Forecast Combination

|

|

|

- Patricia Hardy

- 5 years ago

- Views:

Transcription

1 Forecast Combination In the press, you will hear about Blue Chip Average Forecast and Consensus Forecast These are the averages of the forecasts of distinct professional forecasters. Is there merit to averaging (combining) different forecasts? Or is it better to focus on selecting the best forecast?

2 GDP Forecast Let s consider forecasting GDP growth for 010Q1 (first estimate to be released April 30) GDP growth for the four quarters of Q1 009Q 009Q3 009Q4 6.4% 0.7%.% 5.6%

3 Models In p.s. #10, you considered models for GDP AR(3) plus 3 lags of dt3 AR(3) plus 3 lags of dt1 AR(3) plus 3 lags of spread1 AR(3) plus 3 lags of spread10 AR(3) plus 3 lags of junk The model with junk spread had the lowest AIC Let s reconsider the number of lags

4 AIC for different lag structures junk yield lags AR(1) AR() * 554 AR(3) The model with AR lags and lags of junk has the lowest AIC But the models with 1 and 3 AR lags have nearly the same AIC And the models with 3 lags of junk are quite close too

5 Forecasts junk yield lags AR(1) AR() * 4.3 AR(3) The point forecasts are quite different The model selected by AIC is much higher than the AR model The model with 3 lags of junk have quite different forecasts

6 Average Forecast The average of the 1 forecasts is ˆ y average = 1 = 4.4 This is similar to a consensus or Blue Chip forecast. You could imagine these 1 forecasts as coming from different forecasters. Is it useful to combine the forecasts?

7 Pseudo Out of Sample Experiment Split the sample Estimation period: 1954Q 1994Q4 (30 years) Evaluation period: 1995Q1 009Q4 (15 years) Estimate the 1 models using 1954Q 1994Q4 Fix the parameter estimates Use these models to forecast 1995Q1 009Q4 Also, take the average forecast for each period Create out of sample errors for the 1 models And the out of sample error for the average forecast Compare the performance of the methods by RMSE A simplified version of predictive least square (PLS)

8 Out of Sample RMSE RMSE junk yield lags AR(1) AR() *.3 AR(3) RMSE Average forecast.18 The comparisons based on out ofsample RMSE are similar to AIC on full sample The lowest RMSE is.3, achieved by the model with lags of each But the RMSE of the average forecasts (the average across all 1 forecasts) is.18 We achieve a much lower RMSE by this simple averaging! Why? Why is it useful to combine forecasts? Can we do better than a simple equal weighted average?

9 Theory of Forecast Combination Suppose you have forecasts f 1 and f for y Suppose they are unbiased with variances var(f 1 ) and var(f ) and suppose they are uncorrelated. Then if you take a weighted average f = wf w) ( f The variance of the average is var( f ) = w var ( ) f + (1 w) var( f ) 1

10 Equal weights If w=1/ then ( f ) var( ) 1 + f var var( f ) = 4

11 Optimal Weights Minimizing with respect to w, the optimal weight The weight on forecast 1 is inversely proportional to its variance 1 ) (1 ) var( σ w σ w f + = = + = σ σ σ σ σ σ w

12 Multiple Forecasts In general, if you have forecasts f 1,, f M a forecast combination is f = w f + w f + L+ 1 1 w M f M Where the weights are non negative and w 1 + w + L+ wm = 1

13 Optimal weights When the forecasts are uncorrelated, the optimal weights are w m = σ 1 σ m + σ + L+ σ M The weight on the m th forecast is inversely proportional to its variance If they have the same variance, then the weights are all equal

14 Bates Granger Combination Bates and Granger (1969) An early influential paper Suggested using empirical weights based on out ofsample forecast variances w m = ˆ σ 1 ˆ σ m + ˆ σ + L+ ˆ σ Even though this was derived under the assumption of uncorrelated forecasts, this method can work well in practice. M

15 Bates Granger Implementation Take a series of (pseudo) out of sample forecasts and forecast errors Compute forecast variance (square of RMSE) Invert. Normalize by sum across all models

16 Example RMSE junk yield lags AR(1) AR() AR(3) Take the first model with RMSE=.46 Square and invert to find 0.16 Sum across all 1 models is.14 Divide 0.16/.14=0.08 This is the weight for this model/forecast Because the RMSE is similar across models, the weights are very similar, all 0.08 or 0.09 Bates Granger weights essentially are the same as equal weights

17 Granger Ramanathan Combination Granger and Ramanathan (1984) Introduced a regression method to combine forecasts Similar to a Mincer Zarnowitz regression Regress the actual value on the forecasts Two forecasts: y + t = β 1 f1 t + β ft e t

18 Multiple Forecasts y = β f + β f + L+ β f + t 1 1t t M Mt e t Should use a constrained regression Omit intercept Enforce non negative coefficients Constrain coefficients to sum to one

