NBER WORKING PAPER SERIES BANK FAILURES AND OUTPUT DURING THE GREAT DEPRESSION. Jeffrey A. Miron Natalia Rigol

|

|

|

- Lewis Garrett

- 5 years ago

- Views:

Transcription

1 NBER WORKING PAPER SERIES BANK FAILURES AND OUTPUT DURING THE GREAT DEPRESSION Jeffrey A. Miron Natalia Rigol Working Paper NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA September 2013 We thank Jaron Cordero, Linxi Wu, and Stephanie Hurder for superb research assistance. John Lapp, Randall Parker, Greg Mankiw, Tom Sargent, Kate Waldock and participants at the Wake Forest conference The Federal Reserve Was a Bad Idea provided helpful comments on an earlier draft. The views expressed herein are those of the authors and do not necessarily reflect the views of the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peerreviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications by Jeffrey A. Miron and Natalia Rigol. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including notice, is given to the source.

2 Bank Failures and Output During the Great Depression Jeffrey A. Miron and Natalia Rigol NBER Working Paper No September 2013 JEL No. E32 ABSTRACT In response to the Financial Crisis of 2008, macroeconomic policymakers employed a range of tools designed to prevent failures of large, complex financial institutions ( banks ). The Treasury and the Fed justified these actions by arguing that bank failures exacerbate output declines, rather than just reflecting output losses that have already occurred. This view is consistent with economic models based on credit market imperfections, but it is an empirical question as to whether the feedback from failures to output losses is substantial. This paper examines the relation between bank failures and output by re-considering Bernanke s (1983) analysis of the Great Depression. We find little indication that bank failures exerted a substantial or sustained impact on output during this period. Jeffrey A. Miron Department of Economics Harvard University Cambridge, MA and NBER miron@fas.harvard.edu Natalia Rigol Department of Economics MIT Cambridge, MA nrigol@mit.edu

3 I. Introduction In response to the Financial Crisis of 2008, macroeconomic policymakers employed several tools designed to prevent the failure of large and complex financial institutions ( banks ). 1 Most importantly, the Treasury injected capital directly into banks, and the Fed expanded its balance sheet by purchasing roughly $1.3 trillion in mortgage-backed securities (Fuster and Willen 2010). The Federal Housing Finance Agency also placed Fannie Mae and Freddie Mac into conservatorship, and the Treasury supplied $100 billion of capital to each agency. The Treasury and the Fed justified these actions by appealing to the claim that bank failures contribute to output declines, rather than just reflecting output losses that have already occurred. This proposition stems from theoretical perspectives (e.g., Bernanke and Gertler 1985) and has been supported by certain empirical work (e.g., Bernanke 1983, Bernanke and James 1991). Economists as a group supported the Fed and Treasury policies, mainly from concern that widespread bank failures would exacerbate the recession. A few even speculated that failure to support banks would risk another Great Depression. Yet government aid to failing banks has costs, whether or not that support calms recessions. Most importantly, moral hazard generated by the prospect of bailouts can distort lending and investment decisions toward excessively risky projects or sectors. More broadly, the prospect of bailouts might increase uncertainty, delay appropriate adjustments as banks wait for policymakers to decide whether and whom to bail out, generate strategic actions by banks seeking to profit from bailouts, or reward politically connected banks rather than systemically crucial ones. In assessing the wisdom of bailouts, therefore, it is important to know whether the feedback from bank failures to output is substantial or modest. If failures have a large impact on output, bailouts are potentially desirable even if they generate their own costs. If failures have a modest impact on output, the case for bailouts is less convincing. 1 Some of the financial institutions targeted by these actions were not banks per se, but we use the term bank throughout for ease of presentation. 2

4 This paper examines evidence on the relation between bank failures and output by reconsidering the findings in Bernanke (1983). Bernanke (1983) appears to show that bank failures had a substantial impact on output during the Great Depression. We argue that the data provide little support for this proposition. Our conclusion follows, in part, because determining whether failures cause or reflect output losses is difficult. But the conclusion also follows because even under the most generous identifying assumption, the impact of bank failures during the Great Depression does not appear to have been large or persistent. II: Bank Failures and Output During the Great Depression In attempting to understand the Great Depression, Bernanke (1983) argues that the Friedman and Schwartz (1963) monetary explanation is incomplete because theoretical models of money cannot easily explain the protracted non-neutrality necessary to account for the length of the downturn from Further, Bernanke suggests that the declines in money were not sufficient to explain the magnitude of the fall in output over the same period. Bernanke therefore proposes that bank failures had a non-monetary effect on the real economy through credit rationing since failures made credit scarcer for borrowing firms. In his view, banks act as low-cost credit intermediaries who collect funds from lenders and evaluate the risk of borrowers. The non-trivial and costly-to-replicate service that the banking system provides is to differentiate between good and bad borrowers. Bank failures therefore decrease intermediation capital, raise the cost of loans, and reduce output because alternative sources of credit intermediation cannot arise quickly or in sufficient quantity after banks fail. 2 Bernanke s Empirical Strategy To quantify the importance of monetary versus non-monetary factors in generating the output declines of , Bernanke estimates the equation 2 Following Fisher (1933), Bernanke also argues that debt deflation in the 1930s decreased the net worth of both borrowers and banks, destroying intermediaries and available credit. 3

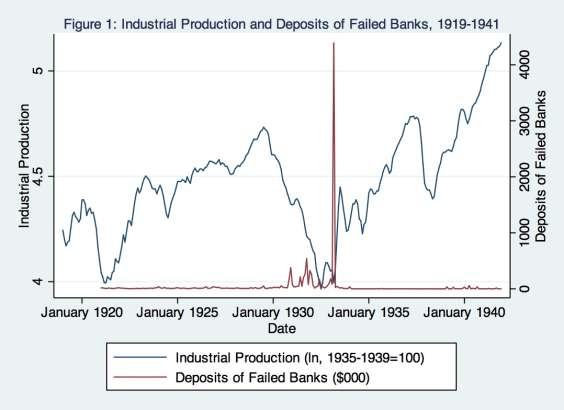

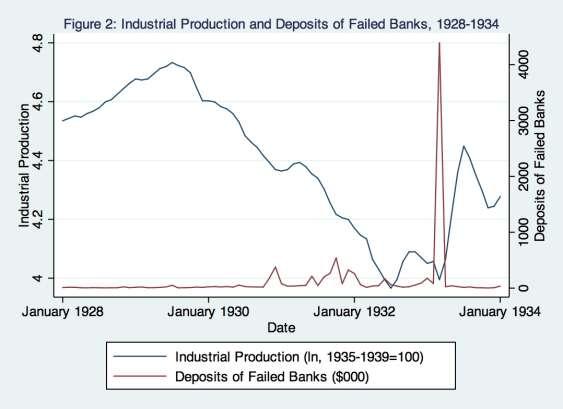

5 y t = a(l) y t-1 + b(l) (m t t-1 m t ) + c(l) DBANKS t + d(l) DFAILS t + e t where y t m t - t-1m t DBANKS t DFAILS t is the log growth rate of monthly industrial production; is the growth rate of M1 less the predicted growth rate; is the first difference of real deposits of failing banks; and is the first difference of real liabilities of failing businesses. Bernanke creates the monetary surprises as residuals from a regression of the growth rate of M1 on four lags of the growth rate of industrial production, wholesale prices, and M1 itself (Bernanke 1983, p. 268). Bernanke also estimates a version of Equation (1) in which he replaces the money surprises with price surprises, defined analogously. Under the null hypothesis that bank and business failures play no independent role in the propagation of output, DBANKS and DFAILS should not enter Equation (1). Instead, the only impact of bank failures should occur via their impact on the money stock, consistent with the Friedman and Schwartz view that monetary shocks generated the lion s share of the output declines during the downturn. In this case, the monetary surprise variable, m t - t-1m t, should explain most of the behavior of output. Overview of the Data Before examining estimates of Equation (1), we consider the raw data. Figure 1 displays the log of monthly industrial production along with the real value of deposits in failed banks for Bernanke s sample period, 1919:1 1941:12. 3 Figure 2 shows these same data for to facilitate closer 3 In constructing the time series for the value of deposits in failed banks and the value of commercial failures, we had to face two issues that Bernanke does not explain in his original paper. First, to construct both series we had to combine several data sources. The Federal Reserve Bulletin provides monthly data on deposits in failed commercial banks for January 1921 December 1936 and three different overlapping series for commercial failures (January 1894 August 1938, June December 1939, and January 1939 December 1968). The FDIC provides data on deposits in failed insured commercial banks and savings associations for January 1934 December These series are not equal for the overlapping time periods. We employ the Fed Bulletin bank failure series for 4

