured debt and unsubordinated debentures. 9-38

39 Types of Bonds (cont.) Initial Offering Market Bonds are classified by where they were originally issued (in the domestic bond market or not). For example, Eurobonds are issued in a foreign country but are denominated in domestic currency. For example, a US corporation issuing bonds in Germany in US dollars. 9-39

40 Types of Bonds (cont.) Abnormal Risk Junk, or high-yield, bonds have a belowinvestment grade bond rating. These bonds have a high risk of default as the firms that issued these bonds are facing severe financial problems. 9-40

41 Types of Bonds (cont.) Coupon Level Bonds with a zero or very low coupon are called zero coupon bonds. These bonds are issued at substantial discounts from their par value and promise to repay a zero or very low coupon rate each year. The par value is repaid at the maturity of the bond. 9-41

42 Types of Bonds (cont.) Amortizing or Non-Amortizing The payments from amortizing bonds, like a home mortgage, include both the interest and principal. The payments from a non-amortizing bonds include only interest. At maturity, the bonds repay the par value of bond. 9-42

43 Types of Bonds (cont.) Convertibility Convertible bonds are debt securities that can be converted into a firm s stock at a prespecified price. 9-43

44 9.5 Determinants of Interest Rates

45 Determinants of Interest Rates As we observed earlier, bond prices vary inversely with interest rates. Therefore in order to understand bond pricing we need to know the determinants of interest rates. 9-45

46 Real Rate of Interest and the Inflation Premium (cont.) The nominal return or interest rate on a note or bond can be thought of including four basic components: 9-46

47 I. Real Rate of Interest and the Inflation Premium Quotes of interest rates in the financial press are commonly referred to as the nominal (or quoted) interest rates. Real rate of interest adjusts the nominal rate for the expected effects of inflation. 9-47

48 Fisher Effect The relationship between the nominal rate of interest, r nominal, the anticipated rate of inflation, r inflation, and the real rate of interest is known as the Fisher effect. 9-48

49 II. Default Premium In addition to accounting for the time value of money and inflation, the interest rate that a firm s bonds pay must also offer a default premium i.e. risk that the issuer will fail to repay interest and principal in a timely manner. 9-49

50 III. Maturity Premium The Term Structure of Interest Rates Long-term bonds are more sensitive to interest rate changes. Maturity premium is the compensation that investors demand for bearing interest rate risk on long-term bonds. 9-50

51 Chapter 10 Stock Valuation

52 Slide Contents Learning Objectives Principles Used in This Chapter 1.Common Stock characteristics 2.The Approach to Valuing Common Stock 3.Preferred Stock 4.The Stock Market Key Terms 9-52

53 Learning Objectives 1. Identify the basic characteristics and features of common stock and use the discounted cash flow model to value common shares. 2. Use the price to earnings (P/E) ratio to value common stock. 3. Identify the basic characteristics and features of preferred stock and value preferred shares. 4. Use the secondary market for common stock. 9-53

54 10.1 Common Stock Characteristics

55 Common Stock Common stockholders are the owners of the firm. They elect the firm s board of directors who in turn appoint the firm s top management team. 9-55

56 Common Stock Characteristics Claim on Income Common stockholders have the right to the firm s income that remains after bondholders and preferred stockholders have been paid. The common stockholders either receive cash payments in the form of dividends or the firm s management reinvests the earnings in the firm. 9-56

57 Common Stock Characteristics (cont.) Claim on Assets In case of liquidation, common stockholders have residual claim on assets. However, bankrupt firms rarely have enough assets to satisfy the claims of stockholders. 9-57

58 Common Stock Characteristics (cont.) Voting Rights In general, common shareholders are the only security holders given the right to vote. Common shareholders have the right to elect the board of directors and approve any changes in the corporate charter. Some firms have multiple classes of stock with different voting rights. 9-58

59 Common Stock Characteristics (cont.) Agency Costs and Common Stock In theory, common stockholders elect the board and effectively control the firm through their representatives on the board. In reality, stockholders are given a slate of nominees (list of candidates) for the board selected by the management. As a result, management effectively elects the board and thus the board may have more allegiance (trust) to the managers than to the shareholders. This may lead to agency problems. 9-59

60 10.2 Valuing Common Stock

61 Valuing Common Stock Using the Discounted Dividend Model Like bonds, common stock s value is equal to the present value of all future cash flows that the stockholder expects to receive from owning the shares of stock. However, unlike bonds, the future cash flows in the form of dividends are not fixed. Thus the value of common stock is derived from discounting expected dividend. 9-61

62 Basic Concept of the Stock Valuation Model Example 10.1 Consider a situation in which we are valuing a share of common stock that we plan to hold for only one year. What will be the value of the stock today if it pays a dividend of $2.00, is expected to have a price of $75 and the investor s required rate of return is 12%? 9-62

63 Basic Concept of the Stock Valuation Model (cont.) Value of Common stock = Present Value of future cash flows = Present Value of (dividend + expected price) = ($2+$75) (1.12) 1 = $

64 Basic Concept of the Stock Valuation Model (cont.) Example 10.2 Continue example What will be the value of common stock if you hold the stock for two years and sell it for $82? 9-64

65 Basic Concept of the Stock Valuation Model (cont.) Value of Common stock = Present Value of future cash flows = Present Value of (dividends + expected price) = {($2) (1.12) 1 } + {($2+$82) (1.12) 2 } = $

66 Basic Concept of the Stock Valuation Model (cont.) Since stocks do not have a maturity period, we can consider the value of stock to be equal to the present value of future expected dividends. Valuing common stocks using general discounted cash flow model is made difficult as analyst has to forecast each of the future dividends. This problem is greatly simplified if we assume that dividends grow at a fixed or constant rate. 9-66

67 The Constant Dividend Growth Rate Model If the firm s cash dividend grow by a constant rate each year, then the common stock can be valued as follows: 9-67

68 The Constant Dividend Growth Rate Model (cont.) V cs = Value of a share of common stock D 0 = Annual cash dividend in the year of valuation g = annual growth rate in the dividend D 1 = expected dividend for the end of year 1 r cs = the common stockholder s required rate of return 9-68

69 Checkpoint 10.1: Check Yourself What is the value of a share of common stock that paid $6 dividend at the end of last year and is expected to pay a cash dividend every year from now to infinity, with that dividend growing at a rate of 5 percent per year, if the investor s required rate of return is 12% on that stock? 9-69

