LCH.CLEARNET LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE

|

|

|

- Bonnie Austin

- 5 years ago

- Views:

Transcription

1

2

3

4

5 LCH.CLEARNET LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE

6 Clearing House Procedures Clear Service principles specified in the Clear Transaction submitted to the Clearing House and as set forth in the ISDA 2006 Definitions Floating Rate The Floating Rate Options shall have the meanings given to them in the ISDA 2000 Definitions or the ISDA 2006 Definitions, as applicable, provided that where the rate for a Reset Date is not available following the application of such definitions, the Clearing House will determine an applicable rate at its sole discretion. Each such rate will be provided in regular reports by the Clearing House to members. (a) Applying Floating Rate Options The Clearing House will determine the rate applicable on a Reset Date in respect of a Clear Contract as set out in the paragraph above. Such rate will be applied to the appropriate floating legs and the coupon payments calculated. The coupon payments will be adjusted to fall on actual business days according to the Calendar(s) and Business Day Convention specified. (b) Negative Rate Method SCMs should note the provisions of section 3.3 of Part A of the Product Specific Contract Terms and Eligibility Criteria Manual as published on the Clearing House's website regarding the applicability of the Negative Rate Method to a Clear Contract. Clear Clearing Members may, in the circumstances, wish to ensure that any trade submitted for registration follows that Negative interest Rate Method Calculation of Inflation Indices (a) The Index level used for calculating the Floating Rate is determined according to the 2008 ISDA Inflation Definitions in respect of the following indices (or successor indices from time to time):. The descriptions of the relevant Indices for the purposes of these calculations are as follows: (i) (ii) EUR Excluding Tobacco-Non-revised Consumer Price Index means the Nnon-revised Index of Consumer Prices excluding Tobacco, or relevant Successor Index, measuring the rate of inflation in the European Monetary Union excluding tobacco, expressed as an index and published by the relevant Index Sponsor. The first publication or announcement of a level of such index for a Reference Month shall be final and conclusive and later revisions to the level for such Reference Month will not be used in any calculations.; FRC Excluding Tobacco-Non-Revised Consumer Price Index means the Nnon-revised Index of Consumer Prices LCH Limited January 2017

7 Clearing House Procedures Clear Service excluding Tobacco, or relevant Successor Index, measuring the rate of inflation in France excluding tobacco expressed as an index and published by the relevant Index Sponsor. The first publication or announcement of a level of such index for a Reference Month shall be final and conclusive and later revisions to the level for such Reference Month will not be used in any calculations.; (iii) (iv) GBP Non-revised Retail Price Index (UKRPI) means the Nnon-revised Retail Price Index All Items in the United Kingdom, or relevant Successor Index, measuring the all items rate of inflation in the United; and Kingdom expressed as an index and published by the relevant Index Sponsor. The first publication or announcement of a level of such index for a Reference Month shall be final and conclusive and later revisions to the level for such Reference Month will not be used in any calculations. USA Nnon-revised index of Consumer Prices for All Urban Consumer (CPI-U) before seasonal adjustment in the United Stateson-revised Consumer Price Index Urban (CPI-U) means the Non-revised index of Consumer Prices for All Urban Consumers (CPI-U) before seasonal adjustment, or relevant Successor Index, measuring the rate of inflation in the United States expressed as an index and published by the relevant Index Sponsor. The first publication or announcement of a level of such index for such Reference Month shall be final and conclusive and later revisions to the level for such Reference Month will not be used in any calculations Index Final 1.9 Initial Margin The Clearing House will calculate the Index Final by taking the relevant Index level for the applicable Reference Month. In the event of no Index being available the Clearing House will, at its sole discretion, determine a value for the Index level. The Clearing House will require SCMs to transfer Collateral in respect of their initial margin obligations. This amount will be determined by the prevailing market conditions and the expected time to close out the portfolio. The Portfolio Approach to Rate Scenarios (PAIRS) will be used to calculate initial margin requirements for Clear Contracts. Separate initial margin calculations are performed for an SCM's Proprietary Accounts and for each Individual Segregated Client Account and Omnibus Segregated Account (other than an Affiliated Client Omnibus Gross Segregated Account). In respect of each Omnibus Gross Segregated Clearing Client (other than a Combined Omnibus Gross Segregated Clearing Client) separate initial margin calculations are performed in respect of the Clear Contracts entered into by the relevant SCM on behalf of LCH Limited January 2017

8

9 FCM PROCEDURES OF THE CLEARING HOUSE LCH LIMITED

10 FCM Procedures FCM Clear Day count fractions will be applied to deal legs independently as they are communicated via the matched format message. Where the FCM Clear Transaction is submitted under the ISDA 2006 Definitions, the Clearing House will calculate Day Count Fractions in accordance with the principles specified in the FCM Clear Transaction submitted to the Clearing House and as set forth in the ISDA 2006 Definitions. (l) Floating Rate The Floating Rate Options shall have the meanings given to them in the ISDA 2000 Definitions or the ISDA 2006 Definitions, as applicable, provided that where the rate for a Reset Date is not available following the application of such definitions, the Clearing House will determine an applicable rate at its sole discretion. Each such rate will be provided in regular reports by the Clearing House to members. (m) Applying Floating Rate Options The Clearing House will determine the rate applicable on a Reset Date in respect of a Clear Contract as set out in paragraph (l) above. Such Rate will be applied to the appropriate floating legs and the coupon payments calculated. The coupon payments will be adjusted to fall on actual Business according to the Calendar(s) and Business Day Convention specified. (n) Negative Rate Method FCM Clearing Member should note the provisions of Section 3.2 of Part A of Schedule 1 to the FCM Product Specific Contract Terms And Eligibility Criteria Manual regarding the applicability of the Negative Rate Method, to an FCM Clear Contract. FCM Clearing Members may, in the circumstances, wish to ensure that any trade submitted for registration follows that Negative interest Rate Method. (o) Calculation of Inflation Indices The Index level used for calculating the Floating Rate is determined according to the 2006 ISDA Definitions. The descriptions of the relevant Indices for the purposes of these calculations are as follows in respect of the following indices (or successor indices from time to time): (i) EUR Excluding Tobacco-Non-revised Consumer Price Index means the Nnon-revised Index of Consumer Prices excluding Tobacco, or relevant Successor Index, measuring the rate of inflation in the European Monetary Union excluding tobacco, expressed as an index and published by the relevant Index Sponsor. The first publication or announcement of a level March 2017

11 FCM Procedures FCM Clear of such index for a Reference Month shall be final and conclusive and later revisions to the level for such Reference Month will not be used in any calculations.; (ii) (iii) (iv) FRC Excluding Tobacco-Non-Revised Consumer Price Index means the Nonnon-revised Index of Consumer Prices excluding Tobacco, or relevant Successor Index, measuring the rate of inflation in France excluding tobacco expressed as an index and published by the relevant Index Sponsor. The first publication or announcement of a level of such index for a Reference Month shall be final and conclusive and later revisions to the level for such Reference Month will not be used in any calculations.; GBP Non-revised Retail Price Index (UKRPI) means the Nnon-revised Retail Price Index All Items in the United Kingdom, or relevant Successor Index, measuring the all items rate of inflation in the United Kingdom expressed as an index and published by the relevant Index Sponsor. The first publication or announcement of a level of such index for a Reference Month shall be final and conclusive and later revisions to the level for such Reference Month will not be used in any calculations.; and USD Non-revised Consumer Price Index Urban (CPI- U) means the Nnon-revised index of Consumer Prices for All Urban Consumers (CPI-U) before seasonal adjustment, or relevant Successor Index, measuring the rate of inflation in the United States expressed as an index and published by the relevant Index Sponsor. The first publication or announcement of a level of such index for such Reference Month shall be final and conclusive and later revisions to the level for such Reference Month will not be used in any calculations. (p) Index Final Initial Margin The Clearing House shall calculate the Index Final by taking the relevant Index level for the applicable Reference Month. In the event of no Index level being available the Clearing House shall, in its sole discretion, determine a value for the Index level. The Clearing House will require FCM Clearing Members to furnish it with Initial Margin. This amount will be determined by the prevailing market conditions and the expected time to close out the portfolio. The Portfolio Approach to Rate Scenarios (PAIRS) will be used to calculate Initial Margin requirements for FCM Clear Contracts. Separate Initial Margin calculations are performed for an FCM Clearing Member's house H and client C accounts and, within a C account, March 2017

12

13 Tenor Amendments March 2017 PRODUCT SPECIFIC CONTRACT TERMS AND ELIGIBILITY CRITERIA MANUAL

14 Product Specific Contract Terms and Eligibility Criteria Manual (b) notional interest rate swaps having the characteristics set out in the table below: Instrument Acceptable Currencies USD Acceptable Rate Options (as further set out in Article 7.1 of the 2000 ISDA Definitions and Article 7.1 of the 2006 ISDA Definitions) USD-LIBOR- Types Rate Maximum Residual Term 18,675 Amount (Min - Max of the relevant unit) USD USD-LIBOR- Basis 18,675 EUR EUR-LIBOR- Rate 18,675 EUR EUR-LIBOR- Basis 18,675 EUR EUR- EURIBOR- REUTERS Rate 18,675 EUR EUR- EURIBOR- REUTERS Basis 18,675 GBP GBP-LIBOR- Rate 18,675 GBP GBP-LIBOR- Basis 18,675 CAD CAD-CDOR- BA Rate 18,67511,375 CAD CAD-CDOR- BA Basis 18,67511,375 JPY JPY-LIBOR- Rate 18,67515,025 JPY JPY-LIBOR- Basis 18,67515,025 AUD AUD-BBR- BBSW Rate 11,375 AUD AUD-BBR- BBSW Basis 11,375 NOK NOK-NIBOR- OIBOR Rate 5,700 NOK NOK-NIBOR- OIBOR Basis 5,700 PLN PLN-WIBOR- WIBO Rate 5,700 LCH.Clearnet Limited January 2017

15 Product Specific Contract Terms and Eligibility Criteria Manual (c) Forward interest rate agreements having the characteristics set out in the table below: Instru ment Forwar d Rate Agreem ent Accept able Curre ncies CHF Acceptabl e Rate Options (as further set out in Section 7.1 of the 2006 ISDA Definitio ns) CHF- LIBOR- Types Fixed v floating currenc y Maximu m Residua l Term 1,225 days Amount (Min - Max of the relevant unit FRA Tenors 1w, 1m, 2m, 3m, 6m, 1y Minim um and Maxim um FRA Terms () Min 3 Max 375 Forwar d Rate Agreem ent CZK CZK- PIBOR- PRBO Fixed v floating 1,225 days 1w, 2w 1m, 2m, 3m, 6m, 9m, 1y Min 3 Max 375 Forwar d Rate Agreem ent DKK DKK- CIBOR2- DKNA13 Fixed v floating 1,225 days 1w, 1m, 2m, 3m, 4m, 5m, 6m, 9m, 1y Min 3 Max 375 Forwar d Rate Agreem ent EUR EUR- LIBOR- Fixed v floating 1,225 days 1w, 1m, 2m, 3m, 6m, 1y Min 3 Max 375 Forwar d Rate Agreem ent EUR EUR- Fixed v EURIBO floating R - REUTER S 1,225 days 1w, 2w, 1m, 2m, 3m, 6m, 7m, 8m, 9m, 1y Min 3 Max 375 Forwar d Rate Agreem ent GBP GBP- LIBOR- Fixed v floating 1,225 days 1w, 1m, 2m, 3m, 6m, 1y Min 3 Max 375 Forwar d Rate Agreem ent HUF HUF- BUBOR- REUTER S Fixed v floating 1,225 days 1w, 2w 1m, 2m, 3m, 4m, 5m, 6m, 7m, 8m, 9m, 10m, 11m, 1y Min 3 Max 375 Forwar d Rate Agreem ent JPY JPY- LIBOR- Fixed v floating 1,225 days 1w,, 2w 1m, 2m, 3m, 4m, 5m, 6m, 7m, 8m, 9m, 10m, 11m, 1y Min 3 Max 375 Forwar d Rate Agreem NOK NOK- NIBOR- OIBOR Fixed v floating 1,225 days 1w, 1m, 2m, 3m, 4m, 5m, 6m, 7m, 8m, 9m, 10m, 11m, 1y Min 3 Max LCH.Clearnet Limited September 2016

