Evolution of MLPs...1. MLP Taxation Issues...2 General Partners...3. Atoms The MLP Marketplace...6

|

|

|

- Collin Mark Phelps

- 6 years ago

- Views:

Transcription

1

2 Evolution of MLPs...1 MLP Taxation Issues...2 General Partners...3 Atoms The MLP Marketplace...6 Investable Market and Benchmarks...8 Historical Performance...9 Inflation Correlation...11 MLP Asset Class Assumptions...12 Next Steps...14 Appendix...15

3 Evolution of MLPs A trivia question sure to stump 99% of the general public is, What does Celtics great Larry Bird and Peanuts legend Snoopy have in common? Answer: They have both been employed by an MLP. The first Master Limited Partnership (MLP) was launched in 1981 to hold oil and gas assets spun out of the Apache Corporation in order to raise capital from smaller investors. The corporate structure experienced rapid growth in the 1980s, including the Boston Celtics in 1986 and Cedar Fair (owners of Knott s Berry Farm) in The diversity of businesses organizing under the MLP structure caused the U.S. Congress to be concerned that corporations would continue to do so to avoid corporate taxation. The 1987 Tax Reform Act limited publicly traded partnerships to real estate, natural resources and dividend and interest income. (In turn, the Celtics lost their status although Cedar Fair remains an MLP today.) The majority of MLPs today are energy-related businesses, with investment firms comprising a much smaller portion of the total universe. Investing in energy MLPs as an asset class has garnered much attention recently. While their risk profile is equity-like, MLPs offer a relatively steady (and high) level of income. However, there are specific risks associated with MLP investing particularly taxation issues that must be understood before investing. In the following research paper, Wilshire Consulting will detail the investment opportunity, highlight historical performance and discuss unique aspects of the asset class. MLP 101 A Master Limited Partnership (MLP) is a public partnership that is traded on a stock exchange. It is a legal structure that combines individual limited partnerships into one large entity to make the ownership interests more marketable, with a general partner operating the business. Ownership of a share of an MLP, called a unit, makes the purchaser a limited partner (LP). This is akin to the ownership of a share of common stock making an investor a company owner (although voting rights are limited within an MLP). Taxation of MLP and common stock earnings, however, is very different. An MLP is a pass-through entity that is taxed at the unit holder level on an individual tax return and generally is not subject to federal or state income tax at the partnership level. This eliminates the double taxation that applies to common stock where the corporation pays taxes on its income and then shareholders also pay on dividends received. Another legal structure that might be found in an MLP portfolio is called a Limited Liability Company (LLC), which is a hybrid between a partnership and a corporation. There are some differences between the two but, for tax purposes, they are similar. Tax issues concerning MLP investments are further complicated for institutional investors by their tax-exempt status, which we will explore in a later section.

4 To qualify for their favorable tax treatment, an MLP must generate 90% of their income from what the IRS terms as qualified sources (generally activities related to natural resources). However, they are not legally required to pass through a certain percentage of their income to unit holders to maintain the tax status. That said they are generally required by their limited partnership agreement to distribute a large percentage of their current operating cash flow on a quarterly basis. A major difference between MLP income and that of stocks and bonds is that an MLP pays a distribution, rather than a dividend, a portion of which may qualify as a return of an investor s capital. The end result is a very different tax liability. Energy MLPs have been garnering interest in the institutional investment arena lately. An energy MLP may engage in any number of activities to abide by IRS requirements exploration, development, production, mining, processing, refining, storage, marketing or transportation. The list of relevant natural resources includes oil and gas, minerals, geothermal energy and timber. This is clearly a broad spectrum of businesses however the majority of energy MLPs engage primarily in the midstream portion of the energy chain i.e. pipelines, storage terminals, gathering, processing. We will see later that pipelines can offer MLPs the best ability to meet the ongoing distributions that have been promised, although it should be noted that MLP businesses have expanded to include the exploration and production of oil and natural gas, coal leasing and mining and shipping. Taxation Issues 1 Tax issues concerning MLP investments are complicated. Although Wilshire is not a tax advisor, the issue needs to be addressed in any MLP primer. To individual or taxable investors, MLPs provide a tax advantaged investment as a significant portion of cash distributions are initially considered a return of capital and, therefore, are tax deferred. However, tax-exempt institutional investors face a complication with MLPs as they may produce Unrelated Business Taxable Income (UBTI). According to the IRS, if an exempt organization regularly carries on a trade or business not substantially related to its exempt purpose the organization is subject to tax on its income from that unrelated trade or business. Further, each of these terms is defined by the IRS. Investing in an MLP means the exempt entity is now a partner engaged in operating a business, and therefore subject to UBTI law. In other words, the organization (pension, endowment) is engaging in an unrelated business (oil transportation, processing, etc.). Through discussions with investment managers, we have learned that their typical public pension plan client considers themselves a sovereignty and therefore not eligible for taxation from the federal government. Corporate plans and endowments, however, 1 The information contained in this paper is not intended as legal, accounting, tax, investment or other professional advice. Prior to any decisions or actions which may affect your personal or business finances, you should consult a qualified professional advisor who understands your particular factual situation.

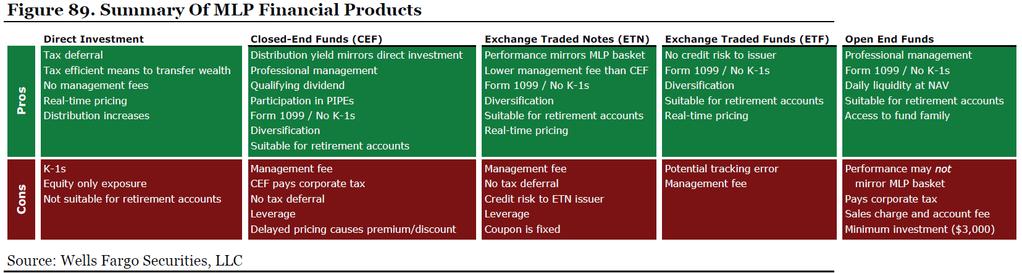

5 cannot make this claim. Additionally, MLP managers can take steps to limit or manage the UBTI by establishing different investment vehicles for holding the assets. The vehicles that are utilized by MLP managers have both pros and cons depending upon the legal structure of the investor. Due to a tax drag effect (or lack thereof) in the varying investment vehicles, a starkly different realized net return could result through time. The primary vehicles used today to implement an MLP allocation are separate account or direct investment, closed-end fund, open-end fund, Exchange Traded Fund (ETF) and Exchange Traded Note (ETN). A separate account is the most tax efficient way to implement the asset class because this structure allows for tax deferral and avoids double taxation. However, an investor would be burdened with K-1s from every investment or even multiple K-1s from varying tax jurisdictions. Closed-end funds have been created to relieve the K-1 tax burden and UBTI. Because the funds are structured as a C-corporation, the fund is obligated to recognize a deferred tax that ultimately reduces the tax benefit provided by the asset class and could result in lower realized cumulative returns. It is important to note that some managers have employed leverage in closed-end funds to counteract the tax drag in the fund. ETFs and open-end funds are similar to closed-end funds in that they minimize the K-1 burden at the cost of an added tax drag to the investment. ETNs carry a unique risk as an investor in an ETN assumes credit risk from the counterparty that sold the note. The decision to implement this asset class can be confusing and the investment vehicle discussion above is just a summary of some of the nuances of each vehicle 2. Ultimately, institutional investors should seek guidance from tax advisors and decide for themselves whether they can manage any tax exposure. General Partners The General Partner (GP) of an MLP is the operating business partner. The MLP has a legal document that defines the rights of the GP and LP. This document is referred to as the Partnership Agreement (PA). Historically, the PA has not granted much power to the LP to exercise influence relative to common equity at public corporations. The PA also sets the Incentive Distribution Rights (IDRs) granted to the GP. An IDR gives the GP a disproportionate share of the incremental cash flow relative to the equity ownership structure. A GP typically owns around 2% of the partnership equity but at the high split 2 A table with more detail has been added to the appendix, which was produced in a Wells Fargo piece. A link to the full report is

6 level a GP could receive 50% of the incremental cash flow. An IDR is meant to incentivize the GP to raise the quarterly cash distribution by improving profits. The specific arrangement is important as LPs need to understand that they will begin to receive a smaller portion of the incremental cash distribution, limiting the upside and decreasing the rate of improvement in yield. Some MLP companies actually package GP interest in a separate MLP and offer them for purchase on the open market, giving investors the opportunity to effectively become a GP without of course having to go to work in the morning. The more recent trend in MLPs has been to focus on growing operations but an IDR can increase the cost of equity and render the MLP less competitive to an MLP with a lower IDR. Therefore, the industry trend has been to cut IDRs or even collapse the GP and MLP into one structure. There are only a few MLPs left that are stuck at the high split level. In addition to the IDRs, there are a couple other idiosyncrasies of the MLP structure that could open the door for conflicts of interest such as related party transactions, high defense take mechanisms and vulnerability of MLP assets to a GP bankruptcy. The main point is that not all MLPs are created equal and that investors need to be diligent in their research of the securities that they buy. We will now take a step back and discuss the energy sector, in general, to provide some important context on how it operates and the layout of its various businesses. Atoms 101 Before discussing energy investments of today, we will briefly discuss atomic events of yesterday actually, a little further back. Millions of years ago, the remains of plants and animals decayed and built into thick layers. This matter was, in time, covered by layers of sand and silt, which eventually hardened into rock. Pressure and heat changed some of these remains into coal, some into oil (petroleum) and some into natural gas. Today, drilling through these layers of sand, silt and rock in the right locations brings deposits of oil and/or gas. These natural resources then need to be transported and refined before they can be used. Exhibit 1 highlights the general transmission and processing of natural gas, specifically. However, once familiar with industry terms, the handling of oil can easily be understood.

