Section 4 The Exchange Rate in the Long Run

|

|

|

- Charlotte O’Neal’

- 6 years ago

- Views:

Transcription

1 Secion 4 he Exchange Rae in he Long Run 1

2 Conen Objecives Purchasing Power Pariy A Long-Run PPP Model he Real Exchange Rae Summary 2

3 Objecives o undersand he law of one price and purchasing power pariy (PPP). o undersand PPP as a heory of long-run exchange rae deerminaion. o undersand he real exchange rae. 3

4 Purchasing Power Pariy he Law of One Price: Idenical goods mus be priced idenically. Commodiy Price Pariy: Goods in differen counries mus sell for he same price, when heir prices are expressed in he same currency. 4

5 Purchasing Power Pariy Commodiy Price Pariy: US k P = S( USD / CAD) P Where P us k is he USD price of commodiy k in he U.S., P kc is he CAD price of commodiy k in Canada, S(USD/CAD) is he price of CAD in USD. C k 5

6 6

7 Purchasing Power Pariy In he real world, CPP may no hold for he following reasons: ransacion Coss: ariffs, ransporaion coss, insurance fees, and oher such coss mean ha i may no be possible o make arbirage profis even in he presence of price differences across counries. Nonraded Goods: Several goods, such as services (haircus) are nonradable. 7

8 Purchasing Power Pariy Quoas: Quoas and oher such barriers o rade resric he abiliy o make arbirage profis. Imperfec Compeiion: Imperfec compeiion in commodiy markes may preven prices from being equalized across counries. For example, price discriminaion, enry coss, and menu coss would preven CPP 8

9 Purchasing Power Pariy In an economy wih many goods, purchasing power is defined in erms of a represenaive bundle of goods. I describes he number of baskes of goods you can buy. he price level is he price of a paricular baske of goods. he mos common price index is he Consumer Price Index (CPI). 9

10 Purchasing Power Pariy Absolue Purchasing Power Pariy: Idenical baskes of goods in differen counries mus sell for he same price, when heir prices are expressed in he same currency. 10

11 Purchasing Power Pariy Absolue Purchasing Power Pariy: US P = S( USD / CAD) P Where P us is he USD price of a baske of goods in he U.S., P c is he CAD price of a baske of goods in Canada, S(USD/CAD) is he price of CAD in USD C 11

12 Purchasing Power Pariy In he real world, Absolue PPP may no hold for he following reasons: Violaions of CPP: Absolue PPP is unlikely o hold if CPP is violaed. ha is, if he individual goods in he represenaive consumpion baske do no saisfy CPP, hen PPP is likely o be violaed. 12

13 Purchasing Power Pariy Differences in Baskes: Absolue PPP will no hold if he composiion of he baskes differs across counries. For example, he presence of non-raded goods would make baskes differen across counries 13

14 Purchasing Power Pariy he Relaive PPP hypohesis saes ha he percenage change in he exchange rae reflecs he difference beween inflaion a home and abroad. Relaive Purchasing Power Pariy: P P US US = S S ( USD / CAD) ( USD / CAD) P P C C 14

15 Purchasing Power Pariy Relaive PPP can also be expressed as: US 1 + π, = [1 + ( S S ) / S ] (1 + π, C ) he linear version of relaive PPP is: π US C, = π, + ( S S ) / S 15

16 Purchasing Power Pariy Where π is he inflaion rae: π, = ( P P ) / P 16

17 Purchasing Power Pariy Relaive PPP saes ha inflaion differences beween counries should be refleced in percenage changes in he exchange rae. For example, if he inflaion rae is 5 % in he US and 2 % in Canada, hen he Canadian dollar should appreciae by 3 %. 17

18 Purchasing Power Pariy If prices in he US are rising faser han in Canada, Canada's expors are becoming relaively cheaper. his should arac imporers, hereby increasing Canadian ne expors and reducing US ne expors. his should generae a relaively higher demand for CAD and promoe an appreciaion of he CAD agains he USD. 18

19 A Long-Run PPP Model he Moneary approach o he exchange rae he Fundamenal Equaion: Price levels and he Demand for Money: P h = M h / L( i h, Y h ) f P = M f / L( i f, Y f ) 19

20 A Long-Run PPP Model Specific predicions from he moneary approach o longrun exchange rae deerminaion: Money supplies An increase in he USD money supply causes a proporional long-run depreciaion of he USD agains foreign currencies. Ineres raes A rise in he ineres rae on USD asses causes a depreciaion of he USD agains foreign currencies. Oupu levels A rise in U.S. oupu causes an appreciaion of he USD agains foreign currencies. 20

21 A Long-Run PPP Model he inernaional ineres rae difference is he difference beween expeced naional inflaion raes. Recall UIP: h f, Recall Relaive PPP: e i = i + ( S S ) /, S π h f e, = π, + ( S S ) / S 21

22 A Long-Run PPP Model So, π eh ef e, = π, + ( S S ) / S And he ineres differenial is: i h i f = π eh π ef,,,, 22

23 A Long-Run PPP Model he Real Ineres Rae: ( 1+ r ) = (1 + i ) /(1 + π,,, ) r = i π e,,, he Fisher Relaion (Real Ineres Pariy): r h = r f,, 23

24 A Long-Run PPP Model A simple numerical example. Assume ha: P = USD 100/Baske, P = USD 101/Baske and i, =0.03 oday, period If I have USD x = USD 100, I can buy 1 baske: B y = USD x / P = (USD 100)/(USD 100/Baske) = B 1 24

25 A Long-Run PPP Model If inves, I ge USD x = USD 103: USD x = (1+ i, ) USD x = (1+0.03)USD 100 = USD 103 If I have USD x = USD 103, I can buy 1.02 baske: B y = USD x / P = USD 103/USD 101/Baske = B 1.02 Inflaion is 1+π, =1.01 (1+π, )=P /P =(USD 101/B)/(USD 100/B) =

26 A Long-Run PPP Model USD rae of reurn is 3 percen: 1+ i, =USD x /USD x = 1.03 Real rae of reurn is 2 percen: (1+r, ) = B y / B y = b1.02/b1 = 1.02 hus, (1+r, ) = (1+ i, ) P /P = (1+ i, )/ (1+π, ) Or r, = i, -π, = =

27 A Long-Run PPP Model he Fisher Effec A rise in a counry s expeced inflaion rae generaes an equal rise in he ineres rae: i, =r, + π e, In he long run, inflaion is a moneary phenomenon: 1+π, = M /M 27

28 A Long-Run PPP Model he Fisher Effec M i i 2 = i 1 + π growh = π + π growh = π i 1 P 0 ime S 0 ime Slope = π + π Slope = π + π Slope = π Slope = π 0 ime 0 ime 28

29 A Long-Run PPP Model Jump in prices: 1+π, = P / P = M M / L( i / L( i,,, Y, Y ) ) Jump in ineres rae for consan also force prices o jump. USD consanly depreciaes and jumps because of absolue PPP. 29

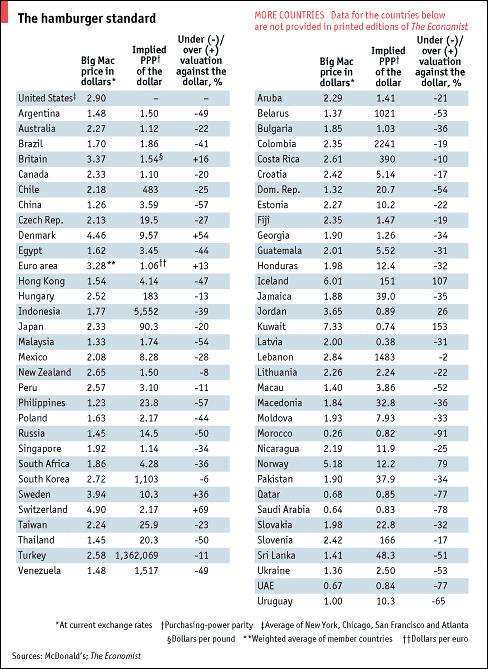

30 he Real Exchange Rae Recen empirical evidence suggess ha PPP does no hold in he shor run. I is a good approximaion for he currencies of counries experiencing hyperinflaion. Prices of idenical goods differ subsanially across counries (he Economis and he Big Mac Index). PPP (or somehing like i) appears o hold in he longrun. ha is, he real exchange rae is rend revering. 30

31 he Real Exchange Rae his empirical evidence also suggess ha domesic and foreign baskes of goods on which price levels are compued are differen across counries. 31

32 he Real Exchange Rae he informaion summarized by PPP may sill be useful o deermine he compeiive posiion of a paricular counry. he Real Exchange Rae summarizes his informaion. he Real Exchange Rae is: Q( US / C) = S( USD / CAD) P US P C 32