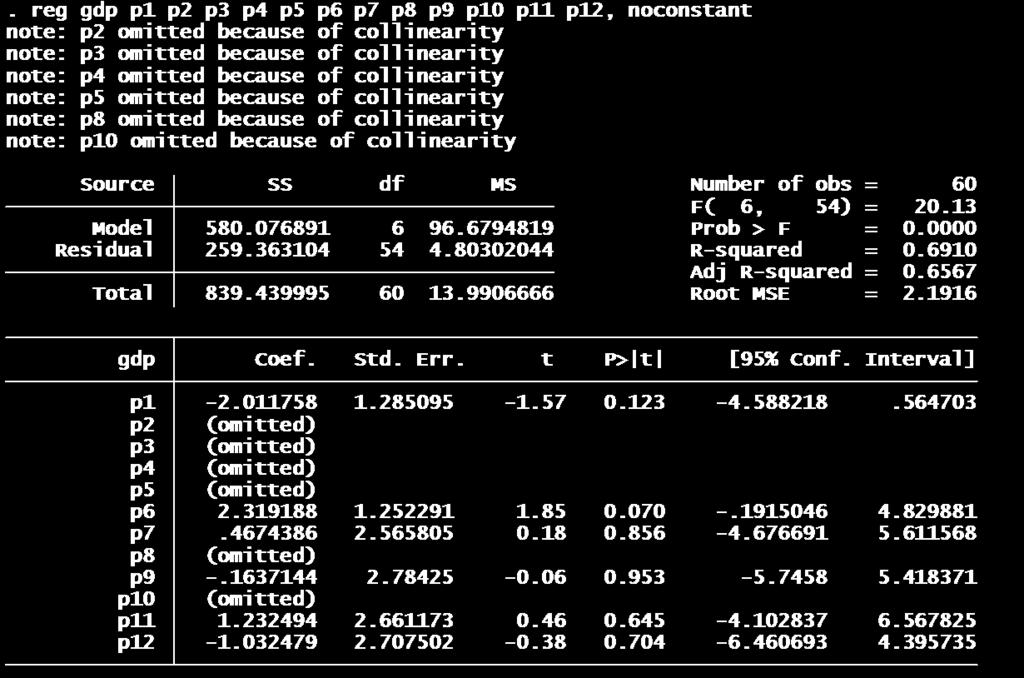

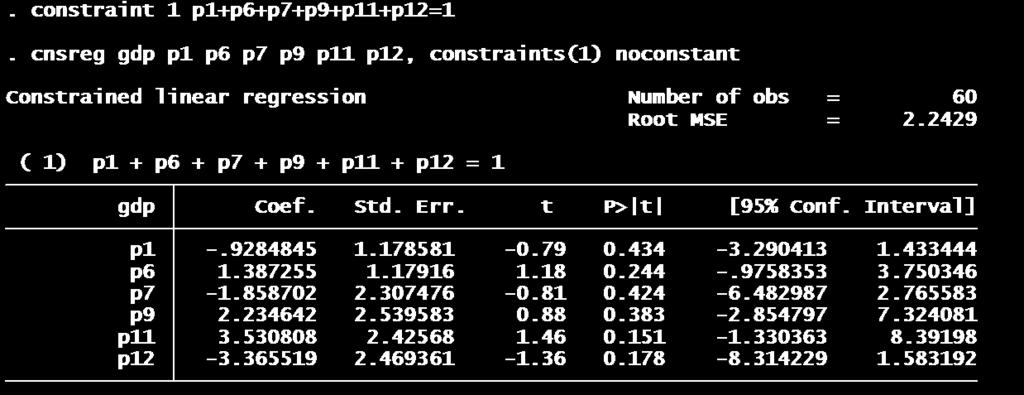

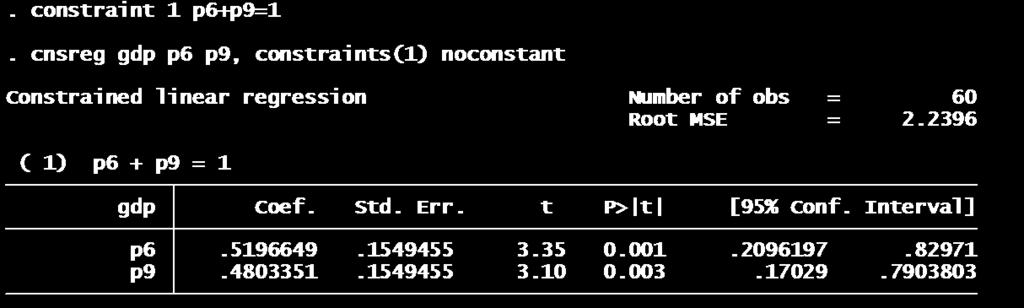

19 STATA implementation reg option noconstant removes the intercept Constrained regression command cnsreg enforces linear constraints defined by constraint For example, if you regress gdp on (p 1,p,p 3,p 4 ).constraint 1 p1+p+p3+p4=1.cnsreg gdp p1 p p3 p4, constraints(1) noconstant

20 Non negativity In STATA it is difficult to enforce the non negative condition on the weights You can do this manually Estimate the regression Eliminate a forecast with the most negative weight Restimate Keep eliminating forecasts until only positive weights are found. Another problem If the forecasts are highly correlated, STATA may exclude redundant forecasts That is okay, they were not helping anyway.

21 Example

22 Example

23 Granger Ramanathan Weights and Forecast We found the following estimated weights Model 6: 0.5 Model 9: 0.48 Combination Forecast 0.5* *5.3=4.7%

24 Bayesian Model Averaging In our discussion of model selection, we pointed out that Bayes theorem says that when there are a set of models, one of which is true, then the probability that a model is true given the data is P BIC ( M D) exp 1 These can be used for forecast weights This is a simplified form of Bayesian model averaging (BMA) which is very popular

25 BMA formula We can write the weights as follows Let BIC* be the smallest BIC The BIC of the best fitting model Let ΔBIC=BIC BIC* be the BIC difference = = Δ = M m m m m m m w w w BIC w 1 * * * exp

26 Implementation Compute BIC for each model Find best fitting BIC* Compute difference ΔBIC and exp( ΔBIC/) Sum up all values and re normalize

27 BIC junk yield lags AR(1) * 571 AR() AR(3) ΔBIC/ junk yield lags AR(1) AR() AR(3) weight junk yield lags AR(1) AR() AR(3) BMA puts the most weight on the model with the smallest BIC It puts very little weight on a model which has a BIC value quite different from the minimum In some cases, several models receive similar weight In this example, most weight (75%) goes on the model with the AR(1) plus lags of the junk spread 15% also on AR() plus lags

28 BMA Weights and Forecast BMA Forecast 0.75* *5.1+.0* *4.7+.0*4.3 =5.1%

29 Weighted AIC (WAIC) Some authors have suggested replacing BIC with AIC in the weight formula w m AIC exp There is not a strong theoretical foundation for this suggestion But, it is simple and works quite well in practice.

30 WAIC formula Let AIC* be the smallest AIC The AIC of the best fitting model ΔAIC=AIC AIC* is the AIC difference = = Δ = M m m m m m m w w w AIC w 1 * * * exp

31 AIC junk yield lags AR(1) * 554 AR() AR(3) ΔAIC/ junk yield lags AR(1) AR() AR(3) weight junk yield Lags AR(1) AR() AR(3) WAIC splits weight more than BMA It puts 4% on each of the three models with the best nearequivalent AIC Puts positive weight on 6 models Puts zero weight on 6 models

32 WAIC Forecast WAIC Forecast.4*5.+.4*5.1+.4* * * *4.4 =4.95%

33 Advantages of Combination Methods When the selection criterion (AIC, BIC) are very close for competing models, it is troubling to select one over the other based on a small different In this setting WAIC and BMA will give the two models near equal weight If the selection criterion are different, simple averaging gives all models the same weight, which seems naïve. In this setting WAIC and BMA will give the models different weight And will give zero weight if the different is sufficiently large If the difference in the criterion is above 10.

34 GDP Combination Forecasts AIC Selection: 5.1% BIC Selection: 5.% Simple Average: 4.4% Bates Granger combination: 4.4% Granger Ramanathan combination: 4.7% BMA: 5.1% WAIC: 4.95%

35 Example: Unemployment Rate Estimated on AIC AIC weights BIC BIC weights AR(4) AR(5) *.74 AR(6) AR(7) AR(8) AR(9) AR(10) AR(11) AR(1) AR(13) 1808* AR(14) AR(15) AR(16) AR(17) AR(18) AR(19) AR(0)

36 Out of Sample RMSE Method RMSE AIC.145 BIC.145 BMA.145 WAIC.145 Best Model (AR(1)).143

37 Which should you use? Current research suggests that combination methods achieve lower MSFE than selection BMA achieves lower MSFE than BIC WAIC achieves lower MSFE than AIC Naïve combination (simple averaging) works quite well But the other methods can do better WAIC works well in practice Bates Granger also works well in many settings

38 Forecast Intervals How do you construct intervals for a combination forecast? Do not combine forecast intervals Given the weights, you can construct the sequence of sample forecasts and forecast errors Use these errors as you have before to construct the forecast interval Compute the RMSE of the combination forecast error

STAT 509: Statistics for Engineers Dr. Dewei Wang. Copyright 2014 John Wiley & Sons, Inc. All rights reserved.

