Solow Growth Analysis: Further Analysis of the Model s Progression Through Time. Patricia Bellew James Madison University

|

|

|

- Winifred Small

- 5 years ago

- Views:

Transcription

1 Volume 1 Number 1 Fall 2011 JURF Journal of Undergraduate Research in Finance Solow Growth Analysis: Further Analysis of the Model s Progression Through Time Patricia Bellew James Madison University In the 1950 s Robert Solow created a system of equations that would combine the input of labor and capital to generate a model of a country s economic path. Our objective is to take a closer look at the Solow growth model. We will analyze this system of differential equations to learn more about the growth of economies in both developed and emerging countries, and what factors play an important role in a country s economic welfare. In doing so we will be able to see stable and unstable solutions, characteristics of each model, and adapt the Solow model to provide more realistic results. We will collect archived data for different countries from the World Data Bank to use as coefficients for our modified differential systems and compare the resulting projections to historical data. We found that by allowing for more economic variables, the Solow Growth Model creates a more realistic path prediction. 1. Introduction We present a descriptive analysis of the Solow growth model, also called the Neoclassical growth model, and how different rate parameters affect an economies path through time. The Solow growth model has many variations, including equations that take into account changes caused by increases in technology and the value of education to a country. These variations of the Solow growth model are our main focus. They will tell us more about how changes in education and technology affect a country s economy over time. With this information, we can see which countries follow similar paths. Our goal is to better understand United States economic fluctuations, and to compare them to the fluctuations of other countries. 2. Solow Growth Model There are two equations that comprise the Solow growth model: the production function, PF, and the capital accumulation equation, CAE. The production function, PF, is the equation that displays the relationship of the inputs of an economy to the outputs. For the base case Solow model, we assume a Cobb-Douglass PF: (1) That is, output, Y, is equal to total capital, K, raised to some number α, between 0 and 1, multiplied by the input of labor, L, raised to the. The equation exhibits constant returns to scale. This means that for every 1% change in the total input, the output given by the PF will also change by 1%. Choosing α is one of the most important initial steps when solving the Solow model, since α determines the shape of the function. We can estimate this parameter by fitting the resulting PF to historical data. The CAE is the base differential equation

2 (DE) for the Solow model. This DE gives the change in capital, K, in terms of Y and K. In this simple Solow model, there are two growth rates: the savings rate, s, and the capital depreciation rate, d.: (2) The change in capital is gross investment, sy, minus total depreciation, dk. We can alter the PF and CAE to represent the model of our choosing, and use historical data from different countries to model the progression of their economic state over time. To see this development we must first select a starting year and enter the collected data into the equations above for all constant variables. Next, we must find data from the selected starting year to represent the variables that change over time; these will be our initial conditions, IC. The result will be a graph showing the path that the country s economy is expected to follow, taking into account changes in both labor and capital. This can be compared to the actual path depicted in the graphs in Appendix A. A more detailed graph of our results would be presented in the form of a phase portrait, which shows the steady state solution and how each point on the graph will move if our IC is chosen at that distance from the equilibrium. A steady state solution is defined as the equation that generates. In other words, we find the parameters that, if plugged into K, cause capital to be constant over time. The further an economy is below its steady state, the faster the economy should grow. The further an economy is above its steady state, the slower the economy should grow (Jones 98). This is the theory behind the Neoclassical growth model. It assumes poorer countries should catch up to the wealthy, causing all to converge, and follow the same economic path. However, mitigating factors, both positive and negative, will cause one or both of the country s rate parameters to adjust. When this change happens the entire model will shift and become an entirely new graph. How do we account for these shocks? We can use the flexibility of the Solow model and create our own systems of differential equations to model how specific shock factors affect an economic path. We select 8 of the countries that Charles I. Jones also investigated in Introduction to Economic Growth. We study 4 rich countries (France, Spain, United Kingdom, and the U.S.), and 4 poor countries (China, India, Uganda, and Zimbabwe). We collect the needed data from both the book and from The World Bank. The parameters that we needed to retrieve for our problems were the following: Adjusted savings as a percent of GNI, GDP per capita, GDP per person employed, labor force total, number of resident patent applications, population growth, and number of researchers in R&D. We will discuss later how each of these are incorporated in the Solow growth model we are studying. 3. Changing the α Parameter There are three general cases we consider. The first is when α from equation (1) is equal to 1. It then follows that the total output would be equal to the input of capital since the PF would be. This means that, in this economy, output is only generated from the input of capital, and no labor is factored in. If this is true, then the CAE may be written solely in terms of K, taking the form: (3) Within this case there are two variations that we will focus on: (a) both s and d are constants, and (b) when d is a constant, but. The first variation, where s and d are constants, would have a solution of the form (4) The C and (s-d) in this solution are constant. From now on we will assume the d for each country is.05, since this is the rate of depreciation that Charles I. Jones used in his book. The only variable would be time, t. If, then over time the amount of capital in the economy will increase. Conversely, if, the capital will deplete to zero and the economy will fail. This is plausible because, with a depreciation rate less than savings rate, a country with this characteristic will save faster than depreciation can take value away. Also, with more savings there is more capacity to reinvest in capital, and since the PF is derived from capital the economy will flourish. If d is bigger than s, over time capital will deplete faster than the rate at which the economy saves and the country will not have the ability to continue at this low state. We choose to represent the savings rate with adjusted net national savings as a percent of GNI, archived in the World Data Bank from because, in Introduction to Economic Growth, it states that the American savings rate was.056 and when we average the data, the rate was approximately As we see, the American rate we use is less than this. This is because we need to shorten the time interval the data is averaged over because our data set didn t start recording the

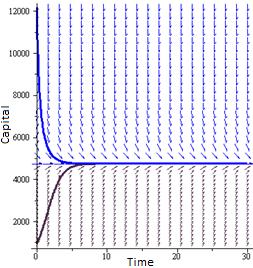

3 GDP per person working until 1980, and we wanted to keep it consistent throughout all the examples. Therefore, we adjust the time line to be The phase portraits shown below are examples of the properties described above. For more examples, all graphs are displayed in the appendix. American, making the, while in china the,. The United States economy is decreasing at an exponential rate to an equilibrium, while China s economy is increasing exponentially. The arrows displayed on the graphs represent the direction the country s economy moves along the solution curves. United States China China s path increases with no equilibrium because without any outside factors if savings is greater than depreciation there will be no limit to the growth. Conversely, the U.S. levels off because, after almost 1,000 years of depreciation outweighing savings, the economy would run out of savings to invest in capital, and the resulting economic state would be at zero. The IC s used for these graphs were the GDP per capita from 1980 for each country. The DE would be at a steady state solution, if, or. The first condition makes, and the second can only occur when, since K is a constant multiplied by an exponential. This model does not seem to be a good representation of an economy because the graphs look identical, which should not be true. Since an economy s structure is built from many contributing factors, we would assume that the model of an economy would have more freedom in its movements. Also, some of the forecasted economies, such as Zimbabwe, will converge to zero after a very low number of years. The phase portrait for Zimbabwe, as shown in the appendix part 1a, suggests that after 500 years the economy will have no capital left and will stay that way. For the second variation (b) from equation (2) we chose to explore when the savings rate is governed by the amount of capital. One way we can represent this is to assume savings is. When looking at the phase portraits we noticed that if the value of β was close to 1, the slope of the models were unreasonably steep. Therefore, we arbitrarily chose β for this system to be.0002 to try and model the economic path as best we can. Under these circumstances, together with an α of 1, the CAE would be: (5) The following equilibriums would create a steady state solution: The solution to this DE is:, where, and K=0 (6) The graphs of this solution are a perfect example of the Neoclassical growth theory. If the IC of a country started above the equilibrium the capital would decrease, while the IC s below the equilibrium would increase. The phase portraits for this system all converge to the same equilibrium, which is just under 5,000. Shown below are samples of the structure the model creates for the economies. The first graph is to show all the countries in comparison to each other, while the second is to show the typical form the graphs render. Again, we used GDP per capita for 1980 as the IC,, and the s corresponding to each country to form these graphs. (7)

