Investor Presentation. June 2015

|

|

|

- Griselda Martin

- 5 years ago

- Views:

Transcription

1 Investor Presentation June 2015

2 Forward-Looking Statement and Cautionary Note Variations If no further specification is included, comparisons are made against the same period of the last year. Rounding Numbers may not total due to rounding. Financial Information Excluding budgetary and volumetric information, the financial information included in this report and the annexes hereto is based on unaudited consolidated financial statements prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board ( IFRS ), which PEMEX has adopted effective January 1, Information from prior periods has been retrospectively adjusted in certain accounts to make it comparable with the unaudited consolidated financial information under IFRS. For more information regarding the transition to IFRS, see Note 23 to the consolidated financial statements included in Petróleos Mexicanos 2012 Form 20-F filed with the Securities and Exchange Commission (SEC) and its Annual Report filed with the Comisión Nacional Bancaria y de Valores (CNBV). EBITDA is a non-ifrs measure. We show a reconciliation of EBITDA to net income in Table 33 of the annexes to PEMEX s Results Report as of March 31, Budgetary information is based on standards from Mexican governmental accounting; therefore, it does not include information from the subsidiary companies or affiliates of Petróleos Mexicanos. It is important to mention, that our current financing agreements do not include financial covenants or events of default that would be triggered as a result of our having negative equity. Methodology We might change the methodology of the information disclosed in order to enhance its quality and usefulness, and/or to comply with international standards and best practices. Foreign Exchange Conversions Convenience translations into U.S. dollars of amounts in Mexican pesos have been made at the exchange rate at close for the corresponding period, unless otherwise noted. Due to market volatility, the difference between the average exchange rate, the exchange rate at close and the spot exchange rate, or any other exchange rate used could be material. Such translations should not be construed as a representation that the Mexican peso amounts have been or could be converted into U.S. dollars at the foregoing or any other rate. It is important to note that we maintain our consolidated financial statements and accounting records in pesos. As of March 31, 2015, the exchange rate of MXN = USD 1.00 is used. Fiscal Regime Starting January 1, 2015, Petróleos Mexicanos fiscal regime is ruled by the Ley de Ingresos sobre Hidrocarburos (Hydrocarbons Income Law). Since January 1, 2006 and until December 31, 2014, PEP was subject to a fiscal regime governed by the Federal Duties Law, while the tax regimes of the other Subsidiary Entities were governed by the Federal Revenue Law. The Special Tax on Production and Services (IEPS) applicable to automotive gasoline and diesel is established in the Production and Services Special Tax Law Ley del Impuesto Especial sobre Producción y Servicios. If the final price is higher than the producer price, the IEPS is paid by the final consumer. On the opposite, the IEPS has been absorbed by the Secretary of Finance and Public Credit (SHCP) and credited to PEMEX. In this case, also known as negative IEPS, the IEPS credit to PEMEX has been included in Other income (expenses) in its Income Statement. PEMEX s producer price is calculated in reference to that of an efficient refinery operating in the Gulf of Mexico. Up to 2014 the final price was stablished by the SHCP. In 2015 the SHCP set a cap for the final price based on the inflation expectations. In 2016 and 2017 the SHCP will do the same; and, based on economic competitions conditions, the price will be determined by the market since Hydrocarbon Reserves In accordance with the Hydrocarbons Law, published in the Official Gazette on August 11, 2014, the National Hydrocarbons Commission (CNH) will establish and will manage the National Hydrocarbons Information Center, comprised by a system to obtain, safeguard, manage, use, analyze, keep updated and publish information and statistics related; which includes estimations, valuation studies and certifications. As of January 1, 2010, the Securities and Exchange Commission (SEC) changed its rules to permit oil and gas companies, in their filings with the SEC, to disclose not only proved reserves, but also probable reserves and possible reserves. Nevertheless, any description of probable or possible reserves included herein may not meet the recoverability thresholds established by the SEC in its definitions. Investors are urged to consider closely the disclosure in our Form 20-F and our Annual Report to the CNBV and SEC, available at Forward-looking Statements This report contains forward-looking statements. We may also make written or oral forward-looking statements in our periodic reports to the CNBV and the SEC, in our annual reports, in our offering circulars and prospectuses, in press releases and other written materials and in oral statements made by our officers, directors or employees to third parties. We may include forward-looking statements that address, among other things, our: exploration and production activities, including drilling; activities relating to import, export, refining, petrochemicals and transportation of petroleum, natural gas and oil products; projected and targeted capital expenditures and other costs, commitments and revenues, and liquidity and sources of funding. Actual results could differ materially from those projected in such forward-looking statements as a result of various factors that may be beyond our control. These factors include, but are not limited to: changes in international crude oil and natural gas prices; effects on us from competition, including on our ability to hire and retain skilled personnel; limitations on our access to sources of financing on competitive terms; our ability to find, acquire or have the right to access additional hydrocarbons reserves and to develop them; uncertainties inherent in making estimates of oil and gas reserves, including recently discovered oil and gas reserves; technical difficulties; significant developments in the global economy; significant economic or political developments in Mexico, including developments relating to the implementation of the Energy Reform (as described in our most recent Annual Report and Form 20-F); developments affecting the energy sector; and changes in our legal regime or regulatory environment, including tax and environmental regulations. Accordingly, you should not place undue reliance on these forward-looking statements. In any event, these statements speak only as of their dates, and we undertake no obligation to update or revise any of them, whether as a result of new information, future events or otherwise. These risks and uncertainties are more fully detailed in our most recent Annual Report filed with the CNBV and available through the Mexican Stock Exchange ( and our most recent Form 20-F filing filed with the SEC ( These factors could cause actual results to differ materially from those contained in any forward-looking statement. 1

3 Content PEMEX today Energy Reform New era of PEMEX Financials 2

4 A Transformation is Underway Benefits for PEMEX Benefits for the Industry 1 Round Zero: reserve base largely intact 12.4 MMMboe proved reserves low replacement cost 1 Open and regulated industry 2 Management and budgetary autonomy 2 Collaboration with companies along the entire value chain 3 Corporate governance 3 Clear distribution of roles 4 New procurement, compensation and fiscal regime 4 Sustainable development of resources 5 Addressing pension liabilities 5 Additional investment and job creation 3

5 A Snapshot of PEMEX Today Exploration and Production Crude oil production: 2,300 Mbd 1 Natural gas production: 5,753 MMcfd 1,3 75% of crude oil output is produced offshore 1P 4 reserves-life: 9.6 years Production mix 1 : 51% heavy crude; 38% light crude; 12% extra-light crude Downstream Refining capacity: 1,690 Mbd Strategically positioned infrastructure JVs and associations with key operators in the Mexican petrochemical and natural gas transportation industries International 8th largest oil producer worldwide 2 Crude oil exports: 1,263 Mbd 1 3rd largest oil exporter to the USA Long-term relationship with USGC refiners JV with Shell in Deer Park, Texas Total revenues 5 USD billion LTM Domestic sales Exports Services Revenues Proved Reserves MMMboe 8% 2% 2% 1% 0% Southeast Tampico-Misantla Burgos 87% Veracruz Deepwater Sabinas 1. January 2015-March PIW Ranking 3. Does not include nitrogen 4. As of January 1, PEMEX Audited and Unaudited financial statements 4

6 Round Zero Maintains Our Strong Reserve Base 2P Reserves MMMboe 100% = % 83% Total prospective resources MMMboe Conventional resources Unconventional resources % 2P Reserves MMMboe 100% = % Prospective resources MMMboe 100% = % 57% Requested and assigned areas Total Assigned areas Unassigned areas Conventional (Excludes deepwater) Conventional (Excludes deepwater) Unrequested areas % of prospective resources 21% 79% Non conventional and deeptwater Non conventional and deeptwater Resolution PEMEX obtained: 100% of its 2P Reserves request 68% of its Prospective Resources request Rationale Sustain current output levels, while holding onto strategic exploratory prospects to facilitate organic growth in the future Objective Strengthen PEMEX and maximize its long-term value for Mexico 1 Includes: Southern, Burgos and other Northern. 2 Includes: Perdido and Holok-Han. Note: Reserves as of January 1, Note: This slide is presented based on the announcement and reports made by the Ministry of Energy. 5

Sabinas Tampico- Misantla Veracruz Oil")

7 Distribution of PEMEX s Reserves 1 MMMboe (billion barrels of oil equivalent) Sabinas Tampico- Misantla Veracruz Oil and Gas Gas Burgos Deep Sea Exploration Gulf of Mexico Yucatan Platform Basin Prospective Reserves Cum. Resources Prod. 1P 2P 3P Non Conv. (90%) (50%) (10%) Conv. Southeastern Tampico Misantla Burgos Veracruz Sabinas Deepwater Total PEMEX Total Mexico As of January 1, Numbers may not total due to rounding. 3 As of January 1, Southeastern Development and Exploitation Projects Exploration Projects 6

8 Industry Cost Leader Production Costs a,b USD / boe Finding & Development Costs a,c,d, e USD / boe Benchmarking: Production Costs 1 USD / boe Benchmarking: Finding & Development Costs 2,3 USD / boe Petrobras Total Chevron 17.1 Shell Shell Statoil BP Petrobras Conoco Chevron Eni ENI Exxon Conoco Total 9.24 Exxon Statoil 8.51 BP PEMEX 7.91 PEMEX a) Data in nominal values. b) Source: 20-F Form (2014 & 2012). c) PEMEX estimates- 3-year moving average. d) Includes indirect administration expenses. e) Calculations based on proved reserves. 1. Source: Annual Reports and SEC Reports Estimates based on John S. Herold Company Performance Metrics year moving average performance calculations. Note: The sum of these figures is for general illustration purposes only, due to the fact that proved reserves replacement rate does not equal 100% on every case, and because F&D costs are relative to total proved reserves, rather than total developed proved reserves. The sum of these should be used as an estimate. 7