6 examination of the timing. These graphs suggest three conclusions about the relation between output and failures. At the broad-brush level, an impact of bank failures on output does not leap from the graphs. Industrial production fluctuated significantly during parts of the interwar period that experienced few bank failures. In particular, industrial production declined 28.8 percent over a span of fifteen months, from the cyclical peak in July, 1929 to the first wave of bank failures in November,1930. That magnitude decline almost half the overall drop makes it plausible that bank failures were partly a response to adverse economic conditions, whether or not failures contributed to output losses. At a more detailed level, these data are consistent with the view that failures reduce output, since in November 1930, October 1931, and March 1933, a reduction in output (relative to the downward trend) occurs simultaneously with a spike in failures. The output declines in these periods were not by themselves enormous, and failures do not appear to have had a persistent impact on the output path, but some correlation is apparent. The graphs also suggest that one particular observation the bank holiday in March, 1933, declared by President Franklin Roosevelt on March 6th might play a substantial role in driving the correlation between failures and output declines. The real value of deposit liabilities of suspended banks in March, 1933 was seven times larger than the second largest value, in October, As it turns out, our conclusions based on the regressions presented below are consistent with the impressions provided by this graphical examination. We conclude that failures plausibly had some impact on output, but this impact is sensitive to the identifying assumption about timing, is not especially large or persistent, and is somewhat sensitive to exclusion of the bank holiday from the sample and append the FDIC series for For commercial failures, we employ the series for January 1921 August 1938, the series for September 1938 December 1939, and the series for January 1940 December Our results are not sensitive to these choices. In addition, Bernanke notes that both commercial and bank failures are scaled by the wholesale price index but does not specify the base year for that index. Following the normalization of industrial production, we set =100. 5

7 Regression Results Table 1 presents our replication of the results from Bernanke s 1983 paper (Table 2, Equations (1) - (4)). 4 Our estimates are close, but not identical to, those reported in Bernanke. 5 The coefficients on the contemporaneous money or price surprises are positive and significant, consistent with the Friedman and Schwartz view that money played a role in the propagation of the Depression. The lagged monetary surprises are never significant while the first lags of the price surprises are. The coefficients on the contemporaneous and lagged values of the liabilities of failed banks are both negative and significant. This is the crucial result in Bernanke s paper; it suggests that even after controlling for the impact of bank failures on the stock of money, bank failures played an additional, nonmonetary role in generating the output declines of the period. The coefficients on the business liabilities variables are negative but inconsistent in significance, so they provide no independent confirmation of Bernanke s hypothesis. These results are thus consistent with Bernanke s conclusions. We now examine whether these results are robust to certain specification issues. The Bank Holiday As Bernanke notes and Figures 1-2 illustrate, bank failures were unusually high in March It is not obvious whether to include this observation in gauging the impact of failures on output, since the mechanism by which banks closed during this episode (an economy-wide, government-imposed shutdown) was not identical to the more usual mechanism. We take no position on this issue and instead examine alternative empirical approaches to dealing with this observation. 4 Bernanke reports OLS standard errors, and we do so as well to facilitate comparison. The conclusions from both the simultaneous and lagged estimates are not changed with HAC standard errors. 5 We have attempted to replicate Bernanke s estimates precisely, so far without success. Two possible explanations for the discrepancies are data revisions and the normalization of the wholesale price index. No parameters we have tried produce Bernanke s estimates exactly. 6

8 Bernanke s reported results include the March, 1933 data. Bernanke notes that he tried an alternate specification in which he scaled this observation to 15% of its reported value (p.270), and that under this modification, the bank failure coefficients retain high significance. We obtain the same result with our data; this approach to handling the March, 1933 observation does not produce a material change in Bernanke s results (Table 2, Regressions (5) - (6)). We then estimate regressions dropping all observations that require the value of bank failures in March Regressions (7)-(8) of Table 2 show the results. In this specification, the bank and business failure variables still enter negatively, consistent with Bernanke s hypothesis, but the coefficients lose their statistical significance. Thus, exclusion of the Bank Holiday does not reverse Bernanke s results but does weaken them substantially. It is not obvious whether results that exclude the bank holiday are more or less informative than those that include this observation. On the one hand, the number of failures and the quantity of deposits involved was enormous in March, This implies that this observation is most relevant to episodes like the recent crisis in which many large banks appeared to be at risk of failure. On the other hand, the exact nature of these suspensions differed from those arising endogenously, since those during the bank holiday were nationwide, applied to all banks, and imposed by government decree. Identification A crucial issue in interpreting Bernanke s results is whether causation runs mainly from bank failures to output declines or from output declines to bank failures. Bernanke recognizes this issue and explains why he believes his regressions measure the impact of failures on output, rather than the reverse, but we do not find his reasoning persuasive. Bernanke states, To conclude that the observed correlations support the theory outlined in this paper requires an additional assumption, that failures of banks and commercial firms are not caused by (anticipations) of future changes in output. To the extent that, say, bank runs are caused by the receipt of bad news about next month s industrial production, the fact that bank failures tend to lead production declines does not prove that the bank problems are helping to cause the decline (p.271). 7

9 We find this description of the identifying assumption confusing. Bernanke seems to suggest that his equation suffers from simultaneous equations bias only if anticipations of future output declines can increase bank failures. But as his regressions are specified, they are subject to such bias so long as current output declines can affect current failures. The ideal way to resolve this issue is to instrument for contemporaneous bank failures, but we are not aware of convincing instruments. An alternative approach is to assume it takes at least a month for bank failures to disrupt credit intermediation and thereby lower output. Under this assumption, any contemporaneous relation between output and failures is assumed to represent the impact of output on failures. We can then determine the effects of failures on output by excluding contemporaneous failures from the regressions. At a minimum, it seems reasonable to consider this specification. Table 3 presents the results. In these regressions, bank failures have no predictive power for output; indeed, the coefficients on bank failures imply that failures predict increases in output. Thus, if the identifying assumption implicit in Table 3 is correct, these data and this specification provide no evidence (indeed, contradict) the view that bank failures cause output declines. Whether this identifying assumption is convincing is impossible to say on a priori grounds. Thus, it is not correct to interpret Table 3 as showing that Bernanke s conclusions are invalid. But the Table 3 results do show that under an alternate and plausible identifying assumption, the interwar data do not support these conclusions. The Magnitude of the Effects A different issue in the assessment of Bernanke s conclusions is the quantitative importance of bank failures in contributing to declines in output, whatever identifying assumption one makes. The raw data examined above did not seem to suggest a large impact, but we reconsider this issue based on the estimated regressions reported in Table 1. Thus, we return to Bernanke s identifying assumption that all of the contemporaneous correlation between output and failures reflects the influence of failures on output. 8

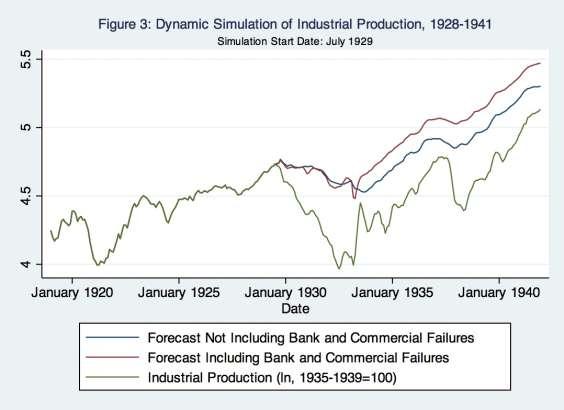

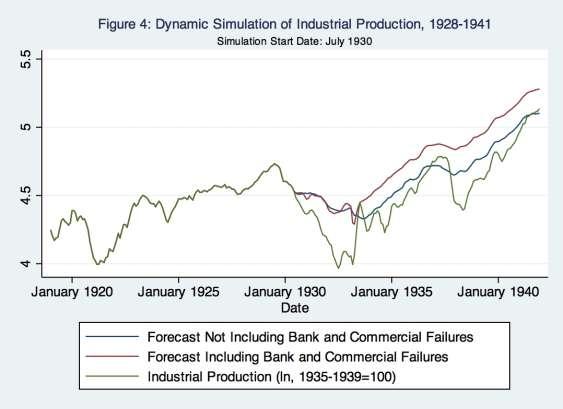

10 Figures 3 and 4 display forecasts of the log of industrial production, along with the actual values, based on estimates of Regressions (1) and (3) that exclude and include, respectively, the bank and business failure variables. We present two sets of forecasts, beginning in July 1929 and July The first date is the peak of Industrial Production, while the second date is the forecast start date used by Bernanke. We construct the forecasts in the following way: first, we generate the fitted value for the growth rate of industrial production for the first month of the forecast period using the relevant regression. Second, we set the forecasted log of industrial production in the first forecast month equal to the log of industrial production in the last month of the non-forecast period plus the predicted growth rate from that period to the first forecast period. Third, we forecast the growth rate from the first to the second month in the forecast period using the forecasted value from the first period and the relevant regression. For all subsequent months, we set the forecasted log of industrial production equal to the forecasted log of industrial production for the previous month plus the growth rate predicted using the relevant regression and all previous forecasted values. The figures suggest that Bernanke s credit variables have minimal impact on the ability of such regressions to explain the decline in output from the peak of Industrial Production in 1929 to the trough in The purely monetary equation does a reasonable job: it gets the direction of most ups and downs correct, and it explains a non-trivial percentage of the decline in output. The equation augmented with the failure variables, however, does not improve the forecast between 1929 and Thus, even under Bernanke s identifying assumption, in which credit variables are statistically significant determinants of output growth, they are not quantitatively important determinants of that growth. III. Discussion The results we have presented, by themselves, shed light on our understanding of the Great Depression. As Bernanke confirmed, monetary factors do appear to have played a major role in the downturn, consistent with the work of Friedman and Schwartz. But the main avenue through which bank 9