7 Exhibit 1 Natural Gas Roadmap Source: U.S. EPA Natural Gas STAR Program The Upstream activities of the energy sector involve drilling and operating wells. Gathering refers to collection and transportation from wells in typically smaller, shorter pipelines to larger trunk pipelines and eventually refineries and processing facilities. Midstream activities, the primary focus of MLP companies, involve separation and processing and then either storage or transmission to the Downstream, end-users. Processing of natural gas consists of separating and cleaning the raw material into methane, the main ingredient of the natural gas that is utilized Downstream, and byproducts such as butane, ethane and propane (often called natural gas liquids, NGL). There are two important differences between natural gas and petroleum systems with respect to MLPs. Crude oil, too, needs to be refined and separated into different types of fuel such as gasoline or jet fuel. However, there is very little exposure to oil refineries within the MLP market. In fact, there are relatively few publicly held refineries in the U.S. and they pay little in terms of current yield, particularly versus the average MLP. Second, refined oil products can be delivered in a variety of ways trucking, railroad although pipelines are the most efficient while transmission lines are the only way to transport natural gas.

8 The MLP Marketplace Now that we have discussed the energy delivery process and industry jargon, we will present the composition of the MLP investment opportunity. Wilshire finds that there were nearly 70 MLPs in the Wilshire 5000 Total Market Index SM (full float) as of the year-end 2010, mostly in the Pipeline sector. 3 The total market capitalization of these companies at year-end was $218 billion. The REIT market can be used as a point of reference for these statistics as the asset class is well established within the institutional investment community. Again as of year-end, the Wilshire U.S. REIT Index SM consisted of just fewer than 100 names with a total market capitalization of $323 billion. While the MLP market is just two-thirds the size of the REIT market, it is still large enough to be considered by many institutional investors. Exhibit 2 contains a summary of the sector allocation, or business focus, for the identified MLPs within the broad market index. Exhibit 2 MLP Universe Business Focus Exploration & Production 5.4% Propane 5.1% Coal 5.6% Shipping Other 2.2% 2.5% Petroleum Transportation 27.3% Gathering & Processing 14.5% Source: Wilshire Atlas SM, Wilshire Consulting Natural Gas Pipelines 37.4% The majority of a market-weighted allocation to MLPs would be to the most stable Midstream activities oil and natural gas pipelines. However, the MLP landscape has broadened through the years to include companies with a focus on propane, coal and maritime shipping. We will review the major segments and their business risks, starting Upstream and working towards finished products delivery. It should be noted that a 3 Although MLPs are represented in the full cap version of the Wilshire 5000 Total Market Index, they are not included in the free float-adjusted version due to tax complications and a lack on meaningful inclusion in active portfolios by investment managers.

9 majority of MLPs deal in more than one market segment. Throughout this paper we will categorize companies based on their largest business exposure. Exploration and Production (E&P) companies are firmly in the Upstream and have the greatest commodity price exposure, by far, of all the MLPs. Companies within this segment acquire and develop oil and gas properties and their assets can include both producing and non-producing reserves. However, under proper management, these companies should contribute to a broad MLP portfolio as the current yields on E&P MLPs within the Wilshire 5000 are higher than the average for the total MLP market. There are a handful of Coal MLPs that are also natural resource producers and therefore are exposed to changing prices. More specifically, electricity demand is the major factor on price as electric utility companies are the primary consumers of coal. Propane MLPs market and distribute a post-processing product so that their main risk is changing demand due to high prices and alternative heating sources. Such businesses are not directly exposed to commodity prices as they operate on a cost plus fixed margin pricing structure. We touched on the function of Gathering and Processing (G&P) companies in the last section. Also mentioned was the lack of much oil refinery business within the MLP market so that nearly everything in G&P is natural gas based. Profits from a gathering pipeline are typically fee-based (per unit of natural gas gathered), although some natural gas gatherers operate on a percentage basis that would expose the business to fluctuating prices. Gathering pipelines, in general, are somewhat commodity sensitive as changes in the price of a natural resource can affect producer or refiner activity in other words, both sides of a gathering pipeline. Cash flow from a gathering business can also be affected by the depletion of existing wells and the need to connect to new wells. Processing contracts for natural gas vary widely and can result in various degrees of commodity price sensitivity. Capital expenditures for processing companies are expected to be higher than pipeline MLPs as they employ less long-lived assets. While gathering pipelines collect and transport raw gas from producing wells, the Natural Gas Pipelines MLP segment refers to transmission lines that receive natural gas from gathering systems (if it does not need to be processed) and other sources and delivers it to Downstream end-users or storage facilities. Pipelines can move gas within a state (intrastate) or among multiple states (interstate). Revenues from a transmission pipeline are typically very stable due to a number of reasons. Pipeline operators charge a tariff on capacity rather than volume, generally reserved with shippers using long-term contracts and are government regulated. The Federal Energy Regulatory Commission (FERC) regulates interstate pipelines and establishes well defined maximum tariffs. Intrastate pipelines share many of the same business conditions except that they are regulated by the state in which they operate. The Petroleum Transportation segment includes both gathering and transmission lines that transport crude oil and the resulting refined products. Crude oil is found in varying

10 degrees of sulfur content (sweet to sour) and viscosity (light to heavy) and refineries differ in their ability to process it so that pipelines play an important role in properly allocating the raw material. Pipeline operators generally charge a fixed-fee per barrel so that they are not exposed to regular and volatile changes in oil prices although a prolonged rise in crude could lead to less oil consumption. Like with natural gas, interstate crude oil pipeline operators are regulated by the FERC, which allows the companies to adjust their tariffs based on a Producer Price Index-plus rate of change. Investable Market and Benchmarks In the previous section, we outlined the MLP market in terms of total market capitalization. Like any publicly traded security, every share outstanding is not necessarily in the hands of public investors, some shares may be owned by the company itself. We can look to MLP indices to get a sense of the capitalization available for purchase and the relevant market segment allocation. There are two major MLP indices the Alerian MLP Index and S&P MLP Index. The Alerian index is a composite of 50 (by definition) energy MLPs with an inception date of December 29, The S&P index includes data beginning in July 2001 and contained 40 companies as of year-end Currently, Alerian is the more inclusive index by not just number of names but also their target market capitalization minimum inclusion requirement is $250 million versus $300 million for the S&P index and their minimum volume requirement is lower. Despite different construction methodologies, the market exposure of the two indices is similar. The adjusted, publicly available market capitalization of the Alerian index was $139 billion at year-end while the S&P index equaled $125 billion. (By comparison, the available (i.e. float-adjusted) capitalization of the Wilshire U.S. REIT Index was $302 billion.) Each index contains eight of the same MLPs in their ten largest names, which then comprise more than 50% of each index (51% for Alerian, 57% for S&P). Further, the Alerian top ten equals 58% of the index and the S&P top ten equals a 63% allocation with the two largest MLPs comprising more than 25% of each index. These statistics highlight the fact that there is meaningful name concentration within the MLP asset class in addition to the obvious Energy sector concentration. Exhibit 3 contains the segment allocation by available market capitalization for each index at year-end using the same definitions described in the previous section.

11 Exhibit 3 MLP Index Exposures Natural Gas Pipelines 32.9% Alerian Gathering & Processing 11.2% Natural Gas Pipelines 32.4% S&P Gathering & Processing 9.7% Petroleum Transportation 37.1% Source: Wilshire Atlas, Wilshire Consulting Coal 3.7% Shipping 2.0% Exploration & Production 6.8% Propane 6.3% Petroleum Transportation 43.2% Exploration & Production 3.0% Propane 6.6% Coal 3.4% Shipping 1.6% Again, both benchmarks are similar in construction although the S&P index includes less of the Upstream activities exploration and production and, to some extent, gathering and processing. Given Alerian s more inclusive methodology and its longer history we will use their index in the next section to study the historical performance of the MLP asset class versus other investment opportunities. Historical Performance From a yield perspective, MLPs have trended with other comparable, high yielding asset classes namely REITs and high yield bonds. In Exhibit 4, we can see that MLP yields, in general, have been coming down for the last 15 years, from near 9% to around 6%.

12 Rolling 3-Year Total Return Yield 25.0% Exhibit 4 Yield Environment 20.0% 15.0% 10.0% 5.0% 0.0% Source: Wilshire Compass Yields on MLPs have been consistently between the yields of REIT equities and high yield bonds. Further, yields from the MLP market have been more consistent, less volatile, than the other two asset classes although all yields did spike during the credit crisis. The total return on MLPs also has been strong since their inception, typically outperforming other like asset classes. Additionally, as we will discuss in a later section, yield is a major driver of forward-looking, expected returns for MLPs. Exhibit 5 shows a rolling three-year total return for the three asset classes from the previous exhibit plus commodities % MLP REIT High Yield Exhibit 5 Rolling 3-Year Total Return 30.00% 20.00% 10.00% 0.00% % % % % Source: Wilshire Compass MLP REIT High Yield Commodities

13 Perhaps most interesting from the above exhibit is how well MLPs did during the credit crisis, in a relative sense. Although prices fell, MLPs performed much better than the other asset classes and rebounded the strongest. Finally, the correlation statistics in Exhibit 6, generated from quarterly total returns, show that there is a potential diversification benefit from investing in MLPs. Exhibit 6 Historical Risk & Correlation December, 1995 to June, 2011 MLP US Equity REIT High Yield Utilities Commodities US CPI Risk 16.0% 18.6% 23.2% 10.7% 18.9% 18.0% 1.9% Correlation MLP 1.00 US Equity REIT High Yield Utilities Commodities US CPI (0.06) Source: Wilshire Compass There are a few statistics from above that are worth highlighting. The correlation between MLPs and U.S. Equity (typically the largest asset class held in a balanced portfolio) of 0.33 is relatively low. Although MLPs operate mainly within the Energy sector, there appears to be some diversification benefit versus a commodities portfolio as suggested by the 0.42 correlation. The correlation of 0.27 versus inflation is a complicated observation. Looking at other asset classes versus inflation, the REIT and high yield bond results over this discrete period of time are much higher (and positive) than Wilshire s current assumptions, which can be found in the appendix. Also, the realized correlation for commodities of 0.53 is more than double our assumption of 0.20 between inflation and commodities. We will discuss further an MLP portfolio s sensitivity to inflation in the next section. Inflation Correlation There are very few asset classes that maintain their value, or hedge, against inflation spikes 4. Wilshire expects that MLPs will be one of those investments but not to the degree that the full historical data suggests (0.28). The correlation of a number of asset classes versus inflation has jumped recently in part due to the increased volatility of inflation itself. Exhibit 7 contains rolling correlations during the history of the Alerian MLP Index and a longer look at the relationship between high yield and inflation. 4 For additional research on inflation and implications for investing, please see Wilshire s Inflation Indepth: The In-s and De-s of Price Movements (2010).