9 Building on Our Significant Infrastructure Production Capacity Refining Atmospheric distillation capacity 1,602 Mbd Gas Processing Sour Nat Gas 4.5 Bcf Cryogenic 5.9 Bcf Condensate Sweetening 144 Mbd Fractioning 568 Mbd Sulfur Recovery 3,256 t/d Petrochemical MMt nominal per year Infrastructure Refining 6 Refineries Fleet: 21 tankers Storage of 13.5 MMb of Refined Products 14,176 km of pipelines Gas 70 Plants in 11 Gas Processing Centers 12,678 km of pipelines Petrochemical 8 Petrochemical Plants 8,357 Pipeline Network (km) ,097 1, ,691 9,975 16,800 Camargo Salamanca Guadalajara Monterrey Nat gas Oil Burgos Cadereyta Arenque Poza Rica Tula Refined and Petrochemicals Products Oil & Gas Reynosa Madero Producer Zone Refinery Petrochemical Center Gas Processing Center Sales Point Pipeline Maritime Route Cd. México Matapionche Pajaritos Morelos San Martín La Venta Cd. Pemex Cosoleacaque Minatitlán N. Pemex Cangrejera Cactus Salina Cruz Petrochemical LPG Gasoline Fuel Oil Jet Fuel 8

10 Content PEMEX today Energy Reform New era of PEMEX Financials 9

Approval of 9 new laws and amendment")

August 13 2014 Round One The Ministry of Energy and the National Hydrocarbons Commission 2 previewed the blocks that will comprise Round One October 2014 On October 7 th, the new Board of Directors")

11 The Milestones of the Energy Reform Constitutional Reform (December 20, 2013) March 21 August Round Zero & Resolution The Ministry of Energy 1 prioritized PEMEX s request for exploratory blocks and producing fields, and defined their dimensions August August Secondary Legislation Potential collaboration agreements (farm-outs, JVs) Approval of 9 new laws and amendment of 12 existing laws Detailed distribution of responsibilities Structure and process for awarding contracts PEMEX defined areas susceptible to collaboration agreements (JVs, farm-outs, etc.) August Round One The Ministry of Energy and the National Hydrocarbons Commission 2 previewed the blocks that will comprise Round One October 2014 On October 7 th, the new Board of Directors was formed On October 14 th, the following committees were established: Audit, Human Resources and Compensation, Strategy and Investments, and lastly, Acquisitions, Leasing, Works and Services December 2015 PEMEX 3 as a State Productive Enterprise 1 SENER 2 CNH 3 PEMEX will be able to work on assignments and contracts during these 24 months 10

12 Updating an Outdated Energy Model Constitutional Reform A clear distribution of roles: owner, regulator, operating entities and operating companies Secondary Legislation The Ministry of Energy dictates the energy policy and coordinates the regulatory entities through the Coordinating Council of the Energy Sector Regulatory entities Operating entities The Ministry of Finance defines fiscal regime, economic terms of contracts and manages resources from exploration and production through the Mexican Petroleum Fund for Stabilization and Development 1 2 ASEA 3 4 CENAGAS 5 Operating companies 6 Other participants 1. Comisión Nacional de Hidrocarburos 2. Comisión Reguladora de Energía 3. Agencia de Seguridad, Energía y Ambiente 4. Centro Nacional de Control de Energía. 5. Centro Nacional de Control de Gas Natural. 6. Comisión Federal de Electricidad. New creation 11

13 Regulated by the Ministry of Energy and the CRE Regulated by the Ministry of Energy and the CNH Quick Take on the New Energy Sector in Mexico Assignments Exploration and Production Contracts Migration Transboundary Hydrocarbon Reservoirs 1. Production-sharing 2. Profit-sharing 3. Licenses 4. Services + Third Parties Third Parties Possibility of direct assignment to PEMEX State participation ( 20%) Comply with international treaties PEMEX to continue commercialization for next 3 years and open to private thereafter Refining Natural gas Transportation, storage and distribution Industrial Transformation (Downstream & Petrochemical) Permits (SENER) Permits (SENER) CENAGAS 1 Permits (CRE 2 ) 1 Centro Nacional de Control del Gas Natural (National Center for Natural Gas Control) 2 Regulation and permits for transportation, storage and distribution not related to pipelines, and for LPG retail will be granted by the Ministry of Energy (SENER) until December 31,

")

14 The Fiscal Regime Exploration and Production Assignments (Round Zero) Migration Contracts (Round One) New fiscal regime PEMEX Licenses Production- Sharing or Profit-Sharing Contracts Signing Bonus 1. Contractual Fee for the Exploratory Phase 2. Royalties 3. Compensation considering Operating Income or Contractual Value of the Hydrocarbons 4. Hydrocarbons Exploration & Extraction Tax 5. Income Tax Oil Fund Income Tax SHCP Industrial Transformation Hydrocarbons Revenue Law Income Tax Law 13

15 Content PEMEX today Energy Reform New era of PEMEX Financials 14

16 Unified Corporate Services Corporate Governance and Structure Strengthen Corporate Governance Board Committees Audit Human Resources and Compensation SENER SHCP State Representatives 1 Independent Members Strategy and Investments Acquisitions, Leasing, Works and Services New Corporate Structure Upstream 2 10 members Drilling Cogeneration 2 Ammonia Fertilizers Industrial Transformation Ethylene Polymers 1 Do not have to be active public servants 2 Approved by the Board of Directors as of May 22, 2015 Logistics Finance Human Resources Procurement Other Flexible legal framework governed by the principles of private law. A special regime for: acquisition and procurement, compensation, budget, debt, subsidiaries and affiliates. 15

17 New Internal Committees to Support Management Executive Committee Operational Committee Ethics Committee Provide support on strategic management Integrated by: Director General Finance Planning IT and Business Processes Alliances and New Business Officer Installed on February 3, 2015 Provide support on operational management, decision making and systemic review of operations Integrated by: Director General Planning Finance E&P Industrial Transformation PMI Installed on February 16, 2015 Provide support to overview the implementation and enforcement of the Codes of Ethics and Conduct Integrated by: Corporate Director of Management Deputy Director of Human Resources and Labor Relations Representatives of each Corporate Direction, Subsidiary Companies, Affiliates and the Internal Control Unit Installed on February 25,

18 Status of the New Structure On March 27, 2015, PEMEX s Board of Directors adopted creation resolutions for the new state productive subsidiaries, the new Organic Statute of Petróleos Mexicanos and made several executive appointments and reappointments. Both creation resolutions and the new Organic Statute of PEMEX were published in the Official Gazette of the Federation last Tuesday, April 28th. All of this, has laid the necessary foundations for the future of the company, that will gradually revert the recent trend observed on our results. Pemex Exploration and Production and Pemex Cogeneration and Services came into effect on May 22,

Profit Sharing Duty Fixed amount per km 2 (amount increases with time) % of")

19 Fiscal Regime for Assignments Key Takeaways 1. Simple 2. Resembles typical tax scheme 3. Gradual reduction of fiscal burden Duties and Royalties Hydrocarbon Exploration Duty Hydrocarbon Extraction Duty (Royalty) Profit Sharing Duty Fixed amount per km 2 (amount increases with time) % of the value of extracted hydrocarbons (% based on hydrocarbon price levels) Value of extracted Hydrocarbons - COST CAP % % % % % X Rate onward 70.00% 68.75% 67.50% 66.25% 65.00% Taxes Hydrocarbon Exploration and Extraction Activity Tax Income Tax (ISR) Fixed amount for exploration per km 2 + fixed amount for extraction per km 2 100% of investments in: exploration, EOR 1 and non-capitalizable maintenance. Allowable deductions: 25% of investments in: extraction and development. 10% of investments in: storage and transport infrastructure. 1 Enhanced Oil Recovery 18

20 PEMEX Strategy in Partnerships is Focused on Three Main Major Objectives Migrate the current E&P Service Contracts (FPWC 1 and EPIC 2 ) into Exploration and Extraction Contracts (EEC) Under the new legal framework, the existing contracts with the corresponding contractors will be migrated into EEC By improving fiscal terms, contractors will gain access to additional resources, currently classified as prospective or contingent, hence enhancing the reserves and production for the contractor as well as earnings and taxes for the State Establish partnerships for selected assigned fields to PEMEX in Round Zero Selected fields assigned to PEMEX in Round Zero will be farmed out The farm-outs will enable the development of fields with high technical complexity or high CAPEX requirements which otherwise would remain underutilized Position PEMEX for partnerships in next rounds PEMEX will develop technical and organizational capabilities to compete for new blocks Capabilities acquired will allow to improve PEMEX s position to compete for blocks in future bidding rounds 1. FPWC. Financed Public Work Contracts 2. EPIC. Exploration and Production Integrated Contracts 19