33 he Real Exchange Rae he real exchange rae is he relaive price of a foreign baske of goods in erms of a domesic baske of goods. For example, assume ha he price level is CAD 150 per baske of Canadian goods in Canada and USD 100 per baske of US goods in he US. Also assume ha he exchange rae is USD 0.65/CAD. 33

34 he Real Exchange Rae he real exchange rae is hen: USD0.65 / CAD CAD150 / Q( US / C) = US USD100 / B US C Q( US / C) = B / B B C ha is, he Canadian baske is cheaper han he American baske, which suggess ha he American economy is somewha less compeiive han he Canadian economy. Anoher inerpreaion is ha he coss of living are lower in Canada. 34

35 he Real Exchange Rae Real depreciaion of he USD A rise in he real home price of a foreign baske of goods. A rise in he real USD/CAD exchange rae A fall in he purchasing power of a USD in Canada relaive o he purchasing power of he USD in he U.S. 35

36 he Real Exchange Rae he real exchange rae is he relaive price of a foreign baske of goods. In he long run, his relaive price is deermined by he supply and demand for baskes of goods. 36

37 he Real Exchange Rae hese marke forces can be summarized by: An increase in world relaive demand for Canadian goods causes an increase in he price of he Canadian baske of goods and an increase in he real exchange rae. An increase in world relaive supply of Canadian goods causes a reducion in he price of he Canadian baske of goods and a reducion in he real exchange rae. 37

38 he Real Exchange Rae Nominal and Real Exchange Raes he real exchange rae is mean revering. he half life of changes in he real exchange rae is several years long. So, relaive PPP holds in he long-run. he real and nominal exchange raes are highly correlaed. C S( USD / CAD) P Q( US / C) = US P his suggess ha prices are sicky. 38

39 39 he Real Exchange Rae he real exchange rae and real ineres pariy. he relaive version of he real exchange rae is: or US C US C P P P P S S Q Q / / = US C S S S Q Q Q,, ) ( +π π =

40 40 he Real Exchange Rae Uncovered Ineres Pariy Real Exchange Rae: Real Ineres Rae: e C US S S S i i + =,, eus ec e e S S S Q Q Q,, ) ( +π π = e i r,,, π =

41 41 he Real Exchange Rae Real Ineres Pariy (Par II) Uncovered Ineres Pariy e C US Q Q Q r r + =,, e C US S S S i i + =,,

42 he Real Exchange Rae he real ineres pariy condiion saes ha differences in expeced real ineres raes depend on expeced movemens in he real exchange rae. 42

43 he Real Exchange Rae An inerpreaion of real ineres pariy r, = r *, + Q he real ineres rae is a measure or he real reurn o capial. he higher ha reurn, he higher he growh rae of he economy. So, if r>r*, he home economy is growing faser and mus see is compeiiveness improves. ha is, he real exchange rae (he price of a foreign baske of goods) mus rise. e Q Q 43

44 Summary Absolue PPP saes ha he purchasing power of any currency is he same in any counry: Relaive PPP predics ha percenage changes in exchange raes equal differences in naional inflaion π P = S *, = π, + ( he real ineres rae is: P e r, = i, π, * S S ) / S 44

45 Summary he real exchange rae is he price of a foreign * baske of goods: SP Q Real ineres pariy is: P If boh UIP and PPP hold: = r = r *,, If only UIP holds: r US, C = r, + Q e Q Q 45

46 Summary here are sizeable movemens in he real exchange rae. hese movemens are long-lasing, bu no permanen. hus, relaive PPP holds in he long run. he real and nominal exchange raes are highly correlaed. 46

CHAPTER CHAPTER18. Openness in Goods. and Financial Markets. Openness in Goods, and Financial Markets. Openness in Goods,

Openness in Goods and Financial Markes CHAPTER CHAPTER18 Openness in Goods, and Openness has hree disinc dimensions: 1. Openness in goods markes. Free rade resricions include ariffs and quoas. 2. Openness

Openness in Goods and Financial Markes CHAPTER CHAPTER18 Openness in Goods, and Openness has hree disinc dimensions: 1. Openness in goods markes. Free rade resricions include ariffs and quoas. 2. Openness

Final Exam Answers Exchange Rate Economics

Kiel Insiu für Welwirhschaf Advanced Sudies in Inernaional Economic Policy Research Spring 2005 Menzie D. Chinn Final Exam Answers Exchange Rae Economics This exam is 1 ½ hours long. Answer all quesions.

Kiel Insiu für Welwirhschaf Advanced Sudies in Inernaional Economic Policy Research Spring 2005 Menzie D. Chinn Final Exam Answers Exchange Rae Economics This exam is 1 ½ hours long. Answer all quesions.

1. To express the production function in terms of output per worker and capital per worker, divide by N: K f N

THE LOG RU Exercise 8 The Solow Model Suppose an economy is characerized by he aggregae producion funcion / /, where is aggregae oupu, is capial and is employmen. Suppose furher ha aggregae saving is proporional

THE LOG RU Exercise 8 The Solow Model Suppose an economy is characerized by he aggregae producion funcion / /, where is aggregae oupu, is capial and is employmen. Suppose furher ha aggregae saving is proporional

ANSWER ALL QUESTIONS. CHAPTERS 6-9; (Blanchard)

") ANSWER ALL QUESTIONS CHAPTERS 6-9; 18-20 (Blanchard) Quesion 1 Discuss in deail he following: a) The sacrifice raio b) Okun s law c) The neuraliy of money d) Bargaining power e) NAIRU f) Wage indexaion

ANSWER ALL QUESTIONS CHAPTERS 6-9; 18-20 (Blanchard) Quesion 1 Discuss in deail he following: a) The sacrifice raio b) Okun s law c) The neuraliy of money d) Bargaining power e) NAIRU f) Wage indexaion

Spring 2011 Social Sciences 7418 University of Wisconsin-Madison

Economics 32, Sec. 1 Menzie D. Chinn Spring 211 Social Sciences 7418 Universiy of Wisconsin-Madison Noes for Econ 32-1 FALL 21 Miderm 1 Exam The Fall 21 Econ 32-1 course used Hall and Papell, Macroeconomics

Economics 32, Sec. 1 Menzie D. Chinn Spring 211 Social Sciences 7418 Universiy of Wisconsin-Madison Noes for Econ 32-1 FALL 21 Miderm 1 Exam The Fall 21 Econ 32-1 course used Hall and Papell, Macroeconomics

Two ways to we learn the model

Two ways o we learn he model Graphical Inerface: Model Algebra: The equaion you used in your SPREADSHEET. Corresponding equaion in he MODEL. There are four core relaionships in he model: you have already

Two ways o we learn he model Graphical Inerface: Model Algebra: The equaion you used in your SPREADSHEET. Corresponding equaion in he MODEL. There are four core relaionships in he model: you have already

Econ 546 Lecture 4. The Basic New Keynesian Model Michael Devereux January 2011

Econ 546 Lecure 4 The Basic New Keynesian Model Michael Devereux January 20 Road map for his lecure We are evenually going o ge 3 equaions, fully describing he NK model The firs wo are jus he same as before:

Econ 546 Lecure 4 The Basic New Keynesian Model Michael Devereux January 20 Road map for his lecure We are evenually going o ge 3 equaions, fully describing he NK model The firs wo are jus he same as before:

Stylized fact: high cyclical correlation of monetary aggregates and output

SIMPLE DSGE MODELS OF MONEY PART II SEPTEMBER 27, 2011 Inroducion BUSINESS CYCLE IMPLICATIONS OF MONEY Sylized fac: high cyclical correlaion of moneary aggregaes and oupu Convenional Keynesian view: nominal

SIMPLE DSGE MODELS OF MONEY PART II SEPTEMBER 27, 2011 Inroducion BUSINESS CYCLE IMPLICATIONS OF MONEY Sylized fac: high cyclical correlaion of moneary aggregaes and oupu Convenional Keynesian view: nominal

Macroeconomics II A dynamic approach to short run economic fluctuations. The DAD/DAS model.

Macroeconomics II A dynamic approach o shor run economic flucuaions. The DAD/DAS model. Par 2. The demand side of he model he dynamic aggregae demand (DAD) Inflaion and dynamics in he shor run So far,

Macroeconomics II A dynamic approach o shor run economic flucuaions. The DAD/DAS model. Par 2. The demand side of he model he dynamic aggregae demand (DAD) Inflaion and dynamics in he shor run So far,

FINAL EXAM EC26102: MONEY, BANKING AND FINANCIAL MARKETS MAY 11, 2004

FINAL EXAM EC26102: MONEY, BANKING AND FINANCIAL MARKETS MAY 11, 2004 This exam has 50 quesions on 14 pages. Before you begin, please check o make sure ha your copy has all 50 quesions and all 14 pages.