STAT 509: Statistics for Engineers Dr. Dewei Wang Applied Statistics and Probability for Engineers Sixth Edition Douglas C. Montgomery George C. Runger 7 Point CHAPTER OUTLINE 7-1 Point Estimation 7-2

STAT 509: Statistics for Engineers Dr. Dewei Wang Applied Statistics and Probability for Engineers Sixth Edition Douglas C. Montgomery George C. Runger 7 Point CHAPTER OUTLINE 7-1 Point Estimation 7-2

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2014, Mr. Ruey S. Tsay. Solutions to Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2014, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2014, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

A RIDGE REGRESSION ESTIMATION APPROACH WHEN MULTICOLLINEARITY IS PRESENT

Fundamental Journal of Applied Sciences Vol. 1, Issue 1, 016, Pages 19-3 This paper is available online at http://www.frdint.com/ Published online February 18, 016 A RIDGE REGRESSION ESTIMATION APPROACH

Fundamental Journal of Applied Sciences Vol. 1, Issue 1, 016, Pages 19-3 This paper is available online at http://www.frdint.com/ Published online February 18, 016 A RIDGE REGRESSION ESTIMATION APPROACH

Business Cycle. Measures of the business cycle include. All of these require leading indicators of the business cycle

Leading Indicators Good forecasting is often determined by finding leading indicators variables which reduce the MSE of multi-step forecast errors Leading indicators move in advance of the forecast variable

Leading Indicators Good forecasting is often determined by finding leading indicators variables which reduce the MSE of multi-step forecast errors Leading indicators move in advance of the forecast variable

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2010, Mr. Ruey S. Tsay. Solutions to Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2010, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2010, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

The histogram should resemble the uniform density, the mean should be close to 0.5, and the standard deviation should be close to 1/ 12 =

Chapter 19 Monte Carlo Valuation Question 19.1 The histogram should resemble the uniform density, the mean should be close to.5, and the standard deviation should be close to 1/ 1 =.887. Question 19. The

Chapter 19 Monte Carlo Valuation Question 19.1 The histogram should resemble the uniform density, the mean should be close to.5, and the standard deviation should be close to 1/ 1 =.887. Question 19. The

Web Appendix. Are the effects of monetary policy shocks big or small? Olivier Coibion

Web Appendix Are the effects of monetary policy shocks big or small? Olivier Coibion Appendix 1: Description of the Model-Averaging Procedure This section describes the model-averaging procedure used in

Web Appendix Are the effects of monetary policy shocks big or small? Olivier Coibion Appendix 1: Description of the Model-Averaging Procedure This section describes the model-averaging procedure used in

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay. Solutions to Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (30 pts) Answer briefly the following questions. Each question has

Chapter 5 Univariate time-series analysis. () Chapter 5 Univariate time-series analysis 1 / 29

Chapter 5 Univariate time-series analysis 1 / 29") Chapter 5 Univariate time-series analysis () Chapter 5 Univariate time-series analysis 1 / 29 Time-Series Time-series is a sequence fx 1, x 2,..., x T g or fx t g, t = 1,..., T, where t is an index denoting

Chapter 5 Univariate time-series analysis () Chapter 5 Univariate time-series analysis 1 / 29 Time-Series Time-series is a sequence fx 1, x 2,..., x T g or fx t g, t = 1,..., T, where t is an index denoting

Linear Regression with One Regressor

Linear Regression with One Regressor Michael Ash Lecture 9 Linear Regression with One Regressor Review of Last Time 1. The Linear Regression Model The relationship between independent X and dependent Y

Linear Regression with One Regressor Michael Ash Lecture 9 Linear Regression with One Regressor Review of Last Time 1. The Linear Regression Model The relationship between independent X and dependent Y

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2017, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2017, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Describe

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2017, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (40 points) Answer briefly the following questions. 1. Describe

Discussion of No-Arbitrage Near-Cointegrated VAR(p) Term Structure Models, Term Premia and GDP Growth by C. Jardet, A. Monfort and F.

Term Structure Models, Term Premia and GDP Growth by C. Jardet, A. Monfort and F.") Discussion of No-Arbitrage Near-Cointegrated VAR(p) Term Structure Models, Term Premia and GDP Growth by C. Jardet, A. Monfort and F. Pegoraro R. Mark Reesor Department of Applied Mathematics The University

Discussion of No-Arbitrage Near-Cointegrated VAR(p) Term Structure Models, Term Premia and GDP Growth by C. Jardet, A. Monfort and F. Pegoraro R. Mark Reesor Department of Applied Mathematics The University

Combining Forecasts From Nested Models

Combining Forecasts From Nested Models Todd E. Clark and Michael W. McCracken* March 2006 RWP 06-02 Abstract: Motivated by the common finding that linear autoregressive models forecast better than models

Combining Forecasts From Nested Models Todd E. Clark and Michael W. McCracken* March 2006 RWP 06-02 Abstract: Motivated by the common finding that linear autoregressive models forecast better than models

Chapter 8. Markowitz Portfolio Theory. 8.1 Expected Returns and Covariance

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Chapter 8 Markowitz Portfolio Theory 8.1 Expected Returns and Covariance The main question in portfolio theory is the following: Given an initial capital V (0), and opportunities (buy or sell) in N securities

Economics 413: Economic Forecast and Analysis Department of Economics, Finance and Legal Studies University of Alabama

Problem Set #1 (Linear Regression) 1. The file entitled MONEYDEM.XLS contains quarterly values of seasonally adjusted U.S.3-month ( 3 ) and 1-year ( 1 ) treasury bill rates. Each series is measured over

Problem Set #1 (Linear Regression) 1. The file entitled MONEYDEM.XLS contains quarterly values of seasonally adjusted U.S.3-month ( 3 ) and 1-year ( 1 ) treasury bill rates. Each series is measured over

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay. Solutions to Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (42 pts) Answer briefly the following questions. 1. Questions

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2009, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (42 pts) Answer briefly the following questions. 1. Questions

Optimal Portfolio Inputs: Various Methods

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

Optimal Portfolio Inputs: Various Methods Prepared by Kevin Pei for The Fund @ Sprott Abstract: In this document, I will model and back test our portfolio with various proposed models. It goes without

APPLYING MULTIVARIATE

Swiss Society for Financial Market Research (pp. 201 211) MOMTCHIL POJARLIEV AND WOLFGANG POLASEK APPLYING MULTIVARIATE TIME SERIES FORECASTS FOR ACTIVE PORTFOLIO MANAGEMENT Momtchil Pojarliev, INVESCO

Swiss Society for Financial Market Research (pp. 201 211) MOMTCHIL POJARLIEV AND WOLFGANG POLASEK APPLYING MULTIVARIATE TIME SERIES FORECASTS FOR ACTIVE PORTFOLIO MANAGEMENT Momtchil Pojarliev, INVESCO

Rowan University Department of Electrical and Computer Engineering

Rowan University Department of Electrical and Computer Engineering Estimation and Detection Theory Fall 203 Practice EXAM Solution This is a closed book exam. One letter-size sheet is allowed. There are

Rowan University Department of Electrical and Computer Engineering Estimation and Detection Theory Fall 203 Practice EXAM Solution This is a closed book exam. One letter-size sheet is allowed. There are

Construction of daily hedonic housing indexes for apartments in Sweden

KTH ROYAL INSTITUTE OF TECHNOLOGY Construction of daily hedonic housing indexes for apartments in Sweden Mo Zheng Division of Building and Real Estate Economics School of Architecture and the Built Environment

KTH ROYAL INSTITUTE OF TECHNOLOGY Construction of daily hedonic housing indexes for apartments in Sweden Mo Zheng Division of Building and Real Estate Economics School of Architecture and the Built Environment

MTH6154 Financial Mathematics I Stochastic Interest Rates

MTH6154 Financial Mathematics I Stochastic Interest Rates Contents 4 Stochastic Interest Rates 45 4.1 Fixed Interest Rate Model............................ 45 4.2 Varying Interest Rate Model...........................

