Valuing Early-Stage Bioscience Companies

|

|

|

- Sharon Manning

- 5 years ago

- Views:

Transcription

1 Valuing Early-Stage Bioscience Companies November 17, 2014 Gregory Phipps Managing Director, Investment

2 The Challenge Valuation mix of (black) art & science In start-up/early-stage, valuation exercise more art than science, with heavy dose of negotiation thrown in by the investment source (VC s, angels, etc.) Valuation may be used for both negotiated price for equity investment purposes, Founder/Partner buy-out scenarios (more common than you think), marital dissolutions, and third-party acquisitions Absence of historic, or (often) accurate means to predict future revenues and cash flow, makes it virtually impossible to use traditional models like Discounted Cash Flow (DCF) for most bioscience companies How do we do it then? 2

3 Sources of Funding for Ontario Bioscience Companies Federal & Provincial Government Public Subsidies/Grants Entrepreneurial support programs Contribution agreements Research & development Tax Credits Publicly supported funds Private Industry Angels Venture Capital Strategic Alliances Discovery & Fundamental Research Pre Commercialization Proof of Concept Product Development Commercialization Market Entry SDTC, NRC IRAP, CIHR Grants, CFDC CSBF, Community Futures Loans Programs SDTC, NRC IRAP, Going Global Science/Tech SR&ED Tax Credits, Provincial R&D ITCs BDC VC Funds Growth 3

4 CDN Bioscience Companies CVCA Segmentation Human Biotech Companies: Developers of technology promoting drug development, disease treatment, and a deeper understanding of living organisms. Includes human, animal, and industrial biotechnology products and services. Also included are biosensors, and biotechnology equipment. Other Biotech: For human vs. other biotech, we re looking at the application of the biotechnology, usually either for use in human medicine, or for other processes like industrial, biofuel, agriculture, or veterinary use. Pharmaceutical Companies: The discovery and development of drug, medications, and other pharmacologically active substances for use in the medical diagnosis, cure, treatment, or prevention of disease. Medical Companies: Manufactures and/or sells medical instruments and devices including medical diagnostic equipment, medical therapeutic devices, and other health-related products such as medical monitoring equipment. Source: Canadian Venture Capital Association 4

5 VC Dollars Invested in CDN Bioscience Companies $250 $200 C$ millions $150 $100 $50 $ First Half 2014 Human Biotech Other Biotech Pharmaceuticals Medical Source: Canadian Venture Capital Association 5

6 Alternative Methods to DCF (Simplified) Venture Capital Method First Chicago Method Berkus Method Scorecard Method Comparables Negotiation WAG 6

7 Before We Start: Glossary Pre-Money: the value of a company BEFORE investment Post-Money: the value of a company AFTER investment is received Return On Investment (ROI): the increase in value of an investment divided by the cost of the investment Present Value (PV): value today Terminal Value: anticipated selling price/exit for a company in the future (liquidity event such as M&A or IPO) 7

8 Venture Capital Method (Bill Sahlman, Harvard) Often used to value pre-revenue, early-stage companies Expected exit price/terminal value is estimated, and then one calculates back to the current post-money If we know the value of something in the future and we know what kind of ROI we need to induce us to make an investment, then we figure out its Present Value to us Present Value (PV) = value of a company today 8

9 Venture Capital Method VC Method is used for very early-stage companies Incorporates some elements of Discounted Cash Flow method insomuch that we apply a risk premium (expressed as return/discount/hurdle rate) and are determining PV, but it is based on the future Terminal Value rather than cash flows Terminal Value = anticipated selling price of the company at a point in the future (TBD) ROI is a multiple of invested cash, regardless of the time since investment Assumes no more shares are issued 9

10 Venture Capital Method 1. Forecast future results 2. Determine likely value at that point (ex. look for comparable M&A or IPO transactions) 3. Convert future values back to present values = Post-Money Valuation 4. Share price is determined, includes Employee Stock Ownership Plan (ESOP) Terminal (exit) Value Post-Money valuation = ROI or Post-Money valuation = Terminal Value anticipated ROI 10

11 Venture Capital Method CASE STUDY: A VC is looking at three companies. She is unwilling to invest unless she can obtain an annualized return of 30% from her $1M investment. Medical Device Company A M&A Therapeutics Company B IPO Diagnostics Company C M&A Revenue $22,500,000 $0 $16,000,000 IPO/M&A Value or Multiple 4X Sales IPOs, Phase II, similar pipeline and market size 3X Sales Terminal Value $90,000,000 $135,000,000 $48,000,000 Values and multiples are determined based on current appropriate comparables from recent public or private company transactions. 11

12 Venture Capital Method Company A Company B Company C Terminal Value $90,000,000 $135,000,000 $48,000,000 Post Money = Terminal Value/30 (ROI) Subtract Investment $3,000,000 $4,500,000 $1,600,000 $1,000,000 $1,000,000 $1,000,000 Pre-Money = PV $2,000,000 $3,500,000 $600,000 Price per share will be the Pre-Money Valuation divided by the number of shares outstanding including ESOP that is needed after the financing. 12

13 Venture Capital Method "Venture Capital Method" of Valuation INPUT Amount to Invest $ 1,000,000 Net Income $ 8,000,000 Year 5 Average P/E Ratio of Profitable Comparable Companies 10 Shares Currently Outstanding 9,989,640 Target Rate of Return 50% OUTPUT Discounted Terminal Value $ 10,534,979 Required Percentage Ownership for the VC 9.49% Number of New Shares Required for the VC's Investment 1,047,683 Price per New Share $ 0.95 Implied Pre-money Valuation $ 9,534,979 Implied Post-money Valuation $ 10,534,979 13

14 First Chicago Method First Chicago approach simply does three different projections: Best, Worst and Survival scenarios & assigns probability estimates to each i.e. Success - 30% chance; Failure - 20% chance; and Survival - 50% chance When utilized, the First Chicago method results in a separate valuation for each of the three potential outcomes These are than added and the valuation and pricing is determined Variations are seen often in public company valuations 14

15 First Chicago Method *Fill all Yellow Highlighted Areas Variables Success Sideways Survival Failure Base Revenue: 0.45 (Average of provided data) Revenue growth rate from base: 120.0% 50.0% 5.0% Projected Liquidation Year 5 With Failure: 1 After Tax Profit Margin: 20.0% 7.0% PE Ratio at Liquidity: 15 7 *From Comparables etc. (P/E of 15 is long term historical average Discount Rate: 30.0% *Internal Hurdle Probability of Each Scenario: 30.0% 50.0% 20.0% Investment Amount: 0.5 Calculations Success Sideways Survival Failure Revenue Growth Rate (From Base Of???) Revenue Level After 3 Years Revenue Level After 5 Years Net Income at Liquidity Value of Company At Liquidity PV of Company Using Discount Rate of???? Expected PV Of The Company Under Each Separate Scenario Expected PV Of The Company

16 Berkus Method Dave Berkus noted angel investor, speaker, author Method only really used or accurate for pre-revenue companies Still requires subject evaluation/assessment of key value metrics I have renamed it the Keg Steakhouse Method or A La Carte Menu Method Cast your vote for best name! 16

17 Berkus Method Valuation Metric Cool idea/concept/tech Experienced management Prototype/build = PoC for bioscience Strategic relationships Board of Directors Paying customers/traction (IP for bioscience) Value $.5 million $.5 million $.25 million $.25 million $.25 million <> $.5 - $1 million 17

Roasted garlic mashed (Board) Sautéed mushrooms(customers) Twice-baked")

18 The Keg Steakhouse Method Keg Fries (Management) Mixed vegetables (Productized) Rice Pilaf (Distribution partner) Roasted garlic mashed (Board) Sautéed mushrooms(customers) Twice-baked potato (IP) 18