FINAL EXAM EC26102: MONEY, BANKING AND FINANCIAL MARKETS MAY 11, 2004 This exam has 50 quesions on 14 pages. Before you begin, please check o make sure ha your copy has all 50 quesions and all 14 pages.

External balance assessment:

Exernal balance assessmen: Balance of paymens Macroeconomic Analysis Course Banking Training School, Sae Bank of Vienam Marin Fukac 30 Ocober 3 November 2017 Economic policies Consumer prices Economic

Exernal balance assessmen: Balance of paymens Macroeconomic Analysis Course Banking Training School, Sae Bank of Vienam Marin Fukac 30 Ocober 3 November 2017 Economic policies Consumer prices Economic

2. Quantity and price measures in macroeconomic statistics 2.1. Long-run deflation? As typical price indexes, Figure 2-1 depicts the GDP deflator,

1 2. Quaniy and price measures in macroeconomic saisics 2.1. Long-run deflaion? As ypical price indexes, Figure 2-1 depics he GD deflaor, he Consumer rice ndex (C), and he Corporae Goods rice ndex (CG)

1 2. Quaniy and price measures in macroeconomic saisics 2.1. Long-run deflaion? As ypical price indexes, Figure 2-1 depics he GD deflaor, he Consumer rice ndex (C), and he Corporae Goods rice ndex (CG)

Technological progress breakthrough inventions. Dr hab. Joanna Siwińska-Gorzelak

Technological progress breakhrough invenions Dr hab. Joanna Siwińska-Gorzelak Inroducion Afer The Economis : Solow has shown, ha accumulaion of capial alone canno yield lasing progress. Wha can? Anyhing

Technological progress breakhrough invenions Dr hab. Joanna Siwińska-Gorzelak Inroducion Afer The Economis : Solow has shown, ha accumulaion of capial alone canno yield lasing progress. Wha can? Anyhing

International transmission of shocks:

Inernaional ransmission of shocks: A ime-varying FAVAR approach o he Open Economy Philip Liu Haroon Mumaz Moneary Analysis Cener for Cenral Banking Sudies Bank of England Bank of England CEF 9 (Sydney)

Inernaional ransmission of shocks: A ime-varying FAVAR approach o he Open Economy Philip Liu Haroon Mumaz Moneary Analysis Cener for Cenral Banking Sudies Bank of England Bank of England CEF 9 (Sydney)

MA Advanced Macro, 2016 (Karl Whelan) 1

1") MA Advanced Macro, 2016 (Karl Whelan) 1 The Calvo Model of Price Rigidiy The form of price rigidiy faced by he Calvo firm is as follows. Each period, only a random fracion (1 ) of firms are able o rese

MA Advanced Macro, 2016 (Karl Whelan) 1 The Calvo Model of Price Rigidiy The form of price rigidiy faced by he Calvo firm is as follows. Each period, only a random fracion (1 ) of firms are able o rese

Macroeconomics. Part 3 Macroeconomics of Financial Markets. Lecture 8 Investment: basic concepts

Macroeconomics Par 3 Macroeconomics of Financial Markes Lecure 8 Invesmen: basic conceps Moivaion General equilibrium Ramsey and OLG models have very simple assumpions ha invesmen ino producion capial

Macroeconomics Par 3 Macroeconomics of Financial Markes Lecure 8 Invesmen: basic conceps Moivaion General equilibrium Ramsey and OLG models have very simple assumpions ha invesmen ino producion capial

CURRENCY CHOICES IN VALUATION AND THE INTEREST PARITY AND PURCHASING POWER PARITY THEORIES DR. GUILLERMO L. DUMRAUF

CURRENCY CHOICES IN VALUATION AN THE INTEREST PARITY AN PURCHASING POWER PARITY THEORIES R. GUILLERMO L. UMRAUF TO VALUE THE INVESTMENT IN THE OMESTIC OR FOREIGN CURRENCY? Valuing an invesmen or an acquisiion

CURRENCY CHOICES IN VALUATION AN THE INTEREST PARITY AN PURCHASING POWER PARITY THEORIES R. GUILLERMO L. UMRAUF TO VALUE THE INVESTMENT IN THE OMESTIC OR FOREIGN CURRENCY? Valuing an invesmen or an acquisiion

(1 + Nominal Yield) = (1 + Real Yield) (1 + Expected Inflation Rate) (1 + Inflation Risk Premium)

= (1 + Real Yield) (1 + Expected Inflation Rate) (1 + Inflation Risk Premium)") 5. Inflaion-linked bonds Inflaion is an economic erm ha describes he general rise in prices of goods and services. As prices rise, a uni of money can buy less goods and services. Hence, inflaion is an

5. Inflaion-linked bonds Inflaion is an economic erm ha describes he general rise in prices of goods and services. As prices rise, a uni of money can buy less goods and services. Hence, inflaion is an

Balance of Payments. Second quarter 2012

Balance of Paymens Second quarer 2012 Balance of Paymens Second quarer 2012 Saisics Sweden 2012 Balance of Paymens. Second quarer 2012 Saisics Sweden 2012 Producer Saisics Sweden, Balance of Paymens and

Balance of Paymens Second quarer 2012 Balance of Paymens Second quarer 2012 Saisics Sweden 2012 Balance of Paymens. Second quarer 2012 Saisics Sweden 2012 Producer Saisics Sweden, Balance of Paymens and

ECO 301 MACROECONOMIC THEORY UNIVERSITY OF MIAMI DEPARTMENT OF ECONOMICS PRACTICE FINAL EXAM Instructor: Dr. S. Nuray Akin

ECO 301 MACROECONOMIC THEORY UNIVERSITY OF MIAMI DEPARTMENT OF ECONOMICS PRACTICE FINAL EXAM Insrucor: Dr. S. Nuray Akin Name: ID: Insrucions: This exam consiss of 12 pages; please check your examinaion

ECO 301 MACROECONOMIC THEORY UNIVERSITY OF MIAMI DEPARTMENT OF ECONOMICS PRACTICE FINAL EXAM Insrucor: Dr. S. Nuray Akin Name: ID: Insrucions: This exam consiss of 12 pages; please check your examinaion

ECONOMIC GROWTH. Student Assessment. Macroeconomics II. Class 1

Suden Assessmen You will be graded on he basis of In-class aciviies (quizzes worh 30 poins) which can be replaced wih he number of marks from he regular uorial IF i is >=30 (capped a 30, i.e. marks from

Suden Assessmen You will be graded on he basis of In-class aciviies (quizzes worh 30 poins) which can be replaced wih he number of marks from he regular uorial IF i is >=30 (capped a 30, i.e. marks from

Inventory Investment. Investment Decision and Expected Profit. Lecture 5

Invenory Invesmen. Invesmen Decision and Expeced Profi Lecure 5 Invenory Accumulaion 1. Invenory socks 1) Changes in invenory holdings represen an imporan and highly volaile ype of invesmen spending. 2)

Invenory Invesmen. Invesmen Decision and Expeced Profi Lecure 5 Invenory Accumulaion 1. Invenory socks 1) Changes in invenory holdings represen an imporan and highly volaile ype of invesmen spending. 2)

SMALL MENU COSTS AND LARGE BUSINESS CYCLES: AN EXTENSION OF THE MANKIW MODEL

SMALL MENU COSTS AND LARGE BUSINESS CYCLES: AN EXTENSION OF THE MANKIW MODEL 2 Hiranya K. Nah, Sam Houson Sae Universiy Rober Srecher, Sam Houson Sae Universiy ABSTRACT Using a muli-period general equilibrium

SMALL MENU COSTS AND LARGE BUSINESS CYCLES: AN EXTENSION OF THE MANKIW MODEL 2 Hiranya K. Nah, Sam Houson Sae Universiy Rober Srecher, Sam Houson Sae Universiy ABSTRACT Using a muli-period general equilibrium

a. If Y is 1,000, M is 100, and the growth rate of nominal money is 1 percent, what must i and P be?

Problem Se 4 ECN 101 Inermediae Macroeconomics SOLUTIONS Numerical Quesions 1. Assume ha he demand for real money balance (M/P) is M/P = 0.6-100i, where is naional income and i is he nominal ineres rae.

Problem Se 4 ECN 101 Inermediae Macroeconomics SOLUTIONS Numerical Quesions 1. Assume ha he demand for real money balance (M/P) is M/P = 0.6-100i, where is naional income and i is he nominal ineres rae.