16 Product Specific Contract Terms and Eligibility Criteria Manual Instru ment Accept able Curre ncies Acceptabl e Rate Options (as further set out in Section 7.1 of the 2006 ISDA Definitio ns) Types currenc y Maximu m Residua l Term Amount (Min - Max of the relevant unit FRA Tenors ent 375 Minim um and Maxim um FRA Terms () Forwar d Rate Agreem ent PLN PLN WIBOR_ WIBO Fixed v floating 1,225 days 1w, 2w 1m, 3m, 6m, 9m, 1y Min 3 Max 375 Forwar d Rate Agreem ent SEK SEK- STIBOR- SIDE Fixed v floating 1,225 days 1w, 1m, 2m, 3m, 6m, 9m, 1y Min 3 Max 375 Forwar d Rate Agreem ent USD USD- LIBOR- Fixed v floating 1,225 days 1w, 1m, 2m, 3m, 6m, 1y Min 3 Max 375 (d) Vanilla inflation rate swaps with constant notional principal having the characteristics set out in the table below; Instrument Vanilla inflation rate swaps with constant notional principal Acceptable Currencies GBP Maximum Acceptable Indices 9 Types Residual Term GBP Nonrevised Retail Price Index (UKRPI) See Annex A (oo)(i) for definition Fixed vs. Floating 18,325 Amount (Min - Max of the relevant unit) ,999,999, Vanilla inflation rate swaps with constant notional principal USD USD Nonrevised Consumer Price Index Urban (CPI-U) See Annex A (pp)(i) for definition Fixed vs. Floating 11, ,999,999, Vanilla inflation rate swaps with EUR FRC Excluding Tobacco-Non- Fixed vs. Floating 11, ,999,999, References in this column are to the 2008 ISDA Inflation Derivatives Definitions LCH.Clearnet Limited September 2016

17 Product Specific Contract Terms and Eligibility Criteria Manual Fraction SWIFT Code Actual/365, Actual/Actual... ACT/365 (See Article 4.16(b) for definition) Actual/365 (Fixed)... AFI/365 (See Article 4.16(c) for definition) Actual/ ACT/360 (See Article 4.16(d) for definition) 30/360,360/360, Bond Basis /360 (See Article 4.16(e) for definition) 30E/ E/360 (See Article 4.16(f) for definition) Business Day Conventions The Business Day Convention specified in the Economic Terms must be one of the following: Following (see Article 4.12(i) of the ISDA 2000 Definitions and Article 4.12 (i) of the ISDA 2006 Definitions for definition) Modified Following (see Article 4.12(ii) of the ISDA 2000 Definitions and Article 4.12(ii) of the ISDA 2006 Definitions for definition) Preceding (see Article 4.12(iii) of the ISDA 2000 Definitions and Article 4.12(iii) of the ISDA 2006 Definitions for definition) For inflation swaps and vanilla interest rate swaps with constant notional principal Clear does not support trades where a different business day convention is used for: fixed period end dates and the termination date float period end dates and the termination date Minimum and Maximum Residual Term of the Trade (Termination date Today) Trades in respect of vanilla interest rate swaps with constant notional principal and variable notional swaps are subject to a minimum and maximum Residual Term on the day they are received by Clear. Minimum Residual Term of trade: Termination date - Today >= 1 + settlement lag where settlement lag is: 1 day for EUR, USD, GBP, and CAD and MXN denominated trades 2 days for JPY, CHF, AUD, DKK, HKD, NZD, SEK, NOK, PLN, ZAR, SAD, HUF &, CZK & MXN denominated trades LCH.Clearnet Limited September 2016

18 Product Specific Contract Terms and Eligibility Criteria Manual Maximum Residual Term of trade: Termination date - Today <= 3,670 days for HKD, ZAR, SGD, HUF & CZK (10 years) Termination date Today <= 3,850 days for CZK, HKD, HUF, MXN, SGD & ZARMXN (10.5 years) Termination date - Today <= 5,495 days for NZD Termination date Today <= 5,700 days for NOK, NZD & PLN (15.5 years) Termination date - Today <= 10,970 days for AUD, CAD, CHF & SEK (30 years) Termination date Today <= 11,375 days for AUD, CAD, DKK, SEK & CHF (31 years)dkk Termination date Today <= 14,62015,025 days for JPY (40 41 years) Termination date Today <= 18,27518,675 days for GBP, EUR & USD (50 51 years) Maximum Residual Term to Maturity for Forward Rate Agreements The maximum residual term to maturity for forward rate agreements is as follows: Currency EUR, JPY, USD, GBP, CHF, DKK, NOK, PLN, SEK, CZK & HUF... CHF, DKK, NOK, PLN, SEK, CZK, HUF... Maximum Residual Term to Maturity ,225 days (3.3 years) 740 days (2 years) The Clearing House will accept inflation swaps for registration: (a) in the case of uninterpolated indices, up to the end of the month prior to the final Reference Month; and (b) in the case of interpolated indices, up to the end of the final Reference Month Designated Maturity The Designated Maturity must be no less than one month and no more than twelve months. The Clearing House will, excepting stub periods, only accept a Designated Maturity that is a whole calendar month Calculation Periods (See Article 4.13 of the ISDA 2000 Definitions and Article 4.13 of the ISDA 2006 Definitions for definition.) For vanilla interest rate swaps with constant notional principal and variable notional swaps the Clearing House will only accept non standard Calculation Periods ("stub periods") at either the start or end of the contract. Transactions with stub periods at LCH.Clearnet Limited September 2016

19

20 TENOR AMENDMENTS MARCH 2017 FCM PRODUCT SPECIFIC CONTRACT TERMS AND ELIGIBILITY CRITERIA MANUAL

21 (b) notional interest rate swaps having the characteristics set out in the table below; Instrument Acceptable Currencies Acceptable Rate Options (as further set out in Article 7.1 of the 2000 ISDA Definitions and Article 7.1 of the 2006 ISDA Definitions) Types Maximum Residual Term Amount (Min - Max of the relevant unit) USD USD-LIBOR- Rate 18,675 USD USD-LIBOR- Basis 18,675 USD USD-LIBOR- Zero Coupon 18,675 EUR EUR-LIBOR- Rate 18,675 EUR EUR-LIBOR- Basis 18,675 EUR EUR-LIBOR- Zero Coupon 18,675 EUR EUR- EURIBOR- REUTERS Rate 18,675 EUR EUR- EURIBOR- REUTERS Basis 18,675 EUR EUR- EURIBOR- REUTERS Zero Coupon 18,675 GBP GBP-LIBOR- Rate 18,675 FCM Product Specific Manual January 2017

22 Instrument Acceptable Currencies Acceptable Rate Options (as further set out in Article 7.1 of the 2000 ISDA Definitions and Article 7.1 of the 2006 ISDA Definitions) Types Maximum Residual Term Amount (Min - Max of the relevant unit) GBP GBP-LIBOR- Basis 18,675 GBP GBP-LIBOR- Zero Coupon 18,675 CAD CAD-CDOR- BA Rate 18,67511,3 75 CAD CAD-CDOR- BA Basis 18,67511,3 75 JPY JPY-LIBOR- Rate 18,67515,0 25 JPY JPY-LIBOR- Basis 18,67515,0 25 AUD AUD-BBR- BBSW Rate 11,375 AUD AUD-BBR- BBSW Basis 11,375 NOK NOK-NIBOR- OIBOR Rate 5,700 NOK NOK-NIBOR- OIBOR Basis 5,700 PLN PLN-WIBOR- WIBO Rate 5,700 FCM Product Specific Manual January 2017

23 Instrument Acceptable Currencies Acceptable Rate Options (as further set out in Article 7.1 of the 2000 ISDA Definitions and Article 7.1 of the 2006 ISDA Definitions) Types Maximum Residual Term Amount (Min - Max of the relevant unit) PLN PLN-WIBOR- WIBO Basis 5,700 SEK SEK-STIBOR- SIDE Rate 11,375 SEK SEK-STIBOR- SIDE Basis 11,375 (c) Forward interest rate agreements having the characteristics set out in the table below; Instrument Acceptable Currencies Acceptable Rate Options (as further set out in Section 7.1 of the 2006 ISDA Definitions) Types Maximum Residual Term Amount (Min - Max of the relevant unit FRA Tenors Minimum and Maximum FRA Terms () Forward Rate Agreement CHF CHF-LIBOR- Fixed v floating 1,225 days 1w, 2w, Min 3 1m, 2m, 3m, 4m, Max 375 5m, 6m, 7m, 8m, 9m, 10m, 11m, 1y Forward Rate Agreement CZK CZK-PIBOR- PRBO Fixed v floating 1,225 days 1w, 2w Min 3 1m, 2m, 3m, 6m, Max 375 9m, 1y Forward Rate Agreement DKK DKK- CIBOR2- DKNA13 Fixed v floating 1,225 days 1w, 1m, Min 3 2m, 3m, 4m, 5m, Max 375 6m, 9m, FCM Product Specific Manual January 2017

24 Instrument Acceptable Currencies Acceptable Rate Options (as further set out in Section 7.1 of the 2006 ISDA Definitions) Types Maximum Residual Term Amount (Min - Max of the relevant unit FRA Tenors Minimum and Maximum FRA Terms () 1y Forward Rate Agreement EUR EUR-LIBOR- Fixed v floating 1,225 days 1w, 2w Min 3 1m, 2m, 3m, 4m, Max 375 5m, 6m, 7m, 8m, 9m, 10m, 11m, 1y Forward Rate Agreement EUR EUR- EURIBOR - REUTERS Fixed v floating 1,225 days 1w, 2w, Min 3 1m, 2m, 3m, 6m, Max 375 9m, 1y Forward Rate Agreement GBP GBP-LIBOR - Fixed v floating 1,225 days 1w, 2w, Min 3 1m, 2m, 3m, 4m, Max 375 5m, 6m, 7m, 8m, 9m, 10, 11m, 1y Forward Rate Agreement HUF HUF- BUBOR- REUTERS Fixed v floating 1,225 days 1w, 2w Min 3 1m, 2m, 3m, 4m, Max 375 5m, 6m, 7m, 8m, 9m, 10m, 11m, 1y Forward Rate Agreement JPY JPY-LIBOR- Fixed v floating 1,225 days 1w, 2w Min 3 1m, 2m, 3m, 4m, Max 375 5m, 6m, 7m, 8m, 9m, 10m, 11m, 1y Forward Rate Agreement NOK NOK-NIBOR- OIBOR Fixed v floating 1,225 days 1w, 1m, Min 3 2m, 3m, 4m, 5m, Max 375 6m, 7m, 8m, 9m, 10m, 11m, 1y Forward Rate Agreement PLN PLN WIBOR_WIB O Fixed v floating 1,225 days 1w, 2w Min 3 1m, 3m, 6m, 9m, Max 375 1y FCM Product Specific Manual January 2017