19 Scorecard Method Not really a valuation method in itself Ranks various factors consider predictors of entrepreneurial success Somewhat subjective but balanced on the whole Best for comparing a number of companies against each other, by type, or by region Company with an avg. product/technology (100% of norm), a strong team (125% of norm) and a large market opportunity (150% of norm). The company can get to positive cash flow with a single angel round of investment (100% of norm). Looking at the strength of the competition in the market, the target is weaker (75% of norm) but early customer feedback on the product is excellent (Other = 100%). The company needs some additional work on building sales channels and partnerships (80% of norm). Using this data, we can complete the following calculation: 19

20 Scorecard Method Comparison factor Range Company Factor Team/Management 30% max 125% Size of Opportunity 25% max 150% Product/Technology 15% max 100% Competition 10% max 75% Sales partnerships 10% max 80% Additional investment 5% max 100% Other factors 5% max 100% SUM 100%

21 Comparables Accurate, reasonable approach to valuation, in the absence of, or willingness, to apply other valuation methods Simply research valuations, of similar companies who have raised equity capital, at same stage, in same region Regional pricing applies. Valuations in Canada are NOT the same as US (Boston, San Fran etc.) We use DowJones VentureSource and PitchBook to research comparable valuations as reported in VC deals Lots of information is private, do your research 21

22 Databases 22

23 Databases 23

24 Databases 24

25 Negotiation Used more often than not Follows traditional, age-old premise of value : what a willing seller and a willing buyer agree upon Can be considered a reasonable foundation value (starting point), on which to apply future/next valuation exercises 25

26 Wild Ass Guess 26

27 Bonus: Venture Capital Math $1 million at a $3 million pre-money valuation leading to a $4 million post money valuation. The math works out that the investor owns 25% of the company post deal ($1 million invested / $4 million valuation) and assuming 1 million shares, each share would be valued at $3 / share ($3,000,000 pre-money / 1 million shares = $3/ share). Investors own 25%, the founders own 75%. But ESOP complicates it, and impacts price/share Assuming a 15% option pool post funding then you need a 20% option pool pre funding (because the pool gets diluted by 25% also when the VC invests their money). So your 100% of the company is down to 80% even before VC funding. The VC s $1 million still buys them 25% of your company it s you who has diluted to 60% ownership rather than 75%. The price/share is actually $2.40 (not $3.00), which is $3,000,000 pre-money/ 1,250,000 shares (because you had to create the 250,000 share options). Thus the true pre-money is only $2.4 million (and not $3 million) because $2.40 per share * 1 million pre-money outstanding shards = $2.4 million 27

28 Thank you! 28

Valuation of Early Stage Companies A quick primer and discussion

Valuation of Early Stage Companies A quick primer and discussion April 29, 2016 A brief introduction Venture Carolina: 501(c)(3) that educates investors and entrepreneurs to help improve the market for

Valuation of Early Stage Companies A quick primer and discussion April 29, 2016 A brief introduction Venture Carolina: 501(c)(3) that educates investors and entrepreneurs to help improve the market for

Hello. TODAY S EARLY-STAGE INVESTMENT VEHICLES. Michael Horten

Hello. TODAY S EARLY-STAGE INVESTMENT VEHICLES Michael Horten June 7, 2017 THE CHANGING Angel Financing LANDSCAPE Traditional Approach to Angel Financing Emulate the VC community by using Series A preferred

Hello. TODAY S EARLY-STAGE INVESTMENT VEHICLES Michael Horten June 7, 2017 THE CHANGING Angel Financing LANDSCAPE Traditional Approach to Angel Financing Emulate the VC community by using Series A preferred

Startup Valuation Methodology SVM. Prabir Mishra Managing Partner SAATRA Capital Advisory

Startup Valuation Methodology SVM Prabir Mishra Managing Partner SAATRA Capital Advisory How do we value a Startup? The most difficult question How do we value? Any clue? Depends on Investor? NO, Yes,

Startup Valuation Methodology SVM Prabir Mishra Managing Partner SAATRA Capital Advisory How do we value a Startup? The most difficult question How do we value? Any clue? Depends on Investor? NO, Yes,

Valuing Biotechnology Companies. Neil J. Beaton, CPA/ABV/CFF, CFA, ASA Alvarez & Marsal Valuation Services, LLC October 9, 2017

Valuing Biotechnology Companies Neil J. Beaton, CPA/ABV/CFF, CFA, ASA Alvarez & Marsal Valuation Services, LLC October 9, 2017 Agenda: Foundations Valuation Techniques Unique Aspects to Consider Foundations

Valuing Biotechnology Companies Neil J. Beaton, CPA/ABV/CFF, CFA, ASA Alvarez & Marsal Valuation Services, LLC October 9, 2017 Agenda: Foundations Valuation Techniques Unique Aspects to Consider Foundations

Valuation. Advanced Starter Seminars. Brussels, 23 November Thomas Crispeels

Valuation Advanced Starter Seminars Brussels, 23 November 2017 Thomas Crispeels Funding a High-Technology Company Start-up Case Study Source Start-up case study Lecture by Rudy Dekeyser VIB Tech Transfer

Valuation Advanced Starter Seminars Brussels, 23 November 2017 Thomas Crispeels Funding a High-Technology Company Start-up Case Study Source Start-up case study Lecture by Rudy Dekeyser VIB Tech Transfer

BUSINESS PLAN SCANNER + COMPANY PROFILE

STEVIA 1931 BV BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: Stevia 1931 BV Contact email: [email protected] Report date: 04.04.2016 Scalable business Demand validated Internationalization

STEVIA 1931 BV BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: Stevia 1931 BV Contact email: [email protected] Report date: 04.04.2016 Scalable business Demand validated Internationalization

Qbic Fund Venture Capital. Guy Huylebroeck Advanced Starters Seminar 16 October 2014

Qbic Fund Venture Capital Guy Huylebroeck Advanced Starters Seminar 16 October 2014 Contents I. VCs and how they work Qbic Fund Highlights Business Accelerator Sources of Capital Fund structure What does

Qbic Fund Venture Capital Guy Huylebroeck Advanced Starters Seminar 16 October 2014 Contents I. VCs and how they work Qbic Fund Highlights Business Accelerator Sources of Capital Fund structure What does

How to value your start-up Dr. Patrik Frei January 2016 San Francisco

How to value your start-up Dr. Patrik Frei January 2016 San Francisco Overview Introduction to Valuation Valuation of start-up companies Valuation of a therapeutic Product Q & A 2 Venture Valuation Mission

How to value your start-up Dr. Patrik Frei January 2016 San Francisco Overview Introduction to Valuation Valuation of start-up companies Valuation of a therapeutic Product Q & A 2 Venture Valuation Mission

Financing sources for life science projects and companies Dr. Aitana Peire May 2017 International Exploitation Training FFH2.

Financing sources for life science projects and companies Dr. Aitana Peire May 2017 International Exploitation Training FFH2.0, Prague Venture Valuation Mission Independent assessment and valuation of

Financing sources for life science projects and companies Dr. Aitana Peire May 2017 International Exploitation Training FFH2.0, Prague Venture Valuation Mission Independent assessment and valuation of

The Funding Landscape for Small Biopharma Ventures,

HEALTHCARE The Funding Landscape for Small Biopharma Ventures, 2010-2015 Trends, strategies and priorities By Gaurav Misra Gaurav Misra Gaurav Misra specializes in pharmaceutical licensing, valuations

HEALTHCARE The Funding Landscape for Small Biopharma Ventures, 2010-2015 Trends, strategies and priorities By Gaurav Misra Gaurav Misra Gaurav Misra specializes in pharmaceutical licensing, valuations

Starting a New Venture-Decision Time

Starting a New Venture-Decision Time The question: Form a business now OR continue to grow the science and development within the university. This is a cost-benefit analysis and you re definitely not ready

Starting a New Venture-Decision Time The question: Form a business now OR continue to grow the science and development within the university. This is a cost-benefit analysis and you re definitely not ready

Accessed by. from :6268. Accessed by. from :6268

KULABRANDS, INC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: kulabrands, Inc Contact email: peter@kulabrands.com Valuation set on: 01.08.2017 Report date: 08.06.2017 The

KULABRANDS, INC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: kulabrands, Inc Contact email: peter@kulabrands.com Valuation set on: 01.08.2017 Report date: 08.06.2017 The

Alternative Approaches to Valuing Early Stage Companies

1 Alternative Approaches to Valuing Early Stage Companies New Jersey Entrepreneurial Network (NJEN) November 18, 2015 event Mario M. Casabona 2 The Objective of this Presentation - What are the value drivers?