4 China France India Spain Uganda UK US Zimbabwe India One fact that should be pointed out is that when an IC was chosen above the equilibrium, the path would decrease at a faster pace than the slope resulting from an IC below the equilibrium. This model also does not seem to be a reasonable fit to a real economy because it suggests that the path will be monotonic, and will increase or decrease based on whether the IC is above or below an equilibrium. Also, shown in this picture, all countries converge in less than 15 years and since the data used started in 1980 we know that this did not happen. The second case we will examine is when α from equation (1) is 0. If this is true, then and the CAE would be,. This implies that the output in this economy is derived directly from labor, and capital arises from savings of labor minus the depreciation of capital. Because we are adding a new variable to the calculations, L, we must know the rate of change of labor, L, and find the solution for both DE s. Within this case we will focus on the following three variations: (a), (b), (c) (8) We choose this fractional structure to give the equations more flexibility for a general case as well as for the form of their solutions. For the β, ϒ, and δ parameters we will arbitrarily choose these values to get the best graphical representative of an economy. Their values are based on the viability of the graphs produced under those conditions. The first, case a, is the assumption that labor force grows at some constant rate n. If this is true, then. As in Jones Introduction to Economic Growth, we will assume, for this case, that the rate n is the same rate as population growth. Because of this, when we run simulations the n will be the average population growth for a specific country over the time period that we are studying. Therefore, if the population increases by 1% then the labor force also increases by 1%. There will be an equilibrium solution at The solution to this problem is when, (9) where represents the IC, which will be the GDP per person working from 1980, and yields the new labor force total when multiplying it by that IC. This is plausible because if your output is generated solely from labor and the population increases over time then your output will also increase at the same rate. Similar to the first problem in section 1, when, the path of the country s economy will be increasing, and when it will be decreasing. The equilibrium solutions are when,. Since the solution is in exponential form, the phase portrait is also much like those in section 1.

, Case b.")

5 US UK France Spain This model does not seem to be a suitable fit, as they do not converge to any equilibruim. There are still only two shapes created by this model and, again, they are based on only the two parameters, s and d. Had this been a true model of these economies, the American and United Kingdom paths are more efficient because if output is only produced from labor it wouldn t be logical to increase capital as France and Spain do. If growth is not constant, there are many alterations that could be made to show how the labor changes through time. Again, we will be looking at equations (8b), Case b., and (8c), Case c. The equation in Case b. was chosen to have L be governed only by L, but for Case c. we wanted to see how letting L depend on K as well would change the shape of the model. When drawing the graphs for Case b., if we choose a ϒ that is too small the country s paths travel at a slope abnormally close to 0. So, for this system we will choose ϒ to be.02. Since δ is in the denominator, small values of δ cause computational problems for Maple and the graphs show negative values for both the labor and the capital. Because of this we will make. Also, to keep constant with the previous problems we will also choose The equilibrium from Case b. would be: (10) The phase portraits for this equation do not converge to any equilibrium. With, L would be increasing or decreasing at a constant rate, causing labor to move monotonically. Below are some examples, and as, the function will always be increasing.

6 China India Uganda Zimbabwe For Case c., the equilibrium solutions are when K=0, and L=0. The difference between this solution and the previous, where L doesn t depend on the amount of capital, is that the countries from Case b. grow exponentially, while the paths the same countries take in Case c. are much more gradual. They both, however, are only functional over a very short period of time. There are some computational errors introduced in some country s economic paths after 1-2 years. Illustrations of the graphs from Case c. are shown below. US UK France Spain In the next section we look into the more general case, when base case equation to include more model changing factors., and change sections of the 4. Education and Technology in the Solow Model Now we will discuss the Solow model when we introduce the concept of changes in technology. A technological change is considered an important economic factor that could alter the original path created by previous parameters. We will assume A is the number of ideas that evolve into new technology and use the number of resident patent applications as the IC, retrieved from the World Data Bank. There are three production function options to choose from to find the solution to the model. The three choices are as follows; Hicks-Neutral Technology:, (11) Solow-Neutral Technology: (12) Harrod-neutral technology:. (13) We will continue to follow Solow s work and use equation (12) the Solow-neutral technology production function. The PF will be, and new CAE will take the form. Again, n is population growth rate, g is technological growth and d is the depreciations rate. This means that now the change in capital is the total savings from investment minus the increase in cost due to a change in labor force per capital, minus change in capital due to technology, minus the depreciation of capital per worker. We add the term because the more advances there are, the less capital will be needed to produce the same amount.

7 Since we have three variables that change over time, K(t), L(t), and A(t), we will need three DE s. Therefore we will also assume that, (14) the equation from Jones Introduction to Economic Growth, where δ is the constant rate of change of ideas, and is calculated by. The parameter ρ will be the percent of the labor population that is involved in research and will be calculated by taking the number of researchers and dividing it by the total labor force. We will estimate λ, which accounts for the overlap that may occur in research projects. For example, if there are two or more firms working simultaneously to produce the same piece of technology, the time and energy that one of those firms could spend researching something else is wasted. Finally, φ accounts for the advantage that researchers currently have because of the technology that has already come into existence. Lastly, we will introduce the value of education to the Solow model. The more a person is educated, the faster or more efficiently they are expected to produce. There may, however, be a point where the additional time spent learning instead of working will be outweighed by the value of experience. In this situation, it would be better suited for the individual to stop education and become a worker to gain experience. Also, if the education in a country is not up to par, their economy may suffer. The model we are introducing was created by Robert E. Lucas, Jr.(1988). In his version of the Solow model, there are new variables and equations. (15) where h is human capital per person. Lucas assumes that human capital evolves according to, (16) where u is time spent working and 1-u is time spent accumulating skill. (Jones 98) We will be using and adapting this model to fit with the one we are creating. As in Introduction to Economic Growth, we will assume that u is the average number of years a person spends educating themselves, and that H is skilled labor, calculated as, where ψ is the percent increase in wages from every additional year in school. We will use the u s that are listed in the appendix of Introduction to Economic Growth, as well as use the same assumption, that. Now it is important to list all the equations we have just described to get a better look at the system we ve generated. (17) (18) (19) (20) (21) The parameters for the phase portraits of this new system seem to be insignificant. Whether φ was or.8 the graphs were essentially the same, economically and financially. Because of insufficient data Zimbabwe and Uganda could not be modeled. For the ones that could be examined, the data used was from since the number of patents was not recorded until then. An important characteristic to point out is that they take on different shapes depending on the IC. They seem to move monotonically in the same way, yet they all still have slightly different slopes and forms from each other. This system seems to be the best representation because, although they only increase, the graphs seem to move like you would expect an economy would, seemingly unpredictable. Some will be moving in the same direction and then diverge from each other. With more research and data on mitigating factors, a better system could be created using the same techniques. Another possible case to explore is if L does not grow at a constant rate. This may bring our model closer to portraying true economic movements more successfully.

8 China France India Spain UK US 5. Conclusion A reoccurring pattern in the cases we examined was that capital and labor were always constantly growing. The only difference in the models is the rate at which they increased. Most of these fluctuations are actually exponential. Granted some of these growth projections predict thousands of years from now, however, our previous assumption was that the economic growth would at least have some of the same properties the Neoclassical model described. The only models that had decreasing capital was the first case, which did not take into account the change in labor, and the one with labor growing at a constant rate. This suggests that with labor and capital changing they will always be increasing unless some outside factor pulls them down. We expected some countries, most likely the poorer ones, would have an inefficient level of education which would pull the labor and capital lines down. Without proper education the amount of capital would suffer. Also, we expected the technology gap to be another negative factor in the economy. More wealthy countries have the resources for R&D that most poor countries do not. The lack of technology was expected to hinder the less fortunate countries and level their capital and labor lines. A theory that could explain why this was not depicted in the graphs is because the poor countries utilize the technological advances of the wealthy without the expense for R&D, causing them to be more well of then they originally would have been. We could also look into the fact that we may have overlooked an important factor that would cause these lines to decrease, or level off. Some of these factors could be the possibility of war. If we could somehow get the percent chance of war for each country we could include it in our prediction method. Another option would be to investigate limited resources. When resources are low, less labor and capital is used pertaining to that source. For example, if a forest was being cut down to produce chairs and there were limited trees, we might slow production, use less workers and machinery to allow for the resource to replenish itself. Finally, an economy is hugely impacted by natural disasters. The earthquakes in Japan are a prime example of this. Many resources will be put into rebuilding this economy instead of the normal production distribution. In Japan, the 1995 Great Hanshin earthquake struck directly beneath the modern industrialized urban area of Kobe. It killed more than 6,000 people and resulted in an estimated $100 billion in damages, or about 2 percent of Japan s gross national product (scawthorn et al., 1997) (Chung and Okuyama). If we gathered all the information on natural disasters for each country and applied it to our model perhaps this extremely influential factor would help level the economic path.

