The Black-Scholes-Merton Model

|

|

|

- Dominick Chapman

- 5 years ago

- Views:

Transcription

and this was reposted on Monday, February 18 at 9:45 AM.")

1 Normal (Gaussian) Distribution Probability Density ? Cumulative Probability Slide 13 in this slide set was corrected (d 1 was set up wrong, although the solution was correct) and this was reposted on Monday, February 18 at 9:45 AM. The Black-Scholes-Merton Model... pricing options and calculating some Greeks 019 Gary R. Evans. This slide set by Gary R. Evans is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International License.

2 Conceptually calculating what a 110 OTM call option should be worth if the present price of the stock is (1) We know how to calculate the probability that the price will be above 100. () What, though, will be the value of that domain?... in 16 days

dr Negative values 1.")

3 Remembering from our homework... Standard normal density function The cumulative distribution is integrating from left to right π = We did this integration and subtracted it from 1! If SS = ln P str Psto σ d π SS itm = 1-4 (SNDF) dr Negative values Positive values

4 ... and knowing this will come in handy when we look at Black-Scholes-Merton: This has a negative value when done this way (for an OTM option).. π = If SS = ln P sto Pstr σ d BSM does this integration for the same problem! then π itm = SS 4 (SNDF) dr

5 How Black-Scholes-Merton works... The Black-Scholes-Merton model is used to price European options (which assumes that they must be held to expiration) and related custom derivatives. It takes into account that you have the option of investing in an asset earning the risk-free interest rate. It acknowledges that the option price is purely a function of the volatility of the stock's price (the higher the volatility the higher the premium on the option). Black-Scholes-Merton treats a call option as a forward contract to deliver stock at a contractual price, which is, of course, the strike price.

6 The Essence of the Black-Scholes Approach Only volatility matters, the mu (drift) is not important. The option's premium will suffer from time decay as we approach expiration (Theta in the European model). The stock's underlying volatility contributes to the option's premium (Vega). The sensitivity of the option to a change in the stock's value (Delta) and the rate of that sensitivity (Gamma) is important [these variables are represented mathematically in the Black-Scholes DE]. Option values arise from arbitrage opportunities in a world where you have a risk-free choice.

7 The BSM Model: European Options C SN( d ) Ke N( d ) 1 r t 365 C = theoretical call value S = current stock price N = standard normal probability distribution integrated to point d x. t = days until expiration K = option strike price r = risk free interest rate daily stock volatility d d 1 ln ln d d t 1 S K r 365 t S K r 365 t t t Note: Hull's version (13.0) uses annual volatility. Note the difference.

8 Breaking this down... C SN( d ) Ke N( d ) 1 r t 365 This term discounts the price of the stock at which you will have the right to buy it (the strike price) back to its present value using the risk-free interest rate. Let's assume in the next slide that r = 0. d 1 ln S K r 365 t t Dividing by this term (the standard deviation of stock's daily volatility adjusted for time) turns the distribution into a standard normal distribution with a standard deviation of 1.

9 ... or simplifying it some (r is zero) This is the absolute log growth spread between the strike price and the stock price. We are calculating the cumulative probability to this standard normal point. CP d 1 SP ln d STR SP STR 1 d This normalizes it to standard normal (the numerator is now number of standard deviations. ).... assume that r is 0 and t is 1: μ is zero so this is the log-normal zero mean adjustment

10 What role is being played by half variance?? Let s look at this simplified where we have a call at the money exactly, with these assumptions, assuming r = 0: 1.. d 1 = ln Sto Str + σ t ln = 0 σ t Stock price = 100 Strike price = Sigma = 0.00 days = d 1 = σ t σ t 4. d 1 = σ t

11 In this example, we are pricing a call that is expiring in 16 days. The price of the stock is $100 and the call strike price is $100. Because BSM does not allow drift, the expected value of the stock in 16 days is $100. If you own this call, you have the right to buy the stock for $100 in 16 days, no matter what the price. Why does this have any value at all?

12 σ t + σ t σ t This spread is what gives the ATM option value... and it is equal to the duration-volatility adjusted random draw.

13 An example (back to the full model)... Consider an otm option with 16 days to expiration. The strike price is 110 and the price of the stock is 100 and the stock has an daily volatility of 0.0. Assume an interest rate of 0.01 (1% annual). The set-up for d1 was incorrect in the original slide posted.. this is correct and consistent with the Jupyter Notebook black_scholes_merton_logical.ipynb d 1 = ln 100/ = d = d = 1.59 C = 100csnd e csnd 1.59 =

14 Using the BSM Model There are variations of the Black-Scholes model that prices for dividend payments (within the option period). See Hull section 13.1 to see how that is done (easy to understand). However, because of what is said below, you really can't use BSM to estimate values of options for dividend-paying American stocks There is no easy estimator for American options prices, but as Hull points out in chapter 9 section 9.5, with the exception of exercising a call option just prior to an exdividend date, "it is never optimal to exercise an American call option on a nondividend paying stock before the expiration date." The BSM model can be used to estimate "implied volatility". To do this, however, given an actual option value, you have to iterate to find the volatility solution (see Hull's discussion of this in 13.1). This procedure is easy to program and not very timeconsuming in even an Excel version of the model. For those of you interest in another elegant implied volatility model, see Hull's discussion of the IVF model in 6.3. There you will see a role played by delta and vega, but again you would have to iterate to get the value of the sensitivity of the call to the strike price.

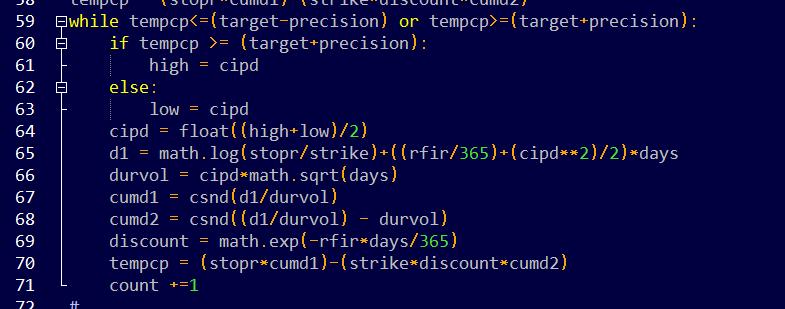

15 Doing this in Python for a Call

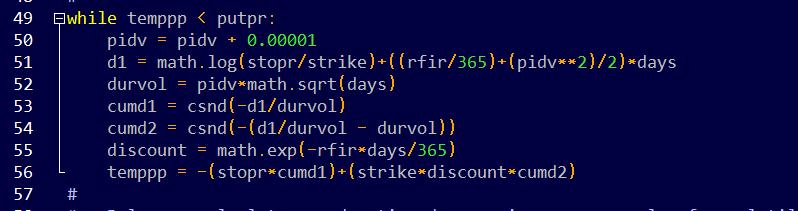

16 Doing this in Python for a Put.. a couple of important sign changes.

17 Calculating implied volatility with B/S: d 1 ln SP STR Very easy to do: Once Black-Scholes is structured, you can use an iterative technique to solve for σ. Name: Date: Gary R. Evans October 7, 011 Put Option Implicit Daily Volatility (IDV) Calculator Stock Symbol: DIA Price: Month: Dec Put Strike: Price: 3.50 Expiration date: 1/17/011 Interest rate: Days to maturity today: Days to maturity override: Implied daily volatility: One-day time decay: Version 3.4 Aug 16, Calculate