21 Bringing New Partnerships On-Board 2P Reserves (MMboe) 2 CAPEX (USD billion) Fields 2.6 Phase Poza Rica-Altamira and Burgos 22 existing contracts 1 Phase 2 1, ATG and Burgos Shallow waters Bolontikú, Sinán and Ek Onshore Rodador, Ogarrio and Cárdenas-Mora Farm-outs Extra heavy oil Ayatsil-Tekel-Utsil Deepwater (gas) Kunah-Piklis Deepwater (oil) Trión and Exploratus Total 4, Aug 2014 / Dec 2015 CIEP & COPF contract migration (first block) Jan / Dec 2015 CIEP & COPF - Second block Nov 2014 / Dec Farm-outs Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec 1 Public Financed Works Contracts, Integrated Exploration & Production Contracts. 2 MMboe million barrels of oil equivalent. 3 3P Reserves 20

22 Future Production Frontiers Deepwater Infrastructure 1 Shale Potential 2 United States Gulf of Mexico United States Mexico Mexico Cuba 1 Source: National Geographic. 2 Source: CNH with information from North Dakota Department of Mineral Resources, Oklahoma Geological Survey, Texas Railroad Commission, Bureau of Ocean Energy Management, Oil &Gas Journal Well Forecast for

23 Downstream Business Portfolio: Main Projects Refining Gas Processing Petrochemicals Cogeneration Challenges: Increase operational efficiency Infrastructure for better fuels Main Projects: Investments in supply infrastructure (Project Gulf- Center), Refineries reconfiguration Clean fuels projects Challenges: Expand gas pipeline network Capture trading opportunities Main Projects: Finish Los Ramones project Transoceanic Corridor Project for propane, gas and refined products Challenges: Integrate value chains: ethane, methane and aromatics Main Projects: Fertilizers strategy, Ethylene oxide and monoethylene glycol projects Modernization of Aromatics Train Challenges: Take advantage of PEMEX s power cogeneration potential Main Projects: Cogeneration projects 22

24 New Business Models - Downstream PEMEX has developed successful strategic alliances in our downstream activities Project Deer Park Gas Pipelines PEMEX Mexichem Partner PEMEX s Participation 1. Joint Venture 2. Oil supply 1. Joint Venture 1. Joint Venture 2. Fixed assets 3. Supply of raw materials Objective Operations Startup Refine Mexican heavy crude oil and increase gasoline supply to Mexico Natural Gas and LPG transportation to power plants in the northern region of Mexico Increase production of vinyl chloride

Los Ramones Phase I Ownership structure (Gasoductos de Chihuahua): 50% PGPB.")

25 Los Ramones Pipeline Project Los Ramones Phase II: North Ownership structure (TAG Pipelines Norte): 45% BlackRock/First Reserve 1 30% PGPB 1 25% IEnova Gasoductos 1 Start of Operations: December 2015 Capacity: 1.4 bcf; 42 diameter. Investment: USD 1.3 billion Length: 452 km (Los Ramones, NL to San Luis Potosi, SLP) Los Ramones Phase I Ownership structure (Gasoductos de Chihuahua): 50% PGPB. 50% IEnova Gasoductos Start of Operations: December 2014 Capacity: 1.0 bcf (2014) up to 2.1 bcf (2015); 48 diameter Investment: USD 0.6 billion Length: 116 km (Agua Dulce, TX to Los Ramones, NL) Los Ramones Phase II: South Ownership structure: (TAG Pipelines Sur): 50% GDF Suez 1 45% BlackRock/First Reserve 1 5% PGPB 1 Start of Operations: December 2015 Capacity: 1.4 bcf; 42 diameter Investment: USD 0.9 billion Length: 291 km (San Luis Potosi, SLP to Apaseo el Alto, GTO) Associations of PEMEX with: BlackRock - First Reserve.- The purpose of this association is to acquire a joint interest in phase two of the Los Ramones pipeline of approximately 45% of this phase. (1) Indirect ownership: the company or group does not directly own the share of the project, but a subsidiary or affiliate company from the company or group. 24

26 Content PEMEX today Energy Reform New era of PEMEX Financials 25

27 Income Statement Evolution Income Statement USD billion Income before taxes and duties Taxes and duties EBITDA Total sales Historically, from 2009 to 2014, taxes have accounted for 118% of operating income and 129% of beforetax profits. In 2015, taxes amounted to 212% of operating income and 45 times before-tax profits, respectively LTM 1Q15 Sales Q15 Operating Income Q15 EBITDA Q15 Petrochemical 2.0% Petrochemical -2.6% Petrochemical -0.4% Gas 9.9% Gas -0.6% Gas 1.3% Refining 34.6% Refining -22.4% Refining -5.8% E&P 53.4% E&P 125.6% E&P 104.9% 26

28 PEMEX One of the Most Profitable Companies in 2014 Gross Margin 50.3% 45.5% EBITDA Margin 55.56% 34.79% 15.1% 13.6% 13.3% 12.5% 18.99% 14.09% 12.32% 9.40% Statoil PEMEX Shell Chevron Exxon BP PEMEX Statoil Chevron Exxon Shell BP Operating Margin 38.87% Before Tax Margin 30.38% 18.08% 10.26% 9.34% 6.50% 5.11% 18.03% 16.23% 14.15% 6.72% 1.40% PEMEX Statoil Chevron Exxon Shell BP PEMEX Statoil Chevron Exxon Shell BP Source: Bloomberg and PEMEX 2014 Audited Financial Statements 27

29 Balance Sheet Evolution Liability and Equity Profile USD billion (5) (9) (21) (14) (52) (56) In addition to internal cash flows, PEMEX has resorted to financial markets to finance its investment projects. Pension liability generates costs and distortions in our financial statements. Our negative equity is a result of accumulated losses and the distortions derived from pension liabilities Q15 Equity Mkt Debt Pension Liability Other Liabilities 28

30 Price Sensitivity 2015 Price Sensitivity 2015: -$1 USD/b USD million (287) 69 (164) (356) Exports Domestic Sales Imports DUC DEH Total Considering current production and the Mexican Mix price 3, if the crude oil price decreases by $1 USD/b, its effect on PEMEX s main accrued items for 2015 will have an aggregate decrease of $164 USD million 4. This is a result of two effects: Crude oil cash flows: net positive effect due a short position (duties > exports) Petroleum products cash flows: net negative effect due to a long position (net domestic sales > imports) 1. Profit Sharing Duty (Derecho por la Utilidad Compartida- DUC). 2. Hydrocarbon Extraction Duty (Derecho de Extracción de Hidrocarburos- DEH). 3. Estimated 2015 Mexican Mix Average Price of USD 45 per barrel. 4. Price correlations between crude oil and refined products are considered. 29

31 Investing To Meet Our Long-term Goals USD billion % Pemex-Corporate 1.3% Pemex- Gas & Basic Petrochemicals CAPEX Distribution USD billion 2.2% Pemex- Petrochemicals 21.2% 14% Pemex-Refining 78.8% 82% Pemex- Exploration & Production E 2016E 2017E 2018E 2019E Figures are nominal and may not total due to rounding. Includes upstream maintenance expenditures. E means Estimated. CAPEX for 2015 is MXN$ billion. Figures for 2015 include the budget adjustments announced as of the date if this report. PEMEX s investment records are in pesos. Figures have been converted at the following average historical exchange rates: MXN /USD for 2011, MXN /USD for 2012, MXN /USD for 2013 and MXN /USD for For 2015 and subsequent years, an exchange rate of $13.40 MXN/USD is used. Investment figures for are under review and must be approved by the Board of PEMEX, along with the elaboration of the 2016 Budget (est. July 2015). Upstream Downstream 30

32 CAPEX Financing Net Indebtedness USD MMM 27.6% 25.0% 7.4% Total debt as of March 2015 is USD 84 billion which represents 0.9x sales and 1.7x EBITDA 14.4% % % 63.8% E2015 Net Indebtedness CAPEX 3,000 2,000 1,000 Stabilization of crude production Mbd 0 Modernization of infrastructure Salamanca Cadereyta Tula Madero Minatitlán Salina Cruz Higher investment in exploration Reserve Replacement Rate- 1 1P and 3P 1. As of January 1, P includes discoveries, developments, revisions and delineations.3p replacement rate only considers new discoveries. Reflects reserve replacements conducted by PEMEX. Source: PEMEX Financial Statements 150% 100% 50% 0% 1P 3P

33 Debt Profile By Currency 1,2 By Interest Rate 1,2 By Instrument 1,2 By Currency Exposure 1,2 1% 1% 4% 7% 21% 66% 27% 73% 4% 2% 6% 11% 18% 59% 1% 23% 0% 75% Dollar UDIS Yens Euros British Pounds Pesos Fixed Floating Int. Bonds ECAs Domestic Bank Loans Cebures Int. Bank Loans Others Dollar Euros Pesos UDI 32 Term Structure Consolidated Debt 1,2 USD MMM As of March 31, Sums may not total due to rounding Does not include accrual interest

34 Financing Program 2015 Source Programmed USD billion Domestic Markets International Markets Loans Export Credit Agencies (ECAs) Others Net Indebtedness

35 Financial Strategy Options International Market Issues Diversify sources of financing in efficient and deep markets (Japan, Middle East). Recurring emissions USD 1 billion. Debt management in order to keep the interest curve both liquid and efficient. New Structures Structured Products (Development Capital Certificates) Issues in MXN MXN is both more efficient in terms of cost and has less depth than the USD. Continue using mechanisms which contribute to increasing the liquidity, terms and volumes of the MXN: Predictable and frequent issuer. Diversified investor base. Issue re-openings. Market Maker programs. Bank Loans Increase the amount and term of revolving credit lines. Bank loans used to complete the financial program, if necessary. Revolving facilities As of February 27, 2015, syndicated revolving credit lines for liquidity management in the amounts of USD 4.5 billion and MXN 23.5 billion. Export Credit Agencies (ECAs) ECAs do not compete with other sources of financing and offer term and cost benefits. Continue with bond issues guaranteed by the US-EXIM. Reach agreements with the Export Bank of China and the Export Import Bank of Korea. Search ECA financing with other entities that currently do not have a business relationship with PEMEX. 34