11 failures mattered seems to have been through their impact on the money supply, rather than via a credit intermediation channel. Our results do not deal directly with whether bank failures during the recent financial crisis would have generated a deeper or longer recession than occurred, had the Treasury and Fed not taken the actions that forestalled these failures. This is because the two episodes differed in important respects. Perhaps most significantly, bank failures during the Great Depression occurred mainly for large numbers of small banks; bank failures during the recent episode would plausibly have involved small numbers of large, interconnected banks. Thus our results shed little direct light over whether Too-Big-to-Fail concerns were valid. To the extent U.S. experience during the Great Depression and especially the view that bank failures played a significant, independent role during that period formed the intellectual foundation for Treasury and Fed actions, however, our results suggest a hint of caution. If the Great Depression does not constitute evidence for Too-Big-to-Fail, then what historical episodes do provide that evidence? We leave that question for another day. 10

12 References Bernanke, Ben (1983), Non-Monetary Effects of the Financial Crisis in the Propagation of the Great Depression, American Economic Review, 73(3), Bernanke, Ben and Mark Gertler (1987), Banking in General Equilibrium, in New Approaches to Monetary Economics, W. Barnett and K. Singleton, eds., New York: Cambridge University Press. Bernanke, Ben and Harold James (1991), The Gold Standard, Deflation, and Financial Crisis in the Great Depression: An International Comparison, in R. G. Hubbard, ed., Financial Markets and Financial Crises, Chicago: University of Chicago Press. Fisher, Irving (1933), The Debt-Deflation Theory of Great Depressions, Econometrica, 1, Friedman, Milton and Anna J. Schwarz (1963), A Monetary History of the United States, , New York: National Bureau of Economic Research. Fuster, Andreas and Paul Willen (2010), $1.25 Trillion is Still Real Money: Some Facts About the Effects of the Federal Reserve's Mortgage Market Investments, Federal Reserve Bank of Boston Public Policy Discussion Paper No

13 Table 1: Replications of Bernanke Table 2 (1) (2) (3) (4) VARIABLES Equation 1 Equation 2 Equation 3 Equation 4 IP t ** 0.554** 0.615** 0.613** (10.19) (9.02) (9.85) (9.78) IP t * (-1.94) (-0.97) (-2.17) (-1.34) Money t 0.443** 0.273* (3.75) (2.40) Money t (0.77) (0.42) Money t (0.42) (1.36) Money t (1.29) (1.24) Price t 0.598** 0.595** (5.28) (4.50) Price t ** 0.314* (4.11) (2.31) Price t (1.21) (0.07) Price t (-1.20) (-0.86) DBANKS t ** ** (-5.85) (-6.10) DBANKS t ** ** (-2.80) (-2.83) DFAILS t * (-2.47) (-1.81) DFAILS t * (-2.22) (-1.49) Constant (0.94) (1.09) (1.43) (1.08) RMSE Observations OLS t-statistics included in parentheses. Sample: January December 1941 (Regressions 1 and 2); January December (Regressions 3 and 4). * significant at 5%; ** significant at 1% 12

14 Table 2: Bank Holiday: Omitting and Scaling March 1933 (5) (6) (7) (8) VARIABLES Scaled Eq. 3 Scaled Eq. 4 Omitted Eq. 3 Omitted Eq. 4 IP t ** 0.599** 0.585** 0.609** (9.71) (9.50) (9.50) (9.69) IP t * (-2.05) (-1.39) (-1.72) (-1.18) Money t 0.344** 0.320** (3.05) (2.86) Money t (0.62) (1.47) Money t * (1.03) (2.06) Money t (1.46) (1.58) DBANKS t ** ** (-5.04) (-4.73) (-1.66) (-0.90) DBANKS t * * (-2.41) (-2.23) (-0.75) (-0.43) DFAILS t (-1.45) (-0.83) (-1.65) (-1.54) DFAILS t * (-2.32) (-1.53) (-1.58) (-1.22) Price t 0.593** 0.546** (4.37) (4.01) Price t * 0.289* (2.43) (2.10) Price t (0.71) (0.01) Price t (-0.38) (-0.75) Constant (1.41) (1.05) (1.03) (0.90) RMSE Observations OLS t-statistics included in parentheses. Sample: January December Regressions 5 and 6: March 1933 bank failures scaled by Regressions 7 and 8: March 1933 bank failures set to missing. * significant at 5%; ** significant at 1%. 13

15 Table 3: Identification: Excluding Contemporaneous Bank Failures (9) (10) (11) (12) VARIABLES Eq. 3 Eq. 4 Eq. 3 Eq. 4 IP t ** 0.605** 0.657** 0.637** (9.53) (9.01) (9.59) (9.26) IP t * * (-1.98) (-1.36) (-2.01) (-1.50) Money t 0.462** 0.449** (3.95) (3.82) Money t (0.42) (0.72) Money t (0.15) (0.29) Money t (0.97) (0.70) Price t 0.701** 0.715** (5.07) (5.14) Price t ** 0.425** (3.10) (2.89) Price t (1.05) (1.09) Price t (-0.33) (-0.43) DBANKS t e e e e-06 (0.35) (0.27) (1.16) (1.14) DFAILS t (-1.11) (-0.46) (-0.94) (-0.20) DBANKS t e e-06 (1.52) (1.59) DFAILS t (0.16) (0.59) Constant (1.32) (0.94) (1.32) (0.97) RMSE Observations OLS t-statistics included in parentheses. Sample: January December * significant at 5%; ** significant at 1%. 14

16 15

17 16

Financial Fragility and the Lender of Last Resort

READING 11 Financial Fragility and the Lender of Last Resort Desiree Schaan & Timothy Cogley Financial crises, such as banking panics and stock market crashes, were a common occurrence in the U.S. economy

READING 11 Financial Fragility and the Lender of Last Resort Desiree Schaan & Timothy Cogley Financial crises, such as banking panics and stock market crashes, were a common occurrence in the U.S. economy

Empirically Evaluating Economic Policy in Real Time. The Martin Feldstein Lecture 1 National Bureau of Economic Research July 10, John B.

Empirically Evaluating Economic Policy in Real Time The Martin Feldstein Lecture 1 National Bureau of Economic Research July 10, 2009 John B. Taylor To honor Martin Feldstein s distinguished leadership

Empirically Evaluating Economic Policy in Real Time The Martin Feldstein Lecture 1 National Bureau of Economic Research July 10, 2009 John B. Taylor To honor Martin Feldstein s distinguished leadership

Paper Published in the February 2005 Journal of Business & Economic Research Why the Quantity of Money Still Matters

Paper Published in the February 5 Journal of Business & Economic Research Why the Quantity of Money Still Matters Michael Cosgrove, College of Business, University of Dallas Daniel Marsh, College of Business,

Paper Published in the February 5 Journal of Business & Economic Research Why the Quantity of Money Still Matters Michael Cosgrove, College of Business, University of Dallas Daniel Marsh, College of Business,

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer NOTES ON THE MIDTERM

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer NOTES ON THE MIDTERM Preface: This is not an answer sheet! Rather, each of the GSIs has written up some

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer NOTES ON THE MIDTERM Preface: This is not an answer sheet! Rather, each of the GSIs has written up some

Commentary: Challenges for Monetary Policy: New and Old

Commentary: Challenges for Monetary Policy: New and Old John B. Taylor Mervyn King s paper is jam-packed with interesting ideas and good common sense about monetary policy. I admire the clearly stated

Commentary: Challenges for Monetary Policy: New and Old John B. Taylor Mervyn King s paper is jam-packed with interesting ideas and good common sense about monetary policy. I admire the clearly stated

