HCA Value for Money Metrics - Technical Note

|

|

|

- Dennis Wiggins

- 5 years ago

- Views:

Transcription

1 Consultation Response: HCA Value for Money Metrics - Technical Note Joseph Carr - November

2 The Author 2

3 Contents The Author... 2 Contents... 3 Executive Summary... 4 Introduction... 6 HCA VfM Metrics - Consultation... 8 Metric 1 Reinvestment % Metric 2 New supply delivered % Metric 3 Gearing % Metric 4 Earnings Before Interest, Tax, Depreciation, Amortisation, Major Repairs Included (EBITDA MRI) Interest Cover % Metric 5 Headline social housing cost per unit Metric 6 Operating Margin % Metric 7 Return on capital employed (ROCE) APPENDIX 1 About the David Tolson Partnership Limited APPENDIX 2 DTP s Treasury & Business Planning Team APPENDIX 3 DTP HCA Metrics for HousingBrixx APPENDIX 4 HCA VfM Metrics - Approach to Analysis APPENDIX 5 Sector Scorecard Working Group Indicators The HCA Metrics Calculator for HousingBrixx is available from DTP at dtp.uk.com 3

4 Executive Summary 1. The Homes and Communities Agency (HCA) is consulting on metrics which will allow the regulator to make meaningful comparisons of economy, efficiency and effectiveness across the sector based on information derived from the Annual Accounts Regulatory Returns Financial Viability Assessment (FVA) only. 2. The proposed Metrics form part of the 2017 Consultation on the Value for Money Standard. The HCA s stated intention is that the proposed VfM Standard would move the focus of the HCA s regulatory approach away from the primarily narrative selfassessment to include focused reporting by providers on targets, including a suite of metrics to be defined, from time to time, by the regulator. 3. The introduction of Value for Money Metrics (VfM Metrics) alongside the HCA s proposed VfM Standard are intended to enhance accountability, consistency and transparency across the sector. VfM Metrics are an improvement on the HCA s unit cost analysis as a means of assessing housing association performance. VfM Metrics should also improve value for money reporting consistency, currently delivered through each housing association s individual Value for Money Self- Assessment, for which there is no prescribed format. We understand that the HCA will also measure these proposed Metrics against FFR forecasts, which are not in the public domain and for reasons of confidentiality will not publish their findings. 4. With the approval of the organisations concerned, DTP has conducted an extensive review of FORECAST performance against the proposed HCA VfM Metrics, based on information extracted from 33 Financial Forecast Return business plans submitted by housing associations to the HCA in In our opinion these housing associations represent a reasonable cross section of the housing association sector. The DTP review reveals wide variations in the HCA VfM Metrics results which may make meaningful comparison difficult. 5. DTP s review of HCA VfM Metrics for 33 housing associations has confirmed a wide variation in results. On the face of it, the variation has much to do with differences in business models, appetite for risk, the type and age of the association, development activity etc. 6. The HCA acknowledges that no single set of Metrics can capture all the measures that matter to each individual association. Registered Providers will be required to set their own strategic objectives and report on them annually in their accounts. Individual housing associations will need to ensure that they include bespoke narrative to support their results, alongside the use of their own metrics and peer comparison as required at Paragraph 2.2 a) of the proposed new VfM Standard. Despite this we believe that there is a significant risk that the proposed VfM Metrics will be compared crudely and misused as a basis for housing association league tables. 7. Encouragingly, the proposed HCA VfM Metrics have been mainly drawn from Sector Scorecard indicators piloted by the Sector Scorecard Working Group (SSWG). Disappointingly the proposed HCA VfM Metrics are exclusively financial and exclude qualitative measures which are likely to be more important to tenants. 4

5 8. There are some specific technical issues. For example, VfM Metrics 1 and 2, which measure reinvestment and new homes developed respectively, improve on the corresponding SSWG indicators, as they include homes purchased, as well as homes developed. However, the proposed calculations need to be refined to eliminate errors, aid consistency and avoid double counting. 9. Section 2.2 a) of the proposed VfM Standard requires registered housing associations to: annually publish evidence in the statutory accounts to enable stakeholders to understand the provider s: a) Performance against its own value for money targets and any metrics set out by the regulator, and how that performance compares to peers; b) Measurable plans to address any areas of underperformance, including clearly stating any areas where improvements would not be appropriate and the rationale for this. In this report we have drawn attention to a higher than expected number of exceptions to the norm; all of which can be explained. 10. Our overall concern is that it is not possible to make meaningful comparisons of economy, efficiency and effectiveness from the metrics alone. The Metrics should facilitate greater transparency and consistency of performance reporting for all housing associations and their stakeholders, but it is clear that in addition to carefully selecting their own measures, each RP will need to provide careful explanation and interpretation where their FFR shows any areas of underperformance relative to the VfM metrics of their peers. 5

6 Introduction 11. This is the (DTP) response to the Value For Money Metrics Technical Note, issued by the Homes and Communities Agency (the HCA) on 27 September DTP is an independent consultancy providing high quality advice and support to affordable housing providers, charities and commercial organisations across the UK. Our mission is to help businesses improve and deliver better services to their customers. See Appendices 1 and 2 for further information about DTP. 13. DTP is pleased to respond to the informal consultation on the HCA VfM Metrics Technical Note. We welcome the approach taken by the HCA to introduce a suite of VfM Metrics to augment the proposed VfM Standard. This should enhance the accountability, consistency and transparency of reporting. 14. Section 2.2 a) of the proposed VfM Standard requires registered housing associations to: annually publish evidence in the statutory accounts to enable stakeholders to understand the provider s: a) Performance against its own value for money targets and any metrics set out by the regulator, and how that performance compares to peers; b) Measurable plans to address any areas of underperformance, including clearly stating any areas where improvements would not be appropriate and the rationale for this. 15. The SSWG has independently conducted a pilot exercise using a set of 15 efficiency and effectiveness indicators and they have published a report of the results from the pilot entitled Sector Scorecard analysis report The SSWG Scorecard has been designed to enable housing association boards to compare performance and efficiency of their peers. It is entirely based on historic information provided by the participants, some of which is not available from the statutory accounts and so could not form part of the HCA VfM Metrics. 16. Their report states that they will evaluate the results and the value of each measure by considering areas such as variability, timescale and calculation, as well as the proposed set of measures that the English Regulator is currently consulting on. They plan to make the Scorecard fully operational in The current SSWG indicators are detailed at Appendix The 15 SSWG Scorecard indicators are organised into five headings (A to E, each with 3 sub-divisions) which include predictable measures such as financial viability, productivity and profitability, but uniquely, also a measure for customer satisfaction. Post-Grenfell, the public s psyche is very keenly attuned to the needs of social housing residents and so, it is extremely difficult to exaggerate the importance of echoing the opinion of residents in order to provide greater accountability, consistency and transparency. 18. The proposed VfM Metrics consist of seven measures (two split into further subcategories) and they encompass all but seven of the SSWG indicators, although 6

7 the calculation of some indicators included in the Metrics differs. The missing SSWG indicators are self-excluded as the VfM Metrics are predicated on housing associations FVA submissions - for ease of regulatory compliance. 19. Specifically, the SSWG Scorecard indicators for occupancy, responsive repairs, rent collection, overhead spend, s invested in communities, s invested in new housing supply and customer satisfaction have been excluded from VfM Metrics. These measures, and perhaps indicators on health and safety and average rent and service charges, are precisely the ones likely to be of most interest to housing association residents. 20. Using the information in the Technical Note, DTP has created a HCA Metrics calculator in a HousingBrixx report for its clients (see Appendix 3). In contrast to the Sector Scorecard pilot and the HCA Metrics, which are both a look back exercise, the DTP HCA Metrics calculator HousingBrixx is forward-looking. It uses the proposed HCA Metrics and applies them to the client s business plan, thus providing a 30-year forecast of results. 21. Thirty three DTP clients agreed to share their business plan data anonymously, enabling DTP to carry out an extensive review and comparison of the HCA proposed metrics, based on information extracted from Financial Forecast Return business plans submitted to the HCA in For the purpose of this report we have focussed our comments on the first 10 years results. DTP s response to the Consultation is based on our analysis of the results; our approach to the analysis is shown in Appendix The 33 housing associations involved reflect the diversity of the sector as a whole, having the following characteristics: Varying in size, owning on average just over 11,000 homes; Based primarily in the North East and North West of England, but also including housing associations from the South East, South West and Scotland; and Are a mixture of both traditional and large scale voluntary transfer associations (LSVTs). 23. DTP s sample of 33 housing associations reveals the wide variation in activity that would be anticipated, given the range of organisations involved. This varies from a relatively new LSVT with an ongoing decent homes programme, a small black and minority ethnic housing association, through to a regional housing association with a complex group structure and a very active development programme. To compare the activities of RPs without a narrative on their profile would be crude - at best meaningless and at worst misleading. Given the HCA s requirement for explaining underperformance, it could lead to a situation where each individual entity will need make the case as to why it is not average (if that were the case). In our opinion, highlighting differences is likely to encourage a greater convergence in performance rather than exceptional performance because RPs might prefer to look average to avoid additional scrutiny by the HCA. 24. The rich vein of information collected by DTP from the review allows us to be broadly supportive of the approach taken by the HCA. Nonetheless, we offer a number of considerations and recommendations in the following sections which we feel will be important for implementation of VfM Metrics to be meaningful. 7

