STRUCTURING INNOVATIVE SUKUK FOR INFRASTRUCTURE FINANCING

|

|

|

- Silvester Shelton

- 6 years ago

- Views:

Transcription

1 STRUCTURING INNOVATIVE SUKUK FOR INFRASTRUCTURE FINANCING 1 ST ANNUAL ISLAMIC FINANCE CONFERENCE: SUKUK FOR INFRASTRUCTURE FINANCING AND FINANCIAL INCLUSION STRATEGY 17 MAY 2016 JAKARTA, REPUBLIC OF INDONESIA MICHAEL J.T. MCMILLEN Menteri Keuangan, Republik Indonesia Islamic Development Bank Other Generous Sponsors

2 Consider select issues relating to issuance of innovative sukuk for infrastructure financing. Two areas of focus: Private sector issuances. Fundamentals of infrastructure finance. OBJECTIVE Synergy point: use infrastructure finance innovations to assist in the development of other aspects of sukuk markets. 2

3 INNOVATION FOR AN EXISTING SUCCESS STORY? Remarks today relate to innovation to change to an area of Islamic finance that must be characterized as an existing success story. The growth in sukuk issuances since 2002, and throughout the economic downturn, has been inspiring. Total Global Sukuk Issuances (November 7) US$ 88 billion 2009 US$ 38 billion 2014 US$ 116 billion 3

4 ISSUERS 2014 Total Global Issuances Sovereign 67% Quasi-Sovereign 16% Corporate 22% Are these allocations credible? Source: Zawya Islamic Sukuk Quarterly Bulletin, Issue 20, Q

5 SECTORS - INFRASTRUCTURE Sector Percent in 2014 (rounded) Governmental 46 Financial Services 18 Transport 12 Telecommunications 10 Power and Utilities 5 Construction 4 Real Estate 4 Other 2 Source: Zawya Islamic Sukuk Quarterly Bulletin, Issue 20, Q Are these allocations meaningful? 5

6 SHARI AH STRUCTURES What drove this shift in issuances? Increase in murabaha issuances seems to correlate with sovereign infrastructure financing. Need to explore further. Structure Percent in 2014 (rounded) Murabaha 59 Murabaha Mudaraba 3 Murabaha - Musharaka 1 63 Ijara 11 Musharaka 10 Bai Bithaman Ajil 8 Wakala 3 Al-Istithmar 4 I Wakala-Bel-Istithmar 1 Salam 1 Mudaraba 1 Source: Zawya Islamic Sukuk Quarterly Bulletin, Issue 20, Q

7 GAPS IN THE SUCCESS STORY Those statistics are both reassuring and disquieting. Much progress has been made, to be sure. But these statistics also point to some gaps in the sukuk story, to areas in which we have made insufficient progress. 7

8 CONCLUSIONS FROM STATISTICS Significant under-reporting of sovereign credit. Focus should be the ultimate credit, not issuer identity. Designation as a corporate issuance, tells us nothing of who owns the corporate or what the ultimate credit is. Corporate leases or sales to a sovereign? Government share of risk is too high: adverse effects on private sector. Sukuk al-murabaha issuances increased dramatically. Are we favoring convenience over correspondence to underlying fundamentals of infrastructure finance? 8

9 Why are there so few private sector issuances? What matters need to be addressed? CONSTRAINTS ON PRIVATE SECTOR INVOLVEMENT 9

10 WHY NO RATED PRIVATE SECTOR CREDITS? Private sector issuances cannot be easily rated. Of the five key rating categories, the most significant in terms of precluding ratings are legal and regulatory. Special purpose vehicles: difficulties in formation and ensuring bankruptcy remoteness. Bankruptcy and insolvency: true sale; substantive consolidation. Collateral security. Systemic legal factors and mechanisms. OIC jurisdictions: not possible to get satisfactory legal opinions, which means no ratings. 10

11 TRUE SALE Transfer of the securitized assets from the asset originator to the SPV issuer: is this really a true sale? If yes: creditors of the asset originator cannot reach the transferred assets in a bankruptcy of the asset originator. If no: creditors of the asset originator will reach the transferred assets; sukuk holders deprived of cash flows and assets. No (or exceedingly few) sukuk satisfy true sale requirements: repurchase obligations; rights of originator in residual value; etc. Result: no ratings. 11

12 COLLATERAL SECURITY Some, if not most, sukuk transactions involve collateral security interests. Sometimes the cost of transferring the assets (title) is prohibitive (fees, taxes, notification costs, other costs and expenses, type of property, etc), and a security interest structure is the only realistic structure. Other times, collateral security laws are mandatorily applicable to the assets. In most OIC jurisdictions, it is difficult, if not impossible, to say that the security interests are first prior perfected security interests. Result: no rating. 12

13 REFORM IS ESSENTIAL Substantive legal reform and systemic reform is necessary with respect to all the aforementioned factors. Islamic finance should take the lead; shape the outcome from inception rather than making piecemeal amendments to principles designed for interest-based finance. Examples: UNCITRAL, World Bank, EBRD and IFC initiatives in the areas of collateral security and bankruptcy. Suggestion: Sukuk issuances on assets in jurisdictions that do not have these infirmities (e.g., the US) to build the markets (primary and secondary) and participation with non-islamic institutions. 13

14 Why are governments involved? What risks are to be allocated and how? What sectors will take risks and finance? INFRASTRUCTURE FUNDAMENTALS What techniques are appropriate and will be used? 14

15 WHAT IS INFRASTRUCTURE FINANCE? Finance of ownership, design, construction, operation and maintenance of large capital-intensive enabling assets: assets with some public purpose. Often monopolistic, single-purpose (single-location) assets. Electricity. Transportation. Telecommunication. Water. Oil and gas. Petrochemicals. Mining. Other natural resources. Roads. Bridges and tunnels. Airports. Railways. Other transportation. Waste water and sewage. Hospitals and health care. Schools. 15

16 FINANCING CHARACTERISTICS Large, capital intensive projects. Cash flows necessitate long tenors for payout. Expropriation risks are high. Post-closing renegotiations are commonplace (incomplete contracts). Banks are reluctant to finance infrastructure. 16

17 WHY AND WHO? Three critical, and interrelated, inquiries in determining when and how to innovate, particularly as to risk allocations: Why is the infrastructure project being financed in a particular manner? What is the motivation? Who owns and who operates the infrastructure project, and what blends of ownership and operation risks are appropriate for a given project? Who finances the infrastructure project? 17

18 STRUCTURE RESPONSIVE TO WHY AND WHO The answers to those questions determine: Objectives of structure. Risk allocations and participations among participants. Financing structure, including: Capital elements. Organizational elements. Contractual elements. 18

19 WHY? Government Motivations: Enhance public services? Accelerate economic growth? Supplement revenues? Achieve cost efficiencies? Political considerations? Fiscal rule constraints? Accounting considerations? Other non-economic considerations? Many of these factors introduce economic inefficiencies. Neither good nor bad; but must be recognized and accommodated. 19

20 WHO OWNS AND WHO OPERATES? Who owns and who operates? How much regulation and how much outsourcing? These questions must be separately analyzed. Depends upon the why. Government. Public sector - private sector combinations. Private sector. 20

21 WHO FINANCES? What sector(s) will take risks and finance? Depends upon the why and who answers. Government. Private corporate. Mixed: public-private partnerships (PPP). Project finance: a structural methodology. 21

22 DISTINCT CONCEPTS FOR INFRASTRUCTURE Infrastructure: defined by asset type. Project finance: defined by the degree of recourse available to the financiers. PPPs (public private partnerships): defined by the entities involved (public and private) in sharing project risks. Some, not all, infrastructure projects are project financed. Some, not all, infrastructure projects involve PPPs. Some, not all, project financings involve infrastructure. Some, not all, PPPs involve infrastructure. 22

23 PROJECT FINANCE AND PPPS Project finance is financing of an economic unit in which the lenders/financiers look to: operational cash flows, and collateral (cash flows and project assets). Defined from financier/lender vantage. Isolate risks and then reallocate risks: greater efficiency and certainty. 23