Portfolio investments accounted for the largest outflow of SEK 77.5 billion in the financial account, which gave a net outflow of SEK billion.

BALANCE OF PAYMENTS DATE: 27-11-27 PUBLISHER: Saisics Sweden Balance of Paymens and Financial Markes (BFM) Maria Falk +46 8 6 94 72, maria.falk@scb.se Camilla Bergeling +46 8 6 942 6, camilla.bergeling@scb.se

BALANCE OF PAYMENTS DATE: 27-11-27 PUBLISHER: Saisics Sweden Balance of Paymens and Financial Markes (BFM) Maria Falk +46 8 6 94 72, maria.falk@scb.se Camilla Bergeling +46 8 6 942 6, camilla.bergeling@scb.se

Macroeconomics II THE AD-AS MODEL. A Road Map

Macroeconomics II Class 4 THE AD-AS MODEL Class 8 A Road Map THE AD-AS MODEL: MICROFOUNDATIONS 1. Aggregae Supply 1.1 The Long-Run AS Curve 1.2 rice and Wage Sickiness 2.1 Aggregae Demand 2.2 Equilibrium

Macroeconomics II Class 4 THE AD-AS MODEL Class 8 A Road Map THE AD-AS MODEL: MICROFOUNDATIONS 1. Aggregae Supply 1.1 The Long-Run AS Curve 1.2 rice and Wage Sickiness 2.1 Aggregae Demand 2.2 Equilibrium

Revisiting exchange rate puzzles

Revisiing exchange rae puzzles Charles Engel and Feng Zhu Absrac Engel and Zhu (207) revisi a number of major exchange rae puzzles and conduc empirical ess o compare he behaviour of real exchange raes

Revisiing exchange rae puzzles Charles Engel and Feng Zhu Absrac Engel and Zhu (207) revisi a number of major exchange rae puzzles and conduc empirical ess o compare he behaviour of real exchange raes

MONETARY POLICY IN MEXICO. Monetary Policy in Emerging Markets OECD and CCBS/Bank of England February 28, 2007

MONETARY POLICY IN MEXICO Moneary Policy in Emerging Markes OECD and CCBS/Bank of England February 8, 7 Manuel Ramos-Francia Head of Economic Research INDEX I. INTRODUCTION II. MONETARY POLICY STRATEGY

MONETARY POLICY IN MEXICO Moneary Policy in Emerging Markes OECD and CCBS/Bank of England February 8, 7 Manuel Ramos-Francia Head of Economic Research INDEX I. INTRODUCTION II. MONETARY POLICY STRATEGY

OPTIMUM FISCAL AND MONETARY POLICY USING THE MONETARY OVERLAPPING GENERATION MODELS

Kuwai Chaper of Arabian Journal of Business and Managemen Review Vol. 3, No.6; Feb. 2014 OPTIMUM FISCAL AND MONETARY POLICY USING THE MONETARY OVERLAPPING GENERATION MODELS Ayoub Faramarzi 1, Dr.Rahim

Kuwai Chaper of Arabian Journal of Business and Managemen Review Vol. 3, No.6; Feb. 2014 OPTIMUM FISCAL AND MONETARY POLICY USING THE MONETARY OVERLAPPING GENERATION MODELS Ayoub Faramarzi 1, Dr.Rahim

Output: The Demand for Goods and Services

IN CHAPTER 15 how o incorporae dynamics ino he AD-AS model we previously sudied how o use he dynamic AD-AS model o illusrae long-run economic growh how o use he dynamic AD-AS model o race ou he effecs

IN CHAPTER 15 how o incorporae dynamics ino he AD-AS model we previously sudied how o use he dynamic AD-AS model o illusrae long-run economic growh how o use he dynamic AD-AS model o race ou he effecs

The macroeconomic effects of fiscal policy in Greece

The macroeconomic effecs of fiscal policy in Greece Dimiris Papageorgiou Economic Research Deparmen, Bank of Greece Naional and Kapodisrian Universiy of Ahens May 22, 23 Email: dpapag@aueb.gr, and DPapageorgiou@bankofgreece.gr.

The macroeconomic effecs of fiscal policy in Greece Dimiris Papageorgiou Economic Research Deparmen, Bank of Greece Naional and Kapodisrian Universiy of Ahens May 22, 23 Email: dpapag@aueb.gr, and DPapageorgiou@bankofgreece.gr.

Problem 1 / 25 Problem 2 / 25 Problem 3 / 11 Problem 4 / 15 Problem 5 / 24 TOTAL / 100

Deparmen of Economics Universiy of Maryland Economics 35 Inermediae Macroeconomic Analysis Miderm Exam Suggesed Soluions Professor Sanjay Chugh Fall 008 NAME: The Exam has a oal of five (5) problems and

Deparmen of Economics Universiy of Maryland Economics 35 Inermediae Macroeconomic Analysis Miderm Exam Suggesed Soluions Professor Sanjay Chugh Fall 008 NAME: The Exam has a oal of five (5) problems and

The Global Factor in Neutral Policy Rates

The Global acor in Neural Policy Raes Some Implicaions for Exchange Raes Moneary Policy and Policy Coordinaion Richard Clarida Lowell Harriss Professor of Economics Columbia Universiy Global Sraegic Advisor

The Global acor in Neural Policy Raes Some Implicaions for Exchange Raes Moneary Policy and Policy Coordinaion Richard Clarida Lowell Harriss Professor of Economics Columbia Universiy Global Sraegic Advisor

Process of convergence dr Joanna Wolszczak-Derlacz. Lecture 4 and 5 Solow growth model (a)

") Process of convergence dr Joanna Wolszczak-Derlacz ecure 4 and 5 Solow growh model a Solow growh model Rober Solow "A Conribuion o he Theory of Economic Growh." Quarerly Journal of Economics 70 February

Process of convergence dr Joanna Wolszczak-Derlacz ecure 4 and 5 Solow growh model a Solow growh model Rober Solow "A Conribuion o he Theory of Economic Growh." Quarerly Journal of Economics 70 February

The Death of the Phillips Curve?

The Deah of he Phillips Curve? Anhony Murphy Federal Reserve Bank of Dallas Research Deparmen Working Paper 1801 hps://doi.org/10.19/wp1801 The Deah of he Phillips Curve? 1 Anhony Murphy, Federal Reserve

The Deah of he Phillips Curve? Anhony Murphy Federal Reserve Bank of Dallas Research Deparmen Working Paper 1801 hps://doi.org/10.19/wp1801 The Deah of he Phillips Curve? 1 Anhony Murphy, Federal Reserve

Economic Growth Continued: From Solow to Ramsey

Economic Growh Coninued: From Solow o Ramsey J. Bradford DeLong May 2008 Choosing a Naional Savings Rae Wha can we say abou economic policy and long-run growh? To keep maers simple, le us assume ha he

Economic Growh Coninued: From Solow o Ramsey J. Bradford DeLong May 2008 Choosing a Naional Savings Rae Wha can we say abou economic policy and long-run growh? To keep maers simple, le us assume ha he

Economics 301 Fall Name. Answer all questions. Each sub-question is worth 7 points (except 4d).

.") Name Answer all quesions. Each sub-quesion is worh 7 poins (excep 4d). 1. (42 ps) The informaion below describes he curren sae of a growing closed economy. Producion funcion: α 1 Y = K ( Q N ) α Producion

Name Answer all quesions. Each sub-quesion is worh 7 poins (excep 4d). 1. (42 ps) The informaion below describes he curren sae of a growing closed economy. Producion funcion: α 1 Y = K ( Q N ) α Producion

San Francisco State University ECON 560 Summer 2018 Problem set 3 Due Monday, July 23

San Francisco Sae Universiy Michael Bar ECON 56 Summer 28 Problem se 3 Due Monday, July 23 Name Assignmen Rules. Homework assignmens mus be yped. For insrucions on how o ype equaions and mah objecs please

San Francisco Sae Universiy Michael Bar ECON 56 Summer 28 Problem se 3 Due Monday, July 23 Name Assignmen Rules. Homework assignmens mus be yped. For insrucions on how o ype equaions and mah objecs please

Capital Controls and Interest Rate Parity

Capial Conrols and Ineres Rae Pariy Evidences from China, 1999-2004 LIU Li-Gang & Ichiro Oani Recen Discussions on Capial Conrols During and afer he Asian Financial Crises Example. Malaysia Impossible

Capial Conrols and Ineres Rae Pariy Evidences from China, 1999-2004 LIU Li-Gang & Ichiro Oani Recen Discussions on Capial Conrols During and afer he Asian Financial Crises Example. Malaysia Impossible

