TURKISH STATISTICAL INSTITUTE (FINANCIAL SECTOR) S.12

|

|

|

- Lewis Gregory

- 5 years ago

- Views:

Transcription

1 (FINANCIAL SECTOR) S.12

2 THE MEASUREMENT OF FINANCIAL SERVICES Financial corporations consist of all resident corporations that are principally engaged in providing financial services, including insurance and pension funding services, to other institutional units. Financial services are the result of financial intermediation, financial risk management, liquidity transformation or auxiliary financial activities. As the provision of financial services is typically subject to strict regulation, it is usually the case that units providing financial services do not produce other goods and services and financial services are not provided as secondary production

3 Financial corporations can be divided into three broad classes, namely,. financial intermediaries, financial auxiliaries other financial corporations.

4 FINANCIAL CORPORATION SECTOR AND SUBSECTOR Financial corporations Central bank Deposit-taking corporations except the central bank Money market funds (MMFs) Non-MMF investment funds Other financial intermediaries except insurance corporations and pension funds Financial auxiliaries Captive financial institutions and moneylenders Insurance corporations Pension Funds S12 S121 S122 S123 S124 S125 S126 S127 S128 S129

5 NACE Units Data Source Central Bank (S.121) Banks (Commercial, Participation and Investment) (S.122) Financial Leasing Companies(S.125) Consumer Financing Companies(S.125) Asset Management Companies and Factoring Companies (S.125) Agricultural Credit Cooperatives (S.125) Insurance Companies (life and non-life) (S.128-S.129) Pension Funding(S.128-S.129) Reinsurance Company(S.128) Foundations and chests (found in the pension commitments to members) (S.128-S.129) Capital Market Board (CMB) (S.126) Saving Deposit and Insurance Fund (SDIF) (S.126) Banking Regulation and Supervision Agency (BRSA) (S.126) Interbank Card Centre (S.126) Istanbul Stock Exchange (S.126) Exchange Offices (S.126) Credit Surety Cooperatives of Turkish Craftsmen and Artisans (S.126) Istanbul Gold Exchange (S.126) VAT Repayment Companies (S.126) Credit Guarantee Fund (S.126) Central Institution of Record (S.126) Derivatives Exchange (S.126) Insurance Agents (S.126) Insurance Brokers (S.126) Insurance Experts (S.126) Portfolio Management Companies (S.126) Central Bank of The Republic of Turkey Banking Regulation and Supervision Agency Survey, Administrative data Undersecretariat of Treasury (UT), Agricultural Insurance Pool (AIP), Turkish Catastrophe Insurance Pool (TCIP) General Directorate of Foundations Administrative data Survey, Administrative data

6 S.122 Data Source Source Type Deposit Banks Nace Rev.2: Development and Investment Banks Nace Rev.2: Participation Banks (Islamic Banks) Nace Rev.2: Banking Regulation and Supervision Agency Banking Regulation and Supervision Agency Banking Regulation and Supervision Agency Administrative Records Administrative Records Administrative Records

7 S.125 Data Source Source Type Consumer Finance Corporations Nace Rev.2: Banking Regulation and Supervision Agency Administrative Records Factoring Nace Rev.2: Financial Leasing Nace Rev.2: Securities Investment Associations, Real Estate Investment Associations Nace Rev.2: Asset Management Companies Nace Rev.2: Banking Regulation and Supervision Agency Banking Regulation and Supervision Agency Turkish Statistical Institute Turkish Statistical Institute Administrative Records Administrative Records Survey Survey

8 S.121 Central Bank As long as the central bank is a separate institutional unit, it is always allocated to the financial corporations sector, even if it is primarily a non-market producer. Output of the Central Bank (CB) is divided into: market output; non-market output. The CB output is calculated in two stages

9 S.121 Central Bank The non market output of the central bank is measured as the sum of costs such as its intermediate consumption, compensation of employees, consumption of fixed capital and other taxes less subsidies on production in line with the ESA 2010 (Table ). Annual detailed profit/loss table of Central Bank of Republic of Turkey (CBRT) is used for all ESA transactions. The data doesn t need any adjustment. FISIM is not calculated for the central bank for not necessary conceptually. According to ESA 2010, the non-market output (P.13) of the central bank output has been entirely allocated to the intermediate consumption of other financial intermediaries.

10 S.121 Central Bank P.11: Commissios and Fees P13/R (Non-market output) = P2/U + P51c/U + D1/U-P11 The central bank's market output (P11/R) was moved to the intermediate consumption (P22/U) of sector S122, as instructed in Section of ESA No FISIM output and No FISIM IC were calculated for the central bank.

11 S.121

12

13 S.122 Deposit-taking corporations except the central bank Deposit-taking corporations except the central bank have financial interme- diation as their principal activity. To this end, they have liabilities in the form of deposits or financial instruments (such as short-term certificates of deposits) that are close sub- stitutes for deposits. The liabilities of deposit-taking corporations are typically included in measures of money broadly defined

14 S.122 In general, this subsector comprises: a) Commercial banks b) Savings banks c) Agricultural credit banks d) Cooperative credit banks and credit unions e) Specialized banks or other financial corporations if they take deposits or issue close substitutes for deposits (for example, corporations engaged in granting mortgages, including building societies and mortgage banks, merchant banks, and municipal credit institutions, including regional or provincial credit institutions which accept deposits)

15 S.122 The following institutional units are not deposit-takingcorporations: a) Head offices which oversee and manage other units of a group consisting predominantly of deposit-taking corporations except the central bank, but which are not deposit-taking corporations themselves. They are classified as financial auxiliaries (S126); b) Non-profit institutions recognized as independent legal entities serving deposit-taking corporations, but not engaged in financial intermediation. They are classified as financial auxiliaries (S126); c) Holding corporations, which are allocated to the captive financial institutions and money lenders subsector (S127), even if all their subsidiary corporations are deposit-taking corporations

16 Defining and classifying head offices and holding companies The 2008 SNA and the BPM6 classify head offices according to their main activity either as a non-financial corporation (S11) or, by conven- tion, as a financial auxiliary (S126). Holding companies are always included in the financial corporations subsector captive financial institu- tions and moneylenders (S127), irrespective of whether all their subsidiary corporations are financial or non-financial corporations Head offices Holding companies Description in ISIC Rev.4 and NACE Rev.2 ISIC Rev.4 Class 7010 (NACE Rev. 2, class 70.10) SIC Rev.4 Class 6420 (NACE Rev. 2 class 64.20):

17 SAS project for 64 Nace

18 S.122 The accounting data structure codes for banking (which are also in Figure ) are; Receivables: Group 5 (500...): interest receivables Group 7 (700...): non-interest income Expenses: Group 6 (600...): interest expense Group 8 (800...): non-interest expense According to the income statement of banks at figure , output and intermediate consumption are estimated by using the codes of groups 7-8, respectively. Codes of Group 5-6 are used for estimating FISIM.

