Risks For The Long Run And The Real Exchange Rate

|

|

|

- Winifred Terry

- 5 years ago

- Views:

Transcription

1 Riccardo Colacito, Mariano M. Croce

2 Overview International Equity Premium Puzzle Model with long-run risks Calibration Exercises Estimation Attempts & Proposed Extensions Discussion

3 International Equity Premium Puzzle Asset returns imply a highly volatile stochastic discount factor governing returns on domestic and foreign currency denominated assets. Currency exchange rates should adjust to adjust to prevent arbitrage opportunities but variance of depreciation rate is low. Implication is a high correlation between stochastic discount factors, but cross-country correlation of consumption is low. Need highly correlated component of consumption growth...

4 International Equity Premium Puzzle Two countries: home (h) and foreign (f) with m i t = log(m i t): E t [exp(m f t+1)r f t+1] = 1 = E t [exp(m h t+1)r h t+1] If the foreign asset is traded in the home country, with exchange rate e t, E t [exp(mt+1)r f t+1] f = 1 = E t [exp(mt+1) h e t+1 R e t+1]. f t If markets are complete: π t+1 = m f t+1 m h t+1 where π t+1 = log(e t+1 /e t ). (Backus, Foresi and Telmer 1996)

5 International Equity Premium Puzzle Var(π t+1 ) = Var(m f t+1 m h t+1) ρ m h,m f = σ2 m h + σ 2 m f σ 2 π 2σ m hσ m f σ 2 m i >.20 from Hansen-Jagannathan bounds σ 2 π Implies that ρ m h,mf >.96 but covariance in consumption is only 27%. In a one county model, consumption growth does not vary enough to explain the excess return over the risk free rate. In a two country model, consumption growth does not co-vary enough to keep track of the movements in the exchange rate.

6 Model: Preferences Two countries (i {h, f }), each with a representative consumer, each with a single county-specific good. Complete home bias- each country derives utility only from its own endowment. Epstein-Zin preferences: Ut i = {(1 δ)(ct i ) 1 γ θ + δ[e t [(U i t+1) 1 γ ]] 1/θ } θ 1 γ δ is discount rate, γ is CRRA, ψ is IES, θ = 1 γ 1 1/ψ

7 Model: Assets E t [M i t+1r i j,t+1] = 1 m i t+1 = log M i t+1 = θ log δ θ ψ ci t+1 + (θ 1) log R i c,t+1 where R i t+1 is the return on the asset that pays dividend stream {C i t }. R i t+1 = v i c,t v i c,t exp c t+1 where vc,t+1 i is the price-consumption ratio in country i. Complete markets: exchange rate adjusts to equalize returns across countries. In equilibrium, autarky in goods and asset holdings. (Not a model of trade.)

8 Model: Consumption Process Consumption follows an exogenous law of motion: c i t = x i t 1 + ɛ i c,t x i t = ρ x x i t 1 + ɛ i x,t Shocks are i.i.d. with correlations governed by Σ: [ɛ h c,tɛ f c,tɛ h x,tɛ f x,t] N(0, Σ) Σ = σ 2 [ Hc 0 0 φ 2 eh x ] [ 1 ρ hf c H c = ρ hf c 1 ] [ 1 ρ hf x H x = ρ hf x 1 ]

9 Model: First-Order Approximations First-order Taylor approximation for price-consumption ratio ( ) vc,t i = vc i (ψ 1) 1 + ψ(1 ρ x δ) x t i Solutions to first-order approximation of model: mt+1 i = log δ 1 ψ x t i + δ 1 1 ψ 1 ρ hf ɛ i x,t+1 + ɛ i c,t+1 x e t+1 = mt+1 f mt+1 h e t r i c,t+1 = r c + 1 ψ x i t + δ 1 1 ψ 1 ρ x δ ɛi x,t+1 + ɛ i c,t+1 r i f,t+1 = r f + 1 ψ x i t where r i f,t+1 is the log risk-free rate and r j is the average log return on asset j.

10 Model: Two Propositions Proposition 1. For a given choice of parameters, and provided that ρ h,f x > ρc h,f, the lowest cross country correlation of the stochastic discount factor is achieved (uniquely) by (ψ, ρ x ) = ( 1 δ, γ 0) where 1 2ρx δ+δ2 δ = δ 2 (1 ρ 2 x ). Proposition 2. For a given choice of parameters, the lowest volatility of the depreciation rate is achieved for ρ hf x = 1.

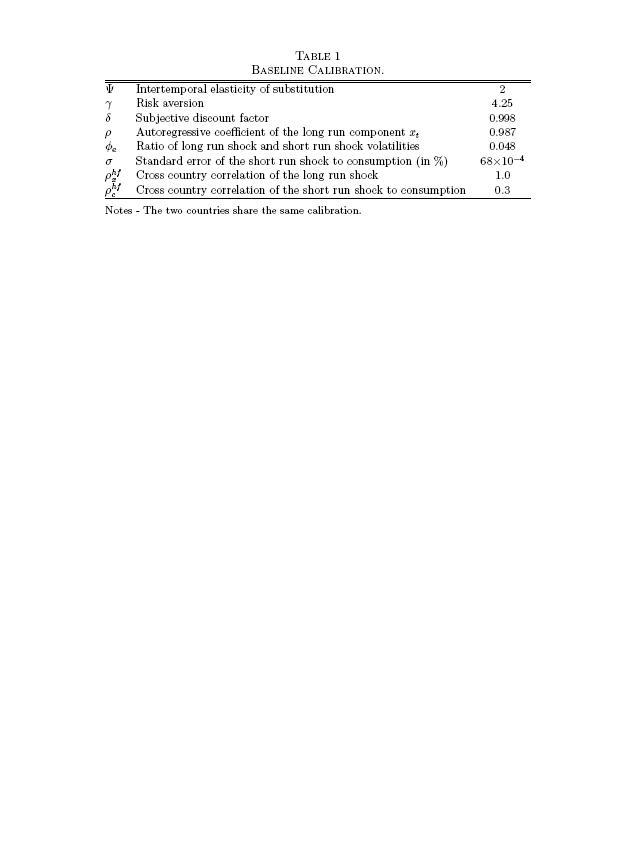

11 Calibration: Baseline

12 Calibration: Varying Paramters

13 Calibration: Matching Other Moments Introduce dividend growth process: d i t = µ d + λx t 1 + ɛ i d,t [ɛ h c,tɛ f c,tɛ h x,tɛ f x,tɛ h d,t ɛf d,t ] N(0, Σ) [ ] [ Σ 0 Σ = 0 σ 2 φ 2 d H H d = σ 2 1 ρ hf d d ρ hf d 1 ]

14 Calibration: Matching other Moments

15 Calibration: Matching other Moments Match most moments fairly well including correlation of excess returns. Correlation of risk-free rate is one: depends only on x i t which are perfectly correlated. Add stochastic volatility: Doesn t change results, correlation of risk-free rate drops to.98

16 Estimation of Long Run Risks Attempts to estimate the persistent component Compare frequency spectra with and without predictable component. Can t distinguish two cases. Use Kalman filter to estimate state-space system. Estimates reasonably close to calibrated values but very large standard errors. Estimate state space system with additional data from Germany and Japan. Doesn t tighten confidence intervals. Simulated Method of Moments estimation with additional moments. Get tighter estimates for consumption laws of motion but not for preference parameters or dividend process.