18 Notational differences: Call Put

Market Volatility and Risk Proxies

Market Volatility and Risk Proxies... an introduction to the concepts 019 Gary R. Evans. This slide set by Gary R. Evans is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International

Market Volatility and Risk Proxies... an introduction to the concepts 019 Gary R. Evans. This slide set by Gary R. Evans is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International

Chapter 9 - Mechanics of Options Markets

Chapter 9 - Mechanics of Options Markets Types of options Option positions and profit/loss diagrams Underlying assets Specifications Trading options Margins Taxation Warrants, employee stock options, and

Chapter 9 - Mechanics of Options Markets Types of options Option positions and profit/loss diagrams Underlying assets Specifications Trading options Margins Taxation Warrants, employee stock options, and

Mathematics of Finance Final Preparation December 19. To be thoroughly prepared for the final exam, you should

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

P&L Attribution and Risk Management

P&L Attribution and Risk Management Liuren Wu Options Markets (Hull chapter: 15, Greek letters) Liuren Wu ( c ) P& Attribution and Risk Management Options Markets 1 / 19 Outline 1 P&L attribution via the

P&L Attribution and Risk Management Liuren Wu Options Markets (Hull chapter: 15, Greek letters) Liuren Wu ( c ) P& Attribution and Risk Management Options Markets 1 / 19 Outline 1 P&L attribution via the

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane.

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 20 Lecture 20 Implied volatility November 30, 2017

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 20 Lecture 20 Implied volatility November 30, 2017

Greek Maxima 1 by Michael B. Miller

Greek Maxima by Michael B. Miller When managing the risk of options it is often useful to know how sensitivities will change over time and with the price of the underlying. For example, many people know

Greek Maxima by Michael B. Miller When managing the risk of options it is often useful to know how sensitivities will change over time and with the price of the underlying. For example, many people know

FIN FINANCIAL INSTRUMENTS SPRING 2008

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

FIN-40008 FINANCIAL INSTRUMENTS SPRING 2008 The Greeks Introduction We have studied how to price an option using the Black-Scholes formula. Now we wish to consider how the option price changes, either

How to Trade Options Using VantagePoint and Trade Management

How to Trade Options Using VantagePoint and Trade Management Course 3.2 + 3.3 Copyright 2016 Market Technologies, LLC. 1 Option Basics Part I Agenda Option Basics and Lingo Call and Put Attributes Profit

How to Trade Options Using VantagePoint and Trade Management Course 3.2 + 3.3 Copyright 2016 Market Technologies, LLC. 1 Option Basics Part I Agenda Option Basics and Lingo Call and Put Attributes Profit

Simple Formulas to Option Pricing and Hedging in the Black-Scholes Model

Simple Formulas to Option Pricing and Hedging in the Black-Scholes Model Paolo PIANCA DEPARTMENT OF APPLIED MATHEMATICS University Ca Foscari of Venice pianca@unive.it http://caronte.dma.unive.it/ pianca/

Simple Formulas to Option Pricing and Hedging in the Black-Scholes Model Paolo PIANCA DEPARTMENT OF APPLIED MATHEMATICS University Ca Foscari of Venice pianca@unive.it http://caronte.dma.unive.it/ pianca/

Financial Markets & Risk

Financial Markets & Risk Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Session 3 Derivatives Binomial

Financial Markets & Risk Dr Cesario MATEUS Senior Lecturer in Finance and Banking Room QA259 Department of Accounting and Finance c.mateus@greenwich.ac.uk www.cesariomateus.com Session 3 Derivatives Binomial

Lecture Quantitative Finance Spring Term 2015

and Lecture Quantitative Finance Spring Term 2015 Prof. Dr. Erich Walter Farkas Lecture 06: March 26, 2015 1 / 47 Remember and Previous chapters: introduction to the theory of options put-call parity fundamentals

and Lecture Quantitative Finance Spring Term 2015 Prof. Dr. Erich Walter Farkas Lecture 06: March 26, 2015 1 / 47 Remember and Previous chapters: introduction to the theory of options put-call parity fundamentals

TEACHING NOTE 98-04: EXCHANGE OPTION PRICING

TEACHING NOTE 98-04: EXCHANGE OPTION PRICING Version date: June 3, 017 C:\CLASSES\TEACHING NOTES\TN98-04.WPD The exchange option, first developed by Margrabe (1978), has proven to be an extremely powerful

TEACHING NOTE 98-04: EXCHANGE OPTION PRICING Version date: June 3, 017 C:\CLASSES\TEACHING NOTES\TN98-04.WPD The exchange option, first developed by Margrabe (1978), has proven to be an extremely powerful

Trading Options for Potential Income in a Volatile Market

Trading Options for Potential Income in a Volatile Market Dan Sheridan Sheridan Mentoring & Brian Overby TradeKing TradeKing is a member of FINRA & SIPC Disclaimer Options involve risks and are not suitable

Trading Options for Potential Income in a Volatile Market Dan Sheridan Sheridan Mentoring & Brian Overby TradeKing TradeKing is a member of FINRA & SIPC Disclaimer Options involve risks and are not suitable

Option Selection With Bill Corcoran

Presents Option Selection With Bill Corcoran I am not a registered broker-dealer or investment adviser. I will mention that I consider certain securities or positions to be good candidates for the types

Presents Option Selection With Bill Corcoran I am not a registered broker-dealer or investment adviser. I will mention that I consider certain securities or positions to be good candidates for the types

Option Trading and Positioning Professor Bodurtha

1 Option Trading and Positioning Pooya Tavana Option Trading and Positioning Professor Bodurtha 5/7/2011 Pooya Tavana 2 Option Trading and Positioning Pooya Tavana I. Executive Summary Financial options

1 Option Trading and Positioning Pooya Tavana Option Trading and Positioning Professor Bodurtha 5/7/2011 Pooya Tavana 2 Option Trading and Positioning Pooya Tavana I. Executive Summary Financial options

Read chapter 9 and review lecture 9ab from Econ 104 if you don t remember this stuff.