1 Alternative Approaches to Valuing Early Stage Companies New Jersey Entrepreneurial Network (NJEN) November 18, 2015 event Mario M. Casabona 2 The Objective of this Presentation - What are the value drivers?

SESSION 9B: VENTURE DEALS & STAGED FINANCINGS

Copyright 2014 by the Board of Trustees of the Leland Stanford Junior University and Stanford Technology Ventures Program (STVP). This document may be reproduced for educational purposes only. AUTUMN 2014

Copyright 2014 by the Board of Trustees of the Leland Stanford Junior University and Stanford Technology Ventures Program (STVP). This document may be reproduced for educational purposes only. AUTUMN 2014

Accessed by. from :6601. Accessed by. from :6601

TROUVAILLE, LLC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: Trouvaille, LLC Contact email: guest46637@equidam.com Valuation set on: 15.01.2018 Report date: 27.02.2018 The

TROUVAILLE, LLC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: Trouvaille, LLC Contact email: guest46637@equidam.com Valuation set on: 15.01.2018 Report date: 27.02.2018 The

GULF COAST CANNAMEDS, INC

GULF COAST CANNAMEDS, INC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: Gulf Coast CannaMeds, Inc Contact email: jgrimesgulfcoast@gmail.com Valuation set on: 01.09.2017 Report

GULF COAST CANNAMEDS, INC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: Gulf Coast CannaMeds, Inc Contact email: jgrimesgulfcoast@gmail.com Valuation set on: 01.09.2017 Report

Angel Investing. Introduction and Discussion. July 26, 2016 Milton Sigelmann

Welcome! Angel Investing Introduction and Discussion July 26, 2016 Milton Sigelmann Angel Investor - Definition An individual who provides capital for a business start-up, usually in exchange for convertible

Welcome! Angel Investing Introduction and Discussion July 26, 2016 Milton Sigelmann Angel Investor - Definition An individual who provides capital for a business start-up, usually in exchange for convertible

STREAMING TELEVISION INC.

STREAMING TELEVISION INC. BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: Streaming Television Inc. Contact email: email63731@equidam.com Valuation set on: 20.06.2018 Report

STREAMING TELEVISION INC. BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: Streaming Television Inc. Contact email: email63731@equidam.com Valuation set on: 20.06.2018 Report

Index 367. F Fashion drugs 102 FDA 69, 70 Feed rate 234, 262 most likely 328 Financial option valuation 59 Financial options 38 Fund raising 5

References AUTM (2005) AUTM U.S. Licensing Survey: FY 2004. (Survey summary of the AUTM U.S. Licensing Survey: FY 2004) Black, F. and Scholes, M. (1973) The Pricing of Options and Corporate Liabilities

References AUTM (2005) AUTM U.S. Licensing Survey: FY 2004. (Survey summary of the AUTM U.S. Licensing Survey: FY 2004) Black, F. and Scholes, M. (1973) The Pricing of Options and Corporate Liabilities

Public versus private funding opportunities for life sciences

Public versus private funding opportunities for life sciences Dr. Patrik Frei June 2012 Meet4Lifescience, Basel Agenda Financing trends Financing sources Public Financing sources Equity Financing sources

Public versus private funding opportunities for life sciences Dr. Patrik Frei June 2012 Meet4Lifescience, Basel Agenda Financing trends Financing sources Public Financing sources Equity Financing sources

Fashion drugs 70 FDA 10, 18 Feed rate 173, 194 most likely 238 Financial option valuation 57 Financial options 36 Fund raising 5

References AUTM (2005) AUTM U.S. Licensing Survey: FY 2004. (Survey summary of the AUTM U.S. Licensing Survey: FY 2004) Black, F. and Scholes, M. (1973). The Pricing of Options and Corporate Liabilities

References AUTM (2005) AUTM U.S. Licensing Survey: FY 2004. (Survey summary of the AUTM U.S. Licensing Survey: FY 2004) Black, F. and Scholes, M. (1973). The Pricing of Options and Corporate Liabilities

Αμοιβαία Κεφάλαια και Εναλλακτικές Επενδύσεις. Private Equities

Αμοιβαία Κεφάλαια και Εναλλακτικές Επενδύσεις Private Equities Private Equity Private equity funds are organized as limited partnerships that are not publicly traded. The investors in private equity are

Αμοιβαία Κεφάλαια και Εναλλακτικές Επενδύσεις Private Equities Private Equity Private equity funds are organized as limited partnerships that are not publicly traded. The investors in private equity are

Accessed by. from :5440

SQUIRREL CAPITAL INVESTMENTS INC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: Squirrel Capital Investments Inc Contact email: guest46929@equidam.com Valuation set on: 15.03.2018

SQUIRREL CAPITAL INVESTMENTS INC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: Squirrel Capital Investments Inc Contact email: guest46929@equidam.com Valuation set on: 15.03.2018

Accessed by. from : Accessed by. from :27243

MEG MEDIA, INC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: MEG Media, INC Contact email: guest47169@equidam.com Valuation set on: 04.05.2018 Report date: 07.05.2018 The

MEG MEDIA, INC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: MEG Media, INC Contact email: guest47169@equidam.com Valuation set on: 04.05.2018 Report date: 07.05.2018 The

Executive Compensation in Privately Owned Businesses: How It s the Same and How It s Very Different

Executive Compensation in Privately Owned Businesses: How It s the Same and How It s Very Different Don Delves, Director, Willis Towers Watson June 6, 2017 2017 Willis Towers Watson. All rights reserved.

Executive Compensation in Privately Owned Businesses: How It s the Same and How It s Very Different Don Delves, Director, Willis Towers Watson June 6, 2017 2017 Willis Towers Watson. All rights reserved.

Money That s What I Want (Everyone wants it Angels & Entrepreneurs) 5 Feb 2014

5 Feb 2014") Money That s What I Want (Everyone wants it Angels & Entrepreneurs) 5 Feb 2014 Mike Volker Innovation Office Simon Fraser University Innovation is the key to growth Talent: Universities R&D Orgs Investors

Money That s What I Want (Everyone wants it Angels & Entrepreneurs) 5 Feb 2014 Mike Volker Innovation Office Simon Fraser University Innovation is the key to growth Talent: Universities R&D Orgs Investors

William Blair 35 th Annual Growth Stock Conference. June 9, 2015 NYSE: Q. Copyright 2014 Quintiles

William Blair 35 th Annual Growth Stock Conference June 9, 2015 Copyright 2014 Quintiles NYSE: Q Forward Looking Statements and Use of Non-GAAP Financial Measures This presentation contains forward-looking

William Blair 35 th Annual Growth Stock Conference June 9, 2015 Copyright 2014 Quintiles NYSE: Q Forward Looking Statements and Use of Non-GAAP Financial Measures This presentation contains forward-looking

STREAMING TELEVISION, INC

STREAMING TELEVISION, INC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: Streaming Television, Inc Contact email: guest47122@equidam.com Valuation set on: 02.07.2018 Report