70 Solve (cont.) V cs = $6*(1+0,05) ( ) = $6.30 ( ) = $ = $90 Thus the value of common stock is $

71 The Comparable Approach to Valuing Common Stock This method estimates the value of the firm s stock as a multiple of some measure of firm s performance, such as the firm s earnings per share, book value per share, sales per share, cash flow per share, where the multiple is determined by the multiples observed from comparable companies. The most common metric (ratio) is earnings per share (EPS Earnings for end of year per share). 9-71

72 Define the P/E Ratio Valuation Model Price/Earnings ratio (P/E ratio) is a popular measure of stock valuation. P/E ratio (Current Price/ Earnings) is a relative value model because it tells the investor how many dollars investors are willing to pay for each dollar of the company s earnings. 9-72

73 Define the P/E Ratio Valuation Model (cont.) V cs = the value of common stock of the firm. P/E 1 = the price earnings ratio for the firm based on the current price per share divided by earnings for end of year 1. E 1 = estimated earnings per share of common stock for the end of year

74 Checkpoint 10.2: Check Yourself After some careful analysis and reflection on the valuation of the Heals shares the company CFO suggested that the earnings projection are too conservative and earnings for the coming year could easily jump to $2.00. What does this do for your estimate of the value of Heals shares if P/E ratio equal ith 22,61? 9-74

75 Solve What does this do for your estimate of the value of Heals shares if P/E ratio equal ith 22,61 and earnings for the coming year could easily jump to $2.00? V cs = $2 = $

76 10.3 Preferred Stock

77 Features of Preferred Stock Dividend: In general, size of preferred stock dividend is fixed, and it is either stated as a dollar amount or as a percentage of the preferred stock s par value. Unlike common stockholders, preferred stockholders receive the same fixed dividend regardless of how well the firm does. 9-77

78 Features of Preferred Stock (cont.) Multiple Classes: If a company chooses, it can issue more than one class of preferred stock, and each class can have different characteristics. For example, Public Storage (PSA) has 16 different issues of preferred stock outstanding that vary in terms of dividend, convertibility, seniority. 9-78

79 Features of Preferred Stock (cont.) Claims on Assets and Income: In the event of bankruptcy, preferred stockholders have priority over common stock. However, they have lower priority than the firm s debt holders. Firm must pay dividends on preferred stock prior to paying dividend on common stock. 9-79

80 Features of Preferred Stock (cont.) Claims on Assets and Income (cont.) Most preferred stock carry a cumulative feature. Cumulative feature requires that all past unpaid dividends to be paid before any common stock dividends can be declared. Thus preferred stocks are less risky than common stocks but more risky than bonds. 9-80

81 Features of Preferred Stock (cont.) Preferred Stock as a Hybrid Security Like common stocks, preferred stocks do not have a fixed maturity date. Also, like common stocks, nonpayment of dividends does not lead to bankruptcy of the firm. Like debt, preferred stocks have a fixed dividend. Also, most preferred stocks are periodically retired even though there is no stated maturity date. 9-81

82 Valuing Preferred Stock Since preferred stockholders generally receive a fixed dividend and the stocks are perpetuities (non-maturing), it can be valued using the present value of perpetuity equation introduced as in chapter

83 Valuing Preferred Stock (cont.) Since preferred stockholders generally receive a fixed dividend and the stocks are perpetuities (non-maturing), V ps = the value of a share of preferred stock D ps = the annual preferred stock dividend r ps = the market yield or the rate of return on the preferred stock s promised dividend 9-83

84 Checkpoint 10.3: Check Yourself What is the present value of a share of preferred stock that pays a dividend of $12 per share if the market s yield on similar issues of preferred stock is 8%? 9-84

85 Solve V ps = $12.08 = $150 Thus the present value of this preferred stock is $

86 10.4 The Stock Market

87 The Stock Market New securities trade in the primary market while currently outstanding securities trade in the secondary market. The corporation receives money from sale of its securities only in the primary market. 9-87

88 The Stock Market (cont.) There are two types of secondary markets: Organized exchanges where trading occurs at a physical location; and Over-the-counter market where trading occurs over the telephone or through computer networks. 9-88

89 Organized Exchanges The New York Stock Exchange (NYSE), also called the Big Board, is the oldest of all organized exchanges and the largest organized exchange in the world. While the NYSE is considered an organized exchange because of its physical location, the majority of its trades are done electronically without a face-to-face meeting of traders. 9-89

90 Organized Exchanges (cont.) The American Stock Exchange (AMEX) is the nation s second largest, floor-based exchange. However, in terms of volume, the AMEX is a distant number two with less than 5% of that on the NYSE. AMEX merged with NASDAQ in 1998 but continues to operate as a separate entity. 9-90

91 Over-the-Counter (OTC) Market The over-the-counter market is a network of dealers that has no listing or membership requirements. Today, the OTC market is electronic with Nasdaq leading the way. OTC listings generally include companies too new or too small to be eligible for listing on a major exchange. 9-91

FIN Chapter 10. Stock Valuation. Liuren Wu

FIN 3000 Chapter 10 Stock Valuation Liuren Wu Overview 1. Common Stock Identify the basic characteristics and features of common stock and use the discounted cash flow model to value common shares. 2.

FIN 3000 Chapter 10 Stock Valuation Liuren Wu Overview 1. Common Stock Identify the basic characteristics and features of common stock and use the discounted cash flow model to value common shares. 2.

Chapter 10. Learning Objectives Principles Used in This Chapter 1.Common Stock 2.The Comparables Approach to Valuing Common

Chapter 10 Learning Objectives Principles Used in This Chapter 1.Common Stock 2.The Comparables Approach to Valuing Common Stock 3.Preferred Stock 4.The Stock Market 1. Identify the basic characteristics

Chapter 10 Learning Objectives Principles Used in This Chapter 1.Common Stock 2.The Comparables Approach to Valuing Common Stock 3.Preferred Stock 4.The Stock Market 1. Identify the basic characteristics

Stock valuation. Chapter 10

Stock valuation Chapter 10 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk Reward Tradeoff. Principle 3: Cash Flows are the Source of Value. Principle

Stock valuation Chapter 10 1 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk Reward Tradeoff. Principle 3: Cash Flows are the Source of Value. Principle

DEBT VALUATION AND INTEREST. Chapter 9

DEBT VALUATION AND INTEREST Chapter 9 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value

DEBT VALUATION AND INTEREST Chapter 9 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value

I. Introduction to Bonds

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

University of California, Merced ECO 163-Economics of Investments Chapter 10 Lecture otes I. Introduction to Bonds Professor Jason Lee A. Definitions Definition: A bond obligates the issuer to make specified