17 Estimation: MLE Estimates

18 Estimation: Additional Countries

19 Estimation: Additional Moments

20 Extensions Additional factors to match yield curve evidence. Yield curves have sharper features at low frequencies but can t be identified in one-factor model.

21 Extensions Economic interpretations of x t. Include wider set of moments. Relaxing home bias assumption to study traded and non-traded goods.

22 Discussion Paper shows how long run risk can be used to solve international equity premium puzzle. Results are very sensitive to high persistence and high cross-country correlation. Attempt to estimate the model but are unable to properly identify parameters or to provide evidence that the persistent component is present. No discussion of approximation errors.

23 Discussion Is there hope of identifying model? Look at country pairs where would expect less correlation in consumption process. Is there more freedom from the data to lower the correlation? Relax home bias assumption. Implications for bi-lateral trade?

Risks for the Long Run and the Real Exchange Rate

Risks for the Long Run and the Real Exchange Rate Riccardo Colacito - NYU and UNC Kenan-Flagler Mariano M. Croce - NYU Risks for the Long Run and the Real Exchange Rate, UCLA, 2.22.06 p. 1/29 Set the stage

Risks for the Long Run and the Real Exchange Rate Riccardo Colacito - NYU and UNC Kenan-Flagler Mariano M. Croce - NYU Risks for the Long Run and the Real Exchange Rate, UCLA, 2.22.06 p. 1/29 Set the stage

International Asset Pricing and Risk Sharing with Recursive Preferences

p. 1/3 International Asset Pricing and Risk Sharing with Recursive Preferences Riccardo Colacito Prepared for Tom Sargent s PhD class (Part 1) Roadmap p. 2/3 Today International asset pricing (exchange

p. 1/3 International Asset Pricing and Risk Sharing with Recursive Preferences Riccardo Colacito Prepared for Tom Sargent s PhD class (Part 1) Roadmap p. 2/3 Today International asset pricing (exchange

Skewness in Expected Macro Fundamentals and the Predictability of Equity Returns: Evidence and Theory

Skewness in Expected Macro Fundamentals and the Predictability of Equity Returns: Evidence and Theory Ric Colacito, Eric Ghysels, Jinghan Meng, and Wasin Siwasarit 1 / 26 Introduction Long-Run Risks Model:

Skewness in Expected Macro Fundamentals and the Predictability of Equity Returns: Evidence and Theory Ric Colacito, Eric Ghysels, Jinghan Meng, and Wasin Siwasarit 1 / 26 Introduction Long-Run Risks Model:

Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles

: A Potential Resolution of Asset Pricing Puzzles, JF (2004) Presented by: Esben Hedegaard NYUStern October 12, 2009 Outline 1 Introduction 2 The Long-Run Risk Solving the 3 Data and Calibration Results

: A Potential Resolution of Asset Pricing Puzzles, JF (2004) Presented by: Esben Hedegaard NYUStern October 12, 2009 Outline 1 Introduction 2 The Long-Run Risk Solving the 3 Data and Calibration Results

Volatility Risk Pass-Through

Volatility Risk Pass-Through Ric Colacito Max Croce Yang Liu Ivan Shaliastovich 1 / 18 Main Question Uncertainty in a one-country setting: Sizeable impact of volatility risks on growth and asset prices

Volatility Risk Pass-Through Ric Colacito Max Croce Yang Liu Ivan Shaliastovich 1 / 18 Main Question Uncertainty in a one-country setting: Sizeable impact of volatility risks on growth and asset prices

Asset Pricing with Heterogeneous Consumers

, JPE 1996 Presented by: Rustom Irani, NYU Stern November 16, 2009 Outline Introduction 1 Introduction Motivation Contribution 2 Assumptions Equilibrium 3 Mechanism Empirical Implications of Idiosyncratic

, JPE 1996 Presented by: Rustom Irani, NYU Stern November 16, 2009 Outline Introduction 1 Introduction Motivation Contribution 2 Assumptions Equilibrium 3 Mechanism Empirical Implications of Idiosyncratic

International Asset Pricing with Recursive Preferences

International Asset Pricing with Recursive Preferences Riccardo Colacito Mariano M. Croce Abstract Focusing on US and UK, we document that both the Backus and Smith (1993) finding, concerning the low correlation

International Asset Pricing with Recursive Preferences Riccardo Colacito Mariano M. Croce Abstract Focusing on US and UK, we document that both the Backus and Smith (1993) finding, concerning the low correlation

Comprehensive Exam. August 19, 2013

Comprehensive Exam August 19, 2013 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question. Good luck! 1 1 Menu

Comprehensive Exam August 19, 2013 You have a total of 180 minutes to complete the exam. If a question seems ambiguous, state why, sharpen it up and answer the sharpened-up question. Good luck! 1 1 Menu

Currency Risk Factors in a Recursive Multi-Country Economy

Currency Risk Factors in a Recursive Multi-Country Economy R. Colacito M.M. Croce F. Gavazzoni R. Ready NBER SI - International Asset Pricing Boston July 8, 2015 Motivation The literature has identified

Currency Risk Factors in a Recursive Multi-Country Economy R. Colacito M.M. Croce F. Gavazzoni R. Ready NBER SI - International Asset Pricing Boston July 8, 2015 Motivation The literature has identified

Heterogeneous Firm, Financial Market Integration and International Risk Sharing

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Heterogeneous Firm, Financial Market Integration and International Risk Sharing Ming-Jen Chang, Shikuan Chen and Yen-Chen Wu National DongHwa University Thursday 22 nd November 2018 Department of Economics,

Money, Sticky Wages, and the Great Depression

Money, Sticky Wages, and the Great Depression American Economic Review, 2000 Michael D. Bordo 1 Christopher J. Erceg 2 Charles L. Evans 3 1. Rutgers University, Department of Economics 2. Federal Reserve

Money, Sticky Wages, and the Great Depression American Economic Review, 2000 Michael D. Bordo 1 Christopher J. Erceg 2 Charles L. Evans 3 1. Rutgers University, Department of Economics 2. Federal Reserve

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns Leonid Kogan 1 Dimitris Papanikolaou 2 1 MIT and NBER 2 Northwestern University Boston, June 5, 2009 Kogan,

Growth Opportunities, Investment-Specific Technology Shocks and the Cross-Section of Stock Returns Leonid Kogan 1 Dimitris Papanikolaou 2 1 MIT and NBER 2 Northwestern University Boston, June 5, 2009 Kogan,

Consumption and Portfolio Decisions When Expected Returns A

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

Consumption and Portfolio Decisions When Expected Returns Are Time Varying September 10, 2007 Introduction In the recent literature of empirical asset pricing there has been considerable evidence of time-varying