STREAMING TELEVISION, INC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: Streaming Television, Inc Contact email: guest47122@equidam.com Valuation set on: 02.07.2018 Report

The Fairshare Model A Performance-Based Capital Structure for Companies Seeking Venture Capital via a CrowdFunded Initial Public Offering (IPO)

") The Fairshare Model A Performance-Based Capital Structure for Companies Seeking Venture Capital via a CrowdFunded Initial Public Offering (IPO) The Nuts & Bolts slide deck for experts in capital structures

The Fairshare Model A Performance-Based Capital Structure for Companies Seeking Venture Capital via a CrowdFunded Initial Public Offering (IPO) The Nuts & Bolts slide deck for experts in capital structures

24 th Annual Health Sciences Tax Conference

24 th Annual Health Sciences Tax Conference Understanding the tax impact of joint ventures and December 10, 2014 Disclaimer EY refers to the global organization, and may refer to one or more, of the member

24 th Annual Health Sciences Tax Conference Understanding the tax impact of joint ventures and December 10, 2014 Disclaimer EY refers to the global organization, and may refer to one or more, of the member

Session 09 Venture Finance and Teams Tom Byers

Session 09 Venture Finance and Teams Tom Byers Copyright 2006 by the Board of Trustees of the Leland Stanford Junior University and Stanford Technology Ventures Program (STVP). This document may be reproduced

Session 09 Venture Finance and Teams Tom Byers Copyright 2006 by the Board of Trustees of the Leland Stanford Junior University and Stanford Technology Ventures Program (STVP). This document may be reproduced

Workshop Business Angels. Valuation Valuation is an art, not a science!

Workshop Business Angels Valuation Valuation is an art, not a science! Jean-Pierre Vuilleumier Managing Director CTI Invest Contact: vui@cti-invest.ch +41 79 251 32 09 4.11.2008 1 Overview of possible

Workshop Business Angels Valuation Valuation is an art, not a science! Jean-Pierre Vuilleumier Managing Director CTI Invest Contact: vui@cti-invest.ch +41 79 251 32 09 4.11.2008 1 Overview of possible

UNDERSTANDING EQUIDAM VALUATION

UNDERSTANDING EQUIDAM VALUATION Office: Marconistraat 16, 3029 AK Rotterdam Phone: +31 (0) 10 26 81 465 E-mail: info@equidam.com WHAT IS EQUIDAM Equidam is the leading provider of online business valuation.

UNDERSTANDING EQUIDAM VALUATION Office: Marconistraat 16, 3029 AK Rotterdam Phone: +31 (0) 10 26 81 465 E-mail: info@equidam.com WHAT IS EQUIDAM Equidam is the leading provider of online business valuation.

Accessed by. from : Accessed by. from :24550

WORKDONE INC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: WorkDone Inc Contact email: guest47053@equidam.com Valuation set on: 09.04.2018 Report date: 05.06.2018 The Team

WORKDONE INC BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: WorkDone Inc Contact email: guest47053@equidam.com Valuation set on: 09.04.2018 Report date: 05.06.2018 The Team

BUSINESS PLAN SCANNER + COMPANY PROFILE

ETELLIGENT INC. BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: etelligent Inc. Contact email: barbara@nwweddingdirectory.com Valuation set on: 05.03.2018 Report date: 05.03.2018

ETELLIGENT INC. BUSINESS PLAN SCANNER + COMPANY PROFILE Contacts The idea Company full name: etelligent Inc. Contact email: barbara@nwweddingdirectory.com Valuation set on: 05.03.2018 Report date: 05.03.2018

TAX INCENTIVES FOR GROWING HEALTH SCIENCE COMPANIES

TAX INCENTIVES FOR GROWING HEALTH SCIENCE COMPANIES 0 1 CONTENTS Executive Summary... 1 Introduction... 3 Recommendations : Government of Canada... 5 Recommendations : Government of Ontario... 7 References...

TAX INCENTIVES FOR GROWING HEALTH SCIENCE COMPANIES 0 1 CONTENTS Executive Summary... 1 Introduction... 3 Recommendations : Government of Canada... 5 Recommendations : Government of Ontario... 7 References...

VALUING YOUR OPPORTUNITY How industry and investors evaluate your project or company

VALUING YOUR OPPORTUNITY How industry and investors evaluate your project or company Dr. Patrik Frei September 2015 Brisbane Overview Introduction Valuation of start-up companies Valuation of a therapeutic

VALUING YOUR OPPORTUNITY How industry and investors evaluate your project or company Dr. Patrik Frei September 2015 Brisbane Overview Introduction Valuation of start-up companies Valuation of a therapeutic

Financing Your Tech Company - Angel and VCC Sources

Financing Your Tech Company - Angel and VCC Sources BCTIA Tech Forum Speakers Series February 23, 2006 By Basil Peters Building Company Value Founding = 10% Equal Tactics & Strategy = 40% Exit Strategy

Financing Your Tech Company - Angel and VCC Sources BCTIA Tech Forum Speakers Series February 23, 2006 By Basil Peters Building Company Value Founding = 10% Equal Tactics & Strategy = 40% Exit Strategy

Venture Capital and Company Valuations in Biotech

Venture Capital and Company Valuations in Biotech Venture Valuation VV AG Badenerstr. 18 8004 Zurich Switzerland Phone +41 (43) 321 86 60 Fax + 41 (43) 321 86 61 info@venturevaluation.ch Agenda - Swiss

Venture Capital and Company Valuations in Biotech Venture Valuation VV AG Badenerstr. 18 8004 Zurich Switzerland Phone +41 (43) 321 86 60 Fax + 41 (43) 321 86 61 info@venturevaluation.ch Agenda - Swiss

Venture Capital Method: Valuation Problem Set Solutions

9-802-162 REV: OCTOBER 10, 2002 WALTER KUEMMERLE Venture Capital Method: Valuation Problem Set Solutions This note provides detailed solutions to questions 1 through 4 of the Venture Capital Method - Valuation

9-802-162 REV: OCTOBER 10, 2002 WALTER KUEMMERLE Venture Capital Method: Valuation Problem Set Solutions This note provides detailed solutions to questions 1 through 4 of the Venture Capital Method - Valuation

NEXT EDGE BIO-TECH PLUS FUND

NEXT EDGE BIO-TECH PLUS FUND Investing in companies of the future: A unique well defined process of investing in North American small and mid-capitalization Biotechnology companies. INVESTMENT OBJECTIVE

NEXT EDGE BIO-TECH PLUS FUND Investing in companies of the future: A unique well defined process of investing in North American small and mid-capitalization Biotechnology companies. INVESTMENT OBJECTIVE

What you need to know to succeed in doing deals and fundraising Dr. Patrik Frei May 2014 Seoul BioKorea

What you need to know to succeed in doing deals and fundraising Dr. Patrik Frei May 2014 Seoul BioKorea Overview Introduction to Valuation Valuation of a companies Valuation of a therapeutic Product Q

What you need to know to succeed in doing deals and fundraising Dr. Patrik Frei May 2014 Seoul BioKorea Overview Introduction to Valuation Valuation of a companies Valuation of a therapeutic Product Q

Agenda. Venture Capital and Valuations

Venture Capital and Valuations Venture Valuation VV AG Badenerstr. 18 8004 Zurich Switzerland Phone +41 (43) 321 86 60 Fax + 41 (43) 321 86 61 info@venturevaluation.ch Agenda - Venture Capital - Why Valuation?

Venture Capital and Valuations Venture Valuation VV AG Badenerstr. 18 8004 Zurich Switzerland Phone +41 (43) 321 86 60 Fax + 41 (43) 321 86 61 info@venturevaluation.ch Agenda - Venture Capital - Why Valuation?