9 GDP per Capita References Bernard, Andrew B., Jones, Charles I., Technology and Convergence The Economic Journal, Vol. 106 No. 437 (1996): Print Chang, Stephanie E., Okuyama, Yasuhide, Modeling Spatial and Economic Impacts of Disasters. New York: Springer-Verlag Berlin Heidelberg New York, Print. De Long, J. Bradford, Productivity Growth, Convergence, and Welfare: Comment The American Economic Review, Vol. 78 No. 5 (1988): Print Fabiao, Fatima Solow Model, An Economic Dynamical System of Growth Applied Mathematical Sciences, Vol. 3 No. 58 (2009): Print Griliches, Zvi, Education, Human Capital, and Growth: A personal Perspective Journal of Labor Economics, Vol. 15 No. 1 (1997): Print Hansen, Gary D, Prescott, Edward C. Malthus to Solow The American Economic Review, Vol. 92 No. 4 (2002): Print Howitt, Peter, Endogenous Growth and Cross-Country Income Differences The American Economic Review, Vol. 90 No. 4 (2000): Print Jones, Bas, Nahuis, Richard, A general Purpose Technology Explains the Solow Paradox and Wage Inequality Economic Letters, 74 (2002): Print Jones, Charles I., Introduction to Economic Growth. New York: W.W. Norton & Company, Inc., Print. Pritchett, Lant, Where Has All the Education Gone? The World Bank Economic Review, Vol. 15 No. 3 (2001): Print Solow, Robert M., Technical Change and the Aggregate Production Function The Review of Economics and Statistics, Vol. 39 No. 3 (1957): Print World Data Bank. (2011). World Development Indicators (WDI) and Global Development Finance(GDF). Retrieved from s=ny.gdp.mktp.cd&period= Appendix A China France India Spain Uganda United Kingdom United States Zimbabwe Year

10 GDP per Worker China France India Spain Uganda United Kingdom United States Zimbabwe Year 1980 Savings rate GDP per Capita GDP per worker population growth rate China France India Spain Uganda United Kingdom United States Zimbabwe Appendix B, s and =.05 are constants:, United States China

11 France India Spain Uganda United Kingdom Zimbabwe

, d")

12 China and India France and Spain Uganda and Zimbabwe United States and United Kingdom Appendix C Part 1b), d is a constant,,, United States China

13 France India Spain Uganda

14 United Kingdom Zimbabwe China India Uganda US France Spain UK Zimbabwe China India Uganda Zimbabwe United States And China United States and India

15 United States and Spain United States and Uganda United States and United Kingdom United States and Zimbabwe

16 Appendix D, s and d are constant,, United States China France India Spain Uganda United Kingdom Zimbabwe

17 United States and United Kingdom France and Spain

18 Uganda and Zimbabwe United Kingdom and Zimbabwe

19 Appendix E, s and d are constant,,, UK US Zimbabwe China and India

20 China India Uganda Zimbabwe France Spain UK US

21 France and Spain

22 Appendix F, s and d constant,,, China India Uganda Zimbabwe France Spain UK US

23 France and Spain United States and United Kingdom

24 United States China Appendix G Add Technology and Education Data Used %pop in research # of patent apps 1995 u for 1995 delta: growth of ideas New savings rate China France India Spain United Kingdom United States

25 China France India Spain UK US Spain and China

26 United States China France India

Chapter 2 Savings, Investment and Economic Growth

George Alogoskoufis, Dynamic Macroeconomic Theory Chapter 2 Savings, Investment and Economic Growth The analysis of why some countries have achieved a high and rising standard of living, while others have

George Alogoskoufis, Dynamic Macroeconomic Theory Chapter 2 Savings, Investment and Economic Growth The analysis of why some countries have achieved a high and rising standard of living, while others have

MA Macroeconomics 11. The Solow Model

MA Macroeconomics 11. The Solow Model Karl Whelan School of Economics, UCD Autumn 2014 Karl Whelan (UCD) The Solow Model Autumn 2014 1 / 38 The Solow Model Recall that economic growth can come from capital

MA Macroeconomics 11. The Solow Model Karl Whelan School of Economics, UCD Autumn 2014 Karl Whelan (UCD) The Solow Model Autumn 2014 1 / 38 The Solow Model Recall that economic growth can come from capital

Introduction to economic growth (3)

") Introduction to economic growth (3) EKN 325 Manoel Bittencourt University of Pretoria M Bittencourt (University of Pretoria) EKN 325 1 / 29 Introduction Neoclassical growth models are descendants of the

Introduction to economic growth (3) EKN 325 Manoel Bittencourt University of Pretoria M Bittencourt (University of Pretoria) EKN 325 1 / 29 Introduction Neoclassical growth models are descendants of the

LEC 2: Exogenous (Neoclassical) growth model

growth model") LEC 2: Exogenous (Neoclassical) growth model Development of the model The Neo-classical model was an extension to the Harrod-Domar model that included a new term productivity growth The most important

LEC 2: Exogenous (Neoclassical) growth model Development of the model The Neo-classical model was an extension to the Harrod-Domar model that included a new term productivity growth The most important

5.1 Introduction. The Solow Growth Model. Additions / differences with the model: Chapter 5. In this chapter, we learn:

Chapter 5 The Solow Growth Model By Charles I. Jones Additions / differences with the model: Capital stock is no longer exogenous. Capital stock is now endogenized. The accumulation of capital is a possible

Chapter 5 The Solow Growth Model By Charles I. Jones Additions / differences with the model: Capital stock is no longer exogenous. Capital stock is now endogenized. The accumulation of capital is a possible

5.1 Introduction. The Solow Growth Model. Additions / differences with the model: Chapter 5. In this chapter, we learn:

Chapter 5 The Solow Growth Model By Charles I. Jones Additions / differences with the model: Capital stock is no longer exogenous. Capital stock is now endogenized. The accumulation of capital is a possible

Chapter 5 The Solow Growth Model By Charles I. Jones Additions / differences with the model: Capital stock is no longer exogenous. Capital stock is now endogenized. The accumulation of capital is a possible

Growth. Prof. Eric Sims. Fall University of Notre Dame. Sims (ND) Growth Fall / 39

Growth Fall / 39") Growth Prof. Eric Sims University of Notre Dame Fall 2012 Sims (ND) Growth Fall 2012 1 / 39 Economic Growth When economists say growth, typically mean average rate of growth in real GDP per capita over

Growth Prof. Eric Sims University of Notre Dame Fall 2012 Sims (ND) Growth Fall 2012 1 / 39 Economic Growth When economists say growth, typically mean average rate of growth in real GDP per capita over

Chapter 2 Savings, Investment and Economic Growth

Chapter 2 Savings, Investment and Economic Growth In this chapter we begin our investigation of the determinants of economic growth. We focus primarily on the relationship between savings, investment,

Chapter 2 Savings, Investment and Economic Growth In this chapter we begin our investigation of the determinants of economic growth. We focus primarily on the relationship between savings, investment,

The Theory of Economic Growth

The Theory of The Importance of Growth of real GDP per capita A measure of standards of living Small changes make large differences over long periods of time The causes and consequences of sustained increases

The Theory of The Importance of Growth of real GDP per capita A measure of standards of living Small changes make large differences over long periods of time The causes and consequences of sustained increases

The Theory of Economic Growth

The Theory of 1 The Importance of Growth of real GDP per capita A measure of standards of living Small changes make large differences over long periods of time The causes and consequences of sustained

The Theory of 1 The Importance of Growth of real GDP per capita A measure of standards of living Small changes make large differences over long periods of time The causes and consequences of sustained

ECO 4933 Topics in Theory

ECO 4933 Topics in Theory Introduction to Economic Growth Fall 2015 Chapter 2 1 Chapter 2 The Solow Growth Model Chapter 2 2 Assumptions: 1. The world consists of countries that produce and consume only

ECO 4933 Topics in Theory Introduction to Economic Growth Fall 2015 Chapter 2 1 Chapter 2 The Solow Growth Model Chapter 2 2 Assumptions: 1. The world consists of countries that produce and consume only

Topic 3: Endogenous Technology & Cross-Country Evidence

EC4010 Notes, 2005 (Karl Whelan) 1 Topic 3: Endogenous Technology & Cross-Country Evidence In this handout, we examine an alternative model of endogenous growth, due to Paul Romer ( Endogenous Technological

EC4010 Notes, 2005 (Karl Whelan) 1 Topic 3: Endogenous Technology & Cross-Country Evidence In this handout, we examine an alternative model of endogenous growth, due to Paul Romer ( Endogenous Technological

3.1 Introduction. 3.2 Growth over the Very Long Run. 3.1 Introduction. Part 2: The Long Run. An Overview of Long-Run Economic Growth

Part 2: The Long Run Media Slides Created By Dave Brown Penn State University 3.1 Introduction In this chapter, we learn: Some tools used to study economic growth, including how to calculate growth rates.