Stock Price, Risk-free Rate and Learning

Stock Price, Risk-free Rate and Learning Tongbin Zhang Univeristat Autonoma de Barcelona and Barcelona GSE April 2016 Tongbin Zhang (Institute) Stock Price, Risk-free Rate and Learning April 2016 1 / 31

Stock Price, Risk-free Rate and Learning Tongbin Zhang Univeristat Autonoma de Barcelona and Barcelona GSE April 2016 Tongbin Zhang (Institute) Stock Price, Risk-free Rate and Learning April 2016 1 / 31

A Long-Run Risks Explanation of Predictability Puzzles in Bond and Currency Markets

A Long-Run Risks Explanation of Predictability Puzzles in Bond and Currency Markets Ravi Bansal Ivan Shaliastovich June 008 Bansal (email: ravi.bansal@duke.edu) is affiliated with the Fuqua School of Business,

A Long-Run Risks Explanation of Predictability Puzzles in Bond and Currency Markets Ravi Bansal Ivan Shaliastovich June 008 Bansal (email: ravi.bansal@duke.edu) is affiliated with the Fuqua School of Business,

Groupe de Travail: International Risk-Sharing and the Transmission of Productivity Shocks

Groupe de Travail: International Risk-Sharing and the Transmission of Productivity Shocks Giancarlo Corsetti Luca Dedola Sylvain Leduc CREST, May 2008 The International Consumption Correlations Puzzle

Groupe de Travail: International Risk-Sharing and the Transmission of Productivity Shocks Giancarlo Corsetti Luca Dedola Sylvain Leduc CREST, May 2008 The International Consumption Correlations Puzzle

Welfare Costs of Long-Run Temperature Shifts

Welfare Costs of Long-Run Temperature Shifts Ravi Bansal Fuqua School of Business Duke University & NBER Durham, NC 27708 Marcelo Ochoa Department of Economics Duke University Durham, NC 27708 October

Welfare Costs of Long-Run Temperature Shifts Ravi Bansal Fuqua School of Business Duke University & NBER Durham, NC 27708 Marcelo Ochoa Department of Economics Duke University Durham, NC 27708 October

Term Premium Dynamics and the Taylor Rule. Bank of Canada Conference on Fixed Income Markets

Term Premium Dynamics and the Taylor Rule Michael Gallmeyer (Texas A&M) Francisco Palomino (Michigan) Burton Hollifield (Carnegie Mellon) Stanley Zin (Carnegie Mellon) Bank of Canada Conference on Fixed

Term Premium Dynamics and the Taylor Rule Michael Gallmeyer (Texas A&M) Francisco Palomino (Michigan) Burton Hollifield (Carnegie Mellon) Stanley Zin (Carnegie Mellon) Bank of Canada Conference on Fixed

Why Surplus Consumption in the Habit Model May be Less Pe. May be Less Persistent than You Think

Why Surplus Consumption in the Habit Model May be Less Persistent than You Think October 19th, 2009 Introduction: Habit Preferences Habit preferences: can generate a higher equity premium for a given curvature

Why Surplus Consumption in the Habit Model May be Less Persistent than You Think October 19th, 2009 Introduction: Habit Preferences Habit preferences: can generate a higher equity premium for a given curvature

A Note on the Economics and Statistics of Predictability: A Long Run Risks Perspective

A Note on the Economics and Statistics of Predictability: A Long Run Risks Perspective Ravi Bansal Dana Kiku Amir Yaron November 14, 2007 Abstract Asset return and cash flow predictability is of considerable

A Note on the Economics and Statistics of Predictability: A Long Run Risks Perspective Ravi Bansal Dana Kiku Amir Yaron November 14, 2007 Abstract Asset return and cash flow predictability is of considerable

Optimal Portfolio Composition for Sovereign Wealth Funds

Optimal Portfolio Composition for Sovereign Wealth Funds Diaa Noureldin* (joint work with Khouzeima Moutanabbir) *Department of Economics The American University in Cairo Oil, Middle East, and the Global

Optimal Portfolio Composition for Sovereign Wealth Funds Diaa Noureldin* (joint work with Khouzeima Moutanabbir) *Department of Economics The American University in Cairo Oil, Middle East, and the Global

Disaster risk and its implications for asset pricing Online appendix

Disaster risk and its implications for asset pricing Online appendix Jerry Tsai University of Oxford Jessica A. Wachter University of Pennsylvania December 12, 2014 and NBER A The iid model This section

Disaster risk and its implications for asset pricing Online appendix Jerry Tsai University of Oxford Jessica A. Wachter University of Pennsylvania December 12, 2014 and NBER A The iid model This section

The Lost Generation of the Great Recession

The Lost Generation of the Great Recession Sewon Hur University of Pittsburgh January 21, 2016 Introduction What are the distributional consequences of the Great Recession? Introduction What are the distributional

The Lost Generation of the Great Recession Sewon Hur University of Pittsburgh January 21, 2016 Introduction What are the distributional consequences of the Great Recession? Introduction What are the distributional

Household income risk, nominal frictions, and incomplete markets 1

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Household income risk, nominal frictions, and incomplete markets 1 2013 North American Summer Meeting Ralph Lütticke 13.06.2013 1 Joint-work with Christian Bayer, Lien Pham, and Volker Tjaden 1 / 30 Research

Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles

THE JOURNAL OF FINANCE VOL. LIX, NO. 4 AUGUST 004 Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles RAVI BANSAL and AMIR YARON ABSTRACT We model consumption and dividend growth rates

THE JOURNAL OF FINANCE VOL. LIX, NO. 4 AUGUST 004 Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles RAVI BANSAL and AMIR YARON ABSTRACT We model consumption and dividend growth rates

Explaining basic asset pricing facts with models that are consistent with basic macroeconomic facts

Aggregate Asset Pricing Explaining basic asset pricing facts with models that are consistent with basic macroeconomic facts Models with quantitative implications Starting point: Mehra and Precott (1985),

Aggregate Asset Pricing Explaining basic asset pricing facts with models that are consistent with basic macroeconomic facts Models with quantitative implications Starting point: Mehra and Precott (1985),

Identifying Long-Run Risks: A Bayesian Mixed-Frequency Approach

Identifying : A Bayesian Mixed-Frequency Approach Frank Schorfheide University of Pennsylvania CEPR and NBER Dongho Song University of Pennsylvania Amir Yaron University of Pennsylvania NBER February 12,

Identifying : A Bayesian Mixed-Frequency Approach Frank Schorfheide University of Pennsylvania CEPR and NBER Dongho Song University of Pennsylvania Amir Yaron University of Pennsylvania NBER February 12,

Asset pricing in the frequency domain: theory and empirics

Asset pricing in the frequency domain: theory and empirics Ian Dew-Becker and Stefano Giglio Duke Fuqua and Chicago Booth 11/27/13 Dew-Becker and Giglio (Duke and Chicago) Frequency-domain asset pricing

Asset pricing in the frequency domain: theory and empirics Ian Dew-Becker and Stefano Giglio Duke Fuqua and Chicago Booth 11/27/13 Dew-Becker and Giglio (Duke and Chicago) Frequency-domain asset pricing