25 Instrument Acceptable Currencies Acceptable Rate Options (as further set out in Section 7.1 of the 2006 ISDA Definitions) Types Maximum Residual Term Amount (Min - Max of the relevant unit FRA Tenors Minimum and Maximum FRA Terms () Forward Rate Agreement SEK SEK- STIBOR- SIDE Fixed v floating 1,225 days 1w, 1m, Min 3 2m, 3m, 6m, 9m, Max 375 1y Forward Rate Agreement USD USD-LIBOR- Fixed v floating 1,225 days 1w, 2w Min 3 1m, 2m, 3m, 4m, Max 375 5m, 6m, 7m, 8m, 9m, 10m, 11m, 1y (d) Vanilla inflation rate swaps with constant notional principal having the characteristics set out in the table below; Instrument Acceptable Currencies Acceptable Indices 8 Types Maximum Residual Term Amount (Min - Max of the relevant unit Vanilla inflation rate swaps with constant notional principal GBP GBP Nonrevised Retail Price Index (UKRPI) See Annex A (oo)(i) for definition Fixed vs. Floating 18,67518, ,999,999, Vanilla inflation rate swaps with constant notional principal USD USD Nonrevised Consumer Price Index Urban (CPI-U) See Annex A (pp)(i) for definition Fixed vs. Floating 11, ,999,999, Vanilla inflation rate swaps with constant notional principal EUR FRC Excluding Tobacco-Non- Revised Consumer Price Index See Annex A (l)(i) for Fixed vs. Floating 11, ,999,999, References in this column are to the 2008 ISDA Inflation Derivatives Definitions. FCM Product Specific Manual January 2017

26 (ii) float period end dates and the termination date (c) Minimum and Maximum Residual Term of the Trade (Termination date Today) Trades in respect of vanilla interest rate swaps with constant notional principal and variable notional swaps are subject to a minimum and maximum Residual Term on the day they are received by Clear. (i) Minimum Residual Term of trade: Termination date - Today >= 1 + settlement lag where settlement lag is: 1 day for EUR, USD, GBP, and CAD and MXN denominated trades 2 days for JPY, CHF, AUD, DKK, HKD, NZD, SEK, NOK, PLN, ZAR, SAD, HUF &, CZK & MXN denominated trades (ii) Maximum Residual Term of trade: Termination date - Today <= 3,670 days for HKD, NZD, ZAR, SAD, HUF & CZK (10 years) Termination date Today <= 3,850 days for CZK, HKD, HUF, SGD, ZAR & MXN (10.5 years) Termination date Today <= 5,700 days for NOK, NZD & PLN (15.5 years) Termination date - Today <= 10,970 days for AUD, CAD, CHF & SEK (30 years) Termination date Today <= 11,375 days for AUD, CAD, DKK, CHF & SEK (31 years)dkk Termination date Today <= 14,62015,025 days for JPY (40 41 years) Termination date Today <= 18,27518,675 days for GBP, EUR & USD (50 51 years) (iii) Maximum Residual Term to Maturity for Forward Rate Agreements The maximum residual term to maturity for forward rate agreements is as follows: Currency EUR, JPY, USD, GBP, CHF, DKK, NOK, PLN, SEK, CZK & HUF Maximum Residual Term to Maturity ,225 days (3.3 years) FCM Product Specific Manual January 2017

27 AUD, CAD, CHF, DKK, NOK, NZD, PLN, SEK, ZAR, CZK, HUF 740 days (2 years) The Clearing House will accept FCM Clear Transactions that are inflation swaps for registration: (a) in the case of uninterpolated indices, up to the end of the month prior to the final Reference Month; and (b) in the case of interpolated indices, up to the end of the final Reference Month. (d) Designated Maturity The Designated Maturity must be no less than one month and no more than twelve months. The Clearing House will, excepting stub periods, only accept a Designated Maturity that is a whole calendar month. (e) Calculation Periods (See Article 4.13 of the ISDA 2000 Definitions and Article 4.13 of the ISDA 2006 Definitions for definition.) The Clearing House will only accept non-standard Calculation Periods ("stub periods") at the start and/or the end of a contract. For variable notional swaps the stub rate should be detailed either as a percentage (i.e., 5.5%), an interpolation (i.e., 1 month / 3 months) or as a designated maturity (i.e., 1 month). Stub Rates within the Final Stub are calculated via interpolation or as a designated maturity. For interpolated coupons, payment dates must fall between the rolled dates, according to the Modified Following business day convention, of the specified designated maturities. Where this does not occur and extrapolation would be required, Clear will reject the trade. The minimum stub period of a variable notional swap accepted by Clear is 1 + Currency Settlement Lag. The minimum stub rate tenor must be >= 1 week for IRS and basis swap and >=1 month for zero coupon swaps. Clear also calculates floating periods subject to 'IMM settlement dates as per ISDA definitions. (f) Up-Front Fees Eligibility of FCM Clear Transactions Any up-front fees due under an FCM Clear Transaction will form part of the first Variation Margin payment made in connection with such FCM Clear Transaction. FCM Clear Transactions with respect to which an FCM Client or an Affiliate is an Executing Party and which are denominated in a One-Day Currency where the up-front fee is due to settle on the day of registration are not eligible for clearing. FCM Product Specific Manual January 2017

28

29 LCH.CLEARNET LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE

30 Clearing House Procedures Clear Service Clear Clearing Member and FCM Clearing Member (as the case may be) and such Clear Clearing Member(s) or such Clear Clearing Member and such FCM Clearing Member shall transfer such Collateral to the Clearing House prior to registration upon request of the Clearing House. In respect of a Clear Contract resulting from a Clear Transaction that is a Sub-Block US Trading Venue Transaction, the Clear Clearing Member in whose name such Clear Contract is registered shall transfer to the Clearing House sufficient Collateral in respect of such Clear Contract at such time after the registration of such Clear Contract as the Clearing House shall require. Notwithstanding the foregoing, (i) if the Clearing House registers a Clear Contract resulting from a Clear Transaction that is not a Sub-Block US Trading Venue Transaction where one or both of the relevant Clear Clearing Members has not provided sufficient Collateral prior to registration, the Clear Clearing Members shall be bound by the terms of the Clear Contract relating thereto arising under Regulation 47 (and in particular by paragraphs (c), (h) and (i) thereof) and any other applicable provision of the Rulebook; and (ii) if the Clearing House rejects a Clear Transaction that is a Sub-Block US Trading Venue Transaction for reasons of insufficient Collateral, the Clearing House shall not be liable to any Clear Clearing Member or anyone else with regard to the registration (or lack of registration or re-registration) of any such Clear Transaction. Upon a Clear Transaction being submitted to the Clearing House for registration and the conditions to registration specified in Regulation 55 (Registration of Clear Contracts) having been satisfied in respect of the related Clear Contract(s), the Clear clearing system will respond, after processing, with a message confirming the registration. The registration notification message will be sent using the Clear Clearing Member reporting system (including by way of the originating Approved Trade Source System). The definitive report of a registered Clear Contract will be shown within the Clear Clearing Member reporting system (see Section 1.1.3) on the Clear Clearing Member reporting account Backloading of Existing Trades A Clear Transaction that has a Trade Date of greater than ten calendar days prior to the date of submission is considered a backloaded trade by the Clearing House (a "Backloaded Trade"). Due to the nature of Backloaded Trades, Clear Clearing Members should note that a relatively large amount of Collateral is required to register such trades. The Clearing House provides the facility for Clear Clearing Members to load such eligible existing Clear Transactions, through an Approved Trade Source System (currently, MarkitWire, Bloomberg and Tradeweb). Where the Clearing House approves additional Approved Trade Source Systems for these purposes, it will notify Clear Clearing Members via a member circular. Backloading requires bilateral agreement between the relevant Executing Parties and acceptance by the Clear Clearing Member(s) or the Clear Clearing Member and the FCM Clearing Member (as the case may be) of the full LCH Limited January 2017

31 Clearing House Procedures Clear Service particulars required by the Clearing House for each such Clear Transaction. At least once every Business Day, the Clearing House will carry out a process (each a "Backload Registration Cycle") for the registration of Backloaded Trades which have been presented for clearing or with respect to which the Clearing House has received the one or more Necessary Consents, if any. Following each Backload Registration Cycle, the Clearing House will calculate the increase in Collateral required to register the Backloaded Trade(s) and will notify each relevant Clear Clearing Member (the "Backload Margin Call"). The Backload Margin Call will be for the entire amount of additional Collateral required in connection with the Backloaded Trade(s), and the Backload Margin Call cannot be satisfied by and will not take into account Clear Tolerance (i.e. Clear Tolerance is not available for this purpose), or any available MER Cover or, Client Buffer or any form of excess Collateral (other than that which has been expressly allocated for that purpose, as described in the paragraph below). In connection with a Backload Margin Call, following the time that a Clear Clearing Member is required to deliver to the Clearing House the Collateral associated with such Backload Margin Call (the "Backload Margin Call Deadline"), the Clearing House will issue such Clear Clearing Member a subsequent margin call to deliver Collateral in respect of any increase in Clear Tolerance utilisation as of the time of the Backload Margin Call Deadline (if any). Where an individual Clear Clearing Member determines that the Backloaded Trade(s) that it is submitting for registration will lead to an aggregate change (be it either an increase or decrease) in the net present value of its portfolio of Clear Contracts in excess of a threshold amount (the "Individual Backload Value Threshold") as published by the Clearing House from time to time, it shall notify the Clearing House before the end of the Business Day preceding the relevant Backload Registration Cycle. In the event that the Clearing House does not receive such notification and the change in net present value of the Clear Clearing Member s portfolio of Clear Contracts is in excess of the Individual Backload Value Threshold the Clearing House may, in its sole discretion, exclude that Clear Clearing Member from the Backload Registration Cycle or postpone or cancel the entire Backload Registration Cycle. Where a Clear Clearing Member notifies the Clearing House of a change in net present value in excess of the Individual Backload Value Threshold, the Clearing House shall inform the Clear Clearing Member whether it will be required to pre-fund the Backload Margin Call and, if so, how Collateral should be delivered such that it will be made available for a Backload Registration Cycle. In the event that the aggregate Backload Margin Call required from all Clear Clearing Members participating in a Backload Registration Cycle is in excess of a pre-determined threshold amount (the "Aggregate Backload Margin Threshold") as published by the Clearing House from time to time, LCH Limited January 2017