Part 2: The Long Run Media Slides Created By Dave Brown Penn State University 3.1 Introduction In this chapter, we learn: Some tools used to study economic growth, including how to calculate growth rates.

). In Ch. 9, when we add technological progress, k is capital per effective worker (k = K

. In Ch. 9, when we add technological progress, k is capital per effective worker (k = K") Economics 285 Chris Georges Help With Practice Problems 3 Chapter 8: 1. Questions For Review 1,4: Please see text or lecture notes. 2. A note about notation: Mankiw defines k slightly differently in Chs.

Economics 285 Chris Georges Help With Practice Problems 3 Chapter 8: 1. Questions For Review 1,4: Please see text or lecture notes. 2. A note about notation: Mankiw defines k slightly differently in Chs.

Testing the predictions of the Solow model: What do the data say?

Testing the predictions of the Solow model: What do the data say? Prediction n 1 : Conditional convergence: Countries at an early phase of capital accumulation tend to grow faster than countries at a later

Testing the predictions of the Solow model: What do the data say? Prediction n 1 : Conditional convergence: Countries at an early phase of capital accumulation tend to grow faster than countries at a later

ECON Chapter 6: Economic growth: The Solow growth model (Part 1)

") ECON3102-005 Chapter 6: Economic growth: The Solow growth model (Part 1) Neha Bairoliya Spring 2014 Motivations Why do countries grow? Why are there poor countries? Why are there rich countries? Can poor

ECON3102-005 Chapter 6: Economic growth: The Solow growth model (Part 1) Neha Bairoliya Spring 2014 Motivations Why do countries grow? Why are there poor countries? Why are there rich countries? Can poor

Economic Growth: Extensions

Economic Growth: Extensions 1 Road Map to this Lecture 1. Extensions to the Solow Growth Model 1. Population Growth 2. Technological growth 3. The Golden Rule 2. Endogenous Growth Theory 1. Human capital

Economic Growth: Extensions 1 Road Map to this Lecture 1. Extensions to the Solow Growth Model 1. Population Growth 2. Technological growth 3. The Golden Rule 2. Endogenous Growth Theory 1. Human capital

Check your understanding: Solow model 1

Check your understanding: Solow model 1 Bill Gibson March 26, 2017 1 Thanks to Farzad Ashouri Solow model The characteristics of the Solow model are 2 Solow has two kinds of variables, state variables

Check your understanding: Solow model 1 Bill Gibson March 26, 2017 1 Thanks to Farzad Ashouri Solow model The characteristics of the Solow model are 2 Solow has two kinds of variables, state variables

Introduction to economic growth (2)

") Introduction to economic growth (2) EKN 325 Manoel Bittencourt University of Pretoria M Bittencourt (University of Pretoria) EKN 325 1 / 49 Introduction Solow (1956), "A Contribution to the Theory of Economic

Introduction to economic growth (2) EKN 325 Manoel Bittencourt University of Pretoria M Bittencourt (University of Pretoria) EKN 325 1 / 49 Introduction Solow (1956), "A Contribution to the Theory of Economic

ECON 450 Development Economics

ECON 450 Development Economics Classic Theories of Economic Growth and Development The Empirics of the Solow Growth Model University of Illinois at Urbana-Champaign Summer 2017 Introduction This lecture

ECON 450 Development Economics Classic Theories of Economic Growth and Development The Empirics of the Solow Growth Model University of Illinois at Urbana-Champaign Summer 2017 Introduction This lecture

Macroeconomics Lecture 2: The Solow Growth Model with Technical Progress

Macroeconomics Lecture 2: The Solow Growth Model with Technical Progress Richard G. Pierse 1 Introduction In last week s lecture we considered the basic Solow-Swan growth model (Solow (1956), Swan (1956)).

Macroeconomics Lecture 2: The Solow Growth Model with Technical Progress Richard G. Pierse 1 Introduction In last week s lecture we considered the basic Solow-Swan growth model (Solow (1956), Swan (1956)).

Macroeconomics. Review of Growth Theory Solow and the Rest

Macroeconomics Review of Growth Theory Solow and the Rest Basic Neoclassical Growth Model K s Y = savings = investment = K production Y = f(l,k) consumption L = n L L exogenous population (labor) growth

Macroeconomics Review of Growth Theory Solow and the Rest Basic Neoclassical Growth Model K s Y = savings = investment = K production Y = f(l,k) consumption L = n L L exogenous population (labor) growth

Intermediate Macroeconomics,Assignment 3 & 4

Intermediate Macroeconomics,Assignment 3 & 4 Due May 4th (Friday), in-class 1. In this chapter we saw that the steady-state rate of unemployment is U/L = s/(s + f ). Suppose that the unemployment rate

Intermediate Macroeconomics,Assignment 3 & 4 Due May 4th (Friday), in-class 1. In this chapter we saw that the steady-state rate of unemployment is U/L = s/(s + f ). Suppose that the unemployment rate

Intermediate Macroeconomics,Assignment 4

Intermediate Macroeconomics,Assignment 4 Due May 6th (Friday), in-class 1. Two countries, Richland and Poorland, are described by the Solow growth model. They have the same Cobb Douglas production function,,

Intermediate Macroeconomics,Assignment 4 Due May 6th (Friday), in-class 1. Two countries, Richland and Poorland, are described by the Solow growth model. They have the same Cobb Douglas production function,,

Jean Monnet Chair in European Integration Studies Prof. PASQUALE TRIDICO Università Roma Tre

Jean Monnet Chair in European Integration Studies Prof. PASQUAE TRIDICO Università Roma Tre Two inputs,, A production function Cobb-Douglas Y= F, = 1 0 < < 1 Constant return to scale (decreasing marginal

Jean Monnet Chair in European Integration Studies Prof. PASQUAE TRIDICO Università Roma Tre Two inputs,, A production function Cobb-Douglas Y= F, = 1 0 < < 1 Constant return to scale (decreasing marginal

Traditional growth models Pasquale Tridico

1. EYNESIN THEORIES OF ECONOMIC GROWTH The eynesian growth models are models in which a long run growth path for an economy is traced out by the relations between saving, investements and the level of

1. EYNESIN THEORIES OF ECONOMIC GROWTH The eynesian growth models are models in which a long run growth path for an economy is traced out by the relations between saving, investements and the level of

1 The Solow Growth Model

1 The Solow Growth Model The Solow growth model is constructed around 3 building blocks: 1. The aggregate production function: = ( ()) which it is assumed to satisfy a series of technical conditions: (a)

1 The Solow Growth Model The Solow growth model is constructed around 3 building blocks: 1. The aggregate production function: = ( ()) which it is assumed to satisfy a series of technical conditions: (a)

Lastrapes Fall y t = ỹ + a 1 (p t p t ) y t = d 0 + d 1 (m t p t ).

y t = d 0 + d 1 (m t p t ).") ECON 8040 Final exam Lastrapes Fall 2007 Answer all eight questions on this exam. 1. Write out a static model of the macroeconomy that is capable of predicting that money is non-neutral. Your model should

ECON 8040 Final exam Lastrapes Fall 2007 Answer all eight questions on this exam. 1. Write out a static model of the macroeconomy that is capable of predicting that money is non-neutral. Your model should

14.05 Intermediate Applied Macroeconomics Exam # 1 Suggested Solutions

14.05 Intermediate Applied Macroeconomics Exam # 1 Suggested Solutions October 13, 2005 Professor: Peter Temin TA: Frantisek Ricka José Tessada Question 1 Golden Rule and Consumption in the Solow Model

