The Development of Alternative Financing Sources for SMEs & the Assessment of SME Credit Risk

|

|

|

- Silvester Bridges

- 5 years ago

- Views:

Transcription

1 The Development of Alternative Financing Sources for SMEs & the Assessment of SME Credit Risk Dr. Edward Altman NYU Stern School of Business GSCFM Program NACM Washington D.C. June 26,

2 Scoring Systems 2

3 Scoring Systems 3

4 Major Agencies Bond Rating Categories 4

5 A B O U T U S START We incorporated in April 2016 in UK and in July 2016 in Italy and became partner of the Italian stock exchange in August

6 MODELS We have developed models for all countries in Europe each segmented by industry sectors 2017 TECHNOLOGY Together with our partner CERTUA Ltd, we have designed and developed our platform to implement our models

7 GOVERNANCE We have selected and appointed our Board members and Advisors 2018 CLIENTS We have built a diverse customer base including bank and non-bank lenders, funds, rating agencies and SMEs themselves

8 O U R V I S I O N BECOME THE MARKET STANDARD TO ASSESS THE CREDIT RISK OF SMEs We are now ready to bring our innovations to U.S. and Asia to facilitate SME lending by providing the most advanced and predictive tools to assess their credit risk 8

9 WHY IS A CREDIBLE AND SOUND RISK MODEL FOR SMEs INCREASINGLY RELEVANT? Several signs seem to suggest that the longest benign cycle in the history may be coming to an end soon. What impact would that have on the outstanding debt towards SME? 9

10 Bank lending to SMEs 140, ,000 10,000 8,000 Are UK banks becoming less interested in the SME lending market? 100,000 80,000 6,000 Source: UK Finance, SME Finance Update Q ,000 40,000 20,000 # approved SME loans & OD (LHS) m approved SME loans & OD (RHS) 4,000 2,000 Banks approved almost 70,000 loans to SMEs this quarter and success rates remain high, with eight out of 10 applications getting the green light. Demand for finance amongst SMEs 0 0 has increased, particularly among production and manufacturing industries. 10

11 Many SMEs will accept a slower growth rather than borrowing to grow faster Strongly agree 23% Strongly disagree 2% 47% Disagree 10% Agree Neither 18% Source: BDRC Continental SME Finance Monitor, Q

12 Use of external finance and willingness to use in the future 45% 40% 35% 30% Why did SMEs become adverse to debt? 25% 20% Source: BDRC Continental, SME Finance Monitor Q % 10% 5% 0% Use external finance and willing to use it in the future Use external finance Do not use it but willing but not willing to use it to in the future Do not use it and not willing to Lack of awareness and understanding of financial products can also reflect a more fundamental apathy and perceived absence of relevance to business owners. There is, after all, no reason for an entrepreneur to take the time to educate themselves on forms of finance if they have no intention of ever requiring or applying for external finance. Not least, doing so is time consuming and any ultimate first-time application is fraught with the real possibility of rejection. 12

13 billion Growth in UK peer2peer business lending and non-bank invoice finance 4 3 Invoice Finance Peer 2 peer Are alternative lenders becoming the preferred choice? 2 1 Source: AltFi Data and Author compilation, non-bank SME lending Q Non-bank lenders values continue to grow. According to AltFi Data, total lending in 2017 exceeded 5bn, an increase of 45% on This brings the total to 13.4bn since started recording data in * * forecasts 13

14 SME Z-Score trends 15.0% 10.0% 5.0% 0.0% SME credit risk profile is worsening across all sectors Source: Wiserfunding, SME Finance Review, Q % We run our models on more than 3 million active SMEs in the -10.0% UK and we have consistently observed similar trends across -15.0% Construction & real estate Retail & wholesale regions and sectors with worsening credit risk profile and increasing amount of debt. Manufacturing Services 14

15 THE Z-SCORE The history and the legacy of a tool that has changed the way we assess the risk profile of companies

16 Why has the Altman Z-Score been successful over the past 50 years? Simplicity 5 financial indicators with objective weightings Affordability basically free Predictivity 80% to 90% accuracy ratio Credibility More than studies have been written regarding this model 16

17 Z-Score (1968) Component Definitions and Weightings 17

18 Zones of Discrimination: Original Z - Score Model (1968) 18

19")

19 Estimating Probability of Default (PD) and Probability of Loss Given Defaults (LGD) 19

20 Median Z-Score by S&P Bond Rating for U.S. Manufacturing Firms:

21 Marginal and Cumulative Mortality Rate Actuarial Approach 21

22 Mortality Rates by Original Rating All Rated Corporate Bonds* Years After Issuance AAA Marginal 0.00% 0.00% 0.00% 0.00% 0.01% 0.02% 0.01% 0.00% 0.00% 0.00% Cumulative 0.00% 0.00% 0.00% 0.00% 0.01% 0.03% 0.04% 0.04% 0.04% 0.04% AA Marginal 0.00% 0.00% 0.18% 0.05% 0.02% 0.01% 0.03% 0.04% 0.03% 0.04% Cumulative 0.00% 0.00% 0.18% 0.23% 0.25% 0.26% 0.29% 0.33% 0.36% 0.40% A Marginal 0.01% 0.02% 0.09% 0.10% 0.07% 0.04% 0.02% 0.22% 0.05% 0.03% Cumulative 0.01% 0.03% 0.12% 0.22% 0.29% 0.33% 0.35% 0.57% 0.62% 0.65% BBB Marginal 0.29% 2.26% 1.20% 0.95% 0.46% 0.20% 0.21% 0.15% 0.15% 0.31% Cumulative 0.29% 2.54% 3.71% 4.63% 5.07% 5.26% 5.46% 5.60% 5.74% 6.03% BB Marginal 0.89% 2.01% 3.79% 1.95% 2.38% 1.52% 1.41% 1.07% 1.38% 3.07% Cumulative 0.89% 2.88% 6.56% 8.38% 10.57% 11.92% 13.17% 14.10% 15.28% 17.88% B Marginal 2.84% 7.62% 7.71% 7.73% 5.71% 4.44% 3.58% 2.03% 1.70% 0.71% Cumulative 2.84% 10.24% 17.16% 23.57% 27.93% 31.13% 33.60% 34.94% 36.05% 36.50% CCC Marginal 8.05% 12.36% 17.66% 16.21% 4.87% 11.58% 5.38% 4.76% 0.61% 4.21% Cumulative 8.05% 19.42% 33.65% 44.40% 47.11% 53.23% 55.75% 57.86% 58.11% 59.88% *Rated by S&P at Issuance Based on 3,454 issues Source: S&P Global Ratings and Author's Compilation 22

23 Mortality Losses by Original Rating All Rated Corporate Bonds* Years After Issuance AAA Marginal 0.00% 0.00% 0.00% 0.00% 0.01% 0.01% 0.01% 0.00% 0.00% 0.00% Cumulative 0.00% 0.00% 0.00% 0.00% 0.01% 0.02% 0.03% 0.03% 0.03% 0.03% AA Marginal 0.00% 0.00% 0.01% 0.02% 0.01% 0.01% 0.00% 0.01% 0.01% 0.01% Cumulative 0.00% 0.00% 0.01% 0.03% 0.04% 0.05% 0.05% 0.06% 0.07% 0.08% A Marginal 0.00% 0.01% 0.03% 0.03% 0.04% 0.04% 0.02% 0.01% 0.04% 0.02% Cumulative 0.00% 0.01% 0.04% 0.07% 0.11% 0.15% 0.17% 0.18% 0.22% 0.24% BBB Marginal 0.20% 1.47% 0.68% 0.56% 0.24% 0.14% 0.07% 0.08% 0.08% 0.16% Cumulative 0.20% 1.67% 2.34% 2.88% 3.12% 3.25% 3.32% 3.40% 3.47% 3.63% BB Marginal 0.53% 1.14% 2.26% 1.09% 1.35% 0.74% 0.79% 0.49% 0.70% 1.05% Cumulative 0.53% 1.66% 3.89% 4.93% 6.22% 6.91% 7.65% 8.10% 8.74% 9.70% B Marginal 1.88% 5.33% 5.30% 5.18% 3.76% 2.41% 2.33% 1.12% 0.88% 0.50% Cumulative 1.88% 7.11% 12.03% 16.59% 19.73% 21.66% 23.49% 24.34% 25.01% 25.38% CCC Marginal 5.33% 8.65% 12.45% 11.43% 3.39% 8.58% 2.28% 3.30% 0.37% 2.66% Cumulative 5.33% 13.52% 24.29% 32.94% 35.21% 40.77% 42.12% 44.03% 44.24% 45.72% *Rated by S&P at Issuance Based on 2,894 issues Source: S&P Global Ratings and Author's Compilation 23

