Cherry Picking MREITs with Acquisition Potential

|

|

|

- Caroline Burke

- 5 years ago

- Views:

Transcription

1 MREITs Cherry Picking MREITs with Acquisition Potential By The Kenanga Research Team l research@kenanga.com.my NEUTRAL Maintain NEUTRAL. MREITs 2Q16 results were in line, while upsides are seen from major leases expiries in PAVREIT and SUNREIT and earnings risks, if any, have been accounted for. Fundamentals are mostly intact as we expect modest earnings growth from MREITs in our universe with an average of % in FY16-17E. At current levels, MREITs under our coverage are commanding modest gross dividend yields of % in FY17E, while our On Our Radar Top Pick, MQREIT (TB; TP: RM1.35), is commanding superior gross yields of 6.5% in FY17E on stable earnings. Maintain our 10- year MGS target of 3.60%. We reiterate our NEUTRAL view on MREITs as the sector lacks a strong near-term catalyst as most upsides have been priced in, evident from decent YTD gains of % for MREITs under our coverage. However, we recommend investors to look out for selected MREITs with visible acquisition pipeline in FY17, with selected picks on more resilient MREITs with acquisition potential (i.e. PAVREIT, SUNREIT, KLCC, AXREIT), which may lend some excitement to earnings growth should the acquisitions are sizeable and earnings accretive. Preferred MREITs include KLCC (OP; TP: RM8.25), PAVREIT (OP: TP: RM2.15) and SUNREIT (OP; TP: RM1.85) for earnings resiliency from strong asset stability and earnings excitement from acquisition potential. Meanwhile, we have MARKET PERFORM call on AXREIT (TP: RM1.80), CMMT (TP: RM1.65), and IGBREIT (TP: RM1.66). 2Q16 results within expectations, similar to 1Q16. QoQ, bottom-line growth was slightly negative (-2% to -10% RNI QoQ) due to lower topline mostly due to seasonality factors from lower turnover rent, and weaker margins, which was slightly worse off than 1Q16, as expected. YoY, all MREITs saw positive topline and bottom line growth (2%-8% RNI YoY), save for AXREIT, which was down slightly (-3%) on higher operating and financing cost for new acquisitions. MREITs were mostly positive YoY on the back of positive reversions of mid-to-high single digits for leases up for expiry, which was largely within our expectations. As such, we believe fundamentals are intact as we have accounted for mid-to-high single digit reversions for most MREITs under our coverage. All in, we made no changes to earnings as results were in line, which was similar to 1Q16. Our calls and TPs were also unchanged, but we upgraded AXREIT s TP to RM1.80 (from RM1.76) post results on adjustments of valuations for the development of Axis PDI. IGBREIT was the top performer under our coverage. IGBREIT emerged as the top gainer YTD, appreciating by 22.4% to RM1.64 as of report cut-off date (15 th Sep 2016), which we reckon may be due to its asset stability from high occupancy (>99%) and stable double-digit reversions, while gross yield before the share price run-up was fairly attractive at 6.2%, above our MREITs average of 5.8% back then. All in, MREITs under our coverage saw positive YTD gains as investors continue to seek safe havens and stable returns in light of volatile markets, outperforming the FBMKLCI (-2%) and FBM Small Cap (-4%) to date. Note that share prices for both SUNREIT and PAVREIT have also increased by 17.8% and 13.5% YTD, respectively, in line with our OUTPERFORM recommendation throughout MREITs Annual Gains Year KLCC SUNREIT CMMT IGBREIT PAVREIT AXREIT % 24.0% 25.0% -2.9% 27.5% 19.5% % -20.0% -22.2% -10.5% -7.9% -6.4% % 22.6% 2.1% 10.1% 14.1% 23.5% % -3.9% -3.5% 2.3% 6.2% -9.4% 2016 YTD 8.4% 17.8% 10.1% 22.4% 13.5% 3.7% Major renewals for PAVREIT and SUNREIT, which we have accounted for in our estimates. To recap, FY16 is a major lease expiry year for PAVREIT (69.0% of NLA), from Pavilion Shopping Mall (PSM) of which we expect single-digit rental reversions. As such, we anticipate % growth in FY16-17E RNI as the positive reversions will accrete mostly in FY17. Additionally, SUNREIT will experience major lease expiries for two of its largest assets, namely; (i) Sunway Pyramid (56.7% of asset NLA), and (ii) Sunway Carnival (58.0%of asset NLA). Although SUNREITs leases up for expiry in FY17E constitute only22% of portfolio NLA, both these assets make up 67% of SUNREITs gross rental income (GRI) as Sunway Pyramid alone makes up 58.2% of the Groups GRI. Based on our channel checks, the retail segment remains soft in CY16 and likely CY17. Hence, in order to be prudent, we maintain our mid-to-high single-digit reversion in FY17 for the abovementioned assets translating to 3-8% growth in FY17-18E RNI for SUNREIT. Save for PAVREIT and SUNREIT, other MREITs under our coverage have 22-30% of leases up for expiry in FY16, and 18-34% in FY17 of NLA which we have already accounted for in our estimates. As such, we believe fundamentals are mostly intact while we expect modest earnings growth from MREITs in our universe at an average of % in FY16-17E. PP7004/02/2013(031762) Page 1 of 7

2 Asset acquisitions moving at a slower pace than FY15, greenfield development to the rescue. YTD, for MREITs under our coverage, there was only two asset acquisition by AXREIT that totalled RM75.0m vs. five assets in CY15 totalling RM1.2b. The acquisitions by AXREIT in FY16 were small industrial facilities, and we did not see any acquisitions for retail or office assets for MREITs under our coverage. We believe this is likely due to the challenging cap rate environment as REITs are finding it tough to acquire yield accretive assets in the current low cap rate conditions (4-6% cap rates for retail assets and 6-8% for industrial assets). The silver lining is the Securities Commissions (SC) s Proposed MREITs Guidelines, which recently obtained public feedback for a list of 16 new proposals, among which was for the development of greenfield assets. To date, two MREITs (SUNREIT and AXREIT) have already come forward to seek SC s exemption to develop greenfield, with AXREIT targeting to spend RM210.9m on development cost for Axis PDI, while SUNREIT acquired a vacant land adjacent to Sunway Carnival mall in Penang for RM17.2m. Going forward, we believe MREITs would prefer to take on greenfield development (i.e. development cost) instead of asset acquisitions from 3 rd parties due to lower cash capital outlays required. However, greenfield development may only accrete in the long run (over 2-4 years), while near-term earnings excitement will still come from asset acquisitions should the yields are favourable. All in positive on SC s list of Proposals, as we expect news flow primarily related to Proposal 1 to 4 to bode well for share price sentiment and valuations, with minimal impact to earnings in the near term. Overall, besides Proposal 1, Proposals 2 to 4 are expected to be beneficial to unitholders as it is catered towards facilitating earnings growth by increasing the scope of permitted activities by MREITs, making it easier for MREITs to secure tenants or minimise vacant space. We maintain our 10-year MGS target of 3.60%. We expect the 10-year MGS to remain close to current level of 3.60%. We believe the 10-year MGS will remain range bound and close to current levels of 3.59% as; (i) We do not anticipate further downside bias to the 10-year MGS as it is already hovering at 60bps above the current OPR rate of 3.00%, while historical data suggests that the 10-year MGS trades at 70bps on average to the OPR since CY12 (range bound between 50 to 88bps). Going forward, our in-house economist expects OPR rate to be maintained at 3.00% in FY17, as such, we expect minimal downsides to the MGS from here on. (ii) (iii) Additionally, we believe downsides to the 10-year MGS are limited as foreign shareholdings of the MGS have reached an all-time high of 51.9% (vs % over the past four years) which we believe may be due to the fact that investors may have limited options for stable returns. We do not expect significant upsides to the 10-year MGS as markets have already priced in one US Fed rate hike by year end. This concurs with our view that the US Fed will implement at least one interest rate hike by 1Q17, while anything more than one rate hike may prompt us to re-look at our MGS estimates with a slight upside bias. That being said, going forward, we believe US rate hikes will not significantly affect the MGS as the frequency of rate hikes will be minimal and while any increase will be on a gradual basis. 10-yr MGS vs. OPR YTD 2016 CY2015 CY2014 CY2013 CY2012 Average 10-yr MGS Average OPR Foreign Shareholding of the MGS 49.3% 46.4% 45.4% 45.3% 40.9% -Max 51.9% 48.5% 48.4% 48.3% 44.4% -Min 47.1% 43.5% 41.9% 41.4% 38.5% Sensitivity Analysis of MREITs TP's based on 10-yr MGS level 10-yr MGS level (%) KLCC TP SUNREIT CMMT TP AXREIT TP IGBREIT PAVREIT Source: Kenanga Research Maintain NEUTRAL on MREITs, with selected picks on more resilient MREITs with an acquisition potential. The sector lacks a strong near-term catalyst going forward as most upsides have been priced in, evident from decent YTD gains for MREITs under our coverage of % (as of our cut of date on 15 th Sep 2016). As such, we maintain NEUTRAL on MREITs for now, but investors can look out for selected REITs with a visible acquisition pipeline in FY17, (i.e. PAVREIT, SUNREIT, KLCC, AXREIT), which may lend some excitement to earnings growth, should: (i) the acquisitions are sizeable (>5% accretion to bottom-line), (ii) with attractive asset yields (>7.5% NPI yield for industrial assets, >6.5% NPI yield for retail assets). At current levels, MREITs are commanding gross yields of %. (refer to table in page 3) PP7004/02/2013(031762) Page 2 of 7