14.05 Intermediate Applied Macroeconomics Exam # 1 Suggested Solutions October 13, 2005 Professor: Peter Temin TA: Frantisek Ricka José Tessada Question 1 Golden Rule and Consumption in the Solow Model

An endogenous growth model with human capital and learning

An endogenous growth model with human capital and learning Prof. George McCandless UCEMA May 0, 20 One can get an AK model by directly introducing human capital accumulation. The model presented here is

An endogenous growth model with human capital and learning Prof. George McCandless UCEMA May 0, 20 One can get an AK model by directly introducing human capital accumulation. The model presented here is

ECON 256: Poverty, Growth & Inequality. Jack Rossbach

ECON 256: Poverty, Growth & Inequality Jack Rossbach What Makes Countries Grow? Common Answers Technological progress Capital accumulation Question: Should countries converge over time? Models of Economic

ECON 256: Poverty, Growth & Inequality Jack Rossbach What Makes Countries Grow? Common Answers Technological progress Capital accumulation Question: Should countries converge over time? Models of Economic

Chapter 9 Dynamic Models of Investment

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 9 Dynamic Models of Investment In this chapter we present the main neoclassical model of investment, under convex adjustment costs. This

Road Map to this Lecture

Economic Growth 1 Road Map to this Lecture 1. Steady State dynamics: 1. Output per capita 2. Capital accumulation 3. Depreciation 4. Steady State 2. The Golden Rule: maximizing welfare 3. Total Factor

Economic Growth 1 Road Map to this Lecture 1. Steady State dynamics: 1. Output per capita 2. Capital accumulation 3. Depreciation 4. Steady State 2. The Golden Rule: maximizing welfare 3. Total Factor

ECON 6022B Problem Set 1 Suggested Solutions Fall 2011

ECON 6022B Problem Set Suggested Solutions Fall 20 September 5, 20 Shocking the Solow Model Consider the basic Solow model in Lecture 2. Suppose the economy stays at its steady state in Period 0 and there

ECON 6022B Problem Set Suggested Solutions Fall 20 September 5, 20 Shocking the Solow Model Consider the basic Solow model in Lecture 2. Suppose the economy stays at its steady state in Period 0 and there

The Role of Physical Capital

San Francisco State University ECO 560 The Role of Physical Capital Michael Bar As we mentioned in the introduction, the most important macroeconomic observation in the world is the huge di erences in

San Francisco State University ECO 560 The Role of Physical Capital Michael Bar As we mentioned in the introduction, the most important macroeconomic observation in the world is the huge di erences in

The Romer Model: Policy Implications

The Romer Model: Policy Implications Prof. Lutz Hendricks Econ520 February 16, 2017 1 / 29 Policies have level effects What are the effects of government policies? We may expect policies to affect saving

The Romer Model: Policy Implications Prof. Lutz Hendricks Econ520 February 16, 2017 1 / 29 Policies have level effects What are the effects of government policies? We may expect policies to affect saving

Macroeconomic Models of Economic Growth

Macroeconomic Models of Economic Growth J.R. Walker U.W. Madison Econ448: Human Resources and Economic Growth Summary Solow Model [Pop Growth] The simplest Solow model (i.e., with exogenous population

Macroeconomic Models of Economic Growth J.R. Walker U.W. Madison Econ448: Human Resources and Economic Growth Summary Solow Model [Pop Growth] The simplest Solow model (i.e., with exogenous population

Advanced Macroeconomics 9. The Solow Model

Advanced Macroeconomics 9. The Solow Model Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) The Solow Model Spring 2015 1 / 29 The Solow Model Recall that economic growth can come from

Advanced Macroeconomics 9. The Solow Model Karl Whelan School of Economics, UCD Spring 2015 Karl Whelan (UCD) The Solow Model Spring 2015 1 / 29 The Solow Model Recall that economic growth can come from

Chapter 7 Externalities, Human Capital and Endogenous Growth

George Alogoskoufis, Dynamic Macroeconomics, 2016 Chapter 7 Externalities, Human Capital and Endogenous Growth In this chapter we examine growth models in which the efficiency of labor is no longer entirely

George Alogoskoufis, Dynamic Macroeconomics, 2016 Chapter 7 Externalities, Human Capital and Endogenous Growth In this chapter we examine growth models in which the efficiency of labor is no longer entirely

Testing the predictions of the Solow model:

Testing the predictions of the Solow model: 1. Convergence predictions: state that countries farther away from their steady state grow faster. Convergence regressions are designed to test this prediction.

Testing the predictions of the Solow model: 1. Convergence predictions: state that countries farther away from their steady state grow faster. Convergence regressions are designed to test this prediction.

Solow instead assumed a standard neo-classical production function with diminishing marginal product for both labor and capital.

Module 5 Lecture 34 Topics 5.2 Growth Theory II 5.2.1 Solow Model 5.2 Growth Theory II 5.2.1 Solow Model Robert Solow was quick to recognize that the instability inherent in the Harrod- Domar model is

Module 5 Lecture 34 Topics 5.2 Growth Theory II 5.2.1 Solow Model 5.2 Growth Theory II 5.2.1 Solow Model Robert Solow was quick to recognize that the instability inherent in the Harrod- Domar model is

Lecture notes 2: Physical Capital, Development and Growth

Lecture notes 2: Physical Capital, Development and Growth These notes are based on a draft manuscript Economic Growth by David N. Weil. All rights reserved. Lecture notes 2: Physical Capital, Development

Lecture notes 2: Physical Capital, Development and Growth These notes are based on a draft manuscript Economic Growth by David N. Weil. All rights reserved. Lecture notes 2: Physical Capital, Development

Infrastructure and Urban Primacy: A Theoretical Model. Jinghui Lim 1. Economics Urban Economics Professor Charles Becker December 15, 2005

Infrastructure and Urban Primacy 1 Infrastructure and Urban Primacy: A Theoretical Model Jinghui Lim 1 Economics 195.53 Urban Economics Professor Charles Becker December 15, 2005 1 Jinghui Lim (jl95@duke.edu)

Infrastructure and Urban Primacy 1 Infrastructure and Urban Primacy: A Theoretical Model Jinghui Lim 1 Economics 195.53 Urban Economics Professor Charles Becker December 15, 2005 1 Jinghui Lim (jl95@duke.edu)

Chapter 4. Economic Growth

Chapter 4 Economic Growth When you have completed your study of this chapter, you will be able to 1. Understand what are the determinants of economic growth. 2. Understand the Neoclassical Solow growth

Chapter 4 Economic Growth When you have completed your study of this chapter, you will be able to 1. Understand what are the determinants of economic growth. 2. Understand the Neoclassical Solow growth

Growth 2. Chapter 6 (continued)

") Growth 2 Chapter 6 (continued) 1. Solow growth model continued 2. Use the model to understand growth 3. Endogenous growth 4. Labor and goods markets with growth 1 Solow Model with Exogenous Labor-Augmenting

Growth 2 Chapter 6 (continued) 1. Solow growth model continued 2. Use the model to understand growth 3. Endogenous growth 4. Labor and goods markets with growth 1 Solow Model with Exogenous Labor-Augmenting

Macroeconomic Models of Economic Growth

Macroeconomic Models of Economic Growth J.R. Walker U.W. Madison Econ448: Human Resources and Economic Growth Course Roadmap: Seemingly Random Topics First midterm a week from today. What have we covered

Macroeconomic Models of Economic Growth J.R. Walker U.W. Madison Econ448: Human Resources and Economic Growth Course Roadmap: Seemingly Random Topics First midterm a week from today. What have we covered

Business Cycles II: Theories

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

Macroeconomic Policy Class Notes Business Cycles II: Theories Revised: December 5, 2011 Latest version available at www.fperri.net/teaching/macropolicy.f11htm In class we have explored at length the main

Chapter 3 The Representative Household Model

George Alogoskoufis, Dynamic Macroeconomics, 2016 Chapter 3 The Representative Household Model The representative household model is a dynamic general equilibrium model, based on the assumption that the

George Alogoskoufis, Dynamic Macroeconomics, 2016 Chapter 3 The Representative Household Model The representative household model is a dynamic general equilibrium model, based on the assumption that the

Savings, Investment and Economic Growth

Chapter 2 Savings, Investment and Economic Growth In this chapter we begin our investigation of the determinants of economic growth. We focus primarily on the relationship between savings, investment,

Chapter 2 Savings, Investment and Economic Growth In this chapter we begin our investigation of the determinants of economic growth. We focus primarily on the relationship between savings, investment,

Economic Growth: Malthus and Solow Copyright 2014 Pearson Education, Inc.

