Chapter 16. Distributions Treated As Section 751(b) Exchanges. Receipt of Excess Cold Assets. Example Receipt of Excess Hot Assets

|

|

|

- Alaina Randall

- 5 years ago

- Views:

Transcription

If Excess Hot Assets Are Distributed: then the partnership is treated as if it made a hypothetical distribution of the partner's proportionate share of Cold assets")

1 Chapter 16 Distributions Treated As Section 751(b) Exchanges Receipt of Excess Cold Assets 1)If Excess Cold Assets Are Distributed: then the partnership is treated as if it made a hypothetical distribution of the partner's proportionate share of Hot assets followed by a fictional sale of these Hot assets by the partner back to the partnership at fair market value in exchange for the excess Cold assets actually received in the distribution. 2 Receipt of Excess Hot Assets 2) If Excess Hot Assets Are Distributed: then the partnership is treated as if it made a hypothetical distribution of the partner's proportionate share of Cold assets followed by a fictional sale of these Cold assets by the partner back to the partnership at fair market value in exchange for the excess Hot assets actually received in the distribution. 3 Example

2 Example 16-1 Jack and Jill Liquidate JJ Partnership Assets Tax Basis FMV Cash To Jack $100, ,000 Accts. Rec. To Jill $0 100,000 Inventory To Jill $40, ,000 Land To Jack $60,000 $100,000 Totals $200,000 $400,000 5 Example Four Steps Step One: Determine the Deemed Distribution a current distribution. Step Two: The Deemed Exchange by the Distributee Partner 7 Step Three: The Deemed Exchange by the Partnership Step Four: The Remaining Proportionate Distribution (current or liquidating). 8

3 Example Example Example Example

4 Example 16-3 Not a Service Partnership 16-6 ABC Partnership ABC Partnership January 1, 2005 Partner's Cash $ 26,000 $ 26,000 Basis Accounts Receivable $ - $ 26,000 Total Assets $ 26,000 $ 52,000 Agnes (50%) $ 13,000 $ 26,000 $ 13,000 Bob (25%) $ 6,500 $ 13,000 $ 6,500 Cao (25%) $ 6,500 $ 13,000 $ 6,500 Total Equity $ 26,000 $ 52,000 Four Steps Illustrated 13 Example 16-3 $26,000 Cash to Agnes Not a Service Php. So No IRC sec. 736(a) Pyt. 14 Example 16-4 Not a Service Php All A/R to Agnes Even if a Service Php. IRC sec. 736(a) is not triggered Example Partner X is liquidated for $25,000 cash 16

5 Example 16-5 Basis Value Cash $25,000 $25,000 Inventory 15,000 25,000 Land 8,000 25,000 TOTAL $48,000 $75,000 Capital Accounts Partner X $16,000 $25,000 Partner Y 16,000 25,000 Partner Z 16,000 25,000 TOTAL $48,000 $75, FMV of Partnership Assets Example X s Interest X s Interest Actual Before After Distribution Distribution Distribution Fictional Proportionate Distribution 2 3 = 4 Difference 5 4 = 6 Hot Assets: Inventory $25,000 $8,333 $0 $8,333 $0 ($8,333) Cold Assets: Cash $25,000 $8,333 $0 $8,333 $25,000 $16,667 Land $25,000 $8,333 $0 $8,333 $0 ($8,333) Net $8, Summary of Tax Consequences to Partner X: Ordinary income of $3,333 on the deemed exchange. Capital gain of $5,667 on the proportionate distribution of money. 19 Tax Consequences to Partnership/Continuing Partners: The partnership increases its inside basis in the inventory by $3,333. If a Sec. 754 election were in effect, then the Partnership would increase the inside basis in the Land by $5,667 Partner X s Sec. 731(a)(1) gain. 20

6 Distributee Partner Reporting Reporting Section 751(b) Exchanges The distributee partner shall submit with the partner s return a statement showing the computation of any income, gain, or loss to the partner Partnership Reporting A partnership which distributes [disproportionately] shall submit with its return for the year of the distribution a statement showing the computation of any income, gain, or loss to the partnership under the provisions of section 751(b)

7 Example 16-8 (Reg (g) Example (5) Modified) Partnership ABC makes a distribution to partner C which reduces C s interest in capital and profits from one-third to onefifth. The current distribution consists of: $5,000 in cash, and $7,500 of accounts receivable (basis $7,500). The partnership uses the accrual method of accounting. 1 Before Distribution to C ABC Partnership Partner's Cash $ 15,000 $ 15,000 Basis Accounts Receivable $ 9,000 $ 9,000 Inventory $ 21,000 $ 30,000 Land Parcel #1 $ 42,000 $ 48,000 Land Parcel #2 $ 9,000 $ 9,000 Total Assets $ 96,000 $ 111,000 Current Liabilities $ 15,000 $ 15,000 Mortage Payable $ 21,000 $ 21,000 Total Debt $ 36,000 $ 36,000 A (1/3) $ 20,000 $ 25,000 $ 32,000 B (1/3) $ 20,000 $ 25,000 $ 32,000 C (1/3) $ 20,000 $ 25,000 $ 32,000 Total Debt and Equity $ 96,000 $ 111,000 2 After the distribution, C's share of the partnership liabilities is reduced by $4,800 from $12,000 (1/3 of $36,000) to $7,200 (1/5 of $36,000). 3 Presence of section 751 property. The partnership has no unrealized receivables; however, both the inventory and accounts receivables are Section 751 inventory items. The inventory items of the partnership, in the aggregate, have appreciated substantially in value. (Sec. 751(d)(1)) The fair market value of all partnership inventory items, $39,000 (inventory $30,000, and accounts receivable $9,000), exceeds 120 percent of the $30,000 adjusted basis of such items to the partnership. 4

8 Four General Steps in a Section 751 Exchange 1) Step One: Identify the fictional current distribution, if any. 2) Step Two: Calculate the tax impact of the fictional exchange on the distributee partner. 3) Step Three: Calculate the tax impact of the fictional exchange on the partnership. 4) Step Four: Calculate the tax impact of the remaining actual proportionate distribution to the distributee partner (current or liquidating). Exchange Table Beginning C's Interest C's Interest Fictional Actual Difference Partnership Before After Proportionate Distribution 5 = 4-3 Assets at Distribution Distribution Distribution FMV 33% 20% 3 = 1-2 Sect 751 Asts: Accts. Rec. $ 9,000 $ 3,000 $ 300 $ 2,700 $ 7,500 $ 4,800 Inventory $ 30,000 $ 10,000 $ 6,000 $ 4,000 $ - $ (4,000) Total $ 39,000 $ 13,000 $ 6,300 $ - $ 800 Non-751 Asts. Cash $ 15,000 $ 5,000 $ 2,000 $ 3,000 $ 9,800 $ 6,800 Parcel #1 $ 48,000 $ 16,000 $ 9,600 $ 6,400 $ - $ (6,400) Parcel #2 $ 9,000 $ 3,000 $ 1,800 $ 1,200 $ - $ (1,200) Total $ 72,000 $ 19,000 $ 13,400 $ (800) 5 6 Debt Relief is Treated Like a Cash Distribution In Column 4, the distribution of cash includes C s $4,800 reduction of debt. (Sec. 752) Total money Distributed = $9,800 (Actual cash of $5,000 + debt relief of $4,800.) Step One: Identify the fictional current distribution. Column 5 shows that C received $800 of excess 751 assets accounts receivable. Therefore, the fictional distribution involves a distribution of $800 of cold assets. The partners can agree which cold assets (worth $800) are fictionally distributed to the partner. Here the partnership agrees that the cold asset fictionally distributed is Parcel #1 worth $800: 7 8

9 Exchange Table Beginning C's Interest C's Interest Fictional Actual Difference Partnership Before After Proportionate Distribution 5 = 4-3 Assets at Distribution Distribution Distribution FMV 33% 20% 3 = 1-2 Sect 751 Asts: Accts. Rec. $ 9,000 $ 3,000 $ 300 $ 2,700 $ 7,500 $ 4,800 Inventory $ 30,000 $ 10,000 $ 6,000 $ 4,000 $ - $ (4,000) Total $ 39,000 $ 13,000 $ 6,300 $ - $ 800 Non-751 Asts. Cash $ 15,000 $ 5,000 $ 2,000 $ 3,000 $ 9,800 $ 6,800 Parcel #1 $ 48,000 $ 16,000 $ 9,600 $ 6,400 $ - $ (6,400) Parcel #2 $ 9,000 $ 3,000 $ 1,800 $ 1,200 $ - $ (1,200) Total $ 72,000 $ 19,000 $ 13,400 $ (800) Step One: Parcel #1, by agreement, worth $800 is fictionally distributed: Inside Basis FMV Parcel #1 $700 * $800 * (42,000 48,000 X 800 = 700) 9 10 Step One: C s outside basis is reduced by $700 in the fictional distribution from $32,000 to $31,300*. *($32, = $31,300) Step Two: Calculate the tax impact of the fictional exchange on the distributee partner C recognizes $100 on his fictional exchange of $800 value ($700 basis) of parcel #1 in exchange for the $800 of accounts receivable ( ). C s basis in the $800 of purchased A/R is $800 (cost)

10 Step Three: Calculate the tax impact of the fictional exchange on the partnership No gain to the partnership because it is treated as receiving $800 value of parcel #1 in exchange for accounts receivable with an $800 basis (value = basis for the A/R). The partnership s basis in Parcel #1 increases to $800 (up $100). 13 Step Four: Calculate the tax impact of the remaining actual proportionate distribution: Total Fictional Distribution - Purchase = Balance Cash $9,800 - = $9,800 Accts Rec 7, = $6,700 C s Beginning outside basis: $32,000 Fictional Distribution of Parcel #1 <700> Cash Distribution <$9,800> Accounts Rec. (value = basis) < 6,700> Ending Outside basis 14, Example: Balance Sheet Before Distribution Before Distribution to C ABC Partnership Partner's Cash $ 15,000 $ 15,000 Basis Accounts Receivable $ 9,000 $ 9,000 Inventory $ 21,000 $ 30,000 Land Parcel #1 $ 42,000 $ 48,000 Land Parcel #2 $ 9,000 $ 9,000 Total Assets $ 96,000 $ 111,000 Current Liabilities $ 15,000 $ 15,000 Mortage Payable $ 21,000 $ 21,000 Total Debt $ 36,000 $ 36,000 A (1/3) $ 20,000 $ 25,000 $ 32,000 B (1/3) $ 20,000 $ 25,000 $ 32,000 C (1/3) $ 20,000 $ 25,000 $ 32,000 Total Debt and Equity $ 96,000 $ 111, Tax Basis Partnership Accounting Entries Debit: Parcel #1 $100 C s Equity $12,400 Credit: Cash $5,000 Accounts Receivable $7,500 16

