North Carolina Supplemental Retirement Board of Trustees. Loren de Mey, Assistant Investment Director. Date: August 11, 2017

|

|

|

- Britton Black

- 5 years ago

- Views:

Transcription

1 To: From: North Carolina Supplemental Retirement Board of Trustees Loren de Mey, Assistant Investment Director Date: August 11, 2017 Subject: GoalMaker and Glidepath Review Background As part of the Board s general fiduciary duties regarding plan design, the Board is responsible for selecting, monitoring, and approving changes to any model asset allocations, including the glidepaths across allocations, that are offered in the Plans. The categories of model allocations/glidepaths include (1) off-the-shelf options (such as Morningstar s allocations and glidepath offered through Prudential s GoalMaker service); and (2) modified versions of off-the shelf options (such as the modified Morningstar version currently used by the Board). 1 The choice of an off-the-shelf option and the decision of how (if at all) to modify the allocations/glidepath are fiduciary obligations of the Board, and the Board relies on investment experts from the Investment Management Division (IMD) and Mercer in making these decisions. On March 23, 2017, the Supplemental Retirement Board (Board) approved a recommendation of the Supplemental Investment Subcommittee on the Glidepath Project. The recommendation was to instruct IMD staff to develop a plan with Prudential to finalize the material changes to the glidepath of the GoalMaker service based on the 2013 Mercer recommendations (i.e., those that were deferred until after the 2015 unbundling) with no incremental fees. As identified by IMD for the Board, those changes included: 1. Smoothing the glidepath; and/or 2. Adding a through retirement or income component to the glidepath GoalMaker / Glidepath Review As of June 30, 2017, there were $4.6 billion in total assets in GoalMaker (44% of total assets in the 401k and 457 Plans). 61% of all participants and 93% of new participants were using GoalMaker. As a reminder, Morningstar provides the underlying asset allocation framework supporting Prudential s GoalMaker service and is currently enhancing the model portfolios with GoalMaker. IMD and Mercer used this new model, developed by Morningstar, as the starting point in their analysis. The new GoalMaker model is a 3 x 9 model (That is, the model includes three risk settings and nine retirement 1 A third alternative fully-customized allocations/glidepaths using a delegated investment manager or investment consultant was previously considered by the Board. 1

2 target years, with 6 target years in the pre-retirement phase and 3 in the post-retirement phase (See Appendix B). The new GoalMaker model improves upon the current model in the following ways: 1. Offers options for participants through retirement, by adding three age-related groupings in the post-retirement phase. 2. Adds additional exposure to growth assets for younger participants, while adding fixed income and stable value assets for participants approaching or in retirement. 3. Smooths the glidepath by adding additional age groupings so participants will experience less abrupt asset allocation changes as they move through the glidepath. To better understand some of the discussion and recommendations, it is important to understand the following: 1. This new GoalMaker model is created by Morningstar under contract with Prudential to be provided as an alternative to Prudential s defined contribution clients that also desire glidepath smoothing as opposed to Standard GoalMaker (which is a 3 x 4 model). 2. Morningstar s Standard GoalMaker has been used by Mercer and the SRP Board to create and authorize the customized North Carolina GoalMaker Model Portfolios. In other words, the current North Carolina glidepath is a customized version of Prudential s Standard GoalMaker model as approved by the SRP Board in 2013 (See Appendix A). 3. Morningstar s Lifetime Asset Allocation Indexes are their best ideas model target date funds with a glidepath for three different risk levels and 14 target dates (i.e., 3 x 14 model). 4. Morningstar periodically updates the Standard GoalMaker model based on updated methodology and capital market assumptions and communicates changes to Prudential. IMD reviewed the alternative 3 x 9 GoalMaker model, including reviewing the reasonableness of the following: 1. Morningstar s glidepath modeling (i.e., methodology and assumptions) and their Lifetime Asset Allocation Indexes (See Appendix C); 2. Any major deviations between the glidepaths of the Lifetime Asset Allocation Indexes and the alternative 3 x 9 GoalMaker, including the mapping of individual sector/style constituents between the two glidepaths; 3. Any major deviations between the glidepaths of the alternative 3 x 9 GoalMaker and the North Carolina GoalMaker Model Portfolio, including the mapping of individual sector/style constituents between the glidepaths; and 4. Throughout the analysis, the allocation to growth and fixed income assets provided by the Prudential model was maintained. IMD analyzed all of the above, reviewed the analysis with Mercer, and proposes the following components of new North Carolina GoalMaker Model Portfolios for the Board s consideration in September. 2

3 1. Adopt Prudential s new GoalMaker 3 x 9 model with recommended modifications, as outlined in Mercer s presentation, including the following modifications: a. Capping the SMID allocation at 30% in the longer-dated funds and scaling down to 20% as participants near retirement to be more in line with the SMID weighting within the Russell 3000 Index (Prudential s proposed model included a significant overweight to SMID throughout the glidepath); b. Increasing the allocation to International Equity to be more in line with the weighting within the MSCI ACWI Index (The allocation to International Equity will decrease as participants approach retirement); and c. Adding an Inflation Sensitive allocation (discussed in greater detail below). i. The Inflation Sensitive allocation would be implemented with a passive U.S. Treasury Inflation Protected Securities ( TIPS ) allocation. ii. The changes would improve the inflation protection for participants approaching or in retirement. iii. The TIPs allocation will be mainly funded through a reduction in the stable value allocation. 2. Utilize only a passive allocation for U.S. Large Cap (i.e., the current glidepath uses both active and passive U.S. Large Cap) 3. Utilize only an active allocation for fixed income (i.e., the current glidepath model uses both active and passive fixed income) 4. Eliminate active Global Equity and replacing it with passive U.S. Large Cap and active International Equity Inflation Sensitive Modification a. Recommend removing the NC Global Equity Fund from the core fund line-up b. Approximately 94% of the assets within the Global Equity Fund are from the GoalMaker allocation. If this change is made, only $60 million would remain in the Global Equity Fund (the self-directed assets), and investment management fees would increase 10 basis points to 0.675% for those remaining assets (given the break points on the current fee schedule). IMD staff and Mercer recommend utilizing an expanded Inflation Sensitive allocation. The current North Carolina GoalMaker Model Portfolios utilize a Real Assets allocation to the PIMCO Inflation Responsive Multi Asset Fund (IRMAF), and the new GoalMaker 3 x 9 Model decreases this allocation as participants age into and through retirement (See Chart 1). This decrease occurs because the portfolio is roughly half allocated to growth-oriented assets, rather than inflation hedging. 3

4 Chart 1: Morningstar s New GoalMaker 3 x 9 Model (Moderate Portfolio) Within the Mercer peer group of target date funds, there is instead an Inflation Sensitive allocation, which increases as participants approach retirement. This basic approach is consistent with the Morningstar methodology utilized within Morningstar s Lifetime Asset Allocation Indexes as can be seen in Chart 2. Chart 2: Morningstar s Lifetime Asset Allocation Indexes (Moderate Portfolio) The Supplemental Plans current Inflation Sensitive investment offering, the PIMCO IRMAF, does not correspond closely to the asset categories that Morningstar modeled within their Lifetime Asset Allocation Indexes. The PIMCO IRMAF does have exposure to TIPS, but also has exposure to growthoriented and higher volatility assets such as REITs, currencies, and commodities. Given these exposures, 4

5 IMD staff and Mercer do not believe it would be in the best interests of participants to materially increase the allocations to IRMAF (i.e., growth assets) as participants approach retirement. Therefore, IMD staff and Mercer are recommending adding in a TIPS allocation to the GoalMaker Model for inflation hedging purposes. The allocations to TIPS would increase for those participants approaching or in retirement. Fees The new proposed GoalMaker model including the new implementation (active/passive split) reduces fees on the GoalMaker portfolios between7-15 basis points (based on fees as of 6/30/17, which include the recently negotiated fee reductions). Further details on fees can be seen on page 29 of the Mercer presentation. Summary of Recommendations (for Board Vote in September) Following is a summary of key points to be presented to the Board for a vote during its September meeting. 1. Approve moving to new GoalMaker Model (moving from 3 x 4 model to 3 x 9 model). 2. Approve Mercer s recommendations to the new model, including the addition of a TIPS allocation. 3. Approve all implementations, including: a. Fully passive for U.S. Large Cap Equity change from current GoalMaker b. Fully active for Fixed Income change from current GoalMaker c. Fully active for International Equity no change from current GoalMaker d. Fully active for Small / Mid U.S. Equity no change from current GoalMaker 4. Replace Global Equity in model portfolios with Passive U.S. Large Cap and Active International Equity 5. Remove NC Global Equity Fund from the Plans Core Menu 6. Add Passive TIPS Fund to Core Menu Any recommended changes to the glidepath and GoalMaker portfolios that are approved by the Board in September 2017 are expected to be implemented in June 2018, given the 8-9 month lead time required by Prudential. Summary The proposed GoalMaker Model reduces fees and adds value for participants by enhancing the model in several ways: going through retirement; smoothing the glidepath with less abrupt asset allocation changes; and optimizing the active/passive mix of investment strategies. The new model adds additional exposure to growth assets for younger participants, while increasing fixed income and inflation hedging allocations for those participants approaching and in retirement. 5

6 Appendix A: Current GoalMaker Allocations (highlighted changes are changes that will be implemented along with the Plan Design changes, effective September 29, 2017) Conservative The objective of the Conservative Model Allocation is to achieve long term growth in excess of inflation with a minimal risk of capital loss over a full market cycle. C01 C02 C03 C04 Conservative 0-5 Yrs 6-10 Yrs Yrs 16+ Yrs NC Large Cap Value 1% 2% 3% 3% NC Large Cap Index 4% 4% 7% 8% NC Large Cap Growth 1% 2% 3% 3% NC Large Cap Core 2% 4% 6% 6% NC Small / Mid Cap Value 2% 3% 5% 7% NC Small / Mid Cap Index 0% 0% 0% 0% NC Small / Mid Cap Growth 2% 3% 5% 7% NC Small / Mid Cap Core 4% 6% 10% 14% NC Global Equity 6% 10% 15% 23% NC International 3% 5% 7% 11% NC International Index 0% 0% 0% 0% NC Fixed Income 16% 14% 12% 10% NC Fixed Income Index 17% 14% 13% 10% NC Stable Value 40% 35% 22% 10% NC Inflation Sensitive 8% 8% 8% 8%, 11 pt 6