Chapter 7 Economic Growth: Malthus and Solow Copyright Chapter 7 Topics Economic growth facts Malthusian model of economic growth Solow growth model Growth accounting 1-2 U.S. Per Capita Real Income Growth

Chapter 7 Economic Growth: Malthus and Solow Copyright Chapter 7 Topics Economic growth facts Malthusian model of economic growth Solow growth model Growth accounting 1-2 U.S. Per Capita Real Income Growth

Growth and Ideas. Chad Jones Stanford GSB. October 14, Growth and Ideas p. 1

Growth and Ideas Chad Jones Stanford GSB October 14, 2015 Growth and Ideas p. 1 U.S. GDP per Person Growth and Ideas p. 2 Why? The average American is 15 times richer today than in 1870. How do we understand

Growth and Ideas Chad Jones Stanford GSB October 14, 2015 Growth and Ideas p. 1 U.S. GDP per Person Growth and Ideas p. 2 Why? The average American is 15 times richer today than in 1870. How do we understand

ECON MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University. J.Jung Chapter 8 - Economic Growth Towson University 1 / 64

ECON 202 - MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University J.Jung Chapter 8 - Economic Growth Towson University 1 / 64 Disclaimer These lecture notes are customized for the Macroeconomics

ECON 202 - MACROECONOMIC PRINCIPLES Instructor: Dr. Juergen Jung Towson University J.Jung Chapter 8 - Economic Growth Towson University 1 / 64 Disclaimer These lecture notes are customized for the Macroeconomics

Chapter 5 Fiscal Policy and Economic Growth

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 5 Fiscal Policy and Economic Growth In this chapter we introduce the government into the exogenous growth models we have analyzed so far.

George Alogoskoufis, Dynamic Macroeconomic Theory, 2015 Chapter 5 Fiscal Policy and Economic Growth In this chapter we introduce the government into the exogenous growth models we have analyzed so far.

Dynamic Macroeconomics

Chapter 1 Introduction Dynamic Macroeconomics Prof. George Alogoskoufis Fletcher School, Tufts University and Athens University of Economics and Business 1.1 The Nature and Evolution of Macroeconomics

Chapter 1 Introduction Dynamic Macroeconomics Prof. George Alogoskoufis Fletcher School, Tufts University and Athens University of Economics and Business 1.1 The Nature and Evolution of Macroeconomics

I. The Solow model. Dynamic Macroeconomic Analysis. Universidad Autónoma de Madrid. Autumn 2014

I. The Solow model Dynamic Macroeconomic Analysis Universidad Autónoma de Madrid Autumn 2014 Dynamic Macroeconomic Analysis (UAM) I. The Solow model Autumn 2014 1 / 38 Objectives In this first lecture

I. The Solow model Dynamic Macroeconomic Analysis Universidad Autónoma de Madrid Autumn 2014 Dynamic Macroeconomic Analysis (UAM) I. The Solow model Autumn 2014 1 / 38 Objectives In this first lecture

The Solow Model and Standard of Living

Undergraduate Journal of Mathematical Modeling: One + Two Volume 7 2017 Spring 2017 Issue 2 Article 5 The Solow Model and Standard of Living Eric Frey University of South Florida Advisors: Arcadii Grinshpan,

Undergraduate Journal of Mathematical Modeling: One + Two Volume 7 2017 Spring 2017 Issue 2 Article 5 The Solow Model and Standard of Living Eric Frey University of South Florida Advisors: Arcadii Grinshpan,

What we ve learned so far. The Solow Growth Model. Our objectives today 2/11/2009 ECON 206 MACROECONOMIC ANALYSIS. Chapter 5 (2 of 2)

") ECON 206 MACROECONOMIC ANALYSIS What we ve learned so far Roumen Vesselinov Class # 7 The key equations of the Solow Model are these: The production function And the capital accumulation equation How do

ECON 206 MACROECONOMIC ANALYSIS What we ve learned so far Roumen Vesselinov Class # 7 The key equations of the Solow Model are these: The production function And the capital accumulation equation How do

I. The Solow model. Dynamic Macroeconomic Analysis. Universidad Autónoma de Madrid. Autumn 2014

I. The Solow model Dynamic Macroeconomic Analysis Universidad Autónoma de Madrid Autumn 2014 Dynamic Macroeconomic Analysis (UAM) I. The Solow model Autumn 2014 1 / 33 Objectives In this first lecture

I. The Solow model Dynamic Macroeconomic Analysis Universidad Autónoma de Madrid Autumn 2014 Dynamic Macroeconomic Analysis (UAM) I. The Solow model Autumn 2014 1 / 33 Objectives In this first lecture

ECONOMIC CONVERGENCE AND THE GLOBAL CRISIS OF : THE CASE OF BALTIC COUNTRIES AND UKRAINE

ISSN 1822-8011 (print) ISSN 1822-8038 (online) INTELEKTINĖ EKONOMIKA INTELLECTUAL ECONOMICS 2014, Vol. 8, No. 2(20), p. 135 146 ECONOMIC CONVERGENCE AND THE GLOBAL CRISIS OF 2008-2012: THE CASE OF BALTIC

ISSN 1822-8011 (print) ISSN 1822-8038 (online) INTELEKTINĖ EKONOMIKA INTELLECTUAL ECONOMICS 2014, Vol. 8, No. 2(20), p. 135 146 ECONOMIC CONVERGENCE AND THE GLOBAL CRISIS OF 2008-2012: THE CASE OF BALTIC

Chapter 7. Economic Growth I: Capital Accumulation and Population Growth (The Very Long Run) CHAPTER 7 Economic Growth I. slide 0

CHAPTER 7 Economic Growth I. slide 0") Chapter 7 Economic Growth I: Capital Accumulation and Population Growth (The Very Long Run) slide 0 In this chapter, you will learn the closed economy Solow model how a country s standard of living depends

Chapter 7 Economic Growth I: Capital Accumulation and Population Growth (The Very Long Run) slide 0 In this chapter, you will learn the closed economy Solow model how a country s standard of living depends

Department of Economics Shanghai University of Finance and Economics Intermediate Macroeconomics

Department of Economics Shanghai University of Finance and Economics Intermediate Macroeconomics Instructor: Min Zhang Answer 2. List the stylized facts about economic growth. What is relevant for the

Department of Economics Shanghai University of Finance and Economics Intermediate Macroeconomics Instructor: Min Zhang Answer 2. List the stylized facts about economic growth. What is relevant for the

EC 205 Macroeconomics I

EC 205 Macroeconomics I Macroeconomics I Chapter 8 & 9: Economic Growth Why growth matters In 2000, real GDP per capita in the United States was more than fifty times that in Ethiopia. Over the period

EC 205 Macroeconomics I Macroeconomics I Chapter 8 & 9: Economic Growth Why growth matters In 2000, real GDP per capita in the United States was more than fifty times that in Ethiopia. Over the period

Technical change is labor-augmenting (also known as Harrod neutral). The production function exhibits constant returns to scale:

. The production function exhibits constant returns to scale:") Romer01a.doc The Solow Growth Model Set-up The Production Function Assume an aggregate production function: F[ A ], (1.1) Notation: A output capital labor effectiveness of labor (productivity) Technical

Romer01a.doc The Solow Growth Model Set-up The Production Function Assume an aggregate production function: F[ A ], (1.1) Notation: A output capital labor effectiveness of labor (productivity) Technical

ECN101: Intermediate Macroeconomic Theory TA Section

ECN101: Intermediate Macroeconomic Theory TA Section (jwjung@ucdavis.edu) Department of Economics, UC Davis October 27, 2014 Slides revised: October 27, 2014 Outline 1 Announcement 2 Review: Chapter 5

ECN101: Intermediate Macroeconomic Theory TA Section (jwjung@ucdavis.edu) Department of Economics, UC Davis October 27, 2014 Slides revised: October 27, 2014 Outline 1 Announcement 2 Review: Chapter 5

Convergence of Life Expectancy and Living Standards in the World

Convergence of Life Expectancy and Living Standards in the World Kenichi Ueda* *The University of Tokyo PRI-ADBI Joint Workshop January 13, 2017 The views are those of the author and should not be attributed

Convergence of Life Expectancy and Living Standards in the World Kenichi Ueda* *The University of Tokyo PRI-ADBI Joint Workshop January 13, 2017 The views are those of the author and should not be attributed

KGP/World income distribution: past, present and future.