$")

11 Example: Balance Sheet After Distribution After Distributions to C ABC Partnership Partner's Cash $ 10,000 $ 10,000 Basis Accounts Receivable $ 1,500 $ 1,500 Inventory $ 21,000 $ 30,000 Land Parcel #1 $ 42,100 $ 48,000 Land Parcel #2 $ 9,000 $ 9,000 Total Assets $ 83,600 $ 98,500 Current Liabilities $ 15,000 $ 15,000 Mortage Payable $ 21,000 $ 21,000 Total Debt $ 36,000 $ 36,000 A (40%) $ 20,000 $ 25,000 $ 34,400 B (40%) $ 20,000 $ 25,000 $ 34,400 C (20%) $ 7,600 $ 12,500 $ 14,800 Total Debt and Equity $ 83,600 $ 98, Example 16-9 Section 751(b) All Cash Liquidating Distribution 18 See balance sheet on next slide. Assume that Josey is liquidated for $400,000 cash. The partnership is not a professional service partnership. 19 Before Liquidation of Josey for $400,000 Cash MLSJ Partnership January 1, 2004 Partner's Cash $ 1,400,000 $ 1,400,000 Basis Accounts Receivable $ - $ 200,000 Total Assets $ 1,400,000 $ 1,600,000 Liabilities $ - Moe $ 350,000 $ 400,000 $ 350,000 Larry $ 350,000 $ 400,000 $ 350,000 Shirley $ 350,000 $ 400,000 $ 350,000 Josey $ 350,000 $ 400,000 $ 350,000 Total Debt and Equity $ 1,400,000 $ 1,600,000 20

12 Before Liquidation of Josey for $400,000 Cash MLSJ Partnership January 1, 2004 Partner's CashGain of $50,000 $ 1,400,000 $ 1,400,000 Basis Accounts Receivable $ - $ 200,000 Total Assets $ 1,400,000 $ 1,600,000 Liabilities $ - $400,000 cash - $350,000 O.B. Moe $ 350,000 $ 400,000 $ 350,000 Larry $ 350,000 $ 400,000 $ 350,000 Shirley $ 350,000 $ 400,000 $ 350,000 Josey= $50,000 $ 350,000 $ 400,000 $ 350,000 Total Debt and Equity $ 1,400,000 $ 1,600,000 The entire distribution falls under Code Sec. 736(b) because it represents Josey s interest in partnership property. The distribution is disproportionate so Code Sec. 751(b) applies Beginning J's Interest J's Interest Fictional Actual Difference Partnership Before After Proportionate Distribution 5 = 4-3 Assets at Distribution Distribution Distribution FMV 25% 0% 3 = 1-2 Sect 751 Asts: Accts. Rec. $ 200,000 $ 50,000 $ - $ 50,000 $ - $ (50,000) Non-751 Asts. Cash $ 1,400,000 $ 350,000 $ - $ 350,000 $ 400,000 $ 50,000 Note that the 751 Exchange is based upon FMV Reading the table: The positive $50,000 cash in column 5 indicates that Josey received excess cold assets (cash) in the distribution. 23 Steps One and Two Beginning J's Interest J's Interest Fictional Actual Difference Partnership Before After Proportionate Distribution 5 = 4-3 Assets at Distribution Distribution Distribution FMV 25% 0% 3 = 1-2 Sect 751 Asts: Accts. Rec. $ 200,000 $ 50,000 $ - $ 50,000 $ - $ (50,000) Non-751 Asts. Cash $ 1,400,000 $ 350,000 $ - $ 350,000 $ 400,000 $ 50,000 Step One: Josey is fictionally treated as if she received $50,000 of accounts receivable (her proportionate share of 751 assets). Step Two: Josey fictionally sells the accounts receivable to the partnership in exchange for cash of $50,000. Josey recognizes ordinary income of $50,000 on the sale. 24

13 Step Three Beginning J's Interest J's Interest Fictional Actual Difference Partnership Before After Proportionate Distribution 5 = 4-3 Assets at Distribution Distribution Distribution FMV 25% 0% 3 = 1-2 Sect 751 Asts: Accts. Rec. $ 200,000 $ 50,000 $ - $ 50,000 $ - $ (50,000) Non-751 Asts. Cash $ 1,400,000 $ 350,000 $ - $ 350,000 $ 400,000 $ 50,000 Step Three: The partnership fictionally pays cash for the accounts receivable and does not recognize gain. The partnership has a $50,000 cost basis in the acquired accounts receivables. 25 Step Four Step Four: The Remaining Distribution Total distribution of $400,000 cash: $50,000 of the cash received in the fictional exchange. The remaining $350,000 (400,000 50,000): Josey s remaining outside basis $350,000 Proportionate Cash Distribution.. <350,000> Remaining Outside Basis 0 26 Ending Balance Sheet After Liquidation of Josey for $400,000 Cash MLSJ Partnership January 2, 2004 Partner's Cash $ 1,000,000 $ 1,000,000 Basis Accounts Receivable $ 50,000 $ 200,000 Total Assets $ 1,050,000 $ 1,200,000 Liabilities Moe $ 350,000 $ 400,000 $ 350,000 Larry $ 350,000 $ 400,000 $ 350,000 Shirley $ 350,000 $ 400,000 $ 350,000 Total Debt and Equity $ 1,050,000 $ 1,200,000 Example Section 751(b) Liquidating Distribution with Cash and Debt Relief 27 28

14 Example See balance sheet on next slide. Assume that Josey is liquidated for: $150,000 of cash. $250,000 of debt relief The partnership is not a service partnership Before Liquidation of Josey for $150,000 Cash + Debt Relief MLSJ Partnership January 1, 2004 Partner's Cash $ 1,400,000 $ 1,400,000 Basis Accounts Receivable $ - $ 200,000 Total Assets $ 1,400,000 $ 1,600,000 Liabilities $ 1,000,000 $ 1,000,000 Moe $ 100,000 $ 150,000 $ 350,000 Larry $ 100,000 $ 150,000 $ 350,000 Shirley $ 100,000 $ 150,000 $ 350,000 Josey $ 100,000 $ 150,000 $ 350,000 Total Debt and Equity $ 1,400,000 $ 1,600, Before Liquidation of Josey for $150,000 Cash + Debt Relief MLSJ Partnership January 1, 2004 Partner's Gain of $50,000 Cash $ 1,400,000 $ 1,400,000 Basis Accounts Receivable $ - $ 200,000 Total Assets $ 1,400,000 $ 1,600,000 Liabilities $ 1,000,000 $ 1,000,000 $150,000 cash + $250,000 deemed cash Moe $ 100,000 $ 150,000 $ 350,000 Larry $ 100,000 $ 150,000 $ 350,000 Shirley - $350,000 $ 100,000 O.B. $ 150,000 $ 350,000 Josey $ 100,000 $ 150,000 $ 350,000 Total Debt and Equity $ 1,400,000 $ 1,600,000 = $50, The entire distribution falls under Code Sec. 736(b) because it represents Josey s interest in partnership property. The distribution is disproportionate so Code Sec. 751(b) applies. 32

15 Steps One and Two Beginning J's Interest J's Interest Fictional Actual Difference Partnership Before After Proportionate Distribution 5 = 4-3 Assets at Distribution Distribution Distribution FMV 25% 0% 3 = 1-2 Sect 751 Asts: Accts. Rec. $ 200,000 $ 50,000 $ - $ 50,000 $ - $ (50,000) Non-751 Asts. Cash $ 1,400,000 $ 350,000 $ - $ 350,000 $ 400,000 $ 50,000 Josey s debt relief of $250,000 is treated like an actual distribution of cash (150K + 250K = 400K). Reading the table: The positive $50,000 cash in column 5 indicates that Josey received excess cold assets (cash) in the distribution Beginning J's Interest J's Interest Fictional Actual Difference Partnership Before After Proportionate Distribution 5 = 4-3 Assets at Distribution Distribution Distribution FMV 25% 0% 3 = 1-2 Sect 751 Asts: Accts. Rec. $ 200,000 $ 50,000 $ - $ 50,000 $ - $ (50,000) Non-751 Asts. Cash $ 1,400,000 $ 350,000 $ - $ 350,000 $ 400,000 $ 50,000 Step One: Josey is fictionally treated as if she received $50,000 of accounts receivable (her proportionate share of 751 assets). Step Two: Josey fictionally sells the accounts receivable to the partnership in exchange for cash of $50,000. Josey recognizes ordinary income of $50,000 on the sale. 34 Step Three Beginning J's Interest J's Interest Fictional Actual Difference Partnership Before After Proportionate Distribution 5 = 4-3 Assets at Distribution Distribution Distribution FMV 25% 0% 3 = 1-2 Sect 751 Asts: Accts. Rec. $ 200,000 $ 50,000 $ - $ 50,000 $ - $ (50,000) Non-751 Asts. Cash $ 1,400,000 $ 350,000 $ - $ 350,000 $ 400,000 $ 50,000 Step Three: In the fictional exchange, the partnership pays cash for the accounts receivable and does not recognize gain. The partnership has a $50,000 cost basis in the purchased accounts receivable. Step Four Step Four: The Remaining Distribution She received a total distribution of $400,000 cash (including $250,000 of debt relief as money): $50,000 of the cash is deemed to be received in the deemed exchange. The remaining $350,000 (400,000 50,000): Josey s remaining outside basis $350,000 Proportionate Cash Distribution.. <350,000> Remaining Outside Basis