LECTURE NOTES 10 ARIEL M. VIALE

LECTURE NOTES 10 ARIEL M VIALE 1 Behavioral Asset Pricing 11 Prospect theory based asset pricing model Barberis, Huang, and Santos (2001) assume a Lucas pure-exchange economy with three types of assets:

LECTURE NOTES 10 ARIEL M VIALE 1 Behavioral Asset Pricing 11 Prospect theory based asset pricing model Barberis, Huang, and Santos (2001) assume a Lucas pure-exchange economy with three types of assets:

Arbitrage-Free Bond Pricing with Dynamic Macroeconomic Models

Arbitrage-Free Bond Pricing with Dynamic Macroeconomic Models Michael F. Gallmeyer Burton Hollifield Francisco Palomino Stanley E. Zin Revised: February 2007 Abstract We examine the relationship between

Arbitrage-Free Bond Pricing with Dynamic Macroeconomic Models Michael F. Gallmeyer Burton Hollifield Francisco Palomino Stanley E. Zin Revised: February 2007 Abstract We examine the relationship between

The Bond Premium in a DSGE Model with Long-Run Real and Nominal Risks

The Bond Premium in a DSGE Model with Long-Run Real and Nominal Risks Glenn D. Rudebusch Eric T. Swanson Economic Research Federal Reserve Bank of San Francisco Conference on Monetary Policy and Financial

The Bond Premium in a DSGE Model with Long-Run Real and Nominal Risks Glenn D. Rudebusch Eric T. Swanson Economic Research Federal Reserve Bank of San Francisco Conference on Monetary Policy and Financial

Risks For the Long Run: A Potential Resolution of Asset Pricing Puzzles

Risks For the Long Run: A Potential Resolution of Asset Pricing Puzzles Ravi Bansal and Amir Yaron ABSTRACT We model consumption and dividend growth rates as containing (i) a small long-run predictable

Risks For the Long Run: A Potential Resolution of Asset Pricing Puzzles Ravi Bansal and Amir Yaron ABSTRACT We model consumption and dividend growth rates as containing (i) a small long-run predictable

Examining the Bond Premium Puzzle in a DSGE Model

Examining the Bond Premium Puzzle in a DSGE Model Glenn D. Rudebusch Eric T. Swanson Economic Research Federal Reserve Bank of San Francisco John Taylor s Contributions to Monetary Theory and Policy Federal

Examining the Bond Premium Puzzle in a DSGE Model Glenn D. Rudebusch Eric T. Swanson Economic Research Federal Reserve Bank of San Francisco John Taylor s Contributions to Monetary Theory and Policy Federal

Oil Price Uncertainty in a Small Open Economy

Yusuf Soner Başkaya Timur Hülagü Hande Küçük 6 April 212 Oil price volatility is high and it varies over time... 15 1 5 1985 199 1995 2 25 21 (a) Mean.4.35.3.25.2.15.1.5 1985 199 1995 2 25 21 (b) Coefficient

Yusuf Soner Başkaya Timur Hülagü Hande Küçük 6 April 212 Oil price volatility is high and it varies over time... 15 1 5 1985 199 1995 2 25 21 (a) Mean.4.35.3.25.2.15.1.5 1985 199 1995 2 25 21 (b) Coefficient

SOLUTION Fama Bliss and Risk Premiums in the Term Structure

SOLUTION Fama Bliss and Risk Premiums in the Term Structure Question (i EH Regression Results Holding period return year 3 year 4 year 5 year Intercept 0.0009 0.0011 0.0014 0.0015 (std err 0.003 0.0045

SOLUTION Fama Bliss and Risk Premiums in the Term Structure Question (i EH Regression Results Holding period return year 3 year 4 year 5 year Intercept 0.0009 0.0011 0.0014 0.0015 (std err 0.003 0.0045

What Do International Asset Returns Imply About Consumption Risk-Sharing?

What Do International Asset Returns Imply About Consumption Risk-Sharing? (Preliminary and Incomplete) KAREN K. LEWIS EDITH X. LIU June 10, 2009 Abstract An extensive literature has examined the potential

What Do International Asset Returns Imply About Consumption Risk-Sharing? (Preliminary and Incomplete) KAREN K. LEWIS EDITH X. LIU June 10, 2009 Abstract An extensive literature has examined the potential

International Asset Pricing with Risk-Sensitive Agents

International Asset Pricing with Risk-Sensitive Agents Riccardo Colacito Mariano M. Croce Abstract We propose a frictionless general equilibrium model in which two international consumers with recursive

International Asset Pricing with Risk-Sensitive Agents Riccardo Colacito Mariano M. Croce Abstract We propose a frictionless general equilibrium model in which two international consumers with recursive

Financial Integration and Growth in a Risky World

Financial Integration and Growth in a Risky World Nicolas Coeurdacier (SciencesPo & CEPR) Helene Rey (LBS & NBER & CEPR) Pablo Winant (PSE) Barcelona June 2013 Coeurdacier, Rey, Winant Financial Integration...

Financial Integration and Growth in a Risky World Nicolas Coeurdacier (SciencesPo & CEPR) Helene Rey (LBS & NBER & CEPR) Pablo Winant (PSE) Barcelona June 2013 Coeurdacier, Rey, Winant Financial Integration...

Introduction. The Model Setup F.O.Cs Firms Decision. Constant Money Growth. Impulse Response Functions

F.O.Cs s and Phillips Curves Mikhail Golosov and Robert Lucas, JPE 2007 Sharif University of Technology September 20, 2017 A model of monetary economy in which firms are subject to idiosyncratic productivity

F.O.Cs s and Phillips Curves Mikhail Golosov and Robert Lucas, JPE 2007 Sharif University of Technology September 20, 2017 A model of monetary economy in which firms are subject to idiosyncratic productivity

Empirical Test of Affine Stochastic Discount Factor Model of Currency Pricing. Abstract

Empirical Test of Affine Stochastic Discount Factor Model of Currency Pricing Alex Lebedinsky Western Kentucky University Abstract In this note, I conduct an empirical investigation of the affine stochastic

Empirical Test of Affine Stochastic Discount Factor Model of Currency Pricing Alex Lebedinsky Western Kentucky University Abstract In this note, I conduct an empirical investigation of the affine stochastic

Explaining International Business Cycle Synchronization: Recursive Preferences and the Terms of Trade Channel

1 Explaining International Business Cycle Synchronization: Recursive Preferences and the Terms of Trade Channel Robert Kollmann Université Libre de Bruxelles & CEPR World business cycle : High cross-country

1 Explaining International Business Cycle Synchronization: Recursive Preferences and the Terms of Trade Channel Robert Kollmann Université Libre de Bruxelles & CEPR World business cycle : High cross-country

Is asset-pricing pure data-mining? If so, what happened to theory?