19 The template of income statement of banks NAME OF BANK CODE OF BANK NAME OF FORM : MONTHLY INCOME STATEMENT CURRENCY UNIT : BILLION TRY PERIOD:/. ACCOUNT CODES AND NAMES DOMESTIC BRANCHES GENERAL CODE NAME ORGANIZATION ABROAD 500 INTEREST TAKEN FROM DISCOUNT AND NEGOTIATION BILLS-TRY 501 INTEREST TAKEN FROM DISCOUNT AND NEGOTIATION BILLS-FX 502 INTEREST TAKEN FROM FACTORING RECEIVABLES-TRY 503 INTEREST TAKEN FROM FQACTORING RECEIVABLES-FX 504 INTEREST TAKEN FROM PRECIOUS METAL LOANS-TRY 608 INTEREST GIVEN TO TRY DEPOSIT (NON RESIDENT PERSONS ANA INSTITUTIONS) 610 INTEREST GIVEN TO TRY DEPOSIT (RESIDENT INSTITUTIONS) 611 INTEREST GIVEN TO FOREIGN EXCHANGE DEPOSIT ACCOUNTS 614 INTEREST GIVEN TO PRECIOUS METAL DEPOSIT ACCOUNTS-TRY 700 COMMISSION TAKEN FROM DISCOUNT ANA NEGOTIATION BILLS-TRY 701 COMMISSION TAKEN FROM DISCOUNT ANA NEGOTIATION BILLS-FX 702 COMMISSION ANA FEES TAKEN FROM FACTORING RECEIVABLES-TRY 810 PERSONNEL EXPENSES-TRY 811 PERSONNEL EXPENSES-FX CONSOLIDA TED

20 P.1 Output P.11 Market output P.111 Market Output (exc. FISIM) P.112 Market Output (FISIM) P.12 Output for own final use R&D, OAS (Own Account Software) P.13 Non-market output Central Bank

21 S.125:Other financial intermediaries, except insurance corporations and pension funds In particular, this subsector may be further subdivided into: Financial corporations engaged in the securitization of assets; Security and derivative dealers (operating on own account); Financial corporations engaged in lending, including financial leasing,9hire purchase and the provision of personal or commercial finance; Central clearing counterparties. These organizations provide clearing and settlement transactions in securities and derivatives. Clearing relates to identifying the obligations of both parties to the transaction, while settlement is the exchange of the securities or derivatives and the correspond- ing payment. The central clearing counterparties involve themselves in the transaction and mitigate counterparty risk;

22 S.125:Other financial intermediaries, except insurance corporations and pension funds Specialized financial corporations that assist other corporations in raising funds in equity and debt markets and provide strategic advisory services for mergers, acquisitions and other types of financial transactions. These corporations are sometimes known as investment banks. In addition to assisting with the raising of funds for their corporate clients, such corporations invest their own funds, including in private equity, in hedge funds dedicated to venture capital, and in collateralized lending. However, if such corporations take deposits or close substitutes for deposits, they are classified as deposittaking corporations;

23 S.125:Other financial intermediaries, except insurance corporations and pension funds Specialized financial corporations that provide the following: Short-term financing for corporate mergers and takeovers. Export/import finance. Factoring services. Venture capital and development capital firms. Loans against mortgage on real estate by issuing mortgage bonds.

24 S.126 Financial auxiliaries Financial auxiliaries consist of financial corporations that are principally en- gaged in activities associated with transactions in financial assets and liabilities or with providing the regulatory context for these transactions, but in circumstances that do not involve the auxiliary taking ownership of the financial assets and liabilities being transacted.

25 S.126 The most common types of financial auxiliaries are the following: (a) Insurance brokers, salvage and claims adjusters (whether employed by the insurance corporation, an independent adjuster or a public adjuster employed by the policyholder), and insurance and pension consultants; (b) Loan brokers, securities brokers who arrange trades between security buyers and sellers but do not purchase and hold securities on their own account, investment advisers, etc.; (c) Flotation corporations that manage the issue of securities; (d) Corporations whose principal function is to guarantee, by endorsement, bills and similar instruments; (e) Corporations that arrange derivative and hedging instruments, such as swaps, options and futures (without issuing them); (f) Corporations providing infrastructure for financial markets, including those providing transaction processing and settlement activities, such as for credit card transactions, as well as securities depository companies, custodians, clearing offices and nominee companies;

26 S.126 g) Managers of pension funds, mutual funds, etc. (but not the funds they manage); (h) Corporations providing stock exchange, insurance exchange, and commodity and derivative exchange; (i) Foreign exchange bureaux; (j) Non-profit institutions recognized as independent legal entities serving financial corporations, but that do not themselves provide financial services; (k) Head offices of financial corporations that are principally engaged in con- trolling financial corporations or groups of financial corporations, but that do not themselves conduct the business of financial corporations; (l) Central supervisory authorities of financial intermediaries and financial markets when they are separate institutional units.

27 S.126 Output of activities auxiliary to financial services and insurance activities is calculated by directly survey data compiling of business statistics except Capital Market Board (CMB), Saving Deposit and Insurance Fund (SDIF) and Banking Regulation and Supervision Agency (BRSA). The output of these institutions is to be measured as the sum of the costs from administrative data. Additionally, R & D, own account software and FISIM adjustments are made.

28 Thanks for your attention

The financial corporations sector and its subsectors

The financial corporations sector and its subsectors IFC Workshop on Developing and Improving Sectoral Financial Accounts 20-21 January 2016 Algiers, Algeria United Nations Statistics Division Outline

The financial corporations sector and its subsectors IFC Workshop on Developing and Improving Sectoral Financial Accounts 20-21 January 2016 Algiers, Algeria United Nations Statistics Division Outline

Session 5 Links Between Private&Public Accounting System and National Accounts

Session 5 Links Between Private&Public Accounting System and National Accounts Ahmet Kürşad Dosdoğru The data sources Compilation Process of FS Content The data sources SUT 2012 R&D Survey Revenue Administration

Session 5 Links Between Private&Public Accounting System and National Accounts Ahmet Kürşad Dosdoğru The data sources Compilation Process of FS Content The data sources SUT 2012 R&D Survey Revenue Administration

Identification of Institutional Sectors and Financial Instruments

3 Identification of Institutional Sectors and Financial Instruments Introduction 3.1 In the Guid e, as in the 2008 SNA and BPM6, institutional units and the instruments in which they transact are grouped

3 Identification of Institutional Sectors and Financial Instruments Introduction 3.1 In the Guid e, as in the 2008 SNA and BPM6, institutional units and the instruments in which they transact are grouped

2008 SNA- FINANCIAL SECTOR

2008 SNA- FINANCIAL SECTOR Training Workshop on Banking, Insurance and Financial Statistic 08-11 January 2017, Dhaka, Bangladesh Moorashin Javan Statistic centre of Iran 1 Outline of presentation Financial

2008 SNA- FINANCIAL SECTOR Training Workshop on Banking, Insurance and Financial Statistic 08-11 January 2017, Dhaka, Bangladesh Moorashin Javan Statistic centre of Iran 1 Outline of presentation Financial

NACE Rev. 2 - Structure and explanatory notes SECTION K FINANCIAL AND INSURANCE ACTIVITIES

NACE Rev. 2 - Structure and explanatory notes SECTION K FINANCIAL AND INSURANCE ACTIVITIES This section includes financial service activities, including insurance, reinsurance and pension funding activities

NACE Rev. 2 - Structure and explanatory notes SECTION K FINANCIAL AND INSURANCE ACTIVITIES This section includes financial service activities, including insurance, reinsurance and pension funding activities

Islamic finance in the System of National Accounts

Islamic finance in the System of National Accounts Consultative Meeting on Developing Islamic Financial Industry Database of OIC Member Countries 24 September 2017 Mugla, Turkey Benson Sim United Nations

Islamic finance in the System of National Accounts Consultative Meeting on Developing Islamic Financial Industry Database of OIC Member Countries 24 September 2017 Mugla, Turkey Benson Sim United Nations

Main changes in the 2008 SNA Part I

Main changes in the 2008 SNA Part I Regional Workshop on Measuring the Informal Sector and the Non-Observed Economy 4-7 October 2015 Tehran, Islamic Republic of Iran United Nations Statistics Division

Main changes in the 2008 SNA Part I Regional Workshop on Measuring the Informal Sector and the Non-Observed Economy 4-7 October 2015 Tehran, Islamic Republic of Iran United Nations Statistics Division

OVERVIEW OF CONCEPTS AND DEFINITIONS

OVERVIEW OF CONCEPTS AND DEFINITIONS Venkat Josyula Developing and Improving Sectoral Financial Accounts Algiers, January 20-21, 2016 The views expressed herein are those of the author and should not necessarily

OVERVIEW OF CONCEPTS AND DEFINITIONS Venkat Josyula Developing and Improving Sectoral Financial Accounts Algiers, January 20-21, 2016 The views expressed herein are those of the author and should not necessarily

The methodological basis for the compilation of the financial accounts is the ESA2010 (the European System of Accounts).