16 Ending Balance Sheet After Liquidation of Josey for $150,000 Cash + Debt Relief MLSJ Partnership January 2, 2004 Partner's Cash $ 1,250,000 $ 1,250,000 Basis Accounts Receivable $ 50,000 $ 200,000 Total Assets $ 1,300,000 $ 1,450,000 Liabilities $ 1,000,000 $ 1,000,000 Moe $ 100,000 $ 150,000 $ 433,333 Larry $ 100,000 $ 150,000 $ 433,333 Shirley $ 100,000 $ 150,000 $ 433,333 Total Debt and Equity $ 1,300,000 $ 1,450,000 Example 16-11: Section 751(b) Liquidating Distribution involving both Sec 736(a) and (b) See balance sheet on next slide. Assume that Josey is liquidated for $1,300,000 of cash. The partnership is not a service partnership. 39 Before Liquidation of Josey for $1,300,000 Cash MLSJ Partnership January 1, 2004 Partner's Cash $ 1,400,000 $ 1,400,000 Basis Accounts Receivable $ - $ 200,000 Unstated Goodwill $ - $ 2,400,000 Total Assets $ 1,400,000 $ 4,000,000 Liabilities $ - Moe $ 350,000 $ 1,000,000 $ 350,000 Larry $ 350,000 $ 1,000,000 $ 350,000 Shirley $ 350,000 $ 1,000,000 $ 350,000 Josey $ 350,000 $ 1,000,000 $ 350,000 Total Debt and Equity $ 1,400,000 $ 4,000,000 40

17 Before Liquidation of Josey for $1,300,000 Cash MLSJ Partnership January 1, 2004 Partner's Gain of $950,000 Cash $ 1,400,000 $ 1,400,000 Basis Accounts Receivable $ - $ 200,000 Unstated Goodwill $ - $ 2,400,000 Total Assets $ 1,400,000 $ 4,000,000 $1,300,000 cash Liabilities $ - - $350,000 O.B. Moe $ 350,000 $ 1,000,000 $ 350,000 Larry $ 350,000 $ 1,000,000 $ 350,000 Shirley = $950,000 $ 350,000 $ 1,000,000 $ 350,000 Josey $ 350,000 $ 1,000,000 $ 350,000 Total Debt and Equity $ 1,400,000 $ 4,000, Assume that Josey receives a premium of $300,000, which the partnership agreement characterizes as a payment for prior services, in addition to her $1,000,000 share of partnership property. 42 Sec. 736(a) Payment $300,000 of the distribution is a Sec. 736(a) payment (a premium over the partner s $1,000,000 share of partnership property). Reg (a)(3). The payment is fixed, therefore: $300,000 of ordinary income to Josey; Sec. 736(b) Payment The remaining $1,000,000 distribution ($1,300,000 - $300,000) is a Sec. 736(b) payment in exchange for Josey s interest in partnership property. The Section 736(b) distribution is disproportionate (too much cash) and Sec. 751(b) applies. $300,000 deduction to the continuing partners

18 The Sec 751(b) Exchange Table Beginning J's Interest J's Interest Fictional Actual Difference Partnership Before After Proportionate Sec 736(b) 5 = 4-3 Assets at Distribution Distribution Distribution Distribution FMV 25% 0% 3 = 1-2 Sect 751 Asts: Accts. Rec. $ 200,000 $ 50,000 $ - $ 50,000 $ - $ (50,000) Non-751 Asts. Cash $ 1,400,000 $ 350,000 $ - $ 350,000 $ 1,000,000 $ 650,000 Goodwill $ 2,400,000 $ 600,000 $ 600,000 $ - $ (600,000) Total $ 3,800,000 $ 950,000 $ 50,000 Reading the table: The positive $50,000 cash in column 5 indicates that Josey received $50,000 excess cold assets (cash) in the distribution. 45 Sec. 751(b) Exchange Table Question: Given that Josey already received $300,000 of the cash under Code Sec 736(a), how can Josey s predistribution share of the cash be $350,000 (25% X $1,400,000) in calculating the Sec 751 exchange (the Sec 736(b) portion)? Answer: The $300,000 Sec 736(a) payment is treated as paid exclusively from the other partners share of the cash (an expense to the other partners). Therefore, Josey s share of the cash can be regarded as $350, Steps One and Two Beginning J's Interest J's Interest Fictional Actual Difference Partnership Before After Proportionate Distribution 5 = 4-3 Assets at Distribution Distribution Distribution FMV 25% 0% 3 = 1-2 Sect 751 Asts: Accts. Rec. $ 200,000 $ 50,000 $ - $ 50,000 $ - $ (50,000) Non-751 Asts. Cash $ 1,400,000 $ 350,000 $ - $ 350,000 $ 1,000,000 $ 650,000 Goodwill $ 2,400,000 $ 600,000 $ 600,000 $ - $ (600,000) Total $ 3,800,000 $ 950,000 $ 50,000 Step One: Josey is fictionally treated as if she received $50,000 of accounts receivable (her proportionate share of 751 assets). Step Two: Josey fictionally sells the accounts receivable to the partnership in exchange for cash of $50,000. Josey recognizes ordinary income of $50,000 on the sale. 47 Step Three Beginning J's Interest J's Interest Fictional Actual Difference Partnership Before After Proportionate Distribution 5 = 4-3 Assets at Distribution Distribution Distribution FMV 25% 0% 3 = 1-2 Sect 751 Asts: Accts. Rec. $ 200,000 $ 50,000 $ - $ 50,000 $ - $ (50,000) Non-751 Asts. Cash $ 1,400,000 $ 350,000 $ - $ 350,000 $ 1,000,000 $ 650,000 Goodwill $ 2,400,000 $ 600,000 $ 600,000 $ - $ (600,000) Total $ 3,800,000 $ 950,000 $ 50,000 Step Three: In the fictional exchange, the partnership pays cash for the accounts receivable and does not recognize gain. The partnership has a $50,000 cost basis in the accounts receivable. 48

19 Step Four Step Four: Josey received a total Sec 736(b) distribution of $1,000,000 cash: $50,000 of the cash is deemed to be received in the fictional sale under Section 751 (Josey recognized ordinary income of $50,000 on the fictional sale of zero basis A/R) 49 Step Four The remaining $950,000 (1,000,000 50,000) is analyzed under the normal proportionate liquidating distribution rules: Josey s pre-distrib. outside basis $350,000 Proportionate Cash Distribution.. <950,000> Section 731(a) Gain (LTCG) 600,000 Assuming the partnership makes a timely Sec 754 election, the partnership increases its basis in the goodwill by $600,000 (per Code Sec 734) and the partnership can amortize that basis increase over 15 years (a Sec. 197 intangible). 50 Summary of Tax Impact on Josey Josey received a liquidating cash distribution of $1,300,000. Tax Treatment: $300,000 of ordinary income ( 736(a) and 707(c)) $ 50,000 of ordinary income per Sec 751(b) $350,000 tax free return of outside basis (Sec 731) $600,000 LTCG per Code Sec 731(a). 51 Balance Sheet Before Before Liquidation of Josey for $1,300,000 Cash MLSJ Partnership January 1, 2004 Partner's Cash $ 1,400,000 $ 1,400,000 Basis Accounts Receivable $ - $ 200,000 Unstated Goodwill $ - $ 2,400,000 Total Assets $ 1,400,000 $ 4,000,000 Liabilities $ - Moe $ 350,000 $ 1,000,000 $ 350,000 Larry $ 350,000 $ 1,000,000 $ 350,000 Shirley $ 350,000 $ 1,000,000 $ 350,000 Josey $ 350,000 $ 1,000,000 $ 350,000 Total Debt and Equity $ 1,400,000 $ 4,000,000 52

20 Tax Basis Partnership Accounting Entries Sec 736(a) Transaction Debit: Credit: Guaranteed Pyt. $300,000* Cash $300,000 * The guaranteed payment reduces the equity of Moe, Larry and Shirley (each) by $100, Tax Basis Partnership Accounting Entries Sec 736(b) Transaction Debit: Accounts Rec $50,000 Goodwill $600,000* Josey s Equity $350,000 Credit: Cash $1,000,000 * Assuming a Section 754 election is made 54 Balance Sheet After After Liquidation of Josey for $1,300,000 Cash MLSJ Partnership January 1, 2004 Partner's Cash $ 100,000 $ 100,000 Basis Accounts Receivable $ 50,000 $ 200,000 Unstated Goodwill $ 600,000 $ 2,400,000 Total Assets $ 750,000 $ 2,700,000 Liabilities $ - Moe $ 250,000 $ 900,000 $ 250,000 Larry $ 250,000 $ 900,000 $ 250,000 Shirley $ 250,000 $ 900,000 $ 250,000 Example 16-12: Liquidating Distribution involving a service partnership with unstated goodwill and unrealized receivables Sec 736(a) and (b) Total Debt and Equity $ 750,000 $ 2,700,

21 See balance sheet on next slide. Assume that Josey is liquidated for $1,300,000 of cash. Josey is a general partner in a service partnership 57 Before Liquidation of Josey for $1,300,000 Cash MLSJ Partnership January 1, 2004 Partner's Cash $ 1,400,000 $ 1,400,000 Basis Accounts Receivable $ - $ 200,000 Unstated Goodwill $ - $ 2,400,000 Total Assets $ 1,400,000 $ 4,000,000 Liabilities $ - Moe $ 350,000 $ 1,000,000 $ 350,000 Larry $ 350,000 $ 1,000,000 $ 350,000 Shirley $ 350,000 $ 1,000,000 $ 350,000 Josey $ 350,000 $ 1,000,000 $ 350,000 Total Debt and Equity $ 1,400,000 $ 4,000, Before Liquidation of Josey for $1,300,000 Cash MLSJ Partnership January 1, 2004 Partner's Gain of $950,000 Cash $ 1,400,000 $ 1,400,000 Basis Accounts Receivable $ - $ 200,000 Unstated Goodwill $ - $ 2,400,000 Total Assets $ 1,400,000 $ 4,000,000 $1,300,000 cash Liabilities $ - - $350,000 O.B. Moe $ 350,000 $ 1,000,000 $ 350,000 Larry $ 350,000 $ 1,000,000 $ 350,000 Shirley = $950,000 $ 350,000 $ 1,000,000 $ 350,000 Josey $ 350,000 $ 1,000,000 $ 350,000 Total Debt and Equity $ 1,400,000 $ 4,000, Sec. 736(a) Payment $950,000 of the distribution is a Sec. 736(a) payment. The payment is fixed, therefore: $950,000 of ordinary income to Josey; $950,000 deduction to the continuing partners. 60