Here is your teacher waiting for Steve Wynn to come on down so I could explain index options to him. He never showed so I guess that t he will have to download this lecture and figure it out like everyone

Here is your teacher waiting for Steve Wynn to come on down so I could explain index options to him. He never showed so I guess that t he will have to download this lecture and figure it out like everyone

Fin 4200 Project. Jessi Sagner 11/15/11

Fin 4200 Project Jessi Sagner 11/15/11 All Option information is outlined in appendix A Option Strategy The strategy I chose was to go long 1 call and 1 put at the same strike price, but different times

Fin 4200 Project Jessi Sagner 11/15/11 All Option information is outlined in appendix A Option Strategy The strategy I chose was to go long 1 call and 1 put at the same strike price, but different times

Monte Carlo Simulations

Is Uncle Norm's shot going to exhibit a Weiner Process? Knowing Uncle Norm, probably, with a random drift and huge volatility. Monte Carlo Simulations... of stock prices the primary model 2019 Gary R.

Is Uncle Norm's shot going to exhibit a Weiner Process? Knowing Uncle Norm, probably, with a random drift and huge volatility. Monte Carlo Simulations... of stock prices the primary model 2019 Gary R.

The Greek Letters Based on Options, Futures, and Other Derivatives, 8th Edition, Copyright John C. Hull 2012

The Greek Letters Based on Options, Futures, and Other Derivatives, 8th Edition, Copyright John C. Hull 2012 Introduction Each of the Greek letters measures a different dimension to the risk in an option

The Greek Letters Based on Options, Futures, and Other Derivatives, 8th Edition, Copyright John C. Hull 2012 Introduction Each of the Greek letters measures a different dimension to the risk in an option

Evaluating Options Price Sensitivities

Evaluating Options Price Sensitivities Options Pricing Presented by Patrick Ceresna, CMT CIM DMS Montréal Exchange Instructor Disclaimer 2016 Bourse de Montréal Inc. This document is sent to you on a general

Evaluating Options Price Sensitivities Options Pricing Presented by Patrick Ceresna, CMT CIM DMS Montréal Exchange Instructor Disclaimer 2016 Bourse de Montréal Inc. This document is sent to you on a general

FINANCIAL MATHEMATICS WITH ADVANCED TOPICS MTHE7013A

UNIVERSITY OF EAST ANGLIA School of Mathematics Main Series UG Examination 2016 17 FINANCIAL MATHEMATICS WITH ADVANCED TOPICS MTHE7013A Time allowed: 3 Hours Attempt QUESTIONS 1 and 2, and THREE other

UNIVERSITY OF EAST ANGLIA School of Mathematics Main Series UG Examination 2016 17 FINANCIAL MATHEMATICS WITH ADVANCED TOPICS MTHE7013A Time allowed: 3 Hours Attempt QUESTIONS 1 and 2, and THREE other

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane.

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 9 Lecture 9 9.1 The Greeks November 15, 2017 Let

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 2017 9 Lecture 9 9.1 The Greeks November 15, 2017 Let

Completeness and Hedging. Tomas Björk

IV Completeness and Hedging Tomas Björk 1 Problems around Standard Black-Scholes We assumed that the derivative was traded. How do we price OTC products? Why is the option price independent of the expected

IV Completeness and Hedging Tomas Björk 1 Problems around Standard Black-Scholes We assumed that the derivative was traded. How do we price OTC products? Why is the option price independent of the expected

Merton s Jump Diffusion Model. David Bonnemort, Yunhye Chu, Cory Steffen, Carl Tams

Merton s Jump Diffusion Model David Bonnemort, Yunhye Chu, Cory Steffen, Carl Tams Outline Background The Problem Research Summary & future direction Background Terms Option: (Call/Put) is a derivative

Merton s Jump Diffusion Model David Bonnemort, Yunhye Chu, Cory Steffen, Carl Tams Outline Background The Problem Research Summary & future direction Background Terms Option: (Call/Put) is a derivative

Risk Neutral Valuation, the Black-

Risk Neutral Valuation, the Black- Scholes Model and Monte Carlo Stephen M Schaefer London Business School Credit Risk Elective Summer 01 C = SN( d )-PV( X ) N( ) N he Black-Scholes formula 1 d (.) : cumulative

Risk Neutral Valuation, the Black- Scholes Model and Monte Carlo Stephen M Schaefer London Business School Credit Risk Elective Summer 01 C = SN( d )-PV( X ) N( ) N he Black-Scholes formula 1 d (.) : cumulative

Derivative Securities Fall 2012 Final Exam Guidance Extended version includes full semester

Derivative Securities Fall 2012 Final Exam Guidance Extended version includes full semester Our exam is Wednesday, December 19, at the normal class place and time. You may bring two sheets of notes (8.5

Derivative Securities Fall 2012 Final Exam Guidance Extended version includes full semester Our exam is Wednesday, December 19, at the normal class place and time. You may bring two sheets of notes (8.5

2 f. f t S 2. Delta measures the sensitivityof the portfolio value to changes in the price of the underlying

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

Sensitivity analysis Simulating the Greeks Meet the Greeks he value of a derivative on a single underlying asset depends upon the current asset price S and its volatility Σ, the risk-free interest rate

MATH 476/567 ACTUARIAL RISK THEORY FALL 2016 PROFESSOR WANG. Homework 3 Solution

MAH 476/567 ACUARIAL RISK HEORY FALL 2016 PROFESSOR WANG Homework 3 Solution 1. Consider a call option on an a nondividend paying stock. Suppose that for = 0.4 the option is trading for $33 an option.

MAH 476/567 ACUARIAL RISK HEORY FALL 2016 PROFESSOR WANG Homework 3 Solution 1. Consider a call option on an a nondividend paying stock. Suppose that for = 0.4 the option is trading for $33 an option.

Attempt QUESTIONS 1 and 2, and THREE other questions. Do not turn over until you are told to do so by the Invigilator.