14 Rolling 3-Year Correlation to Inflation Rolling 3-Year Correlation to Inflation Exhibit 7 Correlation to Inflation (0.20) (0.40) (0.60) (0.80) (1.00) (0.20) (0.40) (0.60) (0.80) (1.00) MLP REIT High Yield Commodities Source: Wilshire Compass High Yield The longer history of the high yield correlation is much more in line with Wilshire s assumption (-0.08) than if we would look at the more recent period. Also in Exhibit 7 we can see that all four asset classes experienced spikes in correlation near the end of Finally, we can observe that the MLP correlation is typically lower than that for commodities. Therefore, it is our belief that there will be some positive relationship between MLPs and inflation but that it will be quite moderate, and likely below our commodity to inflation correlation of This relationship is supported by the dynamics of the MLP asset class. The largest segment, oil and natural gas pipelines, are regulated by FERC which allows operators to increase tariffs annually by an indexed rate, currently equal to the Producer Price Index (PPI) + 1.3%. While PPI and the Consumer Price Index (CPI) do trend together, PPI is more volatile although typically runs at a lower rate than CPI. Therefore, changes in CPI should find their way into MLP revenues although there is enough noise to mute the final correlation statistic. As with all asset classes, the observed correlations of MLPs will vary as economic regimes change. For example, higher energy prices should increase the supply of oil and natural gas, driving up demand for the Midstream businesses that dominate the MLP asset class. However, a sustained decline in economic development would have the opposite effect. MLP Asset Class Assumptions Wilshire maintains assumptions for a number of asset classes that are comprised of forward-looking return forecasts and historically supported risk estimations. As MLPs are prominently a yield-returning asset class, we will look to both the current yield and potential for yield increases in the future to formulate a return assumption. Our starting

15 point is the 12-month trailing average yield for an MLP benchmark 5, which is similar to Wilshire's methodology for REITS, another yield-based asset class. Our forecast for the growth in distributions is based on the regulated tariff increase allowance of the two largest segments of the MLP asset class natural gas pipelines and petroleum transportation currently PPI + 1.3%. While Wilshire does not forecast PPI, we do forecast the broader measure of inflation, CPI (currently 2.25%). As more than 50 years of data suggests that PPI runs at about 85% of CPI, we adjust our inflation forecast accordingly. Additionally, we do not assume that a full 1.3% premium will flow through to income for two reasons. First, the 1.3% is a maximum with no guarantees that operators will be successful in consistently achieving that level. Second, MLPs, in general, have significant discretion as to what they determine is available cash and may reinvest some of that premium back into the business. Therefore, we assume that future distributions will increase by one-half of the maximum regulated premium, which we believe is a conservative approach. Exhibit 8 walks through the basic calculation for Wilshire s current MLP return assumption and highlights the importance of the goingin yield as the major driver of our forecast. Exhibit 8 Wilshire MLP Return Assumption Methodology Date Yield Jan % 12-Month Average Yield 6.8% Feb % Mar % Inflation Assumption 2.3% Apr % Adjusted for PPI (85%) 1.9% May % Jun % FERC Regulated Increase 1.3% Jul % One-half of increase 0.7% Aug % Sep % Oct % Return Assumption Nov % Avg Yield + PPI + Premium 9.4% Dec % (6.8%) + (1.9%) + (0.7%) We round the above assumption to 9.50% in keeping with our standard methodology. Another standard practice for Wilshire is to look to rolling 10-year data for our risk and correlation statistics. For MLPs, the data is somewhat limited as the Alerian index has an inception of The observed risk on the index has moved during that time between 13% and 18%, increasing through time. Our analysis currently suggests an assumed risk on the asset class of 17%. Wilshire regularly revisits our risk and correlation assumptions and will continue to do so as more MLP data becomes available. Assumed correlation statistics for MLPs versus other asset classes have been included in the appendix. 5 Wilshire's MLP assumptions methodology utilizes the Alerian MLP index as the asset class benchmark.

16 Next Steps From a return/risk perspective, the MLP asset class is very attractive. However, the asset class is still relatively new in the institutional marketplace and warrants a cautious approach. The size of the investment opportunity is small with a total market capitalization smaller than any of the top ten largest U.S. companies the name and sector concentration is considerable and the tax issues are complicated. For those investors that decide to include MLPs within their portfolio, the next discussion worth having is how to implement them within a broad portfolio. Given their limited market capitalization and economic exposures, considering them as part of an overall allocation to real assets is a reasonable first step. As the MLP marketplace continues to develop, Wilshire will monitor their progression in order to better understand this unique investment opportunity.

17 Wilshire 2011 Return, Risk & Correlation Matrix Equity Fixed Income Real Assets Dev Glbl LT ex-us Real Estate US ex-us Emg ex-us Glbl Prvt Core Core LT High Bond US Glbl US Stock Stock Stock Stock Stock Mkts Cash Bond Bond Treas TIPS Yield (Hdg) RES RES Cmdty MLP CPI Expected Return (%) Expected Risk (%) Correlations: US Stock 1.00 Dev ex-us Stock (USD) Emerging Mkt Stock Global ex-us Stock Global Stock Private Markets Cash Equivalents Core Bond LT Core Bond LT Treasury TIPS High Yield Bond Non-US Bond (Hdg) US RE Securities Global RE Securities Commodities MLP Inflation (CPI)

18

19

Asset Class Review APR. 24, Master Limited Partnerships

APR. 24, 2013 INVESTOR EDUCATION GLOBAL INVESTMENT COMMITTEE Asset Class Review OVERVIEW AUTHOR Master Limited Partnerships DESCRIPTION. Master limited partnerships (MLPs) operate physical assets such

APR. 24, 2013 INVESTOR EDUCATION GLOBAL INVESTMENT COMMITTEE Asset Class Review OVERVIEW AUTHOR Master Limited Partnerships DESCRIPTION. Master limited partnerships (MLPs) operate physical assets such

Master Limited Partnership (MLP) Overview

Overview") Master Limited Partnership (MLP) Overview ENERGY SECTOR REPORT 17 October 2017 ANALYST(S) Andy Pusateri, CFA This publication is for informational purposes only. While Edward Jones' Research Department

Master Limited Partnership (MLP) Overview ENERGY SECTOR REPORT 17 October 2017 ANALYST(S) Andy Pusateri, CFA This publication is for informational purposes only. While Edward Jones' Research Department

MASTER LIMITED PARTNERSHIP PRIMER MLP 101

MASTER LIMITED PARTNERSHIP PRIMER MLP 101 THIRD QUARTER 2009 This presentation is for information purposes only. It is not an offer of, or a solicitation for, the sale of any security, product or service.

MASTER LIMITED PARTNERSHIP PRIMER MLP 101 THIRD QUARTER 2009 This presentation is for information purposes only. It is not an offer of, or a solicitation for, the sale of any security, product or service.

MASTER LIMITED PARTNERSHIPS (MLPS)

") ABSTRACT MLPs are publicly listed partnerships that invest primarily in the energy sector. The market has grown substantially in the past several years and is expected to continue to grow as the U.S. energy

ABSTRACT MLPs are publicly listed partnerships that invest primarily in the energy sector. The market has grown substantially in the past several years and is expected to continue to grow as the U.S. energy

MLP Market Overview. Emily Hsieh, Director of Operations. Tulsa MLP Conference

MLP Market Overview Emily Hsieh, Director of Operations Tulsa MLP Conference 1 About Alerian 2 About Alerian Real-time MLP Index MLP ETN $14 billion in index-linked products MLP ETF 85% market share for

MLP Market Overview Emily Hsieh, Director of Operations Tulsa MLP Conference 1 About Alerian 2 About Alerian Real-time MLP Index MLP ETN $14 billion in index-linked products MLP ETF 85% market share for

Cushing 30 MLP Index (TICKER: MLPX)

") Cushing 30 MLP Index (TICKER: MLPX) INDEX METHODOLODGY GUIDE Version: Original Document Final v1 November 2009 Swank Energy Income Advisors, LP 3300 Oak Lawn Avenue Suite 650 Dallas, Texas 75219 www.cushingmlpindex.com

Cushing 30 MLP Index (TICKER: MLPX) INDEX METHODOLODGY GUIDE Version: Original Document Final v1 November 2009 Swank Energy Income Advisors, LP 3300 Oak Lawn Avenue Suite 650 Dallas, Texas 75219 www.cushingmlpindex.com