BDO KNOWS: VALUATION OF PORTFOLIO COMPANY INVESTMENTS IMPORTANT REMINDERS AN ALERT FROM THE BDO FINANCIAL SERVICES PRACTICE BACKGROUND

JANUARY 2019 www.bdo.com AN ALERT FROM THE BDO FINANCIAL SERVICES PRACTICE BDO S ASSET MANAGEMENT PRACTICE BDO s Asset Management Services practice provides assurance, tax and advisory services to asset

JANUARY 2019 www.bdo.com AN ALERT FROM THE BDO FINANCIAL SERVICES PRACTICE BDO S ASSET MANAGEMENT PRACTICE BDO s Asset Management Services practice provides assurance, tax and advisory services to asset

Data Mining the Venture-Backed Company Charter

Data Mining the Venture-Backed Company Charter By Jonathan D. Gworek mbbp.com Corporate IP Licensing & Strategic Alliances Employment & Immigration Taxation Litigation 781-622-5930 Data Mining the Venture

Data Mining the Venture-Backed Company Charter By Jonathan D. Gworek mbbp.com Corporate IP Licensing & Strategic Alliances Employment & Immigration Taxation Litigation 781-622-5930 Data Mining the Venture

Connecting with Angel Investors 3 Apr 2013

Connecting with Angel Investors 3 Apr 2013 Mike Volker Innovation Office Simon Fraser University Innovation is the key to growth Talent: Universities R&D Orgs Investors Entrepreneurs are the Champions

Connecting with Angel Investors 3 Apr 2013 Mike Volker Innovation Office Simon Fraser University Innovation is the key to growth Talent: Universities R&D Orgs Investors Entrepreneurs are the Champions

New Brunswick Capital Markets Report 2016

New Brunswick Capital Markets Report 2016 OCTOBER 2016 FCNB.CA 85 Charlotte Street, suite 300 Saint John, NB E2L 2J2 506 658-3060 225 King Street, suite 200 Fredericton, NB E3B 1E1 866 933-2222 Acknowledgement

New Brunswick Capital Markets Report 2016 OCTOBER 2016 FCNB.CA 85 Charlotte Street, suite 300 Saint John, NB E2L 2J2 506 658-3060 225 King Street, suite 200 Fredericton, NB E3B 1E1 866 933-2222 Acknowledgement

Next Edge Bio-Tech Plus Fund

Next Edge Bio-Tech Plus Fund Profile as of March 29, 2019 Investing in companies of the future: A unique, well defined process of investing in North American small and mid-capitalization biotechnology

Next Edge Bio-Tech Plus Fund Profile as of March 29, 2019 Investing in companies of the future: A unique, well defined process of investing in North American small and mid-capitalization biotechnology

Executive Compensation Trend Report

2017 Executive Compensation Trend Report Published: October 30, 2017 Advanced HR, Inc. www.advanced hr.com info@advanced hr.com 415.362.2200 We are pleased to present the 2017 Executive Compensation Trend

2017 Executive Compensation Trend Report Published: October 30, 2017 Advanced HR, Inc. www.advanced hr.com info@advanced hr.com 415.362.2200 We are pleased to present the 2017 Executive Compensation Trend

VENTURE PERSPECTIVES EMERGING ENTERPRISE CENTER AT FOLEY HOAG NEW ENGLAND EDITION

VENTURE PERSPECTIVES EMERGING ENTERPRISE CENTER AT FOLEY HOAG NEW ENGLAND EDITION MAY Quarterly Review of Seed, Series A and Series B/Later Round Financings: First Quarter Activity Level of New England

VENTURE PERSPECTIVES EMERGING ENTERPRISE CENTER AT FOLEY HOAG NEW ENGLAND EDITION MAY Quarterly Review of Seed, Series A and Series B/Later Round Financings: First Quarter Activity Level of New England

Session 12. Stock Options

Session 12 Stock Options Slide 1 Agenda Barbara Arneson Case Stock Options Slide 2 Barbara Arneson Case What is the number of shares outstanding at BioGene as of May 31, 2006? What is its current PE ratio?

Session 12 Stock Options Slide 1 Agenda Barbara Arneson Case Stock Options Slide 2 Barbara Arneson Case What is the number of shares outstanding at BioGene as of May 31, 2006? What is its current PE ratio?

2017 Venture Capital Trends Summary

2017 Venture Capital Trends Summary Prepared by: Hitesh Kothari, Partner, RSM US LLP hitesh.kothari@rsmus.com, +1 212 372 1087 November 2017 Overview In the last 10 years, the deal flow in the venture

2017 Venture Capital Trends Summary Prepared by: Hitesh Kothari, Partner, RSM US LLP hitesh.kothari@rsmus.com, +1 212 372 1087 November 2017 Overview In the last 10 years, the deal flow in the venture

Starting a New Venture. October 11, 2018 Frank Grassler, J.D. VP For Technology Development

Starting a New Venture October 11, 2018 Frank Grassler, J.D. VP For Technology Development Starting a New Venture Decision Time The question: Form a business now OR continue to grow the science and development

Starting a New Venture October 11, 2018 Frank Grassler, J.D. VP For Technology Development Starting a New Venture Decision Time The question: Form a business now OR continue to grow the science and development

Company Valuation. Gideon Shalom Bendor Managing Partner

2 Company Valuation Gideon Shalom Bendor Managing Partner Why try to value a company? Investment purpose M&A and Pre-IPO Tax (409A) Financial Reporting (PPA, ASC 820) ESOP (Employee Stock Option Plan,

2 Company Valuation Gideon Shalom Bendor Managing Partner Why try to value a company? Investment purpose M&A and Pre-IPO Tax (409A) Financial Reporting (PPA, ASC 820) ESOP (Employee Stock Option Plan,

Valuation and Due Diligence in Acquiring Intellectual Assets

Valuation and Due Diligence in Acquiring Intellectual Assets - Measuring the Flagpole - Joseph J. Berghammer Banner & Witcoff, Ltd. Chicago, IL Due Diligence Assessment and Minimization of Risk Valuation

Valuation and Due Diligence in Acquiring Intellectual Assets - Measuring the Flagpole - Joseph J. Berghammer Banner & Witcoff, Ltd. Chicago, IL Due Diligence Assessment and Minimization of Risk Valuation

Introduction. PEs: the invesment process and the Value Creation

Introduction PEs: the invesment process and the Value Creation 1 Contents - Introduction - PE Stages and Investment Process - Initial Strategic Definition: Types of deal and PEs - Deal Sourcing - Initial

Introduction PEs: the invesment process and the Value Creation 1 Contents - Introduction - PE Stages and Investment Process - Initial Strategic Definition: Types of deal and PEs - Deal Sourcing - Initial

Bridging the Gap in Deal Valuation. Wednesday April 12, 2017

Bridging the Gap in Deal Valuation Wednesday April 12, 2017 Bridging the Gap in Deal Valuation Speakers: Clare Fisher, Vice President, Interim Head of Transactions, Shire Greg Miller, MBA, MPH, Vice President

Bridging the Gap in Deal Valuation Wednesday April 12, 2017 Bridging the Gap in Deal Valuation Speakers: Clare Fisher, Vice President, Interim Head of Transactions, Shire Greg Miller, MBA, MPH, Vice President

Executive Compensation Checklist for Pre-IPO Companies

TRENDS & ISSUES Executive Compensation Checklist for Pre-IPO Companies AUTHOR Peter Lupo Managing Director Venture-backed private companies maintain executive compensation programs that are significantly

TRENDS & ISSUES Executive Compensation Checklist for Pre-IPO Companies AUTHOR Peter Lupo Managing Director Venture-backed private companies maintain executive compensation programs that are significantly

Bioindustry in Alberta

BIOINDUSTRY Bioindustry in Alberta State of the Industry 2007 ADVISORY Prepared by: The information contained herein is of a general nature and is not intended to address the circumstances of any particular

BIOINDUSTRY Bioindustry in Alberta State of the Industry 2007 ADVISORY Prepared by: The information contained herein is of a general nature and is not intended to address the circumstances of any particular

Management Report of Fund Performance

Management Report of Fund Performance Covington Venture Fund Inc. Series V For The Period Ended January 31, 2010 [in $000 s except for per share amounts, number of shares and percentages] Table of Contents...