UNIVERSITY OF EAST ANGLIA School of Mathematics Main Series UG Examination 2016 17 FINANCIAL MATHEMATICS MTHE6026A Time allowed: 3 Hours Attempt QUESTIONS 1 and 2, and THREE other questions. Notes are

UNIVERSITY OF EAST ANGLIA School of Mathematics Main Series UG Examination 2016 17 FINANCIAL MATHEMATICS MTHE6026A Time allowed: 3 Hours Attempt QUESTIONS 1 and 2, and THREE other questions. Notes are

Options Markets: Introduction

17-2 Options Options Markets: Introduction Derivatives are securities that get their value from the price of other securities. Derivatives are contingent claims because their payoffs depend on the value

17-2 Options Options Markets: Introduction Derivatives are securities that get their value from the price of other securities. Derivatives are contingent claims because their payoffs depend on the value

... especially dynamic volatility

More about volatility...... especially dynamic volatility Add a little wind and we get a little increase in volatility. Add a hurricane and we get a huge increase in volatility. (c) 2017, Gary R. Evans

More about volatility...... especially dynamic volatility Add a little wind and we get a little increase in volatility. Add a hurricane and we get a huge increase in volatility. (c) 2017, Gary R. Evans

Lecture 6: Option Pricing Using a One-step Binomial Tree. Thursday, September 12, 13

Lecture 6: Option Pricing Using a One-step Binomial Tree An over-simplified model with surprisingly general extensions a single time step from 0 to T two types of traded securities: stock S and a bond

Lecture 6: Option Pricing Using a One-step Binomial Tree An over-simplified model with surprisingly general extensions a single time step from 0 to T two types of traded securities: stock S and a bond

Trading Options for Potential Income in a Volatile Market

Trading Options for Potential Income in a Volatile Market Dan Sheridan Sheridan Mentoring & Brian Overby TradeKing TradeKing is a member of FINRA & SIPC October 19 & 20, 2011 Disclaimer Options involve

Trading Options for Potential Income in a Volatile Market Dan Sheridan Sheridan Mentoring & Brian Overby TradeKing TradeKing is a member of FINRA & SIPC October 19 & 20, 2011 Disclaimer Options involve

A Brief Analysis of Option Implied Volatility and Strategies. Zhou Heng. University of Adelaide, Adelaide, Australia

Economics World, July-Aug. 2018, Vol. 6, No. 4, 331-336 doi: 10.17265/2328-7144/2018.04.009 D DAVID PUBLISHING A Brief Analysis of Option Implied Volatility and Strategies Zhou Heng University of Adelaide,

Economics World, July-Aug. 2018, Vol. 6, No. 4, 331-336 doi: 10.17265/2328-7144/2018.04.009 D DAVID PUBLISHING A Brief Analysis of Option Implied Volatility and Strategies Zhou Heng University of Adelaide,

... possibly the most important and least understood topic in finance

Correlation...... possibly the most important and least understood topic in finance 2017 Gary R. Evans. This lecture is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International

Correlation...... possibly the most important and least understood topic in finance 2017 Gary R. Evans. This lecture is licensed under a Creative Commons Attribution-NonCommercial-ShareAlike 4.0 International

Financial Risk Management

Financial Risk Management Professor: Thierry Roncalli Evry University Assistant: Enareta Kurtbegu Evry University Tutorial exercices #3 1 Maximum likelihood of the exponential distribution 1. We assume

Financial Risk Management Professor: Thierry Roncalli Evry University Assistant: Enareta Kurtbegu Evry University Tutorial exercices #3 1 Maximum likelihood of the exponential distribution 1. We assume

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 2017 Instructor: Dr. Sateesh Mane.

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 217 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 217 13 Lecture 13 November 15, 217 Derivation of the Black-Scholes-Merton

Queens College, CUNY, Department of Computer Science Computational Finance CSCI 365 / 765 Fall 217 Instructor: Dr. Sateesh Mane c Sateesh R. Mane 217 13 Lecture 13 November 15, 217 Derivation of the Black-Scholes-Merton

UCLA Anderson School of Management Daniel Andrei, Derivative Markets MGMTMFE 406, Winter MFE Final Exam. March Date:

UCLA Anderson School of Management Daniel Andrei, Derivative Markets MGMTMFE 406, Winter 2018 MFE Final Exam March 2018 Date: Your Name: Your email address: Your Signature: 1 This exam is open book, open

UCLA Anderson School of Management Daniel Andrei, Derivative Markets MGMTMFE 406, Winter 2018 MFE Final Exam March 2018 Date: Your Name: Your email address: Your Signature: 1 This exam is open book, open

CHAPTER 10 OPTION PRICING - II. Derivatives and Risk Management By Rajiv Srivastava. Copyright Oxford University Press

CHAPTER 10 OPTION PRICING - II Options Pricing II Intrinsic Value and Time Value Boundary Conditions for Option Pricing Arbitrage Based Relationship for Option Pricing Put Call Parity 2 Binomial Option

CHAPTER 10 OPTION PRICING - II Options Pricing II Intrinsic Value and Time Value Boundary Conditions for Option Pricing Arbitrage Based Relationship for Option Pricing Put Call Parity 2 Binomial Option

Trading Volatility Using Options: a French Case

Trading Volatility Using Options: a French Case Introduction Volatility is a key feature of financial markets. It is commonly used as a measure for risk and is a common an indicator of the investors fear

Trading Volatility Using Options: a French Case Introduction Volatility is a key feature of financial markets. It is commonly used as a measure for risk and is a common an indicator of the investors fear

The Black-Scholes Model

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

The Black-Scholes Model Liuren Wu Options Markets (Hull chapter: 12, 13, 14) Liuren Wu ( c ) The Black-Scholes Model colorhmoptions Markets 1 / 17 The Black-Scholes-Merton (BSM) model Black and Scholes

Market risk measurement in practice

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: October 23, 2018 2/32 Outline Nonlinearity in market risk Market

Lecture notes on risk management, public policy, and the financial system Allan M. Malz Columbia University 2018 Allan M. Malz Last updated: October 23, 2018 2/32 Outline Nonlinearity in market risk Market

TradeOptionsWithMe.com

TradeOptionsWithMe.com 1 of 18 Option Trading Glossary This is the Glossary for important option trading terms. Some of these terms are rather easy and used extremely often, but some may even be new to

TradeOptionsWithMe.com 1 of 18 Option Trading Glossary This is the Glossary for important option trading terms. Some of these terms are rather easy and used extremely often, but some may even be new to

Math 239 Homework 1 solutions

Math 239 Homework 1 solutions Question 1. Delta hedging simulation. (a) Means, standard deviations and histograms are found using HW1Q1a.m with 100,000 paths. In the case of weekly rebalancing: mean =

Math 239 Homework 1 solutions Question 1. Delta hedging simulation. (a) Means, standard deviations and histograms are found using HW1Q1a.m with 100,000 paths. In the case of weekly rebalancing: mean =

Manage Complex Option Portfolios: Simplifying Option Greeks Part II

Manage Complex Option Portfolios: Simplifying Option Greeks Part II Monday, 11 th September 7:30 PM IST 2:00 PM GMT 10:00 AM EST A Pioneer Algo Trading Training Institute Streamlined Investment Management

Manage Complex Option Portfolios: Simplifying Option Greeks Part II Monday, 11 th September 7:30 PM IST 2:00 PM GMT 10:00 AM EST A Pioneer Algo Trading Training Institute Streamlined Investment Management

Introduction to Financial Derivatives

55.444 Introduction to Financial Derivatives Weeks of November 18 & 5 th, 13 he Black-Scholes-Merton Model for Options plus Applications 11.1 Where we are Last Week: Modeling the Stochastic Process for