KGP/World income distribution: past, present and future. Lecture notes based on C.I. Jones, Evolution of the World Income Distribution, JEP11,3,1997, pp.19-36 and R.E. Lucas, Some Macroeconomics for the

KGP/World income distribution: past, present and future. Lecture notes based on C.I. Jones, Evolution of the World Income Distribution, JEP11,3,1997, pp.19-36 and R.E. Lucas, Some Macroeconomics for the

Economic Growth I Macroeconomics Finals

Economic Growth I Macroeconomics Finals Introduction and the Solow growth model Martin Ellison Nuffield College Hilary Term 2016 The Wealth of Nations Performance of economy over many years Growth a recent

Economic Growth I Macroeconomics Finals Introduction and the Solow growth model Martin Ellison Nuffield College Hilary Term 2016 The Wealth of Nations Performance of economy over many years Growth a recent

Chapter 10 Aggregate Demand I

Chapter 10 In this chapter, We focus on the short run, and temporarily set aside the question of whether the economy has the resources to produce the output demanded. We examine the determination of r

Chapter 10 In this chapter, We focus on the short run, and temporarily set aside the question of whether the economy has the resources to produce the output demanded. We examine the determination of r

The Effect of Interventions to Reduce Fertility on Economic Growth. Quamrul Ashraf Ashley Lester David N. Weil. Brown University.

The Effect of Interventions to Reduce Fertility on Economic Growth Quamrul Ashraf Ashley Lester David N. Weil Brown University December 2007 Goal: analyze quantitatively the economic effects of interventions

The Effect of Interventions to Reduce Fertility on Economic Growth Quamrul Ashraf Ashley Lester David N. Weil Brown University December 2007 Goal: analyze quantitatively the economic effects of interventions

Capital Income Tax Reform and the Japanese Economy (Very Preliminary and Incomplete)

") Capital Income Tax Reform and the Japanese Economy (Very Preliminary and Incomplete) Gary Hansen (UCLA), Selo İmrohoroğlu (USC), Nao Sudo (BoJ) December 22, 2015 Keio University December 22, 2015 Keio

Capital Income Tax Reform and the Japanese Economy (Very Preliminary and Incomplete) Gary Hansen (UCLA), Selo İmrohoroğlu (USC), Nao Sudo (BoJ) December 22, 2015 Keio University December 22, 2015 Keio

1 Four facts on the U.S. historical growth experience, aka the Kaldor facts

1 Four facts on the U.S. historical growth experience, aka the Kaldor facts In 1958 Nicholas Kaldor listed 4 key facts on the long-run growth experience of the US economy in the past century, which have

1 Four facts on the U.S. historical growth experience, aka the Kaldor facts In 1958 Nicholas Kaldor listed 4 key facts on the long-run growth experience of the US economy in the past century, which have

The Solow Growth Model. Martin Ellison, Hilary Term 2017

The Solow Growth Model Martin Ellison, Hilary Term 2017 Solow growth model 2 Builds on the production model by adding a theory of capital accumulation Was developed in the mid-1950s by Robert Solow of

The Solow Growth Model Martin Ellison, Hilary Term 2017 Solow growth model 2 Builds on the production model by adding a theory of capital accumulation Was developed in the mid-1950s by Robert Solow of

Chapter 6: Long-Run Economic Growth

Chapter 6: Long-Run Economic Growth Yulei Luo SEF of HKU October 10, 2013 Luo, Y. (SEF of HKU) ECON2220: Macro Theory October 10, 2013 1 / 34 Chapter Outline Discuss the sources of economic growth and

Chapter 6: Long-Run Economic Growth Yulei Luo SEF of HKU October 10, 2013 Luo, Y. (SEF of HKU) ECON2220: Macro Theory October 10, 2013 1 / 34 Chapter Outline Discuss the sources of economic growth and

E-322 Muhammad Rahman CHAPTER-6

CHAPTER-6 A. OBJECTIVE OF THIS CHAPTER In this chapter we will do the following: Look at some stylized facts about economic growth in the World. Look at two Macroeconomic models of exogenous economic growth

CHAPTER-6 A. OBJECTIVE OF THIS CHAPTER In this chapter we will do the following: Look at some stylized facts about economic growth in the World. Look at two Macroeconomic models of exogenous economic growth

Economic Growth II. macroeconomics. fifth edition. N. Gregory Mankiw. PowerPoint Slides by Ron Cronovich Worth Publishers, all rights reserved

CHAPTER EIGHT Economic Growth II macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved Learning objectives Technological progress

CHAPTER EIGHT Economic Growth II macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved Learning objectives Technological progress

Macroeconomic Theory I: Growth Theory

Macroeconomic Theory I: Growth Theory Gavin Cameron Lady Margaret Hall Michaelmas Term 2004 macroeconomic theory course These lectures introduce macroeconomic models that have microfoundations. This provides

Macroeconomic Theory I: Growth Theory Gavin Cameron Lady Margaret Hall Michaelmas Term 2004 macroeconomic theory course These lectures introduce macroeconomic models that have microfoundations. This provides

(S-I) + (T-G) = (X-Z)

+ (T-G) = (X-Z)") Question 1 Tax revue in the country is recorded at 40 Euros, net savings are equal to 40 Euros. The investments are a third of the size of government spending, there is a budget deficit of 20 and the current

Question 1 Tax revue in the country is recorded at 40 Euros, net savings are equal to 40 Euros. The investments are a third of the size of government spending, there is a budget deficit of 20 and the current

I. The Solow model. Dynamic Macroeconomic Analysis. Universidad Autónoma de Madrid. September 2015

I. The Solow model Dynamic Macroeconomic Analysis Universidad Autónoma de Madrid September 2015 Dynamic Macroeconomic Analysis (UAM) I. The Solow model September 2015 1 / 43 Objectives In this first lecture

I. The Solow model Dynamic Macroeconomic Analysis Universidad Autónoma de Madrid September 2015 Dynamic Macroeconomic Analysis (UAM) I. The Solow model September 2015 1 / 43 Objectives In this first lecture

Savings, Investment and the Real Interest Rate in an Endogenous Growth Model

Savings, Investment and the Real Interest Rate in an Endogenous Growth Model George Alogoskoufis* Athens University of Economics and Business October 2012 Abstract This paper compares the predictions of

Savings, Investment and the Real Interest Rate in an Endogenous Growth Model George Alogoskoufis* Athens University of Economics and Business October 2012 Abstract This paper compares the predictions of

ECN101: Intermediate Macroeconomic Theory TA Section

ECN101: Intermediate Macroeconomic Theory TA Section (jwjung@ucdavis.edu) Department of Economics, UC Davis November 4, 2014 Slides revised: November 4, 2014 Outline 1 2 Fall 2012 Winter 2012 Midterm:

ECN101: Intermediate Macroeconomic Theory TA Section (jwjung@ucdavis.edu) Department of Economics, UC Davis November 4, 2014 Slides revised: November 4, 2014 Outline 1 2 Fall 2012 Winter 2012 Midterm:

Growth, Capital Accumulation, and the Economics of Ideas

Chapter 8 MODERN PRINCIPLES OF ECONOMICS Third Edition Growth, Capital Accumulation, and the Economics of Ideas Outline The Solow Model and Catching-Up Growth The Investment Rate and Conditional Convergence

Chapter 8 MODERN PRINCIPLES OF ECONOMICS Third Edition Growth, Capital Accumulation, and the Economics of Ideas Outline The Solow Model and Catching-Up Growth The Investment Rate and Conditional Convergence

Notes VI - Models of Economic Fluctuations

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

Notes VI - Models of Economic Fluctuations Julio Garín Intermediate Macroeconomics Fall 2017 Intermediate Macroeconomics Notes VI - Models of Economic Fluctuations Fall 2017 1 / 33 Business Cycles We can