3 MQREIT (TRADING BUY; TP: RM1.35) our Top Pick. We recently released an On Our Radar report (dated 30 th Sep 2016) on MQREIT with a Trading Buy call as we like the stock for its earnings stability and undemanding valuations. Post placement by 4Q16, MQREIT will move into the large cap MREIT space (>RM1.0b), increasing its market cap to c.rm1.3b (from RM820m) implying better trading liquidity and added institutional shareholding from placements to EPF. However, we believe the stock is still trading at a discount to large cap MREITs, at 6.5% on FY17E gross yields vs % for large cap MREITs under our coverage, albeit its stable earnings profile. Additionally, MQREIT s earnings prospect appears solid due to its stable asset profile as the Group had recently acquired Menara Shell, a fully-tenanted asset with a long-term lease, while existing assets are also on long-term leases (avg. 5 years). Going forward, portfolio occupancy is expected to remain healthy at >97% with minimal lease expiries ( % in FY16-17) capping downside risk, while MQREITs is backed by two sponsors for future acquisitions. We like MQREIT as it warrants 14% total returns) on a conservative ppt spread to our 10-year MGS target of 3.60%. Preferred MREITs under our coverage include KLCC (OP; TP: RM8.25), PAVREIT (OP: TP: RM2.15) and SUNREIT (OP; TP: RM1.85). We continue to like KLCC and PAVREIT for their earnings resiliency as both REITs have maintained strong asset stability, with KLCC s assets on long-term leases (i.e. 15 years) and a triple-net-lease (TNL) basis, while PAVREIT s occupancy is strong at >97%. Additionally, both these REITs have low gearing s ( x), allowing for sizeable acquisitions or greenfield potential based on SC s new proposed guidelines, while further clarity on its asset acquisition pipeline will be a positive re-rating catalyst for the stock. As for SUNREIT, we maintain our OUTPERFORM call for its income contribution from Sunway Putra Place and visible acquisition pipeline, thanks to its parent, SUNWAY. Risks to our call. Factors that may affect our call include: (i) worse-than-expected consumer spending, (ii) cost-push factors that result in weaker-than-expected rental reversions, (iii) U.S. Fed increasing interest rates in a more aggressive manner, and (iv) further decline in oil prices and weaker MYR, which may increase pressure on the 10-year MGS. MREITs Peer Comparison MREITs Last Price as at 15/9/16 GDPS FY Gross Yield based on last price Target Gross Yield Gross yield spread to 10-yr MGS 10-yr MGS targ et Current Call Share price upside Total Returns KLCC FYDec17E 5.2% 4.80% 1.20% 3.60% OP % 12.4% S UNR EIT FYJun17/18E 6.1% 5.70% 2.10% 3.60% OP % 13.3% CM M T FYDec17E 5.9% 5.40% 1.80% 3.60% MP % 14.1% AXR EIT FYDec17E 5.8% 5.45% 1.85% 3.60% MP % 10.9% IGB R EIT FYDec17E 5.3% 5.20% 1.60% 3.60% MP % 5.9% PAVR EIT FYDec17E 5.4% 4.40% 0.80% 3.60% OP % 26.8% Source: Kenanga Research This section is intentionally left blank. PP7004/02/2013(031762) Page 3 of 7

4 Peer Comparison NAME Price (15/9/16) Mkt Cap PER (x) Est. NDiv. Yld. ** Historical ROE P/BV Net Profit (RMm) FY16/17 NP Growth FY17/18 NP Growth (RMm) FY15/16 FY16/17 FY17/18 (%) (%) (x) FY15/16 FY16/17 FY17/18 (%) (%) Target Price Rating M-REIT & PROPERTY INVESTMENT UNDER COVERAGE KLCCSS * , % 9.2% % 6.7% 8.25 OUTPERFORM Pavilion REIT , % 7.4% % 13.0% 2.15 OUTPERFORM IGB REIT* MARKET , % 6.9% % 1.9% 1.66 PERFORM Sunway REIT* , % 8.0% % 6.9% 1.85 OUTPERFORM CapitaMalls (M) Trust* , % 10.5% % 4.8% 1.65 MARKET Axis REIT* , % 7.2% % 5.9% 1.80 * Core NP and Core PER ** KLCCSS, CMMT, AXREIT, PAVREIT and IGBREIT based on FYDec16E and SUNREIT on FYJun17E/FY18E PERFORM MARKET PERFORM CONSENSUS NUMBERS YTL Hospitality REIT , % 3.4% % -13% n.a. BUY Al-'Aqar Healthcare BUY -11% 1% REIT , % 8.0% AmanahRaya REIT % 9.0% % 3% n.a. BUY AmFIRST REIT % 8.0% % 0% n.a. SELL Hektar REIT % 0.5% % 4% 1.57 BUY MRCB-Quill REIT % 7.8% % -5% 1.34 BUY Tower REIT n.a. n.a. n.a. 5.1% n.a. n.a. n.a. n.a. n.a. BUY UOA REIT % 16.4% % 0% n.a. BUY Atrium REIT n.a. n.a. n.a. 6.6% n.a. n.a. n.a. n.a. n.a. BUY Al-Salam REIT n.a % n.a. n.a. n.a n.a. 18% n.a. BUY Source: Kenanga Research PP7004/02/2013(031762) Page 4 of 7

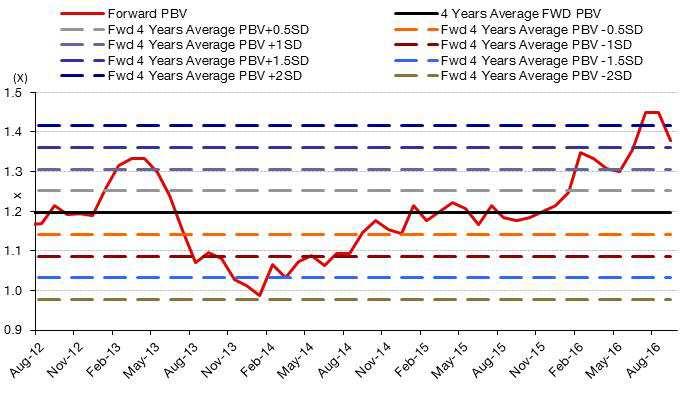

5 MREITS FWD PBV KLCC: Fwd PBV Band SUNREIT: Fwd PBV Band CMMT: Fwd PBV Band AXREIT: Fwd PBV Band IGBREIT: Fwd PBV Band PAVREIT: Fwd PBV Band PP7004/02/2013(031762) Page 5 of 7

6 MREITS FWD PER KLCC: Fwd PER Band SUNREIT: Fwd PER Band CMMT: Fwd PER Band AXREIT: Fwd PER Band IGBREIT: Fwd PER Band PAVREIT: Fwd PER Band PP7004/02/2013(031762) Page 6 of 7

7 Stock Ratings are defined as follows: Stock Recommendations OUTPERFORM : A particular stock s Expected Total Return is MORE than 10% (an approximation to the 5-year annualised Total Return of FBMKLCI of 10.2%). MARKET PERFORM : A particular stock s Expected Total Return is WITHIN the range of 3% to 10%. UNDERPERFORM : A particular stock s Expected Total Return is LESS than 3% (an approximation to the 12-month Fixed Deposit Rate of 3.15% as a proxy to Risk-Free Rate). Sector Recommendations*** OVERWEIGHT : A particular sector s Expected Total Return is MORE than 10% (an approximation to the 5-year annualised Total Return of FBMKLCI of 10.2%). NEUTRAL : A particular sector s Expected Total Return is WITHIN the range of 3% to 10%. UNDERWEIGHT : A particular sector s Expected Total Return is LESS than 3% (an approximation to the 12-month Fixed Deposit Rate of 3.15% as a proxy to Risk-Free Rate). ***Sector recommendations are defined based on market capitalisation weighted average expected total return for stocks under our coverage. This document has been prepared for general circulation based on information obtained from sources believed to be reliable but we do not make any representations as to its accuracy or completeness. Any recommendation contained in this document does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may read this document. This document is for the information of addressees only and is not to be taken in substitution for the exercise of judgement by addressees. Kenanga Investment Bank Berhad accepts no liability whatsoever for any direct or consequential loss arising from any use of this document or any solicitations of an offer to buy or sell any securities. Kenanga Investment Bank Berhad and its associates, their directors, and/or employees may have positions in, and may effect transactions in securities mentioned herein from time to time in the open market or otherwise, and may receive brokerage fees or act as principal or agent in dealings with respect to these companies. Published and printed by: KENANGA INVESTMENT BANK BERHAD (15678-H) 8th Floor, Kenanga International, Jalan Sultan Ismail, Kuala Lumpur, Malaysia Telephone: (603) Facsimile: (603) Website: Chan Ken Yew Head of Research PP7004/02/2013(031762) Page 7 of 7

Axis REIT UNDERPERFORM. Splitting for Better Liquidity. Quick Bites. Price /Ex-Price: RM3.55/RM1.78 TP/Ex-Split: RM3.27/RM1.64

Axis REIT Splitting for Better Liquidity By Sarah Lim l sarahlim@kenanga.com.my News Proposed a 1:2 share split, essentially doubling its unit base from 547.8m to 1.1b units. Comments We were positively

Axis REIT Splitting for Better Liquidity By Sarah Lim l sarahlim@kenanga.com.my News Proposed a 1:2 share split, essentially doubling its unit base from 547.8m to 1.1b units. Comments We were positively

NEUTRAL. MREITs. 2QCY14 Inline, Door Still Open For European QE

MREITs 2QCY14 Inline, Door Still Open For European QE By Sarah Lim l sarahlim@kenanga.com.my NEUTRAL We downgrade MREITs to NEUTRAL. MREITs 2QCY14 results were mostly inline, with the exception of AXREIT.