7 Moderate The objective of the Moderate Model Allocation is moderate growth of principal with limited downside risk over a market cycle., 11 pt Moderate M01 M02 M03 M Yrs 6-10 Yrs Yrs 16+ Yrs NC Large Cap Value 2% 3% 4% 5% NC Large Cap Index 5% 7% 7% 10% NC Large Cap Growth 2% 3% 4% 5% NC Large Cap Core 4% 6% 8% 10% NC Small / Mid Cap Value 4% 5% 7% 10% NC Small / Mid Cap Index 0% 0% 0% 0% NC Small / Mid Cap Growth 4% 5% 7% 10% NC Smann / Mid Cap Core 8% 10% 10% 20% NC Global Equity 11% 15% 19% 25% NC International 6% 7% 9% 12% NC International Index 0% 0% 0% 0% NC Fixed Income 13% 12% 10% 4% NC Fixed Income Index 13% 13% 10% 5% NC Stable Value 31% 21% 14% 5% NC Inflation Sensitive 9% 9% 9% 9% Aggressive The primary investment objective of the Aggressive Model Allocation is to maximize growth of principal Aggressive A01 A02 A03 A Yrs 6-10 Yrs Yrs 16+ Yrs NC Large Cap Value 3% 4% 5% 6% NC Large Cap Index 7% 7% 8% 11% NC Large Cap Growth 3% 4% 5% 6% NC Large Cap Core 6% 8% 10% 12% NC Small / Mid Cap Value 6% 7% 9% 11% NC Small / Mid Cap Index 0% 0% 0% 0% NC Small / Mid Cap Growth 6% 7% 9% 11% NC Small / Mid Cap Core 12% 14% 18% 22% NC Global Equity 16% 19% 24% 30% NC International 8% 9% 12% 15% NC International Index 0% 0% 0% 0% NC Fixed Income 12% 10% 5% 0% NC Fixed Income Index 12% 10% 6% 0% NC Stable Value 17% 13% 7% 0% NC Inflation Sensitive 10% 10% 10% 10% over the long term with a reasonable level of overall volatility. 7

8 Appendix B: Prudential s new GoalMaker Model (3x9) Conservative Pre-Retirement Post-Retirement Years to Retirement US Large 28% 24% 21% 17% 14% 13% 11% 11% 10% SMID Growth 9% 8% 7% 6% 5% 4% 3% 2% 2% SMID Value 9% 8% 7% 6% 5% 4% 3% 2% 2% International Stocks 19% 17% 14% 11% 9% 6% 5% 4% 4% Emerging 8% 7% 5% 4% 3% 2% 2% 1% 0% Bonds 11% 15% 17% 20% 23% 26% 27% 28% 28% SV 11% 17% 25% 32% 37% 42% 46% 49% 51% Real Assets 5% 4% 4% 4% 4% 3% 3% 3% 3% Equity 73% 64% 54% 44% 36% 29% 24% 20% 18% Bonds 22% 32% 42% 52% 60% 68% 73% 77% 79% Alternatives 5% 4% 4% 4% 4% 3% 3% 3% 3% Total 100% 100% 100% 100% 100% 100% 100% 100% 100% Moderate Pre-Retirement Post-Retirement Years to Retirement US Large 33% 31% 28% 24% 22% 17% 16% 16% 14% SMID Growth 11% 10% 9% 8% 7% 6% 5% 4% 3% SMID Value 11% 10% 9% 8% 7% 6% 5% 4% 3% International Stocks 22% 21% 19% 17% 13% 11% 10% 7% 7% Emerging 9% 8% 7% 6% 5% 4% 3% 3% 2% Bonds 4% 7% 11% 15% 19% 23% 25% 26% 27% SV 3% 7% 11% 17% 22% 28% 32% 36% 40% Real Assets 7% 6% 6% 5% 5% 5% 4% 4% 4% Equity 86% 80% 72% 63% 54% 44% 39% 34% 29% Bonds 7% 14% 22% 32% 41% 51% 57% 62% 67% Alternatives 7% 6% 6% 5% 5% 5% 4% 4% 4% Total 100% 100% 100% 100% 100% 100% 100% 100% 100% 8

9 Aggressive Pre-Retirement Post-Retirement Years to Retirement US Large 31% 32% 31% 29% 28% 25% 22% 22% 20% SMID Growth 12% 12% 11% 10% 9% 8% 7% 6% 5% SMID Value 12% 12% 11% 10% 9% 8% 7% 6% 5% International Stocks 25% 24% 23% 22% 19% 15% 13% 12% 11% Emerging 10% 10% 9% 8% 6% 5% 4% 3% 2% Bonds 2% 2% 5% 8% 12% 17% 20% 21% 23% SV 1% 1% 3% 6% 11% 16% 22% 25% 29% Real Assets 7% 7% 7% 7% 6% 6% 5% 5% 5% Equity 90% 90% 85% 79% 71% 61% 53% 49% 43% Bonds 3% 3% 8% 14% 23% 33% 42% 46% 52% Alternatives 7% 7% 7% 7% 6% 6% 5% 5% 5% Total 100% 100% 100% 100% 100% 100% 100% 100% 100% 9

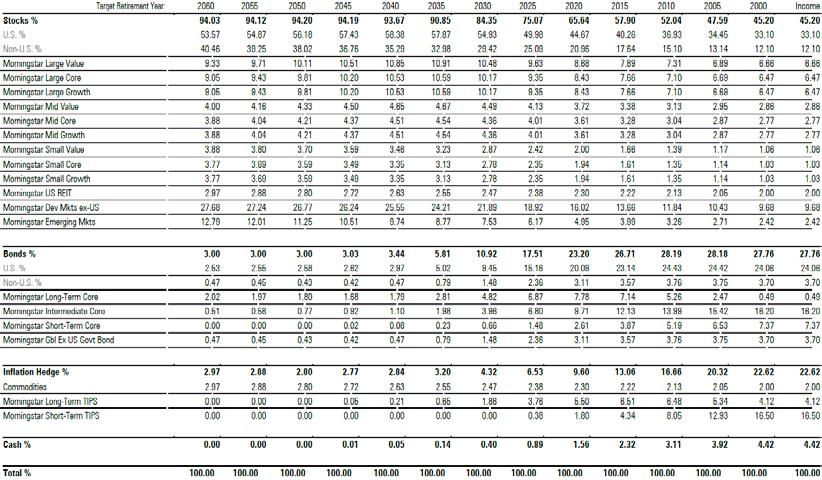

10 Appendix C: Morningstar Lifetime Allocation Indexes Conservative Moderate 10

11 Aggressive 11

12 To: From: North Carolina Supplemental Retirement Board of Trustees Loren de Mey, Assistant Investment Director Date: August 11, 2017 Subject: GoalMaker and Glidepath Review Background As part of the Board s general fiduciary duties regarding plan design, the Board is responsible for selecting, monitoring, and approving changes to any model asset allocations, including the glidepaths across allocations, that are offered in the Plans. The categories of model allocations/glidepaths include (1) off-the-shelf options (such as Morningstar s allocations and glidepath offered through Prudential s GoalMaker service); and (2) modified versions of off-the shelf options (such as the modified Morningstar version currently used by the Board). 1 The choice of an off-the-shelf option and the decision of how (if at all) to modify the allocations/glidepath are fiduciary obligations of the Board, and the Board relies on investment experts from the Investment Management Division (IMD) and Mercer in making these decisions. On March 23, 2017, the Supplemental Retirement Board (Board) approved a recommendation of the Supplemental Investment Subcommittee on the Glidepath Project. The recommendation was to instruct IMD staff to develop a plan with Prudential to finalize the material changes to the glidepath of the GoalMaker service based on the 2013 Mercer recommendations (i.e., those that were deferred until after the 2015 unbundling) with no incremental fees. As identified by IMD for the Board, those changes included: 1. Smoothing the glidepath; and/or 2. Adding a through retirement or income component to the glidepath GoalMaker / Glidepath Review As of June 30, 2017, there were $4.6 billion in total assets in GoalMaker (44% of total assets in the 401k and 457 Plans). 61% of all participants and 93% of new participants were using GoalMaker. As a reminder, Morningstar provides the underlying asset allocation framework supporting Prudential s GoalMaker service and is currently enhancing the model portfolios with GoalMaker. IMD and Mercer used this new model, developed by Morningstar, as the starting point in their analysis. The new GoalMaker model is a 3 x 9 model (That is, the model includes three risk settings and nine retirement 1 A third alternative fully-customized allocations/glidepaths using a delegated investment manager or investment consultant was previously considered by the Board. 1

13 target years, with 6 target years in the pre-retirement phase and 3 in the post-retirement phase (See Appendix B). The new GoalMaker model improves upon the current model in the following ways: 1. Offers options for participants through retirement, by adding three age-related groupings in the post-retirement phase. 2. Adds additional exposure to growth assets for younger participants, while adding fixed income and stable value assets for participants approaching or in retirement. 3. Smooths the glidepath by adding additional age groupings so participants will experience less abrupt asset allocation changes as they move through the glidepath. To better understand some of the discussion and recommendations, it is important to understand the following: 1. This new GoalMaker model is created by Morningstar under contract with Prudential to be provided as an alternative to Prudential s defined contribution clients that also desire glidepath smoothing as opposed to Standard GoalMaker (which is a 3 x 4 model). 2. Morningstar s Standard GoalMaker has been used by Mercer and the SRP Board to create and authorize the customized North Carolina GoalMaker Model Portfolios. In other words, the current North Carolina glidepath is a customized version of Prudential s Standard GoalMaker model as approved by the SRP Board in 2013 (See Appendix A). 3. Morningstar s Lifetime Asset Allocation Indexes are their best ideas model target date funds with a glidepath for three different risk levels and 14 target dates (i.e., 3 x 14 model). 4. Morningstar periodically updates the Standard GoalMaker model based on updated methodology and capital market assumptions and communicates changes to Prudential. IMD reviewed the alternative 3 x 9 GoalMaker model, including reviewing the reasonableness of the following: 1. Morningstar s glidepath modeling (i.e., methodology and assumptions) and their Lifetime Asset Allocation Indexes (See Appendix C); 2. Any major deviations between the glidepaths of the Lifetime Asset Allocation Indexes and the alternative 3 x 9 GoalMaker, including the mapping of individual sector/style constituents between the two glidepaths; 3. Any major deviations between the glidepaths of the alternative 3 x 9 GoalMaker and the North Carolina GoalMaker Model Portfolio, including the mapping of individual sector/style constituents between the glidepaths; and 4. Throughout the analysis, the allocation to growth and fixed income assets provided by the Prudential model was maintained. IMD analyzed all of the above, reviewed the analysis with Mercer, and proposes the following components of new North Carolina GoalMaker Model Portfolios for the Board s consideration in September. 2