3. Long-Run Economic Growth

Intermediate Macroeconomics 3. Long-Run Economic Growth Contents 1. Measuring Economic Growth 2. Growth Accounting 3. Empirical Studies A. International Growth Comparisons B. Growth Accounting 4. Neoclassical

Intermediate Macroeconomics 3. Long-Run Economic Growth Contents 1. Measuring Economic Growth 2. Growth Accounting 3. Empirical Studies A. International Growth Comparisons B. Growth Accounting 4. Neoclassical

macro macroeconomics Economic Growth I Economic Growth I I (chapter 7) N. Gregory Mankiw

N. Gregory Mankiw") macro Topic CHAPTER 4: SEVEN I (chapter 7) macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved (ch. 7) Chapter 7 learning objectives

macro Topic CHAPTER 4: SEVEN I (chapter 7) macroeconomics fifth edition N. Gregory Mankiw PowerPoint Slides by Ron Cronovich 2002 Worth Publishers, all rights reserved (ch. 7) Chapter 7 learning objectives

IN THIS LECTURE, YOU WILL LEARN:

IN THIS LECTURE, YOU WILL LEARN: the closed economy Solow model how a country s standard of living depends on its saving and population growth rates how to use the Golden Rule to find the optimal saving

IN THIS LECTURE, YOU WILL LEARN: the closed economy Solow model how a country s standard of living depends on its saving and population growth rates how to use the Golden Rule to find the optimal saving

Part A: Answer Question A1 (required) and Question A2 or A3 (choice).

and Question A2 or A3 (choice).") Ph.D. Core Exam -- Macroeconomics 10 January 2018 -- 8:00 am to 3:00 pm Part A: Answer Question A1 (required) and Question A2 or A3 (choice). A1 (required): Cutting Taxes Under the 2017 US Tax Cut and

Ph.D. Core Exam -- Macroeconomics 10 January 2018 -- 8:00 am to 3:00 pm Part A: Answer Question A1 (required) and Question A2 or A3 (choice). A1 (required): Cutting Taxes Under the 2017 US Tax Cut and

Incentives and economic growth

Econ 307 Lecture 8 Incentives and economic growth Up to now we have abstracted away from most of the incentives that agents face in determining economic growth (expect for the determination of technology

Econ 307 Lecture 8 Incentives and economic growth Up to now we have abstracted away from most of the incentives that agents face in determining economic growth (expect for the determination of technology

Business Cycles II: Theories

International Economics and Business Dynamics Class Notes Business Cycles II: Theories Revised: November 23, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm In the previous lecture

International Economics and Business Dynamics Class Notes Business Cycles II: Theories Revised: November 23, 2012 Latest version available at http://www.fperri.net/teaching/20205.htm In the previous lecture

Why thinking about economic growth? Kaldor facts old and new Basic tools and concepts

Prof. Dr. Thomas Steger Economic Growth Lecture WS 13/14 1. Motivation and Basic Concepts Why thinking about economic growth? Kaldor facts old and new Basic tools and concepts Why thinking about economic

Prof. Dr. Thomas Steger Economic Growth Lecture WS 13/14 1. Motivation and Basic Concepts Why thinking about economic growth? Kaldor facts old and new Basic tools and concepts Why thinking about economic

ECON 450 Development Economics

ECON 450 Development Economics Classic Theories of Economic Growth and Development The Solow Growth Model University of Illinois at Urbana-Champaign Summer 2017 Introduction In this lecture we start the

ECON 450 Development Economics Classic Theories of Economic Growth and Development The Solow Growth Model University of Illinois at Urbana-Champaign Summer 2017 Introduction In this lecture we start the

Class Notes. Intermediate Macroeconomics. Li Gan. Lecture 7: Economic Growth. It is amazing how much we have achieved.

Class Notes Intermediate Macroeconomics Li Gan Lecture 7: Economic Growth It is amazing how much we have achieved. It is also to know how much difference across countries. Nigeria is only 1/43 of the US.

Class Notes Intermediate Macroeconomics Li Gan Lecture 7: Economic Growth It is amazing how much we have achieved. It is also to know how much difference across countries. Nigeria is only 1/43 of the US.

Part 1: Short answer, 60 points possible Part 2: Analytical problems, 40 points possible

Midterm #1 ECON 322, Prof. DeBacker September 25, 2018 INSTRUCTIONS: Please read each question below carefully and respond to the questions in the space provided (use the back of pages if necessary). You

Midterm #1 ECON 322, Prof. DeBacker September 25, 2018 INSTRUCTIONS: Please read each question below carefully and respond to the questions in the space provided (use the back of pages if necessary). You

Macroeconomics I, UPF Professor Antonio Ciccone SOLUTIONS PROBLEM SET 1

Macroeconomics I, UPF Professor Antonio Ciccone SOLUTIONS PROBLEM SET 1 1.1 (from Romer Advanced Macroeconomics Chapter 1) Basic properties of growth rates which will be used over and over again. Use the

Macroeconomics I, UPF Professor Antonio Ciccone SOLUTIONS PROBLEM SET 1 1.1 (from Romer Advanced Macroeconomics Chapter 1) Basic properties of growth rates which will be used over and over again. Use the

Components of Economic Growth

Components of Economic Growth Components of Economic Growth 1. Capital Accumulation: savings from present income invested to increase future output and income New factories, equipment, etc., increase the

Components of Economic Growth Components of Economic Growth 1. Capital Accumulation: savings from present income invested to increase future output and income New factories, equipment, etc., increase the

Part A: Answer Question A1 (required) and Question A2 or A3 (choice).

and Question A2 or A3 (choice).") Ph.D. Core Exam -- Macroeconomics 13 August 2018 -- 8:00 am to 3:00 pm Part A: Answer Question A1 (required) and Question A2 or A3 (choice). A1 (required): Short-Run Stabilization Policy and Economic Shocks

Ph.D. Core Exam -- Macroeconomics 13 August 2018 -- 8:00 am to 3:00 pm Part A: Answer Question A1 (required) and Question A2 or A3 (choice). A1 (required): Short-Run Stabilization Policy and Economic Shocks

INTERMEDIATE MACROECONOMICS

INTERMEDIATE MACROECONOMICS LECTURE 5 Douglas Hanley, University of Pittsburgh ENDOGENOUS GROWTH IN THIS LECTURE How does the Solow model perform across countries? Does it match the data we see historically?

INTERMEDIATE MACROECONOMICS LECTURE 5 Douglas Hanley, University of Pittsburgh ENDOGENOUS GROWTH IN THIS LECTURE How does the Solow model perform across countries? Does it match the data we see historically?

Midterm Examination Number 1 February 19, 1996

Economics 200 Macroeconomic Theory Midterm Examination Number 1 February 19, 1996 You have 1 hour to complete this exam. Answer any four questions you wish. 1. Suppose that an increase in consumer confidence

Economics 200 Macroeconomic Theory Midterm Examination Number 1 February 19, 1996 You have 1 hour to complete this exam. Answer any four questions you wish. 1. Suppose that an increase in consumer confidence

How Rich Will China Become? A simple calculation based on South Korea and Japan s experience

ECONOMIC POLICY PAPER 15-5 MAY 2015 How Rich Will China Become? A simple calculation based on South Korea and Japan s experience EXECUTIVE SUMMARY China s impressive economic growth since the 1980s raises

ECONOMIC POLICY PAPER 15-5 MAY 2015 How Rich Will China Become? A simple calculation based on South Korea and Japan s experience EXECUTIVE SUMMARY China s impressive economic growth since the 1980s raises

The Empirical Study on the Relationship between Chinese Residents saving rate and Economic Growth

2017 4th International Conference on Business, Economics and Management (BUSEM 2017) The Empirical Study on the Relationship between Chinese Residents saving rate and Economic Growth Zhaoyi Xu1, a, Delong

2017 4th International Conference on Business, Economics and Management (BUSEM 2017) The Empirical Study on the Relationship between Chinese Residents saving rate and Economic Growth Zhaoyi Xu1, a, Delong

Objectives of Macroeconomics ECO403

Objectives of Macroeconomics ECO403 http//vustudents.ning.com Actual budget The amount spent by the Federal government (to purchase goods and services and for transfer payments) less the amount of tax

Objectives of Macroeconomics ECO403 http//vustudents.ning.com Actual budget The amount spent by the Federal government (to purchase goods and services and for transfer payments) less the amount of tax