.") 3. FINANCIAL ACCOUNTS METHODOLOGY 3.1 ESA2010 methodology The methodological basis for the compilation of the financial accounts is the ESA2010 (the European System of Accounts). The financial accounts

3. FINANCIAL ACCOUNTS METHODOLOGY 3.1 ESA2010 methodology The methodological basis for the compilation of the financial accounts is the ESA2010 (the European System of Accounts). The financial accounts

Financial Intermediation Services Indirectly Measured

APPENDIX 3 Financial Intermediation Services Indirectly Measured Overview A3.1 The 2008 SNA and BPM6 intermediation services indirectly measured (FISIM) comprises service output for which producers do

APPENDIX 3 Financial Intermediation Services Indirectly Measured Overview A3.1 The 2008 SNA and BPM6 intermediation services indirectly measured (FISIM) comprises service output for which producers do

Definitions and concepts for the statistical reporting of investment funds Banque centrale du Luxembourg

In case of discrepancies between the French and the English text, the French text shall prevail Definitions and concepts for the statistical reporting of investment funds Banque centrale du Luxembourg

In case of discrepancies between the French and the English text, the French text shall prevail Definitions and concepts for the statistical reporting of investment funds Banque centrale du Luxembourg

TURNOVER/ OUTPUT OF THE ACTIVITIES AUXILIARY TO FINANCIAL SERVICES, EXCEPT INSURANCE AND PENSION FUNDING (ISIC 66.1) IN MALAYSIA

IN MALAYSIA") 31st meeting of the Voorburg Group on Service Statistics 19th to 23rd September 2016 Zagreb Croatia TURNOVER/ OUTPUT OF THE ACTIVITIES AUXILIARY TO FINANCIAL SERVICES, EXCEPT INSURANCE AND PENSION FUNDING

31st meeting of the Voorburg Group on Service Statistics 19th to 23rd September 2016 Zagreb Croatia TURNOVER/ OUTPUT OF THE ACTIVITIES AUXILIARY TO FINANCIAL SERVICES, EXCEPT INSURANCE AND PENSION FUNDING

Definitions and concepts for the statistical reporting of insurance corporations Banque centrale du Luxembourg

In case of discrepancies between the French and the English text, the French text shall prevail Definitions and concepts for the statistical reporting of insurance corporations Banque centrale du Luxembourg

In case of discrepancies between the French and the English text, the French text shall prevail Definitions and concepts for the statistical reporting of insurance corporations Banque centrale du Luxembourg

Lesson 2: 2008 SNA- Changes from 1993 SNA

Lesson 2: 2008 SNA- Changes from 1993 SNA Fourth Intermediate Level e-learning Course on System of National Accounts September-November 2014 1 Outline of presentation 1993 SNA revision process Main Changes

Lesson 2: 2008 SNA- Changes from 1993 SNA Fourth Intermediate Level e-learning Course on System of National Accounts September-November 2014 1 Outline of presentation 1993 SNA revision process Main Changes

Content. SNA 2008 changes. A global revision process MAJOR SNA ISSUES 1/28/ FINANCIAL SERVICES AND FINANCIAL ACCOUNTS

Content SNA 2008 changes December 2013 Background to the update Financial services and financial accounts Capital issues Public administration Others 1 2 1. Background to the update to ESA 2010 A global

Content SNA 2008 changes December 2013 Background to the update Financial services and financial accounts Capital issues Public administration Others 1 2 1. Background to the update to ESA 2010 A global

Definitions and concepts for the statistical reporting of financial companies Banque centrale du Luxembourg

In case of discrepancies between the French and the English text, the French text shall prevail Definitions and concepts for the statistical reporting of financial companies Banque centrale du Luxembourg

In case of discrepancies between the French and the English text, the French text shall prevail Definitions and concepts for the statistical reporting of financial companies Banque centrale du Luxembourg

SNA/M1.18/6.a. 12 th Meeting of the Advisory Expert Group on National Accounts, November 2018, Luxembourg. Agenda item: 6.a.

SNA/M1.18/6.a 12 th Meeting of the Advisory Expert Group on National Accounts, 27-29 November 2018, Luxembourg Agenda item: 6.a. Islamic finance in the national accounts Introduction At its 11 th meeting

SNA/M1.18/6.a 12 th Meeting of the Advisory Expert Group on National Accounts, 27-29 November 2018, Luxembourg Agenda item: 6.a. Islamic finance in the national accounts Introduction At its 11 th meeting

Definitions and concepts for the statistical reporting of securitisation vehicles Banque centrale du Luxembourg

In case of discrepancies between the French and the English text, the French text shall prevail Definitions and concepts for the statistical reporting of securitisation vehicles Banque centrale du Luxembourg

In case of discrepancies between the French and the English text, the French text shall prevail Definitions and concepts for the statistical reporting of securitisation vehicles Banque centrale du Luxembourg

16 May 2014 Regulation No Regulation for Compiling the Monthly Financial Position Report of Monetary Financial Institutions

1 (Unofficial translation) 16 May 2014 Regulation No. 132 Riga Regulation for Compiling the Monthly Financial Position Report of Monetary Financial Institutions Note. As amended by Latvijas Banka's Regulation

1 (Unofficial translation) 16 May 2014 Regulation No. 132 Riga Regulation for Compiling the Monthly Financial Position Report of Monetary Financial Institutions Note. As amended by Latvijas Banka's Regulation

1. METHODOLOGICAL EXPLANATIONS FOR EXTERNAL STATISTICS

1. METHODOLOGICAL EXPLANATIONS FOR EXTERNAL STATISTICS External statistics are a sublimate of several individual statistical surveys for compiling, processing and disseminating data on stocks and/or transactions

1. METHODOLOGICAL EXPLANATIONS FOR EXTERNAL STATISTICS External statistics are a sublimate of several individual statistical surveys for compiling, processing and disseminating data on stocks and/or transactions

31 st Meeting of the Voorburg Group on Service Statistics 19th - 23rd September 2016 Zagreb Croatia

31 st Meeting of the Voorburg Group on Service Statistics 19th - 23rd September 2016 Zagreb Croatia Activities Auxiliary to Financial Services, Except Insurance/Takaful and Pension Funding (ISIC 66.1)

31 st Meeting of the Voorburg Group on Service Statistics 19th - 23rd September 2016 Zagreb Croatia Activities Auxiliary to Financial Services, Except Insurance/Takaful and Pension Funding (ISIC 66.1)

References Monthly balance sheet summaries are prepared from monthly reports submitted by operating insurance companies.

Metadata Insurance companies 1. General Title Accounts of insurance companies. Supervisor of statistics Central Bank of Iceland, Statistics Purpose Data are compiled to make it possible to follow the evolution

Metadata Insurance companies 1. General Title Accounts of insurance companies. Supervisor of statistics Central Bank of Iceland, Statistics Purpose Data are compiled to make it possible to follow the evolution

used: 1 - Reported used: 1 - Reported used: 1 - Reported used: 1 - Reported

Instructions for ECB add-ons (Pension Funds) PFE.01.01 Content of the submission [Pension funds with ECB add-ons] COLUMN/ ROW ITEM INSTRUCTIONS C0010/ER0020 C0010/ER0050 C0010/ER0090 C0010/ER1100 PFE.02.01

Instructions for ECB add-ons (Pension Funds) PFE.01.01 Content of the submission [Pension funds with ECB add-ons] COLUMN/ ROW ITEM INSTRUCTIONS C0010/ER0020 C0010/ER0050 C0010/ER0090 C0010/ER1100 PFE.02.01

ISWGNA Task Force on Islamic Banking. Sectorization of Islamic Financial Corporations and Windows. Russell Krueger

ISWGNA Task Force on Islamic Banking Sectorization of Islamic Financial Corporations and Windows Russell Krueger Economic and Social Commission for Western Asia (ESCWA) Beirut October 24 26, 2017 5 Overview

ISWGNA Task Force on Islamic Banking Sectorization of Islamic Financial Corporations and Windows Russell Krueger Economic and Social Commission for Western Asia (ESCWA) Beirut October 24 26, 2017 5 Overview