32

33 FCM PROCEDURES OF THE CLEARING HOUSE LCH LIMITED

34 FCM Procedures FCM Clear such FCM Clear Contract results from an FCM US Trading Venue Transaction, no later than the Clearing House s receipt of the relevant FCM Clear Transaction details (and thereafter maintain) sufficient Margin in respect of such FCM Contract. In determining whether sufficient Margin for registration is available, the Clearing House will take into account any Available FCM Buffer, MER and Clear Tolerance. Available FCM Buffer or MER will always be applied prior to taking into account any available Clear Tolerance. In respect of an FCM Clear Contract resulting from an FCM Clear Transaction that is a Sub-Block US Trading Venue Transaction, the FCM Clearing Member in whose name such FCM Clear Contract is registered shall furnish the Clearing House with sufficient Margin in respect of such FCM Clear Contract at such time after the registration of such FCM Clear Contract as the Clearing House shall require. Notwithstanding the foregoing: (A) if the Clearing House registers an FCM Clear Contract resulting from an FCM Clear Transaction that is not a Sub-Block US Trading Venue Transaction where one or both of the relevant FCM Clearing Members has not furnished sufficient Margin prior to registration, the FCM Clearing Members shall be bound by the terms of the FCM Clear Contract relating thereto arising under FCM Regulation 45 (and in particular by paragraphs (c), (i) and (j) thereof) and any other applicable provision of the FCM Rulebook; and (B) if the Clearing House rejects an FCM Clear Transaction that is a Sub-Block US Trading Venue Transaction for insufficient Margin, the Clearing House shall not be liable to any FCM Clearing Member or anyone else with regard to the registration (or lack of registration or re-registration) of any such FCM Clear Transaction. Upon an FCM Clear Transaction being submitted to the Clearing House for registration and the conditions to registration specified in FCM Regulation 45 (Registration of FCM Clear Contracts; Novation and Post-Novation Compression; Clear Accounts) having been satisfied in respect of the related FCM Clear Contract(s), the Clear clearing system will respond, after processing, with a message confirming the registration. The registration notification message will be sent using the Clear Clearing Member reporting system (including by way of the originating Approved Trade Source System). The definitive report of a registered Clear Contract will be shown within the Clear Clearing Member reporting system (see Section 2.1.1(c)) on the Clear Clearing Member reporting account. (ii) Backloaded Trades: An FCM Clear Transaction that has a Trade Date of greater than ten calendar days prior to the date of submission is considered a backloaded trade by the Clearing House (a Backloaded Trade ). Due to the nature of Backloaded Trades, FCM Clearing Members March 2017

35 FCM Procedures FCM Clear should note that a relatively large amount of cover is required in order to register such trades. The Clearing House provides the facility for FCM Clearing Members to load such eligible existing FCM Clear Transactions, through an FCM Approved Trade Source System (currently only MarkitWire). Where the Clearing House approves additional FCM Approved Trade Source Systems for these purposes, it will notify FCM Clearing Members via member circular. Backloading requires bilateral agreement between the relevant Executing Parties and acceptance by the FCM Clearing Member(s) and the Clear Clearing Member, if any, of the full particulars required by the Clearing House for each such FCM Clear Transaction. At least once every Business Day, the Clearing House will carry out a process for the registration of Backloaded Trades (each, a Backload Registration Cycle ) which have been submitted for clearing or with respect to which the Clearing House has received the one or more FCM Acceptances, if any. Following each Backload Registration Cycle, the Clearing House will calculate the increase in Required Margin required to register the Backloaded Trade(s) and will notify each relevant FCM Clearing Member (the Backload Margin Call ). The Backload Margin Call will be for the entire amount of Margin calculated by the increase in Required Margin, and the Backload Margin Call cannot be satisfied by and will not take into account Clear Tolerance (i.e., Clear Tolerance is not available for this purpose), or any available MER Cover, or FCM Buffer or Excess Margin (other than that which has been expressly allocated for that purpose, as described in the paragraph below). In connection with a Backload Margin Call, following the time that an FCM Clearing Member is required to furnish the Clearing House with the Margin associated with such Backload Margin Call (the Backload Margin Call Deadline ), the Clearing House will issue such FCM Clearing Member a subsequent margin call to furnish Margin in respect of any Clear Tolerance utilisation as of the time of the Backload Margin Call Deadline (if any). Where an individual FCM Clearing Member determines that the Backloaded Trade(s) that it is submitting for registration will lead to an aggregate change in the net present value of its portfolio of FCM Clear Contracts in excess of a threshold amount (the "Individual Backload Value Threshold") as published by the Clearing House from time to time, it shall notify the Clearing House before the end of the Business Day preceding the Backload Registration Cycle. In the event that the Clearing House does not receive such notification and the change in net present value of the FCM Clearing Member s portfolio of FCM Clear Contracts is in excess of the Individual Backload Value Threshold the Clearing House may, in its sole discretion, exclude that FCM Clearing Member from the Backload Registration Cycle or postpone or cancel the entire Backload Registration Cycle March 2017

36

Appendix I Procedure Section 2C (SwapClear Clearing Service)

") Appendix I Procedure Section 2C (Clear Clearing Service) LCH.CLEARNET LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE Clearing House Procedures Clear Service Any NPV Payment made by an SCM to

Appendix I Procedure Section 2C (Clear Clearing Service) LCH.CLEARNET LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE Clearing House Procedures Clear Service Any NPV Payment made by an SCM to

LCH Limited Self Certification: Rule Changes on the addition of SOFR Swaps as eligible SwapClear products

VIA CFTC PORTAL June 26 2018 Mr Christopher Kirkpatrick Commodity Futures Trading Commission 115 21 st Street NW Three Lafayette Centre Washington DC 20581 LCH Limited Self Certification: Rule Changes

VIA CFTC PORTAL June 26 2018 Mr Christopher Kirkpatrick Commodity Futures Trading Commission 115 21 st Street NW Three Lafayette Centre Washington DC 20581 LCH Limited Self Certification: Rule Changes

Product Specific Contract Terms and Eligibility Criteria Manual

Appendix I Product Specific Contract s and Eligibility Criteria Manual PRODUCT SPECIFIC CONTRACT TERMS AND ELIGIBILITY CRITERIA MANUAL Product Specific Contract s and Eligibility Criteria Manual PART B

Appendix I Product Specific Contract s and Eligibility Criteria Manual PRODUCT SPECIFIC CONTRACT TERMS AND ELIGIBILITY CRITERIA MANUAL Product Specific Contract s and Eligibility Criteria Manual PART B

VIA CFTC PORTAL SUBMISSION. 29 September 2017

VIA CFTC PORTAL SUBMISSION 29 September 2017 Mr. Christopher Kirkpatrick Commodity Futures Trading Commission 1155 21 st Street NW Three Lafayette Centre Washington DC 20581 Dear Mr. Kirkpatrick: Pursuant

VIA CFTC PORTAL SUBMISSION 29 September 2017 Mr. Christopher Kirkpatrick Commodity Futures Trading Commission 1155 21 st Street NW Three Lafayette Centre Washington DC 20581 Dear Mr. Kirkpatrick: Pursuant

FCM PRODUCT SPECIFIC CONTRACT TERMS AND ELIGIBILITY CRITERIA MANUAL

FCM PRODUCT SPECIFIC CONTRACT TERMS AND ELIGIBILITY CRITERIA MANUAL CONTENTS Clause Page SCHEDULE 1 FCM Swapclear... 1 Part A FCM Swapclear Contract Terms... 1 Part B Product Eligibility Criteria for Registration

FCM PRODUCT SPECIFIC CONTRACT TERMS AND ELIGIBILITY CRITERIA MANUAL CONTENTS Clause Page SCHEDULE 1 FCM Swapclear... 1 Part A FCM Swapclear Contract Terms... 1 Part B Product Eligibility Criteria for Registration

Please find attached as appendices the Submission Cover Sheet and the relevant changes to the LCH.Clearnet rulebook.

VIA EMAIL TO: SUBMISSIONS@CFTC.GOV 20 September 2013 Ms. Melissa Jurgens Commodity Futures Trading Commission 1155 21 st Street NW Three Lafayette Centre Washington DC 20581 Dear Ms. Jurgens: Pursuant

VIA EMAIL TO: SUBMISSIONS@CFTC.GOV 20 September 2013 Ms. Melissa Jurgens Commodity Futures Trading Commission 1155 21 st Street NW Three Lafayette Centre Washington DC 20581 Dear Ms. Jurgens: Pursuant

Chapter 901 Interest Rate Swaps Contract Terms

90101. SCOPE OF CHAPTER Chapter 901 Interest Rate Swaps Contract Terms The terms and conditions of each IRS Contract shall be defined by this Chapter, as supplemented by the ISDA Definitions (and where

90101. SCOPE OF CHAPTER Chapter 901 Interest Rate Swaps Contract Terms The terms and conditions of each IRS Contract shall be defined by this Chapter, as supplemented by the ISDA Definitions (and where

Classes of OTC derivatives that LCH Limited has been authorised to clear as notified to ESMA under Regulation 648/2012

Classes of OTC derivatives that LCH Limited has been authorised to clear as notified to ESMA under Regulation 648/2012 In accordance with Article 6 of Regulation (EU) No 648/2012 of the European Parliament

Classes of OTC derivatives that LCH Limited has been authorised to clear as notified to ESMA under Regulation 648/2012 In accordance with Article 6 of Regulation (EU) No 648/2012 of the European Parliament

Public Register for the Clearing Obligation under EMIR

Public Register for the Clearing Obligation under EMIR In accordance with Article 6 of Regulation (EU) No 648/2012 of the European Parliament and of the Council of 4 July 2012 on OTC derivatives, central

Public Register for the Clearing Obligation under EMIR In accordance with Article 6 of Regulation (EU) No 648/2012 of the European Parliament and of the Council of 4 July 2012 on OTC derivatives, central