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

Intermediary Balance Sheets Tobias Adrian and Nina Boyarchenko, NY Fed Discussant: Annette Vissing-Jorgensen, UC Berkeley Objective: Construct a general equilibrium model with two types of intermediaries:

FINANCIAL SECTOR SHOCKS IN A CREDIT VIEW MODEL WORKING PAPER SERIES

WORKING PAPER NO. 2011 01 FINANCIAL SECTOR SHOCKS IN A CREDIT VIEW MODEL By Burton A. Abrams WORKING PAPER SERIES The views expressed in the Working Paper Series are those of the author(s) and do not necessarily

WORKING PAPER NO. 2011 01 FINANCIAL SECTOR SHOCKS IN A CREDIT VIEW MODEL By Burton A. Abrams WORKING PAPER SERIES The views expressed in the Working Paper Series are those of the author(s) and do not necessarily

NBER WORKING PAPER SERIES ARE GOVERNMENT SPENDING MULTIPLIERS GREATER DURING PERIODS OF SLACK? EVIDENCE FROM 20TH CENTURY HISTORICAL DATA

NBER WORKING PAPER SERIES ARE GOVERNMENT SPENDING MULTIPLIERS GREATER DURING PERIODS OF SLACK? EVIDENCE FROM 2TH CENTURY HISTORICAL DATA Michael T. Owyang Valerie A. Ramey Sarah Zubairy Working Paper 18769

NBER WORKING PAPER SERIES ARE GOVERNMENT SPENDING MULTIPLIERS GREATER DURING PERIODS OF SLACK? EVIDENCE FROM 2TH CENTURY HISTORICAL DATA Michael T. Owyang Valerie A. Ramey Sarah Zubairy Working Paper 18769

Working Paper Series Department of Economics Alfred Lerner College of Business & Economics University of Delaware

Working Paper Series Department of Economics Alfred Lerner College of Business & Economics University of Delaware Working Paper No. 2003-09 Do Fixed Exchange Rates Fetter Monetary Policy? A Credit View

Working Paper Series Department of Economics Alfred Lerner College of Business & Economics University of Delaware Working Paper No. 2003-09 Do Fixed Exchange Rates Fetter Monetary Policy? A Credit View

THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.)

") Chapter 12 THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of central banking and monetary

Chapter 12 THE FEDERAL RESERVE AND MONETARY POLICY Macroeconomics in Context (Goodwin, et al.) Chapter Overview In this chapter, you will be introduced to a standard treatment of central banking and monetary

Chapter 10: Classical Business Cycle Analysis: Market-Clearing Macroeconomics

Chapter 10: Classical Business Cycle Analysis: Market-Clearing Macroeconomics Cheng Chen SEF of HKU November 2, 2017 Chen, C. (SEF of HKU) ECON2102/2220: Intermediate Macroeconomics November 2, 2017 1

Chapter 10: Classical Business Cycle Analysis: Market-Clearing Macroeconomics Cheng Chen SEF of HKU November 2, 2017 Chen, C. (SEF of HKU) ECON2102/2220: Intermediate Macroeconomics November 2, 2017 1

NBER WORKING PAPER SERIES U.S. GROWTH IN THE DECADE AHEAD. Martin S. Feldstein. Working Paper

NBER WORKING PAPER SERIES U.S. GROWTH IN THE DECADE AHEAD Martin S. Feldstein Working Paper 15685 http://www.nber.org/papers/w15685 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

NBER WORKING PAPER SERIES U.S. GROWTH IN THE DECADE AHEAD Martin S. Feldstein Working Paper 15685 http://www.nber.org/papers/w15685 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

The role of asymmetric information on investments in emerging markets

The role of asymmetric information on investments in emerging markets W.A. de Wet Abstract This paper argues that, because of asymmetric information and adverse selection, forces other than fundamentals

The role of asymmetric information on investments in emerging markets W.A. de Wet Abstract This paper argues that, because of asymmetric information and adverse selection, forces other than fundamentals

Monetary Policy and Asset Price Volatility Ben Bernanke and Mark Gertler

Monetary Policy and Asset Price Volatility Ben Bernanke and Mark Gertler 1 Introduction Fom early 1980s, the inflation rates in most developed and emerging economies have been largely stable, while volatilities

Monetary Policy and Asset Price Volatility Ben Bernanke and Mark Gertler 1 Introduction Fom early 1980s, the inflation rates in most developed and emerging economies have been largely stable, while volatilities

Macroeconomic Policy during a Credit Crunch

ECONOMIC POLICY PAPER 15-2 FEBRUARY 2015 Macroeconomic Policy during a Credit Crunch EXECUTIVE SUMMARY Most economic models used by central banks prior to the recent financial crisis omitted two fundamental

ECONOMIC POLICY PAPER 15-2 FEBRUARY 2015 Macroeconomic Policy during a Credit Crunch EXECUTIVE SUMMARY Most economic models used by central banks prior to the recent financial crisis omitted two fundamental

The Stock Market Crash Really Did Cause the Great Recession

The Stock Market Crash Really Did Cause the Great Recession Roger E.A. Farmer Department of Economics, UCLA 23 Bunche Hall Box 91 Los Angeles CA 9009-1 rfarmer@econ.ucla.edu Phone: +1 3 2 Fax: +1 3 2 92

The Stock Market Crash Really Did Cause the Great Recession Roger E.A. Farmer Department of Economics, UCLA 23 Bunche Hall Box 91 Los Angeles CA 9009-1 rfarmer@econ.ucla.edu Phone: +1 3 2 Fax: +1 3 2 92

Macroeconomic Effects from Government Purchases and Taxes. Robert J. Barro and Charles J. Redlick Harvard University

Macroeconomic Effects from Government Purchases and Taxes Robert J. Barro and Charles J. Redlick Harvard University Empirical evidence on response of real GDP and other economic aggregates to added government

Macroeconomic Effects from Government Purchases and Taxes Robert J. Barro and Charles J. Redlick Harvard University Empirical evidence on response of real GDP and other economic aggregates to added government

The Gertler-Gilchrist Evidence on Small and Large Firm Sales

The Gertler-Gilchrist Evidence on Small and Large Firm Sales VV Chari, LJ Christiano and P Kehoe January 2, 27 In this note, we examine the findings of Gertler and Gilchrist, ( Monetary Policy, Business

The Gertler-Gilchrist Evidence on Small and Large Firm Sales VV Chari, LJ Christiano and P Kehoe January 2, 27 In this note, we examine the findings of Gertler and Gilchrist, ( Monetary Policy, Business

Monetary Theory and Policy. Fourth Edition. Carl E. Walsh. The MIT Press Cambridge, Massachusetts London, England

Monetary Theory and Policy Fourth Edition Carl E. Walsh The MIT Press Cambridge, Massachusetts London, England Contents Preface Introduction xiii xvii 1 Evidence on Money, Prices, and Output 1 1.1 Introduction

Monetary Theory and Policy Fourth Edition Carl E. Walsh The MIT Press Cambridge, Massachusetts London, England Contents Preface Introduction xiii xvii 1 Evidence on Money, Prices, and Output 1 1.1 Introduction

Lecture notes 10. Monetary policy: nominal anchor for the system

Kevin Clinton Winter 2005 Lecture notes 10 Monetary policy: nominal anchor for the system 1. Monetary stability objective Monetary policy was a 20 th century invention Wicksell, Fisher, Keynes advocated

Kevin Clinton Winter 2005 Lecture notes 10 Monetary policy: nominal anchor for the system 1. Monetary stability objective Monetary policy was a 20 th century invention Wicksell, Fisher, Keynes advocated

Chapter 2. Literature Review

Chapter 2 Literature Review There is a wide agreement that monetary policy is a tool in promoting economic growth and stabilizing inflation. However, there is less agreement about how monetary policy exactly

Chapter 2 Literature Review There is a wide agreement that monetary policy is a tool in promoting economic growth and stabilizing inflation. However, there is less agreement about how monetary policy exactly

Bachelor Thesis Finance

Bachelor Thesis Finance What is the influence of the FED and ECB announcements in recent years on the eurodollar exchange rate and does the state of the economy affect this influence? Lieke van der Horst

Bachelor Thesis Finance What is the influence of the FED and ECB announcements in recent years on the eurodollar exchange rate and does the state of the economy affect this influence? Lieke van der Horst

The Great Depression: An Overview by David C. Wheelock

The Great Depression: An Overview by David C. Wheelock Why should students learn about the Great Depression? Our grandparents and great-grandparents lived through these tough times, but you may think that

The Great Depression: An Overview by David C. Wheelock Why should students learn about the Great Depression? Our grandparents and great-grandparents lived through these tough times, but you may think that

The Great Recession How Bad Is It and What Can We Do?