24 What are the components of our models? Step 1 Financial variables We use 8 to 14 financial ratios specific to SMEs covering leverage, liquidity, profitability and coverage Step 2 Corporate governance We collect a vast amount of structured and unstructured data on directors and the company sourcing from several databases Step 3 Macroeconomic variables To ensure the stability of the model across time, we use industry specific macroeconomic data to help predicting the market outlook 24

25 W I N N I N G S T R A T E G Y Replicate the human behavior to increase accuracy, stability and credibility Financials How is the business doing? Corporate governance Who is managing it? Macroeconomics What is the context? 25

26 The UK SME Z-Score models 26

27 The UK SME Z-Score models 27

28 A Full Risk Assessment 28

29 Assessing the Credit Worthiness of Italian SMEs and Mini-bond Issuers Dr. Edward I. Altman, Professor of Finance, NYU Stern & Co-founder, Wiserfunding Ltd., London, England

30 The importance of SMEs SMEs comprise a major share of economic activity in advanced economies. They account for over 95% of enterprises, 60% of employment and over 50% of value added in the Private sector. In the EU, SMEs have created 85% of net new jobs from 2002/2010. After the last financial crisis, being heavily reliant on traditional bank lending, the majority of SMEs were faced with significant financing constraints in a deleveraging environment and with restricted credit availability from banks. Despite recent central banks supportive stimulus, capital market bond financing is increasingly attractive. Non-bank market-based financing increasingly appeared as an option to improve the flow of credit to SMEs, while enhancing diversity and widening participation in the financial system. Since 2012, new channels have become increasingly important for SMEs to satisfy their funding needs. Examples of these new sources of funding are crowdfunding, P2P lending, equity participation, securitizations, and Mini-bonds. However, in Europe, SME financing is still heavily reliant on bank lending. 30

SMEs not receiving")

")

31 SMEs Access to Finance Reliance on bank financing by SMEs (in%) SMEs not receiving most of the amount of bank loan requested (as % of total SMEs requesting bankloans) 31

32 New Funding Opportunities: CROWDFUNDING Crowdfunding has emerged as one of the strongest channels for SME financing across Europe, but has achieved limited success in Italy so far. 32

Size Of High-Yield Bond Market 1978 2019 (Mid-year US$ billions) US Market $1,800 $1,600 $1,400 $1,200 $1,000 $1,669 Source: NYU Salomon Center estimates using")

33 (Billions) $ (Billions) Size Of High-Yield Bond Market (Mid-year US$ billions) US Market $1,800 $1,600 $1,400 $1,200 $1,000 $1,669 Source: NYU Salomon Center estimates using Credit Suisse, S&P and Citi data $800 $600 $400 $200 $ * Western Europe Market Source: Credit Suisse *Includes non-investment grade straight corporate debt of issuers with assets located in or revenues derived from Western Europe, or the bond is denominated in a Western European currency. Floating-rate and convertible bonds and preferred stock are not included. 33

34 The Italian Mini-bond Market Europe High-yield bond market is still lagging behind the US one, but the growth has accelerated in the last 3 years. In Italy, the market for SME bonds is known as Extra-MOT PRO Minibond market. The new segment of the Extra-MOT market dedicated to listing of bonds, commercial paper, and project finance bonds started in February The total amount of listed issuances since February 2013 is 307, for a total issued amount of about 9,4B. As of October 2018, there is 8,1B outstanding, from 224 issues. In H2 2018, 30 new issues have been launched. We believe Mini-bonds can be a success in Italy as long as the market supplies an attractive risk/return tradeoff to investors as well as affordable and flexible financing for borrowers. 34

35 What are the constraints to the success of the Italian ExtraMOT PRO Mini-bond market? All bond investments face three main risks (Market, Liquidity and Credit), but it is credit risk that is perhaps most critical for relatively unknown, smaller enterprises. Since the ExtraMOT PRO market is still quite young, there are not as yet aggregate default and recovery statistics. We prefer, therefore, to concentrate on issuer default & return analytics based on Italian SME experience. The objective of our model is to help: Italian SMEs to grow and succeed by assessing their risk profile and suggesting what would be the best funding option for them Lenders and investors to assess the risk-return trade offs in investing in either individual or portfolios of Italian SME mini-bonds 35

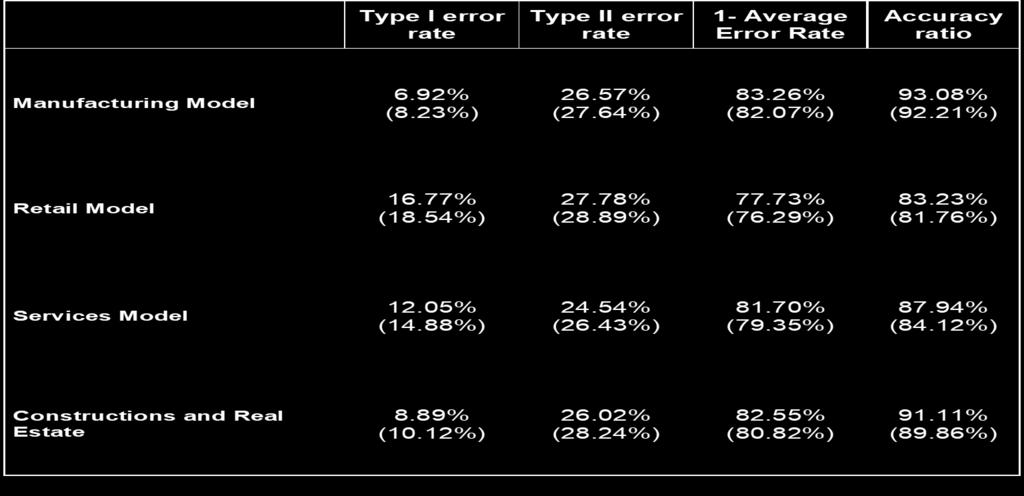

36 SME Z I -Score: Summary of Results We segmented the Italian SMEs by industrial sectors and developed four default prediction models for Manufacturing, Services, Retail and Real Estate firms. Models have been developed on a representative sample of more the SMEs located in the north of Italy and then certified for their relevance at national level. Prediction power of the models is significantly high due to the use of informative variables and appropriate techniques applied. In addition to the Score, Firms/Analysts/Investors also receive an estimated Bond Rating Equivalent and Probability of Default. The SME Z I -Score improves the matching of demand and supply in the capital markets between SMEs looking for funding options and investors. 36

37 The Dataset Initially, financial data of 15,362 active and 1,000 non-active companies were extracted from AIDA (BvD) covering the years 2004 to 2014 (1). Few companies (1,852) had to be dropped due to missing financial information. The shape and size of the final development sample is reported below Number Percentage Non -defaulted firms 13, % Defaulted firms % Total 1 4, % (1): We thank CLASSIS Capital and ASSOLOMBARDA for supporting this research by providing Italian SMEs data 37

38 Frequency Frequency Italian SMEs Profile 2500 Total Assets Sales Total Assets ( m) Sales ( m) Total Assets ( m) Sales ( m) ,1% ,6% ,6% Category < ,5% ,8% Category < <15 77,7% <15 76,7% 38

39 Frequency Italian SMEs Profile Number of employees Number of employees ,4% >200 5,8% 0,8% Category < > Number of employees <50 78,0% 39

40 Count Sector Analysis Sector Performance Defaulted Non-defaulted Sector 0 Agriculture Constructions & RE Financial services Manufacturing Mining PA Retail Services 40

41 Variables Selection Consistent with a large number of studies, we choose five accounting ratio categories describing the main aspects of a company s financial profile: liquidity, profitability, leverage, coverage and activity. For each one of these categories, we create a number of financial ratios identified in the literature as being most successful in predicting firms bankruptcy and transform them in highly predictive variables Next, we apply a statistical forward stepwise selection procedure to the selected variables and estimate the full model for each of the four sectors eliminating the least helpful covariates, one by one, until all the remaining input variables are efficient, i.e. their significance level is above the chosen critical level. 41

42 The Results 42

.")

and the incidence of default given a certain bond rating when the bond was first issued.")