8 HCA VfM Metrics - Consultation 25. To help explain the HCA s approach to the proposed VfM Metrics, the Consultation Paper Technical Note contains the following introduction: 1.1. Alongside the proposed changes to the Value for Money Standard the regulator is proposing to introduce a separate document setting out a limited number of metrics to measure economy, efficiency and effectiveness on a comparable basis across the sector The Value for Money (VfM) metrics suite would provide a new tool for registered providers to demonstrate that they are making best use of their assets and resources to stakeholders, including tenants and the regulator. These metrics will not form part of the Standard itself. This technical note sets out the details of the range of metrics that the regulator could use, including the calculation of each measure, and the source of the data We recognise the sector s diversity and understand that no single set of metrics can capture all of the measures that matter to each individual association. The proposed changes to the VfM Standard would, subject to the outcome of the consultation launched on 27 September 2017, require registered providers to set their own strategic objectives and report on progress on these targets annually in their accounts. This approach would permit individual providers to report on their own bespoke targets, which reflect the individual needs of the organisation, and might include, for example: progress on particular development, regeneration or major repairs schemes; housing quality; or tenant satisfaction The proposed set of standard metrics defined by the regulator is intended to achieve the different, but complementary, objective of providing measures with wide applicability which permit comparison across the sector. In combination with each provider s own published strategic targets, these standard metrics will allow interested stakeholders to not only review the progress of each provider in terms of its own objectives, but also do so in the context of common performance measures that permit meaningful comparison with other organisations The regulator has therefore used a number of principles to select this range of measures. The regulator has sought to use existing regulatory data in order to minimise interference and potential burdens on providers. The proposed suite of VfM metrics is therefore restricted to data derived from registered providers Annual Accounts regulatory returns Financial Viability Assessment (FVA) only The regulator proposes to use FVA data as the basis of the metrics because it is derived from existing audited accounts. There would therefore be no additional data collection requirements for providers and all metrics are derived from data that is already in the public domain in providers own accounts and the Global Accounts data-set. In devising the metrics, we have ensured that they can be calculated by all providers from existing data Whilst no range of measures can be completely exhaustive, the selection of metrics is intended to support understanding of a range of different components of Value for Money (economy, efficiency and effectiveness). Our role in relation to consumer regulation is limited by statute. Consequently the Value for Money metrics primarily focus on financial and output measures which can be derived from FVA returns that providers already submit to the regulator. The metrics include output measures alongside cost data, and measures of the efficiency with which providers use both their resources and their assets. This includes the degree of investment by registered providers to existing stock as well as new supply. The regulator recognises that providers will also have a range of other, often non-financial, measures to monitor their performance which they can also set out as part of their wider value for money reporting to stakeholders Registered providers financial performance is based upon their activity across a range of business streams, including non-social housing activity in unregistered subsidiaries and joint ventures. Providing a full picture of the value for money of the provider s activity therefore involves taking a view across this full range of business streams. The majority of metrics are therefore set at group level and take account of non-social housing income and expenditure as 8

9 well as social housing. However, there are a number of core activities common to all providers, principally social housing lettings. In order to permit like for like comparison on this core function, the headline social housing cost per unit metric is based on social housing activity only 26. The consultation seeks feedback on the proposed selection of metrics and their calculation. In particular, the HCA would welcome views on whether the proposed suite of measures captures the key aspects of performance, or whether there are other measures, derived from FVA data, that should be included instead. 27. The following section of this report describes each of the proposed HCA VfM metrics and comments on them in turn. In addition to an opinion on whether the proposed suite of measures capture meaningful aspects of performance, (economy, efficiency and effectiveness) we have also commented on their limitations. 9

10 Metric 1 Reinvestment % HCA explanation - This metric looks at the investment in properties (existing stock as well as new supply) as a percentage of the value of total properties held. 28. VfM Metric 1 - Reinvestment % does not align directly to a SSWG indicator. This Metric looks at the total investment in properties as a percentage of the value of properties held, thus providing an alternative investment measurement to SSWG indicators B1 and B2, Chart 1: DTP analysis VfM Metric 1 30% 25% 20% 15% 10% 5% 0% Metric 1 - Reinvestment % Standard deviation Mean Min Max 29. VfM Metric 1 Reinvestment does not appear to be a good indicator of economy, efficiency and effectiveness: RPs with data points below the mean are not necessarily underinvesting; and RPs above the mean are not necessarily over-spending. The age and history of the existing stock and rate of delivery of new stock will influence the data. Around 68% of the data points are within One Standard Deviation (1xSD) of the mean and this is a consistent result across the 10 years. This metric has the least correlation of all the proposed HCA VfM metrics. 32% or over 3 in 10 have a poor correlation, this would seem to be a high proportion for this to be used as a metric for any meaningful comparison. By including both existing stock and new supply the result can be easily distorted; development activity, even in large RPs, is rarely evenly spread. The first 4 data points of the max line is a Large Scale Voluntary Transfer (LSVT) with an exceptional investment programme in the first 4 years. The cost of new units, or their net income, both a good measure of economy, would be invisible under this measure. 10

11 Metric 2 New supply delivered % HCA explanation The New supply metric sets out the number of new social housing and non-social housing units that have been acquired or developed in the year as a proportion of total social housing units and non-social housing units managed at period end. It is proposed that registered providers will report on two New supply ratios: A) New supply delivered (Social housing units) B) New supply delivered (Non-social housing units) 30. VfM Metric 2 - New supply delivered % is aligned to SSWG indicator B2, Units Developed (as % of units owned). However, there are a number of key differences: Metric 2 improves on the corresponding SSWG indicator as it includes homes acquired as well as homes developed; It is usefully subdivided into two metrics, one for social housing and one for nonsocial housing. This would capture commercial activity (often carried out in joint ventures), which housing associations are increasingly engaged in as a means of funding regulated activity; and The total homes acquired/developed is divided by total homes in management at the year-end. 31. VfM Metric 2 is potentially superior to the corresponding SSWG indicator, as it reflects total investment in homes developed as well as acquired. This is particularly relevant to smaller housing associations, which tend to increase supply by purchasing homes off-the-shelf. However, the definition for Metric 2 should be refined to calculate genuinely new supply divided by properties owned (to eliminate transfers between associations). Chart 2A: DTP analysis VfM Metric 2A 7% 6% 5% 4% 3% 2% 1% 0% Metric 2A) New Supply Delivered % (Social housing units) Standard deviation Mean Min Max 11

12 32. Expressing Metric 2 as a percentage of total stock holdings allows, for example, new housing supply of housing associations of differing sizes to be more readily compared. However, it is unclear why Metric 2 uses homes in management at the year-end as the denominator as opposed to homes owned (as in the SSWG indicator). The latter would seem more logical as the numerator will include all homes owned by the association owned and managed. 33. VfM Metric 2 New supply delivered % does not appear to be a good indicator of economy, efficiency and effectiveness: All of the providers in our sample forecast have at least some development activity. Half of the providers forecast no development beyond 2023; this is not necessarily lack of ambition and may reflect a decision to model committed developments only, to demonstrate compliance with the HCA 18 month liquidity measure. Initially around 78% of the data points are within 1xSD of the mean; however, this increases to over 85% within 5 years. The previous bullet point suggests that this outturn is influenced more by financial modelling preferences than actual development appetite. The max line in 2018 is a small RP with a large development completing in that year only, the max line in 2019 is a medium size RP with a large development completing in that year only. 34. Whilst there is a further metric, 2B) New Supply Delivered (Non-social housing units), the results of this analysis are skewed as the numerator includes outright sale units but the denominator (non-social housing units managed at the period end) has no carrying balance of outright sales units. 12