14 1. Adopt Prudential s new GoalMaker 3 x 9 model with recommended modifications, as outlined in Mercer s presentation, including the following modifications: a. Capping the SMID allocation at 30% in the longer-dated funds and scaling down to 20% as participants near retirement to be more in line with the SMID weighting within the Russell 3000 Index (Prudential s proposed model included a significant overweight to SMID throughout the glidepath); b. Increasing the allocation to International Equity to be more in line with the weighting within the MSCI ACWI Index (The allocation to International Equity will decrease as participants approach retirement); and c. Adding an Inflation Sensitive allocation (discussed in greater detail below). i. The Inflation Sensitive allocation would be implemented with a passive U.S. Treasury Inflation Protected Securities ( TIPS ) allocation. ii. The changes would improve the inflation protection for participants approaching or in retirement. iii. The TIPs allocation will be mainly funded through a reduction in the stable value allocation. 2. Utilize only a passive allocation for U.S. Large Cap (i.e., the current glidepath uses both active and passive U.S. Large Cap) 3. Utilize only an active allocation for fixed income (i.e., the current glidepath model uses both active and passive fixed income) 4. Eliminate active Global Equity and replacing it with passive U.S. Large Cap and active International Equity Inflation Sensitive Modification a. Recommend removing the NC Global Equity Fund from the core fund line-up b. Approximately 94% of the assets within the Global Equity Fund are from the GoalMaker allocation. If this change is made, only $60 million would remain in the Global Equity Fund (the self-directed assets), and investment management fees would increase 10 basis points to 0.675% for those remaining assets (given the break points on the current fee schedule). IMD staff and Mercer recommend utilizing an expanded Inflation Sensitive allocation. The current North Carolina GoalMaker Model Portfolios utilize a Real Assets allocation to the PIMCO Inflation Responsive Multi Asset Fund (IRMAF), and the new GoalMaker 3 x 9 Model decreases this allocation as participants age into and through retirement (See Chart 1). This decrease occurs because the portfolio is roughly half allocated to growth-oriented assets, rather than inflation hedging. Chart 1: Morningstar s New GoalMaker 3 x 9 Model (Moderate Portfolio) 3

15 Within the Mercer peer group of target date funds, there is instead an Inflation Sensitive allocation, which increases as participants approach retirement. This basic approach is consistent with the Morningstar methodology utilized within Morningstar s Lifetime Asset Allocation Indexes as can be seen in Chart 2. Chart 2: Morningstar s Lifetime Asset Allocation Indexes (Moderate Portfolio) The Supplemental Plans current Inflation Sensitive investment offering, the PIMCO IRMAF, does not correspond closely to the asset categories that Morningstar modeled within their Lifetime Asset Allocation Indexes. The PIMCO IRMAF does have exposure to TIPS, but also has exposure to growthoriented and higher volatility assets such as REITs, currencies, and commodities. Given these exposures, IMD staff and Mercer do not believe it would be in the best interests of participants to materially increase the allocations to IRMAF (i.e., growth assets) as participants approach retirement. 4

16 Therefore, IMD staff and Mercer are recommending adding in a TIPS allocation to the GoalMaker Model for inflation hedging purposes. The allocations to TIPS would increase for those participants approaching or in retirement. Fees The new proposed GoalMaker model including the new implementation (active/passive split) reduces fees on the GoalMaker portfolios between7-15 basis points (based on fees as of 6/30/17, which include the recently negotiated fee reductions). Further details on fees can be seen on page 29 of the Mercer presentation. Summary of Recommendations (for Board Vote in September) Following is a summary of key points to be presented to the Board for a vote during its September meeting. 1. Approve moving to new GoalMaker Model (moving from 3 x 4 model to 3 x 9 model). 2. Approve Mercer s recommendations to the new model, including the addition of a TIPS allocation. 3. Approve all implementations, including: a. Fully passive for U.S. Large Cap Equity change from current GoalMaker b. Fully active for Fixed Income change from current GoalMaker c. Fully active for International Equity no change from current GoalMaker d. Fully active for Small / Mid U.S. Equity no change from current GoalMaker 4. Replace Global Equity in model portfolios with Passive U.S. Large Cap and Active International Equity 5. Remove NC Global Equity Fund from the Plans Core Menu 6. Add Passive TIPS Fund to Core Menu Any recommended changes to the glidepath and GoalMaker portfolios that are approved by the Board in September 2017 are expected to be implemented in June 2018, given the 8-9 month lead time required by Prudential. Summary The proposed GoalMaker Model reduces fees and adds value for participants by enhancing the model in several ways: going through retirement; smoothing the glidepath with less abrupt asset allocation changes; and optimizing the active/passive mix of investment strategies. The new model adds additional exposure to growth assets for younger participants, while increasing fixed income and inflation hedging allocations for those participants approaching and in retirement. 5

17 Appendix A: Current GoalMaker Allocations (highlighted changes are changes that will be implemented along with the Plan Design changes, effective September 29, 2017) Conservative The objective of the Conservative Model Allocation is to achieve long term growth in excess of inflation with a minimal risk of capital loss over a full market cycle. C01 C02 C03 C04 Conservative 0-5 Yrs 6-10 Yrs Yrs 16+ Yrs NC Large Cap Value 1% 2% 3% 3% NC Large Cap Index 4% 4% 7% 8% NC Large Cap Growth 1% 2% 3% 3% NC Large Cap Core 2% 4% 6% 6% NC Small / Mid Cap Value 2% 3% 5% 7% NC Small / Mid Cap Index 0% 0% 0% 0% NC Small / Mid Cap Growth 2% 3% 5% 7% NC Small / Mid Cap Core 4% 6% 10% 14% NC Global Equity 6% 10% 15% 23% NC International 3% 5% 7% 11% NC International Index 0% 0% 0% 0% NC Fixed Income 16% 14% 12% 10% NC Fixed Income Index 17% 14% 13% 10% NC Stable Value 40% 35% 22% 10% NC Inflation Sensitive 8% 8% 8% 8%, 11 pt 6

18 Moderate The objective of the Moderate Model Allocation is moderate growth of principal with limited downside risk over a market cycle., 11 pt Moderate M01 M02 M03 M Yrs 6-10 Yrs Yrs 16+ Yrs NC Large Cap Value 2% 3% 4% 5% NC Large Cap Index 5% 7% 7% 10% NC Large Cap Growth 2% 3% 4% 5% NC Large Cap Core 4% 6% 8% 10% NC Small / Mid Cap Value 4% 5% 7% 10% NC Small / Mid Cap Index 0% 0% 0% 0% NC Small / Mid Cap Growth 4% 5% 7% 10% NC Smann / Mid Cap Core 8% 10% 10% 20% NC Global Equity 11% 15% 19% 25% NC International 6% 7% 9% 12% NC International Index 0% 0% 0% 0% NC Fixed Income 13% 12% 10% 4% NC Fixed Income Index 13% 13% 10% 5% NC Stable Value 31% 21% 14% 5% NC Inflation Sensitive 9% 9% 9% 9% Aggressive The primary investment objective of the Aggressive Model Allocation is to maximize growth of principal Aggressive A01 A02 A03 A Yrs 6-10 Yrs Yrs 16+ Yrs NC Large Cap Value 3% 4% 5% 6% NC Large Cap Index 7% 7% 8% 11% NC Large Cap Growth 3% 4% 5% 6% NC Large Cap Core 6% 8% 10% 12% NC Small / Mid Cap Value 6% 7% 9% 11% NC Small / Mid Cap Index 0% 0% 0% 0% NC Small / Mid Cap Growth 6% 7% 9% 11% NC Small / Mid Cap Core 12% 14% 18% 22% NC Global Equity 16% 19% 24% 30% NC International 8% 9% 12% 15% NC International Index 0% 0% 0% 0% NC Fixed Income 12% 10% 5% 0% NC Fixed Income Index 12% 10% 6% 0% NC Stable Value 17% 13% 7% 0% NC Inflation Sensitive 10% 10% 10% 10% over the long term with a reasonable level of overall volatility. 7

19 Appendix B: Prudential s new GoalMaker Model (3x9) Conservative Pre-Retirement Post-Retirement Years to Retirement US Large 28% 24% 21% 17% 14% 13% 11% 11% 10% SMID Growth 9% 8% 7% 6% 5% 4% 3% 2% 2% SMID Value 9% 8% 7% 6% 5% 4% 3% 2% 2% International Stocks 19% 17% 14% 11% 9% 6% 5% 4% 4% Emerging 8% 7% 5% 4% 3% 2% 2% 1% 0% Bonds 11% 15% 17% 20% 23% 26% 27% 28% 28% SV 11% 17% 25% 32% 37% 42% 46% 49% 51% Real Assets 5% 4% 4% 4% 4% 3% 3% 3% 3% Equity 73% 64% 54% 44% 36% 29% 24% 20% 18% Bonds 22% 32% 42% 52% 60% 68% 73% 77% 79% Alternatives 5% 4% 4% 4% 4% 3% 3% 3% 3% Total 100% 100% 100% 100% 100% 100% 100% 100% 100% Moderate Pre-Retirement Post-Retirement Years to Retirement US Large 33% 31% 28% 24% 22% 17% 16% 16% 14% SMID Growth 11% 10% 9% 8% 7% 6% 5% 4% 3% SMID Value 11% 10% 9% 8% 7% 6% 5% 4% 3% International Stocks 22% 21% 19% 17% 13% 11% 10% 7% 7% Emerging 9% 8% 7% 6% 5% 4% 3% 3% 2% Bonds 4% 7% 11% 15% 19% 23% 25% 26% 27% SV 3% 7% 11% 17% 22% 28% 32% 36% 40% Real Assets 7% 6% 6% 5% 5% 5% 4% 4% 4% Equity 86% 80% 72% 63% 54% 44% 39% 34% 29% Bonds 7% 14% 22% 32% 41% 51% 57% 62% 67% Alternatives 7% 6% 6% 5% 5% 5% 4% 4% 4% Total 100% 100% 100% 100% 100% 100% 100% 100% 100% 8