24 PROJECT FINANCING OF INFRASTRUCTURE Collateral availability importance increases where asset is a monopolistic public good - infrastructure. Cannot move the asset. Monopolistic off-taker. Limited operators. Political risks (expropriation, direct and creeping). Must structure remedies that allow collateral realization. 24

25 WHAT IS A PUBLIC-PRIVATE PARTNERSHIP? Many (and diverse) definitions and conceptions. Generally: collaboration between public and private sectors, with risk sharing as between each sector. 25

26 MOTIVES, INVOLVEMENTS, RISK ALLOCATIONS Motivations and involvements influence risk allocations. Consider the fundamental elements: Operational elements: who has operational risks for design, construction, operation, management, maintenance, etc.? Ownership elements: who has ownership risks at each stage? Regulation motives: government control, decision-making and cash-flow rights. Outsourcing motives: private investor gets control, decisionmaking and fees and/or profit sharing. Incentives/disincentives relative to each. 26

27 WHO - ULTIMATELY PAYS? Who, ultimately, pays for the infrastructure project? The public? Taxpayers? Which taxpayers? The private sector? Users? And how do they pay? Broad-based taxation? Targeted taxation of groups or geographies? General fees? Direct usage fees? Tariffs? 27

28 STRUCTURES Analysis of these factors will determine much of the structure: Government build and operate Concession: private build and operate Public-private partnerships rubric encompasses, among others: Build, own, operate, transfer (BOOT) or design, build, finance, operate (DBF)) Build, operate, transfer (BOT) Build, own, operate (BOO) Build, lease, transfer (BLT), or design, build, operate, maintain (DBOM) Build, transfer, operate (BTO) These are all quite different in terms of risk allocations. These all use Shariʿah-compliant contracts. 28

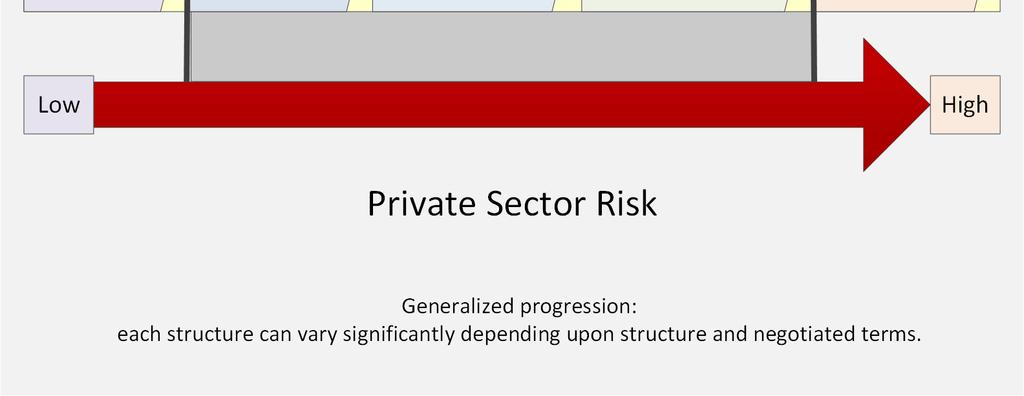

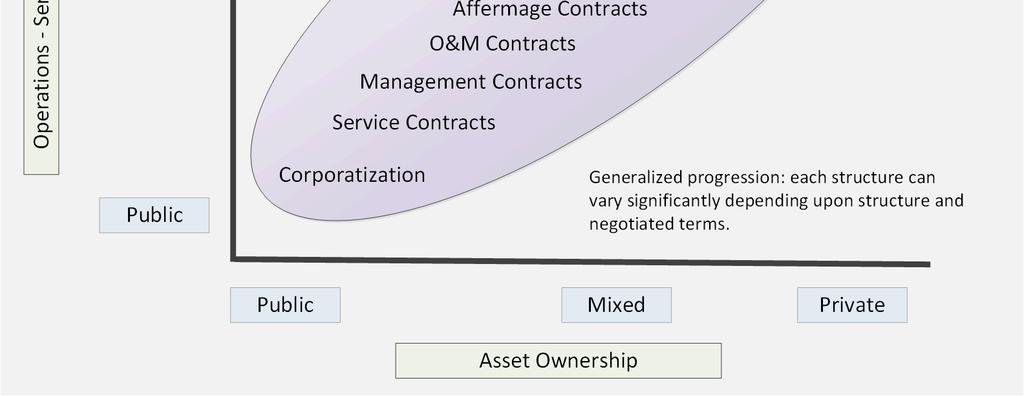

29 PRIVATE RISK PROGRESSION 29

30 OWNERSHIP AND OPERATIONAL RISK 30

31 RISK-REWARD CONTINUUM 31

32 CONCLUSION OPPORTUNITIES EXIST

33 CONCLUSION Structure to infrastructure finance fundamentals and focus on deliberate risk allocations. Motivations why Distribution of ownership and operational risks - who Transactional involvements - who Move to development of private sector issuances. Take the lead in fundamental structural reforms: SPVs Bankruptcy and insolvency Collateral security Systemic legal structure and functioning. 33

34 SUGGESTION: DATA AND STATISTICS Our data and statistics are a significant limitation on our ability to innovate and progress. Classification schemes (for all categories) are poorly defined and inconsistent. The data and statistics are: not publicly available. not rigorous or consistent. not transparent. lacking in inter-correlative depth. Must improve our classification, collection, management and dissemination in every regard. 34

35 MUCH ADO ABOUT NOTHING BASED OR BACKED In Islamic finance: much ado about whether an arrangement is asset backed or asset based. My view: much of that discussion is misinformed and misguided: further, more nuanced, consideration is needed. For a transaction that is not a true sale, but is subject to a first prior perfected security interest, the asset transfer is delated pending default or another trigger event. Asset-based then becomes asset-backed. A strong first prior perfected security interest may transfer essentially all indicia of ownership even before asset transfer. 35

36 THANK YOU

Sukuk restructuring. Chapter Introduction A Case for restructuring. 232 Global Islamic Finance Report (GIFR 2011)

") Chapter 29 Sukuk restructuring 29.1 Introduction A sukuk transaction is restructured either as a result of an originator s default or voluntary restructuring due to merger, acquisition or general corporate

Chapter 29 Sukuk restructuring 29.1 Introduction A sukuk transaction is restructured either as a result of an originator s default or voluntary restructuring due to merger, acquisition or general corporate

From PLI s Course Handbook Islamic Financing: A Comparative Analysis of Sukuk and Conventional Bonds and Securitizations #15105

From PLI s Course Handbook Islamic Financing: A Comparative Analysis of Sukuk and Conventional Bonds and Securitizations #15105 14 SECURITIZATION GLOSSARY Submitted by: Mark Adelson Nomura Securities International,

From PLI s Course Handbook Islamic Financing: A Comparative Analysis of Sukuk and Conventional Bonds and Securitizations #15105 14 SECURITIZATION GLOSSARY Submitted by: Mark Adelson Nomura Securities International,

Analysis of the Sukuk Market. Dubai, April 25, 2007

Analysis of the Sukuk Market Dubai, April 25, 2007 Overview Introduction What is a Sukuk? Types of Sukuk Composition of the Sukuk Market Breakdown of the Sukuk Market Expected Growth of the Sukuk Market

Analysis of the Sukuk Market Dubai, April 25, 2007 Overview Introduction What is a Sukuk? Types of Sukuk Composition of the Sukuk Market Breakdown of the Sukuk Market Expected Growth of the Sukuk Market

GROUP CONSOLIDATED FINANCIAL STATEMENTS

In the Name of Allah The most Gracious and Merciful Emirates Islamic Bank (Public Joint Stock Company) Head Office 3rd Floor, Building 16, Dubai Health Care City, Dubai Tel.: +97 1 4 3160336 Fax: +97 1

In the Name of Allah The most Gracious and Merciful Emirates Islamic Bank (Public Joint Stock Company) Head Office 3rd Floor, Building 16, Dubai Health Care City, Dubai Tel.: +97 1 4 3160336 Fax: +97 1