43 The Bond Rating Equivalent In order to provide additional measures of credit worthiness, we introduce the concept of Bond Rating Equivalents (BRE) and Probabilities of Default (PD). Our benchmarks for determining these two critical variables are comparisons to the financial profiles of thousands of companies rated by one of the major international rating agencies (Standard & Poor s) and the incidence of default given a certain bond rating when the bond was first issued. The latter is based on updated data from E. Altman s Mortality Rate Approach (Altman, Journal of Finance, 1989). Source: Altman & Kuehne, NYU Salomon Centre,

44 Risk Profile of Mini-bond issuers (2015) Bond Rating Equivalent # SMEs % SMEs Avg. Coupon Yield AA 2 2% 0,057 A 4 4% 0,062 BBB 24 25% 0,065 BB 18 19% 0,055 B 31 32% 0,059 CCC 14 14% 0,065 CC 2 2% 0,030 C 2 2% 0,060 Source: Firms listed on Borsa Italiana Extra MOT, calculations by the authors Applying our SME Z I -Score on the mini-bond issuers as of 2015, we find that: Risk profile of SMEs doesn t seem to influence the bond pricing; Majority of existing mini-bond issuers classified as non-investment grade; The risk profile of the mini-bond issuers is better (i.e. less risky) than total SME sample. Source: Firms listed on Borsa Italiana Extra MOT, calculations by the authors 44

45 Wiserfunding Ltd.: Helping Italian SMEs to Succeed Mission is to support small business growth by reducing information asymmetry by providing a common set of information to all market participants. The SME Z I -Score should not to be used in isolation. Other factor (e.g. debt capacity, cash flow, recovery profile, market outlook, directors experience) are assessed when evaluating SMEs financial strength. We believe that by providing lenders/investors and small businesses with the same set of information, we can help them speak the same language. We are working with Classis Capital, Borsa Italiana, Confindustria, several PMI organizations and SMEs to apply our model effectively. 45

Z-Score History & Credit Market Outlook

Z-Score History & Credit Market Outlook Dr. Edward Altman NYU Stern School of Business CT TMA New Haven, CT September 26, 2017 1 Scoring Systems Qualitative (Subjective) 1800s Univariate (Accounting/Market

Z-Score History & Credit Market Outlook Dr. Edward Altman NYU Stern School of Business CT TMA New Haven, CT September 26, 2017 1 Scoring Systems Qualitative (Subjective) 1800s Univariate (Accounting/Market

Credit Markets: Is It a Bubble?

Credit Markets: Is It a Bubble? Dr. Edward Altman NYU Stern School of Business 2015 Luncheon Conference TMA, NY Chapter New York January 21, 2015 1 1 Is It a Bubble? Focus on Default Rates in Credit Markets

Credit Markets: Is It a Bubble? Dr. Edward Altman NYU Stern School of Business 2015 Luncheon Conference TMA, NY Chapter New York January 21, 2015 1 1 Is It a Bubble? Focus on Default Rates in Credit Markets

The Evolution of the Altman Z-Score Models & Their Applications to Financial Markets

The Evolution of the Altman Z-Score Models & Their Applications to Financial Markets Dr. Edward Altman NYU Stern School of Business STOXX Ltd. London March 30, 2017 1 Scoring Systems Qualitative (Subjective)

The Evolution of the Altman Z-Score Models & Their Applications to Financial Markets Dr. Edward Altman NYU Stern School of Business STOXX Ltd. London March 30, 2017 1 Scoring Systems Qualitative (Subjective)

Are You Prepared for a Credit Downturn? A Conversation with Dr. Edward Altman

Are You Prepared for a Credit Downturn? A Conversation with Dr. Edward Altman Agenda Introduction & Housekeeping Keynote: Are We in a Credit Bubble? Q&A 2 Welcome! Dr. Edward Altman Professor of Finance

Are You Prepared for a Credit Downturn? A Conversation with Dr. Edward Altman Agenda Introduction & Housekeeping Keynote: Are We in a Credit Bubble? Q&A 2 Welcome! Dr. Edward Altman Professor of Finance

50 Years of Z-Score: What Have We Learned and Where Are We in the Credit Cycle?

50 Years of Z-Score: What Have We Learned and Where Are We in the Credit Cycle? Dr. Edward Altman NYU Stern School of Business CFA Credit Risk Seminar CFA India Society Mumbai, India February 06, 2019

50 Years of Z-Score: What Have We Learned and Where Are We in the Credit Cycle? Dr. Edward Altman NYU Stern School of Business CFA Credit Risk Seminar CFA India Society Mumbai, India February 06, 2019

Evolution of bankruptcy prediction models

Evolution of bankruptcy prediction models Dr. Edward Altman NYU Stern School of Business 1 st Annual Edward Altman Lecture Series Warsaw School of Economics Warsaw, Poland April 14, 2016 1 Scoring Systems

Evolution of bankruptcy prediction models Dr. Edward Altman NYU Stern School of Business 1 st Annual Edward Altman Lecture Series Warsaw School of Economics Warsaw, Poland April 14, 2016 1 Scoring Systems

First Trust Intermediate Duration Preferred & Income Fund Update

1st Quarter 2015 Fund Performance Review & Current Positioning The First Trust Intermediate Duration Preferred & Income Fund (FPF) produced a total return for the first quarter of 2015 of 3.84% based on

1st Quarter 2015 Fund Performance Review & Current Positioning The First Trust Intermediate Duration Preferred & Income Fund (FPF) produced a total return for the first quarter of 2015 of 3.84% based on

External data will likely be necessary for most banks to

CAPITAL REQUIREMENTS Estimating Probability of Default via External Data Sources: A Step Toward Basel II Banks considering their strategies for compliance with the Basel II Capital Accord will likely use

CAPITAL REQUIREMENTS Estimating Probability of Default via External Data Sources: A Step Toward Basel II Banks considering their strategies for compliance with the Basel II Capital Accord will likely use

Dr. Altman on the Mammoth Debt Problem

WEBINAR Dr. Altman on the Mammoth Debt Problem Annotated Slides Latest Saved Version: 7/6/2018 HIGHLIGHTS EDITION Here s why this is a very bad time to let down your guard. - Jerry Flum Dr. Edward Altman

WEBINAR Dr. Altman on the Mammoth Debt Problem Annotated Slides Latest Saved Version: 7/6/2018 HIGHLIGHTS EDITION Here s why this is a very bad time to let down your guard. - Jerry Flum Dr. Edward Altman

Managing a Financial Turnaround The GTI Case

Managing a Financial Turnaround The GTI Case Dr. Edward I. Altman Stern School of Business New York University Corporate Credit Scoring Models and the Bond Rating Equivalence 2 Forecasting Distress With

Managing a Financial Turnaround The GTI Case Dr. Edward I. Altman Stern School of Business New York University Corporate Credit Scoring Models and the Bond Rating Equivalence 2 Forecasting Distress With

IRMC Florence, Italy June 03, 2010

IRMC Florence, Italy June 03, 2010 Dr. Edward Altman NYU Stern School of Business General and accepted risk measurement metric International Language of Credit Greater understanding between borrowers and

IRMC Florence, Italy June 03, 2010 Dr. Edward Altman NYU Stern School of Business General and accepted risk measurement metric International Language of Credit Greater understanding between borrowers and

Estimating Default Probabilities of Corporate Bonds over Various Investment Horizons

Estimating Default Probabilities of Corporate Bonds over Various Investment Horizons Edward I. Altman Max L. Heine Professor of Finance NYU Stern School of Business New York City In advance of forthcoming

Estimating Default Probabilities of Corporate Bonds over Various Investment Horizons Edward I. Altman Max L. Heine Professor of Finance NYU Stern School of Business New York City In advance of forthcoming

The Evolution & Applications of the Altman Z-Score Family of Models

The Evolution & Applications of the Altman Z-Score Family of Models Dr. Edward Altman NYU Stern School of Business GSCFM Program NACM Washington D.C. June 26, 2019 1 Scoring Systems Qualitative (Subjective)

The Evolution & Applications of the Altman Z-Score Family of Models Dr. Edward Altman NYU Stern School of Business GSCFM Program NACM Washington D.C. June 26, 2019 1 Scoring Systems Qualitative (Subjective)