20 Aggressive Pre-Retirement Post-Retirement Years to Retirement US Large 31% 32% 31% 29% 28% 25% 22% 22% 20% SMID Growth 12% 12% 11% 10% 9% 8% 7% 6% 5% SMID Value 12% 12% 11% 10% 9% 8% 7% 6% 5% International Stocks 25% 24% 23% 22% 19% 15% 13% 12% 11% Emerging 10% 10% 9% 8% 6% 5% 4% 3% 2% Bonds 2% 2% 5% 8% 12% 17% 20% 21% 23% SV 1% 1% 3% 6% 11% 16% 22% 25% 29% Real Assets 7% 7% 7% 7% 6% 6% 5% 5% 5% Equity 90% 90% 85% 79% 71% 61% 53% 49% 43% Bonds 3% 3% 8% 14% 23% 33% 42% 46% 52% Alternatives 7% 7% 7% 7% 6% 6% 5% 5% 5% Total 100% 100% 100% 100% 100% 100% 100% 100% 100% 9

21 Appendix C: Morningstar Lifetime Allocation Indexes Conservative Moderate 10

22 Aggressive 11

WHEREAS, at its meeting on December 14, 2017, the Board adopted a strategy and a manager for the NC TIPS Fund;

SUPPLEMENTAL RETIREMENT PLAN OF NORTH CAROLINA WHEREAS, the North Carolina Department of State Treasurer and the Supplemental Retirement Board of Trustees (the Board ) administer the Supplemental Retirement

SUPPLEMENTAL RETIREMENT PLAN OF NORTH CAROLINA WHEREAS, the North Carolina Department of State Treasurer and the Supplemental Retirement Board of Trustees (the Board ) administer the Supplemental Retirement

North Carolina Supplemental Retirement Plans Annual Review. March 2012

North Carolina Supplemental Retirement Plans Annual Review March 2012 Agenda Overview and Recommendations Inflation Sensitive Options Fund Structure Review GoalMaker Review SMID Cap Growth Investment Operations

North Carolina Supplemental Retirement Plans Annual Review March 2012 Agenda Overview and Recommendations Inflation Sensitive Options Fund Structure Review GoalMaker Review SMID Cap Growth Investment Operations

Updated North Carolina 403(b) Program Model Allocations

Program Model Allocations") NORTH CAROLINA DEPARTMENT OF STATE TREASURER INVESTMENT MANAGEMENT DIVISION JANET COWELL TREASURER KEVIN SIGRIST CHIEF INVESTMENT OFFICER To: From: CC: Supplemental Retirement Board of Trustees Kevin SigRist

NORTH CAROLINA DEPARTMENT OF STATE TREASURER INVESTMENT MANAGEMENT DIVISION JANET COWELL TREASURER KEVIN SIGRIST CHIEF INVESTMENT OFFICER To: From: CC: Supplemental Retirement Board of Trustees Kevin SigRist

Plan Enhancements June 2018 NC 401(k), NC 457, 403(b)

, NC 457, 403(b)") Plan Enhancements June NC 401(k), NC 457, 403(b) Important Changes for All Participants Treasury Inflation Protected Securities (TIPS) Index Funds will be added to all three Plans. In the NC 403(b), the

Plan Enhancements June NC 401(k), NC 457, 403(b) Important Changes for All Participants Treasury Inflation Protected Securities (TIPS) Index Funds will be added to all three Plans. In the NC 403(b), the

GoalMaker 2.0 Implementation NC 401(k), NC 457, NC 403(b)

, NC 457, NC 403(b)") GoalMaker 2.0 Implementation NC 401(k), NC 457, NC 403(b) Participants in GoalMaker More than 190,000 participants across all three Plans utilize GoalMaker (GM). Today s discussion is focused on this total

GoalMaker 2.0 Implementation NC 401(k), NC 457, NC 403(b) Participants in GoalMaker More than 190,000 participants across all three Plans utilize GoalMaker (GM). Today s discussion is focused on this total

North Carolina. Performance Evaluation Report. Fourth Quarter 2017

North Carolina Performance Evaluation Report Fourth Quarter 207 Performance Summary - Quarter in Review 2 NC CURRENT INVESTMENT STRUCTURE Tier I Target Date Funds Tier II - A Passive Core Options Tier

North Carolina Performance Evaluation Report Fourth Quarter 207 Performance Summary - Quarter in Review 2 NC CURRENT INVESTMENT STRUCTURE Tier I Target Date Funds Tier II - A Passive Core Options Tier

North Carolina Supplemental Retirement Plans. Performance Review First Quarter 2017

North Carolina Supplemental Retirement Plans Performance Review First Quarter 2017 Asset Allocation Summary Current Asset Allocation As of March 31, 2017 Prior Period Asset Allocation As of December 31,

North Carolina Supplemental Retirement Plans Performance Review First Quarter 2017 Asset Allocation Summary Current Asset Allocation As of March 31, 2017 Prior Period Asset Allocation As of December 31,

FLORIDA RETIREMENT SYSTEM. Investment Plan Investment Policy Statement

FLORIDA RETIREMENT SYSTEM Investment Plan Investment Policy Statement I. PURPOSE The Florida Retirement System Investment Plan Investment Policy Statement (IPS) serves as the primary statement of Trustee

FLORIDA RETIREMENT SYSTEM Investment Plan Investment Policy Statement I. PURPOSE The Florida Retirement System Investment Plan Investment Policy Statement (IPS) serves as the primary statement of Trustee

Above and Beyond The Latest in Investment Menu Innovations

Above and Beyond The Latest in Investment Menu Innovations Moderator: Jayson Davidson, Hyas Group Speakers: Steve Toole, State of North Carolina Brendan Curran, State Street Global Advisors Order of the

Above and Beyond The Latest in Investment Menu Innovations Moderator: Jayson Davidson, Hyas Group Speakers: Steve Toole, State of North Carolina Brendan Curran, State Street Global Advisors Order of the

FlexChoice Access. Investment Line-up by Asset Class or Category

FlexChoice Access Investment Line-up by Asset Class or Category Simplifying the FlexChoice Access Fund Choices With FlexChoice Access, you now have the opportunity to design a portfolio to help meet client

FlexChoice Access Investment Line-up by Asset Class or Category Simplifying the FlexChoice Access Fund Choices With FlexChoice Access, you now have the opportunity to design a portfolio to help meet client

Target Retirement Performance Update

Target Retirement Update Q1 2017 CIT Strategy Highlights As of March 31, 2017 The State Street Target Retirement Collective Trust Strategies posted quarterly returns ranging from +2.44% (Income Strategy)

Target Retirement Update Q1 2017 CIT Strategy Highlights As of March 31, 2017 The State Street Target Retirement Collective Trust Strategies posted quarterly returns ranging from +2.44% (Income Strategy)

DRAFT MINUTES SUPPLEMENTAL RETIREMENT BOARD OF TRUSTEES

DRAFT MINUTES SUPPLEMENTAL RETIREMENT BOARD OF TRUSTEES The regular quarterly meeting of the Supplemental Retirement Board of Trustees was called to order at 9:03 a.m., September 20, 2018, by the Chair,

DRAFT MINUTES SUPPLEMENTAL RETIREMENT BOARD OF TRUSTEES The regular quarterly meeting of the Supplemental Retirement Board of Trustees was called to order at 9:03 a.m., September 20, 2018, by the Chair,

VRS Investment Policy Statement For An Unbundled Defined Contribution Plan Structure

VRS Investment Policy Statement For An Unbundled Defined Contribution Plan Structure Approved by the Board of Trustees: February 16, 2012 Last Updated February 9, 2017* The Virginia Retirement System (VRS)

VRS Investment Policy Statement For An Unbundled Defined Contribution Plan Structure Approved by the Board of Trustees: February 16, 2012 Last Updated February 9, 2017* The Virginia Retirement System (VRS)

FLORIDA RETIREMENT SYSTEM. Investment Plan Investment Policy Statement

FLORIDA RETIREMENT SYSTEM Investment Plan Investment Policy Statement I. PURPOSE The Florida Retirement System Investment Plan Investment Policy Statement (IPS) serves as the primary statement of Trustee

FLORIDA RETIREMENT SYSTEM Investment Plan Investment Policy Statement I. PURPOSE The Florida Retirement System Investment Plan Investment Policy Statement (IPS) serves as the primary statement of Trustee

University of Maine System Investment Policy Statement Defined Contribution Retirement Plans

University of Maine System Investment Policy Statement Defined Contribution Retirement Plans As Updated at the December 8, 2016, Investment Committee Meeting Page 1 of 19 Table of Contents Section Statement

University of Maine System Investment Policy Statement Defined Contribution Retirement Plans As Updated at the December 8, 2016, Investment Committee Meeting Page 1 of 19 Table of Contents Section Statement

The Looming Liability of Target Date Funds

The Looming Liability of Target Date Funds Proliferation of Target Date Funds (TDFs) One of the most widely used investment options in defined contribution (DC) plans 70% of total DC assets by 2020 1 TDF

The Looming Liability of Target Date Funds Proliferation of Target Date Funds (TDFs) One of the most widely used investment options in defined contribution (DC) plans 70% of total DC assets by 2020 1 TDF

FLORIDA RETIREMENT SYSTEM. Public Employee Optional Retirement Program Investment Policy Statement

FLORIDA RETIREMENT SYSTEM Public Employee Optional Retirement Program Investment Policy Statement I. PURPOSE The Public Employee Optional Retirement Program Investment Policy Statement (IPS) serves as

FLORIDA RETIREMENT SYSTEM Public Employee Optional Retirement Program Investment Policy Statement I. PURPOSE The Public Employee Optional Retirement Program Investment Policy Statement (IPS) serves as

Going Beyond Style Box Investing

Going Beyond Style Box Investing NCPERS Presented by Erin Doyle Orekhov, Client Portfolio Manager May 22, 2017 For financial professional or qualified institutional investor use only. Not for inspection

Going Beyond Style Box Investing NCPERS Presented by Erin Doyle Orekhov, Client Portfolio Manager May 22, 2017 For financial professional or qualified institutional investor use only. Not for inspection

The Northern Trust Focus Funds Glidepath Exhibit

N O R T H E R N T R U S T G L O B A L I N V E S T M E N T S The Northern Trust Focus Funds Glidepath Exhibit northerntrust.com Asset Allocation Framework Our asset allocation framework considers asset