Islamic Capital Market Overview & Role of Sukuk

Islamic Capital Market Overview & Role of Sukuk Islamic Finance A Paradigm Shift In Africa 28th 29th March 2011 Crowne Plaza Hotel Nairobi, Kenya Ijlal Ahmed Alvi Chief Executive Officer IIFM 1) Introduction

Islamic Capital Market Overview & Role of Sukuk Islamic Finance A Paradigm Shift In Africa 28th 29th March 2011 Crowne Plaza Hotel Nairobi, Kenya Ijlal Ahmed Alvi Chief Executive Officer IIFM 1) Introduction

EXPLANATORY NOTE ON ISSUANCE AND SUBSCRIPTION OF SUKUK IN LABUAN INTERNATIONAL BUSINESS AND FINANCIAL CENTRE

EXPLANATORY NOTE ON ISSUANCE AND SUBSCRIPTION OF SUKUK IN LABUAN INTERNATIONAL BUSINESS AND FINANCIAL CENTRE 1.0 Introduction 1.1 As part of the efforts to facilitate and promote the development of the

EXPLANATORY NOTE ON ISSUANCE AND SUBSCRIPTION OF SUKUK IN LABUAN INTERNATIONAL BUSINESS AND FINANCIAL CENTRE 1.0 Introduction 1.1 As part of the efforts to facilitate and promote the development of the

Appendix A: Securities Commission

Appendix A: Securities Commission Malaysia Guidelines on Sukuk 1 In order for the market players to issue a Sukuk under Ijarah sukuk or otherwise, they have to comply with the Securities Commission Malaysia

Appendix A: Securities Commission Malaysia Guidelines on Sukuk 1 In order for the market players to issue a Sukuk under Ijarah sukuk or otherwise, they have to comply with the Securities Commission Malaysia

Islamic Instruments for Asset Management

Islamic Instruments for Asset Management Professor Rodney Wilson IRTI 15th Distance Learning Programme Intermediate Level Course Tuesday, March 20, 2012 Contents Islamic asset management vehicles Advantages

Islamic Instruments for Asset Management Professor Rodney Wilson IRTI 15th Distance Learning Programme Intermediate Level Course Tuesday, March 20, 2012 Contents Islamic asset management vehicles Advantages

RISING UP TO THE CHALLENGES IN ISLAMIC LIQUIDITY MANAGEMENT

RISING UP TO THE CHALLENGES IN ISLAMIC LIQUIDITY MANAGEMENT An Exchange s Perspective November 2010 Raja Teh Maimunah Global Head, Islamic Markets Contemporary Issues Managing liquidity is arguably the

RISING UP TO THE CHALLENGES IN ISLAMIC LIQUIDITY MANAGEMENT An Exchange s Perspective November 2010 Raja Teh Maimunah Global Head, Islamic Markets Contemporary Issues Managing liquidity is arguably the

Securitization & Financial Development in MENA Dr. Nasser Saidi* 1 Keynote speech at Securitisation World: MENA 2007 Conference Dubai, 18 March 2007

Securitization & Financial Development in MENA Dr. Nasser Saidi* 1 Keynote speech at Securitisation World: MENA 2007 Conference Dubai, 18 March 2007 Ladies and Gentlemen: 1. Thank you for inviting me to

Securitization & Financial Development in MENA Dr. Nasser Saidi* 1 Keynote speech at Securitisation World: MENA 2007 Conference Dubai, 18 March 2007 Ladies and Gentlemen: 1. Thank you for inviting me to

Dubai Islamic Bank P.J.S.C. Consolidated financial statements for the year ended 31 December 2015

Consolidated financial statements These audited financial statements are subject to the Central Bank of the UAE approval and adoption by shareholders at the annual general meeting. Report and consolidated

Consolidated financial statements These audited financial statements are subject to the Central Bank of the UAE approval and adoption by shareholders at the annual general meeting. Report and consolidated

Fixed Income Securities Shari a Perspective

SBP Research Bulletin Volume 3, Number 1, 2007 Fixed Income Securities Shari a Perspective Muhammad Imran Usmani 1. Introduction Fixed income securities have been popular around the world in raising finance

SBP Research Bulletin Volume 3, Number 1, 2007 Fixed Income Securities Shari a Perspective Muhammad Imran Usmani 1. Introduction Fixed income securities have been popular around the world in raising finance

Dubai Islamic Bank P.J.S.C. Consolidated financial statements for the year ended 31 December 2016

Consolidated financial statements Report and consolidated financial statements Pages Independent auditors report 1-8 Consolidated statement of financial position 9 Consolidated statement of profit or loss

Consolidated financial statements Report and consolidated financial statements Pages Independent auditors report 1-8 Consolidated statement of financial position 9 Consolidated statement of profit or loss

Islamic Financing Products and Concepts, Current Market Trends and Opportunities. Nadim Khan, Partner, Herbert Smith LLP July 2010

Islamic Financing Products and Concepts, Current Market Trends and Opportunities Nadim Khan, Partner, Herbert Smith LLP July 2010 1 Overview Introduction to Islamic Finance The Key Products The Compliance

Islamic Financing Products and Concepts, Current Market Trends and Opportunities Nadim Khan, Partner, Herbert Smith LLP July 2010 1 Overview Introduction to Islamic Finance The Key Products The Compliance

AAOIFI S NEW AND REVISED ACCOUNTING STANDARDS ON SUKUK AND THEIR EXPECTED IMPACT ON MARKET

AAOIFI S NEW AND REVISED ACCOUNTING STANDARDS ON SUKUK AND THEIR EXPECTED IMPACT ON MARKET COMCEC WORKING GROUP MEETING 29 MARCH 2018 OMAR MUSTAFA ANSARI ACTING SECRETARY GENERAL AAOIFI AGENDA INTRODUCTION

AAOIFI S NEW AND REVISED ACCOUNTING STANDARDS ON SUKUK AND THEIR EXPECTED IMPACT ON MARKET COMCEC WORKING GROUP MEETING 29 MARCH 2018 OMAR MUSTAFA ANSARI ACTING SECRETARY GENERAL AAOIFI AGENDA INTRODUCTION

Abu Dhabi Islamic Bank PJSC INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2011 (UNAUDITED)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2011 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 September 2011 (Unaudited) Contents Page Report on review of interim

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2011 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 September 2011 (Unaudited) Contents Page Report on review of interim

Creating tax efficient Shari a compliant solutions in Russia

CHAPTER 11 Creating tax efficient Shari a compliant solutions in Russia 11.1 Introduction A growing number of businesses in Russia are becoming more interested in using Shari a compliant financial instruments.

CHAPTER 11 Creating tax efficient Shari a compliant solutions in Russia 11.1 Introduction A growing number of businesses in Russia are becoming more interested in using Shari a compliant financial instruments.

Shariah compliant securitization challenges under Kuwait Law & Practice a Case Study

Shariah compliant securitization challenges under Kuwait Law & Practice a Case Study ALEX SALEH Partner & Head of Kuwait Office 19 October 2015 OUR REGIONAL FOOTPRINT ABOUT AL TAMIMI & COMPANY With a focus

Shariah compliant securitization challenges under Kuwait Law & Practice a Case Study ALEX SALEH Partner & Head of Kuwait Office 19 October 2015 OUR REGIONAL FOOTPRINT ABOUT AL TAMIMI & COMPANY With a focus

Islamic Repo & Collateralization Possibilities and the Role of Sukuk

Islamic Repo & Collateralization Possibilities and the Role of Sukuk Euroclear Treasury & Collateral Management Conference Thursday, 11 th February 2010 Emirates Palace, Abu Dhabi Mr. Ijlal Ahmed Alvi

Islamic Repo & Collateralization Possibilities and the Role of Sukuk Euroclear Treasury & Collateral Management Conference Thursday, 11 th February 2010 Emirates Palace, Abu Dhabi Mr. Ijlal Ahmed Alvi

Global Sukuk and Liquidity Market Evaluating the future of global Sukuk markets

Global Sukuk and Liquidity Market Evaluating the future of global Sukuk markets 6 th Kuala Lumpur Islamic Finance Forum 2 nd -6 th November 2009 Ijlal A Alvi, Chief Executive Officer, IIFM Contents 1.