13 Metric 3 Gearing % HCA explanation This metric assesses how much of the adjusted assets are made up of debt and the degree of dependence on debt finance. It is often a key indicator of a registered provider s appetite for growth 35. VfM Metric 3 Gearing % is identical to the corresponding SSWG indicator B3, Gearing. DTP s sample of 33 housing associations shows a spread in gearing, typical of the sector. 36. In our assessment, housing association gearing appears to vary due to the business model, appetite for risk, type and age of the association, loan covenant restrictions, margins achieved, development activity, etc. and is simply an indicator of appetite for growth. Chart 3: DTP analysis VfM Metric 3 100% 90% 80% 70% 60% 50% 40% 30% 20% 10% 0% Metric 3 - Gearing % Standard deviation Mean Min Max 37. VfM Metric 3 - Gearing % does not appear to be a good indicator of economy, efficiency and effectiveness: This metric has been adopted by some lenders as a financial covenant, which is more likely to influence borrowing appetite. The HCA believes this to be a key indicator of appetite for growth. Gearing might be interpreted as a key indicator of capacity; it cannot indicate appetite for growth, which would be predicated on an RP s willingness to take on risk. 73% of our sample of RPs fall within 1xSD of the mean and there is a wide range between max and min, with significant outliers. The max line is a mature LSVT in the North of England that has undertaken a regular programme of development since transfer. The min line is a group that includes a mature LSVT in its group structure. The LSVT has minimal opportunities for development. The DTP review emphasises the need for detailed narrative to accompany the VfM Metrics, along with the identification of appropriate peers from which to draw meaningful comparison and identify best practice, to drive up standards. 13

14 Metric 4 Earnings Before Interest, Tax, Depreciation, Amortisation, Major Repairs Included (EBITDA MRI) Interest Cover % HCA explanation The EBITDA MRI interest cover measure is a key indicator for liquidity and investment capacity. It seeks to measure the level of surplus that a registered provider generates against interest payments (the measure avoids any distortions stemming from the depreciation charge). 38. VfM Metric 4 - EBITDA MRI interest Cover % is identical to the corresponding SSWG indicator A3, EBITDA MRI (as % interest). 39. The DTP review reveals a typical spread in interest cover amongst the 33 housing associations this is more a reflection of the range of legitimate social missions and operating environments than on inherent differences in performance. Chart 4: DTP analysis VfM Metric % Metric 4 - EBITDA MRI Interest Cover % 900% 700% 500% 300% 100% -100% -300% -500% Standard deviation Mean Min Max 40. VfM Metric 4 - Earnings Before Interest, Tax, Depreciation, Amortisation, Major Repairs Included (EBITDA MRI) Interest Cover % appears to be a good indicator of capacity but is not either an indicator of liquidity or a measure of economy, efficiency and effectiveness: This metric has been adopted by many lenders as a financial covenant. 80% of our sample of RPs fall within 1xSD of the mean. This metric has the greatest correlation of all the chosen metrics and the correlation improves over time. The max line is one LSVT in the early years and another in later years. The min line is an LSVT that does not have this metric as a covenant ratio in its loan agreement. 41. The narrow range of the standard deviation compared to the other metrics and the adoption of this metric by lenders as a financial covenant, leads us to believe that housing associations are tailoring their capacity to meet a covenant target built on this metric. However, the danger is that an unsophisticated commentator might misinterpret this Metric in the absence of sufficient context. 14

15 Metric 5 Headline social housing cost per unit HCA explanation The unit cost metric assesses the headline social housing cost per unit as defined by the regulator 42. This metric is unlike the others in that it gives no context for being proposed as a metric, presumably because it is already commonly used. 43. VfM Metric 5 Headline Social Housing Cost Per Unit is identical to the corresponding SSWG indicator E1, Headline social housing cost per unit. DTP s review showed one association with social housing cost per unit that was consistently 30% below the mean and, at the other extreme, an association with costs 60% above the mean, with significant variation between. Chart 5: DTP analysis VfM Metric 5 6,000 5,000 4,000 3,000 2,000 1,000 0 Metric 5 - Headline social housing cost per unit Standard deviation Mean Min Max 44. VfM Metric 5 - Headline social housing cost per unit appears to be a good comparator, but without some background explanation and an understanding of the RP is not a good indicator of economy, efficiency and effectiveness: 72% of our sample of RPs fall within 1xSD of the mean. However, the correlation to the mean reduces over time. The max line is one LSVT in the early years and a London based housing association from year 3 onwards. The min line is a mature urban LSVT in the early years, in later years it is a small urban housing association; in both cases they are located in the North of England. Associations with higher costs were often specialist and more urban-centred, but not invariably so. The use of all Metrics must always be as a can-opener to investigate perceived variances from the average amongst peers. 15

16 Metric 6 Operating Margin % HCA explanation The Operating Margin demonstrates the profitability of operating assets before exceptional expenses are taken into account. Increasing margins are one way to improve the financial efficiency of a business. In assessing this ratio, it is important that consideration is given to registered providers purpose and objectives (including their social objectives). Further consideration should also be given to specialist providers who tend to have lower margins than average. It is proposed that registered providers will report on two Operating Margin ratios: A) Operating Margin (social housing lettings only) B) Operating Margin (overall) 45. VfM Metric 6A and 6B Operating margin % is the equivalent to the two SSWG indicators A1 and A2, Operating margin (overall) and Operating margin (social housing units) as it is also further sub-divided into an overall operating margin and a social housing operating margin. Chart 6A: DTP analysis VfM Metric 6A 50% 40% 30% 20% 10% 0% -10% Metric 6A) Operating margin % (social housing lettings only) Standard deviation Mean Min Max 46. VfM Metric 6A Operating margin % social housing lettings only appears to be a good headline comparator because it is easily understood; without some explanation it is not a good indicator of economy, efficiency and effectiveness: This is one of the components of metric 4 but shows less correlation in metrics 6A and 6B than in metric 4. The correlation to the mean worsens over time, this is the opposite to metric 4. 68% of our sample of RPs fall within 1xSD of the mean compared to 80% of metric 4. This could be explained by differentials in rent levels. The income part of operating margin is controlled; realistically therefore only reductions in costs could be used to improve the ratio. Therefore, this is only a 16

17 relative measure of operating costs to income. Changes to operating margin over time would be worth explaining but comparisons between housing associations should be undertaken with care. The min line is mainly one immature LSVT whose rents are low because they have not converged. The max line is a small urban housing association in early years and a large but more rural housing association in later years. VfM Metric 6B Operating margin % (overall) (Chart 6B below) shows an almost identical position to Chart 6A. Chart 6B: DTP analysis VfM Metric 6B 50% 45% 40% 35% 30% 25% 20% 15% 10% 5% 0% -5% Metric 6B) - Operating margin (overall) Standard deviation Mean Min Max 47. In theory the DTP review perhaps could have revealed a wider variation in the overall operating margin than the social housing operating margin. This might be expected, as housing associations are involved in varying degrees with non-social activity and this would be apparent from published mission statements. However in reality the differences between the two metrics appear to be slight. 17

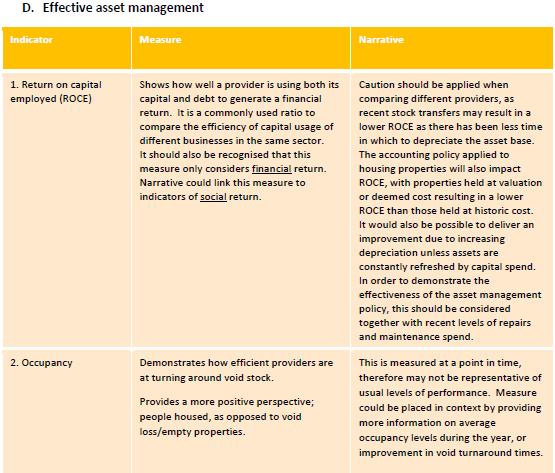

18 Metric 7 Return on capital employed (ROCE) HCA explanation This metric compares operating surplus to total assets less current liabilities and is a common measure in the commercial sector to assess the efficient investment of capital resources. The ROCE metric would support registered providers with a wide range of capital investment programmes 48. VfM Metric 7 Return on Capital Employed (ROCE) is identical to the corresponding SSWG indicator D1, ROCE. Chart 7: DTP analysis VfM Metric 7 11% 9% 7% 5% 3% 1% -1% Metric 7 - Return on capital employed (ROCE) Standard deviation Mean Min Max 49. VfM Metric 7 - Return on capital employed (ROCE) appears to be a good headline comparator, but without explanation is not a good indicator of economy, efficiency and effectiveness: 75% of our sample of RPs fall within 1xSD of the mean. This correlation remains static over time. The max line is distorted by an LSVT that has not completed its investment programme. The min line is a rural ex LSVT. 50. This metric ignores interest payable which can be a key difference between housing associations overall net return. However, with this degree of variation, stakeholders would benefit from knowing more about the reporting housing association to make a useful comparison. 18

19 APPENDIX 1 About the David Tolson Partnership Limited Established in 2006, the David Tolson Partnership Limited ( DTP ) is an independent consultancy providing high quality advice and support to affordable housing providers, charities and commercial organisations across the UK. Our mission is to help businesses improve and deliver better services to their customers. The business was set up by David Tolson, who has over 30 years experience in the housing sector. David was previously the Managing Director of Tribal s Housing and Local Government Consultancy, and before that a Group Director of what is now the Places for People Group. Our core team are all experienced practitioners who understand organisational pressures and constraints and have operated at Board and/or Management team level in complex organisations. We believe this differentiates us from our competitors and gives us a unique place in the market. We recognise the need to provide practical innovative solutions and to support their implementation. We pride ourselves on always providing a bespoke and client specific service, and seek to work in long-term productive partnerships. DTP is Authorised and Regulated by the Financial Conduct Authority (authorised firm reference number ). Further information on DTP can be found at