22 Section 736(a) Portion The $950,000 ($1,300,000 - $350,000) Sec. 736(a) portion consists of: 1) $300,000, a premium (Reg (a)(3)). 2) $600,000, Josey s share of unstated goodwill. 3) $50,000, Josey s share of unrealized receivables. (Code Sec. 736(b)(2)) 61 Sec. 736(b) Payment The remaining $350,000 distribution ($1,300,000 - $950,000) is a Sec. 736(b) payment for Josey s interest in partnership property. The Section 736(b) distribution is proportionate (so Sec 751(b) does not apply) and the distribution simply reduces Josey s outside basis--tax free--from $350,000 to zero. 62 Summary of Tax Impact on Josey Josey received a liquidating cash distribution of $1,300,000. Tax Treatment: $950,000 of ordinary income ( 736(a) and 707(c)) $350,000 tax free return of outside basis 63 Balance Sheet Before Before Liquidation of Josey for $1,300,000 Cash MLSJ Partnership January 1, 2004 Partner's Cash $ 1,400,000 $ 1,400,000 Basis Accounts Receivable $ - $ 200,000 Unstated Goodwill $ - $ 2,400,000 Total Assets $ 1,400,000 $ 4,000,000 Liabilities $ - Moe $ 350,000 $ 1,000,000 $ 350,000 Larry $ 350,000 $ 1,000,000 $ 350,000 Shirley $ 350,000 $ 1,000,000 $ 350,000 Josey $ 350,000 $ 1,000,000 $ 350,000 Total Debt and Equity $ 1,400,000 $ 4,000,000 64

23 Tax Basis Partnership Accounting Entries Sec 736(a) Transaction Debit: Credit: Guaranteed Pyt. $950,000* Cash $950,000 Tax Basis Partnership Accounting Entries Sec 736(b) Transaction Debit: Josey s Equity $350,000 Credit: Cash $350,000 * The guaranteed payment reduces the equity of Moe, Larry and Shirley (each) by $316, The Section 754 election is now irrelevant 66 Balance Sheet After After Liquidation of Josey for $1,300,000 Cash MLSJ Partnership January 1, 2004 Partner's Cash $ 100,000 $ 100,000 Basis Accounts Receivable $ 200,000 Unstated Goodwill $ 2,400,000 Total Assets $ 100,000 $ 2,700,000 Liabilities $ - Self-Study Problem 14 Moe $ 33,333 $ 900,000 $ 33,333 Larry $ 33,333 $ 900,000 $ 33,333 Shirley $ 33,334 $ 900,000 $ 33,334 Total Debt and Equity $ 100,000 $ 2,700,

24

25 73 74

Chapter 16. Distributions Treated As Section 751(b) Exchanges

Exchanges") Chapter 16 Distributions Treated As Section 751(b) Exchanges Receipt of Excess Cold Assets 1)If Excess Cold Assets Are Distributed: then the partnership is treated as if it made a hypothetical distribution

Chapter 16 Distributions Treated As Section 751(b) Exchanges Receipt of Excess Cold Assets 1)If Excess Cold Assets Are Distributed: then the partnership is treated as if it made a hypothetical distribution

Proportionate v. Disproportionate Distributions

Distributions In General Current Distributions Liquidating Distributions Money 15-4 Property 15-5 Example 15-1 15-5 Proportionate v. Disproportionate Distributions 4 Example 15-1 Partnership Assets Ptr.

Distributions In General Current Distributions Liquidating Distributions Money 15-4 Property 15-5 Example 15-1 15-5 Proportionate v. Disproportionate Distributions 4 Example 15-1 Partnership Assets Ptr.

Section. 754 Election. With Distributions

Section 754 Election With Distributions 76 1 754 Election Activates Sec. 743 Sales, Exchanges, Deaths Sec. 734 Distributions 2 Two Upward Adjustment Triggers in Sec. 734 3 1) Distributee recognizes sec.

Section 754 Election With Distributions 76 1 754 Election Activates Sec. 743 Sales, Exchanges, Deaths Sec. 734 Distributions 2 Two Upward Adjustment Triggers in Sec. 734 3 1) Distributee recognizes sec.

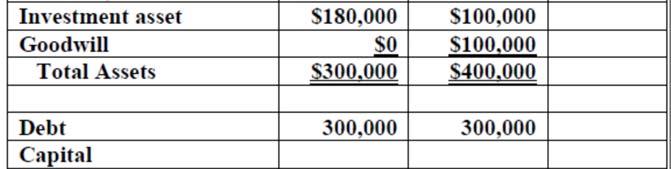

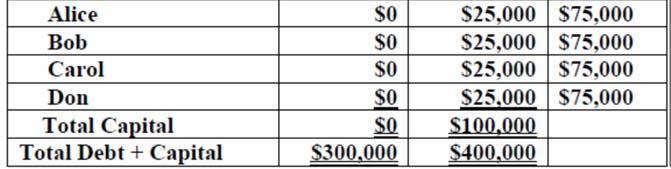

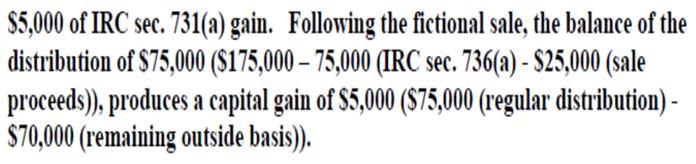

REG (Oct. 31, 2014) -- Proposed Regulations on Partner s Treatment of U/R and Inventory with Distributions

-- Proposed Regulations on Partner s Treatment of U/R and Inventory with Distributions") generating ordinary income to Alice of $20,000 ($25,000 - $5,000). 2 The fictional distribution of inventory reduced Alice s outside basis to $70,000 ($75,000 - $5,000); therefore, the remaining $75,000

generating ordinary income to Alice of $20,000 ($25,000 - $5,000). 2 The fictional distribution of inventory reduced Alice s outside basis to $70,000 ($75,000 - $5,000); therefore, the remaining $75,000

Death of a Partner Death of a Partner 17-3

Death of a Partner 17-2 Tax year closes with respect to deceased partner (not Php). Passive losses may be deducted on final return (reduced by basis step-up). Decedent s IRC sec. 743(b) adjustment disappears

Death of a Partner 17-2 Tax year closes with respect to deceased partner (not Php). Passive losses may be deducted on final return (reduced by basis step-up). Decedent s IRC sec. 743(b) adjustment disappears

Sale or Exchange of a Partnership Interest

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

General Rule Capital Gain or Loss. Sec Example 12-1 Sale. General rule: a sale by a partner generates capital gain or loss.

General Rule Capital Gain or Loss Sec. 741 12-3 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses. Same for: Sale

General Rule Capital Gain or Loss Sec. 741 12-3 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses. Same for: Sale

Staff Tax Training Partnerships & LLCs (Form 1065) Case Solutions

Case Solutions") Staff Tax Training Partnerships & LLCs (Form 1065) Case Solutions DISCLAIMER All problems, exercises, activities, etc., have at least one suggested solution, even if there may be more than one way to solve

Staff Tax Training Partnerships & LLCs (Form 1065) Case Solutions DISCLAIMER All problems, exercises, activities, etc., have at least one suggested solution, even if there may be more than one way to solve

Sale or Exchange of a Partnership Interest

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

5 Sale or Exchange of a Partnership Interest 1 General rule: a sale by a partner generates capital gain or loss. Exception for seller s share of partnership hot asset gains or losses (sec. 751(a)) 2 Amount

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests THURSDAY, JULY 9, 2015, 1:00-2:50 pm Eastern This program is approved for 2 CPE credit hours.

CHAPTER 22 NONLIQUIDATING DISTRIBUTIONS. Problems, page 684

204 CHAPTER 22 NONLIQUIDATING DISTRIBUTIONS Problems, page 684 22-1. X does not recognize gain on the distribution because the amount of cash distributed is less than X's outside basis immediately before

204 CHAPTER 22 NONLIQUIDATING DISTRIBUTIONS Problems, page 684 22-1. X does not recognize gain on the distribution because the amount of cash distributed is less than X's outside basis immediately before

Form 1065 Schedule K-1 Analysis Basis Calculations & Distributions for Partnerships & LLCs Case Suggested Solutions

Form 1065 Schedule K-1 Analysis Basis Calculations & Distributions for Partnerships & LLCs Case Suggested Solutions DISCLAIMER All problems, exercises, activities, etc., have at least one suggested solution,

Form 1065 Schedule K-1 Analysis Basis Calculations & Distributions for Partnerships & LLCs Case Suggested Solutions DISCLAIMER All problems, exercises, activities, etc., have at least one suggested solution,

IRC Section 734 Adjustments: Applying the 754 Election to Distributions of Partnership Property

FOR LIVE PROGRAM ONLY IRC Adjustments: Applying the 754 Election to Distributions of Partnership Property THURSDAY, AUGUST 10, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

FOR LIVE PROGRAM ONLY IRC Adjustments: Applying the 754 Election to Distributions of Partnership Property THURSDAY, AUGUST 10, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION FOR THE LIVE PROGRAM This

IRC 751 "Hot Asset" Treatment: New Rules for Calculating Ordinary Income Recharacterization

Presenting a live 90-minute webinar with interactive Q&A IRC 751 "Hot Asset" Treatment: New Rules for Calculating Ordinary Income Recharacterization New IRS Proposal on Determining Partners' Share of Section

Presenting a live 90-minute webinar with interactive Q&A IRC 751 "Hot Asset" Treatment: New Rules for Calculating Ordinary Income Recharacterization New IRS Proposal on Determining Partners' Share of Section

MACNY. Tax Implications of a Business Transaction. May 10, 2017

MACNY Tax Implications of a Business Transaction May 10, 2017 Thomas J. Giufre Fust Charles Chambers LLP Review of the Different Types of Entities C Corporation: Entity level taxation Two levels of taxation

MACNY Tax Implications of a Business Transaction May 10, 2017 Thomas J. Giufre Fust Charles Chambers LLP Review of the Different Types of Entities C Corporation: Entity level taxation Two levels of taxation

Buying and Selling Pass-Through Entities. Presented By Sno Barry, CPA, MST, Principal Justin Morren, CPA, Senior Tax Specialist

Buying and Selling Pass-Through Entities Presented By Sno Barry, CPA, MST, Principal Justin Morren, CPA, Senior Tax Specialist Agenda 1 Asset vs. Stock Sale 3 Partnerships Buyer and Seller perspective

Buying and Selling Pass-Through Entities Presented By Sno Barry, CPA, MST, Principal Justin Morren, CPA, Senior Tax Specialist Agenda 1 Asset vs. Stock Sale 3 Partnerships Buyer and Seller perspective

Tax Issues in Sale of Partnership and LLC Interests. November 3, MACPA: 2014 Advanced Tax Institute Conference