Passive Opportunities for Master Limited Partnerships (MLP) Investors: The Morningstar MLP Index Family

Investors: The Morningstar MLP Index Family") Passive Opportunities for Master Limited Partnerships (MLP) Investors: The Morningstar MLP Index Family By Jason Stevens, Director of Energy Equity Research Morningstar Research Paper April 2013 Introduction

Passive Opportunities for Master Limited Partnerships (MLP) Investors: The Morningstar MLP Index Family By Jason Stevens, Director of Energy Equity Research Morningstar Research Paper April 2013 Introduction

Master Limited Partnerships 101:

Master Limited Partnerships 101: Presentation to the American Association of Individual Investors Silicon Valley Chapter April 16, 2011 2010 National Association of Publicly Traded Partnerships 1 Master

Master Limited Partnerships 101: Presentation to the American Association of Individual Investors Silicon Valley Chapter April 16, 2011 2010 National Association of Publicly Traded Partnerships 1 Master

ASSET ALLOCATION REPORT

2018 ASSET ALLOCATION REPORT INTRODUCTION We invite you to review Omnia Family Wealth s 2018 report on expected asset class returns for the next 10 years. While we believe these forecasts reflect a reasonable

2018 ASSET ALLOCATION REPORT INTRODUCTION We invite you to review Omnia Family Wealth s 2018 report on expected asset class returns for the next 10 years. While we believe these forecasts reflect a reasonable

Finding Income with MLPs

Finding Income with MLPs Webinar November 1, 2016 Disclosures (1/2) Investing involves risk, including the possible loss of principal. International investments may involve risk of capital loss from unfavorable

Finding Income with MLPs Webinar November 1, 2016 Disclosures (1/2) Investing involves risk, including the possible loss of principal. International investments may involve risk of capital loss from unfavorable

The Case for Midstream Energy Equities

INSIGHTS The Case for Midstream Energy Equities May 2018 203.621.1700 2018, Rocaton Investment Advisors, LLC EXECUTIVE SUMMARY Midstream energy equities, including Master Limited Partnership ( MLPs ),

INSIGHTS The Case for Midstream Energy Equities May 2018 203.621.1700 2018, Rocaton Investment Advisors, LLC EXECUTIVE SUMMARY Midstream energy equities, including Master Limited Partnership ( MLPs ),

MLP Investing: Weighing The Costs And Benefits Of MLP Investment Options. January Curt Pabst, Managing Director, Eagle Global Advisors

January 2011 MLP Investing: Weighing The Costs And Benefits Of MLP Investment Options Curt Pabst, Managing Director, Eagle Global Advisors Master Limited Partnerships (MLPs) have materially outperformed

January 2011 MLP Investing: Weighing The Costs And Benefits Of MLP Investment Options Curt Pabst, Managing Director, Eagle Global Advisors Master Limited Partnerships (MLPs) have materially outperformed

Q Energy Infrastructure & MLP Strategy

Q4 2015 Energy Infrastructure & MLP Strategy 1360 East Ninth Street, Suite 1100 Cleveland, Ohio 44114 MAI Capital Management Overview MAI s heritage dates back to 1973 Privately held, independent SEC registered

Q4 2015 Energy Infrastructure & MLP Strategy 1360 East Ninth Street, Suite 1100 Cleveland, Ohio 44114 MAI Capital Management Overview MAI s heritage dates back to 1973 Privately held, independent SEC registered

Master Limited Partnerships (MLPs) Demystified June 2014

Demystified June 2014") Master Limited Partnerships (MLPs) Demystified June 2014 Brett Bennett, CFA Senior Vice President, Senior Investment Analyst Many investors are seeking additional strategies to help improve portfolio diversification

Master Limited Partnerships (MLPs) Demystified June 2014 Brett Bennett, CFA Senior Vice President, Senior Investment Analyst Many investors are seeking additional strategies to help improve portfolio diversification

CENTER COAST MLP FOCUS FUND

CENTER COAST MLP FOCUS FUND MLP Investing and MLP Concentrated Mutual Funds We are pleased to provide you with the following information pertaining to master limited partnership ( MLP ) investing. MLPs

CENTER COAST MLP FOCUS FUND MLP Investing and MLP Concentrated Mutual Funds We are pleased to provide you with the following information pertaining to master limited partnership ( MLP ) investing. MLPs

GOLDMAN SACHS TRUST. Goldman Sachs MLP Energy Infrastructure Fund Goldman Sachs MLP & Energy Fund

GOLDMAN SACHS TRUST Goldman Sachs MLP Energy Infrastructure Fund Goldman Sachs MLP & Energy Fund Supplement dated March 30, 2018 to the Summary Prospectuses, Statutory Prospectus and Statement of Additional

GOLDMAN SACHS TRUST Goldman Sachs MLP Energy Infrastructure Fund Goldman Sachs MLP & Energy Fund Supplement dated March 30, 2018 to the Summary Prospectuses, Statutory Prospectus and Statement of Additional

Deutsche Global Infrastructure Fund (TOLLX)

") Global Infrastructure Fund (TOLLX) A step beyond MLPs Important risk information Any fund that concentrates in a particular segment of the market will generally be more volatile than a fund that invests

Global Infrastructure Fund (TOLLX) A step beyond MLPs Important risk information Any fund that concentrates in a particular segment of the market will generally be more volatile than a fund that invests

GPs vs MLPs AN OVERVIEW OF THE GENERAL PARTNERS OF MASTER LIMITED PARTNERSHIPS

AN OVERVIEW OF THE GENERAL PARTNERS OF MASTER LIMITED PARTNERSHIPS MLPs AND GPs Master Limited Partnerships, or MLPs, are tax pass-through entities that derive 90 percent of their income from the exploration,

AN OVERVIEW OF THE GENERAL PARTNERS OF MASTER LIMITED PARTNERSHIPS MLPs AND GPs Master Limited Partnerships, or MLPs, are tax pass-through entities that derive 90 percent of their income from the exploration,

Master Limited Partnerships

Frank Benham, CAIA Managing Principal Director of Research, Christopher P. Tehranian Principal Head of Infrastructure Research, Edmund A. Walsh Vice President, Steven Hartt, CAIA Principal, 45 Description

Frank Benham, CAIA Managing Principal Director of Research, Christopher P. Tehranian Principal Head of Infrastructure Research, Edmund A. Walsh Vice President, Steven Hartt, CAIA Principal, 45 Description

Evolution of midstream energy

Evolution of midstream energy As we look at the changing landscape for midstream energy, we continue to see companies simplifying their structure by either eliminating incentive distribution rights (IDRs)

Evolution of midstream energy As we look at the changing landscape for midstream energy, we continue to see companies simplifying their structure by either eliminating incentive distribution rights (IDRs)

Tortoise Talk. Energy update

Tortoise Talk Energy update First quarter 2018 Tortoise Talk First Quarter 2018 The broad energy market had a volatile start to the year with strong performance in January that turned sharply negative

Tortoise Talk Energy update First quarter 2018 Tortoise Talk First Quarter 2018 The broad energy market had a volatile start to the year with strong performance in January that turned sharply negative

MLP INVESTMENT REVIEW & OUTLOOK (March 31, 2018)

") () Three Months Ended 3/31/18 Total Returns Alerian Total Return Index -11.12% Ten Year US Treasury Yield* 2.74% Alerian Total Return Index Yield* 8.80% Spread versus Ten Year Treasury* 6.06% *Quarter

() Three Months Ended 3/31/18 Total Returns Alerian Total Return Index -11.12% Ten Year US Treasury Yield* 2.74% Alerian Total Return Index Yield* 8.80% Spread versus Ten Year Treasury* 6.06% *Quarter

NuStar Energy, L.P. NEUTRAL ZACKS CONSENSUS ESTIMATES (NS-NYSE) SUMMARY

SUMMARY") March 13, 2015 NuStar Energy, L.P. Current Recommendation Prior Recommendation Underperform Date of Last Change 09/26/2013 Current Price (03/12/15) $60.71 Target Price $63.00 NEUTRAL SUMMARY (NS-NYSE)

March 13, 2015 NuStar Energy, L.P. Current Recommendation Prior Recommendation Underperform Date of Last Change 09/26/2013 Current Price (03/12/15) $60.71 Target Price $63.00 NEUTRAL SUMMARY (NS-NYSE)

The Cushing Royalty & Income Fund

Base Prospectus $300,000,000 The Cushing Royalty & Income Fund Common Shares Preferred Shares Debt Securities Subscription Rights for Common Shares and/or Preferred Shares Investment Objective. The Cushing

Base Prospectus $300,000,000 The Cushing Royalty & Income Fund Common Shares Preferred Shares Debt Securities Subscription Rights for Common Shares and/or Preferred Shares Investment Objective. The Cushing

BROAD COMMODITY INDEX

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS AUGUST 2018 120.00% 100.00% 80.00% 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) -80.00% ABCERI S&P

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS AUGUST 2018 120.00% 100.00% 80.00% 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) -80.00% ABCERI S&P

DESIGNED FOR TODAY S AND TOMORROW S INVESTMENT CHALLENGES

DESIGNED FOR TODAY S AND TOMORROW S INVESTMENT CHALLENGES PRUDENTIAL REAL ASSETS FUND EFFECTIVE JUNE 11, 2018, THE FUND S NEW NAME WILL BE PGIM REAL ASSETS FUND. FUND SYMBOLS WILL NOT CHANGE. Potential

DESIGNED FOR TODAY S AND TOMORROW S INVESTMENT CHALLENGES PRUDENTIAL REAL ASSETS FUND EFFECTIVE JUNE 11, 2018, THE FUND S NEW NAME WILL BE PGIM REAL ASSETS FUND. FUND SYMBOLS WILL NOT CHANGE. Potential