An enduring question in macroeconomics: does monetary policy have any important effects on the real (i.e, real GDP, consumption, etc) economy?

economy?") ONETARY OLICY IN THE INFINITE-ERIOD ECONOY: SHORT-RUN EFFECTS NOVEBER 6, 20 oneary olicy Analysis: Shor-Run Effecs IS ONETARY OLICY NEUTRAL? An enduring quesion in macroeconomics: does moneary policy have

ONETARY OLICY IN THE INFINITE-ERIOD ECONOY: SHORT-RUN EFFECTS NOVEBER 6, 20 oneary olicy Analysis: Shor-Run Effecs IS ONETARY OLICY NEUTRAL? An enduring quesion in macroeconomics: does moneary policy have

Topic 6: Financial Integration and Interest Rate Parity Part 1: Backround on interest rate parity conditions

Topic 6: Financial Inegraion and Ineres Rae Pariy Par : Backround on ineres rae pariy condiions In his lecure we sudy some puzzles in inernaional financial markes, regarding he relaionship beween ineres

Topic 6: Financial Inegraion and Ineres Rae Pariy Par : Backround on ineres rae pariy condiions In his lecure we sudy some puzzles in inernaional financial markes, regarding he relaionship beween ineres

Balance of Payments. Third quarter 2009

Balance of Paymens Third quarer 2009 Balance of Paymens Third quarer 2009 Saisics Sweden 2009 Balance of Paymens. Third quarer 2009 Saisics Sweden 2009 Producer Saisics Sweden, Balance of Paymens and

Balance of Paymens Third quarer 2009 Balance of Paymens Third quarer 2009 Saisics Sweden 2009 Balance of Paymens. Third quarer 2009 Saisics Sweden 2009 Producer Saisics Sweden, Balance of Paymens and

Lecture 23: Forward Market Bias & the Carry Trade

Lecure 23: Forward Marke Bias & he Carry Trade Moivaions: Efficien markes hypohesis Does raional expecaions hold? Does he forward rae reveal all public informaion? Does Uncovered Ineres Pariy hold? Or

Lecure 23: Forward Marke Bias & he Carry Trade Moivaions: Efficien markes hypohesis Does raional expecaions hold? Does he forward rae reveal all public informaion? Does Uncovered Ineres Pariy hold? Or

Inflation Accounting. Advanced Financial Accounting

Inflaion Accouning Advanced Financial Accouning Inflaion: Definiions Decrease in purchasing power of money due o an increase in he general price level A process of seadily rising prices resuling in diminishing

Inflaion Accouning Advanced Financial Accouning Inflaion: Definiions Decrease in purchasing power of money due o an increase in he general price level A process of seadily rising prices resuling in diminishing

Chapter 12 Fiscal Policy, page 1 of 8

Chaper 12 Fiscal olicy, page 1 of 8 fiscal policy and invesmen: fiscal policy refers o governmen policy regarding revenue and expendiures fiscal policy is under he capial resources secion of he ex because

Chaper 12 Fiscal olicy, page 1 of 8 fiscal policy and invesmen: fiscal policy refers o governmen policy regarding revenue and expendiures fiscal policy is under he capial resources secion of he ex because

How Risky is Electricity Generation?

How Risky is Elecriciy Generaion? Tom Parkinson The NorhBridge Group Inernaional Associaion for Energy Economics New England Chaper 19 January 2005 19 January 2005 The NorhBridge Group Agenda Generaion

How Risky is Elecriciy Generaion? Tom Parkinson The NorhBridge Group Inernaional Associaion for Energy Economics New England Chaper 19 January 2005 19 January 2005 The NorhBridge Group Agenda Generaion

What is Driving Exchange Rates? New Evidence from a Panel of U.S. Dollar Bilateral Exchange Rates

Wha is Driving Exchange Raes? New Evidence from a Panel of U.S. Dollar Bilaeral Exchange Raes Jean-Philippe Cayen Rene Lalonde Don Colei Philipp Maier Bank of Canada The views expressed are he auhors and

Wha is Driving Exchange Raes? New Evidence from a Panel of U.S. Dollar Bilaeral Exchange Raes Jean-Philippe Cayen Rene Lalonde Don Colei Philipp Maier Bank of Canada The views expressed are he auhors and

Macroeconomics. Typical macro questions (I) Typical macro questions (II) Methodology of macroeconomics. Tasks carried out by macroeconomists

Typical macro questions (II) Methodology of macroeconomics. Tasks carried out by macroeconomists") Macroeconomics Macroeconomics is he area of economics ha sudies he overall economic aciviy in a counry or region by means of indicaors of ha aciviy. There is no essenial divide beween micro and macroeconomics,

Macroeconomics Macroeconomics is he area of economics ha sudies he overall economic aciviy in a counry or region by means of indicaors of ha aciviy. There is no essenial divide beween micro and macroeconomics,

The real exchange rate of the rand and competitiveness of South Africa s trade

MPRA Munich Personal RePEc Archive The real exchange rae of he rand and compeiiveness of Souh Africa s rade Elvis Monga Universiy of Cape Town 15. December 26 Online a hp://mpra.ub.uni-muenchen.de/1192/

MPRA Munich Personal RePEc Archive The real exchange rae of he rand and compeiiveness of Souh Africa s rade Elvis Monga Universiy of Cape Town 15. December 26 Online a hp://mpra.ub.uni-muenchen.de/1192/

Non-Traded Goods and Real Exchange Rate Volatility in a Two-Country DSGE Model

Inernaional Journal of Economics and Finance; Vol. 7, No. 2; 205 ISSN 96-97X E-ISSN 96-9728 Published by Canadian Cener of Science and Educaion Non-Traded Goods and Real Exchange Rae Volailiy in a Two-Counry

Inernaional Journal of Economics and Finance; Vol. 7, No. 2; 205 ISSN 96-97X E-ISSN 96-9728 Published by Canadian Cener of Science and Educaion Non-Traded Goods and Real Exchange Rae Volailiy in a Two-Counry

SIMPLE DSGE MODELS OF MONEY DEMAND: PART I OCTOBER 14, 2014

SIMPLE DSGE MODELS OF MONEY DEMAND: PART I OCTOBER 4, 204 Inroducion BASIC ISSUES Money/moneary policy issues an enduring fascinaion in macroeconomics How can/should cenral bank conrol he economy? Should

SIMPLE DSGE MODELS OF MONEY DEMAND: PART I OCTOBER 4, 204 Inroducion BASIC ISSUES Money/moneary policy issues an enduring fascinaion in macroeconomics How can/should cenral bank conrol he economy? Should

DEBT INSTRUMENTS AND MARKETS

DEBT INSTRUMENTS AND MARKETS Zeroes and Coupon Bonds Zeroes and Coupon Bonds Ouline and Suggesed Reading Ouline Zero-coupon bonds Coupon bonds Bond replicaion No-arbirage price relaionships Zero raes Buzzwords

DEBT INSTRUMENTS AND MARKETS Zeroes and Coupon Bonds Zeroes and Coupon Bonds Ouline and Suggesed Reading Ouline Zero-coupon bonds Coupon bonds Bond replicaion No-arbirage price relaionships Zero raes Buzzwords

Money/monetary policy issues an enduring fascination in macroeconomics. How can/should central bank control the economy? Should it/can it at all?

SIMPLE DSGE MODELS OF MONEY PART I SEPTEMBER 22, 211 Inroducion BASIC ISSUES Money/moneary policy issues an enduring fascinaion in macroeconomics How can/should cenral bank conrol he economy? Should i/can

SIMPLE DSGE MODELS OF MONEY PART I SEPTEMBER 22, 211 Inroducion BASIC ISSUES Money/moneary policy issues an enduring fascinaion in macroeconomics How can/should cenral bank conrol he economy? Should i/can

You should turn in (at least) FOUR bluebooks, one (or more, if needed) bluebook(s) for each question.