The CreditRiskMonitor FRISK Score

Read the Crowdsourcing Enhancement white paper (7/26/16), a supplement to this document, which explains how the FRISK score has now achieved 96% accuracy. The CreditRiskMonitor FRISK Score EXECUTIVE SUMMARY

Read the Crowdsourcing Enhancement white paper (7/26/16), a supplement to this document, which explains how the FRISK score has now achieved 96% accuracy. The CreditRiskMonitor FRISK Score EXECUTIVE SUMMARY

FYB. FINANCIAL YEARBOOK GERMANY/EU PRIVAT E E QUITY AND CORPORATE FINANCE F OR YOUR BUSINESS ALTERNAT IVE TYPES OF FINANCING

www.fyb.de e nglish e dition FYB FINANCIAL YEARBOOK GERMANY/EU 2017 PRIVAT E E QUITY AND CORPORATE FINANCE ALTERNAT IVE TYPES OF FINANCING THE REFERENCE S OURCE FOR AND E NTREPRENEURS INVESTORS F OR YOUR

www.fyb.de e nglish e dition FYB FINANCIAL YEARBOOK GERMANY/EU 2017 PRIVAT E E QUITY AND CORPORATE FINANCE ALTERNAT IVE TYPES OF FINANCING THE REFERENCE S OURCE FOR AND E NTREPRENEURS INVESTORS F OR YOUR

Mapping of Spread Research credit assessments under the Standardised Approach

30 October 2014 Mapping of Spread Research credit assessments under the Standardised Approach 1. Executive summary 1. This report describes the mapping exercise carried out by the Joint Committee to determine

30 October 2014 Mapping of Spread Research credit assessments under the Standardised Approach 1. Executive summary 1. This report describes the mapping exercise carried out by the Joint Committee to determine

BEST S CREDIT RATING METHODOLOGY (BCRM)

") JANUARY 2018 BEST S CREDIT RATING METHODOLOGY (BCRM) AN OVERVIEW This overview document provides a quick look at the components of Best's Credit Rating Methodology (BCRM) and rating process. For more information

JANUARY 2018 BEST S CREDIT RATING METHODOLOGY (BCRM) AN OVERVIEW This overview document provides a quick look at the components of Best's Credit Rating Methodology (BCRM) and rating process. For more information

Bonds explained. Member of the London Stock Exchange

Bonds explained Member of the London Stock Exchange Killik & Co We pride ourselves on being a relationship firm. Each client has their own dedicated Broker, who acts as the single point of contact to provide

Bonds explained Member of the London Stock Exchange Killik & Co We pride ourselves on being a relationship firm. Each client has their own dedicated Broker, who acts as the single point of contact to provide

A NEW APPROACH TO FUNDING UK BUSINESSES

A NEW APPROACH TO FUNDING UK BUSINESSES Contents Why should the UK care about finding alternatives to traditional bank funding? Why should the UK care about finding alternatives to traditional bank funding?...

A NEW APPROACH TO FUNDING UK BUSINESSES Contents Why should the UK care about finding alternatives to traditional bank funding? Why should the UK care about finding alternatives to traditional bank funding?...

Rating Methodology Banks and Financial Institutions

CREDIT RATING INFORMATION AND SERVICES LIMITED Rating Methodology Banks and Financial Institutions CREDIT RATING PHILOSOPHY CRISL follows structured rating methodologies for each sectors of the national

CREDIT RATING INFORMATION AND SERVICES LIMITED Rating Methodology Banks and Financial Institutions CREDIT RATING PHILOSOPHY CRISL follows structured rating methodologies for each sectors of the national

COMPREHENSIVE ANALYSIS OF BANKRUPTCY PREDICTION ON STOCK EXCHANGE OF THAILAND SET 100

COMPREHENSIVE ANALYSIS OF BANKRUPTCY PREDICTION ON STOCK EXCHANGE OF THAILAND SET 100 Sasivimol Meeampol Kasetsart University, Thailand fbussas@ku.ac.th Phanthipa Srinammuang Kasetsart University, Thailand

COMPREHENSIVE ANALYSIS OF BANKRUPTCY PREDICTION ON STOCK EXCHANGE OF THAILAND SET 100 Sasivimol Meeampol Kasetsart University, Thailand fbussas@ku.ac.th Phanthipa Srinammuang Kasetsart University, Thailand

CREDIT RATING INFORMATION & SERVICES LIMITED

Rating Methodology BANKS AND FINANCIAL INSTITUTIONS CREDIT RATING INFORMATION & SERVICES LIMITED Nakshi Homes (4th & 5th Floor), 6/1A, Segunbagicha, Dhaka 1000, Bangladesh Tel: 717 3700 1, Fax: 956 5783

Rating Methodology BANKS AND FINANCIAL INSTITUTIONS CREDIT RATING INFORMATION & SERVICES LIMITED Nakshi Homes (4th & 5th Floor), 6/1A, Segunbagicha, Dhaka 1000, Bangladesh Tel: 717 3700 1, Fax: 956 5783

Bank Flows and Basel III Determinants and Regional Differences in Emerging Markets

Public Disclosure Authorized THE WORLD BANK POVERTY REDUCTION AND ECONOMIC MANAGEMENT NETWORK (PREM) Economic Premise Public Disclosure Authorized Bank Flows and Basel III Determinants and Regional Differences

Public Disclosure Authorized THE WORLD BANK POVERTY REDUCTION AND ECONOMIC MANAGEMENT NETWORK (PREM) Economic Premise Public Disclosure Authorized Bank Flows and Basel III Determinants and Regional Differences

European crossover bonds. A sweet spot?

European crossover bonds A sweet spot? Demand for crossover credit Record low government bond yields and extraordinary easing measures in the aftermath of the global financial crisis have facilitated the

European crossover bonds A sweet spot? Demand for crossover credit Record low government bond yields and extraordinary easing measures in the aftermath of the global financial crisis have facilitated the

What will Basel II mean for community banks? This

COMMUNITY BANKING and the Assessment of What will Basel II mean for community banks? This question can t be answered without first understanding economic capital. The FDIC recently produced an excellent

COMMUNITY BANKING and the Assessment of What will Basel II mean for community banks? This question can t be answered without first understanding economic capital. The FDIC recently produced an excellent

Standard & Poor s Ratings Services Credit Ratings, Research & Analytics

Standard & Poor s Ratings Services Credit Ratings, Research & Analytics Providing Valued Research and Opinions for Market Participants As part of the world s financial infrastructure, Standard & Poor s

Standard & Poor s Ratings Services Credit Ratings, Research & Analytics Providing Valued Research and Opinions for Market Participants As part of the world s financial infrastructure, Standard & Poor s

Assessing Capital Markets Union

6 Assessing Capital Markets Union Quarterly Assessment by Paul Richards Summary It is too early to make an assessment of Capital Markets Union, but not too early to give a market view of the tests by which

6 Assessing Capital Markets Union Quarterly Assessment by Paul Richards Summary It is too early to make an assessment of Capital Markets Union, but not too early to give a market view of the tests by which

Special Report on. Edward I. Altman with Suresh Ramayanam

New York University Salomon Center Leonard N. Stern School of Business Special Report on Default and Returns in the High-Yield Bond Market 2006 in Review and Outlook by Edward I. Altman with Suresh Ramayanam

New York University Salomon Center Leonard N. Stern School of Business Special Report on Default and Returns in the High-Yield Bond Market 2006 in Review and Outlook by Edward I. Altman with Suresh Ramayanam

PANAFRICAN CREDIT RATING AGENCY. Tel: +(225) (225) Fax:+(225)

(225) Fax:+(225)") PANAFRICAN CREDIT RATING AGENCY Public Limited Company with a Board of Directors with a share capital of CFAF 100,000,000 Accredited by the Capital Market authority (CMA) of Rwanda Ref/CMA/July/3047/2015

PANAFRICAN CREDIT RATING AGENCY Public Limited Company with a Board of Directors with a share capital of CFAF 100,000,000 Accredited by the Capital Market authority (CMA) of Rwanda Ref/CMA/July/3047/2015

Preferred and Capital Securities Fund: Bank Fundamentals Haven t Been This Strong in Decades

Preferred and Capital Securities Fund: Bank Fundamentals Haven t Been This Strong in Decades June 5, 2018 by Philippe Bodereau, Yuri Garbuzov, Jeff Helsing of PIMCO SUMMARY Given the strength in bank fundamentals,