Chapter. Corporate Bonds. Corporate Bonds. Corporate Bond Basics, I. Corporate Bond Basics, II. Corporate Bond Basics, III. Types of Corporate Bonds

Chapter 18 Corporate Bonds Corporate Bonds Our goal in this chapter is to introduce the specialized knowledge concerning trading corporate bonds. Money managers who buy and sell corporate bonds possess

Chapter 18 Corporate Bonds Corporate Bonds Our goal in this chapter is to introduce the specialized knowledge concerning trading corporate bonds. Money managers who buy and sell corporate bonds possess

Understanding Interest Rates

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

Money & Banking Notes Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (PV): A dollar paid to you one year from now is less valuable than a dollar paid to you today. Why? -

CHAPTER 9 DEBT SECURITIES. by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

CHAPTER 9 DEBT SECURITIES by Lee M. Dunham, PhD, CFA, and Vijay Singal, PhD, CFA LEARNING OUTCOMES After completing this chapter, you should be able to do the following: a Identify issuers of debt securities;

Bonds and Their Valuation

Chapter 7 Bonds and Their Valuation Key Features of Bonds Bond Valuation Measuring Yield Assessing Risk 7 1 What is a bond? A long term debt instrument in which a borrower agrees to make payments of principal

Chapter 7 Bonds and Their Valuation Key Features of Bonds Bond Valuation Measuring Yield Assessing Risk 7 1 What is a bond? A long term debt instrument in which a borrower agrees to make payments of principal

Security Analysis. Bond Valuation

Security Analysis Bond Valuation Background on Bonds Bonds represent long-term debt securities Contractual Promise to pay future cash flows to investors The issuer of the bond is obligated to pay: Interest

Security Analysis Bond Valuation Background on Bonds Bonds represent long-term debt securities Contractual Promise to pay future cash flows to investors The issuer of the bond is obligated to pay: Interest

FIN 6160 Investment Theory. Lecture 9-11 Managing Bond Portfolios

FIN 6160 Investment Theory Lecture 9-11 Managing Bond Portfolios Bonds Characteristics Bonds represent long term debt securities that are issued by government agencies or corporations. The issuer of bond

FIN 6160 Investment Theory Lecture 9-11 Managing Bond Portfolios Bonds Characteristics Bonds represent long term debt securities that are issued by government agencies or corporations. The issuer of bond

KEY CONCEPTS AND SKILLS

Chapter 5 INTEREST RATES AND BOND VALUATION 5-1 KEY CONCEPTS AND SKILLS Know the important bond features and bond types Comprehend bond values (prices) and why they fluctuate Compute bond values and fluctuations

Chapter 5 INTEREST RATES AND BOND VALUATION 5-1 KEY CONCEPTS AND SKILLS Know the important bond features and bond types Comprehend bond values (prices) and why they fluctuate Compute bond values and fluctuations

1) Which one of the following is NOT a typical negative bond covenant?

Which one of the following is NOT a typical negative bond covenant?") Questions in Chapter 7 concept.qz 1) Which one of the following is NOT a typical negative bond covenant? [A] The firm must limit dividend payments. [B] The firm cannot merge with another firm. [C] The

Questions in Chapter 7 concept.qz 1) Which one of the following is NOT a typical negative bond covenant? [A] The firm must limit dividend payments. [B] The firm cannot merge with another firm. [C] The

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 14-2 Bond Characteristics Bonds are debt. Issuers are borrowers and holders are

CHAPTER 14 Bond Prices and Yields McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. 14-2 Bond Characteristics Bonds are debt. Issuers are borrowers and holders are

Fixed income security. Face or par value Coupon rate. Indenture. The issuer makes specified payments to the bond. bondholder

Bond Prices and Yields Bond Characteristics Fixed income security An arragement between borrower and purchaser The issuer makes specified payments to the bond holder on specified dates Face or par value

Bond Prices and Yields Bond Characteristics Fixed income security An arragement between borrower and purchaser The issuer makes specified payments to the bond holder on specified dates Face or par value

Questions 1. What is a bond? What determines the price of this financial asset?

BOND VALUATION Bonds are debt instruments issued by corporations, as well as state, local, and foreign governments to raise funds for growth and financing of public projects. Since bonds are long-term

BOND VALUATION Bonds are debt instruments issued by corporations, as well as state, local, and foreign governments to raise funds for growth and financing of public projects. Since bonds are long-term

A CLEAR UNDERSTANDING OF THE INDUSTRY

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

A CLEAR UNDERSTANDING OF THE INDUSTRY IS CFA INSTITUTE INVESTMENT FOUNDATIONS RIGHT FOR YOU? Investment Foundations is a certificate program designed to give you a clear understanding of the investment

1. Transaction balances refer to cash kept on hand by a firm to pay everyday expenses.

Chapter 16 Financial Management and Securities Markets / Questions 1. Transaction balances refer to cash kept on hand by a firm to pay everyday expenses. 2. Lockbox systems are beneficial to companies

Chapter 16 Financial Management and Securities Markets / Questions 1. Transaction balances refer to cash kept on hand by a firm to pay everyday expenses. 2. Lockbox systems are beneficial to companies

Financial Investment

Financial Investment Dagmar Linnertová Dagmar.linnertova@mail.muni.cz Seminars Excercises in a seminars evaluated by lecturer Questions as a preparation for final test (2, 1 or 0 points) maximum points

Financial Investment Dagmar Linnertová Dagmar.linnertova@mail.muni.cz Seminars Excercises in a seminars evaluated by lecturer Questions as a preparation for final test (2, 1 or 0 points) maximum points

Chapter 11: Financial Markets Section 2

Chapter 11: Financial Markets Section 2 Objectives 1. Describe the characteristics of bonds as financial assets. 2. Identify different types of bonds. 3. Describe the characteristics of other types of

Chapter 11: Financial Markets Section 2 Objectives 1. Describe the characteristics of bonds as financial assets. 2. Identify different types of bonds. 3. Describe the characteristics of other types of

Financial Markets I The Stock, Bond, and Money Markets Every economy must solve the basic problems of production and distribution of goods and

Financial Markets I The Stock, Bond, and Money Markets Every economy must solve the basic problems of production and distribution of goods and services. Financial markets perform an important function

Financial Markets I The Stock, Bond, and Money Markets Every economy must solve the basic problems of production and distribution of goods and services. Financial markets perform an important function

Investments 10th Edition Bodie Test Bank Full Download:

Investments 10th Edition Bodie Test Bank Full Download: http://testbanklive.com/download/investments-10th-edition-bodie-test-bank/ Chapter 02 Asset Classes and Financial Instruments Multiple Choice Questions

Investments 10th Edition Bodie Test Bank Full Download: http://testbanklive.com/download/investments-10th-edition-bodie-test-bank/ Chapter 02 Asset Classes and Financial Instruments Multiple Choice Questions

CHAPTER 7. Stock Valuation

Principles of Managerial Finance Solution Lawrence J. Gitman CHAPTER 7 Stock Valuation INSTRUCTOR S RESOURCES Overview This chapter continues on the valuation process introduced in Chapter 6 for bonds.