Management Report of Fund Performance Covington Venture Fund Inc. Series V For The Period Ended January 31, 2010 [in $000 s except for per share amounts, number of shares and percentages] Table of Contents...

Quarterly and Annual Review of Series A and Series B/Later Round Financings: Q4 and Year Activity Level of New England Series A Transactions

VENTURE PERSPECTIVES EMERGING ENTERPRISE CENTER AT FOLEY HOAG FEBRUARY 2011 Quarterly and Annual Review of Series A and Series B/Later Round Financings: Q4 and Year Activity Level of New England Series

VENTURE PERSPECTIVES EMERGING ENTERPRISE CENTER AT FOLEY HOAG FEBRUARY 2011 Quarterly and Annual Review of Series A and Series B/Later Round Financings: Q4 and Year Activity Level of New England Series

Quarterly Review of Series A Financings and Series B and Later Round Financings: Second Quarter 2011

VENTURE PERSPECTIVES EMERGING ENTERPRISE CENTER AT FOLEY HOAG SEPTEMBER Quarterly Review of Series A Financings and Series B and Later Round Financings: Second Quarter Activity Level of New England Series

VENTURE PERSPECTIVES EMERGING ENTERPRISE CENTER AT FOLEY HOAG SEPTEMBER Quarterly Review of Series A Financings and Series B and Later Round Financings: Second Quarter Activity Level of New England Series

Valuing Investments in Start-Ups

Valuing Investments in Start-Ups Travis W. Harms, CFA, CPA/ABV Senior Vice President Mercer Capital harmst@mercercapital.com 901.685.2120 AICPA 2017 Forensic & Valuation Services Conference 1 Topics to

Valuing Investments in Start-Ups Travis W. Harms, CFA, CPA/ABV Senior Vice President Mercer Capital harmst@mercercapital.com 901.685.2120 AICPA 2017 Forensic & Valuation Services Conference 1 Topics to

Financing Trends for Q2 2014

THE ENTREPRENEURS REPORT Private Company Financing Trends 1H 2014 Price and Preference By Herb Fockler, Partner, and Eric Little, Knowledge Management Manager, Palo Alto It is a truth universally acknowledged

THE ENTREPRENEURS REPORT Private Company Financing Trends 1H 2014 Price and Preference By Herb Fockler, Partner, and Eric Little, Knowledge Management Manager, Palo Alto It is a truth universally acknowledged

IP Valuation and Forming University Startups

IP Valuation and Forming University Startups Budapest, September 15 17, 2015 Professor John Orcutt University of New Hampshire School of Law 1 AGENDA 1. License v. startup strategy 2. Introduction to valuing

IP Valuation and Forming University Startups Budapest, September 15 17, 2015 Professor John Orcutt University of New Hampshire School of Law 1 AGENDA 1. License v. startup strategy 2. Introduction to valuing

CYNAPSUS THERAPEUTICS INC.

CYNAPSUS THERAPEUTICS INC. Condensed Interim Consolidated Financial Statements For the Three Months Ended (Expressed in Canadian Dollars) Unaudited NOTICE OF NO AUDITOR REVIEW OF CONDENSED INTERIM CONSOLIDATED

CYNAPSUS THERAPEUTICS INC. Condensed Interim Consolidated Financial Statements For the Three Months Ended (Expressed in Canadian Dollars) Unaudited NOTICE OF NO AUDITOR REVIEW OF CONDENSED INTERIM CONSOLIDATED

Equity/M&A Brand. Experience Knowledge Relationships Insight. Building a New Private Equity/M&A Practice Brand

Building A Private Equity/M&A Brand Carroll D. Hurst, CPA Partner Keiter CPAs churst@keitercpa.com Building a New Private Equity/M&A Practice Brand Steps: I. Evaluate market size/competition II. Determine

Building A Private Equity/M&A Brand Carroll D. Hurst, CPA Partner Keiter CPAs churst@keitercpa.com Building a New Private Equity/M&A Practice Brand Steps: I. Evaluate market size/competition II. Determine

November Deal Metrics Survey. A survey of Australian VC and PE deal activity in FY2012. In association with

November Deal Metrics Survey A survey of Australian VC and PE deal activity in FY In association with AVCAL Deal Metrics Report Message from the Chief Executive Welcome to the AVCAL and Pacific Strategy

November Deal Metrics Survey A survey of Australian VC and PE deal activity in FY In association with AVCAL Deal Metrics Report Message from the Chief Executive Welcome to the AVCAL and Pacific Strategy

Compendium of Guidelines, Policies and Procedures

Patented Medicine Prices Review Board REVISED MARCH 2008 Compendium of Guidelines, Policies and Procedures Patented Medicine Prices Review Board Box L40 Standard Life Centre 333 Laurier Avenue West Suite

Patented Medicine Prices Review Board REVISED MARCH 2008 Compendium of Guidelines, Policies and Procedures Patented Medicine Prices Review Board Box L40 Standard Life Centre 333 Laurier Avenue West Suite

ROADMAP FROM CONCEPT TO IPO.

The ENTREPRENEUR S ROADMAP FROM CONCEPT TO IPO www.nyse.com/entrepreneur Download the electronic version of the guide at: www.nyse.com/entrepreneur 38 409A VALUATIONS AND OTHER COMPLEX EQUITY COMPENSATION

The ENTREPRENEUR S ROADMAP FROM CONCEPT TO IPO www.nyse.com/entrepreneur Download the electronic version of the guide at: www.nyse.com/entrepreneur 38 409A VALUATIONS AND OTHER COMPLEX EQUITY COMPENSATION

CRS Electronics Inc. Management Discussion and Analysis. Fourth Quarter and the Year Ended December 31, Dated: April 16, 2010

CRS Electronics Inc. - Management Discussion and Analysis Fourth Quarter and Year Ended December 31, 2009 CRS Electronics Inc. Management Discussion and Analysis Fourth Quarter and the Year Ended December

CRS Electronics Inc. - Management Discussion and Analysis Fourth Quarter and Year Ended December 31, 2009 CRS Electronics Inc. Management Discussion and Analysis Fourth Quarter and the Year Ended December

An Impact Brief September The Rich Get Richer. Are Canadian VCs inadvertently limiting their returns?

An Impact Brief September 2017 The Rich Get Richer Are Canadian VCs inadvertently limiting their returns? Contents The Rich Get Richer 3 Introduction 5 Capital Requirements 8 The Link to Growth 14 Correlation

An Impact Brief September 2017 The Rich Get Richer Are Canadian VCs inadvertently limiting their returns? Contents The Rich Get Richer 3 Introduction 5 Capital Requirements 8 The Link to Growth 14 Correlation

EDUCATIONAL NOTES TO THE SIMPLE AGREEMENT FOR FUTURE EQUITY (SAFE) April 2017

April 2017") EDUCATIONAL NOTES TO THE SIMPLE AGREEMENT FOR FUTURE EQUITY (SAFE) April 2017 The SAFE as investment instrument came into being at the Y Combinator accelerator in Silicon Valley in late 2013. It addressed

EDUCATIONAL NOTES TO THE SIMPLE AGREEMENT FOR FUTURE EQUITY (SAFE) April 2017 The SAFE as investment instrument came into being at the Y Combinator accelerator in Silicon Valley in late 2013. It addressed

The Business Environment Facing Emerging Companies Today

A Report Presented By: Foley & Lardner LLP December 13, 2007 Page 2 EXECUTIVE SUMMARY Emerging company executives, investors and advisors have expressed greater uncertainty in the current market, however

A Report Presented By: Foley & Lardner LLP December 13, 2007 Page 2 EXECUTIVE SUMMARY Emerging company executives, investors and advisors have expressed greater uncertainty in the current market, however

NOVOHEART HOLDINGS INC. Condensed Consolidated Interim Financial Statements. Three and six months ended December 31, 2017 and 2016.