Preferred and Capital Securities Fund: Bank Fundamentals Haven t Been This Strong in Decades June 5, 2018 by Philippe Bodereau, Yuri Garbuzov, Jeff Helsing of PIMCO SUMMARY Given the strength in bank fundamentals,

Americo Todisco. The estimate of default probability in Internal Rating Systems. SAS Forum International Copenhagen June

SAS Forum International Copenhagen 2004 15-17 June The estimate of default probability in Internal Rating Systems Americo Todisco University of Siena, Faculty of Economics Doctorate Program in Law & Economics

SAS Forum International Copenhagen 2004 15-17 June The estimate of default probability in Internal Rating Systems Americo Todisco University of Siena, Faculty of Economics Doctorate Program in Law & Economics

Financial Reporting and Credit Ratings

Financial Reporting and Credit Ratings Greg Jonas Managing Director CARE Conference NAPA, CA April 20, 2007 Agenda Background about credit ratings Calculation, process, role of financial reporting Accounting

Financial Reporting and Credit Ratings Greg Jonas Managing Director CARE Conference NAPA, CA April 20, 2007 Agenda Background about credit ratings Calculation, process, role of financial reporting Accounting

Strategic Banking Corporation of Ireland. SFA Business bytes, Cork May 2016

Strategic Banking Corporation of Ireland SFA Business bytes, Cork May 2016 1 SBCI Key Objectives Reinforce Ireland s economic recovery by improving funding and access to finance mechanisms for the economy

Strategic Banking Corporation of Ireland SFA Business bytes, Cork May 2016 1 SBCI Key Objectives Reinforce Ireland s economic recovery by improving funding and access to finance mechanisms for the economy

Chapter II. Section 1. The following text is added at the beginning:

Appendix 26 approved by the Polish Financial Supervision Authority on September 2nd 2015, to the Base Prospectus of of mbank Hipoteczny S.A. (formerly BRE Bank Hipoteczny S.A.), approved by the Polish

Appendix 26 approved by the Polish Financial Supervision Authority on September 2nd 2015, to the Base Prospectus of of mbank Hipoteczny S.A. (formerly BRE Bank Hipoteczny S.A.), approved by the Polish

JPMORGAN ETFS (IRELAND) ICAV. USD Ultra-Short Income UCITS ETF. 21 December 2017

ICAV. USD Ultra-Short Income UCITS ETF. 21 December 2017") JPMORGAN ETFS (IRELAND) ICAV USD Ultra-Short Income UCITS ETF 21 December 2017 (A sub-fund of JPMorgan ETFs (Ireland) ICAV, an Irish collective asset-management vehicle constituted as an umbrella fund

JPMORGAN ETFS (IRELAND) ICAV USD Ultra-Short Income UCITS ETF 21 December 2017 (A sub-fund of JPMorgan ETFs (Ireland) ICAV, an Irish collective asset-management vehicle constituted as an umbrella fund

BONDS AND CREDIT RATING

BONDS AND CREDIT RATING 2017 1 Typical Bond Features The indenture - a written agreement between the borrower and a trust company - usually lists Amount of Issue, Date of Issue, Maturity Denomination (Par

BONDS AND CREDIT RATING 2017 1 Typical Bond Features The indenture - a written agreement between the borrower and a trust company - usually lists Amount of Issue, Date of Issue, Maturity Denomination (Par

Life Capital. Thierry Léger, CEO Life Capital Ian Patrick, CFO Life Capital

Life Capital Thierry Léger, CEO Life Capital Ian Patrick, CFO Life Capital Life Capital is performing well in a challenging macro environment Today s agenda Life Capital creates alternative access to attractive

Life Capital Thierry Léger, CEO Life Capital Ian Patrick, CFO Life Capital Life Capital is performing well in a challenging macro environment Today s agenda Life Capital creates alternative access to attractive

CREDIT RATINGS AND THE BIS REFORM AGENDA. Edward I. Altman. and. Anthony Saunders. First Draft: February 10, 2001 Second Draft: March 28, 2001

CREDIT RATINGS AND THE BIS REFORM AGENDA by Edward Altman* and Anthony Saunders* First Draft: February 10, 2001 Second Draft: March 28, 2001 Edward I. Altman Anthony Saunders Stern School of Business,

CREDIT RATINGS AND THE BIS REFORM AGENDA by Edward Altman* and Anthony Saunders* First Draft: February 10, 2001 Second Draft: March 28, 2001 Edward I. Altman Anthony Saunders Stern School of Business,

CREDIT RATINGS AND THE BIS REFORM AGENDA. Edward I. Altman. and. Anthony Saunders. First Draft: February 10, 2001 Second Draft: March 28, 2001

CREDIT RATINGS AND THE BIS REFORM AGENDA by Edward Altman* and Anthony Saunders* First Draft: February 10, 2001 Second Draft: March 28, 2001 Edward I. Altman Anthony Saunders Stern School of Business,

CREDIT RATINGS AND THE BIS REFORM AGENDA by Edward Altman* and Anthony Saunders* First Draft: February 10, 2001 Second Draft: March 28, 2001 Edward I. Altman Anthony Saunders Stern School of Business,

The Evolution & Applications of the Altman Z-Score Family of Models

The Evolution & Applications of the Altman Z-Score Family of Models Dr. Edward Altman NYU Stern School of Business National Chemical Credit Association New York May 18, 2017 1 Scoring Systems Qualitative

The Evolution & Applications of the Altman Z-Score Family of Models Dr. Edward Altman NYU Stern School of Business National Chemical Credit Association New York May 18, 2017 1 Scoring Systems Qualitative

Supplementary Notes on the Financial Statements (continued)

") The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2013 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2013 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

Franklin Floating Rate Daily Access Fund Advisor Class

Franklin Floating Rate Daily Access Fund Advisor Class High Yield Fixed Income Product Profile Product Details 1 Fund Assets $3,639,447,605.70 Fund Inception Date 05/01/2001 Number of Securities 207 Including

Franklin Floating Rate Daily Access Fund Advisor Class High Yield Fixed Income Product Profile Product Details 1 Fund Assets $3,639,447,605.70 Fund Inception Date 05/01/2001 Number of Securities 207 Including

Bank of America Merrill Lynch Leveraged Finance Conference. November 29, 2016 NYSE: RDN

Bank of America Merrill Lynch Leveraged Finance Conference November 29, 2016 NYSE: RDN www.radian.biz 1 AGENDA Post Crisis U.S. Housing Market What is Private Mortgage Insurance? Strong Business Fundamentals

Bank of America Merrill Lynch Leveraged Finance Conference November 29, 2016 NYSE: RDN www.radian.biz 1 AGENDA Post Crisis U.S. Housing Market What is Private Mortgage Insurance? Strong Business Fundamentals

COLLATERALIZED LOAN OBLIGATIONS (CLO) Dr. Janne Gustafsson

Dr. Janne Gustafsson") COLLATERALIZED LOAN OBLIGATIONS (CLO) 4.12.2017 Dr. Janne Gustafsson OUTLINE 1. Structured Credit 2. Collateralized Loan Obligations (CLOs) 3. Pricing of CLO tranches 2 3 Structured Credit WHAT IS STRUCTURED

COLLATERALIZED LOAN OBLIGATIONS (CLO) 4.12.2017 Dr. Janne Gustafsson OUTLINE 1. Structured Credit 2. Collateralized Loan Obligations (CLOs) 3. Pricing of CLO tranches 2 3 Structured Credit WHAT IS STRUCTURED

High Yield. LarrainVial Seminario Mercados Globales - Ideas Hans Stoter Head of Credit Investments ING Investment Management

High Yield Hans Stoter Head of Credit Investments ING Investment Management LarrainVial Seminario Mercados Globales - Ideas 2010 Santiago, Lima May 11 13, 2010 What is High Yield Corporate debt with rating

High Yield Hans Stoter Head of Credit Investments ING Investment Management LarrainVial Seminario Mercados Globales - Ideas 2010 Santiago, Lima May 11 13, 2010 What is High Yield Corporate debt with rating

Credit Risk Management: A Primer. By A. V. Vedpuriswar

Credit Risk Management: A Primer By A. V. Vedpuriswar February, 2019 Altman s Z Score Altman s Z score is a good example of a credit scoring tool based on data available in financial statements. It is

Credit Risk Management: A Primer By A. V. Vedpuriswar February, 2019 Altman s Z Score Altman s Z score is a good example of a credit scoring tool based on data available in financial statements. It is