Principles of Managerial Finance Solution Lawrence J. Gitman CHAPTER 7 Stock Valuation INSTRUCTOR S RESOURCES Overview This chapter continues on the valuation process introduced in Chapter 6 for bonds.

Financial Markets Econ 173A: Mgt 183. Capital Markets & Securities

Financial Markets Econ 173A: Mgt 183 Capital Markets & Securities Financial Instruments Money Market Certificates of Deposit U.S. Treasury Bills Money Market Funds Equity Market Common Stock Preferred

Financial Markets Econ 173A: Mgt 183 Capital Markets & Securities Financial Instruments Money Market Certificates of Deposit U.S. Treasury Bills Money Market Funds Equity Market Common Stock Preferred

CHAPTER 4 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk

4-1 CHAPTER 4 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk 4-2 Key Features of a Bond 1. Par value: Face amount; paid at maturity. Assume $1,000. 2. Coupon

4-1 CHAPTER 4 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk 4-2 Key Features of a Bond 1. Par value: Face amount; paid at maturity. Assume $1,000. 2. Coupon

Lecture 4. The Bond Market. Mingzhu Wang SKKU ISS 2017

Lecture 4 The Bond Market Mingzhu Wang SKKU ISS 2017 Bond Terminologies 2 Agenda Types of Bonds 1. Treasury Notes and Bonds 2. Municipal Bonds 3. Corporate Bonds Financial Guarantees for Bonds Current

Lecture 4 The Bond Market Mingzhu Wang SKKU ISS 2017 Bond Terminologies 2 Agenda Types of Bonds 1. Treasury Notes and Bonds 2. Municipal Bonds 3. Corporate Bonds Financial Guarantees for Bonds Current

FINC3019 FIXED INCOME SECURITIES

FINC3019 FIXED INCOME SECURITIES WEEK 1 BONDS o Debt instrument requiring the issuer to repay the lender the amount borrowed + interest over specified time period o Plain vanilla (typical) bond:! Fixed

FINC3019 FIXED INCOME SECURITIES WEEK 1 BONDS o Debt instrument requiring the issuer to repay the lender the amount borrowed + interest over specified time period o Plain vanilla (typical) bond:! Fixed

4. Understanding.. Interest Rates. Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1

4. Understanding. Interest Rates Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1 Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright

4. Understanding. Interest Rates Copyright 2007 Pearson Addison-Wesley. All rights reserved. 4-1 Present Value A dollar paid to you one year from now is less valuable than a dollar paid to you today Copyright

Chapter 3: Debt financing. Albert Banal-Estanol

Corporate Finance Chapter 3: Debt financing Albert Banal-Estanol Debt issuing as part of a leverage buyout (LBO) What is an LBO? How to decide among these options? In this chapter we should talk about

Corporate Finance Chapter 3: Debt financing Albert Banal-Estanol Debt issuing as part of a leverage buyout (LBO) What is an LBO? How to decide among these options? In this chapter we should talk about

: Corporate Finance. Corporate Decisions

380.760: Corporate Finance Lecture 6: Corporate Financing Professor Gordon M. Bodnar 2009 Gordon Bodnar, 2009 Corporate Decisions Investment decision vs. financing decision until now we have focused on

380.760: Corporate Finance Lecture 6: Corporate Financing Professor Gordon M. Bodnar 2009 Gordon Bodnar, 2009 Corporate Decisions Investment decision vs. financing decision until now we have focused on

Test Bank for Investments Global Edition 10th Edition by Zvi Bodie, Alex Kane and Alan J. Marcus

Test Bank for Investments Global Edition 10th Edition by Zvi Bodie, Alex Kane and Alan J. Marcus Link download full: https://digitalcontentmarket.org/download/test-bankfor-investments-global-edition-10th-edition-by-bodie

Test Bank for Investments Global Edition 10th Edition by Zvi Bodie, Alex Kane and Alan J. Marcus Link download full: https://digitalcontentmarket.org/download/test-bankfor-investments-global-edition-10th-edition-by-bodie

Long-Term Liabilities. Record and Report Long-Term Liabilities

SECTION Long-Term Liabilities VII OVERVIEW What this section does This section explains transactions, calculations, and financial statement presentation of long-term liabilities, primarily bonds and notes

SECTION Long-Term Liabilities VII OVERVIEW What this section does This section explains transactions, calculations, and financial statement presentation of long-term liabilities, primarily bonds and notes

Purpose of the Capital Market

BOND MARKETS Purpose of the Capital Market Original maturity is greater than one year, typically for long-term financing or investments Best known capital market securities: Stocks and bonds Capital Market

BOND MARKETS Purpose of the Capital Market Original maturity is greater than one year, typically for long-term financing or investments Best known capital market securities: Stocks and bonds Capital Market

Chapter 10. The Bond Market

Chapter 10 The Bond Market Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds are like money market instruments, but they have maturities that exceed one year. These include

Chapter 10 The Bond Market Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds are like money market instruments, but they have maturities that exceed one year. These include

Important Information about Investing in

Robert W. Baird & Co. Incorporated Important Information about Investing in \ Bonds Baird has prepared this document to help you understand the characteristics and risks associated with bonds and other

Robert W. Baird & Co. Incorporated Important Information about Investing in \ Bonds Baird has prepared this document to help you understand the characteristics and risks associated with bonds and other

The Cost of Capital. Principles Applied in This Chapter. The Cost of Capital: An Overview

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital. Chapter 14

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

The Cost of Capital Chapter 14 Principles Applied in This Chapter Principle 1: Money Has a Time Value. Principle 2: There is a Risk-Return Tradeoff. Principle 3: Cash Flows Are the Source of Value. Principle

STOCK VALUATION Chapter 8

STOCK VALUATION Chapter 8 OUTLINE 1. Common & Preferred Stock A. Rights B. The Annual Meeting & Voting C. Dividends 2. Stock Valuation A. Zero Growth Dividends B. Constant Growth Dividends C. Non-constant