20 APPENDIX 2 DTP s Treasury & Business Planning Team DTP s Treasury and Business Planning team comprises seven experienced professionals who between them provide treasury and business planning support to over a wide range of clients throughout the UK. Adrian Jolliffe (a.jollliffe@dtp.uk.com ), is the Director responsible for the team. He is a recognised expert in treasury management in the social housing sector. Prior to joining DTP in 2008, Adrian had 10 years experience as a senior consultant and Director at Tribal Treasury Services and 20 years experience in financial services, working at a senior level in Barclays Bank and Nationwide Building Society. Clive Eccleston (c.eccleston@dtp.uk.com ), has worked in financial services for more than 30 years. Clive s experience in treasury, finance and business planning is far reaching and includes staff and board member training, evaluation and renegotiation of loan portfolios including covenants, and creation of group borrowing vehicles. Andy Chapman (a.chapman@dtp.uk.com ), has worked with housing associations and local authorities for more than 20 years. He is a specialist in financial planning and modelling and an expert in the use of HousingBrixx. He has developed many bespoke spreadsheet models for areas such as rent setting and asset management, through to full business planning models. Richard Skinner (r.skinner@dtp.uk.com ), has over 30 years experience in the housing sector, working for and with many housing associations in the North of England and Scotland. He is an experienced financial model builder and advanced spreadsheet and HousingBrixx user, specialising in finance and business plan modelling. Sue Thiele (s.thiele@dtp.uk.com ), is an experienced senior finance manager, having worked in social housing for more than 18 years. Her specialisms are treasury management, financial planning and providing interim support. She has experience in managing large group loan portfolios and the implementation and update of both individual and consolidated business plans of complex group structures using either HousingBrixx or Excel. Alison Jennings (a.jennings@dtp.uk.com ), is a treasury specialist with more than 18 years experience in the social housing sector. Prior to joining DTP, Alison worked for the Homes and Communities Agency as a Senior Financial Analyst. She has also worked in a number of treasury roles for North West Housing Associations and has experience in the management of group loan portfolios, cashflow forecasting and liquidity management and business plan modelling using HousingBrixx. Paul Hackett (p.hackett@dtp.uk.com ) has almost 20 years experience of social housing finance with a background that encompasses both local authorities and housing associations. Paul has extensive experience in long term financial planning, financial modelling, capital scheme appraisals, housing transfers, compiling bids and risk analysis. He has expertise in both Excel and HousingBrixx based models. 20

21 APPENDIX 3 DTP HCA Metrics for HousingBrixx VALUE FOR MONEY METRICS - SUMMARY Metric 1 - Reinvestment % Metric 2A) - New supply delivered % (Social housing units) Metric 2B) - New supply delivered % (Non-social housing units) Metric 3 - Gearing % Metric 4 - EBITDA-MRI Interest Cover % Metric 5 - Headline social housing cost per unit a) Management cost per unit b) Service charge cost per unit c) Maintenance cost per unit d) Major Repairs cost per unit e) Other social housing cost per unit Metric 6A) Operating Margin % (social housing lettings only) Metric 6B) Operating Margin % (overall) Metric 7 Return on Capital Employed (ROCE) BUSINESS PLAN ASSUMPTIONS CPI RPI LIBOR 21

22 APPENDIX 4 HCA VfM Metrics - Approach to Analysis The information used in the analysis is extracted from financial forecasts in HousingBrixx. Although 30 years information is available we have chosen to compare the first 10 years. To try and make the analysis accessible to non-specialists we have chosen to limit the scope of our analysis to the following comparative measures: Mean the diagrams show the unweighted average of the data in each year. Range the diagrams show the highest and lowest in the range of data, either side of the mean. Standard Deviation* in each case we have calculated 1 x SD. The diagrams show how uniform (or not) a range of data points are, relative to the average (mean). Percentage within 1 X SD we refer to the proportion of data points that fall within 1 x SD. A narrow band either side of the mean indicates that most of the data points are very close to the average and so are highly correlated. A wide standard deviation band means that the numbers are spread out and less correlated. It would suggest a lack of uniformity and that any comparison to this measure may therefore prove to be little better than comparison to a random distribution. *To calculate the standard deviation of a range of numbers: Work out the Mean (the simple average of the numbers) Then for each number: subtract the Mean and square the result. Then work out the mean of those squared differences. Calculate the square root of the result. Alternatively in excel, use the formula =STDEV(A1:A2) where A1:A2 is the range you want to calculate. 22

23 APPENDIX 5 Sector Scorecard Working Group Indicators 23

24 24

25 25

Strategic report (continued)

") Strategic report (continued) Value for Money (VFM) The Association annually reviews its. The Board comprehensively updated these during 2017/18 as part of the development of a new over-arching strategy

Strategic report (continued) Value for Money (VFM) The Association annually reviews its. The Board comprehensively updated these during 2017/18 as part of the development of a new over-arching strategy

THE GROWING IMPORTANCE OF GROUP STRUCTURE ARRANGEMENTS IN THE HOUSING ASSOCIATION SECTOR IN ENGLAND

THE GROWING IMPORTANCE OF GROUP STRUCTURE ARRANGEMENTS IN THE HOUSING ASSOCIATION SECTOR IN ENGLAND This sector study summarises what was learnt about Housing Association (HA) group structures during the

THE GROWING IMPORTANCE OF GROUP STRUCTURE ARRANGEMENTS IN THE HOUSING ASSOCIATION SECTOR IN ENGLAND This sector study summarises what was learnt about Housing Association (HA) group structures during the

Global accounts of housing associations 2007

Global accounts of housing associations 2007 THE NATIONAL AFFORDABLE HOMES AGENCY March 2008 p1 Global accounts of housing associations 2007 Contents Introduction A B Executive summary Operating and financial

Global accounts of housing associations 2007 THE NATIONAL AFFORDABLE HOMES AGENCY March 2008 p1 Global accounts of housing associations 2007 Contents Introduction A B Executive summary Operating and financial

Railway Housing Association. Value for Money Strategy

Railway Housing Association Value for Money Strategy 2016-21 1 Executive Summary 1.1 Railway Housing Association (RHA) recognises that Value for Money (VFM) is a fundamental consideration for all housing

Railway Housing Association Value for Money Strategy 2016-21 1 Executive Summary 1.1 Railway Housing Association (RHA) recognises that Value for Money (VFM) is a fundamental consideration for all housing

A Proposed Performance and Accountability Frameworkfor Community Development Finance in the UK

A Proposed Performance and Accountability Frameworkfor Community Development Finance in the UK by Sam Colin, Danyal Sattar, Thomas Fisher and Ed Mayo, NEF and Andy Mullineux, University of Birmingham research

A Proposed Performance and Accountability Frameworkfor Community Development Finance in the UK by Sam Colin, Danyal Sattar, Thomas Fisher and Ed Mayo, NEF and Andy Mullineux, University of Birmingham research

Guidance from the HCA Understanding unit costs is an increasingly important part of the HCA s assessment of VfM.

Key points: Value for Money (VfM) reporting is still of variable quality. VfM benchmarking is now common practice. More RPs now provide a return on assets and plans of how to deal with underperforming

Key points: Value for Money (VfM) reporting is still of variable quality. VfM benchmarking is now common practice. More RPs now provide a return on assets and plans of how to deal with underperforming

Value for Money Statement Year to 30 th September 2017

Value for Money Statement Year to 30 th September 2017 Introduction The Hyelm Group is committed to finding ways to provide excellent services whilst at the same time seeking to reduce costs and improve

Value for Money Statement Year to 30 th September 2017 Introduction The Hyelm Group is committed to finding ways to provide excellent services whilst at the same time seeking to reduce costs and improve

Outline Capital Investment Strategy

Outline Capital Investment Strategy INDEX FOREWORD 1. INTRODUCTION 2. PURPOSE 3. SUMMARY 4. INFLUENCES ON CAPITAL INVESTMENT 5. CURRENT CAPITAL EXPENDITURE 6. COMMERCIAL PROPERTY INVESTMENT STRATEGY 7.

Outline Capital Investment Strategy INDEX FOREWORD 1. INTRODUCTION 2. PURPOSE 3. SUMMARY 4. INFLUENCES ON CAPITAL INVESTMENT 5. CURRENT CAPITAL EXPENDITURE 6. COMMERCIAL PROPERTY INVESTMENT STRATEGY 7.