N O R T H E R N T R U S T G L O B A L I N V E S T M E N T S The Northern Trust Focus Funds Glidepath Exhibit northerntrust.com Asset Allocation Framework Our asset allocation framework considers asset

flexpath vs. Vanguard Target Retirement

flexpath vs. Vanguard Target Retirement Average Scores Vanguard flexpath Index 9.0 9.4 3(38) Investment Manager with IPS Vanguard No flexpath Yes Number Asset Classes Vanguard flexpath 4 7 Vanguard Average

flexpath vs. Vanguard Target Retirement Average Scores Vanguard flexpath Index 9.0 9.4 3(38) Investment Manager with IPS Vanguard No flexpath Yes Number Asset Classes Vanguard flexpath 4 7 Vanguard Average

NORTH CAROLINA SUPPLEMENTAL RETIREMENT PLANS

HEALTH WEALTH CAREER NORTH CAROLINA SUPPLEMENTAL RETIREMENT PLANS INVESTMENT STRATEGY DISCUSSION F E B R U A R Y 1 5, 2 0 1 7 Liana Magner, CFA Kelly Henson Will Dillard, CFA MERCER 2016 0 CONTENT DC Trends

HEALTH WEALTH CAREER NORTH CAROLINA SUPPLEMENTAL RETIREMENT PLANS INVESTMENT STRATEGY DISCUSSION F E B R U A R Y 1 5, 2 0 1 7 Liana Magner, CFA Kelly Henson Will Dillard, CFA MERCER 2016 0 CONTENT DC Trends

FLORIDA RETIREMENT SYSTEM. Investment Plan Investment Policy Statement

FLORIDA RETIREMENT SYSTEM Investment Plan Investment Policy Statement I. PURPOSE The Florida Retirement System Investment Plan Investment Policy Statement (IPS) serves as the primary statement of Trustee

FLORIDA RETIREMENT SYSTEM Investment Plan Investment Policy Statement I. PURPOSE The Florida Retirement System Investment Plan Investment Policy Statement (IPS) serves as the primary statement of Trustee

The UPMC Savings Plan: Information about your investment options, fees, and other expenses

UPMC Annual Fee Disclosure Notice January 2018 The UPMC Savings Plan: Information about your investment options, fees, and other expenses The UPMC Savings Plan (Savings Plan or Plan ) is a great way to

UPMC Annual Fee Disclosure Notice January 2018 The UPMC Savings Plan: Information about your investment options, fees, and other expenses The UPMC Savings Plan (Savings Plan or Plan ) is a great way to

NORTH CAROLINA SUPPLEMENTAL RETIREMENT PLANS

HEALTH WEALTH CAREER NORTH CAROLINA SUPPLEMENTAL RETIREMENT PLANS SECOND QUARTER PERFORMANCE REVIEW AGENDA Capital Markets Review Second Quarter Performance Appendix MERCER 2017 1 CAPITAL MARKETS REVIEW

HEALTH WEALTH CAREER NORTH CAROLINA SUPPLEMENTAL RETIREMENT PLANS SECOND QUARTER PERFORMANCE REVIEW AGENDA Capital Markets Review Second Quarter Performance Appendix MERCER 2017 1 CAPITAL MARKETS REVIEW

Voya Target Date: A Holistic Approach to Target Date Design

Voya Target Date: A Holistic Approach to Target Date Design May 2018 Paul Zemsky, CFA Chief Investment Officer, Multi-Asset Strategies and Solutions Halvard Kvaale, CIMA Head of Manager Research and Selection

Voya Target Date: A Holistic Approach to Target Date Design May 2018 Paul Zemsky, CFA Chief Investment Officer, Multi-Asset Strategies and Solutions Halvard Kvaale, CIMA Head of Manager Research and Selection

PLAN NEWS. See inside for details.

United Launch Alliance 401(k) Savings Plan PLAN NEWS Changes to Your Investment Options United Launch Alliance (ULA) regularly reviews the funds in the 401(k) Savings Plan to make sure they offer a combination

United Launch Alliance 401(k) Savings Plan PLAN NEWS Changes to Your Investment Options United Launch Alliance (ULA) regularly reviews the funds in the 401(k) Savings Plan to make sure they offer a combination

Voya Target Date: A Holistic Approach to Target Date Design

Voya Target Date: A Holistic Approach to Target Date Design Paul Zemsky, CFA Chief Investment Officer, Multi-Asset Strategies and Solutions Jody Hrazanek Head of Strategy Design and Implementation Halvard

Voya Target Date: A Holistic Approach to Target Date Design Paul Zemsky, CFA Chief Investment Officer, Multi-Asset Strategies and Solutions Jody Hrazanek Head of Strategy Design and Implementation Halvard

Conservative Risk Fund

Release Date: 09-30-2018 Conservative Risk Fund... Morningstar Category Blended Allocation--30% to 50% Equity Investment Information Investment Strategy The Conservative Risk Fund invests in a combination

Release Date: 09-30-2018 Conservative Risk Fund... Morningstar Category Blended Allocation--30% to 50% Equity Investment Information Investment Strategy The Conservative Risk Fund invests in a combination

CalPERS 457 Plan Target Retirement Date Funds

Asset Allocation CalPERS 457 Plan Target Retirement Date s December 31, 2017 Overview Target Retirement Date s (the "" or "s") are a series of diversified funds, each of which has a predetermined underlying

Asset Allocation CalPERS 457 Plan Target Retirement Date s December 31, 2017 Overview Target Retirement Date s (the "" or "s") are a series of diversified funds, each of which has a predetermined underlying

GIPS List of Composite Descriptions

GIPS List of Composite Descriptions Updated 5/12/14 Concentrated Growth Composite-330 Concentrated Growth portfolios, benchmarked to the Russell 1000 Growth Index, take concentrated positions in larger

GIPS List of Composite Descriptions Updated 5/12/14 Concentrated Growth Composite-330 Concentrated Growth portfolios, benchmarked to the Russell 1000 Growth Index, take concentrated positions in larger

RESPONSES TO QUESTIONS FROM PROPOSERS FOR SFDCP S TARGET DATE FUND INVESTMENT MANAGEMENT REQUEST FOR PROPOSAL

RESPONSES TO QUESTIONS FROM PROPOSERS FOR SFDCP S TARGET DATE FUND INVESTMENT MANAGEMENT REQUEST FOR PROPOSAL To All Proposers: Please review this document for responses to all the questions posed by investment

RESPONSES TO QUESTIONS FROM PROPOSERS FOR SFDCP S TARGET DATE FUND INVESTMENT MANAGEMENT REQUEST FOR PROPOSAL To All Proposers: Please review this document for responses to all the questions posed by investment

UC Retirement Savings Plans Fund Descriptions (click on fund name to reach the specific fund description)

") UC Retirement Savings Plans Fund Descriptions (click on fund name to reach the specific fund description) UC PATHWAY FUND UC Pathway Income Fund UC Pathway Fund 2015 UC Pathway Fund 2020 UC Pathway Fund

UC Retirement Savings Plans Fund Descriptions (click on fund name to reach the specific fund description) UC PATHWAY FUND UC Pathway Income Fund UC Pathway Fund 2015 UC Pathway Fund 2020 UC Pathway Fund

ROCHESTER INSTITUTE OF TECHNOLOGY Investment Policy

ROCHESTER INSTITUTE OF TECHNOLOGY Investment Policy Revised and Approved March 10, 2014 1. Purpose The financial objective of the endowment portfolio is to provide a sustainable level of income distribution

ROCHESTER INSTITUTE OF TECHNOLOGY Investment Policy Revised and Approved March 10, 2014 1. Purpose The financial objective of the endowment portfolio is to provide a sustainable level of income distribution

Dear Participant: Please refer to Part IV of the attached document for information on who to call with questions.

Dear Participant: You are receiving the attached notification as the result of a regulation passed by the Department of Labor (DOL) in October 2010. This participant fee disclosure regulation, referred

Dear Participant: You are receiving the attached notification as the result of a regulation passed by the Department of Labor (DOL) in October 2010. This participant fee disclosure regulation, referred

Target-Date Funds: Not as Simple as Set It and Forget It

Target-Date Funds: Not as Simple as Set It and Forget It This article includes checklists for issues defined contribution plan sponsors must address under new disclosure rules as part of their due diligence

Target-Date Funds: Not as Simple as Set It and Forget It This article includes checklists for issues defined contribution plan sponsors must address under new disclosure rules as part of their due diligence

North Carolina Supplemental Retirement Plans

North Carolina Supplemental Retirement Plans STATEMENT OF INVESTMENT POLICY JUNE 2012 CONTENTS I. PURPOSE II. RESPONSIBILITIES OF PARTICIPANTS III. RESPONSIBLE PARTIES IV. PLAN STRUCTURE V. INVESTMENT

North Carolina Supplemental Retirement Plans STATEMENT OF INVESTMENT POLICY JUNE 2012 CONTENTS I. PURPOSE II. RESPONSIBILITIES OF PARTICIPANTS III. RESPONSIBLE PARTIES IV. PLAN STRUCTURE V. INVESTMENT

AAA INVESTMENT POLICY STATEMENT. American Anthropological Association Investment Policy Statement

AAA INVESTMENT POLICY STATEMENT American Anthropological Association Investment Policy Statement Finance Committee recommended October 23, 2013 Executive Board adopted, November 1, 2013 EXECUTIVE SUMMARY

AAA INVESTMENT POLICY STATEMENT American Anthropological Association Investment Policy Statement Finance Committee recommended October 23, 2013 Executive Board adopted, November 1, 2013 EXECUTIVE SUMMARY

VIRGINIA POLYTECHNIC INSTITUTE AND STATE UNIVERSITY OPTIONAL RETIREMENT AND CASH MATCH PLANS INVESTMENT POLICY STATEMENT

VIRGINIA POLYTECHNIC INSTITUTE AND STATE UNIVERSITY OPTIONAL RETIREMENT AND CASH MATCH PLANS INVESTMENT POLICY STATEMENT May 2007 TABLE OF CONTENTS Page EXECUTIVE SUMMARY...1 PURPOSE OF THE INVESTMENT

VIRGINIA POLYTECHNIC INSTITUTE AND STATE UNIVERSITY OPTIONAL RETIREMENT AND CASH MATCH PLANS INVESTMENT POLICY STATEMENT May 2007 TABLE OF CONTENTS Page EXECUTIVE SUMMARY...1 PURPOSE OF THE INVESTMENT

Fairfax County Public Schools 457(b) Plan. Investment Policy Statement

Plan. Investment Policy Statement") Fairfax County Public Schools 457(b) Plan Investment Policy Statement September 2016 CONTENTS I. Overview & Purpose II. III. IV. Roles and Responsibilities Investment Objectives Investment Guidelines V.