55.444 Introduction to Financial Derivatives Weeks of November 18 & 5 th, 13 he Black-Scholes-Merton Model for Options plus Applications 11.1 Where we are Last Week: Modeling the Stochastic Process for

last problem outlines how the Black Scholes PDE (and its derivation) may be modified to account for the payment of stock dividends.

may be modified to account for the payment of stock dividends.") 224 10 Arbitrage and SDEs last problem outlines how the Black Scholes PDE (and its derivation) may be modified to account for the payment of stock dividends. 10.1 (Calculation of Delta First and Finest

224 10 Arbitrage and SDEs last problem outlines how the Black Scholes PDE (and its derivation) may be modified to account for the payment of stock dividends. 10.1 (Calculation of Delta First and Finest

Hedging with Options

School of Education, Culture and Communication Tutor: Jan Röman Hedging with Options (MMA707) Authors: Chiamruchikun Benchaphon 800530-49 Klongprateepphol Chutima 80708-67 Pongpala Apiwat 808-4975 Suntayodom

School of Education, Culture and Communication Tutor: Jan Röman Hedging with Options (MMA707) Authors: Chiamruchikun Benchaphon 800530-49 Klongprateepphol Chutima 80708-67 Pongpala Apiwat 808-4975 Suntayodom

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing We shall go over this note quickly due to time constraints. Key concept: Ito s lemma Stock Options: A contract giving

Lecture Note 8 of Bus 41202, Spring 2017: Stochastic Diffusion Equation & Option Pricing We shall go over this note quickly due to time constraints. Key concept: Ito s lemma Stock Options: A contract giving

( ) since this is the benefit of buying the asset at the strike price rather

since this is the benefit of buying the asset at the strike price rather") Review of some financial models for MAT 483 Parity and Other Option Relationships The basic parity relationship for European options with the same strike price and the same time to expiration is: C( KT

Review of some financial models for MAT 483 Parity and Other Option Relationships The basic parity relationship for European options with the same strike price and the same time to expiration is: C( KT

Appendix: Basics of Options and Option Pricing Option Payoffs

Appendix: Basics of Options and Option Pricing An option provides the holder with the right to buy or sell a specified quantity of an underlying asset at a fixed price (called a strike price or an exercise

Appendix: Basics of Options and Option Pricing An option provides the holder with the right to buy or sell a specified quantity of an underlying asset at a fixed price (called a strike price or an exercise

Top Five Things You Should Know Before Buying an Option

Top Five Things You Should Know Before Buying an Option Disclaimers Options involve risks and are not suitable for all investors. Prior to buying or selling options, an investor must receive a copy of

Top Five Things You Should Know Before Buying an Option Disclaimers Options involve risks and are not suitable for all investors. Prior to buying or selling options, an investor must receive a copy of

MATH6911: Numerical Methods in Finance. Final exam Time: 2:00pm - 5:00pm, April 11, Student Name (print): Student Signature: Student ID:

: Student Signature: Student ID:") MATH6911 Page 1 of 16 Winter 2007 MATH6911: Numerical Methods in Finance Final exam Time: 2:00pm - 5:00pm, April 11, 2007 Student Name (print): Student Signature: Student ID: Question Full Mark Mark 1

MATH6911 Page 1 of 16 Winter 2007 MATH6911: Numerical Methods in Finance Final exam Time: 2:00pm - 5:00pm, April 11, 2007 Student Name (print): Student Signature: Student ID: Question Full Mark Mark 1

MA 1125 Lecture 05 - Measures of Spread. Wednesday, September 6, Objectives: Introduce variance, standard deviation, range.

MA 115 Lecture 05 - Measures of Spread Wednesday, September 6, 017 Objectives: Introduce variance, standard deviation, range. 1. Measures of Spread In Lecture 04, we looked at several measures of central

MA 115 Lecture 05 - Measures of Spread Wednesday, September 6, 017 Objectives: Introduce variance, standard deviation, range. 1. Measures of Spread In Lecture 04, we looked at several measures of central

Derivatives Analysis & Valuation (Futures)

") 6.1 Derivatives Analysis & Valuation (Futures) LOS 1 : Introduction Study Session 6 Define Forward Contract, Future Contract. Forward Contract, In Forward Contract one party agrees to buy, and the counterparty

6.1 Derivatives Analysis & Valuation (Futures) LOS 1 : Introduction Study Session 6 Define Forward Contract, Future Contract. Forward Contract, In Forward Contract one party agrees to buy, and the counterparty

Capital Projects as Real Options

Lecture: X 1 Capital Projects as Real Options Why treat a corporate investment proposal as an option, rather than as equity + bond (DCF valuation)?! Many projects (especially strategic ones) look more

Lecture: X 1 Capital Projects as Real Options Why treat a corporate investment proposal as an option, rather than as equity + bond (DCF valuation)?! Many projects (especially strategic ones) look more

.5 M339W/389W Financial Mathematics for Actuarial Applications University of Texas at Austin Sample In-Term Exam 2.5 Instructor: Milica Čudina

.5 M339W/389W Financial Mathematics for Actuarial Applications University of Texas at Austin Sample In-Term Exam 2.5 Instructor: Milica Čudina Notes: This is a closed book and closed notes exam. Time:

.5 M339W/389W Financial Mathematics for Actuarial Applications University of Texas at Austin Sample In-Term Exam 2.5 Instructor: Milica Čudina Notes: This is a closed book and closed notes exam. Time:

The objective of Part One is to provide a knowledge base for learning about the key

PART ONE Key Option Elements The objective of Part One is to provide a knowledge base for learning about the key elements of forex options. This includes a description of plain vanilla options and how

PART ONE Key Option Elements The objective of Part One is to provide a knowledge base for learning about the key elements of forex options. This includes a description of plain vanilla options and how

F A S C I C U L I M A T H E M A T I C I

F A S C I C U L I M A T H E M A T I C I Nr 38 27 Piotr P luciennik A MODIFIED CORRADO-MILLER IMPLIED VOLATILITY ESTIMATOR Abstract. The implied volatility, i.e. volatility calculated on the basis of option

F A S C I C U L I M A T H E M A T I C I Nr 38 27 Piotr P luciennik A MODIFIED CORRADO-MILLER IMPLIED VOLATILITY ESTIMATOR Abstract. The implied volatility, i.e. volatility calculated on the basis of option

Math 181 Lecture 15 Hedging and the Greeks (Chap. 14, Hull)

") Math 181 Lecture 15 Hedging and the Greeks (Chap. 14, Hull) One use of derivation is for investors or investment banks to manage the risk of their investments. If an investor buys a stock for price S 0,

Math 181 Lecture 15 Hedging and the Greeks (Chap. 14, Hull) One use of derivation is for investors or investment banks to manage the risk of their investments. If an investor buys a stock for price S 0,

Derivative Securities

Derivative Securities he Black-Scholes formula and its applications. his Section deduces the Black- Scholes formula for a European call or put, as a consequence of risk-neutral valuation in the continuous

Derivative Securities he Black-Scholes formula and its applications. his Section deduces the Black- Scholes formula for a European call or put, as a consequence of risk-neutral valuation in the continuous

Webinar Presentation How Volatility & Other Important Factors Affect the Greeks

Webinar Presentation How Volatility & Other Important Factors Affect the Greeks Presented by Trading Strategy Desk 1 Fidelity Brokerage Services, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917.