MREITs 2QCY14 Inline, Door Still Open For European QE By Sarah Lim l sarahlim@kenanga.com.my NEUTRAL We downgrade MREITs to NEUTRAL. MREITs 2QCY14 results were mostly inline, with the exception of AXREIT.

MARKET PERFORM. FY15 Below Expectations. Results Note. Price: RM1.21 Target Price: RM1.39. By The Kenanga Research Team /

MRCB FY15 Below Expectations By The Kenanga Research Team / research@kenanga.com.my Period Actual vs. Expectations 4Q15/FY15 FY15 core net loss of RM74.7m was below market and our core net profit expectations

MRCB FY15 Below Expectations By The Kenanga Research Team / research@kenanga.com.my Period Actual vs. Expectations 4Q15/FY15 FY15 core net loss of RM74.7m was below market and our core net profit expectations

Malaysian Resources Corp

Malaysian Resources Corp Sunnier Days By Adrian Ng l adrian.ng@kenanga.com.my FY17 CNP of RM101.2m came in above our, but below consensus, full-year estimates, at 130%/91%. Property sales of RM1.4b also

Malaysian Resources Corp Sunnier Days By Adrian Ng l adrian.ng@kenanga.com.my FY17 CNP of RM101.2m came in above our, but below consensus, full-year estimates, at 130%/91%. Property sales of RM1.4b also

Pharmaniaga MARKET PERFORM. 1Q15 Inline but Rich Valuations. Results Note. Price: RM6.91 Target Price: RM6.95. PP7004/02/2013(031762) Page 1 of 5

Page 1 of 5") Pharmaniaga 1Q15 Inline but Rich Valuations By the Kenanga Research Team l research@kenanga.com.my Period 1Q15 Actual vs. Expectations 1Q15 PATAMI of RM31.8m (+21% YoY) came in at 32% and 31% of our and

Pharmaniaga 1Q15 Inline but Rich Valuations By the Kenanga Research Team l research@kenanga.com.my Period 1Q15 Actual vs. Expectations 1Q15 PATAMI of RM31.8m (+21% YoY) came in at 32% and 31% of our and

A Weak Quarter. Results Note. Price: RM3.70 Target Price: RM3.70. By Sarah Lim l PP7004/02/2013(031762) Page 1 of 5

Page 1 of 5") IJM Land Berhad A Weak Quarter By Sarah Lim l sarahlim@kenanga.com.my Period 3Q15/9M15 OUTPERFORM Share Price Performance Price: RM3.70 Target Price: RM3.70 Actual vs. Expectations Dividends Key Results

IJM Land Berhad A Weak Quarter By Sarah Lim l sarahlim@kenanga.com.my Period 3Q15/9M15 OUTPERFORM Share Price Performance Price: RM3.70 Target Price: RM3.70 Actual vs. Expectations Dividends Key Results

Sunway Berhad. OUTPERFORM Price: RM2.65 Target Price: RM3.08 KENANGA RESEARCH. Within expectations. Results Note KENANGA RESEARCH.

Results Note 02 December 2013 Sunway Berhad Within expectations Period 3Q13 / 9M13 Actual vs. Expectations Dividends None as expected. Key Results Highlights At 73% of our full-year FY13 estimates, the

Results Note 02 December 2013 Sunway Berhad Within expectations Period 3Q13 / 9M13 Actual vs. Expectations Dividends None as expected. Key Results Highlights At 73% of our full-year FY13 estimates, the

Below Expectations. Results Note. Price: RM6.95 Target Price: RM4.89. By Desmond Chong l PP7004/02/2013(031762) Page 1 of 5

Page 1 of 5") UMW Holdings Below Expectations By Desmond Chong l cwchong@kenanga.com.my Period Actual vs. Expectations Dividends Key Result Highlights 4Q15 / FY15 Below expectations. The group reported 4Q15 normalised

UMW Holdings Below Expectations By Desmond Chong l cwchong@kenanga.com.my Period Actual vs. Expectations Dividends Key Result Highlights 4Q15 / FY15 Below expectations. The group reported 4Q15 normalised

Rough Start. Results Note. Price: RM5.40 Target Price: RM4.95. By Desmond Chong l

UMW Holdings Rough Start By Desmond Chong l cwchong@kenanga.com.my 1Q16 core PATAMI of RM16.9m (>100% QoQ; -90% YoY) came in way below estimates, making up only 5% of both our and consensus estimates.

UMW Holdings Rough Start By Desmond Chong l cwchong@kenanga.com.my 1Q16 core PATAMI of RM16.9m (>100% QoQ; -90% YoY) came in way below estimates, making up only 5% of both our and consensus estimates.

Rubber Glove KENANGA RESEARCH NEUTRAL. Resilient sales volume growth in Sector Update KENANGA RESEARCH PP7004/02/2013(031762)

") Sector Update 03 April 2013 Rubber Glove Resilient sales volume growth in 2012 NEUTRAL We maintain a Neutral rating on the rubber glove sector. According to Malaysian Rubber Export Promotion Council (MREPC)

Sector Update 03 April 2013 Rubber Glove Resilient sales volume growth in 2012 NEUTRAL We maintain a Neutral rating on the rubber glove sector. According to Malaysian Rubber Export Promotion Council (MREPC)

Above Expectations. Results Note. Price: RM1.69 Target Price: RM1.85. By Adrian Ng l

WCT Holdings Bhd Above Expectations By Adrian Ng l adrian.ng@kenanga.com.my 1Q16 core net profit (C) of RM32.0m came in above our but within consensus expectations accounting for 37% and 22% of estimates,

WCT Holdings Bhd Above Expectations By Adrian Ng l adrian.ng@kenanga.com.my 1Q16 core net profit (C) of RM32.0m came in above our but within consensus expectations accounting for 37% and 22% of estimates,

Braving tough times. Company Update. Price: RM3.06. Target Price of RM3.23.

Sunway Berhad MARKET Price: RM3.06 Braving tough times Target Price: RM3.23 By Adrian Ng l adrian.ng@kenanga.com.my; Sarah Lim l sarahlim@kenanga.com.my Yesterday, we attended SUNWAY s briefing hosted

Sunway Berhad MARKET Price: RM3.06 Braving tough times Target Price: RM3.23 By Adrian Ng l adrian.ng@kenanga.com.my; Sarah Lim l sarahlim@kenanga.com.my Yesterday, we attended SUNWAY s briefing hosted

Shaping a Sustainable Future

Sunway Berhad MARKET PERFORM Cum/Ex-Price: RM3.73/RM1.60 Shaping a Sustainable Future Cum/Ex-Target Price: RM3.87/RM1.66 By Adrian Ng l adrian.ng@kenanga.com.my; Sarah Lim l sarahlim@kenanga.com.my We

Sunway Berhad MARKET PERFORM Cum/Ex-Price: RM3.73/RM1.60 Shaping a Sustainable Future Cum/Ex-Target Price: RM3.87/RM1.66 By Adrian Ng l adrian.ng@kenanga.com.my; Sarah Lim l sarahlim@kenanga.com.my We

All About Valuations. Sector Update

Sector Update Construction All About Valuations By Adrian Ng l adrian.ng@kenanga.com.my NEUTRAL We reiterate our NEUTRAL call on the sector due to: (i) slow contract award news flow for 017, (ii) heightened

Sector Update Construction All About Valuations By Adrian Ng l adrian.ng@kenanga.com.my NEUTRAL We reiterate our NEUTRAL call on the sector due to: (i) slow contract award news flow for 017, (ii) heightened

Held Back in Anticipation of 2017 Budget

Automotive Held Back in Anticipation of 2017 Budget By the Kenanga Research Team l research@kenanga.com.my UNDERWEIGHT We maintain our UNDERWEIGHT rating on the AUTOMOTIVE sector given the outweighing

Automotive Held Back in Anticipation of 2017 Budget By the Kenanga Research Team l research@kenanga.com.my UNDERWEIGHT We maintain our UNDERWEIGHT rating on the AUTOMOTIVE sector given the outweighing

Small Acquisition in Bangsar South

UOA Development Bhd Small Acquisition in Bangsar South By Sarah Lim l sarahlim@kenanga.com.my News UOAD announced that it has acquired 2 ordinary shares of RM1.00 each in Fabullane Development S/B which