Fairfax County Public Schools 457(b) Plan Investment Policy Statement September 2016 CONTENTS I. Overview & Purpose II. III. IV. Roles and Responsibilities Investment Objectives Investment Guidelines V.

Portfolio Allocation Models. for Lincoln Financial Group s Variable Life Insurance Products

Portfolio Allocation Models for Lincoln Financial Group s Variable Life Insurance Products 40% (Conservative) Allocation Model M s Portfolio Allocation Models for Lincoln Financial Group s Variable Insurance

Portfolio Allocation Models for Lincoln Financial Group s Variable Life Insurance Products 40% (Conservative) Allocation Model M s Portfolio Allocation Models for Lincoln Financial Group s Variable Insurance

PRUDENTIAL DAY ONE SM FUNDS

PRUDENTIAL DAY ONE SM FUNDS Preparing for the first day of retirement, and all the days thereafter with target date funds Prudential Day One Funds are offered through Prudential Retirement Insurance and

PRUDENTIAL DAY ONE SM FUNDS Preparing for the first day of retirement, and all the days thereafter with target date funds Prudential Day One Funds are offered through Prudential Retirement Insurance and

C.1. Capital Markets Research Group Asset-Liability Study Results. December 2016

December 2016 2016 Asset-Liability Study Results Capital Markets Research Group Scope of the Project Asset/Liability Study Phase 1 Review MCERA s current investment program. Strategic allocation to broad

December 2016 2016 Asset-Liability Study Results Capital Markets Research Group Scope of the Project Asset/Liability Study Phase 1 Review MCERA s current investment program. Strategic allocation to broad

ASTUTE SMA PLATFORM. Approved Product List. Dated 22 December 2015

ASTUTE SMA PLATFORM Approved Product List Dated 22 December 2015 This Approved Product List is issued by Praemium Australia Limited (ABN 92 117 611 784, AFSL 297956). The information in this document forms

ASTUTE SMA PLATFORM Approved Product List Dated 22 December 2015 This Approved Product List is issued by Praemium Australia Limited (ABN 92 117 611 784, AFSL 297956). The information in this document forms

2016 NCRS Asset Liability Study: Phase 2

2016 NCRS Asset Liability Study: Phase 2 April 19, 2016 2016 NCRS Asset Liability Study: Phase 1 Updated the baseline asset allocation assumptions Created three Scenario-Based Asset Allocation Model Portfolios

2016 NCRS Asset Liability Study: Phase 2 April 19, 2016 2016 NCRS Asset Liability Study: Phase 1 Updated the baseline asset allocation assumptions Created three Scenario-Based Asset Allocation Model Portfolios

EVESTMENT INSTITUTIONAL INVESTMENT INTELLIGENCE CONFERENCE

EVESTMENT INSTITUTIONAL INVESTMENT INTELLIGENCE CONFERENCE 2018 Trends Update: Industry Themes Data Driven Insight Peter Laurelli Global Head of Research, evestment John Molesphini Global Head of Strategic

EVESTMENT INSTITUTIONAL INVESTMENT INTELLIGENCE CONFERENCE 2018 Trends Update: Industry Themes Data Driven Insight Peter Laurelli Global Head of Research, evestment John Molesphini Global Head of Strategic

TIAA-CREF Lifecycle Funds: Methodology and Design

Introduction The TIAA-CREF Lifecycle Funds are a target retirement date fund family that includes a total of 12 funds: 11 target retirement date funds at five-year intervals for retirement dates 2010 through

Introduction The TIAA-CREF Lifecycle Funds are a target retirement date fund family that includes a total of 12 funds: 11 target retirement date funds at five-year intervals for retirement dates 2010 through

Your guide to upcoming changes to your 401(k) Plan Farm Credit Foundations Defined Contribution/401(k) Plan

Plan Farm Credit Foundations Defined Contribution/401(k) Plan") Your guide to upcoming changes to your 401(k) Plan Farm Credit Foundations Defined Contribution/401(k) Plan John Hancock Retirement Plan Services, LLC and Farm Credit Foundations are not affiliated and

Your guide to upcoming changes to your 401(k) Plan Farm Credit Foundations Defined Contribution/401(k) Plan John Hancock Retirement Plan Services, LLC and Farm Credit Foundations are not affiliated and

Investment Options. Selecting the Right Retirement Plan Investments

Investment Options Selecting the Right Retirement Plan Investments 451986 Comprehensive Fund Selection Designed for Retirement Savings The investment options available in our retirement products are carefully

Investment Options Selecting the Right Retirement Plan Investments 451986 Comprehensive Fund Selection Designed for Retirement Savings The investment options available in our retirement products are carefully

Quarterly Asset Class Report Global Equity

Quarterly Asset Class Report Global Equity canterburyconsulting.com Canterbury Consulting ( CCI ) is an SEC registered Investment Adviser. Information pertaining to CCI's advisory operations, services,

Quarterly Asset Class Report Global Equity canterburyconsulting.com Canterbury Consulting ( CCI ) is an SEC registered Investment Adviser. Information pertaining to CCI's advisory operations, services,

GOAL ENGINEER SERIES PORTFOLIO HIGHLIGHTS:

GOAL ENGINEER SERIES The Goal Engineer Series combines Northern Trust s asset allocation, portfolio construction and risk management expertise with Engineered Equity TM and active fixed income strategies

GOAL ENGINEER SERIES The Goal Engineer Series combines Northern Trust s asset allocation, portfolio construction and risk management expertise with Engineered Equity TM and active fixed income strategies

D E F I N I T I O N O F D U T I E S O B J E C T I V E S

UNIVERSITY OF UTAH E NDOWMENT POOL INVESTMENT IMPLEMENTATION STRATEGY CONTENTS May, 2015 O V E R V I E W D E F I N I T I O N O F D U T I E S O B J E C T I V E S A S S E T A L L O C A T I O N / I N V E

UNIVERSITY OF UTAH E NDOWMENT POOL INVESTMENT IMPLEMENTATION STRATEGY CONTENTS May, 2015 O V E R V I E W D E F I N I T I O N O F D U T I E S O B J E C T I V E S A S S E T A L L O C A T I O N / I N V E

Saving for the Future MONDELĒZ GLOBAL LLC TIP PLAN. Investment Options Guide

Saving for the Future MONDELĒZ GLOBAL LLC TIP PLAN Investment Options Guide Effective August 31, 2016 TARGET DATE FUNDS The Target Date Funds are designed as an all-in-one approach for participants looking

Saving for the Future MONDELĒZ GLOBAL LLC TIP PLAN Investment Options Guide Effective August 31, 2016 TARGET DATE FUNDS The Target Date Funds are designed as an all-in-one approach for participants looking

INVESTMENT POLICY STATEMENT CITY OF DOVER POLICE PENSION PLAN

INVESTMENT POLICY STATEMENT CITY OF DOVER POLICE PENSION PLAN August 2016 INVESTMENT POLICY STATEMENT CITY OF DOVER POLICE PENSION PLAN Table of Contents Section Page I. Purpose and Background 2 II. Statement

INVESTMENT POLICY STATEMENT CITY OF DOVER POLICE PENSION PLAN August 2016 INVESTMENT POLICY STATEMENT CITY OF DOVER POLICE PENSION PLAN Table of Contents Section Page I. Purpose and Background 2 II. Statement

STRATEGY OVERVIEW. Long/Short Equity. Related Funds: 361 Domestic Long/Short Equity Fund (ADMZX) 361 Global Long/Short Equity Fund (AGAZX)

361 Global Long/Short Equity Fund (AGAZX)") STRATEGY OVERVIEW Long/Short Equity Related Funds: 361 Domestic Long/Short Equity Fund (ADMZX) 361 Global Long/Short Equity Fund (AGAZX) Strategy Thesis The thesis driving 361 s Long/Short Equity strategies

STRATEGY OVERVIEW Long/Short Equity Related Funds: 361 Domestic Long/Short Equity Fund (ADMZX) 361 Global Long/Short Equity Fund (AGAZX) Strategy Thesis The thesis driving 361 s Long/Short Equity strategies

Capital Market Assumptions

Capital Market Assumptions December 31, 2015 Contents Contents... 1 Overview and Summary... 2 CMA Building Blocks... 3 GEM Policy Portfolio Alpha and Beta Assumptions... 4 Volatility Assumptions... 6 Appendix:

Capital Market Assumptions December 31, 2015 Contents Contents... 1 Overview and Summary... 2 CMA Building Blocks... 3 GEM Policy Portfolio Alpha and Beta Assumptions... 4 Volatility Assumptions... 6 Appendix:

YOUR GUIDE TO GETTING STARTED

Rochester Regional Health 401(k) Defined Contribution Plan Invest in your retirement and yourself today, with help from the Rochester Regional Health 401(k) Defined Contribution Plan and Fidelity. YOUR

Rochester Regional Health 401(k) Defined Contribution Plan Invest in your retirement and yourself today, with help from the Rochester Regional Health 401(k) Defined Contribution Plan and Fidelity. YOUR

PGIM INVESTMENTS UPDATE

PGIM INVESTMENTS Bringing you the investment managers of Prudential Financial, Inc. PGIM INVESTMENTS UPDATE Prudential Mutual Funds to be renamed PGIM Mutual Funds Prudential Closed-end Funds to be renamed

PGIM INVESTMENTS Bringing you the investment managers of Prudential Financial, Inc. PGIM INVESTMENTS UPDATE Prudential Mutual Funds to be renamed PGIM Mutual Funds Prudential Closed-end Funds to be renamed

Amended as of January 1, 2018

THE WALLACE FOUNDATION INVESTMENT POLICY Amended as of January 1, 2018 1. INVESTMENT GOAL The investment goal of The Wallace Foundation (the Foundation) is to earn a total return that will provide a steady

THE WALLACE FOUNDATION INVESTMENT POLICY Amended as of January 1, 2018 1. INVESTMENT GOAL The investment goal of The Wallace Foundation (the Foundation) is to earn a total return that will provide a steady

THE FREEDOM UMA. Unified Managed Account Strategies

THE FREEDOM UMA Unified Managed Account Strategies Freedom UMA Effective investment planning cannot be left to chance. It requires research, consultation, planning, execution and constant monitoring. When