Project finance")

36 New Financing Alternatives Fund Raising in the O&G Industry 1 PEMEX Financing Program % 31% 2% 13% 50% 10% 85% Bonds Bank loans Project finance Equity Bonds (domestic, international markets, ECAs) Project finance Bank Loans International markets: 34.7% Domestic markets: 42.2% ECAs: 8.1% 1. Additional financial flexibility 2. PEMEX could explore new financing opportunities already available in the industry 1 Source: ThomsonONE 35

37 Financial Discipline Budget Adjustment Premises To minimize crude and gas production effects To minimize the impacts on reserves replacement To maintain the capacity to supply the national petroleum products market To minimize the impacts on safety and reliability of our infrastructure while complying with environmental standards 2015 Budget Adjustment MXN billion To minimize potential impacts on our future competitiveness in the opening of the petroleum products market To increase PEMEX s profitability Original Final 36

38 Background and Necessary Update of the Pension Scheme Mexico: Life Expectancy Years In 1942, the retirement conditions were established: 55 years of age 25 years of work Up to 80% of wage The life expectancy growth has had an exponential effect in the pension liability. Accrued Obligations 1 MXN billion 1,494 42% Active employees Current pensions 10% 48% Accrued obligations Reform objectives Current pensions and active employees Based on the following conditions, the Federal Government will recognize with an amount equal to the savings achieved through the negotiation and amendment of the Collective Bargaining Agreement: Individual account regime for new employees Gradual adjustment of the retirement parameters of active employees 1. As of March 31,

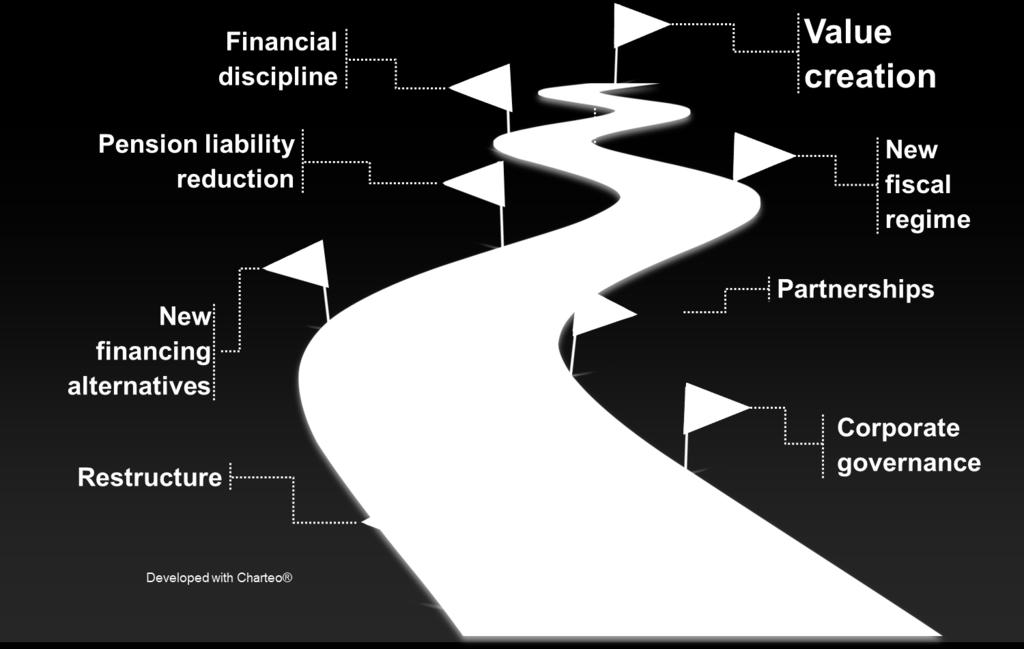

39 What differentiates PEMEX Strengths Human capital Execution flexibility Selected participation in new projects Sustainability mandate through corporate governance, and social & environmental responsibility Improved efficiencies through collaboration Diverse reserve portfolio (regional and Production stabilization Additional efficiency requirements in production and processing Industrial safety and security Increasing financing requirements Human resource attrition Pension liability technological) Technology deployment opportunities Financial autonomy and new fiscal regime Challenges 38

40 Future Goals 39

41 Investor Relations (+52 55)

The new O&G context in Mexico. October 2014

The new O&G context in Mexico October 2014 Forward-Looking Statement and Cautionary Note Variations If no further specification is included, comparisons are made against the same period of the last year.

The new O&G context in Mexico October 2014 Forward-Looking Statement and Cautionary Note Variations If no further specification is included, comparisons are made against the same period of the last year.

Mexico s Energy Reform & PEMEX as a State Productive Enterprise. October 2014

Mexico s Energy Reform & PEMEX as a State Productive Enterprise October 2014 Forward-Looking Statement and Cautionary Note Variations If no further specification is included, comparisons are made against

Mexico s Energy Reform & PEMEX as a State Productive Enterprise October 2014 Forward-Looking Statement and Cautionary Note Variations If no further specification is included, comparisons are made against

PEMEX Outlook. TENEMOS LA ENERGÍA August 2016

PEMEX Outlook TENEMOS LA ENERGÍA August 2016 Disclaimer Variations If no further specification is included, comparisons are made against the same realized period of the last year. Rounding Numbers may

PEMEX Outlook TENEMOS LA ENERGÍA August 2016 Disclaimer Variations If no further specification is included, comparisons are made against the same realized period of the last year. Rounding Numbers may

Petróleos Mexicanos: 2019 Financial and Operating Outlook

Antonio M. Amor Refinery Salamanca, Gto. Mex. Petróleos Mexicanos: 2019 Financial and Operating Outlook January 2019 New York Forward-Looking Statement & Cautionary Note Variations If no further specification

Antonio M. Amor Refinery Salamanca, Gto. Mex. Petróleos Mexicanos: 2019 Financial and Operating Outlook January 2019 New York Forward-Looking Statement & Cautionary Note Variations If no further specification

Mexico s Energy Reform & PEMEX as a State Productive Enterprise. December 2014

Mexico s Energy Reform & PEMEX as a State Productive Enterprise December 2014 Forward-Looking Statement and Cautionary Note Variations If no further specification is included, comparisons are made against

Mexico s Energy Reform & PEMEX as a State Productive Enterprise December 2014 Forward-Looking Statement and Cautionary Note Variations If no further specification is included, comparisons are made against

Preliminary Results as of March 31, May 3, 2017

Preliminary Results as of March 31, 2017 May 3, 2017 Variations Forward-Looking Statement & Cautionary Note If no further specification is included, comparisons are made against the same realized period

Preliminary Results as of March 31, 2017 May 3, 2017 Variations Forward-Looking Statement & Cautionary Note If no further specification is included, comparisons are made against the same realized period

PEMEX Outlook DCF-A /19 de Octubre de 2004

PEMEX Outlook DCF-A /19 de Octubre de 2004 Forward-looking Statement Disclaimer This presentation contains forward-looking statements. We may also make written or oral forward-looking statements in our

PEMEX Outlook DCF-A /19 de Octubre de 2004 Forward-looking Statement Disclaimer This presentation contains forward-looking statements. We may also make written or oral forward-looking statements in our

Petróleos Mexicanos Investor Presentation

Antonio M. Amor Refinery Salamanca, Gto. Mex. Petróleos Mexicanos Investor Presentation February 18, 2019 Forward-Looking Statement & Cautionary Note Variations If no further specification is included,

Antonio M. Amor Refinery Salamanca, Gto. Mex. Petróleos Mexicanos Investor Presentation February 18, 2019 Forward-Looking Statement & Cautionary Note Variations If no further specification is included,

Results as of the 4 th Quarter 2010

Results as of the 4 th Quarter 2010 March 1, 2011 Content 4Q10 Main Highlights Upstream Downstream Financial Results Questions and Answers 2 4Q10 Financial Highlights Billion pesos Billion dollars 2009

Results as of the 4 th Quarter 2010 March 1, 2011 Content 4Q10 Main Highlights Upstream Downstream Financial Results Questions and Answers 2 4Q10 Financial Highlights Billion pesos Billion dollars 2009

Preliminary Results First Quarter April 26, 2013

Preliminary Results First Quarter 2013 April 26, 2013 Forward-Looking Statement and Cautionary Note (1/2) Variations If no further specification is included, changes are made against the same period of

Preliminary Results First Quarter 2013 April 26, 2013 Forward-Looking Statement and Cautionary Note (1/2) Variations If no further specification is included, changes are made against the same period of

Results as of the 3 rd Quarter of 2010

Results as of the 3 rd Quarter of 2010 October 29, 2010 Forward-Looking Statement and Cautionary Note (1/2) Variations If no further specification is included, changes are made against the same period

Results as of the 3 rd Quarter of 2010 October 29, 2010 Forward-Looking Statement and Cautionary Note (1/2) Variations If no further specification is included, changes are made against the same period

Investor Meeting. December 2013

Investor Meeting December 2013 1 Forward-Looking Statements and Cautionary Note Variations If no further specification is included, changes are made against the same period of the last year. Rounding Numbers

Investor Meeting December 2013 1 Forward-Looking Statements and Cautionary Note Variations If no further specification is included, changes are made against the same period of the last year. Rounding Numbers