UOA Development Bhd Small Acquisition in Bangsar South By Sarah Lim l sarahlim@kenanga.com.my News UOAD announced that it has acquired 2 ordinary shares of RM1.00 each in Fabullane Development S/B which

George Kent (M) Bhd Broadly Within

Bhd Broadly Within") George Kent (M) Bhd Broadly Within 1Q19 C of RM18.9m came in broadly within expectations at 13% each of our/consensus estimates. No dividends declared, as expected. No changes to FY19-20E earnings. Upgrade

George Kent (M) Bhd Broadly Within 1Q19 C of RM18.9m came in broadly within expectations at 13% each of our/consensus estimates. No dividends declared, as expected. No changes to FY19-20E earnings. Upgrade

Dismal 2Q15. Results Note. Price: RM8.49 Target Price: RM8.93. By Desmond Chong l PP7004/02/2013(031762) Page 1 of 6

Page 1 of 6") UMW Holdings Dismal 2Q15 By Desmond Chong l cwchong@kenanga.com.my Period 2Q15/ 1H15 Actual vs. Expectations Below expectations. The group reported 2Q15 normalised PATAMI of RM70.4m (-60% QoQ and YoY),

UMW Holdings Dismal 2Q15 By Desmond Chong l cwchong@kenanga.com.my Period 2Q15/ 1H15 Actual vs. Expectations Below expectations. The group reported 2Q15 normalised PATAMI of RM70.4m (-60% QoQ and YoY),

Below Expectations. Results Note. Price: RM8.28 Target Price: RM6.73. By Desmond Chong l PP7004/02/2013(031762) Page 1 of 6

Page 1 of 6") UMW Holdings Below Expectations By Desmond Chong l cwchong@kenanga.com.my Period 3Q15/9M15 Actual vs. Expectations Below expectations. The group reported 3Q15 normalised PATAMI of RM81.7m (+54% QoQ and

UMW Holdings Below Expectations By Desmond Chong l cwchong@kenanga.com.my Period 3Q15/9M15 Actual vs. Expectations Below expectations. The group reported 3Q15 normalised PATAMI of RM81.7m (+54% QoQ and

Look Out for Delivery

Sector Update Construction Look Out for Delivery By Adrian Ng l adrian.ng@kenanga.com.my NEUTRAL We reiterate our NEUTRAL call on the sector due to: (i) slower contract award news flow for 017, (ii) heightened

Sector Update Construction Look Out for Delivery By Adrian Ng l adrian.ng@kenanga.com.my NEUTRAL We reiterate our NEUTRAL call on the sector due to: (i) slower contract award news flow for 017, (ii) heightened

Hua Yang Berhad OUTPERFORM KENANGA RESEARCH. Affordable Housing Advantage. Company Update. Target Price: RM2.91 KENANGA RESEARCH

Company Update 29 October 2013 Hua Yang Berhad OUTPERFORM Price: RM2.11 Affordable Housing Advantage Target Price: RM2.91 HUAYANG held a briefing yesterday which reaffirmed our positive view based on these

Company Update 29 October 2013 Hua Yang Berhad OUTPERFORM Price: RM2.11 Affordable Housing Advantage Target Price: RM2.91 HUAYANG held a briefing yesterday which reaffirmed our positive view based on these

Replenishes in Landbank in KL

Sunway Berhad MARKET PERFORM Cum/Ex-Price : RM3.93/RM1.68 Replenishes in Landbank in KL Cum/Ex-Target Price : RM3.87/RM1.66 By Adrian Ng l adrian.ng@kenanga.com.my; Sarah Lim l sarahlim@kenanga.com.my

Sunway Berhad MARKET PERFORM Cum/Ex-Price : RM3.93/RM1.68 Replenishes in Landbank in KL Cum/Ex-Target Price : RM3.87/RM1.66 By Adrian Ng l adrian.ng@kenanga.com.my; Sarah Lim l sarahlim@kenanga.com.my

Dijaya Corporation Berhad

Quick Bites 16 April 2013 Dijaya Corporation Berhad OUTPERFORM Price: RM1.55 Landbanking in Kota Kemuning Target Price: RM2.15 News Proposed acquisition cum development of 1,172ac land in Kota Kemuning

Quick Bites 16 April 2013 Dijaya Corporation Berhad OUTPERFORM Price: RM1.55 Landbanking in Kota Kemuning Target Price: RM2.15 News Proposed acquisition cum development of 1,172ac land in Kota Kemuning

Sunway Iskandar: Where Living Takes Place

OUTPERFORM Price: RM3.21 Sunway Iskandar: Where Living Takes Place Target Price: RM3.62 By Sarah Lim l sarahlim@kenanga.com.my; Adrian Ng l adrian.ng@kenanga.com.my We visited (SUNWAY) s flagship development

OUTPERFORM Price: RM3.21 Sunway Iskandar: Where Living Takes Place Target Price: RM3.62 By Sarah Lim l sarahlim@kenanga.com.my; Adrian Ng l adrian.ng@kenanga.com.my We visited (SUNWAY) s flagship development

Ho Hup Construction RESEARCH. I m Back! On Our Radar. Kenanga Trading Buy RM1.55 Consensus N.A. N.A. KENANGA RESEARCH.

RESEARCH On Our Radar 31 December 2013 Ho Hup Construction I m Back! INVESTMENT MERIT Coming Back. HOHUP is poised to make a comeback after an extended break from the property & construction scene following

RESEARCH On Our Radar 31 December 2013 Ho Hup Construction I m Back! INVESTMENT MERIT Coming Back. HOHUP is poised to make a comeback after an extended break from the property & construction scene following

On Our Radar Review - Property

Review - Property Calling it A Day By the Kenanga Research Team l research@kenanga.com.my The property sector is expected to remain challenging for the year due to tighter lending liquidity, potential

Review - Property Calling it A Day By the Kenanga Research Team l research@kenanga.com.my The property sector is expected to remain challenging for the year due to tighter lending liquidity, potential

Hua Yang Berhad OUTPERFORM KENANGA RESEARCH. 1 st Landbanking in FY14. Quick Bites. Price: RM3.09. Target Price: RM3.52 KENANGA RESEARCH.

Quick Bites 18 June 2013 Hua Yang Berhad OUTPERFORM Price: RM3.09 1 st Landbanking in FY14 Target Price: RM3.52 News Proposed acquisition of 3.73ac in Sri Kembangan for RM56.9m or RM250psf. The land is

Quick Bites 18 June 2013 Hua Yang Berhad OUTPERFORM Price: RM3.09 1 st Landbanking in FY14 Target Price: RM3.52 News Proposed acquisition of 3.73ac in Sri Kembangan for RM56.9m or RM250psf. The land is

Attractive and Stable Yields

MRCB-Quill REIT Attractive and Stable Yields By Marie Vaz l msvaz@kenanga.com.my We are initiating coverage on MRCB-Quill REIT (MQREIT) s with an OUTPERFORM call and TP of RM1.41. MQREIT s earnings prospect

MRCB-Quill REIT Attractive and Stable Yields By Marie Vaz l msvaz@kenanga.com.my We are initiating coverage on MRCB-Quill REIT (MQREIT) s with an OUTPERFORM call and TP of RM1.41. MQREIT s earnings prospect

Malaysia Bond Flows Update

Malaysia Bond Flows Update Foreign net selloff lower in August, foreign buying to increase on improving fundamentals Economics Kenanga Investment Bank Berhad T: 603-2172 0880 OVERVIEW Foreign selloff moderated.

Malaysia Bond Flows Update Foreign net selloff lower in August, foreign buying to increase on improving fundamentals Economics Kenanga Investment Bank Berhad T: 603-2172 0880 OVERVIEW Foreign selloff moderated.

Not Rated Thiam Chiann Wen ext:1664

MENARA TA ONE, 22 JALAN P. RAMLEE, 50250 KUALA LUMPUR, MALAYSIA TEL: +603-20721277 / FAX: +603-20325048 IPO Monday, 3 September 2012 FBM KLCI: 1,646.11 Sector: REIT IGB Real Estate Investment Trust Fair

MENARA TA ONE, 22 JALAN P. RAMLEE, 50250 KUALA LUMPUR, MALAYSIA TEL: +603-20721277 / FAX: +603-20325048 IPO Monday, 3 September 2012 FBM KLCI: 1,646.11 Sector: REIT IGB Real Estate Investment Trust Fair

Not Going Anywhere Yet

Not Going Anywhere Yet By Sean Lim Ooi Leong l sean.lim@kenanga.com.my NEUTRAL Volatile oil prices are expected to stay despite recent recovery from the bottom premised on slower supply-demand rebalancing

Not Going Anywhere Yet By Sean Lim Ooi Leong l sean.lim@kenanga.com.my NEUTRAL Volatile oil prices are expected to stay despite recent recovery from the bottom premised on slower supply-demand rebalancing

Sunway Berhad OUTPERFORM RESEARCH. Penang Expansion. Quick Bites. Target Price: RM3.08 KENANGA RESEARCH. 18 December 2013

RESEARCH Quick Bites 18 December 2013 Sunway Berhad OUTPERFORM Price: RM2.64 Penang Expansion Target Price: RM3.08 News SUNWAY s wholly-owned subsidiary, Sunway City (Penang), has proposed to acquire 24.5ac,