VIA CFTC PORTAL. 13 January 2017

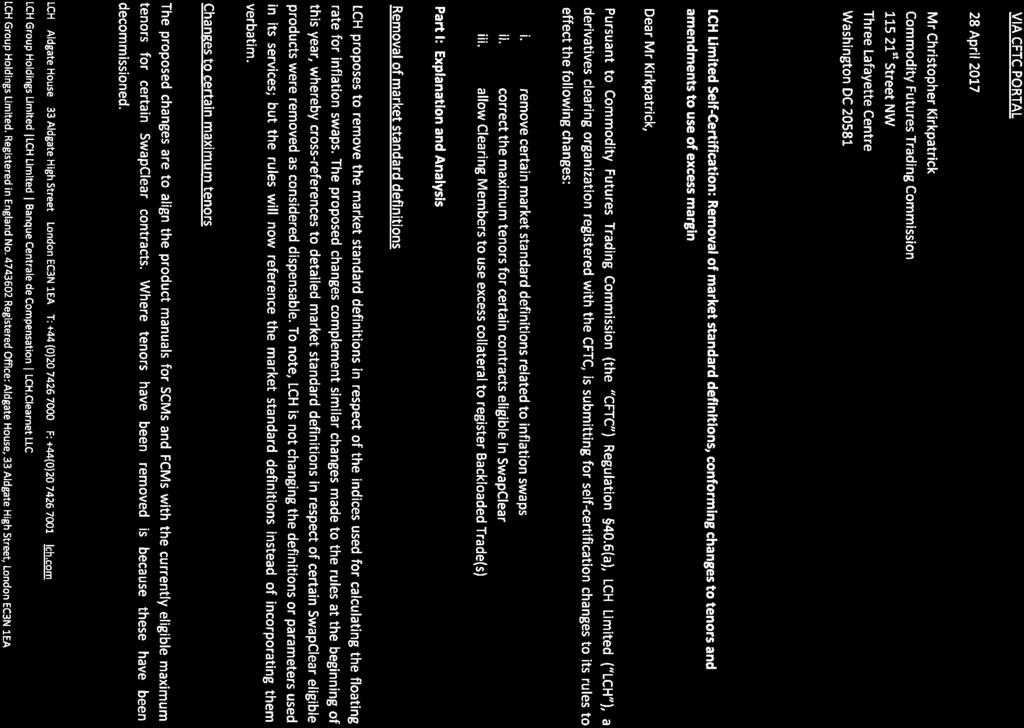

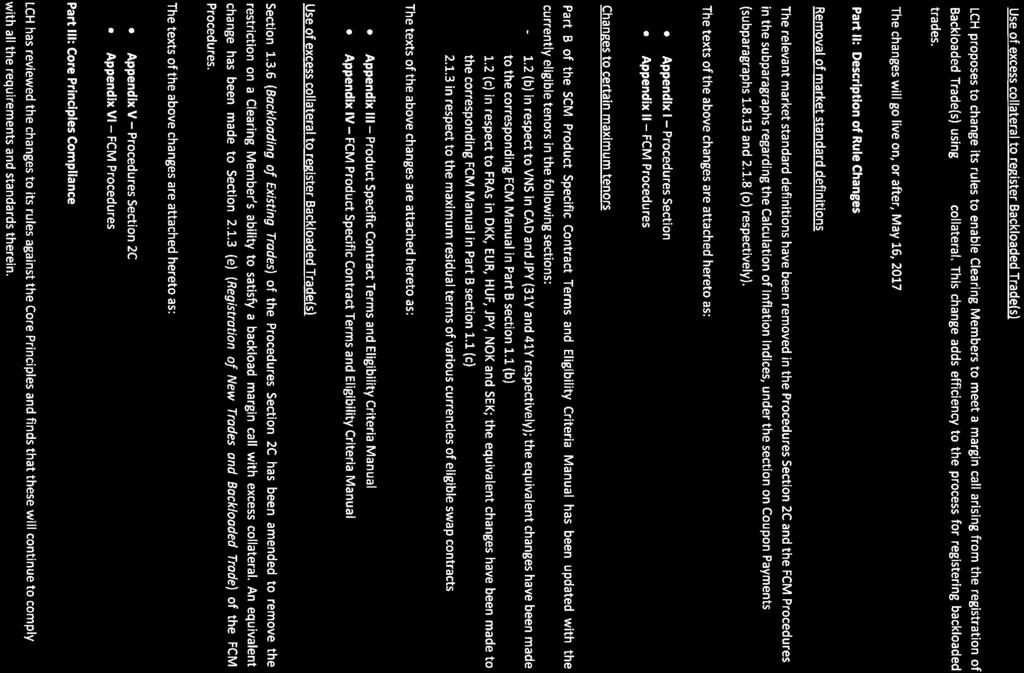

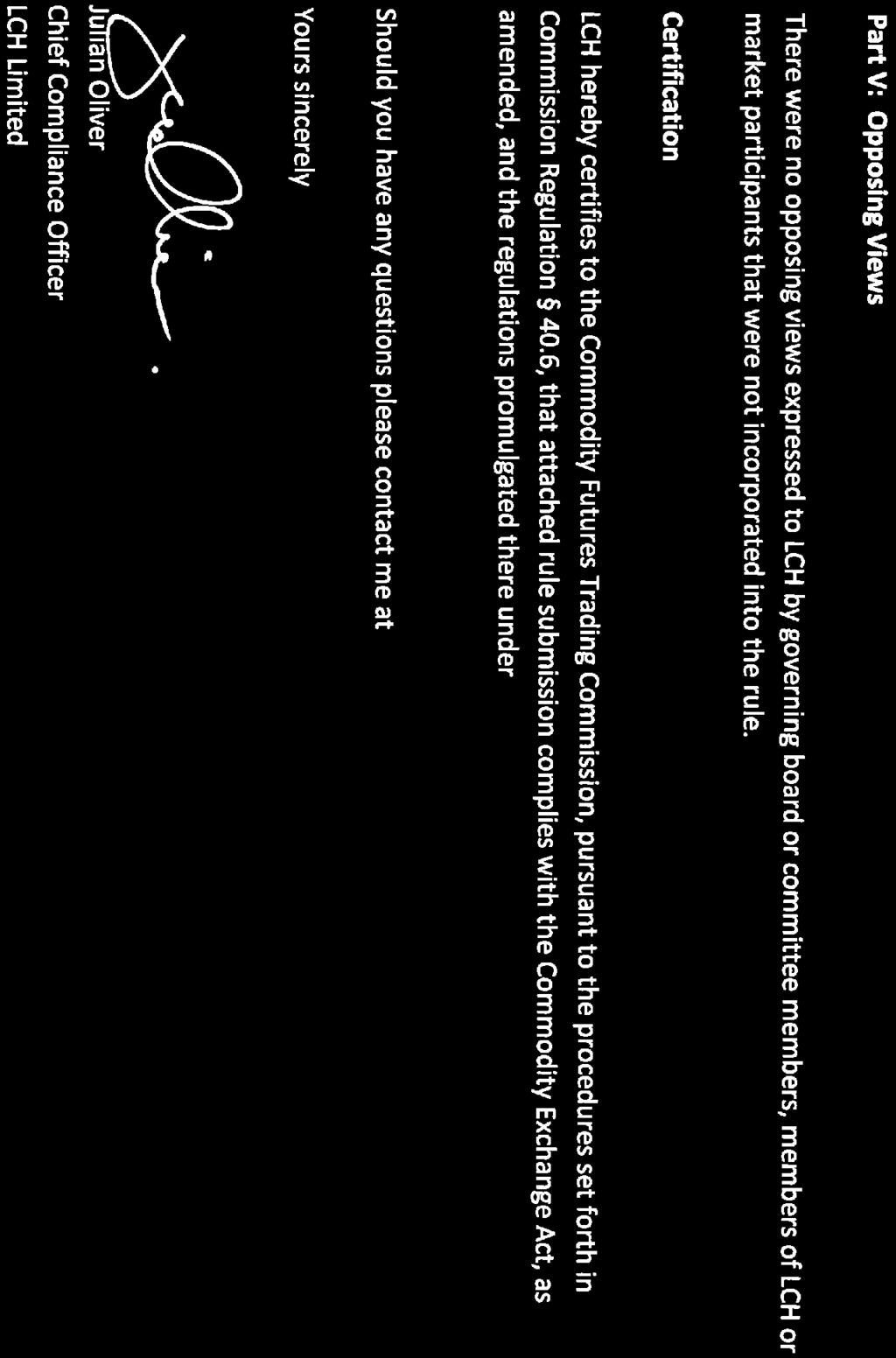

VIA CFTC PORTAL 13 January 2017 Mr Christopher Kirkpatrick Commodity Futures Trading Commission 115 21 st Street NW Three Lafayette Centre Washington DC 20581 LCH Limited Self-Certification: Removal of

VIA CFTC PORTAL 13 January 2017 Mr Christopher Kirkpatrick Commodity Futures Trading Commission 115 21 st Street NW Three Lafayette Centre Washington DC 20581 LCH Limited Self-Certification: Removal of

LCH LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE

LCH LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE CONTENTS Section Page 1. Swapclear Clearing Service... 1 1.1 The Clearing Process... 1 1.2 Operating Times and Calendars... 4 1.3 Registration...

LCH LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE CONTENTS Section Page 1. Swapclear Clearing Service... 1 1.1 The Clearing Process... 1 1.2 Operating Times and Calendars... 4 1.3 Registration...

Public Register for the Clearing Obligation under EMIR

Last update 2 December Public Register for the Clearing Obligation under EMIR In accordance with Article 6 of Regulation (EU) No 648/2012 of the European Parliament and of the Council of 4 July 2012 on

Last update 2 December Public Register for the Clearing Obligation under EMIR In accordance with Article 6 of Regulation (EU) No 648/2012 of the European Parliament and of the Council of 4 July 2012 on

LCH LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE

LCH LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE CONTENTS Section Page 1. Swapclear Clearing Service... 1 1.1 The Clearing Process... 1 1.2 Operating Times and Calendars... 4 1.3 Registration...

LCH LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE CONTENTS Section Page 1. Swapclear Clearing Service... 1 1.1 The Clearing Process... 1 1.2 Operating Times and Calendars... 4 1.3 Registration...

Appendix A Notice of this submission provided to SwapClear Clearing Members

Appendix A Notice of this submission provided to SwapClear Clearing Members To SwapClear Clearing Members From David Horner, Head of SwapClear Business Risk Date 13 September 2016 Subject VNS in PLN/SEK/NOK

Appendix A Notice of this submission provided to SwapClear Clearing Members To SwapClear Clearing Members From David Horner, Head of SwapClear Business Risk Date 13 September 2016 Subject VNS in PLN/SEK/NOK

Interest Rate Swaps: Risk Model CME Group. All rights reserved.

Interest Rate Swaps: Risk Model 2017 Disclaimer Futures trading is not suitable for all investors, and involves the risk of loss. Futures are a leveraged investment, and because only a percentage of a

Interest Rate Swaps: Risk Model 2017 Disclaimer Futures trading is not suitable for all investors, and involves the risk of loss. Futures are a leveraged investment, and because only a percentage of a

Chapter VIII of the Clearing Conditions of Eurex Clearing AG. Clearing of OTC Derivative Transactions

Chapter VIII of the Clearing Conditions of Eurex Clearing AG Clearing of OTC Derivative Transactions As of 04.12.2017 Page 1 Chapter VIII Preamble Preamble This Chapter VIII forms an integral part of the

Chapter VIII of the Clearing Conditions of Eurex Clearing AG Clearing of OTC Derivative Transactions As of 04.12.2017 Page 1 Chapter VIII Preamble Preamble This Chapter VIII forms an integral part of the

ASX Futures Operating Rules

ASX Futures Operating Rules Foreign Clearing Participants and other Clearing Participants with Overseas Activity 4.15A (a) A Clearing Participant that proposes to locate or relocate any part of its business

ASX Futures Operating Rules Foreign Clearing Participants and other Clearing Participants with Overseas Activity 4.15A (a) A Clearing Participant that proposes to locate or relocate any part of its business

FCM PROCEDURES OF THE CLEARING HOUSE LCH.CLEARNET LIMITED

FCM PROCEDURES OF THE CLEARING HOUSE LCH.CLEARNET LIMITED Contents CONTENTS Clause Page 1. FCM Clearing Member Status... 1 1.1 FCM Clearing Member Application Procedure... 1 1.2 Criteria for FCM Clearing