Investor Presentation. August 2017

Investor Presentation August 2017 Content 1 A Snapshot of Mexico & PEMEX Upstream Midstream & Downstream Overall Financial Performance Business Outlook 1 Mexico Snapshot Today, Mexico s fundamentals are

Investor Presentation August 2017 Content 1 A Snapshot of Mexico & PEMEX Upstream Midstream & Downstream Overall Financial Performance Business Outlook 1 Mexico Snapshot Today, Mexico s fundamentals are

Investor Meeting. August 2013

Investor Meeting August 2013 1 Forward-Looking Statements and Cautionary Note Variations If no further specification is included, changes are made against the same period of the last year. Rounding Numbers

Investor Meeting August 2013 1 Forward-Looking Statements and Cautionary Note Variations If no further specification is included, changes are made against the same period of the last year. Rounding Numbers

Overview. Rolando Galindo Head of Investor Relations Office. May 20 th, 2014

Overview Rolando Galindo Head of Investor Relations Office May 20 th, 2014 1 Forward-Looking Statement and Cautionary Note Variations If no further specification is included, changes are made against the

Overview Rolando Galindo Head of Investor Relations Office May 20 th, 2014 1 Forward-Looking Statement and Cautionary Note Variations If no further specification is included, changes are made against the

A Path Towards Improved Profitability

A Path Towards Improved Profitability Jaime del Rio Head of Investor Relations Bonds, Loans and Derivatives Mexico City February 6, 2018 Content 1 2 Lower Oil Prices: How has PEMEX Adapted its Corporate

A Path Towards Improved Profitability Jaime del Rio Head of Investor Relations Bonds, Loans and Derivatives Mexico City February 6, 2018 Content 1 2 Lower Oil Prices: How has PEMEX Adapted its Corporate

Investor Presentation. May 2017

Investor Presentation May 2017 Content 1 A Snapshot of Mexico & PEMEX Upstream Midstream & Downstream Overall Financial Performance Business Outlook 1 Mexico Snapshot Today, Mexico s fundamentals are stronger,

Investor Presentation May 2017 Content 1 A Snapshot of Mexico & PEMEX Upstream Midstream & Downstream Overall Financial Performance Business Outlook 1 Mexico Snapshot Today, Mexico s fundamentals are stronger,

Mexico s Energy Reform. November, 2014

Mexico s Energy Reform November, 2014 Fundamental Principles of the Energy Reform 1 Hydrocarbons in the subsurface belong to the Nation. 2 3 Free market access and direct and fair competition amongst state-owned

Mexico s Energy Reform November, 2014 Fundamental Principles of the Energy Reform 1 Hydrocarbons in the subsurface belong to the Nation. 2 3 Free market access and direct and fair competition amongst state-owned

Preliminary Results Second Quarter July 26, 2013

Preliminary Results Second Quarter 2013 July 26, 2013 1 Forward-Looking Statement and Cautionary Note (1/2) Variations If no further specification is included, changes are made against the same period

Preliminary Results Second Quarter 2013 July 26, 2013 1 Forward-Looking Statement and Cautionary Note (1/2) Variations If no further specification is included, changes are made against the same period

Investor Presentation. March 2018

Investor Presentation March 2018 Content 1 PEMEX Snapshot 2 Upstream 3 Midstream & Downstream 4 Financial Performance 1 PEMEX: Integrated Oil & Gas Company Upstream Downstream Midstream Commercialization

Investor Presentation March 2018 Content 1 PEMEX Snapshot 2 Upstream 3 Midstream & Downstream 4 Financial Performance 1 PEMEX: Integrated Oil & Gas Company Upstream Downstream Midstream Commercialization

Investor Presentation. March 2017

Investor Presentation March 2017 Content 1 A Snapshot of Mexico & PEMEX E&P Midstream & Downstream Financial Outlook of PEMEX 2016 Results 1 Mexico Snapshot Today, Mexico s fundamentals are stronger, allowing

Investor Presentation March 2017 Content 1 A Snapshot of Mexico & PEMEX E&P Midstream & Downstream Financial Outlook of PEMEX 2016 Results 1 Mexico Snapshot Today, Mexico s fundamentals are stronger, allowing

PEMEX Outlook. January, 2006

PEMEX Outlook January, 2006 1 Forward-looking Statement This presentation contains forward-looking statements. We may also make written or oral forward-looking statements in our periodic reports to the

PEMEX Outlook January, 2006 1 Forward-looking Statement This presentation contains forward-looking statements. We may also make written or oral forward-looking statements in our periodic reports to the

Investor Presentation. November 2017

Investor Presentation November 2017 Content 1 A Snapshot of PEMEX Upstream Midstream & Downstream Overall Financial Performance Business Outlook 1 O&G: The Industry Moving the World According to the IEA,

Investor Presentation November 2017 Content 1 A Snapshot of PEMEX Upstream Midstream & Downstream Overall Financial Performance Business Outlook 1 O&G: The Industry Moving the World According to the IEA,

Preliminary Results as of December 31, February 26, 2018

Preliminary Results as of December 31, 2017 February 26, 2018 Variations Forward-Looking Statement & Cautionary Note If no further specification is included, comparisons are made against the same realized

Preliminary Results as of December 31, 2017 February 26, 2018 Variations Forward-Looking Statement & Cautionary Note If no further specification is included, comparisons are made against the same realized

Hydrocarbon Reserves as of January 1, April 26, 2013

Hydrocarbon Reserves as of January 1, 2013 April 26, 2013 1 Forward-Looking Statements This presentation contains forward-looking statements. We may also make written or oral forward-looking statements

Hydrocarbon Reserves as of January 1, 2013 April 26, 2013 1 Forward-Looking Statements This presentation contains forward-looking statements. We may also make written or oral forward-looking statements

Investor Presentation. January 2018

Investor Presentation January 2018 Content 1 A Snapshot of PEMEX Upstream Midstream & Downstream Overall Financial Performance Business Outlook 1 O&G: The Industry Moving the World According to the IEA,

Investor Presentation January 2018 Content 1 A Snapshot of PEMEX Upstream Midstream & Downstream Overall Financial Performance Business Outlook 1 O&G: The Industry Moving the World According to the IEA,

The New Upstream Sector in Mexico: First Steps

The New Upstream Sector in Mexico: First Steps by Héctor Arangua and Lorenza Molina I. Overview A. Now & Then We are being spectators of a historic transformation as one of the greatest changes in the

The New Upstream Sector in Mexico: First Steps by Héctor Arangua and Lorenza Molina I. Overview A. Now & Then We are being spectators of a historic transformation as one of the greatest changes in the

Preliminary Results February 28, 2013

Preliminary Results 2012 February 28, 2013 Forward-Looking Statement and Cautionary Note (1/2) Variations If no further specification is included, changes are made against the same period of the last year.

Preliminary Results 2012 February 28, 2013 Forward-Looking Statement and Cautionary Note (1/2) Variations If no further specification is included, changes are made against the same period of the last year.

Hydrocarbon Reserves as of January 1, March 30, 2011

Hydrocarbon Reserves as of January 1, 2011 March 30, 2011 Forward-Looking Statements This presentation contains forward-looking statements. We may also make written or oral forward-looking statements in

Hydrocarbon Reserves as of January 1, 2011 March 30, 2011 Forward-Looking Statements This presentation contains forward-looking statements. We may also make written or oral forward-looking statements in

Investor Presentation. December 2017

Investor Presentation December 2017 Content 1 A Snapshot of PEMEX Upstream Midstream & Downstream Overall Financial Performance Business Outlook 1 O&G: The Industry Moving the World According to the IEA,

Investor Presentation December 2017 Content 1 A Snapshot of PEMEX Upstream Midstream & Downstream Overall Financial Performance Business Outlook 1 O&G: The Industry Moving the World According to the IEA,

New Perspectives & Opportunities in the Oil & Gas Sector in Mexico. March 2014

New Perspectives & Opportunities in the Oil & Gas Sector in Mexico March 2014 Agenda: - Timetable after Energy Reform - New distribution of roles - Future investment opportunities in Mexico s energy -

New Perspectives & Opportunities in the Oil & Gas Sector in Mexico March 2014 Agenda: - Timetable after Energy Reform - New distribution of roles - Future investment opportunities in Mexico s energy -

Petróleos Mexicanos 2013 Outlook HSBC Mexico CEO/CFO Roundtable

Petróleos Mexicanos 2013 Outlook HSBC Mexico CEO/CFO Roundtable February 21, 2013 1 Forward-Looking Statement and Cautionary Note (1/3) Variations If no further specification is included, changes are made

Petróleos Mexicanos 2013 Outlook HSBC Mexico CEO/CFO Roundtable February 21, 2013 1 Forward-Looking Statement and Cautionary Note (1/3) Variations If no further specification is included, changes are made

Investor Presentation. March, 2013

Investor Presentation March, 2013 1 Forward-Looking Statement and Cautionary Note (1/3) Variations If no further specification is included, changes are made against the same period of the last year. Rounding

Investor Presentation March, 2013 1 Forward-Looking Statement and Cautionary Note (1/3) Variations If no further specification is included, changes are made against the same period of the last year. Rounding

PEMEX Main Statistics of Production. Upstream Total hydrocarbons (Mboed) 2,888 2, % (290) 3,037 2, % (337)

2,888 2, % (290) 3,037 2, % (337)") Annexes Upstream Total hydrocarbons (Mboed) 2,888 2,597-10.1% (290) 3,037 2,700-11.1% (337) Downstream Main Statistics of Production Liquid hydrocarbons (Mbd) 2,103 1,904-9.5% (200) 2,190 1,977-9.7% (213)