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

The Great Recession How Bad Is It and What Can We Do? Helen Roberts Clinical Associate Professor in Economics, Associate Director University of Illinois at Chicago Center for Economic Education Recession

MA Advanced Macroeconomics 3. Examples of VAR Studies

MA Advanced Macroeconomics 3. Examples of VAR Studies Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) VAR Studies Spring 2016 1 / 23 Examples of VAR Studies We will look at four different

MA Advanced Macroeconomics 3. Examples of VAR Studies Karl Whelan School of Economics, UCD Spring 2016 Karl Whelan (UCD) VAR Studies Spring 2016 1 / 23 Examples of VAR Studies We will look at four different

Monetary Economics. The Quantity Theory of Money. Seyed Ali Madanizadeh. February Sharif University of Technology

Monetary Economics The Quantity Theory of Money Seyed Ali Madanizadeh Sharif University of Technology February 2014 Quantity Theory of Money Equation of Exchange M t V t = P t y t where M t is the stock

Monetary Economics The Quantity Theory of Money Seyed Ali Madanizadeh Sharif University of Technology February 2014 Quantity Theory of Money Equation of Exchange M t V t = P t y t where M t is the stock

FRBSF ECONOMIC LETTER

FRBSF ECONOMIC LETTER 211-15 May 16, 211 What Is the Value of Bank Output? BY TITAN ALON, JOHN FERNALD, ROBERT INKLAAR, AND J. CHRISTINA WANG Financial institutions often do not charge explicit fees for

FRBSF ECONOMIC LETTER 211-15 May 16, 211 What Is the Value of Bank Output? BY TITAN ALON, JOHN FERNALD, ROBERT INKLAAR, AND J. CHRISTINA WANG Financial institutions often do not charge explicit fees for

Chapter 26 Transmission Mechanisms of Monetary Policy: The Evidence

Chapter 26 Transmission Mechanisms of Monetary Policy: The Evidence Multiple Choice 1) Evidence that examines whether one variable has an effect on another by simply looking directly at the relationship

Chapter 26 Transmission Mechanisms of Monetary Policy: The Evidence Multiple Choice 1) Evidence that examines whether one variable has an effect on another by simply looking directly at the relationship

THE FED AND THE NEW ECONOMY

THE FED AND THE NEW ECONOMY Laurence Ball and Robert R. Tchaidze December 2001 Abstract This paper seeks to understand the behavior of Greenspan s Federal Reserve in the late 1990s. Some authors suggest

THE FED AND THE NEW ECONOMY Laurence Ball and Robert R. Tchaidze December 2001 Abstract This paper seeks to understand the behavior of Greenspan s Federal Reserve in the late 1990s. Some authors suggest

DEMAND FOR MONEY. Ch. 9 (Ch.19 in the text) ECON248: Money and Banking Ch.9 Dr. Mohammed Alwosabi

ECON248: Money and Banking Ch.9 Dr. Mohammed Alwosabi") Ch. 9 (Ch.19 in the text) DEMAND FOR MONEY Individuals allocate their wealth between different kinds of assets such as a building, income earning securities, a checking account, and cash. Money is what

Ch. 9 (Ch.19 in the text) DEMAND FOR MONEY Individuals allocate their wealth between different kinds of assets such as a building, income earning securities, a checking account, and cash. Money is what

Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison

DEPARTMENT OF ECONOMICS JOHANNES KEPLER UNIVERSITY LINZ Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison by Burkhard Raunig and Johann Scharler* Working Paper

DEPARTMENT OF ECONOMICS JOHANNES KEPLER UNIVERSITY LINZ Money Market Uncertainty and Retail Interest Rate Fluctuations: A Cross-Country Comparison by Burkhard Raunig and Johann Scharler* Working Paper

NBER WORKING PAPER SERIES A BRAZILIAN DEBT-CRISIS MODEL. Assaf Razin Efraim Sadka. Working Paper

NBER WORKING PAPER SERIES A BRAZILIAN DEBT-CRISIS MODEL Assaf Razin Efraim Sadka Working Paper 9211 http://www.nber.org/papers/w9211 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

NBER WORKING PAPER SERIES A BRAZILIAN DEBT-CRISIS MODEL Assaf Razin Efraim Sadka Working Paper 9211 http://www.nber.org/papers/w9211 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge,

Module 31. Monetary Policy and the Interest Rate. What you will learn in this Module:

Module 31 Monetary Policy and the Interest Rate What you will learn in this Module: How the Federal Reserve implements monetary policy, moving the interest to affect aggregate output Why monetary policy

Module 31 Monetary Policy and the Interest Rate What you will learn in this Module: How the Federal Reserve implements monetary policy, moving the interest to affect aggregate output Why monetary policy

Comment. John Kennan, University of Wisconsin and NBER

Comment John Kennan, University of Wisconsin and NBER The main theme of Robert Hall s paper is that cyclical fluctuations in unemployment are driven almost entirely by fluctuations in the jobfinding rate,

Comment John Kennan, University of Wisconsin and NBER The main theme of Robert Hall s paper is that cyclical fluctuations in unemployment are driven almost entirely by fluctuations in the jobfinding rate,

Márcio G. P. Garcia PUC-Rio Brazil Visiting Scholar, Sloan School, MIT and NBER. This paper aims at quantitatively evaluating two questions:

Discussion of Unconventional Monetary Policy and the Great Recession: Estimating the Macroeconomic Effects of a Spread Compression at the Zero Lower Bound Márcio G. P. Garcia PUC-Rio Brazil Visiting Scholar,

Discussion of Unconventional Monetary Policy and the Great Recession: Estimating the Macroeconomic Effects of a Spread Compression at the Zero Lower Bound Márcio G. P. Garcia PUC-Rio Brazil Visiting Scholar,

An Estimate of the Effect of Currency Unions on Trade and Growth* First draft May 1; revised June 6, 2000

An Estimate of the Effect of Currency Unions on Trade and Growth* First draft May 1; revised June 6, 2000 Jeffrey A. Frankel Kennedy School of Government Harvard University, 79 JFK Street Cambridge MA

An Estimate of the Effect of Currency Unions on Trade and Growth* First draft May 1; revised June 6, 2000 Jeffrey A. Frankel Kennedy School of Government Harvard University, 79 JFK Street Cambridge MA

Review of. Financial Crises, Liquidity, and the International Monetary System by Jean Tirole. Published by Princeton University Press in 2002

Review of Financial Crises, Liquidity, and the International Monetary System by Jean Tirole Published by Princeton University Press in 2002 Reviewer: Franklin Allen, Finance Department, Wharton School,

Review of Financial Crises, Liquidity, and the International Monetary System by Jean Tirole Published by Princeton University Press in 2002 Reviewer: Franklin Allen, Finance Department, Wharton School,

Sample Exam 1: QEII Labor Market Rescue?

Sample Exam 1: QEII Labor Market Rescue? It seems the people who most need an economic recovery are the last to benefit. Currently the U.S. is experiencing a slow recovery, and like the last two, a jobless

Sample Exam 1: QEII Labor Market Rescue? It seems the people who most need an economic recovery are the last to benefit. Currently the U.S. is experiencing a slow recovery, and like the last two, a jobless

Long Run Money Neutrality: The Case of Guatemala

Long Run Money Neutrality: The Case of Guatemala Frederick H. Wallace Department of Management and Marketing College of Business Prairie View A&M University P.O. Box 638 Prairie View, Texas 77446-0638

Long Run Money Neutrality: The Case of Guatemala Frederick H. Wallace Department of Management and Marketing College of Business Prairie View A&M University P.O. Box 638 Prairie View, Texas 77446-0638

ECON 1000 Contemporary Economic Issues (Spring 2018) The Stabilization Function of Government

The Stabilization Function of Government") ECON 1000 Contemporary Economic Issues (Spring 2018) The Stabilization Function of Government Relevant Readings from the Required Textbooks: Chapter 7, Gross Domestic Product and Economic Growth Chapter

ECON 1000 Contemporary Economic Issues (Spring 2018) The Stabilization Function of Government Relevant Readings from the Required Textbooks: Chapter 7, Gross Domestic Product and Economic Growth Chapter

Volume Author/Editor: Kenneth Singleton, editor. Volume URL:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Japanese Monetary Policy Volume Author/Editor: Kenneth Singleton, editor Volume Publisher:

This PDF is a selection from an out-of-print volume from the National Bureau of Economic Research Volume Title: Japanese Monetary Policy Volume Author/Editor: Kenneth Singleton, editor Volume Publisher:

Revisionist History: How Data Revisions Distort Economic Policy Research

Federal Reserve Bank of Minneapolis Quarterly Review Vol., No., Fall 998, pp. 3 Revisionist History: How Data Revisions Distort Economic Policy Research David E. Runkle Research Officer Research Department

Federal Reserve Bank of Minneapolis Quarterly Review Vol., No., Fall 998, pp. 3 Revisionist History: How Data Revisions Distort Economic Policy Research David E. Runkle Research Officer Research Department

Discussion. Benoît Carmichael

Discussion Benoît Carmichael The two studies presented in the first session of the conference take quite different approaches to the question of price indexes. On the one hand, Coulombe s study develops

Discussion Benoît Carmichael The two studies presented in the first session of the conference take quite different approaches to the question of price indexes. On the one hand, Coulombe s study develops

Can the Fed Predict the State of the Economy?