MTH6154 Financial Mathematics I Stochastic Interest Rates Contents 4 Stochastic Interest Rates 45 4.1 Fixed Interest Rate Model............................ 45 4.2 Varying Interest Rate Model...........................

Mathematics of Finance Final Preparation December 19. To be thoroughly prepared for the final exam, you should

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

Mathematics of Finance Final Preparation December 19 To be thoroughly prepared for the final exam, you should 1. know how to do the homework problems. 2. be able to provide (correct and complete!) definitions

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay. Solutions to Final Exam.

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2011, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (32 pts) Answer briefly the following questions. 1. Suppose

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2010, Mr. Ruey S. Tsay Solutions to Final Exam

The University of Chicago, Booth School of Business Business 410, Spring Quarter 010, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (4 pts) Answer briefly the following questions. 1. Questions 1

The University of Chicago, Booth School of Business Business 410, Spring Quarter 010, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (4 pts) Answer briefly the following questions. 1. Questions 1

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay. Solutions to Final Exam

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (30 pts) Answer briefly the following questions. 1. Suppose that

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay Solutions to Final Exam Problem A: (30 pts) Answer briefly the following questions. 1. Suppose that

Working Paper Series. Flow of conjunctural information and forecast of euro area economic activity. No 925 / August 2008

Working Paper Series No 925 / Flow of conjunctural information and forecast of euro area economic activity by Katja Drechsel and Laurent Maurin WORKING PAPER SERIES NO 925 / AUGUST 28 FLOW OF CONJUNCTURAL

Working Paper Series No 925 / Flow of conjunctural information and forecast of euro area economic activity by Katja Drechsel and Laurent Maurin WORKING PAPER SERIES NO 925 / AUGUST 28 FLOW OF CONJUNCTURAL

CHAPTER III METHODOLOGY

CHAPTER III METHODOLOGY 3.1 Description In this chapter, the calculation steps, which will be done in the analysis section, will be explained. The theoretical foundations and literature reviews are already

CHAPTER III METHODOLOGY 3.1 Description In this chapter, the calculation steps, which will be done in the analysis section, will be explained. The theoretical foundations and literature reviews are already

Subject CS1 Actuarial Statistics 1 Core Principles. Syllabus. for the 2019 exams. 1 June 2018

` Subject CS1 Actuarial Statistics 1 Core Principles Syllabus for the 2019 exams 1 June 2018 Copyright in this Core Reading is the property of the Institute and Faculty of Actuaries who are the sole distributors.

` Subject CS1 Actuarial Statistics 1 Core Principles Syllabus for the 2019 exams 1 June 2018 Copyright in this Core Reading is the property of the Institute and Faculty of Actuaries who are the sole distributors.

Lecture 3: Factor models in modern portfolio choice

Lecture 3: Factor models in modern portfolio choice Prof. Massimo Guidolin Portfolio Management Spring 2016 Overview The inputs of portfolio problems Using the single index model Multi-index models Portfolio

Lecture 3: Factor models in modern portfolio choice Prof. Massimo Guidolin Portfolio Management Spring 2016 Overview The inputs of portfolio problems Using the single index model Multi-index models Portfolio

Final Exam Suggested Solutions

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

University of Washington Fall 003 Department of Economics Eric Zivot Economics 483 Final Exam Suggested Solutions This is a closed book and closed note exam. However, you are allowed one page of handwritten

Homework #4 Suggested Solutions

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Homework #4 Suggested Solutions Problem 1. (7.2) The following table shows the nominal returns on the U.S. stocks and the rate

JEM034 Corporate Finance Winter Semester 2017/2018 Instructor: Olga Bychkova Homework #4 Suggested Solutions Problem 1. (7.2) The following table shows the nominal returns on the U.S. stocks and the rate

Application to Portfolio Theory and the Capital Asset Pricing Model

Appendix C Application to Portfolio Theory and the Capital Asset Pricing Model Exercise Solutions C.1 The random variables X and Y are net returns with the following bivariate distribution. y x 0 1 2 3

Appendix C Application to Portfolio Theory and the Capital Asset Pricing Model Exercise Solutions C.1 The random variables X and Y are net returns with the following bivariate distribution. y x 0 1 2 3

Jet Fuel-Heating Oil Futures Cross Hedging -Classroom Applications Using Bloomberg Terminal

Jet Fuel-Heating Oil Futures Cross Hedging -Classroom Applications Using Bloomberg Terminal Yuan Wen 1 * and Michael Ciaston 2 Abstract We illustrate how to collect data on jet fuel and heating oil futures

Jet Fuel-Heating Oil Futures Cross Hedging -Classroom Applications Using Bloomberg Terminal Yuan Wen 1 * and Michael Ciaston 2 Abstract We illustrate how to collect data on jet fuel and heating oil futures

FINC 430 TA Session 7 Risk and Return Solutions. Marco Sammon

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

FINC 430 TA Session 7 Risk and Return Solutions Marco Sammon Formulas for return and risk The expected return of a portfolio of two risky assets, i and j, is Expected return of asset - the percentage of

Case Study: Heavy-Tailed Distribution and Reinsurance Rate-making

Case Study: Heavy-Tailed Distribution and Reinsurance Rate-making May 30, 2016 The purpose of this case study is to give a brief introduction to a heavy-tailed distribution and its distinct behaviors in

Case Study: Heavy-Tailed Distribution and Reinsurance Rate-making May 30, 2016 The purpose of this case study is to give a brief introduction to a heavy-tailed distribution and its distinct behaviors in

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay. Solutions to Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (34 pts) Answer briefly the following questions. Each question has

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2012, Mr. Ruey S. Tsay Solutions to Midterm Problem A: (34 pts) Answer briefly the following questions. Each question has

Data Analysis and Statistical Methods Statistics 651

Data Analysis and Statistical Methods Statistics 651 http://www.stat.tamu.edu/~suhasini/teaching.html Lecture 10 (MWF) Checking for normality of the data using the QQplot Suhasini Subba Rao Checking for

Data Analysis and Statistical Methods Statistics 651 http://www.stat.tamu.edu/~suhasini/teaching.html Lecture 10 (MWF) Checking for normality of the data using the QQplot Suhasini Subba Rao Checking for

A Comparative Study of Various Forecasting Techniques in Predicting. BSE S&P Sensex

NavaJyoti, International Journal of Multi-Disciplinary Research Volume 1, Issue 1, August 2016 A Comparative Study of Various Forecasting Techniques in Predicting BSE S&P Sensex Dr. Jahnavi M 1 Assistant

NavaJyoti, International Journal of Multi-Disciplinary Research Volume 1, Issue 1, August 2016 A Comparative Study of Various Forecasting Techniques in Predicting BSE S&P Sensex Dr. Jahnavi M 1 Assistant

Window Width Selection for L 2 Adjusted Quantile Regression

Window Width Selection for L 2 Adjusted Quantile Regression Yoonsuh Jung, The Ohio State University Steven N. MacEachern, The Ohio State University Yoonkyung Lee, The Ohio State University Technical Report

Window Width Selection for L 2 Adjusted Quantile Regression Yoonsuh Jung, The Ohio State University Steven N. MacEachern, The Ohio State University Yoonkyung Lee, The Ohio State University Technical Report