Annexes Upstream Total hydrocarbons (Mboed) 2,888 2,597-10.1% (290) 3,037 2,700-11.1% (337) Downstream Main Statistics of Production Liquid hydrocarbons (Mbd) 2,103 1,904-9.5% (200) 2,190 1,977-9.7% (213)

México Proposed Reforms for the O&G Industry. Antonio Juárez Director AMESPAC

México Proposed Reforms for the O&G Industry Antonio Juárez Director AMESPAC 1 AMESPAC Was created in 2009 to bring together private companies that perform O&G services for Pemex Looks to concur, integrate

México Proposed Reforms for the O&G Industry Antonio Juárez Director AMESPAC 1 AMESPAC Was created in 2009 to bring together private companies that perform O&G services for Pemex Looks to concur, integrate

Implementing Mexico's Energy Reform. Luis Fernando Herrera Deputy General Director of Hydrocarbons Administration

Implementing Mexico's Energy Reform Luis Fernando Herrera Deputy General Director of Hydrocarbons Administration February, 2015 Despite an increase in investment in exploration and production, Mexican

Implementing Mexico's Energy Reform Luis Fernando Herrera Deputy General Director of Hydrocarbons Administration February, 2015 Despite an increase in investment in exploration and production, Mexican

México Proposed Reforms for the O&G Industry

México Proposed Reforms for the O&G Industry Antonio Juárez Director AMESPAC 1 Introduction 2 AMESPAC Was created in 2009 to bring together private companies that perform O&G services for Pemex Looks to

México Proposed Reforms for the O&G Industry Antonio Juárez Director AMESPAC 1 Introduction 2 AMESPAC Was created in 2009 to bring together private companies that perform O&G services for Pemex Looks to

Energy Reform Hydrocarbon Sector

Energy Reform Hydrocarbon Sector On August 12, 2014, the energy reform package of secondary laws became effective. It revolutionizes and permits private participation in the up-, mid- and downstream of

Energy Reform Hydrocarbon Sector On August 12, 2014, the energy reform package of secondary laws became effective. It revolutionizes and permits private participation in the up-, mid- and downstream of

Mexico s Energy Reform Institutional framework

Mexico s Energy Reform Institutional framework Juan Carlos Zepeda March, 2014 www.cnh.gob.mx Reserves and prospective resources Basin Accumalated Production Reserves Prospective Resources 1P 2P 3P Conv.

Mexico s Energy Reform Institutional framework Juan Carlos Zepeda March, 2014 www.cnh.gob.mx Reserves and prospective resources Basin Accumalated Production Reserves Prospective Resources 1P 2P 3P Conv.

THE OPENING OF MEXICO S ENERGY SECTOR

THE OPENING OF MEXICO S ENERGY SECTOR Insight into Mexico s Energy Reform Dallas Parker Gabriel Salinas Mayer Brown LLP February 11, 2014 Overview of Presentation INTRODUCTION I. UPSTREAM II. MIDSTREAM

THE OPENING OF MEXICO S ENERGY SECTOR Insight into Mexico s Energy Reform Dallas Parker Gabriel Salinas Mayer Brown LLP February 11, 2014 Overview of Presentation INTRODUCTION I. UPSTREAM II. MIDSTREAM

Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of December 31, ,2

March 1, 2011 Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of December 31, 2010 1,2 Fourth quarter 2010 summary Total revenues from sales and services increased

March 1, 2011 Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of December 31, 2010 1,2 Fourth quarter 2010 summary Total revenues from sales and services increased

PEMEX Main Statistics of Production

Annexes Main Statistics of Production Upstream Total hydrocarbons (Mboed) 3,629 3,538-2.5% (91) 3,648 3,597-1.4% (50) Liquid hydrocarbons (Mbd) 2,549 2,441-4.2% (108) 2,563 2,496-2.6% (67) Crude oil (Mbd)

Annexes Main Statistics of Production Upstream Total hydrocarbons (Mboed) 3,629 3,538-2.5% (91) 3,648 3,597-1.4% (50) Liquid hydrocarbons (Mbd) 2,549 2,441-4.2% (108) 2,563 2,496-2.6% (67) Crude oil (Mbd)

Newsletter Fall 2014

Newsletter Fall 2014 MEXICO S REVOLUTIONARY ENERGY REFORM: SIX TAKEAWAYS John D. Furlow and Gabriel Salinas 1 Near the end of 2013, Mexican President Enrique Peña Nieto signed into law a sweeping constitutional

Newsletter Fall 2014 MEXICO S REVOLUTIONARY ENERGY REFORM: SIX TAKEAWAYS John D. Furlow and Gabriel Salinas 1 Near the end of 2013, Mexican President Enrique Peña Nieto signed into law a sweeping constitutional

PEMEX Main Statistics of Production

Annexes Main Statistics of Production Upstream Total hydrocarbons (Mboed) 3,703 3,668-0.9% (35) 3,697 3,653-1.2% (45) Liquid hydrocarbons (Mbd) 2,594 2,566-1.1% (28) 2,588 2,564-1.0% (25) Crude oil (Mbd)

Annexes Main Statistics of Production Upstream Total hydrocarbons (Mboed) 3,703 3,668-0.9% (35) 3,697 3,653-1.2% (45) Liquid hydrocarbons (Mbd) 2,594 2,566-1.1% (28) 2,588 2,564-1.0% (25) Crude oil (Mbd)

Building & Operating Offshore Infrastructure in Mexico; a New Paradigm

Building & Operating Offshore Infrastructure in Mexico; a New Paradigm IPLOCA 2017 Mexico City Carlos Morales Gil 1 Content 1. Legal Framework 2. The Institutions And Its Role 3. Opportunities For Operators

Building & Operating Offshore Infrastructure in Mexico; a New Paradigm IPLOCA 2017 Mexico City Carlos Morales Gil 1 Content 1. Legal Framework 2. The Institutions And Its Role 3. Opportunities For Operators

Results as of the 3 rd Quarter October 28, 2011

Results as of the 3 rd Quarter 2011 October 28, 2011 1 Forward-Looking Statement and Cautionary Note(1/2) Variations If no further specification is included, changes are made against the same period of

Results as of the 3 rd Quarter 2011 October 28, 2011 1 Forward-Looking Statement and Cautionary Note(1/2) Variations If no further specification is included, changes are made against the same period of

Results of PEMEX 1 as of December 31,

February 27, 2017 2016 Results Results of PEMEX 1 as of December 31, 2016 2 2015 2016 (MXN billion) Variation 2016 (USD billion) Total Sales 1,166.4 1,079.5-7.4% 52.2 Highlights 2,154 Mbd production exceeds

February 27, 2017 2016 Results Results of PEMEX 1 as of December 31, 2016 2 2015 2016 (MXN billion) Variation 2016 (USD billion) Total Sales 1,166.4 1,079.5-7.4% 52.2 Highlights 2,154 Mbd production exceeds

Mexican Energy Sector Investment Opportunities Post Reform

Mexican Energy Sector Investment Opportunities Post Reform Eagle Ford Consortium 3rd Annual Conference Antonio Juárez Director AMESPAC 1 AMESPAC It was created in 2009 to bring together private companies

Mexican Energy Sector Investment Opportunities Post Reform Eagle Ford Consortium 3rd Annual Conference Antonio Juárez Director AMESPAC 1 AMESPAC It was created in 2009 to bring together private companies

Results of PEMEX 1 as of December 31,

February 27, 2017 2016 Results Results of PEMEX 1 as of December 31, 2016 2 2015 2016 (MXN billion) Variation 2016 (USD billion) Total Sales 1,166.4 1,079.5-7.4% 52.2 Highlights 2,154 Mbd production exceeds

February 27, 2017 2016 Results Results of PEMEX 1 as of December 31, 2016 2 2015 2016 (MXN billion) Variation 2016 (USD billion) Total Sales 1,166.4 1,079.5-7.4% 52.2 Highlights 2,154 Mbd production exceeds

PEMEX 1 Presents its Results for the First Quarter of 2018

PEMEX 1 Presents its Results for the First Quarter of 2018 Mexico City, April 27, 2018 Investor Relations ri@pemex.com Tel (52 55) 1944 9700 www.pemex.com/en/investors Key Highlights The first quarter

PEMEX 1 Presents its Results for the First Quarter of 2018 Mexico City, April 27, 2018 Investor Relations ri@pemex.com Tel (52 55) 1944 9700 www.pemex.com/en/investors Key Highlights The first quarter

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 6-K

6-K 1 c01389e6vk.htm FORM 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 6-K REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE

6-K 1 c01389e6vk.htm FORM 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 6-K REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE

Energy Reform Analysis, Implementation and Compliance

Energy Reform Analysis, Implementation and Compliance Reform s key aspects Pemex and CFE will be granted with greater autonomy an a new character as State Productive Enterprises (Empresas Productivas del

Energy Reform Analysis, Implementation and Compliance Reform s key aspects Pemex and CFE will be granted with greater autonomy an a new character as State Productive Enterprises (Empresas Productivas del

Oil & Gas Industry in Mexico. February 2018

Oil & Gas Industry in Mexico February 2018 Update Oil & Gas Industry Page 2 Update Oil & Gas Industry Mexico s Oil & Gas Reform Contract Regimes LFD Bidding Rounds CEE PSC 3. Private Farmouts License PEP