Workshop on Islamic Finance in the National Accounts. Conceptual Issues in Measuring Islamic Finance in National Accounts

Workshop on Islamic Finance in the National Accounts 24 26 October 2017 Beirut, Lebanon Conceptual Issues in Measuring Islamic Finance in National Accounts Alick Nyasulu Statistician/Statistical Institute

Workshop on Islamic Finance in the National Accounts 24 26 October 2017 Beirut, Lebanon Conceptual Issues in Measuring Islamic Finance in National Accounts Alick Nyasulu Statistician/Statistical Institute

National Accounts of Tajikistan

National Accounts of Tajikistan Nilyufar Khuseynova Spesialist of SNA and financial statistics department Introduction of SNA -93 The practical introduction of System of National Accounts in Tajikistan

National Accounts of Tajikistan Nilyufar Khuseynova Spesialist of SNA and financial statistics department Introduction of SNA -93 The practical introduction of System of National Accounts in Tajikistan

Measuring and Recording Financial Services

MEETING OF THE TASK FORCE ON FINANCIAL INTERMEDIATION SERVICES INDIRECTLY MEASURED (FISIM) Hosted by the IMF March 3 & 4, 2011 IMF Headquarters 1 (HQ1) Room 2-530, 700 19 th Street N.W., Washington D.C.

MEETING OF THE TASK FORCE ON FINANCIAL INTERMEDIATION SERVICES INDIRECTLY MEASURED (FISIM) Hosted by the IMF March 3 & 4, 2011 IMF Headquarters 1 (HQ1) Room 2-530, 700 19 th Street N.W., Washington D.C.

Holdings of Irish Government Bond Return

Holdings of Irish Government Bond Return Notes on Compilation and Online Reporting Guide (September 2018) Further Enquiries to IE_SHS@centralbank.ie Section 1: - Notes on Compilation Irish Government Bonds

Holdings of Irish Government Bond Return Notes on Compilation and Online Reporting Guide (September 2018) Further Enquiries to IE_SHS@centralbank.ie Section 1: - Notes on Compilation Irish Government Bonds

Diversification of Islamic Financial Instruments in Turkey

Republic of Turkey Undersecretariat of Treasury Diversification of Islamic Financial Instruments in Turkey Utku ŞEN Treasury Expert 9 th MEETING OF THE COMCEC FINANCIAL COOPERATION WORKING GROUP October

Republic of Turkey Undersecretariat of Treasury Diversification of Islamic Financial Instruments in Turkey Utku ŞEN Treasury Expert 9 th MEETING OF THE COMCEC FINANCIAL COOPERATION WORKING GROUP October

Financial services provided in association with. interest charges on loans and deposits

Financial services provided in association with interest charges on loans and deposits Regional Course on 2008 SNA (Special Topics): Improving Exhaustiveness of GDP Coverage 31 August-4 September 2015

Financial services provided in association with interest charges on loans and deposits Regional Course on 2008 SNA (Special Topics): Improving Exhaustiveness of GDP Coverage 31 August-4 September 2015

SURVEY ON EXTERNAL FINANCIAL STATISTICS (EFS) REPORTING INSTRUCTIONS

REPORTING INSTRUCTIONS") SURVEY ON EXTERNAL FINANCIAL STATISTICS (EFS) REPORTING INSTRUCTIONS Statistics Department Balance of Payments Section July 2015 80 Kennedy Avenue, CY-1076 Nicosia, Cyprus Postal Address: P.O.Box 25529,

SURVEY ON EXTERNAL FINANCIAL STATISTICS (EFS) REPORTING INSTRUCTIONS Statistics Department Balance of Payments Section July 2015 80 Kennedy Avenue, CY-1076 Nicosia, Cyprus Postal Address: P.O.Box 25529,

TURNOVER/OUTPUT MEASURES IN BANKING AND CREDIT GRANTING INDUSTRIES IN NORWAY. Tore Halvorsen Statistics Norway

1 TURNOVER/OUTPUT MEASURES IN BANKING AND CREDIT GRANTING INDUSTRIES IN NORWAY 24th Voorburg Group meeting Oslo 2009 Tore Halvorsen Statistics Norway Characteristics of the banking and credit granting

1 TURNOVER/OUTPUT MEASURES IN BANKING AND CREDIT GRANTING INDUSTRIES IN NORWAY 24th Voorburg Group meeting Oslo 2009 Tore Halvorsen Statistics Norway Characteristics of the banking and credit granting

Economic and Social Council

United Nations Economic and Social Council ECE/CES/GE.20/2014/21 Distr.: General 07 April 2014 Original: English Economic Commission for Europe Conference of European Statisticians Group of Experts on

United Nations Economic and Social Council ECE/CES/GE.20/2014/21 Distr.: General 07 April 2014 Original: English Economic Commission for Europe Conference of European Statisticians Group of Experts on

REGULATION (EU) No 1011/2012 OF THE EUROPEAN CENTRAL BANK of 17 October 2012 concerning statistics on holdings of securities (ECB/2012/24)

No 1011/2012 OF THE EUROPEAN CENTRAL BANK of 17 October 2012 concerning statistics on holdings of securities (ECB/2012/24)") L 305/6 Official Journal of the European Union 1.11.2012 REGULATION (EU) No 1011/2012 OF THE EUROPEAN CENTRAL BANK of 17 October 2012 concerning statistics on holdings of securities (ECB/2012/24) THE GOVERNING

L 305/6 Official Journal of the European Union 1.11.2012 REGULATION (EU) No 1011/2012 OF THE EUROPEAN CENTRAL BANK of 17 October 2012 concerning statistics on holdings of securities (ECB/2012/24) THE GOVERNING

Methodological notes on the financial accounts and the financial balance sheets of the system of national accounts of the Russian Federation

Methodological notes on the financial accounts and the financial balance sheets of the system of national accounts of the Russian Federation The financial accounts and the financial balance sheets are

Methodological notes on the financial accounts and the financial balance sheets of the system of national accounts of the Russian Federation The financial accounts and the financial balance sheets are

BANK MELLAT, HEAD OFFICE: TAHRAN-IRAN İSTANBUL TURKEY MAIN, ANKARA AND İZMİR BRANCHES INDEPENDENT AUDITOR S REPORT, FINANCIAL STATEMENTS AND NOTES

BANK MELLAT, HEAD OFFICE: TAHRAN-IRAN İSTANBUL TURKEY MAIN, ANKARA AND İZMİR BRANCHES INDEPENDENT AUDITOR S REPORT, FINANCIAL STATEMENTS AND NOTES FOR THE YEAR ENDED 31 DECEMBER 2017 (TRANSLATED INTO ENGLISH

BANK MELLAT, HEAD OFFICE: TAHRAN-IRAN İSTANBUL TURKEY MAIN, ANKARA AND İZMİR BRANCHES INDEPENDENT AUDITOR S REPORT, FINANCIAL STATEMENTS AND NOTES FOR THE YEAR ENDED 31 DECEMBER 2017 (TRANSLATED INTO ENGLISH

LAO PDR SCHEDULE OF SPECIFIC COMMITMENTS FOR FINANCIAL SERVICES UNDER AFAS

FINANCIAL SERVICES, EXCLUDING INSURANCE Horizontal Commitments Applicable to the Financial Services Sector Financial institutions in Lao PDR must adopt a specific legal form. All the commitments are subject

FINANCIAL SERVICES, EXCLUDING INSURANCE Horizontal Commitments Applicable to the Financial Services Sector Financial institutions in Lao PDR must adopt a specific legal form. All the commitments are subject

CFTC s and U.S. Prudential Regulators Margin and Segregation Rules for Uncleared Swaps Definition of Financial End User

(1) A bank holding company or an affiliate thereof; a savings and loan holding company; a U.S. intermediate holding company established or designated for purposes of compliance with 12 CFR 252.153; or

(1) A bank holding company or an affiliate thereof; a savings and loan holding company; a U.S. intermediate holding company established or designated for purposes of compliance with 12 CFR 252.153; or