Webinar Presentation How Volatility & Other Important Factors Affect the Greeks Presented by Trading Strategy Desk 1 Fidelity Brokerage Services, Member NYSE, SIPC, 900 Salem Street, Smithfield, RI 02917.

The Black-Scholes Equation

The Black-Scholes Equation MATH 472 Financial Mathematics J. Robert Buchanan 2018 Objectives In this lesson we will: derive the Black-Scholes partial differential equation using Itô s Lemma and no-arbitrage

The Black-Scholes Equation MATH 472 Financial Mathematics J. Robert Buchanan 2018 Objectives In this lesson we will: derive the Black-Scholes partial differential equation using Itô s Lemma and no-arbitrage

Implied Volatility Surface

Implied Volatility Surface Liuren Wu Zicklin School of Business, Baruch College Options Markets (Hull chapter: 16) Liuren Wu Implied Volatility Surface Options Markets 1 / 1 Implied volatility Recall the

Implied Volatility Surface Liuren Wu Zicklin School of Business, Baruch College Options Markets (Hull chapter: 16) Liuren Wu Implied Volatility Surface Options Markets 1 / 1 Implied volatility Recall the

4. Black-Scholes Models and PDEs. Math6911 S08, HM Zhu

4. Black-Scholes Models and PDEs Math6911 S08, HM Zhu References 1. Chapter 13, J. Hull. Section.6, P. Brandimarte Outline Derivation of Black-Scholes equation Black-Scholes models for options Implied

4. Black-Scholes Models and PDEs Math6911 S08, HM Zhu References 1. Chapter 13, J. Hull. Section.6, P. Brandimarte Outline Derivation of Black-Scholes equation Black-Scholes models for options Implied

Advanced Corporate Finance. 5. Options (a refresher)

") Advanced Corporate Finance 5. Options (a refresher) Objectives of the session 1. Define options (calls and puts) 2. Analyze terminal payoff 3. Define basic strategies 4. Binomial option pricing model 5.

Advanced Corporate Finance 5. Options (a refresher) Objectives of the session 1. Define options (calls and puts) 2. Analyze terminal payoff 3. Define basic strategies 4. Binomial option pricing model 5.

FINANCIAL MATHEMATICS WITH ADVANCED TOPICS MTHE7013A

UNIVERSITY OF EAST ANGLIA School of Mathematics Main Series UG Examination 2016 17 FINANCIAL MATHEMATICS WITH ADVANCED TOPICS MTHE7013A Time allowed: 3 Hours Attempt QUESTIONS 1 and 2, and THREE other

UNIVERSITY OF EAST ANGLIA School of Mathematics Main Series UG Examination 2016 17 FINANCIAL MATHEMATICS WITH ADVANCED TOPICS MTHE7013A Time allowed: 3 Hours Attempt QUESTIONS 1 and 2, and THREE other

CHAPTER 9. Solutions. Exercise The payoff diagrams will look as in the figure below.

CHAPTER 9 Solutions Exercise 1 1. The payoff diagrams will look as in the figure below. 2. Gross payoff at expiry will be: P(T) = min[(1.23 S T ), 0] + min[(1.10 S T ), 0] where S T is the EUR/USD exchange

CHAPTER 9 Solutions Exercise 1 1. The payoff diagrams will look as in the figure below. 2. Gross payoff at expiry will be: P(T) = min[(1.23 S T ), 0] + min[(1.10 S T ), 0] where S T is the EUR/USD exchange

Skew Hedging. Szymon Borak Matthias R. Fengler Wolfgang K. Härdle. CASE-Center for Applied Statistics and Economics Humboldt-Universität zu Berlin

Szymon Borak Matthias R. Fengler Wolfgang K. Härdle CASE-Center for Applied Statistics and Economics Humboldt-Universität zu Berlin 6 4 2.22 Motivation 1-1 Barrier options Knock-out options are financial

Szymon Borak Matthias R. Fengler Wolfgang K. Härdle CASE-Center for Applied Statistics and Economics Humboldt-Universität zu Berlin 6 4 2.22 Motivation 1-1 Barrier options Knock-out options are financial

e.g. + 1 vol move in the 30delta Puts would be example of just a changing put skew

Calculating vol skew change risk (skew-vega) Ravi Jain 2012 Introduction An interesting and important risk in an options portfolio is the impact of a changing implied volatility skew. It is not uncommon

Calculating vol skew change risk (skew-vega) Ravi Jain 2012 Introduction An interesting and important risk in an options portfolio is the impact of a changing implied volatility skew. It is not uncommon

A NEW APPROACH TO MERTON MODEL DEFAULT AND PREDICTIVE ANALYTICS WITH APPLICATIONS TO RECESSION ECONOMICS TOMMY LEWIS

A NEW APPROACH TO MERTON MODEL DEFAULT AND PREDICTIVE ANALYTICS WITH APPLICATIONS TO RECESSION ECONOMICS TOMMY LEWIS BACKGROUND/MOTIVATION Default risk is the uncertainty surrounding how likely it is that

A NEW APPROACH TO MERTON MODEL DEFAULT AND PREDICTIVE ANALYTICS WITH APPLICATIONS TO RECESSION ECONOMICS TOMMY LEWIS BACKGROUND/MOTIVATION Default risk is the uncertainty surrounding how likely it is that

Weekly Options SAMPLE INVESTING PLANS

Weekly Options SAMPLE INVESTING PLANS Disclosures All investing plans are provided for informational purposes only and should not be considered a recommendation of any security, strategy, or specific portfolio

Weekly Options SAMPLE INVESTING PLANS Disclosures All investing plans are provided for informational purposes only and should not be considered a recommendation of any security, strategy, or specific portfolio

ECON FINANCIAL ECONOMICS

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

ECON 337901 FINANCIAL ECONOMICS Peter Ireland Boston College Fall 2017 These lecture notes by Peter Ireland are licensed under a Creative Commons Attribution-NonCommerical-ShareAlike 4.0 International

Credit Risk in Banking

Credit Risk in Banking CREDIT RISK MODELS Sebastiano Vitali, 2017/2018 Merton model It consider the financial structure of a company, therefore it belongs to the structural approach models Notation: E

Credit Risk in Banking CREDIT RISK MODELS Sebastiano Vitali, 2017/2018 Merton model It consider the financial structure of a company, therefore it belongs to the structural approach models Notation: E