Global Sukuk and Liquidity Market Evaluating the future of global Sukuk markets 6 th Kuala Lumpur Islamic Finance Forum 2 nd -6 th November 2009 Ijlal A Alvi, Chief Executive Officer, IIFM Contents 1.

Infrastructure: An emerging real asset class

Market & Investment Insights Infrastructure: An emerging real asset class LISA FERRARO, MANAGING DIRECTOR AND PORTFOLIO MANAGER, ENERGY AND INFRASTRUCTURE Article Highlights: Infrastructure including roads,

Market & Investment Insights Infrastructure: An emerging real asset class LISA FERRARO, MANAGING DIRECTOR AND PORTFOLIO MANAGER, ENERGY AND INFRASTRUCTURE Article Highlights: Infrastructure including roads,

Guide to Islamic Finance in Russia

in Russia Part I: Infrastructure 2009 About the Guide 2 This Islamic Finance Guide in Russia is the result of research work by specialists of IFC Linova, corroborated in practice and expressed for the

in Russia Part I: Infrastructure 2009 About the Guide 2 This Islamic Finance Guide in Russia is the result of research work by specialists of IFC Linova, corroborated in practice and expressed for the

Abu Dhabi Islamic Bank PJSC INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2010 (UNAUDITED)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2010 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Contents Page Report on review of interim condensed consolidated financial

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 SEPTEMBER 2010 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Contents Page Report on review of interim condensed consolidated financial

Qatar International Islamic Bank (Q.P.S.C)

") CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017 CONSOLIDATED STATEMENT OF INCOME For the year ended 31 December 2017 Notes Income from financing activities 24 1,418,995 1,261,932 Net income from

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017 CONSOLIDATED STATEMENT OF INCOME For the year ended 31 December 2017 Notes Income from financing activities 24 1,418,995 1,261,932 Net income from

السالم عليكم ورحمة هللا وبركاته

Ref. 0417/3130/AR 3 rd April 2017 Dr. Hamed Merah Secretary General Accounting & Auditing Organization for Islamic Financial Institutions (AAOIFI) Al Nakheel Tower Office 1001, Building 1074 Road 3622

Ref. 0417/3130/AR 3 rd April 2017 Dr. Hamed Merah Secretary General Accounting & Auditing Organization for Islamic Financial Institutions (AAOIFI) Al Nakheel Tower Office 1001, Building 1074 Road 3622

Euromoney Conference Kuwait April 2011 Financing Development Development Financing

Euromoney Conference Kuwait April 2011 Financing Development Development Financing Agenda 1- Benefits of Islamic Finance 2 - Precedents of Islamic Finance in Financing Development 3 - Aspects of Kuwait

Euromoney Conference Kuwait April 2011 Financing Development Development Financing Agenda 1- Benefits of Islamic Finance 2 - Precedents of Islamic Finance in Financing Development 3 - Aspects of Kuwait

ASPE AT A GLANCE. Section Financial Instruments

ASPE AT A GLANCE Section 3856 - Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial

ASPE AT A GLANCE Section 3856 - Financial Instruments December 2014 Section 3856 Financial Instruments Effective Date Fiscal years beginning on or after January 1, 2011 1 SCOPE Applies to all financial

EBRD s Perspective on Islamic Finance

EBRD s Perspective on Islamic Finance Jim Turnbull Associate Director, Head of DCM, LC2 Izmir - October 2018 Need of Global Infrastructure in Developing Countries ~$1 Trillion Investment Gap ~$1 Trillion

EBRD s Perspective on Islamic Finance Jim Turnbull Associate Director, Head of DCM, LC2 Izmir - October 2018 Need of Global Infrastructure in Developing Countries ~$1 Trillion Investment Gap ~$1 Trillion

Sukuk An Alternative to Bonds & A Viable Liquidity Management Tool for Financial Institutions. ISMAIL IDLE Chief Executive Officer

Sukuk An Alternative to Bonds & A Viable Liquidity Management Tool for Financial Institutions by ISMAIL IDLE Chief Executive Officer (1) Sukuk as a viable alternative to Conventional Bonds: DEFINING Sukuk

Sukuk An Alternative to Bonds & A Viable Liquidity Management Tool for Financial Institutions by ISMAIL IDLE Chief Executive Officer (1) Sukuk as a viable alternative to Conventional Bonds: DEFINING Sukuk

NOTES TO THE FINANCIAL STATEMENTS 1. BACKGROUND INFORMATION The Yemen Kuwait Bank for Trade and Investment - Yemeni Joint Stock Company (YJSC) (the Bank) was established on January 1, 1977 in accordance

NOTES TO THE FINANCIAL STATEMENTS 1. BACKGROUND INFORMATION The Yemen Kuwait Bank for Trade and Investment - Yemeni Joint Stock Company (YJSC) (the Bank) was established on January 1, 1977 in accordance

New Sukuk Products A Case for Microfinance Sector. Salman Syed Ali

New Sukuk Products A Case for Microfinance Sector Salman Syed Ali Achievements of Current Global Islamic Pluses Grew from small and gaining in size and coverage Entered into financing of large-scale long-term

New Sukuk Products A Case for Microfinance Sector Salman Syed Ali Achievements of Current Global Islamic Pluses Grew from small and gaining in size and coverage Entered into financing of large-scale long-term

Accounting, Auditing & Corporate Governance Standards for Islamic Banks & Islamic Financial Institutions with reference to AAOIFI

Accounting, Auditing & Corporate Governance Standards for Islamic Banks & Islamic Financial Institutions with reference to AAOIFI About AAOIFI The Accounting and Auditing Organization for Islamic Financial

Accounting, Auditing & Corporate Governance Standards for Islamic Banks & Islamic Financial Institutions with reference to AAOIFI About AAOIFI The Accounting and Auditing Organization for Islamic Financial

BANK ALJAZIRA (A Saudi Joint Stock Company)

") BANK ALJAZIRA UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE THREE MONTH AND SIX MONTH PERIODS ENDED 30 JUNE 2018 FOR THE SIX MONTH PERIOD ENDED 30 JUNE 2018 1. GENERAL These

BANK ALJAZIRA UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS FOR THE THREE MONTH AND SIX MONTH PERIODS ENDED 30 JUNE 2018 FOR THE SIX MONTH PERIOD ENDED 30 JUNE 2018 1. GENERAL These

AHLI UNITED BANK K.S.C.P KUWAIT CONSOLIDATED FINANCIAL STATEMENT 31 DECEMBER 2017

AHLI UNITED BANK K.S.C.P KUWAIT CONSOLIDATED FINANCIAL STATEMENT 31 DECEMBER 2017 Kuwait C o n t e n t s Page Independent Auditors Report 1-5 Consolidated Statement of Profit or Loss 6 Consolidated Statement

AHLI UNITED BANK K.S.C.P KUWAIT CONSOLIDATED FINANCIAL STATEMENT 31 DECEMBER 2017 Kuwait C o n t e n t s Page Independent Auditors Report 1-5 Consolidated Statement of Profit or Loss 6 Consolidated Statement

DEVELOPMENT OF LIQUIDITY MANAGEMENT INSTRUMENTS: CHALLENGES AND OPPORTUNITIES

DEVELOPMENT OF LIQUIDITY MANAGEMENT INSTRUMENTS: CHALLENGES AND OPPORTUNITIES By Abdul Rais Abdul Majid Chief Executive Officer International Islamic Financial Market (IIFM) International Conference on

DEVELOPMENT OF LIQUIDITY MANAGEMENT INSTRUMENTS: CHALLENGES AND OPPORTUNITIES By Abdul Rais Abdul Majid Chief Executive Officer International Islamic Financial Market (IIFM) International Conference on