Infrastructure debt: Ready to ride on the road to rising rates

Primer: building a case for infrastructure finance Infrastructure debt: Ready to ride on the road to rising rates November 17 Marketing material for professional investors or advisers only In an environment

Primer: building a case for infrastructure finance Infrastructure debt: Ready to ride on the road to rising rates November 17 Marketing material for professional investors or advisers only In an environment

CREDIT UNIVERSITY March 9, 2012

CREDIT UNIVERSITY March 9, 2012 CREDIT UNIVERSITY Outline Overview, Virtuous Circle, and Scope of Operations Understanding the Drivers of the Business and Ford Credit Profit Reporting Ford Credit Business

CREDIT UNIVERSITY March 9, 2012 CREDIT UNIVERSITY Outline Overview, Virtuous Circle, and Scope of Operations Understanding the Drivers of the Business and Ford Credit Profit Reporting Ford Credit Business

Altman-NYU Salomon Center Distressed Debt Indexes and Related Default Analyses

Altman-NYU Salomon Center Distressed Debt Indexes and Related Default Analyses There are three Altman-NYU Salomon Center indexes related to defaulted debt: the Index of Defaulted Public Bonds which commenced

Altman-NYU Salomon Center Distressed Debt Indexes and Related Default Analyses There are three Altman-NYU Salomon Center indexes related to defaulted debt: the Index of Defaulted Public Bonds which commenced

Supplementary Notes on the Financial Statements (continued)

") The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2014 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2014 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

Emerging Market Sovereign Bonds: Does It Cost More To Issue Under English Law?

Consultation Draft April 10, 2014 Emerging Market Sovereign Bonds: Does It Cost More To Issue Under English Law? Sergio Kurlat and Dilip Ratha Development Prospects Group The World Bank 1 Introduction

Consultation Draft April 10, 2014 Emerging Market Sovereign Bonds: Does It Cost More To Issue Under English Law? Sergio Kurlat and Dilip Ratha Development Prospects Group The World Bank 1 Introduction

Fixed income. income investors. Michael Korber Head of Credit. August 2009

Fixed income Old lessons re-learned for income investors Michael Korber Head of Credit August 2009 Role of fixed income in a portfolio The role of fixed income in a portfolio a fixed or floating rate of

Fixed income Old lessons re-learned for income investors Michael Korber Head of Credit August 2009 Role of fixed income in a portfolio The role of fixed income in a portfolio a fixed or floating rate of

Predicting Online Peer-to-Peer(P2P) Lending Default using Data Mining Techniques

Lending Default using Data Mining Techniques") Predicting Online Peer-to-Peer(P2P) Lending Default using Data Mining Techniques Jae Kwon Bae, Dept. of Management Information Systems, Keimyung University, Republic of Korea. E-mail: jkbae99@kmu.ac.kr

Predicting Online Peer-to-Peer(P2P) Lending Default using Data Mining Techniques Jae Kwon Bae, Dept. of Management Information Systems, Keimyung University, Republic of Korea. E-mail: jkbae99@kmu.ac.kr

Section 1. Long Term Risk

Section 1 Long Term Risk 1 / 49 Long Term Risk Long term risk is inherently credit risk, that is the risk that a counterparty will fail in some contractual obligation. Market risk is of course capable

Section 1 Long Term Risk 1 / 49 Long Term Risk Long term risk is inherently credit risk, that is the risk that a counterparty will fail in some contractual obligation. Market risk is of course capable

Mapping of the FERI EuroRating Services AG credit assessments under the Standardised Approach

30 October 2014 Mapping of the FERI EuroRating Services AG credit assessments under the Standardised Approach 1. Executive summary 1. This report describes the mapping exercise carried out by the Joint

30 October 2014 Mapping of the FERI EuroRating Services AG credit assessments under the Standardised Approach 1. Executive summary 1. This report describes the mapping exercise carried out by the Joint

SME and Entrepreneurship Financing: Policy Responses to the Global Crisis and the way forward to recovery

SME and Entrepreneurship Financing: Policy Responses to the Global Crisis and the way forward to recovery AECM Seminar Managing the Recovery: the role of the guarantee schemes in a changing environment

SME and Entrepreneurship Financing: Policy Responses to the Global Crisis and the way forward to recovery AECM Seminar Managing the Recovery: the role of the guarantee schemes in a changing environment

Theviewsexpresedinthesepapersandpresentationsarethoseoftheauthor(s)only,and

only,and") Theviewsexpresedinthesepapersandpresentationsarethoseoftheauthor(s)only,and thepresenceofthem,oroflinkstothem,ontheimfwebsitedoesnotimplythattheimf,its ExecutiveBoard,oritsmanagementendorsesorsharestheviewsexpresedinthepapersor

Theviewsexpresedinthesepapersandpresentationsarethoseoftheauthor(s)only,and thepresenceofthem,oroflinkstothem,ontheimfwebsitedoesnotimplythattheimf,its ExecutiveBoard,oritsmanagementendorsesorsharestheviewsexpresedinthepapersor

Eurozone Economic Watch. July 2018

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

Eurozone Economic Watch July 2018 Eurozone: A shift to more moderate growth with increased downward risks BBVA Research - Eurozone Economic Watch July 2018 / 2 Hard data improved in May but failed to recover

ELITE Thinking Long Term

ELITE Thinking Long Term ELITE What ELITE is a programme designed to help SMEs prepare and structure for the next stage of growth through the access to long term financing opportunities Who ELITE is dedicated

ELITE Thinking Long Term ELITE What ELITE is a programme designed to help SMEs prepare and structure for the next stage of growth through the access to long term financing opportunities Who ELITE is dedicated

Simple Fuzzy Score for Russian Public Companies Risk of Default

Simple Fuzzy Score for Russian Public Companies Risk of Default By Sergey Ivliev April 2,2. Introduction Current economy crisis of 28 29 has resulted in severe credit crunch and significant NPL rise in

Simple Fuzzy Score for Russian Public Companies Risk of Default By Sergey Ivliev April 2,2. Introduction Current economy crisis of 28 29 has resulted in severe credit crunch and significant NPL rise in

PILLAR 3 DISCLOSURE CITIBANK BERHAD

CITIBANK BERHAD PILLAR 3 DISCLOSURE CONTENTS Introduction Capital Adequacy Capital Structure Risk Management Credit Risk Securitization Market Risk Operational Risk Equities Interest Rate Risk/ Rate of

CITIBANK BERHAD PILLAR 3 DISCLOSURE CONTENTS Introduction Capital Adequacy Capital Structure Risk Management Credit Risk Securitization Market Risk Operational Risk Equities Interest Rate Risk/ Rate of

New York University Salomon Center Leonard N. Stern School of Business. Special Report On

New York University Salomon Center Leonard N. Stern School of Business Special Report On Defaults and Returns in the High-Yield Bond and Distressed Debt Market: The Year 2011 in Review and Outlook By Edward

New York University Salomon Center Leonard N. Stern School of Business Special Report On Defaults and Returns in the High-Yield Bond and Distressed Debt Market: The Year 2011 in Review and Outlook By Edward

A Guide to Investing In Corporate Bonds

A Guide to Investing In Corporate Bonds Access the corporate debt income portfolio TABLE OF CONTENTS What are Corporate Bonds?... 4 Corporate Bond Issuers... 4 Investment Benefits... 5 Credit Quality and

A Guide to Investing In Corporate Bonds Access the corporate debt income portfolio TABLE OF CONTENTS What are Corporate Bonds?... 4 Corporate Bond Issuers... 4 Investment Benefits... 5 Credit Quality and

IRISH LIFE ASSURANCE PLC

IRISH LIFE ASSURANCE PLC Step-up Perpetual Capital Notes Presentation to European Fixed Income Investors Peter Fitzpatrick, Group Finance Director David McCarthy, Group Chief Financial Officer David Gantly,

IRISH LIFE ASSURANCE PLC Step-up Perpetual Capital Notes Presentation to European Fixed Income Investors Peter Fitzpatrick, Group Finance Director David McCarthy, Group Chief Financial Officer David Gantly,

For professional advisers only. Schroders. for Bonds. Strength. in bonds. Best Large Fixed-Interest House

For professional advisers only Schroders for Bonds Strength in bonds Best Large Fixed-Interest House Why Schroders for bonds? Experience: Schroders has a long and successful history, commencing in 1804.