FCM PROCEDURES OF THE CLEARING HOUSE LCH.CLEARNET LIMITED Contents CONTENTS Clause Page 1. FCM Clearing Member Status... 1 1.1 FCM Clearing Member Application Procedure... 1 1.2 Criteria for FCM Clearing

Cash-Settled Forward (CSFs)

") Cash-Settled Forward (CSFs) CSFs provide FX market participants with a clearable alternative to the predominant deliverable products in the G20 and several other pairs. These products serve as a viable

Cash-Settled Forward (CSFs) CSFs provide FX market participants with a clearable alternative to the predominant deliverable products in the G20 and several other pairs. These products serve as a viable

Basis point. GBP per million GBP or EUR per million EUR

Inflation; Inflation Swaps - EUR/GBP & Inflation Bonds - EUR Execution Type Instrument Annual Rev Thresholds Rate Rate Type Notes Volume Match or Electronic GBP - ZC/Spread/Fly EUR - ZC/Spread/Fly GBP

Inflation; Inflation Swaps - EUR/GBP & Inflation Bonds - EUR Execution Type Instrument Annual Rev Thresholds Rate Rate Type Notes Volume Match or Electronic GBP - ZC/Spread/Fly EUR - ZC/Spread/Fly GBP

BGC Brokers L.P. OTF Rate Cards Effective Apr 1st 2018

Inflation; Inflation Swaps - EUR/GBP & Inflation Bonds - EUR Execution Type Instrument Annual Rev Thresholds Rate Rate Type Notes Volume Match or Electronic GBP - ZC/Spread/Fly EUR - ZC/Spread/Fly GBP

Inflation; Inflation Swaps - EUR/GBP & Inflation Bonds - EUR Execution Type Instrument Annual Rev Thresholds Rate Rate Type Notes Volume Match or Electronic GBP - ZC/Spread/Fly EUR - ZC/Spread/Fly GBP

Margin Service API - Developer Guide

Margin Service API - Developer Guide Developers new to CME Group's Margin Service API can refer to this flowchart for development guidance. Hyperlinks take you to examples and further information where

Margin Service API - Developer Guide Developers new to CME Group's Margin Service API can refer to this flowchart for development guidance. Hyperlinks take you to examples and further information where

BGC Brokers L.P. OTF Rate Cards Effective Oct 2nd 2018

Inflation; Inflation Swaps - EUR/GBP & Inflation Bonds - EUR Execution Type Instrument Annual Rev Thresholds Rate Rate Type Notes Volume Match or Electronic GBP - ZC/Spread/Fly EUR - ZC/Spread/Fly GBP

Inflation; Inflation Swaps - EUR/GBP & Inflation Bonds - EUR Execution Type Instrument Annual Rev Thresholds Rate Rate Type Notes Volume Match or Electronic GBP - ZC/Spread/Fly EUR - ZC/Spread/Fly GBP

Research Note. Actual Cleared Volumes vs. Mandated Cleared Volumes: Analyzing the US Derivatives Market. July 2018

July 2018 Research Note Actual Cleared Volumes vs. Mandated Cleared Volumes: Encouraging the clearing of standardized derivatives has been a major priority for policy-makers. This has primarily been pursued

July 2018 Research Note Actual Cleared Volumes vs. Mandated Cleared Volumes: Encouraging the clearing of standardized derivatives has been a major priority for policy-makers. This has primarily been pursued

FCM REGULATIONS OF THE CLEARING HOUSE LCH LIMITED

FCM REGULATIONS OF THE CLEARING HOUSE LCH LIMITED Contents CONTENTS Regulation Page Regulation 1 Definitions... 2 Chapter I - SCOPE... 32 Regulation 2 Obligations of the Clearing House to each FCM Clearing

FCM REGULATIONS OF THE CLEARING HOUSE LCH LIMITED Contents CONTENTS Regulation Page Regulation 1 Definitions... 2 Chapter I - SCOPE... 32 Regulation 2 Obligations of the Clearing House to each FCM Clearing

Chapter VIII of the Clearing Conditions of Eurex Clearing AG. Clearing of OTC Derivative Transactions

Chapter VIII of the Clearing Conditions of Eurex Clearing AG Clearing of OTC Derivative Transactions As of 09.10.2017 Page 2 **********************************************************************************

Chapter VIII of the Clearing Conditions of Eurex Clearing AG Clearing of OTC Derivative Transactions As of 09.10.2017 Page 2 **********************************************************************************

SwapAgent Clearing the Way for Non-Cleared

SwapAgent Clearing the Way for Non-Cleared Now Supporting Cross-Currency Swaps SwapAgent simplifies the processing, margining and settlement of non-cleared derivatives Driving Efficiencies for Non-Cleared

SwapAgent Clearing the Way for Non-Cleared Now Supporting Cross-Currency Swaps SwapAgent simplifies the processing, margining and settlement of non-cleared derivatives Driving Efficiencies for Non-Cleared

VIA CFTC PORTAL. 28 December 2017

VIA CFTC PORTAL 28 Mr Christopher Kirkpatrick Commodity Futures Trading Commission 115 21 st Street NW Three Lafayette Centre Washington DC 20581 LCH Limited Self Certification: Rule Changes on Treatment

VIA CFTC PORTAL 28 Mr Christopher Kirkpatrick Commodity Futures Trading Commission 115 21 st Street NW Three Lafayette Centre Washington DC 20581 LCH Limited Self Certification: Rule Changes on Treatment

SEF Rule 804. Equity Derivatives Product Descriptions

SEF Rule 804 Equity Derivatives Product Descriptions Products Rule 804 (1) Total Return Swaps & Price Return Swaps (2) Total Return Index Swaps Product Specifications SEF Rule 804(1) Total Return Swaps

SEF Rule 804 Equity Derivatives Product Descriptions Products Rule 804 (1) Total Return Swaps & Price Return Swaps (2) Total Return Index Swaps Product Specifications SEF Rule 804(1) Total Return Swaps

Date: 30 November Effective Date: 7 December 2016

Number: Segment: C-IRS-05/2016 IRS Circular Subject: Summary Date: 30 November 2016 Effective Date: 7 December 2016 Replaces: C-IRS-02/2016 Terms, additional definitions and eligibility criteria for the

Number: Segment: C-IRS-05/2016 IRS Circular Subject: Summary Date: 30 November 2016 Effective Date: 7 December 2016 Replaces: C-IRS-02/2016 Terms, additional definitions and eligibility criteria for the

TERMS AND CONDITIONS FOR BANKS

TERMS AND CONDITIONS FOR BANKS Valid as of 1 st August, 2017 1 General principles of fees and commissions collection: 1. This Table concerns: a) domestics banks; b) foreign banks; c) banks with LORO account;

TERMS AND CONDITIONS FOR BANKS Valid as of 1 st August, 2017 1 General principles of fees and commissions collection: 1. This Table concerns: a) domestics banks; b) foreign banks; c) banks with LORO account;

EMIR FAQ 1. WHAT IS EMIR?

EMIR FAQ The following information has been compiled for the purposes of providing an overview of EMIR and is not legal advice. The information is only accurate at date of publication and is subject to

EMIR FAQ The following information has been compiled for the purposes of providing an overview of EMIR and is not legal advice. The information is only accurate at date of publication and is subject to

LCH SA CDS Clearing Procedures Section 5 - CDS Clearing Operations 9 April 2018

LCH SA CDS Clearing Procedures Section 5-9 April 2018 Classification: Public CONTENTS SECTION 5 - CDS CLEARING OPERATIONS 5.1 THE CDS CLEARING SERVICE... 3 5.2 BACKLOADING TRANSACTIONS... 3 5.3 CLEARING

LCH SA CDS Clearing Procedures Section 5-9 April 2018 Classification: Public CONTENTS SECTION 5 - CDS CLEARING OPERATIONS 5.1 THE CDS CLEARING SERVICE... 3 5.2 BACKLOADING TRANSACTIONS... 3 5.3 CLEARING

c) Notice of ESMA s Product Intervention Decisions in relation to contracts for differences and binary options

Notice of ESMA s Product Intervention Decisions in relation to contracts for differences and binary options") Leverage Policy Introduction TFI Markets Ltd has established a leverage policy which applies to all its retail customers. The purpose of the policy is to set out the leverage practices of the Company in

Leverage Policy Introduction TFI Markets Ltd has established a leverage policy which applies to all its retail customers. The purpose of the policy is to set out the leverage practices of the Company in

FCM REGULATIONS OF THE CLEARING HOUSE LCH.CLEARNET LIMITED

FCM REGULATIONS OF THE CLEARING HOUSE LCH.CLEARNET LIMITED CONTENTS Regulation Page Regulation 1 Definitions... 2 Chapter I - SCOPE... 24 Regulation 2 Obligations of the Clearing House to each FCM Clearing

FCM REGULATIONS OF THE CLEARING HOUSE LCH.CLEARNET LIMITED CONTENTS Regulation Page Regulation 1 Definitions... 2 Chapter I - SCOPE... 24 Regulation 2 Obligations of the Clearing House to each FCM Clearing

FCM PROCEDURES OF THE CLEARING HOUSE LCH LIMITED

FCM PROCEDURES OF THE CLEARING HOUSE LCH LIMITED Contents CONTENTS Clause Page 1. FCM Clearing Member Status... 2 1.1 FCM Clearing Member Application Procedure... 2 1.2 Criteria for FCM Clearing Member

FCM PROCEDURES OF THE CLEARING HOUSE LCH LIMITED Contents CONTENTS Clause Page 1. FCM Clearing Member Status... 2 1.1 FCM Clearing Member Application Procedure... 2 1.2 Criteria for FCM Clearing Member

1. Deposit products Current accounts 01 Attorney, Notary escrow account 01 Deposit accounts in CZK 02 Deposit accounts in foreign currency 02

Strana 2 z 5 1. Deposit products Current accounts 01 Attorney, Notary escrow account 01 Deposit accounts in CZK 02 Deposit accounts in foreign currency 02 2. Loan products Base rates 04 Overdraft and short

Strana 2 z 5 1. Deposit products Current accounts 01 Attorney, Notary escrow account 01 Deposit accounts in CZK 02 Deposit accounts in foreign currency 02 2. Loan products Base rates 04 Overdraft and short

Fallbacks for Derivatives Background and Role of A Vendor. January 2019

Fallbacks for Derivatives Background and Role of A Vendor January 2019 IBOR Fallbacks: ISDA s Work ISDA is currently undertaking work to amend the 2006 ISDA Definitions to implement fallbacks for: LIBOR

Fallbacks for Derivatives Background and Role of A Vendor January 2019 IBOR Fallbacks: ISDA s Work ISDA is currently undertaking work to amend the 2006 ISDA Definitions to implement fallbacks for: LIBOR

DBIQ Interest Rate Curve Creation Process

15 December 2017 Index Guide Interest Rate Curve Creation Process Summary This document describes the primary price sources for market data used by the Deutsche Bank Index Quant group ( ), a research function

15 December 2017 Index Guide Interest Rate Curve Creation Process Summary This document describes the primary price sources for market data used by the Deutsche Bank Index Quant group ( ), a research function

LCH.CLEARNET LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE

LCH.CLEARNET LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE Clearing House Procedures SwapClear Service 1.2 Operating Times and Calendars 1.2.1 Opening Days The Clearing House will publish a