The Saudi Sukuk Market

The Saudi Sukuk Market For comments and queries please contact: Brad Bourland Chief Economist jadwaresearch@jadwa.com Paul Gamble Head of Research pgamble@jadwa.com or the author: Haitham al-fayez Senior

The Saudi Sukuk Market For comments and queries please contact: Brad Bourland Chief Economist jadwaresearch@jadwa.com Paul Gamble Head of Research pgamble@jadwa.com or the author: Haitham al-fayez Senior

Structured Finance : Asset Based Finance and Covered

1 Structured Finance : Asset Based Finance and Covered Moyn UDDIN Executive Director Al Waha Capital PJSC Dubai, December 15th, 2010 DIFC Conference Center Covered Bond Basics 2 Basic Structure Security

1 Structured Finance : Asset Based Finance and Covered Moyn UDDIN Executive Director Al Waha Capital PJSC Dubai, December 15th, 2010 DIFC Conference Center Covered Bond Basics 2 Basic Structure Security

SUKUK MARKET AND REGULATIONS IN PAKISTAN

SUKUK MARKET AND REGULATIONS IN PAKISTAN Introduction There has been a concerted push by regulatory authorities in Pakistan in the last few years to promote the Islamic finance industry. Recently, the

SUKUK MARKET AND REGULATIONS IN PAKISTAN Introduction There has been a concerted push by regulatory authorities in Pakistan in the last few years to promote the Islamic finance industry. Recently, the

New Sukuk Products A Case for Microfinance Sector. Salman Syed Ali

New Sukuk Products A Case for Microfinance Sector Salman Syed Ali 1 Achievements of Current Global Islamic Finance Pluses Grew from small and gaining in size and coverage Entered into financing of large-scale

New Sukuk Products A Case for Microfinance Sector Salman Syed Ali 1 Achievements of Current Global Islamic Finance Pluses Grew from small and gaining in size and coverage Entered into financing of large-scale

Property Finance Based on Covered Bonds and Sukuk: Requirements in Respect of Legal Certainty of Property Rights. Dr. Klaus Peter Follak

Property Finance Based on Covered Bonds and Sukuk: Requirements in Respect of Legal Certainty of Property Rights Dr. Klaus Peter Follak Requirements of Sustainable Property Finance There is an urgent need

Property Finance Based on Covered Bonds and Sukuk: Requirements in Respect of Legal Certainty of Property Rights Dr. Klaus Peter Follak Requirements of Sustainable Property Finance There is an urgent need

An Overview of Sukuk and its Application In Global Fixed Income Markets

An Overview of Sukuk and its Application In Global Fixed Income Markets Sukuk, commonly known as Islamic bonds, are a recent entry to the world of finance. (Sukuk were used extensively in the Middle Ages,

An Overview of Sukuk and its Application In Global Fixed Income Markets Sukuk, commonly known as Islamic bonds, are a recent entry to the world of finance. (Sukuk were used extensively in the Middle Ages,

Al Salam Bank-Bahrain B.S.C.

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017 CONSOLIDATED STATEMENT OF FINANCIAL POSITION Note ASSETS Cash and balances with banks and Central Bank 4 66,351 131,990 Sovereign Sukuk 357,778 358,269

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2017 CONSOLIDATED STATEMENT OF FINANCIAL POSITION Note ASSETS Cash and balances with banks and Central Bank 4 66,351 131,990 Sovereign Sukuk 357,778 358,269

Dubai Islamic Bank P.J.S.C. Review report and condensed consolidated interim financial information for the nine-month period ended 30 September 2017

Review report and condensed consolidated interim financial information Review report and condensed consolidated interim financial information (Unaudited) Pages Independent auditors report on review of

Review report and condensed consolidated interim financial information Review report and condensed consolidated interim financial information (Unaudited) Pages Independent auditors report on review of

AL SALAM BANK-BAHRAIN B.S.C. BASEL II - PILLAR III DISCLOSURES

AL SALAM BANK-BAHRAIN B.S.C. BASEL II - PILLAR III DISCLOSURES 31 st December 2009 Table of contents Table of contents 1. Introduction... 3 2. Financial Performance and Position... 4 3. Capital structure...

AL SALAM BANK-BAHRAIN B.S.C. BASEL II - PILLAR III DISCLOSURES 31 st December 2009 Table of contents Table of contents 1. Introduction... 3 2. Financial Performance and Position... 4 3. Capital structure...

The Role of PT. Sarana Multi Infrastruktur in Infrastructure Development

The Role of PT. Sarana Multi Infrastruktur in Infrastructure Development 1 OUTLINE Background Profile Framework Financing Policy Challenges Target 2 BACKGROUND Rationale 1. Global economic condition 2.

The Role of PT. Sarana Multi Infrastruktur in Infrastructure Development 1 OUTLINE Background Profile Framework Financing Policy Challenges Target 2 BACKGROUND Rationale 1. Global economic condition 2.

Diversification of Islamic Financial Instruments in Turkey

Republic of Turkey Undersecretariat of Treasury Diversification of Islamic Financial Instruments in Turkey Utku ŞEN Treasury Expert 9 th MEETING OF THE COMCEC FINANCIAL COOPERATION WORKING GROUP October

Republic of Turkey Undersecretariat of Treasury Diversification of Islamic Financial Instruments in Turkey Utku ŞEN Treasury Expert 9 th MEETING OF THE COMCEC FINANCIAL COOPERATION WORKING GROUP October

Public-Private Partnership (PPP) Contracts

Contracts") 25 29 June 2018 London / United Kingdom Introduction A key motivation for governments considering public-private partnerships (PPPs) is the possibility of bringing in new sources of financing for funding

25 29 June 2018 London / United Kingdom Introduction A key motivation for governments considering public-private partnerships (PPPs) is the possibility of bringing in new sources of financing for funding

Dubai Islamic Bank P.J.S.C. Review report and condensed consolidated interim financial information for the nine-month period ended 30 September 2015

Review report and condensed consolidated interim financial information Review report and condensed consolidated interim financial information (Unaudited) Pages Independent auditors report on review of

Review report and condensed consolidated interim financial information Review report and condensed consolidated interim financial information (Unaudited) Pages Independent auditors report on review of

SABA ISLAMIC BANK (Yemeni Joint Stock Company) SANA A, REPUBLIC OF YEMEN

SANA A, REPUBLIC OF YEMEN") (Yemeni Joint Stock Company) SANA A, REPUBLIC OF YEMEN CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT (Yemeni Joint Stock Company) SANA A, REPUBLIC OF YEMEN CONSOLIDATED FINANCIAL STATEMENTS

(Yemeni Joint Stock Company) SANA A, REPUBLIC OF YEMEN CONSOLIDATED FINANCIAL STATEMENTS AND INDEPENDENT AUDITOR S REPORT (Yemeni Joint Stock Company) SANA A, REPUBLIC OF YEMEN CONSOLIDATED FINANCIAL STATEMENTS

ABU DHABI COMMERCIAL BANK P.J.S.C. Review report and condensed consolidated interim financial information for the six month period ended June 30, 2013

ABU DHABI COMMERCIAL BANK P.J.S.C. Review report and condensed consolidated interim financial information for the six month period ended June 30, 2013 ABU DHABI COMMERCIAL BANK P.J.S.C. Review report and

ABU DHABI COMMERCIAL BANK P.J.S.C. Review report and condensed consolidated interim financial information for the six month period ended June 30, 2013 ABU DHABI COMMERCIAL BANK P.J.S.C. Review report and

Bank Muscat (SAOG) NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2012

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS YEAR ENDED 31 DECEMBER 2012") YEAR ENDED 1 LEGAL STATUS AND PRINCIPAL ACTIVITIES Bank Muscat (SAOG) (the Bank or the Parent Company) is a joint stock company incorporated in the Sultanate of Oman and is engaged in commercial and investment

YEAR ENDED 1 LEGAL STATUS AND PRINCIPAL ACTIVITIES Bank Muscat (SAOG) (the Bank or the Parent Company) is a joint stock company incorporated in the Sultanate of Oman and is engaged in commercial and investment

The DFSA Rulebook. Islamic Finance Rules (IFR) IFR/VER12/01-18

IFR/VER12/01-18") The DFSA Rulebook Islamic Finance Rules (IFR) IFR/VER12/01-18 Contents The contents of this module are divided into the following chapters, sections and appendices: 1. INTRODUCTION... 1 1.1 Application...