STOCK VALUATION Chapter 8 OUTLINE 1. Common & Preferred Stock A. Rights B. The Annual Meeting & Voting C. Dividends 2. Stock Valuation A. Zero Growth Dividends B. Constant Growth Dividends C. Non-constant

Valuing Bonds. Professor: Burcu Esmer

Valuing Bonds Professor: Burcu Esmer Valuing Bonds A bond is a debt instrument issued by governments or corporations to raise money The successful investor must be able to: Understand bond structure Calculate

Valuing Bonds Professor: Burcu Esmer Valuing Bonds A bond is a debt instrument issued by governments or corporations to raise money The successful investor must be able to: Understand bond structure Calculate

Test Bank for Investments 8th Canadian Edition by Bodie Kane Marcus Perrakis Ryan

Test Bank for Investments 8th Canadian Edition by Bodie Kane Marcus Perrakis Ryan Link download full: http://testbankair.com/download/test-bank-for-investments-8thcanadian-edition-by-bodie-kane-marcus-perrakis-ryan/

Test Bank for Investments 8th Canadian Edition by Bodie Kane Marcus Perrakis Ryan Link download full: http://testbankair.com/download/test-bank-for-investments-8thcanadian-edition-by-bodie-kane-marcus-perrakis-ryan/

Chapter 8. Money and Capital Markets. Learning Objectives. Introduction

Chapter 8 Money and Capital Markets Learning Objectives Visualize the structure of the government bond market Explain the interaction of Eurodollars, CDs, and Repurchase agreements and their connection

Chapter 8 Money and Capital Markets Learning Objectives Visualize the structure of the government bond market Explain the interaction of Eurodollars, CDs, and Repurchase agreements and their connection

Financing the Enterprise

Financing the Enterprise McGraw-Hill/Irwin Copyright 2014 by The McGraw-Hill Companies, Inc. All rights reserved. CHAPTER 14 Accounting and Financial Statements CHAPTER 15 Money and the Financial System

Financing the Enterprise McGraw-Hill/Irwin Copyright 2014 by The McGraw-Hill Companies, Inc. All rights reserved. CHAPTER 14 Accounting and Financial Statements CHAPTER 15 Money and the Financial System

Savings and Investment

Lecture Notes for Chapter 3 of MACROECONOMICS: An Introduction Savings and Investment Copyright 2000-2009 by Charles R. Nelson 1/8/09 In this chapter we will discuss- How savings becomes investment. Banks

Lecture Notes for Chapter 3 of MACROECONOMICS: An Introduction Savings and Investment Copyright 2000-2009 by Charles R. Nelson 1/8/09 In this chapter we will discuss- How savings becomes investment. Banks

1. Which of the following is not a characteristic of a money market instrument?

Test Bank for Investments 8th Canadian Edition by Bodie Kane Marcus Perrakis Ryan Link download full: https://testbankservice.com/download/test-bank-for-investments-8thcanadian-edition-by-bodie-kane-marcus-perrakis-ryan/

Test Bank for Investments 8th Canadian Edition by Bodie Kane Marcus Perrakis Ryan Link download full: https://testbankservice.com/download/test-bank-for-investments-8thcanadian-edition-by-bodie-kane-marcus-perrakis-ryan/

International Finance

International Finance FINA 5331 Lecture 2: U.S. Financial System William J. Crowder Ph.D. Financial Markets Financial markets are markets in which funds are transferred from people and Firms who have an

International Finance FINA 5331 Lecture 2: U.S. Financial System William J. Crowder Ph.D. Financial Markets Financial markets are markets in which funds are transferred from people and Firms who have an

The following pages explain some commonly used bond terminology, and provide information on how bond returns are generated.

1 2 3 Corporate bonds play an important role in a diversified portfolio. The opportunity to receive regular income streams from corporate bonds can be appealing to investors, and the focus on capital preservation

1 2 3 Corporate bonds play an important role in a diversified portfolio. The opportunity to receive regular income streams from corporate bonds can be appealing to investors, and the focus on capital preservation

Summary. Chapter 6. Bond Valuation

Summary Chapter 6 Bond Valuation Learning objectives: This chapter will help you understand the important concepts relating to bonds and bond investing including bonds valuation. It will also take you

Summary Chapter 6 Bond Valuation Learning objectives: This chapter will help you understand the important concepts relating to bonds and bond investing including bonds valuation. It will also take you

Bond Prices and Yields

Bond Characteristics 14-2 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture gives

Bond Characteristics 14-2 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture gives

Markets: Fixed Income

Markets: Fixed Income Mark Hendricks Autumn 2017 FINM Intro: Markets Outline Hendricks, Autumn 2017 FINM Intro: Markets 2/55 Asset Classes Fixed Income Money Market Bonds Equities Preferred Common contracted

Markets: Fixed Income Mark Hendricks Autumn 2017 FINM Intro: Markets Outline Hendricks, Autumn 2017 FINM Intro: Markets 2/55 Asset Classes Fixed Income Money Market Bonds Equities Preferred Common contracted

Appendix A Financial Calculations

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

Derivatives Demystified: A Step-by-Step Guide to Forwards, Futures, Swaps and Options, Second Edition By Andrew M. Chisholm 010 John Wiley & Sons, Ltd. Appendix A Financial Calculations TIME VALUE OF MONEY

CHAPTER 14. Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS. Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved.

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

CHAPTER 14 Bond Prices and Yields INVESTMENTS BODIE, KANE, MARCUS McGraw-Hill/Irwin Copyright 2011 by The McGraw-Hill Companies, Inc. All rights reserved. INVESTMENTS BODIE, KANE, MARCUS 14-2 Bond Characteristics

Advanced Financial Management Bachelors of Business (Specialized in Finance) Study Notes & Tutorial Questions Chapter 3: Cost of Capital

Study Notes & Tutorial Questions Chapter 3: Cost of Capital") Advanced Financial Management Bachelors of Business (Specialized in Finance) Study Notes & Tutorial Questions Chapter 3: Cost of Capital 1 INTRODUCTION Cost of capital is an integral part of investment

Advanced Financial Management Bachelors of Business (Specialized in Finance) Study Notes & Tutorial Questions Chapter 3: Cost of Capital 1 INTRODUCTION Cost of capital is an integral part of investment

Chapter 13. Introduction to Corporate Finance and Governance

Chapter 13 Introduction to Corporate Finance and Governance 13-2 Topics Covered Creating Value with Financing Decisions Common Stock Preferred Stock Corporate Debt Convertible Securities Patterns of Corporate

Chapter 13 Introduction to Corporate Finance and Governance 13-2 Topics Covered Creating Value with Financing Decisions Common Stock Preferred Stock Corporate Debt Convertible Securities Patterns of Corporate

CHAPTER 14. Bond Characteristics. Bonds are debt. Issuers are borrowers and holders are creditors.