RESEARCH Quick Bites 18 December 2013 Sunway Berhad OUTPERFORM Price: RM2.64 Penang Expansion Target Price: RM3.08 News SUNWAY s wholly-owned subsidiary, Sunway City (Penang), has proposed to acquire 24.5ac,

NAGA Warrants 2017 Seventh Issuance

2017 Seventh Issuance Index-linked Structured Warrants for Trading Relief Rebound By Lawrence Yeo Eng Chien l lawrenceyeo@kenanga.com.my Just last week, all three major US indices (the Dow, S&P500 and

2017 Seventh Issuance Index-linked Structured Warrants for Trading Relief Rebound By Lawrence Yeo Eng Chien l lawrenceyeo@kenanga.com.my Just last week, all three major US indices (the Dow, S&P500 and

NAGA Warrants 2016 Final Issuance

NAGA Warrants 2016 Final Issuance Positioning for Year-end Window Dressing By the Kenanga Research Team l research@kenanga.com.my Unless the FBMKLCI miraculously climbs beyond the 1,692 mark next week,

NAGA Warrants 2016 Final Issuance Positioning for Year-end Window Dressing By the Kenanga Research Team l research@kenanga.com.my Unless the FBMKLCI miraculously climbs beyond the 1,692 mark next week,

Topline Driven Growth BUY. Last Traded: RM4.19

C O M P A N Y U P D A T E Wednesday, March 14, 2018 FBMKLCI: 1,864.03 Sector: Finance THIS REPORT IS STRICTLY FOR INTERNAL CIRCULATION ONLY* AMMB Holdings Berhad TP: RM4.70 (+12.2%) Topline Driven Growth

C O M P A N Y U P D A T E Wednesday, March 14, 2018 FBMKLCI: 1,864.03 Sector: Finance THIS REPORT IS STRICTLY FOR INTERNAL CIRCULATION ONLY* AMMB Holdings Berhad TP: RM4.70 (+12.2%) Topline Driven Growth

Buying Titiwangsa Land

Mah Sing Group Berhad Buying Titiwangsa Land By Sarah Lim l sarahlim@kenanga.com.my Proposed acquisition of 3.56 ac freehold residential land in Titiwangsa, KL for RM60m. The TOD project will be an affordable

Mah Sing Group Berhad Buying Titiwangsa Land By Sarah Lim l sarahlim@kenanga.com.my Proposed acquisition of 3.56 ac freehold residential land in Titiwangsa, KL for RM60m. The TOD project will be an affordable

Market Access. M&A Securities. Results Review 1Q15. Malayan Banking Bhd BUY (TP: RM10.70) Stabilizing Period. Results Review

Stabilizing Period. Results Review") M&A Securities Results Review 1Q15 PP14767/09/2012(030761) Malayan Banking Bhd BUY (TP: RM10.70) Friday, May 29, 2015 Stabilizing Period Results Review Actual vs. expectation. Malayan Banking Berhad (Maybank)

M&A Securities Results Review 1Q15 PP14767/09/2012(030761) Malayan Banking Bhd BUY (TP: RM10.70) Friday, May 29, 2015 Stabilizing Period Results Review Actual vs. expectation. Malayan Banking Berhad (Maybank)

Market Access. M&A Securities. Results Review (1Q15) TSH Resources Berhad HOLD (TP: RM2.38) A Tough Quarter - More Room to Grow.

TSH Resources Berhad HOLD (TP: RM2.38) A Tough Quarter - More Room to Grow.") M&A Securities Results Review (1Q15) PP14767/09/2012(030761) TSH Resources Berhad Thursday, May 21, 2015 HOLD (TP: RM2.38) A Tough Quarter - More Room to Grow Results Review Actual vs. expectations. TSH

M&A Securities Results Review (1Q15) PP14767/09/2012(030761) TSH Resources Berhad Thursday, May 21, 2015 HOLD (TP: RM2.38) A Tough Quarter - More Room to Grow Results Review Actual vs. expectations. TSH

Introduction. to Real Estate Investment Trust ( REIT )

") Introduction [ TOPIC ] to Real Estate Investment Trust [ DATE ] ( REIT ) 28 April 2012 DISCLAIMER This presentation may contain forward-looking statements that involve risks and uncertainties. Actual future

Introduction [ TOPIC ] to Real Estate Investment Trust [ DATE ] ( REIT ) 28 April 2012 DISCLAIMER This presentation may contain forward-looking statements that involve risks and uncertainties. Actual future

Sime Darby SIME MK Sector: Plantation

9MFY17 results below expectations SIME s 9MFY17 core net profit of RM1.58bn (+64.2% yoy) came in below expectations. The variance was mainly due to a lower-thanexpected contribution from the property and

9MFY17 results below expectations SIME s 9MFY17 core net profit of RM1.58bn (+64.2% yoy) came in below expectations. The variance was mainly due to a lower-thanexpected contribution from the property and

NAGA Warrants 2017 Sixth Issuance

2017 Sixth Issuance Buy on Weakness at 1,720-1,750 Zone By Lawrence Yeo Eng Chien l lawrenceyeo@kenanga.com.my Despite gains in regional markets and the US markets climbing to fresh record highs, the Malaysian

2017 Sixth Issuance Buy on Weakness at 1,720-1,750 Zone By Lawrence Yeo Eng Chien l lawrenceyeo@kenanga.com.my Despite gains in regional markets and the US markets climbing to fresh record highs, the Malaysian

On Our Technical Watch

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Index Basic Data 52-week High 1,729.13 (in Million) 52-week Low 1,600.92 KLCI Vol 85.75 Current Level 1,665.32 Bursa

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Index Basic Data 52-week High 1,729.13 (in Million) 52-week Low 1,600.92 KLCI Vol 85.75 Current Level 1,665.32 Bursa

Not Rated Thiam Chiann Wen Tel:

MENARA TA ONE, 22 JALAN P. RAMLEE, 50250 KUALA LUMPUR, MALAYSIA TEL: +603-20721277 / FAX: +603-20325048 IPO Thursday, 10 Sept 2015 FBM KLCI: 1,603.36 Sector: REIT Al-Salam Real Estate Investment Trust

MENARA TA ONE, 22 JALAN P. RAMLEE, 50250 KUALA LUMPUR, MALAYSIA TEL: +603-20721277 / FAX: +603-20325048 IPO Thursday, 10 Sept 2015 FBM KLCI: 1,603.36 Sector: REIT Al-Salam Real Estate Investment Trust

Market Access. Results Review 1Q16. M&A Securities. Digi.Com Berhad. Equipped for Competition BUY (TP:RM5.75) Results Review

Results Review") M&A Securities Results Review 1Q16 PP14767/09/2012(030761) Digi.Com Berhad BUY (TP:RM5.75) Monday, April 25, 2016 Equipped for Competition Results Review Actual vs. expectations. Digi.Com (Digi) started

M&A Securities Results Review 1Q16 PP14767/09/2012(030761) Digi.Com Berhad BUY (TP:RM5.75) Monday, April 25, 2016 Equipped for Competition Results Review Actual vs. expectations. Digi.Com (Digi) started

On Our Technical Watch

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Index Basic Data 52-week High 1,729.13 (in Million) 52-week Low 1,600.92 KLCI Vol 199.37 Current Level 1,662.92 Bursa

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Index Basic Data 52-week High 1,729.13 (in Million) 52-week Low 1,600.92 KLCI Vol 199.37 Current Level 1,662.92 Bursa

Market Access. Results Review (4Q14) M&A Securities. Genting Plantations Berhad. Hit by Plantation-Malaysia Segment. Thursday, May 28, 2015

M&A Securities. Genting Plantations Berhad. Hit by Plantation-Malaysia Segment. Thursday, May 28, 2015") M&A Securities Results Review (4Q14) PP14767/09/2012(030761) Genting Plantations Berhad Thursday, May 28, 2015 HOLD (TP: RM10.77) Hit by Plantation-Malaysia Segment Results Review Actual vs. expectations.

M&A Securities Results Review (4Q14) PP14767/09/2012(030761) Genting Plantations Berhad Thursday, May 28, 2015 HOLD (TP: RM10.77) Hit by Plantation-Malaysia Segment Results Review Actual vs. expectations.

KLCCP Stapled Group. Financial Results 1st Quarter ended 31 March May 2015

KLCCP Stapled Group Financial Results 1st Quarter ended 31 March 2015 5 May 2015 Disclaimer These materials contain historical information of the Company which should not be regarded as an indication of

KLCCP Stapled Group Financial Results 1st Quarter ended 31 March 2015 5 May 2015 Disclaimer These materials contain historical information of the Company which should not be regarded as an indication of

Sime Darby SIME MK Sector: Plantation

A good end to the year Sime Darby s (SIME) FY17 core net profit of RM2.69bn (+1.4% yoy) came in above expectations. The variance was mainly due to higherthan-expected contribution from the plantation and

A good end to the year Sime Darby s (SIME) FY17 core net profit of RM2.69bn (+1.4% yoy) came in above expectations. The variance was mainly due to higherthan-expected contribution from the plantation and

Petra Energy PENB MK Sector: Oil & Gas

Small hiccup, turnaround remains in motion Petra Energy (PENB) remains a strong contender to win the upcoming modification, construction and maintenance (MCM) contract from Petronas, which is to be split

Small hiccup, turnaround remains in motion Petra Energy (PENB) remains a strong contender to win the upcoming modification, construction and maintenance (MCM) contract from Petronas, which is to be split

Market Access. M&A Securities. Results Review 1Q16. Malayan Banking Berhad. Hampered by Loan Loss. Monday, May 30, 2016 HOLD (TP: RM9.