Can the Fed Predict the State of the Economy? Tara M. Sinclair Department of Economics George Washington University Washington DC 252 tsinc@gwu.edu Fred Joutz Department of Economics George Washington

Can the Fed Predict the State of the Economy? Tara M. Sinclair Department of Economics George Washington University Washington DC 252 tsinc@gwu.edu Fred Joutz Department of Economics George Washington

Part III. Cycles and Growth:

Part III. Cycles and Growth: UMSL Max Gillman Max Gillman () AS-AD 1 / 56 AS-AD, Relative Prices & Business Cycles Facts: Nominal Prices are Not Real Prices Price of goods in nominal terms: eg. Consumer

Part III. Cycles and Growth: UMSL Max Gillman Max Gillman () AS-AD 1 / 56 AS-AD, Relative Prices & Business Cycles Facts: Nominal Prices are Not Real Prices Price of goods in nominal terms: eg. Consumer

Financial Crises and the Great Recession

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

Financial Crises and the Great Recession ECON 30020: Intermediate Macroeconomics Prof. Eric Sims University of Notre Dame Spring 2018 1 / 40 Readings GLS Ch. 33 2 / 40 Financial Crises Financial crises

Econ 102 Final Exam Name ID Section Number

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

Econ 102 Final Exam Name ID Section Number 1. Assume that the economy is contracting and unemployment is rising. Which of the following would be a logical explanation for a sudden fall in the unemployment

Comments on Jeffrey Frankel, Commodity Prices and Monetary Policy by Lars Svensson

Comments on Jeffrey Frankel, Commodity Prices and Monetary Policy by Lars Svensson www.princeton.edu/svensson/ This paper makes two main points. The first point is empirical: Commodity prices are decreasing

Comments on Jeffrey Frankel, Commodity Prices and Monetary Policy by Lars Svensson www.princeton.edu/svensson/ This paper makes two main points. The first point is empirical: Commodity prices are decreasing

ECS 3701 Monetary Economics

ECS 3701 Monetary Economics Boston UNISA 2015 26: Transmission Mechanisms of Monetary Policy Errol Goetsch 078 573 5046 errol@xe4.org Lorraine 082 770 4569 lg@xe4.org www.facebook.com/groups/ecs3701 Page

ECS 3701 Monetary Economics Boston UNISA 2015 26: Transmission Mechanisms of Monetary Policy Errol Goetsch 078 573 5046 errol@xe4.org Lorraine 082 770 4569 lg@xe4.org www.facebook.com/groups/ecs3701 Page

Macro theory: A quick review

Sapienza University of Rome Department of economics and law Advanced Monetary Theory and Policy EPOS 2013/14 Macro theory: A quick review Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma1.it Theory:

Sapienza University of Rome Department of economics and law Advanced Monetary Theory and Policy EPOS 2013/14 Macro theory: A quick review Giovanni Di Bartolomeo giovanni.dibartolomeo@uniroma1.it Theory:

VII. Short-Run Economic Fluctuations

Macroeconomic Theory Lecture Notes VII. Short-Run Economic Fluctuations University of Miami December 1, 2017 1 Outline Business Cycle Facts IS-LM Model AD-AS Model 2 Outline Business Cycle Facts IS-LM

Macroeconomic Theory Lecture Notes VII. Short-Run Economic Fluctuations University of Miami December 1, 2017 1 Outline Business Cycle Facts IS-LM Model AD-AS Model 2 Outline Business Cycle Facts IS-LM

Estimating the Impact of Changes in the Federal Funds Target Rate on Market Interest Rates from the 1980s to the Present Day

Estimating the Impact of Changes in the Federal Funds Target Rate on Market Interest Rates from the 1980s to the Present Day Donal O Cofaigh Senior Sophister In this paper, Donal O Cofaigh quantifies the

Estimating the Impact of Changes in the Federal Funds Target Rate on Market Interest Rates from the 1980s to the Present Day Donal O Cofaigh Senior Sophister In this paper, Donal O Cofaigh quantifies the

Choose the one alternative that best completes the statement or answers the question.

Econ 330 Spring 2017: EXAM 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If market participants notice that a variable

Econ 330 Spring 2017: EXAM 1 Name ID Section Number MULTIPLE CHOICE. Choose the one alternative that best completes the statement or answers the question. 1) If market participants notice that a variable

Opening Remarks. Alan Greenspan

Opening Remarks Alan Greenspan Uncertainty is not just an important feature of the monetary policy landscape; it is the defining characteristic of that landscape. As a consequence, the conduct of monetary

Opening Remarks Alan Greenspan Uncertainty is not just an important feature of the monetary policy landscape; it is the defining characteristic of that landscape. As a consequence, the conduct of monetary

EMPIRICAL ASSESSMENT OF THE PHILLIPS CURVE

EMPIRICAL ASSESSMENT OF THE PHILLIPS CURVE Emi Nakamura Jón Steinsson Columbia University January 2018 Nakamura-Steinsson (Columbia) Phillips Curve January 2018 1 / 55 BRIEF HISTORY OF THE PHILLIPS CURVE

EMPIRICAL ASSESSMENT OF THE PHILLIPS CURVE Emi Nakamura Jón Steinsson Columbia University January 2018 Nakamura-Steinsson (Columbia) Phillips Curve January 2018 1 / 55 BRIEF HISTORY OF THE PHILLIPS CURVE

Why Money Matters: A Fourth Natural Experiment

Why Money Matters: A Fourth Natural Experiment James R. Lothian* February 15, 2010 Abstract: Milton Friedman (2005,2006) compared the behavior of money supply, nominal income and stock prices in the United

Why Money Matters: A Fourth Natural Experiment James R. Lothian* February 15, 2010 Abstract: Milton Friedman (2005,2006) compared the behavior of money supply, nominal income and stock prices in the United

ECON Intermediate Macroeconomic Theory

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

ECON 3510 - Intermediate Macroeconomic Theory Fall 2015 Mankiw, Macroeconomics, 8th ed., Chapter 12 Chapter 12: Aggregate Demand 2: Applying the IS-LM Model Key points: Policy in the IS LM model: Monetary

Boston Library Consortium IVIember Libraries

Digitized by the Internet Archive in 2011 with funding from Boston Library Consortium IVIember Libraries http://www.archive.org/details/speculativedynam00cutl2 working paper department of economics SPECULATIVE

Digitized by the Internet Archive in 2011 with funding from Boston Library Consortium IVIember Libraries http://www.archive.org/details/speculativedynam00cutl2 working paper department of economics SPECULATIVE

Macroeconomics: Principles, Applications, and Tools

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 14 The Federal Reserve and Monetary Policy Learning Objectives 14.1 Explain the role of demand and supply in the money market.

Macroeconomics: Principles, Applications, and Tools NINTH EDITION Chapter 14 The Federal Reserve and Monetary Policy Learning Objectives 14.1 Explain the role of demand and supply in the money market.

Prediction errors in credit loss forecasting models based on macroeconomic data

Prediction errors in credit loss forecasting models based on macroeconomic data Eric McVittie Experian Decision Analytics Credit Scoring & Credit Control XIII August 2013 University of Edinburgh Business

Prediction errors in credit loss forecasting models based on macroeconomic data Eric McVittie Experian Decision Analytics Credit Scoring & Credit Control XIII August 2013 University of Edinburgh Business

Solutions to PSet 5. October 6, More on the AS/AD Model

Solutions to PSet 5 October 6, 207 More on the AS/AD Model. If there is a zero interest rate lower bound, is fiscal policy more or less effective than otherwise? Explain using the AS/AD model. Is the United

Solutions to PSet 5 October 6, 207 More on the AS/AD Model. If there is a zero interest rate lower bound, is fiscal policy more or less effective than otherwise? Explain using the AS/AD model. Is the United

NBER WORKING PAPER SERIES ON QUALITY BIAS AND INFLATION TARGETS. Stephanie Schmitt-Grohe Martin Uribe

NBER WORKING PAPER SERIES ON QUALITY BIAS AND INFLATION TARGETS Stephanie Schmitt-Grohe Martin Uribe Working Paper 1555 http://www.nber.org/papers/w1555 NATIONAL BUREAU OF ECONOMIC RESEARCH 15 Massachusetts

NBER WORKING PAPER SERIES ON QUALITY BIAS AND INFLATION TARGETS Stephanie Schmitt-Grohe Martin Uribe Working Paper 1555 http://www.nber.org/papers/w1555 NATIONAL BUREAU OF ECONOMIC RESEARCH 15 Massachusetts

Bubbles, Liquidity and the Macroeconomy

Bubbles, Liquidity and the Macroeconomy Markus K. Brunnermeier The recent financial crisis has shown that financial frictions such as asset bubbles and liquidity spirals have important consequences not

Bubbles, Liquidity and the Macroeconomy Markus K. Brunnermeier The recent financial crisis has shown that financial frictions such as asset bubbles and liquidity spirals have important consequences not

CAN MONEY SUPPLY PREDICT STOCK PRICES?