Latin American E&P Outlook

Latin American E&P Outlook Society of Petroleum Engineers April 20, 2017 www.stratasadvisors.com UPSTREAM MIDSTREAM DOWNSTREAM FUEL & TRANSPORT Who We Are Stratas Advisors is a global consulting and advisory

Latin American E&P Outlook Society of Petroleum Engineers April 20, 2017 www.stratasadvisors.com UPSTREAM MIDSTREAM DOWNSTREAM FUEL & TRANSPORT Who We Are Stratas Advisors is a global consulting and advisory

233 S. Detroit Ave., Suite 100 (918)

") 233 S. Detroit Ave., Suite 100 Tulsa Oklahoma 74120 Tulsa, (918) 582 6864 Pinnacle s Investment Expertise One of the first private funds of Publicly Traded Master Limited Partnerships in the U.S. Investing

233 S. Detroit Ave., Suite 100 Tulsa Oklahoma 74120 Tulsa, (918) 582 6864 Pinnacle s Investment Expertise One of the first private funds of Publicly Traded Master Limited Partnerships in the U.S. Investing

Master Limited Partnerships Solid, Stable Growth

2012 Master Limited Partnerships Solid, Stable Growth Offices: New York: 520 Madison Avenue 26 th Floor New York, NY 10022 212-396-5900 Palm Beach: 324 Royal Palm Way Suite 226 Palm Beach, FL 33480 561-833-6789

2012 Master Limited Partnerships Solid, Stable Growth Offices: New York: 520 Madison Avenue 26 th Floor New York, NY 10022 212-396-5900 Palm Beach: 324 Royal Palm Way Suite 226 Palm Beach, FL 33480 561-833-6789

July J.P. Morgan Structured Investments. The J.P. Morgan Efficiente Plus 5 Index (Net ER) Strategy Guide

Strategy Guide") July 2017 J.P. Morgan Structured Investments The J.P. Morgan Efficiente Plus 5 Index (Net ER) Strategy Guide Important Information The information contained in this document is for discussion purposes

July 2017 J.P. Morgan Structured Investments The J.P. Morgan Efficiente Plus 5 Index (Net ER) Strategy Guide Important Information The information contained in this document is for discussion purposes

NAPTP Annual MLP Investor Conference NASDAQ: CPNO. May 12, 2010

NAPTP Annual MLP Investor Conference NASDAQ: CPNO May 12, 2010 Disclaimer Statements made by representatives of Copano Energy, L.L.C. ( Copano ) during this presentation will include forward-looking statements,

NAPTP Annual MLP Investor Conference NASDAQ: CPNO May 12, 2010 Disclaimer Statements made by representatives of Copano Energy, L.L.C. ( Copano ) during this presentation will include forward-looking statements,

BP Capital TwinLine Energy Fund Class A Ticker: BPEAX Class I Ticker: BPEIX. Summary Prospectus March 30, 2018

BP Capital TwinLine Energy Fund Class A Ticker: BPEAX Class I Ticker: BPEIX Summary Prospectus March 30, 2018 Before you invest, you may want to review the Fund s prospectus, which contains more information

BP Capital TwinLine Energy Fund Class A Ticker: BPEAX Class I Ticker: BPEIX Summary Prospectus March 30, 2018 Before you invest, you may want to review the Fund s prospectus, which contains more information

Aspiriant Risk-Managed Equity Allocation Fund RMEAX Q4 2018

Aspiriant Risk-Managed Equity Allocation Fund Q4 2018 Investment Objective Description The Aspiriant Risk-Managed Equity Allocation Fund ( or the Fund ) seeks to achieve long-term capital appreciation

Aspiriant Risk-Managed Equity Allocation Fund Q4 2018 Investment Objective Description The Aspiriant Risk-Managed Equity Allocation Fund ( or the Fund ) seeks to achieve long-term capital appreciation

COHEN & STEERS MLP INCOME AND ENERGY OPPORTUNITY FUND, INC. 280 PARK AVENUE NEW YORK, NEW YORK (800) STATEMENT OF ADDITIONAL

STATEMENT OF ADDITIONAL") COHEN & STEERS MLP INCOME AND ENERGY OPPORTUNITY FUND, INC. 280 PARK AVENUE NEW YORK, NEW YORK 10017 (800) 330-7348 STATEMENT OF ADDITIONAL INFORMATION, DATED MARCH 25, 2013 THIS STATEMENT OF ADDITIONAL

COHEN & STEERS MLP INCOME AND ENERGY OPPORTUNITY FUND, INC. 280 PARK AVENUE NEW YORK, NEW YORK 10017 (800) 330-7348 STATEMENT OF ADDITIONAL INFORMATION, DATED MARCH 25, 2013 THIS STATEMENT OF ADDITIONAL

IPAA Private Capital Conference. Peter Bowden January 21, 2014

IPAA Private Capital Conference Peter Bowden January 21, 2014 Historical MLP Capital Raising Activity ($ in Billions) Since 2010, there has been significant growth in institutional demand for debt and

IPAA Private Capital Conference Peter Bowden January 21, 2014 Historical MLP Capital Raising Activity ($ in Billions) Since 2010, there has been significant growth in institutional demand for debt and

MICHIGAN CRUDE OIL PRODUCTION: ALTERNATIVES TO ENBRIDGE LINE 5 FOR

MICHIGAN CRUDE OIL PRODUCTION: ALTERNATIVES TO ENBRIDGE LINE 5 FOR TRANSPORTATION Prepared for National Wildlife Federation By London Economics International LLC 717 Atlantic Ave, Suite 1A Boston, MA,

MICHIGAN CRUDE OIL PRODUCTION: ALTERNATIVES TO ENBRIDGE LINE 5 FOR TRANSPORTATION Prepared for National Wildlife Federation By London Economics International LLC 717 Atlantic Ave, Suite 1A Boston, MA,

MANAGED FUTURES INDEX

MANAGED FUTURES INDEX COMMENTARY + STRATEGY FACTS JULY 2017 CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 120.00% 100.00% 80.00% 60.00% 40.00% 20.00% 0.00% AMFERI BARCLAY BTOP50 CTA INDEX S&P 500 S&P

MANAGED FUTURES INDEX COMMENTARY + STRATEGY FACTS JULY 2017 CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 120.00% 100.00% 80.00% 60.00% 40.00% 20.00% 0.00% AMFERI BARCLAY BTOP50 CTA INDEX S&P 500 S&P

BROAD COMMODITY INDEX

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS JULY 2018 100.00% 80.00% 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) -80.00% ABCERI S&P GSCI ER BCOMM

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS JULY 2018 100.00% 80.00% 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) -80.00% ABCERI S&P GSCI ER BCOMM

TransMontaigne Partners L.P. (NYSE TLP) Wells Fargo th Annual Energy Symposium December 10 th, 2013

Wells Fargo th Annual Energy Symposium December 10 th, 2013") TransMontaigne Partners L.P. (NYSE TLP) Wells Fargo 2013 12 th Annual Energy Symposium December 10 th, 2013 Forward Looking Statements All statements, other than statements of historical facts, contained

TransMontaigne Partners L.P. (NYSE TLP) Wells Fargo 2013 12 th Annual Energy Symposium December 10 th, 2013 Forward Looking Statements All statements, other than statements of historical facts, contained

This Webcast Will Begin Shortly

This Webcast Will Begin Shortly If you have any technical problems with the Webcast or the streaming audio, please contact us via email at: webcast@acc.com Thank You! 1 Master Limited Partnerships (MLPs):

This Webcast Will Begin Shortly If you have any technical problems with the Webcast or the streaming audio, please contact us via email at: webcast@acc.com Thank You! 1 Master Limited Partnerships (MLPs):

Master Limited Partnerships (MLPs)

") 1Q 2017 Master Limited Partnerships (MLPs) Distinct Focus on Yield VanEck Vectors High Income Infrastructure MLP ETF (YMLI) VanEck Vectors High Income MLP ETF (YMLP) ETF disclosure This material does not

1Q 2017 Master Limited Partnerships (MLPs) Distinct Focus on Yield VanEck Vectors High Income Infrastructure MLP ETF (YMLI) VanEck Vectors High Income MLP ETF (YMLP) ETF disclosure This material does not

PROSPECTUS. ALPS ETF Trust. March 31, Alerian MLP ETF (NYSE ARCA: AMLP) Alerian Energy Infrastructure ETF (NYSE ARCA: ENFR)

Alerian Energy Infrastructure ETF (NYSE ARCA: ENFR)") March 31, 2016 ALPS ETF Trust PROSPECTUS Alerian MLP ETF (NYSE ARCA: AMLP) Alerian Energy Infrastructure ETF (NYSE ARCA: ENFR) An ALPS Advisors Solution The Securities and Exchange Commission has not approved

March 31, 2016 ALPS ETF Trust PROSPECTUS Alerian MLP ETF (NYSE ARCA: AMLP) Alerian Energy Infrastructure ETF (NYSE ARCA: ENFR) An ALPS Advisors Solution The Securities and Exchange Commission has not approved

MARTIN MIDSTREAM PARTNERS L.P. Deutsche Bank Leveraged Finance Conference September 29, 2015

MARTIN MIDSTREAM PARTNERS L.P. Deutsche Bank Leveraged Finance Conference September 29, 2015 USE OF NON-GAAP FINANCIAL MEASURES This presentation includes certain non-gaap financial measures such as EBITDA

MARTIN MIDSTREAM PARTNERS L.P. Deutsche Bank Leveraged Finance Conference September 29, 2015 USE OF NON-GAAP FINANCIAL MEASURES This presentation includes certain non-gaap financial measures such as EBITDA