Tax Issues in Sale of Partnership and LLC Interests November 3, 2014--MACPA: 2014 Advanced Tax Institute Conference Outline Tax Classification of Partnerships and LLCs Tax Consequences in General to Seller

Tax Issues in Sale of Partnership and LLC Interests November 3, 2014--MACPA: 2014 Advanced Tax Institute Conference Outline Tax Classification of Partnerships and LLCs Tax Consequences in General to Seller

IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests

FOR LIVE PROGRAM ONLY IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests WEDNESDAY, JULY 26, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

FOR LIVE PROGRAM ONLY IRC 751 "Hot Assets": Calculating and Reporting Ordinary Income in Disposition of Partnership or LLC Interests WEDNESDAY, JULY 26, 2017, 1:00-2:50 pm Eastern IMPORTANT INFORMATION

Corporate Tax Segment 3 Corporate Formation

Corporate Tax Segment 3 Corporate Formation University of Leiden International Tax Center May 2007 Professor William P. Streng University of Houston Law Center 4/30/2007 (c) William P. Streng 1 Formation

Corporate Tax Segment 3 Corporate Formation University of Leiden International Tax Center May 2007 Professor William P. Streng University of Houston Law Center 4/30/2007 (c) William P. Streng 1 Formation

BASIC PARTNERSHIP TAX II SALES, DISGUISED SALES & TERMINATIONS

BASIC PARTNERSHIP TAX II SALES, DISGUISED SALES & TERMINATIONS TABLE CONTENTS PART I... 1 SALES & EXCHANGEs OF PARTNERSHIP INTERESTS... 1 A. General Rules Transferor/Selling Partner... 1 B. General Rules

BASIC PARTNERSHIP TAX II SALES, DISGUISED SALES & TERMINATIONS TABLE CONTENTS PART I... 1 SALES & EXCHANGEs OF PARTNERSHIP INTERESTS... 1 A. General Rules Transferor/Selling Partner... 1 B. General Rules

AMERICAN BAR ASSOCIATION SECTION OF TAXATION REPORT TO THE HOUSE OF DELEGATES RECOMMENDATION

AMERICAN BAR ASSOCIATION SECTION OF TAXATION REPORT TO THE HOUSE OF DELEGATES RECOMMENDATION 1 2 3 4 5 6 RESOLVED, That the American Bar Association recommends that Section 751(b) of the Internal Revenue

AMERICAN BAR ASSOCIATION SECTION OF TAXATION REPORT TO THE HOUSE OF DELEGATES RECOMMENDATION 1 2 3 4 5 6 RESOLVED, That the American Bar Association recommends that Section 751(b) of the Internal Revenue

Basis Adjustments for Partnerships and LLCs: Tax Law Challenges Navigating Complex Basis Rules and Avoiding Pitfalls in Section 754 Elections

Presenting a live 110 minute teleconference with interactive Q&A Basis Adjustments for Partnerships and LLCs: Tax Law Challenges Navigating Complex Basis Rules and Avoiding Pitfalls in Section 754 Elections

Presenting a live 110 minute teleconference with interactive Q&A Basis Adjustments for Partnerships and LLCs: Tax Law Challenges Navigating Complex Basis Rules and Avoiding Pitfalls in Section 754 Elections

Current. Law. A partnership interest other than a capital interest. Rev Proc IRS Administrative Concession For Vested Profits Only Interest

Current 5-1 Law Sections 83 and 721; Rev Procs 93-27 & 2001-43 1 Rev Proc 93-27 IRS Administrative Concession For Vested Profits Only Interest 5-6 2 Rev Proc 93-27 5-6 Profits Interest Profits Intererst

Current 5-1 Law Sections 83 and 721; Rev Procs 93-27 & 2001-43 1 Rev Proc 93-27 IRS Administrative Concession For Vested Profits Only Interest 5-6 2 Rev Proc 93-27 5-6 Profits Interest Profits Intererst

Partnership Basis and Distributions: Navigating Sections , 751(b) and 755

and 755") Presenting a live 110-minute teleconference with interactive Q&A Partnership Basis and Distributions: Navigating Sections 731-737, 751(b) and 755 WEDNESDAY, JULY 17, 2013 1pm Eastern 12pm Central 11am

Presenting a live 110-minute teleconference with interactive Q&A Partnership Basis and Distributions: Navigating Sections 731-737, 751(b) and 755 WEDNESDAY, JULY 17, 2013 1pm Eastern 12pm Central 11am

Corporate Taxation Chapter Two: Corporate Formation

Presentation: Corporate Taxation Chapter Two: Corporate Formation Professors Wells January 21, 2015 Key Statutory Provision: 351, 357, 358, 362, 368(c), 1032, 1223(1), 1223(2), 1245(b)(3), 118, 195, 212(3),

Presentation: Corporate Taxation Chapter Two: Corporate Formation Professors Wells January 21, 2015 Key Statutory Provision: 351, 357, 358, 362, 368(c), 1032, 1223(1), 1223(2), 1245(b)(3), 118, 195, 212(3),

Chapter Two - Formation of a Corporation

Chapter Two - Formation of a Corporation Fundamental income tax elements: 1) Transferor: 351(a) - nonrecognition treatment applicable to the asset transferor (if certain conditions are met); otherwise:

Chapter Two - Formation of a Corporation Fundamental income tax elements: 1) Transferor: 351(a) - nonrecognition treatment applicable to the asset transferor (if certain conditions are met); otherwise:

Partnerships/LLCs Section 754 Election and Basis Adjustments

CHECKPOINT LEARNING WEBINARS Partnerships/LLCs Section 754 Election and Basis Adjustments Partnerships/LLCs Section 754 Election and Basis Adjustments Presented by: Laurie A. Stillwell, CPA CHECKPOINT

CHECKPOINT LEARNING WEBINARS Partnerships/LLCs Section 754 Election and Basis Adjustments Partnerships/LLCs Section 754 Election and Basis Adjustments Presented by: Laurie A. Stillwell, CPA CHECKPOINT

I Want Out Tax Considerations In Exiting a Partnership

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2013 I Want Out Tax Considerations In Exiting

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 2013 I Want Out Tax Considerations In Exiting

Ch. 8 - Taxable Corporate Acquisitions/Dispositions

Ch. 8 - Taxable Corporate Acquisitions/Dispositions Corporate ownership & disposition options: 1) Sale of stock transfer mechanics are easy to accomplish; LT capital gain treatment to the individual seller

Ch. 8 - Taxable Corporate Acquisitions/Dispositions Corporate ownership & disposition options: 1) Sale of stock transfer mechanics are easy to accomplish; LT capital gain treatment to the individual seller

SEAGATE TECHNOLOGY PLC CONDENSED CONSOLIDATED BALANCE SHEETS (In millions) (Unaudited)

(Unaudited)") CONDENSED CONSOLIDATED BALANCE SHEETS (In millions) ASSETS June 30, (a) Current assets: Cash and cash equivalents $ 2,285 $ 2,539 Accounts receivable, net 1,209 1,199 Inventories 1,014 982 Other current

CONDENSED CONSOLIDATED BALANCE SHEETS (In millions) ASSETS June 30, (a) Current assets: Cash and cash equivalents $ 2,285 $ 2,539 Accounts receivable, net 1,209 1,199 Inventories 1,014 982 Other current

Partnership Accounting

Partnership Accounting - Partner Capital Accounts - A partnership keeps track of each partner s economic investment in the partnership through a financial record called a capital account. A partner s opening

Partnership Accounting - Partner Capital Accounts - A partnership keeps track of each partner s economic investment in the partnership through a financial record called a capital account. A partner s opening

PPC 1065 Deskbook Practice Aids. Industry-leading tools for tax professionals

PPC 1065 Deskbook Practice Aids Industry-leading tools for tax professionals PPC 1065 DESKBOOK PPC 1065 DESKBOOK PRACTICE AIDS 2 1065 Worksheets WORKSHEET W101: Carryforward Worksheet Partner's Outside

PPC 1065 Deskbook Practice Aids Industry-leading tools for tax professionals PPC 1065 DESKBOOK PPC 1065 DESKBOOK PRACTICE AIDS 2 1065 Worksheets WORKSHEET W101: Carryforward Worksheet Partner's Outside

IRS Audit Guide Intro to Sec. 704(b) confirms flexibility of partnerships

confirms flexibility of partnerships") 7-1 Determining the Partners Distributive Shares Chapter 7 1 IRS Audit Guide Intro to Sec. 704(b) confirms flexibility of partnerships 2 S Shareholders report pro-rata share of S corp. income. Partners

7-1 Determining the Partners Distributive Shares Chapter 7 1 IRS Audit Guide Intro to Sec. 704(b) confirms flexibility of partnerships 2 S Shareholders report pro-rata share of S corp. income. Partners

C Corporation S Corporation LLC. and LLLP. Legal Entity? Same entity as owner Separate entity from owner. Taxed separate from Owner

Legal Entity? Same entity as owner Separate entity from owner Taxed separate from Owner Separate entity from owner, unless piercing or reverse piercing applies Separate entity from owner, unless piercing

Legal Entity? Same entity as owner Separate entity from owner Taxed separate from Owner Separate entity from owner, unless piercing or reverse piercing applies Separate entity from owner, unless piercing

ConsolidationAfterTwoYears.xls-Part 1 (c) John Bildersee 2002

John Bildersee 2002") ConsolidationAfterTwoYears.xls-Part 1 (c) John Bildersee 2002 Cost of acquisition 1,200,000 Life Proportionate Discount Annual Book value of Subsidiary 1,000,000 Purchase premium 300,000 Revaluation Adjustmnt

ConsolidationAfterTwoYears.xls-Part 1 (c) John Bildersee 2002 Cost of acquisition 1,200,000 Life Proportionate Discount Annual Book value of Subsidiary 1,000,000 Purchase premium 300,000 Revaluation Adjustmnt

ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES. Consolidated Financial Statements as of December 31, 2015

ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements as of 2015 ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements As of 2015 Table

ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements as of 2015 ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements As of 2015 Table

Charitable Lead Annuity Trust

Charitable Lead Annuity Trust An Illustration of an Inter Vivos Charitable Lead Annuity Trust AN ANALYSIS PREPARED EXCLUSIVELY FOR Transfer $1M ShopRight, Inc. to 20-Year Shark-Fin CLAT 1 Disclaimer This