LCH.CLEARNET LIMITED PROCEDURES SECTION 2C SWAPCLEAR CLEARING SERVICE Clearing House Procedures SwapClear Service 1.2 Operating Times and Calendars 1.2.1 Opening Days The Clearing House will publish a

ICE CLEAR EUROPE. List of Permitted Cover and Limits on Collateral

ICE CLEAR EUROPE List of Permitted Cover and Limits on Collateral September 2017 Permitted Collateral & Haircuts he following table lists the Permitted Cover ICE Clear Europe Members may lodge to meet

ICE CLEAR EUROPE List of Permitted Cover and Limits on Collateral September 2017 Permitted Collateral & Haircuts he following table lists the Permitted Cover ICE Clear Europe Members may lodge to meet

The respective UK Statutory Instrument is The Markets in Financial Instruments (Amendment) (EU Exit) Regulations 2018 No

(EU Exit) Regulations 2018 No") Via CFTC Portal 19 March 2019 Mr Christopher Kirkpatrick Commodity Futures Trading Commission 1155 21 st Street NW Three Lafayette Centre Washington DC 20581 LCH Limited Self-Certification: rule changes

Via CFTC Portal 19 March 2019 Mr Christopher Kirkpatrick Commodity Futures Trading Commission 1155 21 st Street NW Three Lafayette Centre Washington DC 20581 LCH Limited Self-Certification: rule changes

LCH LIMITED PROCEDURES SECTION 3 FINANCIAL TRANSACTIONS

LCH LIMITED PROCEDURES SECTION 3 FINANCIAL TRANSACTIONS CONTENTS Section Page 1. Financial Transactions... 1 1.1 Accounts and ledgers... 1 1.2 Financial Transaction Reporting... 2 1.3 Protected Payments

LCH LIMITED PROCEDURES SECTION 3 FINANCIAL TRANSACTIONS CONTENTS Section Page 1. Financial Transactions... 1 1.1 Accounts and ledgers... 1 1.2 Financial Transaction Reporting... 2 1.3 Protected Payments

Terms and Conditions of Lykke FX Colored Coins Issuance

Terms and Conditions of Lykke FX Colored Coins Issuance 31 DECEMBER 2016 BACKGROUND INFORMATION The Terms and Conditions governs the issuance of certificates of IOUs (referred as ) by Lykke Corp UK Ltd.,

Terms and Conditions of Lykke FX Colored Coins Issuance 31 DECEMBER 2016 BACKGROUND INFORMATION The Terms and Conditions governs the issuance of certificates of IOUs (referred as ) by Lykke Corp UK Ltd.,

COMMISSIONS, CHARGES & MARGIN SCHEDULE

COMMISSIONS, CHARGES & MARGIN SCHEDULE Effective as of 30th July 2018 30 July 2018 This schedule outlines the various commissions, charges, margins, interest, any other rates and important information

COMMISSIONS, CHARGES & MARGIN SCHEDULE Effective as of 30th July 2018 30 July 2018 This schedule outlines the various commissions, charges, margins, interest, any other rates and important information

Technical Handbook. as of 1 January January

Technical Handbook as of 1 January 2017 1 January 2017 1 Table of Contents Section I Payments Article 1: Account management and processing of payment orders 3 Article 2: Processing of payment orders in

Technical Handbook as of 1 January 2017 1 January 2017 1 Table of Contents Section I Payments Article 1: Account management and processing of payment orders 3 Article 2: Processing of payment orders in

LCH SA CDS Clearing Procedures

LCH SA CDS Clearing Procedures Section 5-1 August 2016 CONTENTS SECTION 5 - CDS CLEARING OPERATIONS 5.1 THE CDS CLEARING SERVICE... 3 5.2 BACKLOADING TRANSACTIONS... 3 5.3 CLEARING OF CLIENT TRADE LEGS...

LCH SA CDS Clearing Procedures Section 5-1 August 2016 CONTENTS SECTION 5 - CDS CLEARING OPERATIONS 5.1 THE CDS CLEARING SERVICE... 3 5.2 BACKLOADING TRANSACTIONS... 3 5.3 CLEARING OF CLIENT TRADE LEGS...

AMENDMENT CREDIT SUPPORT ANNEX

Exhibit J-AMEND Amend Method for CSA (Japanese Law) or Replicate-and-Amend Method for CSA (Japanese Law) This Exhibit to the ISDA 2016 Variation Margin Protocol is applicable if the Agreed Method is Amend

Exhibit J-AMEND Amend Method for CSA (Japanese Law) or Replicate-and-Amend Method for CSA (Japanese Law) This Exhibit to the ISDA 2016 Variation Margin Protocol is applicable if the Agreed Method is Amend

Intragroup Margin Exemption Disclosure Under The European Market Infrastructure Regulation

Intragroup Margin Exemption Disclosure Under The European Market Infrastructure Regulation The European Market Infrastructure Regulation (EMIR) sets out minimum risk-mitigation techniques that apply to

Intragroup Margin Exemption Disclosure Under The European Market Infrastructure Regulation The European Market Infrastructure Regulation (EMIR) sets out minimum risk-mitigation techniques that apply to

Chapter 5. Rules and Policies AMENDMENTS TO ONTARIO SECURITIES COMMISSION RULE TRADE REPOSITORIES AND DERIVATIVES DATA REPORTING

Chapter 5 Rules and Policies 5.1.1 Amendments to OSC Rule 91-507 Trade Repositories and Derivatives Data Reporting AMEDMETS TO OTARIO SECURITIES COMMISSIO RULE 91-507 TRADE REPOSITORIES AD DERIVATIVES

Chapter 5 Rules and Policies 5.1.1 Amendments to OSC Rule 91-507 Trade Repositories and Derivatives Data Reporting AMEDMETS TO OTARIO SECURITIES COMMISSIO RULE 91-507 TRADE REPOSITORIES AD DERIVATIVES

Technical Handbook. 15 June June

Technical Handbook 15 June 2017 15 June 2017 1 Table of Contents Section I Payments Article 1: Account management and processing of payment orders 3 Article 2: Processing of payment orders in TARGET2 6

Technical Handbook 15 June 2017 15 June 2017 1 Table of Contents Section I Payments Article 1: Account management and processing of payment orders 3 Article 2: Processing of payment orders in TARGET2 6

TRADITION SEF PLATFORM SUPPLEMENT 1 TRAD-X INTEREST RATES TRADING PLATFORM. ( Trad-X Platform )

") TRADITION SEF PLATFORM SUPPLEMENT 1 TRAD-X INTEREST RATES TRADING PLATFORM ( Trad-X Platform ) This Tradition SEF Platform Supplement to the Tradition SEF Rulebook, (the Rulebook ) sets out the additional

TRADITION SEF PLATFORM SUPPLEMENT 1 TRAD-X INTEREST RATES TRADING PLATFORM ( Trad-X Platform ) This Tradition SEF Platform Supplement to the Tradition SEF Rulebook, (the Rulebook ) sets out the additional

Networks of counterparties in the centrally cleared EU-wide interest rate derivatives market 1

Networks of counterparties in the centrally cleared EU-wide interest rate derivatives market 1 Pawe l Fiedor Sarah Lapschies Lucia Országhová,, European Systemic Risk Board Secretariat Národná banka Slovenska

Networks of counterparties in the centrally cleared EU-wide interest rate derivatives market 1 Pawe l Fiedor Sarah Lapschies Lucia Országhová,, European Systemic Risk Board Secretariat Národná banka Slovenska

To enhance financial stability by providing risk mitigation services to the global FX market

IOSCO-CONFYN 2012 Financial Stability in a Period of Volatility www.cls-group.com Gerard Hartsink Chairman of the Board November 2012 CLS and the CLS Logo are registered trademarks of CLS UK Intermediate

IOSCO-CONFYN 2012 Financial Stability in a Period of Volatility www.cls-group.com Gerard Hartsink Chairman of the Board November 2012 CLS and the CLS Logo are registered trademarks of CLS UK Intermediate

Amendments to 1. Multilateral Instrument Trade Repositories and Derivatives Data Reporting is

Office of the Yukon Superintendent of Securities Ministerial Order Enacting Rule: 2016/05 Amendment effective in Yukon: September 30, 2016 Amendments to Multilateral Instrument 96-101 Trade Repositories

Office of the Yukon Superintendent of Securities Ministerial Order Enacting Rule: 2016/05 Amendment effective in Yukon: September 30, 2016 Amendments to Multilateral Instrument 96-101 Trade Repositories

STANDARD TARIFF SCALE STOCK, ADR, ETF

AMERIABANK CJSC 17TR PL 72-20 Page 1/8 ANNEX 1 TO BROKERAGE SERVICE AGREEMENT Brokerage Service Fees for AMERIA GLOBAL TRADING Terminal STANDARD TARIFF SCALE STOCK, ADR, ETF Table 1 USA Canada Mexico Austria

AMERIABANK CJSC 17TR PL 72-20 Page 1/8 ANNEX 1 TO BROKERAGE SERVICE AGREEMENT Brokerage Service Fees for AMERIA GLOBAL TRADING Terminal STANDARD TARIFF SCALE STOCK, ADR, ETF Table 1 USA Canada Mexico Austria

CFTC Expands Interest Rate Swap Clearing Requirements

26 October 2016 Practice Groups: Derivatives & Structured Products Investment Management, Hedge Funds and Alternative Investments Global Government Solutions CFTC Expands Interest Rate Swap Clearing Requirements

26 October 2016 Practice Groups: Derivatives & Structured Products Investment Management, Hedge Funds and Alternative Investments Global Government Solutions CFTC Expands Interest Rate Swap Clearing Requirements

LCH SA CDS Clearing Procedures

LCH SA CDS Clearing Procedures Section 2-4 January 2018 Contents CONTENTS SECTION 2 MARGIN AND PRICE ALIGNMENT INTEREST 2.1 OVERVIEW... 1 2.2 MARGIN... 1 2.3 EXCESS COLLATERAL AND THE CLIENT COLLATERAL

LCH SA CDS Clearing Procedures Section 2-4 January 2018 Contents CONTENTS SECTION 2 MARGIN AND PRICE ALIGNMENT INTEREST 2.1 OVERVIEW... 1 2.2 MARGIN... 1 2.3 EXCESS COLLATERAL AND THE CLIENT COLLATERAL

Amendments to the Clearing Conditions of Eurex Clearing AG; Lending CCP: Introduction of clearing for Austrian and Italian equities

eurex clearing circular 087/17 Date: 14 September 2017 Recipients: All Clearing Members, Non-Clearing Members, Basic Clearing Members, FCM Clients and Registered Customers of Eurex Clearing AG and Vendors

eurex clearing circular 087/17 Date: 14 September 2017 Recipients: All Clearing Members, Non-Clearing Members, Basic Clearing Members, FCM Clients and Registered Customers of Eurex Clearing AG and Vendors

Cross Currency Swaps. Savill Consulting 1

Cross Currency Swaps Savill Consulting 1 A forward FX rate is calculated using a no-arbitrage pricing model Assume a US-based investor has US$10.50 million to invest and a 12-mo time horizon. The current

Cross Currency Swaps Savill Consulting 1 A forward FX rate is calculated using a no-arbitrage pricing model Assume a US-based investor has US$10.50 million to invest and a 12-mo time horizon. The current