Delek US Holdings, Inc./ Delek Logistics Partners, LP Wells Fargo Energy Symposium December 2013

Delek US Holdings, Inc./ Delek Logistics Partners, LP Wells Fargo Energy Symposium December 2013 Safe Harbor Provision Delek US Holdings and Delek Logistics Partners, LP are traded on the New York Stock

Delek US Holdings, Inc./ Delek Logistics Partners, LP Wells Fargo Energy Symposium December 2013 Safe Harbor Provision Delek US Holdings and Delek Logistics Partners, LP are traded on the New York Stock

Commodity Exchange Traded Funds

Commodity Exchange Traded Funds Tim Simard NBC Commodities 14-person Calgary-based team running both a client-driven and strategic trading operation Collective team experience in excess of 250 years in

Commodity Exchange Traded Funds Tim Simard NBC Commodities 14-person Calgary-based team running both a client-driven and strategic trading operation Collective team experience in excess of 250 years in

YORKVILLE VARIABLE DISTRIBUTION MLP UNIVERSE INDEX

YORKVILLE VARIABLE DISTRIBUTION MLP UNIVERSE INDEX A Complete Study of Fundamentals, Returns, Risk, and Correlations Analysis & Intellectual Property by: Index Calculation & Maintenance by: 950 Third Avenue,

YORKVILLE VARIABLE DISTRIBUTION MLP UNIVERSE INDEX A Complete Study of Fundamentals, Returns, Risk, and Correlations Analysis & Intellectual Property by: Index Calculation & Maintenance by: 950 Third Avenue,

MARTIN MIDSTREAM PARTNERS L.P. Bank of America High Yield Energy & Power Leveraged Finance Conference JUNE 2, 2015

MARTIN MIDSTREAM PARTNERS L.P. Bank of America High Yield Energy & Power Leveraged Finance Conference JUNE 2, 2015 USE OF NON-GAAP FINANCIAL MEASURES This presentation includes certain non-gaap financial

MARTIN MIDSTREAM PARTNERS L.P. Bank of America High Yield Energy & Power Leveraged Finance Conference JUNE 2, 2015 USE OF NON-GAAP FINANCIAL MEASURES This presentation includes certain non-gaap financial

Revisiting MLP Performance as Interest Rates Rise

Revisiting MLP Performance as Interest Rates Rise November 2018 With the 10-year Treasury yield touching levels in 2H18 that have not been seen for years, it seems like an opportune time to revisit MLP

Revisiting MLP Performance as Interest Rates Rise November 2018 With the 10-year Treasury yield touching levels in 2H18 that have not been seen for years, it seems like an opportune time to revisit MLP

AMLP Alerian MLP

Alerian MLP ETF ETF.com segment: Equity: U.S. MLPs Competing ETFs: MLPI, MLPB, AMJ, AMU, MLPG Related ETF Channels: U.S., Smart-Beta ETFs, Sectors, MLPs, Energy, Alerian MLP Infrastructure, Dividends,

Alerian MLP ETF ETF.com segment: Equity: U.S. MLPs Competing ETFs: MLPI, MLPB, AMJ, AMU, MLPG Related ETF Channels: U.S., Smart-Beta ETFs, Sectors, MLPs, Energy, Alerian MLP Infrastructure, Dividends,

Guide to MLP Investing. Global Trend Events Las Vegas

Guide to MLP Investing Global Trend Events Las Vegas 1 Table of Contents About Alerian 3 Overview of MLPs 11 MLP Performance 16 Energy Renaissance 21 MLP Investment Options 28 Current Issues and Risks

Guide to MLP Investing Global Trend Events Las Vegas 1 Table of Contents About Alerian 3 Overview of MLPs 11 MLP Performance 16 Energy Renaissance 21 MLP Investment Options 28 Current Issues and Risks

2015 Jefferies Energy Conference Pete Bowden Global Head of Midstream Energy Investment Banking November Jefferies LLC Member SIPC

2015 Jefferies Energy Conference Pete Bowden Global Head of Midstream Energy Investment Banking November 2015 Jefferies LLC Member SIPC Current Macro Environment 1 Production / Consumption (MMBbl/d) Stock

2015 Jefferies Energy Conference Pete Bowden Global Head of Midstream Energy Investment Banking November 2015 Jefferies LLC Member SIPC Current Macro Environment 1 Production / Consumption (MMBbl/d) Stock

2018 Summary Prospectus

April 1, 2018 Global X MLP & Energy Infrastructure ETF NYSE Arca, Inc.: MLPX 2018 Summary Prospectus Before you invest, you may want to review the Fund's prospectus, which contains more information about

April 1, 2018 Global X MLP & Energy Infrastructure ETF NYSE Arca, Inc.: MLPX 2018 Summary Prospectus Before you invest, you may want to review the Fund's prospectus, which contains more information about

Low Correlation Strategy Investment update to 31 March 2018

The Low Correlation Strategy (LCS), managed by MLC s Alternative Strategies team, is made up of a range of diversifying alternative strategies, including hedge funds. A distinctive alternative strategy,

The Low Correlation Strategy (LCS), managed by MLC s Alternative Strategies team, is made up of a range of diversifying alternative strategies, including hedge funds. A distinctive alternative strategy,

MARKET UPDATE AUGUST 14, 2015

EDGE is an independent financial firm whose objective advice helps individuals and institutions realize their goals in the areas of investment management and corporate finance. The Edge Research Team s

EDGE is an independent financial firm whose objective advice helps individuals and institutions realize their goals in the areas of investment management and corporate finance. The Edge Research Team s

BROAD COMMODITY INDEX

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS JUNE 2017 80.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% -80.00% ABCERI S&P GSCI ER BCOMM ER

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS JUNE 2017 80.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% -80.00% ABCERI S&P GSCI ER BCOMM ER

Tortoise MLP Fund, Inc.

Tortoise MLP Fund, Inc. SM Yield Growth Quality 2014 3rd Quarter Report August 31, 2014 Steady Wins C o m p a n y a t a G l a n c e Tortoise MLP Fund, Inc. (NYSE: NTG) offers a closed-end fund strategy

Tortoise MLP Fund, Inc. SM Yield Growth Quality 2014 3rd Quarter Report August 31, 2014 Steady Wins C o m p a n y a t a G l a n c e Tortoise MLP Fund, Inc. (NYSE: NTG) offers a closed-end fund strategy

The Compelling Case for Value

The Compelling Case for Value July 2, 2018 SOLELY FOR THE USE OF INSTITUTIONAL INVESTORS AND PROFESSIONAL ADVISORS 0 Jan-75 Jan-77 Jan-79 Jan-81 Jan-83 Jan-85 Jan-87 Jan-89 Jan-91 Jan-93 Jan-95 Jan-97

The Compelling Case for Value July 2, 2018 SOLELY FOR THE USE OF INSTITUTIONAL INVESTORS AND PROFESSIONAL ADVISORS 0 Jan-75 Jan-77 Jan-79 Jan-81 Jan-83 Jan-85 Jan-87 Jan-89 Jan-91 Jan-93 Jan-95 Jan-97

Q Energy Infrastructure & MLP Strategy

Q2 2017 Energy Infrastructure & MLP Strategy 1360 East 9th Street, Suite 1100 Cleveland, Ohio 44114 MAI Capital Management Overview Heritage dating back to 1973 Privately held, independent SEC registered

Q2 2017 Energy Infrastructure & MLP Strategy 1360 East 9th Street, Suite 1100 Cleveland, Ohio 44114 MAI Capital Management Overview Heritage dating back to 1973 Privately held, independent SEC registered

FINANCIAL AND OPERATING SUMMARY

FINANCIAL AND OPERATING SUMMARY ($000s except per share amounts) December 31, Dec 31, 2017 Sep 30, 2017 % Change 2017 2016 % Change Financial highlights Oil sales 64,221 50,563 27 % 217,194 149,701 45

FINANCIAL AND OPERATING SUMMARY ($000s except per share amounts) December 31, Dec 31, 2017 Sep 30, 2017 % Change 2017 2016 % Change Financial highlights Oil sales 64,221 50,563 27 % 217,194 149,701 45

MANAGED FUTURES INDEX

MANAGED FUTURES INDEX COMMENTARY + STRATEGY FACTS JULY 2018 CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 120.00% 100.00% 80.00% 60.00% 40.00% 20.00% 0.00% AMFERI BARCLAY BTOP50 CTA INDEX S&P 500 S&P

MANAGED FUTURES INDEX COMMENTARY + STRATEGY FACTS JULY 2018 CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 120.00% 100.00% 80.00% 60.00% 40.00% 20.00% 0.00% AMFERI BARCLAY BTOP50 CTA INDEX S&P 500 S&P

BROAD COMMODITY INDEX

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS APRIL 2017 80.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% -80.00% ABCERI S&P GSCI ER BCOMM ER

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS APRIL 2017 80.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% -80.00% ABCERI S&P GSCI ER BCOMM ER

Tortoise Energy Infrastructure Corp.