FOUR bluebooks, one (or more, if needed) bluebook(s) for each question.") UCLA Deparmen of Economics Spring 05 PhD. Qualifying Exam in Macroeconomic Theory Insrucions: This exam consiss of hree pars, and each par is worh 0 poins. Pars and have one quesion each, and Par 3 has

UCLA Deparmen of Economics Spring 05 PhD. Qualifying Exam in Macroeconomic Theory Insrucions: This exam consiss of hree pars, and each par is worh 0 poins. Pars and have one quesion each, and Par 3 has

Discussion of Cook and Devereux: Sharing the Burden: International Policy Cooperation. Gernot Müller

Discussion of Cook and Devereux: Sharing he Burden: Inernaional Policy Cooperaion in a Liquidiy Trap Gerno Müller Universiy of Bonn The paper Quesion: Opimal global policy response o counry specific shock

Discussion of Cook and Devereux: Sharing he Burden: Inernaional Policy Cooperaion in a Liquidiy Trap Gerno Müller Universiy of Bonn The paper Quesion: Opimal global policy response o counry specific shock

ECON Lecture 5 (OB), Sept. 21, 2010

, Sept. 21, 2010") 1 ECON4925 2010 Lecure 5 (OB), Sep. 21, 2010 axaion of exhausible resources Perman e al. (2003), Ch. 15.7. INODUCION he axaion of nonrenewable resources in general and of oil in paricular has generaed

1 ECON4925 2010 Lecure 5 (OB), Sep. 21, 2010 axaion of exhausible resources Perman e al. (2003), Ch. 15.7. INODUCION he axaion of nonrenewable resources in general and of oil in paricular has generaed

Output Growth and Inflation Across Space and Time

Oupu Growh and Inflaion Across Space and Time by Erwin Diewer Universiy of Briish Columbia and Universiy of New Souh Wales and Kevin Fox Universiy of New Souh Wales EMG Workshop 2015 Universiy of New Souh

Oupu Growh and Inflaion Across Space and Time by Erwin Diewer Universiy of Briish Columbia and Universiy of New Souh Wales and Kevin Fox Universiy of New Souh Wales EMG Workshop 2015 Universiy of New Souh

Inflation and globalisation: a modelling perspective

Inflaion and globalisaion: a modelling perspecive Charles Engel 1 Absrac This paper examines some sandard open-economy New Keynesian models o address he quesion of how globalisaion affecs he inflaion process

Inflaion and globalisaion: a modelling perspecive Charles Engel 1 Absrac This paper examines some sandard open-economy New Keynesian models o address he quesion of how globalisaion affecs he inflaion process

Microeconomic Sources of Real Exchange Rate Variability

Microeconomic Sources of Real Exchange Rae Variabiliy By Mario J. Crucini and Chris Telmer Discussed by Moren O. Ravn THE PAPER Crucini and Telmer find ha (a) The cross-secional variance of LOP level violaions

Microeconomic Sources of Real Exchange Rae Variabiliy By Mario J. Crucini and Chris Telmer Discussed by Moren O. Ravn THE PAPER Crucini and Telmer find ha (a) The cross-secional variance of LOP level violaions

Federal Reserve Bank of St. Louis Review, Third Quarter 2015, 97(3), pp

, pp") Moneary Policy in Small Open Economies: The Role of Exchange Rae Rules Ana Maria Sanacreu Undersanding he coss and benefis of alernaive moneary policy rules is imporan for economic welfare. Wihin he conex

Moneary Policy in Small Open Economies: The Role of Exchange Rae Rules Ana Maria Sanacreu Undersanding he coss and benefis of alernaive moneary policy rules is imporan for economic welfare. Wihin he conex

Financial Econometrics (FinMetrics02) Returns, Yields, Compounding, and Horizon

Returns, Yields, Compounding, and Horizon") Financial Economerics FinMerics02) Reurns, Yields, Compounding, and Horizon Nelson Mark Universiy of Nore Dame Fall 2017 Augus 30, 2017 1 Conceps o cover Yields o mauriy) Holding period) reurns Compounding

Financial Economerics FinMerics02) Reurns, Yields, Compounding, and Horizon Nelson Mark Universiy of Nore Dame Fall 2017 Augus 30, 2017 1 Conceps o cover Yields o mauriy) Holding period) reurns Compounding

Chapter 7 Monetary and Exchange Rate Policy in a Small Open Economy

George Alogoskoufis, Inernaional Macroeconomics, 2016 Chaper 7 Moneary and Exchange Rae Policy in a Small Open Economy In his chaper we analyze he effecs of moneary and exchange rae policy in a shor run

George Alogoskoufis, Inernaional Macroeconomics, 2016 Chaper 7 Moneary and Exchange Rae Policy in a Small Open Economy In his chaper we analyze he effecs of moneary and exchange rae policy in a shor run

Origins of currency swaps

Origins of currency swaps Currency swaps originally were developed by banks in he UK o help large cliens circumven UK exchange conrols in he 1970s. UK companies were required o pay an exchange equalizaion

Origins of currency swaps Currency swaps originally were developed by banks in he UK o help large cliens circumven UK exchange conrols in he 1970s. UK companies were required o pay an exchange equalizaion

INSTITUTE OF ACTUARIES OF INDIA

INSIUE OF ACUARIES OF INDIA EAMINAIONS 23 rd May 2011 Subjec S6 Finance and Invesmen B ime allowed: hree hours (9.45* 13.00 Hrs) oal Marks: 100 INSRUCIONS O HE CANDIDAES 1. Please read he insrucions on

INSIUE OF ACUARIES OF INDIA EAMINAIONS 23 rd May 2011 Subjec S6 Finance and Invesmen B ime allowed: hree hours (9.45* 13.00 Hrs) oal Marks: 100 INSRUCIONS O HE CANDIDAES 1. Please read he insrucions on

Cheap Labor Meets Costly Capital: The Impact of Devaluations on Commodity Firms

Cheap Labor Mees Cosly Capial: The Impac of Devaluaions on Commodiy Firms Krisin J. Forbes MIT-Sloan and NBER Augus 5, 200 Absrac: This paper examines how devaluaions affec he relaive cos of labor and

Cheap Labor Mees Cosly Capial: The Impac of Devaluaions on Commodiy Firms Krisin J. Forbes MIT-Sloan and NBER Augus 5, 200 Absrac: This paper examines how devaluaions affec he relaive cos of labor and

An Introduction to PAM Based Project Appraisal

Slide 1 An Inroducion o PAM Based Projec Appraisal Sco Pearson Sanford Universiy Sco Pearson is Professor of Agriculural Economics a he Food Research Insiue, Sanford Universiy. He has paricipaed in projecs

Slide 1 An Inroducion o PAM Based Projec Appraisal Sco Pearson Sanford Universiy Sco Pearson is Professor of Agriculural Economics a he Food Research Insiue, Sanford Universiy. He has paricipaed in projecs

CHAPTER CHAPTER26. Fiscal Policy: A Summing Up. Prepared by: Fernando Quijano and Yvonn Quijano

Fiscal Policy: A Summing Up Prepared by: Fernando Quijano and vonn Quijano CHAPTER CHAPTER26 2006 Prenice Hall usiness Publishing Macroeconomics, 4/e Olivier lanchard Chaper 26: Fiscal Policy: A Summing

Fiscal Policy: A Summing Up Prepared by: Fernando Quijano and vonn Quijano CHAPTER CHAPTER26 2006 Prenice Hall usiness Publishing Macroeconomics, 4/e Olivier lanchard Chaper 26: Fiscal Policy: A Summing

Yield Curve Construction and Medium-Term Hedging in Countries with Underdeveloped Financial Markets

Local ineres rae risk approach Empirical resuls Supplemen Yield Curve Consrucion and Medium-Term Hedging in Counries wih Underdeveloped Financial Markes Model based pricing and valuaion M. Cincibuch 1

Local ineres rae risk approach Empirical resuls Supplemen Yield Curve Consrucion and Medium-Term Hedging in Counries wih Underdeveloped Financial Markes Model based pricing and valuaion M. Cincibuch 1

Do Real Exchange Rate Appreciations Matter for Growth?* by Matthieu Bussière, Claude Lopez and Cédric Tille

Do eal Exchange ae Appreciaions Maer for Growh?* by Mahieu Bussière Claude Lopez and Cédric ille o. 9 Mai 04 Kiel Insiue for he World Economy Kiellinie 66 405 Kiel Germany Kiel Working Paper 9 Mai 04 Do

Do eal Exchange ae Appreciaions Maer for Growh?* by Mahieu Bussière Claude Lopez and Cédric ille o. 9 Mai 04 Kiel Insiue for he World Economy Kiellinie 66 405 Kiel Germany Kiel Working Paper 9 Mai 04 Do

Ch. 10 Measuring FX Exposure. Is Exchange Rate Risk Relevant? MNCs Take on FX Risk

Ch. 10 Measuring FX Exposure Topics Exchange Rae Risk: Relevan? Types of Exposure Transacion Exposure Economic Exposure Translaion Exposure Is Exchange Rae Risk Relevan?? Purchasing Power Pariy: Exchange

Ch. 10 Measuring FX Exposure Topics Exchange Rae Risk: Relevan? Types of Exposure Transacion Exposure Economic Exposure Translaion Exposure Is Exchange Rae Risk Relevan?? Purchasing Power Pariy: Exchange