The DFSA Rulebook Islamic Finance Rules (IFR) IFR/VER12/01-18 Contents The contents of this module are divided into the following chapters, sections and appendices: 1. INTRODUCTION... 1 1.1 Application...

Mawarid Finance P.J.S.C. Consolidated Financial Statements

Consolidated Financial Statements Consolidated Financial Statements Page Directors' report 1-2 Independent auditors' report 3-7 Consolidated statement of financial position 8 Consolidated statement of

Consolidated Financial Statements Consolidated Financial Statements Page Directors' report 1-2 Independent auditors' report 3-7 Consolidated statement of financial position 8 Consolidated statement of

Mawarid Finance P.J.S.C. Consolidated Financial Statements for the year ended 31 December 2015

Consolidated Financial Statements Consolidated Financial Statements Page Directors' report 1-2 Independent auditors' report 3-4 Consolidated statement of financial position 5 Consolidated statement of

Consolidated Financial Statements Consolidated Financial Statements Page Directors' report 1-2 Independent auditors' report 3-4 Consolidated statement of financial position 5 Consolidated statement of

Consolidated Financial Statements

In the Name of Allah The most Gracious and Merciful (Public Joint Stock Company) Head Office 13th Floor, Office Tower, Dubai Festival City, Dubai Tel.: +97 1 4 2287474 Fax: +97 1 4 2227321 P.O. Box: 6564,

In the Name of Allah The most Gracious and Merciful (Public Joint Stock Company) Head Office 13th Floor, Office Tower, Dubai Festival City, Dubai Tel.: +97 1 4 2287474 Fax: +97 1 4 2227321 P.O. Box: 6564,

Notes to the consolidated financial statements

Notes to the consolidated financial statements As at 31 December 1 ACTIVITIES BBK B.S.C. (the Bank ), a public shareholding company, was incorporated in the Kingdom of Bahrain by an Amiri Decree in March

Notes to the consolidated financial statements As at 31 December 1 ACTIVITIES BBK B.S.C. (the Bank ), a public shareholding company, was incorporated in the Kingdom of Bahrain by an Amiri Decree in March

EMIRATES NBD BANK PJSC

GROUP CONSOLIDATED FINANCIAL STATEMENTS These Audited Preliminary Financial Statements are subject to Central Bank of UAE Approval and adoption by Shareholders at the Annual General Meeting GROUP CONSOLIDATED

GROUP CONSOLIDATED FINANCIAL STATEMENTS These Audited Preliminary Financial Statements are subject to Central Bank of UAE Approval and adoption by Shareholders at the Annual General Meeting GROUP CONSOLIDATED

AL RAJHI BANKING AND INVESTMENT CORPORATION (A SAUDI JOINT STOCK COMPANY)

") AL RAJHI BANKING AND INVESTMENT CORPORATION INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) FOR THE THREE - MONTH PERIOD ENDED 31 MARCH 2018 1. GENERAL Al Rajhi Banking and Investment

AL RAJHI BANKING AND INVESTMENT CORPORATION INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) FOR THE THREE - MONTH PERIOD ENDED 31 MARCH 2018 1. GENERAL Al Rajhi Banking and Investment

Draft PPP Policy Outline

Note 7 May 2012 Draft PPP Policy Outline This note is the seventh in a series of notes on developing a comprehensive policy, legal, and institution framework for public-private partnership (PPP) programs.

Note 7 May 2012 Draft PPP Policy Outline This note is the seventh in a series of notes on developing a comprehensive policy, legal, and institution framework for public-private partnership (PPP) programs.

OMAN ARAB BANK SAOC. Report and financial statements for the year ended 31 December 2017

OMAN ARAB BANK SAOC Report and financial statements for the year ended 31 December 2017 OMAN ARAB BANK SAOC Report and financial statements for the year ended 31 December 2017 Page Independent auditor

OMAN ARAB BANK SAOC Report and financial statements for the year ended 31 December 2017 OMAN ARAB BANK SAOC Report and financial statements for the year ended 31 December 2017 Page Independent auditor

EMIRATES NBD BANK PJSC

GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS FOR THE THREE MONTHS PERIOD ENDED 31 MARCH 2018 GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Contents Page Independent auditor s report

GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS FOR THE THREE MONTHS PERIOD ENDED 31 MARCH 2018 GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Contents Page Independent auditor s report

Regulation of Islamic Finance in the UK and France

Regulation of Islamic Finance in the UK and France Mohammad Farrukh Raza Managing Director IFAAS UK & France Islamic Finance Regulation Mechanisms in Post-crisis Period 3 rd Astana Economic Forum Astana

Regulation of Islamic Finance in the UK and France Mohammad Farrukh Raza Managing Director IFAAS UK & France Islamic Finance Regulation Mechanisms in Post-crisis Period 3 rd Astana Economic Forum Astana

Tatagroprombank. Talk on Islamic Finance. Kazan -17 June Alberto G. Brugnoni - ASSAIF

Tatagroprombank Talk on Islamic Finance Kazan -17 June 2013 Alberto G. Brugnoni - ASSAIF CONTENTS OF THE TALK WHAT IS ISLAMIC FINANCE ISLAMIC MODES OF FINANCE AVAILABLE TO SMEs ISLAMIC TRADE FINANCE ISLAMIC

Tatagroprombank Talk on Islamic Finance Kazan -17 June 2013 Alberto G. Brugnoni - ASSAIF CONTENTS OF THE TALK WHAT IS ISLAMIC FINANCE ISLAMIC MODES OF FINANCE AVAILABLE TO SMEs ISLAMIC TRADE FINANCE ISLAMIC

AL SALAM BANK-BAHRAIN B.S.C. BASEL II - PILLAR III DISCLOSURES

AL SALAM BANK-BAHRAIN B.S.C. BASEL II - PILLAR III DISCLOSURES 30 th June 2010 Table of contents Table of contents 1. Introduction... 3 2. Financial Performance and Position... 4 3. Capital structure...

AL SALAM BANK-BAHRAIN B.S.C. BASEL II - PILLAR III DISCLOSURES 30 th June 2010 Table of contents Table of contents 1. Introduction... 3 2. Financial Performance and Position... 4 3. Capital structure...

ENDED DECEMBER 31, 1. GENERAL These financial statements comprise the financial statements of Bank AlJazira (the Bank ) and its subsidiaries (collectively referred to as the Group ). Bank AlJazira is a

ENDED DECEMBER 31, 1. GENERAL These financial statements comprise the financial statements of Bank AlJazira (the Bank ) and its subsidiaries (collectively referred to as the Group ). Bank AlJazira is a

Bank Address P O Box 1423, Postal Code 133, Muscat, Sultanate of Oman

Page 6 1 LEGAL STATUS AND PRINCIPAL ACTIVITIES Bank Nizwa SAOG ("the Bank") was registered in the Sultanate of Oman as a public joint stock company under registration number 1152878 on 15 August 2012.

Page 6 1 LEGAL STATUS AND PRINCIPAL ACTIVITIES Bank Nizwa SAOG ("the Bank") was registered in the Sultanate of Oman as a public joint stock company under registration number 1152878 on 15 August 2012.