54 JOURNAL FOR ECONOMIC EDUCATORS, 8(2), FALL 2008 CAN MONEY SUPPLY PREDICT STOCK PRICES? Sara Alatiqi and Shokoofeh Fazel 1 ABSTRACT A positive causal relation from money supply to stock prices is frequently

54 JOURNAL FOR ECONOMIC EDUCATORS, 8(2), FALL 2008 CAN MONEY SUPPLY PREDICT STOCK PRICES? Sara Alatiqi and Shokoofeh Fazel 1 ABSTRACT A positive causal relation from money supply to stock prices is frequently

Inflation Targeting and Inflation Prospects in Canada

Inflation Targeting and Inflation Prospects in Canada CPP Interdisciplinary Seminar March 2006 Don Coletti Research Director International Department Bank of Canada Overview Objective: answer questions

Inflation Targeting and Inflation Prospects in Canada CPP Interdisciplinary Seminar March 2006 Don Coletti Research Director International Department Bank of Canada Overview Objective: answer questions

Box 1.3. How Does Uncertainty Affect Economic Performance?

Box 1.3. How Does Affect Economic Performance? Bouts of elevated uncertainty have been one of the defining features of the sluggish recovery from the global financial crisis. In recent quarters, high uncertainty

Box 1.3. How Does Affect Economic Performance? Bouts of elevated uncertainty have been one of the defining features of the sluggish recovery from the global financial crisis. In recent quarters, high uncertainty

Did Wages Reflect Growth in Productivity?

Did Wages Reflect Growth in Productivity? The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters. Citation Published Version Accessed

Did Wages Reflect Growth in Productivity? The Harvard community has made this article openly available. Please share how this access benefits you. Your story matters. Citation Published Version Accessed

Toward a New Global Recession? Economic Perspectives for 2016 and Beyond

Field Notes February 3rd, 2016 Toward a New Global Recession? Economic Perspectives for 2016 and Beyond by Jose A. Tapia FOR SWPM, DH, AS, DF, GD & DL What economists call macroeconomic variables are numbers

Field Notes February 3rd, 2016 Toward a New Global Recession? Economic Perspectives for 2016 and Beyond by Jose A. Tapia FOR SWPM, DH, AS, DF, GD & DL What economists call macroeconomic variables are numbers

NBER WORKING PAPER SERIES LIQUIDITY RISK AND SYNDICATE STRUCTURE. Evan Gatev Philip Strahan. Working Paper

NBER WORKING PAPER SERIES LIQUIDITY RISK AND SYNDICATE STRUCTURE Evan Gatev Philip Strahan Working Paper 13802 http://www.nber.org/papers/w13802 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

NBER WORKING PAPER SERIES LIQUIDITY RISK AND SYNDICATE STRUCTURE Evan Gatev Philip Strahan Working Paper 13802 http://www.nber.org/papers/w13802 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts

THE RELATIONSHIP BETWEEN MONEY AND EXPENDITURE IN 1982

THE RELATIONSHIP BETWEEN MONEY AND EXPENDITURE IN 1982 Robert L. Hetzel Introduction The behavior of the money supply and the relationship between the money supply and the public s expenditure have recently

THE RELATIONSHIP BETWEEN MONEY AND EXPENDITURE IN 1982 Robert L. Hetzel Introduction The behavior of the money supply and the relationship between the money supply and the public s expenditure have recently

MONEY SUPPLY ANNOUNCEMENTS AND STOCK PRICES: THE UK EVIDENCE

«ΣΠΟΥΔΑΙ», Τόμος 41, Τεύχος 4ο, Πανεπιστήμιο Πειραιώς / «SPOUDAI», Vol. 41, No 4, University of Piraeus MONEY SUPPLY ANNOUNCEMENTS AND STOCK PRICES: THE UK EVIDENCE By N. P. Tessaromatis P. E. Triantafillou

«ΣΠΟΥΔΑΙ», Τόμος 41, Τεύχος 4ο, Πανεπιστήμιο Πειραιώς / «SPOUDAI», Vol. 41, No 4, University of Piraeus MONEY SUPPLY ANNOUNCEMENTS AND STOCK PRICES: THE UK EVIDENCE By N. P. Tessaromatis P. E. Triantafillou

The Global Financial Crisis

The Global Financial Crisis Franklin Allen Wharton School University of Pennsylvania April 27, 2009 What caused the crisis? The conventional wisdom is that the basic cause of the crisis was bad incentives

The Global Financial Crisis Franklin Allen Wharton School University of Pennsylvania April 27, 2009 What caused the crisis? The conventional wisdom is that the basic cause of the crisis was bad incentives

deposit insurance Financial intermediaries, banks, and bank runs

deposit insurance The purpose of deposit insurance is to ensure financial stability, as well as protect the interests of small investors. But with government guarantees in hand, bankers take excessive

deposit insurance The purpose of deposit insurance is to ensure financial stability, as well as protect the interests of small investors. But with government guarantees in hand, bankers take excessive

Monetary Policy and EMU Introduction Why Study Money and Monetary Policy?

Monetary Policy and EMU Introduction Why Study Money and Monetary Policy? Evidence suggests that money plays an important role in generating business cycles Recessions and expansions affect all of us Monetary

Monetary Policy and EMU Introduction Why Study Money and Monetary Policy? Evidence suggests that money plays an important role in generating business cycles Recessions and expansions affect all of us Monetary

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9 THE CONDUCT OF POSTWAR MONETARY POLICY FEBRUARY 14, 2018 I. OVERVIEW A. Where we have been B.

UNIVERSITY OF CALIFORNIA Economics 134 DEPARTMENT OF ECONOMICS Spring 2018 Professor David Romer LECTURE 9 THE CONDUCT OF POSTWAR MONETARY POLICY FEBRUARY 14, 2018 I. OVERVIEW A. Where we have been B.

ECONOMIC GROWTH 1. THE ACCUMULATION OF CAPITAL

ECON 3560/5040 ECONOMIC GROWTH - Understand what causes differences in income over time and across countries - Sources of economy s output: factors of production (K, L) and production technology differences

ECON 3560/5040 ECONOMIC GROWTH - Understand what causes differences in income over time and across countries - Sources of economy s output: factors of production (K, L) and production technology differences

Economic Brief. How Might the Fed s Large-Scale Asset Purchases Lower Long-Term Interest Rates?

Economic Brief January, EB- How Might the Fed s Large-Scale Asset Purchases Lower Long-Term Interest Rates? By Renee Courtois Haltom and Juan Carlos Hatchondo Over the past two years the Federal Reserve

Economic Brief January, EB- How Might the Fed s Large-Scale Asset Purchases Lower Long-Term Interest Rates? By Renee Courtois Haltom and Juan Carlos Hatchondo Over the past two years the Federal Reserve

Test of the bank lending channel: The case of Hungary

Theoretical and Applied Economics Volume XXI (2014), No. 1(590), pp. 115-120 Test of the bank lending channel: The case of Hungary Yu HSING Southeastern Louisiana University yhsing@selu.edu Abstract. This

Theoretical and Applied Economics Volume XXI (2014), No. 1(590), pp. 115-120 Test of the bank lending channel: The case of Hungary Yu HSING Southeastern Louisiana University yhsing@selu.edu Abstract. This

Economic Fundamentals

CHAPTER 5 Economic Fundamentals INTRODUCTION Economics, put simply, is the study of shortages supply vs. demand. As the demand for a product or service rises, the price of those goods or services will

CHAPTER 5 Economic Fundamentals INTRODUCTION Economics, put simply, is the study of shortages supply vs. demand. As the demand for a product or service rises, the price of those goods or services will

Introduction. Learning Objectives. Chapter 17. Stabilization in an Integrated World Economy

Chapter 17 Stabilization in an Integrated World Economy Introduction For more than 50 years, many economists have used an inverse relationship involving the unemployment rate and real GDP as a guide to

Chapter 17 Stabilization in an Integrated World Economy Introduction For more than 50 years, many economists have used an inverse relationship involving the unemployment rate and real GDP as a guide to

causing the crisis and what lessons can be drawn for its future conduct?