Value for Money self-assessment

Value for Money self-assessment 2016-17 1 Contents 1. Introduction 2. Our approach to VfM 3. The regulatory requirements 4. How we make the best use of our assets 5. How our operating costs compare to

Value for Money self-assessment 2016-17 1 Contents 1. Introduction 2. Our approach to VfM 3. The regulatory requirements 4. How we make the best use of our assets 5. How our operating costs compare to

National Housing Federation submission to the second consultation on the tax deductibility of corporate interest expense

4 August 2016 National Housing Federation submission to the second consultation on the tax deductibility of corporate interest expense Submission by email: BEPSinterestconsultation@hmtreasury.gsi.gov.uk

4 August 2016 National Housing Federation submission to the second consultation on the tax deductibility of corporate interest expense Submission by email: BEPSinterestconsultation@hmtreasury.gsi.gov.uk

Social Housing Financial State of the Sector FY16/17

Social Housing Financial State of the Sector FY16/17 Presenting the definitive headline financial results from the Vantage Global Accounts Plus analysis. October 2017 yourvantage.co.uk Contents Introduction

Social Housing Financial State of the Sector FY16/17 Presenting the definitive headline financial results from the Vantage Global Accounts Plus analysis. October 2017 yourvantage.co.uk Contents Introduction

BUSINESS PLAN 2018/ /23

Warwickshire Rural Housing Association BUSINESS PLAN 2018/19 2022/23 Tel: 0300 1234 009 Website: www.warwickshirerha.org.uk Twitter: Follow @WarksRural WARWICKSHIRE RURAL HOUSING ASSOCIATION BUSINESS PLAN

Warwickshire Rural Housing Association BUSINESS PLAN 2018/19 2022/23 Tel: 0300 1234 009 Website: www.warwickshirerha.org.uk Twitter: Follow @WarksRural WARWICKSHIRE RURAL HOUSING ASSOCIATION BUSINESS PLAN

Value for Money Self-Assessment 2017/18

Value for Money Self-Assessment 2017/18 Leeds Federated - Value for Money Self-Assessment 2017/18 This is Leeds Federated s Value for Money Self-Assessment for 2017/18. A version can also be found on our

Value for Money Self-Assessment 2017/18 Leeds Federated - Value for Money Self-Assessment 2017/18 This is Leeds Federated s Value for Money Self-Assessment for 2017/18. A version can also be found on our

Tax-advantaged venture capital schemes streamlining the advance assurance service

Consultation Response Tax-advantaged venture capital schemes streamlining the advance assurance service January 2017 1 Question 1. In what context are you responding to this consultation? 1.1 We are the

Consultation Response Tax-advantaged venture capital schemes streamlining the advance assurance service January 2017 1 Question 1. In what context are you responding to this consultation? 1.1 We are the

Value for money Self assessment statement 2014/15

Value for money Self assessment statement 2014/15 for you for your community not for profit Value for money (VFM) self-assessment 2014/15 Index 1. VFM and TRH Page 3 2. VFM performance targets 2014/15

Value for money Self assessment statement 2014/15 for you for your community not for profit Value for money (VFM) self-assessment 2014/15 Index 1. VFM and TRH Page 3 2. VFM performance targets 2014/15

Financial health of the higher education sector

October 2014/26 Issues paper This report is for information This report provides an overview of the financial health of the higher education sector in England. The analysis covers the financial forecasts

October 2014/26 Issues paper This report is for information This report provides an overview of the financial health of the higher education sector in England. The analysis covers the financial forecasts

Civil Service Statistics 2008: a focus on gross annual earnings

FEATURE David Matthews and Andrew Taylor Civil Service Statistics 2008: a focus on gross annual earnings SUMMARY This article presents a summary of annual Civil Service statistics for the year ending 31

FEATURE David Matthews and Andrew Taylor Civil Service Statistics 2008: a focus on gross annual earnings SUMMARY This article presents a summary of annual Civil Service statistics for the year ending 31

Treasury and Investment Policy

Date approved: 21 June 2016 Approved by: Parent Board i. Executive Recommendation... 3 ii. TREASURY AND INVESTMENT POLICY STATEMENT... 4 1. TMP 1 - RISK MANAGEMENT... 5 2. TMP 2 - VALUE FOR MONEY AND PERFORMANCE

Date approved: 21 June 2016 Approved by: Parent Board i. Executive Recommendation... 3 ii. TREASURY AND INVESTMENT POLICY STATEMENT... 4 1. TMP 1 - RISK MANAGEMENT... 5 2. TMP 2 - VALUE FOR MONEY AND PERFORMANCE

B.29[19a] Matters arising from our audits of the long-term plans

![B.29[19a] Matters arising from our audits of the long-term plans](/thumbs/95/123081028.jpg "B.29[19a] Matters arising from our audits of the long-term plans") B.29[19a] Matters arising from our audits of the 2018-28 long-term plans Photo acknowledgement: istock LazingBee B.29[19a] Matters arising from our audits of the 2018-28 long-term plans Presented to the

B.29[19a] Matters arising from our audits of the 2018-28 long-term plans Photo acknowledgement: istock LazingBee B.29[19a] Matters arising from our audits of the 2018-28 long-term plans Presented to the

COMBINED SUBMISSION OF SPECIALISED SUPPORTED HOUSING PROVIDERS TO THE CONSULTATION PAPER ON FINANCING SUPPORTED HOUSING

COMBINED SUBMISSION OF SPECIALISED SUPPORTED HOUSING PROVIDERS TO THE CONSULTATION PAPER ON FINANCING SUPPORTED HOUSING Introduction We are the leading specialist housing providers in relation to Specialised

COMBINED SUBMISSION OF SPECIALISED SUPPORTED HOUSING PROVIDERS TO THE CONSULTATION PAPER ON FINANCING SUPPORTED HOUSING Introduction We are the leading specialist housing providers in relation to Specialised

DCLG consultation Increasing the borrowing capacity of stock transfer housing associations

DCLG consultation Increasing the borrowing capacity of stock transfer housing associations CIH response May 2015 Emailed to: lsvt.valuation@communities.gsi.gov.uk 1 Introduction 1. The Chartered Institute

DCLG consultation Increasing the borrowing capacity of stock transfer housing associations CIH response May 2015 Emailed to: lsvt.valuation@communities.gsi.gov.uk 1 Introduction 1. The Chartered Institute

COMMENT LETTER 7 RECEIVED FROM PROPERTY INSTITUTE OF NEW ZEALAND

June 20 10 COMMENT LETTER 7 RECEIVED FROM PROPERTY INSTITUTE OF NEW ZEALAND EXPOSURE DRAFT PROPOSED NEW INTERNATIONAL VALUATION STANDARDS QUESTIONS FOR RESPONDENTS The International Valuation Standards

June 20 10 COMMENT LETTER 7 RECEIVED FROM PROPERTY INSTITUTE OF NEW ZEALAND EXPOSURE DRAFT PROPOSED NEW INTERNATIONAL VALUATION STANDARDS QUESTIONS FOR RESPONDENTS The International Valuation Standards

Basel Committee on Banking Supervision Second consultative document on Revisions to the Standardised Approach for credit risk

Basel Committee on Banking Supervision Second consultative document on Revisions to the Standardised Approach for credit risk A response by the Intermediary Mortgage Lenders Association, London, UK 4th

Basel Committee on Banking Supervision Second consultative document on Revisions to the Standardised Approach for credit risk A response by the Intermediary Mortgage Lenders Association, London, UK 4th

Housing Alliance Potential Changes to the Investment Framework for Credit Unions Consultation Paper CP109

Housing Alliance Potential Changes to the Investment Framework for Credit Unions Consultation Paper CP109 June 2017 Introduction The Housing Alliance is pleased to have the opportunity to make a submission

Housing Alliance Potential Changes to the Investment Framework for Credit Unions Consultation Paper CP109 June 2017 Introduction The Housing Alliance is pleased to have the opportunity to make a submission

INDEPENDENT AUDITOR S REPORT TO THE MEMBERS OF GKN PLC

INDEPENDENT AUDITOR S REPORT TO THE MEMBERS OF GKN PLC Report on the audit of the financial statements Opinion Basis for opinion In our opinion: > > the financial statements give a true and fair view of

INDEPENDENT AUDITOR S REPORT TO THE MEMBERS OF GKN PLC Report on the audit of the financial statements Opinion Basis for opinion In our opinion: > > the financial statements give a true and fair view of

Summary of consultation feedback:

Summary of consultation feedback: Future funding of supported housing 20 December 2017 Summary of key points: This briefing summarises the feedback we have received from housing associations to date on

Summary of consultation feedback: Future funding of supported housing 20 December 2017 Summary of key points: This briefing summarises the feedback we have received from housing associations to date on

Effectiveness Efficiency. Economy. Great homes and services Strong and vibrant communities. Value for Money Statement 2016/17