THE VALIDITY OF PPP THEORY IN SOUTH AFRICA: A COINTEGRATION APPROACH 1

THE VALIDITY OF PPP THEORY IN SOUTH AFRICA: A COINTEGRATION APPROACH 1 Oludele, A. Akinboade & Daniel Makina Universiy Of Souh Africa, P.O. Box 392, Unisa 0003, Preoria ABSTRACT The paper explores he validiy

THE VALIDITY OF PPP THEORY IN SOUTH AFRICA: A COINTEGRATION APPROACH 1 Oludele, A. Akinboade & Daniel Makina Universiy Of Souh Africa, P.O. Box 392, Unisa 0003, Preoria ABSTRACT The paper explores he validiy

Forecasting and Monetary Policy Analysis in Emerging Economies: The case of India (preliminary)

") Forecasing and Moneary Policy Analysis in Emerging Economies: The case of India (preliminary) Rudrani Bhaacharya, Pranav Gupa, Ila Panaik, Rafael Porillo New Delhi 19 h November This presenaion should

Forecasing and Moneary Policy Analysis in Emerging Economies: The case of India (preliminary) Rudrani Bhaacharya, Pranav Gupa, Ila Panaik, Rafael Porillo New Delhi 19 h November This presenaion should

9 NEW KEYNESIAN MODELS OF AGGREGATE DEMAND

Economics 314 Coursebook, 2019 Jeffrey Parker 9 NEW KEYNESIAN MODELS OF AGGREGATE DEMAND Chaper 9 Conens A. Topics and Tools... 2 B. Romer s New Keynesian IS/LM and IS/MP... 3 Uiliy maximizaion... 3 Consumpion

Economics 314 Coursebook, 2019 Jeffrey Parker 9 NEW KEYNESIAN MODELS OF AGGREGATE DEMAND Chaper 9 Conens A. Topics and Tools... 2 B. Romer s New Keynesian IS/LM and IS/MP... 3 Uiliy maximizaion... 3 Consumpion

Empirical analysis on China money multiplier

Aug. 2009, Volume 8, No.8 (Serial No.74) Chinese Business Review, ISSN 1537-1506, USA Empirical analysis on China money muliplier SHANG Hua-juan (Financial School, Shanghai Universiy of Finance and Economics,

Aug. 2009, Volume 8, No.8 (Serial No.74) Chinese Business Review, ISSN 1537-1506, USA Empirical analysis on China money muliplier SHANG Hua-juan (Financial School, Shanghai Universiy of Finance and Economics,

Capital Flows, Institutions, and Financial Fragility

Capial Flows, Insiuions, and Financial Fragiliy By Wipawin Promboon Kenan-Flagler Business School UNC-Chapel Hill February 11, 2009 Model Esimaion Globalizaion Liberalizaion Greaer volume of capial flows:

Capial Flows, Insiuions, and Financial Fragiliy By Wipawin Promboon Kenan-Flagler Business School UNC-Chapel Hill February 11, 2009 Model Esimaion Globalizaion Liberalizaion Greaer volume of capial flows:

Ch. 1 Multinational Financial Mgmt: Overview. International Financial Environment. How Business Disciplines Are Used to Manage the MNC

Ch. Mulinaional Financial Mgm: Overview Topics Goal of he MNC Theories of Inernaional Business Inernaional Business Mehods Inernaional Opporuniies Exposure o Inernaional Risk MNC's Cash Flows & Valuaion

Ch. Mulinaional Financial Mgm: Overview Topics Goal of he MNC Theories of Inernaional Business Inernaional Business Mehods Inernaional Opporuniies Exposure o Inernaional Risk MNC's Cash Flows & Valuaion

Changes in the Terms of Trade and Canada s Productivity Performance Revised April 14, 2008

1 Changes in he Terms of Trade and Canada s Produciviy Performance Revised April 14, 2008 W. Erwin Diewer 1 Discussion Paper 08-05 Deparmen of Economics Universiy of Briish Columbia Vancouver, Canada,

1 Changes in he Terms of Trade and Canada s Produciviy Performance Revised April 14, 2008 W. Erwin Diewer 1 Discussion Paper 08-05 Deparmen of Economics Universiy of Briish Columbia Vancouver, Canada,

A Canadian Business Sector Data Base and New Estimates of Canadian TFP Growth November 24, 2012

1 A Canadian Business Secor Daa Base and New Esimaes of Canadian TFP Growh November 24, 2012 W. Erwin Diewer 1 and Emily Yu, 2 Discussion Paper 12-04, Deparmen of Economics, Universiy of Briish Columbia,

1 A Canadian Business Secor Daa Base and New Esimaes of Canadian TFP Growh November 24, 2012 W. Erwin Diewer 1 and Emily Yu, 2 Discussion Paper 12-04, Deparmen of Economics, Universiy of Briish Columbia,

Appendix B: DETAILS ABOUT THE SIMULATION MODEL. contained in lookup tables that are all calculated on an auxiliary spreadsheet.

Appendix B: DETAILS ABOUT THE SIMULATION MODEL The simulaion model is carried ou on one spreadshee and has five modules, four of which are conained in lookup ables ha are all calculaed on an auxiliary

Appendix B: DETAILS ABOUT THE SIMULATION MODEL The simulaion model is carried ou on one spreadshee and has five modules, four of which are conained in lookup ables ha are all calculaed on an auxiliary

Supplement to Chapter 3

Supplemen o Chaper 3 I. Measuring Real GD and Inflaion If here were only one good in he world, anchovies, hen daa and prices would deermine real oupu and inflaion perfecly: GD Q ; GD Q. + + + Then, he

Supplemen o Chaper 3 I. Measuring Real GD and Inflaion If here were only one good in he world, anchovies, hen daa and prices would deermine real oupu and inflaion perfecly: GD Q ; GD Q. + + + Then, he

*Corresponding author Keywords: CNH, Currency Intervention Index, Central Bank Reaction Function, Exchange Rate Intervention.

016 3rd Inernaional Conference on Advanced Educaion and Managemen (ICAEM 016) ISBN: 978-1-60595-380-9 Exchange Rae Inervenion by Cenral Bank: Based on he Influence of he Hong Kong Offshore RMB Exchange

016 3rd Inernaional Conference on Advanced Educaion and Managemen (ICAEM 016) ISBN: 978-1-60595-380-9 Exchange Rae Inervenion by Cenral Bank: Based on he Influence of he Hong Kong Offshore RMB Exchange

Unemployment and Phillips curve

Unemploymen and Phillips curve 2 of The Naural Rae of Unemploymen and he Phillips Curve Figure 1 Inflaion versus Unemploymen in he Unied Saes, 1900 o 1960 During he period 1900 o 1960 in he Unied Saes,

Unemploymen and Phillips curve 2 of The Naural Rae of Unemploymen and he Phillips Curve Figure 1 Inflaion versus Unemploymen in he Unied Saes, 1900 o 1960 During he period 1900 o 1960 in he Unied Saes,

REPUBLIC OF KENYA MINISTRY OF FINANCE MONTHLY DEBT BULLETIN

REPUBLIC OF KENYA MINISTRY OF FINANCE MONTHLY DEBT BULLETIN MARCH 2012 1.0 PUBLIC DEBT 1.1 Inroducion As a end March 2012, public and publicly guaraneed deb sood a Kshs 1,564.20 billion or 46.9 percen

REPUBLIC OF KENYA MINISTRY OF FINANCE MONTHLY DEBT BULLETIN MARCH 2012 1.0 PUBLIC DEBT 1.1 Inroducion As a end March 2012, public and publicly guaraneed deb sood a Kshs 1,564.20 billion or 46.9 percen

Real Exchange Rate, Competitiveness and Policy Implications: a formal analysis of alternative macro models. Massimiliano La Marca *

Real Exchange Rae, Compeiiveness and Policy Implicaions: a formal analysis of alernaive macro models Massimiliano La Marca * (5/24/04) he paper provides a broad overview on he definiion, deerminaion and

Real Exchange Rae, Compeiiveness and Policy Implicaions: a formal analysis of alernaive macro models Massimiliano La Marca * (5/24/04) he paper provides a broad overview on he definiion, deerminaion and

Beggar-thyself or beggar-thy-neighbour? The welfare e ects of monetary policy

Beggar-hyself or beggar-hy-neighbour? The welfare e ecs of moneary policy Juha Tervala and Philipp Engler February 28, 2 Absrac The paper analyses wheher moneary expansion is a beggar-hyself or beggar-hy-neighbour

Beggar-hyself or beggar-hy-neighbour? The welfare e ecs of moneary policy Juha Tervala and Philipp Engler February 28, 2 Absrac The paper analyses wheher moneary expansion is a beggar-hyself or beggar-hy-neighbour