Basic Regression Analysis with Time Series Data

with Time Series Data Chapter 10 Wooldridge: Introductory Econometrics: A Modern Approach, 5e The nature of time series data Temporal ordering of observations; may not be arbitrarily reordered Typical

with Time Series Data Chapter 10 Wooldridge: Introductory Econometrics: A Modern Approach, 5e The nature of time series data Temporal ordering of observations; may not be arbitrarily reordered Typical

Bayesian Linear Model: Gory Details

Bayesian Linear Model: Gory Details Pubh7440 Notes By Sudipto Banerjee Let y y i ] n i be an n vector of independent observations on a dependent variable (or response) from n experimental units. Associated

Bayesian Linear Model: Gory Details Pubh7440 Notes By Sudipto Banerjee Let y y i ] n i be an n vector of independent observations on a dependent variable (or response) from n experimental units. Associated

Optimal Window Selection for Forecasting in The Presence of Recent Structural Breaks

Optimal Window Selection for Forecasting in The Presence of Recent Structural Breaks Yongli Wang University of Leicester Econometric Research in Finance Workshop on 15 September 2017 SGH Warsaw School

Optimal Window Selection for Forecasting in The Presence of Recent Structural Breaks Yongli Wang University of Leicester Econometric Research in Finance Workshop on 15 September 2017 SGH Warsaw School

σ e, which will be large when prediction errors are Linear regression model

Linear regression model we assume that two quantitative variables, x and y, are linearly related; that is, the population of (x, y) pairs are related by an ideal population regression line y = α + βx +

Linear regression model we assume that two quantitative variables, x and y, are linearly related; that is, the population of (x, y) pairs are related by an ideal population regression line y = α + βx +

Economics 424/Applied Mathematics 540. Final Exam Solutions

University of Washington Summer 01 Department of Economics Eric Zivot Economics 44/Applied Mathematics 540 Final Exam Solutions I. Matrix Algebra and Portfolio Math (30 points, 5 points each) Let R i denote

University of Washington Summer 01 Department of Economics Eric Zivot Economics 44/Applied Mathematics 540 Final Exam Solutions I. Matrix Algebra and Portfolio Math (30 points, 5 points each) Let R i denote

CHAPTER 8: INDEX MODELS

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

Chapter 8 - Index odels CHATER 8: INDEX ODELS ROBLE SETS 1. The advantage of the index model, compared to the arkowitz procedure, is the vastly reduced number of estimates required. In addition, the large

MEASURING PORTFOLIO RISKS USING CONDITIONAL COPULA-AR-GARCH MODEL

MEASURING PORTFOLIO RISKS USING CONDITIONAL COPULA-AR-GARCH MODEL Isariya Suttakulpiboon MSc in Risk Management and Insurance Georgia State University, 30303 Atlanta, Georgia Email: suttakul.i@gmail.com,

MEASURING PORTFOLIO RISKS USING CONDITIONAL COPULA-AR-GARCH MODEL Isariya Suttakulpiboon MSc in Risk Management and Insurance Georgia State University, 30303 Atlanta, Georgia Email: suttakul.i@gmail.com,

High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]

![High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]](/thumbs/79/79153367.jpg "High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5]") 1 High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5] High-frequency data have some unique characteristics that do not appear in lower frequencies. At this class we have: Nonsynchronous

1 High-Frequency Data Analysis and Market Microstructure [Tsay (2005), chapter 5] High-frequency data have some unique characteristics that do not appear in lower frequencies. At this class we have: Nonsynchronous

Problems and Solutions

1 CHAPTER 1 Problems 1.1 Problems on Bonds Exercise 1.1 On 12/04/01, consider a fixed-coupon bond whose features are the following: face value: $1,000 coupon rate: 8% coupon frequency: semiannual maturity:

1 CHAPTER 1 Problems 1.1 Problems on Bonds Exercise 1.1 On 12/04/01, consider a fixed-coupon bond whose features are the following: face value: $1,000 coupon rate: 8% coupon frequency: semiannual maturity:

We consider three zero-coupon bonds (strips) with the following features: Bond Maturity (years) Price Bond Bond Bond

with the following features: Bond Maturity (years) Price Bond Bond Bond") 15 3 CHAPTER 3 Problems Exercise 3.1 We consider three zero-coupon bonds (strips) with the following features: Each strip delivers $100 at maturity. Bond Maturity (years) Price Bond 1 1 96.43 Bond 2 2

15 3 CHAPTER 3 Problems Exercise 3.1 We consider three zero-coupon bonds (strips) with the following features: Each strip delivers $100 at maturity. Bond Maturity (years) Price Bond 1 1 96.43 Bond 2 2

MODEL SELECTION CRITERIA IN R:

1. R 2 statistics We may use MODEL SELECTION CRITERIA IN R R 2 = SS R SS T = 1 SS Res SS T or R 2 Adj = 1 SS Res/(n p) SS T /(n 1) = 1 ( ) n 1 (1 R 2 ). n p where p is the total number of parameters. R

1. R 2 statistics We may use MODEL SELECTION CRITERIA IN R R 2 = SS R SS T = 1 SS Res SS T or R 2 Adj = 1 SS Res/(n p) SS T /(n 1) = 1 ( ) n 1 (1 R 2 ). n p where p is the total number of parameters. R

Intro to GLM Day 2: GLM and Maximum Likelihood

Intro to GLM Day 2: GLM and Maximum Likelihood Federico Vegetti Central European University ECPR Summer School in Methods and Techniques 1 / 32 Generalized Linear Modeling 3 steps of GLM 1. Specify the

Intro to GLM Day 2: GLM and Maximum Likelihood Federico Vegetti Central European University ECPR Summer School in Methods and Techniques 1 / 32 Generalized Linear Modeling 3 steps of GLM 1. Specify the

Chapter 9: Sampling Distributions

Chapter 9: Sampling Distributions 9. Introduction This chapter connects the material in Chapters 4 through 8 (numerical descriptive statistics, sampling, and probability distributions, in particular) with

Chapter 9: Sampling Distributions 9. Introduction This chapter connects the material in Chapters 4 through 8 (numerical descriptive statistics, sampling, and probability distributions, in particular) with

Amath 546/Econ 589 Univariate GARCH Models

Amath 546/Econ 589 Univariate GARCH Models Eric Zivot April 24, 2013 Lecture Outline Conditional vs. Unconditional Risk Measures Empirical regularities of asset returns Engle s ARCH model Testing for ARCH

Amath 546/Econ 589 Univariate GARCH Models Eric Zivot April 24, 2013 Lecture Outline Conditional vs. Unconditional Risk Measures Empirical regularities of asset returns Engle s ARCH model Testing for ARCH

Regularizing Bayesian Predictive Regressions. Guanhao Feng

Regularizing Bayesian Predictive Regressions Guanhao Feng Booth School of Business, University of Chicago R/Finance 2017 (Joint work with Nicholas Polson) What do we study? A Bayesian predictive regression

Regularizing Bayesian Predictive Regressions Guanhao Feng Booth School of Business, University of Chicago R/Finance 2017 (Joint work with Nicholas Polson) What do we study? A Bayesian predictive regression

Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models

The Financial Review 37 (2002) 93--104 Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models Mohammad Najand Old Dominion University Abstract The study examines the relative ability

The Financial Review 37 (2002) 93--104 Forecasting Stock Index Futures Price Volatility: Linear vs. Nonlinear Models Mohammad Najand Old Dominion University Abstract The study examines the relative ability