M&A Securities Results Review 1Q16 PP14767/09/2012(030761) Malayan Banking Berhad Monday, May 30, 2016 HOLD (TP: RM9.10) Hampered by Loan Loss Results Review Actual vs. expectations. Malayan Banking Bhd

M&A Securities Results Review 1Q16 PP14767/09/2012(030761) Malayan Banking Berhad Monday, May 30, 2016 HOLD (TP: RM9.10) Hampered by Loan Loss Results Review Actual vs. expectations. Malayan Banking Bhd

MMC MMC MK Sector: Utilities

Weakness continues into 2Q MMC reported a lacklustre set of earnings for 1H17, as PATAMI of RM118m (-3 yoy) was below expectations. 1H17 results constituted 22% of our and consensus full year forecast.

Weakness continues into 2Q MMC reported a lacklustre set of earnings for 1H17, as PATAMI of RM118m (-3 yoy) was below expectations. 1H17 results constituted 22% of our and consensus full year forecast.

Likely To Miss Earnings KPI

UEM Sunrise Likely To Miss Earnings KPI By Sarah Lim l sarahlim@kenanga.com.my MARKET PERFORM Last Price: RM1.18 Target Price: RM1.28 Period Actual vs. Expectations Dividends Key Results Highlights Outlook

UEM Sunrise Likely To Miss Earnings KPI By Sarah Lim l sarahlim@kenanga.com.my MARKET PERFORM Last Price: RM1.18 Target Price: RM1.28 Period Actual vs. Expectations Dividends Key Results Highlights Outlook

Banking Sector. (Neutral) Higher Assets Yield Offers Brighter Income Prospects

Higher Assets Yield Offers Brighter Income Prospects") M&A Securities Sector Update: Banking PP14767/09/2012(030761) Wednesday, June 08, 2016 Banking Sector (Neutral) Higher Assets Yield Offers Brighter Income Prospects Banking sector underperformed in 1Q16

M&A Securities Sector Update: Banking PP14767/09/2012(030761) Wednesday, June 08, 2016 Banking Sector (Neutral) Higher Assets Yield Offers Brighter Income Prospects Banking sector underperformed in 1Q16

Bumi Armada BAB MK Sector: Oil & Gas

Clearer skies from here on BAB reported a 2Q17 revenue of RM694.4m (+71.8% qoq, +72.4% yoy) and headline profit of RM116.6m (+142.3% qoq, +122.5% yoy). After adjusting for the one-offs (big-ticket items

Clearer skies from here on BAB reported a 2Q17 revenue of RM694.4m (+71.8% qoq, +72.4% yoy) and headline profit of RM116.6m (+142.3% qoq, +122.5% yoy). After adjusting for the one-offs (big-ticket items

Market Access. Results Review (2Q15) M&A Securities. Genting Plantations Berhad. Hit by Plantation-Malaysia Segment. Wednesday, August 26, 2015

M&A Securities. Genting Plantations Berhad. Hit by Plantation-Malaysia Segment. Wednesday, August 26, 2015") M&A Securities Results Review (2Q15) PP14767/09/2012(030761) Genting Plantations Berhad Wednesday, August 26, 2015 HOLD (TP: RM9.66) Hit by Plantation-Malaysia Segment Results Review Actual vs. expectations.

M&A Securities Results Review (2Q15) PP14767/09/2012(030761) Genting Plantations Berhad Wednesday, August 26, 2015 HOLD (TP: RM9.66) Hit by Plantation-Malaysia Segment Results Review Actual vs. expectations.

CIMB Group Holdings Berhad TP: RM7.50 (+8.4%) Sluggishness All Around

Sluggishness All Around") A Member of the TA Group MENARA TA ONE, 22 JALAN P. RAMLEE, 50250 KUALA LUMPUR, MALAYSIA TEL: +603-20721277 / FAX: +603-20325048 COMPANY UPDATE Wednesday, August 13, 2014 FBM KLCI: 1,850.39 Sector: Finance

A Member of the TA Group MENARA TA ONE, 22 JALAN P. RAMLEE, 50250 KUALA LUMPUR, MALAYSIA TEL: +603-20721277 / FAX: +603-20325048 COMPANY UPDATE Wednesday, August 13, 2014 FBM KLCI: 1,850.39 Sector: Finance

CapitaLand & REITs Corporate Day, Bangkok. CapitaLand Malaysia Mall Trust Corporate Presentation

CapitaLand & REITs Corporate Day, Bangkok CapitaLand Malaysia Mall Trust Corporate Presentation 0 17 August 2018 Disclaimer These materials may contain forward-looking statements that involve assumptions,

CapitaLand & REITs Corporate Day, Bangkok CapitaLand Malaysia Mall Trust Corporate Presentation 0 17 August 2018 Disclaimer These materials may contain forward-looking statements that involve assumptions,

Building Materials. By Lum Joe Shen / ; Voon Yee Ping, CFA /

Building Materials Heavy on Metal NEUTRAL By Lum Joe Shen / lumjs@kenanga.com.my ; Voon Yee Ping, CFA / voonyp@kenanga.com.my Overall, we maintain our NEUTRAL view on the Building Materials sector despite

Building Materials Heavy on Metal NEUTRAL By Lum Joe Shen / lumjs@kenanga.com.my ; Voon Yee Ping, CFA / voonyp@kenanga.com.my Overall, we maintain our NEUTRAL view on the Building Materials sector despite

PUBLIC INVESTMENT BANK

PUBLIC INVESTMENT BANK PublicInvest Research Results Review Wednesday, February 28, 2018 KDN PP17686/03/2013(032117) PRESTARIANG Outperform DESCRIPTION An ICT service provider focusing on ICT training

PUBLIC INVESTMENT BANK PublicInvest Research Results Review Wednesday, February 28, 2018 KDN PP17686/03/2013(032117) PRESTARIANG Outperform DESCRIPTION An ICT service provider focusing on ICT training

On Our Technical Watch

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,757.99 (in Million) 52-week Low 1,611.88 KLCI Vol 137.65 Current Level 1,754.42 Bursa Vol

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,757.99 (in Million) 52-week Low 1,611.88 KLCI Vol 137.65 Current Level 1,754.42 Bursa Vol

On Our Technical Watch

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,759.76 (in Million) 52-week Low 1,611.88 KLCI Vol 140.99 Current Level 1,738.18 Bursa Vol

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,759.76 (in Million) 52-week Low 1,611.88 KLCI Vol 140.99 Current Level 1,738.18 Bursa Vol

Financial Results for 3 rd Quarter November 2017

Financial Results for 3 rd Quarter 2017 2 November 2017 Important Notice This presentation shall be read in conjunction with OUE Commercial REIT s Financial Results announcement for 3Q 2017 dated 2 November

Financial Results for 3 rd Quarter 2017 2 November 2017 Important Notice This presentation shall be read in conjunction with OUE Commercial REIT s Financial Results announcement for 3Q 2017 dated 2 November

Uchi Tech UCHI MK Sector: Technology

Still all about its yields Uchi s stock price has righfully re-rated over the past 2 years on its attractive valuations and above-average dividend yields. While the latter remains attractive at just under

Still all about its yields Uchi s stock price has righfully re-rated over the past 2 years on its attractive valuations and above-average dividend yields. While the latter remains attractive at just under

On Our Technical Watch

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,759.76 (in Million) 52-week Low 1,611.88 KLCI Vol 129.13 Current Level 1,740.60 Bursa Vol

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,759.76 (in Million) 52-week Low 1,611.88 KLCI Vol 129.13 Current Level 1,740.60 Bursa Vol

Hong Leong Bank Berhad Surprised provisions but better to be prudent

25 August 2017 4QFY17 Results Review Hong Leong Bank Berhad Surprised provisions but better to be prudent Revert to NEUTRAL Unchanged Target Price (TP): RM15.70 INVESTMENT HIGHLIGHTS FY17 was slightly

25 August 2017 4QFY17 Results Review Hong Leong Bank Berhad Surprised provisions but better to be prudent Revert to NEUTRAL Unchanged Target Price (TP): RM15.70 INVESTMENT HIGHLIGHTS FY17 was slightly

PUBLIC INVESTMENT BANK

PublicInvest Research Sector Update Friday, July 14, 2017 KDN PP17686/03/2013(032117) Property Neutral FBM PROPERTY INDEX (m) Volume (m) KLPRP Index 600 500 400 300 200 100 0 Jul-16 Aug-16 Oct-16 Nov-16

PublicInvest Research Sector Update Friday, July 14, 2017 KDN PP17686/03/2013(032117) Property Neutral FBM PROPERTY INDEX (m) Volume (m) KLPRP Index 600 500 400 300 200 100 0 Jul-16 Aug-16 Oct-16 Nov-16