Did monetary policy play a role in causing the crisis and what lessons can be drawn for its future conduct? Remarks prepared by Charles (Chuck) Freedman for the panel discussion at the conference on Economic

Did monetary policy play a role in causing the crisis and what lessons can be drawn for its future conduct? Remarks prepared by Charles (Chuck) Freedman for the panel discussion at the conference on Economic

The Velocity of Money and Nominal Interest Rates: Evidence from Developed and Latin-American Countries

The Velocity of Money and Nominal Interest Rates: Evidence from Developed and Latin-American Countries Petr Duczynski Abstract This study examines the behavior of the velocity of money in developed and

The Velocity of Money and Nominal Interest Rates: Evidence from Developed and Latin-American Countries Petr Duczynski Abstract This study examines the behavior of the velocity of money in developed and

Is monetary policy in New Zealand similar to

Is monetary policy in New Zealand similar to that in Australia and the United States? Angela Huang, Economics Department 1 Introduction Monetary policy in New Zealand is often compared with monetary policy

Is monetary policy in New Zealand similar to that in Australia and the United States? Angela Huang, Economics Department 1 Introduction Monetary policy in New Zealand is often compared with monetary policy

The trade balance and fiscal policy in the OECD

European Economic Review 42 (1998) 887 895 The trade balance and fiscal policy in the OECD Philip R. Lane *, Roberto Perotti Economics Department, Trinity College Dublin, Dublin 2, Ireland Columbia University,

European Economic Review 42 (1998) 887 895 The trade balance and fiscal policy in the OECD Philip R. Lane *, Roberto Perotti Economics Department, Trinity College Dublin, Dublin 2, Ireland Columbia University,

Test Questions. Part I Midterm Questions 1. Give three examples of a stock variable and three examples of a flow variable.

Test Questions Part I Midterm Questions 1. Give three examples of a stock variable and three examples of a flow variable. 2. True or False: A Laspeyres price index always overstates the rate of inflation.

Test Questions Part I Midterm Questions 1. Give three examples of a stock variable and three examples of a flow variable. 2. True or False: A Laspeyres price index always overstates the rate of inflation.

The Taylor Rule: A benchmark for monetary policy?

Page 1 of 9 «Previous Next» Ben S. Bernanke April 28, 2015 11:00am The Taylor Rule: A benchmark for monetary policy? Stanford economist John Taylor's many contributions to monetary economics include his

Page 1 of 9 «Previous Next» Ben S. Bernanke April 28, 2015 11:00am The Taylor Rule: A benchmark for monetary policy? Stanford economist John Taylor's many contributions to monetary economics include his

1. Under what condition will the nominal interest rate be equal to the real interest rate?

Practice Problems III EC 102.03 Questions 1. Under what condition will the nominal interest rate be equal to the real interest rate? Real interest rate, or r, is equal to i π where i is the nominal interest

Practice Problems III EC 102.03 Questions 1. Under what condition will the nominal interest rate be equal to the real interest rate? Real interest rate, or r, is equal to i π where i is the nominal interest

Inflation Persistence and Relative Contracting

[Forthcoming, American Economic Review] Inflation Persistence and Relative Contracting by Steinar Holden Department of Economics University of Oslo Box 1095 Blindern, 0317 Oslo, Norway email: steinar.holden@econ.uio.no

[Forthcoming, American Economic Review] Inflation Persistence and Relative Contracting by Steinar Holden Department of Economics University of Oslo Box 1095 Blindern, 0317 Oslo, Norway email: steinar.holden@econ.uio.no

The Lack of an Empirical Rationale for a Revival of Discretionary Fiscal Policy. John B. Taylor Stanford University

The Lack of an Empirical Rationale for a Revival of Discretionary Fiscal Policy John B. Taylor Stanford University Prepared for the Annual Meeting of the American Economic Association Session The Revival

The Lack of an Empirical Rationale for a Revival of Discretionary Fiscal Policy John B. Taylor Stanford University Prepared for the Annual Meeting of the American Economic Association Session The Revival

ECONOMIC COMMENTARY. Unemployment after the Recession: A New Natural Rate? Murat Tasci and Saeed Zaman

ECONOMIC COMMENTARY Number 0-11 September 8, 0 Unemployment after the Recession: A New Natural Rate? Murat Tasci and Saeed Zaman The past recession has hit the labor market especially hard, and economists

ECONOMIC COMMENTARY Number 0-11 September 8, 0 Unemployment after the Recession: A New Natural Rate? Murat Tasci and Saeed Zaman The past recession has hit the labor market especially hard, and economists

Banking Crises and Real Activity: Identifying the Linkages

Banking Crises and Real Activity: Identifying the Linkages Mark Gertler New York University I interpret some key aspects of the recent crisis through the lens of macroeconomic modeling of financial factors.

Banking Crises and Real Activity: Identifying the Linkages Mark Gertler New York University I interpret some key aspects of the recent crisis through the lens of macroeconomic modeling of financial factors.

Inflation Uncertainty, Investment Spending, and Fiscal Policy

Inflation Uncertainty, Investment Spending, and Fiscal Policy by Stephen L. Able Business investment for new plant and equipment accounts for about 10 per cent of current economic activity, as measured

Inflation Uncertainty, Investment Spending, and Fiscal Policy by Stephen L. Able Business investment for new plant and equipment accounts for about 10 per cent of current economic activity, as measured

EC202 Macroeconomics

EC202 Macroeconomics Koç University, Summer 2014 by Arhan Ertan Study Questions - 3 1. Suppose a government is able to permanently reduce its budget deficit. Use the Solow growth model of Chapter 9 to

EC202 Macroeconomics Koç University, Summer 2014 by Arhan Ertan Study Questions - 3 1. Suppose a government is able to permanently reduce its budget deficit. Use the Solow growth model of Chapter 9 to

Characteristics of the euro area business cycle in the 1990s

Characteristics of the euro area business cycle in the 1990s As part of its monetary policy strategy, the ECB regularly monitors the development of a wide range of indicators and assesses their implications

Characteristics of the euro area business cycle in the 1990s As part of its monetary policy strategy, the ECB regularly monitors the development of a wide range of indicators and assesses their implications

Principles of Macroeconomics. Twelfth Edition. Chapter 13. The Labor Market in the Macroeconomy. Copyright 2017 Pearson Education, Inc.

Principles of Macroeconomics Twelfth Edition Chapter 13 The Labor Market in the Macroeconomy Copyright 2017 Pearson Education, Inc. 13-1 Copyright Copyright 2017 Pearson Education, Inc. 13-2 Chapter Outline

Principles of Macroeconomics Twelfth Edition Chapter 13 The Labor Market in the Macroeconomy Copyright 2017 Pearson Education, Inc. 13-1 Copyright Copyright 2017 Pearson Education, Inc. 13-2 Chapter Outline

1 The empirical relationship and its demise (?)

") BURNABY SIMON FRASER UNIVERSITY BRITISH COLUMBIA Paul Klein Office: WMC 3635 Phone: (778) 782-9391 Email: paul klein 2@sfu.ca URL: http://paulklein.ca/newsite/teaching/305.php Economics 305 Intermediate

BURNABY SIMON FRASER UNIVERSITY BRITISH COLUMBIA Paul Klein Office: WMC 3635 Phone: (778) 782-9391 Email: paul klein 2@sfu.ca URL: http://paulklein.ca/newsite/teaching/305.php Economics 305 Intermediate

19.2 Exchange Rates in the Long Run Introduction 1/24/2013. Exchange Rates and International Finance. The Nominal Exchange Rate

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Chapter 19 Exchange Rates and International Finance By Charles I. Jones International trade of goods and services exceeds 20 percent of GDP in most countries. Media Slides Created By Dave Brown Penn State

Archimedean Upper Conservatory Economics, November 2016 Quiz, Unit VI, Stabilization Policies

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The federal budget tends to move toward _ as the economy. A. deficit; contracts B. deficit; expands C.

Multiple Choice Identify the choice that best completes the statement or answers the question. 1. The federal budget tends to move toward _ as the economy. A. deficit; contracts B. deficit; expands C.

Chapter 10. Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics. Chapter Preview

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

Chapter 10 Conduct of Monetary Policy: Tools, Goals, Strategy, and Tactics Chapter Preview Monetary policy refers to the management of the money supply. The theories guiding the Federal Reserve are complex

Productivity, monetary policy and financial indicators

Productivity, monetary policy and financial indicators Arturo Estrella Introduction Labour productivity is widely thought to be informative with regard to inflation and it therefore comes up frequently

Productivity, monetary policy and financial indicators Arturo Estrella Introduction Labour productivity is widely thought to be informative with regard to inflation and it therefore comes up frequently