Black-Scholes Call and Put Equation and Comparative Static Parameterizations

Option Greeks Latest Version: November 14, 2017 This Notebook describes how to use Mathematica to perform generate graphs of the so-called option "Greeks". Suggestions concerning ways to improve this notebook,

Option Greeks Latest Version: November 14, 2017 This Notebook describes how to use Mathematica to perform generate graphs of the so-called option "Greeks". Suggestions concerning ways to improve this notebook,

OPTION POSITIONING AND TRADING TUTORIAL

OPTION POSITIONING AND TRADING TUTORIAL Binomial Options Pricing, Implied Volatility and Hedging Option Underlying 5/13/2011 Professor James Bodurtha Executive Summary The following paper looks at a number

OPTION POSITIONING AND TRADING TUTORIAL Binomial Options Pricing, Implied Volatility and Hedging Option Underlying 5/13/2011 Professor James Bodurtha Executive Summary The following paper looks at a number

The Impact of Volatility Estimates in Hedging Effectiveness

EU-Workshop Series on Mathematical Optimization Models for Financial Institutions The Impact of Volatility Estimates in Hedging Effectiveness George Dotsis Financial Engineering Research Center Department

EU-Workshop Series on Mathematical Optimization Models for Financial Institutions The Impact of Volatility Estimates in Hedging Effectiveness George Dotsis Financial Engineering Research Center Department

Black-Scholes-Merton (BSM) Option Pricing Model 40 th Anniversary Conference. The Recovery Theorem

Option Pricing Model 40 th Anniversary Conference. The Recovery Theorem") Black-Scholes-Merton (BSM) Option Pricing Model 40 th Anniversary Conference The Recovery Theorem October 2, 2013 Whitehead Institute, MIT Steve Ross Franco Modigliani Professor of Financial Economics

Black-Scholes-Merton (BSM) Option Pricing Model 40 th Anniversary Conference The Recovery Theorem October 2, 2013 Whitehead Institute, MIT Steve Ross Franco Modigliani Professor of Financial Economics

Important Concepts LECTURE 3.2: OPTION PRICING MODELS: THE BLACK-SCHOLES-MERTON MODEL. Applications of Logarithms and Exponentials in Finance

Important Concepts The Black Scholes Merton (BSM) option pricing model LECTURE 3.2: OPTION PRICING MODELS: THE BLACK-SCHOLES-MERTON MODEL Black Scholes Merton Model as the Limit of the Binomial Model Origins

Important Concepts The Black Scholes Merton (BSM) option pricing model LECTURE 3.2: OPTION PRICING MODELS: THE BLACK-SCHOLES-MERTON MODEL Black Scholes Merton Model as the Limit of the Binomial Model Origins

2018 Copyright ETNtrade. Where the Elite Trade. January 2, 2018

Where the Elite Trade Introduction to Basic Options and Option Application January 2, 2018 Today s Presenter: Dave Meldeau ETNtrade President ETNtrade OptionDave @ETNtrade @OptionDave By printing and/or

Where the Elite Trade Introduction to Basic Options and Option Application January 2, 2018 Today s Presenter: Dave Meldeau ETNtrade President ETNtrade OptionDave @ETNtrade @OptionDave By printing and/or

The Black-Scholes Model

The Black-Scholes Model Inputs Spot Price Exercise Price Time to Maturity Rate-Cost of funds & Yield Volatility Process The Black Box Output "Fair Market Value" For those interested in looking inside the

The Black-Scholes Model Inputs Spot Price Exercise Price Time to Maturity Rate-Cost of funds & Yield Volatility Process The Black Box Output "Fair Market Value" For those interested in looking inside the

MATH4143: Scientific Computations for Finance Applications Final exam Time: 9:00 am - 12:00 noon, April 18, Student Name (print):

:") MATH4143 Page 1 of 17 Winter 2007 MATH4143: Scientific Computations for Finance Applications Final exam Time: 9:00 am - 12:00 noon, April 18, 2007 Student Name (print): Student Signature: Student ID: Question

MATH4143 Page 1 of 17 Winter 2007 MATH4143: Scientific Computations for Finance Applications Final exam Time: 9:00 am - 12:00 noon, April 18, 2007 Student Name (print): Student Signature: Student ID: Question

Mathematics of Financial Derivatives

Mathematics of Financial Derivatives Lecture 8 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. The Greek letters (continued) 2. Volatility

Mathematics of Financial Derivatives Lecture 8 Solesne Bourguin bourguin@math.bu.edu Boston University Department of Mathematics and Statistics Table of contents 1. The Greek letters (continued) 2. Volatility

Hedging. MATH 472 Financial Mathematics. J. Robert Buchanan

Hedging MATH 472 Financial Mathematics J. Robert Buchanan 2018 Introduction Definition Hedging is the practice of making a portfolio of investments less sensitive to changes in market variables. There

Hedging MATH 472 Financial Mathematics J. Robert Buchanan 2018 Introduction Definition Hedging is the practice of making a portfolio of investments less sensitive to changes in market variables. There

P2.T5. Market Risk Measurement & Management. Bionic Turtle FRM Practice Questions Sample

P2.T5. Market Risk Measurement & Management Bionic Turtle FRM Practice Questions Sample Hull, Options, Futures & Other Derivatives By David Harper, CFA FRM CIPM www.bionicturtle.com HULL, CHAPTER 20: VOLATILITY

P2.T5. Market Risk Measurement & Management Bionic Turtle FRM Practice Questions Sample Hull, Options, Futures & Other Derivatives By David Harper, CFA FRM CIPM www.bionicturtle.com HULL, CHAPTER 20: VOLATILITY

Bear Market Strategies Time Spreads And Straddles

The Option Pit Method Bear Market Strategies Time Spreads And Straddles Option Pit BMS- Time Spreads and Straddles What we will cover: Simple Capital Allocation Stock Replacement Time Frame The Juiced

The Option Pit Method Bear Market Strategies Time Spreads And Straddles Option Pit BMS- Time Spreads and Straddles What we will cover: Simple Capital Allocation Stock Replacement Time Frame The Juiced

Option Pricing. Simple Arbitrage Relations. Payoffs to Call and Put Options. Black-Scholes Model. Put-Call Parity. Implied Volatility

Simple Arbitrage Relations Payoffs to Call and Put Options Black-Scholes Model Put-Call Parity Implied Volatility Option Pricing Options: Definitions A call option gives the buyer the right, but not the

Simple Arbitrage Relations Payoffs to Call and Put Options Black-Scholes Model Put-Call Parity Implied Volatility Option Pricing Options: Definitions A call option gives the buyer the right, but not the

Credit Risk and Underlying Asset Risk *

Seoul Journal of Business Volume 4, Number (December 018) Credit Risk and Underlying Asset Risk * JONG-RYONG LEE **1) Kangwon National University Gangwondo, Korea Abstract This paper develops the credit

Seoul Journal of Business Volume 4, Number (December 018) Credit Risk and Underlying Asset Risk * JONG-RYONG LEE **1) Kangwon National University Gangwondo, Korea Abstract This paper develops the credit

B. Combinations. 1. Synthetic Call (Put-Call Parity). 2. Writing a Covered Call. 3. Straddle, Strangle. 4. Spreads (Bull, Bear, Butterfly).