Market Access. Results Review 4Q15. M&A Securities. Digi.Com Berhad. Survives the Headwinds BUY (TP:RM5.90) Results Review

Results Review") M&A Securities Results Review 4Q15 PP14767/09/2012(030761) Digi.Com Berhad BUY (TP:RM5.90) Wednesday, February 10, 2016 Results Review Survives the Headwinds Current Price (RM) New Fair Value (RM) Previous

M&A Securities Results Review 4Q15 PP14767/09/2012(030761) Digi.Com Berhad BUY (TP:RM5.90) Wednesday, February 10, 2016 Results Review Survives the Headwinds Current Price (RM) New Fair Value (RM) Previous

KINDLY REFER TO THE LAST PAGE OF THIS PUBLICATION FOR IMPORTANT DISCLOSURES

16 August 2018 2QFY18 Results Review Public Bank Berhad Higher than expected interim dividend Maintain BUY Unchanged Target Price (TP): RM27.30 INVESTMENT HIGHLIGHTS Earnings within expectations Net profit

16 August 2018 2QFY18 Results Review Public Bank Berhad Higher than expected interim dividend Maintain BUY Unchanged Target Price (TP): RM27.30 INVESTMENT HIGHLIGHTS Earnings within expectations Net profit

On Our Technical Watch

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,759.76 (in Million) 52-week Low 1,611.88 KLCI Vol 84.65 Current Level 1,733.93 Bursa Vol

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,759.76 (in Million) 52-week Low 1,611.88 KLCI Vol 84.65 Current Level 1,733.93 Bursa Vol

On Our Technical Watch

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,759.76 (in Million) 52-week Low 1,611.88 KLCI Vol 112.14 Current Level 1,735.84 Bursa Vol

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,759.76 (in Million) 52-week Low 1,611.88 KLCI Vol 112.14 Current Level 1,735.84 Bursa Vol

Market Access. Results Review (1Q16) M&A Securities. Tan Chong Motor Holdings Bhd. Lacking the X-Factor SELL (TP: RM1.

M&A Securities. Tan Chong Motor Holdings Bhd. Lacking the X-Factor SELL (TP: RM1.") M&A Securities Results Review (1Q16) PP14767/09/2012(030761) Tan Chong Motor Holdings Bhd Wednesday, May 11, 2016 SELL (TP: RM1.87) Lacking the X-Factor Results Review Actual vs. expectations. Tan Chong

M&A Securities Results Review (1Q16) PP14767/09/2012(030761) Tan Chong Motor Holdings Bhd Wednesday, May 11, 2016 SELL (TP: RM1.87) Lacking the X-Factor Results Review Actual vs. expectations. Tan Chong

PUBLIC INVESTMENT BANK

PUBLIC INVESTMENT BANK PublicInvest Research Results Review Thursday, November 26, 2015 KDN PP17686/03/2013(032117) PRESTARIANG Outperform DESCRIPTION An ICT service provider focusing on ICT training and

PUBLIC INVESTMENT BANK PublicInvest Research Results Review Thursday, November 26, 2015 KDN PP17686/03/2013(032117) PRESTARIANG Outperform DESCRIPTION An ICT service provider focusing on ICT training and

Market Access. Results Review 2Q16. M&A Securities. RHB Capital Berhad. Recovery in Decent Traction. Thursday, August 25, 2016 BUY (TP: RM5.

M&A Securities Results Review 2Q16 PP14767/09/2012(030761) RHB Capital Berhad BUY (TP: RM5.80) Thursday, August 25, 2016 Recovery in Decent Traction Results Review Actual vs. expectations. RHB Bank Berhad

M&A Securities Results Review 2Q16 PP14767/09/2012(030761) RHB Capital Berhad BUY (TP: RM5.80) Thursday, August 25, 2016 Recovery in Decent Traction Results Review Actual vs. expectations. RHB Bank Berhad

China Lilang (1234 HK)

") HONG KONG EQUITY Investment Research Ethel Ng +852 2103 9415 ethel.ng@hk.oskgroup.com 1H12 Results Review China Lilang (1234 HK) Strong growth amidst the storm BUY Target Price Previous Price HKD7.94 HKD8.73

HONG KONG EQUITY Investment Research Ethel Ng +852 2103 9415 ethel.ng@hk.oskgroup.com 1H12 Results Review China Lilang (1234 HK) Strong growth amidst the storm BUY Target Price Previous Price HKD7.94 HKD8.73

Market Access. M&A Securities. Results Review 1Q15. BIMB Holdings Bhd BUY (TP:RM4.84) Brilliant Beginning. Results Review

Brilliant Beginning. Results Review") M&A Securities Results Review 1Q15 PP14767/09/2012(030761) BIMB Holdings Bhd BUY (TP:RM4.84) Wednesday, May 27, 2015 Brilliant Beginning Results Review Actual vs. expectation. BIMB Holdings Berhad (BIMB)

M&A Securities Results Review 1Q15 PP14767/09/2012(030761) BIMB Holdings Bhd BUY (TP:RM4.84) Wednesday, May 27, 2015 Brilliant Beginning Results Review Actual vs. expectation. BIMB Holdings Berhad (BIMB)

KPJ Healthcare Berhad Moving on cautiously into FY16

14 January 2016 Corporate Update KPJ Healthcare Berhad Moving on cautiously into FY16 INVESTMENT HIGHLIGHTS Cautious outlook for FY16 Expansion plan to resume Overseas operation to remain subdued in FY16

14 January 2016 Corporate Update KPJ Healthcare Berhad Moving on cautiously into FY16 INVESTMENT HIGHLIGHTS Cautious outlook for FY16 Expansion plan to resume Overseas operation to remain subdued in FY16

PUBLIC INVESTMENT BANK

PUBLIC INVESTMENT BANK PublicInvest Research Company Update Monday, November 02, 2015 KDN PP17686/03/2013(032117) MALAYSIA STEEL WORKS (KL) Neutral DESCRIPTION New Rolling Mill One of the smallest steelmakers

PUBLIC INVESTMENT BANK PublicInvest Research Company Update Monday, November 02, 2015 KDN PP17686/03/2013(032117) MALAYSIA STEEL WORKS (KL) Neutral DESCRIPTION New Rolling Mill One of the smallest steelmakers

IHH Healthcare IHH MK Sector: Healthcare & Pharmaceuticals

Inpatient admissions accelerated in 1Q16 Core net profit grew by a tepid 5% yoy in 1Q16, but we deemed this in-line with expectations. Revenue and EBITDA grew by 24% yoy and 17% yoy in the quarter, driven

Inpatient admissions accelerated in 1Q16 Core net profit grew by a tepid 5% yoy in 1Q16, but we deemed this in-line with expectations. Revenue and EBITDA grew by 24% yoy and 17% yoy in the quarter, driven

Tropicana TRCB MK Sector: Property

Disposal of 251 acres of land in Johor We are positive on Tropicana s announcement to dispose 251.6 acres of freehold land in Gelang Patah, as this will reduce its exposure in Johor, as well as lock in

Disposal of 251 acres of land in Johor We are positive on Tropicana s announcement to dispose 251.6 acres of freehold land in Gelang Patah, as this will reduce its exposure in Johor, as well as lock in

Star Media STAR MK Sector: Media

Print remains under pressure We expect prospects for the print media industry to remain weak in 2016 given the challenging market environment, poor consumer sentiment as well as the structurally declining

Print remains under pressure We expect prospects for the print media industry to remain weak in 2016 given the challenging market environment, poor consumer sentiment as well as the structurally declining

Market Access. M&A Securities. Company Update. Tenaga Nasional Berhad. Accepting 3B Project. Thursday, July 09, 2015 BUY (TP: RM15.

M&A Securities Company Update PP14767/09/2012(030761) Tenaga Nasional Berhad BUY (TP: RM15.20) Thursday, July 09, 2015 Accepting 3B Project Latest Development Submit letter of acceptance. TNB has announced

M&A Securities Company Update PP14767/09/2012(030761) Tenaga Nasional Berhad BUY (TP: RM15.20) Thursday, July 09, 2015 Accepting 3B Project Latest Development Submit letter of acceptance. TNB has announced

PUBLIC INVESTMENT BANK

PUBLIC INVESTMENT BANK PublicInvest Research Results Review Tuesday, May 23, 2017 KDN PP17686/03/2013(032117) PRESTARIANG Outperform DESCRIPTION An ICT service provider focusing on ICT training and certification

PUBLIC INVESTMENT BANK PublicInvest Research Results Review Tuesday, May 23, 2017 KDN PP17686/03/2013(032117) PRESTARIANG Outperform DESCRIPTION An ICT service provider focusing on ICT training and certification

Market Access. M&A Securities. Company Update. Tenaga Nasional Berhad. A Look into Debt. Tuesday, July 14, 2015 BUY (TP: RM15.20) Latest Development

Latest Development") M&A Securities Company Update PP14767/09/2012(030761) Tenaga Nasional Berhad BUY (TP: RM15.20) Tuesday, July 14, 2015 A Look into Debt Latest Development Debt position. Tenaga Nasional Bhd (TNB) core business

M&A Securities Company Update PP14767/09/2012(030761) Tenaga Nasional Berhad BUY (TP: RM15.20) Tuesday, July 14, 2015 A Look into Debt Latest Development Debt position. Tenaga Nasional Bhd (TNB) core business