Composition of Foreign Assets: The. Valuation-Effect and Monetary Policy

Composiion of Foreign Asses: The Valuaion-Effec and Moneary Policy Mahias Hoffmann and Caroline Schmid January 3s 7 Absrac Over he las wo decades, he globalizaion of financial markes has become an imporan

Composiion of Foreign Asses: The Valuaion-Effec and Moneary Policy Mahias Hoffmann and Caroline Schmid January 3s 7 Absrac Over he las wo decades, he globalizaion of financial markes has become an imporan

BUDGET ECONOMIC AND FISCAL POSITION REPORT

BUDGET ECONOMIC AND FISCAL POSITION REPORT - 2004 Issued by he Hon. Miniser of Finance in Terms of Secion 7 of he Fiscal Managemen (Responsibiliy) Ac No. 3 of 1. Inroducion Secion 7 of he Fiscal Managemen

BUDGET ECONOMIC AND FISCAL POSITION REPORT - 2004 Issued by he Hon. Miniser of Finance in Terms of Secion 7 of he Fiscal Managemen (Responsibiliy) Ac No. 3 of 1. Inroducion Secion 7 of he Fiscal Managemen

The U.S. Current Account Deficit and the Expected Share of World Output

FEDERAL RESERVE BANK OF SAN FRANCISCO WORKING PAPER SERIES The U.S. Curren Accoun Defici and he Expeced Share of World Oupu Charles Engel Universiy of Wisconsin and NBER John H. Rogers Board of Governors

FEDERAL RESERVE BANK OF SAN FRANCISCO WORKING PAPER SERIES The U.S. Curren Accoun Defici and he Expeced Share of World Oupu Charles Engel Universiy of Wisconsin and NBER John H. Rogers Board of Governors

South African Reserve Bank Working Paper Series WP/17/01

Souh African Reserve Bank Working Paper Series WP/17/1 The Quarerly Projecion Model of he SARB Byron Boha, Shaun de Jager, Franz Ruch and Rudi Seinbach Auhorised for disribuion by Chris Loewald Sepember

Souh African Reserve Bank Working Paper Series WP/17/1 The Quarerly Projecion Model of he SARB Byron Boha, Shaun de Jager, Franz Ruch and Rudi Seinbach Auhorised for disribuion by Chris Loewald Sepember

Expectations and Exchange Rate Policy

Rober M. La Follee School of Public Affairs a he Universiy of Wisconsin-Madison Working Paper Series La Follee School Working Paper No. 2006-008 hp://www.lafollee.wisc.edu/publicaions/workingpapers Expecaions

Rober M. La Follee School of Public Affairs a he Universiy of Wisconsin-Madison Working Paper Series La Follee School Working Paper No. 2006-008 hp://www.lafollee.wisc.edu/publicaions/workingpapers Expecaions

Multiple Choice Questions Solutions are provided directly when you do the online tests.

SOLUTIONS Muliple Choice Quesions Soluions are provided direcly when you do he online ess. Numerical Quesions 1. Nominal and Real GDP Suppose han an economy consiss of only 2 ypes of producs: compuers

SOLUTIONS Muliple Choice Quesions Soluions are provided direcly when you do he online ess. Numerical Quesions 1. Nominal and Real GDP Suppose han an economy consiss of only 2 ypes of producs: compuers

Nominal Rigidities, Asset Returns and Monetary Policy

Nominal Rigidiies, Asse Reurns and Moneary Policy Erica X.N. Li and Francisco Palomino November 4, 211 Absrac We sudy he asse pricing implicaions of price and wage rigidiies in a quaniaive general equilibrium

Nominal Rigidiies, Asse Reurns and Moneary Policy Erica X.N. Li and Francisco Palomino November 4, 211 Absrac We sudy he asse pricing implicaions of price and wage rigidiies in a quaniaive general equilibrium

Fundamental Basic. Fundamentals. Fundamental PV Principle. Time Value of Money. Fundamental. Chapter 2. How to Calculate Present Values

McGraw-Hill/Irwin Chaper 2 How o Calculae Presen Values Principles of Corporae Finance Tenh Ediion Slides by Mahew Will And Bo Sjö 22 Copyrigh 2 by he McGraw-Hill Companies, Inc. All righs reserved. Fundamenal

McGraw-Hill/Irwin Chaper 2 How o Calculae Presen Values Principles of Corporae Finance Tenh Ediion Slides by Mahew Will And Bo Sjö 22 Copyrigh 2 by he McGraw-Hill Companies, Inc. All righs reserved. Fundamenal

Working Paper No. 421 Global rebalancing: the macroeconomic impact on the United Kingdom

Working Paper No. 421 Global rebalancing: he macroeconomic impac on he Unied Kingdom Alex Haberis, Boan Markovic, Karen Mayhew and Pawel Zabczyk April 2011 Working Paper No. 421 Global rebalancing: he

Working Paper No. 421 Global rebalancing: he macroeconomic impac on he Unied Kingdom Alex Haberis, Boan Markovic, Karen Mayhew and Pawel Zabczyk April 2011 Working Paper No. 421 Global rebalancing: he

CHAPTER 3. REAL EXCHANGE RATE AND COMMODITY EXPORTS PRICES

CHAPTER 3. REAL EXCHANGE RATE AND COMMODITY EXPORTS PRICES 3.1 Inroducion Many sudies ha have been conduced on he behaviour of he real exchange rae in developing counries emphasised he imporance of he

CHAPTER 3. REAL EXCHANGE RATE AND COMMODITY EXPORTS PRICES 3.1 Inroducion Many sudies ha have been conduced on he behaviour of he real exchange rae in developing counries emphasised he imporance of he

NOMINAL RIGIDITIES IN A DSGE MODEL: THE PERSISTENCE PUZZLE OCTOBER 14, 2010 EMPIRICAL EFFECTS OF MONETARY SHOCKS. Empirical Motivation

NOMINAL RIGIDITIES IN A DSGE MODEL: THE PERSISTENCE PUZZLE OCTOBER 4, 200 Empirical Moivaion EMPIRICAL EFFECTS OF MONETARY SHOCKS Hump-shaped responses o moneary shocks (Chrisiano, Eichenbaum, and Evans

NOMINAL RIGIDITIES IN A DSGE MODEL: THE PERSISTENCE PUZZLE OCTOBER 4, 200 Empirical Moivaion EMPIRICAL EFFECTS OF MONETARY SHOCKS Hump-shaped responses o moneary shocks (Chrisiano, Eichenbaum, and Evans

US TFP Growth and the Contribution of Changes in Export and Import Prices to Real Income Growth

US TFP Growh and he Conribuion of Changes in Expor and Impor Prices o Real Income Growh Erwin Diewer (UBC; UNSW) Paper Prepared for he IARIW-UNSW Conference on Produciviy: Measuremen, Drivers and Trends

US TFP Growh and he Conribuion of Changes in Expor and Impor Prices o Real Income Growh Erwin Diewer (UBC; UNSW) Paper Prepared for he IARIW-UNSW Conference on Produciviy: Measuremen, Drivers and Trends

The Simple Analytics of Price Determination

Econ. 511b Spring 1997 C. Sims The Simple Analyics of rice Deerminaion The logic of price deerminaion hrough fiscal policy may be bes appreciaed in an exremely lean model. We include no sochasic elemens,

Econ. 511b Spring 1997 C. Sims The Simple Analyics of rice Deerminaion The logic of price deerminaion hrough fiscal policy may be bes appreciaed in an exremely lean model. We include no sochasic elemens,

Question 1 / 15 Question 2 / 15 Question 3 / 28 Question 4 / 42

Deparmen of Applied Economics Johns Hopkins Universiy Economics 602 Macroeconomic Theory and olicy Final Exam rofessor Sanjay Chugh Fall 2008 December 8, 2008 NAME: The Exam has a oal of four (4) quesions

Deparmen of Applied Economics Johns Hopkins Universiy Economics 602 Macroeconomic Theory and olicy Final Exam rofessor Sanjay Chugh Fall 2008 December 8, 2008 NAME: The Exam has a oal of four (4) quesions

Order Flow in the South: Anatomy of the Brazilian FX Market

Order Flow in he Souh: Anaomy of he Brazilian FX Marke Thomas Y. Wu ;y Ocober 21, 2005 Absrac This paper conribues o he microsrucure approach o he exchange raes research by aking a closer look on he FX

Order Flow in he Souh: Anaomy of he Brazilian FX Marke Thomas Y. Wu ;y Ocober 21, 2005 Absrac This paper conribues o he microsrucure approach o he exchange raes research by aking a closer look on he FX