Economy Effectiveness Efficiency Value for Money Statement 2016/17 Great homes and services Strong and vibrant communities Value for money statement Purpose of this statement: to articulate and demonstrate

Economy Effectiveness Efficiency Value for Money Statement 2016/17 Great homes and services Strong and vibrant communities Value for money statement Purpose of this statement: to articulate and demonstrate

Strategic report. Value for Money. 17 Peabody Annual Report and Financial Statements Financial review

Strategic report Value for Money 17 Peabody Annual Report and Financial Statements 2017 Our Group Value for Money (VfM) self-assessment This self-assessment covers the performance of the Peabody Group

Strategic report Value for Money 17 Peabody Annual Report and Financial Statements 2017 Our Group Value for Money (VfM) self-assessment This self-assessment covers the performance of the Peabody Group

Mid Year Business Update. November 2016

Mid Year Business Update November 2016 Executive Summary 2015/16 was another year of significant growth, diversification and continued strong financial performance. Two new partner organisations, both

Mid Year Business Update November 2016 Executive Summary 2015/16 was another year of significant growth, diversification and continued strong financial performance. Two new partner organisations, both

THE BOARD OF THE PENSION PROTECTION FUND. Guidance in relation to Contingent Assets. Type A Contingent Assets: Guarantor strength 2018/2019

THE BOARD OF THE PENSION PROTECTION FUND Guidance in relation to Contingent Assets Type A Contingent Assets: Guarantor strength 2018/2019 This draft document will be published in final form as part of

THE BOARD OF THE PENSION PROTECTION FUND Guidance in relation to Contingent Assets Type A Contingent Assets: Guarantor strength 2018/2019 This draft document will be published in final form as part of

What is the impact of ORR s inflation proposals on Network Rail?

What is the impact of ORR s inflation proposals on Network Rail? Note prepared for Network Rail September 3rd 2012 1 Introduction and summary There is a well-established precedent for using some form of

What is the impact of ORR s inflation proposals on Network Rail? Note prepared for Network Rail September 3rd 2012 1 Introduction and summary There is a well-established precedent for using some form of

Stochastic Modelling: The power behind effective financial planning. Better Outcomes For All. Good for the consumer. Good for the Industry.

Stochastic Modelling: The power behind effective financial planning Better Outcomes For All Good for the consumer. Good for the Industry. Introduction This document aims to explain what stochastic modelling

Stochastic Modelling: The power behind effective financial planning Better Outcomes For All Good for the consumer. Good for the Industry. Introduction This document aims to explain what stochastic modelling

Market trend analysis. Issue 2 March 2018

Market trend analysis Link Asset Services Welcome to the second issue of the Market Trend Analysis from Link Asset Services. This year we analyse the visible market trends through our datasets across the

Market trend analysis Link Asset Services Welcome to the second issue of the Market Trend Analysis from Link Asset Services. This year we analyse the visible market trends through our datasets across the

Mid-Year Review

Mid-Year Review 2014-15 Update on Strategy and Financial Projections Wheatley group Contents 02 03 04 05 05 06 07 10 12 Investing in our future Strong performance Meeting customers needs Platform for growth

Mid-Year Review 2014-15 Update on Strategy and Financial Projections Wheatley group Contents 02 03 04 05 05 06 07 10 12 Investing in our future Strong performance Meeting customers needs Platform for growth

ANNUAL VALUE FOR MONEY STATEMENT 2016/17

ANNUAL VALUE FOR MONEY STATEMENT Page 2 INTRODUCTION What Is BCHA? BCHA is a specialist housing and housing-related support provider, helping people who are homeless and vulnerable to access the right

ANNUAL VALUE FOR MONEY STATEMENT Page 2 INTRODUCTION What Is BCHA? BCHA is a specialist housing and housing-related support provider, helping people who are homeless and vulnerable to access the right

The 2017/18 Levy Policy Statement

The 2017/18 Levy Policy Statement December 2016 Foreword This policy statement confirms our plans for the 2017/18 levy, the final levy year of the second triennium. We aim to keep the rules stable across

The 2017/18 Levy Policy Statement December 2016 Foreword This policy statement confirms our plans for the 2017/18 levy, the final levy year of the second triennium. We aim to keep the rules stable across

Civil Service Statistics 2009: A focus on gross annual earnings

Economic & Labour Market Review Vol 4 No 4 April 10 ARTICLE David Matthews and Andrew Taylor Civil Service Statistics 09: A focus on gross annual earnings SUMMARY This article presents a summary of annual

Economic & Labour Market Review Vol 4 No 4 April 10 ARTICLE David Matthews and Andrew Taylor Civil Service Statistics 09: A focus on gross annual earnings SUMMARY This article presents a summary of annual

Housing Solutions Value for Money self-assessment

Notes Housing Solutions Value for Money self-assessment For the year ended 31 March 2017 1 Our year in summary Increased our turnover by 6% from 43 million to 46 million Increased EBITDA as a % of turnover

Notes Housing Solutions Value for Money self-assessment For the year ended 31 March 2017 1 Our year in summary Increased our turnover by 6% from 43 million to 46 million Increased EBITDA as a % of turnover

Opinion Draft Regulatory Technical Standard on criteria for establishing when an activity is to be considered ancillary to the main business

Opinion Draft Regulatory Technical Standard on criteria for establishing when an activity is to be considered ancillary to the main business 30 May 2016 ESMA/2016/730 Table of Contents 1 Legal Basis...

Opinion Draft Regulatory Technical Standard on criteria for establishing when an activity is to be considered ancillary to the main business 30 May 2016 ESMA/2016/730 Table of Contents 1 Legal Basis...

Firm Foundations: The Future of Housing in Scotland

Firm Foundations: The Future of Housing in Scotland Attached Paper 1 Shared Equity The Future of Shared Equity Seminar Discussion Summary In July 2007, the Joseph Rowntree Foundation hosted a seminar on

Firm Foundations: The Future of Housing in Scotland Attached Paper 1 Shared Equity The Future of Shared Equity Seminar Discussion Summary In July 2007, the Joseph Rowntree Foundation hosted a seminar on

Review of the thin capitalisation arm s length debt test

13 March 2014 Review of the thin capitalisation arm s length debt test The Australian Private Equity and Venture Capital Association Limited (AVCAL) welcomes the opportunity to comment on the Board of

13 March 2014 Review of the thin capitalisation arm s length debt test The Australian Private Equity and Venture Capital Association Limited (AVCAL) welcomes the opportunity to comment on the Board of

Working Capital Strategies to Drive Shareholder Value

Working Capital Strategies to Drive Shareholder Value Working Capital Strategies to Drive Shareholder Value By Ian Fleming, Managing Director, Working Capital Advisory, HSBC The value of working capital

Working Capital Strategies to Drive Shareholder Value Working Capital Strategies to Drive Shareholder Value By Ian Fleming, Managing Director, Working Capital Advisory, HSBC The value of working capital

Clarify and define the actual versus perceived role and function of rating organizations as they currently exist;

Executive Summary The purpose of this study was to undertake an analysis of the role, function and impact of rating organizations on mutual insurance companies and the industry at large. More specifically,

Executive Summary The purpose of this study was to undertake an analysis of the role, function and impact of rating organizations on mutual insurance companies and the industry at large. More specifically,

Weaver Vale Housing Trust. Value for Money Self - Assessment 2017

Weaver Vale Housing Trust Value for Money Self - Assessment 2017 Executive Summary This Executive Summary gives an overview of the information presented in this report. It highlights the good performance

Weaver Vale Housing Trust Value for Money Self - Assessment 2017 Executive Summary This Executive Summary gives an overview of the information presented in this report. It highlights the good performance

Guide to Risk and Investment - Novia

www.canaccord.com/uk Guide to Risk and Investment - Novia This document is important. Its purpose is to help with understanding investment in financial markets, the associated risks and the potential returns.

www.canaccord.com/uk Guide to Risk and Investment - Novia This document is important. Its purpose is to help with understanding investment in financial markets, the associated risks and the potential returns.