CIMB Group CIMB MK Sector: Banking

Group s outlook stabilizing We believe that the CIMB Group is on track for an earnings recovery subsequent to being bogged down with hefty provision costs from Indonesia as well as a restructuring and

Group s outlook stabilizing We believe that the CIMB Group is on track for an earnings recovery subsequent to being bogged down with hefty provision costs from Indonesia as well as a restructuring and

PUBLIC INVESTMENT BANK

PUBLIC INVESTMENT BANK PublicInvest Research Results Review Friday, February 26, 2016 KDN PP17686/03/2013(032117) PRESTARIANG Outperform DESCRIPTION An ICT service provider focusing on ICT training and

PUBLIC INVESTMENT BANK PublicInvest Research Results Review Friday, February 26, 2016 KDN PP17686/03/2013(032117) PRESTARIANG Outperform DESCRIPTION An ICT service provider focusing on ICT training and

Market Access. Results Review (4Q16) M&A Securities. Scientex Berhad. Unstoppable Growth Amid Challenging Times. Tuesday, September 27, 2016

M&A Securities. Scientex Berhad. Unstoppable Growth Amid Challenging Times. Tuesday, September 27, 2016") Market Access M&A Securities Results Review (4Q16) PP14767/04/2012(029 Tuesday, September 27, 2016 Scientex Berhad Unstoppable Growth Amid Challenging Times BUY (TP: RM8.33) Current Price (RM) New Target

Market Access M&A Securities Results Review (4Q16) PP14767/04/2012(029 Tuesday, September 27, 2016 Scientex Berhad Unstoppable Growth Amid Challenging Times BUY (TP: RM8.33) Current Price (RM) New Target

CAPITAMALLS MALAYSIA TRUST

CAPITAMALLS MALAYSIA TRUST Malaysia s Largest Pure-Play Shopping Mall REIT Presentation Slides for CIMB Retail Investors Selangor 10 November 2010 Disclaimer The information in this presentation is qualified

CAPITAMALLS MALAYSIA TRUST Malaysia s Largest Pure-Play Shopping Mall REIT Presentation Slides for CIMB Retail Investors Selangor 10 November 2010 Disclaimer The information in this presentation is qualified

On Our Technical Watch

By Lawrence Yeo / lawrenceyeo@kenanga.com.my; Steven Chan / steven.chan@kenanga.com.my; Muhammad Afif Bin Zulkaplly / muhammad.afif@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High

By Lawrence Yeo / lawrenceyeo@kenanga.com.my; Steven Chan / steven.chan@kenanga.com.my; Muhammad Afif Bin Zulkaplly / muhammad.afif@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High

Market Access. Company Note. M&A Securities. Nestle Malaysia Berhad. Steering Away From Turbulence. Tuesday, June 21, 2016 HOLD (TP: RM79.

M&A Securities Company Note PP14767/09/2012(030761) Nestle Malaysia Berhad Steering Away From Turbulence 1Q16 results review. To recap, Nestle Malaysia Berhad (Nestle) registered its 1Q16 revenue at RM1.3

M&A Securities Company Note PP14767/09/2012(030761) Nestle Malaysia Berhad Steering Away From Turbulence 1Q16 results review. To recap, Nestle Malaysia Berhad (Nestle) registered its 1Q16 revenue at RM1.3

On Our Technical Watch

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,757.99 (in Million) 52-week Low 1,611.88 KLCI Vol 174.33 Current Level 1,748.30 Bursa Vol

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,757.99 (in Million) 52-week Low 1,611.88 KLCI Vol 174.33 Current Level 1,748.30 Bursa Vol

NAGA Warrants 2016 November Issuance

2016 November Issuance Heightened Volatility Ahead By Lawrence Yeo Eng Chien l lawrenceyeo@kenanga.com.my Donald Trump s victory in the US Presidential Elections came as a massive shock to the investment

2016 November Issuance Heightened Volatility Ahead By Lawrence Yeo Eng Chien l lawrenceyeo@kenanga.com.my Donald Trump s victory in the US Presidential Elections came as a massive shock to the investment

On Our Technical Watch

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,729.13 (in Million) 52-week Low 1,611.88 KLCI Vol 166.34 Current Level 1,708.08 Bursa Vol

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High 1,729.13 (in Million) 52-week Low 1,611.88 KLCI Vol 166.34 Current Level 1,708.08 Bursa Vol

Hua Yang Berhad TP: RM1.09 (+2.4%) Subdued Results, Timely Launch of Projects the Key

Subdued Results, Timely Launch of Projects the Key") MENARA TA ONE, 22 JALAN P. RAMLEE, 50250 KUALA LUMPUR, MALAYSIA TEL: +603-20721277 / FAX: +603-20325048 C O M P A N Y U P D A T E Thursday, 19 January 2017 FBMKLCI: 1,665.02 Sector: Property Hua Yang Berhad

MENARA TA ONE, 22 JALAN P. RAMLEE, 50250 KUALA LUMPUR, MALAYSIA TEL: +603-20721277 / FAX: +603-20325048 C O M P A N Y U P D A T E Thursday, 19 January 2017 FBMKLCI: 1,665.02 Sector: Property Hua Yang Berhad

Make Hay While the Sun Shines

Property Developers Make Hay While the Sun Shines By Sarah Lim l sarahlim@kenanga.com.my ; Adrian Ng l adrian.ng@kenanga.com.my UNDERWEIGHT We are downgrading PROPERTY to UNDERWEIGHT from NEUTRAL. We believe

Property Developers Make Hay While the Sun Shines By Sarah Lim l sarahlim@kenanga.com.my ; Adrian Ng l adrian.ng@kenanga.com.my UNDERWEIGHT We are downgrading PROPERTY to UNDERWEIGHT from NEUTRAL. We believe

Market Access. Results Review (3Q15) M&A Securities. Dutch Lady Milk Industries Berhad. Double Whammy. Wednesday, November 18, 2015 HOLD (TP: RM47.

M&A Securities. Dutch Lady Milk Industries Berhad. Double Whammy. Wednesday, November 18, 2015 HOLD (TP: RM47.") Market Access M&A Securities Results Review (3Q15) PP14767/4/212(296 Dutch Lady Milk Industries Berhad Double Whammy Results Review Actual vs. expectations. Dutch Lady Milk Industries Berhad (Dutch Lady)

Market Access M&A Securities Results Review (3Q15) PP14767/4/212(296 Dutch Lady Milk Industries Berhad Double Whammy Results Review Actual vs. expectations. Dutch Lady Milk Industries Berhad (Dutch Lady)

UOA Development UOAD MK Sector: Property

Dividend play In 2016, UOA has thus far launched two projects and plans to launch a third development this year. The total estimated gross development value (GDV) of these three projects is RM3.2bn. Unbilled

Dividend play In 2016, UOA has thus far launched two projects and plans to launch a third development this year. The total estimated gross development value (GDV) of these three projects is RM3.2bn. Unbilled

Market Access. M&A Securities. Results Review 1Q15. Axiata Group Berhad. Slow in Recovery. Wednesday, May 20, 2015 HOLD (TP:RM7.

M&A Securities Results Review 1Q15 PP14767/09/2012(030761) Axiata Group Berhad Wednesday, May 20, 2015 HOLD (TP:RM7.40) Slow in Recovery Results Review Actual vs. expectations. Axiata Group Bhd (Axiata)

M&A Securities Results Review 1Q15 PP14767/09/2012(030761) Axiata Group Berhad Wednesday, May 20, 2015 HOLD (TP:RM7.40) Slow in Recovery Results Review Actual vs. expectations. Axiata Group Bhd (Axiata)

On Our Technical Watch

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data Technical Ratings 52-week High 1,729.13 (in Million) 52-week Low 1,600.92 KLCI Vol 93.61 Current Level

By the Kenanga Research Team l research@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data Technical Ratings 52-week High 1,729.13 (in Million) 52-week Low 1,600.92 KLCI Vol 93.61 Current Level

On Our Technical Watch

By Lawrence Yeo / lawrenceyeo@kenanga.com.my; Steven Chan / steven.chan@kenanga.com.my; Muhammad Afif Bin Zulkaplly / muhammad.afif@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High

By Lawrence Yeo / lawrenceyeo@kenanga.com.my; Steven Chan / steven.chan@kenanga.com.my; Muhammad Afif Bin Zulkaplly / muhammad.afif@kenanga.com.my Figure 1: Daily Charting FBMKLCI Basic Data 52-week High

Market Access. M&A Securities. Results Review 2Q15. Axiata Group Berhad. Satisfactory, Need to Push in 2H15. Friday, August 21, 2015 HOLD (TP:RM7.

M&A Securities Results Review 2Q15 PP14767/09/2012(030761) Axiata Group Berhad Friday, August 21, 2015 HOLD (TP:RM7.10) Satisfactory, Need to Push in 2H15 Results Review Actual vs. expectations. Axiata

M&A Securities Results Review 2Q15 PP14767/09/2012(030761) Axiata Group Berhad Friday, August 21, 2015 HOLD (TP:RM7.10) Satisfactory, Need to Push in 2H15 Results Review Actual vs. expectations. Axiata