Chapter Two. Overview of the Financial System

- 12 - Chapter Two Overview of the Financial System Introduction 2.1 As noted in Chapter 1, FSIs are calculated and disseminated for the purpose of assisting in the assessment and monitoring of the strengths

- 12 - Chapter Two Overview of the Financial System Introduction 2.1 As noted in Chapter 1, FSIs are calculated and disseminated for the purpose of assisting in the assessment and monitoring of the strengths

The Financial System and Banking Sector in Turkey

The Financial System and Banking Sector in Turkey October 2009, Istanbul Contents 1. Impacts of Recent Developments on the Turkish Economy and the Sector 1.1. Economic Performance 1.2. Measures adopted

The Financial System and Banking Sector in Turkey October 2009, Istanbul Contents 1. Impacts of Recent Developments on the Turkish Economy and the Sector 1.1. Economic Performance 1.2. Measures adopted

FINANCIAL DERIVATIVES

FINANCIAL DERIVATIVES A SUPPLEMENT TO THE FIFTH EDITION (1993) OF THE BALANCE OF PAYMENTS MANUAL INTERNATIONAL MONETARY FUND Library of Congress Cataloging-in-Publication Data Financial derivatives, a

FINANCIAL DERIVATIVES A SUPPLEMENT TO THE FIFTH EDITION (1993) OF THE BALANCE OF PAYMENTS MANUAL INTERNATIONAL MONETARY FUND Library of Congress Cataloging-in-Publication Data Financial derivatives, a

BULGARIAN NATIONAL BANK ANNUAL REPORT 2012 APPENDIX

BULGARIAN NATIONAL BANK ANNUAL REPORT 2012 APPENDIX CONTENTS 1 Macroeconomic Indicators 5 2 Monetary and Financial Statistics 2.1. Balance Sheet of the BNB 9 2.2. Monetary Survey 10 2.3. BNB Analytical

BULGARIAN NATIONAL BANK ANNUAL REPORT 2012 APPENDIX CONTENTS 1 Macroeconomic Indicators 5 2 Monetary and Financial Statistics 2.1. Balance Sheet of the BNB 9 2.2. Monetary Survey 10 2.3. BNB Analytical

Changes in the methodology and classifications of the balance of payments and the international investment position statistics

Changes in the methodology and classifications of the balance of payments and the international investment position statistics BPM6 Implementation In October 2014 Eurostat starts data dissemination according

Changes in the methodology and classifications of the balance of payments and the international investment position statistics BPM6 Implementation In October 2014 Eurostat starts data dissemination according

Financial Sector Delineation in ESA 2010

Financial Sector Delineation in ESA 2010 Implementation in the Netherlands (Paul den Boer) Subsectoring of financial corporations ESA 1995 ESA 2010 S.121 The central bank S.121 Central bank S.122 Other

Financial Sector Delineation in ESA 2010 Implementation in the Netherlands (Paul den Boer) Subsectoring of financial corporations ESA 1995 ESA 2010 S.121 The central bank S.121 Central bank S.122 Other

Statistics National Specific Template 1 (SNST.1) Notes on Compilation

Notes on Compilation") Statistics National Specific Template 1 (SNST.1) Notes on Compilation May 2016 For further information or comments: Email: insurance.statistics@centralbank.ie Table of contents Section 1: Introduction...

Statistics National Specific Template 1 (SNST.1) Notes on Compilation May 2016 For further information or comments: Email: insurance.statistics@centralbank.ie Table of contents Section 1: Introduction...

Report of the. Expert Group Meeting on Financial Flows and Balances. Washington, D.C. - September 6-15, Bureau of Statistics

Report of the Expert Group Meeting on Financial Flows and Balances Washington, D.C. - September 6-15, 1988 Bureau of Statistics International Monetary Fund April 1989 Executive Summary An Inter-Secretariat

Report of the Expert Group Meeting on Financial Flows and Balances Washington, D.C. - September 6-15, 1988 Bureau of Statistics International Monetary Fund April 1989 Executive Summary An Inter-Secretariat

Financial Services. IMF Statistics Department

Financial Services IMF Statistics Department Outline Financial Services Central Bank Other financial services Provided in return for explicit charges; Provided in association with interest charges on loans

Financial Services IMF Statistics Department Outline Financial Services Central Bank Other financial services Provided in return for explicit charges; Provided in association with interest charges on loans

CPC Ver Alternative Structure for Division 71

CPC Ver. 1.0 Alternative Structure for Division 71 C o r r e s p o n d i n g Group Class Subclass Title ISIC SECTION 7 Division 71 FINANCIAL AND RELATED SERVICES; REAL ESTATE SERVICES; AND RENTAL AND LEASING

CPC Ver. 1.0 Alternative Structure for Division 71 C o r r e s p o n d i n g Group Class Subclass Title ISIC SECTION 7 Division 71 FINANCIAL AND RELATED SERVICES; REAL ESTATE SERVICES; AND RENTAL AND LEASING

Asia-Pacific Economic Statistics Week Seminar Component Bangkok, 2 4 May 2016

Asia-Pacific Economic Statistics Week Seminar Component Bangkok, 2 4 May 2016 Name of author: Nazaria Baharudin, Siti Salwani Ismail and Badrul Hisham Md Khalid Organization: Department of Statistics Malaysia

Asia-Pacific Economic Statistics Week Seminar Component Bangkok, 2 4 May 2016 Name of author: Nazaria Baharudin, Siti Salwani Ismail and Badrul Hisham Md Khalid Organization: Department of Statistics Malaysia

The 2008 SNA: Impact on GDP and implementation status

The 2008 SNA: Impact on GDP and implementation status Seminar Component of Asia-Pacific Economic Statistics Week 2-4 May 2016 Bangkok, Thailand United Nations Statistics Division Outline of presentation

The 2008 SNA: Impact on GDP and implementation status Seminar Component of Asia-Pacific Economic Statistics Week 2-4 May 2016 Bangkok, Thailand United Nations Statistics Division Outline of presentation

Institutional Sectors

[ 05 ] Institutional Sectors Paul McCarthy National Accounts Workshop Washington - DC, October 25-26, 2010 Institutional units An institutional unit is an economic entity capable, in its own right, of

[ 05 ] Institutional Sectors Paul McCarthy National Accounts Workshop Washington - DC, October 25-26, 2010 Institutional units An institutional unit is an economic entity capable, in its own right, of

Basel II Pillar 3 disclosures

Basel II Pillar 3 disclosures 6M10 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

Basel II Pillar 3 disclosures 6M10 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG and its consolidated

Country Report UZBEKISTAN

Regional Course on SNA 2008 (Special Topics): Improving Exhaustiveness of GDP Coverage 22 30 August 2016 Daejeon, Republic of Korea Country Report UZBEKISTAN Data sources and estimation methods for compiling

Regional Course on SNA 2008 (Special Topics): Improving Exhaustiveness of GDP Coverage 22 30 August 2016 Daejeon, Republic of Korea Country Report UZBEKISTAN Data sources and estimation methods for compiling

DISCUSSION PAPER FOR COMMENTS. Conceptual issues in Measuring Islamic Finance National Accounts Alick Mjuma Nyasulu 1

WORKSHOP ON ISLAMIC BANKING IN NATIONAL ACCOUNTS 24-26 October 2017, Beirut, Lebanon DISCUSSION PAPER FOR COMMENTS Conceptual issues in Measuring Islamic Finance National Accounts Alick Mjuma Nyasulu 1

WORKSHOP ON ISLAMIC BANKING IN NATIONAL ACCOUNTS 24-26 October 2017, Beirut, Lebanon DISCUSSION PAPER FOR COMMENTS Conceptual issues in Measuring Islamic Finance National Accounts Alick Mjuma Nyasulu 1

Working Party on Financial Statistics

Unclassified COM/STD/DAF(2012)28 COM/STD/DAF(2012)28 Unclassified Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development 24-Sep-2012 English

Unclassified COM/STD/DAF(2012)28 COM/STD/DAF(2012)28 Unclassified Organisation de Coopération et de Développement Économiques Organisation for Economic Co-operation and Development 24-Sep-2012 English