Oil & Gas Industry in Mexico February 2018 Update Oil & Gas Industry Page 2 Update Oil & Gas Industry Mexico s Oil & Gas Reform Contract Regimes LFD Bidding Rounds CEE PSC 3. Private Farmouts License PEP

Mexican Oil & Gas industry Investment opportunities post reform

Mexican Oil & Gas industry Investment opportunities post reform Eagle Ford Consortium Meeting January 29th 2014 Texas A&M International University Student Center Ballroom Laredo, Texas Antonio Juárez January

Mexican Oil & Gas industry Investment opportunities post reform Eagle Ford Consortium Meeting January 29th 2014 Texas A&M International University Student Center Ballroom Laredo, Texas Antonio Juárez January

Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of March 31,

Corporate Finance Office May 4, 2010 Investor Relations Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of March 31, 2010 1 During the first quarter of 2010, recorded

Corporate Finance Office May 4, 2010 Investor Relations Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of March 31, 2010 1 During the first quarter of 2010, recorded

Petroleos Mexicanos (PEMEX): Lack of Fiscal Autonomy Constrains Production Growth and Raises Financial Leverage

: Lack of Fiscal Autonomy Constrains Production Growth and Raises Financial Leverage") Special Comment January 2003 Contact Phone New York Alexandra S. Parker 1.212.553.1653 John Diaz Thomas Coleman Petroleos Mexicanos (PEMEX): Lack of Fiscal Autonomy Constrains Production Growth and Raises

Special Comment January 2003 Contact Phone New York Alexandra S. Parker 1.212.553.1653 John Diaz Thomas Coleman Petroleos Mexicanos (PEMEX): Lack of Fiscal Autonomy Constrains Production Growth and Raises

Accountability and transparency

Accountability and transparency Oil and gas fiscal system in Mexico By Pedro Luna Ministry of Finance, Mexico World Bank Headquarters, Washington, DC - Black Auditorium - March 3 rd 4th 1 Mexico s intergovernmental

Accountability and transparency Oil and gas fiscal system in Mexico By Pedro Luna Ministry of Finance, Mexico World Bank Headquarters, Washington, DC - Black Auditorium - March 3 rd 4th 1 Mexico s intergovernmental

MEXICAN STOCK EXCHANGE

STOCK EXCHANGE CODE: PEMEX QUARTER: 4 YEAR: 28 PETROLEOS MEXICANOS BALANCE SHEETS AUDITED INFORMATION TO DECEMBER 31 OF 28 AND 27 (Thousand Pesos) CONSOLIDATED Final Printing REF S CONCEPTS CURRENT YEAR

STOCK EXCHANGE CODE: PEMEX QUARTER: 4 YEAR: 28 PETROLEOS MEXICANOS BALANCE SHEETS AUDITED INFORMATION TO DECEMBER 31 OF 28 AND 27 (Thousand Pesos) CONSOLIDATED Final Printing REF S CONCEPTS CURRENT YEAR

Page 1 of 50 6-K 1 y64756e6vk.htm UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE

Page 1 of 50 6-K 1 y64756e6vk.htm UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE

Investor Presentation. March 2012

Investor Presentation March 2012 Forward-Looking Statement and Cautionary Note (1/3) Variations If no further specification is included, changes are made against the same period of the last year. Rounding

Investor Presentation March 2012 Forward-Looking Statement and Cautionary Note (1/3) Variations If no further specification is included, changes are made against the same period of the last year. Rounding

Mexican Energy Reform Adrian Lajous Center on Global Energy Policy June 2014

UPSTREAM REFORM Round Zero, which deals with Pemex legacy assets, already underway The opening of the Mexican upstream to private investment will be a multi-stage, complex process. The first stage known

UPSTREAM REFORM Round Zero, which deals with Pemex legacy assets, already underway The opening of the Mexican upstream to private investment will be a multi-stage, complex process. The first stage known

Mexican Energy Reform, The Case for a New Geophysical Data Market

Mexican Energy Reform, The Case for a New Geophysical Data Market Rafael Alférez February 18st, 2014 www.cnh.gob.mx 1 OUTLINE Mexico Hidrocarbons Facts Energy Reform (upstream) Oil and Gas Potential of

Mexican Energy Reform, The Case for a New Geophysical Data Market Rafael Alférez February 18st, 2014 www.cnh.gob.mx 1 OUTLINE Mexico Hidrocarbons Facts Energy Reform (upstream) Oil and Gas Potential of

PEMEX Unaudited Financial Results Report as of June 30, 2009

Corporate Finance Office Investor Relations (5255) 1944 9700 ri@dcf.pemex.com PEMEX Unaudited Financial Results Report as of June 30, 2009 July 30, 2009. PEMEX, Mexico s oil and gas company and the eleventh

Corporate Finance Office Investor Relations (5255) 1944 9700 ri@dcf.pemex.com PEMEX Unaudited Financial Results Report as of June 30, 2009 July 30, 2009. PEMEX, Mexico s oil and gas company and the eleventh

2018 THIRD QUARTER RESULTS. Ticker BMV: IENOVA Mexico City, October 24, Page 1

2018 THIRD QUARTER RESULTS Ticker BMV: IENOVA Mexico City, October 24, 2018 We are the first private sector, publicly traded energy infrastructure company on the Mexican Stock Exchange and one of the largest

2018 THIRD QUARTER RESULTS Ticker BMV: IENOVA Mexico City, October 24, 2018 We are the first private sector, publicly traded energy infrastructure company on the Mexican Stock Exchange and one of the largest

SHIFTING INTO 2018: A SNAPSHOT OF MEXICO S ENERGY SECTOR

SHIFTING INTO 2018: A SNAPSHOT OF MEXICO S ENERGY SECTOR More than four years have passed since the much-awaited approval and consequent implementation of the constitutional energy reform. During this

SHIFTING INTO 2018: A SNAPSHOT OF MEXICO S ENERGY SECTOR More than four years have passed since the much-awaited approval and consequent implementation of the constitutional energy reform. During this

PETRÓLEOS MEXICANOS (Exact name of registrant as specified in its charter)

") Page 1 of 48 6-K 1 d436050d6k.htm FORM 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 6-K REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE

Page 1 of 48 6-K 1 d436050d6k.htm FORM 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 6-K REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE

1 ST QUARTER 2018 EARNINGS WEBCAST. May 09, 2018

1 ST QUARTER 2018 EARNINGS WEBCAST May 09, 2018 DISCLAIMER Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes constitute

1 ST QUARTER 2018 EARNINGS WEBCAST May 09, 2018 DISCLAIMER Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes constitute

PEMEX unaudited financial results report as of September 30, 2006

(5255) 1944 9700 November 6, 2006 PEMEX unaudited financial results report as of September 30, 2006 Financial highlights PEMEX, Mexico s oil and gas company and the ninth largest integrated oil company

(5255) 1944 9700 November 6, 2006 PEMEX unaudited financial results report as of September 30, 2006 Financial highlights PEMEX, Mexico s oil and gas company and the ninth largest integrated oil company

Mexico s Energy Reform

Mexico s Energy Reform Lourdes Melgar, Ph.D. Undersecretary of Hydrocarbons Ministry of Energy February 7, 2014 CONSTITUTIONAL AMENDMENT A historic constitutional energy reform was approved in Mexico in

Mexico s Energy Reform Lourdes Melgar, Ph.D. Undersecretary of Hydrocarbons Ministry of Energy February 7, 2014 CONSTITUTIONAL AMENDMENT A historic constitutional energy reform was approved in Mexico in

PEMEX 1 Presents its Results for the Fourth Quarter of 2017

PEMEX 1 Presents its Results for the Fourth Quarter of 2017 Mexico City, February 26, 2018 Investor Relations ri@pemex.com Tel (52 55) 1944 9700 www.pemex.com/en/investors Key Highlights 2017 was a stabilization

PEMEX 1 Presents its Results for the Fourth Quarter of 2017 Mexico City, February 26, 2018 Investor Relations ri@pemex.com Tel (52 55) 1944 9700 www.pemex.com/en/investors Key Highlights 2017 was a stabilization

3 rd QUARTER 2018 EARNINGS WEBCAST. November 12 th, 2018

3 rd QUARTER 2018 EARNINGS WEBCAST November 12 th, 2018 1 Important notice Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF

3 rd QUARTER 2018 EARNINGS WEBCAST November 12 th, 2018 1 Important notice Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF

2 nd QUARTER 2018 EARNINGS WEBCAST. August 8 th, 2018

2 nd QUARTER 2018 EARNINGS WEBCAST August 8 th, 2018 1 Important notice Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes

2 nd QUARTER 2018 EARNINGS WEBCAST August 8 th, 2018 1 Important notice Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes

Interna. A changing world: Mexico facing the 21 st century energy revolution

Interna A changing world: Mexico facing the 21 st century energy revolution CONTENT: 1. Global Outlook of the Oil & Gas sector 2. International Lessons 3. Oil & Gas sector in Mexico today 4. Assessing

Interna A changing world: Mexico facing the 21 st century energy revolution CONTENT: 1. Global Outlook of the Oil & Gas sector 2. International Lessons 3. Oil & Gas sector in Mexico today 4. Assessing

Results of PEMEX 1 as of December 31,

April 30, 2016 Fourth Quarter 2015 (net of IEPS) Results of PEMEX 1 as of December 31, 2015 2 2014 2015 (MXN billion) Variation 2015 (USD billion) Total Sales 366.6 264.3-27.9% 15.4 Operating Income 93.1