THE FREEDOM UMA Unified Managed Account Strategies Freedom UMA Effective investment planning cannot be left to chance. It requires research, consultation, planning, execution and constant monitoring. When

NATIONWIDE ASSET ALLOCATION INVESTMENT PROCESS

Nationwide Funds A Nationwide White Paper NATIONWIDE ASSET ALLOCATION INVESTMENT PROCESS May 2017 INTRODUCTION In the market decline of 2008, the S&P 500 Index lost more than 37%, numerous equity strategies

Nationwide Funds A Nationwide White Paper NATIONWIDE ASSET ALLOCATION INVESTMENT PROCESS May 2017 INTRODUCTION In the market decline of 2008, the S&P 500 Index lost more than 37%, numerous equity strategies

Information Regarding Your Retirement Account LEECH LAKE BAND OF OJIBWE GOVERNMENT 401(K) October 14, 2017

October 14, 2017") Information Regarding Your Retirement Account LEECH LAKE BAND OF OJIBWE GOVERNMENT 401(K) October 14, 2017 The information in this document is designed to provide you important information about your company

Information Regarding Your Retirement Account LEECH LAKE BAND OF OJIBWE GOVERNMENT 401(K) October 14, 2017 The information in this document is designed to provide you important information about your company

Attractive option for college saving

Tomorrow s Scholar 529 Age-Based Portfolios Attractive option for college saving... connecting to the future Not FDIC Insured May Lose Value No Bank Guarantee INVESTMENT MANAGEMENT Introduction The goal

Tomorrow s Scholar 529 Age-Based Portfolios Attractive option for college saving... connecting to the future Not FDIC Insured May Lose Value No Bank Guarantee INVESTMENT MANAGEMENT Introduction The goal

MERCER MULTI-MANAGER FUNDS QUARTERLY REPORT THREE MONTHS TO 31 DECEMBER 2016

MERCER MULTI-MANAGER FUNDS QUARTERLY REPORT THREE MONTHS TO 31 DECEMBER 2016 MERCER MULTI-MANAGER FUNDS QUARTERLY REPORT CONTENTS ECONOMY & MARKETS 1 FINANCIAL MARKET RETURNS TO 31 DECEMBER 2016 QUARTER

MERCER MULTI-MANAGER FUNDS QUARTERLY REPORT THREE MONTHS TO 31 DECEMBER 2016 MERCER MULTI-MANAGER FUNDS QUARTERLY REPORT CONTENTS ECONOMY & MARKETS 1 FINANCIAL MARKET RETURNS TO 31 DECEMBER 2016 QUARTER

2017 Investment Management Division Major Initiatives

2017 Investment Management Division Major Initiatives March 29, 2017 Taken Off the List 1. Research and develop Long-term Stewardship ( ESG ) policies and strategies 2. Transition oversight of Ancillary

2017 Investment Management Division Major Initiatives March 29, 2017 Taken Off the List 1. Research and develop Long-term Stewardship ( ESG ) policies and strategies 2. Transition oversight of Ancillary

TOPS Managed Risk Balanced ETF Portfolio TOPS Managed Risk Moderate Growth ETF Portfolio TOPS Managed Risk Growth ETF Portfolio

TOPS Managed Risk Balanced ETF Portfolio TOPS Managed Risk Moderate Growth ETF Portfolio TOPS Managed Risk Growth ETF Portfolio Class 3 shares Class 4 shares PROSPECTUS May 1, 2017 1-855-572-5945 This

TOPS Managed Risk Balanced ETF Portfolio TOPS Managed Risk Moderate Growth ETF Portfolio TOPS Managed Risk Growth ETF Portfolio Class 3 shares Class 4 shares PROSPECTUS May 1, 2017 1-855-572-5945 This

Topic Five: Case Study: Asset Allocation at the Texas Teacher Retirement System

Topic Five: Case Study: Asset Allocation at the Texas Teacher Retirement System Case Study: Asset Allocation at Texas Teacher Retirement System Background: The Teacher Retirement System of Texas (TRS)

Topic Five: Case Study: Asset Allocation at the Texas Teacher Retirement System Case Study: Asset Allocation at Texas Teacher Retirement System Background: The Teacher Retirement System of Texas (TRS)

A Panel of TIAA-CREF Portfolio Managers: Who s Managing Your Money? April 14, 2011

A Panel of TIAA-CREF Portfolio Managers: Who s Managing Your Money? April 14, 2011 Disclosure You should consider the investment objectives, risks, charges and expenses carefully before investing. Please

A Panel of TIAA-CREF Portfolio Managers: Who s Managing Your Money? April 14, 2011 Disclosure You should consider the investment objectives, risks, charges and expenses carefully before investing. Please

CITY OF VIRGINIA BEACH DEFERRED COMPENSATION PLAN. Statement of Investment Policy

CITY OF VIRGINIA BEACH DEFERRED COMPENSATION PLAN Statement of Investment Policy Board Approved August 10, 2016 TABLE OF CONTENTS Page INTRODUCTION... 2 OBJECTIVES OF THE PLANS... 2 INVESTMENT OPTIONS

CITY OF VIRGINIA BEACH DEFERRED COMPENSATION PLAN Statement of Investment Policy Board Approved August 10, 2016 TABLE OF CONTENTS Page INTRODUCTION... 2 OBJECTIVES OF THE PLANS... 2 INVESTMENT OPTIONS

LifePath Index 2030 Fund H

Blend Moderate Quality Inc Risk Profile This investment option may be most appropriate for someone willing to balance the risk of principal fluctuation with the potential for greater capital growth over

Blend Moderate Quality Inc Risk Profile This investment option may be most appropriate for someone willing to balance the risk of principal fluctuation with the potential for greater capital growth over

FLORIDA RETIREMENT SYSTEM DEFINED BENEFIT PLAN INVESTMENT POLICY STATEMENT

FLORIDA RETIREMENT SYSTEM DEFINED BENEFIT PLAN INVESTMENT POLICY STATEMENT I. DEFINITIONS Absolute Real Target Rate of Return - The total rate of return by which the FRS Portfolio must grow, in excess

FLORIDA RETIREMENT SYSTEM DEFINED BENEFIT PLAN INVESTMENT POLICY STATEMENT I. DEFINITIONS Absolute Real Target Rate of Return - The total rate of return by which the FRS Portfolio must grow, in excess

United of Omaha Life Insurance Company Companion Life Insurance Company mutual of omaha retirement services

United of Omaha Life Insurance Company Companion Life Insurance Company mutual of omaha retirement services 25927477 Investment Options GET RETIREMENT RIGHT 213196 For producer and plan sponsor use only.

United of Omaha Life Insurance Company Companion Life Insurance Company mutual of omaha retirement services 25927477 Investment Options GET RETIREMENT RIGHT 213196 For producer and plan sponsor use only.

City of LA 457 Plan Plan Structure Review International Equity

August 17, 2010 City of LA 457 Plan Plan Structure Review International Equity Devon Muir, CFA, Los Angeles Eileen Kwei, CFA, San Francisco www.mercer.com Contents Introduction Current Situation International

August 17, 2010 City of LA 457 Plan Plan Structure Review International Equity Devon Muir, CFA, Los Angeles Eileen Kwei, CFA, San Francisco www.mercer.com Contents Introduction Current Situation International

UBS Financial Services Inc. Retirement Plan Asset Allocation Guide

ab UBS Financial Services Inc. Retirement Plan Asset Allocation Guide Planning how to invest for your retirement may be one of the most important decisions you ll ever make. Asset allocation is a strategy

ab UBS Financial Services Inc. Retirement Plan Asset Allocation Guide Planning how to invest for your retirement may be one of the most important decisions you ll ever make. Asset allocation is a strategy

Voya Target Retirement Fund Series

Voya Target Retirement Fund Series The Target Date Choice to Help Keep Retirement Goals on Track Holistic Retirement Solution Sophisticated Glide Path Design Open Architecture Approach Blend of Active

Voya Target Retirement Fund Series The Target Date Choice to Help Keep Retirement Goals on Track Holistic Retirement Solution Sophisticated Glide Path Design Open Architecture Approach Blend of Active

Investment Option Performance

Investment Option Performance Data as of: 8/1/2018 The investment funds in this Investment Option Performance Report reflect the investment options currently offered under your plan. MassMutual has not

Investment Option Performance Data as of: 8/1/2018 The investment funds in this Investment Option Performance Report reflect the investment options currently offered under your plan. MassMutual has not

UBS Financial Services Inc. Retirement Plan Asset Allocation Guide

ab UBS Financial Services Inc. Retirement Plan Asset Allocation Guide Planning how to invest for your retirement may be one of the most important decisions you ll ever make. Asset allocation is a strategy

ab UBS Financial Services Inc. Retirement Plan Asset Allocation Guide Planning how to invest for your retirement may be one of the most important decisions you ll ever make. Asset allocation is a strategy

Quarterly Portfolio Guide

An Educational Guide for Individuals Quarterly Portfolio Guide December 31, 2013 Insight into the underlying funds of Variable Universal Life III (VUL III) Insurance Investment Strategies 1 of 78 VUL III

An Educational Guide for Individuals Quarterly Portfolio Guide December 31, 2013 Insight into the underlying funds of Variable Universal Life III (VUL III) Insurance Investment Strategies 1 of 78 VUL III

Building an Investment Strategy

Building an Investment Strategy Building an investment strategy that meets your risk tolerance and investment objectives is critical to successfully preparing for retirement. There are three key steps

Building an Investment Strategy Building an investment strategy that meets your risk tolerance and investment objectives is critical to successfully preparing for retirement. There are three key steps

Building and Managing a Diversified Portfolio

Building and Managing a Diversified Portfolio Craig L. Israelsen, Ph.D. Designer of the Portfolio Presentation AAII Silicon Valley Chapter April 14, 2018 Based on research by Craig L. Israelsen, Ph.D.

Building and Managing a Diversified Portfolio Craig L. Israelsen, Ph.D. Designer of the Portfolio Presentation AAII Silicon Valley Chapter April 14, 2018 Based on research by Craig L. Israelsen, Ph.D.

CP#32-08 Investment Policy

Investment Policy Approved: 07/19/08 Revised: 5/11/2017 Charter of the ICC Investment Management Program Committee 1.0 Introduction: The Board of Directors of The International Code Council, Inc. (the

Investment Policy Approved: 07/19/08 Revised: 5/11/2017 Charter of the ICC Investment Management Program Committee 1.0 Introduction: The Board of Directors of The International Code Council, Inc. (the

Get ready Your Plan is on the move!