Consultation on Proposed Changes to the Treasury Management Code and Cross Sectoral Guidance Notes

Consultation on Proposed Changes to the Treasury Management Code and Cross Sectoral Guidance Notes Closes 30 th September 2017 INTRODUCTION The first version of the Treasury Management in the Public Services:

Consultation on Proposed Changes to the Treasury Management Code and Cross Sectoral Guidance Notes Closes 30 th September 2017 INTRODUCTION The first version of the Treasury Management in the Public Services:

Griffith University. Preparing strata title communities for climate change survey: On line questionnaire findings summary for survey respondents

Griffith University Preparing strata title communities for climate change survey: On line questionnaire findings summary for survey respondents This report provides a summary of findings arising from Griffith

Griffith University Preparing strata title communities for climate change survey: On line questionnaire findings summary for survey respondents This report provides a summary of findings arising from Griffith

Work and Pensions Select Committee Inquiry into governance and best practice in workplace pension provision

Work and Pensions Select Committee Inquiry into governance and best practice in workplace pension provision Introduction 1. With the advent of automatic enrolment, questions of governance and best practice

Work and Pensions Select Committee Inquiry into governance and best practice in workplace pension provision Introduction 1. With the advent of automatic enrolment, questions of governance and best practice

A Discussion Document on Assurance of Social and Environmental Valuations

A Discussion Document on Assurance of Social and Environmental Valuations Social Value UK Winslow House, Rumford Court, Liverpool, L3 9DG +44 (0)151 703 9229 This document is not intended to be an assurance

A Discussion Document on Assurance of Social and Environmental Valuations Social Value UK Winslow House, Rumford Court, Liverpool, L3 9DG +44 (0)151 703 9229 This document is not intended to be an assurance

Value for Money Self-Assessment Approved by bpha Board 18 July 2017

Self-Assessment 2016-17 Approved by bpha Board 18 July 2017 Content of Self-Assessment Report 1 Value for Money (VfM) Introduction and Regulatory Requirements... 1 1.1 Regulatory requirement... 1 1.2 Overall

Self-Assessment 2016-17 Approved by bpha Board 18 July 2017 Content of Self-Assessment Report 1 Value for Money (VfM) Introduction and Regulatory Requirements... 1 1.1 Regulatory requirement... 1 1.2 Overall

FINANCE COMMITTEE DEMOGRAPHIC CHANGE AND AGEING POPULATION SUBMISSION BY AUDIT SCOTLAND

FINANCE COMMITTEE DEMOGRAPHIC CHANGE AND AGEING POPULATION SUBMISSION BY AUDIT SCOTLAND Introduction 1. Audit Scotland carries out the external audit of the majority of public sector bodies in Scotland.

FINANCE COMMITTEE DEMOGRAPHIC CHANGE AND AGEING POPULATION SUBMISSION BY AUDIT SCOTLAND Introduction 1. Audit Scotland carries out the external audit of the majority of public sector bodies in Scotland.

Kyrgyz Republic: Borrowing by Individuals

Kyrgyz Republic: Borrowing by Individuals A Review of the Attitudes and Capacity for Indebtedness Summary Issues and Observations In partnership with: 1 INTRODUCTION A survey was undertaken in September

Kyrgyz Republic: Borrowing by Individuals A Review of the Attitudes and Capacity for Indebtedness Summary Issues and Observations In partnership with: 1 INTRODUCTION A survey was undertaken in September

Clarion Housing Group Value for Money Statement 2017

Clarion Housing Group Value for Money Statement 2017 Value for Money Highlights Value for Money Highlights Clarion Housing Group is a business for social purpose. First and foremost we are a social landlord

Clarion Housing Group Value for Money Statement 2017 Value for Money Highlights Value for Money Highlights Clarion Housing Group is a business for social purpose. First and foremost we are a social landlord

Draft Registration of Overseas Entities Bill

17 September 2018 To: transparencyandtrust@beis.gov.uk Introduction 1. The British Property Federation (BPF) represents the commercial real estate sector. We promote the interests of those with a stake

17 September 2018 To: transparencyandtrust@beis.gov.uk Introduction 1. The British Property Federation (BPF) represents the commercial real estate sector. We promote the interests of those with a stake

Our Commitment to Value for Money (VfM) 2017 Self-Assessment. Benchmarking Report

2017 Self-Assessment. Benchmarking Report") Our Commitment to Value for Money (VfM) 2017 Self-Assessment Benchmarking Report 1. Who do we compare ourselves with? 2. Summary overview 3. External benchmarking 3.1 Overall performance 3.2 What do our

Our Commitment to Value for Money (VfM) 2017 Self-Assessment Benchmarking Report 1. Who do we compare ourselves with? 2. Summary overview 3. External benchmarking 3.1 Overall performance 3.2 What do our

Peer & Independent review Feedback and additional guidance paper august 2009

Peer & Independent review Feedback and additional guidance paper august 2009 2 Disclaimer This paper is intended to provide up to date feedback and additional guidance to that contained within Lloyd s

Peer & Independent review Feedback and additional guidance paper august 2009 2 Disclaimer This paper is intended to provide up to date feedback and additional guidance to that contained within Lloyd s

About this report Executive summary The Retail Team Salaries Top Level Manager salary... 5

Salaries 06 Contents About this report... Executive summary... 3 The Retail Team... 4 Salaries... 5 Top Level salary... 5 Performance related bonuses for Top Level s... 5 Salary tables... 6 Impact of the

Salaries 06 Contents About this report... Executive summary... 3 The Retail Team... 4 Salaries... 5 Top Level salary... 5 Performance related bonuses for Top Level s... 5 Salary tables... 6 Impact of the

Recovering the costs of the Office for Professional Body Anti-Money Laundering Supervision (OPBAS): fees proposals

: fees proposals") Recovering the costs of the Office for Professional Body Anti-Money Laundering Supervision (OPBAS): fees proposals Consultation paper CP17/35 Published by the Financial Conduct Authority (FCA) Comments

Recovering the costs of the Office for Professional Body Anti-Money Laundering Supervision (OPBAS): fees proposals Consultation paper CP17/35 Published by the Financial Conduct Authority (FCA) Comments

Market Oversight. Draft guidance for providers

Market Oversight Draft guidance for providers January 2015 Contents 1. Introduction to Market Oversight 4 What is Market Oversight for? 4 Why and how was the scheme developed? 5 How we have developed our

Market Oversight Draft guidance for providers January 2015 Contents 1. Introduction to Market Oversight 4 What is Market Oversight for? 4 Why and how was the scheme developed? 5 How we have developed our

Methodology and Inputs for the 2017 Valuation: Initial assessment. Technical discussion document for sponsoring employers

NOTE: This document was first circulated to stakeholders in February 2017 as part of the Trustee's preparations for the 2017 valuation. In December 2017, a formal actuarial report was submitted to the

NOTE: This document was first circulated to stakeholders in February 2017 as part of the Trustee's preparations for the 2017 valuation. In December 2017, a formal actuarial report was submitted to the

THE PANEL ON TAKEOVERS AND MERGERS DEALINGS IN DERIVATIVES AND OPTIONS

RS 2005/2 Issued on 5 August 2005 THE PANEL ON TAKEOVERS AND MERGERS DEALINGS IN DERIVATIVES AND OPTIONS STATEMENT BY THE CODE COMMITTEE OF THE PANEL FOLLOWING THE EXTERNAL CONSULTATION PROCESSES ON DISCLOSURE

RS 2005/2 Issued on 5 August 2005 THE PANEL ON TAKEOVERS AND MERGERS DEALINGS IN DERIVATIVES AND OPTIONS STATEMENT BY THE CODE COMMITTEE OF THE PANEL FOLLOWING THE EXTERNAL CONSULTATION PROCESSES ON DISCLOSURE

blackrock consensus funds simple, transparent investment solutions

blackrock consensus funds simple, transparent investment solutions for professional investors only Tony Stenning Head of BlackRock UK Retail Business We ve developed BlackRock Consensus Funds as our core

blackrock consensus funds simple, transparent investment solutions for professional investors only Tony Stenning Head of BlackRock UK Retail Business We ve developed BlackRock Consensus Funds as our core

Local Heat & Energy Efficiency Strategies, and Regulation of District Heating

Local Heat & Energy Efficiency Strategies, and Regulation of District Heating Response by the Council of Mortgage Lenders to the Scottish Government consultation paper Introduction 1. The CML is the representative

Local Heat & Energy Efficiency Strategies, and Regulation of District Heating Response by the Council of Mortgage Lenders to the Scottish Government consultation paper Introduction 1. The CML is the representative

INVESTMENT POLICY. January Approved by the Board of Governors on 12 December Third amendment approved with effect from 1 January 2019

INVESTMENT POLICY January 2019 Approved by the Board of Governors on 12 December 2016 Third amendment approved with effect from 1 January 2019 1 Contents SECTION 1. OVERVIEW SECTION 2. INVESTMENT PHILOSOPHY-

INVESTMENT POLICY January 2019 Approved by the Board of Governors on 12 December 2016 Third amendment approved with effect from 1 January 2019 1 Contents SECTION 1. OVERVIEW SECTION 2. INVESTMENT PHILOSOPHY-

Housing and Regeneration Cabinet Committee. The Review of HRA Subsidy System and Council Rents Cabinet Member for Community Services

AGENDA ITEM: 5 Page nos. 1 7 Meeting Date 9 March 2009 Subject Report of Summary Housing and Regeneration Cabinet Committee The Review of HRA Subsidy System and Council Rents Cabinet Member for Community

AGENDA ITEM: 5 Page nos. 1 7 Meeting Date 9 March 2009 Subject Report of Summary Housing and Regeneration Cabinet Committee The Review of HRA Subsidy System and Council Rents Cabinet Member for Community

2015 National Clubs Census

2015 National Clubs Census Detailed Report FINAL August 2016 Contents Page Key Findings 3 Introduction 6 Approach 8 Limitations 10 Results 12 National Australian Capital Territory New South Wales Queensland

2015 National Clubs Census Detailed Report FINAL August 2016 Contents Page Key Findings 3 Introduction 6 Approach 8 Limitations 10 Results 12 National Australian Capital Territory New South Wales Queensland

Innovation and growth factsheet series

Innovation and growth factsheet series 13 March 2017 Introduction This factsheet 1 provides a high-level overview of finance relevant to universities funding local growth, regeneration and capital projects.