Is asset-pricing pure data-mining? If so, what happened to theory? Michael Wickens Cardiff Business School, University of York, CEPR and CESifo Lisbon ICCF 4-8 September 2017 Lisbon ICCF 4-8 September

Is asset-pricing pure data-mining? If so, what happened to theory? Michael Wickens Cardiff Business School, University of York, CEPR and CESifo Lisbon ICCF 4-8 September 2017 Lisbon ICCF 4-8 September

Prospect Theory and Asset Prices

Prospect Theory and Asset Prices Presenting Barberies - Huang - Santos s paper Attila Lindner January 2009 Attila Lindner (CEU) Prospect Theory and Asset Prices January 2009 1 / 17 Presentation Outline

Prospect Theory and Asset Prices Presenting Barberies - Huang - Santos s paper Attila Lindner January 2009 Attila Lindner (CEU) Prospect Theory and Asset Prices January 2009 1 / 17 Presentation Outline

Skewness in Expected Macro Fundamentals and the Predictability of Equity Returns: Evidence and Theory

Skewness in Expected Macro Fundamentals and the Predictability of Equity Returns: Evidence and Theory Riccardo Colacito Eric Ghysels Jinghan Meng Abstract We show that introducing time-varying skewness

Skewness in Expected Macro Fundamentals and the Predictability of Equity Returns: Evidence and Theory Riccardo Colacito Eric Ghysels Jinghan Meng Abstract We show that introducing time-varying skewness

Recursive Allocations and Wealth Distribution with Multiple Goods: Existence, Survivorship, and Dynamics

Recursive Allocations and Wealth Distribution with Multiple Goods: Existence, Survivorship, and Dynamics R. Colacito M. M. Croce Zhao Liu Abstract We characterize the equilibrium of a complete markets

Recursive Allocations and Wealth Distribution with Multiple Goods: Existence, Survivorship, and Dynamics R. Colacito M. M. Croce Zhao Liu Abstract We characterize the equilibrium of a complete markets

International Asset Pricing with Risk Sensitive Rare Events

International Asset Pricing with Risk Sensitive Rare Events Riccardo Colacito Mariano M. Croce Abstract We propose a frictionless general equilibrium model in which two international consumers with recursive

International Asset Pricing with Risk Sensitive Rare Events Riccardo Colacito Mariano M. Croce Abstract We propose a frictionless general equilibrium model in which two international consumers with recursive

Equilibrium Yield Curve, Phillips Correlation, and Monetary Policy

Equilibrium Yield Curve, Phillips Correlation, and Monetary Policy Mitsuru Katagiri International Monetary Fund October 24, 2017 @Keio University 1 / 42 Disclaimer The views expressed here are those of

Equilibrium Yield Curve, Phillips Correlation, and Monetary Policy Mitsuru Katagiri International Monetary Fund October 24, 2017 @Keio University 1 / 42 Disclaimer The views expressed here are those of

The Eurozone Debt Crisis: A New-Keynesian DSGE model with default risk

The Eurozone Debt Crisis: A New-Keynesian DSGE model with default risk Daniel Cohen 1,2 Mathilde Viennot 1 Sébastien Villemot 3 1 Paris School of Economics 2 CEPR 3 OFCE Sciences Po PANORisk workshop 7

The Eurozone Debt Crisis: A New-Keynesian DSGE model with default risk Daniel Cohen 1,2 Mathilde Viennot 1 Sébastien Villemot 3 1 Paris School of Economics 2 CEPR 3 OFCE Sciences Po PANORisk workshop 7

Chapter 5 Macroeconomics and Finance

Macro II Chapter 5 Macro and Finance 1 Chapter 5 Macroeconomics and Finance Main references : - L. Ljundqvist and T. Sargent, Chapter 7 - Mehra and Prescott 1985 JME paper - Jerman 1998 JME paper - J.

Macro II Chapter 5 Macro and Finance 1 Chapter 5 Macroeconomics and Finance Main references : - L. Ljundqvist and T. Sargent, Chapter 7 - Mehra and Prescott 1985 JME paper - Jerman 1998 JME paper - J.

Risk Premia and the Conditional Tails of Stock Returns

Risk Premia and the Conditional Tails of Stock Returns Bryan Kelly NYU Stern and Chicago Booth Outline Introduction An Economic Framework Econometric Methodology Empirical Findings Conclusions Tail Risk

Risk Premia and the Conditional Tails of Stock Returns Bryan Kelly NYU Stern and Chicago Booth Outline Introduction An Economic Framework Econometric Methodology Empirical Findings Conclusions Tail Risk

The Equilibrium Term Structure of Equity and Interest Rates

The Equilibrium Term Structure of Equity and Interest Rates Taeyoung Doh Federal Reserve Bank at Kansas City Shu Wu University of Kansas June 15, 017 Abstract We develop an equilibrium asset pricing model

The Equilibrium Term Structure of Equity and Interest Rates Taeyoung Doh Federal Reserve Bank at Kansas City Shu Wu University of Kansas June 15, 017 Abstract We develop an equilibrium asset pricing model

Long-Run Risk, the Wealth-Consumption Ratio, and the Temporal Pricing of Risk

Long-Run Risk, the Wealth-Consumption Ratio, and the Temporal Pricing of Risk By Ralph S.J. Koijen, Hanno Lustig, Stijn Van Nieuwerburgh and Adrien Verdelhan Representative agent consumption-based asset

Long-Run Risk, the Wealth-Consumption Ratio, and the Temporal Pricing of Risk By Ralph S.J. Koijen, Hanno Lustig, Stijn Van Nieuwerburgh and Adrien Verdelhan Representative agent consumption-based asset

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

Idiosyncratic risk, insurance, and aggregate consumption dynamics: a likelihood perspective Alisdair McKay Boston University June 2013 Microeconomic evidence on insurance - Consumption responds to idiosyncratic

ESSAYS ON ASSET PRICING PUZZLES

ESSAYS ON ASSET PRICING PUZZLES by FEDERICO GAVAZZONI Submitted in Partial Fulfillment of the Requirements for the Degree of DOCTOR OF PHILOSOPHY at the Carnegie Mellon University David A. Tepper School

ESSAYS ON ASSET PRICING PUZZLES by FEDERICO GAVAZZONI Submitted in Partial Fulfillment of the Requirements for the Degree of DOCTOR OF PHILOSOPHY at the Carnegie Mellon University David A. Tepper School

Booms and Busts in Asset Prices. May 2010

Booms and Busts in Asset Prices Klaus Adam Mannheim University & CEPR Albert Marcet London School of Economics & CEPR May 2010 Adam & Marcet ( Mannheim Booms University and Busts & CEPR London School of

Booms and Busts in Asset Prices Klaus Adam Mannheim University & CEPR Albert Marcet London School of Economics & CEPR May 2010 Adam & Marcet ( Mannheim Booms University and Busts & CEPR London School of

Asset Pricing in Production Economies

Urban J. Jermann 1998 Presented By: Farhang Farazmand October 16, 2007 Motivation Can we try to explain the asset pricing puzzles and the macroeconomic business cycles, in one framework. Motivation: Equity

Urban J. Jermann 1998 Presented By: Farhang Farazmand October 16, 2007 Motivation Can we try to explain the asset pricing puzzles and the macroeconomic business cycles, in one framework. Motivation: Equity

Long Run Labor Income Risk

Long Run Labor Income Risk Robert F. Dittmar Francisco Palomino November 00 Department of Finance, Stephen Ross School of Business, University of Michigan, Ann Arbor, MI 4809, email: rdittmar@umich.edu

Long Run Labor Income Risk Robert F. Dittmar Francisco Palomino November 00 Department of Finance, Stephen Ross School of Business, University of Michigan, Ann Arbor, MI 4809, email: rdittmar@umich.edu

NBER WORKING PAPER SERIES INVESTOR INFORMATION, LONG-RUN RISK, AND THE TERM STRUCTURE OF EQUITY. Mariano M. Croce Martin Lettau Sydney C.