April 30, 2016 Fourth Quarter 2015 (net of IEPS) Results of PEMEX 1 as of December 31, 2015 2 2014 2015 (MXN billion) Variation 2015 (USD billion) Total Sales 366.6 264.3-27.9% 15.4 Operating Income 93.1

Third Quarter 2015 Financial Results

Third Quarter 2015 Financial Results October 23, 2015 Information regarding forward-looking statements This presentation contain statements that are not historical fact and constitute forward-looking statements

Third Quarter 2015 Financial Results October 23, 2015 Information regarding forward-looking statements This presentation contain statements that are not historical fact and constitute forward-looking statements

Mexican energy reform Privatization creates new opportunities and prospects

Mexican energy reform Privatization creates new opportunities and prospects Mexico is experiencing a historic shift in its energy sector, primarily due to 2013 legislation that allows private investment

Mexican energy reform Privatization creates new opportunities and prospects Mexico is experiencing a historic shift in its energy sector, primarily due to 2013 legislation that allows private investment

Full Year 2017 EARNINGS WEBCAST. March 05, 2018

Full Year 2017 EARNINGS WEBCAST March 05, 2018 DISCLAIMER Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes constitute

Full Year 2017 EARNINGS WEBCAST March 05, 2018 DISCLAIMER Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes constitute

SECURITIES AND EXCHANGE COMMISSION Washington, D.C FORM 6-K

6-K 1 d765080d6k.htm 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 6-K REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE

6-K 1 d765080d6k.htm 6-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 6-K REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE

Results of PEMEX 1 as of December 31,

February 27, 2015 Results of PEMEX 1 as of December 31, 2014 2 Fourth Quarter (Oct.-Dec.) 2013 2014 (MXN billion) Variation 2014 (USD billion) Total Sales 409.5 365.2-10.8% 24.8 Operating Income 136.5

February 27, 2015 Results of PEMEX 1 as of December 31, 2014 2 Fourth Quarter (Oct.-Dec.) 2013 2014 (MXN billion) Variation 2014 (USD billion) Total Sales 409.5 365.2-10.8% 24.8 Operating Income 136.5

Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of December 31,

Corporate Finance Office March 3, 2010 Investor Relations Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of December 31, 2009 1 In 2009, PEMEX s net loss decreased

Corporate Finance Office March 3, 2010 Investor Relations Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of December 31, 2009 1 In 2009, PEMEX s net loss decreased

MEXICO S ENERGY REFORM AND INVESTMENT OPPORTUNITIES

MEXICO S ENERGY REFORM AND INVESTMENT OPPORTUNITIES NASCO REGIONAL COMPETITIVENESS SUMMIT Corpus Chris8, Texas April 28th, 2015 1 Oil Perspective Hydrocarbons revenues represented 32% of the federal budget

MEXICO S ENERGY REFORM AND INVESTMENT OPPORTUNITIES NASCO REGIONAL COMPETITIVENESS SUMMIT Corpus Chris8, Texas April 28th, 2015 1 Oil Perspective Hydrocarbons revenues represented 32% of the federal budget

International Shale Development Challenges & Opportunities: Mexico & Argentina

International Shale Development Challenges & Opportunities: Mexico & Argentina October 5, 2016 Chuck Whisman, Global Energy Market Director, CH2M Charles.Whisman@ch2m.com Upstream Oil & Gas Impact in Mexico

International Shale Development Challenges & Opportunities: Mexico & Argentina October 5, 2016 Chuck Whisman, Global Energy Market Director, CH2M Charles.Whisman@ch2m.com Upstream Oil & Gas Impact in Mexico

REPSOL NET INCOME INCREASES BY 41%

JANUARY-SEPTEMBER 2017 EARNINGS Press release Madrid, November 3rd, 2017 6 pages REPSOL NET INCOME INCREASES BY 41% Repsol earned a net profit of 1.583 billion euros in the first nine months of 2017, 41%

JANUARY-SEPTEMBER 2017 EARNINGS Press release Madrid, November 3rd, 2017 6 pages REPSOL NET INCOME INCREASES BY 41% Repsol earned a net profit of 1.583 billion euros in the first nine months of 2017, 41%

Petroleos Mexicanos. Update following ratings stabilization. CREDIT OPINION 13 April Update. Summary

CREDIT OPINION Update following ratings stabilization Update Summary Domicile Mexico City, Ciudad de Mexico, Mexico Long Term Rating Baa3 Type LT Issuer Rating - Fgn Curr Outlook Stable Exhibit 1 Reserve

CREDIT OPINION Update following ratings stabilization Update Summary Domicile Mexico City, Ciudad de Mexico, Mexico Long Term Rating Baa3 Type LT Issuer Rating - Fgn Curr Outlook Stable Exhibit 1 Reserve

Mexico midstream. Opportunities for investors who move now

Mexico midstream Opportunities for investors who move now opp With energy reform in Mexico under way, companies are eager to participate in the Mexican oil and gas renaissance. One of the biggest opportunities

Mexico midstream Opportunities for investors who move now opp With energy reform in Mexico under way, companies are eager to participate in the Mexican oil and gas renaissance. One of the biggest opportunities

3 rd QUARTER 2017 EARNINGS WEBCAST. November 09, 2017

3 rd QUARTER 2017 EARNINGS WEBCAST November 09, 2017 DISCLAIMER Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes

3 rd QUARTER 2017 EARNINGS WEBCAST November 09, 2017 DISCLAIMER Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes

RESULTS AS OF SEPTEMBER 30, 2017

RESULTS AS OF SEPTEMBER 30, 2017 Mexico City, October 27, 2017 PEMEX 1 presents its financial and operating results for the third quarter of 2017 (3Q17 2 ). 1. Key highlights PEMEX guaranteed fuel supply

RESULTS AS OF SEPTEMBER 30, 2017 Mexico City, October 27, 2017 PEMEX 1 presents its financial and operating results for the third quarter of 2017 (3Q17 2 ). 1. Key highlights PEMEX guaranteed fuel supply

October 25, 2013 Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of September 30,

October 25, 2013 Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of September 30, 2013 2 Third Quarter (Jul.-Sept.) 2012 2013 Variation 2013 (Ps. Billion) (U.S.$Billion)

October 25, 2013 Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of September 30, 2013 2 Third Quarter (Jul.-Sept.) 2012 2013 Variation 2013 (Ps. Billion) (U.S.$Billion)

July 27 th, 2012 Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of June 30,

July 27 th, 2012 Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of June 30, 2012 1 Second Quarter (Apr.-Jun.) 2011 2012 Variation 2012 (Ps. Billion) (U.S.$Billion)

July 27 th, 2012 Financial Results of Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of June 30, 2012 1 Second Quarter (Apr.-Jun.) 2011 2012 Variation 2012 (Ps. Billion) (U.S.$Billion)

Management results. Shareholder s Meeting April 2015

Management results Shareholder s Meeting April 2015 1 Disclaimer Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes

Management results Shareholder s Meeting April 2015 1 Disclaimer Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes

Note: For definitions of Moody's most common ratio terms please see the accompanying User's Guide.

Credit Opinion: Petroleos Mexicanos Global Credit Research - 23 Dec 2009 Mexico City, Mexico Ratings Category Moody's Rating Issuer Rating Senior Unsecured NSR Senior Unsecured -Dom Curr Aaa.mx NSR BACKED

Credit Opinion: Petroleos Mexicanos Global Credit Research - 23 Dec 2009 Mexico City, Mexico Ratings Category Moody's Rating Issuer Rating Senior Unsecured NSR Senior Unsecured -Dom Curr Aaa.mx NSR BACKED

PETRÓLEOS MEXICANOS (Exact name of registrant as specified in its charter)

") 6 K 1 d923061d6k.htm FORM 6 K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 6 K REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a 16 OR 15d 16 UNDER THE SECURITIES EXCHANGE

6 K 1 d923061d6k.htm FORM 6 K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 6 K REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a 16 OR 15d 16 UNDER THE SECURITIES EXCHANGE

Investor Presentation. June 2012

Investor Presentation June 2012 Forward-Looking Statement and Cautionary Note (1/3) Variations If no further specification is included, changes are made against the same period of the last year. Rounding

Investor Presentation June 2012 Forward-Looking Statement and Cautionary Note (1/3) Variations If no further specification is included, changes are made against the same period of the last year. Rounding

July 29, 2011 Financial Results of Petróleos Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of June 30,

July 29, 2011 Financial Results of Petróleos Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of June 30, 2011 1 Second Quarter (Apr.-Jun.) 2010 2011 Variation 2011 (Ps. Bn) (U.S.$Bn)

July 29, 2011 Financial Results of Petróleos Petróleos Mexicanos, Subsidiary Entities and Subsidiary Companies as of June 30, 2011 1 Second Quarter (Apr.-Jun.) 2010 2011 Variation 2011 (Ps. Bn) (U.S.$Bn)

INVESTOR PRESENTATION. As of August 2018

INVESTOR PRESENTATION As of August 2018 Important notice Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes constitute

INVESTOR PRESENTATION As of August 2018 Important notice Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes constitute

Second Quarter 2018 Financial Results

Second Quarter 2018 Financial Results July 25, 2018 Information regarding forward-looking statements This presentation contain statements that are not historical fact and constitute forward-looking statements

Second Quarter 2018 Financial Results July 25, 2018 Information regarding forward-looking statements This presentation contain statements that are not historical fact and constitute forward-looking statements

Investor Presentation. As of December 2016

Investor Presentation As of December 2016 1 Important Notice Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes constitute

Investor Presentation As of December 2016 1 Important Notice Safe harbor statement under the US Private Securities Litigation Reform Act of 1995. This document contains statements that YPF believes constitute