For professional advisers only Schroders for Bonds Strength in bonds Best Large Fixed-Interest House Why Schroders for bonds? Experience: Schroders has a long and successful history, commencing in 1804.

The Development of Asian Bond Markets and the Role of the Credit Guarantee and Investment Facility

2015/FMP/WKSP2/018 Session 4.2 The Development of Asian Bond Markets and the Role of the Credit Guarantee and Investment Facility Submitted by: Credit Guarantee and Investment Facility (CGIF) Workshop

2015/FMP/WKSP2/018 Session 4.2 The Development of Asian Bond Markets and the Role of the Credit Guarantee and Investment Facility Submitted by: Credit Guarantee and Investment Facility (CGIF) Workshop

Housing Treasury Financing Risk

Housing Treasury Financing Risk B5: Key developments in the bank lending and private placement markets Speaker: Chair: Phil Jenkins Partner Centrus Advisors Paul Jackson Treasury Independent Housing Treasury

Housing Treasury Financing Risk B5: Key developments in the bank lending and private placement markets Speaker: Chair: Phil Jenkins Partner Centrus Advisors Paul Jackson Treasury Independent Housing Treasury

Eaton Vance Management Two International Place Boston, MA 02110

Eaton Vance Management Two International Place Boston, MA 02110 www.eatonvance.com Form ADV Part 2A January 31, 2018 This brochure provides information about the qualifications and business practices of

Eaton Vance Management Two International Place Boston, MA 02110 www.eatonvance.com Form ADV Part 2A January 31, 2018 This brochure provides information about the qualifications and business practices of

How to set up an Investment Platform?

How to set up an Investment Platform? CDP experience as National Promotional Institution Martina Colombo, CDP Business Development Brussels, November 21 st 2017 The role of CDP as National Promotional

How to set up an Investment Platform? CDP experience as National Promotional Institution Martina Colombo, CDP Business Development Brussels, November 21 st 2017 The role of CDP as National Promotional

Senior Floating Rate Loans: The Whole Story

Senior Floating Rate Loans: The Whole Story Mutual fund shares are not guaranteed or insured by the FDIC, the Federal Reserve Board or any other agency. The investment return and principal value of an

Senior Floating Rate Loans: The Whole Story Mutual fund shares are not guaranteed or insured by the FDIC, the Federal Reserve Board or any other agency. The investment return and principal value of an

Contents. Supplementary Notes on the Financial Statements (unaudited)

") The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2015 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

The Hongkong and Shanghai Banking Corporation Limited Supplementary Notes on the Financial Statements 2015 Contents Supplementary Notes on the Financial Statements (unaudited) Page Introduction... 2 1

1Q 2017 FORD CREDIT EARNINGS REVIEW

1Q 2017 FORD CREDIT EARNINGS REVIEW April 27, 2017 FC1 FORD CREDIT STRATEGY ORIGINATE SERVICE FUND Support Ford and Lincoln sales Strong dealer relationships Full spread of business Consistent underwriting

1Q 2017 FORD CREDIT EARNINGS REVIEW April 27, 2017 FC1 FORD CREDIT STRATEGY ORIGINATE SERVICE FUND Support Ford and Lincoln sales Strong dealer relationships Full spread of business Consistent underwriting

Mapping of Scope Rating s credit assessments under the Standardised Approach

30 October 2014 Mapping of Scope Rating s credit assessments under the Standardised Approach 1. Executive summary 1. This report describes the mapping exercise carried out by the Joint Committee to determine

30 October 2014 Mapping of Scope Rating s credit assessments under the Standardised Approach 1. Executive summary 1. This report describes the mapping exercise carried out by the Joint Committee to determine

FROM BILLIONS TO TRILLIONS: TRANSFORMING DEVELOPMENT FINANCE POST-2015 FINANCING FOR DEVELOPMENT: MULTILATERAL DEVELOPMENT FINANCE

DEVELOPMENT COMMITTEE (Joint Ministerial Committee of the Boards of Governors of the Bank and the Fund on the Transfer of Real Resources to Developing Countries) DC2015-0002 April 2, 2015 FROM BILLIONS

DEVELOPMENT COMMITTEE (Joint Ministerial Committee of the Boards of Governors of the Bank and the Fund on the Transfer of Real Resources to Developing Countries) DC2015-0002 April 2, 2015 FROM BILLIONS

Wealth Adviser Briefing

Wealth Adviser Briefing Peer-to-peer lending Understanding the risk profile of RateSetter Prepared by RateSetter, the UK s leading peer-to-peer lending platform An exclusive insight into peer-to-peer lending

Wealth Adviser Briefing Peer-to-peer lending Understanding the risk profile of RateSetter Prepared by RateSetter, the UK s leading peer-to-peer lending platform An exclusive insight into peer-to-peer lending

CREDIT & DEBT MARKETS Research Group

Working Paper Series CREDIT & DEBT MARKETS Research Group DEFAULTS AND RETURNS IN THE HIGH YIELD BOND MARKET: THE YEAR 2003 IN REVIEW AND MARKET OUTLOOK Edward I. Altman Gonzalo Fanjul S-CDM-04-01 Defaults

Working Paper Series CREDIT & DEBT MARKETS Research Group DEFAULTS AND RETURNS IN THE HIGH YIELD BOND MARKET: THE YEAR 2003 IN REVIEW AND MARKET OUTLOOK Edward I. Altman Gonzalo Fanjul S-CDM-04-01 Defaults

HIGH-YIELD CORPORATE BONDS

HIGH-YIELD (Agreement of Purchaser) Account Name Account Number Rep. No. HY I/We represent and agree as follows: Piper Jaffray Copy Terms. I or me means the client(s). You means Piper Jaffray. High-Yield

HIGH-YIELD (Agreement of Purchaser) Account Name Account Number Rep. No. HY I/We represent and agree as follows: Piper Jaffray Copy Terms. I or me means the client(s). You means Piper Jaffray. High-Yield

Understanding Investments in Collateralized Loan Obligations ( CLOs )

") Understanding Investments in Collateralized Loan Obligations ( CLOs ) Disclaimer This document contains the current, good faith opinions of Ares Management Corporation ( Ares ). The document is meant for

Understanding Investments in Collateralized Loan Obligations ( CLOs ) Disclaimer This document contains the current, good faith opinions of Ares Management Corporation ( Ares ). The document is meant for

Transforming and innovating

Transforming and innovating Eric Rutten CEO Aegon Bank KBW conference May 16, 2018 Helping people achieve a lifetime of financial security 2 Summary Cornerstone of strategy Aegon Bank is a focused player

Transforming and innovating Eric Rutten CEO Aegon Bank KBW conference May 16, 2018 Helping people achieve a lifetime of financial security 2 Summary Cornerstone of strategy Aegon Bank is a focused player

Bank Capital Relief. October 2018

Bank Capital Relief October 2018 Table of contents Executive summary.... 1 What is a bank capital relief strategy?... 1 Role within a portfolio... 4 Potential considerations... 4 Conclusion... 6 Executive

Bank Capital Relief October 2018 Table of contents Executive summary.... 1 What is a bank capital relief strategy?... 1 Role within a portfolio... 4 Potential considerations... 4 Conclusion... 6 Executive

Taiwan Ratings. An Introduction to CDOs and Standard & Poor's Global CDO Ratings. Analysis. 1. What is a CDO? 2. Are CDOs similar to mutual funds?