Abu Dhabi Commercial Bank PJSC

Abu Dhabi Commercial Bank PJSC Review report and condensed consolidated interim financial information for the nine month period ended September 30, Table of contents Report on review of condensed consolidated

Abu Dhabi Commercial Bank PJSC Review report and condensed consolidated interim financial information for the nine month period ended September 30, Table of contents Report on review of condensed consolidated

Queen Alia International Airport The Role of IFC in Facilitating Private Investment in a Large Airport Project

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Jordan s Queen Alia International Airport, located in Amman, was named best airport of

Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Jordan s Queen Alia International Airport, located in Amman, was named best airport of

Queen Alia International Airport The Role of IFC in Facilitating Private Investment in a Large Airport Project

www.ifc.org/thoughtleadership Note 35 April 2017 Queen Alia International Airport The Role of IFC in Facilitating Private Investment in a Large Airport Project In 2007 Jordan lacked the financial resources

www.ifc.org/thoughtleadership Note 35 April 2017 Queen Alia International Airport The Role of IFC in Facilitating Private Investment in a Large Airport Project In 2007 Jordan lacked the financial resources

CONTRIBUTION OF ISLAMIC FINANCE TO THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT 13 NOVEMBER 2017

CONTRIBUTION OF ISLAMIC FINANCE TO THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT 13 NOVEMBER 2017 AUTHOR: HABIB AHMED Durham University Business School, Durham University, United Kingdom habib.ahamed@durham.ac.uk

CONTRIBUTION OF ISLAMIC FINANCE TO THE 2030 AGENDA FOR SUSTAINABLE DEVELOPMENT 13 NOVEMBER 2017 AUTHOR: HABIB AHMED Durham University Business School, Durham University, United Kingdom habib.ahamed@durham.ac.uk

Securitization and Structuring Sukuk

Securitization and Structuring Sukuk Workshop on Developing Sukuk Markets Arab Monetary Fund World Bank Group Abu Dhabi, UAE April 19, 2015 Zamir Iqbal, PhD. The World Bank Global Islamic Finance Development

Securitization and Structuring Sukuk Workshop on Developing Sukuk Markets Arab Monetary Fund World Bank Group Abu Dhabi, UAE April 19, 2015 Zamir Iqbal, PhD. The World Bank Global Islamic Finance Development

Sukuk Market Overview & Structural Trends

Sukuk Market Overview & Structural Trends IIFM Industry Seminar on Islamic Capital Market, Liquidity Management & Risk Mitigation Instruments Morning Pre-Conference Day Session, 19 th Annual World Islamic

Sukuk Market Overview & Structural Trends IIFM Industry Seminar on Islamic Capital Market, Liquidity Management & Risk Mitigation Instruments Morning Pre-Conference Day Session, 19 th Annual World Islamic

EMIRATES NBD BANK PJSC

GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS FOR THE NINE MONTHS PERIOD ENDED 30 SEPTEMBER GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Contents Page Independent auditor s report

GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS FOR THE NINE MONTHS PERIOD ENDED 30 SEPTEMBER GROUP CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS Contents Page Independent auditor s report

RISK-BASED TAX AUDIT REVENUE GENERATION IN NIGERIA

RISK-BASED TAX AUDIT REVENUE GENERATION IN NIGERIA A Presentation at the CITN 2018 Lagos MPTP December 4, 2018 Venue: Tax Professionals House CITN Secretariat Alausa, Ikeja-Lagos Seyi Katola, FCTI Presentation

RISK-BASED TAX AUDIT REVENUE GENERATION IN NIGERIA A Presentation at the CITN 2018 Lagos MPTP December 4, 2018 Venue: Tax Professionals House CITN Secretariat Alausa, Ikeja-Lagos Seyi Katola, FCTI Presentation

Preserver Alternative Opportunities Fund Institutional Shares PAOIX Retail Shares PAORX

PROSPECTUS December 29, 2017 Preserver Alternative Opportunities Fund Institutional Shares PAOIX Retail Shares PAORX Preserver Partners, LLC 8700 Trail Lake Drive West, Suite 105 Memphis, Tennessee 38125

PROSPECTUS December 29, 2017 Preserver Alternative Opportunities Fund Institutional Shares PAOIX Retail Shares PAORX Preserver Partners, LLC 8700 Trail Lake Drive West, Suite 105 Memphis, Tennessee 38125

Interbank Money Market Operations:

Interbank Money Market Operations: -developing Shari ah compliant solutions - potential for Islamic liquidity management AAOIFI World Bank Annual Conference on Islamic Banking and Finance 14 th -15 th

Interbank Money Market Operations: -developing Shari ah compliant solutions - potential for Islamic liquidity management AAOIFI World Bank Annual Conference on Islamic Banking and Finance 14 th -15 th

Shariah Guidelines for Sukuk. Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014

Shariah Guidelines for Sukuk Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014 0 Outline of Presentation Page Credentials Mufti Ismail Ebrahim [2] Islamic Financial Services Products Mufti Ismail

Shariah Guidelines for Sukuk Mufti Ismail Ebrahim Shariah Advisor Malta, October 2014 0 Outline of Presentation Page Credentials Mufti Ismail Ebrahim [2] Islamic Financial Services Products Mufti Ismail

AL RAJHI BANKING AND INVESTMENT CORPORATION (A SAUDI JOINT STOCK COMPANY)

") AL RAJHI BANKING AND INVESTMENT CORPORATION INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) FOR THE THREE - MONTH AND NINE - MONTH PERIODS ENDED 30 SEPTEMBER 2018 1. GENERAL Al Rajhi

AL RAJHI BANKING AND INVESTMENT CORPORATION INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED) FOR THE THREE - MONTH AND NINE - MONTH PERIODS ENDED 30 SEPTEMBER 2018 1. GENERAL Al Rajhi

Mobilizing Islamic Finance for Long Term Financing: Lessons From Conventional Finance. Ana Carvajal

Mobilizing Islamic Finance for Long Term Financing: Lessons From Conventional Finance Ana Carvajal Istanbul, November 2015 The Context: Gaps in long term finance Infrastructure Financing gap estimated

Mobilizing Islamic Finance for Long Term Financing: Lessons From Conventional Finance Ana Carvajal Istanbul, November 2015 The Context: Gaps in long term finance Infrastructure Financing gap estimated

Public-Private Partnership Monitor Key Trends and Findings

Office of Public Private Partnership Public-Private Partnership Monitor Key Trends and Findings 23 November 2017 PPP Monitor Benefits and Key Findings PPP Monitor The PPP Monitor tracks the development

Office of Public Private Partnership Public-Private Partnership Monitor Key Trends and Findings 23 November 2017 PPP Monitor Benefits and Key Findings PPP Monitor The PPP Monitor tracks the development

Islamic Finance More Than Window Dressing?

Islamic Finance More Than Window Dressing? This article considers the most common structures employed in Islamic finance and deals with some of the criticisms surrounding its practice. Introduction Islamic

Islamic Finance More Than Window Dressing? This article considers the most common structures employed in Islamic finance and deals with some of the criticisms surrounding its practice. Introduction Islamic

OMAN ARAB BANK SAOC. Report and financial statements for the year ended 31 December 2017

OMAN ARAB BANK SAOC Report and financial statements for the year ended 31 December 2017 OMAN ARAB BANK SAOC Report and financial statements for the year ended 31 December 2017 Page Independent auditor

OMAN ARAB BANK SAOC Report and financial statements for the year ended 31 December 2017 OMAN ARAB BANK SAOC Report and financial statements for the year ended 31 December 2017 Page Independent auditor

The DFSA Rulebook. Prudential Investment, Insurance Intermediation and Banking Module (PIB) Appendix 5

Appendix 5") Appendix 5 All provisions shown as struck through in this appendix have been moved to the Islamic Finance Rules Module of the DFSA Rulebook. Please see the destination table for further information. The

Appendix 5 All provisions shown as struck through in this appendix have been moved to the Islamic Finance Rules Module of the DFSA Rulebook. Please see the destination table for further information. The

SUKUK, an Emerging Asset Class

SUKUK, an Emerging Asset Class Ibrahim Mardam-Bey CEO, Siraj Capital Ltd November, 2007 DEFINITION AAOIFI Standard 17: investment Sukuk are certificates of equal value representing undivided shares in

SUKUK, an Emerging Asset Class Ibrahim Mardam-Bey CEO, Siraj Capital Ltd November, 2007 DEFINITION AAOIFI Standard 17: investment Sukuk are certificates of equal value representing undivided shares in