. 2. Writing a Covered Call. 3. Straddle, Strangle. 4. Spreads (Bull, Bear, Butterfly).") 1 EG, Ch. 22; Options I. Overview. A. Definitions. 1. Option - contract in entitling holder to buy/sell a certain asset at or before a certain time at a specified price. Gives holder the right, but not

1 EG, Ch. 22; Options I. Overview. A. Definitions. 1. Option - contract in entitling holder to buy/sell a certain asset at or before a certain time at a specified price. Gives holder the right, but not

About Black-Sholes formula, volatility, implied volatility and math. statistics.

About Black-Sholes formula, volatility, implied volatility and math. statistics. Mark Ioffe Abstract We analyze application Black-Sholes formula for calculation of implied volatility from point of view

About Black-Sholes formula, volatility, implied volatility and math. statistics. Mark Ioffe Abstract We analyze application Black-Sholes formula for calculation of implied volatility from point of view

Department of Mathematics. Mathematics of Financial Derivatives

Department of Mathematics MA408 Mathematics of Financial Derivatives Thursday 15th January, 2009 2pm 4pm Duration: 2 hours Attempt THREE questions MA408 Page 1 of 5 1. (a) Suppose 0 < E 1 < E 3 and E 2

Department of Mathematics MA408 Mathematics of Financial Derivatives Thursday 15th January, 2009 2pm 4pm Duration: 2 hours Attempt THREE questions MA408 Page 1 of 5 1. (a) Suppose 0 < E 1 < E 3 and E 2

Valuing Put Options with Put-Call Parity S + P C = [X/(1+r f ) t ] + [D P /(1+r f ) t ] CFA Examination DERIVATIVES OPTIONS Page 1 of 6

![Valuing Put Options with Put-Call Parity S + P C = [X/(1+r f ) t ] + [D P /(1+r f ) t ] CFA Examination DERIVATIVES OPTIONS Page 1 of 6](/thumbs/77/75506899.jpg "Valuing Put Options with Put-Call Parity S + P C = [X/(1+r f ) t ] + [D P /(1+r f ) t ] CFA Examination DERIVATIVES OPTIONS Page 1 of 6") DERIVATIVES OPTIONS A. INTRODUCTION There are 2 Types of Options Calls: give the holder the RIGHT, at his discretion, to BUY a Specified number of a Specified Asset at a Specified Price on, or until, a

DERIVATIVES OPTIONS A. INTRODUCTION There are 2 Types of Options Calls: give the holder the RIGHT, at his discretion, to BUY a Specified number of a Specified Asset at a Specified Price on, or until, a

Financial Derivatives Section 5

Financial Derivatives Section 5 The Black and Scholes Model Michail Anthropelos anthropel@unipi.gr http://web.xrh.unipi.gr/faculty/anthropelos/ University of Piraeus Spring 2018 M. Anthropelos (Un. of

Financial Derivatives Section 5 The Black and Scholes Model Michail Anthropelos anthropel@unipi.gr http://web.xrh.unipi.gr/faculty/anthropelos/ University of Piraeus Spring 2018 M. Anthropelos (Un. of

Introduction to Financial Derivatives

55.444 Introduction to Financial Derivatives November 5, 212 Option Analysis and Modeling The Binomial Tree Approach Where we are Last Week: Options (Chapter 9-1, OFOD) This Week: Option Analysis and Modeling:

55.444 Introduction to Financial Derivatives November 5, 212 Option Analysis and Modeling The Binomial Tree Approach Where we are Last Week: Options (Chapter 9-1, OFOD) This Week: Option Analysis and Modeling:

covered warrants uncovered an explanation and the applications of covered warrants

covered warrants uncovered an explanation and the applications of covered warrants Disclaimer Whilst all reasonable care has been taken to ensure the accuracy of the information comprising this brochure,

covered warrants uncovered an explanation and the applications of covered warrants Disclaimer Whilst all reasonable care has been taken to ensure the accuracy of the information comprising this brochure,

Hedging Effectiveness of Options on Thailand Futures Exchange

Hedging Effectiveness of Options on Thailand Futures Exchange Jirapat Amornsiripanuwat Faculty of Commerce and Accountancy, Thammasat University Email : meng.jirapat@gmail.com The author thanks Mr. Chirasakdi

Hedging Effectiveness of Options on Thailand Futures Exchange Jirapat Amornsiripanuwat Faculty of Commerce and Accountancy, Thammasat University Email : meng.jirapat@gmail.com The author thanks Mr. Chirasakdi

Topical: Natural Gas and Propane prices soar... Source: Energy Information Administration, data are from reports released Jan 23, 2014.

Volatility and Risk... an introduction to the concepts Topical: Natural Gas and Propane prices soar... $5 $2 Source: Energy Information Administration, data are from reports released Jan 23, 2014. ...

Volatility and Risk... an introduction to the concepts Topical: Natural Gas and Propane prices soar... $5 $2 Source: Energy Information Administration, data are from reports released Jan 23, 2014. ...

Sensex Realized Volatility Index (REALVOL)

") Sensex Realized Volatility Index (REALVOL) Introduction Volatility modelling has traditionally relied on complex econometric procedures in order to accommodate the inherent latent character of volatility.

Sensex Realized Volatility Index (REALVOL) Introduction Volatility modelling has traditionally relied on complex econometric procedures in order to accommodate the inherent latent character of volatility.

Presents Mastering the Markets Trading Earnings

www.mastermindtraders.com Presents Mastering the Markets Trading Earnings 1 DISCLAIMER Neither MasterMind Traders or any of its personnel are registered broker-dealers or investment advisors. We may mention

www.mastermindtraders.com Presents Mastering the Markets Trading Earnings 1 DISCLAIMER Neither MasterMind Traders or any of its personnel are registered broker-dealers or investment advisors. We may mention

Valuing Stock Options: The Black-Scholes-Merton Model. Chapter 13

Valuing Stock Options: The Black-Scholes-Merton Model Chapter 13 1 The Black-Scholes-Merton Random Walk Assumption l Consider a stock whose price is S l In a short period of time of length t the return

Valuing Stock Options: The Black-Scholes-Merton Model Chapter 13 1 The Black-Scholes-Merton Random Walk Assumption l Consider a stock whose price is S l In a short period of time of length t the return