Manual on the Changes between ESA 95 and ESA 2010

EUROPEAN COMMISSION EUROSTAT Directorate C: National Accounts, Prices and Key Indicators Manual on the Changes between ESA 95 and ESA 2010 The Manual on the Changes between ESA 95 and ESA 2010 sets out

EUROPEAN COMMISSION EUROSTAT Directorate C: National Accounts, Prices and Key Indicators Manual on the Changes between ESA 95 and ESA 2010 The Manual on the Changes between ESA 95 and ESA 2010 sets out

State of Oklahoma 2005 Finance & Insurance Cluster Analysis

DEFINITION OF INDUSTRY The Finance and Insurance industry cluster consists of establishments that are primarily engaged in or assist in transactions that involve the creation, liquidation, or change in

DEFINITION OF INDUSTRY The Finance and Insurance industry cluster consists of establishments that are primarily engaged in or assist in transactions that involve the creation, liquidation, or change in

Methodological Sheet

Methodological Sheet Harmonised Monetary Statistics according to Regulation (EU) No 1071/2013 of the European Central Bank of 24 September 2013 concerning the balance sheet of the monetary financial institutions

Methodological Sheet Harmonised Monetary Statistics according to Regulation (EU) No 1071/2013 of the European Central Bank of 24 September 2013 concerning the balance sheet of the monetary financial institutions

Notes to the Consolidated Financial Statements

Deutsche Bank 02 Consolidated Financial Statements 181 Notes to the Consolidated Financial Statements Notes to the Consolidated Financial Statements Notes to the Consolidated Financial Statements 01 Significant

Deutsche Bank 02 Consolidated Financial Statements 181 Notes to the Consolidated Financial Statements Notes to the Consolidated Financial Statements Notes to the Consolidated Financial Statements 01 Significant

Revised Basel III Leverage Ratio Visual Memorandum

Revised Basel III Leverage Ratio Visual Memorandum January 21, 2014 2014 Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 Davis Polk & Wardwell LLP Notice: This publication, which we believe

Revised Basel III Leverage Ratio Visual Memorandum January 21, 2014 2014 Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 Davis Polk & Wardwell LLP Notice: This publication, which we believe

FAQs on Conversion from BPM5 to BPM6 (including FAQs on BPM6 Sign Convention)

") FAQs on Conversion from BPM5 to BPM6 (including FAQs on BPM6 Sign Convention) The IMF Statistics Department (STA) started publishing balance of payments (BOP) and International Investment Position (IIP)

FAQs on Conversion from BPM5 to BPM6 (including FAQs on BPM6 Sign Convention) The IMF Statistics Department (STA) started publishing balance of payments (BOP) and International Investment Position (IIP)

notice Measuring Shadow Banking in the Irish National Accounts 1 Figure 1 Potential Shadow Banking Assets

An Phríomh-Oifig Staidrimh Central Statistics Office information notice Measuring Shadow Banking in the Irish National Accounts 1 3,500 Figure 1 Potential Shadow Banking Assets 3,000 Assets ( billion)

An Phríomh-Oifig Staidrimh Central Statistics Office information notice Measuring Shadow Banking in the Irish National Accounts 1 3,500 Figure 1 Potential Shadow Banking Assets 3,000 Assets ( billion)

9. FISIM: Calculation, allocation and impact on GNI

9. FISIM: Calculation, allocation and impact on GNI Introduction The FISIM calculation is defined in Council Regulation (EEC) no. 448/98 of 16 February 1998 and implemented by Council Regulation (EC) No

9. FISIM: Calculation, allocation and impact on GNI Introduction The FISIM calculation is defined in Council Regulation (EEC) no. 448/98 of 16 February 1998 and implemented by Council Regulation (EC) No

Chapter 7 The Time Value of Money... Chapter 8 Risk and Its Measurement... Chapter 9 Analysis of Financial Statements...

TEST BANK This part of the Instructor's Manual presents a test bank of true/false statements, multiple choice questions, and, where appropriate, additional problems. The problems are similar to those in

TEST BANK This part of the Instructor's Manual presents a test bank of true/false statements, multiple choice questions, and, where appropriate, additional problems. The problems are similar to those in

NATIONAL BANK OF THE REPUBLIC OF MACEDONIA

NATIONAL BANK OF THE REPUBLIC OF MACEDONIA Pursuant to Article 64 paragraph 1 item 22 of the Law on the National Bank of the Republic of Macedonia ( Official Gazette of the Republic of Macedonia No. 3/2002,

NATIONAL BANK OF THE REPUBLIC OF MACEDONIA Pursuant to Article 64 paragraph 1 item 22 of the Law on the National Bank of the Republic of Macedonia ( Official Gazette of the Republic of Macedonia No. 3/2002,

Primary Income. Introduction. Compensation of Employees

13 Primary Income Introduction 13.1 Primary income represents the return that accrues to resident institutional units for their contribution to the production process or for the provision of financial

13 Primary Income Introduction 13.1 Primary income represents the return that accrues to resident institutional units for their contribution to the production process or for the provision of financial

Alberta Regulation 187/97. Alberta Treasury Branches Act ALBERTA TREASURY BRANCHES REGULATION. Table of Contents

Alberta Regulation 187/97 Alberta Treasury Branches Act REGULATION Filed: October 9, 1997 Made by the Lieutenant Governor in Council (O.C. 444/97) pursuant to section 34 of the Alberta Treasury Branches

Alberta Regulation 187/97 Alberta Treasury Branches Act REGULATION Filed: October 9, 1997 Made by the Lieutenant Governor in Council (O.C. 444/97) pursuant to section 34 of the Alberta Treasury Branches

Chart of Accounts Manual MAIN DOCUMENT

Chart of Accounts Manual MAIN DOCUMENT (September 2018) TABLE OF CONTENT Page ACRONYMS 8 1. INTRODUCTION 10 2. GENERAL GUIDELINES 11 2.1 Legal basis 11 2.2 Scope and objective 11 2.3 CoA reports 11 2.4

Chart of Accounts Manual MAIN DOCUMENT (September 2018) TABLE OF CONTENT Page ACRONYMS 8 1. INTRODUCTION 10 2. GENERAL GUIDELINES 11 2.1 Legal basis 11 2.2 Scope and objective 11 2.3 CoA reports 11 2.4

Guide to Japan s Flow of Funds Accounts

Guide to Japan s Flow of Funds Accounts Research and Statistics Department Bank of Japan Introduction The Bank of Japan has been compiling the Flow of Funds Accounts Statistics (the FFA) since 1958, covering

Guide to Japan s Flow of Funds Accounts Research and Statistics Department Bank of Japan Introduction The Bank of Japan has been compiling the Flow of Funds Accounts Statistics (the FFA) since 1958, covering

ANNEX TO THE PROTOCOL TO IMPLEMENT THE FOURTH PACKAGE OF COMMITMENTS ON FINANCIAL SERVICES UNDER THE ASEAN FRAMEWORK AGREEMENT ON SERVICES

ANNEX TO THE PROTOCOL TO IMPLEMENT THE FOURTH PACKAGE OF COMMITMENTS ON FINANCIAL SERVICES UNDER THE ASEAN FRAMEWORK AGREEMENT ON SERVICES SCHEDULE OF SPECIFIC COMMITMENTS ASEAN FRAMEWORK AGREEMENT ON

ANNEX TO THE PROTOCOL TO IMPLEMENT THE FOURTH PACKAGE OF COMMITMENTS ON FINANCIAL SERVICES UNDER THE ASEAN FRAMEWORK AGREEMENT ON SERVICES SCHEDULE OF SPECIFIC COMMITMENTS ASEAN FRAMEWORK AGREEMENT ON

EN ANNEX III ANNEX V REPORTING ON FINANCIAL INFORMATION

Table of contents EN ANNEX III ANNEX V REPORTING ON FINANCIAL INFORMATION General instructions... 4 1. References... 4 2. Conventions... 6 3. Consolidation... 7 4. Accounting portfolios of financial instruments...