Charitable Lead Annuity Trust An Illustration of an Inter Vivos Charitable Lead Annuity Trust AN ANALYSIS PREPARED EXCLUSIVELY FOR Transfer $1M ShopRight, Inc. to 20-Year Shark-Fin CLAT 1 Disclaimer This

American Bar Association Section of Taxation Comments on Proposed Regulations Under Section 751(b)

") COMMENTS ON PROPOSED REGULATIONS UNDER SECTION 751(b) 661 American Bar Association Section of Taxation Comments on Proposed Regulations Under Section 751(b) Abstract The American Bar Association Section

COMMENTS ON PROPOSED REGULATIONS UNDER SECTION 751(b) 661 American Bar Association Section of Taxation Comments on Proposed Regulations Under Section 751(b) Abstract The American Bar Association Section

ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES. Consolidated Financial Statements as of December 31, 2016

ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements as of 2016 ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements As of 2016 Table

ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements as of 2016 ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements As of 2016 Table

Flip Charitable Remainder Unitrust

Flip Charitable Remainder Unitrust An Illustration of the Use of a Net Income with Make-up Charitable Remainder Unitrust that "Flips" or Converts to a Standard Charitable Remainder Unitrust in Year 7 AN

Flip Charitable Remainder Unitrust An Illustration of the Use of a Net Income with Make-up Charitable Remainder Unitrust that "Flips" or Converts to a Standard Charitable Remainder Unitrust in Year 7 AN

Basis Calculations & Distributions for Pass-Thru Entities Case Suggested Solutions

Calculations & Distributions for Pass-Thru Entities Case Suggested Solutions Suggested Solution Disclaimer All problems, exercises, activities, etc., have at least one suggested solution, even if there

Calculations & Distributions for Pass-Thru Entities Case Suggested Solutions Suggested Solution Disclaimer All problems, exercises, activities, etc., have at least one suggested solution, even if there

ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES. Consolidated Financial Statements as of December 31, 2014

ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements as of 2014 ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements as of 2014 Table

ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements as of 2014 ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements as of 2014 Table

Business Entities GENERAL PARTNERSHIP

Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation must be met. Implementation expenses

Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation must be met. Implementation expenses

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

ACCOUNTING CYCLE FOR A MERCHANDISING BUSINESS ORGANIZED AS A CORPORATION page 97. Source documents are checked, and transactions are analyzed.. Transactions are recorded in journals. 5. Journal entries

Profit or loss recorded to Retained Earnings

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Cash basis Recognizes transactions when cash or equivalents DIAGRAM OF T-ACCOUNTS METHODS & ORGS Balance Sheet as of 12/31/2100 Accrual basis Follows the matching principle and recognizes Assets = Liabilities

Chapter 14. Statement of Cash Flows

1 Chapter 14 Statement of Cash Flows 2 Figure 14-1 3 Definition of Cash Cash consists of coin, currency, and available funds on deposit at the bank. Negotiable instruments such as money orders, certified

1 Chapter 14 Statement of Cash Flows 2 Figure 14-1 3 Definition of Cash Cash consists of coin, currency, and available funds on deposit at the bank. Negotiable instruments such as money orders, certified

Business Entities GENERAL PARTNERSHIP

THE PRUDENTIAL INSURANCE OF AMERICA Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation

THE PRUDENTIAL INSURANCE OF AMERICA Business Entities General Entity Tax Characteristics and Executive Benefits Using Life Insurance LIABILITY EASE OF FORMATION State law requirements for incorporation

ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES. Consolidated Financial Statements as of December 31, 2013

ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements as of 2013 ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements as of 2013 Table

ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements as of 2013 ITURAN LOCATION AND CONTROL LTD. AND ITS SUBSIDIARIES Consolidated Financial Statements as of 2013 Table

Spreadsheet versus T-Account

Chapter 21 The Statement of Cash Flows Part 2 The Mechanics of the T-Account Approach Intermediate Accounting II Dr. Chula King Spreadsheet versus T-Account Spreadsheet Approach Columns Balance Sheet:

Chapter 21 The Statement of Cash Flows Part 2 The Mechanics of the T-Account Approach Intermediate Accounting II Dr. Chula King Spreadsheet versus T-Account Spreadsheet Approach Columns Balance Sheet:

CONSOLIDATED BALANCE SHEET

CONSOLIDATED BALANCE SHEET December 31, 2017 A S S E T S CURRENT ASSETS: Cash and time deposits 31,380 Accounts receivable trade 98,188 Inventories 1,096 Short-term loans receivable 46,282 Deferred tax

CONSOLIDATED BALANCE SHEET December 31, 2017 A S S E T S CURRENT ASSETS: Cash and time deposits 31,380 Accounts receivable trade 98,188 Inventories 1,096 Short-term loans receivable 46,282 Deferred tax

Distributions. 9/30/2011 (c) William P. Streng 1

William P. Streng 1") Chapter 4 Nonliquidating Distributions Dividends - i.e., operating distributions IRC 301(a) - Subchapter C, Part A. Alternative dividend classification systems: 1) Federal income tax income tax; e&p 2)

Chapter 4 Nonliquidating Distributions Dividends - i.e., operating distributions IRC 301(a) - Subchapter C, Part A. Alternative dividend classification systems: 1) Federal income tax income tax; e&p 2)

Table 1 HARRIS CORPORATION FY '18 Second Quarter Summary CONDENSED CONSOLIDATED STATEMENT OF INCOME (Unaudited)

") Table 1 CONDENSED CONSOLIDATED STATEMENT OF INCOME (In millions, except per share amounts) Revenue from product sales and services $ 1,535 $ 1,449 $ 2,948 $ 2,869 Cost of product sales and services (999)

Table 1 CONDENSED CONSOLIDATED STATEMENT OF INCOME (In millions, except per share amounts) Revenue from product sales and services $ 1,535 $ 1,449 $ 2,948 $ 2,869 Cost of product sales and services (999)

Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II

Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II William R. Skinner Partner, Fenwick & West wrskinner@fenwick.com Steven D. Bortnick Partner, Pepper Hamilton bortnicks@pepperlaw.com

Opting Out of PFIC Tax-and-Interest Treatment: Making QEF Elections on Form 8621 Part II William R. Skinner Partner, Fenwick & West wrskinner@fenwick.com Steven D. Bortnick Partner, Pepper Hamilton bortnicks@pepperlaw.com

Table 1 HARRIS CORPORATION FY '18 Third Quarter Summary CONDENSED CONSOLIDATED STATEMENT OF INCOME (Unaudited)

") Table 1 CONDENSED CONSOLIDATED STATEMENT OF INCOME March 30, 2018 March 31, 2017 March 30, 2018 March 31, 2017 (In millions, except per share amounts) Revenue from product sales and services $ 1,568 $

Table 1 CONDENSED CONSOLIDATED STATEMENT OF INCOME March 30, 2018 March 31, 2017 March 30, 2018 March 31, 2017 (In millions, except per share amounts) Revenue from product sales and services $ 1,568 $

Determining a Partner's Share on Unrealized Receivables at the Liquidation of the Partner's Interest

University of Connecticut DigitalCommons@UConn Faculty Articles and Papers School of Law 2000 Determining a Partner's Share on Unrealized Receivables at the Liquidation of the Partner's Interest Stephen

University of Connecticut DigitalCommons@UConn Faculty Articles and Papers School of Law 2000 Determining a Partner's Share on Unrealized Receivables at the Liquidation of the Partner's Interest Stephen

2011 LIMITED LIABILTY COMPANY (LLC) & PARTNERSHIP FEDERAL TAX UPDATE

& PARTNERSHIP FEDERAL TAX UPDATE") 2011 LIMITED LIABILTY COMPANY (LLC) & PARTNERSHIP FEDERAL TAX UPDATE Gregory L. Gandy, CPA Tax Partner, BiggsKofford 630 Southpointe Court, Suite 200 Colorado Springs, CO 80906 719-579-9090 ggandy@biggskofford.com

2011 LIMITED LIABILTY COMPANY (LLC) & PARTNERSHIP FEDERAL TAX UPDATE Gregory L. Gandy, CPA Tax Partner, BiggsKofford 630 Southpointe Court, Suite 200 Colorado Springs, CO 80906 719-579-9090 ggandy@biggskofford.com

Financial Statements for Fiscal 2003 (April 1, 2003 to March 31, 2004) Nippon Steel Chemical Co., Ltd.

Nippon Steel Chemical Co., Ltd.") Financial Statements for Fiscal 2003 (April 1, 2003 to March 31, 2004) Nippon Steel Chemical Co., Ltd. 1 Consolidated Operating Performances 2004 2003 Increase or decrease 2004 from previous term Net sales

Financial Statements for Fiscal 2003 (April 1, 2003 to March 31, 2004) Nippon Steel Chemical Co., Ltd. 1 Consolidated Operating Performances 2004 2003 Increase or decrease 2004 from previous term Net sales

International Income Taxation Chapter 10

Presentation: International Income Taxation Chapter 10 Professor Wells March 29, 2012 Overview of 367 Tax-free treatment under the Subchapter C rules 367(a): Governs transfer of appreciated property by

Presentation: International Income Taxation Chapter 10 Professor Wells March 29, 2012 Overview of 367 Tax-free treatment under the Subchapter C rules 367(a): Governs transfer of appreciated property by

Mastering Tax Complexities in the Sale of Partnership and LLC Interests

Mastering Tax Complexities in the Sale of Partnership and LLC Interests WEDNESDAY, JUNE 17, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit

Mastering Tax Complexities in the Sale of Partnership and LLC Interests WEDNESDAY, JUNE 17, 2015, 1:00-2:50 pm Eastern IMPORTANT INFORMATION This program is approved for 2 CPE credit hours. To earn credit

Corporate Taxation Chapter Eight: Taxable Acquisitions

Presentation: Corporate Taxation Chapter Eight: Taxable Acquisitions Professors Wells March 9, 2015 Chapter 8 Taxable Corporate Acquisitions/Dispositions Corporate ownership disposition options: 1) Sale

Presentation: Corporate Taxation Chapter Eight: Taxable Acquisitions Professors Wells March 9, 2015 Chapter 8 Taxable Corporate Acquisitions/Dispositions Corporate ownership disposition options: 1) Sale

Flip Charitable Remainder Unitrust

Flip Charitable Remainder Unitrust An Illustration of the Use of a Net Income with Makeup Charitable Remainder Unitrust that "Flips" or Converts to a Standard Charitable Remainder Unitrust in Year 10 AN