NBER WORKING PAPER SERIES INVESTOR INFORMATION, LONG-RUN RISK, AND THE TERM STRUCTURE OF EQUITY Mariano M. Croce Martin Lettau Sydney C. Ludvigson Working Paper 12912 http://www.nber.org/papers/w12912

NBER WORKING PAPER SERIES INVESTOR INFORMATION, LONG-RUN RISK, AND THE TERM STRUCTURE OF EQUITY Mariano M. Croce Martin Lettau Sydney C. Ludvigson Working Paper 12912 http://www.nber.org/papers/w12912

A Structural Explanation of Comovements in Inflation across Developed Countries

A Structural Explanation of Comovements in Inflation across Developed Countries Jesus A Bejarano 4228 TAMU, College Station, TX, 77843, USA Abstract Inflation is highly positively correlated across the

A Structural Explanation of Comovements in Inflation across Developed Countries Jesus A Bejarano 4228 TAMU, College Station, TX, 77843, USA Abstract Inflation is highly positively correlated across the

Chapter 5 Univariate time-series analysis. () Chapter 5 Univariate time-series analysis 1 / 29

Chapter 5 Univariate time-series analysis 1 / 29") Chapter 5 Univariate time-series analysis () Chapter 5 Univariate time-series analysis 1 / 29 Time-Series Time-series is a sequence fx 1, x 2,..., x T g or fx t g, t = 1,..., T, where t is an index denoting

Chapter 5 Univariate time-series analysis () Chapter 5 Univariate time-series analysis 1 / 29 Time-Series Time-series is a sequence fx 1, x 2,..., x T g or fx t g, t = 1,..., T, where t is an index denoting

ASSET PRICING WITH LIMITED RISK SHARING AND HETEROGENOUS AGENTS

ASSET PRICING WITH LIMITED RISK SHARING AND HETEROGENOUS AGENTS Francisco Gomes and Alexander Michaelides Roine Vestman, New York University November 27, 2007 OVERVIEW OF THE PAPER The aim of the paper

ASSET PRICING WITH LIMITED RISK SHARING AND HETEROGENOUS AGENTS Francisco Gomes and Alexander Michaelides Roine Vestman, New York University November 27, 2007 OVERVIEW OF THE PAPER The aim of the paper

Sentiments and Aggregate Fluctuations

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen June 15, 2012 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations June 15, 2012 1 / 59 Introduction We construct

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen June 15, 2012 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations June 15, 2012 1 / 59 Introduction We construct

Long Run Risks and Financial Markets

Long Run Risks and Financial Markets Ravi Bansal December 2006 Bansal (email: ravi.bansal@duke.edu) is affiliated with the Fuqua School of Business, Duke University, Durham, NC 27708. I thank Dana Kiku,

Long Run Risks and Financial Markets Ravi Bansal December 2006 Bansal (email: ravi.bansal@duke.edu) is affiliated with the Fuqua School of Business, Duke University, Durham, NC 27708. I thank Dana Kiku,

Introduction Model Results Conclusion Discussion. The Value Premium. Zhang, JF 2005 Presented by: Rustom Irani, NYU Stern.

, JF 2005 Presented by: Rustom Irani, NYU Stern November 13, 2009 Outline 1 Motivation Production-Based Asset Pricing Framework 2 Assumptions Firm s Problem Equilibrium 3 Main Findings Mechanism Testable

, JF 2005 Presented by: Rustom Irani, NYU Stern November 13, 2009 Outline 1 Motivation Production-Based Asset Pricing Framework 2 Assumptions Firm s Problem Equilibrium 3 Main Findings Mechanism Testable

Frequency of Price Adjustment and Pass-through

Frequency of Price Adjustment and Pass-through Gita Gopinath Harvard and NBER Oleg Itskhoki Harvard CEFIR/NES March 11, 2009 1 / 39 Motivation Micro-level studies document significant heterogeneity in

Frequency of Price Adjustment and Pass-through Gita Gopinath Harvard and NBER Oleg Itskhoki Harvard CEFIR/NES March 11, 2009 1 / 39 Motivation Micro-level studies document significant heterogeneity in

Asset Prices and the Return to Normalcy

Asset Prices and the Return to Normalcy Ole Wilms (University of Zurich) joint work with Walter Pohl and Karl Schmedders (University of Zurich) Economic Applications of Modern Numerical Methods Becker

Asset Prices and the Return to Normalcy Ole Wilms (University of Zurich) joint work with Walter Pohl and Karl Schmedders (University of Zurich) Economic Applications of Modern Numerical Methods Becker

M.I.T Fall Practice Problems

M.I.T. 15.450-Fall 2010 Sloan School of Management Professor Leonid Kogan Practice Problems 1. Consider a 3-period model with t = 0, 1, 2, 3. There are a stock and a risk-free asset. The initial stock

M.I.T. 15.450-Fall 2010 Sloan School of Management Professor Leonid Kogan Practice Problems 1. Consider a 3-period model with t = 0, 1, 2, 3. There are a stock and a risk-free asset. The initial stock

Leisure Preferences, Long-Run Risks, and Human Capital Returns

Leisure Preferences, Long-Run Risks, and Human Capital Returns Robert F. Dittmar Francisco Palomino Wei Yang February 7, 2014 Abstract We analyze the contribution of leisure preferences to a model of long-run

Leisure Preferences, Long-Run Risks, and Human Capital Returns Robert F. Dittmar Francisco Palomino Wei Yang February 7, 2014 Abstract We analyze the contribution of leisure preferences to a model of long-run

Evaluating International Consumption Risk Sharing. Gains: An Asset Return View

Evaluating International Consumption Risk Sharing Gains: An Asset Return View KAREN K. LEWIS EDITH X. LIU October, 2012 Abstract Multi-country consumption risk sharing studies that match the equity premium

Evaluating International Consumption Risk Sharing Gains: An Asset Return View KAREN K. LEWIS EDITH X. LIU October, 2012 Abstract Multi-country consumption risk sharing studies that match the equity premium

RECURSIVE VALUATION AND SENTIMENTS

1 / 32 RECURSIVE VALUATION AND SENTIMENTS Lars Peter Hansen Bendheim Lectures, Princeton University 2 / 32 RECURSIVE VALUATION AND SENTIMENTS ABSTRACT Expectations and uncertainty about growth rates that

1 / 32 RECURSIVE VALUATION AND SENTIMENTS Lars Peter Hansen Bendheim Lectures, Princeton University 2 / 32 RECURSIVE VALUATION AND SENTIMENTS ABSTRACT Expectations and uncertainty about growth rates that

Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles

Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles Ravi Bansal Amir Yaron December 2002 Abstract We model consumption and dividend growth rates as containing (i) a small longrun predictable

Risks for the Long Run: A Potential Resolution of Asset Pricing Puzzles Ravi Bansal Amir Yaron December 2002 Abstract We model consumption and dividend growth rates as containing (i) a small longrun predictable

Online Appendix for Variable Rare Disasters: An Exactly Solved Framework for Ten Puzzles in Macro-Finance. Theory Complements

Online Appendix for Variable Rare Disasters: An Exactly Solved Framework for Ten Puzzles in Macro-Finance Xavier Gabaix November 4 011 This online appendix contains some complements to the paper: extension

Online Appendix for Variable Rare Disasters: An Exactly Solved Framework for Ten Puzzles in Macro-Finance Xavier Gabaix November 4 011 This online appendix contains some complements to the paper: extension

The Life Cycle Model with Recursive Utility: Defined benefit vs defined contribution.