Table of contents EN ANNEX III ANNEX V REPORTING ON FINANCIAL INFORMATION General instructions... 4 1. References... 4 2. Conventions... 6 3. Consolidation... 7 4. Accounting portfolios of financial instruments...

Matrix of Flow of Detailed Funds in the System of National Accounts of Mexico

RESTRICTED CONFERENCE ON STRENGTHENING SECTORAL POSITION AND FLOW DATA IN THE MACROECONOMIC ACCOUNTS Jointly organized by the IMF and OECD February 28 March 2, 2011 IMF Headquarters 2 (HQ2) Conference

RESTRICTED CONFERENCE ON STRENGTHENING SECTORAL POSITION AND FLOW DATA IN THE MACROECONOMIC ACCOUNTS Jointly organized by the IMF and OECD February 28 March 2, 2011 IMF Headquarters 2 (HQ2) Conference

Glossary A B C D E F G H I J K L M N O P Q R S T U V W X Y Z. adjusted change

Glossary A B C D E F G H I J K L M N O P Q R S T U V W X Y Z A adjusted change algo algorithmic trading amount outstanding B bank banking office banks and securities firms bilateral netting agreement BIS

Glossary A B C D E F G H I J K L M N O P Q R S T U V W X Y Z A adjusted change algo algorithmic trading amount outstanding B bank banking office banks and securities firms bilateral netting agreement BIS

The Production of Financial Corporations and Price/Volume Split of Financial Services And Non-Life Insurance Services

BOPCOM-05/37 Eighteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C., June 27 July 1, 2005 The Production of Financial Corporations and Price/Volume Split of Financial

BOPCOM-05/37 Eighteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C., June 27 July 1, 2005 The Production of Financial Corporations and Price/Volume Split of Financial

The System of National Accounts SNA. Original text of amended paragraphs

The System of National Accounts 1993-1993 SNA Original text of amended paragraphs In 1999 the UNSC during its 30th session endorsed the proposal of a mechanism for incremental updating of the 1993 SNA

The System of National Accounts 1993-1993 SNA Original text of amended paragraphs In 1999 the UNSC during its 30th session endorsed the proposal of a mechanism for incremental updating of the 1993 SNA

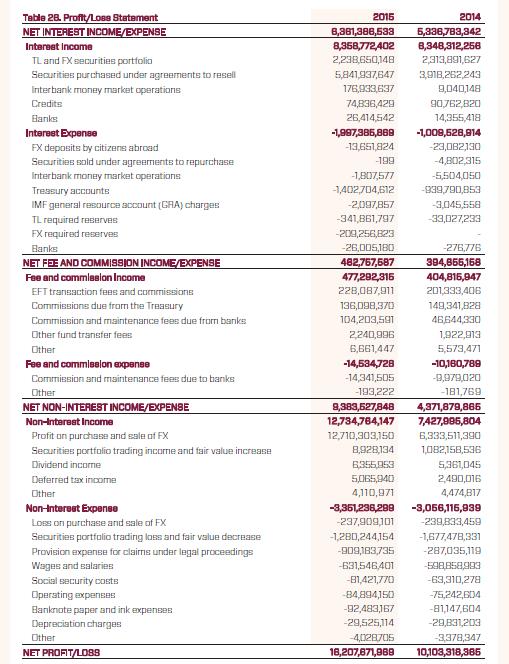

T.C. ZİRAAT BANKASI A.Ş. UNCONSOLIDATED STATEMENT OF CASH FLOWS

ATTACHMENT 1-E T.C. ZİRAAT BANKASI A.Ş. UNCONSOLIDATED STATEMENT OF CASH FLOWS A. CASH FLOWS FROM BANKING OPERATIONS Note (01/01/2007-30/06/2007) (01/04/2006-30/06/2006) 1.1 Operating profit before changes

ATTACHMENT 1-E T.C. ZİRAAT BANKASI A.Ş. UNCONSOLIDATED STATEMENT OF CASH FLOWS A. CASH FLOWS FROM BANKING OPERATIONS Note (01/01/2007-30/06/2007) (01/04/2006-30/06/2006) 1.1 Operating profit before changes

Islamic Finance in National Accounts- Palestine. Amina Khasib

Islamic Finance in National Accounts- Palestine Amina Khasib Banks in Palestine All Banks in Palestine 2016 Conventional Banks Islamic Banks 15 Banks 304 Branches 622 ATM 3 Banks 46 Branches 15% 16% ATM

Islamic Finance in National Accounts- Palestine Amina Khasib Banks in Palestine All Banks in Palestine 2016 Conventional Banks Islamic Banks 15 Banks 304 Branches 622 ATM 3 Banks 46 Branches 15% 16% ATM

Session 5 Supply, Use and Input-Output Tables. The Use Table

Session 5 Supply, Use and Input-Output Tables The Use Table Introduction A use table shows the use of goods and services by product and by type of use for intermediate consumption by industry, final consumption

Session 5 Supply, Use and Input-Output Tables The Use Table Introduction A use table shows the use of goods and services by product and by type of use for intermediate consumption by industry, final consumption

In various tables, use of - indicates not meaningful or not applicable.

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

Basel II Pillar 3 disclosures 2008 For purposes of this report, unless the context otherwise requires, the terms Credit Suisse Group, Credit Suisse, the Group, we, us and our mean Credit Suisse Group AG

Current practice and status of the national accounts compilation in Uzbekistan

Current practice and status of the national accounts compilation in Uzbekistan Regional Course on SNA 2008 (Special Topics): Improving Exhaustiveness of GDP Coverage 22 30 August 2016 Daejeon, Republic

Current practice and status of the national accounts compilation in Uzbekistan Regional Course on SNA 2008 (Special Topics): Improving Exhaustiveness of GDP Coverage 22 30 August 2016 Daejeon, Republic

Financial Statements

Financial Statements I. Balance sheets (Statements of financial position) II. Statements of off-balance sheet items III. Income statements IV. Statements of income and expenses recognized under equity

Financial Statements I. Balance sheets (Statements of financial position) II. Statements of off-balance sheet items III. Income statements IV. Statements of income and expenses recognized under equity

IMF COMMITTEE ON BALANCE OF PAYMENTS STATISTICS BALANCE OF PAYMENTS TECHNICAL EXPERT GROUP (BOPTEG)

") IMF COMMITTEE ON BALANCE OF PAYMENTS STATISTICS BALANCE OF PAYMENTS TECHNICAL EXPERT GROUP (BOPTEG) ISSUES PAPER (BOPTEG) # 27A THE TREATMENT OF NON-MONETARY GOLD IN THE MACRO ECONOMIC ACCOUNTS Executive

IMF COMMITTEE ON BALANCE OF PAYMENTS STATISTICS BALANCE OF PAYMENTS TECHNICAL EXPERT GROUP (BOPTEG) ISSUES PAPER (BOPTEG) # 27A THE TREATMENT OF NON-MONETARY GOLD IN THE MACRO ECONOMIC ACCOUNTS Executive

CHAPTER. Special circumstances

CHAPTER 14 Special circumstances Chapter 14 Special circumstances 14. Special circumstances 14.1 Financial Institutions 14.1.1 Collective Investment Vehicles Collective Investment Vehicles are the main

CHAPTER 14 Special circumstances Chapter 14 Special circumstances 14. Special circumstances 14.1 Financial Institutions 14.1.1 Collective Investment Vehicles Collective Investment Vehicles are the main

Lesson VIII Domestic Economy and External Transactions - revisited

Lesson VIII Domestic Economy and External Transactions - revisited Domestic economy revisited Non-residents ownership of land and other natural resources Branch of multi-nationals & multi-territory institutional

Lesson VIII Domestic Economy and External Transactions - revisited Domestic economy revisited Non-residents ownership of land and other natural resources Branch of multi-nationals & multi-territory institutional

Advanced Finance Dr. Parviz Aghili

Sharif University of Technology Graduate School of Management and Economics Advanced Finance Dr. Parviz Aghili 1390-91 2 nd term Introduction The financial system is the mechanism through which loanable

Sharif University of Technology Graduate School of Management and Economics Advanced Finance Dr. Parviz Aghili 1390-91 2 nd term Introduction The financial system is the mechanism through which loanable

BOM/BSD 18/March 2008 BANK OF MAURITIUS. Guideline on. Standardised Approach to Credit Risk

BOM/BSD 18/March 2008 BANK OF MAURITIUS Guideline on Standardised Approach to Credit Risk Revised December 2017 2 TABLE OF CONTENTS INTRODUCTION... 5 Purpose... 5 Authority... 5 Scope of application...