NOVOHEART HOLDINGS INC Condensed Consolidated Interim Financial Statements Three and six months ended December 31, 2017 and 2016 (Unaudited) Condensed Consolidated Interim Statement of Financial Position

NOVOHEART HOLDINGS INC Condensed Consolidated Interim Financial Statements Three and six months ended December 31, 2017 and 2016 (Unaudited) Condensed Consolidated Interim Statement of Financial Position

ITA IoT Capital Conference

ITA IoT Capital Conference Presented by November 17, 2015 Disclosures IMPORTANT DISCLOSURES AND INFORMATION ABOUT THE USE OF THIS DOCUMENT With the exception of information about FASC, the information

ITA IoT Capital Conference Presented by November 17, 2015 Disclosures IMPORTANT DISCLOSURES AND INFORMATION ABOUT THE USE OF THIS DOCUMENT With the exception of information about FASC, the information

Valuation of start-ups

Valuation of start-ups We ready to begin? Introduction Valuation is one of the biggest hurdles to overcome when taking on an equity investment. Nobody truly knows the value of a company without historical

Valuation of start-ups We ready to begin? Introduction Valuation is one of the biggest hurdles to overcome when taking on an equity investment. Nobody truly knows the value of a company without historical

Accelerator Curriculum 2012 Module: Capitalization

Accelerator Curriculum 2012 Module: Capitalization Andrew Ritten Faegre Baker Daniels LLP 8993441 Bio Andrew Ritten Joined Faegre Baker Daniels corporate group in 1993 Education: Yale University B.A. History,

Accelerator Curriculum 2012 Module: Capitalization Andrew Ritten Faegre Baker Daniels LLP 8993441 Bio Andrew Ritten Joined Faegre Baker Daniels corporate group in 1993 Education: Yale University B.A. History,

AXIAL FOR CEOS THE GUIDE TO PRIVATE COMPANY VALUATION THE SELLER SERIES

AXIAL FOR CEOS THE GUIDE TO PRIVATE COMPANY VALUATION Table of Contents Private Company Valuation Methods... 4 Valuing Add-Ons vs. Platforms... 9 Benefits & Drawbacks of Add-On Acquisitions... 10 Valuation

AXIAL FOR CEOS THE GUIDE TO PRIVATE COMPANY VALUATION Table of Contents Private Company Valuation Methods... 4 Valuing Add-Ons vs. Platforms... 9 Benefits & Drawbacks of Add-On Acquisitions... 10 Valuation

Financial and Consumer Services Commission

New Brunswick Capital Markets Report 2014 October 2014 Financial and Consumer Services Commission FCNB.CA 85 Charlotte Street, suite 300 Saint John, NB E2L 2J2 1 866 933-2222 225 King Street, suite 200

New Brunswick Capital Markets Report 2014 October 2014 Financial and Consumer Services Commission FCNB.CA 85 Charlotte Street, suite 300 Saint John, NB E2L 2J2 1 866 933-2222 225 King Street, suite 200

Introduction to Venture Capital Week 3 About Due Diligence, Valuation, Negotiation, and Mistakes you shouldn t make in the process

Introduction to Venture Capital Week 3 About Due Diligence, Valuation, Negotiation, and Mistakes you shouldn t make in the process School of Business and Economics TIME Research Area Innovation & Entrepreneurship

Introduction to Venture Capital Week 3 About Due Diligence, Valuation, Negotiation, and Mistakes you shouldn t make in the process School of Business and Economics TIME Research Area Innovation & Entrepreneurship

Strategizing Mainland China Investment Exit through Indirect Equity Transfers

Strategizing Mainland China Investment Exit through Indirect Equity Transfers www.pwccn.com In the past few years, China has been enjoying a major boom in the growth of innovation activities under its

Strategizing Mainland China Investment Exit through Indirect Equity Transfers www.pwccn.com In the past few years, China has been enjoying a major boom in the growth of innovation activities under its

Executive Compensation: Insights from the 2014 CompStudy Survey of Venture-Backed Companies

Life Sciences Edition Executive Compensation: Insights from the 2014 CompStudy Survey of Venture-Backed Companies LIFE SCIENCES EDITION Today s moderator Bryan Pearce Global Leader EY Entrepreneur Of The

Life Sciences Edition Executive Compensation: Insights from the 2014 CompStudy Survey of Venture-Backed Companies LIFE SCIENCES EDITION Today s moderator Bryan Pearce Global Leader EY Entrepreneur Of The

ISHARES NASDAQ BIOTECHNOLOGY ETF (IBB)

") ISHARES NASDAQ BIOTECHNOLOGY ETF (IBB) $106.77 USD Risk: High Zacks ETF Rank 3 - Hold Fund Type Issuer Benchmark Index Health Care ETFs BLACKROCK NASDAQ BIOTECHNOLOGY INDEX IBB Sector Weights Date of Inception

ISHARES NASDAQ BIOTECHNOLOGY ETF (IBB) $106.77 USD Risk: High Zacks ETF Rank 3 - Hold Fund Type Issuer Benchmark Index Health Care ETFs BLACKROCK NASDAQ BIOTECHNOLOGY INDEX IBB Sector Weights Date of Inception

E Session 9 Venture Finance Tom Byers

E145 2007 Session 9 Venture Finance Tom Byers Copyright 2007 by the Board of Trustees of the Leland Stanford Junior University and Stanford Technology Ventures Program (STVP). This document may be reproduced

E145 2007 Session 9 Venture Finance Tom Byers Copyright 2007 by the Board of Trustees of the Leland Stanford Junior University and Stanford Technology Ventures Program (STVP). This document may be reproduced

AMERICAN INVESTMENT COUNCIL. Performance Update 2017 Q1

AMERICAN INVESTMENT COUNCIL Performance Update 2017 Q1 Private Equity Performance Benchmarks (as of March 31, 2017) Private Equity Benchmark Returns (Horizon IRR) 1 1-Year 3-Year 5-Year 10-Year BISON Private

AMERICAN INVESTMENT COUNCIL Performance Update 2017 Q1 Private Equity Performance Benchmarks (as of March 31, 2017) Private Equity Benchmark Returns (Horizon IRR) 1 1-Year 3-Year 5-Year 10-Year BISON Private

Valuation Case Study: Jazz Pharmaceuticals [JAZZ] How to Make an Investment Decision