The Life Cycle Model with Recursive Utility: Defined benefit vs defined contribution. Knut K. Aase Norwegian School of Economics 5045 Bergen, Norway IACA/PBSS Colloquium Cancun 2017 June 6-7, 2017 1. Papers

The Life Cycle Model with Recursive Utility: Defined benefit vs defined contribution. Knut K. Aase Norwegian School of Economics 5045 Bergen, Norway IACA/PBSS Colloquium Cancun 2017 June 6-7, 2017 1. Papers

The Shape of the Term Structures

The Shape of the Term Structures Michael Hasler Mariana Khapko November 16, 2018 Abstract Empirical findings show that the term structures of dividend strip risk premium and volatility are downward sloping,

The Shape of the Term Structures Michael Hasler Mariana Khapko November 16, 2018 Abstract Empirical findings show that the term structures of dividend strip risk premium and volatility are downward sloping,

Achieving Actuarial Balance in Social Security: Measuring the Welfare Effects on Individuals

Achieving Actuarial Balance in Social Security: Measuring the Welfare Effects on Individuals Selahattin İmrohoroğlu 1 Shinichi Nishiyama 2 1 University of Southern California (selo@marshall.usc.edu) 2

Achieving Actuarial Balance in Social Security: Measuring the Welfare Effects on Individuals Selahattin İmrohoroğlu 1 Shinichi Nishiyama 2 1 University of Southern California (selo@marshall.usc.edu) 2

Term Premium Dynamics and the Taylor Rule 1

Term Premium Dynamics and the Taylor Rule 1 Michael Gallmeyer 2 Burton Hollifield 3 Francisco Palomino 4 Stanley Zin 5 September 2, 2008 1 Preliminary and incomplete. This paper was previously titled Bond

Term Premium Dynamics and the Taylor Rule 1 Michael Gallmeyer 2 Burton Hollifield 3 Francisco Palomino 4 Stanley Zin 5 September 2, 2008 1 Preliminary and incomplete. This paper was previously titled Bond

Sentiments and Aggregate Fluctuations

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen March 15, 2013 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations March 15, 2013 1 / 60 Introduction The

Sentiments and Aggregate Fluctuations Jess Benhabib Pengfei Wang Yi Wen March 15, 2013 Jess Benhabib Pengfei Wang Yi Wen () Sentiments and Aggregate Fluctuations March 15, 2013 1 / 60 Introduction The

Endogenous Trade Participation with Incomplete Exchange Rate Pass-Through

Endogenous Trade Participation with Incomplete Exchange Rate Pass-Through Yuko Imura Bank of Canada June 28, 23 Disclaimer The views expressed in this presentation, or in my remarks, are my own, and do

Endogenous Trade Participation with Incomplete Exchange Rate Pass-Through Yuko Imura Bank of Canada June 28, 23 Disclaimer The views expressed in this presentation, or in my remarks, are my own, and do

Optimal monetary policy when asset markets are incomplete

Optimal monetary policy when asset markets are incomplete R. Anton Braun Tomoyuki Nakajima 2 University of Tokyo, and CREI 2 Kyoto University, and RIETI December 9, 28 Outline Introduction 2 Model Individuals

Optimal monetary policy when asset markets are incomplete R. Anton Braun Tomoyuki Nakajima 2 University of Tokyo, and CREI 2 Kyoto University, and RIETI December 9, 28 Outline Introduction 2 Model Individuals

A Long-Run Risks Model of Asset Pricing with Fat Tails

Florida International University FIU Digital Commons Economics Research Working Paper Series Department of Economics 11-26-2008 A Long-Run Risks Model of Asset Pricing with Fat Tails Zhiguang (Gerald)

Florida International University FIU Digital Commons Economics Research Working Paper Series Department of Economics 11-26-2008 A Long-Run Risks Model of Asset Pricing with Fat Tails Zhiguang (Gerald)

Entry, Trade Costs and International Business Cycles

Entry, Trade Costs and International Business Cycles Roberto Fattal and Jose Lopez UCLA SED Meetings July 10th 2010 Entry, Trade Costs and International Business Cycles SED Meetings July 10th 2010 1 /

Entry, Trade Costs and International Business Cycles Roberto Fattal and Jose Lopez UCLA SED Meetings July 10th 2010 Entry, Trade Costs and International Business Cycles SED Meetings July 10th 2010 1 /

CEO Attributes, Compensation, and Firm Value: Evidence from a Structural Estimation. Internet Appendix

CEO Attributes, Compensation, and Firm Value: Evidence from a Structural Estimation Internet Appendix A. Participation constraint In evaluating when the participation constraint binds, we consider three

CEO Attributes, Compensation, and Firm Value: Evidence from a Structural Estimation Internet Appendix A. Participation constraint In evaluating when the participation constraint binds, we consider three

Household Debt, Financial Intermediation, and Monetary Policy

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

Household Debt, Financial Intermediation, and Monetary Policy Shutao Cao 1 Yahong Zhang 2 1 Bank of Canada 2 Western University October 21, 2014 Motivation The US experience suggests that the collapse

Reviewing Income and Wealth Heterogeneity, Portfolio Choice and Equilibrium Asset Returns by P. Krussell and A. Smith, JPE 1997

Reviewing Income and Wealth Heterogeneity, Portfolio Choice and Equilibrium Asset Returns by P. Krussell and A. Smith, JPE 1997 Seminar in Asset Pricing Theory Presented by Saki Bigio November 2007 1 /

Reviewing Income and Wealth Heterogeneity, Portfolio Choice and Equilibrium Asset Returns by P. Krussell and A. Smith, JPE 1997 Seminar in Asset Pricing Theory Presented by Saki Bigio November 2007 1 /

Is the Value Premium a Puzzle?