Conversion of Financial Terms of IBRD and IDA Loans and Financing Instruments. Bank Access to Information Policy Designation Public

Bank Directive Conversion of Financial Terms of IBRD and IDA Loans and Financing Instruments Bank Access to Information Policy Designation Public Catalogue Number TRE7.02-DIR.102 Issued July 11, 2018 Effective

Bank Directive Conversion of Financial Terms of IBRD and IDA Loans and Financing Instruments Bank Access to Information Policy Designation Public Catalogue Number TRE7.02-DIR.102 Issued July 11, 2018 Effective

Operational Efficiency for Offshore RMB

Operational Efficiency for Offshore RMB Lisa O Connor, SWIFT May 2012 SWIFT s role Facilitate RMB transactions & automation Broaden industry understanding Provide business insights Provide a global network

Operational Efficiency for Offshore RMB Lisa O Connor, SWIFT May 2012 SWIFT s role Facilitate RMB transactions & automation Broaden industry understanding Provide business insights Provide a global network

ORGANISED TRADING FACILITY RATE CARD

ORGANISED TRADING FACILITY RATE CARD EFFECTIVE DATE: 1 MAY 2018 Head office : 130 Wood Street - London EC2V 6DL - ed Kingdom Louis Capital Markets UK LLP: Authorised and regulated in the ed Kingdom by

ORGANISED TRADING FACILITY RATE CARD EFFECTIVE DATE: 1 MAY 2018 Head office : 130 Wood Street - London EC2V 6DL - ed Kingdom Louis Capital Markets UK LLP: Authorised and regulated in the ed Kingdom by

LCH Aldgate House 33 Aldgate High Street London EC3N 1EA T: +44 (0) F: +44 (0) lch.com

F: +44 (0) lch.com") VIA CFTC PORTAL 10 August 2017 Mr Christopher Kirkpatrick Commodity Futures Trading Commission 115 21 st Street NW Three Lafayette Centre Washington DC 20581 LCH Limited Self Certification: Allocation

VIA CFTC PORTAL 10 August 2017 Mr Christopher Kirkpatrick Commodity Futures Trading Commission 115 21 st Street NW Three Lafayette Centre Washington DC 20581 LCH Limited Self Certification: Allocation

INTERNATIONAL DEVELOPMENT ASSOCIATION BOARD OF GOVERNORS. Resolution No. 211

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION BOARD OF GOVERNORS Resolution No. 211 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized WHEREAS:

Public Disclosure Authorized INTERNATIONAL DEVELOPMENT ASSOCIATION BOARD OF GOVERNORS Resolution No. 211 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized WHEREAS:

Financial Institutions Payment Services Cut-off times

Financial Institutions Payment Services Cut-off times ING Belgium SA/NV May 2017 1. Commercial payments in EUR Value date Payments initiated by your bank for third party 16:45 1 D Payments initiated by

Financial Institutions Payment Services Cut-off times ING Belgium SA/NV May 2017 1. Commercial payments in EUR Value date Payments initiated by your bank for third party 16:45 1 D Payments initiated by

FX Liquidity and Market Metrics: New Results Using CLS Bank Settlement Data. Online Appendix: Supplemental Tables and Figures February 2, 2019

FX Liquidity and Market Metrics: New Results Using CLS Bank Settlement Data Online Appendix: Supplemental Tables and Figures February 2, 2019 Joel Hasbrouck NYU Stern Richard M. Levich NYU Stern Joel Hasbrouck,

FX Liquidity and Market Metrics: New Results Using CLS Bank Settlement Data Online Appendix: Supplemental Tables and Figures February 2, 2019 Joel Hasbrouck NYU Stern Richard M. Levich NYU Stern Joel Hasbrouck,

STANDARD TARIFF SCALE

AMERIABANK CJSC 17TR PL 72-20 Page 1/7 Approved by Management Board Decision 09/81/16 as of June 03, 2016 Chairman of the Management Board General Director Artak Hanesyan June 06, 2016 ANNEX 1 TO BROKERAGE

AMERIABANK CJSC 17TR PL 72-20 Page 1/7 Approved by Management Board Decision 09/81/16 as of June 03, 2016 Chairman of the Management Board General Director Artak Hanesyan June 06, 2016 ANNEX 1 TO BROKERAGE

Service description. Corporate Access Payables Appendix Norway

Service description Corporate Access Payables Appendix Norway Table of contents Page 2 of 13 1 APPENDIX NORWAY... 3 2 GENERAL OVERVIEW OF THE NORWEGIAN PAYMENT INFRASTRUCTURE... 3 2.1 AVAILABLE PAYMENT

Service description Corporate Access Payables Appendix Norway Table of contents Page 2 of 13 1 APPENDIX NORWAY... 3 2 GENERAL OVERVIEW OF THE NORWEGIAN PAYMENT INFRASTRUCTURE... 3 2.1 AVAILABLE PAYMENT

ALERT. U.S. Banking Regulators Finalize Minimum Margin Requirements for Uncleared Swaps. Asset Management. January 8, 2016

Asset Management ALERT January 8, 2016 U.S. Banking Regulators Finalize Minimum Margin Requirements for Uncleared Swaps On October 22, 2015, the Federal Deposit Insurance Corporation (the FDIC ) and the

Asset Management ALERT January 8, 2016 U.S. Banking Regulators Finalize Minimum Margin Requirements for Uncleared Swaps On October 22, 2015, the Federal Deposit Insurance Corporation (the FDIC ) and the

Chapter Year Euro Interest Rate Swap Futures

Chapter 57 10-Year Euro Interest Rate Swap Futures 57100. SCOPE OF CHAPTER This chapter is limited in application to trading of 10-Year Euro Interest Rate Swap ( EUR IRS ) futures. The procedures for trading,

Chapter 57 10-Year Euro Interest Rate Swap Futures 57100. SCOPE OF CHAPTER This chapter is limited in application to trading of 10-Year Euro Interest Rate Swap ( EUR IRS ) futures. The procedures for trading,

Collateral Account Segregation Holding and processing collateral with LCH Ltd

Collateral Account Segregation Holding and processing collateral with LCH Ltd 17 January 2018 Contents 1. Introduction... 5 1.1 Who We Are... 5 1.2 About This Document... 5 1.3 Enquiries... 6 2. Account

Collateral Account Segregation Holding and processing collateral with LCH Ltd 17 January 2018 Contents 1. Introduction... 5 1.1 Who We Are... 5 1.2 About This Document... 5 1.3 Enquiries... 6 2. Account

Terms and conditions - International payments - Personal Clients

Terms and conditions - International payments - Personal Clients Do you plan to make an international payment? Or are you to receive a payment from a country outside Denmark? In Terms and conditions -

Terms and conditions - International payments - Personal Clients Do you plan to make an international payment? Or are you to receive a payment from a country outside Denmark? In Terms and conditions -

Dear Security Holder. 9 June 2017

Dear Holder Re: ETFS Foreign Exchange Limited (the Company ) Accounting period ended 31 December 2016 UK Information to Holders 9 June 2017 The of the Company set out below have been approved as s by HM

Dear Holder Re: ETFS Foreign Exchange Limited (the Company ) Accounting period ended 31 December 2016 UK Information to Holders 9 June 2017 The of the Company set out below have been approved as s by HM

Approved by Management committee of Danske Bank A/S Latvia branch (Meeting No 39/2014 from 24 September 2014) Effective from 01 of December 2014

Effective from 01 of December 2014") Approved by Management committee of Danske Bank A/S Latvia (Meeting No 39/2014 from 24 September 2014) Effective from 01 of December 2014 DANSKE BANK A/S LATVIA BRANCH PRICELIST - FOR PRIVATE CUSTOMERS

Approved by Management committee of Danske Bank A/S Latvia (Meeting No 39/2014 from 24 September 2014) Effective from 01 of December 2014 DANSKE BANK A/S LATVIA BRANCH PRICELIST - FOR PRIVATE CUSTOMERS

Terms and conditions - International payments - Corporate Clients

Terms and conditions - International payments - Corporate Clients Does your company plan to make an international payment? Or are you to receive a payment from a country outside Denmark? In Terms and conditions

Terms and conditions - International payments - Corporate Clients Does your company plan to make an international payment? Or are you to receive a payment from a country outside Denmark? In Terms and conditions

LCH SA CDS Clearing Supplement

LCH SA CDS Clearing Supplement 13 December 2017 This document is for use with the clearing of index linked credit derivative transactions, single name credit derivative transactions and swaption transactions

LCH SA CDS Clearing Supplement 13 December 2017 This document is for use with the clearing of index linked credit derivative transactions, single name credit derivative transactions and swaption transactions

PROCEDURES SECTION 4 MARGIN AND COLLATERAL

LCH.CLEARNET LIMITED PROCEDURES SECTION 4 MARGIN AND COLLATERAL CONTENTS Section Page 1. Collateral... 1 1.1 General Information... 1 1.2 Documentation... 5 1.3 Instructions via CMS... 7 1.4 Settlement

LCH.CLEARNET LIMITED PROCEDURES SECTION 4 MARGIN AND COLLATERAL CONTENTS Section Page 1. Collateral... 1 1.1 General Information... 1 1.2 Documentation... 5 1.3 Instructions via CMS... 7 1.4 Settlement

ISDA Glossary of Selected Provisions from the 2006 ISDA Definitions ~ Vietnamese Translation

ISDA Glossary of Selected Provisions from the 2006 ISDA Definitions ~ Vietnamese Translation [Apr 25, 2011] 1 OBJECTIVES of the ISDA Glossary of Selected Provisions from the 2006 ISDA Definitions ~ Vietnamese

ISDA Glossary of Selected Provisions from the 2006 ISDA Definitions ~ Vietnamese Translation [Apr 25, 2011] 1 OBJECTIVES of the ISDA Glossary of Selected Provisions from the 2006 ISDA Definitions ~ Vietnamese

DRAFT. Triennial Central Bank Survey of Foreign Exchange and OTC Derivatives Markets. Reporting guidelines for turnover in April 2019

DRAFT Triennial Central Bank Survey of Foreign Exchange and OTC Derivatives Markets Reporting guidelines for turnover in April 2019 Monetary and Economic Department May 2018 Table of Contents A. Introduction...

DRAFT Triennial Central Bank Survey of Foreign Exchange and OTC Derivatives Markets Reporting guidelines for turnover in April 2019 Monetary and Economic Department May 2018 Table of Contents A. Introduction...

Payment transaction information

Payment Transaction Payment transaction information Payment instructions will be processed on the same business day if we receive them before the relevant cut-off time on that day. Our business days are

Payment Transaction Payment transaction information Payment instructions will be processed on the same business day if we receive them before the relevant cut-off time on that day. Our business days are

ILLUSTRATIVE SCENARIOS FOR GEF-5 CONTRIBUTIONS

Fifth Meeting for the Fifth Replenishment of the GEF Trust Fund March 9-10, 2010 Rome, Italy GEF/R.5/27 February 16, 2010 ILLUSTRATIVE SCENARIOS FOR GEF-5 CONTRIBUTIONS (PREPARED BY THE WORLD BANK AS TRUSTEE)