BOM/BSD 18/March 2008 BANK OF MAURITIUS Guideline on Standardised Approach to Credit Risk Revised December 2017 2 TABLE OF CONTENTS INTRODUCTION... 5 Purpose... 5 Authority... 5 Scope of application...

Accounts, Indicators and Policy Use with 2008 SNA Framework

Accounts, Indicators and Policy Use with 28 SNA Framework Regional Seminar on Developing a Programme for the Implementation Programme of the 28 SNA and the Implementation Strategy for the SEEA Central

Accounts, Indicators and Policy Use with 28 SNA Framework Regional Seminar on Developing a Programme for the Implementation Programme of the 28 SNA and the Implementation Strategy for the SEEA Central

Supply and Use Tables for Macedonia. Prepared by: Lidija Kralevska Skopje, February 2016

Supply and Use Tables for Macedonia Prepared by: Lidija Kralevska Skopje, February 2016 Contents Introduction Data Sources Compilation of the Supply and Use Tables Supply and Use Tables as an integral

Supply and Use Tables for Macedonia Prepared by: Lidija Kralevska Skopje, February 2016 Contents Introduction Data Sources Compilation of the Supply and Use Tables Supply and Use Tables as an integral

HUNGARY ACT ON THE CAPITAL MARKET

HUNGARY ACT ON THE CAPITAL MARKET Important Disclaimer This does not constitute an official translation and the translator and the EBRD cannot be held responsible for any inaccuracy or omission in the

HUNGARY ACT ON THE CAPITAL MARKET Important Disclaimer This does not constitute an official translation and the translator and the EBRD cannot be held responsible for any inaccuracy or omission in the

Interest Rate Risk Management Refresher. April 29, Presented to: Howard Sakin Section I. Basics of Interest Rate Hedging?

Interest Rate Risk Management Refresher April 29, 2011 Presented to: Howard Sakin 410-237-5315 Section I Basics of Interest Rate Hedging? 1 What Is An Interest Rate Hedge? Interest rate hedges are contracts

Interest Rate Risk Management Refresher April 29, 2011 Presented to: Howard Sakin 410-237-5315 Section I Basics of Interest Rate Hedging? 1 What Is An Interest Rate Hedge? Interest rate hedges are contracts

BOM/BSD 18/March 2008 BANK OF MAURITIUS. Guideline on. Standardised Approach to Credit Risk

BOM/BSD 18/March 2008 BANK OF MAURITIUS Guideline on Standardised Approach to Credit Risk Revised February 2018 i Table of Contents INTRODUCTION... 1 Purpose... 1 Authority... 1 Scope of application...

BOM/BSD 18/March 2008 BANK OF MAURITIUS Guideline on Standardised Approach to Credit Risk Revised February 2018 i Table of Contents INTRODUCTION... 1 Purpose... 1 Authority... 1 Scope of application...

Consolidated Statement of Income

Interim Consolidated Financial Statements Consolidated Statement of Income (Unaudited) (Canadian $ in millions, except as noted) For the three months ended January 31, October 31, July 31, April 30, January

Interim Consolidated Financial Statements Consolidated Statement of Income (Unaudited) (Canadian $ in millions, except as noted) For the three months ended January 31, October 31, July 31, April 30, January

Eighteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C., June 27 July 1, 2005

BOPCOM-05/26 Eighteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C., June 27 July 1, 2005 Fee on Securities Lending and Reversible Gold Transactions BALANCE OF PAYMENTS

BOPCOM-05/26 Eighteenth Meeting of the IMF Committee on Balance of Payments Statistics Washington, D.C., June 27 July 1, 2005 Fee on Securities Lending and Reversible Gold Transactions BALANCE OF PAYMENTS

Guidelines for the OECD questionnaire on INSTITUTIONAL INVESTORS ASSETS AND LIABILITIES. (Table 7II)

") Guidelines for the OECD questionnaire on INSTITUTIONAL INVESTORS ASSETS AND LIABILITIES (Table 7II) 2016 1 INSTRUCTIONS FOR THE DATA QUESTIONNAIRE AND METHODOLOGICAL SURVEY COMPILATION Questionnaire structure

Guidelines for the OECD questionnaire on INSTITUTIONAL INVESTORS ASSETS AND LIABILITIES (Table 7II) 2016 1 INSTRUCTIONS FOR THE DATA QUESTIONNAIRE AND METHODOLOGICAL SURVEY COMPILATION Questionnaire structure

8 Changes from BPM5. Chapter 3. Accounting Principles. Chapter 1. Introduction. Chapter 2. Overview of the Framework APPENDIX

APPENDIX 8 Changes from BPM5 A detailed list of individual changes made in this edition of the Manual is provided below. The comparison is with BPM5, as amended by The Recommended Treatment of Selected

APPENDIX 8 Changes from BPM5 A detailed list of individual changes made in this edition of the Manual is provided below. The comparison is with BPM5, as amended by The Recommended Treatment of Selected

Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016

Page 1 of 93 Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016 Print Summary Results of the September 2016 Survey Summary The September 2016 Senior Credit Officer Opinion Survey

Page 1 of 93 Senior Credit Officer Opinion Survey on Dealer Financing Terms September 2016 Print Summary Results of the September 2016 Survey Summary The September 2016 Senior Credit Officer Opinion Survey

The New Treatment of Reinsurance in SNA 2008: Implementation and Impact

The New Treatment of Reinsurance in SNA 2008: Implementation and Impact Wolfgang Eichmann (Federal Statistical Office of Germany) Paper Prepared for the IARIW 33 rd General Conference Rotterdam, the Netherlands,

The New Treatment of Reinsurance in SNA 2008: Implementation and Impact Wolfgang Eichmann (Federal Statistical Office of Germany) Paper Prepared for the IARIW 33 rd General Conference Rotterdam, the Netherlands,

The Belgian shadow banking sector with a focus on other financial intermediaries (OFIs) 1

1") IFC-National Bank of Belgium Workshop on "Data needs and Statistics compilation for macroprudential analysis" Brussels, Belgium, 18-19 May 2017 The Belgian shadow banking sector with a focus on other financial

IFC-National Bank of Belgium Workshop on "Data needs and Statistics compilation for macroprudential analysis" Brussels, Belgium, 18-19 May 2017 The Belgian shadow banking sector with a focus on other financial

COMMUNIQUE ON PRINCIPLES REGARDING İTMK. (Serial: III, No: 33) SECTION ONE Objective, Scope, Justification and Definitions

SECTION ONE Objective, Scope, Justification and Definitions") COMMUNIQUE ON PRINCIPLES REGARDING İTMK (Serial: III, No: 33) SECTION ONE Objective, Scope, Justification and Definitions Purpose and scope Article 1- (1)This By-law is to regulate the principles regarding

COMMUNIQUE ON PRINCIPLES REGARDING İTMK (Serial: III, No: 33) SECTION ONE Objective, Scope, Justification and Definitions Purpose and scope Article 1- (1)This By-law is to regulate the principles regarding

Session 2 Financial Sector & National Accounts

Session 2 Financial Sector & National Accounts Ahmet Kürşad Dosdoğru Content Supply and Use Tables&FS Ins. Sector Accounts&FS Financial Accounts&FS Regional Accounts&FS Exhaustiveness&FS Financial services

Session 2 Financial Sector & National Accounts Ahmet Kürşad Dosdoğru Content Supply and Use Tables&FS Ins. Sector Accounts&FS Financial Accounts&FS Regional Accounts&FS Exhaustiveness&FS Financial services