درس هفتم یادگیري ماشین. (Machine Learning) دانشگاه فردوسی مشهد دانشکده مهندسی رضا منصفی

دانشگاه فردوسی مشهد دانشکده مهندسی رضا منصفی") یادگیري ماشین توزیع هاي نمونه و تخمین نقطه اي پارامترها Sampling Distributions and Point Estimation of Parameter (Machine Learning) دانشگاه فردوسی مشهد دانشکده مهندسی رضا منصفی درس هفتم 1 Outline Introduction

یادگیري ماشین توزیع هاي نمونه و تخمین نقطه اي پارامترها Sampling Distributions and Point Estimation of Parameter (Machine Learning) دانشگاه فردوسی مشهد دانشکده مهندسی رضا منصفی درس هفتم 1 Outline Introduction

Chapter 8: Sampling distributions of estimators Sections

Chapter 8 continued Chapter 8: Sampling distributions of estimators Sections 8.1 Sampling distribution of a statistic 8.2 The Chi-square distributions 8.3 Joint Distribution of the sample mean and sample

Chapter 8 continued Chapter 8: Sampling distributions of estimators Sections 8.1 Sampling distribution of a statistic 8.2 The Chi-square distributions 8.3 Joint Distribution of the sample mean and sample

Introduction to the Maximum Likelihood Estimation Technique. September 24, 2015

Introduction to the Maximum Likelihood Estimation Technique September 24, 2015 So far our Dependent Variable is Continuous That is, our outcome variable Y is assumed to follow a normal distribution having

Introduction to the Maximum Likelihood Estimation Technique September 24, 2015 So far our Dependent Variable is Continuous That is, our outcome variable Y is assumed to follow a normal distribution having

Chapter 7: Estimation Sections

1 / 40 Chapter 7: Estimation Sections 7.1 Statistical Inference Bayesian Methods: Chapter 7 7.2 Prior and Posterior Distributions 7.3 Conjugate Prior Distributions 7.4 Bayes Estimators Frequentist Methods:

1 / 40 Chapter 7: Estimation Sections 7.1 Statistical Inference Bayesian Methods: Chapter 7 7.2 Prior and Posterior Distributions 7.3 Conjugate Prior Distributions 7.4 Bayes Estimators Frequentist Methods:

Name: 1. Use the data from the following table to answer the questions that follow: (10 points)

") Economics 345 Mid-Term Exam October 8, 2003 Name: Directions: You have the full period (7:20-10:00) to do this exam, though I suspect it won t take that long for most students. You may consult any materials,

Economics 345 Mid-Term Exam October 8, 2003 Name: Directions: You have the full period (7:20-10:00) to do this exam, though I suspect it won t take that long for most students. You may consult any materials,

Multiple Regression. Review of Regression with One Predictor

Fall Semester, 2001 Statistics 621 Lecture 4 Robert Stine 1 Preliminaries Multiple Regression Grading on this and other assignments Assignment will get placed in folder of first member of Learning Team.

Fall Semester, 2001 Statistics 621 Lecture 4 Robert Stine 1 Preliminaries Multiple Regression Grading on this and other assignments Assignment will get placed in folder of first member of Learning Team.

Black-Litterman Model

Institute of Financial and Actuarial Mathematics at Vienna University of Technology Seminar paper Black-Litterman Model by: Tetyana Polovenko Supervisor: Associate Prof. Dipl.-Ing. Dr.techn. Stefan Gerhold

Institute of Financial and Actuarial Mathematics at Vienna University of Technology Seminar paper Black-Litterman Model by: Tetyana Polovenko Supervisor: Associate Prof. Dipl.-Ing. Dr.techn. Stefan Gerhold

How High A Hedge Is High Enough? An Empirical Test of NZSE10 Futures.

How High A Hedge Is High Enough? An Empirical Test of NZSE1 Futures. Liping Zou, William R. Wilson 1 and John F. Pinfold Massey University at Albany, Private Bag 1294, Auckland, New Zealand Abstract Undoubtedly,

How High A Hedge Is High Enough? An Empirical Test of NZSE1 Futures. Liping Zou, William R. Wilson 1 and John F. Pinfold Massey University at Albany, Private Bag 1294, Auckland, New Zealand Abstract Undoubtedly,

A VALUATION MODEL FOR INDETERMINATE CONVERTIBLES by Jayanth Rama Varma

A VALUATION MODEL FOR INDETERMINATE CONVERTIBLES by Jayanth Rama Varma Abstract Many issues of convertible debentures in India in recent years provide for a mandatory conversion of the debentures into

A VALUATION MODEL FOR INDETERMINATE CONVERTIBLES by Jayanth Rama Varma Abstract Many issues of convertible debentures in India in recent years provide for a mandatory conversion of the debentures into

Homework Assignments

Homework Assignments Week 1 (p. 57) #4.1, 4., 4.3 Week (pp 58 6) #4.5, 4.6, 4.8(a), 4.13, 4.0, 4.6(b), 4.8, 4.31, 4.34 Week 3 (pp 15 19) #1.9, 1.1, 1.13, 1.15, 1.18 (pp 9 31) #.,.6,.9 Week 4 (pp 36 37)

Homework Assignments Week 1 (p. 57) #4.1, 4., 4.3 Week (pp 58 6) #4.5, 4.6, 4.8(a), 4.13, 4.0, 4.6(b), 4.8, 4.31, 4.34 Week 3 (pp 15 19) #1.9, 1.1, 1.13, 1.15, 1.18 (pp 9 31) #.,.6,.9 Week 4 (pp 36 37)

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2013, Mr. Ruey S. Tsay. Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2013, Mr. Ruey S. Tsay Midterm ChicagoBooth Honor Code: I pledge my honor that I have not violated the Honor Code during this

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2013, Mr. Ruey S. Tsay Midterm ChicagoBooth Honor Code: I pledge my honor that I have not violated the Honor Code during this

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2013, Mr. Ruey S. Tsay. Final Exam

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2013, Mr. Ruey S. Tsay Final Exam Booth Honor Code: I pledge my honor that I have not violated the Honor Code during this

The University of Chicago, Booth School of Business Business 41202, Spring Quarter 2013, Mr. Ruey S. Tsay Final Exam Booth Honor Code: I pledge my honor that I have not violated the Honor Code during this

Maximum Likelihood Estimation

Maximum Likelihood Estimation EPSY 905: Fundamentals of Multivariate Modeling Online Lecture #6 EPSY 905: Maximum Likelihood In This Lecture The basics of maximum likelihood estimation Ø The engine that

Maximum Likelihood Estimation EPSY 905: Fundamentals of Multivariate Modeling Online Lecture #6 EPSY 905: Maximum Likelihood In This Lecture The basics of maximum likelihood estimation Ø The engine that

Estimation after Model Selection

Estimation after Model Selection Vanja M. Dukić Department of Health Studies University of Chicago E-Mail: vanja@uchicago.edu Edsel A. Peña* Department of Statistics University of South Carolina E-Mail:

Estimation after Model Selection Vanja M. Dukić Department of Health Studies University of Chicago E-Mail: vanja@uchicago.edu Edsel A. Peña* Department of Statistics University of South Carolina E-Mail:

Statistics for Business and Economics

Statistics for Business and Economics Chapter 7 Estimation: Single Population Copyright 010 Pearson Education, Inc. Publishing as Prentice Hall Ch. 7-1 Confidence Intervals Contents of this chapter: Confidence