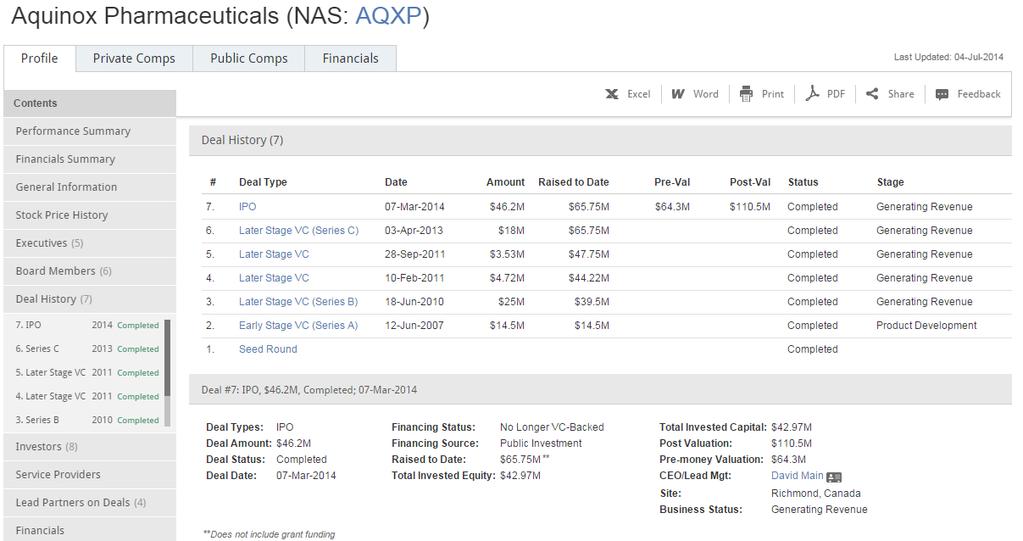

![Valuation Case Study: Jazz Pharmaceuticals [JAZZ] How to Make an Investment Decision](/thumbs/79/78919310.jpg "Valuation Case Study: Jazz Pharmaceuticals [JAZZ] How to Make an Investment Decision") Valuation Case Study: Jazz Pharmaceuticals [JAZZ] How to Make an Investment Decision Step 1 Reviewing the Numbers For a case study like this, always start with the numbers. You will not have enough time

Valuation Case Study: Jazz Pharmaceuticals [JAZZ] How to Make an Investment Decision Step 1 Reviewing the Numbers For a case study like this, always start with the numbers. You will not have enough time

Biotech Financing Update. Dec 2017-Feb 2018

Biotech Financing Update Dec 2017-Feb 2018 Biotech Financing Update Overall figures These figures capture biotech financing data from December 2017 and take a first look at how the sector is doing in 2018

Biotech Financing Update Dec 2017-Feb 2018 Biotech Financing Update Overall figures These figures capture biotech financing data from December 2017 and take a first look at how the sector is doing in 2018

Secondary Market: Evolution and Recent Trends

Secondary Market: Evolution and Recent Trends Emmanuel Roubinowitz, Ponte Partners Internet Securities Event March 16, 2016 1 Secondary Overview Acquisition of shares in PE/VC funds or PE/VC backed companies

Secondary Market: Evolution and Recent Trends Emmanuel Roubinowitz, Ponte Partners Internet Securities Event March 16, 2016 1 Secondary Overview Acquisition of shares in PE/VC funds or PE/VC backed companies

Wells Fargo Middle Market Opportunities Forum Presentation

Wells Fargo Middle Market Opportunities Forum Presentation December 7, 2016 www.tpvg.com FORWARD LOOKING STATEMENT Some of the statements in this presentation constitute forward-looking statements, which

Wells Fargo Middle Market Opportunities Forum Presentation December 7, 2016 www.tpvg.com FORWARD LOOKING STATEMENT Some of the statements in this presentation constitute forward-looking statements, which

We can now calculate our investment s expected future value, depicted in the table below. Exit Valuation (V) Probability (P)

Probability (P)") 2017 In theory, start-up valuation is similar to the valuation of any company. First, estimate the amount of money the company will make for its shareholders (typically through an acquisition or IPO).

2017 In theory, start-up valuation is similar to the valuation of any company. First, estimate the amount of money the company will make for its shareholders (typically through an acquisition or IPO).

Measuring Nova Scotia s Results in Health Research

Collins Management Consulting & Research Ltd. Measuring Nova Scotia s Results in Health Research 2009 Update Report Health Research 2009 Update Report Prepared on behalf of the Nova Scotia Health Research

Collins Management Consulting & Research Ltd. Measuring Nova Scotia s Results in Health Research 2009 Update Report Health Research 2009 Update Report Prepared on behalf of the Nova Scotia Health Research

CMU: Measuring progress and planning for success

CMU KPI Report CMU: Measuring progress and planning for success Third anniversary of CMU: timely opportunity to review the progress on achieving the CMU s vital aims Produced by AFME with the support of

CMU KPI Report CMU: Measuring progress and planning for success Third anniversary of CMU: timely opportunity to review the progress on achieving the CMU s vital aims Produced by AFME with the support of

Venture Capital at BDC. Nazmin Alani, Managing Director

Venture Capital at BDC Nazmin Alani, Managing Director Development Bank Role in Commercializing IP Technology Transfer Conference: Jožef Stefan Institute, Slovenia October 7-8, 2010 Presentation Outline

Venture Capital at BDC Nazmin Alani, Managing Director Development Bank Role in Commercializing IP Technology Transfer Conference: Jožef Stefan Institute, Slovenia October 7-8, 2010 Presentation Outline

Innovation and Growth Financing in Europe and Germany

Arno Fuchs, FCF Fox Corporate Finance GmbH Innovation and Growth Financing in Europe and Germany Status Quo: Achievements, Competitive View & Forward Strategy March 22 nd, 218 Development of Venture Capital

Arno Fuchs, FCF Fox Corporate Finance GmbH Innovation and Growth Financing in Europe and Germany Status Quo: Achievements, Competitive View & Forward Strategy March 22 nd, 218 Development of Venture Capital

Quarterly Review of Series A Financings and Series B and Later Round Financings: First Quarter 2011

VENTURE PERSPECTIVES EMERGING ENTERPRISE CENTER AT FOLEY HOAG JUNE Quarterly Review of Series A Financings and Series B and Later Round Financings: First Quarter Activity Level of New England Series A

VENTURE PERSPECTIVES EMERGING ENTERPRISE CENTER AT FOLEY HOAG JUNE Quarterly Review of Series A Financings and Series B and Later Round Financings: First Quarter Activity Level of New England Series A

2017 KLICK HEALTH CONSUMER SURVEY HEALTHCARE INNOVATION KLICK HEALTH CONSUMER SURVEY ON HEALTHCARE INNOVATION

KLICK HEALTH CONSUMER SURVEY ON SURVEY METHODOLOGY: An online omnibus survey was conducted between May 19 and May 21, 2017 through MARU/Matchbox among 1,012 randomly selected American adults who are also

KLICK HEALTH CONSUMER SURVEY ON SURVEY METHODOLOGY: An online omnibus survey was conducted between May 19 and May 21, 2017 through MARU/Matchbox among 1,012 randomly selected American adults who are also

Top 10 Tax Tips You Need to Succeed or The Tax Act is Your Friend. Selected Issues in the Lifecycle of a Tech Company

Selected Issues in the Lifecycle of a Tech Company Warren Nimchuk, Don Furney and Peter van Bodegom March 26, 2002 Vancouver BC You Need to Succeed or The Tax Act is Your Friend Warren Nimchuk and Don

Selected Issues in the Lifecycle of a Tech Company Warren Nimchuk, Don Furney and Peter van Bodegom March 26, 2002 Vancouver BC You Need to Succeed or The Tax Act is Your Friend Warren Nimchuk and Don

CBI - 10th Life Sciences Accounting and Reporting Congress. March 18, 2014

CBI 0th Life Sciences Accounting and Reporting Congress March 8, 204 Introductions Brent Sabatini Director Technical Accounting & Controls Prateep Menon, CFA Principal Life Sciences Advisory Services One

CBI 0th Life Sciences Accounting and Reporting Congress March 8, 204 Introductions Brent Sabatini Director Technical Accounting & Controls Prateep Menon, CFA Principal Life Sciences Advisory Services One

Venture Finance. Ann Tuesday, February 16, 2010

Venture Finance Ann Miura-Ko ann@maplesinvestments.com @annimaniac Agenda What is this thing called Venture Capital? Accounting for Entrepreneurs What is Venture Capital INSTITUTIONAL INVESTORS (Limited

Venture Finance Ann Miura-Ko ann@maplesinvestments.com @annimaniac Agenda What is this thing called Venture Capital? Accounting for Entrepreneurs What is Venture Capital INSTITUTIONAL INVESTORS (Limited