Is the Value Premium a Puzzle? Job Market Paper Dana Kiku Current Draft: January 17, 2006 Abstract This paper provides an economic explanation of the value premium puzzle, differences in price/dividend

Is the Value Premium a Puzzle? Job Market Paper Dana Kiku Current Draft: January 17, 2006 Abstract This paper provides an economic explanation of the value premium puzzle, differences in price/dividend

Implementing an Agent-Based General Equilibrium Model

Implementing an Agent-Based General Equilibrium Model 1 2 3 Pure Exchange General Equilibrium We shall take N dividend processes δ n (t) as exogenous with a distribution which is known to all agents There

Implementing an Agent-Based General Equilibrium Model 1 2 3 Pure Exchange General Equilibrium We shall take N dividend processes δ n (t) as exogenous with a distribution which is known to all agents There

Macroeconomics Sequence, Block I. Introduction to Consumption Asset Pricing

Macroeconomics Sequence, Block I Introduction to Consumption Asset Pricing Nicola Pavoni October 21, 2016 The Lucas Tree Model This is a general equilibrium model where instead of deriving properties of

Macroeconomics Sequence, Block I Introduction to Consumption Asset Pricing Nicola Pavoni October 21, 2016 The Lucas Tree Model This is a general equilibrium model where instead of deriving properties of

Bank Capital Requirements: A Quantitative Analysis

Bank Capital Requirements: A Quantitative Analysis Thiên T. Nguyễn Introduction Motivation Motivation Key regulatory reform: Bank capital requirements 1 Introduction Motivation Motivation Key regulatory

Bank Capital Requirements: A Quantitative Analysis Thiên T. Nguyễn Introduction Motivation Motivation Key regulatory reform: Bank capital requirements 1 Introduction Motivation Motivation Key regulatory

Supplementary online material to Information tradeoffs in dynamic financial markets

Supplementary online material to Information tradeoffs in dynamic financial markets Efstathios Avdis University of Alberta, Canada 1. The value of information in continuous time In this document I address

Supplementary online material to Information tradeoffs in dynamic financial markets Efstathios Avdis University of Alberta, Canada 1. The value of information in continuous time In this document I address

Behavioral Theories of the Business Cycle

Behavioral Theories of the Business Cycle Nir Jaimovich and Sergio Rebelo September 2006 Abstract We explore the business cycle implications of expectation shocks and of two well-known psychological biases,

Behavioral Theories of the Business Cycle Nir Jaimovich and Sergio Rebelo September 2006 Abstract We explore the business cycle implications of expectation shocks and of two well-known psychological biases,

Long-Run Productivity Risk: A New Hope for Production-Based Asset Pricing

Long-Run Productivity Risk: A New Hope for Production-Based Asset Pricing Mariano Massimiliano Croce Abstract This study examines the intertemporal distribution of productivity risk. Focusing on post-war

Long-Run Productivity Risk: A New Hope for Production-Based Asset Pricing Mariano Massimiliano Croce Abstract This study examines the intertemporal distribution of productivity risk. Focusing on post-war

Collateral Constraints and Multiplicity

Collateral Constraints and Multiplicity Pengfei Wang New York University April 17, 2013 Pengfei Wang (New York University) Collateral Constraints and Multiplicity April 17, 2013 1 / 44 Introduction Firms

Collateral Constraints and Multiplicity Pengfei Wang New York University April 17, 2013 Pengfei Wang (New York University) Collateral Constraints and Multiplicity April 17, 2013 1 / 44 Introduction Firms

Understanding Tail Risk 1

Understanding Tail Risk 1 Laura Veldkamp New York University 1 Based on work with Nic Kozeniauskas, Julian Kozlowski, Anna Orlik and Venky Venkateswaran. 1/2 2/2 Why Study Information Frictions? Every

Understanding Tail Risk 1 Laura Veldkamp New York University 1 Based on work with Nic Kozeniauskas, Julian Kozlowski, Anna Orlik and Venky Venkateswaran. 1/2 2/2 Why Study Information Frictions? Every

Volatility Risk Pass-Through

Volatility Risk Pass-Through R. Colacito, M. M. Croce, Y. Liu, I. Shaliastovich Abstract We show novel empirical evidence on the significance of output volatility (vol) shocks for both currency and international

Volatility Risk Pass-Through R. Colacito, M. M. Croce, Y. Liu, I. Shaliastovich Abstract We show novel empirical evidence on the significance of output volatility (vol) shocks for both currency and international

Asset Pricing with Left-Skewed Long-Run Risk in. Durable Consumption

Asset Pricing with Left-Skewed Long-Run Risk in Durable Consumption Wei Yang 1 This draft: October 2009 1 William E. Simon Graduate School of Business Administration, University of Rochester, Rochester,

Asset Pricing with Left-Skewed Long-Run Risk in Durable Consumption Wei Yang 1 This draft: October 2009 1 William E. Simon Graduate School of Business Administration, University of Rochester, Rochester,

Pierre Collin-Dufresne, Michael Johannes and Lars Lochstoer Parameter Learning in General Equilibrium The Asset Pricing Implications

Pierre Collin-Dufresne, Michael Johannes and Lars Lochstoer Parameter Learning in General Equilibrium The Asset Pricing Implications DP 05/2012-039 Parameter Learning in General Equilibrium: The Asset

Pierre Collin-Dufresne, Michael Johannes and Lars Lochstoer Parameter Learning in General Equilibrium The Asset Pricing Implications DP 05/2012-039 Parameter Learning in General Equilibrium: The Asset

Bond Market Exposures to Macroeconomic and Monetary Policy Risks

Carnegie Mellon University Research Showcase @ CMU Society for Economic Measurement Annual Conference 15 Paris Jul 4th, 9:3 AM - 11:3 AM Bond Market Exposures to Macroeconomic and Monetary Policy Risks

Carnegie Mellon University Research Showcase @ CMU Society for Economic Measurement Annual Conference 15 Paris Jul 4th, 9:3 AM - 11:3 AM Bond Market Exposures to Macroeconomic and Monetary Policy Risks

The Costs of Losing Monetary Independence: The Case of Mexico

The Costs of Losing Monetary Independence: The Case of Mexico Thomas F. Cooley New York University Vincenzo Quadrini Duke University and CEPR May 2, 2000 Abstract This paper develops a two-country monetary

The Costs of Losing Monetary Independence: The Case of Mexico Thomas F. Cooley New York University Vincenzo Quadrini Duke University and CEPR May 2, 2000 Abstract This paper develops a two-country monetary

A Unified Theory of Bond and Currency Markets

A Unified Theory of Bond and Currency Markets Andrey Ermolov Columbia Business School April 24, 2014 1 / 41 Stylized Facts about Bond Markets US Fact 1: Upward Sloping Real Yield Curve In US, real long

A Unified Theory of Bond and Currency Markets Andrey Ermolov Columbia Business School April 24, 2014 1 / 41 Stylized Facts about Bond Markets US Fact 1: Upward Sloping Real Yield Curve In US, real long

1 Explaining Labor Market Volatility

Christiano Economics 416 Advanced Macroeconomics Take home midterm exam. 1 Explaining Labor Market Volatility The purpose of this question is to explore a labor market puzzle that has bedeviled business

Christiano Economics 416 Advanced Macroeconomics Take home midterm exam. 1 Explaining Labor Market Volatility The purpose of this question is to explore a labor market puzzle that has bedeviled business