Bond Characteristics 14-2 CHAPTER 14 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture

Bond Characteristics 14-2 CHAPTER 14 Bond Prices and Yields Bonds are debt. Issuers are borrowers and holders are creditors. The indenture is the contract between the issuer and the bondholder. The indenture

Part A: Corporate Finance

Finance: Common Body of Knowledge Review Part A: Corporate Finance Time Value of Money Financial managers always want to determine how much a periodic receipt of future cash flow is worth in today s dollars.

Finance: Common Body of Knowledge Review Part A: Corporate Finance Time Value of Money Financial managers always want to determine how much a periodic receipt of future cash flow is worth in today s dollars.

Bonds and Their Value

140 Yost Rocks, Inc. wants to borrow money, and it decides to issue bonds. Each bondholder lends the firm money today for 30 years at 12 percent interest.yost Rocks pays each bondholder $120 per year and

140 Yost Rocks, Inc. wants to borrow money, and it decides to issue bonds. Each bondholder lends the firm money today for 30 years at 12 percent interest.yost Rocks pays each bondholder $120 per year and

Reading. Valuation of Securities: Bonds

Valuation of Securities: Bonds Econ 422: Investment, Capital & Finance University of Washington Last updated: April 11, 2010 Reading BMA, Chapter 3 http://finance.yahoo.com/bonds http://cxa.marketwatch.com/finra/marketd

Valuation of Securities: Bonds Econ 422: Investment, Capital & Finance University of Washington Last updated: April 11, 2010 Reading BMA, Chapter 3 http://finance.yahoo.com/bonds http://cxa.marketwatch.com/finra/marketd

Chapter 6. Stock Valuation

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Investments 4: Bond Basics

Personal Finance: Another Perspective Investments 4: Bond Basics Updated 2017/06/28 1 Objectives A. Understand risk and return for bonds B. Understand bond terminology C. Understand the major types of

Personal Finance: Another Perspective Investments 4: Bond Basics Updated 2017/06/28 1 Objectives A. Understand risk and return for bonds B. Understand bond terminology C. Understand the major types of

AGENDA LEARNING OBJECTIVES THE COST OF CAPITAL. Chapter 14. Learning Objectives Principles Used in This Chapter. financing.

Chapter 14 THE COST OF CAPITAL AGENDA Learning Objectives Principles Used in This Chapter 1. The Cost of Capital: An Overview 2. Determining the Firm s Capital Structure Weights 3. Estimating the Costs

Chapter 14 THE COST OF CAPITAL AGENDA Learning Objectives Principles Used in This Chapter 1. The Cost of Capital: An Overview 2. Determining the Firm s Capital Structure Weights 3. Estimating the Costs

ACC 501 Solved MCQ'S For MID & Final Exam 1. Which of the following is an example of positive covenant? Maintaining firm s working capital at or above some specified minimum level Furnishing audited financial

ACC 501 Solved MCQ'S For MID & Final Exam 1. Which of the following is an example of positive covenant? Maintaining firm s working capital at or above some specified minimum level Furnishing audited financial

I. Asset Valuation. The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset.

1 I. Asset Valuation The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset. 2 1 II. Bond Features and Prices Definitions Bond: a certificate

1 I. Asset Valuation The value of any asset, whether it is real or financial, is the sum of all expected future earnings produced by the asset. 2 1 II. Bond Features and Prices Definitions Bond: a certificate

FIXED INCOME ANALYSIS WORKBOOK

FIXED INCOME ANALYSIS WORKBOOK CFA Institute is the premier association for investment professionals around the world, with over 124,000 members in 145 countries. Since 1963 the organization has developed

FIXED INCOME ANALYSIS WORKBOOK CFA Institute is the premier association for investment professionals around the world, with over 124,000 members in 145 countries. Since 1963 the organization has developed

Fixed-Income Securities: Defining Elements

The following is a review of the Fixed Income: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. Cross-Reference to CFA Institute Assigned Reading

The following is a review of the Fixed Income: Basic Concepts principles designed to address the learning outcome statements set forth by CFA Institute. Cross-Reference to CFA Institute Assigned Reading

MONEY MARKET FUND GLOSSARY

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

MONEY MARKET FUND GLOSSARY 1-day SEC yield: The calculation is similar to the 7-day Yield, only covering a one day time frame. To calculate the 1-day yield, take the net interest income earned by the fund

Chapter 6. Stock Valuation

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Chapter 6 Stock Valuation Comprehend that stock prices depend on future dividends and dividend growth Compute stock prices using the dividend growth model Understand how growth opportunities affect stock

Bonds and Other Financial Instruments

SECTION 4 Bonds and Other Financial Instruments OBJECTIVES KEY TERMS TAKING NOTES In Section 4, you will discuss why people buy bonds describe the different kinds of bonds explain the factors that affect

SECTION 4 Bonds and Other Financial Instruments OBJECTIVES KEY TERMS TAKING NOTES In Section 4, you will discuss why people buy bonds describe the different kinds of bonds explain the factors that affect

Bond and Common Share Valuation

Bond and Common Share Valuation Lakehead University Fall 2004 Outline of the Lecture Bonds and Bond Valuation The Determinants of Interest Rates Common Share Valuation 2 Bonds and Bond Valuation A corporation

Bond and Common Share Valuation Lakehead University Fall 2004 Outline of the Lecture Bonds and Bond Valuation The Determinants of Interest Rates Common Share Valuation 2 Bonds and Bond Valuation A corporation

COPYRIGHTED MATERIAL FEATURES OF DEBT SECURITIES CHAPTER 1 I. INTRODUCTION

CHAPTER 1 FEATURES OF DEBT SECURITIES I. INTRODUCTION In investment management, the most important decision made is the allocation of funds among asset classes. The two major asset classes are equities

CHAPTER 1 FEATURES OF DEBT SECURITIES I. INTRODUCTION In investment management, the most important decision made is the allocation of funds among asset classes. The two major asset classes are equities

Lesson 9 Debt and Equity Financing

Lesson 9 Balance Sheet Lesson 9 Debt and Equity Financing Assets: Current Assets: Accounts receivable Less: Allowance for Uncollectible A/R Inventories Prepaid Expenses Long-Term Assets: Property and Equipment