Statistics for Business and Economics Chapter 7 Estimation: Single Population Copyright 010 Pearson Education, Inc. Publishing as Prentice Hall Ch. 7-1 Confidence Intervals Contents of this chapter: Confidence

Effects of skewness and kurtosis on model selection criteria

Economics Letters 59 (1998) 17 Effects of skewness and kurtosis on model selection criteria * Sıdıka Başçı, Asad Zaman Department of Economics, Bilkent University, 06533, Bilkent, Ankara, Turkey Received

Economics Letters 59 (1998) 17 Effects of skewness and kurtosis on model selection criteria * Sıdıka Başçı, Asad Zaman Department of Economics, Bilkent University, 06533, Bilkent, Ankara, Turkey Received

**BEGINNING OF EXAMINATION** A random sample of five observations from a population is:

**BEGINNING OF EXAMINATION** 1. You are given: (i) A random sample of five observations from a population is: 0.2 0.7 0.9 1.1 1.3 (ii) You use the Kolmogorov-Smirnov test for testing the null hypothesis,

**BEGINNING OF EXAMINATION** 1. You are given: (i) A random sample of five observations from a population is: 0.2 0.7 0.9 1.1 1.3 (ii) You use the Kolmogorov-Smirnov test for testing the null hypothesis,

Categorical Outcomes. Statistical Modelling in Stata: Categorical Outcomes. R by C Table: Example. Nominal Outcomes. Mark Lunt.

Categorical Outcomes Statistical Modelling in Stata: Categorical Outcomes Mark Lunt Arthritis Research UK Epidemiology Unit University of Manchester Nominal Ordinal 28/11/2017 R by C Table: Example Categorical,

Categorical Outcomes Statistical Modelling in Stata: Categorical Outcomes Mark Lunt Arthritis Research UK Epidemiology Unit University of Manchester Nominal Ordinal 28/11/2017 R by C Table: Example Categorical,

u (x) < 0. and if you believe in diminishing return of the wealth, then you would require

< 0. and if you believe in diminishing return of the wealth, then you would require") Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Chapter 8 Markowitz Portfolio Theory 8.7 Investor Utility Functions People are always asked the question: would more money make you happier? The answer is usually yes. The next question is how much more

Study Guide on Testing the Assumptions of Age-to-Age Factors - G. Stolyarov II 1

Study Guide on Testing the Assumptions of Age-to-Age Factors - G. Stolyarov II 1 Study Guide on Testing the Assumptions of Age-to-Age Factors for the Casualty Actuarial Society (CAS) Exam 7 and Society

Study Guide on Testing the Assumptions of Age-to-Age Factors - G. Stolyarov II 1 Study Guide on Testing the Assumptions of Age-to-Age Factors for the Casualty Actuarial Society (CAS) Exam 7 and Society

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay. Midterm

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay Midterm ChicagoBooth Honor Code: I pledge my honor that I have not violated the Honor Code during this

Booth School of Business, University of Chicago Business 41202, Spring Quarter 2016, Mr. Ruey S. Tsay Midterm ChicagoBooth Honor Code: I pledge my honor that I have not violated the Honor Code during this

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty Gary Schurman MB, CFA August, 2012 The Capital Asset Pricing Model CAPM is used to estimate the required rate of return

Derivation Of The Capital Asset Pricing Model Part I - A Single Source Of Uncertainty Gary Schurman MB, CFA August, 2012 The Capital Asset Pricing Model CAPM is used to estimate the required rate of return

Final Exam - section 1. Thursday, December hours, 30 minutes

Econometrics, ECON312 San Francisco State University Michael Bar Fall 2013 Final Exam - section 1 Thursday, December 19 1 hours, 30 minutes Name: Instructions 1. This is closed book, closed notes exam.

Econometrics, ECON312 San Francisco State University Michael Bar Fall 2013 Final Exam - section 1 Thursday, December 19 1 hours, 30 minutes Name: Instructions 1. This is closed book, closed notes exam.

P2.T8. Risk Management & Investment Management. Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, 3rd Edition.

P2.T8. Risk Management & Investment Management Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, 3rd Edition. Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM and Deepa Raju

P2.T8. Risk Management & Investment Management Jorion, Value at Risk: The New Benchmark for Managing Financial Risk, 3rd Edition. Bionic Turtle FRM Study Notes By David Harper, CFA FRM CIPM and Deepa Raju

Chapter 7: Estimation Sections

1 / 31 : Estimation Sections 7.1 Statistical Inference Bayesian Methods: 7.2 Prior and Posterior Distributions 7.3 Conjugate Prior Distributions 7.4 Bayes Estimators Frequentist Methods: 7.5 Maximum Likelihood

1 / 31 : Estimation Sections 7.1 Statistical Inference Bayesian Methods: 7.2 Prior and Posterior Distributions 7.3 Conjugate Prior Distributions 7.4 Bayes Estimators Frequentist Methods: 7.5 Maximum Likelihood

The Relationship between Foreign Direct Investment and Economic Development An Empirical Analysis of Shanghai 's Data Based on

The Relationship between Foreign Direct Investment and Economic Development An Empirical Analysis of Shanghai 's Data Based on 2004-2015 Jiaqi Wang School of Shanghai University, Shanghai 200444, China

The Relationship between Foreign Direct Investment and Economic Development An Empirical Analysis of Shanghai 's Data Based on 2004-2015 Jiaqi Wang School of Shanghai University, Shanghai 200444, China

Discussion of The Term Structure of Growth-at-Risk

Discussion of The Term Structure of Growth-at-Risk Frank Schorfheide University of Pennsylvania, CEPR, NBER, PIER March 2018 Pushing the Frontier of Central Bank s Macro Modeling Preliminaries This paper

Discussion of The Term Structure of Growth-at-Risk Frank Schorfheide University of Pennsylvania, CEPR, NBER, PIER March 2018 Pushing the Frontier of Central Bank s Macro Modeling Preliminaries This paper

Monetary Economics Final Exam

316-466 Monetary Economics Final Exam 1. Flexible-price monetary economics (90 marks). Consider a stochastic flexibleprice money in the utility function model. Time is discrete and denoted t =0, 1,...

316-466 Monetary Economics Final Exam 1. Flexible-price monetary economics (90 marks). Consider a stochastic flexibleprice money in the utility function model. Time is discrete and denoted t =0, 1,...

Homework Assignments

Homework Assignments Week 1 (p 57) #4.1, 4., 4.3 Week (pp 58-6) #4.5, 4.6, 4.8(a), 4.13, 4.0, 4.6(b), 4.8, 4.31, 4.34 Week 3 (pp 15-19) #1.9, 1.1, 1.13, 1.15, 1.18 (pp 9-31) #.,.6,.9 Week 4 (pp 36-37)

Homework Assignments Week 1 (p 57) #4.1, 4., 4.3 Week (pp 58-6) #4.5, 4.6, 4.8(a), 4.13, 4.0, 4.6(b), 4.8, 4.31, 4.34 Week 3 (pp 15-19) #1.9, 1.1, 1.13, 1.15, 1.18 (pp 9-31) #.,.6,.9 Week 4 (pp 36-37)

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS. 20 th May Subject CT3 Probability & Mathematical Statistics

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 20 th May 2013 Subject CT3 Probability & Mathematical Statistics Time allowed: Three Hours (10.00 13.00) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1.