Flip Charitable Remainder Unitrust An Illustration of the Use of a Net Income with Makeup Charitable Remainder Unitrust that "Flips" or Converts to a Standard Charitable Remainder Unitrust in Year 10 AN

CONVENIENCE TRANSLATION INTO ENGLISH OF CONDENSED INTERIM CONSOLIDATED FINANCIAL STATEMENTS ORIGINALLY ISSUED IN TURKISH

CONVENIENCE TRANSLATION INTO ENGLISH OF CONDENSED INTERIM CONSOLIDATED FINANCIAL STATEMENTS ORIGINALLY ISSUED IN TURKISH CONDENSED CONSOLIDATED BALANCE SHEETS AT 30 SEPTEMBER 2017 AND 31 DECEMBER 2016

CONVENIENCE TRANSLATION INTO ENGLISH OF CONDENSED INTERIM CONSOLIDATED FINANCIAL STATEMENTS ORIGINALLY ISSUED IN TURKISH CONDENSED CONSOLIDATED BALANCE SHEETS AT 30 SEPTEMBER 2017 AND 31 DECEMBER 2016

Distributions. 9/28/2012 (c) William P. Streng 1

William P. Streng 1") Chapter 4 Nonliquidating Distributions Dividends - i.e., operating distributions See IRC 301(a) - Subchapter C, Part A. Alternative dividend classification systems: 1) Federal income tax income tax; e&p

Chapter 4 Nonliquidating Distributions Dividends - i.e., operating distributions See IRC 301(a) - Subchapter C, Part A. Alternative dividend classification systems: 1) Federal income tax income tax; e&p

Entertainment and Meals

Entertainment and Meals Entertainment. Deductions are eliminated for entertainment expenses under Sec. 274(a)(1) expenses directly related to or associated with entertainment. Effective: Amounts incurred

Entertainment and Meals Entertainment. Deductions are eliminated for entertainment expenses under Sec. 274(a)(1) expenses directly related to or associated with entertainment. Effective: Amounts incurred

FINANCIAL RESULTS. Consolidated Financial Statements - Fiscal Year Ended March 31, Consolidated Balance Sheets

FINANCIAL RESULTS Consolidated Financial Statements - Fiscal Year Ended March 31, 2007-1. Consolidated Balance Sheets (ASSETS) Prior Year End Current Year End (As of March 31, 2006) (As of March 31, 2007)

FINANCIAL RESULTS Consolidated Financial Statements - Fiscal Year Ended March 31, 2007-1. Consolidated Balance Sheets (ASSETS) Prior Year End Current Year End (As of March 31, 2006) (As of March 31, 2007)

POU CHEN CORPORATION AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS March 31, 2013 December 31, 2012 March 31, 2012 January 1, 2012 ASSETS Amount % Amount % Amount % Amount % CURRENT ASSETS Cash and cash equivalents (Notes 4 and 6) $ 29,346,249

CONSOLIDATED BALANCE SHEETS March 31, 2013 December 31, 2012 March 31, 2012 January 1, 2012 ASSETS Amount % Amount % Amount % Amount % CURRENT ASSETS Cash and cash equivalents (Notes 4 and 6) $ 29,346,249

CONSOLIDATED BALANCE SHEET

CONSOLIDATED BALANCE SHEET December 31, 2018 A S S E T S CURRENT ASSETS: Cash and time deposits 51,215 Accounts receivable-trade 95,065 Inventories 5,405 Short-term loans receivable 43,021 Deferred tax

CONSOLIDATED BALANCE SHEET December 31, 2018 A S S E T S CURRENT ASSETS: Cash and time deposits 51,215 Accounts receivable-trade 95,065 Inventories 5,405 Short-term loans receivable 43,021 Deferred tax

Financial Statement Balance Sheet

Financial Statement Balance Sheet Accounting Title 2014/3/31 2013/12/31 2013/3/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 4,556,450 4,372,738 3,960,180

Financial Statement Balance Sheet Accounting Title 2014/3/31 2013/12/31 2013/3/31 Balance Sheet Assets Current assets Cash and cash equivalents Total cash and cash equivalents 4,556,450 4,372,738 3,960,180

Table 1 HARRIS CORPORATION FY '18 First Quarter Summary CONDENSED CONSOLIDATED STATEMENT OF INCOME (Unaudited)

") Table 1 CONDENSED CONSOLIDATED STATEMENT OF INCOME September 29, 2017 (In millions, except per share amounts) Revenue from product sales and services $ 1,413 $ 1,420 Cost of product sales and services

Table 1 CONDENSED CONSOLIDATED STATEMENT OF INCOME September 29, 2017 (In millions, except per share amounts) Revenue from product sales and services $ 1,413 $ 1,420 Cost of product sales and services

Consolidated Financial Statements and Primary Notes

Consolidated Financial Statements and Primary Notes (1) Consolidated Balance Sheet (As of March 31, 2017) Second Quarter of (As of Assets Current assets Cash and deposits 344,093 401,566 Notes and accounts

Consolidated Financial Statements and Primary Notes (1) Consolidated Balance Sheet (As of March 31, 2017) Second Quarter of (As of Assets Current assets Cash and deposits 344,093 401,566 Notes and accounts

SEAGATE TECHNOLOGY PLC CONDENSED CONSOLIDATED BALANCE SHEETS

CONDENSED CONSOLIDATED BALANCE SHEETS (In millions) ASSETS Current assets: Cash and cash equivalents $ 1,125 $ 2,479 Short-term investments 6 6 Accounts receivable, net 1,318 1,735 Inventories 868 993

CONDENSED CONSOLIDATED BALANCE SHEETS (In millions) ASSETS Current assets: Cash and cash equivalents $ 1,125 $ 2,479 Short-term investments 6 6 Accounts receivable, net 1,318 1,735 Inventories 868 993

Distributions. 10/1/13 (c) William P. Streng 1

William P. Streng 1") Chapter 4 Nonliquidating Distributions Dividends - i.e., operating distributions See IRC 301(a) - Subchapter C, Part A. Alternative dividend classification systems: 1) Federal income tax income tax; &

Chapter 4 Nonliquidating Distributions Dividends - i.e., operating distributions See IRC 301(a) - Subchapter C, Part A. Alternative dividend classification systems: 1) Federal income tax income tax; &

Table 1 HARRIS CORPORATION FY '17 Third Quarter Summary CONDENSED CONSOLIDATED STATEMENT OF INCOME (Unaudited)

") Table 1 CONDENSED CONSOLIDATED STATEMENT OF INCOME Quarter Ended Three Quarters Ended March 31, 2017 April 1, 2016 (A) March 31, 2017 April 1, 2016 (A) (In millions, except per share amounts) Revenue from

Table 1 CONDENSED CONSOLIDATED STATEMENT OF INCOME Quarter Ended Three Quarters Ended March 31, 2017 April 1, 2016 (A) March 31, 2017 April 1, 2016 (A) (In millions, except per share amounts) Revenue from

CONSOLIDATED FINANCIAL STATEMENTS These Consolidated Financial Statements were publicly released in the Japanese language on November 9, 2016.

CONSOLIDATED FINANCIAL STATEMENTS These Consolidated Financial Statements were publicly released in the Japanese language on November 9, 2016. (1)Consolidated balance sheet 2016/3/31 2016/9/30 Assets Current

CONSOLIDATED FINANCIAL STATEMENTS These Consolidated Financial Statements were publicly released in the Japanese language on November 9, 2016. (1)Consolidated balance sheet 2016/3/31 2016/9/30 Assets Current

Consolidated Financial Statements (1) Consolidated Balance Sheets

Consolidated Balance Sheets") Consolidated Financial Statements (1) Consolidated Balance Sheets End of consolidated (as of End of consolidated (as of Assets Current assets Cash and time deposits 25,726 34,157 Notes and accounts receivable

Consolidated Financial Statements (1) Consolidated Balance Sheets End of consolidated (as of End of consolidated (as of Assets Current assets Cash and time deposits 25,726 34,157 Notes and accounts receivable

Choice of Entity. Danny Santucci

Choice of Entity Danny Santucci Table of Contents Chapter 1 Sole Proprietorship... 1 Learning Objectives... 1 Introduction... 1 Advantages... 1 Disadvantages... 1 Formation... 1 Start-Up Expenses... 2

Choice of Entity Danny Santucci Table of Contents Chapter 1 Sole Proprietorship... 1 Learning Objectives... 1 Introduction... 1 Advantages... 1 Disadvantages... 1 Formation... 1 Start-Up Expenses... 2

Student Learning Outcomes

Chapter 2 Topic 1 Consolidated Statements: Date of Acquisition Dr. Chula King Advanced Accounting The University of West Florida 1 Student Learning Outcomes Net asset acquisition versus stock acquisition

Chapter 2 Topic 1 Consolidated Statements: Date of Acquisition Dr. Chula King Advanced Accounting The University of West Florida 1 Student Learning Outcomes Net asset acquisition versus stock acquisition

Course Level: Overview. This program is appropriate for professionals at all organizational levels. (24 Credits)

") Partnership Taxation Course Description & Study Guide The program will examine tax issues relating to the formation and operation of partnerships. Participants will gain a familiarity with basic areas

Partnership Taxation Course Description & Study Guide The program will examine tax issues relating to the formation and operation of partnerships. Participants will gain a familiarity with basic areas

Consolidated Balance Sheet - 1/2

Consolidated Balance Sheet March 31, 212 ASSETS CURRENT ASSETS: Cash and cash equivalents (Notes 8 and 19) Time deposits over three months (Note 19) Receivables (Note 19): Trade notes (Note 11) Trade accounts

Consolidated Balance Sheet March 31, 212 ASSETS CURRENT ASSETS: Cash and cash equivalents (Notes 8 and 19) Time deposits over three months (Note 19) Receivables (Note 19): Trade notes (Note 11) Trade accounts

NOL Treatment on Federal Corporate and Individual Tax Returns: Challenges for Preparers

NOL Treatment on Federal Corporate and Individual Tax Returns: Challenges for Preparers Navigating Computation, Sect. 382 Limitation, Carryback/Carryforward and Other Rules FRIDAY, NOVEMBER 16, 1:00-2:50

NOL Treatment on Federal Corporate and Individual Tax Returns: Challenges for Preparers Navigating Computation, Sect. 382 Limitation, Carryback/Carryforward and Other Rules FRIDAY, NOVEMBER 16, 1:00-2:50