Lesson 9 Balance Sheet Lesson 9 Debt and Equity Financing Assets: Current Assets: Accounts receivable Less: Allowance for Uncollectible A/R Inventories Prepaid Expenses Long-Term Assets: Property and Equipment

CHAPTER 8. Valuing Bonds. Chapter Synopsis

CHAPTER 8 Valuing Bonds Chapter Synopsis 8.1 Bond Cash Flows, Prices, and Yields A bond is a security sold at face value (FV), usually $1,000, to investors by governments and corporations. Bonds generally

CHAPTER 8 Valuing Bonds Chapter Synopsis 8.1 Bond Cash Flows, Prices, and Yields A bond is a security sold at face value (FV), usually $1,000, to investors by governments and corporations. Bonds generally

1 SOURCES OF FINANCE

1 SOURCES OF FINANCE 2 3 TRADE CREDIT Trade credit is a form of short-term finance. It has few costs and security is not required. Normally a supplier will allow business customers a period of time after

1 SOURCES OF FINANCE 2 3 TRADE CREDIT Trade credit is a form of short-term finance. It has few costs and security is not required. Normally a supplier will allow business customers a period of time after

Corporate Finance FINA4330. Nisan Langberg Phone number: Office: 210-E Class website:

Corporate Finance FINA4330 Nisan Langberg Phone number: 743-4765 Office: 210-E Class website: http://www.bauer.uh.edu/nlangberg/ What material can be found online? Syllabus Outline of lecture notes Homework

Corporate Finance FINA4330 Nisan Langberg Phone number: 743-4765 Office: 210-E Class website: http://www.bauer.uh.edu/nlangberg/ What material can be found online? Syllabus Outline of lecture notes Homework

2) Which NYSE member is typically an employee of a brokerage company such as Merrill Lynch?

Which NYSE member is typically an employee of a brokerage company such as Merrill Lynch?") Questions in Chapter 8 concept.qz 1) A is an owner of a seat on the New York Stock Exchange. [A] broker [B] dealer [C] member [D] floor trader [E] specialist [A] :This is an individual who arranges security

Questions in Chapter 8 concept.qz 1) A is an owner of a seat on the New York Stock Exchange. [A] broker [B] dealer [C] member [D] floor trader [E] specialist [A] :This is an individual who arranges security

Reporting and Interpreting Bonds

Reporting and Interpreting Bonds CHAPTER 10 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Not Barry and not James Slide 2 Understanding the Business The mixture of debt and equity used to finance

Reporting and Interpreting Bonds CHAPTER 10 McGraw-Hill/Irwin 2009 The McGraw-Hill Companies, Inc. Not Barry and not James Slide 2 Understanding the Business The mixture of debt and equity used to finance

FIN 684 Fixed-Income Analysis Corporate Debt Securities

FIN 684 Fixed-Income Analysis Corporate Debt Securities Professor Robert B.H. Hauswald Kogod School of Business, AU Corporate Debt Securities Financial obligations of a corporation that have priority over

FIN 684 Fixed-Income Analysis Corporate Debt Securities Professor Robert B.H. Hauswald Kogod School of Business, AU Corporate Debt Securities Financial obligations of a corporation that have priority over

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 1 Introduction and Overview

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 1 Introduction and Overview Today: I. Description of course material II. Course mechanics, schedule III. Big picture of funding sources

FUNDING INVESTMENTS FINANCE 238/738, Spring 2008, Prof. Musto Class 1 Introduction and Overview Today: I. Description of course material II. Course mechanics, schedule III. Big picture of funding sources

Chapter 02: Asset Classes and Financial Instruments

Test Bank for Investments and Portfolio Management 9th Edition by Bodie, Kane, Marcus Link download full Test Bank for Investments and Portfolio Management 9th Edition by Bodie, Kane, Marcus: https://digitalcontentmarket.org/download/test-bank-for-investments-and-portfolio-management-

Test Bank for Investments and Portfolio Management 9th Edition by Bodie, Kane, Marcus Link download full Test Bank for Investments and Portfolio Management 9th Edition by Bodie, Kane, Marcus: https://digitalcontentmarket.org/download/test-bank-for-investments-and-portfolio-management-

Part 6 Financing the Enterprise

Part 6 Financing the Enterprise 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may

Part 6 Financing the Enterprise 2016 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or distribution in any manner. This document may

ACC 501 Quizzes Lecture 1 to 22

ACC501 Business Finance Composed By Faheem Saqib A mega File of MiD Term Solved MCQ For more Help Rep At Faheem_saqib2003@yahoocom Faheemsaqib2003@gmailcom 0334-6034849 ACC 501 Quizzes Lecture 1 to 22

ACC501 Business Finance Composed By Faheem Saqib A mega File of MiD Term Solved MCQ For more Help Rep At Faheem_saqib2003@yahoocom Faheemsaqib2003@gmailcom 0334-6034849 ACC 501 Quizzes Lecture 1 to 22

A Comprehensive Look at the CECL Model

A Comprehensive Look at the CECL Model Table of Contents SCOPE... 3 CURRENT EXPECTED CREDIT LOSS MODEL... 3 LOSS PROBABILITIES... 5 MEASUREMENT OF EXPECTED CREDIT LOSSES... 5 Individual Versus Pooled Assessment...

A Comprehensive Look at the CECL Model Table of Contents SCOPE... 3 CURRENT EXPECTED CREDIT LOSS MODEL... 3 LOSS PROBABILITIES... 5 MEASUREMENT OF EXPECTED CREDIT LOSSES... 5 Individual Versus Pooled Assessment...

FIN Chapter 14. Cost of Capital. Liuren Wu

FIN 3000 Chapter 14 Cost of Capital Liuren Wu Overview 1. Understand the concepts underlying the firm s overall cost of capital and the purpose of its calculation. 2. Evaluate a firm s capital structure,

FIN 3000 Chapter 14 Cost of Capital Liuren Wu Overview 1. Understand the concepts underlying the firm s overall cost of capital and the purpose of its calculation. 2. Evaluate a firm s capital structure,

20. Investing 4: Understanding Bonds

20. Investing 4: Understanding Bonds Introduction The purpose of an investment portfolio is to help individuals and families meet their financial goals. These goals differ from person to person and change

20. Investing 4: Understanding Bonds Introduction The purpose of an investment portfolio is to help individuals and families meet their financial goals. These goals differ from person to person and change

Securities Analysis 3FB3 February 25 th, 2014

Chapter 2: Financial Markets and Instruments 2.1 The Money Market The money market is a subsector of the fixed income market. It consists of ST debt securities that usually are highly marketable. Many