Innovation and growth factsheet series 13 March 2017 Introduction This factsheet 1 provides a high-level overview of finance relevant to universities funding local growth, regeneration and capital projects.

Value for Money. Self Assessment Summary 2016

Value for Money Self Assessment Summary 2016 Executive Summary Wythenshawe Community Housing Group Limited () was established in April 2013 when Parkway Green Housing Trust (PGHT) and Willow Park Housing

Value for Money Self Assessment Summary 2016 Executive Summary Wythenshawe Community Housing Group Limited () was established in April 2013 when Parkway Green Housing Trust (PGHT) and Willow Park Housing

VALUE FOR MONEY REPORT 2017

VALUE FOR MONEY REPORT 2017 1 CONTENTS EXECUTIVE SUMMARY 1 EXECUTIVE SUMMARY INTRODUCTION 3 Our Value for Money approach 3 Our operating environment 4 OVERALL PERFORMANCE 5 Operating surplus 5 Operating

VALUE FOR MONEY REPORT 2017 1 CONTENTS EXECUTIVE SUMMARY 1 EXECUTIVE SUMMARY INTRODUCTION 3 Our Value for Money approach 3 Our operating environment 4 OVERALL PERFORMANCE 5 Operating surplus 5 Operating

Pricing Cost Assurance and Analysis Service (CAAS) Estimates Constraints

Estimates Constraints") Pricing Cost Assurance and Analysis Service (CAAS) Estimates Constraints None. Authoritative Guidance Summary 1. Cost Assurance and Analysis Service (CAAS) provide a range of services for the Defence Equipment

Pricing Cost Assurance and Analysis Service (CAAS) Estimates Constraints None. Authoritative Guidance Summary 1. Cost Assurance and Analysis Service (CAAS) provide a range of services for the Defence Equipment

The BBC s commercial activities: a landscape review

A picture of the National Audit Office logo Report by the Comptroller and Auditor General BBC The BBC s commercial activities: a landscape review HC 721 SESSION 2017 2019 7 MARCH 2018 4 Key facts The BBC

A picture of the National Audit Office logo Report by the Comptroller and Auditor General BBC The BBC s commercial activities: a landscape review HC 721 SESSION 2017 2019 7 MARCH 2018 4 Key facts The BBC

Planned and Cyclical Maintenance Policy

M3 Planned and Cyclical Maintenance Policy Date of Approval Review Date August 2016 August 2019 Planned and Cyclical Maintenance 1. Policy Context The introduction of this new comprehensive policy on Planned

M3 Planned and Cyclical Maintenance Policy Date of Approval Review Date August 2016 August 2019 Planned and Cyclical Maintenance 1. Policy Context The introduction of this new comprehensive policy on Planned

SCOTTISH FUNDING COUNCIL CAPITAL PROJECTS DECISION POINT PROCESS

SCOTTISH FUNDING COUNCIL CAPITAL PROJECTS DECISION POINT PROCESS Incorporating amendments by Scottish Futures Trust (Proposals for Decision Points 2 5 Only) Executive summary... 1 Section 1: Introduction

SCOTTISH FUNDING COUNCIL CAPITAL PROJECTS DECISION POINT PROCESS Incorporating amendments by Scottish Futures Trust (Proposals for Decision Points 2 5 Only) Executive summary... 1 Section 1: Introduction

A guide to the incremental borrowing rate Assessing the impact of IFRS 16 Leases. Audit & Assurance

A guide to the incremental borrowing rate Assessing the impact of IFRS 16 Leases Audit & Assurance Given a significant number of organisations are unlikely to have the necessary historical data to determine

A guide to the incremental borrowing rate Assessing the impact of IFRS 16 Leases Audit & Assurance Given a significant number of organisations are unlikely to have the necessary historical data to determine

EMPLOYERS LIABILITY CLAIMS BENCHMARKING

EMPLOYERS LIABILITY CLAIMS BENCHMARKING Claims analysis of the UK s largest construction companies Risk analysis and insight Benchmarking Exercise 3 INTRODUCTION JLT Construction has a track record of

EMPLOYERS LIABILITY CLAIMS BENCHMARKING Claims analysis of the UK s largest construction companies Risk analysis and insight Benchmarking Exercise 3 INTRODUCTION JLT Construction has a track record of

june 07 tpp 07-3 Service Costing in General Government Sector Agencies OFFICE OF FINANCIAL MANAGEMENT Policy & Guidelines Paper

june 07 Service Costing in General Government Sector Agencies OFFICE OF FINANCIAL MANAGEMENT Policy & Guidelines Paper Contents: Page Preface Executive Summary 1 2 1 Service Costing in the General Government

june 07 Service Costing in General Government Sector Agencies OFFICE OF FINANCIAL MANAGEMENT Policy & Guidelines Paper Contents: Page Preface Executive Summary 1 2 1 Service Costing in the General Government

VALUE FOR MONEY (VFM) STATEMENT SUMMARY 2015/16

STATEMENT SUMMARY 2015/16") VALUE FOR MONEY (VFM) STATEMENT SUMMARY 2015/16 Approach Our approach to Value for Money (VFM) SUCCESS IN VFM Success in VFM and efficiency is the same as success in achieving our strategic objectives.

VALUE FOR MONEY (VFM) STATEMENT SUMMARY 2015/16 Approach Our approach to Value for Money (VFM) SUCCESS IN VFM Success in VFM and efficiency is the same as success in achieving our strategic objectives.

RE: Transaction Costs Disclosure: Improving Transparency in Workplace Pensions: Call for Evidence

6 May 2015 Department for Work and Pensions Transparency Team Department for Work and Pensions 3rd Floor West, Zone G Quarry House Leeds, LS2 7UA Submitted via email to: Ms Carol McGinley and Mr Michael

6 May 2015 Department for Work and Pensions Transparency Team Department for Work and Pensions 3rd Floor West, Zone G Quarry House Leeds, LS2 7UA Submitted via email to: Ms Carol McGinley and Mr Michael

Evaluation of the dispersion of profitability within the comparator sets used in Annex 9 of Ofcom s pay TV phase three document

within the comparator sets used in Annex 9 of Ofcom s pay TV phase three document A report for British Sky Broadcasting Limited 16 September 2009 Final report [date] 1 Important Notice This report has

within the comparator sets used in Annex 9 of Ofcom s pay TV phase three document A report for British Sky Broadcasting Limited 16 September 2009 Final report [date] 1 Important Notice This report has

A Snap Shot of the LGBT Sector. #LGBTResilience

A Snap Shot of the LGBT Sector #LGBTResilience August 2016 Foreword Paul Roberts, Chief Executive Officer at LGBT Consortium LGBT Consortium is passionate about working with its Membership to explore how

A Snap Shot of the LGBT Sector #LGBTResilience August 2016 Foreword Paul Roberts, Chief Executive Officer at LGBT Consortium LGBT Consortium is passionate about working with its Membership to explore how

DISCUSSION DOCUMENT ASSURANCE REPORTING ON PENSION TRUSTEES

DISCUSSION DOCUMENT ASSURANCE REPORTING ON PENSION TRUSTEES (December 2011 AAF Pension Trustee Supplement 1 to ICAEW AAF 02/07) Background The Occupational Pension Schemes (Independent Trustee) Regulations

DISCUSSION DOCUMENT ASSURANCE REPORTING ON PENSION TRUSTEES (December 2011 AAF Pension Trustee Supplement 1 to ICAEW AAF 02/07) Background The Occupational Pension Schemes (Independent Trustee) Regulations

ARCH and NFA November 2017 RAISING THE ROOF Analysis of Housing Revenue Account Headroom

ARCH and NFA November 2017 RAISING THE ROOF Analysis of Housing Revenue Account Headroom Summary Report Contents Executive Summary 1 1. Introduction and Background 7 2. Methodology 10 3. Analysis of trends

ARCH and NFA November 2017 RAISING THE ROOF Analysis of Housing Revenue Account Headroom Summary Report Contents Executive Summary 1 1. Introduction and Background 7 2. Methodology 10 3. Analysis of trends