INSTITUTE OF ACTUARIES OF INDIA EXAMINATIONS 20 th May 2013 Subject CT3 Probability & Mathematical Statistics Time allowed: Three Hours (10.00 13.00) Total Marks: 100 INSTRUCTIONS TO THE CANDIDATES 1.

Model Construction & Forecast Based Portfolio Allocation:

QBUS6830 Financial Time Series and Forecasting Model Construction & Forecast Based Portfolio Allocation: Is Quantitative Method Worth It? Members: Bowei Li (303083) Wenjian Xu (308077237) Xiaoyun Lu (3295347)

QBUS6830 Financial Time Series and Forecasting Model Construction & Forecast Based Portfolio Allocation: Is Quantitative Method Worth It? Members: Bowei Li (303083) Wenjian Xu (308077237) Xiaoyun Lu (3295347)

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay. Final Exam

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay Final Exam GSB Honor Code: I pledge my honor that I have not violated the Honor Code during this

Graduate School of Business, University of Chicago Business 41202, Spring Quarter 2007, Mr. Ruey S. Tsay Final Exam GSB Honor Code: I pledge my honor that I have not violated the Honor Code during this

8.1 Estimation of the Mean and Proportion

8.1 Estimation of the Mean and Proportion Statistical inference enables us to make judgments about a population on the basis of sample information. The mean, standard deviation, and proportions of a population

8.1 Estimation of the Mean and Proportion Statistical inference enables us to make judgments about a population on the basis of sample information. The mean, standard deviation, and proportions of a population

Efficient Management of Multi-Frequency Panel Data with Stata. Department of Economics, Boston College

Efficient Management of Multi-Frequency Panel Data with Stata Christopher F Baum Department of Economics, Boston College May 2001 Prepared for United Kingdom Stata User Group Meeting http://repec.org/nasug2001/baum.uksug.pdf

Efficient Management of Multi-Frequency Panel Data with Stata Christopher F Baum Department of Economics, Boston College May 2001 Prepared for United Kingdom Stata User Group Meeting http://repec.org/nasug2001/baum.uksug.pdf

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities - The models we studied earlier include only real variables and relative prices. We now extend these models to have

Topic 4: Introduction to Exchange Rates Part 1: Definitions and empirical regularities - The models we studied earlier include only real variables and relative prices. We now extend these models to have

Internet Appendix: High Frequency Trading and Extreme Price Movements

Internet Appendix: High Frequency Trading and Extreme Price Movements This appendix includes two parts. First, it reports the results from the sample of EPMs defined as the 99.9 th percentile of raw returns.

Internet Appendix: High Frequency Trading and Extreme Price Movements This appendix includes two parts. First, it reports the results from the sample of EPMs defined as the 99.9 th percentile of raw returns.

Identification and Estimation of Dynamic Games when Players Belief Are Not in Equilibrium

Identification and Estimation of Dynamic Games when Players Belief Are Not in Equilibrium A Short Review of Aguirregabiria and Magesan (2010) January 25, 2012 1 / 18 Dynamics of the game Two players, {i,

Identification and Estimation of Dynamic Games when Players Belief Are Not in Equilibrium A Short Review of Aguirregabiria and Magesan (2010) January 25, 2012 1 / 18 Dynamics of the game Two players, {i,

PARAMETRIC AND NON-PARAMETRIC BOOTSTRAP: A SIMULATION STUDY FOR A LINEAR REGRESSION WITH RESIDUALS FROM A MIXTURE OF LAPLACE DISTRIBUTIONS

PARAMETRIC AND NON-PARAMETRIC BOOTSTRAP: A SIMULATION STUDY FOR A LINEAR REGRESSION WITH RESIDUALS FROM A MIXTURE OF LAPLACE DISTRIBUTIONS Melfi Alrasheedi School of Business, King Faisal University, Saudi

PARAMETRIC AND NON-PARAMETRIC BOOTSTRAP: A SIMULATION STUDY FOR A LINEAR REGRESSION WITH RESIDUALS FROM A MIXTURE OF LAPLACE DISTRIBUTIONS Melfi Alrasheedi School of Business, King Faisal University, Saudi

Log-linear Modeling Under Generalized Inverse Sampling Scheme

Log-linear Modeling Under Generalized Inverse Sampling Scheme Soumi Lahiri (1) and Sunil Dhar (2) (1) Department of Mathematical Sciences New Jersey Institute of Technology University Heights, Newark,

Log-linear Modeling Under Generalized Inverse Sampling Scheme Soumi Lahiri (1) and Sunil Dhar (2) (1) Department of Mathematical Sciences New Jersey Institute of Technology University Heights, Newark,

Copyright 2011 Pearson Education, Inc. Publishing as Addison-Wesley.

Appendix: Statistics in Action Part I Financial Time Series 1. These data show the effects of stock splits. If you investigate further, you ll find that most of these splits (such as in May 1970) are 3-for-1

Appendix: Statistics in Action Part I Financial Time Series 1. These data show the effects of stock splits. If you investigate further, you ll find that most of these splits (such as in May 1970) are 3-for-1

Institute of Actuaries of India Subject CT6 Statistical Methods

Institute of Actuaries of India Subject CT6 Statistical Methods For 2014 Examinations Aim The aim of the Statistical Methods subject is to provide a further grounding in mathematical and statistical techniques

Institute of Actuaries of India Subject CT6 Statistical Methods For 2014 Examinations Aim The aim of the Statistical Methods subject is to provide a further grounding in mathematical and statistical techniques

Equity, Vacancy, and Time to Sale in Real Estate.

Title: Author: Address: E-Mail: Equity, Vacancy, and Time to Sale in Real Estate. Thomas W. Zuehlke Department of Economics Florida State University Tallahassee, Florida 32306 U.S.A. tzuehlke@mailer.fsu.edu

Title: Author: Address: E-Mail: Equity, Vacancy, and Time to Sale in Real Estate. Thomas W. Zuehlke Department of Economics Florida State University Tallahassee, Florida 32306 U.S.A. tzuehlke@mailer.fsu.edu

Assessing Model Stability Using Recursive Estimation and Recursive Residuals

Assessing Model Stability Using Recursive Estimation and Recursive Residuals Our forecasting procedure cannot be expected to produce good forecasts if the forecasting model that we constructed was stable

Assessing Model Stability Using Recursive Estimation and Recursive Residuals Our forecasting procedure cannot be expected to produce good forecasts if the forecasting model that we constructed was stable

Chapter 14. Descriptive Methods in Regression and Correlation. Copyright 2016, 2012, 2008 Pearson Education, Inc. Chapter 14, Slide 1

Chapter 14 Descriptive Methods in Regression and Correlation Copyright 2016, 2012, 2008 Pearson Education, Inc. Chapter 14, Slide 1 Section 14.1 Linear Equations with One Independent Variable Copyright

Chapter 14 Descriptive Methods in Regression and Correlation Copyright 2016, 2012, 2008 Pearson Education, Inc. Chapter 14, Slide 1 Section 14.1 Linear Equations with One Independent Variable Copyright

Public Economics. Contact Information

Public Economics K.Peren Arin Contact Information Office Hours:After class! All communication in English please! 1 Introduction The year is 1030 B.C. For decades, Israeli tribes have been living without

Public Economics K.Peren Arin Contact Information Office Hours:After class! All communication in English please! 1 Introduction The year is 1030 B.C. For decades, Israeli tribes have been living without