Chapter 2: Financial Markets and Instruments 2.1 The Money Market The money market is a subsector of the fixed income market. It consists of ST debt securities that usually are highly marketable. Many

Chapter 6. October Chapter Outline. 6.3 Capital Market Securities: Long-Term Debt. 6.5 Difference between Debt and Equity Capital

Chapter 6 Financial Markets, Institutions and Securities October 2003 Chapter Outline 6.1 Financial Markets and Institutions 6.2 The Money Market 6.3 Capital Market Securities: Long-Term Debt 6.4 Capital

Chapter 6 Financial Markets, Institutions and Securities October 2003 Chapter Outline 6.1 Financial Markets and Institutions 6.2 The Money Market 6.3 Capital Market Securities: Long-Term Debt 6.4 Capital

Chapter 5. Interest Rates and Bond Valuation. types. they fluctuate. relationship to bond terms and value. interest rates

Chapter 5 Interest Rates and Bond Valuation } Know the important bond features and bond types } Compute bond values and comprehend why they fluctuate } Appreciate bond ratings, their meaning, and relationship

Chapter 5 Interest Rates and Bond Valuation } Know the important bond features and bond types } Compute bond values and comprehend why they fluctuate } Appreciate bond ratings, their meaning, and relationship

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.notes638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.notes638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed

Debt. Last modified KW

Debt The debt markets are far more complicated and filled with jargon than the equity markets. Fixed coupon bonds, loans and bills will be our focus in this course. It's important to be aware of all of

Debt The debt markets are far more complicated and filled with jargon than the equity markets. Fixed coupon bonds, loans and bills will be our focus in this course. It's important to be aware of all of

MBF1223 Financial Management Prepared by Dr Khairul Anuar

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.mba638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed a

MBF1223 Financial Management Prepared by Dr Khairul Anuar L4 Bonds & Bonds Valuation www.mba638.wordpress.com Bonds - Introduction A bond is a debt instrument issued by a borrower which has borrowed a

Chapter 12. The Bond Market

Chapter 12 The Bond Market Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds are like money market instruments, but they have maturities that exceed one year. These include

Chapter 12 The Bond Market Chapter Preview In this chapter, we focus on longer-term securities: bonds. Bonds are like money market instruments, but they have maturities that exceed one year. These include

Measuring Interest Rates

Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (present discounted value): A dollar paid to you one year from now is less valuable than a dollar paid to you today Why? A

Chapter 4 Understanding Interest Rates Measuring Interest Rates Present Value (present discounted value): A dollar paid to you one year from now is less valuable than a dollar paid to you today Why? A

Powered by TCPDF (www.tcpdf.org) 10.1 Fixed Income Securities Study Session 10 LOS 1 : Introduction (Fixed Income Security) Bonds are the type of long term obligation which pay periodic interest & repay

Powered by TCPDF (www.tcpdf.org) 10.1 Fixed Income Securities Study Session 10 LOS 1 : Introduction (Fixed Income Security) Bonds are the type of long term obligation which pay periodic interest & repay

Chapter 2 Firms and the Financial Market

Chapter 2 Firms and the Financial Market Slide Contents Learning Objectives Principles Used in this Chapter 1.The Basic Structure of the U.S. Financial Markets 2.The Financial Marketplace Financial Institutions

Chapter 2 Firms and the Financial Market Slide Contents Learning Objectives Principles Used in this Chapter 1.The Basic Structure of the U.S. Financial Markets 2.The Financial Marketplace Financial Institutions

VINSCSC2-PTB Summer Street, Boston, MA 02210

Fidelity Variable Insurance Products Asset Manager Portfolio Asset Manager: Growth Portfolio Government Money Market Portfolio Investment Grade Bond Portfolio Strategic Income Portfolio Initial Class,

Fidelity Variable Insurance Products Asset Manager Portfolio Asset Manager: Growth Portfolio Government Money Market Portfolio Investment Grade Bond Portfolio Strategic Income Portfolio Initial Class,

FUNDAMENTALS OF THE BOND MARKET

FUNDAMENTALS OF THE BOND MARKET Bonds are an important component of any balanced portfolio. To most they represent a conservative investment vehicle. However, investors purchase bonds for a variety of

FUNDAMENTALS OF THE BOND MARKET Bonds are an important component of any balanced portfolio. To most they represent a conservative investment vehicle. However, investors purchase bonds for a variety of

Bond Basics QAM Perspectives September 2017

Quadrant s regular newsletter that highlights topics we believe will affect markets or are important in understanding them. Know what you own, and know why you own it. - Peter Lynch (Portfolio Manager,

Quadrant s regular newsletter that highlights topics we believe will affect markets or are important in understanding them. Know what you own, and know why you own it. - Peter Lynch (Portfolio Manager,

Chapter 5. Topics Covered. Debt vs. Equity: Debt. Valuing Stocks

Chapter 5 Valuing Stocks Topics Covered Preferred Stock and Common Stock Properties Valuing Preferred Stocks Valuing Common Stocks - the Dividend Discount Model No growth Constant growth Variable growth

Chapter 5 Valuing Stocks Topics Covered Preferred Stock and Common Stock Properties Valuing Preferred Stocks Valuing Common Stocks - the Dividend Discount Model No growth Constant growth Variable growth

ISS RATHORE INSTITUTE. Strategic Financial Management

1 ISS RATHORE INSTITUTE Strategic Financial Management Solution Booklet By CA. Gaurav Jain 100% Conceptual Coverage Not a Crash Course More than 400 Questions covered in Just 30 Classes Complete Coverage

1 ISS RATHORE INSTITUTE Strategic Financial Management Solution Booklet By CA. Gaurav Jain 100% Conceptual Coverage Not a Crash Course More than 400 Questions covered in Just 30 Classes Complete Coverage

CHAPTER 5 Bonds and Their Valuation

5-1 5-2 CHAPTER 5 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk Key Features of a Bond 1 Par value: Face amount; paid at maturity Assume $1,000 2 Coupon

5-1 5-2 CHAPTER 5 Bonds and Their Valuation Key features of bonds Bond valuation Measuring yield Assessing risk Key Features of a Bond 1 Par value: Face amount; paid at maturity Assume $1,000 2 Coupon

A guide to investing in hybrid securities

A guide to investing in hybrid securities Before you make an investment decision, it is important to review your financial situation, investment objectives, risk tolerance, time horizon, diversification

A guide to investing in hybrid securities Before you make an investment decision, it is important to review your financial situation, investment objectives, risk tolerance, time horizon, diversification