Get ready Your Plan is on the move! November 2018 The is merging with the Bass Pro Group, LLC 401(k) Plan this January. Bass Pro Shops and Cabela s will soon have a unified 401(k) retirement savings program

Get ready Your Plan is on the move! November 2018 The is merging with the Bass Pro Group, LLC 401(k) Plan this January. Bass Pro Shops and Cabela s will soon have a unified 401(k) retirement savings program

Asset Allocation Study

Asset Allocation Study The Metropolitan St. Louis Sewer District August 2016 Pavilion Advisory Group Inc. 227 W. Monroe Street, Suite 2020 Chicago, IL 60606 Phone: 312-798-3200 Fax: 312-902-1984 www.pavilioncorp.com

Asset Allocation Study The Metropolitan St. Louis Sewer District August 2016 Pavilion Advisory Group Inc. 227 W. Monroe Street, Suite 2020 Chicago, IL 60606 Phone: 312-798-3200 Fax: 312-902-1984 www.pavilioncorp.com

RBC Strategic Asset Allocation Models

Page 1 of 7 United States Traditional Fixed Income Only Last updated: March 218 Fixed Income Only The focus is capital preservation. The portfolio is only invested in fixed income asset classes. The investor

Page 1 of 7 United States Traditional Fixed Income Only Last updated: March 218 Fixed Income Only The focus is capital preservation. The portfolio is only invested in fixed income asset classes. The investor

CITY OF YORK MUNICIPAL PENSION FUNDS

Approved: February 28, 2007 Revised: November 2009 Asset Allocation Table Updated: February 2010 Reviewed for continuity: February 2016 Revised: May 2016 Revised: August 2016 CITY OF YORK MUNICIPAL PENSION

Approved: February 28, 2007 Revised: November 2009 Asset Allocation Table Updated: February 2010 Reviewed for continuity: February 2016 Revised: May 2016 Revised: August 2016 CITY OF YORK MUNICIPAL PENSION

Investment and Spending Policy Approved November 5, 2015

Investment and Spending Policy Approved November 5, 2015 College of Southern Maryland Foundation Mason Investment Advisory Services Table of Contents I. Executive Summary... 1 II. Introduction... 2 III.

Investment and Spending Policy Approved November 5, 2015 College of Southern Maryland Foundation Mason Investment Advisory Services Table of Contents I. Executive Summary... 1 II. Introduction... 2 III.

Complete Guide to Investing. 5 th Edition

Complete Guide to Investing 5 th Edition Chapter 1 Getting Started as an Investor... 1 Learning Objectives... 1 Introduction... 1 Investing... 2 What Are the Sources of Money for Investing?... 2 What Are

Complete Guide to Investing 5 th Edition Chapter 1 Getting Started as an Investor... 1 Learning Objectives... 1 Introduction... 1 Investing... 2 What Are the Sources of Money for Investing?... 2 What Are

State of Alaska Department of Revenue. Alaska Retirement Management Board

State of Alaska Department of Revenue Alaska Retirement Management Board March 2016 Department of Revenue Alaska Retirement Management Board Fiduciary of the Fund AS 14.25.007 Consider status of the fund

State of Alaska Department of Revenue Alaska Retirement Management Board March 2016 Department of Revenue Alaska Retirement Management Board Fiduciary of the Fund AS 14.25.007 Consider status of the fund

A distinctive solution for your plan and employees. TIAA-CREF Lifecycle Funds

A distinctive solution for your plan and employees TIAA-CREF Lifecycle Funds TIAA has nearly 100 years of experience managing money for retirement and nearly 60 years of asset allocation experience. Our

A distinctive solution for your plan and employees TIAA-CREF Lifecycle Funds TIAA has nearly 100 years of experience managing money for retirement and nearly 60 years of asset allocation experience. Our

PALM TRAN, INC./ATU LOCAL 1577 PENSION FUND INVESTMENT PERFORMANCE PERIOD ENDING MARCH 31, 2011

PALM TRAN, INC./ATU LOCAL 1577 PENSION FUND INVESTMENT PERFORMANCE PERIOD ENDING MARCH 31, 2011 NOTE: For a free copy of Part II (mailed w/i 5 bus. days from request receipt) of Burgess Chambers and Associates,

PALM TRAN, INC./ATU LOCAL 1577 PENSION FUND INVESTMENT PERFORMANCE PERIOD ENDING MARCH 31, 2011 NOTE: For a free copy of Part II (mailed w/i 5 bus. days from request receipt) of Burgess Chambers and Associates,

Ventura Managed Account Portfolios Superannuation (including Pension)

") VENTURA MANAGED ACCOUNT PORTFOLIOS Ventura Managed Account Portfolios Superannuation (including Pension) Investment Model Menu 1 July 2016 This PDS is issued by Diversa Trustees Limited (the Trustee) ABN

VENTURA MANAGED ACCOUNT PORTFOLIOS Ventura Managed Account Portfolios Superannuation (including Pension) Investment Model Menu 1 July 2016 This PDS is issued by Diversa Trustees Limited (the Trustee) ABN

TEL FAX cookstreetconsulting.com

TEL 303.333.7770 1.800.318.7770 FAX 303.333.7771 cookstreetconsulting.com Contents 1 Market Review 2 Plan Overview 3 Investment Due Diligence Appendix Appendix 3 1 Market Review 5 Q2 2017 Economic Review

TEL 303.333.7770 1.800.318.7770 FAX 303.333.7771 cookstreetconsulting.com Contents 1 Market Review 2 Plan Overview 3 Investment Due Diligence Appendix Appendix 3 1 Market Review 5 Q2 2017 Economic Review

(Modern Portfolio Theory Review)

") (Modern Portfolio Theory Review) IFS-A76898 Charts 1-9 Reminder: You must include the Modern Portfolio Theory Disclosure pages with all charts you select to use, either individually or as a group. Information

(Modern Portfolio Theory Review) IFS-A76898 Charts 1-9 Reminder: You must include the Modern Portfolio Theory Disclosure pages with all charts you select to use, either individually or as a group. Information

MERCER SUPER INVESTMENT TRUST QUARTERLY REPORT THREE MONTHS TO 30 JUNE 2018

MERCER SUPER INVESTMENT TRUST QUARTERLY REPORT THREE MONTHS TO 0 JUNE 2018 Mercer Superannuation (Australia) Limited (MSAL) ABN 79 004 717 5, Australian Financial Services Licence #25906 is the trustee

MERCER SUPER INVESTMENT TRUST QUARTERLY REPORT THREE MONTHS TO 0 JUNE 2018 Mercer Superannuation (Australia) Limited (MSAL) ABN 79 004 717 5, Australian Financial Services Licence #25906 is the trustee

MERCER SUPER INVESTMENT TRUST QUARTERLY REPORT THREE MONTHS TO 31 DECEMBER 2017

MERCER SUPER INVESTMENT TRUST QUARTERLY REPORT THREE MONTHS TO 1 DECEMBER 2017 Mercer Superannuation (Australia) Limited (MSAL) ABN 79 004 717 5, Australian Financial Services Licence #25906 is the trustee

MERCER SUPER INVESTMENT TRUST QUARTERLY REPORT THREE MONTHS TO 1 DECEMBER 2017 Mercer Superannuation (Australia) Limited (MSAL) ABN 79 004 717 5, Australian Financial Services Licence #25906 is the trustee

What s in a Name: White-Label Funds in DC Plans

What s in a Name: White-Label Funds in DC Plans October 2014 Hewitt EnnisKnupp, An Aon Company 2014 Aon plc What s in a Name? That which we call a rose by any other name would smell as sweet. Much like

What s in a Name: White-Label Funds in DC Plans October 2014 Hewitt EnnisKnupp, An Aon Company 2014 Aon plc What s in a Name? That which we call a rose by any other name would smell as sweet. Much like

See the following page for important information about your plan investments.

This notice contains important information about changes to the MMC 401(k) Savings and Retirement Plan. Please review it carefully. If you have any questions about the changes to the plan, the plan s investments,

This notice contains important information about changes to the MMC 401(k) Savings and Retirement Plan. Please review it carefully. If you have any questions about the changes to the plan, the plan s investments,

A Smarter Way to Manage Your Retirement Plan

A Smarter Way to Manage Your Retirement Plan United of Omaha Life Insurance Company A Mutual of Omaha Company Introducing SmartPlan Enterprise SM SmartPlan is a quick and easy way to learn about your retirement

A Smarter Way to Manage Your Retirement Plan United of Omaha Life Insurance Company A Mutual of Omaha Company Introducing SmartPlan Enterprise SM SmartPlan is a quick and easy way to learn about your retirement

Class 1 Shares Class 2 Shares Investor Class Shares. Class 1 shares Class 2 shares Class 3 shares Class 4 shares Investor Class shares

TOPS Conservative ETF Portfolio TOPS Balanced ETF Portfolio TOPS Moderate Growth ETF Portfolio TOPS Growth ETF Portfolio TOPS Aggressive Growth ETF Portfolio Class 1 Shares Class 2 Shares Investor Class

TOPS Conservative ETF Portfolio TOPS Balanced ETF Portfolio TOPS Moderate Growth ETF Portfolio TOPS Growth ETF Portfolio TOPS Aggressive Growth ETF Portfolio Class 1 Shares Class 2 Shares Investor Class

Aiming at a Moving Target Managing inflation risk in target date funds

Aiming at a Moving Target Managing inflation risk in target date funds Executive Summary This research seeks to help plan sponsors expand their fiduciary understanding and knowledge in providing inflation

Aiming at a Moving Target Managing inflation risk in target date funds Executive Summary This research seeks to help plan sponsors expand their fiduciary understanding and knowledge in providing inflation

Comments on File Number S (Investment Company Advertising: Target Date Retirement Fund Names and Marketing)

") January 24, 2011 Elizabeth M. Murphy Secretary Securities and Exchange Commission 100 F Street, NE Washington, D.C. 20549-1090 RE: Comments on File Number S7-12-10 (Investment Company Advertising: Target

January 24, 2011 Elizabeth M. Murphy Secretary Securities and Exchange Commission 100 F Street, NE Washington, D.C. 20549-1090 RE: Comments on File Number S7-12-10 (Investment Company Advertising: Target