Taxation of Corporations and their Shareholders

Taxation of Corporations and their Shareholders Documents for Lecture on Chapter 3 Property Dispositions UNC Charlotte MACC Program January 25, 2017 UNC Charlotte MACC Program Chapter 3 Lecture Materials-2017

Taxation of Corporations and their Shareholders Documents for Lecture on Chapter 3 Property Dispositions UNC Charlotte MACC Program January 25, 2017 UNC Charlotte MACC Program Chapter 3 Lecture Materials-2017

ITURAN LOCATION AND CONTROL LTD. Consolidated Interim Financial Statements as of June 30, 2017

Consolidated Interim Financial Statements as of June 30, 2017 Consolidated Financial Statements as of June 30, 2017 Table of Contents Page Consolidated Interim Financial Statements: Balance Sheets 2-3

Consolidated Interim Financial Statements as of June 30, 2017 Consolidated Financial Statements as of June 30, 2017 Table of Contents Page Consolidated Interim Financial Statements: Balance Sheets 2-3

Effective Tax Planning For Partnerships:

When used properly, an IRC 754 election can be an important tool for an estate planning or business planning attorney. It can make a big difference in the tax burden of a company s partners and should

When used properly, an IRC 754 election can be an important tool for an estate planning or business planning attorney. It can make a big difference in the tax burden of a company s partners and should

Tangible Property Regulations and Tax Update for the Oil and Gas Industry

and Tax Update for the Oil and Gas Industry Laura Roman, CPA, CMAP Partner, Tax and Strategic Business Services 0 Repair Regulations Affect almost all taxpayers Govern capitalizing and deducting expenditures

and Tax Update for the Oil and Gas Industry Laura Roman, CPA, CMAP Partner, Tax and Strategic Business Services 0 Repair Regulations Affect almost all taxpayers Govern capitalizing and deducting expenditures

Learning Objectives. LO1 Journalize and post closing entries for a service business organized as a proprietorship.

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Learning Objectives LO1 Journalize and post closing entries for a service business organized as a proprietorship. Lesson 8-1 Need for Permanent and Temporary Accounts Accounts used to accumulate information

Via Technologies, Inc. and Subsidiaries Consolidated Financial Statements for the Six Months Ended June 30, 2015 and 2014

Via Technologies, Inc. and Subsidiaries Consolidated Financial Statements for the Six Months Ended June 30, 2015 and 2014-1 - CONSOLIDATED BALANCE SHEETS June 30, 2015 (Reviewed) December 31, 2014 (Audited)

Via Technologies, Inc. and Subsidiaries Consolidated Financial Statements for the Six Months Ended June 30, 2015 and 2014-1 - CONSOLIDATED BALANCE SHEETS June 30, 2015 (Reviewed) December 31, 2014 (Audited)

ZORLU ENERJİ ELEKTRİK ÜRETİM A.Ş. CONDENSED INTERIM CONSOLIDATED BALANCE SHEETS AS OF 30 SEPTEMBER 2013 AND 31 DECEMBER 2012

CONDENSED INTERIM CONSOLIDATED BALANCE SHEETS AS OF 30 SEPTEMBER 2013 AND 31 DECEMBER 2012 Audited ASSETS Note 30.09.2013 31.12.2012 Current Assets 471,526 594,414 Cash and Cash Equivalents 5 172,119 187,379

CONDENSED INTERIM CONSOLIDATED BALANCE SHEETS AS OF 30 SEPTEMBER 2013 AND 31 DECEMBER 2012 Audited ASSETS Note 30.09.2013 31.12.2012 Current Assets 471,526 594,414 Cash and Cash Equivalents 5 172,119 187,379

ASPEED TECHNOLOGY INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS (In Thousands of New Taiwan Dollars) June 30, 2018 December 31, 2017 (Audited) June 30, 2017 June 30, 2018 December 31, 2017 (Audited) June 30, 2017 ASSETS Amount % Amount %

CONSOLIDATED BALANCE SHEETS (In Thousands of New Taiwan Dollars) June 30, 2018 December 31, 2017 (Audited) June 30, 2017 June 30, 2018 December 31, 2017 (Audited) June 30, 2017 ASSETS Amount % Amount %

Form 926 Reporting Transfers to Foreign Corporations: Avoiding Harsh Penalties

Form 926 Reporting Transfers to Foreign Corporations: Avoiding Harsh Penalties Ensuring Consistency Between FATCA, FBAR, Form 5471 and Other Foreign Asset Forms TUESDAY, AUGUST 30, 2016, 1:00-2:50 pm Eastern

Form 926 Reporting Transfers to Foreign Corporations: Avoiding Harsh Penalties Ensuring Consistency Between FATCA, FBAR, Form 5471 and Other Foreign Asset Forms TUESDAY, AUGUST 30, 2016, 1:00-2:50 pm Eastern

Table 1 HARRIS CORPORATION FY '19 First Quarter Summary CONDENSED CONSOLIDATED STATEMENT OF INCOME (Unaudited)

") Table 1 CONDENSED CONSOLIDATED STATEMENT OF INCOME September 28, September 29, (In millions, except per share amounts) Revenue from product sales and services $ 1,542 $ 1,410 Cost of product sales and

Table 1 CONDENSED CONSOLIDATED STATEMENT OF INCOME September 28, September 29, (In millions, except per share amounts) Revenue from product sales and services $ 1,542 $ 1,410 Cost of product sales and

RICHWAVE TECHNOLOGY CORPORATION

PARENT COMPANY ONLY BALANCE SHEETS September 30, 2018 (Reviewed) December 31, 2017 (Audited) September 30, 2017 (Reviewed) ASSETS Amount % Amount % Amount % CURRENT ASSETS Cash $ 475,477 24 $ 175,046 11

PARENT COMPANY ONLY BALANCE SHEETS September 30, 2018 (Reviewed) December 31, 2017 (Audited) September 30, 2017 (Reviewed) ASSETS Amount % Amount % Amount % CURRENT ASSETS Cash $ 475,477 24 $ 175,046 11

Saint Elizabeth Medical Center, Inc. For the Year Ended December 31, 2017

I N T E R I M U N A U D I T E D C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S Saint Elizabeth Medical Center, Inc. For the Year Ended December 31, 2017 Unaudited Consolidated Financial

I N T E R I M U N A U D I T E D C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S Saint Elizabeth Medical Center, Inc. For the Year Ended December 31, 2017 Unaudited Consolidated Financial

Tax reform. Supplement to KPMG s Handbook, Accounting for Income Taxes US GAAP. April 19, kpmg.com/us/frv

Tax reform Supplement to KPMG s Handbook, Accounting for Income Taxes US GAAP April 19, 2018 kpmg.com/us/frv Contents Contents Foreword... 1 About this supplement... 2 1. Overview and SEC relief... 4 2.

Tax reform Supplement to KPMG s Handbook, Accounting for Income Taxes US GAAP April 19, 2018 kpmg.com/us/frv Contents Contents Foreword... 1 About this supplement... 2 1. Overview and SEC relief... 4 2.

M&A Tax Aspects for Portfolio Companies

M&A Tax Aspects for Portfolio Companies November 26, 2008 Doron Sadan, Tax Partner The purpose of this document is to highlight certain U.S. Federal 1 tax issues and Israeli tax issues. The information

M&A Tax Aspects for Portfolio Companies November 26, 2008 Doron Sadan, Tax Partner The purpose of this document is to highlight certain U.S. Federal 1 tax issues and Israeli tax issues. The information

Taxable Canadian Corporation

Section 85 rollover Typical Scenarios Sole proprietorship converting to Corp Transferring assets with built in gain to a Corp (eg. Publicly traded stocks, intangible assets) Less Commonly seen: Transferring

Section 85 rollover Typical Scenarios Sole proprietorship converting to Corp Transferring assets with built in gain to a Corp (eg. Publicly traded stocks, intangible assets) Less Commonly seen: Transferring

Sales $ 407,444 $ 396,064 $ 1,602,580 $ 1,515,608 Cost of sales (258,660) (242,460) (1,021,230) (952,221)

(242,460) (1,021,230) (952,221)") CONSOLIDATED STATEMENTS OF INCOME (Unaudited) (Dollar amounts in thousands, except per share data) 2018 2017 2018 2017 Sales $ 407,444 $ 396,064 $ 1,602,580 $ 1,515,608 Cost of sales (258,660) (242,460)

CONSOLIDATED STATEMENTS OF INCOME (Unaudited) (Dollar amounts in thousands, except per share data) 2018 2017 2018 2017 Sales $ 407,444 $ 396,064 $ 1,602,580 $ 1,515,608 Cost of sales (258,660) (242,460)

Accounting Cheat Sheet

DIAGRAM OF TACCOUNTS Assets = Balance Sheet as of 12/31/20 Liabilit ies + = + Equity METHODS & ORGS Accrual basis Follows the matching principle and recognizes transactions as they occur (GAAP Method)

DIAGRAM OF TACCOUNTS Assets = Balance Sheet as of 12/31/20 Liabilit ies + = + Equity METHODS & ORGS Accrual basis Follows the matching principle and recognizes transactions as they occur (GAAP Method)

Federal Taxation on Disposition of Partnership Interests

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1994 Federal Taxation on Disposition of Partnership

College of William & Mary Law School William & Mary Law School Scholarship Repository William & Mary Annual Tax Conference Conferences, Events, and Lectures 1994 Federal Taxation on Disposition of Partnership

Taxation of Corporations and their Shareholders

Taxation of Corporations and their Shareholders Documents for Lecture on Chapter 7 Part 1. Dividends and other distributions Part 2. Stock Redemptions UNC Charlotte MACC Program Turner School of Accountancy

Taxation of Corporations and their Shareholders Documents for Lecture on Chapter 7 Part 1. Dividends and other distributions Part 2. Stock Redemptions UNC Charlotte MACC Program Turner School of Accountancy

Reporting Installment Sales and Repossessions

Reporting Installment Sales and Repossessions GAIL ABBOTT, EA FOR BLUE RIDGE CHAPTER OF VIRGINIA SOCIETY OF ENROLLED AGENTS OCTOBER 19, 2016 What is an Installment Sale? Sale of Property where you receive

Reporting Installment Sales and Repossessions GAIL ABBOTT, EA FOR BLUE RIDGE CHAPTER OF VIRGINIA SOCIETY OF ENROLLED AGENTS OCTOBER 19, 2016 What is an Installment Sale? Sale of Property where you receive