Al Baraka Islamic Bank B.S.C. (c) Basel III, Pillar III Disclosures. 30 June 2017

Basel III, Pillar III Disclosures. 30 June 2017") 30 June 2017 Content Page 1 INTRODUCTION 3 2 CAPITAL ADEQUACY 3 3 RISK MANAGEMENT a) Credit risk 8 b) Market risk 19 c) Equity of Investment Accountholders 23 d) Off-balance sheet equity of Investment

30 June 2017 Content Page 1 INTRODUCTION 3 2 CAPITAL ADEQUACY 3 3 RISK MANAGEMENT a) Credit risk 8 b) Market risk 19 c) Equity of Investment Accountholders 23 d) Off-balance sheet equity of Investment

STATUTORY DISCLOSURES UNDER BASEL II FRAMEWORK

STATUTORY DISCLOSURES UNDER BASEL II FRAMEWORK sohar islamic in giving back to our community Bank Sohar received the Golden Excellence Award for Corporate Social Responsibility for the second consecutive

STATUTORY DISCLOSURES UNDER BASEL II FRAMEWORK sohar islamic in giving back to our community Bank Sohar received the Golden Excellence Award for Corporate Social Responsibility for the second consecutive

Risk transfer versus risk sharing in the Islamic finance contracts: professional accounting view

Risk transfer versus risk sharing in the Islamic finance contracts: professional accounting view 1 O M A R M U S T A F A A N S A R I A S S I S T A N T S E C R E T A R Y G E N E R A L A C C O U N T I N

Risk transfer versus risk sharing in the Islamic finance contracts: professional accounting view 1 O M A R M U S T A F A A N S A R I A S S I S T A N T S E C R E T A R Y G E N E R A L A C C O U N T I N

Training workshop PPP in health sector

EU Health Facility, Vietnam Training workshop PPP in health sector Session 9 Tran Duy Hung Senior PPP and Finance Expert Da Nang, 1-3 December, 2016 1 Content Healthcare PPP structures/options Financing

EU Health Facility, Vietnam Training workshop PPP in health sector Session 9 Tran Duy Hung Senior PPP and Finance Expert Da Nang, 1-3 December, 2016 1 Content Healthcare PPP structures/options Financing

The Certified Islamic Specialist in Accounting

1 The Certified Islamic Specialist in Accounting Introduction: Financial accounting plays a vital role in the measurement and establishment of financial events and facts taking place in banks to determine

1 The Certified Islamic Specialist in Accounting Introduction: Financial accounting plays a vital role in the measurement and establishment of financial events and facts taking place in banks to determine

Attendance at the Singapore Due Diligence 2012 is strictly by invitation only. The content of this presentation is intended solely for invited guests

should not be reproduced or distributed to persons other than the invited guests. Overview of Islamic Finance Hanifah Hashim Head of Fixed Income (Malaysia) Franklin Templeton Investments September 26,

should not be reproduced or distributed to persons other than the invited guests. Overview of Islamic Finance Hanifah Hashim Head of Fixed Income (Malaysia) Franklin Templeton Investments September 26,

Deloitte A Middle East Point of View - Fall 2016 Islamic Finance

16 Islamic megabank The redeemer? 17 Liquidity instruments available to Islamic Banks are few, with many lacking universal Sharia approval across jurisdictions. As a result, IFIs face greater difficulty

16 Islamic megabank The redeemer? 17 Liquidity instruments available to Islamic Banks are few, with many lacking universal Sharia approval across jurisdictions. As a result, IFIs face greater difficulty

Abu Dhabi Islamic Bank PJSC INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 JUNE 2012 (UNAUDITED)

") INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 JUNE 2012 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Contents Page Report on review of interim condensed consolidated financial

INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS 30 JUNE 2012 (UNAUDITED) INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS Contents Page Report on review of interim condensed consolidated financial

An Introduction to PPP s

An Introduction to PPP s AAPA Facilities Engineering Seminar San Diego November 8 th, 2007 Presented by Manju Chandrasekhar Vice President Halcrow, Inc. Outline A Definition of PPP s Principles of PPP

An Introduction to PPP s AAPA Facilities Engineering Seminar San Diego November 8 th, 2007 Presented by Manju Chandrasekhar Vice President Halcrow, Inc. Outline A Definition of PPP s Principles of PPP

Contribution of Islamic Finance to the 2030 Agenda for Sustainable Development (with special reference to infrastructure finance)

") Contribution of Islamic Finance to the 2030 Agenda for Sustainable Development (with special reference to infrastructure finance) Habib Ahmed Durham University Business School, UK 1 Infrastructure Investment

Contribution of Islamic Finance to the 2030 Agenda for Sustainable Development (with special reference to infrastructure finance) Habib Ahmed Durham University Business School, UK 1 Infrastructure Investment

Ghana Infrastructure Investment Fund Investment Policy Statement. As approved by the Board of Directors on April 6, 2017

Ghana Infrastructure Investment Fund Investment Policy Statement As approved by the Board of Directors on April 6, 2017 1 Table of Contents 1. Introduction...4 1.1. Purpose of the Policies and Guidelines...4

Ghana Infrastructure Investment Fund Investment Policy Statement As approved by the Board of Directors on April 6, 2017 1 Table of Contents 1. Introduction...4 1.1. Purpose of the Policies and Guidelines...4

There are fundamental differences between these. The diagrams set out below explain the mechanics of how each sukuk operates.

ISLAMIC FINANCE From 2013, Islamic finance becomes part of the Paper P4 syllabus, following its introduction to Paper F9 two years ago. This article looks at Islamic finance as a growing and important

ISLAMIC FINANCE From 2013, Islamic finance becomes part of the Paper P4 syllabus, following its introduction to Paper F9 two years ago. This article looks at Islamic finance as a growing and important

International Islamic Liquidity Management Corporation

International Islamic Liquidity Management Corporation An Overview of Liquidity Management Issues for Institutions Offering Islamic Financial Services March 9 th, 2016/ Jumada Al- Awwal 29, 1437 IRTI Eminent

International Islamic Liquidity Management Corporation An Overview of Liquidity Management Issues for Institutions Offering Islamic Financial Services March 9 th, 2016/ Jumada Al- Awwal 29, 1437 IRTI Eminent

Sameh I. Mobarek Senior Counsel Energy, LEGPS Member, Global Expert Team on Public-Private Partnerships. PPP Financing Overview

Sameh I. Mobarek Senior Counsel Energy, LEGPS Member, Global Expert Team on Public-Private Partnerships PPP Financing Overview What is a Public-Private Partnership? A PPP is a long-term (5 to 30 year)

Sameh I. Mobarek Senior Counsel Energy, LEGPS Member, Global Expert Team on Public-Private Partnerships PPP Financing Overview What is a Public-Private Partnership? A PPP is a long-term (5 to 30 year)

Al Salam Bank-Bahrain B.S.C.

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2016 CONSOLIDATED STATEMENT OF FINANCIAL POSITION Note BD '000 BD '000 ASSETS Cash and balances with banks and Central Bank 5 131,990 152,572 Sovereign Sukuk

CONSOLIDATED FINANCIAL STATEMENTS 31 DECEMBER 2016 CONSOLIDATED STATEMENT OF FINANCIAL POSITION Note BD '000 BD '000 ASSETS Cash and balances with banks and Central Bank 5 131,990 152,572 Sovereign Sukuk

AL SALAM BANK-BAHRAIN B.S.C. BASEL II - PILLAR III DISCLOSURES

AL SALAM BANK-BAHRAIN B.S.C. BASEL II - PILLAR III DISCLOSURES 31 st December 2010 Table of contents Table of contents 1. Introduction...3 2. Financial Performance and Position...4 3. Capital structure...6

AL SALAM BANK-BAHRAIN B.S.C. BASEL II - PILLAR III DISCLOSURES 31 st December 2010 Table of contents Table of contents 1. Introduction...3 2. Financial Performance and Position...4 3. Capital structure...6