An Introduction to CDOs and Standard & Poor's Global CDO Ratings Analysts: Thomas Upton, New York Standard & Poor's Ratings Services has been rating collateralized debt obligation (CDO) transactions since

An Introduction to CDOs and Standard & Poor's Global CDO Ratings Analysts: Thomas Upton, New York Standard & Poor's Ratings Services has been rating collateralized debt obligation (CDO) transactions since

Basel II Pillar 3 Disclosures Year ended 31 December 2009

DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore Notice to Banks No. 637 (Notice on Risk Based Capital Adequacy Requirements

DBS Group Holdings Ltd and its subsidiaries (the Group) have adopted Basel II as set out in the revised Monetary Authority of Singapore Notice to Banks No. 637 (Notice on Risk Based Capital Adequacy Requirements

ExtraMOT PRO. Borsa Italiana answer to the Italian corporates needs

ExtraMOT PRO Borsa Italiana answer to the Italian corporates needs ExtraMOT PRO 04/2016 10/2016 03/2017 Introduction of the segment for green and social bond 03/2013 03/2015 The launch of the market for

ExtraMOT PRO Borsa Italiana answer to the Italian corporates needs ExtraMOT PRO 04/2016 10/2016 03/2017 Introduction of the segment for green and social bond 03/2013 03/2015 The launch of the market for

7 Forum Internacional de Credito SERASA 21 November 2006 Sao Paulo - Brazil

7 Forum Internacional de Credito SERASA 21 November 2006 Sao Paulo - Brazil Edward I. Altman NYU Leonard N. Stern School of Business Gabriele Sabato ABN AMRO Risk Management - Amsterdam Possible Effects

7 Forum Internacional de Credito SERASA 21 November 2006 Sao Paulo - Brazil Edward I. Altman NYU Leonard N. Stern School of Business Gabriele Sabato ABN AMRO Risk Management - Amsterdam Possible Effects

Transforming and innovating

Transforming and innovating Eric Rutten December 1, 2017 CEO Aegon Bank Helping people achieve a lifetime of financial security 1 Summary Cornerstone of strategy Aegon Bank is a focused player in financial

Transforming and innovating Eric Rutten December 1, 2017 CEO Aegon Bank Helping people achieve a lifetime of financial security 1 Summary Cornerstone of strategy Aegon Bank is a focused player in financial

1Q 2018 Investor Presentation. May 2018

1Q 2018 Investor Presentation May 2018 Forward-Looking Statements This presentation, including the accompanying oral presentation (collectively, this presentation ), does not constitute an offer to sell

1Q 2018 Investor Presentation May 2018 Forward-Looking Statements This presentation, including the accompanying oral presentation (collectively, this presentation ), does not constitute an offer to sell

Presentation at Bank of America Merrill Lynch Banking & Insurance Conference

Presentation at Bank of America Merrill Lynch Banking & Insurance Conference Brady W. Dougan, Chief Executive Officer Credit Suisse London, October 1, 2009 Cautionary statement Cautionary statement regarding

Presentation at Bank of America Merrill Lynch Banking & Insurance Conference Brady W. Dougan, Chief Executive Officer Credit Suisse London, October 1, 2009 Cautionary statement Cautionary statement regarding

Rating of European sovereign bonds and its impact on credit default swaps (CDS) and government bond yield spreads

and government bond yield spreads") Rating of European sovereign bonds and its impact on credit default swaps (CDS) and government bond yield spreads Supervised by: Prof. Günther Pöll Diploma Presentation Plass Stefan B.A. 21 th October

Rating of European sovereign bonds and its impact on credit default swaps (CDS) and government bond yield spreads Supervised by: Prof. Günther Pöll Diploma Presentation Plass Stefan B.A. 21 th October

The case for lower rated corporate bonds

The case for lower rated corporate bonds Marcus Pakenham Fixed income product specialist December 3 Introduction Where should fixed income investors be positioned over the medium term? We expect that government

The case for lower rated corporate bonds Marcus Pakenham Fixed income product specialist December 3 Introduction Where should fixed income investors be positioned over the medium term? We expect that government

Outlook of Trade Finance and Credit Insurance in the Global Trade Digitalisation

Change Picture Outlook of Trade Finance and Credit Insurance in the Global Trade Digitalisation Isidoro Unda CEO - Atradius IACPM 2018 Spring Conference Objectives Analyse the global trade market and Trade

Change Picture Outlook of Trade Finance and Credit Insurance in the Global Trade Digitalisation Isidoro Unda CEO - Atradius IACPM 2018 Spring Conference Objectives Analyse the global trade market and Trade

CIT Restructuring Plan Management Presentation. October 2009

CIT Restructuring Plan Management Presentation October 2009 Important Notices This presentation contains forward-looking statements within the meaning of applicable federal securities laws that are based

CIT Restructuring Plan Management Presentation October 2009 Important Notices This presentation contains forward-looking statements within the meaning of applicable federal securities laws that are based

SHARE DEALING. Income GeneratoR. Halifax Structured Products

SHARE DEALING Income GeneratoR Halifax Structured Products Contents Page 1. Who is involved in the Income Generator? 3 2. Product Overview 4 3. How does the Income Generator work? 6 4. Is the Income Generator

SHARE DEALING Income GeneratoR Halifax Structured Products Contents Page 1. Who is involved in the Income Generator? 3 2. Product Overview 4 3. How does the Income Generator work? 6 4. Is the Income Generator

D C CC CCC B BB BBB A AA AAA

If you want to know more, ASKMORE TM modefinance s credit report. Almost every day millions of people around the world are wondering the real creditworthiness of the companies with which they are in business.

If you want to know more, ASKMORE TM modefinance s credit report. Almost every day millions of people around the world are wondering the real creditworthiness of the companies with which they are in business.

S&P Global Ratings Definitions

S&P Global Ratings s Table Of Contents I. GENERAL-PURPOSE CREDIT RATINGS A. Issue Credit Ratings B. Issuer Credit Ratings II. CREDITWATCH, RATING OUTLOOKS, LOCAL CURRENCY AND FOREIGN CURRENCY RATINGS A.

S&P Global Ratings s Table Of Contents I. GENERAL-PURPOSE CREDIT RATINGS A. Issue Credit Ratings B. Issuer Credit Ratings II. CREDITWATCH, RATING OUTLOOKS, LOCAL CURRENCY AND FOREIGN CURRENCY RATINGS A.

Private Equity Overview

Private Equity Overview June 10, 2010 State Universities Retirement System Rob Parkinson, Associate Agenda Asset Class Overview Market Update SURS Private Equity Portfolio Asset Class Overview Benefits

Private Equity Overview June 10, 2010 State Universities Retirement System Rob Parkinson, Associate Agenda Asset Class Overview Market Update SURS Private Equity Portfolio Asset Class Overview Benefits

Crowd-sourced Credit Transition Matrices and CECL

Crowd-sourced Credit Transition Matrices and CECL 4 th November 2016 IACPM Washington, D.C. COLLECTIVE INTELLIGENCE FOR GLOBAL FINANCE Agenda Crowd-sourced, real world default risk data a new and extensive

Crowd-sourced Credit Transition Matrices and CECL 4 th November 2016 IACPM Washington, D.C. COLLECTIVE INTELLIGENCE FOR GLOBAL FINANCE Agenda Crowd-sourced, real world default risk data a new and extensive

Raising finance for Europe s small & medium-sized businesses

Raising finance for Europe s small & medium-sized businesses A practical guide to obtaining loan, bond and equity funding Association for Financial Markets in Europe www.afme.eu Disclaimer This guide should

Raising finance for Europe s small & medium-sized businesses A practical guide to obtaining loan, bond and equity funding Association for Financial Markets in Europe www.afme.eu Disclaimer This guide should

The Credit Research Initiative (CRI) National University of Singapore

National University of Singapore") 2018 The Credit Research Initiative (CRI) National University of Singapore First version: March 2, 2017, this version: May 7, 2018 Introduced by the Credit Research Initiative (CRI) in 2011, the Probability

2018 The Credit Research Initiative (CRI) National University of Singapore First version: March 2, 2017, this version: May 7, 2018 Introduced by the Credit Research Initiative (CRI) in 2011, the Probability

Bankers lose interest!

1 Bankers lose interest! Bankers lose interest! How changing financial regulations affect all investors 1 Bankers lose interest! Contact: Doug Steevens Senior Portfolio Manager +44 (0)20 7086 9312 douglas.steevens@aonhewitt.com

1 Bankers lose interest! Bankers lose interest! How changing financial regulations affect all investors 1 Bankers lose interest! Contact: Doug Steevens Senior Portfolio Manager +44 (0)20 7086 9312 douglas.steevens@aonhewitt.com

JPMORGAN ETFS (IRELAND) ICAV. EUR Ultra-Short Income UCITS ETF. 10 July 2018

ICAV. EUR Ultra-Short Income UCITS ETF. 10 July 2018") JPMORGAN ETFS (IRELAND) ICAV EUR Ultra-Short Income UCITS ETF 10 July 2018 (A sub-fund of JPMorgan ETFs (Ireland) ICAV, an Irish collective asset-management vehicle constituted as an umbrella fund with

JPMORGAN ETFS (IRELAND) ICAV EUR Ultra-Short Income UCITS ETF 10 July 2018 (A sub-fund of JPMorgan ETFs (Ireland) ICAV, an Irish collective asset-management vehicle constituted as an umbrella fund with