Y i e l d G r o w t h Q u a l i t y 2006 Annual Report Tortoise Energy Infrastructure Corp. TYG Steady Wins Company at a Glance Tortoise Energy Infrastructure Corp. is a pioneering closed-end investment

Y i e l d G r o w t h Q u a l i t y 2006 Annual Report Tortoise Energy Infrastructure Corp. TYG Steady Wins Company at a Glance Tortoise Energy Infrastructure Corp. is a pioneering closed-end investment

Dividend Growth as a Defensive Equity Strategy August 24, 2012

Dividend Growth as a Defensive Equity Strategy August 24, 2012 Introduction: The Case for Defensive Equity Strategies Most institutional investment committees meet three to four times per year to review

Dividend Growth as a Defensive Equity Strategy August 24, 2012 Introduction: The Case for Defensive Equity Strategies Most institutional investment committees meet three to four times per year to review

TRANSAMERICA FUNDS ANNUAL REPORT

TRANSAMERICA FUNDS ANNUAL REPORT OCTOBER 31, 2017 ASSET ALLOCATION FUNDS TRANSAMERICA ASSET ALLOCATION CONSERVATIVE PORTFOLIO TRANSAMERICA ASSET ALLOCATION MODERATE GROWTH PORTFOLIO TRANSAMERICA ASSET

TRANSAMERICA FUNDS ANNUAL REPORT OCTOBER 31, 2017 ASSET ALLOCATION FUNDS TRANSAMERICA ASSET ALLOCATION CONSERVATIVE PORTFOLIO TRANSAMERICA ASSET ALLOCATION MODERATE GROWTH PORTFOLIO TRANSAMERICA ASSET

MLP Market Update. August 21, 2008

MLP Market Update August 21, 2008 Table of Contents MLP Performance YTD Commodity Prices Impact on Business Fundamentals Access to Capital Valuations Positive Asymmetric Returns Conclusions Disclosure

MLP Market Update August 21, 2008 Table of Contents MLP Performance YTD Commodity Prices Impact on Business Fundamentals Access to Capital Valuations Positive Asymmetric Returns Conclusions Disclosure

Tortoise MLP Fund, Inc.

Tortoise MLP Fund, Inc. SM Yield Growth Quality 2014 1st Quarter Report February 28, 2014 Steady Wins C o m p a n y a t a G l a n c e Tortoise MLP Fund, Inc. (NYSE: NTG) offers a closed-end fund strategy

Tortoise MLP Fund, Inc. SM Yield Growth Quality 2014 1st Quarter Report February 28, 2014 Steady Wins C o m p a n y a t a G l a n c e Tortoise MLP Fund, Inc. (NYSE: NTG) offers a closed-end fund strategy

Merrill Lynch Conference Real Assets, Real Earnings, Real Cash September 2003

Merrill Lynch Conference Real Assets, Real Earnings, Real Cash September 003 Forward Looking Statements This presentation contains forward looking statements, including these, within the meaning of Section

Merrill Lynch Conference Real Assets, Real Earnings, Real Cash September 003 Forward Looking Statements This presentation contains forward looking statements, including these, within the meaning of Section

Income Investing basics

Income Investing basics investment options that can offer income, growth, and diversification Key questions to consider: What are your income-oriented investment options? What is the role of income in

Income Investing basics investment options that can offer income, growth, and diversification Key questions to consider: What are your income-oriented investment options? What is the role of income in

EMLP First Trust North American Energy Infrastructure Fund

First Trust North American Energy Infrastructure Fund ETF.com segment: Equity: U.S. MLPs Competing ETFs: AMZA, MLPA, MLPX, TPYP, IMLP Related ETF Channels: North America, No Underlying Index, Active Management,

First Trust North American Energy Infrastructure Fund ETF.com segment: Equity: U.S. MLPs Competing ETFs: AMZA, MLPA, MLPX, TPYP, IMLP Related ETF Channels: North America, No Underlying Index, Active Management,

Building a Better Inflation Hedge: The Case for Real Assets

INSIGHTS Building a Better Inflation Hedge: The Case for Real Assets March 2014 203.621.1700 rocaton.com 2014, Rocaton Investment Advisors, LLC EXECUTIVE SUMMARY After witnessing the U.S. equity market

INSIGHTS Building a Better Inflation Hedge: The Case for Real Assets March 2014 203.621.1700 rocaton.com 2014, Rocaton Investment Advisors, LLC EXECUTIVE SUMMARY After witnessing the U.S. equity market

U.S. OIL & GAS SNAPSHOT

U.S. THOMSON REUTERS LPC FEBRUARY 2016 Colm (C.J.) Doherty Director of Analysis colm.doherty@thomsonreuters.com 646-223-6821 U.S. Key Points Slides 3-4 Oil & Gas Institutional Loan Defaults Slide 5 Oil

U.S. THOMSON REUTERS LPC FEBRUARY 2016 Colm (C.J.) Doherty Director of Analysis colm.doherty@thomsonreuters.com 646-223-6821 U.S. Key Points Slides 3-4 Oil & Gas Institutional Loan Defaults Slide 5 Oil

ENERGY TRANSFER EQUITY

ENERGY TRANSFER EQUITY Credit Suisse MLP & Energy Logistics Conference June 10 th 2014 Jamie Welch Group CFO LEGAL DISCLAIMER This presentation relates to a meeting among members of management of Energy

ENERGY TRANSFER EQUITY Credit Suisse MLP & Energy Logistics Conference June 10 th 2014 Jamie Welch Group CFO LEGAL DISCLAIMER This presentation relates to a meeting among members of management of Energy

MANAGED FUTURES INDEX

MANAGED FUTURES INDEX COMMENTARY + STRATEGY FACTS JUNE 2018 CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 120.00% 100.00% 80.00% 60.00% 40.00% 20.00% 0.00% AMFERI BARCLAY BTOP50 CTA INDEX S&P 500 S&P

MANAGED FUTURES INDEX COMMENTARY + STRATEGY FACTS JUNE 2018 CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) 120.00% 100.00% 80.00% 60.00% 40.00% 20.00% 0.00% AMFERI BARCLAY BTOP50 CTA INDEX S&P 500 S&P

Marathon Petroleum Corporation

January 19, 2015 Marathon Petroleum Corporation (MPC-NYSE) Current Recommendation SUMMARY DATA NEUTRAL Prior Recommendation Underperform Date of Last Change 01/07/2014 Current Price (01/16/15) $77.56 Target

January 19, 2015 Marathon Petroleum Corporation (MPC-NYSE) Current Recommendation SUMMARY DATA NEUTRAL Prior Recommendation Underperform Date of Last Change 01/07/2014 Current Price (01/16/15) $77.56 Target

A Compelling Case for Leveraged Loans

A Compelling Case for Leveraged Loans EXECUTIVE SUMMARY In the current market environment, there are a number of compelling reasons to invest in leveraged loans. In a situation where most assets are trading

A Compelling Case for Leveraged Loans EXECUTIVE SUMMARY In the current market environment, there are a number of compelling reasons to invest in leveraged loans. In a situation where most assets are trading

March 07, Dear Friends and Investors,

March 07, 2018 Dear Friends and Investors, The following market overview for the month of February, 2018 has been produced by the Fund s Senior Portfolio Manager, Steven Goldman. We trust that you ll find

March 07, 2018 Dear Friends and Investors, The following market overview for the month of February, 2018 has been produced by the Fund s Senior Portfolio Manager, Steven Goldman. We trust that you ll find

2017 Annual Report Closed-End Funds

Annual Report 2017 2017 Annual Report Closed-End Funds Midstream focused Tortoise Energy Infrastructure Corp. (NYSE: TYG) Tortoise MLP Fund, Inc. (NYSE: NTG) Tortoise Pipeline & Energy Fund, Inc. (NYSE:

Annual Report 2017 2017 Annual Report Closed-End Funds Midstream focused Tortoise Energy Infrastructure Corp. (NYSE: TYG) Tortoise MLP Fund, Inc. (NYSE: NTG) Tortoise Pipeline & Energy Fund, Inc. (NYSE:

UBS One-on-One MLP Conference

UBS One-on-One MLP Conference January 13, 2015 Strong. Innovative. Growing. 1 Forward-Looking Statements This presentation contains forward-looking statements within the meaning of the federal securities

UBS One-on-One MLP Conference January 13, 2015 Strong. Innovative. Growing. 1 Forward-Looking Statements This presentation contains forward-looking statements within the meaning of the federal securities

MASTER LIMITED PARTNERSHIPS: IMPLICATIONS FOR US ENERGY INFRASTRUCTURE

MASTER LIMITED PARTNERSHIPS: IMPLICATIONS FOR US ENERGY INFRASTRUCTURE by Elizabeth Arnason & Alexandra Cagan John Buley, Professor of the Practice, Fuqua School of Business, Advisor April 27 th, 2018

MASTER LIMITED PARTNERSHIPS: IMPLICATIONS FOR US ENERGY INFRASTRUCTURE by Elizabeth Arnason & Alexandra Cagan John Buley, Professor of the Practice, Fuqua School of Business, Advisor April 27 th, 2018

2018 1st Quarter Report Closed-End Funds

Quarterly Report February 28, 2018 2018 1st Quarter Report Closed-End Funds Midstream focused Tortoise Energy Infrastructure Corp. (NYSE: TYG) Tortoise MLP Fund, Inc. (NYSE: NTG) Tortoise Pipeline & Energy

Quarterly Report February 28, 2018 2018 1st Quarter Report Closed-End Funds Midstream focused Tortoise Energy Infrastructure Corp. (NYSE: TYG) Tortoise MLP Fund, Inc. (NYSE: NTG) Tortoise Pipeline & Energy

on Energy and Tax Policy Submitted to the Subcommittee on Select Revenue Measures of the House Committee on Ways and Means

Statement of Bruce Heine, Director of Government Affairs, Magellan Midstream Partners on behalf of the National Association of Publicly Traded Partnerships on Energy and Tax Policy Submitted to the Subcommittee

Statement of Bruce Heine, Director of Government Affairs, Magellan Midstream Partners on behalf of the National Association of Publicly Traded Partnerships on Energy and Tax Policy Submitted to the Subcommittee

Prospectus. Global X MLP ETF NYSE Arca, Inc: MLPA. Global X MLP Natural Gas ETF* NYSE Arca, Inc: [ ] April 1, *Not open for investment.

![Prospectus. Global X MLP ETF NYSE Arca, Inc: MLPA. Global X MLP Natural Gas ETF* NYSE Arca, Inc: [ ] April 1, *Not open for investment.](/thumbs/83/88163287.jpg "Prospectus. Global X MLP ETF NYSE Arca, Inc: MLPA. Global X MLP Natural Gas ETF* NYSE Arca, Inc: [ ] April 1, *Not open for investment.") Global X MLP ETF NYSE Arca, Inc: MLPA Global X MLP Natural Gas ETF* NYSE Arca, Inc: [ ] Prospectus April 1, 2018 *Not open for investment. The Securities and Exchange Commission ( SEC ) has not approved

Global X MLP ETF NYSE Arca, Inc: MLPA Global X MLP Natural Gas ETF* NYSE Arca, Inc: [ ] Prospectus April 1, 2018 *Not open for investment. The Securities and Exchange Commission ( SEC ) has not approved

Can LOOP Ever Be a Gulf Coast Cushing? Part 2 Searching for a sour crude benchmark.

? Can LOOP Ever Be a Gulf Coast Cushing? Part 2 Searching for a sour crude benchmark. Morningstar Commodities Research 10 April 2017 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

? Can LOOP Ever Be a Gulf Coast Cushing? Part 2 Searching for a sour crude benchmark. Morningstar Commodities Research 10 April 2017 Sandy Fielden Director, Oil and Products Research +1 512 431-8044 sandy.fielden@morningstar.com

Green Investment Management, Inc.

Complete List of Composites 7/12/2017 Complete List of Composites Composite Name GIM Composites Tax Aware 50/50 Tax Aware 60/40 Tax Aware 75/25 Tax Free Bond Guardian Composites Alternatives Balanced 60/40

Complete List of Composites 7/12/2017 Complete List of Composites Composite Name GIM Composites Tax Aware 50/50 Tax Aware 60/40 Tax Aware 75/25 Tax Free Bond Guardian Composites Alternatives Balanced 60/40

2014 MASTER LIMITED PARTNERSHIP INVESTOR CONFERENCE MAY 22, 2014

2014 MASTER LIMITED PARTNERSHIP INVESTOR CONFERENCE MAY 22, 2014 FORWARD-LOOKING STATEMENTS Certain statements and information in this presentation may constitute forward-looking statements. The words

2014 MASTER LIMITED PARTNERSHIP INVESTOR CONFERENCE MAY 22, 2014 FORWARD-LOOKING STATEMENTS Certain statements and information in this presentation may constitute forward-looking statements. The words

BROAD COMMODITY INDEX

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS JANUARY 2018 100.00% 80.00% 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) -80.00% ABCERI S&P GSCI ER

BROAD COMMODITY INDEX COMMENTARY + STRATEGY FACTS JANUARY 2018 100.00% 80.00% 60.00% 40.00% 20.00% 0.00% -20.00% -40.00% -60.00% CUMULATIVE PERFORMANCE ( SINCE JANUARY 2007* ) -80.00% ABCERI S&P GSCI ER

Florida United Methodist Foundation Cautious As Of: September 30, 2017

Cautious Low 0.85% The Cautious Portfolio is designed for a short-term investment horizon and/or risk-averse investor. It seeks a regular and constant income stream, high liquidity and muted volatility.

Cautious Low 0.85% The Cautious Portfolio is designed for a short-term investment horizon and/or risk-averse investor. It seeks a regular and constant income stream, high liquidity and muted volatility.

Corporate Development and Capital Markets Mike Morgan

Corporate Development and Capital Markets Mike Morgan Agenda General Partner Incentive Math or Morality? KMR vs. KMP Price Capital Expenditures Sustaining Cap Ex Expansion Cap Ex Proposed Dividend Policy

Corporate Development and Capital Markets Mike Morgan Agenda General Partner Incentive Math or Morality? KMR vs. KMP Price Capital Expenditures Sustaining Cap Ex Expansion Cap Ex Proposed Dividend Policy

Citi One-On-One MLP / Midstream Infrastructure Conference. August 20, 2014 Strong. Innovative. Growing.

Citi One-On-One MLP / Midstream Infrastructure Conference August 20, 2014 Strong. Innovative. Growing. 1 Forward-Looking Statements This presentation contains forward-looking statements within the meaning

Citi One-On-One MLP / Midstream Infrastructure Conference August 20, 2014 Strong. Innovative. Growing. 1 Forward-Looking Statements This presentation contains forward-looking statements within the meaning

Manager Comparison Report June 28, Report Created on: July 25, 2013

Manager Comparison Report June 28, 213 Report Created on: July 25, 213 Page 1 of 14 Performance Evaluation Manager Performance Growth of $1 Cumulative Performance & Monthly s 3748 3578 348 3238 368 2898

Manager Comparison Report June 28, 213 Report Created on: July 25, 213 Page 1 of 14 Performance Evaluation Manager Performance Growth of $1 Cumulative Performance & Monthly s 3748 3578 348 3238 368 2898

ALERIAN MLP ETF ALERIAN ENERGY INFRASTRUCTURE ETF

ALERIAN MLP ETF ALERIAN ENERGY INFRASTRUCTURE ETF NYSE ARCA: AMLP NYSE ARCA: ENFR SUPPLEMENT DATED AUGUST 4, 2015 TO THE PROSPECTUS DATED MARCH 31, 2015, AS SUPPLEMENTED JULY 1, 2015, AND STATEMENT OF

ALERIAN MLP ETF ALERIAN ENERGY INFRASTRUCTURE ETF NYSE ARCA: AMLP NYSE ARCA: ENFR SUPPLEMENT DATED AUGUST 4, 2015 TO THE PROSPECTUS DATED MARCH 31, 2015, AS SUPPLEMENTED JULY 1, 2015, AND STATEMENT OF

Kayne Anderson. Capital Advisors, L.P. MODERATOR PANELISTS

MODERATOR PANELISTS About Alerian Market intelligence provided through industry-leading benchmarks and analytics Alerian launched the first real-time MLP index Over $9 billion is directly linked to the

MODERATOR PANELISTS About Alerian Market intelligence provided through industry-leading benchmarks and analytics Alerian launched the first real-time MLP index Over $9 billion is directly linked to the

Term Deposits. Deposit Review May Background on Term Deposits

Deposit Review May Term Deposits Simon Fletcher Head of Research (+61) 3 9670 8615 simon.fletcher@bondadviser.com.au Ethan Xing Quantitative Analyst (+61) 3 9670 8615 ethan.xing@bondadviser.com.au With

Deposit Review May Term Deposits Simon Fletcher Head of Research (+61) 3 9670 8615 simon.fletcher@bondadviser.com.au Ethan Xing Quantitative Analyst (+61) 3 9670 8615 ethan.xing@bondadviser.com.au With

Brookfield. MLPs are down more than 50% from the August 2014 high, near the largest drawdown in the history of the sector.

Brookfield Why MLPs, and Why Now? Public Securities Group By several measures, MLPs are more attractively valued today than they have been in many years. Yet concerns over low oil prices and the challenges

Brookfield Why MLPs, and Why Now? Public Securities Group By several measures, MLPs are more attractively valued today than they have been in many years. Yet concerns over low oil prices and the challenges

Kinder Morgan Management, LLC (Exact name of registrant as specified in its charter)

") KMR Form 10-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year

KMR Form 10-K UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year

2018 Summary Prospectus

April 1, 2018 Global X MLP ETF NYSE Arca, Inc.: MLPA 2018 Summary Prospectus Before you invest, you may want to review the Fund's prospectus, which contains more information about the Fund and its risks.

April 1, 2018 Global X MLP ETF NYSE Arca, Inc.: MLPA 2018 Summary Prospectus Before you invest, you may want to review the Fund's prospectus, which contains more information about the Fund and its risks.

Credit Suisse MLP and Energy Logistics Conference

Credit Suisse MLP and Energy Logistics Conference New York City June 2014 www.magellanlp.com Forward-Looking Statements Portions of this document constitute forward-looking statements as defined by federal

Credit Suisse MLP and Energy Logistics Conference New York City June 2014 www.magellanlp.com Forward-Looking Statements Portions of this document constitute forward-looking statements as defined by federal

Total

The following report provides in-depth analysis into the successes and challenges of the Northcoast Tactical Growth managed ETF strategy throughout 2017, important research into the mechanics of the strategy,

The following report provides in-depth analysis into the successes and challenges of the Northcoast Tactical Growth managed ETF strategy throughout 2017, important research into the mechanics of the strategy,

TORTOISE MLP FUND, INC. STATEMENT OF ADDITIONAL INFORMATION

TORTOISE MLP FUND, INC. STATEMENT OF ADDITIONAL INFORMATION Tortoise MLP Fund, Inc., a Maryland corporation (the Company, we, us, or our ), is a non-diversified, closed-end management investment company

TORTOISE MLP FUND, INC. STATEMENT OF ADDITIONAL INFORMATION Tortoise MLP Fund, Inc., a Maryland corporation (the Company, we, us, or our ), is a non-diversified, closed-end management investment company

Q&A Market Implications of Tax Reform

IN-D EPTH A NALYSIS OF TIMELY INVESTMENT TOPICS Q&A Market Implications of Tax Reform December 27, 2017 Investment Strategy Team Key Takeaways» The Tax Cuts and Jobs Act was signed into law on December

IN-D EPTH A NALYSIS OF TIMELY INVESTMENT TOPICS Q&A Market Implications of Tax Reform December 27, 2017 Investment Strategy Team Key Takeaways» The Tax Cuts and Jobs Act was signed into law on December